Annual Report 1950 - SEC.gov

248

Sixteenth Annual Report of the Securities and Exchange Commission Fiscal Year Ended June 30, 1950 UNITED S'TATES GOV,ERNMENT PRINTING OFFICE, WASHINGTON: IUO For lillIeby the Superintendent ot Documents, U. S. GuYerom.nt PrinU ... Olll.,. Wuhlnilon 25, D. C. Price 55cents -

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Annual Report 1950 - SEC.gov

Sixteenth Annual Report

of the

Securities and Exchange

Commission

Fiscal Year Ended June 30, 1950

UNITED S'TATES GOV,ERNMENT PRINTING OFFICE, WASHINGTON: IUO

For lillIeby the Superintendent ot Documents, U. S. GuYerom.nt PrinU ... Olll.,.Wuhlnilon 25, D. C. Price 55cents-

II

SECURITIES AND EXCHANGE COMMISSION

Headquarters Office

425 Second Street'NW.

Washington 25, D. C.

COMMISSIONERS

HARRY A. McDoNALD, Chairman.DONALD C. COOK, Vice-OhairmanRICHARD B. MCENTIRE

PAUL R. ROWEN

EDWARD T. MCCORMICK

ORVAL L. Dnbors, Secretary

LEITER OF TRANSMI1TAL

SECURITIES AND EXCHANGE C01\IMISSION,

Washington, D.O., January 31, 1951.SIR: I have the honor to transmit to you the Sixteenth Annual

Report of the Securities and Exchange Commission, in accordancewith the provisions of section 23 (b) of the Securities Exchange Actof 1934, approved June 6, 1934; section 23 of the Public UtilityHolding Company Act of 1935, approved August 26, 1935; section46 (a) of the Investment Company Act of 1940,approved August 22,1940, section 216 of the Investment Advisers Act of 1940, approvedAugust 22, 1940,and section 3 of the act of April 25, 1949,amendingthe Bretton Woods Agreements Act.

Respectfully,HARRY A. McDoNALD,

Ohairman.THE PRESIDENT OF THE SEN ATE,

THE SPEAKER OF THE HOUSE OF REPRESENTATIVES,

Washington, D. O.III

5

1123344444

677778888999

1010111112121518181920

TABLE OF CONTENTSPage

Foreword_________________________________________________________ XICommissioners and staff officers___________________________________ __ XVIRegional and branch offiees., ________________________________________ xv

PART I

ADMINISTRATION OF THE SECURITIES ACT OF 1933The registration process

Purpose of registrationExamination procedureEffective date of registration statement;Time required for registration

The volume of securities registeredVolume of all securities registeredVolume of securities registered for cash sale

A. All securitiesB. Stocks and bondsC. All securities registered for cash sale for the accounts of

issuers-by type of issuerD. Use of investment bankers as to securities registered for

cash sale for the accounts of issuersAll new securities offered for cash sale

Registered securitiesUnregistered securities

CorporateNoncorporate

Total registered and unregistered securitiesRegistration statements filed

Disposition of registration statementsOther documents filed under the act

Exemption from registration under the actExempt offerings under regulation AExempt offerings under regulation A-MExempt offerings under regulation B

Confidential written reports under regulation BOil and gas investigations

Formal actions under section 8Stop-order proceedings under section 8 (d)

Deficiencies discovered in examination of registration statementsChanges in rules, regulations and forms

Regulation BW-Reports of International Bank for Reconstruction,Regulation A-General exemption of small issues

Litigation under the act

PART II

ADMINISTRATION OF THE SECURITIES EXCHANGE ACT OF1934

Regulation of exchanges and exchange trading; ___________________ 23Registration of exehanges.L, , _ ________________________ 23Disciplinary actions by exchanges against membera, ___________ 26

Registration of securities on exchanges___________________________ 26Examination of applications and reports______________________ 26Statistics of securities registered on exchanges_________________ 28Temporary exemption of substituted or additional securities., ___ 28Special offerings on exchangea.; _ ____ ______________ 29Secondary distributions approved by exchanges; __ ____________ 30

V

_ _ _ _ _ _ _ _ _ _

_

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

_ _

VI TABLE OF COKTENTS

PART II-Continued

ADMINISTRATION OF THE SECURITIES EXCHAKGE ACT OF1934-Continued

Termination of registration under section 19 (a) (2)Unlisted trading privileges on exchanges

Applications for unlisted trading privilegesDelisting of securities from exchanges

Securities delisted by applicationSecurities delis ted by certificationSecurities removed from listing on exempted exchanges

Manipulation and StabilizationManipulation

Trading investigationsStabilization

Security transactions of corporation insidersReports of transactions and holdingsPublication of data reportedPreventing unfair use of inside information

Statistics of ownership reportsSolicitations of proxies, consents, and authorizations

Statistics of proxy statementsExamination of proxies

Regulation of brokers and dealersRegistration

Administrative proceedingsRecord of broker-dealer proceedings

Broker-dealer insI?ectionsPricing practicesFinancial reports

Supervision of N ASD activity~~e~b~rship---~---------------------------------------- __ Disciplinary actions

Changes in rules, regulations, and formsForm 10Form 10- KForm 8-KForm 9-KForm 8Rule X-12A-4

Litigation under the act,Inju?~tio~ actions_:Participation as amUU8 cunaeAppellate proceedingsKaiser-Frazier investigation and litigation with Otis & Co

Page3131343535353636363838393940404141424243434445505151525252535353545454545455565858

PART IIIADMINISTRATION OF THE PUBLIC UTILITY HOLDING COM-

PANY ACT OF 1935The public utility industry under the acL________________________ 60Progress under section II-over-all summary _ __ __________________ 62Progress under section ll-survey of individual systems____________ 65Cities Service Co_____ __ ____ ___ ____ _____ _ 65The Commonwealth & Southern Corp____________________________ 67Electric Bond and Share Co_____________________________________ 68

American & Foreign Power Co., Inc_________________________ 69American Power & Light Co________________________________ 70Electric Power & Light Corp________________________________ 71National Power & Light Co_________________________________ 72

General Public Utilities Corp , _ _ _ __ ____ _ 73International Hydro-Electric System______ __ ___ 74Long Island Lighting Co_ ___ _______________ _______ _ ___ 76The Middle"West Corp____ __ __ _____________________ ____________ 77National Gas & Electric Corp___________________________________ 78

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

_ _ _ _ _ _ _ _ _

~ _ _ _ _

TABLE OF CONTENTS VII

PART III-Continued

ADMINISTRATION OF THE PUBLIC UTILITY HOLDING COMPANY ACT 0%" 1935-Continued

New England Public Service Co ................................. Niagara Hudson Power Cor .......h.. .............. North Continent Utilities & ~ ~ o ~ & ~ o ~ . ~ . ~ . ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ Standard Power and Light Gorp.-Standard Gas and Electric Co. The United Corp .......................................... The United Li h t & Railways Co ............................

The continuing hol8ing company systems ......................... American Gas m d Electric Co .............................. American Natural Gas Co.................................. Central and South West Cor ......................... The Columbia Gas System, ~ I : : : I ........................ Consolidated Natural Gas Ca ............................... Delaware Pawer & Light Co ................................ Interstate Power Co ....................................... Middle South Utilities, Inc ................................. National Fuel Gaa Co ...................................... New England Electric System ............................... Xew England Gas & Electric Association ..................... Northern Natural Gas Co.................................. Northern States Power Co .................................. Ohio Edison Co ........................................... The Southern Co .......................................... Utah Power and Light Co ................................... The West Penn Electrio Co ..................................

Issues of seeuntiea, assumptions of liabilities and alterations of rights. . Competitive bldding ............................................ Cooperation with State and Local regulatory authorities ............ Litigation under the act ........................................

Actions to enforce voluntary plans under section 11 (e)........ Petitions to review orders of the Commission under section 24 (a) . Enforcement proceedings under section 11 (e).. ...............; Petitions to review orders of the Commission .................. Petitions for intervention ...................................

PAR'l'I('11'.4TIOY OF THE CO3lhllJSION I S CORPORVI'E KE-011(:.4TlZ.4TlOY.3 I'NLIER C1f.4l'TEH ...........?(OF T11E 13AXKIt17PTC'\' ACT, AS AMENDED

Commission's functions under chapter X......................... The Commission ss a party to proceedings ........................ Summary of activitis ..........................................

Activities relating to the trusteeship ......................... Problems in the administration of the estate .................. Responsibilities of fiduciaries ................................ Activities with respect to allowances .........................

Institution of chapter X proceedings ............................. .......................... XPlans of reorganization under chapter

Fairness ofplan ........................................... Feasibility of plan ......................................... Consummation of plan .....................................

Advisory rep0 rt.. .............................................

ADMINISTRATION OF T H E TRUST INDENTURE ACT OF.......1820 Kature of trust indenture regulation . . . . . . . . . . . . . . . . . . . . . . lntraration r i r h Seeuritie~.4ct of 1833. . . . . . . . . . . . . . . . . . . Stari.+trrs of inderrturclr qualified.. . . . . . . . . . . . . . . . . . . . . .

