COMPANY UPDATE NOT RATED - Baroda E-Trade

24

COMPANY UPDATE BOB Capital Markets Ltd is a wholly owned subsidiary of Bank of Baroda Important disclosures, including any required research certifications, are provided at the end of this report. NOT RATED PRATAAP SNACKS | Packaged Foods | 21 December 2021 Emerging contender in booming snacks business ▪ Fast-growing player in savoury packaged snacks. Strengthening of processes (to stabilise RM cost) and distribution channels to spur growth Ruchitaa Maheshwari [email protected] Source: NSE | Price as of 20 Dec 2021 Stock performance Source: NSE ▪ Aggressive expansion into sweet snacks planned over the next 2-3 years – a relatively untapped high-margin, high-growth category ▪ Targeting 18‐20% revenue CAGR over three years and 8-10% margins. Trading at ~33x FY21 EV/EBITDA; we do not have a rating on the stock We interacted with the management of Prataap Snacks (PSL, Not Rated) to gain insights into the company’s efforts towards achieving stated growth and profitability targets. Key takeaways: Value for money + Innovations + Strong distribution reach to drive growth: PSL is one of the fastest growing organized players in the attractive savory segment. PSL has established itself in a highly competitive intensity by a) value for money player, b) constantly focussing on new innovations and expanding its product profile, c) streamlining its distribution channel (from 3 tier to 2 tier by removing super stockists), d) ~2mn retail outlets spread across 31 States & UT, e) faster market replenishment, f) emphasis on popular flavours, g) relevant marketing schemes and h) tapping newer geographies in order to accelerate its revenue growth trajectory. PSL has not only multiplied its market share (1% to ~6% from 2010 to 2020) in just ten years, but also expanded pan India. Management envisages these initiatives to lead to 18‐20% revenue CAGR and 8-10% EBITDA margin over FY21-FY24E. Geographical expansion to fuel growth: PSL has a strong presence in Madhya Pradesh, Mumbai, Delhi, Haryana, West Bengal and Orissa (+50% of revenue). It sees large, untapped potential in Uttar Pradesh, Bihar, Punjab, J&K and South India, and is looking to expand its footprint in these areas. Deepening distribution in existing markets: PSL is tapping potential outlets by enrolling new retailers through tele-calling. These additional outlets could provide a ~30% jump in revenue. Till now, PSL has tapped an additional 60,000 outlets and plans to add 250,000 by Apr’22. The tele-callers will also push other products which were not being sold earlier, thereby increasing traction across the product line. PLI scheme to bolster revenue: Under the government’s PLI scheme (base year 2019-20), PSL will receive an incentive of 7.5% of the incremental sales on all its products except potato chips for the first four years, followed by 6.75% in FY26 (base year FY22) and 6% in FY27 (base year FY23). As the company’s financials got impacted due to the covid, management expects benefit to flow in from FY23. 420 710 1,000 1,290 1,580 1,870 Dec-18 Mar-19 Jun-19 Sep-19 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Sep-21 Dec-21 DIAMOND NSE Nifty (Relative) Ticker/Price DIAMOND IN/Rs 841 Market cap US$ 296.5mn Free float 29% 3M ADV US$ 0.4mn 52wk high/low Rs 855/Rs 485 Promoter/FPI/DII 72%/5%/21%

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of COMPANY UPDATE NOT RATED - Baroda E-Trade

COMPANY UPDATE

BOB Capital Markets Ltd is a wholly owned subsidiary of Bank of Baroda

Important disclosures, including any required research certifications, are provided at the end of this report.

NOT

RATED PRATAAP SNACKS | Packaged Foods | 21 December 2021

Emerging contender in booming snacks business

▪ Fast-growing player in savoury packaged snacks. Strengthening of

processes (to stabilise RM cost) and distribution channels to spur growth

Ruchitaa Maheshwari

Source: NSE | Price as of 20 Dec 2021

Stock performance

Source: NSE

▪ Aggressive expansion into sweet snacks planned over the next 2-3

years – a relatively untapped high-margin, high-growth category

▪ Targeting 18‐20% revenue CAGR over three years and 8-10% margins.

Trading at ~33x FY21 EV/EBITDA; we do not have a rating on the stock

We interacted with the management of Prataap Snacks (PSL, Not Rated) to

gain insights into the company’s efforts towards achieving stated growth and

profitability targets. Key takeaways:

Value for money + Innovations + Strong distribution reach to drive growth: PSL

is one of the fastest growing organized players in the attractive savory segment. PSL

has established itself in a highly competitive intensity by a) value for money player, b)

constantly focussing on new innovations and expanding its product profile, c)

streamlining its distribution channel (from 3 tier to 2 tier by removing super stockists),

d) ~2mn retail outlets spread across 31 States & UT, e) faster market replenishment, f)

emphasis on popular flavours, g) relevant marketing schemes and h) tapping newer

geographies in order to accelerate its revenue growth trajectory. PSL has not only

multiplied its market share (1% to ~6% from 2010 to 2020) in just ten years, but also

expanded pan India. Management envisages these initiatives to lead to 18‐20%

revenue CAGR and 8-10% EBITDA margin over FY21-FY24E.

Geographical expansion to fuel growth: PSL has a strong presence in Madhya

Pradesh, Mumbai, Delhi, Haryana, West Bengal and Orissa (+50% of revenue). It

sees large, untapped potential in Uttar Pradesh, Bihar, Punjab, J&K and South

India, and is looking to expand its footprint in these areas.

Deepening distribution in existing markets: PSL is tapping potential outlets by

enrolling new retailers through tele-calling. These additional outlets could provide a

~30% jump in revenue. Till now, PSL has tapped an additional 60,000 outlets and

plans to add 250,000 by Apr’22. The tele-callers will also push other products which

were not being sold earlier, thereby increasing traction across the product line.

PLI scheme to bolster revenue: Under the government’s PLI scheme (base year

2019-20), PSL will receive an incentive of 7.5% of the incremental sales on all its

products except potato chips for the first four years, followed by 6.75% in FY26

(base year FY22) and 6% in FY27 (base year FY23). As the company’s financials

got impacted due to the covid, management expects benefit to flow in from FY23.

