Effect of Money on Nigeria's Economic Growth

51

MONETARY POLICY IN NIGERIA – THE IMPACT OF MONETARY POLICY ON NIGERIA’S ECONOMIC GROWTH Monetary Policy in Nigeria - Developing countries growth policies are better delivered as full packages since fiscal and monetary policies are inextricable, except in terms of the instruments and implementing authorities. However, monetary policy appears more potent in correcting short term macroeconomic maladjustments because of the frequency in applying and altering the policy tools, relative ease of its decision process and the sheer nature of the sector which propagates its effect to the real economy – the financial system. The main objective of monetary policy in Nigeria is to ensure price and monetary stability. This is mainly achieved by causing savers to avail investors of surplus funds for investment through appropriate interest rate structures; stemming wide fluctuations in the exchange rate of the naira: proper supervision of banks and related institutions to ensure financial sector soundness; maintenance efficient payments system; applying deliberate polices to expand the scope of the

Transcript of Effect of Money on Nigeria's Economic Growth

MONETARY POLICY IN NIGERIA – THE IMPACT OF MONETARY

POLICY ON NIGERIA’S ECONOMIC GROWTH

Monetary Policy in Nigeria - Developing countries

growth policies are better delivered as full packages

since fiscal and monetary policies are inextricable,

except in terms of the instruments and implementing

authorities. However, monetary policy appears more

potent in correcting short term macroeconomic

maladjustments because of the frequency in applying and

altering the policy tools, relative ease of its

decision process and the sheer nature of the sector

which propagates its effect to the real economy – the

financial system.

The main objective of monetary policy in Nigeria is to ensure

price and monetary stability. This is mainly achieved

by causing savers to avail investors of surplus funds

for investment through appropriate interest rate

structures; stemming wide fluctuations in the exchange

rate of the naira: proper supervision of banks and

related institutions to ensure financial sector

soundness; maintenance efficient payments system;

applying deliberate polices to expand the scope of the

financial system so that interior economics, which a re

largely informal, are financially included. Financial

inclusion is

Particularly important in the sense that the larger it

is larger is the interest rate sensitivity of

production and aggregate demand and so the more

effective monetary policy is.

The economy of Nigeria is faced with unemployment low

investment and high inflation rate and these factors

mitigate against the growth of the economy. Thus

adopting monetary policy in manipulating the

fluctuations experienced so far in the economy, CBN

undertakes both concretionary and expansionary measures

in tackling the problems observed above. Therefore, the

need is felt to research on the impact of monetary

policy on the economic growth of Nigeria. Thus, the

following research questions sharpen the focus of the

problem.

Does monetary policy have any significant impact on

Nigeria’s economic growth?

Is there any long-run relationship between monetary

policy and economic growth in Nigeria?

The general objective of this study is to examine the impact of monetary

policy on Nigeria ‘s economic growth.

The specific objectives include:

To determine the effect of monetary policy on the

Nigerian economic growth

To ascertain the long- run relationship between

monetary policy and economic growth in Nigeria.

WORKING HYPOTHESIS

1. Ho: Monetary Policy does not have significant impact

on Nigeria’s economy.

2. Ho: There is no long-run relationship between

monetary policy and economic in Nigeria.

SIGNIFICANCE OF THE STUDY

As the Central Bank of Nigeria is undertaking policies

that will promote the economic growth of Nigeria , this

study will act as a source of information on various

ways of adopting monetary policy and its instruments

for stabilizing the economy. It will guide the policy

makers towards policy initiation.

It will help students and researcher to do further work

related to this research project.

SCOPE OF THE STUDY

The study covers the impact of monetary policy on

Nigeria ‘s economic growth in the period 1970 to 2009.

In the course of the analysis, effects shall the period

under review.

PERATIONANL DEFINITION OF THE RESARCH CONCEPTS

Social sciences concepts have received avalanche of

definitions, and as such, on one definition has all it

takes for universal acceptability. However, the

following concepts, as defined below, are relevant to

the study.

i . Effects are the result or an out come of something.

Ii. Money in an policy is a measure designed to

regulate money in an economy ( Erb 1995).

Iii money supply refers to the stock of liquid assets

held within an economy at a point in time ( Tirwall

1974).

iv. Inflation means a sustained rise in the average

price of a standard basket of goods and services,

without a corresponding increase in the quantity of

those goods and services (Oyejidi 1972).

v. Gross domestic product ( GDP) is the market value of

final domestic production of goods service during a

given period, usually Year.

REVIEW OF RELATED LITERATURE

THEORTICAL LITERATURE

Monetary theory has undergone a vast and complex

evolution since the study of the economic phenomenon

first came into limelight, It has drawn the attention

of many researches with different views on the role

and dimensions of money in attaining macro- economic

objectives. Consequently, there are quite a number of

studies aimed at establishing relationship between the

stock of money and other economic aggregates such as

inflation and output.

In this chapter we will take a look at the different

schools of thought, their views of the role of money

in attaining policy objectives alongside are view the

necessary literature relating to this study.

THE CLASSICAL MONETARY THEORY

The classical school evolved through concerted efforts

and contribution of economists like Jean Baptist Say,

Adam Smith, david Richardo, Pigu and others who shared

the same beliefs . The classical model attempts to

explain the determination, savings and investment with

respect to money.

The classical model on say’s law markets which states

that ‘’ supply creates its own demand. ‘ Thus classical

economists believe that the economy automatically tends

towards full employment level by laying emphasis on

price level and on how best to eliminate inflation

(Amacher and UIbrich, 1986)

The classical economists decided upon the quantity.

