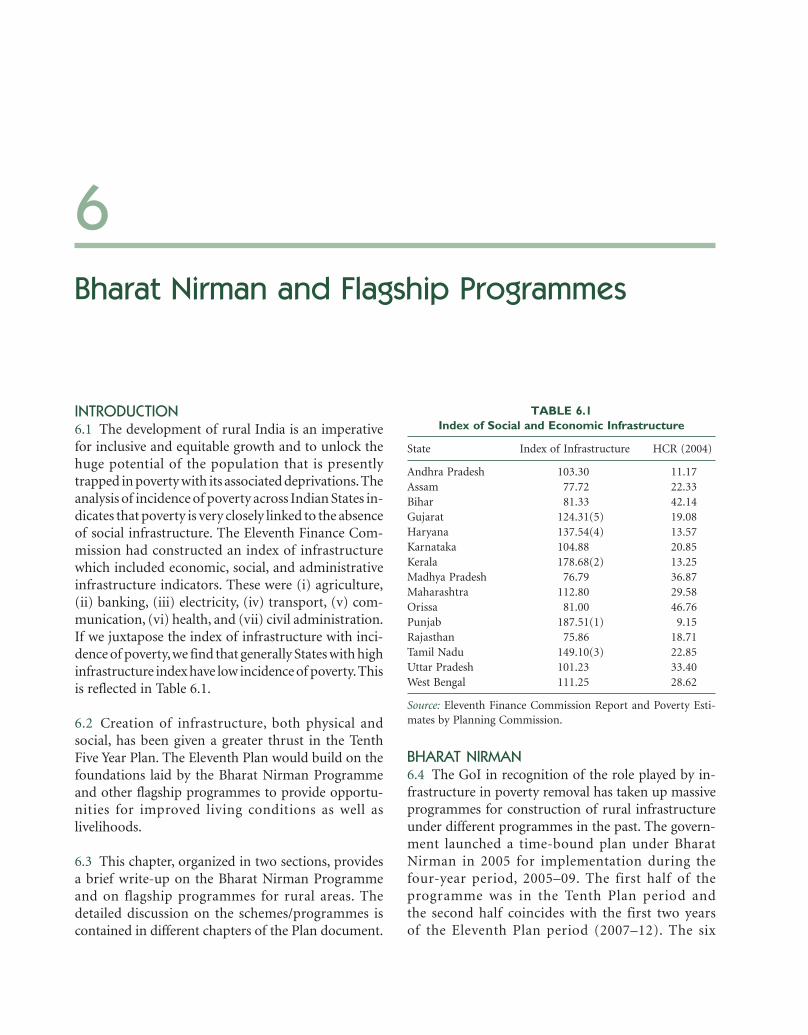

Eleventh Five Year Plan - Centre for Social Justice

537

Eleventh Five Year Plan 2007-12 VOLUME III VOLUME III AGRICULTURE, RURAL DEVELOPMENT, INDUSTRY, SERVICES, AND PHYSICAL INFRASTRUCTURE Eleventh Five Year Plan 2007-12 Planning Commission Government of India

-

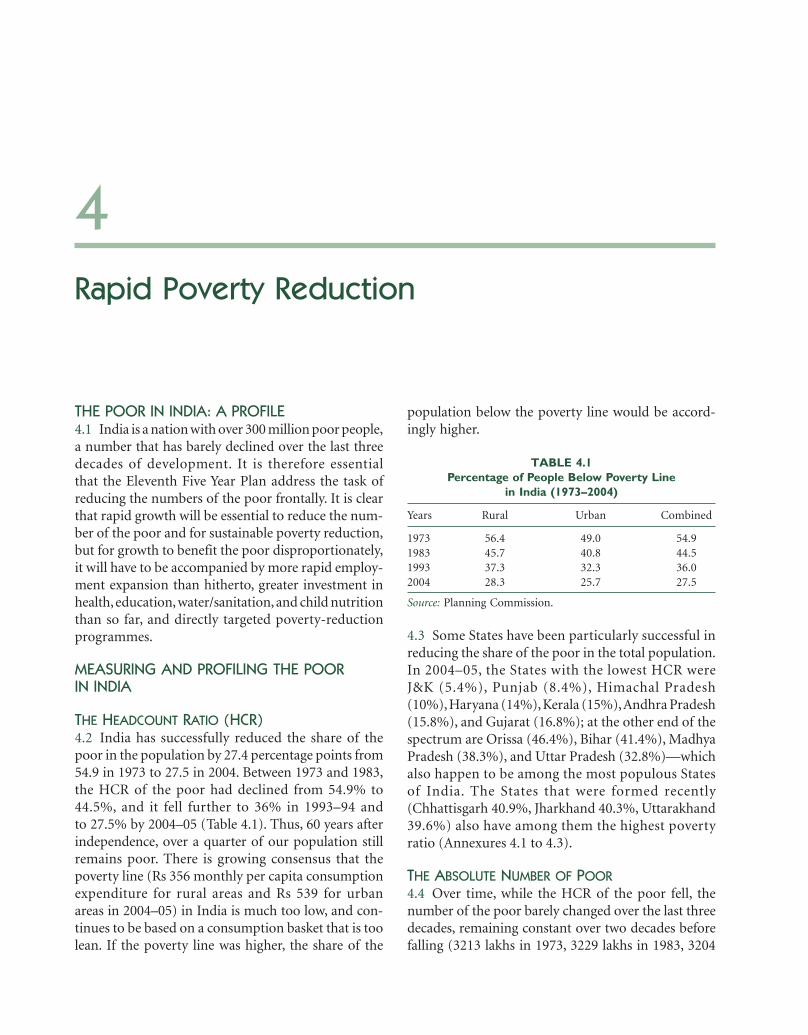

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Eleventh Five Year Plan - Centre for Social Justice

Eleventh Five Year Plan 2007-121www.oup.com

Volu

me III

Published by:

ElEvEnth FivE YEar Plan 2007-12

This Five Year Plan document focuses on inclusive growth. The document is divided into three volumes. Volume I: Inclusive Growth—details the vision,

policies, and strategies of the key sectors and gives the macroeconomic framework and financing of the Plan; Volume II: Social Sector—provides plans

for Education, Sports, Art and Culture, Health and Family Welfare, Nutrition and Social Safety Net, Drinking Water and Sanitation, and Women and Child Rights; and Volume III: Agriculture, Rural Development, Industry, Services, and Physical

Infrastructure—includes chapters on the respective sectors.

Rs 000

9 780195 696509

ISBN 0-19-569650-6

V o l u m e I I I

agrIculture, rural deVelopment, Industry, serVIces, and physIcal Infrastructure

Eleventh Five Year Plan2007-12

Planning Commission Government of Indiawww.planningcommission.gov.in

Planning Commission Government of India

Eleventh Five Year Plan(2007–2012)

Agriculture, Rural Development, Industry,Services and Physical Infrastructure

Volume III

Planning CommissionGovernment of India

1YMCA Library Building, Jai Singh Road, New Delhi 110 001

Oxford University Press is a department of the University of Oxford. It furthers theUniversity’s objective of excellence in research, scholarship, and education

by publishing worldwide in

Oxford New York

Auckland Cape Town Dar es Salaam Hong Kong Karachi Kuala LumpurMadrid Melbourne Mexico City Nairobi New Delhi Shanghai Taipei Toronto

With offices in

Argentina Austria Brazil Chile Czech Republic France Greece GuatemalaHungary Italy Japan Poland Portugal Singapore South Korea Switzerland

Thailand Turkey Ukraine Vietnam

Oxford is a registered trademark of Oxford University Pressin the UK and in certain other countries

Published in IndiaBy Oxford University Press, New Delhi

© Planning Commission (Government of India) 2008

The moral rights of the author have been asserted

First published 2008

All rights reserved. No part of this publication may be reproduced or transmitted, in any form or by any means,electronic or mechanical, including photocopying, recording or by any information storage and retrieval system,

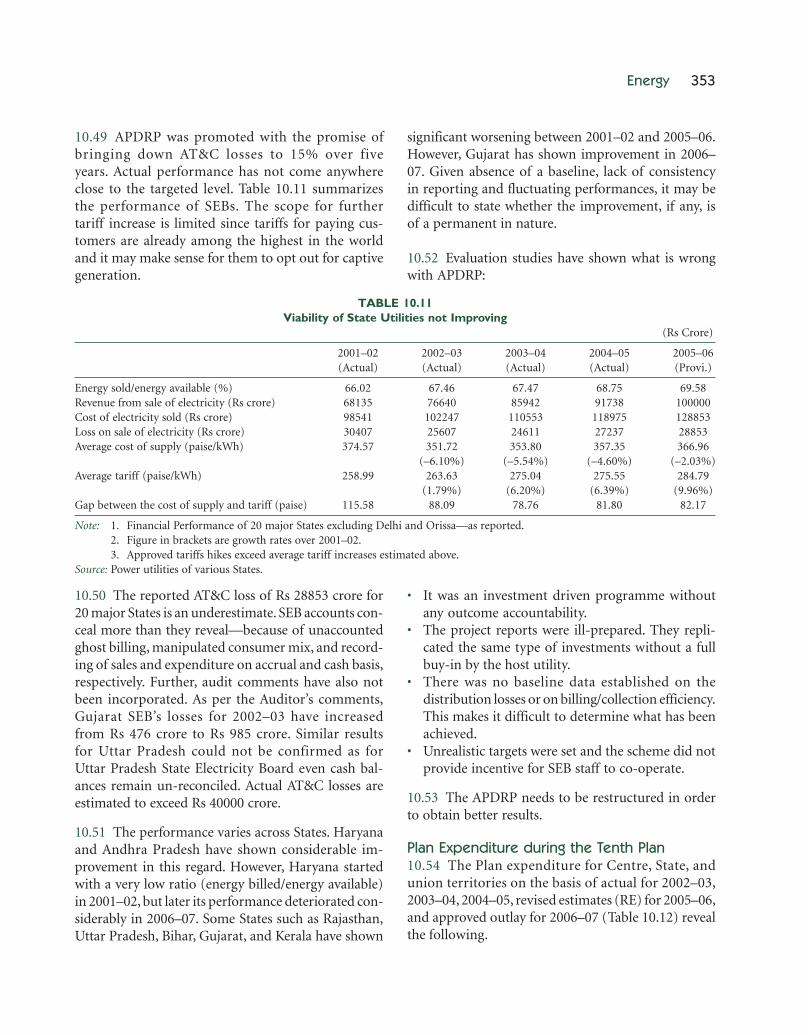

without permission in writing from Planning Commission, Government of India

ISBN-13: 978-0-19-569650-9ISBN-10: 0-19-569650-6

Published by Oxford University PressYMCA Library Building, Jai Singh Road, New Delhi 110 001

On behalf of Planning Commission, Government of India, Yojna Bhawan,Sansad Marg, New Delhi 110 001

1Contents

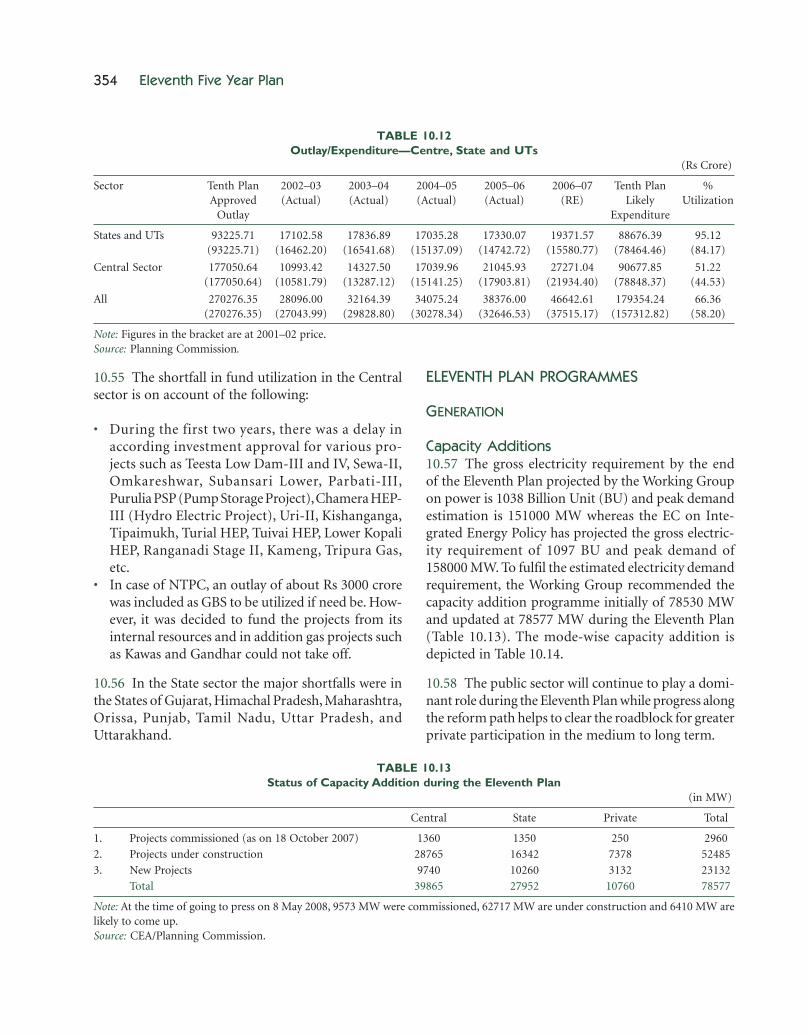

List of Tables vList of Figures ixList of Boxes xList of Annexures xiiList of Acronyms xiv

