Democratic and Popular Republic of Algeria

106

Re-port No. 12534-At Democratic and Popular Republic of Algeria Rteview of Agricultural Policies and Agricultural Services 1 987-1 993 December 29,1t994 Natural Resources and EnvironmentDivision Maghreb and Iran Department Middle East and North Africa Regional Office w. X ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~...X v > f a _ w o S rA \ ¢~~~., c, ' ,' .i S*'; }44<<_j, ,,'2-,4' 3~~ MIRGRPIS - ; yetSC 254A Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Democratic and Popular Republic of Algeria

Re-port No. 12534-At

Democratic and Popular Republic of AlgeriaRteview of Agricultural Policies and Agricultural Services1 987-1 993

December 29,1t994

Natural Resources and Environment DivisionMaghreb and Iran DepartmentMiddle East and North Africa Regional Office

w. X

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~...X

v > f a _ w o S rA \ ¢~~~., c, ' , ' .i

S*'; }44<<_j, ,,'2-,4'

3~~ MIRGRPIS -

; yetSC 254A

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

DEMOCRATIC AND POPULAR REPUBLIC OF ALGERIA

REVIEW OF AGRICULTURAL POLICIES AND AGRICULTURAL SERVICES1987 - 1993

CURRENCY EQUIVALENTS

Currency Unit = Algerian Dinar (DA)

Official Exchange Rate (DA per US$)

Period End of Period Period Average

1988 6.731 5.9151989 9.032 7.6091990 12.191 8.9581991 21.392 18.4731992 22.781 21.8361993 24.120 23.345April 1994 36.000

FISCAL YEAR

January 1 - December 31

WEIGHTS AND MEASURES

Metric System

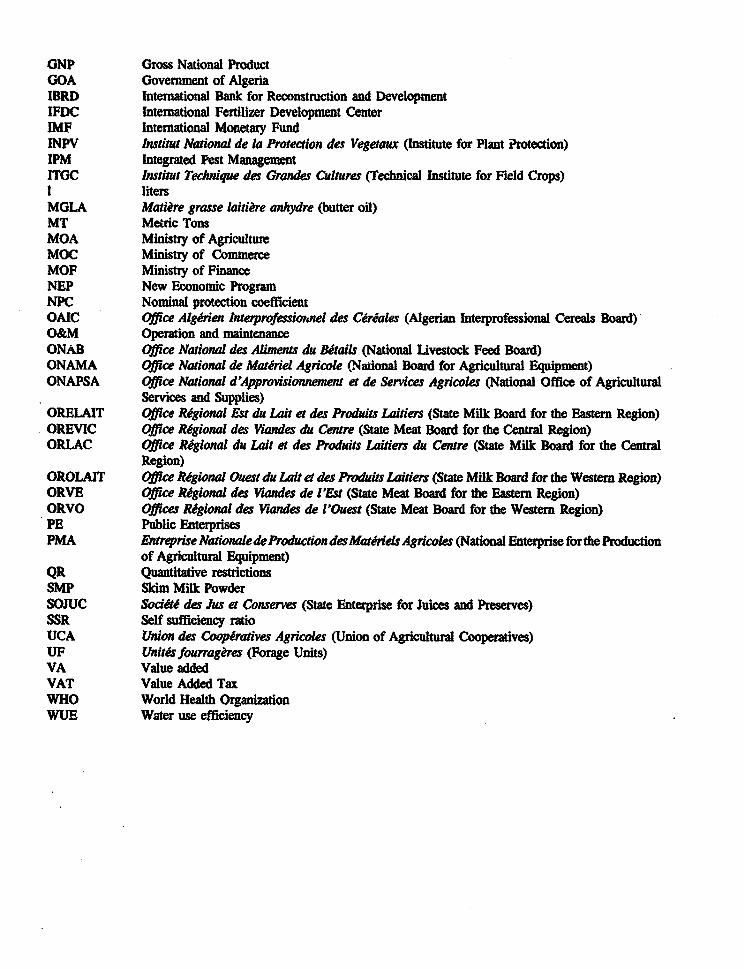

ABDREVIAT!ONS AND ACRONYMS

Al Artificial InseminationASMIDAL Entreprise Nationale des Engrais et de Produits Phytosaitaires (National Enterprise for the

Production of Fertilizers and Plant Protection Chemicals)AVN Autonte vetennaire nationale (National Veterinay Authority)BADR Algenan Agricultural Development BankCAH ComitE ad hoC (ad hoc Conmrmce tor Imports)CASAP Coopaves Agricoles de Serices et dApprousionnement (Agricultural Input Supply

Cooperatives)CCLS Coopratives des CEreales et Lgumes Secs (Cooperatives for Cereals and Pulses)CDC Cahiers des Charges (Import Permits)CEM Country Economic MemorandumCNCC Centre Nationale de Cont&ole et Cerdficaion des Semences at Plamtes (National Center for the

Control and Certification of Seeds and Plants)CNP Conseil Natonal de la Planification (National Planning Council)COOPAPI Coopfrtives Apicoles (Apiculture Cooperatives)COOPSEL CoopEaives de Services de I'Eevage Born et Ovin (Cooperative for ivesatock Services)COOPSEM Coopives de Semen ces (3eed Production Cooperatives)COPAVI Cooperadves de la Producitn Avicole (Poultry Cooperatives)DA Algerian dinarDAS Domaines Agricoles Socai aS (Socialist State Farms)DOP Direcdion de l'Organlsatic 3de la Producion (Directorate of Production)DP Direction de la Planifcation (Directorate of Planning)DR Direction de la Regulaion (Directorate of Regulon)DRC Domesdc resource costDRVF Diection de la Reckerche, de la Vulgarisadon et de la Fomzation (Directorate of Research,

Extension and Trining)DSA Directions des Services Agricoles (Directorates of Agriculu Services)DSV Direcion des Services Vaernaires (Directorate of Veterinary Services)EAC F&ploitatonos agricolks collectf (Agricultural Cooperative Farms)EAI E&loitations agricoks individuelles (Agricultural Individual Farms)EC European ConuityEDI4MA Entrepnse de Disiibution de Madcines et Matiel Agricole (Enterpise for the Distribution of

Agricutural Machinery and Equipment)EEP Export Enhanemen ProgramENAFLA Ewrepise Nationake Algriene des Fruits et Lgumaes (State Enterprise for Marketing Fresh

Fruits and Vegetables)ENAFROID Entreprise Nationale du Froid (National Enterprise for Frozen Foods)ENAPAL EwtrepriseNationale&l Approvisionnement enProdisAlimentaires (National Enterprise forFood

Supply)ENASUCRE Entreprise Nationale du Sucre (State Enterprise for Sugar Procesing)ENCG Entrepmse Nationale des Corps Gras (State Enterprise for Processig Fats and Oils)ENIAL Entreprise Natonale de Developpement des Industries Aimnentaires (State Enterprise for the

Development of Food ndustries)ERIAD Entreprise Regionale des Indtries Cereakeres et D*ives (State Regional Enterprise for Cereal

Processing)ESW Economic and Sector WorkFAO Food and Agrculture Organization of the United NationsGDP Gross Domestic ProductGD JMMA Groupens d 'lntrets Commnwu pour la Distributon et 1, "inmance du Materil Agricol et

de la Pete Hydradique (Apex Orgnization for the 1DIMN-A)

GNP Gross National ProductGOA Government of AlgeriaIBRD Intemnational Bank for Reconstruction and DevelopmentIFDC International Ferilizer Development CenterIMF International Monetary FundINPV Institut National de la Protection des Vegetaux (Institute for Plant Protection)IPM Integrated Pest ManagementITGC Insihut Techmqye des Grandes CWltures (Technical insttute for Field Crops)I litersMGLA Matiere grasse lainere anhydre (butter oil)MT Metric TonsMOA Ministry of AgricultureMOC Ministry of CommerceMOF Ministry of FinanceNEP New Economic ProgramNPC Nominal protection coefficientOAIC Office Algenen Interprofessiornel des Cirales (Algerian Interprofessional Ceras Board)O&M Operation and maintenanceONAB Office National des Aliments du Betails (National Livestock Feed Board)ONAMA Office National de Materiel Agricole (National Board for Agricultural Equipment)ONAPSA Office National d'Appropmsionnement et de Serices Agricoles (National Office of Agricultural

Services and Supplies)ORELAfT Office Regional Est du Lait et des Produdt Laitiers (State Milk Board for the Eastern Region)OREVIC Office R&gional des Vuades du Centre (State Meat Board for the Central Region)ORLAC Office Regional du Lait et des Prodiats Laiders du Centre (State Milk Board for the Central

Region)OROLAIT Office R)gional Ozest du Lait et des Prod*d:s Laiders (State Milk Board for the Western Region)ORVE Office Regional des Viandes de l'Est (Stae Meat Board for the Eastern Region)ORVO Offices Regional des Vuindes de l'Ouest (State Meat Board for the Western Region)PE Public EnterprisesPMA Enreprise NationaledeProducton desMatrielsAgricoles (National Enterprise for the Prduction

of Agricultural Equipment)QR Quantitative restrictionsSMP Skdm Milk PowderSOJUC Societe des Jus et Conserves (State Enterprise for Juices and Preserves)SSR Self sufficiency ratioUCA Union des Cooperatives Agricoles (Union of Agricultural Cooperatives)UF Unitesfourrageres (Forage Units)VA Value addedVAT Value Added TaxWHO World Health OrganizationWUE Water use efficiency

DEtMOCRATIC AND POPULAR REPUBLIC OF ALGERIAREVIEW OF AGRICULTURAL POLICIES AND AGRICULTURAL SERVICES

1987 - 1993

Table of Contents Pape

ExecutiveSummary . ............................................... I

1. Introduction ...................................................... 1

2. Recent Performae of the Agricultmal Secor ................................. 2Genea ....................... ......................... 2Agroecological Issues ................................................ 3Idgation ........ ........................................ 3Crop Production: Climatic Conditions and Produicdon Stability ........................ 4Livestock Production ................................................. S

3. Macroeconomic Policies Affecting the Agricultural Sector and Agricultura Services. 7Fisal Meurs twards Agriculture. 7Production Subsidies. 8Trde and Forein Exchange Regimes .11Rural Finance and Interest Rate Policies .14Employment .iSReflecion on Policy Objectives. 15

4. Output Distribution and Markeing Services ........... .................. I.... 17Current Status of Marketixb ............................................ 17'Administrative Agricultural Markeing Channels ......... ..................... 17

Ces ............................................. 17The Dairy Subsector ........................................... 19Oilseeds ............................................ 19Sugar ..................................................... 19

Agrtural Marketing by the Private Sector . .................................. 19Fruits and Vegetables .......................................... 20Livestock ............................................. 21

