CIMA F2 - Financial Management Workbook Q & A - Mapit ...

255

F2 Financial Management Q & A www.mapitaccountancy.com CIMA F2 - Financial Management Workbook Q & A

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of CIMA F2 - Financial Management Workbook Q & A - Mapit ...

F2 Financial Management Q & A www.mapitaccountancy.com

CIMA F2 - Financial Management

Workbook Q & A

F2 Financial Management Q & A www.mapitaccountancy.com

Group Accounts

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1

Additional Information

Almeria today acquired all the shares in Murcia for $300m.

The Fair Value of the NCI at acquisition was 0.

Required

Prepare the consolidated statement of financial position for the Almeria group

Almeria Murcia

Non Current Assets

Tangible 100 100

Investment in Murcia 300

Current Assets

Inventory 40 200

Receivables 60 100

Cash 200 200

700 600

Ordinary Shares 160 100

Accumulated Profits 240 200

Equity 400 300

Non Current Liabilities 100 200

Current Liabilities 200 100

700 600

F2 Financial Management Q & A www.mapitaccountancy.com

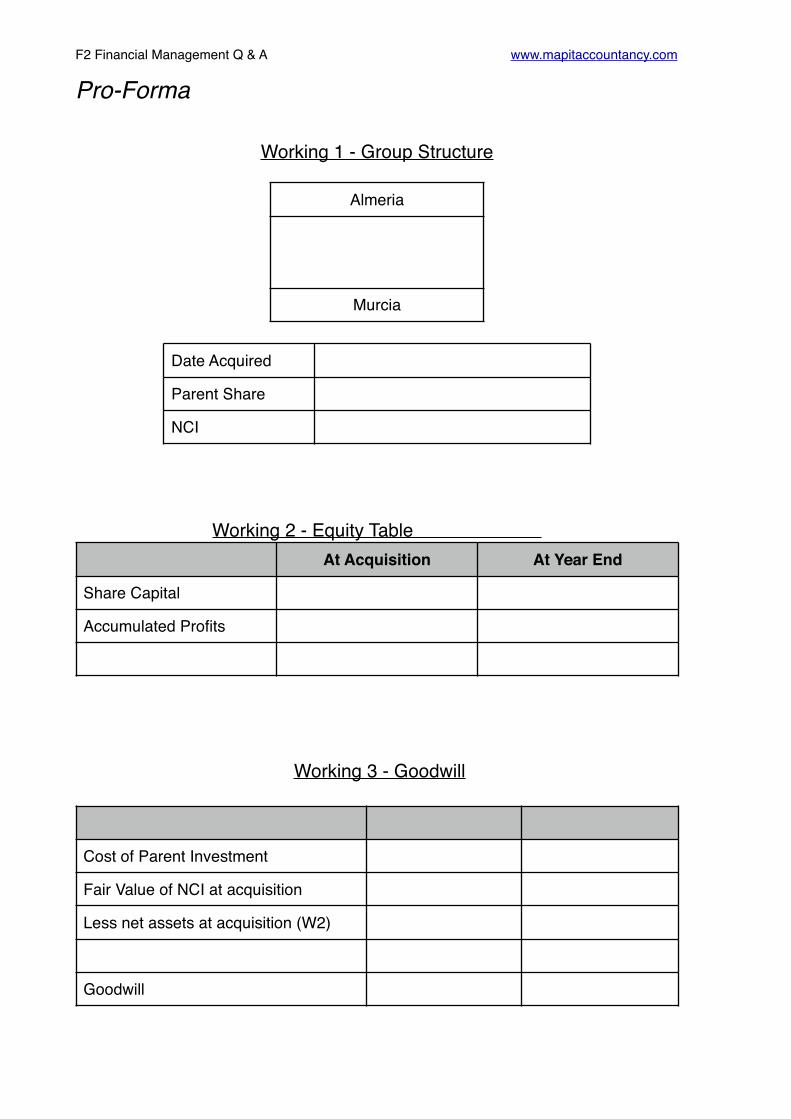

Pro-Forma

Working 1 - Group Structure

Working 2 - Equity Table

Working 3 - Goodwill

Almeria

Murcia

Date Acquired

Parent Share

NCI

At Acquisition At Year End

Share Capital

Accumulated Profits

Cost of Parent Investment

Fair Value of NCI at acquisition

Less net assets at acquisition (W2)

Goodwill

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition

NCI% of Sub Post-Acq Profits

Value of NCI at Year End

$

Parent’s Accumulated Profits

Add: Parent % of the subsidiary’s post acquisition profits

F2 Financial Management Q & A www.mapitaccountancy.com

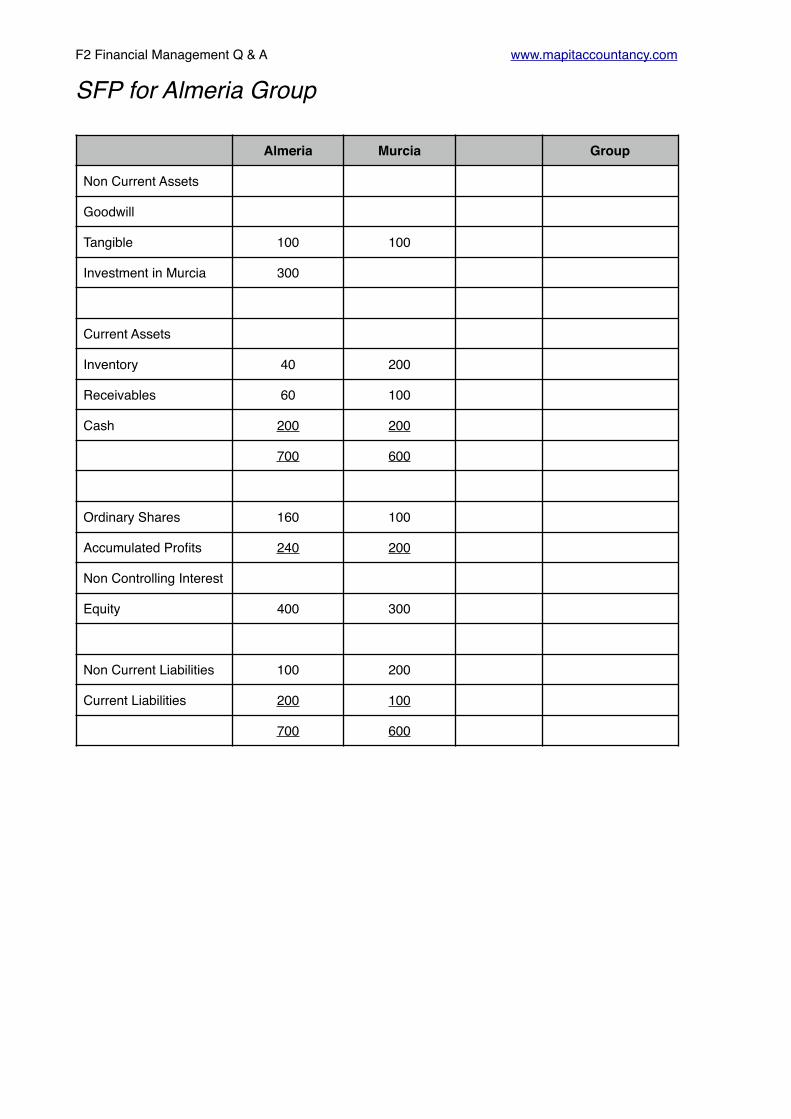

SFP for Almeria Group

Almeria Murcia Group

Non Current Assets

Goodwill

Tangible 100 100

Investment in Murcia 300

Current Assets

Inventory 40 200

Receivables 60 100

Cash 200 200

700 600

Ordinary Shares 160 100

Accumulated Profits 240 200

Non Controlling Interest

Equity 400 300

Non Current Liabilities 100 200

Current Liabilities 200 100

700 600

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Working 1 - Group Structure

Working 2 - Equity Table

Working 3 - Goodwill

Almeria

↓100%

Murcia

Date Acquired TODAY

Parent Share 100%

NCI 0%

At Acquisition At Year End

Share Capital 100 100

Accumulated Profits 200 200

300 300

Cost of Parent Investment 300

Fair Value of NCI 0

Less net assets at acquisition (W2) -300

Goodwill 0

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition 0

NCI% of Sub Post-Acq Profits 0

Value of NCI at Year End 0

$

Parent’s Accumulated Profits 240

Add: Parent % of the subsidiary’s post acquisition profits Nil

240

F2 Financial Management Q & A www.mapitaccountancy.com

SFP for Almeria Group

Almeria Murcia Group

Non Current Assets

Goodwill None (W3) Nil

Tangible 100 100 100 + 100 200

Investment in Murcia 300 Cancel out Nil

Current Assets

Inventory 40 200 40 + 200 240

Receivables 60 100 60 +100 160

Cash 200 200 200 + 200 400

700 600 1000

Ordinary Shares 160 100 Parent 160

Accumulated Profits 240 200 W5 240

Non Controlling Interest W4 Nil

Equity 400 300 400

Non Current Liabilities 100 200 100 + 200 300

Current Liabilities 200 100 200 + 100 300

700 600 1000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 2

Additional Information

Ant today acquired 160m of the 200m shares in Dec.

The Fair Value of the NCI was 50.

Required

Prepare the consolidated statement of financial position for the Ant group

Ant Dec

Assets 500 500

Investment in Dec 350

850 500

Ordinary Shares 100 200

Accumulated Profits 250 100

Equity 350 300

Liabilities 500 200

850 500

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 2 Pro-Forma

Working 1- Group Structure

Working 2- Equity Table

Working 3 - Goodwill

↓

Date Acquired

Parent Share

NCI

At Acquisition At Year End

Share Capital

Accumulated Profits

Cost of Parent Investment

Fair Value of NCI at acquisition

Less net assets at acquisition (W2)

Goodwill

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition

NCI% of Sub Post-Acq Profits

Value of NCI at Year End

$

Parent’s Accumulated Profits

Add: Parent % of the subsidiary’s post acquisition profits

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of Financial Position for Ant Group

Ant Dec Group

Goodwill

Assets 500 500

Investment in Dec

350

850 500

Ordinary Shares

100 200

Accumulated Profits

250 100

NCI

Equity 350 300

Liabilities 500 200

850 500

F2 Financial Management Q & A www.mapitaccountancy.com

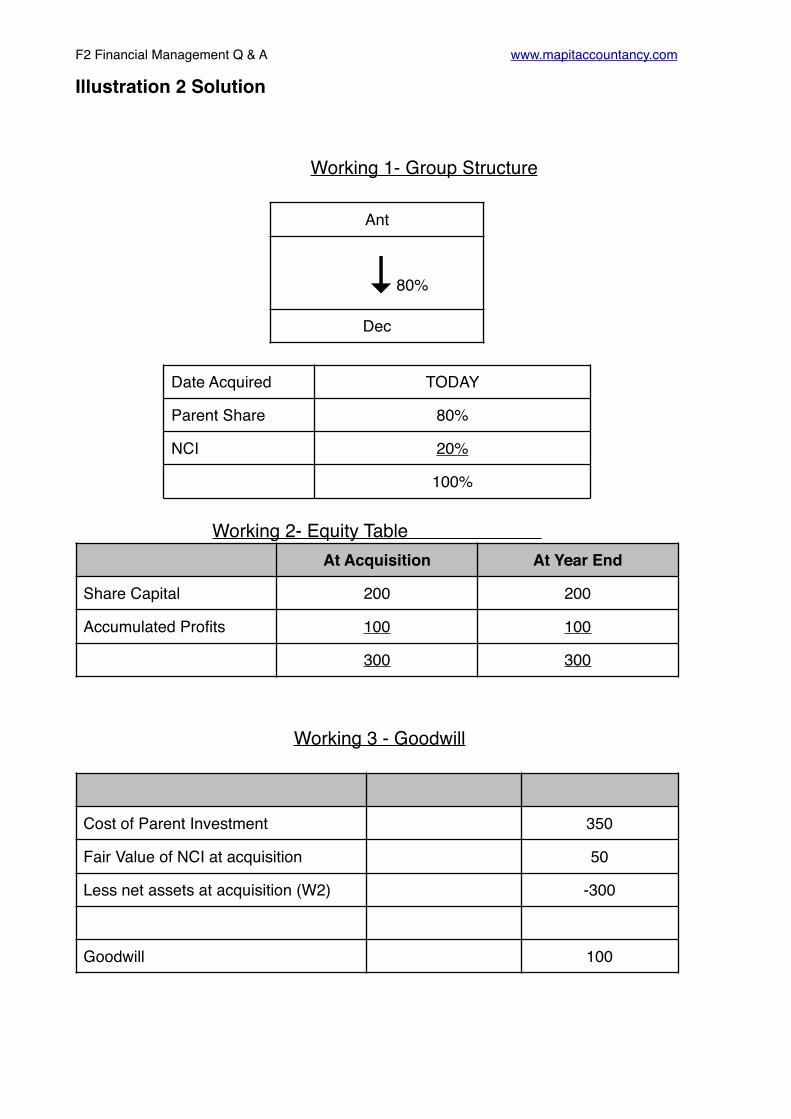

Illustration 2 Solution

Working 1- Group Structure

Working 2- Equity Table

Working 3 - Goodwill

Ant

↓80%

Dec

Date Acquired TODAY

Parent Share 80%

NCI 20%

100%

At Acquisition At Year End

Share Capital 200 200

Accumulated Profits 100 100

300 300

Cost of Parent Investment 350

Fair Value of NCI at acquisition 50

Less net assets at acquisition (W2) -300

Goodwill 100

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition 50

NCI% of Sub Post-Acq Profits 0

Value of NCI at Year End 50

$

Parent’s Accumulated Profits 250

Add: Parent % of the subsidiary’s post acquisition profits Nil

250

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of Financial Position for Ant Group

Ant Dec Group

Goodwill W3 100

Assets 500 500 500 + 500 1000

Investment in Dec

350 Cancelled in Goodwill W3

Nil

850 500 1100

Ordinary Shares

100 200 Parent Only 100

Accumulated Profits

250 100 W5 250

NCI W4 50

Liabilities 500 200 500 +200 700

850 500 1100

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 3

Additional Information

Evan acquired 150m shares in Dando one year ago when the reserves of Dando were $40m. The Fair Value of the NCI on the date of acquisition was $100m.

Required

Prepare the consolidated statement of financial position for the Evan group.

Evan Dando

Assets 200 350

Investment in Dando 500

Current Assets 200 300

900 650

Ordinary Shares ($1) 200 200

Accumulated Profits 250 100

Equity 450 300

Non Current Liabilities 280 200

Liabilities 170 150

900 650

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Working 1- Group Structure

Working 2 - Equity Table

Working 3 - Goodwill

↓

Date Acquired

Parent Share

NCI

At Acquisition At Year End

Share Capital

Accumulated Profits

Cost of Parent Investment

Fair Value of NCI at acquisition

Less net assets at acquisition (W2)

Goodwill

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition

NCI% of Sub Post-Acq Profits

Value of NCI at Year End

$

Parent’s Accumulated Profits

Add: Parent % of the subsidiary’s post acquisition profits

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of Financial Position for Evan Group

Evan Dando Group

Goodwill

Assets 200 350

Investment in Dando

500

Current Assets 200 300

900 650

Ordinary Shares ($1)

200 200

Accumulated Profits

250 100

NCI

Equity 450 300

Non Current Liabilities

280 200

Liabilities 170 150

900 650

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Working 1- Group Structure

Working 2 - Equity Table

Working 3 - Goodwill

Evan

↓75%

Dando

Date Acquired 1 Year Ago

Parent Share 75%

NCI 25%

100%

At Acquisition At Year End

Share Capital 200 200

Accumulated Profits 40 100

240 300

Cost of Parent Investment 500

Fair Value of NCI at acquisition 100

Less net assets at acquisition (W2) -240

Goodwill 360

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition 100

NCI% of Sub Post-Acq Profits (25% x 60m) 15

Value of NCI at Year End 115

$

Parent’s Accumulated Profits 250

Add: Parent % of the subsidiary’s post acquisition profits

(75% x 60m) 45

295

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of Financial Position for Evan Group

Evan Dando Group

Goodwill W3 360

Assets 200 350 200 + 350 550

Investment in Dando

500 Cancelled out in W3.

Nil

Current Assets 200 300 200 + 300 500

1410

Ordinary Shares ($1)

Parent Only 200

Accumulated Profits

W5 295

NCI W4 115

570

Non Current Liabilities

280 200 280 + 200 480

Liabilities 170 150 170 + 150 320

1410

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 4

Additional Information

Virtual acquired 60m shares in Insanity one year ago when the reserves of Insanity were $60m. The Fair Value of the NCI at that date was $120m.

Required

Prepare the consolidated statement of financial position for the Virtual group

Virtual Insanity

Assets 1000 800

Investment in Insanity 600

Current Assets 400 200

2000 1000

Ordinary Shares ($1) 800 100

Accumulated Profits 750 400

Equity 1550 500

Non Current Liabilities 250 300

Liabilities 200 200

2000 1000

F2 Financial Management Q & A www.mapitaccountancy.com

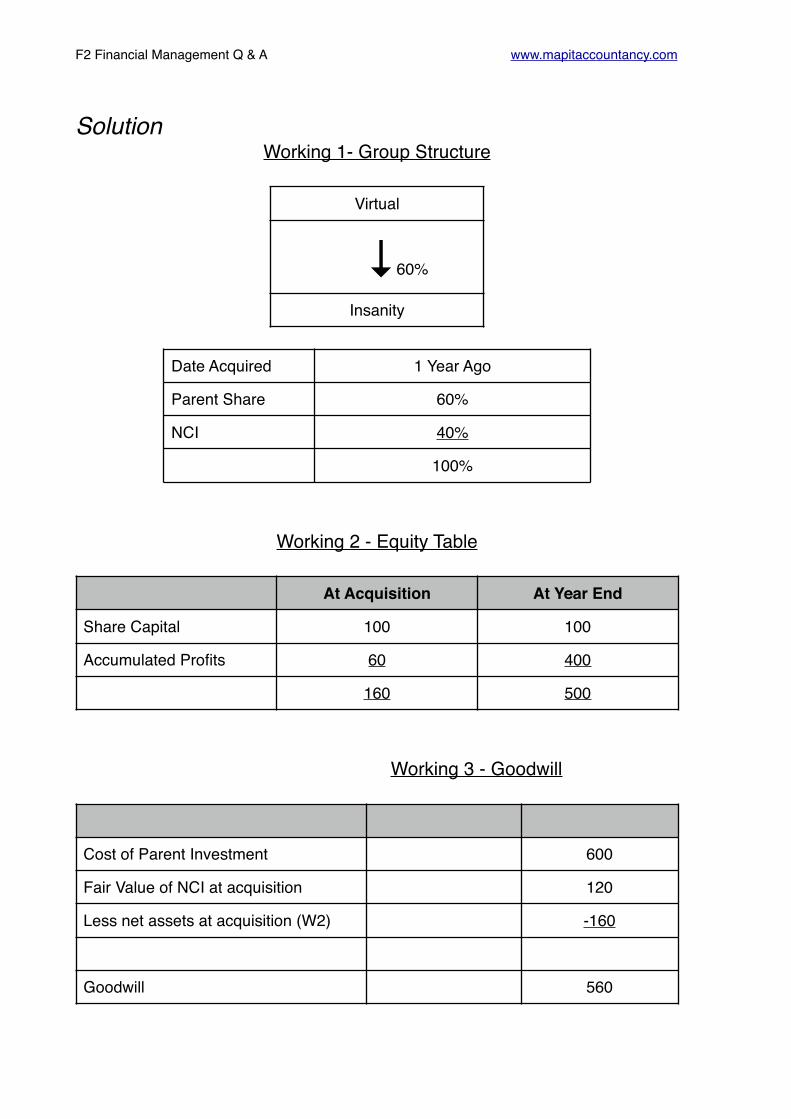

SolutionWorking 1- Group Structure

Working 2 - Equity Table

Working 3 - Goodwill

Virtual

↓60%

Insanity

Date Acquired 1 Year Ago

Parent Share 60%

NCI 40%

100%

At Acquisition At Year End

Share Capital 100 100

Accumulated Profits 60 400

160 500

Cost of Parent Investment 600

Fair Value of NCI at acquisition 120

Less net assets at acquisition (W2) -160

Goodwill 560

F2 Financial Management Q & A www.mapitaccountancy.com

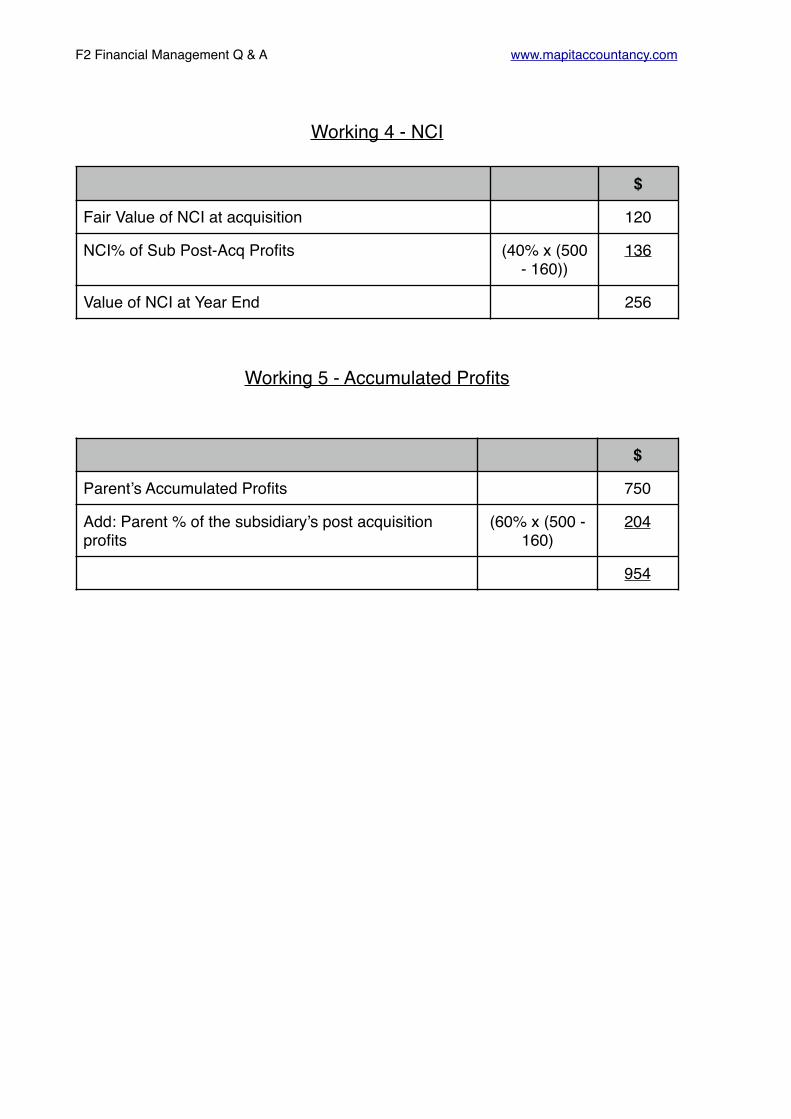

Working 4 - NCI

Working 5 - Accumulated Profits

$

Fair Value of NCI at acquisition 120

NCI% of Sub Post-Acq Profits (40% x (500 - 160))