Theory of money as the determinant of the general price

level. Theory shows how money affects the economy. It

may be considered in terms of the ‘’ quation of

Exchang’’. This equation 2.1

Implying that changes in the price level can be changes

in the stcok of money. . The equation of exchange can

be startsd thus:

Mv= py 2.1

Mv = py

Where py = Gnp

Mv= Total Expenditure= GNP

M= stock of money

P= General price level

V= Income Velocity of money

Y =The Flow of Real goods and services

MV= measures the total value of transactions t within

a given period of time (total expenditure PY measures

the value of goods currently produced and sold ( total

product in value GNP). The relationship is derived from

the fact that ina closed economy, anything a single

purchased by one person is simultaneously sold by

another ( two parts of with money equals the average

stock of money in existence (m) goods and services

( velocity v).

THE QUANTITY OF MONEY

The classical economists did not introduce the role of

money in their model in terms of its demand and supply.

Insteady introduced money by using the quantity theory.

In short, related the level of economic commodity

price to the quantity of money in the economy and the

level of its commodity production. Two very similar

‘’quantity theory’’ formulations were used to explain

the level of price VIz ; the transactions formulation

or the Cambridge equation.

In the transaction version – associated with Fisher and

Newcomb, some assumptions were made, Viz : that the

quantity of money (m) is determined independently of

other variable, velocity of circulation (V) is taken as

constant, the volume of transactions (T) is also

considered constant. Thus of price (p) and the

assumption of full employment of the economy, the

equation of exchange is given as;

MV = PT, which can readily establish the production

that – the level of price is a function of the supply

of money . That is, p= F(m) which implies that, any

change in price. In cash balances version – associated

with Walras, Marshell, Wicksell and pigou, the

neoclassical school)(Cambridge school), changed the

focus of the quantity theory of without changing its

underlying assumptions. This version , focuses on the

fraction (K) of income, held as money balances. The

Cambridge version can be expressed as:

M= kpy

Where

K= Fraction of income

M =Quantity of money

P= price level

Y=value of goods and services

The K in the Cambridge equation is merely inversion of

V, the income Velocity of money balances, in the

original formulation of quantity theory. This version

directs attention to the determinants of demand for

money, rather than the effects of changes in the

supply money .’ Anyanwu (1993).

KEYNESIAN AND MONETARY PLOICY

The Keynesian model assumes a close economy and a

perfect competitive market with fairly price- interest

aggregate supply function. The economy is also assumed

not to exist at employment equilibrium and also that it

works only in the short run because asKey nes aptly

puts it ‘’ In the long run, we also will be dead’’. In

this analysis too, money supply is said to be

exogenously determined if wealth holderonly have one

choice between holding bouds. The Keyesian theory is

rooted on one notion of price rigidity and possibility

of an economy setting at a less than full employment

level of output, income and employment. The Keynesian

macro economy brought into focus the issue of output

rather than prices as being responsible for changing

economic conditions. In other records, they were not

interested in the quantity theory perse.

From the Keynesian in the mechanism, monetary policy

works by influencing interest rate which influences

investment decisions and consequently, output and

income via the multiplies process (Amacher and Ulbrich,

1989).

THE MONETAIST THEORY

The monetarist essential, quantity theorist who adopted

Fisher’s equation of exchange to illustrate their

theory, as a theory of demand for money and not a

theory of output price and money income by making a

functional relationship between the quantity of real

balances demanded a limited number of Variable (Essia,

1997) .

Monetarists like Friedman (1963) emphasized money

supply as the key factor affecting the wellbeing of

the economy. Thus , in order to promote steady of

growth rate, the money supply should grow at a fixed

rate, instead of being regulated and altered by the

monetary authority (ies). Keyness on the other hand,

maintained that monetary policy alone is ineffective in

stimulating economic activity because it works through

indirect interest rate rate mechanism .

Friedman equally argued that since money supply is

substitutive not just for bonds but also for many goods

and services, changes in money supply will therefore

have both direct and indirect effects on spending and

investment respectively. Brunner and Meltzer modeled

spending the demand for money will depend upon the

relative rates of return available or different

competing assets in which wealth can be.

THE MODERN APPROACH

The modern approach is the restatement of the quantity

theory in modern terms. It resulted in a new and more

sophisticated the quantity theory and in manner

amenable to empirical test.

It view s velocity of circulation as a stable function

of a limited number of key variables. That is,

velocity bears a stable and predictable relationship to

a limited number of other variables, and determiners

how much money people will hold rather than motive for

holding more and sees money as the main type of asset

which yields a flow of services to its holders,

according to the functions it performs (Fried man

1956).

In determining the factors influencing money demand ,

Friedman casts it in function is as follows.

Md = F(rb, re,P, 1/P .dp/dt w, w, u )

Where :

R b= Interest return or Yields on bonds

Re = Rate of return on equities

P= the price level

1/p . dp/dt = ratio of price change overtime w

W= ratio of non human wealth

W= wealth of the economic actor or permanent income

U= tastes and preferences.

Therefore , the demand for money according to this

approach, is not a fixed quantum , but varies in a

predictable fashion with the return on bonds and

equalities, the price level expectation, ratio of human

on non human wealth , or permanent income and tastes

and preferences.

