Derivatives Risk Exposure, Volatility of Firm’s Value, and Going Concern Audit Opinion

30

Derivatives Risk Exposure, Volatility of Firm’s Value, and Going Concern Audit Opinion Abstract This study aims to explain the effects of risk exposure on the going-concern audit opinion mediated by volatility of firm's value. First, it examined the effects of risk exposure on volatility of firm's value, and the second the effect of volatility of firm's value on a going concern audit opinion. By using path analysis methodology, the study found that risk of covenant violation and the risk of foreign currency exchange rate positives indirectly affect the going-concern audit opinion which mediated by volatility of firm's value. The effect of volatility of firm's value on a going concern audit opinion and the finding as well are the contributions of this study. Keywords: Risk exposure, volatility of firm's value, the Going-concern audit opinion, Information asymmetry 1. Introduction The bankruptcy of the twenty of U.S. major companies during 2001 and 2002 made the public question the credibility of the accounting profession. Twelve of them did not receive an explanatory paragraph that reflects there is a problem of business continuity (going concern) to the consolidated audit opinion before going bankrupt. This condition is seen as a failure of auditors to comply with SAS 59 which requires the auditor to evaluate conditions or events during the audit that raise doubts about the sustainability of the company. (Venuti, 2004). It is dilemmatic to auditors when issuing a going-concern audit opinion. The issuance of this opinion, it worries will accelerate the bankruptcy process (self-fulfilling prophecy), but if the auditors do not publish it, the auditors do not give early warning about the company's business going concern’s issues to relevant parties.

-

Upload

indonesiabankingschool -

Category

Documents

-

view

0 -

download

0

Transcript of Derivatives Risk Exposure, Volatility of Firm’s Value, and Going Concern Audit Opinion

Derivatives Risk Exposure, Volatility of Firm’s Value, and Going Concern Audit Opinion

Abstract

This study aims to explain the effects of risk exposure on the going-concern audit

opinion mediated by volatility of firm's value. First, it examined the effects of risk exposure on

volatility of firm's value, and the second the effect of volatility of firm's value on a going

concern audit opinion. By using path analysis methodology, the study found that risk of

covenant violation and the risk of foreign currency exchange rate positives indirectly affect

the going-concern audit opinion which mediated by volatility of firm's value. The effect of

volatility of firm's value on a going concern audit opinion and the finding as well are the

contributions of this study.

Keywords:

Risk exposure, volatility of firm's value, the Going-concern audit opinion, Information

asymmetry

1. Introduction

The bankruptcy of the twenty of U.S. major companies during 2001 and 2002 made

the public question the credibility of the accounting profession. Twelve of them did not

receive an explanatory paragraph that reflects there is a problem of business continuity

(going concern) to the consolidated audit opinion before going bankrupt. This condition is

seen as a failure of auditors to comply with SAS 59 which requires the auditor to evaluate

conditions or events during the audit that raise doubts about the sustainability of the

company. (Venuti, 2004).

It is dilemmatic to auditors when issuing a going-concern audit opinion. The issuance

of this opinion, it worries will accelerate the bankruptcy process (self-fulfilling prophecy), but

if the auditors do not publish it, the auditors do not give early warning about the company's

business going concern’s issues to relevant parties.

Empirical findings found that the going-concern audit opinion give a signal to users of

financial statements that the company is having problems about financial difficulties and

possible bankruptcy in the future. Companies that received going-concern audit opinion

indicated to have a risk of financial distress, technical default, liquidation, and loan default

(JF Mutchler, 1985; Mutchler et al., 1997; Wilkins, 1997; Constantinides, 2002; Styron, 1993;

Fanny & Saputra, 2000; Setyarno et al., 2006; Lam & Mensah, 2006; Gaganis & Pasiouras,

2007; Bhimani et al., 2009). Going-concern audit opinion was also shown to mitigate

market’s surprise about announcement of companies’ bankruptcy (Chen & Church, 1996;

Holder-Webb & Wilkins, 2000; Blackwood, 2002).

Existing research has not considered the possible risks arising from derivative

transactions that would cause the failure of auditors to capture signals of fraud and going-

concern problems of the company. In general, derivative instruments can be used for two

purposes that are contrary to the impact of risks, namely (i) hedging, which reduce risk

exposure, and (ii) trading by speculative motives which have an impact on increasing risk

exposure. In practice, derivative financial transactions for the hedging purpose are often

ineffective, so the impact on risk is similar to speculative transactions. Thus, speculative

hedging will lead to volatility of firm’s value is higher than the effective hedging (Zhang,

2009). Auditors are required to use the optimal audit strategy, so as to distinguish

companies that use derivative instruments for hedging purposes (effective hedging) and

companies that use complex derivative strategies (Cummins et al, 1998).

Derivatives strategy of the firm will affect the nature of the distribution company's

operating cash flow and solvency levels of the company. Companies that use derivative

instruments for hedging purposes (effective hedging) could increase the company's

solvency, thereby reducing the probability of having a default. While companies with

complex derivative strategies allow for large losses, which disturb the stability of the

company's solvency and increase the probability of default. The auditors’ ability to

distinguish derivative strategies will reduce the possibility of the auditor failed to detect a

material misstatement of the financial statements of clients, including corporate default risk

due to complex derivative strategies.

Empirical studies have shown that derivative risk exposures affect the volatility of the

firm’s value (Berkman & Bradbury, 1996; Guay, 1999; Rossieta, 2010). Volatility of firm’s

value (total risk), market risk (market risk), and firms specific risk are the reason of company

to use derivative instruments for hedging purpose (Guay, 1999). The higher volatility of firm’s

value, the greater probability of companies failed to meet their obligation, so the higher of the

risk of company's going concern problem.

Therefore, this study aims to give an explanation for the problem of research, either

(i) the effect of risks exposure managed by derivative instruments on the volatility of firm’s

value, (ii) the effect of the volatility of firm’s value on the possibility of the auditor issued a

going-concern audit opinion, and (iii) the effects of exposure derivatives risks on going-

concern audit opinion which is mediated by the volatility of firm’s value. The second and third

research problems, either the findings are the main contribution of this research. To answer

the problems of research, this study used path analysis which is integrated two models that

estimated by a cross section regression and logistic regression. Sample is limited only on

non-banking public companies which are indicated using financial derivative instrument to

manage risks.

2. Theoretical Framework and Hypothesis Development

2.1 Agency Theory, Information Asymmetry and Financial Reporting Risk

The agency relationship between the principals and the agents can cause problems

when both sides maximize their utility, so the agents no longer act in accordance with the

interests of principals. Agency problems rise such as agency costs, information asymmetry,

moral hazards, and adverse selection (Jensen & Meckling, 1976; Rossieta, 2009). Financial

accounting reporting system could be a mechanism to control (reduce) adverse selection,

moral hazard problems and mitigate the problem of information asymmetry. (Healy &

Palepu, 2001).

