Economies of diversification in the banking industry : A frontier approach

21

Journal of Monetary Economics 31 (1993) 229-249. North-Holland Economies of diversification in the banking industry A frontier approach* Gary D. Ferrier University of Arkansas, Fayetteville. AR 72701, USA Shawna Grosskopf Sourhem Illinois University. Carbondale, IL 62901, USA Kathy J. Hayes Southern Methodis University, Dallas, TX 75275, USA Suthathip Yaisawarng Union College, Schenectady, NY 12308. USA Received November 1991, final version received December 1992 This paper defines a new measure, economies of diversification, to examine the cost effect of product line expansion. This measure is a special case of expansion path subadditivity and contains economies of scope as a special case. A nonparametric frontier technique which isolates the effects of inefficiency and scale is used to measure economies of diversification. Applied to a set of 468 U.S. depository institutions operating in 1984, we find slight diseconomies of diversification. Dis- economies of diversification and inefficiency due to the overutilization of resources are found to be more important determinants of bank costs than is the failure to operate at optimal scale. Keywords: Economies of diversification; Nonparametric frontier; Banking 1. Introduction Recent changes in banking laws and regulations have allowed commercial banks to expand their services into new product lines and geographic areas. Correspondence to: Kathy J. Hayes, Department of Economics, Southern Methodist University, Dallas, TX 75275, USA. *The authors thank, without implicating, Allen N. Berger, Rolf Fire, David B. Humphrey, C.A. Knox Lovell, and an anonymous referee for their valuable comments on earlier drafts of this paper. 0304-3932/93/%06.00 0 1993-Elsevier Science Publishers B.V. All rights reserved

Transcript of Economies of diversification in the banking industry : A frontier approach

Journal of Monetary Economics 31 (1993) 229-249. North-Holland

Economies of diversification in the banking industry

A frontier approach*

Gary D. Ferrier University of Arkansas, Fayetteville. AR 72701, USA

Shawna Grosskopf Sourhem Illinois University. Carbondale, IL 62901, USA

Kathy J. Hayes Southern Methodis University, Dallas, TX 75275, USA

Suthathip Yaisawarng Union College, Schenectady, NY 12308. USA

Received November 1991, final version received December 1992

This paper defines a new measure, economies of diversification, to examine the cost effect of product line expansion. This measure is a special case of expansion path subadditivity and contains economies of scope as a special case. A nonparametric frontier technique which isolates the effects of inefficiency and scale is used to measure economies of diversification. Applied to a set of 468 U.S. depository institutions operating in 1984, we find slight diseconomies of diversification. Dis- economies of diversification and inefficiency due to the overutilization of resources are found to be more important determinants of bank costs than is the failure to operate at optimal scale.

Keywords: Economies of diversification; Nonparametric frontier; Banking

1. Introduction

Recent changes in banking laws and regulations have allowed commercial banks to expand their services into new product lines and geographic areas.

Correspondence to: Kathy J. Hayes, Department of Economics, Southern Methodist University, Dallas, TX 75275, USA.

*The authors thank, without implicating, Allen N. Berger, Rolf Fire, David B. Humphrey, C.A. Knox Lovell, and an anonymous referee for their valuable comments on earlier drafts of this paper.

0304-3932/93/%06.00 0 1993-Elsevier Science Publishers B.V. All rights reserved

230 G.D. Ferrier et al., Economies of diversification in banking

These changes have also allowed other depository institutions to begin offering products traditionally offered by commerical banks.’ The profusion of mergers and acquisitions which has swept through the banking industry in recent years’ may have also altered the cost structure of banking. In addition, Ferrier and Love11 (1990) and Berger and Humphrey (1991) find that production inefficien- cies are important determinants of bank costs. In light of the changes in the marketplace and recent empirical findings, the cost structure of the banking industry3 warrants further scrutiny. Concern has been expressed about the competitive viability of smaller, less diversified banks as opposed to larger, more diversified banks in this new environment. In addition, the benefits to savings and loan institutions, mutual savings banks, and credit unions of increased product offerings need to be assessed. The focus of this paper is to examine the impact of product diversification on the cost structure of banking using a fron- tier cost approach. In particular, we will compare the frontier costs of more diversified banks with those which are more specialized to identify which types of banks may have a cost advantage. The effect of product line expansion on cost will be referred to as economies of diversification.

Little evidence of scope economies has been found in the banking industry. In a review article of thirteen cost studies of relatively small banks, Clark (1988) concludes that there is little evidence of global economies of scope in banking. Working with a sample of the largest U.S. banks, Hunter, Timme, and Yang (1990) conclude that banks do not experience much in the way of economies of scope. This work has relied primarily on parametric techniques for measuring economies of scope and did not allow for the possibility of inefficient firm behavior.4 In addition, traditional parametric techniques have implicitly im- posed the same cost structure on diversified and specialized firms when testing for product mix economies by estimating a common cost function for both types of firms. Finally, these techniques do not typically sort out gains (losses) due to differences in operating efficiencies and gains (losses) due to diversification.

r For example, the Depository Institutions Deregulation and Monetary Control Act of 1980 and the Garn-St. Germain Act of 1982 allowed mortgage issuing institutions (saving and loans and mutual savings banks) to offer commercial and consumer loans in addition to mortgage loans.

‘During the 1980s commercial bank mergers and acquisitions averaged 300 per year [Rose (1989)J Many mergers and acquisitions involving thrifts also occurred.

3 In this paper the terms ‘banking industry’ and ‘banks’ will be used to refer to commercial banks, mutual savings banks, savings and loans, and credit unions, all of which are included in the data set used in the empirical work in this paper.

4A number of published studies [e.g., Aly, Grabowski, Pasurka, and Rangan (1990), Berger and Humphrey (1991) Elyasiani and Mehdian (1990), Evanoff, Israilevich, and Merris (1990), and Ferrier and Lovell (1990)] use parametric and/or nonparametric frontier techniques to study the efficiency of banks and to characterize the scale economies present in banking. Only Berger and Humphrey (1991) and Ferrier and Lovell (1990) address the issue of product mix economies under a frontier framework. Using a ‘thick frontier’ approach Berger and Humphrey find average diseconomies of scope of 15X-20% for U.S. banks; using a composed error cost frontier Ferrier and Love11 find little evidence of cost complementarities between pairs of products in a translog cost system.

