![Dr T Malakoutian.ppt [Compatibility Mode]](https://static.fdokumen.com/doc/165x107/63364bfed2b7284203084459/dr-t-malakoutianppt-compatibility-mode.jpg)

Cost of Capital [Compatibility Mode

12

15/02/13 1 3-0 3-1 1. Understand the methods used to estimate a firm’s cost of equity capital 2. Know how to determine a firm’s cost of debt 3. Know how to determine a firm’s overall cost of capital (the weighted average cost of capital or WACC) 4. Divisional and Project costs of capital 5. Flotation costs and the WACC Why cost of capital is important Calculate cost of equity Calculate weighted average cost of capital ( WACC) Divisional and Project Costs of Capital 3-2

Transcript of Cost of Capital [Compatibility Mode

15/02/13

1

3-0

3-1

1. Understand the methods used to estimate a firm’s cost of equity capital

2. Know how to determine a firm’s cost of debt

3. Know how to determine a firm’s overall cost of capital (the weighted average cost of capital or WACC)

4. Divisional and Project costs of capital5. Flotation costs and the WACC

ûWhy cost of capital is importantûCalculate cost of equityûCalculate weighted average cost of capital (

WACC)û Divisional and Project Costs of Capital

3-2

15/02/13

2

3-3

ûWe know that the return earned on assets depends on the risk of those assets

û The return to an investor is the same as the cost to the company

ûOur cost of capital provides us with an indication of how the market views the risk of our assets

ûKnowing our cost of capital can also help us determine our required return for capital budgeting projects

3-4

û The required return is the same as the appropriate discount rate. It is based on the risk of the cash flows

ûWe need to know the required return for an investment before we can compute the NPV and make a decision about whether or not to take the investment

ûWe need to earn at least the required return to compensate our investors for the financing they have provided

3-5

û The cost of equity is the return required by equity investors given the risk of the cash flows from the firm. Risk includes both ¡ Business risk, and¡ Financial risk

û There are two major methods for determining the cost of equity¡ Dividend growth model¡ Capital Asset Pricing Model (CAPM)

15/02/13

3

3-6

ûStart with the DGM formula (from HBCO408 Financial Management) and re-arrange to solve for RE

gPDR

gRDP

E

E

+=

−=

0

1

10

Remember that D1 = D0(1+g)

3-7

ûSuppose that a company is expected to pay a dividend of $1.58 per share next year. ûThe company has experienced a steady

growth in dividends of 5% per year over recent years and the market expects this to continue. ûThe company’s current share price is $25. ûWhat is the estimated cost of equity?

%3.11113.05.2558.1

==+=ER

3-8

ûOne method for estimating the growth rate is to use the historical average, for example:Year Dividend Percent Change2006 1.23 -2007 1.302008 1.362009 1.432010 1.50

(1.30 – 1.23) / 1.23 = 5.7%(1.36 – 1.30) / 1.30 = 4.6%(1.43 – 1.36) / 1.36 = 5.1%(1.50 – 1.43) / 1.43 = 4.9%