According to Zhao (2004), information asymmetry plays a decisive role in corporate

risk management policies. Hedging can reduce information asymmetry between managers

and investors about the costs and risks faced by the company. The higher information

asymmetry between managers and investors, the company further reduces hedging to

convey signal about the quality of the firm value to investors along with the increasing

volatility of the firm’s value while raising the cost of bankruptcy. Companies convey

information about the benefits of hedging (signaling cost) to reduce the cost of bankruptcy.

2.2 Use of Derivatives to Manage Risk and Volatility of Firm’s Value

Companies have benefit from the use of derivative instruments for hedging purposes,

as it can enhance shareholder value by exploiting market imperfections, the tax structure,

existence of bankruptcy problems, information asymmetry, and agency problems that lead to

agency costs (Muller & Verschoor, 2005). Company obtained benefit from the use of

derivative instruments for hedging purposes to decrease some types of risks exposure.

Nevertheless, when hedging is not effective, the derivative transaction will have a similar

impact to derivative transactions for trading, which increases the volatility of the firm’s value.

(i) Risk of Bankruptcy

Company that faces the problem of bankruptcy is usually a company that has a

variant of the firm’s value, leverage, and high capital costs (Rossieta, 2010). Hedging

activities reduce the variability of firm’s value in the future, thereby reducing the probability of

occurrence of bankruptcy costs and increase firm value (Smith & Stulz, 1985; Rossieta,

2010). Conversely, the use of derivative instruments for trading purposes could increase the

risk of bankruptcy, thereby increasing the volatility of firm’s value. In this study, bankruptcy

costs are assumed identical with the theoretical risk of bankruptcy due to the higher costs of

bankruptcy, the more likely a company will be completely bankrupt. The greater cost of

capital, the more likely company will face bankruptcy, so the higher the volatility of firm’s

value.

Previous researches (Nance et al., 1993; Berkman and Bradbury, 1996; Fok et al.,

1997; Guay and Kothari, 2003; Muller and Verschoor, 2005; Faff and Marshall, 2005; Zhang,

2009; Rossieta, 2010) have provide empirical evidence of the claim of Smith and Stulz

(1985) that the derivative instruments for hedging purposes to enhance shareholder value

because it can reduce the risk of bankruptcy, except in research of Nance et al. (1993) and

Fok et al. (1997).

Based on the above arguments, then arranged the following hypothesis 1 (H1):

H1: The level of cost of capital positively affects on the volatility of firm’s value that having

derivative transactions.

(ii) Fluctuation Risk Due Taxes

Companies that use derivative instruments for hedging purposes have benefit from a

progressive tax rate structure (Rossieta, 2010). Through hedging, the more convex

company's tax rate function, the greater the reduction in tax payable acquired firms (Nance

et al., 1993). If hedging can reduce variability of income before taxes, then the value of the

firm after taxes will increase due to reduced risk of fluctuations in income (Berkman &

Bradbury, 1996; Rossieta, 2010)

This study followed Rossieta (2010) by using the profit after tax to measure of

income growth associated with the distribution of profit after tax which is claimed by the

parties concerned with the wealth of firms (value firms). If each party is assured to obtain the

wealth distribution company based on its right, then the volatility of firm value will decline.

This tax benefit is a ratio of earnings growth on the growth of tax. If profit growth is greater

than tax growth, the company expected having benefits from fluctuations in earnings and a

progressive tax rate schedule due to the use of derivative instruments. The greater the tax

benefit obtained by the company, the smaller the tax payment, so that volatility will decrease.

Therefore, it developed the hypothesis 2 (H2) as follows:

H2: The Benefits of tax rates negatively affects the volatility of firm’s value that entered into

derivative transactions.

(iii) Risk of Agency Problems

As an agent of shareholders, managers faced problem of conflict of interest between

shareholders and bondholders as underinvestment problems (Berkman & Bradbury, 1996 in

Rossieta, 2010). The use of derivative instruments mitigates conflicts of interest between

shareholders and debt holders to overcome the problem of underinvestment problem.

Managers do not always realize that positive NPV projects because of short-term liquidity

problems due to bondholders always take part fixed investment results (interest payments),

while shareholders do not necessarily get the rest. Hedging can mitigate the conflict between

shareholders and debtholders by reducing fluctuations in cash flow (cash flow stability),

reducing the risk of default, and create future cash flow to shareholders, thus increasing the

value of the firm (Berkman & Bradbury, 1996; Nance et al., 1993; Rossieta, 2010).

Therefore, firms with high short-term liquidity tends to reduce the use of derivative

instruments for hedging purposes, thereby increasing the potential for future cash flows and

increase the volatility of the company. Conversely, companies with low liquidity tend to use

derivative instruments for hedging purposes in order to maintain stability in the future cash

flows, reducing liquidity risk due to underinvestment problem, which could reduce the

volatility of firms (Nance, Clifford W. Smith, & Smithson, 1993).

Based on these arguments, it developed the hypothesis 3 (H3) as follows:

H3: firm's short-term liquidity negatively affects the volatility of firm’s value that entered into

derivative transactions.

Derivative instruments also can be used to accommodate the interests of managers

in terms of meeting earnings targets. This occurred because the accounting numbers (profit)

is often used as a basis for the preparation of contract agreements and the basis of

manager’s compensations, so that managers will strive to meet profit targets to achieve

corporate goals and maximize their own interests. Derivative instruments for hedging

purposes can be used managers to maintain profit fluctuations.

Hedging can limit manager’s policy by maintaining variants accounting numbers to

achieve profit and avoid the risk of default on the debt covenant violations in its activities. For

example, managers will consider every positive NPV projects and consider its impact on the

stability of cash flows and firm value (Smith & Stulz, 1985; Rossieta, 2010). Conversely, the

use of derivative instruments for trading can increase the risk of default because of violation

of debt covenants, thus increasing the volatility of firm’s value and reduce the value of the

firm.

In other words, derivative instruments can be used to accommodate the interests of

managers to meet profit targets and to avoid violating debt covenants by managing the risk

of fluctuations in earnings, thereby reducing the volatility of the company. Conversely, the

use of derivative instruments with opportunistic motivation is to obtain the current year profit

target will affect the fluctuations in profits and may result in violation of covenants, thereby

increasing the volatility of the company. Based on these arguments then developed the

hypothesis 4a (H4a) and hypothesis 4b (H4b) as follows:

H4a: Fluctuations in profit due to the use of derivative instruments positively affects on the

volatility of firm’s value.

H4b: The risk of debt violation of covenants is affected by fluctuations in earnings due to the

use of derivative instruments positively affects on the volatility of firm’s value.

