accountancy and financial management – ii

51

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of accountancy and financial management – ii

ACCOUNTANCY ANDFINANCIAL

MANAGEMENT – II(AS per Revised Syllabus of Mumbai University for F.Y.B.Com., II Semester)

Rajiv MishraM.Com., MBA, M.Phil., NET,

Lecturer at N.E.S. Ratnam College of Arts,Science and Commerce for BBI & Co-ordinator for M.Com.,

Bhandup (W), Mumbai-400 078.Visiting Faculty at N.G. Acharya, D.K Marathe, V.K. Menon College, Pragati College,

Dnyansadhana College and Vikas College for M.Com., BBI, BMS, BFM and BAF.

MUMBAI NEW DELHI NAGPUR BENGALURU HYDERABAD CHENNAI PUNE LUCKNOW AHMEDABAD ERNAKULAM BHUBANESWAR INDORE KOLKATA GUWAHATI

Pratima SinghM.Com., M.Phil., B.Ed.,Vice Principal & HOD,Account Department,

Chandrabhan Sharma College.

Dr. Vijaybharti JainM.Com., (Gold Medalist), Ph.D.,

Assistant Professor,Gurukul College.

Rajendra B. VareM.Com., M.A., MBA, M.Phil., B.Ed.,

I/c Principal, Shivaji ShikshanSanstha College (Night),

Mumbai.

Asif BaigM.Com., B.Ed., M.Phil., MBA, NETHOD. Accounts at Gurukul College,

Ghatkopar.

CMA (Dr.) Kinnari ThakkarM.Com., ACMA, CS., Ph.D.,

MBA (Finance),Principal, SIES College ofCommerce & Economics,

Sion (E), Mumbai.

H.G. PradhanM.Com., M.Phil., UGC NET,

Assistant Professor at WesternCollege, Sanpada and

Vikas College, Vikhroli.

Published by : Mrs. Meena Pandey for Himalaya Publishing House Pvt. Ltd.,“Ramdoot”, Dr. Bhalerao Marg, Girgaon, Mumbai - 400 004.Phone: 022-23860170/23863863, Fax: 022-23877178E-mail: [email protected]; Website: www.himpub.com

Branch Offices :New Delhi : “Pooja Apartments”, 4-B, Murari Lal Street, Ansari Road, Darya Ganj,

New Delhi - 110 002. Phone: 011-23270392, 23278631; Fax: 011-23256286Nagpur : Kundanlal Chandak Industrial Estate, Ghat Road, Nagpur - 440 018.

Phone: 0712-2738731, 3296733; Telefax: 0712-2721216Bengaluru : No. 16/1 (Old 12/1), 1st Floor, Next to Hotel Highlands, Madhava Nagar,

Race Course Road, Bengaluru - 560 001.Phone: 080-22286611, 22385461, 4113 8821, 22281541

Hyderabad : No. 3-4-184, Lingampally, Besides Raghavendra Swamy Matham, Kachiguda,Hyderabad - 500 027. Phone: 040-27560041, 27550139

Chennai : New-20, Old-59, Thirumalai Pillai Road, T. Nagar, Chennai - 600 017.Mobile: 9380460419

Pune : First Floor, "Laksha" Apartment, No. 527, Mehunpura, Shaniwarpeth(Near Prabhat Theatre), Pune - 411 030. Phone: 020-24496323/24496333;Mobile: 09370579333

Lucknow : House No 731, Shekhupura Colony, Near B.D. Convent School, Aliganj,Lucknow - 226 022. Phone: 0522-4012353; Mobile: 09307501549

Ahmedabad : 114, “SHAIL”, 1st Floor, Opp. Madhu Sudan House, C.G. Road, Navrang Pura,Ahmedabad - 380 009. Phone: 079-26560126; Mobile: 09377088847

Ernakulam : 39/176 (New No: 60/251) 1st Floor, Karikkamuri Road, Ernakulam, Kochi – 682011.Phone: 0484-2378012, 2378016; Mobile: 09387122121

Bhubaneswar : 5 Station Square, Bhubaneswar - 751 001 (Odisha).Phone: 0674-2532129, Mobile: 09338746007

Indore : Kesardeep Avenue Extension, 73, Narayan Bagh, Flat No. 302, IIIrd Floor,Near Humpty Dumpty School, Indore - 452 007 (M.P.). Mobile: 09303399304

Kolkata : 108/4, Beliaghata Main Road, Near ID Hospital, Opp. SBI Bank,Kolkata - 700 010, Phone: 033-32449649, Mobile: 7439040301

Guwahati : House No. 15, Behind Pragjyotish College, Near Sharma Printing Press,P.O. Bharalumukh, Guwahati - 781009, (Assam).Mobile: 09883055590, 08486355289, 7439040301

DTP by : SunandaPrinted at : Rose Fine Art, Mumbai. On behalf of HPH.

© AuthorsNo part of this publication may be reproduced, stored in a retrieval system, or transmitted in any formor by any means, electronic, mechanical, photocopying, recording and/or otherwise without the priorwritten permission of the publisher.

First Edition : 2016

Preface

It is a matter of great pleasure to present this new edition of the book on Accountancy andFinancial Management – II to the students and teachers of F.Y.B.Com., Semester II, University ofMumbai. This book is written on lines of syllabus instituted by the University. The book presents thesubject matter in a simple and convincing language.

I owe a great many thanks to a great many people who helped and supported me during thewriting of this book which includes Principal, Coordinator, and Students of K.M. College, DAV,Ratnam College, K.J. Somaiya, Vivekananda Education Society, Vikas College, R.J. College of theB.Com., BBI, BMS, BAF and BFM section.

My deepest thanks to Mr. Manoj Sharma of the Nitin Godiwala College who was the strengthto me always.

I would also thank all of them who have been a part of this book and helped me knowinglyor unknowingly. I also extend my heartfelt thanks to my family S.N. Mishra (Father), Sunita S.Mishra (Mother), Sanjiv S. Mishra (Brother), Rupa R. Mishra (Wife), Yash R. Mishra (Son) andwell-wishers would have been a distant reality.

Special Thanks/Acknowledgements

(1) Prof. Mrs. Rina Saha Principal – N.E.S. Ratnam College(2) Prof. Manoj Sharma Principal – Nitin Godiwala College(3) Prof. Ajay Bhamre Principal – RADAV College(4) Prof. Probol Gupta Vice-principal – RADAV College(5) Prof. R.K. Patra Sr. Vice-principal – Vikas College(6) Prof. Vinayak Mulay Vice-principal – Vikas College(7) Dr. Kinnary Thakkar Reader Commerce – Mumbai University(8) CA Rajiv Khurana HOD Accountancy – RADAV College(9) Prof. Riya Rupani BMS and BBI Coordinator – N.E.S. Ratnam College

(10) Prof. Sandip Gupta BMS Coordinator – K.J. Somaiya College(11) Prof. Jyotsna Shilpi BMS Coordinator – Vikas College(12) Prof. Selvi BMS Coordinator – R. Jhunjhunwala College(13) Prof. Mukesh Kanojia BMS Coordinator – R.D. National College(14) Prof. Bhupinder Saini BMS Coordinator – RADAV College(15) Prof. Bhavdas C.M. Sr. Lecturer – V.E.S College(16) Prof. Nitin Agarwal Lecturer – Gurukul College(17) Prof. Kursheed Shaikh Lecturer – Narayan Guru College(18) Prof. Mrunmayee Thatte Lecturer – Joshi Bedekar College(19) Prof. Jia Makhija Lecturer – N.E.S. Ratnam College(20) Prof. Kedar Pandey Lecturer – Nitin Godiwala College

Author

Syllabus

ACCOUNTANCY AND FINANCIAL MANAGEMENT - IIF.Y.B.Com., Semester II

Topics at Glance

Sr. No. Topics No. of Lectures

Module 1 Accounting from Incomplete Records 15

Module 2 Consignment Accounts 15

Module 3 Branch Accounts 15

Module 4 Accounting with the Use of Accounting Software 15

Detailed Syllabus

Module Topics No. of Lectures

1 Accounting from Incomplete Records 15IntroductionProblems on preparation of final accounts of ProprietaryTrading Concern (conversion method)

2 Consignment Accounts 15Accounting for consignment transactionsValuation of stockInvoicing of goods at higher price (excluding overriding commission, normal/abnormal losses)

3 Branch Accounts 15Meaning/Classification of branchAccounting for Dependent Branch not maintainingfull books:Debtors methodStock and debtors method

4 Accounting with the Use of Accounting Software 15IntroductionPreparation of books and trial balance with the useof accounting software

Paper PatternInternal Assessment

1. Question Paper Pattern for Periodical Class Test for Courses at UG Programmes Written ClassTest 20 Marks

Sr. No. Particulars Marks

1 Match the Column/Fill in the Blanks/Multiple Choice Questions (½ Mark each) 05 Marks

2 Answer in One or Two Lines (Concept Based Questions) (1 Mark each) 05 Marks

3 Answer in Brief (Attempt any Two of the Three) (5 Marks each) 10 Marks

Question Paper PatternMaximum Marks: 75 Duration: 2½ HoursQuestions to be Set: 05All questions are compulsory carrying 15 Marks each.

Q.1 Objective Questions 15 Marks(A) Sub-questions to be asked 10 and to be answered any 08(B) Sub-questions to be asked 10 and to be answered any 07(*Multiple Choice/True or False/Match the Columns/Fill in the Blanks)

Q.2 Full Length Practical Question 15 MarksOR

Q.2 Full Length Practical Question 15 MarksQ.3 Full Length Practical Question 15 Marks

ORQ.3 Full Length Practical Question 15 Marks

Q.4 Full Length Practical Question 15 MarksOR

Q.4 Full Length Practical Question 15 MarksQ.5 (A) Theory Questions 08 Marks

(B) Theory Questions 07 MarksOR

Q.5 Short Notes 15 MarksTo be asked 05To be answered 03

Note: Full length question of 15 Marks may be divided into two sub-questions of 08 and 07 Marks.

1. Accounting from Incomplete Records 1 – 43

2. Consignment Accounts 44 – 70

3. Branch Accounts 71 – 109

4. Accounting with the Use of Accounting Software 110 – 127

Contents

The Single Entry System is really no system at all for keeping accounts. Under this system, onlysuch accounts are kept as seem to be absolutely necessary. Usually, the accounts that are kept arethose relating to cash/credit customers and creditors. One may not find accounts relating to fixedassets, purchases, sales, expenses, incomes, etc. Thus, one may find that some transactions are notrecorded at all, some transactions are recorded only in one of their aspects while, for some others,both the aspects are recorded. Goods sold on credit will be recorded only in the account of thecustomer concerned. Cash received from him will be recorded both in the Cash Acount and in theaccount of the customer. Purchase of machinery on credit will not be recorded at all till payment ismade.

This system of recording transactions is very defective. No trial balance can be taken out andhence accuracy of books cannot be proved. Chances of mischief of fraud remaining undetected arehigh. Trading and Profit and Loss Account cannot be prepared and, hence, the proprietor will have nofirm idea of profit earned or loss suffered. Balance sheet, called statement of affairs here, is preparedin an unsatisfactory manner. The assets and liabilities are not proved from records but are put down byphysical inspection and on estimated basis. In spite of all the defects, the system is quite popular withsmall firms which cannot afford to spend money on proper accounting.

Meaning

Incomplete Record of Accounting means absence of double entry, i.e., both aspects of thetransaction not recorded which is incomplete, unscientific and unsatisfactory system.