Average = (5.7 + 4.6 + 5.1 + 4.9) / 4 = 5.1%

Alternative: use geometric average

15/02/13

4

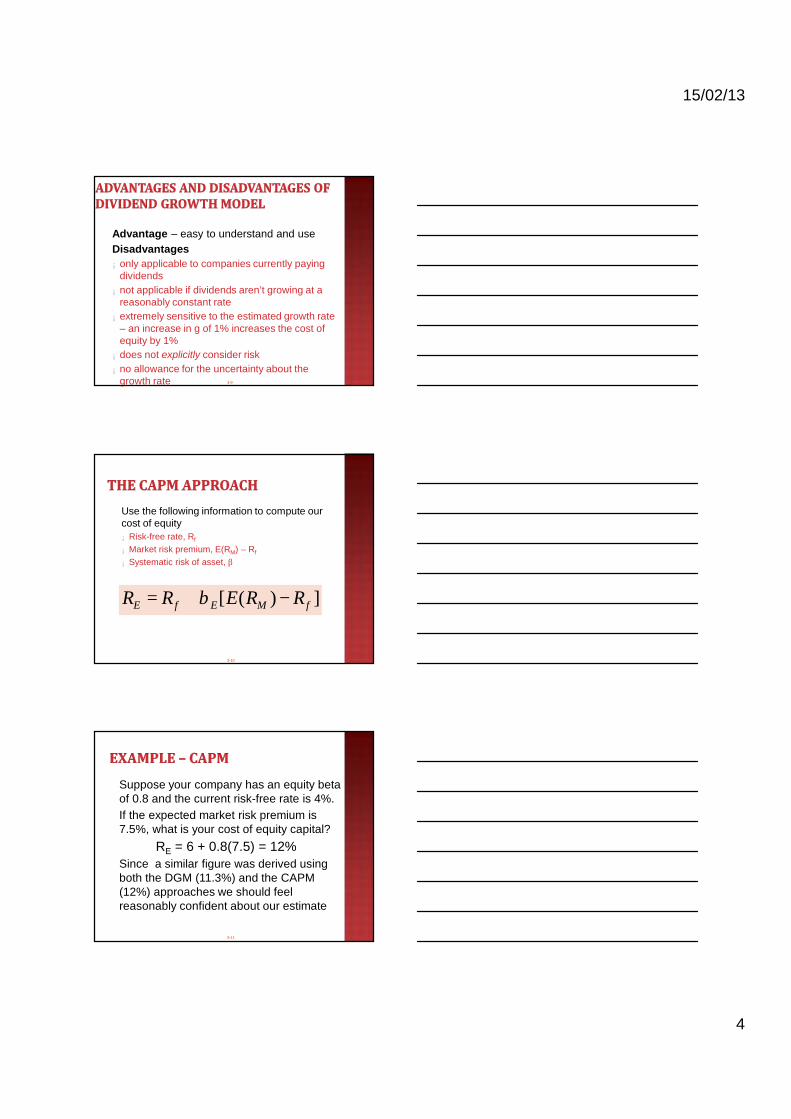

3-9

ûAdvantage – easy to understand and useûDisadvantages¡ only applicable to companies currently paying

dividends¡ not applicable if dividends aren’t growing at a

reasonably constant rate¡ extremely sensitive to the estimated growth rate

– an increase in g of 1% increases the cost of equity by 1%¡ does not explicitly consider risk¡ no allowance for the uncertainty about the

growth rate

3-10

ûUse the following information to compute our cost of equity¡ Risk-free rate, Rf

¡ Market risk premium, E(RM) – Rf

¡ Systematic risk of asset, β

])([ fMEfE RRERR −+= β

3-11

ûSuppose your company has an equity beta of 0.8 and the current risk-free rate is 4%.ûIf the expected market risk premium is

7.5%, what is your cost of equity capital?RE = 6 + 0.8(7.5) = 12%

ûSince a similar figure was derived using both the DGM (11.3%) and the CAPM (12%) approaches we should feel reasonably confident about our estimate

15/02/13

5

3-12

ûAdvantages¡ Explicitly adjusts for systematic (beta) risk ¡ Applicable to all companies, as long as we can

estimate betaûDisadvantages¡ Have to estimate the expected market risk premium

which varies over time¡ Have to estimate beta which also varies over time¡ We are using the past to predict the future, which is not

always reliable

3-13

ûSuppose our company has a beta of 1.5. The market risk premium is expected to be 7% and the current risk-free rate is 6%.

ûAnalysts’ estimates indicate that our dividends will grow at 5% per year and our last dividend was $2.

ûOur stock is currently selling for $18 ûWhat is our cost of equity?¡ Using SML: RE = ¡ Using DGM: RE =

3-14

û The cost of debt is the required return on our company’s debt

ûWhere there are active bond markets the focus is on the cost of long-term debt or bonds.

û (Where the bond market is under-developed the focus is on medium to long term bank loans).

