Competition; *Electronics; Employment Aigher E - ERIC

452

ED 245 883 TITLE INSTITUTION REPORT NO PUB DATE NOTE AVAILABLE FROM PUB TYPE EDRS PRICE DESCRIPTORS IDENTIFIERS ABSTRACT DOCU'tENT RESUME SE 044 576 International Competitiveness in Electronics. Congress of the U.S., Washington, D.C. Office of Technology Assessment. OTA-ISC-200 Nov 83 547p. Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402. Reports Evaluative/Feasibility (142) MF02/PC22 Plus Postage. Automation; *Competition; *Electronics; Employment Patterns; Engineering Education; Financial Support; Aigher Education; *Industry; *International Relations; *International Trade; Manufacturing; *Policy; Science Education; Secondary Education; Technology *Industrial Policy; United States This assessment continues the Office of Technology Assessment's (OTA) exploration of the meaning of industrial policy in the United States context, while also examining the industrial policies of several U.S. economic rivals. The major focus is on electronics, an area which virtually defines "high technology" of the 1980's. The assessment sets the characteristics of the technology itself alongside other forces that exert major influences over international competitiveness. Specific areas addressed include: electronics technology; srr,,Acture, trade, and competitiveness in the international electronics industry; quality, reliability, and automation in manufacturing; role of financing in competitiveness and electronics; human resources (education, training, management); employment effects; national industrial policies; and U.S. trade policies and-their effects. The report concludes by outlining five options for a U.S. industrial policy, drawing on electronics for examples of past and prospective impacts, as well as on OTA's previous studies of the steel and automotive induStries. A detailed summary and iltroductory comments are included. Also included in appendices are case studies in the development and marketing of electronics products, a discussion of offshore manufacturing, and a glossary of terms used in the assessment. (J1,0 *-********************************************************************** * Reproductions supplied by EDRS are the best that can be made * * from the original document. , * *************-*******p*******************,*************-:*****************

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Competition; *Electronics; Employment Aigher E - ERIC

ED 245 883

TITLEINSTITUTION

REPORT NOPUB DATENOTEAVAILABLE FROM

PUB TYPE

EDRS PRICEDESCRIPTORS

IDENTIFIERS

ABSTRACT

DOCU'tENT RESUME

SE 044 576

International Competitiveness in Electronics.Congress of the U.S., Washington, D.C. Office ofTechnology Assessment.OTA-ISC-200Nov 83547p.Superintendent of Documents, U.S. Government PrintingOffice, Washington, DC 20402.Reports Evaluative/Feasibility (142)

MF02/PC22 Plus Postage.Automation; *Competition; *Electronics; EmploymentPatterns; Engineering Education; Financial Support;Aigher Education; *Industry; *InternationalRelations; *International Trade; Manufacturing;*Policy; Science Education; Secondary Education;Technology*Industrial Policy; United States

This assessment continues the Office of TechnologyAssessment's (OTA) exploration of the meaning of industrial policy inthe United States context, while also examining the industrialpolicies of several U.S. economic rivals. The major focus is onelectronics, an area which virtually defines "high technology" of the1980's. The assessment sets the characteristics of the technologyitself alongside other forces that exert major influences overinternational competitiveness. Specific areas addressed include:electronics technology; srr,,Acture, trade, and competitiveness in theinternational electronics industry; quality, reliability, andautomation in manufacturing; role of financing in competitiveness andelectronics; human resources (education, training, management);employment effects; national industrial policies; and U.S. tradepolicies and-their effects. The report concludes by outlining fiveoptions for a U.S. industrial policy, drawing on electronics forexamples of past and prospective impacts, as well as on OTA'sprevious studies of the steel and automotive induStries. A detailedsummary and iltroductory comments are included. Also included inappendices are case studies in the development and marketing ofelectronics products, a discussion of offshore manufacturing, and aglossary of terms used in the assessment. (J1,0

*-*********************************************************************** Reproductions supplied by EDRS are the best that can be made *

* from the original document. , *

*************-*******p*******************,*************-:*****************

O

Inte ationaompetitiveness

In ElectronicsUS. DEPARTMENT OF EDUCATION

NATIONAL INSTITUTE OF EDUCATIONEDUCATIONAL RESOURCES INFORMA.TION

I CENTER IER1Ci

This document has been reproduced asrecewed from the person or organaationonginatmg ItMinor changes nave been made to improvereproduction quality,

Ponts of view or opinions Staled in this docd-ment do not necessarily represent official NIEposition or policy.

44

L13. ;" CONGRESS OF THE UNITED STATES*tee* Office of Technology Assessment

41Wastfington. D. C. 20610

Office of Technology =assessment

Congressional Board of th-. r.:41:h. Congress

MORRIS K. UDALL, Arzr:::-1,

TED STEVENS. Alaska,.

Senate

ORRIN G. HATCHUtah

CHARLES McC. MATHIAS. JR-Mary land

EDWARD M. KENNEDYMassachusetts

ERNEST F.. HOLLINGSSouth Carolina

CLAIBORNE PELLRhode Island

CHARLES N. KIMBALL. ChairmanMidwest Research Institute

EARL BEISTLINEUniversity of Alaska

CHARLES A. BOWSHERGeneral Accounting Office

CLAIRE T. DEDRICKCalifornia Land Commission

House

E. BROV' ", JR.' California

..7,":";"1-IN D.

Michigan

.:`..A,R.RY WINN, Ill.Kansas

CLAYA.F.NCE E.Ohio

'1..'90PER EVAIowa

JOHN H. G -1.717-.."N'..5

Advisory Courmif

JAMES C. FLETCHMtUniversity of Pittsburgh

S. DAVID FREEMANTennessee Palley Authority

GILBERT GUDECongressional Research Service

CARL N. HODGESUniversity of Arizona .

Director

RAC) '14,Um, f

Hamlweekt & Quist

DAVID PUTTERGeneral \P. Mors Corp.

LEWIS THOMASMemorLI Sloan-Kettering

I. Cancer Center

JOHN H. GIBBONS

The Technology Assessment Board approves the reh:ase of this report. The views expressed in this report are notnecessarily those of the Board, OTA Advisory Council, or of individual 'members thereof.

International--C

in Electronics

OTA Reports are the principal documentation of formal assessment projects.These projects are approved in advance by the Technology Assessment Board.At the conclusion of a project, the Board has the opportunity to review the report,but its release does not necessarily imply endorsement of the results by the Boardor its individual members.

CONGRESS OF THE UNITED STATES

Office of Technolnly Assessmentvidsn.ngton.o C 20510

Recommended Citation:International Competitiveness in Electronics (Washington, D.C.: U.S. Congress, Officeof Technology Assessment, OTA-ISC-200, November 1983).

Library of Congress Catalog Card Number 83-600610

For sale by the Superintendent of Documents,U.S. Government Printing Office, Washington, D.C. 20402

Foreword

This assessment, requested by the Senate Committee on Commerce, Science,and Transportation, the House Committee on Ways and Means, and the joint Eco-nomic Committee, completes a series of three reports on the competitiveness ofU.S. industries. The series began with Technology and Steel Industry Competitive-ness and continued with U.S. industrial Competitiveness: A Comparison of Steel,Electronics, and Aufoinobiles.

Today. the subject of international competitiveness has more visibility amongthe general public than ever before. it has emerged as one of the primary economicissues facing Congress. Debates over "reindustrialization" and "industrial policy"beginning several years ago have been renewed. This assessment continues OTA'sexploration of the meaning of industrial policy in the U.S. context, while also ex-amining the industrial policies of several of our economic rivals.

Electronics virtually defines "high technology" in the 1980's. Th;s assessmentsets the characteristics of the technology itselfa technology already of such ubiq-uity that microprocessors and computers outnumber people in the United Statesalongside other forces that exert major influences over international com-petitiveness. These factors range from human resources and costs of capital to thepriorities that corporate managers place on manufacturing Technologies and thequality of their products. The report concludes by outlining five options for a U.S.industrial policy, drawing on electronics for examples of past and prospective im-pacts, as well as on OTA's previous studies of the steel and automobile industries.

OTA is grateful for the assistance of the advisory panel for this assessment,as well as for the help provided by many individuals in other parts of the FederalGovernment. OTA assumes full responsibility for the report.

JOHN H. GIBBONSDirector

lit

Electronics Advisory Pane!

Jack C. ActonGreensburg, Pa.

Steve BeckmanAFL-CIO

A. Terry BrixTemar Ltd.

Richard P. CaseIBM Corp.

Ruth Schwartz CowanSUNY-Stony Brook

William Kay DainesAmerican Retail Federation

Leonard DietchZenith Radio Corp.

Katherine Seelman, ChairpersonNew York, N, Y.

Richard A_ KraftMatsushita Industrial Co,

E. Floyd KvammeApple. C.."61711Tater-inc.

Geraldine McArdleReston, rVa.

Charles PhippsTexas Instruments, Inc.

K. M. PooleBell Laboratories

Benjamin t`,.t RosenSevin .Rosen Management Co.

Kate WilhelmEugene, Dreg.

Isaiah Frank Robert B. WoodJohns Hopkins University International Brotherhood of Electrical

F. Willard Griffith II Workers

GC International Michael Y. Yoshinu

Robert R. Johnson Harvard Business School

Mosaic Systems Inc.

iv 7

International Competitiveness in Electronics Project Staff

Lionel S. johns, Assistant Director, OTAEnergy, Materials, and International Security Division

Peter Sharfman, Program Managerinternational Security and Commerce Program

1Tt't

Martha Caldwell HarrisRobert R. Miller*

Contributors

Robert Fisher*

Robert Rarog*

L. W. Borgman 84 Co.Princeton, N.J.

Consultant Services Institute, Inc.Livingston, N.J.

Developing World Industry &Technology, Inc,

Washington, D.C.,

Hamilton Herman, et al.Potomac, Md.H. C. Lir

Untverrsiry -6f-Ivta-ryta

OTA Publishinn Staff

OTA contract p

Phillip Otterness*

Barbara Sachs*

ContractorsMary Ann MaguireUniversity of Maryland, College Park

Mitsubishi Research Institute, Inc.Tokyo, Japan

Richard W. MoxonUniversity of Washington, SeattleSterling Hobe Corp.Washington, D.C.

John H. Wheatley, et al.University of Washington, Seattle

John C. Holmes, Publishing OfficerJohn Bergling Kathie S. Boss Debra M. Datcher Joe Henson

Glenda Lawing Linda A. Leahy Cheryl J. Manning

Contents

Chapter Page1. Part A: Summary 3

Part B: Extended Summary 232. Introduction 553. Electronics Technology 67t. trucTure and i rade in the international Electronics industry 107

5. Competitiveness in the International Electronics Industry 163

6. Manufacturing: Quality, Reliability, and Automation 2177. Financing: Its Role in Competitiveness in Electronics 2538. Human Resources: Education, Training, Management 3019. Employment Effects 343

10. National Industrial Policies 37711. U.S. Trade Policies and Their Effects 429

12. Federal Policies Affecting Electronics: Options for the United States 463Appendix A: Glossary 505Appendix B: Offshore Manufacturing 510Appendix C: Case Studies in the Development and Marketing

of Electronics Products 520Index 539

vii

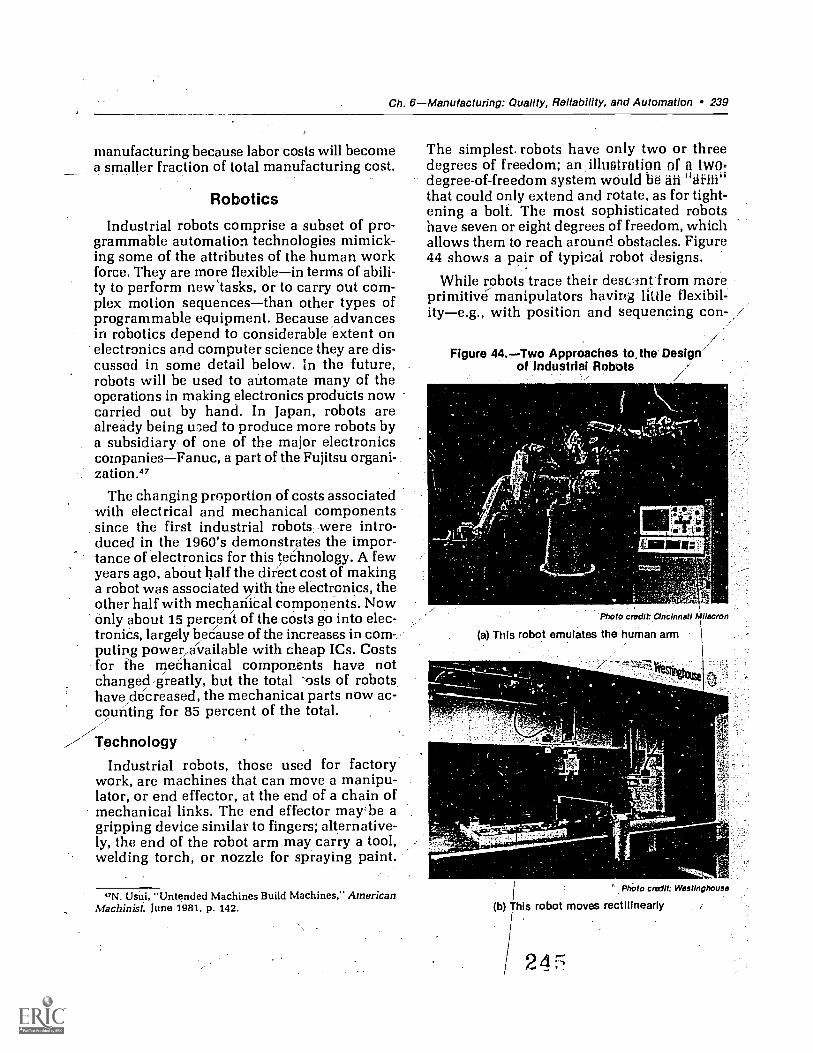

CHAPTER 1

Part A: Summary

Contents

Firiciings 5

i: lli*:_li,ulliptlIlll.ti l'ilSaillli ilI illti l......:^). Lit.i.l.,:ftnlit., fliiUStr I i.1' --',II.:',. 1-.1-, L. ;p',, ,- 1 1

15

Cr)nciusif):.! IJ

2

l\lartri$();; G./11:1/11tl'iti allf1 5

'I 11fi Ii( j Ii1r)1)if 111.10.giat.lqi Cirtsuit l'ruciuct;()p. Liltv 11

t;t 1)tica!-; 72

T.)+, 1 (:(ouptit..:r ht. Value:

:1!:(1 P:\1H)ri,, 11111 1.:(plip!noW.1....11;1,-, H. I )

