Economic Review: Spring 1979: Money, Prices, and Exchange Rates

46

FEDERAL RESERVE BANK OF SAN FRANCISCO ECONOMIC REVIEW SPRING 1979

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Economic Review: Spring 1979: Money, Prices, and Exchange Rates

FEDERAL RESERVE BANKOF SAN FRANCISCO

ECONOMICREVIEW

SPRING 1979

The Federal Reserve Bank of San Francisco’s Economic Review is published quarterly by the Bank’s Research and Public Information Department under the supervision of Michael W. Reran, Senior Vice President. The publication is edited by William Burke, with the assistance of Karen Rusk (editorial) and William Rosenthal (graphics).

For free copies of this and other Federal Reserve publications, write or phone the Public Information Section, Federal Reserve Bank of San Francisco, P.O. Box 7702, San Francisco, California 94120. Phone (415) 544-2184.

Money, Prices and Exchange Rates

I. Introduction and Summary 5

II. Estimating the Underlying Inflation RateJohn L. Scadding 7

...Som e time w ill be required to reduce the rate of imbedded in fla tion— about 7 percent— to the level of the early 1960’s.

III. Money and Exchange Rates— 1974-79Michael W. Keran 19

. . .A m ajor share of recent U.S. exchange-rate movements can be explained by the divergence of U.S. m onetary policies from those of Germany, Japan and Switzerland.

IV. Has a Strong U.S. Economy Meant a Weak Dollar?Michael Bazdarich 35

...R ecen t U.S. evidence does not support the view that strong econom ic grow th necessarily weakens exchange rates.

Editorial com m ittee fo r th is issue:John Judd, Charles Pigott, Rose McElhattan

The newspapers and academic journals are fullof theories (sometimes contradictory theories)which attempt to explain each striking newdevelopment occuring in this era of rapidly risingprices and wildly fluctuating exchange rates.Consider, for example, several important policyoriented questions which have arisen during thepast year or two. What is the basic underlyingrate of inflation? Do speculative influences explain the steep drop in the dollar's value duringthe 1977-78 period? Or has the very strength ofthe U.S. economy led to the decline in the valueof the nation's currency? The task of analysis, asthe following articles indicate, is to apply sophisticated tests to the available statistical evidence,as a means of devising correct answers to thesequestions-and therefore correct policy solutions to the nation's problems.

In analyzing the recent inflation, John Scadding says, "Only the systematic changes in pricesare of any use in forecasting future prices; bydefinition, the unsystematic, transitory changescontain no information about the future courseof prices." He then presents a model of howindividuals might rationally extract informationabout the underlying inflation rate from observed price changes, and then use that information to forecast future prices.

Scadding argues that successively higher levelsof inflation have become imbedded in the economy since 1960. The underlying inflation ratefluctuated around 1.7 percent until the late1960's, averaged about 4.8 percent in the 1971-73period, and hovered around 7.0 percent in theexpansion of the late 1970's. "Neither the1969-70 nor the 1973-75 recession made a sizable dent in the underlying rate; the most theyseemed capable of doing was to stabilize theinflation rate until some new disturbance carriedit to a higher plateau."

The ingrained rate of inflation currently perceived by the market is very high by historical

5

standards, and has stubbornly remained at thislevel throughout the current expansion. "Thispersistence of a high perceived underlying inflation rate doubtless has given inflation an important momentum of its own as market participants, in an effort to protect themselves againstfuture inflation, build this perception into theirwage and price demands."

This point leads Scadding to a second important conclusion-"Even if aggregate demandgrowth could be moderated, pressure for priceand wage increases would continue to emanatefrom the cost side for a considerable time." Theimplication for the real economy is not reassuring, since output and employment may have toremain below normal levels for a fairly protracted time if any significant progress is to be madeagainst inflation.

Michael Keran, in his contribution, analyzesthe reasons for the decline in the internationalvalue of the dollar over the 1977-78 period. Hequickly dismisses the popular impression thatthe dollar was driven down by speculators with avested interest in an undervalued dollar, notingthat speculation tends to drive the value of acurrency towards a long-run equilibrium valuedetermined by economic fundamentals. Thosespeculators who most clearly perceive the underlying fundamentals and accordingly take a position in the exchange market will generally makethe most profits, while those speculators who goagainst the fundamentals will generally losemoney. Because of this self-selection process, theobserved value of the dollar should not deviatesignificantly from the level consistent with economic fundamentals for more than a short periodof time.

Keran concentrates on explaining movementsin the exchange value of the dollar against thecurrencies of seven other major industrial countries in the 1974-79 period of flexible exchangerates. He first summarizes the apparent

monetary-policy considerations which shapedmonetary developments during this period. Thenhe shows that actual changes in the "excessmoney supply"-nominal money supply less realmoney demand-led to changes in prices andexchange rates in a way consistent with economic theory and empirical statistical tests. He baseshis analysis on two propositions: I) the exchangerate between two domestic currencies will adjustto reflect changes in the relative domestic purchasing power of the currencies; and 2) domesticmonetary developments are a major determinantof domestic inflation rates, and thus of thedomestic purchasing power of a given currency.

Keran estimates his equations with two alternative measures-money, and money plus quasimoney. The former is the narrow definition ofmoney including currency and demand deposits.This primarily satisfies the means-of-paymentmotive for holding money. The latter is thebroader definition which includes currency, demand deposits and quasi-monetary deposits ofcommercial banks. This measure includes asubstantial store-of-value motive for holdingmoney. Both definitions provided statisticallysignificant results, although the broader measuregave generally superior results. "Given the dollar's role as both an international means ofpayment and store of value, the superiority of thebroader measure of money is not surprising."

Keran concludes that an important share ofthe exchange-rate movements since 1975 can beexplained by monetary factors, rather than byspeculation or changes in such real factors as theterms of trade. His study also implies thatforeign-exchange markets adjust much morequickly than domestic commodity markets tochanges in domestic monetary conditions. Because these exchange rate changes can affect the

6

dollar price of internationally traded goods, theemergence of flexible exchange rates can shortenthe lag between money and prices.

Michael Bazdarich raises the question ofwhether the recent strength in the U.S. economyhas led to the weakness of the dollar. Accordingto the theory in question, fast economic growthin a country causes an acceleration in its importsand therefore a deterioration in its trade balance.This ultimately would lead to a depreciation ofthe domestic currency.

Bazdarich questions this approach, arguinginstead that true economic growth, as evidencedby rapid growth in productive capacity, or potential GNP, typically strengthens the domesticcurrency. "Growth of this type implies improving supply and wealth conditions, which canmore than offset the effects of rising demand onthe trade balance. Sharp cyclical increases inGNP, on the other hand, can weaken the domestic currency. These movements typically involvean increase in demand with no change in productive capacity, and so do not generate any offsetting effects to the rise in imports."

Bazdarich argues that the popular analysis hasmissed this important distinction. His statisticaltests indicate no support for the argument thattruly strong growth in an economy will necessarily tend to weaken exchange rates. "Indeed,recent. U.S. evidence suggests that the oppositehas been the case. The 'strong economy, weakcurrency'explanation of the dollar's decline thusdoes not appear to have any hard theoretical orempirical evidence to support it." Bazdarich'sfindings-which parallel Keran's-suggest thatrecent GNP increases have been mostly cyclical,caused perhaps by an overly expansionary policy, and for that reason have been associated witha falling dollar.

John L. Scadding*

It is widely recognized that every wiggle in theconsumer price index or in the GNP implicitprice deflator does not signify a change in whatwe typically mean by inflation. Inflation is usually defined as an on-going, systematic rise inprices, while many of the influences which operate to produce month-to-month or even quarterto-quarter changes in prices-like strikes, cropfailures, temporary dislocations due to inclementweather and the like-do not persist. Indeed,their effects are unsystematic and ephemeral.

Only the systematic changes in prices are ofany use in forecasting future prices; by definition, the unsystematic, transitory changes contain no information about the future course ofprices. The persistence of relatively high andvariable rates of inflation in recent years hasmeasurably increased the marketplace's stake inefficiently forecasting prices. One would expecttherefore that the marketplace makes some attempt to discriminate between the systematicforces operating on prices-the things that determine the underlying inflation rate-and theshort run, transitory and unsystematic part ofprice changes. I

This paper presents a model of how individuals might rationally extract information aboutthe underlying inflation rate from observed pricechanges, and how they might use that information to forecast future prices. The model is thenestimated by assuming that people use theseforecasts, among other things, to determine howmuch to spend on consumption.

