Eirles Two Limited

73

Eirles Two Limited Directors’ report and financial statements For the year ended 31 December2014 Registered number 327009

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Eirles Two Limited

Eirles Two Limited

Directors’ report andfinancial statements

For the year ended31 December2014

Registered number 327009

Eirles Two Limited

Contents Page

Directors and other information 1 -2

Directors’ report 37

Statement of Directors responsibilities 8

Independent auditor’s report 9— 10

Statement of financial position 11

Statement of comprehensive income 12

Statement of cash flows 13

Statement of changes in equity 14

Notes to the financial statements 15—71

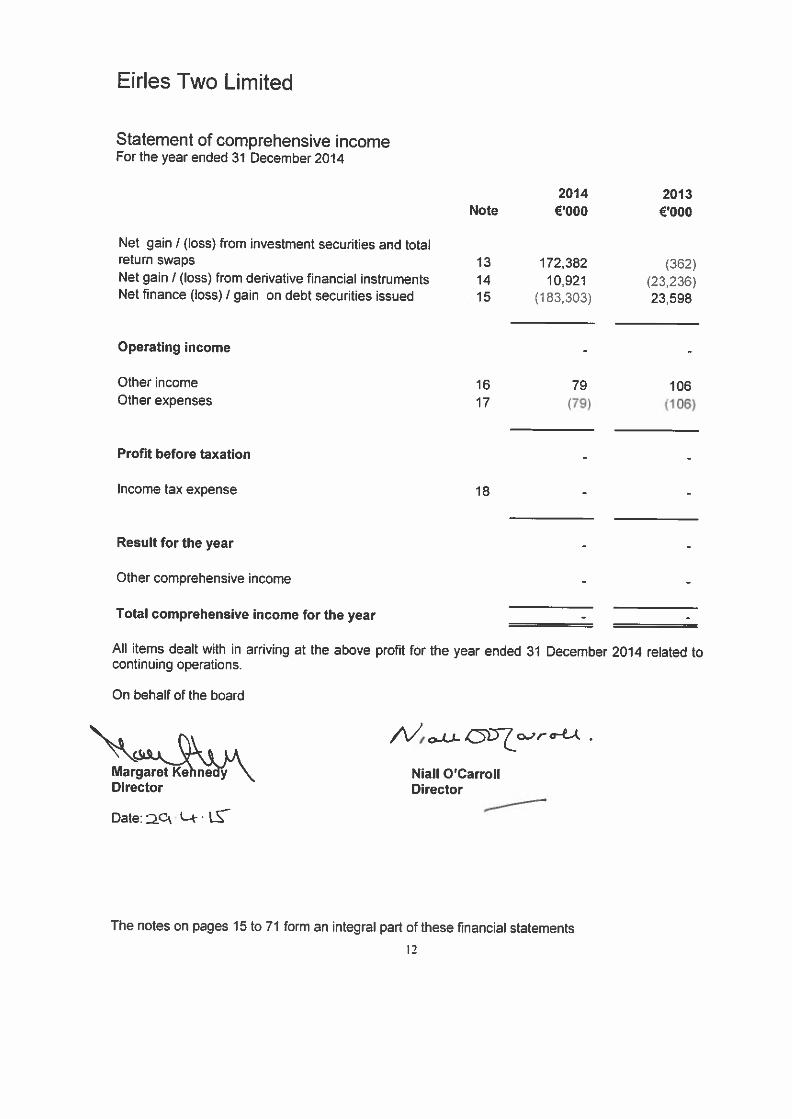

Eirles Two Limited

Directors and other information

Directors Michael Whelan (Irish) (resignation: 27 February 2015)Niall O’Carroll (Irish)Liam Quirke (Irish)Margaret Kennedy (Irish) (appointment: 27 February 2015)

Registered office 6th Floor, Pinnacle 2Eastpoint Business ParkDublin 3Ireland

Trustee The Law Debenture Corporation p.l.c.Fifth Floor100 Wood StreetLondon EC2V 7EXUnited Kingdom

Deutsche Trustee Company LimitedWinchester House1 Great Winchester StreetLondon EC2N 208United Kingdom

Bank of New York MellonRiverside TwoSir John Rogersons QuayGrand Canal DockDublin 2Ireland

Administrator & Deutsche International Corporate Services (Ireland) LimitedCompany Secretary 61h Floor, Pinnacle 2

Eastpoint Business ParkDublin 3Ireland

Independent auditor KPMGChartered Accountants, Statutory Audit Firm1 Harbourmaster PlaceI FSCDublin 1Ireland

Arranger Deutsche Bank AG, London BranchPC Box 4416 BishopsgateLondon EC2P 2ATUnited Kingdom

Eirles Two Limited

Directors and other information

Bankers Deutsche Bank AG, London BranchPC Box 4416 BishopsgateLondon EC2P 2ATUnited Kingdom

Bank of New York MellonRiverside TwoSir John Rogersons QuayGrand canal DockDublin 2Ireland

Listing Agents Deutsche Bank Luxembourg 8k2 Boulevard Konrad AdenauerL-1115Luxembourg

Deutsche Bank AG, London BranchPD Box 4416 BishopsgateLondon EC2P 2ATUnited Kingdom

Solicitor Matheson70 Sir John Rogerson’s QuayDublinIreland

Swap Counterparty Deutsche Bank AG, London BranchPD Box 4416 BishopsgateLondon EC2P 2ATUnited Kingdom

BNP Paribas. London Branch10 Harewood AvenueLondon NW16MUnited Kingdom

7

Eirles Two Limited

Directors’ Report

The Directors present the annual report and audited financial statements of Eirles Two Limited (theCompany”) for the year ended 31 December 2014.

Principal activities, business review and future developmentsThe Eirles Two Limited program was set up in April 2000 to issue multiple series of debt securities,with the rating on each series independent of the other (if applicable). This means that Eirles TwoLimited (the company” or the ‘issuer’) can issue various series of debt securities ranging from AAAto non-rated. This gives the sponsor greater flexibility in what it can finance through this vehicle andit reduces the cost of issuing.

Eirles Two was set up as a segregated multi issuance Special Purpose Entity. Each Series isgoverned by a separate Supplemental Programme Memorandum (5PM). Each Series consists ofan investment in collateral from the proceeds of the issuance of debt securities.

The Programme offers investors the opportunity to invest in a portfolio of investments, the“investment securities and total return swaps”, and alter the interest rate risk and credit risk profile ofthe portfolio through the use of derivative instruments.

The Company has established a EUR 10,000.000,000 Multi-Issuance Programme (the“Programme”) to issue debt securities and/or other secured limited recourse indebtedness. Debtsecurities will be issued in Series (each a ‘Series”) and the terms and conditions of the debtsecurities of each Series will be set out in a Supplemental Programme Memorandum for such Series(each a “Supplemental Programme Memorandum”).

Each series of debt securities will be secured as set out in the terms and conditions of the Debtsecurities including a first fixed charge over certain collateral, primarily in the form of investmentsecurities, total return swaps or cash, as set out in the relevant Supplemental ProgrammeMemorandum (the “Collateral”) and a first fixed charge over funds held by the Agents under theAgency Agreement (each as defined in the terms and conditions of the Debt securities). EachSeries may also be secured by an assignment of the Company’s rights under a Swap Agreementand/or Option Agreement andlor Repurchase Agreement and/or Credit Support Document (each asdefined in the terms and conditions of the debt securities) and any additional security as may bedescribed in the relevant Supplemental Programme Memorandum (together the “MortgagedProperty”). For details of the assets held by the Company at the end of the year. refer to note 7 forthe investment securities and total return swaps.

The credit risk of the investment securities and total return swaps is borne by either the, Company’sswap counterparty (in cases where a default swap transaction has been entered into for thatparticular series) or the Company’s holders of debt securities. Refer to note 4 (b) (i) and 22 (a) forfurther details about how the Company manages credit risk.

For every new issuance of debt securities, Deutsche Bank AG London, as arranger, transfers to theCompany an amount of USD 200 as corporate benefit (income). This income is taxable under Irishlaw at a current rate of 25% and the net amount is retained as the profit for the year.

As arranger, Deutsche Bank AG, London Branch also agreed to reimburse the Company againstany costs, fees, expenses or out-goings incurred. Deutsche Bank AG, London Branch is also theswap coupterparty for all series.

The Company made a net gain on investment securities and total return swap of EUR 172m (2013:net loss EUR 0.36m) for the year and a net gain on derivative financial instruments of EUR llm(2013: net loss EUR 23m).

3

Eirles Two Limited

Directors’ Report (continued)

Principal activities, business review and future developments (continued)Due to the limited recourse nature of the debt securities issued and as the return on those issuedsecurities is directly linked to the performance of the investment securities, total return swaps andderivative financial instruments! the Company made a corresponding net loss of EUR 183m (2013:net gain EUR 24m) on the debt securities in issue for the year.

As at 31 December 2014, the fair value of the Company’s total debt securities issued was EUR1.091m (2Q13: EUR 1.218m). The company had no new series issued (2013: 3 new issues) duringthe year. Refer to Note 7 and 9 for further details.

No series have matured during the year whereas Series 325, 326, 327, 328, 329, 334 and 360 wereredeemed in full.

The following series are currently in issue as at year end date: Series 49, 91, 164, 176, 191, 192,194, 195, 200, 205, 215, 216, 229, 254, 255, 298, 299, 309, 312, 316, 319, 345, 347, 351, 352, 353,354, 355, 357, 361, 363, 364, 365, and 366.

Series 3, 4. 5. 6, 25, 26, 27, 28, 29, 30, 31, 37, 39, 41, 54. 57, 83, 86, 95, 111 (Class B), 124, 130,138, 154, 155. 169 (Class B), 170, 190, 204, 206, 249, 250. 253, 289. 302, 314 and 315 have neverbeen issued.

Results and dividends for the yearThe results for the year are set out on page 12. The Directors do not recommend the payment of adividend for the year under review.

Changes in Directors during the yearThere were no changes in Directors during the year.

Risks and uncertaintiesThe principal risks and uncertainties facing the Company relate to the debt securities issued,investment securities and total return swap and derivative instruments held by the Company. Theseare explained in Notes 4 and 22 of the financial statements along with the risk managementframework in place to deal with these risks.

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associatedwith the Company’s processes, personnel and infrastructure, and from external factors other thancredit, market and liquidity risks such as those arising from legal and regulatory requirements andgenerally accepted standards of corporate behaviour. Operational risks arise from all of theCompany’s operations.

Directors, secretary and their interestsThe Directors and secretary who held office on 31 December 2014 did not hold any shares in theCompany at that date, or during the year. There were no contracts of any significance in relation tothe business of the Company in which the Directors had any interest, as defined in the CompaniesAct 1990. at anytime during the year.

