COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: A REVISION

11

ABSTRACT When facing with any process involving financial valuation it is of a crucial importance to find and use the accurate discount rate. CAPM provides us with an accurate and very commonly used solution to solve the pro- blem, but it requires the estimation of the Beta, which is quite difficult, especially when talking about non-quo- ted companies. For many years, text books have suggested to look for a quoted company with a strong simila- rity with the one to be priced in order to use its Beta. Nevertheless, this may bring up an important problem, since both companies could show different leverage, which would also affect to Taxes and Betas. Both academics and practitioners usually use the wildly renowned formulation by Hamada, but we think that this proposal may introduce important biases, insofar as it only takes Corporation Tax into account, and not Personal Income Tax. In this paper we introduce the effect of Personal Income Tax in a simple and original way that can be useful for Financial practice. Keywords: Cost of funds, Levered Beta, Hamada equation, Tax effects. JEL Classification: G31, G32. RESUMEN En el proceso de valoración de empresas y, en general, en cualquier tipo de valoración financiera, es muy importante acertar con el tipo de descuento. El CAPM aporta una solución “elegante” y muy utilizada para resolver el problema, pero se encuentra con la dificultad del cálculo de la Beta, sobre todo en empresas no coti- zadas. Desde hace años, los libros de texto recomiendan buscar empresas cotizadas similares y utilizar sus Betas. Sin embargo, existe una dificultad: las empresas tienen diferente grado de apalancamiento, lo que tam- bién afecta a los impuestos y a la Beta. Académicos y “practitioners” utilizan para resolver este problema la conocida fórmula de Hamada, pero cre- emos que su planteamiento tiene el problema de considerar el impuesto de sociedades, pero no el de la renta de las personas físicas. Nosotros introducimos el impuesto sobre la renta de una manera que creemos que es sencilla y original, lo que puede ser de gran utilidad en la práctica financiera. Palabras claves: Coste de los fondos, Beta apalancada, Fórmula de Hamada, Efecto de los impuestos. Clasificación JEL: G31, G32. Recibido: 31 de enero de 2014 Aceptado: 20 de febrero de 2014 * Departamento de Finanzas de la Universidad de Deusto. Autor de contacto: Javier Santibáñez Grúber ([email protected]) ANÁLISIS FINANCIERO 6 Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani and Miller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller y el CAPM: una propuesta Análisis Financiero, n.º 124. 2014. Págs.: 6-16 Javier Santibáñez*, Leire Alcañiz* y Fernando Gómez-Bezares* Cost of funds on the basis of Modigliani and Miller and CAPM propositions: a revision Coste de los fondos bajo las hipótesis de Modiagliani y Miller y el CAPM: una propuesta

Transcript of COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: A REVISION

ABSTRACTWhen facing with any process involving financial valuation it is of a crucial importance to find and use theaccurate discount rate. CAPM provides us with an accurate and very commonly used solution to solve the pro-blem, but it requires the estimation of the Beta, which is quite difficult, especially when talking about non-quo-ted companies. For many years, text books have suggested to look for a quoted company with a strong simila-rity with the one to be priced in order to use its Beta. Nevertheless, this may bring up an important problem,since both companies could show different leverage, which would also affect to Taxes and Betas.Both academics and practitioners usually use the wildly renowned formulation by Hamada, but we think thatthis proposal may introduce important biases, insofar as it only takes Corporation Tax into account, and notPersonal Income Tax. In this paper we introduce the effect of Personal Income Tax in a simple and originalway that can be useful for Financial practice.

Keywords: Cost of funds, Levered Beta, Hamada equation, Tax effects.JEL Classification: G31, G32.