420

710

1,000

1,290

1,580

1,870

Dec

-18

Mar

-19

Jun-

19

Sep

-19

Dec

-19

Mar

-20

Jun-

20

Sep

-20

Dec

-20

Mar

-21

Jun-

21

Sep

-21

Dec

-21

DIAMOND NSE Nifty (Relative)

Ticker/Price DIAMOND IN/Rs 841

Market cap US$ 296.5mn

Free float 29%

3M ADV US$ 0.4mn

52wk high/low Rs 855/Rs 485

Promoter/FPI/DII 72%/5%/21%

PRATAAP SNACKS

EQUITY RESEARCH 2 21 December 2021

Contents

Emerging player in packaged snacks ............................................................ 3

Diverse product portfolio, improving mix ........................................................ 3

Focus on innovation, value for money and premiumisation ........................... 4

Sweet snacks a nascent but large opportunity ............................................... 6

Strong distribution network and expanding footprint ...................................... 8

Optimisation of distribution channels to reduce cost and improve margin ..... 9

Strong distribution network coupled with expanding footprint via outsourcing ........................................................................................................................ 9

Synergy with Avadh Snacks ......................................................................... 10

Credible initiatives to contain margin volatility .............................................. 11

Financial Analysis ......................................................................................... 13

PLI scheme to augment revenues ................................................................ 13

High operating leverage with no major capex in pipeline ............................. 14

Working capital intensity inherently low........................................................ 14

Sequoia Capital’s investment in PSL ........................................................... 15

Indian snack industry booming .................................................................... 16

PSL vs. DFM Foods ..................................................................................... 16

Company Background ................................................................................... 18

Management profile ........................................................................................ 20

Financials ........................................................................................................ 21

PRATAAP SNACKS

EQUITY RESEARCH 3 21 December 2021

Emerging player in packaged snacks

We interacted with Amit Kumat, MD & CEO, and Sumit Sharma, CFO of PSL to gain

insights into the company’s growth plans and future outlook. Headquartered in Indore,

Madhya Pradesh, the company has established a sizeable presence across the

country, driven by a focus on product innovation, geographic expansion, effective

marketing and optimised distribution.

PSL currently sells more than 11mn packs per day and has multiplied its market share

from 1% to ~6% over 2010-20. Products are sold under three brands – the parent

‘Yellow Diamond’ brand for potato chips, extruded snacks and traditional Indian salty

snacks (namkeen), ‘Rich Feast’ for its recently launched sweet snacks, and the newly

acquired ‘Avadh’ (savoury) brand. The company has demonstrated the ability to

compete with regional players on their own turf and gain market leadership, which

reflects its strong brand positioning.

Diverse product portfolio, improving mix

PSL initially started out with chips/crisps under the Yellow Diamond brand and rapidly

expanded its product line. Today, it offers a bevy of snacks including crisps (katori),

pipes, samosas (trikon), rings, chips, sticks (namkeen chulbule), puffs and popcorn. In

October 2018, PSL acquired Gujarat-based Avadh Snacks which offers a

complementary salty snack portfolio, besides entering the sweet snack category in

H2FY18 with the launch of mini cakes.

Entry into newer categories has helped PSL achieve nearly double pace revenue

growth of 27% over FY13-FY17 (while catering to a wide range of taste preferences and

consumer segments, including adults and children), where snack industry grew by

14.7% CAGR during the same period. Per management, extruded snacks have the

highest margin as they are less volatile in terms of raw material pricing (corn, gram

flour), followed by potato chips (medium margin) and other savoury items (low margins

due to high regional competition).

The extruded and sweet categories – favorites among children – were hard hit during

the pandemic due to school closures. PSL aims to raise the contribution of sweet

snacks from the current ~3% of revenue to 7-8% by FY25. As these earn higher

gross margins than salty snacks, management expects the improving mix coupled with

opening up of the economy post pandemic to aid margin expansion from H2FY22.

PRATAAP SNACKS

EQUITY RESEARCH 4 21 December 2021

Fig 1 – PSL’s product portfolio and competitor profile

Category Launch PSL’s brand Flavours SKUs (Rs) Competitors

Potato Chips FY05 Yellow Diamond

Plain Salted, Cream ‘n’ Onion, Tom-Chi, Nimbu Masala, Yummy Masala,

Tangy Tomato, Plain Upvas, Black Pepper and Magic Masala 5, 10, 20, 50

Lays (Pepsico), Bingo (ITC), Balaji, Parle’s Wafers, Haldirams

Extruded Snacks

FY06 Chulbule Tangy Tomato, Teekha Tadka, Noodle Masala, Taza Tomato, Achari

Chatka, Tango Mango and Cream ‘N’ Onion 5, 10, 20, 50

Kurkure (Pepsico), Balaji, Crax (DFM Foods), Bingo (ITC), Taka Tak (Haldiram)

FY10 Wheels Chatpata Masala and Tomato Ketchup 5

FY10 Scoops Masala and Tomato 5

FY11 Puffs Cocktail, Tomato, Pudina and Punjabi Tadka 5

FY12 Rings Masala, Tomato, Mango Chutney, and Chilli Cheese 5, 10, 15

FY18 Seven Wonders

Lentil Crackers – Cumin & Black pepper, Lentil Crackers – Cream & Onion,

Lentil Crackers – Sweet Mango Chutney, Veggie Straws – Masala Tikka,

Veggie Straws – PeriPeri, Quinoa Chips – Cheese Garlic

30

FY18 Kurves Four Flavours 5

Namkeen 2012 Yellow Diamond

Moong Dal, Chhana Dal, Chana Masala –Heeng Jeera flavour, All-in-One,

Aloo Bhujiya, Bhujia Sev, Punjabi Tadka, Ratlami Sev, Tasty Shing Bhujia,

Mixture, Falahari Chivda – Meetha and sweet and salty flavours, Khatta

Meetha, Banana Wafers – Black Pepper and Mamra, Garlic Sev Mamra,

Masala Matar, Chana Choorand Salted flavours, Cornflake Mixture, Bhel,

Plain Sev Peanuts – Classic and Black Pepper flavours

5, 10, 30, 70 Haldirams, Lehar (Pepsico), Balaji, Bikaji Foods

Sweet Snacks

2018 Rich Feast Orange, Strawberry, Vanilla and Chocolate 5 Britannia, Lotte, Sunfeast, Monginis, Cadbury, Pilsbury, Moonfills

Source: Company, BOBCAPS Research

Focus on innovation, value for money and premiumisation

PSL focuses on understanding local consumer tastes and preferences through

innovative product launches at competitive prices. Its product portfolio extends across

strategic price points and pack sizes (over 100 SKUs), with prices ranging from

Rs 5 to Rs 100. This enables the company to target India’s large bottom-of-the-pyramid

population that is gradually shifting from the unorganised to the formal market.

Furthermore, the possibility of premiumisation of product portfolio also remains high

given new launches are now on the health and wellness platform which command

higher operating margin; its sweet snacks venture also commands higher gross margin.

Fig 2 – Portfolio spread across strategic price points and pack sizes

Source: Company, BOBCAPS Research

PRATAAP SNACKS

EQUITY RESEARCH 5 21 December 2021

Innovative launches

In order to tap regional markets, PSL plays with flavour profiles. For instance, the

company uses pepper-based variants (Ratlami) in the north and sweet variants in

the west. This has helped it garner nationwide acceptance for its products.

In a bid to attract the younger population (children), PSL offers toys inside snack

packets. In addition, it has tied up with the producers of cartoons to use characters

such as ‘Motu & Patlu’ for its promotional campaigns.

In 2017, PSL ventured into the healthy snacks category with its brand ‘7Wonders’.

This business has seen a slow pickup and hence there are no plans to launch the

brand in the near term. However, the company has the structure in place to remain

relevant in the event of a consumer shift towards healthier alternatives.