(iv) Risk Exposure of Foreign Currency Exchange Rate

Companies involved in global business can not be separated from the risk of

exchange rate movements of foreign currencies. The movement of foreign currency

exchange rates increases the default risk of the company if the company has no sufficient

assets in foreign currency to cover liabilities in foreign currency (adequate net open

position). Therefore, the company has a higher risk exposure in foreign currency exchange

rates compared with purely domestic firms (Rossieta, 2010). Derivative instruments for

hedging purposes can reduce the risk exposure arising from exchange rate movements of

foreign currencies, so as to enhance shareholder value (Muller & Verschoor, 2005;

Sribunnak and Wong, 2004; Fok et al., 1997; Berkman and Bradbury, 1996 .) The greater

the company's net open position, the greater the risk of currency exchange rate movements,

so that volatility of firm’s value will increase. Based on the above arguments, then arranged

hypothesis 5 (H5) as follows:

H5: The amount of net open position positively effects on volatility of firm value that entered

into derivative transactions.

2.3 Volatility of Firm’s Value and Going Concern Audit Opinion

Going-concern assumption is more determined by the consideration or assessment

of the auditor (Venuti, 2004). Management is responsible to provide an assessment of the

company's business continuity under the assumption of going concern with due respect to

the ability of the company's liquidity. As SAS No. 34, Paragraphs 17 and 18 Pedoman

Standar Akuntansi Keuangan (PSAK-Indonesia Guidelines for the Financial Accounting

Standards) regulates going concern issues for management in preparing financial

statements. The financial statements have to be prepared based on the going concern

assumption. Management should disclose the reason of company does not meet the

assumption.

Capital market liberalization on the one hand increasing liquidity of capital markets

that preferred by investors and speculators, but on the other hand has increased the volatility

of the company (Tickell, 2000). This situation encouraged investors and speculators to get

profit from derivative instruments, especially with the availability of derivative products for

hedging purposes with relatively low cost. However, derivative products are not able to

directly affect the price of underlying assets of the derivative product. The wider of the

difference in price between derivative products and the underlying assets, then the wider

risks faced by investors and speculators. Empirical research shows that the risk exposure of

derivative instruments (even if used for hedging purposes) affects the volatility of firm’s

value. However, studies that tested the effect of risk exposure of derivative instruments on

going concern audit opinion still hard to find.

In general, the auditing process is often obtained noise signals on the status of the

fairness of financial statements, especially for companies that use the strategy of complex

derivative instruments. This happened because of the auditor difficult to obtain actual

information about the actions of managers that reduce the firm’s value, allowing the auditor

obtaining the less accurate information about his client. This condition leading the auditor

issuing a false audit opinion which is the client's derivatives strategy is one of the functions

of the audit process (John and John, 2006). In this study the volatility of the firm’s value

treated as one indicator of going concern problem.

If the company uses derivative instruments with efficient motivation, then the volatility

of firm’s value will be reduced, thereby decreasing the possibility of going-concern problems

in the future. Based on the above arguments, it is concluded that the greater volatility of firm

value, the greater the going concern risk faced by the company, so that the greater the

probability to obtain going-concern audit opinion. Therefore, then arranged hypothesis 6 (H6)

as follows:

H6: Volatility of firm’s value due to the use of derivative instruments positively effects on

going-concern audit opinion.

It is hard to find empirical research that examines the effect of risk exposure on

going-concern audit opinion in the published literature documentations, so this study use

volatility of firm’s value as a variable that explains the influence of risk exposure on the

going-concern audit opinion, as shown in Figure 3.3 (appendix 4) which are arranged on the

hypotheses 7-11 as follows:

Mediated by volatility of firm’s vale, the risk of capital cost (H7), the risk of

fluctuations in taxes rate (H8), risk of short-term liquidity (H9), the risk of fluctuations in

income (H10a), the risk level of debt (H10b), and the risk of net open position (H11)

influence going concern audit opinion for the companies who use derivative instruments.

3 Methods Research

3.1 Data and Sample

This study use secondary data in the form of annual reports, financial reports, daily

stock prices, and daily composite stock price index of public company listed on the Indonesia

Stock Exchange (IDX). Samples were selected using purposive sampling method with the

criteria as follows: (i) public company as registered in Indonesia Stock Exchange (IDX) from

2001 to 2008, except those engaged in finance and banking industry. The sample is

restricted until 2008 to control the impact of changes in tax laws since there is one variable

(TARBIT) that measures the benefits of a progressive tax rate; (ii) reports its financial

statements on the Indonesia Stock Exchange during the period of observation; (iii) the

companies that indicated use derivative instruments. The identifications are (a) has

disclosure regarding the adoption of SFAS No. 55 (1999) on Accounting for Derivatives and

Hedging, (b) using keywords such as stock options, currency futures, swaps, LIBOR,

SIBOR, and the like; (iv) the availability of the daily stock price data during the observation

period.

3.2 Research Models

There are two models used in this study. The first model is used to answer the first

research problem, the influence of risk exposure on the volatility of firm’s value, as well as to

test the hypothesis 1 and hypothesis 5.

iiii

iiii

AbsNOPDERLnEarning

CRTARBITstressCostVolatilityFV

_

1__

654

3210 (3.1)

Predicted sign of the coefficient for each variable are: cost_stress1 is positive (+), tarbit is

negative (-), CR is negative (-), LnEarning is positive (+), DER is positive (+), and NOP_Abs

is positive (+).

The second model is used to answer the second and third research problems in this

study, which are the influences of the volatility of firm’s value on going-concern audit opinion

as well as answering the influence of risk exposure on the going-concern audit opinion

mediated by the volatility of firm’s value. The model is well to test the sixth hypothesis (H6)

until the eleventh hypothesis (H11).

iiiii

i

i LnSizeBetaZSCOREVolatilityFVGC

GC

43210 _

1 (3.2)

Predicted sign of the coefficient for each variable are: FV_Volatility is positive (+), ZSCORE

is negative (-), Beta is positive (+), and LnSize is negative (-). The descriptions of two

models are presented in the appendix 1. Data will be analyzed using cross section

regression approach for the first model and logistic regression for the second model. Both

models will be integrated and analyzed using path analysis to answer the third research

problems concerning the influence of risk exposure on the going-concern audit opinion

mediated by the volatility of firm’s value.

3.3 Definition and Research Variables

3.3.1 First Research Model

The dependent variable in the first model is the volatility of firm’s value. Volatility

used on market-based as reflected in the price with the assumptions market is efficient and

rational, so that the information available in the market can establish prices (Ball and Brown,

1968). Volatility of firm value is measured by a standard deviation of annualized 30 days

(instruments) daily stock returns (Rossieta, 2010).

The independent variables in the first model:

(i) The cost of capital (COST_STRESS), a proxy to measure bankruptcy risk, is the cost

incurred by the company from obtaining funding in the form of loans or bonds from

third parties. The cost of capital is measured by the ratio of interest expense on debt

(%).

(ii) The benefits due to tax (TARBIT), a proxy for measuring the risk of fluctuations in

taxes payment in the use of derivative instruments. This variable was measured by

using the ratio of the tax growth to earnings growth.

