Economy of Israel

170

Vol.1-2014 Israel - Killer or Leader? With 20 years Economic Overview The report is based on the authors’ opinion and the facts collected which may or may not be agreed by the readers. Disagreement with any part of this report is welcomed. Asim Siddiqui, Daniyal Kaleem and Saniya Salah Udddin

Transcript of Economy of Israel

Vol.1-2014

Israel - Killer or Leader?

With 20 years Economic Overview

The report is based on the authors’ opinion and the facts collected which may or may not be agreed by the readers.

Disagreement with any part of this report is welcomed.

Asim Siddiqui, Daniyal Kaleem and Saniya Salah Udddin

Daniyal, Asim and Saniya

2

By,

Daniyal Kaleem

Muhammad Asim Siddiqui

Saniya Salah Uddin

Daniyal, Asim and Saniya

3

Dedicated to,

Dr. Tahir Ali

Chairman

Department of Commerce

University of Karachi

Daniyal, Asim and Saniya

4

Serial # Chapter Page #

1 Acknowledgement 5

2 Introduction _______________________ 6 -9

2.1 Objective ………………………………………….. 7

2.2 Preface ………………………………………….. 8

2.3 Summary …………………………………………. 9

3 History __________________________ 10-20

3.1 Judaism-Background …………………………... 11-12

3.2 Formation of Israel …………………………….. 13-18

3.3 Overview ………………………………………. 19

3.4 Map …………………………………………….. 20

4 Economic Indicators ______________ 21-22

World Bank, CIA & United Nations …………... 22

5 Economic Performance _____________ 23-136

5.1 GDP 1995-2014 ……………………………….. 24

5.1-A Graph …………………………………………... 25

5.1-B Reasons for Variation …………………………... 26-28

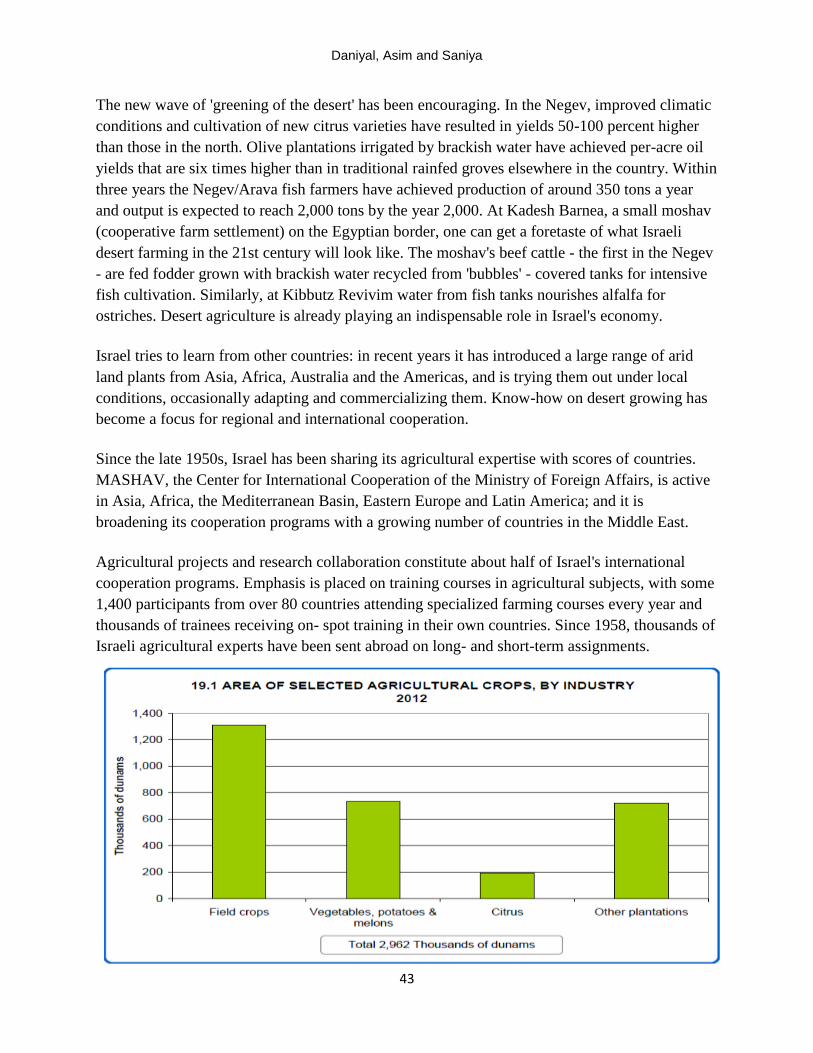

5.2 Agriculture ----------------------------------------------- 29-62

5.2-A Introduction …………………………………….. 30

5.2-B History ………………………………………...... 31-32

5.2-C A Glance …………………………………………. 33-34

5.2-D Analysis, Planning, Research, Government ……… 35-38

5.2-E Irrigation and Technology ………………………. 39-42

5.2-E Fruits …………………………………………….. 43-46

5.2-F Vegetables ………………………………………... 47

5.2-G Dairy Farming …………………………………….. 48

5.2-H Poultry and Beef ………………………………….. 49

5.2-I Aqua Culture ……………………………………... 50

5.2-J Mari Culture ……………………………………... 51

5.2-K Floriculture ………………………………………… 52-54

5.2-L Bee Keeping ………………………………………. 55-56

5.2-M Economy, World Market, Future ………………….. 57-60

5.2-N Challenges …………………………………………. 61-62

5.3 Industry ------------------------------------------------------ 63-103

5.3-A Introduction …………………………………….. 64

5.3-B High-Tech Industry …………………………...... 65-68

5.3-C Defense Industry ...………………………………. 69-74

Daniyal, Asim and Saniya

5

5.3-D Aerospace Industry ………………….………… 75-76

