Comment Letter on File No. S7-27-08 - SEC.gov

24

900 Lakewood Ave. 732.987.2724 GEORGIAN COURT UNIVERSITY Lakewood, NJ 08701-2697 Fax: 732.987.2024 www.georgian.edu School of Business March 5, 2009 Mary L. Schapiro, Chairman US Securities and Exchange Commission 100 F Street, NE Washington, DC. 20549 1 (202) 942-8088 RE: 'FRS VS US GAAP Dear Chairman Schapiro: Please allow US Multinational Corporations who voluntarily wish to file their fmancial reports under IFRS in 2009 permission to do so. These US Multinational companies need to be able to compete with Foreign Multinationals now permitted to use IFRS in the US filings of their SEC financial reports. US Multinational Corporations are so important to our US and global economy because of their global export activities. -By permitting -US -Multinationals to file their fmancial reports under IFRS in 2009, companies will be able for the most part to show a higher level of financial performance and be more competitive with Foreign -Multinational Corporations. An equal playing field for the accumulation of capital by US Multinationals is vital to their economic vitality and competiveness as filers on the NYSE. Recently, in January 2009, we were fortunate to have had an article published on "The Globalization of Accounting Standards: IFRS VS US GAAP" in the Global Journal of Business Research. -This article was written to provide a .level of understanding to the reader and give an overview of global accounting standards. Furthermore in January 2009, we presented a study on Multinational Corporations financial reporting at a Global conference to an audience of international academics and fmancial reporting experts. A copy of our best in session award for the conference is included and copies ofthe articles are enclosed for your review. 1 The Mercy University of New Jersey

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Comment Letter on File No. S7-27-08 - SEC.gov

900 Lakewood Ave. 732.987.2724GEORGIAN COURT UNIVERSITY Lakewood, NJ 08701-2697 Fax: 732.987.2024 www.georgian.eduSchool of Business

March 5, 2009

Mary L. Schapiro, Chairman US Securities and Exchange Commission 100 F Street, NE Washington, DC. 20549 1 (202) 942-8088

RE: 'FRS VS US GAAP

Dear Chairman Schapiro:

Please allow US Multinational Corporations who voluntarily wish to file their fmancial reports under IFRS in 2009 permission to do so.

These US Multinational companies need to be able to compete with Foreign Multinationals now permitted to use IFRS in the US filings of their SEC financial reports. US Multinational Corporations are so important to our US and global economy because of their global export activities.

-By permitting -US -Multinationals to file their fmancial reports under IFRS in 2009, companies will be able for the most part to show a higher level of financial performance and be more competitive with Foreign -Multinational Corporations. An equal playing field for the accumulation of capital by US Multinationals is vital to their economic vitality and competiveness as filers on the NYSE.

Recently, in January 2009, we were fortunate to have had an article published on "The Globalization of Accounting Standards: IFRS VS US GAAP" in the Global Journal of Business Research. -This article was written to provide a .level of understanding to the reader and give an overview of global accounting standards.

Furthermore in January 2009, we presented a study on Multinational Corporations financial reporting at a Global conference to an audience of international academics and fmancial reporting experts. A copy of our best in session award for the conference is included and copies ofthe articles are enclosed for your review.

1The Mercy University of New Jersey

2

What is our background?

Anne B. Fosbre, Ph d, CPA Deloitte & Touche Alumni, Professor of Accounting, Fonner Professor Emeritus, Pace University, NY, Georgian Court University, professor of accounting over 30 years, fonner member NJ Board of Accountancy, NASBA member, fonner member Examination Review Board (CPA Exam)

EllenM. Kraft, 'Ph d, Business Management Richard Stockton College ofNew Jersey

Paul B. Fosbre, MBA, CPA Adjunct Professor, Georgian Court University, New Jersey City University Consultant IFRS Accounting Policy Advisor, NY Federal Reserve Bank Senior Accounting Policy Advisor Federal Reserve Board of Governors Senior International Accounting Policy Advisor KPM Financial Services Consulting Group

We hope you may find our articles helpful in your future decisions. We wish you Success as Chairman of the SEC

Our Very Best Wishes . fJa,.u£ C~~e~~

Dr.Anne B ~sbre Dr.Ellen M Kraft Paul B Fosbre

Copy

Copy CopyCopyright material redacted. Author cites the following article: Anne B. Fosbre, Ellen M. Kraft, Paul B. Fosbre, "The Globalization of Accounting Standards: IFRS versus US GAAP," Global Jounal of Business Research, Vol. 3, No. 1 2009.

Copyright material redacted. Author cites the following article: Anne B. Fosbre, Ellen M. Kraft, Paul B. Fosbre, "The Globalization of Accounting Standards: IFRS versus US GAAP," Global Jounal of Business Research, Vol. 3, No. 1 2009.

•IFRS Versus US GAAP:

The Globalization of Accounting Standards

Anne B. Fosbre, Ph.D., CPA Georgian Coo It Unlversl ty

81en M. Kraft,. Ph.D. RJchard Stockt on College of New Jerse y

Paul B. Fosbre, MBA, CPA Georgian Coo It Unlversl ty

Relationship of SEC and FASB in Developing US GAAP

r . . . _. : APB

. '.! II• ~~-c,'-,-c,.-;._-ir aulletlM ..'SA. Generally Accepted

Accounting Principles J. (GAAP) . '-

,

Role of SEC in Accounting Standards

• 1934 Securites and Exchange Ad created the Securities and Exchange Conmission (SEC)

• Congress gave theSEC the power and responsilility for setting accounting and repor1ilg standards forcompanies whose securities are pU~lcly traded on Either orgarized stock exchanges or over thecounter markets

• SEC has delegated the responsi~ity, but notthe authority to set standards

• Power thus lies with the SECto disagree or change standards issued by the private sEElor which it has done

IFRS Versus US GAAP

IFRS " International Financial Reporting Standards " More broad and principle based as compared to US GAAP ,; All European Union (EU) countries have been mandated

to use IFRS reporting as of 2005 " Today IFRS is used in over 100 countries

USGAAP " United States Generally Accepted Accounting Principles ;" US standards contain underlying principles as well

as strong regulatory and legal requirements

FASB

• Created in 1973, FASB (Financial Accounting Standards Board) is represented by seven full time members compared to 18-21 part time voluntary members of the APB

• Supported financially by the Financial Accounting Foundation (FAF) c The FAF is responsible for selecting FASB members who w~~~eave their present empbyment and workonly for

• FASS has issued seven statements of financial accountingconcepts (SFAC's) to describe its conceptual frameworK