I. Agriculture

1. AGRICULTURE 3

2. WATER MANAGEMENT AND IRRIGATION 43

3. FOREST 65

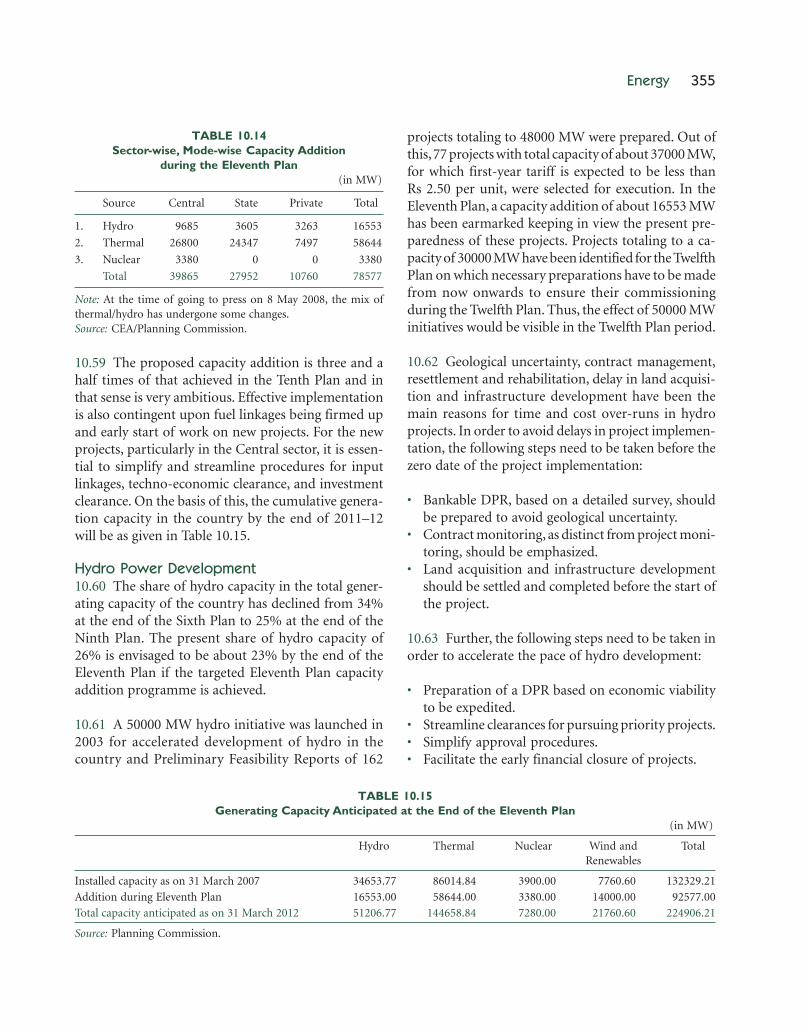

II. Rural Development

4. RAPID POVERTY REDUCTION 79

5. ENSURING RURAL AND URBAN LIVELIHOODS 104

6. BHARAT NIRMAN AND FLAGSHIP PROGRAMMES 129

III. Industry7. INDUSTRY 139

7.1 Industry including Small and Medium Enterprises (SMEs) 1397.2 Minerals 206

IV. Services8. SERVICES 239

8.1 Construction 2398.2 Tourism 245

8.3 IT and IT-Enabled Services 2518.4 Financial Services 259

V. Physical Infrastructure09. TRANSPORT 279

9.1 Integrated Transport System 2799.2 Railways 2799.3 Roads 2899.4 Shipping 3089.5 Ports 3149.6 Civil Aviation 320

10. ENERGY 342

11. URBAN INFRASTRUCTURE, HOUSING, BASIC SERVICES AND POVERTY ALLEVIATION 394

12. COMMUNICATIONS AND INFORMATION TECHNOLOGY 423

12.1 Telecommunications 42312.2 Information Technology 43112.3 India Post 43812.4 Information and Broadcasting 444

Appendix

PROJECTED GBS FOR THE ELEVENTH PLAN 455

iv Contents

1Tables

1.1 Average GDP Growth Rates—Overall and in Agriculture 41.2 Growth Rates of National State Domestic Product (NSDP) from Agriculture 41.3 Growth Rate in Output of Various Sub-sectors of Agriculture 51.4 Trend Growth Rate in Area, Input Use, Credit and Capital Stock in

Agriculture—1980–81 to 2005–06 61.5 Investment in Agriculture 81.6 Region-specific Factors Causing Low Productivity 91.7 Outlay and Expenditure of Ministry of Agriculture during the Tenth Five Year Plan 101.8 Production and Distribution of Seeds 161.9 Changing Share of Private and Public Sector in Seeds Production 17

1.10 Credit Flow to Agriculture Sector by Co-operatives 211.11 Progress of Reforms in Agricultural Markets (APMC Act) as on March 2008 23

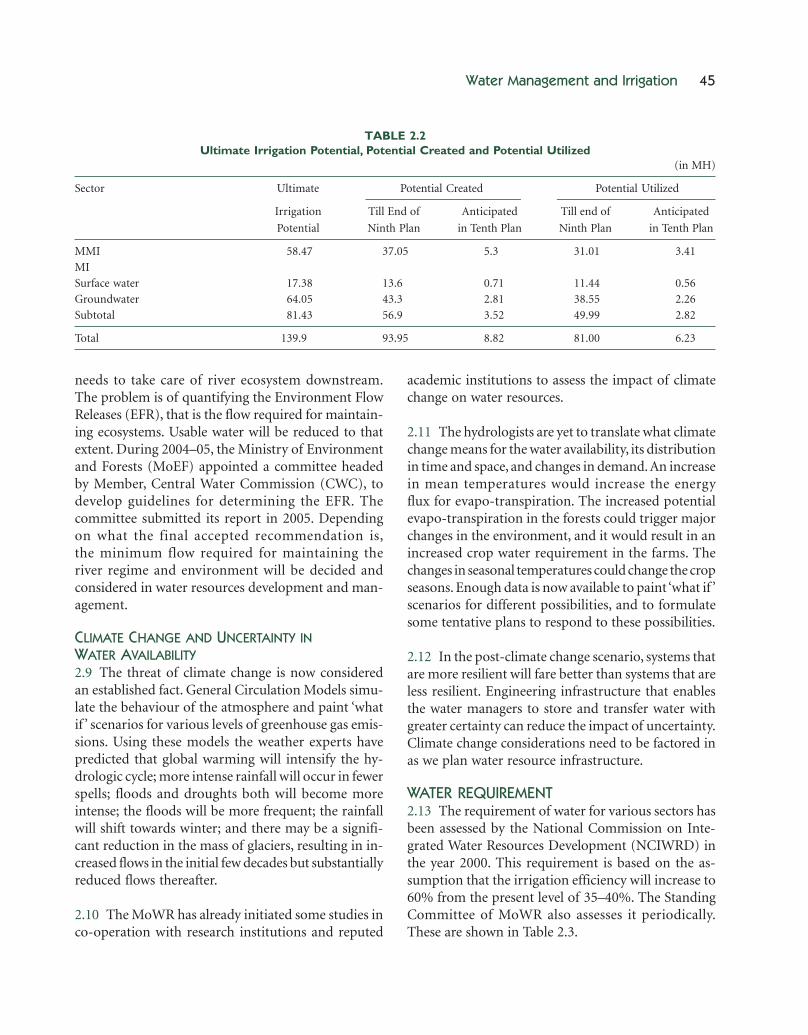

2.1 Estimates of Water Resources in India 442.2 Ultimate Irrigation Potential, Potential Created and Potential Utilized 452.3 Water Requirement for Various Sectors 462.4 Physical Progress under CAD and Water Management (CADWM)

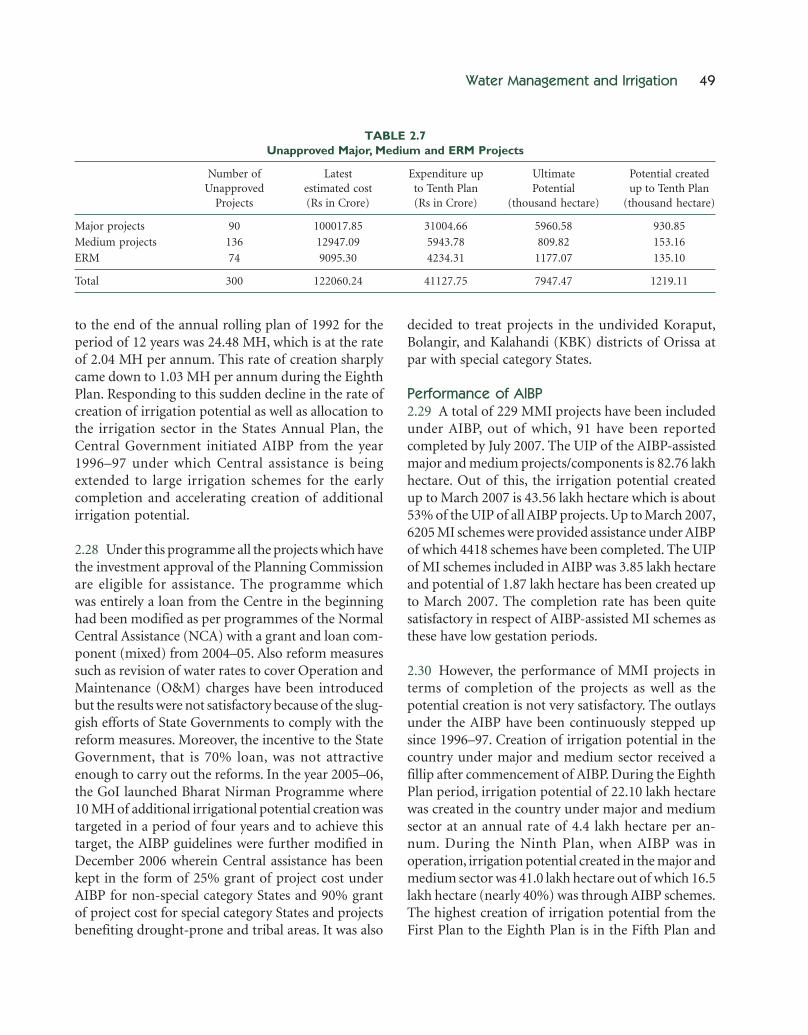

Programme in the Tenth Plan 472.5 Physical and Financial Performance of MMI Sector during the Tenth Plan 472.6 Spillover Major, Medium and ERM Projects into the Eleventh Plan 482.7 Unapproved Major, Medium and ERM Projects 492.8 Performance of AIBP Projects 502.9 Physical and Financial Performance of MI Sector during the Tenth Plan 50

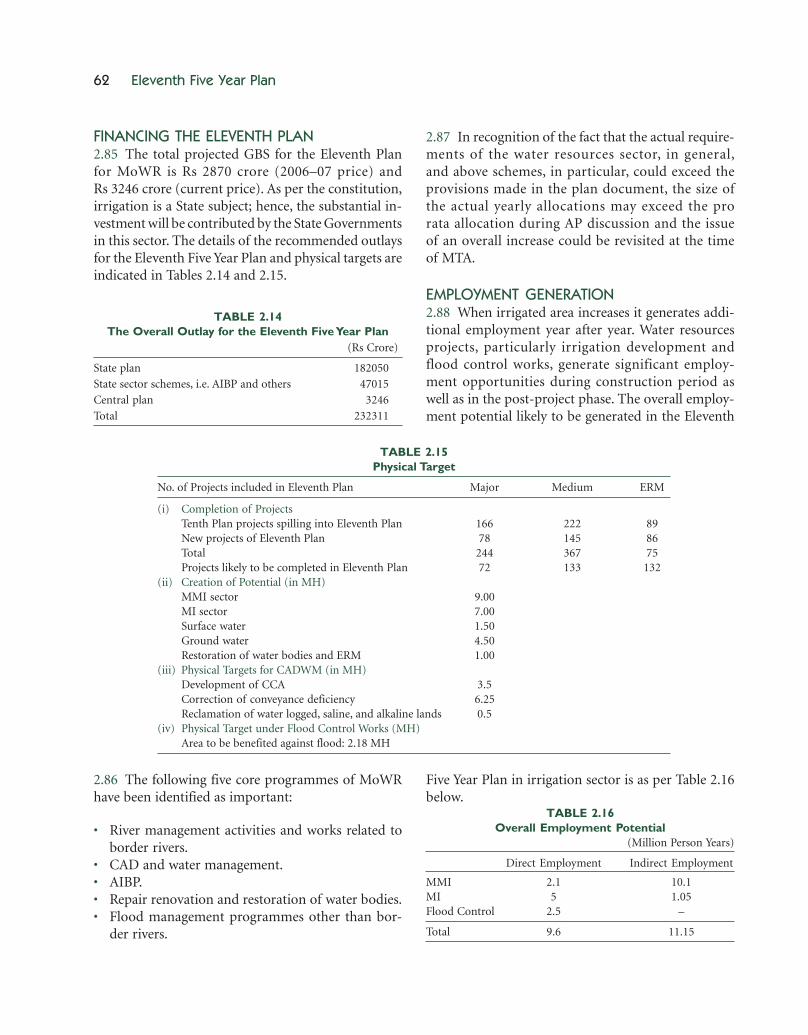

2.10 Financial Performance in Flood Management during the Tenth Plan 522.11 Flood Damage and Relief in the Tenth Plan 522.12 Progress of Inter-linking of Rivers 572.13 State-wise Number of WUAs Formed and Irrigated Area Covered 592.14 The Overall Outlay for the Eleventh Five Year Plan 622.15 Physical Target 622.16 Overall Employment Potential 62

4.1 Percentage of People Below Poverty Line in India (1973–2004) 794.2 Number of Persons Below Poverty Line in India (1973–2004) 80

4.3 Percentage of Households by Asset-holding Categories, by Social Group 814.4 Land Owned per Household by Social Group, 2003 824.5 Incidence of Indebtedness by Social Group 824.6 Health and Nutrition Indicators by Social Groups in 2005–06 (NFHS-3) 834.7 Gross Enrolment, Dropout at Primary Stage (I–V) by Social Groups, 2004–05 835.1 Performance of Handloom Sector during the Tenth Plan Period 1085.2 Performance of Handicraft Sector during the Tenth Plan Period 1115.3 Performance of Powerloom Sector during the Tenth Plan Period 1135.4 Performance of Sericulture Sector during the Tenth Plan 1155.5 Tenth Plan Achievements and Eleventh Plan Targets for Wool Sector 1185.6 Performance of the KVI Sector during the Tenth Five Year Plan 1205.7 Performance of Coir Industry during the Tenth Plan Period 1215.8 Performance of FPI Sector during the Tenth Plan Period 1235.9 Year-wise Physical Targets for the Eleventh Plan for FPI (MSME Manufacturing Units) 125

A5.1 Indian Clusters—An Overview 1276.1 Index of Social and Economic Infrastructure 1296.2 Targets under Bharat Nirman 1306.3 Irrigation Targets under Bharat Nirman 1306.4 Physical Progress of Bharat Nirman during 2005–07 131