It is a system which only records cash and personal accounts. It is always incomplete double Entry.

Features

1. Prepared by sole trading concern and partnership firm: This system was prepared byonly sole trading and partnership firm since there are no legal requirement of bookkeepingunder double entry system, i.e., registration not required compulsorily for sole trading concernand partnership firm.

2. Not uniform: The uniformity concept is missing under this system as the system differs orvaries from one business organisation to another business organisation for maintaining theirbooks of accounts.

ACCOUNTING FROM

INCOMPLETE

ReCORDS

Chapter

1

2 Accountancy and Financial Management – II

3. No rule: No fixed rules are followed under this system as no hard and fast rules are issued byany authorised accounting regulatory bodies.

4. Record of one aspect: This system ignores both aspects of the transaction, i.e., double entryis not passed. So, only one aspect of the transaction is recorded.

5. Personal as well as business aspect: This system always take care of proprietor’s personalas well as business transaction, i.e., Cash Book under this system also takes care of personalreceipts and payments of proprietor apart from keeping recorded of business receipts andpayments.

COMPUTATION OF PROFIT OR LOSS

There are two methods of incomplete record system for accounting:

A. Statement of Affairs Method (Networth Method)

B. Conversion Method

CONVERSION METHOD

Under this method, the organisation prepares Final Accounts which requires the following way:Trading and Profit & Loss A/c

Particulars Amt (`̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Opening Stock xx By SalesTo Purchase: Cash x Cash x Credit x Credit x Less: Return (x) xxLess: Drawing (x) xxTo Direct Expenses xx By Closing Stock xxTo Gross Profit x By Gross Loss x

xxx xxxTo Gross Loss x By Gross Profit xTo Revenue Expenses By Other Income xx Office Expenses x Selling Expenses x Financial Expenses xx xxTo Net Profit xx By Net Loss x

xxx xxx

Accounting from Incomplete Records 3

Balance SheetLiabilities `̀̀̀̀ Assets `̀̀̀̀

Capital xx Fixed Assets:Add: Net profit x Cost xxLess: Net loss (x) xxx Less: Depreciation x xxLess: Drawings (x) xxx Investment xLoan x Current Assets & Advances xxCurrent Liabilities x Miscellaneous Expenses x

xxx xxx

Working Notes:

Dr. 1. Debtors Accounts Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Balance b/d x By Cash Bank xTo Bill Receivable (Dishonoured) x By Bills Receivable A/c xTo Bank A/c (Cheque Dishonoured) x By Discount Ac xTo Credit Sales x By Bad Debt A/c x

By Sales Return A/c xBy Balance c/d x

xx xxDr. 2. Creditors Account Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Cash/Bank xx By Balance b/d xxTo Bills Payable(Dishonoured) xx By Bills Payable (Dishonoured) xxTo Bills Receivable (Endorsed) x By Debtors (Endorsed bill x

dishonoured)To Discount x By Cash Bank (ChequesTo Purchase Return x Dishonoured) xTo Balance c/d x By Credit Purchase x

xx xxDr. 3. Bills Receivable A/c Cr.

Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Balance b/d xx By Cash Bank xxTo Debtors A/c xx By Discount xx

By Debtors (Bill dishonoured) xxBy Creditors (Bills Receivable endorsed) xxBy Balance c/d xx

xx xx

4 Accountancy and Financial Management – II

Dr. 4. Bills Payable A/c Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Cash Bank xx By Balance b/d xxTo Creditors xx By Creditors xx(Bill Payable Dishonoured)To Balance c/d xx

xxx xxx

Dr. 5. Revenue Expense A/c Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Balance b/d xx By Balance b/d (o/s in beginning) xxTo Cash Bank (Expenses Paid) x By Profit & Loss A/c xxTo Balance c/d (o/s at end) x By Balance c/d x

xx xx

Dr. 6. Revenue Income A/c Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Balance b/d xx By Balance b/d xxTo P & L A/c xx By Cash Bank (received) xxTo Balance c/d x By Balance c/d xx

xxx xxx

Dr. 7. Fixed Assets A/c Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Balance b/d xx By Cash Bank (Sale) xTo Bank (Purchase) x By Loss on Sale xTo Profit on Sale x By Depreciation x

By Balance c/d xxxx xx

Dr. 8. Cash/Bank A/c Cr.Particulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Balance b/d xx By Balance b/d (Overdraft) xTo Cash Sales x By Cash Purchase xTo Collection from Debtors x By Creditors xTo Bills Receivable x By Bills Paid xTo Capital Introduced x By Drawing xTo Sale of Fixed Asset x By Fixed Assets Purchase xTo Miscellaneous Income x By Balance c/d xxTo Balance c/d

xxx xxx

Accounting from Incomplete Records 5

9. Stock/Goods A/cParticulars Amt ( `̀̀̀̀) Particulars Amt ( `̀̀̀̀)To Opening Stock x By Cost of Goods Sold xTo Purchase x By Closing Stock x

xx xx

STEPS FOR SOLVING PROBLEM

Step 1: Prepare Trading A/c

For cash sales and purchase, prepare Cash/Bank A/c.

For credit sales and purchase, prepare Debtors A/c and Creditors A/c.

For opening and closing stock, prepare Stock A/c.

Step 2: Prepare P & L A/c

For expenses, prepare Revenue Expense A/c.

For other income, prepare Revenue Income A/c.

Step 3: For beginning capital, prepare opening Balance Sheet

Step 4: Prepare Balance Sheet at the end of the year

Prepare Bills Receivable A/c and Payable A/c.

Prepare Fixed Asset A/c.

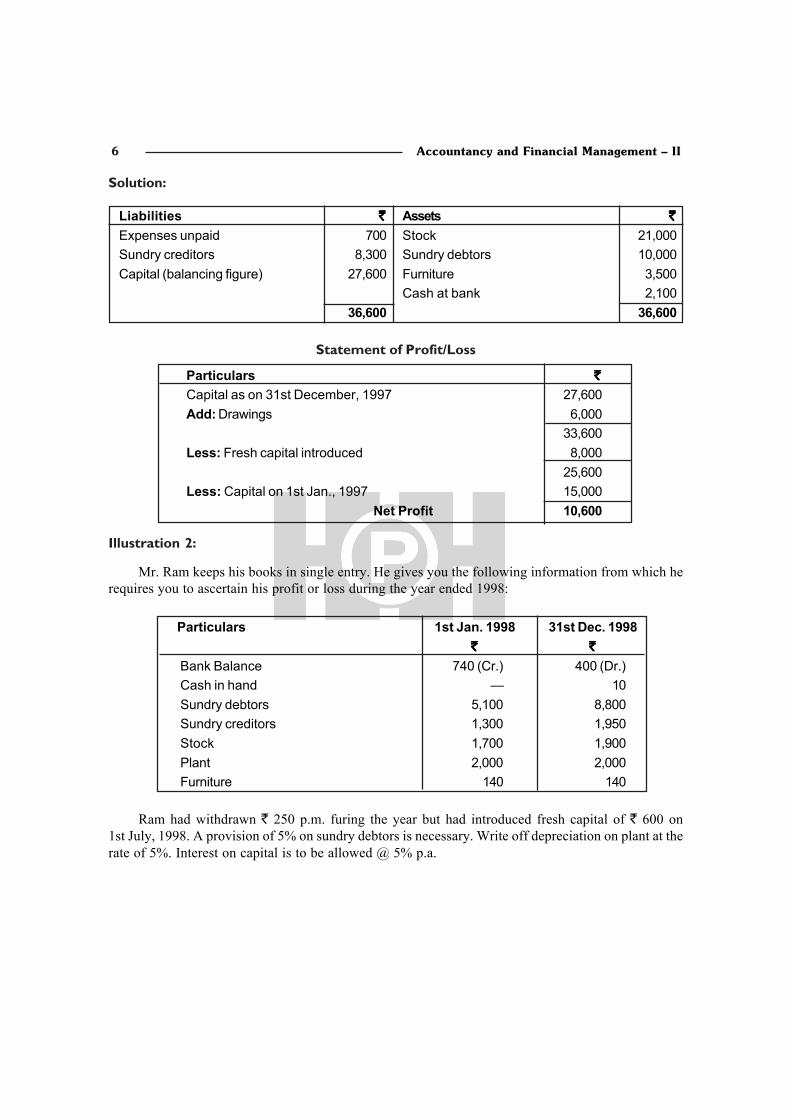

Illustration 1:

Chandra commenced business on 1st January, 1997 with a capital of ` 15,000. On 1st July,1997, he introduced a further capital of ` 8,000. During the year, he withdrew ` 500 p.m. for domesticuse. On 31st December, 1997, his assets and liabilities were:

`̀̀̀̀

Stock 21,000Debtors 10,000Furniture 3,500Cash at bank 2,100Expenses unpaid 700Sundry creditors 8,300

6 Accountancy and Financial Management – II

Solution:

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Expenses unpaid 700 Stock 21,000Sundry creditors 8,300 Sundry debtors 10,000Capital (balancing figure) 27,600 Furniture 3,500

Cash at bank 2,10036,600 36,600

Statement of Profit/Loss

Particulars `̀̀̀̀

Capital as on 31st December, 1997 27,600Add: Drawings 6,000

33,600Less: Fresh capital introduced 8,000

25,600Less: Capital on 1st Jan., 1997 15,000

Net Profit 10,600

Illustration 2:

Mr. Ram keeps his books in single entry. He gives you the following information from which herequires you to ascertain his profit or loss during the year ended 1998:

Particulars 1st Jan. 1998 31st Dec. 1998`̀̀̀̀ `̀̀̀̀

Bank Balance 740 (Cr.) 400 (Dr.)Cash in hand — 10Sundry debtors 5,100 8,800Sundry creditors 1,300 1,950Stock 1,700 1,900Plant 2,000 2,000Furniture 140 140

Ram had withdrawn ` 250 p.m. furing the year but had introduced fresh capital of ` 600 on1st July, 1998. A provision of 5% on sundry debtors is necessary. Write off depreciation on plant at therate of 5%. Interest on capital is to be allowed @ 5% p.a.

Accounting from Incomplete Records 7

Solution:

Mr. RamStatement of Affairs

Particulars 1.1.1998 31.12.1998Plant 2,000 2,000Less: Depreciation @ 5% Nil 2,000 100 1,900Furniture 140 140Stock 1,700 1,900Sundry debtors 5,100 8,800Less: Provision @ 5% Nil 5,100 440 8,360Cash in hand 10Cash in bank 400

8,940 12,710Less: Sundry creditors 1,300 1,950Bank overdraft 740 2,040 — 1,950Capital 6,900 10,760

Statement of Profit/Loss

Particulars `̀̀̀̀

Capital as on December 31,1998 1,0760Less: Capital as on January 1, 1998 6,900

3,860Add: Drawings 3,000

6,860Less: Capital introduced 600Net Profit before interest on capital 6,260Less: Interest on capital @ 5% 360Profit during the year 5,900

Working Note:

Interest on capital:On ̀ 6,900 @5% for full year 345On ̀ 600 @5% for 6 months 15

360

Illustration 3:

Shah and Rao are partners sharing profits and losses in the ratio of 3 : 2 after carging interest oncapital @ 6% p.a. Interest on drawings is to be ignored. On 1st July, 1998, their position was as under:

8 Accountancy and Financial Management – II

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Sundry creditors 14,300 Machinery 20,000Capitals: Stock 12,000

Shah 20,000 Sundry debtors 11,000 Rao 15,000 35,000 Cash at bank 4,000

Furniture 2,000Prepaid insurance 300

49,300 49,300

During the year ended 30th June, 1999, Shah had drawn ` 5,000 and Rao had drawn ` 3,500 fortheir private purposes. On 30th June, 1999, the assets and liabilities were:

`

Sundry debtors 12,000Stock 18,000Cash at bank 4,500Prepaid insurance 200Sundry creditors 13,700Expenses owing 600

Machinery and Furniture were the same as previoulsy but a depreciation @ 10% p.a. was to bewritten off. Prepare statement of profit for 1998-99 and the statement of affairs as at 30th June, 1999.

