efCo^r.amrofft - Karnataka Forest Department

109

THE KARNATAKA FOREST ACCOUNT CODE CONTENTS Chapters Page No. 1239 ^ Introduction — Extent of application ,T r. . 1239 " Definitions 1241 111 Classification of Transactions 1^ System of Accountants and Relation with Audit 12 9 1253 ^ Appropriations and Control of Expenditure 1263 ^ Cash Accounts 1274 ^ Works Accounts VIII Accounts of Timber, Stores, Tools and Plant Live-stock and Sandalwood IX Accounts, Returns rendered by Forest Department Officers .... X Acaruntsofthea«efCo^r.amrofft^ Forests-DepartmentalCheckofAccounts,etc. ^I Audit by Accountant-General appendix 1320 I Classification of Forest Revenue and Expenditure • II Annual Plan of Operations ^1-A Rules for the Maintenance of the Field Note-book .. ^ll'B Rules for Maintenance of Measurement Book . • • • Classification of the Articles by the Non-Consumable) which are normally purchase y ,^3^3 Department _ i-ias ^ Accounts to be maintained and rendered by Forest 1233 AKLJ PUBUCATION

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of efCo^r.amrofft - Karnataka Forest Department

THE

KARNATAKA

FOREST ACCOUNT CODE

CONTENTS

Chapters Page No.

1239^ Introduction — Extent of application,T r. . 1239" Definitions

1241111 Classification of Transactions

1^ System of Accountants and Relation with Audit 12 91253^ Appropriations and Control of Expenditure 1263

^ Cash Accounts1274

^ Works Accounts

VIII Accounts of Timber, Stores, Tools and PlantLive-stock and Sandalwood

IX Accounts, Returns rendered by Forest Department Officers ....X Acaruntsofthea«efCo^r.amrofft^Forests-DepartmentalCheckofAccounts,etc.

^I Audit by Accountant-General

appendix

1320

I Classification of Forest Revenue and Expenditure •II Annual Plan of Operations^1-A Rules for the Maintenance of the Field Note-book . .^ll'B Rules for Maintenance of Measurement Book . • • •

Classification of the Articles by theNon-Consumable) which are normally purchase y ,^3^3Department _ i-ias

^ Accounts to be maintained and rendered by Forest1233

AKLJ PUBUCATION

1234 KARNATAKA FOREST ACCOUNT CODE CONTENTS CONTENTS KARNATAKA FOREST ACCOUNT CODE 1233

FORMS INDEX

Form

No.

Particulars Reference

to paraPage No.

FACl Preparation of annual budget estimates 39 1353

FAC2 Form of intimation of greints 40 1352

FAC3 Statement showing the total revenue andexpenditure

63 1353

FAC4 Summaiy of revenue and expenditure 63 1370

|fAC5 Works cash book 70 1387

|fAC6 Cash balance report 81 1387

|fAC7 General cash book 86 1388

|fAC8 Register of cheque and receipts books 99 1389

|FAC9 Form of muster roll 104 1389

|facio Measurement book 112 1392

FACll Register of field note book/measurementbook

112 1392

FAC12 Field note book 113 1393

FAC13 (Receipts and disposals of animals and(birds

154-C 1393

|fAC 14 (History record of animals and birds 154-C 1394

|fAC15 Register of sanctioned estimates 123 1395

(FAC 16 (Intimation to the sanctioned estimates 123 1395

|faC17 Register of sanctioned works 123 1395

(FAC 18 Completion report of works 123 1396

|fAC19 Consolidated works voucher 124 1396

FAC 20 Consolidated statement of completionreport

128 1397

IfAC21 Marking list of trees 132(a) 1398

Form

No.

Particulars Reference P

to para'age No.

FAC 22 Register of trees marked and felled 132(b) 1398 J

FAC 23 Monthly progress report in respect ofmaterials prepared and despatched

132(b)(2) 1399

FAC 24 Monthly progress of logging operationscarried out in respect of teak/jungle wood

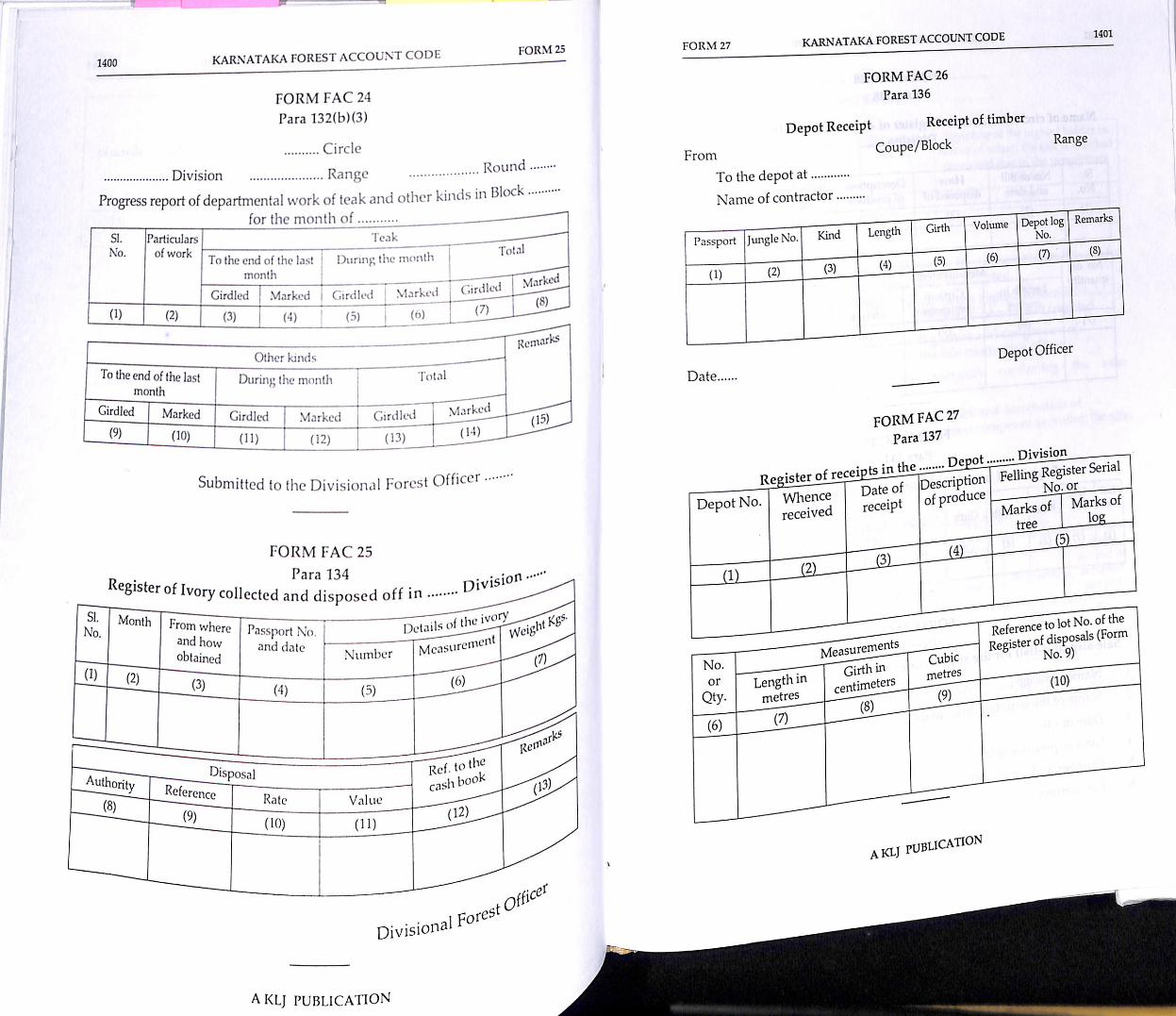

132(b)(3) 1l400

FAC 25 Register of ivory collected and disposedoff

134 400

FAC 26 Depot receipt |l36 1401 1

FAC 27 Register of receipts of Timber and otherproduce

137 1401

FAC 28 Register of disposals from the depots ofthe division

138 1402

FAC 29 Lot roll of auction sales |l41 1402 1

FAC 30 Bid list|l42 1402 1

FAC 31 Register of special supplies |l44 1403

FAC 32 Register of retail sales of timber |l45 1404 1

FAC 33 Register of receipts, disposals and balanceof timber and other forest produce in thedepot

146 1404

FAC 34 Register of disposals of sawn timberaccount out-turn for the month of

148 1404

FAC 35 Stock register of sawn timber passed andrejected

148 1405

FAC 35-A Register of trees felled and converted 1152 1405

FAC 36-A Register of livestock 154 1406

FAC 36-B

FAC 37

Work turned out by elephants ^52Statement showing the sales of timber and 155other produce removed by Governmentagency during the month of... I

1406

1407

aklj publicationAKLJ PUBLICATION

1236 KARNATAKA FOREST ACCOUNT CODE CONTENTS

Form

No.

Particulars Reference

to paraPage No.

FAG 38 Register of outstandings on account ofrevenue for the month of...

158 1407

FAG 39 Revenue realised from the forest producecut and collected by consumers andpurchasers

156 1408

FAG 40 Demand, collection and balance of forestrevenue for the quarter ending...

158 1408

FAG 41 Register of fee grants of timber and otherproduce

159 1409

FAG 42 Register of right and privilege holders 160 1410

FAG 43 Statement showing the drift andconfiscated forest produce

161 1410

FAG 44 Register of collection and removal ofsandalwood in range/depot

162 1411

FAC45 Register of sandal trees removed fromprivate lands

162 1412

FAC46 Acknowledgment of sandalwoodremoved from private holdings

162 1413

FAG 471

Passport for transport of roughsandalwood in the depot

163 1414

[fag 48 Receipt of rough sandalwood in depots 163 1415

FAG 49 r

1 ̂Register showing the details of roughandalwood in the depot

163 1416

FAG 50

1 p

.egister of rough sandalwood issued toepot for preparation and out-turn ofrepared wood

