Annual Report 1975 - SEC.gov

238

94th Congress, 2d Session f) 5, -...';e CUI'I'.f i~ s .) ;, J.. -";.0'. ,.I .t n '7 ~ ~ n J IJ7 . '. :- ( ;) , . ~~~Sb f\NNUAL ItJiS REPORT 1-f1p;L/ L\'/' \ of the / . fEE for the fiscal ~~~ed ~~June30, 197~ - - - •

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Annual Report 1975 - SEC.gov

94th Congress, 2d Session

f) 5, -...';e CUI'I'.f i ~ s .) ;, J.. -";.0'. ,.I .t n '7 ~ ~ nJ IJ7 . '. :- ( ;) ,

. ~~~Sb f\NNUALItJiS REPORT 1-f1p;L/L\'/' \ of the / .

fEEfor thefiscal

~~~ed~~June30,

197~

- - - •

SECURITIES AND EXCHANGE COMMISSION

Headquarters Office500 North Capitol StreetWashington, D.C. 20549

COMMISSIONERS

RODERICK M HILLS, ChairmanPHILIP A. LOOMIS, JR.JOHN R. EVANSA. A. SOMMER, JRIRVING M. POLLACK

GEORGE A FITZSIMMONS, Secretary

'CommlSSloner Sommer resigned from the Commission, effective April 2, 1976

For sale by the Superintendent of Documents, U S Government Printing OfficeWashington, 0 C 20402-Prlce $2 30 (paper cover)

Stock Number 046-000-00106-1Class Number SE 1 1 975

•

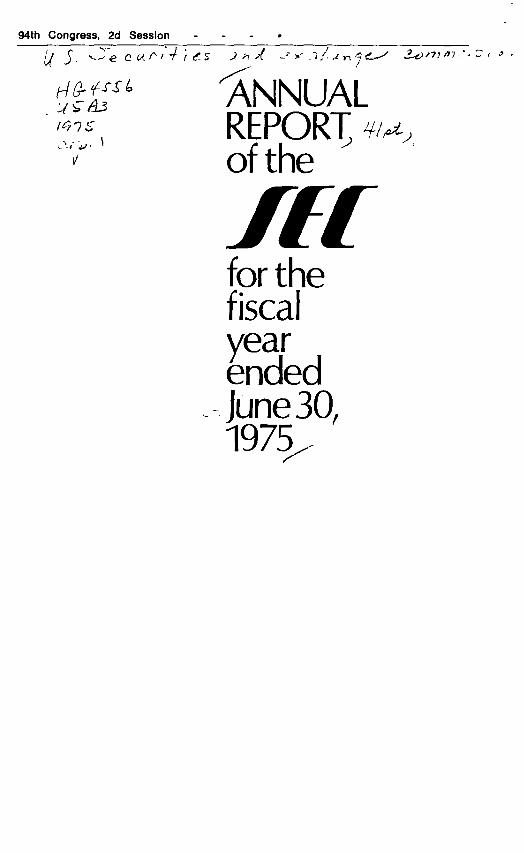

LETTER OF TRANSMITTAL

SECURITIES AND EXCHANGE COMMISSIONWashington, D.C.

Sirs. On behalf of the Securities and Exchange Commission,I have the honor to transmit to you the Forty-First AnnualReport of the Commission covering the fiscal year July 1. 1974to June 30. 1975, In accordance with the provrsrons of Section 23(b)of the Secunties Exchange Act of 1934, as amended,Section 23 of the Public Utility Holding Company Act of 1935;Section 46(a) of the Investment Company Act of 1940; Section 216of the Investment Advisers Act of 1940; Section 3 of the Actof June 29. 1949 amending the Bretton Woods Agreement Act;Section 11(b) of the Inter-Amencan Development Bank Act;and Section 11 (b) of the ASian Development Bank Act

Respectfully,

RODERICK M HILLSChairman

THE PRESIDENT OF THE SENATETHE SPEAKER OF THE HOUSE OF REPRESENTATIVES,

Washington, D.C.

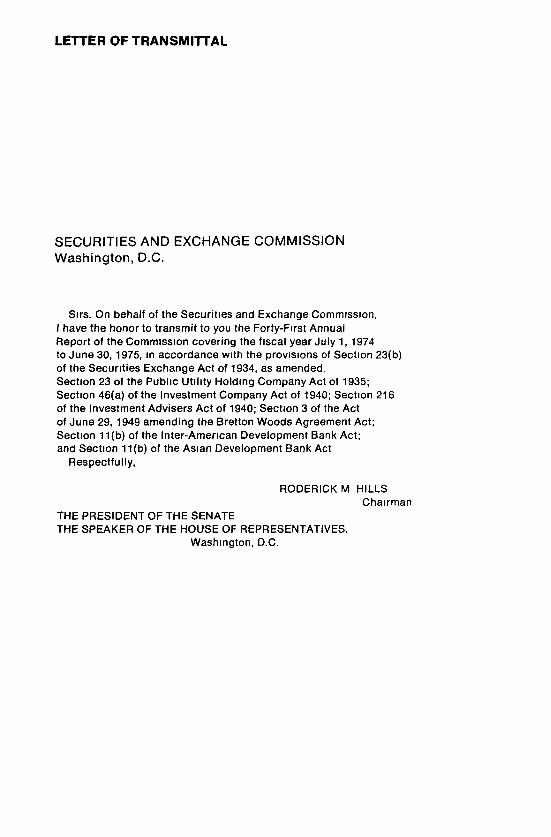

zo(J)(J)

ouUJc..!'Z<:cuxUJ

cz<(J)UJI-0::::JUUJ(J)

IV

~~

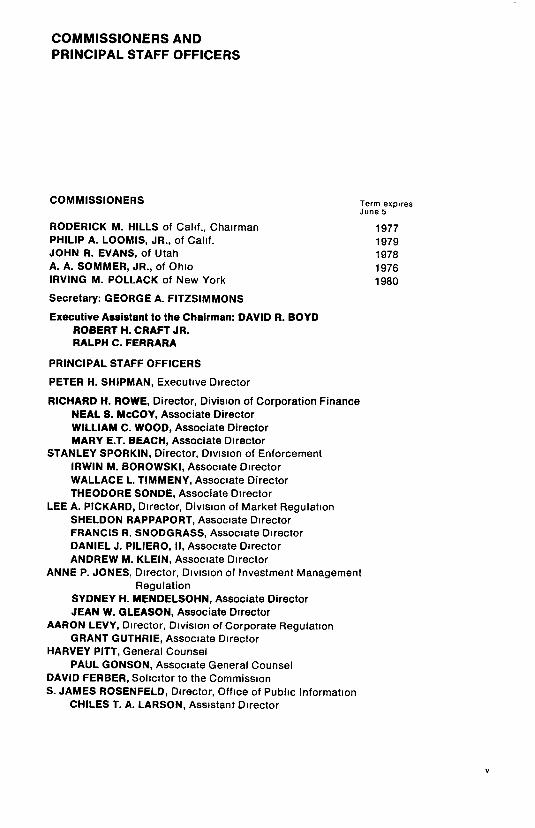

COMMISSIONERS ANDPRINCIPAL STAFF OFFICERS

COMMISSIONERS Term expiresJune 5

RODERICK M. HILLS of cant., ChairmanPHILIP A. LOOMIS, JR., of Calif.JOHN R. EVANS, of UtahA. A. SOMMER, JR., of OhioIRVING M. POLLACK of New York

Secretary: GEORGE A. FITZSIMMONS

Executive Assistant to the Chairman: DAVID R. BOYDROBERT H. CRAFT JR.RALPH C. FERRARA

PRINCIPAL STAFF OFFICERS

PETER H. SHIPMAN, Executive Director

RICHARD H. ROWE, Director, Division of Corporation FinanceNEAL S. McCOY, Associate DirectorWILLIAM C. WOOD, Associate DirectorMARY E.T. BEACH, Associate Director

STANLEY SPORKIN, Director, Drvrsion of EnforcementIRWIN M. BOROWSKI, Associate DirectorWALLACE L. TIMMENY, Associate DirectorTHEODORE SONDE, Associate Director

LEE A. PICKARD, Director, Dlvrsron of Market RegulationSHELDON RAPPAPORT, Associate DirectorFRANCIS R. SNODGRASS, Associate DirectorDANIEL J. PILIERO, II, ASSOCiate DirectorANDREW M. KLEIN, ASSOCiate Director

ANNE P. JONES, Director, DIVISion of Investment ManagementRegulation

SYDNEY H. MENDELSOHN, Associate DirectorJEAN W. GLEASON, Associate Director

AARON LEVY, Director, Division of Corporate RegulationGRANT GUTHRIE, ASSOCiate Director

HARVEY PITT, General CounselPAUL GONSON, ASSOCiate General Counsel

DAVID FERBER, Solicttor to the OommlssronS. JAMES ROSENFELD, Director, Office of Public Information

CHILES T. A. LARSON, ASSistant Director

19771979197819761980

v

JOHN C. BURTON, Chief AccountantA. CLARENCE SAMPSON, Associate Chief Accountant

J. RICHARD ZECHER, Director of Economic and Policy ResearchGENE L. FINN, Chief Economist, Office of Economic Research

BERNARD WEXLER, Director, Office of Opinions and ReviewWILLIAM S. STERN, Associate DirectorHERBERT V. EFRON, Associate Director

WARREN E. BLAIR, Chief Administrative Law JudgeFRANK J. DONATY, ComptrollerRICHARD J. KANYAN, Service OfficerALBERT FONTES, Director, Office of PersonnelJAMES C. FOSTER, Director, Office of Reports and Information

ServicesFRANKLIN E. STULTZ, Associate DIrector

RALPH L. BELL, Director, Office of Data Processing

VI

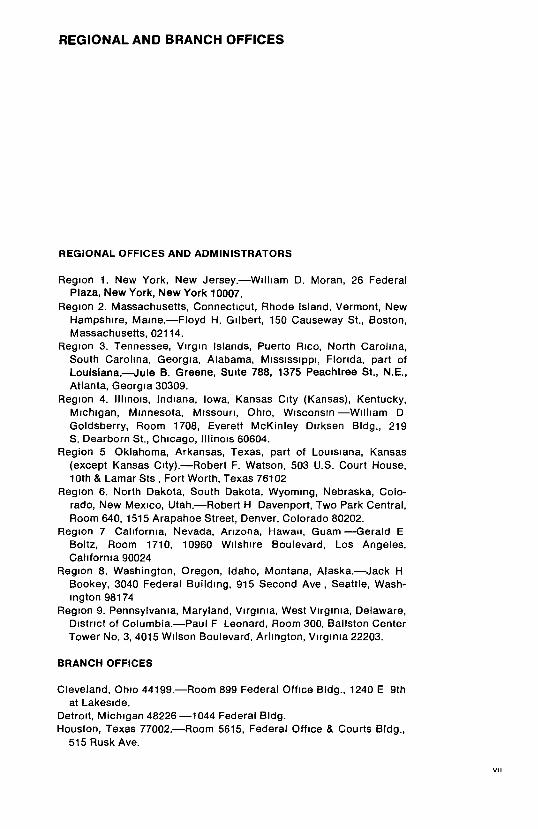

REGIONAL AND BRANCH OFFICES

REGIONAL OFFICES AND ADMINISTRATORS

Region t. New York, New Jersey.-Wlillam D. Moran, 26 FederalPlaza, New York, New York 10007.

Region 2. Massachusetts, Connecticut, Rhode Island, Vermont, NewHampshire, Malne.-Floyd H. Gilbert, 150 Causeway St., Boston,Massachusetts, 02114.

Region 3. Tennessee, Virgin Islands, Puerto RICO, North Carolina,South Carolina, Georgia, Alabama, MISSISSiPPi, Florida, part ofLoulstana-c-Jule B. Greene, SUite 788, 1375 Peachtree St., N.E.,Atlanta, Georgia 30309.

Region 4. lllrnors, Indiana, Iowa, Kansas City (Kansas), Kentucky,Michigan, Minnesota, MISSOUri, Ohro, Wisconsin -William DGoldsberry, Room 1708, Everett McKinley Dirksen Bldg., 219S. Dearborn St., Chicago, lllinors 60604.

Region 5 Oklahoma, Arkansas, Texas, part of LOUISiana, Kansas(except Kansas Clty).-Robert F. Watson, 503 U.S. Court House,10th & Lamar Sts, Fort Worth, Texas 76102

Region 6. North Dakota, South Dakota, Wyoming, Nebraska, Colo-rado, New MeXICO, Utah.-Robert H Davenport, Two Park Central,Room 640, 1515 Arapahoe Street, Denver, Colorado 80202.

Region 7 California, Nevada, Arizona, Hawau, Guam -Gerald EBoltz, Room 1710, 10960 Wilshire Boulevard, Los Angeles,California 90024

RegIOn 8. Washington, Oregon, Idaho, Montana, Ataska-s-Jack HBookey, 3040 Federal Building, 915 Second Ave, Seattle, Wash-rnqton 98174

Region 9. Pennsylvania, Maryland, Virginia, West Virginia, Delaware,District of Columbia.-Paul F Leonard, Room 300, Ballston CenterTower No.3, 4015 Wilson Boulevard, Arlington, Virginia 22203.

BRANCH OFFICES

Cleveland, Ohio 44199.-Room 899 Federal Office Bldg., 1240 E 9that Lakeside.

Detroit, Michigan 48226 -1044 Federal Bldg.Houston, Texas 77002.-Room 5615, Federal Office & Courts Bldg.,

515 Rusk Ave.

VII

Miami, Florida 33131.-SUIte 701 DuPont Plaza Center, 300 BiscayneBoulevard Way.

Philadelphia, Pennsylvania 19106.-Federal Bldg., Room 2204.600 Arch St.

St. LOUIS,MIssouri 63101 -Room 1452, 210 North Twelfth St.Salt Lake City, Utah 84111.-Room 6004, Federal Reserve Bank

Bldg .• 120 South State St.San Francisco, California 94102.--450 Golden Gate Ave., Box 36042

VIII

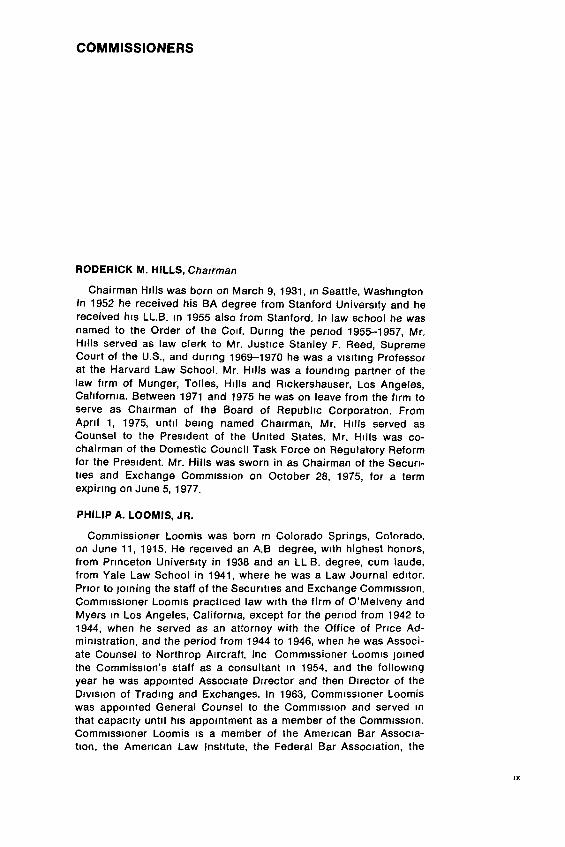

COMMISSIONERS

RODERICK M. HILLS, Chairman

Chairman Hills was born on March 9,1931, In Seattle, WashingtonIn 1952 he received his BA degree from Stanford Unlversrty and hereceived hrs LL.B. In 1955 also from Stanford. In law school he wasnamed to the Order of the COif. DUring the period 1955-1957, Mr.Hills served as law clerk to Mr. Justrce Stanley F. Reed, SupremeCourt of the U.S.• and during 1969-1970 he was a vtsrtmq Professorat the Harvard Law School. Mr. Hills was a foundrng partner of thelaw firm of Munger, Tolles, Hills and Hrckershauser, Los Angeles,California. Between 1971 and 1975 he was on leave from the firm toserve as Chairman of the Board of RepubliC Corporation. FromApril 1, 1975, until berng named Chairman, Mr. Hills served asCounsel to the Presrdent of the United States. Mr. Hills was co-chairman of the Domestic Council Task Force on Regulatory Reformfor the President. Mr. Hills was sworn in as Chairman of the Securi-ties and Exchange Commission on October 28, 1975, for a termexpiring on June 5, 1977.

PHILIP A. LOOMIS, JR.