7.1.1 Growth Rates 1397.1.2 Sectoral Share in GDP 1407.1.3 Trends in the Performance of Industrial Sub-Sectors —Annual Growth Rate 1417.1.4 Gross Capital Formation and Capital Formation in Manufacturing 1417.1.5 Employment in Organized Manufacturing 1437.1.6 Contribution of Non-departmental Enterprises to GDP at Factor Cost (Current Price) 1537.1.7 Macro View of Central Public Sector Enterprises 1547.1.8 Performance Indicators of State-level Public Enterprises 1557.1.9 Projection of Growth in Vehicle Production and Exports in the Eleventh Five Year Plan 166

7.1.10 Capacity, Production, and Export of Cement 1707.1.11 Projected Shipbuilding Order Book Turnover 1867.1.12 Plan Outlays for the Last Three Five Year Plans for VSE Sector 1957.1.13 Chinese Town and Village Enterprises (TVEs) Exports 1967.1.14 Definition of MSMEs 1977.1.15 Year-wise Physical Targets for the Eleventh Plan 203

7.2.1 Production and Imports of Lead–Zinc Concentrate 2127.2 2 Minerals—Unrealized Potential 2138.2.1 Contribution of Travel and Tourism (T&T) in GDP and Employment in 2007 2458.2.2 Tourists Arrivals in India 2468.2.3 Tourism Receipts 2468.3.1 Growth of IT-ITES Professionals in India—Indian IT Sector:

Knowledge Professionals Employed 2538.3.2 Manpower Requirements for IT-ITES in India 2548.3.3 Indian IT-ITES Exports Forecast 2007–2012 2598.4.1 Growth Rate (Real) of Financial Services (Banking and Insurance) 2598.4.2 Savings and Loan Accounts 2608.4.3 Credit Access of Farmer Households 2618.4.4 Flow of Credit to Agriculture 262

vi Tables

8.4.5 Distribution of Outstanding Credit of SCBs according to the Size of the Credit Limit 2628.4.6 Sector-wise Distribution of Outstanding Credit of SCBs 2638.4.7 Artisan and Village Industries and Other Small-Scale Industries 2638.4.8 Average Population per Branch Office 2699.2.1 Physical Targets and Achievements 2809.2.2 Productivity Performance 2819.2.3 Throw Forward of Projects 2859.2.4 Projection of Freight Traffic in the Eleventh Five Year Plan vis-à-vis

Achievements in the Ninth and Tenth Plans 2879.2.5 Projection of Passenger Traffic in the Eleventh Five Year Plan vis-à-vis

Achievements in the Ninth and Tenth Plans 2879.2.6 Eleventh Five Year Plan—Requirement for Rolling Stock 2889.3.1 Achievements on National Highways 2909.3.2 Corridor-wise Details of Progress on the Golden Quadrilateral as on 31 August 2007 2919.3.3 Status of NHDP and Other NHAI Projects as on 31 August 2007 2929.3.4 Connectivity Status under PMGSY (as on 31 March 2007)—Targets versus Achievements 2949.3.5 Shortfall in Funds for Road Maintenance in the Tenth Plan 2959.3.6 Phasing of Expressway by the Study Group of MoSRTH 2979.3.7 Estimated Targets for the Eleventh Five Year Plan 3039.4.1 Financial Performance of the Shipping Sector in the Tenth Plan 3089.4.2 Increase in Tonnage 3099.5.1 Tenth Plan Cargo Traffic Targets and Achievements 3149.5.2 Tenth Plan—Capacity Added to Major Ports 3159.5.3 Tenth Plan—Productivity Parameters of Major Ports 3159.5.4 Capacity Creation and Projected Traffic in Major Ports in the Eleventh Plan 3179.6.1 Financial Performance of Air India 3249.6.2 Growth in Capacity and Traffic during the Tenth Plan 3249.6.3 Financial Performance of Indian Airlines 3259.6.4 Growth in Capacity and Traffic during the Tenth Plan 3259.6.5 Financial Performance of Airports Authority of India 3269.6.6 Financial Performance of Pawan Hans Helicopters Ltd 3269.6.7 Financial Performance of Air India Charters Ltd 32710.1 Projected Primary Energy Requirement for India, 2030 34310.2 Trends in Demand and Supply of Primary Energy 34510.3 Source-wise Energy Demand 34610.4 Percentage Demand met from Domestic Sources 34610.5 Projected Commercial Energy Requirement for 2011–12 at the Rate of 9% Growth 34710.6 Growth Rates of Domestic Supply 34710.7 Installed Capacity Addition during the Tenth Plan 35110.8 All-India Cumulative Generating Capacity 35110.9 Cumulative Achievements of Transmission Lines at the End of the Tenth Plan 352

10.10 Summary of Investment Component of APDRP (as on 31 August 2007) 35210.11 Viability of State Utilities not Improving 35310.12 Outlay/Expenditure—Centre, State and UTs 35410.13 Status of Capacity Addition during the Eleventh Plan 35410.14 Sector-wise, Mode-wise Capacity Addition during the Eleventh Plan 35510.15 Generating Capacity Anticipated at the End of the Eleventh Plan 355

Tables vii

10.16 Fuel Requirement during 2011–12 35710.17 Physical Programmes—Petroleum and Natural Gas 36510.18 Outlays/Expenditure—Petroleum and Natural Gas 36510.19 Crude Oil Production 36810.20 Natural Gas Production 36810.21 LNG Supply Projections during the Eleventh Plan 36910.22 Projected Crude Oil and Natural Gas Production from Overseas 36910.23 Public Sector Outlays for the Eleventh Plan 37010.24 Accretion of Coal Reserves over the Years 37210.25 Company-wise/Scheme-wise Expenditure during the Tenth Plan 37510.26 Household Energy Consumption in India (July 1999–June 2000) 38410.27 Estimated Medium-term (2032) Potential and Cumulative Achievements

as on 31 March 2007 38610.28 Progress in Grid Interactive Renewable Power 38710.29 Capital Costs and the Typical Cost of Generated Electricity from the Renewable Options 38710.30 Power Generation through Grid Interactive Renewable Power 38710.31 Financial Outlays Proposed for the Eleventh Plan 38810.32 Physical Targets Proposed for the Eleventh Plan 38810.33 Proposed R&D Initiatives in the Eleventh Plan 390

11.1 City/Town-wise Average Access to Drinking Water 40211.2 Funds Requirement—Urban Basic Services 40411.3 Proposed Flow of Funds 40411.4 Comparison of Poverty Estimates Based on Uniform Recall Period 40511.5 Comparison of Poverty Estimates Based on Mixed Recall Period 40511.6 Number of Persons below Poverty Line in Urban and Rural Areas 40511.7 Social Housing Schemes 40711.8 Urban Local Bodies/Parastatals which have been Granted Permission for

Issue of Tax-Free Bonds 41811.9 Outlay and Expenditure 420

11.10 Funds Requirement 42211.11 Sources of Funding 42211.12 Slum Population—Census 2001 42211.13 Population, Housing and Basic Amenities 422

12.1.1 Telecom Network Status in India as on March 2007 42312.1.2 Private Sector Participation (as on 31 March 2006) 42412.1.3 Status of Telecom Indicators in Some Countries as on December 2005 42412.1.4 Expansion of Telecom Network—Public and Private Operators and Fixed and Mobile

(PSUs and Private Operators) during the Tenth Plan Period (2002–07) 42512.1.5 Performance of Telecom Equipment Manufacturing Sector during the Tenth Plan 42612.4.1 Annual Growth of Indian Entertainment and Media Industry 445

viii Tables

1Figures

2.1 Expenditure on Irrigation 462.2 Categorization of Blocks/Mandals/Talukas as on March 2004 51

7.1.1 Share in World Exports of Manufactured Goods 1427.1.2 Starting a Business—Time, and Procedures 1447.1.3 Closing a Business—Time, and Recovery Rate 1457.1.4 Contribution of States to Output and Employment in Manufacturing 1607.1.5 Auto Components—Projection of Turnover and Exports 1677.1.6 Cement—Export, Project Demand and Capacity needed by 2011–12 1707.1.7 Share (Value of Output) of Different Segments of Chemical Industry in India 1737.1.8 Domestic Sales and Exports of Pharmaceuticals 1747.1.9 Pharmaceuticals—Exports, Retail Sale and Institutional Sale by 2011–12 175

7.1.10 Demand of Fertilizer by 2011–12 1787.1.11 Indian Leather Exports—Changing Structure 1807.1.12 Projected Growth of India’s Exports of Leather and Leather Products 1807.1.13 Relative Scale of Operation of Plastic Processing Industry 1837.1.14 Ownership-wise Distribution 1907.1.15 Project Cost Sanctioned under TUFS 1937.1.16 Growth of the SME Sector in India 1987.1.17 Availability of Credit for SSI and Tiny Units 201

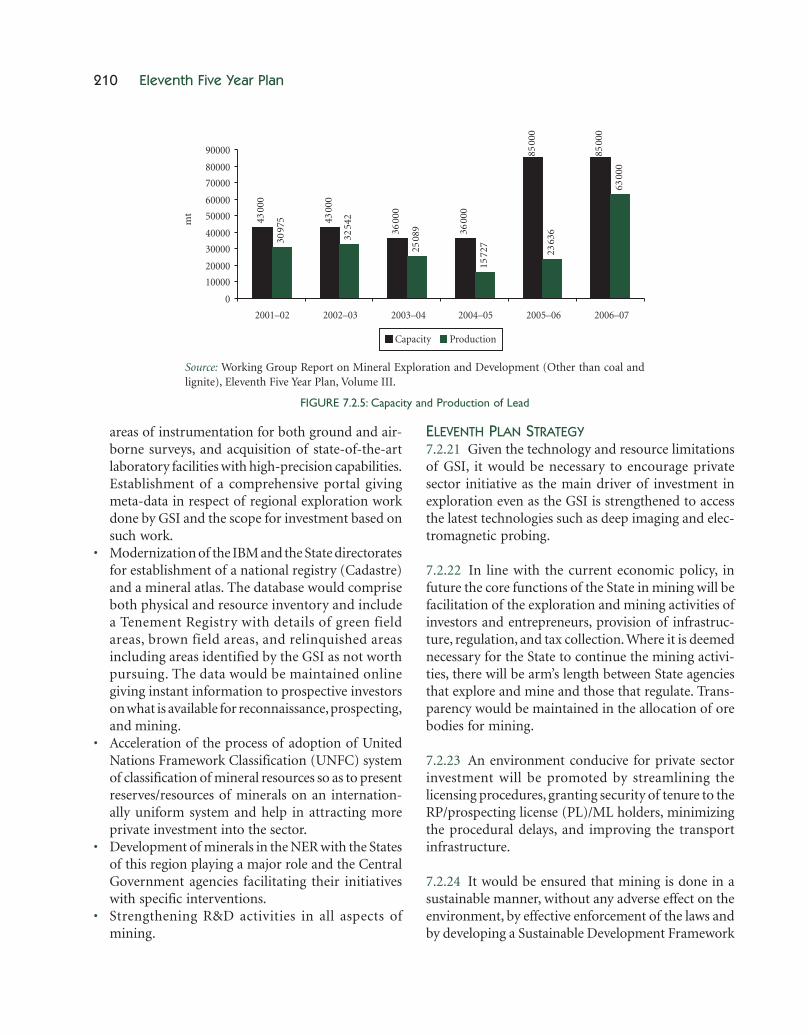

7.2.1 Approvals of Reconnaissance Permit 2077.2.2 Production and Export of Aluminium 2087.2.3 Capacity, Production and Export of Copper 2087.2.4 Capacity and Production of Zinc 2097.2.5 Capacity and Production of Lead 21010.1 Estimated Sector-wise Demand for Coal in 2011–12 376

12.4.1 Indian Entertainment and Media Industry—Status and Projections 445

1Boxes

1.1 Strengths and Weaknesses of Watershed Development Projects in India after 1994 273.1 Avoided Deforestation Incentive Mechanism for States 735.1 Untapped Domestic and International Markets for Traditional Crafts 1055.2 Hope Looms 1085.3 Eleventh Plan Schemes—Handicrafts 1125.4 Eleventh Plan Schemes 1195.5 From Poverty to Prosperity 125

7.1.1 Autonomous Institutions in Industry Sector 1577.1.2 Industrial Area Development Schemes 1587.1.3 Dwindling of a Vibrant Sector 2007.1.4 Small Success 2048.1.1 Holistic Human Resource Development (HRD)—Construction Industry

Development Council (CIDC) 2419.2.1 Expansion of Chinese and Indian Railways (1992–2002)—A Comparison 2829.2.2 Dedicated Freight Corridors (DFCs) 2839.2.3 Throw Forward—A Way Forward 2859.2.4 Fare–Freight Ratio of World Railways 2859.2.5 Public–Private Partnership (PPP) 2869.3.1 Initiatives taken to Expedite Completion of Quality Road Projects 2939.3.2 Modernization of Maintenance Management 2969.3.3 Initiatives taken to Facilitate Private Sector Investment 2969.3.4 Road Sector Objectives for the Eleventh Plan 3009.3.5 Innovations by some State Governments 3019.3.6 Some Options of Resource Mobilization for Rural Roads 3019.5.1 Tariff Setting Mechanism 31910.1 Integrated Energy Policy 34310.2 Energy Equivalence 34510.3 Private Sector Participation 35711.1 Vision 39411.2 Strategy of Urban Development 39511.3 Status of Urban Services 402

11.4 Objectives for Urban Poverty Alleviation 40611.5 Slums 40611.6 Integrated Slum Development 40611.7 Spread of Slums 40611.8 Housing Construction and Ownership 40711.9 New Focus in SJSRY 408

11.10 Housing Stock 41011.11 Housing Shortage and Requirement 41111.12 Investment Requirement 41211.13 Financing of Housing Loans 41211.14 Best Practices in Public Transport 421

12.2.1 Major Government Initiatives 43212.2.2 Indicative List of Successful Initiatives in the States 43312.3.1 Basic Profile of the Postal Sector 439

Boxes xi

1Annexures

1.1 Plan Outlays for the Centre, States and UTs 411.2 Degraded Lands Developed under Various Watershed Development

Programmes—since Inception upto the Tenth Five Year Plan 421.3 Projection for Central Sector GBS–Ministry-wise for the Eleventh Plan 422.1 Plan-wise Cumulative Potential Created and Utilized 644.1 Headcount Ratio and Number of Poor Persons Below Poverty Line in India (Combined) 1004.2 Headcount Ratio and Number of Poor Persons Below Poverty Line in India (Rural) 1014.3 Headcount Ratio and Number of Poor Persons Below Poverty Line in India (Urban) 1024.4 Percentage of Population Below Poverty Line by Social Groups—2004–05 1035.1 Cluster Development in India—Towards a Reinvigorated Cluster Approach 127

