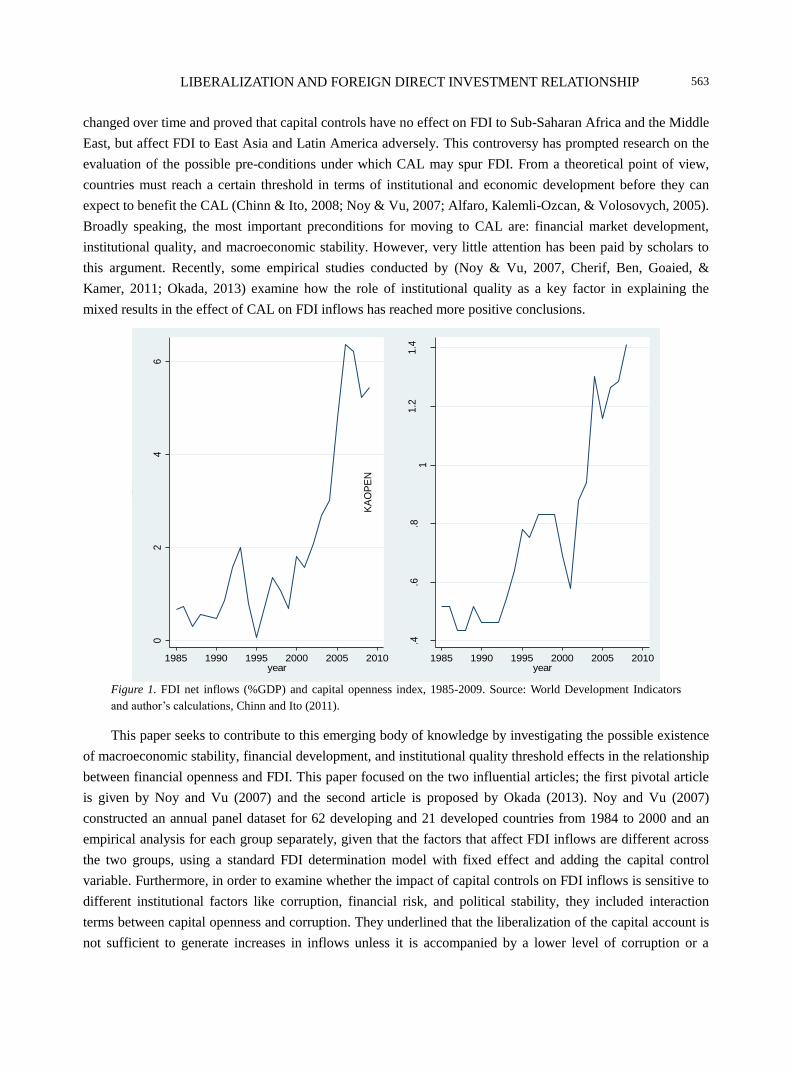

Chinese Business Review (ISSN 1537-1506) Vol.13, No.9, 2014

67

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Chinese Business Review (ISSN 1537-1506) Vol.13, No.9, 2014

Chinese Business Review

Volume 13, Number 9, September 2014 (Serial Number 135)

David

David Publishing Company

www.davidpublishing.com

PublishingDavid

Publication Information: Chinese Business Review is published monthly in hard copy (ISSN 1537-1506) and online by David Publishing Company located at 240 Nagle Avenue #15C, New York, NY 10034, USA.

Aims and Scope: Chinese Business Review, a monthly professional academic journal, covers all sorts of researches on Economic Research, Management Theory and Practice, Experts Forum, Macro or Micro Analysis, Economical Studies of Theory and Practice, Finance and Finance Management, Strategic Management, and Human Resource Management, and other latest findings and achievements from experts and scholars all over the world. Editorial Board Members: Kathleen G. Rust (USA) Moses N. Kiggundu (Canada) Helena Maria Baptista Alves (Portugal) Marcello Signorelli (Italy) Doaa Mohamed Salman (Egypt) Amitabh Deo Kodwani (Poland) Lorena Blasco-Arcas (Spain) Yutaka Kurihara (Japan) Shelly SHEN (China)

Salvatore Romanazzi (Italy) Saeb Farhan Al Ganideh (Jordan) GEORGE ASPRIDIS (Greece) Agnieszka Izabela Baruk (Poland) Goran Kutnjak (Croatia) Elenica Pjero (Albania) Kazuhiro TAKEYASU (Japan) Mary RÉDEI (Hungary) Bonny TU (China)

Manuscripts and correspondence are invited for publication. You can submit your papers via Web Submission, or E-mail to [email protected], [email protected]. Submission guidelines and Web Submission system are available at http://www.davidpublishing.org, http://www.davidpublishing.com. Editorial Office: 240 Nagle Avenue #15C, New York, NY 10034, USA E-mail: [email protected]

Copyright©2014 by David Publishing Company and individual contributors. All rights reserved. David Publishing Company holds the exclusive copyright of all the contents of this journal. In accordance with the international convention, no part of this journal may be reproduced or transmitted by any media or publishing organs (including various websites) without the written permission of the copyright holder. Otherwise, any conduct would be considered as the violation of the copyright. The contents of this journal are available for any citation, however, all the citations should be clearly indicated with the title of this journal, serial number and the name of the author.

Abstracted / Indexed in: Database of EBSCO, Massachusetts, USA Ulrich’s Periodicals Directory, USA ProQuest/CSA Social Science Collection, PAIS, USA Cabell’s Directory of Publishing Opportunities, USA Summon Serials Solutions, USA ProQuest Google Scholar Chinese Database of CEPS, OCLC ProQuest Asian Business and Reference Index Copernicus, Poland Qualis/Capes index, Brazil NSD/DBH, Norway Universe Digital Library S/B, ProQuest, Malaysia Polish Scholarly Bibliography (PBN), Poland

SCRIBD (Digital Library), USA PubMed, USA Open Academic Journals Index (OAJI), Russian Electronic Journals Library (EZB), Germany Journals Impact Factor (JIF) (0.5) WZB Berlin Social Science Center, Germany UniMelb, Australia NewJour, USA InnoSpace, USA Publicon Science Index, USA Turkish Education Index, Turkey Universal Impact factort, USA BASE, Germany WorldCat, USA

Subscription Information: Print $520 Online $360 Print and Online $680 David Publishing Company, 240 Nagle Avenue #15C, New York, NY 10034, USA Tel: +1-323-984-7526, 323-410-1082 Fax: +1-323-984-7374, 323-908-0457 E-mail: [email protected] Digital Cooperative Company: www.bookan.com.cn

David Publishing Company

www.davidpublishing.com

DAVID PUBLISHING

D

Chinese Business Review

Volume 13, Number 9, September 2014 (Serial Number 135)