Commissioner Loomis was born rn Colorado Springs, Colorado,on June 11, 1915. He received an A.B degree, With highest honors,from Princeton Unlversity in 1938 and an LL B. degree, cum laude,from Yale Law School in 1941, where he was a Law Journal editor.Prior to Joming the staff of the Securities and Exchange Oornrrussron,Commissioner Loornrs practiced law With the firm of O'Melveny andMyers rn Los Angeles, California, except for the period from 1942 to1944, when he served as an attorney with the Office of Price Ad-ministration, and the period from 1944 to 1946, when he was Associ-ate Counsel to Northrop Aircraft, Inc Commissioner Loornrs jomedthe Oomrnisaron's staff as a consultant rn 1954, and the totlowmqyear he was appointed ASSOCiate Director and then Director of theDIVISion of Tradmg and Exchanges. In 1963, Commissioner Loomiswas appointed General Counsel to the Commission and served In

that capacity until hrs apporntment as a member of the Commission.Commissioner Loomis IS a member of the American Bar ASSOCia-tion, the American Law Institute, the Federal Bar Association, the

rx

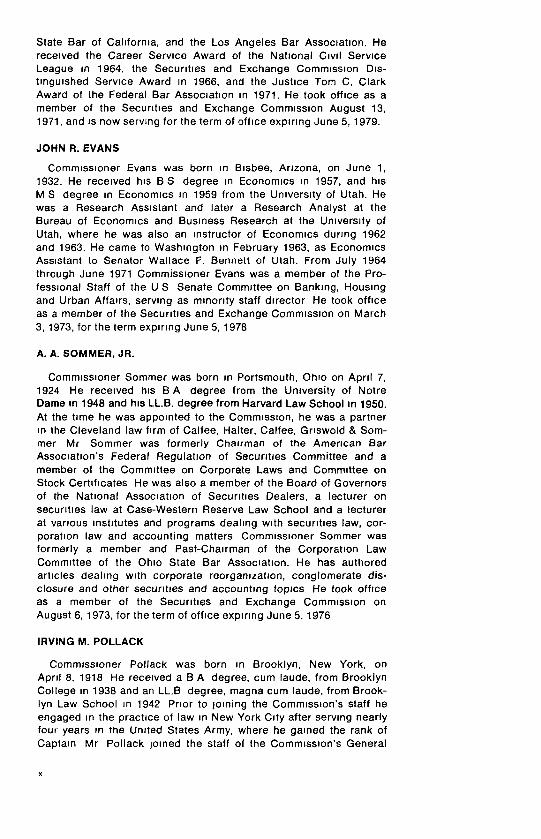

State Bar of California, and the Los Angeles Bar Assocratron. Hereceived the Career Service Award of the National CIvil ServiceLeague In 1964, the Securities and Exchange Commission DIs-tmqurshed Service Award In 1966, and the Justice Tom C. ClarkAward of the Federal Bar Association In 1971. He took office as amember of the Securities and Exchange Commission August 13,1971, and IS now serving for the term of office expiring June 5, 1979.

JOHN R. EVANS

Cornrrusarorrer Evans was born In Bisbee, Arizona, on June 1,1932. He received his B S degree In Economics In 1957, and hisM S degree In Economics In 1959 from the University of Utah. Hewas a Research Assistant and later a Research Analyst at theBureau of Economics and Business Research at the University ofUtah, where he was also an Instructor of Economics durinq 1962and 1963. He came to Washington In February 1963, as EconomicsASSistant to Senator Wallace F. Bennett of Utah. From july 1964through June 1971 Commissroner Evans was a member of the Pro-tessronal Staff of the U S Senate Committee on Banking, HOUSingand Urban Affairs, serving as minority staff director He took officeas a member of the Securities and Exchange Commission on March3, 1973, for the term expiring June 5, 1978

A. A. SOMMER, JR.

Commissioner Sommer was born In Portsmouth, Ohro on April 7,1924 He received hrs B A degree from the University of NotreDame In 1948 and hiS LL.B. degree from Harvard Law School In 1950.At the time he was appointed to the Commission, he was a partnerIn the Cleveland law firm of Calfee, Halter, Calfee, Griswold & Som-mer Mr Sommer was formerly Chairman of the American BarASSOCiation's Federal RegulatIOn of Securities Committee and amember of the Committee on Corporate Laws and Committee onStock Certrtrcates He was also a member of the Board of Governorsof the National ASSOCiatIOn of Securities Dealers, a lecturer onsecunties law at Case-Western Reserve Law School and a lecturerat various institutes and programs dealing With securities law, cor-poratron law and accounting matters Oornmrssroner Sommer wasformerly a member and Past-Chairman of the Corporation LawCommittee of the Ohio State Bar ASSOCiatIOn. He has authoredarticles dealing With corporate reorganization, conglomerate dis-closure and other secunnes and accounting tOPiCS He took officeas a member of the Securities and Exchange Comrnrssron onAugust 6, 1973, for the term of office expiring June 5, 1976

IRVING M. POLLACK

Cornrrusstoner Pollack was born In Brooklyn, New York, onApril 8, 1918 He received a B A degree, cum laude, from BrooklynCollege In 1938 and an LL.B degree, magna cum laude, from Brook-lyn Law School In 1942 Prior to JOining the Cornrmssron's staff heengaged In the practice of law In New York City after serving nearlyfour years In the United States Army, where he gained the rank ofCaptain Mr Pollack JOined the staff of the Cornmrssron's General

Counsel In October 1946 He was promoted from time to trrne toprogressively more responsible positions In that office and In 1956became an Assistant General Counsel. A career employee, Mr.Pollack became DIrector of the Drvrsron of Enforcement In August1972 when the SEC's drvisrons were reorganized. He had beenDirector of the Divrston of Trading and Markets since August 1965,and previously served as Associate DIrector since October 1961In 1967 Mr. Pollack was awarded the SEC Distinguished ServIceAward for Outstanding Career Service, and in 1968 he was a co-recrprent of the Rockefeller PublIC Service Award In the field of law,legislation and regulation Mr. Pollack took the oath of office onFebruary 13, 1974 as a member of the Securities and ExchangeCommission, and is now serving for the term exprrrnq June 5, 1980

XI

TABLE OF CONTENTS

Organizational chart.Commission and principal staff officersRegional and branch officesBiographies of Comrnissroners

Part 1

IMPORTANT DEVELOPMENTSMarket regulation

The Securities Acts Amendments of 1975The national market system.. ..RegulatIOn of clearing aqencres and transfer

agents ... . . .Munclpal secuntres ,Cornmlssron ratesBrokers and dealers ..Accounts and records

Commission rates ....Development of the national market system ...Consolidated tape .. ..Composite quotation systemShort sale regulationOption market regulation ..Uniform net capital rule.Development of uniform broker-dealer reporting

system .. .Key Regulatory reportProposed Rule 17a-18 ....Proposed Rule 17a-19 ..Formation of the report coordinating groupFinancial and operational reports.Assessment forms and proceduresRegistration formsTrading forms

Broker-dealer model compliance gUideDisclosure related matters .

Beneficial ownership and tender offers.Annual reports to security holders.

IV

VVII

IX

3333

4566778

1113141517

17171718181818191919191920

XIII

IMPORTANT DEVELOPMENTS-ContinuedProjectionsThe Rule 140 series

Rule 144Rule 145Rule 146Rule 147

Adoption of Rule 240Disclosure of 011 and gas reserves

Coordination with the Federal Power Com-rnrssion on filings which Include naturalgas esn mates

Gold purchasing and investingPOSSible disclosure of environmental and other

SOCially Significant mattersInvestment Companies

Mutual Fund distnbuuonImproved communication with InvestorsPrice competition at the underwriter levelPrice competition at the retail level

Variable life InsuranceStatus of broker-dealers as Investment advrsersInstitutional DisclosureSale of Investment adviser

Significant Cases Involving Secunties Acts.Silver and gold Investments ..Cornmisston litigation.

Part 2

2122222222232324

2424

25262626272728282929293435

THE DISCLOSURE SYSTEM 45Public offering the 1933 Securities Act 45

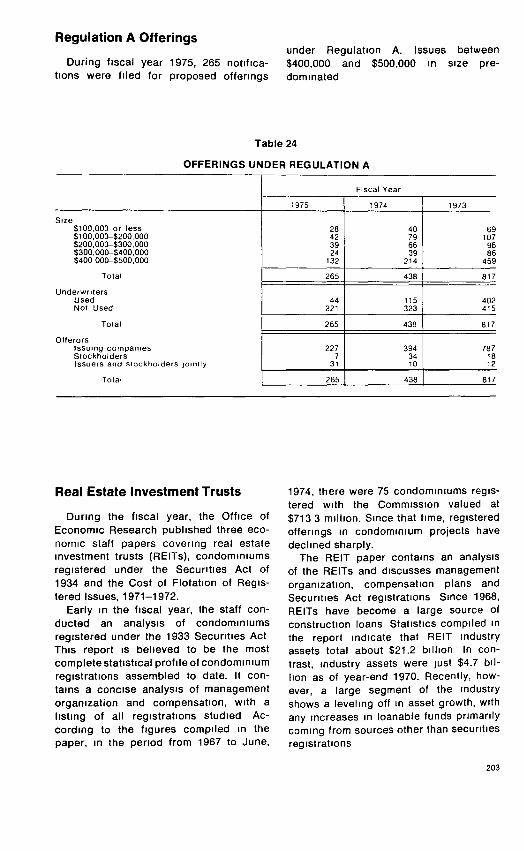

Information provided 45ReVieWing process 46Time for reqrstratron 46Financral analysis and examination 46Office of oil and gas 47Tax shelters 47DIVidend reinvestment plans 47

Small Issue exemption 47RegulatIOn A 48Regulation B 48Regulation E 49Regulation F 49

Continuing disclosure' the 1934 Securities ExchangeAct 49

Heqrstration on exchanges 49Over-the-counter reqrstration 49Exemptions 49Penodrc reports 49Proxy soucrtanons 49Takeover bids, large acqursmons 51Insider Reporting . 52

Accounting 52

XIV

THE DISCLOSURE SYSTEM-ContinuedRelations with the accounting professionAccounting and auditing standardsOther developments

Exemptions for mternatronal banksTrust Indenture Act of 1939Freedom of Inforrnatron ActFreedom of lntorrnatron Act Lrtiqatron

Part 3

REGULATION OF SECURITIES MARKETSRegulatIOn of exchanges

ReqrstratronDelrsunqExchange disciplinary action

Exchange rulesExchange mspectrons

New York Stock Exchange specialist inspectionChicago Board Options Exchange inspection.Amencan Stock Exchange Options program in-

specnonPreliminary inspection of contemplated

Philadelphia-Baltimore-Washington Stock Ex-change Option pilot

Supervrsion of the Natronal Assocranon of SecuntresDealers

NASD rulesNASD mspectionsNASD drsctplmary actionsReview of NASD drscrpnnary actionsReview of NASD membership actronNASDAQ Issuer removal

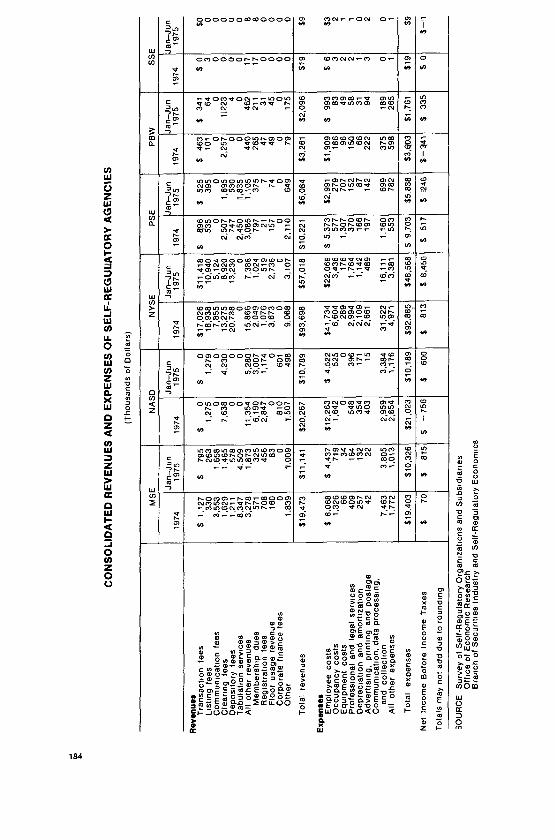

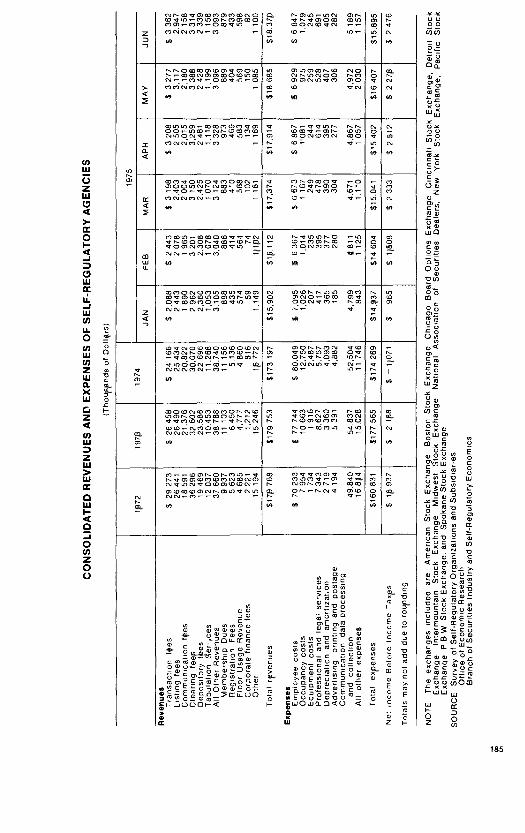

Expenses and operations of self-regulatory orqaruza-nons

Financial results of the NASDNASD budgetFinancial results of New York Stock ExchangeBoston Stock Exchange, Chicago Board Options

Exchange and Midwest Stock ExchangeAmencan Stock Exchange, Detroit Stock Ex-

change, PBW Stock Exchange and SpokaneStock Exchange

Cincinnati Stock Exchange, Intermountain StockExchange and Pacific Stock Exchange

Broker-dealer regulationReqrstrauonRecordkeepinqFinancial responsibilityBroker-dealer exarrunationsEarly warning and surveillanceTraining programRegulatIOn of broker-dealer trading In goldRegulatory burden on the small broker-dealer

53545557595961

656565666666676768

69

69

69707172727374

74757676

77

78

78787879797980828384

xv

REGULATION OF SECURITIES MARKET5-ContinuedClearance and settlement 85Securities Investor Protection Corporation 86

litigation related to SPIC 86Commission rule changes related to SPIC. 86

SECO broker-dealers 86Exemptions 87Other Commission rule changes and developments 88

Mortgage market exemptions 88RegUlatory problems posed by "going private" 88Foreign Access to United States Securities Mar-

kets 89Real estate Investment contract secunties . 89

Confirmation Requirements for penodic transactions 89Short seiling Into secondary offering 89

Part 4

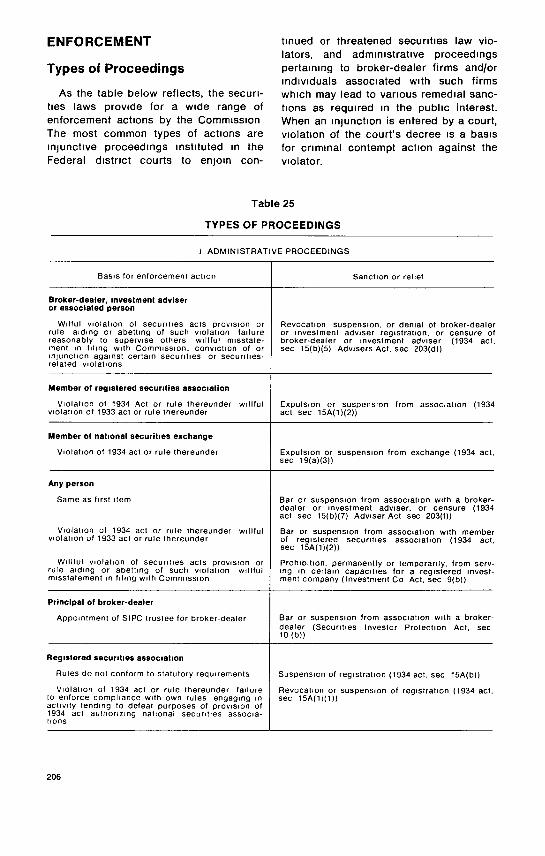

ENFORCEMENT 95Detection 95

Complaints 95Market Surveillance 95

tnvesnqanons 96litigation mvolvmq Commission investigations 96Enforcement Proceedings 97Administrative proceedings 98Applications for relief from drsquauncatrons 101Trading suspensions 101Delinquent reports program 102CIVil proceedings 103Participation as amicus currae 115Criminal proceedings 116

Organized Crime program 119Cooperation With other enforcement agencies. 121

SWISS treaty 122Foreign restricted list 122

Part 5

INVESTMENT COMPANIES AND ADVISERS 127Number of registrants. 127Legislation 128Rules 128

Amendment to Rule 17d--1 128Amendment to Rule 17a-7 129Temporary Rule 6a-2{T) 129Investment company confirmation requirements 130Brochure rule 130Investment adviser record-keeping requirements 130

Regulatory safeguards-the NASD sales load rule 131Applications 131Other developments 133

"Money market" funds 133Sale of partrcipanons In certificates of deposit 133ASSignments of Investment advisory contracts 133

XVI

INVESTMENT COMPANIES AND ADVISERS-ContinuedRegistratIOn of foreign Investment companies 134NASD ann-reciprocal rule 134Two-tier real estate companies 135Variable annuity Illustrations 135Employee Retirement Income Security 136Securities depository system 136

Part 6

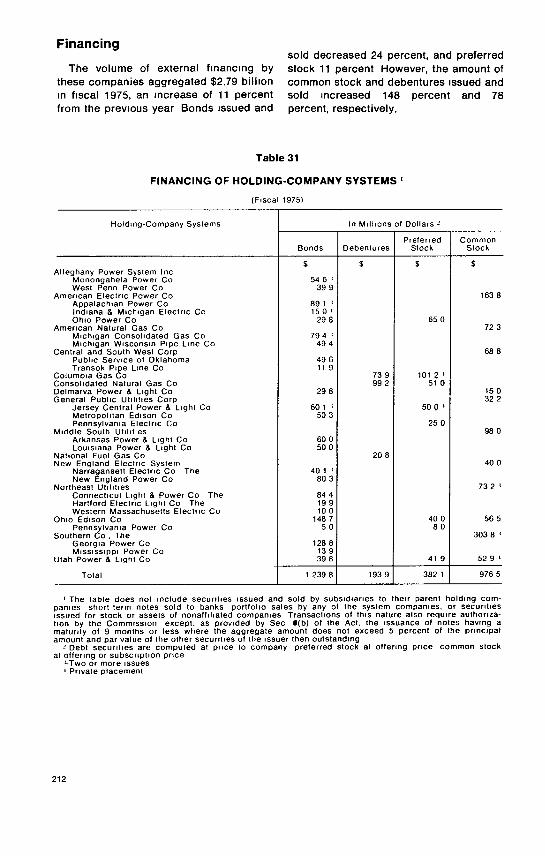

PUBLIC UTILITY HOLDING COMPANIESCornposttronProceedingsFinancing

VolumeFinancing of fuel and gas suppliesCornpetmve bidding

Part?