4

Eirles Two Limited

Directors’ Report (continued)

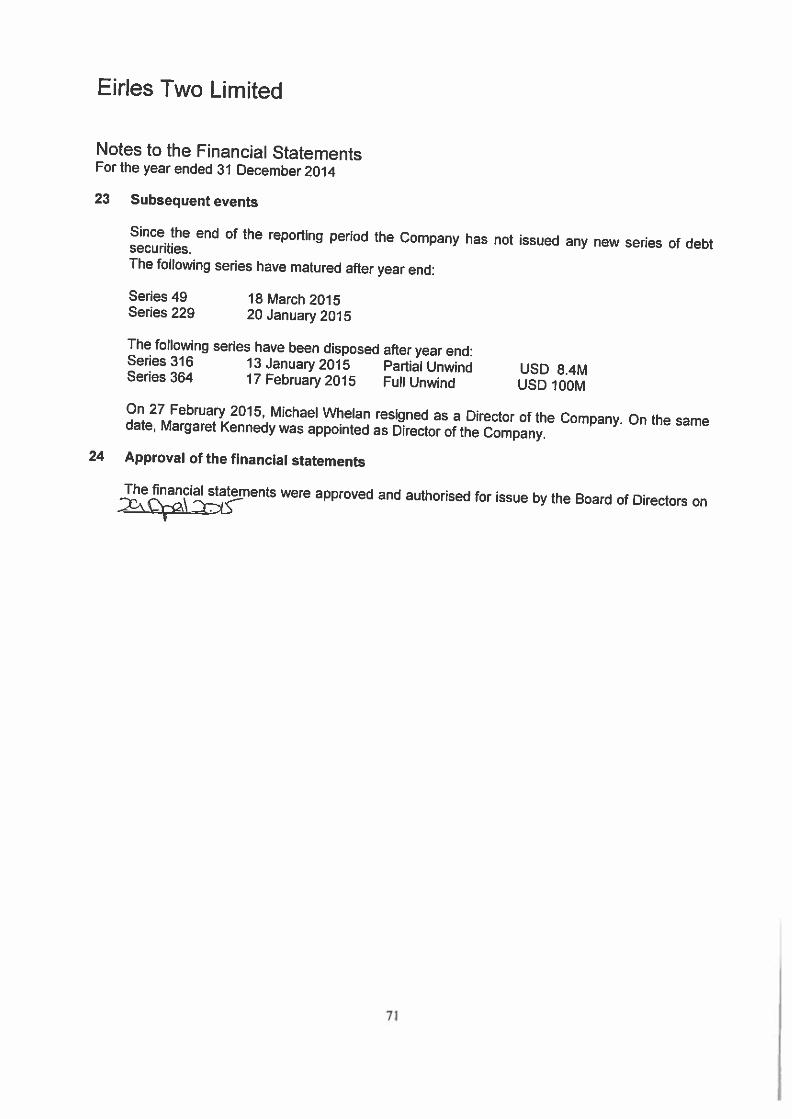

Subsequent eventsSince the end of the reporting period the Company has not issued any new series of debt securities.The following series have matured after year end:Series 49 18 March 2015Series 229 20 January 2015The following series have been disposed after year end:Series 316 13 January 2015 Partial Unwind USD 8.4MSeries 364 17 February 2015 Full Unwind USD lOOMOn 27 February 2015, Michael Whelan resigned as a Director of the Company. On the same date,Margaret Kennedy was appointed as Director of the Company.

Corporate Governance StatementThe Board of Directors (the Board”) is responsible for establishing and maintaining adequateinternal control and risk management systems for the Company in relation to the financial reportingprocess. Such systems are designed to manage rather than eliminate the risk of failure to achievethe Company’s financial reporting objectives and can only provide reasonable and not absoluteassurance against material misstatement or loss.The Board has established processes regarding internal control and risk management systems toensure its effective oversight of the financial reporting process. These include appointing DeutscheInternational Corporate Services (Ireland) (the Administrator’) to maintain the accounting records ofthe Company independently of Eirles Two Limited (the Servicer’) and the Trustee. TheAdministrator is contractually obliged to maintain proper books and records and to that end performsreconciliations of its records to those of the Servicer and the Trustee.The Administrator is also contractually obliged to prepare the annual report including financialstatements for review and approval by the Board. The Board evaluates and discusses significantaccounting and reporting issues as the need arises.From time to time, the Board also examines and evaluates the Administrator’s financial accountingand reporting routines and monitors and evaluates the external auditors’ performance, qualificationsand independence. The Administrator has operating responsibility for internal control in relation tothe financial reporting process and reports to the Board.The Board is responsible for assessing the risk of irregularities whether caused by fraud or error infinancial reporting and ensuring that the processes are in place for the timely identification of internaland external matters with a potential effect on financial reporting. The Board has also put in placeprocesses to identify changes in accounting rules and recommendations and to ensure that thesechanges are accurately reflected in the Company’s financial statements.The Administrator is contractually obliged to design and maintain control structures to manage therisks which the Board judges to be significant for internal control over financial reporting. Thesecontrol structures include segregation of responsibilities and specific control activities aimed atdetecting or preventing the risk of significant deficiencies in financial reporting for every significantaccount in the financial statements and the related notes in the Company’s annual report.The Board delegates the asset valuation function to DB AG, London Branch (the swapcounterpady/originator”) who operates a sophisticated system of controls to ensure appropriatevaluation of the assets except for Series 229 whose valuation is delegated to BNP Paribas. All thevalues for the financial instruments held by the Company have been provided by the swapcounterparty. In our opinion, DB AG, London Branch is the most appropriate and reliable source ofsuch fair values in its capacity as the swap counterparty. We are satisfied that the amounts asstated in the Company’s financial statements represent a reasonable approximation of those values.

)

Eirles Two Limited

Directors’ Report (continued)

Corporate Governance Statement (continued)The Company’s policies and the Board’s instructions with relevance for financial reporting areupdated and communicated via appropriate channels, such as e-mail, correspondence andmeetings to ensure that all financial reporting information requirements are met in a complete andaccurate manner. The Board has an annual process to ensure that appropriate measures are takento consider and address the shortcomings identified and measures recommended by theindependent auditors.

Given the contractual obligations on the Administrator, the Board has concluded that there iscurrently no need for the Company to have a separate internal audit function in order for the Boardto perform effective monitoring and oversight of the internal control and risk management systems ofthe Company in relation to the financial reporting process.

No person has a significant direct or indirect holding of securities in the Company. No person hasany special rights of control over the Company’s share capital.

There are no restrictions on voting rights.

Appointment and replacement of Directors and amendments to the Articles of AssociationWith regard to the appointment and replacement of Directors, the Company is governed by itsArticles of Association and Irish Statute comprising the Companies Acts, 1963 to 2013. The Articlesof Association themselves may be amended by special resolution of the shareholders.

Powers of DirectorsThe board is responsible for managing the business affairs of the Company with the Articles ofAssociation. The Directors may delegate certain functions to the administrator and other partiessubject to the supervision and direction by the Directors. The Directors have delegated the day today administration of the Company to the administrator as stated above.

Transfer of sharesThe instrument of transfer of any share shall be executed by or on behalf of the transferor and, incases where the share is not fully paid, by or on behalf of the transferee. The transferor shall bedeemed to remain the holder of the share until the name of the transferee is entered on the registerin respect thereof. If the Directors refuse to register a transfer, they shall, within two months afterthe date on which the transfer was lodged by the Cornpany, send to the transferee notice of therefusal.

Audit committeeThe sole business of the Company relates to the issuing of asset-backed debt securities. TheCompany invests in investment securities and total return swaps and writes credit default swaps inorder to secure return to its investors. It also enters into certain derivatives to hedge out interest rateand currency risk exposures arising between asset and liability mismatches.

Under Regulation 91(9)(d) of the European Communities (Statutory Audits) (Directive 2006/431EC)Regulations 2010 (the “Regulations”). which were published by the Irish Minister for Enterprise,Trade and Innovation on 25 May 2010, such a Company may avail itself of an exemption from therequirement to establish an audit committee.

6

Eirles Two Limited

Directors’ Report (continued)

Audit committee (continued)Given the contractual obligations of the administrator and the limited recourse nature of thesecurities issued by the Company, the board of Directors has concluded that there is currently noneed for the Company to have a separate audit committee in order for the board to perform effectivemonitoring and oversight of the internal control and risk management systems of the Company inrelation to the financial reporting process. Accordingly, the Company has availed itself of theexemption under Regulation 91(19)(d) of the Regulations.

credit EventDuring the year, credit event arised in Series 91 with reference entity BWIC 2006 1A C2. The creditevent with respect to reference entity to which the notes are credit linked did not result in theoccurrence of any payment under the relevant credit default swap agreement or early redemption inwhole or in part in accordance with the terms of the notes due to sufficient headroom in place.

Accounting recordsThe Directors believe that they have complied with the requirements of Section 202 of theCompanies Act, 1990 with regard to the books of account by engaging a service provider whoemploys accounting personnel with the appropriate expertise and by providing adequate resourcesto the finance function. The books of account of the Company are maintained at 61h Floor, Pinnacle2. Eastpoint Business Park! Dublin 3.

Independent auditorIn accordance with Section 160(2) of the Companies Act, 1963, KPMG, Chartered Accountants,Statutory Audit Firm, have signified their willingness to continue in office.

On behalf of the board

AMargaret Kennedy Niall O’carrol)Director Director

Date:lCtt.4.

7

Eirles Two Limited

Statement of Directors’ responsibilities in respect of Directors’ report and thefinancial statements

The Directors are responsible for preparing the Directors Report and financial statements, inaccordance with applicable law and regulations.

Company law requires the Directors to prepare financial statements for each financial year. Underthat law, the Directors have elected to prepare the financial statements in accordance withInternational Financial Reporting Standards (IFRS&’) as adopted by the European Union. (‘EU”)and applicable law.

The financial statements are required by law to give a true and fair view of the state of affairs of theGroup and Company and of their profit or loss for that period. In preparing the financial statements,the Directors are required to:• select suitable accounting policies and then apply them consistently;• make judgments and estimates that are reasonable and prudent;• state whether they have been prepared in accordance with IFRS5 as adopted by the EU; and• prepare the financial statements on the going concern basis unless it is inappropriate to

presume that the Company will continue in business.

The Directors are also required by the Transparency (Directive 20041109/EC) Regulations 2007 (the“Transparency Regulations”), to include a management report containing a fair review of thebusiness and a description of the principal risks and uncertainties facing the company.

The Directors are responsible for keeping proper books of account that disclose with reasonableaccuracy at any time the financial position of the Company and enable them to ensure that itsfinancial statements comply with the Companies Acts, 1963 to 2013. They have generalresponsibility for taking such steps as are reasonably open to them to safeguard the assets of theCompany and to prevent and detect fraud and other irregularities. The Directors are alsoresponsible for preparing a Directors’ Report that complies with the requirements of the CompaniesAct, 1963 to 2013.

Responsibility Statement, in accordance with the Transparency Regulations

Each of the Directors, whose names and functions are listed on page 1 of these FinancialStatements confirm that, to the best of each person’s knowledge and belief;

• the financial statements, prepared in accordance with lFRSs as adopted by the EU asapplied in accordance with the provisions of the Companies Acts 1963 to 2013, give a trueand fair view of the assets, liabilities and financial position of the Company at 31 December2014 and its result for the year then ended; and

• the Directors’ Report contained in the Annual Report includes a fair review of thedevelopment and performance of the business and the position of the company, togetherwith a description of the principal risks and uncertainties that it faces.

On behalf f the board

fV< a-t1- r 0L’tMargaret Kenne Niall O’CarrollDirector Director

Date:r.

8

KPMGAudit1 Harbou,rrster P!aceIFSCDubtn 1Ire!ad

Independent auditor’s report to the members of Lines Two Limited

We have audited the financial statements (‘‘financial statements”) of Eirles Two Limited for the yearended 31 December 2014 which comprise Statement of Financial Position, Statement ofComprehensive Income, Statement of Cash Flows, Statement of Changes in Equity and the relatednotes. The financial reporting framework that has been applied in their preparation is Irish law andInternational Financial Reporting Standards (WRSs) as adopted by the European Union.