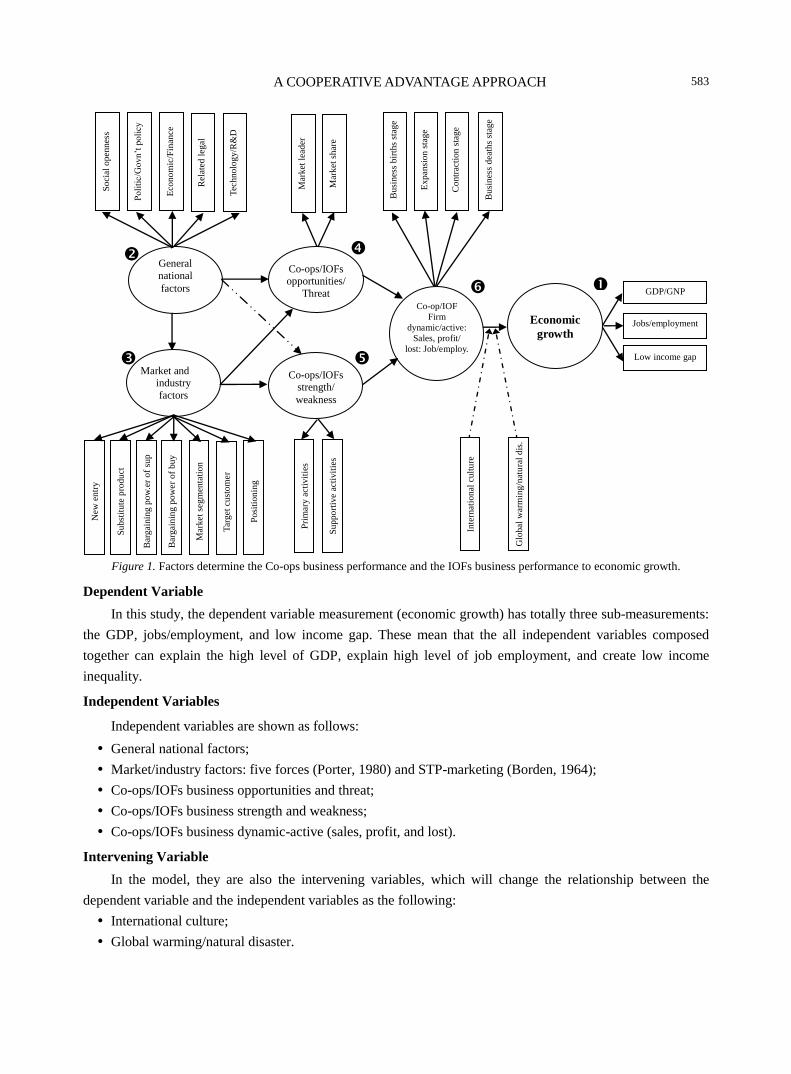

Contents

Economics

Impact of Financial Development on the Environmental Quality in Iran 537

Hadi Esmaeilpour Moghadam, Mohammad Reza Lotfalipour

Sino-European Trade Competition in Latin America and the Caribbean 552

Wioletta Nowak

Threshold Effects in the Capital Account Liberalization and Foreign Direct

Investment Relationship 562

Gammoudi Mouna, Cherif Mondher

Management

Cooperation Between Co-operative Business Organization and Investor Owned Firm

to Stimulate Economic Growth of a Country: A Cooperative Advantage Approach 578

Chanchai Petchprapunkul

Characteristics of Organizational Leadership and Motivation As a Factor of Change

in the Public Health System 586

Slobodanka Krivokapić

Chinese Business Review, September 2014, Vol. 13, No. 9, 537-551 doi: 10.17265/1537-1506/2014.09.001

Impact of Financial Development on the Environmental

Quality in Iran

Hadi Esmaeilpour Moghadam, Mohammad Reza Lotfalipour

Ferdowsi University of Mashhad, Mashhad, Iran

In recent decades, undesirable environmental changes, such as global warming and greenhouse gases emission,

have raised worldwide concerns. In order to achieve higher growth rate, environmental problems emerged from

economic activities have turned into a controversial issue. The aim of this study is to investigate the effect of

financial development on environmental quality in Iran. For this purpose, the statistical data over the period from

1970 to 2011 were used. Also by using the Auto Regression Model Distributed Lag (ARDL), short-term and

long-term relationships among the variables of model were estimated and analyzed. The results show that financial

development accelerates the degradation of the environment; however, the increase in trade openness reduces the

damage to environment in Iran. Error correction coefficient shows that in each period, 53% of imbalances would be

justified and will approach their long-run procedure. Structural stability tests show that the estimated coefficients

were stable over the period.

Keywords: financial development, trade, Auto Regression Model Distributed Lag (ARDL)

Introduction

Environmental pollution and protecting the environment have been the global issues that have even now

entered the political domain of countries. According to the Kyoto Protocol (Retrieved from http://www.unfccc.

int), countries of the world have taken appropriate executive measures to preserve the environment as common

public goods, they have also introduced some penalties for the world’s major polluting countries. In Iran, due to

the existence of large reserves of fossil fuels, to save energy is not taken seriously. Climate change caused by

increasing concentrations of greenhouse gases is seen as an important factor in changing the world’s climate, to

the extent that in many cases, a small change in the weather condition may end in severe changes in the

intensity and number of natural disasters and economic loss. Therefore, this is especially important because of

some abnormal environmental effects at different stages of the production, conversion, and consumption of

energy. Pattern of development in the energy sector would be acceptable only with minimum damage to the

environment. Pollutants and greenhouse gases arising from the activities of energy sector have undeniable

environmental effects at the regional and global level. Pollutant gases cause acid rain, health risks to humans

and other creatures, climate change, and global warming. In this study, environmental quality index is a

combination of various contaminants that is obtained by Principal Component Analysis (PCA).

Hadi Esmaeilpour Moghadam, M.A. Student in Economics, Ferdowsi University of Mashhad, Iran. Mohammad Reza Lotfalipour, professor, Ferdowsi University of Mashhad, Iran. Correspondence concerning this article should be addressed to Hadi Esmaeilpour Moghadam, P.O. Box: 9177948974, Azadi Sq,

Mashhad, Iran. E-mail: [email protected].

DAVID PUBLISHING

D

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

538

Many studies concentrated on the relationship between environmental pollution and economic growth in

recent years, and the impact of financial development on the environment has received little attention. However,

financial development through various channels could be effective on the quality of the environment: (1)

Financial development through providing the necessary capitals for industrial and factory activities may lead to

environmental pollutions (Sadorsky, 2010); (2) financial intermediaries may access to the environmental

friendly new technology that can improve the environment (Tamazian, Chousa, & Vadlamannati, 2009); (3)

financial development may provide more financial resources with less financial costs, for instance, for

environmental projects (Tamazian et al., 2009; Tamazian & Rao, 2010).

This study investigates the effect of financial development on environmental quality in Iran over the

period from 1970 to 2011. In this study, the environmental quality index is the combination of various

pollutants which is obtained with the PCA. The paper is organized as follows: Part 2 of theoretical framework

discusses the importance of economic and financial development for environmental quality, Part 3 presents a

review of the literature, Part 4 presents data description and the econometric procedure, and the last two parts

comprise the study results and conclusions.

Theoretical Framework

Environmental Kuznets Curve

Greenhouse gases emission from fossil fuels and other human activities are serious threat to global

temperature. Changes in weather patterns may disrupt the environment and human activities.

A number of studies argue that the relationship between economic growth and environmental degradation

follows an inverted U curve. This inverted U is known as environmental Kuznets curve (EKC). Accordingly,

the use of natural resources and energy to achieve high economic growth increases the primary stages of

industrialization process due to the high priority of production and employment over clean environment and

low-technology, and consequently enhances the emission of pollution. At this stage, economic agents cannot

supply the costs of reducing pollution due to the low per capita income, and thus the environmental impacts of

economic growth are ignored. However, per capita income will improve the quality of the environment in the

next stages of industrialization process after reaching certain level of per capita income, so that in such situation,

the indicators of environmental pollution reduce with regard to the importance of clean environment, high

technology, and appropriate environmental laws and regulations.

Also the relationship between financial development and environmental degradation can be expressed in

the form of an inverted U relationship. So in the primary stages of financial development, because of the high

priority of growth over clean environment, just financial development increases the volume of industrial

activities. But in the next stages and after reaching to favorable growth, financial development will improve the

quality of the environment, by investing in environmental projects and taking access to high technologies

(Shahbaz, Hye, Tiwari, & Leitão, 2013a).

The first experimental study on the EKC was conducted by Grossman and Krueger (1991) in a report

format as the environmental effects of the North American free trade agreement. They reviewed the

relationship between air quality and economic growth in the 42 countries and concluded that the relationship

between economic growth and the concentration of suspended particles in the air and sulfur dioxide is in the

form of inverted U. This study was the basis for the next studies in this field.

Several studies, including Shafik (1994); Selden and Song (1994); Cole, Rayner, and Bates (1997); Lieb

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

539

(2004); Aldy (2005); Song, Zheng, and Tong (2008); and Iwata, Okada, and Samreth (2009), tested the

hypothesis of EKC. Although the hypothesis of EKC has been confirmed in the most of studies, the results of

some studies suggest the existence of a uniform or third degree forms relationship between pollution emissions

and economic growth.

Impact of Financial Development and Trade on Environmental Quality

Despite many studies about the relationship between economic growth and environmental quality, a

number of researchers, including Tamazian and Rao (2010), Zhang (2011), Pao and Tsai (2011), Jalil and

Feridun (2011), Shahbaz et al. (2013a), and Shahbaz, Solarin, Mahmood, and Arouri (2013b), considered

financial development as an important factor affecting the environmental quality in recent years.

Well-developed capital markets and the strong banking system can promote the progress of technology and

productivity. Capital of technologies that need large sums of investment can easily be provided in the

developed financial systems (Tamazian et al., 2009). The financial markets provide the implementation of such

technologies with risk sharing for investors.

Further development of financial sector can facilitate more investment with low cost, which also includes

investment in environmental projects. Ability to increase such investments in environmental protection as the

work of the public sector can be important for states in the local, state, and national levels (Tamazian & Rao,

2010). Corporate access to advanced and clean technologies, with the financial development that decreases CO2

emissions and increases domestic production, financial and investment regulations are promoted for the benefit

of environmental quality (Yuxiang & Chen, 2010). Financial systems with better performance release

restrictions of the foreign financing provision which prevents industrial and corporative development and make

way for economic growth (Levine, 2005). Thus, financing provision for industrial large activities can increase

environmental pollutions.

The effects of trade liberalization on environment are separated into three effects: scale effect,

composition effect, and technology effect. The effect of scale represents the change in the size of the economic

activities, second effect represents the change in the composition or basket of the manufactured goods, and the

effect of technology represents the change in the production technology, especially shift to clean technologies.