CORPORATE REORGANIZATIONSChapter X rulesSummary of acnvines ,Administrative mattersTrustee's rnvestrqanons and statementsPlans of reorganizationActivities with regard to allowancesIntervention In Chapter XI

PartS

SEC MANAGEMENT OPERATIONSOrqaruzatronal chargesInformation handlingConsumer servicesAcnvrty under Freedom of Information ActPersonnel management

HecrurtrnentPersonnel management evaluationTraining and development

Office spaceFmarrcral management

Part 9

141141141143143143143

149149150150151153156158

167167167168169169169169170170171

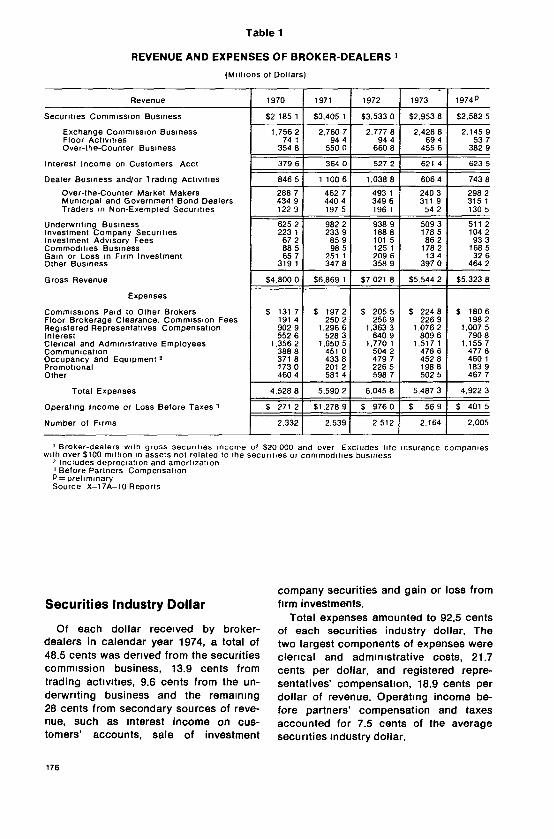

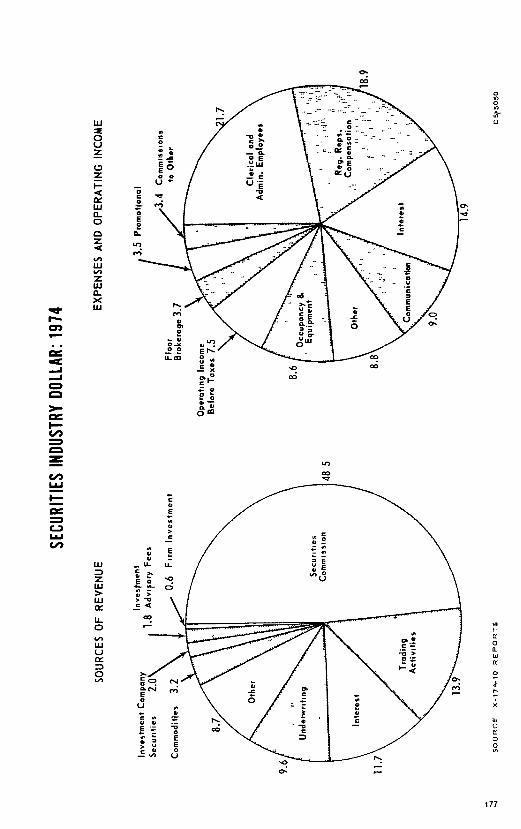

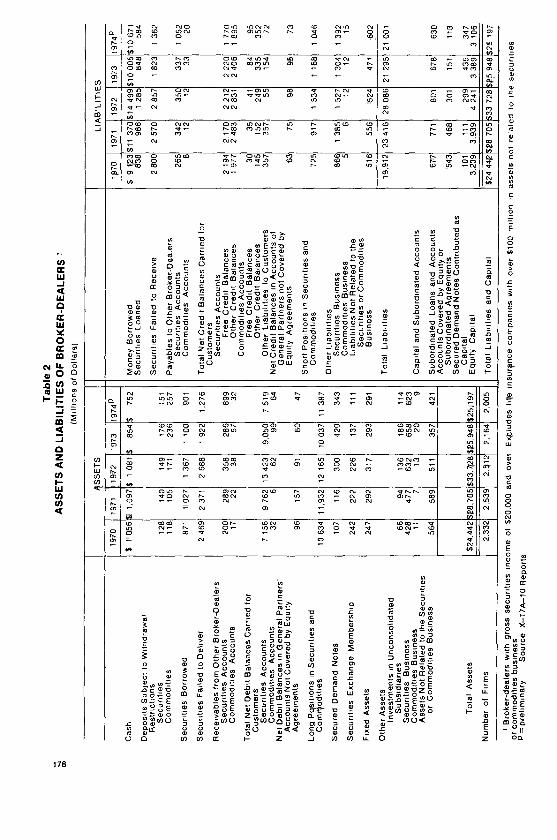

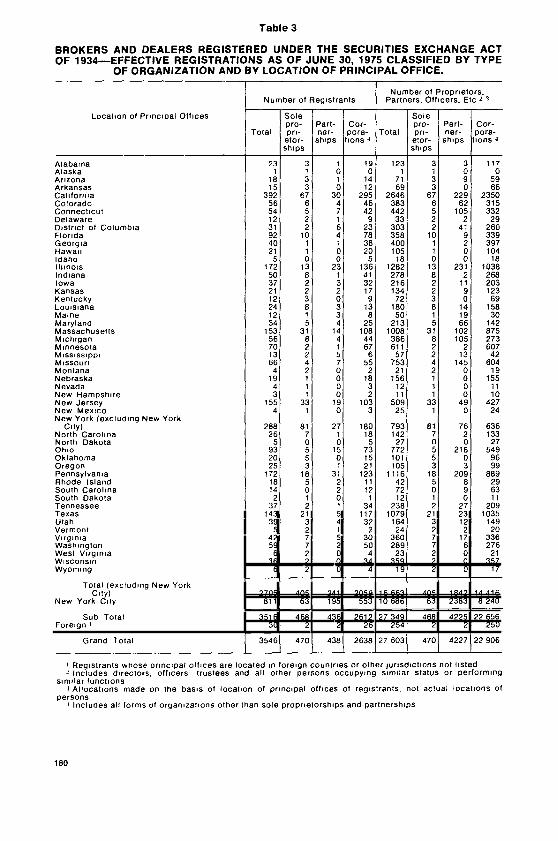

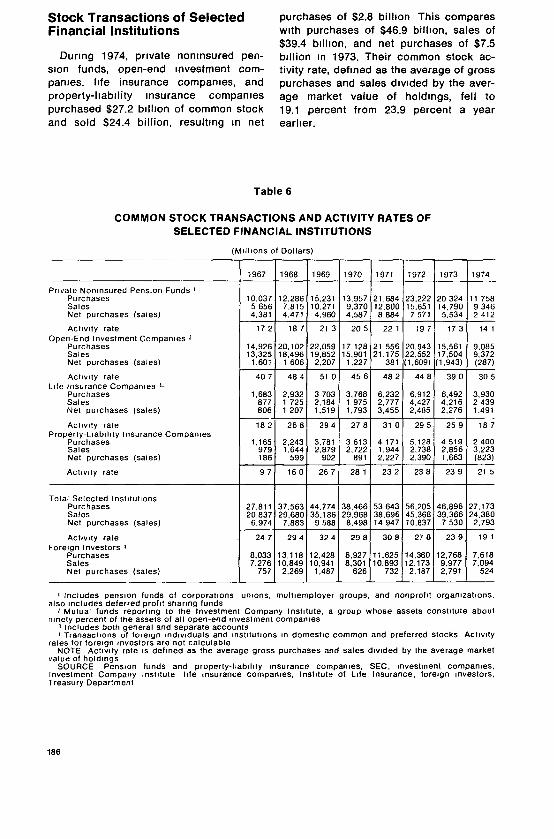

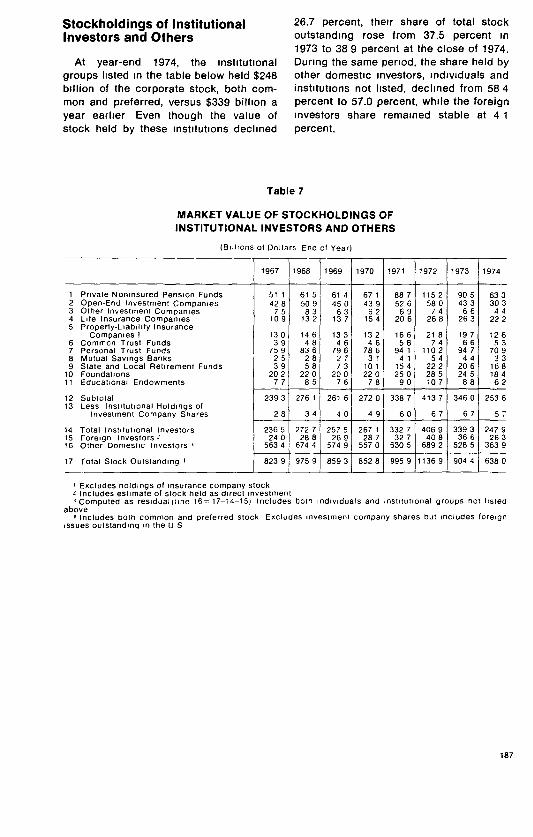

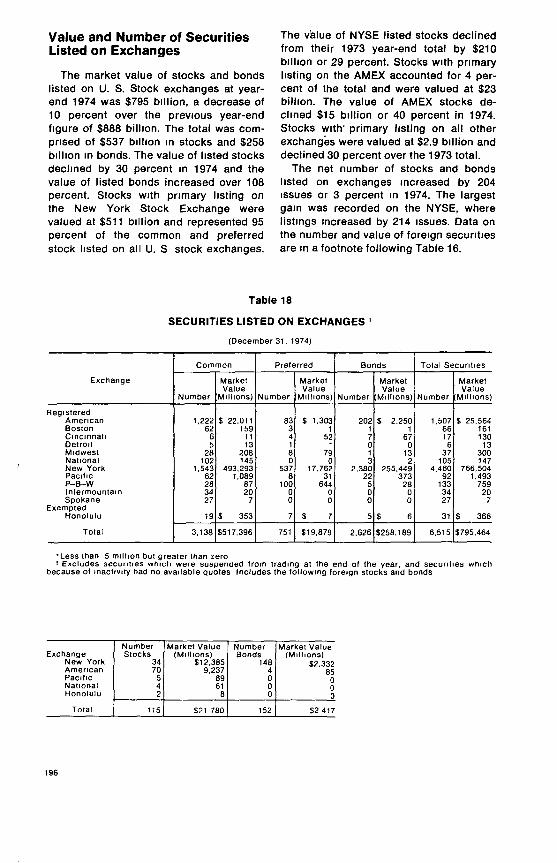

STATISTICS 175The secunnes Industry 175

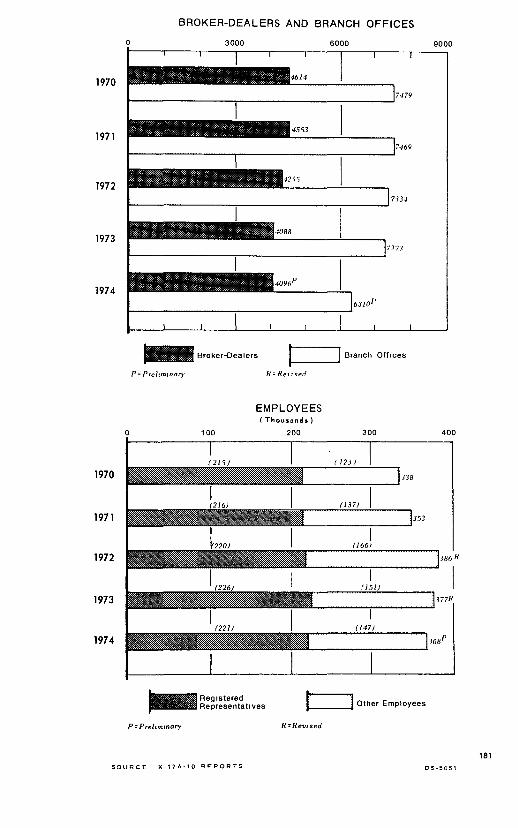

Income and expenses 175Table 1 Broker-dealer Income and expenses 176Securities Industry dollar 176Chart. SecurJ!les Industry dollar 1974 177Assets and habihnes 179Table 2: Assets and nabruties of broker-dealers 178Broker-dealers, branch offices, employees 179Table 3. Location of broker-dealers 180Chart: Broker-dealers and branch offices 181

XVII

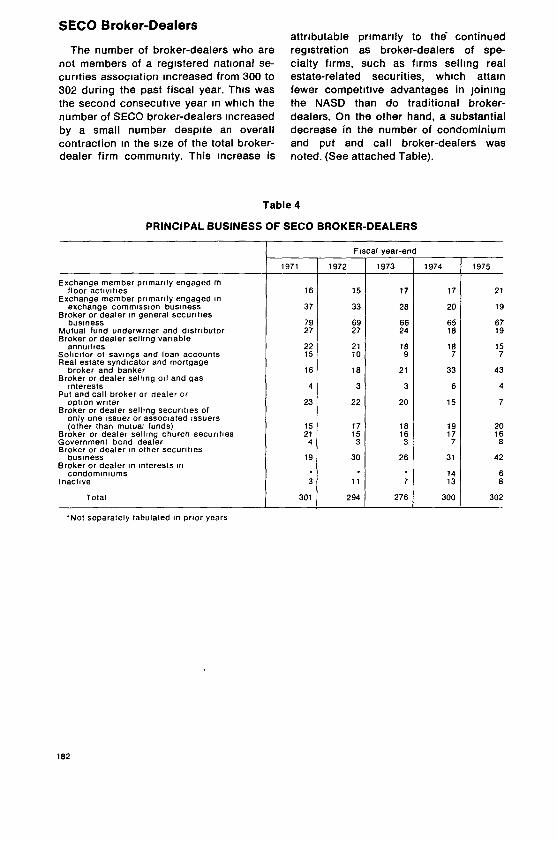

STATISTlCS-ContinuedSECD broker-dealer 182Table 4. Principal business of SECD broker-

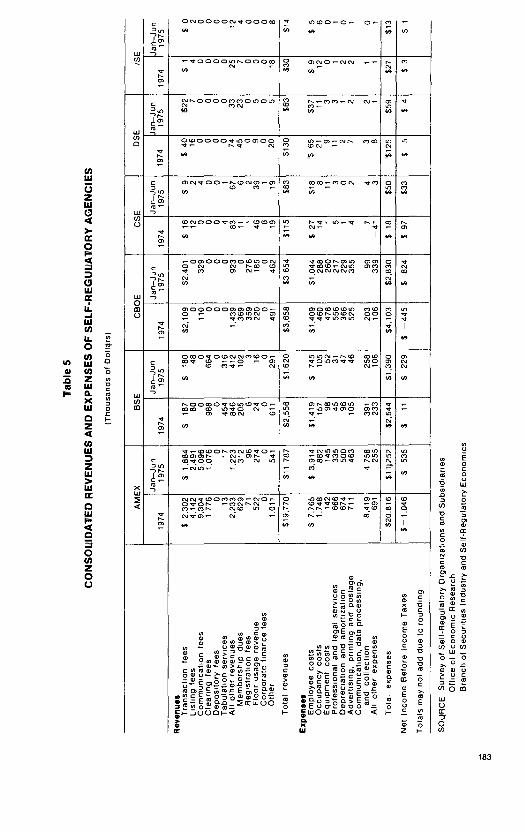

dealers 182Table 5. Consolidated Revenues and expenses of

self regulatory agencies 183Financial institutions.. ... . . . . . . . . 186

Stock transactions.. .. 186Table 6: Common stock transactions and activity

rates of selected financial msutunons: 1967-1974 186

Stockholdrnqs 187Table 7. Market value of stockholdmqs of institu-

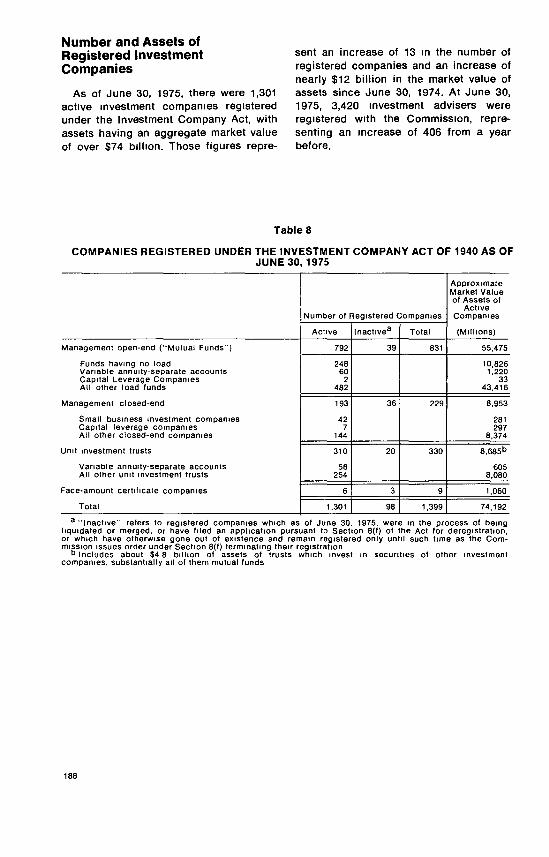

tional Investors and others 1967-1974 187Number and assets of registered Investment com-

panies 188Table 8: Companies registered under the Invest-

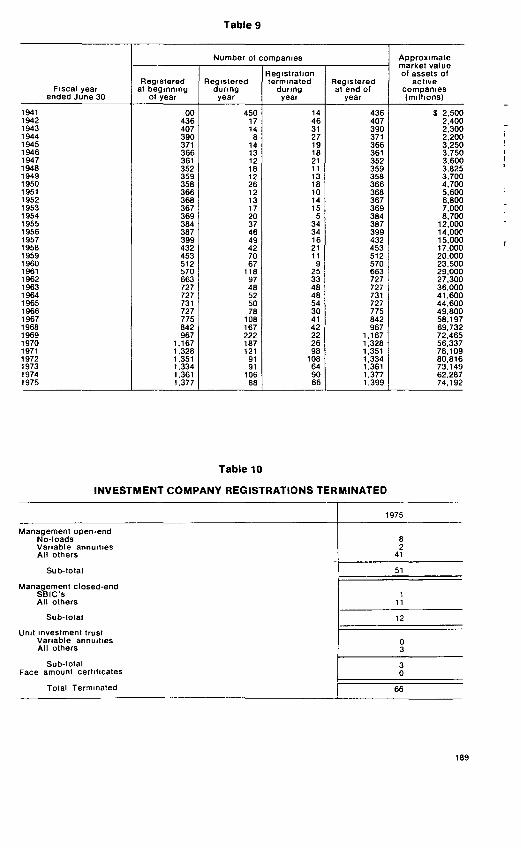

ment Company Act of 1940as of June 30,1975 188Table 9' Number of Investment companies: 1941-

1975 189Table 10: Investment company reqrstratrons ter-

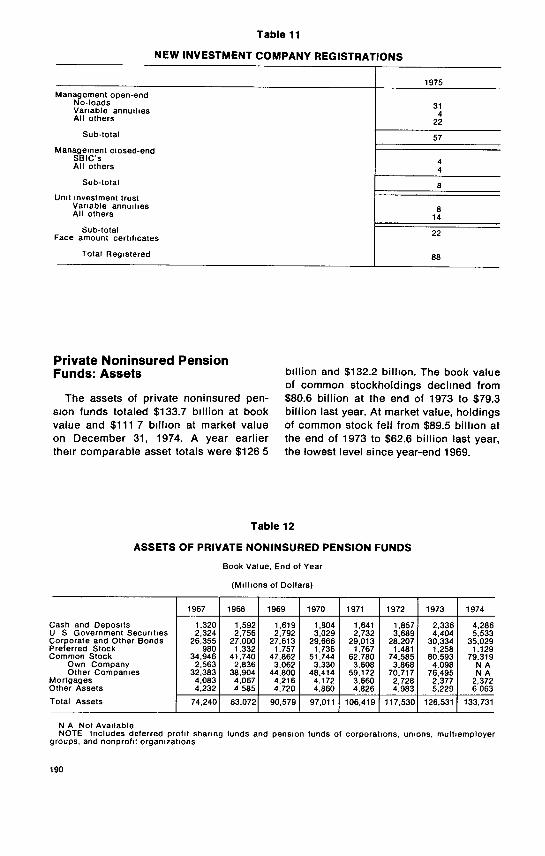

minated 189Table 11. New Investment company registrations 190Private nornsured pension funds: assets 190Table 12 Assets of private norunsured pension

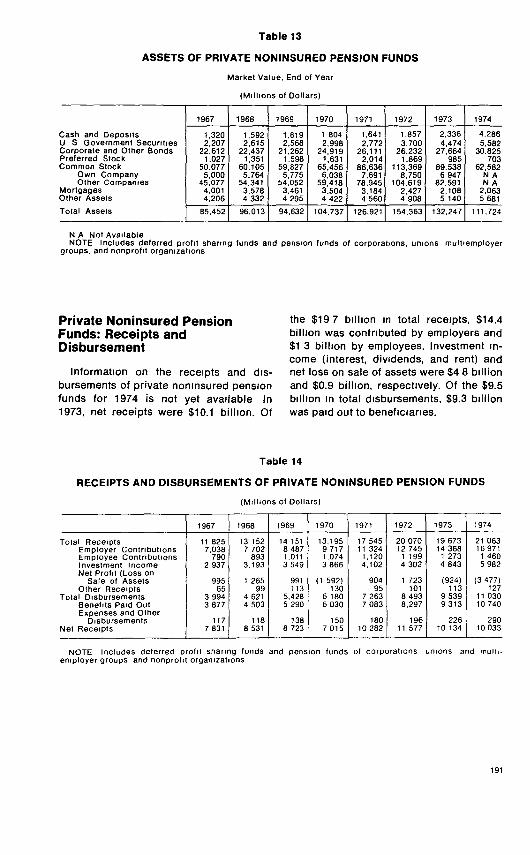

funds book value: 1967-1974 190Table 13. Assets of private noninsured pension

funds. market value: 1967-1974 191Private non Insured pension funds. receipts and

disbursements 191Table 14 Receipts and disbursements of private

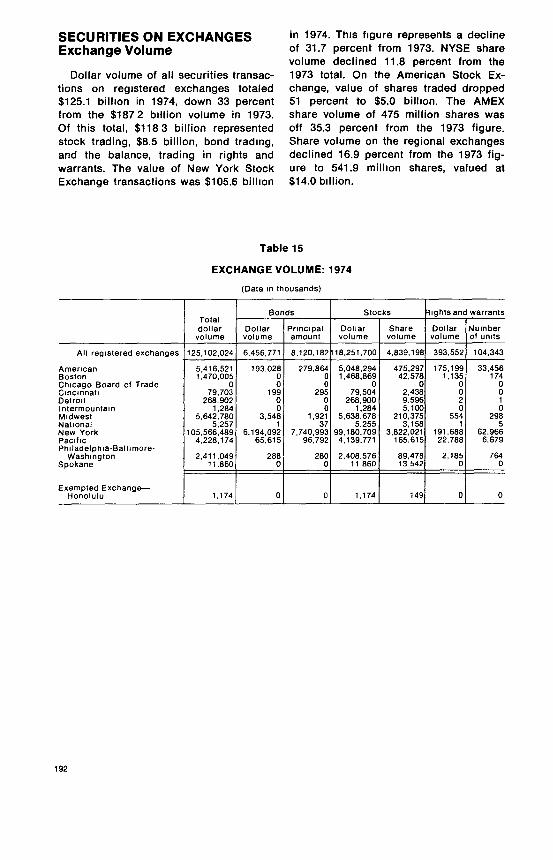

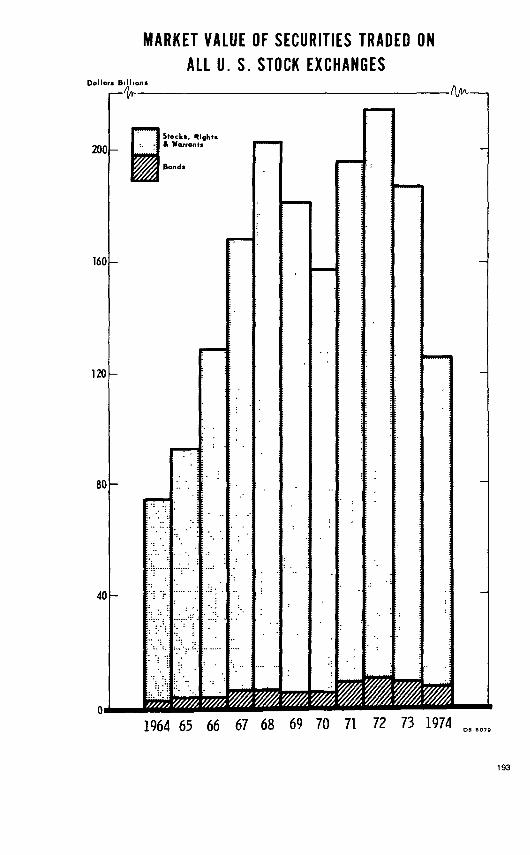

non Insured pension funds: 1967-1974 191Securities on exchanges. 192

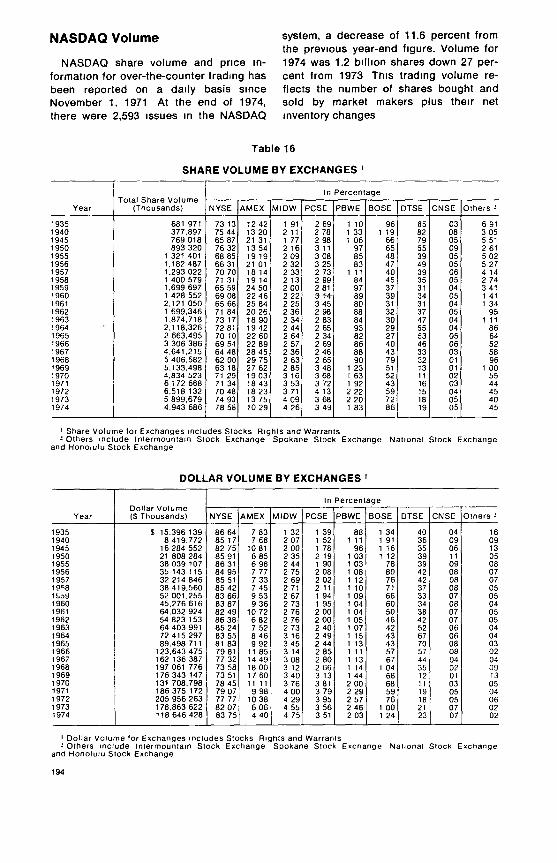

Exchange volume 192Table 15. Exchange volume 1974 192NASDAQ volume 194Table 16 Share volume and dollar volume by ex-

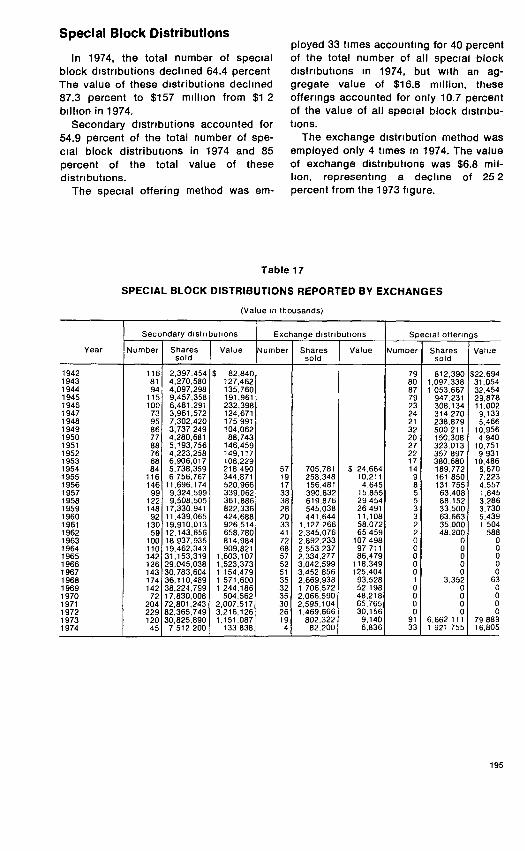

changes 194Special block distribution 195Table 17. Special block distributions reported by

exchanges 195Value and number of securities listed on ex-

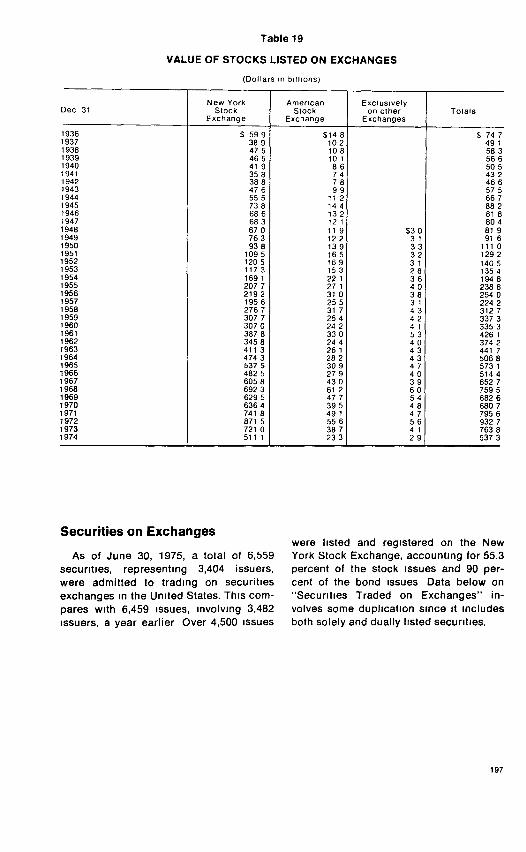

changes 196Table 18 Securities listed on exchanges 196Table 19 Value of stocks listed on exchanges

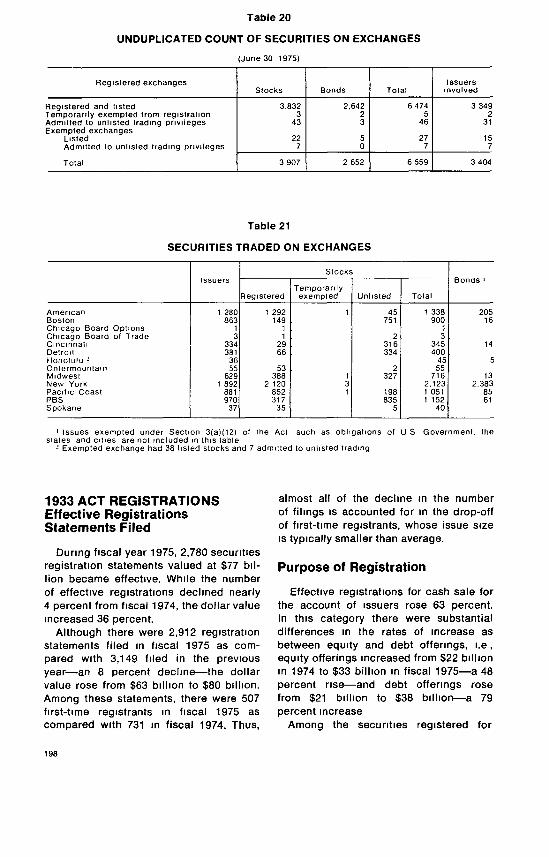

1936-1974 197Securities on exchanges 197Table 20 Unduplicated count of securities on ex-

changes . 198Table 21 Securities traded on exchanges. 198

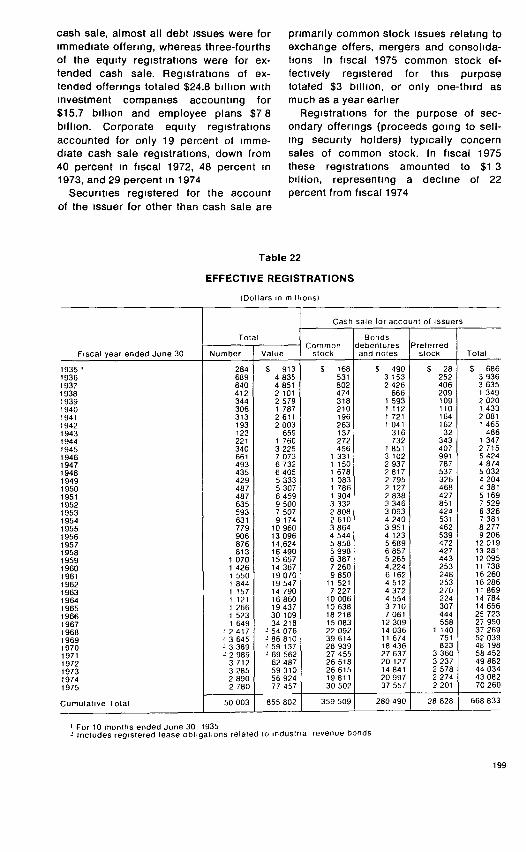

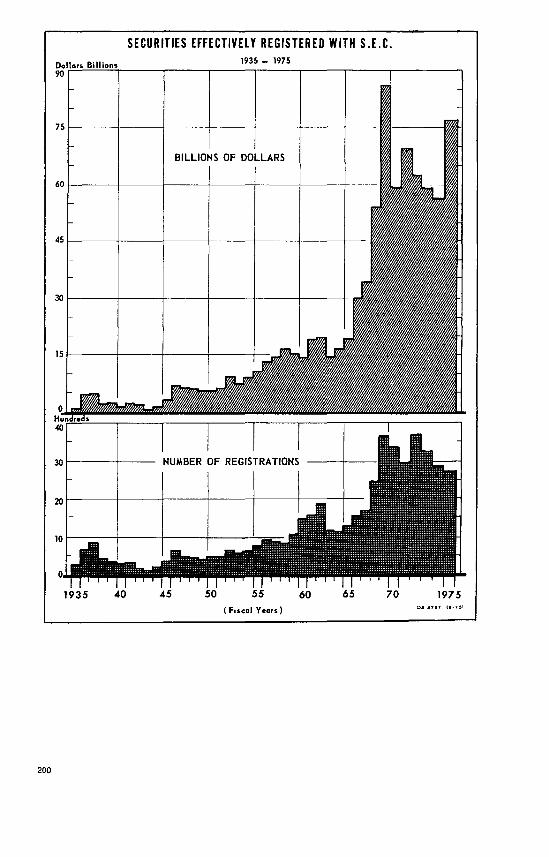

1933 Act reg rstratrons 198Effective registrations statements flied 198Table 22 Effective registrations 199Chart. Securities effectively registered with SEC 200

XVIII

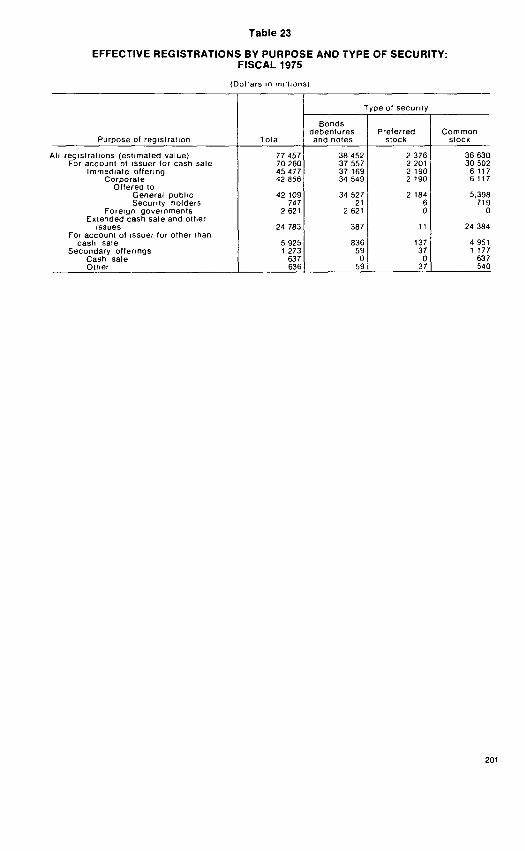

STA T1STICS-ContinuedTable 23. Effective registratIOns by purpose and

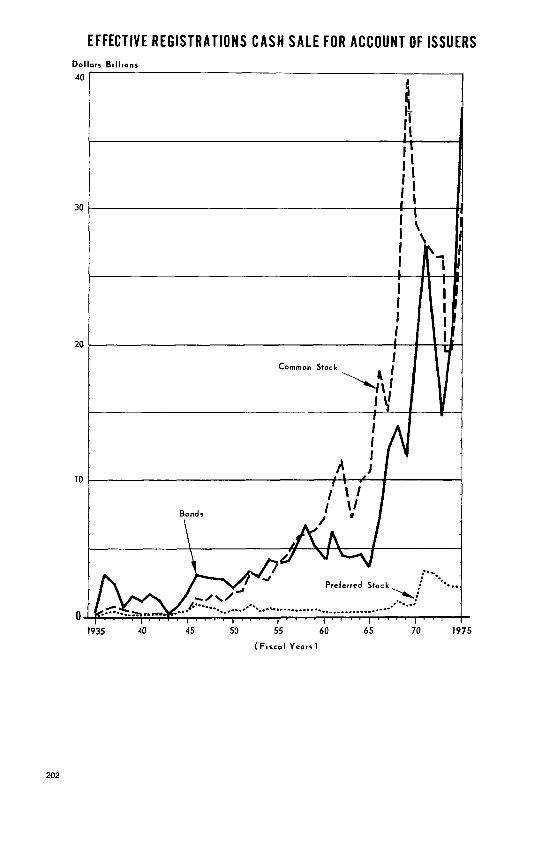

type of security. fiscal 1975 201Chart Effective reqistratrons cash sale for ac-

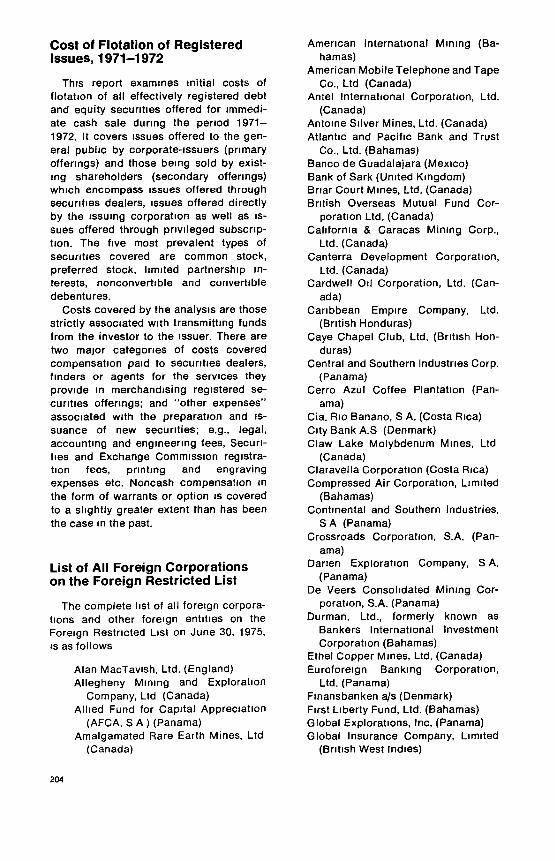

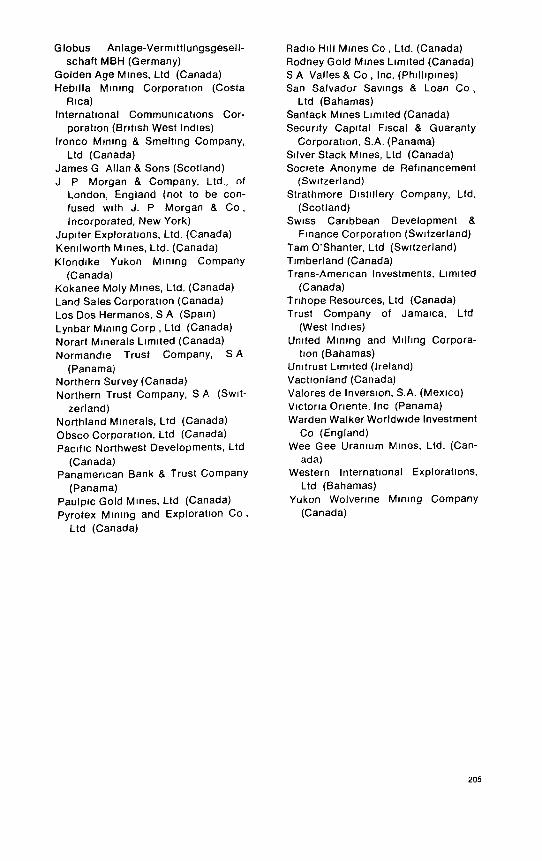

count of Issuers 202Regulation A offerings 203Table 24: Offerings under Regulation A 203Real estate Investment trusts 203Cost of flotation of registered Issuers, 1971-1972 204List of all foreign corporations on foreign re-

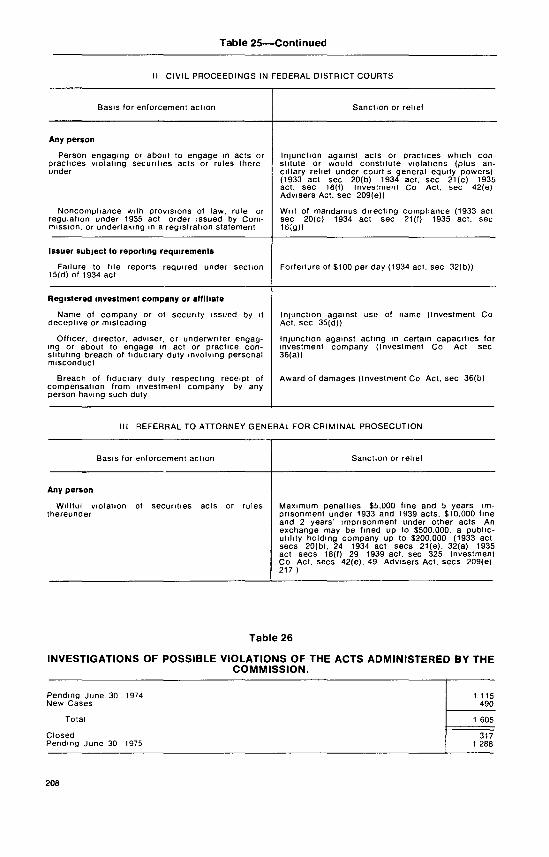

stricted list 204Enforcement 206

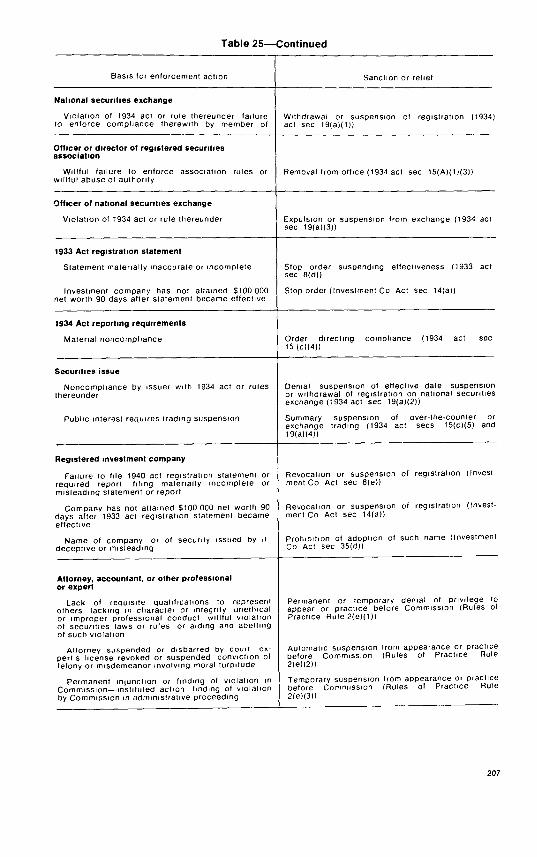

Types of proceedings 206Table 25' Types of proceedings 206Table 26 Investigations of possible violations of

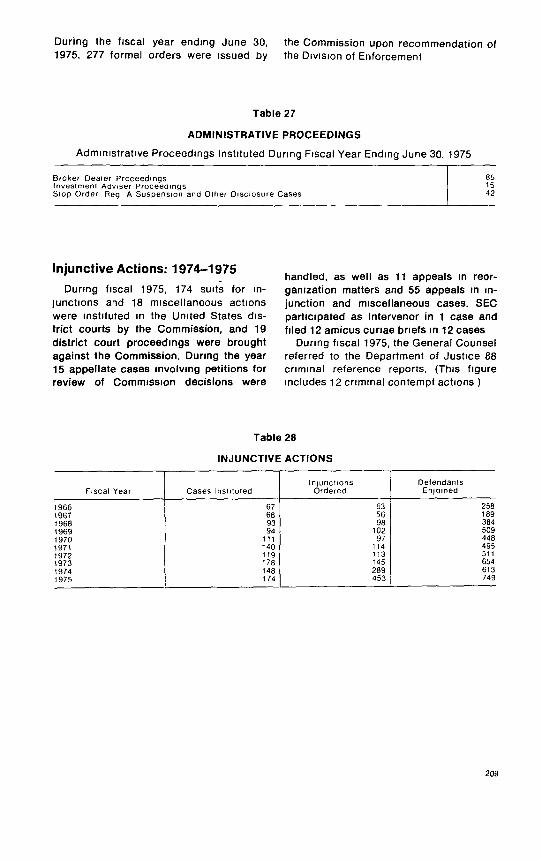