G.D. Ferrier et al., Economies of diversification in banking 231

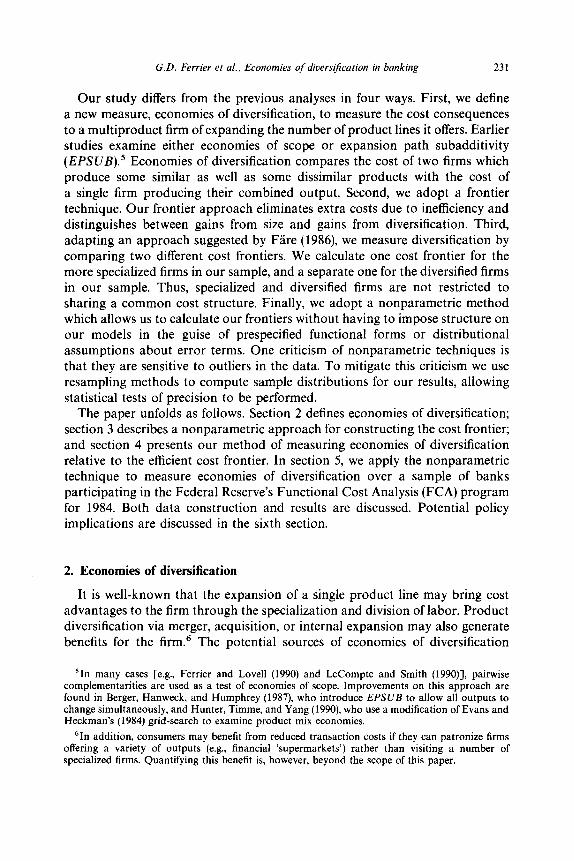

Our study differs from the previous analyses in four ways. First, we define a new measure, economies of diversification, to measure the cost consequences to a multiproduct firm of expanding the number of product lines it offers. Earlier studies examine either economies of scope or expansion path subadditivity (EPSUB).’ Economies of diversification compares the cost of two firms which produce some similar as well as some dissimilar products with the cost of a single firm producing their combined output. Second, we adopt a frontier technique. Our frontier approach eliminates extra costs due to inefficiency and distinguishes between gains from size and gains from diversification. Third, adapting an approach suggested by Fare (1986), we measure diversification by comparing two different cost frontiers. We calculate one cost frontier for the more specialized firms in our sample, and a separate one for the diversified firms in our sample. Thus, specialized and diversified firms are not restricted to sharing a common cost structure. Finally, we adopt a nonparametric method which allows us to calculate our frontiers without having to impose structure on our models in the guise of prespecified functional forms or distributional assumptions about error terms. One criticism of nonparametric techniques is that they are sensitive to outliers in the data. To mitigate this criticism we use resampling methods to compute sample distributions for our results, allowing statistical tests of precision to be performed.

The paper unfolds as follows. Section 2 defines economies of diversification; section 3 describes a nonparametric approach for constructing the cost frontier; and section 4 presents our method of measuring economies of diversification relative to the efficient cost frontier. In section 5, we apply the nonparametric technique to measure economies of diversification over a sample of banks participating in the Federal Reserve’s Functional Cost Analysis (FCA) program for 1984. Both data construction and results are discussed. Potential policy implications are discussed in the sixth section.

2. Economies of diversification

It is well-known that the expansion of a single product line may bring cost advantages to the firm through the specialization and division of labor. Product diversification via merger, acquisition, or internal expansion may also generate benefits for the firm.6 The potential sources of economies of diversification

‘In many cases [e.g., Ferrier and Love11 (1990) and LeCompte and Smith (1990)], pairwise complementarities are used as a test of economies of scope. Improvements on this approach are found in Berger, Hanweck, and Humphrey (1987) who introduce EPSUB to allow all outputs to change simultaneously, and Hunter, Timme, and Yang (1990) who use a modification of Evans and Heckman’s (1984) grid-search to examine product mix economies.

‘In addition, consumers may benefit from reduced transaction costs if they can patronize firms offering a variety of outputs (e.g., financial ‘supermarkets’) rather than visiting a number of specialized firms. Quantifying this benefit is, however, beyond the scope of this paper.

232 G.D. Ferrier et al., Economies of diversification in banking

include excess capacity in fixed inputs and the joint use of public inputs.7 Diversification may provide the firm with the opportunity to grow despite the presence of diminishing marginal returns in a given product line, to avoid/reduce the risks faced by firms specializing in the production of a more limited portfolio of goods and services, and to expand sales beyond the limits of any given market, whether these limits are given by demand or supply factors. The latter point is especially pertinent for banks operating in states where branching restrictions limit the geographical size of the market.

We now formalize the notion of diversification economies and compare it with economies of scope and expansion path subadditivity. Let y = (Yt, . . ‘9 yM) E rWy be the vector of outputs produced from the vector of inputs x=(x~,...,x~)ERN+. This technological relationship can be summarized by the input requirement set, L(y) = {x:x produces y). As is well-known, technology can also be completely described by the cost function

c(y,w)=min{wx’:xEL(y)}, (1) X

where w = (wl, . . . , wN) E R”, + is the vector of input prices. Baumol, Panzar, and Willig (1982, def. 4B1, pp. 71-72) formally define

economies of scope as follows. Let U be the set of outputs produced by a firm. Consider a subset of the firm’s outputs, S c U, and let P = { T1, T,, . . . , Tk} denote a nontrivial partition of S. There are economies of scope at ys with respect to the partition P if

i$l C(YTii WI ’ 4Ysi w). (2)

Note that economies of scope is a special case of subadditivity’ where the output vectors of specialized firms are restricted to be orthogonal to one another. For the three-output case, i.e., y = ( y,, y,, y3), economies of scope are said to exist if9

C(Y,,O, 0; WI + 40, Y2, y3; WI > C(Y,, Y2, Y3; w). (3)

‘Bailey and Friedlaender (1982) provide an excellent discussion of the sources of economies of scope in general; Berger, Hanweck, and Humphrey (1987) offer a more thorough discussion of the sources of scope economies in banking.

sSubadditivity exists when c:= 1 c(y,) > c(y), where I?= 1 yi = y. Scope is the special case where

the yi are orthogonal to one another.

90nly one possible partition of the output set is shown in (3). Scope economies could be calculated relative to any nontrivial partition.

