Greater Angila Limited ATP approval decison letter and policy ...

1 Internship Report“Credit Policy and Performance Analysis”

Pubali Bank Limited View Prepared for

Mr. Kamruzzaman Titu

Prepared By Suvongkar Banik

Roll No: 9952235

Reg No:9997502

BBA

2

National University of Bangladesh

Gazipur, Bangladesh

Internship Report on

“Credit Policy and Performance Analysis” – A Pubali Bank Limited View”

3

Letter of Transmittal

June, 30,2014

Mr. Kamruzzaman Titu

Lecturer, School of Business

Bangladesh Institute of Science And Technology (BIST)

122, New Kakrail, Dhaka-1000

Subject: Submission of the Internship Report.

Dear Sir,

4I am intended very happy of submitting the internshipreport entitled “Credit Policy and PerformanceAnalysis” – A Pubali Bank Limited View”. A report isbased on my internship program.

The whole report is prepared on the basis of practicalexperiences in Pubali Bank Limited, Foreign ExchangeBranch, analyzing Annul Report, Prospectus, variousacademic books and journals and Internet also. I havefollowed your guidelines as per your direction. I havetried enough to furnish all the materials. What I haveachieved during the service period I shall be highlygrateful if you kindly accept this Internship Report.This report is one of very significant as it is one ofthe most important requirements of completing BBAprogram this report is a brief’ summary of work andexperience gained during the service period. I will bepleased to answer any query of you thereby.

Sincerely yours,

Suvongkar Banik

BBA (Major in Finance)

Roll No: 9952235

Reg No: 9997502

STUDENT’S DECLARATION

5

I declare that the report entitled “An Internship Report on “Credit Policy and Performance Analysis” – A Pubali Bank Limited. Pubali Bank Limited, Foreign Exchange Branch, submitted as requirements of BBA of National University, Bangladesh was prepared by me. I wastried my best to collect necessary information that made the report specific and original. I may assure you that the report was uniquely prepared by me.

Suvongkar Banik

National university of Bangladesh

BBA (Major in Finance)

6 Roll No: 9952235

Reg No: 9997502

The successful accomplishment of this project work isthe outcome of the contribution of number of people,especially those who have given the time and effort toshare their thoughts and suggestions to improve thereport.

At the beginning, I would like to pay my humblegratitude to the Almighty Allah for giving me theability to work hard under pressure & complete theresearch paper successfully. However, the spaceinvolved does not allow us to mention everybodyindividually. It gives me immense pleasure to thank alarge number of individuals for their cordialcooperation and encouragement who have contributeddirectly or indirectly in preparing this project. .

I would like to thank my honorable course instructor“Mr. Kamruzzaman Titu” for asking me to prepare thisreport and for providing me proper guidance to work onthis company analysis. It is an opportunity for me totranslate into action the directives of my learnedinstructor and prove my worth in the preparation of thereport confidently. I gathered a lot of knowledge and

ACKNOWLEDGEMENT

7information and practical experience while working onit. I really want to express my heartiest gratitude tohim for his valuable advice and time that he gave me,which helped me prepare this company analysis.

I am very grateful to Mr.Zeauddin Ahmed,AGM of PubaliBank Foreign Exchange Branch, where I completed myinternship program and all the employees especiallySenior Officer of Loan Department Mr.M.A.Khair Khan,SPO,Mr. Swapan Kumar Mridha, Principal Officer, Mr. MD.Nasiruddin, Senior Officer, Mrs. Amina Akter, SeniorOfficer and Mr. S.M. Noman Farhad , Officer of PBL, fortheir hearty co-operation in the learning process aboutPubali Bank: General Banking System & Loan Proceduresin particular. I would also convey my thanks to all theemployees for their beloved manners and attitudes shownto me during the program.

Last of all I would like to express my thanks to theauthors, researchers, article writers whose books andarticles I consulted and my family who helped me inevery stage of the report by providing valuableinformation and suggestion in respect of preparing thisreport.

Abbreviations

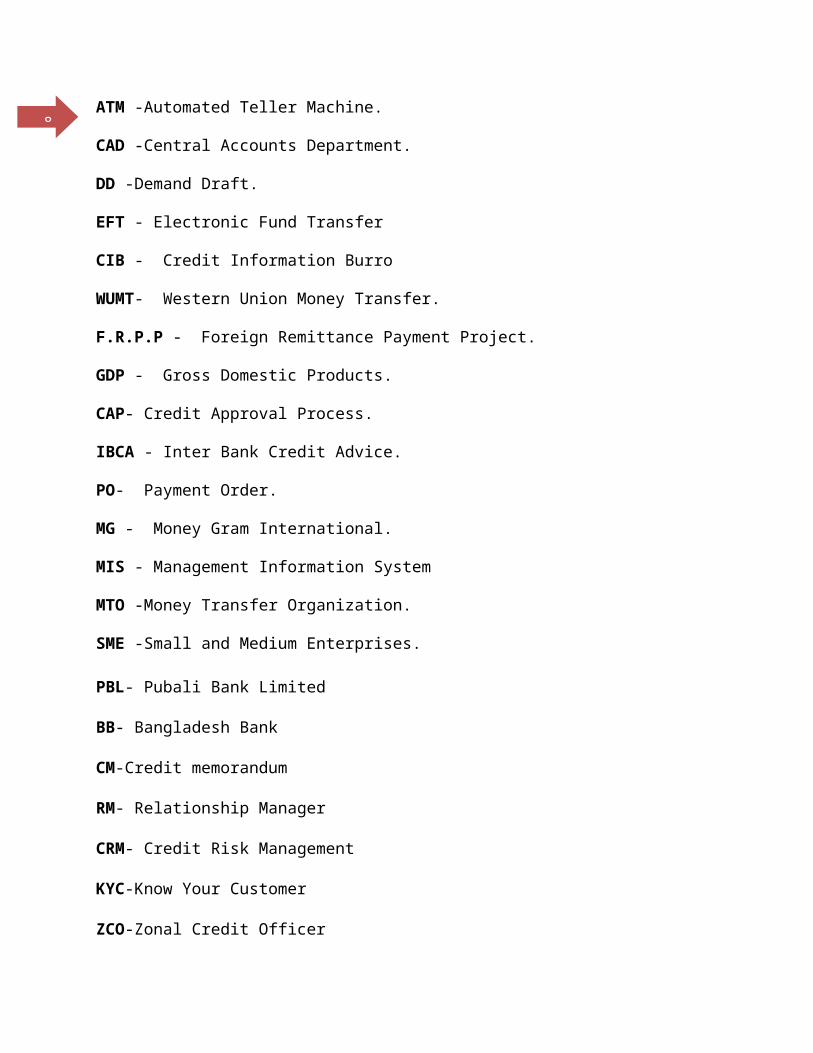

8ATM -Automated Teller Machine.

CAD -Central Accounts Department.

DD -Demand Draft.

EFT - Electronic Fund Transfer

CIB - Credit Information Burro

WUMT- Western Union Money Transfer.

F.R.P.P - Foreign Remittance Payment Project.

GDP - Gross Domestic Products.

CAP- Credit Approval Process.

IBCA - Inter Bank Credit Advice.

PO- Payment Order.

MG - Money Gram International.

MIS - Management Information System

MTO -Money Transfer Organization.

SME -Small and Medium Enterprises.

PBL- Pubali Bank Limited

BB- Bangladesh Bank

CM-Credit memorandum

RM- Relationship Manager

CRM- Credit Risk Management

KYC-Know Your Customer

ZCO-Zonal Credit Officer

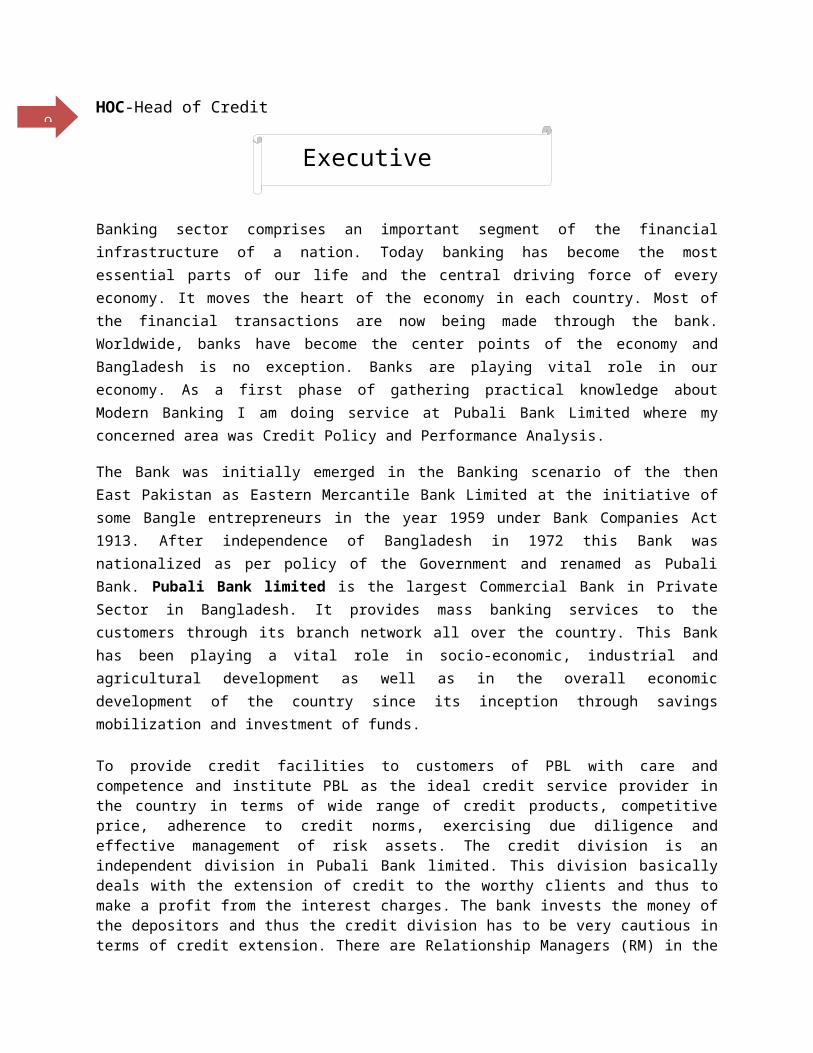

9HOC-Head of Credit

Banking sector comprises an important segment of the financialinfrastructure of a nation. Today banking has become the mostessential parts of our life and the central driving force of everyeconomy. It moves the heart of the economy in each country. Most ofthe financial transactions are now being made through the bank.Worldwide, banks have become the center points of the economy andBangladesh is no exception. Banks are playing vital role in oureconomy. As a first phase of gathering practical knowledge aboutModern Banking I am doing service at Pubali Bank Limited where myconcerned area was Credit Policy and Performance Analysis.

The Bank was initially emerged in the Banking scenario of the thenEast Pakistan as Eastern Mercantile Bank Limited at the initiative ofsome Bangle entrepreneurs in the year 1959 under Bank Companies Act1913. After independence of Bangladesh in 1972 this Bank wasnationalized as per policy of the Government and renamed as PubaliBank. Pubali Bank limited is the largest Commercial Bank in PrivateSector in Bangladesh. It provides mass banking services to thecustomers through its branch network all over the country. This Bankhas been playing a vital role in socio-economic, industrial andagricultural development as well as in the overall economicdevelopment of the country since its inception through savingsmobilization and investment of funds.

To provide credit facilities to customers of PBL with care andcompetence and institute PBL as the ideal credit service provider inthe country in terms of wide range of credit products, competitiveprice, adherence to credit norms, exercising due diligence andeffective management of risk assets. The credit division is anindependent division in Pubali Bank limited. This division basicallydeals with the extension of credit to the worthy clients and thus tomake a profit from the interest charges. The bank invests the money ofthe depositors and thus the credit division has to be very cautious interms of credit extension. There are Relationship Managers (RM) in the

Executive Summary

10branches who have the responsibility to gather valued client where thebank can invest. When a client applies for certain amount of credit,the credit officers first assess the financial and operationalviability of the client and prepare a call report. If the boardapproves of disbursement and the client fulfills all the necessarylegal and procedural requirements, then only the loan is sanctioned. Asanction advice is prepared and provided to the client. Beforeextension of loans, a comprehensive credit risk appraisal is done andannual reviews are made. A credit memorandum (CM) is prepared by theRelationship Manager (RM) which includes the findings of suchassessment. The RM used to be the owner of the customer relationshipand he / she is held responsible for complying with all the policiesand guidelines of Bangladesh bank, bank laws, PBL policies andguidelines etc. According to Bangladesh Bank guidelines, all Banksshould adopt a credit risk grading system. Therefore, PBL has dulyimplemented a credit risk grading policy in its credit risk assessmentprogram. The system defines the risk profile of borrower’s to ensurethat account management, structure and pricing are commensurate withthe risk involved. (Focus Group on Credit Risk Management, (2005),Credit Risk Management: Industry Best Practices, Managing Core Risksof Financial Institutions, Bangladesh Bank). Before commencing thecredit approval process, a proper credit analysis is done throughCredit Memorandum. No credit facility may be approved unless asatisfactory presentation package has been prepared. To minimizecredit losses, monitoring procedures and systems are in place thatprovides an early indication of the deteriorating financial health ofa borrower.

As a modern bank PBL should go for a technological revolution in allover the organization. The project will be costly but not impossibleusing our own technology. Bangladeshi programmers and technicians canbe used here for reducing the cost. The automation in credit policyand performance analysis will establish PBL as a pioneer of newgeneration banking in Bangladesh. Also PBL will able to grow morerapidly than present.

Table of

11 Description

Page no

1.0 Chapter One: Introduction 12

1.1 Origin of the Report: 12 1.2 Background: 12 1.3 Objectives of the report: 13 1.4 Scope: 13 1.5 Sources of information: 14 1.6 Methodology: 14 1.7 Limitations: 152.0 Chapter Two: Pubali Bank Limited 15 2.1 Background of Pubali Bank Limited:

15

2.2 Vision Statement: 16 2.3 Mission Statement: 16 2.4 Goals of Pubali Bank Limited:

16

2.5 Core Objectives: 17 2.6 Business Objectives: 17 2.7 Strategies: 17 2.8 Business Philosophy of Pubali Bank Limited:

17

2.9 Strength of Pubali Bank Limited:

18

2.10 Board of Directors: 19 2.11 Capital Position: 19 2.12 Product and Services: 19 2.13 New Product and Services: 21 2.14 Correspondent Banking Relation:

21

2.15 Corporate Social 21

12 Responsibility (CSR): 2.16 SWOT ANALYSIS: 23 2.17 Pubali Bank Limited: Online Banking:

23

2.18 Deposits: 25 2.19 Advances: 25 2.20 Investments: 25 2.21 Position of Profit & loss:

26

2.22 Human Resources: 26 2.23 Pubali Bank Limited’s FiveYears’ Financial Positions:

27

3.0 Chapter Three: Credit Policy of Pubali Bank Limited

28

3.1 Credit Overview in Pubali Bank Limited:

28

3.2 Types of Advances: 28 3.3 Portfolio Management of Credit:

29

3.4 Selection of Borrower: 30 3.5 Processing of Credit: 30 3.5.1 Credit Report: 31 3.5.2 CIB Report: 31 3.5.3 Visiting Client: 32 3.5.4 Credit Line Application Form:

32

3.5.5 Supporting Documents:

34

3.5.6 Analysis of Client’s account:

34

13 3.6 Project Financing Evaluation:

35

3.6.1 Project Evaluation:

35

3.6.2 Technical & Market Appraisal:

36

3.6.3 Financial Projections and analysis:

38

3.6.4 Managerial Aspect:

39

3.6.5 Socio-economic Aspect:

39

3.7 Pricing of Loan: 39 3.8 Approval Process: 40 3.9 Post sanctions process: 41 3.10 Documentation: 41 3.11 Creation of Charges over Securities:

42

3.12 Securities and Advances: 43 3.13 DISBURSEMENT: 43 3.14 Monitor/ Control of CreditOperations:

45

3.14.1 Control of overdrawn accounts:

45

3.14.2 Control of loans:

47

3.14.3 Control of other Credit facilities:

48

3.15 Handling of Delinquent Loan/Advance:

50

3.15.1 Identificationof Delinquent Advances:

50

3.15.2 Monitoring of 51

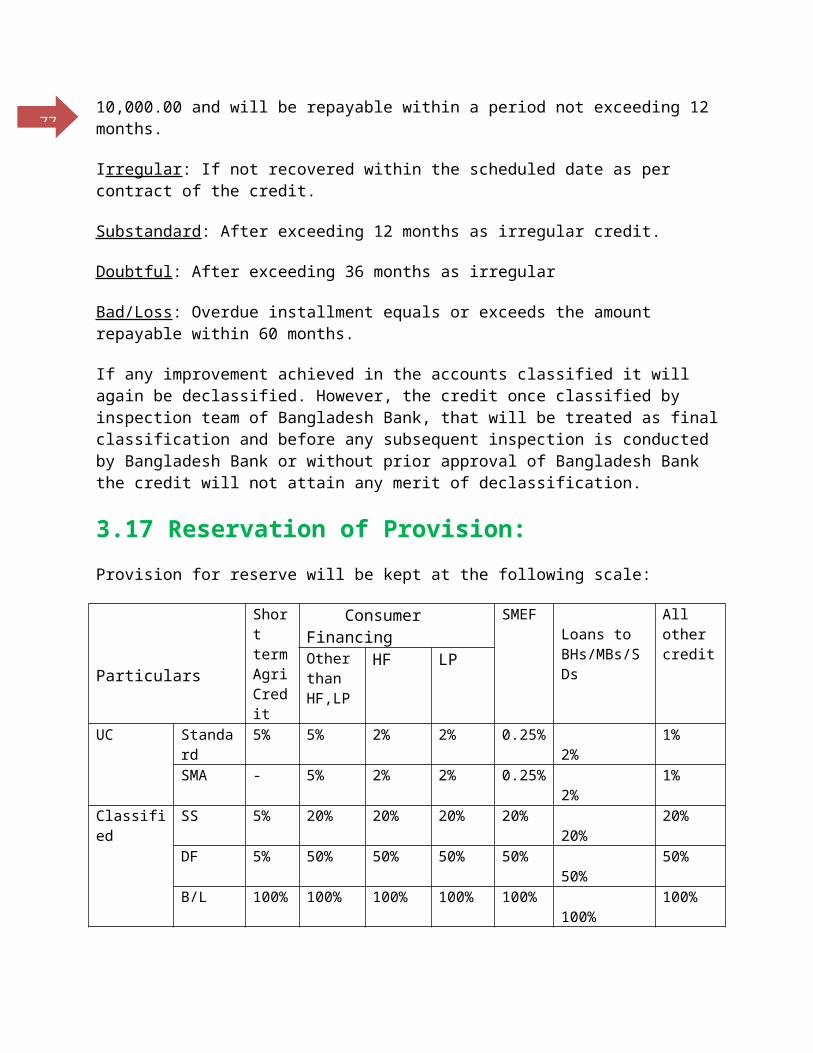

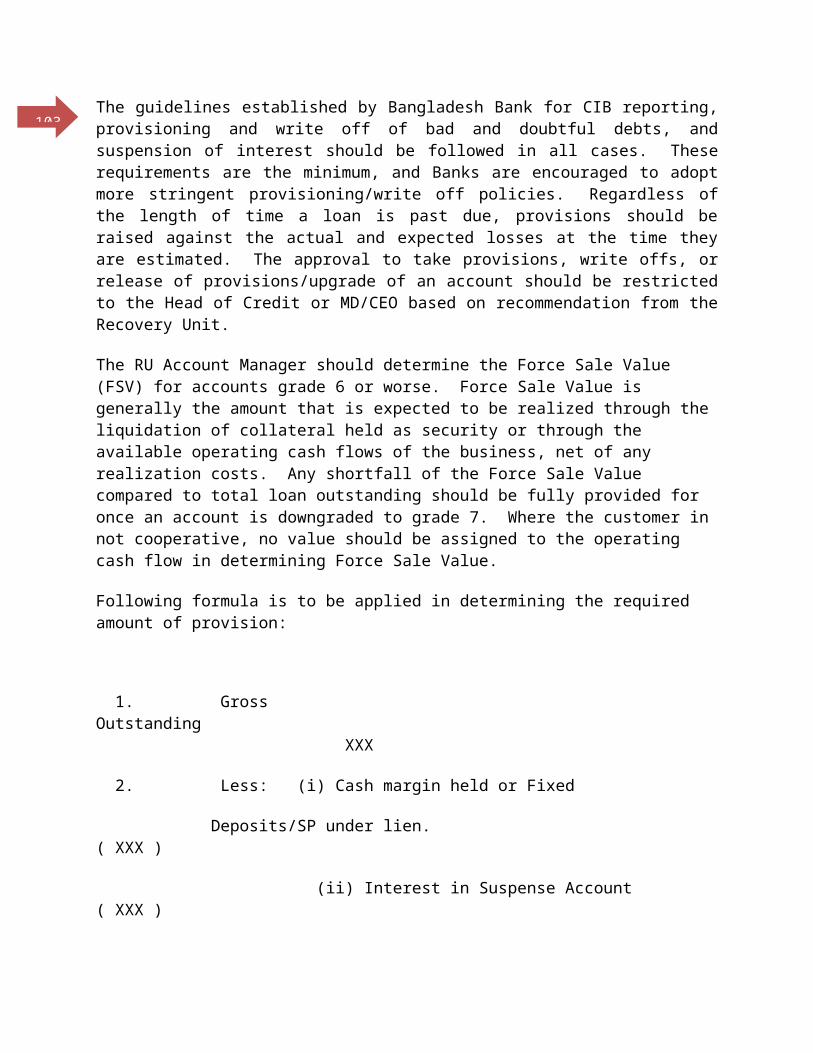

14 the delinquent accounts: 3.16 Loan Classification- Provisioning:

51

3.17 Reservation of Provision: 53 3.18 Treatment of Interest Suspense:

54

3.19 Identification of Possible Recourses for Recovery of Delinquent Debts:

54

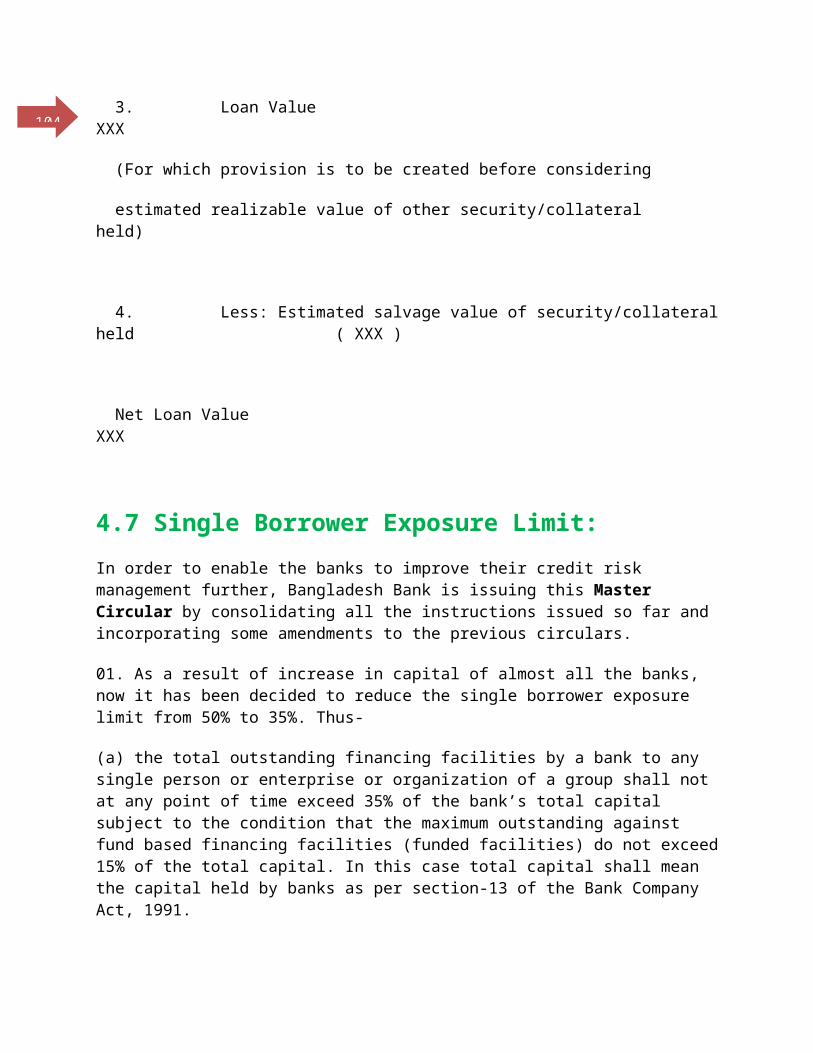

3.20 Litigation and Costs: 54 3.21 Loan Loss Provision: 55 3.22 Write Off: 554.0 Chapter Four: Credit Management Guidelines by Bangladesh Bank

56

4.1 Policy Guidelines: 56 4.1.1 Lending Guidelines:

56

4.1.2 Credit Assessment: 58 4.1.3 Risk grading: 60 4.2 Preferred Organizational Structure & Responsibilities:

64

4.3 Procedural guideline: 64 4.4 Credit Administration: 66 4.4.1Disbursement: 66 4.4.2 Custodial Duties: 66 4.4.3 Compliance Requirements:

67

4.5 Credit Monitoring: 67 4.6 Credit Recovery: 68 4.6.1 NPL Account Management:

69

4.6.2 Account Transfer Procedures:

69

15 4.6.3 Non Performing Loan (NPL) Monitoring:

70

4.6.4 NPL Provisioning and Write Off:

70

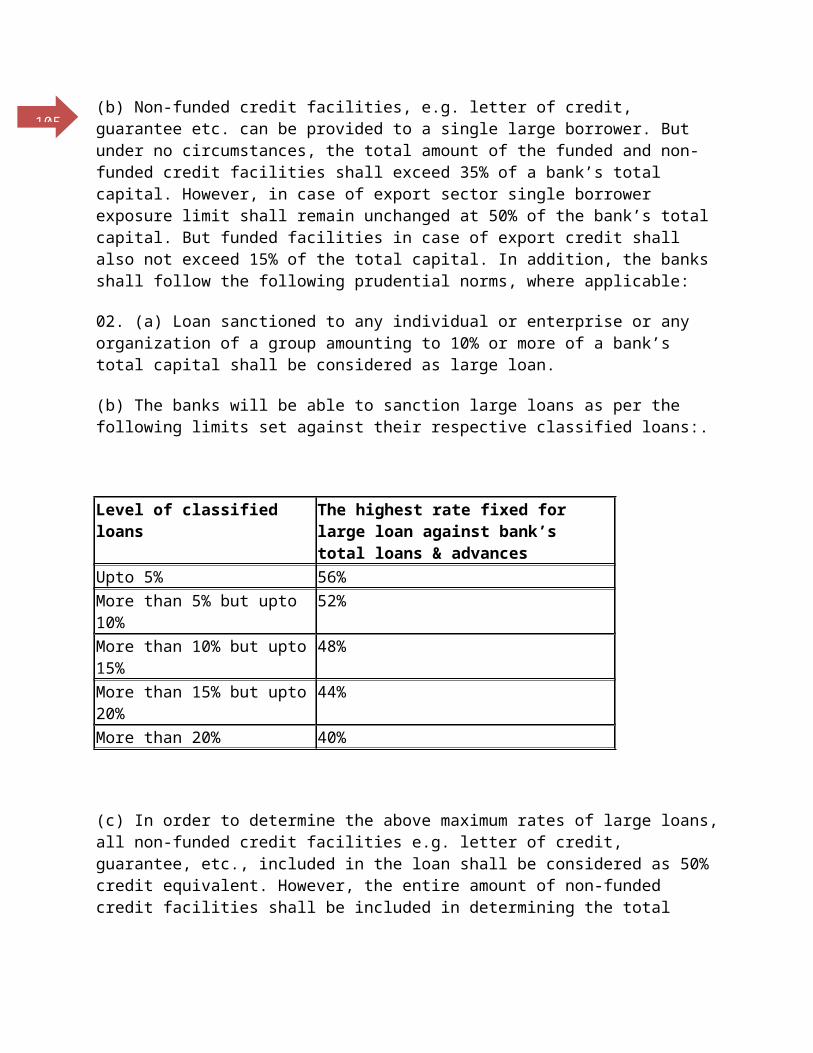

4.7 Single Borrower Exposure Limit:

71

5.0 Chapter Five: Policy Comparison with Bangladesh Bank

74

5.1 Portfolio Comparison: 74 5. 2 Single Borrower/ Group Limits:

74

5.3 Credit Assessment: 74 5.4 Risk grading: 75 5.5 Approval Authorities: 76 5.6 Credit Process: 76 5.7 Segregation of Duties: 76 5.8 Preferred Organizational Structure:

77

5. 9 Approval Process: 77 5.10 Credit Administration: 77 5.11 Credit Monitoring: 85 5.12 Credit Recovery: 85 5.13 Account Transfer Procedures:

86

5.14 Non-performing Loan Account Management:

86

6.0 Chapter Six:Operational Performance of Pubali Bank Ltd.

87

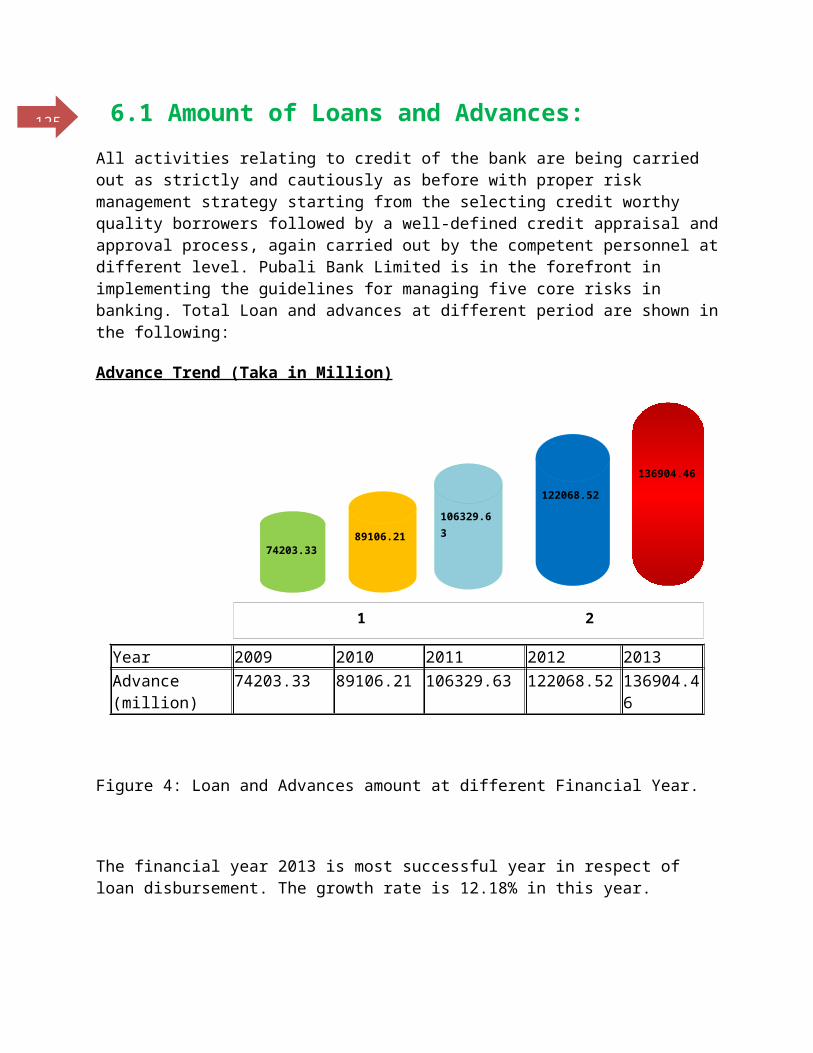

6.1 Amount of Loans and Advances:

87

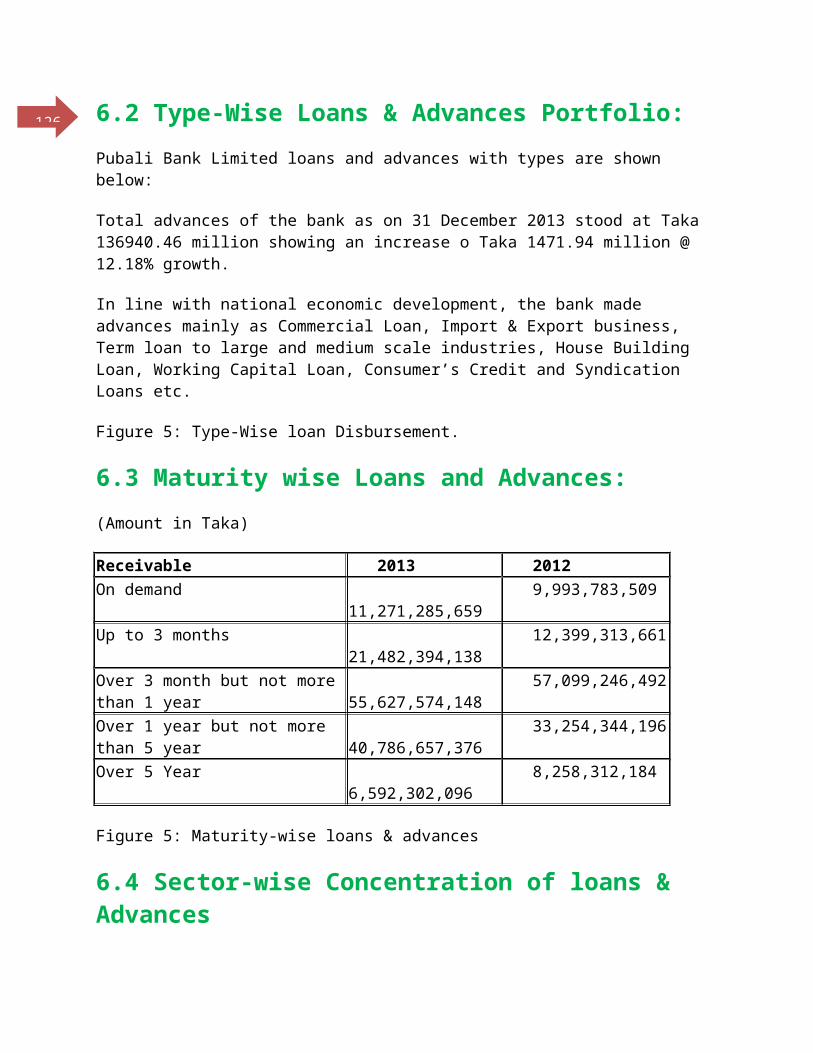

6.2 Type-Wise Loans & Advances Portfolio:

88

6.3 Maturity wise Loans andAdvances:

88

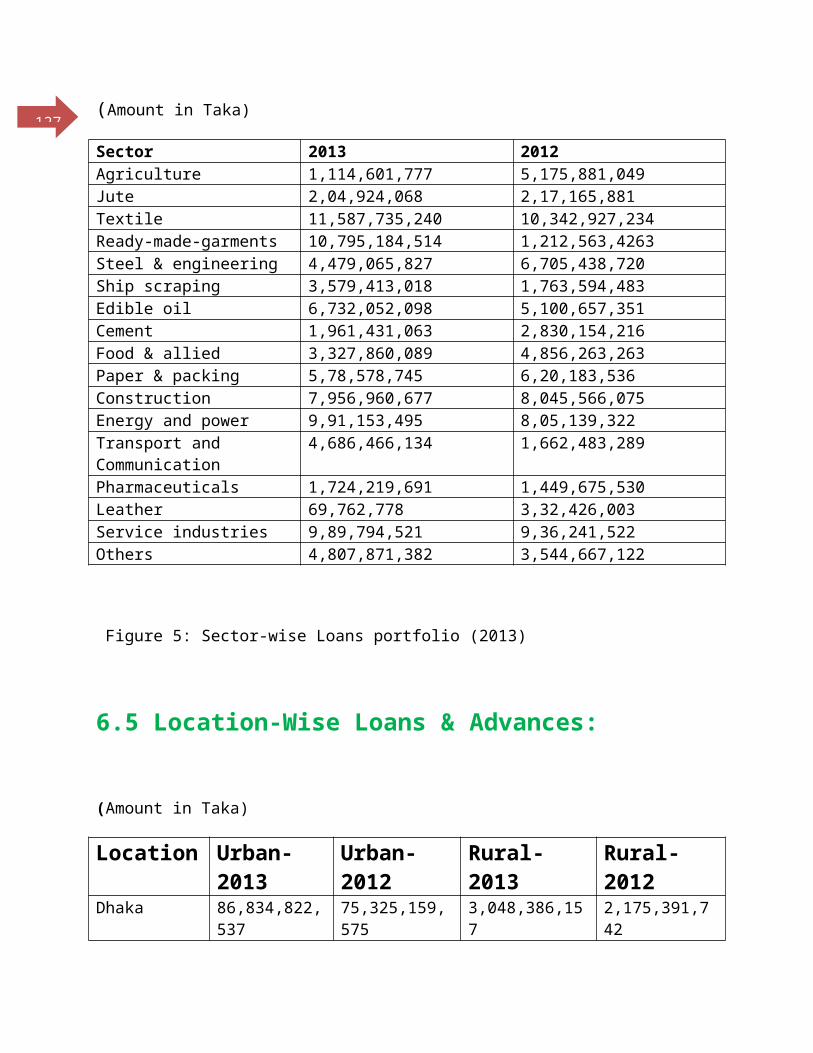

6.4 Sector-wise Concentration of loans & Advances:

88

6.5 Location-Wise Loans & Advances:

89

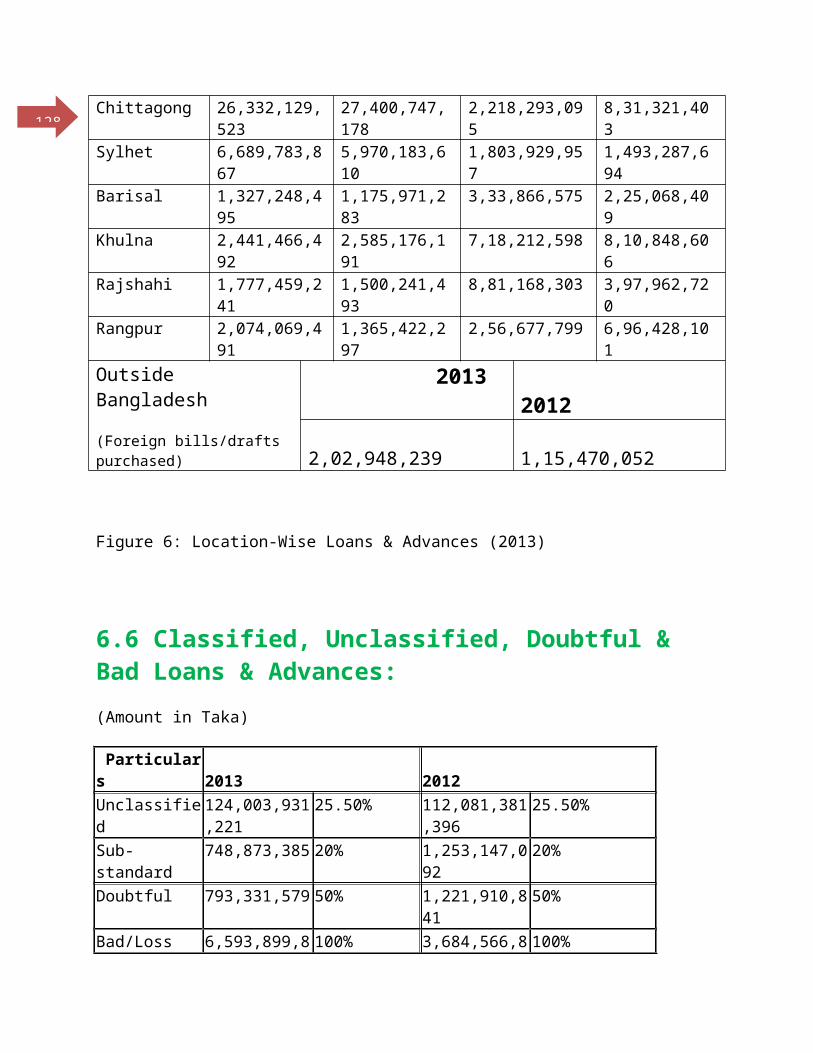

6.6 Classified, Unclassified, Doubtful & Bad Loans & Advances:

90

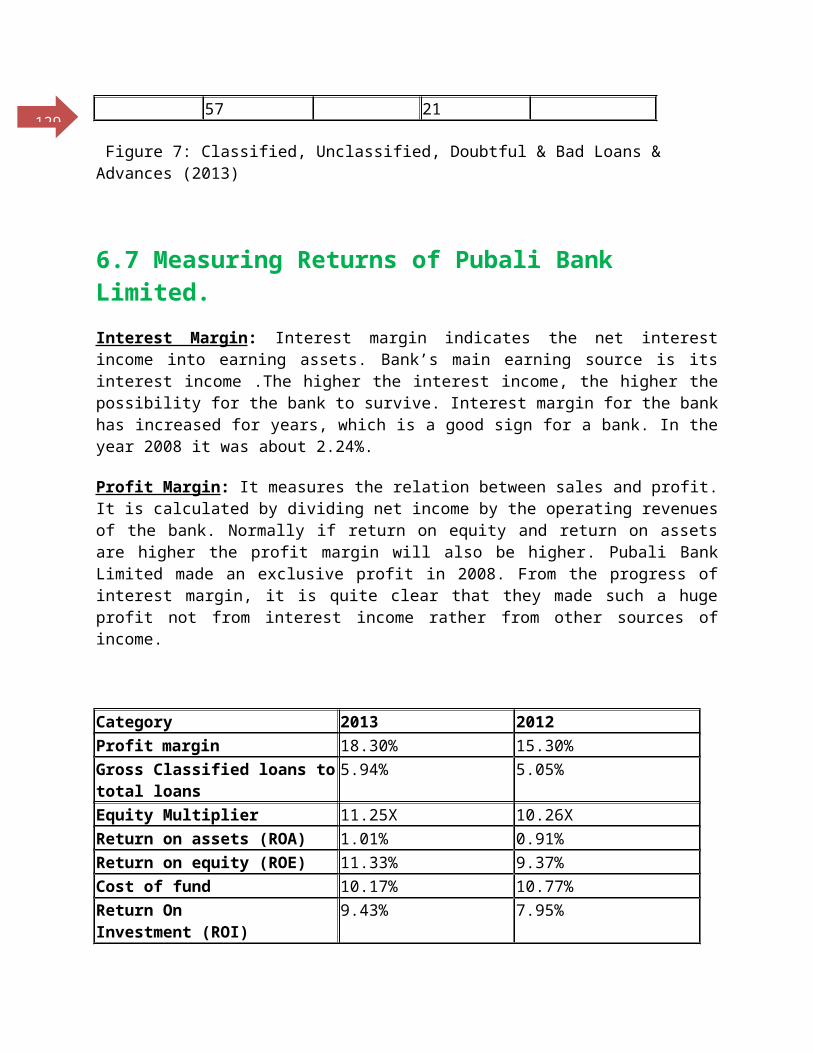

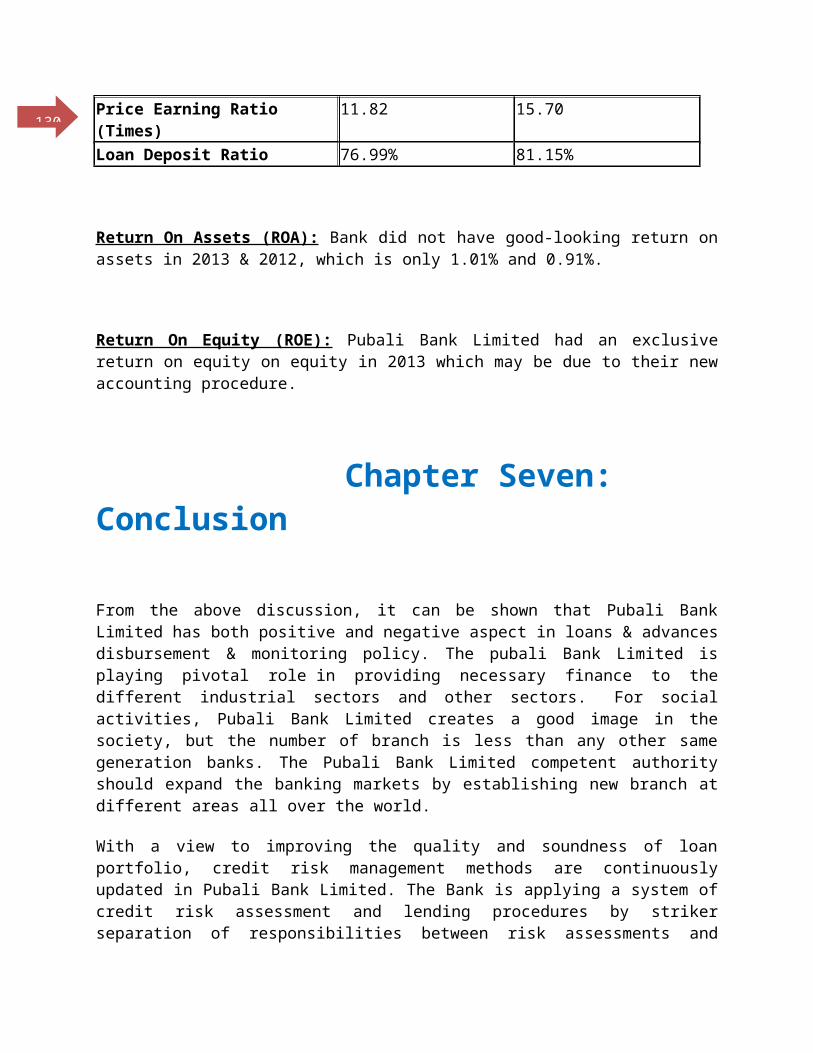

6.7 Measuring Returns of Pubali Bank Limited:

90

7.0 Chapter Seven: Conclusion 91

16

Chapter One: Introduction

1.1 Origin of the Report:The research paper has conducted on “Credit Policy andPerformance Analysis of Pubali Bank Limited”. This report is apartial requirement of Research Paper of BBA program. Beforepreparation this report I am more experienced in my Bank’spractical activities & on the job training at Pubali BankLimited, foreign exchange Branch, Dhaka. Practical problems havearranged me for preparing this type of Research.

17 1.2 Background:Throughout the last few years Bangladesh has been experiencing arapid and significant change in the banking sector. Not only inour country, all over the world the dimension of banking has beenchanging rapidly mainly due to the technological innovation,globalization and deregulation. This change all over the worldhas significantly affected the banking industry of our country,the result of which is the change in this sector in our country.Now the condition is such that banks must compete in the marketplace both with local institutions as well as foreign ones.

Pubali Bank Limited is the successor of the erstwhile EasternMercantile Bank Limited incorporated in 1959 under the CompaniesAct 1913. Eastern Mercantile Bank Ltd was nationalized underBangladesh Bank's (Nationalization) Order 1972 and was renamed asPubali Bank.

It was denationalized on 30 June 1983 under the Bangladesh Bank's(Nationalization) Amendment Ordinance 1983. Since inception thisBank has been playing a vital role in socio-economic, industrialand agricultural development as well as in the overall economicdevelopment of the country through savings mobilization andinvestment of funds. After being handed over to the privateownership and management, Pubali Bank consolidated its businessand profitability and earned profits in the years 1985 to 1989.However with the increase in classified loans and advancesespecially to Govt. and Semi Govt. sector, and due to theimplementation of the financial sector reform program of theGovt. in 1989 requiring strict classification provision, the Bankfell into catastrophe and started to incur loss.

Through the efforts of the management, the Bank started makingoperating profit from 1994. In 1996 Bangladesh Bank identifiedPubali Bank as a problem bank considering the capital inadequacy,provision shortfall, amount of classified loans etc and the Boardsigned a Memorandum of Understanding with the central bank toregularly report on the improvements in these areas. Pubali Bankhas improved its performance in the recent years.

18The Bank expanded its operation through opening 5 new branches atdifferent places during the year 2013. As such the total numberof branches of the bank stand at 423 all over the country.