Review of Consraints in Agricultual Marketing Services ......................... 21

Thi seor work s based on several missions undertain in 19 anl 1993. We adnowwdge wh gratiudethe cooperation, contrbutons and commnts of the Algeran authorities. The Task ger s Mr. KutluSomel (abo contibut on agricultural policy and crop producton) and the contributors are Mr. MiNdDeba e ( and marketug); Mr. Ian Goldin (agricultural tae); Mr. Lauent Madi(livesock sector); Mr. Harald Stier (agricultural inputs); Mr. Orhan Dogan (consu,tant,issues); Mr. Noman Kanafi (consltant, agricultura machinery); Mr. Hendrik KuIh (consulant,seeds); Mr. Villy Nilsen (consultant, agricultural macinery); Mr. Ronald Phlips (cooperaves); and Mr. Gary Reusch6 (consultan, seeds). Mr. John Mclntire is the peer reviewe. Mr.MYp _ Sinha I the Acding Naturl lRores and wir m n tDivision Chif and the County

Dpawtmnt Diredr s Mr. Daiel Ridhie. Support frm the Danish Trust Fod s grptefulyadcowleged for thework of Mess. Kanfani and Niesen.

ii

5. Lnput Distribution and Marketing and Other Agricultural Services .................... 23Seeds ................... .................. 23Fertilizers .................. 25Pesticides . 27Agricultu ral Machinery and Equipment 28Livestock Services ................ ............... 30

Sanitary Control and Veterinary Services ............... 30Livestock Input Supply ............... 31

Review of Constraints in Input Supply and Provision of Agricultural Services ............ 31

6. Structural and Institutional Issues ........................................ 33Land Tenure ..................................................... 33Cooperatives ..................................................... 34Public Administration for Agriculture ................. .................... 36Research and Extension ................ ........ ........ 37

7. Conclusions and Recommendations ........................ 38

Statistical Annex ... 46

The following technical docments, which were used in the preparation of this report, are available on a restrictedbasis:

Agricultural Policy Issues (in English)The Trade Dimension (in Engish)Agricultural Marketing (in English)The Livestock Sector (in English)Agroecological Issues in Nordhem Algeria (in French, unedited)Agricultural Cooperatives: Issues, Prospects and Challenges (in English)Fertilizer and Chemical Input Distribution (in English)Seeds Subsector (two reports; in English, unedited)Agriculual Machinery and Equipmet (in English, unedited)

DEMOCRATIC AND POPULAR REPUBLIC OF ALGERIAREVIEW OF AGRICULTURAL POLICIS AND AGRICULTURAL SERVICES

197 -1993

Executive S_mmary

1. Background. In 1987, Algeria began taking major steps towards the economic transformationof the agricultural sector. The dismantling of the state farms and their transformaton into individual andcollective private farms have changed the basic structure of the agricultural sector. Other actions includedprivatizing some cooperatives and giving autonomy to some of the large public enterprises (PE) involved in inputproduction and service provision, including marketing, while remaining under public ownership through holdingcompanies (Fonds de particpion). Considerably more challenging work lies ahead in agricultural reform inAlgeria. Private farms and farmers are more numerous as compared to the situation uuder socialist organizationand are also more diffused over space. The needs of this new organization have to be addressed in the areas ofinput and service provision, including diverse areas as marketing, storage, credit, input supply, and tecnicalinforation. The monopolistic PE that served the socialist farms have to be adapted and restruchtred to servethese private fanmers under competitive market conditions and the private sector has to assume a higher role inproviding agricultural services. This transformation will involve considerable structural and macroeconomicadjustment, involving macroeconomic prices; public expenditures; the directon, level and sustainabiity ofagricultural subsidies; public ownership; etc. The sector's ability to absorb these impacts is critical to the successof the adjustment program. lhe objecdive of the sector work is to assess specific issues n the transformanonprocess ofAlgerian agriculture pertaining to agricultural services, to review recent policy developments affectngthe agricultural sector and to develop optionsfor change to ensure that an evenual adjustmtprogram inducesad eqate supply response andpromotesflexiblity, efficiency, producty and stability In agricutual production.The term 'agricultmua services" is used broadly to cover, e.g., the adminision, research and extension,wholesale and retail marketing (including imports and exports) of agricultural products and inpUtS and theorganization of agroindustry, etc., with the associated regulatory frmnework.

2. The analysis in this document focuses on conditions that existed until mid-1993, when the studywas concluded. Considerable progess has been achieved in inproving macroeconomic conditions as a result ofthe Stabilization Program initiated in April 1994. Some of the policy changes have affected the agriultural sectordirecdy; while an effort has been made to record these changes in this document, they are not analyzed in depthas this would merit another study. '

3. Agriculture contributes around 11-15 percent of total value added (VA) and 11-12 percent ofGDP. It receives around 8-10 percent of total investment and absorbs around 25 percent of labor. The twoconsecutive seasons of outsanding output due to favorable weather conditions in 1991 and 1992 have resultedin real growth rates of 23.0 and 4.8 percent in agricultural VA (in 1980 prices), but 1993 was anotherdisappointing year due to drought and the same situation is expected for 1994. Food imports of US$1.9 biUlionand US$1.75 biSlion comprised 19.5 and 22.5 percent of total imports in 1990 and 1991 respectively. The foodself sufficiency ratio (SSR), is low, particularly in cereals, pulses, edible oil and milk, and there are technicallimits to increasing SSR. Imports of agricultural inputs and equipment increse the dendence of the agriculturalsector on the international market.

4. Agriculural Policies. The pervasive nature of implicit and explicit supports in agriculture, aswell as the inconsistency between some of the policy measures require some reflection on policy objectives. Thebasic issues are that (a) it is difficult to find an explicit statement of policy objectives that go beyond therhetorical; and (b) there is a high degree of confusion of efficiency and equity objectives. Other issues arewhether: (c) any of the explicit objectives are realistic and economically sound; (d) some of the policy objectivesimplicit in the measures taken are realistic and consistnt; and (e) the policy measures taken are the best toachieve the given objectives.

ii

5. One ovefriding Government objective to increase the degree of self sicaency focusing aboveall on cereals for human consumpton. These policies lack the critical component of addressing the issue ofstabibly of production. As such, any consequent gains in production will be opportunistic and ephemeral. Therealism of these policies, when the overall SSR is around 20 percent, is doubtful. They thwart the developmentof products for import substitution or exports, where Algeria could have comparative advantage.

6. Improving the economic efficency of production did not appear to te a policy objective. Bothinputs and products received significant implicit and/or explicit subsidies and the consequent distortions werecompounded by inefficiencies in marketing and distribution due particularly to PE dominance and price andmargin controls, and finally, consumer subsidies.

7. Equity objectives predominated and the main tool used for this purpose was pdrEquation wherebytransport and handling costs or margins or prices were equalized over the country. This constrained private sectorinvolvement in such markets, prevented spatial and temporal arbitrage, caused bunching of harvest deliveries andresulted in inefficient input provision that lacked price incentives to differentiate among markets based on realcosts.

8. The policy objective ofprovidingfood at low cost to conswners affects agriculture adversely. Theprice and margin controls used to achieve these objectives, as well as the use of PE to implement them,

fecuively served as barriers to entry for the private sector and precluckd their involvement in these markets.While targeting welfare support to vulnerable groups would be justified, subsidizing all consumers would not.

9. In some cases the effects of the policies implied results that were in essence income tranfers toagriculture. Given the limited resources for such purposes, the objectives can not be achieved in an equitablemanner. The use of prices and interest rates to achieve income and equity objectives result in market distortionsthat affect efficiency. While income policies may be justified, direct compenaion would be less distortionaly.

10. Concems about enmplymen objectives were undermined by policies that encouraged the use ofcapa intesive technologies. In this respect, further study is necessary to assess the possible existence ofsegmented labor markets and a dualistic farm structure. The potential of private sector rural services in creatingemployment has not been adequately assessed due to the PE dominance in these areas.

11. Maintaining the natural resource base, as an objective, needs to be supported by a set ofconsistent policies. The limited defensive efforts in agroecological protection are defeated by price policies thatencouraged the expansion of production into marginal and ecologically fragile areas.

12. The appauent confusion in policy objectives and policy tools reflected (a) the difficulty theauthorities face in the transition from a planned, socialist sector to a market oriented sector domiated by privatefarmers; (b) the pervasive paternalistic and benevolent attitude of the policy makers and administrators,compounded by recent political developments, and the preoccupaion with providing food at low cost toconsumers; and (c) the need to develop policy analysis capabilities in the public administation for agriculture.

13. Since mid-1994, the economic and structal reform activities initated by the StabilizationProgram have started to rect some of these distortions. Medim term adjustment programs are being developedto design and sequence the economic, structura and instiutional changes under a market economy. Private sectoropeaions are also expanding.

14. Cofstraints in Agricultural Marketg Services. The Algerian agricultural marketing systemcould be improved substantially with respect to the three basic functions: (i) the exchange ofproducts; (ii) theechange of risk; and (ill) the exc*ange of informauion. The current marketing system of allocating of producs

iii

entails high and unnecessary costs throughout the agricultural and food marketing chains, both private and public.This poor performance results mainly from (i) high post-harvest losses or deterioration along the marketing chain;(ii) inefficient transporation; (iii) poor storage conditions and insufficient availability of storage facilities; and(iv) inefficient disfiibution of consumer products at the retail level. Four constraints have been identified:

a. the strong Government market intervention polices implemented through parastatals affect shortto medium term positions taken by private entrepreneurs in the market;

b. the preferential treatment and monopolistic position of the parastatals in marketing chains, inaccess to foreign exchange and credit, serve as barriers to entry for the private sector;

c. the poor infrastructure and equipment at the wholesale level (i.e., between farmers andprocessing and distribution enterprises); and

d. a poor regulatory environment, where some positive developments have been taking place sincemid-1993.

15. Constraints in Input Supply and Provision of Agricultu Services. The basic constraints ininput supply and related agricultual services stem from: (i) the inability of the PE to adapt in the face of anagricultural sector now composed of private farmers; (ii) the maintained privileges of PE monopolies in accessto resources such as foreign exchange, subsidies, credit, etc., but subject to overall resource consmints; (fii) theGovenmient interventions in prices, margins and other controls such as effective QR; and (iv) as a consequence,the limited involvement and experience of the private sector in these areas.

16. The PE involved in input supply and provision of services have traditionally served the statefams under a planned, socialist system, characterized by central decisions on input use based on techimcalcriteria. Furthermore, the scale of the state farms was considerably larger as compared to the average privatefarm size today. These private farmers are economic agents that are sensitive to and respond to economic stimuli,and are more dispersed over space. The PE have not responded to the needs of this new structure and havecontnued to behave and produce as before, without adequate assessment of market stmcture, demand or logistics.