136

Value of NCI at Year End 256

$

Parent’s Accumulated Profits 750

Add: Parent % of the subsidiary’s post acquisition profits

(60% x (500 - 160)

204

954

F2 Financial Management Q & A www.mapitaccountancy.com

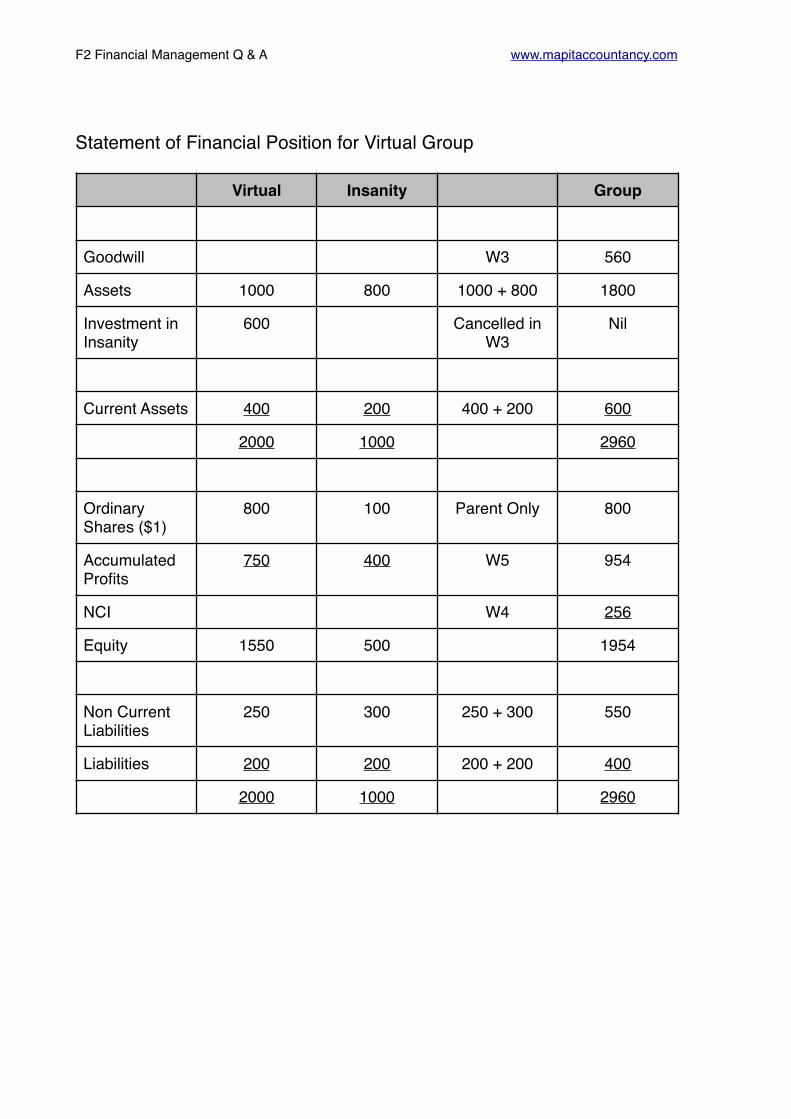

Statement of Financial Position for Virtual Group

Virtual Insanity Group

Goodwill W3 560

Assets 1000 800 1000 + 800 1800

Investment in Insanity

600 Cancelled in W3

Nil

Current Assets 400 200 400 + 200 600

2000 1000 2960

Ordinary Shares ($1)

800 100 Parent Only 800

Accumulated Profits

750 400 W5 954

NCI W4 256

Equity 1550 500 1954

Non Current Liabilities

250 300 250 + 300 550

Liabilities 200 200 200 + 200 400

2000 1000 2960

F2 Financial Management Q & A www.mapitaccountancy.com

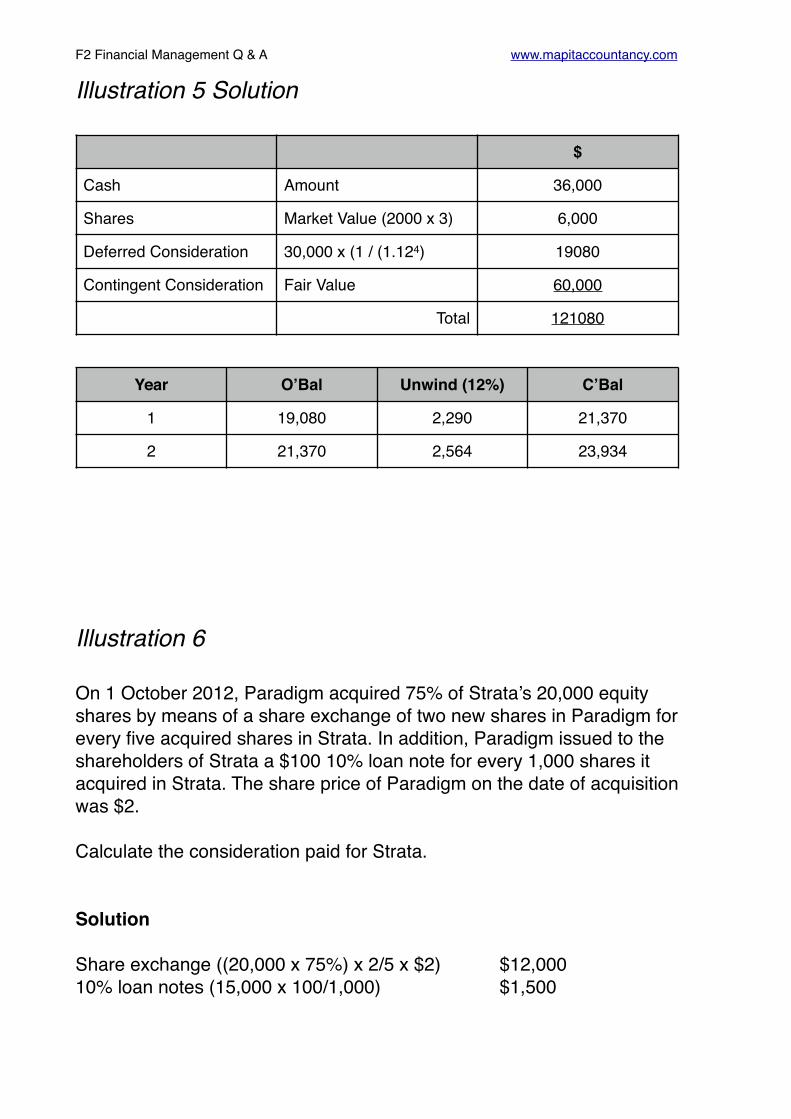

Illustration 5

Jabba acquired 100% of the shares in Hutt two years ago.

The consideration was as follows:

1. Cash of $36,000.2. 2000 Shares in Jabba (the share price is currently $3).3. $30,000 to be paid four years after the date of acquisition. The

relevant discount rate is 12%4. If the group meets certain targets there will be a further payment with

fair value of $60,000 at a later date.

Required:

(i) Calculate the fair value of the consideration which Jabba has given in purchasing the investment in Hutt.

(ii)Show the value of the liability in the Statement of Financial Position for the deferred consideration at the end of the current year.

(iii)What is the charge to the Statement of Profit or Loss in the current period related to the deferred consideration?

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 5 Solution

Illustration 6

On 1 October 2012, Paradigm acquired 75% of Strata’s 20,000 equity shares by means of a share exchange of two new shares in Paradigm for every five acquired shares in Strata. In addition, Paradigm issued to the shareholders of Strata a $100 10% loan note for every 1,000 shares it acquired in Strata. The share price of Paradigm on the date of acquisition was $2.

Calculate the consideration paid for Strata.

Solution

Share exchange ((20,000 x 75%) x 2/5 x $2) $12,00010% loan notes (15,000 x 100/1,000) $1,500

$

Cash Amount 36,000

Shares Market Value (2000 x 3) 6,000

Deferred Consideration 30,000 x (1 / (1.124) 19080

Contingent Consideration Fair Value 60,000

Total 121080

Year O’Bal Unwind (12%) C’Bal

1 19,080 2,290 21,370

2 21,370 2,564 23,934

F2 Financial Management Q & A www.mapitaccountancy.com

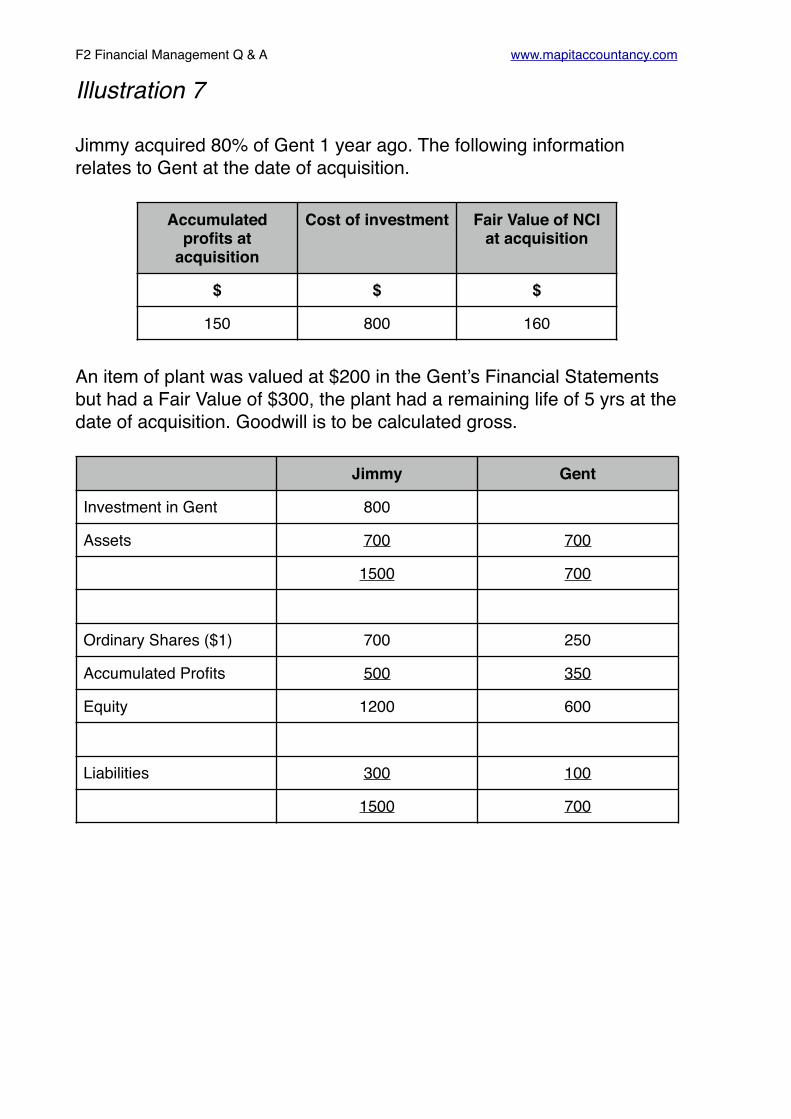

Illustration 7

Jimmy acquired 80% of Gent 1 year ago. The following information relates to Gent at the date of acquisition.

An item of plant was valued at $200 in the Gent’s Financial Statements but had a Fair Value of $300, the plant had a remaining life of 5 yrs at the date of acquisition. Goodwill is to be calculated gross.

Accumulated profits at

acquisition

Cost of investment Fair Value of NCI at acquisition

$ $ $

150 800 160

Jimmy Gent

Investment in Gent 800

Assets 700 700

1500 700

Ordinary Shares ($1) 700 250

Accumulated Profits 500 350

Equity 1200 600

Liabilities 300 100

1500 700

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionWorking 1- Group Structure

Working 2 - Equity Table

Jimmy

↓80%

Gent

Date Acquired 1 Year Ago

Parent Share 80%

NCI 20%

100%

At Acquisition At Year End

Share Capital 250 250

Accumulated Profits 150 350

Fair Value Adjustment 100 100

Additional Depreciation -20

500 680

F2 Financial Management Q & A www.mapitaccountancy.com

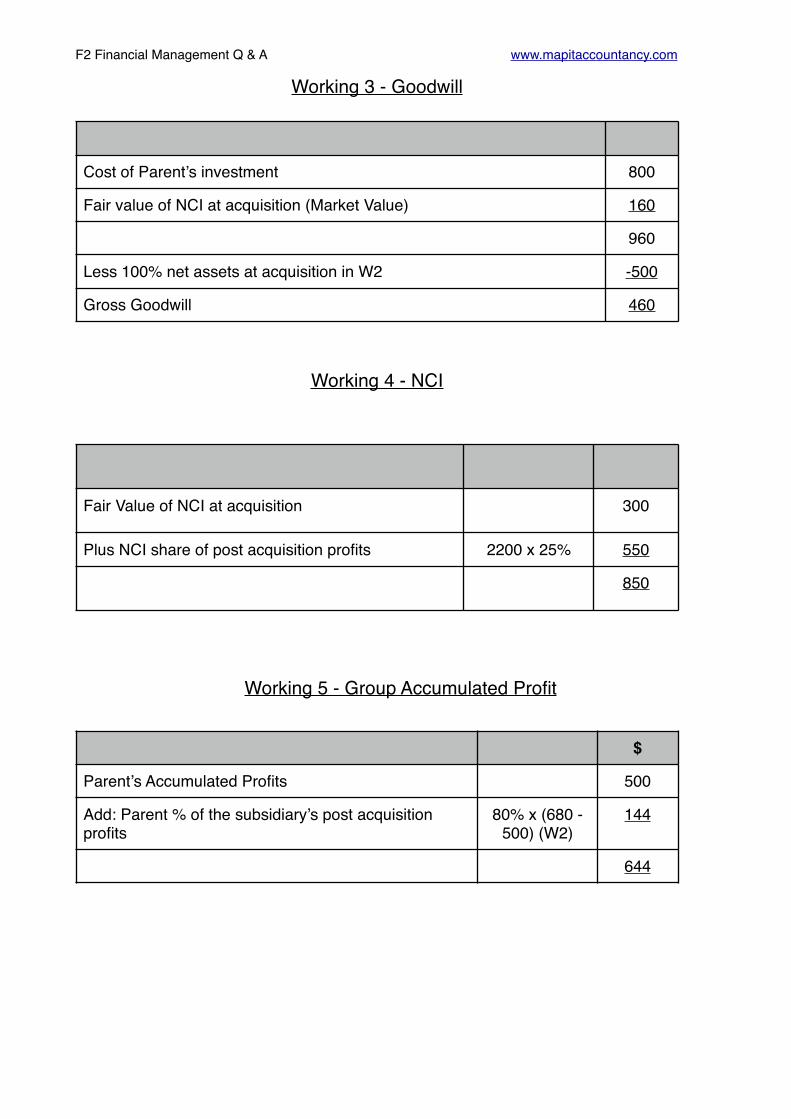

Working 3 - Goodwill

Working 4 - NCI

Working 5 - Group Accumulated Profit

Cost of Parent’s investment 800

Fair value of NCI at acquisition (Market Value) 160

960

Less 100% net assets at acquisition in W2 -500

Gross Goodwill 460

Fair Value of NCI at acquisition 300

Plus NCI share of post acquisition profits 2200 x 25% 550

850

$

Parent’s Accumulated Profits 500

Add: Parent % of the subsidiary’s post acquisition profits

80% x (680 - 500) (W2)

144

644

F2 Financial Management Q & A www.mapitaccountancy.com

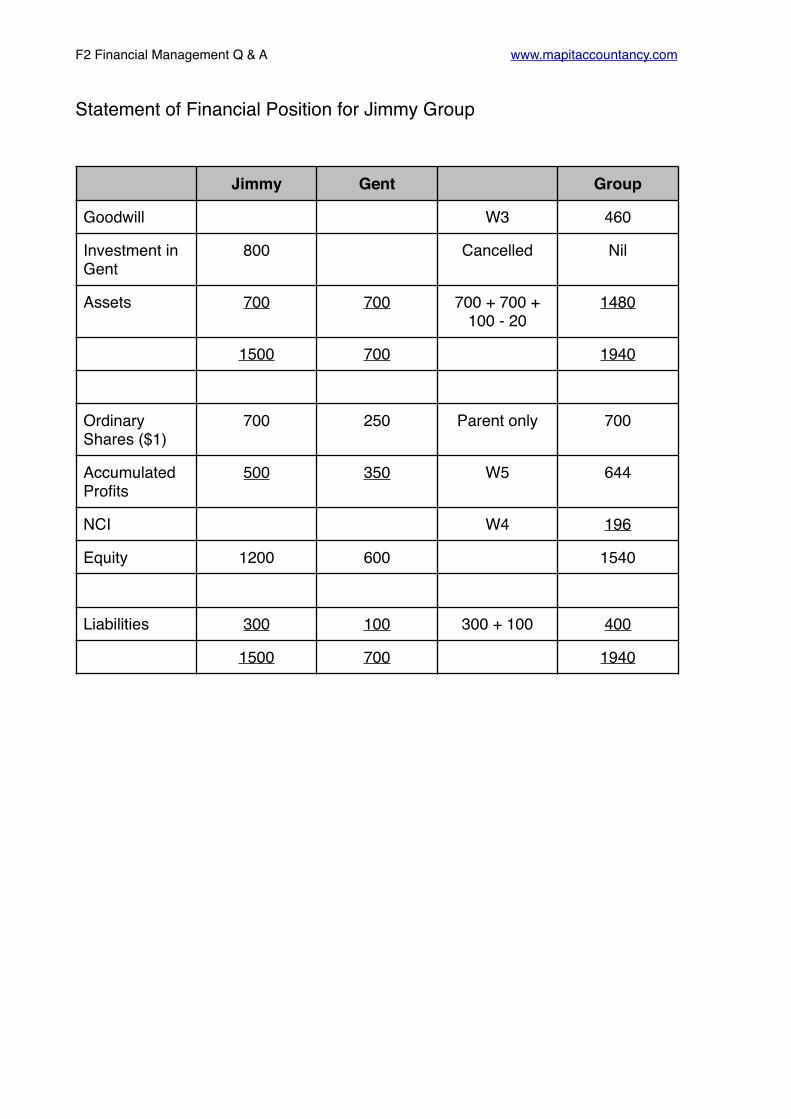

Statement of Financial Position for Jimmy Group

Jimmy Gent Group

Goodwill W3 460

Investment in Gent

800 Cancelled Nil

Assets 700 700 700 + 700 + 100 - 20

1480

1500 700 1940

Ordinary Shares ($1)

700 250 Parent only 700

Accumulated Profits

500 350 W5 644

NCI W4 196

Equity 1200 600 1540

Liabilities 300 100 300 + 100 400

1500 700 1940

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 8

Devil acquired 90% of Detail 2 years ago. The following information relates to Gent at the date of acquisition.