7.1.1 Industrial Investment Proposals 2177.1.2 Investment Projects Benefiting from Loans from Banks/FIs in 2004–05, 2005–06

and 2006–07 2177.1.3 Composition of Exports and Growth Rates 2187.1.4 Performance of CPSEs during the Tenth Five Year Plan 2197.1.5 State-wise and Year-wise Investment Intentions (IEMs + LOIs + DILs) 2207.1.6 State-wise Investment Projects Benefiting from Loans from Banks/FIs

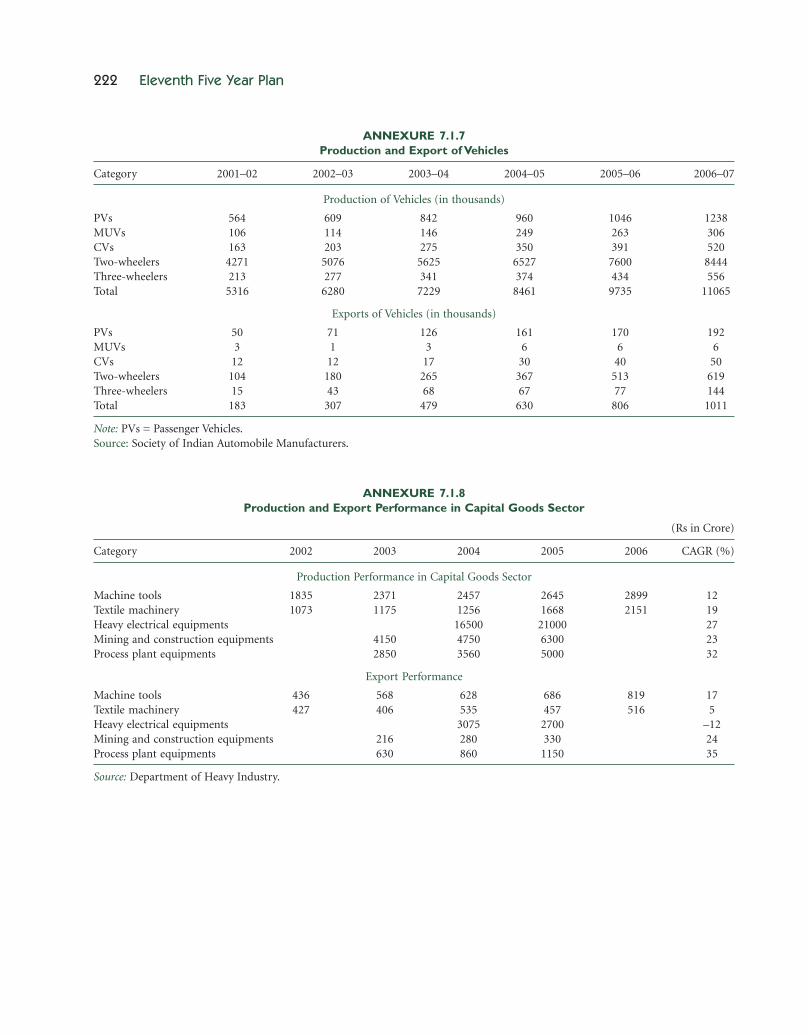

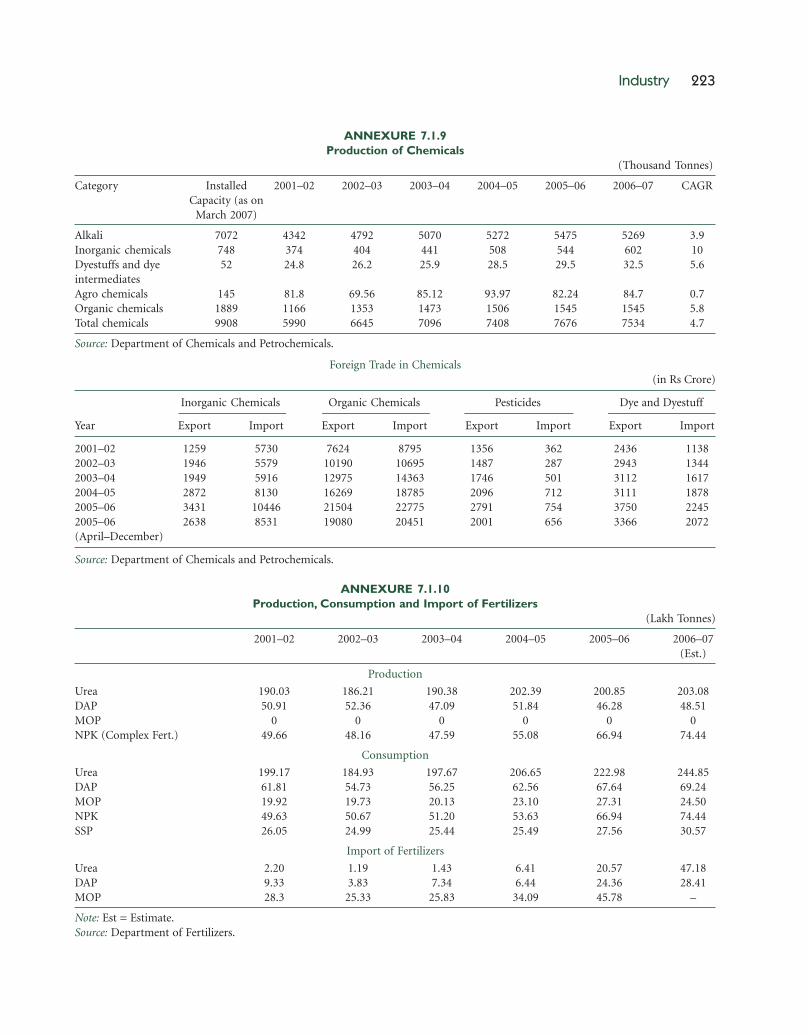

during 2004–05, 2005–06 and 2006–07 2217.1.7 Production and Export of Vehicles 2227.1.8 Production and Export Performance in Capital Goods Sector 2227.1.9 Production of Chemicals 223

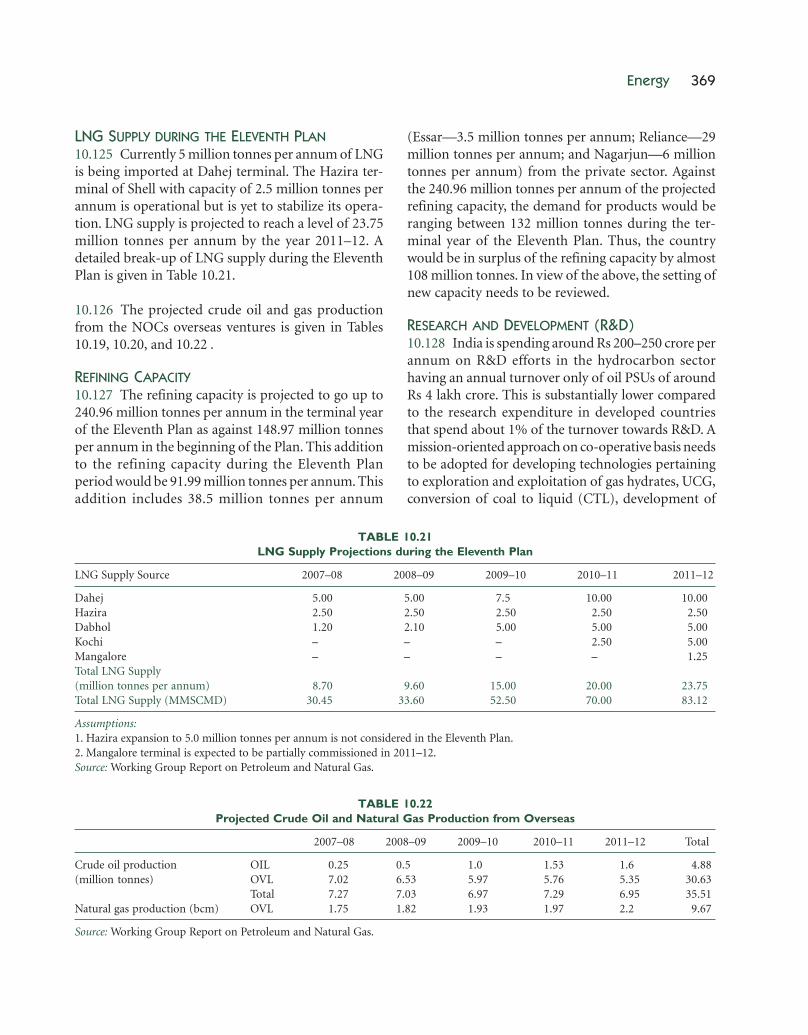

7.1.10 Production, Consumption and Import of Fertilizers 2237.1.11 Production, Import and Export of Paper and Paperboard 2247.1.12 Production, Import and Export of Newsprint 2247.1.13 Performance of Commodity Polymers and Synthetic Fibres 2247.1.14 Production, Import and Export of Finished Steel 2257.1.15 Estimated Requirement of Raw Material and Other Inputs in Steel Production by 2011–12 2257.1.16 Production, Consumption and Export of Sugar during 2002–03 to 2006–07 2257.1.17 Production of Cloth—Year on Year Growth 2267.1.18 Exports of Textiles and Clothing during the Tenth Five Year Plan 2267.1.19 The Tenth Plan Outlay and Anticipated Expenditure and the Eleventh Plan Outlay 227

7.1.20 Performance of SSIs, Year 2001–01 to 2006–07 2287.1.21 Export Destination (Country) of SSI Products 2287.1.22 Participation of Women in SSI Sector, State-wise 2297.1.23 Schemes for MSME 230

7.2.1 Organization/Company-wise Actual Expenditure in theTenth Five Year Plan—Ministry of Mines 232

7.2.2 Life Indices of Important Minerals 2327.2.3 Estimated Apparent Consumption, Domestic Production,

Resource Situation and Life Index of Selected Minerals 2337.2.4 Material Balance of Principal Non-ferrous Metals 2347.2.5 Iron Ore Availability—Haematite (as on 1 April 2005) 2347.2.6 Iron Ore Availability—Magnetite (as on 1 April 2005) 2347.2.7 Physical Targets Proposed by GSI for some Important Activities for the

Eleventh Plan (2007–12) 2357.2.8 Physical Targets Proposed by IBM and MECL for some Important

Activities for the Eleventh Plan (2007–12) 2357.2.9 Expansion Projects of NALCO—Capacity Additions 236

7.2.10 Scheme-wise Break-up of Eleventh Plan Outlays at Current Price—Ministry of Mines 2368.2.1 Financial and Physical Performance of Tourism during the Tenth Five Year Plan 2739.2.1 Resource Mobilization for the Tenth Five Year Plan 3299.2.2 Gross Budgetary Support 3299.3.1 Financial and Physical Performance 3309.3.2 Central Road Sector Outlay and Expenditure—At Current and Constant

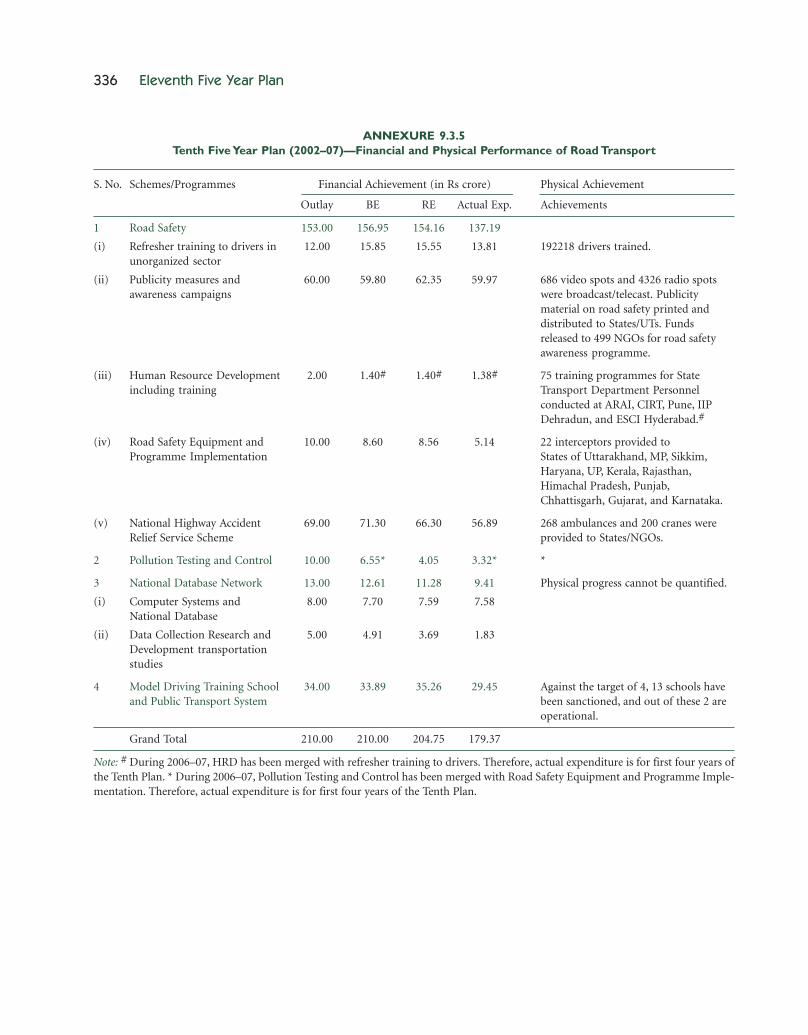

Price for the Tenth Plan 3329.3.3 Plan-wise Addition to NH Length 3339.3.4 Bharat Nirman—Targets for New Connectivity 3349.3.5 Tenth Five Year Plan (2002–07)—Financial and Physical Performance of Road Transport 3369.3.6 State-wise Sanctions and Releases of Central Share in Respect of

Model Driving Training School—Status as on 31 March 2007 3379.3.7 Physical Performance of State Road Transport Corporations/Undertakings 3389.5.1 Year-wise Physical Targets and Achievements during the Tenth Plan—

Major Ports (Commodity-wise) 3399.5.2 Year-wise Physical Targets and Achievements during the Tenth Plan—