17. The PE have continued to have privileged access to the scarcer foreign exchange resources forimports of inputs, raw maWials, machinery, equipment and spare parts. Furtherore, the PE have continuedto be the media through which Government input subsidy programs are implemented. This has effectively reducedpart c. the market risk for the PE, but this option is not available to the private sector. As effective barriers toentry me gradually decreased it will be possible to have more participation of the private sector.

18. The Govermment administered prices and margins and piriquation schemes effectively block.private sector involvement in input supply. Although, most agricultural input subsidies have been eliminated onApril 1994 in conformity with the IMF Stand By agreement, the private sector will not be able to provideservices in these areas in a competitive manner if it is not allowed to differentiate between market segments. Suchcontrols and panterritorial pricing also encourage inefficient production in unsuitable areas, as wel as adverselyaffecting retail operations, especially by the input supply cooperatives. While social reasons may justifyGovermment intervention in well targeted, specific areas, panterritorial control and uniform prices and/or marginscan not be justified.

19. Land Temwe. Land tenure is a fundamental problem. Currentily, four main modes of rights overland exist in Algeria. These are (i) Pilot Farms under the jurisdiction of the public domain; (ii) individual privatefarms (EAI) and collective private farms (EAC); (iii) the traditional private sector farms (melk); and (iv) the landin the steppe areas under the jurisdiction of the national domain but where tribes exercise a usage right. The basic

iv

issues now are the resolution of ownership rights for the EAC and EAI and registering the property rights of thetraditional private farmers. One problem area is that the cooperative and collective operations expected of theEAC have not worked. Centrifugal forces are thus changing the EAC into defacto EAI. There are currently somepreliminary moves to turn this into a de jure situation. However, the central authorities' concern to maintainviable farm sizes and prevent fragmentation and parcellization may be slowing the process. Knowledge about landtenure issues and land use patterns needs to be improved at the policy making level. A conmmittee has beenforned to advise the policy makers on the issues and propose action, legislation, etc., and there are positivedevelopments. Yet, the task at hand is monumental and it has to be recognized that it wiUl take considerable timeand resources to develop a land tenure system that is conducive to efficient use of resources through the marketsystem and does not pose major equity problems. The linkages with rural finance (collateral requirements) haveto be considered, and, manageable market systems and the associated legal fraework for the sale, inheritanceand rental of land (for cash or in kind returns) need to be organized. However, above all, adequate policy signalsmust be given to fanmers that they are the owners of the land in order to promote investments in land andefficient exploitation of resources. Under the Cadastre Project supported by the Bank, resoes have beenallocated for a study on agricultural land tenure.

20. Cooperatives. Since independence, Cooperatves have been state sponsored organizations thatserved as instruments for implementing agricultural policy. The cooperatives maintained close ties with the PE,which either supplied goods to or purchased products from the cooperatives. The present transformation of theAlgerian cooperative system was initiated in 1988 but there is a wide variation in the extent to which cooperativeshave transformed themselves from govermmental agencies to private enterprises. The most important system ofcooperatives involved in cereals and pulses, the CCLS, have been left out of the legal framework of privadzaion.The CCLS are not cooperatives in any sense of the concept, and in their present status appear to be anunnecessary stage in the distribution of imported commodities. Their restructring within a broader frameworkof the distribution of agricultural commodities should be a priority. The privatized cooperatives, especially thoseinvolved in input supply, face an overwhelming debt burden arising from their patrimoine, i.e., assessed valueof infrasucture and stock when the new, privauzed cooperatives were formed. Thepatrmomne reflects not theeconomic but the accounting value of outdated and depreciated infrastructure and equipment as well as lossesincurred as a consequence of implementing govermment policies under socialist agriculture. It is necessary toreview the debt position of the cooperatives, release them from any liability on the pautriine, and establish asetlement mechanism for cooperative debts, in such a manner as to relieve them from dependence on theGoverment. The defacto monopoly position of PE in the supply of key agricultural inputs effectively preventcooperatives from engagg in activities such as importng seeds and other inputs. This condition is exacerbatedby Govermnent controls over prices and margins for inputs which squeeze cooperative profits.

21. Research and Extension. Traditionally, the organization and orientation of agricultural resarchin Algeria was geared to the socialist sector. Extension emphasized conveying the technical information necessaryto realize production plans to the limited number of state farms. Hence, the main challenge to the research andextension system today is to reorient itself to the needs of private farmers guided by profit motives under marketconditions with real resource constraints and climate and market risks. The limited resources of the publicresearch and extension organizations essentially require that they be used effectively in priority areas. A Researchand Exension Project is under implementaion with Bank financing (Loan 3216-AL). On the other hand, privatesector research and extension should be allowed and encouraged.

22. Public AdminLstrton for Agricutre. MOA is the focal public organ for the concepualizon,development and execution of agricultural policy. MOC, MOF and CNP are also involved in the policy processesin coordination with MOA. There are two related issues: (a) the higher role for market forces and private sectoroperations will require a reorientation towards new perspectives for the processes and methods of agriculturalpolicy; (b) policy objectives have to be subjected to critical assessment of feasibility, cost and alternatives. It istherefore important to develop agricultural policy analysis capacity in the MOA, with close linlges to CNP,

v

MOC, MOP and the universities. Commitment from the Government, backed by sustainable resource allocation,should be supported by a program of technical assistance.

23. Conclusions and Rmmendations. Algerian agriculture maifests serious problems thatconstrain its potential. These problems emanate from (i) the policy dimension, pertining to both the generalmacroecononmc enviromnent and to the agricultural sector specifically; and (i;) structurl, institutional andtechnical constraints, related to land temnre, agroindustrial structure, marketing, input supply, cooperatives,research and extension on appropriate technologies and the regulatory environment. The soluton of majormacroeconomic problems, such as those related to the management of the foreign exchange and trade regimes,the financial sector and the interest rate, and budgetary management, will require a well designed and sequencedadJusment program, which should take into consideration the potential impact on the agricultural sector.Problems of a policy and structural nature that pertain specifically to the agricultural sector also need to beaddressed within an agricutural sector adjustment program.

24. On broad macroeconomic issues, those pertaining to the foreign exchange and trade regime areof critical importance to agriculture:

a. imported inputs entail implicit subsidies due to the overvalued exchange rate, resuting ininefficient use due to distorted prices; better targeted subsidies should be more transparent in thebudget and shoudd not use the exchange rate as the medium;

b. before the macroeconomic stabilization program, the limited foreign exchange from officialresources were effectively rationed through administrative processes and QR imposeu - theCAH and, while imports with foreign exchange from the 'paraliel" market and own sources wereallowed for the private sector, it was not permitted to reflect the higher foreign exchange costson product and service prices; this caused various compensatory measures, such as over-invoicing, to recover costs. Starting April 1994 and following the macroeconomic stabilizationprogrm, the CAH has been dissolved and the QR have been removed except for (i) strategiccommodities where imports by the private sector would be based on professional, technical andcommercial competence; and (ii) the temporary suspension of many competng imports to allowdomestic production to develop; on the other hand, imports with foreign exchange from the"parallel" market and own sources are no longer allowed;

c. the overvalued exchange rate renders nontradables expensive and discourages foreign investment;on April 1994, the DA was devalued by 50 percent, but the gap between the official exchangerate and the parallel market rate remains substantial; the macroeconomic stabilization programcalls for the gradual liberalization of the exchange rate leading to the introduction of an inter-bank foreign exchange market by mid-1995;

d. the privileged access of the PE to foreign exchange perpetuated their inefficiencies and crowdedout the private sector, serving as a barrier to entry; the first trade liberalizing measures underthe Stand-By agreement should facilitate the private sector access to foreign exchange;

e. the wedge between the official and market exchange rates incorporates transactions costs and riskpremia, which are rents accruing to agents not directly involved in producton and services; and

f. foreign exchange retention schemes discriminated against agricultural exports at 50 percent, whilethe global retention rate was 100 percent; after mid-1994, the foreign exchange retention rate isunified at 50 percent for all types of exports (except for hydrocarbons and mine products).

vi

25. Larger concerns such as the management of the foreign debt will be influential in the resolutionof the issues surrounding the foreign exchange and trade regimes. A thorough discussion of these issues can befound inthe Country Economic hlemoranium (CEM) (Report No. 12048-AL). The fundamental recommendationis also appropriate for agriculture: the target should be to unify bhe foreign exchange rate and limit thetransactions that can benefit from a preferential rate to be funded from official sources to a narrow positive list.Foreign exchange at the unified rate should be available competively to all econoniic agents. Any preferentialtreatment and privileged access to foreign exchange accorded to PE should be explicidy eliminated.

26. The focus on agricultural production to improve self sufficiency should be reevaluated with thefocus on food security and efficient use of resources. The technical limits on incteasing SSR in food imply thatagrictltvual resources, especially in those areas endowed with better soils, irrigation and higher rainfall, shouldbe used more efficiently to diversify production, in particular, focusing on high value products that can alsoinduce high value added processing, destined for segmented markets and exports.

27. The second issue of a broad macroeconomic nature pertains to the financial sector and interestrate policies. The interest rate is negative in real terms and more so for agriculture. Financial sector issues needto be addressed in general terms but, the specific problems and needs of the agricultural sector have to be noted.The higher transactions costs and risks associated with agricultural production would make rural finance a lowpriority in lending portftmtos of conmnercial financial institutions. Hence, compensatory measures such assubsidizing the transactioms costs of rural finance may have to be considered. Under aUl circumstances, positivereal interest rates are recommended for agriculture as well to reduce the bias towards capital intensive technologychoices and to ='romote more labor intensive methods that will promote labor absorption in the face of high ruralunemployment. Rural financial institutions and policies will need to be assessed with a thorough study.

28. Another fundamental structural problem arises from the industrialiation model adopted inAlgeria. This model emphasized an industrial structure under public ownership with large scale, capital intensiveoperatons, which, in turn, promoted import dependence to assure timely supply of standardized and uniforminputs in large amounts. As a copsequence, domestic sources of supply were either neglected or treated asproblem areas that could only survive with state support. This model was of limited use in creating employmentand absorbing labor, in contradiction with the existing factor proportions in the country. This structure has hencecontributed significantly to the current problems of unemployment, compounded by policies that subsidized capitalintensive methods, even m the agricultral sector. Hence, future focus on agroindustry and agricultural servicesshould be on smaller scale, labor intensive private sector operations.

29. The main target of agricultural reform and adjustnent should be to accord a higher role for theprivate sector (including cooperatives) and market forces. This will require a three pronged approach:

a. review and adjustment of the regulatory enviromnent to identify and implement changes that willfacilitate private sector operations under narket conditions; including, Government policies, suchas price and margin controls,pgriquaton, subsidies, access to foreign exchange, etc., that serveas effective barriers to entry for the private sector;

b. limiting the monopoly powers of the PE through restructuring and privatization and creatngmore competition through private sector participation to enhance efficiency of markets; and

c. investment in agricultural services, emphasizng those that can be managed by the private sector.