163 1417

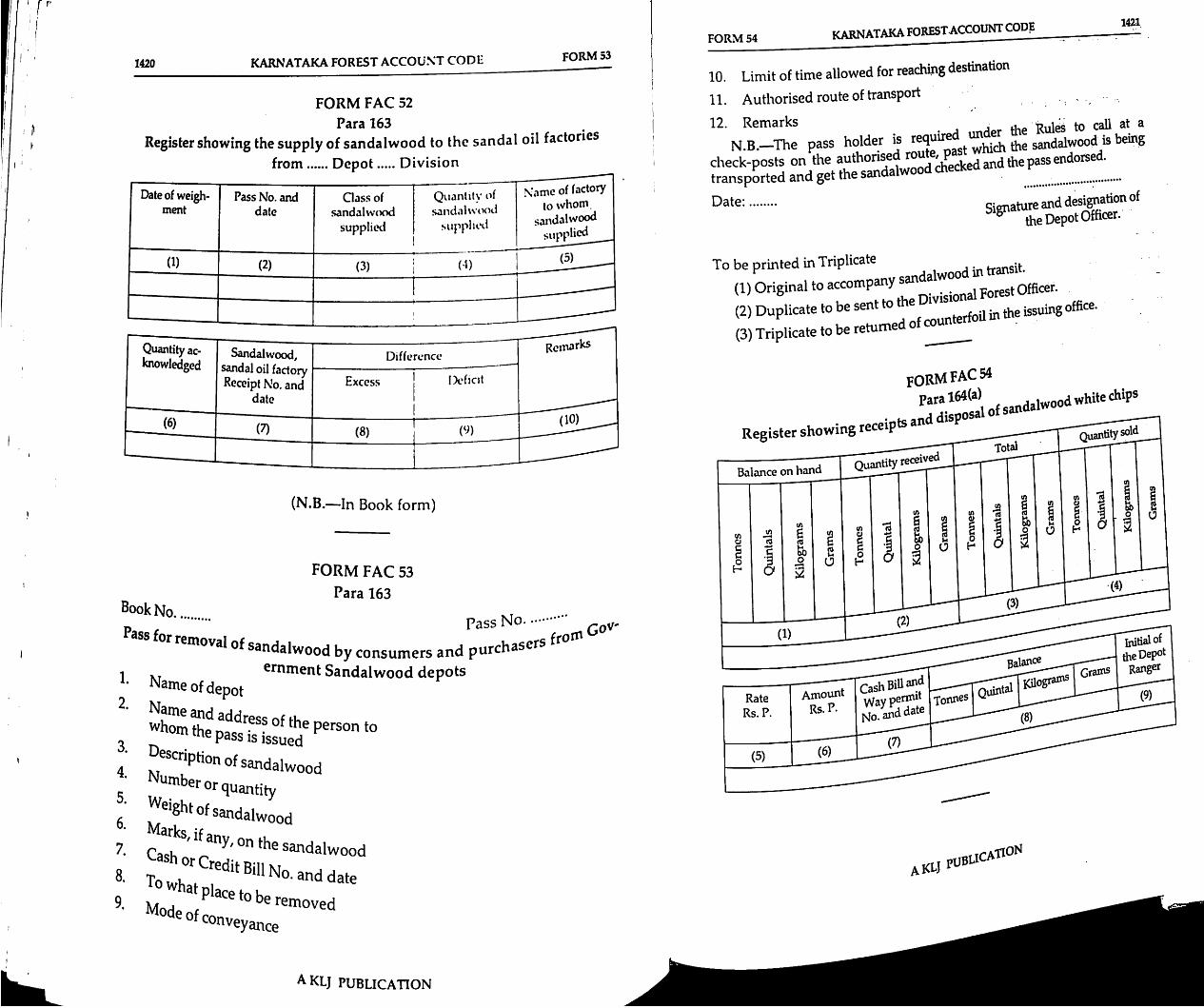

[fag 51 Retail sale of sandalwood in depot163 1419

FAG 52 StSL

atement showing the sandalwoodpplied to sandalwood oil factories

163 1420

FAG 53 R(ar

Jmoval of sandalwood by consumersid purchasers 163 1420

AKLJ PUBLICATION

CONTENTS KARNATAKA FOREST ACCOUNT CODE 1237

Form

No.

Particulars FReference 1

to para'age No.

FAG 54 Sale of white chips in depot L64(a) 1421 1FAG 55 Abstract of statement showing the

quantity of rough sandalwood sent to theDivisional Forest Officer by the depot

164(b) 1422

FAG 56 Abstract of monthly transactions ofsandalwood asserted in the sandalwood

depot

164 1423

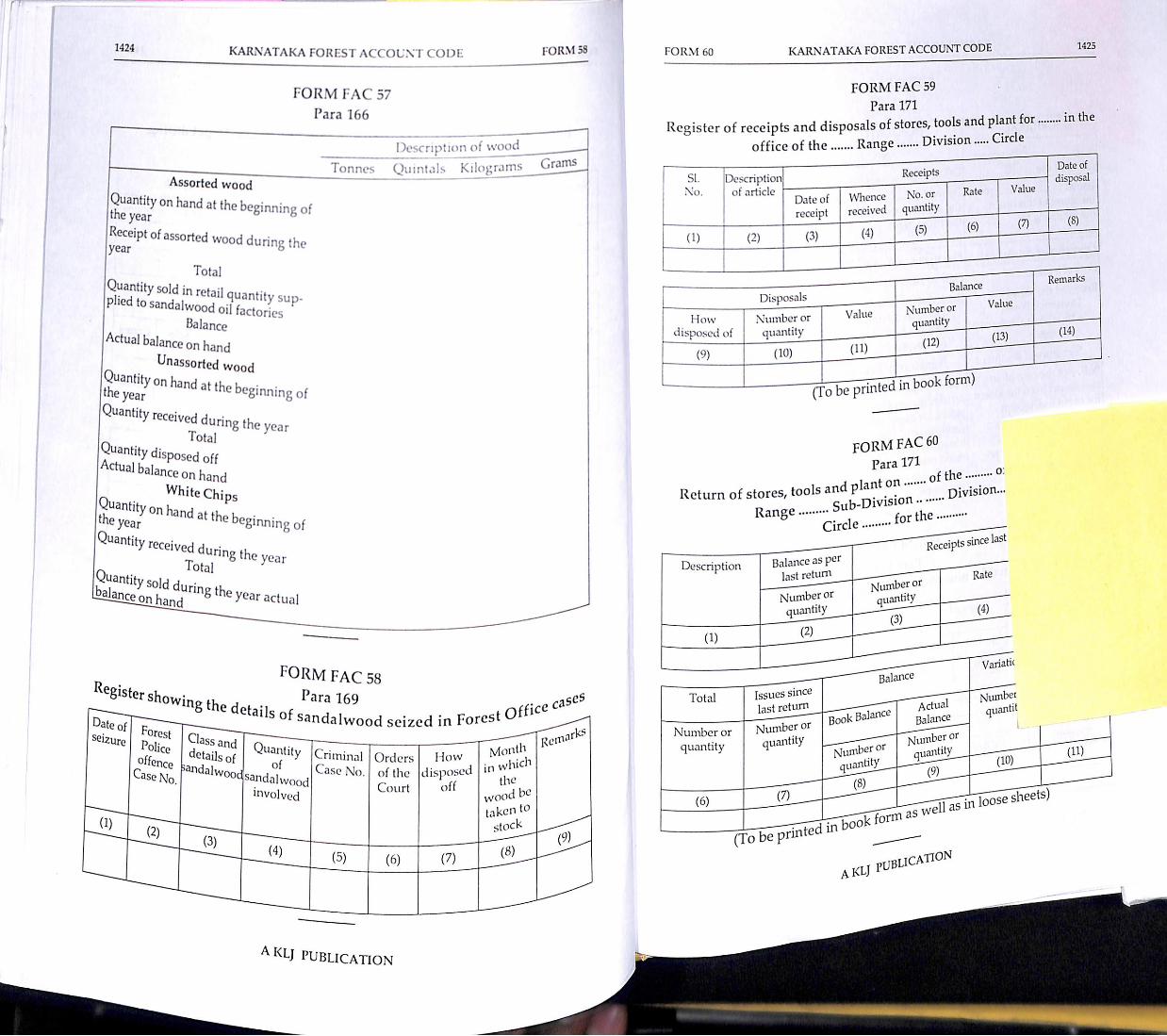

FAG 57 Stock taking of sandalwood 166 1424 1

FAG 58 Register showing the details ofsandalwood seized

169 1424

FAG 59 Register of receipts and disposals of tools,stores and plant

171 1425

fag 60 Return of stores, tools and plants for 171 1425 1

FAG 61 Invoice Form 171 1426 1

FAG 62 Register of consumable and non-consumable articles

174 1426

FAG 63 Voucher Form 183 1427

fag 64 Register of cheques drawn 194 1427 1

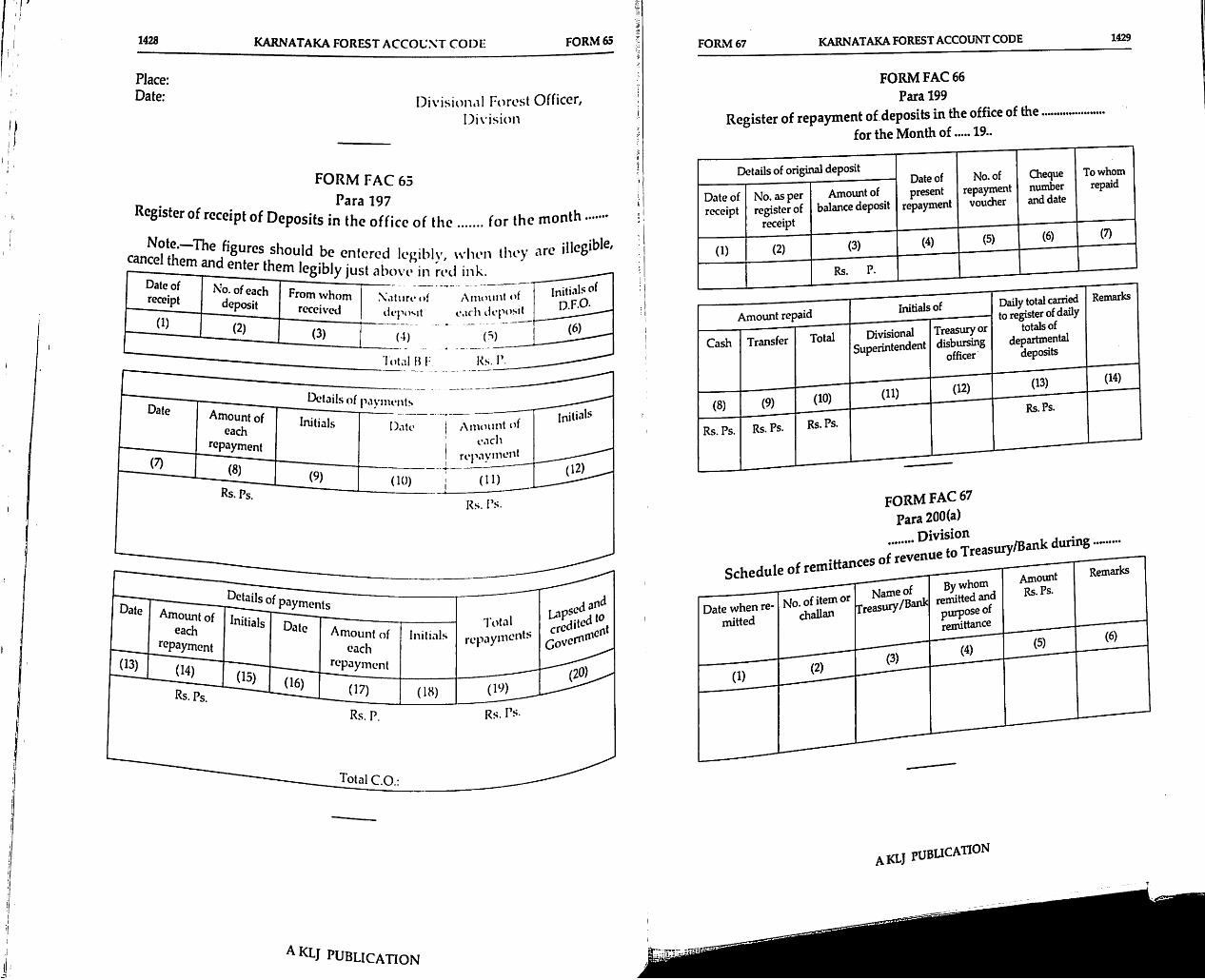

FAG 65 Register of receipts of forest deposits 197 1428

FAG 66 Register of repayment of forest deposits 199 1429 1

FAG 67 Schedule of forest remittances 200(a) 1429 1

fag 68 Detailed statement of advances 201(a) 1430 1

FAG 69 Find indent Form205 1430 1

fag 70 Register of disallowances 210 1431 1

FAC 71 Register of debits and credits 215 1432

FAG 72 Register showing rent recovered from....for the month of...