CHAPTER 1

Part A: Summary

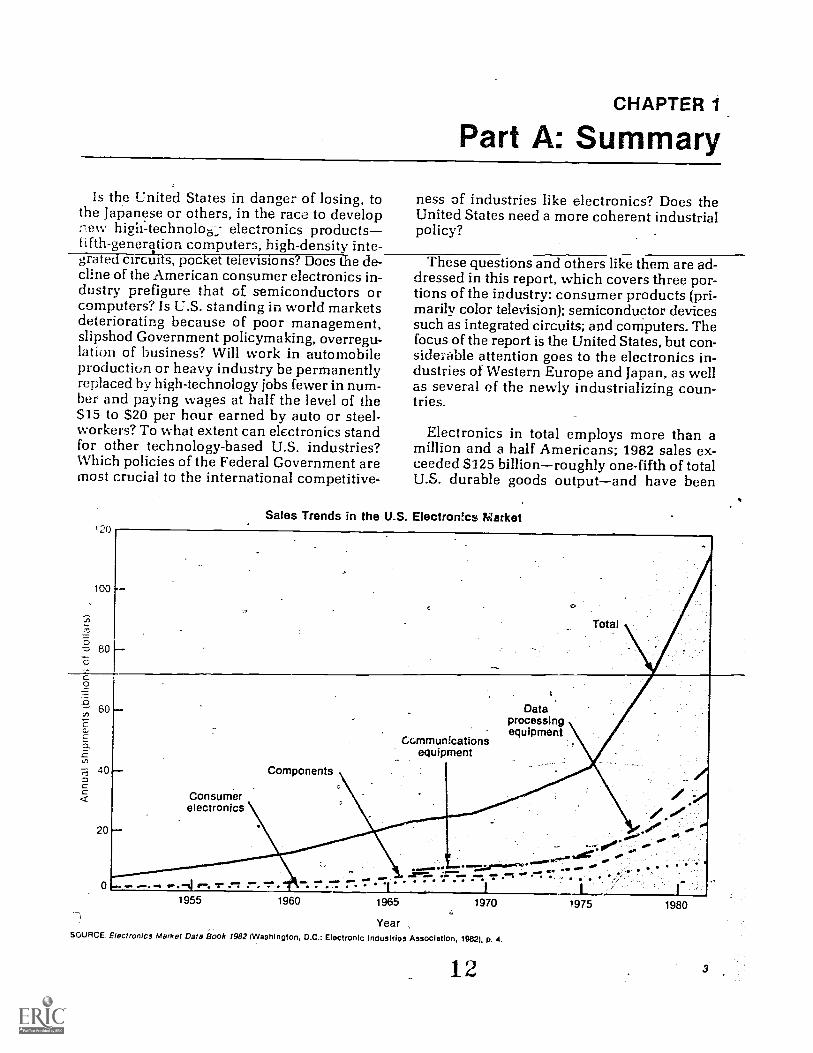

Is the United States in danger of losing, tothe Japanese or others, in the race to developnew high-technolog; electronics products! ifth-generation computers, high-density inte-grated circuits, pocket televisions? Does the de-cline of the American consumer electronics in-dustry prefigure that of semiconductors orcomputers? Is U.S. standing in world marketsdeteriorating because of poor management,slipshod Government policymaking, overregu-lation of business? Will work in automobileproduction or heavy industry be permanentlyreplaced by high-technology jobs fewer in num-ber and paying wages at half the level of the$15 to $20 per hour earned by auto or steel-workers? To what extent can electronics standfor other technology-based U.S. industries?Which policies of the Federal Government areinost crucial to the international competitive-

120

100

80

60

40

20

ness of industries like electronics? Does theUnited States need a more coherent industrialpolicy?

These questions and others like them are ad-dressed in this report, which covers three por-tions of the industry: consumer products (pri-marily color television); semiconductor devicessuch as integrated circuits; and computers. Thefocus of the report is the United States, but con -side: able attention goes to the electronics in-dustries of Western Europe and Japan, as wellas several of the newly industrializing coun-tries.

Electronics in total employs more than amillion and a half Americans; 1982 sales ex-ceeded $125 billionroughly one-fifth of totalU.S. durable goods outputand have been

Sales Trends in the U.S. Electronics Market

Consumerelectronics

Components

C

Communicationsequipment

Dataprocessingequipment

Total

1- "-mt 11.. irnp

1955

IM I1960

:,...'. *414.... .°. anima.. .. m.....:drm11..."r , E.

minim . jro :. ....g 9. .17 .., . . .. -

.1 I L :'''1965

YearSOURCE: Electronics Market Data Book 1982 (Washington, D.C.: Electronic Industries Association, 1982), P. 4.

1970

12

19751-

1980

4 International Competitiveness in Electronics

growing at nearly 15 percent per year; the sec-tor is an export leader, with a surplus of about$3 billion on a total trade volume of nearly $50billion. The industry's products feed manyother portions of the U.S. economy. Not onlydoes the Nation's defense depend heavily onelectronic technologies, but both manufac-turing and service industriesranging from theproduction of numerically controlled machinetools to banking and insuranceuse electronicproducts both directly and indirectly.

The competitiveness of firms and industriesrefers to the ability of firms in one country todesign, develop, manufacture, and market theirproducts competition with firms and indus-tries in other countries. At several pointsbelow, shares of the U.S. market or of worldmarkets are used as examples of trendsin in-ternational competitiveness; in fact, however,competitiveness is a more subtle concept.While market share is one possible indicator,it is only indirectly related to competitiveness.

How an industry will fare in internationalcompetition depends on factors ranging fromtechnology itself, to industrial policies pursuedby national governments, to the human re-sourcestechnicians to upper-level manag-ersavailable in a given country. In somecases, competitiveness is primarily a functionof prices, hence manufacturing coststhem--selves determined by wage rates, labor produc-tivities, the design of both products and man-ufacturing processes. This is the case in con-sumer electronics. In higher technology por-tions of the industry, one firm may 7--e able tooffer products that are beyond the technicalcapabilities of its rivalse.g., high-density in-tegrated circuits, advanced computer software.Where this is true, costs are less important.

From the Federal perspective, shifts in theinternational competitiveness .of American in-dustries have ramifications far beyond mattersof trade balances and foreign economic policy,even military security. The competitive stand-ing of a nation's industries will determine quite

13

directly its gross domestic product, and there-fore the standard of living of its citizens.

The linkage between competitiveness andemploymentin the aggregate, in particularsectors, or in particular occupational catego-riesis much looser. Industries can rise incompetitiveness while declin ng in employ-mentthe case in the U.S. textile industry inrecent years. In other cases, competitivenessmay remain high, output may expand, but do-mestic employment may grow relatively slowlycompared to output; this has been the case inboth the U.S. semiconductor and computer in-dustries. Similarly, domestic employment isonly loosely related to trends in foreign invest-ment or to government policies directed at con-trolling flows of imported goods; trade protec-tion has helped the employment picture in theU.S. consumer electronics industry no morethan it has in the steel industry or the automo-bile industry.

While the competitiveness of a given sectorof the U.S. economy depends on both domesticand international economic forces, the domes-tic contexte.g., people and institutions here,not overseas--generally carries the most weightin determining which industries will grow incompetitiveness, which decline. As a result,public policies with domestic objectives exertthe most influence over trends in internationalcompetitiveness. These are matters of indus-trial policy. OTA uses this .term in a neutralsense to refer to tha body of regulations, laws,and other policy instruments that affect the ac-tivities of industry and the resources, includinghuman capital, that the Nation's economy de-pends on. The United States has not in the pasthad a self-conscious industrial policy, in.partbecause it had no need for one. The lesson ofthe U.S. electronics industry, along with indus -.tries like steel and automobiles that PTA hasexamined previously, is that future internation-al competitiveness may well depend on a morecoherent and consistent approach by, the Fed-eral Government to matters of industrial policy.

Ch. 1Part A: Summary 5

Principal FindingsU.S. Competitiveness in Electronics

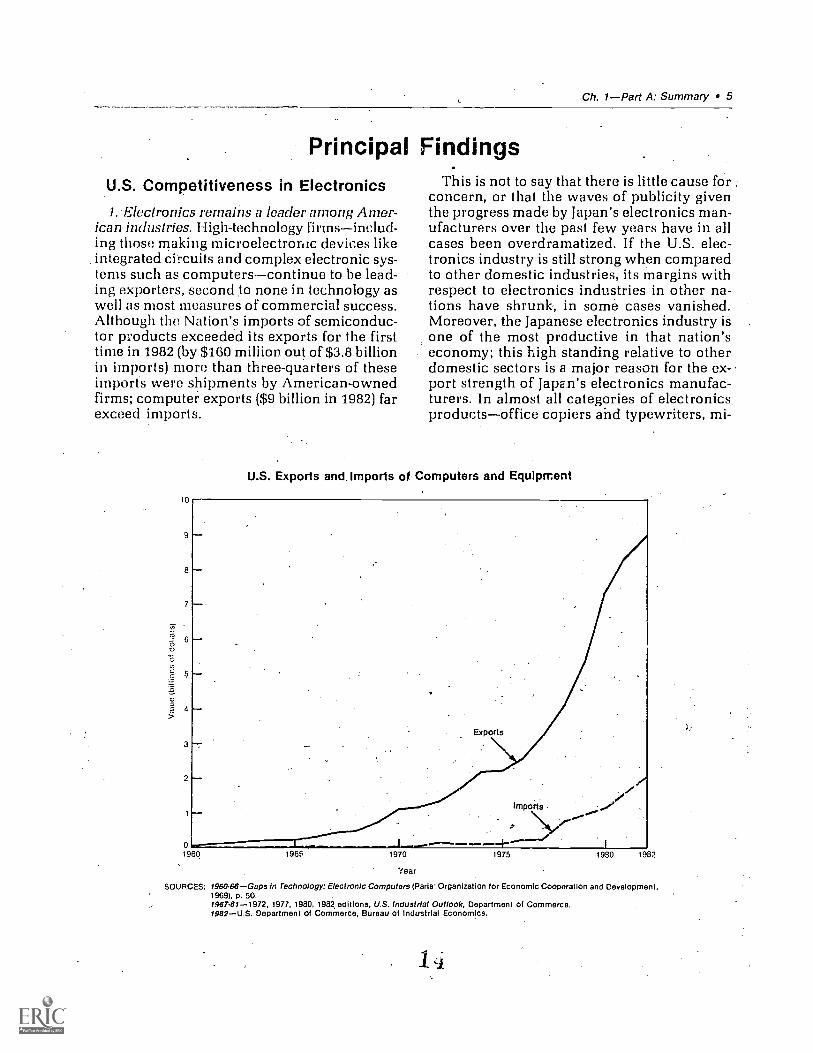

1. 'Electronics remains a leader among Amer-ican industries. High-technology firmsinclud-ing those making microelectronic devices likeintegrated circuits and complex electronic sys-tems such as computerscontinue to be lead-ing exporters, second ,to none in technology aswell as Most measures of commercial success.Although the Nation's imports of semiconduc-tor products exceeded its exports for the firsttime in 1982 (by $160 million out of $3.8 billionin imports) more than three-quarters of theseimports were shipments by American-ownedfirms; computer exports ($9 billion in 1982) farexceed imports.

r.6

0

O

C0

4

10

8

5

This is not to say that there is little cause forconcern, or that the waves of publicity giventhe progress made by Japan's electronics man-ufacturers over the past few years have in allcases been overdramatized. If the U.S. elec-tronics industry is still strong when comparedto other domestic industries, its margins withrespect to electronics industries in other na-tions have shrunk, in some cases vanished.Moreover, the Japanese electronics industry isone of the most productive in that nation'seconomy; this high standing relative to otherdomestic sectors is a major reason for the ex-port strength of Japan's electronics manufac-turers. In almost all categories of electronicsproductsoffice copiers and typewriters, mi-

U.S. Exports and. Imports of Computers and Equipment

0 es1960 1965 1970 1975 1980 1982

Year

SOURCES: 1960.66 Gaps In rechnology: Electronic Computers (Paris: Organization for Economic Cooperation and Development.1969), p. 50,1987.81-1972, 1977, 1980, 1982 editions, U.S. Industrial Outlook, Department of Commerce.1982U.S. Department of Commerce, Bureau of industrial Economics.

6 International Competitiveness In Electronics

croelectronics, communications equipmentand consumer goodsthe U.S.-Japan trade bal-ance is strongly negative (see ch. 4).

2'. Just as the competitive positions of a na-hylastries will differ, with Some rising

and othorSdeclining, so competitive positionswithin an industry like electronics will vary.Likewise, within one portion of the industry,such as color television manufacturing, somefirms will at any given time be more competi-tive than others.

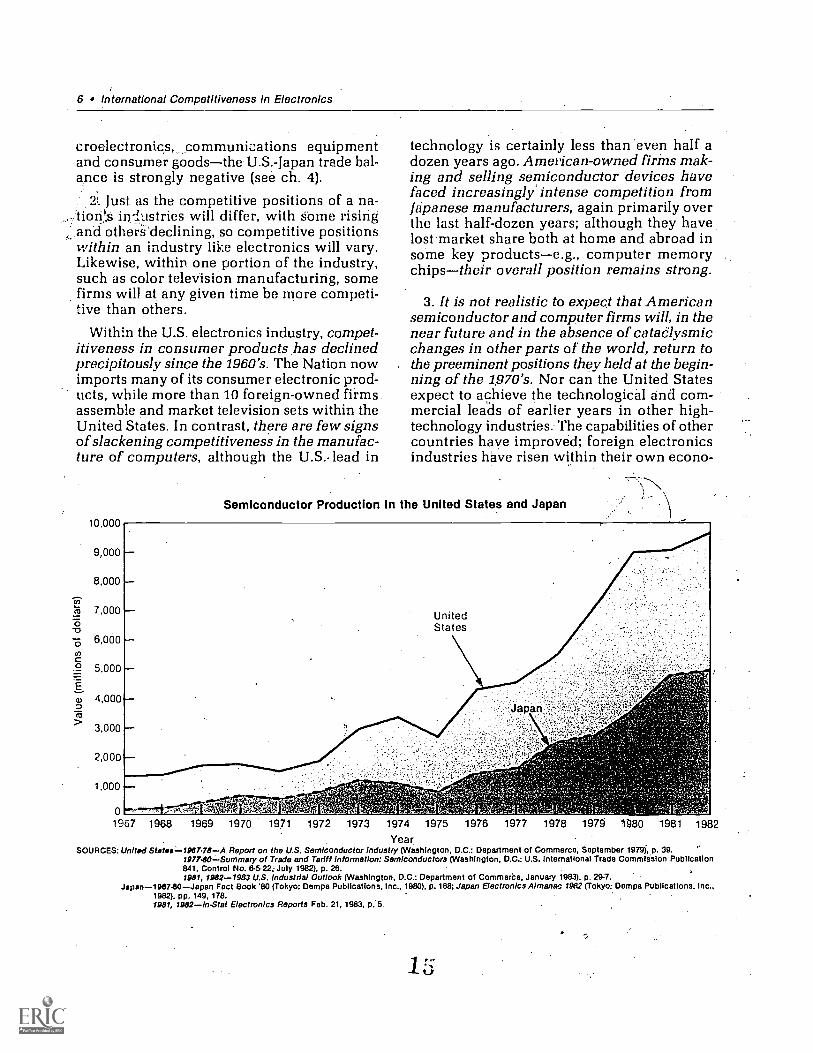

Within the U.S. electronics industry, compet-itiveness in consumer products has declinedprecipitously since the 1960's. The Nation nowimports many of its consumer electronic prod-ucts, while more than 10 foreign-owned firmsassemble and market television sets within theUnited States. In contrast, there are few signsof slackening competitiveness in the manufac-ture of computers, although the U.S., lead in

10.000

9,000

8,000

7.0000

-6 6,000l)C2 5,000

Ea) 4,000

3,000

2,000

1,000

01967 1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 'I'g80 1981 1982

YearSOURCES: United Statee=1987.78A Report on the U.S. Semiconductor Industry (Washington, D.C.: Department of Commerce, September 1979j, p. 39.