(iii) The current ratio (CR), a proxy for measuring short-term liquidity risk as a result of the

use of derivative instruments to overcome the risk of agency problems

(underinvestment problem). This variable was measured by the ratio of current assets

to current liabilities for the period (%).

(iv) The level of income (LNEARNING), a proxy for measuring manager performance

incentives in firms that use derivative instruments. This variable is measured by natural

logarithm net income.

(v) The level of debt (DER), a proxy for measuring the risk of debt covenant violations at

companies using derivative instruments. The level of debt (DER) reflects the

company's capital structure. DER measured by the ratio of total liabilities divided by

equity market value.

(vi) The absolute of net open position (NOP_Abs), a proxy for measuring the risk of

exchange rate movements of foreign currencies due to the instruments or contracts

with foreign parties. Net open position (NOP_Abs) is the company's financial net

position in foreign currencies to manage risk exposure caused by exchange rate

fluctuations .This variable is measured by the proportion of the absolute difference

between assets and liabilities denominated in foreign currencies to total book value of

equity (% )

3.3.2 Second Research Model

Dependent variable of second model of this research is going-concern audit opinion

as set out in the (Indonesia) Statement of Auditing Standard N0. 30 (PSA No.30). The types

of going-concern audit opinion provided by the auditor in this research are (i) an unqualified

opinion with explanatory paragraph relating to entity’s going concern problem or emphasis of

a matter, (ii) unqualified opinion with the exception or adverse opinion, or (iii) disclaimer. This

variable is measured using dummy variables with value 1 for firm i that received going-

concern audit opinion and 0 otherwise.

Independent variable used in the second research model is the volatility of firm’s

value (FV_Volatility) as used as the dependent variable in the first model. To control other

factors that affect the going-concern audit opinion, this study used three control variables,

namely: (i) the financial distress condition (ZSCORE), (ii) market risk (Beta), and, (iii) firm

size (SIZE). Variable ZSCORE that used to measure financial distress condition is the

Altman Z "-Score model (1993):

Z "= 6:56 (X1) + 3:26 (X2) + 6.72 (X3) + 1:05 (x4) (3.3)

Z "is the overall index; X1 is working capital / total assets; X2 is the retained earnings / total

assets; X3 is earnings before interest and taxes / total assets; and X4 is the book value of

equity / book value of total liabilities. Because Indonesia is a developing country, it added

+3.25 to the constants in equation (3.3) above to obtain the Altman index Z''-Score (1993).

The second variable, namely market risk (Beta) is the market risk information that

may affect the going-concern audit opinion. Beta is measured by a beta coefficient of

regression of return company i with the daily composite stock return for one year. The third

control variable, namely firm size (SIZE). Size of company is the representation of

accounting systems, internal control of the company, and public attention. This variable was

measured by the natural logarithm of total assets of the company (lnSIZE).

4 Data Analysis

4.1 Descriptive Statistics and Correlations Test

Table 4.2 (Appendix 2) presents descriptive statistics that illustrate mean, median,

and data distributions. Table 4.1 (appendix 1) shows there are 104 observations after

passing through the sample selection procedure based on purposive sampling. Forty-seven

percent (49 of 104 observations) firms received going-concern audit opinion, so it shows that

composition of the two groups of firms that received going-concern audit opinion and non-

going concern audit opinion nearly equal. Based on the minimum value, maximum, and

standard deviation above, it shows that the data distribution is relatively large. Only a going-

concern, market beta, and size of company variables that data distributions are relatively

normal compared to others. It is indicated only the data that is used to measure variables in

the second model is adequate to test the research hypothesis. These results are then

consistent with the results of correlation test and regression test.

Correlation test between variables used in the first model were tested using the

Pearson Correlation presented in Table 4.3 (appendix 4) giving an initial indication that only

a covenant violation risk exposure and risk of exchange rate movements of foreign

currencies that have a positively (as predicted) correlated to the volatility of the firm’s value.

While the risk of fluctuation of income level negatively (not according to predictions)

correlated to the volatility of firm’s value. While the correlation between variables used in the

second model presented in Table 4.4 (appendix 4) giving an early indication that all these

variables in both models significant correlated on going-concern audit opinion, except for

variable market beta is not significant but the direction is positive as prediction.

4.2 Classical Assumption Test and Goodness of Fit Test

Based on the classical assumption test, the first research model is free from

problems of normality, multicollinearity, heteroscedasticity, and autocorrelation. Normality

test results show the data spread around the diagonal line and follow the direction of the

diagonal line. Kolgomorov-Smirnov Test (KS) is worth 0147 and not significant.

Multicollinearity test results the value of each variable TOL more than 0.1 and VIF values

less than 10. Heteroscedasticity test is using an informal test (graph) and formal testing

(statistical analysis). Based on the scatterplots seen that the data spread randomly, do not

form a specific pattern, and scattered both above and below the number 0 on the axis Y.

Similarly, Park test results indicate p value of each variable in the top 5% and not significant,

so the null hypothesis can not be rejected. Thus the both results, graphs and statistical

analysis, model free from the problem of heteroscedasticity. Autocorrelation test using

Durbin-Watson test (DW Test). After treatment by adjusting data with rho’s value, the model

did not have problem of autocorrelation as indicated by the value of DW in between du and

4-du or are in the reception area of null hypothesis that there is no positive or negative

autocorrelation.

The second research model is estimated using logistic regression. Normality test

results show this model is free from problems of normality assumptions. Goodness of fit test

using the Hosmer and Lemeshow's Goodness of Fit Test, obtained that Chi-square

significance value above 5%, in other words that data is fitted with the model. Test of validity

of the model using Cox and Snell R Square and Negelkerke R Square. The value of Cox and

Snell R Square and Negelkerke R. Square respectively is 31.7% and 42.3%.