216 1432

fag 73 Register of sales tax adjusted 217 1433 1

AKLJ PUBLICATION

1238 KARNATAKA FOREST ACCOUNT CODECONTENTS

Fonn

No.

Particulars Reference

to para

Page No.

FAG 74 Account current Form 218 1433

FAG 75 Classified abstract of revenue for themonth of....

218 1448

FAG 76 Classified abstract of expenditure for themonth of....

218 1448

FAC77 Objection book of the DivisionalSuperintendent

85(8)(b) 1449

FAC78 Satement showing the arrears in annualverification of stocks T and P livestock inthe Division

238 1449

FAC79 Statement of arrears in realisation of forestrevenue of....

238 1450

FAC 80 Satement showing the number of cases offorest offences pending to end of 31stMarch

38 1450

FAC81 Statement of review report on theworking of schemes costing over 5 lakhsfor the year

239 1451

FAC 82 Form of PWG 31-A1451

FAC 83 Proforma for Estimate 121 1452

FAC 84 Piece Work Agreement 125 1452

FAC 85 Contract Certificate 125 1453

AKLJ PUBLICATION

THE

KARNATAKA

FOREST ACCOUNT CODE

(As amended by Notification Nos. AHFF 2 LFFI87 dated 13-10-1987and AHFF 13 FAF 92, dated 30-3-199o)

CHAPTER I

Introduction—Extent of Application

1. Tlie Rules contained in this ^tlTtlTeprocedure to be followed by ° keeping in their offices oftransactions relating to Forest ep . accounts to the Controllingaccounts of such transactions an ren supplementary to theOfficers and the Account^^ ^ode, the KamatakaFinancial Rules contained m rnnHneent Expenditure. Insofar as theyTreasury Code and accounts of Forests Department Officers,deal with the initial and compiled acc ^ ̂ Comptroller andthey are based on

2. This Code generally embodies allForest Department except— Department; and

(i) Administrative matters in general contained in theSatScfvU i^^es Rules and the Kamataka Financial Code.

CHAPTER 11Definitions

3. Unless there be ^ tlae sense hereinterms defined in this Chapter are

'"r 1. H.- o,» s sComptroller and Auditor GeneralGovernment of Accountant General;

(i) "AccounUntGen " denotes formal sanction— X

iquirement of such

1239

AKLJ PUBLICATION

1240 KARNATAKA FOREST ACCOUNT CODE CUP. II

Administrative Department. It is an Administrative order of theDepartment to execute certain specified works under powers delegated to them to meet the Administrative needs of the Department;

(iii) "Book transfer".—^Tliis term is applied to the process whereby financial transactions which do not involve the giving or receiving ofcash or of stock materials that are brought to account. Such transactions may either effect the books of a single Accounting Officer orthey may involve operation in the books of more than one Accounting Officer whose accounts are ultimately incorporated in theaccounts of Government provided there is no book transfer between the Divisions in case of sales and supplies effected from oneDivision to other Forest Division;

(iv) "Competent Authority".—Tlie term 'Competent Authority' meansGovernment or any other authority to whom the relevant powershave been delegated by Government;

(v) Contract". The term 'contract' means any kind of undertakingwritten expressed or implied by a person not being a Governmentservant or by a firm for the construction, maintenance or repairs ofwork or for the supply of materials or for the performance of anyservice in connection with the execution of work or supply of materials;

(vi) "Contractor".—^The term 'Contractor' means a person or persons ora firm that has made such an undertaking, but often its use isrestricted to contractors for the execution of works or for services inconnection therewith;

(vii) "Direction Office".—^This term indicates the office of an Administrative Officer who has one or more Divisional Officers workingunder his jurisdiction and is not himself entrusted with the execution of works or with the receipt or disbursement of public money,Le., the Chief Conservator of Forests and Officers of the Conservator of Forests' rank, but if such an Officer is also entrusted with thereceipt and disbursement of public money, he is treated as a Divisional Officer for purposes of this Code;

"Divisional Officer".—This term is applied to an Executive Officerof the Forest Department who is not subordinate to another executive or Disbursing Officer of the Department, even though the Executive charge held by him may not be recognised as a "Division"by the Government. Thus, the officer-in-charge of an independentSub-Division is also treated as a Divisional Officer for purpose ofthis Code;

"Government" means State Government unless the context impliesotherwise;

"Quantity".—In the accounts of works, this expression is used todescribe the extent of work done, supplies made or services performed when these can be measured, weighed or counted;

AKLJ PUBLICATION

(viii)

(ix)

(X)

CHP. Ill KARNATAKA FOREST ACCOUNT CODE 1241

(xi) "Rate".—In estimates of cost, contracts, contractors' bills andvouchers, generally, rate means the consideration allowed for eadiunit of work, supply or other service;

(xii) "Range Forest Officer".—Tliis designation is used to describethose Government Servants who are non-gazetted subordmatesand who are placed in responsible executive clrarge of r^ge worksunder the orders of the officer-in-charge of a recognised Division orSub-Division and the accounts of whose transaction are thereforeultimately mcorporated in those of the Division or Sub-Division;

(xiii) "Sub-Divisional Forest Officcr".-Tliis desi^ation is applied primarily to a Government servant of an Assistant Consei^atorForests' status who holds the charge of a recognised Sub-Division;

(xivf "Advance to Contractors".—This term denotes the amounts paid' ̂ on secuTty to the contractors as 'Advances' before the execuhon or

completion of the works and recoverable from the Contractorsbills subsequently;

M -ApproFM.»--:™V™s-jpida";jof.h.' .u» b, Go,.™-

ment to meet 'Charged' expenditure;, « 1. uohirnc —Tills term denotes the various re-(xvi) "Annual Reports and the closure of tlie

ports or returns to be p p ^ office. Department and theyears' accounts) by the /Administrative and Accounting mat-

j- ^ orivanrp of a fixed sum of money

^IvTtol's—ff disbursements of recurrmg nature.

CHAPTER HIClassification of Transactions

4. lire functions of the Forest Depar^entj^e^^^^^

ing soil fertility; i j--

(xvii)

ing soil fertility, the forests so as to obtain the(b) the exploitation and permanent maintenance and

maximum yield '"/the people, agriculture and mdustnes mthe supply of the needs of the pe ̂ j g ofthe matter of forest ^ment of forests, the con-

struction of roads and briag

AKLJ PUBLICATION

1242 KARNATAKA FOREST ACCOUNT CODE CHP. Ill

up of remote and inaccessible forest areas, and the construction ofbuildings required by the Department in connection with the administration and working of the forests and preservation of wildlife;

(c) the conduct of research into silviculture, utilisation and other problems affecting the regeneration and development of forests andwild life.

5. The transactions of charges and receipts pertaining to the ForestDepartment are classified in the accounts of the Divisional Officers underthe appropnate expenditure or revenue heads concerned.

inwtn Establishment—'Permanent Establishment'includes all officers of whatever rank who are required for the ordinaryadmmistration of the forests on permanent basis.

Temporary Establishment' will include non-permanentestaWishment and entertamed for the general purpose of a Division or

for purposes of general supervision as distinct from theactual execution of the work or works and is continued from time to time.

Creadon o%mpor5,%°'(b) The appointoents to posts of temporary establishments are made in

accordance with the procedure laid down in general recruitment rules asper powers delegated to the various officers of the Department.

(c) The leave, travelling and other allowancesestablishment are governed by the provisions of K.C.S.Rs.

9. Labour. Under Labour is included all bonci fide manual labouremployed, whether.—

(i) on the reaping, collection, fashioning, removal, transport and saleof forest produce;

(ii) on the feed and upkeep of live-stock;

(iii) on the construction and maintenance of tools and plant;(iv) on the construction and maintenance of communications and

buildings;

(v) on tlie demarcation, improvement, extension and protection of forests;

(vi) on Wild Life Works; and

(vii) similar other works.

Note.~No establishment, temporary or permanent can be broughtunder this category. ^

nf maistries or gangers are included under the heada our, ut any higher supervisory personnel is distinctly excluded.

of temporary

aklj publication

CHP. Ill KARNATAKA FOREST ACCOUNT CODE 1243

Tlie following items shall not be included under labour.—(a) Crews of boats permanently maintained for the use of the depart

ment;

(b) Gardeners, tope-watcliers and other workmen permanently employed;

(c) Watchmen and sweepers employed in permanent depots or build-ings;

(d) Letter carriers employed under special circumstances for more thana month at a time;

(e) Temporary office establishments, i.e., persons entertained for anyclerical work.

10. Tire wages of labourers will be shown in the Muster Rolls andcharged to appropriate heads of expenditure.

^ J I „ rnmoetent to sanction the employment of11. Forest Officers, who ^^mpet employed is notlabour, are personally responsible to ensure mat m fretained for a period longer than is actually necessary.

J . uiici,n,ent —(11 Works establishment will mclude12. Work charged estabhshme . U execution of workssuch establishment, as is ^ to the concerned works. Whenwhose pay and allowances are temporary establishment arethe employees borne on 'he .Penn^J for the timeemployed on the works of this na , substitutes on thebeing charged direct to the works^ -n^e W the headregular establishment should however 5-E,l.bli.hm.nt- unto j m., b. mployrf

(ii) Employees borne on j important works or schemes.

sub-head in the case of concerned s Competent Authority for(iv) In all cases prevmus is necessary which should

employment on work charg .specify in respect of each appom ^

(a) the rate and the scale p Y(b) the period of sanction; jhe per-(c) full name of the works and

son engaged would e p charged establishment will(v) Increments of .*'^%'"'S:frroi?ure''iweTm respect of regular

be regulated according to Pestablishment. urci-impnt should be maintained for

(vi) The service books of dates of the accrual of increments,each incumbent for watchmg the correetc.

aklj pubucation

1244 KARNATAKA FOREST ACCOUiVT CODECHP. Ill

ur ieaye and T.A. Rules of the members of the work chargedestablishment, if they belong to the permanent or temporary establishmentwould be governed by the leave and T.A. Rules of K.C.S.Rs. Tlie leave andi.A. ot the other members of the work diarged establishment will howeverbe regulated as per orders issued by Government from time to time.