EMPIRCAL LITERATURE

Aaogu (1998) sees monetary policy as actions by

monetary authorities to influence the national economic

objectives by controlling or influencing the quantity

and direction of money supply, credit and the cost of

credit. This according to him is aimed at ensuring

adequate supply of money to support financial

accommodation for growth and development programmes

for sustainable growth and development on the one hand

and , stabilizing various sectors of the , economy

for sustainable growth and development on the other.

Monetary policy can seen as employing the central

Bank’s control of the money supply as an instrument

for achieving the objectives of economy policy

(Johnson 1962 ). Similarly, from a synthesis of most of

the literature and in the context of the Nigerian

situation , Ubogu (1985) defines monetary policy as an

attempt by the monetary authorities to the level

aggregate economic activities by controlling the

quantity and direction of money and credit

availability . Vaish 9 1979) is the view that the

theoretical roots monetary policy go the way of the

quantity theory money, which according to him ,

remains a central theme in the theory The quantity

theory

State that a change in money supply , ceteris paribus ,

results in a proportional change in he price level .

The controversies in monetary theory and policy have

centered on what has come to be called the transmission

mechanism , the channel by which money supply

influences economic activity .In interest rate, move

to bring the demand for money into equally supply , the

new level of interest rates in turn influences both

consumption and interest spending hence the of out put

(Johnson , 1962 ). Changes in money supply are to be

compatible with the rate of inflation, This change

affect s the wealth of the public and therefore

influences their spending plans even without changes

rates. The interest rate channel, in any fails to apply

in countries where interest rates are not freely

variable but are fixed .Inrush cases, credit is

allocated by some non-price criteria, hence

availability and costs become the channel of

influence (Ubogu, 1985) . Economists, and mainly of the

classical, school, argue that expectations of

individuals and firms play an important role in

transmitted the effect of monetary policy actions

while this debate goes no, many hold the view that;

the relative strength of the various channels of

transmission of monetary policy is likely to very from

country to over time, depending on institutional

arrangements and economic circumstances. It may also be

the case that the time lags inherent in the various

channels of transmission differ. Another area of

debate in monetary theory policy where differences

remain relatively wide is the question of the efficacy

of monetary policy in nominal changes. Here, the

difference in views range from that of the Keynesians

who argue that monetary policy could influence real

output , in both the short and long runs, to the neo-

classical who argue that no such change in real

output is possible even in the short run. The

monetarist is captured by an aggregate supply curve

which is upward sloping to a point represented by full

employment , which is the natural rate and vertical

thereafter. This shape of the aggregated supply curve

allows for inflation/output trade-off, `

In the short but not in the long run. The neo-classical

aggregate supply curves, in contrast to both of these,

are vertical at the full employment level, thereby

precluding any inflation/output trade off even in the

short run. An important point worth stressing from the

policy point of view, is the empirical fact that a

close relationship is found to exist between money

supply and nominal income in all countries. It follows

perhaps logically from this, that if production cannot

adjust in the short run, due to whatever bottlenecks,

monetary action is likely to cause changes in prices

(Dornbusch and Fischer 2004).

As noted earlier, monetary policy refers to the

combination of measures designed to regulate the value,

supply a cost of money in an economy in consonance with

the expected level of economic activity. One of the

principal functions of the Central Bank of Nigeria

(CBN) is to formulate and execute monetary policy to

promote monetary stability and a sound financial

system. The CBN carried out this responsibility on

behalf of the federal government through a process

outlined in the Central Bank of Nigeria decree 24, 1991

and the banks and other financial institution decree

25, 1991 as amended. In formulating and executing

monetary policy, the governor of the CBN is required to

make proposal to the president of the Federal Republic

of Nigeria who has the power to accept or amend such

proposals. Thereafter the CBN is obliged to implement

the monetary policy approved by the president (CBN)

1996).

The CBN is also empowered by the two enabling laws, to

direct the banks and other financial institutions to

carry out certain duties in pursuit of the approved

monetary policy. Usually, the monetary policy to be

pursued is detailed out in the form of guidelines are

generally operated within a fiscal year but the

elements could be amended in the course of those

particular years. Penalties are normally prescribed for

non- compliance with specific provisions in the

guidelines.

The aims of monetary policy are basically to control

inflation maintain a health balance of payments

position in order to safeguard the external value of

the national currency and promote adequate and

sustainable level of economic growth and development.

OBJECTIVES OF MONETARY POLICY

Asogu, (1998) defined monetary policy as a measure

designed to influence the availability, cost and

direction of money and credit in pursuit of specified

economic goals. Monetary policy is art of the overall

economic policy that regulates the level of money

supply and credit in the economy in order to achieve

some desired policy objective. By monetary policy

objectives, we mean the ultimate objectives of

macroeconomic policy. The objectives include:

The maintenance of price stability; maintenance of

balance of payment equilibrium; attainment of high rate

of employment; accelerating the pace of economic growth

and development; exchange rate stability and the

maintenance of Price Stability.

In the modern economy, the price level tends to be

sticky if not rigid in the downward direction, so that

the problem of price level stability has essentially

been that of avoiding inflation. Inflation erodes the

purchasing power of economic agents and introduces

uncertainty and other vices. Price stability is

therefore, necessary not only to remove these vices but

also to restore confidence and maintain international

competitiveness.

The Maintenance of Balance of Payments Equilibrium:

In the case of maintenance of balance of payments

equilibrium, policy will be directed at influencing the

components of the balance of payments- the current and

the capital account in such a way that the balance of

payments is always in equilibrium. For instance,

monetary policy affects the interest rate and high

interest rates attract capital inflows and hence

influence the balance of payments. Which this level of

development and growth are attained depends upon the

resource available to the country.