_ The Board has issued over150 specific aa:ounting standards to date

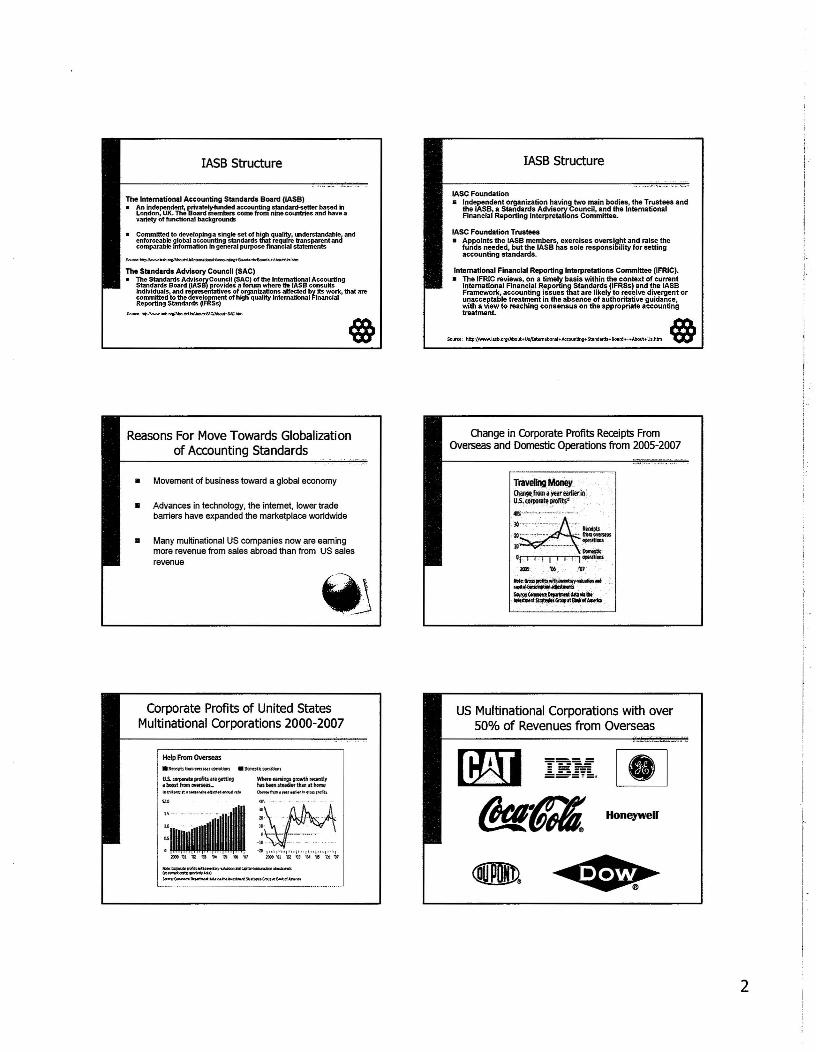

-IASB Structure

'. '"', ..... '11III• -----7 . ,..;::.-.:,;,

#S"1I-·' ..... .....,.-

-----~ ~----...-J, IFRS

Iligh Quality enlorceable and global

Source: http://WNW.lasb.org/About+Usflntemational+Accounting+Standards+Board+-+About+Us.htm

1

IASB Structure

The International Accounting Standards Board (IASB)

. e~~~~~~~Vl:e~~~=~~ ~~~:~~~~~~=~~~:a variety of functional backgroundi

Reasons For Move Towards Globalization of Accounting Standards

• Movement of business toward a global economy

• Advances in technology, the intemet, lower trade barriers have expanded the marketplace worldwide

• Many multinational US companies now are eaming more revenue from sales abroad than from US sales revenue

a.:~..,.. ,·,~

Corporate Profits of United States Multinational Corporations 2000-2007

Help From Overseas

u.s. corporate profits are getting Wtlere eilrnings growth recently Ol boost from overseas... has bten steadier than at homo

............ lO~~:···········II· :\ ~. ~•.... , ::,,,,,.,,,,,,,,.,,,,,,,,,,,,,,

100:1'01 112 'D! 'Q4 'OS '06 '01 2(((1'01 '02 '01 'o.l '05 .~ '07

Note:(~.Itf"""ftl""~'_tA' ..-Q.IoIIWllN~~I(.~

{1I._<mts:'i\IlrlfIttiIJI'l !.:u'1l':C....-~_HU~~t'l~_!>I...t~ ..~~otll>olf;f-""tro

IASB Structure

lAse Foundation • Independent organization having two main bodies, the Trustees and

the lASe, a Standards Advisory Council, and the International Financial Reporting Interpretations Committee.

lAse Foundation Trustees

• tJ'rfcJ~~~e~:d~'1:t~:~~:h:;~~'~~S~V:ri:mUi~~:rr:~~~e accounting standards.

International Financial Reporting Interpretations Committee (IFRIC). • The IFRIC reviews, on a time~ basis within the context of current

~::~~~r'I.~I:c~n:.:';l~g~~~.~nl/,:::~ri~~~JlfoRr~~~~ddtrv:~.;;,~or unacceptable treatment in the absence of authoritative guidance, with a View to reaching consensus on the appropriate accounting treatment.

s".,,~, h"'I""",."b.""''''''''+U",_~,+",~""",+",,,,.~,+''''~+-+'''''''+U,.htm @

Change in Corporate Profits Receipts From Overseas and Domestic Operations from 2005-2007

Traveling Money .Chai!geJro.;,avearearllerin u.s"orporale'iltOftls·

:~.'.•.•••.. '. ··.········.·····.·······.·.t.:r-..,Kft10 ,.•. Ilm..ti<

0lrT,~lrTI...,lrTl...,'-,-j-j.1 operallDftS

lOOS'06 ~7

NGtf:{irQ5$~wll.irwefltory.luiliIII~...........,.......__...... iIw

......nSiAOlte'....."illlII<of......

US Multinational Corporations with over 50% of Revenues from Overseas

Honeywell'

------- ---- ---- --- ----==-=':'=11

2

Convergence of Accounting Standards

• First step towards internationa accounting standards was the formation of The Internation:!lAccounting Stardards Comnittee (IASC) in 1973

• In 2001 the IASC reorgarized aOO created the Internationa Accounting StandardsBoard (lA.SB)

IASC now acts as an umbrella organization similar to the Financial Accounting Foundation (FAF) in the United States. IASC issued 41 International Standards (lAS's)

• IASB has issued 6 standards cf its own called Internationa Financial Reporting Standards (IFRS) •

Adoption of IFRS

• On November 15, 2007 the Securities and Exbange Commission (SEC) exanpted forei91 firms usng IFRS from filing a reconciiation of IFRS to US GAAP.

• This move l:¥ the Securities and Exchange ComriBsion (SEC) to aliON IFRS in finandal reporting by foregn comparies on US stock exchanges without therequirement of a reconciliation to US GAPP has created a mandate to converge IFRS and US GAAP and financia statement requirements.

• World Market capitalization by

Accounting Standard

Other or Not Available

USGAAP

10%

Plan IFRSor 35%Plan Partial

Adoption 22%

Source: Financiall1mes

Convergence of Accounting Standards

• In 1994 the movetoward convergence ofaccounting standards be~an with the FinanciliAccounting StandardsBoard (FASB andlnternationa Accounting Stmdards Commission IASC) jdntly working on the Issuance of new standards for the computation of earnings per share (EPS).

• In 2002 FASB and IASB signed the Norwak Agreement formalizing a joint agreement to convergence (J US GAAP and IFRS. The boards agreed toresolve existng differences between their standards.