û The required return is best estimated by computing the yield-to-maturity on existing debt

ûWe may also use estimates of current interest rates based on the bond rating we expect when we issue new debt

û The cost of debt is NOT the coupon rate !!

15/02/13

6

3-15

ûSuppose a company has a bond issue currently outstanding that has 8 years left to maturity. ûThe coupon rate is 9% with interest paid

semiannually. The bonds current trade at $945.80 per $1000 (face value) bond or 94.58%ûWhat is the cost of debt?

3-16

ûReminders¡ Preferred stock generally pays a constant dividend

each period¡ Dividends are expected to be paid every period

foreverûPreferred stock is a perpetuity, so we take the

perpetuity formula (P = CF/r), rearrange and solve for RP

û In this case, RP (cost of preferred stock) is:ûRP = D / P0

3-17

ûA company has preferred stock that has an annual dividend (D) of $3.

û If the current price of preferred stock is $25, what is the cost (required return) of preferred stock?

ûRP = $3 / $25 = 12%ûThis is the current market required rate of

return on preferred stock issued by the company (its opportunity cost)

15/02/13

7

3-18

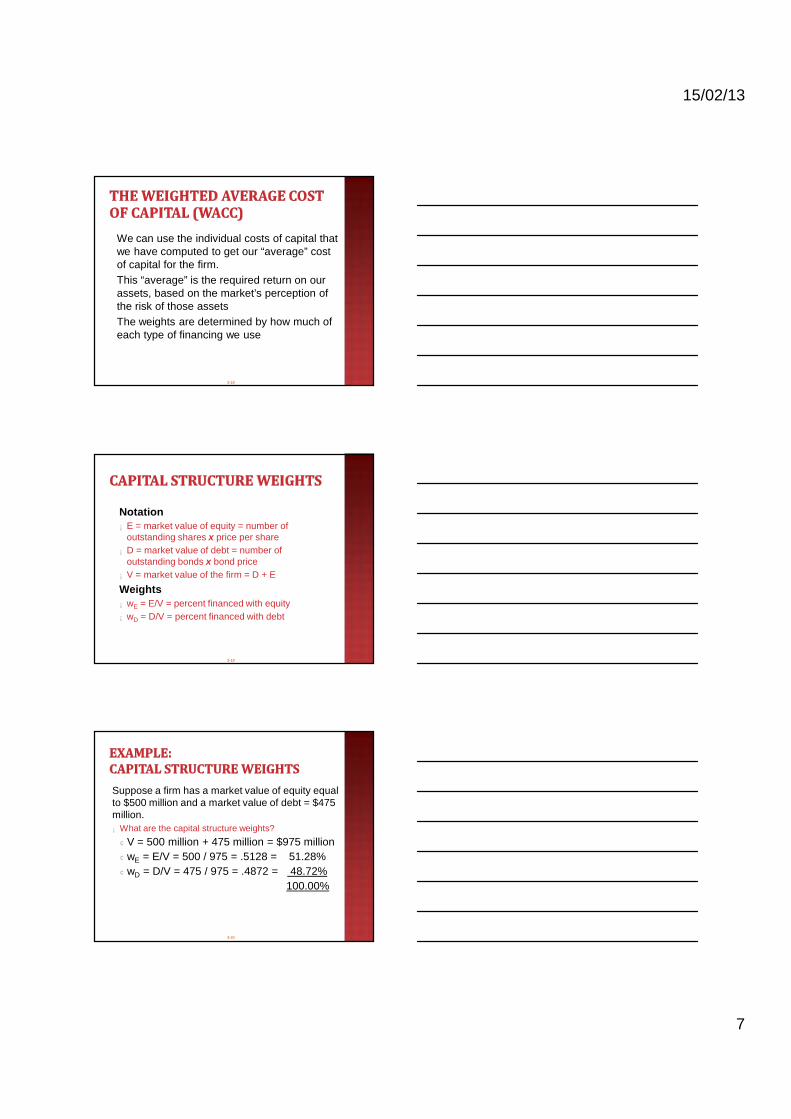

ûWe can use the individual costs of capital that we have computed to get our “average” cost of capital for the firm.