5 Discussion and Conclusion

5.1 The Effect of Risks Exposure on Volatility of Firm’s Value

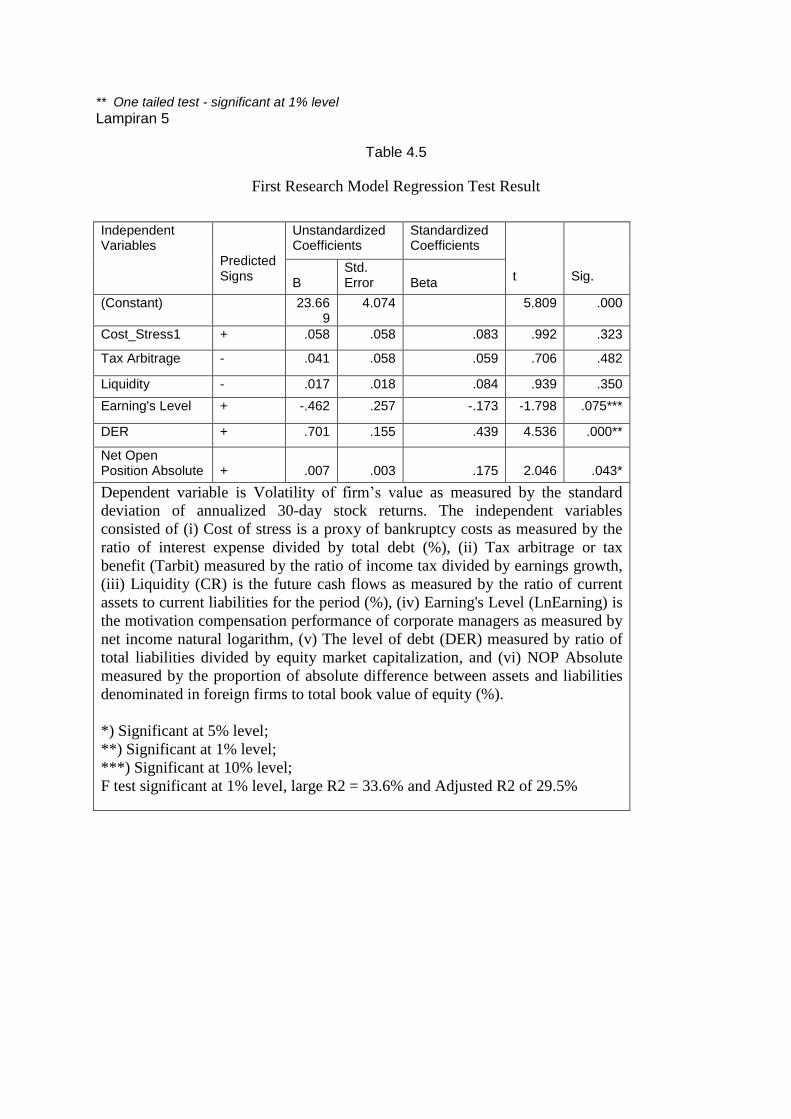

The result of statistical estimation of the first model (Appendix 5) by using a cross

section regression showed that risk exposure is simultaneously significant effect on the

volatility of firm’s value. Bankruptcy risk (cost of stress), the benefits of progressive tax rates

(tarbit), the stability of future cash flows (current ratio), the level of income (LnEarning), the

level of debt (DER), and the risk of exchange rate movements of foreign currencies

(NOP_Abs) simultaneously significant influence the volatility of firm’s value at 1%

significance level. These six variables explain the volatility of firm’s value amounted to 29.5%

and the rest influenced by other factors beyond the research model. Partial test results (t

statistics) of each variable described below.

a. Research Hypothesis 1 (H1)

The result of regression test showed that β1 coefficient is the regression coefficient of

the cost of capital (cost of stress) is positive (as predicted) with a value of significance (p

value) is greater than the alpha value of 0.1. Therefore, research hypothesis which states

that the level of capital cost positively influence on the volatility of firm’s value that entered

into derivative transactions rejected.

b. Research Hypothesis 2 (H2)

The result of regression test showed that β2 coefficient is the regression coefficient of

tax arbitrage (tarbit) is positive (contrary to predictions) with a value of significance (p value)

is greater than the alpha value of 0.05. Therefore, research hypothesis which states that the

benefits of tax rates negatively affect the volatility of a firm’s value that entered into

derivative transactions rejected.

c. Research Hypothesis 3 (H3)

The result of regression test showed that β3 coefficient is the regression coefficient of

liquidity (CR) is positive (contrary to prediction) and significance value (p value) is greater

than the alpha value 0.1. Therefore, research hypothesis which states that the firm's short-

term liquidity risk negatively affects the volatility of firms’ value that entered into derivative

transactions rejected.

d. Research Hypothesis 4a (H4a) and H4b

The result of regression test showed that β4 coefficient is the regression coefficient of

Earning's level (LnEarning) is negative (does not match predictions) but the value of

significance (p value) is smaller than the alpha value of 0.1. Therefore, research hypothesis

(H4a), which states that the fluctuations in the rate of profit due to the use of derivative

instruments positively influence on the volatility of firm’s value rejected.

This is due to not meeting the assumption of manager incentives in the form of the

benefits of using derivative instruments in order to achieve year-end profit target. That is

payoff between expected risk and return does not support the profit target at end of period.

The behavior of managers who avoid risk (risk averse) from the volatility of firm’s value due

to derivative instruments, reducing the possibility of managers use derivative instruments if

the manager believes year-end earnings will exceed profit targets, so the volatility of firm

value decreases (Smith and Stulz, 1985).

The result of regression test showed that β5 coefficient is the regression coefficient of

level of debt (DER) is positive (as predicted) and significance value (p value) less than the

alpha value of 0.001. Therefore, research hypothesis (H4b) which states that the risk of debt

is affected by fluctuations in earnings due to the use of derivative instruments positively

influence on the volatility of firm’s value can not be rejected. This result can be interpreted

that if the accounting numbers as one of the considerations of debt contracts, encouraged

companies to use derivatives to achieve the target of covenant. The more managers are

motivated to use derivative instruments, the greater the fluctuations in earnings and the

higher the likelihood the company violated the provisions of debt contracts, so the volatility of

company value will increase.

e. Research Hypothesis 5 (H5)

The result of regression test showed that β6 coefficient is the regression coefficient of

absolute net open position (NOP_Abs) is positive (as predicted) and significance value (p

value) less than the value of alpha 0.05. Therefore, research hypothesis which states that

the amount of net open positions negatively affect the volatility of firm value can not be

rejected. The results could be interpreted that the greater the amount of net foreign assets

denominated in foreign currencies with their obligations, the greater the risk exposure to

exchange rate fluctuations of foreign currency, thereby reducing the volatility of firm’s value.

5.2 The Effect of Volatility of Firm’s Value on Going Concern Audit Opinion

The result of second model estimation (Appendix 6) is obtained that the β7 coefficient

as a coefficient regression of volatility of firm’s value (FV_Volatility) is positive (as predicted)

and significance value (p value) less than the alpha value of 0.1. Therefore, research

hypothesis (H6) which states that the volatility of firm’s value resulting from the use of

derivative instruments positively effects on the going concern audit opinion can not be

rejected. This suggests that the greater volatility of firm’s value, the greater the risk the

company, the more likely to face going concern problems, thus raising the possibility the

company obtained a going-concern audit opinion. Thus it can be said that the volatility of

firm’s value due to the use of derivative instruments can be used as one risk factor that may

be considered by auditors in issuing the going-concern audit opinion.

The three regression coefficients of control variables confirmed with the research

prediction and the value of significance (p value) less than the value of alpha 0.05 or in other

words, these three variables have a significant effect on the going-concern audit opinion.