In 2018, the company launched ‘Nachos’ in four flavours at a unique price point of

Rs 10. This caused a major disruption in the market and prompted other players to

bring out offerings at the same price.

In H2FY18, the company entered into sweet snacks with the launch of ‘Yum Pie’

under the Rich Feast brand at a Rs 5 price point. This chocolate, jam-based snack

with a cake-like base differs from existing products in the market and is aimed at

consumers in the age group of 4-15. Further, to expand the sweet portfolio, the

company has launched ‘Yum Cake’, ‘Choco Vanila Cake’ and ‘Cookie Cake’ in

2019, followed by ‘Cup Cake, ‘Tiffin Cake’ and ‘Sandwich Cake’ in 2020.

In 2021, PSL introduced plain-cut chips, puffed crisp balls (puchka), noodle pellets

and rusks, with a goal to increase home consumption. Per management, customer

acceptance has been high in noodle pellets. To cater to the large audience, plans

are underway to roll out eggless Swiss rolls and cupcakes priced at Rs 10 each by

end-December 2021.

VFM (value for money) strategy

PSL focuses on delivering products that are either priced lower than bigger brands or

offer more per pack. The emphasis is on offering a value proposition to the price-

conscious consumer. For instance, when Frito-Lay was offering 22gm of potato chips in

a Rs 5 pack, PSL offered 30gm for the same amount – a strategy that has helped the

company grow at 20-25% in the past 5-6 years. Its pricing strategy has pushed several

bigger competitors to also offer value packs in an effort to stay ahead in the market.

Pack sizes also play a key role in conversion from unorganized to organized. Small

packs of Rs 5 and Rs 10 contribute 70-80% of sales in India’s snack market. For PSL,

~80% of sales come from products priced at Rs 5, 10-12% from Rs 10 products and the

balance from high-value packs. The company’s distribution strategy thus includes

establishing a strong base in tier B, C and D sales outlets where the Rs 5 SKU is a

bestseller.

PSL achieves this by (1) increasing its presence near schools and tuition centres for

sales of rings, wheels and sweet snacks which are a favourite amongst children, and

(2) selling namkeen at outlets near tobacco and liquor shops where uptake is higher.

This also increases the per-dealer offtake growth rate.

PRATAAP SNACKS

EQUITY RESEARCH 6 21 December 2021

Sweet snacks a nascent but large opportunity

The Indian sweet and candy market is valued at ~US$ 664mn, with sugar confectionery

holding a 70% share (US$ 461mn) and chocolate confectionery accounting for the

remainder (US$ 203mn).

There is a huge untapped growth opportunity in the sweet snacks segment on account

of current segmentation of offerings and changing lifestyles of consumers. Traditionally,

consumers seeking a sweet snack have had limited options such as chocolates or

traditional Indian sweets. Alternatives in a convenient size with attractive packaging

have not been comprehensively addressed in the Indian market. The volume weight

ratio for sweets snacks is favorable for manufacturers, leading to lower logistics cost

and relatively higher gross margin.

Given the potential of the industry had and has a global reach, a lot of brands in their

early days made a name for themselves in the space. A few of the renowned ones are

Haldirams, Balaji, Bikano, Bikaji, Prataap Snacks, Cornitos – the brands have not only

achieved local but also a global footprint. In fact, the branded segment covers about

30% of this market and is growing at 10-12%. With the use of automation and better

shelf life, the segment is all set to only grow further.

At the same time, consumers are exhibiting a growing preference for western sweets,

especially chocolate-based confectionaries, due to exposure to media and the internet

and higher living standards. In addition, concerns related to hygiene and quality due to

a lack of established processes to manufacture Indian sweets is also driving this shift.

Rich Feast brand garnering good response

At ~Rs 30bn, the sweet market is currently just 10% of salty snacks is expected to grow

more than 15% over the next 4-5 years. Within sweet snacks, cake is an evolving

category that has witnessed some major developments in formats, pricing and variants

in the last few years. PSL too has entered this segment under the Rich feast brand with

a launch of – (a) Cup Cake (b) Tiffin Cake (c) Sandwich Cake and (d) Cookie cakes, in

three different flavor- (Chocolate, Strawberry, Vanilla and Tuti fruity). The product has

evinced good response and demand is picking up. To enhance its sweet product basket

PSL is in the process of launching few more products in the market. The management

has maintained to launch only eggless sweet as the target audience is huge.

To make its presence felt and garner market share, management is following its

strategy of ‘more for less price’. For instance, Pillsbury Choco Cookie Cake offers 11gm

for Rs 5 and PSL offers 16gm at the same rate and same product profile. Given the

good response to its products, the company plans to roll out eggless Swiss rolls and

cupcakes priced at Rs 10 each by end-Dec’21.

