draft-report-informal-sector-17-march-2021.pdf - Niesbud

226

1 Comprehensive Study for Preparation of a Policy/Scheme for Providing Support for Formalizing Informal Sector through Entrepreneurship Promotion Final Draft of Consulting Report Submitted to NIESBUD An autonomous body under administrative control of the Ministry of Skill Development and Entrepreneurship, Government of India By MDI GURGAON 17.03.2021

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of draft-report-informal-sector-17-march-2021.pdf - Niesbud

1

Comprehensive Study for Preparation of a Policy/Scheme for Providing Support for Formalizing Informal Sector through

Entrepreneurship Promotion

Final Draft of Consulting Report Submitted to

NIESBUD An autonomous body under administrative control of the Ministry of Skill

Development and Entrepreneurship, Government of India

By

MDI GURGAON

17.03.2021

2

Table of Contents ExecutiveSummary ................................................................................................................. 6

Chapter1-OrganizationofReport&MappingofChapterswithTermsofReference(ToR) ....................................................................................................................................... 13

1.1Introduction ....................................................................................................................................... 13 1.2MinistryofSkilldevelopmentandEntrepreneurship(MSDE)........................................................ 15 1.2.1.DirectorateGeneralofTraining(DGT) .............................................................................................. 15 1.2.2NationalSkillDevelopmentAgency(NSDA) ....................................................................................... 17 1.2.3NationalSkillDevelopmentCorporation(NSDC) ............................................................................... 17 1.2.4NationalSkillDevelopmentFund(NSDF) .......................................................................................... 18 1.2.5TheIndianInstituteofEntrepreneurship(IIE) ................................................................................... 18 1.2.6TheNationalInstituteforEntrepreneurshipandSmallBusinessDevelopment(NIESBUD) ............... 18 1.2.7SectorSkillCouncils(SSC) .................................................................................................................. 18 1.2.8Trainees/Beneficiaries ...................................................................................................................... 19 1.2.9CapacityDevelopers ........................................................................................................................... 19 1.3Conceptual/OperationalDefinitionsofmajorconceptsusedinthereport .................................. 19 1.3.1InformalSector .................................................................................................................................. 19 1.3.2FormalSector .................................................................................................................................... 21 1.3.3Formalization .................................................................................................................................... 21 1.3.4UnorganizedSector............................................................................................................................ 21 1.3.5CapacityBuilding ............................................................................................................................... 22 1.3.6Entrepreneurship ............................................................................................................................... 22 1.3.7EntrepreneurialSkills ........................................................................................................................ 22 1.4ApproachtoStudy .............................................................................................................................. 22 1.5BriefaboutApproachesofFormalization ........................................................................................ 23 1.6ScopeofthepresentstudyandBroadOrganizationofthereport ................................................. 25 1.6.1ConductingaComprehensiveStudy,throughtheexistingdatabases(alreadycommissionedStudies,PrivateReportsetc.)tounderstandtheInformalSector............................................................................. 25 1.6.2ExploringPotentialRoleofMSDE ...................................................................................................... 26 1.7Conclusion .......................................................................................................................................... 32

Chapter2-ReviewofliteratureofthestudiesonInformalsector ................................... 34 2.1Introduction ....................................................................................................................................... 34 2.2StudiesbyInternationalScholars/organizations .......................................................................... 34 2.3StudiesbyIndianScholars/OrganizationsintheIndianContext .................................................. 39 2.4SummarizationofMajorFindings&EvolutionofBroadThemesforFormalizationFramework

........................................................................................................................................................................ 44 2.5Conclusion .......................................................................................................................................... 48

Chapter3-MappingtheCurrentAvailableDatabasesfortheEstimation,ClassificationandPrioritizationoftheInformalSector ............................................................................ 51

3.1.Formal-InformalEnterpriseClassification ................................................................................... 51 3.1.1Introduction ....................................................................................................................................... 51 3.1.2Informal-FormalClassificationLandscapeinIndia ............................................................................ 52

3

3.2SizeoftheFormalandInformalSectors .......................................................................................... 59 3.2.1Overview ............................................................................................................................................ 59 3.2.2Sectorwiseestimation ....................................................................................................................... 60 3.2.3EstimateofManufacturing,Tradeandotherservicesenterprisesaspertheircategories–RuralV/sUrbanandOAEV/sEstablishment. ............................................................................................................ 67 3.2.4StateWiseEstimation ........................................................................................................................ 68 3.2.5Discussion .......................................................................................................................................... 72 3.3PrioritizationofSectors .................................................................................................................... 73 3.3.1Overview ........................................................................................................................................... 73 3.3.2.EmployeeProductivityindifferentsectorsofinformalenterprises(GVAPW) .................................... 74 3.3.3Distributionofinformalenterprisesbasedontheireconomiccontribution(GVAPE) ......................... 76 3.3.4.Classificationofinformalenterprisesaspertheirinclusiveness ........................................................ 78 3.3.5Majorstatewiseprioritizationofsectors/subsectorsbasedonanefficientandcomprehensiveensemble-basedfeatureselectionmethodology .......................................................................................... 81 3.3.6WomenEntrepreneurDatabasedPriorityRankingusingEconomicCensusdata.............................. 84 3.4Conclusion .......................................................................................................................................... 89

Chapter4-Mappingthepoliciesandsupportprovidedtoinformalsector .................... 92 4.1.Introduction ....................................................................................................................................... 92 4.2GovernmentInitiativesforInformalSector ..................................................................................... 92 4.2.1FinancialCapitalandInsurancesupport ........................................................................................... 92 4.2.2KnowledgeCapitalSupport................................................................................................................ 95 4.2.3InfrastructureCapitalSupport........................................................................................................... 99 4.3SupportbyLargeScaleNGOs .......................................................................................................... 110 4.3.1FinancialCapitalandInsuranceSupport ......................................................................................... 110 4.3.2KnowledgeCapitalSupport.............................................................................................................. 111 4.3.3InfrastructureCapitalSupport......................................................................................................... 114 4.4SocialImpactEnterprises ................................................................................................................ 118 4.4.1FinancialCapital .............................................................................................................................. 118 4.4.2InfrastructuralandTechnologicalCapital ....................................................................................... 118 4.4.3KnowledgeCapital ........................................................................................................................... 119 4.4.4Others .............................................................................................................................................. 119 4.5PrivateSectorCSRActivities ........................................................................................................... 119 4.5.1FinancialCapitalInitiatives ............................................................................................................. 119 4.5.2Infrastructure&TechnologicalCapitalInitiatives ........................................................................... 120 4.5.3KnowledgeCapital ........................................................................................................................... 121 4.5.4.Others ............................................................................................................................................. 124 4.6TechnologyFirms ............................................................................................................................. 124 4.6.1FinancialCapitalInitiatives ............................................................................................................. 124 4.6.2Infrastructure&TechnologicalCapitalInitiatives ........................................................................... 124 4.6.3KnowledgeCapital ........................................................................................................................... 125 4.7GigEconomy ..................................................................................................................................... 126

Chapter5-InformalMicro-entrepreneurs:ChallengesandIssues ................................ 129 5.1Introduction ..................................................................................................................................... 129 5.2ReviewofCaseStudiesinthecontextofIndianInformalSector .................................................. 129 5.2.1InformalManufacturingSector ....................................................................................................... 129 5.2.2StreetFoodVendors ......................................................................................................................... 136

4

5.2.3MarketVendors................................................................................................................................ 139 5.2.4ChallengesfacedbyIndianmicro-entrepreneurs ............................................................................. 142 5.3WorkingModeofPrivateOrganizations........................................................................................ 143 5.4InternationalBestPractices ........................................................................................................... 145 5.4.1TheSouthAfricanExperience .......................................................................................................... 145 5.4.2TheMexicanExperience ................................................................................................................... 146 5.4.3TheBrazilExperience ...................................................................................................................... 146 5.4.4TheKenyaExperience ...................................................................................................................... 148 5.5ConcludingRemarks ........................................................................................................................ 150

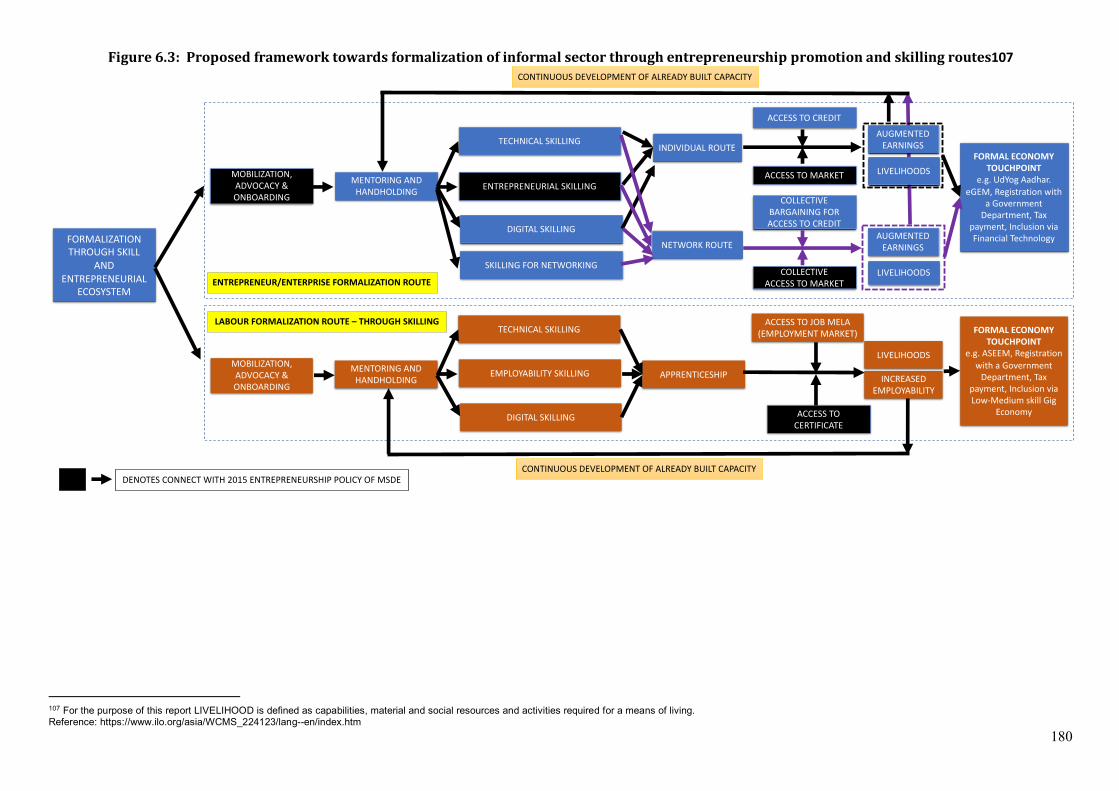

Chapter6-PolicyRecommendationsandFrameworkforMSDEtoSupportFormalizationofInformalEnterprisesthroughEntrepreneurship ............................... 153