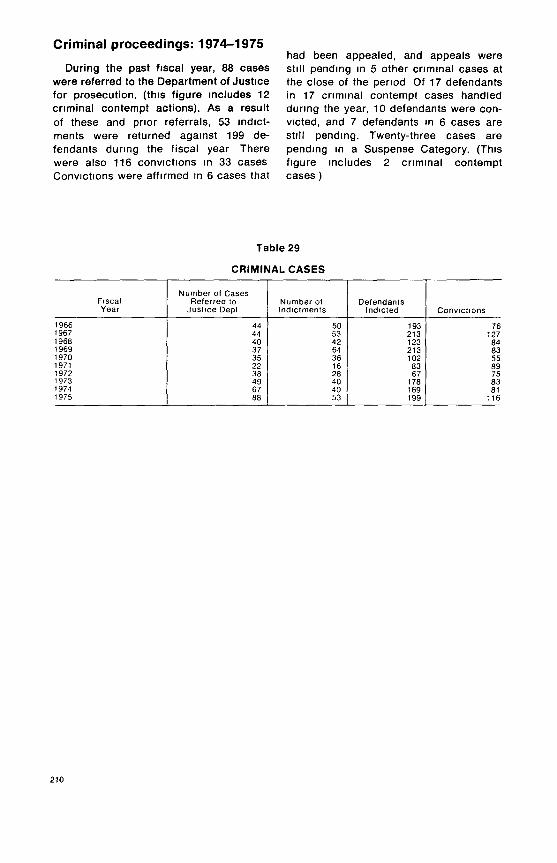

the acts administered by the Cornrnrssron 208Table 27: Administrative proceedings 209Injunctive actions: 1974-1975 209Table 28: Injunctive actions 209Criminal proceedings: 1974-1975 210Table 29: Criminal cases 210

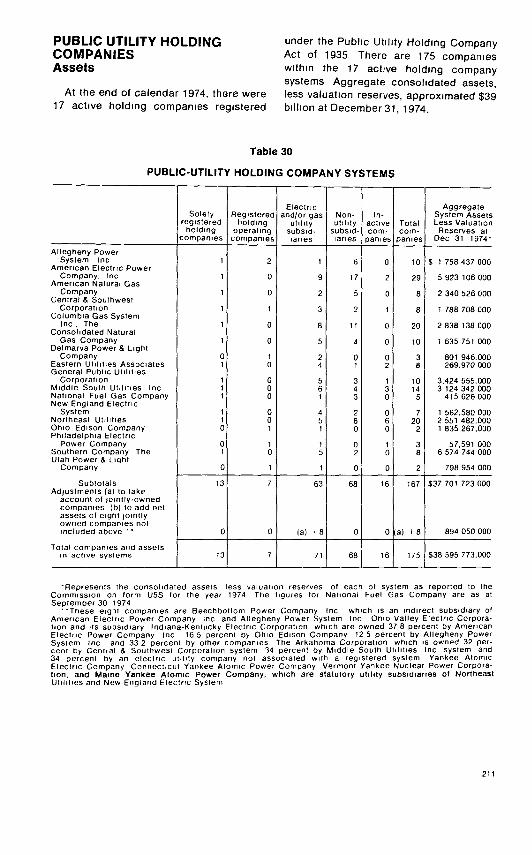

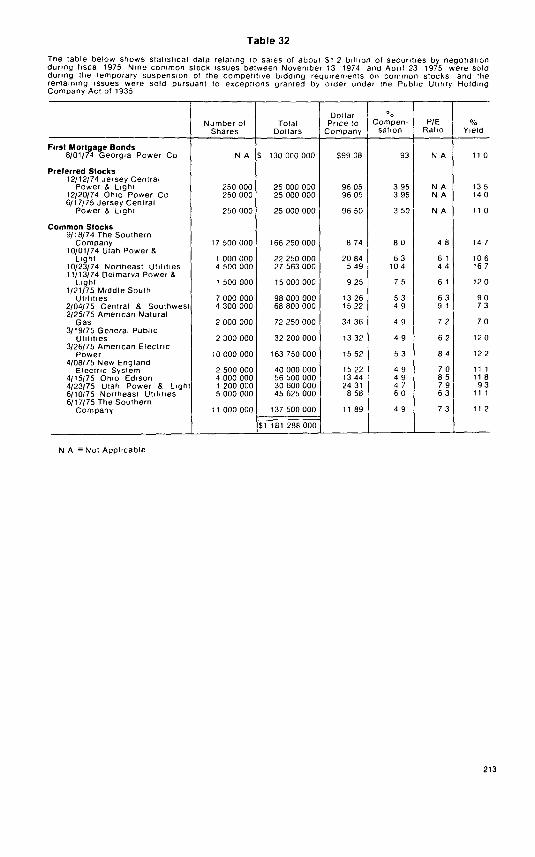

Public nlrty holding companies 211Assets 211Table 30. Public utility holding company systems 211Fmancmq 212Table 31: Fmancrnq of holding company systems 212Table 32. Issuers of holding company system

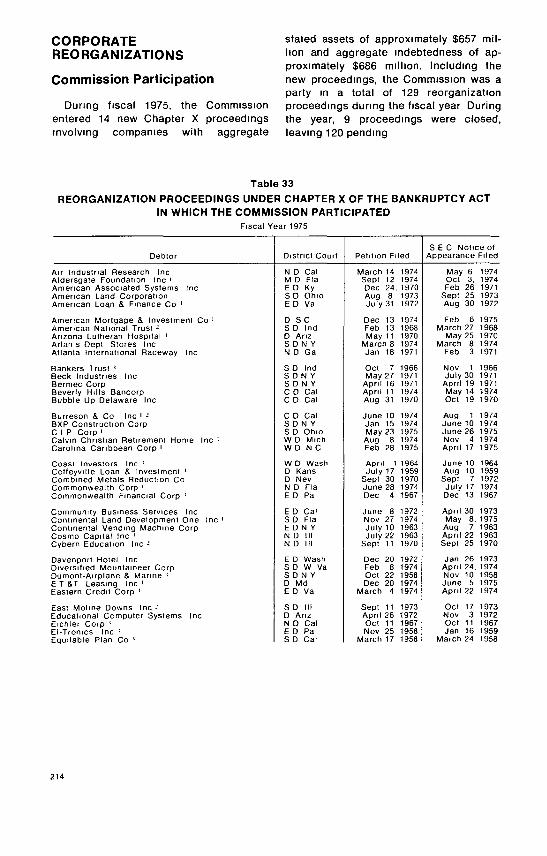

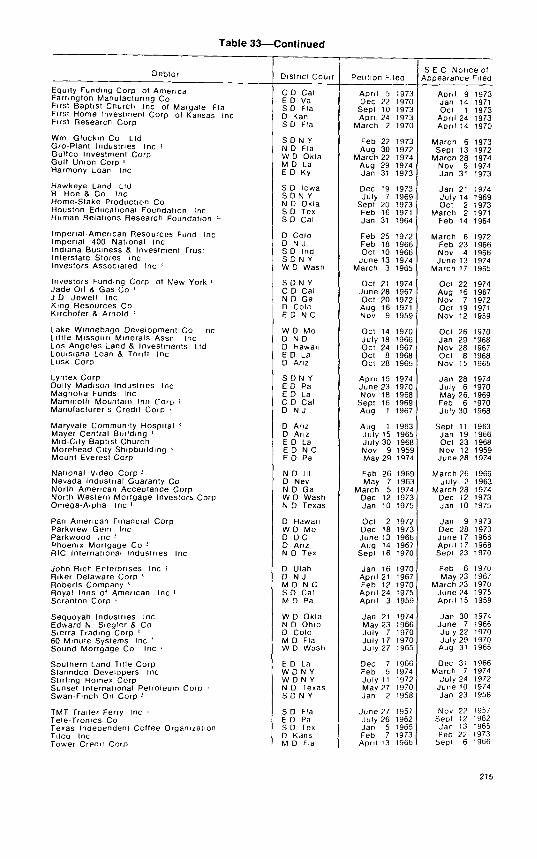

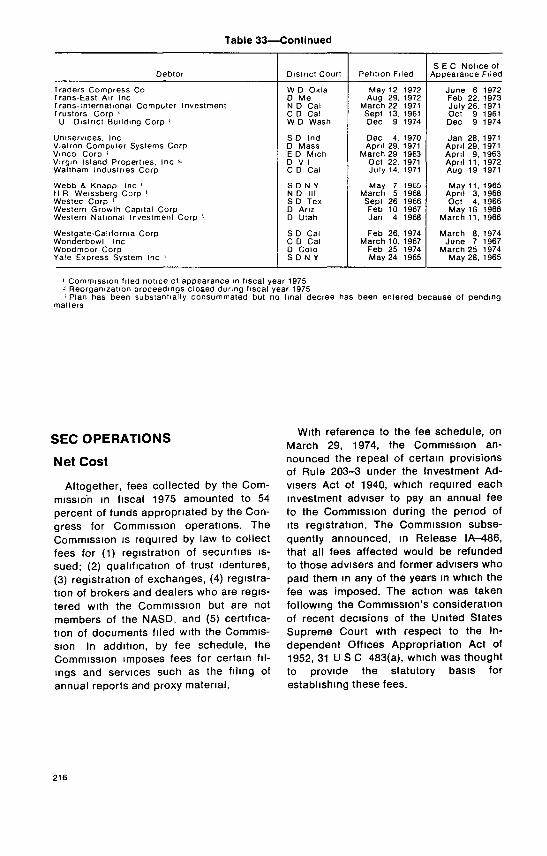

securities fiscal 1975 213Corporate Reorganizations 214

Comrmsston particrpanon 214Table 33: ReorganizatIOn proceedings under

Chapter X of the Bankruptcy Act In which theCommission particrpated 214

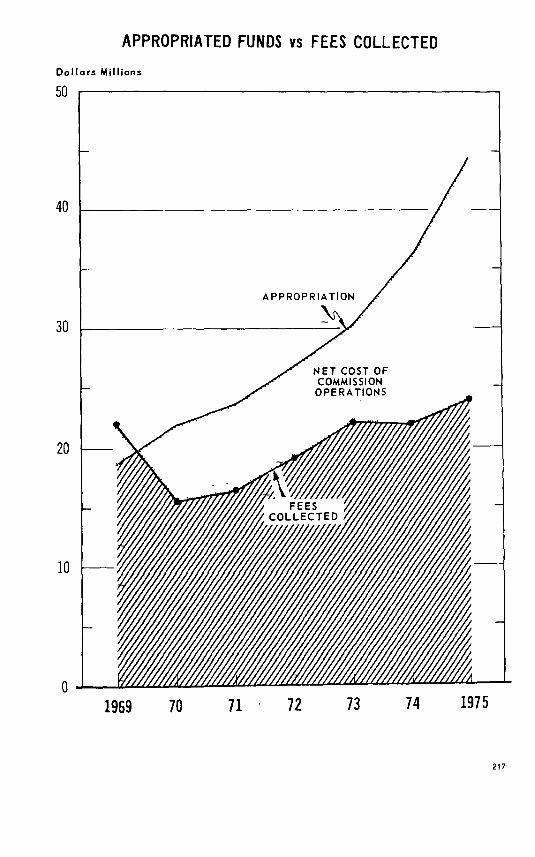

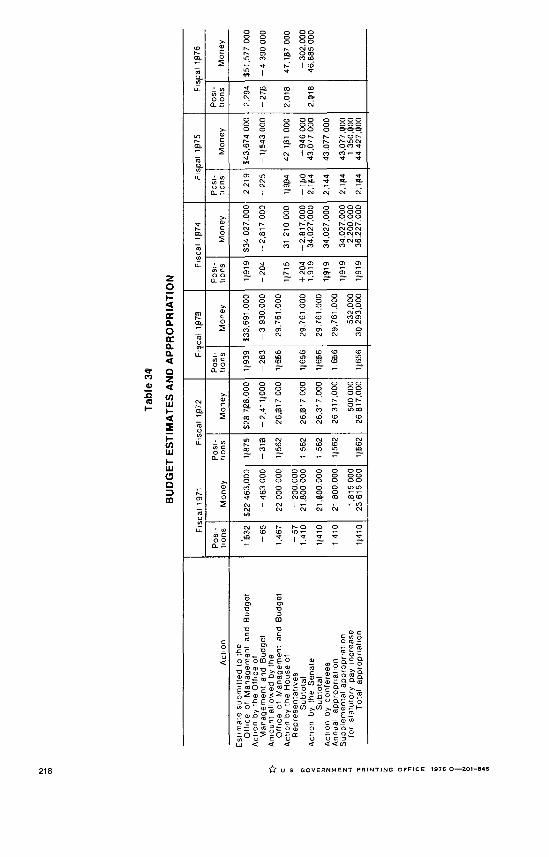

SEC Operations. 216Net cost 216Chart. Appropriated funds vs. fees collected 217Table 34' Budget estimates and appropnatrcn 218

XIX

PART 1POR NT

DEVE~ P ENTS

MARKET REGULATION

During the past year, the Commissionundertook several actions of far-reachingImportance to the seountres Industry, thesecurities markets and the investing pub-lic. At the same time, the Congresspassed legislation enhancing and clarify-Ing the Commission's authority over thesecurities markets and the securitiesIndustry

Perhaps the most significant actiontaken by the Commission was ItS adop-non of Securities Exchange Act Rule19b-3 on January 23, 1975. That rulerequired the elrrrunatron of fixed commis-sion rates on exchange transactions as ofMay 1, 1975--endlng a practice whichhad existed for over 175 years on thenation's securities exchanges. The deer-sron to adopt Rule 19b-3 came afternearly a decade of study by the Com-mission, the Congress and many others.In adopting Rule 19b-3, the Commissionbecame the first federal requlatory agencyto substitute competitive pricing for apreviously sanctioned system of pricefixing within an Industry.

Among other things, the system of fixedcomrrussron rates was seen as hinderingprogress toward the implementation ofa national market system. The Comrrus-sron has continued ItS efforts toward thedevelopment of such a system, includingprogress toward the introduction of aconsolidated tape for reporting securitiestransactions and a composite quotationsystem.

PART 1IMPORTANT

DEVELOPMENTS

The Commission and the Congress havebeen acting together to take all necessaryand appropriate steps to assure thatsecuntres transactions are effected fairlyand efficiently at the best available price,that competition IS enhanced within thesecunties industry, and that informationwith respect to quotations and transac-tions be made more fully available tobrokers, dealers and Investors. Much ofthe Commission's work over the past yearhas been directed toward the realizationof those goals.

The Securities Acts Amendmentsof 1975

The Securities Acts Amendments of19751, enacted June 4, 1975, significantlyrevise and expand the Securities Ex-change Act of 1934 Among other things,the Commission IS directed to facrtitatethe establishment of a national marketsystem for securities and a nationwidesystem for the clearance and settlementof securities transactions, clarify andstrengthen the Commission's oversightrole with respect to self-regulatory or-ganizations, and provide for broad regu-lation of brokers, dealers, and bankstrading In mumcrpal secuntres. The 1975Amendments further contain new pro-visrons relating to fixed commrssron rates,trading on national securities exchanges,the payment for research services withbrokerage comrmssrons, and registrationand regulation of brokers and dealers 2

The National Market System The Com-

3

rmssion IS directed to facilitate the es-tablishment of a national market systemfor securities In accordance with thefindings and objectives stated In Section11A(a)(1) The heart of the national mar-ket system will be cornrnurucatron sys-tems that dtssimmate last sale andquotation information for secuntresqualified for trading In the national mar-ket system These communication sys-tems, which will link all markets forqualified secuntres, are to be designedto foster ettrcrency, enhance competition,Increase the information available tobrokers, dealers and Investors, tacrlrtatethe offsetting of Investors' orders andcontribute to best execution of such or-ders. To acrueve those