PRATAAP SNACKS

EQUITY RESEARCH 7 21 December 2021

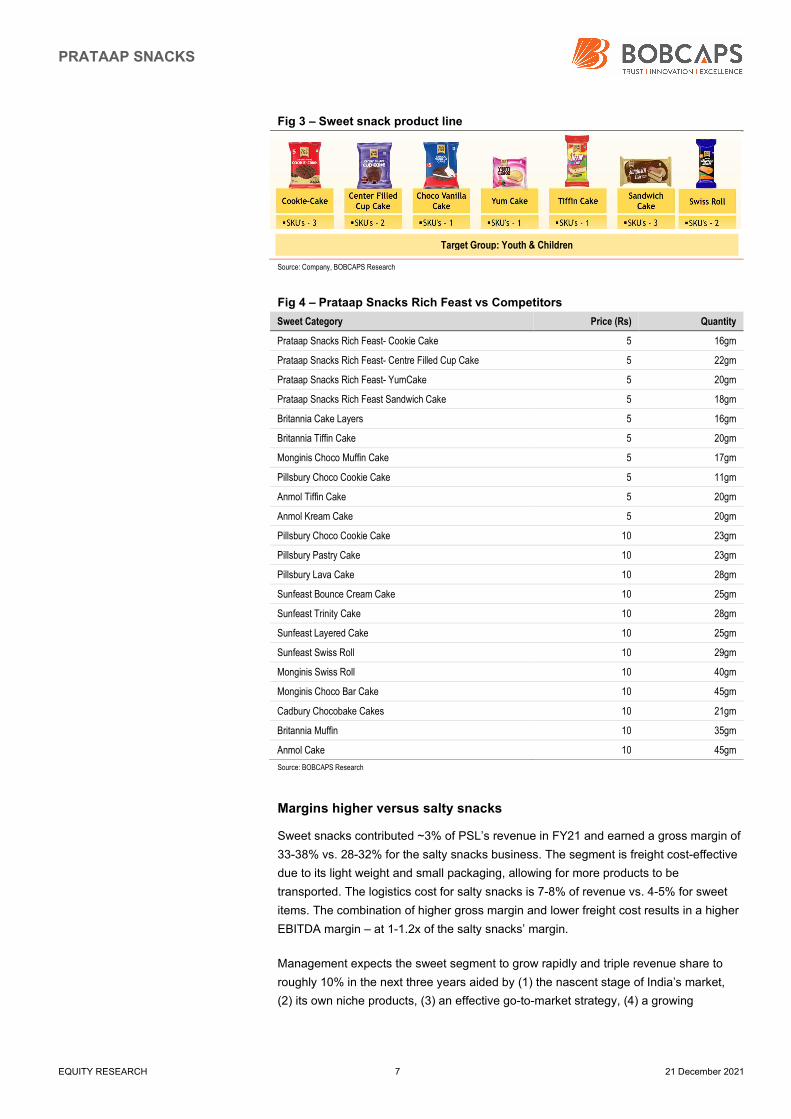

Fig 3 – Sweet snack product line

Source: Company, BOBCAPS Research

Fig 4 – Prataap Snacks Rich Feast vs Competitors

Sweet Category Price (Rs) Quantity

Prataap Snacks Rich Feast- Cookie Cake 5 16gm

Prataap Snacks Rich Feast- Centre Filled Cup Cake 5 22gm

Prataap Snacks Rich Feast- YumCake 5 20gm

Prataap Snacks Rich Feast Sandwich Cake 5 18gm

Britannia Cake Layers 5 16gm

Britannia Tiffin Cake 5 20gm

Monginis Choco Muffin Cake 5 17gm

Pillsbury Choco Cookie Cake 5 11gm

Anmol Tiffin Cake 5 20gm

Anmol Kream Cake 5 20gm

Pillsbury Choco Cookie Cake 10 23gm

Pillsbury Pastry Cake 10 23gm

Pillsbury Lava Cake 10 28gm

Sunfeast Bounce Cream Cake 10 25gm

Sunfeast Trinity Cake 10 28gm

Sunfeast Layered Cake 10 25gm

Sunfeast Swiss Roll 10 29gm

Monginis Swiss Roll 10 40gm

Monginis Choco Bar Cake 10 45gm

Cadbury Chocobake Cakes 10 21gm

Britannia Muffin 10 35gm

Anmol Cake 10 45gm

Source: BOBCAPS Research

Margins higher versus salty snacks

Sweet snacks contributed ~3% of PSL’s revenue in FY21 and earned a gross margin of

33-38% vs. 28-32% for the salty snacks business. The segment is freight cost-effective

due to its light weight and small packaging, allowing for more products to be

transported. The logistics cost for salty snacks is 7-8% of revenue vs. 4-5% for sweet

items. The combination of higher gross margin and lower freight cost results in a higher

EBITDA margin – at 1-1.2x of the salty snacks’ margin.

Management expects the sweet segment to grow rapidly and triple revenue share to

roughly 10% in the next three years aided by (1) the nascent stage of India’s market,

(2) its own niche products, (3) an effective go-to-market strategy, (4) a growing

Target Group: Youth & Children

PRATAAP SNACKS

EQUITY RESEARCH 8 21 December 2021

distribution network for salty products, and (5) a focus on the key Rs 5 price point and

on high-demand eggless products where the competition is less and market is huge.

Fig 5 – Sweet snacks: Portfolio synergies

Particulars Salty Snacks Sweet Snacks

Price Points Rs 5, 10, 20, 40, 80 Rs 5

Gross Margin 28-32% 33-38%

Volatility in Raw Material prices Medium to High Low

Freight Cost as a % of revenue 7-8% 4-5%

MRP on the vehicle (Rs) 16,000-20,000 30,000-35,000

Distributor Margin @ ~7.5% (Rs) 1,200-1,500 2,250-2,625

Variable Costs Same Same

Entry Barrier Low to Medium Medium to High

Source: Company, BOBCAPS Research

Fig 6 – With increasing contribution of sweets and streamlining of distribution channel, freight cost likely to decline

Source: Company, BOBCAPS Research

Strong distribution network and expanding footprint

PSL has a reach of ~2mn outlets and currently serves 31 states and union territories

across India. The company effectively uses these distribution network to increase its

penetration into the existing key markets North and West. The company is also

increasing its presence in Gujarat (highest snacks market in terms of per capita

consumption) and Southern markets as these markets are largely dominated by

regional players with highly competitive intensity. Further, the East market continues to

grow led by increasing demand in extruded snacks particularly rings and specific flavors

like cream and onion. PSL expects to replicate the same model in southern markets

and garner market share and brand loyalty going forward.

PSL is tapping potential outlets by enrolling new retailers through tele-calling.

These additional outlets could provide a ~30% jump in revenue, per management.

So far this year, the company has tapped an additional 60,000 outlets and plans

to add 250,000 more by Apr’22.

7.5

7.2

7.1 7.1

6.8

6.9

7.0

7.1

7.2

7.3

7.4

7.5

7.6

FY18 FY19 FY20 FY21

(%) Freight Cost as a % of Sales

PRATAAP SNACKS

EQUITY RESEARCH 9 21 December 2021

Optimisation of distribution channels to reduce cost and

improve margin

PSL follows a traditional three-tier distribution channel model (~95% of sales) of super

stockists, distributors and retailers. The company first distributes its product to super

stockists who are appointed to operate and maintain outlets/warehouses for sale to

distributors and dealers. Generally, these super stockists have formal agreement with

the company for 3-5 years. Currently, PSL has a network of 245 super stockists and

more than 4,300 distributors.

After strongly establishing itself, the company to follow two-tier distribution channel

model (just like its competitor Balaji Snacks) under which the company will do away with

the super stockists and will trade directly with distributors followed by retailers. This

move will start in the big city where the smaller distributors will be consolidated.

However, the company will continue to follow the three-tier distribution model in the

rural area as the job of super stockists is to replenish the distributor and retailers.

The company pays 2.5%-3% margin to the super stockists, and ~3% margin is

paid as a reimbursement of secondary freight. Distributor is paid 7.5%-8% margin

and retailers are paid to the tune of 15%-20% margin. After removing super

stockists from the scene, management expects to save huge cost of ~6% and

operating margin to improve by ~4%. As of now, management expects margin to

improve by 2-2.5% over a period of two years and will be visible from Q4FY22

onwards.

Strong distribution network coupled with expanding footprint

via outsourcing

PSL operates through 15 manufacturing facilities, of which 7 are in-house and 8 are on

contract manufacturing basis. The company follows asset light model where the

contract manufacturing which stood at ~4% in FY16 has increased to 24% in FY21

and 25% in H1FY22. The company is targeting the contribution to increase to 30%

in next 2-3 years. To enable optimum efficiency in the distribution and to reach

out to a more expansive market, the company is increasingly employing an asset-

light 3P (Production Preparation Process) third party manufacturing model. This

model is based on proximity to the target market, enabling faster replenishments,

and is expected to reduce freight costs. Along with lower logistics costs, the 3P

model results in lower capex. Going forward, this asset-light model will help in

yielding better margins and thereby drive higher return on capital employed.