An item of plant was valued at $300 in the Gent’s Financial Statements but had a Fair Value of $200.

The plant subject to the fair value adjustment had a remaining life of 4 yrs at the date of acquisition. Goodwill is to be calculated Gross.

Accumulated profits at

acquisitionCost of

investmentFair Value of NCI

at acquisition

$ $ $

250 1000 55

Devil Detail

Investment in Detail 1000

Assets 600 800

1600 800

Ordinary Shares ($1) 650 100

Accumulated Profits 250 500

Equity 900 600

Liabilities 700 200

1500 700

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionWorking 1- Group Structure

Working 2 - Net Assets Subsidiary

Devil

↓90%

Detail

Date Acquired 2 Years Ago

Parent Share 90%

NCI 10%

100%

At Acquisition At Year End

Share Capital 100 100

Accumulated Profits 250 500

Fair Value Adjustment -100 -100

Additional Depreciation (2yrs) 50

250 550

300

F2 Financial Management Q & A www.mapitaccountancy.com

Working 3 - Goodwill

Working 4 - NCI

Working 5 - Group Accumulated Profit

Cost of Parent’s investment 1000

Fair value of NCI at acquisition (Market Value) 55

1055

Less 100% net assets at acquisition in W2 -250

Gross Goodwill 805

Fair Value of NCI at acquisition 55

Plus NCI share of post acquisition profits 10% x 300 (W2) 30

85

$

Parent’s Accumulated Profits 250

Add: Parent % of the subsidiary’s post acquisition profits

90% x 300 (W2)

270

520

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of Financial Position for Devil Group

Devil Detail

Goodwill 1000 W3 805

Assets 600 800 600 + 800 - 100 + 50

1350

1600 800 2155

Ordinary Shares ($1)

650 100 Parent 650

Accumulated Profits

250 500 W5 520

NCI W4 85

Equity 900 600

Liabilities 700 200 700 + 200 900

1500 700 2155

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 9

Evaro Co. Acquired 80% of Stando Co. one year ago and the following detail is relevant:

At the date of acquisition the following was relevant:

i) An item of plant was valued at $100m in the Gent’s Financial Statements but had a Fair Value of $50m, the plant had a remaining life of 10 yrs at the date of acquisition.

ii)Stando Co. owns an internally generated brand worth $20m on the date of acquisition that has a useful economic life of 20 years.

iii)At the date of acquisition a court case against Stando Co. is in process which has resulted in a contingent liability of $25m being disclosed in their financial statements. By the year end Stando Co. had won the court case resulting with no payment as a result.

Required

Compete the Equity Table (W2) based on the above information for Stando. Co.

At Acquisition$m

At Year End$m

Share Capital 100 100

Accumulated Profits 250 500

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

At Acquisition$m

At Year End$m

Share Capital 100 100

Accumulated Profits 250 500

Fair Value of Plant -50 -50

Remove Depreciation (50/10) 5

Brand 20 20

Amortization on Brand -1

Contingent Liability -25 0

295 574

F2 Financial Management Q & A www.mapitaccountancy.com

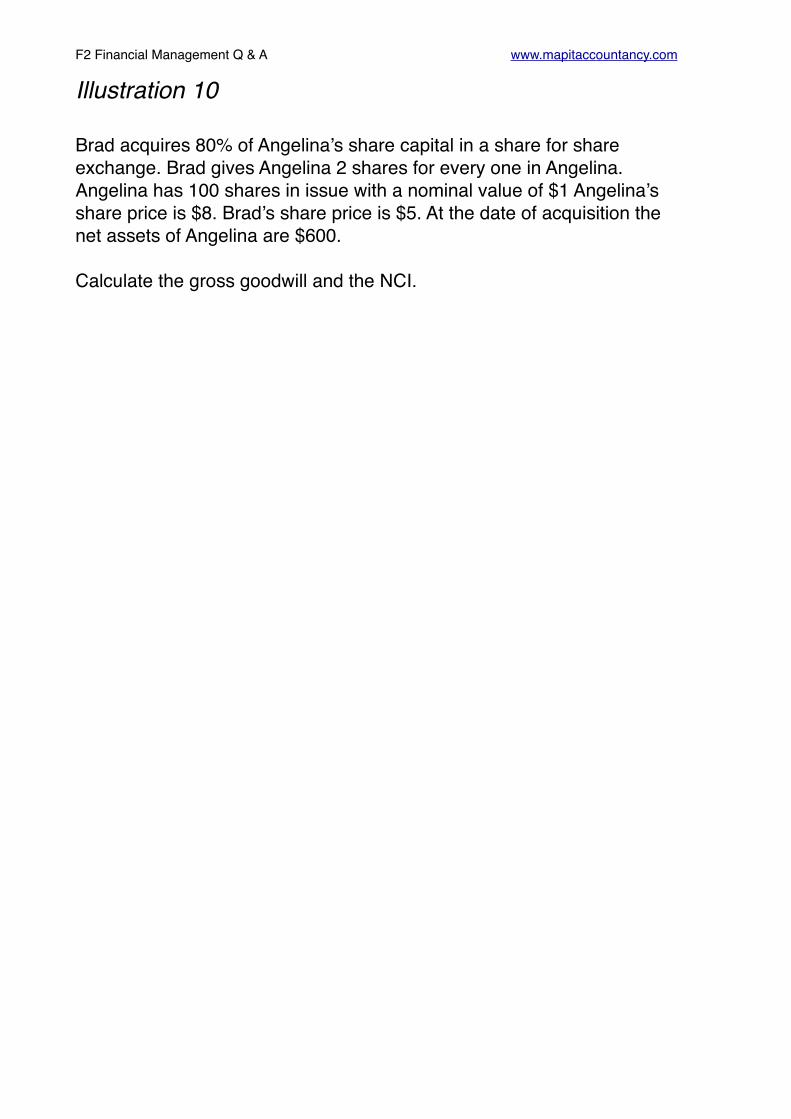

Illustration 10

Brad acquires 80% of Angelina’s share capital in a share for share exchange. Brad gives Angelina 2 shares for every one in Angelina. Angelina has 100 shares in issue with a nominal value of $1 Angelina’s share price is $8. Brad’s share price is $5. At the date of acquisition the net assets of Angelina are $600.

Calculate the gross goodwill and the NCI.

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Consideration

Brad is purchasing 80% of 100 shares = 80 shares

He is issuing 2 shares for each of the 80 he is purchasing (80 x 2) = 160

Each of the 160 shares is worth $5 so consideration is (160 x 5) = $800

Goodwill

Cost of Parent’s investment 800

Fair value of NCI at acquisition (Market Value) 160

960

Less 100% net assets at acquisition in W2 -600

Gross Goodwill 360

F2 Financial Management Q & A www.mapitaccountancy.com

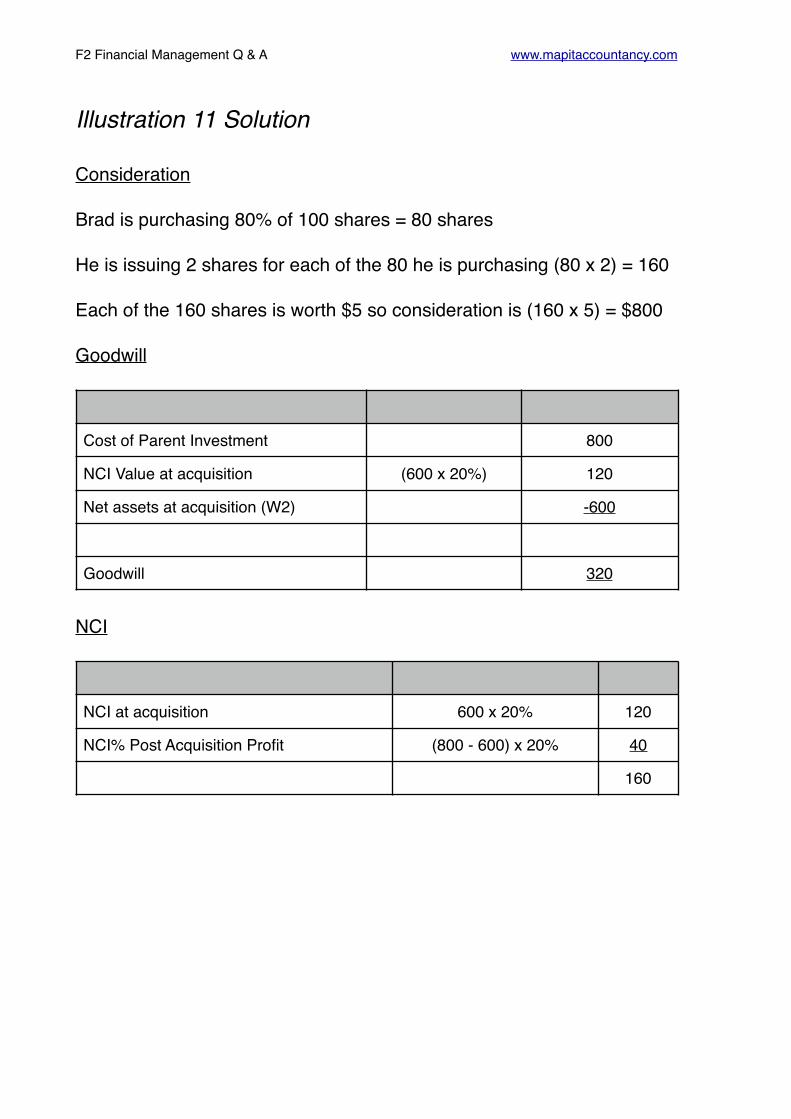

Illustration 11

Brad acquires 80% of Angelina’s share capital in a share for share exchange. Brad gives Angelina 2 shares for every one in Angelina. Angelina has 100 shares in issue with a nominal value of $1. Brad’s share price is $5. At the date of acquisition the net assets of Angelina are $600.

Calculate the goodwill arising using the proportionate method and the NCI.

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 11 Solution

Consideration

Brad is purchasing 80% of 100 shares = 80 shares

He is issuing 2 shares for each of the 80 he is purchasing (80 x 2) = 160

Each of the 160 shares is worth $5 so consideration is (160 x 5) = $800

Goodwill

NCI

Cost of Parent Investment 800

NCI Value at acquisition (600 x 20%) 120

Net assets at acquisition (W2) -600

Goodwill 320

NCI at acquisition 600 x 20% 120

NCI% Post Acquisition Profit (800 - 600) x 20% 40

160

F2 Financial Management Q & A www.mapitaccountancy.com

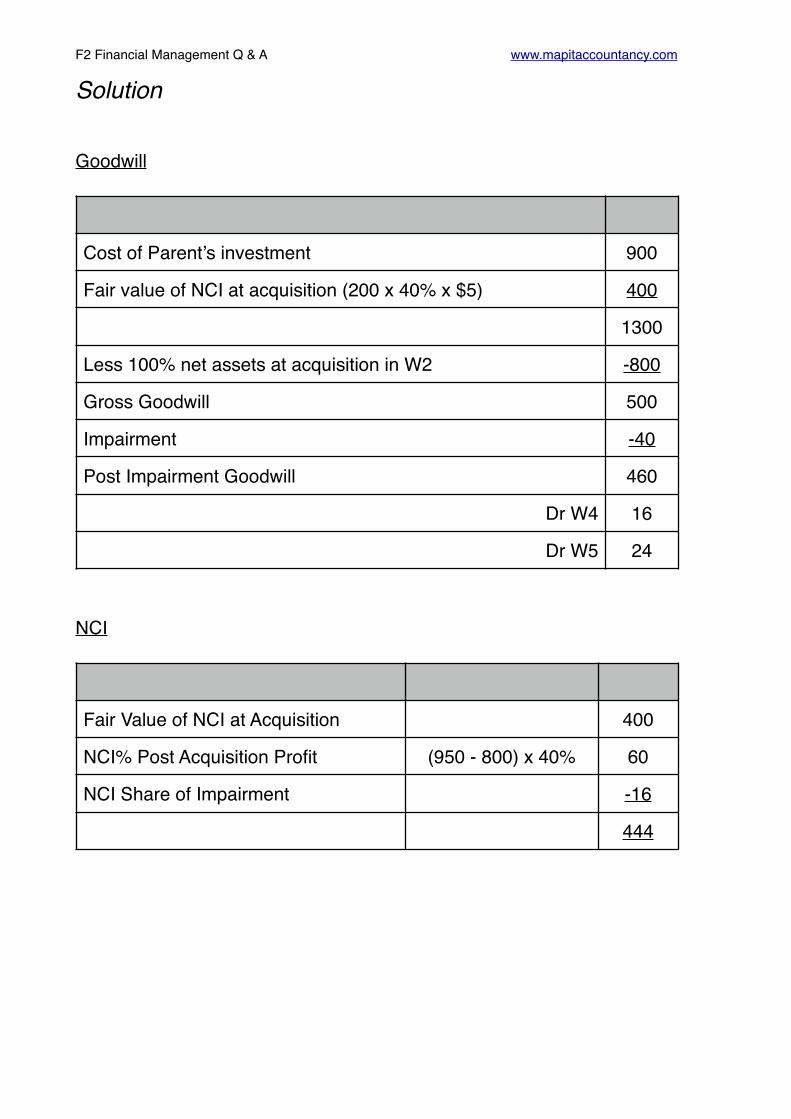

Illustration 12

(i)Archie acquires 60% of Mitchell’s share capital with consideration of $900. Mitchell has 200 shares in issue with a share price is $5. At the date of acquisition the net assets of Mitchell were $800 and are $950 at the year end. At the year end the retained earnings of Archie were $1,000.

An impairment review has been carried out on the goodwill at the year end which has found it to be impaired by $40.

Calculate the gross goodwill, the retained earnings and the NCI at the year end.

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Goodwill

NCI

Cost of Parent’s investment 900

Fair value of NCI at acquisition (200 x 40% x $5) 400

1300

Less 100% net assets at acquisition in W2 -800

Gross Goodwill 500

Impairment -40

Post Impairment Goodwill 460

Dr W4 16

Dr W5 24

Fair Value of NCI at Acquisition 400

NCI% Post Acquisition Profit (950 - 800) x 40% 60

NCI Share of Impairment -16

444

F2 Financial Management Q & A www.mapitaccountancy.com

Retained Earnings

Parent 1000

NCI% Post Acquisition Profit (950 - 800) x 60% 90

Parent Share of Impairment -24

1066

F2 Financial Management Q & A www.mapitaccountancy.com

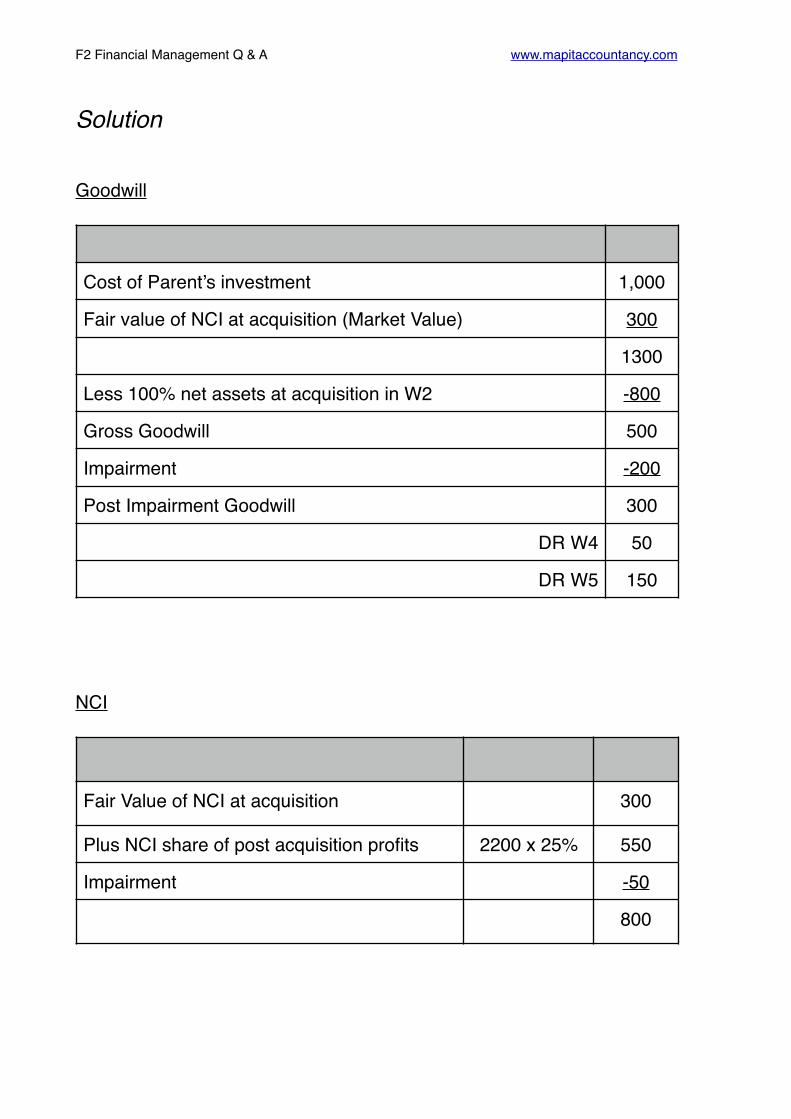

Illustration 12 (ii)

French acquired 75% of Shambles several years ago.

If French has $1500 of retained earnings at the year end, calculate the gross goodwill, retained earnings for the group and the NCI at the year end.

Cost of Investment

Fair Value of NCI at

acquisition

Net assets at acquisition

Net assets at year end

Goodwill Impairment at

Y/E

$ $ $ $ $

1,000 300 800 3,000 200

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Goodwill

NCI

Cost of Parent’s investment 1,000

Fair value of NCI at acquisition (Market Value) 300

1300

Less 100% net assets at acquisition in W2 -800

Gross Goodwill 500

Impairment -200

Post Impairment Goodwill 300

DR W4 50

DR W5 150

Fair Value of NCI at acquisition 300

Plus NCI share of post acquisition profits 2200 x 25% 550

Impairment -50

800

F2 Financial Management Q & A www.mapitaccountancy.com

Retained Earnings

Parent 1500

NCI% Post Acquisition Profit 2200 x 75% 1650

Parent Share of Impairment -150

3000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 12 (iii)

Pinky acquired 80% of Brain 4 years ago. The following information is relevant:

Goodwill is calculated gross and is subject to an annual impairment review. In the current year goodwill has been impaired by $20.