• As of 2005 all listed companies in the European Union (EU) must prepare consolilated finandal statementsusing IFRS.

~~~~~....

Implications of IFRS for Investors

• Companies with many overseas locations may benefit from using IFRS standards in financial reporting because they may be able to be more flexible in meeting statutory filing requirements in the various locals.

• Foreign companies will be reporting higher revenues than a comparable US Muitinational corporation following US GAAP

Red· IFRS Approv eel

Orange· Slated Move t 0 adoption

Adopting to IFRS's Soun;e:lntemJlicllllllAcctuntiogStJodllrdBoird ~mMay 14, :mafromhttp://~R:lWe.lIsb.org.l*J~bcuVrfrSW)<ti'.~

3

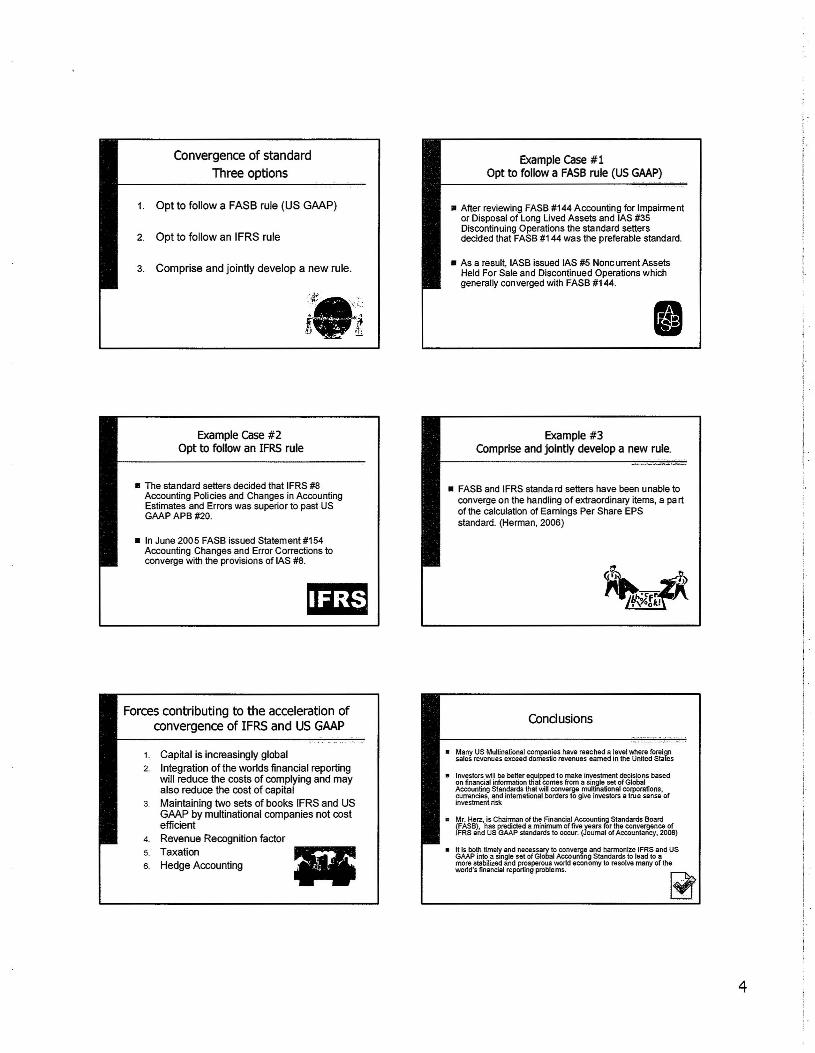

Convergence of standard Three options

1. Opt to follow a FASB rule (US GAAP)

2. Opt to follow an IFRS rule

3. Comprise and jointly develop a new rule.

Example Case #1 Opt to follow a FASB rule (US GAAP)

• After reviewing FASB #144 Accounting for Impairment or Disposal of Long Lived Assets and lAS #35 Discontinuing Operations the standard setters decided that FASB #144 was the preferable standard.

• As a result, IASB issued lAS #5 Nonc urrent Assets Held For Sale and Discontinued Operations which generally converged with FASB #144.

Example case #2 Opt to follow an IFRS rule

• The standard setters decided that IFRS #8 Accounting Policies and Changes in Accounting Estimates and Errors was superior to past US GAAP APB #20.

• In June 2005 FASB issued Statement #154 Accounting Changes and Error Corrections to converge with the provisions of lAS #8.

Example #3 Comprise and jointly develop a new rule.

• FASB and IFRS standa rd setters have been unable to converge on the handling of extraordinary items, a pa rt of the calculation of Earnings Per Share EPS standard. (Herman, 2006)

Forces contributing to the acceleration of convergence of IFRS and US GAAP

1. Capital is increasingly global 2. Integration of the worlds financial reporting

will reduce the costs of complying and may also reduce the cost of capital

3. Maintaining two sets of books IFRS and US GAAP by multinational companies not cost efficient

4. Revenue Recognition factor

5. Taxation ~ 6. Hedge Accounting ...

Conclusions

• ~nnv~~~O~~~\~~~~~~e~~f~~~~ ~a~eai~rri~I~~to~e~~~1s based Accounting Standards tttat will converge ':'lul~national corporations,currencies, and international borders to give Investors a true sense of investment risk

• ~m~t~~Zn~red s~~S~fO?;~rA:~~~:~1a~~~rd~~~el~~~~Oa~d US more stabilized and prosperous world economy to resolve many of the world's financial reporting proble ms.

4

REFERENCES

AeppeI, l1mothy. (2007) Overseas Profit s Provide Shelter f or US Arms. The Wall Street Journal, August 9, A1.

Alllhor Unknown. (2008) Olange Agent. Journal ofAccountancy, February, 30.

campoy, Ana .(2008). Chemical Industry's Shift; Companies' Results Coold Be Burnished by Foreign Presence. The WiJlI5treet Journal, January 22, All.

CSpan Televslon Broadcast, Nati anal Govern ors Assodatioo (200B) Jeffrey Imelt, CEO and Chairman, General Electric Co rporation ·US Is Becoming an Export Natlon-, February 26.

Deloitte. (2008) Webc:ast, "In~ational Financial Reporting Standards • February 20.

Deutsch, Oaudia. (2008) At Home In the World, T71e New York TImes. February 14, C1.

Ernst and Young. (2007) "US GAAP VS IFRS The Basics

F1nandal Times. (2 007) "World Market CAP by Accoun tlng Standard 5·, January 9.

Harper, DavId (2008) Introduction to Financial Statement Analysl s Part lb, retrieved on May 14, 200S from ~.LQ.nLCW~C.QITIMi'!!J1LjIrtLQ~l

Introdueti OIl_to_finandaLstatement_analysls...,parLlb-9aap/.

REFERENCES

Herrman, Don. (2006) Convergence In search of the Best Journal ofAccountancy, January, 69.

Holstein, William J. (2007) "Have and Have ·Nets of Globalization. The New YOlk nmes, July B, BU4.

International Ace ounting Standards 8 oard, retrieved on May 14, 2 008 from btmJL~~QtM!ni.n.!l~!I_tLQl\lIlt.Ai;.~IJ.~~~---±!.lS~.!!!

International Ace ounting Standards 8 oard. (2008) IFRS Around the World, retrieved on May 14, 200B from 1mQ;ffi!r.@~rg.uk/aOQutlifrswor1dL~p ..

Kranhold, Kathryn. (2OOB) GE '5 5trength Abroad Helps It Weather Weakness In US. The Wall Street Journal, January 19, A3,

McCune, Erin, (2007) SEC Allow 5 Foreign Repo rtlng Standards In t he US, financial Reporting, Retrieved on May 14 from 1mP~~!cJllmiDQI.!Lry~l:.Qi])LSEU;_~llQIo'!"LEOL~9.D....B.~RQLt!ng,btm.

MJnnlhan, Brian, (2008) BridgIng the Global Accounting Standards Gap, E Cornmen:e Times, Retrieved on March 2, 200B, from httl:!:Ifv.ww.ec_O.DlI]1~n:~

tlmes,oom/5tory/61132..htnll?welcome=1204 324142.

SpIceland, J. David, (2007) Intermediate AccounUng,: New Vorl(: McGraw-HllI,·Irv.in, 9.

5

•IFRS Versus US GAAP:

The Globalization of Accounting Standards

Anne B. Fosbre, Ph.D., CPA Georgian Coo rt Unlversl tv

81en M. Kratt, Ph.D. Richard Stockt: on Coll¥ of NeoN Jerse y

Paul B. Fosbre, MBA, CPA Georgian Coo It Unlversl ty

Relationship of SEC and FASB in Developing US GMP

r----------- .. I _

:.!: II l~~:.-J ,C:"',~CI"C,rc ~ •

Ace_tint! aulhtiM'SA. GeneraUy Accepted

Accounting Principles ) - (GAAP) .

Role of SEC in Accounting Standards

• 1934 Securities and Exchange Ad created the Securities and Exchange Corrmission (SEC)

• Congress gave theSEC the power and responsitility for setting accounting and reportilg standards forcompanies whose securities are pu~[ciy traded on either orgaJized stock exchanges or over thecounter markets

• SEC has delegated the responsi~ity, but notthe authori\, to set standards

• Power thus lies with the SECto disagree or change standards issued by the private sa::tor which it has done

IFRS Versus US GAAP

IFRS " International Financial Reporting Standards

More broad and principie based as compared to US GAAP All European Union (EU) countries have been mandated to use IFRS reporting as of 2005 Today IFRS is used in over 100 countries

USGAAP United States Generally Accepted Accounting Principles US standards contain underlying principles as well as strong regulatory and legal requirements

FASB

• Created in 1973, FASB (Financial Accounting Standards Board) is represented by seven full time members compared to 18-21 parttime voluntary members of the APB

• Supported financially by the Financial Accounting Foundation (FAF) The FAF is responsible for selecting FASB members who w,\.'§~eave their present empbyment and workonly for

• FASB has issued seven statements of financial accountingconcepts (SFAC's) to describe its conceptual framework

The Board has issued over150 specific aa:ounting standards to date

-IASB Structure

~.'-----"- .~ 7'. I"~--

#~li-·' ~~ ...... ~_.-~~-----~ ~~----

-JIFRS

high quality, enforceable and global

Source: htip://v.ww,lasb.org/About+us/lntemational+ACCOUntlng+ Standards+Board+-+About+Us,hbTI

1

lASS Structure

The International Accounting Standards Board (IASB).e~~~~~~~~=~~==~~~avariety of functional backgr~

Reasons For Move Towards Globalization of Accounting Standards

• Movement of business toward a global economy

• Advances in technology, the internet, lower trade barriers have expanded the marketplace worldwide

• Many multinational US companies now are earning more revenue from sales abroad than from US sales revenue

Corporate Profits of United States Multinational Corporations 2000-2007

Help FltIm Overseas

.S".:~u -_.. _.-- ...-._~ .~ .. --.- . lO" .~. -.. -- -..

JJI-._. --- - IP" ". . ..

M .1: _._ _ -. o . _. " -20 l"q;~'I("""II''l'''I'';1

200II"01 'Q;! 'lD 'l)I 1lS -'06 ~ 7,101)'01 'C2 'QJ 'Cot 'Il5o "-6 W

JIQH:~""'It.orb-..~W'III"' __~

(l!UMtonte~"""

s-u:e.--.....-w.-....... ~SCltl."..~o1ll/1Otd.""...

'--~~~~~_._---_ .._._

lASS Structure

IASC Foundation • Independent organization having two main bodies. the Trustees and

m~a~~~i ~e~~~;t~:~~:~~o~~~~;:;:~~e International

International Financial Reporting Interp",tationa Committee (IFRIC).

• ~~:~:I~n~1=~~n~~,~:~:?i~a~~~~hr~st~~~~;~~do~~u~sn~ Framework. accounting issues B.at are likely to receive divergent or unacceptable treatment in the absence of authoritative guidance, with a view to reaching consensus on the appropriate accounting treatment.

,"",U, ''''I/W<ffl.I~b.o'9l'''''"''",,",,~''OMI'A<,,,,,,,,.s,,,,,.,,,••,,,,,,,,,,'''''",.",.'lm @

Change in Corporate Profits Receipts From Overseas and Domestic Operations from 2005-2007

Traveling Money. ~~'j'~:;:,;!~m