The effect of the scale increases environmental degradation and the effect of technology reduces environmental

degradation in trade liberalization. The effect of composition depends on the type of relative advantage. So

according to the concept of comparative advantage, if a country has advantage in the polluting goods and has

expertise in its production, then composition effect negatively influences the environment due to the changes in

the composition of the country’s manufactured goods to polluting goods; and if due to comparative advantage,

the combination of a country’s manufactured goods changes to clean ones, then the composition effect will

have positive influence on the environment. Generally, following trade liberalization if the effect of technology

dominates the scale and composition effects (in a country with a comparative advantage in polluting industries)

or if the effect of technology and composition (in a country with a comparative advantage in clean industries)

dominates the effect of scale, then trade liberalization will lead to positive environmental outcomes (Grossman

& Krueger, 1991).

Literature Review

Many studies have been conducted on the relationship between economic growth and environmental

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

540

quality. A number of researchers have examined the role of factors such as energy consumption (Ang, 2007;

Alam, Fatima, & Butt, 2007), foreign trade (Halicioglu, 2009), electricity consumption growth and

population growth (Tol, Pacala, & Socolow, 2006), human resources and capital (Soytas, Sari, & Ewing, 2007)

on the environment. Financial development has been considered as one of the effective factors on the

environment.

Tamazian et al. (2009) examined the effect of financial development in the BRIC (Brazil, Russia, India,

and China) countries using the modeling approach of the standard reduced form during 1992 to 2004. Results

showed that higher levels of financial and economic development reduce environmental pollution, while

financial liberalization and financial openness are crucial factors for reducing CO2 emissions. In addition,

adopting policies relevant to financial liberalization and openness to attract greater levels of research and

development (R&D) and foreign direct investment (FDI) may reduce environmental pollution in these

countries.

Tamazian and Rao (2010) in their study examined the effects of financial and institutional development on

CO2 emissions in 24 countries in transition period from 1993 to 2004. The results confirmed the existence of

EKC. The importance of institutional quality and financial development on environmental performance was

also confirmed. Based on the results, financial development had a positive effect on the environmental

protection in the countries in transition. Results also indicated that financial liberalization might be harmful to

the quality of the environment if it is not implemented in a strong organizational structure. Trade openness in

these countries has led to an increase in pollution.

Using panel cointegration and Granger causality test for BRIC countries, Pao and Tsai (2010) examined

the relationship between long-term and dynamic causality of carbon dioxide emissions, energy consumption,

FDI, and GDP. The results indicate that in the long-run equilibrium, carbon dioxide emissions compared to

energy consumption are elastic and compared to FDI are inelastic. The results also confirm the EKC hypothesis

in the studied countries.

Zhang (2011) examined the effect of financial development on CO2 emissions in China during the period

from 1994 to 2009, and employed techniques such as Johansson cointegration vector, Granger causality test,

and variance analysis. The results show that the financial development of China acts as an important stimulus in

rising the greenhouse emissions. The size and scale of financial intermediaries were more important than other

indicators of financial development. Nevertheless, the effect of financial intermediaries is far weaker. The size

and scale of China’s stock market have relatively greater effect on carbon emissions, while FDI, due to its small

share from GDP, has the least effect on Carbon emissions. Using the ARDL model, Jalil and Feridun (2011)

also examined the effects of growth, financial development, and energy consumption on CO2 emissions in

China in the two periods 1953-2006 and 1987-2006. In their study, the share of cash debt from GDP, the share

of commercial bank assets from total assets of the banking system, and the share of foreign assets and liabilities

from GDP were used as indicators of financial development. The results showed that financial development

contributes to reducing environmental pollution in China. The results also confirmed the existence of EKC in

China.

Shahbaz et al. (2013b) examined the effect of financial development on economic growth and energy

consumption, CO2 emissions in Malaysia from 1971 to 2011. The results showed financial development in

Malaysia led to decrease in CO2 emissions, while, economic growth and energy consumption increased CO2

emissions. In another study, Shahbaz et al. (2013a) examined the effect of economic growth, energy

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

541

consumption, financial development, and trade openness on CO2 emissions in the period from 1975 to 2011 in

Indonesia. In their study, real per capita domestic credit to the private sector was considered as a measure of

financial development. Results showed that economic growth and energy consumption in Indonesia increased

CO2 emissions, while, financial development and trade will diminish them. Furthermore, inverted U

relationship between financial development and CO2 dissemination was also confirmed.

Ozturk and Acaravci (2013) examined the effect of financial development, trade, economic growth, and

energy consumption on CO2 emissions over the period from 1960 to 2007 in Turkey, using the cointegration

approach. Results showed that in the long term, trade increases CO2 emissions, and financial development

variable is not significant on the CO2 emissions. EKC hypothesis was confirmed in Turkey as well.

In Iran, many researchers have studied the factors affecting the environmental quality. A number of

studies have addressed the relationship between environmental quality and economic growth (Pazhouan &

Moradhasel, 2007; Pourkazemi & Ebrahimi, 2008; Salimifar & Dehnavi, 2009; Ghazali & Zibaee, 2009;

Mowlayi, Kavosi Kalashemi, & Rafiei, 2010), energy consumption (Behboodi & Barghi Golazani, 2008;

Lotfalipour, Fallahi, & Ashena, 2010), trade openness (Barqi Askooei, 2008; Behboodi, Fallahi, & Barghi

Golazani, 2010; Agheli, Velaei Yamchi, & Jangavar, 2010; Lotfalipour, Fallahi, & Bastam, 2012), factors of

the labor force and capital (Sharzaei & Haghani, 2009), the value added share of the industrial sector from GDP

(Nasrollahi & Ghaffari Goolak, 2009; Vaseghi & Esmaeili, 2009). Sadeghi and Feshari (2010) in an article

using Johansson’s cointegration approach over the period from 1971 to 2007 with regard to indices of carbon

dioxide emissions and arable land for the environmental quality concluded that in addition to long-run

equilibrium between the export and environmental quality indices, the variables of exports and FDI had a

significant negative impact on environmental quality indices.

Fotros and Maboodi (2010) used econometric approach of Yamamato, investigating the existence and

direction of causality among energy consumption, urbanization, economic growth, and carbon dioxide

emissions over the period from 1971 to 2006. Results indicate a causal relationship among energy consumption,

GDP, urbanization, and carbon dioxide emissions. Estimation of the relationship among carbon dioxide

emissions, energy consumption, urban population and GDP showed that U hypothesis about environmental

pollution and GDP in Iran is true. Sadeghi, Motafaker Azad, Pour Ebadelahan Kovich, and Shabaz Zade

Kheyavi (2012) addressed the causal relationship between carbon dioxide emissions and FDI variables, per

capita energy consumption and GDP in the environmental Kuznets hypothesis in Iran over the period from

1980 to 2008. Results verified the bilateral causal relationship between variables of CO2 emissions and per

capita energy consumption, and unidirectional causal relationship from GDP to per capita energy consumption.

Using panel data and generalized moments approach, Barqi Askooei, Fallahi, and Zhande Khatibi (2012)

estimated the impact of variables such as energy consumption, factory products, economic openness, FDI, and

economic growth on the carbon dioxide emissions for the period from 1990 to 2010 in D8 countries. The

results showed that in the approach of fixed effects, all variables except FDI had a positive and significant

relationship with carbon dioxide emissions.

Materials and Methods

Data

The ARDL can be used for short-term and long-term relations between the dependent and explanatory

variables of the model. The model in this paper is as follows:

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

542

EN FD FD GDP OP (1)

where EN is environmental quality index, FD is financial development, FD2 is square of FD, GDP is gross

domestic product and OP is trade openness.

Using PCA which is based on a linear combination of the original variables on the variance-covariance

matrix and using the following indices, this study tries to extract the general index for financial development

and address all aspects of financial development:

(1) index of financial development depth: the ratio of cash to GDP in current prices;

(2) basic index of financial development: the ratio of domestic bank assets to total assets of commercial

banks and the Central Bank;

(3) index of financial development performance: the ratio of private sector’s debt (to the banking system)

to GDP;

(4) instrumental index of financial development: the ratio of money held by the public to total money

supply;

(5) structural index of financial development: the ratio of banking system claim of private sector to total

banking system credit.

Trade openness index is the ratio of total exports and imports to GDP and environmental quality index is

combinations of Sulfur Oxide pollutants, SO2 and SO3, Nitrogen Oxides of NOX, Carbon Monoxide, SPM

suspended particles, and Carbon Dioxide which are examined in PCA approach. Data on emissions of SO2, SO3,

NOX, CO, and SPM were obtained from energy balance sheet of Ministry of Energy, Department of Power and

Energy. Data on CO2 were collected from Carbon Dioxide Information Analysis Center, data on GDP were

obtained from UNCTAD (United Nations Conference on Trade and Development), and data on indices of

financial development, the financial development squared and trade were obtained from economic reports and

balance sheet of the Central Bank. In this study, the period between 1970 and 2011 was examined, and Microfit

4.0 and Matlab 8.01 were used for the estimation and forecasting.

