Computer-Organized Cost Engineering - Taylor & Francis Group

104

COMPUTER-ORGANIZED COST ENGINEERING

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Computer-Organized Cost Engineering - Taylor & Francis Group

COMPUTER-ORGANIZEDCOST ENGINEERING

COST ENGINEERING

A Series of Reference Books and Textbooks

Editor

KENNETH K. HUMPHREYSAmerican Association of Cost Engineers

Morgantown, West Virginia

1. Applied Cost Engineering, Forrest D. Clark and A. B. Lorenzoni2. Basic Cost Engineering, Kenneth K. Humphreys and Sidney Katell3. Applied Cost and Schedule Control, James A. Bent4. Cost Engineering Management Techniques, James H. Black5. Manufacturing Cost Engineering Handbook, edited by Eric M.

Malstrom6. Project and Cost Engineers' Handbook, Second Edition, Revised

and Expanded, edited by Kenneth K. Humphreys7. How to Keep Product Costs in Line, Nathan Gutman8. Applied Cost Engineering, Second Edition, Revised and Expanded,

Forrest D. Clark and A. B. Lorenzoni9. Managing the Engineering and Construction of Small Projects:

Practical Techniques for Planning, Estimating, Project Control,and Computer Applications, Richard E. Westney

10. Basic Cost Engineering, Second Edition, Revised and Expanded,Kenneth K. Humphreys and Paul Wellman

11. Cost Engineering in Printed Circuit Board Manufacturing, Robert P.Hedden

12. Construction Cost Engineering Handbook, Anghel Patrascu13. Computerized Project Control, Fulvio Drigani14. Cost Analysis for Capital Investment Decisions, Hans J. Lang15. Computer-Organized Cost Engineering, Gideon Samid16. Engineering Project Management, Frederick L. Blanchard

Additional Volumes in Preparation

COMPUTER-ORGANIZEDCOST ENGINEERING

Gideon SamidD & G Sciences

McLean, Virginia

Marcel Dekker, Inc. New York and Basel

library of Congress Cataloging-in-Publicarion Data

Samid, Gideon.Computer-organized cost engineering / Gideon Samid.

p. cm. — (Cost engineering ; 15)Includes bibliographical references and index.ISBN 0-8247-8339-51. Engineering economy. 2. Engineering-Estimates. I. Title,

n. Series: Cost engineering (Marcel Dekker, Inc.); 15.TA177/7.S26 1990 90-3804620' .00285--dc20 OP

This book is printed on acid-free paper.

Copyright © 1990 by Marcel Dekker, Inc. All Rights Reserved.

Neither this book nor any part may be reproduced or transmitted in anyform or by any means, electronic or mechanical, including photocopying,microfilming, and recording, or by any information storage and retrievalsystem, without permission in writing from the publisher.

Marcel Dekker, Inc.270 Madison Avenue, New York, New York 10016

Current printing (last digit):10 9 8 7 6 5 4 3 2 1

PRINTED IN THE UNITED STATES OF AMERICA

Dedicated to my FatherYa'acovSamid

A Fine EngineerA Remarkable Teacher

FOREWORD

The book and the factory, the word and the deed, the plan and its execution, thedreams and their fulfillment... I credit my personal accomplishments in life to myeducation as a child, as a student, and later as a corporate executive, to keep theseaspects in balance, always. It is not easy. At times one is carried away by airydreams, neglecting to consider the cost of his accomplishment. Conversely, onemay be steam-carried by his daily rush, minding the trees, overlooking the forest.The balancing act is an act of art.

Computer-Organized Cost Engineering is a book that reminds its reader of thebalance and the interplay between the desired and the possible. To accomplishanything you may wish for will cost you resources, time, money, and attention.All are exhaustible and, if not managed properly, will run out before your goal isaccomplished. When this happens, it doesn't matter anymore how great your idea,how noble your wish-it is left unrealized. Running a major industrial corporation,I witnessed all too often the dichotomy between those who are good at setting uplofty goals but arc too haughty to mind the dollars and cents and those who knowthe price of all the parts but are blind to the value of the whole. When thisdichotomy is left unbridged, it spells disaster. I spent much of my corporate timebuilding those bridges.

With that perspective, I view Computer-Organized Cost Engineering as a bookthat fills a certain void in the engineering literature. There are plenty of textbooksthat tell how to design a machine or a process, but they rarely address the questionsof how to estimate the cost of their design, how to schedule the work realistically,and how to control the production once it rolls off the drawing board. Costengineering books, on the other hand, tend to dwell on such technicalities of bill ofmaterials, form management, and filing, which quickly bore the engineer whomistakenly perceives cost engineering as clerical in nature. And that is where thisbook is different. It emphasizes the integrity between plans and their cost. Itdescribes the unity between thinking outline and penciling details.

vi Computer-Organized Cost Engineering

This book expresses its cost engineering ideas through the craft of computerscience and information technology, and in that respect it is very timely. Yet itsbasic message of balance and the need to bring the goal, the plan, and its executioninto good harmony is timeless.

Max RatnerChairman of the Board

Forest City Enterprises, Inc.Cleveland, Ohio

PREFACE

Cost engineering spreads across the fertile ground between technology andbusiness. It is the challenge of balance: creativity and order teaming up to build,to put together, to establish. Computer technology unleashed the potential of costengineering. It serves as a platform from which good engineering judgment,experience, and insight can be heard.

This book was written for engineers, for students, and for everyone with theurge to build that which cannot be accomplished in an instant. It is about projectsthat take time, resources, patience, judgment, teamwork, and perseverance. It iswritten with the accent on the original turf on which the profession came into itsown: industrial and residential construction. Yet I have tried to reflect theuniversal appeal of computer-organized cost engineering, and to make the bookreadable to anyone interested in "getting there" within budget and on schedule.

The book reviews the practice, the procedures, and the philosophy of the craftof allocating limited resources to make unlimited dreams come true.

The tools change so fast, the techniques evolve more slowly, but the principlesendure. I learned the principles at home, the techniques in school, the tools atwork.

I was educated as a nuclear engineer and a chemical engineer. I worked in acoal mine, in oil companies, and in defense installations. I practiced with controlhardware, spacecraft, and computers. I was a glorified gofer, an overtitled director,and a satisfied chief engineer. I am proud to uphold a family tradition: anengineering way of life.

I am honored by every reader who turns to this book.

Gideon Samid

ACKNOWLEDGMENT

Always on my mind, my mother. In ways only her own, she encouraged me totake this commitment and see it through. She is not with us today to see the result.I do thank my father, whose actions are a wonder until this very day. My brother,Amnon, helped me with unlimited devotion. My wife, Dvorit, shared the trenchesand the the ups and downs. My daughter Anat, working within D&G Sciences,organized and filed, compiled and edited-with grace, insistence, patience, andstyle. Her contribution is reflected in the artwork, the typesetting, and the generallayout. My son, Yaron, kept me challenged. My editors at Marcel Dekker, Inc.,were forthcoming and supportive. In particular, I wish to mention Hugh Haggerty,who steered me through the last phases, never losing his patience. ProfessorKehat, Mr. Max Ratner, and David Rosoff found the time to review the manuscriptand enlighten me with their professional comments. And then, all the unnamedteachers who taught me a lesson a day throughout my diversified career: Yourfingerprints are all over this book. Thank you indeed.

INTRODUCTION

This book chronicles the spectacular growth of a newborn: computer-organizedcost engineering, an old profession fertilized with a new technology. Suddenly theenvelope of the possible is redrawn. Dormant opportunities are awakened. More isasked of the cost engineer; more is dependent upon him or her. Old ways must bereexamined; new ways must be duly adopted. Excitement is in order, but prudenceis, too. Throughout this book, I have tried to express both enthusiasm and caution,keeping an eye on the opportunity and the risk. Much like a powerful hammer: usefulin construction, but watch your fingers.