I. (a) Disability and other extraordinary pensions and gratuities are incertam cases admissible in accordance with the Rules of the Kamataka CivilServices Rules.

(b) Gratuity.—

(i) Minimum qualifying service which entitles for terminal/death Gratuity.

Ten years continuous service in the respective categories.(ii) Scales of Terminal and Death-Gratuity.

At the rate of one month's pay last drawn at the time of retirementtor each completed year of service. '

(in) Maximum amount of gratuity admissible.

pay upto the date of superannuation, ifthere is no provident Fund Scheme.

(iv) Service counting for Gratuity:

292%^o'fKr^Tj'®" ^ Clause B of Rule2y2-B of K.C.S.RS., may be adopted for this purpose.(v) Procedure for preferring claims, their verification, etc.

The procedure contained in Part IV of K.C.S.Rs. regarding prefer-

SlTof ̂alf to thL. • ^ cases where no service registers are main-

ice'"ren£eT bv T'' Officer will have to certify the details of serv-preoared or nth ^ reference to the acquittance rollsprepared or other records maintained for them.

(vi) Expenditure on Gratuity:

be debitSf tn^ fh gratuity sanctioned to this staff is toment benefits — 4 ~ ̂ account "266 pension and other retire-under the revised PensionE"^^^ allowances - 5 - gratuities"

(vii) Mode of payment of Gratuity:

Wmenrol ^ 292-B of K.C.S.Rs. foris to be follow^ Gratuity on retirement and death cases

sion and thrgTaShv^ such staff may be worked out by the Divi-(Pension) Verificatif^ forwarded to the Accountant Generalcompetent as oer K r q p sanction of the authorityper K.C.S.RS. After certification of the gratuity admis-

aklj publication

CHP. Ill KARNATAKA FOREST ACCOUNT CODE 1245

sible the amount of gratuity will be authorised by the AccountantGeneral in favour of the Divisional Forest Officer concemed Inturn the Divisional Forest Officer, has to draw the amount fromthe treasury for disbursement to the person concerned.

II. Earned Leave.—Tlie authority competent to fill upgrant Earned Leave to sucli members as are emp oye ^ r jfrom year to year upto 1/llth of the period of fand limited to sixty days at a time subject to the followmg condihons.-' ' Leave cannot be claimed as a matter of right. Discretion is reservedauTlwity empowered to grant leave

at any time accordingly to the exigencies of public service.4 o. workduty without leave shall not be ^sence, shall be treated ashis absence and the period ° absence from duty of aextraordinary leave ujij^ment without leave granted bymember of work charged es render suclr person liable tothe Competent Authority, will also renaer pdisciplinary action for misconduct. .hp

. fhp leave allowances to tne(i) that if no substitute is ̂ PP , ^ before the leave com-

"rku-S wove.^ - . Ip^VP-

(a)

(b) A

if any, ot sucn pay u... ^

Exception.—In the case of a lorry die incumbent proceeding onbe appointed against the the rate of pay he was drawmg onleave may be paid the leave allowanthe day before he proceeded on eave.

(ii) that leave shall not except for appUcant has

(2)

condoned oy

(ill) that leave shall not be permissi e^^^^ at the time of granting(1) Unless, so far as can be for a

the leave, the months after the expiry ofperiod of not less than six mleave; and agreement to the effect thatUnless the employee si^^ establishinenthe will resume duty fo, a period of not lessshould his service be ̂ leave (on thethan six months j jy); andforfeiture of his leave s J ^d 90 days, re.,

continuous duty then pertoAKLJ FOBLICATION

1246 karnataka forest account code CHP. Ill

mterrupted, all claims to leave earned upto the date will beforfeited, unless otherwise such interruptions are condoned byCompetent Authority.

III. (1) i^y extraordinary leave enjoyed by a person on the workcharged estabhshment should have the effect of postponing the increment.

(2) (a) Extraordinary leave taken by a person on the work charged^ablishment m excess of 3 months, should constitute a break in service.

such a person resuming duty. Competent Authority may grant higherstartmg pay to which he would have been entitled but for such break inspecial deserving cases.

(b) Casual Leave.—Members of work charged establishment (includingdnvers) of the Forest Department may be allowed casual leave of 15 day^according to the provisions contained in Annexure-B of K.C.S.Rs providedno extra expenditure is incurred on this account by the department. Casualleave is admissible only to those who have put in not less than three vearsof service. ^

Note.-Special casual leave not exceeding 7 days in any one calendaryear on undergoing vasectomy or tubectomy operation on the strength ofMedical Certificate granted by the Medical Officer performing theoperation may be granted to work charged establishment.

establishment, rendered by a person onthe work charged estabhshment should be treated as duty for purpose ofmcrement m the original post on the work charged establislLent

(4) Short spells of officiating service on the reeular estat>Iiclimonfaltering the service on the work charged establishment should be treated ascontmuous for purposes of calculating the leave.

.cfS- officiating service of a member of the work chargedKtabhshment m a post on the regular establishment should not constiLean mterruption of service in the work charged establishment.

work^chareed^PsiaW^'h'"'^''." seniority, service on the temporary orfor incremfnt h an! continuous has been allowed to countservice, when contirnm^ ^ ® temporary and work chargedsenioritv nrnmnf treated as continuous for purposes ofthissenTorfty. ' ®'^'^°''dffis'y be effected on the basis ofestablishment ̂ thp'^Fnr^T n members of the work chargedmanner as is sanrKn ^ i ®P®'^bTient shall be sanctioned in the samecondition that if anv J? regular establishment subject to theholidays due to ^ by them on these

over-time allowance L such LuX^k"'^^ will not be entitled to anyIV^ T* IT'

Members of the work^chame^^ Charged Establishment.—(i)of travelling alhwancp pc ^ will be allowed the same ratesS iowance, as admissible to Government Servants in regularaklj publication

CHP. Ill KARNATAKA FOREST ACCOUNT CODE 1247

establishments under K.C.S.Rs., 1958 as amended from time to time.Wlienever the pay of such establisliment is fixed so as to cover the expensesof journeys also, the claim for travelling allowance will be regulated witireference to the conditions applicable to such cases.

(ii) Wlienever members of work charged establishment are transferredfrom one place to another in the interest of public service, they are alsoentitled to joining time and joining time pay admissible under KarnatakaCivil Services Rules, 1958.

(iii) Advances of T.A. may be paid to the members of the work Aargedestablishment (Forest Department) who have put m a connot less than three years to cover the actual journey expenoffice imprest, subject to the condition that the amount of suA advan^does not exceed the actual travelling allowance admissible to t^^^^respect of the said journey. Such advances if no a jus e pmolovees tothe following month should be recovered from the pay of the employees towhom the advances have been made.

14 Salaries and Allowances.-Claims on account of salariesallowances of Gazetted Government incontingent establishment^fsev^^^^^^

the case may be, if required by rules.Detailed rules in this behalf are contained in the Karnataka FmancialCoJ, .„<! CWil S.r.»s RUa ^IS. Travelling Allowance Brils.—TraveU S ^ prescribed

and non-Gazetted staff, should be F P ..gjsuries or forwarded to theform, and presented for as the case mayAccountant General, for ® Allowance bills requiringbe, as required by rules. Traveumg Controlling Ofhcerscounter-signature should be duly Accountai^t General, forbefore presentation at the , instructions for the preparati^ ofpre-audit before encashment, e ̂ the Karnataka Financial CodeTravelling Allowance Bills are contained mand K.C.S.RS. , • j the Manual of Contingent

16. Contingencies.—Rules Department in respect ofExpenditure should be observe cheaues should not be issue mexpenditure towards contingencies. Chq ^^^^^^ wiU ̂payment of charges on account of th officers and they should betherefore appear in the accounts of Ac Fore ^ Register okept entirely separate in eaA office showing mcontingent expenditure should c P . jy^-heads enumera ethe expenditure incurred un e"Contingencies". are allowed a fixed perrnanent

17. Permanent Advance.—Forest contingencies. The a vance

advance to meet the expendi u

aklj publication

1250 KARNATAKA FOREST ACCOUNT CODE CHP. IV CHP. IV KARNATAKA FOREST ACCOUNT CODE 1251

funds required for all disbursements in connection with the execution oworks or scliemes. He also collects departmental receipts of the Divisionand pays them into the Treasuries or the Banks.

fb) The accounts of these receipts and disbursements (including thetransactions of subordinate Government Servants working ""^er him) a ecompiled under his supervision by the Divisional Superintendents and arerendered monthly to the Accountant-General on due dates.

Thp Divisional Forest Officer is further required to maintain clear

make these accounts available for audit.(d) Personal payments to ̂ 'V ^^r^drllng bX'^

and the {^ttirtRne ̂ K.F.C M.C.Etreasuries in accordance with the g p Accountant General himself

o,»c.„ - p.« .3

omcor h.,

.».cco™„

fully recorded as to afford the "ny case, even though suchthat may be made into the . Les of'the transaction. It isenquiry may be as to the economy or ̂ he measurement andfurther essential that xdHcU and self-contained as to btransactions in general must ^ evidence of facts ifproduceable as a satisfactory \mnz or taking of cash, stores,a Court of Law. All transactions ® ggfons, which have moneyother properties, rights, privileges .i" of a transaction of a rece^P^value should be brought to account. T under the final or theor expenditure should always be rnade a oor remittance head to which it pertains. pivisio^"^^^

25. (a) Relationship with the is responsible notOfficer as a primary Disbursing Officer of the whole Division/ bonly for the financial regularity of the transaction o correctly and ir'also for the maintenance of accounts of the transac , render 1^^accordance with the Rules and Codes. He is further req j.g|^ion in tb^accounts to the Accountant-General for audit and for m pgeneral accounts. j^^is

(b) The Divisional Forest Officer is responsible for the j, ̂ oubtDivision and which should not be allowed to fall into arrears, but

consnil^®'°" which in his opinion cannot be clearCons^!^!Jr °l Accountant-General, he should seek orders ottor of Forests without delay to finalise in consultat

aklj publication

Accountant-General. If the proposal involve extra Cft, sanrton ofCompetent Authority is necessary for employment of additionalestablishment.