Net Assets at year end

Net Assets at acquisition

Cost of investment

Fair Value of NCI at

acquisition

$ $ $ $

150 100 175 25

Pinky Brain

Investment in Pinky 175

Assets 100 100

Inventory 140 200

Receivables 160 100

Bank 125 200

700 600

Ordinary Shares ($1) 160 50

Accumulated Profits 240 100

Equity 400 150

Non current liabilities 100 250

Liabilities 300 100

700 600

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Working 1- Group Structure

Working 2 - Net Assets Subsidiary

Pinky

↓80%

Brain

Date Acquired 4 Years Ago

Parent Share 80%

NCI 20%

100%

At Acquisition At Year End

Share Capital 50 50

Accumulated Profits 50 100

100 150

F2 Financial Management Q & A www.mapitaccountancy.com

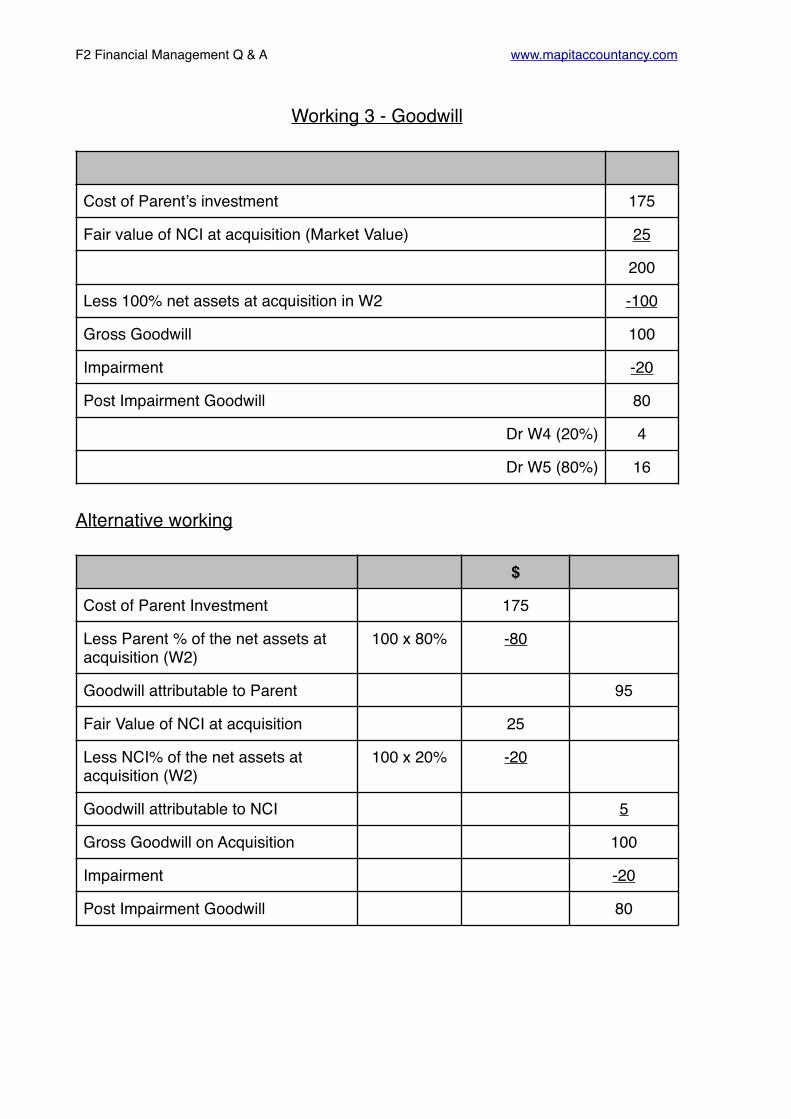

Working 3 - Goodwill

Alternative working

Cost of Parent’s investment 175

Fair value of NCI at acquisition (Market Value) 25

200

Less 100% net assets at acquisition in W2 -100

Gross Goodwill 100

Impairment -20

Post Impairment Goodwill 80

Dr W4 (20%) 4

Dr W5 (80%) 16

$

Cost of Parent Investment 175

Less Parent % of the net assets at acquisition (W2)

100 x 80% -80

Goodwill attributable to Parent 95

Fair Value of NCI at acquisition 25

Less NCI% of the net assets at acquisition (W2)

100 x 20% -20

Goodwill attributable to NCI 5

Gross Goodwill on Acquisition 100

Impairment -20

Post Impairment Goodwill 80

F2 Financial Management Q & A www.mapitaccountancy.com

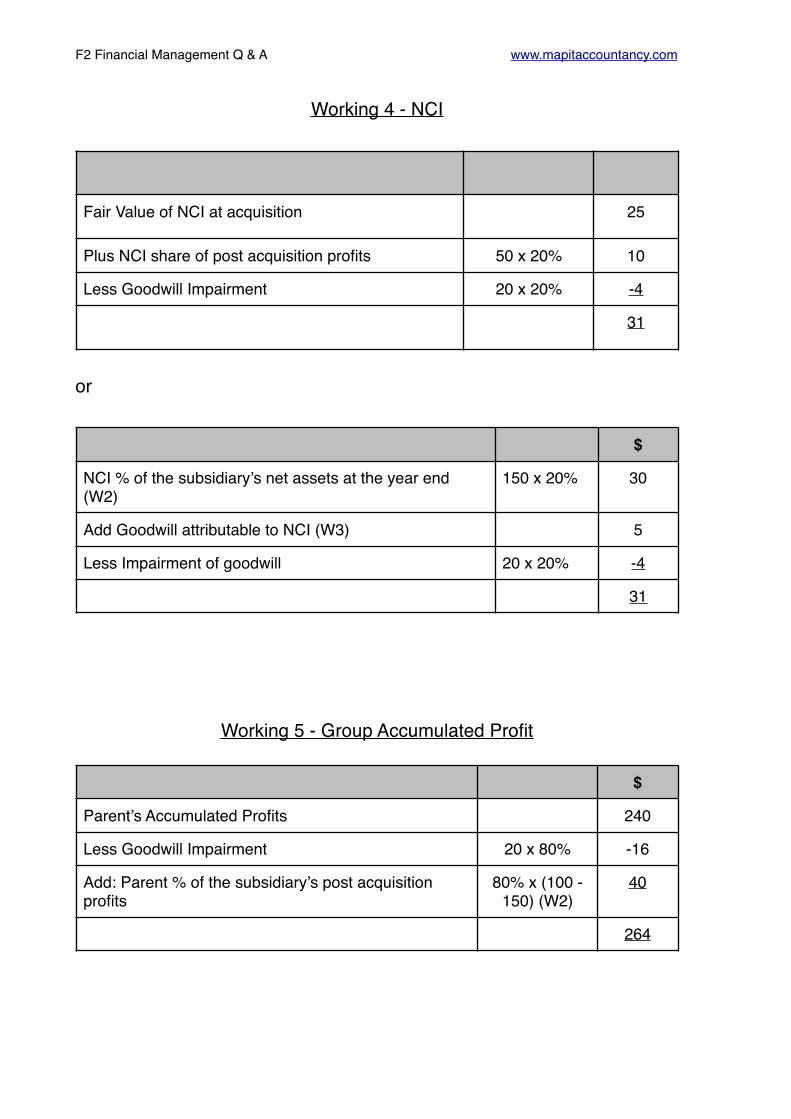

Working 4 - NCI

or

Working 5 - Group Accumulated Profit

Fair Value of NCI at acquisition 25

Plus NCI share of post acquisition profits 50 x 20% 10

Less Goodwill Impairment 20 x 20% -4

31

$

NCI % of the subsidiary’s net assets at the year end (W2)

150 x 20% 30

Add Goodwill attributable to NCI (W3) 5

Less Impairment of goodwill 20 x 20% -4

31

$

Parent’s Accumulated Profits 240

Less Goodwill Impairment 20 x 80% -16

Add: Parent % of the subsidiary’s post acquisition profits

80% x (100 - 150) (W2)

40

264

F2 Financial Management Q & A www.mapitaccountancy.com

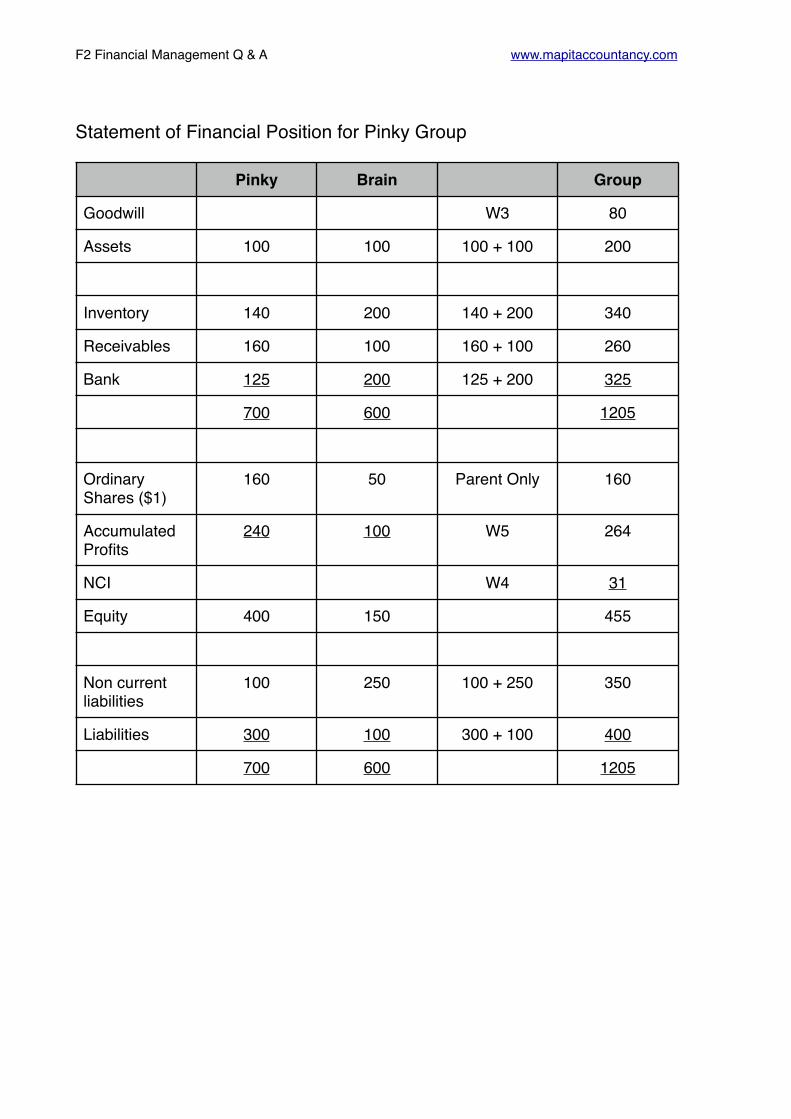

Statement of Financial Position for Pinky Group

Pinky Brain Group

Goodwill W3 80

Assets 100 100 100 + 100 200

Inventory 140 200 140 + 200 340

Receivables 160 100 160 + 100 260

Bank 125 200 125 + 200 325

700 600 1205

Ordinary Shares ($1)

160 50 Parent Only 160

Accumulated Profits

240 100 W5 264

NCI W4 31

Equity 400 150 455

Non current liabilities

100 250 100 + 250 350

Liabilities 300 100 300 + 100 400

700 600 1205

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 13

George owns 80% of the subsidiary Bungle. Goodwill has been calculated on a proportionate basis and at acquisition was $400m.

During the impairment review in the current year it was found that the carrying value of the goodwill has been impaired by $50m

What is the required treatment to deal with the impairment of goodwill?

F2 Financial Management Q & A www.mapitaccountancy.com

Solution

Goodwill on Balance Sheet

Proportionate goodwill 400

Impairment -50

Goodwill after impairment 350

Treatment

DR Retained Earnings (W5) 50

CR Goodwill 50

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 14A Parent company has recorded an asset of $300 goods receivable with a subsidiary.

The subsidiary had recorded this as an initial liability payable of $300 but has just recorded and sent a cheque payment to the parent of $50 leaving the payable balance of $250.

How should this be adjusted for on consolidation?

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionWhen cross casting assets & liabilities:

Less Payables $250 (DR)

Plus Cash at bank $50 (DR)

Less Receivables $300 (CR)

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 15Parent has been selling goods to subsidiary. The parent has recorded an asset of $500 receivable from the subsidiary.

The $500 includes goods worth $100 sent prior to the year end to the subsidiary who has not received them. As a result the subsidiary has a balance of $400 recorded as a liability in payables.

How should this be treated on consolidation?

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionWhen cross casting assets & liabilities:

Less Payables $400 (DR)

Plus Inventory $100 (DR)

Less Receivables $500 (CR)

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 16Arctic is the parent of a subsidiary Monkeys. Extracts of their SFPs are below

The trade payables of Monkeys includes $35m due to Arctic. This was after the deduction of $10m in respect of cash sent by Monkeys but not yet received by Arctic.

The receivables of Arctic at the year end include $70m due from Monkeys. $25m of these goods had been dispatched by Arctic, but were not yet received by Monkeys.

Show the treatment on consolidation.

Arctic Monkeys

Current Assets

Inventory 300 100

Receivables 200 250

Bank 100 50

600 400

Current Liabilities 420 220

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionRemember!

Add the goods/cash in transit

Subtract the inter company current accounts

+/- Item Where? $m

+ Cash in transit Cash at Bank 10

+ Goods in transit Inventory 25

- Inter Company Current Account Payables 35

- inter Company Current Account Receivables 70

Arctic Monkeys Group

Current Assets

Inventory 300 100 300 + 100 + Goods in transit of 25

425

Receivables 200 250 200 + 250 - 70 inter company current account

380

Bank 100 50 100 + 50 + cash in transit 10

160

600 400 965

Current Liabilities

420 220 420 + 220 - inter company current account

35

605

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 17Sea is the parent of a subsidiary Lion. Extracts of their SFPs are below

The trade payables of Lion includes $20m due to Arctic. This was after the deduction of $15m in respect of cash sent by Lion but not yet received by Sea.

The receivables of Sea at the year end include $50m due from Lion. $15m of these goods had been dispatched by Sea, but were not yet received by Lion.

Show the treatment on consolidation.

Sea Lion

Current Assets

Inventory 400 250

Receivables 100 100

Bank 150 100

650 450

Current Liabilities 90 140

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionRemember!

Add the goods/cash in transit

Subtract the inter company current accounts

+/- Item Where? $m

+ Cash in transit Cash at Bank 15

+ Goods in transit Inventory 15

- Inter Company Current Account Payables 20

- inter Company Current Account Receivables 50

Sea Lion Group

Current Assets

Inventory 400 250 400 + 250 + Goods in transit of 15

665

Receivables 100 100 100 + 100 - 50 inter company current account

150

Bank 150 100 150 + 100 + cash in transit 15

265

650 450 965

Current Liabilities

90 140 90 + 140 - inter company current account 20

210

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 18Inter company sales of $400 have occurred in Attila group at a mark up on cost of 25%. At the year end 1/4 of these goods had been sold on. Attila has an 80% interest in Hun.

I. Calculate the PURP.

II. Show the accounting treatment if the parent company is the seller.

III. Show the accounting treatment if the subsidiary company is the seller.

IV. Do parts I - III if the goods had been sold at a margin of 30%.

F2 Financial Management Q & A www.mapitaccountancy.com

Solution (Mark-up)

Parent is seller

Subsidiary is seller

Unsold Inventory Mark-up PURP

(400 x 3/4) = 300 25/125 60

DR/CR Account $ $

DR Accumulated Profits (W5) to decrease 60

CR Inventory to decrease 60

DR/CR Account $ $

DR Accumulated Profits (W5) with parent share to decrease (60 x 80%)

48

DR NCI (W4) with subsidiary share to decrease 12

CR Inventory to decrease 60

F2 Financial Management Q & A www.mapitaccountancy.com

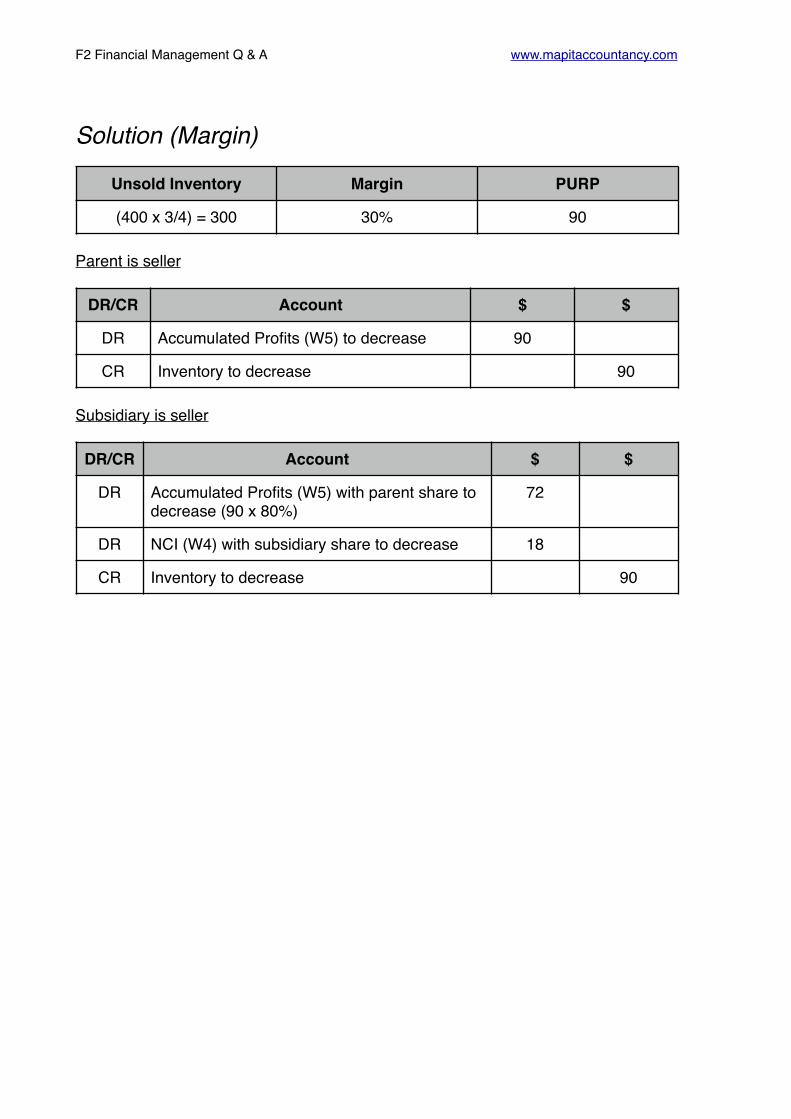

Solution (Margin)

Parent is seller

Subsidiary is seller

Unsold Inventory Margin PURP

(400 x 3/4) = 300 30% 90

DR/CR Account $ $

DR Accumulated Profits (W5) to decrease 90

CR Inventory to decrease 90

DR/CR Account $ $

DR Accumulated Profits (W5) with parent share to decrease (90 x 80%)

72

DR NCI (W4) with subsidiary share to decrease 18

CR Inventory to decrease 90

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 19Argentina owns an 80% share of Messi which it purchased one year ago.

The information below relates to Messi at the date of acquisition.

The income statements for both are:

Other information

I. Argentina sold goods to Messi during the year at a margin of 40% and worth $100m. Half of these goods have been sold on by Messi by the year end.

II. The fair value of Messi’s net assets were equal to their book value at the date of acquisition, with the exception of some machinery which had a useful life of 5 years.

III. Calculate goodwill using the fair value of the NCI at the date of acquisition. At the year end an impairment review has found that the goodwill has been impaired by 10%.

Produce a consolidated Income Statement for the Argentina group.

Ordinary Share Capital

Reserves Fair Value of the net assets

Fair value of the NCI

Cost of the investment

$m $m $m $m $m

200 400 800 200 1900

Argentina Messi

Revenue 8000 3000

Cost of Sales -4000 -1000

Gross Profit 4000 2000

Operating Costs -1500 -1500

Finance Costs -1000 -200

Profit Before Tax 1500 300

Tax -700 -100

Profit for the year 800 200

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 19 SolutionWorking 1- Group Structure

Working 2 - Inter Company

PURP

As the Parent is seller

Remember to remove the total amount of the sales also from sales and cost of sales

Argentina

↓80%

Messi

Date Acquired 1 Year Ago (No time apportionment)

Parent Share 80%

NCI 20%

100%

Unsold Inventory Margin PURP

(100 x 1/2) = 50 40% 20

DR/CR Account $ $

DR Cost of sales to increase 20

CR Inventory to decrease 20

DR/CR Account $ $

DR Revenue to decrease 100

CR Cost of sales to decrease 100

F2 Financial Management Q & A www.mapitaccountancy.com

Working 3 - Goodwill

We don’t need the net assets at the year end, but we do need them at acquisition to calculate goodwill. Be careful - we are given the total and told that the difference is machinery - this will lead to an additional depreciation expense.