Exchange Rate Stability

Fluctuations that may cause further deterioration or

undue appreciation that may lead to overvaluation in a

country’s currency are checked. The Central Bank in its

monetary measures, aims at maintaining adequate level

of foreign exchange rate consistent with the allocative

efficiency

TECHNIQUES OF MONETARY POLICY CONTROL

The techniques by which the stated objectives are

pursued by the monetary authorities can be classified

into two categories:- the Market Control Approach and

the portfolio Control Approach. Market Control

Approach:

This is an indirect or traditional approach of monetary

control.

They include the manipulation of:-

The Open Market Operation and

The Central Bank’s Discount Rate.

Attainment of High Rate of Employment

In the real world situations, the level of employment

that implies full employment is not obvious.

Economists define a situation of full employment as

one where all people who wish to work at the going wage

rate in the labour market will be employed. But it is

not possible that all those seeking employment will be

employment at one time. Even in the period of boom in a

dynamic economy, some people will always be between

jobs or seeking new employment. Thus, the monetary

policy measures aim at attaining a high rate of

employment that should proxy full employment. In other

words, it aims at maintaining a low and stable level of

unemployment, Anyanwu (2003).

Accelerating the pace of Economic Growth and

Development

Monetary policy aims at promoting economic growth and

development. Development may be measured by the level

of income per heard, capital per head, savings per

head, the percentage of unexploited resources amount of

public goods, the extent to which the working class

obtained education. While economic growth may be said

to concern itself with the effect of investment on

raising potential income and hence causes changes in

the living standard of the people. The extent to which

this level of development and growth are attained

depends upon the resource available to the country.

Exchange Rate Stability

Fluctuations that may cause further deterioration or

undue appreciation that may lead to overvaluation in a

country’s currency are checked. The Central Bank in its

monetary measures, aims at maintaining adequate level

of foreign exchange rate consistent with the allocative

efficiency.

TECHNIQUES OF MONETARY POLICY CONTROL

The techniques by which the stated objective are

pursued by the monetary authorities can be classified

into two categories:- the Market Control Approach and

the Portfolio Control Approach.

Market Control Approach:

This is an indirect or traditional approach of monetary

control.

They include the manipulation of:-

The Open Market Operation and

The Central Bank’s Discount Rate.

Open Market Operations

Open market operation refer to the buying and selling

of government and other approved securities by the

Central Bank in the open market. The Central Bank goes

to the public or ‘Open’ market for either long or short

term government securities and buys or sells them

depending on whether the aim is to create or destroy

bank deposits. Increase in the bank deposit implies an

increase in the money supply. Thus, if the Central Bank

wants to reduce the volume of money in circulation

because the economy is irking by inflation, it sells

securities to be public for which the public pays by

writing cheque favoring their deposit accounts. This

will reduce the commercial bank’s balance with the

Central Bank and hence their ability to create money.

Conversely, in times of depression, the Central Bank

buys securities thereby increasing the reserve base of

the commercial banks and hence their loanable funds.

The Central Bank’s Discount Rate

Central Bank’s discount rate measures the price changed

by the Central Bank for financial assistance made

available to the banking sector in the events of

perceived shortages of liquidity, (Chowdhry, 1986). In

other words, it is the rate of interest the Central

Bank charges the commercial banks on founds lent to

them against collateral. The term also applies to the

Central Bank’s activity of discounting bills when

commercial banks by discounting bills, such as,

treasury bills, treasury certificates, commercial bills

and promissory notes of short term duration at the

Central Bank. The lending rates of the commercial

banks’ are closely linked; discount rate induces a fall

in commercial banks’ lending rate and vice versa. The

manipulation of the discount rate helps to control the

volume of money in circulation. For instance, if the

economy experiences inflationary pressure, the Central

Bank raise the discount rate thereby making it very

costly for the commercial banks to obtain founds from

her. Consequently, commercial banks, in turn increase

their lending rate. The effect of the increase in

commercial bank’s lending rate is to reduce the demand

for borrowing, as long as the demand is interest

elastic. This will, in effect, cause investment to

shrink, and employment, income and the general price

level will all fall.

Portfolio Control Approach

Portfolio Control Approach is a direct or non-

traditional approach of monetary control. It works

through the instruments of portfolio constants, namely:

Reserve requirements

Special deposits with the Central Bank

Selective credit controls

Moral suasion

Direct Measures.

Reserve Requirements: Commercial banks are required to

keep some reserves with the Central Bank. By increasing

or decreasing the banks’ reserve requirement, the

Central Bank affects the banks’ ability to lend. When

banks are required to hold more liquid assets in

reserve, fewer assets will be left for them to lend to

the general public. On the other hand, a reduction in

reserve requirement release assets held for this

purpose for lending as loans and advances by the banks.

Special Deposits with the Central Bank: Special

deposits with the Central Bank are additional deposits

over and above the minimum legal reserve requirement

that the commercial banks are made to deposit with the

Central Bank. The mandatory special deposits are a

major measure in reducing the deposits available for

banks to lend to their customers. Though they appear on

the asset side of the bank’s balance sheets, they

cannot be used as part of any reserve base.

Selective Credit Control: This is a measure used by the

Central Bank to control the flow of bank credits to

different sectors of the economy. The Central Bank

directs banks on the cost, volume and direction of

credit to different sectors of the economy. The central

Bank may instruct the bank sector to give more loans to

the preferred sector of the economy- the productive

sector while extending little or no credit to the less

preferred sectors- the service or consumption sector of

the economy. By the use of selective credit control,

monetary policy influences the volume of money in

circulation as well as the allocation of resources.

