China Internal Market Development and Regulation

268

Report No. 12291 CHA China Internal MarketDevelopment and Regulation March 17, 1994 Country Operations Division China and Mongolia Department East Asiaand Pacific Regional Office FOR OFFICIAL USE ONLY I0 ,. . v ~- 5, c' ' 'N~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1 MI1CROGRAPHICS Report No: 12291 CIIA Type: SEC Document offheWoMW'anI~ This docuiient has" a ebictedIuinadmybeue ywm~ol iihe e1act pidaI- f. lb c'ntew. ''ay0't ot6 'e di~~cIo~ed w d&aCtb'w r.' '* .-. . '' .. . ~~~~~-~: .. .3 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of China Internal Market Development and Regulation

Report No. 12291 CHA

ChinaInternal Market Development and Regulation

March 17, 1994

Country Operations DivisionChina and Mongolia DepartmentEast Asia and Pacific Regional Office

FOR OFFICIAL USE ONLY

I0

,. . v ~- 5, c' '

'N~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~1

MI1CROGRAPHICS

Report No: 12291 CIIAType: SEC

Document offheWoMW'anI~

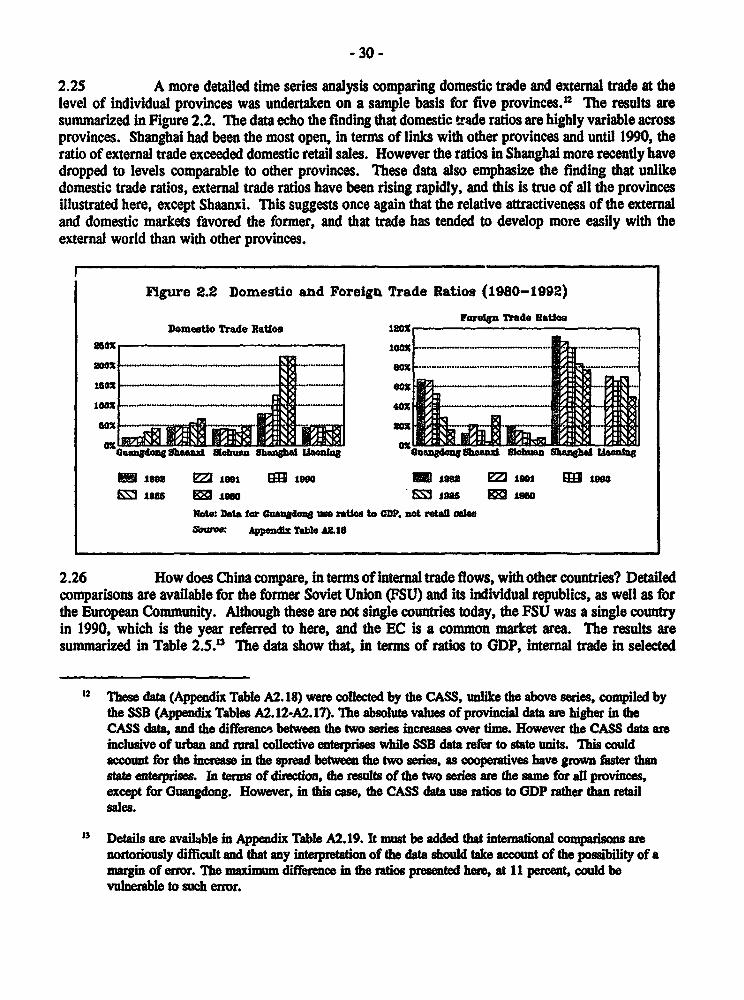

This docuiient has" a ebictedIuinadmybeue ywm~oliihe e1act pidaI- f. lb c'ntew. ''ay0't ot6 'e

di~~cIo~ed w d&aCtb'w r.' '*

.-. . ''

.. . ~~~~~-~: .. .3

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit: Yuan (Y)

(Nominal Official Period Average Rates)

Year Yuan (Y) per US$

1992 5.521991 5.321990 4.781989 3.771988 3.721987 3.7r1986 3.451985 2.941984 2.321983 1.981982 1.891981 1.701980 1.501979 1.561978 1.68

FLSCAL YEAR

January 1 - December 31

WEIGHTS AND MEASURES

Metric System

FOR OFFICIAL USE ONLY

ACRONYMS AND ABBREVIATIONS

ASEAN Association of South-East Asian NationsCASS Chinese Academy of Social SciencesCFSRRI China Economic Systems Reform Research InstituteCFA Communaut6 Financiere AfricaineCFMC Commodities Futures Management CommissionCFTC Commodities Futures Trading CommissionCNCC China National Coal CorporationCNFMGC China Non-FerrouG Metals General CorporationCOV CovarianceDRC Development Research CouncilEC European CommunityECU European Currency UnitETDZ Economic and Technical Development ZonesFEAC Foreign Exchange Adjustment CentersFIMBRA Financial Intermediaries', Managers' and Brokers' Regulatory AssociationFSU Former Soviet UnionFTC Foreign Trade CorporationGITIC Guangdong International Trust and Investment CenterGDP Gross Domestic ProductGNP Gross National ProductGPAIC Guangdong Province Administration of Industry and CommerceGVIO Gross Value of Industrial OutputGVO Gross Value of OutputLAUTRO Life Assurance and Unit Trust Regulatory OrganizationLME London Metal ExchangeMME Ministry of Materials and EquipmentMOC Ministry of CommerceMOFTEC Ministry of Foreign Trade and Economic CooperationNAFTA North American Free Trade AssociationNTHS National Trnmk Highway SystemOEC Office of Economic CooperationSAIC State Administration of Industry and CommerceSCETO State Council Economic and Trade OfficeSCRES State Commission for the Restructuring of the Economic SystemSEZ Special Economic ZoneSHME Shanghai Metals ExchangeSIB Securities and Investments BoardSME Shenzhen Metals ExchangeSOEs State Owned EnterprisesSPC State Planning CouncilSRO Self-Regulatory OrganizationsSTICERD Suntory-Toyota International Center for Economics and Related DisciplinesTVE Township and Village EnterprisesUK United KingdomUSA United States of America

Thds doment has a restricted distn1ution and may be used by recipient only in the perfom of thidrI official duties. Its contents may not otherise be disclosed without Wodd Bank authoion. l

CONTENTS

Executive Summary .................................... xi

Market Senatonand Market Developme .................. 1

A. Introduction 1Factors Affecting Internal Markets 4Objectives of this Report .5

B. The Potential Benefits of Internal Free Markets. 7Forms of Regional Integration. 7The Case for Regional Integration. 8

C. Market Strcture in China .12

Annex 1.1 Calculadtion of Regional Structural Difference Coefficients ...... 16

2 Rect Evolution of China's Internal Markets ........ ............. 20

A. The Impact of Price Reform .20Assessing Price Efficiency: Plan and Market Prices .22Assessing Price Efficiency: Regional Price Differentials 24

B. Interrgional Domestic Trade .26An Analysis of Domestic Trade Flows ...... .......... 29

C. Factor Mobility: Capital .32Factors Affecting nterprovincial Investment .32Profit Retention and Taxation .33Tax Concessions in 'Zones' Established by the Center .35Tax Concessions in 'Zones' Established by Localities .36Other Tax Concessions by Localities .37Regional Cooperation Zones .38Procedures and Practice .38Summary: Tax Policy and Regional Capital Flows .39An Analysis of Evidence .40The Banking System: Interbank Borrowing and Lending 43The Banking System: Payment Clearance and Settlement 45Capital Markets .47

D. Factor Mobility: Labor .47B. Foreign Exchange Mobility .53

Recent Changes .55F. Conclusions .55

- iv -

3 The Distribution System ..................................... 58

A. The Changing Role of the State in Distribution .58B. The Efficiency of the Present Distribution System .63

Evolution of the Materials Distribution System .63The System Today ........................... 67The Efficiency of the Present Materials Distribution System ... 70

C. Parlel Changes in Agriculture. 75Agrcultual Wholesale Markets .75

D. Transpoitation, Telecommunications and Services .76The Raflroad System .78Truck Transportation .78

E. Summay and Implications. 31

Annex 3.1 A Note on Producer Goods Distnbution Systems ................. 82Efficient Distribution Systems ...................... 82Altermative Cbannel Structures ...................... 82Chamel Functions ............................. 83The Evolution of Distnbution Channels for Producer's Goods . . 84Some Comments on Distributor Efficiency .... .......... 86'Best Practice' Tools and Techniques to Minimize Costs ...... 87

4 New Forms of Markes ...................................... 89

A. China's Distinctive Pattern of Development of Commodity Exchanges . 90B. Agricultural Markets .91C. The Metals Exchanges of Shanghai and Shenzhen .93

The Shenzhen Meta Exchange .96The Shanghai Meta Exchange .98

D. An Assessment of Trading on China's Two Metals Exchanges. 101The System of Trading on the Exchanges .101The Costs of Trading on the Exchanges .104The Nature of Trading Activity on the Exchanges .105

E. Policies and Regulations for Commodities and Futures Markets 109The Difficulty of Reconciling Free Markets andContimued Goverment Intervention .109

Financial Safeguards for Participants on the Exchanges 110. Framework of Regulation for Commodity Markets in Chinaand Oder Countries .111

F. Future Prospects for China's Commodity Exchanges ................... 114The Pressures for the Rationalization of the Number ofChinse Commodity Exchanges .................... 114

The Likely Development of Trading on the Exchanges .... ... 115G. Implications for Government Action ............................. 117

Annex 4.1 Commodity Market Trading: A Zero-Sum Game ................. 119

S Market Regaon . ........................................ 121

A. Regulation in a Market Economy .121B. Competition and a Competitive Enviromnent .122

Market Structure: Firm Size and Industrial Concentration 123Potental Changes in Market Structure: Mergers .125Potential Changes in Market Structure: Enterprise Groups 127Market Conduct Issues .134Legal Provisions on Competition .134

C. The Entry of New Firms .136The Role and Functions of the SAIC .136Other Agencies Concerned with Entry .139

D. Other Regulations Affecting Market Structre .140Consumer Protection Related Rules:

Advertizing and Fraudulent Practices .140Protection to Producers: Tridemarks, Patent and Copyright ... 142

E. Conclusions .144

6 Mbarkets ad Government: Future Perspectives ................... 146

A. General Themes - A Synthesis .146B. Policy, Regulation and Administration .149

Price and Quantity Controls .149Internal Trade .149Factor Mobifity. 10Market Reguation .152

C. Physical Constraints and the Management of Distribution .154Distribution Practices and Distribution Facilities .. 154Road Transportation .. 155Commodities and Futures Markets .155

D. The Future Role of the Govermment .156

References ......................................... 158

- vi -

Tables in Text

Table 1.1 Trends in the Branch Composition of China's Industrial Output .... ...... 13Table Al. 1 Comparison of Average Coefficients of Structural Difference .... ....... 19Table 2.1 Ratios of Market to State Prices for Main Materials ................. 23Table 2.2 Plan and Market Prices for Selected Materials (1985-1991) .... ........ 24Table 2.3 Coefficient of Regional Variation of Retail Prices of Major Commodities .... 25Table 2.4 Coefficients of Variation of Materials Prices by Province (1990-1992) ..... 25Table 2.5 China and Other Regional Trading Areas: Interregional Trade .... ....... 31Table 2.6 Interprovincial and Foreign Investment in Selected Provinces .... ....... 41Table 2.7 Mean and Coefficient

of Variation of Effective Tax Rates of 20 Provinces (1986-1990) .... ..... 43Table 3.1 Composition of Total Retail Sales Value by Ownership (1960-1991) ....... 61Table 3.2 Number and Share of Domestic Trade Units

by Ownership and Region (1985-1991) . 61Table 3.3 Retail Trade Services in China and Other Countries.63Table 3.4 China and Other Countries: Employment in Trade and Transport .... ..... 77Table 5.1 Industrial Concentration Ratios for Selected Industries ............... 124Table 5.2 Size Distribution of Industry by Alternative Indices (1991) ............. 125

Figues in Text

Figure 1.1 Reduction in Scope of Price Controls ........................... 2Figure 1.2 External and Domestic Trade Shares ........................... 3Figure 1.3 Coefficients of Structural Difference ........................... 15Figure 2.1 Free Market Prices Relative to State List Prices ........ ............ 23Figure 2.2 Domestic and Foreign Trade Ratios (1980-1992) .................... 30Figure 3.1 Material Supply by Government Contact ........................ 59Figure 3.2 Marketization of Agriculture ................................ 60