G.D. Ferrier et al., Economies of diverst$cation in banking 233

Diseconomies of scope occur if the inequality in (3) is reversed. Baumol, Panzar, and Willig (1982, def. 4B2, p. 73) define the degree of economies of scope at y relative to the product set T as

sc,(y) _ CC(YTi w) + 4 Yu-T-i WI - C(Yi WI1 c(y; w)

(4)

Berger, Hanweck, and Humphrey (1987) define expansion path subadditiuity (EPSUB) as the proportional change in cost in the production of multiple outputs by two firms instead of one firm. The output vectors of the specialized firms are not orthogonal in this case, but do sum to the output vector of the single firm. For the three-output case, expansion path subadditivity is measured by comparing the separate costs of firms A and B with the cost of their merged operation:

EPSUB(y) =

c(yf, y;, y$ w) + c(yf, y,", y;; w) - C(Y;' + YZ Yz” + yz”, y: + yt w) ) c( yf + y;, y2” + Y,", Y3" + YE WI (5)

where the superscripts denote firms and the subscripts denote products. EPSUB is more general than economies of scope,” and is concerned with the costs of larger firms relative to smaller firms, rather than with the cost of joint production versus disjoint production. If EPSUB > 0, then firms A and B can increase their cost competitiveness if they combined their activities; if EPSUB < 0, then the merged firm would be at a cost disadvantage relative to the smaller firms A and B.”

Economies of diversification is a special case of EPSUB and contains econo- mies of scope as a special case. It concerns the situation in which at least one of the outputs is produced by all of the smaller, ‘specialized’ firms (as in EPSUB), while the production of all other outputs is disjoint (as in economies of scope). Consider the case of three outputs and two firms. Suppose that one firm specializes in the production of output 1, the other firm specializes in the production of output 2, while both firms produce some of output 3. Economies of divers$cation are said to exist if

C(Yl’, 0, Y:; w) + c(O, Y,“, Y,“; WI > 4 y:, Y,“, Y3” + yjl; w).

Diseconomies of diversification occur if the inequality in (6) is reversed.

(6)

“‘Economies of scope is the special case of EPSUB where y: = 0, yt = 0, and yf = 0.

“As pointed out by an anonymous referee, EPSUB is intended to test whether it is more cost-effective for a firm to grow or to start a new firm in order to expand output. In this case, firm B is a residual firm which produces the differences in output produced by the larger firm (A plus B) and the smaller firm A. If EPSUE > 0, then firm A should expand to A plus B. If EPSUB < 0, a new firm (i.e., firm E) should be created.

234 G.D. Ferrier et al., Economies of diversification in banking

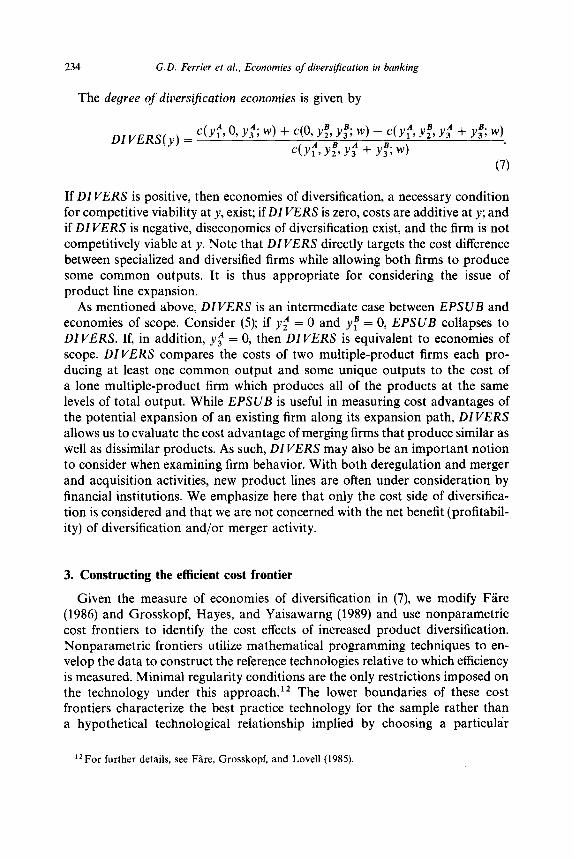

The degree of diversiJication economies is given by

DIVERS(y) = c(y$, 0, y;; w) + c(0, y;, y,“; WI - C(Yl’, Y,“, Y3” + Y,“; 4

C(Y& Y2B9 Y3” + Y& w) (7)

If DIVERS is positive, then economies of diversification, a necessary condition for competitive viability at y, exist; if DZ VERS is zero, costs are additive at y; and if DIVERS is negative, diseconomies of diversification exist, and the firm is not competitively viable at y. Note that DIVERS directly targets the cost difference between specialized and diversified firms while allowing both firms to produce some common outputs. It is thus appropriate for considering the issue of product line expansion.

As mentioned above, DIVERS is an intermediate case between EPSUB and economies of scope. Consider (5); if yt = 0 and yp = 0, EPSUB collapses to DIVERS. If, in addition, yt = 0, then DIVERS is equivalent to economies of scope. DIVERS compares the costs of two multiple-product firms each pro- ducing at least one common output and some unique outputs to the cost of a lone multiple-product firm which produces all of the products at the same levels of total output. While EPSUB is useful in measuring cost advantages of the potential expansion of an existing firm along its expansion path, DIVERS allows us to evaluate the cost advantage of merging firms that produce similar as well as dissimilar products. As such, DIVERS may also be an important notion to consider when examining firm behavior. With both deregulation and merger and acquisition activities, new product lines are often under consideration by financial institutions. We emphasize here that only the cost side of diversifica- tion is considered and that we are not concerned with the net benefit (profitabil- ity) of diversification and/or merger activity.

3. Constructing the efficient cost frontier

Given the measure of economies of diversification in (7), we modify Fare (1986) and Grosskopf, Hayes, and Yaisawarng (1989) and use nonparametric cost frontiers to identify the cost effects of increased product diversification. Nonparametric frontiers utilize mathematical programming techniques to en- velop the data to construct the reference technologies relative to which efficiency is measured. Minimal regularity conditions are the only restrictions imposed on the technology under this approach. I2 The lower boundaries of these cost frontiers characterize the best practice technology for the sample rather than a hypothetical technological relationship implied by choosing a particular

“For further details, see Fire, Grosskopf, and Love11 (1985).

G.D. Ferrier et al., Economies of diversificarion in banking 235

functional form as when estimating a parametric cost function. The motivation for using a frontier technique is straightforward. Economies of product scale and mix (i.e., scale economies and diversification economies) and subadditivity are characteristics of the cost or production surface. We argue that a frontier cost function13 is the appropriate choice for identifying cost economies and subad- ditivity. This methodology has the advantage over the standard cost function approach of being able to correct for deviations from the cost frontier. A by- product of this technique is that it also determines the relative cost efficiency of each firm.