Major Ports (Port-wise) 3399.5.3 Tenth Plan—Outlays and Expenditure in Ports Sector 3409.6.1 Financial Progress of the Civil Aviation Sector during the Tenth Plan 34110.1 Coal Demand/Supply—Sector-wise Break-up 39110.2 Company-wise Coal Production Programme 39210.3 Calorific Values, Units and Conversion Factors 393

12.2.1 Performance of IT Hardware and Software during the Tenth Five Year Plan 45012.2.2 Performance of Export Segment of IT Hardware and Software during the

Tenth Five Year Plan 45012.4.1 Progress of the Plan Expenditure of Communication and Information Sector 451

Annexures xiii

1Acronyms

3G Third GenerationA&N Islands Andaman and Nicobar IslandsAAI Airports Authority of IndiaAAUI Automobile Association of

Upper IndiaABB Asea Brown Boveri LtdACA Additional Central AssistanceACI Aero Club of IndiaACZs Agro-Climatic ZonesADB Asian Development BankAGR Adjusted Gross RevenueAI Air IndiaAIBP Accelerated Irrigation Benefit

ProgrammeAICL Air India Charters LimitedAICRP All-India Co-ordinated Research

ProjectAIDS Acquired Immuno Deficiency

SyndromeAIR All-India RadioALHW Andaman Lakshadweep Harbour

WorksALIMCO Artificial Limbs Manufacturing

CorporationAMR Addition, Modification and

ReplacementANDA Abbreviated New Drug ApplicationAP Annual PlanAP Andhra PardeshAPDRP Accelerated Power Development

and Reforms Programme

APEDA Agricultural and Processed FoodProducts Export DevelopmentAuthority

APES Apparel Parks for ExportsScheme

API Active Pharmaceutical IngredientAPM Administered Price MechanismAPMC Agricultural Product Marketing

CommitteeARAI Automotive Research Association

of IndiaASI Annual Survey of IndustriesAT&C Aggregate Technical and

CommercialATF Aviation Turbine FuelATI Automotive Training InstitutesATM Air Traffic ManagementATMAs Agriculture Technology

Management AgenciesAUWSP Accelerated Urban Water Supply

ProgrammeAVT Artisan, Village, and TinyAWBI Animal Welfare Board of IndiaBALCO Bharat Aluminium Co. LtdBARC Bhabha Atomic Research CentreBC Business CorrespondentsBCAS Bureau of Civil Aviation SecurityBCCL Bharat Coking Coal Limitedbcm billion cubic metreBCPL Brahmaputra Cracker and Polymer

Ltd

Acronyms xv

BCPL Bengal Chemicals andPharmaceuticals Limited

BDDS Bomb Detection and DisposalSquad

BE Budget EstimateBEE Bureau of Energy EfficiencyBG Broad GaugeBHEL Bharat Heavy Electricals LtdBIFR Bureau of Industrial and Financial

ReconstructionBih BiharBIFR Bureau of Industrial and Financial

ReconstructionBIS Bureau of Indian StandardsBkWh billion kilowatt hoursBLA BLA IndustriesBMI Body Mass IndexBMTC Bangalore Metropolitan Transport

CorporationBMTPC Building Materials and Technology

Promotion CouncilBMS Basic Minimum ServicesBOO Build–Own–OperateBOT Build, Operate, and TransferBPCL Bharat Petroleum Corporation LtdBPL Below Poverty LineBPO Business Process OutsourcingBRDB Border Roads Development BoardBRGF Backward Regions Grant FundBRK Brick KilnBRO Border Roads OrganizationBRPL Bongaigaon Refineries and

Petrochemicals LtdBRPSE Board for Reconstruction of Public

Sector EnterprisesBS Budgetary SupportBSNL Bharat Sanchar Nigam LtdBSUP Basic Services to the Urban PoorBt Billion tonneBTKM Billion Tonne Kilometrebtu British Thermal UnitBU Billion UnitC-DOT Centre for Development of

TelematicsCAA Constitution Amendment ActCACP Commission for Agricultural Costs

and Prices

CAD Command Area DevelopmentCAD Computer Aided DesignCADWM Command Area Development and

Water ManagementCAGR Compound Annual Growth RateCAMPA Compensatory Afforestation Fund

Management and PlanningAuthority

CARA Central Adoption Resource AgencyCART Credit Appraisal and Rating ToolCAS Conditional Access SystemCBM Coal Bed MethaneCBOs Community Based OrganizationsCBSP Capacity Building for Service

ProviderCBVS Chanderi Bunkar Vikas SamitiCBWE Central Board for Workers’

EducationCCA Culturable Command AreaCCBs Central Co-operative BanksCCDA Coal Conservation and

Development ActCCEA Cabinet Committee on Economic

AffairsCCL Central Coalfields LimitedCCO Coal Controller OrganizationCDI Coal Dust InjectionCDMA Code Division Multiple AccessCDP City Development PlanCDSCO Central Drugs Standard Control

OrganizationCEA Central Electricity AuthorityCERC Central Electricity Regulatory

CommissionCENVAT Central Value-Added TaxCERT-In Indian Computer Emergency

Response TeamCFC Common Facility CentreCFS Container Freight StationCFt Cubic FeetCGWB Central Ground Water BoardCha ChhattisgarhCHMS Complaints Handling Management

SystemCIC Community Information CentreCIDC Construction Industry

Development Council

xvi Acronyms

CII Confederation of Indian IndustriesCIL Coal India LimitedCIPET Central Institute of Plastics

Engineering and TechnologyCIRT Central Institute of Road

TransportCITES Convention on International Trade

in Endangered Species of WildFauna and Flora

CLA Central Loan AssistanceCLCS Credit-Linked Capital SubsidyCLCSS Credit Linked Capital Subsidy

SchemeCLIFF Community-linked Finance FacilityCMTI Central Manufacturing Technology

InstituteCNS Communication, Navigations and

SurveillanceCoI Committee on InfrastructureCOIN Co-operative Bank Information

NetworkCOSCAP Co-operative Development of

Operational Safety and ContinuingAirworthiness Programme

CPCL Chennai Petroleum CorporationLtd

CPCSEA Committee for the Purpose ofControl and Supervision ofExperiments on Animals

CPDS Chemical Promotion andDevelopment Scheme

CPL Commercial Pilot LicenceCPP Calling Party PaysCPP Captive Power PlantCPPRI Central Pulp and Paper Research

InstituteCPSE Central Public Sector EnterpriseCPSU Central Public Sector UndertakingCRC Chawki Rearing CentreCRF Central Road FundCRRI Central Road Research InstituteCSB Central Silk BoardCSC Common Service CentreCSD Cutter Suction DredgerCSIR Council of Scientific and Industrial

ResearchCSL Cochin Shipyard Ltd

CSO Central Statistical OrganizationCSS Centrally Sponsored SchemesCST Central Sales TaxCTL Coal To LiquidCTSA Central Tibetan School

AdministrationCUM Cubic MetreCUSP Cryogenic Upper Stage ProjectCVs Commercial VehiclesCWC Central Water CommissionCWDB Central Wool Development BoardCZA Central Zoo AuthorityDAC Department of Agriculture and

Co-operationDAE Department of Atomic EnergyDAHDF Department of Animal Husbandry,

Dairying, and FisheriesDAP Di-Ammonium PhosphateDARE Department of Agricultural

Research and EducationDBT Department of BiotechnologyDC Development CommissionerDCI Dredging Corporation of IndiaDD DoordarshanDDHPY Deen Dayal Hathkargha Protsahan

YojanaDDP Desert Development PlanDel DelhiDFC Dedicated Freight CorridorDFID Department for International

DevelopmentDFP Directorate of Field PublicityDFPD Department of Food and Public

DistributionDGCA Directorate General of Civil

AviationDGH Directorate General of

HydrocarbonDGLL Directorate General of Lighthouses

and LightshipsDGMS Directorate General of Mines

SafetyDGPS Differential Global Positioning

SystemsDG (S) Directorate General of ShippingDHI Department of Heavy IndustryDIL Direct Industrial License

Acronyms xvii

DIPP Department of Industrial Policy andPromotion

DIT Department of InformationTechnology

DMF Drug Master FileDMIC Delhi–Mumbai Industry CorridorDPAP Drought Prone Area ProgrammeDPC District Programme Co-coordinatorDPE Department of Public EnterprisesDPR Detailed Project ReportDoDWS Department of Drinking Water

SupplyDOE Directorate of ExtensionDoNER Development of North East RegionDoP Department of PostsDoRTH Department of Road Transport and

HighwaysDoT Department of TelecommunicationsDRDA District Rural Development AgencyDRM Digital Radio MondialeDSIR Department of Scientific and

Industrial ResearchDSL Digital Subscriber LinesDSM Demand Side ManagementDTH Direct To HomeDTO District Transport OfficeDVC Damodar Valley CorporationDWCUA Development of Women and

Children in Urban AreasDWT Dead Weight TonnageE&I Roads of Economic and Interstate

ImportanceE&P Exploration and ProductionEAPs Externally Aided ProjectsEBR Extra Budgetary ResourcesEC Expert CommitteeECBC Energy Conservation Building CodesECE Economic Commission for EuropeECL Eastern Coalfields LimitedEDI Electronic Data InterchangeEDP Entrepreneurship Development

ProgrammeEFC Expenditure Finance CommitteeEFR Environment Flow ReleasesEGS Education Guarantee SchemeEIA Environmental Impact AssessmentEIC Export Inspection Council

EMSC Environmental Measures andSubsidence Control

EOR Enhanced Oil RecoveryERC Expenditure Reform CommitteeERM Extension, Renovation, and

ModernizationERP Enterprise Resource PlanningESA External Support AgenciesEU European UnionEV Electric vehicleEWS Economically Weaker SectionsFAB Fabrication UnitsFAO Food and Agricultural OrganizationFAR Floor Area RatioFASAL Forecasting Agriculture Output

using Space, Agro-Meteorology, andLand-based Observation

FBRs Fast Breeder ReactorsFCI Food Craft InstituteFCRI Fluid Control Research InstituteFDA Forest Development AgencyFDDI Footwear Design and Development

InstituteFDI Foreign Direct InvestmentFICCI Federation of Indian Chambers of

Commerce and IndustryFM Frequency ModulationFO Furnace OilFOB Free On BoardFOIS Freight Operation Information

SystemFPI Food Processing IndustryFPR Flood Prone RiverFR Feasibility ReportFRM Fertilizer Raw MaterialFSI Floor Space IndexFSI Forest Survey of IndiaFTA Free Trade AgreementFTII Film and Television Institute of IndiaFTL Fluorescent Tube LightFWW Four Wheeler WagonG&P Ginning and PressingGAIL Gas Authority of India LtdGbps Gigabits per secondGBS Gross Budgetary SupportGCF Gross Capital FormationGCV Gross Calorific Value

xviii Acronyms

GDCF Gross Domestic CapitalFormation

GDP Gross Domestic ProductGER Gross Enrolment RatioGHz GigahertzGI Geographical IndicationGIS Geographic Information SystemsGLP Good Laboratory PracticesGMP Good Manufacturing PracticeGoI Government of IndiaGoM Group of MinistersGP Gram PanchayatGPS Global Positioning SystemGQ Golden QuadrilateralGRE Graduate Record ExaminationGSI Geological Survey of IndiaGSM Global System for Mobile

CommunicationsGSPC Gujarat State Petroleum

Corporation LimitedGSRDC Gujarat State Road Development

CorporationGST Goods and Service TaxGT Gross TonnagesGuj GujaratGVA Gross Value AddedGWe Gigawatt ElectricalGW-Yr Gigawatt Yearha HectareHACCP Hazard Analysis and Critical

Control PointHar HaryanaHCI Hotel Corporation of IndiaHCL Hindustan Copper LtdHCR Headcount RatioHDTV High Definition TelevisionHEMM Heavy Earth Moving MachineryHEP Hydro Electric ProjectHFC Housing Finance CompanyHH HouseholdHMCPs Hardware Manufacturing Cluster

ParksHP Himachal PradeshHOCL Hindustan Organics Chemicals

LimitedHPC High Powered Inter-Ministerial

Committee

HPCL Hindustan Petroleum CorporationLtd

HPL Hindustan Prefab LimitedHR Human ResourceHRD Human Resource DevelopmentHSL Hindustan Shipyard LtdHUDCO Housing Urban Development

CorporationHZL Hindustan Zinc LtdI&B Information and BroadcastingI&M Industry and MineralsIAY Indira Awaas YojanaIBM Indian Bureau of MinesIBP Indo Burma Petroleum Company

LtdIC Integrated CircuitsICAR Indian Council of Agricultural

ResearchICDS Integrated Child Development

ServicesICE Information, Communication and

EntertainmentICFRE Indian Council of Forestry Research

and EducationICML Integrated Coal Mining LtdICPS Integrated Child Protection

SchemeICRIER Indian Council for Research on

International Economic RelationsICT Information and Communication

TechnologyID Industrial DisputeIDA International Development

AssociationIDLS Integrated Development of

Leather SectorIDSMT Integrated Development of Small

and Medium TownsIDTR Institute of Driving Training and

ResearchIEBR Internal and Extra Budgetary

ResourceIEC Information, Education, and

CommunicationIEM Industrial Entrepreneur

MemorandaIEPR Integrated Energy Policy Report

Acronyms xix

IFFCO Indian Farmers FertilizerCo-operative Ltd

IGCAR Indira Gandhi Centre for AtomicResearch

IGCC Integrated Gasification CombinedCycle

IGRUA Indira Gandhi Rashtriya UranAkademi

IHM Institutes of Hotel ManagementIHSDP Integrated Housing and Slum

Development ProgrammeIID Integrated Infrastructure

DevelopmentIIFM Indian Institute of Forest

ManagementIIM Indian Institute of ManagementIIMC Indian Institute of Mass

CommunicationIIP Index for Industrial ProductionIISCO Indian Iron and Steel CompanyIIT Indian Institute of TechnologyIITM Indian Institute of Tropical

MetereologyIITTMs Indian Institute of Tourism and

Travel ManagementIIUS Industrial Infrastructure

Upgradation SchemeIL&FS Infrastructure Leasing and Financial

Services LtdILCS Integrated Low Cost Sanitation

SchemeILD International long distanceILDP Indian Leather Development

ProgrammeIMD Indian Meteorological DepartmentIMF Irrigation Maintenance FundIMO Instant money-orderIMR Infant Mortality RateIMU Indian Maritime UniversityINCOIS Indian National Centre for Ocean

Information ServicesIndal Indian Aluminium Company LimitedINSA Indian National Shipowners’