30. Technical assistance will be necessary to revi6v the existing regulatory framework and legislationto assess the constrain faced by the private sector. New legislation will need to be developed for considerationby the Goverment that will facilitate private sector operations under market conditions. Conversely, the State

vii

agencies will need to assume a regulatory oversight role as opposed to their traditional role as active participantsin production and provision of agricultural services.

31. Agricultural policies will need to be based on clear, consistent and transparent objectives. Whileit is the prerogative of any Government to influence economic activity, interventions should be selective, entailminirmu distortion and be within budgetary constraints. In agriculture, it is important to direct interventions toinfluence production through product prices rather than input and service priees to reduce distortions. Theelimination of explicit subsidies on most agricultural inputs in April 1994 should improve the situation. However,water and seed prices are still subsidized, and implicit input subsidies are still in place. Social interventiomsshould be well targeted to be effective and to reduce spillover distortionary effects. For these purposes, it isnecessary to develop policy analysis capabilities in the MOA, CNP, MOC and MOF.

32. Certain policy reforms are a prerequisite to the development of agricultural services. Only minordevelopments can be expected in marketing and processing under the current centrally planned environment forthe cereal and dairy subsectors. Reforms in these two key sensitive subsectors need to be based on well designedprograms to ensure sufficient and stable supply. In the dairy subsector, the distortions that produce widedifferences between producer and consumer prices and import costs need to be reduced. Consumer subsidies needto be targeted towards vulnerable groups. Furtemore, the issue of the comparative advantage in milk productionwould need to be addressed, including the role it plays in the portfolio of agricultural products for farmers. Ifprice distortions are reduced, there would be interest by the private sector in developing small to medium sizemarketing and processing activities.

33. In the cereal subsector, reforms in price and trade polici s will be slow. International trade withAlgeria in cereals is conducted under concessional arrangements that defacto use a single Algerian countrpartthat guarante credit and can handle large quantities. Hence, reform in this sector would need to be developedbased on thorough and detailed studies, considering domestic production issues as well. Considering that Algeriaw4ll continue to depend largely on imports for the country's needs over the long run in cereals and cerealproducts, it would be conceivable to select the main port terminals and related facilities to be modernized and/orexpanded, and be put under private sector management.

34. Reforms in the price and trade policy, and demonopolization would be imperative before anyinvolvement in investnents in the sugar and oilseeds subsectors. In both subsectors, restrctrng andrefurbishing of the existing refining facilities would need to be analyzed. Studies looking at the production andmarket potential for oilseeds would also be recomiended. In the fruits and vegetables and livestock subsectorsthere is significant potential for private and public investment but the main issue is to give the private sectoraccess to credit and foreign exchange. It should be noted that price policies have been addressed since 1990.Today, almost 90 percent of tt - products have liberalized prices. However, the remaining products withadministered prices are the most critical for agricultural production.

35. Development of private marketing services would need substantial reform in the role ofGovernment and its agencies in pricing products. Such reform should guarantee enough freedom to emergingentrepreneurs such as merchants, transporters, small processors and retailers, to let them gradually supplant theexisting large PE (i) in offering alternative new outlets for farmers products; (ii) in adding higher value toagricultural products; (ii) in creating jobs; and (iv) in providing better supply (larger quantities, better qualityand efficient services) to the population. The role of the Government, together with the representatives ofentrepreneurs and farmers in each subsector, should focus on rules and enforcement of fair competition andcontracts, consumer health, improved infrastructure and information on market conditions and new technologies.Private sector participation in these markets will increase as barriers to entry are gradually eliminated.

viii

36. RestucturIng, including amvestiture and privatization of agroindustrial enterprises in competitivesubsectors should be a priority. Private sector development has the biggest potential in processing in the cereals,feed, fruit and vegetables and livestock subsectors. The administered prices and margins, and the p0rmqwionpolicies confer indirect preference to parastatals, including large subsidies. These policies discourage privatesector operations in the areas. Privatization should be addresseo, stri with the ERIAD in the milling andbaking industry, ENAPLA, ENAFROID, ENCG, SOJUC, and the regional dairy and meat boards. In most ofthese subsectors, effectve bariers to pnvate sector entry should be removed.

37. In input supply, the dominant position of ONAPSA should be considered with priority with aview towards restructuring and privatization. Similarly, problems associated with other PE such as ONAB,GDIMMA, PMA, ASMIDAL, etc., should be addressed and programs should be developed for restructuring andprivatization. Private enterpnse access to these markets is limited due to adminstered prices and margins,pruatiOdn, and implicit and explicit subsidies to the PE. On policy matters, state controls over prices, marginsand other concrete allocation decisions need to be removed. Under the stipulations of the new agreeent withthe IMP, most explicit input subsidies have been eliminated, but input prces have to be declared and are stillnot market determined.

38. Are for pote investments in agricultural services need to be identified to complement theadjusitm process. Technical and financial support for investment could target three categories of investorsproviding services to farmers:

a. private enterprises providing wholesale marketing and processing services along the agriculturaland food marketing chain; merchants and associations of farmers whose mam activities are (i)to buy or get delivery of agricultural products frm fannewrs and importers; (ii) to condition(clean, dry, sort, package, etc.) these products accordingly with incentives given by the domesticmarkets; (iii) to store; (iv) to transport; (v) to process the products and add service value tothem; and (vi) to manage commercial risks and risks related to price fluctuaions;

b. selected PE, with a strong commitment from Government to demonopolize and privatize, toimprove the handling of domestic and imported socialy sensitive products, and to assist theirreorienation to new, or more focused, acities; and

c. the State and municipalities to improve a number of public and semi-public (in connection withnational or regional professional associations) (i) infrastructure (mainly port facilities to unloadincoming ships, facilitate tansit, inspection, inland transportation, etc., and regional commodityexchanges); and 00i) agencies involved in the priority fields listed above, i.e., regulating andenforcement of fair competition and contracts; consumer health safety; and market information;and training in business administration and marketin. The infrastructural investments shouldemphasize management by the private sector to enhance cost recovery for O&M.

DEMOCRATIC AND POPULAR REPUBLIC OF ALGERIA

REVIEW OF AGRICULTURAL POLICIES AND AGRICULTURAL SERVICES1987 - 1993

1. Introduction

1.1. In 1987, Algeria began taking major steps towards the economic transformation of the agriculturalsector. The dismanling of the state fanns (DAS; Domaie Agnicoles Socialistes) and their transformation intocollectve and ixdividual pnvate farms (EAC/EAI; Exploitations Agricoles Collectives and Exploiations AgncolesIndividuelles) have effectively changed the basic structure of the agricultural sector. Legislation governingcooperatives was changed and most state cooperatives (excluding the cooperatives for cereals and pulses; theCCLS) were given private sector status. Other actions included giving autonomy to some of the large publicenterprises (PE) and parastatals' involved in input production and service provision, including marketing, whileremaining under public ownraship through holdnig companies (Fonds departicipation). The private sector is nowallowed to participate in such agricultural services and is also given the right to import, which, as will beexplained below, remains largely on paper due to the dominance of PE and their preferential access to foreignexchange and credit. State controls over output and input prices remain, covering some critical commodities.

1.2. Considerably more challenging work lies ahead in agncultural reform in Algena after anencouraging start. Private farms and farmers are more numerous as compared to the situation under socialistorganizion and are also more diffused over space. The needs of this new organization have to be addressed inthe areas of input and service provision, including diverse areas as marketing, storage, credit, input supply, andtechnical information. The monopolistic PE that served the socialist farms have to be adapted and restructuredto serve these private farmers under competitive market conditions and the private sector has to assume a higherrole in providing agricultural services.

1.3. The Algerian economy will be undergoing significant adjustments in the medium term. Theorganzation and the management of the agricultural sector will have to be gradually relinquished to market forceswhich can more efficiently determine resource allocation. This transformation will involve considerable structuraland macroeconomic adjustment, involving macroeconomic prices; public expenditures; the direction, level andsustainability of agricultural subsidies; public ownership; etc. The sector's ability to a.,orb these impacts iscritical to the success of the adjustment program. It is necessary to assess policy developnts, and structuraland instiuional bottlenecks in agricultural services3 and develop options for change to ensure that an eventualadjustment program induces and promotes flexibility, efficiency, productivity and stability in agriculturalproduction.

1.4. The objectve of the sector work is to assess specific issues in the transformation process ofAlgerian agriculture pertaining to agricultural services and to review recent policy developments affecting theagricultural sector. After an initial review of the recent production perfonnance, a discussion of themacroeconomic factors affecting agriculture will follow, the most important being the agricultural subsidies; themanagement of the macroeconomic prices of the foreign exchange and interest rates; the trade regime; andemployment policies. This will be followed by focusing on specific issues pertaining to agricultural services onoutput marketing and input supply respectively, and, subsequently, structural and institutional constraints, leadingto conclusions and recommendations. The analysis in this document focuses on conditions that existed until mid-1993, when the study was concluded. Considerable progress has been achieved in improving macroeconomic

In this document, parastatals are used to designate the various public enterprises, marketing boards, etc.

2 The term agricuural senvces is used broadly, covering, e.g., the administration, research and extension, wholesaleand retail marketing (including imports and exports) of agricultural products and inputs and the organization ofagroidustry, etc., with the associated regulatory famework.

2

conditions as a result of the Stabilization Program inidated in April 1994.3 Some of the policy changes haveaffecte the agricultural sector directly; while an effort has been made to record these changes in this document,they are not analyzed in depth as this would merit another study.

1.S. Seeral complementary studies or operations elaborate on certain issues that are not treated indetail in the present report. The 1993 Country Economic Memorandum (CEM) (Report No. 12048-AL) discussesthe broad macroecononic issues, particularly those related to the foreign exchange and trade regimes, as wellas discussing consumer related issues. In 1991, the former were also discussed in the ESW on Exchange andTrade Reionn (Report No. 9508-AL) and the latter were discussed in the ESW on Consumer Subsidy Reform(Report No. 9881-AL). The discussion of agricultural policies in the present report also served as the backgroundfor the CEM. Water related issues are treated in the 1992 ESW, the Water Resources Development StrategyPaper (Report No. 10858-AL), and the irrigation projects under implementation with Bank financing. The 1993Tanort Strategy Note also discusses grain import and transport facilites. The 1993 ESW on EnvironmentalIssues discusses agroecological matters. Agricultural research and extension are being addressed in a pilotResearch and Extension Project (Loan No. 3216-AL). Land tenure matters are to be addressed in a study to befnanced by the Cadaste Project under implementation. The Enterprise and Financial Sector Adjustmeant Lo(EFSAL) addresses financial sector reform and restructuring issues, among others, in two critical PE inagriculral input and machinery production. Rural finance issues were addressed in an Agricultural Credit Loan,which was not extended due to the deterioration in the general conditions in the financial sector. A rural financestudy would be conucted under the proposed Agricultural Services Project. A prices and incentives studyconducted by the Algerian authorities addresses issues of comparative advantage in agricultural production. Thepresent report also updates some of the information in the 1990 ESW, "Algeria: A new Opportunity for Growth"(Report No. 7419-AL). Finally, the present report is in conformity with the 1993 Agricultual Strateg Paper(Report No. 11741-AL).