5.3-E Weapon Industry ………………………………. 77-78

5.3-E Electronics Industry ……….……………………… 79-80

5.3-F Diamond Industry ………………………………… 81-82

5.3-G Textile Industry …………………………………… 83-86

5.3-H Semi-conductor Industry …………………………. 87

5.3-I Chemical Industry ………………………………… 88-90

5.3-J Automative Industry ………………………….…... 91

5.3-K Design Industry …………………………………… 92-93

5.3-L Film Industry …………………………………….. 94-95

5.3-M Tourism Industry …………….………………….. 96

5.3-N Association of Different Industries …………...... 97-102

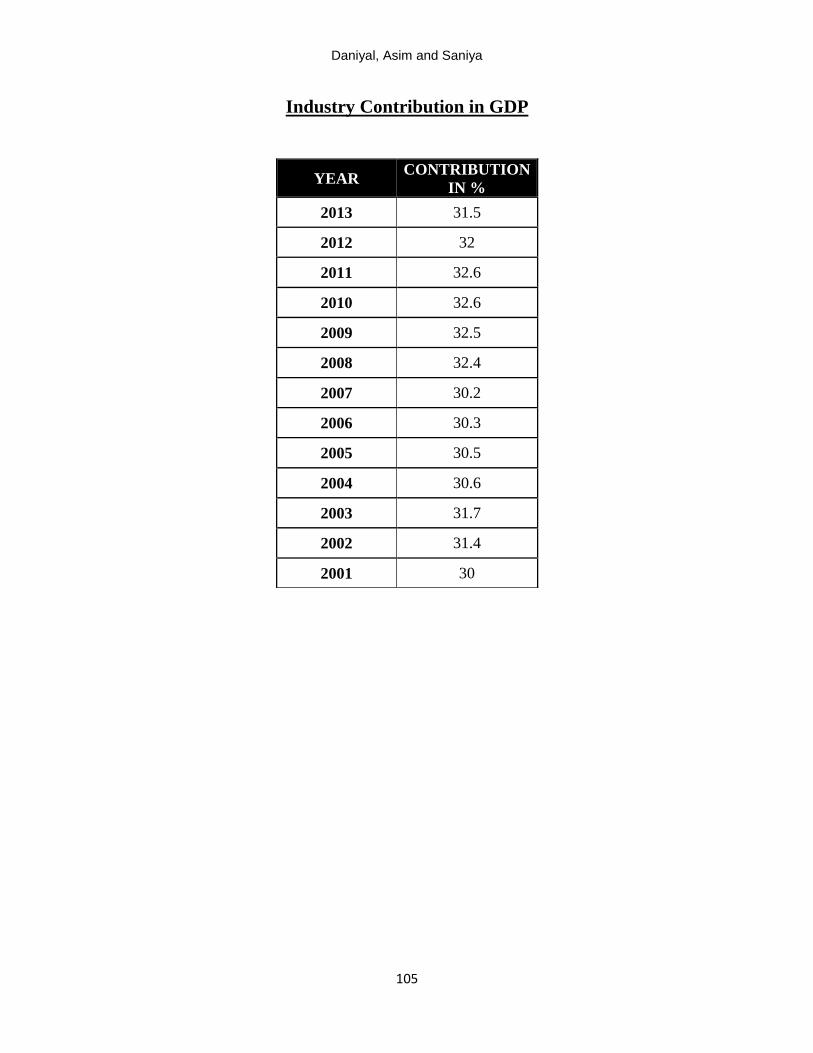

5.3-O Industry and GDP ………………...………........... 103

5.4 Services --------------------------------------------------- 104-136

5.4-A Introduction …………………………………….. 105

5.4-B History ……………………………………………. 106-107

5.4-C Finance ………….………………………........... 108-111

5.4-D Banking …….....…………………………………. 112-113

5.4-E Tourism …………………………….…………… 114-122

5.4-F Trade ….….……..……………………………… 123-126

5.4-G Public Sector …………………………………….. 127-129

5.4-H Health Care ……………………………………… 130-132

5.4-I Education ………………………………………. 133-134

5.4-J Taxation ……………………………………...….. 135

5.4-K Conclusion and Recommendation ……………… 136

6 Current Situation __________________ 137- 145

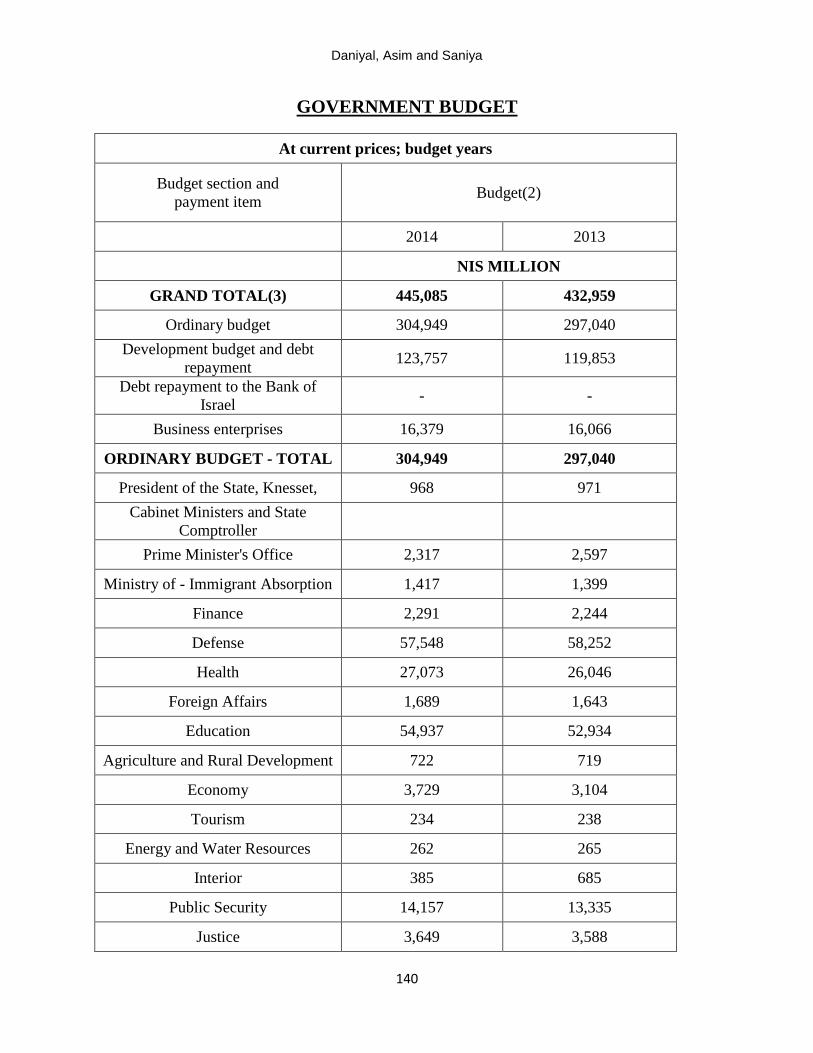

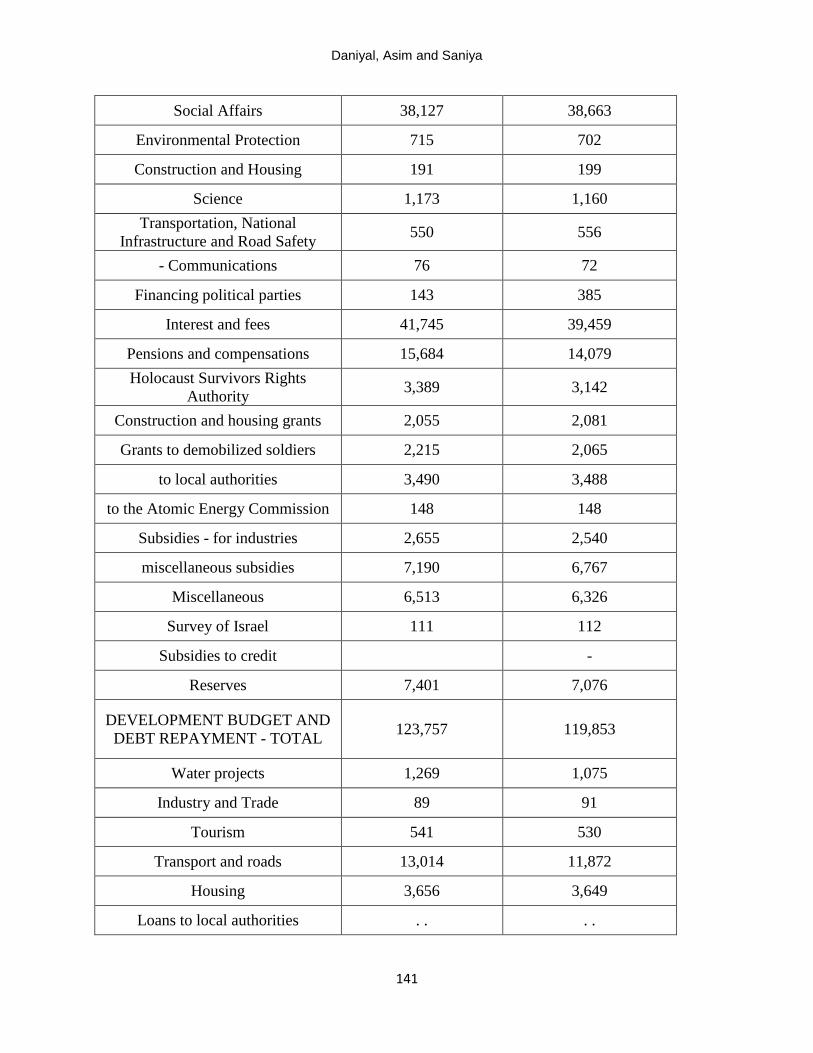

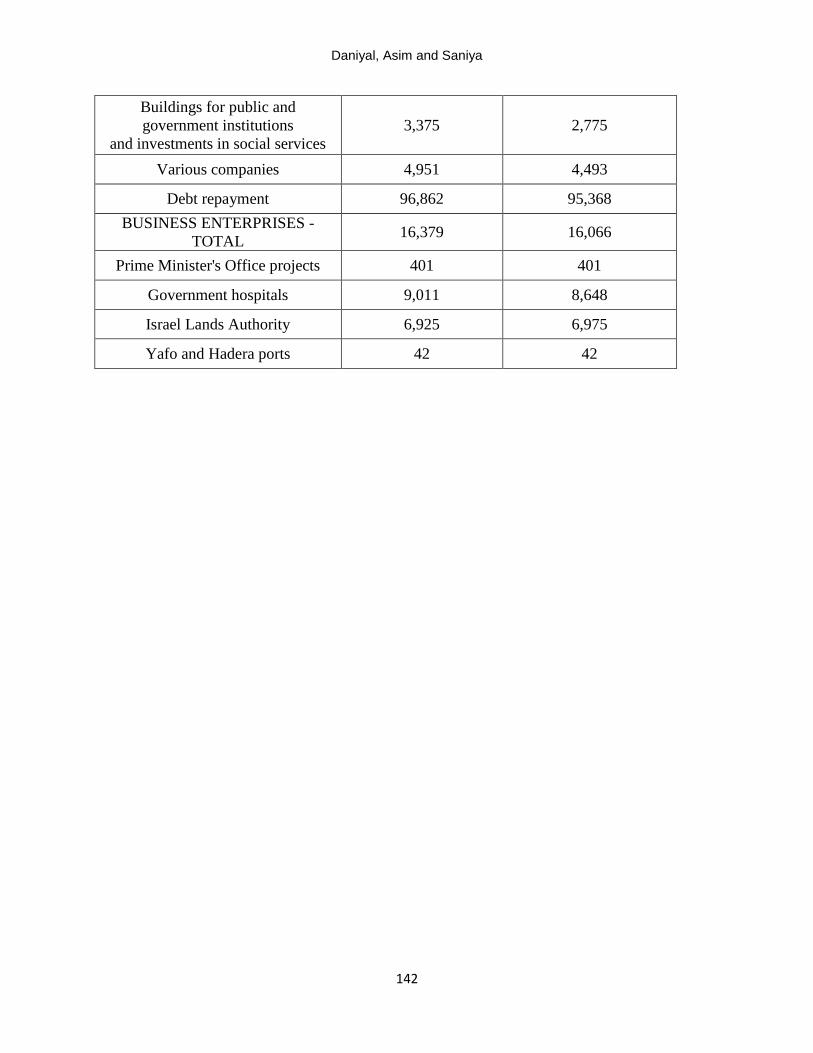

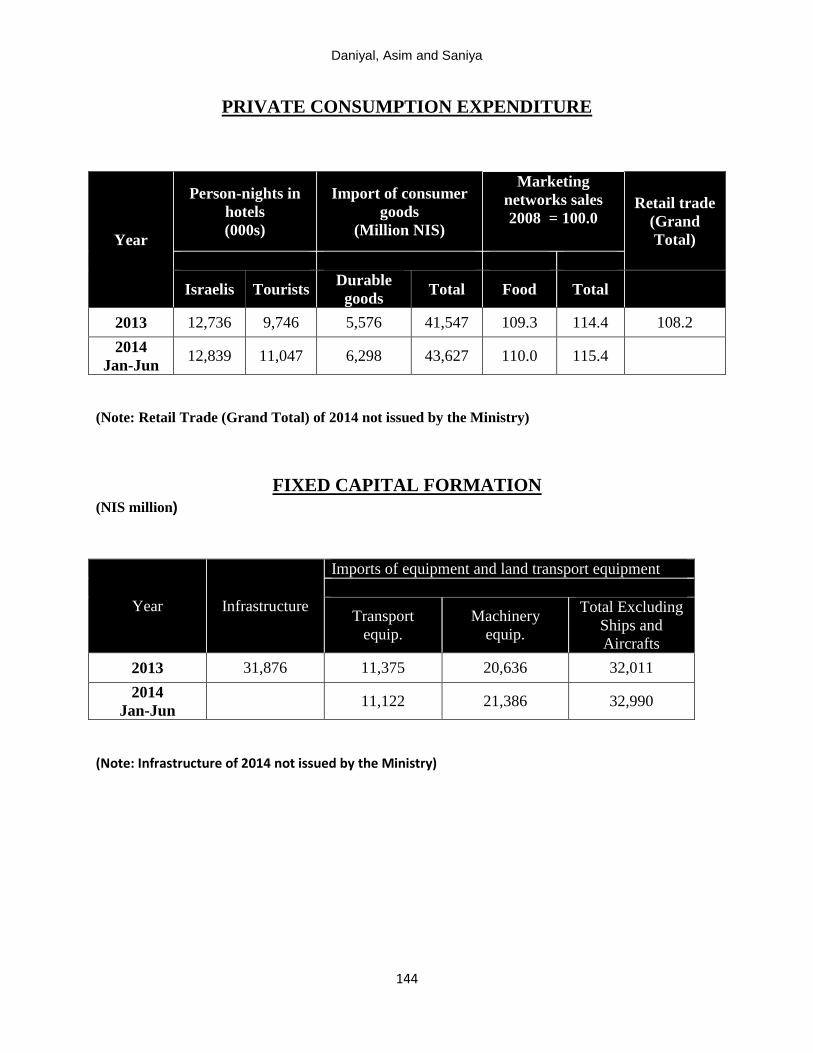

6.1 Budget ……………………………………………… 138-140

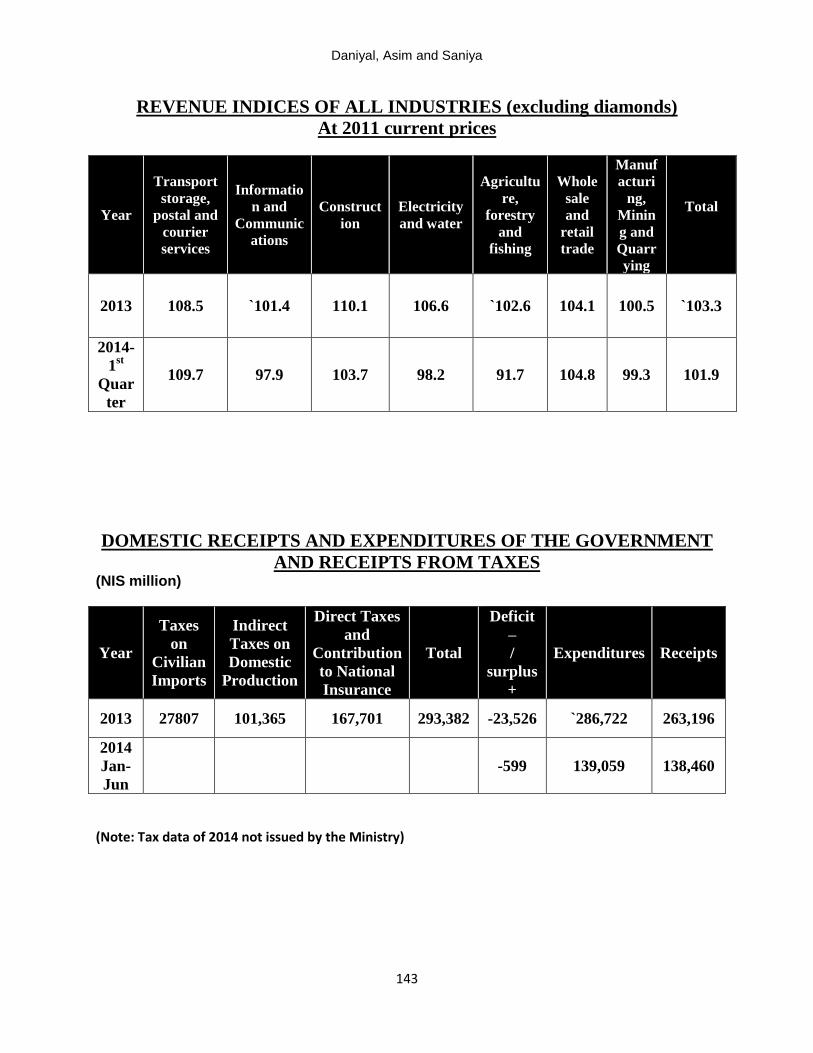

6.2 Revenue Indices & Receipts and Payments ……….. 141

6.3 Private Consumption and Capital Formation ……… 142

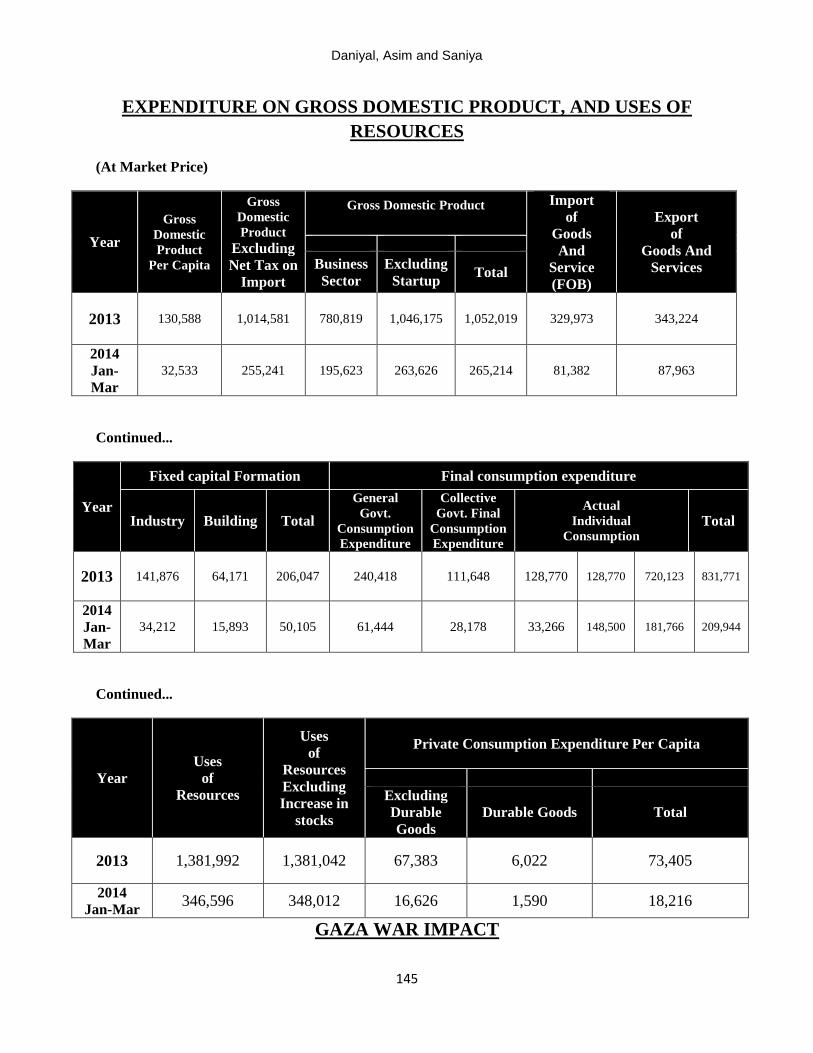

6.4 Expenditure on GDP and Uses of Resources ……… 143

6.3 Gaza War Impact ………………………………… 144-145

7 Summary __________________________ 146-151

7.1 Agriculture ……………………………………………… 147

7.2 Industry ………………………………………………... 148

7.3 Services ………………………………………..……… 149-151

8 Comparison __________________________ 152-160

8.1 Economy of Pakistan …………………………………… 153

World Bank, CIA & United Nations 8.2 Agriculture ………………………………………….. 154-155

8.3 Industry …………………………………………… 156-158

8.4 Services …………………………………………….. 159-160

Daniyal, Asim and Saniya

6

9 Conclusion ___________________________ 161-164

9.1 Recommendation ………………………………………. 162-164

Daniyal, Asim and Saniya

7

Acknowledgement

The report is the mandatory research of the Course, Development Economics, studied in the 4th

Semester of BS program at Department of Commerce, University of Karachi.

1st of all we would like to thanks Allah the Almighty, who give us the opportunity to study at this

department from the best faculty of country.