Traditionally, economists have assumed thateconomic agents form their expectations aboutfuture· events adaptively, i.e., the forecast fornext period is formed by adjusting this period'sforecast by some fraction of this period's forecasterror. Price expectations are commonly mod-

*Associate Professor of Economics, Scarborough College, University of Toronto, and Visiting Scholar, Federal Reserve Bank of San Francisco, Summer 1978.

7

elled this way, although the adaptive model is infact ill-suited for this purpose because it leads tochronic underprediction of prices if prices aregrowing. The reason is fairly obvious. The adaptive model implies that forecast prices are aweighted average of current and past prices,which will always be less than the current levelwhen prices are growing. The forecasting modeldeveloped in this paper represents a generalization of the adaptive model that allows for systematic growth in prices and therefore avoids theproblem of chronic underprediction. The modelhas the added attraction of being derived fromoptimizing behavior, rather than adduced on anad hoc basis as is typically done.

Information about the market's perception ofthe underlying inflation rate is valuable to thepolicy maker for at least two reasons. In the firstplace, such information should provide relatively efficient estimates of ingrained inflation,which presumably is what policy makers areinterested in. Almost by definition it is theproblem-the inflation that won't go away.Certainly the agonizing that goes on in Washington every month over what the price indices aretelling us suggests that the chief preoccupation ofpolicy makers is with the underlying inflationrate. This is understandable, of course, becausethat underlying rate is probably the appropriatetarget for the conventional macroeconomic remedies for inflation: tight money and stringentgovernment budgets. These traditional policytools are too cumbersome, inflexible or blunt intheir impact to be used to counteract everyvagary of the price indices.

The second reason why the policy makershould be interested in how the market estimatesthe underlying inflation rate has to do with theputative trade-off between employment andinflation summarized in the now-familiar Phillips Curve. One popular explanation for thetrade-off is that it is caused by temporary diver-

gences between the perceived or anticipated rateof inflation on the one hand, and the actual rateof inflation on the other. According to this view,a decline in the actual rate of inflation, forexample, produces a (temporary) increase inunemployment and corresponding decline inoutput as perceptions about the course of inflation lag behind events. Obviously the longer ittakes perceptions about inflation to adjust, thelonger will be the adjustment period duringwhich employment and output are below theirfull-employment levels. It follows, therefore,that the costs in terms oflost output and employment ofa successful anti-inflation policy depend,among other things, on the speed with whichperceptions adjust. Knowledge about how themarket estimates the underlying inflation ratewhich presumably comes close to the theoreticalnotion of the perceived rate of inflation-canprovide the policy maker with one estimate ofthis critical parameter.

The estimates of the underlying inflation rateyielded by the model suggest several importantconclusions. First, perceptions of the ingrainedinflation are currently quite high (about sevenpercent) and have been so during all of thecurrent expansion. Second, these perceptions

appear to respond very sluggishly to changes inthe actual inflation rate, which suggests that asuccessful assault on inflation will entail a protracted adjustment period (and possibly one thatinvolves significant losses in output and employment). Finally, this sluggishness in perceptionsmay be attributable to a high variance in theunsystematic part of price changes, which makesit difficult for individuals to distinguish changesin underlying inflation from random movementin the indices. A certain amount of evidencesuggests that this problem has become worsesince 1970.

Section I of our paper develops our basictheory-a standard model of consumption behavior and a sketch of how people might rationally forecast prices. Section II expands on thelatter point with a technical discussion of thetheory of optimal prediction. The reader who isnot interested in the details may skip this sectionand proceed directly to Section III, which discusses the empirical results and presents estimates of the underlying inflation rate. Section IVconcludes the paper with a summary and touchesbriefly on one important policy implication ofthe empirical findings.

I. Basic Theory

(1.1)

Prices and ConsumptionAlmost all modern theories of consumption

start from two fundamental propositions. First,people are free from any significant moneyillusion, i.e., what matters is the amount ofgoodsand services that the dollars allocated to consumption will buy. The second proposition isthat the decision about the amount to spend onconsumption today is part of a broader planwhich encompasses decisions about how muchto spend over a significant and indefinite periodin the future. The first proposition is typicallyincorporated in empirical work by measuringconsumption in real terms, i.e., as consumptionspending deflated by some appropriate priceindex. The second proposition is handled bymaking consumption a function not of currentincome alone, but rather of people's longer-termincome position as measured by their wealth orpermanent income. A familiar and widely-

8

accepted hypothesis about consumptionbehavior-the permanent-income hypothesisembodies these two points in the followingsimple formulation:

C t = BoytPI

Here C is nominal, or current-dollar consumption; P is some price index; l is permanent realincome; and Bo is the marginal (and average)propensity to consume. 2 Note that (1.1) assumesthat all relations are contemporaneous-thattoday's (time t's) consumption depends on today's prices and permanent income. If the timeperiod used as the unit of observation is longenough, this assumption of strict contemporaneity is probably not too far-fetched. A year, forexample, is probably enough time for people tomake consumption plans and to adjust thoseplans as they receive new information about

prices and income. However, the assumption isdoubtless strained for quarterly data such as weuse, and for that reason quarterly consumptionmodels typically assume that consumption adjusts with a lag to changes in prices and income.As is well known, such models are indistinguishable from specifications which make consumption a function of expected, or forecast, pricesand income where the forecasts of a particularvariable are based on its past values. Hence wecan turn (1.1) into a quarterly model by replacingactual prices and permanent income with theirforecast values. We assume that consumptionplans are revised each quarter, and the relevantforecasts therefore are one-period-ahead forecasts, i.e., forecasts for next quarter. Thus consumption plans for the next quarter (time t+1)are made today on the basis of today's forecasts(denoted by bars over the variables) of nextquarter's permanent income and prices:

These unpredictable influences on consumptionwe model as an additive random-error term inthe logarithms of the variables. 3 Thus we complete (1.3), after writing it in logarithms, as

In Ct+1 = InBo + In Y1+1 - (In Pt+1 - In PHI)

+ In Ut+l, (I.4)

where In Ut+1 is a random variable which hasmean zero and which is uncorrelated with theother right-hand variables.

We shall derive estimates of forecast prices byestimating equation (I.4) on quarterly, U.S.postwar data. To do so, however, we must be ableto distinguish the consumption effects of theforecast errors in prices from all of the unpredictable influences captured in In Ut+l. To dothat, we next turn to a discussion of how pricesare forecast.

Equation (1.2) implies that nominal consumption deflated by expected prices should be morestable than nominal consumption deflated byactual prices, which is the usual measure of realconsumption. Or to put the point in a slightlydifferent way, part of the observed variation inthe conventional measure of real consumption isspurious in the sense that it reflects the unintended effect of errors in forecasting prices. Tosee this, let Ct+1 = Ct+l/Pt+l be the conventionalmeasure of real consumption. Then we have

As equation (1.3) makes clear, real consumptiondepends not only on forecast permanent income,but also inversely on the relative error in forecasting prices, (Pt+II Pt).

To complete the specification of the determinants of real consumption, we need to recognizethat there are accidental, unforeseen influenceswhich cause consumption to deviate temporarilyfrom its planned levels-things like illness, sudden trips, unannounced sales, discoveries of newproducts and new places to shop, and so on.

Ct+1 = (C t+l/Pt+J) (Pt+I/Pt+l)

= BoY 1+1 (Pt+l/Pt+l)

(1.2)

(1.3)

9

Forecasting PricesAgain, the problem in forecasting prices is to

separate the systematic, sustained rise in pricesfrom the random and transient. We can visualizethis distinction by thinking of the systematicinfluences as operating to push prices along apath, while the unsystematic forces temporarilydisplace prices away from that path. By definition, only the systematic part of the price changeis predictable, and the problem of forecastingprices therefore comes down to one of extrapolating the systematic, underlying path. Two typesof uncertainty intrude to make this a difficultproblem. First, the underlying inflationary process is not fully understood, so that the systematic path of prices cannot be precisely inferred from. one's model of inflation. Forexample, suppose for the sake of argument thatmonetary growth is the main cause of inflation.Our understanding of the links between moneyand prices is still too imprecise to permit complete certainty about how prices will behavegiven the behavior of money. For this reason, weshould look at the current behavior of pricesthemselves as another indicator of the underlying rate of inflation. However, that introducesthe second source of uncertainty: the prices weactually observe can deviate in an unpredictableway from the underlying inflation path. These

random deviations act like measurement error— they cause observed prices to differ from the underlying prices which we are interested in.

