BAB II TINJAUAN PUSTAKA II.1 Tinjauan Pariwisata Pantai II ...

Econophysics and Sociophysics

Lecture II

R. Mansilla

CEIICH, UNAM

What Statistical Physics has to do with Finance ? Over the previous two decades, physicists had become adept at analyzing systems with many particles interacting heterogeneously and the markets clearly consisted of such particles: the investors. What really complicates things is the fact that “particles” of markets have an adaptive behavior and try to predict what will happen based on past history and their perception of the present. What is difficult to understand is that their performance disturbs the stage on which they want to make decisions. This kind of reflexivity principle has been reported by one of the most lucid market players, George Soros:

G. Soros, The alchemy of finance, John Wiley and Sons, 1987

As a result of this it is impossible to make a deductive reasoning in these systems. So the only way out is to induce future behavior based on the information available. The latter is generally limited

It was the kind of problems that W. Brian Arthur attacked early in 1994.

W. Brain Arthur (1945-)

El Farol Bar 808 Canyon Road

Sta Fe, N.M.

El Farol Bar Problem

In 1988 on Thursday nights the Galway musician Gerry Carty played Irish music at El Farol Bar and the site was not pleasant if crowded. Each week music lovers mulled whether it was worth showing up…and everybody mulled that others also mulled. It was an interesting problem: if many people decide to go, then the bar would be crowded. It would have been better to stay home. If many decided to stay at home, then the bar would be empty and have been a good decision to attend. Note that the right decision was always to be in the minority group. What has this to do with the markets? The decisions of economic agents are also binary: buy or sell. If many choose to buy and sell a few, there is excess demand and prices rise, which benefits the minority group who are the sellers. If many want to sell and buy a few, there is an oversupply and lower prices, benefiting the minority group who are the buyers. The right decision is to be always in the minority group. This verdict is obtained collectively.

The details of the model of W. Brian Arthur

W. Brian Arthur, Inductive Reasoning and Bounded Rationality American Economic Review, 84, pp. 406–411, 1994. • Assume that participants know the number of attendees in

previous weeks …… 44 , 78 , 56 , 15 , 23 , 67 , 84 , 34 , 45 , 76 , 40 , 56 , 35

• Each of the participants have predictive strategies The same as last week [35] A mirror image around 50 of last week [65] The rounded average of the last four weeks [52] Etc. • Each participant use k of the above mentioned strategies • Always use the currently most accurate predictor.

With these rules were developed computer simulations using 100 participants.

• No periodic behavior were found. As Arthur explain: All the cycles are quickly "arbitraged" away so there are no persistent cycles. If several people expect many to go because many went three weeks ago, they will stay home.

• Mean attendance fluctuates always around 60. This number was the threshold to decide whether the bar was full or not.

• Attendance seems to fluctuate chaotically.

One of the indisputable merits of Arthur's model is have done for the first time a multi-agent simulation and recognize the importance of adaptive behavior of the agents within the simulation.

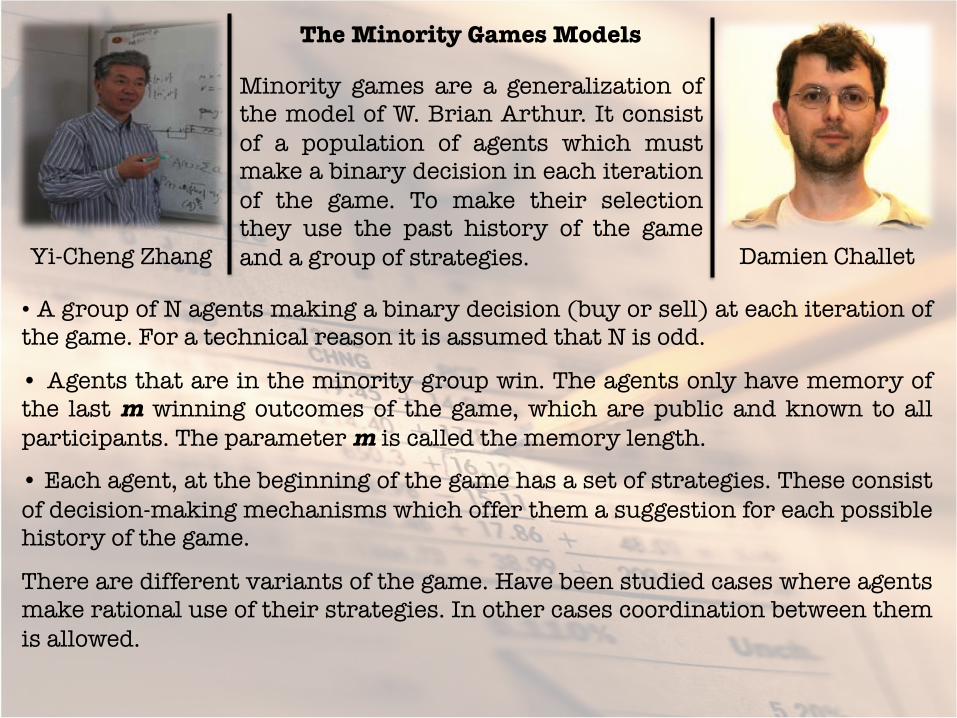

Yi-Cheng Zhang Damien Challet

The Minority Games Models

Minority games are a generalization of the model of W. Brian Arthur. It consist of a population of agents which must make a binary decision in each iteration of the game. To make their selection they use the past history of the game and a group of strategies.

