Economic consequences of United Kingdom’s decision to stay or leave the European Union

14

Economic consequences of United Kingdom’s decision to stay or leave the European Union Peyman Pouryeganeh

Transcript of Economic consequences of United Kingdom’s decision to stay or leave the European Union

Economic consequences of United Kingdom’s decision to stay or leave the European Union

Peyman Pouryeganeh

2

Introduction Assessing the economic consequences of UK’s decision to stay or leave the European Union will require an understanding of the country’s history and its current position within the EU. The United Kingdom joined the European Union on January 1st 1973 with the mere intention of being part of a greater economic force. However, after the revolutions of 1989 and the collapse of communism across Central and Eastern Europe, which led to closer ties between European neighbors, the UK never showed interest in adopting, in its entirety, the “single market” concept or the “four freedoms” of movement of goods, services, people, and money (European Union, 2013). Although, for economic reasons, the UK has consistently shown interest in a deeper European single market, on many occasions, it has demonstrated discomfort with the politics and efforts of other EU members to implement members’ obligations (Kosmopolito, 2011). For the same reason, the country did not adopt euro as its currency in 1999. In addition, and to maintain and control its borders, it did not become a member of the Schengen area and cooperation (European Union, 2013). The economy of the UK is mainly services-‐based with a concentration on financial services although it also maintains capacity in high-‐tech and other industrial sectors (European Union, 2013). With a GDP of €1.9 billion in 2012, the UK’s economy is the third largest in the EU after Germany and France, and accounts for more than 14% of the EU’s total GDP, making it an important member of the European Union (OECD, 2013). On the other hand, nearly half of the UK’s exports go to the EU member countries making EU an indispensable market for the UK’s economy. In this paper we begin by investigating the current economic situation of the EU and the UK. We will then evaluate the benefits and the drawbacks associated with UK’s membership in the European Union, to conclude on whether the economic situation of the UK would be better if it left the EU.

3

Current Economic situation of the EU With only 7% of the world’s population, the EU’s trade with the rest of the world constitutes about 20% of the global non-‐energy exports and imports making it the biggest exporter and the second-‐biggest importer on the planet. Nearly two thirds of the EU’s total trade is done between the EU countries. The United States and China are the EU’s first and second most important trading partners respectively (European Union, 2013).

Real GDP Growth For the first time since the global financial crisis in 2008, the EU’s economy contracted by 0.3% in 2012 (Figure-‐1). In order to understand the possible causes of the downturn, we shall study the change in the aggregate demand which itself may have resulted from a reduction of one or a combination of consumption, business investment, government spending, or net exports.

Figure 1-‐ The EU's real GDP growth rate (Source: Eurostat)

According to OECD (2013), the EU’s total consumption in 2012 increased by USD 126 billion from Q1 to Q3. Government expenditure and net exports also increased by USD 35 billion and USD 176 billion respectively for the same period. Therefore, the deteriorating growth of 2012 can only be linked to the lack of business investment in that year. The European Union’s economy is predicted to shrink by 0.1 percent in 2013, and therefore heading for its first ever back-‐to-‐back years of falling production. Nevertheless, the economy is predicted to stabilize by end of 2013, and a GDP growth of 1.4 percent is forecast for 2014 (Eurostat, 2013).

2004 2005 2006 2007 2008 2009 2010 2011 2012 Real GDP Growth 2.5 2.1 3.3 3.2 0.3 -‐4.3 2.1 1.6 -‐0.3