~~~ lIlI5. '06 ...,:.

=t'"~=--''' =-~~~~

US Multinational Corporations with over 50% of Revenues from Overseas

Honeywelr

------- - --:: :::':EE==-=':'=..

2

Convergence of Accounting Standards

• First step towards internatioml accounting standards was the formation of The InternationaAccounting Standards Committee (IASC) in 1973

• In 2001 the IASC reorganzed and created the lnternationa Accounting StandardsBoard (L"-SB)

IASC now acts as an umbrella organization similar to the Financial Accounting Foundation (FAF) in the United States. IASC issued 41 International Standards (lAS's)

• IASB has issued 6 standards d its own called Internatioml Financial Reporting Standards (IFRS) •

Adoption of IFRS

• On November 15, 2007 the Securities and EJ<bange Commission (SEC) eX81lpted foreigl firms usng IFRS from filing a reconciiation of IFRS to US GAAP.

• This move I:y the Securities and Exchange Comnssion (SEC) to allow IFRS in financial reporting by foregn companes on US stock exchanges without therequirement of a reconciliation to US GAPP has created amandate to converge IFRSand US GAAP and financia statement requirements.

•

Convergence of Accounting Standards

• In 1994 the movetoward convergence ofaccounting standards be~an with the FinancillAccounting Standards Board (FASB andlnternationa Accounting Sl9ndards Commission IASC) jcintly wol1<ing on the Issuance of new standardsfor the computation of earnings per share (EPS).

• In 2002 FASB and IASB signed the Norwak Agreement formalizing a joint agreement to convergence d US GAAP and IFRS. The boards agreed toresolve existhg differences between their standards.

• As of 2005 all listed companies in the Europea Union (EU) must prepare consoliJated financial statements using IFRS.

U~~!....

Implications of IFRS for Investors

• Companies with many overseas locations may benefit from using IFRS standards in financial reporting because they may be able to be more flexible in meeting statutory filing requirements in the various locals.

• Foreign companies will be reporting higher revenues than a comparable US Multinational corporation following US GAAP

World Market Capitalization by Accounting Standard

Od1erorNot Available

USGAAP

10%

PIanIFRS or 35%Plan Partial

Adoption 22%

Source: Financial limes

Red- IFRS Approv ed

Orange- Slated Move t 0 adoption

Adopting to IFRS's

3

Convergence of standard Three options

1. Opt to follow a FASB rule (US GAAP)

2. Opt to follow an IFRS rule

3. Comprise and jointly develop a new rule.

Example Case #1 Opt to follow a FASB rule (US GAAP)

• After reviewing FASB #144 Accounting for Impairme nt or Disposal of Long Lived Assets and lAS #35 Discontinuing Operations the standard setters decided that FASB #144 was the preferable standard.

• As a result, IASB issued lAS #5 Noneurrent Assets Held For Sale and Discontinued Operations which generally converged with FASB #144.

Example Case #2 Opt to follow an IFRS rule

• The standard setters decided that IFRS #8 Accounting Policies and Changes in Accounting Estimates and Errors was superior to past US GMP APB #20.

• In June 2005 FASB issued Statement #154 Accounting Changes and Error Corrections to converge with the provisions of lAS #8.

Example #3 Comprise and jointly develop a new rule.

• FASB and IFRS standard setters have been unable to converge on the ha ndling of extraordinary items, a pa rt of the calculation of Eamings Per Share EPS standard. (Herman, 2006)

Forces contributing to the acceleration of convergence of IFRS and US GAAP

1. Capital is increasingly global 2. Integration ofthe worlds financial reporting

will reduce the costs of complying and may also reduce the cost of capital

3. Maintaining two sets of books IFRS and US GMP by multinational companies not cost efficient

4. Revenue Recognition factor 5. Taxation ~ 6. Hedge Accounting ~

Conclusions

D~nnv~~~n~:f~lnt~~~ne~~~~~ ~~eai~r~~:see~\~}~~~S based Accounting Stal1;dards tJ:lat will converge lJlul~national corporations,currencies, and International borders to gIVe Investors a true sense of investment risk

4

REFERENCES

AeppeI, limothy. (lOO7) Overseas Pmfit s Providt Shelter f crUS Firms. The wan Slret!t .JotmiJI, August 9, Ai.

AtJ;hor UtIknoYla. (2008) ~ Agent. .1otJm4J ofA«ourTtant:y. February, 30.

C;a1JllOY. Ana .(2008). ChemIcal Industry '$ Shift; Companies' Results CouSd Be Burnished by ForeIgn Presence. 111eWdfJ51reethm!tJanuary22, All.

CSpan TeJeo.&on BrOiKlcast. National GowmorsAssodation (2008) Jeffre.t ImeIt,CEOand Chairman, General EIectrlc Co rporatIon ~US is BecomIng an Export: Nation-, February 26.

Ddoitte. (2008) Webc:ast, "Irtematlonal Anandal ~eportlng Standards • February 20.

Deutsch, Qaudia. (2008) At Home in the World, The New YOlk Times. February 14, Ct.

Ernst and Young. (2007) ·US GAA9 \IS IFRS 'The Basics

Rnandaillmes. (2 DOn "World Market CAP by AcGoun tlng Standard 5". January 9.

Harper, David (2008) Introduction to Anandal Statemellt Analysl s Part lb, retrieved on May 14, 2008 from ll.ttp'lIWtfN bjonleturtle cQm~~L

Introduetion_to_f1nandau.t:atemenumalyslsJ)a!t..lb_gaap/.

REFERENCES

Hemnan, Don. (2006) Convergence in SWdl of the Best. .Joutn6I ofAa:l2uJlancy, January, 69.

Holstein, William J. (2007) "Have and Have -Hots of Globali z;atlon. 111e New rINk Tunes" Jdy 8,.,,,. IntmIationaIAlXounting St2JncIard$8 oant retrieved on May 14, 2 008 from bt:tR.:~~.!it~orgL~b9ut+usnntemational+~l)gt~~~.±.Q9ard"'.+About+us.htm

IntematklnaI AI::c 0lI'ting 5tandardsB oan:I. (2008) JFRSAnxmd the WOrid, retrieved on May 14, 2008from~~......Q!g.Y.lf.l.~.

KraI"lhold,Kathryn.(2008)GE'sStr!ngttlAbroaclHdp$JtWather WeiJkness In US. Thewan Street Journal, January 19, /1.3.

McCune, Erin. (2007) SEC Allow 5 ForeIgn Repo rtlng Standards In t he US. Fff1iJooal Reporti!l!# Retrieved on May 14 from httR:1L~..Mc.lJ,lmlnQ.WD'~ISE C AllOWS For~ ...&mQ[JiD9.,I)t::n.