The $200m asset has a useful life of 5 years so the extra depreciation will be $200m x 1/5 = $40m. The treatment for this is:

We can then use this to calculate the goodwill on acquisition

At Acquisition At Year End

Share Capital 200 N/A

Accumulated Profits 400 N/A

Fair Value Adjustment (Balancing figure)

200 N/A

800 N/A

DR/CR Account $ $

DR Cost of sales to increase 40

CR Non current assets to decrease 40

Cost of Parent’s investment 1900

Fair value of NCI at acquisition (Market Value) 200

2100

Less 100% net assets at acquisition in W2 -800

Gross Goodwill 1300

Goodwill impairment

Gross Goodwill 1300

Impairment Loss (1300 x 10%) 130

F2 Financial Management Q & A www.mapitaccountancy.com

The treatment for this is:

Working 4 - Cost of Sales

Working 5 - NCI

DR/CR Account $ $

DR Cost of sales to increase 130

CR Goodwill Intangible Asset to decrease 130

$m

Parent 4000

Subsidiary 1000

Less Inter Company Sales -100

Plus the PURP 20

Plus additional depreciation 40

Plus impairment loss 130

5090

$

NCI % of the subsidiary’s profits in question 200 x 20% 40

Less NCI share of additional depreciation 40 x 20% -8

Less NCI share of Impairment of goodwill 130 x 20% -26

6

F2 Financial Management Q & A www.mapitaccountancy.com

Income statement for Argentina Group

Argentina

Messi Group

Revenue 8000 3000 8000 + 3000 - 100 inter company sales

10900

Cost of Sales -4000 -1000 W4 -5090

Gross Profit 4000 2000 5810

Operating Costs -1500 -1500 1500 + 1500 -3000

Finance Costs -1000 -200 1000 + 200 -1200

Profit Before Tax 1500 300 1610

Tax -700 -100 700 + 100 -800

Profit for the year 800 200 810

Attributable to Parent (Balancing Figure) 804

Attributable to NCI (W5) 6

810

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of Changes in Equity Pro-forma

Share Capital

Share Premium

Revaluation Reserve

Accumulated Profits

NCI Total

O’Balance X X X X X X

Share Issues X X X

Revaluation Gains

X X X

Profit for period

X X X

Less Dividends

(X) (X) (X)

Cl’Balance X X X X X X

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 20Nadal is a 90% subsidiary of Federer. It was acquired one year ago for $4000m. At that time the accumulated profits were $800m.

Income Statements

Statements of Financial Position

Federer Nadal

Revenue 20000 4000

Cost of Sales -12000 -2000

Gross Profit 8000 2000

Distribution Costs -2100 -300

Admin Expenses -1400 -500

Operating Profit 1500 1200

Exceptional Gain Nil 580

Investment Income 90 Nil

Finance Costs -600 -150

Profit Before Tax 3990 1630

Tax -700 -130

Profit for the year 3290 1500

Federer Nadal

Investment in Nadal 4000

Assets 20000 5000

24000 5000

Share Capital 5000 1000

Accumulated Profits 15690 2200

Equity 20690 3200

Liabilities 3310 1800

24000 5000

F2 Financial Management Q & A www.mapitaccountancy.com

Federer Statement of changes in Equity

Nadal Statement of changes in Equity

Other Information:

In the year Federer sold goods to Nadal at a margin of 20%. The total amount sold was $100m, of which a quarter remain in inventory at the year end.

Also during the year Nadal sold $180m of goods to Federer. These goods were sold at a mark up of 50%. Half of the goods remain in inventory at the year end.

At the date of acquisition the fair values of Nadal’s net assets were equal to their book value with the exception of an item of plant that had a fair value of $200m in excess of its carrying value and a remaining useful life of 4 years. Goodwill is to be calculated on a proportionate basis.

Federer paid a dividend during the year of $200m while Nadal paid a dividend of $100m. Federer has recognised the dividend received from Nadal as investment income.

Required

Prepare the consolidated Income Statement, consolidated Statement of Changes in Equity and the consolidated Statement of Financial Position for the Federer group.

Share Capital Accumulated Profits

Total Equity

Opening Balance 5000 12600 17600

Profits for the year 3290 3290

Less Dividends -200 -200

Closing Balance 5000 15690 20690

Share Capital Accumulated Profits

Total Equity

Opening Balance 1000 800 1800

Profits for the year 1500 1500

Less Dividends -100 -100

Closing Balance 1000 2200 3200

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionWorking 1- Group Structure & PURP

PURP

Parent is seller

Subsidiary is seller

Federer

↓90%

Nadal

Date Acquired 1 Year Ago

Parent Share 90%

NCI 10%

100%

Unsold Inventory Margin PURP

(100 x 1/4) = 25 20% 5

DR/CR Account $ $

DR Accumulated Profits (W5) to decrease 5

CR Inventory to decrease 5

Unsold Inventory Margin PURP

(180 x 1/2) = 90 50/150 30

DR/CR Account $ $

DR Accumulated Profits (W5) with parent share to decrease (30 x 90%)

27

DR NCI (W4) with subsidiary share to decrease 3

CR Inventory to decrease 30

F2 Financial Management Q & A www.mapitaccountancy.com

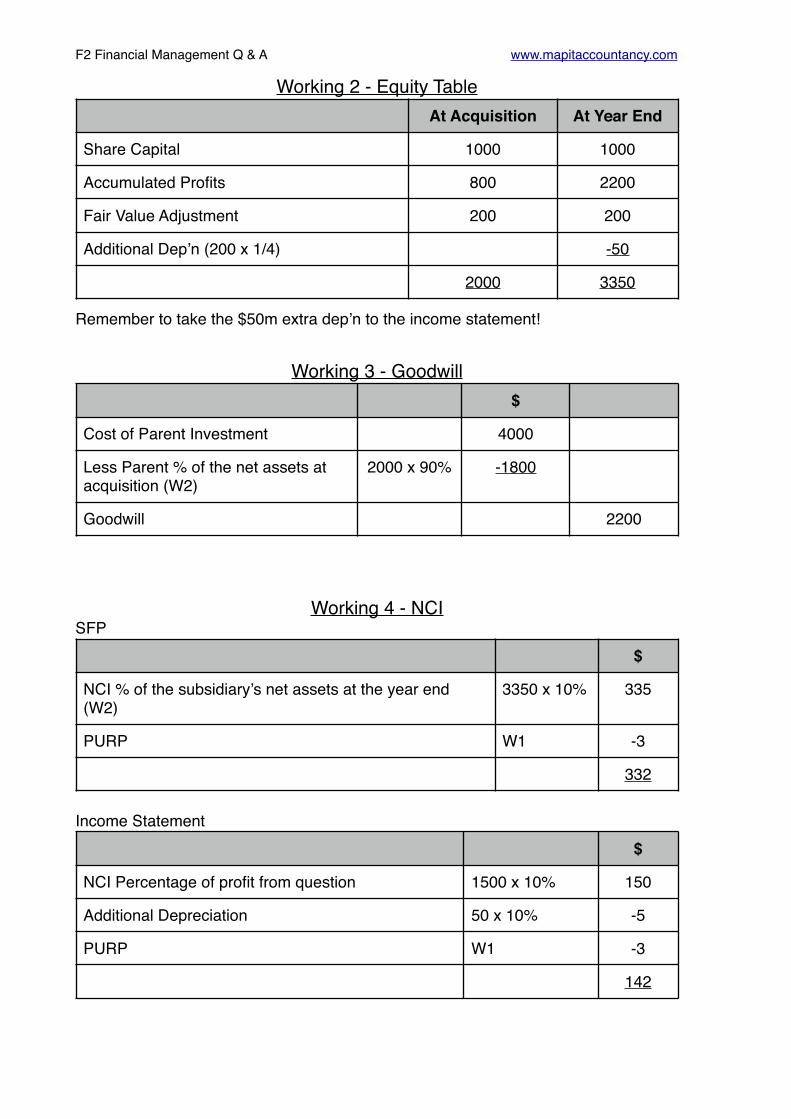

Working 2 - Equity Table

Remember to take the $50m extra dep’n to the income statement!

Working 3 - Goodwill

Working 4 - NCISFP

Income Statement

At Acquisition At Year End

Share Capital 1000 1000

Accumulated Profits 800 2200

Fair Value Adjustment 200 200

Additional Dep’n (200 x 1/4) -50

2000 3350

$

Cost of Parent Investment 4000

Less Parent % of the net assets at acquisition (W2)

2000 x 90% -1800

Goodwill 2200

$

NCI % of the subsidiary’s net assets at the year end (W2)

3350 x 10% 335

PURP W1 -3

332

$

NCI Percentage of profit from question 1500 x 10% 150

Additional Depreciation 50 x 10% -5

PURP W1 -3

142

F2 Financial Management Q & A www.mapitaccountancy.com

Working 5 - Group Accumulated Profit

Income Statement

$

Parent’s Accumulated Profits 15690

PURP 5 + 27 -32

Add: Parent % of the subsidiary’s post acquisition profits

90% x (2000 - 3350) (W2)

1215

16873

Federer Nadal Group

Revenue 20000 4000 20000 + 4000 - 100 - 180

23720

Cost of Sales -12000 -2000 12000 + 2000 - 100 - 180 - 35 -

50

-13805

Gross Profit 8000 2000 9915

Distribution Costs -2100 -300 2100 + 300 -2400

Admin Expenses -1400 -500 1400 + 500 -1900

Operating Profit 1500 1200 5615

Exceptional Gain Nil 580 580

Investment Income 90 Nil Nil

Finance Costs -600 -150 600 + 150 -750

Profit Before Tax 3990 1630 5445

Tax -700 -130 700 + 130 -830

Profit for the year 3290 1500 4615

Attributable to Parent (Balancing Figure)

4473

Attributable to NCI W4 142

4615

F2 Financial Management Q & A www.mapitaccountancy.com

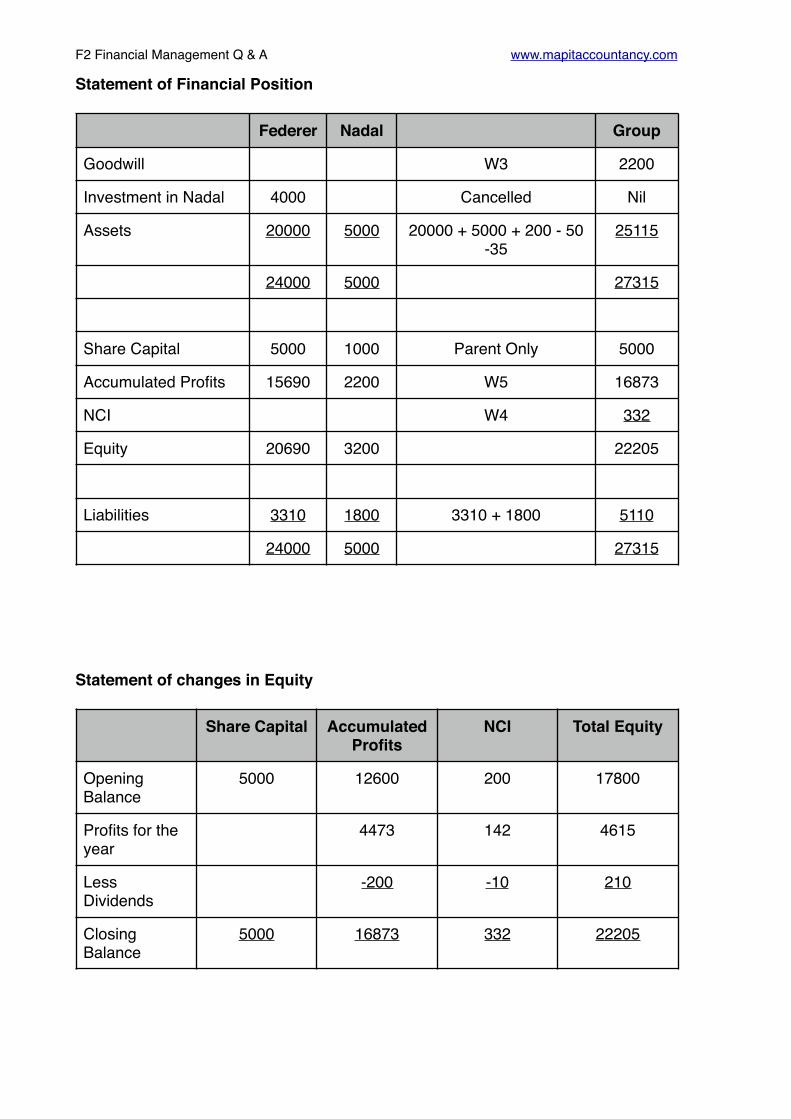

Statement of Financial Position

Statement of changes in Equity

Federer Nadal Group

Goodwill W3 2200

Investment in Nadal 4000 Cancelled Nil

Assets 20000 5000 20000 + 5000 + 200 - 50 -35

25115

24000 5000 27315

Share Capital 5000 1000 Parent Only 5000

Accumulated Profits 15690 2200 W5 16873

NCI W4 332

Equity 20690 3200 22205

Liabilities 3310 1800 3310 + 1800 5110

24000 5000 27315

Share Capital Accumulated Profits

NCI Total Equity

Opening Balance

5000 12600 200 17800

Profits for the year

4473 142 4615

Less Dividends

-200 -10 210

Closing Balance

5000 16873 332 22205

F2 Financial Management Q & A www.mapitaccountancy.com

Associates(IAS 28)

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1 3 years ago Star Ltd. bought 25% of the share capital of Wars Ltd. for consideration of $400,000. Since that time Wars Ltd.has had the following results:

Due to poor trading results and customer service issues, Star Ltd feel that in the current year the investment in Wars Ltd. has been impaired by $20,000.

Show the treatment of War Ltd. in the statement of financial position of Star Group and in the Income statement for the 3 years of the investment.

Solution

Year Profit Dividend Paid By Associate

1 $200,000 0

2 $160,000 $150,000

3 $30,000 0

Year 1 Investment In Associate (SFP)

Initial Investment 400,000

Parent Share of Post Acquisition Profit (200,000) x 25% 50,000

Investment in Associate 450,000

Year 1 Income From Associate (Income Statement)

Parent share of Current Year Income (200,000 x 25%) 50,000

F2 Financial Management Q & A www.mapitaccountancy.com

Year 2 Investment In Associate (SFP)

Initial Investment 400,000

Parent Share of Post Acquisition Profit (200,000 + 160,000) x 25% 90,000

Share of Dividend (150,000 x 25%) -37,500

Investment in Associate 452,500

Year 2 Income From Associate (Income Statement)

Parent share of Current Year Income (160,000 x 25%) 40,000

Year 3 Investment In Associate (SFP)

Initial Investment 400,000

Parent Share of Post Acquisition Profit

(200,000 + 160,000 + 30,000) x 25% 97,500

Share of Dividend (150,000 x 25%) -37,500

Impairment -20,000

Investment in Associate 440,000

Year 3 Income From Associate (Income Statement)

Parent share of Current Year Income (30,000 x 25%) 7500

Impairment -20,000

Loss From Associate -12500

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 2 Inter company sales of $1,300 have occurred in Attila group at a mark up on cost of 30%. At the year end 1/2 of these goods had been sold on. Attila has an 30% interest in Hun.

I. Calculate the PURP.

II. Show the accounting treatment if the parent company is the seller.

III. Show the accounting treatment if the Associate company is the seller.

F2 Financial Management Q & A www.mapitaccountancy.com

Solution (Mark-up)

Parent is seller

Subsidiary is seller

Unsold Inventory Mark-up PURP Group %

(1300 x 1/2) = 650 30/130 150 45

DR/CR Account $ $

DR Accumulated Profits (W5) to decrease 45

CR Investment in Associate 45

DR/CR Account $ $

DR Accumulated Profits (W5) to decrease 45

CR Group Inventory 45

F2 Financial Management Q & A www.mapitaccountancy.com

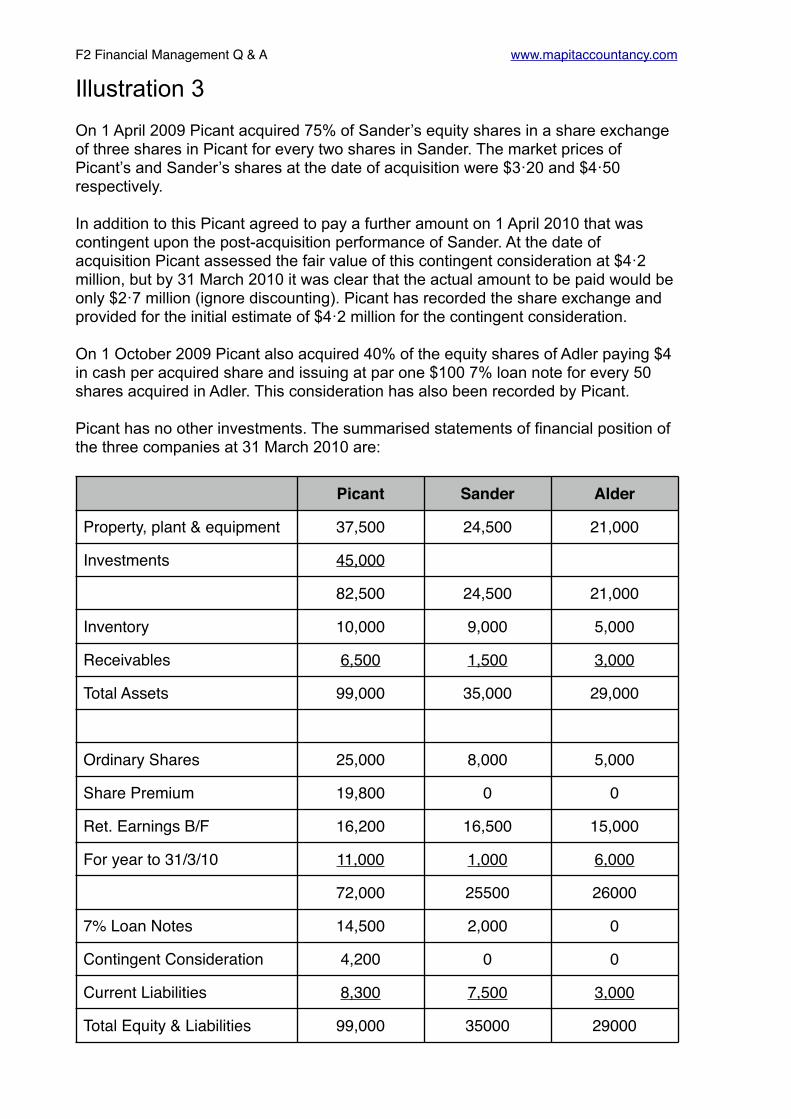

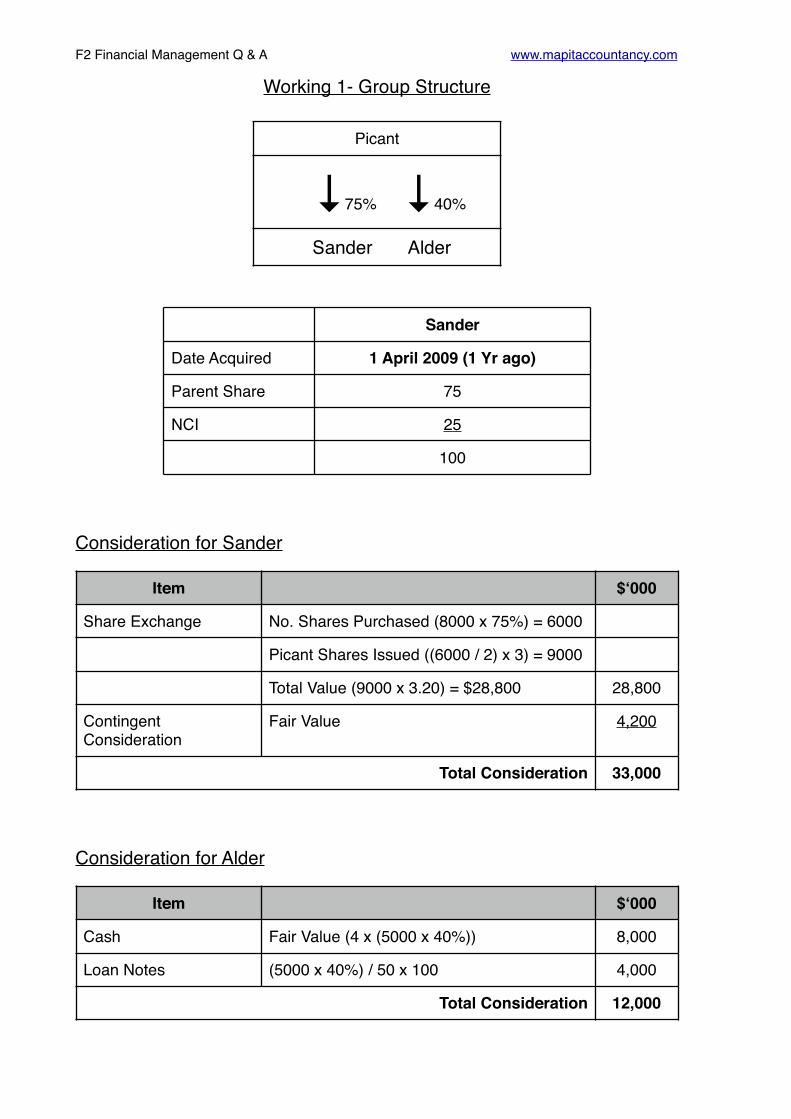

Illustration 3 On 1 April 2009 Picant acquired 75% of Sander’s equity shares in a share exchange of three shares in Picant for every two shares in Sander. The market prices of Picant’s and Sander’s shares at the date of acquisition were $3·20 and $4·50 respectively.