Solution:

Statement of Affairs as at 30th June, 1999

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Sundry creditors 13,700 Machinery 20,000Expenses unpaid 600 Less: Depreciation 2,000 18,000Combined capitals 39,600(balancing figure) Stock 18,000

Sundry debtors 12,000Less: Provision for doubtful debts 600 11,400Cash at bank 4,500Prepaid insurance 200Furniture 2,000Less: Depreciation 200 1,800

53,900 53,900

Accounting from Incomplete Records 9

Statement of Profit or Loss

Particulars `̀̀̀̀ `̀̀̀̀

Capital on 30th June,1999 39,600Add: Drawings:

Shah 5,000Rao 3,500 8,500

48,100Less: Capitals on 1st July, 1998 35,000Net Profit 13,100

Division of Profit:

Profit and Loss (Appropriation) Account for the year ended 30.6.1999

Statement of Affairs of Shah and Rao as at 30th June 1999

Illustration 4:

Following are the assets and liabilities of N and S on April 1, 1994 (N contributing one-and-a-halftimes of S's capital); Plant and Machinery ` 16,000; Stock ` 8,000; Debtors ` 16,000; Cash in handand at bank ` 1,000; Trade Creditors ` 13,000.

The position as on 31st March, 1995 was as follows:

Cash in hand and at bank ` 1,600; Trade Creditors ` 20,200; Debtors ` 8,400; N's drawingsduring the year had been ` 3,000 and S had drawn ` 1,200. Besides this, N had withdrawn ` 4,000 onSeptember 30, 1994 from his capital account. Depreciate Plant and Machinery by 10% and allowinterest on capital at 5% p.a. Interest on drawings is to be ignored. N and S share profit and loss in theratio of 3 : 2.

You are required: to calculate net profit before interest on capital and net profit after interest oncapital.

Solution:

Statement of Affairs as on 1.4.1994Division of Capital between Nand S:

If capital of S is 1, then N's capital will be 1.5 and total capital will be 2.5. Therefore, N's capitalsis: 28,000×1.5/2.5 = ` 16,800 and S's capital is: 28,000×1/2.5 = ` 11,200.

Calculation of Capital as on 31st March, 1995Particulars `̀̀̀̀

Cash in Hand and at Bank 1,600Sundry Debtors 8,800Stock in Trade 8,400Plant and machinery (16,000 – 1600) 14,400

33,200

10 Accountancy and Financial Management – II

Less: Creditors 20,200Net Assets, i.e., Capital of N and S 13,000

CALCULATION OF GROSS PROFIT

Sometimes, Gross Profit is required to be calculated, in addition to Net Profit. Since there is noinformation regarding sales and purchases, Trading Account cannot be prepared. Therefore, initiallynet profit will be calculated by preparing statement of profit as discussed above. Then all expenses,losses and depreciation will be added back. Any income will be deducted. The resultant figure will beGross Profit.

Illustration 5 (Calculation of Gross Profit):

01.01.1998 31.12.1998Sundry Assets 4,00,000 6,50,000Sundry Liabilities 1,20,000 1,90,000Expenses during the year 1998

Salary – ` 10,000; Rent – ` 15,000; Depreciation – ` 8,000; Bad debts – ` 4,000.

During the year 1998, furniture having a book value of ` 7,000 was sold for ` 8,000.

Drawings during the year were ` 9,000.

Calculate Gross Profit and Net Profit.

Solution:

Statement Showing Net Profit for the year ended 31.12.1998

Particulars `̀̀̀̀

Capital as on 31.12.1998 (6,50,000 – 1,90,000) 4,60,000

Add: Drawings 9,000

4,69,000

Less: Capital as on 01.01.1998 (4,00,000 – 1,20,000) 2,80,000

Net Profit 1,89,000

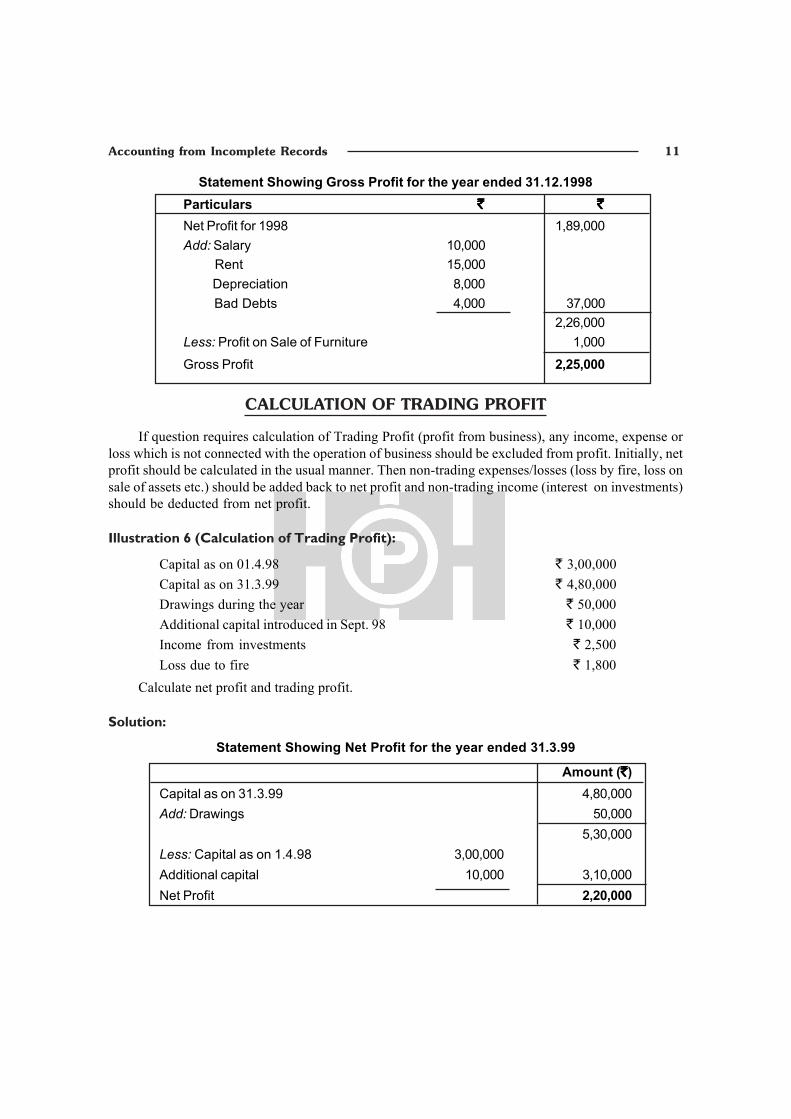

Accounting from Incomplete Records 11

Statement Showing Gross Profit for the year ended 31.12.1998Particulars `̀̀̀̀ `̀̀̀̀

Net Profit for 1998 1,89,000Add: Salary 10,000 Rent 15,000 Depreciation 8,000 Bad Debts 4,000 37,000

2,26,000Less: Profit on Sale of Furniture 1,000

Gross Profit 2,25,000

CALCULATION OF TRADING PROFIT

If question requires calculation of Trading Profit (profit from business), any income, expense orloss which is not connected with the operation of business should be excluded from profit. Initially, netprofit should be calculated in the usual manner. Then non-trading expenses/losses (loss by fire, loss onsale of assets etc.) should be added back to net profit and non-trading income (interest on investments)should be deducted from net profit.

Illustration 6 (Calculation of Trading Profit):

Capital as on 01.4.98 ` 3,00,000Capital as on 31.3.99 ` 4,80,000Drawings during the year ` 50,000Additional capital introduced in Sept. 98 ` 10,000Income from investments ` 2,500Loss due to fire ` 1,800

Calculate net profit and trading profit.

Solution:

Statement Showing Net Profit for the year ended 31.3.99

Amount (`̀̀̀̀)Capital as on 31.3.99 4,80,000Add: Drawings 50,000

5,30,000Less: Capital as on 1.4.98 3,00,000Additional capital 10,000 3,10,000Net Profit 2,20,000

12 Accountancy and Financial Management – II

Statement Showing Trading Profit for the year ended 31.3.99

Particulars `̀̀̀̀

Net Profit for 1999 2,20,000Add: Loss due to Fire 1,800

2,21,800Less: Income from Investments 2,500

Trading Profit 2,19,300

Illustration 7 (Drawings as a Percentage of Net Profit):

Mr. Pawan had following assets and liabilities:

1.4.96 31.3.97

Cash in Hand 5,000 6,000

Bank Balance 12,000 29,000

Stock 25,000 24,000

Sundry Debtors 10,000 18,000

Furniture 20,000 ?

Equipments 30,000 ?

Sundry Creditors 15,000 12,000

During the year, he introduced ` 7,000 as additional capital. He has withdrawn 75% of the profitsearned. Depreciation on furniture and equipments is to be charged @ 10% p.a.

Calculate the Capital and Statement of Profit and Loss for the year ended 31.3.1997.

Solution:

Calculation of CapitalParticulars 1.4.96 31.3.97Sundry Assets:Cash in hand 5,000 6,000Bank Balance 12,000 29,000Stock 25,000 24,000Sundry Debtors 10,000 18,000Furniture 20,000 18,000Equipments 30,000 27,000

1,02,000 1,22,000Less: Sundry Creditors 15,000 12,000Capital 87,000 1,10,000

Accounting from Incomplete Records 13

Statement of Profit and Loss for the year ended 31.3.1997Particulars `̀̀̀̀ `̀̀̀̀

Capital as on 31.3.97 1,10,000Less: Capital as on 1.4.96 87,000Additional Capital 7,000 94,000Net Profits after drawings 16,000

Add: Drawings

×25

7516,00048,000

Net Profit before drawings 64,000

Note: During the year, 75% of the profits have been withdrawn. Therefore, ` 16,000 representsonly 25% of the profits. Hence, profits earned will be ` 64,000.

CORRECTION IN THE VALUE OF ASSETS AND LIABILITIES

Value of assets and liabilities given in the question may require some corrections/adjustments. Insuch a case, values of the assets and liabilities should be corrected before calculating capital (NetAssets).

Illustration 8:

Ramesh carries on business as dressmakers. He does not keep any accounts but wants to ascertainhis profit or loss for the year 1990. He gives you an idea of the assets and liabilities as on 31.3.1989 and31.3.1990 which are as follows:

Particulars 31.12.1989 31.12.1990Cash in Hand 470 430Bank Balance as per Pass Book 6,230 8,170Book Debts 3,100 2,900Stock in Trade 15,000 18,000Investments in D.C.M. Debentures 8,000 3,000Equipment at Cost 6,000 10,000Owing for Supplies 5,000 6,000

On enquiry, you find the following:

(a) Certain cheques for payment for taxes amounting ` 2,500 issued on 28.12.1989 had not beenpresented; these were paid in Jan 1999.