Going forward, the company is expected to increase the 3P model as its lucrative in

terms of expanding rapidly without significant outlay, rapid innovation and rolling swiftly

in the market. However, the company will continue to manufacture innovation driven

products like Sweet snacks due to protection of intellectual property as well as the 3P’s

are inefficient to manufacture such products satisfactorily.

PRATAAP SNACKS

EQUITY RESEARCH 10 21 December 2021

Fig 7 – Strategically located manufacturing facilities to cater to regional demand

Source: Company, BOBCAPS Research

Synergy with Avadh Snacks

In October 2018, PSL acquired an 80% equity stake in Gujarat-based Avadh Snacks

Private Limited (Avadh) for Rs 1.5bn and its board has approved the acquisition of a

further 10.48% stake for Rs 330mn. The balance 9.52% is to be purchased in the next

year and a half. Avadh’s savoury products complement PSL’s existing portfolio and give

the company a foothold in Gujarat, India’s largest salty snacks market.

Access to India’s largest market for salty snacks

Started in 2010, Avadh’s product range includes traditional salty snacks (bhujia,

chevda, fafda and gathiya), and extruded pellets such as wheels, cups and pasta.

Avadh has a manufacturing facility at Rajkot and a well-established direct distribution

network in Gujarat. With a reach of 75,000-1,00,000 retail outlets in Gujarat, it is the

fourth largest player in the state with ~6% market share.

PSL will use this distribution strength to market its products into western India where it

has a limited presence. It aims to increase the capacity of Avadh’s Rajkot plant by

100%, with phase-1 (50% expansion) completed in Jun’20.

Avadh has also entered the states of Maharashtra, Madhya Pradesh and Rajasthan

which form 10% of its revenue and are targeted to contribute 20% in the next 2-3 years.

PSL plans to launch Avadh’s extensive range of pellet-based snacks pan-India by

leveraging Yellow Diamond’s manufacturing and distribution network. The company has

also been increasing its touch points in Gujarat and neighbouring markets by cross-

selling its popular Yellow Diamond products.

PRATAAP SNACKS

EQUITY RESEARCH 11 21 December 2021

Fig 8 – Avadh product portfolio

Source: Company, BOBCAPS Research

Targeting 15% growth in FY23-FY24

Avadh earns lower gross margins (~15% compared to ~30% for PSL) due to its super-

value offerings but garners similar EBITDA margins owing to cheaper distribution costs.

Management is targeting 15% revenue growth from the business in FY23 and FY24 and

is hopeful of replicating the success it has had with the Yellow Diamond brand (also

an acquisition).

Credible initiatives to contain margin volatility

PSL has volatile EBITDA margins and witnessed marked declines in recent years due

to bad potato crops and fluctuations in vegetable oil prices. Raw material forms ~72% of

the total revenue, of which Potatoes form 20% of cost of goods sold, palm oil 15-16%

and packaging 16-17%. To mitigate the risk, management has introduced various

structural changes (outlined below) and expects these initiatives coupled with an

improving product mix to aid 8-10% EBITDA margins over the next three years vs.

6.7%/5.4% in FY20/FY21.

Historically, edible palm oil prices have hovered at Rs 60-65/kg. However, since

Oct’19, prices have skyrocketed to a peak of Rs 142/kg in May’21 and currently

hover at ~Rs 120/kg. As per management, a Rs 5 movement in palm oil price has a

1% impact on EBITDA margin. PSL is mitigating the adverse margin impact

through process reengineering and cost optimisation. If inflationary pressure

persists, a change in grammage will be the last resort.

Being an essential commodity, the company believes that inflation is a short-term

issue and prices are likely to correct soon. The government has reduced customs

duty on palm oil to 30.25% from 35.75% which has already helped lower prices.

Management expects palm oil to settle at ~Rs 100/kg in coming months, giving the

company enough room to achieve double-digit EBITDA margins. While pricing

pressure would continue over the next two quarters due to labour shortages in

Malaysia and Indonesia and higher export duty, PSL believes that benefits from

rationalising its direct distribution channel would help cushion the volatility.

PRATAAP SNACKS

EQUITY RESEARCH 12 21 December 2021

Fig 9 – Crude Palm Oil Price

Source: Investing.com, BOBCAPS Research

In terms of distribution, PSL plans to deliver products directly from its factories to

distributors instead of taking the super-stockist route, to save on the second leg of

logistics cost. As per management, this will drive 2-2.5% margin improvement in

two years’ time, visible from Q4FY22 onwards.

In order to curb potato costs, the company has increased the duration of cold

storage and reduced open buying in the market from 3 months to 1 month to

alleviate price volatility.

To lower packaging costs, it now enters into long-term contracts of 9 months to a

year for laminates vs. short-term contracts earlier. However, off late the packaging

costs have risen massively, giving some knee jerk reaction in the EBITDA margin

volatility.

A&P spend is 1.1% of total revenue and unlikely to increase from this level. The

company is spending Rs 150-160mn on advertisements which will continue going

forward. Further, it is foraying into larger packs that have a different target audience

and hence plans to spend an additional Rs 100mn-120mn annually for the next two

years to build brand equity for umbrella brand ‘Yellow Diamond’.

Other initiatives taken to control cost include: (1) rationalisation of packet size,

(2) change in size of corrugated packing boxes, (3) reduction in trade margin by

0.5-1%, and (4) grammage reduction in non-core SKUs.

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

Jul

20

Aug

20

Sep

20

Oct

20

Dec

20

Jan

21

Feb

21

Apr

21

May

21

Jun

21

Aug

21

Sep

21

Oct

21

Dec

21

(Rs/metric tonne) Crude Palm Oil Price

PRATAAP SNACKS

EQUITY RESEARCH 13 21 December 2021

Financial Analysis

Fig 10 – Revenue Growth

Source: Company, BOBCAPS Research

Fig 11 – Gross Profit & Gross Margin Fig 12 – EBITDA/PAT and Margins

Source: Company, BOBCAPS Research Source: Company, BOBCAPS Research

PLI scheme to augment revenues

Under the PLI scheme approved by the government (base year 2019-20), PSL will

receive an incentive of 7.5% of the incremental sales on all its products except potato

chips for the first four years, followed by 6.75% in FY26 (base year FY22) and 6% in

FY27 (base year FY23). The incentives will be included in other operating income. The

company must meet the condition of a 10% revenue CAGR to enjoy these benefits. As

its financials were affected by Covid-19, management expects PLI benefits to flow from

FY23.

11,70613,938

11,71114.9 19.1

(16.0)

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY19 FY20 FY21

(%)(Rs mn) Net Revenue Growth (R)

3,502

3,991

3,280

29.9

28.628.0

24

25

26

27

28

29

30

31

32

33

34

3,000

3,200

3,400

3,600

3,800

4,000

4,200

FY19 FY20 FY21

(%)(Rs mn) Gross Profit Gross Margin (R)

832937

631446 469

142

7.16.7

5.4

3.83.4

1.20

2

4

6

8

10

0

200

400

600

800

1,000

1,200

1,400

FY19 FY20 FY21

(%)(Rs mn)EBITDA PAT

EBITDA margin (R) PAT margin (R)

PRATAAP SNACKS

EQUITY RESEARCH 14 21 December 2021

High operating leverage with no major capex in pipeline

The company had expensed significant capex of Rs 5.45bn over FY18- FY21 to support

its expanded product profile. Per management, this will provide high operating leverage

and enough room to expand volumes and reach without major capex for the next two

years. In addition, the company is increasing the use of contract manufacturing which

will enable it to expand rapidly without significant investment.