-‐6 -‐4 -‐2 0 2 4

% change

Real GDP Growth

4

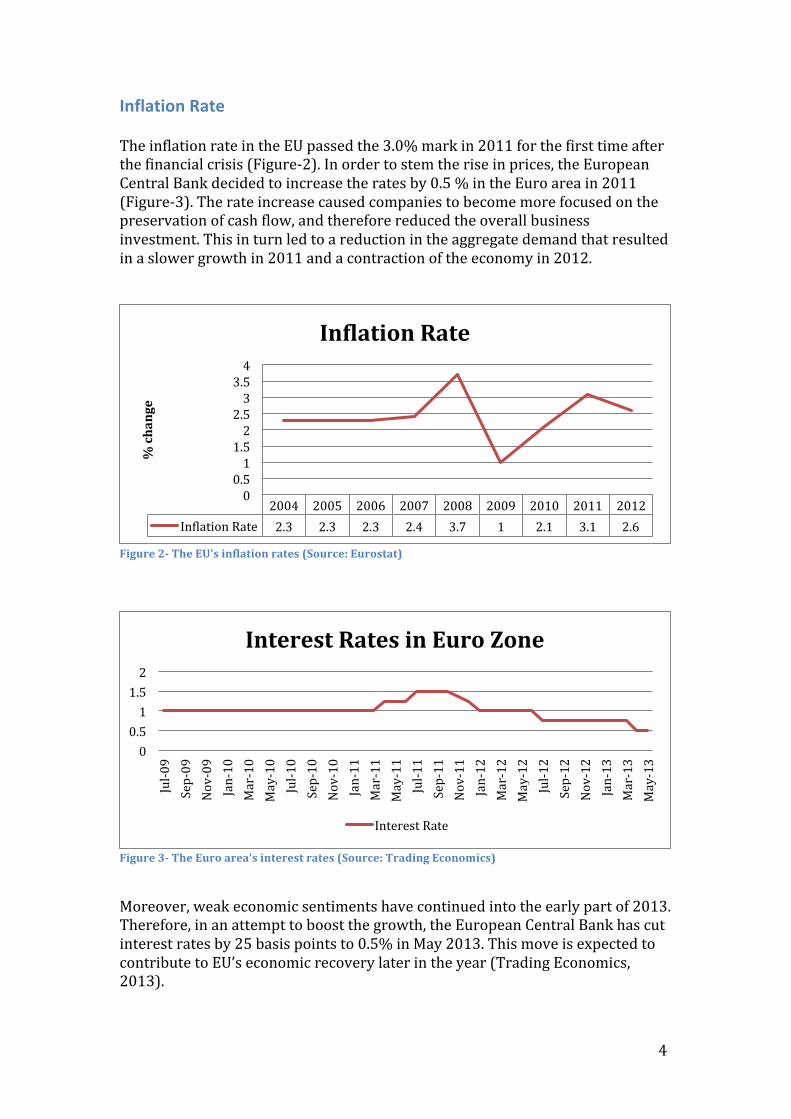

Inflation Rate The inflation rate in the EU passed the 3.0% mark in 2011 for the first time after the financial crisis (Figure-‐2). In order to stem the rise in prices, the European Central Bank decided to increase the rates by 0.5 % in the Euro area in 2011 (Figure-‐3). The rate increase caused companies to become more focused on the preservation of cash flow, and therefore reduced the overall business investment. This in turn led to a reduction in the aggregate demand that resulted in a slower growth in 2011 and a contraction of the economy in 2012.

Figure 2-‐ The EU's inflation rates (Source: Eurostat)

Figure 3-‐ The Euro area's interest rates (Source: Trading Economics)

Moreover, weak economic sentiments have continued into the early part of 2013. Therefore, in an attempt to boost the growth, the European Central Bank has cut interest rates by 25 basis points to 0.5% in May 2013. This move is expected to contribute to EU’s economic recovery later in the year (Trading Economics, 2013).