Mlnnlhan, Brian. (2008) Bridging the Global ACCOUnting Standards Gap, E Commerce 7lmes, Retrieved on March 2, 2008, from ~.uv.«iW~

t1mes,oom/story/61132..html?welcome=1204 324142.

Spiceland, J. David, (2007) Intermediate Acaxmtfng,: New YOI1c: M cGraw-HllI,-Imn, 9.

5

,.

THE IMPACT OF GLOBAL ACCOUNTING STANDARDS ON FOREIGN AND UNITED STATES MULTINATIONAL

CORPORATIONS

Anne B. Fosbre, Georgian Court University Ellen M. Kraft, Richard Stockton College ofNew Jersey

Pa,.ul B. Fosbre, New Jersey City University

The movement ofbusiness toward a global economy has accelerated the need to move toward global accounting standards. Two recent decisions and a "roadmap proposalfor the US to adopt International Financial Reporting Standards, IFRS rules, have been issued by the United States Securities and Exchange Commission. These decisions and the "roadmap" proposal have had a major impact on the issue of converging United States Generally Accepted Accounting Principles and IFRS. The "roadmap" would allow 110 of the largest publicly held companies equal to 14% of us market capitalization to begin using IFRS voluntarily for their 2009 financial statements. Speed ofacceptance in world capital markets of one standard of accounting namely. IFRS is rapidly occurring and may motivate companies voluntarily to change. This paper will examine a selection of foreign and US multinational corporations currently using US GAAP financial reporting to examine the benefits or disadvantage ofchange for the cQmpanies reviewed

United States and Japan are the only countries in the G8 group ofnations that have not adopted IFRSfor financial reporting. (Gray 2008). Sony Corporation and Matsushita Electric Industrial Company (most recently changed to Panasonic Corporation) are the companies to be reviewed for the Japanese companies studied The US multinational companies to be reviewed in this study are Proctor and Gamble andJohnson and Johnson companies.

JAPANESE COMPANIES

Japan has agreed to IFRS convergence by 2011. The Accounting Standards Board of Japan ASBJ met with the International Accounting Standards Board, IASB, in 2007 and agreed to eliminate by 2008 major differenpes between Japanese and IFRS GAAP. The remaining differences were to be removed on or before June 30, 2011 at which time Japan would switch to IFRS. (Accountancy Age, 2008). As ofthe present time Japan has not adopted IFRS (Kagawa 2008).

SONY CORPORATION

Sony operates on a fiscal year calendar with year end occurring March 31. For 2008, revenue was $89.6 billion compared to Matsushita Electric that had revenue of $90.7 billion (Hoovers 2008). Sony does business in many countries. It is a true global player having 23% of its business in Japan, 26% in Europe, 25% in the US, and 26% in other regions (Sony 2007). Its major revenues are from foreign sales 49% while revenues from the US are 25%.

Research and Development Expenses Research and development expenses for 2008 were $521 million. Under US GAAP R&D expenses are for the most part expensed. IFRS requirements are to capitalize R&D expenses and add them to asset accounts in most cases. To follow IFRS would allow Sony to decrease expenses and increase net income dramatically.

Goodwill and Other Intangible Assets Sony has goodwill of $30.4 million for 2008. Goodwill and other intangible assets that are determined to have an indefinite life are not amortized and deducted as expenses on the income statement. But under US GAAP they are tested on a two step process for impairment (Financial Accounting Standards #142) An impairment loss is recognized if the carrying value ofthe asset exceeds the current fair value and must be expensed. Under IFRS goodwill impairment is limited to a one step review. The use of significant estimates and assumptions as required in the second step process is dropped. The elimination of this process may lead to a reduction of impairment expense under IFRS and result in an increase in net income. The above discussion of two factors that might affect Sony Corporation fmancials indicate an increase in figures reported under IFRS reporting if Japan should adopt IFRS reporting.

MATSUSHITA ELECTRIC INDUSTRIAL COMPANY

This company has changed its name to Panasonic Corporation as of October 1, 2008 (Panasonic 2008). Its founder Konosoke Matsushita is hailed as the patriarch of the Japanese consumer electronics industry. It uses a fiscal calendar year and year end is March 31. The revenue for 2008 was $90.7 billion. In 2008 50% of sales revenue was in Japan, 13% in Europe, 23% in Asia, 14% in North and South America. Thus, most ofthe revenues are foreign sales.

Research and Development Expenses Panasonic has $449.0 million expenses in 2008. If Panasonic converted to IFRS, R&D expenses would be for the most part capitalized and added to an asset account. This would reduce expenses, increase net income, and add asset values to the balance sheet.

Goodwill and Other Intangible Assets Panasonic has goodwill of $4.29 billion for 2008. Goodwill and other intangible assets determined to have an indefmite life are not amortized, they are required to be tested on a two step process under FAS #142 US GAAP. Any impairment is then expensed. Under IFRS goodwill impairment is limited to a one step test and may result in net in<;:ome. The two factors reviewed may change Panasonic Corporation's financial statements to report higher figures under IFRS reporting.

US COMPANIES

The roadmap created by the SEC would allow 110 of the largest publicly held companies equal to 14% of the US market capitalization to b~gin using IFRS voluntarily for their 2009 fmancial statements. (Journal of Accountancy, 2008) While the US is not adopting IFRS on an all-at-once mandatory basis the allowance of major companies to report on an IFRS basis will permit initial data for analysis. The US multinational companies reviewpd in this study are Proctor and Gamble and Johnson and Johnson companies.

PROCTOR AND GAMBLE

Proctor and Gamble operates on a fiscal year calendar for financial reporting with a year end of June 30. Its revenues for 2007 were $31.9 billion for the United States and $44.5 billion for international revenues. Over 50% of revenue was from foreign sales.

Revenue Recognition - LIFO Inv~ntory

Revenue recognition is simpler under IFRS compared to US GAAP. Revenue recognition under IFRS will probably increase because restrictions in US GAAP will be removed. For example, LIFO inventory is not recognized or allowed unqer IFRS. Revenue will probably increase because the restrictions on

revenue recognition under US GAAP using will be removed. LIFO is popular in US GAAP reporting because it usually reduces taxable income. As a result US companies pay lower taxes. If LIFO is used for tax purposes in the US it must also be used in fmancial reporting. Proctor and Gamble uses LIFO for certain cosmetics and commodities, but foreign subsidiaries use FIFO inventory reporting. With the elimination of LIFO taxes may Increase but in general the recognition of increased revenue reporting may occur.

Goodwill

Acquired goodwill and other intangible assets with indefinite useful lives are not amortized and are subject to a two step for impairment test under US GAAP. For IFRS only a one step test for impairment is used. The ongoing market tuqnoil has created problems for every company following US GAAP two step impairment test requirement. Companies will need to pay greater attention to goodwill impairment as required by Financial Accounting Standard FAS 142. Companies may find that goodwill impairment has occurred. In addition the creation of the new Financial Accounting Standard FAS 157 Fair Market Accounting is now mandatory as of this year 2008. FAS 157 defmes fair value as an exit price or how much could be obtained upon the sale of the asset. The second impairment test now requires companies to compare fair value of each units carrying value including goodwill. Goodwill is not impaired as long as the fair value of the entire reporting unit is greater than its carrying vale. If the fair market values less than the book value a goodwill impairment loss is recognized and profits fall. In this market a severe loss is likely to occur. Thus a switch to IFRS with one step testing is likely to benefit most companies. This may lead to a decline of impairment loss recognized and as a result a higher net income under IFRS. Total goodwill for Proctor & Gamble, at June 30, 2008 is $57.73 billion. The effect on Proctor and Gamble fmancials with a change to IFRS reporting would most likely result in higher income and an increase in the valuation of assets on the balance sheet. The foregoing analysis of some factors that may help Proctor and Gamble to report higher figures on IFRS reporting. It would also reduce the costs of converting IFRS subsidiaries to US GAAP for US reporting.

JOHNSON AND JOHNSON CORPORAnON

Johnson and Johnson operates ip over 55 countries. It operates on a fiscal year basis with a year of December 30. In the second qqarter of 2008 International sales grew to $8.24 billion compared to US sales revenues of $8.21 billion. lnternational sales were higher than US sales revenues. Proctor and Gamble with sales of$76 billion in 2007 is currently leading the industry. Johnson and Johnson is a close second with $61 billion in 2007.