Fig 13 – With no major capex in offing, FCF & OCF to turn positive

Fig 14 – Return Ratios dampened in FY21 due to Covid

Source: Company, BOBCAPS Research Source: Company, BOBCAPS Research

Working capital intensity inherently low

Working capital intensity of the business remained low at 7.1% in FY20. Inventory days

are low due to the perishable nature of raw material and fast-moving finished goods. A

strong market position allows PSL to enjoy favourable terms with distributors where

dues are settled within a short duration of nine days. PSL also receives credit of ~25

days from its suppliers even though it operates on a cash-and-carry format.

Fig 15 – Ex-cash Working Capital as a % of sales Fig 16 – Working Capital efficiency

Source: Company, BOBCAPS Research Source: Company, BOBCAPS Research

The cash conversion cycle was at 12 days in FY19 which increased to 23 days in FY21

due to a higher inventory cycle. Amid Covid-19, inventory days shot up to 56 during

FY21 which resulted in an increase in ex-cash working capital to 9.6% of sales. The

inventory piled up because 18-20% of PSL’s total revenue comes from institutional

(955)

(509)

483

(301)

954844

(1,000)

(700)

(400)

(100)

200

500

800

1,100

FY19 FY20 FY21

(Rs mn) FCF CFO

7.7 8.0

2.9

8.3 8.0

2.3

7.86.4

1.4

0

2

4

6

8

10

12

14

FY19 FY20 FY21

(%) RoCE RoE RoIC

830

988

1,124

7.1 7.1

9.6

5

6

7

8

9

10

200

400

600

800

1,000

1,200

FY19 FY20 FY21

(%)(Rs mn) Working capital ex-cash WC as % sales (R)

34 32 34

5248

56

2824

30

9 8 8

0

10

20

30

40

50

60

FY19 FY20 FY21

(Days) Working capital days Inventory days Creditor days Debtor Days

PRATAAP SNACKS

EQUITY RESEARCH 15 21 December 2021

sales which includes bus depots, railways, schools, colleges and coaching centres – all

of which slowed down due to lockdown restrictions. Management expects the

vaccination drive and improving mobility to improve the cash conversion cycle.

Fig 17 – Cash Conversion Cycle expected to improve

Source: Company, BOBCAPS Research

Sequoia Capital’s investment in PSL

US-based venture capital firm Sequoia Capital, which has backed companies that now

control US$ 1.4tn of combined stock market value including Apple, Google, YouTube,

Instagram and WhatsApp, holds ~48% stake in PSL.

Fig 18 – Sequoia Capital investment over the years

Year Amount (Rs mn)

2011 620

2012 120

2013 300

2014 250

Source: Company, BOBCAPS Research

12

19

23

0

5

10

15

20

25

FY19 FY20 FY21

(Days) Cash Conversion Cycle

PRATAAP SNACKS

EQUITY RESEARCH 16 21 December 2021

Indian snack industry booming

The packed snacks such as instant and ready-to-cook snacking food items act as the

primary growth drivers for the snacks industry in India. The consumption of package

snacks is growing in India due to hygienic factors, easy availability, numerous choices,

and a rise in the citizens' personal disposable income.

Industry sources estimate India’s snack market at Rs 550bn in 2020, of which organised

players account for Rs 220bn-240bn. The potato chips, extruded and namkeen

segments account for Rs 60bn-75bn each and sweet snacks is a Rs 30bn market. The

country’s snack industry is expected to grow at a 13% CAGR over 2020-26 to reach

US$ 23.4bn.

Apart from a large unorganised sector, brands such as Prataap Snacks, Balaji Wafers,

ITC-Bingo, DFM Foods, Bikanervala, Haldiram’s and PepsiCo are the key players in

India. Indian consumers have diverse regional preferences and tastes, which makes it

important for companies to offer a mix of regional and national flavours and variants.

Packed snacks such as instant and ready-to-cook food items act as the primary growth

drivers for the industry in India.

Consumption of packaged food is growing due to hygiene factors, easy availability,

numerous choices and a rise in disposable income. The Covid-19 induced lockdown

also drove higher snacking as consumers were confined to their homes. When most

economic sectors were adversely hit, lifestyle changes wrought by the pandemic

positively impacted the snack market in India.

PSL vs. DFM Foods

DFM remains confined to North India

DFM Foods was among the first players to enter the extruded snack market and sells its

products under the ‘CRAX’ brand. The company was a pioneer in giving away free toys

with snacks to drive sales to children. However, it has been unable to scale up in terms

of products and geography, still deriving ~75% of its revenue from North India and the

Delhi market.

Southern markets form just 5% of DFM’s total revenue and are difficult to serve as its

plant is located in North India – posing a challenge in the highly competitive, freight-

intensive snacks category. In a bid to expand into different geographies, it is providing a

distributor margin of ~12% in non-northern markets compared to ~7% in North India.

PSL has pan-India reach and distribution

PSL entered the domestic snack market in 2005 with a facility in Indore, followed by an

entry into the western market of Mumbai and northern market of Delhi by taking

advantage of reverse logistics. After gaining critical scale, it further expanded its reach

into eastern states via Guwahati (Assam) and then ventured into South India via

outsourcing. Thus, PSL has uniform revenue contribution across geographies.

PRATAAP SNACKS

EQUITY RESEARCH 17 21 December 2021

The company enjoys a first-mover advantage in terms of early investment in a pan-India

distribution channel coupled with strategic plant locations that enable it to effectively

respond to market demands, evolving consumer preferences and competitive

pressures. In addition, it is streamlining its distribution channel which will reduce freight

cost and distributor margins going forward. In contrast, DFM’s expansion into different

geographies could attract higher freight cost and distributor margins.

PRATAAP SNACKS

EQUITY RESEARCH 18 21 December 2021

Company Background

Prataap Snacks Ltd. (PSL) is a leading Indian Snack Foods Company. It offers multiple

variants of products across categories of Potato Chips, Extruded Snacks, Namkeen

(traditional Indian snacks) under the popular and vibrant Yellow Diamond brand. It has

recently launched a range of sweet snacks under the distinctive Rich Feast brand. PSL

is focused on offering deep value to consumers through a variety of pack sizes at

attractive price points. Its products are present across 31 States and Union Territories in

India.

Headquartered in Indore, India; PSL operates 15 manufacturing facilities of which 7

facilities are in-house and 8 are on contract manufacturing basis. Its distribution network

includes 245 super stockists and more than 4,300 distributors allowing it extensive

reach across the country.