We begin by introducing some basic notation and proceed with a general discussion of how the reference technologies (cost frontiers) are constructed. Let Y denote an M x K matrix of observed outputs, i.e., M different outputs for each of K firms. Observed inputs are denoted by the matrix X which is of dimension N x K, i.e., there are N different inputs for each of K firms. We construct a piecewise linear reference technology based on these observed outputs and inputs by taking convex combinations of the observed data points and their extensions:

L(y)={x: Y~z2y,X*zIx,zELq),

where L(y) is the input requirement set for output vector y and z is a K x 1 vector of intensity variables from activity analysis. The weak in- equalities in (8) allow for disposability of outputs and inputs. Since the only restriction on the z variables is that they be nonnegative, the technology represented by (8) satisfies constant returns to scale (CRS). This implies that scalar expansions and contractions of the observed input-output vectors are feasible. Constant returns to scale represents long-run optimal scale (consistent with minimum average costs for the firm with the traditional U-shaped average cost curve).

Construction of-the input requirement set is illustrated in fig. 1. Suppose that there are three firms with the same observed output vector y but input vectors corresponding to points D, E, and F. The technology constructed by (8) is bounded by the line segment DE, the vertical extension from point D and the horizontal extension from point E. The lower boundary of the input require- ment set represents the minimal input bundles which can produce the observed output level.

We wish to identify diversification economies in isolation of any scale effects. Thus, we remove any scale inefficiency as well as technical and allocative inefficiency from these diversified firms. We accomplish this by first minimizing

‘3Alternatively, a frontier production function or distance function would also be appropriate.

J.Mon- F

236 G.D. Ferrier et al., Economies of diversification in banking

Xl 0

Fig. 1. Nonparametric reference technology and efficiency measurement.

costs relative to our constant returns reference technology. Minimum efficient cost for firm k may be found by solving the following linear program:

ck *“” = c( yk, wk) = min wk * x’, z.x

(9)

subject to

where the constraints are the technology specified in (8), wk is the vector of observed input prices,14 and c:*‘~~ refers to minimal costs for observation k under constant returns to scale. The measure c:,CRS will be compared with the

r41f input prices are unavailable or unreliable (as they are in our data set), then minimal costs may be calculated as the solution to the following problem for each observation, k = 1, . . , I;,

Ck *,CRS = c( yx) = min 1 I

subject to

where C is the 1 x K vector of observed costs and cI is the cost for firm k. This problem will yield the same solution as (9) if all firms face the same input price vector. See Fare and Grosskopf (1985) for detaiis.

G.D. Ferrier et al., Economies of diver@ication in banking 237

efficient additive frontier (discussed in section 4) to determine the cost effects of changes in diversification alone. As a byproduct of the frontier method, a Farrell (1957) input-based measure of cost efficiency (CE) for observation k

is computed as

k = 1, . . . , K. (10)

In terms of fig. 1, (9) yields minimum costs for the observed output level relative to the constructed frontier L(y). For the firm operating at point F, minimum cost is given by costs at F*, which lies on the isocost curve WW which is tangent to L(y). If all of the firms face the same input prices, then D would be cost-efficient (it is at the tangency between the input requirement set and the isocost curve), but E would not be cost-efficient.

The methodology used here can determine how close to the optimal scale a firm operates. ’ 5, l6 To calculate scale efficiency we compare efficient firm cost under CRS [i.e., the solution to (9)] to efficient firm cost under variable returns to scale ( VRS) (i.e., returns to scale may be constant, increasing, or decreasing). Scale efficiency (SE) may be calculated as [see Fare and Grosskopf (1985)]”

SEk = c~~“““/c~* VRS, k = 1,. . . , K, (11)

where c:,“~~ is minimal cost for firm k relative to a reference technology which satisfies VRS.18 Scale inefficiency is simply a violation of CRS. Thus, if SEI, = 1, then CRS prevail at yk and observation k is scale-efficient. However, if SEI, < 1, then observation k is at a point of increasing or decreasing returns to scale, i.e., observation k is not scale-efficient.

This notion of scale efficiency is illustrated in fig. 2, for the single-output case. The cost set under VRS is bounded by c*,VRS, and the cost set under CRS is bounded by c**~~~. For observation D, scale efficiency is the vertical distance

r5 Firms have achieved an optimal scale of output when scale economies have been exhausted. In this case, unit costs of production have been minimized. See Baumol, Panzar, and Willig (1982) for details.

r6Although DIVERS excludes any extra costs due to scale inefficiency, we compute scale efficiency for diversified banks in order to facilitate a comparison with the existing literature on bank costs.

“For this approach to yield measures of scale efficiency identical to those calculated with input and output quantities only, allocative efficiency must be identical under CRS and VRS and the firms must face the same input prices. Note that, using a linear programming approach, Ferrier and Love11 (1990) found allocative inefficiency to be relatively low for banks. See Fare and Grosskopf (1985) for more details.

‘sMinima1 cost relative to a variable returns (VRS) technology may be calculated by solving (9)

where the additional restriction c,“=, zt = 1 is imposed. This restriction yields a ‘tighter’ fit of the

technology around the data; see fig. 2 and Fare and Grosskopf (1985).

238 G.D. Ferrier et al., Economies of diversification in banking

C c*, VRS

I Y

0 YD

Fig. 2. Nonparametric reference technology and scale efficiency measurement.

between the two cost structure at output y,, i.e., SED = ~~~~~~~~~~~~~~~~ The distance from observed cost to the VRS frontier gives technical efficiency (TE), i.e., for observation D, TE, = ~~~~~~~~~~~~~~~~~~~ Thus SE measures the efficiency of the observed scale of operation relative to the optimal scale of operation, while TE measures technical efficiency at the observed scale of operation.

4. Diversification economies relative to the efficient additive frontier

To determine whether economies of diversification exist, we compare the frontier minimum costs of firms that produce all outputs with the frontier minimum costs of a set of specialized firms which have been summed to impose strict cost additivity. This requires two steps which we summarize here and explain in detail below. First, we calculate minimum costs for the diversified firms separately, i.e., we calculate (9) for the diversified firms in our sample. Second, we construct a cost frontier which satisfies strict additivity by summing our specialized firms lg and calculate the distance of the cost-minimized diversi- fied firms from this minimum additive cost frontier. Our frontier approach allows us to define a ‘cost function’ consistent with its economic meaning as minimum (rather than ‘mean’ observed) costs. Furthermore, specialized and diversified

19By constructing an additive costfrontier, technical and scale inefficiency are removed from these ‘hypothetical’ firms.