Annex Tables

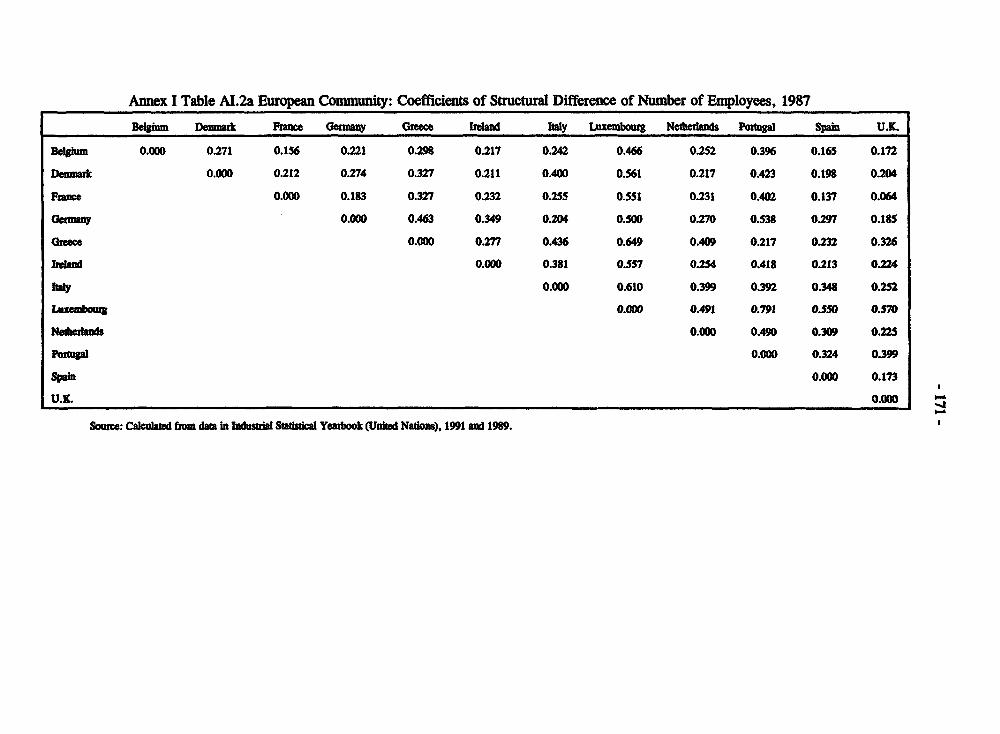

Annex I Table Al. la European Community: Coefficients of Structural Differenceof Number of Firms, 1987 .................................... 168

Annex I Table Al. lb United States: Coefficients of Structural Differenceof Number of Firms, 1987 .................................... 169

Annex I Table AI. lc China: Coefficients of Structural Difference of Numberof Firms, 1991 ............................................ 170

Annex I Table AI.2a European Community: Coefficients of Structural Differenceof Number of Employees, 1987 ................................. 171

Annex I Table AI.2b United States: Coefficients of Structural Differenceof Number of Employees, 1987 ................................. 172

Annex I Table Al.2c China: Coefficients of Structural Differenceof Number of Employees, 1991 .................... ... 173

Annex I table AI.3a European Ccommunity: Coefficients of Structural Differenceof Output Value, 1987 ....................................... 174

- vii -

Annex I Table Al.3b United States: Coefficients of Structural Differenceof Output Value, 1987 . .. 175

Annex I Table Al.3c China: Ciefflcients of StructUral Differenceof Output Va;ue, 1991 .................. t . . . ... . 176

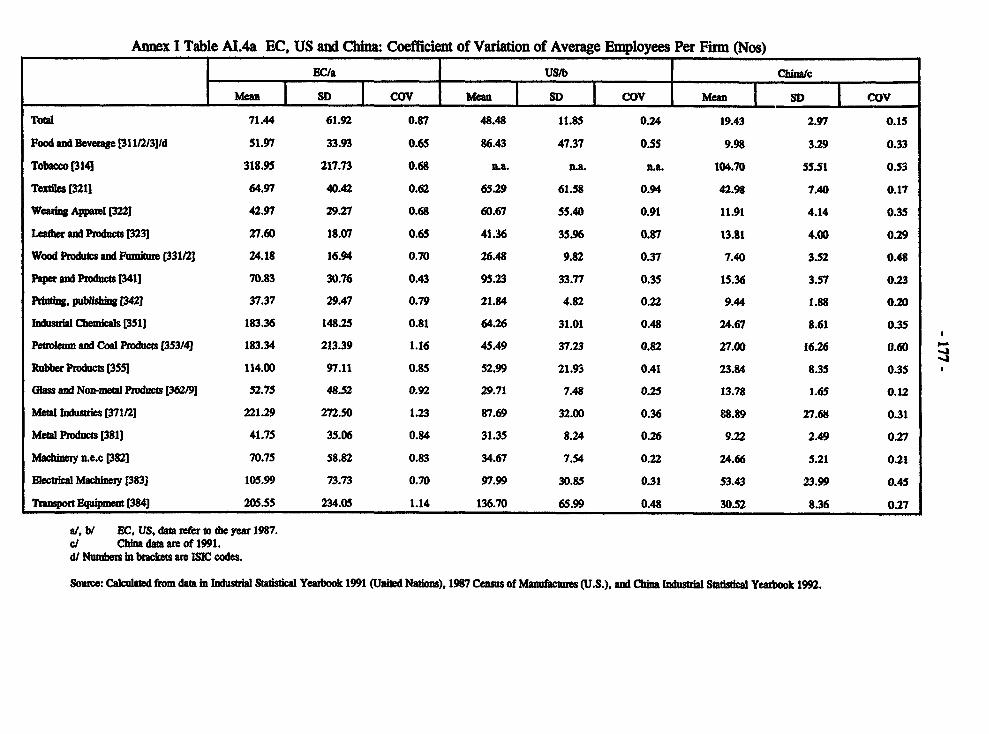

Annex I Table Al.4a EC, US and China: Coefficient of Variationof Average Employees Per Firm (Nos) ............. .. .............. 177

Annex I Table Al.4b EC, US and China: Coefficient of Variationof Average Output Per Firm (US$ million) ........... .. .............. 178

Appendx Tables

Appendix Table Al.l Per Capita National Income by Province (1983-1991) .... ..... 179Appernix Table A1.2 Per capita Investment in Fixed Assets by Provinces (1983-1991) 180Appendix Table A1.3 Per Capita Gross Value of Industrial Output

by Province (excluding village enterprises) (1985-1991) .................. 181Appendix Table A1.4 Per Capita Gross Value of Industrial Output

by Province (includiDg village enterprises) (1985-199i) .................. 182Appendix Table A1.5 Number and Gross Output Value of Industrial Enterpises

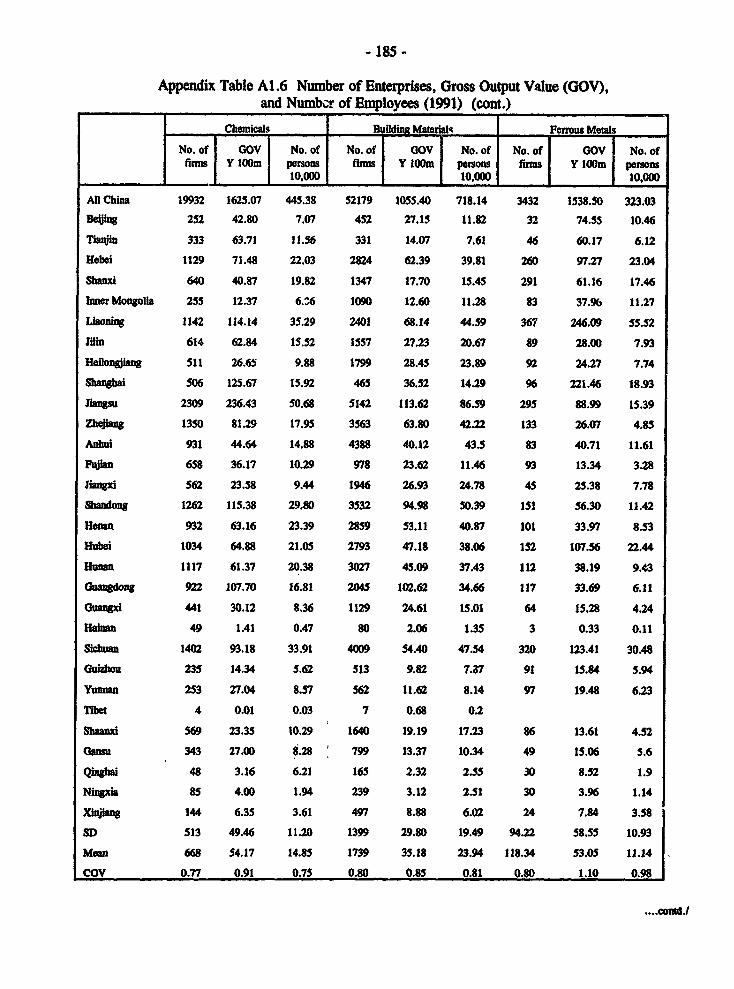

by Ownership (1985-1991) .................................... 183Appendix Table A1.6 Number of Enterprises, Gross Output Value (GOV),

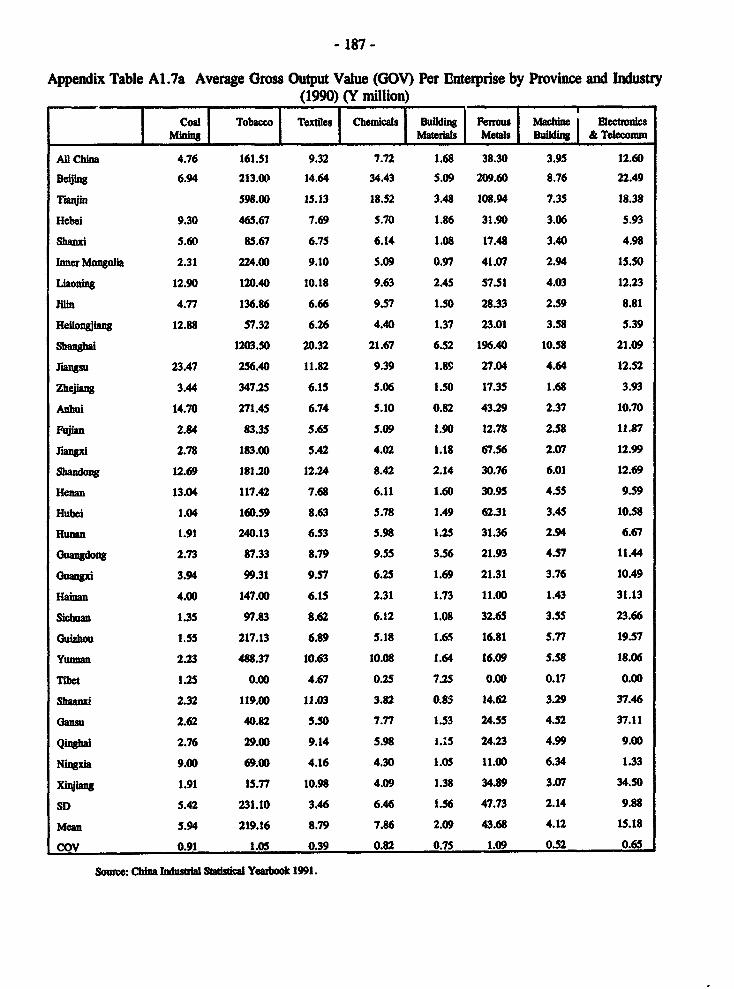

and Number of Employees (1991) ................................ 184Appendix Table Al.7a Average Gross Output Value (GOV) Per Enterprise

by Province and Industry (1990) (Y million) ............. . ............ 187Appendix Table A1.7b Average Gross Output Value (GOV) Per Enterprise