6.1Introduction ..................................................................................................................................... 153 6.1.1ExistingLiterature ........................................................................................................................... 155 6.1.2PrioritySub-SectorstoFocusupon .................................................................................................. 156 6.1.3InsightsfromPrimaryData ............................................................................................................. 160 6.1.4ChallengesfacedduringFormalization ............................................................................................ 165 6.1.5Support/PoliciesandStakeholdersforFormalizationofInformalSector ........................................ 167 6.2.MinistryofSkillDevelopmentandEntrepreneurship(MoSDE)&SkillEcosystem .................... 170 6.2.1Introduction ..................................................................................................................................... 170 6.2.2MajorSchemes,Programs,InitiativesandProjects .......................................................................... 170 6.2.3NationalPolicyforSkillDevelopmentandEntrepreneurship2015 .................................................. 172 6.2.4Keybeneficiariestofocusforproposedformalizationframeworkandkeychallengesfacedbyinformalsector ......................................................................................................................................... 174 6.3FrameworksandApproachesforMoSDEforformalizationofinformalsector .......................... 176 6.3.1Frameworkofformalizationofinformalsectorthroughentrepreneurshippromotionandskillingecosystem ................................................................................................................................................. 177 6.3.2Frameworktowardsaddressingofchallengesofinformalsector .................................................... 183 6.3.3IllustrativeGovernanceStructureandWorkingPlan ....................................................................... 200 6.4Duediligenceprocessesforpartnershipsandstakeholderengagement .......................................... 202 6.5ConcludingRemarks ........................................................................................................................ 204

References ............................................................................................................................ 207

5

Executive Summary

6

ExecutiveSummaryThisreportisfocussedontheformalizationofinformaleconomybyprovidingsupporttotheinformalsectorthroughcapacitybuildingandentrepreneurship.Thestudywasadeskresearch based on secondary data drawn from difference sources viz. NSS 67th & 73rdRounddata,AnnualSurveyof IndustryUnitLeveldataof2010-11&2014-15,Academicstudiesnationalandinternationalinthecontextofinformalsector.Movingtowardsformaleconomyisatalltaskandmultiplestakeholdershavetakenmultipleinitiativestowardsthisend.In2002,ILOlaunchedtheDecentWorkAgendaprovidingsevenkeyavenuestowardsformalizationofaneconomy.Outofthesevenagendapoints,onewas ‘Entrepreneurship,Skills,Finance,ManagementandAccesstoMarkets’.Forfurtheringthisagenda,thisreportfocussedonthe‘spreadanddepth’ofinformallabourandenterprisesinIndia,highlightingthe challenges faced by them and proposing action points for MSDE to enable theirmovement towards Formal Sector. Thereafter, a Frameworkwas developed forMSDE toprovideentrepreneurialsupporttoinformalenterprises,especiallybyaligningthecurrentinitiativestakenbymultiplestakeholdersinInformalSectorandstrengtheningtheexistingsupport.Thereportconsistsof6chapters.

ChapterOnepresentstheorganizationofthereportandmappingofchapterswithrespectivepointsofthetermsofreference(ToR).Itessentiallysummarizesthemajorconstituentsofthereport.Itstartswithintroduction(Section1.1)tothestudywhichalsotalkedaboutthecharacteristicsoftheIndianinformalsector.ItisfollowedbySection1.2whichprovidesabriefonMSDE.Section1.3discussesaboutthedefinitionsofmajorconceptsthatarecentralto this study and serve as anchors for the discussions and propositions through theremainingchaptersofthisstudy.Section1.4discussesabouttheoverarchingapproachandmethodologyof thestudy.Section1.5discusses fewexistingapproachesof formalization.Section1.5formsoneofthebasisforevolutionoffinalrecommendationsinChapter6andalso helps the reader in understanding the connect and relevance of finalization ofconceptualdefinitioninSection1.3.Section1.5servesaspremiseoftheliteraturereviewdoneinChapter2andthesecondarydataconsolidationdoneinChapter3and4.Thiswouldalso form a theoretical lens to absorb the case studies given in Chapter 5. Section 1.6discussestheScopeofthepresentstudyandBroadOrganizationofthereportintermsofToR and the mapping of the expectation of the ToR with contents and deliverablesencompassedinthevariouschaptersofthereport(Table1.1).Thekeycontributionofthischapteristheconceptualizationofkeydefinitionswhichwillusedthroughoutthereport,theapproachandmethodologyofthereportandthemappingofToRwiththechaptersinthisreport.

7

ChapterTwoThischapterpresentsthereviewofliteratureofthestudiesconductedintheinformalsectoraimedatformalizationofinformalsector.Itstartswithintroductiontothechapter (Section 2.1) and is followed by review of studies in informal sector andformalizationdonebyinternationalscholars/organizationswhereinpolicies(Section2.2).These policies can be classified in terms of their domain and the costs and benefits offormalization that arebeing targeted. Section2.3presents the reviewof studiesdonebyIndianscholars/organizationsinthecontextofIndia.Section2.4presentsthesummaryofmajorfindingsandevolutionofbroadthemesforformalizationframeworkandisfollowedbyconclusionofthechapter(Section2.5).

Itisreportedintheliteraturethatinformalitytakesvariousformsindifferentcountriesandnewformshademergeovertimewithinacountry.Therefore,therecanbeno“onesizefitsallpolicy”toregulateorimprovetheconditionsofinformalenterprisesandworkersinanycountryforlongerduration.Therearemanyperspectivesofinformalityanditstransitiontoformalization. These are capital view of formalization, labour view of formalization,technologicalperspective,andgeneralperceptionofcitizensworkingwithor in informalsector.Manystudiesfromdifferentcountriesarereviewedinthepartofthereport.

ThesestudiesincludetheperceptionofscholarsandexpertsforformalizationofinformalsectorMajorityofthemusedthephrasessuchas“formalizationmustbesimpleandeasy”,“formalization must be optimal. There is no scope for either over regulation or lack ofregulation“.Someofthesereportedthatitisweakeningthetraditionaltradeunionandnewformof informalunionsareemerged insomepartof theworldwhichoftenresults in toviolence. It is reported bymany experts and scholar that a new formof formalization ishappening inmany part of theworld that require intervention at different levels by thegovernments.InthecontextofIndianinformalenterprises,thefindingofeconomicstudiesrelated to formalization, impact of recent policy decisions of government specificallydemonetizationandGST,viewsof technologysavvystart-ups,etc.arereviewed.There isneedtobringawarenessamongmassesabouttangiblebenefitsoftheprocess,trainingofentrepreneursformakingthemawareofnewmethodologies,administrativeandproceduralreforms, taxrelated fearand incentives,reviewoflawsandregulations,easier inspectionandcompliance,commoninfrastructurefacilities,increaseefficiencyofpublicprocurement,monetaryincentive,sectoralApproach,andextensionofsocialprotectionetc.

ChapterThreepresentsthemappingofcurrentavailabledatabasestoestimatetheinformalenterprisesanddetailedclassificationsof informalenterprisesundervarioussectorsandsubsectors.This chapteralso includes theprioritisationofmajor sectorsandsub-sectors

8

basedonvitalparameterssuchasGVA,employment,inclusionandgeography.Thechapterisdividedintothreebroadsections.Section3.1exploresthecurrentavailabledatabasesandother available reports to discuss the extent of Informal Sector in India. In this section,mappingof currentavailabledatabases (NSSO, ILO,NAS,NCEUS,CSO,EconomicSurveysMSDE, Reports ofMOSPI etc.) for providing an in-depth overview on extent of informalsector and for elaborating and defining the unorganized and informal sector andidentificationofkeycharacteristics.Section3.2depictsthepictureofthesizedistributionofIndia’s non-agricultural enterprise structure, both formal and informal, and presents apercentage break-up between the formal and informal enterprises under each sector.Section 3.3 encompasses the prioritisation of sectors and subsectors. This prioritisationmostlyusedNSSOdata.FirstSetofPriorityencompassfocusonM15(Manufactureofothernon-metallic mineral products), M2 (Manufacture of food products), M10 (Printing andreproductionofrecordedmedia),M5(Manufactureoftextiles),M14(Manufactureofrubberand plastics products), M17 (Manufacture of fabricated metal products), M24 (Othermanufacturing),M6(Manufactureofwearingapparel)frommanufacturingsector,T3(Otherwholesale trade), T4 (Other retail trade) from Trade sector and S13 (Education), S14(HumanHealth and SocialWork), S1 (Accommodation), S2 (Food service activities), S11(Professional, Scientific andTechnical activities) in Services sector. Similarly second andthird set of priorities are given in the chapter in details and statewise calculations anddetailingsupportedwithsecondarydataintheAnnexures1and2.Subsectionsection3.3.6does prioritisation of sectors using economic census data and with focus on womenentrepreneurs.Finally,Section3.4offerssomeconcludingremarks.