This is not a beginner's book. If you happen to be completely unaware of costengineering, cost estimating, scheduling, and cost control; if project management istotally out of your world; if resource allocation is Greek to you, reading this book mightprove quite confusing. On the other hand, it is not an expert-narrow, jargon-laden dryaccount. Having a rough sense of the above-mentioned topics will make you a targetreader. Some paragraphs may use a term that is not explained in the text, but the thrustof the text is not dependent on these terms (e.g., the term "head" in costing a pump).These are compromises needed to accommodate the professional cost engineer aswell as a wider circle of readers variably removed from the details of the profession.The reason for such a broad net is rooted in the new face of the profession. Computertools now allow more people to practice cost engineering, while professional costengineers are freed of the more clerical parts of their craft and focus on the morethoughtful elements. The changes imply new depth and new breadth. The book tries tofollow both. Attempting to capture the essence of the change in modern cost engineer-ing, yet living with the constraint of scope, the book had to leave out many valuabletopics.

Cost engineers, before the computer, simply ignored the true complexity of theirprofession because they could do nothing about it. They also largely avoided theuncertainty inherent in predicting the future (future cost or schedule) and resortedto deterministic, sometimes arbitrary, formulas. Complexity and uncertainty are thetwo dragons for which the computer is a fit match. But the cost engineer must learnto use the computer for what it's worth. This book tries to help.

Chapter Walk-ThroughThe book is structured in three parts. The first two describe cost engineering and computertechnology, each as viewed by the other, and the third part examines the practice, theprocedures, and the philosophy of integrating the two.

Part One, A Computer Technology View of Cost Engineering, is divided into twochapters: Elements and Business Considerations. Elements provides a run through thethree traditional categories of the profession: cost estimation, scheduling, and costcontrol. Cost estimation is viewed as the centerpiece. The chapter portrays theroutines of construction estimates, and industrial estimates, as well as estimates ofa softer nature. It ends with a section called The Rhythm, which features topics notfitting into one category or another. They show how the three categories are linkedtogether to create a rhythmic sequence. In the second chapter of Part One, Business

2 Computer-Organized Cost Engineering

Considerations, the sections describe the relationship between cost engineering andcontractual commitments, the competitive edge, and the ever-present uncertainty. At onepoint, the very essence of cost engineering—planning—is cast in the metaphor of a crutch:something to walk with but to run without The popular notion of "what iF is analyzed andcritiqued, and its reverse-"if what"-is suggested as a more challenging alternative. The lastsection in this chapter focuses on the dichotomy cost-results and the dynamics of therespective uncertainties: cost uncertainty and result uncertainty. It describes a method forreducing the two in a balanced way.

In Part Two, A Cost Engineering View of Computer Technology, the discussionruns through the practice, the procedures, and the philosophy of the new technology asseen by cost engineers. The first two chapters deal with the tools: tools of the costengineering trade and tools of the computer host. In Tools of the Trade, the sectionsdescribe the dedicated cost engineering software and the general-purpose softwareemerging as the stronger leg, riding on the phenomenal success of personal computers.The discussion is focused on computing software, database software, and graphicstools. The second chapter, Tools of the Host, comes with two sections: one under theheading of Sharing — sharing resources and sharing information; and the other underthe title Frameware — utilities and software aids that constitute a framework in supportof other programs. Naturally these two topics don't even come close to covering therange of computer tools that underlie cost engineering software. The two wereselected for discussion because both are important and seem to fall between the chairs,so to speak. Using a computer, the reader is necessarily using a particular operatingsystem and has probably more documentation about it than he cares to read. A similarpredicament holds for hardware. It is harder to find a good discussion on theavailable tools for sharing resources and sharing information, across the office oracross the globe. The same is true for the various utilities that make the life of acomputer user so much easier.

Procedures, Chapter 5, is in the same bind as the tools chapters. The scope requireda stark elimination of important topics. The selected topics are software engineering(a cursory discussion) and a handful of applications: archiving of cost engineeringdata (the History Accumulator), the power of stochastic processing (Monte Carlo),and then a topic that should not have been there: computer security. Computer crimeis a growing menace, and protection must be a concern at any level of usage. Anothersection brings a practical application for incoporating conflciting expert knowledgethrough a neural network. The section ends with a topic that may seem light: personalspace — the techniques of making our computer-burdened desk a more workableenvironment. The productivity impact is largely underrated.

The last chapter in this part, Concepts, features two sections. The first describessome of the "laws" of handling information mass that have emerged with computertechnology. Issues like data glut, data reliability, documentation, and artificial intel-ligence are assessed, explained, and concisely presented.

The second section of Concepts offers a discussion of the battle against complexity.The sheer number of details involved in some large projects, the interrelations, the

Introduction 3

everything-affects-everything syndrome - these components of the cost engineeringcomplexity are always a challenge. The section runs through the weapons that contain,manage, and ultimately defeat the complexity dragon.

In the third part, A Utility View of Organization, the discussion is about how to engage thenew technology with the old profession-how to use, not abuse, the power of combiningcost engineering with computer technology. The part offers two chapters: Chapter 7,Methodologies, talks about the how-to of computer-organized cost engineering, and Chapter8, In Focus, offers various specific designs the reader can use for programming his ownsoftware and integrating it into his cost engineering environment.

In Methodologies the discussion begins with some organizational principles thatmay serve as guidelines in the process of sorting out a good way to use computer powerwith all its variety vis-a-vis cost engineering through all its aspects. Later sectionsdiscuss the modes of such engagements and how they affect the job descriptionof certain cost engineers. The final section provides a checklist, a sequence of stepsthrough which a cost engineering need may be matched with a computer tool.

In Focus discusses a small variety of specific products. The polar elements repre-sentation of trees offers a practical way to represent a rich body of information aboutprojects and hierarchies in general. T*VIEW is a tool to manage projects that aredefined through one prime hierarchy, and Dispenser(Z) is a detailed case studyof the balanced reduction of uncertainty described in Part One (Business Con-siderations). Chapter 8 closes with a detailed design document for a cash flowproduct that can record transactions as well as manage contractual commitments.

/ hope this chapter walk-through will help some readers focus on their interest andbypass the rest. I also humbly hope that some will flip the pages from first to last and read,or at least scan, this book cover to cover.

Whatever your level of reading, please let me have your comments.

CONTENTS

Dedication HiForeword (Max Ratner) vPreface viiAcknowledgment viii

Introduction 1

Part One A Computer Technology View of Cost Engineering 7

1 Elements 8

2 Business Considerations 80

Part Two A Cost Engineering View of Computer Technology 141

3 Tbols of the Thide 1424 Tbols of the Host 1935 Procedures 2256 Concepts 271

Part Three A Utility View of Organization 307

7 Methodologies 3088 In Focus 346

Appendices 383References 385List of Organizations 392Bibliography 403Index 419

PART ONE

A Computer Technology View of Cost Engineering

Cost engineers are civil engineers, mechanical engineers,aeronautical engineers, and nuclear, chemical, and electricalengineers who take engineering a step further-into a costestimate, into a scheduled plan, into a world of limitedresources.

In the process, they may write a lot of numbers and sumthem up. To the uninitiated, the cost engineer looks like aclerk, or like an accountant. At times he looks like aneconomist. The term "engineering" seems out of place. Howwrong! It is subject-matter expertise that governs theprofession. That is why a new high-rise cannot be estimatedby a clerk, an industrial plant cannot be cost-assessed by aneconomist, and a nuclear reactor cannot be dollar-evaluatedby accountants. The people in these discliplines have theirhands full, and their contribution should not beunderemphasized, but they are not cost engineers.

Computers gave the cost engineer a tool that added a newdimension to the profession. The use of computers in itself isan engineering endeavor, and so today the term "(cost)engineering" has a dual meaning: expertise not only in thesubject matter but also in using computers in the process ofoptimizing resource allocation. The modern cost engineer isa central player in a competitive economy. His or herresponsibility is to find ways to extract more results fromfinite dollars and limited time. And, conversely, he or shetries to engineer a solution to the problem of achieving atarget result with a smaller investment.

Available resources are finite; expressive imagination isinfinite. This anomaly is the challenge of cost engineering.

1Elements

Cost engineering is a two-way window. Looking through this window thebusiness community relates to science and technology. Looking theother way, scientists and engineers hear and see what business wants anddoes.

Cost engineering answers questions: How much does it cost? Howlong will it take? And later, Does it really cost and take as much and aslong as predicted? The cost engineering components that handle thesequestions are cost estimation, scheduling, and cost control, the elementsof cost engineering.1

The difficulty or simplicity of handling these questions depends on (1)the complexity of the subject matter, (2) the prevailing constraints, (3)the extent to which 1 and 2 are given or known.