The next section develops an explicit model of how consumers would rationally forecast prices in the context of these two types of uncertainty. Because the non-technical reader may wish to skip that section, we may summarize the main points here and in Chart 1. The essence of the optimal forecasting scheme is that forecasts are revised each period as new information about prices is received. This new information is used in two ways: (1) to locate the current position of the underlying inflation path (point B) and (2) to determine its slope (line AB), i.e., to determine how fast prices are growing along the underlying path. This latter variable, of course, is what we mean by the underlying inflation rate. The two variables then are used to extrapolate the underlying path, and that extrapolation is used as the forecast of next period’s prices (C).

It is clear from these remarks that the forecast of prices is an estimate of where the underlying path will be tomorrow. When tomorrow comes, however, actual prices in general will differ from this estimate, and the question then is how much of the forecast error to attribute to a mistake in estimating underlying prices, and how much to ascribe to the random deviations of observed

Chart 1Price Paths Over Time

prices from the underlying path. The former of course should be used to revise one’s estimate of where the underlying path (B) is; the latter is merely “noise” and should be disregarded. The theory of optimal prediction provides the following solution to this problem: add to last period’s forecast (E) a fraction (EB) of the forecast error, and use that result as the best estimate of the current position of the underlying path. This fraction, which we denote by K, is a number between 0 and 1. Its value is determined by the amount of random variation found in observed prices. If this measurement error is negligible, so that observed prices stay close to the underlying path, K will be 1, because the estimates of underlying prices should always be adjusted to equal observed prices. At the opposite extreme, where observed prices contain no information about the underlying path, one should disregard the entire forecast error and hence K will be 0.

The new information about prices allows us not only to estimate the current position of the underlying path, but also to re-estimate its position last period. The idea involved here is a familiar one in navigation: a navigator’s current readings allow him both to estimate his current position and to revise his estimate of where he was previously. This approach provides an up- to-date estimate of a second point on the underlying path, which means that the slope of the path can be estimated and hence an estimate of the underlying rate can be calculated. The theory of optimal prediction indicates that the revision in the estimate of last period’s position (DA) should be proportional to the revision in the estimate of the current position (EB). The factor of proportionality, which we denote by D, must lie between 0 and a number less than 1. Its particular value depends upon the amount of knowledge market participants have about the inflationary process. Where knowledge is fairly complete—where one can be reasonably confident about his estimate of the underlying inflation rate—D should be close to 1, so that the revisions in the estimates of today’s and last period’s positions leave the slope of the path unchanged. By the same token, where one has only a vague idea about what causes inflation and therefore must rely heavily on observed price changes as an indicator, D should be close to 0.

10

This will mean that any forecast error leads to arelatively large revision in the estimate of thecurrent location of the path, to relatively littlerevision in the estimate of where the path wasyesterday, and consequently to a relatively largerevision in the rate of growth between the twopoints.

As noted earlier, Chart 1 illustrates the sequence of steps involved in forecasting prices.Logarithms of prices are used here because theempirical results in Section III are expressed inthose terms. This representation also has theadvantage that slopes of straight-line segmentscan be interpreted as rates ofchange-as rates ofinflation, in other words.

Clearly, the estimate of the underlying inflation rate-the slope of the line segment AB-is afunction of how much estimates of the currentand previous locations of the underlying path arerevised, given the forecast errors. Thus the estimate of underlying inflation depends on K andD. It is also clear that the forecast for period t + 1depends on the same factors. These two observations suggest the possibility of obtaining esti-

mates of the underlying inflation rate by usingdata on price forecasts to infer the values of Dand K. Of course, we do not have direct observations on forecast prices. But we do have indirectevidence because real consumption is a function,among other things, of the price-forecast error.However, to deduce the forecast error fromobserved movements in real consumption, wemust be able to isolate its effects from all of theother influences on consumption. In order to dothat, we need to introduce the final result fromSection II-that the forecast error depends onthe sequence of current and past accelerations inprices, i.e., on how fast the rate of inflation hasbeen changing. Hence our methodology consistsof substituting a distributed lag in priceaccelerations for the forecast error in the consumption function (equation 1.4), estimating thedistributed-lag co-efficients, calculating estimates of K and D from these distributed-lagestimates, and, finally, using the estimates of Kand D to calculate estimates of the market'sperception of the underlying inflation rate.

II. Optimal Prediction

Note that this representation of the inflationaryprocess is completely general. It can as easilyaccommodate a pure monetary explanation ofinflation as a cost-push one. The question of

The problem of forecasting prices can beformally characterized as one of forecasting avariable with incomplete knowledge of thecauses of its movements and with errors involvedin its observations. The model sketched here issummarized by equations (2.1a) and (2.1 b). Thefirst describes the path of prices generated by theunderlying inflationary process; the asterisks areused to distinguish these prices-which are notdirectly observed-from actual or observedprices, P. The variable ¢ summarizes all of theavailable information about how fast prices aregrowing along the underlying path. Thus ¢ iswhat we mean by the underlying inflation rate.

(2.1a)

(2.1 b)

11

what causes inflation is essentially a questionabout the determinants of ¢. This, of course, isan important issue, but one which we need notaddress here.

Uncertainty about the inflationary process isrepresented by the random variable, w. Since bydefinition this uncertainty provides no information about prices, we require that it have zeromean and be uncorrelated with its past (andtherefore with past P*s). A common name forrandom variables with these properties is whitenoise. Equation (2.1 b) expresses the point thatprices are measured with error. Thus observedprices (P) differ from underlying prices (P*) by arandom term, v. Again, since v is uninformativeabout inflation, we require that it be white noise,and also that it be uncorrelated with w.

Consider now the problem of forecastingprices in the context of equations (2.1a) and(2.1 b). Before proceeding, we should note thatwhile the following discussion provides only aheuristic justification for our final forecastingequations, it is easy enough to show that these

equations generate minimum mean-square errorforecasts and therefore are optimal in that sense.4

As we noted in the previous section, the problemof forecasting is viewed as a problem in extrapolating the underlying inflationary path. Formallythis can be divided into two parts: (1) determining the current position of the underlying path,i.e., determining what Pi is, to serve as a startingpoint; and (2) determining the rate of change ofp* so that the path can be extrapolated. Let theestimate of the current location of the path be P~and the estimated rate of change, (f)t+l. Thenequation (2.la) suggests that our best forecast oftomorrow's prices, Pt+l, is given by

(2.2)

The estimate Pi is based on two sources ofinformation: all prior information which is incorporated in last period's forecast, Pt, and newinformation received in the form of today'sprices. However, the latter is not fully informative about inflation, which suggests that only afraction of the new information should be incorporated in estimating Pi:

sponds to Ks close to I, while the oppositeranking of uncertainties produces Ks close to 0. 5

We assume that people identify the underlyinginflation rate with the speed at which p* iscurrently changing. In order to determine thatvelocity, it is necessary to know not only what p*currently is, but also what it was last period. LetPi-lit denote the latter. The t-l subscript denotes that this is an estimate of where the underlying path was yesterday; the t subscript indicatesthat is a retrospective estimate, i.e., one madetoday. In general, people's perceptions today ofwhere the underlying path was yesterday willdiffer from where they thought it was at the time.The latter is obviously last period's analogue ofPi, which we denote by Pi-I' The theory ofoptimal prediction indicates that people revisetheir estimate of the last period's position by afraction, D,6 of the revision in their estimate ofthe current position:

(2.3a)

First-order approximations to equations (2.2)and (2.3) yield the following relationship in thelogarithms of forecast prices:

(2.4b)

The factor K is essentially the ratio of theuncertainty about underlying prices to uncertainty about the amount of error in observedprices. The latter is measured by the variance ofv, while the uncertainty in underlying prices is afunction both of this uncertainty and uncertaintyabout the underlying inflationary process .asmeasured by the variance of w. .If we let a~ be thevariance of v, aJ, the variance of w, and a*2 theuncertainty in underlying prices, we have

In Pt+I - In Pt == 4>t+l - (I-K) (In Pt - Pt)(2.5)

It is clear from this expression that our forecasting scheme is a mixed extrapolative-regressiveone of the sort first proposed by deLeeuw (1965)and subsequently used by Modigliani and Sutch(I966), among others, in their work on forecasting interest rates. The extrapolative element is<Pt+ I-the rate at which prices are forecast togrow in the future. The regressive element in theforecast is represented by the second term ontheright-hand side of the expression. It indicatesthat, ceteris paribus, prices are forecast to revertpartially to their present level. The smaller is K,the larger is the influence of this regressiveelement. The estimate of the underlying inflationrate is given by