AssociationIOC Indian Oil CorporationIODP Integrated Ocean Drilling

Programme and Geotechnoic

IOR Improved Oil RecoveryIP Internet ProtocolIPE Institute of Public EnterpriseIPEA International Preliminary

Examining AuthorityIPFT Institute of Pesticides Formulation

TechnologyIPIRTI Indian Plywood Industries Research

and Training InstituteIPM Integrated Pest ManagementIPO Indian Intellectual Property OfficeIPRs Intellectual Property RightsIPTV Internet Protocol TelevisionIR Internal ResourcesIRDA Insurance Regulatory and

Development AuthorityIREDA Indian Renewable Energy

Development AgencyIREP Integrated Rural Energy ProgrammeIRMRA Indian Rubber Manufacturers

Research AssociationIRQP Improvement of Riding Quality

ProgrammeISA International Searching AuthorityISO International Organization for

StandardizationISP Internet Service ProviderIT Information TechnologyITC Industrial Training CentresITES IT-enabled ServicesITI Industrial Training InstituteITS Intelligent Transportation SystemIWAI Inland Waterways Authority of IndiaIWDP Integrated Wasteland Development

ProjectIWT Inland Water TransportJ&K Jammu and KashmirJBIC Japan Bank for International

CooperationJFM Joint Forest ManagementJha JharkhandJKML Jammu and Kashmir Mineral LtdJNNURM Jawaharlal Nehru National Urban

Renewal MissionJNPT Jawaharlal Nehru Port TrustJSMDCL Jharkhand State Mineral

Development Corporation

xx Acronyms

JSPL Jindal Steel and Power LtdJV Joint VentureJVC Joint Venture CompanyK–G Krishna–GodavariKar KarnatakaKBK Koraput, Bolangir, and KalahandiKcal KilocalorieKCCs Kisan Credit CardsKer KeralaKg KilogramKgoe Kilogram of oil equivalentKm KilometreKPO Knowledge Process OutsourcingKRIBHCO Krishak Bharati Co-operative

LimitedKRL Kochi Refineries LtdKV Kilo VoltKVI Khadi and Village IndustriesKVIC Khadi and Village Industries

CommissionKVK Krishi Vigyan KendraKW KilowattKWh Kilowatt hourKWp Kilowatt peakLEAP Lifelong Education and Awareness

ProgrammeLED Light-emitting diodeLIC Life Insurance CorporationLIG Low-Income GroupsLMT Lakh Metric TonnesLNG Liquefied Natural GasLOI Letter of IntentLSIs Large-Scale Industriesm metrem2 square metrem3 cubic metresMah MaharashtraMAMID Mine Accident Analysis and

Modernization of informationDatabase

MAP Medicinal and Aromatic PlantMAT Management Aptitude TestMBC Mail Business CentreMCA Model Concession AgreementMCA Ministry of Corporate AffairsMCDR Mineral Conservation and

Development Rules

MCuM Million Cubic MetresMDM Mid-day MealMDF Mineral Development FundMDR Major District RoadMECL Mineral Exploration Corporation

LtdMEMU Mainline Electric Multiple UnitMFI Micro Finance InstitutionMFPI Ministry of Food Processing

IndustriesMGIRI Mahatma Gandhi Institute for Rural

IndustrializationMH Million HectareMHRD Ministry of Human Resources

DevelopmentMI Minor irrigationMICE Meetings Incentives Conventions

and ExhibitionsMIS Management Information SystemsMITI Model Industrial Training InstituteML Mining LeaseMLAs Members of Legislative AssemblyMMA Macro Management SchemeMMBtu Million British Thermal UnitMMI Major and Medium IrrigationMMP Mission Mode ProjectMMDR Act Mines and Minerals (Development

and Regulation) ActMMSCMD Million Standard Cubic Metres

per DayMNC Multi-National CompanyMNRE Ministry of New and Renewable

EnergyMoA Union Ministry of AgricultureMoC Ministry of CoalMoCA Ministry of Civil AviationMoEF Ministry of Environment and ForestMoHUPA Ministry of Housing and Urban

Poverty AlleviationMoI&B Ministry of Information and

BroadcastingMoP Ministry of PowerMOP Muriate of PotashMORD Ministry of Rural DevelopmentMoSRTH Ministry of Shipping, Road

Transport, and HighwaysMoT Ministry of Tourism

Acronyms xxi

MoU Memorandum of UnderstandingMoWR Ministry of Water ResourcesMP Madhya PradeshMPC Metropolitan Planning CommitteeMPLAD Member of Parliament Local Area

Development ProgrammeMPP Marketing Promotion ProgrammeMPP Multipurpose ProjectMRIN Marketing Research Surveys and

Information NetworkMRO Maintenance, Repair, and

OverhaulMRPL Mangalore Refineries and

Petrochemicals LtdMRP maximum retail priceMRTD Marine Research and Technology

DevelopmentMRTS Mass Rapid Transit SystemMSE Micro and Small EnterpriseMSME Micro, Small, and Medium EnterpriseMSMED Act Micro, Small, and Medium

Enterprises Development ActMSP Minimum Support Pricesmt metric tonnesMTA Mid-Term AppraisalMTNL Mahanagar Telephone Nigam LtdMtoe Million Tonne of Oil EquivalentMU Million UnitMUTP Mumbai Urban Transport ProjectMUV Multi-Utility VehicleMVA Million Volt AmperesMW MegawattMWe Megawatt ElectricalNABARD National Bank for Agriculture and

Rural DevelopmentNAEB National Afforestation and

Eco-development BoardNAEEB National Afforestation,

Ecorestoration, and Eco-development Board

NAEP National Afforestation andEco-Development Project

NAFUS National Fund for the UnorganizedSector

NAIS National Agricultural InsuranceScheme

NAL National Aerospace Laboratories

NALCO National Aluminium Company Ltd.NAP National Afforestation ProgrammeNARDCO National Real Estate Development

CouncilNARS National Agricultural Research

SystemNASSCOM National Association of Software

and ServiceCompaniesNATRIP National Automotive Testing and

R&D Infrastructure ProjectNBC Net Bank CreditNBCC National Building Construction

CorporationNBFC Non-banking Financial CompanyNBO National Building OrganizationNBS Net Budgetary SupportNCA Normal Central AssistanceNCAER National Council for Applied

Economic ResearchNCAOR National Centre for Antarctic and

Ocean ResearchNCCBM National Council for Cement and

Building MaterialsNCDC National Climatic Data CentreNCERT National Council of Educational

Research and TrainingNCEUS National Commission for Enterprises

in the Unorganized SectorNCIWRD National Commission on Integrated

Water Resources DevelopmentNCL Northern Coalfields LtdNCLT National Company Law TribunalNCMP National Common Minimum

ProgrammeNCMRWF National Centre for Medium Range

Weather ForecastNCPCR National Commission for

Protection of Child RightsNCR National Capital RegionNCRPB National Capital Region Planning

BoardNDC National Development CouncilNDE Non-Departmental EnterpriseNDDB National Dairy Development BoardNDMA National Disaster Management

AuthorityNE North East/Eastern

xxii Acronyms

NEC North Eastern CoalfieldsNEDFI North Eastern Development

Finance Corporation LtdNEF National Electricity FundNEF National Equity FundNEF (R&D) National Energy FundNeGP National e-Governance PlanNEIP North East Industrial PolicyNEKRTC North East Karnataka Road

Transport CorporationNELP New Exploration Licensing PolicyNER North Eastern RegionNFBS National Family Benefit SchemeNFDB National Fisheries Development

BoardNFHS National Family Health SurveyNGN Next Generation NetworksNGOs Non-Governmental OrganizationsNH National HighwayNHAI National Highways Authority of IndiaNHB National Housing BankNHDP National Highway Development

ProgrammeNHFDC National Handicapped Finance and

Development CorporationNHM National Horticulture MissionNH (O) National Highways (Original)NHPC National Hydroelectric Power

Corporation LtdNIAM National Institute of Agricultural

MarketingNIC National Informatics CentreNIC National Industrial ClassificationNICFS National Institute of Criminology

and Forensic SciencesNICNET National Informatics Centre

NetworkNID National Institute of DesignNIFM National Institute of Finance

ManagementNIFT National Institute of Fashion

TechnologyNIOT National Institute of Ocean

TechnologyNIPER National Institute of

Pharmaceutical Education andResearch

NITs National Institutes of TechnologyNITA National Institute of Tribal AffairsNLC Neyveli Lignite CorporationNLCPR Non-Lapsable Central Pool of

ResourcesNLD National Long DistanceNLDCP National Livestock Disease Control

ProgrammeNLI National Labour InstituteNLW Non Linked WasheryNMBS National Maternity Benefit SchemeNMCC National Manufacturing

Competitiveness CouncilNMDFC National Minorities Development

and Finance CorporationNMT Non-motorized TransportNNM National Nutrition MissionNOAPS National Old Age Pension SchemeNOCs National Oil CompaniesNOVOD National Oilseeds and Vegetable

Oils Development BoardNPC National Productivity CouncilNPCIL Nuclear Power Corporation of India

LimitedNPK Nitrogen–Phosphorus–PotassiumNPPA National Pharmaceutical Pricing

AuthorityNPS New Pricing SchemeNRAA National Rainfed Area AuthorityNRC National Referral CentreNRC National Research CentreNRCP National River Conservation PlanNREG National Rural Employment

GuaranteeNREGA National Rural Employment

Guarantee ActNREGP National Rural Employment

Guarantee ProgrammeNREGS National Rural Employment

Guarantee SchemeNRHM National Rural Health MissionNRI Non-Resident IndianNRM Natural Resource ManagementNRSA National Remote Sensing AgencyNS–EW North–South and East–WestNSAP National Social Assistance

Programme

Acronyms xxiii

NSC National Seed CorporationNSDP National Slum Development

ProgrammeNSDP National State Domestic ProductNSIC National Small Industries

CorporationNSS National Sample SurveyNSSO National Sample Survey

OrganizationNSVS National Service Volunteer SchemeNTFP Non-Timber Forest ProduceNTH National Test HouseNTKM Net Tonne KilometreNTP New Telecom PolicyNTPC National Thermal Power

CorporationNUIF National Urban Infrastructure FundNUIS National Urban Information SystemNW National WaterwayNWDA National Water Development

AgencyNWDPRA National Watershed Development

Project for Rainfed AreaNWKRTC North West Karnataka Road

Transport CorporationNWP National Water PolicyNYKS Nehru Yuva Kendra SangathanO&M Operation and MaintenanceO&OEG Oil and Oil Equivalent of GasOBCs Other Backward ClassesOECD Organization for Economic

Co-Operation and DevelopmentOEM Original Equipment ManufacturerOFC Optical Fibre CableOIL Oil India LtdOMIFCO Oman India Fertilizer CompanyOMS Output per Man-ShiftOMT Operation, Maintenance, and

TollingONGC Oil and Natural Gas CorporationOOH Out-of-HomeOOIS Ocean Observation and

Information SystemOSVs Offshore Supply VesselsOTC Open Technology CentreOVL ONGC Videsh LtdPAP Project-Affected Person/People

PBITEP Profit before interest, tax, and EPPCC Pulverized Coal CombustionPCO Public Call OfficePCPDS Pharma and Chemical Promotion

and Development SchemePCPIRs Petroleum, Chemicals, and

Petrochemical Investment RegionsPCS Port Community SystemPCUs Passenger Car UnitsPDS public distribution systemPEPSURTC Punjab and East Punjab States

Union Road Transport CorporationPESA Panchayat (Extension to Scheduled

Areas) ActPFDF Pooled Finance Development FundPFMs Postal Finance MartsPGE Platinum Group of ElementsPHE Public Health EngineeringPHED Public Health Engineering

DepartmentPHHL Pawan Hans Helicopters LtdPHM Post-harvest ManagementPHWR Pressurized Heavy Water ReactorPIA Programme Implementation

AgencyPIB Public Investment BoardPIM Participatory Irrigation

ManagementPIU Programme Implementation UnitPL Prospecting LicensePLF Plant Load FactorPLR Prime Lending RatePMEGP Prime Minister’s Employment

Generation ProgrammePMGSY Pradhan Mantri Gram Sadak YojanaPMN Polymettalic NodulesPMRY Prime Minister’s Rozgar YojanaPMS Pavement Management SystemsPOL Petroleum, Oil, and LubricantsPPP Public–Private PartnershipPRIs Panchayati Raj InstitutionsPRODIP Product Development, Design

Intervention, and PackagingPSCs Powerloom Service CentresPSCI Postal Staff College IndiaPSE Public Sector EnterprisePSP Pump Storage Project

xxiv Acronyms

PSU Public Sector UndertakingPun PunjabPURA Provision of Urban Amenities in

Rural AreasPVC Polyvinyl ChloridePWC Pricewaterhouse CoopersPWD Persons With DisabilitiesPWD Public Works DepartmentQCI Quality Council of IndiaQts QuintalsR&D Research and DevelopmentR&M Renovation and ModernizationRaj RajasthanRAS Reclamation of Alkali SoilRBI Reserve Bank of IndiaRCF Rashtriya Chemicals and Fertilizers

LtdRCPs Rural Community PhonesRCSRC Regional Cyber Security Research

CentreRDG Route Dispersal GuidelinesRE Revised EstimateREACH Registration, Evaluation, and

Authorization of ChemicalsREC Rural Electrification Corporation

LtdREGP Rural Employment Generation

ProgrammeRF Radio FrequencyRFI Radio Frequency IdentificationRGGVY Rajiv Gandhi Grameen Vidyutikarn

YojanaRGSY Rashtriya Gram Swaraj YojanaRIDF Rural Infrastructure Development

FundRINL Rashtriya Ispat Nigam LtdRISC Rural Industries Service CentesRKM Route KilometresRKVY Rashtriya Krishi Vikas YojanaRMC Ready-Mix ConcreteRMK Rashtriya Mahila KoshRMS Risk Management SystemRNI Registrar of Newspaper for IndiaROB Road Over BridgeRP Reconnaissance PermitRPO Regional Project OfficeRPS Retention Price Scheme

RR Rural RoadsRRBs Regional Rural BanksRSVY Rashtriya Sam Vikas YojanaRSY Rashtriya Sadbhavana YojanaRTA Regional Trading ArrangementRTKM Revenue Tonne KilometresRTOs Regional Transport AuthoritiesRUB Road Under BridgeRVP River Valley ProjectRW Road WingS&T Science and TechnologySAIL Steel Authority of India Ltd.SARDP-NE Special Accelerated Road