2. Recent Perfornce of the Agricultural Sector

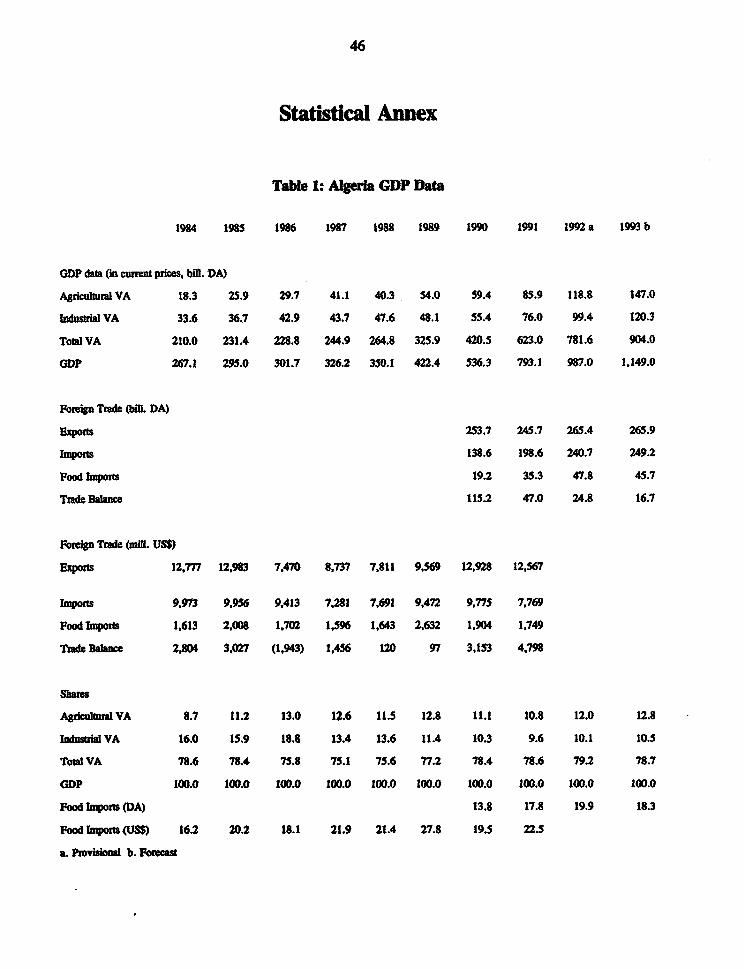

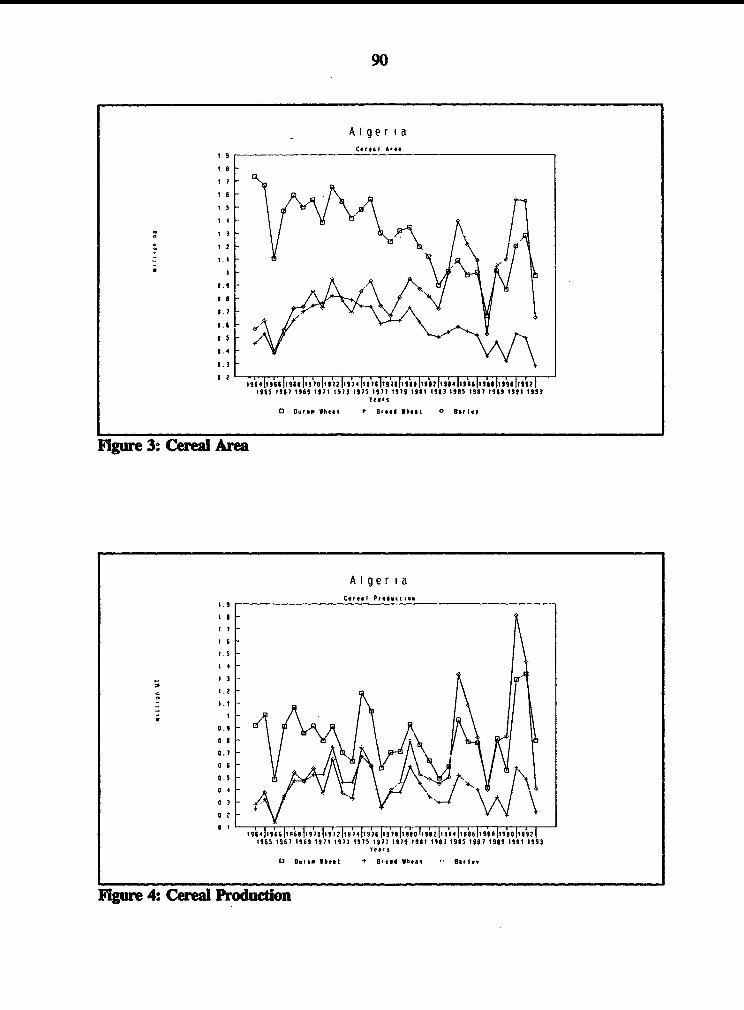

2.1. Genal. Agriculture contributes around 11-15 percent of total value added (VA) and 11-12percent of GODP (Table 1). It receives around 8-10 percent of total investment and absorbs around 25 percent oflabor (Tables 2, 3 and 4). The two consecutive seasons of oustanding output due to favorable weather conditionsin 1991 and 1992 have resulted in real growth rates of 23.0 and 4.8 percent in agricultural VA (in 1980 prices),but 1993 was another disappointing year due to drought and the same situation is expected for 1994.

2.2. Food imports of US$1.90 billion and US$1.75 billion comprised 19.5 and 22.5 percent of totalimports in 1990 and 1991 respectively (Table 1). Within the past decade, the highest share of food imports intotal imports reached 27.8 percent in 1989 after a severe drought, amounting to US$2.63 billion.4 There aretecical limits to increasing the low food self sufficiency ratio (SSR: the percentage of food demand met by

3 In accordance with the Stand-by agreemen of the IMP signed on May 1994, Algei has taken several measurelatd to its macro-economy, specifically: (a) an immedia devaluation of the DA by 50 percent, this will befollowed by a gradud liberalization of the exchange rate by mid-1995; (b) the CAHhas been dissolved and the QRhave been abolished except for 'straegic products where the pnvate sector's right to import is based onprofessional, technical and commera criteria, and the temporary suspension of certain import competig importsto allow domestic production to develop; (c) elimination of agricultural input subsidies -except for water and seeds;(d) an increase in the Central Bak interest rates to an average of 24 percent and elimination of ceilings on lendingrates; and (e) monetary and fiscal policy adjustments.

For purposes of comparison, exports totaled US$ 9.57 billion, US$ 12.93 billion and US$ 12.57 billion in 1989,1990 and 1991 rspectively.

3

domestic production). According to preliminary FAO data, overall SSR is 24 percent (measured in calories) andis projected to increase to 27 percent by the year 2010. The SSR in critical products such as cereals (20, 24)r,pulses (20, 53), vegetable oils (11,17) and milk (38, 24) are projected to continue to be low. Imports ofagricultural inputs and equipment increase the dependence of the agricultural sector to the international market.

2.3. Since 1990, agricultural investments have comprised between 8-10 percent of total investmentsin the economy (Table 2). Around half of these investments have been in irrigation. The remainder is absorbedmostly by agriculture, but forestry has been picking up. Due to their priority, irrigation investments dominatepublic investments in agriculture with a share of over two thirds.

2.4. Agroecologkal Issues. The natural resource base is threatened by several natural or man-madefactors. The consequences are not only jeopardizng the productivity of farm land but also the substantiveinvestments in irrigation. Soil erosion and desertification through the encroachment of sand dunes are the twomain agroecological problems.

2.5. Soil Erosion. The main factor causing soil loss is water erosion, due to heavy runoff in thefragile areas, which are primarily the overgrazed pastures, denuded forest areas, the untilled fallow and theravines and gullies in the watershed areas. In some areas, expansion of production into marginal areas in responseto Govermment price incentives and the use of inappropriate tillage techniques have recendy become more critical.As a consequence, almost 10 million ha of land in the North is considered susceptible to loss of productivity asa result of soil erosion. Currendy, (a) soil erosion in the watershed areas reaches 2,000 MT/km3/year; (b) 120million MT of sedimentation is lost to the sea annually; (c) on average, dams have lost about half their capacitydue to siltation; and (d) the annual reduction of water storing capacity in dams is around 20 million m3. Theseproblems require a concerted research and extension effort (both for erosion control and for promotingapropriate production technologies) along with public works and involvement of local populations i managingthe natural resource base and the environment.

2.6. Deserification. The encroachment of sand dunes results in irreversible loss of agncultural land.Intensive efforts are under way to stabilize dunmes with "barrages verts" and controlling grazing in marginal areas(despite the countervailing pressures from contradictory subsidies to promote livestock production). An exampleof effective controls is observed in Bousaada, where the foramate presence of underground water has allowedland widt highly sandy soils to be allocated to producers. Commercial production on these farms is the bestguarantee for dune stabilization. Similar approaches should be used where the potential of the private sector canbe exploited to counter ecological problems.