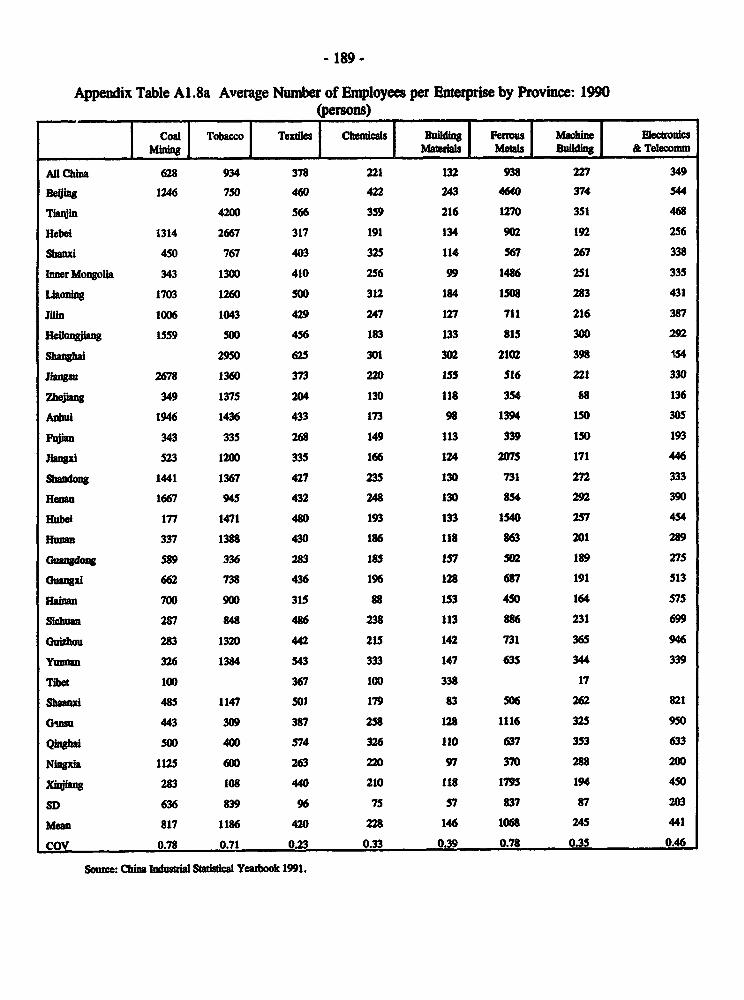

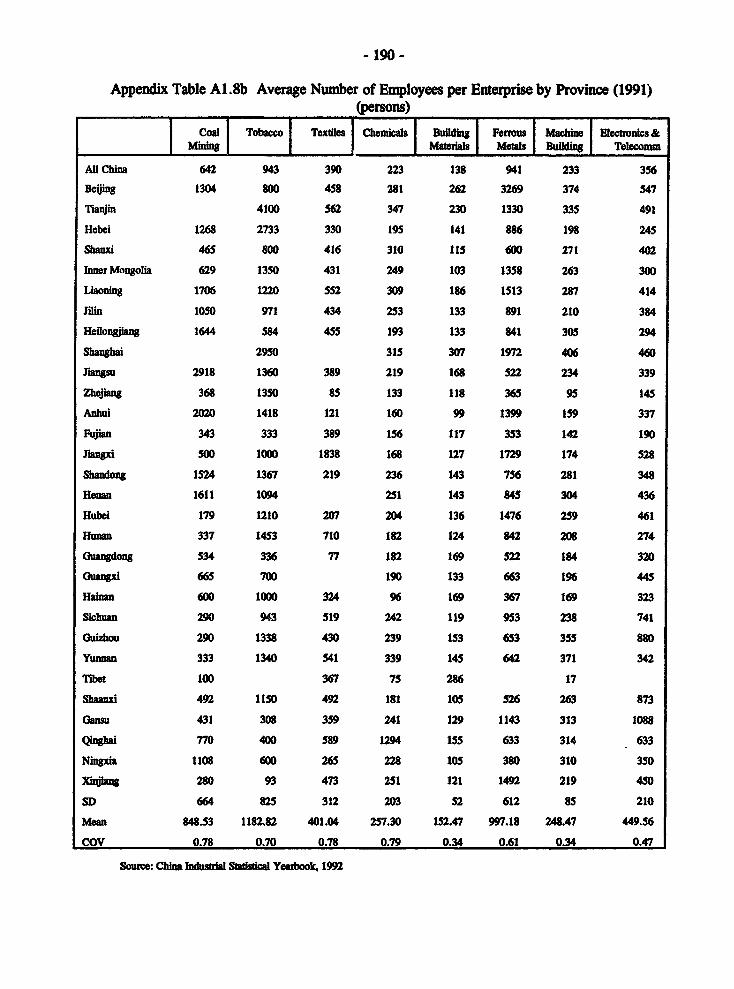

by Province and Industry (1991) (Y million) ......................... 188Appendix Table Al.8a Average Number of Employees per Enterprise by Province: 1990 189Appendix Table A1.8b Average Number of Employees per Enterprise by Province (1991) 190

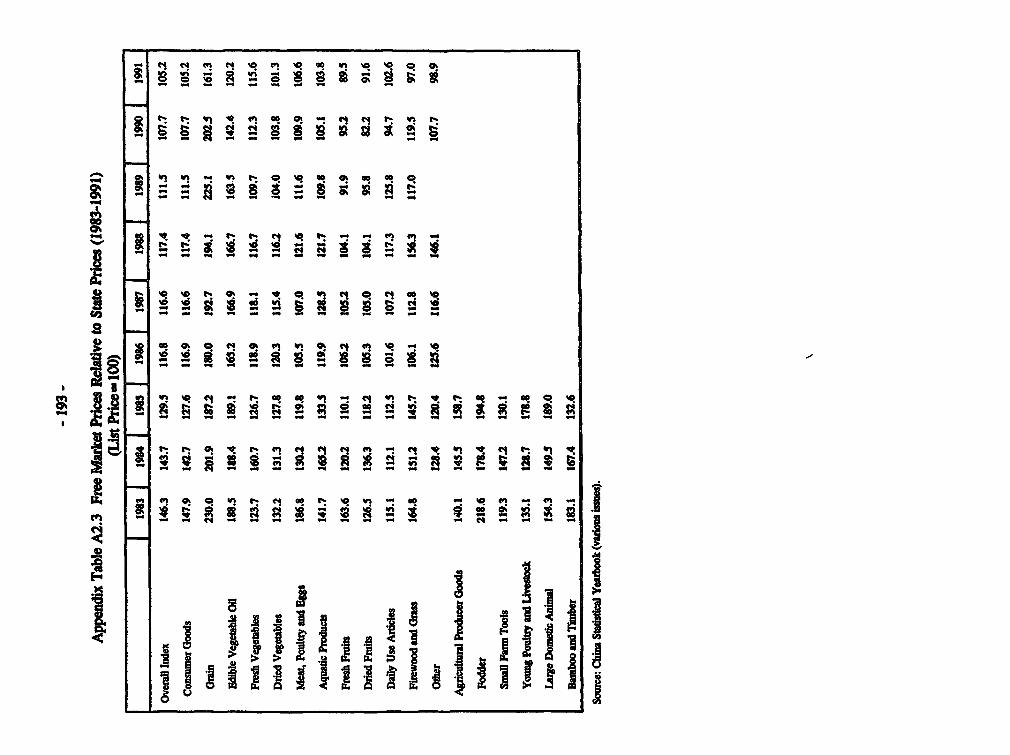

Appendix Table A2.1 Price Controls: Reduction in Scope (1978-1991) ...... ...... 191Appendix Table A2.2 Free Market Price Indices of Consumer Goods ....... ...... 192Appendix Table A2.3 Free Market Prices Relative to State List Prices (1983-1991) .... 193Appendix Table A2.4 Planned and Market Prices of Main Materials (Y/ton) ........ 194Appendix Table A2.5 Planned and Market Prices of Main Materials (1989-1991) ..... 195Appendix Table A2.6 Retail Prices of major Commodities

in 29 Provincial Capitals (1986) ................................ 197Appendix Table A2.7 Retail Prices of Major Commodities

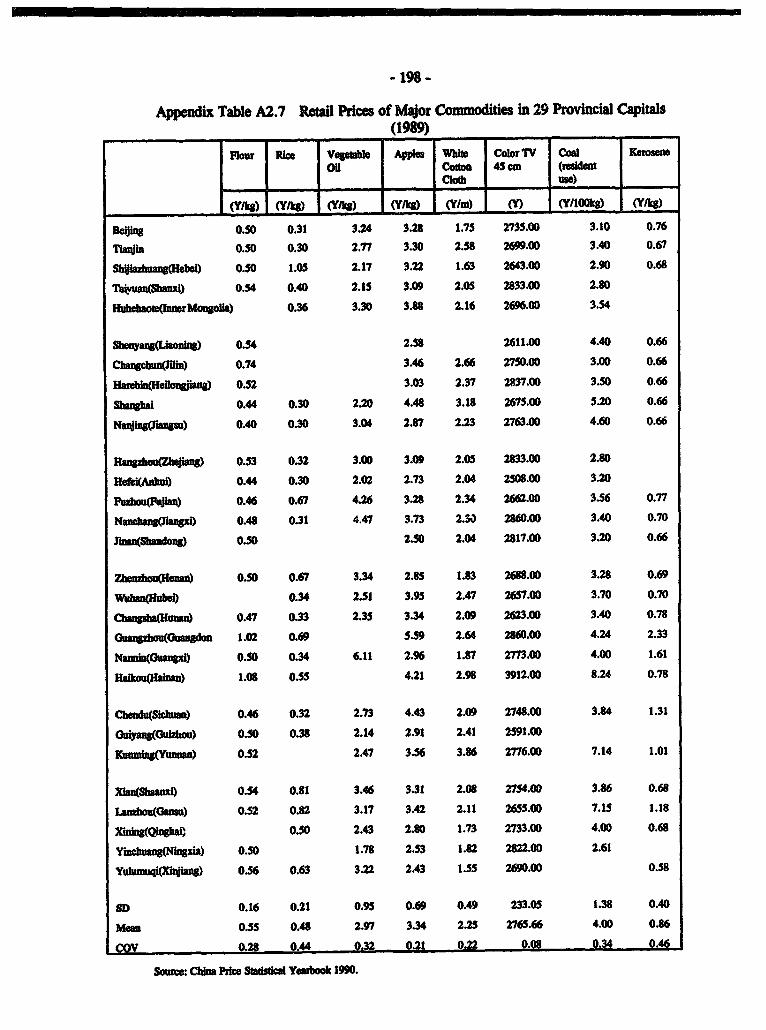

in 29 Provincial Capitals (1989) ....... ........... ................ 198Appendix Table A2.8 Retail Prices of Major Commodities

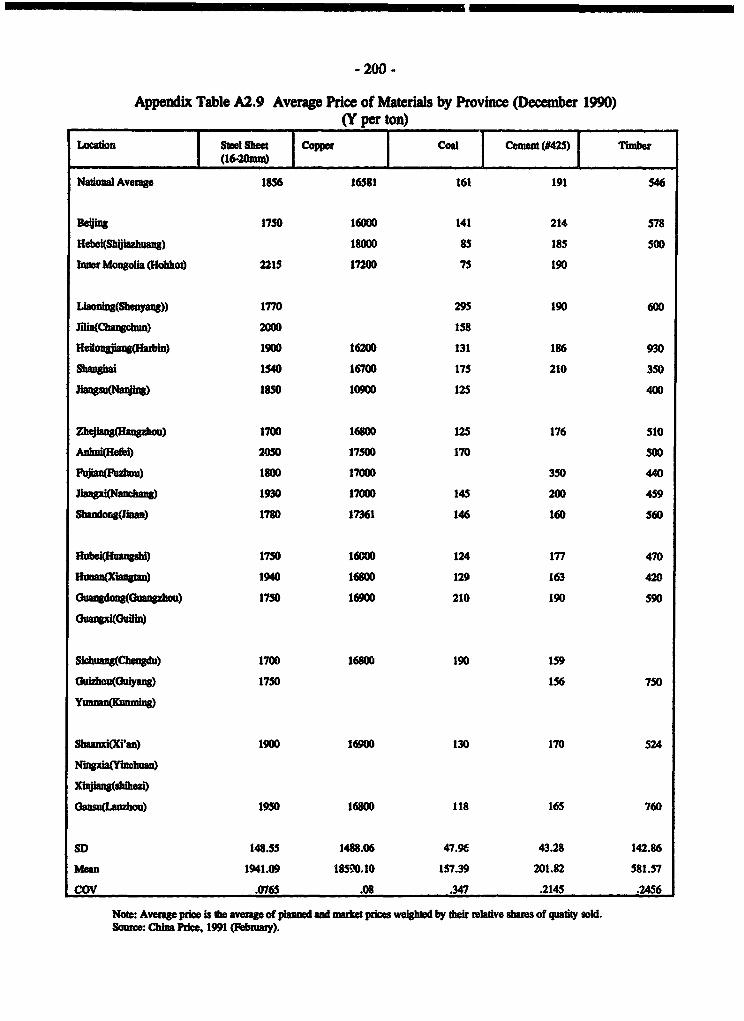

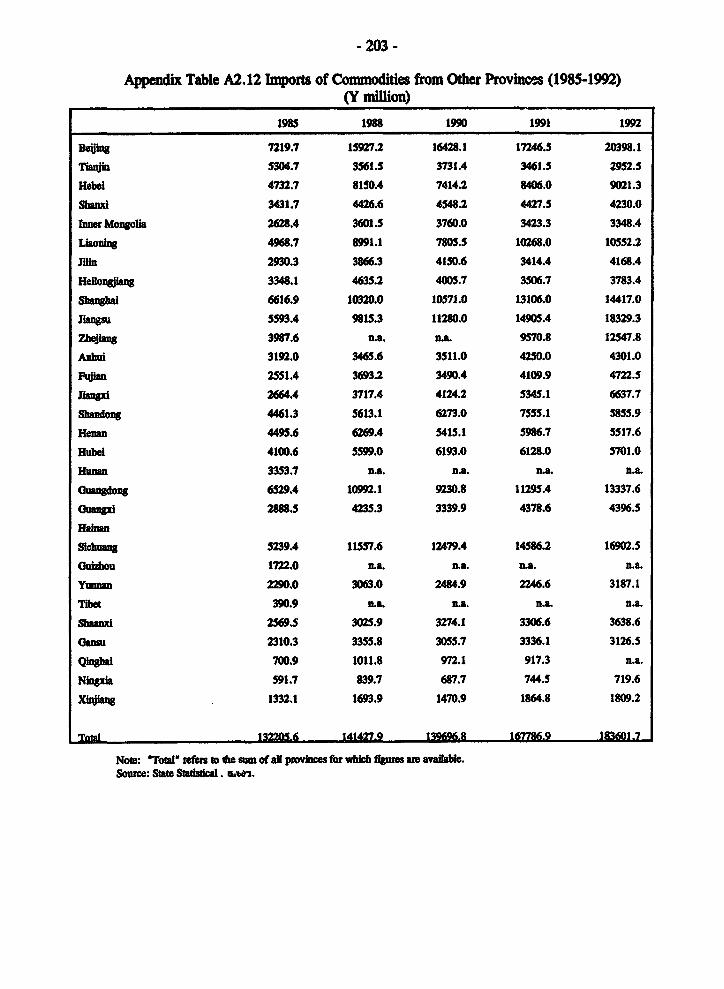

in 29 Provincial Capitals (1991) ................ ....... 199Appendix Table A2.9 Average Price of Materials by Province (ecember 1990) ....... 200Appendix Table A2. 10 Average ?,dce of Materials by Province (December 1991) ...... 201Appendix Table A2. 11 Average Price of Materials by Province (June 1992) . .202Appendix Table A2.12 Imports of Commodities from Other Provinces (1985-1992) ...... 203Appendix Table A2.13 Exports of Commodities to Other Provinces (1985-1992) ...... 204Appendix Table A2.14 Total Domestic Sales within Province (1985-1992) .......... 205Appendix Tablc A2.15 Ratio of Interprovincial Exports