RESUMENEn el proceso de valoración de empresas y, en general, en cualquier tipo de valoración financiera, es muyimportante acertar con el tipo de descuento. El CAPM aporta una solución “elegante” y muy utilizada pararesolver el problema, pero se encuentra con la dificultad del cálculo de la Beta, sobre todo en empresas no coti-zadas. Desde hace años, los libros de texto recomiendan buscar empresas cotizadas similares y utilizar susBetas. Sin embargo, existe una dificultad: las empresas tienen diferente grado de apalancamiento, lo que tam-bién afecta a los impuestos y a la Beta.Académicos y “practitioners” utilizan para resolver este problema la conocida fórmula de Hamada, pero cre-emos que su planteamiento tiene el problema de considerar el impuesto de sociedades, pero no el de la rentade las personas físicas. Nosotros introducimos el impuesto sobre la renta de una manera que creemos que essencilla y original, lo que puede ser de gran utilidad en la práctica financiera.

Palabras claves: Coste de los fondos, Beta apalancada, Fórmula de Hamada, Efecto de los impuestos.Clasificación JEL: G31, G32.

Recibido: 31 de enero de 2014 Aceptado: 20 de febrero de 2014

* Departamento de Finanzas de la Universidad de Deusto. Autor de contacto: Javier Santibáñez Grúber ([email protected])

ANÁLISIS FINANCIERO6

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

Javier Santibáñez*, Leire Alcañiz*y Fernando Gómez-Bezares*

Cost of funds on the basis ofModigliani and Miller and CAPMpropositions: a revisionCoste de los fondos bajo las hipótesisde Modiagliani y Miller y el CAPM: una propuesta

1. INTRODUCTION

When trying to value a company on a cash-flow dis-count basis, it is of a crucial importance to estimate,among other variables, the appropriate discount rate.Assuming the conclusions of the Capital Asset PricingModel (CAPM; Sharpe, 1970), the required return forany investment should depend on its systematic risk,which requires the estimation of the “beta” of the com-pany, usually on the basis of a regression processbetween historical profitability of the studied companyand the one provided by the market as a whole. Howev-er, an additional problem that we usually have to copewith is that not many companies are quoted in the mar-ket, so the process becomes a tough one when trying tocalculate the beta of a non-quoted company. In thosecases, professionals usually try to estimate the beta ofthe company to be priced on the basis of a similar one(this is known as levered Beta calculation); and it isvery common to use the Hamada (1969) formulation,which implicitly assumes that we have to take the effectof Corporation Tax into account.

Nevertheless, Miller (1977) made it clear that it is notonly the Corporation Tax the one to be taken intoaccount, but the Personal Income Tax as well, insofar asif the Tax System as a whole was properly designed(which means that the advantage for leverage in Corpo-ration Tax should be eliminated in the Personal IncomeTax, by treating better income coming from dividendsthan those coming from interest), no advantage wouldbe reached by levering a company (which would take usback to Modigliani and Miller, 1958). While it is a verycomplex problem, as it is difficult to estimate accurate-ly the Tax burden for dividends or interest in the Per-sonal Income Tax1, and even the real Corporation Taxrate that the companies are bearing (because of theeffect of partial exemptions, etc.), we have to be awareof the distortion that we are introducing in the processwhen taking only Corporation Tax (Modigliani andMiller, 1963) into account.

In this paper we will propose an alternative formulationto Hamada (1969) for the estimation of levered betas, inwhich Personal Income Tax is also taken into account

(based on both Modigliani and Miller and CAPMpropositions), which can be seen as a generalization ofthe Hamada one (that would remain as a particular caseof the one that we pose)2.

2. GENERAL FORMULATION

Weighted Average Cost of Capital (WACC) is common-ly calculated as follows:

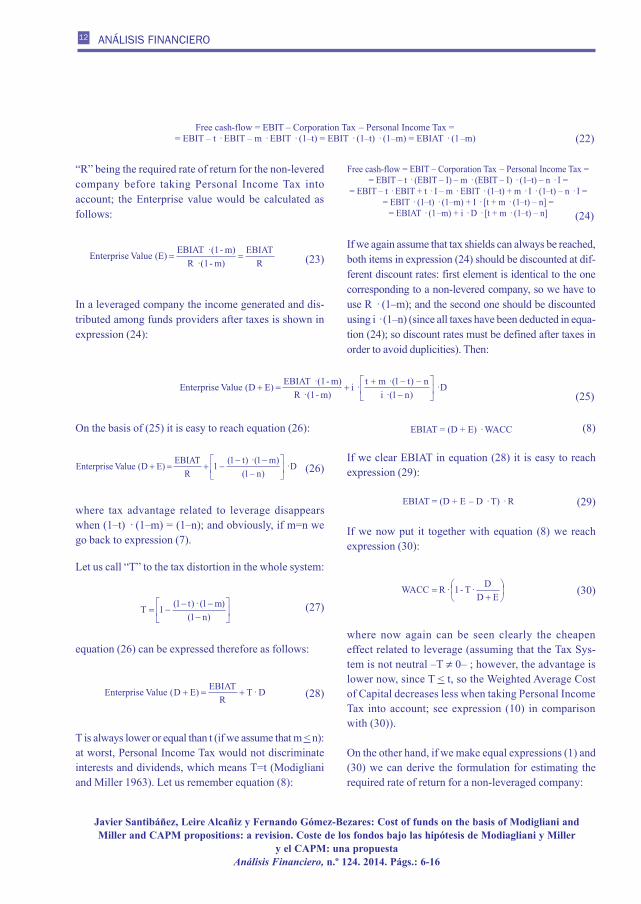

(1)

where:

i Required rate of return for Debtki Net cost of Debtke Cost of EquityWACC Weighted Average Cost of Capitalt Tax rate (Corporation Tax)D Debt (Market value)E Equity (Market value)

Let us assume stable conditions, no growth and that thecompany invests only the necessary amount to maintainthe current value of assets (replacement investment, equalto depreciation, so as to keep constant its cash-flow gener-ation capability); if we do so, the Market value of the firm(understood as Market value of assets) should be calculat-ed as follows (present value of a perpetuity):

(2)

whereas in addition to the previously defined nomen-clature, EBIAT is Earnings Before Interest and AfterTaxes, that is to say, generated profits by assets to paythe whole providers of funds; under the described con-ditions, it should be equal to total payments for financ-ing. In addition:

(3)

COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: ... 7

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

where S is net sales, C is disbursement operating costs,AM is depreciation and amortization (of tangible andintangible fixed assets), and EBIT is Earnings BeforeInterest and Taxes.

3. MODIGLIANI AND MILLER PROPOSITIONS(1958 and 1963)

In their wildly renowned paper of 1958, Modigliani andMiller proposed that the Financial Structure does nothave any impact on the Weighted Average Cost of Cap-ital (and therefore, neither on the value of the firm). The

line of reasoning is quite simple: the capital funds

providers of the company as a whole would ask for a

return depending on the risk of the assets; so if we

assume the assets remain the same, no change should be

expected on the required rate of return for financing

them, even if we use different proportions of Debt and

Equity. In other words, in competitive and efficient

Markets two identical assets could not be priced differ-

ently (that is what would happen if different Financial

Structures for the same assets had different costs).

Modigliani and Miller proposal can be summed up in

figure 1.

ANÁLISIS FINANCIERO8

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

Nevertheless, Corporation Tax changes it all, since itbrings about a distortion due to the different treatment ofinterests and dividends. In fact, interests are deductible(provoking tax savings) from the Tax base, while divi-dends are not; therefore, all the rest remaining the same, ifit is true that under perfect Market conditions the FinancialStructure would be irrelevant, the imperfection mentionedabove would cause an interest for leverage.

The effect of the Corporation Tax advantage can be eas-ily shown. If we assume a non leveraged company (ful-ly Equity financed), the free cash-flow (that under the

formerly proposed conditions could be used for payingdividends) can be expressed as follows:

(4)

whose present value should be calculated using a dis-count rate considering the Assets risk (R). This way, theEnterprise value (that in a non-leveraged companywould be both Assets value and Equity value) should beestimated as follows:

(5)

If we now consider the possibility for the company to bor-row money, the free cash-flow to be distributed amongthe funds providers after Corporation Tax would be:

(6)

where I refers to the Interests to be paid on the Debt (so itis calculated by multiplying the interest rate by the totalamount of Debt), and as can be seen, we face a new situ-ation insofar as there is an additional item in the formulawhich is related to the savings that the interest paymentcauses in the Corporation Tax; if we assume both that thisTax shield can always be accomplished and that lendersdo not assume any risk, this part of the income should bediscounted at the Risk-free rate, and so:

(7)

It can be seen that the Enterprise value can be obtainedby adding to the non-leveraged one a term that growswith Debt (the formerly mentioned Tax shield), so thereis an interest for the company to increase leverage to itsmaximum.

