Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY)

190

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY) Final Report March 2014 Gujarat Urja Vikas Nigam Limited (GUVNL) CONFIDENTIAL

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY)

Cost Benefit Analysis of Kisan Hit Urja Shakti

Yojana (KHUSHY)

Final Report

March 2014

Gujarat Urja Vikas Nigam Limited (GUVNL)

CONFIDENTIAL

MCB ISA A 0 0

P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

10 April 2014

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH

Final Report

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY)

Final Report

March 2014

Gujarat Urja Vikas Nigam Limited (GUVNL)

CONFIDENTIAL

Mott MacDonald, 501 Sakar II, Ellisbridge, Ahmedabad 380 006, Gujarat, India

T +91 (0)79 2657 5550 F +91 (0)79 2657 5558 W www.mottmac.com

Sardar Patel Vidyut Bhavan, Race Course, Vadodara 390007

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Revision Date Originator Checker Approver Description Standard00 December, 2013 BD, RR PM PS Draft Report

01 March, 2014 RR PM PS Final Report

02 May, 2014 RR PM PS Final Report

Issue and revision record

This document is issued for the party which commissioned it and for specific purposes connected with the above-captioned project only. It should not be relied upon by any other party or used for any other purpose.

We accept no responsibility for the consequences of this document being relied upon by any other party, or being used for any other purpose, or containing any error or omission which is due to an error or omission in data supplied to us by other parties.

This document contains confidential information and proprietary intellectual property. It should not be shown to other parties without consent from us and from the party which commissioned it.

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Chapter Title Page

Executive Summary i

Overall Voltage Level/Quality ______________________________________________________________________ i Line break/Unscheduled Breakdowns _______________________________________________________________ i Incidence of Hooking ___________________________________________________________________________ ii Crop Output & Yield ____________________________________________________________________________ ii Transformer Failure ____________________________________________________________________________ ii Motor Failure ii Motor Starter Failure ___________________________________________________________________________ ii Bore Well iii View on continuation of the scheme _______________________________________________________________ iii PGVCL iii Year-Wise Sent Out and Units Billed _______________________________________________________________ iii Year-Wise Details on % Transformer Failure _________________________________________________________ iii Pay Back Period: Feeders Completed in 2008-09 _____________________________________________________ iii Pay Back Period: Feeders Completed in 2009-10 _____________________________________________________ iv Pay Back Period: Feeders Completed in 2010-11 _____________________________________________________ iv Pay Back Period: Feeders Completed in 2011-12 _____________________________________________________ iv Pay Back Period: Feeders Completed in 2012-13 _____________________________________________________ iv Pay Back Period: All Dedicated Feeders ____________________________________________________________ v Pay Back Period: All Scattered Connections _________________________________________________________ v Pay Back Period: Overall (All Feeders) _____________________________________________________________ v DGVCL v Year-Wise Sent Out and Units Billed _______________________________________________________________ v Year Wise % Theoretical Loss ____________________________________________________________________ vi Year-Wise Details on % Transformer Failure _________________________________________________________ vi Pay Back Period: Dedicated Feeders ______________________________________________________________ vi Pay Back Period: Scattered Feeders _______________________________________________________________ vi Pay Back Period: Overall (All Feeders) _____________________________________________________________ vi UGVCL vii Year-Wise Sent Out and Units Billed (Dedicated Feeders) _____________________________________________ vii Year Wise % Theoretical Loss ___________________________________________________________________ vii Year-Wise Details on % Transformer Failure ________________________________________________________ vii Pay Back Period: Dedicated Feeders _____________________________________________________________ vii Pay Back Period: Scattered Feeders ______________________________________________________________ vii Pay Back Period: Overall (All Feeders) ____________________________________________________________ viii MGVCL viii Year-Wise Sent Out and Units Billed (Dedicated Feeders) _____________________________________________ viii Year Wise % Theoretical Loss ___________________________________________________________________ viii Year-Wise Details on % Transformer Failure ________________________________________________________ viii Pay Back Period: Dedicated Feeders _____________________________________________________________ viii Pay Back Period: Scattered Feeders _______________________________________________________________ ix Pay Back Period: Overall (All Feeders) _____________________________________________________________ ix

1 Introduction 1

Contents

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

1.1 Mott MacDonald Group ______________________________________________________________ 1 1.1.1 What we do _______________________________________________________________________ 1 1.1.2 Mott MacDonald India________________________________________________________________ 2 1.2 Gujarat Urja Vikas Nigam Limited (GUVNL) _______________________________________________ 3 1.3 The Project ________________________________________________________________________ 4 1.4 Scope of Work _____________________________________________________________________ 4

Part A: Paschim Gujarat Vij Company Limited (PGVCL) 6

2 Profile of PGVCL 7

2.1 Paschim Gujarat Vij Company Limited ___________________________________________________ 7

3 Implementation of Kisan Hit Urja Shakti Yojana (KHUSHY) – PGVCL 8

4 Consumer Perception of Kisan Hit Urja Shakti Yojana (KHUSHY) – PGVCL 15

4.1 Approach and Methodology __________________________________________________________ 15 4.1.1 Sample Design ____________________________________________________________________ 15 4.1.2 Questionnaire Design _______________________________________________________________ 16 4.2 Key Results of Consumer Perception Study - PGVCL ______________________________________ 17 4.2.1 General Information ________________________________________________________________ 17 4.2.2 Level of Agreement on Technical and Financial Aspects ____________________________________ 20 4.2.3 Assessment of Tangible Benefits Accrued after implementation of KHUSHY ____________________ 27 4.2.4 Single Phase Connection and Bore well Details ___________________________________________ 35 4.2.5 View on continuation of the scheme ____________________________________________________ 36

5 Cost-Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY) – PGVCL 37

5.1 Implementation Details of KHUSHY ____________________________________________________ 38 5.2 Benefits Accrued Under KHUSHY _____________________________________________________ 38 5.2.1 Transmission and Distribution Losses (PGVCL) __________________________________________ 38 5.2.2 Transformer Failures (PGVCL) ________________________________________________________ 40 5.3 Payback Period (PGVCL) ____________________________________________________________ 40 5.3.1 Selection of Baseline Loss/Sent Unit ___________________________________________________ 41 5.3.2 Selection of Cost Realization _________________________________________________________ 41 5.3.3 Cost of Capital ____________________________________________________________________ 41 5.3.4 Savings due to reduction in Transformer Failures _________________________________________ 41 5.4 Pay Back Calculations ______________________________________________________________ 42

Part B: Dakshin Gujarat Vij Company Limited (DGVCL) 45

6 Profile of DGVCL 46

6.1 Dakshin Gujarat Vij Company Limited __________________________________________________ 46

7 Implementation of Kisan Hit Urja Shakti Yojana (KHUSHY) – DGVCL 47

8 Consumer Perception of Kisan Hit Urja Shakti Yojana (KHUSHY) – DGVCL 49

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

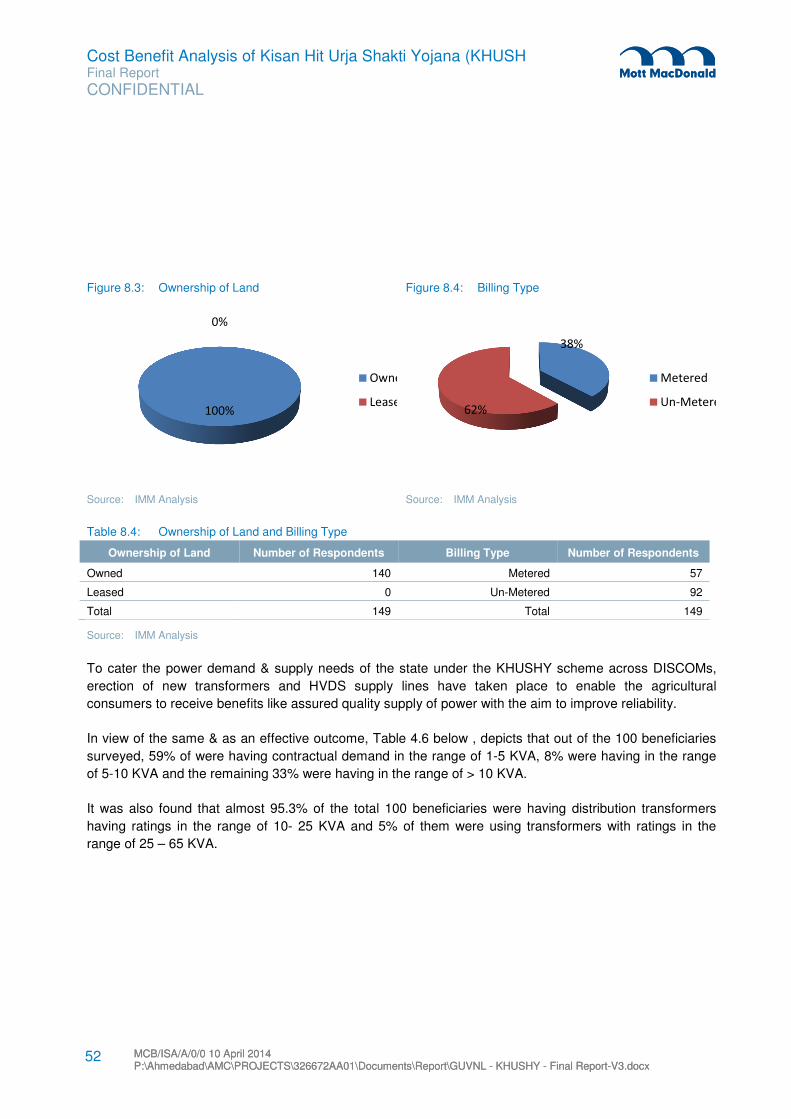

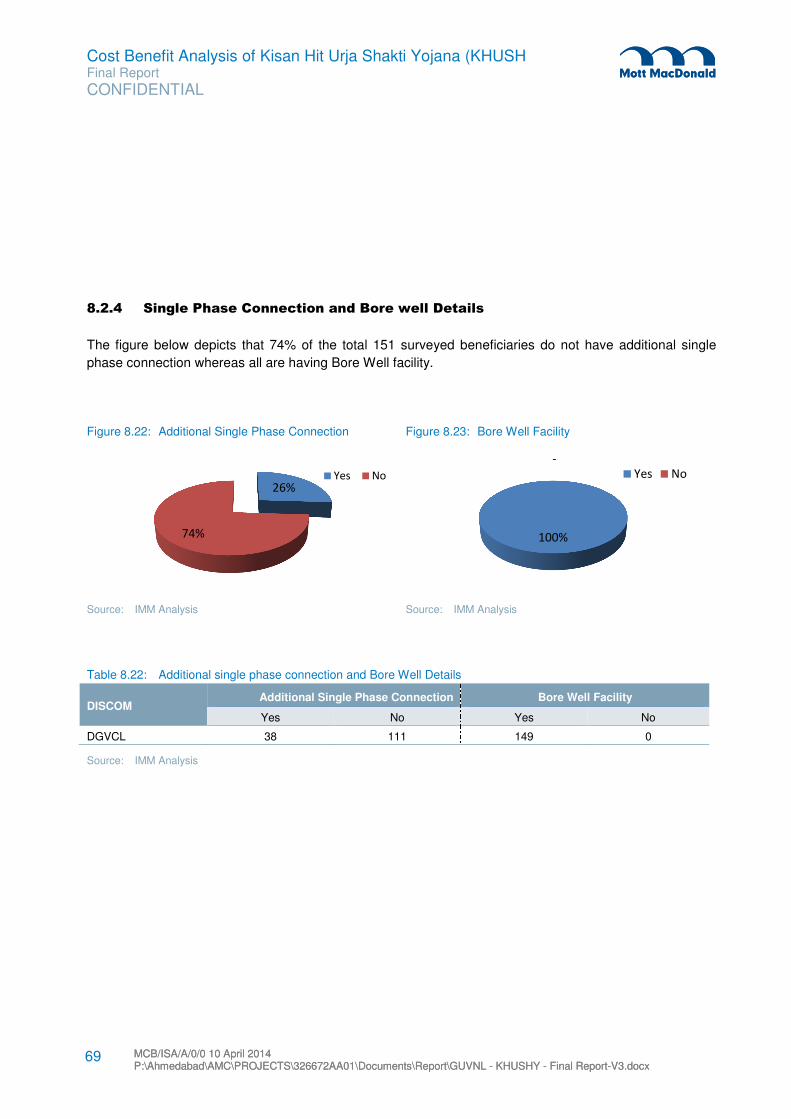

8.1 Approach and Methodology __________________________________________________________ 49 8.1.1 Sample Design ____________________________________________________________________ 49 8.1.2 Questionnaire Design _______________________________________________________________ 50 8.2 Key Results of Consumer Perception Study - DGVCL ______________________________________ 50 8.2.1 General Information ________________________________________________________________ 50 8.2.2 Level of Agreement on Technical and Financial Aspects ____________________________________ 53 8.2.3 Assessment of Tangible Benefits Accrued after implementation of KHUSHY ____________________ 62 8.2.4 Single Phase Connection and Bore well Details ___________________________________________ 69 8.2.5 View on continuation of the scheme ____________________________________________________ 70

9 Cost-Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY) – DGVCL 71

9.1 Implementation Details of KHUSHY ____________________________________________________ 72 9.2 Benefits Accrued Under KHUSHY _____________________________________________________ 72 9.2.1 Transmission and Distribution Losses (DGVCL) __________________________________________ 72 9.2.2 Transformer Failures (DGVCL) _______________________________________________________ 75 9.3 Payback Period (DGVCL) ____________________________________________________________ 75 9.3.1 Selection of Baseline Loss/Sent Unit ___________________________________________________ 76 9.3.2 Selection of Cost Realization _________________________________________________________ 76 9.3.3 Cost of Capital ____________________________________________________________________ 76 9.3.4 Savings due to reduction in Transformer Failures _________________________________________ 76 9.4 Pay Back Calculations ______________________________________________________________ 77

Part C: Uttar Gujarat Vij Company Limited (UGVCL) 78

10 Profile of UGVCL 79

10.1 Uttar Gujarat Vij Company Limited _____________________________________________________ 79

11 Implementation of Kisan Hit Urja Shakti Yojana (KHUSHY) 80

12 Consumer Perception of Kisan Hit Urja Shakti Yojana (KHUSHY) 82

12.1 Approach and Methodology __________________________________________________________ 82 12.1.1 Sample Design ____________________________________________________________________ 82 12.1.2 Questionnaire Design _______________________________________________________________ 83 12.2 Key Results of Consumer Perception Study - UGVCL ______________________________________ 83 12.2.1 General Information ________________________________________________________________ 84 12.2.2 Level of Agreement on Technical and Financial Aspects ____________________________________ 87 12.2.3 Assessment of Tangible Benefits Accrued after implementation of KHUSHY ____________________ 94 12.2.4 Single Phase Connection and Bore well Details __________________________________________ 101 12.2.5 View on continuation of the scheme ___________________________________________________ 101

13 Cost-Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY) – UGVCL 103

13.1 Implementation Details of KHUSHY ___________________________________________________ 104 13.2 Benefits Accrued Under KHUSHY ____________________________________________________ 104 13.2.1 Transmission and Distribution Losses (UGVCL) _________________________________________ 104 13.2.2 Transformer Failures (UGVCL) ______________________________________________________ 107

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

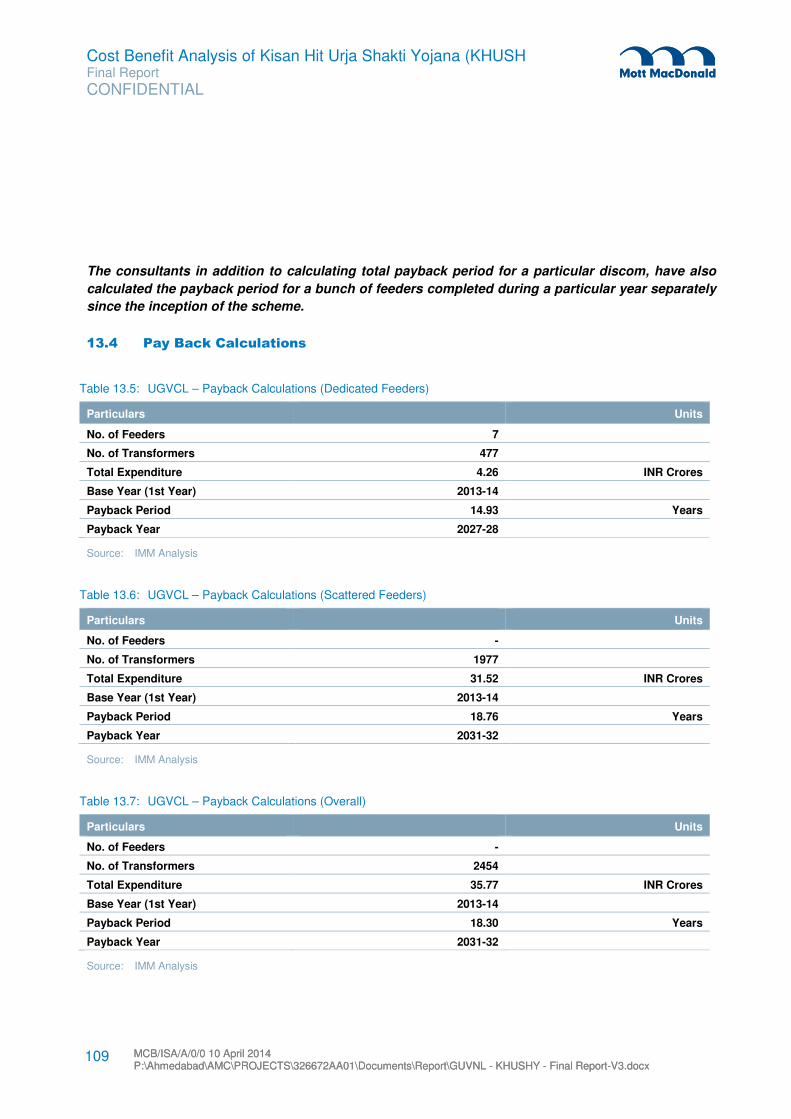

13.3 Payback Period (UGVCL) ___________________________________________________________ 107 13.3.1 Selection of Baseline Loss/Sent Unit __________________________________________________ 108 13.3.2 Selection of Cost Realization ________________________________________________________ 108 13.3.3 Cost of Capital ___________________________________________________________________ 108 13.3.4 Savings due to reduction in Transformer Failures ________________________________________ 108 13.4 Pay Back Calculations _____________________________________________________________ 109

Part D: Madhya Gujarat Vij Company Limited (MGVCL) 110

14 Profile of MGVCL 111

14.1 Madhya Gujarat Vij Company Limited _________________________________________________ 111

15 Implementation of Kisan Hit Urja Shakti Yojana (KHUSHY) – MGVCL 112

16 Consumer Perception of Kisan Hit Urja Shakti Yojana (KHUSHY) – MGVCL 114

16.1 Approach and Methodology _________________________________________________________ 114 16.1.1 Sample Design ___________________________________________________________________ 114 16.1.2 Questionnaire Design ______________________________________________________________ 115 16.2 Key Results of Consumer Perception Study - MGVCL _____________________________________ 115 16.2.1 General Information _______________________________________________________________ 115 16.2.2 Level of Agreement on Technical and Financial Aspects ___________________________________ 118 16.2.3 Assessment of Tangible Benefits Accrued after implementation of KHUSHY ___________________ 125 16.2.4 Single Phase Connection and Bore well Details __________________________________________ 133 16.2.5 View on continuation of the scheme ___________________________________________________ 133

17 Cost-Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSHY) – MGVCL 135

17.1 Implementation Details of KHUSHY ___________________________________________________ 136 17.2 Benefits Accrued Under KHUSHY ____________________________________________________ 136 17.2.1 Transmission and Distribution Losses (MGVCL) _________________________________________ 136 17.2.2 Transformer Failures (MGVCL) ______________________________________________________ 139 17.3 Payback Period (MGVCL) __________________________________________________________ 139 17.3.1 Selection of Baseline Loss/Sent Unit __________________________________________________ 140 17.3.2 Selection of Cost Realization ________________________________________________________ 140 17.3.3 Cost of Capital ___________________________________________________________________ 140 17.3.4 Savings due to reduction in Transformer Failures ________________________________________ 140 17.4 Pay Back Calculations _____________________________________________________________ 141

18 Observations & Recommendations 142

18.1 Consumer Perception of KHUSHY ____________________________________________________ 142 18.1.1 Overall Voltage Level/Quality ________________________________________________________ 142 18.1.2 Line break/Unscheduled Breakdowns _________________________________________________ 142 18.1.3 Incidence of Hooking ______________________________________________________________ 142 18.1.4 Crop Output & Yield _______________________________________________________________ 142 18.1.5 Transformer Failure _______________________________________________________________ 142 18.1.6 Motor Failure ____________________________________________________________________ 143 18.1.7 Motor Starter Failure_______________________________________________________________ 143

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

18.1.8 Bore Well _______________________________________________________________________ 143 18.1.9 View on continuation of the scheme ___________________________________________________ 143 18.2 Estimated Monetary Benefit to Customers ______________________________________________ 144 18.3 Cost Benefit Analysis for DISCOMs ___________________________________________________ 144

Appendices 146

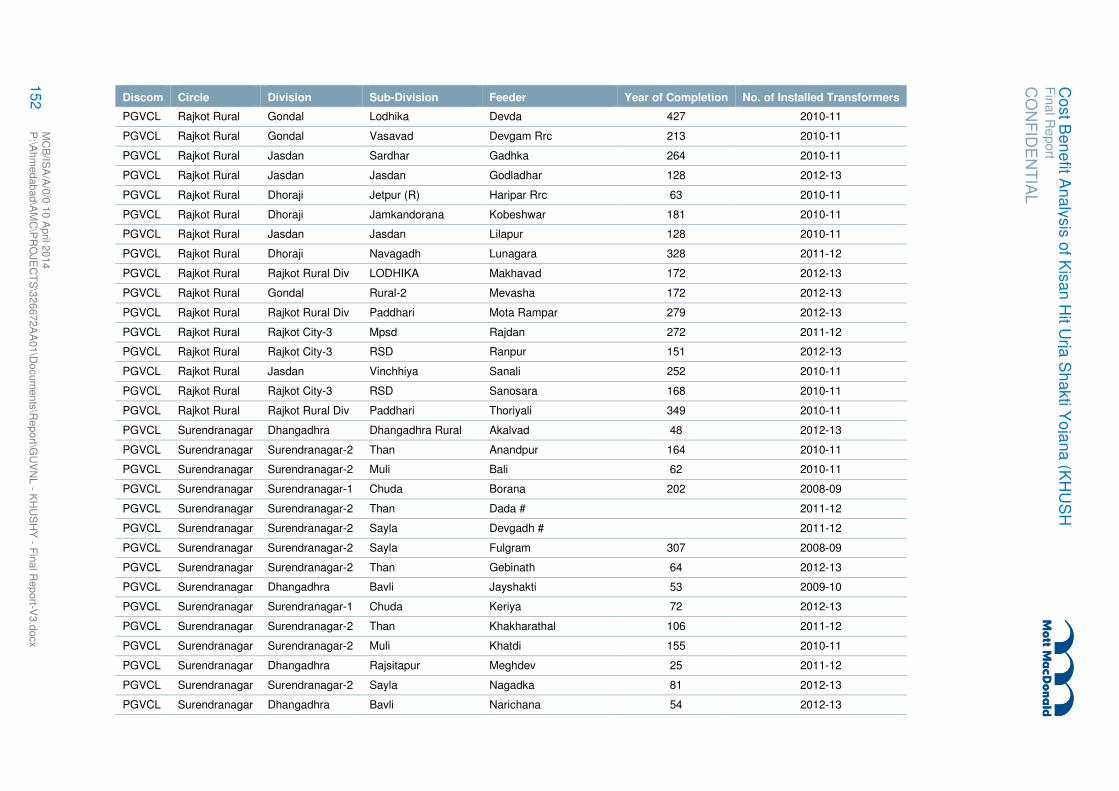

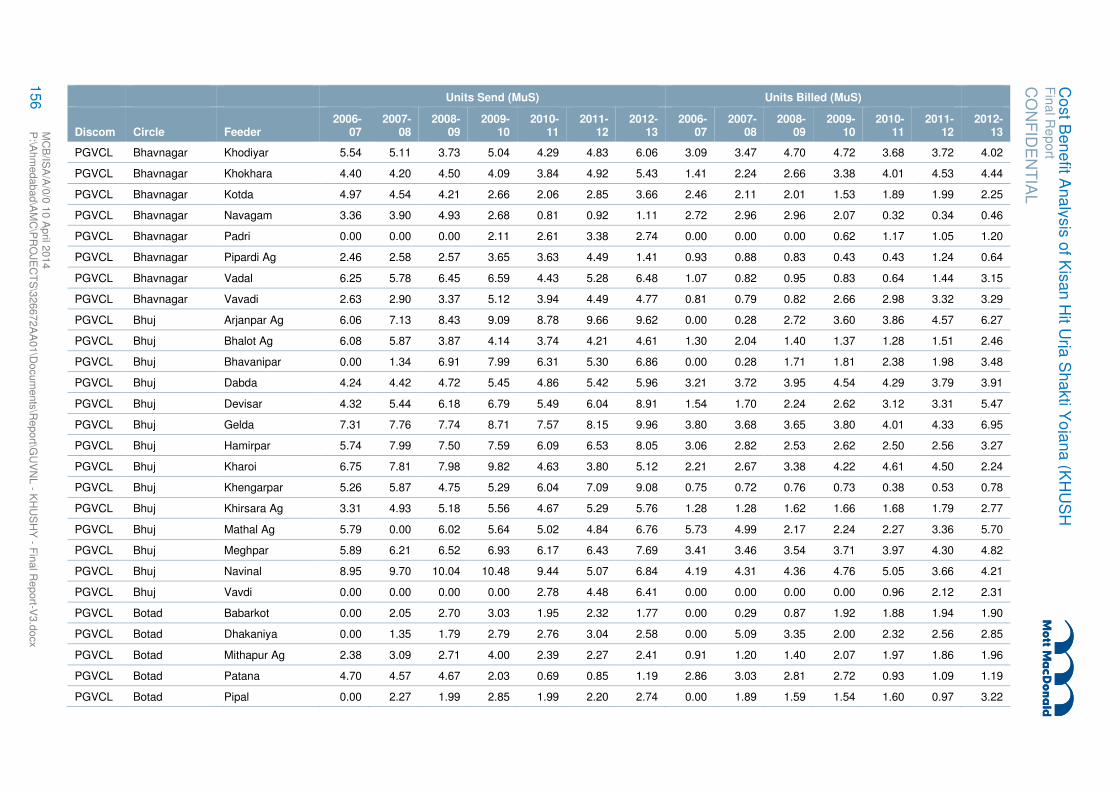

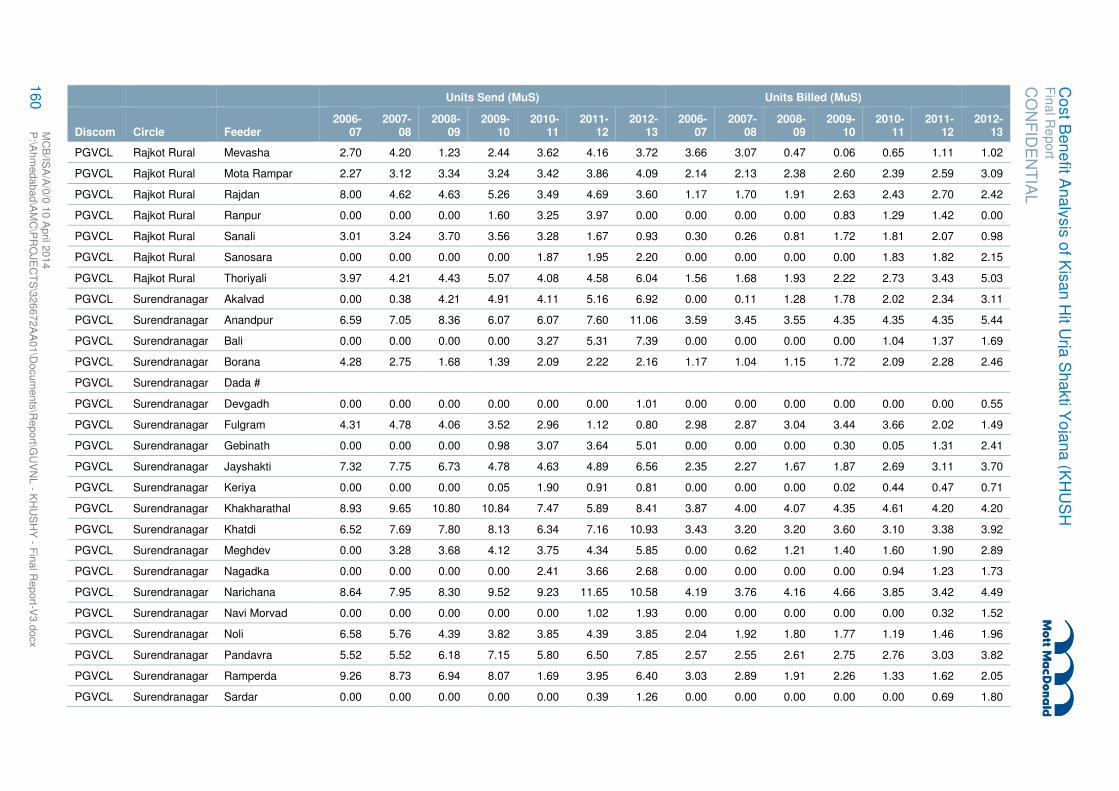

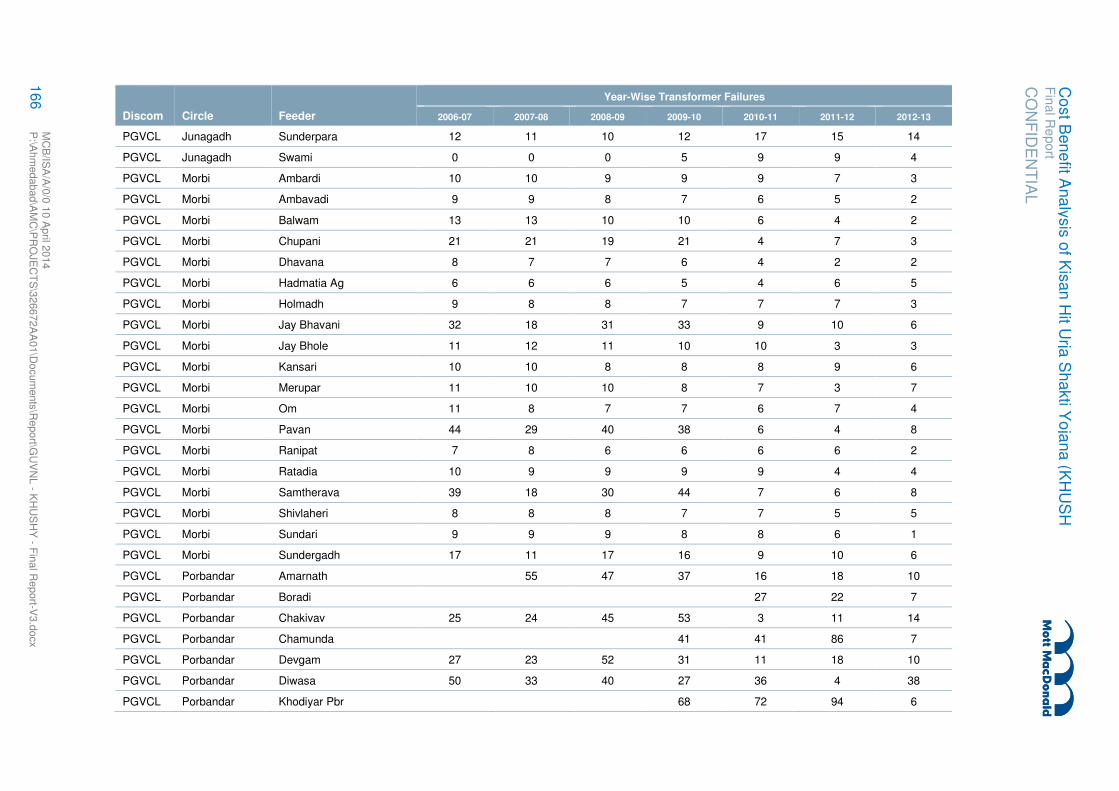

Appendix A. List of Feeders Covered Under KHUSHY _______________________________________________ 147 Appendix B. Feeder Wise Change in Units Billed ___________________________________________________ 154 Appendix C. Feeder-Wise Details on Transformer Failure & Customer Complaints _________________________ 162 Appendix D. Questionnaire ____________________________________________________________________ 169

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

i MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

The Government of Gujarat - through Kisan Hit Urja Shakti Yojana (KHUSHY) scheme - has been

implementing High Voltage Distribution System (HVDS) in place of Low Voltage Distribution System

(LVDS) on identified agricultural feeders. Approximately 65,000 No. of Agricultural consumers are

expected to accrue benefits under this scheme. In this context, GUVNL had engaged the service of Mott

MacDonald Private Limited to conduct a cost benefit analysis (CBA) and agricultural consumer survey to

assess tangible and intangible benefits of KHUSHY scheme.

The KHUSHY scheme has been implemented across all Distribution companies viz. PGVCL, DGVCL,

MGVCL and UGVCL. In total 174 feeders across all the distribution companies have been converted under

this scheme into HVDS. PGVCL and the agricultural consumers have benefitted immensely under this

scheme wherein 157 feeders have been converted into HVDS. All agricultural customers under these

feeders have been allotted dedicated transformers for their connections.

The consumer perception survey had to be done for a sample size of 5% of the total benefitted consumers

which were expected to be around 65000 Nos with an objective to assess the benefits to the consumer

because of the implementation of KHUSHY (HVDS) scheme. The survey has been conducted for 3265

HVDS customers. The distribution of the sample among the distribution companies and further at circle

and feeder level has been done on the basis of the actual conversion of feeders under KHUSHY (HVDS).

The discom wise sample size is as given in the below table

Discom Circle Division Sub-Division No. of Feeders No. of Beneficiaries

PGVCL 10 17 24 29 2865

UGVCL 2 4 5 6 151

DGVCL 3 4 4 5 149

MGVCL 1 1 1 2 100

TOTAL 16 26 34 42 3265

The key observations of the customer perception study for PGVCL are as under

Overall Voltage Level/Quality

There has been a major improvement in the voltage level/quality after the implementation of KHUSHY. The

continuity of power supply would not be effective in absence of low or constantly fluctuating voltage. The

effectiveness of the implementation of the scheme on this parameter is crucial and has led to improve

satisfaction levels of the customers.

Line break/Unscheduled Breakdowns

The incidences of line breaks and unscheduled shutdowns have also drastically decreased after

implementation of KHUSHY.

Executive Summary

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

ii MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Incidence of Hooking

Theft and pilferage account for a substantial part of the high transmission and distribution losses. One of

the objectives of the scheme was to minimize these losses. The various steps and technical interventions

during the scheme have made it cumbersome for the customers indulge in such activities.

Crop Output & Yield

The primary objective of the project was to provide consumers with uninterrupted and quality Power related

benefits. The Crop output & yield are directly dependent on the monsoon & weather conditions. The

electricity has little impact on the crop yield especially in cases where there is levels of underground water

are low.

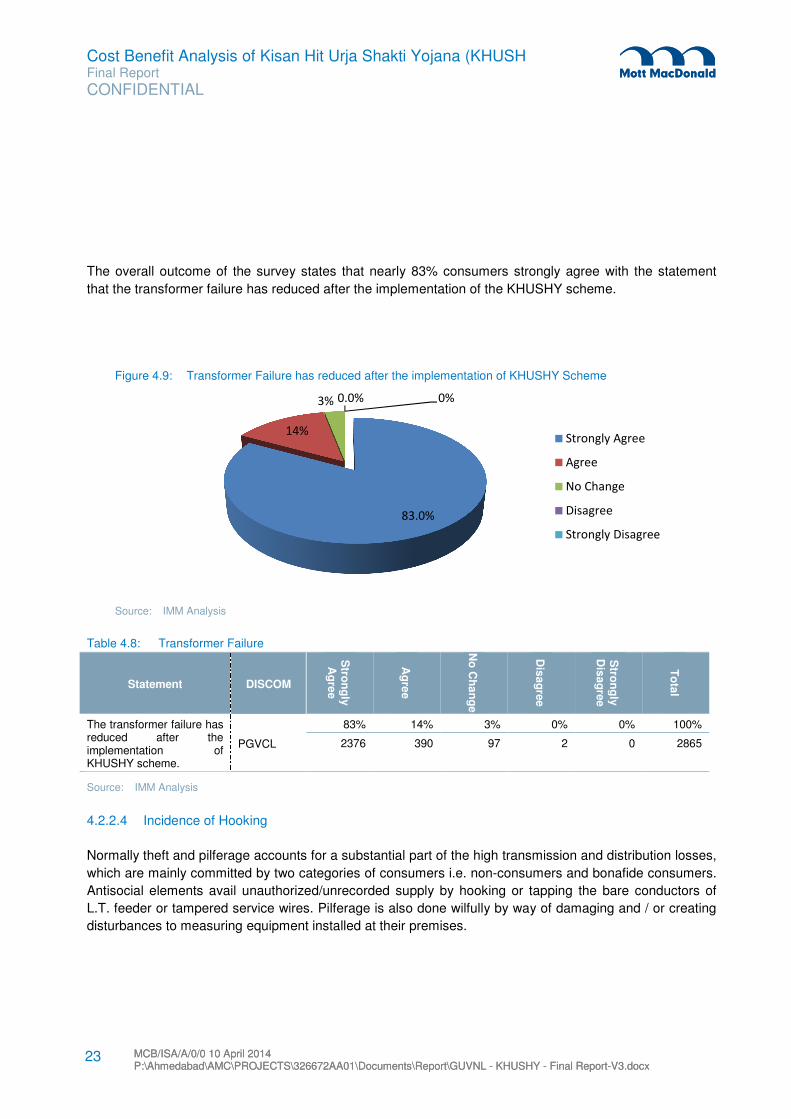

Transformer Failure

The transformer failures have decreased drastically after the implementation of KHUSHY. Majority of the

surveyed customers strongly agree or agree to the statement that the transformer failures have reduced

after the implementation of the scheme.

The survey results show that majority of the customers experienced transformer failures around 3-5 times

while other few experienced it more than 5 times. After the implementation of KHUSHY all the surveyed

customers experienced transformer failure in the bracket of 0-2 times. The results hence show that there

has been a considerable decrease in transformer failure after the implementation of KHUSHY.

The results also show that there has been a considerable decrease in average days loss per transformer

failure after the implementation of KHUSHY.

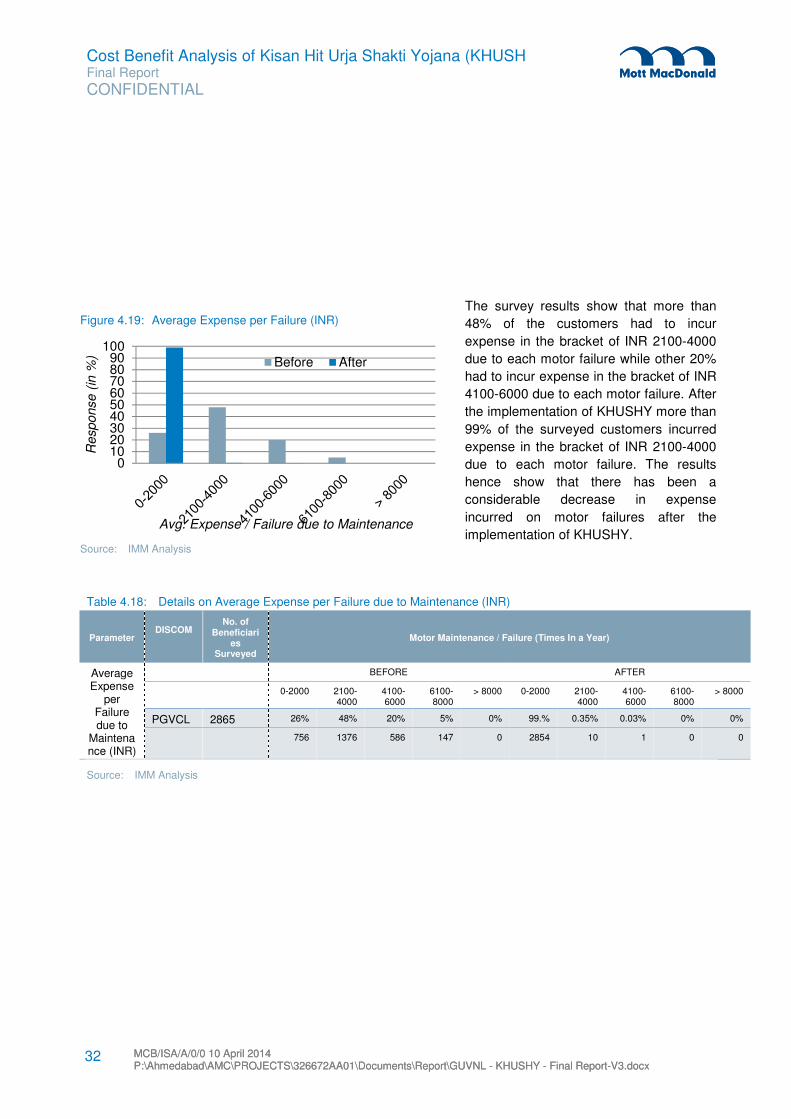

Motor Failure

The survey results show that a major portion of the customers experienced motor failures around 3-5 times

while other few experienced it more than 5 times. After the implementation of KHUSHY all the surveyed

customers experienced motor failures in the bracket of 0-2 times. The results hence show that there has

been a considerable decrease in motor failure after the implementation of KHUSHY.

The results also show that there has been a considerable decrease in average days loss per motor failure

after the implementation of KHUSHY.

The results hence show that there has been a considerable decrease in expense incurred on motor

failures after the implementation of KHUSHY.

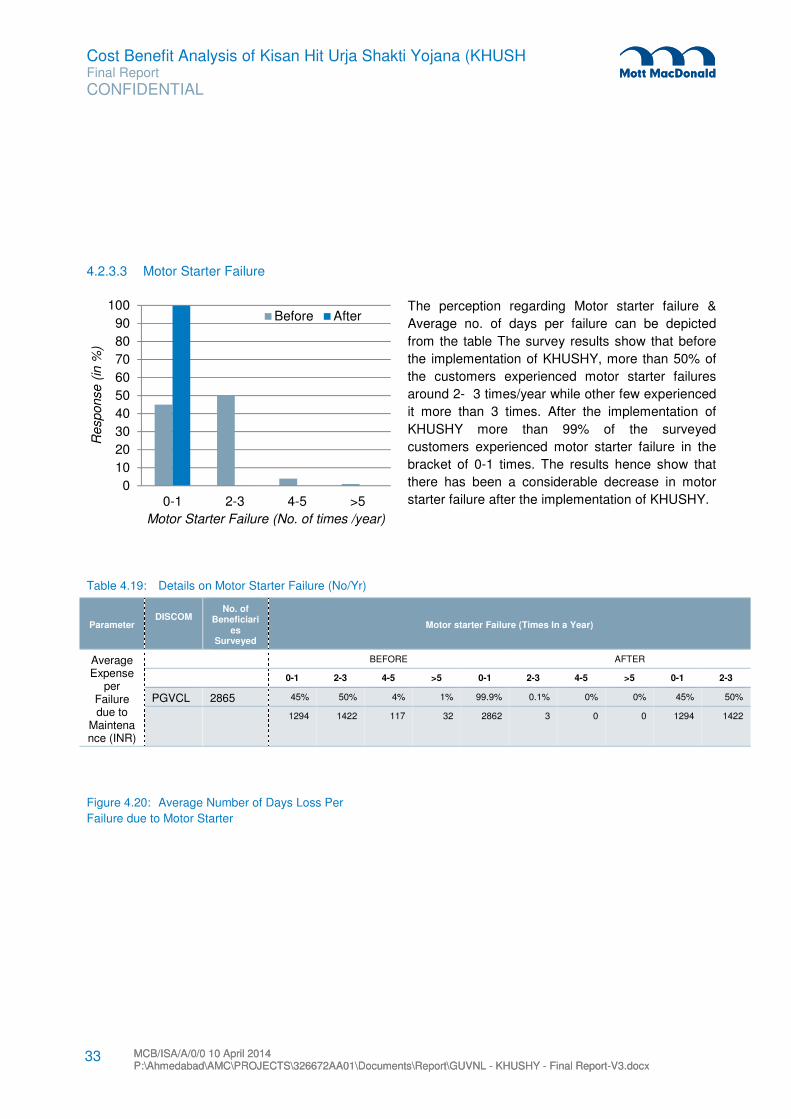

Motor Starter Failure

The survey results show that a major portion of the customers experienced motor starter failures around 2-

3 times/year while other few experienced it more than 3 times. After the implementation of KHUSHY all the

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

iii MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

surveyed customers experienced motor starter failure in the bracket of 0-1 times. The results hence show

that there has been a considerable decrease in motor starter failure after the implementation of KHUSHY.

The results also show that there has been a considerable decrease in average days loss per motor starter

failure after the implementation of KHUSHY.

The results also show that there has been a considerable decrease in expense incurred on motor starter

failures after the implementation of KHUSHY.

Bore Well

The operating hours of the bore well basically depends upon three variables including the monsoon, the

levels of ground water and availability of electricity. The electricity issue have been solved to a large extent

after the implementation of the scheme. The other two variables remaining unpredictable and largely

varying from location to location there, no major increase in the operating hours of the bore wells has been

observed.

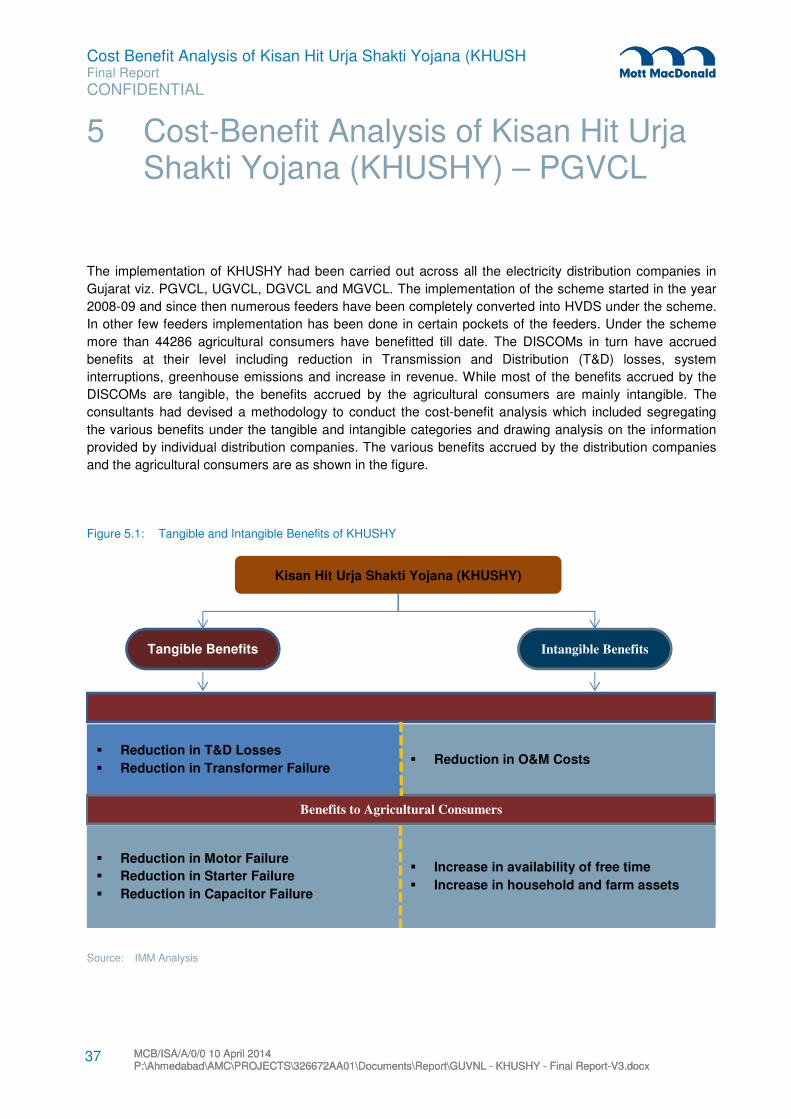

View on continuation of the scheme

Out of the 3865 beneficiaries surveyed, 99% of them are happy & satisfied with the implementation of the

KHUSHY Scheme and have expressed their interest and willingness in support and continuation of the

scheme in other parts of the state.

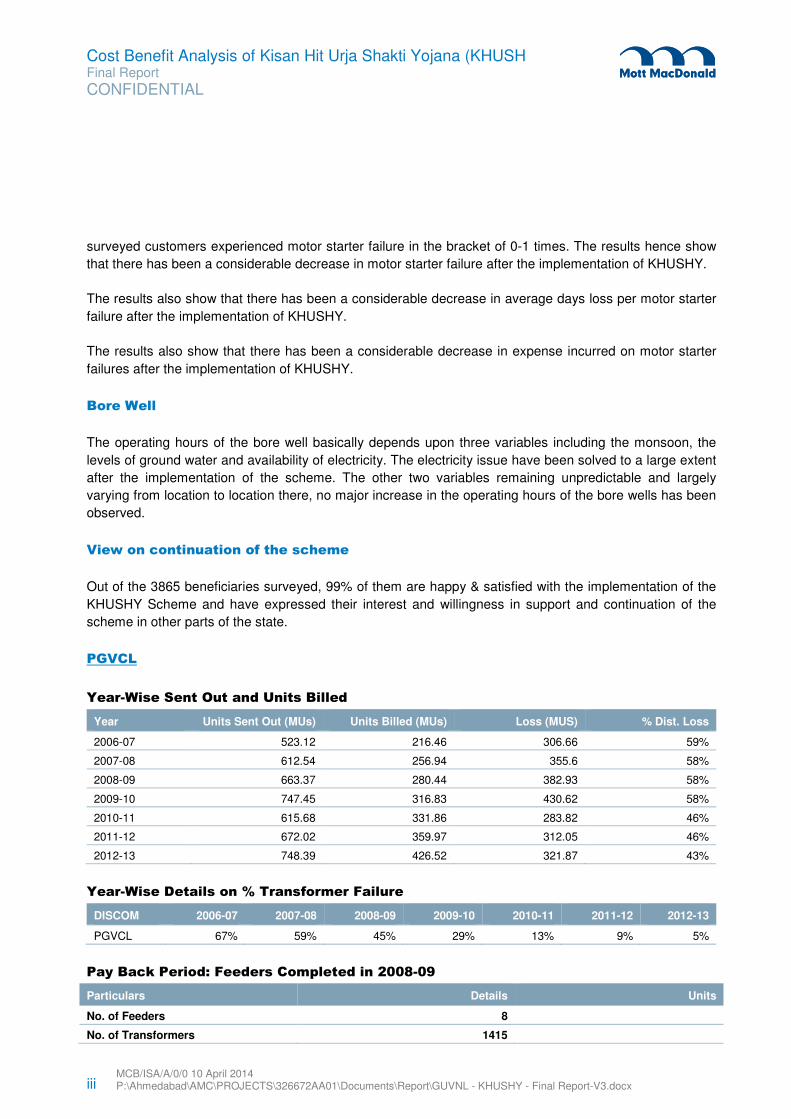

PGVCL

Year-Wise Sent Out and Units Billed

Year Units Sent Out (MUs) Units Billed (MUs) Loss (MUS) % Dist. Loss

2006-07 523.12 216.46 306.66 59%

2007-08 612.54 256.94 355.6 58%

2008-09 663.37 280.44 382.93 58%

2009-10 747.45 316.83 430.62 58%

2010-11 615.68 331.86 283.82 46%

2011-12 672.02 359.97 312.05 46%

2012-13 748.39 426.52 321.87 43%

Year-Wise Details on % Transformer Failure

DISCOM 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

PGVCL 67% 59% 45% 29% 13% 9% 5%

Pay Back Period: Feeders Completed in 2008-09

Particulars Details Units

No. of Feeders 8

No. of Transformers 1415

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

iv MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Particulars Details Units

Total Expenditure 13.6 INR Crores

Base Year (1st Year) 2009-10

Payback Period 2.808 Years

Payback Year 2011-12

Pay Back Period: Feeders Completed in 2009-10

Particulars Details Units

No. of Feeders 8

No. of Transformers 1444

Total Expenditure 16.55 INR Crores

Base Year (1st Year) 2010-11

Payback Period 2.78 Years

Payback Year 2012-13

Pay Back Period: Feeders Completed in 2010-11

Particulars Details Units

No. of Feeders 58

No. of Transformers 11412

Total Expenditure 146.10 INR Crores

Base Year (1st Year) 2011-12

Payback Period 6.22 Years

Payback Year 2017-18

Pay Back Period: Feeders Completed in 2011-12

Particulars Details Units

No. of Feeders 16

No. of Transformers 2080

Total Expenditure 25.09 INR Crores

Base Year (1st Year) 2012-13

Payback Period 5.288 Years

Payback Year 2016-17

Pay Back Period: Feeders Completed in 2012-13

Particulars Details Units

No. of Feeders 71

No. of Transformers 9719

Total Expenditure 105.53 INR Crores

Base Year (1st Year) 2013-14

Payback Period 4.22 Years

Payback Year 2015-16

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

v MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Pay Back Period: All Dedicated Feeders

Particulars Details Units

No. of Feeders 161

No. of Transformers 26070

Total Expenditure 306.88 INR Crores

Base Year (1st Year) 2013-14

Payback Period 3.46 Years

Payback Year 2016-17

Pay Back Period: All Scattered Connections

Particulars Details Units

No. of Feeders -

No. of Transformers 10583

Total Expenditure 149.71 INR Crores

Base Year (1st Year) 2013-14

Payback Period 8.77 Years

Payback Year 2018-19

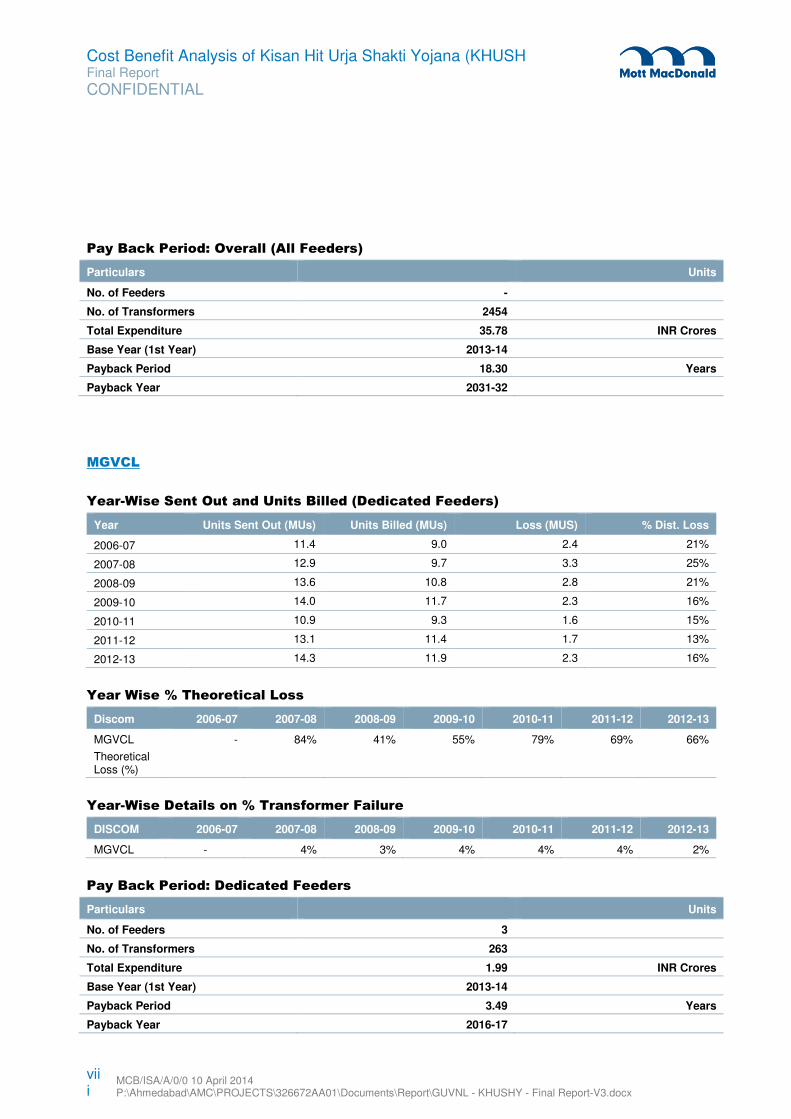

Pay Back Period: Overall (All Feeders)

Particulars Details Units

No. of Feeders 161+Scattered

No. of Transformers 36653

Total Expenditure 456.59 INR Crores

Base Year (1st Year) 2013-14

Payback Period 5.47 Years

Payback Year 2018-19

DGVCL

Year-Wise Sent Out and Units Billed

Year Units Sent Out (MUs) Units Billed (MUs) Loss (MUS) % Dist. Loss

2006-07 14.23 6.80 7.43 52%

2007-08 5.42 3.58 1.84 34%

2008-09 11.48 6.28 5.20 45%

2009-10 14.33 7.39 6.94 48%

2010-11 19.40 10.81 8.59 44%

2011-12 24.68 15.53 9.15 37%

2012-13 21.54 16.46 5.07 24%

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

vi MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

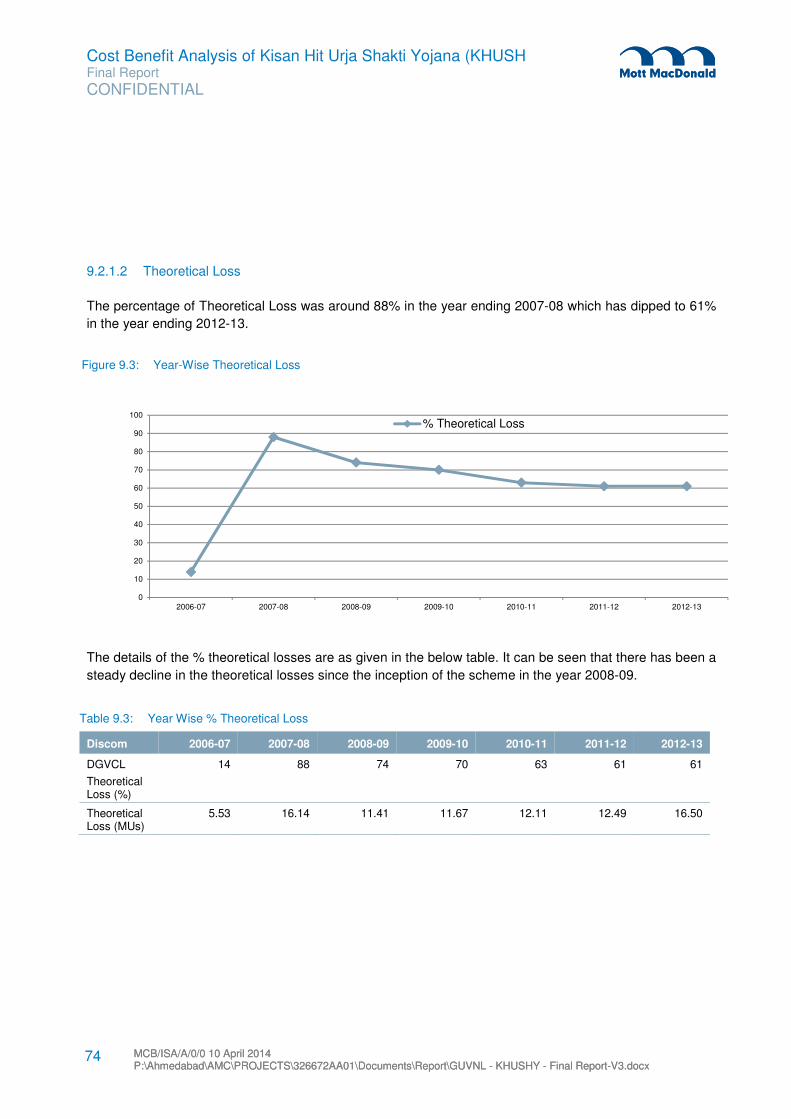

Year Wise % Theoretical Loss

Discom 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

DGVCL

Theoretical Loss (%)

14 88 74 70 63 61 61

Year-Wise Details on % Transformer Failure

DISCOM 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

DGVCL 39% 12% 31% 20% 20% 17% 6%

Pay Back Period: Dedicated Feeders

Particulars Units

No. of Feeders 6

No. of Transformers 283

Total Expenditure 6.22 INR Crores

Base Year (1st Year) 2013-14

Payback Period 15.48 Years

Payback Year 2028-29

Pay Back Period: Scattered Feeders

Particulars Units

No. of Feeders -

No. of Transformers 724

Total Expenditure 4.38 INR Crores

Base Year (1st Year) 2013-14

Payback Period 53.11 Years

Payback Year 2065-66

Pay Back Period: Overall (All Feeders)

Particulars Units

No. of Feeders -

No. of Transformers 1007

Total Expenditure 10.60 INR Crores

Base Year (1st Year) 2013-14

Payback Period 22.16 Years

Payback Year 2034-35

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

vii MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

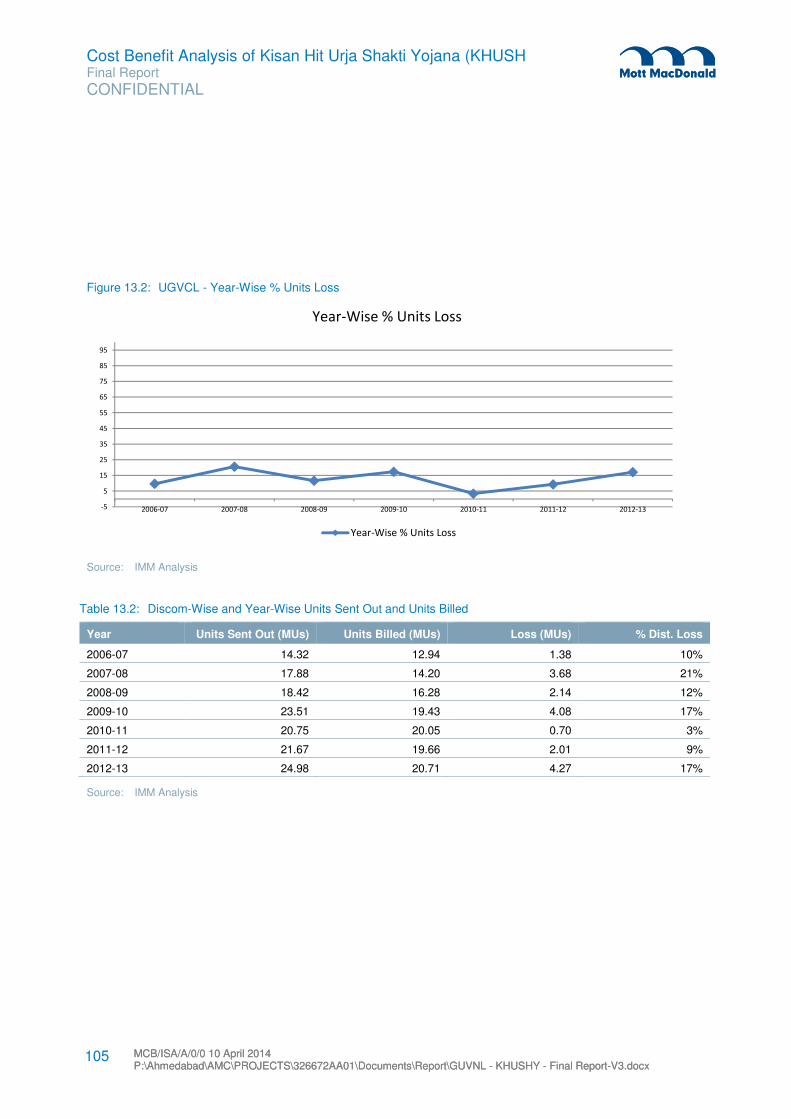

UGVCL

Year-Wise Sent Out and Units Billed (Dedicated Feeders)

Year Units Sent Out (MUs) Units Billed (MUs) Loss (MUS) % Dist. Loss

2006-07 14.32 12.94 1.38 10%

2007-08 17.88 14.2 3.68 21%

2008-09 18.42 16.28 2.14 12%

2009-10 23.51 19.43 4.08 17%

2010-11 20.75 20.05 0.7 3%

2011-12 21.67 19.66 2.01 9%

2012-13 24.98 20.71 4.27 17%

Year Wise % Theoretical Loss

Discom 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

UGVCL

Theoretical Loss (%)

55% 54% 24% 31% 53% 35% 31%

Year-Wise Details on % Transformer Failure

DISCOM 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

UGVCL 14% 16% 9% 5% 5% 7% 4%

Pay Back Period: Dedicated Feeders

Particulars Units

No. of Feeders 7

No. of Transformers 477

Total Expenditure 4.26 INR Crores

Base Year (1st Year) 2013-14

Payback Period 14.93 Years

Payback Year 2027-28

Pay Back Period: Scattered Feeders

Particulars Units

No. of Feeders -

No. of Transformers 1977

Total Expenditure 31.52 INR Crores

Base Year (1st Year) 2013-14

Payback Period 18.76 Years

Payback Year 2031-32

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

viii

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Pay Back Period: Overall (All Feeders)

Particulars Units

No. of Feeders -

No. of Transformers 2454

Total Expenditure 35.78 INR Crores

Base Year (1st Year) 2013-14

Payback Period 18.30 Years

Payback Year 2031-32

MGVCL

Year-Wise Sent Out and Units Billed (Dedicated Feeders)

Year Units Sent Out (MUs) Units Billed (MUs) Loss (MUS) % Dist. Loss

2006-07 11.4 9.0 2.4 21%

2007-08 12.9 9.7 3.3 25%

2008-09 13.6 10.8 2.8 21%

2009-10 14.0 11.7 2.3 16%

2010-11 10.9 9.3 1.6 15%

2011-12 13.1 11.4 1.7 13%

2012-13 14.3 11.9 2.3 16%

Year Wise % Theoretical Loss

Discom 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

MGVCL

Theoretical Loss (%)

- 84% 41% 55% 79% 69% 66%

Year-Wise Details on % Transformer Failure

DISCOM 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

MGVCL - 4% 3% 4% 4% 4% 2%

Pay Back Period: Dedicated Feeders

Particulars Units

No. of Feeders 3

No. of Transformers 263

Total Expenditure 1.99 INR Crores

Base Year (1st Year) 2013-14

Payback Period 3.49 Years

Payback Year 2016-17

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

ix MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

Pay Back Period: Scattered Feeders

Particulars Units

No. of Feeders -

No. of Transformers 2516

Total Expenditure 27.24 INR Crores

Base Year (1st Year) 2013-14

Payback Period 9.50 Years

Payback Year 2022-23

Pay Back Period: Overall (All Feeders)

Particulars Units

No. of Feeders -

No. of Transformers 2910

Total Expenditure 29.29 INR Crores

Base Year (1st Year) 2013-14

Payback Period 8.30 Years

Payback Year -

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

1

1.1 Mott MacDonald Group

Mott MacDonald is a U.K. based uniquely diverse £1 billion global consultancy, delivering leading-edge

solutions for public and private sector clients across 12 core business areas. As one of the world’s largest

employee-owned companies with more than 14,000 staff, the company has principal offices in nearly

50 countries and projects in 140.

Our breadth of skills, sectors, services and global reach makes us uniquely placed to bring our customers:

� Holistic, innovative thinking

� Global experience with local insight

� World-expert practitioners

� Multi-sector perspective

1.1.1 What we do

We work with our customers and use our worldwide resources and experience to:

� Plan, design, procure and deliver projects on any scale

� Provide management consultancy built on technical know-how

� Help shape and implement development policies and programmes

� Advance sustainability and promote the wellbeing of the planet

1.1.1.1 Our service to customers

By staying closely attuned to our customers’ needs and aspirations, we seek to keep ahead of the game,

proactively identifying new service requirements and gearing up to meet them. We understand what our

customer’s need, what’s required to satisfy those needs and we get on with it – adding real value in the

process by saving them as much money and time as possible without ever compromising on quality. We

take pride in every commission, no matter the size.

1.1.1.2 Sustainable solutions

We are committed to working in partnership with our customers and supply chains to incorporate

sustainable solutions into our projects. We are experts in sustainable design, construction and

management, seeking to include sustainability as a driver at the most critical conceptual, planning and

feasibility stages of all our projects – addressing the whole-life costs and impacts from a truly

multidisciplinary viewpoint.

We are also acting to reduce our own impact and have committed to an active programme to make

significant year on year reductions in our per capita carbon emissions.

1 Introduction

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

2

1.1.1.3 Innovation

We pride ourselves in finding ways to solve existing challenges and tackle new ones. The value of our

innovation can be measured by the prestigious awards our people and projects win – over 200 in the last

three years.

1.1.1.4 Our people

Our principal differentiator is the quality of our staff. Our success is fuelled by their dedication, enthusiasm

and ingenuity. Many of our engineers, environmentalists, planners, economists, cost consultants; project

managers, safety experts, IT specialists, educationalists, healthcare advisors and management

consultants are recognised as innovators or world authorities in their fields. Understanding that to work

with the best we must be the best, we promote professional excellence and knowledge management,

which is why continuous learning and skills improvement are ingrained in our company culture.

1.1.1.5 Community spirit

As a multinational company with a global reach, we recognise our obligation to make a positive

contribution to communities in which we work. At a corporate level we engage and support local

communities sponsoring a number of charity projects each year. We also encourage and support our staffs

who invest enormous time and energy in a range of charitable, educational, disaster relief and

development work around the world.

1.1.1.6 Global presence

With major offices and centres of excellence across the globe, we bring our skills and resources directly to

our customers, wherever they or their projects are based. Each office has in-depth knowledge and

understanding of local conditions and practices, backed by our worldwide resources – enabling us to offer

services around the clock, around the world.

1.1.2 Mott MacDonald India

Mott MacDonald in India (hereinafter referred to as MM) has over 1600 staff engaged in planning,

developing and delivering projects across many sectors – from energy, industry, water and environment to

transport, buildings, urban infrastructure and social development. We are making our mark in many areas

of business and industry, serving not only the burgeoning domestic demand but also a wider customer

base in core markets such as industry, infrastructure and health.

1.1.2.1 Our Sectors

MM activities are focussed primarily on the growing need for physical and social infrastructure and the

creation of wealth and employment through manufacturing and the more efficient development of its

resources. These are extraordinarily diverse, ranging across:

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

3

� Buildings

� Communications

� Energy

� Industry and industrial development

� Social development including health and

education

� Transportation infrastructure

� Urban development

� Water and environment

In all these markets, we address business and developmental issues as well as engineering. We aim to

serve the broader needs of our clients to create successful and sustainable projects. We bring to the

market an almost unique combination of management and engineering capability, both local and

worldwide, delivered in India with the maximum use of Indian and international resources.

Our Indian business has exceptional expertise in the industry sector, especially in chemicals,

pharmaceuticals and textiles where we lead the field in business case planning, business

conceptualisation, strategy, financial and demand modelling, basic and detailed engineering, project

management, procurement and validation services for some of the world’s largest chemical and

pharmaceutical manufacturers.

We are also one of the leading transportation and urban infrastructure service providers in India. Our

services in metros are well recognised and we are proud to be associated with Delhi Metro. We are

providing design work on almost 40% of the transport system all over Delhi including a 22km stretch from

the heart of Delhi to the city’s South-east border.

Our Indian experts are also enhancing project delivery for projects globally in key areas such as oil and

gas, water, power, pharmaceuticals, roads and highways, airports and buildings, health and education.

1.2 Gujarat Urja Vikas Nigam Limited (GUVNL)

Gujarat Urja Vikas Nigam Limited (GUVNL) is engaged in the business of bulk purchase and sale of

electricity, Supervision, Co-ordination and facilitation of the activities of its six Subsidiary Companies

including

� GSECL - Engaged in the business of Generation of Electricity.

� GETCO - Engaged in the business of Transmission of Electricity.

� UGVCL - Engaged in the business of Distribution of Electricity in the Northern area of Gujarat.

� DGVCL - Engaged in the business of Distribution of Electricity in the Southern area of Gujarat.

� MGVCL - Engaged in the business of Distribution of Electricity in the Central area of Gujarat.

� PGVCL - Engaged in the business of Distribution of Electricity in the Western area of Gujarat.

One of the basic functions of the Company includes Co-ordination of the activities of its subsidiaries,

business, works to determine their economic and financial objectives/targets and to review, control, guide

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

4

and direct their performance with a view to secure optimum utilization of all resources placed at their

disposal.

1.3 The Project

The Government of Gujarat - through Kisan Hit Urja Shakti Yojana (KHUSHY) scheme - has been

implementing High Voltage Distribution System (HVDS) in place of Low Voltage Distribution System

(LVDS) on identified agricultural feeders. In HVDS, the 11 kV lines are extended nearer to the loads as

much as possible and small size Distribution transformers (e.g. 10, 16 & 25 kVA) are erected and service

connection is released to the consumer through a short LT lines preferably through insulated overhead

cables known as Aerial Bunched Cable (ABC)/PVC Cable. HVDS entails benefits both to DISCOM and

consumer.

Till date, all four DISCOMs (viz. PGVCL, UGVCL, MGVCL and DGVCL) put together have invested around

Rs. 550 Crore under this scheme. The utilities and approximately 65,000 No. of Agricultural consumers are

expected to accrue benefits against this capital expenditure. In this context, GUVNL has engaged the

service of Mott MacDonald Private Limited to conduct a cost benefit analysis (CBA) and agricultural

consumer survey to assess tangible and intangible benefits of KHUSHY scheme.

1.4 Scope of Work

1. Collect circle-wise actual annual costs incurred for conversion of LVDS to HVDS in identified Areas /

feeders across all four DISCOMs of Gujarat:

a. Aggregate capital expenditure covering new equipment / material (e.g. distribution transformer,

conductor, cross arm etc.) and installation & commissioning;

b. Repair and maintenance costs for LVDS and HVDS (e.g. repairing of DTR in case of failure);

c. Interest costs (including interest during construction) on loans (if any)

d. Any other significant costs incurred by utilities which has impact on cost benefit analysis

2. Estimate tangible (quantitative) benefits accrued to DISCOMs due to conversion of LVDS to HVDS.

Consultant will estimate following benefits in monetary terms (to the extent possible and taking

reasonable assumptions, wherever needed):

a. Reduction in AT&C losses

b. Reduction in distribution transformer failure rate

c. Comparison of System interruptions

d. Comparison of Technical Losses (Theoretical Losses)

e. Comparison of per HP sent out units

f. Comparison of Average Ampere Loading on feeders

g. Reduction in greenhouse gas emission due to reduction in AT&C losses.

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

5

3. Identify and list down intangible (qualitative) benefits to utilities and consumers due to conversion of

LVDS to HVDS.

4. Conduct a consumer perception survey of agriculture consumers {for a specific sample size

approximately 5% of total benefited consumers (approximately 65,000 No.) to assess the benefits to the

consumer due to implementation of KHUSHY (HVDS) scheme.

5. Develop a MS Excel based model for assessing total costs; total benefits and overall cost benefit

analysis. (to be submitted to GUVNL with all the calculation formulas)

6. Prepare a report covering cost benefit analysis and outcome of the consumer survey.

7. Verification of data and information provided by GUVNL, DISCOMs and other organization (if any) for

ascertaining its correctness and accuracy.

8. Representing GUVNL before the Govt. of Gujarat or its agencies, Gujarat electricity Regulatory

Commission, any statutory or regulatory body or any public forum for sharing of the results of this study.

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

6

Part A: Paschim Gujarat Vij Company Limited (PGVCL)

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

7

2.1 Paschim Gujarat Vij Company Limited

PGVCL was incorporated on

15th September, 2003 with

certificate of business w.e.f.

15th October, 2003.

Commercial operation of

company started on 1st April

2005. PGVCL is feeding

electricity in 8 districts of

Gujarat namely Rajkot,

Jamnagar, Junagadh,

Porbandar, Bhuj, Bhavnagar,

Surendranagar and Amreli

covering total 83 Talukas. For

better administration and

consumers' conveniences, administrative area of company is divided into 11 circles out of which 6 circles

are under direct control of Corporate Office, 4 circles are under the control of Bhavnagar Zonal Office and

1 circle under the control of Bhuj Zonal Office. PGVCL caters to almost 48,61,565 customers. The areas

covered by UGVCL are as depicted in the figure. The basic details of PGVCL are as illustrated in the table:

Particulars Details

Total Area Covered By Company 99,771 Sq. Kms.

Districts Covered 8

Talukas Covered 83

Villages Covered 5905

Total Consumers of Company 4861565 (As on 30.06.13)

Circles 11

Divisions 44

Sub Divisions 226

Source: PGVCL Website

2 Profile of PGVCL

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

8

High Voltage Distribution System including KHUSHY (Kisan Hit Urja Shakti Yojana) is a scheme with an

objective of eliminating Line losses by installing smaller size of distribution transformers matching with the

load demand of individual consumer or very small group of consumers. The scheme has been largely

implemented in the Agriculture Sector since its roll out in the year 2008-09. The scheme had been aimed in

improving Voltage Profile as well as reduction in Technical loss and associated Commercial Loss. The

scheme had been designed to benefit both the agricultural customers as a result of uninterrupted power

with consistent voltage as well as the distribution companies in the long rum due to drastic decrease in

transmission and distribution losses.

The KHUSHY scheme has been implemented across all Distribution companies viz. PGVCL, DGVCL,

MGVCL and UGVCL. In total 174 feeders across all the distribution companies have been converted under

this scheme into HVDS. PGVCL has benefitted immensely under this scheme wherein 161 feeders have

been converted into HVDS. All agricultural customers under these feeders have been allotted dedicated

transformers for their connections.

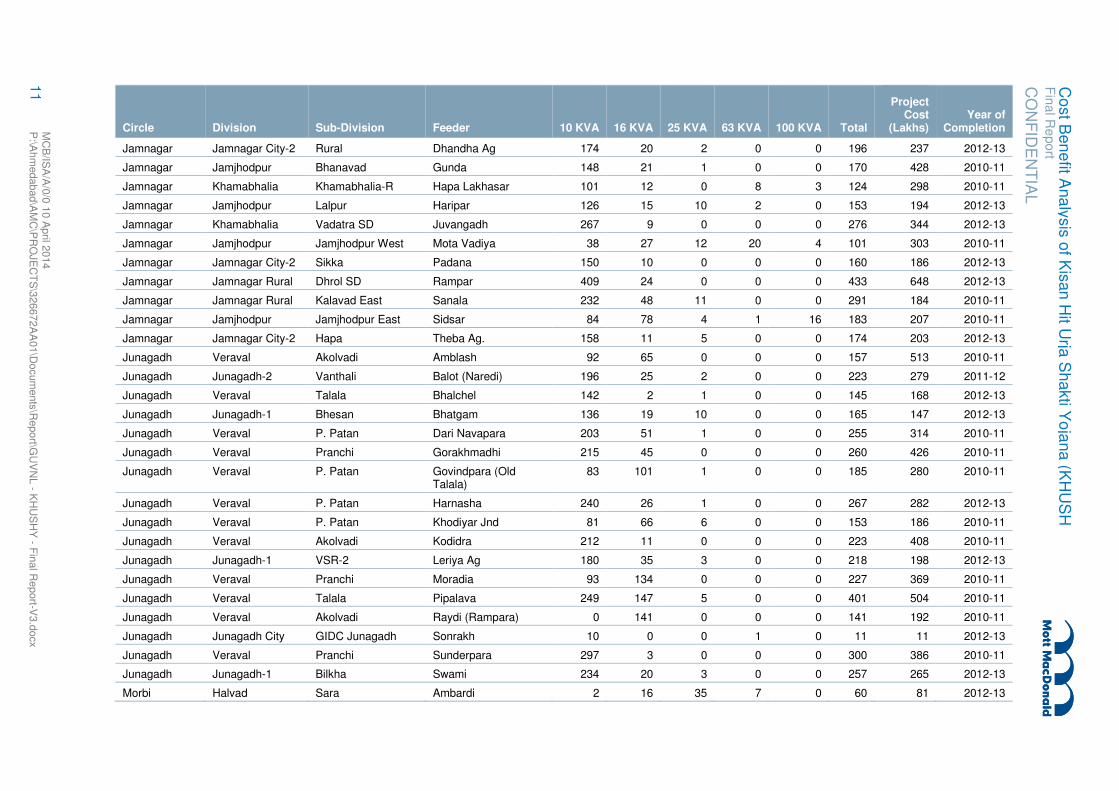

The details of feeders in PGVCL which have been converted into HVDS and the number of transformers

installed are as given in the table:

3 Implementation of Kisan Hit Urja Shakti Yojana (KHUSHY) – PGVCL

CO

NF

IDE

NT

IAL

Fin

al R

eport

Co

st B

en

efit A

na

lysis

of K

isan

Hit U

rja S

ha

kti Y

oja

na

(KH

US

H

9

MC

B/IS

A/A

/0/0

10 A

pril 2

014

P:\A

hm

edabad\A

MC

\PR

OJE

CT

S\3

26672A

A01\D

ocum

ents

\Report\G

UV

NL - K

HU

SH

Y - F

inal R

eport-V

3.d

ocx

Table 3.1: PGVCL Feeder Details

Circle Division Sub-Division Feeder 10 KVA 16 KVA 25 KVA 63 KVA 100 KVA Total

Project Cost

(Lakhs) Year of

Completion

Amreli Una Una-2 Amodra 212 19 0 0 0 231 220 2012-13

Amreli Una Kodinar-2 Anandpur Amr 331 13 2 0 0 346 335 2012-13

Amreli Una Kodinar-1 Balnath 187 38 9 0 0 234 281 2011-12

Amreli Una Kodinar-2 Batheshvar # 2010-11

Amreli Una Kodinar-2 Bhavani 404 10 0 0 0 414 524 2010-11

Amreli Amreli-2 Vadia Dhundhiya Pipaliya 116 41 21 3 0 181 235 2009-10

Amreli Una Kodinar-2 Fafani 233 5 4 0 0 242 296 2010-11

Amreli SKD Jafrabad Fichadi 340 7 0 0 0 347 250 2012-13

Amreli Una Kodinar-2 Gaytri 244 37 3 0 0 284 415 2010-11

Amreli Una Kodinar Gir Devali 360 16 2 0 0 378 436 2009-10

Amreli Amreli-1 Amreli Rural Giriya 74 21 10 1 0 106 144 2012-13

Amreli SKD Rajula Hindorana 172 4 0 0 0 176 250 2010-11

Amreli Una Kodinar-2 Khodiyar # 2011-12

Amreli Amreli-2 Dhari-2 Marvadi 49 54 13 0 0 116 108 2012-13

Amreli Amreli-2 Chalala Morzar 108 21 12 2 0 143 126 2012-13

Amreli Una Kodinar-2 Pichhava Ag 114 3 0 0 0 117 136 2009-10

Amreli Una Kodinar-2 Satyanarayan # 2010-11

Amreli Amreli-1 Babra Valaradi 107 40 15 0 0 162 175 2012-13

Amreli Amreli-2 Kunkavav Vavdi Road 251 48 21 3 0 323 370 2010-11

Bhavnagar Bhavnagar Rural Vartej Bcw 121 53 21 0 0 195 240 2012-13

Bhavnagar Mahuva Jesar Bhandariya 112 14 6 0 0 132 113 2010-11

Bhavnagar Palitana Talaja Borda Ag 111 27 3 0 0 141 113 2009-10

Bhavnagar Mahuva Mahuva R-2 Datha 151 6 2 0 0 159 179 2012-13

Bhavnagar Bhavnagar City-2 Ghogha Hathab 174 14 1 0 0 189 150 2012-13

Bhavnagar Mahuva Jesar Hipavadli 34 33 11 0 0 78 81 2012-13

Bhavnagar Bhavnagar City-2 Mamsa Jaspara 279 30 13 0 0 322 348 2010-11

Bhavnagar Bhavnagar Rural Vartej Khodiyar 4 118 29 2 0 153 164 2008-09

Bhavnagar Bhavnagar Rural Vartej Khokhara 310 46 11 0 0 367 399 2009-10

CO

NF

IDE

NT

IAL

Fin

al R

eport

Co

st B

en

efit A

na

lysis

of K

isan

Hit U

rja S

ha

kti Y

oja

na

(KH

US

H

10

MC

B/IS

A/A

/0/0

10 A

pril 2

014

P:\A

hm

edabad\A

MC

\PR

OJE

CT

S\3

26672A

A01\D

ocum

ents

\Report\G

UV

NL - K

HU

SH

Y - F

inal R

eport-V

3.d

ocx

Circle Division Sub-Division Feeder 10 KVA 16 KVA 25 KVA 63 KVA 100 KVA Total

Project Cost

(Lakhs) Year of

Completion

Bhavnagar Mahuva Mahuva R-2 Kotda 116 18 13 0 0 147 154 2010-11

Bhavnagar Palitana Golidhal Navagam 36 3 0 0 0 39 50 2012-13

Bhavnagar Palitana Talaja Padri 196 7 0 0 0 203 150 2012-13

Bhavnagar Bhavnagar Rural Sanosara Pipardi Ag 86 36 20 0 0 142 163 2012-13

Bhavnagar Mahuva Jesar Vadal 76 33 2 0 0 111 161 2011-12

Bhavnagar Bhavnagar Rural Sanosara Vavadi 151 34 23 0 0 208 220 2010-11

Bhuj Naliya Kothara Arjanpar Ag 7 11 21 21 0 60 86 2012-13

Bhuj Anjar Anjar Rural-1 Bhalot Ag 27 10 24 0 0 61 74 2011-12

Bhuj Anjar Anjar Rural Bhavanipar 33 20 26 22 2 103 100 2010-11

Bhuj Anjar Anjar T Dabda 0 1 18 22 0 41 67 2012-13

Bhuj Naliya Nakhtrana Devisar 25 45 23 5 0 98 133 2010-11

Bhuj Mandvi Mundra Gelda 0 5 33 41 11 90 82 2011-12

Bhuj Anjar Bhimasar Hamirpar 132 95 23 5 0 255 318 2012-13

Bhuj Anjar Bhachau Kharoi 9 2 10 50 9 80 26 2010-11

Bhuj Bhachau Rapar Khengarpar 30 38 26 3 0 97 124 2012-13

Bhuj Bhuj Deshalpar Khirsara Ag 1 5 31 7 0 44 56 2012-13

Bhuj Naliya Nakhtrana Mathal Ag 0 0 1 20 0 21 40 2012-13

Bhuj Mandvi Dahisara Meghpar 1 13 47 12 0 73 98 2012-13

Bhuj Mandvi Mundra Navinal 37 16 61 9 0 123 120 2010-11

Bhuj Bhuj Madhapara Vavdi 3 8 3 0 0 14 19 2012-13

Botad Botad Paliyad Babarkot 94 35 20 0 0 149 187 2009-10

Botad Botad Botad (T-2) Dhakaniya 87 23 3 1 0 114 125 2011-12

Botad Botad Barvala Mithapur Ag 13 126 12 0 0 151 149 2008-09

Botad Gadhada Dhasa Patana 17 266 44 8 1 336 545 2008-09

Botad Gadhada Gadhda-R Pipal 95 20 7 0 0 122 126 2012-13

Botad Botad Botad (R) Ratanvav 11 3 7 0 0 21 23 2012-13

Botad Gadhada DHASA Sitapar 67 22 6 0 0 95 88 2012-13

Botad Botad Botad Zamrala Ag 15 10 5 1 0 31 23 2012-13

Jamnagar Jamnagar City-1 Hapa Aliyabada (New) 18 229 18 1 0 266 231 2008-09

Jamnagar Jamnagar Rural Kalavad West Bamangam 237 32 7 0 0 276 289 2010-11

CO

NF

IDE

NT

IAL

Fin

al R

eport

Co

st B

en

efit A

na

lysis

of K

isan

Hit U

rja S

ha

kti Y

oja

na

(KH

US

H

11

MC

B/IS

A/A

/0/0

10 A

pril 2

014

P:\A

hm

edabad\A

MC

\PR

OJE

CT

S\3

26672A

A01\D

ocum

ents

\Report\G

UV

NL - K

HU

SH

Y - F

inal R

eport-V

3.d

ocx

Circle Division Sub-Division Feeder 10 KVA 16 KVA 25 KVA 63 KVA 100 KVA Total

Project Cost

(Lakhs) Year of

Completion

Jamnagar Jamnagar City-2 Rural Dhandha Ag 174 20 2 0 0 196 237 2012-13

Jamnagar Jamjhodpur Bhanavad Gunda 148 21 1 0 0 170 428 2010-11

Jamnagar Khamabhalia Khamabhalia-R Hapa Lakhasar 101 12 0 8 3 124 298 2010-11

Jamnagar Jamjhodpur Lalpur Haripar 126 15 10 2 0 153 194 2012-13

Jamnagar Khamabhalia Vadatra SD Juvangadh 267 9 0 0 0 276 344 2012-13

Jamnagar Jamjhodpur Jamjhodpur West Mota Vadiya 38 27 12 20 4 101 303 2010-11

Jamnagar Jamnagar City-2 Sikka Padana 150 10 0 0 0 160 186 2012-13

Jamnagar Jamnagar Rural Dhrol SD Rampar 409 24 0 0 0 433 648 2012-13

Jamnagar Jamnagar Rural Kalavad East Sanala 232 48 11 0 0 291 184 2010-11

Jamnagar Jamjhodpur Jamjhodpur East Sidsar 84 78 4 1 16 183 207 2010-11

Jamnagar Jamnagar City-2 Hapa Theba Ag. 158 11 5 0 0 174 203 2012-13

Junagadh Veraval Akolvadi Amblash 92 65 0 0 0 157 513 2010-11

Junagadh Junagadh-2 Vanthali Balot (Naredi) 196 25 2 0 0 223 279 2011-12

Junagadh Veraval Talala Bhalchel 142 2 1 0 0 145 168 2012-13

Junagadh Junagadh-1 Bhesan Bhatgam 136 19 10 0 0 165 147 2012-13

Junagadh Veraval P. Patan Dari Navapara 203 51 1 0 0 255 314 2010-11

Junagadh Veraval Pranchi Gorakhmadhi 215 45 0 0 0 260 426 2010-11

Junagadh Veraval P. Patan Govindpara (Old Talala)