objectives. theCommission IS granted junsdrction overpersons who, by direct or indirect use ofthe malls or any other instrumentality ofInterstate cornrnerce," are engaged In thevarious stages of collecting, processing,distributing or publishing, on a currentand continuing basis, intorrnatron abouttransactions In or quotations for any se-cunty (other than an exempted security)Those persons, who are termed securitiesinformation processors, and their acnvrtlesare subject to registratIOn and regulationby the Commission. The cornmrssron alsomay prescribe rules and regulations re-lating to securities processing activitiesby self-regulatory organizations, membersthereof, brokers or dealers which utrhzeany means of Interstate commerce

Certain new provisrons require theelimination of restrictive rules and prac-trees which either prevent brokers fromobtaining the best price for their custo-mers or hinder market-making activitieswithin the national market system. Suchprovrsions as Sections 6(b), 11A(c),15A(b), 19(b), 19(c), 19(e), and 23(a) seekto prevent any unnecessary or inappro-pnate regulatory burden on competitionand to balance the anti-competitivermplrcanons of any action by any self-regulatory organization or by the Com-rnrssron with the purposes and considera-tions of the Exchange Act. Furthermore,the 1975 Amendments expand the Com-mlssron's authority to regulate marketmakers, specialists, and other dealers

4

(including the authority to prohibit a firmfrom acting both as a dealer and as abroker In a security) to promote faircompetition among such persons andequal protection of all markets for qualr-ned securmes and of all exchangemembers, brokers and dealers.

The Commission IS directed to reviewany and all rules of natronal secuntiesexchanges which hrrut or condrtron theability of members to effect transactronsIn securmes otherwise than on such ex-changes and to report its conclusions toCongress. Institution of proceedings ISrequired where any such rule Imposes aburden upon competition not necessaryor appropriate In furtherance of the Ex-change Act.

The 1975 Amendments also containcertain powers which may be exercisedwith respect to trading In listed securitiesIn the over-the-counter markets. Addr-tronally, the national secuntres exchangesare permitted to commence trading in se-cuntres not otherwise listed by the issueron such exchanges after Commissionreview and approval

Section 11A(d) requires the establish-ment of a National Market Advisory Board.It IS to advise the commrssron on whatsteps are appropriate to facilitate estab-lishment of a national market systemand on significant regulatory proposalsmade by the Commission or any self-regulatory organization. It IS also directedto study the possible need for a new self-regulatory body, the National MarketRegUlatory Board, which would adminis-ter the national market system, and toreport ItS conclusrons to Congress

Requletion of Clearing Agencies andTransfer Agents. The 1975 Amendments(Section 17A) establish a system of regu-lation extending to all facets of the se-cunnes handling process, designed topromote prompt and accurate clearanceand settlement of securities transactrons.Clearing agencies must register withand report to the Commission, which Willreview the rules of such clearing agen-cies to determine whether they complywith the statute's objectives. The primaryenforcement and inspection responsibili-ties over clearing aqencres that are

banks IS assigned to whichever bankregulatory agency is the appropriate reg-ulatory agency. Rulemakmg authorityconcern 109 the safeguardmg of funds andsecurities by bank clearing agencies ISshared by the Commission and the ap-propriate bank regulatory agency.4

The Securities Exchange Act IS furtheramended to require transfer agents, otherthan banks, to register with the Com-mlssion. Bank transfer agents must regis-ter with the appropriate bank regulatoryagency. The Commission is granted broadrulemaking power over all the aspects ofa transfer agent's activities. Nevertheless,as with clearing aqencres, where a trans-fer agent IS a bank, mspecnon and en-forcement responsibilities are vested 10

the appropriate bank regulatory agencyand rulemakmg authority concern 109 thesafeguard 109 of funds and securities bybank transfer agents IS shared by theCommission and the appropriate bankregulatory agency.