An important consequence of the former is that now theWeighted Average Cost of Capital is no longer independ-ent from the leverage, but decreases as Debt rises. In fact,on the basis of expression (2) we can reach equation (8):

(8)

And if we now take equation (7) into account it is easyto see that:

(9)

So if we now equalize expressions (8) and (9) wereach (10):

(10)

where the cost reduction effect related to leverageappears very clearly. In addition, a different formula forestimating the cost of Equity can be raised on the basisof the former; so, if we make equal expressions (1) and(10) we have equation (11):

(11)

4. CAPM

CAPM (Capital Asset Pricing Model) is built on thebasis of Markowitz Model hypothesis, and sets out afundamental relationship between a given asset and therequired rate of return to finance it. The model high-lights the fact that the total risk of any asset can be splitup into Systematic risk and Diversifiable (Non-system-atic) risk. Systematic risk is due to the Market, that is tosay, it is given by the fact that any asset is in some wayrelated to the general economic course, and because ofthat, it has a certain amount of non Diversifiable risk;Non-systematic is the specific risk of the investment(the portion of risk that the Market is unable to explain),so it can be avoided with a proper diversification. If thisis the case and we assume risk-averse individuals,nobody would take avoidable risks, so we all wouldeliminate Diversifiable risks and only Systematic riskwould remain.

The classical measure for Systematic risk is Beta, whichcan be calculated as follows:

COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: ... 9

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

(12)

where COV (Rj , Rm) is the Covariance between thestudied asset and Market returns; and VAR (Rm) is theVariance of the Market returns.

The model poses a positive linear relationship betweenthe required return on any investment and its relevantrisk (measured with Beta), that can be summarized inthe following expression (Security Market Line, SML;the model requires adjustment to the purposed line toany asset correctly valued):

(13)

where E (Rj) is the expected return on the asset, Rf is theRisk-free rate and the Premium is the differencebetween the expected return for the Market and theRisk-free rate.

Under CAPM conditions, all Assets, Equity and Debtshould perfectly adjust to equation (13), so:

(14)(15)(16)

where βa, βi and βe are the Systematic risk measures forthe Assets (assuming non-leveraged company), forDebt and for Equity.

5. INTRODUCING CAPM INTO THE MODIGLIANIAND MILLER PROPOSALS (1958 and 1963)

Combining CAPM and Modigliani and Miller proposi-tions takes us to the classical formulas commonly used

for estimating a company Beta on the basis of observedBetas in the Market. Again, the idea is quite simple: itwould be very difficult to estimate Equity Beta in a non-quoted company, since we have no historical data aboutits returns, so Covariance with the Market would remainunknown3; but in some cases, it could be derived fromthe Beta of a quoted company.

This proposal poses one important problem: even if theactivity of both companies were the same, leveragecould be totally different, so we have to face an adjust-ing process in which first of all, Beta of the observedcompany assets must be inferred from its Equity one(taking both leverage and Beta of Debt into account);and in a second step, Equity Beta of the studied compa-ny would be estimated (again, taking its leverage andthe Beta of Debt into account). This process is com-monly known as “levered Beta calculation”.

Formulation to be used is quite simple to derive. Let usremember that when equaling expressions (1) and (10)(that is to say we accept Modigliani and Miller –1963–propositions) we have:

Clearing R we reach expression (17):

(17)

If we now take into account CAPM (expressions 15 and16), equation (17) becomes the following:

ANÁLISIS FINANCIERO10

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

We then only have to clear Beta of Equity in expression(19), as can be seen in equation (20):

(20)

A particular case of the former happens if we assume fullyguaranteed Debt (no risk taken by Debt providers; whichmeans to assume Beta of Debt equal to zero): it is the for-mula of Hamada (1969) for estimating Beta of Equity:

(21)

NOTE: the whole formulation is applicable for the orig-inal proposal by Modigliani and Miller (1958; we onlyhave to assume Tax Corporate rate equal to zero).