The Value of ZScore Index significant negatively effect on going-concern audit opinion. This

shows that the greater the value of the Z-Score Index, the better the company's financial

condition, the less deal with business going concern problems, thereby reducing the

possibility of company received going-concern audit opinion. Market beta significant

positively affect on going-concern audit opinion. This shows that the greater the market risk,

the greater the company’s risk, the bigger chance a company facing going concern problem,

the greater the possibility of company receiving a going concern audit opinion. Company

size (LnSize) significant negatively effect on going-concern audit opinion. The larger the

company, the less likely the company obtain going-concern audit opinion. This confirms the

argument of Gaganis and Pasiouras (2007), Lam and Mensah (2006), and Mutchler,

Hopwood, and McKeown (1997) which states that the auditor will tend to reduce the

possibility of going concern audit opinion against larger companies because large

companies tend having better the accounting and internal control system, reduce information

asymmetry during the audit assignment, tended to gain greater public attention, so that

tends to be better able to overcome the problem of financial distress in one year ahead. Only

market beta variable that is not in accordance with correlation variables test as described

earlier.

5.3 The Effect of Risks Exposures on Audit Going Concern Audit Opinion Mediated by

Volatility of Firm’s Value

This section explains the role of the volatility of firm’s value as a variable that

mediates the effect of risk exposure managed by derivative transaction on going-concern

audit opinion, as well as answering the third research problems (H7 to H11). This problem is

solved by using path analysis in the diagram 4.1 (Appendix 7).

Based on estimation of the first model, only the variable bankruptcy costs (DER) and

the absolute net open position (NOP_Abs) which supports the hypothesis of the study and

significantly affect the volatility of firm’s value. The second research model estimation results

show that the volatility of firm’s value positively effect on going-concern audit opinion. Thus

the volatility of firm value can be used as variables that mediate the relationship between

exposure risk and going-concern audit opinion. Exposure risks that can be mediated by the

volatility of firm’s value in this study is the risk of covenants violation (H10b) and the risk of

exchange rate movements of foreign currencies (H11)

The number of influence of the risk of covenants violation (DER) on going-concern

audit opinion which is mediated by the volatility of firm’s value is 0.0558 (positive value). This

result suggests that when firms use accounting numbers as incentives in manager contracts,

managers will be motivated to use the instrument to achieve profit targets. The more often

the company uses derivative instruments with opportunistic motivation, it increase earnings

volatility. The greater the fluctuations in earnings, it will increase the likelihood of violations of

covenant targets (DER), so the greater the volatility of firm’s value and raise the possibility of

firms receiving going-concern audit opinion.

The number of influence of exchange rate movements of foreign currency on going-

concern audit opinion which is mediated by the volatility of firm’s value is 0.00108 (positive

value). This empirical evidence indicates that the greater the NOP (the greater the net

difference in foreign currency assets with liabilities), the greater the risk exposure of

exchange rate fluctuations of foreign currency, the greater the volatility of firm’s value, thus

raising the possibility the company received a going-concern audit opinion.

5.4 Sensitivity Tests

This research conducted three additional tests to test consistency of the model used.

First additional test is changing the measurement of the volatility of firm’s value; the second

additional test is decomposing the variables Z-Score, and last test is changing the

measurement of cost of capital. Additional test results provide evidence that relatively

consistent with the results of initial model estimation.

Besides the volatility of firm’s value that affect the going-concern audit opinion, the

three control variables affect the going-concern audit opinion either. Company's financial

condition (ZScore) proved negatively effect on going-concern audit opinion, the market beta

positively effect on going-concern audit opinion, while firm size negatively affect the going-

concern audit opinion.

5.5 Conclusion

This study basically describes the effects of risk exposure on going-concern audit

opinion which is mediated by the volatility of firm’s value. Empirical test results indicate that

exposure risk managed by a derivative instrument, such debt covenant violations and the

risk of exchange rate movements of foreign currencies significant positively affects on the

volatility of firm’s value in Indonesia. Volatility of firm’s value positively significant affects on a

going concern audit opinion. Only debt covenant violation risks and risk of exchange rate

movements of foreign currencies positively significant effects on going-concern audit opinion

mediated by the volatility of firm’s value in Indonesia.

6 Implications and Limitations

The implications of this research indicate that companies using derivative

instruments should consider the use of derivative instruments to manage exposure risk of

the covenant violations and risk of exchange rate movements of foreign currencies that will

increase the volatility of firm’s value and raise the possibility of companies receiving going-

concern audit opinion.

Auditors, as a party who has a role in assessing the fairness of accounting

information of his clients, should consider those kinds of risk during the audit process.

Auditors should asses the effectiveness of firms in managing exposure risks of the use of

derivative instruments, particularly the risk of covenant violations and the risk of exchange

rate movements of foreign currencies, even it declared for hedging purposes. This is related

to the possibility of ineffective hedging has same impact with trading on the volatility of firm’s

value. So the volatility of company firm’s value due to the use of derivative instruments may

be one consideration in issuing going concern audit opinion.

In addition, management should increase the disclosure of information about

company risks associated with derivative transactions in its annual report, so as to minimize

the information asymmetry between management, investors and auditors. If this is done, the

public (including investors and auditors) will be more involved in the governance process

about the possibility risk of the company going-concern, so that all parties can take the

necessary action needed to save the company from possible bankruptcy.

Limitations of the study are difficult to distinguish companies that use derivative

instruments for effective hedging purposes and trading, measurement of market beta that

does not use the adjusted price (such as stock splits and dividend payments), and

measurement of financial distress by Altman's Z-Score Model.

Future research is suggested to improve the methodology and variable

measurements. In terms of methodology, further research could consider using structural

equation modeling. Future studies are advised to use the standard deviation of annualized

monthly returns and volatility changes in the value of the company to measure the volatility

of firm’s value (Guay, 1999).

REFFERENCES Altman, E. I. (2000). Predicting financial distress of companies: Revisiting the Z-Score and

Zeta Models. Journal of Banking & Finance .

Ball, R., & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal

of Accounting Reserach , 159-177.

Berkman, H., & Bradbury, M. E. (1996). Empirical evidence on the corporate use of

derivatives. Financial Management , 5-13.

Bhimani, A., Gulamhussen, M. A., & Lopes, S. (2009). The effectiveness of the auditor's

going-concern evaluation as an external governance mechanism: Evidence from loan

defaults. The International Journal of Accounting , 239–255.

Blackwood, A. H. (2002). Going concern opinions and the market's reaction to bankruptcy

filings after SAS No. 59. USA: Nova Southeastern University.

Calderon, T. G., & Cheh, J. J. (2002). A roadmap for future neural networks research.

International Journal of Accounting Information Systems , 203–236.

Chen, K. C., & Church, B. K. (1996). Going concern opinions and market reaction to

bancruptcy filings. The Accounting Review , 117-128.

Collins, D. W., Kothari, S., Shanken, J., & Sloan, R. G. (1994). Lack of timeliness and noise

as exolanations for the low contemporaneous return-earning association. Jounal of

Accounting and Economics , 18, 289-324.

Constantinides, S. (2002). Auditors', bankers' and insolvency practitioners' "going-concern"

opinion Logit Model. Managerial Auditing Journal , 487.