In addition to this Picant agreed to pay a further amount on 1 April 2010 that was contingent upon the post-acquisition performance of Sander. At the date of acquisition Picant assessed the fair value of this contingent consideration at $4·2 million, but by 31 March 2010 it was clear that the actual amount to be paid would be only $2·7 million (ignore discounting). Picant has recorded the share exchange and provided for the initial estimate of $4·2 million for the contingent consideration.

On 1 October 2009 Picant also acquired 40% of the equity shares of Adler paying $4 in cash per acquired share and issuing at par one $100 7% loan note for every 50 shares acquired in Adler. This consideration has also been recorded by Picant.

Picant has no other investments. The summarised statements of financial position of the three companies at 31 March 2010 are:

Picant Sander Alder

Property, plant & equipment 37,500 24,500 21,000

Investments 45,000

82,500 24,500 21,000

Inventory 10,000 9,000 5,000

Receivables 6,500 1,500 3,000

Total Assets 99,000 35,000 29,000

Ordinary Shares 25,000 8,000 5,000

Share Premium 19,800 0 0

Ret. Earnings B/F 16,200 16,500 15,000

For year to 31/3/10 11,000 1,000 6,000

72,000 25500 26000

7% Loan Notes 14,500 2,000 0

Contingent Consideration 4,200 0 0

Current Liabilities 8,300 7,500 3,000

Total Equity & Liabilities 99,000 35000 29000

F2 Financial Management Q & A www.mapitaccountancy.com

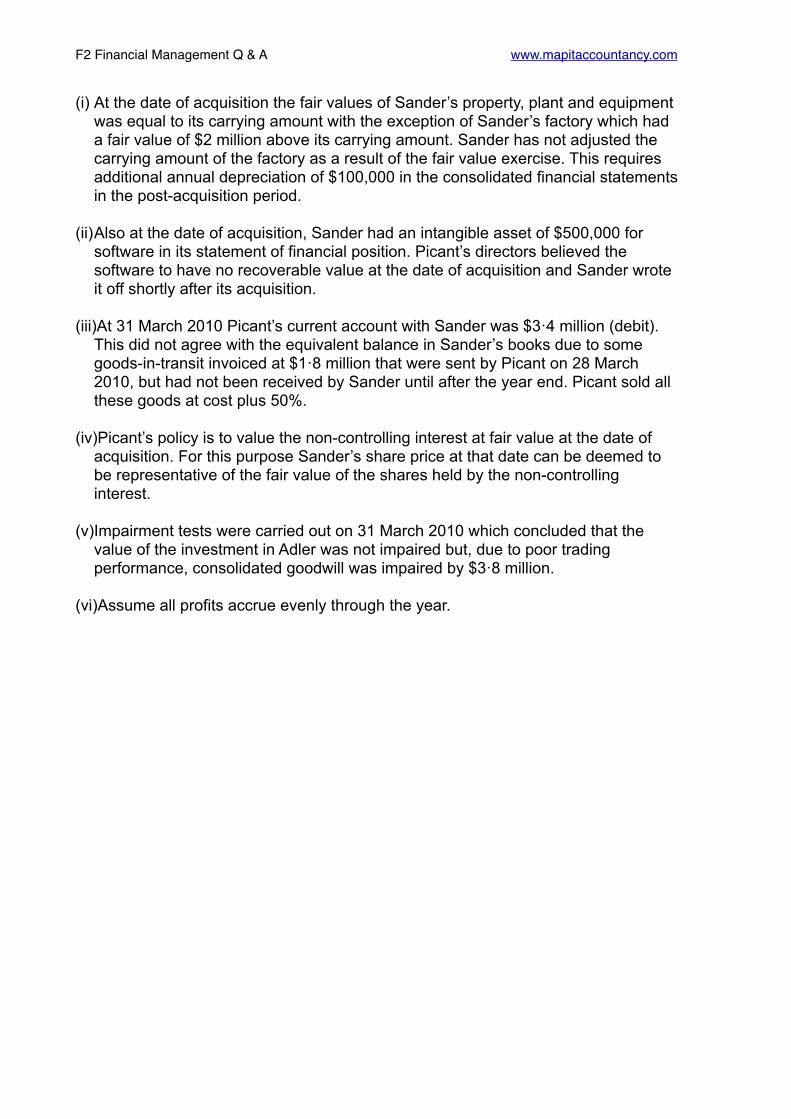

(i) At the date of acquisition the fair values of Sander’s property, plant and equipment was equal to its carrying amount with the exception of Sander’s factory which had a fair value of $2 million above its carrying amount. Sander has not adjusted the carrying amount of the factory as a result of the fair value exercise. This requires additional annual depreciation of $100,000 in the consolidated financial statements in the post-acquisition period.

(ii)Also at the date of acquisition, Sander had an intangible asset of $500,000 for software in its statement of financial position. Picant’s directors believed the software to have no recoverable value at the date of acquisition and Sander wrote it off shortly after its acquisition.

(iii)At 31 March 2010 Picant’s current account with Sander was $3·4 million (debit). This did not agree with the equivalent balance in Sander’s books due to some goods-in-transit invoiced at $1·8 million that were sent by Picant on 28 March 2010, but had not been received by Sander until after the year end. Picant sold all these goods at cost plus 50%.

(iv)Picant’s policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose Sander’s share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest.

(v)Impairment tests were carried out on 31 March 2010 which concluded that the value of the investment in Adler was not impaired but, due to poor trading performance, consolidated goodwill was impaired by $3·8 million.

(vi)Assume all profits accrue evenly through the year.

F2 Financial Management Q & A www.mapitaccountancy.com

Working 1- Group Structure

Consideration for Sander

Consideration for Alder

Picant

↓75% ↓40%

Sander Alder

Sander

Date Acquired 1 April 2009 (1 Yr ago)

Parent Share 75

NCI 25

100

Item $‘000

Share Exchange No. Shares Purchased (8000 x 75%) = 6000

Picant Shares Issued ((6000 / 2) x 3) = 9000

Total Value (9000 x 3.20) = $28,800 28,800

Contingent Consideration

Fair Value 4,200

Total Consideration 33,000

Item $‘000

Cash Fair Value (4 x (5000 x 40%)) 8,000

Loan Notes (5000 x 40%) / 50 x 100 4,000

Total Consideration 12,000

F2 Financial Management Q & A www.mapitaccountancy.com

Working 2 - Net Assets Subsidiary

Working 3 - Goodwill in Sander

At Acquisition At Year End

Share Capital 8,000 8,000

Accumulated Profits 16,500 17,500

Fair Value of Factory 2,000 2,000

Additional Dep’n -100

Software -500

26000 27400

$‘000 $‘000

Cost of Parent Investment 33,000

Fair Value of NCI at acquisition (8,000 x 25%) x $4.5

9,000

Less NCI% of the net assets at acquisition (W2)

-26,000

Gross Goodwill on Acquisition 16,000

Impairment -3,800

Goodwill at year end 12,200

Impairment to Parent in W5 (3,800 x 75%) 2,850

Impairment to NCI in W4 (3,800 x 25%) 950

F2 Financial Management Q & A www.mapitaccountancy.com

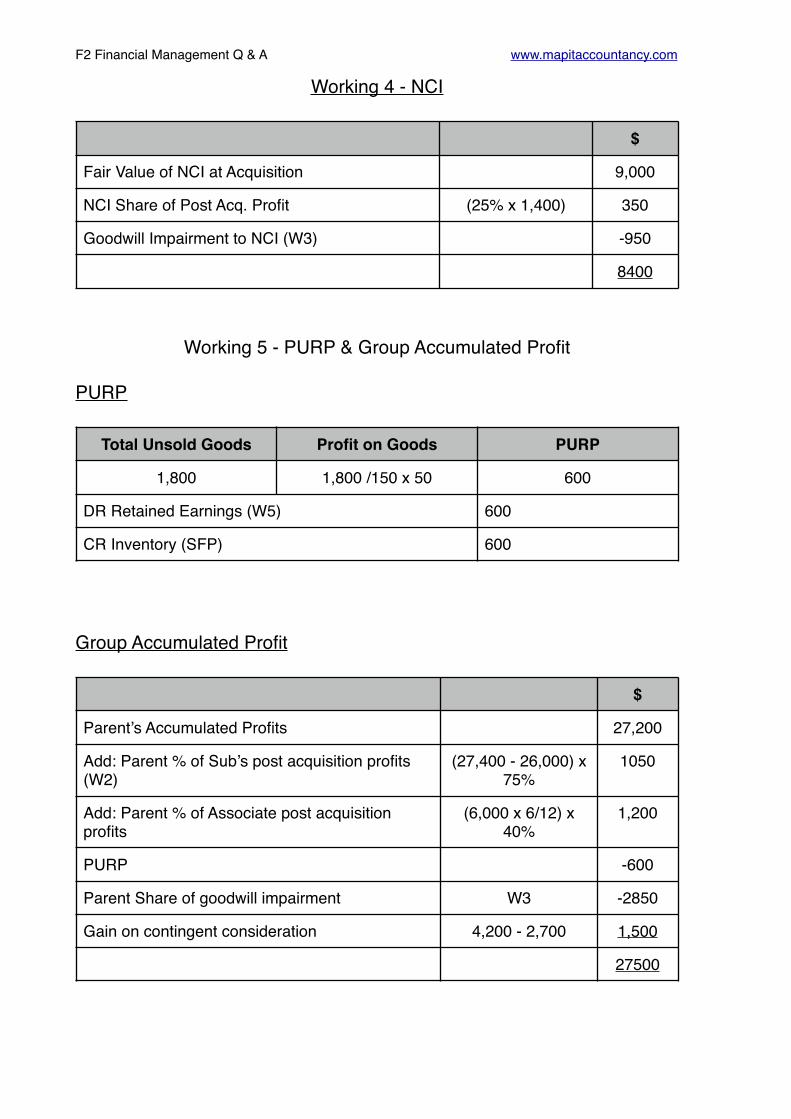

Working 4 - NCI

Working 5 - PURP & Group Accumulated Profit

PURP

Group Accumulated Profit

$

Fair Value of NCI at Acquisition 9,000

NCI Share of Post Acq. Profit (25% x 1,400) 350

Goodwill Impairment to NCI (W3) -950

8400

Total Unsold Goods Profit on Goods PURP

1,800 1,800 /150 x 50 600

DR Retained Earnings (W5) 600

CR Inventory (SFP) 600

$

Parent’s Accumulated Profits 27,200

Add: Parent % of Sub’s post acquisition profits (W2)

(27,400 - 26,000) x 75%

1050

Add: Parent % of Associate post acquisition profits

(6,000 x 6/12) x 40%

1,200

PURP -600

Parent Share of goodwill impairment W3 -2850

Gain on contingent consideration 4,200 - 2,700 1,500

27500

F2 Financial Management Q & A www.mapitaccountancy.com

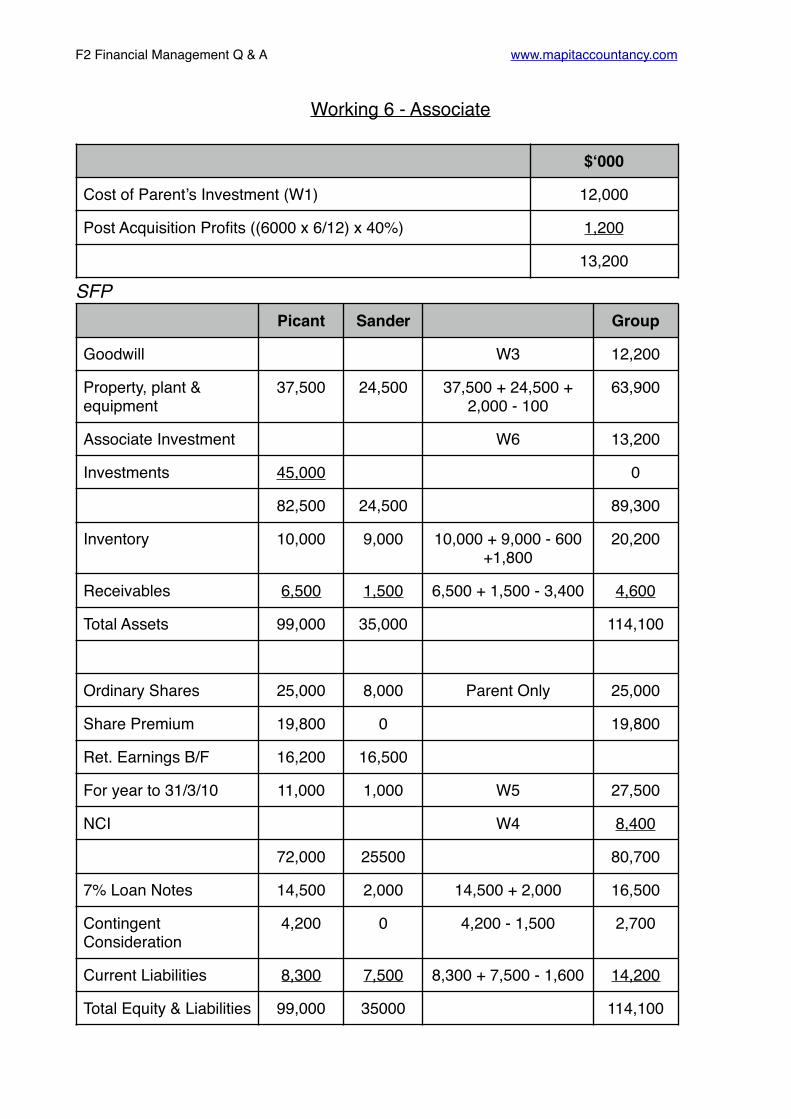

Working 6 - Associate

SFP

$‘000

Cost of Parent’s Investment (W1) 12,000

Post Acquisition Profits ((6000 x 6/12) x 40%) 1,200

13,200

Picant Sander Group

Goodwill W3 12,200

Property, plant & equipment

37,500 24,500 37,500 + 24,500 + 2,000 - 100

63,900

Associate Investment W6 13,200

Investments 45,000 0

82,500 24,500 89,300

Inventory 10,000 9,000 10,000 + 9,000 - 600 +1,800

20,200

Receivables 6,500 1,500 6,500 + 1,500 - 3,400 4,600

Total Assets 99,000 35,000 114,100

Ordinary Shares 25,000 8,000 Parent Only 25,000

Share Premium 19,800 0 19,800

Ret. Earnings B/F 16,200 16,500

For year to 31/3/10 11,000 1,000 W5 27,500

NCI W4 8,400

72,000 25500 80,700

7% Loan Notes 14,500 2,000 14,500 + 2,000 16,500

Contingent Consideration

4,200 0 4,200 - 1,500 2,700

Current Liabilities 8,300 7,500 8,300 + 7,500 - 1,600 14,200

Total Equity & Liabilities 99,000 35000 114,100

F2 Financial Management Q & A www.mapitaccountancy.com

Increasing/Decreasing Holding

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1Vic purchased 10% of the shares in Bob several years ago. The investment cost $17,000 and Vic currently carries the investment at cost in the accounts. Vic has subsequently purchased 45% of the shares in Bob for $120,000. The net assets of Bob have a fair value of $60,000 and the fair value of the original investment is $45,000. The fair value of the NCI is $90,000.

Calculate the gain or loss arising on the subsequent acquisition of shares

Solution 1

Fair value of original investment 45,000

Less the cost of the original investment -17,000

Gain taken to income statement 28,000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 2Vic purchased 10% of the shares in Bob several years ago. The investment cost $17,000 and Vic currently carries the investment at cost in the accounts. Vic has subsequently purchased 45% of the shares in Bob for $120,000. The net assets of Bob have a fair value of $60,000 and the fair value of the original investment is $45,000. The fair value of the NCI is $90,000.

Calculate the gross goodwill arising on the acquisition of Bob.

Solution 2

Working 1- Group Structure

Working 2 - Revaluation

Vic

↓10% ↓45%

Bob

Date 10% Acquired Years Ago

Date 45% Acquired Now

Parent Share 55%

NCI 45%

1

Fair value of original investment 45,000

Less the cost of the original investment -17,000

Gain taken to income statement 28,000

F2 Financial Management Q & A www.mapitaccountancy.com

Working 3 - Goodwill

Fair value of original investment 45,000

Fair value of consideration for second investment 120,000

165,000

Fair value of NCI at acquisition 90,000

Less 100% net assets at acquisition -60,000

Gross Goodwill 195,000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 3Aldo purchased 15% of the shares in Giro several years ago. The investment cost $85,000 and they currently carry it at cost in the accounts. Aldo has subsequently purchased 75% of the shares in Giro for $700,000. The net assets of Giro have a fair value of $750,000 and the fair value of the original investment is now $145,000. The fair value of the NCI on acquisition was $180,000.

Calculate the gross goodwill arising on the acquisition of Giro.

Solution 3

Working 1- Group Structure

Working 2 - Revaluation

Aldo

↓15% ↓75%

Giro

Date 15% Acquired Years Ago

Date 75% Acquired Now

Parent Share 90%

NCI 10%

1

Fair value of original investment 145,000

Less the cost of the original investment -85,000

Gain taken to income statement 60,000

F2 Financial Management Q & A www.mapitaccountancy.com

Working 3 - Goodwill

Fair value of original investment 145,000

Fair value of consideration for second investment 700,000

845,000

Fair value of NCI at acquisition 180,000

Less 100% net assets at acquisition -750,000

Gross Goodwill 275,000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 4A parent has owned 70% of a subsidiary for a long period of time. The NCI in the subsidiary is currently measured at $500,000. If the parent buys another 10% what will the value of the NCI fall to?

Solution 4

$

Current NCI value (30% holding) 500,000

Proportion being purchased (500,000 x 10/30) 166,667

New Value of NCI (500,000 - 166,667) 333,333

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 5A parent has owned 90% of a subsidiary for a long period of time. The NCI in the subsidiary is currently measured at $300,000.

I. The parent acquires all of the remaining shares for consideration of $250,000.

II. The parent acquires 3% of the shares for $200,000 reducing the NCI to 7%.

What is the difference taken to equity in both situations?

Solution 5

I.

II.

$

Amount of cash paid for subsequent investment 250,000

Decrease in the NCI 300,000

Difference to an equity reserve 50,000

$

Amount of cash paid for subsequent investment 200,000

Decrease in the NCI 300,000 x 3/10 90,000

Difference to an equity reserve -110,000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 6Inter purchased 70% of the shares in Milan several years ago. At that time goodwill of $80,000 arose. The net assets of Milan are currently $100,000 and the NCI is $18,000.

I. Calculate the gain arising on disposal if Inter sells it’s entire holding for $350,000.

II. Calculate the gain arising on disposal if Inter sells 30% for $250,000 and the fair value of the residual value is $30,000

F2 Financial Management Q & A www.mapitaccountancy.com

Solution 6I.

II.

$

Sale Proceeds 350,000

Less net assets of sub at date of disposal -100,000

Less all goodwill remaining at disposal -80,000

Plus all NCI at date of disposal 18,000

Plus fair value of any residual holding Nil

Gain to group 188,000

$

Sale Proceeds 250,000

Less net assets of sub at date of disposal -100,000

Less all goodwill remaining at disposal -80,000

Plus all NCI at date of disposal 18,000

Plus fair value of any residual holding 30,000

Gain to group 118,000

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 7For several years Jeremy has owned 70% of Richard. The net assets of Richard at this time are $250,000. The NCI is $68,000 and the gross goodwill is $200,000.

Jeremy has just sold 15% to take the holding to 55% for consideration of $150,000. Calculate the difference arising that will be taken to equity.

F2 Financial Management Q & A www.mapitaccountancy.com

Solution 7

$

DR Amount of cash received for sale of subsequent investment 150,000

CR Increase in the NCI (% of net assets & goodwill)

15% x (250,000 + 200,000) 67,500

CR Difference to an equity reserve (Gain) 82,500

F2 Financial Management Q & A www.mapitaccountancy.com

Vertical Groups

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1Consider a group with the following structure and detail:

Required

Calculate the Goodwill & the NCI at the acquisition date.