2004 2005 2006 2007 2008 2009 2010 2011 2012 Inelation Rate 2.3 2.3 2.3 2.4 3.7 1 2.1 3.1 2.6

0 0.5 1

1.5 2

2.5 3

3.5 4

% change

InFlation Rate

0 0.5 1

1.5 2

Jul-‐09

Sep-‐09

Nov-‐09

Jan-‐10

Mar-‐10

May-‐10

Jul-‐10

Sep-‐10

Nov-‐10

Jan-‐11

Mar-‐11

May-‐11

Jul-‐11

Sep-‐11

Nov-‐11

Jan-‐12

Mar-‐12

May-‐12

Jul-‐12

Sep-‐12

Nov-‐12

Jan-‐13

Mar-‐13

May-‐13

Interest Rates in Euro Zone

Interest Rate

5

Nevertheless, although fine-‐tuning of macroeconomic policy inputs can help the EU accelerate its economic recovery and maintain growth in the near-‐to-‐medium term by increasing the aggregate demand, this will lead to an inflationary boom. The economic growth of the EU in the long run can only be guaranteed through a sustained increase of the aggregate supply. In this fashion, inflation rate can be lowered and maintained below but close to the 2% target level while GDP increases in a gradual manner. Increase in the aggregate supply can be achieved through increase in labor productivity, increase in physical capital, improvement of human capital by education and training, and advancement in technology in order to achieve more efficient levels in production of goods and services (Begg and Ward, 2013).

Unemployment Unemployment is perhaps one of the biggest challenges for the European Union. The EU’s unemployment rate has been constantly increasing following the 2008 financial crisis (Figure-‐4). In March 2013, 26.52 million people were estimated to be unemployed in the EU of which 5.69 million were under the age of 25 (Eurostat, 2013). The deteriorating economy is expected to drive unemployment rate to its new high of 11.1% in 2013, which is expected to remain at the same levels in 2014 (The Economic Times, 2013).

Figure 4-‐ The EU's unemployment rate (Source: OECD & Eurostat)

Current Economic situation of the UK With a population of 62.6 million, representing 0.91 percent of world’s total population, the UK’s trade with the rest of the world constitutes 2% of the global exports and 3.6% of global imports. Nearly half of the UK’s total trade is done with the EU countries. The United States followed by EFTA countries and China are the UK’s other biggest trading partners respectively (Allen, 2012).

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Unemployment Rate 9.2 9 8.3 7.2 7.1 9 9.7 9.7 10.5 10.9

0 2 4 6 8 10 12

Unemployment Rate (%)