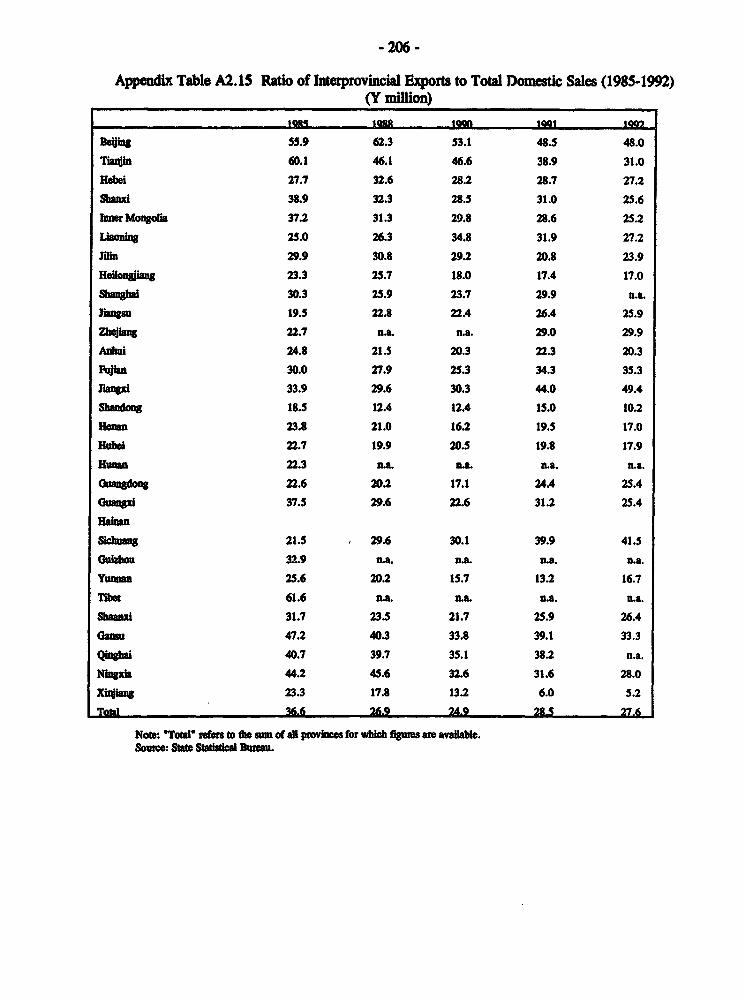

to Total Domestic Sales (1985-1992) .............. .. ............... 206

- viii -

Appendix Table A2.16 Ratio of Inter-provinical Importsto Total Domestic Sales (1985-1992) .............. .. ............... 207

Appendix Table A2.17 Ratio of Inter-provinical Tradeto Total Domestic Sales (1985-1992) ............. .. ............... 208

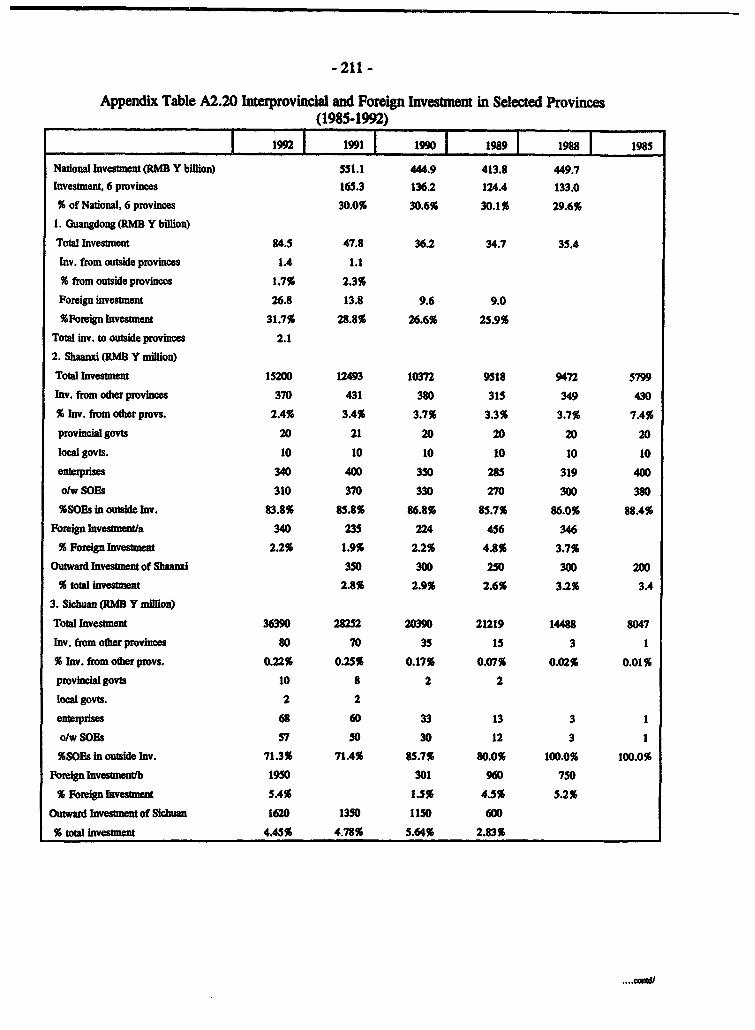

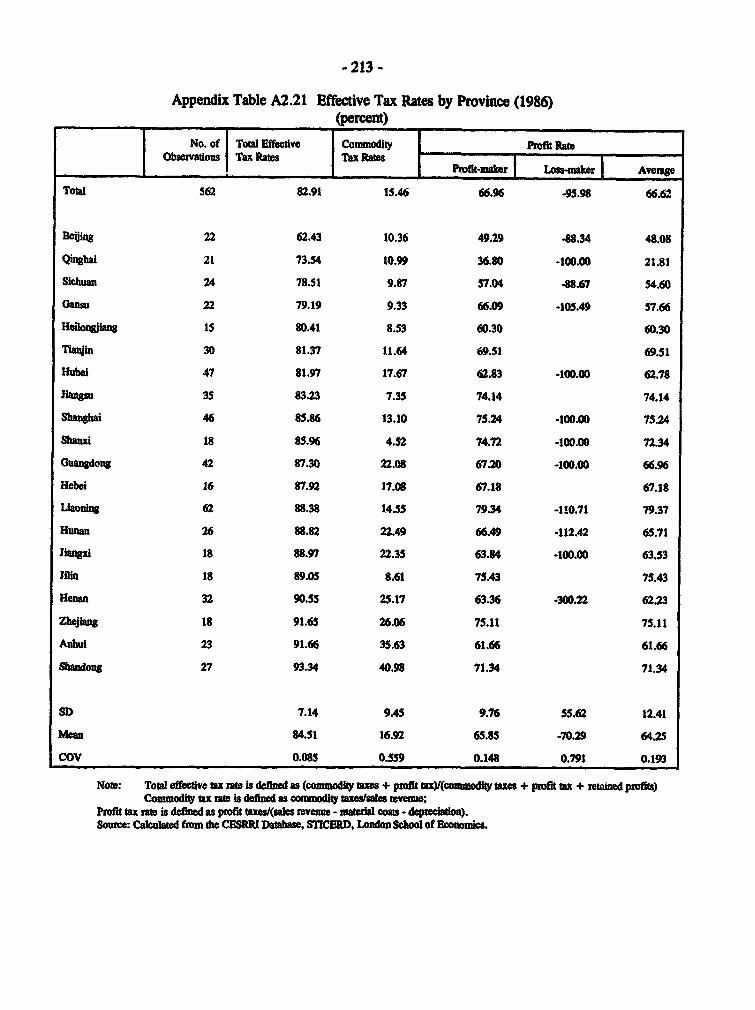

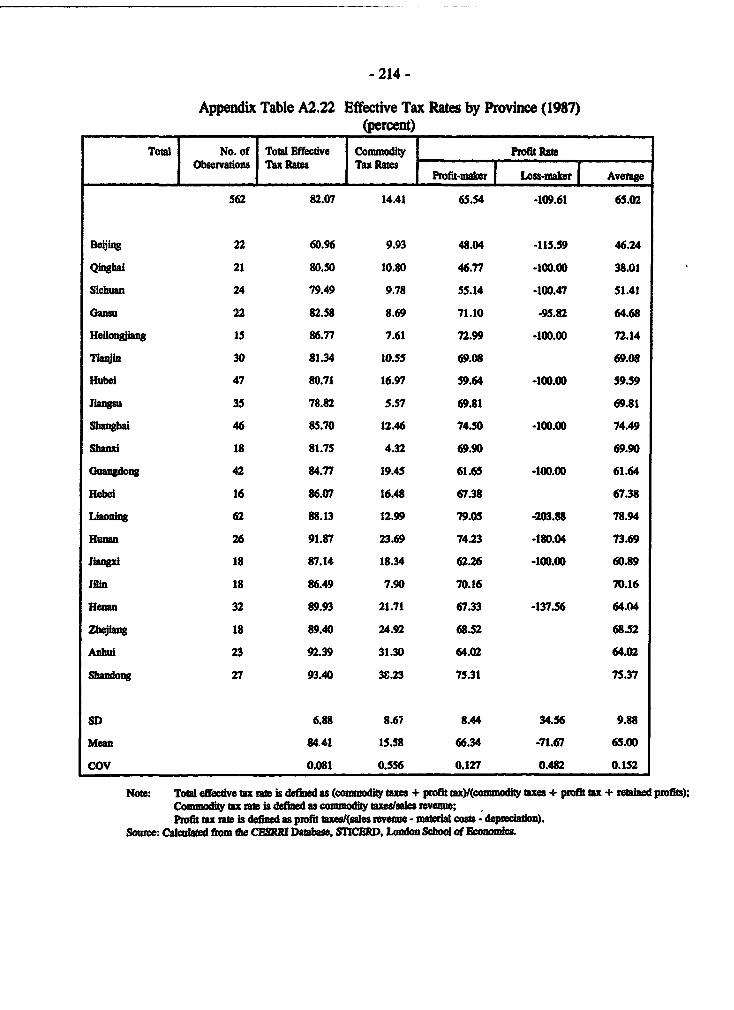

Appendix Table A2.18 Inter-provinical and Foreign Trade (RMB Y billion and %) .... 209Appendix Table A2.19 China and Other Regional Trading Areas: Interregional Trade ... 210Appendix Table A2.20 lnterprovincial and Fo.-eign Investment in Selected Provinces .... 211Appendix Table A2.21 Effective Tax Rates by Province (1986) ................. 213Appendix Table A2.22 Effec*ive Tax Rates by Province (1987) ................. 214Appendix Table A2.23 Effective Tax Rates by Province (1988) ................. 215Appendix Table A2.24 Effective T-x Rates by Province (1989) ................ 216Appendix Table A2.25 Effective Tax Rates by Province (1990) ................ 217

Appendix Table A3.1 Supply by Government Contacts (1981-1991) ............. 218Appendix Table A3.2 Production of Main Products (1981-1991) ........ ........ 219Appendix Table A3.3 Distribution of Retail Sales in Quantity and Value ........... 220Appendix Taole A3.4 Total Value of Retail Sales by Ownership (1960-1991) ........ 221Appendix Table A3.5 Composition of Total Retail Sales by Ownership (1960-1991) .... 222Appendix Table A3.6 Number of Domestic Trade Units

by Ownership and Region (1985-1991) ............. .. .............. 223Appendix Table A3.7 Composition of Dumestic Trade Units

by Ownership and Region (1985-1991) ............. .. .............. 224Appendix Table A3.8 Staff and Outlets of Materials Circulation System (1985-1991) ... 225Appendix Table A3.9 Number of Units and Persomel in Domestic Trade

by Ownership (1985-1991) .................. .................. 226Appendix Table A3.10 Sales of Machinery and Electrical Trading Companies