We have decided to dedicate this report to our honorable Chairman, Dr. Tahir Ali because he is

always been so helpful to his students in every matter. Thanks to the great Chairman for giving

us the best environment and faculty to learn from.

Then we would like to thanks Madam Ayesha Farid who is the course in-charge. She taught all

the chapters that are to be covered in this report in the 3rd

Semester’s course and this semester

also. Then she gave us this report to do which basically not emphasizes on the Israel’s economy

but the main purpose was to identify the flaws in Pakistan’s economy and make it a better

country to live. It was a highly challenging research since our 1st semester and at some moments

we were not very hopeful on completing this report. However, her confidence given to us helped

actually in completion of this difficult research. We thank the great teacher for her cooperation in

this regard.

At last, we would also thanks the other faculty members of this department especially to one of

our greatest teachers, Sir Muhammad Farrukh Aslam who always assisted us in this report.

Daniyal, Asim and Saniya

8

Introduction

Daniyal, Asim and Saniya

9

Objective

Since we started to understand the world countries, we always heard few country names which

were very common to us, like United States of America, United Kingdom, Kingdom of Saudi

Arabia, India, China and Israel.

Israel-A country whose name whenever called was always taken negatively, whenever some

worst, any terrorist attack had occurred. People always used to express hatred for the country.

When we studied the course, Development Economics, we were assigned the economic report of

Israel. Firstly, we also expressed negative emotions as the report was assigned at the time of

Gaza Genocide-2014. We started to research on Israel which gives us very shocking and

unexpected knowledge.

The report carries the history of Israel, the economic position of the country among the world

along with a very detailed 20 years analysis of the country’s economy. The report covers all the

economic sectors which make the country one of the strongest economy of the world. The report

also covers the non-economic sectors which don’t have a direct impact on the economy however

they are considered in the economic plans.

At the end of the report, we have given a 20 years brief economic position of Pakistan. The basic

purpose of the report was to compare our country with the economy of Israel. We have also

given necessary recommendations with reference to Israel to improve the economy of Pakistan.

Daniyal, Asim and Saniya

10

Preface

The State of Israel was founded on 14th

May 1948. The country is located in Western Asia. The

geographical alignment of Israel includes latitude of 31° 30' N and longitude of 34° 45' E. The

particular latitude shows its position in Northern Hemisphere. Israel covers a total area 20,770

sq. km, is the 154th largest country of the world.

Jerusalem, the capital and largest city of Israel is also partly claimed by Palestinians. The city has

major religious significance in the world; this is the birthplace of three major religions: Islam,

Judaism, and Christianity. Israel is the only country in the world following Hebrew calendar,

also called as Jewish calendar.

Israel has since fought several wars with neighboring Arab states, in the course of which it

has occupied the West Bank, Sinai Peninsula, part of South Lebanon, Gaza Strip and the Golan

Heights. It annexed portions of these territories, including East Jerusalem, but the border with the

West Bank is disputed. Israel has signed peace treaties with Egypt and with Jordan, but efforts to

resolve the Israeli–Palestinian conflict have so far not resulted in peace.

It is a developed Middle East country. It is the member country of the Organization for

Economic Co-operation and Development (OECD). The country is considered as the 43rd

largest economy of the world as per GDP 2012. The country has the highest standard of living in

the Middle East.

Daniyal, Asim and Saniya

11

Summary

Israel has a technologically advanced market economy. Cut diamonds, high-technology

equipment, and pharmaceuticals are among the leading exports. Its major imports include crude

oil, grains, raw materials, and military equipment. Israel usually posts sizable trade deficits,

which are covered by tourism and other service exports, as well as significant foreign investment

inflows. Between 2004 and 2011, growth averaged nearly 5% per year, led by exports. The

global financial crisis of 2008-09 spurred a brief recession in Israel, but the country entered the

crisis with solid fundamentals, following years of prudent fiscal policy and a resilient banking

sector. In 2010, Israel formally acceded to the OECD. Israel's economy also has weathered the

Arab Spring because strong trade ties outside the Middle East have insulated the economy from

spillover effects. The economy has recovered better than most advanced, comparably sized

economies, but slowing demand domestically and internationally, and a strong shekel, has

reduced forecasts for the next decade to the 3% level. Natural gas fields discovered off Israel's

coast since 2009 have brightened Israel's energy security outlook. The Tamar and Leviathan

fields were some of the world's largest offshore natural gas finds this past decade. The massive

Leviathan field is not due to come online until 2018, but production from Tamar provided a one

percentage point boost to Israel's GDP in 2013 and is expected to contribute 0.5% growth in

2014. In mid-2011, public protests arose around income inequality and rising housing and

commodity prices. Israel's income inequality and poverty rates are among the highest of OECD

countries and there is a broad perception among the public that a small number of "tycoons" have

a cartel-like grip over the major parts of the economy. The government formed committees to

address some of the grievances but has maintained that it will not engage in deficit spending to

satisfy populist demands. In May 2013 the Israeli government, in a politically difficult process,

passed an austerity budget to reign in the deficit and restore confidence in the government's fiscal

position. Over the long term, Israel faces structural issues, including low labor participation rates

for its fastest growing social segments - the ultra-orthodox and Arab-Israeli communities. Also,

Israel's progressive, globally competitive, knowledge-based technology sector employs only 9%

of the workforce, with the rest employed in manufacturing and services - sectors which face

downward wage pressures from global competition.

Daniyal, Asim and Saniya

12

History

Daniyal, Asim and Saniya

13

Background of Judaism

What is Judaism?

Judaism is the religion, philosophy, and way of life of the Jewish people. Judaism is

a monotheistic religion, with the Torah as its foundational text while part of the larger text

known as the Tanakh or Hebrew Bible, and supplemental oral tradition represented by later texts

such as the Midrash and the Talmud.

Judaism claims a historical continuity spanning more than 3,000 years. Judaism has its roots as a

structured religion in the Middle East during the Bronze Age. Of the major world religions,

Judaism is considered one of the oldest monotheistic religions.

Judaism includes a wide corpus of texts, practices, theological positions, and forms of

organization. Within Judaism there are a variety of movements, most of which emerged

from Rabbinic Judaism, which holds that God revealed his laws

and commandments to Moses on Mount Sinai in the form of both the Written and Oral Torah.

Historically, this assertion was challenged by various groups such as

the Sadducees and Hellenistic Judaism during the Second Temple period;

the Karaites and Sabbateans during the early and later medieval period; and among segments of

the modern reform movements. Liberal movements in modern times such as Humanistic

Judaism may be nontheistic. Today, the largest Jewish religious movements are Orthodox

Judaism, Conservative Judaism and Reform Judaism.

Judaism is considered by religious Jews to be the expression of the covenantal relationship

that God established with the Children of Israel. The Israelites were already referred to as "Jews"

in later books of the Tanakh such as the Book of Esther, with the term Jews replacing the title

"Children of Israel". Judaism's texts, traditions and values strongly influenced later Abrahamic

religions, including Christianity, Islam and the Baha'i Faith. Many aspects of Judaism have also

directly or indirectly influenced secular Western ethics and civil law.

Who are Jews?

The Jews are an ethno religious group and include those born Jewish and converts to Judaism.

The Jewish ethnicity, nationality and religion are strongly interrelated, as Judaism is the

traditional faith of the Jewish nation. Converts to Judaism typically have a status within the

Jewish ethnos equal to those born into it. Conversion is not encouraged by mainstream Judaism,

and is considered a tough task, mainly applicable for cases of mixed marriages

In 2012, the world Jewish population was estimated at about 14 million, or roughly 0.2% of the

total world population. About 42% of all Jews reside in Israel and about 42% reside in the United

States and Canada, with most of the remainder living in Europe, and other minority groups

spread throughout the world in South America, Asia, Africa, and Australia.

Daniyal, Asim and Saniya

14

Christianity and Jews

The most profound difference between traditional Jewish belief and that of Christianity is in its

belief in the expected Messiah. Traditional Jewish belief holds that the Messiah of Israel is yet to

come, while Christians view the Messiah in the personage of Jesus. The disparity between these

two views has often given rise to tension and, occasionally, has spilled over into violence.

One of the basic positions held by Orthodox Jews regarding the Messiah is that he will come

from King David’s lineage and he will bring peace into the world.

Historians and theologians regularly review the changing relationship between

some Christian groups and the Jewish people; the article on Christian–Jewish

reconciliation studies one recent issue.

Islam and Judaism

Both religions claim to arise from the patriarch Abraham, and are therefore considered

Abrahamic religions. Jews have interacted with Muslims since the 7th century,

when Islam originated and spread in the Arabian Peninsula, and many aspects of Islam's core

values, structure, jurisprudence and practice are based on Judaism. Muslim culture and

philosophy have heavily influenced practitioners of Judaism in the Islamic world.

Jews in Muslim countries were not entirely free from persecution—for example, many were

killed, exiled or forcibly converted in the 12th century, Jews were confined to walled quarters

beginning in the 15th century and increasingly since the early 19th century.

In the late 20th century, Jews were expelled from nearly all the Arab countries. Most have

chosen to live in Israel. Israel has since fought several wars with neighboring Arab states after

which it has signed peace treaties with Egypt and Jordan, but efforts to resolve the Israeli–

Palestinian conflict have so far not resulted in peace.

Daniyal, Asim and Saniya

15

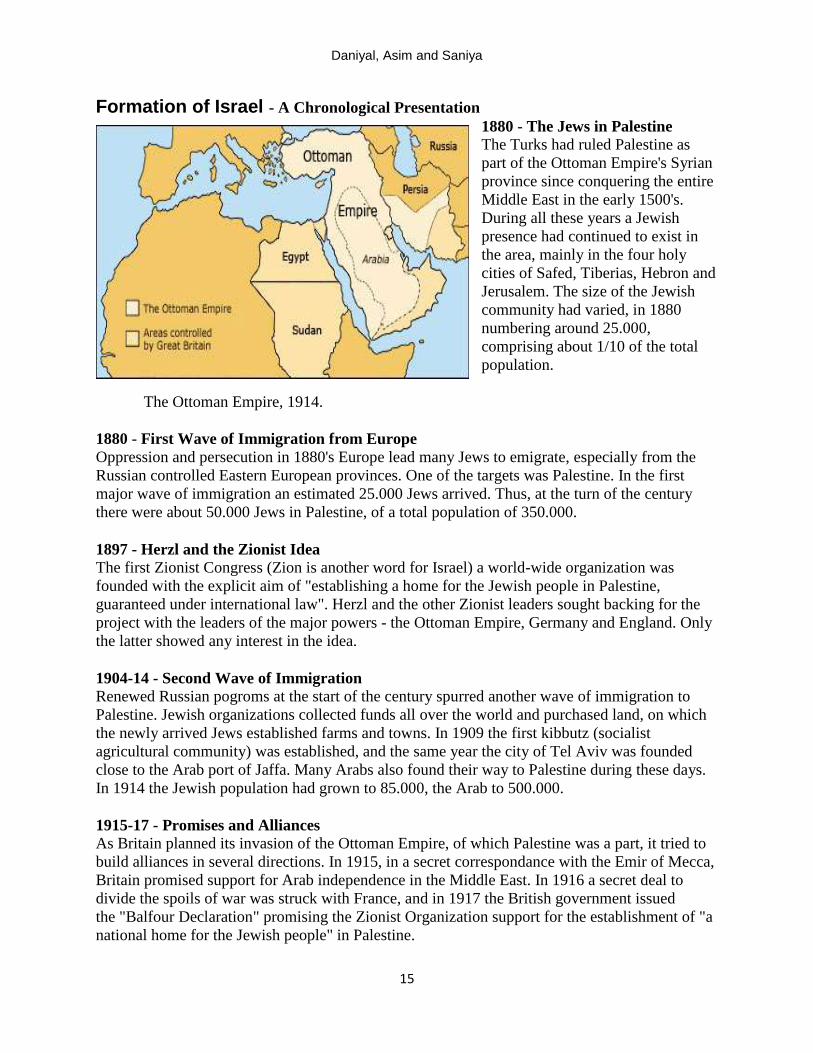

Formation of Israel - A Chronological Presentation

1880 - The Jews in Palestine The Turks had ruled Palestine as

part of the Ottoman Empire's Syrian

province since conquering the entire

Middle East in the early 1500's.

During all these years a Jewish

presence had continued to exist in

the area, mainly in the four holy

cities of Safed, Tiberias, Hebron and

Jerusalem. The size of the Jewish

community had varied, in 1880

numbering around 25.000,

comprising about 1/10 of the total

population.

The Ottoman Empire, 1914.

1880 - First Wave of Immigration from Europe

Oppression and persecution in 1880's Europe lead many Jews to emigrate, especially from the

Russian controlled Eastern European provinces. One of the targets was Palestine. In the first

major wave of immigration an estimated 25.000 Jews arrived. Thus, at the turn of the century

there were about 50.000 Jews in Palestine, of a total population of 350.000.

1897 - Herzl and the Zionist Idea The first Zionist Congress (Zion is another word for Israel) a world-wide organization was

founded with the explicit aim of "establishing a home for the Jewish people in Palestine,

guaranteed under international law". Herzl and the other Zionist leaders sought backing for the

project with the leaders of the major powers - the Ottoman Empire, Germany and England. Only

the latter showed any interest in the idea.

1904-14 - Second Wave of Immigration Renewed Russian pogroms at the start of the century spurred another wave of immigration to

Palestine. Jewish organizations collected funds all over the world and purchased land, on which

the newly arrived Jews established farms and towns. In 1909 the first kibbutz (socialist

agricultural community) was established, and the same year the city of Tel Aviv was founded

close to the Arab port of Jaffa. Many Arabs also found their way to Palestine during these days.

In 1914 the Jewish population had grown to 85.000, the Arab to 500.000.