(b) Stock in Trade is valued at selling price; the mark up in 1989 has 25% selling price but duringthe year 1990 it was 25% on cost.

14 Accountancy and Financial Management – II

(c) Book debts as on 31.3.1989 include ` 1,000 for good sent on sale or returns basis, thecustomers still having the rights to return the goods.

(d) The investments are shown in face value, the purchases have been made at 95.

(e) Half the equipments as on 31.12.1989 was purchased in 1988 and remaining in 1989.Depreciation @10% p.a. on original cost on closing balance is charged.

(f) A cheque for ` 500 was returned by the bank dishonoured on 30.12.1990 and customer haddeposited ` 700 directly into the bank on the same date. Ramesh did not know of there yet.

(g) His drawings during the year 1990 have been at the rate of ` 500.

(h) A cheque issued for ` 3,100 for his income tax was not presented as on 31.12.1990.

You are requested to ascertain the profit earned or loss suffered by Ramesh in 1990.

Solution:

Statement of Affairs of Ramesh as on 31st Dec. 1989

Particulars `̀̀̀̀ Particulars `̀̀̀̀

Sundry Creditors 5,000 Cash 470Capital (Bal. Fig.) 26,000 Bank 3,730

Sundry Debtors 2,100Stock 12,000Investments 7,600Equipments 6,000Less: Depreciation 900 5,100

31,000 31,000

Statement of Affairs of Ramesh as on 31st December, 1990

Particulars `̀̀̀̀ Particulars `̀̀̀̀

Sundry Creditors 6,000 Cash 430Capital (Bal. Fig.) 27,550 Bank 5,070

Book Debts 2,700Stock 14,400Investments 2,850Equipments 10,000Less: Depreciation 1,900 8,100

33,550 33,550

Accounting from Incomplete Records 15

Statement of Profit and Loss for the year ended 31.12.90

Capital as on 31st December, 1990 27,550

Add: Drawings including income tax 9,100

36,650

Less: Capital as on 31.12.89 26,000

Profit for the year 10,650

Working Notes:

(i) Bank Balance: As per Pass Book is given, but bank balance as per Cash Book will be shownin Balance Sheet. Therefore, following adjustments will be required:

Particulars 31.12.1989 (`̀̀̀̀) 31.12.1990 (`̀̀̀̀)

Balance as per Pass Book 6,230 8,170

Less: Unpresented cheques 2,500 3,100

Adjusted Bank Balance 3,730 5,070

Unpresented cheques as on 31.12.1990 for personal income tax of the proprietors will be treatedas drawings.

Illustration 9:

Khan gives some of balance as per his records as on January 1, 2001 and 31st December, 2001:

January 1, 2011 Dec. 31, 2001(`)(`)(`)(`)(`) (`)(`)(`)(`)(`)

Cash and Bank Balance 4,500 3,650Sundry Debtors ? 37,800Sundry Creditors 19,600 21,700Stock in Trade 11,000 13,400Furnitures and Fixtures 16,000 ?Expenses Outstanding 4,100 5,300

He informs you that he always sells goods at margin of 25% on sales but one lot costing ` 1,500had to be sold for ` 1,400 due to damage. The cash book summary, inter alia, showed the followingitems:

`̀̀̀̀ `̀̀̀̀

Paid to Creditors 57,000 Received from Sundry Debtors 76,000Paid to Expenses 20,300 Miscellaneous Receipts 900Paid to furniture 2,500 Drawings 6,000Cash Purchases 6,000

16 Accountancy and Financial Management – II

Discounts allowed and received were ` 650 and ` 300.

Depreciation on Furniture was @ 10%.

Prepare Khan’s trading and profit and loss account for 2001 and his balance sheet as at the end ofthat year.

Solution:

Note: Good deal of information is not available. It will have to be ascertained and hence the followingworkings.

1. To ascertain credit purchase

Sundry Creditors A/cParticulars `̀̀̀̀ Particulars `̀̀̀̀

To Cash 57,000 By Balance b/d 19,600To Discount Received 300 By Purchases 59,400To Balance c/d 21,700 (By Balancing figure)

79,000 79,000

`̀̀̀̀

2. Total PurchaseCredit 59,400Cash 6,000

65,4003. Cost of Goods Sold and Sales

Purchase 65,400Add: Opening Stock 11,000Less: Closing Stock 13,400

76,400Cost of Goods Sold 63,000Less: Item sold below Cost 1,500

61,500Add: Gross profit @ 33½% which is the same as 25% on sales 20,500

82,000Add: Sales below cost 1,400

83,4004. Cash Sales 14,0505. Credit Sales 69,350

Total Sales 83,4006. Opening Balance of Sundry Debtors 41,5007. Opening Balance of Capital 51,600

Accounting from Incomplete Records 17

Cash Book

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 4,500 By Sundry Creditors 57,000To Sundry Debtors 76,000 By Cash Purchases 6,000To Misc. Receipts 900 By Expense 20,300To Cash Sales (Balancing figure) 14,050 By Furniture 2,500

By Drawings 6,000By Balance c/d 3,650

95,450 95,450

Sundry Debtors A/c

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d (Balancing figure) 45,100 By Cash 76,000To Credit Sales 69,350 By Discount 650

By Balance c/d 37,8001,14,450 1,14,450

Balance Sheet as on 1st Jan, 2001

Particulars `̀̀̀̀ Particulars `̀̀̀̀

Sundry Creditors 19,600 Cash and Bank Balance 4,500Expenses Outstanding 4,100 Sundry Debtors 45,100Capital (Balancing figure) 52,900 Stock in Trade 11,000

Furniture and Fixtures 16,00076,600 76,600

Trading and Profit and Loss Account of Khan for the year ended 31st Dec., 2001

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Opening Stock 11,000 By Sales 83,400To Purchases 65,400 By Closing Stock 13,400To Gross Profit c/d 20,400

96,800 96,800To Expenses 21,500 By Gross Profit b/d 20,400To Depreciation 1,725* By Discount Received 300To Discount allowed 650 By Misc. Receipts 900

By Loss 2,27523,875 23,875

Dr. Cr.

Dr. Cr.

18 Accountancy and Financial Management – II

llustration 10:

Bose supplies to you the following information:1st January, 1998 31st Dec., 1998

`̀̀̀̀ `̀̀̀̀Sundry Debtors 18,100 19,300Stock 15,000 14,000Machinery 25,000 —Furniture 4,000 —Sundry creditors 11,000 12,500

Summary of cash transactions for 1998:Receipts `̀̀̀̀ Payments `̀̀̀̀

Opening Balance 500 Payment of creditors 35,000Cash Sale 6,100 Wages 16,000Received from Debtors 73,300 Salaries 15,000Miscellaneous receipts 200 Drawings 4,0200Loan from Dass 10,000 Expenses 11,000(@ 9% on 1st July) Machinery Purchased (1st July) 9,500

Closing Balance 1,60092,100 92,100

Discount allowed were ` 700 and discount received were ` 400. Bad debts written off were` 800. Depreciation is to be written off on furniture @ 5% and Machinery @ 10%. Expenses includeinsurance @ ` 500 p.a. paid up to 31st March, 1999; Wages ` 2,000 are still due.

Prepare Trading and Profit and Loss Account and Balance Sheet relating to 1998.

Solution:

Total Debtors Account (to Ascertain Credit Sales)

Dr. Cr.Date Particulars `̀̀̀̀ Date Particulars `̀̀̀̀

1998 1998Jan.1 To Balance b/d 18,100 Dec.31 By Cash 75,300

To Credit Sales 78,000 By Discount 700(Balancing Figure) By Bad Debts 800

By Balance Debts 19,30096,100 96,100

Accounting from Incomplete Records 19

Purchases A/cDate Particulars `̀̀̀̀ Date Particulars `̀̀̀̀

1998 1998Dec.31 To Cash 35,000 Jan.1 By Balance b/d 11,000

To Discount 400 By Credit PurchasesTo Balance Sheet 12,500 (Balancing Figure) 36,900

47,900 47,900

Balance Sheet as on 1st Jan., 1998

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Sundry Creditors 11,000 Cash 500Capital (Balancing figure) 51,600 Stock 15,000

Sundry Debtors 18,100Machinery 25,000Furniture 4,000

62,600 62,600

Trading and Profit and Loss Account of Bose for the year ended Dec. 31, 1998

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Opening Stock 15,000 By Sales:To Purchases 36,900 Credit 78,000To Wages: Paid 16,000 Cash 6,100 84,100

Add: Outstanding 2,000 18,000 By Closing Stock 14,000To Gross Profit c/d 28,200

98,100 98,100To Salaries 15,000 By Gross Profit b/d 28,200To Expenses: 11,000 By Miscellaneous Receipts 200

Less: Prepaid 125 10,875 By Discount Received 400To Interest on Loan: By Loss 2,200

9% for 6 months on ̀ 10,000 450To Depreciation:

Machinery 2,975Furniture 200 3,175

To Discount allowed 700To Bad Debts 800

31,000 31,000

20 Accountancy and Financial Management – II

Balance Sheet of Bose as at December 31, 1998Liabilities `̀̀̀̀ `̀̀̀̀ Assets `̀̀̀̀ `̀̀̀̀

Sundry Creditors 12,500 Fixed Assets:Wages Unpaid 2,000 Machinery:Loan 10,000 Balance on 1st Jan. 1999 25,000Add: Interest Unpaid 450 10,450 Addition 9,500Capital 34,500Balance on 1st Jan. 1998 51,600 Less: Depreciation 2,975 31,525Less: Loss 2,200 Furniture:

Drawings 4,400 6,200 45,400 Balance on 1st Jan. 1999 4,000Less: Depreciation 200 3,800Current Assets:

Stock 14,000Debtors 19,300Cash 1,600Prepaid Insurance 125

70,350 70,350

Note: Depreciation on Machinery has been calculated as under:`̀̀̀̀

10% on ̀ 25,000 for full year 2,50010% on ̀ 25,000 for six months 475

2,975

llustration 11:

Rajendra carries on business of Retail Traders in consumer goods. He is not able to keep properbooks of accounts. He provides the following information from which you are require to prepare hisfinal accounts for the year 2008 and Balance Sheet as on that date.

The following were the balances of Assets and Liabilities:Particulars 01.01.2008 31.12.2008

Amount (`̀̀̀̀) Amount (`̀̀̀̀)Capital 2,10,000 ?Stock 54,000 61,300Debtors ? 1,80,000Furniture 6,000 6,000Building 90,000 90,000Creditors 48,000 33,000Loan from Deepali 5,000 NilBills Receivable 3,000 2,000Bills Payable 4,000 2,500Cash Balance 500 ?

Accounting from Incomplete Records 21

Analysis of Cash and Bank Book

Manager's Salary 6,000Salaries to Staff 25,000General Expenses 22,500Paid to Creditors 90,000B.R. Honoured 5,000B.P. Paid 4,500Cash Sales 90,000Receipts from Debtors 1,50,000Bank overdraft (01.01.2008) 23,500Interest and Bank Charges 450Personal Drawings 12,000Deepali's Loan repaid with interest 5,500

Additional Information:

(a) Rajendra purchases and sells in cash as well as on credit basis.

(b) During the year, Bills receivable of ` 1,000 was dishonoured.

(c) Further, Bills receivable worth ` 2,500 were endorsed, but out of that also bills receivable of` 1,500 were dishonoured.