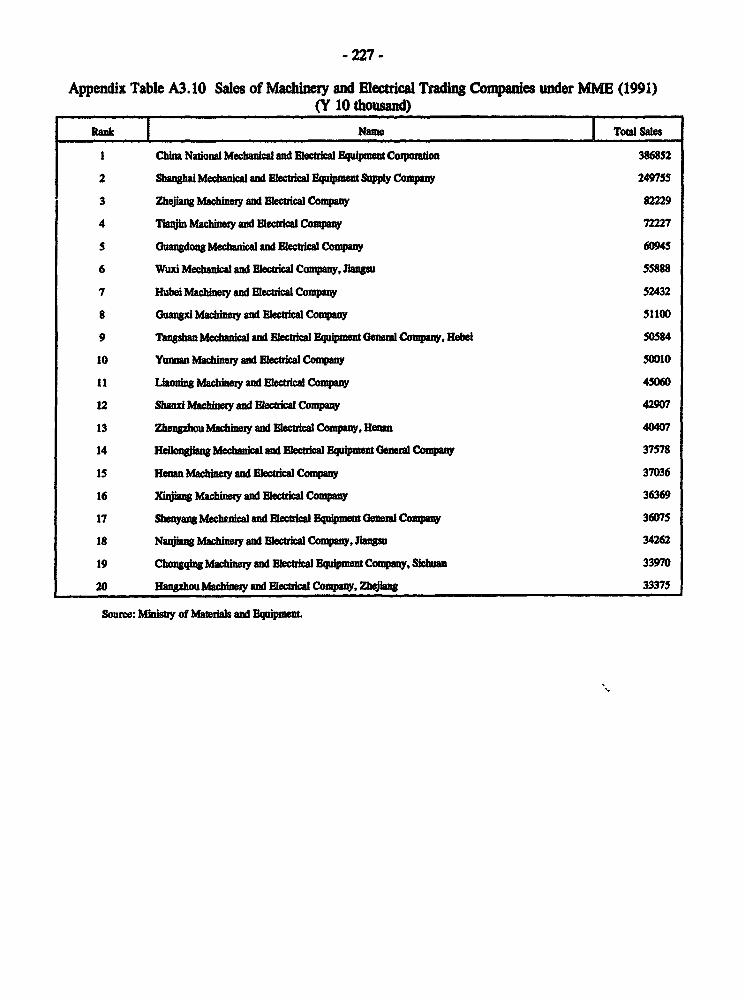

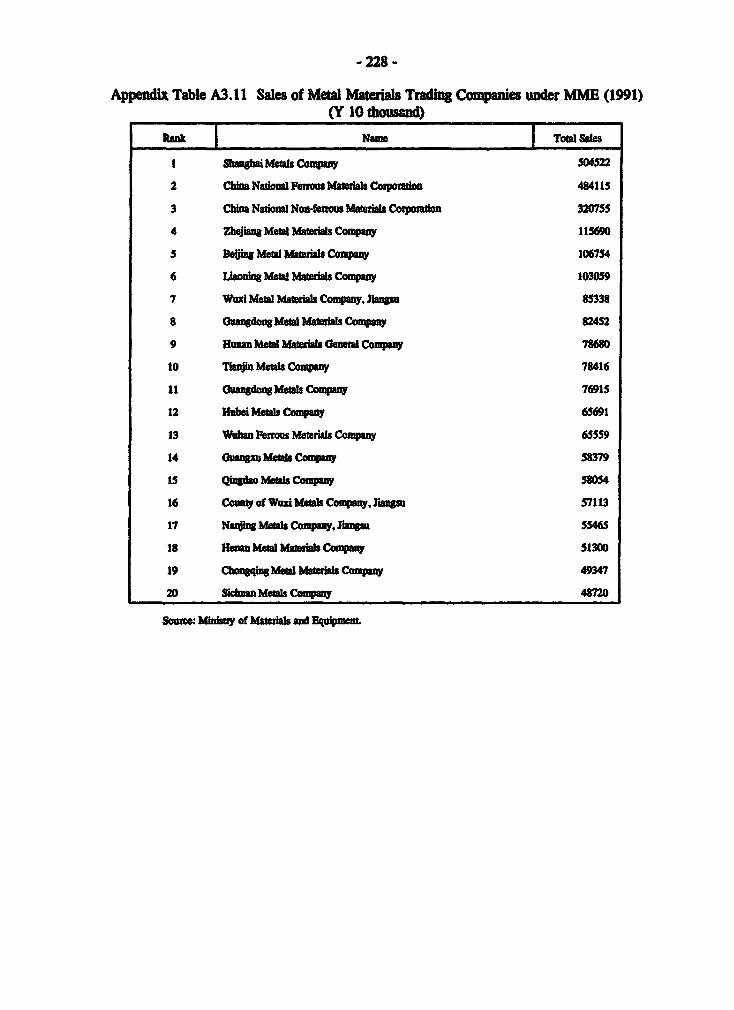

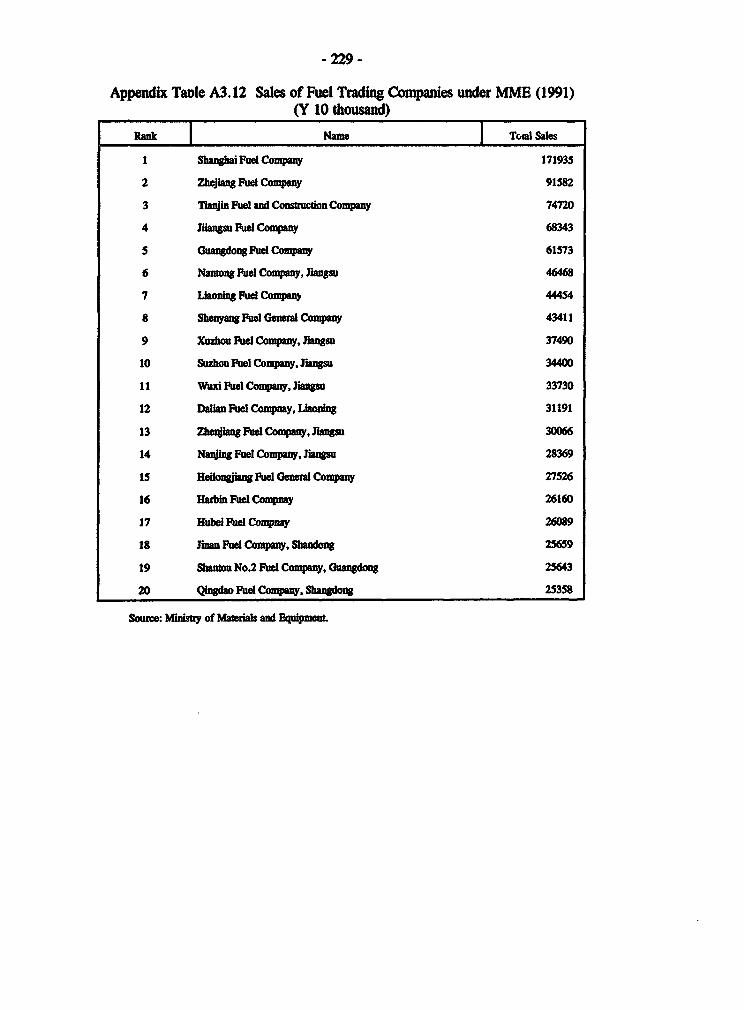

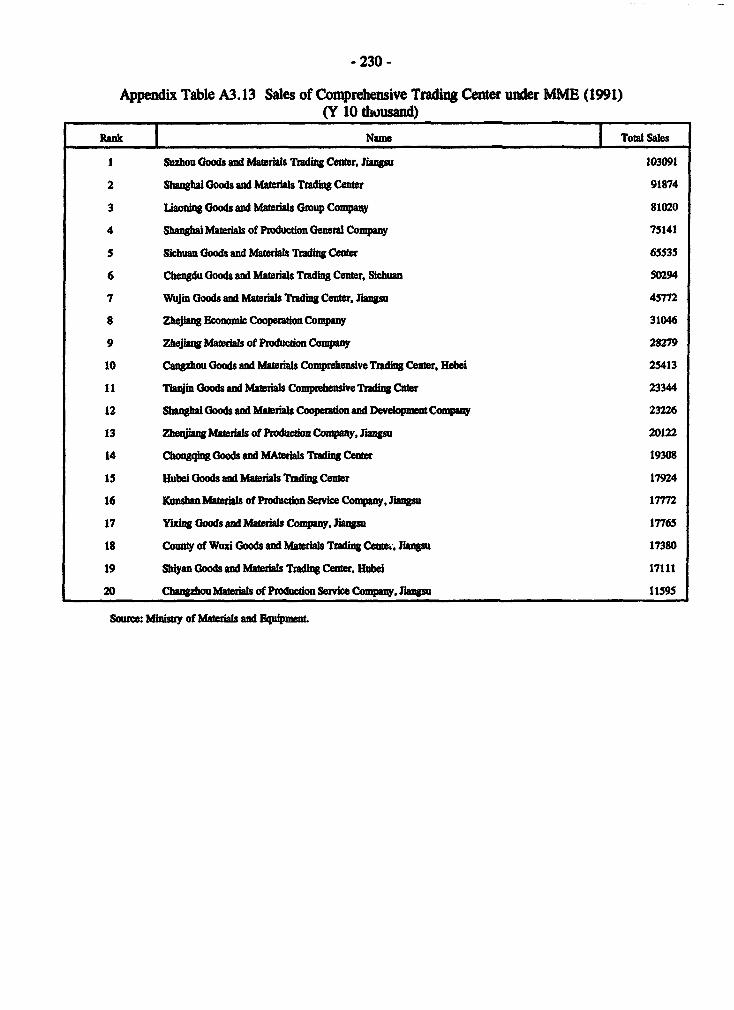

under MME (1991) .................... .................... 227Appendix Table A3.11 Sales of Metal Materials Trading Companies under MME (1991) 228Appendix Table A3.12 Sales of Fuel Trading Companies under MME (1991) .... .... 229Appendix Table A3.13 Sales of Comprehensive Trading Center ulder MME (1991) .... 230Appendix Table A3.14 Purchase, Sales and Inventory of CommercW Units (1962-1991) 231Appendix Table A3.15 Coal Industry: Inventory and Working Capital Requiremes

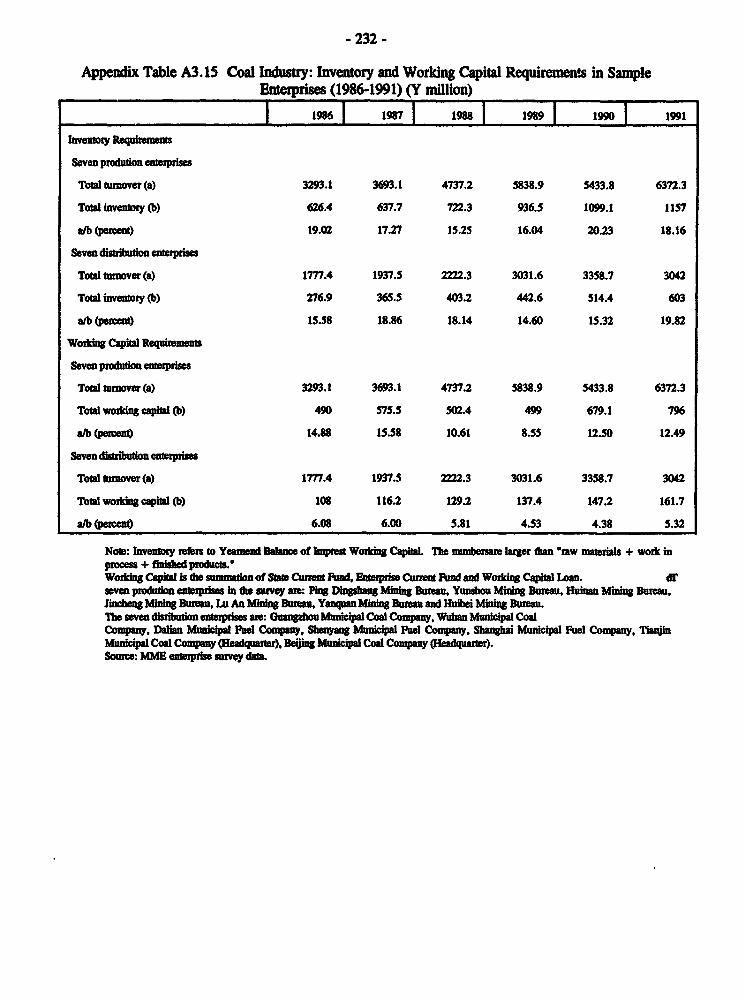

in Sample .............................................. 232Appendix Table A3.16 Cement Industry: Inventory and Working Capital Requirements

in Sample ..... ....................... 233Appendix Table A3.17 Steel Industry: Inventory an . 'orldng Capital Requiemens

in Sample .............................................. 234Appendix Table A3.18 Length of Transportation Routes by Province (1983-1991) .... 235Appendix Table A3.19 Per Capita Length of Transportation Routes

by Province (1983-1991) .................... .................. 236Appendix Table A3.20 Average Shiping Distance of Freight (1962-1991) .......... 237

Appendix Table A4.1 China's Foreign Trade in Non-Ferrous Metals ... ......... 238Appendix Table A4.2 Trading Volume on the Shenzhen Metal Exchange ........... 239Appendix Table A4.3 Trading Volume on the Shanghai Metal Exchange .... ....... 240

Appendix Table A5. la Size Distribution of Industry by Number ofEmployees and Number of Firms (1991) ............................ 241

- lx-

Appendix Table AS.lb Size Distribution of Industry by Number ofEmployees and Persons Employed (1991) ..... 242

Appendix Table AS. lc Size Distribution of Industry by Number ofEmployees and Gross Output Value (1991) .243

Appendix Table A5.2a Size Distribution of Industry by Gross Value ofIndustri Output and Number of Firms (1991) .244

Appendix Table AS.2b Size Distribution of Industry by Gross Value ofIndustrial Output and Number of Employees (1992) .245

Appendix Table A5.2c Size Distribution of Industry by Gross Value ofIndustrial Output and Output Value (1992) ........................... 246

CONTRIBUTORS

This report and its annexes are based on the findings of a preparatory visit to China in November 1992,followed by a full-fledged investigative study during March 1993 in China, jointly undertaken by the WorldBank, the Ministry of Materials and Equipment, and the State Administration of Industry and Commerce,Government of China. In addition to discussions in Beijing, the team visited Shenyang (Liaoning Province),Shanghai Municipality, Suzhou, Wuxi (Jiangsu Province) and Shenzhen (Guangdong Province). Excellentsupport was provided at each location visited by the local departments of the Ministry of Materials as wellas the State Administration of Industry and Commerce.

The World Bank team consisted of Anjali Kuniar (team manager and principal author of this report),Wang Yuan (task coordinator from the Beijing Office of the World Bank), Mark Dutz (competition policy),James Fry (commodities and futures markets), Lawrence Wortzel (distribution systems) and Jun Ma (capitalmobility, data base). Jun Ma also provided able research assistance in Washington and Cathy Song helpedwith document preparation. The Chinese team consisted of Wu Baozhong (task leader from the Ministryof Materials and Equipment), Zhao Jie, Wang Erliog, Li Chenghuai, Qi Xiaojie and Shi Chunling and XuSu (MME). Wang Baotong from the SAIC also accompanied the team on its field visits. Background papersfor this study were prepared by a team led by Tao Fei of the Chinese Academy of Social Scienc, s; by theMinistry of Materials and by the Development Research Council. The team extends its gratitude andappreciation to all the officials from the various govermment agencies, distribution companies and enterpriseswith whom it met.