197740Summaty of Trade and Tariff information: Semiconductors (Washington, D.C.: U.S. International Trade Commission Publication841, Control No. 6 -5.22; July 1982), p. 28.1981, 1982-1983 U.S. Industrial Outlook (Washington, D.C.: Department of Commeice, January 1983), p. 29-7.

Japan-1967-80Japan Fact Book '80 (Tokyo: Dempa Publications, Inc., 1980), p. 188; Japan Electronics Almanac 1982 (Tokyo: Dempa Publications, Inc.,1982), pp. 149, 178.1981, 1982in-Stat Electronics Reports Feb. 21, 1983, p..5.

technology is certainly less than even half adozen years ago. American-owned firms mak-ing and selling semiconductor devices havefaced increasingly' intense competition fromJapanese manufacturers, again primarily overthe last half-dozen years; although they havelost market share both at home and abroad insome key productse.g., computer memorychipstheir overall position remains strong.

3. It is not realistic to expect that Americansemiconductor and computer firms will, in thenear future and in the absence of cataclysmicchanges in other parts of the world, return tothe preeminent positions they held at the begin-ning of the 1.970's. Nor can the United Statesexpect to achieve the technological and com-mercial leads of earlier years in other high-technology industries. The capabilities of othercountries have improved; foreign electronicsindustries have risen within their own econo-

Semiconductor Production in the United States and Japan

_la

Ch. 1Part A: Summary 7

mies; international economic conditions havechanged.

4. The United States can continue to behighly competitive in electronics and othertechnologically driven industries, with U.S.firms remaining leaders in innovation, in in-ternational trade, and in sales and profits athome and abroad. Not only is this possible, itis necessary if the United States is to maintainits standard of living, its military security, andif the U.S. economy is to provide well-payingand satisfying jobs for the Nation's labor force.Electronics is indispensable to a broad rangeof manufacturing and service functions, fromcomputer-aided design of the structures of of:fice buildings to the switching of the telephoneswithin those buildings.

5. Congress could take the initiative in devis-ing programs that would actively support theelectronics industry, and others of comparableimportance. The first requisite is broad nation-al agreement on the role of high-technologysectors like electronics as a driving force forfuture economic growth, a greater degree ofconsensus on where the U.S. economy is nowheading and where it should head. The secondis better understanding of how particularpieces of legislation affect the competitivenessof American industry, which in turn requiresdeveloping the capability of the Federal Gov-ernment for analyzing the sources of compet-itive strength.

The Role of Technology

1. One way to establish a competitive advan-tage in an industry like electronics is throughsuperior technology. Better process technology.e.g., automationcan help reduce costs. Forsimilar products, lower manufacturing costspermit lower selling prices, hence a more com-petitive product. Alternatively, higher profits'may be possible, which can help finance fur-ther improvements. Production technologiesare particularly important in consumer elec-tronics and semiconductors, less so for largecomputers.

2. Superior product technologies may com-mand premium prices in the marketplace, mak-ing manufacturing costs less significant. Prod-uct featuresranging from appearance toquantifiable characteristics such as the per-formance of a computer system in running"benchmark" programscan contribute tocompetitive advantage; in high-technologyfields as in low, product differentiation andastute marketing can be important.

Understanding customer wants and needs isvital to designing successful products; inte-grated circuits that are functionally similar,perhaps even interchangeable, may be differen-tiated through subtle variations in perform-ance; advertising strategies can be built aroundclaims of high quality or rapid delivery'; a broadarray of alternate source suppliers may re-assure prospective purchasers. Manufacturersof computers and peripherals. devote con-siderable effort to industrial design and humanfactors engineering; ease of u e is vital in sell-ing computer systems to first -time customers.

Rapid technical change reates much morescope for product technology as a competitiveweapon in microelectronics and computersthan in consumer electronics. For many years,American semiconductor and computer man-ufacturers prosper 'd by offering products thatfirms elsewhere in the world could not designor build.

Industrial Policy

1. OTA, takes industrial policy to be a neutralterm referring to the group of Federal policiesthat affect competitiveness, productivity, andeconomic efficiencysometimes directly,sometimes through influences on business de-cisions or on individuals. Industries rise andfall in international comWition for many rea-sons. Seldom can single causes be foundmoreSeldom yet simple, straightforward palicyrernedies. Plainly, industrial policy offers noquick fixes for the dilemmas of the U.S. con-sumer electronics industry, nor any sure pre-scriptions that can guarantee the future com-

,

6'

8 International Competitiveness in Electronics

4.

\vissifieisfrodPhoto credit: Mostek Corp.

Portion of a read-only integrated circuit memory

_petitiveness of our microelectronics or comput-er sectors. Just as plainly, competitiveness inelectronicsand in other U.S high-technologyindustrieswill depend on factors including:

capable people, hence on Federal policiesdealing with education and training;capital for new business startups and forexpansion, hence on macroeconomic andtax policies;open markets for American products,hence on foreign economic policy; and.the research base that supports domesticfirms, hence on Federal technology andscience policy.

The job of industrial policy is to evaluate, link,and coordinate the many Federal efforts thatdeal with such concerns.

2. While, international competitiveness isfirmly rooted in the efforts of private com-panies, public policies set many of the rules of

the game. In the United States and in other,parts of the world, business enterprises coalpete in an environment shaped to considerableextent by government industrial policies (in-cluding elements of fiscal, monetary, tax, manpower, trade, and regulatory policies).

Foreign governments are experimenting withindustrial policies intended to aid and supporttheir own electronics industries; virtually allindustrialized and industrializing nations sin-gle out electronics for special treatment. Amer-ican firms seeking to export or to manufactureoverseas must contend with economic andsocial policies of host governments that are'more complex and sophisticated than in thepast. Rather than outright protectionism orother forms of overt discrimination against for-eign firms, host governments now adopt indirect subsidies for their own industriestax in-centives, capital allocations, funding for com-mercially oriented research and development(R&D). At the same time, governments bargainwith foreign multinationals using carrots andsticks such as investment incentives and per-formance requirements while seeking to ac-quire jobs and technology, or to improve theirbalance of payments.

3. Although a well-designed and supportiveindustrial policy is not, by itself, sufficient tobuild competitiveness in a given sector of a na-tion's economy, government policies can, un-der some circumstances, tip the balance. TheUnited States can expect no more than verylimited success in negotiations with other na-tions aimed at minimizing the impacts of thosecountries' industrial policies.

For this and other reasons, a "business-as-usual" approach is unlikely to prove sufficientto the task of maintaining U.S. competitivenessin electronics. Better prospects for strengthen-ing the U.S. position would come with theadoption of more effective industrial. policiesof our own. The American electronics industryfaces only a few major problems, mostly in thetrade arena, that are directly--susceptible toGovernment remedy. On the other hand, Fed-eral agencies could support the industrydirectly and indirectlyin many ways. Few of

17

these would have much visibility. By the sametoken, they would not necessarily cost much.Consistent and careful attention to the manysmaller matters that affect competitivenessdiffusion of technology within the UnitedStates, tax treatment of equipment contribu-tions to universities, the antitrust environmentfor joint R&D, long-term basic researcharethe necessary ingredients in a more coherentand productive industrial policy. A supercom-puter project, to take a current example, maybe glamorous as well as desirable in itself, butis no substitute.. \..

4. The choice of policy tools, and,thr designof individual measures, depend on overall ob-jectives; an industrial policy is the sum of manyparts that can be put together in different`ways.Should CongreSs wish to pursue .a more ..o-ctised industrial policy for the United States,it could choose from among five bro alter-\natives:

A protective strategy aimed at presrmvingthe domestic market base for U.S. indus-tries, along with preservation of existingjobs and job opportunities.Protection and/or support for a limitednum ibe: of industries judged Critical for theU.S. .:!,.7ratolny or. more narrowly, for na-tional semirity.Support for the technological base and inAitutional infrastructure that underlyAmerican industries, with particular atten-ticn to structural adjustwent (e.g., labor

ret;atuing and mobility).Promotion i the glolvil competitiveness of

firms inc'zYstries by encouragingt and or.,,m uwnpf:-:tition in domestic

Js int -7.:iatiDiiA morkets.2 fertwi tvhorc: r3e private sec-

tor when ..-'7cefiling industrialdevehiy-ttent an

.While these five approaches to industrial pol-i(., discussed. in chapter 12, are certainly not114.f.tually _exclusive, they represent distinctlyditerent thrusts, implying different mixes ofpolicy instruments as well as different goals.

Ch. 1Part A: Summary 9

What would be the implications of a decisionto pursue a more coherent industiial policy inthe United States? First and foremost, that toautomatically equate "industiial policy" witha greater degree of Government involvementin the economy is to view the matter from anarbitrarily narrow perspective. Industrialpolicy does not have to run counter to effortsto "get Government off the backs of business."Rather, it should be construed as an effort tomake the inevitableindeed oftentimes desir-able and necessaryFederal involvement amore consistently productive one. It implies aneffort to develop, both politically and institu-tionally, Government policies toward industrythat:

explicitly consider impacts on com-petitiveness and economic efficiency;seek to treat the problems and opportuni-ties of particular industries in the contextof the economy as a whole, rather than inisolation; and,do a better job of relating policy tools topolicy objectives.

Policy Concerns in ElectronicsAmong the elements of industrial policy, the

following are vital for the continuing com-petitiveness of the U.S. electronics industry.They might have rather different places, andbe addressed in different ways, under each ofthe alternatives listed above.

1. High-quality education and training (in-cluding retraining) for engineers, technicians,and other skilled workers.

More than anything else, the competitive po-sition of the United States in high technology,has been built on the human resources avail-able here. A renewed Federal commitment toeducation and training seems called for (seeohs. 8 and 9). Engineering enrollments runningat record levels have swamped the resourcesavailable in colleges and universities; even so,the United States graduated but 63,000 engineers in 1981 compared to 75,000 in ,Japan.

10

10 International Competitiveness in Electronics.

U.S. electronics firms have faced seriousproblems in finding adequate numbers of en-gineers, as well as technicians and service per7sonnel with needed skills and aptitudes. Inade-quaw resources in U.S. engineering schools areharming the quality of education as well as con-straining the numbers of new graduates. Train-ing and retraining for technicians and parapro-fessionals. varies widely in quality and appro-priateness to emerging needs. Many people inthe United States emerge from high schoolquite unprepared to work in technology-basedindustries.

Despite fluctuations in supply and demandover the years., engineers in principle compriseone ''of the most employable occupationalgroups in the labor force; it is hard to imaginean "oversupply" of engineers or of people withgood technical training of any of a wide vari-ety of types in an economy like that of theUnited States, provided that people are will-ing and able to shift jobs according to demandWithin the economy and organizations are will-ing to help them do so.

2. A strong technological basestemmingfrom basic research and applied R&D withlong-term objectives, including the diffusion ofresults, in-fields such as solid-state electronics,optical devices, communications technologies,computer-aided design of circuits and systems,and computer software.

The Federal .Government could not only con-tinue to fund basic research, it could establishnew mechanisms for diffusing the results ofR&D to the private sector, experiment with thesupport of commercially oriented (rather thanmilitary) research, and strengthen tax incen-tives and other encouragements for successfulinnovators.

3. Economic adjustment policies that smoothflows of capital and labor within the economy,aiding growing firms in their efforts to corn

while-

pete hile providing well-paying jobs for. thedomestic labor force.

Structural change is a fact of life in Americanindustries, driven by-the currents of an increas-ingly open international economy (see chs. 4and 5), as well as byjechnological change (ch.

3). Corporations, cities and regions. and peo--ple must adjust to changes, many of which areoutside their control. Federal attention to max-imizing the positive effectives of changee.g.,stimulating growth industrieswhile:amelio-rating the negative impacts, could be Opt1: of thecentral elements in a more coherent industrialpolicy for the United States. Policy initiativesaimed at personnel mobilitywhether \geo-graphic, inter-industry, or within organiza-tionsare one example.

4. Adequate supplies of investment capitalfor new startups as well as rapidly expandingestablished firms.

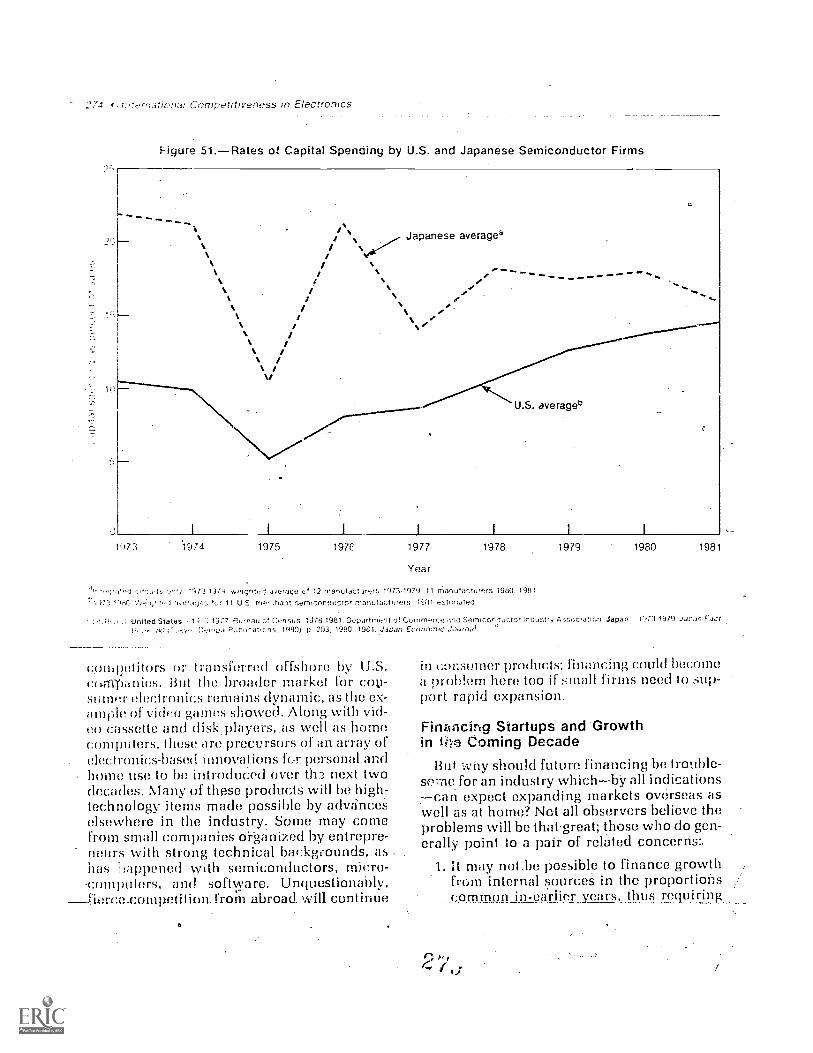

As discussed in chapter 7, venture capitalmarkets in the United States function well,although cyclic downturns are likely to recurand risk capital is often hard to find at earlystages of technology development.