(d) Depreciate furniture and building at 5% p.a.

(e) Create a provision for doubtful debts at ` 6,000.

(f) Discount was allowed by suppliers ` 500.

(g) Salaries to staff was outstanding ` 3,000. General expenses prepaid ` 1000.

Solution:

Opening Balance Sheet (01.01.08)

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Capital 2,10,000 Stock 54,000Creditors 48,000 Debtors (b/f) 1,37,000Loan from Deepali 5,000 Furniture 6,000Bills Payable 4,000 Building 90,000Bank Overdraft 23,500 Bills Receivable 3,000

Cash Balance 5002,90,500 2,90,500

22 Accountancy and Financial Management – II

Debtors A/cParticulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 1,37,000 By Cash & Bank A/c 1,50,000To B/R (Discount) 1,000 By B/R 7,500To Creditors (End bilI discount) 1,500 By Balance c/d 1,80,000To Sales (B/f) 1,98,000

3,37,500 3,37,500

Bills Receivable A/cParticulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 3,000 By Cash/Bank 5,000To Debtors (B/f) 7,500 By Debtors (Discount) 1,000

By Creditors (Endorsed) 2,500By Balance c/d 2,000

10,500 10,500

Creditors A/cParticulars `̀̀̀̀ Particulars `̀̀̀̀

To Cash/Bank 90,000 By Balance b/d 48,000To B/R (endorsed) 2,500 By Debtors (EBO) 1,500To Discount 500 By Purchases (Bal.) 79,500To B/P 3,000To Balance c/d 33,000

1,29,000 1,29,000Bills Payable A/c

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Cash/Bank 4,500 By Balance b/d 4,000To Balance c/d 2,500 By Creditors 3,000

7,000 7,000

Cash/Bank A/cParticulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d (Cash) 500 By Balance b/d (BOD) 23,500To B/R 5,000 By Loan from Deepali (5,000 + 500) 5,500To Sales (Cash) 90,000 By Manager's Salary 6,000To Debtors 1,50,000 By Salaries to staff 25,000

By General Expenses 22,500By Creditors 90,000By B/P 4,500By Interest and Brokerage 450By Drawings 12,000By Balance c/d 56,050

2,45,500 2,45,500

Dr. Cr.

Dr. Cr.

Dr. Cr.

Dr. Cr.

Dr. Cr.

Accounting from Incomplete Records 23

Trading and P & L A/cfor the year ended 31st Dec. 2008

Dr. Cr.Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Opening stock 54,000 By Sales:To Purchases 79,500 Cash 90,000To Gross Profit c/d 2,15,800 Add: Credit 1,98,000 2,88,000

By Closing stock 61,3003,49,300 3,49,300

To Manager’s Salary 6,000 By Gross Profit b/d 2,15,800To Salaries to staff 25,000 By Discount 500Add: Outstanding 3,000 28,000To General Expenses 22,500Less: Prepaid 1,000 21,500To Int. & Bank charges 450To Int. on Deepali’s loan 500To Depreciation: Furniture 300 Building 4,500 4,800To Reserve for B.D. 6,000To Net Profit c/d 1,49,050

2,16,300 2,16,300

Balance Sheet as on 31.12.08

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Capital 2,10,000 Furniture 6,000Add: Net Profit 1,49,050 Less: Depreciation 300 5,700

3,59,050 Building 90,000Less: Drawings 12,000 3,47,050 Less: Depreciation 4,500 85,500Creditors 33,000 Stock 61,300Bills Payable 2,500 Debtors 1,80,000OIs Staff Salary 3,000 Less: R.D.D. 6,000 1,74,000

Bills Receivable 2,000Prepaid General Expenses 1,000CashIBank 56,050

3,85,550 3,85,550

24 Accountancy and Financial Management – II

llustration 12:

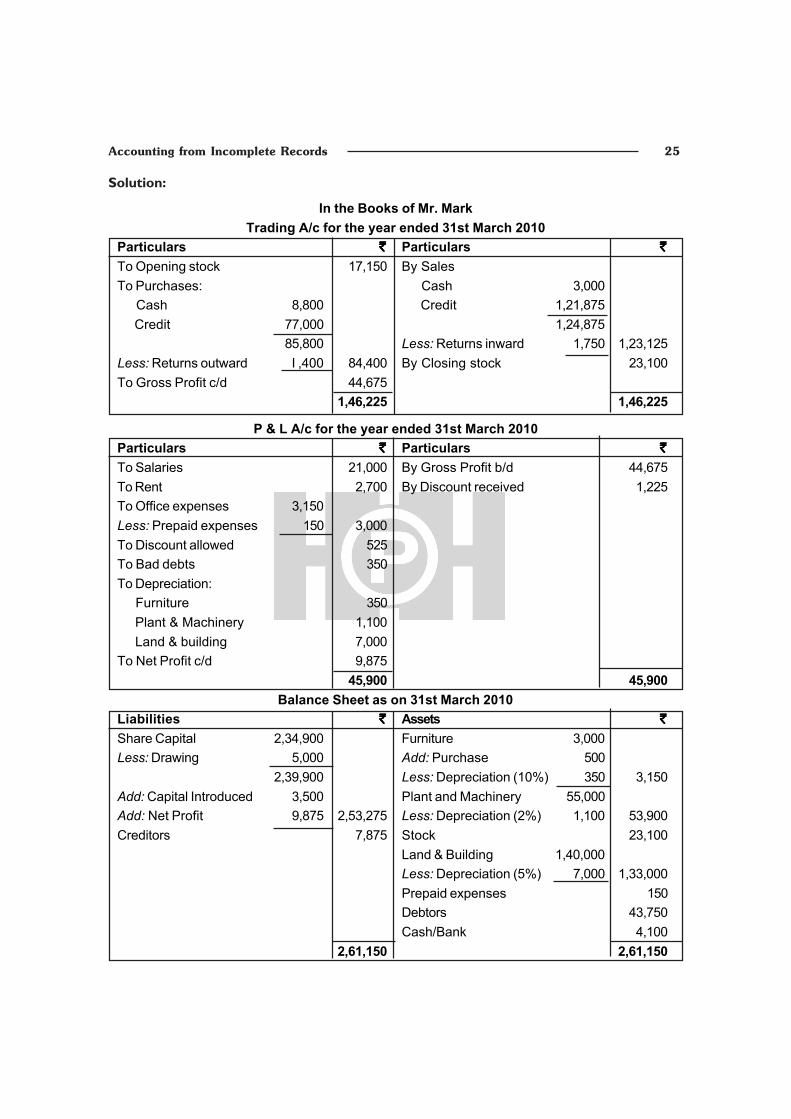

Mr. Mark does not maintain proper books of accounts. From the following information, prepareTrading and Profit and Loss Account for the year ended 31st March, 2010 and a Balance Sheet as onthat date.

Particulars 31.03.2009 31.03.2010`̀̀̀̀ `̀̀̀̀

Debtors 31,500 43,750Stock 17,150 23,1 00Cash and Bank 8,750 ?Creditors 10,500 7,875Furniture 3,000 3,500Plant and Machinery 55,000 55,000Land and Buildings 1,40,000 1,40,000

Analysis of the other transactions are:

Particulars ` ` ` ` `

Cash Collected from Debtors 1,07,000Cash Paid to Creditors 77,000Salaries 21,000Rent 2,700Office Expenses 3,150Drawings 5,000Fresh Capital introduced 3,500Cash Sales 3,000Cash Purchases 8,800Discount Received 1,225Discount Allowed 525Returns Inward 1,750Returns Outward 1,400Bad debts 350

Further Information:

(a) Depreciate Plant and Machinery by 2%, Land and Building by 5% and Furniture by 10%.

(b) Office expenses were prepaid ` 150 on 31st March, 2010.

Accounting from Incomplete Records 25

Solution:

In the Books of Mr. MarkTrading A/c for the year ended 31st March 2010

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Opening stock 17,150 By SalesTo Purchases: Cash 3,000 Cash 8,800 Credit 1,21,875

Credit 77,000 1,24,87585,800 Less: Returns inward 1,750 1,23,125

Less: Returns outward I ,400 84,400 By Closing stock 23,100To Gross Profit c/d 44,675

1,46,225 1,46,225

P & L A/c for the year ended 31st March 2010Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Salaries 21,000 By Gross Profit b/d 44,675To Rent 2,700 By Discount received 1,225To Office expenses 3,150Less: Prepaid expenses 150 3,000To Discount allowed 525To Bad debts 350To Depreciation: Furniture 350

Plant & Machinery 1,100 Land & building 7,000To Net Profit c/d 9,875

45,900 45,900Balance Sheet as on 31st March 2010

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Share Capital 2,34,900 Furniture 3,000Less: Drawing 5,000 Add: Purchase 500

2,39,900 Less: Depreciation (10%) 350 3,150Add: Capital Introduced 3,500 Plant and Machinery 55,000Add: Net Profit 9,875 2,53,275 Less: Depreciation (2%) 1,100 53,900Creditors 7,875 Stock 23,100

Land & Building 1,40,000Less: Depreciation (5%) 7,000 1,33,000Prepaid expenses 150Debtors 43,750Cash/Bank 4,100

2,61,150 2,61,150

26 Accountancy and Financial Management – II

Working Notes:

Statement of Affairs as on 31.03.’09Particulars `̀̀̀̀ Particulars `̀̀̀̀

Capital 2,44,900 Debtors 31,500Creditors 10,500 Stock 17,150

Cash/Bank 8,750Furniture 3,000Plant and Machinery 55,000Land and Building 1,40,000

2,55,400 2,55,400

Dr. Debtors A/c Cr.Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 31,500 By Cash/Bank 1,07,000To Credit sales 1,21,875 By Discount allowed 525

By Bad debts 350By Returns inward 1,750By Balance c/d 43,750

1,53,375 1,53,375

Dr. Creditors A/c Cr.Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Cash/Bank A/c 77,000 By Balance b/d 10,500To Discount received 1,225 By Credit Purchases 77,000To Returns outward 1,400To Balance c/d 7,875

87,500 87,500

Dr. Cash/Bank A/c Cr.

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 8,750 By Creditors 77,000To Debtors 1,07,000 By Salaries 21,000To Capital 3,500 By Rent 2,700To Cash Sales 3,000 By Office Expenses 3,150

By Drawing 5,000By Purchases 8,800By Furniture 500By Balance c/d 4,100

1,22,250 1,22,250

Accounting from Incomplete Records 27

llustration 13:

Mr. Bhopatrao does not maintain proper books of accounts. From the following information,prepare Trading and Profit and Loss Account for the year ended 31st March, 2008 and a Balance Sheetas on that date:

Assets and Liabilities 1.4.2007 (`̀̀̀̀) 31.3.2008 (`̀̀̀̀)Plant and Machinery 1,40,000 1,40,000Furniture 10,000 10,000Stock 44,000 60,000Debtors 81,000 1,12,500Creditors 27,000 22,5006% Investments 50,000 50,000

Analysis of other transactions:Particulars `̀̀̀̀

Cash paid to creditors 1,98,000Cash Received from debtors 2,73,600Salaries 54,000Rent 7,500Office Expenses 19,000Drawings 13 ,500Additional Capital Introduced 10,000Cash Sales 35,000Cash Purchases 25,000Discount Received 3,150Discount Allowed 1,350Returns Inward 4,500Returns Outward 3,600Bad Debts 900Cash as on 1.4.2007 20,000

Depreciate Plant and Machinery @ 5% p.a. and Furniture @ 10% p.a. and also provide interestreceivable on Investments.