(c) Accountant General's inspection.-Tlre Accountant-Generalarranges for the periodical test audit and local inspecton o le arco^the Division aAd Subordinate Offices and theresponsible in making available the initi^ accounts andrequired for the purpose. Tlie Inspecting Officersdrafts of the reports with the Head of the Office inspectmg beforesubmitting them to the Accountant-General and for this purpose, the headofti^^ offfce slmuld arrange to be present at the headquarters dunng theperiod of inspection or atleast on the last day of it unless prevented byexigencies of work.

(d) Hie following procedure should be adopted in dealing with sureports of inspection.—

(i) The report will be sent officially by tlie Accountant-General to dieDivisional Officer concemed who should submit it widi his repliesto the Conservator of Forests within a month of its receipt.

Conservator of Forests,

(iii) Such of the outstanding P^agraphs as areFomste \GtnS7sp^^^^^^ ™ef Conf S Ws

rif Forests should also send to the Account-

this behalf;

(V) Cases involving wherever a question of policy or pro-S .houM b.cedure Accountant-General does not accept proposals

(vi) Tlie cases m whiA Ac® j Forests, as well as generalo, Orim f ,*• "I"'" -J'"'question of importo fo, such orders.ment, will be reported

Note.—1. The dates specih ^j^j-erned.any delay should be noticed seriousty by

2. The Chief °',.°sudi Inspection Reports should mvariablyother Officers dealing with all s P^^ explanations or furtherspecify a time-lunit ^ gydi reports and strictly enforce theinformation on pomts mciuutime-limit.

aklj publication

1252 KARNATAKA FOREST ACCOUNT CODE CHP. IV

3. The Divisional Officer's presence in headquarters to discuss the pointsraised in the draft reports with the Inspecting Officers will not only help inelimination of such of the points included in the draft report as aresatisfactorily explained during the discussion, but also minimise delays intaking further action. Whenever it appears likely that the presence of anySub-Divisional Officer or subordinate will help elucidation of the points inthe report, they should be summoned to be present during the discussion.

4. Inspecting Officers making comments on the confidential recordsshown to them are expected to write all such comments in their own handtreating them as strictly confidential and submit them separately from theregular inspection reports to the Accountant-General.

26. Communication of sanction to the Accountant-General. As ageneral rule, every sanctioning authority is responsible for all sanctions andorders against which audit of receipts or disbursements is to be conductedby the Accountant-General are communicated to him in accordance withsuch procedure as prescribed.

27. Result of audit.—Tlie result of audit are communicated to theDivisional Officer in the form of audit notes, objection statements, letters ormemoranda. They are also communicated in the form of InspectionReports, the procedure relating to which is detailed in the aboveparagraphs, ^lese should receive prompt attention. Replies of theDivisional Officer to these documents should be satisfactory and conipleteand should be submitted with least delay.

28. Objection Statements, Audit Notes and Inspection Reports should bereturned through the Conservator of Forests after the Divisional Officer hasrecorded his replies thereon, but the Conservator of Forests, will passorders m certain matters which he is competent to deal with finally andrecor is remarks on all the other points before returning the abovestatements and reports to the Accountant-General.

29. Once a transaction has been entered in an objection statement orotherwise dealt within one or other documents referred to in the foregoingparas, t le responsibility for having the objection removed will devolve

Officer and the Accountant-General is required to

clearLirc of^ob authorities all important items and serious delays in the

sanfhvin is usually removed by obtaining the requisiterelevanf' necessary recovery, by correcting or completing theinformation voucher, by furnishing necessary documents orspecified nifpT ° ^'^^se securing compliance with the provisions of aas beine TT"" ^ an audit objectionintimaHLof?tc; w>h?^ objection should be held to be in force unlesstimahon of Its withdrawal is received from the Accountant-General.

coming to h^^noHce^S^ objection any traiisactionexcess expenditnrp' r» covered by adequate sanction or involvesr constitute an irregularity. In some cases the

AKLJ PUBLICATION

CHP. V KARNATAKA FOREST ACCOUNT CODE 1253

Divisional Officer may have already taken action to regularise thetransactions. For example in cases of excess over smiction not requirmgrevised estimates, he may have either approved the excess or sou^itsanction of higher authority therefor when the excess ishis powers of sanction. Yet if the necessa^ intimation of ̂ be requisitsanction or approval does not reach the Accoun an - ener UpincDivisional Accountants in which the regularaudited, the Accountant-General will raise the o Ugsupposed to assume that the necessary sanction or ers laaccorded. Tlie Divisional Officer ^bould b,eref°re ̂Accountant-General at the earliest opportunity "^bmation of suchsanctions and orders as are required to be commu^d .T^tei^Snt orfurnish him without waiting for the receipt of le o 1® which theaudit note, all necessary information or documents without whichrelevant transactions cannot be admitted finally m audit.

Note.-Tlie object of this Rule is to obviate ®audit objections but °b)ections ̂ fte transactions and byrequirements of financial n,ay be, such sanctionstaking timely action to ° jn'^vhich a deviation from the rule hasor orders as may be required in cases in wnicn aoccurred.

CHAPTERV

Appropriations and Control of Expenditure

31. Revenue is realised and ib butwhen it falls due under the statutoiy Legislatureexpenditure can be incurred on^iy against g ^ ^ diargedor an appropriahon made V between the voted and chargedexpenditure. Tl"ie incidence of P. r ^ Constitution,is determined by the relevant provisions of the Go

1 inmrred on works or schemes.32. Expenditure can only be in

(i) if sanction either special obeen obtained authorisi g ^gve been provided by(ii) if funds to cover "specific provision for the same has

the Competent 7 gbmates of the concerned year after ap-been made m the budge Conservator of Forests;p™i„8 .h. pl» of ,f ,h. Con-

(iii) if the expenditure thereunder and in accordance with?K^cS mles! regulations and orders issued by Competent

of f'""'' " ° '

AKLJ PUBLICATION

1254 karnataka forest account codeCHP. V

aoDromiaH^^^o ^ divided into primary units ofnecessarv mfn' ^ a ^ divided and sub-divided as may benecessary into secondary units of appropriation.

DeJafnin^fn^l^^v minor and detailed heads of appropriationpertaining to the Forest Department are specified in Appendix I

OnpffLn"""^' ̂ Operations.—(!) Tliere shall be an Annual Plan ofrespect of each forest division. Tlie Annual Plan of

ni^n nf ^ e prepared for both plan and non-plan respectively. TlieDronn«L°fT various works which arenraE- ■ f' durliig ensulng year based Oil llieDronnsort°'i'^ 1 Working Plan and the various schemes which are

1° ™plemented under different budget heads. Wliilenrpviniic ^ i!^ Operations spill over works of the

. be given first priority and only after providing for allicciioi?K works, fresh works should be proposed. The instructionsy le iigher officers from time to time should also be kept in a vieww ̂^0 plan of operations. Tlie Plan of Operations should beimi e 0 the budget head allotment indicated to each division undervarious heads of accounts both plan and non-plan for the year.

(2) In respect of any additional allotment provided during the course ofthe year under any sclieme under plan or non-plan, supplementary plan ofoperations should be prepared and got approved separately.

(3) Tlie Deputy Conservator of Forests shall submit the Plan ofOperations in respect of his division by 20th April of the year. TlieConservator of Forests shall scrutinise the Plan of Operations submitted bythe Deputy Conservator of Forests with reference to the allotment for theyear and approve the plan with such modifications as he may considernecessary and communicate the same to the respective Deputy Conservatorof Forests before the 30th of April of the year.

The Plan of Operation and estimates should be submitted by the Rangeorest Officers to Deputy Conservator of Forests through the Assistant

^conservator of Forests by 10th of April of the year.(4) The Conservator of Forests may call for a meeting of the Deputy

Pta^o^per ̂ during the last week of April to discuss/finalise the®'<ecuted withoue the approval of the Plan of

the Plan nf r/ ®.^°^s®fvator of Forests. However pending approval ofODeratinn m over works which are proposed in the Plan ofv^peration may be executed.]

OfficL, a Officer should submit to the Divisional Forestthan the 10th of Tnno°^n^u^n^ relating to his Range every quarter not later

' September, 10th December and end of Marcli

13-10-1987 substituted by Notification No. AHFF 2 LFFI 87,

aklj

dated

publication

CHP. V karnataka forest account code 1255

showing the extent of progress made during the period under the column"Result of operations" for Non-plan expenditure. In respect of planexpenditure, the progress reports shall be submitted in the form and by thedate prescribed from time to time. The DFO will collect the informationthus obtained and submit the consolidated return to the Conservator ofForests, for the whole Division every quarter.

(6) Tlie Divisional Forest Officer's Annual Report will be based entirelyon the return for the quarter ending Marcli. Tlie Divisional Forest Officerwill be personally held responsible for the careful preparation of all returnsand their punctual submission.

35. The Range being the unit of Administration, the plan of operationsshould be drawn for each Range separately. Tlie Annual P an o opera ionshould provide for fellings, thinnings, etc., according to sanctioned work^plans for extraction of forest produce, control of grazing o ca e,against fire and execution of works of regeneration and ̂ ° ratP<i willexercise of rights which have beer, recorded m the ^necessarily be provided for in these plans, ̂ ae plan o P ,contain detailed rates for the proposed ordma^ 'approximate anticipated cost for all the capital wor s prop

36. Tlie Budget will be framed on the basis of the annual plan ooperations.

37. Tlie Divisional Officer will 5g^X'''of Fores^witiioutHie plan of operations as approved by C , . deviationsintroducing any deviations unless specific PP A„fhoritv in advance,found necessary, is obtained from the • gj-^all amount to anAny ,h. app«,«l Pl'" Scr "11 b.unauthorised expenditure for which th recoverable from theheld personally responsible and the amount shall be recoverDivisional Forest Officer. , j

38. The plan should ordinarily budget estimates on suchsubmitted to the Conservator of Fores s circle-wise should bedates as prescribed by him. Tlie P ° P Chief Conservator of Forestsfurnished by Conservator of Forests, « theaccording to the instructions issue y

39. Annual Budget Eshmates-me during the ensumgreview their requirements of gran , . statement in the prescribedfinancial year, and submit ggity for funds to the extent appliedform explaining clearly therein ie --Q^Qsed works and of all items offor, especially in the case of i -g^QjAjg over and above the usual andexpenditure demanding specia P , ̂ Estimates should be prepared bynormal allotments. ,Hpr eacli minor and detailed heads m thethe Divisional Forests Officers u Conservator of Forests eacliprescribed Form FAC prepare Amiual Budget Estimatesyear. Tlie Conservator of to Hie Chief Conservator of Forests,of the Circle each year fu^^ Estimates for the wholeFrom these Annual Budge

1256 karnataka forest account code CUP. V

State will be prepared by the Chief Conservator of Forests (General) whowill prepare and submit a consolidated copy of such Budget Estimates forf Government in Finance Department as per theca en ar prescribed for regulating the Budget work each year. No new

neads should be introduced without the approval of the Government in theFmance Department.