This report is made solely to the Company’s members, as a body, in accordance with section 193 of theCompanies Act 1990. Our audit work has been undertaken so that we might state to the Company’smembers those matters we are required to state to them in an auditor’s report and for no other purpose.To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other thanthe Company and the Company’s members as a body, for our audit work, for this report, or for theopinions we have formed.

Respective responsibilities of directors and auditor

As explained more fully in the Directors’ Responsibilities Statement set out on page 8, the directors areresponsible forthe preparation of the financial statements giving a true and fair view. Our responsibilityis to audit and express an opinion on the financial statements in accordance with Irish law andInternational Standards on Auditing (UK and Ireland). Those standards require us to comply with theFinancial Reporting Council’s Ethical Standards for Auditors.

Scope of the audit of the financial statements

An audit involves obtaining evidence about the amounts and disclosures in the financial statementssufficient to give reasonable assurance that the financial statements are free from material misstatement,whether caused by fraud or error. This includes an assessment of: whether the accounting policies areappropriate to the company circumstances and have been consistently applied and adequately disclosed;the reasonableness of significant accounting estimates made by the directors; and the overallpresentation of the financial statements. In addition, we read all the financial and non-financialinformation in the annual report to identify material inconsistencies with the audited financialstatements and to identify any information that is apparently materially incorrect based on, or materiallyinconsistent with, the knowledge acquired by us in the course of performing the audit. If we becomeaware of any apparent material misstatements or inconsistencies we consider the implications for ourreport.

Opinion on financial statements

In our opinion:

• the financial statements give a true and fair view, in accordance with WRSs as adopted by the EU,of the state of the Company’s affairs as at 31 December 2014 and of its result for the year thenended; and

• the financial statements have been properly prepared in accordance with the Companies Acts 1963to 2013.

9

KPMG. on Iris, p ar(narsh! and a member fern 0f jh KP.lG nerv.nnkrn,a,naI

Cze,a,n.,rKP.’2 Interanc’aIp a S., as 5rfy

Independent auditor’s report to the members of Eirles Two Limited (continued)

Matters on which we are required to report by the Companies Acts 1963 to 2013

We have obtained all the information and explanations which we consider necessary for the purposesof our audit.

The financial statements are in agreement with the books of account and, in our opinion, proper booksof account have been kept by the Company.

In our opinion the information given in the directors’ report is consistent with the financial statementsand the description in the Corporate Governance Statement of the main features of the internal controland risk management systems in relation to the process for preparing the financial statements isconsistent with the financial statements.

The net assets of the Company, as stated in the Statement of Financial Position are more than half ofthe amount of its called-up share capital and, in our opinion, on that basis there did not exist at 31December 2014 a financial situation which under Section 40(l) of the Companies (Amendment) Act,1983 would require the convening of an extraordinary general meeting of the Company.

Matters on which we are required to report by exception

We have nothing to report in respect of the following:Under the Companies Acts 1963 to 2013 which require us to report to you if, in our opinion thedisclosures of directors’ remuneration and transactions specified by law are not made.

Ailbhe Kennyfor and on behalf ofKPMGChartered Accountants, Statutory Audit FirmI Harbourmaster PlaceJFSCDublin IIreland

Date: 29 April 2015

10

Eirles Two Limited

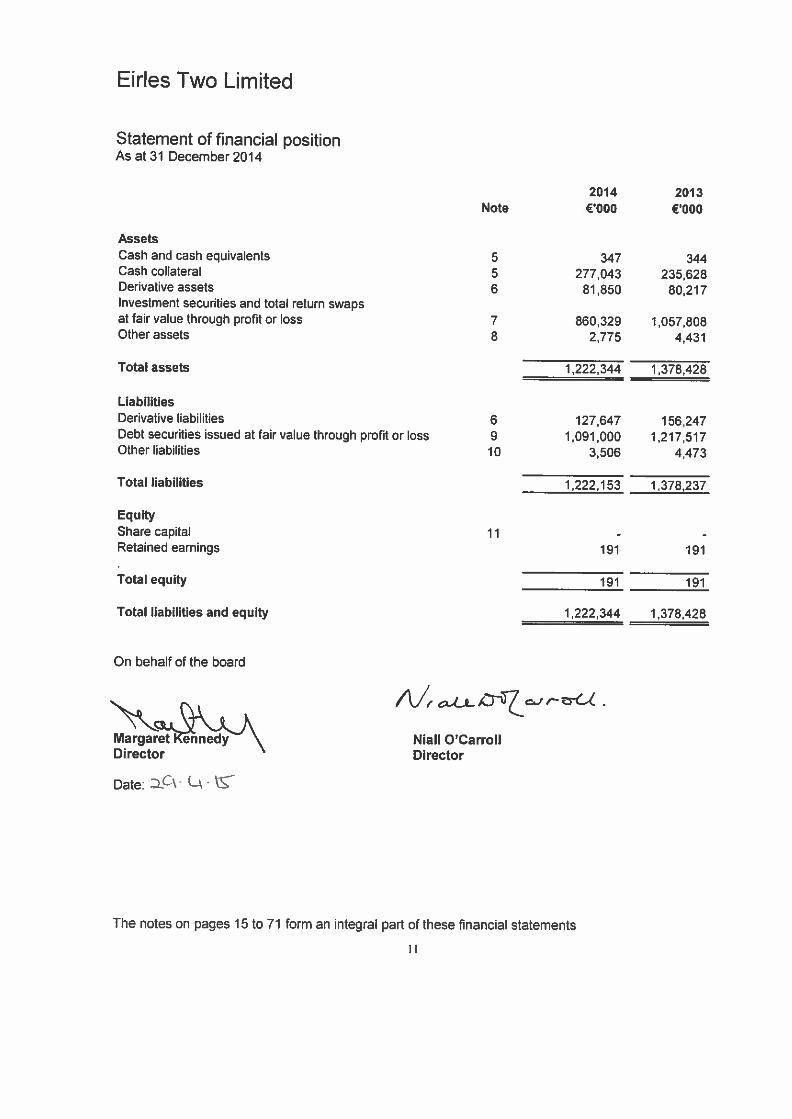

Statement of financial positionAs at 31 December 2014

Cash and cash equivalentsCash collateralDerivative assetsInvestment securities and total return swapsat fair value through profit or lossOther assets

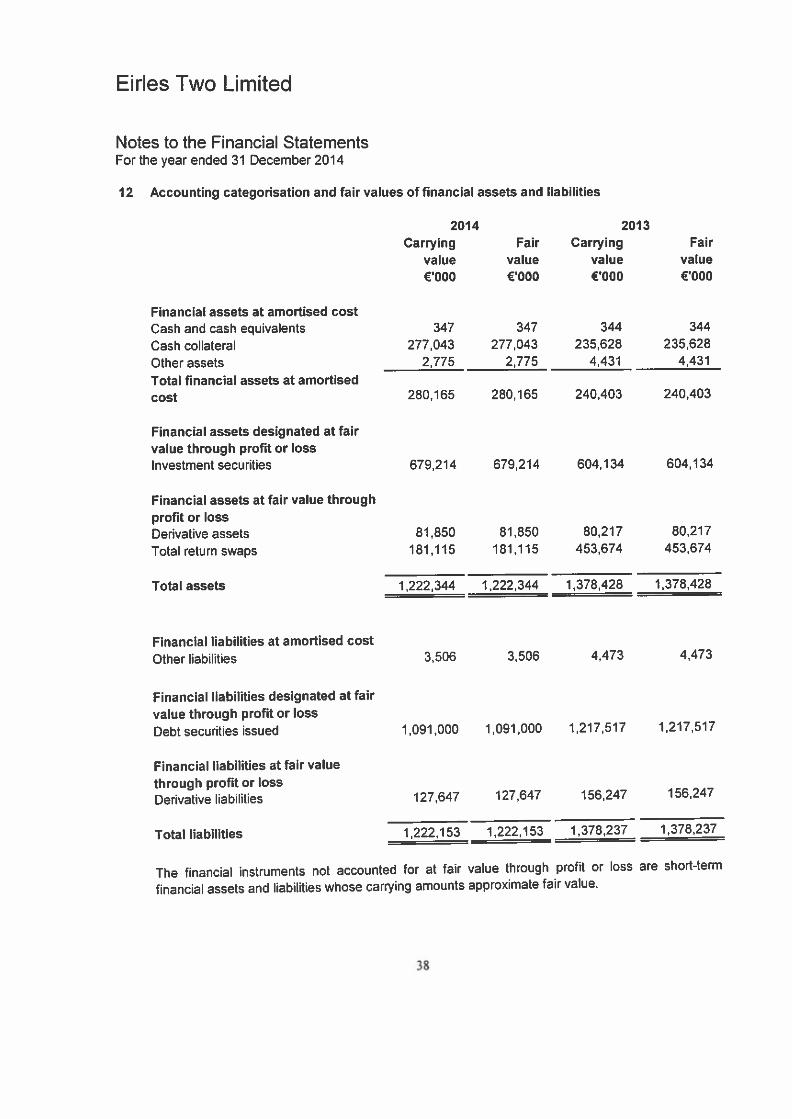

Total assets

LiabilitiesDerivative liabilitiesDebt securities issued at fair value through profit or lossOther liabilities

Total liabilities

q U ityShare capitalRetained earnings

Total equity

Total liabilities and equity

On behalf of the board

AMargaret Kennedy

Date: C\ L

5 347 344277,043 235,628

81,850 80,21756

7 860,329 1,057,8082,775 4,4318

1.222,344 1 378,428

127,647 156,2471,091,000 1,217,517

3,506 4,473

1,222,153 1,378,237

191 191

191 191

1,222,344 1,378,428

Al, 0tCc’rtZ.

Niall o’carrollDirector

The notes on pages 15 to 71 form an integral part of these financial statements

Assets

2014 2013Note €‘OOO €‘OOO

6910

11

Eirles Two Limited

Statement of comprehensive incomeFor the year ended 31 December 2014

2014 2013Note €000 €000

Net gain / (loss) from investment securities and totalreturn swaps 13 172382 (362)Net gain / (loss) from derivative financial instruments 14 10,921 (23,236)Net finance (loss) / gain on debt securities issued 15 (183,303) 23,598