Executive Summary

A. An Overview

i. China's commitment to the creation of a market economy received new emphasis in therecent 8th National People's Congress of March 1993. The congress ratified the decision taken at the14th Party Congress of October 1992, to develop a 'socialist market economy', shifting decisively awayfrom central planning. The Constitution of 1982 was amended to emphasize this shift.

ii. The development of the internal market was fostered by a series of mechanisms intendedto reduce the scope of state intervention:

(1) Progressive price decontrol was first introduced through three categories of prices(planned, guidance and market prices) and the gradual movement of goods from morereglated to less regulated categories. The 'dual track' pricing, introduced in 1985,permitted output above certain target levels to be sold on the free market. The proportionof goods in total domestic retail trade subject to planned prices fell dramatically between1978 and 1991, In favor of 'guidance prices' and free market prices. Goods subject toplanned prices have fallen considerably further, with recent announcements in early 1993of the relaxation of controls on prices of grain and edible oils.

(2) The allocation of goods moved progressively out of the mandatory plan. In 1980, 90percent of industrial goods and 837 production materials were allocated under the plansystem. By 1993, the proportion of industrial goods under the plan had declined to lessthan 10 percent and the number of production materials in this category was reduced to11. At the same time, consumer goods administered by the Ministry of Commercedeclined in number from 274 in 1978 to 14 in 1993.

(3) Distribution systems and chamcis gradually expanded. Formerly, the system of unifiedpurchase and sale of consumer manufactures, and the unified purchase of farm products,by designated government agencies, accounted for virtually all sales. Sales may now bemade to private purchasing agencies or directly to consumers. New 'comprehensive' and'specialized' cistribution agencies have sprung up. Sales undertaken by governmentagencies have also diversified in form and function, and state-owned distribution agenciesare providing new forms of services.

(4) Sophisticated forms of commodities markets, for many agricultural products andIndustrial raw materials have been established. Today there are 21 centrally sponsored

- xii -

commodities exchanges in China, many of which are equipped with advanced computertechnology and newly constructed modern trading facilities.

(5) In conjunction with these policy and real side adjustments, the government has drawn upa major program of legislative change for establishing a framework for a marketeconomy.

iii. Over the last decade, China has made remarkable strides towards the establishment of amarket economy. But the progress achieved so far has been uneven. This report evaluates the extentto which China, through the adoption of the measures described above, has been able to establish well-functioning markets. Well-functioning markets imply markets which transmit accurate signals to economicagents in terms of production decisions and factor allocation. The report distinguishes between theregional or spatial aspect of market functioning, and the movement from plan to market. Foliowing apolicy evaluation, the report analyzes the new systems for allocating and distributing goods that haveevolved in the aftermath of planning. The report also discusses present regulation of markets In thechanging environment.

B. Main Flndings

iv. There are large potential benefits in achieving well-functioning and regionally integiatedinternal markets and other countries have achieved greater market integration through systematic anddeliberate policies (Chapter 1, para 1.21 to 1.30). The report examines China's present Industrialstructure and demonstrates that the composition of output has remained remarkably staic despiteshifts In the ownership of industrial output (para 1.33). The cross-section structure of industi outputby region shows that each major industrial group is located in virually all provinces. Firm size is alsoremarkably similar across provinces.

V. To assess the extent to which China could gain from greater integration of its domesticmarket, the report compares China and other large regional markets. Subject to the caveats that applyto international comparisons with the EC and the US, the findings suggest that regional differences inChina appear relatively small, and there is little evidence of industrial specialization or a well-integratedstructure (para 1.37 and Annex 1.1). Relative to other countries, China Is far from realizing thebenefits of its potentially large internal market. As a consequence of its relatively 'cellular'economicstructure, many benefits, such as scale economies in plant size and the spreading of overheads inmanagement, technology and learning, communications and infrastructure, associated with thedevelopment of industrial 'clusters', have yet to be exploited.

vi. To promote regional trade and specialization, mechanisms for the redistribution ofbenefits among the various regions are needed. Today with the marked relative decline in theproportion of total revenue accruing to the central government, the scope for such redistributivemechanisms is limited. Options for such mechanisms are discussed (Chapter 1, para 1.27 and Chapter6, para 6.21).

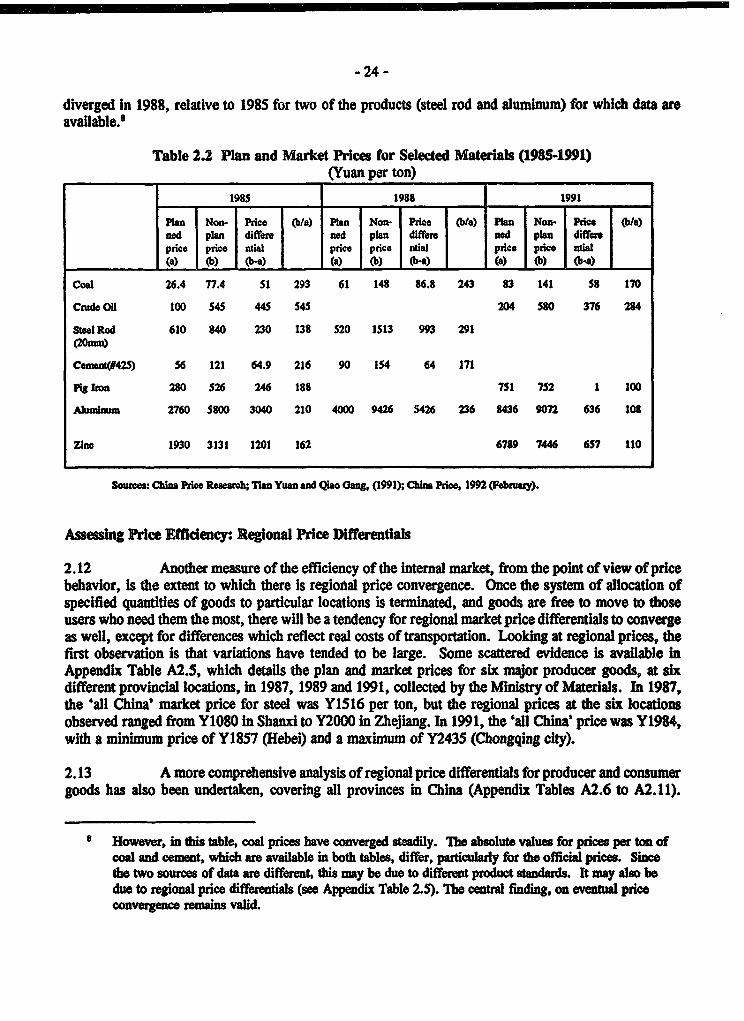

vii. Using a series of measures of price behavior, an analysis shows that there has bee asignificant convergence between plan and market prices (Chapter 2, parn 2.8 to 2.10). Recent price

- xiii -

reforms in early 1993 have consolidated and extended the progress achieved with the dual track system.This shows that China has achieved notable success in replacing the allocative mechanisms of the planningregime with allocation through the market. The reduction in the proportion of goods allocated throughthe plan, as well as the increase in the proportion of goods subject to market prices, has been remarkable.

viii. Progress is less evident in the regional integration of China's markets. Despite the rapiddecline In the number and level of price controls, there are still persistent regional price differentialsamong both producer and consumer goods (para 2.12 to 2.16). Price convergence across regions hasbeen slower and more erratic than convergence between plan and market prices, for specific products.Some divergence in regional prices may have emerged as a consequence of the lifting of price controlsand the reflection of real costs of transport in prices. But eventual price convergence (with transport costadjusted differentials) would still be expected. The present differentials suggest spatial segmentation ofthe internal market.

ix. An analysis of domestic Interprovincial trade In goods indicates that the share of tradeflows across provinces, relative to total retail trade, have declined in many provinces, and on aggregatefor the country as a whole (para 2.17 to 2.29). These declines have occurred at th3 same time as theshares of external trade, and inflows of external investment, have increased In most provinces. From1985 to 1992, overseas exports and imports grew at 17 and 10 percent per year, respectively. Whiledomestic interprovincial trade also rose in absolute terms, its rate of growth at 4.8 percent per year waslow relative to foreign trade and also lower than the 9 percent annual rate of growth of total retail sales.The findings suggest that individual provinces are tending to behave like independent countries, with anincrease in external (overseas) trade and a relative decline in trade flows with each other.

x. A part of the relative decline in internal trade could be ascribed to the reduction in theforced movement of goods under planning. Another explanation is that the partial deregulation of theoutput and selling price of some goods led to incentives to evade public procurement, over 1985 to 1988,in the period of the interprovincial 'trade wars'. Provincial authorities responded with the erection ofexport embargoes. With further relaxations in price and quantity controls, as well as the decline in theshort-lived demand boom, export embargoes became less significant.

xi. The downward trend in interprovincial trade, continuing untl the present, cannot beexplained only by these considerations and requires other explanations. Some relative reduction may bedue to an increase in intraprovincial production as well as consumption, due to the rapid growth intownship and village enterprises. Problems of numerous fees and fines, extracd on the road, legal aswell as illegal are also an explanation. The absence of overarching regulations on iteprovincial tradeimplies that decisions which may limit trade made at the provincial, or lower levels, cannot be easilyovertned. Difficulties of transportation by road as well as by rail also hinder the domestic flow ofgoods. Transport facilities have not grown as fast as output. Mimisterial and jurisdictional barriers haveaggravated spatial segmentation. Difficulties encountered in interprovincial payments and settlementmechanisms have also segmented the internal market.

xii. Cross-provinical investment flows have declined in relative terms (compared to the shareof foreign investments, and relative to provincial GDP) over 1985 to 1992 (para 2.54 to 2.60). The fiscalsystem, and the incentives and authority given to provincial and local governments to raise revenues,provide partial explanations. The separation of profits and taxes was accompanied by the introduction ofprofit retention, as well as an increase in local authorities' taxation powers. It is therefore to theadvantage of local governments to retain enterprises within their jurisdictions. InAtivs for

- xiv -

Interprovincial investment are also confused by the large number of special investment zones, with nmnyauthorized or unauthorized tax concessions.

xiii. Some progress is observed in labor mobility in terms of increased flexibility in the hiringand dismissal of labor in state enterprises, and in determining wages and bonuses. There is less progressin the regional mobility of labor, despite the recent relaxation of urban grain rationing In several locations(para 2.74 to 2.88).

xiv. Foreign exchange had been constrained in its mobility across regions, as regionaldifferentials in swap markets indicated. Recent changes, introduced on January 1, 1994, indicateconsiderable imporvement in the flexibility of access to foreign exchange, as well as simpliflcation of thetrade and exchange control regime. How the new system will operate in practice can only be determinedafter it has been in place for some months. In conclusion, there has been considerable progress in thesubstitution of planned allocation by the price mechanism. Yet, markets for both goods and factorsof production still show signs of regional fragmentation.

xv. The withdrawal of the state from allocation and pricing decisions was not accompaniedby a parallel withdrawal of the state from distribution (Chapter 3, para 3.7 to 3.12). The share of thestate sector (excluding collectives) in distribution, as measured by both the value of retail trade and thenumber of distribution units increased in absolute terms over the last decade. While there was a relativedecline in the state's share over the early years of the reform (1978 to 1985), there was little perceptiblechange from 1985 to 1991.

xvi. Yet, in aggregate, retail trade grew and the level of retail trade services available nowput China above the former Soviet Union, though still below Western Europe (Table 3.3). Innovativechanges have also occurred in the distribution system, in response to other changes in marketmechanisms. They illustrate that the state sector has been able to respond to competitive stimuli and thatchanges in operation are being effected despite relatively gradual changes in ownership. The combinedrequirements of capital-intensive infrastructure and the need to build information networks across largeregions and many entities may make it more difficult for the non-state sector to enter the business ofdistribution, relative to production.

xvii. While the evolution of new forms of distribution in China has been in the right direction,there is scope for better management of distribution functions of existing warehouse facilities, improvedinventory management, delivery scheduling and the development of backchannels for the recycling ofused materials (Annex 3.1).

xviii. In terms of the organization of the distribution of producer goods, some enterprises underthe leadership of material and equipment bureaus and their sponsor, the former Ministry of Materials andEquipment (now a part of the Ministry of Internal Trade) are involved in a wide range of activities,including industry, real estate and construction. This diversification has been in part a response to poorprofitability from their main task of distribution, due to price controls and allocative obligations. Thetwelveenterprise structure of many materials bureaux results from the takeover of the marketng anddistriltion functions of some production bureaus, with agreements to maintain their structures intact.This 12-enterprise structure has developed variations in some areas and firther flexbility is encouragedto adapt to local industrial needs.