1915-17 - Promises and Alliances As Britain planned its invasion of the Ottoman Empire, of which Palestine was a part, it tried to

build alliances in several directions. In 1915, in a secret correspondance with the Emir of Mecca,

Britain promised support for Arab independence in the Middle East. In 1916 a secret deal to

divide the spoils of war was struck with France, and in 1917 the British government issued

the "Balfour Declaration" promising the Zionist Organization support for the establishment of "a

national home for the Jewish people" in Palestine.

Daniyal, Asim and Saniya

16

1917 - The British Invasion As the Ottoman Empire entered World War I on the side of the Central Powers it was now at war

with England, and soon after British troops invaded all of the Ottoman Middle East. In 1917

General Allenby conquered Jerusalem, and one year after Damascus.

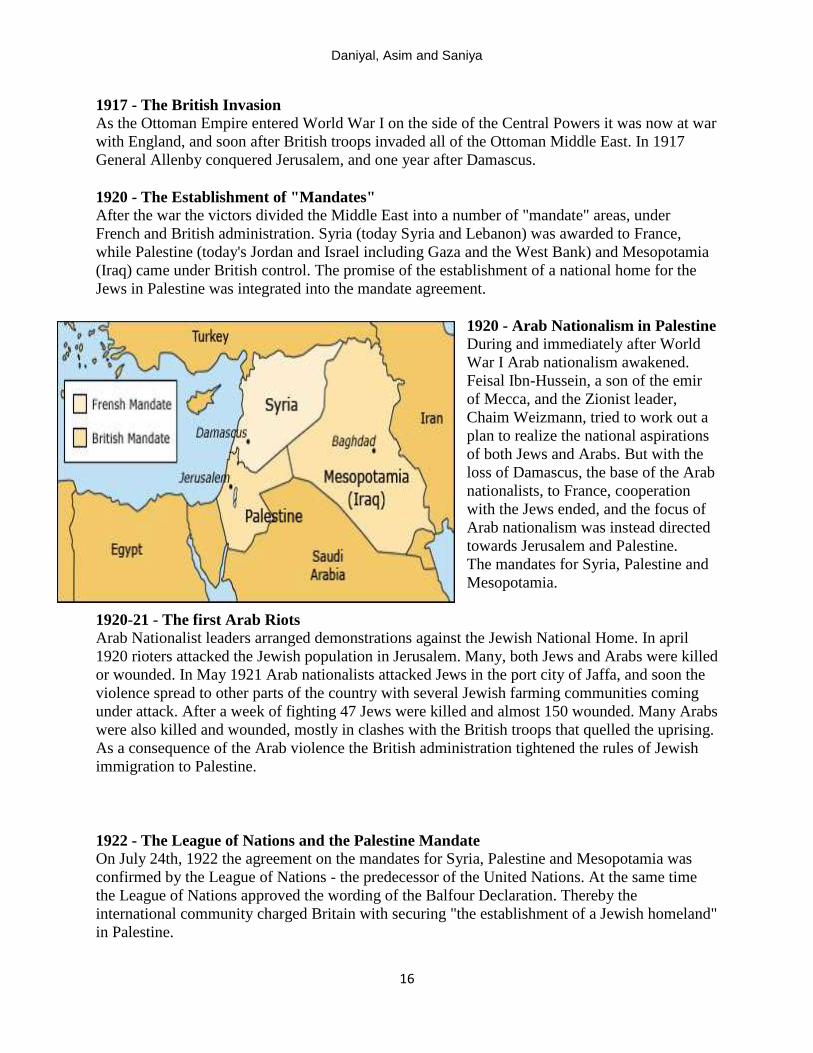

1920 - The Establishment of "Mandates"

After the war the victors divided the Middle East into a number of "mandate" areas, under

French and British administration. Syria (today Syria and Lebanon) was awarded to France,

while Palestine (today's Jordan and Israel including Gaza and the West Bank) and Mesopotamia

(Iraq) came under British control. The promise of the establishment of a national home for the

Jews in Palestine was integrated into the mandate agreement.

1920 - Arab Nationalism in Palestine

During and immediately after World

War I Arab nationalism awakened.

Feisal Ibn-Hussein, a son of the emir

of Mecca, and the Zionist leader,

Chaim Weizmann, tried to work out a

plan to realize the national aspirations

of both Jews and Arabs. But with the

loss of Damascus, the base of the Arab

nationalists, to France, cooperation

with the Jews ended, and the focus of

Arab nationalism was instead directed

towards Jerusalem and Palestine.

The mandates for Syria, Palestine and

Mesopotamia.

1920-21 - The first Arab Riots

Arab Nationalist leaders arranged demonstrations against the Jewish National Home. In april

1920 rioters attacked the Jewish population in Jerusalem. Many, both Jews and Arabs were killed

or wounded. In May 1921 Arab nationalists attacked Jews in the port city of Jaffa, and soon the

violence spread to other parts of the country with several Jewish farming communities coming

under attack. After a week of fighting 47 Jews were killed and almost 150 wounded. Many Arabs

were also killed and wounded, mostly in clashes with the British troops that quelled the uprising.

As a consequence of the Arab violence the British administration tightened the rules of Jewish

immigration to Palestine.

1922 - The League of Nations and the Palestine Mandate On July 24th, 1922 the agreement on the mandates for Syria, Palestine and Mesopotamia was

confirmed by the League of Nations - the predecessor of the United Nations. At the same time

the League of Nations approved the wording of the Balfour Declaration. Thereby the

international community charged Britain with securing "the establishment of a Jewish homeland"

in Palestine.

Daniyal, Asim and Saniya

17

1922 - Jordan Severed from Palestine

In September 1922 Britain and the League og Nations decided that the 3/4 of Palestine east of

the Jordan River would be excluded from the area, in which the Jewish homeland was to be

established. The area was initially awarded limited autonomy under the name of Transjordan, but

was later granted full independence as The Kingdom of Jordan.

1922-23 - Failed Attemps at Arab-Jewish Power Sharing Several attempts were made by the British High Commissioner to Palestine at establishing

various kinds of home-rule for the mandate, in which both Jews and Arabs were to participate.

But the Palestinian Arabs rejected any proposal that included power-sharing with the Jews.

1920's - Development of the "Yishuv" The Jewish community in Palestine (the "Yishuv") developed rapidly in the 1920's. A Jewish

parliament, "Knesset Israel", was established, for which also women could both run and vote.

Responsibility for Jewish religious, culturel and social affairs was transferred to the Knesset.

Later, in 1927, it was also authorized to collect taxes from the Jewish community, and became

responsible for education, health and social welfare within the Jewish sector. Unproductive and

arid land areas were cultivated, industrial businesses were founded, and power plants and other

infrastructure were being built. Hebrew was used as a business language, there was a Hebrew

press, and in 1925 The Hebrew University was inaugurated just outside Jerusalem.

The Arabs also benefitted from the economic growth of the Jewish sector. In 1925 the Jews

made up only about 15% of the population, while accounting for 45% of the mandate's total tax

revenues. Conversely, most of the money was spent on the Arab sector, which, contrary to the

Jewish sector, didn't have any functioning welfare system

1929 - Renewed Arab Attacks on Jews The Muslim leader in Palestine, the Mufti of Jerusalem, Haj Amin al-Husseini, initiated a

campaign of false rumors about Jewish threats against Muslim holy places, followed by calls for

attacks on Jews. Soon Jewish communities all over Palestine were under attack. In some cities

Jews succeeded in defending themselves, but in other areas regular massacres on Jews took

place. In Hebron 67 Jews were murdered, and the rest of the Jewish inhabitants driven out,

ending two thousand years of uninterrupted Jewish presence in the town.

1930-31 - Uncertainty about the Jewish National Home

In reaction to the Arab violence of 1929 the British leadership in Palestine tightened the rules for

Jewish immigration and the sale of land to Jews. But after protests from both The Zionist

Organization and The League of Nations, and an intense debate about Britain's continued support

for the Jewish National Home, the provisions were annulled.

1933 - Jewish Immigration Increasing

Hitler's rise to power in Germany in 1933 resulted in renewed Jewish emigration from Europe,

and Palestine experienced the largest wave of Jewish immigration yet. In the period of 1933-36

an estimated 175.000 Jews arrived, bringing the Jewish population up to around 370.000. The

Arab population too, experienced massive growth during the mandate period, since 1914 almost

doubling to 950.000.

Daniyal, Asim and Saniya

18

1935 - Nazi and Arab Anti-Jewish Propaganda Arab scepticism towards Jewish immigration from Europe was further exacerbated through

German and Italian anti-Jewish propaganda in the Arab World. Arab political commentators

disseminated myths of Zionist plans to kill Arabs and desecrate mosques, and called for a

Palestinian "Jihad" against both Jews and the British. In 1935 the powerful Arab Al-Husseini

clan founded the "Palestine Arab Party", along with an armed militia, "al-Futuwwa", for battle

against the infidels.

1936 - The Arab Revolt In April 1936, as a protest against the immigration policy of the British mandate, the Mufti of

Jerusalem, Haj Amin al-Husseini, organized an general strike and total Arab boykott of the

mandate. Spontaneous violence erupted, followed by organized attacks on Jewish farming

communities by Arab gangs. Civilian Jews were murdered, livestock killed and crops destroyed.

The British accepted a Jewish demand for the arming of 3000 Jewish guards ("ghaffirs"), which,

together with the Jewish underground organization, Haganah, established in reaction to the Arab

riots of the 1920's, partly succeeded in defending Jewish settlements against the Arab attacks.

The revolt and the accompanying strike was quite costly for the Arab community, and by autumn

the strike was called off, and the violence died out.

1937 - The Peel Commission's Partition Plan A British commission of inquiry, led by Lord Robert Peel, was sent to Palestine in order to find a

solution to the conflict. It suggested that the remaining part of the mandate (after the detachment

of Transjordan) be partitioned into two states, one Jewish and one Arab. The north-western fifth

of the area would constitute a Jewish state, the remaining, much larger part, would be Arab,

while a strip from Jerusalem to the port city of Jafffa would remain an international zone. The

plan included a "population swap" in order to make the proposed states as ethnically

homogeneous as possible. Opinions on the issue were divided among the Jews of Palestine, but

the general sentiment pointed towards hesitant acceptance. The Palestinian Arabs, on the other

hand, along with the rest of the Arab World, rejected the plan, which was then abandoned.

1937 - Arab-German Alliance

Nazi-Germany also rejected any partition of Palestine, which could lead to "a Jewish position of

power", and intensified its efforts to strengthen its position among the Arabs. In July 1937 the

Mufti of Jerusalem, Haj Amin al-Husseini, expressed his personal admiration of the new

Germany. The Arab press in Palestine too, showed support for the European Nazism and

fascism, and copied energetically from the European anti-Semitic propaganda. In exchange the

Nazis supplied weapons for the Palestinian Arabs' fight against the Jews.

1937 - The Arab Revolt Resumed

In the autumn of 1937 the Arab revolt was resumed, and attacks on Jewish settlements and

murders of Jewish civilians reached a new high. In 1938 the Haganah adopted a more offensive

strategy and organized mobile units, which staged nightly attacks against Arab guerrilla bases,

inflicting heavy losses on the Mufti's rebels. Also British soldiers were victims of Arab attacks,

prompting Britain to clamp down on the Arab leadership. Mufti Haj Amin escaped to Lebanon,

from where he continued to direct the fighting - not only against Britain and the Jews, but also

against his Arab opponents in Palestine. When the revolt was finally suppressed in August 1939

Daniyal, Asim and Saniya

19

the number of dead had reached 2.394 Jews, 610 British og 3.764 Arabs, including hundreds of

Arab victims of the Mufti's terror.

1938 - Britain's Last Partition Plan In November 1938 the British Woodhead Commission issued a report recommending a partition

plan uniting a Jewish and an Arab state in a common economic union, allowing the Arabs to

enjoy the benefits of progress within the Jewish community. The partition was modified

(compared to the Peel-plan) so that the Jewish state would cover only 1/20 of Palestine, or about

1/100 of the original mandate. The Jews rejected the plan, arguing that the proposed Jewish state

was too small. The Arabs rejected the plan, ruling out any form of Jewish independence or

national self-determination.

1939 - British Abandonment of the Jewish National Home The British government presented a plan severely restricting Jewish immigration to Palestine,

while proposing the establishment of a single Arab majority state, with no specific protection of

the Jewish minority. The leader of the Palestinian Jews, David Ben-Gurion, warned the British

that a Jewish uprising in Palestine could be in every way as destructive as the recently ended

Arab revolt.

1939 - Jewish-British Alliance As tensions mounted between Britain and the Jews of Palestine, the latter were forced to make a

fateful decision: To be with or against Britain in the impending war against Germany. The choice

wasn't difficult. Jewish welfare and security depended on the democratic world. British-Zionist

quarrels had to be suspended for the greater cause. The Jewish community in Palestine threw

itself wholeheartedly into the war on the side of Great Britain.

1939-45 - Palestine during World War II

During World War II many Palestinian Jews were mobilized as soldiers on the side of the allies,

e.g. under the British East Kent Regiment ("The Buffs"), and later in the "Jewish Brigade," while

the rest of the Jewish commumity in Palestine employed all available resources in the production

of equipment, foods and other necessities in support of the allied war effort. The leaders of the

Palestinian Arabs, on the other hand, supported the Nazis. The highest Muslim authority, the

Mufti of Jerusalem, Haj Amin al-Husseini, was especially active, and travelled several times to

Berlin in order to persuade the Nazis to extend their program for the extermination of European

Jewry to also include the Jews of Palestine. In addition al-Husseini helped organize Bosnian

Muslims into the special "Hanzar" SS-division.

1945-48 - Refugees from Europe Despite Jewish support for the victory against Nazi Germany, and the enormous pressure from

refugees in the wake of the Nazi Holocaust, Great Britain, in an attempt to appease the

Palestinian Arabs, continued to enforce strict quotas for Jewish immigration. Some Jews were

smuggled into Palestine, while many perished at sea or ended up in refugee camps in Cyprus. In

respons to Britain's policy on Palestine the Jewish military underground organization, Haganah,

launched a campaign of sabotage against the mandate's installations. Some smaller, but more

radical, Jewish groups carried out regular terror attacks against the British administration in

Palestine.