P

↓80% - 1 Year Ago

S

↓60% - 1 Year Ago

S1

Cost of Investment

Net Assets on Acquisition

FV NCI on Acquisition

S 250 200 60

S1 220 150 100

F2 Financial Management Q & A www.mapitaccountancy.com

Working 1 - Effective Interest in S1

Working 2 - Goodwill in S

Working 3 - Goodwill in S1

Working Total

P’s Direct Interest in S 80%

Non Controlling Interest in S 20%

100%

P’s indirect interest in S1 (80% x 60%) 48%

Non Controlling Interest in S1 (Balancing figure) 52%

100%

$

Cost of Parent Investment 250

Fair Value of NCI at acquisition 60

Less net assets at acquisition -200

Goodwill attributable to Parent 110

$

Cost of Investment 220

Less indirect holding adjustment 220 x 20% -44

Fair Value of NCI at acquisition 100

Less net assets at acquisition -150

Goodwill attributable to Parent 126

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

$

Fair Value of NCI at Acquisition in S 60

Fair Value of NCI at Acquisition in S1 100

Less indirect holding adjustment -44

116

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 2Ozzy acquired a 70% holding in Sharon 2 years ago. Sharon purchased a 60% shareholding in Jack one year ago. The following financial statements relate to the Ozzy group.

Statements of Financial Position Ozzy Sharon Jack

$ $ $

Investment in Sharon 50

Investment in Jack 17

Other assets 25 18 20

75 35 20

Ordinary Shares 50 20 8

Accumulated profits 20 12 8

Equity 70 32 16

Liabilities 5 3 4

75 35 20

Income Statements Ozzy Sharon Jack

$ $ $

Revenue 400 60 85

Operating Costs -395 55 -83

Operating Profit 5 5 2

Tax -3 -2 -1

Profit for Year 2 3 1

Accumulated Profits Sharon Jack

One year ago 3 4

Two years ago 2 3

F2 Financial Management Q & A www.mapitaccountancy.com

Goods worth $8m were sold in the year by Jack to Sharon and by the year end all of these had been sold to a third party.

An impairment review at the year end found the goodwill of Sharon to be impaired by $3m, goodwill is to be calculated gross.

Prepare the consolidated statement of financial position and consolidated income statement for the Ozzy group.

Fair Value of NCI based on effective shareholdings

Sharon Jack

One year ago 8 10

Two years ago 7 6

F2 Financial Management Q & A www.mapitaccountancy.com

SolutionWorking 1- Group Structure

Ozzy’s effective Interest in Jack

Ozzy

↓70% - 2 Years Ago

Sharon

↓60% - 1 Year Ago

Jack

Working Total

Ozzy’s direct interest in Jack 0%

Ozzy’s indirect interest (via Sharon)

(70% x 60%) 42%

Ozzy’s effective interest in Jack 0.42

Non Controlling Interest in Jack (Balancing figure) 0.58

100%

Ozzy’s Direct Interest in Sharon 70%

Non Controlling Interest in Sharon 30%

100%

F2 Financial Management Q & A www.mapitaccountancy.com

Working 2 - Equity Table

Working 3 - Goodwill in Sharon

At Acquisition At Year End

At Acquisition At Year End

Sharon Jack

Share Capital 20 20 8 8

Accumulated Profits 2 12 4 8

22 32 12 16

Cost of Parent’s investment 50

Fair value of NCI at acquisition (Market Value) 7

57

Less 100% net assets at acquisition in W2 -22

Gross Goodwill 35

Impairment -3

Goodwill after Impairment 32

F2 Financial Management Q & A www.mapitaccountancy.com

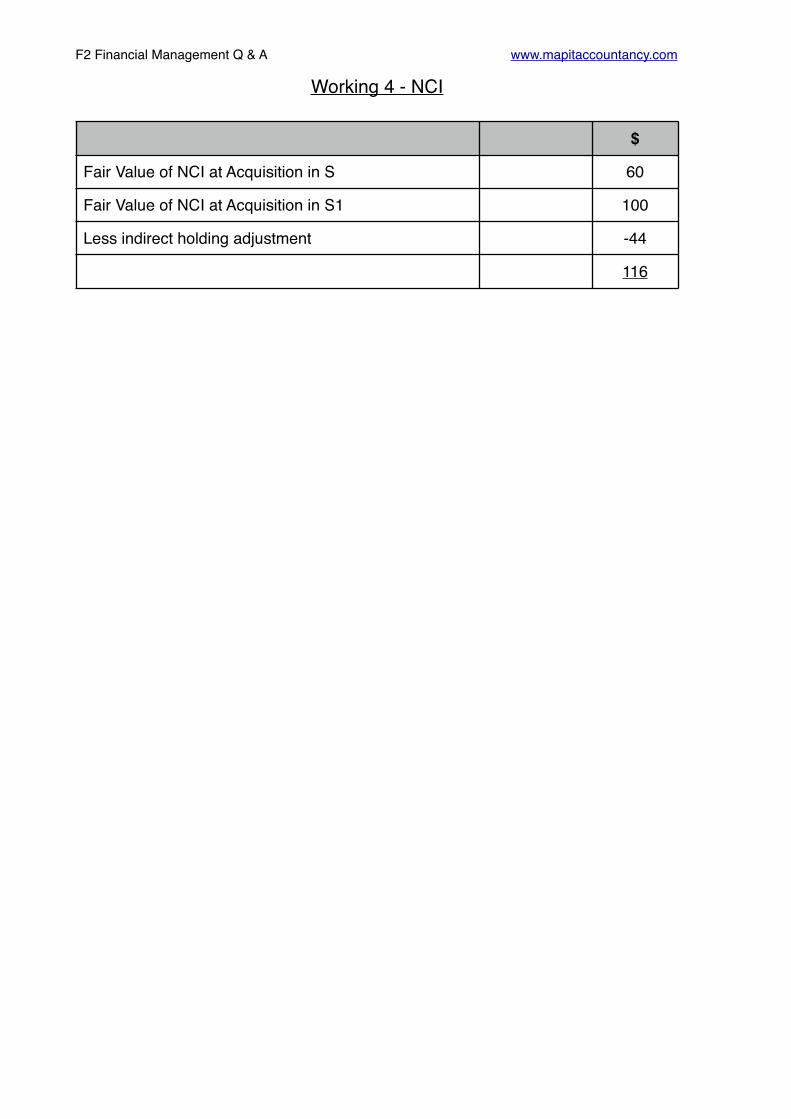

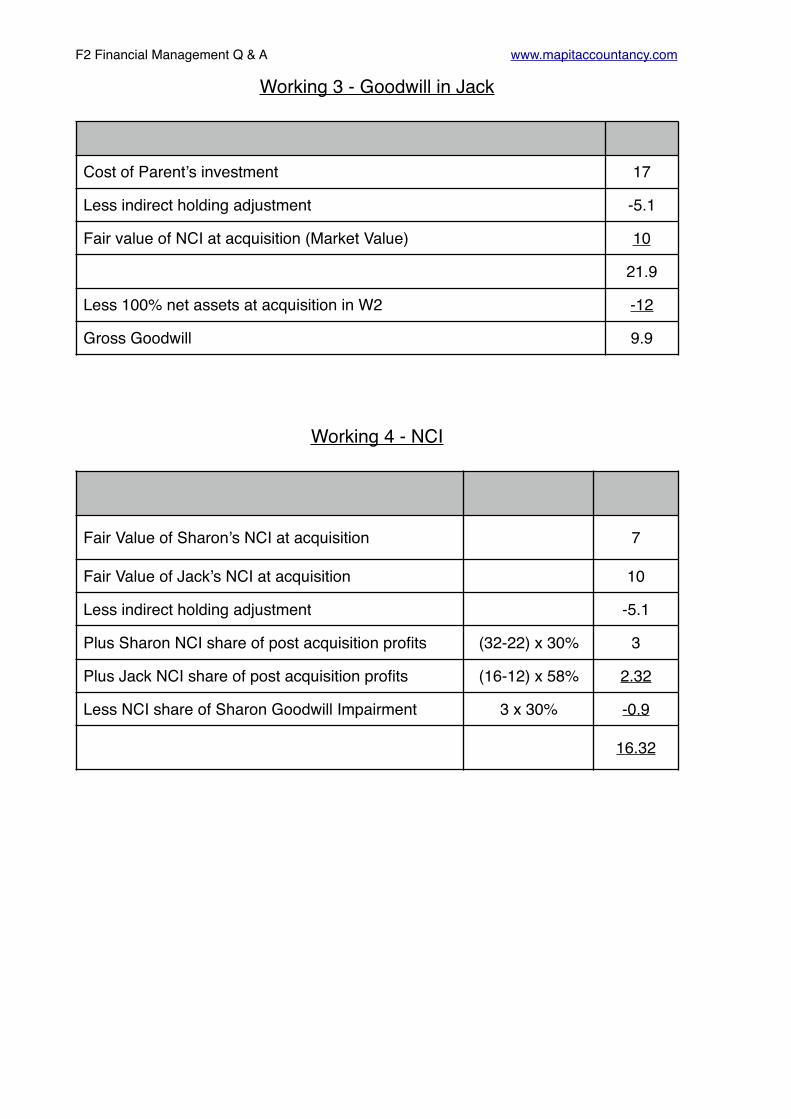

Working 3 - Goodwill in Jack

Working 4 - NCI

Cost of Parent’s investment 17

Less indirect holding adjustment -5.1

Fair value of NCI at acquisition (Market Value) 10

21.9

Less 100% net assets at acquisition in W2 -12

Gross Goodwill 9.9

Fair Value of Sharon’s NCI at acquisition 7

Fair Value of Jack’s NCI at acquisition 10

Less indirect holding adjustment -5.1

Plus Sharon NCI share of post acquisition profits (32-22) x 30% 3

Plus Jack NCI share of post acquisition profits (16-12) x 58% 2.32

Less NCI share of Sharon Goodwill Impairment 3 x 30% -0.9

16.32

F2 Financial Management Q & A www.mapitaccountancy.com

Working 5 - Group Accumulated Profit

Working 6 - NCI (Income Statement)

$

Parent’s Accumulated Profits 20

Less Goodwill Impairment 3 x 70% -2.1

Add: Parent % of Sharon’s post acquisition profits 10 x 70% 7

Add: Parent % of the Jack’s post acquisition profits 4 x 42% 1.68

26.58

Sharon Jack

NCI % of Profit in Question (30% x 3) 0.9 (1 x 58%) 0.58

NCI Share Goodwill Impairment (30% x 3) -0.9

NCI Share Group Profit -0.00 0.58

Total 0.58

F2 Financial Management Q & A www.mapitaccountancy.com

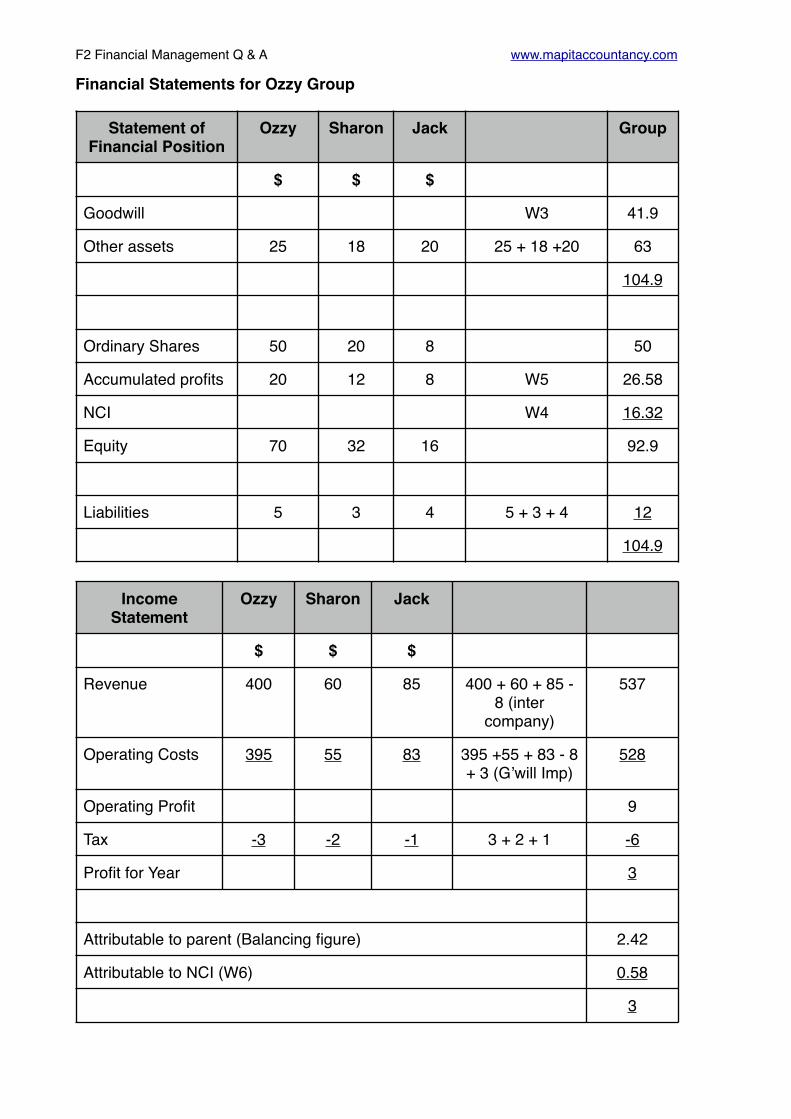

Financial Statements for Ozzy Group

Statement of Financial Position

Ozzy Sharon Jack Group

$ $ $

Goodwill W3 41.9

Other assets 25 18 20 25 + 18 +20 63

104.9

Ordinary Shares 50 20 8 50

Accumulated profits 20 12 8 W5 26.58

NCI W4 16.32

Equity 70 32 16 92.9

Liabilities 5 3 4 5 + 3 + 4 12

104.9

Income Statement

Ozzy Sharon Jack

$ $ $

Revenue 400 60 85 400 + 60 + 85 - 8 (inter

company)

537

Operating Costs 395 55 83 395 +55 + 83 - 8 + 3 (G’will Imp)

528

Operating Profit 9

Tax -3 -2 -1 3 + 2 + 1 -6

Profit for Year 3

Attributable to parent (Balancing figure) 2.42

Attributable to NCI (W6) 0.58

3

F2 Financial Management Q & A www.mapitaccountancy.com

Indirect Associates

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1

The parent has an 60% holding in the subsidiary. The subsidiary has an associate in which it holds 40%. The following information is relevant.

Show the treatment for the associate in the group financial statements.

Subsidiary’s cost of investment in associate 200

Fair value of net assets in associate at acquisition 120

Fair value of net assets in associate at year end 300

F2 Financial Management Q & A www.mapitaccountancy.com

Solution 1

Effective interest & NCI

Parent’s’s indirect interest (via Sub)

(60% x 40%) 24%

NCI (Balancing figure) 16%

Parent’s effective interest 40%

Post Acquisition Profits

Fair value of net assets in associate at year end 300

Fair value of net assets in associate at acquisition -120

Post acquisition profits 180

Carrying Value of Associate $

Cost of Investment 200

Subsidiary share of post acquisition profits (40% x 180) 72

Carrying Value of Associate 272

Treatment

DR Investment in Associate 40% x 180 72

CR Equity W5 (Parent share of post acquisition profits)

24/40 x 72 43.2

CR NCI W4 (NCI share of post acquisition profits) 16/40 x 72 28.8

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1The statements of financial position for 3 companies are as follows:

Other information:

I. John acquired a 60% holding in Paul for $600

II. Paul acquired a 60% holding in Ringo for $200

III. John acquired a 30% holding in Ringo for $75

IV. All of the investments were made on the same date

V. Goodwill is to be calculated gross and no impairment has been recorded

VI. The carrying value of assets & liabilities were the same as the fair values on the date of acquisition

VII. On the date of acquisition the following information was correct:

Prepare the consolidated statement of financial position for John Group.

John Paul Ringo

Investments 675 200

Assets 900 700 400

1575 900 400

Share Capital 300 200 100

Accumulated Profits

700 400 100

Equity 1000 600 200

Liabilities 575 300 200

1575 900 400

Paul Ringo

Accumulated Profits 250 60

Fair value of the effective NCI 100 60

F2 Financial Management Q & A www.mapitaccountancy.com

Solution 1

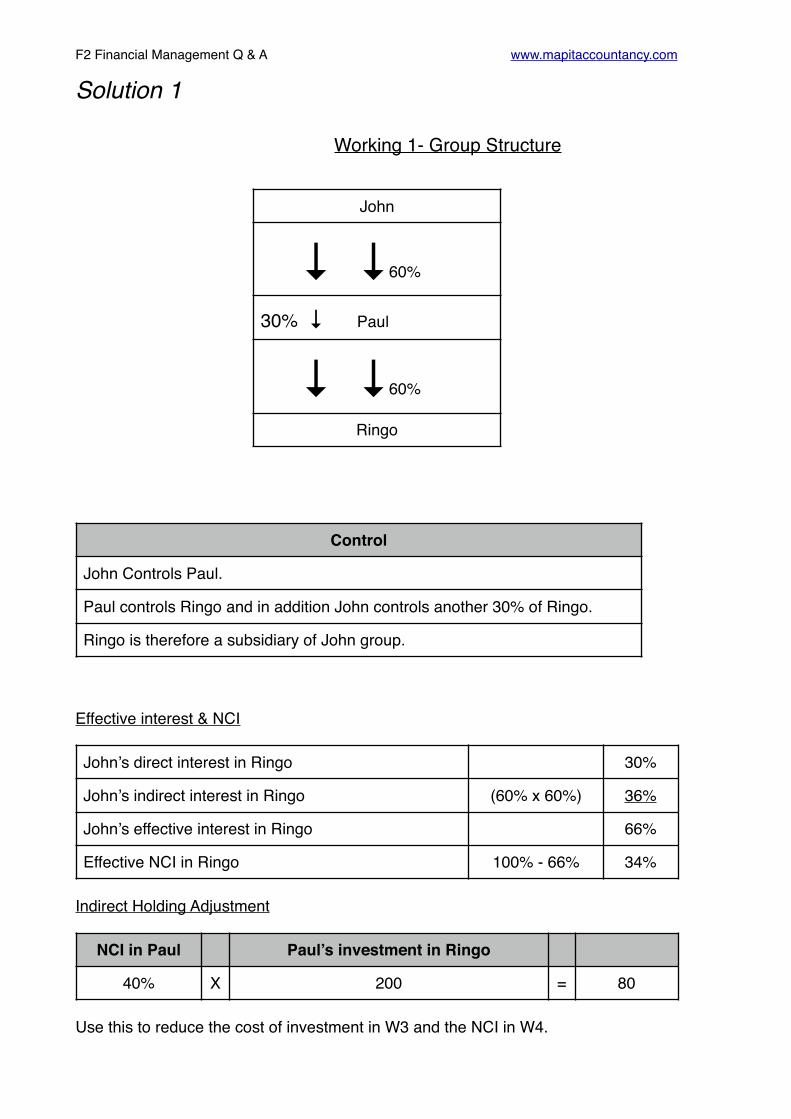

Working 1- Group Structure

Effective interest & NCI

Indirect Holding Adjustment

Use this to reduce the cost of investment in W3 and the NCI in W4.

John

↓ ↓60%

30% ↓ Paul

↓ ↓60%

Ringo

Control

John Controls Paul.

Paul controls Ringo and in addition John controls another 30% of Ringo.

Ringo is therefore a subsidiary of John group.