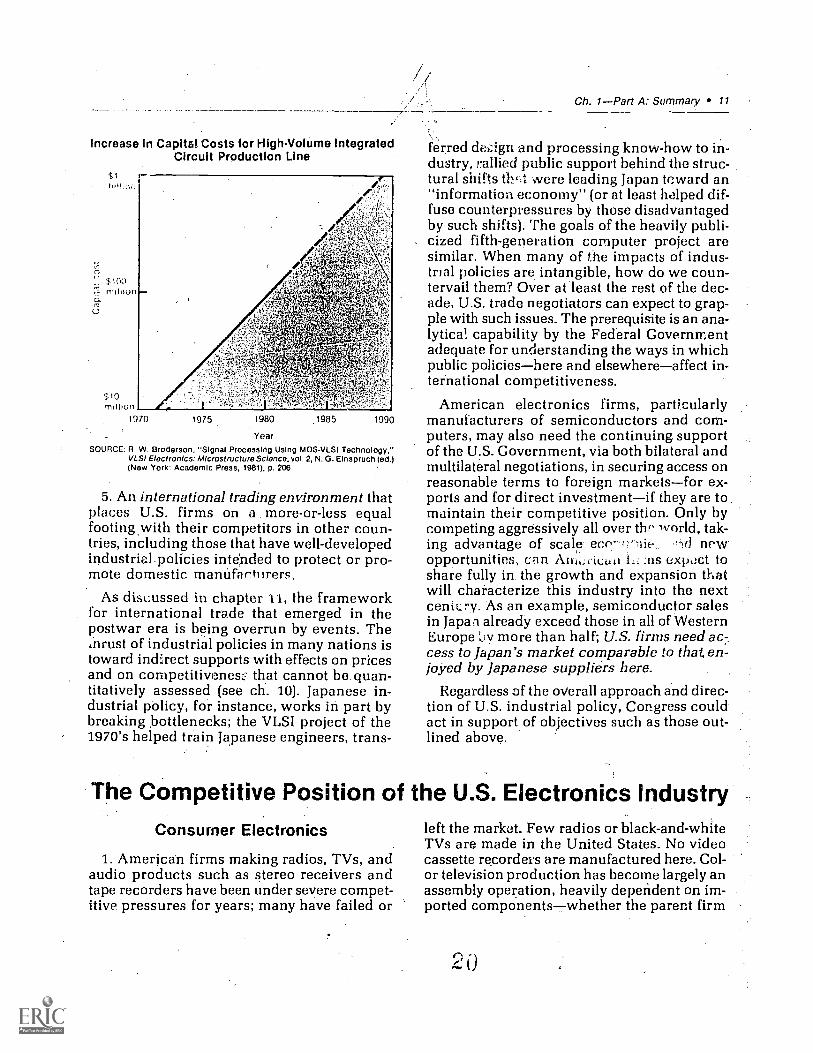

Rapidly growing companies, particularly in'the semiconductor industry, do face severefinancial pressures. These stem from increas-ing capital intensity, due both to higher R&Dexpenses and to production equipment that hasgone up in cost by an order of magnitude overthe past decade, coupled with the preferenceof American managers to finance expansionfrom internally generated funds. Tax policieshave a major influence over sovirces of financ-ing and risk absorption.

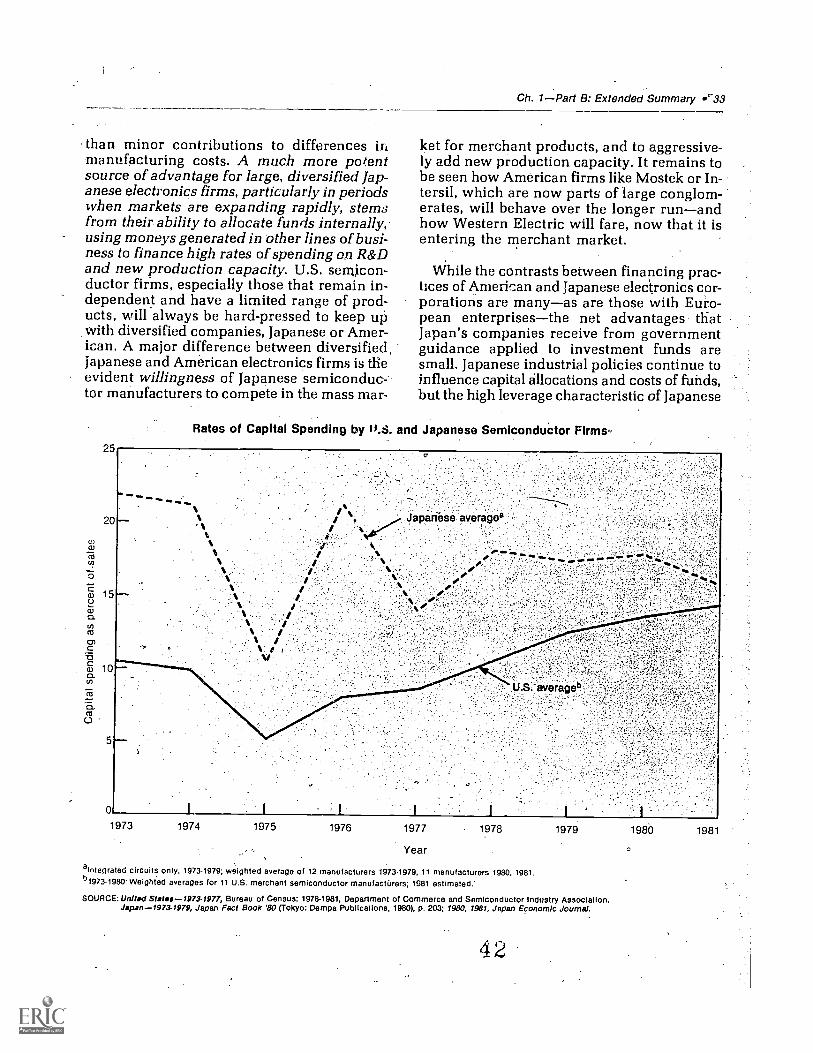

While the advantages are not as great assometimes implied, large diversified electron-ics companies in Japan, and perhaps in someWestern European countries, do benefit fromreal (i.e., inflation-adjusted).costs of capital thatare somewhat lower than for merchant semi-conductor firms in the United States. By them-selves, these differencesmatters of a few per-centage pointsare not enough to weigh heavi-ly in the competitive balance. Constraints onrates of capital spendingdue in part to thepreference of American firms for internal fi-nancingare more likely to be a drag on thecompetitive abilities of U.S. manufacturers.These and other factors, primarily expectationsconcerning ;iflation, tilt the investment deci-sions of American managers toward the short-er term.

Increase in Capita! Costs for HighVolume IntegratedCircuit Production Line

S10million

1910 1975 1980 1985 1990

YearSOURCE: R. W. Broderson, "Signal Processing Using MOSVLSI Technology,

VLSI Electronics: Microstructure Science. vol. 2, N. G. Einspruch (ed.)(New York: Academic Press, 1981), p, 206

5. An international trading environment thatplaces U.S. firms on a more-or-less equalfooting with their competitors in other coun-tries, including those that have well-developedindustrial policies intended to protect or pro-mote domestic manufarturers.

As discussed in chapter 11, the frameworkfor international trade that emerged in thepostwar era is being overrun by events. The,nrust of industrial policies in many nations istoward indirect supports with effects on pricesand on competitivenes: that cannot be quan-titatively assessed (see ch. 10). Japanese in-dustrial policy, for instance, works in part bybreaking bottlenecks; the VLSI project of the1970's helped train Japanese engineers, trans-

Ch. 1Part A: Summary 11

ferred dfii;ign and processing know-how to in-dustry, rallied public support behind the struc-tural shifts th=.t were leading Japan toward an"information economy" (or at least helped dif-fuse counterpressures by those disadvantagedby such shifts). The goals of the heavily publi-cized fifth-generation computer project aresimilar. When many of the impacts of indus-trial policies are intangible, how do we coun-tervail them? Over at least the rest of the dec-ade, U.S. trade negotiators can expect to grap-ple with such issues. The prerequisite is an ana-lytical capability by the Federal Governmentadequate for understanding the ways in whichpublic policieshere and elsewhereaffect in-ternational competitiveness.

American electronics firms, particularlymanufacturers of semiconductors and com-puters, may also need the continuing supportof the U.S. Government, via both bilateral andmultilateral negotiations, in securing access onreasonable terms to foreign marketsfor ex-ports and for direct investmentif they are tomaintain their competitive position. Only bycompeting aggressively all over tho world, tak-ing advantage of scale eciro .,;,d newopportunities, can Atri4,riuun 1- .11S t.:Xlit1Ct toshare fully in the growth and expansion thatwill characterize this industry into the nextcenicry. As an example, semiconductor salesin Japal already exceed those in all of WesternEurope ',.;./ more than half; U.S. firms need ac:-cess to Japan's market comparable to that en-joyed by Japanese suppliers here.

Regardless of the overall approach and direc-tion of U.S. industrial policy, Congress couldact in support of objectives such as those out-lined above.

The Competitive Position of the U.S. Electronics IndustryConsumer Electronics

1. American firms making radios, TVs, andaudio products such as stereo receivers andtape recorders have been under severe compet-itive pressures for years; many have failed or

left the market. Few radios or black-and-whiteTVs are made in the United States. No videocassette recorders are manufactured here. Col-or television production has become largely anassembly operation, heavily dependent on im-ported componentswhether the parent firm

12 International Competitiveness in Electronics

U.S. Sales and imports of Selected Consumer Electronic Products, 1982

U.S, sales(millions of dollars)

Imports(mAlions of dollars)

Import penetration(percent)3

Color television $4,253 $546 12.8%Blackand white TV 507 344 67.9Video cassette recorders 1,303 1,032 100.03Home and auto radiosb 1,579 1,207 76.4Stereo systemsc 1.754 1,342 76.5

$9,396 $4,471 47.6%a8ecause many Items Imported in a given year are not sold until the following year, dividing Imports during a given calendaryear by sates in that same year may give only a rough indication of Import penetration; for Instance, all video cassette recorderssold in the United States are imported even though 1982 sales figures exceed 1982 Import figures.bincluding auto tape players.

cincluding audio tape units and other component equipment.SOURCE: Electronic Market Data Book 1983 (Washington, D.C.: Electronic Industries ASsociatIon, 1983), pp. 8, 19, 31.

is American -owned (RCA, Zenith, GE) or for-eign-owned (Sony, Quasar, Magnavox). In tele-vision manufacture especially, the policies of 250

the Federal Government have contributed tothe plight of the industry. Dumping complaintsagainst importers going back to 1968 havenever bi.en fully resolved. An industry legallyentitled to trade protection has not received it.

2. Nonetheless, trade practices illegal underU.S, Inv e been only one factor in the de-clining competitiveness of the American con-sumer electronics industry. More fundamen-tally, competitive advantages have shifted toother parts of the worldfirst japan, now new-ly industrializing countries like Taiwan andSouth Korea. These countries 'have masteredthe technological requirements for mass-pro-ducing consumer products such as TV sets.They have lower labor costs than the UnitedStates, an adequate corps of skilled workersand engineers, supportive government indus-trial policies, and astute corporate manage-ments.

American firms have been reduced to a reac-tive posture; they have lost the lead in productdesign and development while moving manu-facturing operations to foreign countries inorder to keep their costs competitive. Americanproducts in consumer alectronicase.g., colortelevision receiverscontinue to he competi-tive in performance, quality, and reliability, butthey are no better than imports. The consumerelectronics market is highly price-competitive;without advantages in technology or productfeatures, . American manufacturers will behard-

0 2000II

tz, 1500)

100

50

0

Price Index for Televisions Comparedto All Consumer Durables

1973 1974 1975 1976 1977

Year

1978 1979 1980 1981

SOURCES: Consumer DurablesEconomic Report of the President 1982(Washington, D.C.: U.S. Government Printing Office, February 1982),p. 294.

TelovIslons.Electronic Market Data Book (Washington, D.C.: Elec-tronic Industries Association, 1982), p. 29.

pressed to keep up with their foreign-basedcompetitors. While U.S. firms may continue toinnovate and to be leaders in consumer prod-ucts aimed m. specialized market nichescom-puter games have been a recent examplebroadly speaking, product leadership has beenlost. At least in the short term, prospects fortaking the lead in new generations of high val-ued-added mass market products seem slim.

3. The rise of foreign firms together with pro-tracted trade disputes have contributed to a ma-jor shift .in the structure of the U.S. consumerelectronics industry. The number of firms-hasnot charged greatly since the 1960's; but whileonce there were 16 or 17 American-owned

21

Ch. 1Part A: Summary 13

manufacturers of TVs, today only 4 of 15 withplants in the United States have headquarterShere. Still, the market shares of the traditionalU.S. leadersZenith and RCAhave notchanged much; together these two companiescontinue to hold about 40 percent of the U.S.color TV market. It is the weaker AmericanmanufactUrers that have succumbed.

4. At the same time foreign enterprises wereinvesting in assembly plants in the UnitedStates, American-owned firms were transfer-ring labor-intensive manufacturing operationsto low-wage offshore locations. In general, finalassembly for the U.S. market remains here,with subassembly in Mexico and the Far East.These moves wore driven by foreign competi-tion. t;.S. color TV manufacturers felt they hadlittle option but to move production abroad ifthey were to cut costs and meet their competi-tor's prices.

Offshore production substitutes quite directlyfor jobs in the United States. Nonetheless, ifAmerican firms had not moved offshore, it isquite possible that they would have lost evenmore ground to foreign-based competition,with yet more jobs lost over the longer term.In most cases, transfers of production overseashare net impacts on U.S. employment and onthe U.S.. economy that appear relatively small;improvements in labor productivity, for ex-amplealso- driven by foreign competitionhave been at least as important as a cause ofemployment declines in television manufactur-ing. Needless to say, the impacts on individualsand communities where job losses concentrateare often severe and long-lasting; in 10 yearsthe production work force in consumer elec-tronics has been cut by more than 40 percent,from 85,000 to 50,000.

5. Beginning near the end of the 1970's, Or-derly Marketing Agreements (OMAs) limitedimports of color TVs while encouraging for-eign firms to produce here. The result was toequalize the terms of competition and to mod-erate employment declines in the UnitedStates. Otherwise, the OMAs did little to helpthe U.S. industry rebuild its competitivestrength.