ûThis “average” is the required return on our assets, based on the market’s perception of the risk of those assets

ûThe weights are determined by how much of each type of financing we use

3-19

ûNotation¡ E = market value of equity = number of

outstanding shares x price per share¡ D = market value of debt = number of

outstanding bonds x bond price¡ V = market value of the firm = D + E

ûWeights¡ wE = E/V = percent financed with equity¡ wD = D/V = percent financed with debt

3-20

ûSuppose a firm has a market value of equity equal to $500 million and a market value of debt = $475 million.¡ What are the capital structure weights?¢V = 500 million + 475 million = $975 million¢wE = E/V = 500 / 975 = .5128 = 51.28%¢wD = D/V = 475 / 975 = .4872 = 48.72%

100.00%

15/02/13

8

3-21

ûWe are concerned with after-tax cash flows, so we need to consider the effect of taxes on the various costs of capital

û Interest expense reduces our tax liability¡ this reduction in taxes reduces our cost of debt¡ after-tax cost of debt = RD(1-TC)

ûDividends are not tax deductible, so there is no tax impact on the cost of equity

ûWACC = wERE + wDRD(1-TC)

3-22

ûEquity Information¡ 5 million shares¡ $80 per share¡ Beta = 1.15¡Market risk premium =

7%¡ Risk-free rate = 6%

ûDebt Information¡ $200 million in

outstanding debt (face value)¡ Current quote = 110¡ Coupon rate = 9%,

semiannual coupons¡ 15 years to maturity

ûTax rate = 30%

3-23

ûWhat is the cost of equity?

ûWhat is the cost of debt?

ûWhat is the after-tax cost of debt?

15/02/13

9

3-24

ûWhat are the capital structure weights?

ûWhat is the WACC?

3-25

û Using the WACC as our discount rate is only appropriate for projects that have the same risk as the firm’s current operations

û If we are looking at a project that does NOT have the same risk as the firm, then we need to determine the appropriate discount rate for that project

û Divisions of a firm often require separate discount rates so an overall company WACC may not be very useful for companies that have several divisions with operations facing different levels of risk

3-26

ûAssume a firm’s overall WACC = 15%ûAssume further that the firm is evaluating the

following three projects (these may be in separate divisions)

Risk AdjustedProject Required Return IRR

A 20% 17%B 15% 18%C 10% 12%

15/02/13

10

3-27

ûWhat would happen if we use the WACC for all projects regardless of risk?

ûAssume the firm’s overall WACC = 15%Risk Adjusted

Project Required Return IRRA 20% 17% ACCEPTB 15% 18% ACCEPTC 10% 12% REJECT

û The accept/reject decision is based on WACC

3-28

û In this case the firm should:¡ Reject Project A because:¢ Its required return exceeds its IRR therefore its NPV must be

negative (even though IRR > overall WACC)¡ Accept Project B because:¢ It promises an IRR of 17% which exceeds its required return

of 15% (which is also equal to WACC) ¡ Accept Project C because:¢ It promises an IRR of 12% which exceeds its required return

of 10% (even though its IRR is less than WACC)û If the company uses WACC as the cutoff for all

projects then it will become riskier and its cost of capital will increase

3-29

û Find one or more companies that specialize in the product or service that we are considering

û Compute the beta for each companyû Calculate an average beta*û *Technically we need to unlever the beta for each

company before computing the average and, once the average of the unlevered beta has been found, we then relever to match the capital structure of the firm.