(2.3)

(2.4a)

a*2 == "-- ~t

Clearly K lies on the closed interval [0, I]. Relatively low measurement uncertainty or highprocess uncertainty (low a~ or high a~) corre-

_ ..... A A*<Pt+I == (Pi - Pi-l/t)/ P Hit, (2.6a)

which to a first-order approximation is

12

(f;t+l~ (l-K) (InPt - InPt-l) + K(InP t-lnPt-l) - DK(lnPt - InPt)

as a distributed lag in current and past accelerations in prices:

Since (2.9) is a particular solution of (2.8), thedistributed-lag coefficients, aj, must be functionsof K and D. In particular, we must have

(2.6b)

Equations (2.5) and (2.6b) together yield thefollowing relationship in the logarithms of forecast prices:

In P t+l - In Pt = (I-K) (In Pt - InPt-l)+K(In Pt In Pt-I) + (I-D)K(In Pt - In Pt)

(2.7)

00- _ 21n Pt+l - Pt+1 -k aj Ll In Pt+l-j

j=0 (2.9)

It is clear from equation (2.9) that a constantinflation rate, i.e., Ll21nPt+j = 0 for current andall past periods, produces a zero forecast error.In other words, when prices are growing at asteady rate, the actual and forecast levels ofprices are the same. A permanent change in theinflation rate, on the other hand, produces atransitory (though by no means short-lived)divergence of actual from forecast prices. Thedistributed-lag coefficients trace out the path ofthe forecast error during the transition. Thus therequirement that ao=I indicates that a onepercentage-point increase in the rate of inflationinitially raises actual prices above forecast pricesby exactly the same amount. Thereafter, the gapbetween actual and forecast prices may continueto widen for awhile, or may begin to close; theparticular path followed depends on the valuesof D and K, which determine the speed withwhich forecasts are revised. Ultimately, however,as the last condition on the aj indicates, the gapmust close and in the limit go to zero. Thus in thenew steady-state equilibrium, forecast and actualprices again grow along the same path.

If the last term were missing, (2.1) would implythat the growth rate of forecast prices is anexponentially declining weighted average ofcurrent and past rates of price change-thefamiliar adaptive-expectations result. For forecasting the level of prices, this is clearly suboptimal if a change occurs in the average rate ofgrowth of prices. Consider, for example, whatwould happen if the inflation rate permanentlyincreased. The growth rate of forecast priceswould follow with a lag, and approach as a limitthe new, higher inflation rate. But it would neverexceed the actual inflation rate, and consequently the level of forecast prices would always fallshort of the level of actual prices. For this reason,(2.7) has a term in the forecast error, InPt-lnPt,which is designed to adjust the growth of forecastprices to remove any systematic discrepancybetween actual and forecast prices.

Finally, (2.7) is easily recast in terms offorecast errors to produce

(In Pt+l -In P t+ l ) =[2(l-K) + DK](ln Pt -InPt) - [l-K] (In Pt-l - In P t-]) + Ll2 In Pt+l,

(2.8)

where Ll2 In Pt+l, the second difference in thelogarithm of prices, measures price accelerations, i.e., changes in the rate ofgrowth of prices.Repeated lagging of (2.8) and substitution backinto itself yields a solution for the forecast error

lim aj+ 1 = 0 j-oo (2.10)

(3.1)

InCt+l = InBo + In(yf+I) - k ajLl2

J=O

InPt+l-j + InUt+l

III. Empirical ResultsEstimating the Consumption Function

Our consumption function, after substitutinga distributed lag in price accelerations (denotedby Ll21nPt+l_j) for the forecast error, is

13

For the purpose ofestimation, consumption isdefined to exclude expenditure on new consumer durables, which is more properly treated as aform of savings. 7 Forecast permanent income,Yl+ 1, is computed recursively from the formula

H+l = (I + .0048) (O.IYt + 0.9yn,

where y is measured per capita real income, .0048is the quarterly trend rate of growth of y for theperiod 1947:1-1977:4, and the weights 0.1 and0.9 are taken from Darby (1972).

Measured income is defined as the sum ofdisposable personal income plus undistributedcorporate profits. On theoretical grounds alonethe latter should be included, since permanentincome is viewed as the flow of income generatedby a broadly defined concept of wealth thatincludes corporate wealth. Moreover, empiricalevidence suggests that households treat changesin the value of their equity holdings as part oftheir income. (See, for example, David andScadding [1975].) The implicit price deflator forGNP, rather than the consumer-price index orconsumption-spending deflator, is used to measure P. This is done because a "true" cost-ofliving index-i.e., one that corresponds to thenotion of permanent income-should includethe prices of both current and future consumption. No existing index approaches this ideal, ofcourse, but a broad-based index like the GNPdeflator presumably comes closest, because itimplicitly includes the prices of future consumption through its inclusion of producers'goodspnces.

Two restrictions are imposed in estimating(3.1): (I) the forecast errors are assumed toaverage out to zero over the sample period; and(2) the forecast errors and permanent income areassumed to be uncorrelated. Both are imposedon the grounds that people make efficient forecasts, i.e., that roughly speaking, they· use allavailable information. Consider the firstrestriction. If, for example, the forecast error weresystematically positive, people would ultimatelyrecognize their chronic underforecasting andwould adjust their forecasts upwards to removethe discrepancy. This recognition might takesome time, but not to the extent that errorswould systematically cumulate over our entire

14

sample period of 24 years. Next, consider thesecond restriction. Recall that the permanentincome variable in (3.1) is forecast permanentincome. If this variable were correlated with theforecast error in prices, people could use thisassociation to improve their forecasts of permanent income. It would pay them to do so until theassociation disappeared, i.e., until permanentincome and the forecast error in prices becameuncorrelated.

The two restrictions are easily imposed byestimating (3.1) in two stages. First, real consumption is regressed on a constant and permanent income. The residuals from this estimationare then regressed on the distributed ·lag inaccelerations in prices to obtain estimates of theaj. The latter will be unbiased provided therestrictions are true.

Equation (3.2) reports the results of the firststage regression. The sample period is 1953:31977:4, and both consumption and permanentincome are in per capita terms. The adjustedmUltiple R2

, standard error of estimate, DurbinWatson statistic and estimated first-order serialcorrelation in the error term (p) are shownbelow. The standard errors of the estimatedcoefficients are shown in parentheses beneaththeir respective estimates.

InCt+l = -.2820 + 1.0015 In(yf+d(.0752) (.0573) (3.2)

iP= .9986 D.W. = 1.7458S.E. = .0057 P= .9434

The appropriateness of the restnctlOns imposed in estimating (3.1) can be roughly gaugedby comparing the coefficient estimates in (3.2)with comparable estimates from otherconsumption studies. Such a comparison indicates nosignificant bias in the estimates, which suggeststhat the restrictions may not be unreasonable.Thus the point estimate of the coefficient on yf+ 1,

which measures the permanent-income elasticityof consumption, is effectively unity. Thisagreescompletely with the permanent-income specification of the consumption function, and it issupported by a large body of other evidence}The estimated constant in (3.2) implies a marginal propensity to consume ofapproximately.75.

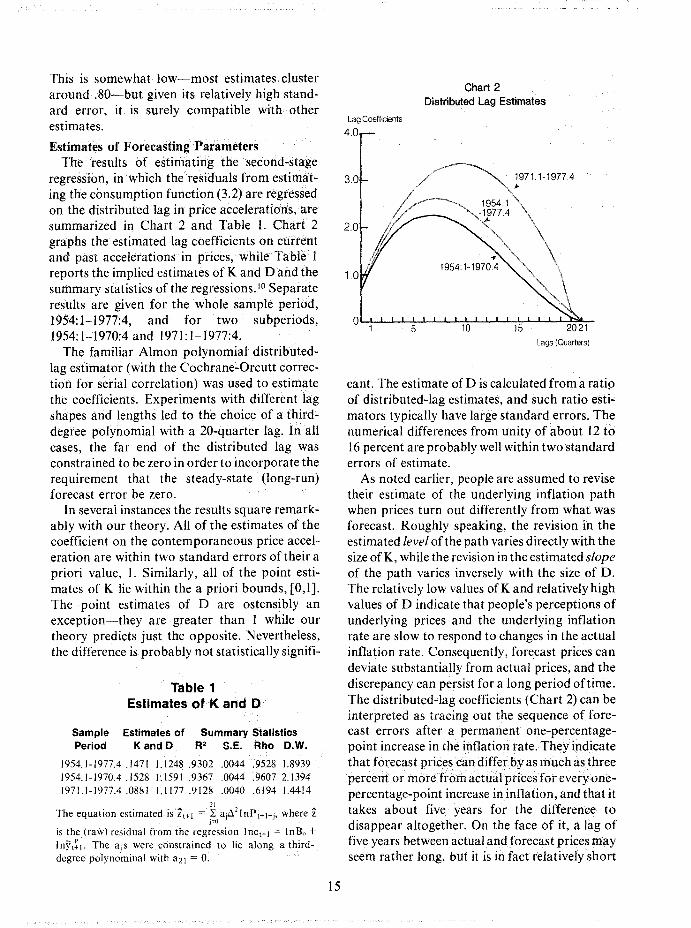

Chart 2Distributed Lag Estimates

cant. The estimate of D is calculated from a ratipof distributed-lag estimates, and such ratio esti-'mators typically have large standard errors. Thenumerical differences from unity of about 12 to16 percent are probably well within two standarderrors of estimate.