6

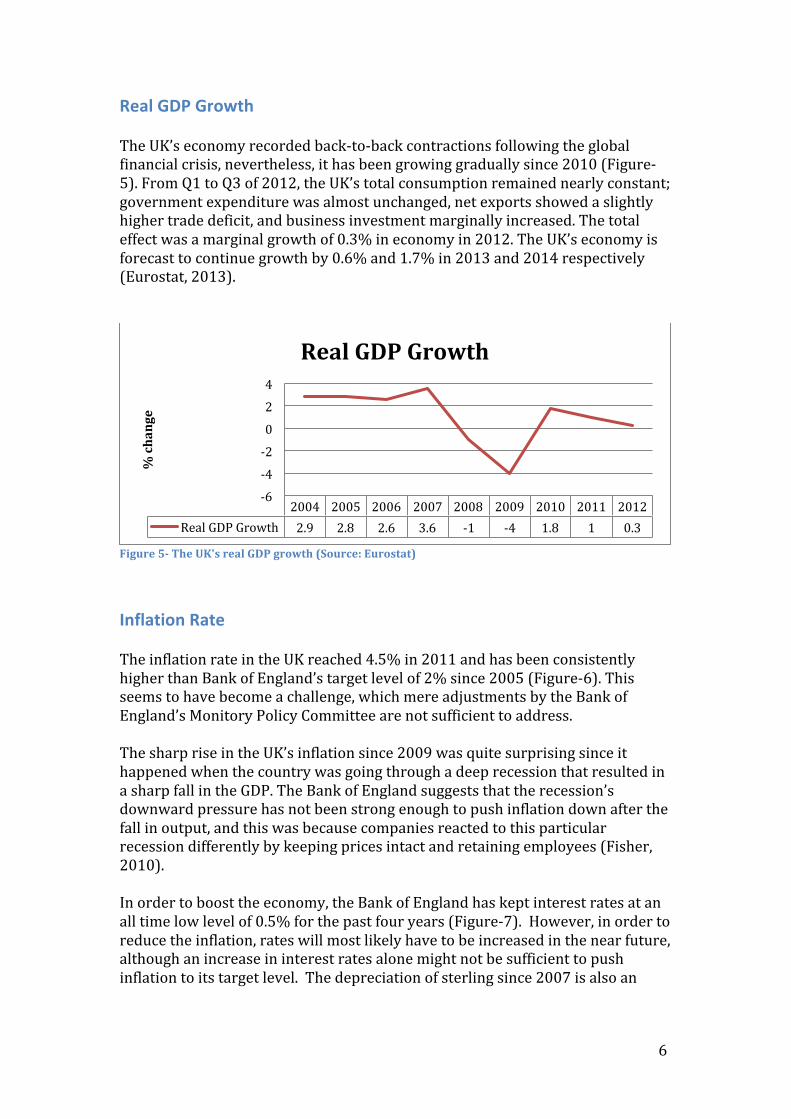

Real GDP Growth The UK’s economy recorded back-‐to-‐back contractions following the global financial crisis, nevertheless, it has been growing gradually since 2010 (Figure-‐5). From Q1 to Q3 of 2012, the UK’s total consumption remained nearly constant; government expenditure was almost unchanged, net exports showed a slightly higher trade deficit, and business investment marginally increased. The total effect was a marginal growth of 0.3% in economy in 2012. The UK’s economy is forecast to continue growth by 0.6% and 1.7% in 2013 and 2014 respectively (Eurostat, 2013).

Figure 5-‐ The UK's real GDP growth (Source: Eurostat)

Inflation Rate The inflation rate in the UK reached 4.5% in 2011 and has been consistently higher than Bank of England’s target level of 2% since 2005 (Figure-‐6). This seems to have become a challenge, which mere adjustments by the Bank of England’s Monitory Policy Committee are not sufficient to address. The sharp rise in the UK’s inflation since 2009 was quite surprising since it happened when the country was going through a deep recession that resulted in a sharp fall in the GDP. The Bank of England suggests that the recession’s downward pressure has not been strong enough to push inflation down after the fall in output, and this was because companies reacted to this particular recession differently by keeping prices intact and retaining employees (Fisher, 2010). In order to boost the economy, the Bank of England has kept interest rates at an all time low level of 0.5% for the past four years (Figure-‐7). However, in order to reduce the inflation, rates will most likely have to be increased in the near future, although an increase in interest rates alone might not be sufficient to push inflation to its target level. The depreciation of sterling since 2007 is also an

2004 2005 2006 2007 2008 2009 2010 2011 2012 Real GDP Growth 2.9 2.8 2.6 3.6 -‐1 -‐4 1.8 1 0.3

-‐6

-‐4

-‐2

0

2

4

% change

Real GDP Growth

7

important factor that directly impacts inflation since it affects the prices for goods and services imported into the UK.

Figure 6-‐ The UK's Inflation Rate (Source: Eurostat)

Figure 7-‐ The UK's Bank Rates History (Source: Bank of England)

Unemployment Unemployment rate in the United Kingdom has been fluctuating between 7.6% and 8.0% since 2009 (Figure-‐8). Although employment in the UK is expected to rise in the next two years, it is envisaged that the unemployment rate may nevertheless slightly increase because the number of new jobs created will not be enough to absorb the growing number of economically active people. The anticipated moderate increase in the UK’s unemployment rate is linked to factors such as planned public spending cuts that are yet to be implemented, slow GDP growth, and increase in labor productivity while demand remains weak (British Chambers of Commerce, 2013).