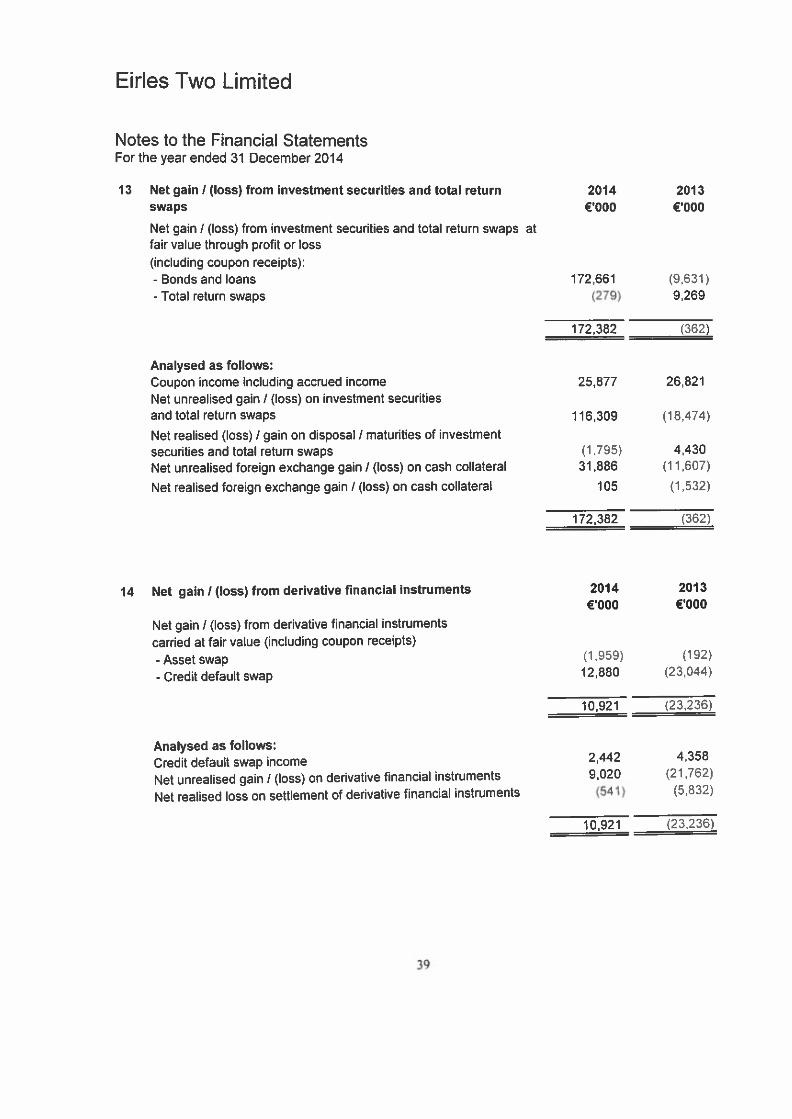

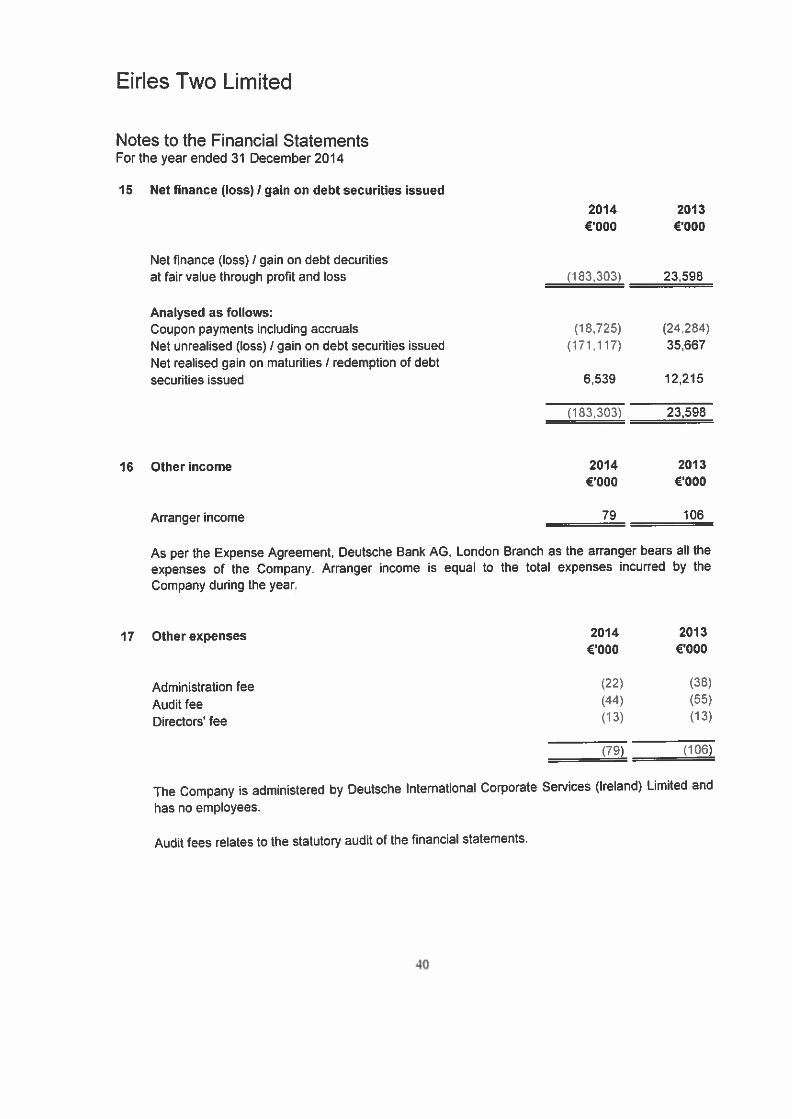

Operating income- -

Other income 16 79 106Otherexpenses 17 (79) (106)

Profit before taxation- -

Income tax expense 18 - -

Resultforthe year- -

Other comprehensive income- -

Total comprehensive income for the year- -

All items dealt with in arriving at the above profit for the year ended 31 December 2014 related tocontinuing operations.

On behalf of the board

CD(ora-LA..

Margaret Ke ne y Niall O’CarrollDirector Director

Date: 2Cs’Lk’

The notes on pages 15 to 71 form an integral part of these financial statements

2

Eirles Two Limited

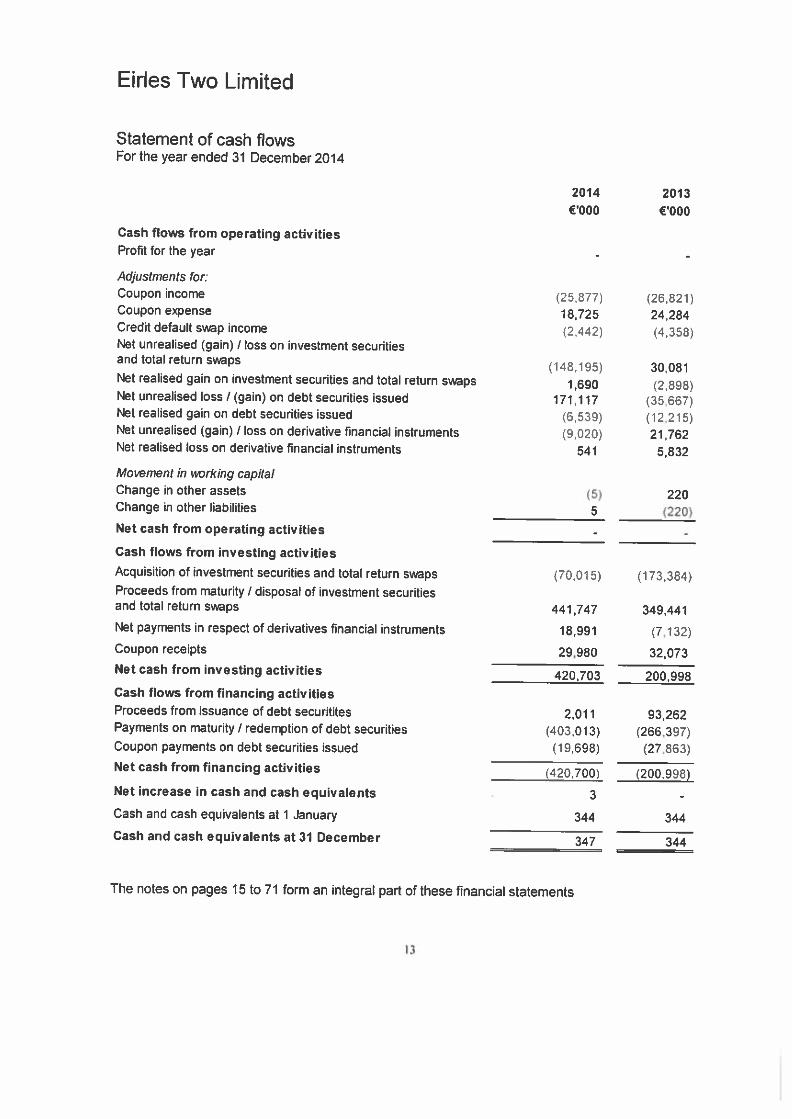

Statement of cash flowsFor the year ended 31 December 2014

Cash flows from operating activitiesProfit for the year

Adjustments forCoupon incomeCoupon expenseCredit default swap incomeNet unrealised (gain) / loss on investment securitiesand total return swaps

Net realised gain on investment securities and total return swapsNet unrealised loss! (gain) on debt securities issuedNet realised gain on debt securities issuedNet unrealised (gain) / loss on derivative financial instrumentsNet realised loss on derivative financial instruments

Movement in working capitalChange in other assetsChange in other liabilities 5Net cash from operating activities

Cash flows from investing activities

2013

(‘000

Acquisition of investment securities and total return swapsProceeds from maturity / disposal of investment securitiesand total return swaps

Net payments in respect of derivatives financial instruments

Coupon receipts

Net cash from investing activities

Cash flows from financing activitiesProceeds from issuance of debt securititesPayments on maturity / redemption of debt securitiesCoupon payments on debt securities issued

Net cash from financing activities

Net increase in cash and cash equivalents

Cash and cash equivalents at 1 January

Cash and cash equivalents at 31 December

(70,015) (173,384)

441747 349,441

18,991 (7,132)

29,980 32073

420,703 200,998

(420700)

3

344

347

93,262(266,397)

(27,863)

(200.998)

344

344

The notes on pages 15 to 71 form an integral part of these financial statements

2014

(‘000

(25.877)18725(2,442)

(148.195)

1,690171.117

(6,539)(9,020)

541

(26,821)24,284(4,358)

30,081

(2.898)(35667)(12,215)21,762

5,832

220(220)

(5)

2,011(403,013)(19,698)

13

Eirles Two Limited

Statement of Changes in EquityFor the year ended 31 December 2014

Share Retainedcapital earnings Total€000 €000 €000

Balance as at 31 December 2012- 191 191

Profit forthe year-2013- - -

Other comprehensive income- - -

Total comprehensive income for the year

Balance as at 31 December 2013 - 191 191

Profit for the year -2014- - -

Other comprehensive income- - -

Total comprehensive income for the year - - -

Balance as at 31 December 2014- 191 191

The notes on pages 15 to 71 form an integral part of these financial statements

14

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

General information

Eirles Two Limited (the ‘Company”) was incorporated on 14 April 2000 in the Republic ofIreland with registered number 327009. The registered office of the Company is at 6th Floor,Pinnacle 2, Eastpoint Business Park, Dublin 3.

The Company is a special purpose vehicle that has been established to issue debt securitiesunder a EUR 10,000,000,000 Multi-issuance note programme.

The program offers investors the opportunity to invest in a portfolio of investments, the“investment securities,” and alter the interest rate risk and credit risk profile of the investmentportfolio through the use of derivative instruments.

The company has no direct employees. The financial statements were authorised for issue bythe Directors on 29 April, 2015.

2 Basis of preparation

(a) Statement of complianceThe financial statements have been prepared in accordance with International FinancialReporting Standards and its interpretations as adopted by the EU (“IFRS”) and inaccordance with the Companies Acts 1963 to 2013.

The accounting policies set out below have been applied in preparing the financialstatements for the year ended 31 December 2014, the comparative information, for 2013presented in these financial statements has been prepared on a consistent basis.

These financial statements have been prepared on a going concern basis.