VIII T~LE OF CONTENTS

147147147151152152153153155156156160162165165166166166167167168169169169170172

PART VIADMINISTRATION OF THE INVESTMENT COMPANY ACT OF

W~ h~Registration under the act___ ____ _ __ ____ 140Types and investment policies of companies formed_______________ 141Sellingliterature_______________________________________________ 141Data on investment companiea.; ___ ___ __ __ _ 142Applications flled; , ____________________________________________ 142Litigation under the act, _______________________________________ 143

PART VIIADMINISTRATION OF THE INVESTMENT ADVISERS ACT OF

1940Registration statlsties, _________________________________ 145Administrative proceedings _____________________________________ 145

PART VIIIOTHER ACTIVITIES OF THE COMMISSION UNDER THE

VARIOUS STATUTESThe Commission in the courts

CivilproceedingsCriminal proceedings

Complaints and InvestigatlonsInvestigations of securities violationsCanadian situation

Securities violations fileActivities of the Commission in accounting and auditing

Examination of financial statementsProposed amendment of regulation S-X

.. Other de,:el!>pme~t~ in accounting and auditingDivision of oplIDon wntmgInternational Bank for Reconstruction and DevelopmentAdvisory and interpretative assistanceConfidential treatment of applications, reports or documentsStatistics and special studies

Saving studyFinancial position of corporationsCapital marketsPersonneLFiscal affairsPublications

Public releasesOther publications

Information for public inspectionPublic hearings

PART IXAPPENDIX-8TATISTICAL TABLES

Table 1. Registrations fully effective under the Securities Act of 1933_ __ 174Part 1. Distribution by months_________________________________ 174Part 2. Breakdown by method of distribution and type of security

of the volume proposed for cash sale for account of is-suers________________________________________________ 175

Part 3. Purpose of registration and industry of registrant- _________ 176Table 2. Claesificatlon by quality and size of new bond issues registered

under the Securities Act of 1933 for cash sale to the generalpublic through investment bankers during the fiscal years 1948,1949, and 1950_ _____ ___________________________________ 177

Part 1. Number of bond issues and aggregate value_______________ 177Part 2. Compensation to distributorB____________________________ 178

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

TABLE OF CONTENT&

PUT IX--Continued

APPENDIX-STATISTICAL TABLES-Continued

IX

PageTable 3. New securities offered for cash sale in the United States________ 179

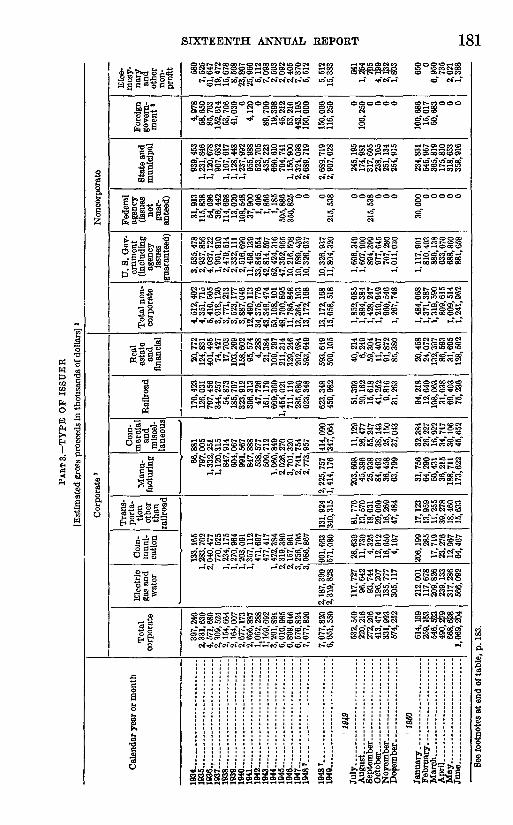

Part 1. Type of offering________________________________________ 179Part 2. Type of security_______________________________________ 180Part 3. Type of issuer_________________________________________ 181Part 4. Private placements of corporate securities_________________ 182

Table 4. Proposed uses of net proceeds from the sale of new corporatesecurities offered for cash sale in the United Btates , ___ ___ 184

Part 1. All corporate__________________________________________ 184Part 2. Public utility _ _ _ __ _______ 185Part 3. IndustriaL ___ __ _ _______ 187Part 4. Railroad., __ ____ _ __ 189Part 5. Real estate and financiaL_______________________________ 190

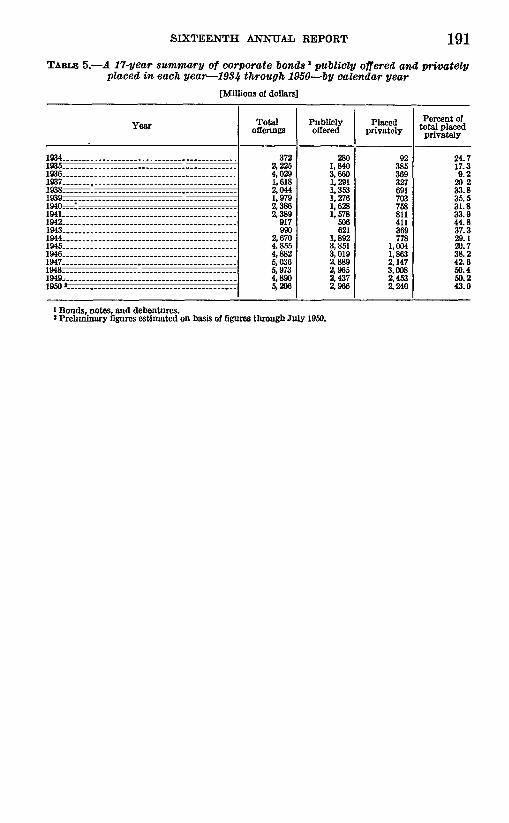

Table 5. A 17-year summary of corporate bonds publicly and privatelyplaced in each year-1934 through 195Q--by calendar yearc , , 191

Table 6. A 17-year summary of new securities offered for cash in theUnited Statesc. , , _ _ _ _ _____________ 192

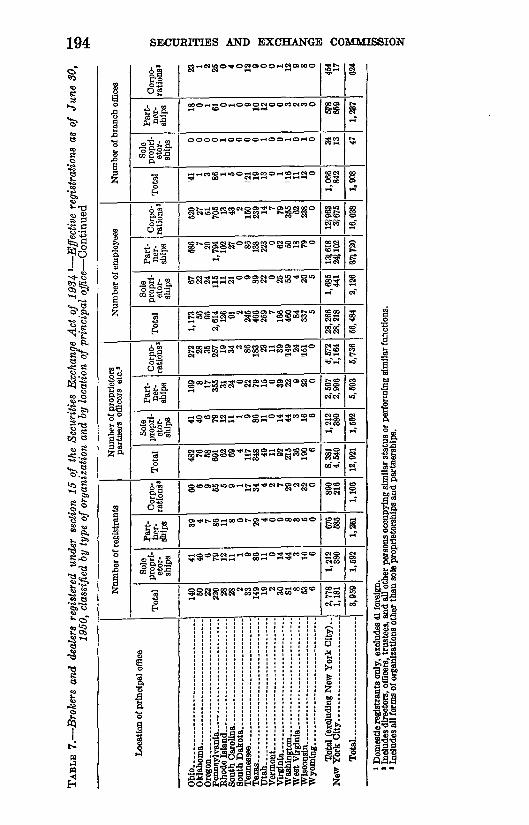

Table 7. Brokers and dealers registered under section 15 of the SecuritiesExchange Act of 1934--effective registrations as of June 30,1950, classified by type of organization and by location ofprincipal offiee , _ __ ___ ___ 193

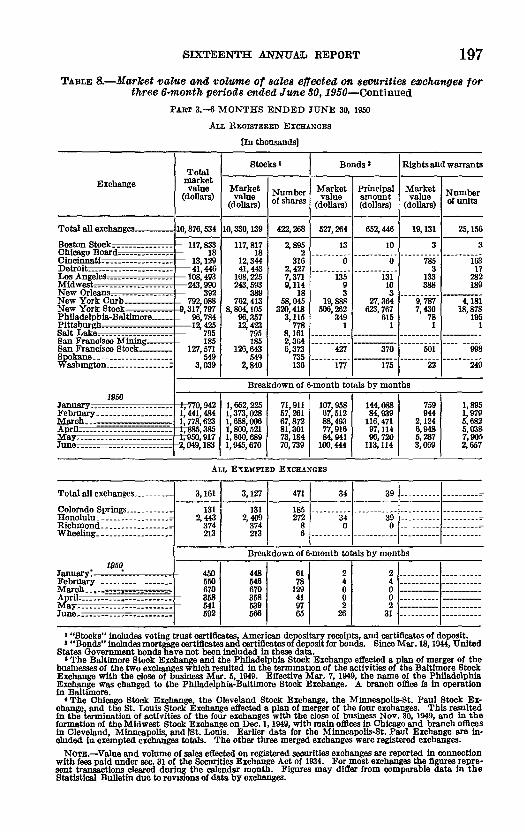

Table 8. Market value and volume of sales effected on securities exchangesfor the three 6-months periods ended June 30, 1950__________ 195

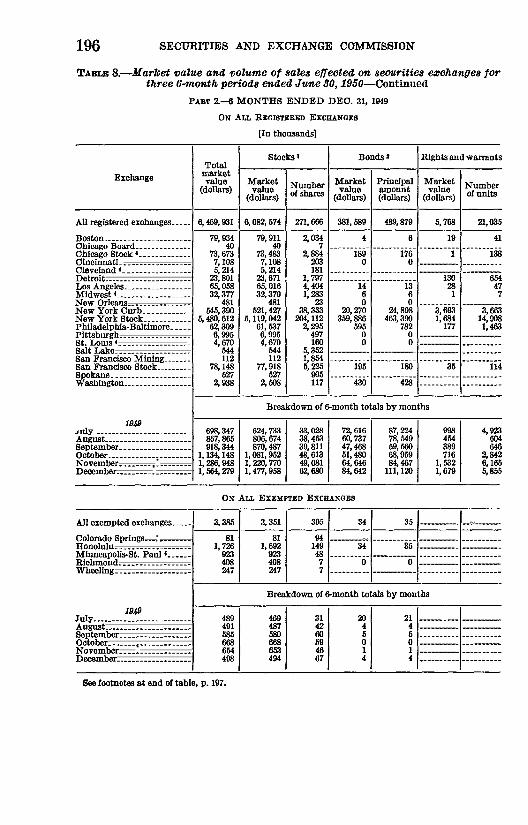

Part 1. Six months ended June 30, 1949__________________________ 195Part 2. Six months ended December 31,1949_____________________ 196Part 3. Six months ended June 30, 1950__________________________ 197

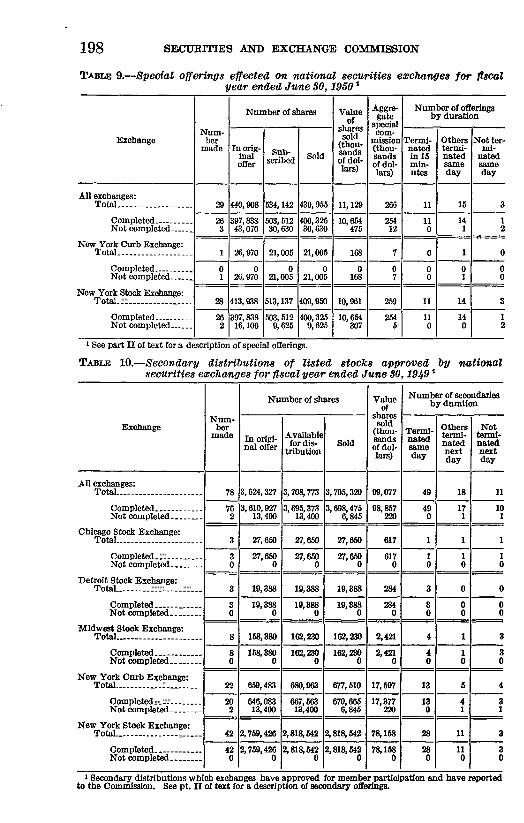

Table 9. Special offerings effected on national securities exchanges forfiscal year ended June 30,1950___________________________ 198

Table 10. Secondary distributions of listed stocks approved by nationalsecurities exchanges for fiscal year ended June 30, 1950______ 198

Table 11. Classification by industry of issuers having securities registeredon national securities exchanges as of June 30, 1949 and as ofJune 30, 1950_ ________ __________ _______________________ 199

Table 12. Number and amount of securities classified according to basis forthe admission to dealing on all exchanges as of June 30, 1950__ 199

Table 13:Part 1. Number and amount of securities classified according to the

number of registered exchanges on which issue was ad-mitted to dealing as of June 30,1950___________________ 200

Part 2. Proportion of registered issues that are also admitted to un-listed trading privileges on other exchanges as of June 30,1950________________________________________________ 200

Part 3. Proportion of issues admitted to unlisted trading privilegesthat are also registered on other exchanges as of June 30,1950________________________________________________ 201

Part 4. Proportion of all issues admitted to dealing on registeredexchanges that are admitted to dealing on more than 1registered exchange as of June 30, 1950__________________ 201

Table 14. Number of issuers having securities admitted to dealings onexchanges as of June 30,1950, classified according to the basisfor admission of their securities to dealing_________________ 201

Table 15. Number of issuers having stocks only, bonds only, and bothstocks and bonds admitted to dealings on exchanges as ofJune 30, 1950_ ______________ ____________________ _______ 201

Table 16. For each exchange as of June 30, 1950, the number of issuersand securities, basis for admission of securities to trading, andthe percentage of stocks and bonds admitted to trading on oneor more other exchanges_________________________________ 202

Table 17. Number of issues admitted to unlisted trading pursuant toclauses 2 and 3 of section 12 (f) of the Securities Exchange Actof 1934 and volume of transactions therein________________ 203

x TABLE OF CONTENTS

PART IX--Continued

APPENDIX-STATIS'I'ICAL TABLES-ContinuedPage

Table 18. Reorganization cases instituted under chapter X and section77-B in which the Commission filed a notice of appearanceand in which the Commission actively participated during thefiscal year ended June 30,1950___________________________ 204

Table 19. Reorganization proceedings in which the Commission partici-pated during the fiscal year ended June 30,1950___________ 204

Table 20. Summary of cases instituted in the courts by the Commissionunder the Seeurities Act of 1933, the Securities Exchange Actof 1934, the Public Utility Holding Company Act of 1935, theInvestment Company Act of 1940, and the InvestmentAdvisers Act of 1940____________________________________ 206

Table 21. Summary of cases instituted against the Commission, cases inwhich the Commission participated as in intervenor or amicuscuriae, and reorganization cases on appeal under chapter X inwhich the Commission participated-pending during thefiscal year ended June 30,1950___________________________ 206

Table 22. Injunctive proceedings brought by Cornmission, under theSecurities Act of 1933, the Securities Exchange Act of 1934, thePublic Utility Holding Company Act of 1935 and the Invest-ment Advisers Act of 1940, which were pending during thefiscal year ended June 30,1950__________________________ 207

Table 23. Indictments returned for violation of the acts administered bythe Commission, the Mail Fraud statute (sec. 338, title 18,U. S. C.), and other related Federal statutes (where the Com-mission took part in the investigation and development of thecase) which were pending during the 1950 fiscal year________ 210

Table 24. Petitions for review of orders of Commission under the SecuritiesAct of 1933, the Securities Exchange Act of 1934, the PublicHolding Company Act of 1935, and the Investment CompanyAct of 1940, pending in circuit courts of appeals during the fiscalyear ended June 30,1950________________________________ 215

Table 25. Contempt proceedings pending during the fiscal year endedJune 30,1950__________________________________________ 216

Part 1. Civil contempt proceedings , ___ 216Part 2. Criminal contempt proceedings___________________________ 216

Table 26. Cases in which the Commission participated as intervenor or asamicus curiae, pending during the fiscal year ended June 30,1950__________________________________________________ 217

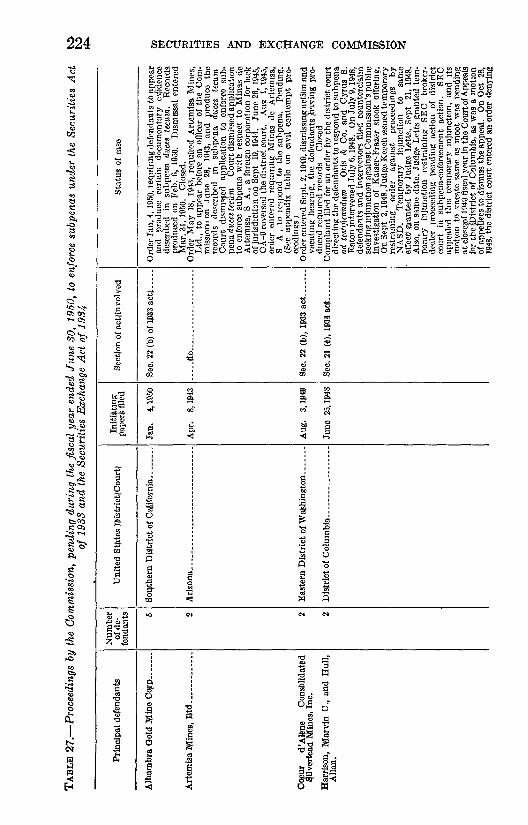

Table 27. Proceedings by the Commission, pending during the fiscal yearended June 30, 1950, to enforce subpenas under the SecuritiesAct of 1933 and the Securities Exchange Act of 1934________ 224

Table 28. Miscellaneous actions against the Commission or employees ofthe Commission during the fiscal year ended June 30, 1950___ 225

Table 29. Actions to enforce voluntary plans under section 11 (e) tocomply with section 11 (b) of the Public Utility HoldingCompany Act of 1935___________________________________ 226

Table 30. Actions under section 11 (d) of the Public Utility Holding Com-pany Act of 1935 to enforce compliance with Commission'sorder issued under section 11 (b) of that act_______________ 228

Table 31. Reorganization cases under chapter X of the National Bank-ruptcy Act in which the Commission participated whenappeals were taken from district court orders __ ____________ 229

Table 32. A 17-year summary of criminal cases developed by the Com-mission-1934 through 1950, by fiscal year________________ 230

Table 33. Summary of criminal cases developed by the Commission whichwere still pending at June 30, 1950-by fiscal year__________ 231

Table 34. A 17-year summary classifying all defendants in criminal casesdeveloped by the Commission-1934 to July 1, 1950________ 231

Table 35. A 17-year summary of all injunction cases instituted by theCommission-1934 to July 1, 1950, by calendar year________ 232

FOREWORD

This is the Sixteenth Annual Report of the Securities and ExchangeCommission. It covers the year July 1, 1949 to June 30, 1950.

The report first outlines the activities of the Commission under themajor statutes entrusted to it and, in later sections, deals with over-allactivities that cut through statutory lines.

For the Securities and Exchange Commission the year was an ex-tremely active one. Financing by industry, the major source of work-load for the Commission, has continued at a high rate. The Commis-sion's job in a particular financing may be the clearance of a registra-tion statement under the Securities Act or the approval of the financingunder the Public Utility Holding Company Act, or it may be, byformal or informal means, to issue an opinion as to whether the financ-ing is exempted from these statutes. In any case the work must bedone thoroughly and promptly-to guard the interest of investorsand to be fair to business whose timing schedules may be closelygeared to market conditions.

This balance of interests is, in our view, essential to the effectivenessof the laws. Thorough performance is a necessity in order to servethe investor whom the laws seek to protect. Unwarranted delays are adisservice to those who must live with and comply with the laws. Thebasic philosophy behind these statutes is that free enterprise is facili-tated by honest and decent relations between investor and management.The Commission stresses the facilitative aspect of these laws.

Past reports of the S. E. C. have outlined its progress toward simpli-fying administration and compliance. Those efforts continue. Theyare--in the context of our disclosure laws-e-eflorts to transform dis-closure on paper into effective information of the investor. Forexample, the Commission has by dint of constant pressure succeededin eliminating from prospectuses destined for investors a good deal oftechnical and confusing detail. This process of simplification has notyet reached the financial statements in prospectuses to the extent theCommission would like to see that done. The accounting professionhas recently been invited to join the Commission in an effort to re-duce the present formal presentation of information in balance sheetsand income statements to homely and understandable terms.

Material problems have faced the Commission in its study of methodsof revising the mechanics of prospectus distribution under t'he Securi-ties Act. These difficulties have delayed the recommendation of statu-tory changes. However, the study has proved to be a fruitful onenevertheless. It has stimulated an active interest in the usefulnessof the prospectus as a vehicle of investor information. It hasprompted active attempts-with revisions already made and more inthe offing-to change the prospectus into a piece of informative litera-ture useful to the layman. It has led to a consideration of thepossibilities of authorizing more informative identifying literature

xt

XII FOREWORD

to be used by distributors in advance of effectiveness of registration.It has resulted in a consideration of the possibility of encouragingpreeffective use of adequate informative material. One possible rulenow being discussed would allow this pre-effective material to besupplemented (after effectiveness) with a simple sheet giving missinginformation about price, yields, and spreads, so that the pre-effectivematerial and the supplemental sheet together would constitute theprospectus. In this way the need for printing and distributing aftereffectiveness a wholly new prospectus (duplicating much of the infor-mation previously circulated) could be avoided.

These rule revisions are designed to encourage investors to readpros.l?ectuses and to stimulate distributor interest in making timelydistribution of adequate information. "Whether they are substitutesfor a revision of the statute, which would make it mandatory to pro-vide a prospectus before selling a security, cannot now be statedwith any assurance.

Of particular significance in this report is the record of our progressunder section 11 of the Public Utility Holdin~ Company Act. Thatsection requires the integration and simplification of holding companysystems, and-under certain circumstances-the elimination of hold-ing companies. These aims are accomplished by voluntary plans,approved by the Commission and, in many cases, by the courts, fordisposal of holding companies' controlling interests in operating com-panies, for reorganization of system companies, or for dissolution oftop or intermediate holding companies.

In the 12 years of active administration of these provisions over$10,000,000,000of assets have been released from jurisdiction under theHolding Company Act. There remain subject to the act about$13,000,000,000of assets in holding company systems; and it is guessedthat the Commission will remain with a $6,000,000,000to $7,000,000,000industry to regulate under the standards of the act.

The completion of this vast program would bring administrationof the Holding Company Act into a new phase. Enormous increasesin utility construction in recent years have put a heavy demand on thestaff for the processing of financing applications. The defense pro-gram will continue to require large outlays by the industry for capitalexpansion, and that work alone will draw heavily on personnelresources no longer committed to the section 11 phase of our work.

Of necessity many duties under the act have had to be rationed inorder to concentrate on the task of integration and simplification. Aresurvey of those duties is in progress.

On January 9, 1950, the Commission transmitted to the Congress areport recommending an amendment to the Securities Exchange Actof 1934 which would extend to investors in unregistered securities theprotections afforded by the act in respect of the availability of publicinformation, the provision of data necessary for intelligent exerciseof the right to vote, and the regulation of insiders' short-term trading.This report supplemented and brought up to date an earlier reportwhich had been submitted on June 19, 1946.

Economic development since 1946, the report indicated, had mademore essential the need for this legislation. Individual holdings ofcash, deposits, and U. S. Government securities were at a record high,

FOREWORD XIII

and yet investment in equity securities had not correspondinglyincreased. Where idle funds were used for the purchase of suchsecurities, they were used largely to increase the investment in securi-ties subject to the protections of the Securities Exchange Act. Thelack of publicity about companies outside of the scope of the act has,in our view, been a substantial factor in the lack of investor interestin these securities. A survey of the financial manuals disclosed thatthere were approximately 1,800 companies which would be coveredby the proposed legislation.

After the receipt of these recommendations by the Commission,there were introduced into the Senate by Senator Frear and into theHouse of Representatives by Representative Sadowski identical billsproviding for the amendment of the Securities Exchange Act inaccordance with the Commission's proposals. Hearings were heldbefore the Senate Banking and Currency Committee, but no committeereport was rendered to the Congress. Senator Frear explained in aspeech delivered on the floor of the Senate that this was caused bythe continuous emergency which faced the Banking and CurrencyCommittee as a result of the Korean War. According to the Senator,it was decided that the subcommittee should further study the legis-lation with a view to action on it at the next session.

COMMISSIONERS AND STAFF OFFICERS

(as of October 20, 1950)Commissioners Te~~~p;re8

HARRYA. McDoNALD, of Michigan, Chairman-______________________ 1951DONALDC. COOK,of l\1ichigan, Vice Chairman_______________________ 1954RICHARDB. McENTIRE, of Kansas_________________________________ 1953PAUL R. ROWEN, of l\1assachusetts_________________________________ 1955EDWARDT. MCCORMICK,of Arizona________________________________ 1952

Secretary: ORVALL. DuBOIS

Staff OfficersBALDWIN B. BANE, Director, Division of Corporation Finance. ANDREW

JACKSON,Associate Director.MORTONE. YOHALEM,Director, Division of Public Utilities.ANTHOX H. LUND, Director, Division of Trading and Exchange. SHERRY

T. McADAM, Jr., Associate Director.ROGERS. FOSTER,General Counsel. LOUIS Loss, Associate General Counsel.EARLE C. KING, Chief Accountant.MICHAELE. l\100NEY,Director, Division of Opinion Writing.JEROMES. KATZIN, Executive Assistant to the Chairman.NATHAND. LoBELL,Executive Adviser to the Commission.HASTINGS P. AVERY,Director, Division of Administrative Services.WILLIAM E. BECKER,Director, Division of Personnel.JAMES J. RIORDAN,Director, Division of Budget and Finance.

XIV

REGIONAL AND BRANCH OFFICES

Regional AdministratorsZone 1-Peter T. Byrne, Equitable Building (Room 2006), 120 Broadway,

New York 5, N. Y.Zone 2-Philip E. Kendrick, Post OfficeSquare Building (Room 501),79 Milk

Street, Boston 9, Mass.Zone 3-William Green, Atlanta National Building (Room 322), Whitehall

and Alabama Streets, Atlanta 3, Ga.Zone 4--Charles J. Odenweller, Jr., Standard Building (Room 1608), 1370

Ontario Street, Cleveland 13, Ohio.Zone 5-Thomas B. Hart, Bankers Building (Room 630), 105 West Adams

Street, Chicago 3, Ill.Zone 6-0ran H. Allred. United States Courthouse (Room 103), Tenth and

Lamar Streets, Fort Worth 2, Tex.Zone 7-John L. Geraghty. Midland Savings Building (Room 822), 444

Seventeenth Rtreet. Denver 2. Colo.Zone 8-Howard A. Judy. Appraisers Building (Room 308). 630 Sansome

Street. San Francisco 11, Calif.Zone 9-James E. Newton. 1411 Fourth Avenue Building (Room 810),

Seattle 1, Wash.Zone lo-E. Russel Kelly, 425 Second Street NW., Washington 25, D. C.

Branch OfficesFederal Building (Room 1074) Detroit 26. Mich.United States Post Office and Courthouse (Room 1737), 312 North Spring

Street, Los Angeles 12, Calif,Pioneer Building (Room 400), Fourth and Roberts Street, St. Paul, Minn.Wright Building (Room 327), Tulsa 3, Okla.United States Courthouse and Customhouse (Room 1006), 1114 Market

Street, St. Louis 1, Mo.

xV

•

PART I

ADMINISTRATION OF THE SECURITIES ACT OF 1933The purpose of the Securities Act of 1933 is to provide full and fair

disclosure and to prevent fraud in the sale of securities in interstateand foreign commerce and through the mails. To this end, the actrequires that issuers of securities to be offered for such public salemust file with the Commission registration statements setting forthprescribed information about the securities; that investors must befurnished, at or before delivery of the security purchased, a copy of arequired prospectus containing the more significant items of suchinformation; and civil and criminal penalties are provided for secu-rities frauds. The act does not authorize the Commission to pass onthe investment merits of securities and it makes representations to thecontrary unlawful.

THE REGISTRATION PROCESS

Purpose of Registration

Unless exempted from the Securities Act, securities offered for salein interstate commerce or by the use of the mails must be registered.Securities for which such exemption is provided consist, in general, ofgovernment and municipal securities and the issues of banks, railroads,cooperatives and other organizations and associations specified in sec-tion 3 (a) of the act or covered by exemptions in rules and regulationsadopted by the Commission, as discussed elsewhere in this report, pur-suant to section 3 (b) of the act. In addition, while the act containsno exemption for securities of governmental or other foreign issuersas such, Public Law 142, 81st Congress, approved by President Tru-man on June 29, 1949,extended a specific exemption to securities issuedor guaranteed by the International Bank for Reconstruction andDevelopment from the registration requirements of both the SecuritiesAct of 1933 and the Securities Exchange Act of 1934.

An integral part of each registration statement is the prospectus,which sets forth the more pertinent information about the securityoffering. As a basic method of direct disclosure to investors, theprospectus plays a vital role in carrying out the purpose of the act.

The registration statement as a whole discloses material factsdealing, among other things, with the character, size, and profitable-ness of the business, its capital structure, the uses to which the companyintends to put the proceeds realized from the sale of the securities,options outstanding against securities of the issuer, remuneration ofofficers and directors, bonus and profit-sharing arrangements, under-writers' commissions, and pending and threatened legal proceedings.

There must also be included in this document certified financial state-ments of the business enterprise.

915841--51----2 1

2 SECURITIES AJ\TJ) EXCHANGE COMMISSION

The information contained in registration statements filed with theCommission is not only made available immediately for public inspec-tion at the officesof the Commission but also forms the basis of wide-spread publicity released by financial news services, financial writers,and newspapers throughout the nation, which further accelerates theprocess of getting this information rapidly before a greatly enlargedfield of potential investors.

While the purpose of registration is thus to secure full and fairdisclosure of material facts about securities to enable prospectiveinvestors to judge the risk involved intelligently, it is not intendedto remove the risk from investment decisions. The Commission is notauthorized under the Securities Act of 1933 to pass on the investmentmerits of securities, and an effective registration statement does notimply that the Commission has in any way passed upon the meritsof or given approval to the securities covered. Section 23 of the actmakes it unlawful to make any contrary representation to any pro-spective purchaser.Examination Procedures

One of the Commission's most important undertakings has beenits development of procedures and techniques, which are constantlyundergoing improvements as dictated by experience, for the fast andthorough examination of registration statements to determine com-pliance with the disclosure requirements of the act. The need forspeed in the examination process arises not only from the statutoryprescription of an effective date of the registration statement, in theordinary case on the twentieth day after its filing, but also from theCommission's desire to avoid unnecessary interference with financingplans.

"'Whereexamination shows the registration statement to be inac-curate or incomplete in disclosure of material information, the Com-mission may resort to its power under section 8 of the act and issuean order preventing or suspending the effectivenessof the registrationstatement. However, the Commission has, during the past five years.continued its policy of exercising this power sparingly. Instead, ithas relied for enforcement mainly upon the long-standing practice ofsecuring an amendment to the registration statement. Accordingly,registrants are informally advised, as promptly as possible after thestatements are filed, of any material misrepresentations or omissionsfound upon examination and they are afforded an opportunity tofile correcting amendments before the statements become effective.This advice is furnished by means of an informal "letter of comment"which indicates what information should be corrected or supple-mented to meet the disclosure standards.

Another informal procedure that has proved effective in speedingthe registration process is the "pre-filing conference" between staffmembers and representatives of registrants and underwriters. In thismanner registrants are encouraged to discuss problems in connectionwith the proposed filing for the purpose of determining in advancewhat types or methods of disclosure may be necessary under the cir-cumstances. This has contributed to the marked reduction in the num-

SIXTEENTH ANNUAL REPORT 3

bel' of instances where the Commission has found it necessary to resortto stop-order proceedings or other formal action under section 8.

Neither the Commission, the issuer, nor the underwriter desires astatement to become effective unless it complies with the act. Often,the staff will ascertain that deficiencies exist in the registration state-ment as filed, or the issuer or underwriter may wish either to amendthe statement or simply to delay its effectiveness because of changesin the securities market or for other business reasons. In such cases,if there is a danger that the registration statement may become effec-tive in defective form or prematurely for the purposes of the issuer orunderwriter, it is customary for the registrant to file a minor amend-ment, called a "delaying amendment," which starts the 20-day wait-ing period running anew.Effective Date of Registration Statement

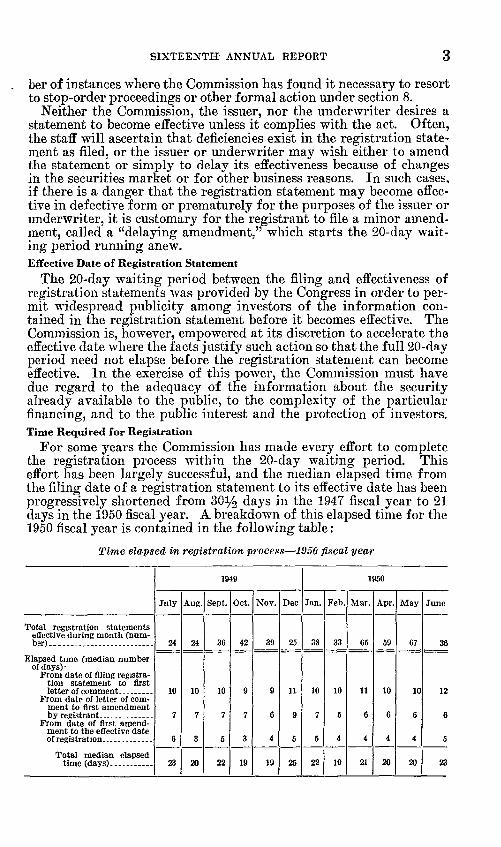

The 20-day waiting period between the filing and effectiveness ofregistration statements was provided by the Congress in order to per-mit widespread publicity among investors of the information con-tained in the registration statement before it becomes effective. TheCommission is, however, empowered at its discretion to accelerate theeffective date where the facts justify such action so that the full20-dayperiod need not elapse before the registration statement can becomeeffective. In the exercise of this power, the Commission must havedue regard to the adequacy of the information about the securityalready available to the public, to the complexity of the particularfinancing, and to the public interest and the protection of investors.Time Required for Registration

For some years the Commission has made every effort to completethe registration process within the 20-day waiting period. Thiseffort has been largely successful, and the median elapsed time fromthe filing date of a registration statement to its effective date has beenprogressively shortened from 30y:! days in the 1947 fiscal year to 21days in the 1950fiscal year. A breakdown of this elapsed time for the1950fiscal year is contained in the following table:

Time elapsed in registration pl'ocess-1950 fiscal year

1949 1950

July Aug. Sept. Oct. Nov. Dec Jan. Feb. Mar. Apr. May June- -- - -- - - - -- - -- --

Total regrstratlon statementseffectiveduring month (num-

39 38 33ber)__________________________ 24 24 36 42 25 65 59 67 36-- - -- - - --Elapsed time (median number

ofdays)'From date of filing ragrstra-

tion statement to firstletter of comment. .... ___ . 10 10 10 9 9 11 10 10 11 10 10 12

From date of letter or com-ment to first amendmentby registrant. ... _______ . .. 7 7 7 7 6 9 7 5 6 6 6 6

From date of first amend-ment to tbe effectivedateor registration ___________ .. 6 3 5 3 4 5 5 4 4 4 4 5

-- - --- -- - - - -- - -- --Total median elapsedtime (days)___________ 23 20 22 19 19 25 22 19 21 20 20 23

-- - - -- - =

4 SECURITIES AND EXCHANGE COMMIS:SION

A.lthough the median elapsed time from filing to effectiveness was21 days in the 1950 fiscal year, this time was 20 days or less in sixmonths of the year, accounting for more than half of all the registra-tion statements which became effective during the year. The Com-mission intends to continue its efforts to bring the total elapsed mediantime down to 20 days or less in all months.'

THE VOLUME OF SECURITIES REGISTEREDVolume of All Securities Registered iu Fiscal Year

1950 1949Total registered $5,307,077,000 $5,333,362,000The amount of securities effectively registered during the 1950 fiscal

year was practically the same as that for the 1949 period.The volume registered in the 1950 fiscal year was distributed over

4872 statements covering 647 issues, as compared with 429 statementscovering 588 issues for the 1949 fiscal year.Volume of securities registered for cash sale

304,736,0004,686,051,000

$4, 381, 314, 000

621,027,0005,307,077,000

19J,9

$4,204,008,000193,870,000

4,397,878,000935,484,000

5,333,362,000

1950

Total registeredfor cash sale _Total registered for other than cashsale _Total of allregisteredsecurities _

A. ALL SECURITIES

Registered for cash sale for accounts ofissuers _Registered for cash sale for accounts ofothers than issuers _

B. STOCKS AND BONDS REGISTERED FOR CASH SALE FOR THE ACCOUNTSOF ISSUERS

Equity securitiesother than preferred stock,Preferred stock _Total allstock _All bonds _TotaL _

1950$1,786,056,000

467,929,0002,253,985,0002,127,330,0004,381,314,000

191,9$1,083,117,000

325,854,0001,408,971,0002,795,036,0004,204,008,000

1There Is no necessary connection between the total time elapsed In the registrationprocess and the 20 day waitIng perIod required by the statute. Under section 8 of theSecuritIes Act a regtstratlon statement becomes ell'ectIve on the 20th day after filing(unless the CommIssIon has accelerated ell'ectIveness). The filing of an amendment to theregistration statement begins the waIting period running anew, unless the CommIssIon hasconsented to or required the filing of the amendment.

After due notice and hearing the CommIssIon may refuse to permit a statement to be-come ell'ective. or may issue a stop-order determinIng the ell'ectiveness of the statement.

In view of the tradition of the CommissIon to rely on careful examination of registrationstatements and the procurement of corrections by voluntary means, emphasis In the regis-tration process is upon correction In response to a stair letter of comment, rather than uponformal procedures to refuse or terminate eftectiveness.

The total time elapsed in the registration process is not completely withIn the control ofthe CommissIon. As will be noted from the chart above, a substantial part of this total timeIncludes the time taken by the registrant to make corrections pursuant to a letter of com-ment and the subsequent time taken to examIne the amended statement.

As the chart shows the median elapsed tIme from the date of filing to the first letter ofcomment runs between 9 and 12 days. The remainder of the time Is consumed by theregistrant In making corrections and In a revIew of those correctIons by the stall'.

Customarily a statement Is declared eftectlve shortly after the receipt of the correctionsmade pursuant to the letter of comment. At times, however, more than one letter isnecessary.

This figure di1l'ers from the 488 shown in the table on p. 176 due to dill'erence inelasslfteatton as to time of ell'ectIveness of registration statements. See appendix table I,footnote 2 for details.

•

SIXTEENTH ANNUAL REPORT 5

(Millions of dollars) I

It should be noted that while the volume of bonds registered byissuers for cash sale decreased substantially, stock so registered showeda marked increase.

From September 1934 through June 1949 new money purposesrepresented 37 percent of the net proceeds expected from the cash saleof issues registered for the accounts of the issuers. In the 1950 fiscalyear new money purposes represented 51 percent of the expected netproceeds for the year-large enough to raise the 16-year average 2points to 39 percent,"

The table below shows the amount of each type of security registeredfor cash sale for the accounts of the issuers in each of the fiscal years1935through 1950as well as the three 5-year totals. In addition to thetotals of the new issues for cash sale, all registrations are shown for thesame periods.

Cash sale for account of issuers

Fiscal year ended June 30 All regis- Total Bonds and Common stocktrations Preferredtaee-ernount stock and certl1lcatescertificates of participation

1935' __________________________________ 913 686 490 28 1681936___________________________________ 4,835 3,936 3,153 252 5311937___________________________________ 4,851 3,635 2.426 406 8021938___________________________________ 2,101 1,349 666 209 4741939___________________________________ 2.579 2,020 1,593 109 3181935--39 15,280 11,626 8,328 1,003 2,293

1940___________________________________ 1,787 1,433 1,112 110 2101941___________________________________ 2,611 2,081 1,721 164 1961942___________________________________ 2,003 1,465 1,041 162 2631943___________________________________ 659 486 316 32 1371944___________________________________ 1,760 1,347 732 343 2721940-44. 8,820 6,812 4,922 812 1,078

1945___________________________________ 3,225 2,715 1,851 407 4561946___________________________________ 7,073 5,424 3,102 991 1,3311947___________________________________ 6,732 4,874 2,937 787 1,1501948 6,405 5,032 2,817 537 1,6781949___________________________________ 5,333 4,204 2,795 326 1,0831945--49____________________________ 28,768 22,249 13,502 3,047 5,698

1950___________________________________ 5,307 4,381 2,127 468 1,786

I Dollar amounts are rounded to millions and will not necessarily add to totals.I For 10 months ended June 30, 1935.

C. ALL SECURITIES REGISTERED FOR CASH SALE FOR THE ACCOUNTS OFISSUERS-BY TYPE OF ISSUEB

Tllpe of IssuerElectric,gas, and water companies _Financialand investment companies _Transportation and communication com-panies 1

Manufacturing companies _Foreign governments _Extractive companies _Merchandising companies _S'erVlcecompames., .Real estatecompanies ._

1950$2,038,227,000

1,067,692,000522,753,000506,304,000175,950,00033,027,00025,370,000

7,582,0004,409,000

19./9$1, 796, 709,000

680,600,000989,911,000679,447,000

o33,495,00014,675,000

9,171,000°Total____________________________ 4,381,314,000 4,204,008,000

IDoes not include companies subject to regulation by the Interstate Commerce Commission and there-fore exempt from registration.

See also appendix table 1, pt. 3.

__________________________--

_________ -----------------

_______________• ___________________

_

- _

•

6 SECUR'ITIES AND EXCHANGE COMMISSION

19J,9$2,758,454,000

557,361,000962,830,000

1950$2,927,787,000

Registrations of securities for cash sale by electric, gas, and watercompanies exceeded by 13 percent their previous high established inthe 1949 fiscal year. Those for the financial and investment com-panies exceeded by 18 percent their previous high established in the1946 fiscal year. These two groups accounted for 47 percent and 24percent respectively of the total for the year. Manufacturing com-panies and transportation and communication companies registeredabout equal amounts, each 12 percent of the total, decreases of 25 and47 percent, respectively, from the amounts of the 1949fiscal year.

D. USE OF INVESTMENT BANKERS AS TO SECURITIES REGISTERED FOR CASHSALE FOR THE ACCOUNTS OF ISSUERS

Amount registered to be sold throughinvestment bankers:

Under agreements to purchase forresaleUnder agreements to use "best efforts"to selL

Total registered to be sold through invest-ment bankers

Total registered to be sold directly to in-vestors by issuers

3,890,617,000

490,698,000

3,315,814,000

888,194,000

Total 4,381,314,000 4,204,008,000

The Commission's Section of Operational Statistics continues tostudy the costs of flotation of security issues. The greatest part ofthese costs continues to be commissions and discount, which are theamounts paid to investment bankers, the balance being distributedamong other expenses such as (a) those not affected by registration:exchange listings, Federal revenue, stamp taxes, State fees and taxes,trustees, transfer agents, etc., (b) those partly affected by registra-tion : printing and engraving, legal fees and expenses, accounting feesand expenses, engineering, appraising, etc., and miscellaneous and(c) those entirely attributable to registration: the S. E. C. filing feeof one one-hundredth of 1 percent of the maximum offering price ofthe securities registered.

During the past 5 calendar years, 1945-49 inclusive, registrationsof all types of securities (for cash sale and otherwise) amounted toapproximately $29,000,000,000. The cost of flotation of these secu-rities was $2.64per hundred dollars of gross proceeds. Of this, com-pensation paid to underwriters amounted to $2.12 and other expensesamounted to $0.52.

In the 1950fiscal year, investment bankers were used in the sale of89 percent of the total registered for cash sale for the accounts ofissuers as compared with 79 percent in the 1949fiscal year. Commit-ments by investment bankers to purchase for resale involved 67 per-cent of the total registered for cash sale for the accounts of issuers,as compared with 66 percent in the 1949fiscal year.~

That part of cost of flotation represented by commissions and dis-counts to investment bankers, but excluding other expenses, is shownior each type of security for each of the past 10 fiscal years. The

See appendix tables 1 and 2 for a more detailed breakdown of the dollar volume ofSecurities Act registrations.

_

_

_

_

-

•

SIXTEENTH ANNUAL REPORT 7

table below covers securities effectively registered for cash sale throughinvestment bankers to the general public for the accounts of the regrs-trants, but does not include securities sold to existing security holdersof the issuers, securities sold to special groups, and securities of invest-ment companies.

Commissions and discounts to investment bankers(Percent ofgross proceeds)

FIScalyear ended Bonds Preferred Common Fiscal year cnded Bonds Preferred CommonJune 30 stock stock June 30 stock stock

194L_____________ 1 8 4 1 144 1946______________ 9 3 1 801942______________ 1 5 4 1 101 1947______________ 9 28 931943______________ 1.7 J 6 97 1948______________ .6 4 5 1021944______________ 1 5 3 1 8 1 1949.-____________ 8 38 7 11945______________ 1 J J 1 93 1950______________ .6 2 7 64

ALL NEW SECURITIES OFFERED FOR CASH SALE'

Registered SecuritiesSecurities effectively registered under the Securities Act of 1933

and actually offered for cash sale during the 1950fiscal year amountedto $3,163,000,000. This total was less than the amount of securitiesoffered in any of the postwar fiscal years; $4,656,000,000were so offeredduring the peak year ended June 1946. The amounts of such offeringsin the last 2 years, valued at actual offering prices, are as follows: 6

Corporate (excluding investment com-panies)Noncorporate (Foreign Government)

TotaLUnregistered Securities

CORPORATE

1950 1949$2,987,000,000 $3,443,000,000

176, 000, 000 0

$3,163,000,000 $3,443,000,000

Some $3,006,000,000of unregistered corporate securities are knownto have been offered for cash sale by issuers in the 1950 fiscal year ascompared with $3,686,000,000 in the 1949 fiscal year. The basis forexemption of these securities from registration is as follows: 7

Basis for exemption from registration: 1950 1949Privately placed issues______________ $2,211,000,000 $2,904, ODD, 000Railroads and other common carriers__ 572,000,000 621,000,000Commercial bank issues , ____________ lID, 000, 000 25, 000, 000Intrastate offerings , ________________ 6, ODD, 000 5, 000, 000Offerings under regulation A 1_ _ _ _ _ _ _ _ 107, 000, 000 121, 000, 000Other exemptions___________________ ° 10,000,000

Total $3,006,000,000 $3,686,000,000I Includes ouly offerings between $100,000and $300,000ill size. See p. 9 [or a more detailed discusslon of

regulation A offuillgs.

See appendix for a detailed statistical breakdown of all securities o[fered for cash salein the United States_

The figures given In this section exclude securities sold through continuous offertng',such as issues of open-end investment companies and employee purchase plans.

7 Where a security may have been exempted from registration for more than one reason.the security was counted only once.

_ _

_

•

•

8 SECURITIES AND EXCHANGE COMMISSION

NONCORPORATE

1949$11, 135, 000, 000

2,512,000,000166,000,000

o10,000,000

The total of unregistered governmental and eleemosynary securitiesoffered for cash sale in the United States during the 1950 fiscal yearwas $15,673,000,000 as compared with $13,823,000,000 in the 1949fiscal year. These totals consist of the following:Issuer: 1950

United States Government $12,068,000,000State and local governments , ________ 3, 482, 000, 000Foreign governments________________ 0International Bank_________________ 101,000,000Miscellaneous nonprofit organlzations , 22,000,000

Total $15,673,000,000 $13,823,000,000

Total Registered and Unregistered Securities

Proceeds from corporate securities flotations, both registered andunregistered, applicable to expansion of fixed and working capitalamounted to $3,940,000,000. This is considerably lower than thevolume of securities sold for this purpose during the 1949 and 1948fiscal years, the amount being approximately $5,800,000,000 in eachof these two periods. Electric and gas companies accounted for 41percent of the new money financing, manufacturing firms 17 percent,communication companies 8 percent, railroads 9 percent, and allothers 25 percent. Securities offered for retirement of outstandingsecurities and repayment of bank loans amounted to $1,601,000,000inthe 1950 fiscal period compared with $921,000,000 in the precedingyear. The increase was due to a substantial rise in the amount ofsecurities refunded, particularly by electric and gas utility companies."

REGISTRATION STATEMENTS FILED

During the 1950 fiscal year 496 registration statements were filedcovering proposed offerings in the aggregate amount of $5,220,654,010.

Number and di8position of registration statements filed

Prior to July I, July I, 1949to Total as of June1949 June 30, 1950 30,1950

Registration statements:8,043 8,639Flied •••..•........ ___ .• _ •. _ .. _._ ....•.•...••. 496

Effective-net ...... __ ..•. _ •.•.•.•............ 6,663 1488 17,144Under stop or refusal order-s-net. .. _____ ...... 182 10 182Withdrawn_ ........................ _. ___ .•. _. 1,145 23 1,168Pending at June 30,1949.•.... _ ... _________ ... 63 -----------.--.--- ------- --- ---- ----Pending at June 30,1950...................... -.-----------.---- 45

8,043 ------- - ----- ----- 8,639Aggregate dollar amount:

$57,962,671,149 $5,Z~O,654,010 $63, 183,325,159As filed___ ••...•............ _ ....... _. __ ..••. _ As etfective •. _ .... __ .. _ •.•• _ .•.•.............. 54,113,698,063 5,307,077,191 59,440,775,254

1 Excludes 2 registration stetements which became etfectlve and were subsequently withdrawn andincludes 1 registration statement previously under stop order.

I 7 registration statements which became etfectlve prior to July I, 1949were withdrawn and are countedin the number withdrawn.

I During the flscel year a stop order was issued agaInst 1registration statement and a stop order on anotherregistration statement was lifted, making no change in the net number of stop order cases.

See appendix table 4 for statistics in greater detatl as to the use of net proceeds fromthe sale of securtttes.

------ -~-- --------

•

SIXTEENTH ANNUAL REPORT 9Additional documents filed in the 1950 ttscal year related to Securities Act

registrationsNature of document: Number

Material amendments to registration statements filed before theeffective date of registration____________________________________ 764

Formal amendments filed before the effective date of registration forthe purpose of delaying the effective date_________________________ 421

Material amendments filed after the effective date of regtstration.L, , 638

Total amendments to registration statements 1,823Supplemental prospectus material, not classified as amendments

to registration statements 1,112Reports filed under section 15 (d) of the Securities Exchange Act

of 1934 pursuant to undertakings contained in registrationstatements under the Securities Act of 1933:

Annualreports___________________________________________ 753Current reports 2,378

EXEMPTION FROM REGISTRATION UNDER THE ACT

The Commission is authorized by section 3 (b) of the act to adoptrules and regulations granting exemptions from the registration re-quirements for issues of securities whose aggregate offering price tothe public does not exceed $300,000.

The Commission has adopted five regulations pursuant to thisauthority: Regulation A, a general exemption for small issues; regula-tion A-R, a special exemption for notes and bonds secured by firstliens on family dwellings; regulation A-M, a special exemption forassessable shares of stock of mining companies; regulation B, anexemption for fractional undivided interests in oil or gas rights, andregulation B-T, an exemption for interests in oil royalty trusts orsimilar types of trusts or unincorporated associations.

Small offerings of securities may be made and sold to the publicpursuant to a section 3 (b) exemption on the basis of a less completedisclosure than that required by the act in the case of a registeredsecurity. For example, regulation A provides for the filing of a simpleletter of notification, containing limited information about the issuerand the offering, with the appropriate regional officeof the Commis-sion, and provides further that the offering may be made five businessdays thereafter.It should be emphasized, however, that exemption from regis-

tration permitted under section 3 (b) carries no exemption from civilliabilities under section 12 for misstatements or omissions, or fromthe criminal liabilities for fraud under section 17. For the properenforcement of these sections, the conditions for the availability of theexemptions provided under section 3 (b) include, with the exceptionof regulation A-R, the requirement that certain minimum informationbe filed with the Commission and that disclosure of certain inform ationbe made in sales literature, if any sales literature is used. While noprospectus need be used, selling literature must be filed in advance ofIts use.Exempt Ofi'erings under Regulation A

In the 1950 fiscal year 1,357 letters of notification were filed underregulation A, covering offerings in the aggregate amount of $171,743,-472, compared with 1,392 filings totaling $186,782,661during the 1949

10 SECURITIES A1-.TDEXCHANGE COMMISSION

fiscal year. The 1950 fiscal year figures include 136 letters of notifica-tion covering stock offerings aggregating $19,909,525 filed by com-panies engaged in some phase of the oil and gas business.

In addition to the 1,357letters of notification filed in the 1950fiscalyear, 1,159 amendments to these letters of notification were receivedand examined and there were 1,844 filings of sales literature to beused in connection with such offerings.

Of 1,345letters of notification covering completed offerings filed inthe 1950fiscal year, 787 covered proposed offerings of $100,000or less;218 covered offerings for more than $100,000and less than $200,000;and 340 covered offerings of more than $200,000 but not more than$300,000. Issuing companies made 1,134of these offerings, stockhold-ers made 199, and both issuers and stockholders joined in making theremaining 12. Commercial underwriters marketed 398of the offermgs,officers and directors or other persons not regularly engaged in theunderwriting business handled 164, and there was no underwritingof the remaining 803.

The procedure for making an exempt offering under regulation Ais simple. All that is necessary is to file the prescribed letter of notifi-cation, and such sales literature as the offeror intends to employ, withthe appropriate regional officeof the Commission five busmess daysbefore the offering is to be made. In processing by the Commission thismaterial is examined in the field and reviewed by the staff at the Com-mission's headquarters. This review involves a search for pertinentinformation in the Commission's extensive files and an examinationto determine whether the exemption provided by the regulation isapplicable to the particular case and whether the information fileddiscloses any violation of any of the acts administered by the Commis-sion. The results of this review are made available promptly to theregional office. The Commission also follows the practice of cooper-ating with the proper local authorities in the States in which the securi-ties are proposed to be offered by furnishing them significant dataabout the proposed offering.Exempt Offerings under Regulation A-M

During the 1950fiscal year the Commission received and examined !)prospectuses covering an aggregate offering price of $303,122for as-sessable shares of mining corporations exempt from registration underthis regulation.Exempt Offerings under Regulation B

The Commission maintains a specialized unit in its headquartersofficeto administer regulation B and to advise and assist with technicalphases of all offerings of oil and gas securities arising under other pro- tvisions of the Securities Act. In addition, the Commission maintains " a petroleum geologist in Tulsa, Okla., who advises the Commission asto the development of tracts and wells in the Mid-Continent andCoastal regions. Development has been active in the Rocky Mountainsduring the 1950 fiscal year.

The exemption from registration provided by regulation B forfractional undivided interests in oil or gas rights is limited to a maxi-mum aggregate offering price of $100,000. Regulation B requires that

SIXTEENTH ANNUAL REPORT 11an offering sheet be filed with the Commission summarizing pertinentinformation regarding the security being offered.

In addition to 136 offerings under regulation A which covered oiland gas securities, 88 offering sheets and 61 amendments were filed un-der regulation B during the 1950 fiscal year. The following actionswere taken on these filings:

Action taken on filmg8 under regulation B

Temporary suspension orders (rule 340 (a ) ) 14Orders terminating proceedings after amendmenL________________________ 8Orders consenting to withdrawal of off'ertng sheet and terminating pro-ceedlng ---____________ 1Orders terminating- effectiveness of offering- sheet (no proceeding pendlng j ; , l)Orders consenting- to withdrawal of offering- sheet (no proceeding- pending) __ 1Orders accepting- amendment of offerin.e; sheet (no proceeding pending) 34

Total orders_____________________________________________________ 66

Oonfidential written reports of sales under regulation B.-Anotherfunction of the Commission in the administration of regulation Bis to determine from confidential written reports of actual salesthat no violations of law occurred in the marketing of oil and gassecurities exempted under this regulation. Such reports are requiredto be filed pursuant to rules 320 (a) and 322 (c) and (d) concerningsales made by broker-dealers to investors and by dealers to otherdealers. During the 1950 fiscal year 1,132such reports were receivedwith respect to aggregate sales of $829,875.

Oil and gas investigations.-Most oil and gas investigations ariseout of complaints received by the Commission. They are conductedprimarily to ascertain whether there has been any violation of sectionr>, which requires registration, or of section 17, which prohibits fraudin securities transactions.

A typical investigation was made in the 1950 fiscal year to deter-mine whether certain claims of profits in sales literature used to selloil royalties under regulation B were misleading. The offering circu-lar claimed that the royalties would return a profit of 8 to 12 per-cent and would be a better investment than most stocks and bonds.The staff made an extensive study of the total income received fromroyalties sold by the offeror under offering sheets relating to as manyas 46 tracts since 1940. Inasmuch as information as to productionand income from these tracts was not a matter of published record,a large part of the necessary data was obtained from the producerand the purchaser of the oil. Itwas found that out of the 46 tractsunder review, only 2 had returned the capital invested, with a profit;4 should eventually do so, with a modest profit; and of the remaining40 tracts only a very few can reasonably be expected ever to returneven as much as the capital invested.

The offeror agreed to cease claiming an 8 to 12 percent yield, toceasecomparing any return on these royalties with that available fromstocks and bonds, and to describe his royalties as liquidating assetsthe return from which cannot be regarded as profit until the capitalinvested has been recovered by the purchaser.

12 SECURITIES AA""DEXCHANGE COMMISSION

The Commission instituted 10 new investigations involving oil andgas securities during the 1950fiscal year and 23 such cases were closed.This brought the total pending during the year to 135 and the numberpending at the close of the year to 112. As a result of evidence de-veloped in two cases, the Commission secured injunctions in the courtsrestraining violations of the registration and antifraud provisions ofthe act. The facts in two other cases were referred to the Departmentof Justice for criminal prosecution, in which the Commission co-operated. The conviction of Claude Cleve Alfred in connection withfraudulent sales of oil securities is mentioned in another section ofthis report.

FORMAL ACTION UNDER SECTION 8

The purpose of the Commission's informal procedures in processingregistration statements is to get registration statements which complywith the requirements of the act before the statements becomeeffective. In almost all cases conference and comment by letter aresufficient both for the needs of the registrant and for the adequateprotection of investors. It is sometimes necessary, however, for theCommission to exercise its powers under section 8 in order to preventa reg-istration statement from becoming effective in deficient or mis-leading form or to suspend the effectiveness of a registration statementwhich has already become effective.

Under section 8 (b) the Commission may institute proceedings todetermine whether It should issue an order to prevent a registrationstatement from becoming effective. Such proceedings are authorizedif the registration statement as filed is on its face inaccurate or incom-plete in any material respect. Under section 8 (d) proceedings may beinstituted at any time to determine whether the Commission shouldissue a stop-order to suspend the effectiveness of a registration state-ment if it appears to the Commission that the registration statementincludes any untrue statement of a material fact or omits to state anymaterial fact required to be stated or otherwise necessary to make thestatements included not misleading. Under section 8 (e) the Com-mission may make an examination to determine whether to issue astop-order under section 8 (d).Stop-order Proceedings under Section 8 (d)

Two stop order proceedings were pending at the beginning of the1950 fiscal year and one was instituted during the year under section8 (d). These cases are described below.

Pan American Gold. Limited. (no personai lialJility)-File No.2-7603.-This Canadian company filed a registration statement cover-ing 1,983,295of its common shares, $1 par value, to be offered at 45cents per share and net about $670,500 to the issuer. According tothe registration statement, these proceeds were to be used (1) for theexploration of a gold mining prospect located in South Dakota,and (2) for the equipment of a South American gold placer miningproperty.

Upon examination the registration statement appeared to containmaterially misleading representations, and in the 1949 fiscal year theCommission authorized a private examination under section 8 (e) to

SIXTEENTH ANNUAL REPORT 13

determine the adequacy and accuracy of certain of these representa-tions and to determine whether stop-order proceedings should be in-stituted. On the basis of testimony adduced at the examination, stop-order proceedings were instituted. Following these proceedings andafter the registrant filed amendments to the registration statementwhich substantially corrected deficiences, the Commission issued itsopinion, deferring issuance of a stop-order pending correction by theregistrant of the remaining deficiencies, at which time the registrationstatement could become effective,"

The Commission found that the original registration statement wasmaterially misleading in numerous respects. The prospectus filed asa part of the original registration statement contained informationto the effect that the registrant's South Dakota property is locatedalong the southern border of the famous Homestake Mine. A map,forming a part of the prospectus, showed what purported to be thesoutheasterly "trend" of the Homestake gold ore bodies into andthrough the registrant's property. This representation was said torest on the authority of United States Geological Survey Atlas Folio219. The Commission found that the map was not supported bysuch folio and that the registrant had no factual basis for portrayingthe extension of the Homestake ore bodies into and through its prop-erty. The prospectus was amended to omit this unjustifiable claimand also to delete a report on the property which the Commission heldto be materially inaccurate, inadequate, and misleading. In additionit was amended to show for the first time that the registrant was awareof several unfavorable geological reports made after exploratorydrilling.

The South American property of the registrant was described orig-ally in the registration statement as being ready for productiveoperation upon installation of mining equipment. The amount ofcommercial gravel said to be available for mining was estimated at aminimum of 5,000,000cubic yards averaging $1 per cubic yard in gold.The planned rate of production was said to be at least 1,000,000cubicyards of gravel per year. The registrant stated that it believed thatoperations on the property should enable it to obtain steady earningpower from this property. The amended registration statement dis-closes that the registrant made no investigation of the property, andhas no factual information about the presence, extent, or character ofgravel deposits on the property. The prospectus, as revised, showsthat the registrant intends to test the property as an initial step inorder to determine whether it warrants the installation of machineryfor production. Specifically, it is stated in the revised prospectus:"If the further exploratory work and shafting as contemplated do notshow sufficient values to justify further development, this propertywill be abandoned."

The Maumee Oil Oorporation-File No. fJ-7976.- This case was com-pleted during the 1950fiscal year although instituted previously. Thecompany was incorporated in Ohio on July 30, 1947 and on May 11,1949 filed a registration statement covering 8,000 shares of no parvalue common stock to be offered at $100 a share. Its assets consisted

Securl ties Act release No. 3368.•

14 SECURITIES A!\'D EXCHANGE COMMISSION

of assignments of oil and gas leases and an undivided one-half interestin four wells (two of which were not productive) in the Beddo field inthe vicinity of Ballinger, Runnels County, Tex. A.fter examinationof the registration statement, stop-order proceedings were institutedon May 27, 1949.

From information developed at the hearing it appeared that theregistration statement failed to disclose that the Beddo field was aninferior field which seldom, if ever, marketed more than 60 percentof its allowable production, and often much less, and that the numberof dry holes in the field exceededthe number of producing wells. Theregistration statement also failed to provide adequate informationwith respect to the wells in which the registrant had an interest. Theprospectus stated that two of the four wells were unproductive, butit failed to state that the other two producing wells had no reasonablechance of profitable production and were bemg operated on a day today basis only because this was more economical than to abandon them.

At the time the registration statement was filed the registrant wasin possession of two reports from geologists which indicated that, atbest, only 5 percent of the registrant's acreage had a reasonable chanceto produce oil in any amount. The Commission held that in suchcircumstances, where there had been significant exploration in the areaindicating that the possibilities of success were extremely remote, itwas misleading to imply a fair chance of profit by describing theoffering as "speculative," or to state or imply that the area in whichthe registrant's properties were located had not been proved, or thatthe registrant's own acreage should be regarded as unproved. Asto the registrant's plan for new drilling, to be financed with proceedsfrom the sale of the securities sought to be registered, it was heldmisleading for the registrant to characterize the projected wells as"exploratory" without disclosing the information in its possessionindicating that since the projected wells were to be located in thevicinity of its existing unprofitable wells there was no reasonablefactual basis for an expectation that new wells would be better thanthe existing wells.

The registration statement and prospectus failed to name Eldrid~eS. Price as a promoter although required to do so by the Commis-sion's rules, and to provide a fair disclosure of the registrant's deal-ings with him. Price, although not an officer,director, or stockholder,sold assignments of oil and gas leases on some 2,677acres of his hold-ings in Runnels County, Tex., to the persons who became the originalshareholders of the company. Price received about $290,340, about92 percent of all the money obtained by the registrant from the saleof securities. The original amount paid to Price was $43.75 an acre,but this was later raised to $100 although Price was apparently at thesame time acquiring additional acreage for about $1 per acre.

The Commission's opinion mentions other omissions and incon-sistencies in the registration statement relating to such matters asthe amount of the offering, the liability of certain shareholders forassessment, the business experience of officers, inaccurate financialstatements, and the failure to file material exhibits." At the close of

10 Securities Act release No. 3354.

SIXTEENTH ANNUAL REPORT 15the 1950 fiscal year the registrant had not attempted to correct thedeficiencies found to exist in its registration statement and the stoporder was still in effect.

Ralph A. Blanchard and George P. Simons, doing business asNorthwest Petroleumr-File No. 2-8243.-The registration statementfiled in this case covered 350 "undivided Fractional Participating In-terests (Oil)" to be offered for sale to the public at an aggregate priceof $175,000. The Commission, alleging generally that there is reason-able cause to believe that the disclosures contained in the registrationstatement and prospectus are inaccurate and incomplete in materialrespects, challenging 19 items specifically, instituted stop-order pro-ceedings during the 1950 fiscal year that were still pending at theclose of the year."

DEFICIENCIES DISCOVERED IN EXAMINATION OF REGISTRATIONSTATEMENTS

The examination of registration statements during the waitingperiod brings to light many deficiencies in the registration statementswhich would, if undiscovered, be published and furnished to investors.These are sometimes corrected; often they are of such material char-acter that the statements are withdrawn on discovery of the deficiency.The following are examples of deficiencies discovered in examinationof registration statements.Overstated Oil Reserves

An oil-producing company filed a registration statement covering$2,937,254of 4% percent senior cumulative interest debentures, dueJanuary 1, 1965; $1,147,150of 5 percent junior income debentures, dueJanuary 1, 1970; 30,500 shares of $5 cumulative class A preferredstock, no par; 51,000shares of $5 cumulative class B preferred stock,no par; and 2,000shares of common stock, no par.

Prior to the formation of the company, the promoters of its predeces-sors had sold working interests in oil leases, in which the promotersretained overriding royalties, to some 350 investors in and aroundBoston. These royalties and other assets were subsequently conveyedto the company by the promoters. The company appears to have beencontinuously short of working capital although, in addition to sub-stantial loans from insurance companies and banks, it had receivedadditional funds from a syndicate composed of some of the originalinvestors in the leases. A plan of reorganization was devised whichprovided for: (1) A large loan from the RFC; (2) the acquisitionof additional 011 properties; (3) the repayment of part of the out-standing loans; and (4) payments in cash and new securities for theproperties owned and to be acquired. The Commission determinedthat the proposed offering of debentures, preferred stock, and commonstock, in addition to cash, to the 350 investors was a public offeringand required the filing of a registration statement.

It became apparent upon review by the Commission of the reportsprepared by various petroleum engineers in respect of the company'soil and gas reserves, and after conference with such engineers, that

11 Securities Act release No. 3367.

16 SECURITIES AND EXCHANGE COMMISSION