Section 17A(e) requires the Com-mission to eliminate the physical move-ment of secunties certificates during thesettlement process. In addition, the Com-rmssron IS directed, in Section 12(m), tostudy the practice of registering securrties10 "street name," i.e., 10 a name otherthan that of the beneficial owner, and toreport to Congress its conclusrons.

MUniCipal Securities. New Section 15BInitiates a comprehensive pattern for theregistration and regulation of brokers,dealers and banks that buy, sell, or effecttransacnons 10 municipal securities aspart of their regular business 10 otherthan a fidUCiary capacity. Issuers of mu-nicipal securities contmue to be exemptfrom the registration provrsions of thefederal secuntres acts.

A MuniCIpal Securities RulemakmgBoard is created to prescnbe rules regu-latmg the acnvmes of brokers, dealersand municipal securities dealers relatmgto transactions 10 mumclpal secunnes,Its scope of authority and responsibilityIS defmed in terms of enumeratedpurposes and standards. Section15B(b)(2)(K), for example, sets forth therequirement that the Board establish theterms and conditions under which any

rnurucrpal secuntres dealer may sell anypart of a new Issue of municipal securitiesto a municipal securities investment port-folio durmg the underwriting period. TheCommission IS required to take affirma-tive action on rules proposed by theBoard and is authonzed to abrogate,add to, or delete from any Board rule.The commrssron may directly regulatefraudulent, manipulative, and deceptiveacts and practices pursuant to Sections10(b) and 15(c) of the Exchange Act.

The Board Will be comprised of repre-sentatives of broker-dealers, banks andthe public, mcludmg Issuers of and in-vestors 10 muruclpat securities. (Sec.15B(b)(1).) The procedures to be fol-lowed in the nomrnatron and election ofmembers of the Board are desrqned toassure fair adrnmrstratron of the Boardand fair representation of all segments ofthe municipal securities industry (Sec.15B(b)(2)(B). The Board IS authorized tohire appropriate staff and to assessmunicipal securities dealers to coverreasonable expenses (Secs. 15B(b) (2)-(I) and (J).

The Board's rulemakmg powers areextensive (Sec. 15B(b)(2)(AHK).) Thepurposes for which the Board can exer-cise its rulemaking authority include:prevention of fraudulent and manipulativeacts and practices; promotion of just andequitable principles of trade; establish-ment of standards for entry mto themunicipal sscuntles business: regulationof selling and underwntrnq practices;procedures for arbitration of intra-Industrydisputes; and deterrninatron of the fre-quency and scope of inspections ofmunicipal securities dealers by the bankrequlatory authorities With respect tobanks and the NASD with respect tosecunnes firms.

The Board does not have any power toconduct Inspections or to enforce its rulesInstead, the Securttles Exchange Act as-signs these responsjblhtres to the NASDfor securities firms which are members ofthe NASD (Secs. 15A(b)(7) and 15B(c)(7).Similarly, such responsibilities are as-signed to the bank regulatory agenciesfor municipal securities dealers wmcnare banks (Secs. 15B(c)(5) and 17(b).

5

As of June 30, 1975, the Commissionhad taken Initial steps to Implement thestatutory goals of Section 15B. On June12, 1975, the Commission announced thesolicitation of recommendations of in-dividuals for appointment to the Munic-rpal Securities Rulemaklng Board.s TheCommission plans to continue to worktoward the creation of a registrationprocess for sscunnes firms and banks en-gaged In the murucipal securities Industryas well as the establishment of cooperativeefforts with appropriate bank regulatoryagencies

Brokers and dealers that buy, sell, oreffect transactions In municipal securitiesand banks that buy and sell such se-cuntres as a part of a regular businessother than In a fiduciary capacity arerequired to register with the Commission(Sec. 15B(a)(1). If a bank engages in thebusiness of trading murucipal securitiesthrough a separately Identifiable depart-ment or divtsion, that department or di-vision rather than the entire bank canregister with the Commission (Secs3(a)(30) and 15B(b)(2)(1I). Brokers anddealers already registered with the Com-rnrssron by reason of their general se-cuntres business are not required tore-reqrster. No person IS permitted toengage In the business of trading Inrnumcipat securities unless registeredWith the Commission and the Commissionhas the authority, In accordance Withspecified procedures, to revoke theregistration of any person found to be inViolation of the Securities Exchange Act,or any rule of the Commission or theBoard (Sec. 15B(c)(2).