PSL has a wide presence that is equally spread in metro cities and urban clusters as

well as in rural areas and Tier 2 and 3 cities and towns. Its products are available at

independent grocers and small retail stores in the lanes and by-lanes of its key markets

and it is now building up its presence in supermarkets, hypermarkets and modern trade

outlets.

PSL continued to launch new products, new flavors and innovation in the market for its

target consumers. Having started with potato chips, the Company today has a

diversified product portfolio into various categories. It has more than 100 SKUs at

strategic price points and pack sizes - starting from Rs 5 till Rs 100. Currently, it sells

more than 11mn packets per day spread over 100 SKUs, which reflects its vibrant

product offerings.

The wide product portfolio of Avadh Snacks is complementary to PSLs existing salty

snack portfolio. Hence, the acquisition of Avadh Snacks has facilitated the Company in

providing a varied mix of regional and national flavors and variants. Further, on the

opportunity dynamics front, Gujarat has one of the highest per capita consumptions of

packaged snacks. All the products of Avadh Snacks are marketed under the brand

Avadh.

Fig 19 – Prataap Snacks timeline

Source: Company, BOBCAPS Research | Note: As per Financial Year

PRATAAP SNACKS

EQUITY RESEARCH 19 21 December 2021

Fig 20 – Prataap Snacks + Avadh Product Portfolio

Source: Company, BOBCAPS Research

PRATAAP SNACKS

EQUITY RESEARCH 20 21 December 2021

Management profile

Arvind Mehta, Chairman and Executive Director: Arvind Mehta was appointed

as an additional Director of the company in May’11. He has over 32 years of

experience in real estate along with over 17 years in the snacks industry and the

financing business. Mehta has a Bachelor’s degree in Commerce.

Amit Kumat, Managing Director and Chief Executive Officer: Amit Kumat was

appointed as an additional Director of the company in May’11 and made CEO in

Jun’16. Kumat has over 25 years of experience in the snacks industry. He has a

Bachelor’s degree in Engineering and a Master’s degree in Science.

Sumit Sharma, Chief Financial Officer: Sumit Sharma has over 19 years of

experience in finance, accounts and taxation. Prior to joining PSL, he worked with

Crompton Greaves during 2005‐06 and Case New Holland Construction (earlier

known as L&T‐Case Equipment) during 2006‐12. Sharma is responsible for the

accounting and reporting, financial planning and taxation functions of the company.

He has been a member of the Institute of Chartered Accountants of India since

Feb’02 and has a Bachelor’s degree in Commerce.

Apoorva Kumat, President – Operations: Prior to joining PSL, Apoorva Kumat

was associated with group company Prakash Snacks and Hello Agro Food

Products. He is involved in the production planning, logistics and sales functions of

the company. He has a Bachelor’s degree in Commerce.

Subhash Bhatt, Vice President – Production: Subhash Bhatt has been with PSL

since Sep’11. Prior to joining the company, he worked with group company

Prakash Snacks and Hello Agro Food Products. He is responsible for managing the

production function of the potato chips and namkeen segments. Bhatt has a

Bachelor’s degree in Technology.

PRATAAP SNACKS

EQUITY RESEARCH 21 21 December 2021

Financials

Income statement

Y/E 31 Mar (Rs mn) FY18 FY19 FY20 FY21

Revenue 10,184 11,706 13,938 11,711

Net Raw Materials 6,862 8,204 9,947 8,431

Power & Fuel Cost 259 269 274 293

Employee Cost 365 415 577 533

Contract labour 262 306 370 316

Freight & forwarding charges 769 841 985 831

Advt & Sales 254 172 150 129

Other Expenses 543 665 699 547

Total Expenditures 9,315 10,874 13,001 11,080

EBITDA 869 832 937 631

EBITDA % 8.5 7.1 6.7 5.4

Depreciation (304) (376) (617) (546)

Interest expense (29) (9) (75) (63)

Other income 80 109 92 88

Profit before tax 617 557 337 111

Taxes (175) (110) 132 31

Minorities and other 0 - - -

Reported Net profit 442 446 469 142

Other Comprehensive income 0 0 0 0

Net profit 442 446 469 142

Source: Company, BOBCAPS Research

Balance sheet summary

Y/E 31 Mar (Rs mn) FY18 FY19 FY20 FY21

Equity capital 117 117 117 117

Reserves 5,078 5,496 5,960 6,115

Net worth 5,195 5,614 6,078 6,232

Minority Interest 0 0 0 0

Debt 107 924 1,649 1,131

Deferred tax liab (net) -58 605 410 344

Total liabilities 5,245 7,143 8,137 7,706

Fixed assets 2,647 2,873 3,591 3,394

Capital Work In Progress 16 67 196 209

Other Intangible assets 44 1,927 1,825 1,726

Goodwill 0 461 461 461

Other non current assets 101 166 538 489

Inventories 897 1,195 1,323 1,307

Sundry debtors 204 308 326 266

Loans & Advances 164 168 187 194

Other current assets 201 231 170 161

Sundry creditors (997) (856) (875) (926)

Other current liabilities & Prov (326) (239) (192) (220)

Cash 2,144 819 538 304

Other Financial Assets 150 23 49 342

Total assets 5,245 7,143 8,137 7,706

Source: Company, BOBCAPS Research

PRATAAP SNACKS

EQUITY RESEARCH 22 21 December 2021

Cashflow summary

Y/E 31 Mar (Rs mn) FY18 FY19 FY20 FY21

Profit before tax 617 557 337 111

Depreciation 304 376 617 546

Tax paid (175) (110) 132 31

Working capital ∆ (143) (663) (132) 157

Other operating items - (461) - -

Operating cashflow 603 (301) 954 844

Capital expenditure (2,967) (654) (1,464) (362)

Free cash flow (2,364) (955) (509) 483

Equity raised 4,778 (4) 19 36

Investments - - - -

Others (295) (1,821) (296) (145)

Debt financing/disposal 107 817 726 (518)

Dividends paid (24) (24) (24) (24)

Equity Buy back - - - -

Capital subsidy - - - -

Other items (58) 663 (196) (66)

Net ∆ in cash 2,144 (1,325) (281) (234)

Opening Cash Flow - 2,144 819 538

Closing Cash Flow 2,144 819 538 304

Source: Company, BOBCAPS Research

Ratio analysis

Y/E 31 Mar FY18 FY19 FY20 FY21

Growth matrix (%)

Revenue growth 14.1 14.9 19.1 (16.0)

Op profit growth 112.5 (4.3) 12.6 (32.7)

EBIT growth 287.8 (12.5) (27.2) (57.9)

Net profit growth 419.6 1.1 5.2 (69.8)

Profitability ratios (%)

EBITDA margin 8.5 7.1 6.7 5.4

Net profit margin 4.3 3.8 3.4 1.2

RoCE 17.4 7.7 8.0 2.9

RoNW 17.0 8.3 8.0 2.3

RoA 8.4 6.2 5.8 1.8

Per share ratios (Rs)