As noted earlier, people are assumed to revisetheir estimate of the underlying inflation pathwhen prices turn out differently from what wasforecast. Roughly speaking, the revision in theestimated level of the path varies directly with thesize of K, while the revision in the estimated slopeof the path varies inversely with the size of D.The relatively low values ofK and relatively highvalues of D indicate that people's perceptions ofunderlying prices and the underlying inflationrate are slow to respond to changes in the actualinflation rate. Consequently, forecast prices candeviate substantially from actual prices, and thediscrepancy can persist for a long period oftime.The. distributed-lag coefficients (Chart 2) can beinterpreted as tracing out the sequence offorecast errors after a permanent one-percentagepoint increase in the inflation rate. They indicatethat forecast prices can differby as much as threepercent or morefrom actualprices for every onepercentage-point increase in inflation, and that ittakes about five years for the difference todisappear altogether. On the face of it,a lag offive years between actual and forecast prices mayseem rather long, but it is in fact relatively short

This is somewhat low-most estimates clusteraround.80~but given its relatively high standard error, it is surely compatible with otherestimates.

Estimates of Forecasting ParametersThe results· of estimating the second-stage

regression, in which the residuals from estirriat~

ing the consumption function (3.2) are regressedon the distributed lag in price accelerations,aresummarized in Chart 2 and Table 1. Chart 2graphs the estimated lag coefficients on currentand past accelerations in prices, while Tablelreports the implied estimates of K and D and thesummary statistics of the regressions. lo Separateresults are given for the whole sample period,1954: 1-1977:4, and for two subperiods,1954:1-1970:4 and 1971:1-1977:4.

The familiar Almon polynomial distributedlag estimator (with the Cochrane~Orcutt correction for serial correlation) was used to estimatethe coefficients. Experiments with different lagshapes and lengths led to the choice ofathirddegree polynomial with a 20~quarter lag. In allcases, the far end of the distributed lag wasconstrained to be zero in order to incorporate therequirement that the steady-state (long-run)forecast error be zero.

In several instances the results square remarkably with our theory. All of the estimates of thecoefficient on the contemporaneous price acceleration are within two standard errors of their apriori value, 1. Similarly, all of the point estimates of K lie within the a priori bounds, [0,1].The point estimates of D are ostensibly anexception-they are greater than 1 while ourtheory predicts just the opposite. Nevertheless,the difference is probably not statistically signifi-

Table 1Estimates of K and D

Sample Estimates of Summary StatisticsPeriod K and D R2 S.E. Rho D.W.

1954.1-1977.4 .1471 1.1248.9302 .0044 .9528 1.89391954.1·1970.4 .1528 1.1591 .9367 .0044 .9607 2.13941971.1-1977.4.0881 1.1177 .9128 .0040 .6194 1.4414

21

The equation estimatediszt+1 = ~ a jC121nPt+l_ j • where Zj::;:O

is the (raw) residual from the regression InCt+1 = InR. +Inytr l . The UjS were constrained to lie along a thirddegree polynominal with aZI = O.

15

Lag Coefficients

4.0

3.0

2.0

1971.1-1977.4~

Lags (Quarters)

by comparison with typical results obtainedfrom studies of the relationship between pricesand interest rates. Some observers have rejectedthese long lags as being implausible, givellourknowledge of how prices are formed. I I However,once errors of measurement are allowed, theymay not be so implausible: where one is unsureabout the amount of information contained inprice movements, it is not irrational to ignorethem unless they continue for a long time.

The low values of K and high values of D alsosuggest that most of the uncertainty in forecasting prices stems from measurement error inprices, i.e., from the fact that a significant partofthe observed variation in prices represents random shocks which are unrelated to systematicinflation. The decline in the value of K for thelater subperiod suggests as well that prices havebecome more unpredictable since 1970. Thispoint has been made elsewhere on the basis ofdifferent evidence, 12 and agrees with one's casualimpression that the price level in the Seventieshas been subject to more frequent and severeshocks than was the case in prior decades.

Estimates of Underlying Inflation Rate_ Estimates of the underlying inflation rate,4>t+1 , along with the actual quarterly inflationrates, are shown in Chart 3. Clearly, the estimates of the underlying inflation rate have thesort of properties one would expect of such aseries: a much greater quarter-to-quarter stability than the actual inflation rate, and an ability totrack faithfully the longer-run movements in theactual inflation rate. However, the underlyinginflation rate can differ from the actual rate forsubstantial periods of time, reflecting the longadjustment lags.

It is also clear that successively higher levels ofinflation have become embedded in the economysince 1960. Thus the underlying inflation ratefluctuated around l.7 percent until the lateSixties, averaged about 4.8 percent from 1971 to1973, and in the current expansion has hoveredaround 7 percent. Apparently, neither the1969-70 nor the 1973-75 recession made a sizable dent in the underlying rate; at most, theyseemed capable only of stabilizing the inflation

Chart 3

Actual and Underlying Inflation Rates

1962 1964 1966 1968

oHf-------,j----,j--

-1 =-~~~-":=~""":_:1954 1956 1958

3

2

4

6.

5

9

8

10

11

Annual Rate (%)

12

7

16

rate until some new disturbance carried it off to ahigher plateau.

There is no evidence that the 1971 priceandwage controls had any noticeable effect on people's perceptions about the underlying inflationrate. The decline in the underlying inflation rateafter the second quarter of J971 was negligiblecompared to the fall in the actual rate, and it didnot last as long. Some numbers make this pointmore forcefully. In the four quarters ending in1971:2, the inflation rate, measured by thegrowth in the GNP implicit price deflator, averaged 5.2 percent. In the four subsequent quarters, inflation declined by nearly 1Yz percentagepoints to 3.8 percent. By comparison, the under-

lying inflation rate was 4.8 percent in the firstperiod, and 4.9 percent in the secondeffectively unchanged, in other words.

Much of the spectacular run-up in inflationrates in late 1973 and in 1974 appears to havebeen treated by economic participants as transitory, and thus was not viewed as symptomatic ofa deterioration in the underlying rate (thoughthat did happen). This perception was borne outby the subsequent sharp decline in inflation ratesafter 1974. By the same token, the underlyingrate did not follow the actual rate down as thelatter fell from its 1974 highs. Again, this perception appears to have been borne out by thebounce-back in inflation rates after mid-1976.

IV. Summary and ConclusionsObviously, the estimates of the underlying Secondly, even if aggregate-demand growth

inflation rate calculated here should not be could be moderated, pressure for price and wageaccepted uncritically. Nevertheless, the congru- increases would continue to emanate from theence of our estimation results with the predic- cost side for a considerable time. The implicationtions of theory, and their conformance with of this for output and employment is not reassur-historical experience, are too striking to be ing. If pressures from inflationary expectationsignored. This congruence lends our estimates a do not abate after growth in aggregate demandhigh degree of plausibility. slows down, the difference presumably has to

Two points seem worth repeating because they come out of real income growth. This is essential-bear on the important question of what a suc- ly the modern explanation for the observedcessful assault on inflation is likely to cost in trade-off between unemployment and inflationterms of lost output and employment. First, the described by the Phillips Curve. This explana-ingrained rate of inflation currently perceived by tion of course stresses the temporary nature ofthe market is dismally high by historical the trade-off. Once expectations of inflationstandards-around 7 percent at an annual rate- have fully caught up with the actual rate, outputand has stubbornly remained at this level and employment are assumed to return to theirthroughout the current expansion. This persis- normal levels. But our finding about the lengthtence of a high perceived underlying inflation of the adjustment period-about five years-rate doubtless has given inflation an important suggests that temporary can still be a long time.momentum oUts own, because market partici- Hence, output and employment may have topants, in an effort to protect themselves against remain below normal levels for a fairly protract-future iI1flation, have built this perception into ed time if any significant progress is to be madetheir wage and price demands. against inflation.