At Present, Pubali Bank is the largest private commercial bankhaving 429 branches and it has the largest real time centralizedonline banking network.

Credit risk management needs to be a robust process that enablesbanks to proactively manage loan portfolios in order to minimizelosses and earn an acceptable level of return for shareholders.Given the fast changing, dynamic global economy and theincreasing pressure of globalization, liberalization,consolidation and dies-intermediation, it is essential that bankshave robust credit risk management policies and procedures thatare sensitive and responsive to these changes. So it is very muchhelpful to me to work my internship is such an area.

1.3 Objectives of the report:Objectives assist the researcher to advance objectively. Thefollowings objectives may be with this identified study aspresented below:

Knowing the credit policy and credit operation model. Knowing lending products of the Pubali Bank Limited. Knowing the interest rates and fees of loans. Knowing the process of selecting borrowers. Knowing about the loan recovery System Knowing about the loan classification. To critically analyze the credit policy of Pubali Bank

Limited. To evaluate the credit performance. To conclude whether the credit policy compliances with

present situation.

19 1.4 Scope:The report is an attempt to state the credit policy of PubaliBank Limited as compared to Bangladesh Bank Credit PolicyGuidelines and to evaluate credit performance. A detailed creditpolicy including borrower selection, credit worthiness analysis,credit approval process, credit disbursement & monitoring, creditadministration etc. has been explained and compared. The creditperformance of bank has analyzed with implementing credit policy.After completion of research, it is helpful to me to understand atotal loans and advanced related works of a bank.

1.5 Sources of Information:The sources of information are both primary and secondary whichhas given as follows:

Primary Sources:

Practical Desk work. Conversation with credit officers and managers. Conversation with clients.

Secondary Source:

Practical case problems. Manual of Credit division. Bangladesh Bank Circulars Annual reports of Pubali Bank Limited. Different manuals, books, existing soft information.

1.6 Methodology:

20Sample Design: The study represents comprehensive data of PubaliBank Limited and Bangladesh Bank credit management guidelines.

Collection of information: To conduct this study considerableinformation and expert opinion will be collected from primary aswell as secondary sources.

Processing of information: A careful and systemic processing ofinformation facilitates comparison and evaluates performance tomake decision whether the policy compliances with presentsituation.

Analysis and interpretation: The information has been collectedwill be duly analyzed and interpreted as to achieve the desiredobjectives. Credit policy data has analyzed by comparison andcredit performance evaluation is done by trend analysis

Final Report Preparation: The final report has been prepared onthe basis of presentation, analysis and interpretation of theinformation.

1.7 LimitationsTo conduct research, there are many problems arisen, which hasthe purpose of the report. The limitations are:

It was very difficult to collect data from such a bigorganization.

Sufficient books, publications, facts and figures arenot available. These constraints narrowed the scope ofaccurate analysis

Difficult to collect information as concern people arereluctant to disclose information.

Credit management is a too big to cover wholly in thislimited scope. It required huge time and huge space tocover. So, I have covered only some important topics ofcredit management.

21 Access to only a number of information sources. Non-availability of secondary data.

Chapter Two: Pubali Bank Limited2.1 Background of Pubali Bank Limited:Pubali Bank Limited (PBL) was incorporated as Eastern MercantileBank Limited in 1959 as per the companies’ act 1913 with 60percent equity owned by the then few East Pakistanis. Rest 40percent shares were owned by the State Bank of Pakistan. Thefounding chairman was Mr. O R Nizam from Chittagong. The otherfew founding members were Mr. M R Siddiqee, Dr. Naimur Rahman,Mr. M H Chowdhury and Khan Bahadur Mojibur Rahaman.After theindependence, as per the nationalization policy of thegovernment, this bank was nationalized by the Bangladesh Bank(Nationalization) Order – 1972 (PO no. 26 of 1972) and wasrenamed as Pubali Bank. After 12 years of nationalization,according to the privatization policy of the government the bankwas privatized in 1984 and renamed as Pubali Bank Limited (PBL).During the denationalization 160 rural branches were handed overto Bangladesh Krishi Bank. The Government of the People'sRepublic of Bangladesh handed over all assets and liabilities ofthe then Pubali Bank to the Pubali Bank Limited. Since thenPubali Bank Limited has been rendering all sorts of CommercialBanking services as the largest bank in private sector throughits branch network all over the country. Now Pubali Limited Bankis the largest private commercial bank having 423 branches allover the world and it has the largest real time centralizedonline banking network.

To provide client services all over Bangladesh it has establisheda wide correspondent banking relationship with a number of localbanks. To facilitate international trade transactions, it has

22arranged correspondent relationship with large number ofinternational banks which are active across the globe.

2.2 Vision Statement:Providing customer centric lifelong banking services. Pubali BankLimited dreams of better Bangladesh, where arts and letters,sports and athletics, music and entertainment, science andeducation, health and hygiene, clean and pollution freeenvironment and above all a society based on morality and ethicsmake all our lives worth living. Pubali Bank Limited’s essenceand ethos rest on a cosmos of creativity and the marvel-magic ofa charmed life that abounds with spirit of life and adventuresthat contributes towards human development.

2.3 Mission Statement: To be the most respected and preferred brand among all

financial services providers in Bangladesh. Providing a superior value proposition to the customers by

fulfilling their financial needs in the fastest and mostappropriate way.

To provide world class finance, capital and risk managementproducts bundled with diversity and differentiation,delivered economically through the client’s choice ofdistribution channel recognizing the unique lifetimefinancial needs of clients.

To build an empowering organization with the structure,career development, training and rewards to ensure thevision is achieved.

Using flexible technology, scale and risk management toensure our services are of superior value.

2.4 Goals of Pubali Bank Limited: Providing appropriate long term returns to our shareholders

and to become the number one bank of all private commercialbank.

23 Serve institutions, corporate, businesses and individuals

through Customer Relationship management (CRM). Develop innovative and new products recognizing the unique

lifetime financial needs of customers. Enhancing Corporate Governance for effective interaction

between various participants i.e. shareholders, board ofdirectors, bank’s management and taking effective decisionto ensure corporate success and economic growth.

Streamlining risk and compliance for shareholdersconfidence, better operating performance and optimal risk-reward outcomes.

Continuous enrichment of its human assets so that theydeliver values to the business.

Strengthening brand image for creating higher customersatisfaction and loyalty.

Adapting latest technologies and responding quickly in fastchanging market scenario for providing uninterruptedservices and business continuity, minimizing risks andmoving towards MIS and DSS.

Enhancing financial inclusion efforts for sustained higheconomic growth and development.

Institutionalize CSR.

2.5 Core Objectives:Pubali Bank Limited believes in its uncompromising commitment tofulfill its customer needs and satisfaction and to become theirfirst choice in banking. Taking cue from its pool of esteemedclientele, Pubali Bank Limited intends to pave the way for a newera in banking that upholds and epitomizes its vaunted Marques“Your Trusted Partner.”

2.6 Business Objectives: Build up a low cost fund base. Make sound loans and investments. Meet capital adequacy requirement at all time. Ensure 100% recovery of all advances. Ensure a satisfied work force.

24 Focus on fee-based income. Adopt appropriate management technology. Install a scientific MIS to monitor Bank’s activities.

2.7 Strategies: Synchronized and steady growth of the bank. Utilize all available resources to develop various plans,

policies and procedures in each of the objective and goals area.

Implement plans, policies and procedures. Draw upon the connections, advice etc. of the foreign

partners. Utilize a team of professional employees. Search for a customized solution of IT for the purpose of

full automation step by step.

2.8 Business Philosophy of Pubali Bank Limited:The objectives of Pubali Bank Limited remain to offer modern &innovative products & services to its client’s in Bangladesh. Thepartnership with FMO is optimistically scene to offer scopesopportunities to draw on modern tools & techniques of bankingfrom western world which could be blended with the currentlyprevalent local customs & practice. The Bank is committed tobeing a sophisticated prominent and professional institution,providing a one window service to its customers. During the firstfive years Pubali Bank Limited Bank’s strategy was focused oncontinuing in provident of internal procedures and operatingstructures, to have a greater control on the quality of ourbusiness and to provide better management direction. After fiveyears of working on the Banks structure, its culture andcontrols, the management is confident that the Bank can moveforward on a rapid growth path. The Pubali Bank Limited’scorporate philosophy is to build its non-funded fee andcommission income stream, thus reducing its reliance on interest

25income alone. Pubali Bank Limited’s focus is to provide onecounter service to the clients covering:

a) Commercial Banking ( Deposit Accounts), b) Consumer Banking(Retail Baking ), c) Traveler Cheque, d) Foreign & InlandRemittances, e) Financial Services, f) Corporate Banking, g)Asset & liability management , h) Liquidity & capital ResourcesManagement, i) Information technology and j) Human Resources.

2.9 Strength of Pubali Bank Limited: Pubali Bank Limited is the largest commercial bank in the

private sector of our country and first Real timeCentralized Online banking network in Bangladesh with 427online branches.

Pubali Bank Limited directors and /or their family membersdo not maintain any sort of bank account with Pubali BankLimited, since its inception.

Pubali Bank Limited’s directors do not avail of anyfacility or even any fee/remuneration from the bank forattending the meetings of the Board/ExecutiveCommittee/Audit Committee.

Pubali Bank Limited’s sponsoring shareholders did not takeany dividend for the initial 5 years in order to increasethe capital base of the bank.

Pubali Bank Limited allows all local remittances such asTT, DD, PO etc. free of cost.

Pubali Bank Limited’s classified loan as on December 31,2013 is only 5.94% of total loans and advances.

Pubali Bank Limited’s authorized capital and paid upcapital as on December 31, 2013 stood at Taka 2000.00 croreand Taka 838.45 crore respectively.

Pubali Bank Limited’s capital adequacy ratio (CAR) as onDecember 31, 2013stood at 11.73% as against BangladeshBank’s minimum requirement of 10.00%.

Pubali Bank Limited maintains general provision onunclassified loans and Advances @3% instead of minimumrequirement of 1% as set forth by Bangladesh Banks loanprovisions.

26 Pubali Bank Limited expands free medical facilities under

its “Rural Health Service Program” to the members of thegeneral public around the rural branches.

Pubali Bank Limited support humanitarian and philanthropicactivities and causes and spends a substantial amount fromits income for these purposes.

pubali Bank Limited promotes different socio-culture andsports activities.

Pubali Bank Limited helps the distressed employees of Ranaplaza tragedy at savar donated tk.2.27 Crore in the reliefFund of our Honorable Prime Minister in 2013.

Pubali Bank Limited provides 12.18% of its total advancesas Term loan and a substantial amount as working capitalloan to support industrial development and boost up exportearnings of the country.

Pubali Bank Limited Global growth has increased veryslightly from an annualized rate of 2.5% in the second halfof 2012 to only 2.75 in the first quarter of 2013.

Pubali Bank Limited has earned an operating profit oftk.813.14 Crore in spite of all national and internationaladversities and able to achieve operating profit growth27.24% in 2013.

Pubali Bank Limited’s objective is not only to make profit,but also simultaneously contribute towards social and humandevelopment through various altruistic activities.

2.10 Board of Directors:Chairman Mr. hafiz Ahmed MazumderVice Chairman Mr. Habibur RahmanDirector Mr. Moniruddin AhmedDirector Mr.Syed Moazzem HussainDirector Mr. Muhammad Faizur RahmanDirector Mr. Ahmed Shafi ChowdhuryDirector Mrs. Suraiya RahamanDirector Mr. Fahim Ahmed Faruk ChowdhuryDirector Mr. Rumana SharifDirector Mr. Mustafa Ahmed

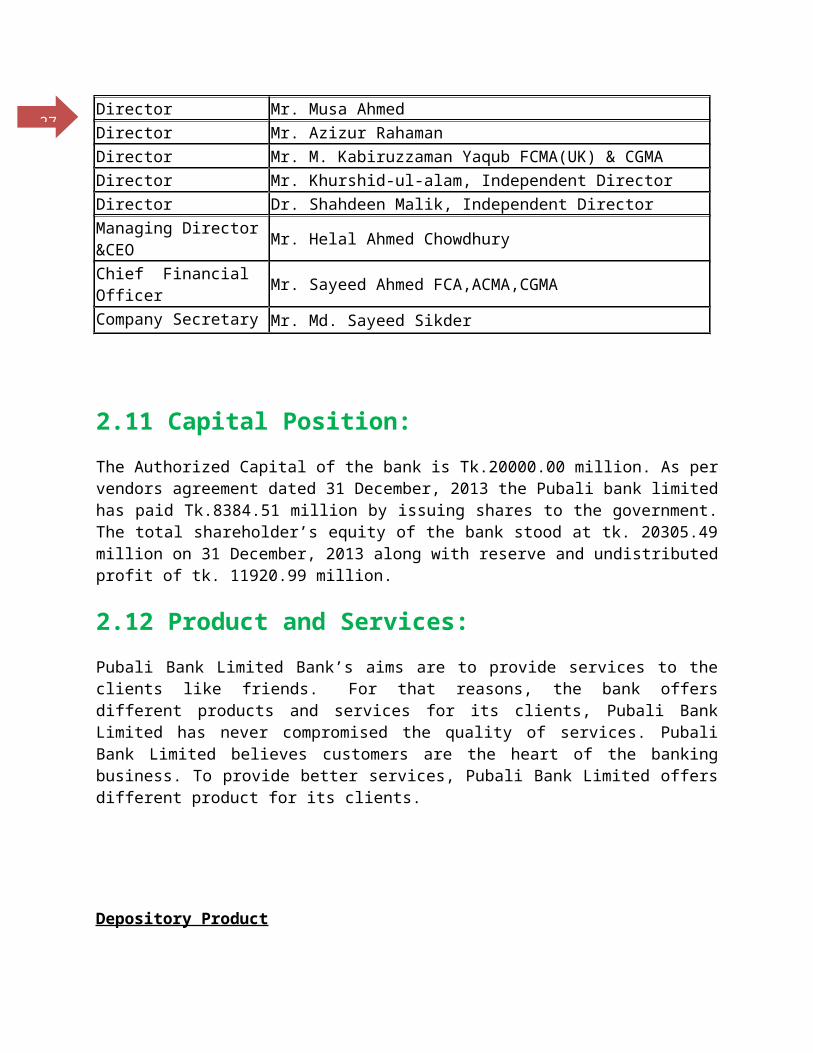

27Director Mr. Musa Ahmed Director Mr. Azizur RahamanDirector Mr. M. Kabiruzzaman Yaqub FCMA(UK) & CGMADirector Mr. Khurshid-ul-alam, Independent DirectorDirector Dr. Shahdeen Malik, Independent DirectorManaging Director&CEO Mr. Helal Ahmed Chowdhury

Chief Financial Officer Mr. Sayeed Ahmed FCA,ACMA,CGMA

Company Secretary Mr. Md. Sayeed Sikder

2.11 Capital Position:The Authorized Capital of the bank is Tk.20000.00 million. As pervendors agreement dated 31 December, 2013 the Pubali bank limitedhas paid Tk.8384.51 million by issuing shares to the government.The total shareholder’s equity of the bank stood at tk. 20305.49million on 31 December, 2013 along with reserve and undistributedprofit of tk. 11920.99 million.

2.12 Product and Services:Pubali Bank Limited Bank’s aims are to provide services to theclients like friends. For that reasons, the bank offersdifferent products and services for its clients, Pubali BankLimited has never compromised the quality of services. PubaliBank Limited believes customers are the heart of the bankingbusiness. To provide better services, Pubali Bank Limited offersdifferent product for its clients.