G.D. Ferrier et al., Economies of divers$cation in banking 239

firms are allowed to face entirely different cost frontiers. Hence, we explicitly recognize that they may not share a common technology, as is generally assumed in the literature.

We derive a cost frontier satisfying strict additivity by constructing hybrid firms for which the costs of a firm specializing in the production of y, and y, are added to the costs of a firm specializing in the production of y2 and y,, where the hybrid firm achieves the same aggregated level of output as produced by the specialized firms. Thus, by construction, these hypo- thetical firms are strictly additive in costs. In the empirical work we construct all possible combinations of specialized banks to yield a set of additive data (c+, Y+).~’ We denote the additive technology formed by the specialized firms as C + (y, w). The efficiency measure and the degree of diversification eco- nomies are calculated as follows:

W, = min{A: A.ck*SCRSE C+(y, w)} (12)

and

DIVER& = ( ,.c:‘~~~ - c:~cRs),c~~cRs (13)

= w,- 1,

wherek = 1,. . . , K indexes the diversified firms and c:.CRS is the minimal cost calculated from (9) for the diversified firms. 21 The resulting efficiency measures, W,, k = 1, . . . , K, yield measures of how far the diversified firms are from the minimum additive cost frontier, given that they are minimizing costs relative to their own frontier and DI VERSk [which is analogous to the definition given in (7)] is interpreted as the percentage by which minimal costs of a diversified firm differ from minimum additive costs for that output vector.

If a diversified firm exhibits economies of diversification, its costs will be less than the corresponding additive frontier costs at that level and mix of outputs, i.e., W, > 1 or DZVERSk > 0. If W, < 1 (i.e., DIVERSk < 0), then the diversified firm exhibits diseconomies of diversification.

“For the three output case, we would have:

(c’, Y ‘) = (CC(Yl”% 0, Y:; w) + cK-4 Y$ Y& w)l, Iv:, Y!. Y: + Y3)

21 Note that C * (y, c) can be specified as linear constraints to be substituted into the programming problem (9) as follows:

C’(y,c) = {(c+,y+): Y+ ‘Z 2 y+. c+ ‘2 5 c+, ZE lq’},

where C+ is the vector of all the possible summed costs and Y+ is the matrix of the corresponding summed outputs.

J. Mm- G

240 G.D. Ferrier et al., Economies of diversification in banking

Fig. 3. Economies of diversification relative to an additive cost frontier.

Fig. 3 illustrates how the cost-minimizing diversified firm is judged relative to an efficient additive frontier for the simple two-output case. Additive firms are denoted by superscript pluses ( + ) and cost-minimized diversified firms are denoted by ‘d’ superscripts. Note that we are assuming that the first step of the procedure has been completed, thus inefficiency has been removed from all firms. Points A and B represent two cost-minimized specialized firms; point E+ is the ‘hybrid’ additive firm formed by combining A and B. The cost of E+, cE’ ,

is the minimal additive cost which belongs to the additive reference technology C + ( y, w) (the plane in fig. 3) constructed from the cost-minimized specialized firms. Points Fd and Gd are two possible cost-minimized diversified firms with the same output level and mix as E ‘. The costs of the diversified firms Fd and Gd are compared to the (hypothetical) additive frontier C’(y, w) to determine whether economies of diversification exist. The measure of economies of diversi- fication, W,, is the ratio of the efficient cost of an additive firm to that of a diversified firm with identical output level and mix. For example, cp is below the additive frontier, indicating that there are economies of diversification at Fd, and Wp = cE+/cF d > 1. On the other hand, cod lies above the additive

G.D. Ferrier et al., Economies of diversificafion in banking 241

frontier, thus IV,, = cE+/cod < 1, indicating that there are diseconomies of diversification at Gd. From this illustration it should be clear that W, is a local measure of diversification where costs of diversified firms are compared to costs of additive firms with the same outputs.

Nonparametric programming models are often criticized for being sensitive to outliers. These models also do not allow the researcher to employ standard statistical tests since measurement error is essentially ignored. In order to address these concerns we employ bootstrapping methods to generate a sampling distribution of the economies of diversification measures for each of the diversified banks in our sample. We do this by taking repeated random samples from our ‘population’ of additive firms (those created from the specialized firms) and calculate DIVERS for our diversified banks relative to each of these random samples. This repeated sampling technique allows us to construct a sampling distribution of DIVERS and to test the statistical significance of our findings.

A mean value of DIVERS based on (13) can be calculated for each of the diversified banks as

DZVERSk = i ((Wki - 1)/Z), k=l,...,K, i=l

(14)

where I is the number of iterations or samples relative to which the degree of diversification economies is calculated.

5. Data and results

Our data set consists of 575 banks participating in the Federal Reserve’s Functional Cost Analysis (FCA) program in 1984. These banks are relatively small, all having deposits of less than $1 billion. Following Berger, Hanweck, and Humphrey (1987), five bank services - demand deposits, time deposits, real estate loans, installment loans, and commercial loans - are considered as bank outputs. ** We adopt the ‘production approach’ to bank activity [see Humphrey (1985)] and use the number of deposit and loan accounts as our metric of bank

22An extensive literature, both theoretical and empirical, concerns itself with the ‘proper’ defini- tion of bank inputs and outputs, The chief focus of this literature has been on the dual nature of deposits as both ‘inputs’ (used in the funding of loans) and ‘outputs’ (providing services to depositors which require the input of labor, etc.) in the banking production/intermediation process. We do not claim any special insights, but do choose to treat deposits as outputs. This is done in recognition of the fact that significant amounts of labor, capital, and material inputs are used in the ‘production’ of deposits, because deposits generate significant value added for banks, and in order to maintain consistency with the majority of previous bank cost studies.

242 G.D. Ferrier et al., Economies of diversification in banking

outputs. 23,24 The total cost of providing these services is the sum of the expenditures on labor, capital, and materials2’

In order to investigate whether and to what degree economies of diversifi- cation exist in the U.S. banking industry, we would like to have homo- geneous samples; i.e., banks operating under similar environments or regula- tions. Some states allow banks to operate multiple branches and some do not, thus we segment our sample into two subgroups - 196 unit-state banks and 379 branching-state banks. Each subgroup is investigated separately.