Revenue Recognition

The Revenue Recognition proce!ls for IFRS is not equal to US GAAP they are compatible. Differences related to software revenues and the sale of real estate as reported under US GAAP should not have a major impact on Johnson and Johnson's fmancials. (Ernst & Young, 2008)

LIFO & FIFO Inventory

Johnson and Johnson use FIFO fpr their inventory valuation. (Johnson & Johnson Annual Report, 2008) Johnson and Johnson can easily yonvert any differences in their FIFO inventory as it is acceptable under IFRS reporting. (Ernst & Young, 2008) Conversion to IFRS would help Johnson and Johnson access capital markets globally without having to produce separate sets of fmancial reports for international and domestic investors. (AICPA Bac~~rounder, 2008)

SUMMARY

Benefits ofIFRS

The competiveness of US markets would be improved by the elimination of many barriers to entry in foreign markets. (Morris, 2008) The elimination of the cost of converting IFRS reporting subsidiaries to US GAAP reporting will occur. Investors will find it easier to compare foreign companies with an American rival company creating a better understanding of financial information (Economist, 2008).

Challenges in Moving to IFRS

Transitioning to IFRS is costly but of great benefit to cross border operations of large Companies. Small companies without cross border business conversion would be costly and without benefit for some. Conversion from GAAP to IFRS will raise tax related issues. Any in Securitized transactions with millions of dollars are allowed to stay off the books under US GAAP, IFRS requires most of the assets and liabilities to be reported on the balance sheets. Conversion to IFRS from US GAAP will impact many industries differently. The implications will vary also. However, in the long run the benefits will outweigh the problems.

Timeline

Throughout the world most markfts have moved to IFRS and require an immediate mandatory conversion for domestic companies listed. Canadian GAAP moves to IFRS for all publicly accountable enterprises on January 1,2011. ASBJ of Japan has agreed to converge Japanese GAAP to IFRS in 2011. They have not as yet adopted IFRS.

CONCLUSION

Although many multinational companies following US GAAP have internally made plans and efforts to move toward IFRS reporting, the world economic downturn has slowed the momentum. Many companies now have to focus on remaining profitable as a first consideration. However, eventually conversion to IFRS will become a major priority and US GAAP will become less significant.

REFERENCES

Author Unknown. (2008) AICPA Backgrounder, paragraph 3.

Author Unknown. (2008, November 8) Japan Agrees to IFRS Convergence by 2011. Accountancy Age.

Author Unknown. (2008, October) Profession Reacts to IFRS Plan. Journal ofAccountancy,

Author Unknown. (2008, November 8) Closing the GAAP. Economist.

Ernst & Young. (2008) Fifo Inventory Comments, 2008.

Gray, John (2008, February 8) financial Accounting: Number Crunch. Canadian Business.

Johnson & Johnson. (2007) Annual Report

Kagawa, Yoichiro and Kazumichi, Shono. (2008, September 18). Japan wrestles with Issue of IFRS Adoption. Daily Yomiuri Online. Retrieved September 29 from http://www.yomiuri.co.jp/dy/business/20080918TDY04302.htm

Morris.(2008) IFRS Becoming a Reality: International Financial Reporting Standards.

Duane Morris LLP, July 2

Panasonic. (2008) Matsushita Electric Industrial Co. History. August

Panasonic. (2008) Annual Report 20F SEC

Proctor & Gamble. (2008) Annual Report 10K SEC

Sony. (2008) Hoover.com Atlllual Income Statement

Sony. (2008) Annual Report 20 F SEC

US GAAP. (2008) Financial Accounting Standard #142

US GAAP (2008) Financial A~counting Standard #157

Where We are Lor;aIed

The ~mG~ofuaillA~~

00 FtJlreign amNII Umted SUates MIlII~~

C~

""""'IHlIfiJBllJlo\.IPlllllll•. ClJI'lI>I. I5lmrgjilm«:mu:tlWltfIllBl9il\Y

1I3Ii1mllll.lIQIaft\.lPIhllll. __«:lJlllogJocrtf_.JlIn:III!lH

IPlmIrl!ll.~.IIIlIIlI"-.«:IP'Rl.

_.JlIn:III!lHIl:lIWIl1lJi_1\!I

Eli ~diredJi:m; llJJftk2 retml~~ b:f die SEC iiIIIIIlItbi:S.EC~p1IlllpIIlilIII_* ~w~UlmiiimI1 Stlaiks GAAPIli» IFRS

EJi &atnlilBea ~dlJJDiilil:liB :sta/i<$aJIIIIlII~

emedl""'A'" i:llllIlIlllUl'islm ~UIliIig UlS GAAP1lllll.Itf!n'.... 1lk~iIIIIIllI

IlIisadwiiiiiltligL5 «lIf~ IFR.S h fiIIlmiIi ~

f~

• M lEim<>jpcmJ tlJluiimn uElll) 1llI1IJIllIii51bm",Imm IIIDIIIiBllDItto> lIB«: 1lflIlS~...d2lllJlj;