Financial Development and Trade in Iran

Figure 1 shows the trend of financial development in Iran. As shown in the period between 1970 and 2011,

financial development has declined and then increased due to imposed war. Overall financial development in

Iran has been increasing. However, the amount of financing for the industrial activities has increased over the

period. Figure 2 shows the amount of financing for the country’s industrial sector compared to other sectors and

activities with incremental growth, and shows that this sector has received more attention than other sectors in

financial development process.

Figure 3 shows the amount of exports and imports in Iran. Exports and imports have increased over the

years of the study.

Industries such as cement, glass, ceramics, iron and steel, pulp and paper, etc. apply a wide range of

environmental effects and release in the air plenty of oxides of Carbon, Sulfur, and Nitrogen.

According to Figure 4 and 5, exports of polluting goods have declined in the period between 1970 and

2011 and have a downward trend. However, the growth in imports of polluting goods compared to total

imported goods has risen. Therefore, the amount of pollutants produced during this period has a downward

trend.

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

543

Figure 1. Financial development and its trend in the period between 1970 and 2011. Source: Economic reports and balance sheet of the central bank.

Figure 2. The financing of industrial activities compared to other activities. Source: Economic reports and balance sheet of the central bank.

Figure 3. Exports and imports in the period from 1970 to 2011. Source: Economic reports and balance sheet of the central bank.

0

5

10

15

20

25

30

35

40

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0

10000

20000

30000

40000

50000

60000

70000

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

import export

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

544

Figure 4. Trend of exporting polluting goods over the period from 1970 to 2011. Source: Economic reports and balance sheet of the central bank.

Figure 5. Trend of importing polluting goods over the period from 1970 to 2011. Source: Economic reports and balance sheet of the central bank.

Model

In this study, Autoregressive Distributed Lag Modeling Approach was employed which was proposed by

Pesaran and Shin (1999). Most of recent studies suggest that ARDL approach is preferable to other approaches

such as Engel-Granger, in examining the cointegration and long-run relationship among the variables. Whether

the variables in the model are I(0) or I(1), this approach is applicable, and in small samples it is relatively more

efficient than other approaches. ARDL Model is as follows:

, ∑ , ′ (2)

where

, 1 (3)

, 1, 2, … , (4)

In the above relationships Yt is the dependent variable and Xit is the independent variable. L is lag operator

and wt is a vector of categorical variables including predetermined variables in the model, such as intercept,

dummy variables, time trend, and other exogenous variables. P is the number of lags used for the dependent

0

5

10

15

20

25

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0

5

10

15

20

25

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

545

variable and q is the number of lags used for the independent variables. Numbers of optimal lags for each of the

explanatory variables could be set by a measure of Akaike, Schwarz-Bayesian, Hanan-Queen, or adjusted

coefficient of determination. In this study, given the small size of the data set, Schwartz-Bayesian measure was

used. Long-run coefficients are calculated as follows:

,

,

1, 2 , …, (5)

ARDL approach consists of two steps to estimate the long-run relationships. First, the dynamic ARDL

model is tested for long-run relationship, and in the next step, long-run and short-run coefficients are estimated.

The second step is conducted only if the long-run relationship is verified in the first step. Having estimated

ARDL dynamic model, this paper tested the following hypothesis:

H ∑ 1 0

H ∑ 1 0 (6)

The null hypothesis implies the absence of a long-run relationship. Quantity t statistics requires to perform

the test as follows:

∑

∑ (7)

If t statistics obtained from the absolute critical values provided by Banerjee, Dolado, and Mester (2012) is

larger, then the null hypothesis based on absence of cointegration is rejected, and long-run relationship is

accepted (Nowferesti, 1999). In the second step, if the presence of cointegration is approved, the long-run

relationship would be estimated.

Study Results

Before the test, reliability of all variables is checked to ensure that none of the variables is I(2). If there is

any I(2) variable in the model, F statistics is not reliable. To ensure variables of time series used in the model

stationary or none-stationary, Augmented Dickey Fuller (ADF) test has been used. Table 1 shows the ADF

test’s results in the level for the variables. Usually the Schwarz Bayesian Criterion (SBC) saves the number of

lags. Therefore, in this study, the number of optimized lags is selected based on SBC criteria. OP variable in the

level, while without trend, is stationary, but for the variables of FD, FD2, GDP, and EN, Absolute Dickey Fuller

statistic in both cases is smaller than the critical values. Therefore, the variables in level are none-stationary and

the unit root hypothesis on the variables is not rejected.

Table 1

Results of Unit Root Tests in the Level

Variables With intercept and without trend * With intercept and trend **

Optimal lag ADF statistics Test results Optimal lag ADF statistics Test results

EN 0 -0.95 Non-stationary 0 -2.11 Non-stationary

FD 1 -0.74 Non-stationary 0 -2.79 Non-stationary

FD2 1 -0.72 Non-stationary 0 -2.44 Non-stationary

GDP 0 2.50 Non-stationary 5 0.25 Non-stationary

OP 9 -4.55 Stationary 9 -3.53 Non-stationary

Notes. * Critical value at the confidence level of 95% in cases without trend is -2.96; ** critical value at the confidence level of 95% in cases with trend is -3.56. Source: Research findings.

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

546

To find the stationary degree of the variables, ADF test was replicated for the first-order difference of the

variables. Test results showed that variables get stationary by making one deduction.

Table 2

Results of Unit Root Tests on the First Difference of the Variables

Variables With intercept and without trend * With intercept and trend **

Optimal lag ADF statistics Test results Optimal lag ADF statistics Test results

EN 0 -5.28 Stationary 0 -5.38 Stationary

FD 0 -3.94 Stationary 0 -3.71 Stationary

FD2 0 -3.84 Stationary 0 -3.60 Stationary

GDP 0 -3.81 Stationary 0 -4.24 Stationary

Notes. * Critical value at the confidence level of 95% in cases without trend is -2.96; ** critical value at the confidence level of 95% in cases with trend is -3.56. Source: Research findings.

Result of estimation of ARDL model is based on the three parts: dynamic, short-run, and long-run

relationships. The following equation as the dynamic relationships among variables can be specified and

estimated:

EN ∑ α EN ∑ FD ∑ FD ∑ GDP ∑ OP U (8)

To estimate the relationship, as the data are on annual basis, the maximum lags were taken two, and using

Schwarz-Bayesian criterion, dynamic relationships among variables were selected. The optimal lags for each of

the variables were set and the model was estimated as ARDL (1, 0, 0, 0, 0). To study the long-run relationship

of the variables, the value of computational statistics of Banerjee et al. (2012) is calculated in the following

way:

.

.3.78 (9)

The value of table of Banerjee et al. (2012) at confidence level of 90% for a model with intercept is equal

to -3.64; thus, the existence of long-run relationship among the variables is confirmed. Having ensured the

long-term relationship, results of estimation would be provided in Table 3.

Table 3

Result of Estimation of Long-run Relationship

Variables Coefficients Standard deviation t statistics Critical value

FD 14.55 6.33 2.30 0.028*

FD2 -0.11 0.06 -1.84 0.074**

GDP 20.84 3.14 6.63 0.000*

OP -38.81 8.56 -4.53 0.000*

Notes. * Significant at 95% confidence level; ** significant at 90% confidence level. Source: Research findings.

As the results of the classic test show the lack of successive correlation among components of disturbances,

properly specified equation and equal variance, the results of long-run relationship are reliable. Results

obtained from Table 3 show that all variables are significant at the 90% confidence interval. The positive

coefficient of GDP (20.84) shows that economic growth in Iran is primarily associated with emission increase.

Coefficient of financial development and trade liberalization is positive and negative respectively, which

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

547

implies that increase in financial development causes rise in environmental degradation; however, trade

increase promotes the quality of the environment. The coefficient of long term emissions relative to variable of

squared financial development is significant and negative (-0.11), which shows that the inverted U relationship

between financial development and environmental quality is true in Iran.

For a more detailed review of the results, changes in the environmental degradation index and financial

development could be estimated in the model according to the coefficients, and assuming that all other

conditions do not change, shown in Figure 6.

Figure 6. Inverted U relationship between financial development and environmental quality for Iran using Matlab. Sources: Research findings.

In this figure, the vertical axis and horizontal axis respectively represent the environmental emissions and

financial development. As it is seen, the curve for Iran is similar to an inverted U and the estimated model fully

meets the theoretical expectations. In the period between 1970 and 2011, Iran was in the first half of the curve,

and financial development for levels higher than 0.72 leads to improved environmental quality. The estimated

error correction model to study adjustment of short-run disequilibrium towards long-run equilibrium is

presented in Table 4.