Of the 196 banks in unit-states, 179 produce all five outputs while the remaining 17 banks do not provide either real estate or commercial loans. Our technique of measuring economies of diversification requires that the additive reference technology be constructed from partially specialized banks which have been summed to (hypothetically) produce all five positive outputs and have strictly additive costs.26

To construct the additive technology we first disaggregate our specialized banks into two groups - banks which do not provide real estate loans and those which do not provide commercial loans. All permutations of observa- tions within each group are formed by adding and subtracting observations pairwise. Results are then used to construct all possible combinations of banks. Any nonpositive values are deleted, yielding a population of 3057 hypothetical unit-state banks with additive cost. The additive frontier is constructed from random samples of these hypothetical banks, removing all technical and scale inefficiency with which these banks may operate.

To ensure the existence of a solution to our linear programming problems, we require that each output of diversified banks (i.e., banks which originally provide all five services) be no less than the minimal, and no greater than the maximal, output of the hypothetical banks. For the unit-state subgroup, 161 diversified banks belong to this admissible region and are included in the sample used to calculate economies of diversification.

23Working with Norwegian bank data, Berg, Forsund, and Jansen (1989) find that efficiency scores are dependent upon whether numbers of accounts or average sizes of accounts are employed as the measure of output, However, they offer no guidance as to which measure ought to be used; thus we use number of accounts in accordance with the ‘production approach’.

24See Berger and Humphrey (1992) for an excellent discussion of output definition and measure- ment concerns in banking cost studies.

25The FCA data do not contain the information needed to derive prices for capital or materials; in our analysis it is assumed that all banks face the same prices for these two inputs. Wage data are available from the FCA data.

26Note that all banks in the sample provide demand and time deposit services. This implies that we do not have complete specialization and therefore can not identify ‘pure’ economies of scope. We are identifying cost savings/dissavings of diversification conditional on the provision of these basic services.

G.D. Ferrier et al., Economies of diversification in banking 243

Table I

Descriptive statistics of outputs and cost.a

Demand deposits Time deposits Real estate loans Installment loans Commercial loans Total cost

Demand deposits Time deposits Real estate loans Installment loans Commercial loans Total cost

__

Standard Mean deviation

(A) Unit-state banks

161 diversified banks

6.408.7 4,227.7 9,189.l 6,583.8

389.3 280.4 2,717.3 2513.5

950.1 615.3 2,125,909.5 2,069,9 10.4

3057 hypothetical banks

17,498.5 9,078.4 16,577.7 8,692.3

449.4 363.1 6,609.3 3,558.0 1,686.O 1,022.9

5,244,265.0 3,085,526.0

Maximum value

23,759.0 37,997.0

1,318.0 14,143.0 3,196.O

15,760,075.1

56,694.0 55,604.O

1,392.9 21,070.O

3,630.O 19,767,770.0

Minimum value

676.0 226.0

29.0 122.0 22.0

148,651.l

3.0 42.0 27.0 47.0

6.0 14405.9

(B) Branch-state banks

307 diversiJied banks

Demand deposits 13,298.3 12,265.3 81,188.O 1,120.o Time deposits 28,091.6 28,422.6 174,159.0 2.962.0 Real estate loans 2,045.5 3,481.2 27,093.O 90.0 Installment loans 5,733.6 5,356.8 28,952.0 273.0 Commercial loans I505.5 I396.5 8,854.0 44.0 Total cost 3,898,398.3 3,794,64 1.4 26,663,696.2 331,638.3

5313 hypoihetical banks

Demand deposits 38,800.9 21,090.7 137,111.0 171.0 Time deposits 115689.0 113,967.6 726,732.0 138.0 Real estate loans 5,465.2 5,678.0 28,999.0 78.0 Installment loans 34,176.6 42,908.8 262,208.O 2.0 Commercial loans 3,537.6 2,932.6 9,055.o 41.0 Total cost 11,545,445.8 7,418,219.6 50,295,656.5 50,789.8

aOutput measures (demand deposits, time deposits, real estate loans, installment loans, and commercial loans) are expressed in number of accounts; total cost is in dollars.

A similar procedure is followed for the 379 branch-state banks. In this group, 336 banks produce all five outputs, 15 banks do not provide real estate loans, 27 banks do not have commercial loans, and one observation does not provide installment loans. We delete the one bank which does not provide installment loans so that all specialized branch-state banks provide a subset of services consisting of demand deposits, time deposits, and installment loans, as was the case for the unit-state

244 G.D. Ferrier et al., Economies of diversiJication in banking

Table 2

Efficiency results of diversified banks.

Mean Standard Maximum deviation value

Minimum value

Technical efficiency Scaler efficiency Potential cost saving

Technical efficiency Scale efficiency Potential cost saving

(A) Unit-state banks

0.685 0.227 0.875 0.168

$1,126,887 $1,669,645

(B) Branch-state banks

0.596 0.212 0.839 0.154

$2,156,330 $2,480,192

l.ooo 0.210 1.000 0.084

$14,437,589 SO

l.CQO 0.170 l.ooO 0.314

$18,279,559 SO

banks. We construct all possible permutations of each specialized group and randomly select 25% of the number of observations from each permutation data set to construct 5313 hypothetical additive branch-state banks.27 Given these hypo- thetical branch-state banks, we obtain 307 diversified banks in the admissible region. Table 1 displays descriptive statistics of the diversified and hypothetical banks in our final sample for both the unit-state and branch-state banks.

Recall that our technique first eliminates technical and scale inefficiency by determining efficient cost, c*.~~~, prior to comparing c* to the minimum additive cost frontier. Thus, the measures of technical and scale efficiency, as well as DIVERS, give us information about the sources of inefficiency for banks. Table 2 reports our findings on technical and scale efficiency, and the potential cost savings were banks to operate on the efficient surface at the optimal scale of output.28 Both unit-state banks and branch-state banks operate with a high degree of technical inefficiency. On average, technical inefficiency pushes costs 46% over the efficient level for unit-state banks and 68% over for branch-state banks. Operating at nonoptimal scales also raises costs above the efficient levels on average for the banks in our sample. Scale inefficiency, however, is a much

l’If we were to use the entire set of permutations of specialized banks, we would have at least 100,000 hypothetical banks, which exceeds the computational capacity of our computer.

“If there are outliers in our diversified samples which form the diversified frontier, our measure of technical efficiency would be biased downward for nonoutliers, but the measure of scale efficiency would be unaffected. However, if the outlier is not part of the frontier, then only that particular outlier’s technical efficiency score would be biased. Investigation of correlations between inputs and outputs as well as their plots (stem and leaf or histogram, boxplot, and normal probability plots) does not reveal any obvious outliers. Nevertheless, the relatively low proportion of efficient branch-state banks (1% for the CRS and 8% for the VRS technologies) would suggest the potential existence of outliers in our sample of diversified branch-state banks. This could possibly bias DIVERS toward economies of diversification.