In this regard, U.S. experience with OMAsrestricting color TV imports has paralleledother cases of import quotas, for instance inthe steel industry. Although the ostensible pur-pose may be to give domestic firms time to re-structure and adjust to changing competitivecircumstances, most cases protected indus-tries continue to react to pressures from abroadrather than taking strong positive steps of theirown; the notion that a respite from import com-petition will, by itself, help corporations restoretheir competitiveness gets little support fromevents in color television.

Semiconductors

1. U.S. manufacturers of semiconductorproducts such as integrated circuits remainhighly competitive in markets all over theworld. American-owned merchant firms--those that produce for the open marketar'aleaders in circuit design and process technol-ogy. While their share of world sales haschanged little over the past few years, with U.S.firms and their subsidiaries still accounting forabout 70 percent of worldwide output of inte-grated circuits,. Japarfe-Se manufacturers havebeen catching up in technology. Nonetheless,U.S. companies have the capability to maintaintheir competitiveness in most world markets.The inroads made by Japanese suppliers ofcommodity-like chips, notably random accessmemories (RA Ms); portend stronger competi-tion in other types of microelectronic devicesbut do not translate automatically into advan-tages for products such as logic chips or milcroprocessor families. There is no reason to ex-pect a loss of competitiveness in advanced mi-croelectronic products paralleling that in con-sumer electronics.

Although foreign manufacturers may some-times have advantagese.g., -supportive gov-ernment industrial policies, as in Japan orWestern Europethe U.S. merchant firmshave their own strengths. Among these are theability to rapidly develop and commercializenew technologies, to anticipate and design forshifting customer needs, and to adapt to chang-ing realities of international competition by

22

14 International Competitiveness in Electronics

entering into joint venture and technologytransfer agreements with both domestic andforeign firms when this is advantageous.

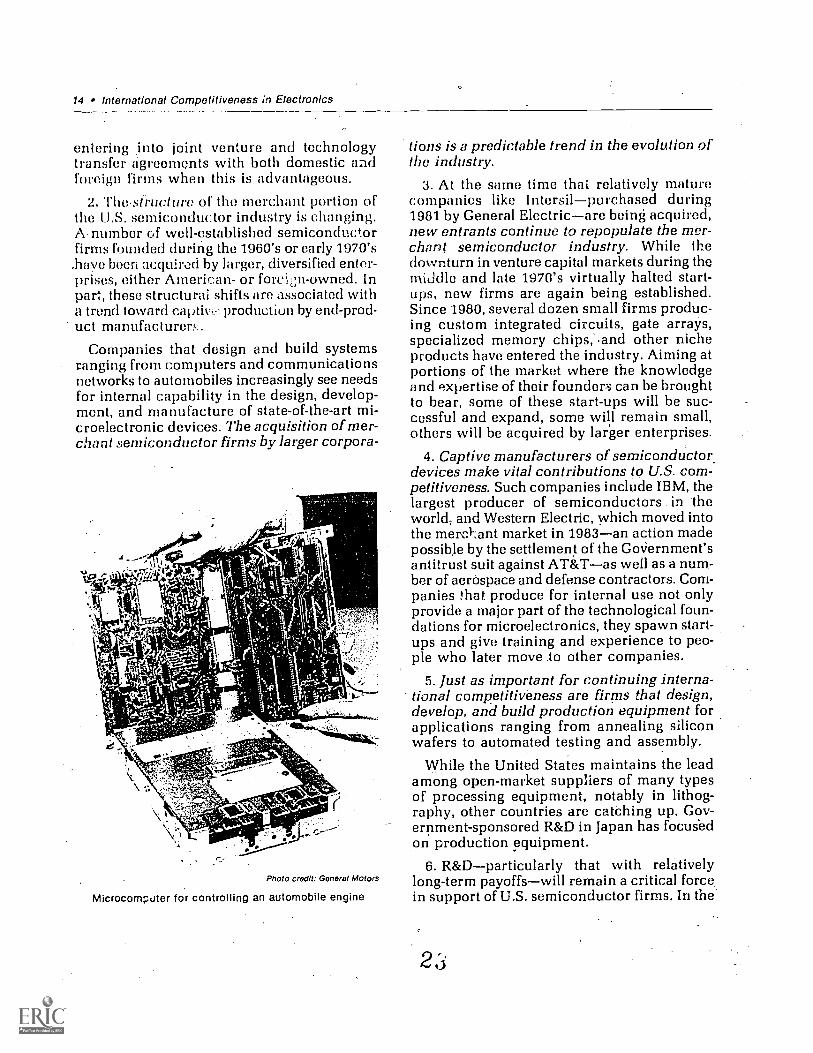

2. The.structure of the merchant portion ofthe U.S. semiconductor industry is changing.A. number of well - established semiconductorfirms founded during the 1960's or early 1970's.have been acquired by larger, diversified enter-prises, either American- or forein-owned. Inparr, these structural shifts are associated witha trend toward aptivi production by end-prod-uct manufacturer;:.

Companies that design and build systemsranging from computers and communicationsnetworks to automobiles increasingly see needsfor internal capability in the design, develop-ment, and manufacture of state-of-the-art mi-croelectronic devices. The acquisition of mer-chant semiconductor firms by larger corpora-

Photo credit: General Motors

Microcomputer for controlling an automobile engine

Lions is a predictable trend in the, evolution ofthe industry.

3. At the same time that relatively maturecompanies like Intersilpurchased during1981 by General Electricare being acquired,new entrants continue to repopulate the mer-chant semiconductor industry. While thedownturn in venture capital markets during themiddle and late 1970's virtually halted start-ups, new firms are again being established.Since 1980, several dozen small firms produc-ing custom integrated circuits, gate arrays,specialized memory chips, ..and other nicheproducts have entered the industry. Aiming atportions of the market where the knowledgeand expertise of their founder3 can be broughtto bear, some of these start-ups will be suc-cessful and expand, some will remain small,others will be acquired by larger enterprises.

4. Captive manufacturers of semiconductor.devices make vital contributions to U.S. com-petitiveness. Such companies include IBM, thelargest producer of semiconductors in theworld, and Western Electric, which moved intothe merchant market in 1983an action madepossible by the settlement of the GoVernment'santitrust suit against AT&Tas well as a num-ber of aerospace and defense contractors. Com-panies that produce for internal use not onlyprovide a major part of the technological foun-dations for microelectronics, they spawn start-ups and give training and experience to peo-ple who later move to other companies.

5. Just as important for continuing interna-tional competitiveness are firms that design,develop, and build production equipment forapplications ranging from annealing siliconwafers to automated testing and assembly.

While the United States maintains the leadamong open-market suppliers of many typesof processing equipment, notably in lithog-raphy, other countries are catching up. Gov-ernment-sponsored R&D in Japan has focusedon production equipment.

6. R&Dparticularly that with relativelylong-term payoffswill remain a critical forcein support of U.S. semiconductor firms. In the

past, much of tho technology base has comefrom larger firms such as II3M and AT&T. Gov-ernment support for research has not been sig-nificant in recent years, although the VeryHigh-speed Integrated Circuit program of theDefense ,Department will have commercialspinoffs.

The U.S. semiconductor industry can nolonger rely on past approaches to R&D andtechnology development. The industry recog-nizes the changing situation, and is develop-ing new mechanisms for strengthening itstechnical foundations; these include closer in-teractions with universities, along with jointVentures and cooperative research efforts. Con-gress and the Federal Government could ac-tively support and encourage both basic andapplied research with longer run payoffs. Thisis one of the surest ways of supporting contin-ued U.S. competitiveness in microelectronics.

Computers

1. American manufacturers of digital com-puters have dominated world markets formany years. Much as U.S. semiconductor firmshave demonstrated the ability to rapidly capi-talize on new technological and market oppor-tunities, so have American computer firmspioneered most of the design concepts thathave driven information processing: network-ing and distributed computing, small businessmachines and minicomputers, time-sharingamong multiple work stations, cheap massstorage, desktop microcomputers.

There are few concrete signs that thisdominance by U.S.-based firms.is threatened.Nevertheless, relative positions within theworld computer' industry will continue to shift,stimulated in many cases by new applicationsof computing power. As the industry continuesto evolve, the technological leads of Americanfirms are likely to shrink, and competitive posi-tions may become more difficult to maintain.Nevertheless, the U.S. lead in worldwide mar-keting of data processing systems is so largethat prospective challengers such as Japan can-not hope for more than modest success overthe rest of the century.

Ch. 1Part A: Summary 15

2. American firms have done a much betterjob than their foreign competitors of balanc-ing what the available technology can doagainst what customers for data processing sys-tems have wanted to accomplish. This has beenan important element in Patterns of competi-tive success, which have depended as heavilyon software that could be easily used by neo-phyte purchasers and was reliablei.e., free of"bugs"as on raw hardware performance.

In fact, foreign computer firms have some-times been able to match the United States.interms of hardwam; by and large, Japan's com-puter marufactUrers can at present. But theirsystems are still behind, mostly because thesoftwareat all levels is not as good: More-over, foreign firms -- whether European or Jap-anesehave not been as adept as Americansat finding new ways to apply their hardware.For example, U.S. firms remain well ahead inoffice automation, point-of-sale terminals forretail merchandisers, and many other applica-tions of distributed intelligence.

3. The ongoing structural alterations in thedata processing industry will be deeper andfarther-reaching than those in microelectronicsor consumer electronics.

Most of the recent technological innovationsin consumer electronics have come from large,well-established firms; new products fromsmall companies have seldom reached massmarkets. In microelectronics, while start-upshave resumed in the United Statesmany striv-ing to establish themselves with the aid of in-novative productsthe path of technologicalevolution seems, for the moment, well charted;there are few signs of sudden change thatwould seriously unsettle the industry. Com-puter technology which depends on micro-electronics, but also on other feeders, primarilysoftwareis potentially more volatile. As newapplications of computing power open win-dows of opportunity for firms in many partsof the world, American manufacturers willface more intense competitive pressures. Dis-tributed intelligence will transform a broadrange of other industries as well.

29.

16 International Competitiveness In Electronics

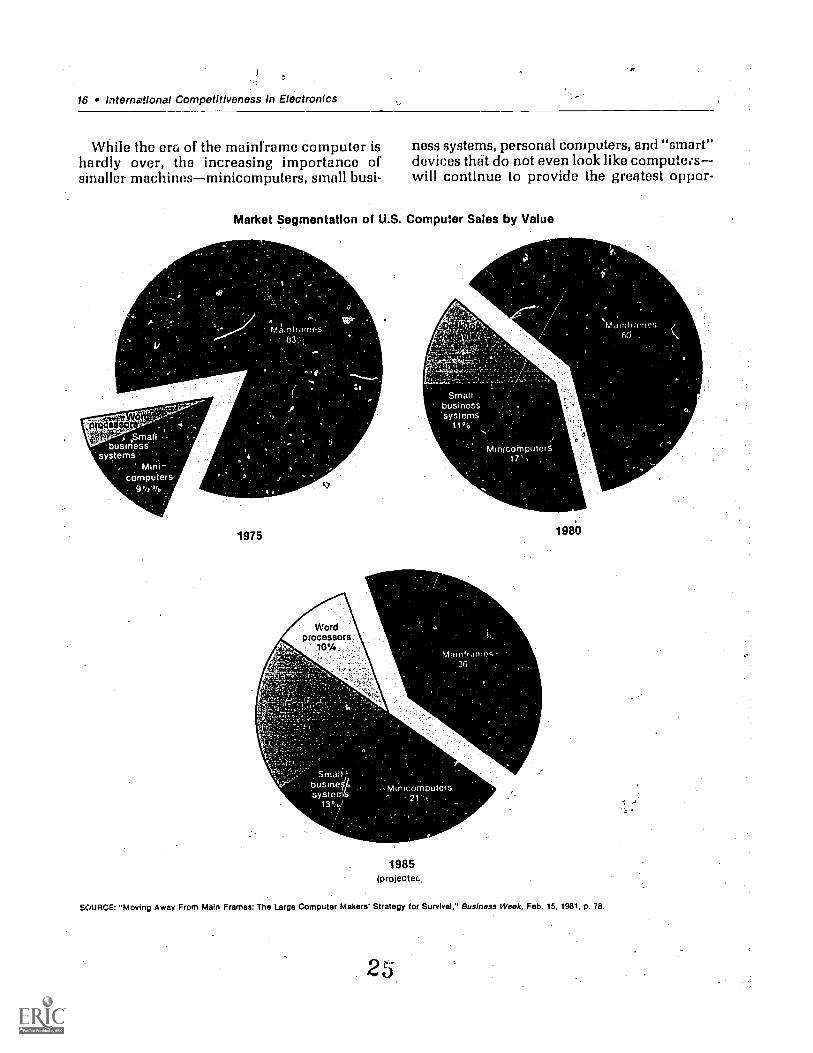

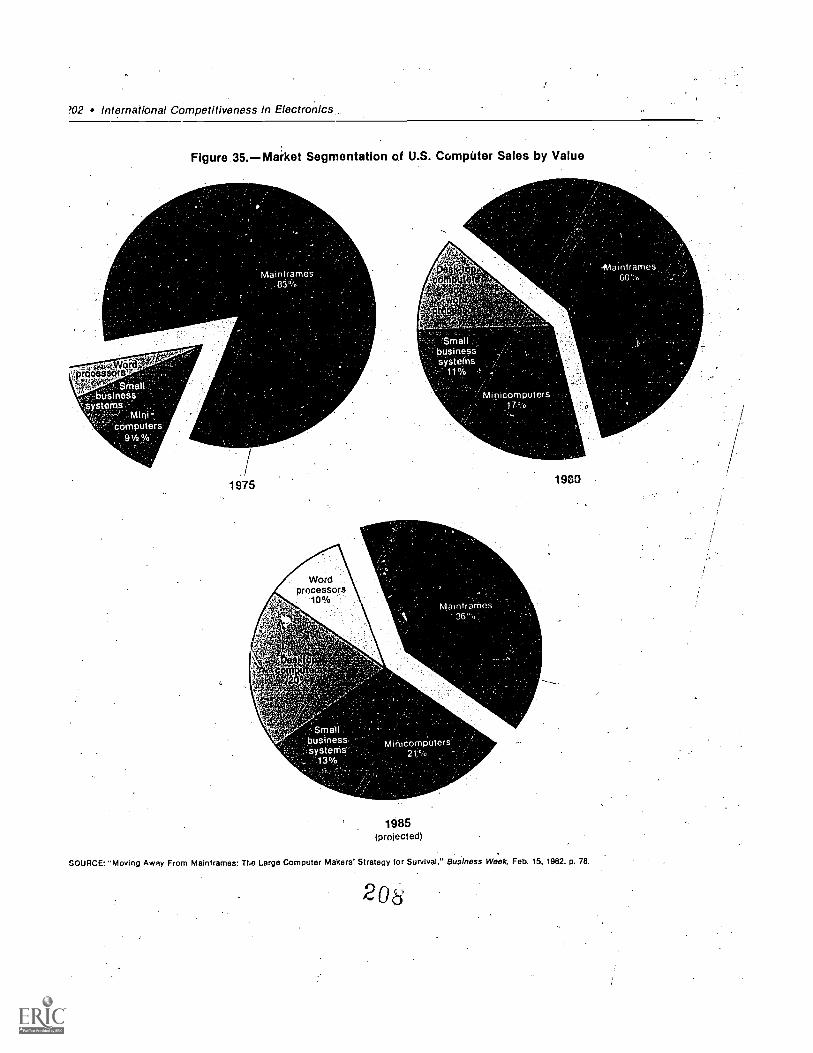

While the err, of the mainframe computer is ness systems, personal computers, and "smart"hardly over, the increasing importance of devices that do not even look like computet.ssinaller machinesminicomputers, small busi- will continue to provide the greatest oppor-

Market Segmentation of U.S. Computer Sales by Value

1975

Wordprocessors

10%

1985(projectec,.