(b) Changes in accounting policies

There were no changes in accounting policies which has a financial impact on theCompany’s financial statements during the year

15

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(c) New standards, amendments or interpretations

(i) Effective for annual periods beginning on 1 January 2014

A number of new standards and interpretations are effective for annual periodsbeginning on or after 1 January 2014. Of these, the following were of relevance tothe company and were considered for adoption:

The amendments to lAS 32 Financial Instruments: Presentation (OffsettingFinancial Assets and Financial Liabilities) clarify the offsetting criteria in lAS 32 byrevising the guidance on when an entity currently has a legally enforceable right toset-off and when gross settlement is considered to be equivalent to net settlement.Based on the new requirements! the Company assessed that at this time norevisions to its previous approach to offsetting of financial assets and financialliabilities arises in the statement of financial position.

IFRS 10 Consolidated Financial Statements establishes a new control-basedmodel for consolidation that replaces the existing requirements of both lAS 27 andSIC-12 Consolidation - Special Purpose Entities. Under the new standard aninvestor controls an investee when (i) it has exposure to variable returns from thatinvestee (H) it has the power over relevant activities of the investee that affectthose returns and (iii) there is a link between that power and those variable returns.The standard includes specific guidance on the question of whether an entity isacting as an agent or principal in its involvement with an investee. Theassessment of control is based on all facts and circumstances and is reassessed ifthere is an indication that there are changes in those facts and circumstances.

The Directors have assessed that IFRS 10 did not have an impact on theCompany as it is a stand-alone entity with no interests that could potentially qualifyas a subsidiary interest. Therefore, based on the new requirements, the Companyassessed that at this there was no implications for the financial statements. As theCompany has no subsidiaries, the IFRS 10 Amendment on Investment Entitiesdoes not apply.

IFRS 12 Disclosure of Interests in Other Entities sets out more comprehensivedisclosures relating to the nature, risks and financial effects of interests insubsidiaries, associates, joint arrangements and unconsolidated structuredentities. Interests are widely defined as contractual and non-contractualinvolvement that exposes an entity to variability of returns from the performance ofthe other entity or operation.

The Directors have assessed that IFRS 12 did not have any impact on theCompany as the Company does not hold any Interest in Other Entities.

16

EirIes Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(c) New standards, amendments or interpretations (continuation)

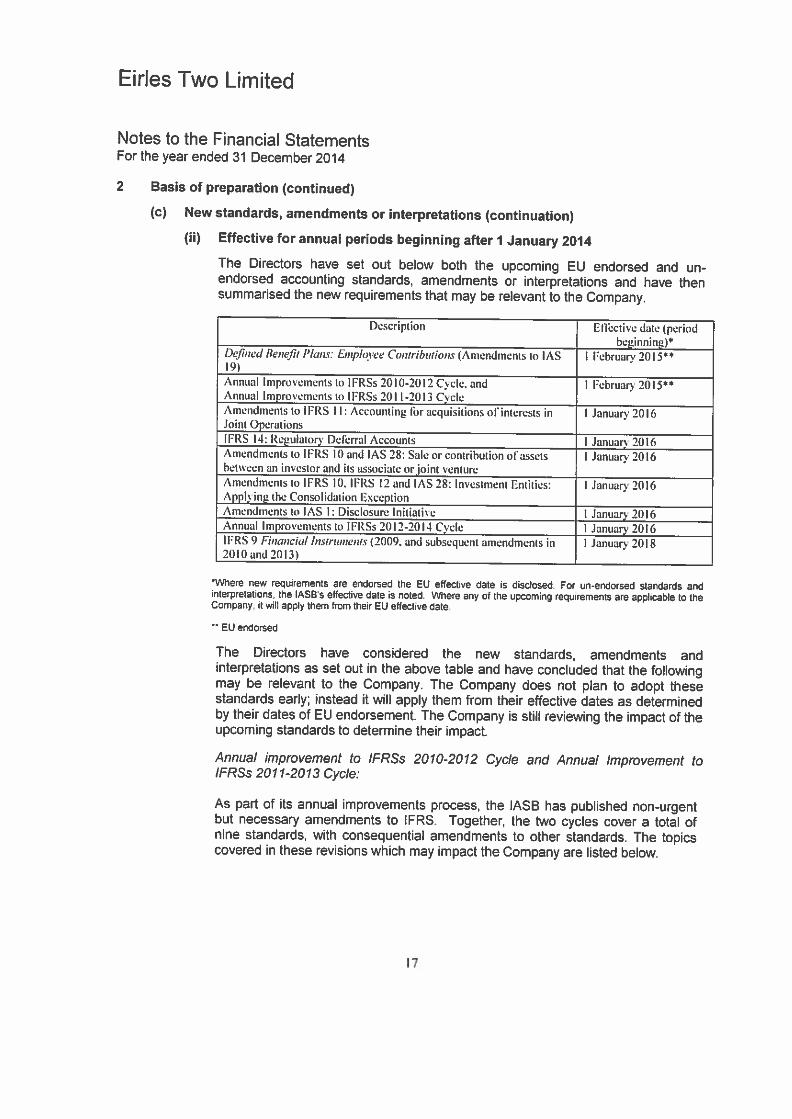

(ii) Effective for annual periods beginning after 1 January 2014

The Directors have set out below both the upcoming EU endorsed and Un-endorsed accounting standards, amendments or interpretations and have thensummarised the new requirements that may be relevant to the Company.

Description Etibctive date (periodL beginning)

Defined Bencjit PIanv Enipiotte Co,nrthzqions (Amendments to lAS I Februan 20 15’H9)

Annual Improvements to lFRSs 2010-2012 Cycle, and I Februan 2015”Annual_Improvements_to_IFRSs_201_1-2013_CeleAmendments to IFRS II: AccounLing for acquisitions olinterests in I January 2016Joint_OperationsIFRS 14: Regulatory Delërral Accounts I January 2016Amendments to IFRS 10 and lAS 28: Sale or contribution oI’assets 1 January 2016hetneen an in\ estor and its associate or joint ventureAmendments to IFRS 10. IFRS 12 and lAS 28: lnvt-sLment Entities: I Januan 2016Applying the Consolidation ExceptionAmendments to lAS I: Disclosure Initiative I January 2016Annual Improvements to IFRSs 2012-2014 Cycle I January 2016IFRS 9 Financial Instruments (2009. and subsequent amendments in I January 20182010 and 2013)

‘Mere new requirements are endorsed the EU effective date is disc!osed For un-encorsed standards andinterpretabors the IASBs effective date is noted. 1ere any of the upcoming requremens are applicable to theCompany. it wi’ apply them from their EU efftve date** EU endorsed

The Directors have considered the new standards, amendments andinterpretations as set out in the above table and have concluded that the followingmay be relevant to the Company. The company does not plan to adopt thesestandards early; instead it will apply them from their effective dates as determinedby their dates of EU endorsement. The Company is still reviewing the impact of theupcoming standards to determine their impact.

Annual improvement to IFASs 2010-2012 Cycle and Annual Improvement toIFRSs 2011-2013 Cycle:

As part of its annual improvements process, the IASB has published non-urgentbut necessary amendments to IFRS. Together, the two cycles cover a total ofnine standards, with consequential amendments to other standards. The topicscovered in these revisions which may impact the company are listed below.

17

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(c) New standards and interpretations (continued)

(i) Effective for annual periods beginning after 1 January 2014 (continued)

Annual Improvements to IFRSS 2010-2012 Cycle:

lAS 24 Related Party Disclosure: This improvement clarifies that an entityproviding key management personnel (KMP) services to the reporting entity or tothe parent of the reporting entity is a related party of the reporting entity. Thereporting entity is not required to disclose the compensation paid or payable bythe management entity to the management entity’s employees or directors.Instead the reporting entity discloses the amounts incurred for the provision of keymanagement personnel services that are provided by the separate managemententity.

Amendments to lAS 1: Disclosure Initiative: The amendments to lAS 1Presentation of Financial statements address some of the concerns expressedabout existing presentation and disclosure requirements and ensure that theentities are able to use judgement where applying lAS 1. The amendments relateto the following; materiality, order of the notes, subtotals, accounting policies anddisaggregation. The impact of these amendments are currently underconsideration by the Company.

IFRS 9 Financial Instruments (2014)

IFRS 9 Financial Instruments issued on 24 July 2014 is the IASB’s replacement oflAS 39’s Financial Instruments: Recognition and Measurement. The Standardincludes requirements for recognition and measurement. impairment,derecognition and general hedge accounting.

Recognition and measurement

Financial assets

1. Investments in debt instruments

The recognition and measurement of financial assets under IFRS 9 is built ona single classification and measurement approach for financial assets thatreflects the business model in which they are managed and their cashflowcharacteristics. There are three measurement methods available for financialassets (a) amortised cost1 (b) fair value through other comprehensive incomeand (c) fair value through profit or loss. The existing lAS 39 categories held-to-maturity, loans and receivables, and available-for-sale are removed.

18

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(c) New standards and interpretations (continued)

(i) Effective for annual periods beginning after 1 January 2014 (continued)

IFRS 9 Financial Instruments (2014) (continued)

Recognition and measurement (continued)

Financial assets (continued)

1. Investments in debt instruments (continued)

(a) Amortised cost

In order for a financial asset to be measured at amortised cost the followingtwo criteria are required;

(i) The asset is held to collect its contractual cash flows; and(U) The asset’s contractual cash flows represent ‘solely payments of

principal and interest’ (SPPI”)

The assessment as to whether cash flows meet this test is made in thecurrency in which the financial asset is denominated. Financial assetsincluded within this category are initially recognised at fair value andsubsequently measured at amoftised cost.

(b) Fair value through other comprehensive income (“FVOCI)

A financial asset is measured at FVDCI if both the following criteria are met

i. The objective of the business model is achieved both by collectingcontractual cash flows and selling financial assets; and

U. The asset’s contractual cash flows represent SPPI.

Financial assets included within the FVOCI category are initiallyrecognised and subsequently measured at fair value. Movements in thecarrying amount should be recognised through other comprehensiveincome (“OCI”), except for the recognition of impairment gains or losses,interest revenue and foreign exchange gains and losses which arerecognised in profit and loss.

(c) Fair value through profit or loss (“FVPL’)

FVPL is the residual category. Financial assets should be classified asFVPL if they do not mee the criteria of FVOCI or amortised cost with anychanges in fair value recorded through profit orloss.

19

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(c) New standards and interpretations (continued)

(i) Effective for annual periods beginning after 1 January 2014 (continued)

IFRS 9 Financial Instruments (2014) (continued)

Recognition and measurement (continued)

Financial assets (continued)

2. Investments in equity instruments

Investments in equity instruments are always measured at fair value. Equityinstruments are those that meet the definition of “equity” from the perspectiveof the issuer as defined in lAS 32: Financial Instruments: Presentation. Equityinstruments that are held for trading are required to be classified at FVPL. Forall other equities, management has the ability to make an irrevocable electionon initial recognition, on an instrument-by-instrument basis, to presentchanges in fair value in DCI rather than profit or loss.

Financial liabilities

The recognition of financial liabilities under IFRS 9 carries forward the treatment oflAS 39, except that IFRS 9 introduces, with some limited exceptions, newrequirements for the accounting for and presentation of changes in the fair value ofan entity’s own debt when the entity has chosen to measure the debt at fair valueusing the fair value option. IFRS 9 requires that the changes in the fair value of anentity’s own credit risk should be recognised in CCI rather than through profit orloss. Amounts in CCI relating to own credit are not reclassified to profit or losseven when the liability is derecognised and the amounts are realised. However,the new standard does allow transfers within equity.