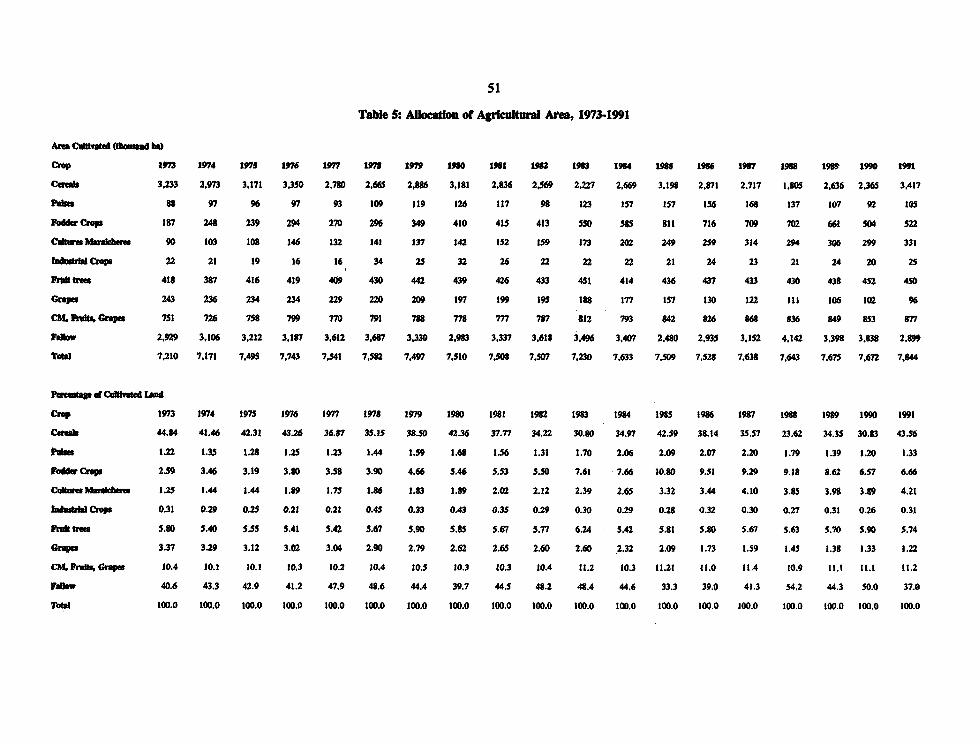

2.7. Irrigation. Irrigated areas make up only about 10 percent of cultivated and 34 percent of arableland (Table 7) and there are plans to expand these areas substantially by the year 2010. The Government giveshigh priority to and allocates a large share of agricultural investments to irrigation. However, there are importantproblems in the management of the water resources and the imgated areas. Overall system efficiency is estimatedat 36 percent. This low system efficiency is compounded by low on-farm water use efficiency (WUE), whichwould imply that as low as only 20 percent of the water harnessed for irrigation is actually converted into plantproduction. In some cases, the exigencies of self sufficiency policies result in the use of valuable irrigated landfor crops with low economic value. These problems are compounded by the lack of effective water charges tocover at least operation and maintenance (O&M) costs. As a consequence, system maintenance is not done in aneffective manner. Soil erosion in the watershed areas has caused irrigated areas to decline by reducing waterstorage capacity in dams as a result of siltation. Hence, the following should be given as high priority asinvestments in expanding irrigated areas: (a) rehabilitation and effective O&M of irrigation systems; (b) effective

The first number in the parentheses is the average SSR for 1988-1990 and the second is the projected SSR for 2010,according to preliminary FAO data.

4

disseminaon of production techiques; and (c) water pricing that promotes higher on-farm WUE. On the otherhand, actions bringing out the natural potentW of the South have been taken in order to increase nationalagricultural production capacity. The encouraging results of the first experiments have shown multiplepossibilities to rapidly increase agricultual production through the exploitation of water resources in fte Southernregions. It is also important to note that economic and social objectives must be taken into consideration in thedevelopment of the South.

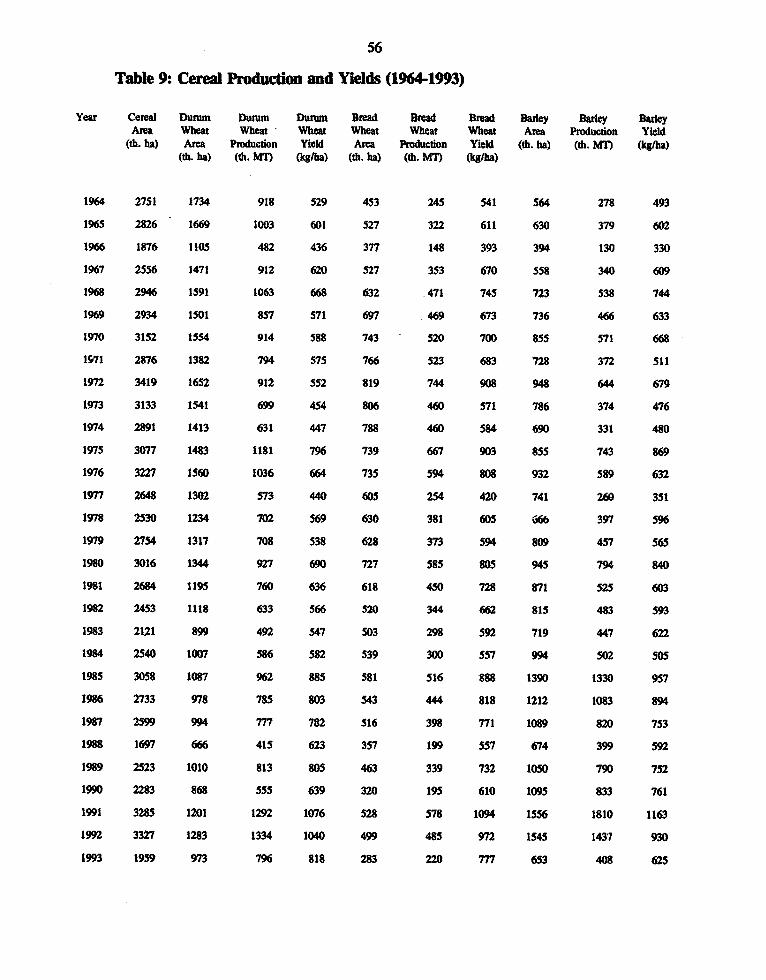

2.8. Crop Production: Climatic Conditions and Production Stabilt. Since the initiation of thereforms in 1987, climatic conditions have exhibited substantial variability, from the extremes of drought in1987/1988 to the record setting harvests of 1990/1991 and 1991/1992 (Tables 8-11). Preliminary results indicatea sharp drop in agricultural production in 1992/1993 due to drought, particularly in cereals with a 38 percentdrop over the previous season. ',here is also a risk that 1994 will present the same disappointing results due todrought. Despite the investments in irrigation and the availability of adaptable techniques of prouction,agricultural production remains highly susceptible to climatic conditions. In this respect, the issue of enhandngstabiity around an increasing trend of production becomes criticil for several reasons.

2.9. From the national perective, the high degree of production variability makes the managementof the sector quite difficult in terms of assuring adequate food supplies in a timely maimer through imports andin terms of developing effective incentives. Storage capacity in cereals and pulses is nearly equal to the averagelevel of domestic production and to about 20 percent of annual consumption. The investment in storage capacityand the opportunity cost of the idle resources stored therein are in effect the premia for the expensive nationalinsurance policies to counter the vagaries of climatic variability. For the farmers, who are invariably risk averseand give high priority to the stability of income and consumption streams, the basic methods of managing therisks of climatic variability are first a reduced level of input use to account for risk, and second, a diversificationof income generating activities in a portfolio of crop and livestock production and off-farm employment.

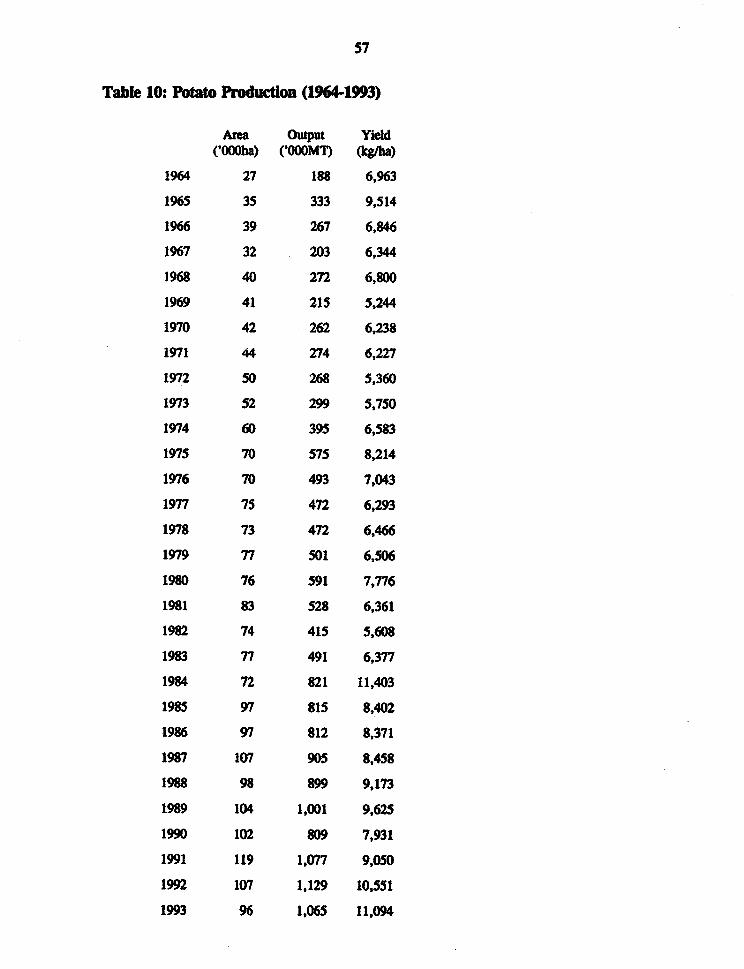

2.10. For several main crops, such as cereals, pulses and potatoes, trend analyses indicate that stabilityaround an increasing trend is a major issue. Regressions for production, area and yields were estimated for theperiod 1964-1992, or 1991 if data were not available, with and without intercept and slope dummy variables forthe period between 1987-1992 (or 1991) to account for the 1987 reforms (Tables 12-14). It may be prematureto expect results as a consequence of the 1987 reforms but the evidence indicates that stability of production isa wajor issue that does need to be addressed by policy makers and researchers.

2.11. For cereals as a whole and specifically for durum and barley, there are statistically significantincreases in the trends after 1987 for area and production but not for yields (Table 12, Figures 3-5). This impliesthat most of the production increases are due to area expansion, into fallow, into marginal lands or at the expenseof other crops. Invariably, these regressions have low correlation coefficients indicating substantial residualvariation around the trend. For bread wheat, there are no statistically significant shifts in trends after 1987, whichindicate a downward trend in area, an insignificant trend in production and hence a slight upward trend in yields.Stability in cereal production depends on sustainable yield increases brought about by the development andeffective extension of adapted improved technologies that are economically viable. While this will not eliminatethe effects of weather totally, it can reduce them and enhance stabfility. Evidence from countries with similaragroecological conditions, such as Turkey, show that this is feasible. The adjustment of the research andextension organization to the new structure of agriculture could expedite effective results in this direction.