1980

SOURCE: "Moving Away From Main Frames: The Large Computer Makers' Strategy for Survival," Business Week, Feb. 15, 1981, p. 78.

25

Ch. 1-Part A: Summary 17.

(unities for growth and expansion. The multi-tude of prospective applications of computingpower will offer new openings for overseasfirms as well as American companies. In someportions of the data processing equipmentiu those still in relative in-fancy. such as desktop machines and standard-ized otilc;0 automation productsforeign firmsmay eventually achieve a greater presence than

:they have managed in mainframe systems orgeneral-purpose minicomputers. To the extentthat computers become mass-market products,manufacturers in other parts of the world arelikely to emerge as more formidable competi-tors.

1%It*

N414

iro .9

)12'.etrair

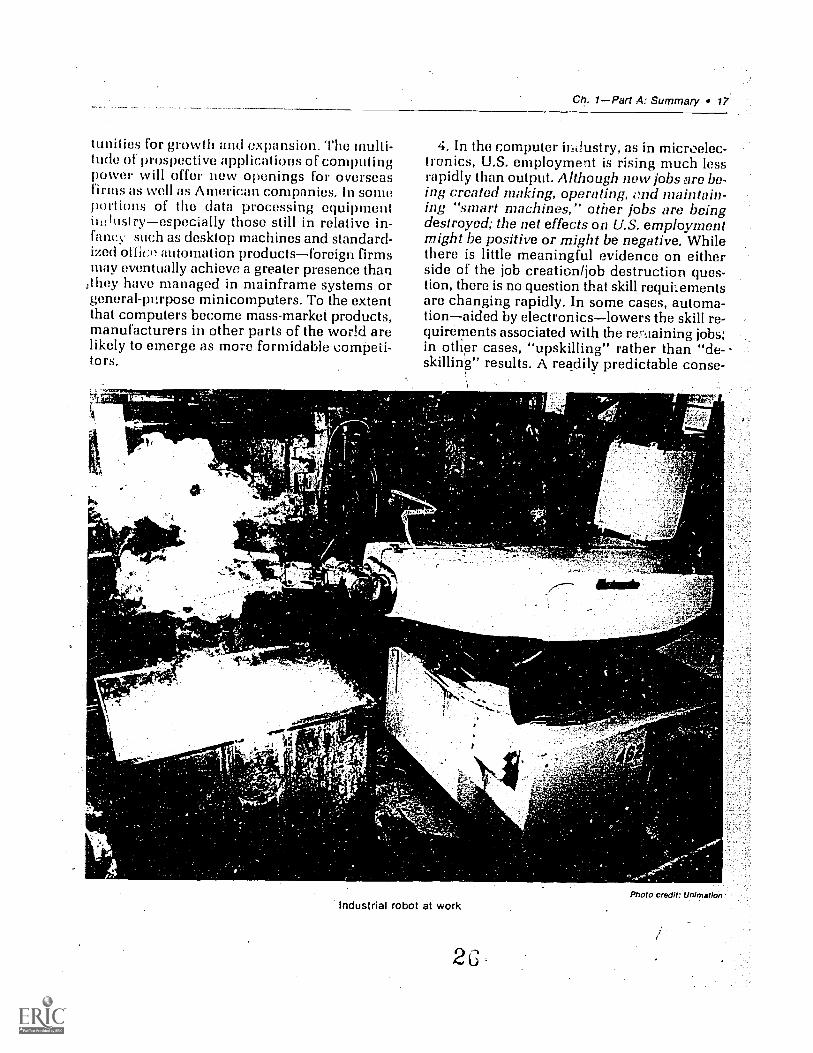

4, In the computer industry, as in microelec-tronics, U.S. employment is rising much lessrapidly than output. Although new jobs are be-ing created making, operating, and maintain-ing "smart machines, other jobs are beingdestroyed; the net effects on U.S. employmentmight be positive or might be negative. Whilethere is little meaningful evidence on eitherside of the job creation/job destruction ques-tion, there is no question that skill requLementsare changing rapidly. In some cases, automa-tionaided by electronicslowers the skill re-quirements associated with the rertiaining jobs:in other cases, "upskilling" rather than "de.-skilling" results. A readily predictable conse-

Industrial robot at work

,--- Nam&

Photo credit: Unirnation

18 lrternational Competitiveness in Electronics

quence has been serious labor market disloca-tions; these seem bound to intensify. Even iflabor market shifts cannot be predicted verywell, the need for adjustment is clear. To theextent that labor market shiftsgeographical,in terms of skills, in terms of wage levelsareunexpected (and some will always be), the im-pacts will be more severe. An obvious implica-tion is that policy responses must emphasizeflexibility.

5. Japan's computer manufacturers will notbe content with narrow or specialized markets.Following strategies similar to those that havesucceeded in consumer electronics anti semi-conductors, Japanese computer firms will at-tempt to establish themselves in selected dataprocessing markets and expand from there.Backed by government efforts such as the fifth-

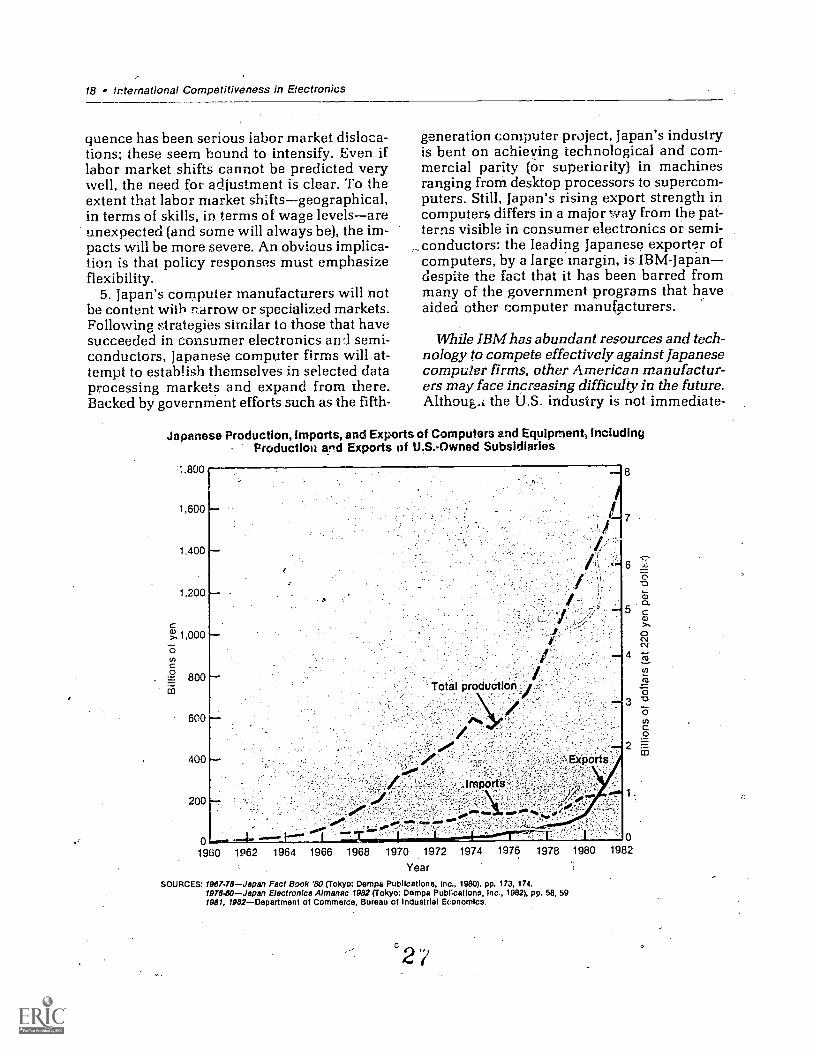

generation computer project, Japan's industryis bent on achieving technological and com-mercial parity (or superiority) in machinesranging from desktop processors to supercom-puters. Still, Japan's rising export strength incomputers differs in a major way from the pat-terns visible in consumer electronics or semi-conductors: the leading Japanese exporter ofcomputers, by a large margin, is IBM-japandespite the fact that it has been barred frommany of the government programs that haveaided other computer manufacturers.

While IBM has abundant resources and tech-nology to compete effectively against Japanesecomputer firms, other American manufactur-ers may face increasing difficulty in the future.AlthouE.,: the U.S. industry is not immediate-

Japanese Production, Imports, and Exports of Computersand Equipment, includingProduction and Exports of U.S.-Owned Subsidiaries

:,800

1,600

1,400

1,200

C>,) 1,000

0C

L2 800co

600

400

200

01960 1962 1964 1966 1968 1970 1972 1974 1976 1978 1980

YearSOURCES: 1987.78Japan Fact Book '80 (Tokyo: Damps Publications, Inc., 1980), pp. 173, 174.

1978-80Japan Electronics Almanac 1982 (Tokyo: Dempa PubKcalions, Inc., 1982), pp. 58, 591981, 1982 Department of Commerce, Bureau of Industrial Economics.

Ch. 1Part A: Summary a 19

ly imperiled, the Federal Government couldhelp ensure future competitiveness through abetter developed, more consistent industrialpolicy, particularly one supporting technologydevelopment and technical education.

6. As computers and their applications con-tinue to spread through the U.S, economy, theFederal Government might act to strengthenthe competitiveness of the industry both direct-ly and indirectly:

"Computer literacy"the ability to effec-Lively utilize smart machines and sys-temswill be a critical skill for the laborforce. Education and training in fieldsranging from traditional modes of quanti-tative thinking (arithmetic, algebra) to soft-ware engineering deserve renewed sup-port. Congress could provide leadership aswell as direct and tangible aid.Federal support aimed at critical bottle-necks in data processing, mostly in soft-ware, could be a vital long-term stimulusfor the American industry. Productivity in

software development has gone up onlyslowly over the years. Financing for educa-tion and training in software engineering,as well as R&D directed at computer archi-tectures, new programing languages,"andartificial intelligence appears appropriate.Smaller firms striving to establish them-selves in the data processing equipment in-dustryparticularly those developing soft-ware, peripherals, and innovative applica-tions of computing powerhave the sameneeds as do U.S. microelectronics firms:not only people with highly developedtechnical skills, but adequate supplies ofcapital for investment in R&D and produc-tion capacity and access to foreign mar-kets.

If effectively implemented, industrial policiesin support of such needs could pay vast divi-dends throughout the-U.S. economy becauseof the multitude of ways in which applicationsof computing power can enhance the compet-itiveness of firms in industries of all types.

ConclusionA nation can never be competitive in all in-

dustries at once. Not only will some rankhigher than others, but places will change overtime. Economies need to adjust; adjustmentbrings pain and distress to firms that encountertrouble, people who lose their jobs, the commu-nities affected. Even within an industry likeelectronicsin the United States, highly com-petitive as a wholesome parts, such as con-sumer electronics, face a far more problematicfuture than others. That s ch events are inevi-table does not mean that at least some of theproblems cannot be anticipated, and Some ofthe distress ameliorated by Government action.Moreover, the Federal Governthent can takepositive actions to support the develocimentand diffusion of technology, human resources,the infrastructure that companies depend onwhen pursuing' their individual competitivestrategies. Government policies can aid grow-ing sectors, help people and institutions adapt

to change. The dynamic of international com-petitiveness is continuous, and calls for a con-tinuing series of policy responses.

People can and will argue endlessly about thesuccesses and failures of industrial policies inother countries, but the primary lesson to bedrawn from foreign experience is simply this:industrial policymaking is a continuing activityof governments everywhere. In the UnitedStates, industrial policy has been left mostlyto the random play of events. Improvement isclearly possible; policymaking can be a pur-poseful activity characterized by learning frompast experience within a framework of empir7ically based analysis. Developing more effec-tive industrial policy for the United States mustbegin in this spirit, While recognizing that theprocess is inherently political. There is no onething that the Federal Government can do thatwill make a big difference for the future com-

2

20 International Competitiveness in Electronics

petitiveness of the U.S. electronics industry,but there are many specific policy concernsthat deserve attention. Only by linking andcoordinating these more effectively can theUnited States expect to develop a coherent andforward-looking approach to industrial policy.

29

Until the Nation begins this task, Americanfirms will continue to find themselves at a dis-advantage when facing rivals based in coun-tries that have turned to industrial policies asa means of enhancing their own competitive-ness.

CHAPTER 1

Part B: Extended Summary

Contents

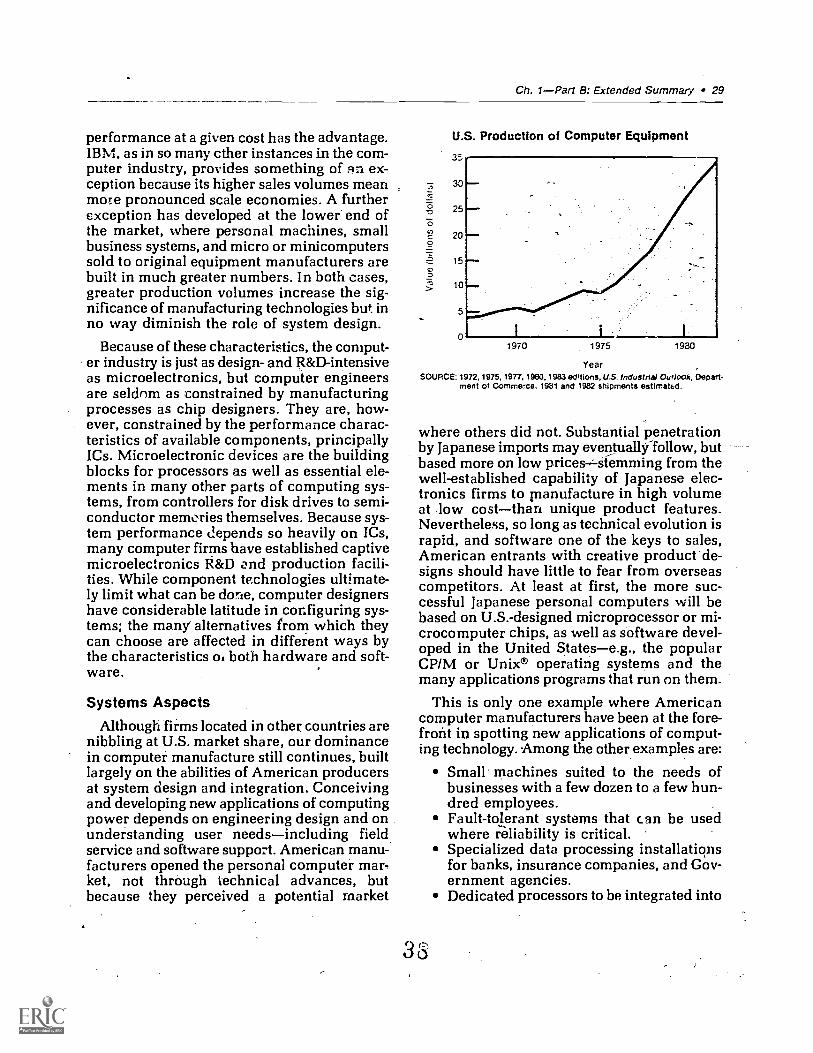

r,t;t:."lechnology 23(:;)n-innic; 23(;ein ic:onduct ors 24:ompnters 28

Finance 31Vt!tittn.4, Capital :31

nanc:ing Growth 32Intematior :1 I)ifferences 32.