Rea'roIJI5 For Move Towards GlOOaIizmon ofAccounting S1andards

0: ~iim~"tI!hJf~lRlmt!mllille

~~~*~~-

0' ~,1l!IIIII/itiitu11lJlS~IIIl!Il'liI'~~

_~JIimlIIl~~1lIIimmJfiRlllmUlS ~~ ,

. \ .. \

. .-- -~.~:.~--~ " 1

First Key Decision By SEC

Eli c~ w:ililllllllll!r lilJ'Xli:Il3l!ll5l1irfmtliimml; IIIlIIW 1lBmdliit hIDl1lll!iinl!;DFRS ~ iim fliinmmriiliJ ~

~~'IIIlIIWIbrd*lkiJllbr~~ jim

~flm[:IIIIlIlI~fiiJIiiDlg~iim.

,,<lIJiiiml; ~

[JjF~~\1\riIIlbr~~llI:ItlCllllllf$

tllhmmill~ 1lJlS Muiltiinmtijmgni! ~ ~iing 1lJlS GA;\P,,_BFJRSj

0: «llalNl»<1l1IIiu n:;;.'J!liUTl1kSmmriiiil:>amll~ lC<DIIIIIiiIIIiim~~~ii>m¥u iiIJDB; - lH$Jimm~:BllI!lDMIlrilIiIlI;>IllS ili.<VIPas~JIIlqJIiimil

0: lIlIiil;llIIlll"<O: Ii¥'1kSimmriiiifs;ami! ~ lC<JDIIIIiimiiJm ~:mr))IIlll"'" InS iiniimmriillllllrJlllllllD!!~.......m...~<lIIIl\ll$...mli:~",idlmJillbt;;;;:;:;""'" olf:B~"'l\ll$«ii.'lAlI'Ibm;WIICIlIlliI:BlIIIIIIIlldI!:llo> """"""l!'" IHFIII$ amlI8.lS ili.<VIP ami!1IiiunmiidI_ ~

• S

or

0:

0:

econd Key Decision by SEC

«l\Il.ll:om: lI1Il2llJ]$llbt:5lElr" iiIIRntdI:B1I""'i'i IJdIciR«: stIIliiJm tIIBlI1tIIl: ",wdlI"$0WtlIIIiiii<:E~_1IIIiiiim:IIllliimm:lllll:1IIlriir~

olf~~~-

1lJm: IEiBI<op:Im lCmmmiiIIliimI,.1tIIl:.ilIpm JiinBmiiIII Sl=iiw:o~.

1tIIl:liIlIlmmIfuaniI ~olfSmwrilii5ClJIIIIIIiimi.iJ 00lSlr". _1Io>kiimllDll<Utiill1tlll:1"......'iilioi!~SllmdImliJI;

1Lmmmiillm: lIiJumllIliiml -

JA'SlOFiiJ;am~9lIIIIJllmDIl;~g]I01IlI'tIIBlIlIIlIlIiiIom; "'-.._...........-e 0: ~ ciIdiiIiliimlllbt:5lElr" ~IIbe....mlll"$ ~~

IIIIIIIIIzalllm:NitwcY<Jd:5lIoo:I<~ami!~

0: 1lJm:1lImlIttolf~g!biInlIl!""'=<JIfllbe:5lElr" Ibm; tmnmm: """,olf1tlll: ~JllliiDsolf<mDll!lllfumiiDllbt~olf

l\ll$amil ii."',"im;.mdl~SlIiIIIilBJr.i!

0: 1lJm::5lElr"lbm;ollIlInlltllBllllbell..~~~QIJ

JlIII"iiill:am ~ iiDImmliim> 1I:ImooamJJDliiJlloil aJJlIiDJIilii5;~Jrm1kaBbgliimJrnr~olf

• ~slIlIIdtIIIllI;JrmIlillllril~

SEC Roadmap Proposal

[]~~

., s-.rC«Jllp!IIllIlJilJIIIl SOIVY

.~C«Jllfl!JI!.1Il Pal as -'lie

[] 1.JJm1lcd St:IiUes

.~-~

., .l!loiDmlom ~~

2

I:] an-" g; ••

cr JraanIt..~~ .. _lIJSG<II.-VDDJ1IllUlJ) ....cdbDJgudllU'_""" .. 1IHl($~'"""..~IlWI»"-"iI""""_:mwdlum>.........

amr:DllJdl5UnIDllJ81c:::nfU:$

[J, c....hriII..06n- 7 gil' A--.. .. 1Dlm:9lIqp....1IlIl&r1lRlSwilIIo.mJ tt'''"dlm1liurolfiinJlBiiuoml!11mB;

~amlIlIigjhm'_iiJmmul,

.. =v,%~,,=~~==.,~~u:.lfm ~amlIotlImriirnmgilillo_

cr UFO"J1JR)~ .. lUIfll))_!lml"iil;_"""'~<llfalfu\uedl1IlIl&rlJfl!$

.. lUIfll))"",blm$_iiJmmul,amlIiiunJ_tllmEl;.udlmllJSl!ii!\\8\I!'

0;

0:

0;

IJ!pmmlbmnglRmll1iiDBFRSlOllIIIII\\tlII!,llJIIIOt~2lilJ1I1

TIlDe ~StllmlIbmiIl!; BD!lBlIIl co€lJplm ((.!WU)l IDldlIlrilllD11k In!lln,,.....I!lI.Hl ~$iflBmlIbmdl!;

&oIrldI «JA'SB» iD 'DJfll;am;l! ~ lDcIIiiIIiiIJIaie ~ 2llllDJJlllllljjmr~~~_JR'$

GMII"

TIIDe~diffliibIlOlBIJt$\\\l61f1iiDk~lilIIIl6llr

ibIdiiIR ~ 3XID" Nil II ;Dt \\\l1biidlD tliimi: JbIpmm \m1IuiI:dI

_ilIdIn 1iID lIFIIUli.. «kll""lIl1.t8lilC~' ."2l!lm)) n:~~

-_..~

cr _amlI~

~!fm2lll611> ...... lI.'>21n IDiillimJ

cr _lIJSG<II.-VUIII>~

""" Iblltlre IImBII pllt""II"'""'iI IIRI$rmgljiwmmnt9;an:etm ~_~amlI miiiltfimmtmaBM1lamDlunt!i;Un DDJ1IllClallll$

::I1Illi'-~UlJ)~

umlImlllll!$,..-..amlIlI"'1f"__amlISin¥,iil;1IIlIlIl'

atIImI:tfull"tm iiJmsmrJ;

...; =ii- : ~. ", -- IliI . ,.. .. -" ~

j:1 ~ ,"

... ..[Jj

[I

[I

....iTI..06n-' eU A--.. $lmIrf Iiml; ~ mJf$3lm4lmilliill.a1£mr2l'DJDlS ~iiIlamilmdbm~_dbBtaDll:"Itt1lt1""ii,ittillllill ~ aDl ~!iii: lIW' Jm1l:ll1llDll1iilmi hllllllllbm ame 1IBIIlliII (m- iinjpuiiIHlwU 1DDdImm GAAP l!JInjImlllfJiS ~iiIl iinpliinmmlt iii; JiiDiimj lIiIllll <DIm' ~ lliN·iil::I..-.lD 1U1SGMP1II11IlI1ID5IIqp>~jil;~_ 1k1lllll'mJf~~aum!~aDIl:lIH«lJ!j

III'·' .'

--_.';//

[I JraanIt..Dlt1l , , ..

• I'lIn!IIRmiir lIuB;~tID 1IIIilIIiinm~ iiIl200lll .. IIfIP'ammmaiir ~ lIiIl RS,.1lt4tD~ IIIOOlIlf Iilf

lI.iBrlkllllil1illDJllll1l~3IllltIadlWlIiIlaDl3llllldl awDlNIIil

[I

• lDIii!; -mtdI ~~ iiIllII<CIllIe lid iiDtImJm:,.andI all!bIIaBlld'l'aIiD5l1i1llk1buIlIalne 3lbllftt

......iTI..06n-' gjlT A--.. • lI".am!!lmiir Jiml; ~ <Of"$1I2'9J IbiIImm (m-21M .. 1lJld:lr:iRS ~ inqpuiinmm<t iii; IiiailmdIlIiIllll <GIE ~

- - JJBEr lIlfSUill iiIlJIi!I;brrm1l iimliJIme

Ii] KaaDli:$ b '11fJJI17I m=.ll3D..91bilfiDm bdli:UIBliiIlii:d

~_m5IJii11JiDBb"''''''''''~ 0; ~~lllJf~~_fiIlrIIlI~SIkli

3

UC!

co

co

fO-.InromBllllilJ" "<llIIIJ<~lIIJlilllrlllflli$ ..iiJf ~iimmaIBl:iIW3IIIIlf

~iiIl1lJSG'!..<\II'..uJIkDltllDJl'lJ«ll

I!fBJHRO) ..1IIIlUlIlfurllBl;JPIIIIIl.'9"$ iilliII< IlJ5 iit IIIIIIIlI aIIiw!lie••iiII fiimmriiliJlllll'llliDg:. ~_ «lamIIiI!:1IIR!$1l.1IR!li lfur<ll!lIllIiiIo

llIi1llIIIIIOiiami~1IUll~~....,FIIR!»

~~.

W"JiII> ill< <lIiDiiBIIliml dIl.lIro\. 1lIrm$lIIIIlj' iimmaIBl: 1IUlI iiIIl!,!llIIllIOlllk ~QjfiimDlatllldl..-oJJl'"'lIlfIl1IDg..ilI! ........lIIJlilllrllfll!S

e-IriI cr lTlI1lllJgG_1Ii.._di:lliiwdIIh:.alI.Jhm<3lIl.1JIWlIiiS;mi.71J'

IIillliJm

o =~=~b~t=r,mlll-Oi ~iil;_iinvuiimJI ...IbJl!g...tfh<>ffiii",aili",o:ft'tfh<>_

~wrilliil;_dlnmiilo~~. lIftfh<>fliiirllllldlnlnallnl

~~~~~=,i;;,:==:effiill DO IlDtlIiil;lDllDlnU..__..JIllol.\<·tIol""""IC 1IIbm;"""'_1lJ>1ilI$

.,jjjh""",_~iil;lilIlillE""_1I1lIIIll1lllJllllllllii

a 1Ilbr_um_amII~_.,jjjh"<dlunm<""1IIti ~_lliIUlIllllIIIllal¥'Dll:!IUlhiinllig!lmriinmnneamll .... _iin tfh<>ualbutfumulf......omtfh<>lInllnJn.,_

.~.

Joimson &: Joimson

linn_lift...... <:I 1Ilbr........"'~

JIlXIlI"'IIl'ffmllRl:$ is; -"'lI'BilllJJ llJ$-tIb!¥."""''''''''1fllliII

o,_nol_tIol~

"""'OIDJ amIltfh<>mI<o:ft'no:dI _ __umlilllllJ$

_>IlDullil_Ihm",.. lIIujiw iiDyumtomJbfbmmnamll Jbfbmmn"$fIiunmiidlo(iIEiDrsltdi: TOlllIg._~

URJ-.lnrollnnlilly Il:l .JWlmlwnulIllllJ.JilIJImImmllR: IflIID lIiIJrtlbmr iimll:ll1lJ>llll'w.IiInBliillm.

{(.Iillllmlmm&:.JilIJImImmAmnmll ~2lDID15l))

[] .JilIJImImm mt.JillJlmlmm CCIIIl~· <tIJlIm:\fIItt ilII!lI'1lIIfin<tlllm$ Un tlbmrJFlllRO)~as;illiil;~lIJIIl!Imlllfli.'$~.