(1) A formal definition of cost engineering is given by Humphreys 1984,1987. Speaking officially as theexecutive director of the American Association of Cost Engineers Humphreys defines a costengineer as "an engineer whose judgment and experience is utilized in the application of scientificprinciples and techniques to problems of cost estimation; cost control; business planning andmanagement science; profitability analysis; and project management, planning and scheduling." It isinteresting to contrast this with an older definition given by Bauman 1964: "Cost Engineer Arelatively new designation for any graduate or professional engineer or equivalent employing histechnical skills in the practice of process cost estimation, cost control, profitability, or the generalengineering economics of capital investment." In most environments today, MBA's and economistswho are not engineers take hold of the overall business planning, and management, pushing thecost engineer into his core elements of cost estimation, scheduling and cost control.

Elements

When 1 and/or 2 comprise a great deal of data computers are calledfor. When they involve complex computations computers are relied onagain. When the data and computation are generally unknown or illdefined computers will help simulate the missing link.

Business does not let go. The answers to the three basic questions arenot enough, Can it cost less? Finish faster? Is it possible to anticipatedisagreements about estimates versus actual costs earlier? Cost en-gineers are put on the spot. General engineering is not shy, either. Canwe do more with the given budget, use the project time better, and allowearlier indication for surprises?

Both business and engineering tap the cost engineer's shoulder: with:If I change my mind later, can it be done without a cost or schedulepenalty?

These questions, driven by a competitive economy, place a greatchallenge at the door of cost engineering.

To meet this challenge, cost engineers had to grow from engineers whodo clerical cost to engineers who do cost as mathematical abstraction.Computers took over the endless summations, the massive data han-dling, even the data entry and data display, and cost engineers moved onto wrestle with the complexity of optimal resource allocation.

(1) One can hardly dispute the importance of resource allocation in any project, and economic activity,yet, it is quite an abstraction, and as a result cost engineering in general remains in relativeobscurity- Webster New World Dictionary 1980 has an entry for civil engineering, but not for costengineering. Even in the engineering community many confuse cost engineering with costestimating or cost accounting. Major Engineering handbooks don't mention cost engineering, noteven as an index entry. Among them Kutz 1986 Mechanical Engineering Handbook, Kong 1983Handbook of Structural Concrete, Grimm 1990 Handbook of HVAC, and Merritt 1983 StandardHandbook for Civil Engineers". On the other end, non-engineering estimators and appraisersfurther blur the distinction of the cost engineering profession. It sounds impressive when anarchitect, or an engineer says: I designed this... or I built this... What can a cost engineer say? Icosted this... I resource-allocated this... The situation is similar to that of an anesthesiologist whocan not claim that he performed the surgery, but it is a fact that his expertise or lack of it willdetermine the recovery of the patient.

10 Computer-Organized Cost Engineering

A resource is anything one can run out of, primarily time and money.Equipment, materials, skills — even job opportunities are all resources.The modern cost engineer builds associations of resources: dollars-timeslots-crew-equipment-material-supervision.

Given n resources of one type and k resources of a second type, thereare n * k possible "pairs" (allocations). Add m resources of a third type,and the number of three parts allocations becomes n * k * m. It growsfast. If there are 10 resource types and there are 100 items of each, thenthe possible allocations become

10010

Given 10 day-long jobs, 10 crews, and 10 calendar days (all areresources), there are 10*10*10 = 1000 theoretical allocations. Some ofthem, taken together, are impossible; others are possible but make noengineering sense; and some that make engineering sense don't makebusiness sense. Some combinations taken together will constitute a goodoverall plan. One of them will be best. Which?

At first glance it may seem that computers, with their legendary speed,will be able simply to go through all the possibilities and offer a selection.A more careful review will show that even if computers becomethousands of times faster than they are today, they will still be far tooslow to crack the full-size allocation challenge. Therefore, it is neces-sary to use faith, experience, intuition, and heuristic — that which is notobjective and mathematical — and through these strive for the bestallocation. Computer-Organized cost engineering is not yet reduced to

(1) See Conway et al 1967 for a thorough discussion of the inherent complexity of scheduling. Also seeHu 1982 for a computer view of the same topic.

(2) Hu 1982 offers excellent examples of the limits of computability. The renowned Dijkstra in page 3in Dahl 1972 gives a simple but illuminating observation. See Gleick 1987 for an enthrallingdiscussion on the modem trend to express complexity with tools of apparent chaos rather than withtools of arbitrary order.

Elements 11

a recipe, expressed in formulas or software. There are recipes and thereis a lot of software, but common sense and judgment are still very muchin the game.

Much heat is generated from disagreements between the two types ofcost engineers: those who are intimidated by computers and rely onmethods that served them for years, and those who are wedded tocomputers and see the entire profession as software to run, or to bewritten. The literature mirrors this division. On one hand are the goodold-fashioned cost engineering books, which make cursory mention ofthe computer, and on the other hand, a new wave of computer books isflooding the market, with little mention of the virtues of classic costengineering.

The prospects of the profession and its good fortune lie in a balancedapproach.2

COST ESTIMATION

Cost estimation is the centerpiece of cost engineering. There are somany reasons costs will change, and prices will vary, that the life of a costestimator is never too cozy. Unlike the design engineer, who deals withlaws of nature — never finicky, constant, or reliable — the elements thatthe estimator manipulates are as dependable as the weather, as constantas a shoreline, and as avoidable as taxes.

Process engineers, architects, and designers can reach a point ofultimate accuracy. The cost estimator cannot. It is a frustration he orshe must bear and live with. The most that a cost engineer can hope for

(1) Some pre computer era books survive the times, see Popper 1970. The "Lang Factors" introducedby Lang in 1947 are still cited, but modern literature like Cheadle 1987, Koenigseker 1982, Clark1979, Jelen 1983, or Winklehaus 1982, as well as Tavakoli 1989, and Prerau 1987 reflect thestrong emphasis on mathematical abstractions, and computer technology.

(2) See Samid 1984, and Samid 1982 for some 'balance1 notes.

12 Computer-Organized Cost Engineering

is a past-perfect estimate. This is a cost estimate based on a perfectanalysis of the past. It is 100% accurate if the future is a mere extrapola-tion of past events. To the extent that the future hides surprises, theestimate will bear discrepancies.

The estimator's goal is to draw the full body of conclusions from thepast and to be ready for anything the future might offer. Let us focus onthese two techniques.

Learning From The Past

From where else? The biggest rival tothe past as a teacher is "wishful think-ing." Keeping the past as the primeteacher is the duty and responsibility ofthe cost engineer. The dynamics areusually as follows. One track: wishfulthinking expects a result, and then his-tory is searched to support it. Tracktwo: history is learned from, but on theway from raw data to respective con-clusions, wishful thinking sneaks in andcontaminates the outcome.

Wishful Thinking

Blocking W

DATAESTIMATES

Data-to-ConclusionProcess

ArbitraryParameters

fig LI producing an estimate

In producing an estimate one tries to use allthe relevant data, avoid wishful thinking andminimize the amount of arbitrary input

The mathematical techniques thatlead to extracting a set of conclusions from a body of data are notwell-founded. They may never be. Therefore the cost engineer has toresort to techniques which are acceptable and thereby defensible. Twodangers loom: (1) that the estimator will overlook some of the con-clusion potential within the data, and (2) that he will see in the past whatis not there — draw conclusions that are not warranted on the basis ofwhat happened before. Often both discrepancies happen simultaneous-ly during the same estimate process. See insert "producing an estimate"(fig i.i).

The techniques in use are (1) sameness, (2) trending, and (3) inter-polations.