FOOTNOTES

1. For some evidence that the market discounts spurious evidence of inflation in the consumer price indexsee, E. Fama, "Interest Rates and Inflation: TheMessage in the Entrails,"American Economic Review,67 (June 1977), pp. 487-96.

2. Some controversy surrounds the proposition implicit in (1.1) that consumption is strictly proportional topermanent income. This restriction was not imposed in

17

the estimation, but the empirical results were so consistent with it that I have written (1.1) in the traditionalform.

3. The variable u, which can be interpreted to be theratio of actual to planned consumption, has a lognormal distribution if we assume, in the usual way, that 1n uis normally distributed. Hence the assumption that themean of 1n u is zero corresponds to assuming that the

median ratio of actual to planned consumption is unity,and it is in this sense that actual and desired consumption are "on average" the same.

4. A good account of the theory involved can be foundin A. Bryson and Y. Ho, Applied Optimal Control (Waltham, Mass.: Blaisdell, 1969J

5. K has a steady-state solution for constant<t>.AIthough obviously we do not wantto assume the latter,we shall assume that the relative variation in <t> is sosmall that K is approximately constant. There .is ampleprecedent in the literature for doing· so, presumablybecause without such a simplification the forecastingproblem has no closed-form solution,

6. The expression for D is

D=

O*~ (1+<t>I) 2+ o~

where, as before, 0*2 measures the uncertainty inunderlying prices and o~ stands for the uncertaintyabout the underlying inflationary process. Clearly D isbounded from above by a number less than 1, while itcannot be less than zero.

7. To be totally consistent, we should add to consumption the imputed service flow from the existing stock ofconsumer durables. We did not do this simply becausequarterly estimates are not readily available; it is doubtful that the omission has any practical significance.

8. For a more thorough discussion of this point,see A.Alchian and B. Klein, "On a Correct Measure of Inflation," Journal of Money, Credit and Banking 5 (February 1973, Part Ill, pp. 173-91.

9. For an up-to-date survey of evidence on the consumption function, see R. Ferber,"Consumer Econom-

ics: A Survey," Journal of Economic Literature 11(December 1973), esp. pp. 1307-08. Estimating (3.1) intwo stages does not appear to have affected the estimates except trivially. When (3.1 J is estimated in onestep, the estimate of the marginal propensity to consume is .78 rather than .75, while the estimated incomeelasticity is .98 rather than 1-differences which arewithout statistical or economic significance. Thedistributed-lag estimates are even less affected: theyare virtually indistinguishable from the estimatesgraphed in Chart 2.

10. The estimates of K and D are obtained by substituting the estimated aj into the restrictions aj+l = (2(1-KJ +DK) aj - (1-KJ aj-l = 0 and solving for K and D. Thechoice of which aj to use is arbitrary: any four consecutive ones will do, and I chose a2 through a5. See G. Boxand G. Jenkins, Time Series Analysis (San Francisco:Holden Day, 1970), page 383.

11. See for example, T. Sargent, "Interest Rates andPrices in the Long Run," Journal of Money, Credit andBanking 5(February 1973, Part 11), pp. 384-449.

12. B. Klein, "Our New Monetary Standard: The Measurement and Effects of Price Uncertainty,1880-1973,"Economic Inquiry 13 (December 1975), pp. 462-84,argues that the shift from a monetary constitutionbased on the gold standard to a managed fiduciarystandard increased uncertainty about future prices. Heplaces the watershed in the mid-Sixties, at the latest.However, my experiments with different subperiodsproduced clear evidence for a break around 1970. Myconjecture is that it took the monetary laxity of the lateSixties to convince the public that monetary arrangements had fundamentally changed-a perception thatwas soon borne out by the collapse of the BrettonWoods System.

REFERENCES

Alchian, Armen and Klein, Benjamin. "On a CorrectMeasure of Inflation," Journal of Money, Credit andBanking 5 (February 1973, Part 1), pp, 173-91.

Box, George, and Jenkins, Gwilym. Time Series Analysis, San Francisco: Holden Day, 1970.

Bryson, Arthur, and Ho, Yu-Chi. Applied Optimal Control, Waltham, Mass.: Blaisdell, 1969.

Darby, Michael. "The Allocation of Transitory IncomeAmong Consumer's Assets," American EconomicReview 62 (December 1972), pp. 928-41.

David, Paul, and Scadding, John.. "Private Savings:Ultrarationality, Aggregation and 'Denison's LaIN',"Journal of Political Economy 82 (March"Aprll1974), pp. 225-50.

de Leeuw, Frank. "A Model of Financial Behavior," in J.Duesenberry, G. Fromm, L. Klein and E. Kuh, eds.,The Brookings Quarterly Econometric Model of

18

the United States, Chicago: Rand McNally, 1965,Chapter 13.

Fama, Eugene. "Interest Rates and Inflation: TheMessage in the Entralls."American Economic Review 67 (June 1977), pp. 487-96.

Ferber, Robert. "Consumer Economics: A Survey,"Journal of Economic Literature 11 (December1973), pp. 1303-43.

Klein, Benjamin. "Our New Monetary Standard: TheMeasurement and Effects of Price Uncertainty,1880-1973," Economic Inquiry 13 (December1975), pp. 461-84.

Modigliani, Franco, and Sutch, Richard. "Innovations inInterest Rate Policy," American Economic Review65 (May 1966), pp. 178-97.

Sargent, Thomas. "Interest Rates and Prices in theLong Run," Journai of Money, Credit and Banking5 (February 1973, Part II), pp. 385-449.

Michael W. Keran*

Why has the international value of the dollardeclined over the past year and a half? There is apopular impression (sometimes reinforced by therhetoric of government officials) that the dollarhas been driven down by speculators who have avested interest in seeing an undervalued dollar.According to this view, the magnitude of thedecline is unrelated to economic fundamentalsand represents the irrational behavior of speculators.

Most economists have difficulty with thisexplanation. A considerable body of evidenceshows that speculation tends to drive the value ofa currency towards the long-run equilibriumvalue; i.e., value determined by economic fundamentals. Those who misjudge fundamentalsand attempt to drive the dollar away from itslong-run equilibrium value will tend to losemoney. On the average they will buy when themarket value is high and sell when the marketvalue is low. Those speculators who most clearlyperceive the underlying fundamentals and accordingly take a position in the exchange marketwill, on average, make the most profits.

What this means is that stabilizing speculationwill tend to be profitable and destabilizing speculation to be unprofitable. 2 The self-selectionprocess of unsuccessful speculators leaving themarket to the successful speculators has important implications for the exchange markets. Inparticular, the observed value of the dollarwould not deviate significantly from the levelconsistent with economic fundamentals for morethan a short period of time.

Two types of economic factors affect the

* Senior Vice President and Director of Research,Federal Reserve Bank of San Francisco. Researchassistance for this article was provided by StephenZeldes.

19

exchange rate-real factors and monetary factors. The real factors have to do with the relativeattractiveness of any two countries' goods, i.e.,how many bushels of U.S. wheat are exchangedfor one Japanese color T. V. set. This is called theterms of trade. The monetary factors have to dowith the purchasing power of a currency. Ifinflation reduces the domestic purchasing powerof the dollar, a parallel decline in the dollar'sforeign purchasing power will be achieved by anexchange-rate adjustment. This is called purchasing power parity.

The purpose of this article is to explain movements in the exchange value of the dollar againstthe currencies of seven other major countries(Canada, France, Germany, Japan, Italy, Switzerland and the U,K,), during the period offlexible exchange rates running from roughly1974 or 1975 through March 1979. The analysisfocuses on whether monetary factors can explaina significant share of the movements of the dollaragainst these seven major currencies. Section Idiscusses the role of monetary factors in influencing prices in general. Section II discusses themonetary and real determinants of exchangerates, with the aid of a model which permits theempirical estimation of the monetary factorsaffecting the exchange rate. In Section III, comparative monetary developments in the U.S. andother industrial countries are analyzed andshown to be in close alignment with observedmovements of exchange rates. Forillal statisticalanalyses confirm that a significant share of thevariation in exchange rates between the dollarand seven other currencies can be explained bymonetary factors. That section provides forecasts of exchange rates based on actual monetarydevelopments in 1978 and forecasts of monetarydevelopments in 1979. Section IV gives a summary and conclusion.