2004 2005 2006 2007 2008 2009 2010 2011 2012 Inelation Rate 1.3 2.1 2.3 2.3 3.6 2.2 3.3 4.5 2.8

0

1

2

3

4

5

% change

InFlation Rate

0 2 4 6 8

Feb-‐04

Jul-‐04

Dec-‐04

May-‐05

Oct-‐05

Mar-‐06

Aug-‐06

Jan-‐07

Jun-‐07

Nov-‐07

Apr-‐08

Sep-‐08

Feb-‐09

Jul-‐09

Dec-‐09

May-‐10

Oct-‐10

Mar-‐11

Aug-‐11

Jan-‐12

Jun-‐12

Nov-‐12

Apr-‐13

Interest Rates

Interest Rates

8

Figure 8-‐ The UK's Unemployment Rate (Source: OECD & British Chambers of Commerce)

Current Account Balance In 2012, the United Kingdom recorded its highest trade deficit since 1989 (Figure-‐9), which corresponded to 3.7% of its GDP. This was caused by a slow growth in manufacturing exports augmented with a surprisingly sharp fall in export of services. Considered a pillar of the UK’s economy, financial services could only earn 1.8 billion Euros in 2012 compared with 31 billion Euros in the previous year. This decrease is believed to have resulted from the regulatory pressure introduced by the Bank of England, which has led banks to reduce their foreign loans in order to boost their lending to local companies and households (Flanders, 2013).

Figure 9-‐ The UK's Trade Balance (Source: Eurostat)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Unemployment Rate 4.7 4.8 5.4 5.3 5.7 7.6 7.8 8 7.8 7.9

0

2

4

6

8

10

Unemployment Rate (%)

2004 2005 2006 2007 2008 2009 2010 2011 2012 Trade Balance -‐37.4 -‐47.7 -‐66.8 -‐51.6 -‐25.1 -‐23.1 -‐56.7 -‐33.5 -‐68.56

-‐80

-‐60

-‐40

-‐20

0

Billion Euro

Current Account Balance

9

The economic benefits and drawbacks for Britain to stay as a member of the European Union Putting politics aside and looking at the issue from a strictly economical and objective perspective, one can identify both positive and negative consequences of the UK remaining within the European Union. EU membership provides Britain with the opportunity of competing in a bigger market with larger number of companies across borders leading to increased efficiency, better utilization of resources, and innovation. This can in turn lower the prices of goods and services manufactured and produced in the UK, reducing inflation rates, and making UK exporters more competitive in markets outside the EU (Booth and Howarth, 2012). By staying with the EU, the United Kingdom will benefit from a higher growth and a faster economic recovery assuming that it will commit itself to the strengthening and deepening of the single market concept. It is estimated that only by including freedom of movement in the areas of energy, telecom, transport, and digital, Britain can boost its GDP by approximately £110 billion (Wright, 2013). On the contrary, by leaving Europe, the UK will risk losing access to its primary market that is worth about £234 billion (Allen, 2012). This could be detrimental to the UK’s economy especially at a time when economic recovery is slow, and unemployment is high. By staying with the EU, Britain will be part of a bigger market for foreign direct investments. Since only most productive firms invest abroad, attracting these investments boosts growth, creates employment, and increases labor skills through knowledge transfer (Booth and Howarth, 2012). However, since the EU’s economy is contracting while the UK’s is slowly recovering, some British economists suggest that now is the best time for Britain to leave the EU in order to attract higher levels of foreign investments (Chu, 2012). Since its drastic fall after the financial crisis of 2008, the British pound (GBP) has been struggling to regain its value (Figure-‐10), which in turn has contributed to an increase in prices for imported goods and services and as a result higher inflation rates. By leaving the EU, Britain will have to face a higher degree of economical uncertainty at least in the near-‐to-‐medium term, which could potentially lead to further devaluation of its currency. A more volatile currency and a slow economy will make Britain a less attractive choice for foreign direct investments. This translates to even slower economic recovery, higher unemployment, and higher inflation rates.