Commission Rates. The 1975 Amend-ments prohibit the Imposition of anyschedule or fixing of rates of commis-sions, allowances, discounts, or otherfees by a national securities exchange tobe charged by ItS members for effectingexchange transactions A temporaryexemption postpones such prohibitionfor odd-lot dealers or for a member actingas broker on the floor of a national se-cunnes exchange for another member.The Commission may permit a nationalsecurities exchange to Impose reasonablefixed commissions (1) prior to November

6

1, 1976, If such fixed rates are found tobe in the publrc Interest, and (2) afterNovember 1, 1976, if the Commissioninstitutes a proceeding and makes cer-tain deterrrunatrons, as set forth In Sec-tion 6(e). Additional provisions, such asSection 6(f) and Section 11A(c), grantauthority to the Commission to remedyproblems affecting the orderliness oftrading on exchanges

The elimination of fixed rates raisedquestions for Investment managers whomay be required to pay a broker for re-lated research services. To protect an in-vestment manager against a claim ofbreach of fiduciary obligation if he paidmore than the lowest available price forexecution and research services, Section28(e) permits him to pay a cornrrusstonfor executing a transaction above thelowest available price If he determines Ingood faith that It was reasonable consrd-ering the value of the brokerage andresearch services provided. The legisla-tive history of that provrsion makes Itclear that Section 28(e) applies only topayments made by a money manager toa member of a national securities ex-change, broker, or dealer for servicesrendered by that particular member,broker or dealer, and that It has no ap-plication whatsoever to a situation Inwhich payment IS made by an Investmentmanager to one broker or dealer forservices rendered by another broker ordealer."

Brokers and Dealers. A Significantamendment to Section 11(a) of the Ex-change Act prohibits, With certain ex-cepnons, any member of a nationalsecuntres exchange from effecting anytransaction on such exchange for its ownaccount, the account of an associatedperson, or an account over which It or anassociated person thereof exercises in-vestment discretion For members of anational securities exchange as of May 1,1975, the proscriptions do not applyuntil May 1, 1978. The Commission ISauthorized to regulate transactions exe-cuted off an exchange or otherwise notprohibited.

The 1975 Amendments expand thescope of the Commission's authonty un-

der Section 15(a) to Include the registra-tion and regulation of brokers and deal-ers who trade exclusively on a nationalsecurities exchange. With respect to newregistrations of all brokers and dealers,the Commission IS required within 45days either to Issue an order grantingsuch registration or institute a proceed-Ing to determine whether registrationshould be denied. Among other sectionsamended, secnon 15(b) authorizes theCommission to adopt uniform standardsfor persons engaged in the securitiesindustry.

Accounts and Records. Section 17 ofthe Exchange Act has been expanded toprovide for record-keeping and reportingrequrrements of the various new regu-lated entities and that certified tmancralfinancial statements of brokers and deal-ers be filed with the Oommlssron andsent to their customers. Section 17(e)(2)permits the adoption of rules prescribingthe form and content of financial state-ments filed pursuant to the Exchange Actand the accounting principles and stand-ards employed in their preparationSection 17(f) requires, in part, (1) theImplementation of a system of reportinginformation about missing, lost, counter-feit, or stolen sscunnes and (2) the finger-printing of the partners, directors, officers,and employees of every member of anational securities exchange, broker,dealer, registered transfer agent, andregistered clearing agency.

Commission Rates

As noted above, the Commission, be-fore passage of the 1975 Amendments,adopted Rule 19b-3,7 eliminating fixedcomrnissrons on exchange transactionsas of May 1,1975. The Commission madea preliminary announcement on August27, 1974,8 of ItS plan to eliminate fixedcornmrssron rates. In September the Com-mtssron formally requested each nationalsecurmes exchange to effect necessarychanges in ItS constitution, rules andpractices so as to eliminate those ele-ments which required exchange membersto charge any person any fixed rate ofcornmrssron.v Only one national securi-

ties exchange indicated that It wouldcomply With the Commission's request,other national sscunnes exchanges in-dicated that they would not comply vol-untarily With the Commission's request.Consequently, the Commission proposedRules 19b-3 and 10b-22 under the Ex-change Act for comment and heldhearings to receive Views, data and ar-guments from interested persons on boththe proposed rules and the proposedeffective date of May 1, 1975.

.......As a result of the hearings, the Com-mission adopted Rule 19b-3 With modi-fications from the form first published forcomment Specifically, the required elimi-nation of "floor brokerage" rates wasdelayed until May 1, 1976. The Commis-sion determined not to adopt proposedRule 10b-22, which related to agreementsamong exchange members for the settingof brokerage rates. The Commission'sadministrative action has been legisla-tively affirmed In Section 6(e) of the 1975Amendments.V After carefu I consideration of all the

arguments advanced In the hearings onRule 19b-3, of the numerous studies madeconcerrunq cornmlssron rates, and of therecent experience of both the Commis-sion and the securities Industry Withfixed rates, the Cornrnisaron set forth asItS basic reason for the adoption of Rule19b--3 the conclusron that, under presentcircumstances, the free play of competi-tion can provide a level and structure ofcornmrssion rates which would betterserve the Interests of the Investing public,the securities markets, the secunnes in-dustry, the natronal economy and thepublic interest than any system of pricefixing which can reasonably be devised.lO

In March 1975, the Oornrnlssron an-nounced a program to morutor the Impactof ItS decision to eliminate fixed rates ofcomrrusslon.'! The program IS designedto determine what effect the absence ofany schedule or fixed rates of commis-sions may have on the pubuc Interest,protection of Investors, and maintenanceof fair and orderly markets. The program,as announced, Included publication forcomment of a proposed rule under theExchange Act reqUiring certain broker-

dealers to file with the Commission reve-nue and expense data and relatedfinancial and other information and noti-fication of changes In membership in-terests In national securities exchanges

The monitoring program has beenanalyzing a sampling of firms to developinformation on effective cornmrssron ratesbeing paid by mdrvtdual and institutionalcustomers to different types of broker-dealer firms; reviewing volume reportsfrom national securities exchanges andthird market firms to determine the drs-tnbution of trading among the variousmarket places; compiling additional in-formation about revenue sources andexpenses of national securities exchangesand registered national securities asso-ciations; and studying the Income, ex-penses, assets and liabilities of specialistsand the activity of certain stocks.

On May 2, 1975, the Oornmrssron an-nounced the adoption of Rule 17a-20and related Form X-17A-20, the approvalof two plans submitted pursuant to para-graph (a)(3) of Rule 17a-20, and theImplementation of other aspects of theprogram to monitor the Impact of theehmmatron of fixed ccmrrussron rates onexchange transactions 12

For the months of May and June, NewYork Stock Exchange (NYSE) broker-dealers Incurred a revenue loss fromcornrrussron rate discounts of approxr-mately $42 million. Thrs revenue loss wasapproximately 7.6 percent of total se-cunnes commission revenue and 4 per-cent of total revenue dunnq thiS periodlndivrdual customers paid slightly moreon small size orders and slightly less onlarge orders. The net effect in June wasa decline averaging 1.5 to 2 percent Inthe cornrnlssron rate charged on all in-divrdual orders. Institutional customers,on the other hand, received discounts Inall order size categories and receivedan average discount of 19 5 percent In themonth of June. The experience With com-petitive rates for non-NYSE firms durrnqthe May and June period was Similar tothat of NYSE member firms.

Based upon the preliminary and in-complete evidence of two months'experience (May-june, 1975) With com-

8

petitrve rates during a period of risingtrading volume, historical trading pat-terns among exchanges and over-the-counter markets appear not to havealtered Similarly, the tmancral conditionof self-regulatory organizations does notappear to have been materially affected.

Development of the NationalMarket System

Advisory Committee on the Implementa-tion of a Central Market System. Asdescnbed In last year's Annual Report,13the Commission established an AdvisoryCommittee on the Implementation of aCentral Market System to assist It In con-nection With ItS proposals for a centralmarket system and to ensure that such asystem would meet the needs of thenation's capital markets In the future,consistent With the publrc Interest and theprotection of Investors.

Specrtrcalty, the Committee was askedto study and to submit recommendationsto the Cornrnissron on such matters as:

a. The appropriate structure forregulatory supervrsron of the centralmarket system;

b The nature and scope of theOomrmssron's role during the processof Implementing the central marketsystem;

c. The ways in which a central mar-ket system should be structured Inorder effectively to meet the needs ofour capital markets, the public interest,the protection of investors and themaintenance of fair and orderly marketsfor securities;

d. The needs and perspectives ofusers of a central market system, in-cluding Issuers of and Investors Insecurities, as well as securities pro-tessronats: and

e. The appropriate resolution offundamental policy Issues relating tothe central market system's operations.The Committee, composed of twelve

persons, eight of whom are from the se-curities Industry, was assisted by mem-bers of the Oommlssron's staff The staffattempted to Identify for the Committeea number of unresolved Issues which the

Committee might consider, including(1) the registration requirements andcaprtal standards appropriate for market-makers granted access to the system,(2) the responsibthtres of market-makerswhen acting as agents in the system;and (3) the responstbtlrtles of market-makers acting as dealers In the system

Certain structural questions were alsoraised: Whether lrrrut orders for pubuccustomers should be held In a consoli-dated limit order book and, If so, whoshould be permitted access to the book,whether specialists or market-makersshould be prohrbited from dealing directlyWith public customers; and how the roleof transactions between customers wouldbe effected Without the use of brokers orspecialists In the central market system.In addition, the staff suggested that theCommittee consider rules on auctiontrading and priorities for public custom-ers' orders in the new central marketsystem.

In a preliminary statement Issued De-cember 11, 1974, 14 the Committee notedthat Its suggestions would be made With-out regard to whether It was feasible toutrhze exrstinq technology to ImplementItS suggestIOns and that although notunanimous its preliminary views didreflect the sense of the Committee as awhole. Particular emphasis was placedon auction-market principles in a centralmarket system, which were consideredthe most effective means of encouragingcompetition among buyers and sellers.The preliminary statement of the Com-mittee set forth specific conclusionswith respect to specialists' net capital,market oontinuity and public preferanceobligations, outlined the manner in whichlimit orders entered with specialistsshould be treated, and descnbed possibletrading limitations to be imposed onspecialists. Stressing the importance ofpreserving the dealer function of brokers,the Committee recognized the importanceof the role played by over-the-counterdealers in the markets and the necessityof providing an adequate opportunity andIncentive for their continued participationin a central market system.

On July 15, 1975, the Comrmttee sub-

mltted to the Commission, In preliminaryform, a Summary Report of its finalconclusrons The Summary Report re-emphasized that the views enunciatedwere not unanimous or endorsed by allmembers without reservation

The Summary Report defined the ob-jectives of the central market system asfollows:

a To provide all Investors WIth themaximum opporturnty to buy and sellsecuritres at the best possrble price,

b To provide the depth and Irqutdrtynecessary to tacrlrtate the ralsrnq ofcapital by issuers; and

c To provide a mechanism for theconsurnrnanon of transactions at areasonable cost.

To accomplish these objectrves, theSummary Report envlsioned that the cen-tral market system must include all trans-acuons In securities listed on exchangesand permit access to all specrahsts,qualified market-makers and qualifiedbroker-dealers

The Committee emphasized thatauction-market principles, including pref-erence for all public orders, would beessentral to the central market systemThe system's rules, according to theSummary Report, should provide that allorders entered for the account of personsother than brokers or dealers would havepreference over orders entered by pro-tesstonals. Among system professionals,however, the orders of specralrsts andmarket-makers would be permitted todisplace orders of other broker-dealersdealing for their own account

An Important role was recommendedfor specialists on the various stockexchanges. The Cornrruttee also recom-mended that the system permit partici-pation of all market-makers, includingthose now dealing In the third market(i.e , over-the-counter trading In secun-nes listed on exchanges). The reportspelled out In some detau respcnsrbrlrnesof specialists and market-makers enter-ing quotations in the system, includingtheir minimum net capital. The SummaryReport indicated that there should betrading and competition among special-

9

IStS and market-makers dealing in thesame secuntres.

The Summary Report stated that bothspecialists and market-makers should berequired to maintain continuous, fair andorderly markets In those securities Inwhich they are registered to deal. TheCommittee, however, drew an Importantdistinction between the two. specraltstswould be assigned to deal In particularsecunues, so that at least one specialrstwould be responsible for maintaining amarket in every listed security; registeredmarket-makers would be permitted to se-lect the secunties In which they dealtMarket-makers would also be permittedto deal with all types of customers, whilespecialrsts would be prohibited from deal-Ing directly with institutional customersand with insiders, officers and directorsof the Issuers of the securities In whichthey made markets

Thrs restriction on speciausts' dealingswas seen to be directly related to theirrole as agents for the limit orders of pub-uc customers. The Committee envrsronedthat limit orders would be guaranteedexposure to all transactions In systemsecunues only if they were placed withspecransts. Although market-makerswould be permitted to hold and executelimit orders, they would guarantee ex-posure of such orders to all system trans-actions only by usmq a specialtst. TheSummary Report recognized "best execu-tion" as the primary duty of brokers In thesystem, detailing certain aspects of thatduty In the context of an operationalcentral market system. The SummaryReport also indicated that the systemshould maximize the opportunities forbrokers to execute orders for their cus-tomers without a specianst or otherqualified market-maker participating Inthe transaction.

A central self-regulatory authority, withthe responsibility and authority to Imposerules and regulations on all specrausts,market-makers and broker-dealers trad-Ing In listed securities was deemed Im-portant by the Committee. Early In ItSconsrderatron. the Committee had recom-mended that such a body be establishedas soon as posstble, In view of the opera-

10

non of the consolidated tape, the diS-semrnatron of quotations In listed se-cunnes and the unftxrnq of commissionrates. SUbsequently, however, the Com-mittee recognized that creation of sucha board would be inappropriate so longas the National Market Advisory Board,called for by the seounnee Acts Amend-ments of 1975, was assiqned responsr-bility to study the governance of thecentral market system. Therefore, it urgedthat the Board and the Oomrrussronmonitor the events taking place towardthe development of a central marketsystem to Insure the existence of an ap-propriate regulatory framework.

The Committee believed the most ef-ticrent and effective structure for govern-Ing the central market system would beprovided by the merger of presentlyexrstrnq exchanges dealing In secuntrssto be Included In the system. The Com-mittee pointed out, however, that while atrue central market system Involves someform of centralized control, a merger ofthe exchanges would not be a pre-requisrte

The Committee concluded ItS summaryreport With a series of recommendationsfor Oornrnlssron action. Included wererecommendations, made early In theCommittee's deliberations, for Impositionof rules dealing with short-seiling andminimum capital requirements for spe-cralrsts and market-makers. The Com-rmssron has already taken action on thesematters. In addition, the Committeerecommended that all specratlsts andmarket-makers be required to maintainbona fide, continuous and competitivetwo-srded quotations for each securityIn which they make a market and thatsuch quotations bear a reasonable rela-tionship to the last sale in those secunnes.

The Committee recognized as par-ticularly important ItS recommendationthat the New York Stock Exchange andthe American Stock Exchange be per-mitted to retain their present rules caus-Ing members to bring all trades Insecurities on those exchanges to therespective trading floors. The Committeerecognized that such rules pertaining tospecmc market centers Will be map-

propriate in the central market systembut concluded that they should not beeliminated until such time as a similarrule can be imposed for the system as awhole A system-wide rule was thoughtto be appropriate when a compositequotation system was In operation, fa-Cilitating members' efforts to achieve bestexecution, and when a consolidated limitorder book was established, makingpossible the execution of public ordersin all market places.

The Commission expects to receive afinal report, with dissenting Views, fromthe Committee In the fall of 1975. It ISanticipated that the work of the CommitteeWill constitute a beginning POint fordeliberations by the new NatIOnal MarketSystem Advisory Board called for by theSecurities Acts Amendments of 1975.15

Consolidated Tape

As previously reported.!" a plan for theconsolidated reporting of price and vol-ume data, filed jorntly by the Amerrcan,Midwest, Pacific, PBW and New YorkStock Exchanges and the National As-sociation of secunues Oealers, Inc.("NASO"), was declared effective by theCommission as of May 17, 1974.17 Thejoint industry plan (the "Plan") providedfor a tape consisting of two separateticker "networks," displayed concur-rently. Network A would report transac-tions In stocks listed on the New YorkStock Exchange ("NYSE") and NetworkB, transactions In stocks listed on theAmerican Stock Exchange ("Amex") andcertain stocks listed only on the partici-pating regional exchanges. Both networkswould report all trades in their respectivestocks, regardless of whether they tookplace on an exchange or In the so-called"third market." In addition, Informationdisseminated over Networks A and Bwould also be available through in-terrogation devices, enabling investorsand market professionals to obtain themost recent last sale price for any stockcovered by the system regardless of themarket of execution. The system was de-signed to be compatible With equipmentpresently found in most brokerage offices.

The Plan contemplated that the con-solidated tape would be put Into opera-tion In two phases beglnnrng Within 20weeks after Commission approval of thePlan. The pilot phrase was to be a 20-week period of experimental operationcovering a limited number of stocks, afterwhich full operation of the consolidatedtape would begin, by reporting and dis-seminating last sale data of eligiblesecurities to be Included in Networks Aand B by means of a high-speed line.Thrs would permit reception of reportedinformation on a current baSIS, regardlessof any delay In the dissemination of theinformation over Networks A and Bcaused by the servicrnq of interrogationdevices.

Actual Implementation of the consoli-dated tape lagged behind the 40-weektime period contemplated by the Plan,pnncipally because the Original estimatewas overly optimistic and failed toanticrpate the technical problems in-herent In the development of the newcomputer system that was required. Also,both the sponsors and the Commissionbelieved that certain regUlatory prob-lems should be addressed before theImplementation of the consolidated tape.

