Chapter v - Wiring diagrams - The Rolls-Royce and Bentley ...

Upload

khangminh22Category

view

0download

0

Kapil Goel Adv 1

Delhi Bench of ITAT In Rolls Royce 40 DTR 289

Kapil Goel B.Com(H) FCA LLBAdvocate Delhi High Court

Kapil Goel Adv 2

Rolls Royce Group Entities

Overseas

Rolls Royce Singapore LtdAssessee/Co

INDIAN CLIENTS

Supply of Spares & Services to OilField equipments Direct/

Independent Equipment Supply

ANR Ltd Indian Party providing

Marketing support

Kapil Goel Adv 3

Outline

Snapshot of the rulingFacts of the case (views of AO and CIT-A)Contentions of assessee before ITATContentions of revenue before ITATITAT Reasoning and AnalysisFinal ConclusionCritical Analysis

Kapil Goel Adv 4

Snapshot of the decisionWhen Head office maintains accounts on mercantile basis, not possible to claim cash system of accounting limitedly for Indian activities : Section 145On reopening u/s 148: Where assessee foreign company had Indian agent for relevant years, for Indian activities and no income from sale of spares in India shown in Indian tax return (either no return or no income)- Valid reopening

Kapil Goel Adv 5

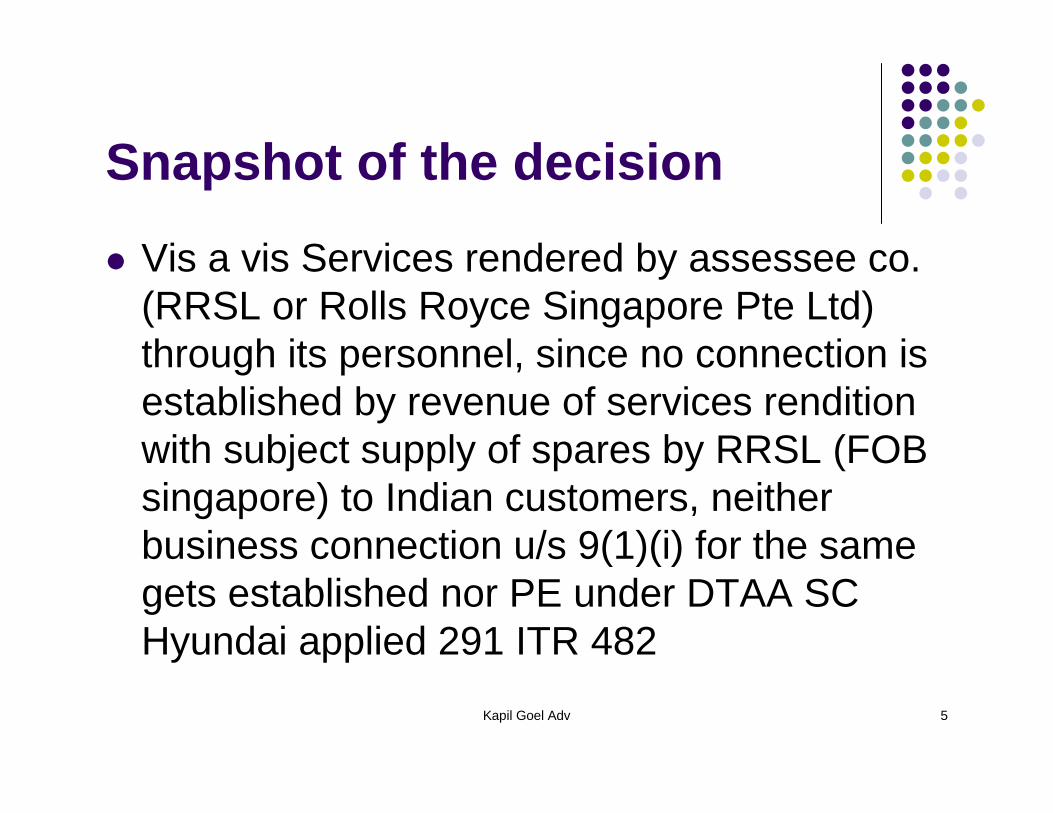

Snapshot of the decision

Vis a vis Services rendered by assessee co. (RRSL or Rolls Royce Singapore Pte Ltd) through its personnel, since no connection is established by revenue of services rendition with subject supply of spares by RRSL (FOB singapore) to Indian customers, neither business connection u/s 9(1)(i) for the same gets established nor PE under DTAA SC Hyundai applied 291 ITR 482