28 Accountancy and Financial Management – II

Solution:

In the Books of Mr. BhopatraoOpening B/S as on 1.4.07

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Capital 3,18,000 P & M 1,40,000Creditors 27,000 Furniture 10,000

Stock 44,000Debtors 81,0006% Investment 50,000Cash in hand 20,000

3,45,000 3,45,000

Debtors A/cDr. Cr.

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 81,000 By Cash 2,73,600To Sales 3,11,850 By Discount 1,350

By Return Investment 4,500By Bad debts 900By Balance c/d 1,12,500

3,92,850 3,92,850

Dr. Creditors A/c Cr.Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Cash 1,98,000 By Balance b/d 27,000To Discount 3,150 By Purchase 2,00,250To Returns Outward 3,600To Balance c/d 22,500

2,27,250 2,27,250

Dr. Cash A/c Cr.

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d 20,000 By Creditors 1,98,000To Debtors 2,73,600 By Salaries 54,000To Capital Introduced 10,000 By Rent 7,500To Cash Sales 35,000 By Office Expenses 19,000

By Drawings 13,500By Cash Purchase 25,000By Balance c/d 21,600

3,38,600 3,38,600

Accounting from Incomplete Records 29

Trading and P&L A/c for the year ended 31st March, 2008Dr. Cr.

Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Opening Stock 44,000 By Sale:To Purchases: Cash 35,000 Cash 25,000 Creditors 3,11,850 Credit 2,00,250 Less: Return (4,500) 3,42,350Less: Return (3,600) 2,21,650 By Closing Stock 60,000To Gross Profit c/d 1,36,700

4,02,350 4,02,350To Salaries 54,000 By Gross Profit b/d 1,36,700To Rent 7,500 By Interest 3,000To Office Expenses 19,000 By Discount received 3,150To Discount allowed 1,350To Bad debts 900To Depreciation: Plant 7,000 Furniture 1,000 8,000To Net Profit c/d 52,100

1,42,850 1,42,850

EXERCISE

1. MURTY Started a Firm on 1st Jan, 1998 with a capital of ` 8,000. On 1st April 1998, heborrowed from his wife a sum of ` 4,000 @ 9% p.a. on 31st December, 1998. His assets andliabilities were:

Cash 600

Stock 9,400

Sundry debtors 7,100

Sundry creditors 4,200

Ascertain the profit or loss made by Murty during the year 1998. Murty had drawn ` 2,500for his domestic use.

[Ans: Profit = `= `= `= `= ` 3,130. Capital as on 31.12.1998 = `̀̀̀̀ 8,630][Hint: It has been that interest on loan is outstanding]

30 Accountancy and Financial Management – II

2. Mr. Krishan keeps his books on ‘single entry system’. His position as on 31st December,1994 was as follows:

Cash in hands ` 200; cash at bank ` 3,500; closing stock ` 10,200; sundry creditors ` 8,000;sundry debtors ` 10,500; plant and machinery ` 19,700; fixtures and fittings ` 3400.

During the year, he received ̀ 20,000 from LIC which he brought in his business. He withdrewfor his personal expenses ` 800 p.m. Further, his personal expenses amounting to ` 2,300were paid from his business account. On 31st December, 1995, his position was as follows:

Cash in hand ` 260; bank overdraft ` 1,740; closing stock ` 13,800; sundry creditors ` 5,600;sundry debtors ` 15,700; plant and machinery ` 25,700; fixtures and fittings ` 4,000.

Prepare statement showing profit or loss made by him for the year ended on 31st December,1995.

[Ans: Profit = `̀̀̀̀ 4,520; Capital on 31.12.1994 = `̀̀̀̀ 39,500; Capital on 31.12.1995 = `̀̀̀̀ 52,120]

3. Mr. A does not maintain double enrty book of accounts. From the following details, determinethe profits for the year and prepare statement of affairs at the end of the year.

1.1.93 (`̀̀̀̀) 31.12.93 (`̀̀̀̀)

Stock 40,000 60,000

Debtors 30,000 40,000

Cash 2,000 1,000

Bank 10,000 5,000

Creditors 15,000 25,000

Outstanding expenses 5,000 8,000

Furniture 2,000 ?

Depreciation @ 10% is to be charged on furniture. Mr. A has withdrawn ` 1,000 per month.` 2,000 was invested by Mr. A in 1993. Bank balance on 1.1.93 is as per Cash Book, but thebank overdraft on 31.12.93 is as per bank statement. Cheques for ` 2,000 drawn in December,1993 have not been encashed within the year.

[Ans: Profit = `̀̀̀̀ 8,800; Capital on 1.1.93 = `̀̀̀̀ 64,000; Capital on 31.12.93 = `̀̀̀̀ 62,800, bank overdraft on 31.12.93 = `̀̀̀̀ 7,000]

4. Patel commenced business on 1st July, 1992 with a capital of ` 20,000. During the yearended 30th June, 1993, he borrowed ` 5,000 from Mr. A and introduced a further capital of` 2,000. Furniture worth ` 3,000 was purchased. Cash in hand ` 450; cash at bank ` 2,500;sundry debtors ` 4,050; stock ` 7,000; bills receivable ` 1,800; sundry creditors ` 750.

Furniture is to be depreciated by 10%. Ascertain the profit or loss made by Patel during theyear ended 30th June, 1993.

[Ans: Net losss = `̀̀̀̀ 6,250]

5. Ali keeps his books by single entry. He gives you the following information from which herequires you to ascertain his profit or loss during 1998:

Accounting from Incomplete Records 31

1.1.1998 (`̀̀̀̀) 31.12.1998 (`̀̀̀̀)Bank balance 740crore 400Cash in hand - 10Sundry debtors 5,300 8,800Sundry creditors 1,500 1,950Stock 1,700 1,900Plant 2,000 2,000

Furniture 140 140

Ali had withdrawn ` 3,000 during the year but had introduced fresh capital of ` 600 on 1stJuly 1998. A provision of 5% on sundry debtors is necessary. Write off depreciation on plant@ 5%. Interest on capital is to be allowed @ 5% p.a.

[Ans: Profit after on capital = `̀̀̀̀ 5,900; Capital as on 1.1.98 = `̀̀̀̀ 6,900; Capital as on 31.12.1998 = `̀̀̀̀ 10,760]

6. Mr. Ramesh had ` 3,30,000 in the bank account on 1.1.1998 when he started his business. Heclose his accounts on 31st March, 1999. His single entry books showed his position asfollows:

31.3.1998 (`̀̀̀̀) 31.3.1999 (`̀̀̀̀)

Cash in hand 2,200 3,300

Stock in trade 20,900 31,900

Debtors 1,100 2,200

Creditors 5,500 3,300

On and from 1.4.1998, he began drawing ` 770 p.m. for his personal expenses from the cashbox of the business. His account with the bank had the following entries:

Deposits (`̀̀̀̀) Withdrawals ( `̀̀̀̀)

1.1.98 33,000

1.1.98 to 31.3.98 2,45,300

1.4.98 to 31.3.99 2,53,000 2,97,000

The above withdrawals included payment by cheque of ` 2,20,000 and ` 66,000 respectivelyduring the period from 1.1.98 to 31.12.98 and from 1.4.98 to 31.12.99, for the purchase ofmachineries for the business. The deposits after 1.1.98 consisted whole of sale price receivedfrom the customers by cheques.

Draw up Mr. Ramesh’s statement of affairs as at 31.3.19978 and 31.3.99 respevtively andwork out his profit or loss for the year ended 31.3.99.

[Ans: Profit = `̀̀̀̀ 46,640; Capital as on 31.3.989 = `̀̀̀̀ 3,23,400; Capital as on 31.3.99 =`̀̀̀̀ 3,60,800; Loss from 1.1.98 to 31.3.98 = `̀̀̀̀ 5,060]

32 Accountancy and Financial Management – II

7. Sethi had declared an income ` 26,000 during 1997 and 1998. The Income Tax Officer thinksthat Sethi has not disclosed his income fully. He asks for your assistance to find out whetherhis impression his correct.

Sethi owed, on December 31.1996, a dwelling house valued at ` 5,000 and had in his firm, acapital of ` 60,000. He also had ` 5,000 in his private Savings Bank Account. He owed` 10,000 to his brother.

It is established that besides the dwelling house, Sethi's assets and liabilities on 31st December,1998 were:

`̀̀̀̀

Cash at bank 1,700

Saving bank account 7,800

Stock 25,000

Sundry debtors 35,000

Furniture & fixtures 6,000

Motor car 16,000

Sundry creditors 20,000

Expenses payable 600

The loan to his brother is no longer outstanding. His living expenses have been @ ` 1,000p.m. Besides, he reported that he made a gift of ` 1,500 to his niece on her marriage.

What advice will you give to the Income Tax Officer?

[Ans: Total income for two year = `̀̀̀̀ 41,400; Capital as on 31.12.96 = `̀̀̀̀ 1,05,000; Capitalas on 31.12.1998 = `̀̀̀̀ 1,20,900]

8. The balance sheet of Key, Tai and Chung on 31st December 1997 was as follows:Balance Sheet as at 31st December, 1997

Particulars `̀̀̀̀ Particulars `̀̀̀̀

Sundry creditors 25,300 Cash 5,400Expenses payable 800 Stock at cost 41,000Loan from Tai 10,000 Sundry debtors 27,900Capitals : Furniture & fixtures 6,100 Kye 20,000 Current account: Tai 15,000 Key 1,500 Chung 10,000 45,000 Chung 1,100 2,600Tai's current account 1,900

83,000 83,000

Accounting from Incomplete Records 33

Profits were shared by the partners in the ratio of Kye, 4/10, Tai 3/10 and Chung 3/10. On31st December, 1998, the various assets and liabilities of the firms were as follows:

Assets `̀̀̀̀ Liabilities `̀̀̀̀

Cash 4,700 Sudry creditors 27,000Stock 45,200 Expenses prepaid 240Sundry debtors 31,400 Loan from Tai 10,000

Furniture & fixtures 5,660

The partners had drawn: ` 6,000 by Kye, ` 5,000 by Tai and ` 4,000 by Chung. Prepare theBalance Sheet of the firm at the end of 1998.

[Ans: Current accounts: Kye = `̀̀̀̀ 620 (cr.); Tai = `̀̀̀̀ 3,590 (cr.) and Chung = `̀̀̀̀ 990 (cr.);Total of balance sheet = `̀̀̀̀ 87,200. It has been assumed that interest on Tai'sloan @ 6% = `̀̀̀̀ 600 is outstanding]

9. Narendra, who keep his books by single entry, has submitted returns to the Income TaxAuthorities showing his income to be as follows:

`̀̀̀̀

Year ending Dec. 31, 1989 7,350

Year ending Dec. 31, 1990 7,400

Year ending Dec. 31, 1991 7,870

Year ending Dec. 31, 1992 13,570

Year ending Dec. 31, 1993 12,140

Year ending Dec. 31, 1994 9,260

The Income Tax Officer is not satisfied as to the accuracy submitted. You are instructed toassist establishing their correctness, and for that prupose you are supplied with the followinginformation:

(a) Business liabilities and assets on 31st Dec. 1988 were, debtors ` 1,450, cash at bank andin hand ` 9,470; stock ` 5,420; creditors 7,320.