10

Another advantage of staying with the EU is the free movement of goods and compliance with only one set of manufacturing standards. Today, the EU follows one set of legislated product regulations, which means that any product meeting these regulations can freely move in the EU’s single market. If Britain decides to leave the EU, it should either follow the EU’s regulations for its domestic production or should follow two different sets of standards for domestic and foreign production, which will be costly for its manufacturers and producers, leading once again to an increase in prices (Booth and Howarth, 2012). Britain makes an annual net contribution of €9 billion to the EU’s budget which is approximately equal to 0.6 percent of its GDP. By leaving the EU, the UK can use this amount as a contribution to its own budget. Nevertheless, the UK currently has a budget deficit that is equal to 8.3 percent of its GDP; therefore, saving the EU budget contribution will not have a substantial impact on the UK’s budget. Moreover, the contribution of members to the EU’s common budget is mostly used to develop post-‐Soviet bloc countries, which in turn will make these countries bigger potential markets for all EU members including Britain in the future (Chu, 2012).

The economic consequences of the UK’s departure from the European Union’s perspective For the EU, Britain is a €305 billion export market, which makes up approximately 2.5 percent of its GDP (Allen, 2012). Since the EU runs a trade surplus with Britain, in the event that Britain decides to leave the European Union, the aggregate demand in the EU could potentially drop by approximately €83 billion per year. This will move the EU’s economy to a new short-‐run equilibrium with lower inflation and GDP. A decrease in inflation will result in an increase in real wages that will force employers to reduce output by cutting employment (Begg and Ward, 2013).

Figure 10-‐ Sterling index (Source: Moneyweek)

11

To bring the economy back to long-‐term equilibrium and avoid an increase in unemployment, the EU will need to either implement the appropriate monetary or fiscal policies to raise the aggregate demand to the levels prior to the UK’s separation or to increase short-‐run supply by cutting wages if accepted by workers (Begg and Ward, 2013). Britain’s decision to leave the European Union can also have a negative impact on the EU’s financial services sector. As suggested by Lilico (2011), Britain has always been an advocate of liberalizing the EU’s highly regulated financial services sector. The EU, on the other hand, continues to support tighter regulations, as the financial crisis and the subsequent recession have been attributed to inadequate regulations in the UK’s and the US’s financial services. At the same time, the world is going through a geo-‐economic shift in which economies in Asia and Latin America are rapidly growing while the EU’s economy is shrinking or at the best barely recovering. These growing economies will be in need of, and are likely to seek from stable economies, less regulated global wholesale financial services, for which the UK has developed a strong expertise (Lilico, 2011). Therefore, in the event that Britain leaves the EU, the EU will risk losing part of its financial services market to the UK.

Conclusion Britain’s economy is growing although not as fast as expected and certainly not at the rates seen prior to the financial crisis. The country’s inflation rates have been higher than its target level of 2 percent since 2005, and its unemployment is at its highest levels in the past ten years and is expected to further increase due to the country’s slow GDP growth, high labor productivity, weak demand, and public spending cuts planned by the government. By leaving the European Union, Britain risks losing access to its primary market that is crucial for its economic growth. It also loses the opportunity of competing in a bigger market with a large number of cross-‐border firms that can be a source of increased efficiency, better utilization of resources, and innovation. Britain will also face a higher degree of economical uncertainty in short-‐to-‐medium term, which could affect its already devaluated currency. The combination of a weaker currency and a slower economy can make Britain a less attractive choice for foreign direct investments, which can further raise the country’s inflation and unemployment. Finally, in the event Britain decides to leave the EU, it shall still comply with the manufacturing standards set by the EU if it wishes to export to this market. This could raise the cost of manufactured goods if Britain decides to follow two different sets of standards for domestic and foreign productions.

12

This being said, leaving the European Union may actually represent some advantages for Britain such as saving the net annual contribution to the EU’s budget, winning a bigger portion of the financial services market, especially to address demand from growing markets. In addition, and as suggested by some economists, this may be the right move at the right time, given the EU’s anticipated contracting economy. In fact, those economists suggest that by exiting the EU, the UK is likely to attract more foreign direct investments. In conclusion, while arguments can be developed both for and against the UK’s separation from the EU, it seems to us that the level of economic uncertainty that could result from this move and its possible negative consequences are sufficient to support status quo. On this basis, we do not believe that the UK’s economic situation would improve if it were to leave the European Union.