I. Money and PricesThe monetary source of exchange-rate

changes is based on two propositions:I) The exchange rate between two domestic

currencies will adjust to reflect changes in therelative domestic purchasing power of the currencies (i.e., purchasing power parity); and

2) Domestic monetary developments are amajor determinant of domestic inflation rates,and thus the domestic purchasing power of agiven currency.

The second of these propositions is the monetary theory of inflation-too much money chasing too few goods. In its simplest form, thistheory can be stated as follows:

In the long run, the inflation rate (% D.P) isdetermined by the difference between the growthof the nominal money supply (% ~MS) and thereal money demand (% ~md). The nominalmoney supply is determined by the governmentthrough its monetary authority. The real demand for money is determined by the privatesector of the economy. The primary motivesbehind the demand for money are as a means ofpayment and as a store of value. The means-ofpayment desire for money is dependent on thevolume of transactions, which in turn is relatedto the level of a country's real income. A rise inreal income leads to a rise in the real demand formoney.3

The store-of-value desire for money dependsupon the following factors:

I) The sophistication of the financial system,and the type and convenience of non-monetaryfinancial assets available to the public;

2) The real interest rate. The higher the realrate paid on monetary assets (e.g., time deposits),the higher the money demand; the higher the realrate paid on non-monetary assets, the lower thereal demand for money.

3) Inflation expectations. The higher the expected inflation rate, the greater the expecteddecline in the value of monetary assets and thusthe lower the real demand for money.

There are a number of ways of translatingthese general principles into an empiricallytestable proposition. Perhaps one of the oldest

ways of stating this relation is via the familiarFisher Equation of Exchange.

This relationship states that, in long-run equilibrium, prices (P) will be equal to the ratio ofmoney supply to the long-run real demand for

(3)

(4)

(5)

(2)

M/P=T/V

md = T/V

MV= PT

P= M/md = M/(T/V) =ME

In long-run equilibrium, demand for realmoney balances must be equal to actual realbalances (M/ P). Thus, using equation (3), weidentify the long-run equilibrium value of M/ Pwith (md) and the long-run values of T and Vwith the determinants of money demand. Thus:

In this expression, where the bars refer to longrun equilibrium values, Trepresents the long-runmeans of payment function of money, while Vrepresents the long-run store of value function.

We next substitute this long-run behavioraldescription of money demand back into theequation of exchange to obtain:

The stock of money (M) times the velocity ofmoney (V) equals the physical volume oftransactions (T) times price level (P).

This is true by definition, analogous to thenational-income definition: National IncomeHousehold Consumption plus Business Investment plus Government Spending. Just as thenational-income definition can be translated intoa statement of economic behavior by makingassumptions about consumption and investmentbehavior, so the Fisher equation ofexchange canbe by making assumptions about the factors thatdetermine the demand for money, i.e., velocityand transactions.

One can make equation 2 into a behavioralrelationship by introducing the demand for realmoney balances. If we rearrange terms in equation 2, we obtain:

(I)% ~P = % ~MS - % ~md

20

money balances. This ratio is defined as excessmoney balances (ME). An expression similar toequation (1) can, of course, be obtained bytaking the time rate of change of all variables in(5) to obtain:

% ~P = %~M - % ~(T/V) = % ~ME (Sa)

This expression summarizes the main point ofthe monetary theory of inflation-that ultimately inflation is determined by excess moneygrowth (%~ ME). This excess money supply isthe key element in the monetary factors whichdetermine the exchange rate.

II. Detennination of Exchange RatesThe exchange rate between the currencies of

any two countries will be determined by twofactors, one monetary and one "real." Theseseparate influences can be summarized in thefollowing way:

Where Ex is the exchange rate between the U.S.dollar and some foreign currency (t). Pus is thelong-run equilibrium price level in the U.S.; Pr isthe long-run equilibrium price level in the foreigncountry; t is the equilibrium terms of trade. Themonetary effects are measured by the relativeprice (Pr{Pus), while the real effects are measured by the terms of trade (t).

I. Real effects: The terms of trade measure thevalue ofone country's goods in terms of the valueof another country's goods, e.g., how manybushels of U.S. wheat it takes to "purchase" oneJapanese T. V. set. A change in the terms of tradecould be caused by a change in technology, thediscovery of new sources of raw material, or asubstantial change in relative prices of importantcommodities, such as a rise in the price of oil.

2. Monetary effects: Exchange rates fluctuateto maintain equality between the domestic andforeign purchasing power of a currency, according to the theory of purchasing-power parity (orPPP). A rise in U.S. prices will reduce thedomestic purchasing power of the dollar. Thiswill increase the demand for lower-priced foreigngoods and assets, which will depreciate the dollarrelative to the foreign currency. The incentive toincrease demand for foreign goods will subsideonly when the dollar has depreciated by anamount equal to the decline in its domesticpurchasing power, assuming foreign-currencyprices are unchanged. Because monetary factorsdetermine the domestic purchasing power of a

Ex = (Pr / Pus) . t (6)

21

currency (for reasons already discussed), so theyalso influence the international exchange valueof that currency.

Purchasing-power parity can be explained in anumber of interrelated ways. Theoretically, themost general explanation is related to the neutrality of money. If the money supply is doubled,all prices will double-or the purchasing powerof money will be reduced by half. For thisproposition to hold for all goods, both domesticand foreign, the exchange value of the domesticcurrency must fall by one-half relative to foreigncurrency (assuming there is no change in theexcess supply of money abroad). In this way, thedomestic and international purchasing power ofthe domestic currency are equal, and the neutrality of money is preserved. If the foreign moneysupply is doubled at the same time as the domestic money supply, the exchange rate will beunchanged, because foreign prices will go up asmuch as domestic prices.

The market mechanism by which the adjustment process operates is sometimes called thelaw of one price. This is based on the propositionthat the same goods will have the same price in allmarkets. For example, the dollar price of wheatin Kansas City will be the same as the yen price inTokyo, given the dollar/yen exchange rate. If theprice of wheat were higher in Tokyo than inKansas City by more than transportation, tariffsand other costs, then sufficient wheat will beshipped to Japan to drive its price toward equality with the U.S. price.

Short vs. Long Run ConsiderationsIn Section I, we emphasized that the relation

between money and prices was a long-run proposition. Equilibrium in the market for goodstakes some time to achieve, because householdsmust change their consumption habits and firms

% ilEx = % il(MEr / MEus) + % ilt (9)

Log Ex = ao + al log (MEr / MEus) (8)

Taking the logs of both sides and making thesimplifying assumption that the terms of tradj::are constant, we can empirically estimate theequation as follows:

(7)Ex = (M& / MBus) . t

The changes in the exchange rate are equal to aconstant term (ao ') which measures the changesin the real factors, plus a coefficient (al') whichmeasures the impact on exchange rates of thechange in the ratio ofthe excess money growth inthe U.S. and in the foreign country. This ishypothesized to equal unity. The time lag inequations 8 and 10 reflects the length of timeneeded by market participants to recognize that

Assuming that the real factors which affectexchange rates-i.e., the terms of trade (%ilt)-change at a constant rate, we obtain theempirically testable equation:

measure of long-term PPP than are currentgoods prices. Second, because prices of tradedgoods increase with a decline in the exchangevalue of the dollar, and because traded goods area significant component of the general priceindex, the time lag between money and pricesmay be shortened when a country moves fromfixed to flexible exchange rates.

Where aa is a measure of an unchanged terms-oftrade effect on the exchange rate, and al is ameasure of the monetary influence on the exchange rate. Its value is expected to be positiveand equal to one. Alternatively, we can expressequation 7 in terms of changes:

The ModelThis discussion can be formalized and an

equation specified for empirical testing. Giveninitial condition values for the exchange rate andexcess money, and substituting equation 5 intoequation 6, we get:

must change their production patterns. It iscostly for households to speculate on inflation bypurchasing goods in excess of consumptionneeds, because the cost of holding "inventories"is high. While anticipatory purchases in a periodof rising prices will occur, the amount is severelylimited. Thus goods prices will adjust only slowlyto a rise in excess money supply.