G.D. Ferrier et al.. Economies of diver@ation in banking 245

Table 3

Frequency distribution of resampling diversification economies.”

State branching regulation

Degree of diversification economies

Economies Additive Diseconomies

Total

Unit-state 4 38 119 161 Branch-state 9 41 251 307

“Based on the following hypothesis at the 0.05 level of significance: H,: mean degree ofdiversifica- tion economies equals zero, H,: mean degree of diversification economies is not equal to zero.

smaller problem than is technical inefficiency. These results are consistent with those of Aly, Grabowski, Pasurka, and Rangan (1990), Berger and Humphrey (1991), and Ferrier and Love11 (1990), all of whom find inefficiencies to be important determinants of bank costs. Unit-state branch banks could produce their observed levels of output with an average cost savings of 12.5% were they to operate at optimal scale; branch-state banks could save even more, on average 17%. If banks were to reorganize to the efficient configurations (i.e., by proportionally reducing input usage to the efficient levels and adjusting opera- tions to the optimal scale), it would result in an average cost savings of $1,126,887 for unit-state banks and $2,156,330 for branch-state banks.

Table 3 reports the number of diversified banks that are located above, on, and below the additive frontier using bootstrapping techniques.” We test each observation for statistical significance against the null hypothesis of cost ad- ditivity at the 5% level of significance. A student-t statistic is calculated from the distribution of bootstrapped values of DIVERS for each firm. Those observa- tions with t-values above 2.023 are designated as exhibiting economies of diversification, while those with t-values below - 2.023 are denoted as experi- encing diseconomies of diversification. All other observations are considered to have additive cost structures.

Only 2.5% (4 of 161) of unit-state banks and 3% (9 of 307) of branch-state banks are found to exhibit statistically significant economies of diversification, i.e., DIVERS > 0. The majority of both types of banks (74% of unit-state and 84% of branch-state banks) were found to lie above the additive frontier, thus displaying statistically significant diseconomies of diversification, i e . ., DIVERS -=c 0.30 Findings on the degree of economies of diversification are

29Recall that the hypothetical banks which define the additive technology were constructed from a relatively small number of specialized banks found in the data set. While small in number, the specialized banks were not necessarily small banks. DIVERS is calculated relative to the additive frontier, and thus is dependent upon the observations which are used to construct the additive technology.

300ur qualitative conclusion would remain the same if we correct for outliers among the diversified banks.

246 G.D. Ferrier et al., Economies of diverstJ5cation in banking

Table 4

Results of diversification economies measure.

Branching type Grand mean

Standard deviation

Maximum value

Minimum value

Unit-state (n = 161) - 0.285 0.223 0.376 - 0.643 Branch-state (n = 307) - 0.219 0.188 1.565 - 0.370

reported in table 4. The grand mean (computed over all iterations for all observations) indicates that diversification raises costs for both unit-state banks (by 28%) and branch-state banks (by 22%). These results are similar to Berger and Humphrey’s (1991) ‘thick frontier’ findings on economies of scope.

In table 5, banks are classified by size as proxied by the total value of loans.31 The patterns of economies of diversification are similar for banks in unit-states and branch-states. Mean values of DIVERS are all negative for all sizes, except for unit-state banks with a total value of loans greater than $250 millions. Diseconomies of diversification exist between the provision of real estate loans and commercial bank loans at every bank size. This result is similar to that found by Berger and Humphrey (1991) using a ‘thick frontier’ approach.

The degree of diseconomies appears to be increasing as bank size increases; i.e., larger banks experience higher costs due to diversification than do smaller banks. This result is confirmed by looking at the frequency distributions of banks exhibit- ing economies of diversification, additive costs, and diseconomies of diversifica- tion. All of the unit-state banks with total loans exceeding $150 million experience cost disadvantages due to diversification. Economies of diversification and addi- tive costs were found for smaller sizes of unit-state banks. Branch-state banks with total loans exceeding $400 million suffer higher costs from diversification. The majority of banks experiencing economies of diversification in our sample have total loans of less than $50 million. Eighty-five percent of our additive cost diversified banks are small banks with total loans of less than $100 million. Our findings for small U.S. banks are similar to those of Hunter, Timme, and Yang (1990), who find that large U.S. banks were not subadditive in their costs.

To summarize, we find broad agreement of our results across banks in unit-states and those in branch-states. Banks in this sample overutilize resources in a variety of ways. The major problem is technical inefficiency. On average these banks have diversified their product lines in a suboptimal manner. Our

“Ideally we would like to use total assets as our proxy of bank size. Unfortunately, we do not have total assets in our data set. Since the total value of all loans represents the major proportion of bank assets in general, we use it as our proxy of bank size. We could also classify banks by the total value of deposits. Because the total value of loans is highly correlated with the total value of deposits (0.79 for unit-state banks and 0.92 for branch-state banks) and are significant at the 1% level, results from the two classifications are similar.

Tab

le

5

Eco

nom

ies

of d

iver

sifi

catio

n by

si

ze.

Gra

nd

mea

n St

anda

rd

devi

atio

n Fr

eque

ncy

a

< 50

- 0.

238

0.24

1 31

3316

1

(A)

Uni

t-st

ate

bank

s

Tot

al

valu

e of

loa

ns

(mill

ions

of

S)

_

50-1

00

100-

150

150-

250

250-

350

> 35

0 T

otal

- 0.

342

- 0.

386

- 0.

455

- 0.

396

0.25

7 -

0.28

5 0.

171

0.12

2 0.

108

0.08

1 0.

223

o/4/

35

O/lj

lS

O/O

/5

O/O

/3

1 /o/

o 4/

38/l

19

~~

(B)

Bra

nch-

stat

e ba

nks

Tot

al

valu

e of

loa

ns

(mill

ions

of

S)

< 50

50

-100

10

0-20

0 20

0-40

0 40

0-60

0 60

0-80

0 80

0-10

00

> 10

00

Tot

al

Gra

nd

mea

n -

0.15

3 -

0.23

6 -

0.26

1 -

0.25

9 -

0.28

5 -

0.28

8 -

0.28

4 -

0.22

8 -

0.21

9 St

anda

rd

devi

atio

n 0.

283

0.11

6 0.

119

0.09

6 0.

026

0.01

6 0.

