Modelling of strata movement with a special reference to caving mechanism in thick seam coal mining

Upload

independentCategory

view

11download

0

ES-1

Global Energy Decisions

Coal Advisory Service Reference Case

Coal Fall 2007

© Copyright 2007, Global Energy Decisions, LLC All rights reserved. No part of this report may be reproduced or transmitted in any form or means, electronic or mechanical, including photocopying, recording, or by any information storage or retrieval system without the permission of Global Energy Decisions, LLC. This report constitutes and contains valuable trade secret information of Global Energy Decisions. Disclosure of any information contained in this report by you and your Company to anyone other than the employees of your Company ("Unauthorized Persons") is prohibited unless authorized in writing by Global Energy Decisions. You will take all necessary precautions to prevent this report from being available to Unauthorized Persons, as defined above, and will instruct and make arrangements with employees of your Company to prevent any unauthorized use of this report. You will not lend, sell, or otherwise transfer this reports (or information contained therein or parts thereof) to any Unauthorized Person without Global Energy Decisions prior written approval. PROPRIETARY AND CONFIDENTIAL Global Energy Advisors 2379 Gateway Oaks Drive, Suite 200 | Sacramento, CA 95833 tel 916-569-0985 | fax 916-569-0999 Global Energy Decisions

The opinions expressed in this report are based on Global Energy Decisions’ judgment and analysis of key factors

expected to affect the outcomes of future power markets. However, the actual operation and results of power markets

may differ from those projected herein. Global Energy Decisions makes no warranties, expressed or implied, including

without limitation, any warranties of merchantability or fitness for a particular purpose, as to this report or other

deliverables or associated services. Specifically, but without limitation, Global Energy Decisions makes no warranty or

guarantee regarding the accuracy of any forecasts, estimates, or analyses, or that such work products will be accepted

by any legal, financial, or regulatory body.

Executive Summary

Coal Reference Case, Fall 2007 ES-1

The purpose of the Coal Reference Case Fall 2007 is to provide a large scope analysis of the U.S. electric-steam coal industry’s historic and current status and Global Energy’s predictions for the industry’s direction over the next 25 years. As mining costs rise, coal seams and reserves deplete, emission regulations change and increase, and some fuels become more competitive over the next 25 years, the allocation of coal in the electric generation industry is certain to see substantial changes.

Recent History And Current Status Of The Coal Industry Historically, the electric power sector has always consumed more coal than any other sector. It has shown significant demand growth and increased its coal demand share from 73 percent in 1975 to 93 percent of total U.S. coal consumption in 2006, a year in which total electric power coal consumption was 1.06 billion short tons. The industrial and coking plant sectors combined for the last 7 percent or approximately 100 million tons of demand in 2006. This steady increase in use over the years in a volatile industry shows coal’s reliability as a fuel source despite any competitive disadvantages it may have. Coal Production

In order to meet increasing demand, mainly from the electricity generation sector, total U.S. coal production has increased by approximately 52 million tons in the past 10 years to 1.16 billion tons. The Powder River Basin has been responsible for nearly all of the increase while most other major producing basins have seen production declines. The Powder River Basin has increased production by 55 percent to 472 million tons in 2006 from 1997 levels. In the same time frame Central Appalachia has seen production decline by 18.6 percent to 236 million tons in 2006. Higher sulfur Illinois Basin coal production has declined 13.4 percent to 96 million tons in response to the Clean Air Act amendments while Northern Appalachia coal production has declined 12.5 percent to 136 million tons since 1997 for the same reason. The only basin to see an increase in production since 1997 was the Rocky Mountain Basin, showing a modest increase of 1.3 percent in the last 10 years with 112 million tons of total production in 2006. While not considered production, coal imports have steadily increased from 15 million tons in 2000 to 36 million tons in 2006, a 142 percent increase. Coal Mine Productivity

All major coal producing basins have seen declines in basin-level productivity since 2001 due to a lack of new mining technology and deteriorating reserve quality. Though accounting for all U.S. gains in coal mine production over the past decade, the Powder River Basin has seen its overall basin-level productivity decline by 16.7 percent to 34.98 tons per miner hour since 2001. In the same time frame Central Appalachia has seen productivity decline by 25 percent to 2.82 tons per miner-hour in 2006. Illinois Basin and Rocky Mountain productivity have also seen very significant declines of 11.26 and 20.34 percent, respectively. Northern Appalachia productivity saw a decrease of only 1.23 percent, the smallest productivity decline of all the major basins since 2001. Decreasing productivity and increasing production indicate more numerous yet smaller coal mines than in the past.

Executive Summary

ES-2

Coal Prices

All major U.S. coal producing basins have experienced tremendous growth in the FOB (free on board) mine prices they receive for their coal over the past decade. In constant dollars weighted average FOB mine prices (includes spot and contract pricing) have increased 32 percent in the United States from 1998 to 2006. Central Appalachia has seen the most significant increase in FOB prices from $25 to $46/ton over this time period, an increase of 84 percent. The Illinois Basin and Northern Appalachia have both seen a 36 percent increase in FOB mine prices, with 2006 prices of $29.92 and $37.39/ton, respectively. Rocky Mountain coal has realized one of the smallest increases on a dollar per ton basis of approximately five dollars/ton, though this does equate to a significant 27 percent increase. The Powder River Basin’s increases in FOB mine prices have been the most modest from $7.83 to $9.11/ton, or 16 percent. Electricity Generation

In 2006, coal-fired power plants generated 50 percent of U.S. electricity. A decade ago the picture was very different. Coal’s share of electricity generation was near 60 percent in 1997, but has since fallen to 50 percent due to a massive build out of cheap (approximately $600/kW) natural gas plants driven by very low natural gas prices in the early portion of this decade. With low gas prices apparently a thing of the past, coal now holds the title of lowest cost fossil fuel for electricity generation. This is reflected in plant utilization rates, which are much higher for coal than for gas. In 2006 the utilization rate, or capacity factor, of coal plants was 71 percent compared to 25 percent for gas plants. Despite the fact that coal’s generation share is smaller than it was 10 years ago, coal production and consumption increased during that time frame as demand for coal as a source for power generation has continued to increase to meet increasing demand for electricity in the United States. Transportation

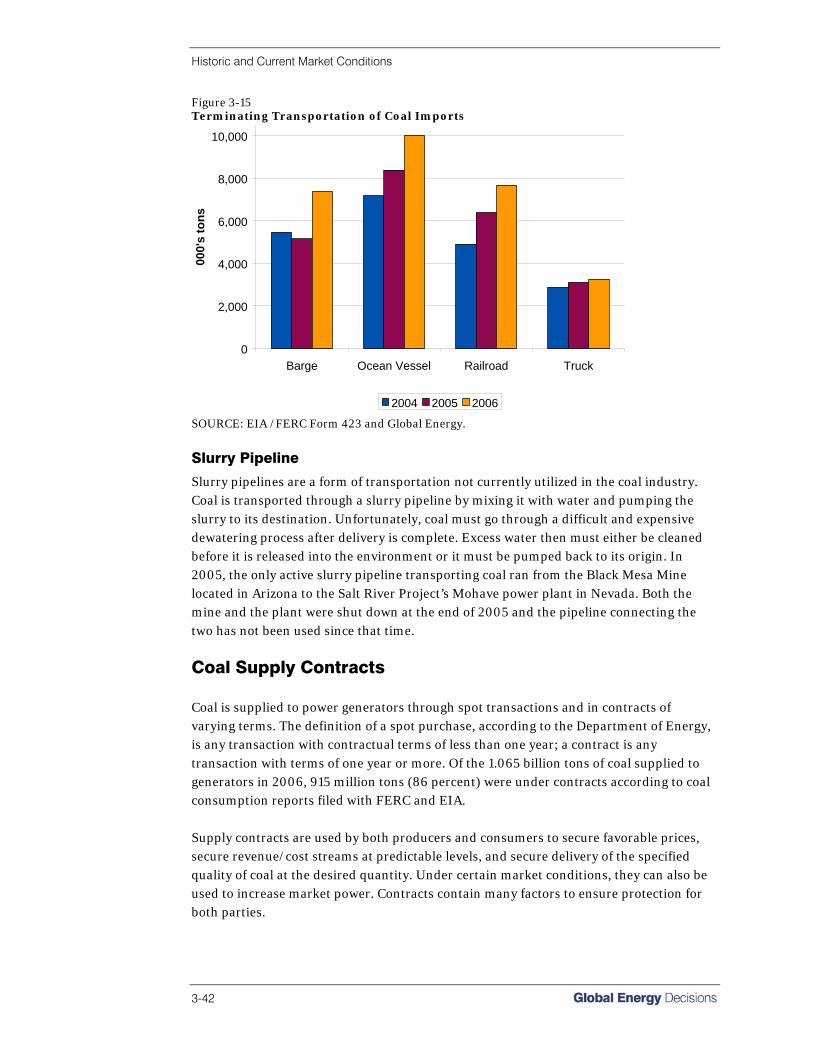

In the coal industry, transportation costs factor strongly in the ultimate delivered price at the plant. For instance, 60 percent of the delivered price of coal produced in the PRB is attributable to transportation costs on average. Rail is the transportation method most heavily relied upon in the coal industry due to the vast geographic area that rail infrastructure covers and its ability to move large amounts of coal long distances through varied terrain. Almost 72 percent of coal deliveries utilize rail transportation for at least a portion of their journey. The Powder River Basin, where the average haul distance is 1,200 miles to the plant and 2,400 miles roundtrip—almost exclusively by rail—is of particular note due to rail transportation capacity issues. The owners of the Joint Line are investing in capacity expansion but this may only be prolonging the inevitable—construction of another railroad to the PRB. Another route for coal out of the PRB is necessary, and the market may provide it with the proposed Tongue River Railroad and/or the Dakota, Minnesota and Eastern Railroad (DM&E). River barges are one of the most economical ways to move coal large distances on a cost per ton-mile basis. The obvious constraint to moving coal via barge is geographic location of coal mines and plants in relation to navigable waterways. In 2006, 161 million tons of

Executive Summary

Coal Reference Case, Fall 2007 ES-3

coal had terminating transportation on river barges. Lake vessels are more constrained by geographic location of plants than river barges and were responsible for only 25 million tons of delivered coal in 2006. Fifty percent of the Illinois Basin’s and Central Appalachia’s deliveries, amounting to nearly 130 million tons, utilized trucks as their first and in some cases only form of transportation in 2006. Ocean vessels account at least in some part for nearly all of the 81 million tons of combined U.S. imports and exports. Contracts

Historically, coal contracts were made for longer terms than they are today. The tendency in the industry has been to shorten contract length as other potentially more reliable means of managing risk (e.g., over-the-counter coal trading) have become more widely available and accepted. The reality is that over 85 percent of coal is delivered under contracts with lengths of one year ore more; a dynamic that is unlikely to change anytime soon because of the risk management tool it provides to both producers and consumers. Mining Costs

Deeper and thinner seams, growing underground mine safety costs, and diminishing opportunities to consolidate reserves will cause production to decrease in Central Appalachia. Some of these same issues will add upward cost pressures in all of the other basins. Trends in Central Appalachia over the last 10 year’s coal production are towards surface mining and away from underground mining. With mountaintop mining under attack from environmentalists in the courts there is an added degree of uncertainty about the future of some operations. This situation affords opportunity for consolidation even with the merger and acquisition activity in the coal industry over the last several years. Opportunities for companies to capitalize on potential synergies and the pressure from low prices and rising costs with some producers particularly exposed provide lots of room for ongoing and potentially big consolidation moves—especially in Central Appalachia. Coal-Fired Generation

Today, 93 percent of coal produced in the United States is used for generating electric power. The forecast for future coal use derives from our current understanding of the coal supply and electric generating markets. In addition to cost pressures, coal faces challenges on the demand side in the form of environmental regulation of power plants and competition from other sources of electric power. Coal plants currently provide the U.S. with the half of its electric supply even though coal’s share of U.S. electricity supply has been reduced to 50 percent from about 59 percent over the past decade. Coal remains far cheaper than natural gas on a delivered basis, even with current environmental costs factored in. Alternatives to coal-fired power each come with a set of advantages and disadvantages: • There are 66 operating nuclear power plants in the U.S. today, which account for 21

percent of U.S. electric power generation. Utilization is at 90 percent so up-rates are not likely to account for much further capacity expansion. Fuel is currently cheap, waste disposal is an ongoing and long-term expense, and adding capacity with new

Executive Summary

ES-4

plants faces long lead-times and public opposition but there are a few in the planning stages.

• Gas capacity is the highest of any other fuel with increasing government and public scrutiny regarding emissions in recent years. Gas has become more desirable due to its low emissions and relatively low construction costs, increasing its contribution to total electricity output to 20 percent of total generation. High fuel costs and volatility are likely to keep utilization levels low, but 60,000 MW are on the drawing board nonetheless.

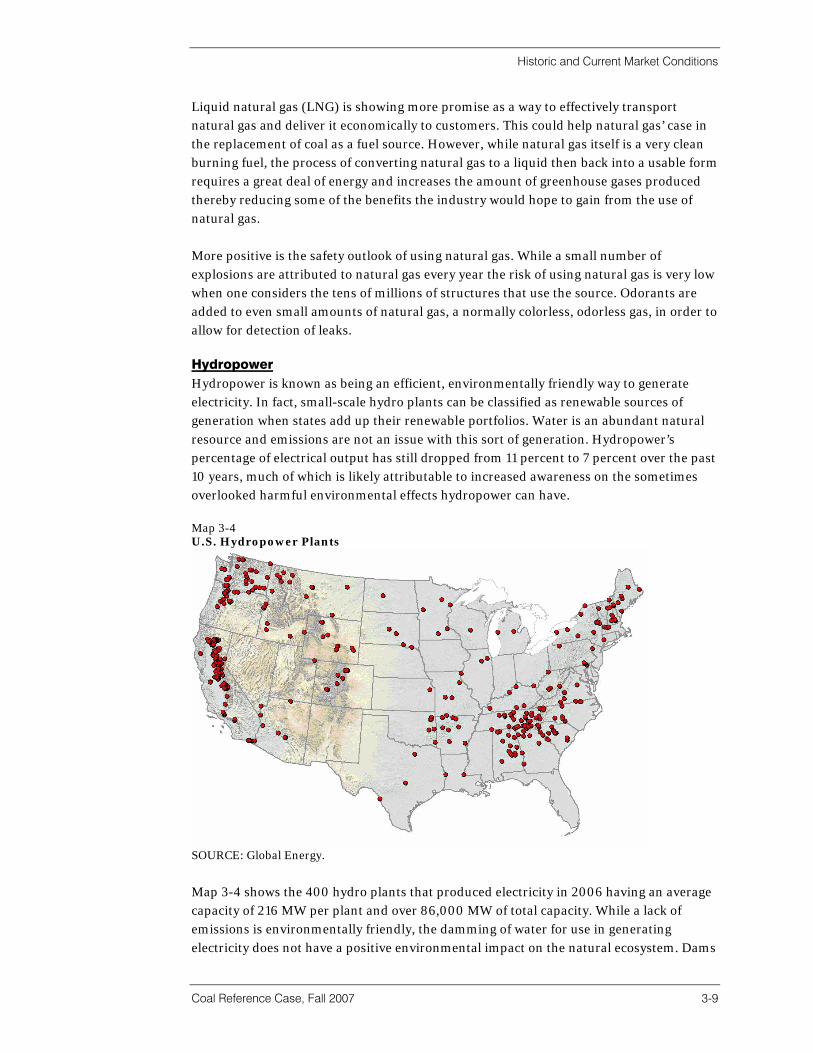

• Hydropower’s percentage of electrical output has dropped from 11 percent to 7 percent over the past 10 years, much of which is likely attributable to increased awareness on the sometimes overlooked harmful environmental effects hydropower can have. Several regions are in the midst of droughts which are lowering output and new, large scale capacity additions are virtually out of the question.

• Renewable energy’s contribution to electricity output is barely 2 percent and remains relatively insignificant. Wind’s contribution will grow as long as subsidies last, but output intermittency and transmission remain as sizeable obstacles. Renewable portfolio standards and carbon regulation will lend support for greater deployment.

Since 1990, net SO2 and NOX emissions at coal burning plants have fallen by 31.3 percent and 33.1 percent, respectively, while the amount of coal burned has increased from 783 million tons/year to 1,015 million tons/year. Nonetheless, utilities continue to face close scrutiny to reduce their emission exposure, which has helped contribute to coal’s decreasing role in the U.S. electricity supply—displaced primarily by gas. Investments in emissions control have resulted in 121 GW of coal-fired capacity that currently has SO2 controls and 306 GW with some form of NOX controls. New emissions limits under the Clean Air Interstate Rule (CAIR) and Clean Air Mercury Rule (CAMR) have spurred a further boom in emissions control equipment installations.

Forecast For The Coal Industry Coal markets are subject to boom and bust cycles with supply and demand constantly in flux and production, contracts, transportation, and stockpiles all playing a role in adding to the uncertainty. In order to address this uncertainty, the Coal Quality Market Model (CQMM) is used by Global Energy to forecast future U.S. consumption, allocation, and price of coal from every mine to every boiler over the 25-year study period. The CQMM relies on data from Global Energy and uses a highly sophisticated network linear program to find the optimal minimum cost solution for the given model input and constraints. Much of the data supplied by Global Energy is extracted from the Velocity Suite, the industry’s leading coal and energy market database. Along with the help of numerous government, public, and private data sources Global Energy has created the most thorough, accurate, and highly representative database achievable. The results from this model represent Global Energy’s forecast and are detailed in the section below.

Executive Summary

Coal Reference Case, Fall 2007 ES-5

Coal Demand Forecast

Coal will remain the single largest contributor to overall U.S. electric supply over the course of this forecast as demonstrated in Figure ES-1. Our forecast shows coal generation will increase almost 28 percent through 2031 though coal’s relative share of the market will decline 4 percent. Gas-fired capacity increases its market share of generation by 10 percent while posting a 227 percent increase; this is the second largest growth in generation in this forecast. The largest relative growth in generation comes from renewables which will experience a 341 percent increase, but still remains only 5 percent of the total U.S. generation. Figure ES-1 Historical and Forecasted Electricity Generation by Fuel

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2026

2031

Year

Gen

erat

ion

(GW

h)

Coal Nuc Gas Water Petro Renew

Historical Forecast

SOURCE: Global Energy.

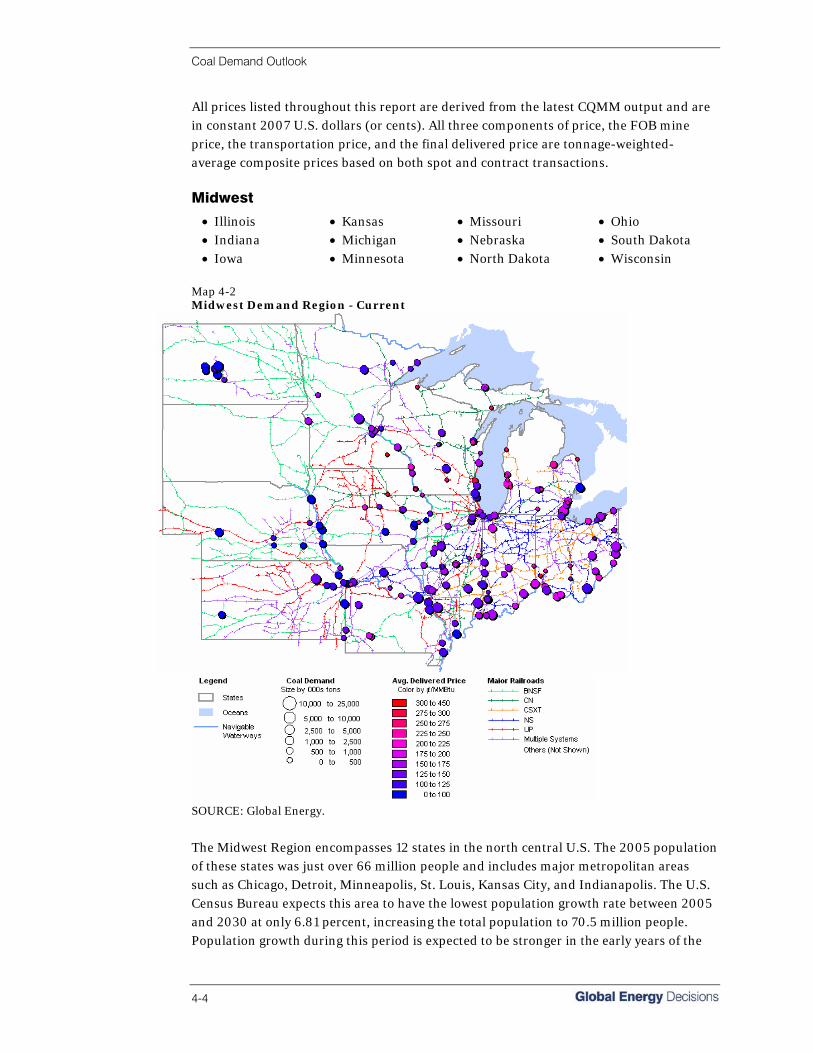

Since U.S. coal demand differs between different regions of the country, Global Energy has partitioned the results into smaller, well-defined demand regions.1 The U.S. regional coal demand forecast can be found in Figure ES-2. Coal demand will differ by region due to several key factors: • Growth in overall electricity demand; • Status of the existing coal fleet, the age of the units, and their utilization rate; • Difficulty in permitting new plants; and • Delivered cost of coal and competing fuels. The Northeast region has the lowest current coal demand and the slightest increase in coal demand of all the regions over the forecast period. With an average growth of 0.5 percent a year, its total demand will increase 13 percent over the 25-year time span. The West region is also relatively flat, increasing 16 percent over 25 years. The Southeast region is expected to increase 24 percent, which equates to over 160,000 GW-hours of

1 Please refer to Section 3 to view a map of the five U.S. demand regions.

Executive Summary

ES-6

coal generation. The Midwest shows growth every year resulting in the highest absolute increase (248,300 GWh or 34 percent since 2007) in coal power demand by 2031. The South Central region, while small, shows the greatest average yearly increase (1.5 percent) and overall increase (44 percent) in coal-fired electricity generation. Figure ES-2 Coal Generation Demand by Region

0

200

400

600

800

1,000

1,200

2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031

Coa

l Dem

and

(000

's G

W-h

r)

Northeast West South Central Southeast Midwest

SOURCE: Global Energy.

Coal Supply Forecast

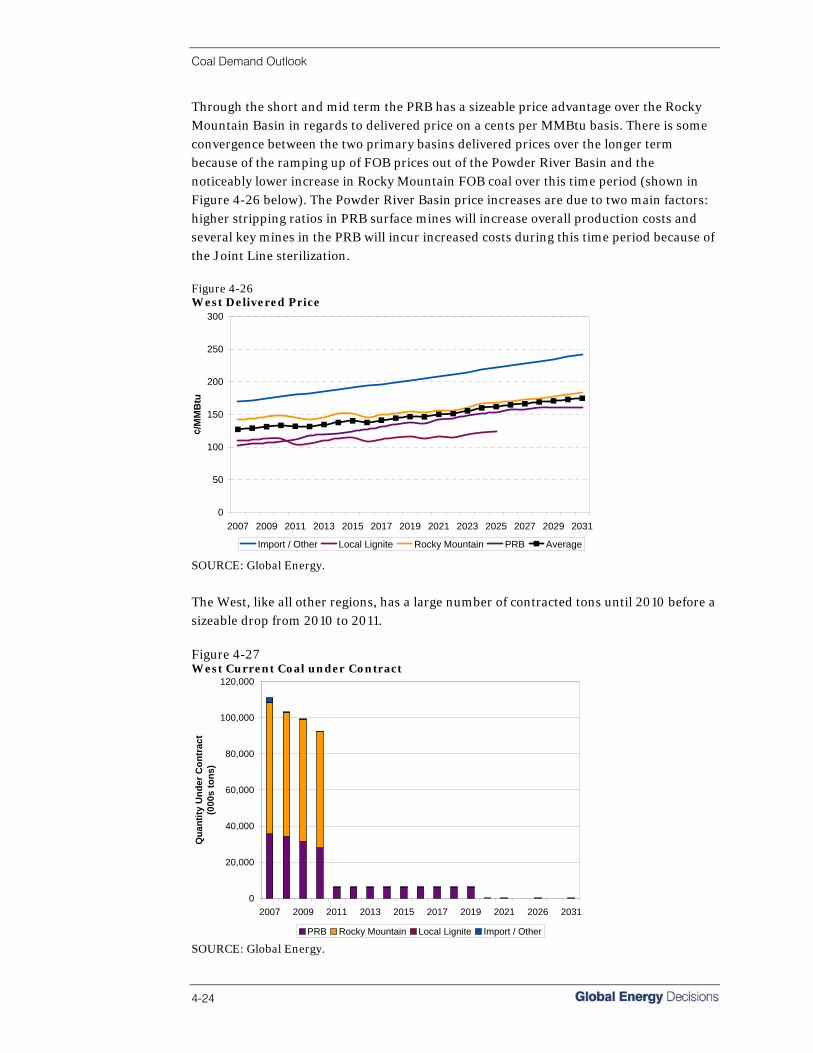

Total deliveries of coal within the U.S. are expected to increase from 1.05 billion tons in 2007 to 1.3 billion tons in 2031, an annual average increase of 1.98 percent. Demand for coal is expected to increase for all basins except for Central and Southern Appalachia, which should see demand decrease by 45 percent and 28 percent, respectively. The largest percentage increase in demand is expected to come from Colombian coal at 178 percent—a 36 million ton increase over the 25-year study period. Demand for PRB coal is forecasted to rise by 50 percent (annual growth of 9.4 million tons/year) and the Illinois Basin should see a 37 percent growth in demand (annual growth of 1.28 million tons/year). Rocky Mountain coal is expected to command a 27 percent increase in demand (annual growth of 1.1 million tons/year). Lignite demand should remain relatively flat. Figure ES-3 details our 25-year forecast for basin-level coal deliveries.

Executive Summary

Coal Reference Case, Fall 2007 ES-7

Figure ES-3 United States Delivered Coal Quantities

-

200

400

600

800

1,000

1,200

1,400

2007 2010 2013 2016 2019 2022 2025 2028 2031

MM

tons

Import / Other Local Lignite Rocky Mountain Illinois Basin

Northern App Central / Southern App PRB

SOURCE: Global Energy.

Mine Fully Allocated Costs

Fully allocated mine costs, which include full production costs including return on capital, are expected to increase over the forecasted period. Although taxes and royalties are expected to decline over the midterm, the cash cost of coal for all U.S. coal basins is expected to rise for a number of reasons: • Decreasing productivity due to thinner and deeper seams; • Limits on the economies of scale ; • Rising prices for fuel, equipment, tires, and explosives; • Competition for skilled labor across the energy sector; and • An aging workforce that is nearing retirement in the East. U.S. coal mine fully allocated costs are expected to decrease over the next five years by about 4 percent, as shown in Figure ES-4. This is a result of increases in production of Powder River Basin coal and decreases in production of Central Appalachian coal. Numerous industry sources have indicated that the MINER Act will add up to $8 per ton of coal extracted from underground mines.

Executive Summary

ES-8

Figure ES-4 U.S. Fully Allocated Mine Costs; 2007-2031 (Constant 2007 Dollars)

20

22

24

26

28

30

32

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

FAC

$/to

n

U.S Fully Allocated Costs

SOURCE: Global Energy.

Global Energy expects fully allocated costs for Appalachian coal mines to increase over the mid term. A significant amount of the Appalachian fully allocated cost increase is due to increased cash costs of complying with the provisions in the MINER Act of 2006, which affects Appalachian mines more than any other region in the United States. Compliance with the new safety regulations will place a heavy burden on all underground mine operators, but the heaviest burden will be on the smaller operators who will be unable to distribute compliance costs over a broad production base. Unless there is significant consolidation of reserves and operations in the East, longwall mining will not be as economical to install. As a result, less efficient, higher cost underground operations will continue in the Appalachian region. Western coal basins (including the Powder River and Rocky Mountain) fully allocated costs are expected to increase by approximately 5-6 percent over the next five years. Increasing coal ratios; seam splitting and washouts; higher input costs for fuel, labor, explosives, tires, and equipment; and increasing tax and royalty costs will all contribute. These cost increases are not expected to be offset by productivity-increasing technological improvements. Productivity is the single largest factor that contributes to a mine’s overall production costs. U.S. coal mines’ aggregate productivity is likely to fluctuate through the mid term. The variability in productivity is mainly due to large volumes of higher cost, lower productivity mines being shut-in and some larger western mines ramping up production as market conditions and prices fluctuate. For example, in 2007 over 43 million tons of production capacity with productivity less than 19.6 tons per miner-hour will go off line. With reserve blocks becoming increasingly difficult to mine we do not expect to see major increases in productivity in the future unless new technologies for extracting coal are developed.

Executive Summary

Coal Reference Case, Fall 2007 ES-9

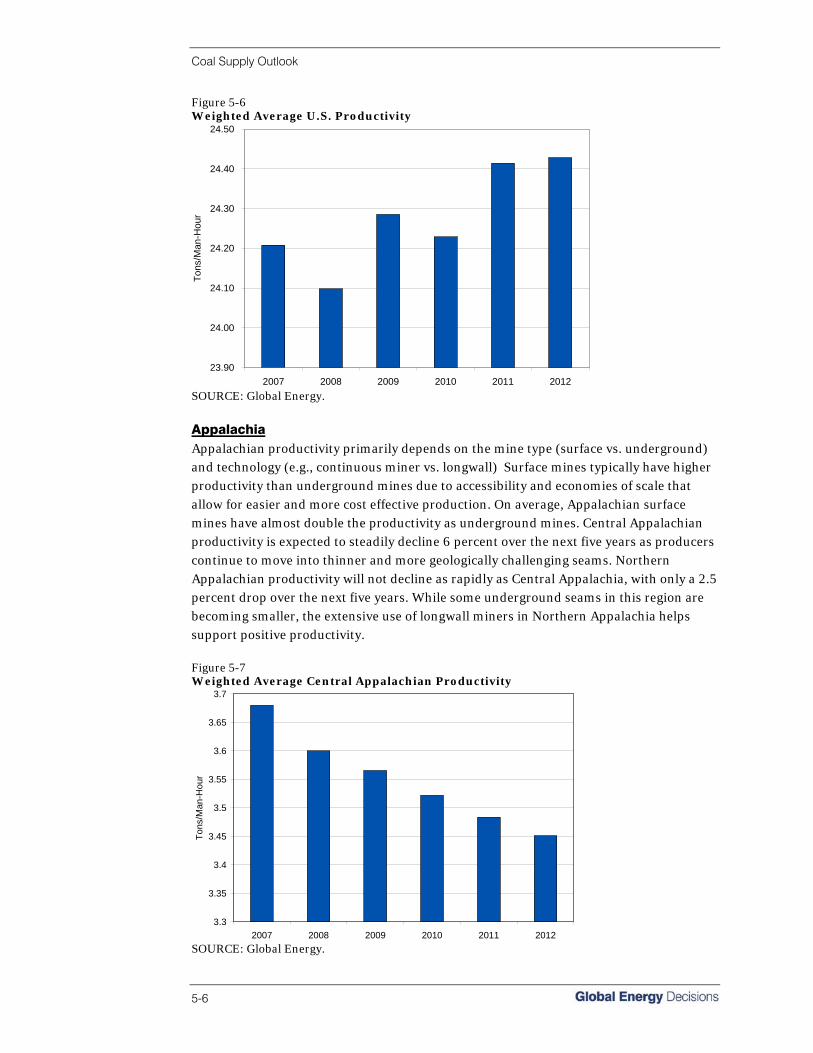

Eastern U.S. productivity (Appalachia and Illinois Basin) primarily depends on the mine type (surface vs. underground) and technology (e.g., continuous miner vs. longwall). Surface mines typically have higher productivity than underground mines due to accessibility and economies of scale that allow for easier and more cost effective production. On average, eastern surface mines have almost twice the productivity as underground mines. Central Appalachian productivity is expected to steadily decline 6 percent over the next five years as producers continue to move into thinner and more geologically challenging seams. Northern Appalachian productivity will not decline as rapidly as Central Appalachia, with only a 2.5 percent drop over the next five years. While some underground seams in this region are becoming smaller, the extensive use of longwall miners in Northern Appalachia helps support positive productivity. Even though Illinois Basin production capacity will grow over the mid-term, productivity is expected to decline through 2010. Productivity in the Powder River Basin is expected to flatten over the next three years, but remain the highest of all the U.S. coal basins. FOB Mine Prices

FOB mine prices (Figure ES-5) will also escalate over the forecasted period due to increasing production costs coupled with growing demand. Unparalleled mining conditions allow the Powder River Basin to have much lower FOB mine prices than other areas with smaller, less productive mines. Increased short-term FOB prices for South American imports will be due to increased U.S. and European demand for the coal while expanded supply with weakened European demand will dampen import coal prices through the long term. Northern Appalachian FOB prices should experience the strongest growth over the mid term due to robust demand. FOB coal price inflation will be tempered by escalating competition among the basins for customers that have the ability to switch to a primarily Btu-centric rather than sulfur-centric coal product. Figure ES-5 FOB Mine Price Forecast by Basin; 2007-2031 (Constant 2007 Dollars)

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

2007 2010 2013 2016 2019 2022 2025 2028 2031

FOB

$/to

n

Central App Colombia Illinois Basin Northern AppPRB Rocky Southern App

SOURCE: Global Energy.

Executive Summary

ES-10

Coal Transportation

Of all the transportation issues facing the U.S. coal markets, the development and expansion of rail in the Powder River Basin will have the biggest impact on U.S. coal consumption patterns. In addition to plans by UP and BNSF to expand the existing lines, there are two major plans to add more transportation capacity out of the PRB: the Dakota, Minnesota & Eastern Railroad and development of the Tongue River Railroad. Increased competition for tonnage from the PRB could be the only check on the two major rail carriers’ stranglehold on western rail pricing, which Global Energy is forecasting to show the greatest increases over the forecast period. Our forecasted 25-year coal transport price inflation assumptions can be found below in Table ES-1. Table ES-1 Global Energy Forecasted 25-Year Coal Transport Price Inflation

Barge Lake Vessel Ocean Vessel Eastern Rail Western Rail

102.8% 106.4% 103.5% 115.3% 127.7%

SOURCE: Global Energy.

Besides western rail pricing and bottlenecks, forecasted coal transportation will be dependent upon a wide variety of factors: • Barge pricing will remain flat but increased river flooding, drought, dam and lock

repair work, and dredging will all factor into barge availability; • Lake vessels will also show little pricing inflation though environmental concerns coupled

with climate change related freezing/thawing patterns could add uncertainty; and • Ocean vessels’ current extremely high pricing should settle down with increased

availability and port expansions on the way. Delivered Price Forecast by Region Increased FOB mine and transportation prices will translate into continued pressure on the delivered price of coal. While the Powder River Basin has extremely low FOB mine prices, the coal produced here has to be transported great distances and in great quantities because of its low heat content. For this reason the eastern regions (Southeast and Northeast) have high delivered coal costs because of higher eastern mining costs or very high transportation rates for cheaper western coal. Colombian imports also keep eastern prices high due to the extremely high transportation costs. For western coal consumers the low price and short hauls equate to retaining the lowest burner-tip price of coal even with considerable inflation over the forecast period. Figure ES-6 below details the changes in regional delivered prices over the course of this forecast.

Executive Summary

Coal Reference Case, Fall 2007 ES-11

Figure ES-6 U.S. Regional Delivered Price of Coal (Constant 2007 $/MMBtu)

1.2

1.4

1.6

1.8

2

2.2

2.4

2.6

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

Del

iver

ed $

/MM

Btu

West Midwest South Central Southeast Northeast SOURCE: Global Energy.

Battlegrounds

Battlegrounds are supply areas in which different basins can deliver coal for the same price on a dollar per MMBtu basis. Map ES-1 shows the areas in 2007 where delivered prices are $2.00/MMBtu or less. The Powder River Basin is able to deliver to a very large geographic area, penetrating nearly all of the areas served by the Illinois Basin and Central Appalachia at this price. While the PRB is able to penetrate central Indiana and Ohio at this price level, this is a rail market that has a higher price than surrounding areas such as the Ohio River and the Great Lakes which can be accessed more cheaply by barge or lake vessel. This is shown clearly below with the “horseshoe” shape the PRB’s $2.00/MMBtu area takes in this region. Competition is currently heaviest in Illinois and the river markets directly surrounding it, as well as into the Ohio River Valley as far east as West Virginia. The main competition will continue to be on the river markets through the mid term, particularly the Ohio River. This remains the only area where all three basins are able to deliver coal under $2.00/MMBtu. The greatest shift in the market occurs through the longer term as Central Appalachia’s production declines and costs continue to increase. The market that is reachable at a delivered price of $2.00/MMBtu shrinks dramatically to contain only a small part of the Ohio River Valley. Meanwhile, increased demand for Illinois Basin coal inflates delivered prices around the basin and into the southeast, leaving the Illinois Basin area and the western half of the Ohio River Valley the only major battleground left at this price range. Competition among these basins will certainly occur elsewhere in the country with the southeast being the likeliest alternate battleground.

Executive Summary

ES-12

Map ES 1 2007 Coal Battleground Areas

SOURCE: Global Energy.

Table of Contents

Coal Reference Case, Fall 2007 i

Executive Summary ES-1 1 Introduction 1-1

Purpose Of Study........................................................................................ 1-1 Organization Of The Report ........................................................................ 1-4

2 Forecast Methodology and Assumptions 2-1

Forecast Methodology ................................................................................ 2-1

• Global Energy’s Approach to Modeling Demand for Electric Power ....................2-1

• Global Energy’s Approach to Modeling Natural Gas Prices.............................2-6

• Global Energy’s Approach to Modeling Emissions Prices ...............................2-8

• Coal Price Volume and Model .........................................................................2-10

• Global Energy’s Coal Cost Model ...................................................................2-14

• Global Energy’s Approach to Modeling Productivity and Production ............2-17

Forecast Assumptions ...............................................................................2-20

• Electricity Demand...........................................................................................2-20

• Natural Gas and Oil Pricing .............................................................................2-22

• Generating Capacity ........................................................................................2-24

• Key Assumptions Applied to the MARKETSYM™ Model................................2-25

• Environmental Issues.......................................................................................2-31

• Transportation Assumptions............................................................................2-38

3 Historic and Current Market Conditions 3-1

Demand For Electricity Generation............................................................. 3-1 • Historic and Current Electricity Generation by Fuel ..........................................3-1

• Historic and Current Electricity Capacity by Fuel ..............................................3-2

Supply Of Coal...........................................................................................3-12 • Historic and Current Coal Consumption by Sector.........................................3-12

• Basin Production and Quality ..........................................................................3-14

• Basin Reserves ................................................................................................3-17

• Basin Costs......................................................................................................3-22

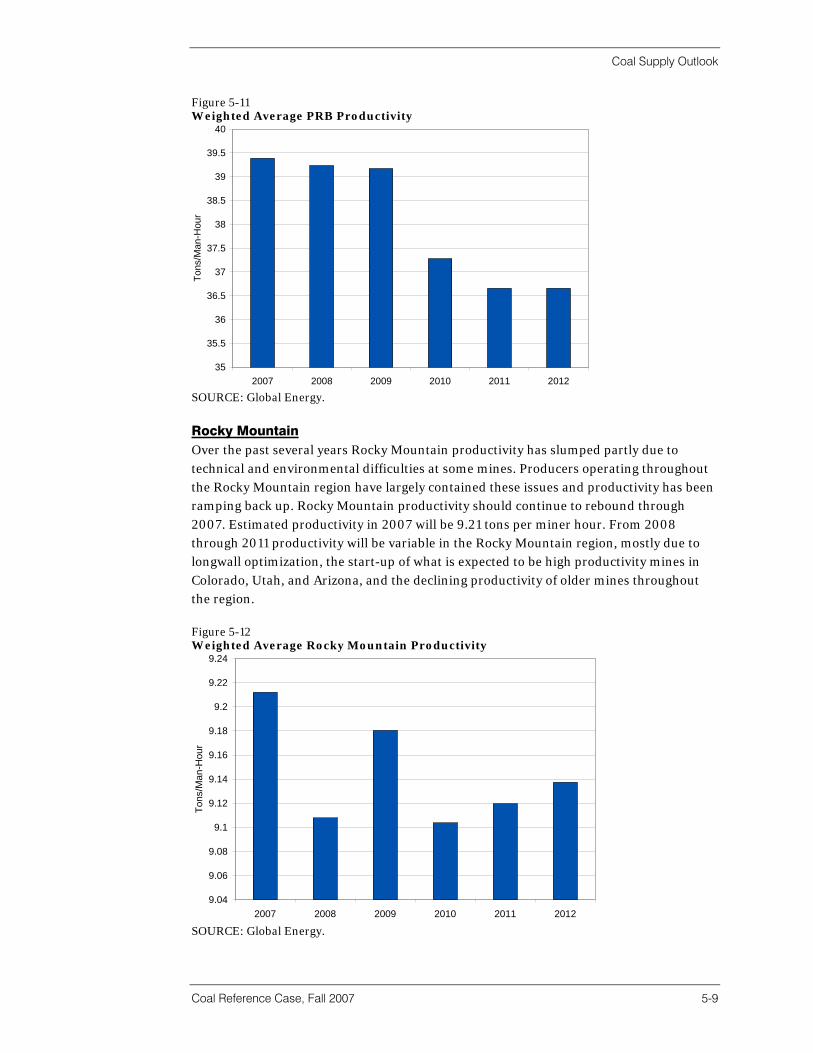

• Non-Utility Coal Consumption .........................................................................3-25

Coal Transportation....................................................................................3-28 • Railroad Transportation ...................................................................................3-28

• River Barge.......................................................................................................3-37

• Truck ................................................................................................................3-39

• Lake Vessel ......................................................................................................3-39

• Ocean Vessel ...................................................................................................3-40

• Slurry Pipeline ..................................................................................................3-42

Table of Contents

ii

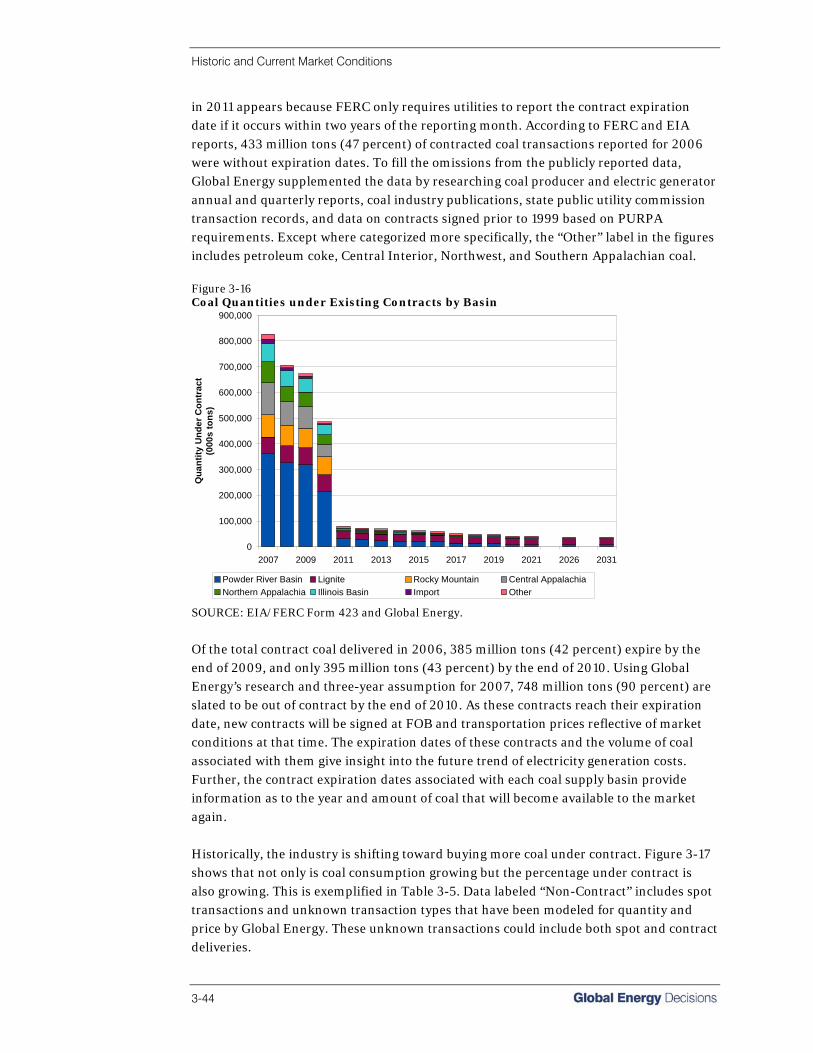

Coal Supply Contracts ...............................................................................3-42 Regulatory Issues.......................................................................................3-48

• Clearn Air Act ...................................................................................................3-49

• Clean Air Mercury Rule ....................................................................................3-54

• Clean Air Interstate Rule ..................................................................................3-56

• Carbon Emissions Regulations .......................................................................3-56

• Mountain Top Removal Mining........................................................................3-62

• The Surface Mine Control and Reclamation Act .............................................3-64

• The Mine Safety and Health Administration ....................................................3-65

Other Issues...............................................................................................3-66

• Industry Consolidation Through Merger and Acquisition (M&A) ....................3-66

• OTC Markets ....................................................................................................3-70

• Foreign Markets ...............................................................................................3-72

4 Coal Demand Outlook 4-1

Demand Region Outlook ............................................................................ 4-1 • Overall U.S. Demand .........................................................................................4-1

Midwest ....................................................................................................... 4-4 Northeast..................................................................................................... 4-9 South Centtral ............................................................................................4-13 Southeast ...................................................................................................4-17

West ...........................................................................................................4-21 Non-Utility Future Coal Consumption ........................................................4-25

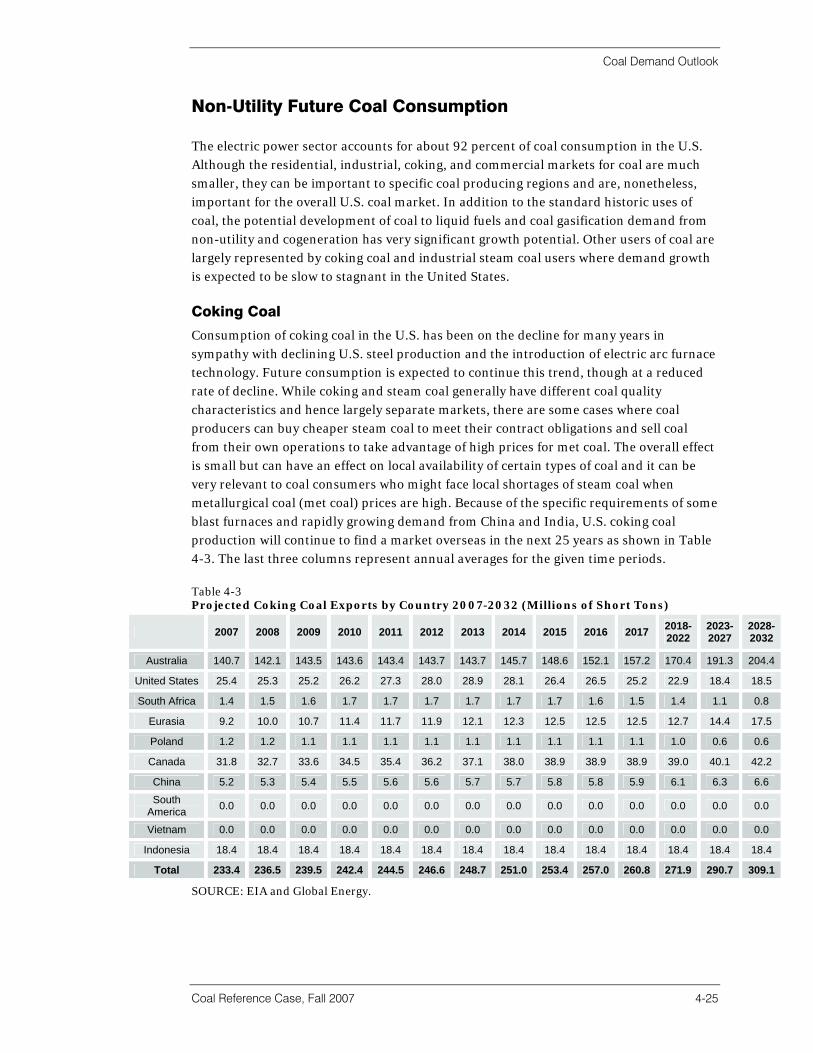

• Coking Coal .....................................................................................................4-25

• Industrial, Commercial, and Residential Coal Use..........................................4-26

• Coal-to-Liquids and Coal-to-Gas ..................................................................... 426

• 25-Year Projections..........................................................................................4-28

5 Coal Supply Outlook 5-1

Forecasted Coal Costs ............................................................................... 5-1

• U.S. Fully Allocated Costs .................................................................................5-1

• Basin Fully Allocated Costs ...............................................................................5-2

• Basin Productivity ..............................................................................................5-5

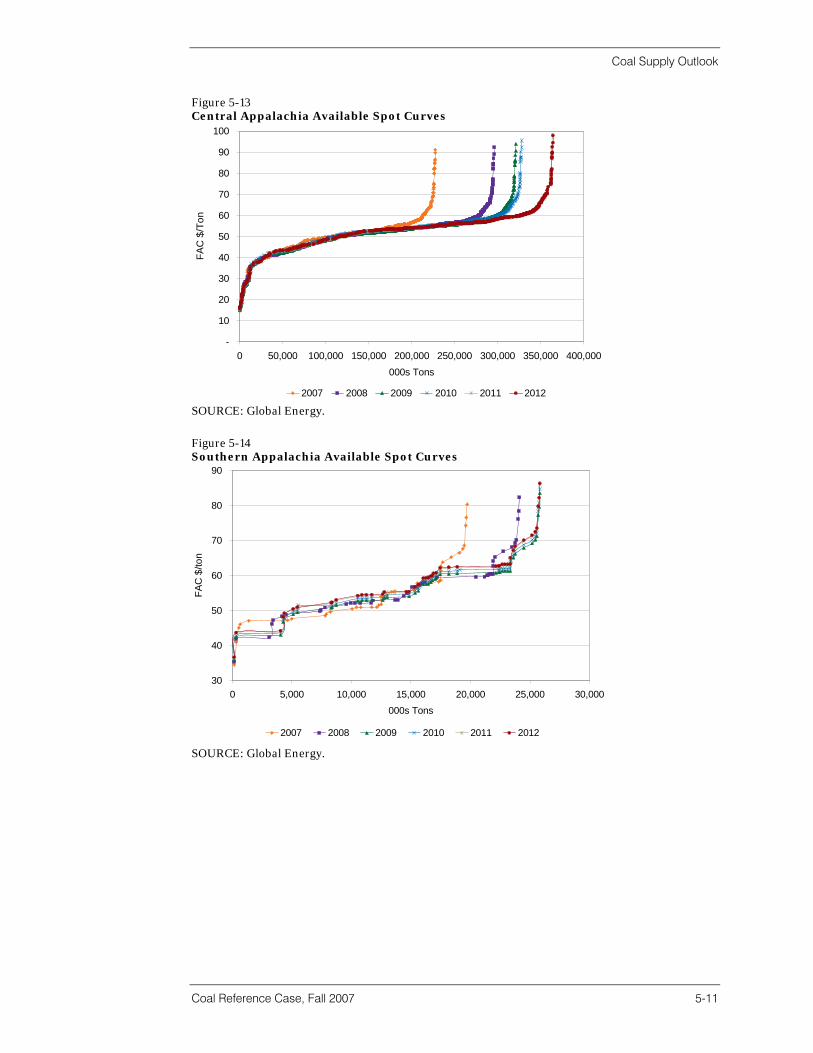

• Avaialble Spot Curves by Basin.......................................................................5-10

FOB And Delivered Prices By Supply Basin And Region ..........................5-14

• Central Appalachia ..........................................................................................5-15

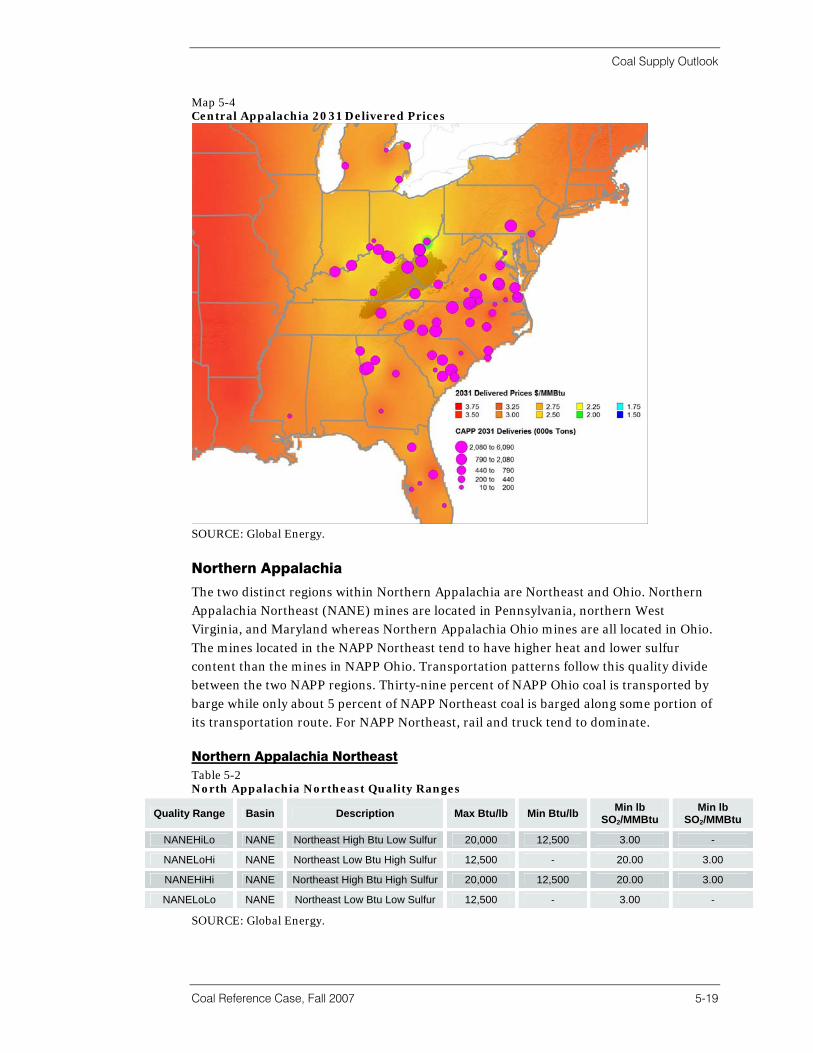

• Norhtern Appalachia........................................................................................5-19

• Illinois Basin .....................................................................................................5-21

• Powder River Basin..........................................................................................5-25

Table of Contents

Coal Reference Case, Fall 2007 iii

• Rocky Mountain Region...................................................................................5-30

• All Other Basins ...............................................................................................5-35

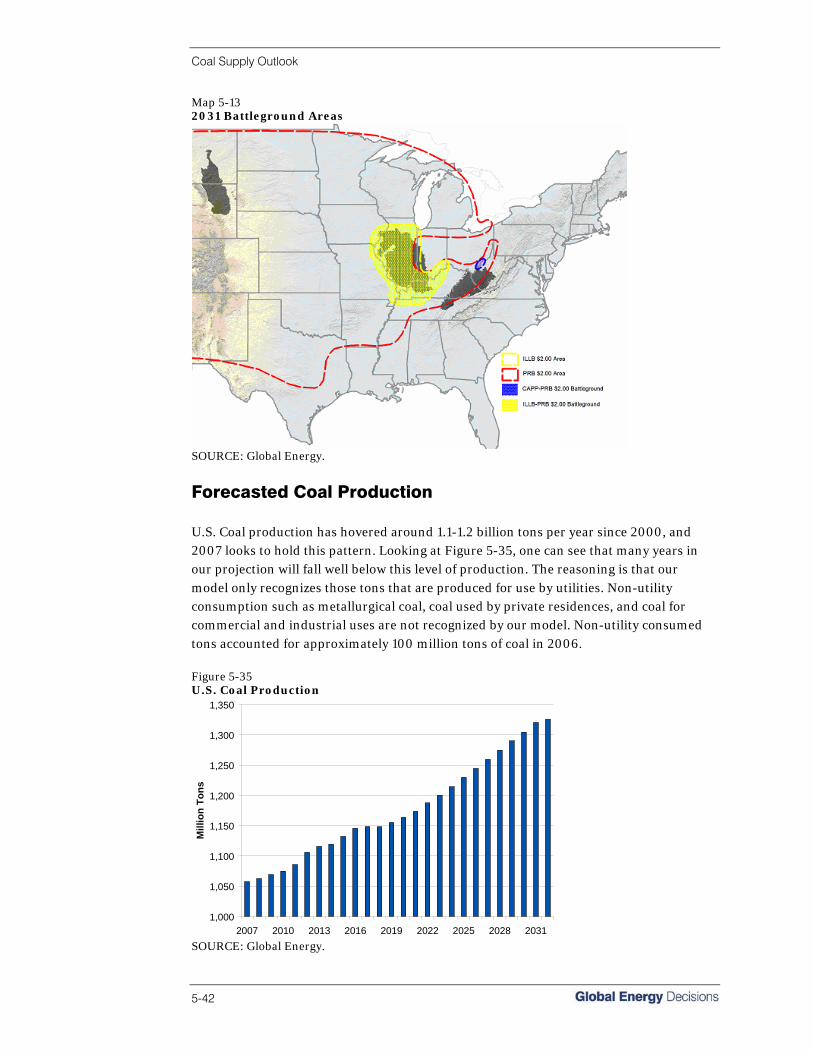

Coal Basin Battleground ............................................................................5-39 Forecasted Coal Production ......................................................................5-42

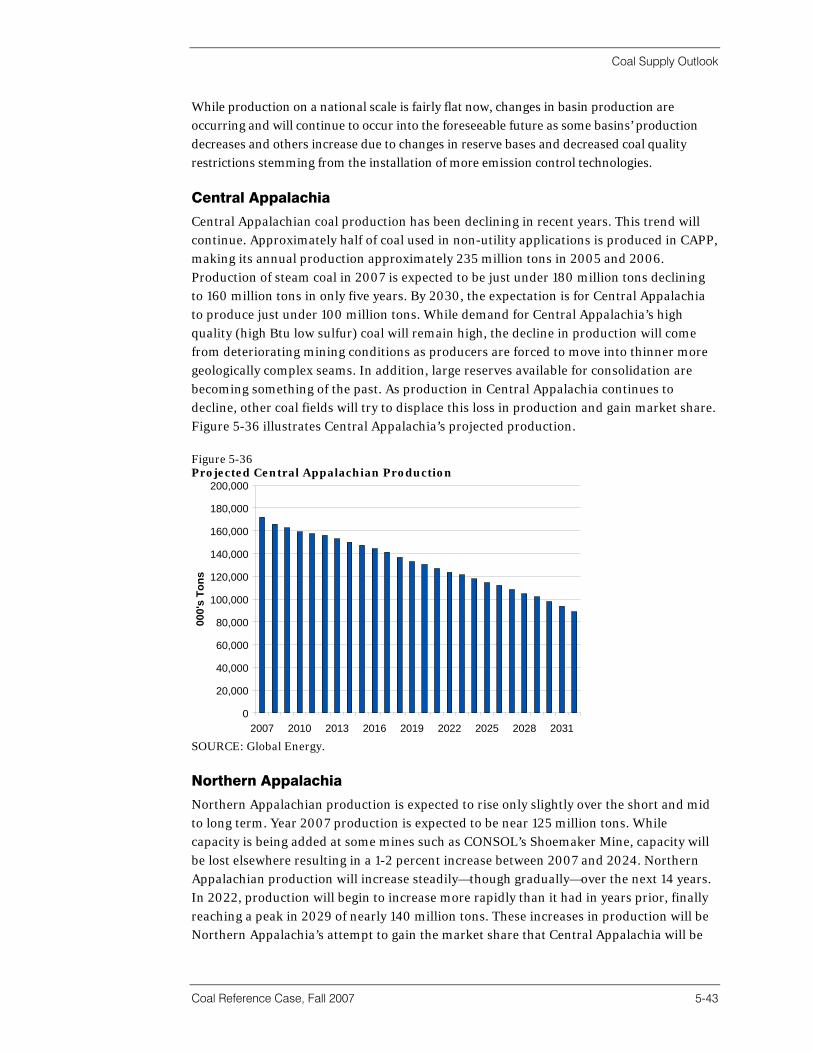

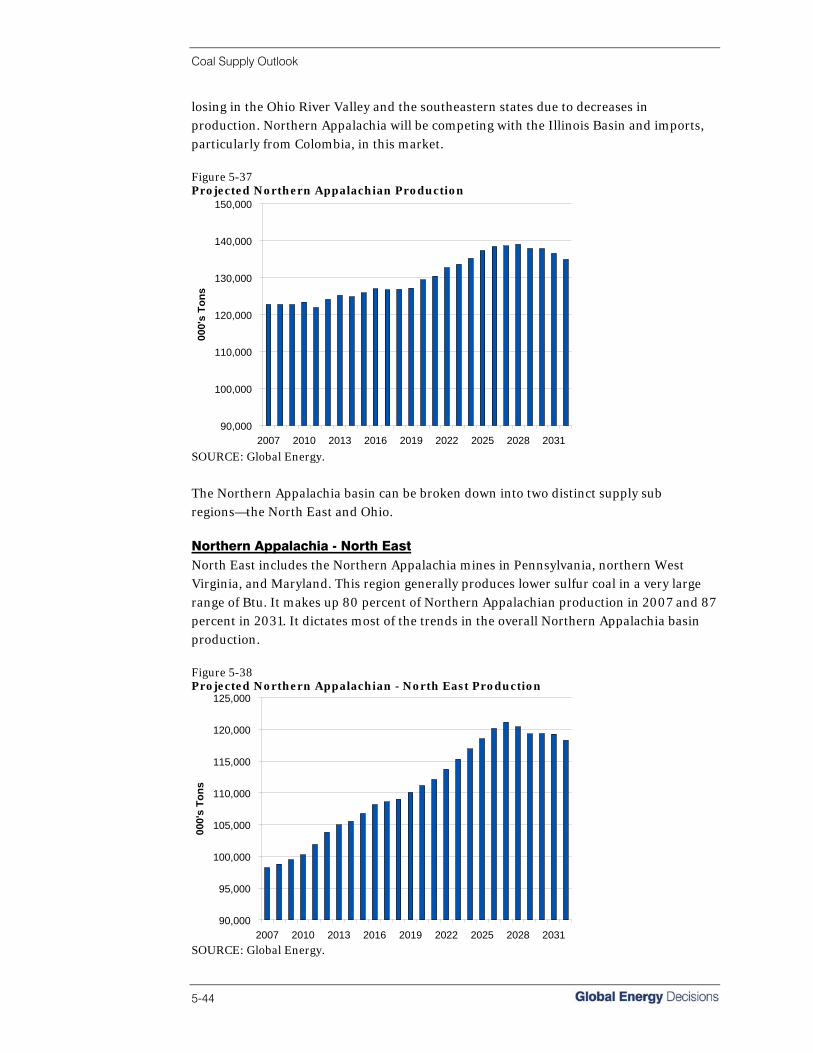

• Central Appalachia ..........................................................................................5-43

• Northern Appalachia........................................................................................5-43

• Illinois Basin ...................................................................................................... 545

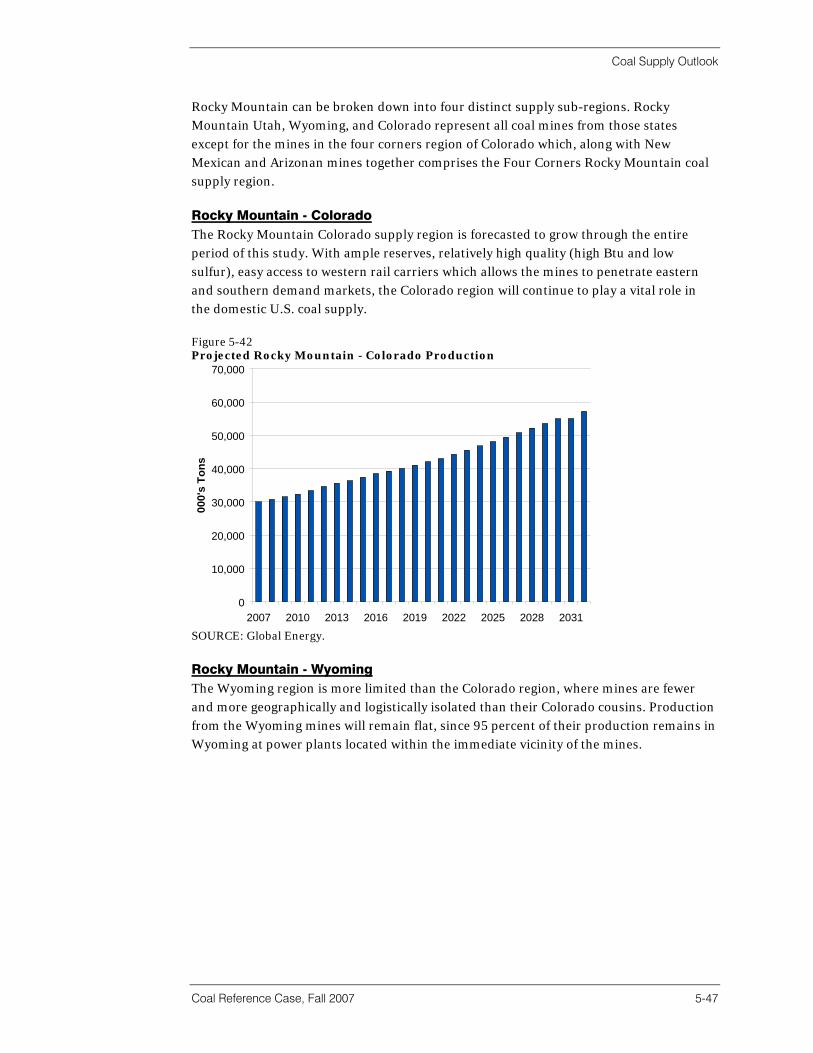

• Rocky Mountain ...............................................................................................5-46

• Powder River Basin..........................................................................................5-49

Future Coal Transportation ........................................................................5-52

• Railroad Transportation ...................................................................................5-53

• Barge Transportation .......................................................................................5-60

• Ocean Vessel Transportation ..........................................................................5-61

Appendix A Demand Region Prices

Appendix B Demand Region Volumes

Appendix C Basin Volumes & Prices

iv

List of Tables

Coal Reference Case, Fall 2007 v

ES-1 Global Energy Forecasted 25-Year Coal Transport Price Inflation..................... ES-10

2-1 Reference Case Gas Price Forecasting Phases......................................................2-6

2-2 Emissions Costs .....................................................................................................2-10

2-3 Historic and Forecasted Economic and Population Growth .................................2-20

2-4 Forecasted Electricity Growth - GWh .....................................................................2-21

2-5 Key Statistics for Future Fuel Mix; 2007-2031........................................................2-22

2-6 Average Market Clearing Price Forecast................................................................2-22

2-7 Natural Gas and Oil Price Forecast; 2007 S/MMBtu .............................................2-24

2-8 Current and Forecasted Capacity (MW) ...............................................................2-24

2-9 Key Statistics for Future Coal Technology; 2007-2031..........................................2-25

2-10 Generic Unit Costs and Operating Characteristics................................................2-27

2-11 Regional Multipliers ................................................................................................2-28

2-12 Capital Structure Characteristics............................................................................2-29

2-13 Cost Assumptions for Emissions Control Equipment............................................2-32

2-14 Effectiveness of Emissions Control Equipment .....................................................2-32

2-15 Reference Case SO2 Allowance Price Forecast .....................................................2-33

2-16 National and CAIR NOX Emissions Prices..............................................................2-36

2-17 Escalation by Transportation Mode .......................................................................2-39

3-1 Electric Power Plants and Average Capacity ...........................................................3-4

3-2 Appalachia Recoverable Resources by Coal Bed.................................................3-18

3-3 Remaining Coal in the Illinois Basin by Coal Bed ..................................................3-19

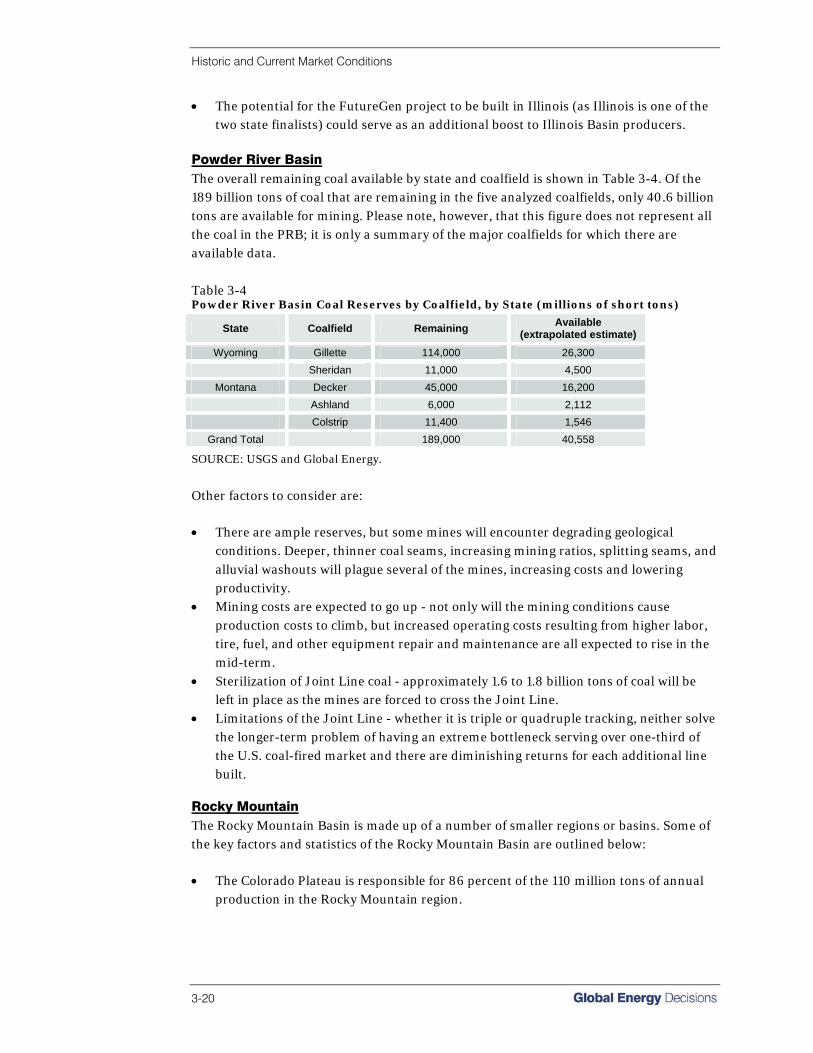

3-4 Powder River Basin Coal Reserves by Coalfield....................................................3-20

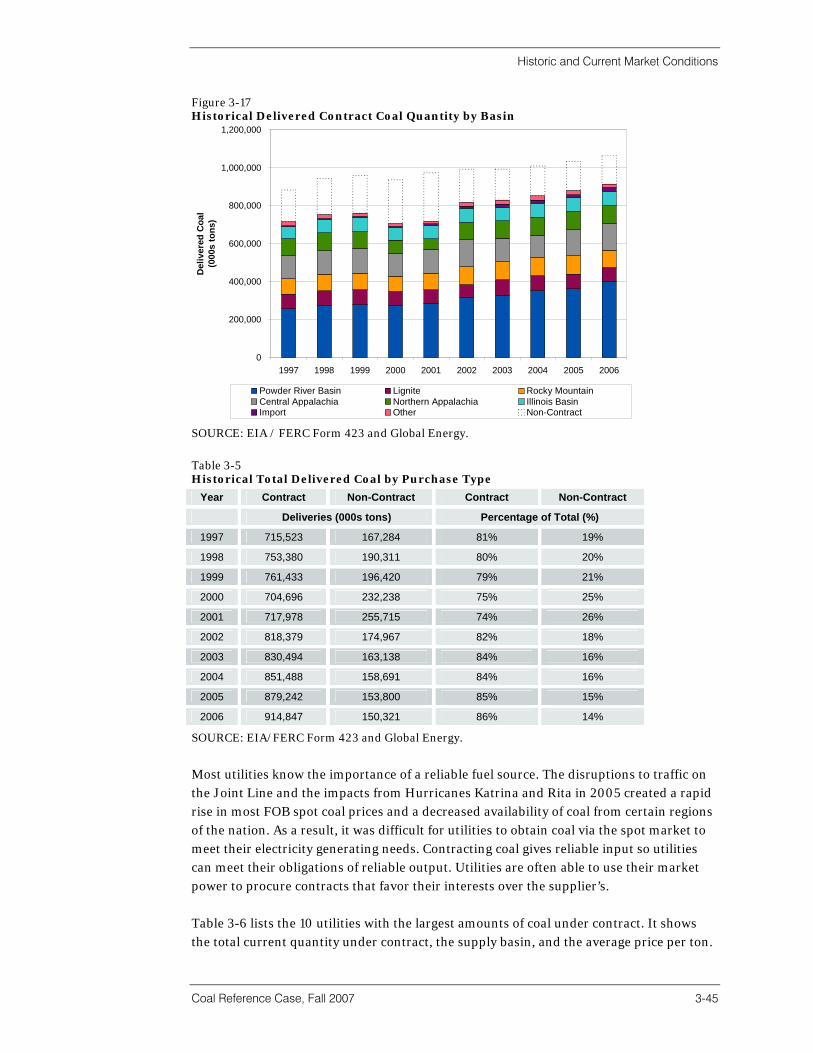

3-5 Historical Total Delivered Coal by Purchase Type.................................................3-45

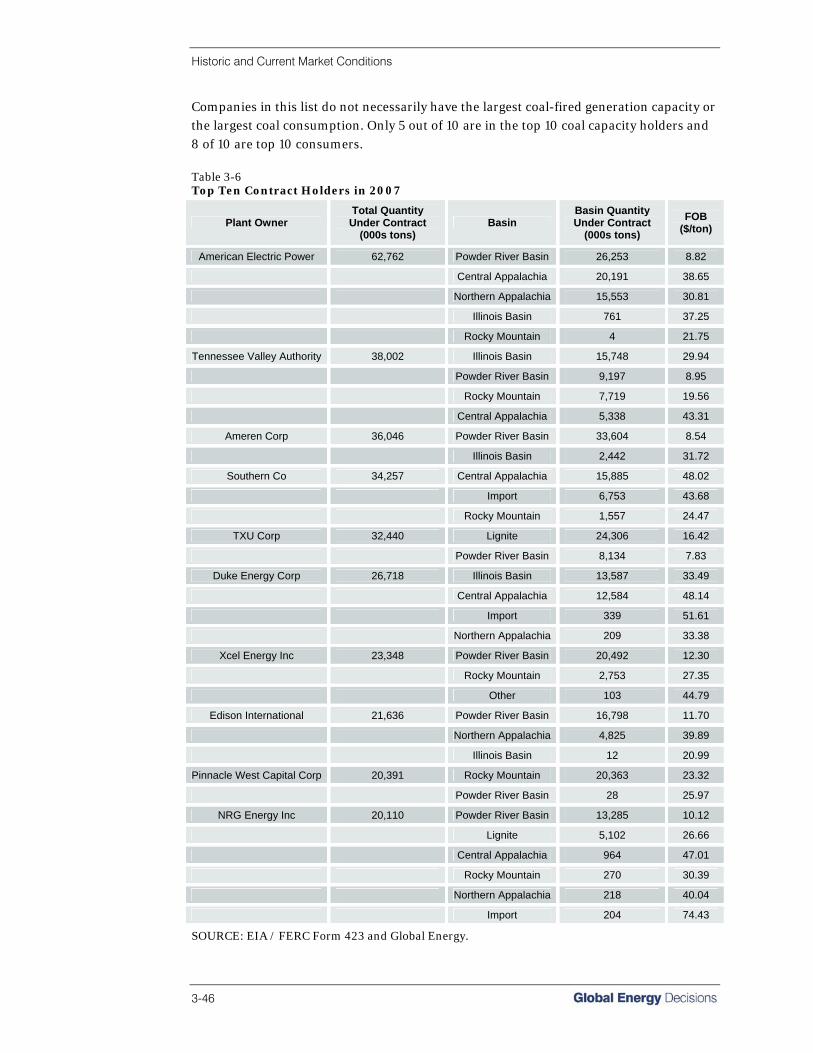

3-6 Top Ten Contract Holders in 2007 .........................................................................3-46

3-7 National Ambient Air Quality Standards.................................................................3-50

3-8 State Mercury Emissions Rules..............................................................................3-55

3-9 Major Federal GHG Emission Reduction Proposals .............................................3-60

3-10 World Steam Coal Trade 2005-2006......................................................................3-73

4-1 Yearly Coal Generation Demand by Region ............................................................4-2

4-2 Approximate Ton Makeup of Coal Source Categories Seen in Figures..................4-3

4-3 Projected Coking Coal Exports by Country; 2007-2032........................................4-25

4-4 Coal-to-Liquids Plants under Development ...........................................................4-27

5-1 Central Appalachia Quality Ranges .......................................................................5-15

List of Tables

vi

5-2 North Appalachia Northeast Quality Ranges .........................................................5-19

5-3 North Appalachia Ohio Quality Ranges .................................................................5-20

5-4 Illinois Basin Quality Ranges ..................................................................................5-21

5-5 Northern Powder River Basin Quality Ranges .......................................................5-25

5-6 Southern Powder River Basin FOB Mine Prices ....................................................5-26

5-7 Rocky Mountain Colorado North Quality Ranges..................................................5-31

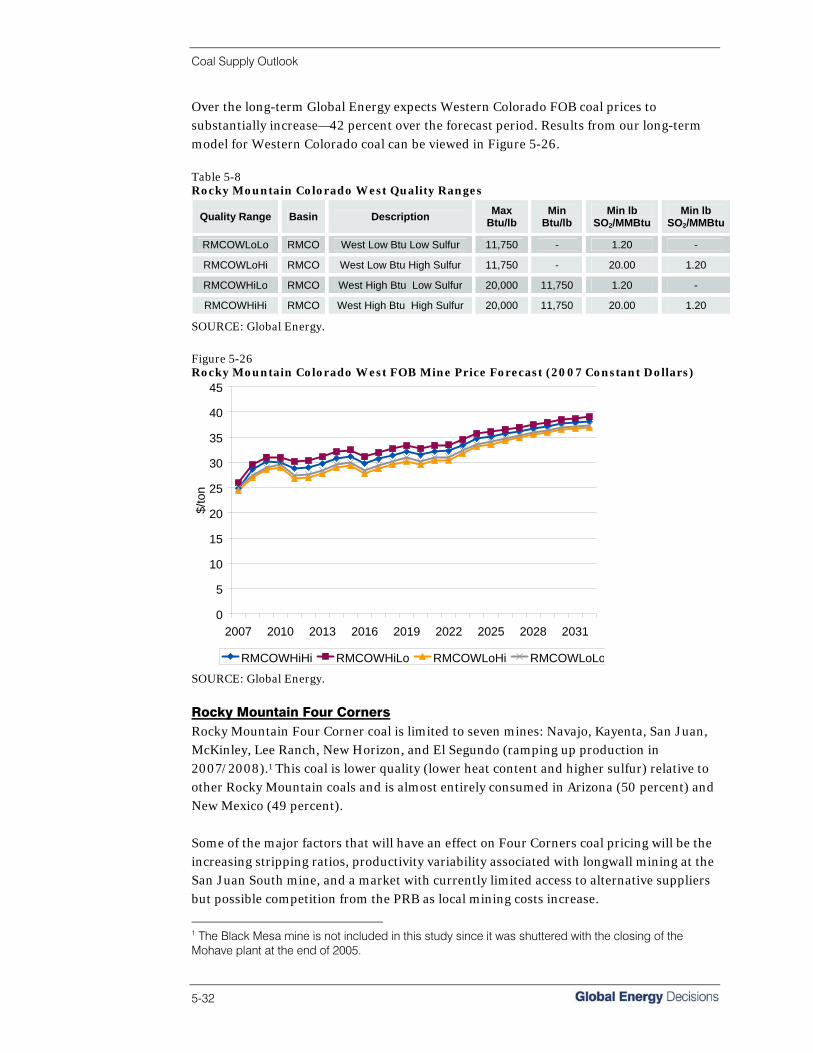

5-8 Rocky Mountain Colorado West Quality Ranges...................................................5-32

5-9 Rocky Mountain Four Corners Quality Ranges......................................................5-33

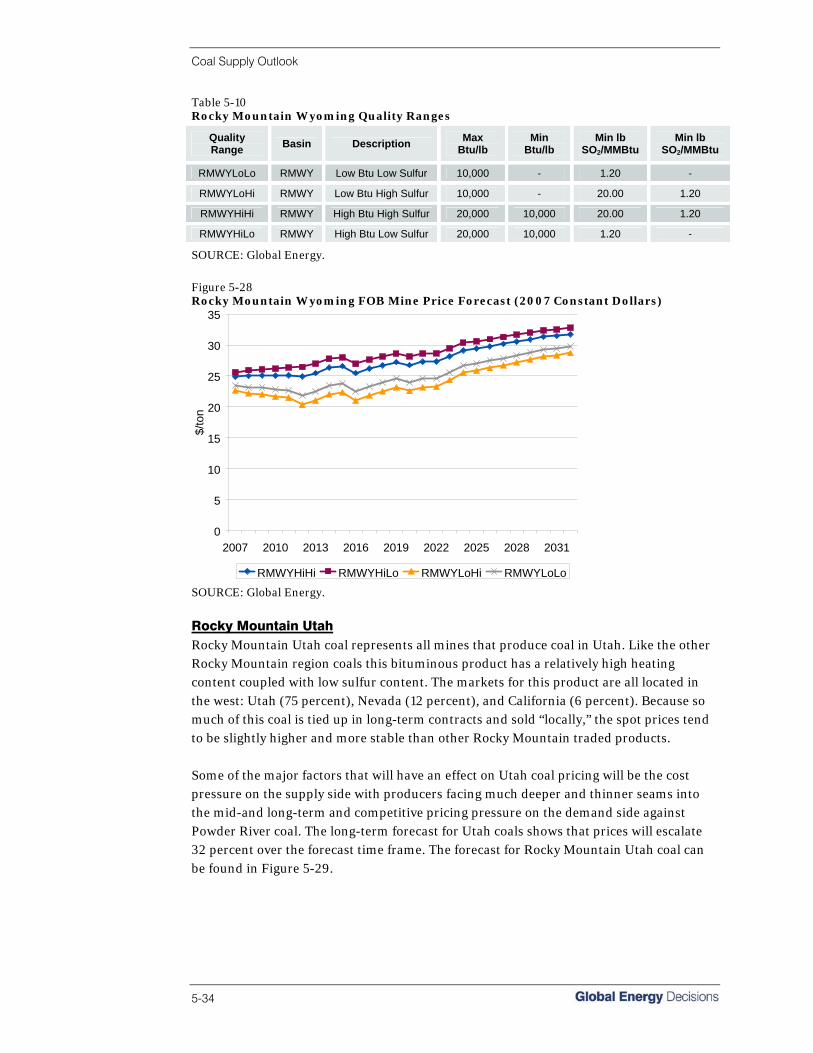

5-10 Rocky Mountain Wyoming Quality Ranges............................................................5-34

5-11 Rocky Mountain Utah Quality Ranges ...................................................................5-35

5-12 Central Interior Quality Ranges...............................................................................5-35

5-13 Northern Lignite Quality Ranges ............................................................................5-36

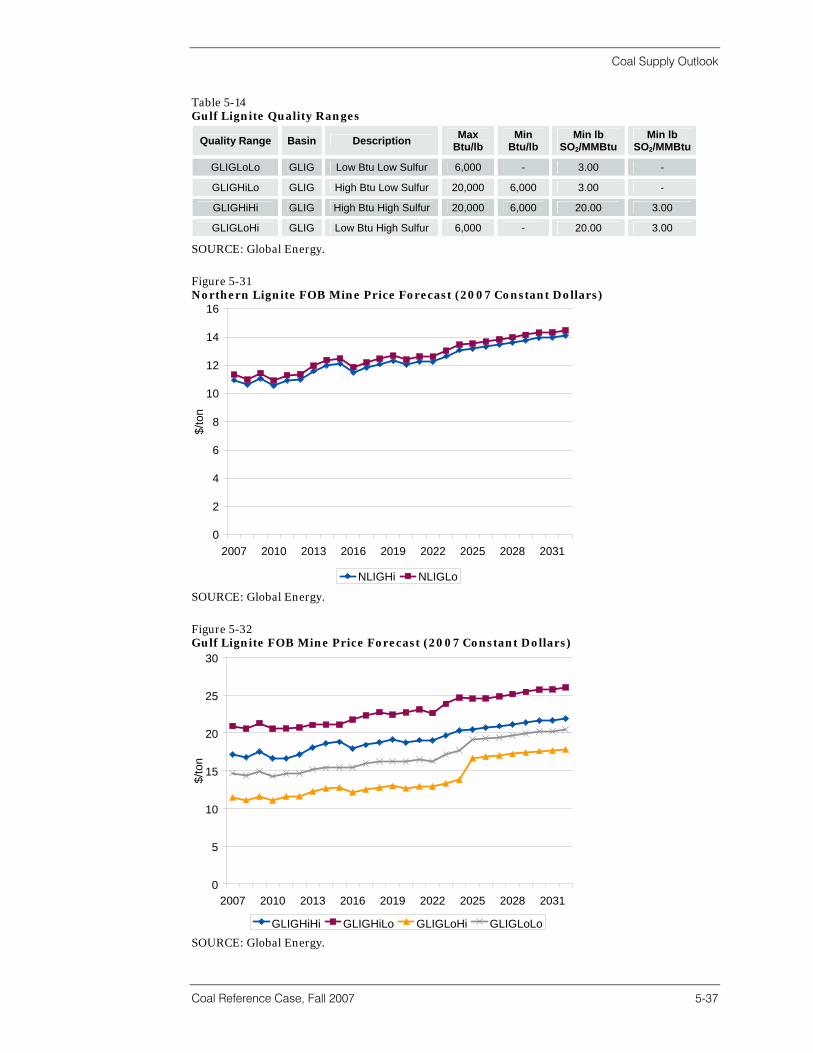

5-14 Gulf Lignite Quality Ranges....................................................................................5-37

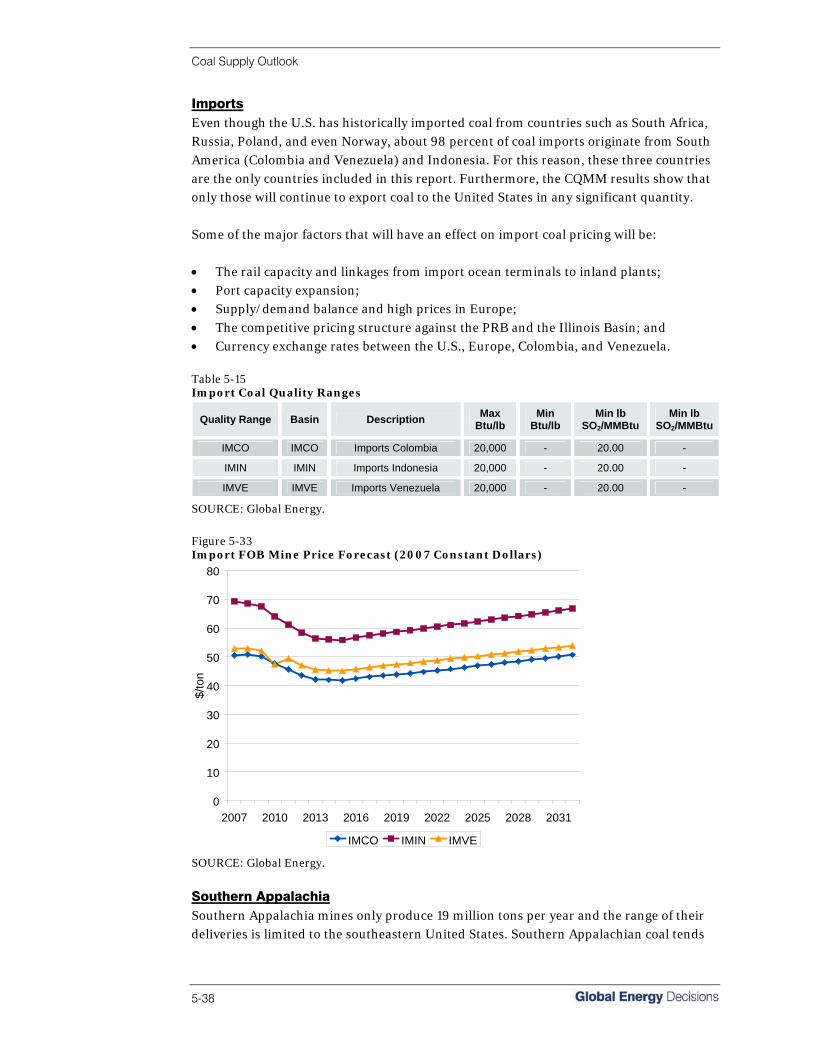

5-15 Import Coal Quality Ranges ...................................................................................5-38

5-16 Southern Appalachia Quality Ranges ....................................................................5-39

5-17 Mill Rates by Transportation Mode.........................................................................5-52

5-18 Potential DM&E PRB Coal Tonnage by Termination .............................................5-56

5-19 Rail Access to Notable Coal Docks .......................................................................5-57

5-20 Import Handling Facility Capacities .......................................................................5-61

List of Figures

Coal Reference Case, Fall 2007 vii

ES-1 Historical and Forecasted Electricity Generation by Fuel..................................... ES-5

ES-2 Coal Generation Demand by Region .................................................................... ES-6

ES-3 United States Delivered Coal Quantities ............................................................... ES-7

ES-4 U.S. Fully Allocated Mine Costs; 2007-2031 (Constant 2007 Dollars) ................. ES-8

ES-5 FOB Mine Price Forecast by Basin; 2007-2031 (Constant 2007 Dollars) ............ ES-9

ES-6 U.S. Regional Delivered Price of Coal (Constant 2007 $/MMBtu)...................... ES-11

1-1 Forecasted Coal Demand ........................................................................................1-1

2-1 Global Energy’s Fuels Analysis Uses an Integrated Cross Commodity Approach 2-1

2-2 Gas Price Seasonal Variation ...................................................................................2-7

2-3 CQMM Logic Flowchart..........................................................................................2-13

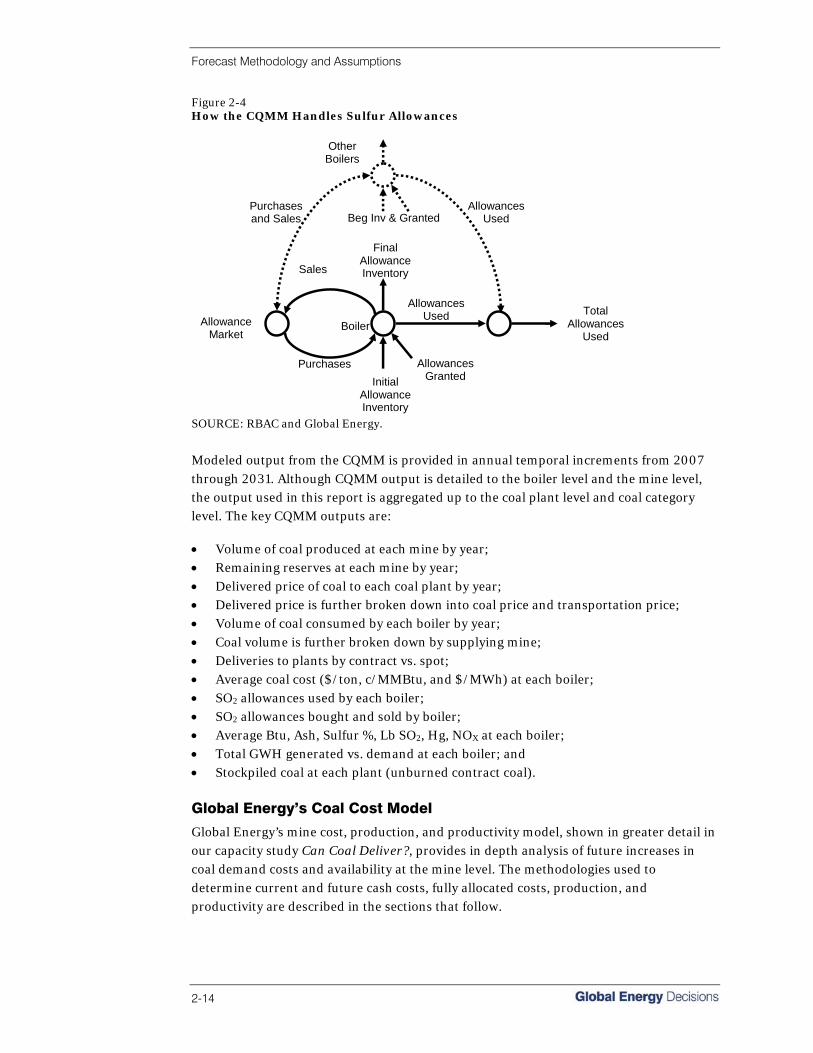

2-4 How the CQMM Handles Sulfur Allowances..........................................................2-14

2-5 Historic GDP and Electricity Generation Growth ...................................................2-21

2-6 Historical and Forecasted Electricity Generation by Fuel......................................2-21

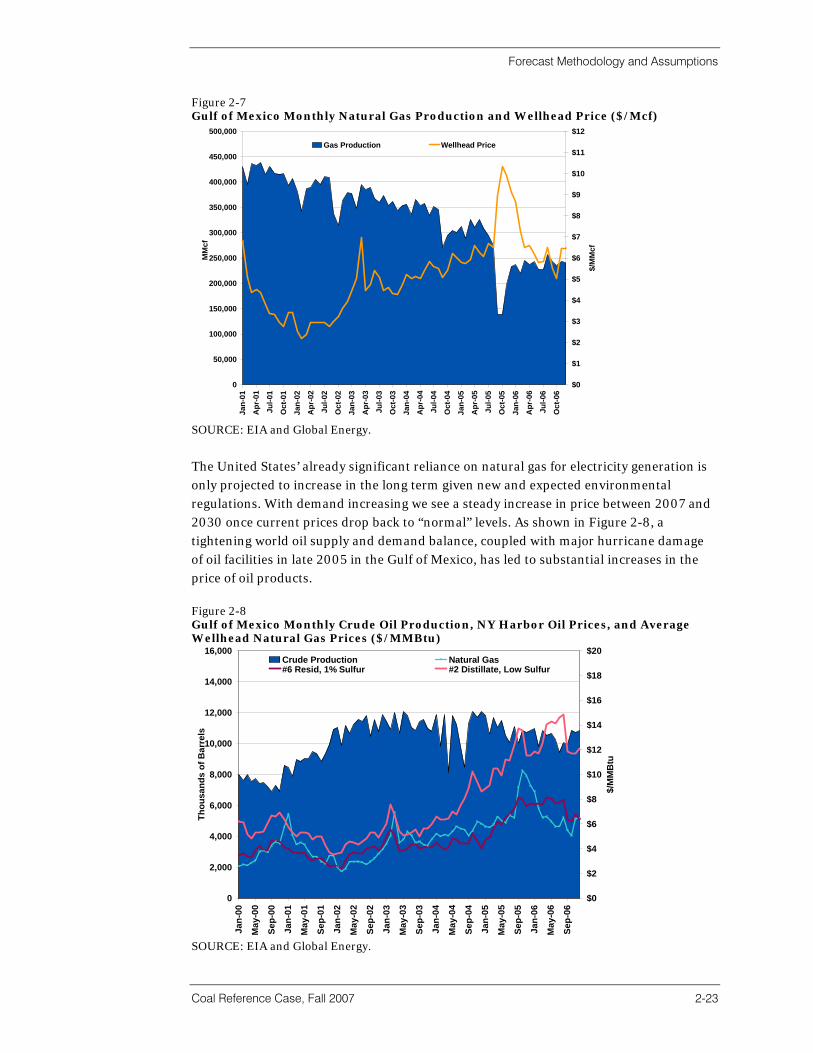

2-7 Gulf of Mexico Monthly Natural Gas Production and Wellhead Price ...................2-23

2-8 Gulf of Mexico Crude Oil Production, NY Harbor Oil Prices, and Average Wellhead Natural Gas Prices..................................................................................2-23

2-9 Historical and Forecasted Electricity Generation by Coal Plant Technology ........2-25

2-10 Forecasted Scrubbed and Un-Scrubbed U.S. Coal Capacity...............................2-33

2-11 National and CAIR NOx Emissions.........................................................................2-35

2-12 SCR Installations by MW Capacity .........................................................................2-35

3-1 Electricity Generation by Region ..............................................................................3-2

3-2 Percentage of Electricity Generation by Fuel ...........................................................3-2

3-3 U.S. Generating Capacity by Fuel Type; 2007.........................................................3-3

3-4 U.S. Capacity Installation Timeline ...........................................................................3-3

3-5 Historic and Current Capacities by Fuel Type .........................................................3-4

3-6 Historic and Current Capacity Factors by Fuel Type...............................................3-5

3-7 Average Delivered Fuel Price to Electric Utilities .....................................................3-8

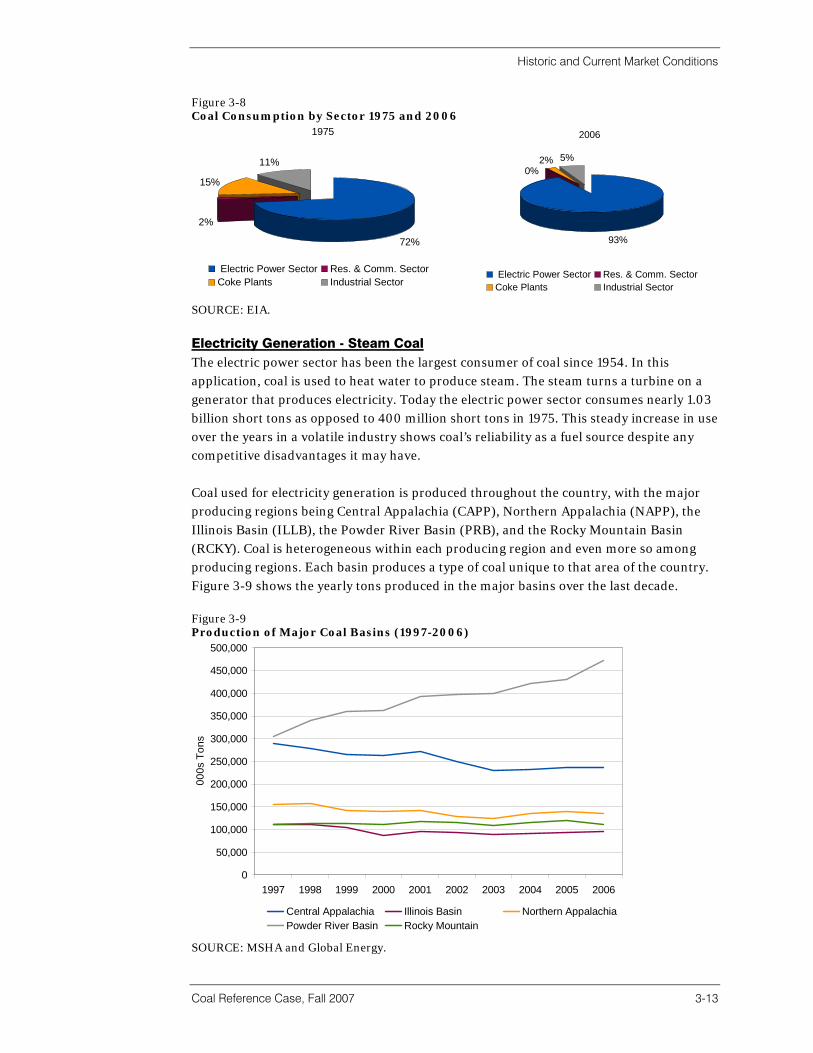

3-8 Coal Consumption by Sector 1975 and 2006........................................................3-13

3-9 Production of Major Coal Basins (1997-2006).......................................................3-13

3-10 U.S. Coal Resources ..............................................................................................3-18

3-11 Coal Mine Productivity by Basin; 1995-2007 .........................................................3-23

3-12 Historical Non-Utility Coal Consumption; 1973-2006 ............................................3-26

3-13 Average Coking Coal Prices in the U.S.; 2001-2007 .............................................3-27

3-14 Rail Cost Adjustment Factor...................................................................................3-35

List of Figures

viii

3-15 Terminating Transportation of Coal Imports ..........................................................3-42

3-16 Coal Quantities under Existing Contracts by Basin ...............................................3-44

3-17 Historical Delivered Contract Coal Quantity by Basin............................................3-45

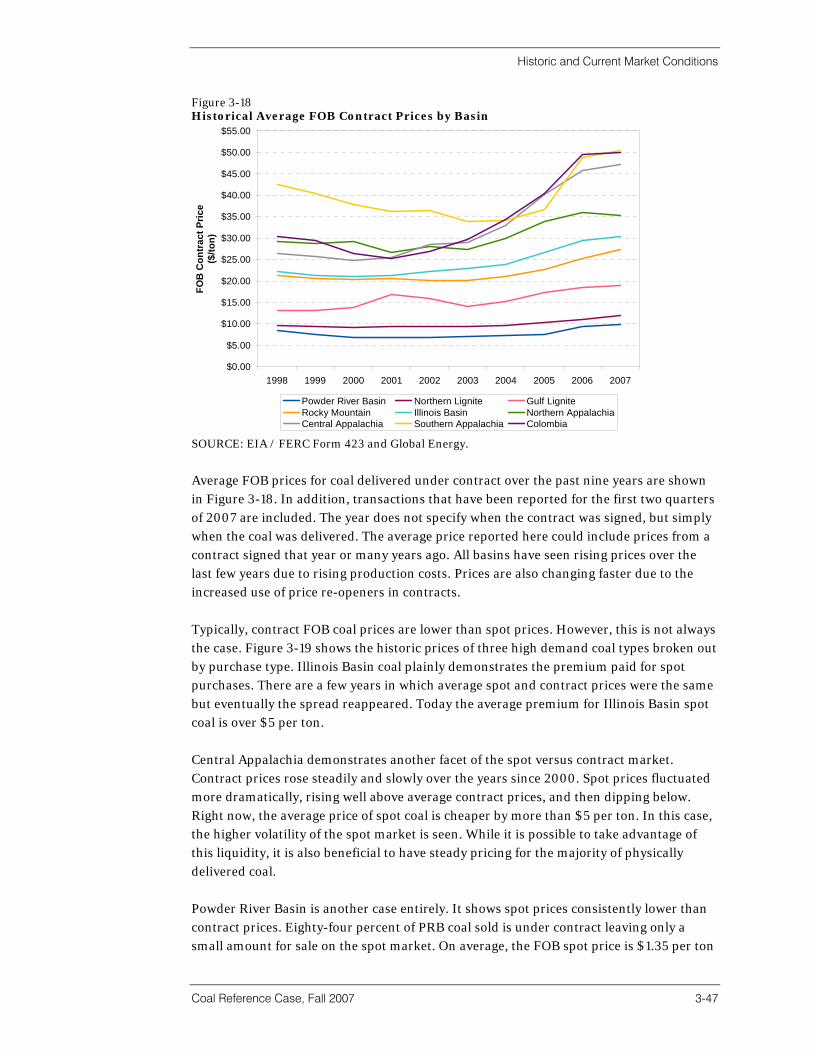

3-18 Historical Average FOB Contract Prices by Basin .................................................3-47

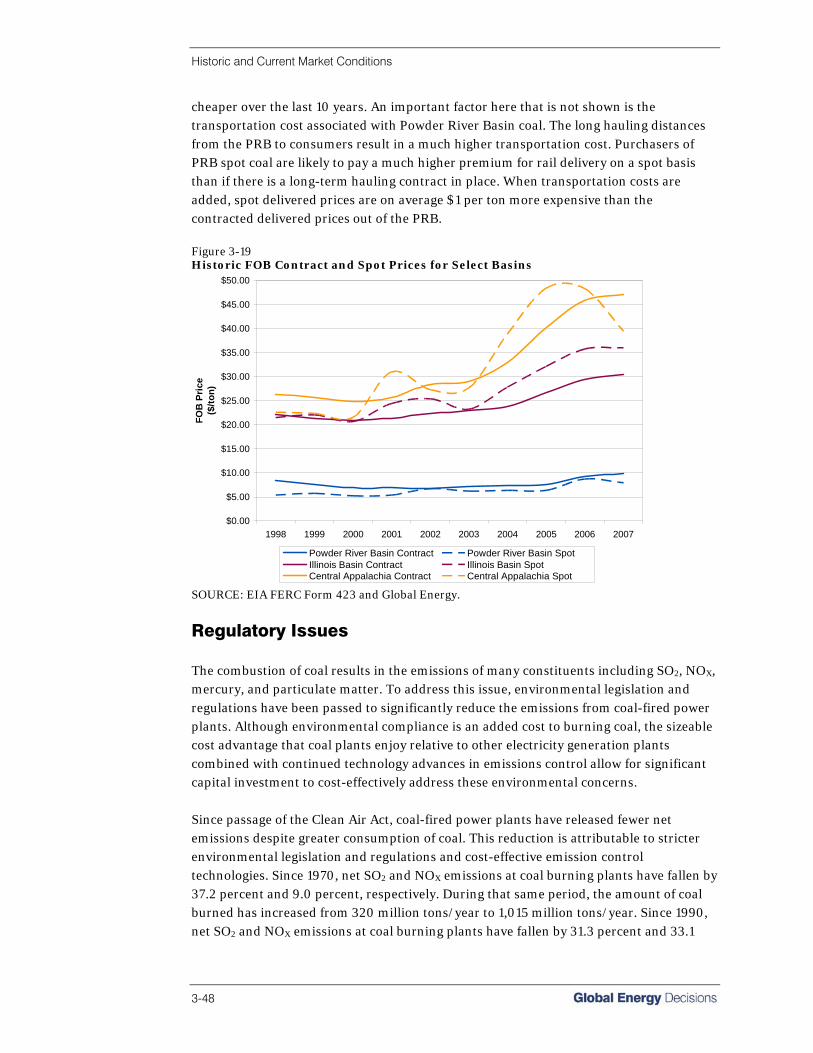

3-19 Historic FOB Contract & Spot Prices for Select Basins .........................................3-48

3-20 Production and Productivity at Surface and Underground Mines in

Central Appalachia; 1990-2007..............................................................................3-63

3-21 Market Concentration for U.S. Coal Producers by Basin; 1990-2007 ...................3-69

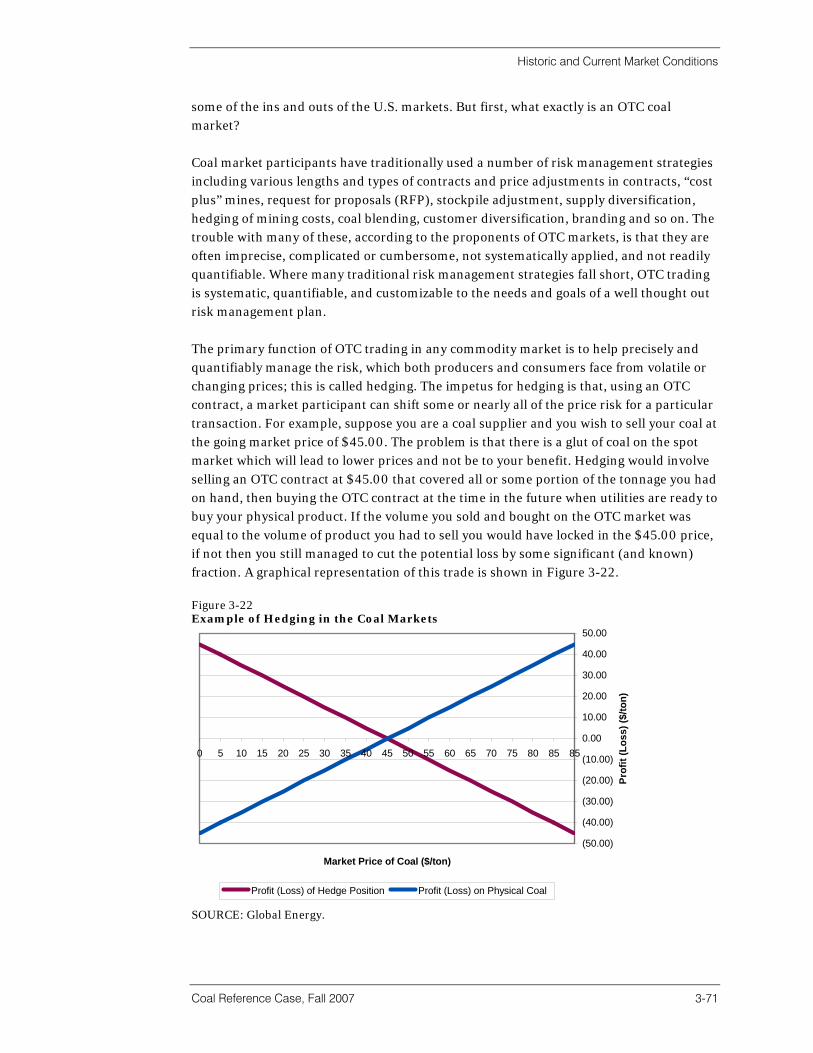

3-22 Example of Hedging in the Coal Markets ..............................................................3-71

4-1 United States Coal Demand by Basin......................................................................4-1

4-2 Coal Generation Demand by Region .......................................................................4-3

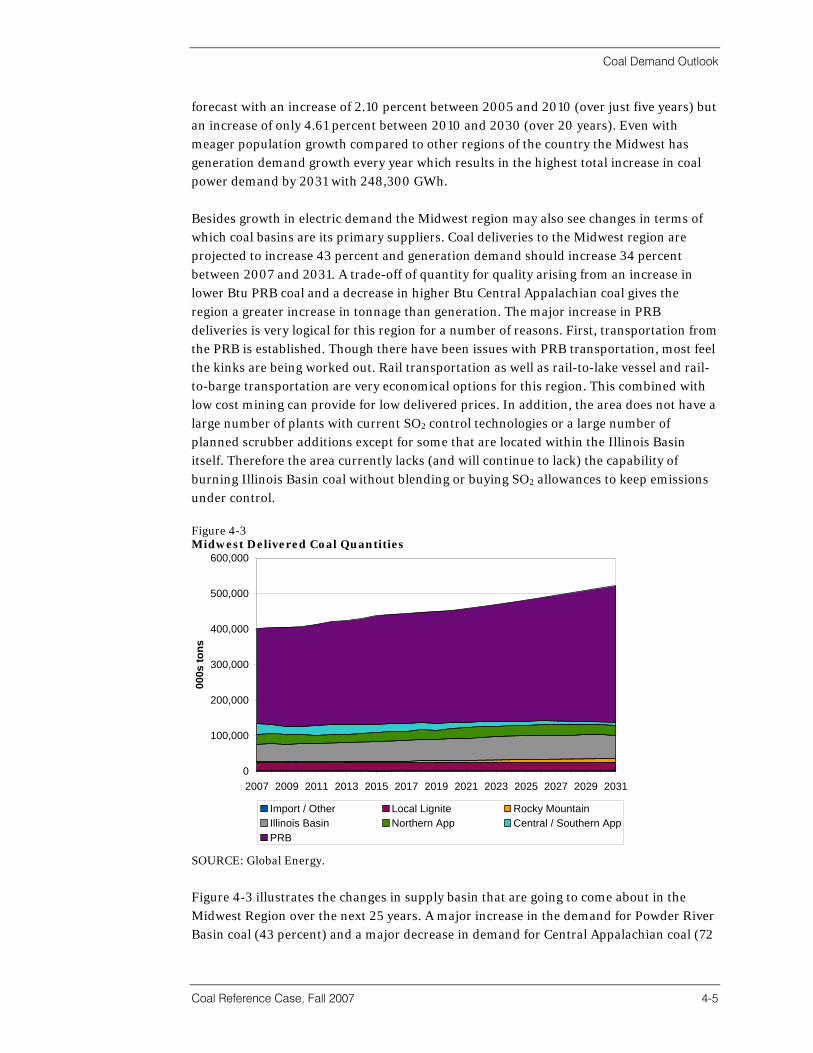

4-3 Midwest Delivered Coal Quantities ..........................................................................4-5

4-4 Midwest FOB Mine Price ..........................................................................................4-6

4-5 Midwest Transportation Cost by Basin ....................................................................4-7

4-6 Midwest Delivered Price ...........................................................................................4-7

4-7 Midwest Coal under Contract...................................................................................4-8

4-8 Northeast Delivered Coal Quantities ......................................................................4-10

4-9 Northeast FOB Mine Price......................................................................................4-11

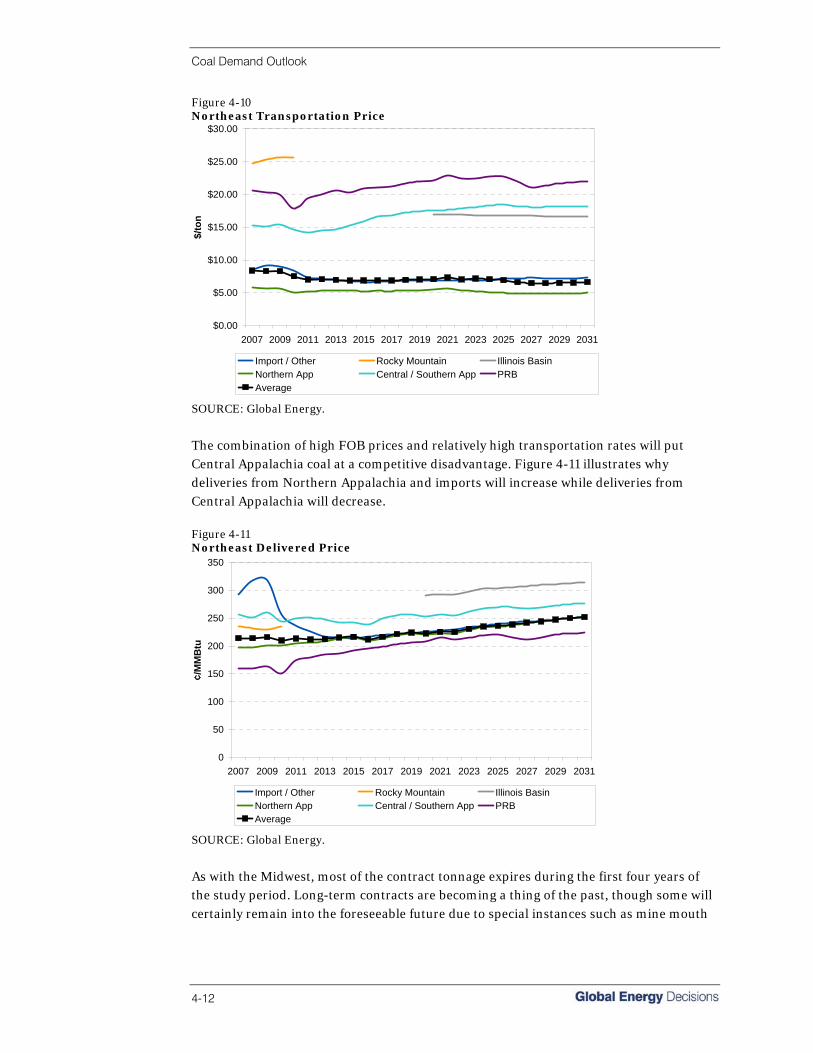

4-10 Northeast Transportation Price...............................................................................4-12

4-11 Northeast Delivered Price.......................................................................................4-12

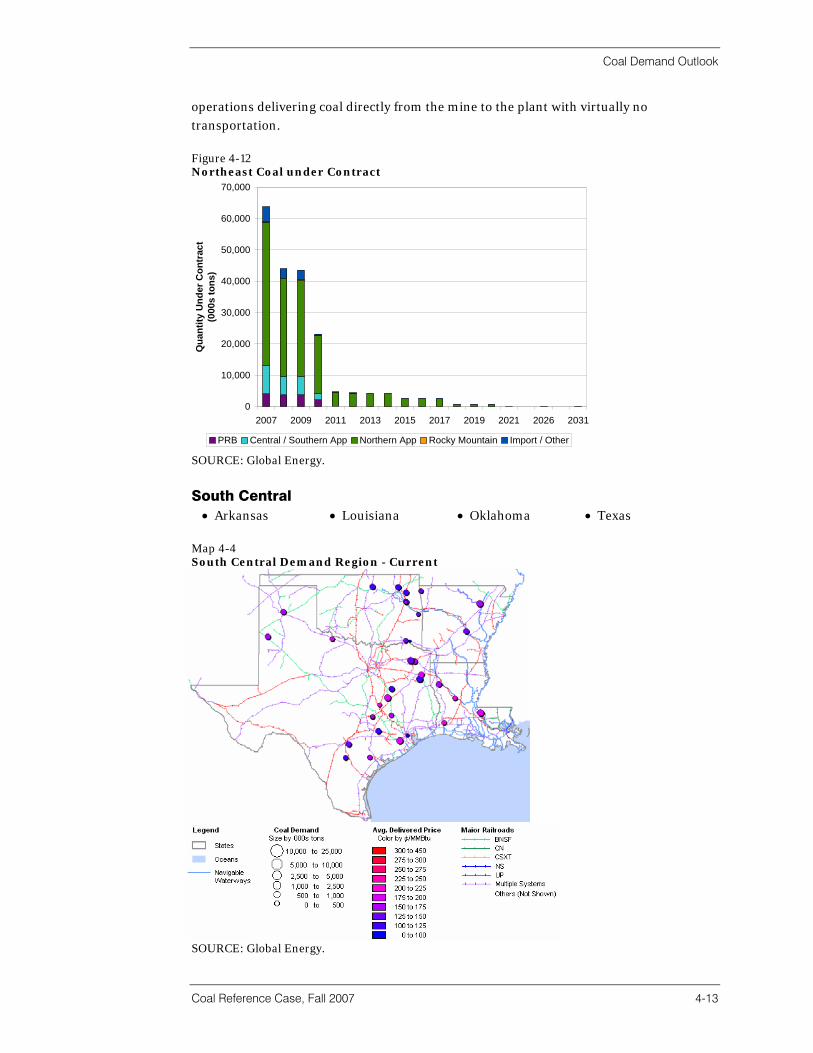

4-12 Northeast Coal under Contract ..............................................................................4-13

4-13 South Central Delivered Coal Quantities................................................................4-14

4-14 South Central FOB Mine Price................................................................................4-15

4-15 South Central Transportation Price ........................................................................4-15

4-16 South Central Delivered Price.................................................................................4-16

4-17 South Central Coal under Contract ........................................................................4-16

4-18 Southeast Delivered Coal Quantities .....................................................................4-18

4-19 Southeast FOB Mine Price .....................................................................................4-18

4-20 Southeast Transportation .......................................................................................4-19

4-21 Southeast Delivered Price ......................................................................................4-20

4-22 Southeast Current Coal under Contract.................................................................4-20

4-23 West Delivered Coal Quantities..............................................................................4-22

4-24 West FOB Mine Price..............................................................................................4-23

4-25 West Transportation Cost .......................................................................................4-23

4-26 West Delivered Price...............................................................................................4-24

List of Figures

Coal Reference Case, Fall 2007 ix

4-27 West Current Coal Under Contract ........................................................................4-24 4-28 Projected Non-Utility Coal Consumption; 2004-2031............................................4-29

5-1 U.S. Fully Allocated Mine Costs ...............................................................................5-1

5-2 Projected Appalachian Fully Allocated Costs ..........................................................5-3

5-3 Projected Illinois Basin Fully Allocated Costs ..........................................................5-4

5-4 Projected PRB Fully Allocated Costs .......................................................................5-4

5-5 Projected Rocky Mountain Fully Allocated Costs ....................................................5-5

5-6 Weighted Average U.S. Productivity ........................................................................5-6

5-7 Weighted Average Central Appalachian Productivity ..............................................5-6

5-8 Weighted Average Northern Appalachian Productivity............................................5-7

5-9 Weighted Average Illinois Basin Productivity ...........................................................5-7

5-10 Stratigraphic Cross Section of Future Mining Conditions at Buckskin Mine...........5-8

5-11 Weighted Average PRB Productivity ........................................................................5-9

5-12 Weighted Average Rocky Mountain Productivity .....................................................5-9

5-13 Central Appalachia Available Spot Curves ............................................................5-11

5-14 Southern Appalachia Available Spot Curves .........................................................5-11

5-15 Northern Appalachia Available Spot Curves..........................................................5-12

5-16 Illinois Basin Available Spot Curves .......................................................................5-12

5-17 Rocky Mountain Available Spot Curves .................................................................5-13

5-18 Powder River Basin Available Spot Curves............................................................5-13

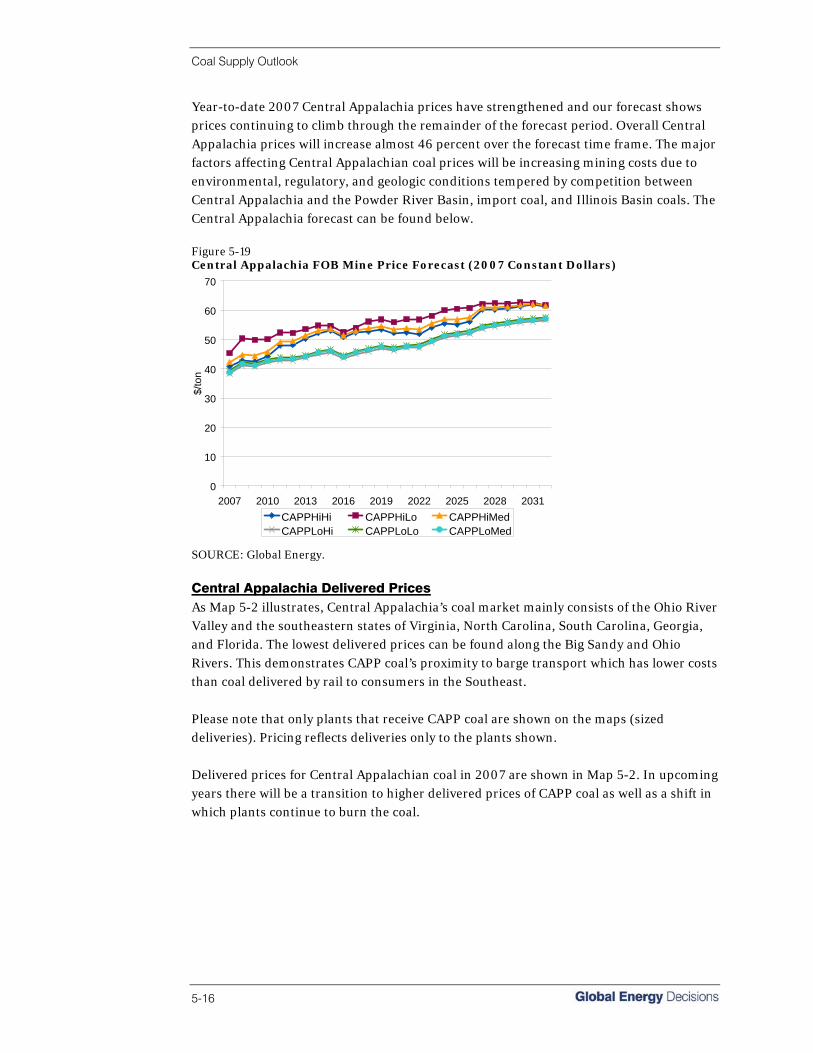

5-19 Central Appalachia FOB Mine Price Forecast .......................................................5-16

5-20 North Appalachia Northeast FOB Mine Price Forecas ..........................................5-20

5-21 Northern Appalachia Ohio FOB Mine Price Forecast ............................................5-21

5-22 Illinois Basin FOB Mine Price Forecast ..................................................................5-22

5-23 Northern Powder River Basin FOB Mine Price Forecast .......................................5-26

5-24 Southern Powder River Basin FOB Mine Price Forecast .......................................5-27

5-25 Rocky Mountain Colorado North FOB Mine Price Forecast ..................................5-31

5-26 Rocky Mountain Colorado West FOB Mine Price Forecast...................................5-32

5-27 Rocky Mountain Four Corner FOB Mine Price Forecast........................................5-33

5-28 Rocky Mountain Wyoming FOB Mine Price Forecast............................................5-34

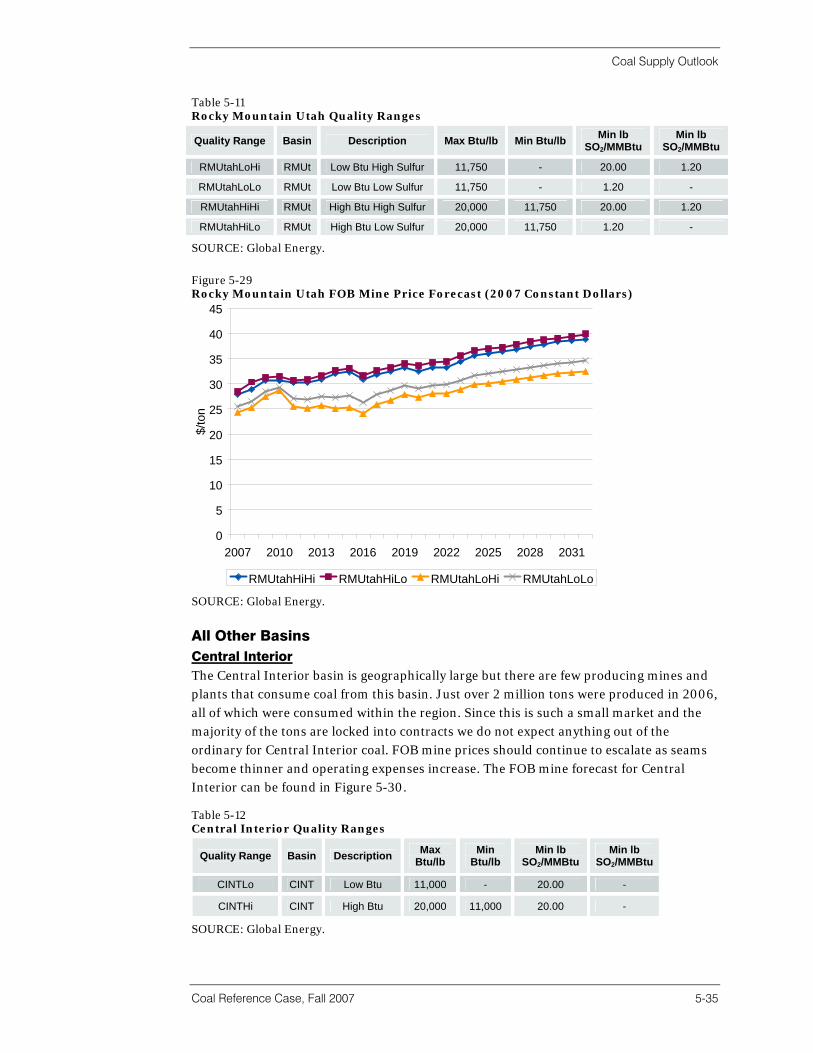

5-29 Rocky Mountain Utah FOB Mine Price Forecast ...................................................5-35

5-30 Central Interior FOB Mine Price Forecast...............................................................5-36

5-31 Northern Lignite FOB Mine Price Forecast ............................................................5-37

5-32 Gulf Lignite FOB Mine Price Forecast ....................................................................5-37

5-33 Import FOB Mine Price Forecast............................................................................5-38

List of Figures

x

5-34 Southern Appalachia FOB Mine Price Forecast ....................................................5-39

5-35 U.S. Coal Production ..............................................................................................5-42

5-36 Projected Central Appalachian Production............................................................5-43

5-37 Projected Northern Appalachian Production .........................................................5-44

5-38 Projected Northern Appalachian - North East Production.....................................5-44

5-39 Projected Northern Appalachian - Ohio Production ..............................................5-45

5-40 Projected Illinois Basin Production.........................................................................5-46

5-41 Projected Rocky Mountain Production...................................................................5-46

5-42 Projected Rocky Mountain - Colorado Production ................................................5-47

5-43 Projected Rocky Mountain - Wyoming Production ................................................5-48

5-44 Projected Rocky Mountain - Four Corners Production ..........................................5-48

5-45 Projected Rocky Mountain - Utah Production........................................................5-49

5-46 Projected Powder River Basin Production .............................................................5-50

5-47 Projected Southern Powder River Basin Production..............................................5-51

5-48 Projected Northern Powder River Basin Production ..............................................5-52

List of Maps

Coal Reference Case, Fall 2007 xi

ES-1 2007 Coal Battleground Areas ............................................................................ ES-12

1-1 Coal Consumption by Source Region......................................................................1-2

2-1 Natural Gas Liquid Market Centers ..........................................................................2-8

3-1 The Five U.S. Coal Demand Regions.......................................................................3-1

3-2 U.S. Nuclear Power Plants .......................................................................................3-5

3-3 U.S. Gas-Fired Power Plants....................................................................................3-7

3-4 U.S. Hydropower Plants ...........................................................................................3-9

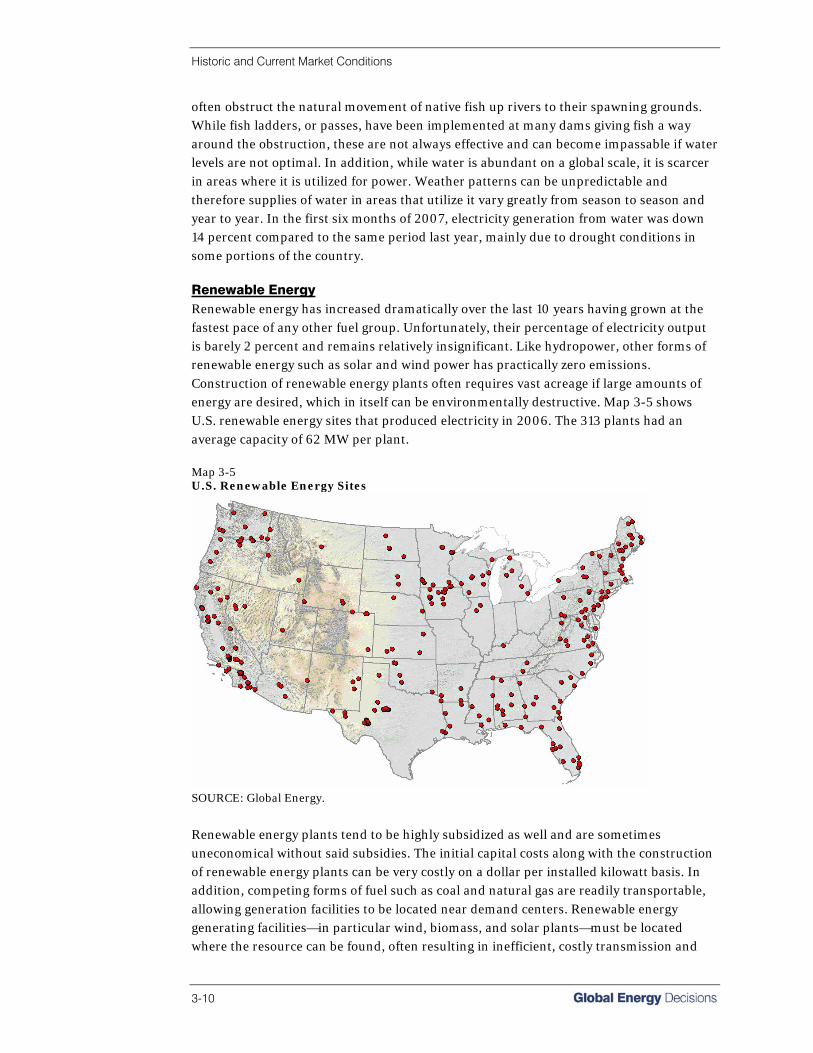

3-5 U.S. Renewable Energy Sites.................................................................................3-10

3-6 U.S. Coal-Fired Power Plants .................................................................................3-11

3-7 U.S. Coal Supply Regions ......................................................................................3-15

3-8 Rail Transportation in Appalachia ..........................................................................3-29

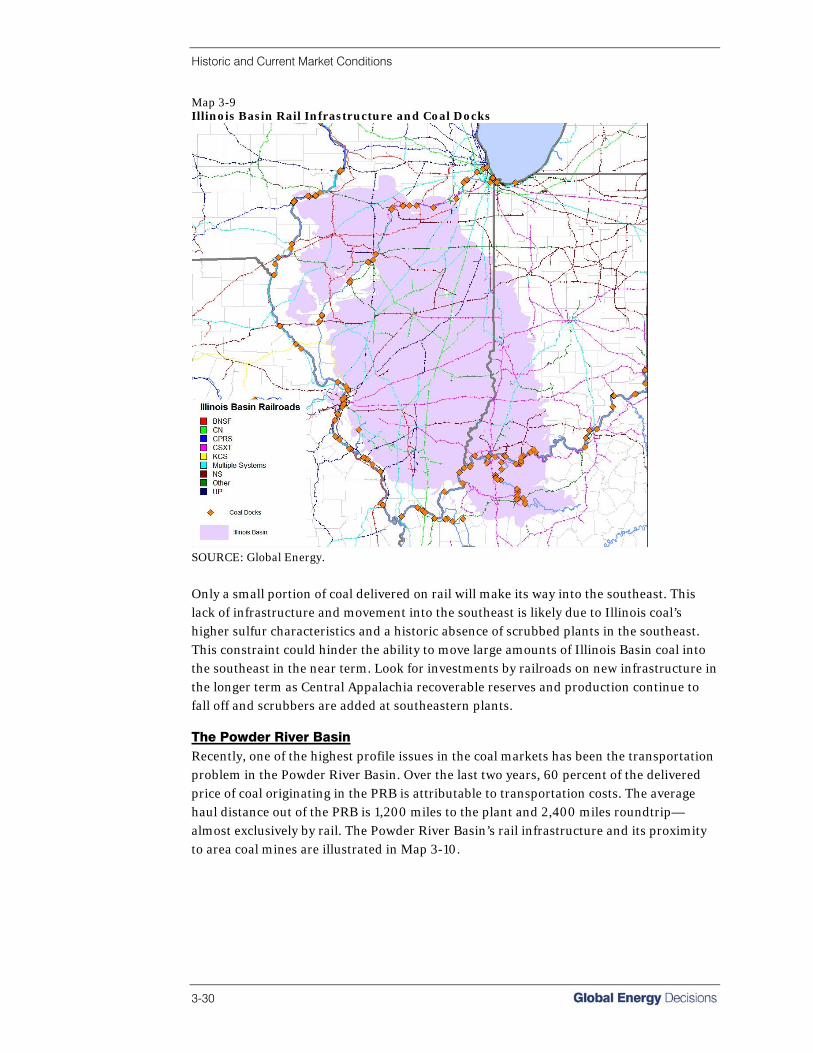

3-9 Illinois Basin Rail Infrastructure and Coal Docks ...................................................3-30

3-10 Rail Transportation in the Powder River Basin .......................................................3-31

3-11 Powder River Basin.................................................................................................3-34

3-12 River Transportation in the Eastern United States. ................................................3-37

3-13 Coal Handling Facilities..........................................................................................3-40

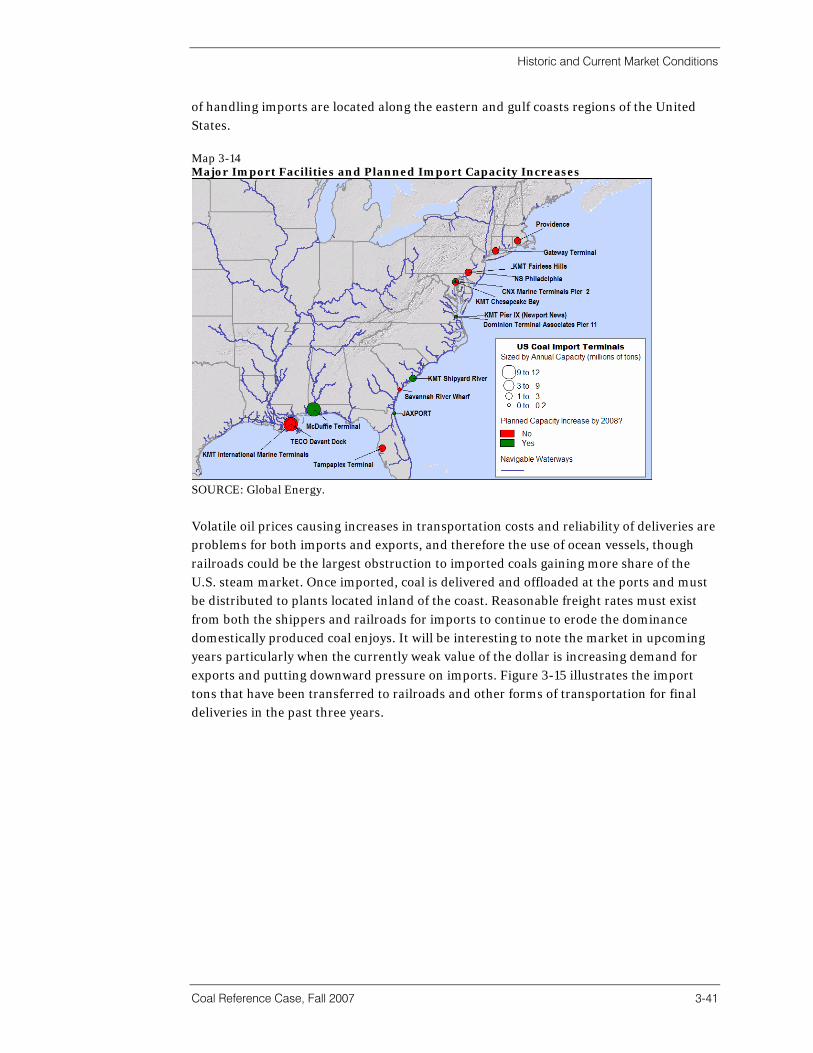

3-14 Major Import Facilities and Planned Import Capacity Increases...........................3-41

3-15 Coal Plant Mercury Emissions in 1999...................................................................3-55

3-16 GHG Reduction Initiatives in North America ..........................................................3-58

4-1 The Five U.S. Coal Demand Regions.......................................................................4-2

4-2 Midwest Demand Region - Current..........................................................................4-4

4-3 Northeast Demand Region - Current .......................................................................4-9

4-4 South Central Demand Region - Current ...............................................................4-13

4-5 Southeast Demand Region - Current.....................................................................4-17

4-6 West Demand Region - Current .............................................................................4-21

5-1 U.S. Coal Supply Regions ......................................................................................5-14

5-2 Central Appalachia 2007 Delivered Prices.............................................................5-17

5-3 Central Appalachia 2015 Delivered Prices.............................................................. 518

5-4 Central Appalachia 2031 Delivered Prices.............................................................5-19

5-5 Illinois Basin 2007 Delivered Prices........................................................................5-23

5-6 Illinois Basin 2015 Delivered Prices........................................................................5-24

5-7 Illinois Basin 2031 Delivered Prices........................................................................5-25

5-8 Powder River Basin 2007 Delivered Prices ............................................................5-28

List of Maps

xii

5-9 Powder River Basin 2015 Delivered Prices ............................................................5-29

5-10 Powder River Basin 2031 Delivered Prices ............................................................5-30

5-11 2007 Battleground Areas .......................................................................................5-40

5-12 2015 Battleground Areas........................................................................................5-41

5-13 2031 Battleground Areas........................................................................................5-42

5-14 Canadian Pacific and DM&E Rail and Potential Coal Plant Market.......................5-55

5-15 Rail Routes in the Powder River Basin ...................................................................5-59

Section 1 Introduction

Introduction

Coal Reference Case, Fall 2007 1-1

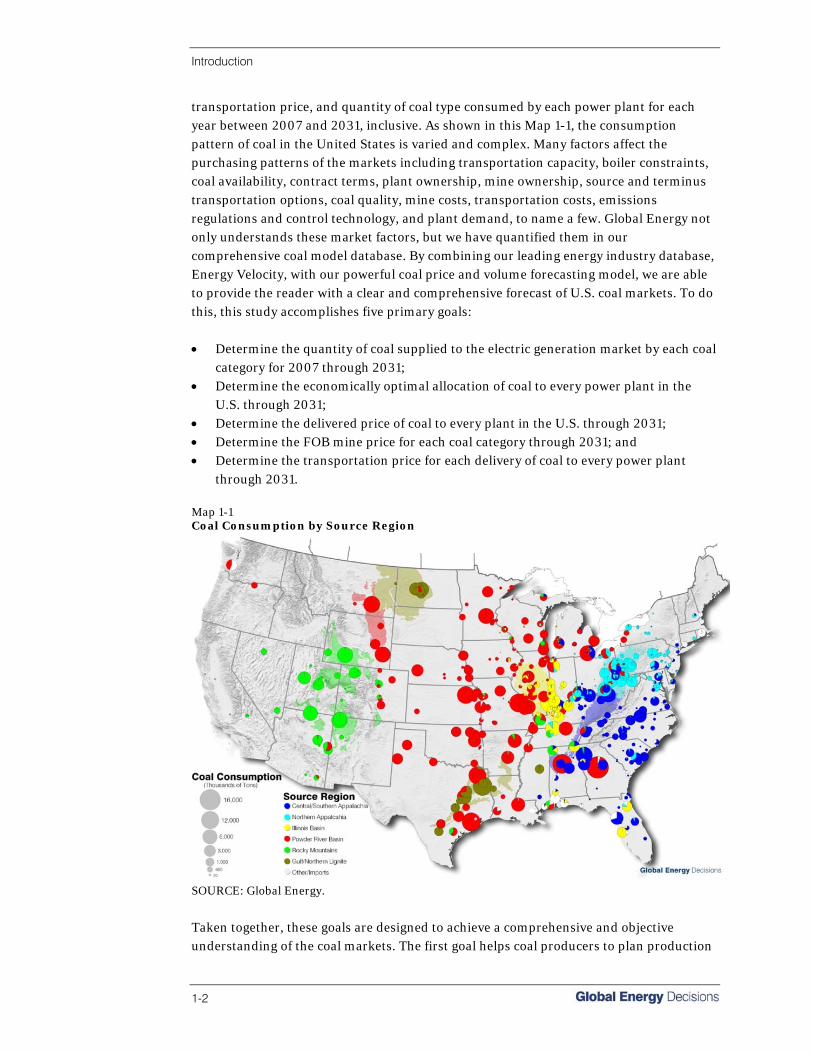

Purpose Of Study The consumption of coal in the United States has grown dramatically over the past five decades principally in response to growing demand for electricity generation. The consistent historic increase in utilization of existing steam-electric coal plants combined with the proposed construction of over 77,000 MW of new coal-fired power plants promises to create a significant increase in future coal demand. Alternative and novel uses for coal such as steel production, liquefaction, gasification, ethanol production, and hydrogen production will create even greater demand for coal. In addition to Global Energy’s forecast of future coal consumption, the Energy Information Agency’s (EIA) Annual Energy Outlook (AEO) and the National Coal Council (NCC) also predict that consumption of coal will significantly rise over the next several decades as shown in Figure 1-1. The AEO reference growth scenario reveals that U.S. coal supply must increase by 465 million tons to meet demand by 2025. Even the AEO low growth scenario adds 323 million tons by 2025. More aggressively, the NCC recommends that U.S. coal supply must increase by 1.3 billion tons by 2025 to meet expected demand for electricity, liquefaction, gasification, and other uses. Figure 1-1 Forecasted Coal Demand

SOURCE: Annual Energy Outlook.

The Global Energy mine capacity study, Can Coal Deliver?, provided an in-depth view of current and future production costs, annual production and productivity associated with every mine in the United States. While Can Coal Deliver? provided detailed analyses of mining issues based on geology, resources, costs, and productivity from 2007 through 2012, the purpose of this study is to provide a large scope analysis of the U.S. coal markets. Specifically, this study provides a highly detailed forecast of coal production and consumption patterns and prices in the U.S. over the next 25 years. Using a state-of-the-art coal price and allocation model, Global Energy has created a forecast of mine price,

Introduction

1-2

transportation price, and quantity of coal type consumed by each power plant for each year between 2007 and 2031, inclusive. As shown in this Map 1-1, the consumption pattern of coal in the United States is varied and complex. Many factors affect the purchasing patterns of the markets including transportation capacity, boiler constraints, coal availability, contract terms, plant ownership, mine ownership, source and terminus transportation options, coal quality, mine costs, transportation costs, emissions regulations and control technology, and plant demand, to name a few. Global Energy not only understands these market factors, but we have quantified them in our comprehensive coal model database. By combining our leading energy industry database, Energy Velocity, with our powerful coal price and volume forecasting model, we are able to provide the reader with a clear and comprehensive forecast of U.S. coal markets. To do this, this study accomplishes five primary goals: • Determine the quantity of coal supplied to the electric generation market by each coal

category for 2007 through 2031; • Determine the economically optimal allocation of coal to every power plant in the

U.S. through 2031; • Determine the delivered price of coal to every plant in the U.S. through 2031; • Determine the FOB mine price for each coal category through 2031; and • Determine the transportation price for each delivery of coal to every power plant

through 2031. Map 1-1 Coal Consumption by Source Region

SOURCE: Global Energy.

Taken together, these goals are designed to achieve a comprehensive and objective understanding of the coal markets. The first goal helps coal producers to plan production

Introduction

Northeast Regional Outlook, Spring 2007 1-3

and manage reserve assets effectively by providing information on coal types that are likely to be in high demand. It also provides utilities with planning tools by determining which coals are likely to be in high demand and thus likely to be more costly. The second goal logically follows, providing producers information about their likely markets and consumers with likely available least cost sources of fuel. A forecast for the delivered price of coal at the plant level gives coal consumers a planning tool for generation asset management. The FOB mine price forecast provides a planning tool for coal producers’ potential revenue streams. And finally, the transportation price forecast provides a planning tool for producers, consumers, and coal transporters. These goals form the core of the study, but understanding the reasoning and logic that underlie forecast results is also essential to a useful forecast. In order to provide context for the forecast, substantiate the findings, and provide the reader with the necessary background, a comprehensive review of the current and historical coal market is necessary. This study also assesses two broad but essential aspects of the coal market: • Alternative electricity generation sources, their current and historic costs and

utilization rates relative to coal as generation sources, and associated financial and environmental risks for each generation type; and

• The coal industry’s place in the current electric generation market based on historic production, productivity, reserves, and costs as well as transportation issues, environmental constraints, changing historical patterns of supply and demand, and coal transaction contracts.

On the surface, this study is intended to make broad brush strokes to describe the fundamentals of coal supply and demand. Its foundation, however, is much more detailed and inclusive and builds a forecast from the most basic data on what is essentially the most granular level possible. This study is driven by the desire to add plant level coal price input to complete Global Energy’s interconnected power market model and to provide a mine level forecast for coal production. This study has given us a better understanding of the complex market dynamics that underlie the coal industry and has enabled us to answer questions such as, “How much Powder River Basin coal will penetrate the eastern coal markets given our understanding of the historic, current, and likely future production, mine costs, transportation rates, plant fuel limitations, environmental regulations, and competition from other basins?” This is a complicated question which demands a comprehensive understanding of all aspects of a fascinating industry. Global Energy, in partnership with RBAC, has developed the Coal Quality Market Model (CQMM) and comprehensive input dataset to forecast the likely consumption patterns of coal at the boiler level over the next 25 years. In other words, we would like to know which boilers will receive coal from which mines. This model essentially acts as a coal router, matching coal supply from individual mines to coal demand at individual boilers. It seeks to find the lowest cost solution for the entire system. The model is designed to

Introduction

1-4

meet the goal of determining the most likely allocation of coal given the cost of producing it at each mine, the possible transportation options and prices, and the demand and limitations of each boiler. When we aggregate the model results we can answer questions like the one posed above with a great deal of precision or adjust the parameters of the model to more accurately reflect our understanding of and expectation for the coal industry. In Global Energy’s MARKETSYM™ model the prices of oil, natural gas, coal, and emissions allowances are inputs utilized to produce outputs of future demand of coal, natural gas, oil, and their contributions to U.S. power generation over the next 25 years. The Global Energy Reference Case Model is a dynamic tool allowing users to create forecasts based on industry factor assumptions made by Global Energy as well as create unique forecasts based on variations of factor assumptions.

Organization Of The Report The report detailing the Fall 2007 Coal Reference Case is divided into six main sections: • The Executive Summary briefly describes the purpose and results of the study; • The Introduction outlines the purpose of the study and describes the organization

of the report; • The Forecast Methodology and Assumptions section outlines how Global

Energy integrates oil, gas, coal, emissions, and power models to produce outputs; describes our CQMM and its scenario and sensitivity capabilities; gives insight into our cost modeling methodology for coal; and analyzes electricity demand and related supply as well as related constraints such as emissions;

• The Historic and Current Market Conditions section outlines demand for electricity, possible generation options and their advantages and disadvantages; paints a picture of coal supply for electricity generation and other uses; addresses issues concerning transportation, emissions, and safety regulations and their possible effect on coal supply and demand; and outlines important contract volumes and expiration dates;

• The Coal Demand Outlook section examines forecasted demand for coal used for electricity by region and coal type as well as outlining historic and future consumption of coal in the coking, industrial, commercial, and residential sectors;

• The Coal Supply Outlook section provides forecasts on costs, productivity, and production; as well as forecasts on prices of steam coal and consumption of steam, industrial, commercial, and residential coal by region; and outlines import price and volume forecasts.

Section 2 Forecast Methodology and Assumptions

Forecast Methodology and Assumptions

Coal Reference Case, Fall 2007 2-1

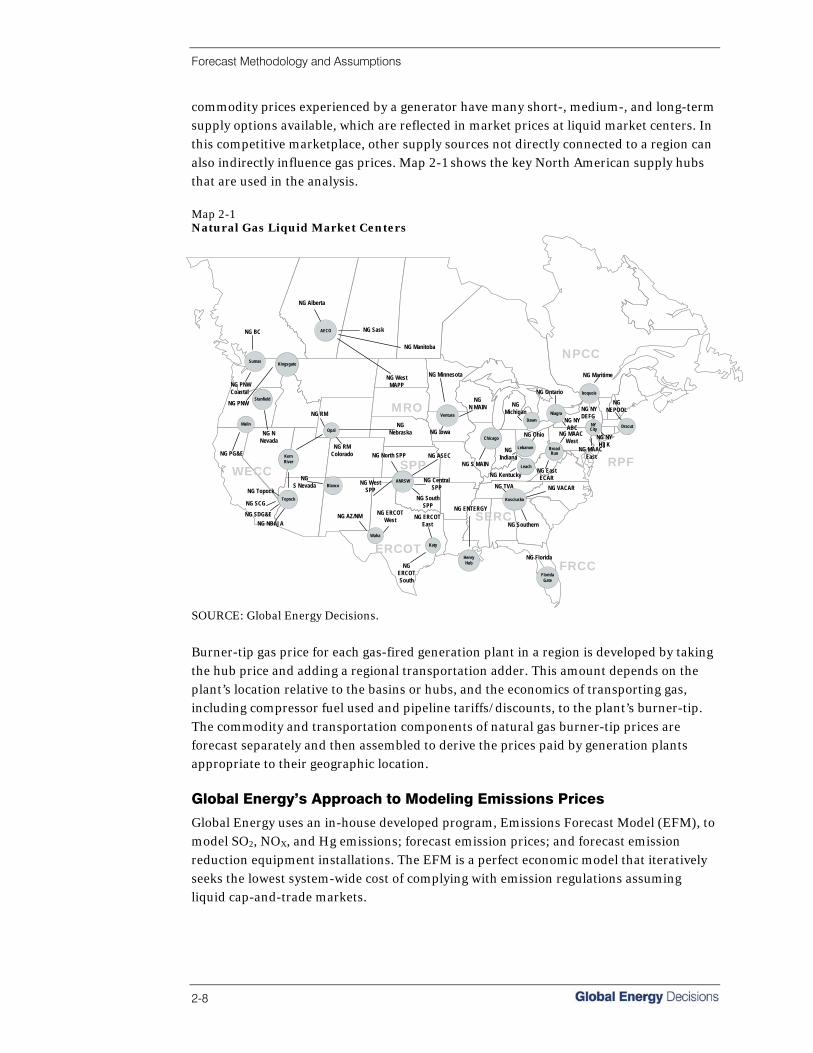

Forecast Methodology Global Energy’s approach to market forecasting integrates model inputs and outputs from our power, emissions, and fuels forecasting models. Figure 2-1 shows how the models in our suite of forecast products are interrelated. The coal model takes the demand for electric power at each coal generating station from the Reference Case forecast, which is tied directly to the gas, oil, coal, and emissions models. Prices for emissions (NOx, SO2, and Hg) allowances at a national and regional level are used as inputs for the Emissions Price forecast. Prices for gas, oil, and coal are taken from the gas, oil, and coal models, respectively, and input to the Power Reference Case, which in turn feeds the fuels and emissions models. Each of the inputs into the coal market model is itself the result of sophisticated modeling techniques as described below. Figure 2-1 Global Energy’s Fuels Analysis Uses an Integrated Cross Commodity Approach

SOURCE: Global Energy.

Global Energy’s Approach to Modeling Demand for Electric Power The MARKETSYM™ Model Global Energy uses a fundamentals-based methodology to forecast power prices in each region of North America. Based on its proprietary MARKETSYM™ system—MARKETSYM™ is a sophisticated, relational database that operates with a state-of-the-art, multi-area, chronological production simulation model—Global Energy simulates the operation of each region of North America. For each region, MARKETSYM™ considers:

Demand

EmissionPrice

Forecast

Price

Oil Model

Coal Model

GasModel

ReferenceCase

ForecastPrice Price

Price

Price

Demand Demand

PricePrice

Demand

EmissionPrice

Forecast

Price

Oil Model

Coal Model

GasModel

ReferenceCase

ForecastPrice Price

Price

Price

Demand Demand

PricePrice

Forecast Methodology and Assumptions

2-2

• Individual power plant characteristics including heat rates, start-up costs, ramp rates, and other technical characteristics of plants;

• Transmission line interconnections, ratings, losses, and wheeling rates; • Forecasts of resource additions and fuel costs over time; • Forecasts of loads for each utility or load serving entity in the region; and • The cost and availability of fuels that supply the plants.

MARKETSYM™ simulates the operation of individual generators, utilities, and control areas to meet fluctuating loads within the region with hourly detail. The model is based on a zonal approach where market areas (zones) are delineated by critical transmission constraints. The simulation is based on a mathematical objective function that minimizes the cost of serving load within the modeled electric system subject to meeting load, a number of operational constraints, as well as the assumed strategic behavior (bidding) of market participants. Monte Carlo analysis is employed to incorporate individual unit forced outages. The result is a long-term price forecast that allows existing and new generators to recover all short- and long-term costs (including financing costs) from the market. To understand how uncertainty regarding power prices, fuel prices, and hydro conditions influence the forecast, Global Energy also prepares a sample stochastic analysis of power prices and generator profitability that explicitly models key stochastic variables and their correlation. As such, Global Energy simulates the price formation in competitive markets using a least cost approach with an explicitly defined scarcity bidding behavior. Three fundamental principles guide the forecast development: • Maintain sufficient reliability in all market areas; • In the short term, benchmark the model against observed historical market prices

and market heat rates; and • In the long term, allow new capacity to recover all costs, including fixed and financing

costs from the energy market.