6. THE EFFECT OF PERSONAL INCOME TAX(MILLER, 1977)

In the work of 1963, Modigliani and Miller assume thatthere is only Corporation Tax, which introduces a distor-

tion, insofar as Debt and Equity are not treated the same.However in 1977, Miller points out that if the Tax Sys-tem as a whole was properly designed, it should notinterfere with the financial decisions of the companies;to put it another way, the function of the Tax System isnot to provide companies with the proper FinancialStructure, but to drain money from the Economic Sys-tem in order to redistribute wealth, accomplish publicinvestments, etc. If so, and if we assume no other Mar-ket imperfections, we would go back to the original pro-posal: Financial Structure is not relevant in order to putvalue on the company (the Financial Objective of thefirm), since the advantage of Debt in Corporation Taxdisappears when considering the Tax System as awhole.

Let us revise the previous formulation, taking now intoaccount that the Personal Income Tax treats differentlyDebt income and Equity income (interests and divi-dends)4. Be “m” the Tax rate for dividends in PersonalIncome Tax, and “n” the one for interests (assumingthat, obviously, m < n).

Let us now first consider a non-leveraged company. Thegenerated income to be distributed among fundsproviders can be seen in equation (22):

Let us compare expression (18) with equation (14), thatindicates the required rate of return on assets in a non-leveraged company under CAPM conditions; it is easy

to derive equation (19) in order to estimate Beta ofassets (assumed that both Beta of Equity and Debt andthe leverage of the observed company are all known):

COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: ... 11

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

(18)

(19)

“R” being the required rate of return for the non-leveredcompany before taking Personal Income Tax intoaccount; the Enterprise value would be calculated asfollows:

(23)

In a leveraged company the income generated and dis-tributed among funds providers after taxes is shown inexpression (24):

If we again assume that tax shields can always be reached,both items in expression (24) should be discounted at dif-ferent discount rates: first element is identical to the onecorresponding to a non-levered company, so we have touse R · (1–m); and the second one should be discountedusing i · (1–n) (since all taxes have been deducted in equa-tion (24); so discount rates must be defined after taxes inorder to avoid duplicities). Then:

ANÁLISIS FINANCIERO12

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

(22)

(24)

(25)

On the basis of (25) it is easy to reach equation (26):

(26)

where tax advantage related to leverage disappearswhen (1–t) · (1–m) = (1–n); and obviously, if m=n wego back to expression (7).

Let us call “T” to the tax distortion in the whole system:

(27)

equation (26) can be expressed therefore as follows:

(28)

T is always lower or equal than t (if we assume that m < n):at worst, Personal Income Tax would not discriminateinterests and dividends, which means T=t (Modiglianiand Miller 1963). Let us remember equation (8):

(8)

If we clear EBIAT in equation (28) it is easy to reachexpression (29):

(29)

If we now put it together with equation (8) we reachexpression (30):

(30)

where now again can be seen clearly the cheapeneffect related to leverage (assuming that the Tax Sys-tem is not neutral –T ≠ 0– ; however, the advantage islower now, since T < t, so the Weighted Average Costof Capital decreases less when taking Personal IncomeTax into account; see expression (10) in comparisonwith (30)).

On the other hand, if we make equal expressions (1) and(30) we can derive the formulation for estimating therequired rate of return for a non-leveraged company:

(31)

Nevertheless, expression (31) is not a logical one, sincethe weights for both cost of Debt and Equity should addup to one (as happens under Modigliani and Millerpropositions when taking only Corporation Tax intoaccount; see expression (17)). This leads us to bringabout a correction in expression (1) that seems to be rea-sonable. Let us remember equation (1) that has beenused both in a world without taxes, and in a single Cor-poration Tax context:

(1)

where “t” is the Corporation Tax rate (that would be zeroin a world without taxes). Under Miller (1977) conditionsit must be said that if the Tax System as a whole was prop-erly designed, dividend collectors should have an advan-tage over interest ones in Personal Income Tax (that is tosay, m<n); and this different treatment would lead lendersto ask for a higher profitability than what they wouldexpect if the aforementioned difference did not happen.