Moral Suasion: This involves the issuing of persuasive

instructions to commercial banks to control the flow of

their credits to the economy. The Central Bank issues

these instructions in its periodic meetings especially

at the Bankers’ Committee Meetings, Annual Dinner of

the Chartered Institute of Bankers of Nigeria and on

other occasions when it meets formally or informally

with the heads of the banking community. Moral suasion

is supposed to be an appeal soliciting for the banks’

voluntary compliance over some credit guidelines.

Direct Measures: The direct measures involves the use

of interest rate ceilings, lending ceilings and

qualitative lending guidelines. The Central Bank may

decide to place a limit on the rate of interest and in

such a situation the rate of interest cannot fluctuate

beyond that limit. The lending ceilings when placed,

will limit the amount of found period of time that

could be lent to the public by the commercial bank.

MONETARY POLICY IN AN ENVIRONMENT OF REGULATED

FINANCIAL SYSTEM

Anyanwu (2003), emphasized that if an economy with

financial regulation starts to observe a fairly steady

upward trend in the velocity of the monetary base M1 and

M3 without a corresponding growth in the gross domestic

product (GDP) the ultimate economic monetary policy

would be in addition to informing the banks (moral

suasion) of this view by way of consultations to

increase the interest rate, raise the special reserve

deposits ratio and thus force the bank to reduce their

asset base. Because of the existence of controls,

change in the reserve ratio have a direct impact on

banks’ lending.

Under the tap system of selling government securities

whereby the price (and not the quality) of these

securities was fixed there was very little risk of

capital losses. Although most nations apply market

operations to affect their liquidity condition, they

are not the primary instrument of monetary policy.

Indeed, it mounts pressure on the primary market,

therefore, discouraging the development of the

secondary market; impairing true portfolio adjustment

is by holders of government debt as well as the

government ability to conduct open market operations.

MONETARY POLICY IN DEREGULATED FINANCIAL SYSTEM

The system of regulatory measures constructed to

protect investors and to maintain confidence in the

stability of financial market and institutions failed

to achieve the set objective as financial institutions

devised other names of operations than their compliance

to the regulatory body controls. As observed by Anyanwu

(2003), the regulations had allowed the banks to emerge

as highly profitable institution but with a declining

market share and at a high cost to depositors. Several

developments according to her, rendered the impact of

regulations of financial institutions a weak tool. One

of such developments is the upsurge of and increase

variability in inflation. Inflation has the potentials

of increasing the opportunity cost of holding moneys

balances. Investors tend to prefer short dated claims

over longer dated claims. Maturity controls imposed on

the banks restricted their ability to meet this demand.

The limited flexibility of banks in the face of high

and variable inflation rates afforded an opportunity

for non-bank financial intermediaries to expand

consequently, money Market Corporation, building

society and credit Unions, experience rapid growth.

Other development is the progressive increase in the

size of government budget deficits. The effect of this

rapid growth places considered pressure on the existing

methods for the sales of public securities.

Osuber (2006) had maintained that monetary authorities

could switch to financial de-regulation to set in

motion changes in both manner in which monetary policy

is transmitted to the real economy and the stability

and interest rate elasticity of the demand for money.

Thus the introduction of tender system of selling

government securities and the move to a floating

exchange rate regime increasing the monetary

authorities potential control over injections of

liquidity into the domestic monetary system thus,

enhancing their ability to use open market operations

to influence domestic monetary condition.

Osuber (2006), pin-pointed that monetary policy in a

deregulated financial system, strengthens the role of

market force in determining operations, and the real

economy through changes in interest rates. With greater

competitions therefore, financial sector, changes in

interest rate, tend to spread quickly through the

whole range of financial assets and liabilities.

Specifically, in the deregulated financial environment,

the value of deposit is determined by both demand and

supply consequently, any tightening of monetary policy

by the monetary authority will induce a rise in deposit

rate resulting in an increase in the supply of deposits

and offsetting to some extend the authorities effort to

reduce the growth of money. Thus, financial

institutions particularly banks are now better able to

protect their deposit base and to sustain their lending

than they had been in the regulated frame work in which

the volume of deposit was primarily determined.

The demand for credit may also have become less

sensitive to interest rate in the deregulated system.

For example, increased use of floating interest rates

and moral suasion and flexible loan packages may result

in less discouragement to marginal borrowers as rate

rises.

MONETARY POLICY AS A TOOL FOR ECONOMIC GROWTH

Consistent and stabilized monetary policy is usually a

set of demand management measures intended to remove

some macroeconomic imbalances, which if allowed to

persist, could be inimical to long-term growth.

According to Anyanwu (2003), countries seeking for

sustainable economic growth after a period of

macroeconomic imbalances must first get stabilized. In

Nigeria, monetary policy effectively implemented is a

veritable tool for stable economic growth.

Efforts for sustainable growth began in Nigeria in the

early 1980’s in response to the emergence and

persistence of unstable macroeconomic developments.

There was need to address basic elements of economic

instability such as the expended government spending

which resulted in large deficits. The instability

variables that needed to be stabilized were:

Excessive government borrowing; rapid monetary

expansion; inflation; chronic overvaluation of national

currency; reduced export competitiveness; introduction

of N200 and N500 currency notes; growth in real GDP

which stood at 2.8 and 3.8 percent in 1999 and 2000

respectively; CBN adoption of Universal Banking (UB) in

Nigeria end of 2000.