(b) Narendra owed his brother ` 4,000 on 31st Dec., 1988. on 15th Feb. 1991. He repaid thisamount, and on 1st Jan., 1994 he lent his brother, ` 3,000.

(c) Narendra owns a house, which he purchased in 1984 for ` 20,000 and a car which hepurchased in 1990 for ̀ 7,500 in 1993 he brought ` 10,000 shares in X Ltd. for ` 7,500.

(d) In 1994, ` 3,000 was stolen from his house.

(e) Narendra estimates that his living expenses have been 1989: ̀ 3,000; 1990: ` 4,000; 1991:` 6,000; 1992, 1993 and 1994: ` 7,000 p.a. exclusive of the amount stolen.

(f) On 31st Dec. 1994, the business liabilities and assets were creditors ` 8,400; debtors` 5,920; cash in hand and at bank ` 19,450, and stock ` 6,740.

34 Accountancy and Financial Management – II

From the information submitted above, prepare a statement showing whether or not theincome declared by Narendra is correct.

[Ans: Total capital on 31.12.1988 = `̀̀̀̀ 23,936; Total capital on 31.12.1994 = `̀̀̀̀ 60,025]

CONVERSION METHOD

10. Calculate credit sales from the following figures:

`̀̀̀̀ `̀̀̀̀

Opening balance of debtors 20,000 Discount allowed 4,000

Cash received form debtors 95,000 Closing balance of debtors 18,000

Bad debts written off 2,000

[Ans: Credit sale = `̀̀̀̀ 99,000]

11. Calculate credit purchase from the following information:

`̀̀̀̀ `̀̀̀̀

Opening balance of creditors 15,000 Discount received 3,000

Cash paid to creditors 80,000 Closing balance of creditors 18,000

B/R endorsed to creditors 7,000

[Ans: Credit purchase = `̀̀̀̀ 93,000]

12. Calculate closing stock from the following figures:

`̀̀̀̀ `̀̀̀̀

Opening stock 12,000 Sales 60,000

Purchases 70,000 Sales returns 2,000

Purchases returns 5,000 Gross profit rate on cost 25%

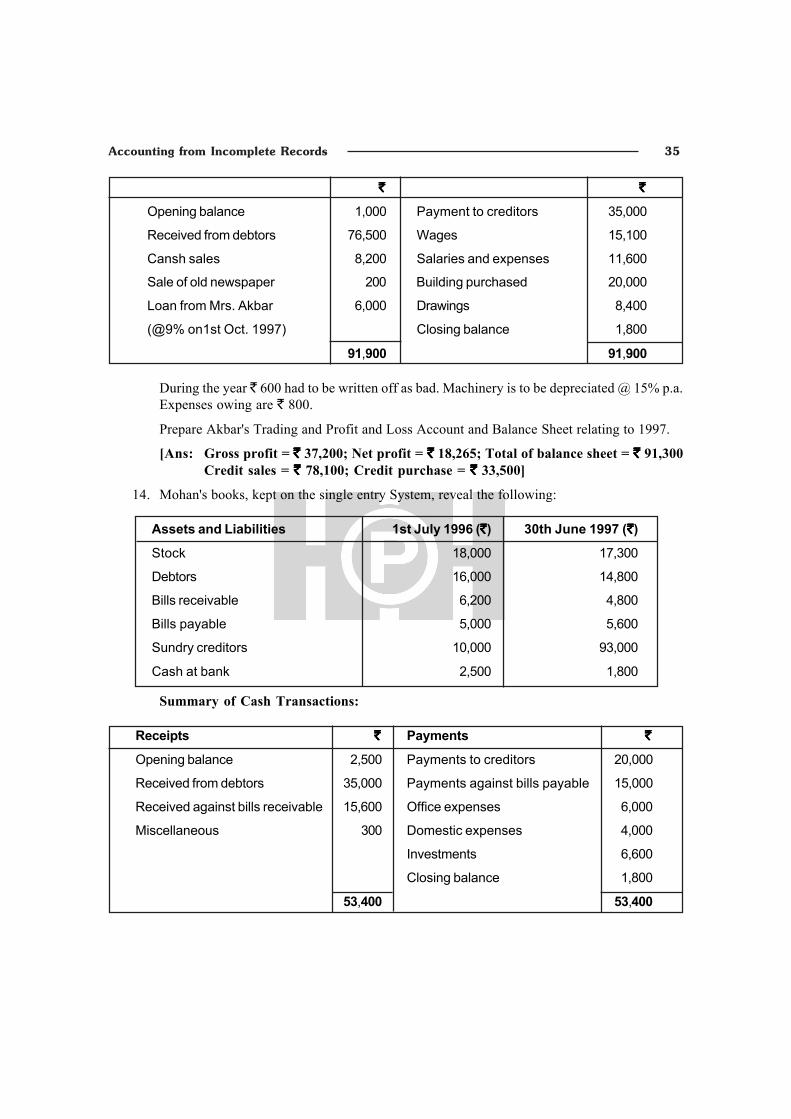

13. Akbar did not keep proper books of account. However, he gives you the following informationrelating to 1997:

Assets and Liabilties 1st Jan., 1997 (`̀̀̀̀) 31st Dec., 1997 ( `̀̀̀̀)

Cash at bank 1,000 1,800

Stock 20,000 19,500

Sundry debtors 15,000 16,000

Machinery 40,000 —

Sundry creditors 20,000 18,500

Accounting from Incomplete Records 35

`̀̀̀̀ `̀̀̀̀

Opening balance 1,000 Payment to creditors 35,000

Received from debtors 76,500 Wages 15,100

Cansh sales 8,200 Salaries and expenses 11,600

Sale of old newspaper 200 Building purchased 20,000

Loan from Mrs. Akbar 6,000 Drawings 8,400

(@9% on1st Oct. 1997) Closing balance 1,800

91,900 91,900

During the year ` 600 had to be written off as bad. Machinery is to be depreciated @ 15% p.a.Expenses owing are ` 800.

Prepare Akbar's Trading and Profit and Loss Account and Balance Sheet relating to 1997.

[Ans: Gross profit = `̀̀̀̀ 37,200; Net profit = `̀̀̀̀ 18,265; Total of balance sheet = `̀̀̀̀ 91,300Credit sales = `̀̀̀̀ 78,100; Credit purchase = `̀̀̀̀ 33,500]

14. Mohan's books, kept on the single entry System, reveal the following:

Assets and Liabilities 1st July 1996 (`̀̀̀̀) 30th June 1997 ( `̀̀̀̀)

Stock 18,000 17,300

Debtors 16,000 14,800

Bills receivable 6,200 4,800

Bills payable 5,000 5,600

Sundry creditors 10,000 93,000

Cash at bank 2,500 1,800

Summary of Cash Transactions:

Receipts `̀̀̀̀ Payments `̀̀̀̀

Opening balance 2,500 Payments to creditors 20,000

Received from debtors 35,000 Payments against bills payable 15,000

Received against bills receivable 15,600 Office expenses 6,000

Miscellaneous 300 Domestic expenses 4,000

Investments 6,600

Closing balance 1,800

53,400 53,400

36 Accountancy and Financial Management – II

Investments consisted of 4% Government Bonds of the face value of ` 8,000 and werepurchased on 1st Jan 1997. Prepare Trading and Profit and Loss Account and Balance Sheetfrom above figures.

[Ans: Gross Profit = `̀̀̀̀ 12,400; Net Profit = `̀̀̀̀ 6,860; Total of Balance Sheet = `̀̀̀̀ 45,460]

15. Desai wants to ascertain the profit he earned during 1998and his balance sheet at the end ofthe year. He does not keep sytematic books of account and can give you only the followinginformation:

Assets and Liabilities Dec 31, 1997 (`̀̀̀̀) Dec 31, 1998 ( `̀̀̀̀)

Sundry debtors 45,000 48,600

Sundry creditors 2,400 ?

Cash 6,300 ?

Furniture and fixtures 11,000 13,600

Stock at cost 25,000 30,000

Transactions during 1998: `̀̀̀̀

Cash received from debtors 80,000

Discount allowed to them 1,400

Bad debts writtenoff 1,800

Cash paid to creditors 64,000

Goods returned by customers 3,000

Goods returned to suppliers 2,000

Expenses paid 5,200

Drawings 9,000

He still owes ` 800 for expenses and the depreciation on furniture and fixtures is 15%. Heaffirms that he always sells goods at cost plus 40%. A provision of 2.5% on debtors isrequired against bad debts. Help Desai.

[Ans: Gross profit = `̀̀̀̀ 24,800; Net profit = `̀̀̀̀ 13,770; Total of Balance Sheet = `̀̀̀̀ 95,870]

Accounting from Incomplete Records 37

16. The books of Moneymaker showed the following figures:

Assets and Liabilities 31.12.95 (`̀̀̀̀) 31.12.96 (`̀̀̀̀)

Cash at bank 3,500 8,500

Cash in hand 410 850

Stock on trade 22,500 25,500

Sundry debtors 18,000 ?

Sundry creditors 8,000 7,300

Bills payable 20,000 18,000

Furniture and fittings 5,000 ?

Outstanding salary 200 ?

The cash book analysis showed the following figures amongst others:

Particulars `̀̀̀̀ Particulars `̀̀̀̀

Receipts from customers 1,05,000 Drawings 6,000

Discount allowed to customers 1,300 Payments to creditors 19,000

Salary upto 31.12.96 2,600 Discount received from creditors 2,600

Rent 3,600 Payment for bills payable 80,000

Sundry trade expenses 8,500

Furniture purchased on 1.7.96 1,000

Depreciation is provided on furniture and fitings @ 10 p.a. No figures are available for totalsales. However, Moneymaker informs you that he maintains a steady gross profit rate of 25%on sales.

Prepare Moneymaker's Trading and Profit and Loss Account for the year ended 31st December,1996 and the balance sheet as at date.

[Ans: Net profit = `̀̀̀̀ 18,217; Total of Balance Sheet = `̀̀̀̀ 58,727; Closing Balance ofDebtors = `̀̀̀̀ 18,427; Furniture and fittings after depreciation = `̀̀̀̀ 5,450; Creditpurchase = `̀̀̀̀ 98,900; Opening capital = `̀̀̀̀ 21,210]

38 Accountancy and Financial Management – II

17. Calculate total sales from the following information:

Particulars `̀̀̀̀

Bills receivable on 1st January 1998 7,800Debtors on 1st January 1998 30,800Cash received on maturity of bills receivable during the month 20,900Cash received from debtors 70,000Bad debts written off 4,800Returns inward 8,700Bills receivable dishonoured 1,800Bills receivable on 31st January 1998 6,000Debtors on 31st January 1998 25,500

Cash sales, during the months 15,900

[Ans: Credit Sales = `̀̀̀̀ 97,300; B/R drawn during the year = `̀̀̀̀ 20,900; Total sales = ` ` ` ` ` 1,13,200]

18. The Balance Sheet of Bose and Dass was as under on 31st December 1997:

Liabilities `̀̀̀̀ Assets `̀̀̀̀

Sundry creditors 11,600 Stock 15,000Bills payable 4,300 Debtors 16,100Capitals: Furniture 4,000 Bose 20,000 Delivery van 13,000

Dass 15,000 35,000 Cash at bank 2,800

The transactions during 1998 were:

Particulars `̀̀̀̀ Particulars `̀̀̀̀

Purchases 30,000 Bills payable issued 7,000

Sales 50,000 Discount received 500

Bills receivable received 6,000 Discount allowed 800

Accounting from Incomplete Records 39

The stock on 31st Dec, 1988 was ` 18,200. Cash transactions were as follows:

Particulars `̀̀̀̀

Received from debtors 45,000

Received against B/R 4,500

Received from sale of O/s gunny bags 200

Payment to creditors 21,500

Payment against B/P 8,000

Expenses (including salaries) 10,000

The balance at Bank on 31st Dec., 1998 was ̀ 4,500. Delievery van is to be depreciated @ 15%.During the year, both partners had withdrawn an equal sum of money. Allowing a commissionof 10% of net profits before such commission to the manager, prepare Trading and Profit andLoss Account and Balance Sheet relating to 1998.