Kapil Goel Adv 6

Snapshot of the decision Vis a vis independent supply of equipment by other group companies of Rolls Royce group, since no connection has established between said equipment supply and subject spares/maintenance services provided by RRSL, no PE under DTAA can be perceived for instant RRSL activities merely because RRSL supplied spares and/or provided services to prior equipment supply to Indian Customers

Kapil Goel Adv 7

Snapshot of the decisionQua Agency PE in form of ANR (P) Ltd Calcutta, ITAT affirmed CIT-A and AO’s view that same is business connection of RRSL and also PE of RRSL resp. under Act and DTAA as ANR is exclusive agent of RRSL in India

Further, business premises of ANR has been held to be fixed place PE under Para 5(1) of RRSL/assessee company

Kapil Goel Adv 8

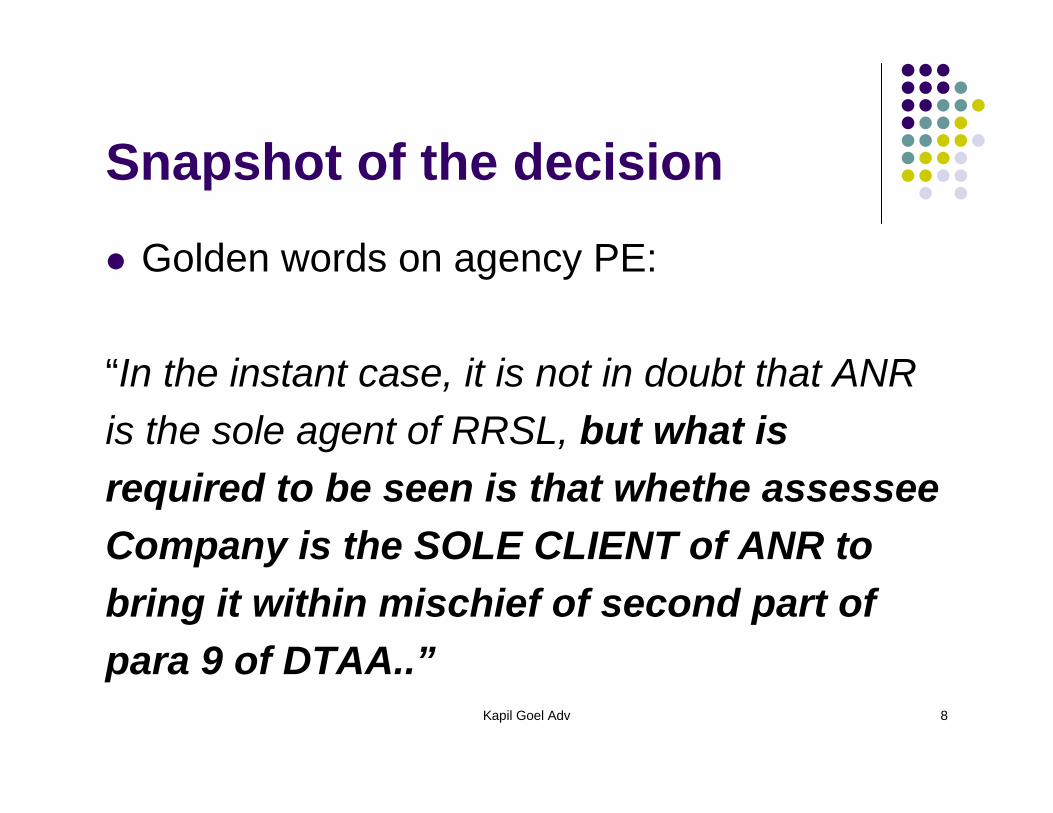

Snapshot of the decision

Golden words on agency PE:

“In the instant case, it is not in doubt that ANR is the sole agent of RRSL, but what is required to be seen is that whethe assessee Company is the SOLE CLIENT of ANR to bring it within mischief of second part of para 9 of DTAA..”

Kapil Goel Adv 9

Snapshot of the decision

The term wholly means entirely, completely, fully, totally, a little less than whole. In terms of percentage, it would mean anything around 90%.

Mr Venkatraman being employee of Rolls Royce Energy Systems India Pvt ltd having no control of RRSL/assessee, cannot constitute service PE of assessee company.