40. Distribution of Grants.—Tlie Chief Conservator of Forests and theConservators of Forests will allot funds to the several Drawing Officers,regulating the distribution of the forest grants sancHoned by Governmentaccordmg to the programme of works (Annual Plan of operations) to be

W^n IT®/ ! I" Divisions. Tlie Chief Conservator ofconv nf thl amounts so allotted in Form FAC 2. AAccLnUt Cen^r o grants so made should also be sent to thewatS^^rthe information. Tlie responsibility ofwatchmg the drawmgs agamst the grants apporHoned by the Chief

SfiiTwL afe sMoh' F°re7te rests with the Drawingwithin the limit of the restrict the drawings and keep themwithm the limit of the allotments under each head as well as each sub-head.

or in wMe^or roKr''"" surrender grants at their disposal in partin whole or apply for more funds if any necessity therefor arises but thelatter course should seldom, if ever be followed. eror arises out tne

The distribution of the total amounts provided in the Budget would bedone according to the requirements of the works or scheme! coTcentdSubsequent transfers or reappropriation would be made by the ComoetentAuthority according to the power delegated to him. All such t!S ore-appropriations of funds should be intimated to the Accountant-Qineral

41. Usually no applications for additional grants should be submittedunless such applications are suDDorted hv f suDmittedshould be Zly explained TRe-appropriation of grants be in urgent cases should Bpreference to the concerned works or schemp«; affp u! •Competent Authority. The application fnr , j.®. ^Pproval of theaccompanied by a le«er should bethe cost of different operations on whir! j detailmg the nature ofincurred. No new charges should be included P''°P°®'=d to bethey are sanctioned by the Comoetent a tf "L ®"dget Estimates untiladd'ed at the end of the LgeTStts" ex'^' !•charges which are anticipated to be incurred du lu"^of Government approval. during the year in anticipation

42. It should be distinctly made clear thaf if • ,of the Budget grant has been entered in a rl l Jdoes not constitute any authority fnr pv ^ estimate of charges thatapproval of the ComfetenrAu^hor fof a!*®mcurred should be obtained in the form nf a expenditureoccasion for such increased expenditure^r^ses

CHP. V KARN ATAKA FOREST ACCOUNT CODE 1257

aklj publication

43. Under the receipt heads the sources of revenue, tlie quantities ofproduce proposed to be removed and the amount expected to be realisedshould be given.

44. (i) Tlie expenditure should be classified under Revenue Expenditureor Capital Expenditure as the case may be.

(ii) Tlie expenditure is either Revenue or Capital, tlie distiriction betweenthe terms being used only for the purpose of definmg tie powers osanction to expenditure by various authorities.

"Revenue" and "Capital" Expenditures;

45. "Revenue" Expenditure comprises the cost of all whrfiare necessary to produce revenue or ^maintenance and the ordinary operations undertaken annually for theimprovement of the forests.—

(a) Cost of tending operations, i.e., thmnin^ improvement, fellings,cleaning, creeper cutting, stubbing out of Kana grass, etc.

(b) Tlie cost of all measures fortions, example, clearingdebris of fellings, boe'ng natural reproduction, reopening

tion of natural death. Forest the preservation of

expenditure is of 'Revenue or pthe principle enunciated herem. represents charges whicli

46. "Capital" Expenditure, o ijnmediate return. Capitaldo not recur annually or whicli ^ ̂ for a series of years, or repaycharges frequently " u rehims or in local benefits of other kmd,themselves only onnplv protection against storms, erosion orsuch as the increase of water supply, ylandslips. regarded as involving

47 Each proposal for such worked out in full detail to

shL that all the measures have been

aklj publication

1258 KARNATAKA FOREST ACCOUNT CODE CHP. V

that the result is likely to be ultimately profitable to such a degree as tojustify the outlay.

48. The principles to be observed in deciding whether an item ofexpenditure should be charged to "Capital" or "Revenue" are as follows.—

(a) "Capital" bears all charges for the first construction and equipmentof a project as well as charges for maintenance on sections notopened for working and charges for such subsequent additions andimprovements as may be sanctioned under the rules by CompetentAuthority. It may also bear charges on account of restoration ofdamages caused by extraordinary casualities, such as flood, fire,etc., and such charges should be recorded under a separate minorhead "Extraordinary replacements".

(b) "Revenue" bears all charges for maintenance and working expenses which include all expenditure for the working and upkeepof the project, as also for such renewals and subsequent replacements, and such additions, improvements or extensions as it maybe considered desirable to cliarge to revenue instead of increasingthe capital cost of the undertakings.

(c) In the case of renewals and replacements of existing works, if thecost really represents an increase in the capital value of the systemand exceeds the cost of the original work by Rs. 1,000 the cost of thenew work should be divided between capital aiid revenue, the portion debited to the latter account being the cost of the originalwork, which should be estimated if the actual cost is not known,and the balance charged to capital. In other cases, the whole cost ofthe new work should be charged to revenue. Tlius a renewal whichdoes not represent a substantial improvement of the original workand which is in all material essentials the same as the latter although it may exceed the cost of that work by more than Rs. 1,000should not be charged to capital but to the revenue account.

Items comprising "Capital" Expenditure:

49. The foUowing items come under "Capital" expenditure.—(i) Construction of permanent roads, tramways, bridges, buildings, ca-

na s, wells, timber slides, saw mills, factories, etc., including equipment of houses, saw mills, factories, etc.

(ii) Purcliase of live-stock, stores, tents, tools and plant.(iii) Purcliase of l^d for plantations and forest purposes, and cash

compensation for extinction of forest rights.(iv) Expenditure on forest settlements and demarcation of Reserves.(v) Cost of Forest Surveys.

Sumerafi^s^^^^ working plans including valuation surveys and

AKLJ PUBLICATION

CHP. V KARNATAKA FOREST ACCOUNT CODE 1259

(vii) Plantations including extensive cultural operations, renewds, adch-tions and improvements under the above items of expenditure willcome under "Capital" expenditure, while ordinary repairs to thecapital works come under "Revenue" expenditure.

50. The necessary funds for works carried out under the supervision ofthe Public Works Department will be provided for in tlie Budget of thisDepartment.

51, Whenever the outlay on any one work or item within the year isexpected to exceed Rs. 10,000, all needful particulars regardmg such workof item must be entered separately in an explanatory note to e u geEstimates.

Note.—Construction of all forest buildings costing not25,000 in each case may be undertaken by the Forest Departmen i e

52. Regarding the details that should be given in tliethe Divisional Forest Officers in justification of the P^P®®? .. ^the following points should be kept in view. Important deviationsfigures of former years should be clearly explaine .

FOREST PRODUCE

53. Timber and other j'oj/jndBamboL.—Government Agency: Timber, Firewood, ̂ , working plans of thecase, the number of trees to be felled accor mg -g workingforests in each Division has to be assesse estimated must beplan, the grounds for proposing fellings .^^roved plan. The Chiefstated, ivith the sanction ° and cost of each operation,Conservator of Forests has full powers. Th depot, etc., in cubicsucli as felling, logging, carting, specifically. If it is proposed tometres per log or otherwise, must be ̂ ^ed rates and cost must becut timber into planks or scantlings, the estimateaspecified. , .v, works.—If previous sanction of

54. Roads, Bridges, Buildings an ° , these works has not beenthe Competent Authority for gi^guid be prepared and gotobtained, a detailed estimate commencement of the work,sanctioned by the Competent Authon y .wgof is covered by budgetprovided the expenditure to be mcurred thereorprovision. „.rks.-(a) Demarcation of

55. DemarcaHon and outlines and mathematicalboundaries.—Perfect symmetry of . Xjg and may be aimed at as isaccuracy of boundary are theorebca y desirable to saaifwe ̂ ypracticable, but to secure these yg plots of land of considerablematerial area of forest, to exclude from ' ̂ j^^g covered beessize whidi have been included m ^i^ivation any compara ve y Sand vegetation and to take , crops are now grow. ®quantity of land on which rice or g j.^ reasons exist rethe boundary line is very irregular, ana

AKLJ PUBLICA-nON

1262 KARNATAKA FOREST ACCOUNT CODE CHP. V

year concerned, the Conservator of Forests shall take into account theworks to be carried out in the Division as per plan of operations drawn up,the special and urgent works to be carried out during the year underspecific orders of higher authorihes and the sanctioned Budget Grantsprovided for expenditure during the year.

67. The amount thus specified by the Conservator of Forests to be drawnby means of cheques from the Bank/Treasury by the Divisional ForestOfficer/Assistant Conservator of Forests in each year, shall be shown in themonthly current account under the "Debt and Remittance Head" — "ForestAdvances", under the column Budget Grants, to watch the overdrafts, ifany, by the Accountant General and shall in addition, be shown in theRegister of Cheques drawn at the end of each month in the followingform.—

(1) Amount authorised to be drawn during the year by the Conservator of Forests;

(2) Amount drawn up to the end of the previous month;

(3) Amount drawn during the month;

(4) Total (Cols. 2 and 3);

(5) Balance amount available for drawal during the year.68. The copy of the monthly Register of Cheques drawn shall be

rendered simultaneously by the Divisional Forest Officer/AssistantConservator of Forests to the Conservator of Forests and to theBanks/Treasuries concerned, who shall watch the overdrafts of funds ifany, from the Bank/Treasury by the Divisional Forest Officer/Assist^itConservator of Forests and if such an event arises, the Bank/Treasury shallrefuse overdrafts and the Conservator of Forests shall call the DivisionalForest Officer to order immediately besides taking such steps as are foundnecessary against the Divisional Forest Officer for such overdrawals.

^[All LOCs issued by the Conservator of Forests to the DeputyConservators of Forests shall expire on the 31st March of the year Nocheques shall be issued after this date. Tl.e Deputy Conservator of Foreststnt'J Accountant General, thetotal cheques drawn figures for the month of March bv Telegram orMuddam on the 1st of April He shall also intimate the number and date ofthe last cheque issued m each of the cheques book in use by him.]

69. The amount drawn by the Divisional Forest Officer/AssistantConservator of Forests from Banks/Treasuries for work each vear shall beadjusted by him during that year alone bv c i i ^ .

over against the relevant budget grants of the succeediL Tear AU final?"asu™ in full ani/rediied to theTreasury and when disallowed and in no case shall such disallowance be

1. Added by Notification No. AHFF 2 LFFI87, dated 13-10-1987AKLJ PUBLICATION

CHP. VI KARNATAKA FOREST ACCOUNT CODE 1263

allowed to continue more than three months from the date of suchdisallowances.

CHAPTER VI

Cash Accounts

70. (a) Cash Accounts for accounting cash transactions.^iere shall betwo Cash Books, viz., (a) Works Cash Book, (b) General Cas oo

(b) General Cash Book.—Receipt of money received and paid at a forestoffice may be divided into two classes.