Table 4

Results of the Estimation of Error Correction Model

Variables Coefficients Standard deviation T-statistics Critical value

dFD 7.76 3.79 2.04 0.049*

dFD2 -0.06 0.03 -1.71 0.096**

dGDP 11.12 3.25 3.42 0.002*

dOP -20.70 6.23 -3.32 0.002*

ECM(-1) -0.53 0.14 -3.80 0.001*

Notes. * Significant at 95% confidence level; ** significant at 90% confidence level. Source: Research findings.

The value of -0.53 was obtained for error correction coefficients in the model, which means a 53%

adjustment in each period to establish a long-run equilibrium. The results of CUSUM and CUSUMSQ tests for

evaluating the estimated coefficients and the results of stability test for short- and long-run coefficients over the

time were shown in Figure 7 and 8.

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

548

Figure 7. Plot of cumulative sum of recursive residuals. Sources: Research finding.

Figure 8. Plot of cumulative sum of squares of recursive residuals. Sources: Research finding.

As in both tests, the statistics were within the 95% confidence intervals, null hypothesis based on the

stability of the coefficients was accepted and at the confidence level of 95%, the obtained results are valid.

Conclusions

Economic growth is one of the most important concerns of human communities. Development process in

Iran, like other developing countries involves the use of the environment and at its degradation at the same

times. Financial intermediaries through financial development may increase technological innovation and

mobilize financial resources to identify the best production technology and make investments in projects

involving clean environment. Nevertheless, financial development may increase financing for industrial

activities which harm the environment.

Due to the different reliability degrees of the variables, long-run ARDL model was employed. The results

show that the coefficient of financial development is positive and significant at the 0.05% probability level, and

suggest that in addition to economic growth, financial development also affects environmental quality in Iran,

and has led to increase environmental pollution. Negative squared coefficient of financial development implies

that inverted U-shaped relationship between financial development and environmental quality is true for Iran.

Results show that Iran is on the upside half of curve and according to predictions made on the basis of the

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

549

financial development of approximately 0.72 in Iran, financial development will lead to improved

environmental quality. Given the high importance of development for developing countries, including Iran, to

support environmental policies is of low priority. Based on the Figure 2, in the years considered, financing for

industrial activity has increased compared to other activities and industries have been inefficient in protection

of the environment. Financial development has made way for destruction of environment. In fact, the

investments were only effective in increasing the size of the industrial activities and have not resulted in

technological advancement in the industry.

Results show that economic growth had a significant and positive impact on emissions. The study’s results

also suggest that increased trade openness has led to improvement of environmental quality in the country. This

could be due to that the goods which produce large quantities of pollutants in the manufacturing process are

imported from other countries like China. As a result, the pollution increases in the exporting countries, and in

Iran as an importing country, pollution reduces due to the reduction in production of polluting goods.

Furthermore, it might be due to decline in export of polluting goods, which reflects low production and reduced

pollution in Iran. The decline in the proportion of heavy polluting products’ export such as cement, glass,

ceramics, iron, and steel, which produce large amounts of pollutants in manufacturing process (Figure 5), and

increased proportion of imports (Figure 4) confirm the results of the model. In addition, economic openness

leads to an increase in imports of high tech intermediary and capital goods that create less pollution in

production process.

References Agheli, L., Velaei Yamchi, M., & Jangavar, H. (2010). Impacts of economic openness on environmental degradation in Iran.

Journal of Strategy, 19, 197-216. Alam, S., Fatima, A., & Butt, M. S. (2007). Sustainable development in Pakistan in the context of energy consumption demand

and environmental degradation. Journal of Asian Economics, 18(5), 825-837. Aldy, J. E. (2005). An environmental Kuznets curve analysis of U.S. state level carbon dioxide emission. Environment &

Development, 14, 48-72. Ang, J. B. (2007). CO2 emissions, energy consumption, and output in France. Energy Policy, 35(10), 4772-4778. Barqi Askooei, M. (2008). Effects of trade liberalization on greenhouse gas emission (carbon dioxide) in the environmental

Kuznets Curve. Journal of Economic Research, 82, 1-22. Barqi Askooei, M., Fallahi, F., & Zhande Khatibi, S. (2012). The effect of factory products and foreign direct investment on CO2

emissions in D8 Member countries. Journal of Economic Modeling, 4, 93-109. Behboodi, D., & Barghi Golazani, E. (2008). Environmental impacts of energy consumption and economic growth in Iran.

Journal of Value Economic, 5(4), 35-53. Behboodi, D., Fallahi, F., & Barghi Golazani, E. (2010). Social and economic factors effective on carbon dioxide emissions per

capita in Iran. Journal of Economic Research, 90, 1-17. Cole, M. A., Rayner, A. J., & Bates, J. M. (1997). The environmental Kuznets curve: An empirical analysis. Environment and

Development Economics, 2(4), 401-416. Fotros, M., & Maboodi, R. (2010). Causal relationship between energy consumption and urban population and environmental

pollution in Iran 1971-2006. Journal of Energy Economics Studies, 27, 1-17. Ghazali, S., & Zibaee, M. (2009). Analysis of the relationship between environmental pollution and economic growth

using panel data: A case study of carbon monoxide emissions. Journal of Economics and Agricultural Development, 2, 128-133.

Grossman, G., & Krueger, A. B. (1991). Environmental impact of a North American free trade agreement. NBER working paper, 3914, 1-57.

Halicioglu, F. (2009). An econometric study of CO2 emissions, energy consumption, income and foreign trade in Turkey. Energy Policy, 37(3), 1156-1164.

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

550

Iwata, H., Okada, K., & Samreth, S. (2010). Empirical study on the environmental Kuznets curve for CO2 in France: The role of nuclear energy. Energy Policy, 38(8), 4057-4063.

Jalil, A., & Feridun, M. (2011). The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Economics, 33(2), 284-291.

Levine, R. (2005). Finance and growth: Theory and evidence. Handbook of economic growth, 1, 865-934. Lieb, C. M. (2004). The environmental Kuznets curve and flow versus stock pollution: The neglect of future damages.

Enviromental and Resource Economics, 29, 483-506. Lotfalipour, M. R., Fallahi, M. A., & Ashena, M. (2010). The relationship between carbon dioxide emissions and economic

growth, energy and trade in Iran. Journal of Economic Researches, 94, 151-173. Lotfalipour, M. R., Fallahi, M. A., & Bastam, M. (2012). Environmental issues and forecasting the carbon dioxide emissions in

the Iran. Journal of Applied Economic Studies in Iran, 3, 81-109. Mowlayi, M., Kavosi Kalashemi, M. & Rafiei, H. (2010). The relationship between carbon dioxide emission and per capita

income and existing environmental Kuznets curve in Iran. Journal of Environmental Sciences, 1, 205-216. Nasrollahi, Z., & Ghaffari Goolak, M. (2009). Economic development and environmental pollution in Kyoto Pact countries and

the countries of Southeast Asia (with emphasis on the environmental Kuznets curve). Journal of Economic Sciences, 35, 105-125.

Nowferesti, M. (1999). Unit root and cointegration in econometrics. Tehran: Institute of Rasa Cultural Services. Ozturk, I., & Acaravci, A. (2013). The long-run and causal analysis of energy, growth, openness and financial development on

carbon emissions in Turkey. Energy Economics, 36, 262-267. Pao, H. T., & Tsai, C. M. (2011). Multivariate Granger causality between CO2 emissions, energy consumption, FDI (foreign

direct investment) and GDP (gross domestic product): Evidence from a panel of BRIC (Brazil, Russian Federation, India, and China) countries. Energy, 36(1), 685-693.

Pazhouan, J., & Moradhasel, N. (2007). Effects of economic growth on air pollution. Journal of Economic Research, 94(7), 141-160. Pesaran, M. H., & Shin, Y. (1999). An Autoregressive Distributed Lag Modeling Approach to cointegration analysis. In S. Strøm

(Ed.), Econometrics and economic theory in the twentieth century: The ragnar Frisch centennial symposium. Cambridge: Cambridge University Press.

Pourkazemi, M., & Ebrahimi, I. (2008). Evaluation of environmental Kuznets curve in the Middle East. Journal of Economic Research, 34, 57-71.

Sadeghi, S., & Feshari, M. (2010). An estimation of long-run relationship between exports and environmental quality index: A case study of Iran. Iranian Journal of Economic Research, 44, 67-83.

Sadeghi, S., Motafaker Azad, M., Pour Ebadelahan Kovich, M., & Shabaz Zade Kheyavi, A. (2012). The causal relationship between carbon dioxide emissions, foreign direct investment, GDP and per capita energy consumption in Iran. Journal of Energy and Environmental Economics, 4, 101-116.

Sadorsky, P. (2010). The impact of financial development on energy consumption in emerging economies. Energy Policy, 38(5), 2528-2535.