Kapil Goel Adv 10

Snapshot of the rulingIn country support services (promotion and marketing services etc) by ANR Ltd constitutes Agency PE (being instrumental in securing orders to RRSL) under subject DTAA (ANR being subject to extensive control and economically dependent on RRSL) – For spares supply

Carrying on of business through a fixed place held to include conduct of RRSL business by ANR from its premises vide Para 1 of Article 5 of Subject DTAA – For spares Supply

Kapil Goel Adv 11

Snapshot of the rulingANR Ltd is business connection u/s 9 of the Act of RRSL vide SC ruling in R.D.Aggarwal and Anglo French Textiles (for spares supply)

Since risk assumed and functions performed by ANR are very limited, profits to be attributed @ 10% of profits from Indian supply of spares (ITAT Inngersoll 4 ITD 654 and Mad HC in Annmalas applied 41 ITR 781) – agent’s commission to be reduced from attributed profits

Kapil Goel Adv 12

Dangerous FindingOn SC Morgan Stanley; BHC Set Satellite :

“After considering the submissions of both the Parties, we are inclined to reject theassessee’s contention that merely because RRSL has been paying commission to ANR, no part of the profit can be further attributed to PE in India cannot be accepted. We have already observed above that the payment of fixed remuneration @ US $40,000 per annum to ANR has not been proved being paid at ALP …”

Kapil Goel Adv 13

Facts in brief

Notices issued u/s 148 for AY 1998-99 to AY 2001-02 (ROI filed only for 01-02) on ground of:

Subsequent regular assessment of AY 2002-03 (Offering FTS on cash basis – held incorrect, to be taxed on accrual basis)No Return filed for any year except AY 2001-2002

(Reopening held valid by CIT-A)

Kapil Goel Adv 14

Facts in brief

Method of accounting changed from cash basis to accrual basis u/s 145 for FTS by AO affirmed by CIT-A reasoning 9(1)(vii) do not permit cash basis for FTS and since global accounts maintained on mercantile basis, no choice to follow cash basis for Indian PE/activities

Kapil Goel Adv 15

Facts in briefAO treated supply of spare parts to Indian customers by RRSL chargeable to tax for:

Assessee’s responsibility flowing from equipment supply by RR group companies, being incidental and obligatory to equipment supplyRRSL maintenance services cannot be isolated from spares supply both being inextricably linked to each otherANR Indian party being dedicated agent for RRSL is business connection/BC and PE under DTAAPresence of Sales Manager Mr V in India

(CIT-A- first appellate authority- affirmed this)

Kapil Goel Adv 16

Facts in brief- AO’s attribution chartAY Spares Supply Services

RenditionIndian Profits attributed

1998-99 90% portion 10% portionTaxed u/s 115A @ 20%

11% profits on 90% spares supply – no attribution …

1999-2K Same Same 11.26% profit rate to ..

2000-01 6% 12.77% profit rate minus 5% general overheads

2001-02 5.35% 13.73% profit rate and 5% overheads

Kapil Goel Adv 17

CIT-A relief on AO’s attributionHeld for AY 2002-03; 03-04 & 04-05 :25% attribution to Indian activities of spares supply

For Other assessment years: 10% attribution rate to be applied

Direction: Applying Global Profit rate to Spares Supply in India- attribute as per above %age

Kapil Goel Adv 18

RRSL Contentions

SB of ITAT in 31 ITD 67 & BHC in 259 ITR 391: Section 145 choice is available to non residents alsoNo mechanism stipulated in Act as to how CASH system can be followed and therefore RRSL maintaining excel sheets and log book – sufficient compliance of the sameBad Reopening u/s 148 for want of “reasons

to believe” qua income escaping asst.

Kapil Goel Adv 19

RRSL Contentions contd…ANR is independent entity, not working solely for RRSL as confirmed by ANR in written confirmation- never doubted by AO u/s 131 from ANRANR is not part of RR Group; RRSL has no right over place of ANR/Its employees/ManagementANR only provides marketing support to RRSL and no services to “outsiders” qua/for RRSLANR never had any power to negotiate and conclude contracts for RRSL; no role of ANR in securing ordersActivities including spares supply to Indian customers, their price discussions, technical aspects etc – take place outside India by RRSL

Kapil Goel Adv 20

RRSL ContentionsOnus to establish PE exists lies on revenue SC in Sofema SA Civil Appeal 5260/2008 (refer Mum ITAT Airlines Roatables)- not fulfilledNo material on record to establish that RRSL used ANR premises in India for Its business (under its control etc)Non compete clause- restricting ANR from marketing competitive products – Conflict of Interest clause