13

References Allen, G., 2012. Library of House of Commons: UK Trade Statistics [pdf] Available at: < http://www.parliament.uk/briefing-‐papers/SN06211> [Accessed 16 May 2013]. Begg, D., Ward, D., 2013. Economics for business. 4th ed. Maidenhead: McGraw-‐Hill. Booth, S., and Howarth, C., 2012. Trading places: Is EU membership still the best option for UK trade? [online] Available at < http://www.europarl.org.uk/ressource/static/files/2012eutrade.pdf> [Accessed 21 May 2013]. British Chambers of Commerce, 2013. BCC Economic Forecast [online] Available at < http://www.britishchambers.org.uk/press-‐office/press-‐releases/bcc-‐economic-‐forecast-‐uk-‐growth-‐reduced-‐in-‐2013-‐and-‐2014,-‐but-‐prospects-‐will-‐improve-‐gradually.html#.UZcm8yt4ZEo> [Accessed 18 May 2013]. Chu, B., 2012. What if Britain left the EU? The Independent [online] Available at < http://www.independent.co.uk/news/world/europe/what-‐if-‐britain-‐left-‐the-‐eu-‐7904469.html> [Accessed 23 May 2013]. European Union, 2013. A growing community, [online] Available at: <http://europa.eu/about-‐eu/eu-‐history/1970-‐1979/index_en.htm> [Accessed 10 May 2013]. Eurostat, 2013. Real GDP growth rate and Unemployment Statistics, [online] Available through University of Warwick Library Website: < http://encore.lib.warwick.ac.uk> [Accessed 13 May 2013]. European Commission, 2013. Trade-‐Countries and regions: China, [online] Available at: http://ec.europa.eu/trade/policy/countries-‐and-‐regions/countries/china/ > [Accessed 15 May 2013]. Fisher, P., 2010. Why is CPI inflation so high?, Based on a talk to Merseyside Young Professionals. Liverpool, 14 June 2010. [online] Available at: < http://www.bankofengland.co.uk/publications/Documents/speeches/2010/speech438.pdf> [Accesses 17 May 2013]. Flanders, S., 2013. Britain, the world and the end of the free lunch?, BBC, [online] Available at < http://www.bbc.co.uk/news/business-‐21956087> [Accessed 18 May 2013]. Kosmopolito, 2011. The UK and the European Union: A difficult relationship, [online] Available at: < http://www.kosmopolito.org/2011/11/15/uk-‐and-‐eu-‐a-‐difficult-‐relationship/> [Accessed 10 May 2013]. Lilico, A., 2011. Open Europe: How to safeguard the UK financial sector in a changing EU. The Telegraph [online] Available at http://blogs.telegraph.co.uk/finance/andrewlilico/100013618/open-‐europe-‐how-‐to-‐safeguard-‐the-‐uk-‐financial-‐sector-‐in-‐a-‐changing-‐eu/ > [Accessed 30 May 2013].

14

OECD, 2013. Main economic indicators: UK, volume 2013/3, [online] Available through: University of Warwick Library Website < http://encore.lib.warwick.ac.uk > [Accessed 10 May 2013]. The Economic Times, 2013. Unemployment in Europe is expected to worsen, [online] Available at: < http://articles.economictimes.indiatimes.com/2013-‐05-‐05/news/39027586_1_european-‐union-‐eurozone-‐countries-‐european-‐central-‐bank > [Accessed 14 May 2013]. Trading Economics, 2013. Euro Area Interest Rate, [online] Available at: < http://www.tradingeconomics.com/euro-‐area/interest-‐rate > [Accessed 14 May 2013]. Wright, O., 2013. British business: We need to stay in the EU – or risk losing up to £92bn a year. The Independent [online] Available at < http://www.independent.co.uk/news/uk/politics/british-‐business-‐we-‐need-‐to-‐stay-‐in-‐the-‐eu-‐-‐or-‐risk-‐losing-‐up-‐to-‐92bn-‐a-‐year-‐8622925.html> [Accessed 20 May 2013].