FACTORS INFLUENCING MONETARY POLICY

According to Anyanwu (2003) a number of variables or

aggregates have tended to influence the monetary

policy. These variables are:

Economic Stability: for the main thrust of monetary

policy to be fully implementable, there should be

macroeconomic stability otherwise a lot of distortions

and lapses will make the targets unrealizable.

Financial Market Efficiency: A special ingredient for

the monetary policy effectiveness is the money market

segment.

Inflation: The scope or magnitude of the inflationary

trends in the economy goes a long way to influence the

monetary policy. With high inflation any, rate the

price stability exchange rate stability and balance of

payments position, will not be fully realized.

LIMITATIONS OF PREVIOUS STUDY

A review of existing empirical studies indicated that –

for middle income economies, monetary policy shocks

have some modest effects on economic parameters.

Genev (2002) for example, using a structural vector

Autoregressive (SVAR) approach, studied the effect of

monetary shock in ten central and Eastern European

(CEE) countries, found some indications that changes in

the exchange rate affect out put. In the same spirit,

Starr (2005) using SVAR model with orthogonaized

identification, found little evidence of real effects

of monetary policy in five common wealth of independent

states (CIS) with notable exception that-changes in

interest rate have a significant impact on output.

However, for developing country like Nigeria, the

evidence is weak and full of puzzles”. For example,

Balogun (2007) used simultaneous equation model to test

the hypothesis of monetary effectiveness in Nigeria,

and found that-rather than promoting growth, domestic

monetary policy was a source of stagnation and

persistent inflation. Again, Chuku (2009) using a

structural Vector Autoregressive (SVAR) approach in

measuring the effect of monetary innovations in Nigeria

found that price based nominal anchors do not have a

significant influence on real economic activity

modestly.

The idiosyncratic evidence (inconsistent with

theoretical expectations), returned from different

investigations in different countries, is what

economists usually referred to as “puzzle”. The three

most common puzzles identified in the literature are:

the liquidity puzzle, the price puzzle and the exchange

rate puzzle. The liquidity puzzle is a finding that-

increase in monetary aggregates is accompanied by an

increase (rather than a decrease) in interest rate.

While the price puzzle is the finding that contraction

monetary policy through positive innovations in the

interest rate seems to lead to an increase (rather than

a decrease) in prices. Yet, the most common in open

economics is the exchange rate puzzle , which is a

finding that an increase in interest rate is associated

with depreciation (rather than appreciation) of the

local currency.

Intuitively, it is discovered that the causes of the

above identified puzzles, are due to inability of the

pervious researchers to specify their model correctly.

For example, Chukwu (2009) in measuring the effect of

monetary policy innovations in Nigeria, did not include

interest rate in his model, which is an important

instrument for monetary policy.

Again, inability of the researchers to use the correct

econometric method in their regression analysis. For

example, Balogum (2007) in determining effectiveness of

monetary policy in Nigeria, applied only simultaneous

equation model, which did not give room to test for

stationarity of data in order to avoid spurious result.

Therefore. It is with the view of annihilating these

puzzles, that the researcher would apply unit root test

and co-integration econometric model, in order to

stationarize the data, and ascertain the long run

relationship between monetary policy and economic

growth in Nigeria.

RESEARCH METHODOLOGY

This chapter focuses on the research method that will

be adopted. Regression analysis based on the classical

linear regression model, otherwise known as Ordinary

Least Square (OLS) technique is chosen by the

researcher. The researcher’s choice of technique is

based not only on its computational simplicity but also

as a result of its optimal properties such as

linearity, unbiasedness, minimum variance, zero mean

value of the random terms, etc (Gujarati 2004).

MODEL SPECIFICATION

In this study, hypothesis has been stated with the view

of examining the impact of monetary policy on

Nigeria’s economic growth. In capturing the study,

these variables were used as proxy. Thus, the model is

represented in a functional form. It is shown as below:

GDP = F (MS, INT, EXCH) ………….. 1.1

Where

GDP = Real Gross Domestic Product

MS = Money Supply

INT = Interest rate

EXCH = Exchange rate

In a linear function, it is represented as follows,

GDP = b0 + b1 MS + b2 INT + b3 EXCH+ Ut …………….. 1.2

Where

b0 = Constant term

b1 = Regression coefficient of MS

b2 = Regression coefficient of INT

b3 = Regression coefficient of EXCH

Ut = Error Term

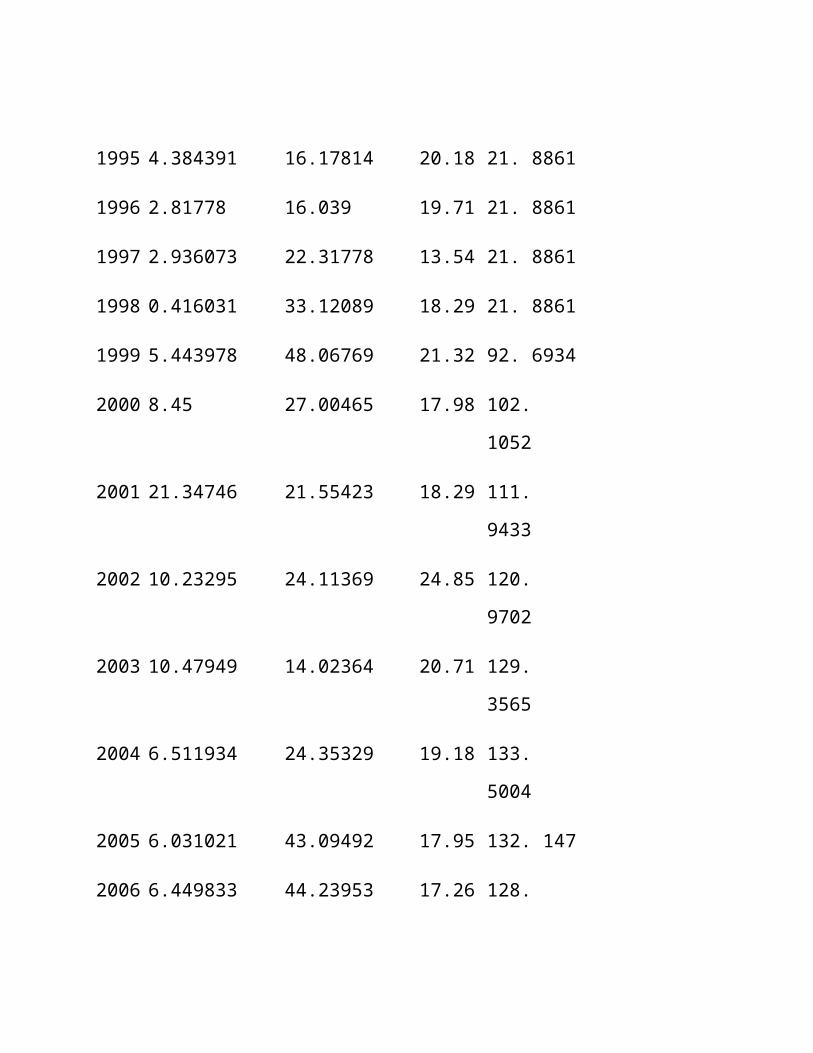

DATA PRESENTATION

Year RGDP

(N=Million)

MS

(=N=Million)

INT

Rate

EXCH

Rate

1970 11.76819 6. 501738 7 0.7143

1971 3.759941 16.61547 7 0.6955

1972 8.526815 25. 31896 7 0.6579

1973 199.806 54. 50246 7 0.6579

1974 70.6816180. 30013 7 0.6299

1975

7.266672

39. 23182 6 0.6159

1976

8.144374

33. 76234 6 0.6265

1977 – 7

32195

1.096369 6 0.6466

1978 2. 28.04118 7 0.606

518109

1979 5.

338587

47.68304 7.5 0.5957

1980 550. 5322 7. 031126 7.5 0.5464

1981 -2.69796 11. 95357 7.75 0.61

1982 -7.0547 15. 39495 10.25 0.6729

1983 -1.09651 11.93011 10 0.7241

1984 9.518966 12.44159 12.5 0.7649

1985 2.45483 4.232502 9.25 0.8938

1986 -0.56556 22.91948 10.5 2.0206

1987 7.357725 34.98785 17.5 4.0179

1988 7.665243 935.3842 16.5 4.5367

1989 13. 01924 -85.408 26.8 7.3916

1990 -0.8114 27.43463 25.5 8.0378

1991 2.2557 47.52662 20.01 9. 9095

1992 1.277907 53.75794 29.8 17. 2984

1993 0.224609 34.49515 18.32 22. 0511

1994 2.162566 19.41172 21 21. 8861

1995 4.384391 16.17814 20.18 21. 8861

1996 2.81778 16.039 19.71 21. 8861

1997 2.936073 22.31778 13.54 21. 8861

1998 0.416031 33.12089 18.29 21. 8861

1999 5.443978 48.06769 21.32 92. 6934

2000 8.45 27.00465 17.98 102.

1052

2001 21.34746 21.55423 18.29 111.

9433

2002 10.23295 24.11369 24.85 120.

9702

2003 10.47949 14.02364 20.71 129.

3565

2004 6.511934 24.35329 19.18 133.

5004

2005 6.031021 43.09492 17.95 132. 147

2006 6.449833 44.23953 17.26 128.

6516

2007 6.407226 57.78557 16.94 125.

8606

2008 6.296026 48.38334 15.94 118.8606

2009 -100 -100 16.7 124.4484

ESTIMATION METHOD AND PROCEDURE

Currently modern economic analysis involve the use of

econometric method where appropriate statistical and

econometric test can be conduced to ensure the validity

and reliability of the data and result, for accurate

projection and prediction of the phenomenon in

question. The multiple equation model is presented by

the real Gross Domestic product (GDP) at current factor

cost as the dependent variable, with the total function

of Money supply (MS), Interest rate (INT) and Exchange

rate (EXCH), as the explanatory variable. The model

being a time series regression estimates, the

researcher will therefore test for the empirical

viability of the model using the ordinary least square

(OLS) analytical technical. The use of OLS method

according to koutsoyians (2001), yields parameter

estimates with optimal properties such as unbiased

minimum variance and efficient, thereby making the

parameter estimates best linear and unbiased (BLUE).

Other reasons include that its computational procedure

is fairly simple, as compared with other econometric

methods.

EVALUATION OF THE ESTIMATED PARATMETERS

Specifically, to carry out a thorough statistical

estimation on this study, the summary statistics R2 S.E,

unit root, co integration and Durbin Watson statistics,

would be conducted at 5% level of significance. For the

evaluation of the estimates as stated by koutsoyianis

(2003), after the estimate of the parameters of an

economic model, the next stage is the evaluation.