Impairment

IFRS 9 requires an entity to recognise expected credit losses on financial assetsmeasured at amortised cost and to update the amount of expected credit lossesrecognised at each reporting date to reflect changes in the credit risk of financialinstruments. This model is forward looking and it eliminates the threshold for therecognition of expected credit losses, so that it is no longer necessary for a triggerevent to have occurred before credit losses are recognised. Consequently moretimely information is provided about expected credit losses. Specifically, IFRS 9generally requires an entity to base its measurement of expected credit losses onreasonable and supportable information that is available without undue cost oreffort, and that includes historical, current and forecast information. In addition,the same impairment model is applied to all financial assets subject to impairmentaccounting.

20

Eiries Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(c) New standards and interpretations (continued)

(I) Effective for annual periods beginning after 1 January 2014 (continued)

IFRS 9 Financial Instruments (2014) (continued)

Hedge accountThg

IFRS 9 introduces a substantial revision to hedge accounting requirements whichwill allow entities better reflect their risk management activities in their financialstatements. The revision was issued in a response to concerns of preparers offinancial statements about the difficulty of appropriately reflecting riskmanagement activities in financial statements. The changes also addressconcerns raised by users of the financial statements about the difficulty ofunderstanding hedge accounting.

The version of IFRS 9 issued in 2014 supersedes all previous versions and ismandatorily effective for periods beginning on or after 1 January 2018 with earlyadoption permitted. For a limited period, previous versions of IFRS 9 may beadopted early if not already done so provided the relevant date of initialapplication is before 1 February 2015. In addition, the own credit changes can beearly applied in isolation without otherwise changing the accounting for financialinstruments. For EU Companies, endorsement by the EU is required, therebylimiting the ability to early adopt this standard.

Given the nature of the Company’s operations, this standard is not expected tohave a material impact on the Company’s financial statements as the Companyadopts fair value accounting in relation to all its significant financial instruments.

(d) Basis of measurement

The financial statements are prepared on the historical cost basis except for thefollowing:• Derivative financial instruments are measured at fair value;• Investment securities and total return swaps designated at fair value through profit

or loss are measured at fair value; and• Debt securities issued designated at fair value through profit or loss are measured at

fair value.

The methods used to measure fair values are discussed further in note 3(a).

21

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

2 Basis of preparation (continued)

(e) Functional and presentation currency

The financial statements are presented in Euro! which is the Company’s functionalcurrency. Functional currency is the currency of the primary economic environment inwhich the entity operates. The issued share capital of the Company is denominated inEuro and the debt securities issued are also primarily denominated in Euro. Thedirectors of the Company believe that Euro most faithfully represents the economiceffects of the underlying transactions! events and conditions.

Except as otherwise indicated, all financial information presented in Euro has beenrounded to the nearest thousand.

(f) Use of estimates and judgements

The preparation of the financial statements in conformity with IFRSs requiresmanagement to make judgments, estimates and assumptions that may affect theapplication of accounting policies and the reported amounts of assets, liabilities, incomeand expenses. The estimates and associated assumptions are based on historicalexperience and various other factors that are believed to be reasonable under thecircumstances, the results of which form the basis of making the judgements aboutcarrying values of assets and liabilities that are not readily apparent from other sources.Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions toaccounting estimates are recognised in the period in which the estimates are revisedand in any future periods affected.

Information about significant areas of estimation, uncertainty and critical judgments inapplying accounting policies that have the most significant effect on the amountsrecognised in the financial statement are described in Notes 22 (e).

(g) Operating segments

The Company has applied IFRS 8 Operating Segments which puts emphasis on the“management approach” to reporting on operating segments.

The Company is engaged as one segment. It involves the repackaging of bonds andother debt instruments, on behalf of investors, which are bought from the market andsubsequently secuhtised to avail of potential market opportunities and risk-returnasymmetries.

Refer to Note 22(a) for further information on the assets.

77

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

3 Significant accounting policies

The accounting policies set out below have been applied consistently to all periods presentedin these financial statements.

(a) Financial instruments

The financial instruments held by the company at fair value through profit or lossincludes the follo’Mng:• Investment securities and total return swaps (TRS);• Derivative financial instruments; and• Debt securities issued.

CategorisationA financial asset or financial liability at fair value through profit or loss is a financial assetor liability that is classified as held-for-trading or designated as at fair value through profitor loss. Other financial instruments are carried at amortised cost.

Derivative financial instruments are carried at fair value through profit or loss. TheCompany has designated the investment securities and total return swaps as well asdebt securities issued at fair value through profit or loss.

Designation at fair value through profit or loss upon initial recognitionThe Company has designated financial assets and liabilities at fair value through profit orloss when either:• The assets or liabilities are managed, evaluated and reported internally on a fair

value basis;• The designation eliminates or significantly reduces an accounting mismatch which

would otherwise arise; or• The asset or liability contains an embedded derivative that significantly modifies

the cash flows that would otherwise be required under the contract.

Investment securities and total return swapsInvestment securities consist of bonds held by the Company and these are designatedas at fair value through profit or loss. Total return swaps consist of credit linked collateralwhich enable the Company to gain exposure and benefit from a reference amount andare carried at fair value through profit or loss. These do not qualify as derivative financialinstruments under lAS 39 Financial Instruments: Recognition and Measurement as thesedo not have minimal initial net investment and therefore are classified as financial assetsat fair value through profit or loss. Investment securities include corporate bonds,government bonds, loans, mortgage bonds and receivable under total return swaps.

23

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

3 Significant accounting policies (continued)

(a) Financial instruments (continued)

Derivative financial instrumentsDerivative financial instruments held for risk management purposes include derivativeassets and liabilities that are used to economically hedge the derivatives at each seriesfrom interest rate or market fluctuations affecting the relevant collateral assets. Suchderivatives are not formally designated into a qualifying hedging relationship andtherefore all changes in their fair value are recognised in the statement ofcomprehensive income. The Company also write credit default swap derivatives thatcreate economic returns for the Company; such derivatives are carried at fair valuethrough profit or loss.

Debt securities issuedThe debt securities issued are initially measured at fair value and are designated asliabilities at fair value through profit or loss when they either eliminate or significantlyreduce an accounting mismatch or contain an embedded derivative that significantlymodifies the cash flows that would otherwise be required under the contract.

Financial assets and liabilities that are not at fair value through profit or lossFinancial assets that are not at fair value through profit or loss and are not quoted in anactive market include cash at bank, deposits with credit institutions and other assets andare categorised as loans and receivables for measurement purposes.

Financial liabilities that are not at fair value through profit or loss include accruedexpenses and other payables. These are categorised as financial liabilities measured atamortised cost, adjusted for initial direct costs in the case of instruments to be carriedsubsequently at amortised costs for measurement purposes.

Recognition and measurementThe Company initially recognises all financial assets and liabilities at fair value on the

trade date, which is the date on which the Company becomes a party to the contractual

provisions of the instruments. From trade date! any gains and losses arising from

changes in fair value of the financial assets or financial liabilities at fair value through

profit or loss are recorded in the statement of comprehensive income.

Financial assets and financial liabilities not categorised as at fair value through profit or

loss are subsequently measured at amortised cost.

DerecognitionThe Company derecognises a financial asset when the contractual rights to the cash

flows from the asset expire, or it transfers the rights to receive the contractual cash flows

on the financial asset in a transaction in which substantially all the risks and rewards of

ownership of the financial asset are transferred. Any interest in transferred financial

assets that is created or retained by the Company is recognised as a separate asset or

liability. The Company derecognises a financial liability when its contractual obligations

are discharged or cancelled or expire.

24

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

3 Significant accounting policies (continued)

(a) Financial instruments (continued)

OffsettingFinancial assets and liabilities are offset and the net amount presented in the statementof financial position when, and only when, the Company has a legal right to offset theamounts and intends either to settle on a net basis or to realise the asset and settle theliability simultaneously. Income and expenses are presented on a net basis only whenpermitted by the accounting standards.

Fair value measurement principlesFair value is the price that would be received to sell an asset or paid to transfer a liabilityin an orderly transaction between market participants at the measurement date of theprincipal or which the Company has access at that time. The fair value of a liabilityreflects its non-performance risk. The determination of fair values of financial assets andfinancial liabilities are based on quoted bid market prices or dealer price quotations forfinancial instruments traded in active markets, where these are available and market isregarded as active if transaction for the asset or liability take place with sufficientfrequency and volume to provide pricing information on an ongoing basis. The Companymeasures instruments quoted in an active market at bid price. For all other financialinstruments fair value is determined by using valuation techniques. Valuation techniquesinclude net present value techniques, the discounted cash flow method, comparison tosimilar instruments for which market observable prices exist, and valuation models. TheCompany uses widely recognised valuation models for determining the fair value ofcommon and simpler financial instruments like call options, interest rate and currencyswaps.

For more complex instruments, the Company uses proprietary models, which usually aredeveloped from recognised valuation models. Some or all of the inputs into these modelsmay not be market observable, and are derived from market prices or rates or areestimated based on assumptions.

(b) Financial liability and equity

The financial instruments issued by the Company are treated as equity (i.e. forming part

of shareholder’s funds) only to the extent that they meet the following two conditions:

• they include no contractual obligations upon the Company to deliver cash or other

financial assets or to exchange financial assets or financial liabilities with another

party under conditions that are potentially unfavourable to the Company; and

• where the instrument will or may be settled in the Company’s own equity

instruments, it is either a non-derivative that includes no obligation to deliver a

variable number of the Company’s own equity instruments or is a derivative that

will be settled by the Company exchanging a fixed amount of cash or other

financial assets for a fixed number of its own equity instruments.

25

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

3 Significant accounting policies (continued)

(b) Financial liability and equity (continued)

To the extent that this definition is not met, the proceeds of issue are classified as afinancial liability.

Finance payments associated with financial liabilities are dealt with as part of theongoing remeasurement of debt securities to fair value. Any payments associated withfinancial instruments that are classified in equity are distributions from the net incomeattributable to equity holders and are recorded directly in equity.

(c) Operating segments

The Company has appUed IFRS 8 Operating Segments which puts emphasis on the“management approach” to reporting on operating segments.

The Company is engaged as one segment. It involves the repackaging of bonds andother debt instruments, on behalf of investors, which are bought from the market andsubsequently securitised to avail of potential market opportunities and risk-returnasymmetries.

Refer to Note 22(a) concentration risk for the geographical segmental information of theassets.

(d) Cash and cash collateral

Cash and cash collateral consist of cash held on deposit which can be terminated within

3 months provided all parties agree to the transaction. These are subject to insignificant

risk of changes in their fair value.

Cash collateral is held as security for issuance of certain debt securities.

Cash and cash collateral are carried at amortised cost in the statement of financial

position.

(e) Foreign currency transaction

Transactions in foreign currencies are translated to the functional currency of the

Company at exchange rates at the dates of the transactions. Monetary assets and

liabilities denominated in foreign currencies at the reporting date are retranslated to the

functional currency at the exchange rate at that date. Non monetary assets and liabilities

denominated in foreign currencies that are measured at fair value are retranslated to the

functional currency at the exchange rate at the date that the fair value was determined.

Foreign currency differences arising on retranslation are recognised through profit or

loss and are included under net gain from investment securities and total return swaps.

derivatives or debt securities issued, as appropriate.

26

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

3 Significant accounting policies (continued)

(f) Net gain I (loss) from investment securities and total return swaps

Net gain I (loss) from investment securities and total return swaps relates to investmentsin bonds and total return swaps, and includes realised income (including couponreceipts), and unrealised fair value changes including foreign exchange differences.