Depository Product

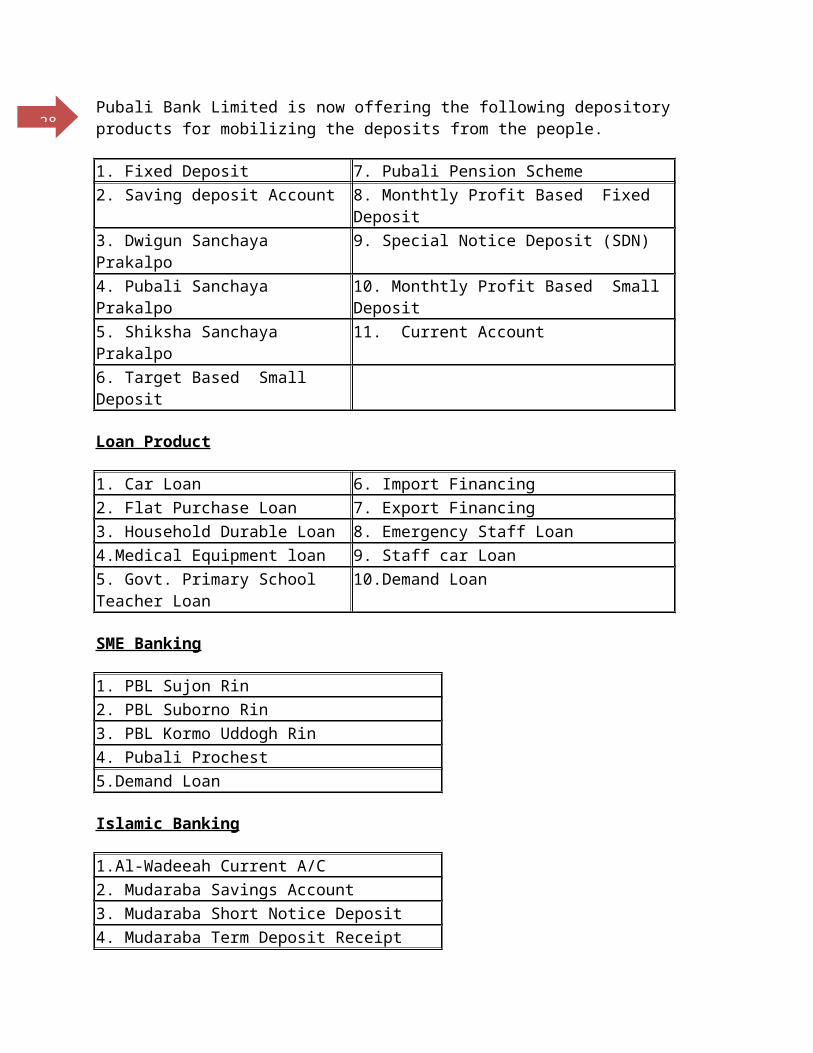

28Pubali Bank Limited is now offering the following depository products for mobilizing the deposits from the people.

1. Fixed Deposit 7. Pubali Pension Scheme2. Saving deposit Account 8. Monthtly Profit Based Fixed

Deposit3. Dwigun Sanchaya Prakalpo

9. Special Notice Deposit (SDN)

4. Pubali Sanchaya Prakalpo

10. Monthtly Profit Based Small Deposit

5. Shiksha Sanchaya Prakalpo

11. Current Account

6. Target Based Small Deposit

Loan Product

1. Car Loan 6. Import Financing2. Flat Purchase Loan 7. Export Financing3. Household Durable Loan 8. Emergency Staff Loan4.Medical Equipment loan 9. Staff car Loan5. Govt. Primary School Teacher Loan

10.Demand Loan

SME Banking

1. PBL Sujon Rin2. PBL Suborno Rin3. PBL Kormo Uddogh Rin4. Pubali Prochest5.Demand Loan

Islamic Banking

1.Al-Wadeeah Current A/C 2. Mudaraba Savings Account3. Mudaraba Short Notice Deposit 4. Mudaraba Term Deposit Receipt

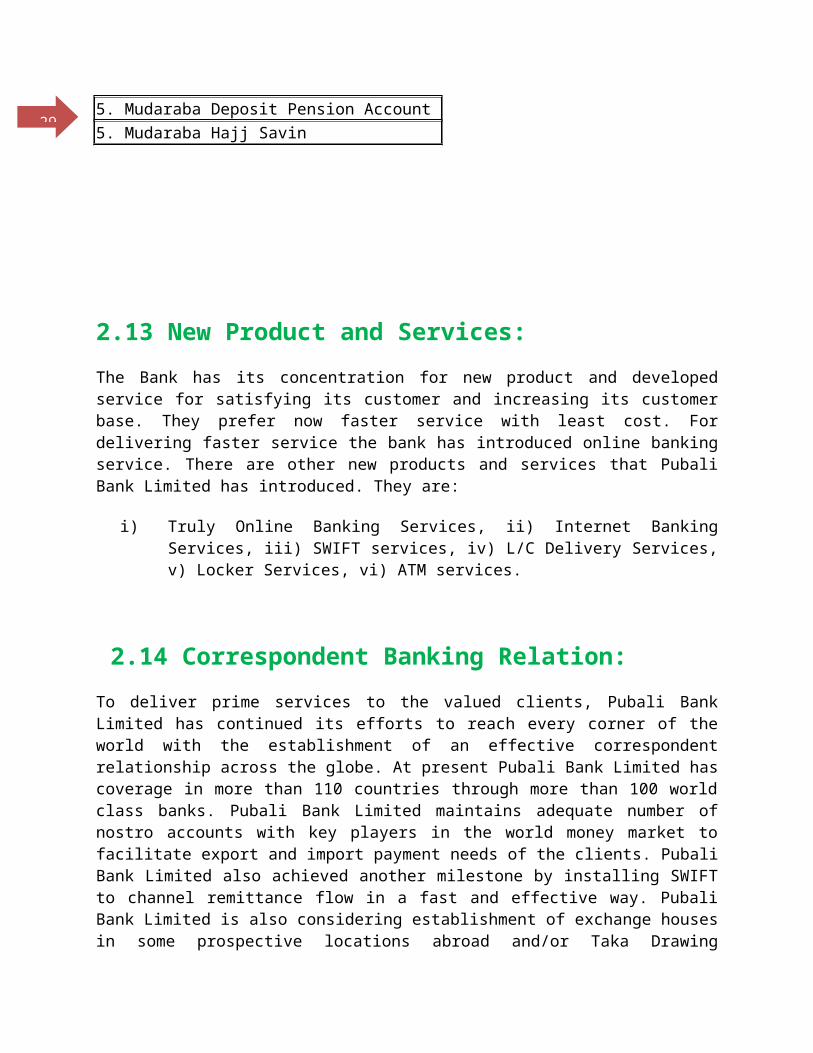

295. Mudaraba Deposit Pension Account5. Mudaraba Hajj Savin

2.13 New Product and Services:The Bank has its concentration for new product and developedservice for satisfying its customer and increasing its customerbase. They prefer now faster service with least cost. Fordelivering faster service the bank has introduced online bankingservice. There are other new products and services that PubaliBank Limited has introduced. They are:

i) Truly Online Banking Services, ii) Internet BankingServices, iii) SWIFT services, iv) L/C Delivery Services,v) Locker Services, vi) ATM services.

2.14 Correspondent Banking Relation:To deliver prime services to the valued clients, Pubali BankLimited has continued its efforts to reach every corner of theworld with the establishment of an effective correspondentrelationship across the globe. At present Pubali Bank Limited hascoverage in more than 110 countries through more than 100 worldclass banks. Pubali Bank Limited maintains adequate number ofnostro accounts with key players in the world money market tofacilitate export and import payment needs of the clients. PubaliBank Limited also achieved another milestone by installing SWIFTto channel remittance flow in a fast and effective way. PubaliBank Limited is also considering establishment of exchange housesin some prospective locations abroad and/or Taka Drawing

30Arrangement with internationally reputed exchange houses tosupport governments effort of a building a comfortable foreignexchange reserve through channeling inward remittance.

2.15 Corporate Social Responsibility (CSR):

Pubali Bank's response to corporate social responsibility is embodied by the concept of responsible banking, which is imbibed in the way we do business and drive the objectives of the Bank to be the best financial institution in Bangladesh. We recognize our obligations to the society, so we are committed to always making informed, reasonable and ethical decision in the manner we carry outOur business, how we treat our employees, and how we relate to our customers.Our CSR initiatives over the years have focused on health care, sports, education and youth development, the arts, philanthropy and charitable activities.

Health Care

Because we believe that good health is a critical condition for rapid socio-economic development of the country, the Bank has donated or funded large volumes to set up state of an art facility to various hospitals across the country to underline its commitment to ensure availability of health service to all at affordable cost and thus saving exodus of foreign currencies.

Pubali Bank Limited has donated Tk. 10 (ten) crore to Dhaka Ahsania Mission, a humanitarian organization, towards setting up a state of the art modern Cancer hospital to alleviate the sufferings of peoplewho have currently no access to specialized medical treatment of Cancer. In Bangladesh, there are minimal cancer facilities and many people in both urban and rural areas of the country are dying due tolack of hospitals and doctors, to serve their cancer needs. It is estimated that there are 1,000,000 people in Bangladesh who already have cancer and 200,000 new patients are added each year. Currently,with existing hospital facilities, Bangladesh has the capability to serve 20,000 patients each year - which means that 180,000 patients

31go altogether unserved - thousands of them will needlessly suffer and ultimately die without any cancer care. The Ashania Mission Cancer and General Hospital will serve approximately 73,000 patientseach year, preventing as many as 40,000 deaths and reducing the suffering of approximately 270,000 patients all over Bangladesh. Pubali Bank Limited has also donated Tk. 2 (two) Crore to ENT CancerHospital. Apart from direct donation, Pubali Bank Limited from the very initiation extended credit to all big hospitals at a concessional rate of interest so that valuable foreign currency can be saved and our people can get healthcare services at affordable cost:BIRDEMIbrahim Cardiac CenterApollo HospitalUnited HospitalSquare HospitalInternational Medical College and HospitalBangladesh Medical College and HospitalLab AidGreen Life Hospital etc.

Our other areas of Corporate Social Responsibility

Regular donations to different educational institutions, disabledorganizations Sports sponsoring- Boat rowing etc.Helping the distress people for treatmentFinancial and other supports have been provided for the complicatedoperation of the own employeesFinancial support for the educational purposes and good result ofthe childrenPBL has been providing magazines and supports for extra curricularactivities to major universities

32Internship facilities to the students of the leading universitiesFor the natural calamity and national tragedy PBL always extendsits hand to help and provide financial support

PBL always extends its support to distress people throughgovernment scheme/contribution to Government Fund etc.

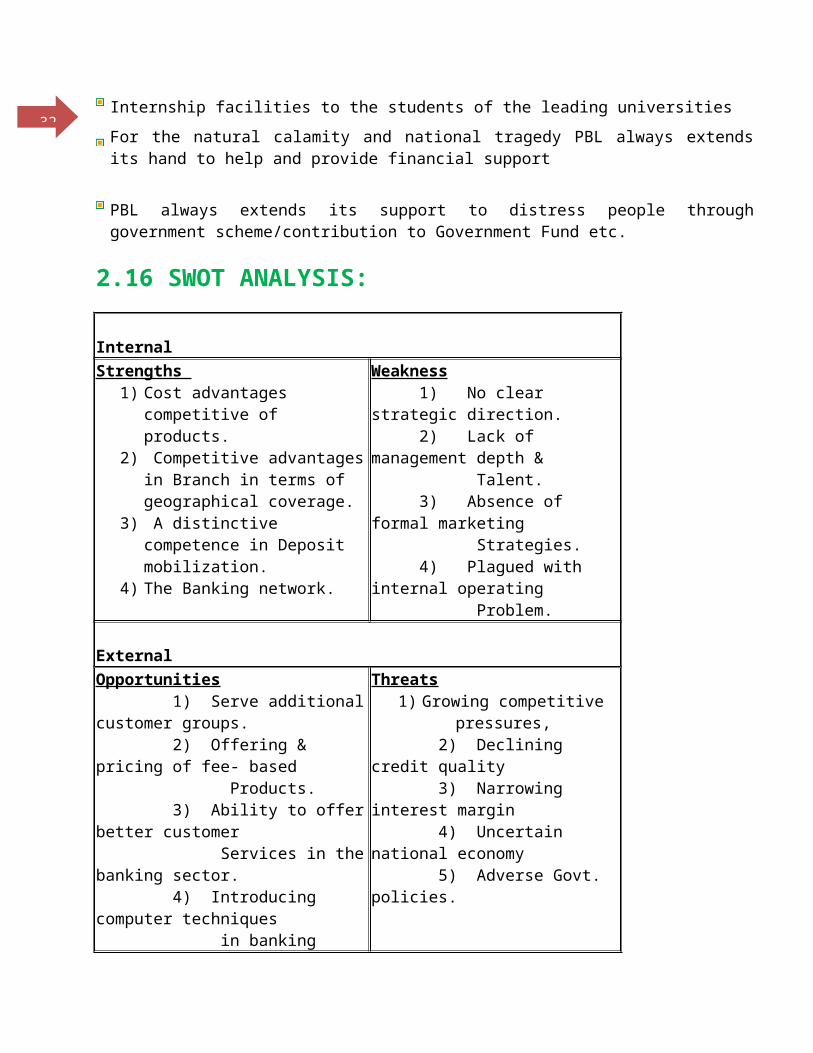

2.16 SWOT ANALYSIS: InternalStrengths

1) Cost advantages competitive of products.

2) Competitive advantagesin Branch in terms of geographical coverage.

3) A distinctive competence in Deposit mobilization.

4) The Banking network.

Weakness 1) No clear strategic direction. 2) Lack of management depth & Talent. 3) Absence of formal marketing Strategies. 4) Plagued with internal operating Problem.

ExternalOpportunities 1) Serve additionalcustomer groups. 2) Offering & pricing of fee- based Products. 3) Ability to offerbetter customer Services in thebanking sector. 4) Introducing computer techniques in banking

Threats1) Growing competitive pressures,

2) Declining credit quality 3) Narrowing interest margin 4) Uncertain national economy 5) Adverse Govt. policies.

33activities.

2.17 Pubali Bank Limited: Online Banking:The year 2013, is a landmark in the history of Pubali BankLimited, as the Bank successfully implemented its online system.Online Banking system provides better services for the customersand makes the bank cost effective. After implementing onlinesystem, customers can enjoy the following world class bankingservices at a reasonable and affordable price through the fullautomated real-time any where any branch banking servicescovering 24 hours a day:

Through Branches:

A customer can avail services with any branch of PubaliBank Limited.

Customer can withdraw or deposit money in any branch ofPubali Bank Limited.

International financial transactions can be carried out bythe on-line SWIFT interface of the banking software.

Customer can enjoy facilities of loan installment paymentsfrom savings/ current accounts, Fund transfer to otheraccounts.

Sweep-out facility, enabling to transfer the money fromany account when it exceeds pre-defined amounts.

Sweep-in facility, enabling to bring money from anotheraccount when the first account balance falls below a pre-defined amount.

Through ATMs:

By using Pubali Bank Limited’s own ATM pools anywhere in the country, the valued customers of the Bank can perform the following functions at any time:

Account balance enquiry.

34 Cash withdrawal 24 hours a day, 7 days a week, and 365 days

a year. Cash deposit to some designated number of ATM’s at any time Mini statement printing. Statement request. Personal Identification number change. Request for cheque book. Fund transfer within his/her own account. Payment of mobile/T&T phone, gas, electricity, water,

internet, credit card bills from the customer’s savings and current account.

Payment of School/College/University fees by debiting one’s savings a/ current account.

Purchase of activation number for Mobile/Internet pre-paid card.

Through Point of Sale (POS) terminals :

Bill settlement at any Pubali Bank Limited POS terminals installed at strategic locations.