Daniyal, Asim and Saniya

20

1947 - The UN Partition Plan

In February 1947 Britain decided to turn over the problem of Palestine to the United Nations,

which had just been established following the end of World War II. A commission appointed by

the UN recommended a partition of the remainder of Palestine into two states, one Jewish and

one Arab, with Jerusalem as an international zone controlled by the UN.

On November 29, 1947 the UN's General Assembly adopted Resolution 181, thus approving the

partition plan. The Jews of Palestine, who by 1947 made up one third of the population, were

unhappy with the area allotted The leaders of the 1.2 million Palestinian Arabs, along with the

rest of the Arab World, rejected the plan, and declared to attack and destroy the Jewish state.

1947-48 - Preparation for War Immediately after the UN's decision on the partition of Palestine into one Jewish and one Arab

state in November 1947 Arab gangs began attacking Jewish communities all over Palestine. As

Britain prepared to pull out its last troops, Jewish and Arab underground militia fought to

position themselves most favorably in anticipation of the imminent Arab invasion. The prospect

of war made tens of thousands of Palestinian Arabs, including most of the elite, leave Palestine.

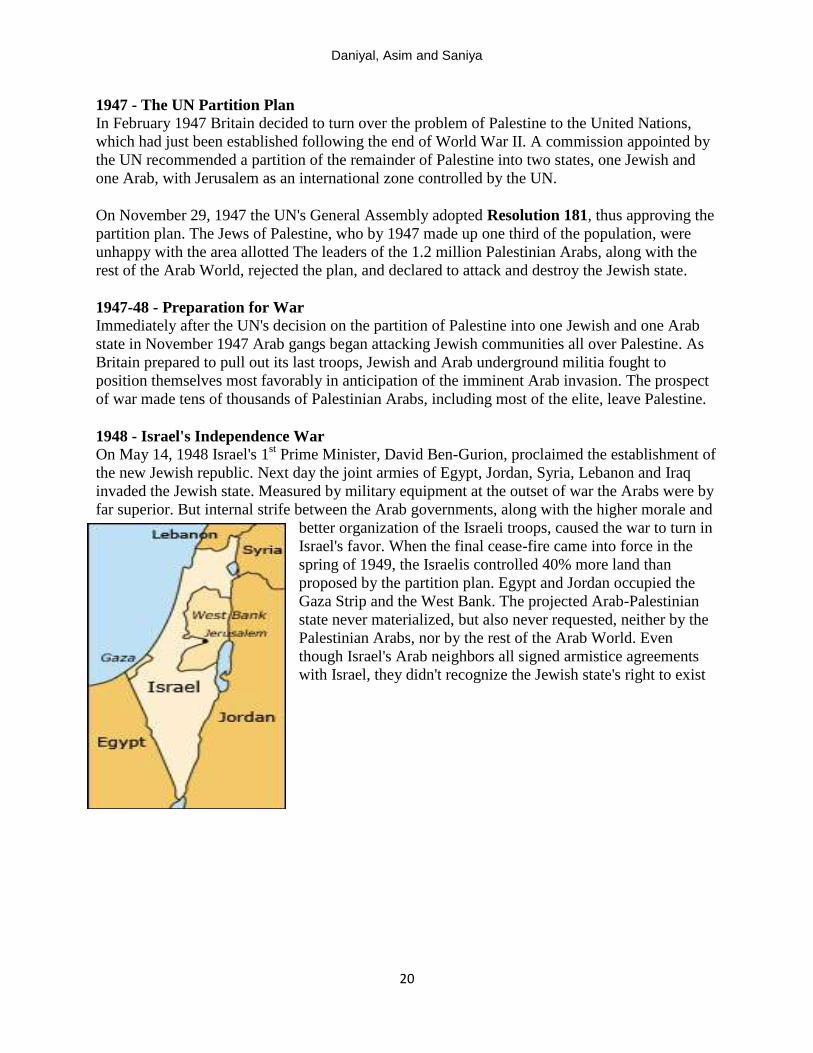

1948 - Israel's Independence War On May 14, 1948 Israel's 1

st Prime Minister, David Ben-Gurion, proclaimed the establishment of

the new Jewish republic. Next day the joint armies of Egypt, Jordan, Syria, Lebanon and Iraq

invaded the Jewish state. Measured by military equipment at the outset of war the Arabs were by

far superior. But internal strife between the Arab governments, along with the higher morale and

better organization of the Israeli troops, caused the war to turn in

Israel's favor. When the final cease-fire came into force in the

spring of 1949, the Israelis controlled 40% more land than

proposed by the partition plan. Egypt and Jordan occupied the

Gaza Strip and the West Bank. The projected Arab-Palestinian

state never materialized, but also never requested, neither by the

Palestinian Arabs, nor by the rest of the Arab World. Even

though Israel's Arab neighbors all signed armistice agreements

with Israel, they didn't recognize the Jewish state's right to exist

Daniyal, Asim and Saniya

21

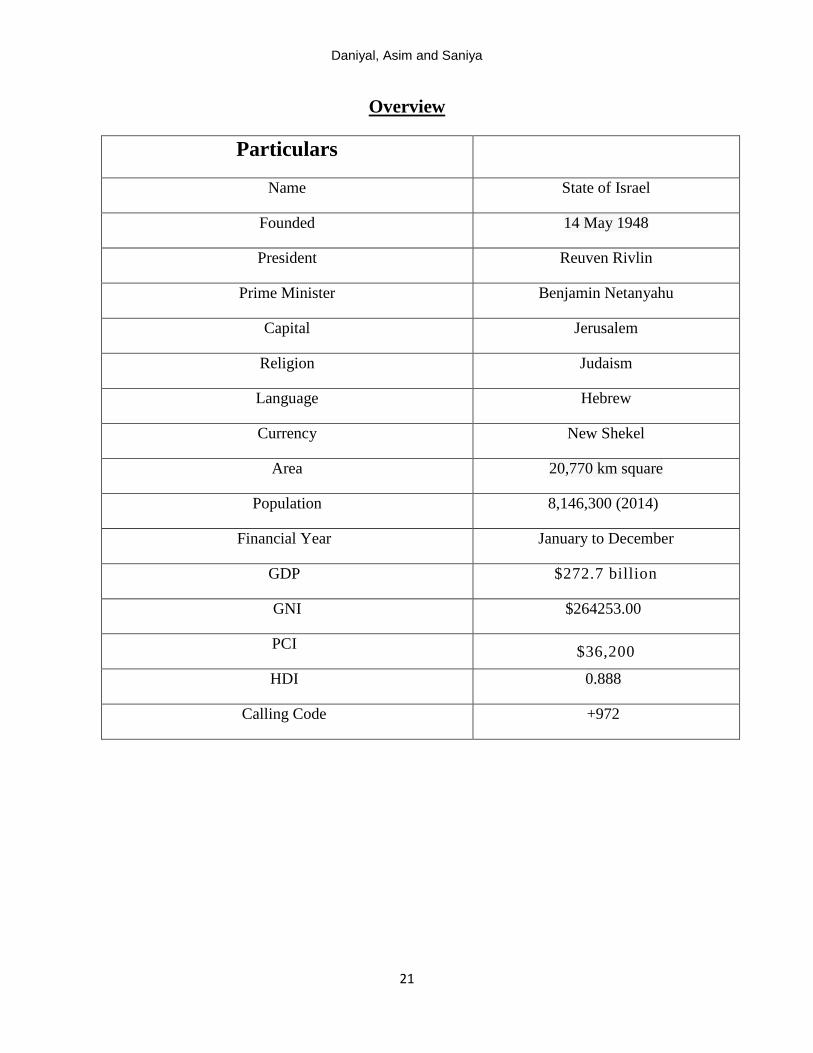

Overview

Particulars

Name State of Israel

Founded 14 May 1948

President Reuven Rivlin

Prime Minister Benjamin Netanyahu

Capital Jerusalem

Religion Judaism

Language Hebrew

Currency New Shekel

Area 20,770 km square

Population 8,146,300 (2014)