004

0.18

8 Fr

eque

ncy”

71

2416

6 l/l

l/9

6 l/2

/50

o/4/

30

O/O

/8

O/O

/4

O/O

/ 1

WI2

9/

41/2

51

~~~

~~__

_ ~_

“Fre

quen

cy

is t

he

num

ber

of b

anks

ex

hibi

ting

econ

omie

s of

div

ersi

fica

tion,

ad

ditiv

ity

of c

osts

, an

d di

seco

nom

ies

of d

iver

sifi

catio

n,

resp

ectiv

ely.

248 G.D. Ferrier et al.. Economies of diverst@tion in banking

results indicate that both unit-state and branch-state banks could reduce costs by not providing either real estate or commercial loans, Banks could improve their competitiveness by changing managerial style and reorganization (i.e., improve technical efficiency) without necessarily diversifying.32 The smallest cost inefficiency is found to be due to nonoptimal scale. Apparently banks in this sample are able to operate close to the correct size in terms of the levels of outputs produced.33

6. Conclusions

We have presented evidence on product mix economies in the banking industry using a cost frontier approach which does not assume that a common technology is faced by both specialized and diversified firms. Our nonparametric technique separates the effects of production inefficiency, scale effects, and product mix effects. After controlling for inefficiency and scale, we find dis- economies of diversification for banks in both unit- and branch-banking states. Resampling methods were used on our results to obtain statistical tests of their significance.

On average, we find a large degree of technical inefficiency, a lesser degree of scale inefficiency, and diseconomies of diversification. These results suggest that a large potential benefit of increased competition would be the likely reduction of the overall level of inefficiency found in the banking industry as banks are forced to use inputs more efficiently. Scale efficiency may be enhanced as banks expand or contract their current product lines. Based on cost considerations, the further expansion of bank services into related areas may not be warranted. However, this cost disadvantage associated with the joint provision of financial services may be offset by other benefits of diversification. For example, by offering a variety of financial services at one location consumers may benefit from reduced transaction costs and the firms may benefit through the diversification of risks, thus enhancing social welfare. These benefits may bring a revenue advantage to banks offering diversi- fied services. Future research could investigate the potential revenue advantages of diversification.

In the face of diseconomies of diversification banks will face greater competi- tion from nonbank ‘banks’ - institutions which produce only loans or deposits - which may be able to outperform banks. Finally, on the cost side, thrifts may fail to benefit from their recently gained right to expand their menu of deposit

32The Pearson correlation coefficient between DIVERS and technical efficiency for unit-state banks (0.198) is relatively small, but is statistically significant at the 5% level. This relationship is not statistically significant for the branch-state banks.

33This may indicate that most banks in our sample operate under constant returns to scale.

G.D. Ferrier et al., Economies of diversification in banking 249

and loan offerings. Depository institutions have available to them large poten- tial benefits in the form of improved operating efficiencies, and may have demand side advantages by serving as financial ‘supermarkets’ to their cus- tomers.

References

Aly, H.Y., R. Grabowski, C. Pasurka, and N. Rangan, 1990, Technical, scale, and allocative efficiencies of US. banking: An empirical investigation, Review of Economics and Statistics 72, 211-218.

Baumol, W.J., J.C. Panzar, and R.D. Willig, 1982, Contestable markets and the theory of industry structure (Harcourt Brace Jovanovich, San Diego, CA).

Bailey, E.E. and A.F. Friedlaender, 1982, Market structure and multiproduct industries, Journal of Economic Literature 20, 1024-1048.

Berg, S.A., F.R. Fsrsund, and E.S. Jansen, 1989, Bank output measurement and the construction of best practice frontiers, Mimeo. (Bank of Norway, Oslo).

Berger, A.N., G.A. Hanweck, and D.B. Humphrey, 1987, Competitive viability in banking: Scale, scope and product mix economies, Journal of Monetary Economics 20, 501-520.

Berger, A.N. and D.B. Humphrey, 1992, Measurement and efficiency issues in commercial banking, in: Z. Griliches, ed., Output measurement in the service sectors (University of Chicago Press, Chicago, IL).

Berger, A.N. and D.B. Humphrey, 1991, The dominance of inefficiencies over scale and product mix economies in banking, Journal of Monetary Economics 28, 117-148.

Clark, J.A., 1988, Economies of scale and scope at depository institutions: A review of the literature, Federal Reserve Bank of Kansas City Economic Review 73, 16633.

Elyasiani, E. and S. Mehdian, 1990, Efficiency in the commercial banking industry: A production frontier approach, Applied Economics 22, 539-551.

Evanoff, D.D., P.R. Israilevich, and R.C. Merris, 1990, Relative price efficiency, technical change, and scale economies for large commercial banks, Journal of Regulatory Economics 2,281-298.

Evans, D.S. and J.J. Heckman, 1984, A test for subadditivity of the cost function with an application to the Bell System, American Economic Review 74, 615-623.

Fare, R., 1986, Addition and efficiency, Quarterly Journal of Economics 51, 861-865. Fare, R. and S. Grosskopf, 1985, A nonparametric cost approach to scale efficiency, Scandinavian

Journal of Economics 87, 594-604. Fare, R., S. Grosskopf, and C.A.K. Lovell, 1985, The measurement of efficiency of production

(Kluwer-Nijhofl Publishing, Boston, MA). Farrell, M.J., 1957, The measurement of productive efficiency, Journal of the Royal Statistical

Society A (General) 120, 253-281. Ferrier, G.D. and C.A.K. Lovell, 1990, Measuring cost efficiency in banking: Econometric and linear

programming evidence, Journal of Econometrics 46, 229-245. Grosskopf, S., K.J. Hayes, and S. Yaisawarng, 1989, Measuring economies of scope: Two frontier

approaches, Mimeo. (Department of Economics, Sourthern Methodist University, Dallas, TX). Humphrey, D.B., 1985, Costs and scale economies in bank intermediation, in: R.C. Aspinwall and R.

Eisenbeis, eds., Handbook of banking strategy (Wiley, New York, NY) 7455783. Hunter, W.C., S.G. Timme, and W.K. Yang, 1990, An examination of cost subadditivity and

multiproduct production in large U.S. banks, Journal of Money, Credit, and Banking 22, 504525.

LeCompte, R.L.B. and SD. Smith, 1990, Changes in the cost of intermediation: The case of savings and loans, Journal of Finance 45, 1337-1346.

Rose, P.J., 1989, Profiles of US. merging banks and the performance outcomes and motivations for recent mergers, in: B.E. Gup, ed., Bank mergers: Current issues and perspectives (Kluwer Academic Publishers, Boston, MA) 3-28.