To make it clearer, let us think about a non-leveragedcompany fully owned by a sole investor. Only by shift-ing Equity for Debt he or she could collect part of theprofitability in the form of interests, which aredeductible from the Corporation Tax Base; so the high-er the leverage, the lower the Corporation Tax to bepaid, and the higher the money collected by that soleowner. But if Debt incomes are treated worse in Person-al Income Tax, the advantage reached in CorporationTax would decrease, and it could disappear if the systemas a whole was properly designed (that is to say, T=0).This way, the tax correction should be given by a taxshield considering the system as a whole (so we mightuse (1–T) instead of (1–t)). Expression (1) can be thenrewritten as follows:

(32)5

Let us deepen on what the former means. Rememberthat T was defined as the measure of the imperfectionrelated to the Tax System as a whole (considering bothCorporation and Personal Income Taxes):

(27)

so:

The former implies that requirement of Debt Providerschanges:

(33)

In other words, the proposed formulation might beseen as a correction to the one we use when only Cor-poration Tax exists, insofar as the tax shield achievedin Corporation Tax could be minored by the PersonalIncome Tax effect (since the item (1–m)/(1–n) shouldlogically be higher than 1 and the decrease of Debtcost is lower; and if we assume m=n we would go backto 1963 Modigliani and Miller case).

Under the proposed conditions, we can equal expres-sions (32) and (30):

(34)

Equation (34) seems to be more reasonable; and we canalso clear the cost of Equity in this proposal, coherentwith Miller (1977):

(35)

COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: ... 13

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

7. INTRODUCTION OF THE CAPM INTO THE MILLER(1977) PROPOSAL

Introducing CAPM into the Miller proposal is againquite simple. As we said earlier, CAPM poses the fol-lowing formulation in order to estimate the required rateof return on Assets, Debt and Equity:

(14)(15)(16)

Let us remember as well equation (34):

(34)

If we now substitute expressions (15) and (16) in equa-tion (34), the required rate of return on the assets in anon-leveraged company would be as follows:

ANÁLISIS FINANCIERO14

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

(36)

(37)

If we now compare expressions (36) and (14) we canderive equation (37), under the assumption that bothBeta of Equity and Beta of Debt, as well as leverage (alldata referred to the observed company) are known:

where the Beta of Equity for the studied company canbe cleared:

(38)

If we assume that Debt is fully guaranteed (Beta of Debtequal to zero), then we have the Hamada formulation

adapted to Miller (1977) propositions, which we callSGHAMM formula (2014).

(39)

NOTE: Observe that all formulation proposed is validfor 1958 Modigliani and Miller propositions (T=0) andalso for 1963 proposal (by substituting T for t).

8. CONCLUSIONS

Formulation most frequently used by practitioners toestimate the appropriate rate of return to be used in theassessment of assets or stocks is based on CAPM andModigliani and Miller (1963) propositions, taking onlythe effect of Corporation Tax into account (Hamada,1969). Insofar as it is also very usual that dividends andinterests are not equally treated in the Personal IncomeTax (in order to eliminate the advantage that Debt has inCorporation Tax; Miller, 1977), the aforementioned for-mulation introduces a distortion in the results to bereached.

In this paper we have developed, on the basis of bothCAPM (Sharpe, 1970) and Modigliani and Millerpropositions (Modigliani and Miller, 1958 and 1963;and Miller, 1977), an alternative formulation whichtakes the effect of both Taxes (Corporation and Person-al Income Tax) into account, and allows to overcome thedistortion mentioned before.