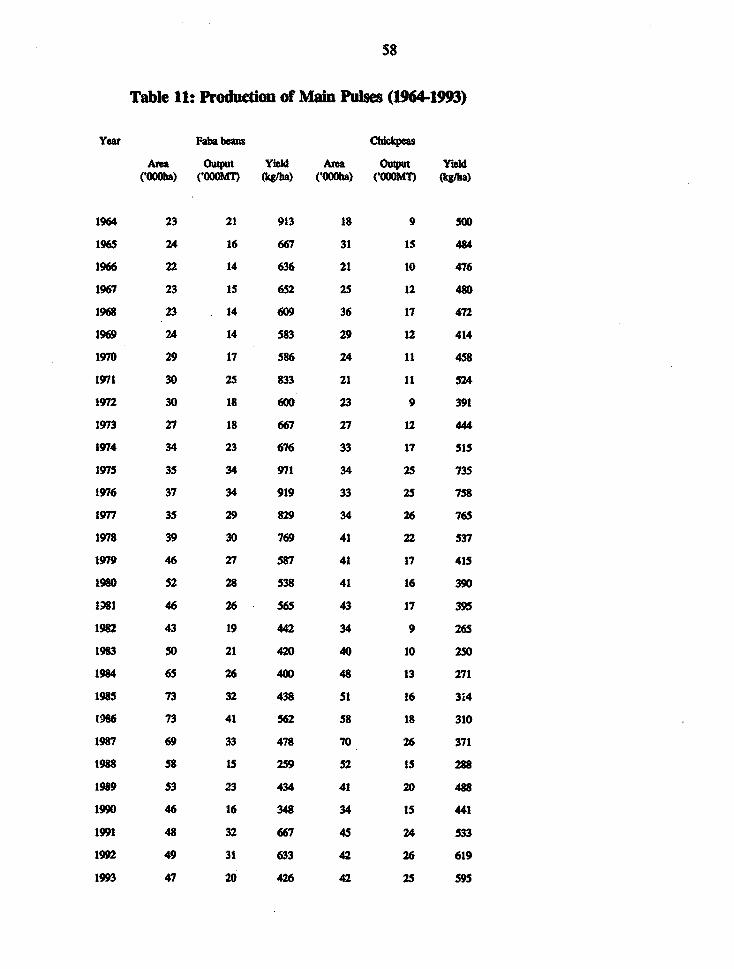

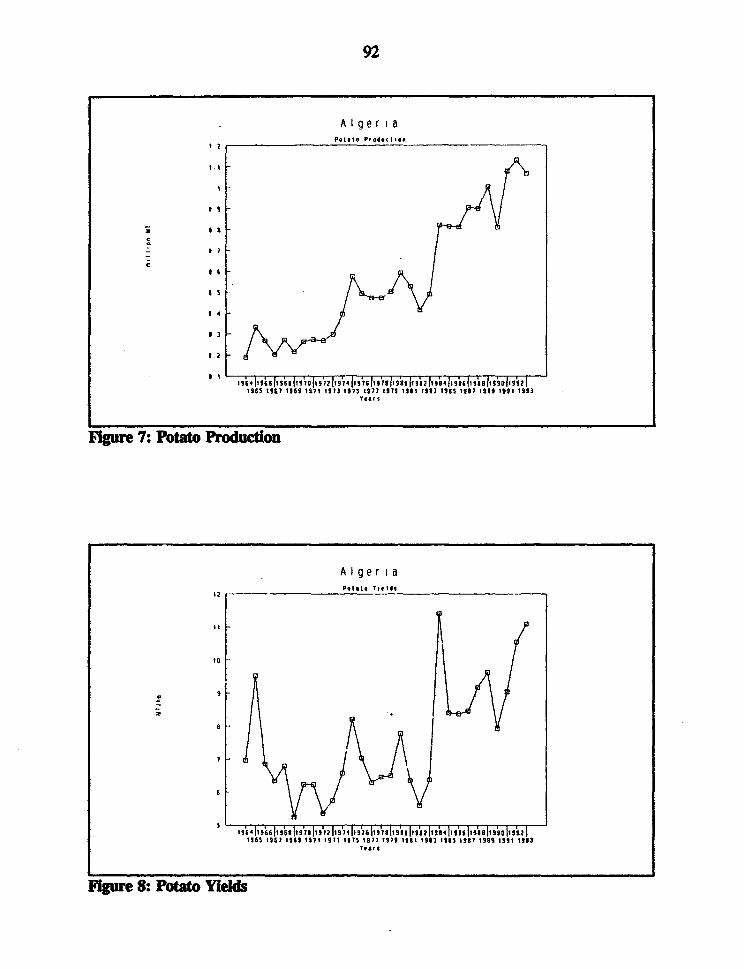

2.12. Similar trend regressions for faba beans, chickpeas and potatoes show varied results (Tables 13-14, Figures 6-11). For faba beans, an irrigated crop and hence not as susceptible to variable rainfall, there arenot only no statistically significant changes in trends after 1987 but yields actually show a significant downwardtrend. For chickpeas, invariably produced under rainfed conditions, the story is exactly the same, except that theresidual unexplained variation is considerably higher. For poatoes, a high priority crop under current

5

Government policies, there are significant upward production and area trends that do not change after 1987 andthere is very little residual variation (i.e., high correlation coefficients). For potato yields however, even thoughthere is a significant upward yield trend which does not change after 1987, the residual variation around the trendis quite high, indicating a high degree of instability.

2.13. IUvestock Production. The livestock sector accounts for around 50 percent of the agriculturalGDP and has been a primary source of agricultural growth. Depending on the subsector, this can be attributedto more liberal market conditions, protection in the form of quantitative restrictions (QR) and high tariffs onimports, or specific incentives provided by the State through price supports and input, particularly feed, subsidies.The State continues to play a pervasive role, especially in the dairy industry, in: (i) input and service delivery;(ii) producer and consumer price setting; and (iii) distribution and marketing. The private sector plays a dominmtrole in production, but it faces obstacles in participating in trade, marketivg and processing, due to the operationsof large monopolistic PE.

2.14. Trends il Livestock Production. The compositon of the Algerian herd is dominated by sheep(Table 15). Over the past 12 years, despite the severe drought of 1984-1987, the ovine populadon grew at 2.5percent anmually, from 13.4 million to 18 million heads. Cattle and goat populations have been stable. In the meatsubsector, because of QR on imports, supply is based mainly on local production (Table 16). The SSR for redmeat has averaged 90 percent for ten years. In 1991, shares in total supply were: poultry, 46 percent; mutton,30 percent; beef, 20 percent; and goat meat, 4 percent. Red meat production grew at an average rate of 6.7percent annually between 1981 and 1992. Meat marketing and processing are dominated by the private sectorwhich controls an estimated 95 percent of transactions, in both official and clandestine markets. The poultryindustry expanded dramatically between 1980 and 1987, with the production of meat increasing from 98,000 to225,000 tons (12.6 percent per year), and the production of eggs from 308 to 2,800 million (37.1 percent peryear). This growth has been achieved primarily in the modern private sector, spurred by high prices in liberalizedmarkets; availability of credit for investments, especially for egg production; and important public investmentsupstream in the production chain whereby the public sector controlled input supply (animal feed, chicks, parentstocks, veterinary products, and equipment). However, the 1987 reforms affected the public sector in poultryinputs adversely. The disrupted input supply, with stges and price increases, affected the economics of bothegg and broiler production, which, in 1992, dropped to 2,068 million eggs and 189,000 tons of meat. Translatedin terms of per capita annual consumption, both egg and meat consumption decreased from 125 eggs and 10 kilosof meat in 1987 to 80 eggs and 7.5 kilos of meat in 1992.

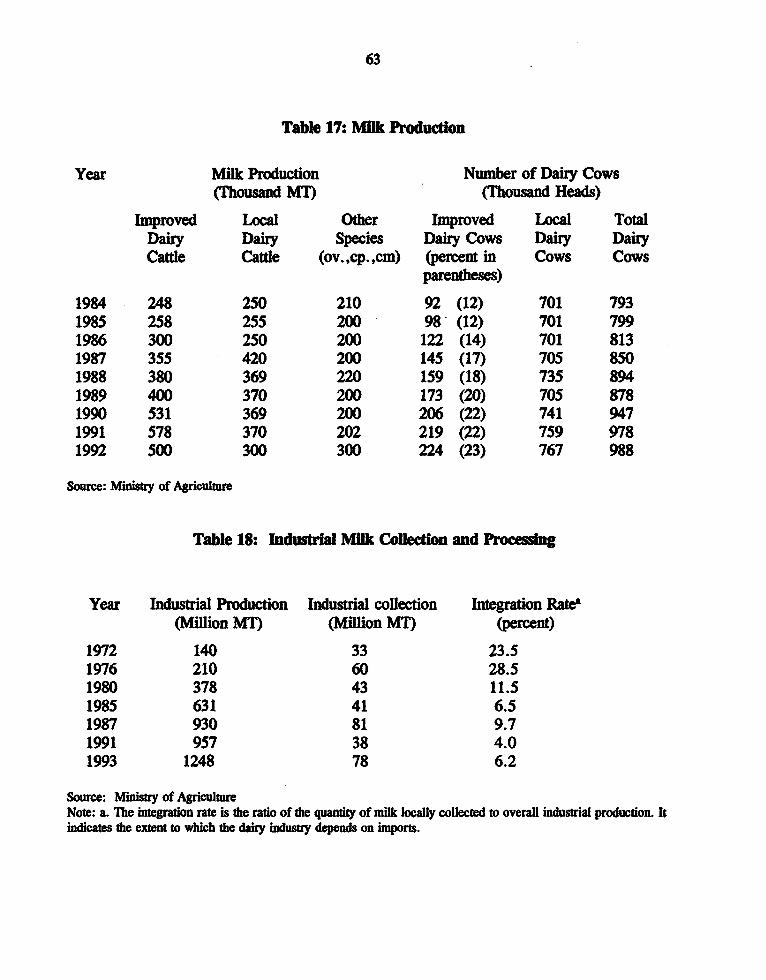

2.15. The Dairy Sector. Since the early 80s the Government has promoted milk production to improveself sufficiency (SSR remained at 35 percent in 1992). Due to consumer subsidies, the consumption of milk isvery high compared to neighboring countries: in 1991, amual per capita milk equivalent consumption of dairyproducts amounted to 116 1 in Algeria, 53 1 in Morocco, and 70 1 in Tunisia, compared with WHOrecommendations of 901. Annual per capita consumption increased from 54.51 in 1969 to 94.5 1 in 1985, andto 116 1 in 1991. Imports represent about 60 percent of the total consumption and 97 percent of the milkprocessed by the national dairy industry (Table 19).

2.16. Milk is supplied from three different sources:

a. Locally produced milk, mainly consumed on-farm or sold in the market, is estimated to amountto 35 percent of the total supply in 1991. Domestic milk production has registered a 75 percentincrease between 1984 and 1991, due to strong Government support (Table 17). However, only3-4 percent of domestic raw milk production is collected by the parastatals. The limited but livelysector of peddlers provide milk direcdy to the consumers or to small businesses which produceyogurt and cheese (Tables 17-18).