In contrast, the market for assets seems toadjust relatively quickly to changes in supply anddemand, because "inventory" adjustments inassets can be achieved at low cost. One canrearrange his portfolio of assets by "instantaneous" buy-and-sell decisions at relatively lowtransactions cost, and generally zero carryingcost. In general, we assume that goods prices in"flow" markets take longer to adjust to shifts insupply and demand than assets prices in "stock"markets.

This distinction has important implicationswith respect to the monetary determinants ofexchange rates. The exchange rate-the international price of the dollar-can be affected byshifts in the international supply and demand fordollars, which in turn depend upon internationaltrade in goods, services, and financial assets.Trade in goods and services changes relativelyslowly in response to changes in income andprices, as is typical of all "flow" markets. Buttrade in financial assets can change quickly, as istypical of all "stock" markets.

The exchange rate, in the short run, thus isdetermined by the capital account of the balanceof payments. A change in the excess moneysupply (once recognized) could translate immediately into a change in the exchange rate. Themonetary effect on the exchange rate would bethe same in magnitude as that on the domesticinflation rate. The only difference would be interms of timing: the effect on the exchange ratewould occur quickly, while the effect on the priceof domestically produced goods would bedelayed.

This analysis has several important implications. First, the exchange rate between the dollarand any foreign currency will measure the equilibrium purchasing power parity of the twocurrencies. If the exchange rate adjusts quicklyand prices adjust slowly to the same excessmoney supply, the exchange rate may be a better

22

the relative excess supplies of money hadchanged. This might well vary between countries, depending upon the country's past monetary policy and inflation experience.4 Introducing time lags into equations 8 and 10produces the basic estimating equations whichwill be considered in the next section.

nlog EXt = ao + raj log (MEr! MEus)t-n

(II)

n~log EXt = ao' + Iaj' ~log(MEriMEuS>t-n

(12)

nWhere I refers to the sum of months in whichchanges in excess money will have their completeeffect on the exchange rate.

UI. Testing the Monetary ApproachWe present evidence here to support the prop

osition that monetary factors explain a significant share of the recent movements in the exchange value of the dollar against seven othercurrencies. First, we present a summary of theapparent monetary-policy considerations whichshaped monetary developments in the 1975-78period. Then we show that the actual changes inthe excess money supply led to changes in pricesand. exchange rates in a way consistent witheconomic theory. Finally, we present formalstatistical tests of the relationship between money and exchange rates which confirm and quantify the empirical relations.

Monetary Policy 1975-78In the summer of 1975, all eight countries in

this study faced a common set of economicproblems-two or more years of double-digitinflation and the recent emergence of a businessrecession which, for most countries, was theworst in the post-World War II period. Differentgovernments (and their monetary authorities)responded to these twin problems in differentways.

In the U.S., the primary goal apparently wasto deal with the historically high unemploymentrate by following a monetary policy which permitted a substantial acceleration in aggregatedemand from 1975 through 1978. Other countries such as Germany, Japan and Switzerland,responding to the historically high inflation rate,apparently followed a monetary policy whichpermitted only a moderate acceleration in aggregate demand.

As a result of this divergence in monetarypolicies, short-run rates of real growth alsodiverged. The U.S. grew at a rate from 1975 to

23

1978 which was above its historical average, butthe reverse was true for Germany, Japan andSwitzerland. Over the longer run, these divergentmonetary policies led to divergent inflation rates.From 1976 to 1978 the inflation rate in the U.S.accelerated, while the inflation rates in Germany,Japan and Switzerland decelerated. Finally, thepolicy divergence between the U.S. and Germany, Japan and Switzerland led to a decline inthe exchange value of the dollar with regard tothe Deutschemark, yen and Swiss franc.

Marshalling the EvidenceIn broad outline, we assert that divergent

monetary policies have been the key factorbehind the divergent economic developmentsand exchange-rate movements of the past severalyears. The evidence in support of this scenario isprovided in Charts I and 2.5 Chart I shows thatfrom 1975 to 1978, the money supply in the U.S.grew at about the same rate as in Switzerland,and more slowly than in Germany and Japan.However, as discussed in the theoretical section,the relevant measure is not the growth in thenominal money supply, but rather the growth inthe excess money supply, which is nominalmoney less real money demand, as is shown inChart 2.

In estimating real money demand, the meansof payment (i.e., transactions) motive was measured by the trend in industrial production, andthe store of value motive for holding money wasmeasured by the trend in velocity. Sixty-monthtrends of these factors were utilized, to reflecttheassumption that reversible cyclical shifts in thecomponents of real money demand would haveno effect on the long-term equilibrium price level

Chart 1Nominal Money Supply

1975=100

(P), and thus no effect on the exchange rate.6 Calculated on that basis, excess money growth in the U.S. was higher in the 1975-78 period than in Germany, Japan and Switzerland (Chart 2).

Domestic Results. The relationship between excess money growth and real output growth is a short-run phenomenon. Thus, we would expect that those countries with the highest excess money growth would, in the short run, exhibit the most rapid growth in real output. The results in Table 1 and Chart 2 confirm that result. The U.S., where growth in excess money has been fastest among the four countries since 1975, has also had the fastest rate of real growth. Germany, with the slowest growth of excess money, has had the slowest real growth, and Japan and Switzerland have fallen in between.7

The relationship between excess money growth and prices is a long-run phenomenon. Thus, excess money-growth patterns would not necessarily be completely reflected in the observed price patterns for consumer and wholesale prices to date. (Tables 2 and 3). For all four countries and for both price indexes, the inflation rate has dropped substantially since 1974. The U.S. and Japan recorded almost the same average consumer-price inflation rate in

the last four years (close to 7 percent)— substantially higher than that observed in Germany (4 percent) and Switzerland (2 percent). In the period 1977.3-1978.3, however, Japan’s inflation rate had decelerated to 4 percent, and the German and Swiss rates have also decelerated, while the U.S. rate has accelerated to almost 8 percent. As a result, the spread in the consumer inflation rates between the U.S. and the other three countries has widened recently in line with the differences in their excess money growth.

The same basic pattern emerges with respect to wholesale prices, but with an even wider spread since 1977.3. For one reason, there is a larger weight of traded goods in the wholesale index than in the consumer index. Thus, changes in the exchange rate which directly affect internationally-traded goods prices will have a larger and more immediate impact on the WPI than on the CPI. This may be the genesis of the vicious vs. virtuous cycle argument. Countries whose monetary policies tend to decelerate inflation experience an immediate favorable impact on the exchange rate which reduces the inflation rate promptly; while countries whose monetary policies tend to accelerate inflation suffer an immediate unfavorable effect on the exchange rate which promptly adds to domestic inflation. This vicious/ virtuous cycle should be considered a

Chart 2

24

reflection of the timing of the monetary impacton prices, rather than as a new destabilizingphenomenon. This subject is discussed further inSection IV.

Exchange Rate Results. These domestic results are broadly consistent with the assumptionsof relatively easy monetary policy in the U.S. andrelatively tight monetary policies in Germany,Japan and Switzerland. To measure the impactof these assumed divergent policies on exchangerates, we have computed a "monetary index"the ratio of the excess money supply in the U.S.to the excess supply in each of the other countries. Each monetary index is scaled to thecorresponding exchange rate by the coefficientsestimated in the equation in the appendix of thisarticle. As indicated in Chart 3, this monetaryindex shows a high degree of correspondencewith the movement in the bilateral exchange rate

Table 1Industrial Production

(Annual Rate ,of Change)

1963-73 1973-75 1975.1-1978.3

Germany 5.1 -4.3 2.1Japan 12.3 -7.5 6.7Switzerland 4.6 -6.7 3.0United States 5.4 -4.7 7.8

Table 2Consumer Price Index

(Annual Rate of Change)

1973.4- 1974.4- 1977.3-1974.4 1978.3 1978.3

Germany 6.5 4.0 2.5Japan 24.4 7.3 4.0Switzerland 8.7 2.0 1.0United States 12.1 6.8 7.9

Table 3Wholesale Price Index

(Annual Rate of Change)

1973.4- 1974.4- 1977.3-

1974.4 1978.3 1978.3

Germany 13.4 2.5 1.2

Japan 23.5 0.9 -3.3

Switzerland 12.7 -2.4 -4.0

United States 22.2 5.6 8.3

25

between the dollar and each of these three currencies. In each case, the monetary index declined in 1974, rose slightly in 1975 and early1976, and then declined substantially throughthe end of 1978. This movement in the monetaryindex is paralleled by a similar movement in theexchange rate. The major decline in the exchangevalue of the dollar was accompanied by a majorexpansion in the excess money supply in the U.S.relative to the other three countries.