Through Internet

Through internet banking of Pubali Bank Limited, the following can be performed:

Checking of account balance. Print-out of account statement for a particular period. Transfer of fund within the customer’s own accounts. Payment of mobile/T&T phone, gas, electricity, water, and

internet bills from the customer’s account. Payment of School/College/University fees by debiting

one’s own account. Purchase activation number of Mobile/Internet pre-paid

cards. Deposit of loan installments

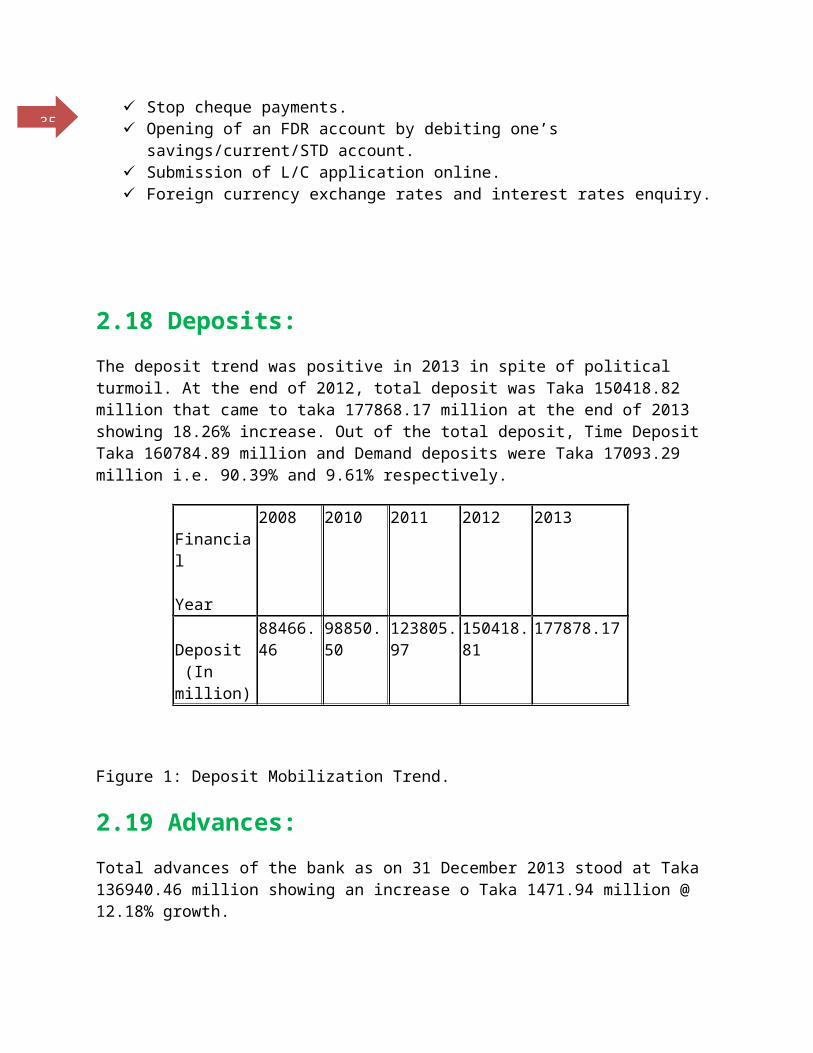

35 Stop cheque payments. Opening of an FDR account by debiting one’s

savings/current/STD account. Submission of L/C application online. Foreign currency exchange rates and interest rates enquiry.

2.18 Deposits:The deposit trend was positive in 2013 in spite of political turmoil. At the end of 2012, total deposit was Taka 150418.82 million that came to taka 177868.17 million at the end of 2013 showing 18.26% increase. Out of the total deposit, Time Deposit Taka 160784.89 million and Demand deposits were Taka 17093.29 million i.e. 90.39% and 9.61% respectively.

Financial Year

2008 2010 2011 2012 2013

Deposit (In million)

88466.46

98850.50

123805.97

150418.81

177878.17

Figure 1: Deposit Mobilization Trend.

2.19 Advances:Total advances of the bank as on 31 December 2013 stood at Taka 136940.46 million showing an increase o Taka 1471.94 million @ 12.18% growth.

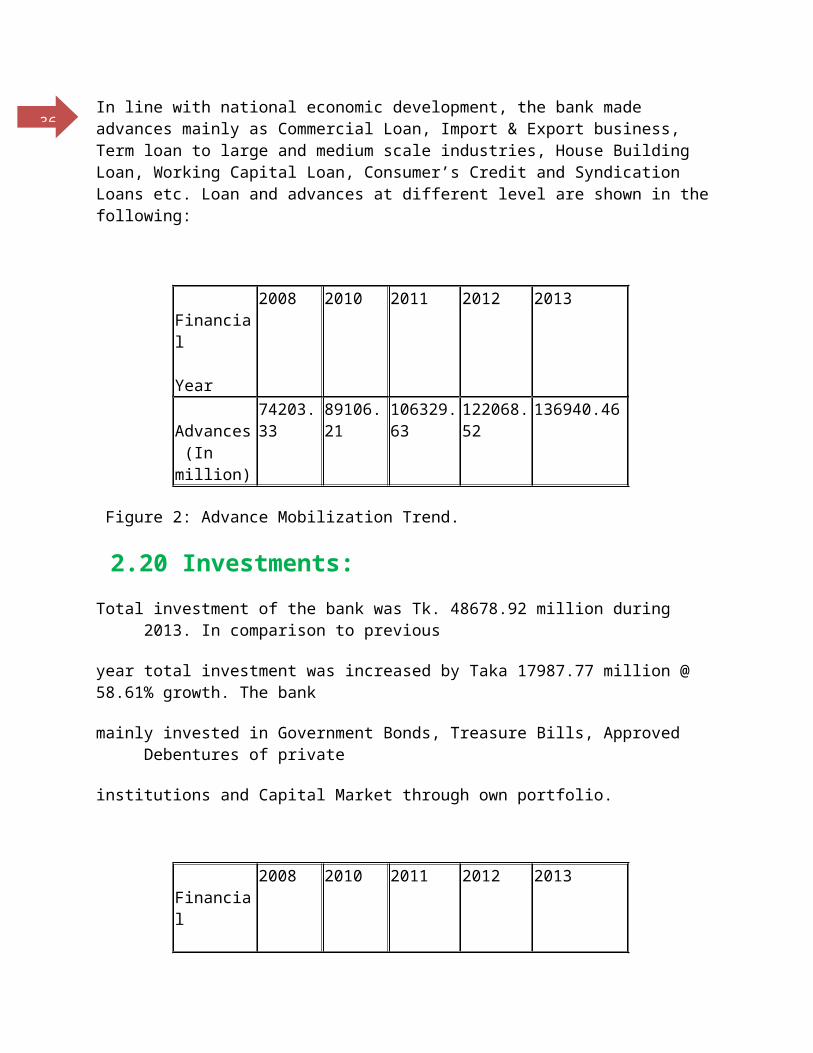

36In line with national economic development, the bank made advances mainly as Commercial Loan, Import & Export business, Term loan to large and medium scale industries, House Building Loan, Working Capital Loan, Consumer’s Credit and Syndication Loans etc. Loan and advances at different level are shown in the following:

Financial Year

2008 2010 2011 2012 2013

Advances (In million)

74203.33

89106.21

106329.63

122068.52

136940.46

Figure 2: Advance Mobilization Trend.

2.20 Investments:Total investment of the bank was Tk. 48678.92 million during

2013. In comparison to previous

year total investment was increased by Taka 17987.77 million @ 58.61% growth. The bank

mainly invested in Government Bonds, Treasure Bills, Approved Debentures of private

institutions and Capital Market through own portfolio.

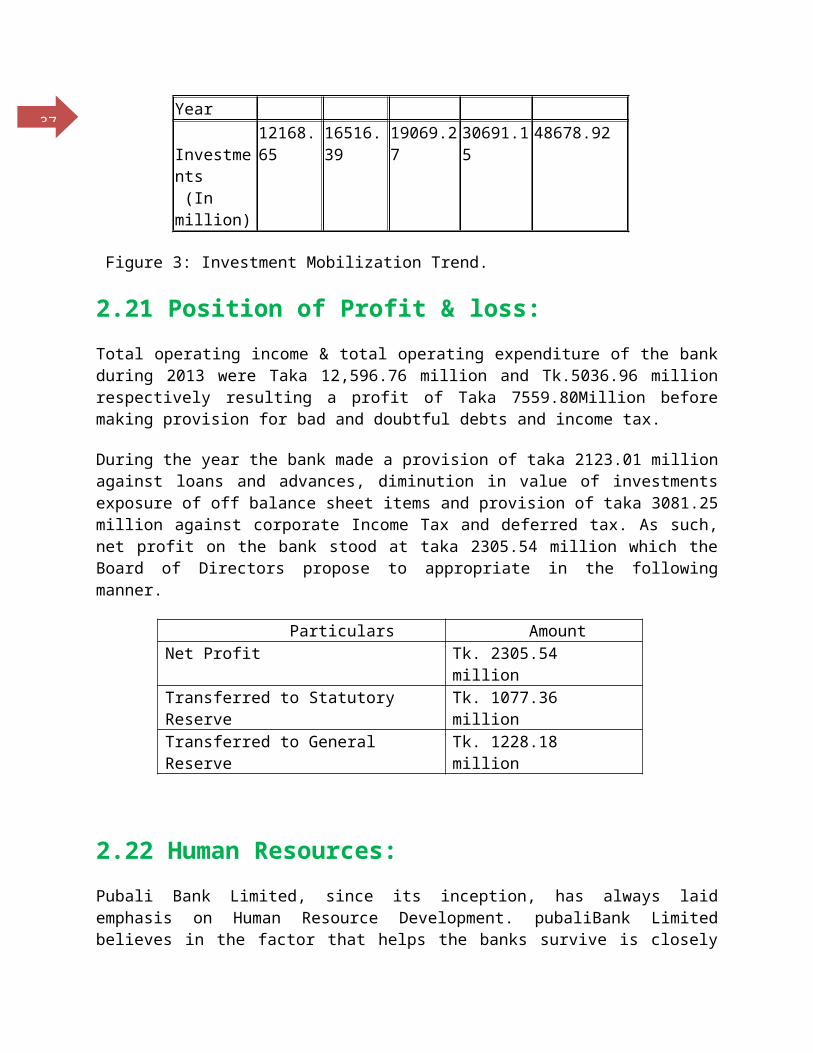

Financial

2008 2010 2011 2012 2013

37Year Investments (In million)

12168.65

16516.39

19069.27

30691.15

48678.92

Figure 3: Investment Mobilization Trend.

2.21 Position of Profit & loss:Total operating income & total operating expenditure of the bankduring 2013 were Taka 12,596.76 million and Tk.5036.96 millionrespectively resulting a profit of Taka 7559.80Million beforemaking provision for bad and doubtful debts and income tax.

During the year the bank made a provision of taka 2123.01 millionagainst loans and advances, diminution in value of investmentsexposure of off balance sheet items and provision of taka 3081.25million against corporate Income Tax and deferred tax. As such,net profit on the bank stood at taka 2305.54 million which theBoard of Directors propose to appropriate in the followingmanner.

Particulars AmountNet Profit Tk. 2305.54

millionTransferred to Statutory Reserve

Tk. 1077.36 million

Transferred to General Reserve

Tk. 1228.18 million

2.22 Human Resources:Pubali Bank Limited, since its inception, has always laidemphasis on Human Resource Development. pubaliBank Limitedbelieves in the factor that helps the banks survive is closely

38interlinked with the quality of service and satisfaction of therequirements of the clientele and that directly depends on thequalification and efficiency of the employees. With thisobjective in view, Pubali Bank Limited excels the performance ofits member of the staff by creating opportunities throughproviding proper training, rewards and recognition. To attractand retain qualified and efficient staff.

Pubali considers human resources to be an essential ingredient ofsuccess for Bank. The Bank is committed to effective managementand development of human resources, go through the process ofstabilization, reform and modernization.

In view of the importance of the management of human resources,internal structures were changed. The accountabilities of theGeneral Manager, Administration were changed to provide greateremphasis on HR Management and development plans are under way formore radical change in the various divisions responsible formanaging human resources.

The General Manager– Human Resources Management and Development, is also leading various activities to modernize HR polices and procedures under the guidance of the HR Advisor. These improvements reflect changing pressures on the Bank and are designed to bring HR practices more in line with good practice ininternational banks Pubali Bank Limited has formulated a number of well thought policies for the welfare of its employees, in theform of gratuity funds, Superannuating fund, employees House Building Loan Scheme, Cycle/ Motorcycle / Car loan scheme, etc.

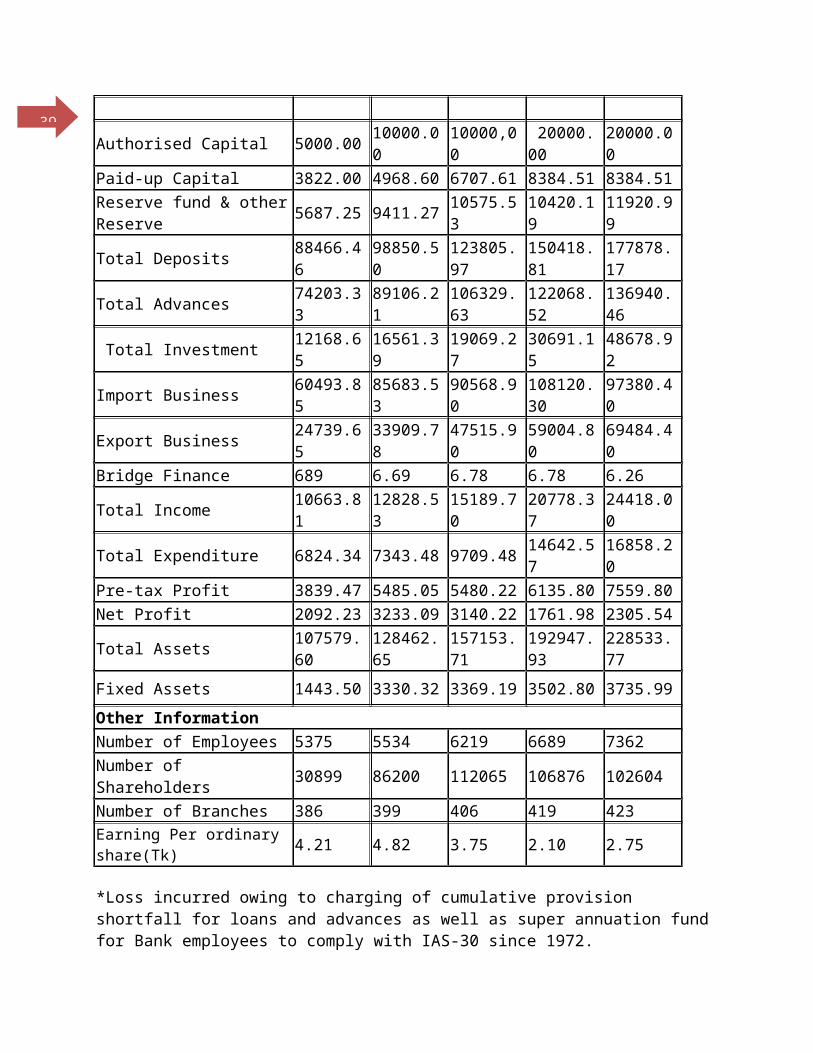

2.23 Pubali Bank Limited’s Five Years’ Financial Positions:

Key Financials (Figures in a million taka)

Particurars 2008 2009 2010 2012 2013

39

Authorised Capital 5000.00 10000.00

10000,00

20000.00

20000.00

Paid-up Capital 3822.00 4968.60 6707.61 8384.51 8384.51Reserve fund & otherReserve 5687.25 9411.27 10575.5

310420.19

11920.99

Total Deposits 88466.46

98850.50

123805.97

150418.81

177878.17

Total Advances 74203.33

89106.21

106329.63

122068.52

136940.46

Total Investment 12168.65

16561.39

19069.27

30691.15

48678.92

Import Business 60493.85

85683.53

90568.90

108120.30

97380.40

Export Business 24739.65

33909.78

47515.90

59004.80

69484.40

Bridge Finance 689 6.69 6.78 6.78 6.26

Total Income 10663.81

12828.53

15189.70

20778.37

24418.00

Total Expenditure 6824.34 7343.48 9709.48 14642.57

16858.20

Pre-tax Profit 3839.47 5485.05 5480.22 6135.80 7559.80Net Profit 2092.23 3233.09 3140.22 1761.98 2305.54

Total Assets 107579.60

128462.65

157153.71

192947.93

228533.77

Fixed Assets 1443.50 3330.32 3369.19 3502.80 3735.99Other InformationNumber of Employees 5375 5534 6219 6689 7362Number of Shareholders 30899 86200 112065 106876 102604

Number of Branches 386 399 406 419 423Earning Per ordinary share(Tk) 4.21 4.82 3.75 2.10 2.75

*Loss incurred owing to charging of cumulative provision shortfall for loans and advances as well as super annuation fund for Bank employees to comply with IAS-30 since 1972.

40 Chapter Three: Credit Policy of Pubali Bank Limited

3.1 Credit Overview in Pubali Bank Limited:In a financial system of any economy, we know, financial surpluses mobilized from surplus economic unit and transferred tothe deficit economic unit. In the banking world, the bank acts asan intermediary in between deficit economic unit & surplus economic unit. Bank mobilizes the fund from surplus economic unitas deposit & makes the fund available to the deficit unit. The style of making the fund available to the deficit unit is nothingbut creation of credit. Credit is in true sense, making provisionof fund by one party to another party under certain terms & conditions.