Salimifar, M., & Dehnavi, J. (2009). Comparing the environmental Kuznets curve in OECD member countries and developing countries: An analysis based on panel data. Journal of Knowledge and Development, 29(16), 181-200.

Selden, T. M., & Song, D. (1994). Environmental quality and development: Is there a Kuznets curve for air pollution emissions? Journal of Environmental Economics and Management, 27(2), 147-162.

Shafik, N. (1994). Economic development and environmental quality: An econometric analysis. Oxford Economic Papers, 46, 757-773.

Shahbaz, M., Hye, Q. M. A., Tiwari, A. K., & Leitão, N. C. (2013a). Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renewable and Sustainable Energy Reviews, 25, 109-121.

Shahbaz, M., Solarin, S. A., Mahmood, H., & Arouri, M. (2013b). Does financial development reduce CO2 emissions in Malaysian economy? A time series analysis. Economic Modelling, 3, 145-152.

Sharzaei, G., & Haghani, M. (2009). Evaluation of causal relationship between carbon emissions and internal revenue, with emphasis on the role of energy. Journal of Economic Research, 68, 75-90.

Song, T., Zheng, T., & Tong, L. (2008). An empirical test of the environmental Kuznets curve in China: A panel cointegration approach. Economic Review, 19(3), 381-392.

Soytas, U., Sari, R., & Ewing, B. T. (2007). Energy consumption, income, and carbon emissions in the United States. Ecological Economics, 62(3-4), 482-489.

IMPACT OF FINANCIAL DEVELOPMENT ON THE ENVIRONMENTAL QUALITY

551

Tamazian, A., & Rao, B. (2010). Do economic, financial and institutional developments matter for environmental degradation? Evidence from transitional economies. Energy Economics, 32(1), 137-145.

Tamazian, A., Chousa, J. P., & Vadlamannati, K. C. (2009). Does higher economic and financial development lead to environmental degradation: Evidence from BRIC countries. Energy Policy, 37(1), 246-253.

Tol, S. J. W., Pacala, R., & Socolow, S. R. (2006). Understanding long term energy use and carbon dioxide emissions in the USA. Humborg: Humborg University Press .

United Nations. (1997). Kyoto Protocol to the United Nations framework convention on climate change. Retrieved from http://www.unfccc.int

Vaseghi, E., & Esmaeili, A. (2009). Evaluation of determining factors in CO2 emissions in Iran (application of environmental Kuznets). Journal of Ecology, 52, 99-110.

Yuxiang, K., & Chen, Z. (2010). Financial development and environmental performance: Evidence from china. Environment and Development Economics, 16, 1-19.

Zhang, Y. J. (2011). The impact of financial development on carbon emissions: An empirical analysis in China. Energy Policy, 39(4), 2197-2203.

Chinese Business Review, September 2014, Vol. 13, No. 9, 552-561 doi: 10.17265/1537-1506/2014.09.002

Sino-European Trade Competition in Latin

America and the Caribbean

Wioletta Nowak

University of Wroclaw, Wroclaw, Poland

The article studies trade in goods between China and the Latin American and Caribbean (LAC) countries and

between the European Union (EU) and LAC during the years from 2000 to 2013. From the beginning of the 21st

century, big changes in LAC’s trade patterns have been observed. The article contains possible explanation of them.

The analysis is based on the ECLAC (Economic Commission for Latin America and the Caribbean) data.

Merchandise trade between China and LAC grew significantly over the period from 2000 to 2013. In 2013, the

value of merchandise exports from China was higher than from the EU-28 in the case of 12 LAC countries. Chinese

imports of goods surpassed the European ones in five countries in the region. In order to increase its exports of

manufactured goods and imports of natural resources and agricultural commodities, China combines trade

arrangements with foreign aid policy. Besides, a rapid development of bilateral diplomatic ties between China and

LAC is observed. The EU-LAC trade relations have worsened during the last decade mainly due to financial crisis

and development of the EU-Asia trade relations.

Keywords: China, merchandise trade, foreign aid, European Union (EU)

Introduction

The European Union (EU) and China (after the United Sates) are the most important trading partners for

the Latin American and Caribbean (LAC). Since the beginning of the 21st century, a rapid expansion of

Sino-Latin trade and economic relations has been observed. China is likely to surpass the EU and be LAC’s

second largest trade partner in a few years. China’s ties with Latin America are not new. However, their

dynamics in recent years were really spectacular. The significant increase in trade between China and LAC

countries was observed after the beginning of the financial crisis. Besides, from 2008, China has become a

major source of financing for many countries in the region. China uses its loans to develop bilateral trade

relations with the LAC states.

After the financial crisis, the EU was mainly concentrated on the struggle against its effects. In order to

restore its economy, the EU developed closer economic and trade relations with Asia. At the same time, the

EU-LAC trade relations have worsened. Although, the EU increased its aid-for-trade with LAC countries, it has

been gradually losing its importance for LAC as a destination for exports and as a source for imports.

In the literature, trade relations between China and Latin America and between the EU and LAC are

mainly examined separately (Bárcena & Rosales, 2010; Bárcena, Prado, Rosales, & Pérez, 2012; Roy, 2012).

Wioletta Nowak, Ph.D., University of Wroclaw, Wroclaw, Poland. Correspondence concerning this article should be addressed to Wioletta Nowak, Institute of Economic Sciences, Uniwersytecka

22/26, 50-145 Wroclaw, Poland. E-mail: [email protected].

DAVID PUBLISHING

D

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

553

The aim of the paper is to study China-LAC and the EU-LAC trade relations in the first decade of the 21st

century using the same data set. The analysis is principally based on the EULAC data.

Development of China-LAC and the EU-LAC Trade Relations

Trade between China and Latin America is dated back to the 1560s. At that time, Chinese ships sailed to

Acapulco in Mexico via Manila. China exported mainly silk, cotton cloths, jewellery, and gun powder to Latin

America, and imported wine, olive, oil, soap, and food. In 1815, this “silk-road” on the sea between China and

Latin America was closed due to an implementation of the Chinese export control policy (Jiang, 2006, p. 69).

In the 19th century, Sino-Latin American relations took a different form. The basis of ties was the Chinese

immigration. Hundreds of thousands of Chinese workers migrated to the Latin American countries (Mexico,

Brazil, Chile, Panama, and Peru) where they mainly worked in mines and on plantations (Ratliff, 2009, p. 2).

After the proclamation of People’s Republic of China in 1949, economic cooperation between China and

LAC was still limited. Trade exchange was insignificant, not to mention investments. The situation was a

consequence of a lack of diplomatic contacts at high governmental levels between China and LAC states and

the poor condition of the Chinese economy.

In the 1950s, Sino-Latin American ties were restricted to visits of individual Latin Americans. LAC

countries began to establish diplomatic relations with China just in the 1970s. The first countries that

recognized People’s Republic of China in the region were Cuba and Chile. Cuba established diplomatic

relations with China in 19601 and Chile 10 years later. Then, other major countries in the region began to

recognize China.2 It happened mainly because of two significant events: In 1971, the government of People’s

Republic of China was recognised as the legal representative of China in the United Nations (UN) and was

given the permanent seat in the UN Security Council; in February 1972, President Richard Nixon visited China,

after which the pressure from the United States declined and Latin countries which were always in the orbit of

the American influence could begin to establish diplomatic relations with China.

China-LAC trade relations accelerated after Deng Xiaoping’s reforms in 1978. China’s rapid economic

growth and its constantly increasing demand for natural resources, food and new markets caused that it had to

find new trade partners. China, among others, turned to resource-rich Latin America.

Until now, China has got preferential access to three markets in the region (Table 1). It signed free trade

agreement (FTA) with Chile, Peru, and Costa Rica. FTAs cover items on the World Trade Organization’s new

trade agenda. It means that they concern not only the deregulation and liberalization of goods markets but also

services and investment. Besides, in 2012, China declared readiness to negotiate with Mercosur (Argentina,

Brazil, Paraguay, Uruguay, and Venezuela) on a free trade area.

Sino-Latin American trade relations are developed and strengthened also during high-level visits. A

significant increase in official visits to LAC by the highest Chinese authorities has been recorded since 2001.

Diplomatic relations were developed and maintained by Jiang Zemin and his successors Hu Jintao and Xi

Jinping (Table 2).

1 After the Sino-Soviet split in the 1960s, Cuba chose the Soviet Union and froze its relation with China. Both countries normalised relations after the collapse of the Soviet Union. 2 In 2014, People’s Republic of China was recognized by 21 LAC countries: Cuba (1960), Chile (1970), Peru (1971), Mexico (1972), Argentina (1972), Guyana (1972), Jamaica (1972), Trinidad and Tobago (1974), Venezuela (1974), Brazil (1974), Suriname (1976), Barbados (1977), Ecuador (1980), Colombia (1980), Antigua and Barbuda (1983), Bolivia (1985), Grenada (1985), Uruguay (1988), Bahamas (1997), Dominica (2004), and Costa Rica (2007).