[Ans: Gross Profit = `̀̀̀̀ 23,200; Net Profit = `̀̀̀̀ 10,035; Total of Balance Sheet = `̀̀̀̀ 53,550;Drawings = `̀̀̀̀ 8,500]

19. X started grocery business on 1st January, 1996 with a capital of ` 10,000. He spent ` 1,500on furniture and fixtures in cash. He maintains his books on single entry. Following figureswere extracted from his books:

Particulars `̀̀̀̀

Sales (inclusive of cash ` 8,000) 20,000

Purchases (inclusive of cash purchase ̀ 2,500) 12,000

Bad debts written off 750

Business expenses 1,050

X used groceries worth ` 1,500 and took ` 1,300 in cash for personal use. On 31st December1996, his sundry debtors were ` 1,250 and sundry creditors ` 1,500. Stock in hand on31st December, 1996 was ` 1,500.

Prepare profit and loss account for the year ended on 31st December, 19996 and balancesheet as on that date.

OBJECTIVE QUESTIONS

A. Multiple Choice Questions

1. Usually, in a single entry system, ______________.

(a) only manual accounts are maintained

(b) only cash and personal accounts are maintained

40 Accountancy and Financial Management – II

(c) only real accounts are maintained

(d) only nominal accounts are maintained

2. Profit can be ascertained from the incomplete records under single entry by using______________.

(a) Statement of Affairs Method (b) Conversion Method

(c) either (a) or (b) above (d) None of (a) or (b)

3. If books are kept under single entry system, credit sales are ascertained by preparing______________.

(a) Total Creditors Account (b) Total Debtors Account

(c) Credit Sales Account (d) Trading Account

4. If books are kept under single entry system, credit purchases are ascertained by preparing______________.

(a) Total Creditors Account (b) Total Debtors Account

(c) Credit Purchases Account (d) Bills Payable Account

5. If books are kept under single entry system, opening stock is ascertained by preparing -______________.

(a) Opening Stock Account (b) Stock Register

(c) Memorandum Trading Account (d) Opening Statement of Affairs

6.Dr. Total Debtors Account Cr.Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d xxx By Cash/Bank xxxTo Balancing Figure xxx By Bad Debts w/o xxx

By Balance c/d xxx Total xxx Total xxx

The balancing figure in the above account is likely to indicate ______________.

(a) Sales returns (b) Credit sales

(c) Bills receivable drawn (d) Discount allowed

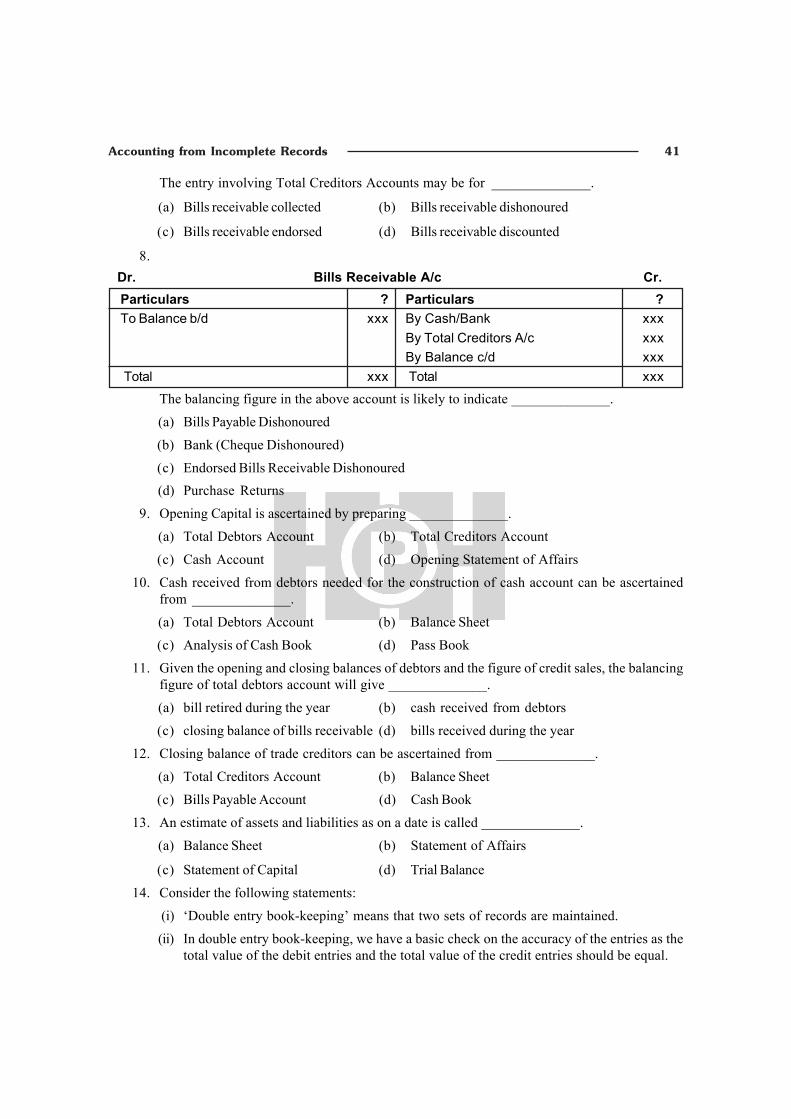

7.Dr. Bills Receivable A/c Cr.Particulars `̀̀̀̀ Particulars `̀̀̀̀

To Balance b/d xxx By Cash/Bank xxxBy Total Creditors A/c xxxBy Balance c/d xxx

Total xxx Total xxx

Accounting from Incomplete Records 41

The entry involving Total Creditors Accounts may be for ______________.

(a) Bills receivable collected (b) Bills receivable dishonoured

(c) Bills receivable endorsed (d) Bills receivable discounted

8.Dr. Bills Receivable A/c Cr.Particulars ? Particulars ?To Balance b/d xxx By Cash/Bank xxx

By Total Creditors A/c xxxBy Balance c/d xxx

Total xxx Total xxx

The balancing figure in the above account is likely to indicate ______________.

(a) Bills Payable Dishonoured

(b) Bank (Cheque Dishonoured)

(c) Endorsed Bills Receivable Dishonoured (d) Purchase Returns

9. Opening Capital is ascertained by preparing ______________.

(a) Total Debtors Account (b) Total Creditors Account

(c) Cash Account (d) Opening Statement of Affairs

10. Cash received from debtors needed for the construction of cash account can be ascertainedfrom ______________.

(a) Total Debtors Account (b) Balance Sheet

(c) Analysis of Cash Book (d) Pass Book

11. Given the opening and closing balances of debtors and the figure of credit sales, the balancingfigure of total debtors account will give ______________.

(a) bill retired during the year (b) cash received from debtors

(c) closing balance of bills receivable (d) bills received during the year

12. Closing balance of trade creditors can be ascertained from ______________.

(a) Total Creditors Account (b) Balance Sheet

(c) Bills Payable Account (d) Cash Book

13. An estimate of assets and liabilities as on a date is called ______________.

(a) Balance Sheet (b) Statement of Affairs

(c) Statement of Capital (d) Trial Balance

14. Consider the following statements:

(i) ‘Double entry book-keeping’ means that two sets of records are maintained.

(ii) In double entry book-keeping, we have a basic check on the accuracy of the entries as thetotal value of the debit entries and the total value of the credit entries should be equal.

42 Accountancy and Financial Management – II

Are the statements true or false?

Statement (i) Statement (ii)

(a) True True(b) True False

(c) False True

(d) False False

15. Which of the following items could appear on the credit side of a Total Debtors account?

(i) Cash received from customers

(ii) Bad debts written off

(iii) Increase in reserve for doubtful debts

(iv) Discounts allowed(v) Sales

(vi) Credits for goods returned by customers

(vii) Cash refunds to customers

(a) (i), (ii), (iv) and (vi) (b) (i), (ii), (iv) and (vii)

(c) (iii), (iv), (v) and (vi) (d) (v) and (vii)

Ans.:1. (b) 2. (c) 3. (b) 4. (a) 5. (c) 6. (b) 7. (c) 8. (d)9. (d) 10. (a) 11. (b) 12. (a) 13. (b) 14. (c) 15. (a)

B. Match the Following Columns:

Column A Column B1. Credit sales (a) Memorandum Trading Account2. Cash Sales (b) Bills Receivable A/c3. Credit Purchases (c) Total Debtors A/c4. Opening Stock (d) Capital A/c5. Opening capital balance (e) Sales A/c6. Bill endorsed (f) Closing Statement of Affairs

(g) Cash/Bank Accounts(h) Opening Statement of Affairs(i) Purchases A/c(j) Total Creditors Account

Ans.:

1. (c), 2. (g), 3. (j), 4. (a), 5. (h), 6. (b)

Accounting from Incomplete Records 43

C. State Whether True or False

1. Single Entry System follows the basic accounting principle of accrual.2. Trial Balance is prepared under Single Entry System in order to verify arithmetical accuracy

of the records.

3. Under Single Entry System, it is not possible to ascertain the gross profit earned by thebusiness.

4. Under Single Entry System, only one journal entry is passed for all the transactions during aday.

5. Under Single Entry System, all entries are passed as well as posted only by one person.6. Under Single Entry System, only one aspect of transaction (either debit or credit) is recorded

for all transactions.

7. Even in Single System, Cash Account may be kept properly with entries made for bothreceipts and payments.

8. Normally, in Single System, credit sales are recorded only in the Debtors A/c but no SalesRegister is maintained.

9. Under Single Entry System, it is not possible to ascertain the net profit earned by the business.10. Income-tax Act allows small traders to adopt single entry system for keeping books of accounts.

11. Conversion method helps in preparing final accounts from records kept under single entrysystem.

12. Under Conversion method, credit sales are ascertained by preparing Sales Register.

13. Under Conversion method, credit purchases are ascertained by preparing Purchase Day Book.14. Under Conversion method, closing stock is ascertained by preparing Stock Register.

15. Under Conversion method, opening capital is ascertained by using the Statement of Affairsmethod.

16. The name single entry system is used because for every transaction only one aspect is recordedin the books of account.

17. Under single entry system, it is not possible to prepare a trial balance unless the missingfigures are ascertained.

18. Limited companies are free to choose either single entry or double entry system of accounting.

19. Under single entry system, the usual accounts maintained are the personal accounts of suppliersand customers and the cash book.

20. Under the conversion method of single entry, credit purchases and credit sales are ascertainedby preparing the total creditors and total debtors accounts respectively.

Ans.:

1. F 2. F 3. T 4. F 5. F 6. F 7. T 8. T

9. T 10. F 11. T 12. F 13. F 14. F 15. T 16. F

17. T 18. F 19. T 20. T.