6

b. Skim milk powder (SMP), imported and reconstituted by the regional daily boards represents 31percent of total supply. The milk industry is dependent on imported milk powder used forreconstituting. Imports represent more than 60 percent of the overall national consumption.Between 1985 and 1992, the dairy boards imported about 700,000 tons of SMP together with175,000 tons of butter oil (matire grasse laWtiAre anhydre, MGLA), representing an average of87,000 tons of SMP a year. The import bill increased from US$80 million in 1985 to US$300million in 1992 due to increases in prices and volumes.

c. Imported Ia/da (ready to use powdered milk) represents 34 percent of total supply; between 1985and 1992, about 580,000 tons of lakda were imported by the public sector.

2.17. Technical Constraints in Livestock Production. Technical constraints are the criticalimpediment to livestock development in Algeria and the Govermment has focused on technical issues for a longterm strategy. To improve the efficiency of livestock producdon, policy issues such as trade restrictions, privatesector development and the dominance of the public sector in production and input supply also need to beaddressed with priority in a long term strategy. The four major technical constraints impeding livestockproduction and productivity in Algeria which need to be addressed with priority are:

a. A structural feedstuff deficit which currently amnounts to 50 percent of the estimated needs of 9.7billion forage units (UF). 6 Of this need, 3.2 billion UF are met by forage and 1.5 billion UFfrom concentrate, mainly barley. A primary factor in this deficit is the low yields of forage cropsand rangelands. Finally, this deficit is aggravated by the poor quality of the cultivated forage andanimal feed, especially in terms of protein content. The balance is covered by increasing grazingpressure on the rangelands, marginal and fallow lands, and increasing the use of straw andstubble.

b. Inadequate delivery of veterinary services prevents improvement in animal health. Lack ofresources for compulsory campaigns and vaccine shortages, especialy in the remote Mkiya,result in very low vaccination coverage and inadequate epidemic surveillance. The privatizationof veterinary services is well advanced. However, the public sector's dominance in input marketshinders further development of private practice. In particular, veterinarians face constraints dueto: (i) limited access to credit; (ii) shortages of adequate veterinary products; and (iii) competitionfrom free public services.

c. Weak genetic improvement programs due to: (i) inadequate artificial insemination (Al)technology,; (ii) lack of a national strategy for selection and performance testing, especially oflocal breeds; and (iii) inadequate follow-up of the performance of improved animals.

d. Deficient livestock management practices which have resulted in productivity declines, especiallysince the 1987 reforms and in the modern sector which was concentrated in the DAS. Also,agricultural services (research, extension, and other production support services such as Al) areinadequate to support small and geographically dispersed farms. As a result of feed grainsubsidies, the use of concentates in ruminant intake, particularly barley, has increased butwithout consequent improvement of livestock productivity.

6 One standard forage unit is the equivalent of the energy provided by one kg of barley.

7

3. M Policies Affecting the Agcultal Sector and Agricultural Services

3.1. Fal Measures towards Agriculture. The Government considers the agricultural sector astrategic sector, which is allocated priority in production subsidies, current public expenditures and publicinvestments.' These expenditures are in addition to the consumer subsidies for several basic commodities (in1993, semolina, flour, bread, milk and baby food) covering the difference between the costs of domesticproduction or the costs of imports and the fixed consumer prices." As these are welfare expenditures, they willnot be discussed here, but they do exert an adverse influence on the efficiency of agricultural narkets and theinterest of the private sector in these markets.

3.2. The planned 1993 budget relatives affecting agriculture were as follows:

Budgetary line item DA billion Percent

Total revenues 336Toull expenditures 504

of which:Curent expenditures for agriculture 281 60.3

of which:Ministry of Agriculture 3.3 0.65Production subsidies 11.6 2.30Seaonl credit interest rate subsidies 0.7 0.14

Consumer subsidies 23.0 4.56

Investment expenditures 200 49.7of which:Agricultural and irrigation investments 18.2 3.61Rural electrification 4.4 0.86Long term credit interest rate subsidies 0.3 0.06

ERIAD 0.42Chambers of Agriculture 0.14

The 1993 Plan defines the following specific pnority areas which appear to be exhaustive of agricultural activities(* indicates that the activity will also benefit from interest rate subsidies): (a) land developmen (*); (b) agriculturalactivities on newly developed lands; (c) hydraulic exploration (*); (d) cmerl, pulse, and forage production; (e)indusi afforestation; (f) water recycling and treatment; (g) inDras ural and on-farm production relatedinvestments; (h) palm groves and other mstic plantations; (i) aquaculture (*); 0) trituration and refining of oilseeds,yeast prduction, sugar refining; (k) fertilizers, fertilizer inputs (*); (1) cold storage of seeds and plants; (m) smalland medium irrigation in zones to be promoted; and (n) storage infrastructure for strategic cereals (*).

In 1992, such expenditures for social safety comprised DA 20 billion of direct assistance and DA 34.3 billion inconsumer subsidies. The planned expenditures from the 1993 Budget were DA 24 bilion and DA 23 billionrespectively.

8

3.3. Current expenditures planned from the 1993 Budget entailed DA11.6 billion of productonsubsidies as price guarantees, DAO.7 billion of interest rate subsidies for seasonal credit and DA3.3 billion forthe Ministry of Agriculture (5.1 per,.ent of the total current expenditures). Only DA6.7 billion of productionsubsidies could be disbursed due to drought. For investment expenditures, explicit allocations were for DA4.35billion for rural electrification and DA18.24 billion for agriculture and hydraulics, together comprising 11.3percent of public investments. In addition, there were capital operations of DAO.3 billion for the long termcomponent of the interest rate subsidies and an unknown amount for the reimbursement of the losses(assainissen en) of the PE input (mainly fertilizer) producers and distributors, due to the Government'sintervention in reducing input prices in 1992. Treasury operations that do not appear on the Budget also coversome of the PE losses. Finally, there are extrabudgetary expenditures (varafiscalite) of DAO.55 billion for theChambers of Agriculture and the regional PE for Cereal Processing (ERIAD). While some of the relativemagnitudes may appear to be small in terms of fiscal burden, their effects on the agricultural sector are quiteimportant. Furthermore, when projected deficits amount to a third of expenditures, all magnitudes need to bescrutinized as potental fiscal burden.

3.4. On taxation, agriculture benefits from a multitude of exemptions. Agricultural incomes arisingfrom the production of cereals and pulses and on-farm poultry production of a non-industrial naure are exemptfrom taxation "permanently" and incomes from agricultural (including livestock) activities are exempt fromtaxation in areas identified as (a) development zones, for a period of 10 years; and (b) in mountain zones, fora period of 5 years. Many agricultural products and inputs are either exempt from or have low rates of VAT.9The sale of live animals, cereals and milk, are also exempt from VAT, while sales operations regarding pulses,rice and aquatic anials and plants are subject to a 7 percent rate. Imported inputs for priority activities andscientific research equipment are exempt from customs levies. The exemptions will be lifted in the financinglegislation (loi desfinances) of 1995. Invements in priority activities are exempt from VAT and imported inputsfor these investments benefit from a low customs levy of 3 percent. Finally, agricultural land and farm buildingsare exempt from taxation except for the EAC and EAI which have to pay for usufruct rights (redevance dejouissance) at a rate varying between 120-1200 DA/ha according to zones.'0 The loi des finances of 1994 hasintrduced a land tax over private agricultural land and has raised the redevance de jouissance for the EAI andEAC from 1200 Dafha to 7500 DA/ha. Construction of buildings for the priority activities benefits from a 5 or10 year exemption, the latter in the case of location in development zones. These exemptions, along with actualproblems of collection, reduce the role of agriculture as a public revenue source.

3.5. Prodution Subsidies. Production is subsidized through output price supports. Furthermore, someprocessed agricultural products are subject to price and margin controls at the production and distribution levels.The list of agricultural products and inputs subject to different levels of control is given in Table 20. Explicitinput subsidies have been eliminated but implicit input subsidies occur at the level of imported inputs whichbenefit from the overvalued exchange rate and some are further exempted from customs levies and VAT. On

9 Veterinaiy medicines, agricultural protection chemicals, sheet plastic for greenhouses and equipment for priorityactivities are exempt from VAT. Animal feeds, fertilizers, poultry inputs and many imported inputs benefit froma reduced VAT rate of 7 percent. Livestock, tomato concentrate and honey sale operations are subject to a 13percent VAT except for red meat which is subject to a slaughter tax. For some higher value fruits and fish, VATis as high as 21-40 percent. Financial activities are subject to VAT of 7 percent for insurance and 10 percet forbank operations.

10 As her is no comprehensive and effective cadastre, land taxation would be difficult to implement. Furthrmore,in some wzlaya, the list of the EAC/EAI beneficiaries has not been compiled, making their taxation difficult.

9

occasion, such as in 92, they benefit from price reductions to be financed by the Budget (assainissemet)."Finally, confounding the objectives of social equity and production efficiency, cereals, pulses and most inputsare subject to panterdtorial price equalization (p&nquaton).

3.6. The main policy ins ent utilized to influence agricultural production is the guaranteed price.These currendy cover cereals, pulses, potatoes, industrial tomatoes, oil grains, sugar beets, onion, garlic, rawcow's milk, tobacco and seeds for cereals, pulses, potatoes, forage grains and garlic (Table 21). The subsidiesimplicit in the guaranteed prices are budgeted for according to the difference between a reference price and theguaranteed price and financed by the 'Fonds de garantie" from the budget. For major comnodities such ascereals and milk, the reference prices are based on imports.)2 For others, there is either an apparenly arbitraryreference price, subject to change, or, the sales price is the reference price, which is bound to be variable unlessalso controlled. The reference and guaranted prices for cereals and pulses in 1993 are as follows:

Cereals Reference Guarnteed Prcent Pulse Reference Guaranteed PercentPrice Price over and Price Price over

(DAMM (DAIMT) Reference Rice (DAAMI) (DA/MT) Reference

Durum wheat 4,082.5 10,250 151 Harkot Beans 11,802.0 29,700 152

Bread wheat (hard) 4,082.5 9,100 123 Lentils 11,802.0 25,250 114

Bread wheat 4,285.0 9,100 112 ChIckpeas 11,802.0 17,200 46

Barley 3,587.5 4,700 31 Rice 11,802.0 14,000 19

Oats 2,890.0 5,100 76 Faba beans 11,802.0 12,900 9

maize 3,M50.0 11,700 260 Feverolles 11,802.0 11,600 -2

Tritkale 3,565.0 7,150 101 Dry peas 11,802.0 13,400 14