Kapil Goel Adv 21

RRSL Contentions

No agency PE in form of ANR : Advance ruling in TVM case 237 ITR 230 and ITAT ruling in Western Union 101 TTJ 56 relied to say ANR independent economically

For off-shore supply of Indian spares parts no taxability in India: SC in IHI 288 ITR 408 and LG Cables relied

Kapil Goel Adv 22

Revenue’s contentions

Valid reopening of cases u/s 148 of the Act-CIT-A reliedMethod of accounting – Cash basis –difference between disclosure of income on “cash” basis vis a vis maintaining of books on cash basis – books maintained not being proved for want of production of them- hence adverse inference to be drawn

Kapil Goel Adv 23

Revenue’s Contentions

On merits, as to PE and BC existed CIT-A orders reliedOn attribution stated in all years 25% attribution must

Kapil Goel Adv 24

ITAT’s analysis/reasoningValid reopening u/s 148 : SC Rajesh Jhaveri Applied 291 ITR 500 : reasonable material in form of subsequent orders/143(3) exists- Reasons not appreciated in light of 3- judge SC ruling in Kelvinator case Jan 2010 – Tangible material- live nexus – seems to be missing

“Therefore what is relevant for section 145(1) is the system of accounting regularly followed by assessee. In present case, the assessee is a foreign company and not its PE in India”

Kapil Goel Adv 25

ITAT’s reasoning and analysis“ In order to determine whether any income from whatever source it is derived, has been recd. Or is deemed to be recd in India or accrues or deems to accrue/arise in India to a non resident during any relevant year, one has to ascertain the system of accounting regularly followed by non resident foreign company….” –For tax and accounting purposes, whether different system possible – refer Chaturvedi and Pithisaria –Seems Yes

Kapil Goel Adv 26

ITAT reasoning

Since revenue has not been able to point out any iota of evidence/material to show and establish that in original contract of supplying equipment by some other co belonging to RR group there exists any condition putting obligation upon Indian buyer or upon RRSL to supply spares necessary to main equipment already supplied by some other entity of RR group under different contract…

Kapil Goel Adv 27

ITAT analysis and reasoningFOB Singapore- Supply of spares by RRSL and prior equipment supply has no joint to connect them, both being independent and separate, hence on that count no taxability in RRSL hands for spares supply (no PE and no BC)

Activities of RRSL and other group entities of RR group are in no way interconnected /interrelated

Revenue’s contention that related activities have been purposely bifercated is based on assumption and presumption

Kapil Goel Adv 28

The question that arises before us is as to whether the RRSL has PE in India with regard to its activity of supplying spares to its clients in India? Test is whether providing services and supply spares are inextricably linked Revenue’s case that every maintenance contract involves certain spares supply, is OK but same is not material to decide the issue:

Kapil Goel Adv 29

Classical Test from ITATWhat is to be seen is whether Indian customer is bound to avail services of RRSL merely because certain spares have been supplied by RRSL or For taking RRSL maintenance services, Indian client is bound to take spares from RRSL

No material brought on record by revenue to support the allegation that services and supply are inter-twinned – Hence on this count also revenue’s charge of taxability of Indian spares supply fails u/Act and DTAA

Kapil Goel Adv 30

Agency PE- ANR Ltd and RRSL under DTAA and Act- ITAT’s views

For deciding agent is not “dependent” – he must be both legally and economically independentRelevant tests:

Freedom given to AgentIndependent agent is responsible for result of his work and not subject to close supervisionExtensive control and detailed instructionsEconomic independence points to earning profit from one’s own entrepreneurial skills and knowledgeOrdinary course action would depend upon customary business practices and not legal arrangements

Kapil Goel Adv 31

Agency PE- ANR Ltd and RRSL under DTAA and Act- ITAT’s views

ANR being restricted to carry activities competing RRSL – this unusual restriction to ITAT, suggest that ANR never intended to act as Independent agent in ordinary course of its business

Since ANR exclusively rendered services in relation to specified products to RRSL-pointer to dependent agent

Kapil Goel Adv 32

Agency PE- ANR Ltd and RRSL under DTAA and Act- ITAT’s views

In confirmation from ANR as filed by RRSL so as to prove RRSL is not sole client of ANR, since there is no disclosure as to following vital facts in said confirmation, same being withheld, necessarily adverse inference is to be drawn to RRSL:

Nature of services provided to others by ANRName of those companies to whom ANR provided servicesAmount of commission earned by ANR from those other companies vis a vis income earned from RRSL

Kapil Goel Adv 33

Agency PE- ANR Ltd and RRSL under DTAA and Act- ITAT’s views

QUA ANR: Activities of making customers aware of products sold by RRSL, making sales presentation and demo’s for RRSL customers, creating commercial environment for RRSL products, making liasion with equipment operators – Held to constitute Fixed place PE of RRSL In India – Under Art 5(1) – Para 96

Kapil Goel Adv 34

Agency PE- ANR Ltd and RRSL under DTAA and Act- ITAT’s views

ANR being instrumental in securing orders and negotiations – Held same in light of “dependent factor” since ANR not proved economically independent – same constitutes Agency PE of RRSL under Para 8/9 of Article 5 of subject DTAA (being subject to extensive control and not acting in ordinary course) –Para 94,95,97,98

Kapil Goel Adv 35

Business Connection ANR Ltd and RRSL under Act- ITAT’s views

Since by role played by ANR in India- RRSL has been enabled to earn income in Singapore from Supply of subject spare parts etc to Indian clients- a real and intimate connection existsNot mere isolated/stray transaction

Hence Section 9(1)(i) Business Connection Exists

Kapil Goel Adv 36

Critical AnalysisWhen once third party confirmation is filed (here ANR stating Independent person), without there being any enquiry from ANR by AO, same cannot be disbelieved – Amounts to giving premium to revenue for lexity on its partRef : Raj HC in 174 Taxman 440 affirming ITAT114 TTJ 697 Ref: Delhi ITAT Mobile Escotel (for doubting commission payment- if summons/131 not issued –it is must to accept commission as genuine)DHC Gennesis Commet 163 Taxman 482

Kapil Goel Adv 37

Critical AnalysisIt is not open to the department while rejecting assessee’s explanation to make presumption that the witness come forward to give false evidence to oblige the assessee Refer All HC in 72 ITR 766.

An explanation given by the assessee has to be considered objectively before AO takes a decision to accept it or reject it that is, department cannot convert a good proof into no proof on mere ipse-dixit (suspicion etc) – Refer SC in 49 ITR 112

Kapil Goel Adv 38

Critical AnalysisRuling contrary to Motorola Special Bench ruling in 95 ITD 269: Relevant Para’s

Ericsson case: Para 120;128 132- (Delhi ITAT alcatel case) – even where employees visited in India – held Indian co place being group subsidiary neither BC nor PE under DTAAMotorola case: Para 220;222;228 : Facility in Gratis etc (preparatory/auxiliary- pre commencement – business)Also APHC on 144 ITR 146 : Virtual Projection TEST not applied correctly in instant caseAlso Onus on Revenue to establish PE – assessee’s reliance on SC Sofema SC- not dealt properly

Kapil Goel Adv 39

Critical Analysis

SC in Morgan Stanley Held Back Office Operations not give rise to PE under India USA DTAA- Also held it Preparatory and Auxiliary in Character 292 ITR 416Securing Orders cannot be equated as done by ITAT with Assistance in order procurements ….vis a vis Agency PEBusiness place of ANR assumed for its functions to be place of RRSL- incorrect

Kapil Goel Adv 40

Critical AnalysisDHC in UAE Exchange Centre: Provision for PE in DTAA reflects eagerness to tax on part of source state, must receive tightest and strictest construction– In nature of deeming provisions- where-ever doubt lean in favor of assessee – not applied – in Present case- here ANR neither was virtual projection of RRSL in India nor ANR did more than what Liaison office of UAE did in India – WHERE DHC held it to be of non B/C and PE character

Citation: 268 ITR 9

Kapil Goel Adv 41

Critical Analysis

Cited precedent of AAR in TVM and ITAT in Western Union- never dealt by ITAT in its order (qua Agency PE etc)

Total Mix up of Attribution Plea of Assessee on basis of SC in Morgan Stanley; BHC Set Satellite – not adjudicated properly

Kapil Goel Adv 42

Thank You

Advocate Kapil Goel9910272806

Copyright © 2022 FDOKUMEN

!["The European Court's love-hate relationship with collecting societies" [1997] 6 European Intellectual Property Review 289](https://static.fdokumen.com/doc/165x107/63347048e9e768a27a100bba/the-european-courts-love-hate-relationship-with-collecting-societies-1997-6.jpg)