(1) Money drawn on bills from the treasury on account of salary, es-tablishment, travelling allowances and contmgencies.

(2) Forest Revenue, Deposits, cash recoveries f 'han 'toe relatagto (1) above and disbursements on account oest Works' or refund of revenue,bursements either -

operations of department. We Htransaction is accounted be notea agams _umn of the Cash Book, the pages of the cash bookbered before it is brought to use. ...rUnrised

(a) Works Cash Book.—Every teTp'afl account in Cashto receive or disburse Government money s cnb-clause (2) above, inBook (Form FAC-5) for transactions ,„_,„(,tions as tliey occur butwhich he should enter not only all monetary transachonsalso book transfers. sub-clause (1) above

(b) General Cash Book.—Money drawn Pshould be accounted in this book. unoKmpnt travelling

Cash recoveries on account ofallowance and contingencies itted into Treasury/B^k anreceived from the Courts should be rem ttea beshould not be credited in the Cash Bookshown in the General Cash Book. members of the

Similarly, all personal advances Cars and ^bUlsDepartment on account of transfers, etc., to themCycles and other conveyances, o transactions per ^ thepresented at the Treasury/Bank and ^^t only shoshould not be brought on into the worksGeneral Cash Book. , and open m^ner. Ai

71. All accounts must be kept "^atever no ̂ par®'®■•eceipts, disbursements and charges of wh^^ ^s and no Ppublic service must be clearly fho^^ . ^ authorised,recounts be permitted, except w le become u

72. Payments must be promptly ma e asaklj poblication

1266 KARNATAKA FOREST ACCOUNT CODE CUP. VI

custody of Government money in his charge and will keep the key of it inhis own possession. As all large payments should be made by cheques andall large payments should be made by cheques and all revenue be paid intothe Treasury/Bank as frequently as possible, ordinarily not exceeding oneweek, the amount on hand at any time need only be very small. Under nocircumstances shall any Forest Officer or subordinate place any privatemoney in the Government Cash Chest. Government money should be keptin a Cash Chest separate from non-Govemment money and kept entirelyout of Government account.

77. Whenever necessary. Government may authorise, the appointmentof Treasurer to be in-charge of the Cash Chest after obtaining adequatesecurity from him.

78. Members of the Office Establishment should not be entrusted with

the collection of Government money, except on account of the pay of theoffice establishments, and for contingent cliarges, which should as a rule bemade payable only to the head of office. Tliey should not be also authorisedto receive payment for forest produce unless specifically allowed to do so.All subordinates who are in the custody of Government money or who dealwith the collection of Forest Revenue should be made to furnish security asprescribed. The Controlling Officers are responsible to see that the securityfurnished is sufficient and is in one of the forms prescribed in Article 355 ofK.F.C. Steps should be taken for periodical check of the currency of thesecurities by the head of the office.

Term 'Cash' Defined

79. The term 'Cash' includes legal tender coin, currency notes.Government Cheques and drafts on scheduled bank, payable on demandand remittance transfer receipts.

Note—1. Government Securities, Deposit Receipts of Baiiks, Debenturesand bonds accepted as Security Deposit under rules of Government, do notfall under the term 'CASH'.

Note—2. Cheques received from private individuals should be treatedas cash only after their encashment. Cheques drawn by GovernmentOfficers in favour of Forest Officers be treated as Cash while they are intransit to the Treasury.

[Note—3, A Government Officer receiving money on behalf ofGovernment must give the payer a receipt in Form 1 of Kamataka Financialode, 1958. T^e procedure prescribed in Article 6 of Kamataka Financialo e, 1958 with regard to obtaining printed receipt books and maintaining

comp ete accounts of the receipt books should be scrupulously followed.]

aq Disbursing Officer should check all the entries in his Cash Bookas possible after the date of their occurrence and he should initia

Notification No. FD AHFF 13 FAF 92, dated 30-3-1995, w.e

aklj publication

CHP. VI KARNATAKA FOREST ACCOUNT CODE 1267

with date after the last entry cliecked. Tlie cash book should be signed byhim at the end of the month and such signature should be understood asfixing his responsibility for all the entries of the month inclusive of closingbalance.

Works Cash Book—II—Checking, Closing and Balancing

81. Tlie Works Cash Book should be closed at the end of eacli month.Tlie account balance at the close of the month should be checked with theactual cash balance on hand and verified by actual count. If any excess ordeficiency is found, it should be entered at once as such in the Cash Bookon the debtor or creditor side, as the case may be. In case of deficiency, itshould be immediately made good by the concerned. This does nothowever preclude the action contemplated to be taken as per provisions ofK.F.C. and other relevant rules. Tlie Range Forest Officers including DepotOfficers and Assistant Conservators of Forests who render accounts toDivisional Forest Officers are required to close their cash books on 25th ofeach month except for Marcli in whicli monthly transactions are to beindicated for full month. A report of the same will be forwarded to theofficer to whom the accounts are submitted. A report of the cash balanceremaining on the last day of each month (Form FAC-6) will be forwardedon that day to the Accountant-General, Kamataka and to the Conservatorof Forests duly indicating therein how mucli represents undisbursed pay,travelling allowance and contingent imprest.

82. Tlie duty of verifying and certifying the monthly c^h bailee mustordinarily be performed by the Divisional Forest Officer/AssistantConservator of Forests in person, but if he be absent on ^the month or is physically "incapacitated by sictaess to perfo^the cash balance may be verified by the Senior ̂ or ~aj„tenLice ofat headquarters (excluding the official enlisted with ttiemamtenance ofcash accounts, the fact of his absence bemg distmctly noted).

83 Without the special permission of Government in each case, not83. Witliout tne sp y allowed to elapse without a personalmore than two months may be . . plrocf offirpr Each suchverification of the cash balance the Divisiona^ Eachverification should be reported to the ccoun r. c ^

84 fal Wherever any defalcation, or loss of public money, theft or fraud,84. (a) Wherever ̂ y u ^ revenue, stores or other property isin connection with the d p :j^«^ediately reported to the immediatediscovered, the fact f ^^fceiw when the matter hasSuperior Officer and to th complete report should be sentbeen fully ® ̂ nt of loss and also the errors committed oriTeg'cS^U^ny!!^^^^^^^^^ - such loss and the prospects ofIts recovery. chapter XXI of K.F.C. regarding

-n.,' o, shouM b.followed.

AKLJ PUBLICATION

1268 KARNATAKA FOREST ACCOUNT CODE CHP. VI

85. Duties and responsibilities of the Divisional Superintendent in theDivisional Forest Office.—(1) Tlie Divisional Superintendent is responsiblefor the compilation, maintenance of the monthly cash accounts of theDivisional Forest Office in accordance with the prescribed rules. He isresponsible to the Divisional Forest Officer. Thus the DivisionalSuperintendent is the ministerial head who is saddled with theresponsibility of compiling and rendering the monthly accounts of theDivisional Forest Officer to the Accountant General.

(2) In the discharge of his duties, the Divisional Superintendent mustkeep himself fully conversant with all the sanctions and orders and withother proceedings of the Divisional Forest Officer and the Range ForestOfficers which may affect actually the Revenue and Expenditure of theDivision.

The Divisional Superintendent should see that the rules and orders inforce are observed in respect of transactions of the Division and shouldbring to the notice of the Divisional Forest Officer immediately he noticesany deviation, for such action as is necessary.

(3) The Divisional Superintendent should see that Divisional Cash Book,Office Contingent Register and the General Cash Book are written up asand when transactions take place. He will be the custodian for the ChequeBooks, Cash Receipt Books, valuable documents and the registers thereof,and vouchers which are to be retained in the Divisional Forest Office.

(4) Cash Accounts of the entire Division should be scrutinised by theDivisional Superintendent in accordance with the rules before they areincorporated in the monthly accounts of the Division. Tlie monthlyschedules to the Cash Accounts in the Divisional Forest Office are gotposted up by him and they are rendered to the Accountant General.

(5) While incorporating the accounts of the Unit Offices with theDivisional Accounts, he will apply certain preliminary checks to the initialaccounts, vouchers, etc., of the Unit Officers who render accounts o "iDivisional Forest Officer to see that.—

(a) They have been received in a complete form;(b) That all sums repayable are duly realised and all realisations are

credited to the proper head of account and in time;(c) The charges are covered by sanction and there is sufficient

ment to cover the charges and are supported bysetting forth the claims and the acknowledgement of the plegally entitled to receive the sum paid;

(d) All vouchers are arithmetically correct and that they are inspects properly prepared in accordance with the rules. He s ̂exercise personal check of arithmetical accuracy of the vouand attest them in token of having checked them;

(e) All items of expenditure are correctly classified;

AKLJ PUBLICATION

CHP. VI KARNATAKA FOREST ACCOUNT CODE 1269

(f) Tlie charges paid are on the basis of the rates sanctioned by theCompetent Authority {e.g., quantities of work done, supplies made,services rendered) certified by the authorised Government servant,and the claims admitted are valid and in order;

(g) Tlie Divisional Superintendent should clieck the works expenditurewith the estimates to ensure the charges incurred are in pursuanceof the objects for whicli the estimates provide. The Divisional Superintendent is personally responsible for the cliecking of the billsfor the work done with the sanctioned estimate, the quantity ofwork done, sanctioned rate, total sanctioned cost so that he maybring to the notice of the Divisional Forest Officer the deviations, ifany, from the sanctioned estimate.

(6) Tlie Divisional Superintendent should see that every payment is sorecorded and receipt is so obtained that second claim against the work onthe same account is impossible and if it represents a remission or refund ofthe sum previously received by the Govemment tliat the amount paid iscorrectly refundable to the payee. It is one of the functions of the DivisionalSuperintendent to see that the expenditure proposed to be incurred orincorporated is within the competency of the Divisional Forest Officer andthat there is sufficient allotment to cover the expenditure incurred orincorporated.

(7) It is also his duty to see to the compilation and rendering of theAnnual Returns to the Accountant-General like the Clearance Register ofRevenue and Forest Deposits, Schedule of Lapsed Deposits, etc., on duedates.

(8) (a) The Divisional Superintendent will list out the objections,omissions and commissions, if any, found out at the time of chectog t iemonthly accounts of the Unit Offices and communicate them to the UnitOfficers concerned under the attestaKon of the Division^ Forest Officer asimmediately as practicable and follow them up till they are cleared orrectified.

(b) Tlie Divisional Superintendent shall maintainForm FAC-77 and record therein the objections overruled ^ =Forest Officer/Assistant Conservator of Forests and submit the s^e to the

Conservator of Forests for his review.

f91 It is the primary responsibility of the Divisional Superintendent tosee?hat tL fnsJection^Reports and Audit Notes are attended to promptlyand replied within the Hme-hmit prescribed.

«0, When |h.