According to him, evaluations consist of deciding

whether the estimated parameters are theoretically

meaningful and statically satisfactory.

The coefficient of determination (R2) is usually

employed in order to evaluate the explanatory power of

the model. The value of the (R2) gives the proportion

of the variation in the dependent variable explained by

changes in the explanatory variables. The value of (R2)

lies between 0 and 1. the higher R2, the greater the

percentage of variation of Y explained by the

regression plan. That is, the better the goodness of

fit. The closer R2 to zero, the worse the fit.

Standard Error test (S.E): It is used to test for the

reliability of the coefficient estimates.

Decision Rule

If S.E < 1/2b1, reject the null hypothesis and

conclude that the coefficient estimate of parameter is

statistically significant. Otherwise accept the null

hypothesis.

Durbin Watson (DW) test: it is used to test for the

presence of autocorrelation (serial correlation).

Decision Rule

If the computed Durbin Watson statistics is less than

the tabulated value of the lower limit, there is

evidence of positive first order serial correlation. If

it is greater than the upper limit there is no evidence

of positive first order serial correlation. However, if

it lies between the lower and upper limit, there is

inconclusive evidence regarding the presence or absence

of positive first order serial correlation.

Unit Root Test: It will be used to test for the

stationarity of the time series data. Augmented

Dickeyfuller (ADF) test will be used in the course of

the test.

Decision Rule

Considering the absolute values, 5% level of

significance will be used.

If the critical value of the ADF tests in less than the

ADF test statistics, we concluded that the time series

data is stationary considering the level it is

differenced. Otherwise, the data is not stationary.

If the data is differenced once before stationarity is

induced, we conclude that the data is integrated of

order one. i.e 1(1), if it is differenced of twice, so

that stationerity is obtained, we say that it is

integrated of order two i.e 1 (2). However, should the

time series become stationary at level, i.e no

differencing, we say that the series is integrated of

order zero i.e 1(0).

Co integrated Test

It is used to test for the long run relationship

between the variables. Johansson co-integration test

will be utilized in the co integration analysis and the

normalized co-integrating coefficient, shall be

ascertained to examiner the nature of the long run

relation between the variables estimated in the model.

REFERENCES

Amacher, R. C. & H.H. Ulbrich, (1986), Principles of

Macroenomics South Western Publishing Co. Cincinnati.

Anyanwu J.C. (1993), Monetary economics theory policy

and institutions. Hybrid publishers Ltd, 6B Oguta Road,

Onisha, Nigeria

Anyanwu, F.A (2003), Public Finance CREMD Publishers,

Owerri.

Asogu, J.O. (1998), An Econometric Analysis of the

Relative potency of Monetary and fiscal policy in

Nigeria. CBN Economic and Financial Review 36, 2.

Balogun E. (2007) “Monetary policy and economic

performance of West Africa monetary zone countries”

MPRA, 3408

Central Bank of Nigeria (1996), “Monetary policy in

Nigeria” (Abuja: CBN ch.3).

Central Bank of Nigeria (1996), “ The Design and

Implementation of Macroeconomic policy” (Abuja: CBN ch.

10.).

Chuku A Chuku (2009), Measuring the effects of monetary

policy innovations in Nigeria. Africa Journal of

accounting, Economics, Finance and Banking Research 5,5

Chowdhury, A.R (1986) “Monetary and fiscal impacts on

Economic activities in Bangladesh”. Bangladesh

Development studies, xiv,2.

Dornbush, R. et a; (2004), Macroeconomics (New Delhi:

Tata McGaw – Hill Publishing company Limited).

Erb, F. (1995): Central Banking, Fourth edition, New

York: St. Martin’s press.

Essis, Uwen (1997), The Evolution of Economics as an

Academic Discipline Journal of Economic Srudies 1.1.

Friedman, (1956), The quantity theory of money – A

restatement in Friedman (ed) studies in the quantity

theory of money University of chikago press

friedman, Schwartz. K (1963), Money and Business Cycles

Review of Economics and Statistics. 45

Genev G. (2002) “Transmission mechanism of monetary

policy in central and eastern Europe”, Report 52,

Centre for social and economic research (CASE) Warsaw

gujarati D.N (2004), Theory of Economics United State

Military Academy West point, Mc Graw – Hill Inc Book

Co- Singapore.

Johnson, H.G. (1962), Monetary Theory and Policy.

American Economic Review vol. LII.

Koutsoyiannis, A. (2001), Theory of Econometrics (New

York: PALGRAVE – Houndmills, Basingstoke, Hampshire RG

21 6x 5 and 175 fifth Avenue).

Koutsoyianis (2003) Theory of Econometrics, Macmillan

press, Great Britain.

Osuber, J.U. (2006) Finance, Principles, Environment

and Decisions, Bill Fred (Nig) Ltd, Owerri.

Oyjide, T.A (1972): “ Dedicit Financing, Inflation and

Capital Formation the Analysis of the Nigerian

Economy”, 1957 – 1970 NJSS vol. 14.

Starr M. (2005), Does money matter in the CIS? Effects

of monetary policy on out and price Journal of

competitive economics (33) 441- 461.

Thirdwall, A,P. (1974), Inflation, Saving and Growth

in Developing Economics; London Macmillan.

Ubogu, R.E. (1985), “Potency of Monetary and Fiscal

Policy Instruments on Economic Activities of African

Countries” Finafrica: Savings and Development IX, 4.

Varish M. C. (1979) Money, Banking and International

Trade (New Daihi: Publishing House P.V.T. Ltd).