John’s direct interest in Ringo 30%

John’s indirect interest in Ringo (60% x 60%) 36%

John’s effective interest in Ringo 66%

Effective NCI in Ringo 100% - 66% 34%

NCI in Paul Paul’s investment in Ringo

40% X 200 = 80

F2 Financial Management Q & A www.mapitaccountancy.com

Working 2 - Net Assets Subsidiary

Working 3 - Goodwill in Paul

Working 3 - Goodwill in Ringo

At Acquisition At Year End

At Acquisition At Year End

Paul Ringo

Share Capital 200 200 100 100

Accumulated Profits 250 400 60 100

450 600 160 200

Cost of Parent’s investment 600

Fair value of NCI at acquisition (Market Value) 100

700

Less 100% net assets at acquisition in W2 -450

Gross Goodwill 250

Cost of Paul’s investment 200

Cost of John’s investment 75

Less indirect holding adjustment -80

Fair value of NCI at acquisition (Market Value) 60

255

Less 100% net assets at acquisition in W2 -160

Gross Goodwill 95

F2 Financial Management Q & A www.mapitaccountancy.com

Working 4 - NCI

Working 5 - Group Accumulated Profit

Fair Value of Paul NCI at acquisition 100

Fair Value of Ringo NCI at acquisition 60

Less indirect holding adjustment -80

Plus Paul NCI share of post acquisition profits (600-450) x 40%

60

Plus Ringo NCI share of post acquisition profits (100 - 60) x 34%

13.6

153.6

$

Parent’s Accumulated Profits 700

Add: Parent % of Paul’s post acquisition profits 150 x 60% 90

Add: Parent % of Ringo’s post acquisition profits 40 x 66% 26.4

816.4

F2 Financial Management Q & A www.mapitaccountancy.com

Statement of financial position for John Group

John Paul Ringo Group

Goodwill W3 (95 + 250)

345

Assets 900 700 400 900 + 700 + 400

2,000

2,345

Share Capital

300 200 100 Parent 300

Accumulated Profits

700 400 100 W5 816

NCI W4 154

Equity 1,270

Liabilities 575 300 200 500 + 300 +200

1,075

2,345

F2 Financial Management Q & A www.mapitaccountancy.com

Changes in Mixed Groups

F2 Financial Management Q & A www.mapitaccountancy.com

Solutions to Lecture Illustrations

Working Total

A’s direct interest in C 25%

A’s indirect interest (via B) (90% x 70%) 63%

A’s effective interest in C 0.88

Non Controlling Interest in C (Balancing figure) 12%

100%

Working Total

D’s direct interest in F 30%

D’s indirect interest (via E) (70% x 40%) 28%

D’s effective interest in F 0.58

Non Controlling Interest in F (Balancing figure) 0.42

100%

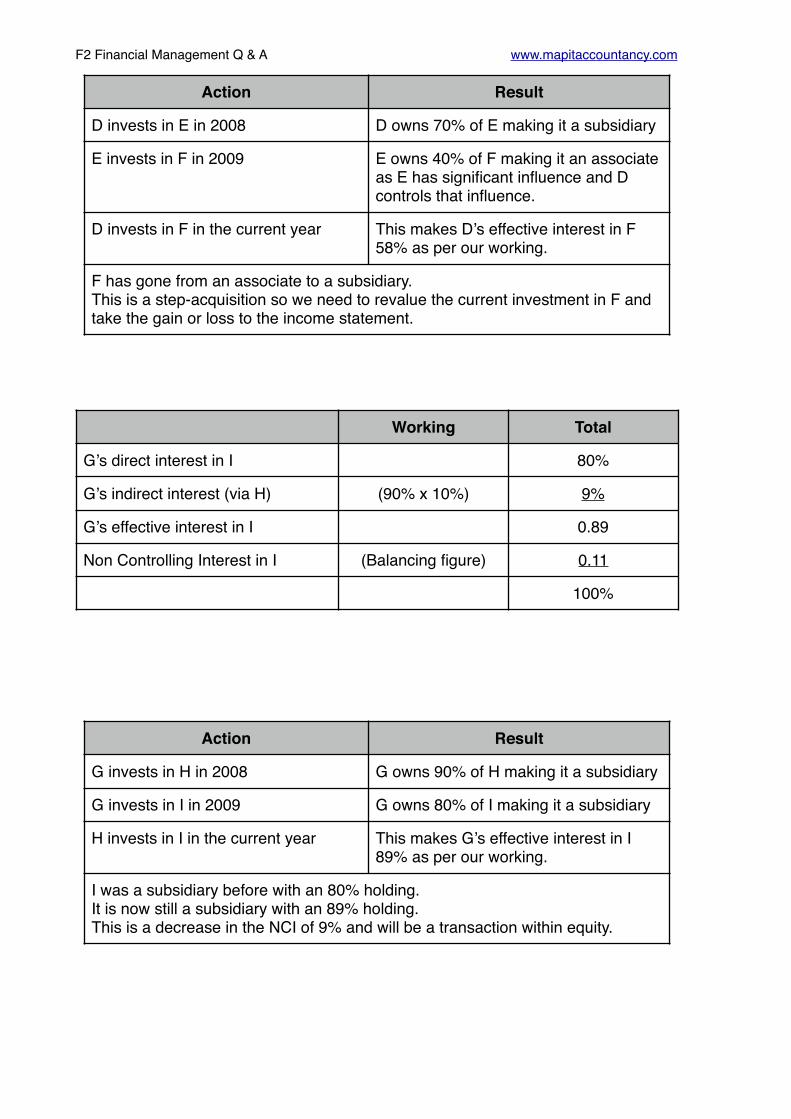

Action Result

D invests in E in 2008 D owns 70% of E making it a subsidiary

D invests in F in 2009 D owns 30% of F making it an associate

E invests in F in the current year This makes D’s effective interest in F 58% as per our working.

F has gone from an associate to a subsidiary.This is a step-acquisition so we need to revalue the current investment in F and take the gain or loss to the income statement.

F2 Financial Management Q & A www.mapitaccountancy.com

Action Result

D invests in E in 2008 D owns 70% of E making it a subsidiary

E invests in F in 2009 E owns 40% of F making it an associate as E has significant influence and D controls that influence.

D invests in F in the current year This makes D’s effective interest in F 58% as per our working.

F has gone from an associate to a subsidiary.This is a step-acquisition so we need to revalue the current investment in F and take the gain or loss to the income statement.

Working Total

G’s direct interest in I 80%

G’s indirect interest (via H) (90% x 10%) 9%

G’s effective interest in I 0.89

Non Controlling Interest in I (Balancing figure) 0.11

100%

Action Result

G invests in H in 2008 G owns 90% of H making it a subsidiary

G invests in I in 2009 G owns 80% of I making it a subsidiary

H invests in I in the current year This makes G’s effective interest in I 89% as per our working.

I was a subsidiary before with an 80% holding.It is now still a subsidiary with an 89% holding.This is a decrease in the NCI of 9% and will be a transaction within equity.

F2 Financial Management Q & A www.mapitaccountancy.com

Action Result

G invests in H in 2008 G owns 90% of H making it a subsidiary

H invests in I in 2009 I is a simple investment of 10%

G invests in I in the current year This makes G’s effective interest in I 89% as per our working.

I was an investment before.It is now a subsidiary with an 89% holding.This is a step acquisition.

F2 Financial Management Q & A www.mapitaccountancy.com

IAS 21 Foreign Currency

F2 Financial Management Q & A www.mapitaccountancy.com

Illustration 1Which of the following statements relating to IAS 21 The effects of changes in foreign exchange rates is correct?

A. The functional currency of a foreign subsidiary is the currency that the group financial statements are presented in.

B. A foreign subsidiary must present it’s financial statements in the presentational currency of the parent.

C. Consideration will be given to the currency of the costs and sales of the entity when determining it’s functional currency.

D. The more autonomous a subsidiary, the more likely it’s functional currency is that of the parent entity.

Answer C

Illustration 2Bulldog Ltd has a year end of 31 January.

On 13th October Bulldog Ltd buys goods from Eagle Inc. a US supplier for $250,000.

On 24th November Bulldog settles the transaction in full.

Exchange rates

13th October £1 : $1.45

24th November £1 : $1.55

Show the accounting entries for these transactions.

F2 Financial Management Q & A www.mapitaccountancy.com

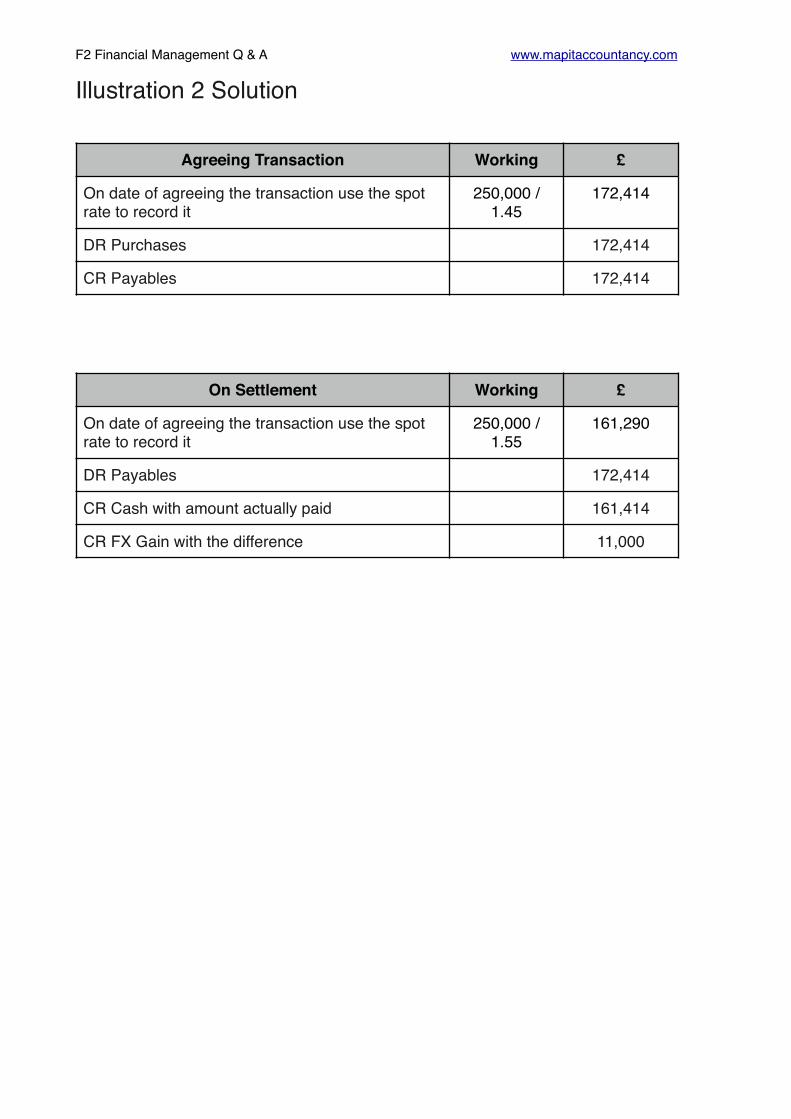

Illustration 2 Solution

Agreeing Transaction Working £

On date of agreeing the transaction use the spot rate to record it

250,000 / 1.45

172,414

DR Purchases 172,414

CR Payables 172,414

On Settlement Working £

On date of agreeing the transaction use the spot rate to record it

250,000 / 1.55

161,290

DR Payables 172,414

CR Cash with amount actually paid 161,414

CR FX Gain with the difference 11,000

F2 Financial Management Q & A www.mapitaccountancy.com

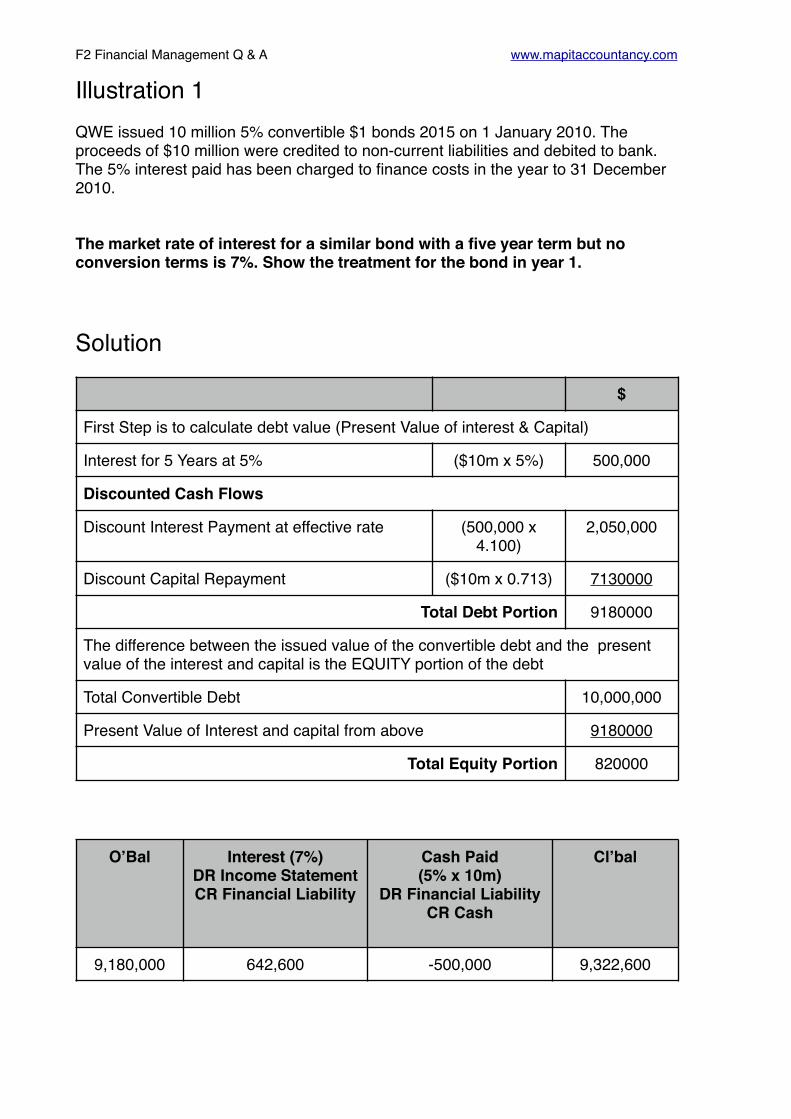

Illustration 3Jeff Ltd. purchases an item of plant on 1st June from a foreign supplier on one month’s credit for €100,000. Jeff is a US company.

Exchange rates

1st June $ = €1.50

21st June $ = €1.40

How will this transaction be dealt with in the accounts for the year to 21st June?

F2 Financial Management Q & A www.mapitaccountancy.com

Solution to Illustration 3

At Purchase Date Working $

The rate at the time of purchase is $ : €1.50 €100,000 / 1.50 66,666

DR Asset 66,666

CR Payables 66,666

At 21st June Working $

The rate at this time is $ : €1.40 €100,000 / 1.40 71,429

The payable must be retranslated at the year end as it is a monetary balance. So........

DR FX Loss (71,429 - 66,666) 4,763

CR Payables (71,429 - 66,666) 4,763

The $4,763 is unrealised so is included in Other Comprehensive Income.

F2 Financial Management Q & A www.mapitaccountancy.com

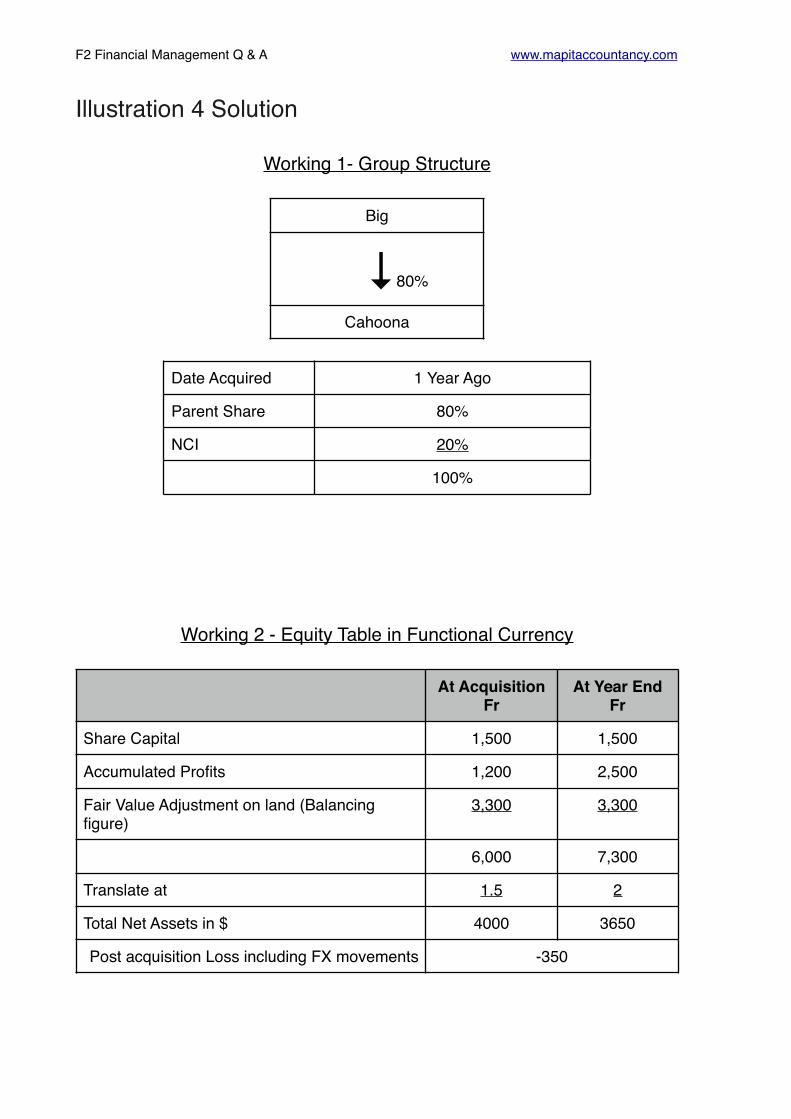

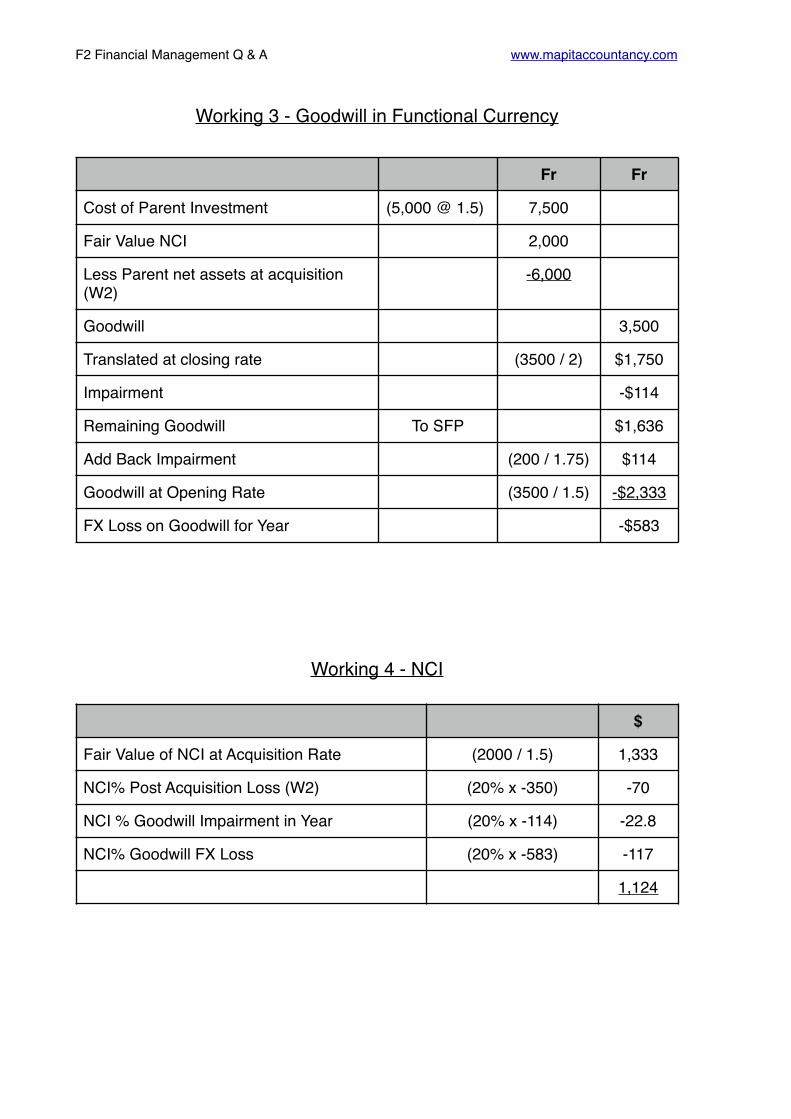

Illustration 4

Big Ltd. acquired 80% of Cahoona Inc. on 1st July 20X1.Cahoona Inc are based in Burgerland where the functional currency is Francs (Fr). The financial statements for the year to 30 June 20X2 are below.

SFP Big$

CahoonaFr

Investment in Cahoona 5000

Non Current Assets 10,000 3,000

Current Assets 5,000 2,000

20000 5,000

Share Capital 6,000 1,500

Retained Earnings 4,000 2,500

Liabilities 10,000 1,000

20,000 5,000

Income Statement Big$

CahoonaFr

Revenue 25,000 35,000

Operating Costs -15,000 -26,250

Profit Before Tax 10,000 8,750

Tax -5,000 -7,450

Profit for the Year 5,000 1,300

F2 Financial Management Q & A www.mapitaccountancy.com

There was no other comprehensive income for either entity in the period.

Other information:

I. The fair value of the net assets of Cahoona was Fr6,000 on the date of acquisition with any increase being attributable to land held at historic cost.

II. Big sold goods to Cahoona during the year for $1,000 cash.

III.The NCI is valued using the Fair Value method at FR 2000 at acquisition.