û Use that average beta along with the CAPM to find the appropriate return for a project of that level of risk

û Problem - often difficult to find pure play companies

15/02/13

11

3-30

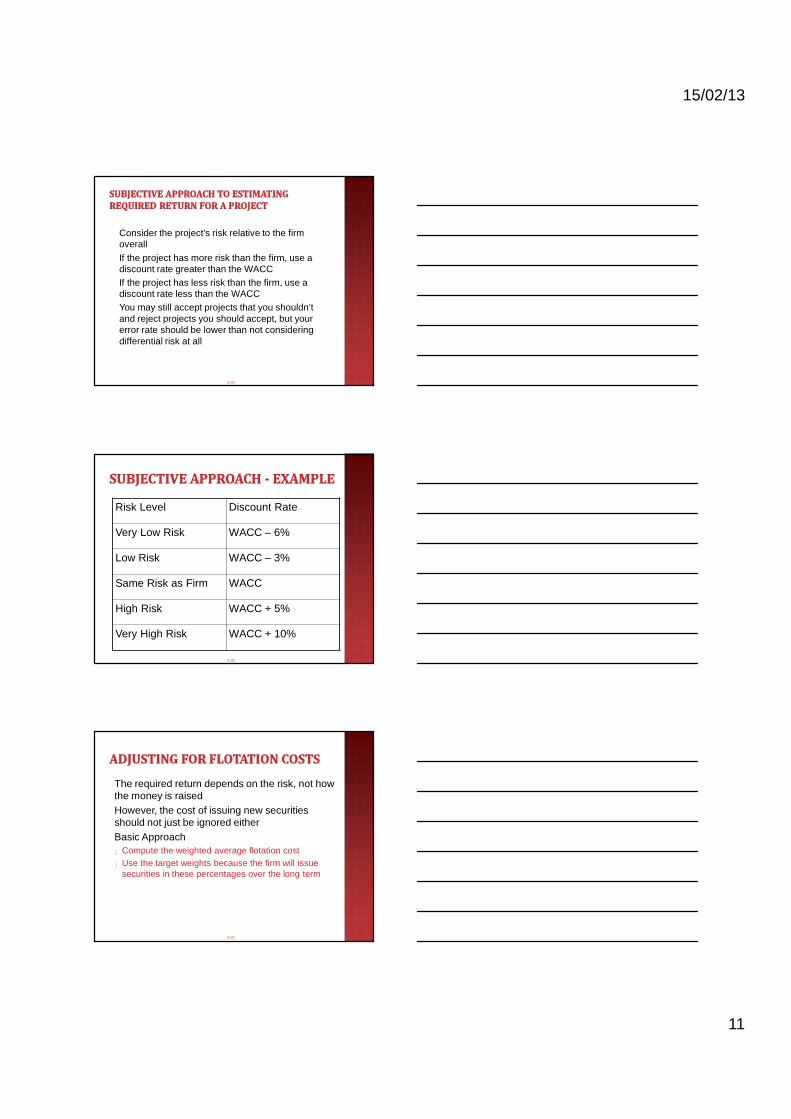

û Consider the project’s risk relative to the firm overall

û If the project has more risk than the firm, use a discount rate greater than the WACC

û If the project has less risk than the firm, use a discount rate less than the WACC

û You may still accept projects that you shouldn’t and reject projects you should accept, but your error rate should be lower than not considering differential risk at all

3-31

Risk Level Discount Rate

Very Low Risk WACC – 6%

Low Risk WACC – 3%

Same Risk as Firm WACC

High Risk WACC + 5%

Very High Risk WACC + 10%

3-32

û The required return depends on the risk, not how the money is raised

ûHowever, the cost of issuing new securities should not just be ignored either

ûBasic Approach¡ Compute the weighted average flotation cost¡ Use the target weights because the firm will issue