Financial Year January to December

GDP $272.7 billion

GNI $264253.00

PCI $36,200

HDI 0.888

Calling Code +972

Daniyal, Asim and Saniya

22

Map

Daniyal, Asim and Saniya

23

Economic

Indicators

Daniyal, Asim and Saniya

24

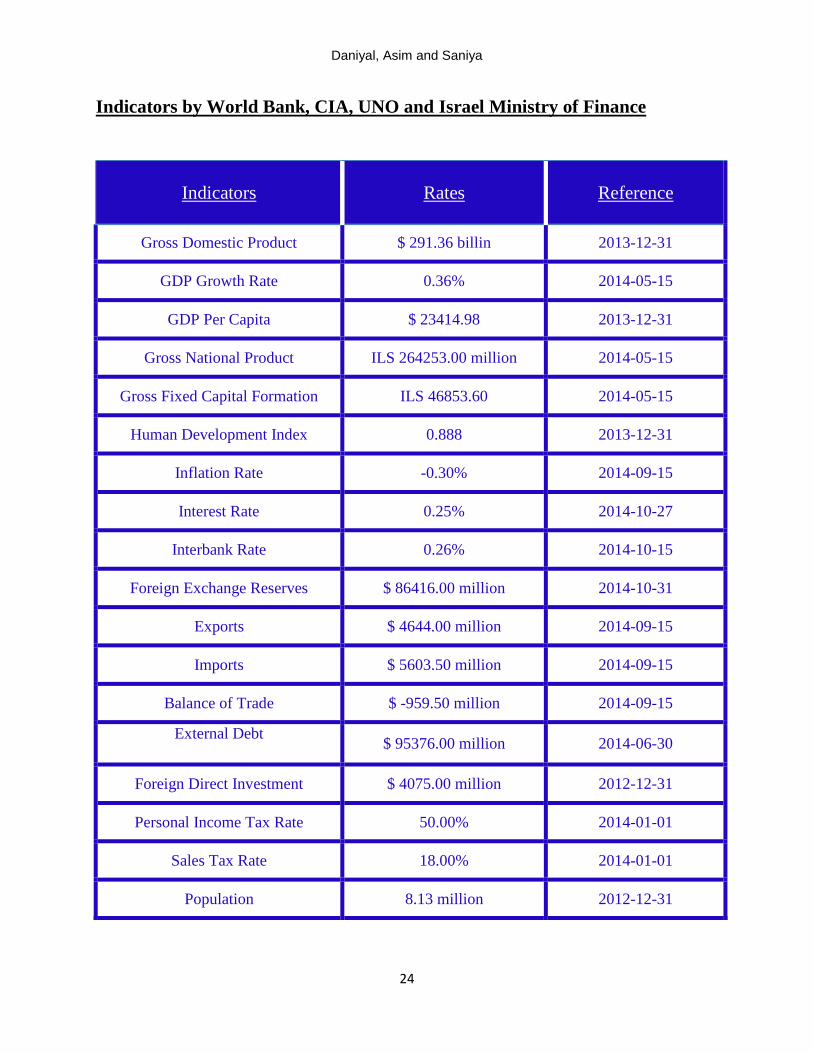

Indicators by World Bank, CIA, UNO and Israel Ministry of Finance

Indicators Rates Reference

Gross Domestic Product $ 291.36 billin 2013-12-31

GDP Growth Rate 0.36% 2014-05-15

GDP Per Capita $ 23414.98 2013-12-31

Gross National Product ILS 264253.00 million 2014-05-15

Gross Fixed Capital Formation ILS 46853.60 2014-05-15

Human Development Index 0.888 2013-12-31

Inflation Rate -0.30% 2014-09-15

Interest Rate 0.25% 2014-10-27

Interbank Rate 0.26% 2014-10-15

Foreign Exchange Reserves $ 86416.00 million 2014-10-31

Exports $ 4644.00 million 2014-09-15

Imports $ 5603.50 million 2014-09-15

Balance of Trade $ -959.50 million 2014-09-15

External Debt $ 95376.00 million 2014-06-30

Foreign Direct Investment $ 4075.00 million 2012-12-31

Personal Income Tax Rate 50.00% 2014-01-01

Sales Tax Rate 18.00% 2014-01-01

Population 8.13 million 2012-12-31

Daniyal, Asim and Saniya

25

Economic

Performance

Daniyal, Asim and Saniya

26

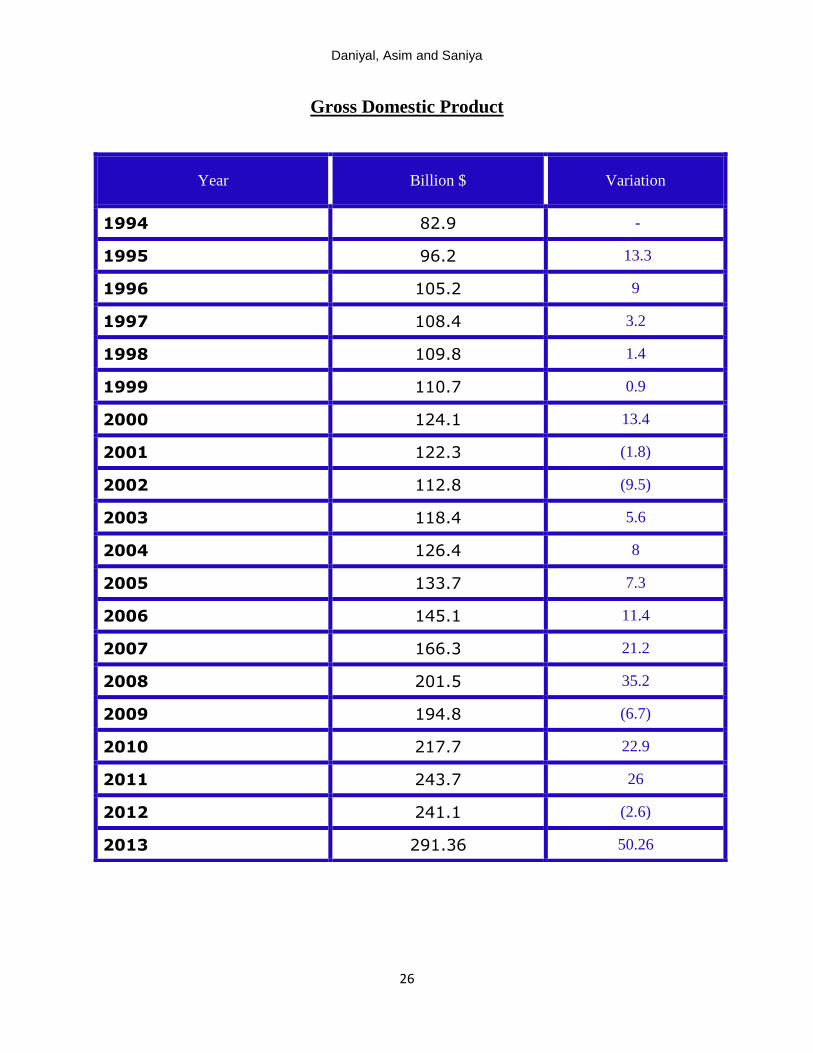

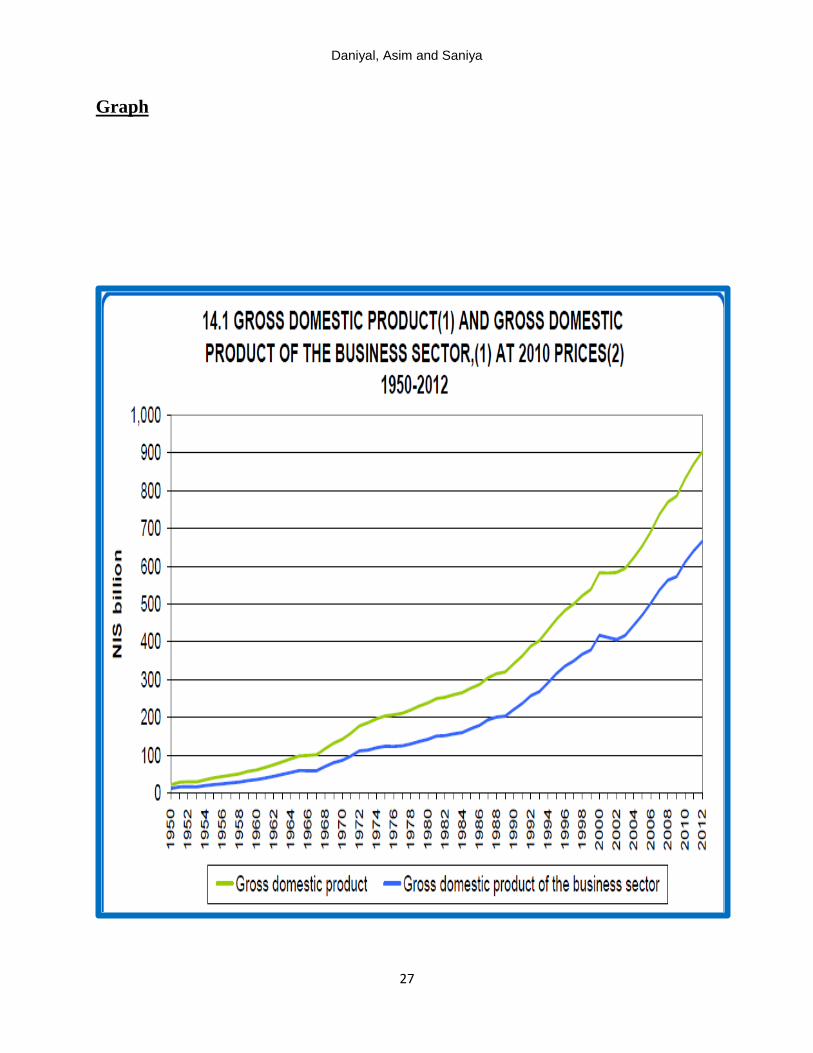

Gross Domestic Product

Year Billion $ Variation

1994 82.9 -

1995 96.2 13.3

1996 105.2 9

1997 108.4 3.2

1998 109.8 1.4

1999 110.7 0.9

2000 124.1 13.4

2001 122.3 (1.8)

2002 112.8 (9.5)

2003 118.4 5.6

2004 126.4 8

2005 133.7 7.3

2006 145.1 11.4

2007 166.3 21.2

2008 201.5 35.2

2009 194.8 (6.7)

2010 217.7 22.9

2011 243.7 26

2012 241.1 (2.6)

2013 291.36 50.26

Daniyal, Asim and Saniya

27

Graph

Daniyal, Asim and Saniya

28

Reasons for Variation in GDP

1995

In 1995, the GDP was increased from $ 82.9 billion dollar to $ 96.2 billion. There was a huge

increase of $ 13.3 billion. In the same year, the assassination of Yitzhak Rabin took place on

November 4, 1995 (12th of Marcheshvan, 5756 on the Hebrew calendar) at 21:30, at the end of

a rally in support of the Oslo Accords at the Kings of Israel Square in Tel Aviv. The assassin, an

Israeli ultranationalist terrorist named Yigal Amir, strenuously opposed Rabin's peace initiative

and particularly the signing of the Oslo Accord. The assassination of Israeli Prime Minister and

Defense Minister Yitzhak Rabin was the culmination of Israeli right-wing dissent over the Oslo

peace process. Rabin, despite his extensive service in the Israeli military, was disparaged

personally by right-wing conservatives and Likud leaders who perceived the Oslo peace process

as an attempt to forfeit the occupied territories

The funeral of Rabin took place on November 6, the day after the assassination, at the Mount

Herzl cemetery in Jerusalem, where Rabin was buried.

2000

In 2000, the GDP was increased from $ 110.7 billion dollar to $ 124.1 billion. There was a huge

increase of $ 13.4 billion. President Clinton announced his invitation to Barak and Arafat on 5

July 2000, to come to Camp David to continue their negotiations on the Middle East peace

process. PALESTINE represented by President Anwar Sadat, and Israel represented by Prime

Minister Menachem Begin. On 11 July, the Camp David 2000 Summit convened, although the

Palestinians considered the summit premature. The summit ended on 25 July, without an

agreement being reached. At its conclusion, a Trilateral Statement was issued defining the agreed

principles to guide future negotiations

The negotiations were based on an all or nothing approach, such that "nothing was considered

agreed and binding until everything was agreed." The proposals were, for the most part, verbal.

As no agreement was reached and there is no official written record of the proposals, some

ambiguity remains over details of the positions of the parties on specific issues Also, Ehud

Barak announces his resignation as prime minister, and says there will be a new election for the

post. He will stay on as caretaker in the meantime.

2006-2007

In 2006 and 2007, the GDP was increased to $ 18.7 billion. The 2006 Lebanon War, also called

the 2006 Israel–Hezbollah War and known in Lebanon as the July War. and in Israel as

the Second Lebanon Warwas a 34-day military conflict in Lebanon, northern Israel and

the Golan Heights. The principal parties were Hezbollah paramilitary forces and the Israeli

Daniyal, Asim and Saniya

29

military. The conflict started on 12 July 2006, and continued until a United Nations-

brokered ceasefire went into effect in the morning on 14 August 2006, though it formally ended

on 8 September 2006 when Israel lifted its naval blockade of Lebanon. Due to unprecedented

Iranian military support to Hezbollah before and during the war, some consider it the first round

of the Iran–Israel proxy conflict, rather than a continuation of the Arab-Israeli conflict.

The conflict was precipitated by the Zar'it-Shtula incident. On 12 July 2006, militants from the

group Hezbollah fired rockets at Israeli border towns as a diversion for an anti-tank

missile attack on two armored Humvees patrolling the Israeli side of the border fence.[

The conflict is believed to have killed at least 1,191–1,300 Lebanese people and 165 Israelis.It

severely damaged Lebanese civil infrastructure, and displaced approximately one million

Lebanese and 300,000–500,000 Israelis.

On 11 August 2006, the United Nations Security Council unanimously approved United Nations

Security Council Resolution 1701 (UNSCR 1701) in an effort to end the hostilities. The

resolution, which was approved by both the Lebanese and Israeli governments the following

days, called for disarmament of Hezbollah, for withdrawal of Israel from Lebanon, and for the

deployment of Lebanese soldiers and an enlarged United Nations Interim Force in

Lebanon (UNIFIL) in the south. UNIFIL was given an expanded mandate, including the ability

to use force to ensure that their area of operations was not used for hostile activities and to resist

attempts by force to prevent them from discharging their duties

ON MARCH 2006, Kadima party wins Israeli elections and Ehud Olmert becomes Prime

Minister. Voter turnout was the lowest ever (63.2%). Hamas ends 16 month long truce as cross

border violence escalates near Gaza.

2008

Israeli satellite Amos-3 is launched into space from the Baikonur Cosmodrome space launch

facility in Kazakhstan. Prime Minister Ehud Olmert announces that he would not seek re-election

as party leader and that he would resign from his position as Prime Minister immediately after a

new Kadima leader was named. One reason for resignation is the corruption scandal in which

Olmert is embattled

The Gaza War, also known as Operation Cast Lead was a three-week armed conflict between

Palestinians in the Gaza Strip and Israel that began on 27 December 2008 and ended on 18

January 2009 in a unilateral ceasefire. An Israeli ground invasion began on January 3. Infantry

commanders were given an unprecedented level of access to coordinate with air, naval, artillery,

intelligence, and combat engineering units during this second phase. Various new technologies

and hardware were also introduced.

Daniyal, Asim and Saniya

30

On January 5, the IDF began operating in the densely populated urban centers of Gaza. The

conflict resulted in between 1,166 and 1,417 Palestinian and 13 Israeli deaths.

In September 2009, a UN special mission, headed by the South African Justice Richard

Goldstone, produced a report accusing both Palestinian militants and the IDF of war crimes and

possible crimes against humanity, and recommended bringing those responsible to justice.

2010

The 2010 Israel–Lebanon border clash occurred on August 3, 2010, between the Lebanese

Armed Forces (LAF) and Israel Defense Forces (IDF), after an IDF team attempted to cut down

a tree on the Israeli side of the Blue Line, near the Israeli kibbutz of Misgav Am and the

Lebanese village of Adaisseh. The Lebanese Army asserted that it opened fire on Israeli soldiers

to contravene the attempt of Israelis to intrude through the border of Lebanon in violation of the

internationally recognized border between Israel and Lebanon

The largest forest fire in Israel's history engulfs a bus carrying cadets from the Israel Prison

Service's officer course en route to evacuate prisoners from the Damun Prison in the area of the

fire, taking 44 lives, including 37 of the cadets and their officers. The fire devastates hundreds of

acres of pine forest on Mount Carmel in northern Israel, close to the city of Haifa, and is

eventually brought under control late on December 5, 2010.

Daniyal, Asim and Saniya

31

AGRICULTURE

Fruits

Vegetables

Dairy farming

Poultry and beef

Aqua culture

Mari culture

Floriculture

Bee keeping

Daniyal, Asim and Saniya

32

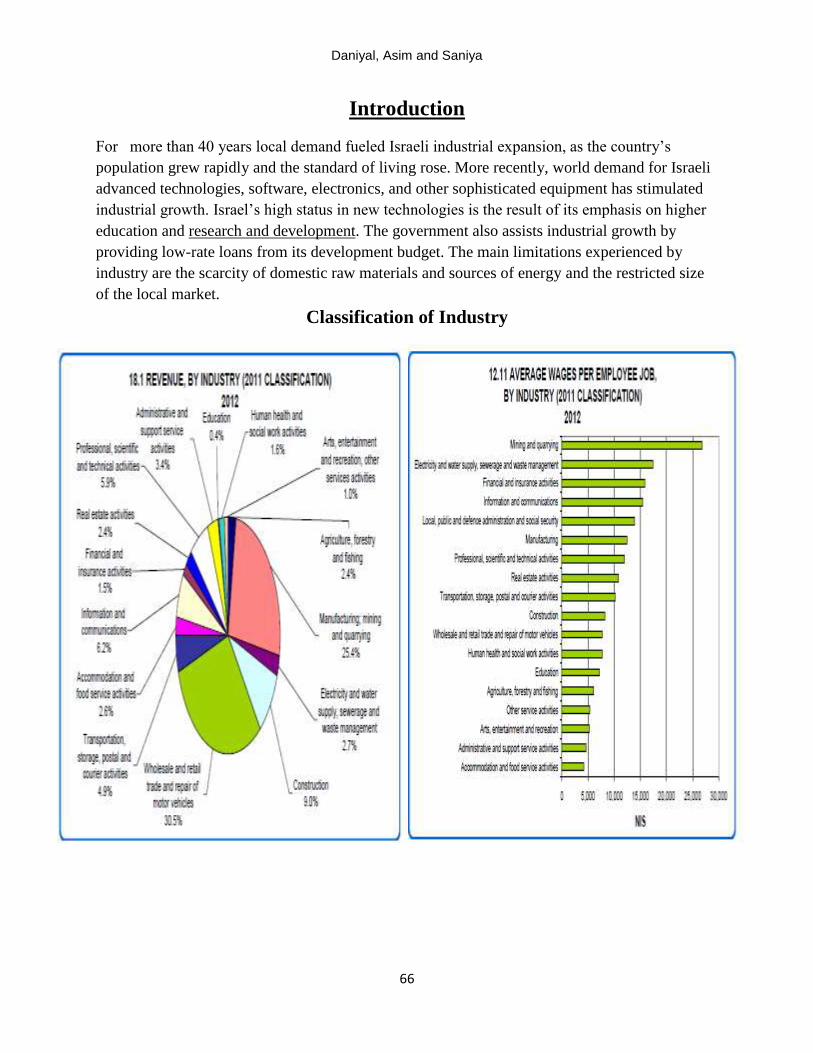

Introduction

Though small in size, Israel's agricultural sector is vibrant and highly advanced. Over the last

two decades, it has undergone a substantial structural change, during which the number of farms

and self-employed farmers has significantly decreased, while the farms themselves have become

much larger and more efficient. Farmers in Israel today are better equipped with highly

developed entrepreneurial skills and the managerial abilities required for coping with the

changing, dynamic world of modern agriculture.