Phase I of the consolidated tape sys-tem was Originally scheduled to com-mence on October 4, 1974. It was deferredfor a two-week period by the Commission,In response to a request by the NYSE, topermit resolution of certain mechanicalproblems the NYSE believed would havearisen as a result of the Commission'samendments to ItS short sale rules-Securities Exchange Act Rules 3b-3,10a--1, and 10a--218 The amendments tothe short sale rules had the effect ofprohibrtmq short sales of a securitylisted on an exchange at a price belowthe last pnor sale (a "minus tick"), or atthe last sale price if the preceedingdifferent sale price had been at a higherprrce (a "zero minus tick"), as reportedon the consolidated system. The amend-ments applied the Commission's shortsale regUlation, for the first time, In auniform manner to all markets In whichtransactions In listed securities occurred,and were part of the Oornmrssron's efforts

11

to resolve certain regulatory problemsbefore the Implementation of the con-solidated tape But after reviewing theproblems created by the uniform shortsale rule, the Commission determined tosuspend the operation of the amend-ments, and the pilot phase of the con-solidated system began operation asrescheduled on October 18,1974

Although full operation of the con-solidated tape system was Originallyscheduled for February 21, 1975, It be-came obVIOUSto all the Plan participantsby mid-January that the February 21deadline could not be met. On February19, 1975, the Consolidated Tape Associa-tion ("CTA"), the governing body for theconsolidated system, Informed the Com-mrssion that, because of testing de-lays and recent problems with the MarketData System of the NYSE, the CTA ex-pected to be able to Implement onlycertain elements on or before June 16,1975.19 Specrncally, It expected that onor before June 16, 1975' (1) last sale dataregarding transactions in all eligible se-cuntres required to be Included In Net-work A of the consolidated system wouldbe reported In accordance with the Planby all Plan participants (other than theAmex) and by four other "reportingparties" (r.e., the Boston Stock Exchange,the Cincinnati Stock Exchange, the De-troit Stock Exchange, and the InstitutionalNetwork Corporation ("Instinet"» to theSecurities Industry Automation Corpora-tion ("SIAC"), the Plan processor, and(2) such last reports would be transmittedby SIAC to vendors of market informationon a low-speed basis. The CTA's letterindicated that maximum effort was beingexpended on making Network A opera-tional as soon as possible, and that SIACwas continuing to program for therequirements of Network B and thehigh-speed line.

On March 3, 1975, after indicating thatit would not object to the delay, the Com-mission stated that It was disappointedby the delay but that It understood thatcertain of the reasons for the delay werebeyond the control of the CTA. The Com-rnissron also stated that the staff wouldbe making inquiry of the CTA as to the

12

reasons for the delay and the future plansof the CTA with respect to the full imple-mentation of the Plan. The CTA responseof March 26, 1975, to staff mqurries re-garding the delay, which detailed de-scnptions of the reasons for testingdelays, was released by the Oomrrussronon May 1, 1975.20The Oornmlssion issuedan Interpretative release specrtymq therequirements 'regarding displays on in-terroqauon systems,21 which helped re-solve questions concerning applicationof Rule 17a-15 to vendors and problemsCited by the CTA In Its March 26 letter.22

Between February and June 1975, thePlan participants conducted an extensivetest program to Insure the accuracy, re-liability and integrity of programming forNetwork A. Personnel from the variousexchanges, SIAC and the vendors sub-jected the system to a broad range ofSimulated market condiuons. All the testsproved successful, and the CTA was ableto fully Implement Network A reportingon a low-speed baSIS on June 16, 1975.The CTA IS currently continuing work onthe remaining elements of the consoli-dated system-Network B and the hlgh-speed line. A final date, however, hasnot yet been set for full implementationof all elements of the consolidated system.Implementation of Network A of the con-solidated tape, while not constitutingfull Implementation of the Plan, IS amajor step toward the eventual achieve-ment of a central market system. Trans-actions executed In markets other thanon the floor of the NYSE are now appear-Ing on moving tickers for the first time.Such transactions are Indicated on thetape by an ampersand tollowrnq thesymbol for the NYSE-listed stock Theampersand, In turn, IS followed by a letterthat Identifies the specrnc market place.

Those letters are' M for Midwest; Pfor Pacrnc: X for PBW; C for Cincinnati;T for NASD (r.e., the third market); ando for Insllnet. The Boston Stock Exchange-Identified by the letter B--was addedto the consolidated tape on July 14, 1975,and the Detroit Stock Exchange--Identi-fled by the letter D-IS expected to beadded to the system sometime In latesummer or early fall, 1975.

The inclusion of NYSE, regional andthird market transactions on a singleconsolidated tape, even on the limitedscale currently In place, enables investorsto make more Informed Judgments regard-ing which market centers offer the mostadvantageous price at a particular time.Even though the Information presented onthe consolidated tape IS essentially his-toncal information, i.e., prices at whichtransactions were effected In the pastrather than prices at which future trans-actions may be effected, such informationshould be useful to Investors In indicatinggeneral trends and temporary price dis-parities between market centers.

In addition to its benefits to Investors,the consolidated tape represents a sig-nificant technological achievement Inthe processing of securities information.The consoltdated tape IS not Just a me-chanical merger of exrstinq ticker net-works but a completely new computersystem tying together all the nation'smarket centers. Sophisticated and com-plex programs had to be developed toInsure that the different equipment andprograms of various exchanges andthe NASD could be accommodated, and,perhaps more important, to Insure that alllast sale reports would be reported on theconsolidated tape in the proper se-quence. All the complex programmingchanges were accomplished successfully,and the CTA and the Commission arepresently looking forward to Implementa-tion of the high-speed line, which for thefirst time Will provide Investors with lastsale reports on a current baSIS, even Inthe event of delays In ticker disseminationdue to mechanical limitations.

Composite Quotation System

When the Commission issued ItS firstproposed rule on composite transactionreporting in March 1972, it also proposeda companion rule-e-Secuntles ExchangeAct Rule 17a-14-governlng the de-velopment of a composite quotationsystem.23 Rule 17a-14, as Originallyproposed, would have required all na-tional securities exchanges to makequotations of their registered specialists

available on a current and contmumqbaSIS to vendors of market Information.Similarly, the NASD would have beenrequired to make available to such ven-dors on a current and continuing baSISquotations of market makers With respectto over-the-counter quotations In se-cunties listed or traded on exchanges.

On August 14, 1974, the Commissionreleased for public comment a substan-tial revrsion to proposed Rule 17a-1424

as a result of the many comments whichhad been received, the recommendationsof the Commission's Advisory Committeeon Market Disclosure regarding a com-posite quotation system, and the Com-mission's experience With Implementationof a consolidated transaction reportingsystem under Rule 17a-15.

The major change In Rule 17a-14 fromthe original proposal was that the revisedrule required the reporting of quotationspursuant to a plan Similar to that requiredby Rule 17a-15. Accordingly, Rule 17a-14,as revised, would have required everynational securities exchange and theNASD to report to the Commission quota-tions of their market makers or specialistsIn listed securities. The quotations wereto be available on a real-time, currentand continuing baSIS.

The Commission received many publiCcomments With respect to ItS August 1974proposal. After considering all of the pub-lic comments, the Commission determinedto adopt a new approach desiqned to in-crease the availability of quotation in-formation without potentially burdensomefederal requlation. On March 11, 1975,the Commission announced that It hadrequested all national secuntrss ex-changes to effect changes in their rulesand practices to be effective on or beforeMay 1, 1975, to eliminate those whichrestricted, or had the effect of restricting,access to or use of quotation informationdisseminated by such exchanges to anyquotation vendor.25 At the same time, theCommission announced that It was defer-ring further consrderation of proposedRule 17a-14 until It had had an oppor-tunity to observe the effects of eliminatingrestrictions on quotation drssemmatron.

In announcing ItS new approach, the

13

Oommrssron reiterated ItS view that quo-tation information, such as that currentlyprovided by some exchanges to theirmembers, IS essential to broker-dealers,whether members or not, In dischargingtheir duty of reasonable diligence In theexecution of customers' orders.26 By re-questing the elimination of exchangerestrictions on quotation drssernrnanon,the Commission Intended that as a resultof competitive forces a composite quota-tion system would develop with a mini-mum of federal regulation.

On May 7, 1975, the Commission an-nounced that It had received responses(to ItS March 11, 1975 request) from allnational secuntres exchanges and that allexchanges either had taken the acllonrequested by the Commission or hadInformed the Commission that they didnot have any rules or practices whichrestricted access to, or use of, such In-torrnatrcn.s" In making ItS announcement,the Commission added that, In ItS View,the actions taken by the various ex-changes would tacrlrtate the establishmentof a central market system, as contem-plated by the Market Structure State-ment 2H and the PolIcy Statement,29 bymaking possible the composite display ofquotation information for multiply tradedsecurities.

Short Sale Regulation

On March 6, 1974, the Commissionproposed amendments to Securrties Ex-change Act Rules 3b-3, 10a-1 and 10a-2In order to establish uniform short salerules, which were considered to be anecessary element of the consolidatedreporting system.30 After analyzing thecomments received on the proposedamendments and concluding that no seri-ous objections had been raised, the Com-mission announced their adoption to beeffective October 4, 1974 (the "OctoberAmendments")."! In a letter to the Com-rrussron, dated October 11,1974, the NewYork Stock Exchange asserted that theOctober Amendments would create in-surmountable technical, operational andregulatory problems

In view of the problems noted by the

14

NYSE, the Commission temporarily sus-pended the effectiveness of the OctoberAmendments to Rules 10a-1 and 10a-2.32The effect of that suspension was to leavethe regulallon of short sales on exchangemarkets as it had existed before adoptionof the October Amendments, while theCommission continued to study the mostefficient, effective and fair manner toachieve uniform short sale regulation Ina central market system.

On March 5, 1975, the Commissionpublished for comment additional pro-posed amendments to Rule 10a-1, (the"March Proposals").33 The Commissionnoted that many persons believed thatshort selling should not be regulated atall, except to the extent It IS used as amanipulative devlce.34 Consrderatron ofsuch arguments, however, had beenhampered by a lack of current statisticalstudies of the pattern of short seiling intoday's markets, particularly on regionalsecurities exchanges and In the thirdmarket. In any event, the Commissionthought It would be premature to considerelimination of short sale regulation (alto-gether or for any class of short sellers)before additional progress was made to-ward the establishment of a centralmarket system. Nevertheless, the Com-mrssron specmcalty encouraged com-ments on the feasibility and probableeffects of exempting from regulation shortsales by persons other than brokers anddealers, or of eliminating short saleregulation entirely.

The Commission acknowtedqed in theannouncement of the March Proposalsthat use of the proposed rules In the con-solidated system might pose certainoperational problems for those exchangema'rkets which regularly experienced ahigh volume In reported securities buthad not yet modernized their facilities sothat access to intormanon reported in aconsolidated system was not immediatelyavailable on the floor of the exchange.For that reason, the March Proposalsprovided, as an alternative to the Com-mrssron's general rule, that any nationalsecurities exchange, by rule, might pro-hibit short sales of reported sscunnesIn ItS own market (i) below the last sale

price on that exchange, or (ii) at the lastsale price, unless that price was abovethe next preceding different sale price.The March Proposals also provided thatshort sa es of reported secuntres effectedon any exchange having such a rulewould have to comply With that exchange'srule and that such compliance wouldconstitute compliance With paragraph (a)of Rule 10a-1, as amended.

Network A of the consolidated systemcommenced operation on June 16, 1975.In order to ensure comparable short saleregulation of all transactions in reportedsecuntres In all markets reporting trans-actions to that system, the Commissionannounced on June 12, 1975, the adop-tion of amendments to Rules 10a-1 and10a-2 (effective June 16, 1975), whichwere Identical, In all material respects, tothe March Proposals.35

Paragraph (a) of Rule 10a-1 will notapply to short sales of any reported se-cunty until last sale information on thatsecurity is made available to vendors ofmarket information on a real-time basis.When such information becomes avail-able on a real-time basis, paragraph (a)of Rule 10a-1 will govern short sales Inall markets (including transactions ef-fected on national secuntres exchangesand In the over-the-counter market)Additionally, national securities ex-changes will have an option either toadopt their own short sale rules, subjectto the Commission's power under Section19 of the Securities Exchange Act, or begoverned by paragraph (b) of Rule 10a-1,the tradrnonal form of the rule, whichapplies only to short sales effected onnational securities exchanges.

Option Market Regulation

By the end of fiscal year 1975, theChicago Board Options Exchange, Inc.("CBOE"), whose option plan were ap-proved by the Commission In the preced-ing fiscal year, had 1,025 members andlisted call options on 67 stocks.36 Theaverage dally volume of options tradedon CBOE reached approximately 53,000contracts, representing 5,300,000 sharesof the underlying stocks."

DUring the past fiscal year, the Com-mission declared effective option plansof two other exchanges, the AmericanStock Exchange (Amex) and the PBWStock Exchange, Inc. ("PBW"). The Com-rmssion declared the Amex option planeffective In December 1974,38 and thatexchange began trading call options onJanuary 7, 1975. By the end of the fiscalyear, the Amex listed options on 40stocks, and had an average dally volumeof 17,016 contracts, representing 1,701,600shares of underlying stock.

In May 1975, the Oomrrussron declaredPBW's option plan effective and that ex-change began trading options on June27,1975.39

In addition to the three exchanges Witheffective option plans, the Pacrtrc StockExchange ("PaCifiC") announced ItS in-tention to initiate options trading and heldseveral discussions with the Oommrssron'sstaff regarding ItS preliminary work on aplan for such a program.

DUring the fiscal year, the CBOE, WithCommission approval, made numerouschanges In ItS option plan under Rule9b-1. For example, In response to Com-mission and CBOE concern about emerg-ing trading patterns in options where theexercise price had fallen substantrallybelow the market price, the CBOErestricted opening transactions In suchoptions.w At the same time, the CBOEprohibited market makers from quotingspreads In such options greater than Y4of $1.41 It also adopted provrsions totacrlrtate more orderly openings of trad-Ing and to eliminate market-makers'ability to gain priority over public ordersThe CBOE also strengthened ItS netcapital and margin rules.

The Arnex option plan, like that of theCBOE, calls for trading In options onstocks with a substantial number ofshares outstanding, Widely held and ac-tively traded. Members of the Amex, atthe time ItS option plans were declaredeffective, automatically obtained optiontrading pnvileqes on that exchange. Ingeneral, the Amex applied contractstandardization methods substantiallyIdentical to those used by the CBOE-that IS, options were made fungible by

15

limiting the contract variables such asexpiration months and the exercise, or"striking", prices.

The Amex options generally are tradedIn a manner very srrmlar to that for othersecuntres traded on that exchange. A rna-jor difference between the Amex's pro-gram and the CBOE's IS that the Amexuses, with certain modifications, a singlespecralist both to make a market and tohandle agency limit orders In Its options,while the CBOE splits the specraustsfunctions between a market-maker(dealer) and a board broker, performingthe agency tuncnon.« One modificationAmex made In ItS floor trading procedureIS that ItS registered floor traders whotrade options are required tp trade In away that assists the spscraust In main-taining a fair and orderly market In op-tions, and may be called upon by eithera floor official or floor broker to makecompetitive quotations In the market.

The PBW's program IS Similar to that ofAmex and CBOE In such areas as thecharacteristics of underlying stocks forItS options, clearing principles, and con-tract term standardization for ItS options.like the Amex, the PBW utruzes its exist-Ing specialrsts for market making in ItSoptions and requires ItS regIstered floortraders to assist the specralrsts PBW'splan, however, Involves for the first timeoptions traded on the same exchange asthe one on which the underlying secuntresare traded Because of this distinctivecharacteristic, the PBW has separated ItSoption floor from the rest of Its tradingfloor to prevent VIsual and direct audi-tory comrnumcatron between the twotrading areas. The PBW also protubrts ItSfloor members who have learned ofcertain large transactions about to beexecuted In an optron or an underlyingsecurity of an option class traded on thePBW from initiating orders In the sameoption until two minutes after the trans-action has been printed on the transactiontape.43 These measures were desiqnedprimarily to bar possrble misuse In PBW'soptron market of mtorrnatron obtained byfloor members relating to activity in anunderlying stock or In a block of options

16

before the information has been publiclydisseminated.

As previously reported,44 on the basisof conclusrons reached tollowmq thecomrmssron's hearings In early 1974 onmultiple-exchange options trading andoptions trading in general, the staff hadsuggested SUbject matters to be ad-dressed by all exchanges concernedbefore the initiation of multiple-exchangeoptions trading or the expansion of theCBOE (which was the only exchange thentrading options). One such recommenda-tion called for a common national clear-ing system. In declaring the Amex optionplan effective, which authorized the initia-tion of multiple-exchange option trading,the Commission noted and approved thejoint establishment by the Amex and theCBOE of the Options Clearing Corpora-tion ("OCC") to Implement a nationalclearing system for all exchange-listedoptlons.ss All exchange-traded optionswere thereafter issued, guaranteed andregistered by the OCC in compliance withfederal securities laws. Moreover, theOCC currently clears and settles alloption transactions effected In exchangetraded options, now also including thoseon the PBW, and it will perform the sametuncnons for those exchanges whichmay later initiate options programs andbecome partlcipants in OCC.

Another recommended prerequisite tomultiple-exchange trading of options wasthe achievement of a common tape forreporting transactions in all listed options.In response, the exchanges concernedset up a policy-making body, the OptionsPrice Reporting Authority ("OPRA"), tocoordinate the establishment and on-gOing administration of a separate com-mon options tape on the floor ofexchanges trading options and after atrial period, If econormcal, to offer ac-cess to the tape to subscnbers, OPRAalso administers orssermnanon of lastsales data concerning options from theparticipating exchanges to vendors ofautomated interrogation devlces.46 Fur-thermore, In response to Oornrrussronstaff recommendations, all the parnclpat-

Ing exchanges have agreed to make op-tion quotations available through thevendors to qualified non-members as wellas to their own members and havereached general agreement regardingstandardization of terms of exchange-traded options These actions have allbeen approved by the Comrmssron.s?

Uniform Net Capital Rule

On June 26, 1975,48 the Commissionannounced the adoption of a Uniform netcapital rule, Securities Exchange ActRule 15c3-1 , effective September 1,1975,subject to transitional provisions whichdelay the effective date of certain pro-vrsrons until January 1, 1976. The adop-tion of the rule followed consideration ofcomments received In response to a re-lease In. which the proposed rule hadbeen re-published for comment 49