Elements 13

SamenessSameness is the most common, most automatic way to learn from thepast. An estimator will record a cost figure and assume that history willreplay itself in the future. In noninflationary times and when technologydoes not shake things too much, this simple method is also the best (whenit applies). It helps if the estimator has a constant supply of recenthistory, whether his own or from external sources. The challenge hereis to keep the massive amount of cost data in an orderly fashion so thatit can be found when needed and used for an estimate. The engineeringchallenge is to ascertain sameness validity; that is, in what case, is anhistorical price likely to be valid asa future COSt figure? { A time dependent variable

TrendingNext to sameness, trending is themost popular learning-from-the-past technique. But unlike same-ness it involves a host ofmathematical techniques that oftensharply disagree. When a cost fig-ure changed in a given pattern in therecent past, what does this say aboutits future behavior? If the es-timator is lucky and the pattern isthat of a straight line, then theprojection seems simple. If therecent pattern is more erratic, then depending on which mathematicaltechnique he uses, the projection will be different and in any case will bemuch less valid (because of diversity of opinions). See insert "forecastinguncertainty (fig 1.2)."

The computer challenge here is to program the various forecastingalgorithms, connect them to the database, and apply them properly. Insome forecasting methods, the trending is based on a simple time series,which are data of one variable (say the cost of a cubic yard of ready-mixconcrete) as it varies over time. In other cases the data of many variablesare taken into account. And the more variables, the more crucial is theconnection between the algorithm and the database.

time

fig 1*2 forecasting uncertainty

The three lines represent three valid options formodeling a trend out of the four data points. Eachmodel incorporates an arbitrary assumption aboutwhat is important and what is not. Often this ar-bitrariness is shrouded in heavy mathematics.

14 Computer-Organized Cost Engineering

InterpolationsThis elaborate technique involves using two or more loosely relatedhistorical cost figures, combining them on an imaginary model of reality,and deducing from this model what a third cost figure should be. Theestimate in this case is only as good as the model. The variety ofmathematical offerings is enormous here, standardization is nonexistent,and the validity of the result is always open to debate.

The respective computer challenge is to keep the historical databasein good order, programming the interpolation model properly, and thentying the two together without a flaw.

Depending on the model itself, the programming challenge will havetwo parts: (1) to ensure that the program reflects what the modelintended, and (2) to write the program efficiently enough so that it doesnot take forever to produce the estimate. The degree to which onesucceeds with the latter challenge is readily obvious. The first challengeis difficult because flaws may thrive, like fungus in the marshes ofcomputer talk, and because of the cryptic appearance of programminginstructions. Read more about this in Chapter 6.

Surprise Readiness (Risk... Contingency...)

If the future holds a "step function" surprise, that is, a surprise withoutany advance notice, then there is no way to be ready for it before thesurprise fully presents itself. For these surprises, readiness is in the formof preconceived "what i f plans. Most surprises, fortunately, send some

(1) Surprise-readiness is discussed under topics of risk, contingency and decision analysis. See French1986 for a modern, analytical account of decision theory. See Saaty 1980,1982 as well as Weiss 1987fora presentation of AHP — Analytical Hierarchy Process — designed to handle complex policyand decision situations. See Brown for a simplified version of decision theory, and see Ghlaseddin1986 on developing a framework for decision support systems. See Graf 1984 for an overview ofcontingency considerations. See Stevenson 1984 for cost estimate contingencies, and see Cabano1989 on the same subject from the point of view of the investor. See Hertz 1983 for riskmanagement and its applications. See Curran 1989 for a recommendation on range estimates tohandle uncertainty. See Belev 1989 of minimizing risk in high-technology programs. See Mathur1989 on risk considerations in capital cost estimating. See Ahuja 198S on resource uncertainty andtheir impact on scheduling. Fischhoff 1981 contemplates the issue of acceptable risk. Wilson f982focuses on risk/benefit analysis. Rowe 1977 offers an insightful anatomy of risk. Gilbreath 1983provides a review of operational risk in managing construction contracts. Charette 1989 andBoehm 1981 do the same for software engineering management.

Elements 15

time dependent variable

telltale signs to announce their coming, and it is the duty of the costestimator to be alert to these signs and interpret them correctly.

The computer proved helpful on both accounts. What if analysis isnow feasible and fast. Advance notice signs can be captured and inter-preted even if they show up as little bits and pieces, scattered all over theplace. See insert "step-function surprise" (fig 1.3).

'What If?"Before the com-puter came to help,cost estimatorscould hardly finishthe most probablecase estimate, andthe notion ofdeveloping addi-tional estimatesbased on differentassumptions wastheoretical. Buttoday it is possible,without much extrawork, to assemblenumerous estimatesbased on many setsof assumptions. Ifsuch estimates areproperly docu-mented, then they collectively amount to surprise readiness. Should oneof the documented cases turn out to be reality, the plan for it will beready.

The problem of course is that there are always too many possibilities,too many tracks on which the future can approach us; it is impossible toplan for them all. A selection process is required, and if reality shows upas an unselected option then all the what if effort is in vain. To accom-modate this variety, some techniques implement a continuum of options.Other take the discrete way. The first approach covers more cases, but

fig 13 step-function surprise

A step-function surprise happens without advance notice, and can not besystematically predicted. Most changes, fortunately, send telltale signs,and some, as depicted, will happen gradually. It is then up to the estimatorto spot them.

16 Computer-Organized Cost Engineering

each case is less defined and not as clearly thought out. The discretemethod covers fewer options but allows for in-depth analysis of each.1

Leading IndicatorsUnforeseen changes that send leading indicators pose a special challengefor the cost estimator. Some indicators come from the general economy,and the estimator can rely on economics experts and publications to alerthim and educate him on their meaning. Inflation, wholesale prices, andconstruction starts are but only three of a host of indices that may applyto a particular estimate and trigger a reevaluation of the figures.2

Other indicators are unique to a project, and the estimator must findthem on his own and do his own interpretation of their impact. If theunion is negotiating higher fees, if electrical subcontractors are over-loaded with work, if a test shows that the material of construction thatwas specified does not withstand the higher than expected reactortemperatures — all these are leading indicators, and the earlier they areallowed to affect the estimate, the better.

ATTRIBUTION VERSUS SUMMATION

There are two fundamental ways to assign a cost figure to an object: (1)attribution and (2) summation. The first is through one of the threemethods mentioned before: sameness, trending, and interpolation; thesecond is based on the simple premise that the cost of the whole is thesum of the cost of its parts. If the cost of the parts is known, then

(1) "What i f and multi-options considerations became very popular in modern literature. See forexample Haneiko 1983, Wilson 1982, Curran 1989, Zimmerman 1983, Mathur 1989, Ahuja 1985, orSamid 1989.

(2) ENR - Engineering News Record, Marshall & Swift (MAS), Nelson, and Chemical Engineering,as well as the Wall Street Journal and Business Week, are some well known publications whichtrack relevant industrywide indices.

(3) Ohlrichs 1981, Samid 1984, and Bullis 1987 offer discussion and illustrations for project-specificindicators. DuBois 1980 presents a study of cost indices. Patterson 1969 forwards a treatise onpreparing and maintaining a construction cost index. Review Winklehaus 1982 for indicatorsspecific to the construction industry. Also refer to Spinney 1985 and Luttwalk 1985 for an intruigingaccount of Pentagon usage of cost indicators.

Elements 17

summation will produce the cost of the original object without uncer-tainty. That is, the uncertainty of cost attribution is left to the parts. Andnow, instead of attributing a cost value to one object, we are faced withdoing the same to many objects. More work is involved but so is a greateropportunity for accuracy and what is often more important, a betterchance to convince others of the validity of the estimate.

This summation-attribution trade-off is reflected in the classes ofestimates: the first estimates, so-called conceptual, are long on attribu-tion and short on summation. At the other end of the spectrum, theopposite is true: extensive summation, and limited attribution. Thevarious estimates between these show a trend in which high-level costattribution is gradually replaced by breakdown to smaller parts andsubsequent summation.

Let us briefly review a simple example and then dwell a bit on thecharacter of summation that is innate to cost estimations.

Office BuildingIf a developer considers an office building in an office park, then veryearly in his considerations he will want a rough estimate. He would beeager to find if he is in the ballpark as far as his financial muscle isconcerned. Definitely this is not the time to do a lot of summations oflittle parts. To attribute a cost figure, one could use the "sameness"approach, that is, take an available cost figure of a similar office buildingin the same park, which was built recently enough, and attribute the samecost to the building being considered. If the office building has to bebuilt far into the future, the estimator can take into account sometrending techniques and plot the total construction cost of similar officebuildings that were built at different times in the past and then extrapo-late these figures to the desired future time frame.1

If the estimator relies on, say, the cost of a hospital in the area and thecost of a school building in the neighborhood, rather than the cost of an

(1) See Wade 1982, Koenigseker 1982, and Jain 1983 for further reading on methodologies for officebuilding indices.