Development Programme for theNorth Eastern Region

SARS Severe Acute RespiratorySyndrome

SAT Scholastic Aptitude TestSAUs State Agricultural UniversitiesSBIRI Small Business Innovation Research

InitiativeSBLP SHGs–bank linkage programmeSC Scheduled CasteSCA Special Central AssistanceSCB Scheduled Commercial BanksSCCL Singareni Collieries Company LtdSCDC Scheduled Caste Development

CorporationSCI Shipping Corporation of IndiaSCP Special Component PalnSDA State Designated AgencySDC Strategic Distribution CentreSDD Song and Drama DivisionSDF Sustainable Development

FrameworkSDF Sugar Development FundSEB State Electricity BoardSECL South Eastern Coalfields LtdSEI–CMM Software Engineering Institute–

Capacity Maturity ModelSERCs State Electricity Regulatory

CommissionsSES Selected Educational StatisticsSEWA Self Employed Women’s

AssociationSEZ Special Economic ZoneSFCI State Farm Corporation of India

Acronyms xxv

SFURTI Scheme of Fund for Regeneration ofTraditional Industries

SGRY Sampoorna Grameen RozgarYojana

SGSY Swaranjayanti Gram SwarozgarYojana

SH State HighwaySHG Self-help GroupSHPI SHG Promoting InstitutionSHTP Special Handicrafts Training ProjectSIAs State Implementing AgenciesSIDBI Small Industries Development Bank

of IndiaSISI Small Industries Service InstitutesSITP Scheme for Integrated Textile ParksSJSRY Swarna Jayanti Shahri Rozgar

YojanaSLDB State Land Development BankSLNA State-level Nodal AgencySLPEs State-level Public EnterprisesSME Small and Medium EnterpriseSMP Statutory Minimum PriceSOCFOD Strengthening of Core Functions

of DGMSSPA School of Planning and

ArchitectureSPS Sanitary and PhytosanitarySPUs State Power UtilitiesSPV Special Purpose VehicleSq M Square MetreSq Km Square KilometreSRs State RoadsSREP Strategic Research Extension PlansSRFTI Satyajit Ray Film and Television

InstituteSRR Seed Replacement RateSRSF Special Railway Safety FundSRTUs State Road Transport UndertakingsSRU Ship Repair UnitSS Secondary SchoolSSA Sarva Shiksha AbhiyanSSCP Sethusamudram Channel ProjectSSIs Small-Scale IndustriesST Scheduled TribeSTD Sexually Transmitted DiseaseSTPI Software Technology Parks of IndiaSWAN State-Wide Area Network

T&CS Thrift and Credit SocietiesT&D Transmission and DistributionT&T Travel and TourismTAT Technical Assistance in Telecom SectorTB TuberculosisTCD Metric Tonnes crushed per dayTCF Trillion Cubic FeetTCIDS Textile Centres Infrastructure

Development SchemeTDSAT Telecom Disputes Settlement and

Appellate TribunalTEC Telecom Engineering CentreTETC Telecom Testing and Security

Certification CentreTFC Twelfth Finance CommissionTISCO Tata Iron and Steel CompanyTMC Technology Mission on CottonTMT Thousand Metric TonneTN Tamil NaduTPD Tonnes Per DayTPY Tonne per YearTRAI Telecom Regulatory Authority of

IndiaTSC Total Sanitation CampaignTSD Trailer Suction DredgerTSP Tribal Sub-PlanTUFS Technology Upgradation Fund

SchemeTVEs Town and Village EnterprisesTWh Trillion Watt hourUAE United Arab EmiratesUCG Underground Coal GasificationUGC University Grants CommissionUHV Useful Heat ValueUIDSSMT Urban Infrastructure Development

Scheme for Small and Medium TownsUIP Ultimate Irrigation PotentialUK United KingdomULBs Urban Local BodiesUMA&N Undersea Cabling between

Mainland and Andaman & Nicobar(A&N) Islands

UMBVS Urmul Marusthali Bunkar VikasSamiti

UMPP Ultra-mega Power ProjectUNCCD United Nations Convention to

Combat Desertification

xxvi Acronyms

UNCTAD United Nations Conference onTrade and Development

UNDP United Nations DevelopmentProgramme

UNFC United Nations FrameworkClassification

UNIDO United Nations IndustrialDevelopment Organization

UP Uttar PradeshUPA United Progressive AllianceURIF Urban Reform Incentive FundUS/USA United States of AmericaUSAID United States Agency for

International DevelopmentUSFDA United Sates Food and Drug

AdministrationUSO Universal Service ObligationUSOF Universal Service Obligation

FundUSP Unique Selling PointUT Union TerritoryUtt UttarakhandVAMBAY Valmiki Ambedkar Awas YojanaVAT Value-Added TaxVGF Viability Gap FundingVLCC Very Large Crude Carrier

VLF Village Level FederationVoIP Voice over Internet ProtocolVPN Virtual Private NetworkVPT Village Public TelephoneVRS Voluntary Retirement SchemeVSAT Very Small Aperture TerminalVSE Village and Small EnterprisesVSNL Videsh Sanchar Nigam LimitedWB West BengalWCCU World Class Central UniversityWCD Women and Child DevelopmentWCL Western Coalfields LtdWDF Watershed Development FundWDPSCA Watershed Development Project for

Shifting Cultivation AreaWHO World Health OrganizationWiFi Wireless FidelityWII Wildlife Institute of IndiaWiMAX Worldwide Interoperability for

Microwave AccessWLL Wireless in Local LoopWMO Wireless Monitoring OrganizationWPC Wireless Planning & Co-ordinationWTO World Trade OrganizationWUA Water Users AssociationZBB Zero Based Budgeting

IAgriculture

1Agriculture

INTRODUCTION1.1 Although its share in Gross Domestic Product(GDP) has declined from over half at Independenceto less than one-fifth currently, agriculture remainsthe predominant sector in terms of employment andlivelihood with more than half of India’s workforceengaged in it as the principal occupation. Agriculturestill contributes significantly to export earnings andis an important source of raw materials as well as ofdemand for many industries.

1.2 India’s agriculture sector has an impressivelong-term record of taking the country out of seriousfood shortages despite rapid population increase.This was achieved through a favourable interplayof infrastructure, technology, extension, and policysupport backed by strong political will. The mainsource of long-run growth was technological augmen-tation of yields per unit of cropped area. This resultedin tripling of foodgrain yields, and foodgrain pro-duction increased from 51 million tonnes in 1950–51to 217 million tonnes in 2006–07. Production of oil-seeds, sugarcane, and cotton have also increasedmore than four-fold over the period, reaching 24million tonnes and 355 million tonnes and 23 millionbales, respectively, in 2006–07.

1.3 But, although GDP from agriculture has morethan quadrupled, from Rs 108374 crore in 1950–51 toRs 485937 crore in 2006–07 (both at 1999–2000 price),the increase per worker has been rather modest. GDP

per agricultural worker is currently around Rs 2000per month, which is only about 75% higher in realterms than in 1950 compared to a four-fold increasein overall real per capita GDP. While slower growth ofGDP in agriculture than non-agriculture is expected,the main failure has been the inability to reduce thedependence of the workforce on agriculture signifi-cantly by creating enough non-farm opportunities toabsorb the labour surplus in rural areas and equip-ping those in agriculture to access such opportunities.Half of those engaged in agriculture are still illiterateand just 5% have completed Higher Secondaryeducation. Incomes and education are of course leastamong agricultural labourers. Even families operat-ing farms now suffer from much smaller holdings(70% below 1 hectare in 2003 compared to 56% in1982), and farming members in such families are twiceas likely to be illiterate as non-farming members.Ensuring food security and farmer welfare thus requiresupport systems to extend technology and scale ben-efits in a sustainable manner to a huge existing work-force in agriculture that lacks non-farm skills and isalso ageing and getting feminized.

RECENT TRENDS AND CONCERNS1.4 The Mid-Term Appraisal (MTA) for the TenthFive Year Plan had drawn attention to the loss ofdynamism in agriculture and allied sectors after themid-1990s. In fact, during the last decade or so Indianagriculture has faced a number of severe challenges,superimposed on the long-term demographics. Recent

4 Eleventh Five Year Plan

trends that have raised concern regarding food secu-rity, farmers’ income, and poverty are:

• Slowdown in growth.• Widening economic disparities between irrigated

and rain-fed areas.• Increased vulnerability to world commodity price

volatility following trade liberalization. This had anadverse effect on agricultural economies of regionsgrowing crops such as cotton and oilseeds.

• Uneven and slow development of technology.• Inefficient use of available technology and inputs.• Lack of adequate incentives and appropriate insti-

tutions.• Degradation of natural resource base.• Rapid and widespread decline in groundwater table,

with particularly adverse impact on small and mar-ginal farmers.

• Increased non-agricultural demand for land andwater as a result of the higher overall GDP growthand urbanization.

• Aggravation in social distress as a cumulativeimpact of the above, reflected in an upsurge infarmers’ suicides.

1.5 Growth of agricultural GDP decelerated from over3.5% per year during 1981–82 and 1996–97 to onlyaround 2% during 1997–98 and 2004–05 (see Table1.1). This deceleration, although most marked in rain-fed areas, occurred in almost all States and coveredalmost all major sub-sectors, including those such ashorticulture, livestock, and fisheries where growth wasexpected to be high (see Table 1.3). Consequently,growth of agricultural GDP has been well below thetarget of 4% set in both Ninth and Tenth Plans. In fact,Tenth Plan growth averaged even less than that during

TABLE 1.1Average GDP Growth Rates—Overall and in Agriculture

(% per Year at 1999–2000 Price)

Period Total Economy Agriculture and Allied Sectors Crops and Livestock

1. Pre-green revolution 1951–52 to 1967–68 3.69 2.54 2.652. Green revolution period 1968–69 to 1980–81 3.52 2.44 2.723. Wider technology dissemination period 1981–82 to 1990–91 5.40 3.52 3.654. Early reforms period 1991–92 to 1996–97 5.69 3.66 3.685. Ninth Plan 1997–98 to 2001–02 5.52 2.50 2.496. Tenth Plan period 2002–03 to 2006–07 7.77 2.47 2.51

of which 2002–03 to 2004–05 6.60 0.89 0.892005–06 to 2006–07 9.51 4.84 4.96

Source: National Accounts Statistics 2008 (New Series), Central Statistical Organization, Ministry of Statistics and ProgrammeImplementation, New Delhi.

TABLE 1.2Growth Rates of National State Domestic Product (NSDP) from Agriculture

(States Ranked by % of Rainfed Area)

State Growth Rate in Rainfed State Growth Rate in RainfedNSDP Agriculture (%) NSDP Agriculture (%)

1984–85 to 1995–96 to 1984–85 to 1995–96 to1995–96 2004–05 1995–96 2004–05

1 2 3 4 5 6 7 8

Punjab 4.00 2.16 3 Gujarat 5.09 0.48 64Haryana 4.60 1.98 17 Rajasthan 5.52 0.30 70Uttar Pradesh 2.82 1.87 32 Orissa –1.18 0.11 73Tamil Nadu 4.95 –1.36 49 Madhya Pradesh 3.63 –0.23 74West Bengal 4.63 2.67 49 Karnataka 3.92 0.03 75Bihar –1.71 3.51 52 Maharashtra 6.66 0.10 83Andhra Pradesh 3.18 2.69 59 Kerala 3.60 –3.54 85All-India 3.62 1.85 60 Assam 1.65 0.95 86

Source: National Accounts Statistics, (State Series) Central Statistical Organization, Ministry of Statistics and Programme Implementa-tion, New Delhi.

Agriculture 5

Ninth Plan because, as was noted in the MTA, growthplummeted to below 1% during its first three years,that is from 2002–03 to 2004–05. There has been someupturn since then and growth has averaged more than4% in the subsequent two years, with early indicationsthat this is likely to be maintained in 2007–08 also. Thisrevival gives hope that at least some of the causesof recent poor agricultural performance are beingreversed and that the Eleventh Plan target, set at 4%,may actually be attainable.

1.6 The improved performance in the second half ofTenth Plan is a welcome development, but there is noreason for complacency. Not only is the period tooshort to reach firm judgment on trends, the prolongeddeceleration over several years has meant that despitethe improvements, per capita output of cereals, pulses,oilseeds, and also of some major vegetables and fruits(e.g., potatoes and bananas) in 2006–07 remainedbelow 1996–97 levels. Moreover, despite significantimports, food prices flared up in 2006. This was un-like during 2000–05 when, although production waseven lower, prices remained subdued because of lowdomestic demand and depressed world prices. Partof the recent production upturn is clearly price-led,following a marked hardening of world commodityprices and possibly also responding to the fact thatdomestic food demand has responded positively tohigher overall GDP growth and the introduction ofRural Employment Guarantee. However, althoughimportant in the short-run, such price response alonecannot be the basis of sustained agricultural growth

at 4%. The recent trend towards diversion of food cropsfor biofuels in surplus countries means that foodsecurity needs a stronger production response basedon tackling supply side problems in the foodgrainssector.

1.7 The supply side performance of agriculture is af-fected by a large number of factors, several of whichinteract among each other. These factors are the natu-ral resource base (including rainfall), technology, in-frastructure (including irrigation), and the economicenvironment comprising price signals and institutions(Table 1.4). Analysis by the Steering Group for the Elev-enth Plan has identified technological change (usingyield potential of varieties of major crops released bythe National Agricultural Research System [NARS] asa proxy), public investment (including investment onirrigation), and diversification (represented by areaunder fruits and vegetables) as the most importantproximate determinants of growth. The SteeringGroup analysis shows (Table 1.4) that progress on firsttwo of these factors slowed down from early 1990s.However, the negative effect in growth was offset byprivate investment, which was the fourth most impor-tant factor in the analysis, because the terms of trade,which affect profitability and thus private investment,improved during 1990–97. As a result, growth contin-ued to be relatively high in this period. However, termsof trade turned against agriculture from 1999–2000to 2004–05 and reduced profitability of farming quitesharply. This occurred partly because of low domesticfood demand and partly because removal of quota

TABLE 1.3Growth Rate in Output of Various Sub-sectors of Agriculture

(Gross Value of Output at 1999–2000 Price)

Period Cereals Pulses and Fruits and Other All Livestock FisheryOilseeds Vegetables Crops Crops

1951–52 to 1967–68 4.19 2.98 2.67 2.42 3.00 1.02 4.681968–69 to 1980–81 3.43 0.97 4.82 2.98 3.00 3.26 3.081981–82 to 1990–91 3.52 5.41 2.84 1.71 2.97 4.78 5.74 1991–92 to 1996–97 2.36 2.92 6.07 2.18 3.09 4.00 7.05Ninth Plan 1997–98 to 2001–02 1.49 –1.43 4.11 3.82 2.25 3.53 2.63Tenth Plan 2002–03 to 2006–07 1.28 4.29 2.97 3.58 2.46 3.69 3.23of which 2002–03 to 2004–05 –1.27 5.95 0.30 1.57 0.42 3.32 1.772005–06 to 2006–07 3.52 1.61 6.97 6.59 5.53 4.23 5.49

Source: New Series of National Accounts Statistics, Central Statistical Organization, Ministry of Statistics and Programme Implementa-tion, New Delhi.