Informal enterprises constitute for millions of unregulated, unlicensed, and untaxedmicroenterprises thatarereferredtoas the“informalsector”.The informal“enterprises”includesmallenterprisesrangingfromwasterecyclingunits,streetvendors,pavementfoodstalls,saleofpiratedbooks,anddigitalproductstohome-basedmanufacturingenterprises.Thesesmallbusinessesormicroenterprisestypicallyoperatedatsmallerscalesofbusiness,withlowlevelsoflabour,littleuseoftechnology,lowphysicalandhumancapital,andlowincomes.Comparedtoformalenterprises,informalenterpriseshavefewerorlessvaluablefactors ofproduction other than their own labour: such as capital, land, and technology.Second, theyalsohave lessbargainingpowertodemand their shareof valueadded.Thevalueoftheirproductionisoftencapturedbyemployers,intermediariesalongthesupplychain, andespecially the lead firmsat the topof the supply chain.Third,definitionsandmeasuresofproductivityvaryfromsectortosector.And,therearefewdirectmeasuresofthe productivity of the informal enterprises. However, the informal enterprises canpotentially contribute to reduction of poverty and inequality, thereby enabling inclusivegrowthfrombelow.Thischapterguidesw.r.tprioritizationofsubsectorswhichwasasource

9

ofinputforthenextchapter–Chapter4.ThiswasalsoasourceofinputforChapter6(TheHowpartoftheformalizationprocess).

ChapterFourpresentsasummatedviewofthesupport/policiesprovidedtoinformalsectorbyvariousstakeholderssuchasCentralandStateGovernments/Ministries,largescaleNGOs,SocialImpactEnterprises,PrivateSectorCSRActivities,TechnologyFirmsetc.Thesupportincludes measures like skilling, reskilling & upskilling development training of theentrepreneurs,recognitionofpriorlearning(RPL),easeofdoingbusiness,financialsupport,newandimprovedtechnologyimplementation,oranyothermeasurewhichwillhelptheseunitstowardscapacitybuildingandpromotingthemtohaveaformaleconomytouchpoint,betterlivelihoodandaugmentedearnings/employability.Chapterfourisdividedintosevensections.Section4.1istheintroduction.Section4.2envisagesthegovernmentpoliciesthatareworking towards informal sectorwitha sub-classificationon thebasisofkey impactareassuchasFinancialcapital/support,infrastructuressupport,technologicalsupportandother relevant support. Similarly, Section 4.3 is about large scale NGOs with a sub-classificationonthebasisofkeyimpactareas,Section4.4isaboutSocialImpactEnterpriseswithasub-classificationonthebasisofkeyimpactareas,Section4.5isaboutPrivateSectorCSRActivitieswithasub-classificationonthebasisofkeyimpactareasandSection4.6isaboutsupportfromTechnologyFirmswithasub-classificationonthebasisofkeyimpactareas.ThereafterthesupportandinitiativesofgigeconomyhavebeencoveredinSection4.7.

ChapterFivereportsvariouscasestudiesfromthecontextofinformalsector,Indianaswellasglobal.Thesecaseshavebeendrawnfromvariousliteraturetounderstandandexplorethechallengefacedbymicro-entrepreneurs,thatmightincludegapsintermsofaccessinggovernmentpolicies, formal/informal training,access tocapital,markets,monitoringandroleplayedbytechnologyplatforms(ifany)etc.Thesecaseshavebeenborrowedfromtherespectivesourcesandhavebeenacknowledgedwhilementioningexcerptfromarespectivestudy.Thesaidchapterisdividedintosixsections.

Section 5.1 is the introductory sectionwhich is followed by Section 5.2 that presents acomparativeanalysisbetweenformalandinformalenterprisestounderstandnotonlytheworkingmode of a private organisation but also the characteristics informal enterprisespossesswhichmightbedetrimentaltotheirexistenceandsubsequentgrowth.Section5.3dealswithcasestudiesoninformalsectorfromthecontextofIndia.InthissectionvariousIndiancases from informal sectorhavebeencollated.The select cases representvariousinformaleconomicactivitiesbeingcarriedoutinIndiaandwhichrangesfromstreetvendorstohandloomweaverstohardcoremanufacturingactivities.Various inferenceshavebeendrawnandreportedinthesaidsection.Someofthecommonalitiesfoundinthesaidcase

10

studies, are no formal training, lack of awareness about the same, access tomarket andcapital and largely barriers and harassment at multiple levels. Section 5.4 reportsinternationalbestpracticeswherein formalisationof informalsectorhasbeenattempted.MostofthesecaseshadaclearindicationaboutGovt.interventions.Thesaidinterventionsprimarily revolve around tax reforms, certification and accreditation and training andeducation as well as credit support. Section 5.5 collates and presents the problem andchallengesfacedbymicro-entrepreneursingeneralandalsospecifictotheIndiancontextespecially issues in terms of access to finance capital, infrastructure capital, knowledgecapital, lowproductivity,lowqualityproductsandlessvalueadditionperemployees,lowprofitabilityetc.Thissectionstartswithgeneralproblemsof informalsector in Indiaandalsoinselectdevelopingcountriesandisfollowedbythechallengesofaccesstofinancialcapital being faced by informal enterprises. Further it highlights the challenges ofinfrastructurecapitalincludingfeaturesofinfrastructurecapital.Itisfollowedbychallengesof knowledge capital wherein data with respect to education level of the workers andvocational training provided to informal sectorworkers, is presented. The challenges ofproductivityalongwithsupportdatafromselectedcountriesispresentedandissuesrelatedproductivity, low quality of products and less value addition per employees are alsodiscussed. Section 5.6 presents the concluding remarks of the chapter. The chapterconcludeswithanotionthatthegradualandincrementalreformscanfetchbetterresultswith respect to formalisation of Indian informal sector vis-à-vis radical and numerousstructuralchangesininformalsector.

ChapterSixaddressesthe ‘how’partof the formalizationof informalenterprisesstartingwithconnectofvariousprecedingchaptersasapremiseforthecurrentchapter.ThisfirstsectionofthechapterincludessummaryoftheextantliteraturefromChapter2,prioritysub-sectorsidentifiedfromchapter3,insightsfromprimarydata(alimitedsample-independentprimarystudythatwasdonefordelvingdeeperintounderstandingofchallengesofinformalsectorsandwayforwardtowardsformalization),summaryofchallengesandissuesfacedbytheinformalsector(fromchapter5)andsummaryofsupport/policiesandstakeholdersforformalizationofinformalsector(fromChapter4).ThisisfollowedbyabriefaboutexistingecosystemofMSDE,majorschemes,programs, initiativesandprojectsofMSDE,NationalPolicy for Skill Development and Entrepreneurship 2015, beneficiaries for the proposedformalization initiatives and possible approach themes for MSDE’s intervention andmapping with existing MSDE’s initiatives (including the National Policy for SkillDevelopment and Entrepreneurship 2015). The next section presents the SuggestedFramework, Approaches, Actions Points andWorking Plan for MSDE for the process offormalization come into the picture. The suggested framework has two parts to it viz.frameworktowardsformalizationofinformalsectorthroughentrepreneurshippromotion(Section6.3.1)andskillingroutes forenterpriseaswellaslabourpartof the framework.

11

Secondpartbeing framework forefficientaddressingof challenges faced informal sector(Section 6.3.2).Section 6.4 outlines the Due diligence processes for partnerships andstakeholderengagementfollowedbytheconclusion.Thekeycontributionofthechapterarethe proposed framework and the operational strategy to address and facilitate theformalization of informal enterprises into formal economy through entrepreneurshippromotion.

12

Organization of Report & Mapping of Chapters with Terms of Reference (ToR)

13

Chapter1-OrganizationofReport&MappingofChapterswithTermsofReference(ToR)

1.1Introduction

InformalsectorinIndiahasbeencontributingtotheoveralleconomyhistorically.ItiswidelyagreedthatIndiastandsatthecuspofthreevitaltransitions,ifitistotransformitselffromanemergingtoadevelopedmarketeconomy.Theseareruraltourban,farmtofactory,andinformaltoformal1.AsperthelatestreportofInternationalLabourOrganisation(ILO),shareofinformalsectorandofnon-agriculturalinformalsector(viz.manufacturing,constructionand trade) in total employment has been 88.2% and 78.1% respectively in India (ILO(2018)).TheterminformalsectorisoftenusedinterchangeablywithunorganizedsectorinIndiaanditsinterpretationisalsoconsistentwiththatofILO(ChenandVanek(2013)).Itconsistsofallunincorporated(notcoveredunderthefactoriesactandthesocialsecuritylegislationslikeEmployeesStateInsuranceActandProvidentFundAct)privateenterprisesowned by individuals or households engaged in the sale and production of goods andservicesoperatedonaproprietaryorpartnershipbasisandwithlessthantentotalworkers.Theoverwhelmingportionofworkersofthepoorandvulnerablegroups(between94%and98%)areinformalworkers,whiletheyconstitutemuchsmallerproportionoftheworkforceinthemiddleclassorhigherincomegroups(NCEUSReport(2009)).