18 Computer-Organized Cost Engineering

office building, then he might use some form of interpolation to assessthe cost of the building in question. It is worth noting that the hospitaland school costs don't have to be actual historical figures: they can bedefinitive or appropriation estimates.

When the estimated ballpark or conceptual cost is within range, thedeveloper will gradually want to substantiate the figures (and if he doesnot care, the lender does), and this is when summation is in order. Theoffice building will be defined according to its parts; each part will beestimated separately, and the numbers added up. The breakdown maytake various forms. It is customary that the first level of breakdown willbe an accounting level, dictated by applicable accounting standards.Accordingly the total cost will be separated according to fixed capital;working capital, associated costs, like insurance and, taxes; and moneypaid to the construction contractor, which is where the heart of costengineering lies. Deeper breakdowns will go into bare site cost versusengineering and management items, and then into battery limit expen-ses, off-site expenses, steel structures, mechanical, instrumentation,electrical — all of which customarily cut along the material-labor-sub-contractor cost element.

Summation, Accuracy, And JustificationWhen the cost of an object is represented as a summary of cost figuresof many of its detail parts and those details are organized in an impressivehierarchy, then altogether the cost statement acquires status and"respect". The psychological impression is universal: a lot of work wasput into this — it must be right. The practical consequence is that if it isnot right one has a hard time proving it.

One line of logic will claim that merely pushing the cost attributionprocess down into the details will not necessarily improve the overallaccuracy. True enough, but on the other hand the details may be bettersuited for cost attribution, and their very multitude invokes a statisticalpremise that claims that the accuracy of the whole is better than theaccuracy of the parts. Without going into statistical formalities, thisimportant premise can be shown through a simple example.

Elements 19

Summation AccuracyLet objects A and B each cost exactly $10. Let us assume that anestimator is likely to estimate each with a 10% accuracy. Using onlyround numbers, each object is equally likely to be estimated as

9 10 11

dollars. Which means that a third of the time it will be estimated

correctly, or a probability of 1/3 for a 0% inaccuracy, and a probability

of 2/3 for 10% estimation inaccuracy.

The object C of which A and B are parts will be estimated through

summation. There are 3 *3 = 9 possible summary combinations, which

will yield the following possible cost estimates for C:

18 19 20 21 22

19 20 21

20

In 3 of the 9 cases, C will be estimated with 0% inaccuracy, which isthe same as for A and B. However there will be 4 of 9 cases (probabilityof 4/9) in which the estimate will be within a 5% range from the exactnumber. And only 2/9 (compared to 2/3) probability that the estimatewill be 10% away from the exact number. In short, the accuracy of thewhole is better than the accuracy of the parts. The same holds in thegeneral case, and thus the more ramified the breakdown, the morebranches in the cost tree, and the smaller the items undergoing costattribution (as opposed to summary), the more accurate the total es-timate. 1

(1) Refer to Paradine 1970, Fry 1965, David 1962, and Anderson 1984 for an in-depth discussion ofsummation accuracy.

20 Computer-Organized Cost Engineering

CONCEPTUAL ESTIMATES

"Conceptual" in this context is euphemism for "inaccurate." These areestimates one prepares when he either has few data to base his estimateon, or not much time to prepare a more thorough estimate, or, of course,a combination of these. Yet these are the estimates that often make orbreak a company. Because it is here that projects are killed before theyare thoroughly looked at. And if you happen to kill your best, mostinnovative ideas, you inevitably retreat as a competitor. If a project isunderestimated in the conceptual stage there are still many milestonesat which it can subsequently be killed or modified, but an idea that waskilled on the basis of a misleading conceptual estimate has no morechances. The question is how to improve the speed and the accuracy ofthis type of crucial estimate. There are several ways: (1) better raw data,(2) better attribution, and (3) increased summary estimates.1

Better Raw Data

Since most conceptual estimates are very poor with cost algorithms andsince most rely on simple "sameness" or "trending" attribution, it iscrucial to have good relevant data. To achieve this, one can (1) build adatabase from common sources, or (2) develop his own private datasource. The selected method depends on the situation. If the estimatorhas to produce ballpark estimates on wide-ranging subjects (as ap-plicable for banks and other lending institutions), then it is impossibleto develop one's personal database. If, on the other hand, the range islimited and the estimates are similar in nature, then a private databaseis in order. It was customary for years to keep data for conceptualestimates in graphic and in book form. These noncomputerized methodsare still popular and probably will be for some time. The more generalthe spectrum of estimate, the more handy the computer becomes. Costnetworks allow anyone with a computer, a telephone, and a password toupdate himself with the latest cost figures on just about anything.

(1) See Bakewell 1985, Ponce 1985, Koenigseker 1982, and Humphreys 1987 for representativediscussions of conceptual estimates. See Page 1984 for a conceptual cost estimating manual. ReviewHollman 1989 for a case study report.

(2) See Samid 1984 for a discussion on the considerations for the build/buy decision.

Elements 21

Better Attribution

Factor estimation is the common name for those "quick and dirty"conceptual cost statements. The term represents the attribution methodwhich takes two or more related cost figures and interpolates them intoan estimate of the object in question. Thus if one wants to build arefinery, he may look at a graph of the cost of refineries of variouscapacities and find an estimated cost.

Prices per unit are another common means. Buildings and structureshave been traditionally expressed as cost per square foot, and this cost isthe basis of conceptual estimates for a building of a known area.

Some factors are so acclaimed in cost engineering tradition that thereis no point in arguing with them, even if better ones can be found. If youestimate an industrial plant, you factor your cost off the equipmentfigures, if you estimate labor, take the labor to material factor, and soon.2

If one is faced with estimates of the same nature over and over again,then it makes a lot of sense to revisit some of those "holy cows" and adjustthem based on recent history. It also makes a lot of sense to use modernpattern recognition techniques to plow relevant data for the purpose offinding new and powerful attribution ratios.

A good ratio or factor is one that ties together a known data item withan unknown one. Thus the price per square foot of building ties togetherthe known area with the unknown cost. Equipment cost is easy toascertain through a phone call to a vendor, and therefore it is a usefulbasis for estimating piping, insulation, electrical, engineering, etc. But

(1) See Means 1987,1988,1990 (different books for different topics). See Richardson 1984,1988,1989.See Marshall & Swift 1981,1982,1984.

(2) Lang, as early as 1947, introduced a set of factors for industrial estimates of chemical plants, andthe concept is alive today. Amazingly, some of the figures are carried over, too often, blindly. SeeLang 1947.

(3) See Naver 1989 for an excellent review of remote access to specific data. See Jordan 1990 for aninformative discussion on PC communication tools, and procedures. See Beardon 1988 for ageneral networks discussion, and see part two in this book under "sharing".

22 Computer-Organized Cost Engineering

these traditional factors are by no means the only ones. Having good andreliable factors means improved conceptual estimates, which in turnmeans a sharper competitive edge.

Increased Summary Estimates

At first glance the idea of running summary rather than attributionestimates in the conceptual mode seems a bit out of place. There is notime to build a cost hierarchy and assign individual cost figures to thebasic elements and then summarize it all. Indeed not, if it is donemanually. The advent of computers gave the ability to create automatedcost hierarchies, feed them with unit prices of common materials andlabor rates, and then perform the summary instantly and produce a coststatement. Conceptual estimates are rough and inaccurate because thedesign engineer has not yet specified the details to be costed. Tominimize this deficiency, the cost estimator will take the role of thedesign engineer and come up with some nominal specifications andbreakdown structures, which are not likely to accurately correspond tothe eventual design but are very likely to produce a conceptual costestimate that is more accurate than plain attribution.

DEFINITIVE ESTIMATES

An estimate deserves the adjective "definitive" when it is a pure sum-mary estimate — when the challenge is to take off the details fromdrawings and specifications and add them up properly, not missing anydetail or double counting any. The computation is simple; the datavolume is the problem.