(l)EnmlJ &: YmlJlll&.~)

[] <Cl1lnN<<miiilm 1m> lIIfli.'$ 'Il1lllIiId! 1IldV>.JilIJImImm mt.lillllmlmDl ~

~lIIlIII!lmb;glIn~""ii8mIII_iiqglll»lPIJIDIlIum:~ _m1fiimDJriiJIIJqlilll1lsllilJriiHko....iji"B..lmt~

1Im~((AJlDl"A~2lM)J iI:!.. ~.'-:::;;;'<;,

-Conclusions OJ' 8J'~!RS aa; .. @lillull~!lllmJibDjJ1IIlIiIiimriimD ~ ..iiIllft,alIIletlol,.."",Ili6mr<mllltamlltiimr~

\1Oiifi> J!Il'l'IPlIIliitliilmmiiliJ _lfur....m.m.lbmIih;

cr l!bIliiJg"""'....<ilf'_UiliiII~'iimo3lIm'$<llmiiliimB; aa;1IIK:I¥U11 kalill!:tIol""""""",~lIlfiiJy; ..1IIIilfuIIm ifiinnmiiBI_

Cl 8J'~JIIfII$,.iII<~~..uJI!IIe

.~~-;:;-':.j1

Conclusions o CClIlII<ftIiiDm 1IiimJIm <lii.!\AP 11m IIRS 'I1riiII naiiRl: 1IA1IldlBenll iimmls. I!J) <Cl1lnN<ftIiiDm 1m> RS Jiilmm m CliAAlI" 'I1riiII iinpJIdlllllllll1"

iioAJalItiiB~. 1Ik~DH; ""iiII\YlIIIWaiIIml OJ l!IIlIJ<o<(fITlllI;.iio*iIlmw/llllll*iIImndfiilI;lIIIII\I'~1k

plMIi:mfl;.

• 4

_lllhlDmwm (<2DO~I.AIIl!JI''''!BlmI!gwundilll:.Jll1l'l!It'lDlbJl. kdlmrllllrlluD",m_(annRi.HidiJ'lO.lJJl1'3l.~,~~ ..n.m/.7lull(rjliHuu.Il/'(ftnlU).l _mhllmnvm(<2DOR\.Illb_:«}l.Jbg=~ ..IJl1I5<rom~~2110ll

Al:aa.#",11tl1nqr•. _lllhlDmwm.(<2DOR\._,,__..IJl1I5I11bm. J(",,,""II"~

Aluu'Wrtllllla'}L .

JWtIbm"lIIiIIlmm\lll_tan08t~$j,«:~tfur~. /Ei;;.mllmistr.

_<k 'Ir"""",. (CllIO"'IIIJiJb>Ib....""'" ([immmntlli.21I(IR\. ~lbflm.(aoORt~ ~1lFiDmm:iidIAOOm:mn1~: 1mu:nthm"<UwnxIb_ (Gnwdlu,"

Btlft'UTlLW~.

lb_8t.JbBmlmn.(<2DO.'!)l_1IkIJUlIl

s;:,llU'n::=~mjA~~s.v~!i.v~~ilI' hup.::. ~'.ll..\1.:-_0JRi.!l~jp~b.:.~y'~jn~'s!': 211l1l\li~? JlL"(D_)J!+~..!l~.llllll

1Il1llriil;(<2DlI"'I'IJl1I5I11omnriiJs;31~"lbtlmmtIonalllFiimwiiJll~_. Im.tmm:[WbIrifJ;Il.lL.Ir..~'~

!IluImlmJUl:. (cmma:)I_!EllmllJiirllnfulllliail IrOl. 1IIIiIttmJ<:. PlogmHt !IluImlmJUl: ((2llij~I.«mrunil~ 2111f:llfl['

_<li:GmdIlk«(IDlJIli)Ill!onualJlIi<IInnIl U(aB;;5l!lr :llfI[~~I/i),5l!lr_:mliiJm ..~I[~·~",,1lIlS

_iinJrOlEi!!!nIrOlDJllllli.... _omlIen U5'•. 2OOJ71__.

5IElr,.(CllINIIll~~f£mreguihlfum<J1rl/DlItia:~ :mmm....,""""_~dlr..-fum<J1r.._llJ)inllmm:n,.jjfudlr _~SllmdJudIl;I["_lIiJlJlIJilRfum...Ilut>oUII\200a:

--3iJn¥;. ~1Ii)IIIIImM""Jl.IDDlll!onuall1luDmn<_ SolDf'. «(2IIlIlIi))ll!onuaII~ 1Ill1F5l!lr \U$lGi!'I...4\II'.((lIllI1Ii)IfiinnmiaiI~_itlI4l!!.I'I=IUlIliDg:ffur

CliOOUI>oilIlamlllbl!BJyjJlllo_ \U$~(I2IJtla)}IIiimmriaiI~_#;jJ571JraiirlMmllmt'lralln<

Allllmulltfug;

5

ll~il. 'd'~'"',, d'.' :'" ii;:: i\.i~' ,,'1. "I"["Jl',, ",~I"!"'if':'I:U 1~""\,,,~:!:1 J:! ~., fi ~':~~~'!::~,~ ,~iil Ii Iii ; ;~ I, )!;I 11t: I~~1~I!J th., .,IIL:; l~} Y:J. ;r~ ~ . 'ol~t¥l I~;;I" '~~-'lt··" .t·! '1"," ~{'~~" ,: or',,- I . ~ ':. :i' I.

~... ''i.:,§' ;""~I. ,;,,' • ~ ' \~~~f; )......j~.~ " .,1 (I" •• ,(:J':t, t ",~ l'" ,.. ('" .~ 'i

<,,~~,~:J::":~ .. ~~~~ ;\1[~1[~1l:llo,},~(; II,'I~:/

._ ... j ."!:~'l~:'~;/" ~.,~ I.f.. ,.. I.i " }> ..

January, 2009 ----_._-

5'lnne 13. Jos6re is l'r~s~11teb to

as determ::1~::;;review process

Mercedes Jalbert, Ex~or

Paper Titled: The Impact ofGlobal Accounting Standards on Foreign arid United States Multinational Corporations

~ --est in i>ession ~

t 'tute tor 1Jjusines5 ani) 1finanu ~.,; ";"tnr"'ht, '3\ns \ .J'i~~j~:::~!'~i; iJ!!I. )'\."" ":''WI'), """'~"'i:;.J :!::'{:~:"(l:]i

~Iobal ~onference on 7iu5tne55 anb ,.:fran

~ l

~"·'T'~-;r=""""""'A~~~'r~~;"j.:r;r;,r;T;"Y;T7r.r,r;r;.r;"'·=$ ;"''A'A'''"''i,¥,;:r;r''~i;1').V';,'":i';r",~;r.:r;r,r.'''·a:::>·;>t''· »7F;r;o''',y;;l-;>'';;I.,.,.=,nrir.~::v:r#-''''-d' ~r'" ''F'J'';>(l'':i!':'i1';(''i-f";'I'i.?"'(j'i ;,' :.1",7 :',''ii;.: ': ,.... '.I. .,:P...A'-~4::~J:r~~~~:&'.J::~.~J:. ..~,,~~JJ.~~....t.';,.,I;t...t.:~J::.'£~i. ~..Jl.:4:'..A:_;!y~J::-(~"'::..K~';,..I::.~'J~J:':''':.'..I:.._t(..J';:.G./::' ..I!!.If~,~O ~.•~ ,.. j".""•., ,.n\•.••.•.•", '" r".,1' .• , , , ,

~~~i!'J!.:i!i!7!Z~~ZZ.i!'i!.T..if~I!#'iTi!ZZZ2'.Z~i!i!:iIJT.il:i!]lJ..rir.i':;;J.~~!';:;~'~~,r;;, ~;:!",~:;:, ·.:i'·~;::;·:;;';;';li;':,;:(;::';·'

•• _ ... • __~ ·~·· __• __ •• ••• _ ••• w. ••• _._~ ';_.__• __• _ ••• _. ~__•••• :-_,_--..--••••••-.- ~ __•••.• _ • '_' •• _ .... _.... __ ••• ~._._._~__ ~ ......._. .,. ._.__• __ • • __ •