Theinformalsector,reportedlyhasbeenlessproductivevis-a-visformalsectorastheformalsectorisdrivenbysize,capitalintensiveproduction,accesstocapital,self-selectionbymoreproductive employers for formal activities, technology, taxation and usage of productivepublic distribution in developing countries including India (Esfahani and Salehi-Isfahani(1989)). The Indian informal sector can be characterized with low wages, seasonalunemployment,absenceofbargainingskills,lackofaccesstocreditandinabilitytoaccessgovernmentschemesandinabilitytotakeadvantageofpolicies.Manystudiessuggestthatinformalsectorentrepreneurs’facedifficultiesingainingaccesstocreditandithasbeenoneoftheirmainhandicapsvis-a-vistheformalsector(Kumar(2001)).Therehasbeenalotofgovernmentinterventionthroughvariouspolicyreformshowevernotmuchimpactcouldbeseenatthegroundlevel.

AccordingtoVenkataratnam(2001)andKapoor(2007),effectivestructuresforintegratingthegovernmentinterventionsandtheintendedrecipientsandbeneficiarieshavenotbeenimplementedduetothedifficultyinbalancingsocio-economiccomplexityofadevelopingcountryandtheapparentshifttowardmarketbasedeconomy.Chauduriet.al.(2006)foundthattheliberalizationoftheIndianeconomyin1991-92hadasignificantnegativeimpactontheinformalsector.Siggel(2010)reasonedoutthreefoldfactorsforthesaiddeviationfrom

1https://www.livemint.com/Opinion/ZmfWEAVMWQ5U1lqv7YDfYI/The-challenge-of-formalizing-the-Indian-economy.html

14

the desired impact of policy reforms for informal sector viz. ineffective reach of tradeliberalization; increased international competitivenessof several industries in the formalsectorthroughtheirsubstantialcostreduction;andsubcontractingrestrictingincreaseinlaborsupplyintheinformalsector.

It ispertinent to say that India’s informaleconomyrequiresa shift toward formalizationwhichnotonlyprovidegrowthtotheoveralleconomybutalsototheworkersintheinformalsectorwithapossible routeoutofpoverty (Siggel (2010)).Given the spreadof informalsector in India, which ismarredwith low productivity and poorwages, it is crucial forGovernmentpoliciesandprogramstoaimatinformalenterpriseswhichcansupportthemto move towards formalization. At its 104th Session (2015), the International LaborConferencealsoadoptedtheRecommendationconcerningthetransitionfromtheinformalto the formal economywherein one of the objectives, was to facilitate the transition ofworkers and economic units from the informal to the formal economy,while respectingworkers’fundamentalrightsandensuringopportunitiesforincomesecurity,livelihoodsandentrepreneurship(ILO(2015)).

Inviewof theabove, thepresentstudyendeavourstoexplore informalsector in India interms of various studies existing in the extant literature, numbers and data available incurrentdatabases,existingpoliciesandschemes inplace for furtheringthe formalizationeffortssothatprioritysectorsforMSDE’sfocusofeffortsandpolicy/scheme/frameworkforMSDE’s considerationandpossible implementation forProvidingsupport for formalizingInformalSectorthroughEntrepreneurshipPromotion.

Themainaimofthischapteristointroducebriefbackgroundaboutinformalsectorandtospecifically conceptualize/operationalize thedefinitionsof informalsector, formalsector,formalization,capacitybuildingandentrepreneurship.ThiswillbefollowedbymappingofTermsof Referencewith various chaptersof the report. The chapter is divided in to sixsectionincludingSection1.1.ofintroduction.Section1.2presentsabriefofMSDE.ThisisfollowedbySection1.3whereintheconceptual/operationaldefinition(s)ofinformalsector,formal sector, formalization, capacity building, entrepreneurship promotion andentrepreneurshipasreferredtointhereportarelisted.Approachtothestudyisbriefedinsection1.4.Itisfollowedbydescriptionofdifferentapproachestoformalizationascitedintheliteratureinsection1.5.Section1.6encompassesthescopeofthepresentstudyasgivenin theTerms of Reference of theRFP alongwith itsmappingwith the various Chapters(Chapter2to7)ofthepresentreport.Thissectionalsogivesanoverarchingviewofthebriefoutlineofthereport.

15

1.2MinistryofSkilldevelopmentandEntrepreneurship(MSDE)

“TheMinistry is responsible for co-ordination of all skill development efforts across thecountry,removalofdisconnectbetweendemandandsupplyofskilledmanpower,buildingthevocationalandtechnicaltrainingframework,skillup-gradation,buildingofnewskills,and innovative thinking not only for existing jobs but also jobs that are to be created”(Source:https://www.msde.gov.in).“TheMinistryaimstoSkillonalargeScalewithSpeedand high Standards in order to achieve its vision of a 'Skilled India'” (Source:https://www.msde.gov.in)

“Itisaidedintheseinitiativesbyitsfunctionalarms–DirectorateGeneralofTraining(DGT),NationalSkillDevelopmentAgency(NSDA),NationalSkillDevelopmentCorporation(NSDC),National Skill Development Fund (NSDF), Indian Institute of Entrepreneurship (IIE),NationalInstituteofEntrepreneurshipandSmallBusinessDevelopment(NIESBUD),and37Sector Skill Councils (SSCs)2 aswell as 187 training partners registeredwithNSDC. TheMinistry also intends to work with the existing network of skill development centres,universitiesandotheralliances in the field.Further, collaborationswith relevantCentralMinistries, Stategovernments, internationalorganizations, industryandNGOshavebeeninitiated for multi-level engagement and more impactful implementation of skilldevelopmentefforts”(Source:https://www.msde.gov.in).

“The present Government has taken multiple initiatives in this direction, with severalGovernmentMinistries/Departmentssupportingentrepreneurshipthroughoneortheotherscheme.However,entrepreneurshipsupport in truesensedoesn’tgetpercolatedtoruralareasduetolackofaccessoftheseschemes.Toovercomethesechallenges,theMinistryofSkill Development andEntrepreneurship (MSDE) is expected towork towards providingnecessarygrowthsupporttoinformalenterprisestoenablethemtomovetowardsformalsectorandthuscontributepositivelytowardsIndia’sgrowthstory”(Source:RFPDocumentof the present study). As per the ministry sources, MSDE is guided with two policyframeworks, i.e., National Skill Development Policy 2009, and National Policy on SkillDevelopmentandEntrepreneurship,2015(Source:https://www.msde.gov.in).

1.2.1.DirectorateGeneralofTraining(DGT)

“TheDirectorateGeneralofTrainingconsistsoftheDirectorateofTrainingandDirectorateofApprenticeTraining.This includesanetworkof IndustrialTraining Institutes (ITIs) inStates; National Skills Training Institutes (NSTIs), National Skills Training Institutes forWomen(NSTI-W)andothercentralinstitutes.AnumberoftrainingProgrammescateringtostudents, trainers and industry requirements are being run through this network. Thebuildingblocksforvocationaltraininginthecountry-IndustrialTrainingInstitutes-playavitalroleintheeconomybyprovidingskilledmanpowerindifferentsectorswithvarying

2 https://www.msde.gov.in/ssc.html

16

levelsof expertise. ITIsareaffiliatedbyNationalCouncil forVocationalTraining (NCVT).DGT also operationalizes the amended Apprentices Act, 1961” (Source:https://dgt.gov.in/About_DGT)

MajorfunctionsoftheDGTare:• Toframeoverallpolicies,normsandstandardsforvocationaltraining.• Todiversify,updateandexpandtraining facilities in termsofcraftsmenandcrafts

instructortraining.• Toorganizeandconductspecializedtrainingandresearchatthespeciallyestablished

trainingInstitutes.• Toimplement,regulateandincreasethescopeoftrainingofapprenticesunderthe

ApprenticesAct,1961.• ToorganizevocationaltrainingProgrammesforwomen.• Toprovidevocationalguidanceandemploymentcounselling.• Assistscheduledcastes/scheduledtribesandpersonswithdisabilitiesbyenhancing

theircapabilitiesforwageemploymentandself-employment”.

The Craftsmen Training Scheme (CTS): “The scheme for training of skilled craftsmen isimplementedthroughGovt.andPvt.IndustrialTrainingInstitutes(ITIs)whichareundertheadministrative and financial control of State Governments or Union TerritoryAdministrations.Durationofthesetrainingcoursesvariesfrom6Months-2Yearsduration,NSQFcompliantcoursesin138Tradeswhichincludes74Engineeringtrades,59TradesintheNon-EngineeringSectorand05coursesforPersonswithDisabilities(PwD)/Divyangjan.Currently,23.15Lakhpersonsareundergoingtrainingin14,491ITIs(bothGovt.&Pvt.)”(Source:https://dgt.gov.in/About_DGT).Accordingtoanotherstatistics23,14,000personsaregoingundertrainingin14,917ITIs.Thenumberofapprenticesare197,053(Source:https://dgt.gov.in/).

TheschemesofDGTincludeSchemeforTraining-craftstrainingscheme(CTS),flexiMOU,dualsystemof training,AdvancedVocationalTrainingScheme (AVTS),ApprenticeshipTraining;Training for Trainers - Crafts Instructor Training Scheme (CITS): Scheme for creation/improvement of training infrastructure- Enhancing Skill Development Infrastructure inNorth Eastern States(ESDI), Skill Development in 47 Districts Affected by Left WingExtremism(LWE), Upgradation of 1396 Govt. ITIs through PPP, Skills Strengthening forIndustrialValueEnhancement (STRIVE),UpgradationofGovernment ITIs intoModel ITI,GradingofITI's,andVocationalTrainingImprovementProject;andschemeforSchemeofPolytechnics.DGTconductsexamination forCITSandpublishes itsresultson itswebsite.DGT has signed different MOU with its partners from industry to achieve the overallobjectivesoftheministry.