Often the difficulty in definitive estimates is not so much to sum thenumbers up, as much as it is to unravel them to defend a cost figurechallenged by a reviewer. The other practical difficulty is the flexibilityto accommodate changes. One has to maintain the data in a high degreeof order if he is to be ready for questions; what if we change the stainless

Elements 23

steel specification to a higher grade? But the more one is ready for suchwhat if questions, the more one has to invest up front in setting the dataaccording to a variety of keys. As always, there is a trade-off that needsto be balanced.

The different computer products that help the estimator in his defini-tive statement will compete more on the appearance of the report thanon anything else, although such emphasis is not generally justified.

Variety In Estimates

The conceptual estimate is the first cost statement; the fully definitiveestimate is the last. Between these, depending on the environment,there may be several others that are a hybrid cost statement, taking partsfrom the conceptual and parts from the definitive. Contractors havetheir own series of estimates, architects have theirs, and owners anddevelopers have different estimates, too. Bidders in various environ-ments have some unique in-between estimates, and banks go by theirprocedures and their preferences. It matters greatly whether the es-timate relates to a new, unheard of project or whether it is anotherinstance of a known quantity. It matters if it is a project to build or aproject to demolish; it is a different series if the estimates relate tobuilding a factory in a distant place where all utilities, support, andinfrastructure must be costed, as opposed to building the same in anindustrial park. A brand-new building is different from a revamp job.The size of the project impacts on the number and appearance of theestimates (and the number of people involved).1 Residential construe-

(1) See Humphreys 1987, and Stewart 1987 for a good exposition of organizing cost estimating data forlarge projects.

24 Computer-Organized Cost Engineering

tion is one story (or more), commercial development is its own case,chemical plants are costed with idiosyncrasies unshared by others, andcosting the construction of an airplane or a nuclear reactor are different;they all come with traditional jargon and specialties. Their underlyingstructure is always the same, and it is this commonality on which this bookis focused (fig 1.4).1

Relative Usefulness ofEstimate

Mid-RangeEstimates

ConceptualEstimate

project process

Irecommended decision zones -

fig 1.4 upgrading class of estimate

As the project progresses it offers more raw data for its estimate. The original conceptual estimate is replacedwith one or more mid-range estimates which in turn are superseded by the definitive statement Points X and Yrepresent the switch over states when the next class of estimate becomes more effective. Throughout the seriesof estimates the owner will make successive go/no-go decisions.

(1) This account focuses on the two extremes: the conceptual estimate and the definitive. Thein-between types are numerous and non-standardized. The American Association of CostEngineers has proposed three types of estimates: the "order of magnitude" estimate with accuracyof -30% to +50%; the "budget" estimate ranging from -15% to +30%, and the "definitive": -5% to+15%. See Humphreys 1987 for a discussion on the various types of estimates. See Humphreys1984,1987 and Stewart 1984 for a clear discussion on types of estimates.

Elements 25

Logical Expressions

Inspired by accounting software, cost engineering was initially limited tousing computers as data containers and fast calculators. It was onlygradually that logic was welcome. When it comes to expressing a pieceof logic, computers excel. Logic and computers go hand in hand. Com-puter languages match or exceed any other language in their ability toexpress logic. Thus, all cost-related logic that appears elsewhere can betranslated into computer language and express itself in the eventualschedule, or cost statement. Such logic appears in contracts, codes,regulations, and standards.

A contract will stipulate conditional cost rates and payments, and thoseconditions can be programmed (see CASH* VIEW in Chapter 8). Thegovernment regulations FAR and DFAR are readily programmable, andso are various municipal guidelines.

Modern construction is inundated with regulations: equal oppor-tunity, safety, and visibility considerations are taken up by governmentbodies and by various independent institutions. The American Instituteof Architects issues General Conditions of the Contract for Construc-tion. Guidelines are published by the American Society for Testing andMaterials (ASTM), the American Concrete Institute (ACI), theAmerican Association of State Highway Officials (AASHO), andnumerous others. Codes like ACI 305-72, Recommended Practice forHot Weather Concreting, or ASTM A325-71, High-Strength Bolts forStructural Steel Joints, may all be translated into computer language.

Objectivity And Adversity In Estimates

Since every estimate is an opinion, it is also biased. Even if the estimatorhas no stakes in the outcome, he nonetheless comes to work with acertain background. If his recent and dominant experience is overes-timating, then he is likely to be wary of another case. The same holds forunderestimation. In practice, however, just about any estimator hassome stake in the outcome, even if it is not on the surface. The relation-ship between a biased estimate and the objective estimate is similar tothat between a subjective sense of justice and its corresponding objectivestate. In the justice system, we have come to realize that the best way toguarantee a minimum bias is the method of adversity: justice is supposed

26 Computer-Organized Cost Engineering

to come through if two opposing attorneys argue for their subjectivepoints of view. Business practice was also refined to a similar solution:an estimator with an interest in a low-cost figure is pitched against anequal professional with an opposite interest. The two argue against eachother in written cost statements, presentations, and the negotiationstable between seller and buyer. This is a good idea when it is keptcivilized. It is important to stress that having two opposing estimators ofequal qualification is very important; otherwise the amateur will be easilyintimidated.

The arguments and counterarguments are best practiced if the twoopposing estimators use the same "sheet of music" — the same computersystem. If they don't, then settling differences may be a hopeless task,since who can tell if the difference is material or due to the software?Ideally the two will use the very same model, agreed upon beforehand,and focus on adjusting input parameters. In the event that an unsettledargument is forwarded to a third estimator, such a one-system approachis a good converging point: asking the two estimators to redefine theirinputs in terms of the selected one system. Since many estimates may betoo elaborate for the entire job, the arbitrator may circle the disagree-ment zone and only that part of the estimate will be imported to thesettlement system.

The Cost Of Estimates

Estimating a project increases its cost because an estimate is an expense,(likewise with regard to scheduling). It is possible to under- or over-dothat investment. It turns out that for smaller projects one tends tooverspend on cost estimating, and for larger projects, the trend is theopposite. The first case is easy to argue: it is not worthwhile to pay anestimator $500 to narrow down a cost of an activity which is rangeestimated between $4000 and $4500. But a $5 million project for whichthe estimator asks for an additional $5000 in order to provide a detailedbreakdown cost report, a sudden attack of frugality may becounterproductive. Imagine the following setting: an executive commit-tee in a city charged with building a new correction facility, will turn to

(1) See Samid 1982 for a discussion on the adverse effects of amateur cost estimating

Elements 27

a professional estimator to estimate the construction cost in order to beable to assess the incoming bids. Often the committee members willcompare total cost only. If a bidder came close enough to the inde-pendently estimated figure, then it looks OK. Why worry about thenumbers in the back pages? Why commission the estimator to provideboring details? A shrewd owner will know why: the total may be in line,but it came about through low-bidding on one account, and overbiddingon the other. A detailed comparison will spot the overbid account, say itwas carpentry, and use the independentlyestimated cost figure to negotiate the pricedown. Armed with details, the owner is likelyto recover the expense of the estimateseveral times over. See insert "The cost ofestimates" (fig 1.5).

%-ratio between cost of estimatesand estimated cost

0.1%

THE NATURE OF ESTIMATESJlOM

estimated cost

Although estimates are everywhere and fig u the cast of estimatespracticed by everyone, hard- core estimatesare reserved for the costlier and longerprojects, and also for projects with high public visibility. Out of the realmof estimates at large, one may cut off the adhoc, instant, "automatic"estimates, and this leaves us with estimates prepared in order, method,and formality and with visibility and justification of assumptions anddetails.

Methodical estimates may be categorized as those that require subjectmatter expertise and those that don't. Estimating the cost of a well-defined inventory is a matter of counting and some multiplication;estimating the cost of gas along a distance-defined trip is also a matterof reading mileage and multiplication. Gradually, and without any clearborderline, the subject matter may become quite complex and the basicrequirement for an estimator turns out to be subject matter expertise.

The subject matter expertise methodical estimates may in turn bedivided into estimates for projects that are large, tangible, and heavy, andto projects that are small, intangible, and light — the rest. For bothcategories one tends to find an S-curve relationship between the ac-

28 Computer-Organized Cost Engineering

accuracy ofestimates

curacy of the estimate and the effort to develop it. See insert "effort andaccuracy of estimates" (fig 1.6).