- xv -

xix. Some of the warehouses owned by tha materials bureaus are old, with inadequateprotection against the elements, leading to spoilage and damage in storage. The location of the newfacilities at the sites of existing storage centers is not optimal. Many warehouses today are located inurban areas where land is scarce and expensive in terms of its opportunity cost. The present level ofmechanization of materials handling and computerization of order placement and inventory managementis very limited. Due to a variety of causes, which may Include internal management and administrationas well as market conditions, the financial condition of some materials bureaus is reported to beprecarious and should be analyzed.

xx. Difficulties caused by trade barriers and distribution problems are compounded by realbottlenecks in transport (para 3.51 to 3.65). The demand for 200 million tons of freight (around 10percent of freight capacity) was estimated to be unsatisfied in 1989. China's rate of investment intransport, at around 1.3 percent of GNP, compares unfavorably with other developing country ratios, of2 to 3.8 percent of GNP (para 3.56). Producer goods depend largely on the railroad system, thatsuffered from underinvestment due to limited revenues resulting from low passenger and freight tariffs.Recent successive raises in tariffs are expected to improve the profitability of the system. The assignmentof freight quotas to specific producers or users also distorted the prices of commodities requiring railfreight.

xxi. On road transportation, the regulation and administration of the trucking business is anissue of concern. Although the entry of new operators of trucking services has grown easier, and pricinghas become more flexible since 1983, there is still overlap in the functions of the multiple agencies whosepermits are required for licensing and registration (the local Transportation Bureaux as well as the PublicSecurity Office). There are also constraints on the time period and permitted uses of 'own account'trucks. Deregulation of trucking tariffs has taken the form of 'decentralized regulation', with the transferof the authority for setting tariffs to the to local Departments of Communications. Consequently, thereare now wide regional variations in tariffs.

xxii. The development of trucking operations is constrained by the lack of freight forwardingand consolidation centers and the limited development of intermodal transportation systems. Such systemsrequire the development of containerized shipping, which China is now beginning to explore.

xxiii. A remarkable number of commodities exchanges have been established in the last twoto three years, in grain, non-ferrous metals, petrochemicals, and agricultural commodities such as rubberand sugar (Chapter 4). A new framework of supervision for the new exchanges was announced, on Nov.4, 1993. The registration of exchanges remains the responsibility of the State Administration of Industryand Commerce, but the responsibility for their supervision has been assigned to the State CouncilSecurities Commission. Day to day administration of such supervision will be entrusted to the ChinaSecurity Supervision and Administation Committee. After scrutiny by this body, all exchanges will bere-registered with the SAIC. There have been wide differences in the operating rules of the variousexchanges. Some regulations (concerning margin deposits and fees) have been at inappropriate levels.Essential elements of commodities market regulations (such as Pidelity funds) did not exist. It is hopedthat under the new framework these difficulties will be resolved.

xxiv. Continued intervention in activities related to the exchange of commodities, such as settingprice ceilings or floors (as in the case of the Zhengzhou grain center), warehousing (through the provisionof differential subsidies, in the metals trade) raises the risk of either undermining the price uncertaintyon which such exchanges depend, or raising the pressure to continually increase government subsidies,

- xvi -

as subsidies are transferred through arbitrage to all market participants. The recent operation of thecommodity exchanges emphasizes the possibility of 'proxy markets' arising in cases where continuedgovernment intervention persists.

xxv. The most striking example provided here of the effects of controls in one market on therest of the economy is the case of foreign exchange speculation through trade on the metals exchanges.If exporters and importers do not have free access to foreign currencies, and there are markets which dealin forward and futures contracts for internationally tradable commodities, these markets will reflectexpected movements in the foreign exchange rate. Hedging or speculative transactions in foreign exchangebecome part of the raison-detre of such exchanges. The large and growing volume of trade on theexchanges suggests that the foreign exchange market is more constrained today than apparent, and pricesignals are consequently distorted (para 4.44 to 4.49).

xxvi. A key issue which China must confront in its experiments with new market forms, andspeciflcally in the area of establishing commodities markets, is that the present large numbers of suchexchanges will probably diminish over time due to a number of factors; the improvement in internalcommunications, closer integration with the world economy and consequently closer links with exchangesoutside the country. Speculative activity will fall as the 'zero-sum' nature of such trade is betterunderstood. The establishment of independent markets, especially in foreign exchange, will hasten thisprocess. There is a likelihood of waste in the establishment of several new exchanges, especially in viewof the presently preferred capital-iatensive methods . f screen-trading which is an expensive option toadopt in the initial stages of an exchange.

xxvii. There is room to improve the efficiency and reduce the cost of trading practices (para4.33 to 4.40). The metals Exchange at Shanghai is a fully computerized screen based system, where theexistence of a trading floor is redundant. The Shenzhen exchange is a combination of an 'open outcry'system, with a large central screen recording bids and buys. In both cases, a simple open outcry ringdealing system may have been preferable on cost grounds. The computerized information entryrequirements slow the trading process and will become a hindrance as the pace of trading accelerates. Italso impedes the growth of trade by 'market makers', trading on their own account and providingessential liquidity to the system. While cultural reticence may be a factor against the adoption of 'openoutcry', its cost advantages for a newly-established should also be considered. In the future, onceexchanges are well-established, they could evolve towards more expensive screen-based trading.

xxviii. China is aware of the need to safeguard competition and develop regulations forcompetitive markets. A law on competition was approved in September 1993, and a new law on consumerprotection has also been adopted. Laws to safeguard market competition through the protection .f patentsand trademarks were approved earlier. The problem of monopoly in China is not pervasive, unlike manyother transforming socialist countries. Consequently, the emphasis should be on market 'conduct' issues,such as the the control of unfair trading practices rather than market 'structure' issues, such as enterprisesize, or mergers and acquisitions. China is today experimenting with the fostering of links betweenenterprises and the formation of enterprise groups and some of the experiments are likely to increaseoperational efficiency, and facilitate interregional investments (5.13 to 5.27).

xxix. Procedures for establishing new enterprises are still onerous (para 5.35 to 5.46). Manydifferent agencies' permits are required and a large discretionary role is given to some agencies, such asthe State Administration for Industry and Commerce (SAIC). Ihe role of the SAIC has expandedenormously over the last few years and it may be undertaking the work entrusted to several different

- xvii -

agencies in market economies (including licensing new establishments, safeguarding competition andregistering 'kew commodity exchanges).

xxx. A large agenda for legal reform is now under preparation as part of the Five-year planfor economic legislation. Many differen. agencies will tackle different aspects of reform, and the processcould be slow, especially In view of the need for drafting assistance required by some of the agenciesconcerned. The World Bank has offered assistance to the Chinese government in this process of legalreform through an Economic Law Reform Project which is currently under preparation.

C. Recommendattons

xxxi. Key recommendations to help China accelerate its movement towards the adoption ofwell-functioning internal markets and an integrated domestic economy are presented below. These aregrouped under four broad heads: (1) increased market integration through trade, price and factor mobility;(2) enhanced efficiency in distribution; (3) better functioning of new markets; and (4) a more appropriateregulatory framework.

Market Integration

xxxii. China's authorities should ift residual controls on prices. So far, they have emphasizedthe prices, or allocation, oa goods. They must now achieve further progress with the decontrol of theprices of both critical consumer goods and producer goods still subject to the Plan and then move towardsprice and quantity restraints on services and on factors of production.

xxxiii. Concerning regional trade policies and the Integration of regional markets:

(1) China must establish a general framework of legislation on interregional trade andprohibit trade barriers, such as internal 'export' embargoes or 'import' restraints;

(2) The myriad fees and fines levied on interstate (and intercounty) trade must be harmonizedacross provinces. A nationwide standardized list of genuine charges should be prepared.The transparency of the procedure followed in each local jurisdiction can be improvedthrough the collection and periodic publication of schedules of tariffs, taxes and othercharges, at a provincial or national level;

(3) Authorities should standardize the collection agencies for fees and publish details ofpersons or agencies responsible for collection; and

(4) Once a list of genuine fees is established, authorities must stop the collection of illegalcharges.

xxxiv. In the context of capital mobility and interprovincial investments, the government should:

(1) Condnue and extend the separation of profits and taxes;

- xviii -

(2) Reduce the Incentives to provincial or lower level authorities to restrict the transfer ofenterprises to other locations through the stricter enforcement of the rule of tax accrualto the home province. Establish an appropriate monitoring system for this; and

(3) Stop the legal and illegal circumventions of the interstate income tax regulation resultingfrom the establishment of special 'zones'. While many illicit zones have receinly beenremoved, the 200-odd which have been permitted to remain are still a non-negligiblenumber.

xxxv. To ensure the equitable distribution of the, benefits of the gaias from increased internaltrade and factor mobility, the Government should consider the establishment of an appropriateredistributive or compensation mechanism. Alternative mechanisms incluee the European Community'sStructural Funds, or the fund suggested in the Bank's recent Budgetary Expenditure study (see Chapter6).

xxxvi. Attention should be turned towards regulations which permit an increase in the regionalmobility of labor. One important reason for restricting labor mobility in the past was urban grainrationing. Some rations have been lifted in early 1993, and many price controls on consumer essentialssuch as grain and edible oils. This is an appropriate moment to begin to lift restraints on labor mobility.

xxxvii. In the context of the recently unified exchange rate, care should be taken to ensure freeaccess to foreign exchange by exporters and importers through the banking system. Besides the widerimplications for efficiency this should increase foreign exchange mobility and also permit the newcommodities markets to fulfil their primary function.

DMbutton Syste

xxxviii. While the evolution of new forms of distribution in China have been in the rightdirection, there are still shortfalls compared to best practice in market economies. A detailed study ofcurrent distribution practices should be undertaken, to investigate the scope for better management ofdistnrbution functions of existing warehouse facilities, through (i) the reduction of partly-loaded truckshipments; (ii) the reduction oe +he number of times goods are handled or moved; (iii) improved inventorymanagement through more reliable shipping from producers and timely information from users; (iv) betterphysical management of warehouse space by arranging goods on a computerized customer order in theorder in which they will be picked up from warehouse shelves; (v) the introduction of 'cross docking'practices to permit vehicles bringing in supplies to be transferred directly to delivery vehicles topurchasers, and (vi) the development of backcbannels for the recycling of used materials.

xxxix. Concerning the range of operations of the former MME and the organization of materialsbureaux, China should:

(1) Accord greater flexibility to the MME in their primary activities, in terms of theprocurement, pricing and distribution of the goods they carry, through the acceleratedlifting of price controls and allocation obligations on these activities;

(2) Discourage the branching out of materials bureaux into unrelated and speculativeactivities such as real estate purchase or construction;

-xix -

(3) Permit the present twelve-enterprise structure to be more flexible and better adapted tothe needs of local industry; and

(4) Encourage value-adding activities at the materials bureaux, to provide additional qualityor convenience for buyers. But research on products distributed may be better integratedwith production enterprises than with distribution enterprises.

xl. Actions to increase future competition through new entrants are also required. Localbureaus should be permitted and encouraged to expand into other localities, and entry into distributionby individuals and collectives could also be encouraged, for example by permitting them to leasewarehouse space from government bureaus.

xli. Detailed studies of the physical facilities of the distributionsystem are recommended. Thecosts and benefits of investing in improved facilities must be evaluated. The evaluation should examinethe potential loration of any proposed new facilities, as well as the relocation of existing urbanwarehouses to points outside major cities. The study should also appraise the costs and benefits of themechanization of materials handling and the computerization of order placement and inventorymanagement.

xlii. A study of the financial condition of the materials bureaus and an esdmation of the extentto which the decline in profitability of the materials bureaus is due to losses made on goods which remainunder planned allocation should be undertaken. The expected improvement in profitablity at materialsbureaus, with recent reductions in the number of goods under planned allocation or controlled prices,should then be calculated. The examination of the profitability of the materials distribution system shouldalso include an evaluation of cash-flow and inventory management, and should be launched as an exercisewhich combines marketing as well as financial expertise. Since the last major round of price decontrolshas just been concluded, this is an appropriate time to begin such an undertaking.

xliii. Detailed recommendations on transport are available in other reports. This report pointsto some key issues affecting distributional efficiency. Regarding railways, the government should:

(1) Undertake successive increases in railway tariffs, to their long run marginal cost levels,to improve profitability and ensure that decisions on industrial location are based on theright parameters; and

(2) Phase out the assignment of freight quotas to specific producers or users, to avoiddistortions in the prices of commodities requiring rail freight.

xliv. On the regulation and administration of the trucidng business, China should:

(1) Remove the overlap in some of the functions of the multiple agencies whose permits arerequired for licensing and registration (the local Transportation Bureaux as well as thePublic Security Office);

(2) Gradually remove constraints on the time period, and permitted uses, of 'own account'trucks;

-xx -

(3) Deregulate altogether the 'decentralized regulation', of trucking tariffs (which has led tothe transfer of the authority for setting tariffs to the to local Departments ofCommunications, and consequent wide regional variations in tariffs);

(4) Develop freight forwarding and cousolidation centers to encourage 'own account' truckersby serving as collection points for goods shipped in less-thaa-truckload quantities; ar4

(5) Further promote the development of containerized shipping to facilitiate intermodaltransportation systems.

New Marets

xlv. A first concern in this area is completion of the overal framework of supervision for thenew exchanges, to be adopted by the new CFMC. The new legislation should take into considerationalternative approaches to the regulation of commodities exchanges, presented in the report (pp 109).Second, once the umbrella legislation is in place, the task of reconciling the differences in operating rulesof different exchanges must be undertaken. Areas of the present legislation which require attention are:the nature of the supervisory Board, the regulations on participation, on transaction fees, and margindeposits. The establishment of provisions for a Fidelity Fund (for protection against default by brokers)is also recommended. Third, the role of the SAIC, as the body best suited to handle the registration ofnew exchanges, should be reevaluated. The SAIC is already considerably overextended and this is a taskrequiring specialized knowledge. In this context, the regulations, recendy adopted by the SAIC, fortraders and brokers on the exchanges, may restrict the number of participants on the new exchanges, andshould therefore be reviewed. It is more desirable to have a smaller munber of exchanges, but with arelatively large number of participants on each, than vice versa. Fourth, the likelihood of considerablewaste in the establishment of several new exchanges, especially in view of the presently preferred capital-intensive methods of trading, must be recognized and more exchanges should only be established if shownto be sustainable in the medium term.