The success story of Israel's agriculture can be attributed in large measure to the Israeli

farmers' responsiveness and willingness to introduce innovations, know-how and technological

transfers. In doing so, the farmers cooperate closely with research and development experts,

extension advisers and agro-technology companies. Israel's agricultural sector serves as an

excellent laboratory for the development of new agro-technologies, which are then disseminated

around the world for the benefit of all.

The structural change undergone by Israel’s agricultural sector has a broader scope: the adoption

of a comprehensive approach to rural development, in which fresh food production– the

backbone of rural life and livelihood everywhere – has leveraged a much larger set of economic

activities, such as food processing and packaging, other industrial projects,various services and

agro-tourism.

The name and essence of Israel’s Ministry of Agriculture was altered in the 1990s to the

“Ministry of Agriculture and Rural Development" while prioritizing environmentally-friendly

agriculture, rural development and food production. The consequent policies pertaining to the

rural population comprise professional assistance and beneficial incentives aimed at developing

infrastructure and services.

Daniyal, Asim and Saniya

33

History

Historically, agriculture has played a more important role in Israeli national life than its

economic contribution would indicate. It has had a central place in Zionist ideology and has been

a major factor in the settlement of the country and the absorption of new immigrants although its

income-producing importance has been minimal. As the economy has developed, the importance

of agriculture has declined even further. For example, by 1979 agricultural output accounted for

just under 6 percent of GDP. In 1985 agricultural output accounted for 5.1 percent of GDP,

whereas manufacturing accounted for 23.4 percent.

In 1981, the year of the last agricultural census (as of 1988), there were 43,000 farm units with

an overall average size of 13.5 hectares. Of these, 19.8 percent were smaller than 1 hectare, 75.7

percent were between 1 and 9 hectares, 3.3 percent were between 10 and 49 hectares, 0.4 percent

were between 50 and 190 hectares, and 0.8 percent were more than 200 hectares. Of the 380,000

hectares under cultivation in that year, 20.8 percent was under permanent cultivation and 79.2

percent under rotating cultivation. The farm units also included a total of 160,000 hectares of

land used for purposes other than cultivation. In general, land was divided as follows: forest, 5.7

percent; pasture, 40.2 percent; cultivated, 21.5 percent, and desert and all other uses, 32.6

percent. Cultivation was based mainly in three zones: the northern coastal plains, the hills of the

interior, and the upper Jordan Valley.

Agricultural activities generally were conducted in cooperative settlements, which fell into two

principal types: kibbutzim and moshavim . Kibbutzim often served strategic or defensive

purposes in addition to purely agricultural functions. In the 1980s, such settlements usually

engaged in mixed farming and had some processing industry attached to them. A moshav

provides its members with credit and other services, such as marketing and purchasing of seeds,

fertilizer, pesticides, and the like. By centralizing some essential purchases, the moshavim were

able to benefit from the advantages of size without having to adopt the kibbutz ideology.

The agricultural sector declined in importance from 1952 to 1985. This decline reflects the rapid

development of manufacturing and services rather than a decrease of agricultural productivity. In

fact, from 1966 through 1984, agriculture was far more productive than industry.

Efficient use of the factors of production and the change in their relative composition explain a

significant portion of the increased productivity in the agricultural sector. From 1955 to 1983, the

agricultural sector cut back on employed persons and increased the use of water, fertilizer, and

pesticides, leading to a substantial increase in productivity.

Daniyal, Asim and Saniya

34

Other factors that contributed to increased productivity included research, training, improved

crop varieties, and better organization. These changes in factor utilization led to a twelvefold

increase in the value of agricultural production, calculated in constant prices, between 1950 and

1983.

In absolute terms, the amount of cultivated land increased from 250,000 hectares in FY 1950 to

440,000 hectares in FY 1984. Of this total, the percentage of irrigated land increased from 15

percent in FY 1950 (37,500 hectares) to around 54 percent in FY 1984 (237,000 hectares). The

amount of water used for agricultural purposes increased from 332 million cubic meters in FY

1950 to 1.2 billion cubic meters in FY 1984.

The most dramatic change over this period was the reduction in the agricultural labor force.

Whereas the number of workers employed in agriculture in the early 1950s reached about

100,000, or 17.4 percent of the civilian labor force, by 1986 it had dropped to 70,000, or 5.3

percent of the civilian labor force.

Agriculture has benefited from high capital inputs and careful development, making full use of

available technology over a long period. Specialization in certain profitable export crops, in turn,

has generated more funds for investment in agricultural production and processing, as has the

development of sophisticated marketing mechanisms. In particular, Israel has had success in

exporting citrus fruit, eggs, vegetables, poultry, and melons.

Another factor important in Israel's agricultural development has been the sector's impressive

performance in foreign trade. The rapid growth of agricultural exports was accompanied by a

general increase in total exports. Between 1950 and 1993, a prominent development was the

decline (by 65 percent) in the importance of citrus fruit exports in relation to total raw

agricultural exports. This decrease was more than balanced by the increase in importance of

processed agricultural products, whose exports increased by 4,000 percent over the same period

Daniyal, Asim and Saniya

35

Israel Agriculture at a Glance

Israel’s agricultural is characterized by an intensive system of production stemming from the

need to overcome the scarcity in natural resources, particularly water and arable land. The

constant growth in agricultural production is due to the close cooperation between researchers,

farmers, and agriculture-related industries. Together they develop and apply new methods in all

agricultural branches. The result is modern agriculture in a country more than half of whose area

is desert. As farmers and scientists have had to contend with a difficult environment and limited

water resources, their experience is especially relevant to the developing world. Its success lies in

the determination and ingenuity of farmers and scientists who have dedicated themselves to

developing a flourishing agriculture, demonstrating to the world that the real value of land is a

function of how it is utilized. The close cooperation between R&D and industry led to the

development of a market-oriented agri-business that exports particularly water solutions.

Agriculture in Israel is the success story of a long, hard struggle against adverse conditions and

of making maximum use of arable land and scarce water. When Jews began resettling their

historic homeland in the late 19th century, their first efforts were directed - mostly for

ideological reasons - to turning barren land into fertile fields. The secret of Israel's present

agricultural success lies in the close interaction between farmers and government-sponsored

researchers, who cooperate in developing and applying sophisticated methods in all agricultural

branches, as well as technological advancement, new irrigation techniques, and innovative agro-

mechanical equipment. Since Israel attained independence in 1948, the total area under

cultivation has increased by a factor of 2.6, to approximately 1.1 million acres. The irrigated land

area increased by a factor of 8, to about 0.6 million acres until the mid 1980s; however, owing to

the growing shortage of water, coupled with intensive urbanization, this is now less than half a

million acres. During the past half century the number of agricultural settlements grew from 400

to 750, but the share of the population living in them has fallen from 12 percent to less than 5%.

Today, most of Israel's food is domestically produced and supplemented by imports, mainly of

grain, oilseeds, meat, coffee, cocoa, and sugar, all of which are more than covered by agricultural

exports. Farm production consists largely of dairy and poultry products. Additionally, a large

variety of flowers, fruit, and vegetables is locally grown, especially in warm areas that give

farmers an early advantage in European markets. During the winter months, Israel is Europe's

greenhouse, exporting melons, tomatoes, cucumbers, peppers, strawberries, kiwis, mangoes,

avocados, a wide variety of citrus fruits, long stemmed roses and spray carnations. The share of

agricultural product of the GNP declined from 11 percent to 2.6 percent between 1950 and 2013,

and the proportion of agricultural exports decreased from 60 percent to less than 2 percent of

total exports. This, despite an absolute increase of annual exports from $20 million in 1950 to

$1.4 billion in 2013 due, inter alia, to the widespread introduction of innovative farming

methods, modern irrigation methods and export policies.

Daniyal, Asim and Saniya

36

exportpoliciespolicies.treatmenexportfa

Daniyal, Asim and Saniya

37

Strategic Planning for Sustainable Agriculture

The Ministry of Agriculture and Rural Development is in the process of defining a strategic plan

and comprehensive framework for agricultural and rural sustainable development, while

preserving the rural landscape and maintaining environmental values. The following principles

are incorporated for the plan:

Efficient use of resources and materials in agricultural activity.

Reduction of both degradable and non-degradable waste.

Reduction of agriculture related hazards and damage to the environment.

Preservation of agricultural land and open space, and maintaining the culture and landscape

values of agriculture.

Preservation of the nature/agriculture balance.

Efficient use of land and resources for rural development.

Preservation of the unique rural character of agricultural communities.

Maintaining rural open space as "green lungs" for the benefit of urban communities.

Promotion of sustainable development in accordance with national concepts and international

agreements.

Incorporating sustainable development principles into purchasing contracts among farmers

and by the Ministry.

Sustainable development for agriculture refers to the wise use of irreversible resources (land,

water, energy) and minimizing the adverse environmental impact of manmade resources used in

agricultural production (fertilizers, pesticides, non-degradable materials). It includes reducing the

use, replacing, and improving these resources as well as treatment for additional agricultural by-

products such as organic waste, spillage and gaseous emissions.

Daniyal, Asim and Saniya

38

Detailed Analysis

Despite the decline in its importance relative to other economic branches, agriculture has been

growing in absolute terms and still plays an important part in Israel's economy, representing

today some 2.0 percent of the Gross Domestic Product and about 3.5 percent of exports.

Agricultural inputs produced in Israel are valued today at over $2 billion, of which 70% are

exported.

Agriculture is of major national importance; in certain areas, such as the Arava and the Jordan

Valley, it provides the sole means of livelihood for the population. In 1996 approximately 73,500

people were involved in farming, constituting about 3.0 percent of the country's workforce.

In monetary terms, Israel produces almost 70% of all its food requirements. It imports much of

its grain, oilseeds, meat and fish, and it’s the sugar, coffee and cocoa. However, these imports are

offset by exports of agricultural produce valued at around $800 million and $600 million worth

of processed foods per annum. Today, just under a quarter of the income of Israel's farmers

derives from the export of fresh produce, including items such as flowers, avocados, out-of-

season vegetables and certain exotic fruits grown for export. In 1996 some 140,000 tons of fruit

and vegetables - 14 percent of the entire crop - were sold to factories for processing and export.

This is a far cry from the situation a century ago. When Jews began resettling their historic

homeland in the late 19th century, their first efforts were directed towards reclaiming the mostly

semi-arid land, much of which was rendered untillable by deforestation, soil erosion and neglect.

Rocky fields were cleared and terraces built in the hilly regions; swampland was drained, and

systematic reforestation begun; soil erosion was counteracted, and salty land washed to reduce

soil salinity.

Since Israel attained its independence in 1948, the total area under cultivation has increased from

165,000 ha. to some 435,000 ha. and the number of agricultural communities has grown from

400 to 900 (including 136 Arab villages). During the same period, agricultural production has

expanded 16-fold, more than three times the rate of the population growth.

Israel's varied climatic, topographical and soil conditions (from sub-tropical to arid, from 400

meters below sea level to 1000 meters above and from sand dunes to heavy alluvial soils) made

it possible to grow a wide range of agricultural produce. The success of the country's agriculture

stems from the determination and ingenuity of farmers and scientists who have dedicated

themselves to developing a flourishing agriculture in a country which is more than half desert,

thus demonstrating that the real value of land is a function of how it is used.

Daniyal, Asim and Saniya

39

Daniyal, Asim and Saniya

40

Research & Development

The fact that agricultural production continued to grow despite severe water and land limitations

was no accident. It was the result of another unique Israeli phenomenon: a close and ongoing

cooperation between researchers, extension workers, farmers and agriculture-related services and

industries. Continuous, application-oriented research and development (R&D) has been carried

out in the country since the beginning of the century. The agricultural sector today is based

almost entirely on science-linked technology, with government agencies, academic institutions,

industry and cooperative bodies working together to seek solutions to problems and meet new

challenges. Dealing with subjects ranging from plant genetics and blight control to arid-zone

cultivation, lsrael's agricultural R&D has developed science-based technologies which have

dramatically enhanced the quantity and quality of the country's produce. The key to this success

lies in the two-way flow of information between research personnel and farmers. Through a

network of extension services (and active farmers' involvement in all R&D stages), problems in

the field are brought directly to the researcher for solutions, and scientific results are quickly

transmitted to the field for trial, adaptation and implementation.

The drive to achieve maximum yields and crop quality has led to new plant varieties, to breeding

of improved animal species and to a wide range of innovations in irrigation and fertization,

machinery, automation, chemicals, cultivation and harvesting. Many of these innovations are

also exported.

Government Involvement

The Ministry of Agriculture supports and supervises the activities of the country's agricultural

sector, including maintenance of high standards for plant and animal health, promotion of

agricultural planning, extension, research and marketing. For many years, agriculture was tightly

controlled, with the allocation of production and water quotas for each crop. At present, only

quotas for milk and some control of eggs, broilers and potatoes are in effect.

Ongoing programs to increase the country's water potential involve rainfall enhancement through

cloud seeding, desalination of brackish water and sewage recycling. The search for more water

has recently led to exploitation of the huge underground reservoir of brackish water in the Negev

desert, which has been found suitable for growing specific crops.

Supervision of the country's water supply includes determining water quotas, progressive prices,

fully controlling groundwater pumping and initiating supply-enhancing projects. A ten-year

program has been introduced recently, which proposes a cut in the supply of improved water for

agriculture; treatment of all urban waste-water; expanded utilization of desalinated brackish

water; a reduction of high water-consuming crops; storing of flood waters; development of

capital-intensive greenhouses; and massive desalination of sea water.