MOUsSigned:IthassignedMOUswithIBM,NIOS,SAP,CISCO,NASSCOM,and(Accenture+Cisco+Quest) Alliance. In addition,MoU for strategic partnership on skill development

17

betweenMSDEandDassaultAviation,andNSTI,RDSDEMumbaiandHPCLMumbaiunderCSR is signed. Further, a letter of understanding between DGT& Reliance Jio Infocommlimitedissigned.

1.2.2NationalSkillDevelopmentAgency(NSDA)

NationalSkillDevelopmentAgency(NSDA)isanautonomousbodyunderMinistryofSkillDevelopment and Entrepreneurship that anchors the National Skill QualificationsFrameworkandalliedqualityassurancemechanismsforsynergizingskillinitiativesinthecountry(Source:https://www.nsda.gov.in/nsda-about-us.html)

TheNationalSkillsQualificationsFramework(NSQF)organizesqualificationsaccordingtoaseriesoflevelsofknowledge,skillsandaptitude.Theselevelsaredefinedintermsoflearningoutcomeswhichthelearnermustpossessregardlessofwhethertheywereacquiredthroughformal, non-formal or informal learning. In that sense, the NSQF is a quality assuranceframework. It is, therefore, anationally integratededucationandcompetencybased skillframeworkthatwillprovideformultiplepathways,horizontalaswellasvertical,bothwithinvocational educationandvocational trainingandamongvocational education, vocationaltraining, general education and technical education, thus linking one level of learning toanother higher level. In addition, it maintains the National Labour Market InformationSystem(LMIS).

As per the dashboard of LMIS, the ecosystem consists of 20350 courses, 45401 trainingcenter,6343trainingproviders,95050trainers,57675assessors,623assessmentbodies,442 certified bodies. According to another statistics, it has data of 9944385 certifiedcandidates. Another functions of NSDA is provide The National Quality AssuranceFramework (NQAF) aims to improve the quality of all education and training/skillsProgrammesinIndia,andNationalSkillResearchDivision(NSRD).WedidnothaveaccesstoLMIS.ItisnotpossibletoknowtypeofdataisstoredwithLMIS.

1.2.3NationalSkillDevelopmentCorporation(NSDC)

“NSDCaimstopromoteskilldevelopmentbycatalyzingcreationoflarge,qualityandfor-profitvocational institutions.Further, theorganizationprovides fundingtobuildscalableandprofitablevocationaltraininginitiatives.Itsmandateisalsotoenablesupportsystemwhich focusesonqualityassurance, informationsystemsandtrainthetraineracademieseither directly or through partnerships. NSDC acts as a catalyst in skill development byprovidingfundingtoenterprises,companiesandorganizationsthatprovideskilltraining.Italso develops appropriate models to enhance, support and coordinate private sectorinitiatives.AsperitsdataasonJuly31,2019,ithad462trainingpartners,11000trainingcenters,2100 jobroles,38SSCs. Ithaspresence in29statesand6unionterritories,andtrained1.12crorepersons.Ithasplaced50.68lakhstrainedpersons.ItsschemesincludePradhanMantriKaushalVikasYojana (PMKVY),PradhanMantriKaushalKendra,Udaan,

18

International Skill Training, and Technical Intern Training Program (TITP)” (Source:https://nsdcindia.org/)

1.2.4NationalSkillDevelopmentFund(NSDF)

TheNationalSkillDevelopmentFundwassetup in2009bytheGovernmentof India forraisingfundsbothfromGovernmentandnon-Governmentsectorsforskilldevelopmentinthe country.TheFund is contributedbyvariousGovernmentsources, andotherdonors/contributorstoenhance,stimulateanddeveloptheskillsofIndianyouthbyvarioussectorspecificprograms.ApublicTrustsetupbytheGovernmentofIndiaisthecustodianoftheFund.TheTrustacceptsdonation,contribution incashorkind fromtheContributors forfurtheranceofobjectivesoftheFund.TheFundisoperatedandmanagedbytheBoardofTrustees. The Chief Executive Officer of the Trust is responsible for day-to-dayadministrationandmanagementoftheTrust.

1.2.5TheIndianInstituteofEntrepreneurship(IIE)

“Indian Institute of Entrepreneurship (IIE) is an autonomous organization under theMinistry of Skill Development & Entrepreneurship. The main aim of the Institute is toprovidetraining,researchandconsultancyactivitiesinSmallandMicroEnterprises(SME),withspecialfocusonentrepreneurshipdevelopment”(Source:http://iie.nic.in/)

1.2.6TheNationalInstituteforEntrepreneurshipandSmallBusinessDevelopment(NIESBUD)

ItisanorganizationoftheMSDE,engagedintraining,consultancy,research,etc.inordertopromote entrepreneurship and Skill Development. The major activities of the InstituteincludeTrainingofTrainers,ManagementDevelopmentProgrammes,Entrepreneurship3-cum-Skill Development Programmes, Entrepreneurship4 Development Programmes andClusterIntervention.

1.2.7SectorSkillCouncils(SSC)

SectorSkillCouncilsaresetupasautonomous industry-ledbodiesbyNSDC.TheycreateOccupationalStandardsandQualificationbodies,developcompetencyframework,conductTraintheTrainerPrograms,conductskillgapstudiesandAssessandCertifytraineesonthecurriculum aligned to National Occupational Standards developed by them (Source:https://www.msde.gov.in/ssc.html. As on date, 37 Sector Skill Councils (SSCs) areoperational.Intotal,thereare39SSCs.Thereareover600CorporateRepresentativesintheGoverningCouncilsoftheseSSCs.

3 Entrepreneurship is the process of designing, launching and running a new business, which is often initially a small business. The people who create these businesses are called entrepreneurs. 4 An entrepreneur is an individual who starts and runs a business with limited resources and planning, and is responsible for all the risks and rewards of his or her business venture. The business idea usually encompasses a new product or service rather than an existing business model.

19

1.2.8Trainees/Beneficiaries

MSDEhas largenumberof traineesasevident fromthedatagivenat theMSDEwebsite.Thesebeneficiariesbelongtodifferentcategories.Thedetailsareavailableinvariousreportsofgovernmentandreportspublishedbytheotherorganizationsandexperts.ThetraineesofMSDEare(i)whohadnotattendedtheschoolandcolleges(maybeatargetpopulationofJSSs),(ii)dropoutsfromuniversities,colleges,andschools,(iii)studentswhocannotaffordthecostofhighereducationandforcedtobearresponsibilitiesofthefamiliesunderforcedcircumstancesbutreadytodosomething,(iv)citizenswhoarewillingtolearnandalsohadwilltostarttheirownbusinessoranyotheractivitytoenhanceearnings,(v)citizenshavingtheirinformalunitsandplanningtotaketheseunitstothenextleveletc.

1.2.9CapacityDevelopers

MSDEhasalargegroupofcapacitydevelopersincludingmastertrainer,trainers,mentors,assessors,contentdeveloper,qualitymonitor,etc.ThesecapacitydevelopersarepartnerofMSDEasan individualorasanorganization.Thedetailsof thesecapacitydevelopersareavailablewithwebsite ofMSDE ormembers of its ecosystem. These are very importantcomponentofecosystemofMSDE.

TheinformationaboutMSDEanditsstakeholdersalongwithresearchdoneinthefirstfivechapters of this report combined with existing policy for entrepreneurship and skilldevelopmentwillpaveway fora frameworkandworkingplan for transitionof informalenterprisestotheformaleconomyusingentrepreneurship.

Fromaresearchstudyperspective,sometentativeconstructs thatwere lookedbyus fordelvingdeeperinsideintothephenomenaoftransmutationofinformaleconomybusinessandentrepreneursintoformaleconomybusinessandentrepreneursaregiveninthenextsection.

1.3 Conceptual/Operational Definitions of major concepts used in thereport

There are various descriptions and definitions of informal sector, formal sector,formalization,capacitybuildingandentrepreneurshipavailableintheliterature.Theaimofthissub-sectionistoenlistsomeoftheavailableconceptualdefinitionsinliteraturefortheaforementioned concepts and to finally present the definition(s) that will be used fordescribing and defining the concepts of informal sector, formal sector, formalization,capacitybuildingandentrepreneurshipinthepresentreport.

1.3.1InformalSector

Theterminformalsectorisusedinterchangeablywithunorganizedsector(Source:ChenandVanek,(2013)).Sincetheveryonset,theconceptanddefinitionofinformalsectorhasbeena subject of debate both at the national and international levels. Hart (1970) first

20

introduced this sectoras unregulatedeconomicenterprises.Followed by InternationalLabourOffice(1972)camewithanofficialdefinitionbasedoncertaincharacteristicsofthe enterprises.Even thoughmost of the international studies have used theterm“informalsector”, Central Statistical Organization (CSO) in India introduces thissector as “unorganized sector” in itsreportonNationalAccountsStatistics.An explicitdefinition of the informal sector in the Indian context distinguishing betweenunorganizedandinformalsectorisprovidedbyNationalSampleSurveyOrganization(2000)5.

Definition1:According to NSSO, the informal sector incorporatestheunincorporatedproprietiesorpartnershipenterprisesoftheAnnualSurveyofIndustries(ASI).Intheunorganized sector, in addition to the unincorporated proprieties or partnershipenterprises,enterprisesrunbycooperativesocieties,trusts,privateandlimitedcompaniesarealsoincluded.Theinformalsectorcan,therefore,beconsideredasasub-setoftheunorganizedsector.