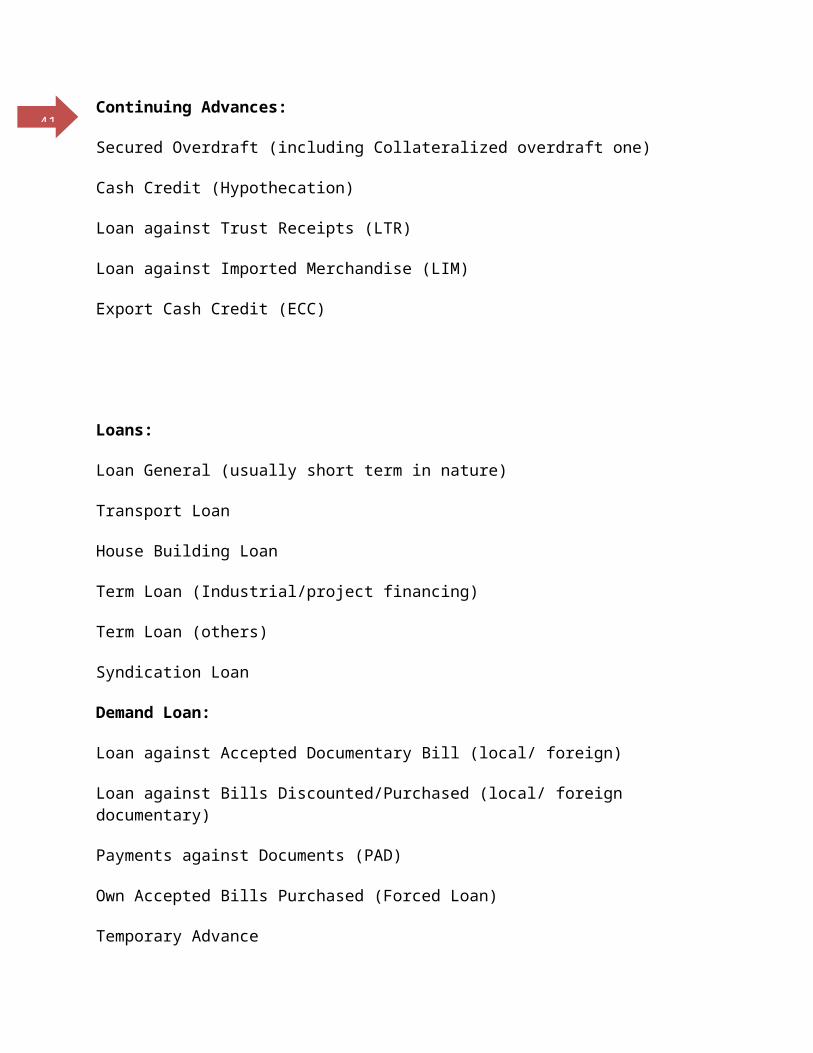

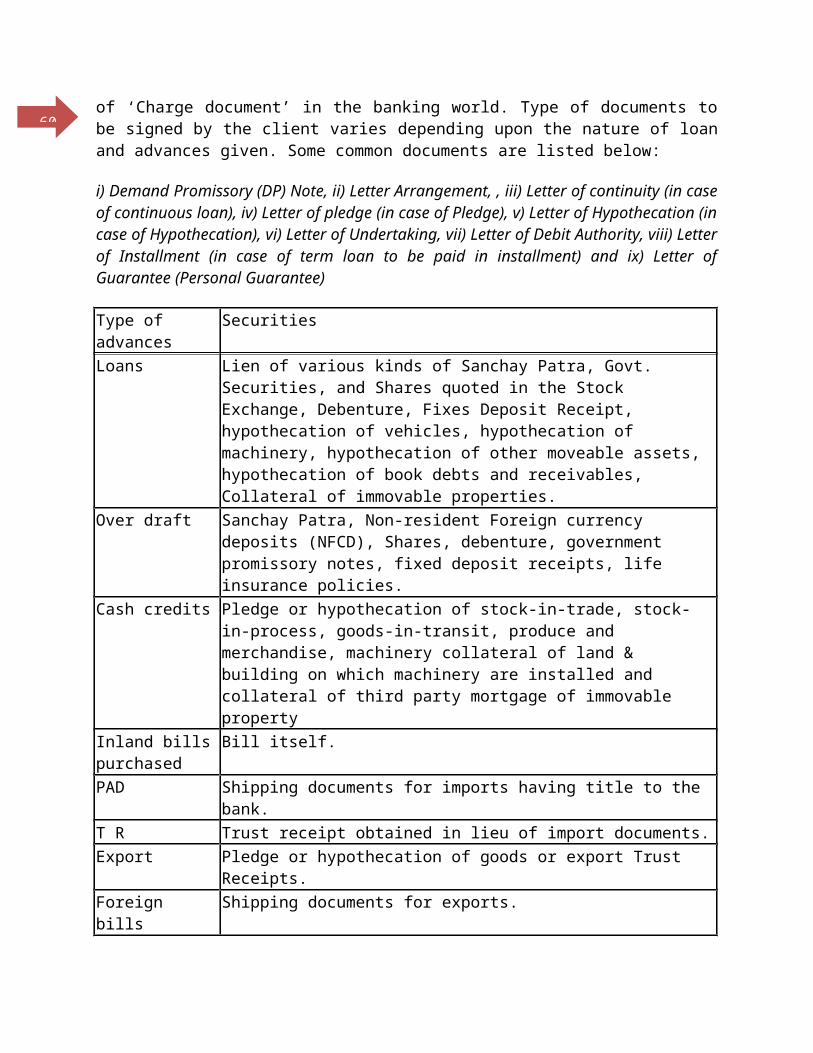

3.2 Types of Advances:The credit facilities granted by the bank are classified under different account heads as under:

Loan (like short/ mid/ long term in nature) Overdrafts (allowing frequent debit/credit transactions

within an agreed limit) Trade related credit facilities (like bills port folio) Short Term Advances (like continuing facilities) Contingent facilities (like Letters of Credit, Letters of

Guarantee)

Generally all facilities, except term loans are repayable on demand. Trade related credit facilities are self-liquidating in nature. Cash Credit /Overdrafts are reviewed annually or at regular intervals in case a closer monitoring of the accounts is necessary.

41Continuing Advances:

Secured Overdraft (including Collateralized overdraft one)

Cash Credit (Hypothecation)

Loan against Trust Receipts (LTR)

Loan against Imported Merchandise (LIM)

Export Cash Credit (ECC)

Loans:

Loan General (usually short term in nature)

Transport Loan

House Building Loan

Term Loan (Industrial/project financing)

Term Loan (others)

Syndication Loan

Demand Loan:

Loan against Accepted Documentary Bill (local/ foreign)

Loan against Bills Discounted/Purchased (local/ foreign documentary)

Payments against Documents (PAD)

Own Accepted Bills Purchased (Forced Loan)

Temporary Advance

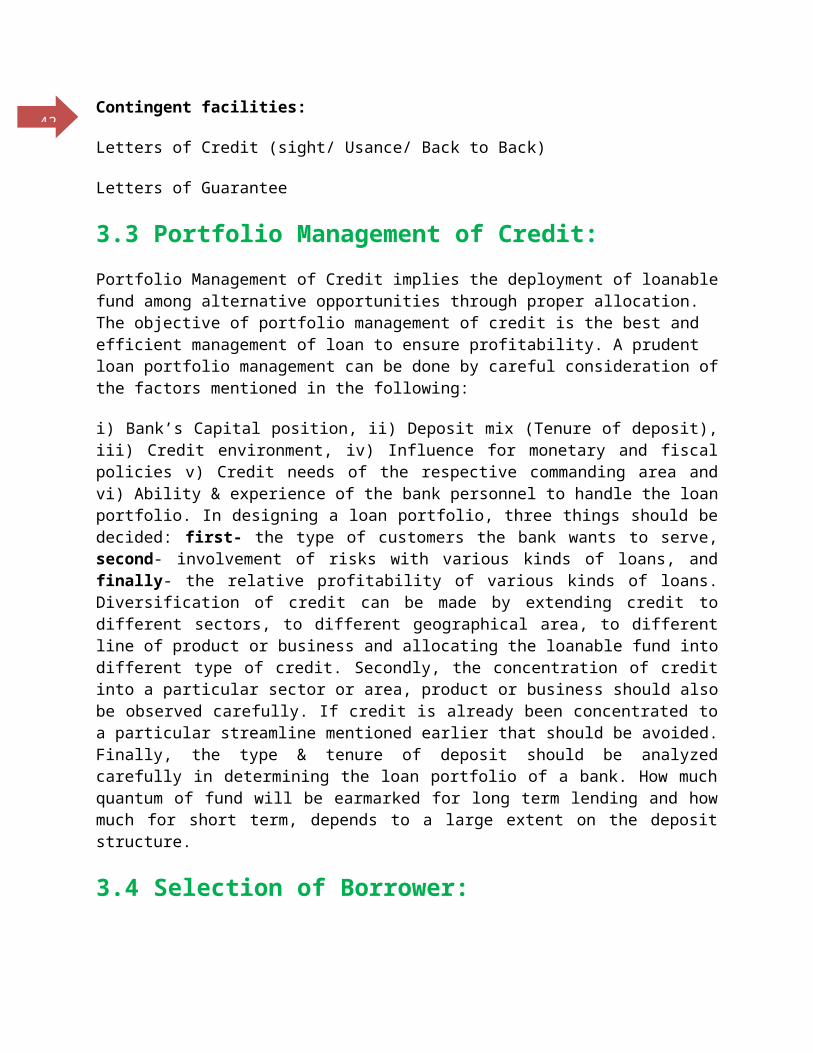

42Contingent facilities:

Letters of Credit (sight/ Usance/ Back to Back)

Letters of Guarantee

3.3 Portfolio Management of Credit:Portfolio Management of Credit implies the deployment of loanablefund among alternative opportunities through proper allocation. The objective of portfolio management of credit is the best and efficient management of loan to ensure profitability. A prudent loan portfolio management can be done by careful consideration ofthe factors mentioned in the following:

i) Bank’s Capital position, ii) Deposit mix (Tenure of deposit),iii) Credit environment, iv) Influence for monetary and fiscalpolicies v) Credit needs of the respective commanding area andvi) Ability & experience of the bank personnel to handle the loanportfolio. In designing a loan portfolio, three things should bedecided: first- the type of customers the bank wants to serve,second- involvement of risks with various kinds of loans, andfinally- the relative profitability of various kinds of loans.Diversification of credit can be made by extending credit todifferent sectors, to different geographical area, to differentline of product or business and allocating the loanable fund intodifferent type of credit. Secondly, the concentration of creditinto a particular sector or area, product or business should alsobe observed carefully. If credit is already been concentrated toa particular streamline mentioned earlier that should be avoided.Finally, the type & tenure of deposit should be analyzedcarefully in determining the loan portfolio of a bank. How muchquantum of fund will be earmarked for long term lending and howmuch for short term, depends to a large extent on the depositstructure.

3.4 Selection of Borrower:

43Selection of borrower is a very significant part of a creditdecision. The borrower should be diagnosed prudently. Degree ofrisk has an inverse relationship with the selection of borrower.Selection of right borrower reduces the risk of non-repayment ofthe loan. To the contrary, degree of risk of non-repaymentincreases with the selection of wrong borrower. In our country,the huge volume of non-performing loan is mainly the result offailure in selecting right borrower. So, if it is found that lineof business is prospective and profitable but the potentialborrower is not right one, the proposal should not beentertained. There are some parameters for selection of aborrower. Some ‘C’s commonly expresses the parameters. And thusthe criteria for selection of a borrower are popularly known as 5C’s such as:

i) Character: Market reputation, morality, family background,and promptness in repayment,

ii) Capacity: Ability to manage the business, ability toemploy the fund in the right

way, ability to overcome unforeseenproblems,

iii) Capital: Equity strength, assets & properties,

iv) Collateral: The easy marketability of the properly given assecurity,

v) Condition: Overall business condition,

If the borrower’s found satisfactory in terms of all C’s onlythen it is suggested to entertain the borrower.

3.5 Processing of Credit:Credit proposals must be prepared for all credit facilities. Theprocessing of a credit proposal falls into mainly two stages asunder:

44 Obtaining due approval of the competent authority

(Discretionary Powers) of Pubali Bank Limited Steps for allowing the client to avail the credit facility.

Management approval levels splits into following authority:

Head Office Credit Committee: The Credit Executive &Recommendation Committee (CRECOM) is responsible to review, andapprove or reject any credit limit proposals on the basis ofapproval lending policy, criteria of lending, sectorial exposure,group exposure and/ or on other genuine grounds. Credit Committeeusually sits on every week or more frequently as the need mayarise. The proposals after thorough discussion/ deliberation iffound suitable is recommended for approval by the ExecutiveCommittee of the Board through the Managing Director:

Delegated authority to the Managing Director: Under delegatedlending authority to the Managing Director, credit proposals, onetime or specific gets approval after scrutiny is done by HeadOffice Credit Division. From time to time the Managing Directormay delegate the branch managers discretionary powers with dueapproval from the competent authority.

Executive Committee of the Board: If the facilities requiredfurther approval from the executive committee of the Board, thenthe proposal send. The credit proposal has been sent to theexecutive committee of the Board if the credit committee thinksto require further approval.

Credit limit proposal originates in the branch. Proposal afterdue checking, analysis is sent with recommendation signed by themanager and the credit officer in-charge. After the creditproposal has been finally approved by the competent authority asthe case may be, the resolution /decision thereof are sent to thebranch for further action as follows:

Convey offer to the borrower and obtain acceptance thereagainst.

45 Branch credit /loan administration perfect the security and

charge documents considering the nature and the terms of thefacility.

Setting –off client file account record.

3.5.1 Credit Report: The branch manager should ensure preparation of credit report onthe client to determine its past record, business performances,market reputation etc. The credit report should contain thefollowing:

1. The nature of client’s business.2. The names of owners and details of their associated business

concerns.3. Net worth of the individual person owing the firm /company

(obtain through declaration at the time of submission ofloan application).

4. The financial health of the business concern.

3.5.2 CIB Report: For processing credit proposals (both funded & non-funded) Banksand Financial Institutions need to obtain mandatory satisfactoryCIB report from Bangladesh Bank. Present criteria for obtainingmandatory CIB report may be changed from time to time at thediscretion of Bangladesh Bank. Branch manager must obtainsatisfactory CIB report prior to processing of credit proposalsand mention the status of the client and its allied concerns/persons of the borrower in the credit line proposal as it isrevealed in the latest CIB report. In CIB report there is anyclassified loan, no farther credit proposal is processed.

3.5.3 Visiting Client:The visit and meeting the client at their door-step may help toconfirm the business decision reach by the manager with regard to

46the client’s financial status, management efficiency andtechnical details about the good sense and services in which theclient deals. This will also help to judge its quality andacceptability as a reliable security. A set of question, whichmay be asked, should be prepared beforehand.

3.5.4 Credit Line Application Form:A credit proposal is its funds or non-funds based at the stage ofprimary scrutiny, credit officers prime consideration is toascertain with reasonable accuracy, due date liquidation ofloan /credit exposure. There are different sections covered inthe credit proposal format which is explained below:

01. Client introduction: Giving the exact name and style of theclient as per registration in case of company. Also indicate thenature of the proposal “Fresh” or “Renewal/ Revision”. Usefigures in denomination of Taka in million, state exact nature ofbusiness/description of the project. Provide business capital/equity capital of the owner based on financial statements.

02. Particulars of owners: State whether proprietor, partners ordirectors. Show the percentage of the shareholdings of thedirectors as per record. Provide declared assets / net worth asthe case may be by individually.

03. Allied concerns: Provide name of allied business concern ofthe owners/ client, their nature of business and their investment/ interest in the business.

04. Credit facility from other banks: Obtain declared statementfrom the client. Also refer to CIB report of Bangladesh Bank.

05. Account maintained with Pubali Bank Limited: State allaccounts including Fixed Deposit, if any, showing averagedeposit/ current deposit.