(g) Net gain I (loss) from derivative financial instruments

Net gain / (loss) from derivative financial instruments relates to the fair value movementson derivatives held by the Company and includes realised and unrealised fair valuechanges, settlements and foreign exchange differences.

(h) Net finance (loss) I gain on debt securities issued

Finance expense on debt securities issued relates to debt securities issued and includesfinancing costs (including coupon payments) realised and unrealised fair value changesand foreign exchange differences.

(i) Taxation

Income tax expense comprises current and deferred tax. Income tax expense isrecognised through profit or loss, in other comprehensive income or directly in equityconsistent with the accounting for the item to which it is related.

current tax is the expected tax payable on the taxable income for the year, using taxrates applicable to the Company’s activities enacted or substantively enacted at thereporting date, and adjustment to tax payable in respect of previous years.

Deferred tax is provided for temporary differences arising between the carrying amounts

of assets and liabilities for financial reporting purposes and the amounts used for

taxation purposes. Deferred tax is not recognised for temporary differences arising on

the initial recognition of assets or liabilities in a transaction that is not a business

combination and that affects neither accounting nor taxable profit. Deferred tax is

measured at the tax rates that are expected to be applied to the temporary differences

when they reverse, based on the laws that have been enacted or substantively enacted

by the reporting date.

A deferred tax asset is recognised only to the extent that it is probable that future taxable

profits will be available against which the asset can be utilised. Deferred tax assets are

reviewed at each reporting date and are reduced to the extent that it is no longer

probable that the related tax benefit will be realised.

(j) Other income and expenses

All other income and expenses are accounted for on an accruals basis.

27

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

3 Significant accounting policies (continued)

(k) Share capital and dividends

Share capital is issued in Euro and is classified as equity. Dividends are recognised as aliability in the period in which they are approved.

4 Financial risk management

(a) Introduction and overview

The Eirles Two Limited programme was set up in April 2000 to issue multiple series ofnotes, with the rating on each series independent of the other (if applicable). Thismeans that Eirles Two Limited (the ‘Company’ or the “issuer”) can issue various seriesof notes ranging from AAA to non-rated. This gives the sponsor greater flexibility in whatit can finance through this vehicle and it reduces issue costs.

Eirles Two Limited was set up as a segregated multi issuance Special Purpose Entity(SPE). The Programme offers investors the opportunity to invest in a portfolio ofinvestments and total retum swaps, the ‘investment securities and total return swap”,and alter the interest rate risk and credit risk profile of the portfolio through the use ofderivative instruments.

This ensures that if one series defaults, the holders of that series are unable to reachother assets of the issuer, which might otherwise have resulted in the issuer’sbankruptcy and the default of the other series of debt securities. The segregation criteriainclude the following:

• The Company is a bankruptcy remote SPE. organised in Ireland.• The Company issues separate series of debt obligations.• Assets relating to any particular series of debt securities are held separately and

apart from the assets relating to any other series.Any swap transaction entered into by the issuer for a series is separate from any

other swap transaction for any other series.• For each series of debt securities, only the trustees are entitled to exercise

remedies on behalf of the debt security holders.• Each series of issued debt securities is reviewed by a recognised rating agency

prior to issuance regardless of whether it is to be rated or not.

Each Series is governed by a separate Supplemental Programme Memorandum (SPM).

Each Series consists of an investment in collateral from the proceeds of the issuance of

debt securities.

28

Fines Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

4 Financial risk management (continued)

(a) Introduction and overview (continued)

The Company has entered into Asset Swap Agreements with Deutsche Bank AG,London Branch. The net proceeds from the issue of the debt securities are paid to theSwap Counterparty to purchase the portfolio of investments securities plus any interestaccrued thereon on behalf of the Company. The credit quality details of the investmentsecurities and total return swap held by the Company are disclosed in note 4(b)(i).During the term of the Asset Swap, the Company pays to the Swap Counterpartyamounts equal to the interest received in respect of the collateral, and on the maturitydate of the collateral will deliver the portfolio or the proceeds of its redemption to theSwap Counterparty. The Company also entered into a number of Credit Default SwapAgreements with Deutsche Bank AG, London Branch. In exchange for the receipt ofpremium income for the relevant series, the Company has sold credit protection on anumber of reference entities.

The Swap Counterparty delivers the collateral to the account of the Company and paysthe Company amounts equal to the interest payable under the debt securities, and if theswap agreement has not terminated prior to the maturity date of the respective notes, asum equal to the redemption amount payable on the debt securities.

The debt securities issued are recorded at fair value which equates to the net proceedsreceived in Euro and are subsequently carried at fair value through profit or loss. Theultimate amount repaid to the holders of these debt securities will depend on theproceeds from the investment securities or total return swaps and any payment theSwap counterparty is obliged to make under the terms of the swap agreement

(b) Risk management framework

The Board of Directors has overall responsibility for the establishment and oversight of the

Company’s risk management framework.

The risk profile of the Company is such that market, credit, liquidity and other risks relating

to the investment securities and total return swap as well as derivative financial

instruments are borne fully by the holders of debt securities issued.

The Company has exposure to the following risks from its use of financial instruments:

(i) Credit risk;(U) Liquidity risk; and(Ni) Market risk.

This note presents information about the Company’s exposure to each of the above risks,

the Company’s objectives, policies and processes for measuring and managing risk and

the Company’s management of capital. Further quantitative disclosures are included in

Note 22 to these financial statements.

The Company does not have any externally imposed capital requirements.

29

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

4 Financial risk management (continued)

(b) Risk management framework (continued)

(i) Credit risk

Credit risk is the risk of the financial loss to the Company if the counterparty to afinancial instrument fails to meet its contractual obligations, and arises principallyfrom the Company’s credit linked securities (investments and total return swaps)and also from the derivative contract that the Company has entered into.

The Company limits its exposure to credit risk by only investing in bonds and totalreturn swaps and only with counterparties that have a credit rating defined in thedocumentation of the relevant series.

The risk of default on these assets and on the underlying reference entities is borneby the swap counterparty and/or the holders of the debt securities as designated inthe priority of payments described in the 5PM of the relevant series.

The credit quality of the Company’s investment securities has been disclosed inNote 22 (a).

The credit risk relating to underlying reference entities as shown in Note 22(d) arisesprincipally from the investment assets and total return swaps which the Companyholds which are credit-hnked to a portfolio of underlying reference entities. Anydefault or “credit events” in the underlying portfolio of reference entities may triggera reduction in the nominal amounts of the debt instrument which the Company holdsdepending on the loss amounts, as well as, other terms and conditions on the debt.Because of the limited recourse nature of the debt securities issued by theCompany, any such losses would ultimately be borne by either the Company’sSwap Counterparty and/or the Company’s holders of debt securities for thatparticular series.

Secondly, the Company has also sold credit protection to Swap Counterparties inreturn for a premium. The corresponding debt securities on which the creditprotection has been sold are credit-linked to the credit quality of the underlyingportfolio of reference entities. Therefore any default or “credit events” in theunderlying portfolio of reference entities might require a specific amount of thecollateral i.e. certain investment securities held by the Company to be delivered tothe Swap Counterparty that has purchased the credit protection from the Company.However, due to the limited recourse nature of the debt securities issued by theCompany any such payments in respect of the credit default swap, i.e. theunderlying portfolio of reference entities would ultimately be borne by the holders ofdebt securities by way of corresponding reduction in the nominal amounts of those

debt securities issued depending on the terms and conditions attached to debtsecurities issued.

30

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

4 Financial risk management (continued)

(b) Risk management framework (continued)

(i) Credit risk (continued)

Refer to Note 6 “Derivative financial instruments” for further details.

The linking of the Company’s issued debt securities to the underlying portfolio ofreference entities is achieved by entering into credit default swap agreements withSwap Counterparties. The credit default swap is a leveraged arrangement.

The aggregate reference portfolio notional amounts are usually substantially higherthan the notional amounts of the credit default swaps and the nominal amounts ofthe debt securities issued. This leverage increases the risk of loss to the Companyand, therefore, to the holders of debt securities.

Refer to the table in Note 22(e) “Fair Values” for further details.

(ii) Liquidity risk

Liquidity risk is the risk that the Company will encounter difficulties in meetingobligations arising from its financial liabilities that are settled by delivering cash oranother financial asset, or that such obligation will have to be settled in a mannerdisadvantage to the Company.

The Company’s obligation to the holders of debt securities of a particular series islimited to the net proceeds upon realisation of the collateral of that series, i.e.investment securities, total return swaps and derivatives. Should the net proceedsbe insufficient to make all payments due in respect of a particular series of Notes,the other assets of the Company are not contractually required to be made availableto meet payment and the deficit is instead borne by the holders of debt securitiesand/or the Swap Counterparties according to established priority of payment.

The timing and amount of proceeds from realising the collateral of each series issubject to market conditions.

There were no liquidity issues experienced by the Company or the SwapCounterparties in respect to meeting its obligations to holders of debt securitiesissued or to swap counterparties. The Company or the Swap Counterparties did notdefault on any of its contractual commitments during the year.

31

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

4 Financial risk management (continued)

(a) Risk management framework (continued)

(iii) Market risk

Market risk is the risk that changes in market prices, such as foreign exchangerates, interest rates and other price risk will affect the company’s income or thevalue of its holdings of financial instruments and receivables under total returnswaps.

The objective of the market risk management is to manage and control market riskexposures within acceptable parameters while optimising the return on risk.

Foreign exchange risk and interest rate risk are economically hedged with the use ofcurrency swap agreements and the asset swap agreements, respectively. Crosscurrency swap is incorporated in the asset swap.

32

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

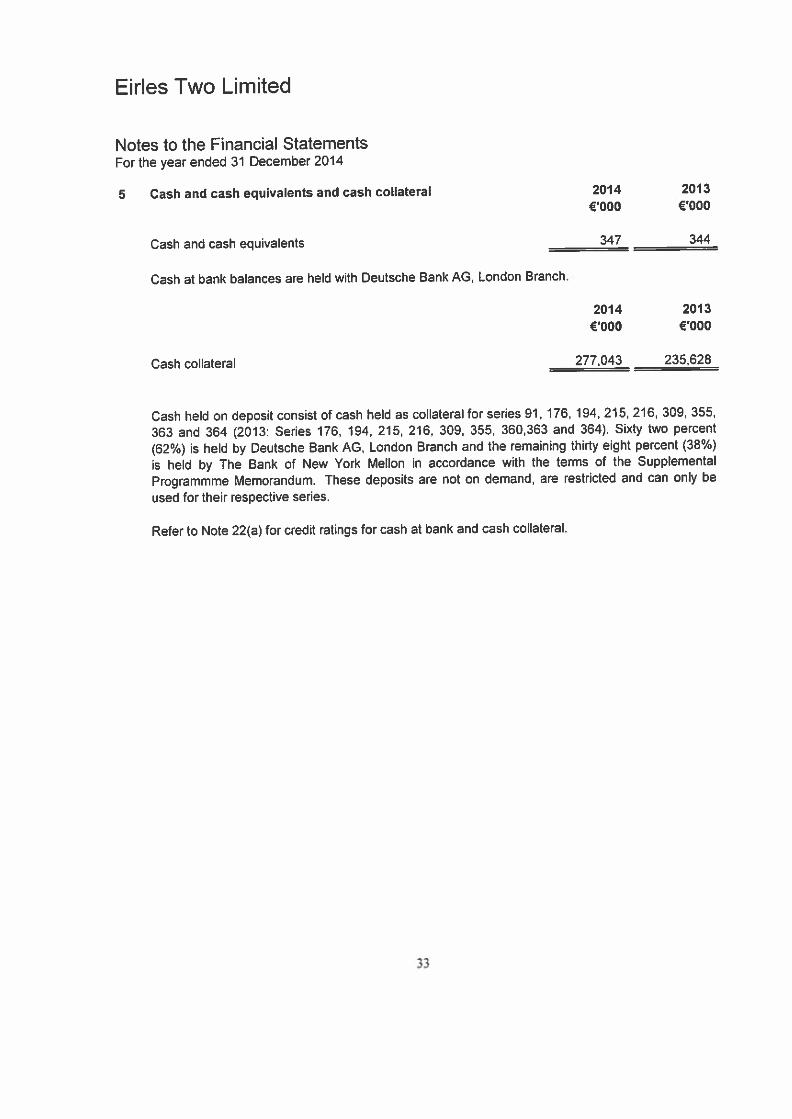

5 Cash and cash equivalents and cash collateral 2014 2013

€000 €000

Cash and cash equivalents 347 344

Cash at bank balances are held with Deutsche Bank AG, London Branch.