securities in these percentages over the long term

15/02/13

12

3-33

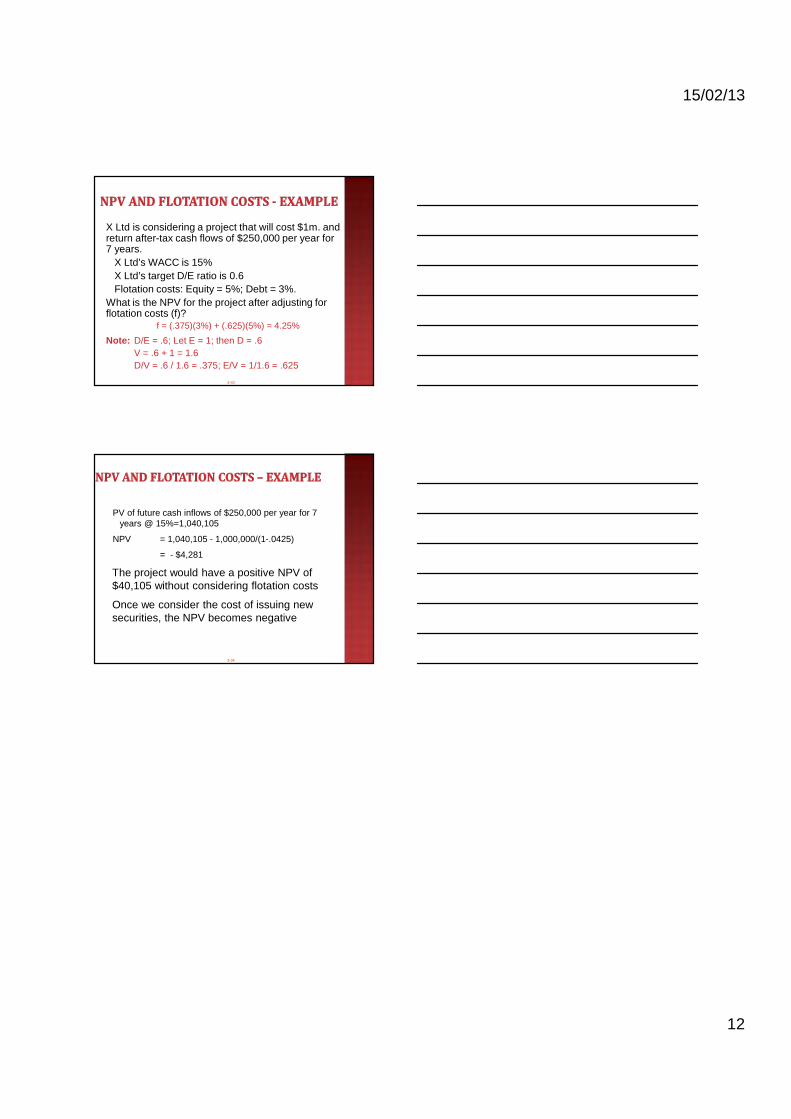

X Ltd is considering a project that will cost $1m. and return after-tax cash flows of $250,000 per year for 7 years. ûX Ltd’s WACC is 15% ûX Ltd’s target D/E ratio is 0.6 û Flotation costs: Equity = 5%; Debt = 3%. What is the NPV for the project after adjusting for flotation costs (f)?

f = (.375)(3%) + (.625)(5%) = 4.25%

Note: D/E = .6; Let E = 1; then D = .6V = .6 + 1 = 1.6D/V = .6 / 1.6 = .375; E/V = 1/1.6 = .625

3-34

PV of future cash inflows of $250,000 per year for 7 years @ 15%=1,040,105

NPV = 1,040,105 - 1,000,000/(1-.0425)

= - $4,281

ûThe project would have a positive NPV of $40,105 without considering flotation costs

ûOnce we consider the cost of issuing new securities, the NPV becomes negative

![Microsoft PowerPoint - powerpoint_to_print.ppt [Read-Only] [Compatibility Mode](https://static.fdokumen.com/doc/165x107/632119038a1d893baa0ce804/microsoft-powerpoint-powerpointtoprintppt-read-only-compatibility-mode.jpg)

![BEE.ppt [Compatibility Mode] - Knowledge Exchange Platform](https://static.fdokumen.com/doc/165x107/631cba156c6907d368016fa0/beeppt-compatibility-mode-knowledge-exchange-platform.jpg)

![Bai10_He thong luu tru.ppt [Compatibility Mode]](https://static.fdokumen.com/doc/165x107/633196767f0d9c38da010add/bai10he-thong-luu-truppt-compatibility-mode.jpg)