Human Resources 34Quantity and Quality 34Continuing Education am: Training 35Preparation for Work in Technology-Based Industries 37NIIII;Welflnilt and Organization 37

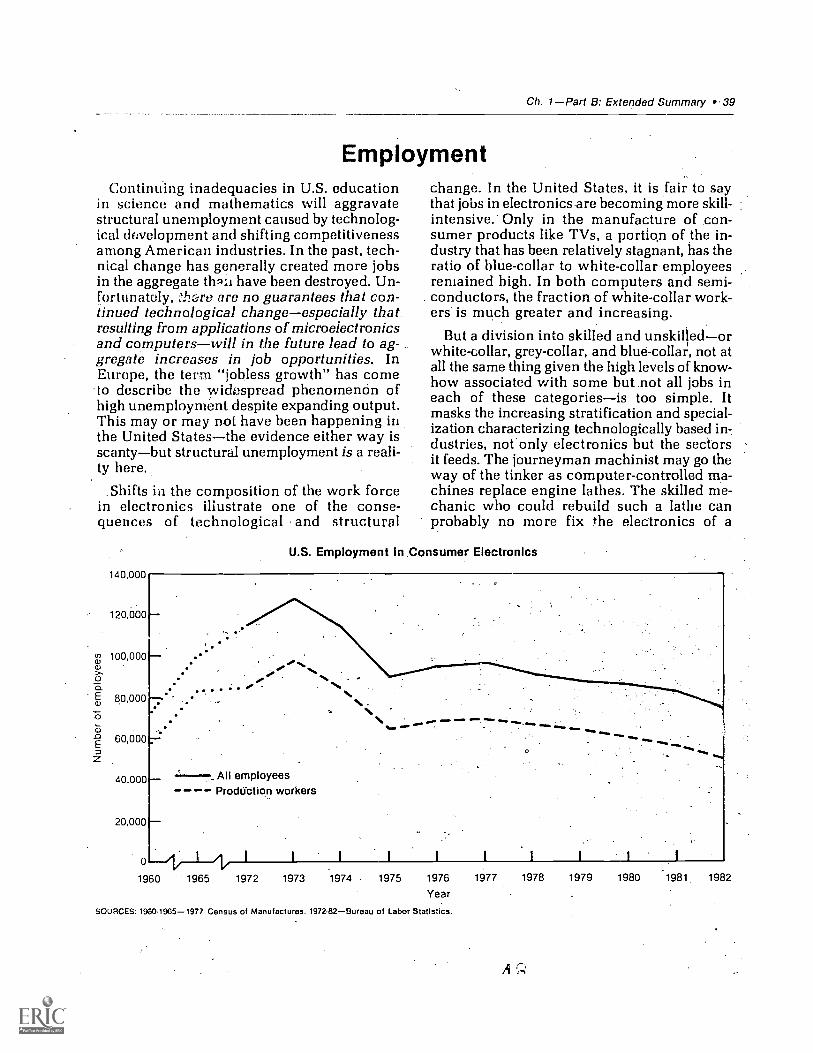

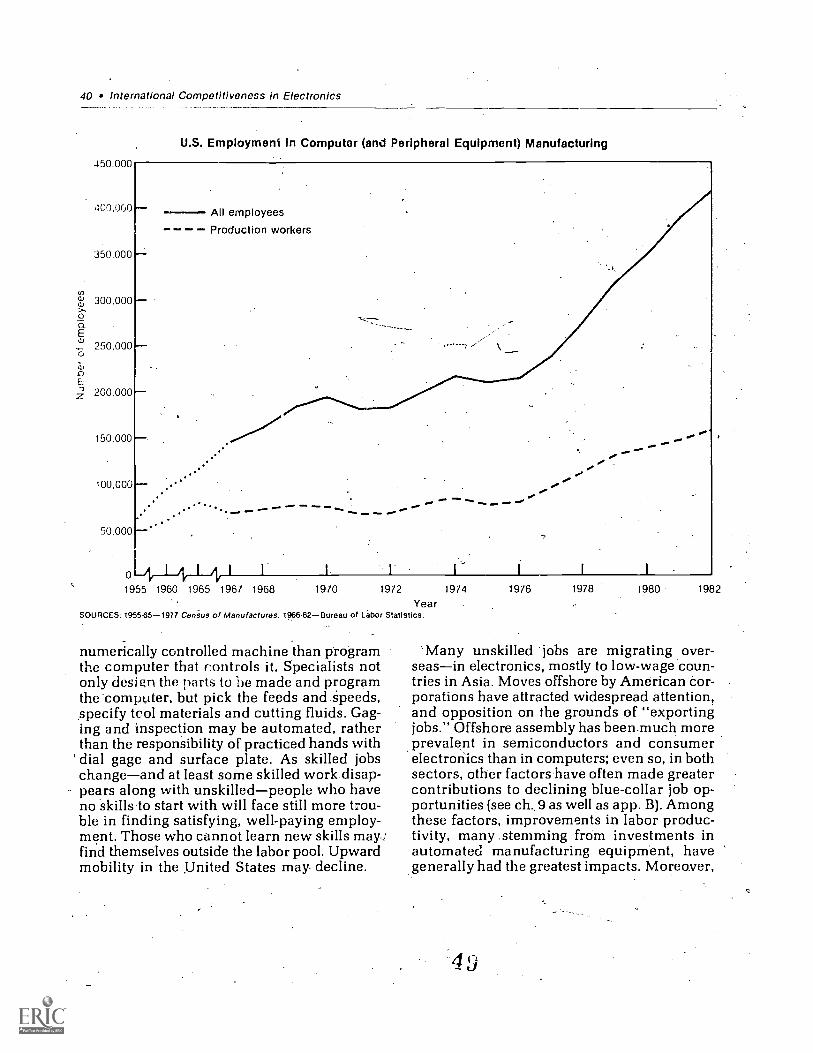

Employment 39

Trade 42Antidumping Enforcement, 42The Environment for World Trade 42

U.S. Industrial Policies 46

List of TablesPage

Color TV Imports into the United States 24World Integrated Circuit Output by Headquarters Location of Producing Firms 27Predicted Growth Rates by Occupational Category in the

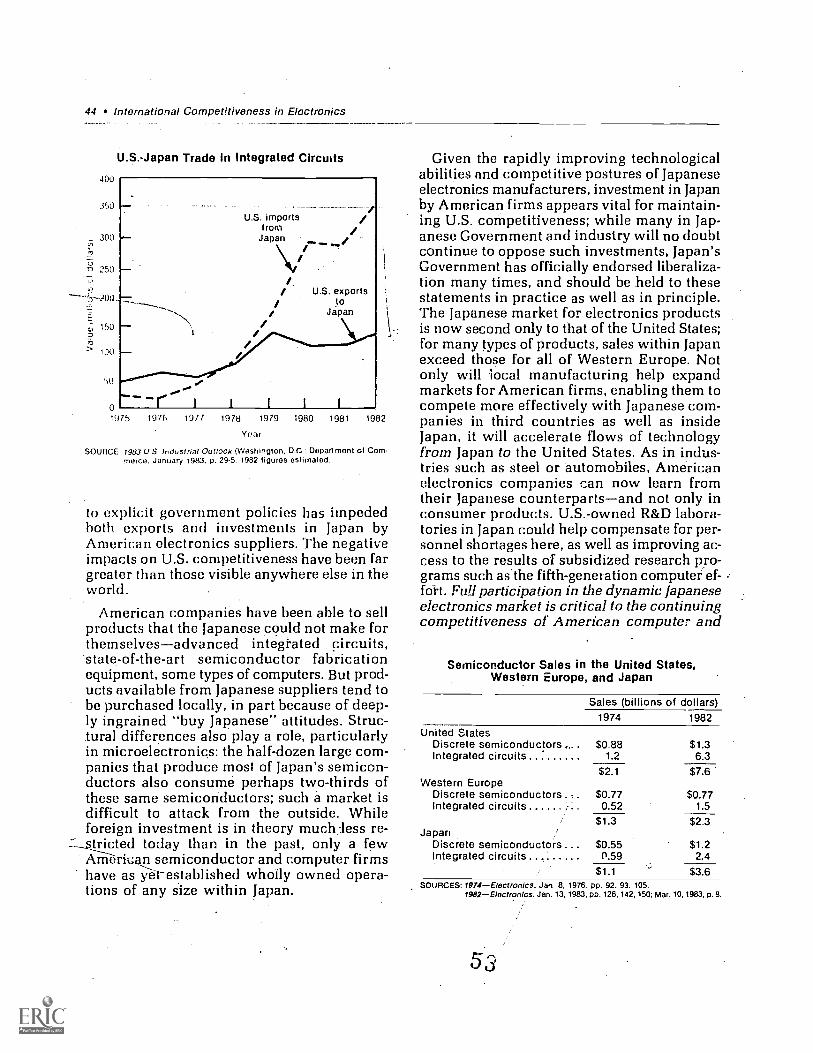

United States Over the 1980's 41Samico-nductor Sales in the United States, Western Europe, and Japan 44

List of FiguresPage

Japan's Production and Exports of Video Cassette Recorders (VCRs) 25.U.S. Semiconductor Sales by Typo 26U.S. Production of Computer Equipment 29Rates of Capital Spending by U.S. and Japanese Semiconductor Firms 33U.S. Employment in'Consumer Electronics 39U.S.Employment in Computer (and Peripheral EquiPment) Manufacturing 40U.S.-japan 'Trade in Integrated Circuits 44Distrilmtion of U.S. Semiconductor Sales by End Market 46

CHAPTER 1

Part B: Extended Summary

Part B of chapter 1 expands upon, withoutrepeating, the findings in the St:- .mary. In parrticular, the sections below highlight the role oftechnology as a force on competitiveness inconsumer electronics, semiconductors, andcomputers, along with factors such as capitalfor investment in research and expanded pro-duction capacity, human resources and theirdevelopment, and industrial and trade policiesboth here and abroad.

The several meanings that can be assignedto the rather amorphous concept "international

competitiveness" are discussed in detail inchapter 5. The viewpoint adopted below is firstthat of the manufacturer. Private companiesdesign, develop, produce", and market goodswhich may have more or less success in themarketplace, more or less positive impact ona nation's competitive position. Later the viewswitches to that of governments and their pol-icies, which act on competitiveness directlyand indirectly by influencing business activ-ities, supporting- education, subsidizing ex-ports, through the climate for capital formationand economic growth.

TechnologyChapter 3 covers electronics technology in

some detail (also see the Glossary, app. A, forexplanations of technical terms). Here the in-teractions between technical capabilities andmarket success are explored.

Consumer Electronics

In consumer electronic products such as coil_or TVs, both product and process technologiesare well-understood and widely fiiffused. Prod-uct differentiation strategies are more impor-tant than technical differences; componenttelevision, stereo sound, and digital chassisdesigns illustrate the frontiers of this nowiarge-ly routine field. Japan's consumer electronicsmanufacturers have benefited from the econo-mies of higher production volumes and per-haps from more extensive automation, but bothprodUct and process technologies in consumerelectronics tend to be standardized, technicalchange to be incremental. Companies any-where in the industrialized world have accessto much the same pool of knowledgethe ex-ceptions being newer product families likevideo cassette recorders (VCRs). Color TV3with similar prOduct features are made notonly in Western Europe, the United States, and

japan, but in developing countries like Taiwanand South Korea. Manufacturing technologiesare similar wherever TVs are built, with labor-intensive operations carried out in low-wagedeveloping countries by European and. Jap-anese firms, as well as American. The resultis a competitive environment in which Ameri-can firms have few unique advantages.