EPS 18.8 19.0 20.0 6.0

Dividend per share 1.0 1.0 1.0 1.0

Cash EPS 31.8 35.1 46.3 29.3

Book value per share 221.5 239.4 259.1 265.7

Valuation ratios (x)

P/E 44.7 44.2 42.0 139.3

P/B 3.8 3.5 3.2 3.2

EV/EBIDTA 20.3 23.8 22.2 32.6

Liquidity ratios

Debtor days 7.3 9.5 8.4 8.2

Inventory days 35.1 52.4 47.9 55.8

Creditor days 39.1 28.4 24.2 30.1

Source: Company, BOBCAPS Research

PRATAAP SNACKS

EQUITY RESEARCH 23 21 December 2021

Disclaimer

Recommendation scale: Recommendations and Absolute returns (%) over 12 months

BUY – Expected return >+15%

HOLD – Expected return from -6% to +15%

SELL – Expected return <-6%

Note: Recommendation structure changed with effect from 21 June 2021

Our recommendation scale does not factor in short-term stock price volatility related to market fluctuations. Thus, our recommendations may not always be strictly in

line with the recommendation scale as shown above.

Rating distribution

As of 30 November 2021, out of 115 rated stocks in the BOB Capital Markets Limited (BOBCAPS) coverage universe, 57 have BUY ratings, 31 have HOLD ratings, 6

are rated ADD*, 2 are rated REDUCE* and 19 are rated SELL. None of these companies have been investment banking clients in the last 12 months. (*Our ADD and

REDUCE ratings are in the process of being migrated to the new recommendation structure.)

Analyst certification

The research analyst(s) authoring this report hereby certifies that (1) all of the views expressed in this research report accurately reflect his/her personal views about

the subject company or companies and its or their securities, and (2) no part of his/her compensation was, is, or will be, directly or indirectly, related to the specific

recommendation(s) or view(s) in this report. Analysts are not registered as research analysts by FINRA and are not associated persons of BOBCAPS.

General disclaimers

BOBCAPS is engaged in the business of Institutional Stock Broking and Investment Banking. BOBCAPS is a member of the National Stock Exchange of India Limited

and BSE Limited and is also a SEBI-registered Category I Merchant Banker. BOBCAPS is a wholly owned subsidiary of Bank of Baroda which has its various

subsidiaries engaged in the businesses of stock broking, lending, asset management, life insurance, health insurance and wealth management, among others.

BOBCAPS’s activities have neither been suspended nor has it defaulted with any stock exchange authority with whom it has been registered in the last five years.

BOBCAPS has not been debarred from doing business by any stock exchange or SEBI or any other authority. No disciplinary action has been taken by any regulatory

authority against BOBCAPS affecting its equity research analysis activities.

BOBCAPS has obtained registration as a Research Entity under SEBI (Research Analysts) Regulations, 2014, having registration No.: INH000000040 valid till

03 February 2025. BOBCAPS is also a SEBI-registered intermediary for the broking business having SEBI Single Registration Certificate No.: INZ000159332 dated 20

November 2017. BOBCAPS CIN Number: U65999MH1996GOI098009.

BOBCAPS prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of

any companies that the analysts cover. Additionally, BOBCAPS prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory

board member of any companies that the analysts cover.

Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions contrary to the

opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations

expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of

interest. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be

illegal. We are not soliciting any action based on this material. It is for the general information of BOBCAPS’s clients. It does not constitute a personal recommendation

or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this

material, clients should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice.

The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any

investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. BOBCAPS does not

provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding any potential investment in certain transactions —

including those involving futures, options, and other derivatives as well as non-investment-grade securities —that give rise to substantial risk and are not suitable for all

investors. The material is based on information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such.

Opinions expressed are our current opinions as of the date appearing on this material only. We endeavour to update on a reasonable basis the information discussed

in this material, but regulatory, compliance, or other reasons may prevent us from doing so.

We and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance of this material, may from time to time have “long” or

“short” positions in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein and may from time to time add to or dispose

of any such securities (or investment). We and our affiliates may act as market makers or assume an underwriting commitment in the securities of companies

discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis, and may also perform or seek to perform

investment banking or advisory services for or relating to these companies and may also be represented in the supervisory board or any other committee of these

companies.

For the purpose of calculating whether BOBCAPS and its affiliates hold, beneficially own, or control, including the right to vote for directors, one per cent or more of the

equity shares of the subject company, the holdings of the issuer of the research report is also included.

BOBCAPS and its non-US affiliates may, to the extent permissible under applicable laws, have acted on or used this research to the extent that it relates to non-US

issuers, prior to or immediately following its publication. Foreign currency denominated securities are subject to fluctuations in exchange rates that could have an

PRATAAP SNACKS

EQUITY RESEARCH 24 21 December 2021

adverse effect on the value or price of or income derived from the investment. In addition, investors in securities such as ADRs, the value of which are influenced by

foreign currencies, effectively assume currency risk. In addition, options involve risks and are not suitable for all investors. Please ensure that you have read and

understood the Risk disclosure document before entering into any derivative transactions.

In the US, this material is only for Qualified Institutional Buyers as defined under rule 144(a) of the Securities Act, 1933. No part of this document may be distributed in

Canada or used by private customers in the United Kingdom.

No part of this material may be (1) copied, photocopied, or duplicated in any form by any means or (2) redistributed without BOBCAPS’s prior written consent.

Company-specific disclosures under SEBI (Research Analysts) Regulations, 2014

The research analyst(s) or his/her relatives do not have any material conflict of interest at the time of publication of this research report.

BOBCAPS or its research analyst(s) or his/her relatives do not have any financial interest in the subject company. BOBCAPS or its research analyst(s) or his/her

relatives do not have actual/beneficial ownership of one per cent or more securities in the subject company at the end of the month immediately preceding the date of

publication of this report.

The research analyst(s) has not received any compensation from the subject company in the past 12 months. Compensation of the research analyst(s) is not based on

any specific merchant banking, investment banking or brokerage service transactions.

BOBCAPS or its research analyst(s) is not engaged in any market making activities for the subject company.

The research analyst(s) has not served as an officer, director or employee of the subject company.

BOBCAPS or its associates may have material conflict of interest at the time of publication of this research report.

BOBCAPS’s associates may have financial interest in the subject company. BOBCAPS’s associates may hold actual / beneficial ownership of one per cent or more

securities in the subject company at the end of the month immediately preceding the date of publication of this report.

BOBCAPS or its associates may have managed or co-managed a public offering of securities for the subject company or may have been mandated by the subject

company for any other assignment in the past 12 months.

BOBCAPS may have received compensation from the subject company in the past 12 months. BOBCAPS may from time to time solicit or perform investment banking

services for the subject company. BOBCAPS or its associates may have received compensation from the subject company in the past 12 months for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory services in a

merger or specific transaction. BOBCAPS or its associates may have received compensation for products or services other than investment banking or merchant

banking or brokerage services from the subject company in the past 12 months.