Definition2:Itconsistsofallunincorporated(notcoveredunderthefactoriesactandthesocial security legislations like Employees State Insurance Act and Provident Fund Act)privateenterprisesownedbyindividualsorhouseholdsengagedinthesaleandproductionofgoodsandservicesoperatedonaproprietaryorpartnershipbasisandwithlessthantentotalworkers(Source:NCEUSReport(2009),page357).

Definition3: “Productionunitsof the informal sectorweredefinedby the15th ICLSasasubsetofunincorporatedenterprisesownedbyhouseholds, i.e.asasubsetofproductionunitswhicharenotconstitutedasseparatelegalentitiesindependentlyofthehouseholdsorhouseholdmemberswhoownthem,andforwhichnocompletesetsofaccounts(includingbalancesheetsofassetsandliabilities)areavailablewhichwouldpermitacleardistinctionoftheproductionactivitiesoftheenterprisesfromtheotheractivitiesoftheirownersandtheidentificationofanyflowsofincomeandcapitalbetweentheenterprisesandtheowner”(HussmannsandMehran(1994)).

Definition4:Theinformalsector,alsoknownastheundergroundeconomy,blackeconomy,shadoweconomy,orgreyeconomy,ispartofacountry’seconomythatisnotrecognizedasnormalincomesources6.

Ifoneweretolookatthemajorfeaturesoftheaforementionedfivedefinitionsthenwewould conclude that Informal Sector Unitsmainly comprise of enterprises notmandatorily coveredunder any of the legislations (acts, laws and rules) of thecountrysuchassocialprotection/welfare,companyregistrationlegislation,labourlegislationorunderthetaxnet;andexcludingillicitactivities.Thisisthedefinition

5 Distinction between Informal and Unorganized Sector: A Study of Total Factor Productivity Growth for Manufacturing Sector in India. Available from:https://www.researchgate.net/publication/268366658_Distinction_between_Informal_and_Unorganized_Sector_A_Study_of_Total_Factor_Productivity_Growth_for_Manufacturing_Sector_in_India [accessed May 26 2020] 6 https://marketbusinessnews.com/financial-glossary/informal-sector-definition-meaning/

21

thatILOinitspoint204in104th InternationalLabourConferenceinJune2015envisaged7.

1.3.2FormalSector

Definition 1: According to IGI global, formal sector encompasses all economic activitiesoperatingwithintheofficiallegalframeworkthatarepayingtaxesonallgeneratedincomes8.

Definition 2: Additional viewpoints about definitions of formal sector, comprehenddistinction between formal and informal sector as (a) whether a worker has a formalcontract;(b)whetheraworkerisaregular/salariedworker(asopposedtoself-employedorcasual);(c)whetherafirmisregisteredwithanybranchofthegovernment;(d)whetherthefirmpaystaxes;and(e)whetheraworkerreceivessocialsecurity9.

Definition3:SociologyGroupdefinesFormalsectoras-“Formalsectorasactivitieswhich are taxed andmonitoredby the government and the activities involved areincluded in the Gross Domestic Product(GDP)” (Source:https://www.sociologygroup.com/formal-informal-sector-differences/)

1.3.3Formalization

Definition1:Broadlytherearetwoviewsonthedebateonformalizingtheinformaleconomy: Capital viewconsiders inclusionofenterprises in the formal taxandfinancialsystems;andlabourviewconsidersinclusionofworkersinthesocialprotectionsystem2.Thisisthebroadworldviewthathasbeenusedasananchorforconceptualizationoftheconceptofformalizationinthereport.

Definition2:Also, formalizationhasbeenconceptualizedbroadlyas theprocessofbringingmorebusinessfirmsandhouseholdsunderthetaxandregulatorynets—whether of corporate tax, personal income tax,GST, provident fund contributions,labourlaws,environmentalregulationsoranyotherregulations10.Thisisthebroadworldviewthathasbeenusedasananchorforoperationalizationofformalizationinthereport.

1.3.4UnorganizedSector

Definition1:Unorganisedsectorisdefinedasthatsetofeconomicactivitiescharacterizedbyrelativeeaseof entry, relianceon indigenousresources, smallscaleofoperations, labour

7 The recommendation defined the term “informal economy” as: “all economic activities by workers and economic units that are—in law or in practice—not covered or insufficiently covered by formal arrangements; and does not cover illicit activities...”. This definition of economic activities and units would cover informal workers and enterprises under any of the legislations such as access to social protection, labour legislation or under the tax net. Formalization of the Informal Economy: Perspectives of Capital and Labour. Available from: https://www.researchgate.net/publication/327731542_Formalization_of_the_Informal_Economy_Perspectives_of_Capital_and_Labour [accessed May 26 2020]. 8 https://www.igi-global.com/dictionary/formal-economy/68313 9https://www.news18.com/news/business/economic-survey-for-the-first-time-estimates-size-of-formal-and-informal-sector-in-india-1645105.html 10 https://www.livemint.com/Opinion/ZmfWEAVMWQ5U1lqv7YDfYI/The-challenge-of-formalizing-the-Indian-economy.html

22

intensiveoperations,relianceonskillsacquiredoutsidetheformaleducationalsystemandunregulatedcompetitivemarket(ILO,1983)11

Definition2:AccordingtoNCEUSReport,2007-"Theunorganizedsectorconsistsofallunincorporatedprivateenterprisesownedbyindividualsorhouseholdsengagedin the sale and production of goods and services operated on a proprietary orpartnershipbasisandwithlessthantentotalworkers"12.

1.3.5CapacityBuilding

Definition: Capacity, according to OECD/DAC ―...is understood as the ability of people,organisationsandsocietyasawholetomanagetheiraffairssuccessfully‖.TheAgenda21ofthe United Nations Conference on Environment and Development (UNCED), CapacityBuildingwasdefinedinthefollowingway:―CapacityBuildingencompassesthecountry’shuman,scientific,technological,organizational,institutionalandresourcecapabilities13.

1.3.6Entrepreneurship

Definition: Entrepreneurship refers to the capacityandwillingness tostart,maintainandcontinuously improve a productive and gainful business venture whilst innovativelymanagingassociatedrisks.Beinginvolvedinalivelihoodactivityforsubsistencepurposesisnotanactofentrepreneurship14

1.3.7EntrepreneurialSkills

Definition:Entrepreneurialskillssuchasinnovativeness,problemsolvingskills,risktaking,customercare,selling(counting,addingandsubtracting–sortingoutchange),confidenceandcommunicationskills10.

1.4ApproachtoStudy

Theoverarchingmethodologyforthisstudyencompassesthefollowingsteps:

Systematic analysisof available secondary informationanddatabases for informal sectorclassification and estimation in India. This involved the following sub-phases: DataCollection,data reduction,datadisplay, anddrawingconclusions;with constant iterationbetween the analytical stages. Data reduction involves selecting, focusing, simplifying,abstracting, and transforming the data in the field notes or transcripts into summaries,coding,testingthemes,etc.Thissorts,discards,andorganizesthedatasothatconclusionscanbedrawn.

11 https://shodhganga.inflibnet.ac.in/bitstream/10603/219828/10/10_chapter%203.pdf 12 http://www.publishingindia.com/GetBrochure.aspx?query=UERGQnJvY2h1cmVzfC8xMTg1LnBkZnwvMTE4NS5wZGY= 13 https://openei.org/w/images/8/80/Best_Practices_in_Capacity_Building_Approaches.pdf 14 https://unevoc.unesco.org/e-forum/INFORMAL_SECTOR_STUDY.pdf

23

Collectionofsecondaryinformation:Collectionofinformationthatisalreadyavailablefromthearchivesanddatastoresfromidentifiedexternalinstitutionsandorganizationsisdone.

Collectionofprimaryinformation:Collectionofprimaryinformationwasdonewithaviewtofill the information gaps to some extent that were arising due to limited secondaryinformation availability/access. Herein it is pertinent to be reiterated that this study isprimarilybasedonsecondarydata.

Providingaccesstoinformation:Thispartofapproachofthestudyisaboutthedisseminationofthefindingsofstudy.Disseminationincludesgovernmentorganizationmayhaveaccesstothecompiledinformationandallowingcivilsocieties/citizens/entrepreneurs/informalsector to benefit from this additional amount of knowledge. This can be done using astakeholderworkshopinlightofthefinaldraftreportofthisstudytohaveaparticipativeconfirmationofthefindingsandsuggestionsofthereport.Thishelpedintheevolutionoftheproposed frameworkof formalizationof informal sector through entrepreneurshippromotion(asgiveninChapter6).

To add rigor and value to this study, this detailed researchwork has employed a pluralresearchdesign(combinationofexploratory,descriptiveandconclusive).Thepurposeistoportraytheaccuratesituationswithrespecttothepoliciesandpolicyinstrumentsconcernedandtheprojectdeliverables.

1.5BriefaboutApproachesofFormalization

Theobjectivesof includingthissectionis tobrieflyexplaintheapproachofformalizationbasedonthesecondarydataavailableintheliterature.