AKLJ PUBLICATION

1270 KARNATAKA FOREST ACCOUNT CODE CHP. VI

over Note detailing the position of the accounts, etc., of the Division andmake it over to his successor and the Divisional Forest Officer.

5^® Assistant Conservator of Forests or other officers whochcques and compile and render the accounts to the

Divfcinnffc 1^6 duties and responsibilities assigned to theOffice ^ps^ntendent will be discharged by the ministerial head of the

Forest ^®"®2cHons referred to in Article 70(2)(b) si/fni, theRolls and Conh^ Cash Book in Form FAC-7, AcquittanceFinancial Corfo Registers in the manner laid down in the KamatakaconSteein Expenditure, and subject to rulesall Inter-DewrtmenM Revenue, Deposits and Advances andDepartments so far a<; fh between Forest and other Publicand works will aknh to Revenue Receipts and Conservancyworks will also be entered in the Forest Works Cash Book.

fSS.xxxxx.]

Departmental Arr^?"!* ^ Revenue realised which enter the Forestpaid into a Treasury/Bank by a Forest

Remittance 882 CaQh credited to the Forest Department as M-rendering accounts tn fho and Adjustments between ofhce

forest produce are CTediited''to'°M^^ contractors or purchasers ofAdjustments between Vfc Remittances—882. Cash Remittances andAccountant-General/Acmn rendering accounts to the sameRemittance ir^to Trea^^p^'^^M Forest Remittances ^receive such sums is nprpL ' u authority of a Forest Office^Forest Officer to whose accm^f ^ depositor must state the name of the

90. The follow-departmental accwnts"^"?!! u'"®'* *'>' R°rest Officers do not enter therespective heads concerned ' ̂ Treasury/Bank to theRemittances and Tt Remittances-882. Cashsame Accountant-General/A ®^®en Offices rendering Accounts to^Remittances into Treasuries'' Officers 111. Forest Remittances—I-

(1) Cash recoveries on ilowance and contin^pn"^^ salaries, establishment, travelling ̂batta received from including subsistance allowance anundisbursed pay. ^ balance of permanent advance anCash recoveries of ntransfer, house buildin^^ advances such as advance of pay onmotor cycle and bicvHp and repair advances, motor car,

AKLJ PUBLICA-nON

(2)

on these advances

hf. 13-7-1995

CHP. VI KARNATAKA FOREST ACCOUNT CODE 1271

91. A Treasury Officer will receive Forest Revenue.—(1) When paid inby a Forest Officer.

(2) Wlien the challan is countersigned by a Forest Officer.

(3) Wlien the Treasury Officer is specially authorised to receive it. Insuch cases, a copy of the challan will be forwarded by the Treasury/Bankdirect to the Divisional Forest Officer in order tliat the Revenue may bebrought to account in the books of the latter.

92. A copy of the Treasury Subsidiary Register showing the amountscredited to the Head "M. Remittances", together with the relevant challans,will be sent monthly by the Treasury to the concerned Divisional ForestOfficer for checking the same with amounts shown in his Cash Book asremitted to the Treasury.

93. ''Manner of Payment".—(a) The Divisional Forest Officers should, asfar as possible, make all their payments for works by dieques. It ispermissible to make payments to suppliers of stores by obtammg ReserveBank drafts in accordance with the rules laid down in tlie Treasury Code.

(b) As a rule, no cheque should be drawn unless it is intended to be p^daway Any cheques drawn in favour of contractors or others should bmade over to them by the Disbursing Officer direct.cheques through the Subordinate Officers maydiscretion and on the responsibility of the Disbursmg ^"^4^®®^^the Subordinate Officer should make no entrykeeps as payments made by cheque will appear in the Cash Book otDisbursing Officer who draws the cheque.

(c) In cases in which theDivisional or Assistant Conservator of Rpoistered Post oncheques, the same may be ® ̂ted below, duly stampedobtaining a Pr^-recei^ed Mn discretionwherever necessary. Conservator of Forests and onof the Divisional Forest Officer/Assistant Conservatorspecific written request by the payee concern .

"Received from ^by'a<ii"stment on account of Biil No.l!'!" :dat;d"". my^avou7(^^^ of work or supplies).

Signature of the Contractor of Supplier."

„ ic a serious irregularity to draw AequesNote.—(1) Usually deposit them in cash chest at the close

are signed by him.aklj publication

1272 KARNATAKA FOREST ACCOUNT CODE CHP. VI

94. Bills.—General instructions regarding the form of Bills, theircompletion and stamping as laid down in Articles 24, 31 and

fin ° I Financial Code should be followed. As far as possible,«!fnro<f ^ applicable to the case should be used. Suppliers ofdpn^rh^ f ? should be encouraged to prefer their claims in thereiprfpH if^fi not prepared on such forms should not beaddiHnnai necessary details of claims. In such cases, theEverv bill cb^ required should be added by the Disbursing Officer.Y uld setforth the unit, rate at which the payment is to be made.

of ^ gener^ rule, every payment including repaymentpurpose mu^t ^ deposited with the Government for whateverthe claims and all ^ voucher setting forth clear particulars ofclassification andcertificate of nnfp nf ro voucliers for repayment of deposits areceipts of deposits shoiyM against the original credits in the register ofThe full name of thp « u (umished in addition to other particulars,including the Head nf given in the estimate and other particularsare debitable or to which the charges admitted on a vouchervoucher are creditable m or other credits shown in theprovided for the oumnc clearly indicated therein in the spaceexhibits any expendihirp^ ^ prominent place. When a voucherto accrue as per instanrp ^^^ch revenue may priirm facie be expectedmaterial from a building n fi? appears in a Bill for removingrepairs, clearing of iun^lp cJ work, either dismantled or undergoingindicate how the old mafprM ^ should be recorded todisposed off and if sold ® ̂ ^^^'^oved or the trees cut, etc., have beenGovernment. ' ̂ ^ proceeds were credited to

the payee's receipt, a cerh^catP f payment by a voucher or bythe Disbursing Officer and r ? Payment as indicated below signed bywith the Memorandum Superior Officer togetherplaced on record and circumstances, should always en^essary. Full particulars nf fb Accountant General, wherewhere this necessitates use nf ̂ should invariably be setforth anrecorded on the Bill itself regular bill form, the certificate may

IHnK u Of paymenti do hereby certify that I h, cwas paid to . personally satisfied myself that a sum ofcash book for that month iVo u '^^e as recorded m my

payment is covered byTyfcv'' ̂ ) ̂nd that no part of theDated. ■' 'r other voucher.

'CounteDisbursing Officer.

rsigned'

aklj publication

CHP. VI KARNATAKA FOREST ACCOUNT CODE 1273

Divisional Forest Officer/Assistant Conservator of Forests/

Conservator of Forests

Dated "

96. Every voucher must bear a Pay Order signed or initialled and datedby the Divisional Forest Officer/Assistant Conservator of Forests. Thisorder should specify the amount payable both in words and figures. All PayOrders must be signed by hand and in ink.

97. Every vouclier should also bear, or have attached to it anacknowledgement of the payment, signed by the person by whom or onwhose behalf the claim is put forward. Tliis acknowledgement should betaken at the time of payment. When the payee signs in the language otherthan Kannada or English, he should be required to note the amount m hisscript in his own handwriting. The said acknowledgement mcludmg ^yremarks made by the Payee should invariably be transliterated m ^epresence of a witness who is familiar with that language and who alsoknows Kannada or English.

Note.-Wlren the Disbursing Officer anticipates «>y «

Kamataka Financial Code.

98. Remittance to Treasury.-Thekeep a remittance book the remittancetreasunes as they are made. This Dooand the challan to be receipted by the treasury.

«. a..,™ dX«Officer and other Officers author indents The required printedfrom the District Treasunes p C. 1 should be obtained byreceipt books, (machine numbere ), jj. officers and distributed tothe Head of the Department or other Con gall Subordinate Officers. , .pceiDt

, r, • f Rnnks should immediately be on receipt(b) Cheque Books and Recei^ Bookbe carefully examined by the dieque leaves contained inconcerned, who should count t le num ^ account of chequeeach and record a certificate of coun w Divisional Forest Officer orand receipt books, etc., should be kept by the DivOther Officer in Form FAC-8. ..^vv,pdiatelv on receipt be

(c) Cheque Books and of the Divisional Forestkept under lock and key m th pOfficer and other Officers conceme

aklj publication

1274 KARNATAKA FOREST ACCOUNT CODE CHP. VII

(d) Counterfoils of used Cheque books should be preserved by theDivisional Forest Officer/other Officers after careful clieck.

(e) Before bringing a new cheque book into use the Divisional ForestOfficer/other Officers will intimate the Treasury/Bank of its number and ofthe serial numbers of cheques it contains.

100. Custody of cash.—Public money in large amounts kept frequentlyinto the custody of the Departmental Officers should be kept in strongtreasure chest secured by double locks of different patterns. All the keys ofthe said lock must not be kept in the same person's custody and as ageneral rule, the keys of one lock should be kept apart from the keys of theother lock and in a different person's custody when practicable. Wheneverthe Cashier or the Superintendent is attached to the Divisional ForestOffice/other Offices, the keys of one of the locks of treasure chest willnecessarily remain in his possession, those of the other locks being keptwith the Divisional Forest Officer/other Officers. The chest should never beopened unless both the custodians of the keys are present. Both of themmust be present at the time it is again locked.

101. The Divisional Forest Officer/other Officer should count the cashatleast once a month, or in the case outstations he or the Sub-DivisionalForest Officer should count it periodically whenever he visits them Theresult of such counting should be recorded in the form of a note in the cashbook showing the date of examination and the amount (in words).

CHAPTER VII

WORKS ACCOUNTS

A. General

102. The initial records upon which the accounts of works are basedare.—

(a) the Muster Roll;

(b) the Measurement Book; and

(c) the Field Note Book.

For the work done by the daUy labour, the subordinate not below therank of a Forest Guard in-charge of the work will prepare a Muster Roll,w 1 wi s ow the work done by this means and the amount payable on

<^0"tract work generally the Field Note

miicfp^nii ""i-u Book will form the basis of account. From theField Nnto R if ® *^'11 prepare the labour reports and from thebills of contrartorsTnd sujjto™"^'

aklj publication

CHP. VII KARNATAKA FOREST ACCOUNT CODE 1275

103. Tlie initial accounts and vouchers connected with charges relatingto works must invariably specify:

(1) the full name of the work as given in the estimate;(2) the name of the component part (or sub-head) of it; and(3) the charges (if any) which are of the nature of recoverable payment

and the names of the contractors or others from whom recoverable.Vl04. Muster Rolls.—(1) Muster rolls shall be maintained eifcer by the

Forest Mali/Forest Guards/duly foUowing the procedure Pjes^bed m theForest Accounts Code. Disbursement of wages, however, ®the Forester/Range Forest Officer fumishmg the necessary certificate ofdisbursement and recording the progress of the output.