Estimating a big structure of any size or purpose is of a certain nature.For one, these are the historically older estimates, the smoother, themore mature, the more methodical, and ingeneral they are quite accurate, since theirassociated uncertainty is relatively limited.Now, one can point to the NASA shuttleand claim that this large, tangible, andheavy item experienced legendary costand time overruns. Indeed there are toomany such examples, but in proportionthey are still minor and limited. Size,visibility, and high expenditure turn theseoverruns into media prey, and theirproblems are amplified out of proportion.Overall in the construction industry, con-tractors are remarkably accurate in es-timating cost. How many softwareprograms experience horrendous dead-line slippage and cost multiplication?How many books planned for a quick 4 to6 months' effort ballooned into 10 years ofunending struggle? How may decades andbillions of dollars ago did the NationalCancer Institute estimate beating cancer?

In general, construction estimates should serve as an example andinspiration for other estimate types. The technical terms "engineering"and "industry" have a certain aura of positive buildup, progress, and —construction. In an attempt to share the ring of the terms, others haveborrowed them handily. The insurance people are now an industry,laboratory work is today genetic engineering, etc. For these terms tojustify their migration, they have to carry over the spirit of the originalterms: construction under constraints, building something with limitedtime and money, quantifying progress — objective cost estimation.

effort to produceestimates ($,time)

fig 1.6 efforts and accuracy of estimates

Below a certain limit, more effort will notimprove estimate accuracy. Same for thehigh limit In between the effort is produc-tive. Point X is a good place to concludean estimate.

Elements 29

Large, Tangible, Heavy (Construction and Manufacturing)Estimates

Construction estimates follow a general pattern that transcends thecharacter of the construction itself. In every construction class, there isone basic physical quantity that carries on its back the result of theestimate as well as many interim cost factors. The most popular by faris the venerable SF (square foot): area. Buildings and structures of allsorts are first and foremost quantified by their total floor area. Cost persquare foot is a value currency that measures residential buildings,commercial establishments, warehouses, schools, and hospitals alike.The SF value is the basic factor in conceptual cost estimates and even indefinitive estimates (calculating marginal and operational costs: floorpolish, safety patrols). Multistory buildings carry a secondary measure:number of stories. In fact, the old image of a professional estimator isone who coughs up the price per square foot of any building specified bykind, location, and year of construction. Quality of building is sum-marized by this magic dollars per square feet: one number telling adifference composed of material difference and differences incraftsmanship. The dollar difference may be more than twofold.

Then there are items that strongly resist SF representation: pipelinesare measured through running feet, as is a fence. A post is captured byits bottom diameter and total height; a storage vessel is measured byvolume; a pump by gallons per minute and head. And if all else fails,there is always the unique case. Every time, however weird, can be

(1) There are plenty of good resources for large, tangible, and heavy construction and manufacturingestimates. See Halpin 1980, Kavanagh 1978, Stevens 1985, Barrie 1978, Winklehaus 1982, Vainner1984 for major construction projects. See Westney 1985 for smaller construction projects. SeeSamid 1989 for some aspects of estimating industrial construction under uncertainty. See Engelke1989 for transportation infrastructure cost. See Wilson 1989, Techwell 1985 for manufacturingestimates. See Langley 1983 for estimating air conditioning systems. See Varela 1989, and Ashford1984 for estimating airport construction. See Brown 1985 for aerospace construction. See Massey1982 for plumbing estimates. See Popper 1970, Bauman 1964, Schweyer 1955, Nelson 1966, Caldwell1975, and RodI 1985 for industrial chemical estimates. See Barrett 1989, Spinney 1985, and Luttwak1985 for weapon systems estimates. See Nigbor 1981 for electronic industrial estimates. SeeKrishnan 1984 for industrial electrical situation. See Halvorsen 1981 for environmental instances.See Doering 1985 for revamp and upgrade estimates. See Hannon 1990, Samid 1990, Kakade 1989,Allcott 1988, and Coen 1989 for estimates of power generation.

30 Computer-Organized Cost Engineering

defined as a unit of itself. The drawback is that it cannot be comparedto other "weirdos."

The total cost of a construction project is expressed as the basicquantity times its per quantity cost (= unit price) plus "other," which arefixed costs unrelated to the quantity.

It is customary to represent cost component per SF Material per squarefoot, labor, engineering per square foot; "extras" and "breaks," too, arerepresented on a SF basis.

The reason that SF is so useful is rooted in (1) the laws of mechanicsand strength of materials, (2) the prevailing codes and regulation, and(3) economy of scale. These reasons also make it very convenient for thecomputer to step in and perform a detailed estimate.

To support a given load, under a given building code, the designer findshimself quite limited in his choices. Shape is a free parameter, but thequantities of concrete and steel are pretty much locked in throughestablished, time-honored formulas. These formulas allow a computerdesign (and a subsequent estimate) to size a building quite accurately.

The most important factor in any structure or building is the support-able load. Considering the natural laws for strength of materials, thesupport needed for a given load depends on the distribution of that loadacross the floor (or the building). Different distributions will requiredifferent minimum structures. Accordingly, a computer program or adesign engineer will have to know the exact location of each load item.Moreover, since load distribution strongly affects the required structure,the cost per square foot would not have been uniform (between variousbuildings) and, hence, not useful. See insert "residential cost figures in1989" (fig 1.7).

Cost/SF is useful and does not vary as implied above because buildingcodes step in and impose a design process based on load/SF. Thisimposition is for the sake of simplicity of calculation and is justified bythe hefty safety factor used for structural calculation. Once every squarefoot of area has to be designed to support a given lbs/SF, the designfreedom is vastly curtailed, and for various shapes, locations, and style

Elements 31

800 1000 1200 1400 1600900 1100 1300 1500

unit area <SF)

fig 1.7 residential cost figures in 1989

The more units in the building, the less the $lsf value.Same for larger size living units. Figures representaverage construction cost in the U.S.

options, the eventual price per square foot converges around the samenumber.

cost's* per unit and building size

In estimating the cost of astorage tank the volume is themost important factor, and thecost is measured per cubic foot orper gallon. Now if only geometrywas the rule, then a given volumecould be constructed in endlessforms. Even if one is limited to acylindrical shape, it is possible toachieve a given volume throughtall and narrow cylinders orthrough wide and short ones.Such design freedom would havemade cost per gallon a nonstarter.Structural considerations wouldkick in for the tall building and make it that much more expensive. Alas,the same structural considerations impose an optimum for thediameter/height ratio. This optimum is normally used, and therefore thecost per gallon is indeed a good index.

Since buildings are designed for people and people come with a narrowheight distribution, it so happens that the height of a given floor in abuilding also comes with a narrow distribution. And if one considers acertain class of building, then that distribution is even narrower. Accord-ingly, specifying floor area implies volume. And so cost items that arevolume dependent are also linear with the floor area (e.g., HVAC). X Thesame is true for wall area factors (e.g., tiles).

This fantastic cost per square foot linearity in buildings created com-petitive pressures for the "soft" cost elements. To be competitive,suppliers of services like various cleaning jobs, installment of publicaddress systems, even decorations and works of art (painting, sculptures,

(1) See Langley 1983 for HVAC estimates

32 Computer-Organized Cost Engineering

and plants), are reduced, measured, and committed on a per square footbasis.

Life is not this easy. The bigger challenge is not in the estimate but inthe cost control process. The SF measure is virtually helpless when itcomes to assessing whether the cost to date is in an overrun state. Thefinal cost is linear with floor area, the cost during construction has almostno relation to the total area, and low productivity, unrelated, but ac-cumulating problems, and poor management may all combine in aninvisible cash crunch. The solution in this case is to devise variousprogress indices, and live by them. A given class of building will have asimilar cost per days since kickoff, similar costs for poured concrete, andso forth. In general, such indices reflect construction practice, and acontractor can use them from one job to the next. They are not souniform across contractors.