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

554

Table 1

Trade Agreements Between China and the Latin American Countries

Agreement name Type Coverage Date of entry into force

Chile to China FTA & EIA Goods & Services 01-Oct-2006 (Goods), 01-Aug-2010 (Services)

China to Costa Rica FTA & EIA Goods & Services 01-Aug-2011

Peru to China FTA & EIA Goods & Services 01-Mar-2010

Note. EIA: Economic Integration Agreement. Source: Retrieved from http://rtais.wto.org/UI/PublicAllRTAList.aspx.

Table 2

Development of Bilateral Ties Between China and Latin America and the Caribbean in the Years 2001-2014

Year Chinese authority Visited LAC countries

2001, April President Jiang Zemin Chile, Argentina, Uruguay, Brazil, Cuba, Venezuela

2003, December Prime Minister Wen Jiabao Mexico

2004, November President Hu Jintao Chile, Brazil, Argentina, Cuba

2005, September President Hu Jintao Mexico

2008, November President Hu Jintao Peru, Costa Rica, Cuba

2009, February Vice President Xi Jinping Mexico, Jamaica, Colombia, Venezuela, Brazil

2010, April President Hu Jintao Brazil

2011, June Vice President Xi Jinping Cuba, Uruguay, Chile

2012, June Prime Minister Wen Jiabao Brazil, Uruguay, Argentina, Chile

2013, May/June President Xi Jinping Trinidad and Tobago, Costa Rica, Mexico,

2014, July President Xi Jinping Brazil, Argentina, Venezuela, Cuba

Moreover, the China Council for the promotion of international trade has initiated so far eight China-Latin

America business summits which are also an important platform for trade cooperation between China and LAC.

The first was held in Santiago, Chile (2007), the second in Harbin, China (2008), and the next in Bogota,

Colombia (2009), Chengdu, China (2010), Lima, Peru (2011), Hangzhou, China (2012), San Jose, Costa Rica

(2013), and Changsha, China (2014).

Europe and LAC are linked through historical, cultural, political, and economic ties which are dated back

to 1492. However, contemporary relations between the EU and LAC were regulated in 1999 during the first

EU-LAC summit which was held in Rio de Janeiro, Brazil. The main achievement of the summit was the

establishment of a strategic partnership between the EU and LAC. Since then, issues referring to a mutual

cooperation in the area of free trade between the regions are discussed during biannual EU-LAC summits. So

far six bi-regional summits have been held in Madrid, Spain (2002), Guadalajara, Mexico (2004), Vienna,

Austria (2006), Lima, Peru (2008), Madrid, Spain (2010), and Santiago, Chile (2013). The summits bring

together heads of state and government from both continents. In the years when the EU-LAC summits do not

take place, the EU and the Rio Group3 meet at ministerial level. In 2010, EU-LAC foundation was created in

order to assist in the implementation of main objectives of the strategic partnership between the regions. The

Foundation has 63 members: the 28 members of the EU, the 33 LAC states, and the EU institutions (Retrieved

from http://eulacfoundation.org/en/about-us).

The EU has privileged relations in trade with the Caribbean and countries of Central America. Besides, the 3 The Rio Group was established by Argentina, Brazil, Colombia, Mexico, Panama, Peru, Uruguay, and Venezuela in 1986. The Group eventually extended to 24 Latin American and Caribbean states.

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

555

EU signed special agreements with Mexico, Chile, Colombia, and Peru (Table 3). All trade agreements

between the EU and LAC relate to deregulation and liberalization of trade in goods and services.

Table 3

Trade Agreements Between the EU and LAC

Agreement name Type Coverage Date of entry into force

EU to CARIFORUM States EPA FTA & EIA Goods & Services 01-Nov-2008 EU to Central America (Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua, and Panama)

FTA & EIA Goods & Services 01-Aug-2013

EU to Chile FTA & EIA Goods & Services 01-Feb-2003 (Goods)

01-Mar-2005 (Services)

EU to Colombia and Peru FTA & EIA Goods & Services 01-Mar-2013

EU to Mexico FTA & EIA Goods & Services 01-Jul-2000 (Goods)

01-Oct-2000 (Services)

Note. CARIFORUM includes 14 CARICOM members and the Dominican Republic. Source: Retrieved from http://rtais.wto.org/UI/PublicAllRTAList.aspx.

In 2000, the EU opened negotiations on free trade area with Mercosur. However, there are some obstacles

in negotiations concerning sectors which are sensitive for both sides. The EU protects its own production of

food via the common agricultural policy and Mercosur wants the access to the European market in agricultural

goods. In turn, Mercosur protects its own production of manufactured goods that are the EU’s basic export

commodities (Roy, 2012, p. 8).

Main Characteristics of Merchandise Trade Between China and LAC and Between the EU and LAC

Europe has been the second major trading partner (after the United States) for LAC for many years.

However, recently, an impressive increase in trade between China and LAC33 (33 countries) has been observed.

In the years 2000-2013, the value of China’s exports in goods to LAC33 increased about 19 times and Chinese

imports in goods from the region increased over 23 times. At that time, the value of the EU25 (25 countries)

exports in goods to LAC33 increased about three times. European merchandise imports increased 2.7 times.

Trends in merchandise trade between the EU25 and LAC33 and between China and LAC33 over the period

2000-2014 are presented in Figure 1.

In 2000, the value of European merchandise exports to LAC33 was 7.7 times higher than Chinese, but 14

years later only 1.2 times. At the beginning of the century, the value of European merchandise imports from

LAC33 was 9.3 higher than China’s imports from the region. In 2013, the EU25 imports value was merely 1.1

higher than the Chinese. The EU has been steadily losing its share in Latin American market to China. If the

average growth rate of Chinese trade with LAC will be maintained, China is likely to be the second important

trading partner for LAC in a few years.

After the beginning of global economic and financial crisis, both China and the EU decreased their trade

with LAC. In 2009 compared to 2008, the Chinese exports declined by 21% and imports by 10%. In the case of

the EU, the figures were respectively 24% and 31%.

The change in the Chinese merchandise trade with selected Latin American countries over the period from

2000 to 2013 is significantly higher. For instance, during last 14 years, the Chinese exports to Colombia and

Peru increased over 40 times. China’s imports from Venezuela and Colombia increased over 100 times. In the

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

556

case of Costa Rica, the increase in the Chinese imports was exceptionally high. In the considered years, the EU

increased its trade with the Latin American countries a few times (Table 4).

Figure 1. EU25 and China’s trade in goods with LAC33 in the years 2000-2013 (USD million). Source: Retrieved from http://www.cepal.org/comercio/ecdata2.

Table 4 Percentage Change in Value of China’s and the European Union’s Trade in Goods With Selected Latin American Countries in the Years 2000-2013

Country China EU25

Country China EU25

Exports Imports Exports Imports Exports Imports Exports Imports

Argentina 1,334% 554% 132% 111% Guatemala 964% 3,676% 132% 82%

Brazil 2,834% 3,249% 243% 155% Mexico 2,069% 1,997% 177% 242%

Chile 1,573% 1,447% 282% 149% Panama 752% 4,208% 153% 119%

Colombia 4,277% 11,158% 334% 356% Peru 4,188% 1,401% 387% 328%

Costa Rica 1,322% 46,041% 76% 116% Uruguay 856% 2,334% 182% 338%

Cuba 491% 522% 83% 71% Venezuela 2,264% 13,742% 96% 76%

Ecuador 3,863% 867% 509% 258%

Source: Retrieved from http://www.cepal.org/comercio/ecdata2.

The rise in the Chinese merchandise trade with selected Latin American countries is much more

impressive in longer period. During the last 20 years, China has been exponentially increased its trade with

countries in the region. China’s exports and imports of goods to its most important Latin American trading

partners are presented in Figure 2.

A fast growth of the merchandise exchange between China and LAC caused that China has already

overtaken the EU in trade with a few countries in the region. In 2013, China exported more commodities than

the EU to 12 Latin American countries: Chile, Panama, Venezuela, Peru, Uruguay, Guatemala, Paraguay,

Honduras, Jamaica, Nicaragua, Haiti, and Dominica. The Chinese imports value of goods was higher than the

European in the case of five countries: Brazil, Chile, Venezuela, Peru, and Uruguay.

Since the beginning of the 21st century, the importance of China as an export market significantly has

been increased in a few LAC countries (Table 5). In 2013, China absorbed almost one fourth of the Chilean

merchandise exports and one fifth of the Brazilian ones. Besides, over 17% of the Peruvian and 14% of the

Uruguayan exports were destined in China. A relatively big increase in the share of exports of goods to China

in total exports was also observed in the case of Colombia, Argentina, and Panama. China still became an

0

50000

100000

150000

200000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Exports of goods

E25 China

0

50000

100000

150000

200000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Imports of goods

E25 China

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

557

unexploited market for Bolivia, Costa Rica, Mexico, or Paraguay. Over the period from 2000 to 2013, China

substantially increased its importance as a source of imports for the LAC countries. In 2013, the most

dependent countries on Chinese commodities were Paraguay (28.3% of its imports came from China), Chile

(19.7%), and Peru (19.4%).