4706. Existing credit lines(s): Give details and nature offacility. The amount of respective limit and the outstandingare on the date of the proposal, state validity/ maturity stateprimary and collateral security in brief.

07. Proposed credit line(s): In case of renewal /revision, thissection should be completed only after careful review of theconduct of the account, Client’s financial requirement, managingof business affairs in terms of available facility (ies). In caseof fresh proposal, and after having a preliminary discussion withthe client to have a clear view of client’s account, his futureplans and financing requirements, the size of limit, period andproposed security to be structured.

08. Analysis of credit proposal: In this section, provide generalbackground of the client, business profile, project details andmanagement aspects of the business house/industry.

09. Third party information: Provide status of up to date CIBreport, Credit checking with other sources such as previous banksaccount transaction.

10. Financial information: This section reflects the financialsoundness of the business concern and information to be collected/ prepared from spreadsheet analysis on the basis of client’smanagement certified financial statements or audited financialreports. Furnish comments on the liquidity, profitability andleverage position of the client. This exercise / assessmentshould be done carefully pinpointing the strong and weak areas.

11. Prospects: Here business prospects market outlook of theproduct to be given. Salient features of the products, pricing,market strategy to be provided in case of manufacturing products.

12. Assessment of financing requirement: Client’s financingrequirement to be assessed on the basis of business cash flow /working capital assessment / future plans. Exact requirement isto be assessed and recommended after preliminary discussion withthe client.

4813. Inadequacy in the documentation: Mention non-fulfillment ofany documentation / mortgage perfection etc. Also indicate auditobjection on client’s account.

14. Collateral security: Give details of security in the form ofland, building, machinery, it’s written down value or surveyedvalue. Also show nature of marketable securities, its face valueand average market value.

15. Risks Analysis: Furnish comments on Credit Risk Gradingexercise, if done, and indicate the CRG rating. Indicate possiblerisks in the business and its mitigation.

16. Accounts/ Business performance: Give details of client’sdeposit/ loan accounts performance last 12 (twelve) months. Showdebit/ credit summation, minimum/ maximum balances, L/Cs opened,export documents negotiated during last 12 months.

17. Bank’s earning: Give break-up of earnings from therelationship last 3 (three) years.

18. Recommendation: Give meaningful comments, consideration ofthe business line with clear recommendation.

19 Proposed facility (ies): Give facility wiseproposed/renewed/restructured loan/ credit limits, purpose of thefacility, source of repayment, pricing of the facility, securitysupport and validity of the facility, other conditions/ specialconditions including requirement of Bangladesh Bank approval tobe highlighted.

3.5.5 Supporting Documents:The branch manager while processing a credit proposal for HeadOffice approval, he must see that the proposal recommended isbased on following supporting documents:

i) at least 90 days before Credit report on the client, ii)Financial statements, iii) Spreadsheet analysis, iv) Net worthanalysis and v) Acceptable security details & vi) CRG report.

49This report should be updated when renewal of credit facilitiesare considered. Third party credit report / CIB report along withcredit report on the client should be kept in the file at thebranch. Business/ financial performance is being analysis base onaudited accounts if they are available.

3.5.6 Analysis of Client’s account:The objective of analyzing financial statements from the point ofview of the bank is to understand the manner in which client’sown resources are employed, its liquidity position, the ratios ofnet worth to borrowing and of current assets to currentliabilities. The analysis should provide answers to followingareas:

1. Borrower’s net worth: To see if the borrower’s net worthjustifies the level of credit facilities being requested. Networth is calculated by total debt liabilities from total assets.From another point of view, the net worth is the owners’ totalinterest in the business made up of paid up capital andaccumulated surplus consisting of written earnings and reserves.

2. Working capital: To see whether the current assets aresufficient to meet the client’s current commitments andliabilities. Working capital is arrived at by deducting thecurrent liabilities from the current assets.

3. Profitability: To see whether sufficient earnings from theoperation of the business are there to repay the bank debtsliving sufficient balance /return on equity.

4. Capital Gearing: To see how much amount of equity is in thebusiness compare with the borrowed funds. As a good bankingproposition substantial equity investment should be insured.

5. Cash flow: When assessing the client’s liquidity position andprofitability, the timing of client’s commitment must beconsidered. His commitments must be spread in such a way that thebusiness would never face a cash shortage in the foreseeablefuture.

50

3.6 Project Financing Evaluation:Systematic analysis is required to be undertaken to provide arational basis for decision making. Socio-economic objectives ofthe country needs to be considered in addition to the soundnessof the project in terms of technical, commercial, financial andmanagement considerations while making investment decision.

3.6.1 Project EvaluationThe proposal may be for a new project or an existing projectrequiring Balancing, Modernization, Replacement and Expansion(BMRE). The project appraises in terms of technical, commercial,financial, management and socio-economic aspects while makinginvestment decision.

The proposal to be developed in the following areas:

a) Cost of the project: The cost of the project represents allfixed capital expenditures incurred or to be incurred foracquisition of its fixed assets and the net working capital torun the project. Proper assessment of the cost of the project isvery important for fixation of debt/equity contribution of theBank. After determining cost of the project, financing plan shallhave to be worked out realistic basis.

b) Means of financing/ Debt-equity ratio: Contribution from thesponsors in the form of paid up capital, director’s loan etc.form part of the equity. Contribution from the bank is consideredas debt. Debt equity ratio should be set in a manner that thesponsors have reasonable stake in the project. In case of BMREproject, debt equity ratio shall be fixed on incremental cost ofthe project.

c) Working Capital: A portion of working capital remains tied upin the business over the years, called net working capital andrequires funding from long term source. The other portion of

51working capital varies from time to time, generally met fromshort-term sources like commercial bank borrowing and creditors.

While computing working capital requirement, Banks policy andBangladesh Bank’s instruction from time to time to be kept inmind. Following are the generally accepted guideline forcalculation of working capital:

Capacity utilization

a) Existing unit : 5% above the last year’s actualcapacity utilization

b) New unit : 60% of attainable capacity/ratedcapacity

d) Credit investigation and selection of sponsors: The creditinvestigation conducted by a banker seeks to evaluate theentrepreneurial ability, managerial experience, business acumen,integrity, reputation and financial worth of promoters applyingfor Bank’s financial assistance for setting up industries or BMREof a project. The credit investigation of the clients also lookfor their individual liabilities for a realistic assessment oftheir worth.

e) Balance sheet and statement of accounts: The analysis offinancial statements of a concern would provide information onliquidity, activity and profitability position of the concern.The financial soundness of a business can be determined by usingdifferent indicators from the Balance Sheet and Profit and LossAccount which is known as the ratio analysis.

f) Bank’s past experience: In many cases, the applicant may havealready availed loans either for the project or for some otherpurposes from Pubali Bank Limited or from different financialinstitutions. In such cases, the credit inquiry will providevaluable information about their worth, dealings and presentstatus of the liabilities. Credit Investigation Report should beobtained from other Banks as well as from other divisions of thesame bank.

52g) Govt. report publications; There is another documentary sourceof information namely the official gazette, press reportsregarding suits by or against persons and parties insolvency andliquidation of particular individual or enterprise, black listingand/or similar punitive action against individuals, firms etc. bythe Govt./Autonomous bodies etc. which are very valuable.

h) Banking Transaction: Clients carry on normal business,maintain deposits and also avail overdraft facilities. A detailedreview of these accounts will give very valuable informationabout the financial standing of the clients.

i) Report from Trade Circle: More information relating tosponsor’s worth, size of business, turnover, integrity,reputation, honesty, business morality conduct etc. of theclients can be obtained from other traders in the same line. Aclient engaged in a manufacturing business must invariably haveconstant trade links with the wholesale market.

j) Source of equity: It may be necessary to raise cash eitherrising of equity through borrowing on the security of thesponsor’s property or through sale of property. Borrowed fundwill be discouraged, if the borrowed fund thus raised is to bepaid back out of earnings of the new project. The sponsors mayhave several other sources of mobilizing equity e.g., cash inhand, bank deposits, dividend income, marketable securities,internal cash generation of the existing business etc. All thesesources should be thoroughly examined.

3.6.2 Technical Appraisal: Following areas to be looked into during technical appraisal:

a) Product, process and the capacity: Product to be identified,production process to be chalk down and capacity of the projectto be determined.

b) Land and location: Location of the project should be suitablewith all infrastructure facilities. Other relevant issues likeproximity to market, availability of raw materials and worker ,

53environmental issues to be looked into before selecting oflocation.

c) Building: The area and nature of construction should bedetermined as per requirement of the project. The estimatesshould be based on quantitative analysis in respect of variousbuilding materials rather than on a flat rate basis.

d) Machinery and equipment: The cost of machinery, spares etc.constitute the largest component of total cost of the project.All costs related to machinery including duty, tax, insurance,freight, installation etc. should be taken into consideration.The value of machinery and equipment should generally bedetermined on the basis of three competitive genuine pricequotations.

e) Other fixed assets: The project should include furniture,fixture, office equipment etc. as per requirement. Preliminaryexpenses, cost for trial production, interest during constructionperiod should also be included in the cost of project. It shouldbe kept in mind that no item is left out and if there is anyrequirement of contingencies.

f) Pre-operating expenses: Initial costs like survey, plan,drawing, salary allowances of the employees duringimplementation, promotional fee, legal documentation fee,consultant fee, commission and interest during constructionperiod etc. are the part of project cost and to be includedduring preparation of project cost.

g) Requirement of raw materials: Item wise requirement of rawmaterials to be quantified and the price and duty structure to bementioned to arrived at the actual cost of raw materials, sourcesof raw materials whether imported or local to be mentioned.Requirement of packing materials should also be taken care of.

h) Requirement of utilities: Requirement of utilities, source andthe cost thereof are to be attended.

54i) Waste disposal: Wastage of raw materials during processing andhandling are to be determined with utmost care. Impact of wastageduring calculation of raw materials and finished goods needs tobe addressed properly. Necessary arrangement for disposal ofwastage is also to be made.

j) Environmental impact and pollution control: Effect onenvironment and pollution hazards may be taken intoconsideration. Measures must be prescribed regarding negativeeffect on environment. Steps required to control the possiblepollution should be identified and mentioned in the report.

Market Appraisal: Market in a broader sense, is termed as the sum of contractsbetween buyers and sellers of a product or service, the price andquantity exchanged and which are determined by the forces ofdemand and supply. Following areas need to attend in the marketappraisal:

i) Application of product and services, ii) Target market –Local/Export, iii) Demand/Supply analysis Substitute andcompetitors, iv) Proposed marketing/Distribution Arrangements, v)Proposed Buyers vi) Price competitiveness, vii) PromotionalAspects.

3.6.3 Financial Projections and analysis:a) Earning forecast: The earnings forecasts measure cost ofproduction and profitability relating to a particular period or anumber of periods as may be used for the purpose of forecasts. Athree-year period is needed to be seen by the Bank to arrive atan investment decision. The earnings forecast involve theestimation of sales and estimation of associated costs that shallhave to be incurred to achieve the projected sales.

b) Estimation of sales: In estimating sales, the quantity to besold is to be determined first and then the selling price to beapplied to estimate the sales in monetary terms.

55c) Estimation of cost of sales: Major items of costs should beidentified and highlighted in estimating the total cost of sales.Some cost items such as those relating to raw materials, rent,tax, insurance, water, power, fuel, interest etc. can beestimated at actual with great deal of accuracy. On the otherhand many of the administrative and sales expenses can beestimated only with rough approximation.

d) Cash flow: One of the major tasks in financial forecasting isto assess the requirement of funds and to find out how thoserequirements can be met. It involves estimation of cost andsources of fund, estimation of income from future operation,liabilities that shall have to be incurred and the proposedinvestment in future assets.

e) Analysis: In case of BMRE loan proposal, the project will haverelevant operating past. The analysis of the past operation of anexisting concern is of great usefulness in predicting, with afair degree of accuracy, the future results of business activityand the future ability of an enterprise to meet its creditobligation. In such cases, the financial statement of the concernfor the past three consecutive years should be reviewed to form acorrect opinion.

f) Ratio analysis: The financial statement of an existing concernor future projections for a proposed investment may be analyzedthrough calculation of a number of financial ratios. Many typesof financial ratios may be calculated and used. But the purposefor which the analysis is made will suggest emphasizing one setof ratios in preference to another.

g) Sensitivity Analysis: Sensitivity analysis provides thepicture of relative changes in overall profitability due tochange in any variable. Usually changes (increase) in materialand other variable cost or changes (decrease) in selling priceare being taken into consideration for making sensitivityanalysis.

h) Break-even analysis: The basic strength of a project lies inits overall profitability. But it is equally important to know

56the point of sales, capacity utilization, level of production orprice to cover the expenses and starts profit earning. The pointof activity at which the project would neither earn profit norincur loss is called Break-even point.

i) Financial Internal Rate of Return (FIRR): Financial rate of return measures the potential earning power of a project considering time value of money covering entire life of the project.

FIRR = Lower discounting rate + (NPV at lower discounting rate/ (NPV at lower discounting rate minus NPV at higher discounting rate) X (Difference between Higher discounting rate minus lower discounting rate))

3.6.4 Managerial Aspect: This is another important aspect of the appraisal. Managerialfeasibility refers to the assessment of ability of managementpersonnel in managing a project efficiently. The followingmanagerial skills should be analyzed:

Technical skill to use knowledge, method and Techniques(acquired from experience, education and training) toperform the job.

Human skill to maintain interpersonal relationship withinor outside the organization.

Conceptual skill to understand the complexities in overallorganization.

3.6.5 Socio-economic Aspect:The observation of this aspect is to see whether the project issocially desirable. How much contribution will be made by theproject to the G. D. P. and how many numbers of employment willbe generated by the project should be ascertained.

57 3.7 Pricing of Loan: Pricing of loan is a great important element in banking business.Because through pricing, bank usually create margin/profit. So itis to be determined carefully. In pricing, four components are tobe calculated prudently otherwise pricing of that loan willcreate a definite loss for the bank. The components are:

i. Interest Expense or Cost of Fund: The interest to be givento the depositor and to central

Banks for borrowing

ii. Administrative Cost

iii. Cost of Capital: Return expected by the investors for theircapital invested in the bank

Iv. Risk Premium

3.8 Approval Process:In order to fully understand Pubali Bank Limited’s proceduresrelating to sanctioning and control of advances a necessary firststep is to examine the Bank’s organization structure.

The organization structure has three levels – Branch, HeadOffice, CRECOM and Executive Committee of the Board (in lieu ofBoard of Directors).

Branch: The first level of organization in Pubali Bank Limited isthe branch. Function of the branch have been split into four maincategories; Advances, Foreign Exchange, General banking, andAccounting & Establishment. The size of the advance functiondepends on the number of borrowers and the size and complexity oftheir accounts.

58The work of the advance department at the branch is to prepareall the detailed schedules in the Credit Line Proposals. Toensure that the security for the advance is perfected and toprovide all information required on the creditworthiness of thecustomer the department also monitors the advances accountsregular basis.

The branch manager or officer-in-charge of advance departmentshould conduct the initial interview with the customer. If theproposal meets Pubali Bank Limited’s lending criteria and iswithin the manager’s discretionary powers, the credit line shouldbe approved by the Manager.

Head Office: The second level of Pubali Bank Limited’sorganization is the Head Office under Managing Director’sdiscretionary power and /or the Credit Committee (CRECOM) formedat Head Office level. The Credit Committee is headed by itsChairman who is at present ex-officio Deputy Managing Director.Other members of the Credit Committee are the departmental headsrelating to credit, credit administration and fund management.Normally Credit Committee is a recommending forum. Credit lineproposals recommended by the Credit Committee are either sanctionunder discretionary power of the Managing Director or anythingbeyond the capacity of the M.D. is sent to the ExecutiveCommittee of the Board for approval.

It is the responsibility of the Credit Committee to review, andapprove or reject all credit line proposals above the branchmanagers’ discretionary powers. Using the powers delegated to itby the Board of Directors, Credit Committee can finally recommendall credit line proposals up to the approved limit of M.D. andExecutive Committee of the Board.

In the Head Office organization structure the reviewingdepartments are known as the Credit Division and LoanAdministration and Monitoring Division .This department’s dealswith all the detailed work of reviewing credit line proposals andcontrolling overdrafts and loans on a continuous basis.

Executive Committee of the Board: