COOPETITION AMONGST HOTELS IN SOUTH AFRICA A ...

178

COOPETITION AMONGST HOTELS IN SOUTH AFRICA A CASE STUDY OF COOPETITION AMONGST FIVE-STAR HOTELS IN CAPE TOWN, SOUTH AFRICA Kerrin Titmas Research report presented in partial fulfilment of the requirements for the degree of Master of Business Administration at the University of Stellenbosch Supervisor: J Volschenk Degree of confidentiality: A December 2012

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of COOPETITION AMONGST HOTELS IN SOUTH AFRICA A ...

COOPETITION AMONGST HOTELS IN SOUTH AFRICA

A CASE STUDY OF COOPETITION AMONGST FIVE-STAR

HOTELS IN CAPE TOWN, SOUTH AFRICA

Kerrin Titmas

Research report presented in partial fulfilment

of the requirements for the degree of

Master of Business Administration

at the University of Stellenbosch

Supervisor: J Volschenk

Degree of confidentiality: A December 2012

ii

Declaration

By submitting this research report electronically, I, Kerrin Titmas, declare that the entirety of the

work contained therein is my own, original work, that I am the owner of the copyright thereof

(unless to the extent explicitly otherwise stated) and that I have not previously in its entirety or in

part submitted it for obtaining any qualification.

K Titmas October 2012

Copyright © 2012 Stellenbosch University All rights reserved

iii

Acknowledgements

My sincere gratitude goes to Jako Volschenk of the University of Stellenbosch Business School,

under whose supervision I compiled this research report. Without his guidance and patience, the

completion of this report would not have been possible. I acknowledge his passion for the

academic world and his desire to make a meaningful contribution to adult learning. His passion for

the topic coopetition certainly was very inspiring.

My appreciation goes to all those who gave willingly of their time to conduct interviews with me in

order to contribute to the of tourism and hospitality research. Lastly, thanks to all my friends who

teased me for taking 4 years to complete my research.

iv

Abstract

Coopetition is the simultaneous cooperation and competition amongst competitors (Gnyawali &

Madhaven, 2001); the objective being mutually beneficial results (Oxford, 2012). It is a fairly new

concept and has not widely been applied to the hospitality industry. Most of the research that exists

on this topic relates to destination marketing, cooperation or competition in tourism and hospitality;

very little looks at coopetition.

The current economic situation, and as its negative impact on the hospitality industry in South

Africa, has provided a need to explore how hotels are able to work together in order to retain their

position in the market as well as gain a competitive edge over one another and other markets.

The primary objective of the research report is to contribute to coopetition theory, specifically in the

hospitality industry. The study is based on research of the interaction between the network of five-

star hotels in Cape Town. It explores their relationships with one another and with other hotels in

South Africa.

The secondary objective is to answer a number of subordinate research questions which provide

insight into the factors that promote or hinder coopetition. It considers the reasons for coopetition,

the role of third parties in the relationship, the impact of geographic location on these relationships,

amongst other factors.

The results of the study have provided insights as to how factors internal and external to the

organisations impact their willingness to cooperate with their competitors. The study determines

reasons for coopetition, activities where it is present and shares the impact of the coopetitive

initiatives to date. It confirms some of the existing theory and highlights areas where there is scope

for future research.

Key words:

Competition

Coopetition

Destination marketing

Hospitality network

v

Table of contents

Declaration ii

Acknowledgements iii

Abstract iv

List of tables x

List of figures xi

List of acronyms and abbreviations xii

CHAPTER 1 ORIENTATION 1

1.1 INTRODUCTION 1

1.2 PROBLEM STATEMENT 1

1.3 RESEARCH OBJECTIVES 1

1.3.1 Primary Objective 2

1.3.2 Secondary Objectives 2

1.4 LITERATURE REVIEW 3

1.4.1 Tourism and hospitality 3

1.4.2 Coopetition 4

1.4.3 Cooperation 5

1.4.4 Competition 5

1.4.5 Business networks 6

1.4.6 Destination marketing 7

1.5 CLARIFICATION OF KEY CONCEPTS 8

1.5.1 Competitive advantage 8

1.5.2 Market 8

1.5.3 Market share 8

1.5.4 Brand equity 8

1.5.5 Hotel occupancy 8

1.5.6 Economic recession 8

1.5.7 Marketing 9

1.5.8 Five-star hotel 9

1.5.9 City of Cape Town 9

1.6 IMPORTANCE / BENEFITS OF THE STUDY 9

1.7 DELIMITATION OF THE STUDY 10

1.8 RESEARCH DESIGN AND METHODOLOGY 10

vi

1.8.1 Sampling 11

1.8.2 Questionnaire design and data collection 11

1.8.2.1 Questionnaire 11

1.8.2.2 Data collection – Interviews 12

1.8.3 Data analysis 12

1.9 CHAPTER OUTLINE 13

1.9.1 Chapter One – Introduction 13

1.9.2 Chapter Two – Literature Review 13

1.9.3 Chapter Three – Research methodology 13

1.9.4 Chapter Four – Analysis and interpretation 13

1.9.5 Chapter Five – Conclusion and recommendations 13

1.10 NATURE AND FORM OF RESULTS 13

1.11 CONCLUSION 14

CHAPTER 2 LITERATURE REVIEW 15

2.1 INTRODUCTION 15

2.2 TOURISM AND HOSPITALITY 15

2.2.1 Tourism 15

2.2.2 Hospitality in South Africa 17

2.3 COOPETITION 21

2.3.1 Definition 21

2.3.2 A form of cooperation or a discipline on its own? 21

2.3.3 Coopetition as a vertical or horizontal relationship 22

2.3.4 Types of coopetition 23

2.3.5 Levels of coopetition 23

2.3.6 Impacts of coopetition 27

2.3.7 Balancing cooperation and competition 28

2.3.8 The role of customers in coopetition 28

2.3.9 The role of third party organizations in coopetition management 29

2.3.10 Critical factors for coopetition to succeed 31

2.3.10.1 Management commitment 31

2.3.10.2 Leadership development of trust 32

2.3.10.3 Long-term commitment 33

2.3.11 Using game theory to explain coopetition 33

2.3.12 Coopetition in tourism 34

vii

2.4 COOPERATION 36

2.4.1 More formal types of cooperation 36

2.4.2 Cooperation amongst competing organisations 39

2.4.3 Causes of conflict in inter-competitor cooperation 39

2.4.4 Barriers to cooperation 40

2.4.5 Formalising cooperative relationships between organisations 40

2.5 COMPETITION 40

2.5.1 Porters Five Forces Model of Competition 41

2.5.2 Driving Forces 44

2.6 BUSINESS NETWORKS 45

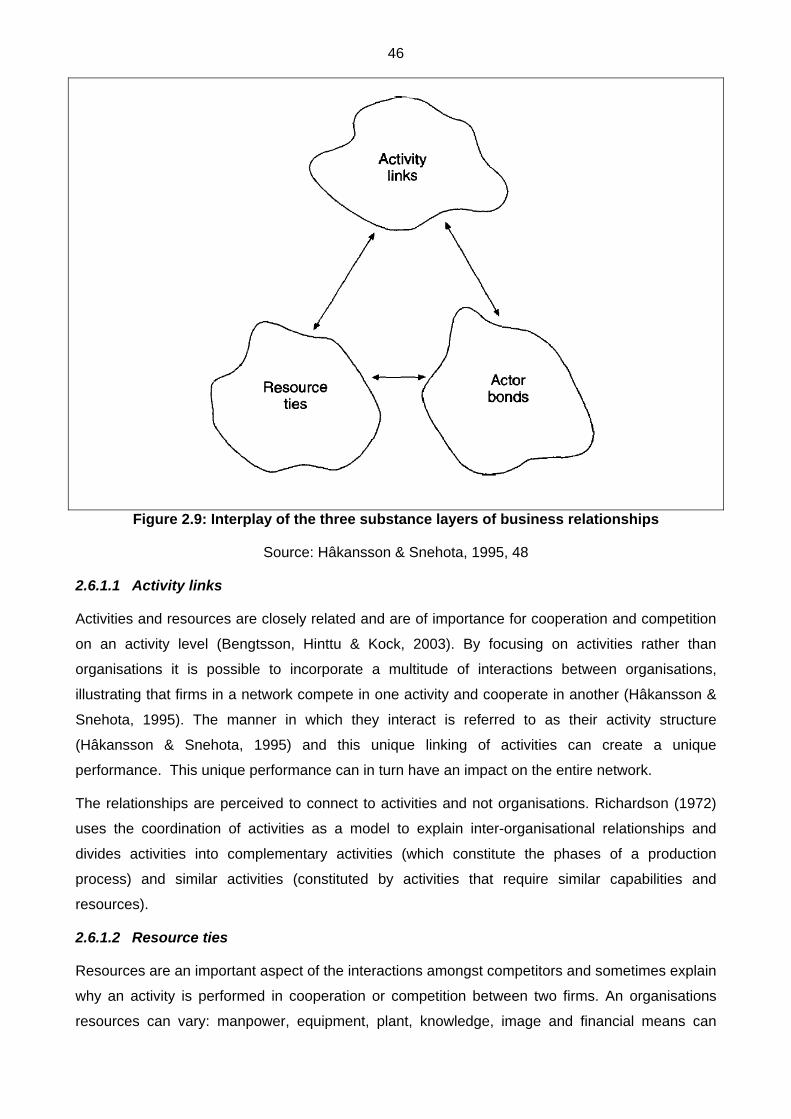

2.6.1 The substance of business relationships 45

2.6.2 Functions of business relationships 47

2.6.3 Relationships between business networks 49

2.6.4 Relationships between competitors in business networks 49

2.6.5 Factors affecting relationships 49

2.6.6 Impacts of change in business networks 50

2.6.7 Networks in tourism marketing 50

2.7 DESTINATION MARKETING 51

2.7.1 Structuring a Destination Marketing Organisation 53

2.7.2 Funding a DMO 54

2.7.3 Key duties of a DMO 54

2.8 SUMMARY 55

CHAPTER 3 RESEARCH METHODOLOGY 56

3.1 INTRODUCTION 56

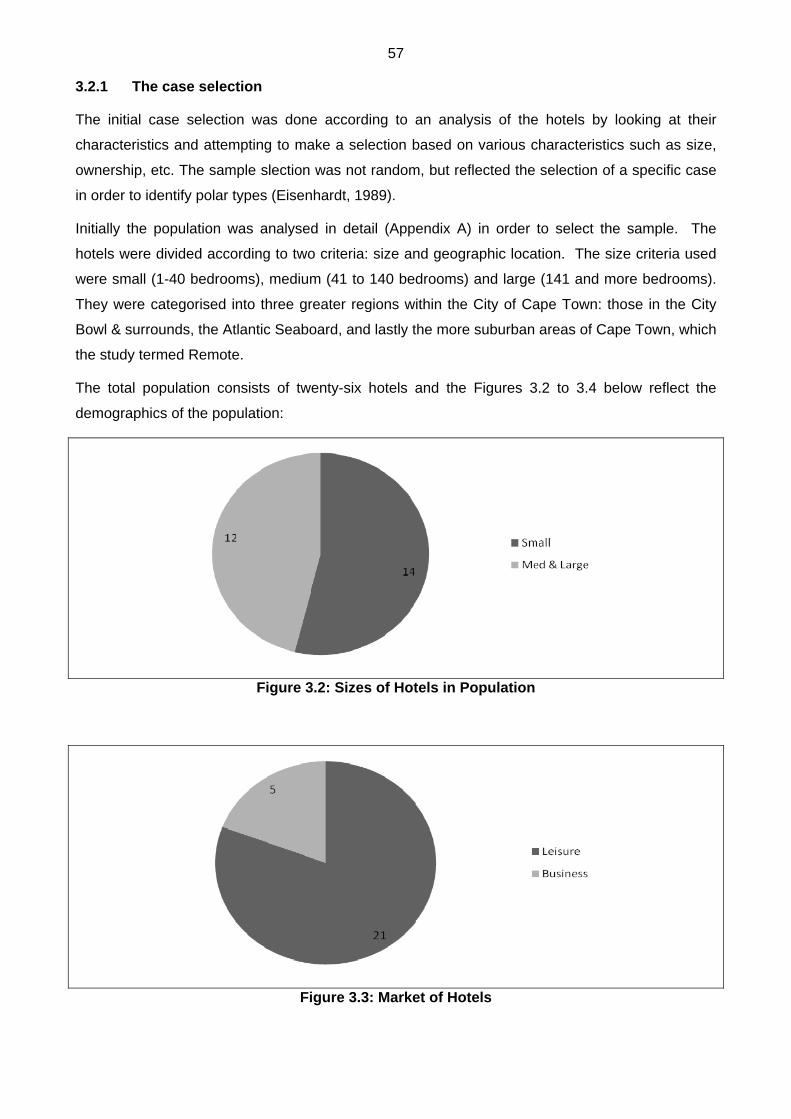

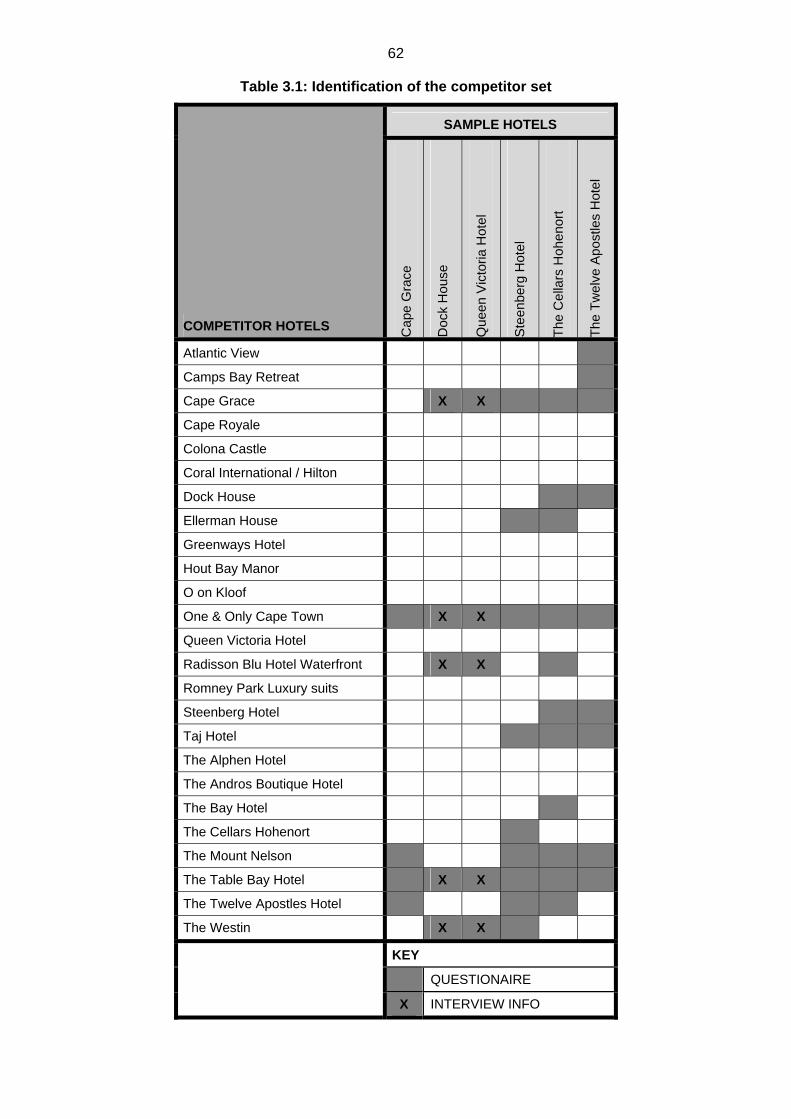

3.2 THE POPULATION AND SAMPLE 56

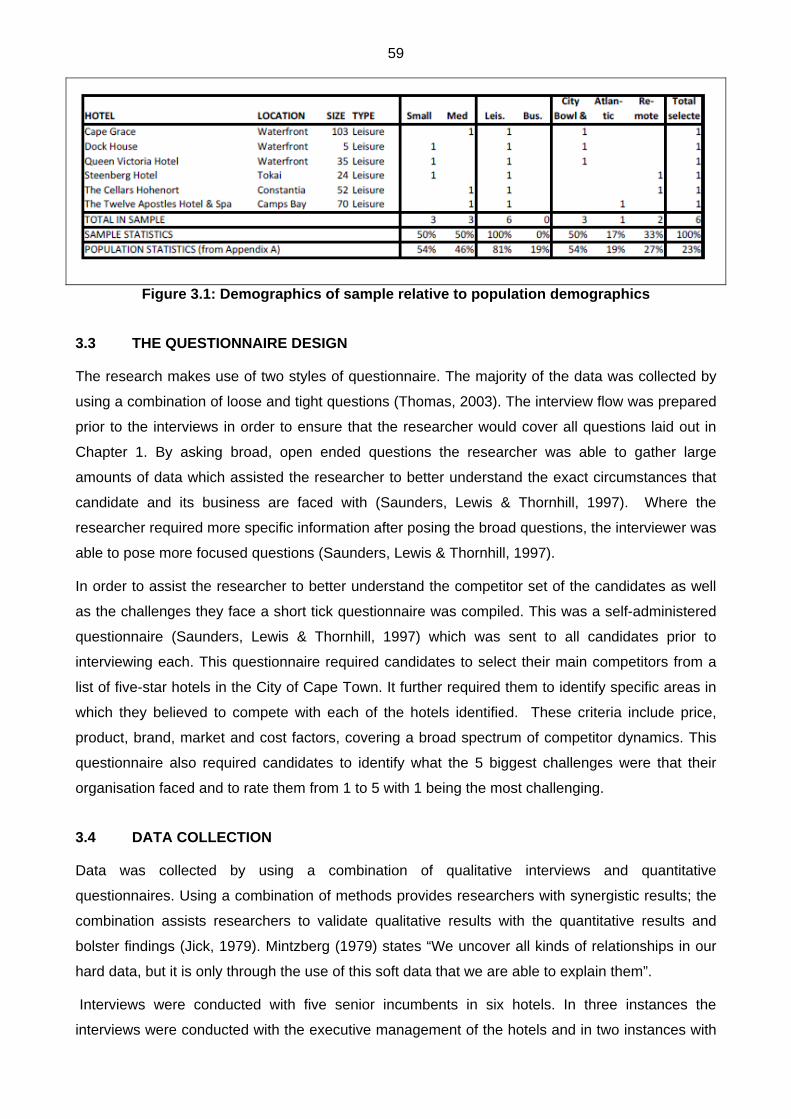

3.2.1 The case selection 57

3.3 THE QUESTIONNAIRE DESIGN 59

3.4 DATA COLLECTION 59

3.5 DATA ANALYSIS 61

3.5.1 Checklist data 61

3.5.2 Interview data 63

3.5.3 Interpretation of the data 63

3.5.4 Potential bias 63

CHAPTER 4 FINDINGS 65

4.1 INTRODUCTION 65

viii

4.2 THE PROFILE OF RESPONDENTS 65

4.3 ANSWERING THE RESEARCH QUESTIONS 65

4.3.1. RQ1: What is the nature of the relationships (both collaborative and competitive) between five star hotels in the City of Cape Town? 65

4.3.2. RQ2: What relationships (both collaborative and competitive) do these hotels have with hotels outside of the region? 68

4.3.3. RQ3: On what level do the hotels consider themselves to be competitors? 71

4.3.4. RQ4: What kinds of activities and initiatives do these hotels collaborate on? 72

4.3.5. RQ5: Why do these hotels collaborate with other competitor hotels? 73

4.3.6. RQ6: What has the impact been of the coopetition initiatives they have engaged in, both with one another and other hotels in South Africa? 73

4.3.7 RQ7: What potential there is to expand on these relationships in order to benefit these hotels? 74

4.3.8 RQ8: What factors contribute to the varied relationships between each of the hotels? 76

4.3.9 RQ9: What role do third parties play in promoting coopetition amongst hotels in the region? 79

4.3.10 RQ10: What factors hinder coopetition amongst the hotels in question? 80

4.3.11 RQ11: What potential exists for future cooperative joint marketing initiatives? 80

4.3.12 RQ12: What differences exist between the coopetition patterns practiced by hotels in similar regions, different regions and with similar product offerings? 81

CHAPTER 5 SUMMARY, CONCLUSION AND RECOMMENDATIONS 83

5.1 INTRODUCTION 83

5.2 SUMMARY OF MAIN FINDINGS 83

5.2.1 Network findings 83

5.2.2 Factors affecting coopetition 85

5.2.3 Reasons to coopete 86

5.2.4 Benefits of coopetition initiatives 86

5.3 RECOMMENDATIONS 86

5.4 FURTHER RESEARCH 87

REFERENCES 88

APPENDIX A: HOTELS IN CITY OF CAPE TOWN 97

APPENDIX B: CHECKLIST 98

APPENDIX C: QUESTIONNAIRE 100

APPENDIX D: INTERVIEW WITH GABY GRAMM – STEENBERG 101

APPENDIX E: INTERVIEW WITH NEIL MARKOVITZ, NEWMARK HOTELS 112

APPENDIX F: INTERVIEW WITH TONY ROMER-LEE, McGRATH COLLECTION 123

ix

APPENDIX G: INTERVIEW WITH ANDREW ROSETTENSTEIN, CAPE GRACE 138

APPENDIX H: INTERVIEW WITH BRETT DAVIDGE, 12 APPOSTLES 145

APPENDIX I: CHECKLIST COMPLETED BY G.GRAMM 153

APPENDIX J: CHECKLIST COMPLETED BY A.ROSETTENSTEIN 155

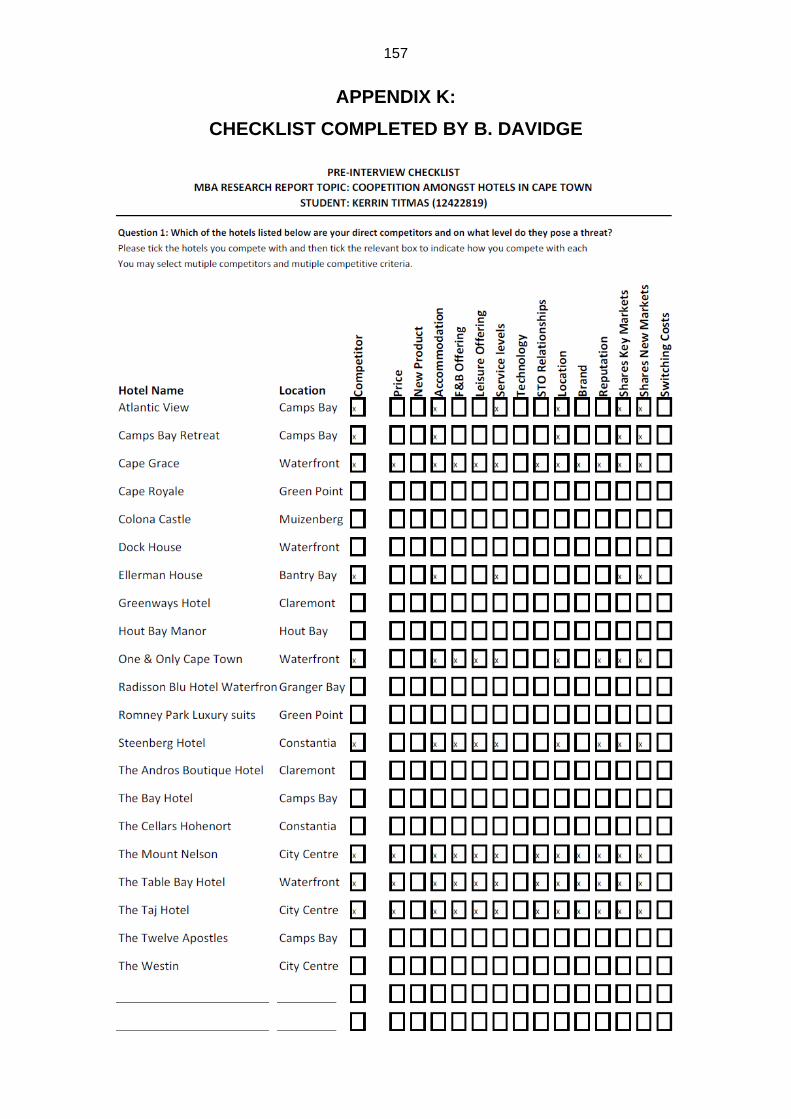

APPENDIX K: CHECKLIST COMPLETED BY B. DAVIDGE 157

APPENDIX L: CHECKLIST COMPLETED BY T.ROMER-LEE 159

APPENDIX M: RESULTS TABLES 161

x

List of tables

Table 1.1: Typology of inter-organisational relationships 3

Table 2.1: Overview of past research on coopetition 22

Table 2.2: Relationships between firms 23

Table 2.3: Types of coopetition 23

Table 2.4: Levels of coopetition 24

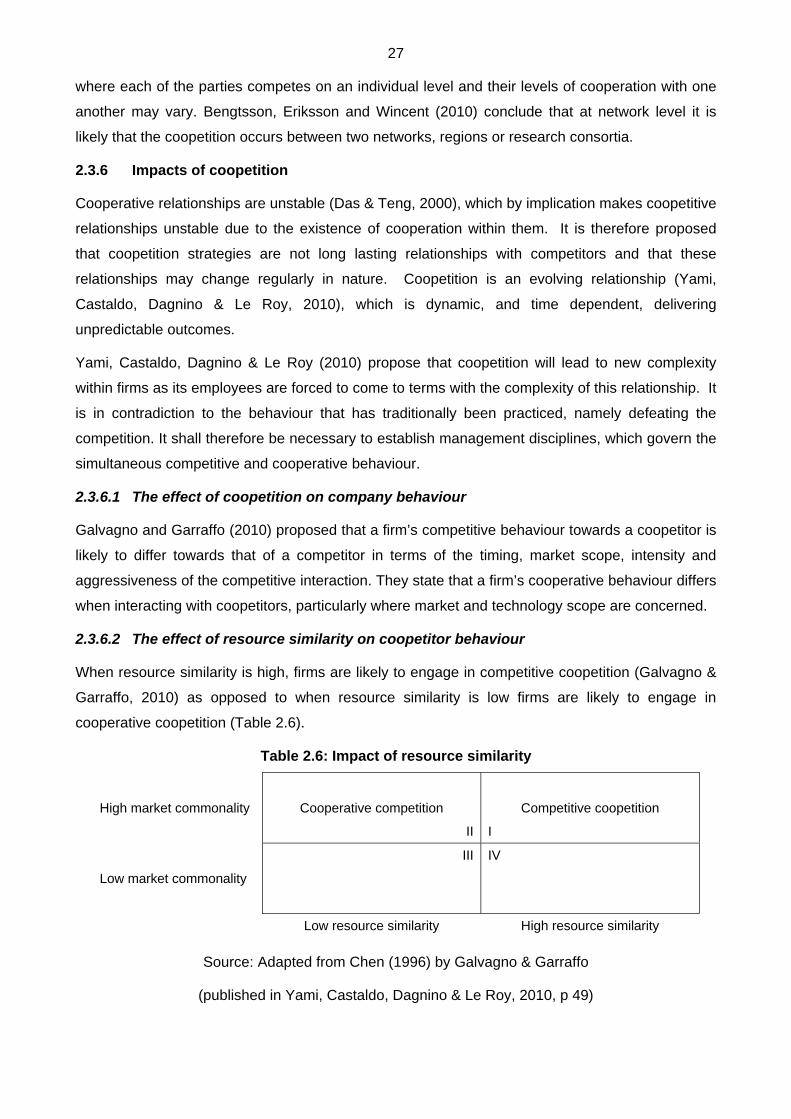

Table 2.6: Impact of resource similarity 27

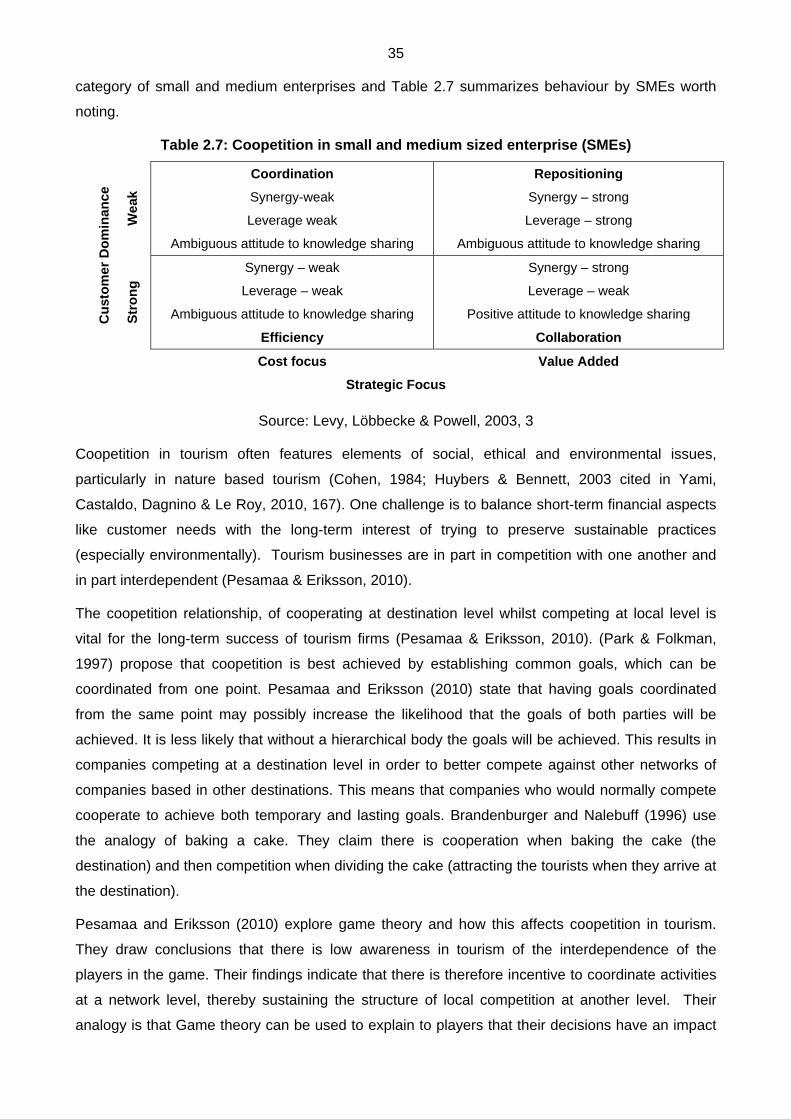

Table 2.7: Coopetition in small and medium sized enterprise (SMEs) 35

Table 2.8: A typology of governance structure 40

Table 3.1: Identification of the competitor set 62

Table 4.1: Respondent profile 65

Table 5.1: Summary of coopetitive activities evident in the networks 85

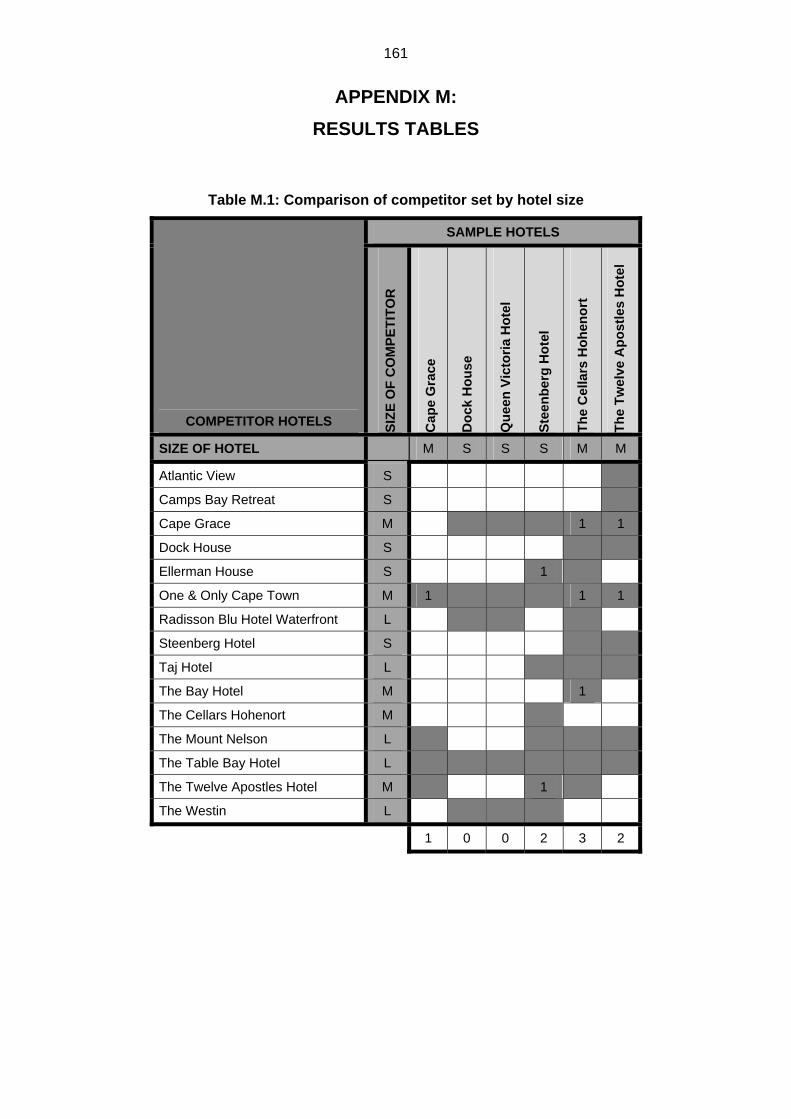

Table M.1: Comparison of competitor set by hotel size 161

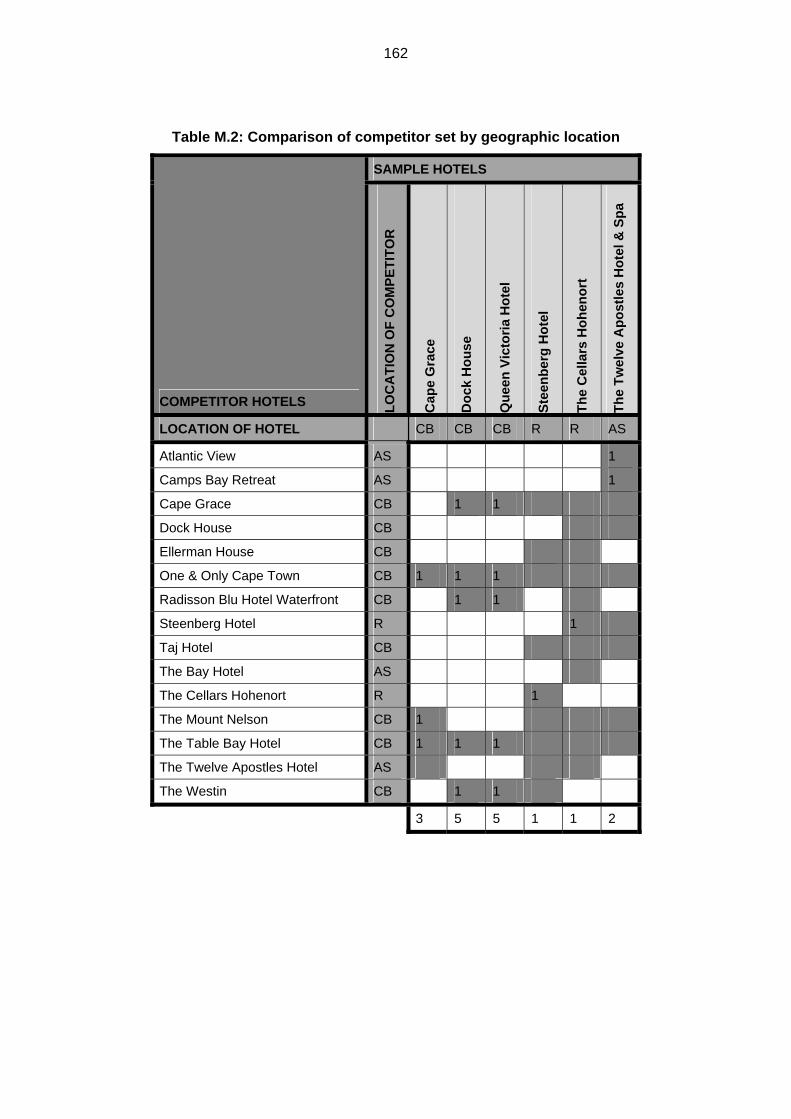

Table M.2: Comparison of competitor set by geographic location 162

Table M.3: Comparison of competitive factors by competitor 163

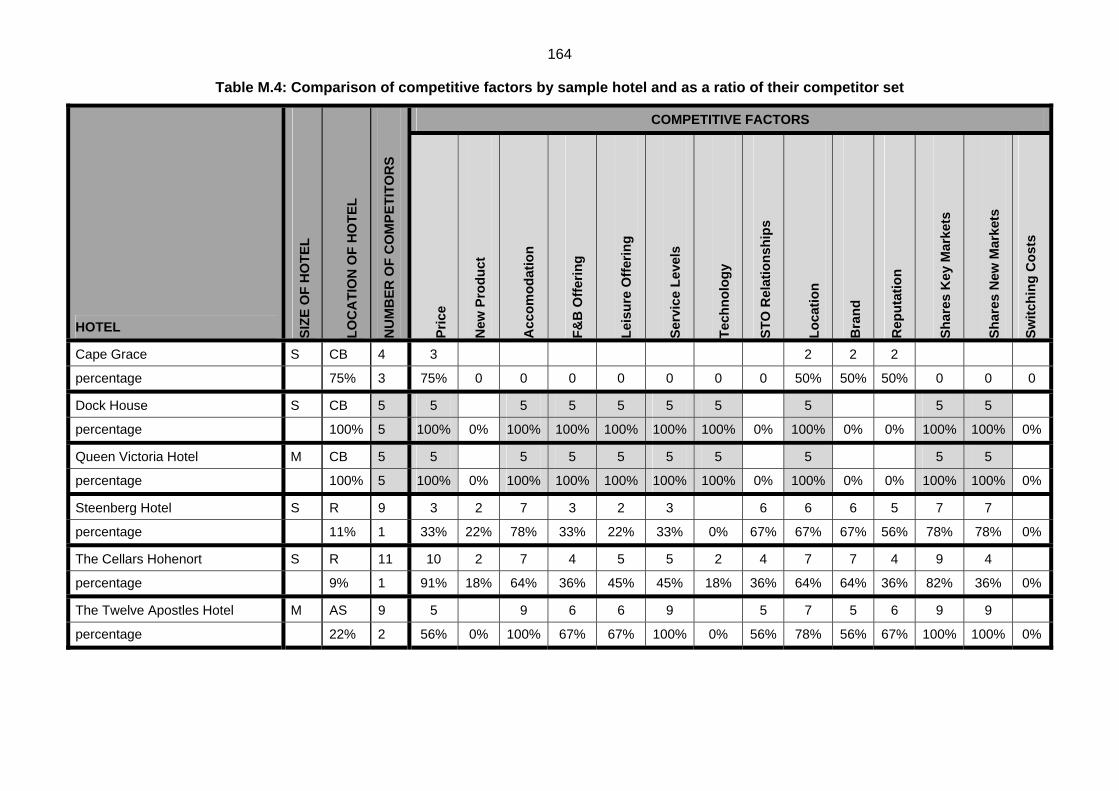

Table M.4: Comparison of competitive factors by sample hotel and as a ratio of their competitor set 164

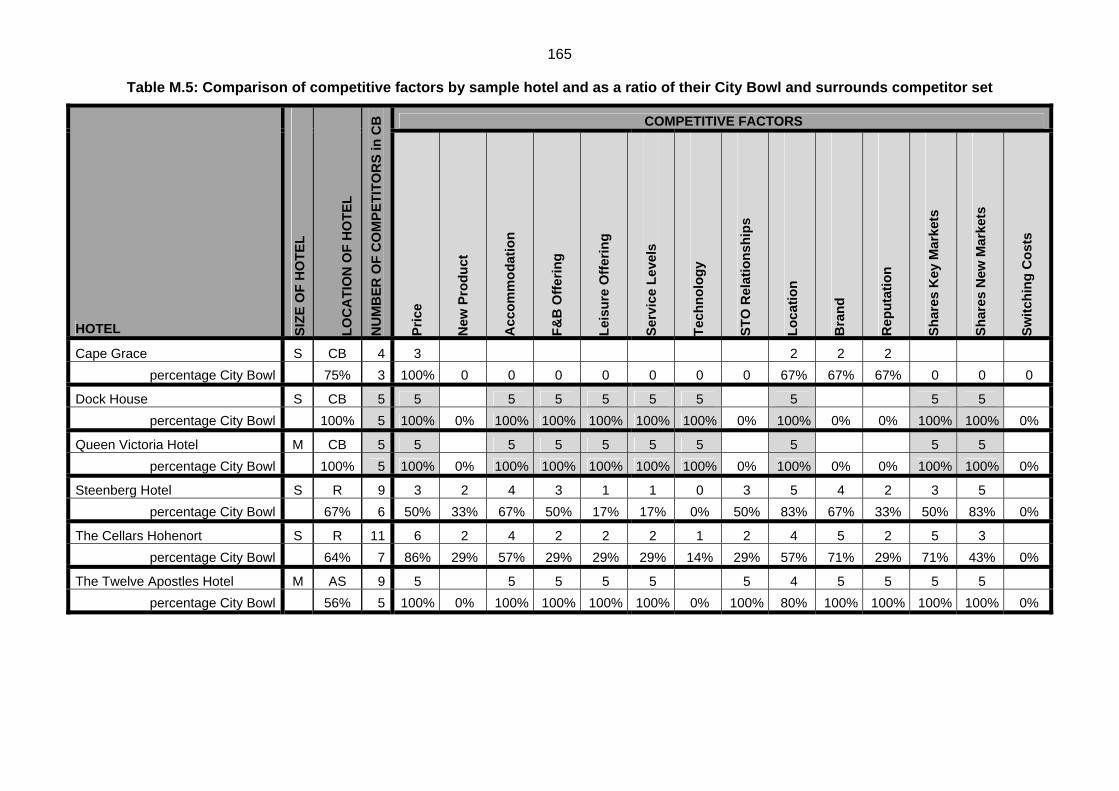

Table M.5: Comparison of competitive factors by sample hotel and as a ratio of their City Bowl and surrounds competitor set 165

Table M.6: Comparison and ranking of key challenges faced by sample hotels 166

xi

List of figures

Figure 1.1: Map of hotel locations 9

Figure 2.1: Domestic and foreign visitors 2004 to 2015 16

Figure 2.2: Accommodation occupancy rates (%) 2006 to 2015 17

Figure 2.3: Number of hotel rooms (thousands) 2005 to 2010 18

Figure 2.4: Hotels - Occupancy rates (%) 2006 to 2015 18

Figure 2.5: Hotels –Summary of statistics 2006 to 2015 19

Figure 2.6: Five-star hotels – Summary of statistics 2006 to 2015 20

Figure 2.7: Total hotel room revenue by category 2010 20

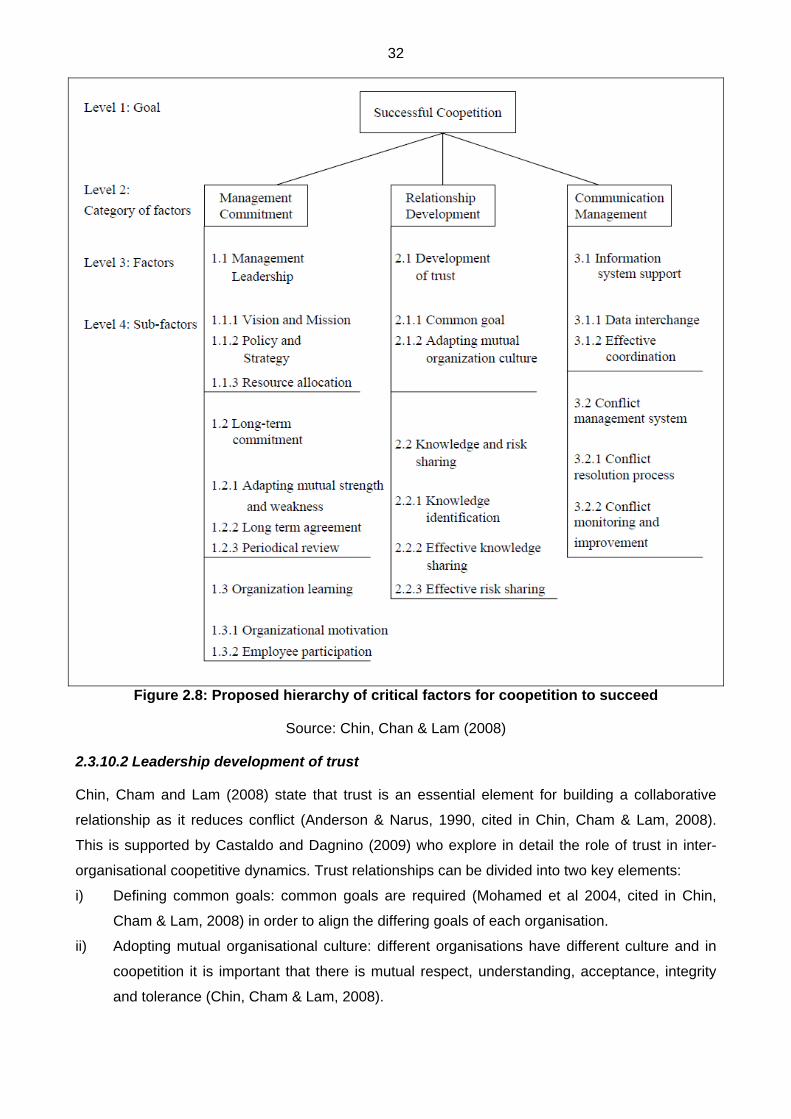

Figure 2.8: Proposed hierarchy of critical factors for coopetition to succeed 32

Figure 2.9: Interplay of the three substance layers of business relationships 46

Figure 2.10: Dyadic function of a business relationship 47

Figure 2.11: Single actor function of a relationship 48

Figure 2.12: Network function of a relationship 48

Figure 3.1: Selection of Population 56

Figure 3.2: Sizes of Hotels in Population 57

Figure 3.3: Market of Hotels 57

Figure 3.4: Geographic location of Hotels 58

Figure 3.1: Demographics of sample relative to population demographics 59

xii

List of acronyms and abbreviations

% Percent

etc. et cetera

FIFA Federated International Football Association

GDP Gross domestic product

GDS Global Distribution System

i.e. that is

LHW Leading Hotels of the World

LTO Local Tourism Organisation

NTA National Tourism Association

NTO National Tourism Organisation

PWC PricewaterhouseCoopers (firm of accountants)

R Rand – South African currency

REVPAR Revenue Per Available Room

RTO Regional Tourism Organisation

SA South Africa

SAGTA South African Golf Tourism Association

SATOUR South African Tourism Association

SME Small to Medium Enterprise

TGCSA Tourism Grading Council of Southern Africa

UNWTO United Nations World Tourism Organisation

1

CHAPTER 1

ORIENTATION

1.1 INTRODUCTION

There is limited research on coopetition theory available that examines the cooperative

relationships amongst competitors in the hospitality industry. Most of the research that is available

considers either the manner in which the hotels cooperate (Porter, 1998; Dyer & Singh, 1998;

Astley & Fombrun, 1983) or compete (Porter, 1980; Zairi, 1996; Ferrier, 2001; D’Aveni, 1994) with

one another, but not how they do both simultaneously.

Little research has considered how hotels that compete for a share of the same market are able to

benefit from cooperation with one another through both formal and informal alliances. With the

increasing number of hotels built globally over the past decade, the downturn in traditional markets

due to the economic recession and the oversupply of hotel accommodation in South Africa it is

important to explore ways in which hotels can work together in order to be sustainable, maintaining

their competitive advantage over one another and other regions.

The specific purpose of this study is to look at the relationships between a number of five-star

hotels in the City of Cape Town and the patterns of coopetition they currently practice. It is an

exploratory study, which compares the behaviour of hotels, and whether there are patterns

relevant to their size, market, geographic location, shareholding and product offering. The study

seeks to highlight similarities and differences in the manner in which they interact with other hotels.

The study further aims to identify how the hotel network currently operates, where the hotels

perceive benefit from their relationships and to explore future opportunities for competitor hotels to

cooperate. The study shall encompass a thorough review of existing literature as well as a series

of one-on-one interviews.

1.2 PROBLEM STATEMENT

The main aim of this study is to answer the following question:

What is the nature of the coopetition relationships between five-star hotels in South Africa and

what potential exists to expand these relationships for the benefit* of these hotels?

*For the purpose of this study, benefit means increase occupancies and/or revenues and/or profits

and/or brand equity.

1.3 RESEARCH OBJECTIVES

The primary research objective was identified prior to formulating the secondary objectives and

providing an overview of the related literature.

2

1.3.1 Primary Objective

This research report is intended to contribute to coopetition theory, specifically in the hospitality

industry. The study is based on research of the current interaction of five-star hotels in the City of

Cape Town with one another and with other hotels in South Africa.

The study was initiated in order to explore the patterns of coopetition that currently exist between

five-star hotels in South Africa. The sample hotels are all located in the City of Cape Town, share

the same broader market, and have similar or complimentary offerings. The study also explores

the relationships these hotels have with hotels outside of this region. It aims to explore the potential

for these hotels to expand their existing marketing networks. It explores whether these hotels use

their networks more for the benefit of their immediate geographic region or across a national

network.

The study explores six hotels, looking at the similarities or differences in patterns of behaviour

amongst them and (1) how they interact with one another i.e. other hotels in the City of Cape

Town, (2) other five-star hotels in South Africa and (3) hotels with an identical product offering or

facility i.e. golf course, winery, etc.

1.3.2 Secondary Objectives

The following subordinate research questions were formulated for this study:

RQ1. What is the nature of the relationships (both collaborative and competitive) between five-

star hotels in the City of Cape Town?

RQ2. What relationships (both collaborative and competitive) do these hotels have with hotels

outside of this region?

RQ3. On what level do the hotels in the study consider themselves competitors?

RQ4. In what kinds of activities and initiatives do these hotels collaborate?

RQ5. Why do these hotels collaborate with other competitor hotels?

RQ6. What has the impact been of the coopetition initiatives they have engaged in, both with

one another and other hotels in SA?

RQ7. What potential there is to expand on these relationships in order to benefit these hotels?

RQ8. What factors contribute to the varied relationships between each of the hotels?

RQ9. What role do third parties play in promoting coopetition amongst hotels in the region?

RQ10. What factors hinder coopetition amongst the hotels in question?

RQ11. What potential exists for future cooperative joint marketing initiatives?

RQ12. What differences exist between the coopetition patterns practiced by hotels in similar

regions, different regions and with similar product offerings?

3

Through the primary and secondary objectives of this research, the study shall bring to light areas,

which it recommends for further study in order to expand on the theory of coopetition in hospitality.

1.4 LITERATURE REVIEW

A thorough review of the literature is provided in Chapter 2, which addresses the questions raised

by the primary and secondary objectives of the study. The literature review first looks at tourism

and particularly the hospitality industry in South Africa in order to give context to the research study

and the need for hotels to cooperate. Next, it broadly outlines coopetition as a concept and then

explores the two components necessary for coopetition, namely cooperation and competition. In

order to provide a better understanding of the relationships that exist in business the literature

review explores business networks, focusing mainly on horizontal networks. It then goes into

specific detail of one particular coopetition relationship which functions across tourism networks

and has been researched in detail, namely destination marketing.

Table 1.1 provides illustrates the varied relationships which exist between organisations, showing

both their vertical and horizontal nature. This provides a good framework from which to explore the

literature.

Table 1.1:- Typology of inter-organisational relationships

Dir

ecti

on

of

Rel

atio

nsh

ip

Ver

tica

l

Arms length exchange Vertical multifaceted

relationships Alliances between buyers

and suppliers

Ho

rizo

nta

l

Traditional competitive markets

Horizontal multifaceted relationships

Alliances between non-competitors

Competition Coopetition Cooperation

Source: Dowling et al. 1996. p 156

1.4.1 Tourism and hospitality

Tourism is a common term, widely used in everyday language. The term often overlaps with the

concepts of holidays, travel, hospitality and leisure. Definitions of tourism are broad and vary

depending on the context. The Concise Oxford Dictionary (1976) defines tourism as “the provision

of things and services that attract tourists”. The United Nations World Tourism Organisation (WTO,

2011) identifies tourism as a key driver for socio-economic progress.

Over the decades, in South Africa and internationally, tourism has experienced continued growth

and has been one of the fastest growing economic sectors in the world. More recently a number of

new destinations have established themselves (WTO, 2011) creating greater competition for a

share of market. Globally the volume of tourism equals and in some instances surpassed that of

the export of oil, food products and automobiles. Tourism is one of the major players in the

4

international arena and is one of the main income sources for many countries (WTO, 2011),

including South Africa (South African Tourism, 2010).

Hospitality is defined by Business Dictionary (2011) as “hotels, motels, inns or such businesses

that provide transitional or short-term lodging, with or without food”. PWC released a study on the

South African hospitality industry (2011) which, following the economic downturn in 2009 and the

2010 FIFA World Cup, predicts how the hospitality industry in South Africa could develop from

2011 until 2015. The study outlines that the global recession affected economic activity and

translated into steep declines in both foreign and domestic travel. It confirms that R13.9billion was

spent on hospitality related activities during the 2010 FIFA World Cup, reflecting a rise in income

during that time, but that in 2011 the market returned to its pre World Cup declining trend. PWC

(2011) projected a fall of 7.1% in revenue in 2011.

The South African economy experienced a long-term growth phase from 1999 until 2008. Real

economic growth averaged at 4% per annum during this period, the longest upward cycle in

history. In 2004, domestic tourism and travel took off and between 2004 and 2006, the number of

visitors to and within South Africa almost doubled. Between 2006 and 2008, there was further

growth of around 9%. During the period, 2005 to 2010 there was a large amount of investment in

new product, and during the period 2005 to 2008, 1600 rooms were introduced to the market. A

further 9700 rooms were added between 2008 and 2010 (PWC, 2011). South Africa now faces an

oversupply of hotel rooms during a stage of economic downturn and low future growth potential.

1.4.2 Coopetition

Bengtsson and Kock (2000) define coopetition as “a dyadic and paradoxical relationship emerging

when two firms are cooperating in some activities, while competing with each other in the

remaining activities”. Brandenburger and Nalebuff (1996) define coopetition as “simultaneous

cooperation and competition”. Gnyawali and Madhaven (2001) were amongst those who

introduced the term.

Bengtsson and Kock (2000) argue that competition and cooperation amongst organisations can

co-exist simultaneously. In order for successful simultaneous cooperation and competition to take

place amongst competitors, certain codes of conduct or ground rules need to be in place. An

example of this is the seven-point code of conduct adopted by the parties studied in Grängsjö and

Gummeson’s study (2006). The parties engaged in the coopetition relationship entered into active

dialogue with one another, were efficient in making decisions and implementing them and treated

one another as equals, irrespective of size of their organization or financial contribution made.

They established a relationship of trust amongst the parties concerned, sharing information,

meeting regularly face to face and lastly having fun whilst engaging.

Coopetition is possible on a variety of levels in organisations and Koza and Lewin (1998) believe

that the proximity of an activity to its customer is relevant to the level of cooperation or competition

5

that occurs. They believe that companies compete in activities close to the customer and

cooperate in activities far from the customer. Proximity of the activity to the customer and trust

relationships are two important concepts, which come up repeatedly in coopetition theory (Putnam,

1993; Morgan & Hunt, 1994). Trust and shared values amongst the parties are as important as

the existence of competition is (Brandenburger & Nalebuff, 1996; Porter, 1998; Gummesson,

2002).

1.4.3 Cooperation

Cooperation is defined by the Shorter Oxford English Dictionary (2006) as the action of working

together for the same purpose or in the same task. It expands this definition as “the combination of

a number of individuals in an economic activity so that all may share in the benefits”. Cooperation

is a concept in direct paradox to competition and transpires when companies, divisions of

companies and functions within companies work together (Dyer & Singh, 1998). Cooperation

focuses on joint strategies for adding value to two or more businesses (Gnyawali & Madhaven,

2001). By cooperating companies strengthen their competitive advantage; forming strategic

alliances, networks and strategic ecosystems (Astley & Fombrun, 1983).

Cooperation describes the links, which bring organisations together, enhancing their ability to

compete in the market place (Lynch, 1990). According to Wang and Krakover (2008) there are four

types of cooperative relationships; namely affiliation, coordination, collaboration and strategic

networks. Another cooperative relationship encountered in the literature review is a strategic

alliance. Where marketing is specifically concerned Palmer (2002) recognised that cooperative

marketing groups are groups of independent businesses who recognise the value of developing a

market as a joint initiative as opposed to doing so alone.

Cooperation amongst companies in geographic proximity is a powerful factor which contributes to

the ability of a cluster of companies and each of the companies within the cluster to gain a

competitive advantage over other companies outside of the grouping (Porter, 1998).

1.4.4 Competition

The Shorter Oxford English Dictionary (2006) defines competition as “the act of competing or

contending with others for supremacy, a position or prize”. It expands on this to incorporate that

competition is “the striving for custom between rival traders in the same commodity” as well as the

“interaction between two or more parties that share a limited environmental resource”. Competition

is a term used commonly in strategic management and refers to inter-firm rivalry (Porter, 1980). In

an economic environment, it exists when two or more parties have a common objective and seek

to outperform one another. In economic terms, one refers to “positive sum”, “zero sum” and

“negative sum” competition. A positive sum competition is one in which all parties are better off,

zero sum is where one party is better off at the expense of the others and negative sum is where

all parties are worse off because of the competition (Wankel, 2009).

6

Any firm entering into competition seeks competitive advantage, which also lies at the heart of

competitive success (Porter, 1985). The literature surrounding competition focuses mainly on

strategies to add value or advantage one business over another (Gnyawali & Madhaven, 2001).

According to traditional views price was the most important competitive factor. Factors that did not

relate to price, like quality and innovation, were believed to play a role, but not be as effective as

the role played by price. In economic literature, the only form of cooperation recognised is price

coordination, yet in more recent literature on the private enterprise economy, it is recognised that

the individuals are independent, yet their activities are interrelated (Jorde & Teece, 1989).

Companies have in more recent years had to adopt aggressive or hypercompetitive behaviour in

order to survive in their relevant markets (D’Aveni, 1994).

As times change business are becoming more market driven in their competition strategies and

they are reorganising their businesses to focus completely on the customer. They are utilising

expertise and resources on their core competencies, designing their product to meet the

customer’s needs, improving the speed of their service delivery, establishing added value and

driving customer orientated innovation (Zairi, 1996).

1.4.5 Business networks

Grant and Baden-Fuller (2004) point out that one of the most important trends in the 25 years prior

to them publishing their work, was the increase in companies forming collaborative relationships or

networks. A network is a structure where threads relate a number of nodes to one another. In a

business network, one can view the nodes as the businesses and the threads as the relationships

that exist between them. Inside a business, the nodes can be the individual business units and the

threads the relationships that exist between each business unit (Hâkansson, 1987).

Hâkansson and Ford (2002) point out that a node directly relates to the existence of a thread and

that the content of the threads is because of investment by both of the counterparts i.e. the nodes

on either end of the thread. The greater the investment the more substantial the content of the

thread will be. The more that is invested in the threads, the stronger they become, but the stronger

they become the more restricting they become to the freedom of each node to change. Put more

simply, as businesses work more closely their relationships strengthen, yet as their relationships

strengthen they are more restricted by these relationships.

Strategic tourism networks are formalised structures that integrate the shared vision of all tourism

organizations involved in the network. They take a system orientation in destination marketing.

There are two types of networks in a destination, namely horizontal and vertical networks and the

structure of these varies depending on the kinds of organisations participating in them. Horizontal

networks are those involving organisations that provide similar services, such as the local

restaurant association, whereas vertical networks involve organisations offering different services

(Wang & Krakover, 2008).

7

A tourist destination is a place where a large number of businesses offer varying services to

tourists. Their co existence and relationships to one another and other stakeholders, form various

networks. Tourists are able to vary their product offering by choosing from different goods and

services provided by companies which are located in close proximity to one another, and the

companies involved ultimately compete for a share of wallet (Wang & Krakover, 2008).It is only

possible to practice destination marketing if both networks are in place (Grängsjö & Gummesson,

2006).

In a study one specific successful tourism network the members adhered to three basic principles,

namely showing enthusiasm, giving time and contributing financially to the network. It was further

found that they had to balance their collective interests versus their individual interests, as well as

cooperate and compete whilst following the seven-point code of conduct mentioned earlier.

Understanding the working relationships i.e. network amongst tourism businesses in a destination

is a critical prerequisite of many destination-marketing programmes (Terpstra & Simonin, 1993).

1.4.6 Destination marketing

Wahab et al. (cit. in Pike, 2004) provided the following definition of tourism destination marketing:

“the management process through which the National Tourist Organisations and/or tourist

enterprises identify their selected tourists, actual and potential, communicate with them to

ascertain and influence their wishes, needs, motivations, likes and dislikes, on local, regional,

national and international levels, and to formulate and adapt their tourist products accordingly in

view of achieving optimal tourist satisfaction thereby fulfilling their objectives”.

Tourism differs from manufactured goods industry in three ways. Firstly, the tourist is brought to

the product i.e. the destination. Secondly, the product is consumed simultaneously to it being

produced and thirdly the production of tourism involves a collective cooperative body as well as

individual business competitors within close proximity (Grängsjö & Gummesson, 2005). The

nature of the tourism entity’s participation in destination marketing can vary from a loosely

connected relationship to a more formal and integrated relationship. Informal affiliations require

loose linkages and merely require participants to express good faith and a similar interest (Bailey &

Koney, 2000) as opposed to formal joint ventures where parties work together closely on a project

(Ring & Van de Ven, 1994).

It seems that coopetition mentality occupies the tourism stakeholders’ mindsets when they

approach destination marketing. The cooperative behaviour and competitive approach adopted by

some of the tourism organisations in Wang and Krakover’s study (2008) is a good illustration of the

coopetition relationship. It clearly shows the hostile relationship on the one hand coupled with the

need to pool resources on the other hand in order to achieve a common goal. The leadership

within the destination marketing organisation and the community is vital to its success.

8

1.5 CLARIFICATION OF KEY CONCEPTS

After a brief introduction to the literature related to the topics discussed and explored in this study,

it is necessary to clarify the key concepts. The importance and benefits of the study is illustrated

thereafter.

1.5.1 Competitive advantage

The fundamental of any business strategy is the quest to improve the company’s financial

performance and strengthen its long-term competitive position. This provides the organisation with

an advantage over its competitors. When one company has a competitive advantage over

another, it has the ability to deliver above average financial results and profits and has a better

chance of sustainability. A company’s competitive advantage is sustainable when parts of its

strategy cause large numbers of buyers to prefer that company’s products or services over those

of a competitor for a long period of time (Hough, 2008).

1.5.2 Market

“An actual or nominal place where forces of demand and supply operate, and where buyers and

sellers interact (directly or through intermediaries) to trade goods, services, contacts or

instruments, for money or barter. Markets include mechanisms or means for (1) determining the

price of the traded item, (2) communicating the price information, (3) facilitating deals and

transactions, and (4) effecting distribution. The market for a particular item is made up of existing

and potential customers who need it and have the ability and the willingness to pay for it”

(Business Dictionary, 2011).

1.5.3 Market share

“A percentage of total sales volume in a market captured by a brand, product, or company”

(Business Dictionary, 2011).

1.5.4 Brand equity

Branding is the name, symbol or term used to identify a product. Brand equity is the value of a

brand’s overall strength in the market (Cannon, Perreault & McCarthy, 2008).

1.5.5 Hotel occupancy

“The rate of occupation or percentage occupation per month or year of the total capacity available

within a hotel during that same period” (Business Dictionary, 2011).

1.5.6 Economic recession

The terms recession and economic recession make reference to a global crisis, which began in

2007, the impact of which is still felt today. It is considered by many economists to be the worst

financial crisis since the 1930’s Great Depression (Reuters, 2012). It resulted in the collapse of a

9

number of large banks and financial institutions, bank bail-outs by national governments globally,

as well as downturns in stock markets around the world; resulting ultimately in recession.

1.5.7 Marketing

“Marketing is the performance of activities that seek to accomplish an organisation’s objectives by

anticipating customer or client need and directing a flow of need-satisfying goods and services

from producer to customer or client” (Cannon, Perreault & McCarthy, 2008). Marketing stresses

that the company’s efforts should focus on its customer’s satisfaction at a profit.

1.5.8 Five-star hotel

A five-star hotel is one that is graded with five stars, (or delivers the equivalent standards to the

graded hotels) by the Tourism Grading Council of Southern Africa. The grading criteria cover

service standards, facilities in the hotel and the level of amenities provided by the hotel. A five-star

grading is the highest grading available and is an indication of luxury amenities, high standards

and personalised service.

1.5.9 City of Cape Town

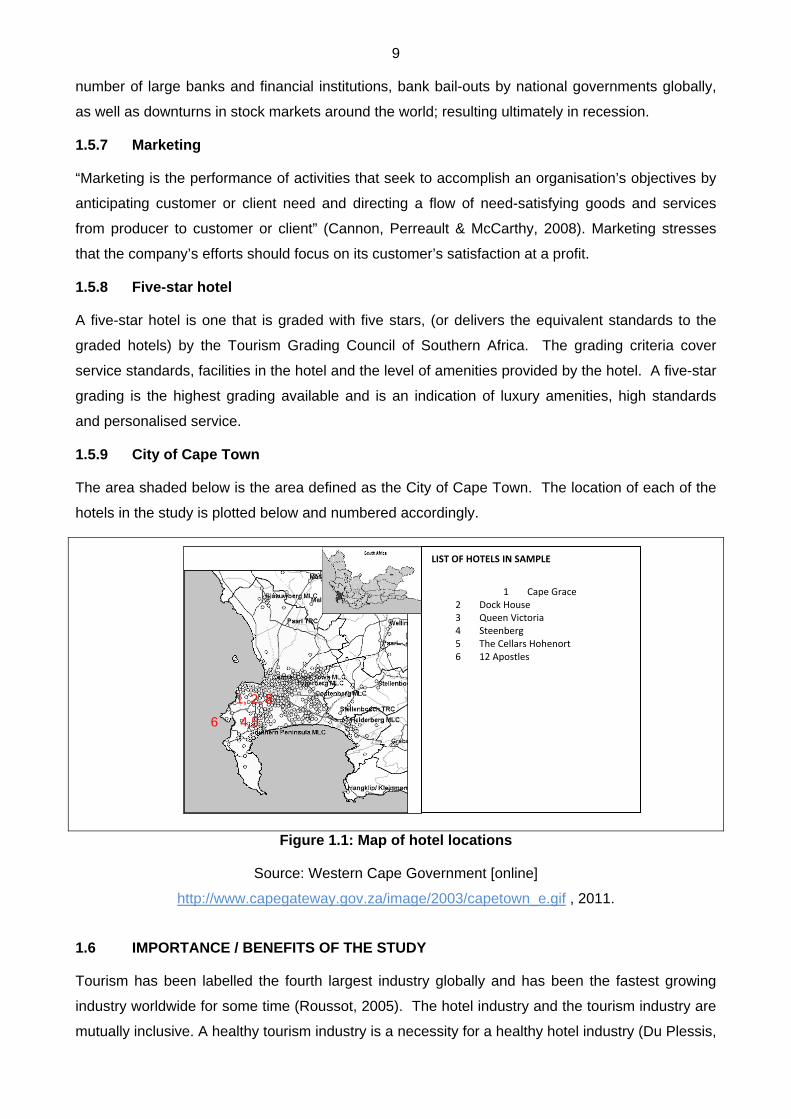

The area shaded below is the area defined as the City of Cape Town. The location of each of the

hotels in the study is plotted below and numbered accordingly.

Figure 1.1: Map of hotel locations

Source: Western Cape Government [online]

http://www.capegateway.gov.za/image/2003/capetown_e.gif , 2011.

1.6 IMPORTANCE / BENEFITS OF THE STUDY

Tourism has been labelled the fourth largest industry globally and has been the fastest growing

industry worldwide for some time (Roussot, 2005). The hotel industry and the tourism industry are

mutually inclusive. A healthy tourism industry is a necessity for a healthy hotel industry (Du Plessis,

LIST OF HOTELS IN SAMPLE

1 Cape Grace 2 Dock House 3 Queen Victoria 4 Steenberg 5 The Cellars Hohenort 6 12 Apostles

1, 2, 8

6 4.5

10

1989). It is estimated that the hotel industry generates 75% of all tourism income globally (Bishop,

2005).

In South Africa accommodation is broken down into (1) hotels, (2) guest house and guest farms

and (3) caravans, camping sites and bush lodges. Although hotels accounted for just over 50% of

the available rooms in South Africa in 2010, they account for 75% of total spend. A number of new

hotels have opened since the economy began to weaken as developers and hoteliers had

committed to the inception of these projects prior to the economic downturn. In Johannesburg

capacity has risen by 30% in the past 3 years, in Cape Town by 20% in 2 years and in Durban by

35% in 3 years. This, coupled with the impact of the economic recession has led to average

occupancies falling from 70.3% to 53.1% in 2010 (PWC, 2011).

It is clear from these statistics that supply outweighs demand and therefore the logical conclusion

is that only the fittest shall survive. It is therefore imperative to explore possibilities for individual

hotels to retain some form of competitive advantage in order to sustain themselves and South

Africa’s position as a tourism destination.

1.7 DELIMITATION OF THE STUDY

The report is a contribution to co-operative marketing theory, specifically addressing how

competitors in the tourism sector develop strategies for joint marketing initiatives and developing

the tourist destinations of (1) the City of Cape Town and (2) South Africa. The proposed research

will focus exclusively on the South African hospitality industry, and more specifically five-star hotels

in the City of Cape Town. It will broadly compare how the hotels interact with one another and with

other hotels in the region and South Africa. It will focus predominantly on their marketing

interaction.

1.8 RESEARCH DESIGN AND METHODOLOGY

Thomas (2003) describes qualitative research as the method, which involves a researcher

describing kinds of characteristics of people and events without comparing the events in terms of

measurements or amounts. Quantitative methods focus attention on measurements and amounts

of the characteristics displayed by peoples or events in a study. For the purposes of this research,

a qualitative approach has been selected in order to facilitate a case study approach.

Thomas (2003) recommends that qualitative methods be utilised when studying the current status

of people and events where the researcher seeks to collect and interpret information about some

phenomenon without concern for quantities. A case study typically consists of a description of one

entity’s actions, explaining their behaviour. It can also take the form of a comparison when the

likeness and difference between two or more entities is analysed.

11

The biggest advantage of a case study is that it allows a researcher to reveal the manner in which

an array of factors has contributed to the unique situation that is in play where the entity or entities

are concerned. A limitation to the case study approach is that generalisations or principles drawn

from one case can be applied to other cases at the risk of error. Readers should not assume that

the results in one case study would be identical with that in another (Thomas, 2003).

1.8.1 Sampling

The qualitative study will make use of a form of non-probability sampling referred to as purposive

sampling. Purposive or judgemental sampling enables the researcher to select cases that will best

enable the researcher to answer the research questions and objectives (Saunders, Lewis &

Thornhill, 1997).

The study pertains to five-star hotels in South Africa. The reason for selecting this population of

hotels is due to the highly competitive nature of interaction in this sector at present. Since the FIFA

2010 World Cup there is an oversupply of hotels in South Africa and particularly in the City of Cape

Town (PWC, 2011). It is therefore of interest to assess what these hotels are doing; if and how

they are interacting with one another and other competitor hotels in order to strengthen their

position in the market.

Interviews shall be conducted with the business heads of the six hotels selected for purposes of

this research, all of which are located in the City of Cape Town and are five-star graded or

equivalent in standard. The study shall examine patterns in response based on the location of each

hotel, its proximity to the competitor hotels it cooperates with. It also examines whether or not they

are more likely to work with directly competing hotels or hotels that complement their offering.

1.8.2 Questionnaire design and data collection

1.8.2.1 Questionnaire

Thomas (2003) refers to four approaches to questions, namely loose-question, tight-question,

converging-question and response-guided approaches. The loose-question approach is used to

elicit interpretations of very general queries. A tight-question strategy is designed to discover a

respondent’s preferences among a limited number of options. The converging-question approach

is designed to incorporate advantages of both loose and tight methods. The interviewer first asks

broad, open-ended questions and then follows the response of the interviewee with additional

more focused questions. Lastly, the response-guided approach allows the interviewer to pose a

question and then based on the answer received to spontaneously create additional questions that

are logical extensions of the initial answer received.

The questionnaire will contain a combination of open questions in order to allow the participants to

be more descriptive (Saunders, Lewis & Thornhill, 1997). The majority of the questions are likely

to begin with the words “why”, “how” and “what” and shall be combined with probing questions in

order to drill down into more specific detail where information is specifically required (Saunders,

12

Lewis & Thornhill, 1997). The probing questions will focus more on the marketing interaction

between the hotels. Very little use of closed questions shall be made in order to ensure that

extensive answers are obtained.

1.8.2.2 Data collection – Interviews

An interview is the most advantageous approach to obtain data, as the answers to the questions

can be quite complex due to their open-ended nature (Easterby-Smith et al., 2002; Healey, 1991;

Jankowicz, 2005). When planning an interview the researcher benefits from deciding on multiple

strategies to best fit the needs of the study (Saunders, Lewis & Thornhill, 1997). The interviews

shall be conducted face to face wherever possible, however where not possible telephonic

interviews shall be conducted. Prior to conducting the interviews permission shall be obtained to

audio-record the interviews. After the interviews, a typist shall be appointed to transcribe the audio-

recordings.

1.8.3 Data analysis

Once the recordings have been transcribed, a thorough analysis of the transcripts shall begin in

order to integrate the related data drawn from the different transcripts, identifying the key themes

and patterns for further analysis and exploration. The data shall be categorised in order to identify

the nature of the relationships between the sample hotels in order to reach conclusions to the

questions this study seeks to answer. A summary of the principal themes that emerge from the

interviews shall be obvious at this point (Saunders, Lewis & Thornhill, 1997). The study will also

compare their responses; in particular, how they are similar and different to one another (Thomas,

2003).

An important challenge in this data analysis process shall be to identify any bias that exists

amongst those interviewed as well as to discover the consistencies and inconsistencies that exist

in their opinions. The steps that shall be followed in the data analysis process are in short:

i) Transcribe the data and identify the major ideas.

ii) Define appropriate units of analysis.

iii) Categorise the data according to the relevant themes that emerge.

iv) Confirm the categories that have emerged.

v) Identify the themes and utilise theory in order to interpret these where necessary.

The data shall be categorised as follows in order to facilitate an analysis:

i) Geographical patterns relating to cooperative relationships.

ii) Types of cooperation practiced and the distance from the customer.

iii) Information relating to the markets where cooperation is most prevalent or most hindered.

iv) The types of marketing activities engaged in between parties.

v) Factors which promote or hinder cooperation.

13

1.9 CHAPTER OUTLINE

In the following section, the structure of the study and the contents of the different chapters is

outlined.

1.9.1 Chapter One – Introduction

Chapter One outlines the research problem and provides the reader with a background to the

research problem and the manner in which the research has been approached. It sketches a

background to the problem, the formal relationship between the hotels and explains briefly the

importance of the research.

1.9.2 Chapter Two – Literature Review

This chapter of the research report will comprise an in-depth literature review. The review, the

content of which is outlined earlier in this chapter, will introduce coopetition. It shall explore

cooperation and competition independently in order to provide a better understanding of how these

two principles can be utilised simultaneously by competitors. Additionally destination marketing, a

form of coopetition utilised in the tourism industry is explored in more detail.

1.9.3 Chapter Three – Research methodology

The primary research and the methodology and format of the questionnaires is discussed and

analysed. The sampling procedure is discussed together with the research into the design of the

questionnaire and the data collection and analysis methods. It will also include the testing of the

questionnaire, re-design and final distribution of the questionnaire.

1.9.4 Chapter Four – Analysis and interpretation

This chapter will contain an analysis of the data collected in order to ascertain what behaviour is

exhibited by the organisations in the sample. The data shall be grouped and sorted as deemed

appropriate in order to facilitate addressing the research question. This chapter can be regarded as

the core of the study as it requires a great deal of interpretation of the results, utilising the literature

review to ascertain how the results fit into the current theory and the expansion thereon.

1.9.5 Chapter Five – Conclusion and recommendations

The last chapter of the study provides a conclusion that is drawn from the data analysed in Chapter

Four. Recommendations are made for ways to further leverage the coopetition relationships that

exist amongst the hotels in South Africa. Shortcomings of the study are explained and

recommendations for future research are highlighted at this point.

1.10 NATURE AND FORM OF RESULTS

The results shall be presented in a written case study. Tables shall be utilised in order to present

summaries of certain of the data, particularly where comparison is required.

14

1.11 CONCLUSION

This chapter has provided an introduction to coopetition, the hospitality and tourism industries. It

provides context for the need to conduct the research. It clearly outlines the primary and secondary

research objectives and the questions that support these, providing a framework for possible

outcomes. It provides an outline of the process the research will follow as well as the methods

used as, laying the foundation for a review of the literature in more detail.

15

CHAPTER 2

LITERATURE REVIEW

2.1 INTRODUCTION

This chapter contains a summary of the literature reviewed in order to facilitate a better

understanding of the research problem and assist with the effective interpretation of the data

gathered.

2.2 TOURISM AND HOSPITALITY

Chapter One establishes that these two concepts are highly interlinked and therefore best explored

together as most of the literature around these topics overlaps or involves the other.

2.2.1 Tourism

Globally tourism contributes to five percent of economic activity. It contributes between six and

seven percent to employment worldwide (both direct and indirect employment). Between 1950 and

2010 international tourism arrivals has expanded at a rate of six comma two percent (6.2%) per

annum and the share of international tourism that is received by emerging and developing

countries has risen from thirty two percent in 1990 to fort seven percent in 2010. International

tourist arrivals grew by nearly seven percent in 2010. The United Nations World Tourism

Organisation forecasts a growth in international tourist arrivals of between four and five percent in

2011 (WTO, 2011).

As tourism grows internationally and new destinations and markets become evident it is

understood that competition will increase and South Africa will need to be on top of its game. In

South Africa, tourism contributed ten comma five percent (10.5%) to GDP in 2008 (South African

Tourism, 2010). It has grown at three times the world average and has created almost a million

jobs since the end of apartheid, overtaking gold exports as an earner of foreign currency (Media

Club South Africa, 2011). It plays a critical role in the country’s economy and is highly susceptible

to the impact of the Rand exchange rates. Whilst a strong currency reduces inflationary pressure

in the economy, it has adverse effects on tourism as it reduces the buying power of foreign visitors

(South African Tourism, 2010).

When looking at historic growth patterns it is important to take note that the FIFA World Cup has

distorted the stats of 2010, resulting in unnaturally high volumes of visitors. The number of foreign

visitors increased fifteen comma one percent (15.1%) in 2010 and there was an increase of

fourteen comma three percent (14.3%) in domestic visitors to 5.13 million. The overall number of

visitors rose by fourteen comma eight percent (14.8%) to 13.2 million in 2010. The number of

visitors is estimated to decline by eight comma seven percent (8.7%) in 2011, as there will be no

16

international attraction to South Africa in the 2011, which can compare with the impact of the 2010

FIFA World Cup (PWC, 2011).

It is predicted that post 2011 the improved economic climate will lead to stead gains in domestic

and foreign travel in South Africa. The number of foreign overnight visitors is projected to rise by

2.1 million between 2011 and 2015. That equates to six comma four percent (6.4%) compound

annual growth, taking the total to R9.6million visitors per annum. When comparing this to the 2010

figures it equates to three comma five percent (3.5%) compound annual growth (PWC, 2011).

On the domestic travel front, the number of visitors is expected to grow by three comma four

percent (3.4%) compounded annually between 2011 and 2015. This equates to an increase of

650 000 visitors. Compared to the 2010 figures growth is expected to decline to zero comma three

percent (0.3%) compounded annually, reaching 5.2 million visitors in 2015. Figure 2.1 below is a

representation of the actual visitor statistics to 2010 and the forecasted statistics to 2015.

Figure 2.1: Domestic and foreign visitors 2004 to 2015

Source: PricewaterhouseCoopers, 2011, 8

The total number of visitors in South Africa will increase to 14.8 million by 2015, a two comma

three percent (2.3%) compound annual increase for 2010, but a five comma three five percent

(5.35%) compounded annual growth from 2011. Growth in travel and tourism will have a positive

impact on the accommodation industry.

When considering tourism it is important to understand what the key drivers are of tourism

revenue. They are the number of foreign arrivals per annum, average spend per day and average

length of stay of tourists (South African Tourism, 2010). These drivers have an impact on the

accommodation sector of the tourism industry, which is also known as hospitality.

17

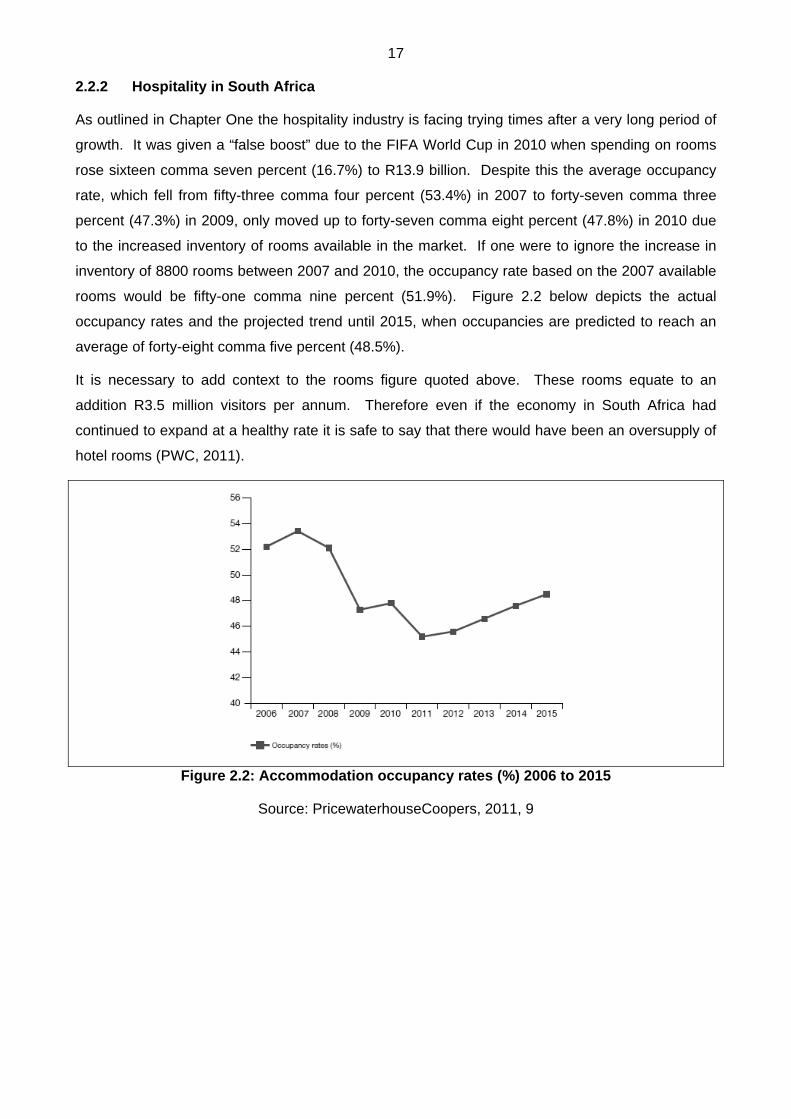

2.2.2 Hospitality in South Africa

As outlined in Chapter One the hospitality industry is facing trying times after a very long period of

growth. It was given a “false boost” due to the FIFA World Cup in 2010 when spending on rooms

rose sixteen comma seven percent (16.7%) to R13.9 billion. Despite this the average occupancy

rate, which fell from fifty-three comma four percent (53.4%) in 2007 to forty-seven comma three

percent (47.3%) in 2009, only moved up to forty-seven comma eight percent (47.8%) in 2010 due

to the increased inventory of rooms available in the market. If one were to ignore the increase in

inventory of 8800 rooms between 2007 and 2010, the occupancy rate based on the 2007 available

rooms would be fifty-one comma nine percent (51.9%). Figure 2.2 below depicts the actual

occupancy rates and the projected trend until 2015, when occupancies are predicted to reach an

average of forty-eight comma five percent (48.5%).

It is necessary to add context to the rooms figure quoted above. These rooms equate to an

addition R3.5 million visitors per annum. Therefore even if the economy in South Africa had

continued to expand at a healthy rate it is safe to say that there would have been an oversupply of

hotel rooms (PWC, 2011).

Figure 2.2: Accommodation occupancy rates (%) 2006 to 2015

Source: PricewaterhouseCoopers, 2011, 9

18

Figure 2.3: Number of hotel rooms (thousands) 2005 to 2010

Source: PricewaterhouseCoopers, 2011, 6

In comparison to the above, looking only at hotels there is a prediction of a further increase of

seven comma one percent (7.1%) room availability in 2011, followed by a further increase of three

comma two percent (3.2%) in 2012. The significant decrease in occupancies in the past 2 years

has discouraged further plans to expand and it is predicted that between 2013 and 2015 a growth

of less than one percent (1%) in room availability will be seen. It is estimated that by 2015 there will

be approximately 66 000 hotel rooms available in South Africa, a compounded annual increase of

two comma three percent (2.3%) from 2010 (PWC, 2011). It is of interest to compare Figure 2.2

above which looks at accommodation as a whole versus Figure 2.4 below which looks at hotels

only.

Figure 2.4: Hotels - Occupancy rates (%) 2006 to 2015

Source: PricewaterhouseCoopers, 2011, 15

19

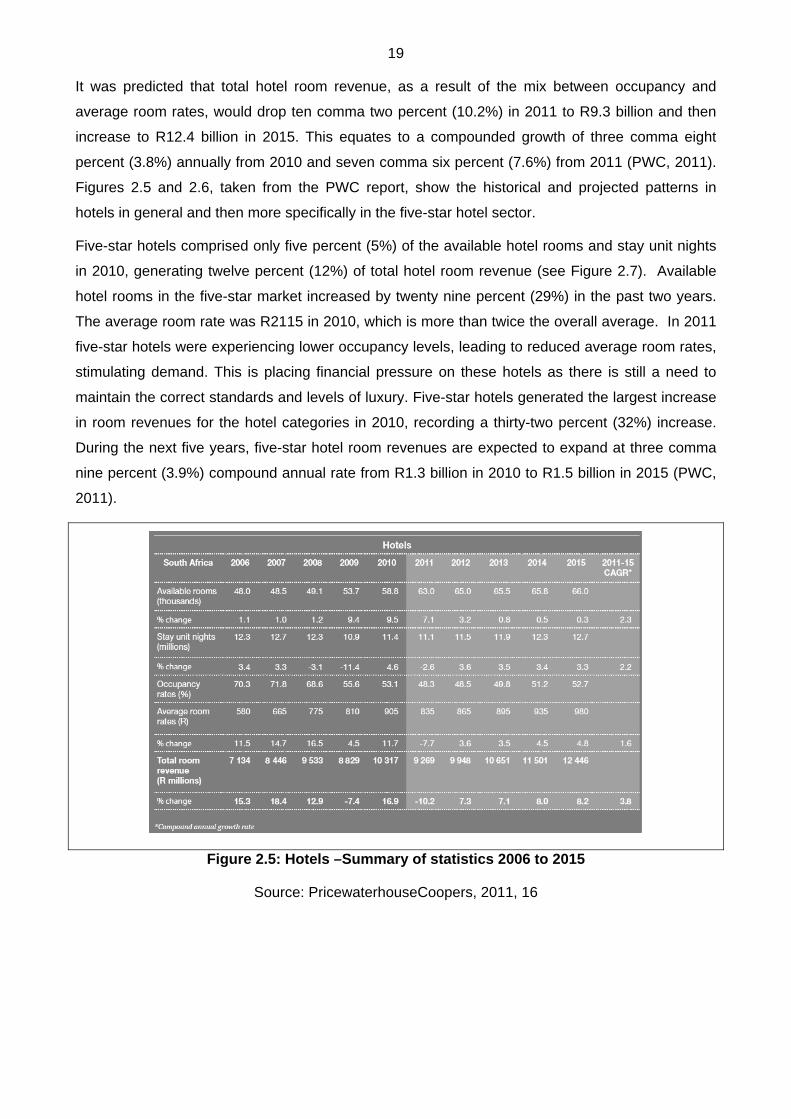

It was predicted that total hotel room revenue, as a result of the mix between occupancy and

average room rates, would drop ten comma two percent (10.2%) in 2011 to R9.3 billion and then

increase to R12.4 billion in 2015. This equates to a compounded growth of three comma eight

percent (3.8%) annually from 2010 and seven comma six percent (7.6%) from 2011 (PWC, 2011).

Figures 2.5 and 2.6, taken from the PWC report, show the historical and projected patterns in

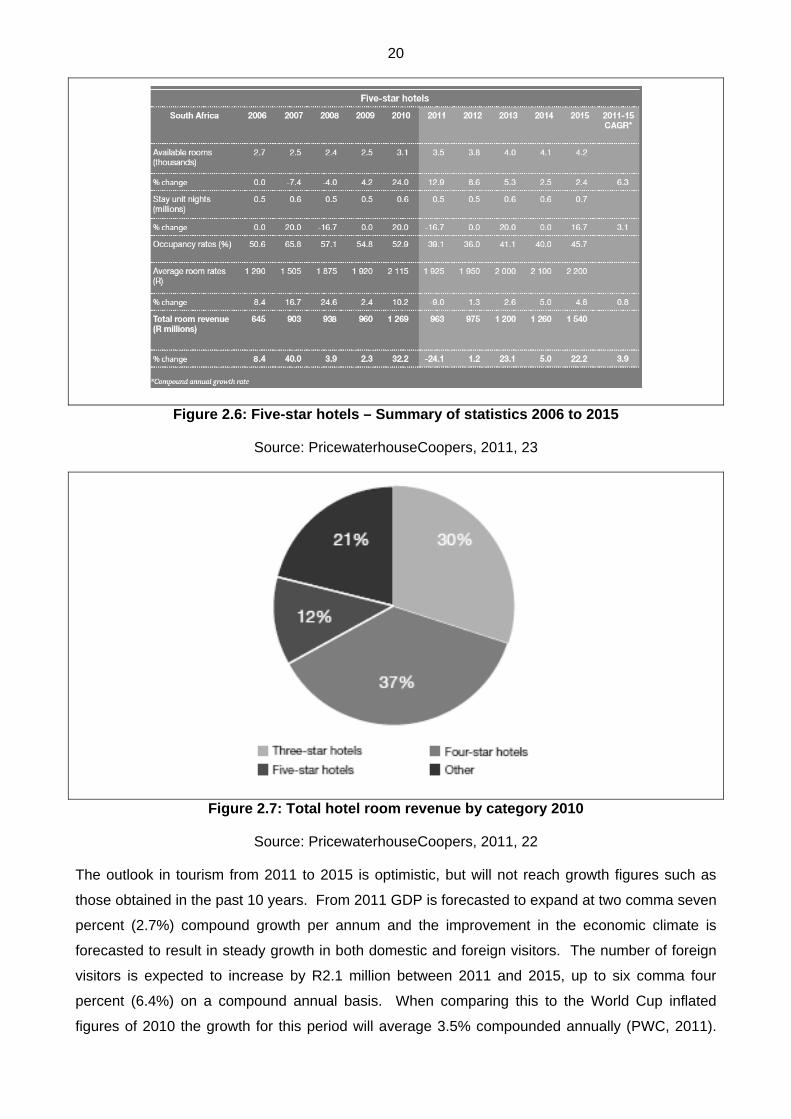

hotels in general and then more specifically in the five-star hotel sector.

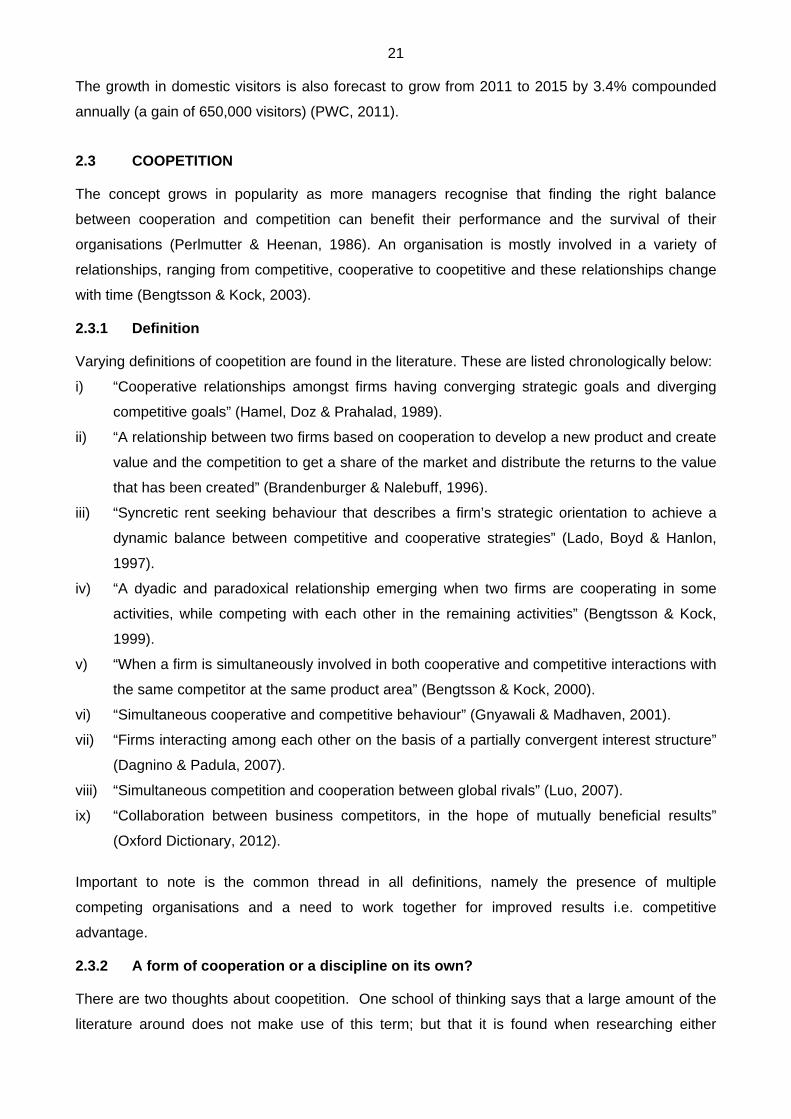

Five-star hotels comprised only five percent (5%) of the available hotel rooms and stay unit nights

in 2010, generating twelve percent (12%) of total hotel room revenue (see Figure 2.7). Available

hotel rooms in the five-star market increased by twenty nine percent (29%) in the past two years.

The average room rate was R2115 in 2010, which is more than twice the overall average. In 2011

five-star hotels were experiencing lower occupancy levels, leading to reduced average room rates,

stimulating demand. This is placing financial pressure on these hotels as there is still a need to

maintain the correct standards and levels of luxury. Five-star hotels generated the largest increase

in room revenues for the hotel categories in 2010, recording a thirty-two percent (32%) increase.

During the next five years, five-star hotel room revenues are expected to expand at three comma

nine percent (3.9%) compound annual rate from R1.3 billion in 2010 to R1.5 billion in 2015 (PWC,

2011).

Figure 2.5: Hotels –Summary of statistics 2006 to 2015

Source: PricewaterhouseCoopers, 2011, 16

20

Figure 2.6: Five-star hotels – Summary of statistics 2006 to 2015

Source: PricewaterhouseCoopers, 2011, 23

Figure 2.7: Total hotel room revenue by category 2010

Source: PricewaterhouseCoopers, 2011, 22

The outlook in tourism from 2011 to 2015 is optimistic, but will not reach growth figures such as

those obtained in the past 10 years. From 2011 GDP is forecasted to expand at two comma seven

percent (2.7%) compound growth per annum and the improvement in the economic climate is

forecasted to result in steady growth in both domestic and foreign visitors. The number of foreign

visitors is expected to increase by R2.1 million between 2011 and 2015, up to six comma four

percent (6.4%) on a compound annual basis. When comparing this to the World Cup inflated

figures of 2010 the growth for this period will average 3.5% compounded annually (PWC, 2011).

21

The growth in domestic visitors is also forecast to grow from 2011 to 2015 by 3.4% compounded

annually (a gain of 650,000 visitors) (PWC, 2011).

2.3 COOPETITION

The concept grows in popularity as more managers recognise that finding the right balance

between cooperation and competition can benefit their performance and the survival of their

organisations (Perlmutter & Heenan, 1986). An organisation is mostly involved in a variety of

relationships, ranging from competitive, cooperative to coopetitive and these relationships change

with time (Bengtsson & Kock, 2003).

2.3.1 Definition

Varying definitions of coopetition are found in the literature. These are listed chronologically below:

i) “Cooperative relationships amongst firms having converging strategic goals and diverging

competitive goals” (Hamel, Doz & Prahalad, 1989).

ii) “A relationship between two firms based on cooperation to develop a new product and create

value and the competition to get a share of the market and distribute the returns to the value

that has been created” (Brandenburger & Nalebuff, 1996).

iii) “Syncretic rent seeking behaviour that describes a firm’s strategic orientation to achieve a

dynamic balance between competitive and cooperative strategies” (Lado, Boyd & Hanlon,

1997).

iv) “A dyadic and paradoxical relationship emerging when two firms are cooperating in some

activities, while competing with each other in the remaining activities” (Bengtsson & Kock,

1999).

v) “When a firm is simultaneously involved in both cooperative and competitive interactions with

the same competitor at the same product area” (Bengtsson & Kock, 2000).

vi) “Simultaneous cooperative and competitive behaviour” (Gnyawali & Madhaven, 2001).

vii) “Firms interacting among each other on the basis of a partially convergent interest structure”

(Dagnino & Padula, 2007).

viii) “Simultaneous competition and cooperation between global rivals” (Luo, 2007).

ix) “Collaboration between business competitors, in the hope of mutually beneficial results”

(Oxford Dictionary, 2012).

Important to note is the common thread in all definitions, namely the presence of multiple

competing organisations and a need to work together for improved results i.e. competitive

advantage.

2.3.2 A form of cooperation or a discipline on its own?

There are two thoughts about coopetition. One school of thinking says that a large amount of the

literature around does not make use of this term; but that it is found when researching either

22

cooperation or competition. It states that it is at times only evident that coopetition is present in the

interaction between two firms when the cooperation is taking place amongst competitors.

Fjeldstad, et al (2004) states that coopetition could become part of the “competitive paradigm” if

cooperation between firms is considered “competitive manoeuvring”, both of which provide a

competitive advantage. This would mean that coopetition is another form of cooperation.

Concepts, which are relevant for cooperation, like trust, opportunism and commitment would be

crucial to coopetitive relationships (Yami, Castaldo, Dagnino & Le Roy, 2010).

The other school believes that coopetition is an entirely separate discipline. Dagnino and Rocco

(2009) stress that coopetition does not emerge from combining cooperation and competition. He

implies that cooperation and competition merge together to form a “new strategic interdependence

between firms” thereby creating value for each firm.

2.3.3 Coopetition as a vertical or horizontal relationship

Coopetition can be found both horizontally in relationships at the same level of the value chain or

between direct competitors; or vertically between suppliers and customers (Bengtsson & Kock,

2000). Table 2.1 summarises some of the literature available. This study focuses on relationships

between competing firms; therefore the literature review explores the horizontal relationships in

more detail.

Table 2.1: Overview of past research on coopetition

Typology of relationship

Objective

Nature/definition Antecedent Outcomes

Vertical relationship Lado, Boyd and Hanlon, 1997; Bengtsson and Kock, 2000; Luo, 2007

Gnyawali and Madhaven, 2001; Gnyawali and Park, 2008

Afuah, 2000; Bengtsson and Kock, 2000; Baldwin and Bengtsson, 2004; Oliver, 2004; Quintana-Garcia and Benavides-Velasco, 2004; Gnyawali, He and Madhaven, 2006; Luo, 2007; Luo, Rindfleisch and Tse, 2007; Ritala, Hallikas and Sissonen, 2008.

Horizontal relationship Hamel, Doz and Prahalad, 1989; Quintana-Garcia and Be Benavides-Velasco, 2004; Bonel and Rocco, 2007; Hokura, 2007.

Source: Yami, Castaldo, Dagnino & Le Roy, Edward Elgar, 2010: 43

Bengtsson and Kock (1999) state that firms can be in a variety of relationships with other firms.

These relationships will depend on their own strength as well as their need for external resources

(Table 2.2). They state that firms should take advantage of the benefits that arise from competition

23

as well as those arising from cooperation. In order to reap the benefits of both types of behaviour

the firm needs to adopt both competitive and cooperative behaviours, namely a coopetition

strategy (Yami, Castaldo, Dagnino & Le Roy, 2010). This contradicts a great deal of research

gathered around competition and cooperation, which imply that the two relationships are mutually

exclusive.

Table 2.2: Relationships between firms

Relative position in the industry

Strong Weak

Need for external resources

Strong Coopetition Cooperation

Weak Competition Coexistence

Source: Bengtsson & Kock, 1999

2.3.4 Types of coopetition

Dagnino and Padula (2002) suggest that there are multiple types of coopetition (Table 2.3) which

depend on the number of competing firms involved in the relationship. They differentiate between

dyadic coopetition and network coopetition. Within each, they further distinguish between simple

and complex forms of coopetition.

Table 2.3: Types of coopetition

Number of firms in the coopetition relationship

Two More than two

Number of activities in the value chain

One Simple dyadic coopetition Simple network coopetition

Multiple Complex dyadic coopetition Complex network coopetition

Source: Dagnino & Padula, 2002

2.3.5 Levels of coopetition

Coopetition research covers four levels of coopetition: individual, organizational, inter-

organizational and network (Yami, Castaldo, Dagnino & Le Roy, 2010). Table 2.4, extracted from

the book Coopetition summarises the research that exists on the four levels. Most relevant to this

study is the theory of inter-organisational and network coopetition relationships.

24

Table 2.4: Levels of coopetition

Coopetition level Drivers

(selected examples)

Process Outcome

(selected examples)

Individual

(for example, Fang, 2006; Hatcher and Ross, 1991; Lindskold, Betz and Walters, 1986; Loch, Galunic and Schneider, 2006; Tjosvold 1986; and Tjosvold and Sun, 2001)

Cultural traits Individual goals Individual morals

and values Personality

In cooperation, individuals strive to get others to be effective and to trust and rely on one another, which lead to shared perspectives and interests. In competition, individuals actively interfere with one another and lack of trust restricts information exchange. A dynamic balance between cooperation and competition is however possible.

Creativity Loyalty Productivity Stress

Organisation

(for example, Alper, Tjosvold and Law, 1998; Chen and Tjosvold, 2008; Loch, Galunic and Schneider, 2006; Tsai, 2002)

Department goals Organisational

values Task structures Team procedures

In cooperation, organizational systems communicate that goal attainment helps teams and departments be successful together, and systems are designed for interdependence and resource sharing. Competition facilitates processes aiming to withhold information and ideas between departments and subunits as pursuing own goals and to obstruct the goal process of others. Organizations must balance incentives to cooperate and to compete in order to ensure both communication and efficiency.

Market knowledge

Organizational coordination

Profits/losses Shared

knowledge and resources

Mutual interorganisational

(for example, Bengtsson and Kock, 2000; Boneland and Rocco, 2007; Das and Teng, 2000; Khanna, Gulati and Nohria, 1998; Levy, Loebbecke, and Powell, 2003)

Resource sharing and acquisition

Reducing the benefits of a competitor

(Changes in) structural conditions (for example, cost structure, competitive focus, advantages of scale)

Oriented towards cooperation, decision processes are accommodative and aim for mutual problem solving, where dyad members are attentive and responsive to the other’s interests. Competition involves less fair, more biased, and less honest behaviour, which makes dyadic members strive to fulfil own interests. A fruitful coopetitive relationship requires balanced power but may be difficult to sustain over long periods of time.

Building channels to foreign markets

Knowledge spill over

New markets, products and processes

Relationship maintenance

Network

(for example, Carayannis and Alexander, 2004; Dei Ottati, 1994; Gnyawali and Madhavan, 2001; Oshri and Weeber, 2006)

Advancing joint interests and pooling resources of common purposes

Networking structure and positions

Social, cultural and regulatory changes

Technological advances and complexity

When cooperating, dependence is based on trust. When competing, dependence is related to an actor’s network strength and position. Conflicts are few in cooperation but arise frequently in competition. There are also clear norms when cooperating. When competing, there are invisible norms and distance between actors. It is difficult to balance coopetition for all parties to reap the benefits, due to vast complexities.

Coordination Expand the total

market Innovation and

differentiation Integrated

strategies

Source: Yami, Castaldo, Dagnino & Le Roy, 2010: 23-25

25

2.3.5.1 Coopetition in inter-organisational relationships

Where cooperation takes place between competitors it rarely does so within the same area where

the cooperating firms compete (Gomes-Casseres, 1994). The main reason for coopetition is to

gain strategic advantage over competitors (Hamel, Doz and Prahalad, 1989). Multiple studies

focus on the relationships between two or more organisations, where all of the organisations in the

relationship are involved in cooperative and competitive relationships simultaneously. The literature

explores a number of theories. Bengtsson and Kock (1999, 2000) utilise industrial organisation and

industrial network theory. Cognitive theory (Thomas & Pollock, 1999), organisational learning

(Khanna, Gulati & Nohria, 1998) and alliance literature (De Rond & Bouchikhi, 2004) are also

explored.

Bengtsson & Kock (2000) claim that competition between firms, is a result of the structural

conditions in an industry. When there is a change in these conditions firms are more likely to work

together, examples are where there has been a change in regulations (Padula & Dagnino, 2007)

and as a result knowledge is shared. Another example is where market conditions require firms to

cooperate in order to take advantage of scale or volume (Mitchell, Dussauge & Garrette, 2002).

Some of the literature suggests that it is easier to achieve coopetition when the competing firms

who engage in the cooperative relationship are equal in size or status (Das & Teng, 2000) and

complementing resources. During the process it is essential that the trust relationship is

established and maintained (Zeng & Chen, 2003). Levy, Löbbecke and Powell (2003) suggest that

if knowledge sharing is managed it can alleviate some of the tension between the rivals.

The short duration of coopetition relationships can largely be attributed to the continuous change in

environment within which they exist as well as the level of cooperation or competition that exists

amongst the parties (Bönel & Rocco, 2007; Dagnino & Padula, 2007). Das and Teng (2000)

attribute the failure of certain coopetitive relationships to an inability to effectively deal with the

tensions that sometimes arise in such relationships.

There are both advantage and disadvantages to coopetitive relationships.

The advantages are:

i) Value creation (Bengtsson & Kock, 2000).

ii) Value sharing (Bengtsson & Kock, 2000).

iii) Increased innovation and creativity (Bengtsson & Kock, 1999).

iv) Achieving growth (Thomas & Pollock, 1999).

v) Remaining competitive (Thomas & Pollock, 1999).

The disadvantages:

i) The development of a trap (Bönel & Rocco, 2007).

ii) The ending of the coopetitive relationship (Bönel & Rocco, 2007).

26

iii) The negative impact of tension on individual employees in each firm (Bengtsson & Kock,

2001).

Bengtsson and Kock (1999) found that competitors tend to cooperate in activities, which are further

away from the customer, whilst they compete in activities close to the customer.

2.3.5.2 Coopetition in networks

As opposed to the simplicity of the coopetition amongst firms in the same industry as explored

above, coopetition exists in networks. The reason for exploring this in more detail is that this form

is often found in the tourism and hospitality industries. Coopetition in networks can appear in the

following forms:

i) Between districts or regions (Dei Ottati, 1994).

ii) Industries (Mariani, 2007).

iii) Research consortia (Carayannis & Alexander, 2004).

iv) Interest groups (Doucet, 2006).

v) Networks of firms (Chaudhri & Samson, 2000; Ims & Jakobsen, 2006).

As is the case with inter-organisational relationships, changes in the environment can cause firms

to engage in coopetitive relationships (Okura, 2007). Reasons for engaging in such relationships

across networks include:

i) The costs and nature of technological systems may lead to joint research and development

projects (Oshri & Weeber, 2006).

ii) The pooling of resources (Carayannis & Alexander, 2004).

iii) Advancing of joint interests (Mariani, 2007).

iv) Reducing the benefits or advantages of competitors by engaging in collusion (Ims &

Jakobsen, 2006; Gnyawali, He & Madhaven, 2006).

In networks, tension is also likely to arise between partners. It can arise because of a number of

factors such as asymmetry of resource input, size of partners or status of partners (Gnyawali &

Madhaven, 2001). There are both advantages and disadvantages to coopetitive relationships

across networks. Advantages include reduced costs (Okura, 2007) and improved innovation and

research and development (Dei Ottati, 1994). On a network level it is far more difficult to maintain

the balance of cooperation and competition in the relationship and thus difficult to ensure that all

involved gain benefits. Network relationships are generally more stable as it is more difficult for one

party to break away from the interdependencies that establish on a network level (Bengtsson,

Eriksson & Wincent, 2010).

Interesting to note is that in many instances it is the formation of a network that gives rise to

competition on a network level but that the individual parties within the network may not actually

compete (Brandenburger & Nalebuff, 1996). This is not the case when considering R&D consortia,

27

where each of the parties competes on an individual level and their levels of cooperation with one

another may vary. Bengtsson, Eriksson and Wincent (2010) conclude that at network level it is

likely that the coopetition occurs between two networks, regions or research consortia.

2.3.6 Impacts of coopetition

Cooperative relationships are unstable (Das & Teng, 2000), which by implication makes coopetitive

relationships unstable due to the existence of cooperation within them. It is therefore proposed

that coopetition strategies are not long lasting relationships with competitors and that these

relationships may change regularly in nature. Coopetition is an evolving relationship (Yami,

Castaldo, Dagnino & Le Roy, 2010), which is dynamic, and time dependent, delivering

unpredictable outcomes.

Yami, Castaldo, Dagnino & Le Roy (2010) propose that coopetition will lead to new complexity