9. BIBLIOGRAPHY

BREALEY, R.A., S.C. MYERS and F. ALLEN (2007): Princi-ples or corporate finance, McGraw–Hill, New York, 9th ed.

GÓMEZ-BEZARES, F. (2014): Dirección financiera, Descléede Brouwer, Bilbao, 5th ed.

GÓMEZ-BEZARES, F. (2012): Elementos de finanzas corpo-rativas, Desclée de Brouwer, Bilbao.

HAMADA, R.S. (1969): “Portfolio analysis, market equilibri-um and corporation finance”, Journal of Finance, March,pp. 13-31.

MILLER, M.H. (1977): “Debt and Taxes”, Journal of finance,32, May, pp. 266–268.

MODIGLIANI, F. and M.H. MILLER (1958): “The cost ofcapital, corporation finance and the theory of invest-ment”, American economic review, 48, June, pp.261–297.

MODIGLIANI, F. and M.H. MILLER (1963): “Corporateincome taxes and the cost of capital: Acorrection”, Amer-ican economic review, 53, June, pp. 433–443.

SHARPE, W.F. (1970): Portfolio theory and capital markets,McGraw–Hill, New York.

APPENDIX

Let us deepen in an alternative way to reach the logic of expres-sion (39). Be “q” the required return (before Personal IncomeTax) for a stock with identical risk (after Taxes) than Debt. Itshould happen that:

(A.1)

so:

(A.2)

Let us remember that:

(A.3)

so:

(A.4)

If we now make equal (1) and (30) we have:

(A.5)

(A.6)

Taking (A.4) into account:

(A.7)

(A.8)

which takes us directly to the logic of (34).

Taking now the CAPM into account, and following the sameprocess than before (from (14) to (39)):

(A.9)(A.10)(A.11)

Substituting (A.10) and (A.11) in (A.8):

COST OF FUNDS ON THE BASIS OF MODIGLIANI AND MILLER AND CAPM PROPOSITIONS: ... 15

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

Taking now (A.9) into account:

ANÁLISIS FINANCIERO16

Javier Santibáñez, Leire Alcañiz y Fernando Gómez-Bezares: Cost of funds on the basis of Modigliani andMiller and CAPM propositions: a revision. Coste de los fondos bajo las hipótesis de Modiagliani y Miller

y el CAPM: una propuestaAnálisis Financiero, n.º 124. 2014. Págs.: 6-16

(A.12)

(A.13)

(A.14)

where the Beta of Equity for the studied company can becleared:

(A.15)

(A.16)

If we assume that Debt (or the proposed stock for which return“q” is required) is fully guaranteed (Beta of Debt equal to zero),we reach again (39):

(A.17)

Notes

1.- And even more in the Corporation Tax, when it is a companythe owner of stock or debt (with different rates depending onthe kind of company). Not to talk about the additional pro-blems that arise when facing with international ownership.

2.- Deeper explanations and formulation of both Modigliani

and Miller propositions and Capital Asset Pricing Model(CAPM) can be found in Gómez-Bezares (2014), chapters5 and 7. Gómez-Bezares (2012) and Brealey, Myers andAllen (2007) may be consulted as well for some particularissues. Formulation related to the inclusion of CAPM inMiller’s proposal (1977) can be seen as original.

3.- Accounting data could be used, but this approach showsimportant theoretical problems.

4.- This was the way the Tax System worked in Spain since1995 to 2007. The changes introduced in Personal IncomeTax in 2007 took us back to a more coherent situation withModigliani and Miller (1963), insofar as interests and divi-dends are since then equally treated (Tax rate of 21%nowadays). Anyway, when trying to measure the impact ofthe distortion, we face a more complicated problem, if wealso take into account that there is an exemption in Perso-nal Income Tax for the first 1.500 euros collected as divi-dends, and that taxation for dividends collected by compa-nies or Mutual Funds has a different treatment.

5.- In this context, “i” should be understood as the requiredreturn for Debt assuming m=n=0; or, in general, if no dis-crimination was made in the Personal Income Tax (that isto say, (1 – m) = (1 – n)). This will be treated in more depthin the Appendix.