Figure 2. China’s exports and imports of goods to Brazil, Chile, Mexico, and Venezuela (USD million) in the years 1994-2013. Source: Retrieved from http://www.cepal.org/comercio/ecdata2.

Table 5

Merchandise Trade of Selected LAC Countries with China in 2000 and 2013 (Percentages of Total Trade)

Country Exports Imports

Country Exports Imports

2000 2013 2000 2013 2000 2013 2000 2013

Argentina 3.0 7.2 4.6 15.4 Ecuador 1.2 2.3 2.2 16.7

Bolivia 0.4 2.6 3.1 12.1 Mexico 0.2 1.7 1.6 16.1

Brazil 2.0 19.0 2.2 15.6 Panama 0.2 6.1 0.6 7.9

Chile 5.0 24.8 5.7 19.7 Paraguay 0.7 0.6 11.5 28.3

Colombia 0.2 8.7 3.0 17.5 Peru 6.4 17.5 3.9 19.4

Costa Rica 0.2 3.3 1.3 9.6 Uruguay 4.0 14.2 3.2 16.9

Source: Retrieved from http://www.cepal.org/comercio/ecdata2.

The EU is still an important export market for most of the LAC countries. For instance, in 2009 over 20%

of Brazil’s, Honduras’ or Panama’s exports were destined in EU27. However, in the years from 2000 to 2009, a

percentage increase in merchandise exports to EU27 was observed only in Ecuador, Honduras, Panama,

0

10000

20000

30000

40000

50000

60000

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Brazil

Exports Imports

0

5000

10000

15000

20000

25000

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Chile

Exports Imports

05000

100001500020000250003000035000

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Mexico

Exports Imports

0

5000

10000

15000

2000019

94

1996

1998

2000

2002

2004

2006

2008

2010

2012

Venezuela

Exports Imports

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

558

Paraguay, Venezuela, and four Caribbean countries. In the case of 18 countries in the region, the share of

merchandise exports of goods to EU27 in their total exports decreased over the considered period (Bárcena &

Rosales, 2010, p. 13).

An analysis of the structure of China’s and Europe’s trade with LAC shows some similarities. Namely,

both sell to LAC mostly manufactured goods and LAC countries send to them mainly resources and raw

materials. China’s exports of goods to Latin America consist principally of electronics, components and parts,

machinery and equipment, textiles and apparel. In other words, China is a source of imports of cheap

manufactured goods for the region (Table 6).

Table 6

Top Five Latin American Trade Partners of China in 2013

China’s exports of goods China’s imports of goods

No. Country Goods No. Country Goods

1 Brazil Telecommunication equipment, optical instruments, electrical machinery

1 Brazil Iron ore and concentrates, seeds and oleaginous fruit, crude petroleum, pulp andwaste paper, sugar and honey

2 Mexico Telecommunication equipment, optical instruments, automatic data processing machines

2 Chile Copper, ores and concentrates of base metals, iron ore and concentrates

3 Chile Telecommunication equipment, footwear, cloths

3 Venezuela Crude petroleum and oils, petroleum products

4 Panama Petroleum products, ships, boats and floating structure

4 Mexico Ores and concentrates of base metals, passenger motor vehicles, microcircuits, transistors

5 Argentina Telecommunication equipment 5 Peru Ores and concentrates of base metals, iron ore and concentrates, copper

Source: Retrieved from http://www.cepal.org/comercio/ecdata2.

Table 7

Top Five Latin American Trade Partners of the European Union in 2013

EU25 exports of goods EU25 imports of goods

No. Country Goods No. Country Goods

1 Brazil

Medicinal and pharmaceutical products, motor vehicle parts and accessories, petroleum products, aircraft and associated equipment

1 Brazil Iron ore and concentrates, feeding stuff for animals, seeds and oleaginous fruit, coffee, crude petroleum

2 Mexico Petroleum products, medicinal and pharmaceutical products, motor vehicle parts and accessories

2 Mexico Crude petroleum and oils, telecommunication equipment, passenger motor vehicles

3 Argentina Petroleum products, motor vehicle parts and accessories, medicinal and pharmaceutical products

3 Chile Copper, ores and concentrates of base metals, fruit and nuts

4 Chile Aircraft and associated equipment, passenger motor vehicles, crude petroleum

4 Argentina Feeding stuff for animals, chemical products, ores and concentrates of base metals

5 Colombia Medicinal and pharmaceutical products, aircraft and associated equipment

5 Colombia Crude petroleum and oils, coal, fruit and nuts

Source: Retrieved from http://www.cepal.org/comercio/ecdata2.

Latin America is important destination for the European medicinal and pharmaceutical products, motor

vehicles and aircraft (Table 7). Latin American exports mainly copper, iron and steel, oil, natural gas, coal,

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

559

soya beans, beef, bananas, and coffee to China and the EU. On average, the LAC countries sell more different

products to the EU than to China (Bárcena et al., 2012, p. 40). Of the LAC countries, only Mexico exports more

technology-intensive products to China and the EU.

Foreign Aid as a Tool of Promoting Trade With LAC Countries

China uses different methods to increase its trade in goods with other countries. One of the most effective

tools is foreign aid. Depending on the region and country, China provides grants, interest-free loans or

concessional loans to countries with which it trades. In the case of the LAC countries, low-interest loans

dominated in the Chinese foreign aid policy. It is estimated that China offered about USD 100 billion to the

region in the years from 2005 to 2013 (Figure 3).

Figure 3. China’s lending to Latin America and the Caribbean in the years 2005-2013 (USD billion). Source: Gallagher, Irwin, and Koleski (2012).

Over 90% of China’s lending to LAC was pledged after 2007. In 2010, China’s loan commitments to the

region were more than combined loans of the Inter-American Development Bank, World Bank, and United

States Export-Import Bank to LAC (Gallagher et al., 2012, p. 1).

During the financial crisis, China provided low-interest loans mainly to four resource-rich countries in the

region: Venezuela (USD 50.6 billion), Argentina (USD 14.1 billion), Brazil (USD 13.4 billion), and Ecuador

(USD 9.9 billion). China was the last resort of financing for countries like Argentina, Ecuador, and Venezuela

that were not able to borrow easily in international capital markets. The data about Chinese lending to LAC in

the years from 2005 to 2013 are presented in Table 8.

Table 8

China’s Lending to Selected Latin American and Caribbean States in the Years 2005-2013 (USD Billion)

Country Value of loans Country Value of loans Country Value of loans

Argentina 14.1 Colombia 0.075 Peru 2.3

Bolivia 0.611 Costa Rica 0.789 Uruguay 0.01

Brazil 13.4 Ecuador 9.9 Venezuela 50.6

Chile 0.15 Mexico 2.4

Source: Gallagher et al. (2012).

Besides, in July 2014, Chinese President Xi Jinping announced additional USD seven billion to Argentina,

USD five billion to Brazil, and USD 5.7 billion in loan and USD five billion in credit line to Venezuela (Lee,

0.231 0

4.8 6.3

13.6

37

17.8

3.5

15

2005 2006 2007 2008 2009 2010 2011 2012 2013

COMPETITION IN LATIN AMERICA AND THE CARIBBEAN

560

2014). A sharp increase in the Chinese financing provided to LAC in the second half of the first decade of 21st

century coincided with the rise of trade in goods between China and countries in the region.

The EU members and institutions have been provided official development assistance to Latin America

and the Caribbean for many years. Since 2001, European grants and concessional loans have been more often

directed to trade-related projects and programmes4. The EU increased its aid-for-trade disbursements to LAC

countries after the Hong Kong WTO Ministerial Conference (Nowak, 2014, p. 77). The European aid-for-trade

to the region in the years 2002-2011 is presented in Figure 4.

Figure 4. The European Union’s aid-for-trade commitments to LAC (USD million, 2011 constant). Source: Retrieved from http://dx.doi.org/10.1787/aid_glance-2013-en.

From the report Aid for Trade at a Glance 2013, it follows that in 2010, the EU provided aid-for-trade to

25 LAC countries. The volumes of aid varied across the states. The EU supported trade-related projects mainly

in the poorest countries of the region: The major ones were Peru, Haiti, Honduras, and Jamaica (Figure 5).

Figure 5. The European Union’s aid-for-trade disbursements to selected LAC countries in 2010 (USD million, 2011 constant). Source: Retrieved from http://dx.doi.org/10.1787/aid_glance-2013-en.

The level of the European aid was lower than China’s aid. It is worth noting that in the years from 2005 to