Cummins, J. D., Phillips, R. D., & Smith, S. D. (1998). Derivatives and corporate risk

management: Participation and volume decisions in the insurance industry. Wharton:

Financial Institutions Centre.

Davis, E. B., & Ashton, R. H. (2002). Threshold adjustment in response to asymmetric loss

functions: The case of auditors' ‘‘substantial doubt’’ thresholds. Organizational

Behavior and Human , 1082–1099.

Faff, R. W., & Marshall, A. (Vol. 36, No. 5, 2005). International evidence on the determinants

of foreign exchange rate exposure of multinational corporations. Journal of

International Business Studies , 539-558.

Fanny, M., & Saputra, S. (2000). Opini audit going concern: Kajian berdasarkan model

prediksi kebangrutan, pertumbuhan perusahaan, dan reputasi kantor akuntan publik

(Studi Emiten Bursa Efek Jakarta). Simposium Nasional Akuntansi VIII. Solo.

Firth, M. (1978). Qualified audit reports: Their impact on investment decisions. The

Accounting Review , 53, 642-650.

Fok, R. C., Carroll, C., & Chiou, M. C. (1997). Determinants of corporate hedging and

derivatives: A revisit. Journal of Economics and Business , 569 585.

Gaganis, C., & Pasiouras, F. (2007). A multivariate analysis of the determinants of auditors'

opinion on Asia Bank. Managerial Auditing Journal , 22 No. 3, 268-287.

Guay, W. R. (1999). The Impact of derivatives on firm risk: An empirical examination of new

derivative users. Journal of Accounting and Economics 26 , 319-351.

Guay, W., & Kothari, S. (2003). How much do firms hedge with derivatives? Journal of

Financial Economics , 423–461.

Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the

capital markets: A review of the empirical disclosure literature. Journal of Accounting

and Economics , 405–440.

Holder-Webb, L. M., & Wilkins, M. S. (2000). The incremental information content of SAS

No. 59 Going Concern Opinions. Journal of Accounting Research , 38 (No. 1), 209-

219.

Hopwood, W., McKeown, J., & Mutchler, J. (1989). A test of the incremental explanatory

power of opinions qualified for consistency and uncertainty. The Accounting Review ,

64 (1), 28-48.

Indonesia, I. A. (2001). Standar profesional akuntan publik. Jakarta: Salemba Empat.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior; agency

costs and ownership structure. Journal of Financial Economics , 305-360.

John, K., & John, T. A. (2006). Managerial incentives, derivatives and stability. Journal of

Financial Stability , 71–94.

Jr, J. J., Bierstaker, J. L., & O’Donnell, E. (2009). Integrating business risk into auditor

judgment about the risk of material misstatement: The influence of a Strategic-

systems-audit approach. Accounting, Organizations and Society , 1-14.

Knechel, W. R. (2007). The business risk audit: Origins, obstacles and opportunities.

Accounting, Organizations and Society , 383–408.

Lam, K. C., & Mensah, Y. M. (January 2006). Auditors' decision making under going concern

uncertainties in low litigation-risk environments: Evidence from Hongkong. Hong Kong

Governance Conference at Hong Kong Baptist University. Hong Kong.

Martin, R. D. (2000). Going-concern uncertainty disclosures and conditions: A comparison of

French, German, and U.S. Practices. Journal of International Accounting, Auditing &

Taxation , 137–158.

Muller, A., & Verschoor, W. F. (2005). The Impact of corporate derivative usage on foreign

exchange risk exposure. Netherlands: Limburg Institute of Financial Economics (LIFE).

Mutchler, J. F. (1985). A Mulitivariate analysis of the auditor's going concern opinion

decision. Journal of Accounting Research , 668-682.

Mutchler, J. F., Hopwood, W., & McKeown, J. M. (1997). The Influence of contrary

information and mitigating factors on audit opinion decisions on. Journal of Accounting

Research , 295-310.

Nance, D. R., Clifford W. Smith, J., & Smithson, C. W. (1993). On the determinants of

corporate hedging. The Journal of Finance , 267-284.

Rance, R. (1999). The application of Altman's Revised Four Variables ZScore Bancruptcy

Prediction Model for retail firms and the influence of asset size and sales growth on

their failure. UMI.

Rossieta, H. (2009). Risk signal, derivatives transactions, and the Indonesian GAAP. 10th

Asian Academic Accounting Association Annual Conference. Istambul, Turkey.

Setyarno, E. B., Januarti, I., & Faisal. (Agustus 2006). Pengaruh kualitas audit, kondisi

keuangan perusahaan, opini audit tahun sebelumnya, pertumbuhan perusahaan

terhadap opini audit going concern. Simposium Nasional Akuntansi IX. Padang.

Smith, C. W., & Stulz, R. M. (1985). The determinants of firms' hedging policies. The Journal

of Financial and Quantitative Analysis , 391-405.

Sribunnak, V., & Wong, M. F. (2004). Foreign exchange sensitivity-analysis disclosures and

market-based risk measures. KPMG−UIUC Conference on Risk, (pp. 1-46).

Styron, W. J. (1993). An empiriacal examination of the going concern audit option: The

auditor's decision regarding continuing going concern opinions and the subsequent

fate on companies that have received going concern opinions. Ann Abror, MI USA:

University Microfilms International.

Tickell, A. (2000). Dangerous derivatives: Controlling and creating risks in international

money. Geoforum, Elsevier Science Ltd , 87-99.

Venuti, E. K. (2004, May). The going-concern assumption revisited: Assessing a company's

future viability. The CPA Journal , p. 40.

Wilkins, M. S. (1997). Technical default, auditors' decisions and future financial distress.

Accounting Horizons , 40.

Zhang, H. (2009). Effect of derivative accounting rules on corporate risk management.

Journal of Accounting and Economics , 244–264.

Zhao, L. (2004). Corporate risk management and asymmetric information. The Quarterly

Review of Economics and Finance , 727–750.

Appendix 1 Table Error! No text of specified style in document..1

Operationalization of Variables

Variables Name of Variables Measurements

Dependent variables

Volatility of firm’s value (FV_Volatility)

Deviation standards of annualized 30 days returns (%)

Going Concern Audit Opinion (GC)

Dummy variable 1 for company receiving going concern audit opinion and 0 otherwise

Independent Variables

Bankruptcy cost (COST_STRESS1)

Ratio of interest expense on debt (%)

Benefits due to tax rates (TARBIT)

ratio of the tax growth to earnings growth

Current Ratio (CR) ratio of current assets to current liabilities for the period (%)

The level of income (LNEarning)

natural logarithm of net income.

The level of debt (DER)

ratio of total liabilities divided by equity market value

Absolute Net Open Position (NOP_Abs)

the proportion of the absolute difference between assets and liabilities denominated in foreign currencies to total book value of equity (% )

Control Variables

Financial Condition (ZSCORE)

Altman Z”-Score Index Model (1993)

Market Risk (Beta)

a beta coefficient of regression of return company i with the daily composite stock return for one year.