6 Eleventh Five Year Plan

restrictions under World Trade Organization (WTO)made Indian farm prices to become more aligned withcorresponding international prices at a time whenthese were in decline. Private investment in agricul-ture stagnated as a result, the area cultivated fell, anddiversification slowed down—all leading to decelera-tion. Moreover, public investment remained lowand technology generation became negligible. Cut-backs following the Fifth Pay Commission in 1997 mayhave contributed to the problem as these cutbacksseverely weakened the reach of critical support insti-tutions—notably co-operatives, seed farms, and theextension system.

1.8 An important reason for recent farm distress wasthat after improving steadily from 1980 to 1997, termsof trade turned against agriculture from 1999 and,almost for the first time in post-independent India,farm prices actually fell at the same time that farm pro-duction decelerated. This not only depressed incomes,but also increased farm debt considerably. More gen-erally, farmers are now subject to greater risk becausevariability of world prices is much higher than whatIndian farmers have been used to in the past. Thereis need to evolve a clear policy on how to deal withthis situation and some suggestions are made later inthis chapter.

1.9 In the meantime, commodity futures markets thatcan potentially reduce price variability have grownmassively in crop coverage and trading volume. AtRs 36.76 lakh crore in 2006–07, futures volumes nowfar exceed the volume of actual physical trade in agri-cultural commodities. But direct participation of farm-ers is negligible and price volatility does not appear tohave reduced. A reason why futures markets are notbeing able to perform efficiently could be that thesemarkets are very new and still in a learning phase.Quality specifications, delivery norms, margin, and lotsize of most commodities traded at the bourses makeit difficult for the average farmers to directly partici-pate in exchange trading as hedgers. There is also aneed to look at legal and regulatory regime and modifythese to enable direct farmers’ participation. For ex-ample, the passage of the Warehousing (Developmentand Regulation) Act 2006 makes possible the intro-duction of a regulated system of warehouse receiptswhich, along with investment in rural marketing in-frastructure, can improve the effective reach of futurestrading. Besides the poor direct participation of farm-ers, which is not unusual, available evidence is also thatindirect benefit through reduced spot price volatilityhas been insignificant so far and the cash–future link-age is not very strong. However, futures markets doappear to have better integrated different spot market

TABLE 1.4Trend Growth Rate in Area, Input Use, Credit and Capital Stock in

Agriculture—1980–81 to 2005–06(% per Year)

Period 1980–81 to 1990–91 1990–91 to 1996–97 1996–97 to 2005–06

Technology# 3.3 2.81 0.00Public sector net fixed capital stock 3.86 1.92 1.42*Gross irrigated area 2.28 2.62 0.51*Electricity consumed in agriculture 14.07 9.44 –0.53@Area under fruits and vegetables 5.60 5.60 2.71@Private sector net fixed capital stock 0.56 2.17 1.17*Terms of trade 0.190 0.95 –1.69*Total net fixed capital stock 2.00 2.06 1.28*NPK use 8.17 2.45 2.30Credit supply 3.72 7.51 14.37*Total cropped area 0.43 0.43 –0.10Net sown area –0.08 0.04 –0.22Cropping intensity 0.51 0.39 0.12

Note: # Yield potential of new varieties released of paddy, rapeseed/mustard, groundnut, wheat, maize, and cotton; * Upto 2003–04;@ Upto 2004–05.

Agriculture 7

prices with each other and with world prices. This canbenefit farmers by reducing local monopsony power,but it can also be problematic if the policy objectiveis to insulate domestic prices from full variability ofworld prices. Unless trade policy is broadly predict-able in advance, futures can too quickly transmit in-ternational price shocks leading to controversy andknee-jerk reactions.

1.10 Another important development of market in-stitutions is the rise of modern food retailing whichoffers the prospect of lower marketing costs and re-duced spoilage leading to lower prices for consumersand higher realization for farmers. Modern retailinghas become controversial partly because those involvedin existing trading mechanisms feel their vested inter-ests threatened. However, although there is room formutually beneficial modernization in this area and thiswill undoubtedly evolve, a legitimate area of concernis that if front-end investment outpaces the backwardlinkage with farmers, the immediate outcome may sim-ply be higher imports and lower farm prices. Clearly,efforts must be made to ensure more efficient spot andfutures markets and more rapid development of thebackward farm linkages of retailing.

1.11 An unfortunate trend over the past two decadeshas been that expenditure control efforts followingfiscal shocks such as the Pay Commissions awards haveled to cutbacks in agricultural investment and exten-sion, but not in subsidies. Budgetary subsidies to agri-culture have increased from around 3% of agricultureGDP in 1976–80 to about 7% in 2001–03. During thesame period, public investment in agriculture declinedfrom over 4% of agriculture GDP to 2%. Most of thesubsidies are on fertilizer, power, and irrigation waterand these have actually contributed to the degrada-tion of natural resources. Further, a considerableamount of Plan expenditure on agriculture is not oninvestment but on subsidies not accounted for in theabove list. Simplistic fiscal rules such as protecting Planexpenditures more than non-Plan expenditures addto the problem. For example, although the Plan sharein States’ total expenditure on agricultural and alliedsectors has improved considerably from a low justafter Fifth Pay Commission, much of this representsincrease in Plan subsidies at the cost of essential

staff, particularly in the extension system and theco-operative sector. With hindsight, it appears that thepolicy of restraining new hiring may have been exces-sive, as is evident from the age composition and highvacancies among extension staff and reduced reach ofco-operatives. Even a relatively small percentagereduction in subsidies can finance relatively largeincrease in public investment in crucial areas such assoil amelioration, watershed development, groundwa-ter recharge, surface irrigation, and other infrastruc-ture and can also allow substantial expansion in thereach of critical farm support systems.

1.12 Nonetheless, an important policy gain of recentyears is the turnaround in public investment in lateryears of the Tenth Plan, reversing years of decline.Overall capital formation in the sector is now 12% ofagricultural GDP, which is the highest in 25 years.This must have contributed to the recent upturn ingrowth. But figures in Table 1.5 also imply that Incre-mental Capital Output Ratio has risen from about 2.5to around 4. Unless efficiency of investment is restored,investment would need to increase much further, toabout 16% of agricultural GDP, to achieve the 4% ag-ricultural growth target.

1.13 In light of the above, the Eleventh Plan certainlyneeds to increase public investment further, from 3%of agricultural GDP to about 4%. But it also needsto do much more to ensure that future growth ismore efficient, sustainable, and inclusive. This can beachieved by focusing on the following:

• With availability of land and water fixed, growth inagriculture can be achieved only by increasingproductivity per unit of these scarce natural re-sources through effective use of improved technol-ogy. The research system has so far focused mainlyon breeding varieties that increase the yield poten-tial of individual crops by enabling more intensiveuse of inputs. Although such research did increasepotential yields substantially in the past, it put lessemphasis on efficient and sustainable use of soilnutrients and water, or on identifying location-specific farming systems with proper mix of cropsand livestock, especially for rain-fed areas. Besides,the potential yields of new varieties being released

8 Eleventh Five Year Plan

seem to have plateaued suggesting that the currentsystem is no longer leading to adequate outcomes.This ‘technology fatigue’ has to be countered bychanging research priorities suitably.

• At the same time, frontline trials of various researchdepartments provide clear evidence of large gapsbetween what can be attained at the farmer’s fieldwith adoption of available technology as comparedto what is obtained with existing practices. Exploit-ing this potential must be the main source of yieldgrowth in the Eleventh Plan because overcomingtechnology fatigue will take time. Moreover, sinceyield gaps vary considerably from crop-to-crop andfrom region-to-region, the strategy must enablespecific plans for each agro-climatic region. As Table1.6 shows, constraints vary considerably even by veryaggregate zones. This will also require much stron-ger links between research, extension, and farmers.

• The pressing need to accelerate agriculture growthshould not be at the cost of sustainability ofour natural resource base, which is starkly limited.Deforestation has affected both soils and waterand this is compounded by soil degradation andoverexploitation of groundwater. Besides watersheddevelopment in watersheds where agriculture isimportant, a concerted effort is needed to afforestupper catchments at higher elevations of river ba-sins. In addition to erosion, salinity, and alkalinity,soils are losing soil carbon and micronutrientsdue to irrational and unbalanced fertilizer use

(Table 1.6). This must be addressed urgently sincethis directly affects input use efficiency. The serious-ness of the problem can be seen from the fact thatnearly two-thirds of our farmlands are in some wayeither degraded or sick and only about one-third arein good health. Rapid expansion of groundwater usefor irrigation was a key factor in the relatively rapidgrowth of agriculture between the mid-1960s andlate 1980s. But further expansion should be strictlymonitored, especially in regions where aquiferlevels have dropped causing concern about futuresustainability. Action on the environmental frontcannot wait in face of a possibly looming adverseclimate change due to global warming.

1.14 For growth to be at all inclusive, the agriculturalstrategy must focus on the 85% of farmers who aresmall and marginal, increasingly female, and who findit difficult to access inputs, credit, and extension or tomarket their output. While some of these farmers mayultimately exit from farming, the overwhelmingmajority will continue to remain in the sector and theobjective of inclusiveness requires that their needsare attended to. For example, credit has grown at un-precedented rates (30% per annum) to other sectorsbut not to small and marginal land holders and womenwho lack collateral security. Besides issues such as rightsto land (especially for women), it is now well recog-nized that the poor are best empowered if they func-tion as a group rather than as individuals. Hence there

TABLE 1.5Investment in Agriculture

(Rs in Crore at 1999–2000 Price)

Year GDP from Gross Capital Formation GCF in Agriculture as %Agriculture (GCF) in Agriculture of GDP from Agriculture

Public Sector Private Sector Total Public Sector Private Sector Total

1980–81 to 1984–85 239678 12007 13132 25139 5.0 5.5 10.51985–86 to 1989–90 274034 9601 14370 23971 3.5 5.2 8.71990–91 to 1994–95 325957 7915 19348 27263 2.4 5.9 8.41995–96 to 1999–2000 383330 7724 22631 30354 2.0 5.9 7.92000–01 407176 7155 31872 39027 1.8 7.8 9.62001–02 433475 8746 39468 48215 2.0 9.1 11.12002–03 398206 7962 38861 46823 2.0 9.8 11.82003–04 441360 9376 35457 44833 2.1 8.0 10.22004–05 441183 12273 36835 49108 2.8 8.3 11.12005–06 468013 15006 39899 54905 3.2 8.5 11.72006–07 485939 17749 43013 60762 3.7 8.9 12.5

Source: National Accounts Statistics 2008 (New Series), Central Statistical Organization, Ministry of Statistics and ProgrammeImplementation, New Delhi.

Agriculture 9

is a need to encourage a ‘group approach’ for the poorand for women to reap economies of scale and beeffective farmers. A group approach could also improvethe bargaining power of small cultivators in contractfarming. The few examples where small and marginalfarmers have benefited from contract farming arethose where they have entered into contracts collec-tively rather than individually. In Punjab, MahindraShubhlabh Services Ltd followed this approach formaize farming with a number of safeguards for riskprotection, etc., built in. Again in South India, theUnited Planter’s Association of South India signedcontracts with women’s self-help groups (SHGs) fortea cultivation. One way forward to encourage mar-ginal farmers and women to form groups for purposesof farming would be to shift at least some of the cur-rent subsidies to be available only to groups of suchfarmers rather than to individuals.

TENTH PLAN OUTLAYS AND EXPENDITURE1.15 Against the projected Tenth Plan outlay ofRs 58933 crore on agriculture and allied sectors, theutilization is about the same as outlay in current pricebut likely to be only around 84% at the 2001–02 price.The utilization in the case of irrigation and floodcontrol sector is also of the same order, that is 85%. Inboth the cases, much larger shortfalls in the first two

years of the Plan were made up in subsequent years.Plan outlays in agriculture and allied sectors and inirrigation and flood control for the Centre, States, andunion territories (UTs) are presented in Annexure 1.1.

1.16 The progress of outlay and expenditure duringthe Plan period for the three departments of the UnionMinistry of Agriculture (MoA), namely, the Depart-ment of Agriculture and Co-operation (DAC), theDepartment of Animal Husbandry, Dairying, andFisheries (DAHDF), and the Department of Agricul-tural Research and Education (DARE) is given inTable 1.7.

1.17 As may be seen, a substantial increase in outlaywas provided to the Ministry of Agriculture since 2004–05 taking the Central Government’s share of total planexpenditure on agriculture and allied sectors (Centreand States) from 33% in 2002–03 to 44% in 2006–07.The Ministry has introduced several new programmesduring Tenth Plan aimed at diversification of agricul-ture, strengthening technology validation, demonstra-tion and dissemination, water saving, and developmentof infrastructure. These include:

• The National Horticulture Mission (NHM) ap-proved by the Cabinet Committee on Economic

TABLE 1.6Region-specific Factors Causing Low Productivity

Agro-climatic Region States/Parts of States Region-specific Constraints

Western Himalayan region-I J&K, HP, Uttaranchal Severe soil erosion, degradation due to heavy rainfall/floods anddeforestation, low SRRs, poor road, poor input delivery, inadequatecommunication infrastructure and marketing

Eastern Himalayan region-II Assam, NE States, Sikkim Aluminium toxicity and soil acidity, soil erosion and floods, shiftingcultivation, low SRRs, non-availability of electricity, poor road, poorinput delivery system and communication infrastructure

Lower and middle gangetic West Bengal, Bihar, Flood/water logging, improper drainage, salinity/alkalinity, arsenicplains regions-III and IV Eastern UP contamination, low SRRs, non-availability of electricity, high popula-

tion growth, poor road and communication infrastructure