• A group of N agents making a binary decision (buy or sell) at each iteration of the game. For a technical reason it is assumed that N is odd.

• Agents that are in the minority group win. The agents only have memory of the last m winning outcomes of the game, which are public and known to all participants. The parameter m is called the memory length.

• Each agent, at the beginning of the game has a set of strategies. These consist of decision-making mechanisms which offer them a suggestion for each possible history of the game.

There are different variants of the game. Have been studied cases where agents make rational use of their strategies. In other cases coordination between them is allowed.

0

1

1

1

0

1

0

0

0

0

0

0

1

1

1

1

0

0

1

1

0

0

1

1

0

1

0

1

0

1

0

1

An example of strategy with m = 3

If the memory of agents is m, then there are distinct histories and therefore the number of different strategies is:

2m

22m

ai, sh ∈ −1, 1{ }Let be the decision agent i made using the strategy s given

the history h. Let:

A(t) = ai , s(t )h(t )

i=1

N

∑ ; σ 2 = A2

There exist a memory size:

mc ≈ log2 zcN( )

for which the magnitude reaches a minimum. This minimum value did not depend on the number of strategies s using the agents if N is large enough. This magnitude could be associated to the volatility of the markets.

σ 2

Bad news…

A. Cavagna developed the following alternative model: at each iteration, when the agents should take its decision, his memory was erased and replaced by a random information common to any agent. As can be seen in the figure above the results were similar to those obtained by Savit et al.

Where was the cheating ?

Nowhere. M. Marsili y D. Challet show that the model can be described as a spin system and, as varies, a dynamical phase transition with symmetry breaking undergoes. The symmetry that gets broken is the equivalence between the two actions: in the symmetric phase both actions are taken by the minority with the same frequency (e.g., there are, on average, as many buyers as sellers). For , in each of the possible states, the minority does more frequently an action than the other one, i.e., the game’s outcome is asymmetric. An asymmetry in the game’s outcome is an opportunity that an agent could in principle exploit to gain.

α = 2m N

α <αc

α >αc

This opened the door for other lines of research

Measure of complexity of Kolmogorov-Chaitin Let define the Kolmogorov-Chaitin measure complexity of a binary string s to the length of the shortest program p that run on a Turing machine T produces the string s.

K(s) =min p , s = T (p){ }This measure of complexity has only been able to calculate explicitly in particular cases, it is generally uncomputable, but its average value on certain families of strings can be calculated. C. Adami, N. J. Cerf, Physical complexity of symbolic sequences, Physica D, 137, pags. 62-69, 2000. The measure of complexity of Kolmogorov-Chaitin is a measure of randomness. Applied to the outputs of minority games should provide an estimate of how random the binary strings the model produces are. Obviously this should be relate to the efficient market hypothesis

C(l) = K(s)s∈B(l )

≈ lα (m)

The results obtained here showed that the more increase the memory length of agents, most random was the overall system response. This is in accordance with the efficient market hypothesis

Definition

We say that an agent is näive if he chosen at random the strategy that will use within the group available to him. We say that an agent is sophisticated if he always chooses the strategy that has given him better results in the past.

C(l) = K(s)s∈B(l )

≈ la(m, s)ϕ+b(m, s)

Where was a measure of the sophistication of the agents. Completely sophisticated Completely naive ϕ = 0

ϕϕ =1

Observatory of financial crises http://www.er.ethz.ch/fco/index

Didier Sornette Professor on the Chair of Entrepreneurial Risks, Department of Management, Technology and Economics (D-TEC) ETH Zurich, Kreuzplatz 5, CH-8032 Zurich, Switzerland

What happens in real markets ?

http://arxiv.org/PS_cache/cond-mat/pdf/0210/0210509v1.pdf

S o r n e t t e a n d J o h a n s e n managed to make an excellent "prediction" of the NASDAQ crash of April 2000. They used the Benioff’s Law to make their prediction.

ε(t) = A+B(tc − t)m 1+C cos ln(tc − t)+φ( )"# $%

The Kolmogorov-Chaitin complexity measure was calculated for several large crashes in the IPC and the NASDAQ. The results were c o mp a r e d w i t h t i m e s where the market was close to the efficiency.

αβ llC =)(

http://arxiv.org/PS_cache/arxiv/pdf/1008/1008.1846v3.pdf

H. Zenil, J. P. Delahaye, AN ALGORITHMIC INFORMATION THEORETIC APPROACH TO THE BEHAVIOUR OF FINANCIAL MARKETS, Journal of Economic Surveys, 25, pags. 431-463, 2011.

Recently new studies been extended this work

FIN

Copyright © 2022 FDOKUMEN