Size of Company (LnSIZE)

natural logarithm of total assets of the company.

Appendix 2 Table Error! No text of specified style in document..2

Sampling Design

Descriptions Amounts

The number of companies listed on the Indonesia Stock Exchange until 2008

393

Delisted companies (14) Companies in the financial industry, banking, and securities (55) Companies do not report the financial statements during the observation period

(78)

Companies do not indicated use of derivative instruments (225) Companies’ share prices data do not available (7) Companies that met the criteria for sample selection 14 Number of year observations 8 Number of firm year observations 112 Outlier data (8) Final samples 104

Appendix 3

Table 4.2

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation Skewness Ratio Statistic Statistic Statistic Statistic Statistic

Firms Value Volatility

104 6.38695 86.92947 31.3827751 17.50866473 5.667

Cost of Stress 1 104 .05910 183.98908 14.1013700 24.33210155 20.716

Tax Arbitrage 104 -227.71860 30.50880 -2.1968225 23.50572626 -37.488

Liquidity 104 11.90836 627.44984 141.7176994 92.36020841 8.706

Earning's Level 104 .00000 22.59800 16.1882673 6.47708123 -7.918

DER 104 .12400 89.64550 4.6323173 11.14530030 23.903

Going Concern 104 0 1 .47 .502 .495

ZScore Index 104 -5.29488 11.18361 5.0629171 3.16110184 -6.472

Market Beta 104 -.37860 2.17618 .9464259 .51977937 -.055

Company Size 104 18.33380 25.11450 21.6562192 1.54156559 1.666

Net Open Position Absolut

104

.00000

4282.2860

7

136.1493077

450.56382032

33.450

Valid N (listwise) 104

Source: Data processed

Appendix 4 Table Error! No text of specified style in document..2

Correlations of Research Variables of Model 1

Firms Value Volatility

Cost of Stress 1

Tax Arbitrage Liquidity

Earning's Level DER

Net Open Position Absolute

Firms Value Volatility 1 .040 .090 -.130 -.451** .505** .262**

Cost of Stress 1 .040 1 -.094 .139 .029 -.034 -.111

Tax Arbitrage .090 -.094 1 .063 -.027 .036 -.027

Liquidity -.130 .139 .063 1 .300** -.329** -.225*

Earning's Level -.451** .029 -.027 .300** 1 -.521** -.081

DER .505** -.034 .036 -.329** -.521** 1 .165*

Net Open Position Absolut

.262** -.111 -.027 -.225* -.081 .165* 1

*) One tailed-test - significant at 5% level , **) One tailed test - significant at 1% level

Table Error! No text of specified style in document..3 Correlations of Research Variables of Model 2

Firms Value Volatility

Going Concern

ZScore Index

Market Beta

Company Size

Firms Value Volatility 1

Going Concern .344** 1 -.397** .139 -.292**

ZScore Index -.384** -.397** 1 .136 .125

Market Beta -.244** .139 .136 1 .305**

Company Size -.443** -.292** .125 .305** 1

*One tailed-test - significant at 5% level

** One tailed test - significant at 1% level Lampiran 5

Table 4.5

First Research Model Regression Test Result

Independent Variables

Predicted Signs

Unstandardized Coefficients

Standardized Coefficients

t

Sig.

B

Std. Error

Beta

(Constant) 23.669

4.074 5.809 .000

Cost_Stress1 + .058 .058 .083 .992 .323

Tax Arbitrage - .041 .058 .059 .706 .482

Liquidity - .017 .018 .084 .939 .350

Earning's Level + -.462 .257 -.173 -1.798 .075***

DER + .701 .155 .439 4.536 .000**

Net Open Position Absolute

+

.007

.003

.175

2.046

.043*

Dependent variable is Volatility of firm’s value as measured by the standard

deviation of annualized 30-day stock returns. The independent variables

consisted of (i) Cost of stress is a proxy of bankruptcy costs as measured by the

ratio of interest expense divided by total debt (%), (ii) Tax arbitrage or tax

benefit (Tarbit) measured by the ratio of income tax divided by earnings growth,

(iii) Liquidity (CR) is the future cash flows as measured by the ratio of current

assets to current liabilities for the period (%), (iv) Earning's Level (LnEarning) is

the motivation compensation performance of corporate managers as measured by

net income natural logarithm, (v) The level of debt (DER) measured by ratio of

total liabilities divided by equity market capitalization, and (vi) NOP Absolute

measured by the proportion of absolute difference between assets and liabilities

denominated in foreign firms to total book value of equity (%).

*) Significant at 5% level;

**) Significant at 1% level;

***) Significant at 10% level;

F test significant at 1% level, large R2 = 33.6% and Adjusted R2 of 29.5%

Appendix 6

Table 4.6

Second Research Model Regression Test Result

Independent Variables

Predicted B S.E. Wald df Sig.

Signs

FV_Volatility + .036 .020 3.218 1 .073**

ZScore - -.374 .122 9.472 1 .002*

Beta + 1.633 .534 9.360 1 .002*

LnSize - -.393 .181 4.709 1 .030*

Constant 7.717 4.188 3.396 1 .065

The dependent variable is the going-concern audit opinion as measured by the dummy variable with value 1 for firm i that received going-concern audit opinion and 0 otherwise. Dependent variable is the volatility of the company (FV_Volatility) as measured by the standard deviation of annualized 30 days the stock returns. Zscore, Beta, and LnSize are control variables. ZScore measured by the Altman Z "-Score Index model (1993) with adjusted for developing countries, Beta is measured by regression coefficient of daily stock return company i with the daily composite stock index returns for a year , and LnSize measured by the natural logarithm of total assets of the company. *) Significant at 5% level **) Significant at 10% level Nagelkerke R Square 42.3%

Table 4.7

Effect of Risk Exposures on Going Concern Audit Opinion mediated by Volatility of Firm’s

Value

Variables Standardized Coefficients

Regression coefficient of FV_Volatility

The Number of Indirect Effects

DER

GC

0.155 0.36 0.155 x 0.36 = 0.0558

NOP_Abs

GC

0.003 0.36 0.003 x 0.36 = 0.00108

i

Appendix 7

Figure 4.1

Path Analysis Diagram of Integrating Research Models 1 and 2 Descriptions:

(i) 8146.0336.0111 2 Re , Number of R2 can be seen on the results of regression models of the first model

(ii) 75961.0423.01ker12 2 RkeNegele , Number of negelkerke R2 can be seen on the results of the regression of second

model

e2= 0.7596

-0.393*

-0.374*

1.633*

0.003*

0.059

0.018

-0.257*

0.155*

Tarbit

CR

LnEarning

DER

NOP_Abs

FV_Volatility Going

Concern

0.36**

ZScore

Beta e1= 0.8146

Cost_Stress1

0.083

LnSIZE