Itisevidentfrommanystudiesthattwosectorofeconomyhavedependencyoneachother.Hassan et al (2010) studied some aspect of formal and informal sectorwithin a generalequilibriumframeworkofadevelopingeconomywithaforeignownedfactorofproduction.They raised questions whether the informal-formal sector relationship is procyclical/complementary–expansionorcontractioninonenecessarilyimpliesanexpansionorcontractionintheother–whentheinformalsectorissubjecttoatechnologicalshock.Theyalsodiscussedtheissuesthatderiveanecessaryandsufficientconditionunderwhichapositiveshocktotheinformalsectorresultsinacontractioninboththesizeoftheurbanformalsectorandtheinformalsector.Theresultsoftheirstudyindicatedthattheinformal-formalsectorrelationshipisprocyclical,itneverthelesscallsintoquestiontheconventionalwisdom on the benefits of intervention in the informal sector of developing economies,particularlywheremultinationalcorporationssub-contractcertainlaborintensivestagesofproductiontotheinformalsector.

Unni(2018)mentionedthattherearetwoviewsonthedebateofformalizingtheinformaleconomy.Theseare(i)capitalviewwhichconsidersinclusionofenterprisesintheformaltaxandfinancialsystems;and(ii)labourviewwhichconsidersinclusionofworkersinthesocial

24

protection system. Unni (2018) further mentioned that those argue about inclusion ofinformalunits in thetaxnetorrecommendtransactingthroughformalbankingchannelsconstitutes formality are more concerned with inclusion of enterprises in formalaccountableandtraceablesystems.ShealsomentionedthatinarecentResearchConferenceontheInformalEconomyinHarvardUniversity,participantsarguedthatthecapitalviewofformalizationisnotformalizationbutjust“Normalization”,allenterprisesandworkersareincluded in the same “net”. From the lens of labour formalization iswhenworkers areincluded in the social security systems. She advocated like many others countries theperspectivefromthelabourviewbetakenintoaccountforformalization.Itwillcoverwiderconsiderations such as redistribution of wealth, tackling poverty, inequality andvulnerability.

WIEGO15mentioned that formalizationof the informaleconomycan takedifferent formssuch as registration, taxation, organization and representation, legal frameworks, socialprotection,businessincentives/support,andmore.Formalizationmeansdifferentthingstodifferentcategoriesoftheinformalworkforce.Whatisneededonpartofregulatorsisanapproach to formalization of the informal economy that is comprehensive in design butcontext-specificinpractice.Theapproachtoformalizationinbitmoredetailisgivenintheformofschemesandsubschemeofformalizationofenterprisesaslistedbelow:

(i) “RegistrationandTaxation16:o Thereisaneedforsimplifiedregistrationproceduresinthecontextofmicro

entrepreneurso Progressiveregistrationfees

(ii) Appropriatelegalandregulatoryframeworks,including:o Enforceablecommercialcontractso Privatepropertyrightso Useofpublicspacefordoingthebusiness

(iii) Benefitsofoperatingformally:o Accesstofinanceandmarketinformationthroughdifferentchannelsincluding

governmentchannels.o Accesstopublicinfrastructureandserviceso Enforceablecommercialcontractso Limitedliability.Asperthepresentregulationfortheproprietorship&

partnershipthereisunlimitedliabilityo Clearbankruptcyanddefaultruleso Accesstogovernmentsubsidiesandincentives,includingprocurementbidsand

15 https://www.wiego.org/rethinking-formalization 16 A tax or tax system is considered progressive if the tax burden as a percentage of income increases as the level of income increases. The degree of progressivity or regressivity can be measured by the ratio of tax burden at the lowest income level to the tax burden at the highest income level.

25

exportpromotionpackageso Membershipinformalbusinessassociationsevenstatusoftheunitisinformal.o Accesstoformalsystemofsocialsecurityshouldbeextendedtoinformalunits”

Informalizingaspecificgroupsofinformalworkers,policymakersandpractitionersshouldchooseappropriateelementsfromthisframeworkandtailortheinterventionstomeetlocalcircumstances/requirements.

1.6ScopeofthepresentstudyandBroadOrganizationofthereport

1.6.1ConductingaComprehensiveStudy,throughtheexistingdatabases(alreadycommissionedStudies,PrivateReportsetc.)tounderstandtheInformalSector

Activities

A1. PerformingaliteraturereviewoftheStudiesconductedintheInformalSectoraimedatformalization.

A2. Mapping the current available database (national as well as state level) such asNCEUS, Economic Survey, MOSPI, NSSO, data available with various relevantMinistriesandotheravailableReports toprovidean in-depthReportonextentofInformalSectorinIndia.(Theanalysiswouldcoverextentof InformalSectorinallStatesandUnionTerritories,providingapercentagebreak-upbetweenformalandinformalenterprisesundereachSector).

A3. Mapping all the Policies and Support provided to Informal Sector by variousstakeholders suchasCentral andStateGovernments/Ministries, large scaleNGOs,Social ImpactEnterprises,PrivateSectorCSRActivities,TechnologyFirmsetc.andidentifying agencieswhich are carrying out the related ground level support andimplementationactivities.

A4. ReviewingCaseStudies,workingmodeofprivateorganizations,internationalbestpracticesetc. tounderstandthechallenge facedbymicro-entrepreneurs, includinggapsintermsofaccessinggovernmentpolicies,formal/informaltraining,accesstocapital,markets,monitoringandroleplayedbytechnologyplatforms(ifany)etc.

Outcomes

O1. EstimationofinformalenterprisesanddetailedclassificationofinformalenterprisesundervariousSectorsandSub-sectors.

O2. Classification of informal enterprises leading to identification of priority sectors(based on various parameters like employment, economic contribution,inclusiveness,geographyetc.)andstates/departments/industryassociationsetc.forMSDEtofocuson.

26

O3. IdentificationofChallenges(KeyIssues) facedbymicro-entrepreneurs,especiallyissuesintermsofaccesstofinancecapital,infrastructurecapital,knowledgecapitaletc.

1.6.2ExploringPotentialRoleofMSDEDiscussing the results of comprehensive desktop research with a Panel of Experts in‘StakeholderWorkshop’withaviewtoidentifyareasofinterventionforMSDEinordertosupport conversion of informal enterprises to formal ones. The Panel will consist ofrepresentativeofstakeholdersintheentrepreneurialspace,suchasenablingagenciesandincubators, impact investors, NGOs, key sector experts, technology firms and financialinstitutionsprovidingsupporttomicro-enterprisesintheinformalsectoraswellaspolicymakingbodies.

Activities

A1. Developing a framework of approach based on possible synergies across thestakeholdersintheeco-systemforfacilitatingformulationofPolicybyMSDE.

A2. ConductingStakeholderWorkshopsaswellas individual interviewstodiscusstheimplicationsofdesktopresearchconducted.

A3. DeliberatinganddiscussingvariousapproachesthatcouldbeadoptedbyMSDEtosupportconversionofinformalenterprisestoformalones.

Outcomes

O1. Validation of action points with the identified stakeholders to create aroadmap/guidelinesforMSDEtoprovidenecessarysupporttoenablemovementofinformal enterprises towards the formal sector through exploring variousapproachesandsolutions,includingdisruptivedigitaltechnologysolutionsasthekeyanchorpoint.ThiswouldalsoincludethepotentialroleofMSDEandthesupportitmayprovidetoinformalenterprisesintermsofskills,training,accesstomarketsandcapital,mentoringandcapacitybuilding.

O2. Providing a solution/working plan in order to align all support schemes gearedtowardsinformalsectortoremoveduplicityandincreaseimpact.

O3. Proposing an operational framework to MSDE for implementation by clearlyidentifyingmission, vision, due diligence processes for partnerships, yearly plans,governancemodel,digitalplatformandsupporteco-systems(compliancehandling,paymentsolutions,B2B,B2CandG2Bnetworkingetc.),convergenceetc.

Giventheaforementionedactivitiesandoutcomes,theresearchteamatMDI,envisagedthepresentreportinamannersuchthatthereispointtopointmappingofthescope(includingvariousactivitiesandoutcomesofthepresentstudy)asgivenintheTermsofReferenceof

27

theRFPalongwiththevariousChapters(Chapter2to7)ofthepresentreport.ThesamehasalsobeendescribedinTable1.1.

28

Table1.1MappingofthescopeofthepresentstudyasgivenintheToRoftheRFPthevariousChaptersofthepresentreport

ChapterS.No.(Asper theReport)

Chapter Title (Asperthereport)

Scope of theStudy&S.No.asperToR

S.No. asper ToRfor therespectiveActivity/Outcome

ActivitytitleasperToR

Outcome title as perToR

2

Literature Reviewsof Studiesconducted in theinformalsector

3.1Conducting aComprehensive Study,through theexistingdatabases(alreadycommissionedStudies,PrivateReports etc.)to understandthe InformalSector

3.1.1.1

Performing aliterature review ofthe Studiesconducted in theInformal Sectoraimed atformalization.

-

3

Mapping thecurrent availabledatabases plusmapping theextentofInformalSector

3.1.1.2

Mappingthecurrentavailable database(national aswell asstate level) such asNCEUS, EconomicSurvey, MOSPI,NSSO,dataavailablewith variousrelevant Ministriesand other availableReports to providean in-depthReporton extent ofInformal Sector inIndia. (The analysiswould cover extentofInformalSectorinallStatesandUnionTerritories,providing apercentage break-up between formaland informalenterprises undereachSector).

-

4

Mapping thepolicies & supportfrom stakeholdersand agenciesworkingonground

3.1.1.3

Mapping all thePoliciesandSupportprovided toInformal Sector byvariousstakeholders suchasCentralandStateGovernments/Ministries, large scaleNGOs,SocialImpactEnterprises, PrivateSector CSR

-

29

ChapterS.No.(Asper theReport)

Chapter Title (Asperthereport)

Scope of theStudy&S.No.asperToR

S.No. asper ToRfor therespectiveActivity/Outcome

ActivitytitleasperToR

Outcome title as perToR

Activities,Technology Firmsetc. and identifyingagencies which arecarrying out therelatedgroundlevelsupport andimplementationactivities.