83 101 1 0 0 185 280 2010-11

Junagadh Veraval P. Patan Harnasha 240 26 1 0 0 267 282 2012-13

Junagadh Veraval P. Patan Khodiyar Jnd 81 66 6 0 0 153 186 2010-11

Junagadh Veraval Akolvadi Kodidra 212 11 0 0 0 223 408 2010-11

Junagadh Junagadh-1 VSR-2 Leriya Ag 180 35 3 0 0 218 198 2012-13

Junagadh Veraval Pranchi Moradia 93 134 0 0 0 227 369 2010-11

Junagadh Veraval Talala Pipalava 249 147 5 0 0 401 504 2010-11

Junagadh Veraval Akolvadi Raydi (Rampara) 0 141 0 0 0 141 192 2010-11

Junagadh Junagadh City GIDC Junagadh Sonrakh 10 0 0 1 0 11 11 2012-13

Junagadh Veraval Pranchi Sunderpara 297 3 0 0 0 300 386 2010-11

Junagadh Junagadh-1 Bilkha Swami 234 20 3 0 0 257 265 2012-13

Morbi Halvad Sara Ambardi 2 16 35 7 0 60 81 2012-13

CO

NF

IDE

NT

IAL

Fin

al R

eport

Co

st B

en

efit A

na

lysis

of K

isan

Hit U

rja S

ha

kti Y

oja

na

(KH

US

H

12

MC

B/IS

A/A

/0/0

10 A

pril 2

014

P:\A

hm

edabad\A

MC

\PR

OJE

CT

S\3

26672A

A01\D

ocum

ents

\Report\G

UV

NL - K

HU

SH

Y - F

inal R

eport-V

3.d

ocx

Circle Division Sub-Division Feeder 10 KVA 16 KVA 25 KVA 63 KVA 100 KVA Total

Project Cost

(Lakhs) Year of

Completion

Morbi Morbi Tankara Ambavadi 15 61 34 0 0 110 125 2012-13

Morbi Morbi Morbi Rural Balwam 0 0 29 8 37 74 60 2012-13

Morbi Halvad Charadva Chupani 0 16 66 44 20 146 85 2010-11

Morbi Halvad Halvad Town Dhavana 1 0 11 19 0 31 62 2012-13

Morbi Morbi Tankara Hadmatia Ag 119 44 15 1 0 179 171 2012-13

Morbi Wankaner Wankaner Rural-1 Holmadh 136 14 0 0 0 150 160 2012-13

Morbi Halvad Sara Jay Bhavani 3 6 25 27 5 66 57 2010-11

Morbi Halvad Sara Jay Bhole 28 44 13 1 0 86 77 2012-13

Morbi Halvad Halvad Town Kansari 3 8 16 14 0 41 62 2012-13

Morbi Halvad Halvad Town Merupar 0 2 8 7 0 17 39 2012-13

Morbi Halvad Charadva Om 4 6 21 4 0 35 31 2012-13

Morbi Halvad Sara Pavan 7 15 34 26 8 90 22 2010-11

Morbi Halvad Sara Ranipat 24 18 18 1 0 61 74 2012-13

Morbi Wankaner Wankaner Rural-2 Ratadia 39 8 2 0 0 49 49 2012-13

Morbi Wankaner Wankaner Rural-2 Samtherava 89 45 21 0 0 155 268 2010-11

Morbi Halvad Halvad Town Shivlaheri 1 3 28 8 0 40 66 2012-13

Morbi Halvad Sara Sundari 5 47 41 8 0 101 116 2012-13

Morbi Halvad Charadva Sundergadh 7 38 62 19 1 127 129 2010-11

Porbandar Keshod-2 Keshod-O&M-1 Amarnath 137 161 4 0 0 302 353 2010-11

Porbandar Porbandar Rural Ranavav Boradi 162 23 0 0 0 185 140 2012-13

Porbandar Keshod-2 Mangrol(R) Chakivav 275 56 0 0 0 331 390 2010-11

Porbandar Porbandar Rural Bagvadar Chamunda 147 2 0 0 0 149 185 2012-13

Porbandar Keshod-O&M-2 Chorwad Devgam 42 165 0 0 0 207 232 2010-11

Porbandar Mangrol Madhavpur Diwasa 69 4 0 0 0 73 93 2011-12

Porbandar Kutiyana RURAL Khodiyar Pbr 93 45 5 0 0 143 147 2012-13

Porbandar Porbandar Rural Bagvadar Mariya 113 3 0 0 0 116 147 2012-13

Porbandar Keshod-1 Rural-1 Nonjalvav 165 35 5 2 0 207 243 2012-13

Porbandar Keshod-2 Keshod-O&M-1 Nunarda 69 93 0 0 0 162 205 2010-11

Porbandar Keshod-2 Mangrol(R) Satmarg 64 111 0 0 0 175 220 2010-11

Porbandar Keshod-2 Mangrol(R) Shepa 278 175 0 0 0 453 543 2010-11

CO

NF

IDE

NT

IAL

Fin

al R

eport

Co

st B

en

efit A

na

lysis

of K

isan

Hit U

rja S

ha

kti Y

oja

na

(KH

US

H

13

MC

B/IS

A/A

/0/0

10 A

pril 2

014

P:\A

hm

edabad\A

MC

\PR

OJE

CT

S\3

26672A

A01\D

ocum

ents

\Report\G

UV

NL - K

HU

SH

Y - F

inal R

eport-V

3.d

ocx

Circle Division Sub-Division Feeder 10 KVA 16 KVA 25 KVA 63 KVA 100 KVA Total

Project Cost

(Lakhs) Year of

Completion

Porbandar Keshod-1 Keshod-O&M-1 Shergadh 265 54 3 0 0 322 356 2011-12

Porbandar Keshod-O&M-2 Mangrol(T) Water Works 178 61 1 0 0 240 293 2010-11

Rajkot City Rajkot City-3 Rajkot Rural Sub-Div

Nakarawadi 202 13 3 0 0 218 138 2012-13

Rajkot City Rajkot City-3 Madhapar Sub-Div Rangpar 200 19 1 0 0 220 255 2012-13

Rajkot Rural Dhoraji Dhoraji (R) Bateshwar 258 24 5 0 0 287 303 2012-13

Rajkot Rural Gondal Kotda Bhadva 165 28 2 0 0 195 237 2010-11

Rajkot Rural Dhoraji Jetpur (R) Dedarva 85 49 18 2 0 154 166 2012-13

Rajkot Rural Gondal Lodhika Devda 420 6 1 0 0 427 519 2010-11

Rajkot Rural Gondal Vasavad Devgam Rrc 197 14 2 0 0 213 258 2010-11

Rajkot Rural Jasdan Sardhar Gadhka 207 57 0 0 0 264 311 2010-11

Rajkot Rural Jasdan Jasdan Godladhar 121 6 1 0 0 128 124 2012-13

Rajkot Rural Dhoraji Jetpur (R) Haripar Rrc 43 20 0 0 0 63 85 2010-11

Rajkot Rural Dhoraji Jamkandorana Kobeshwar 140 36 5 0 0 181 273 2010-11

Rajkot Rural Jasdan Jasdan Lilapur 124 4 0 0 0 128 153 2010-11

Rajkot Rural Dhoraji Navagadh Lunagara 313 13 2 0 0 328 389 2011-12

Rajkot Rural Rajkot Rural Div LODHIKA Makhavad 169 3 0 0 0 172 197 2012-13

Rajkot Rural Gondal Rural-2 Mevasha 151 16 5 0 0 172 175 2012-13

Rajkot Rural Rajkot Rural Div Paddhari Mota Rampar 268 7 4 0 0 279 327 2012-13

Rajkot Rural Rajkot City-3 Mpsd Rajdan 238 27 7 0 0 272 360 2011-12

Rajkot Rural Rajkot City-3 RSD Ranpur 134 13 4 0 0 151 214 2012-13

Rajkot Rural Jasdan Vinchhiya Sanali 232 19 0 0 1 252 357 2010-11

Rajkot Rural Rajkot City-3 RSD Sanosara 166 2 0 0 0 168 218 2010-11

Rajkot Rural Rajkot Rural Div Paddhari Thoriyali 323 25 0 0 1 349 464 2010-11

Surendranagar Dhangadhra Dhangadhra Rural Akalvad 3 27 15 3 0 48 36 2012-13

Surendranagar Surendranagar-2 Than Anandpur 64 89 10 1 0 164 179 2010-11

Surendranagar Surendranagar-2 Muli Bali 1 17 37 7 0 62 45 2010-11

Surendranagar Surendranagar-1 Chuda Borana 0 200 2 0 0 202 111 2008-09

Surendranagar Surendranagar-2 Than Dada # 2011-12

Surendranagar Surendranagar-2 Sayla Devgadh # 2011-12

CO

NF

IDE

NT

IAL

Fin

al R

eport

Co

st B

en

efit A

na

lysis

of K

isan

Hit U

rja S

ha

kti Y

oja

na

(KH

US

H

14

MC

B/IS

A/A

/0/0

10 A

pril 2

014

P:\A

hm

edabad\A

MC

\PR

OJE

CT

S\3

26672A

A01\D

ocum

ents

\Report\G

UV

NL - K

HU

SH

Y - F

inal R

eport-V

3.d

ocx

Circle Division Sub-Division Feeder 10 KVA 16 KVA 25 KVA 63 KVA 100 KVA Total

Project Cost

(Lakhs) Year of

Completion

Surendranagar Surendranagar-2 Sayla Fulgram 0 302 5 0 0 307 160 2008-09

Surendranagar Surendranagar-2 Than Gebinath 40 20 4 0 0 64 57 2012-13

Surendranagar Dhangadhra Bavli Jayshakti 17 11 20 5 0 53 68 2009-10

Surendranagar Surendranagar-1 Chuda Keriya 69 2 1 0 0 72 72 2012-13

Surendranagar Surendranagar-2 Than Khakharathal 32 64 10 0 0 106 138 2011-12

Surendranagar Surendranagar-2 Muli Khatdi 41 65 39 10 0 155 114 2010-11

Surendranagar Dhangadhra Rajsitapur Meghdev 0 11 9 5 0 25 33 2011-12

Surendranagar Surendranagar-2 Sayla Nagadka 70 9 2 0 0 81 83 2012-13

Surendranagar Dhangadhra Bavli Narichana 1 23 23 7 0 54 50 2012-13

Surendranagar Surendranagar-1 LSDR Navi Morvad # 2008-09

Surendranagar Surendranagar-2 Sayla Noli 129 61 10 0 2 202 219 2010-11

Surendranagar Surendranagar-2 SRSD Pandavra 54 40 15 12 0 121 140 2011-12

Surendranagar Surendranagar-2 Muli Ramperda 4 6 20 6 0 36 23 2010-11

Surendranagar Surendranagar-1 LSDR Sardar # 2008-09

Surendranagar Dhangadhra Bavli Siddhanath 4 2 27 24 1 58 81 2009-10

Total 17993 5779 1627 549 122 26070 30687.56

# Data Included in Parent Feeder

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

15

The primary beneficiaries of Kisan Hit Urja Shakti Yojana (KHUSHY) are the agricultural consumers and

the individual distribution companies. While the agricultural consumers were expected to benefit with

quality voltage, freedom from frequent interruptions, timely supply or power, reduction of maintenance

costs, the distribution companies were expected to benefit from drastically reduced transmission and

distribution losses. To understand the actual benefits accrued by the agricultural consumers and in line

with the terms of reference a consumer perception study of agricultural consumers was conducted. The

approach and methodology adopted for the study is as given below

4.1 Approach and Methodology

The consultants have adopted a scientific methodology for the current study which was finalized in

consultation with GUVNL. The basic approach was primarily to design a sample which would represent all

the distribution companies adequately and to extract information from the consumers on several

parameters which can give a holistic understanding of the impact of the scheme.

4.1.1 Sample Design

As per the terms of reference the consumer perception survey had to be done for a sample size of 5% of

the total benefitted consumers which stand at around 65000 Nos. to assess the benefits to the consumer

due to implementation of KHUSHY (HVDS) scheme. Hence the sample size for the survey had to be

around 3250 Nos. The survey has been conducted for 3265 HVDS customers. The distribution of the

sample among the distribution companies and further at circle and feeder level has been done on the basis

of the actual conversion of feeders under KHUSHY (HVDS).

The details of sample design for PGVCL is as under

Table 4.1: Details of conversion of feeders under KHUSHY

Discom Circle Division Sub-Division No. of Feeders No. of Beneficiaries

PGVCL 10 17 24 29 2865

Source: Information submitted by DISCOMs

The sample distribution for the consumer perception study PGVCL is as given in the table below

Table 4.2: Sample Distribution

Discom Circle Division Sub-Division Name of Feeder No. of Beneficiaries

PGVCL Bhavnagar

Bhavnagar City – 2 Ghogha Hathab 110

Bhavnagar Rural Vartej Khokhara 173

Vavdi Sanosar 79

Jamnagar Jamjhodpur Bhanvad Gunda 151

Jamjhodpur- East

Sidsar 95

4 Consumer Perception of Kisan Hit Urja Shakti Yojana (KHUSHY) – PGVCL

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

16

Discom Circle Division Sub-Division Name of Feeder No. of Beneficiaries

Junagadh JND - 1 Bhesan Bhatgam 106

Bilkha Swami 180

Kutch Anjar Anjar - R1 Bhalot 71

Bachau Rapar Khengarpar 78

Bhuj Madhapar Vavdi 33

Morbi Halvad Sara Ambavadi 118

Morbi Tankara Hadmatiya 119

Porbandar Porbandar – R Ranavav Bordi 110

Kutiyana Khodiyar 147

RRC RRD Paddhari Mota Rampar 139

Gondal Lodhika Devda 72

Lodhika Devda/Und 60

Jetpur Dedarava Dedarava 38

Lunagara Kerali 32

Dedarava Rupavati 50

Dedarava Arab Timbdi 55

Kobeshwar AG Dadvi 11

Kobeshwar AG Kanavadala 34

Surendranagar SNR1 Chuda Borana 113

LSDR Navi Morvad 109

Amreli Amreli-2 Kukavav Vavdi Road 189

Talali AG 136

Botad Botad Gadhada-R Pipal 88

Gadhada Dhasa Patana 37

Sitapar 132

Total PGVCL 2865

Source: IMM Field Survey

4.1.2 Questionnaire Design

The consultants have used a pre-designed questionnaire as a research tool for the consumer perception

study. The approach while designing the questionnaire was to extract information on several parameters

as to understand the overall impact on the agricultural consumers. The details which the questionnaire

fetched broadly included the following

� Location Details including district, taluka, Discom, circle, division, subdivision and feeder details.

� General Information including name of beneficiary, address, contact details, number of family

members, source of income, land area, cultivation area, ownership of land, year of connection, billing

type, contract demand, connected load, transformer rating etc.

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

17

� Technical Details including voltage quality, line break or shutdown details, transformer failure,

incidence of hooking, crop output and yield, aricultural income etc, power usage details etc.

� Operational Details including average number of days loss per failure, motor maintenance, average

expense per failure, operating days of borewell, operating hours of borewell, number of crops cultivated

during year, income per acre, primary type of crop etc.

� Socio Economic Details including type of house, house hold assets, farm assets, number of cattle etc.

� Broad view and suggestion on the implementation of KHUSHY

The questionnaire includes 51 broad questions in total. A copy of the questionnaire has been appended

with the report.

4.2 Key Results of Consumer Perception Study - PGVCL

The consultants have surveyed a total of 2865 agricultural consumers across PGVCL. The key survey

results are as given below

4.2.1 General Information

The General Information including name of beneficiary, address, contact details, number of family

members, source of income, land area, cultivation area, ownership of land, year of connection, billing type,

contract demand, connected load, transformer rating etc. we gathered during the field survey. The analysis

of the same are given in subsequent sections.

4.2.1.1 Source of Income

Economic resources have a significant direct impact on family wellbeing, as family members depend on

each other to meet basic needs and attain a certain standard of living. Changes to economic

circumstances (such as reduced income or wealth, or increased expenditure needs) may prevent a family

from being able afford necessary or desirable items or services. It is coherent that in order to sustain the

family wellbeing (dependency of family members on the head of the family), The source of income needs

to be upheld.

From the below table 4.4 the relationship between the family wellbeing and the source of income can be

depicted. Out of the 2865 beneficiaries surveyed, 100% have their major source of income as Agriculture

with 72% of them having 4-7 dependent family members, 11% having 1-4 family members dependent,

13% having 7-10 family members dependent and 4% having >10 family members dependent on the

income & earnings of the head of the household.

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

18

Figure 4.1: Number of Family Members Figure 4.2: Source of Income

Source: IMM Analysis Source: IMM Analysis

Table 4.3: Number of Family Members and Source of Income

No of Family Members No of Respondents Primary Source of Income No of Respondents

1-4 300 Agriculture 2865

4-7 2054

7-10 371

>10 122

Total 2865 Total 2865

Source: IMM Analysis

Continuing to achieve the economic prosperity it is equally important to have ownership of the assets &

basic amenities (such as land, house, utilities etc.) which are contributing in the family well-fare and at the

same time in maintaining the living standards.

Out of 2865 Beneficiaries surveyed, 96 % of them were having land of their own whereas only 6% of the

totals were using land on lease for cultivation of crops and carry out their agricultural activities. It was also

observed that 62% of them were having Metered connections whereas 38% of them were un-metered

connections.

11%

72%

13%

4%

1-3

4-7

7-10

>10

100%

0%

Agriculture

Others

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

19

Figure 4.3: Ownership of Land Figure 4.4: Billing Type

Source: IMM Analysis Source: IMM Analysis

Table 4.4: Ownership of Land and Billing Type

Ownership of Land Number of Respondents Billing Type Number of Respondents

Owned 2753 Metered 1777

Leased 112 Un-Metered 1088

Total 2865 Total 2865

Source: IMM Analysis

To cater the power demand & supply needs of the state under the KHUSHY scheme across DISCOMs,

erection of new transformers and HVDS supply lines have taken place to enable the agricultural

consumers to receive benefits like assured quality supply of power with the aim to improve reliability.

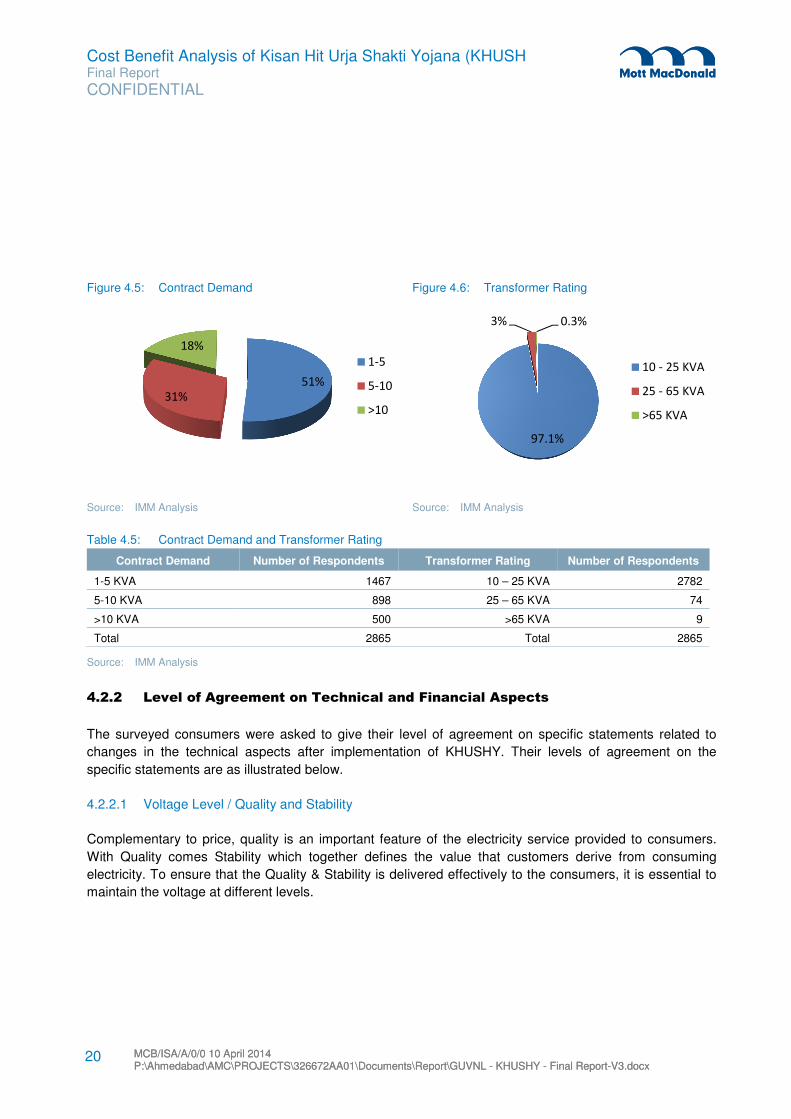

In view of the same & as an effective outcome, Table 4.6 below , depicts that out of the 2865 beneficiaries

surveyed, 51% of were having contractual demand in the range of 1-5 KVA, 31% were having in the range

of 5-10 KVA and the remaining 18% were having in the range of > 10 KVA.

It was also found that almost 97% of the total 2865 beneficiaries were having distribution transformers

having ratings in the range of 10- 25 KVA, 3% of them were using transformers with ratings in the range of

25 – 65 KVA and only 0.3% were having transformers with ratings in the range of > 65 KVA.

96%

4%

Owned

Leased 62%

38%

Metered

Un-Metered

Cost Benefit Analysis of Kisan Hit Urja Shakti Yojana (KHUSH Final Report

CONFIDENTIAL

MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx MCB/ISA/A/0/0 10 April 2014 P:\Ahmedabad\AMC\PROJECTS\326672AA01\Documents\Report\GUVNL - KHUSHY - Final Report-V3.docx

20

Figure 4.5: Contract Demand Figure 4.6: Transformer Rating

Source: IMM Analysis Source: IMM Analysis

Table 4.5: Contract Demand and Transformer Rating

Contract Demand Number of Respondents Transformer Rating Number of Respondents

1-5 KVA 1467 10 – 25 KVA 2782

5-10 KVA 898 25 – 65 KVA 74

>10 KVA 500 >65 KVA 9

Total 2865 Total 2865

Source: IMM Analysis

4.2.2 Level of Agreement on Technical and Financial Aspects

The surveyed consumers were asked to give their level of agreement on specific statements related to

changes in the technical aspects after implementation of KHUSHY. Their levels of agreement on the

specific statements are as illustrated below.

4.2.2.1 Voltage Level / Quality and Stability

Complementary to price, quality is an important feature of the electricity service provided to consumers.

With Quality comes Stability which together defines the value that customers derive from consuming

electricity. To ensure that the Quality & Stability is delivered effectively to the consumers, it is essential to

maintain the voltage at different levels.

51%

31%

18%

1-5

5-10

>10

97.1%

3% 0.3%

10 - 25 KVA

25 - 65 KVA

>65 KVA