Daniyal, Asim and Saniya

41

Irrigation

Near the Desert Plant Research Station of Ben-Gurion University in Be'er Sheva is a farm

cultivated over 2,000 years ago by the earliest desert farmers, the Nabateans. Their agricultural

methods were astonishingly sophisticated. By building terraces and clearing the soil of stones,

every drop of runoff water was collected and then diverted to the lower-lying fields and orchards.

The methods have changed, but saving water and making optimal use of scarce land still

characterizes agriculture in the region.

Water saving has been the farmers' leitmotif since the State of Israel was founded in 1948. The

country has ten major companies producing irrigation and filtration equipment, all internationally

active. In no other field of agricultural technology has Israel so excelled.

In terms of annual rainfall, 60% of the country may be defined as arid or semi-arid. Rain falls

only between November and April, with uneven distribution of yearly precipitation, ranging

from 28 inches (70 cm.) in the north to less than two inches (five cm.) in the south. Annual

renewable water resources amount to some 1.6 billion cu.m., about 75 percent of which is used

for agriculture. Of the latter, two thirds is potable - a share which is likely to decrease

substantially in the coming years as more sewage treatment plants come on line.

In the past 30 years agricultural output has increased almost fivefold* with hardly any increase in

the amount of water used. This reflects technological advances of different types - water

efficiency went up by about 30% and crops with higher yields and market-value were

introduced. To reduce water consumption for agriculture, advanced water-saving techniques

(notably the drip system) were applied, which direct the water flow straight to the root zone of

plants. Also, computerized irrigation systems were used and greenhouse agriculture was

significantly expanded. Israeli engineers and agriculturalists created the revolutionary drip

irrigation system, which has reduced water consumption by 50-70 percent compared with gravity

irrigation, and by 10-20% compared to sprinkler irrigation. At present, scientists are testing the

first generation of ultra-low application rate "minute irrigation" drip emitters for soil-less media

in greenhouses, emitters with 100-200 cc/h flow rates. Considered even more advanced than the

drip system, they will create optimal air-water relationships in the plants' root zone and, being

more efficient, save yet more water. Micro-spraying and micro-sprinkling irrigation accessories

have also been developed, mainly for use in orchards, where each tree is irrigated by its

individual sprayer.

To overcome regional imbalances in water availability, most of the country's freshwater sources

have been joined in the National Water Carrier, an integrated network of pumping stations,

reservoirs, canals and pipelines which transfers water from the north, where most of the sources

are, to the agricultural areas of the semi-arid south. As a result, the amount of irrigated farmland

has increased from 30,000 ha. in 1948 to some 186,400 ha. today.

Daniyal, Asim and Saniya

42

Mechanization and Agro technology

In order to lower costs, increase yields, improve quality and save manpower, innovative

agricultural machinery and electronic equipment have been locally designed and manufactured,

and are widely used. Intensive experimentation on the drawing board and in the field has

resulted, inter alia, in the development of heavy-duty soil preparation machinery; advanced

tillage, planting, harvesting and transplanting equipment adaptable to intensive farming; and

diverse irrigation systems, ranging from sprinklers to computerized drip irrigation. Automated

milking and dairy herd management systems and egg-collecting equipment, computerized

feeding systems and production-recording computers have been introduced, as well as machinery

for the grading, packing, storing and transporting of produce. Locally-developed agro

technologies include computerized fertilization, which injects fertilizers through the irrigation

system, and advanced temperature and humidity control methods, which provide healthy

environments for poultry, flowers, out-of-season vegetables and the like.

Growing Crops in the Desert

Since 1948, the sparsely populated desert area between Be'er Sheva and Eilat has played an

important role in agricultural production. More than 40 percent of the country's vegetables and

field crops are grown in the Arava and Negev and 90 percent of the melons exported come from

the Arava.

Today, partly because of Jewish Agency and Government programs to promote settlement, and

partly because the supply of farmland in the country's densely populated central region is

shrinking (only 20 percent of the country's total land area of 22,000 sq. km is arable, and a

growing share is used for housing), the importance of the southern Negev and Arava for farming

is increasing. In the process, the pattern of farming in the desert is also undergoing change, with

new varieties of crops suited to the region's conditions being developed and introduced, along

with animal husbandry, hitherto confined to more northern areas.

The common advantages of the two regions are their long hours of sunshine and relatively high

temperatures, as well as the fact that land is relatively cheap and abundant and adequate water

(saline or recycled) is available. The further south one goes, the earlier crops ripen. This makes it

possible to grow for export to Europe during the winter months - October through March - when

prices are highest, with less expenditure of energy than required elsewhere.

Until the 1990s, the accent was on field crops, vegetables, fruit and dates. These branches

continue to expand in the Negev and Arava, and in addition giant citrus groves (10,000 acres),

have been planted by industrial companies in the northern Negev. Attempts to expand the

growing of flowers, grapes for wine, olives for oil, cattle for meat, ostriches and fish are now

taking off.

Daniyal, Asim and Saniya

43

The new wave of 'greening of the desert' has been encouraging. In the Negev, improved climatic

conditions and cultivation of new citrus varieties have resulted in yields 50-100 percent higher

than those in the north. Olive plantations irrigated by brackish water have achieved per-acre oil

yields that are six times higher than in traditional rainfed groves elsewhere in the country. Within

three years the Negev/Arava fish farmers have achieved production of around 350 tons a year

and output is expected to reach 2,000 tons by the year 2,000. At Kadesh Barnea, a small moshav

(cooperative farm settlement) on the Egyptian border, one can get a foretaste of what Israeli

desert farming in the 21st century will look like. The moshav's beef cattle - the first in the Negev

- are fed fodder grown with brackish water recycled from 'bubbles' - covered tanks for intensive

fish cultivation. Similarly, at Kibbutz Revivim water from fish tanks nourishes alfalfa for

ostriches. Desert agriculture is already playing an indispensable role in Israel's economy.

Israel tries to learn from other countries: in recent years it has introduced a large range of arid

land plants from Asia, Africa, Australia and the Americas, and is trying them out under local

conditions, occasionally adapting and commercializing them. Know-how on desert growing has

become a focus for regional and international cooperation.

Since the late 1950s, Israel has been sharing its agricultural expertise with scores of countries.

MASHAV, the Center for International Cooperation of the Ministry of Foreign Affairs, is active

in Asia, Africa, the Mediterranean Basin, Eastern Europe and Latin America; and it is

broadening its cooperation programs with a growing number of countries in the Middle East.

Agricultural projects and research collaboration constitute about half of Israel's international

cooperation programs. Emphasis is placed on training courses in agricultural subjects, with some

1,400 participants from over 80 countries attending specialized farming courses every year and

thousands of trainees receiving on- spot training in their own countries. Since 1958, thousands of

Israeli agricultural experts have been sent abroad on long- and short-term assignments.

Daniyal, Asim and Saniya

44

High-Tech Farming

Economists discussing the country's farming choices sometimes draw an analogy between a

kilogram of exported tomatoes, which might fetch around five dollars, and a kilo of hybrid

tomato seeds, which today may be selling abroad for $7,000. High-tech farming, it is suggested,

is the only way to survive. Indeed, market forces at home and abroad, and a scarcity of land,

labor and water are forcing major changes on Israeli agriculture. Increasingly, there is a shift

from extensively-farmed, mass-produced crops to intensive growing of niche products based on

scientific and technological R&D, such as hybrid, virus-resistant tomatoes or tissue-culture

propagated banana-tree saplings. The country's farmers face increasing competition. On the one

hand, ties with the Palestinian Authority have caused an influx of vegetables and poultry,

depressing prices. On the other hand, readjustment of world trade patterns in the wake of the

GATT agreement has led - for the first time in Israel's history - to imports of fresh and processed

produce from Europe and the US. On the export side, Israeli products like citrus and flowers face

stiff competition from other producers in the Mediterranean region and farther afield, while

avocados, one of the largest exports, have been facing cut-throat competition in Europe from

Mexican growers.

As in other countries, Israeli agriculture has been forced to employ fewer and fewer people. The

work force shrank almost 40 percent between 1960 (121,000) and 1996 (73,500). However, these

persons are producing and exporting more. In the early 1950s one full-time agricultural

employee fed 17 people. In 1994, one full-time worker produced food for 90 persons.

Most of Israel's agriculture is organized on cooperative principles which evolved in the country

during the first decades of the 20th century. Motivated by both ideology and circumstances, the

early pioneers set up two unique forms of agricultural settlements: the kibbutz, a collective

community in which the means of production are communally owned and each member's work

benefits all; and the moshav, a cooperative village where each family maintains its own

household and works its own land, while purchasing and marketing are conducted cooperatively.

Both provided a means to realize the pioneers' dream of rural communities based on social

equality, cooperation and mutual aid. Their output today comprises the lion's share of the

country's fresh produce, as well as many processed food products, both for the domestic market

and for export, and almost all meat, poultry and fish.

Daniyal, Asim and Saniya

45

Agriculture - by Branches

FRUITS

In 2012, the area covered by fruit orchards, excluding citrus groves, was about 37,000 hectares.

In addition, there are 21,000 hectares of oil olives grown without additional irrigation, mostly in

the Arab sector. Produce reached 690,000 tons of fruit in 2012. The main fruit crops are bananas,

146,000 tons; apples, 110,000 tons; avocados, 90,000 tons; and table grapes, 75,000 tons. Fruit

accounts for 20% of the total agricultural production in Israel. Even though most of the fruit

production is for local consumption, in 2011 Israel exported 55,000 tons of avocados, 18,000

tons of persimmons, 15,000 tons of mangoes, 15,000 tons of dates and 16,000 tons of

pomegranates. The varied climate lends itself to a wide variety of fruit crops. In hilly and

mountainous areas, for example, deciduous fruit trees, which have chilling requirements, are

grown, while in the coastal plain or valleys, tropical and subtropical fruit trees can be grown In

the arid Arava, dates are grown successfully. Due to the varied climate and the advanced

technologies for growing fruit trees under protected conditions (greenhouses and shade-houses)

during the cold season, fruit can also be picked out of season, thereby prolonging the marketing

period and improving fruit quality A number of leading growers have succeeded in reaching

peak yields in Israel, for example: apples, 90 tons/ha; bananas, 100 tons/ha; plums, 50 tons/ha;

peaches and nectarines, 70 tons/ha; mangoes, 75 tons/ha; and pears, 50 tons/ha.

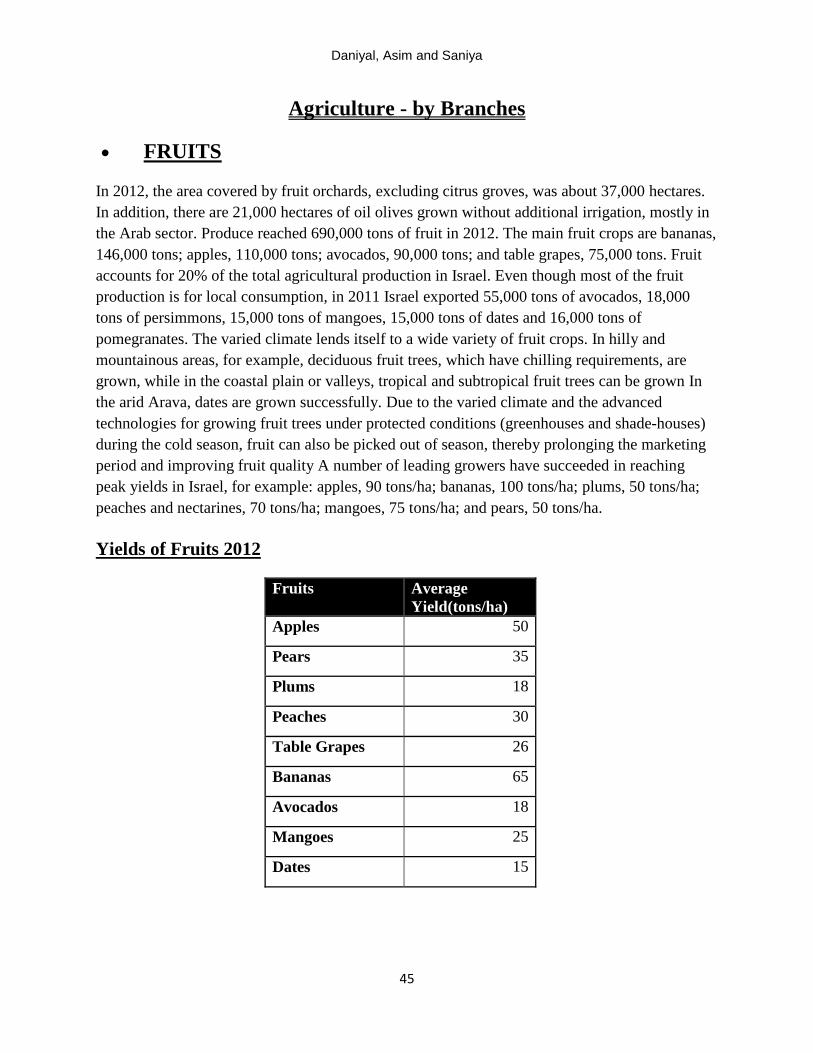

Yields of Fruits 2012

Fruits Average

Yield(tons/ha)

Apples 50

Pears 35

Plums 18

Peaches 30

Table Grapes 26

Bananas 65

Avocados 18

Mangoes 25

Dates 15

Daniyal, Asim and Saniya

46

Storage

The use of advanced technologies enables the marketing of high quality fruit which can reach the

overseas consumer a few days after picking. Fruit can also be stored under refrigeration for long

periods. Advanced storage technologies are employed in the cooling houses and sorting and

packing facilities, as well as in the domestic and export distribution network.

Mechanization

Several mechanical means have been developed in order to increase the efficiency of handling

fruit. For example, a hydraulic lift with a booth allows the worker to reach the highest branches.

The lift can be steered, guided from tree to tree and raised or lowered to the desired height. In

addition to the standard model, a particularly high model has been developed for picking dates.

Research and Development