5

Reviewing CaseStudies andIdentification ofChallengesfacedbytheinformalsector

3.1.1.4

Reviewing CaseStudies, workingmode of privateorganizations,international bestpractices etc. tounderstand thechallenge faced bymicro-entrepreneurs,including gaps interms of accessinggovernmentpolicies,formal/informaltraining, access tocapital, markets,monitoringandroleplayed bytechnologyplatforms (if any)etc.

-

3

Mapping thecurrent availabledatabases plusmapping theextentofInformalSector

3.1.2.1 -

Estimationof informalenterprises anddetailed classificationofinformalenterprisesunder various SectorsandSub-sectors.

3Identification ofPrioritySectors

3.1.2.2 -

Classification ofinformal enterprisesleading toidentification ofprioritysectors(basedonvariousparameterslike employment,economiccontribution,inclusiveness,

30

ChapterS.No.(Asper theReport)

Chapter Title (Asperthereport)

Scope of theStudy&S.No.asperToR

S.No. asper ToRfor therespectiveActivity/Outcome

ActivitytitleasperToR

Outcome title as perToR

geography etc.) andstates/departments/industry associationsetc. forMSDE to focuson.

5

Reviewing CaseStudies andIdentification ofChallengesfacedbytheinformalsector

3.1.2.3 -

Identification ofChallenges (KeyIssues)facedbymicro-entrepreneurs,especially issues interms of access tofinance capital,infrastructure capital,knowledgecapitaletc.

6

Roadmap/Guidelines for MSDE tosupportFormalization ofInformalSector

3.2 ExploringPotential RoleofMSDE

3.2.2.1

Developing aframework ofapproach based onpossible synergiesacross thestakeholders in theeco- system forfacilitatingformulation ofPolicybyMSDE.

-

DependsonProposedStake-HolderWorkshop

3.2.2.2

ConductingStakeholderWorkshops as wellas individualinterviews todiscuss theimplications ofdesktop researchconducted.

--

6 +Results ofProposedStakeHolderWorkshop

3.2.2.3

Deliberating anddiscussing variousapproaches thatcouldbeadoptedbyMSDE to supportconversion ofinformalenterprises toformalones.

-

6Roadmap/Guidelines for MSDE tosupport

3.2.3.1 -

Validation of actionpoints with theidentifiedstakeholdersto create a

31

ChapterS.No.(Asper theReport)

Chapter Title (Asperthereport)

Scope of theStudy&S.No.asperToR

S.No. asper ToRfor therespectiveActivity/Outcome

ActivitytitleasperToR

Outcome title as perToR

Formalization ofInformalSector

roadmap/guidelinesfor MSDE to providenecessary support toenable movement ofinformal enterprisestowards the formalsector throughexploring variousapproaches andsolutions, includingdisruptive digitaltechnology solutionsas the key anchorpoint. Thiswould alsoinclude the potentialrole of MSDE and thesupportitmayprovidetoinformalenterprisesin terms of skills,training, access tomarkets and capital,mentoring andcapacitybuilding.

6

Roadmap/Guidelines for MSDE tosupportFormalization ofInformalSector

3.2.3.2

Providing a solution/working plan in orderto align all supportschemes gearedtowards informalsector to removeduplicity and increaseimpact.

6

Roadmap/Guidelines for MSDE tosupportFormalization ofInformalSector

3.2.3.3 -

Proposing anoperationalframework to MSDEfor implementationbyclearly identifyingmission, vision, duediligenceprocessesforpartnerships, yearlyplans, governancemodel,digitalplatformand support eco-systems (compliancehandling, paymentsolutions, B2B, B2Cand G2B networkingetc.),convergenceetc.

32

1.7Conclusion

Thissectionessentiallysummarizesthemajorconstituentsofthischapter.Section1.1wasthe introduction to the study which also talked about Section 1.3 discussed about thedefinitionsofmajor concepts that are central to this studywith the finalized definitionswhichwillbeanchoredto–fordiscussionsandpropositionsthroughoutthisstudy.Section1.4discussedabouttheapproachandmethodologyofthestudy.Section1.5discussedfewapproaches of formalization. Section 1.5 forms one of the basis for evolution of finalrecommendationsinChapter6andalsohelpsthereaderinunderstandingtheconnectandrelevanceof finalizationofconceptualdefinition inSection1.3.Also,oncesection1.5hasbeen read through the readerwould be able to appreciate the literature reviewdone inChapter2andthesecondarydataconsolidationdoneinChapter3and4.ThiswouldalsoformatheoreticallenstoabsorbthecasestudiesgiveninChapter5.Section1.6discussedtheScopeofthepresentstudyandBroadOrganizationofthereportintermsofToRandthemappingoftheexpectationoftheToRwithcontentsanddeliverablesencompassedinthevariouschaptersofthereport.

33

Review of literature of the studies on Informal sector

34

Chapter2-ReviewofliteratureofthestudiesonInformalsector

2.1Introduction

Informalitytakesvariousformsindifferentcontexts,andnewformsofinformalityemergeovertime(withinacountry).Therearemanyperspectivesofinformalitysuchasthecapitalviewofformalization,labourviewofformalization,technologicalperspective,andageneralperceptionofcitizensworkingwithorintheinformalsectorofaneconomy.Thischapterpresents a review of extant literature in the informal sector aimed at formalization. Inaddition,thischapteralsopresentsnewtrendsastheyemergedinrecentyearsacrossselecteconomiesintheworld,e.g.India.

Thechapterisprimarilydividedintofivesections,includingtheintroductionsection.Thesecond section (2.2) discusses the studies and suggestions provided by internationalscholarsandexpertsforformalizinginformalsector.Someofthestudiesalsomentionedthata new form of formalization is happening in many parts of the world, and it requiresintervention at different levels by the governments. Section 2.3 presents the efforts andsuggestionsofthescholarsandexpertsinthecontextofIndianinformalenterprises;itisfollowed by Summarization of Major Findings and Evolution of Broad Themes forFormalization Framework in section 2.4. Section 2.5 encompasses the conclusion of thechapter.

2.2StudiesbyInternationalScholars/organizations

In international extant literaturemanydifferentpolicieshavealreadybeen implementedthroughouttheworldtosupporttheformalizationofinformalenterprises.Thesepoliciescanbeclassifiedintermsoftheirdomainandthecostsandbenefitsofformalizationthatarebeing targeted. In 2011, the Donor Committee for Enterprise Development suggested aclassificationintoninedifferentbusinessenvironmentdomains(DCED,2011)17:

1. Business registration and licensing; adapting business registration and licensingregimes to simplify the administrative processes of registration (for example, onestopshopintegratingallproceduresnecessaryforbusinessregistration).

2. Simplificationoftaxationpolicyandadministration,inordertoeasetaxcompliance(for example, by introducing more transparent and simplified tax reporting, anddifferentiating tax schemes formicro enterprises, farmers and currently informalenterprises).

3. Landownershipandtitling;reforming incompletecadastersandonerousorcostlylandregistrationsystemsandenablingfemaleownershipoflandandassets,inorder

17 DCED (August 2011), “How Business Environment Reform can promote formalization”, annex to: “Supporting Business Environment Reform, Practical Guidance for Development Agencies”, Donor Committee for Enterprise Development.

35

toenableenterprisestoworkfromapermanentlocationandtoraisecapitalthroughland-basedcollateral.

4. Labourandlabour-relatedissues;giventheneedforregulationtoguaranteeaproperfunctioning of the labour market, basic social protection for workers and skillsdevelopment, the costs of complying with these regulations should be as low aspossible.

5. Judicial reform; reducing transaction costs, improving the quality of governancemethodsandimprovingaccesstojusticeinbureaucraticadministration.

6. Intellectualproperty rights; improvingtheenforcementof existing laws regardingtrademarksandotherpropertyrights, inordertoprovideeconomicopportunitiesunderlegaloperation.

7. Improvedaccesstofinancialservices;increasetheaccessofpoorwomenandmentothefullrangeoffinancialservices,inordertoreducethecostsofraisingcapital.

8. Access to information about business regulation and rules; awareness (andunderstanding) of existing business regulations and rules is a prerequisite forenterprisestoregister.

9. Incentives for reform and communicating these to informal enterprises.Formalization should introduce the benefits of compliance with the legal andregulatory framework.Microandsmallenterprisesshouldsee formalizationasanopportunityforgreateraccesstomarketsandgrowth.

Governmentitself(beinganimportantclientinvariousmarketsforproductsandservices)could be added as a tenth domain. For example, a percentage of public orders could bereservedfor formalmicroandsmallenterprises(MSEs),whichcouldencourage informalMSEstoformalize(IshengomaandKappel,2006)18.Together,thevariouscombinationsofdomain and targeted costs and benefits could be used to develop a detailed typology ofpoliciestoformalizeinformalenterprises.

Table2.1Typologyofformalizationpolicies,bydomainandthetargetedcostsandbenefitsofformalization.(Source:Panteia,2014)

Targetedcostsandbenefitsofformalization

S.No Domain Entrycosts

Taxes,feesandsocial

contributions

Compliancecosts

Permanentlocation

Accesstobusiness

developmentservices

Accesstonew

markets

1Businessregistrationandlicensing

X X X

2Tax policy andadministration

X X

18 Ishengoma, E. and R. Kappel (2006), “Formalization of informal enterprises: economic growth and poverty”, Eschborn: Economic Reform and Private Sector Development Section, GTZ.

36

Targetedcostsandbenefitsofformalization

S.No Domain Entrycosts