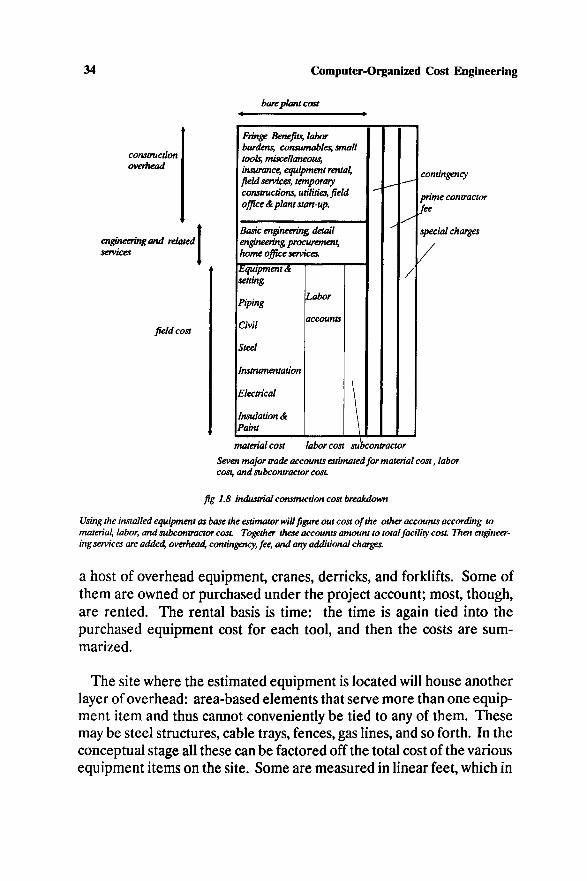

In estimating the construction of a chemical plant, the SF is replacedwith gallons per day — the throughput of the prime products. Thereactor in which the desired reaction takes place may be the functionalheart of the entire process. The know-how of the exact quantities of rawmaterials, catalysts, temperature and pressure variations, rates of masstransfer, heat transfer, etc., took perhaps years to research. But theydon't much affect the cost of the plant itself (a notable exception is thereaction control system). The heavy cost times are the containers of thematerials (usually fluids), the pumps that move them about, and the pipesthat facilitate the movement. These cost items are determined by thethroughout, and by the nature of the materials. A gamma radioactivematerial needs to be handled in a certain way that depends on itsradiation level. The size of the various storage tanks depends on storagepolicy, which is usually a consideration of the bigger economic picture,and operational continuity. Unlike the typical building, which is passiveonce built, an industrial plant requires heavy power, the facilities ofwhich have to be built. Since most chemical reactions are heat sensitive,such plants require heavy cost in heat exchangers, heating and coolingfacilities, and the power source to get it all moving. A plant will requirehigh-pressure steam, a high-capacity electrical substation, and possiblyvarious combustion facilities. All in all, it is an order of magnitude morecomplex than the geometry- controlled building estimate.

Elements 33

This industrial complexity is handled with the same approach: lookingfor a quantity to carry, define, and measure prices by. There is no easySF measure, and the common measure is based on the prime equipmentitems: the reactors, the storage vessels, the pumps, the substation, andso forth. Most of these items can readily be associated with a cost figurethrough standard tables or, better, by calling up a vendor. Then thepurchased equipment cost becomes the "carrier." Installing it will beestimated as a percentage of the purchased cost, the required foundationas another percentage, piping, instruments, paint, insulation — all thecost accounts are expressed as a cost ratio derived from the equipmentcost.

The explanation for the success of such ratios is not as solid as it is withbuildings. Generally more expensive equipment is heavier and biggerand thus requires a larger foundations and more paint area, more insula-tion, more instrumentation, and more piping. Since the materialspecified for the main equipment item is usually the same or similar tothe pipe specification, a more expensive item will require more expen-sive pipes. See insert "industrial construction cost breakdown" (fig 1.8).

These equipment cost factors are simply the best one could practicallyidentify. They predate the computer era and were used for years forconceptual, even appropriation-level estimates. 1 Today the idea is toquantify these "dressings" of the main equipment items through directdesign estimation (destimation), and the ratios are compiled to keep theold-timers happy. Also, these factors were meaningful with regard tomore standardized, so-called heavy industry. Not too many heavy instal-lations are built any more in the United States, and the trend today istoward specialty chemicals, pharmaceutical processes. (1) The old ratiosare no longer valid, and (2) new ratios are hard to come by since the costcenter of gravity shifts from tanks and pipelines to high-tech specialtyinstruments and modular reactors.

The per equipment cost ratio help estimate the immediate environ-ment of a major equipment item. To finish them all in place, one needs

(1) See Lang 1947, Ohlrichs 1981

34 Computer-Organized Cost Engineering

bare plant cost

constructionoverhead

engineering and related Iservices I

field cost

Fringe Benefits, laborburdens, consumables, smalltools, miscellaneous,insurance, equipment rental,field services, temporaryconstructions, utilities, fieldoffice & plant start-up.

Basic engineering detailengineering procurement,home office services.

Equipment Asetting.

Piping

Civil

Steel

Instrumentation

Electrical

Insulation &Paint

Labor

accounts

\

/

contingency

prime contractorfee

special charges

material cost labor cost subcontractor

Seven major trade accounts estimated for material cost, laborcost, and subcontractor cost

fig 1.8 industrial construction cost breakdown

Using the installed equipment as base the estimator wilt figure out cost of the other accounts according tomaterial, labor, and subcontractor cost Together these accounts amount to total facility cost Then engineer-ing services are added, overhead, contingency, fee, and any additional charges.

a host of overhead equipment, cranes, derricks, and forklifts. Some ofthem are owned or purchased under the project account; most, though,are rented. The rental basis is time: the time is again tied into thepurchased equipment cost for each tool, and then the costs are sum-marized.

The site where the estimated equipment is located will house anotherlayer of overhead: area-based elements that serve more than one equip-ment item and thus cannot conveniently be tied to any of them. Thesemay be steel structures, cable trays, fences, gas lines, and so forth. In theconceptual stage all these can be factored off the total cost of the variousequipment items on the site. Some are measured in linear feet, which in

Elements 35

turn is based on site area, which once again leans on the installedequipment. So, in a very loose way, such a linear factor makes sense.Installing and constructing these area items also requires an overheadaccount for forklifts, cranes, etc., another factor.1

At this point the so-called battery limits have been accounted for. Inthe surroundings of the equipment, one finds the rest of the cost itemslocated within the perimeter of the total plant area. These are theadministrative building and control room, as well as work items likelandscaping, excavation, drainage, and demolition. In many instancesthese are based on the characteristics of the site and have little to do withthe nature or the cost of the equipment. These work items, like theprevious ones, require overhead cost in the form of service equipment.When all the site cost items are accounted for, it is time to top it all offwith cost elements that reference the entire project but are rather lesstangible. These are engineering services, home office follow-up, inven-tory, licensing, accommodations, start-up cost, royalties, insurance,taxes, spare parts, consumables, and finally contingencies andcontractor's fee. Some of these cost elements depend on the accumulat-ing cost so far, and others are fixed price.

This cost structure shows the centrality of the prime equipment items.All other cost elements are computed by their reference.

A similar situation is found in estimating military installations andmilitary forces: a prime unit is selected and is made the anchor for theentire estimate. Accordingly, navies measure themselves by ship count.The U.S. Navy is in the midst of a long debate over the 600-ship navyplan. For the outsider, the emphasis on ships is not too clear: ships comewith a variety of missions, sizes, and costs — what's the point of countingships? The point is simple: there is no better unit. Like the area of abuilding and the equipment items in an industrial installation, so areships to the navy: they carry the cost computation and the cost expres-

(1) See Halpin 1980 chapter 9 for a good overview of equipment cost considerations. See Dataquest1982 for equipment rental rates.

36 Computer-Organized Cost Engineering

sions "on their backs." Similarly, the air force is talking airplanes orwings. What about the army? No clear-cut unit there. In fact, there aretwo competing methods: one that measures fighting units, like divisionsor tanks. The other counts people, since the army is the most people-in-tensive force. The army estimate begins with a war-fighting model foreach world arena. In the model only engagement units are counted, andit is assumed that the support is there. Once the fighting forces arequantified, the army uses established linear factors to assess supportrequirements. Repair units, medical units, military police units, etc., arecomputed and expressed as a ratio derived from the engagement unit.

Master Plan Estimates