2014 2013

€000 €000

Cash collateral 277043 235,628

Cash held on deposit consist of cash held as collateral for series 91, 176, 194, 215, 216, 309, 355,

363 and 364 (2013: Series 176, 194, 215, 216. 309, 355, 360,363 and 364). Sixty two percent

(62%) is held by Deutsche Bank AG, London Branch and the remaining thirty eight percent (38%)

is held by The Bank of New York Mellon in accordance with the terms of the Supplemental

Programmme Memorandum. These deposits are not on demand, are resthcted and can only be

used for their respective series.

Refer to Note 22(a) for credit ratings for cash at bank and cash collateral.

3)

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

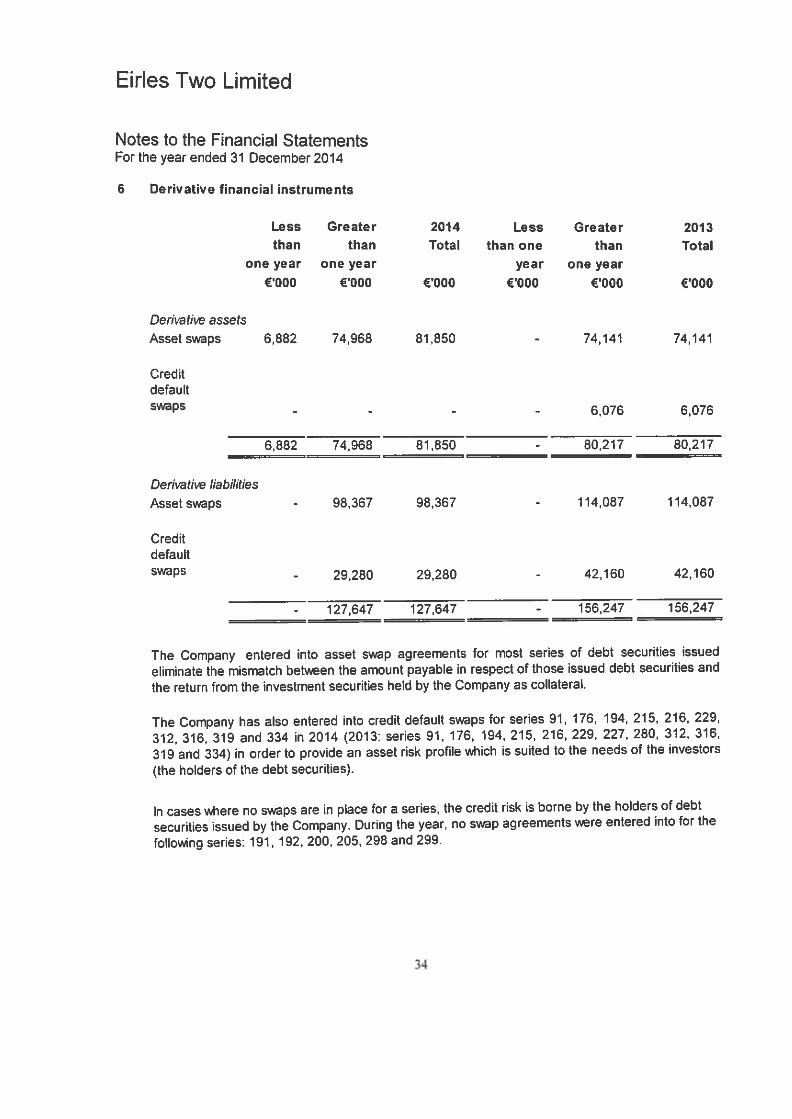

6 Derivative financial instruments

Less Greater 2014 Less Greater 2013than than Total than one than Total

one year one year year one year

(‘000 (‘000 (‘000 (‘000 (‘000 (‘000

Derivative assets

Asset swaps 6,882 74,968 81,850 - 74,141 74,141

CreditdefaultSWaps - - -

- 6,076 6,076

6,882 74,968 81,850 - 80,217 80,217

Derivative liabilities

Asset swaps - 98,367 98.367 - 114,087 114,087

Creditdefaultswaps

- 29,280 29,280 - 42,160 42,160

- 127,647 127,647 - 156,247 156,247

The Company entered into asset swap agreements for most series of debt securities issued

eliminate the mismatch between the amount payable in respect of those issued debt securities and

the return from the investment securities held by the Company as collateral.

The Company has also entered into credit default swaps for series 91, 176, 194, 215, 216, 229,

312, 316, 319 and 334 in 2014 (2013: series 91, 176, 194, 215, 216, 229, 227, 280, 312, 316,

319 and 334) in order to provide an asset risk profile which is suited to the needs of the investors

(the holders of the debt securities).

In cases where no swaps are in place for a series, the credit risk is borne by the holders of debt

securities issued by the Company. During the year, no swap agreements were entered into for the

follo’Mng series: 191, 192, 200, 205, 298 and 299.

34

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

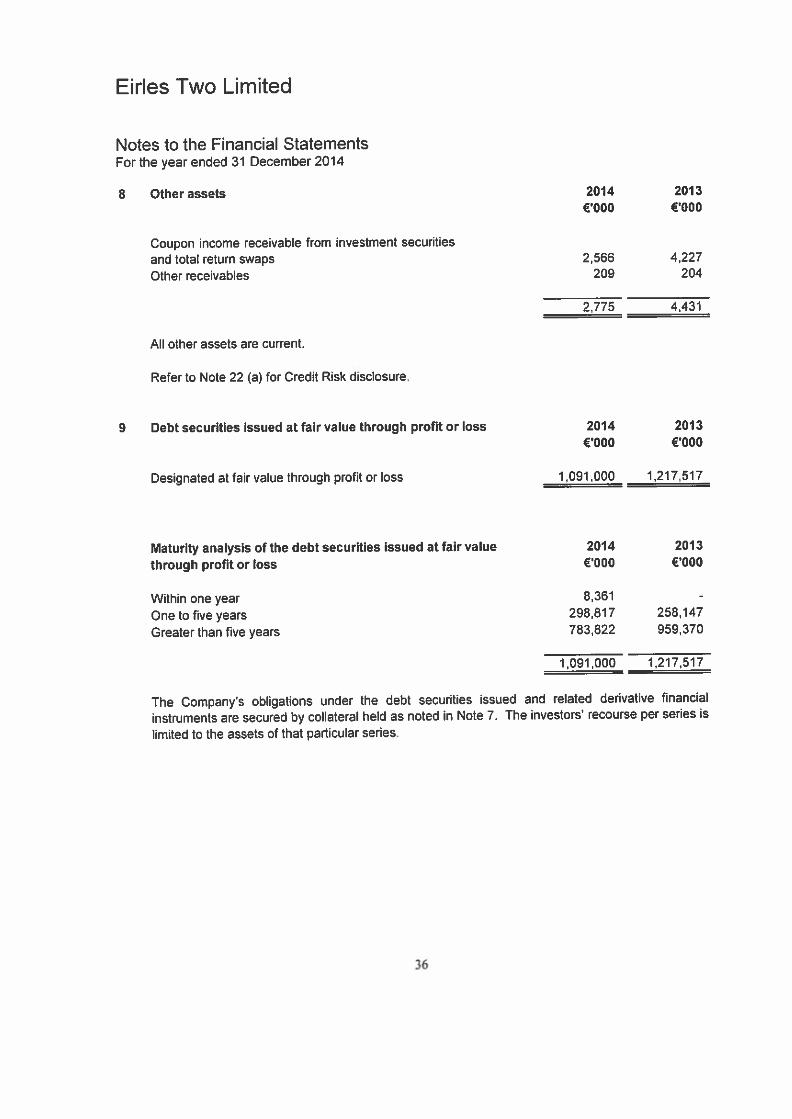

8 Other assets 2014 2013€000 €‘OOD

coupon income receivable from investment securities

and total return swaps 2566 4227

Other receivables 209 204

2)775 4,431

All other assets are current.

Refer to Note 22 (a) for Credit Risk disclosure.

9 Debt securities issued at fair value through profit or loss 2014 2013€000 €000

Designated at fair value through profit or loss 1,091,000 1,217,517

Maturity analysis of the debt securities issued at fair value 2014 2013

through profit or loss €000 €000

Within one year 8,361 -

One to five years 298,817 258,147

Greater than five years 783,822 959,370

1,091,000 1,217,517

The Company’s obligations under the debt securities issued and related derivative financial

instruments are secured by collateral held as noted in Note 7. The investors’ recourse per series is

limited to the assets of that particular series,

36

Eirles Two Limited

Notes to the Financial StatementsFor the year ended 31 December 2014

7 Investment securities and total return swaps at fair valuethrough profitor loss 2014 2013

€000 €000

Designated at fair value through profit or lossBonds 679,214 604,134

Total return swap 181,115 453674

860,329 1,057,808

Maturity analysis of investment securities and total return swaps

at fair value through profit or loss

Within one year 2,112 17,393

One to five years 335,060 296,916

Greater than five years 523,157 743,499

860,329 1,057,808

The carrying value of all of the above assets of the Company represents their maximum exposure

to credit risk. The credit risk is eventually transferred to the Swap Counterparty or the holders of

debt securities through the credit default swap. The Company is then exposed to credit risk in

respect of the CDS Swap Counterpafty. The investment securities and total return swaps are held

as collateral for debt securities issued by the Company.

The Company has issued certain passthrough series of notes which do not meet the recognition

criteria under lAS 39 - Financial Instruments: Recognition and Measurement since inception. As at

31 December 2014, the passthrough series in issue were 191, 192, 200, 205, 298 and 299. All the

series as mentioned as at 31 December 2014 were not recognised in the financial statements for

the year ended 31 December 2013.

Total return swapsUnder these arrangements the proceeds from the issuance of debt securities are held on deposit

with the Swap Counterparty under the swap agreement. The deposit is synthetically linked to the

credit performance of a portfolio of reference entities through a credit default swap. The Swap

Counterparty provides a return that replicates the return due to the holders of the debt securities

and also reimburses certain the expenses related to the series.

In the event that any of these reference entities default, a notice is served to the Company. The

receivable under total return swap is reduced by an amount equal to the amount in the default as

determined by the calculation agent with reference to the defaulted reference entity and the

Company’s obligation under the debt securities is also reduced by the same amount as per the

terms of the SPM.