Differences in both product and process tech-nologies for televisions were greater during thelate 1960's and early 1970's whet Japanesefirms were beginning to invade the U.S. mar-ket. Then, firms in Japan moved more quicklythan their American counterparts toward solid-state chassis designs. By using transistors andintegrated circuits (ICs), they were able to im- .

prove the reliability of their products, and moreeasily automate portions of the productionprocess. Automation helped compensate forcomponent costs that at the time were" higherfor transistorized designS than for those rely-ing on vacuum tubes. Reliability was particu-larly important to Japanese firms because theydid not have service organizations or, dealernetworks within the United States. To increase -

their market shares, they needed to sell through.retail outlets such as discount chains. To

23

24 International Competitiveness in Electronics

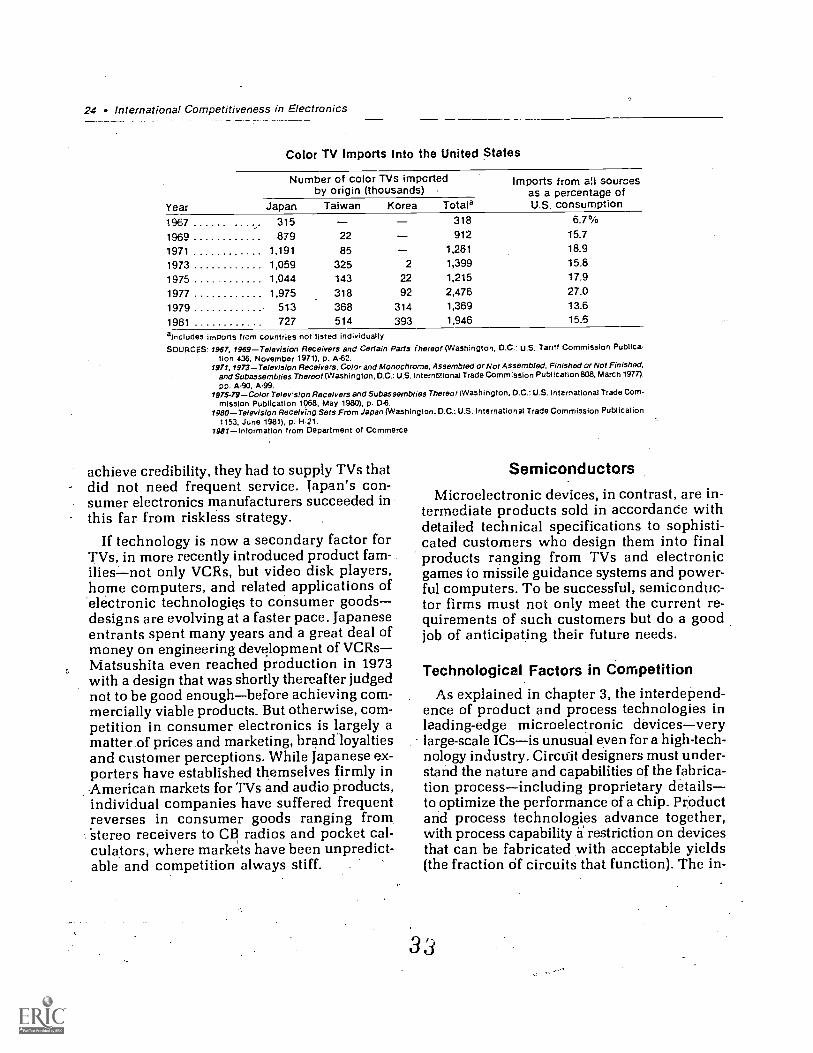

Color TV Imports Into the United States

Year

Number of color TVs impertedby origin (thousands)

Imports from all sourcesas a percentage ofU.S. consumptionJapan Taiwan Korea Total a

1967 315 318 6.7%

1969 879 22 912 15.7

1971 1,191 85 1,281 18.9

1973 1,059 325 2 1,399 15.8

1975 1,044 143 22 1,215 17.9

1977 1,975 318 92 2,476 27.0

1979 513 368 314 1,369 13.6

1981 727 514 393 1,946 15.6

aincludes imports from countries not listed individually.SOURCES: 1967. 1969Television Receivers and Certain Pads Thereof (Washington, D.C.: U.S. Tariff Commission Publica-

tion 436, November 1971), p. A62.1971.1973Television Receivers, Color and Monochrome, Assembled or Not Assembled, Finished or Not Finished,

and Subassemblies Thereof (Washington, D.C.: U.S. Interntnonal Trade Commission Publication 808, March 1977).pp. A-90, A99.

1975.79Color Telev'sion Receivers and Subassemblies Thereof (Washington, D.C.: U.S. International Trade Com-mission Publication 1068, May 1980). p. D-6.

1980Television Receiving Sets From Japan (Washington, D.C.: U.S. International Trade Commission Publication1153. June 1981), p. H.21.

1981Information from Department of Commerce

achieve credibility, they had to supply TVs thatdid not need frequent service. Japan's con-sumer electronics manufacturers succeeded inthis far from riskless strategy.

If technology is now a secondary factor forTVs, in more recently introduced product fam-iliesnot only VCRs, but video disk players,home computers, and related applications ofelectronic technologies to consumer goodsdesigns are evolving at a faster pace. Japaneseentrants spent many years and a great deal ofmoney on engineering development of VCRsMatsushita even reached production in 1973with a design that was shortly thereafter judgednot to be good enoughbefore achieving com-mercially viable products. But otherwise, com-petition in consumer electronics is largely amatter. of prices and marketing, brand loyaltiesand customer perceptions. While Japanese ex-porters have established themselves firmly inAmerican markets for TVs and audio products,individual companies have suffered frequentreverses in consumer goods ranging fromStereo receivers to CB radios and pocket cal-culators, where markets have been unpredict-able and competition always stiff.

SemiconductorsMicroelectronic devices, in contrast, are in-

termediate products sold in accordance withdetailed technical specifications to sophisti-cated customers who design them into finalproducts ranging from TVs and electronicgames to missile guidance systems and power-ful computers. To be successful, semiconduc-tor firms must not only meet the current re-quirements of such customers but do a goodjob of anticipating their future needs.

Technological Factors in Competition

As explained in chapter 3, the interdepend-ence of product and process technologies inleading-edge microelectronic devicesverylarge-scale ICsis unusual even for a high-tech-nology industry. Circuit designers must under-stand the nature and capabilities of the fabrica-tion processincluding proprietary detailsto optimize the performance of a chip. Productand process technologies advance together,with process capability a restriction on devicesthat can be fabricated with acceptable yields(the fraction of circuits that function). The in-

33

12

I

10

7

5

5

3

2

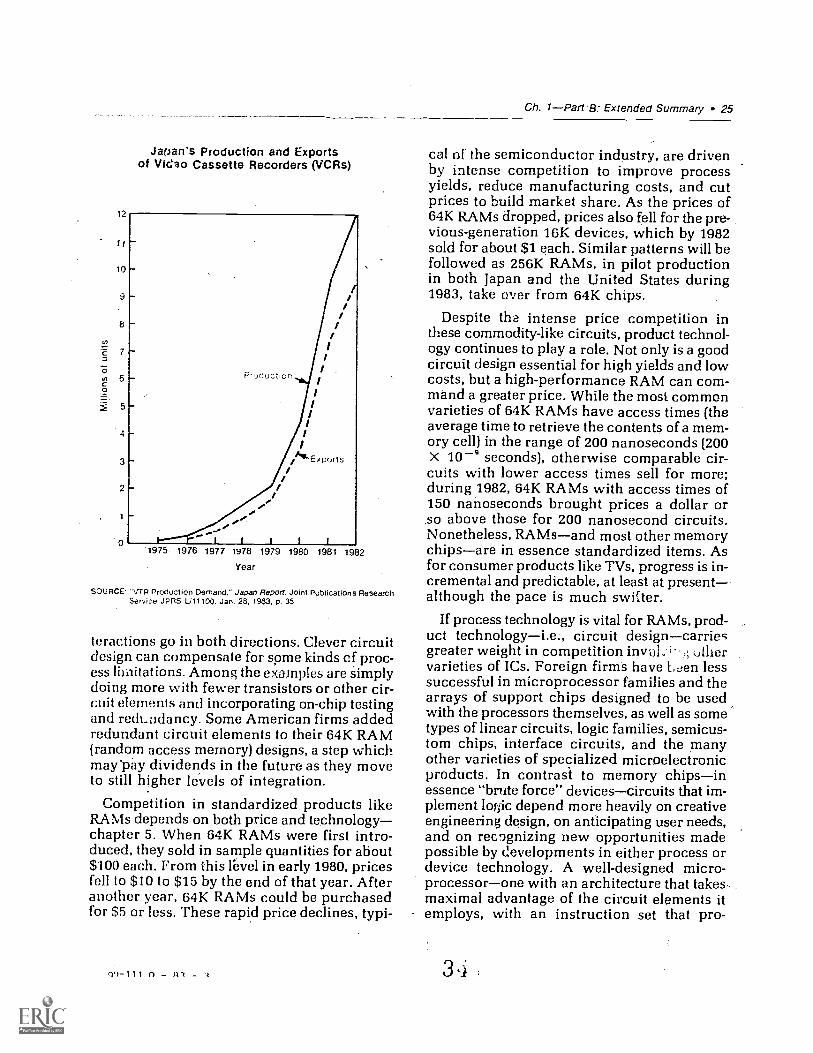

Japan's Production and Exportsof Vireo Cassette Recorders (VCRs)

1975 1976 1977 1978 1979 1980 1981 1982

Year

Ch. 1Part'8: Extended Summary 25

SOURCE "VTR Production Demand," Japan Report. Joint Publications ResearchService JPRS 011100. Jan. 28, 1983. P. 35

teractions go in both directions. Clever circuitdesign can compensate for some kinds cf proc-ess limitations. Among the examples are simplydoing more with fewer transistors or other cir-cuit elements and incorporating on-chip testingand redundancy. Some American firms addedredundant circuit elements to their 64K RAM(random access memory) designs, a step whichmay 'pay dividends in the future as they moveto still higher levels of integration.

Competition in standardized products likeRAMs depends on both price and technologychapter 5. When 64K RAMs were first intro-duced, they sold in sample quantities for about$100 each. From this level in early 1980, pricesfell to $10 to $15 by the end of that year. Afteranother year, 64K RAMs could be purchasedfor $5 or less. These rapid price declines, typi-

r),)- 1 1 1 - fl z -

cal of the semiconductor industry, are drivenby intense competition to improve processyields, reduce manufacturing costs, and cutprices to build market share. As the prices of64K RAMs dropped, prices also fell for the pre-vious-generation 16K devices, which by 1982sold for about $1 each. Similar patterns will befollowed as 256K RAMs, in pilot productionin both japan and the United States during1983, take over from 64K chips.

Despite the intense price competition inthese commodity-like circuits, product technol-ogy continues to play a role. Not only is a goodcircuit design essential for high yields and lowcosts, but a high-performance RAM can corn-mend a greater price. While the most commonvarieties of 64K RAMs have access times (theaverage time to retrieve the contents of a mem-ory cell) in the range of 200 nanoseconds (200X 10 seconds), otherwise comparable cir-cuits with lower access times sell for more;during 1982, 64K RAMs with access times of150 nanoseconds brought prices a dollar orso above those for 200 nanosecond circuits..Nonetheless, RAMsand most other memorychipsare in essence standardized items. Asfor consumer products like TVs, progress is in-cremental and predictable, at least at presentalthough the pace is much swirder.

If process technology is vital for RAMs, prod-uct technologyi.e., circuit designcarriesgreater weight in competition invol. ;` uthervarieties of ICs. Foreign firms have Len lesssuccessful in microprocessor families and thearrays of support chips designed to be usedwith the processors themselves, as well as sometypes of linear circuits, logic families, semicus-tom chips, interface circuits, and the manyother varieties of specialized microelectronicproducts. In contrast to memory chipsinessence "brute force" devicescircuits that im-plement Ionic depend more heavily on creativeengineering design, on anticipating user needs,and on recognizing new opportunities madepossible by developments in either process ordevice technology. A well-designed micro-processorone with an architecture that takes,maximal advantage of the circuit elements itemploys, with an instruction set that pro-

3,4

26 International Competitiveness in Electronics

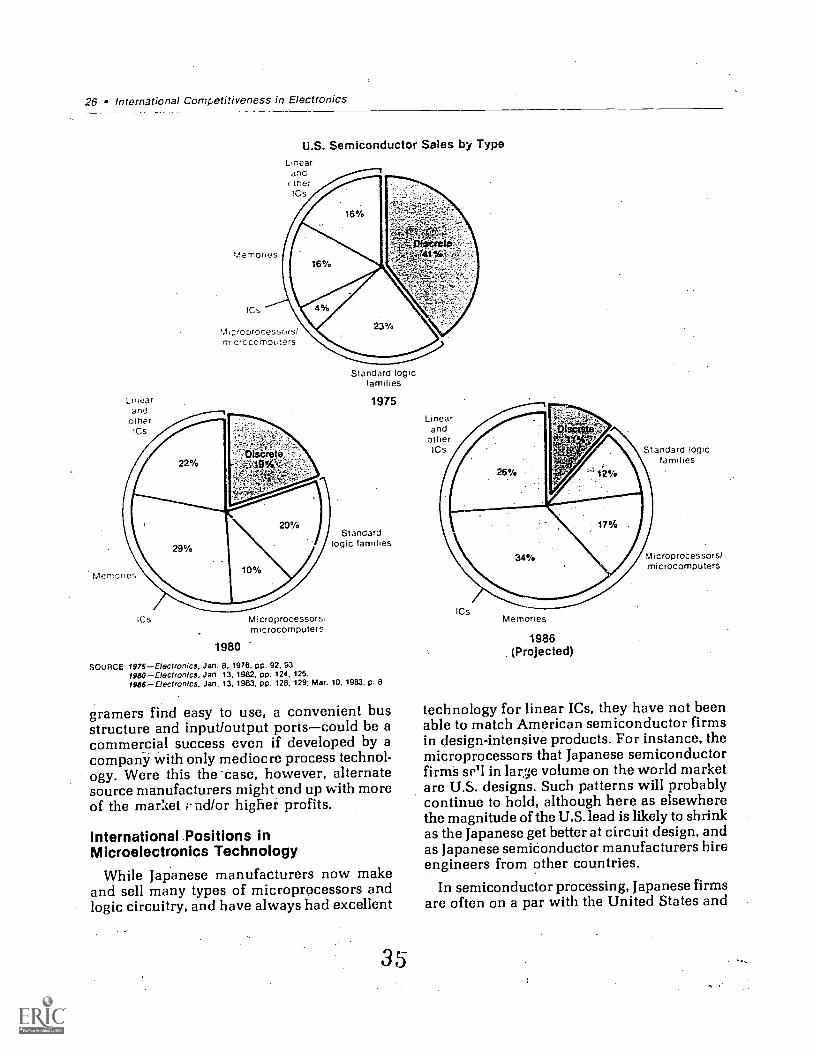

Linearand

otherICs

Memories

ICs

U.S. Semiconductor Sales by TypeLinear

and(tilerICs

Microrocessorsimicrocomovre.rs

ICs Microprocessors!microcomputers

1980

Standard logicfamilies

1975

Standardlogic families

SOURCE: 1975 El ec !tonics, Jan. 8, 1978, pp. 92, 93.1986 ElecfronIcs, Jan. 13, 1982, pp. 124, 125.1946 El e c t ro nics, Jan. 13, 1983, pp. 128, 129; Mar, 10, 1983, p. 8

gramers find easy to use, a convenient busstructure and input/output portscould be acommercial success even if developed by acompany with only mediocre process technol-ogy. Were this the 'case, however, alternatesource manufacturers might end up with moreof the market ;' ad/or higher profits.

International Positions inMicroelectronics Technology

While Japanese manufacturers now makeand sell many types of microprocessors andlogic circuitry, and have always had excellent

35

LinearandotherICs Standard logrc

families

ICsMemories

1986(Projected)

Microprocessors/microcomputers

technology for linear ICs, they have not beenable to match American semiconductor firmsin design-intensive products. For instance, themicroprocessors that Japanese semiconductorfirms se'l in large volume on the world marketare U.S. designs. Such patterns will probablycontinue to hold, although here as elsewherethe magnitude of the U.S. lead is likely to shrinkas the Japanese get better at circuit design, andas Japanese semiconductor manufacturers hireengineers from other countries.

In semiconductor processing, Japanese firmsare often on a par with the United States and

Ch. 1Part B: Extended Summary 27

may. be better in some cases. One reason hasbeen the VLSI research project and its severalfollow-ons, orchestrated and partially fundedby Japan's Government. By 1983, Japanesemanufacturers were, as a group, further alongin production plans for process-intensive 256KRAMs than their American competitors. Proc-ess control also exerts a major influence overquality: nevertheless, if a few years ago thequality of some types of Japanese ICsspecif-ically, RAM chipswas higher than suppliedby American firms, today any differences aremuch smaller (see ch. 6).