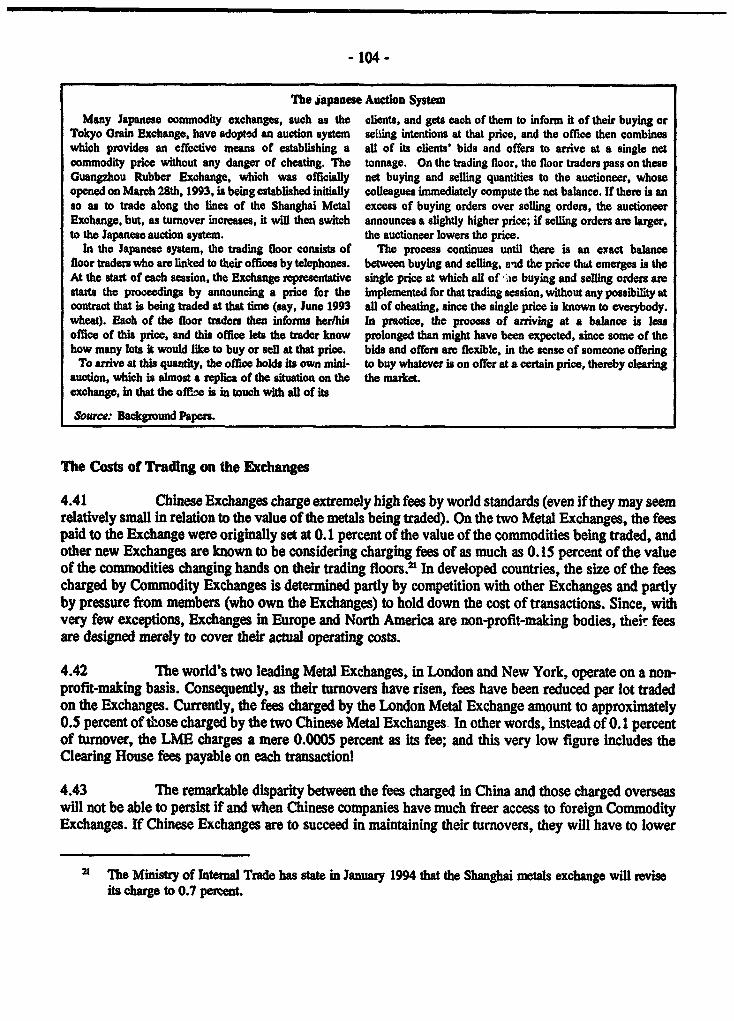

xlvi. In terms of the physical organization of the new exchanges, the following improvementscan be pointed out. First, the adoption of a simple open outcry ring dealing system should be considered,as an alternative to the present computerized system, not only in all new exchanges, but also in theexisting ones, ast the time when the next increase in computer requirements is reviewed. Objections to'open outcry' based on their vulnerability to fraud, are exaggerated. However if this a majorconsideration, the 'Japanese Auction System' could be introduced, in which there is a single price for allbuying and selling orders for a given trading session.

xlvii. Meanwhile, trading costs can be reduced with the utilization of the facilities at a giventrading center by more than one exchange. Since most exchanges at present do not trade every day of theweek, or all hours of the day, this should be feasible.

Ma*et Regukaion

xlviii. FMrst, there is little evidence of monopoly, in the sense of industrial structure, in China.The regulatory emphasis should therefore be on market conduct issues. Care must be exercised to notsnuff out early experiments with enterprise groups, with unduly restrictive regulations on mergers.

-xxi -

xlix. Second, entry for new enterprises should be simplified. The administration of the processof entry and exit may sometimes be as important as the law. Third, the functions of the SAIC and otheragencies should be redefined to make them more transparent and reduce the discretionary element presenttoday in the granting of approvals. Fourth, some of the functions of the SAIC (such as the monitoringof unfair practices, monitoring cases of fraud in labelling and trademarks, and taking care of enterpriseentry requirements), should be delegated to more specialized agencies in the future. Finally, it shouldbe noted th.at a proliferation of new laws, sometimes conflicting in scope, or in terms of agenciesconcerned, could be counterproductive. Care must also be taken to counter any tendencies to permit theinterests of the agencies drafting the laws to dominate the new draft legislation.

1Market Segmentation and Market Development

A. Introduction

1.1 China's commitment to the creation of a market economy, which has been the centralplank of its program of economic reform, received new emphasis in the 8th National People's Congressof March 1993. The congress ratified the decision, already taken at the 14th Party Congress of October1992, to develop a 'socialist market economy', shifting decisively away from central planning. TheConstitution of 1982 was amended to emphasize this shift of policy towards the development of 'socialismwith Chinese characteristics'. These decisions reflect the culmination of a series of policy shifts whichbegan in December 1978, when the Third Plenum of the 11th Party Congress announced for the first timethat planning and markets could be compatible. Over the subsequent period, futher policypronouncements steadily moved China towards the goal of an increase in the role of its markets and adecline in central planning.'

1.2 Shifts in administrative responsibility had been introduced in parallel to the changes inpolicy direction. In 1982, internal distribution functions for consumer goods were consolidated underthe Ministry of Commerce, which merged the Ministry of Grains and the National Trading Corporationwith the former Ministry of Commerce. In 1988, the Ministry of Materials was established, by adecision of the State Council to gradually abolish the material supply and marketing organizations ofindividual ministries, and consolidate the supply and marketing responsibility of producer goods at thenational level though enterprises under the new Ministry. Finally, in 1993, at the 8th National People'sCongress, it was decided that the erstwhile Ministries of Commerce and Materials would be merged ina single new Ministry of Internal Trade.

1.3 The development of the internal market was fostered by a series of mechanisms intendedto reduce the scope of state intervention. A first key element of the strategy was progressive pricedecontrol, through the introduction of three categories of prices, planned prices, guidance prices andmarket prices and the gradual movement of goods from more regulated to less regulated categories,together with 'dual track' pricing, introduced in 1985, which permitted output above certain target levels

I Following the success of agncultural maiket reforms after 1979, the 12th Congress of the Party aimedto use nadcet regulation as a supplement to planning, and in October 1984 it called for a furtherreduction in the scope of madatory planning and its replacement by 'guidance planning'. The 13thCongress of 1987 adopted the goal of 'letting the state regulate tL3 market, and letting the market guidethe enterprises'. The evolution of the politics of market reform is taced in White (1993).

-2-

to be sold on the free market.2 The proportion of goods in total domestic retail trade subject to plannedprices fell dramatically between 1978 and 1991 (Figure 1.1), in favor of 'guidance prices' and freemarket prices. Goods subject to planned prices have fallen considerably aurther, with recentannouncements in early 1993 of the relaxation of controls on prices of grain and edible oils.

Figure 1.1 Ieduot1on In Scope of Price controls(Peroentage)(1978-1991)

L1 t1 t993

1 Iliad Ples 1 Gulded Priew UmI Fe" Pdie

1.4 Second, the allocation of goods was progressively moved out of the mandatory plan. In1980, 90 percent of industrial goods, and 837 production materials were allocated under the plan system.By early 1993, the proportion of industrial goods under the plan had declined to 12 percent and thenumber of production materials in this category has been reduced to 11. At the same time, consumergoods whose planned allocation was administered by the Ministry of Commerce declined in number from274 in 1978 to 14 in 1993. Third, a diversification of distribution systems and channels was graduallypermitted. Formerly, the system of unified purchase and sale of consumer manufactures, as well as theunified purchase of farm products, by designated government agencies, accounted for virtually all sales.3

Sales may now be made to private purchasing agencies, or directly to consumers. A variety of newforms of markets are evolving as a consequence, including sophisticated commodity exchanges andcomprehensive as well as specialized distribution centers.

2 Explored furtr in Chapter 2. Descriptions of the progress of price reform in China may be tracedthrough Byrd (1987), Wu and Zhao (1987) and World Bank (1990a&b). Sectodal details are given inWorld Bank (1992) 'China: The Achievements and Challenges of Price Reform', Albouy (1991) and acompanrtive pepective is offered in RIjaran (1991).

3 The Unified Purchase system dated from 1951, wben it was introduced with an Implementing Decisionof the State Council. Manufachtued consumer goods were classified under three categories, accordingto whether they were deemed to be essential goods, items of mass demand, or others. The purchaseand sale of goods in the first two categories were handled by the central government, while goods inthe third category were handled by local governments. Agrcultural goods were similarly grouped andgoods in the first two categories were subject to 'monopoly purchase' and 'designated purchase',respectively, at statedetermined prices. Goods in the third category were subject to purchase atnegotiated prices.

- 3 -

1.5 At the same time as these measures to improve the functioning of the internal market werebeing introduced, China also adopted an 'open door' policy towards foreign trade and investment. It Isclear that China has made rapid strides in the development of its external trade. In recent years, from1985 to 1992, exports and imports grew at 17 and 10 percent per year, respectively. While domesticinterprovincial trade also rose in absolute terms, its rate of growth at 4.8 percent per year was lowrelative to foreign trade, and also lower than the 9 percent annual rate of growth of total retail sales(Figure 1.2). As a consequence, while the share of external trade in GDP increased, the share ofinterprovincial trade in domestic retail sales declined.

Figure 1.2 External and Domestic Trade Shares

GBX 7~~~~~~~~ox.40o% . t%

50%307o .. 1- . 640% *- -

ZoSa *-** -11- 111|1-- -1 . 3 80% . -_lox. I

1985 1988 1990 1991 1992 1985 1988 1990 1991 1992

i hternal Trade / GDP I Dro= Trade/ReLSalee

fomwe Appendix Table P.10 nd WM Bank hti

1.6 Together with the finding of the relative decline in domestic trade, there are reports ofdifficulties encountered in the processes of internal trade, both in terms of the difficulties of establishingnew forms of markets, as well as obstacles created by authorities in some provinces, which restrict theinflow or outflow of goods and factors in their provinces. These difficulties are compounded by realbottlenecks in transport, storage and distribution. It has recently been estimated that the demand foraround 200 million tons of freight, or around 10 percent of freight capacity, remained unsatisfied in 1989.China's rate of investment in transport has averaged around 1.3 percent of GNP, while other developingnations' investments in transport ranged from 2 to 3.8 percent of GNP.4

1.7 The limited extent to which internal trade exists has sometimes been attributed to theuniquely 'cellular' structure of the economy.' Though geographically vast, it has been pointed out thatattempts at achieving the local self-sufficiency emphasized in the Maoist era led to a duplication ofindustrial pattern by province. The inefficient location of industry was compounded by dispersal resultingfrom the 'Third Front' policy, of moving industrial enterprises towards the interior. In later years, (aspointed out today by some government officials), with increasing dencentralization, local governmentofficials sometimes established 'repetitive and non-economic industries with a view to increasing local

4 World Bank (1992). Report No. 10592-CHA.

5 Commented on by Donnithome (1972), and later by Lyons (1987). Recent evidence, particularly in theprovinces around Shanghad, has been described by W. Huang (1992).

4-

fiscal revenues, or local employment, or even to "chase achievements" during their official careers. In1987, 80 factories in 21 provinces produced refrigerators, over a hundred factories in 26 provincesproduced televisions and 300 factories in 28 provinces could produce washing machines. The pattern wasreinforced by the nature of the planning mechanism and the decentralization of investment decisions inthe early 1980s at the provincial level. As a consequence, industrial plant is frequently undersized. Onereason why provincial and local authorities have sometimes limited the entry of goods from otherprovinces is to attempt to shelter these small and relatively inefficient enterprises. This protection resultsultimately in higher prices for consumers and inefficient production. While there are now some signsof change, impediments to regional trade flows still exist in a variety of forms. A major potentialeconomic advantage, the large internal market, is diminished as a consequence.

Factors Affecting Internal Markets

1.8 As the preceding paragraphs suggest, there is a wide range of factors which determinemarket structure and affect the functioning of markets, beginning, first, with a broad group of governmentpolicies. Most important among these are decisions regarding resource allocation and resourcedistribution systems, and price determination systems. Decisions to remove goods from the system ofcentrally-planned procurement, allocation and distribution implied by the unified purchase and salessystems represent major moves towards the creation of markets. The relaxation or removal of pricecontrols, which permits prices to be determined by the forces of market demand and supply, is also acritical element of market creating policies.

1.9 Another key factor in the creation of efficient markets is the spatial integration of marketswithin an economy. The geographical size of China's internal market offers huge potential benefits fromsuch integration, in terms of increased efficiency in industrial structure as well as in the deployment offactors and pricing of goods. The policies affecting the realization of market integration are those whichrelate to the mobility of goods and factors of production. The extent to which goods, or factors ofproduction such as labor and capital, are permitted to move freely within the country depends not onlyon the establishment of distribution systems, but also on both national and local level policy decisions tofacilitate, or at least allow, their movement. In international trade, such constraints on trade flows ingoods take the form of tariff or non-tariff barriers. In internal trade, tariff barriers in the form ofcodified specific or ad valorem levies on goods entering or leaving provinces are rare, within a country.6

In the case of China, there are no such formal tariffs, but there many accounts of ad hoc charges, feesand tolls on goods entering or leaving provinces, and in economic terms their equivalence to tariffs maybe established. Moreover the uncertainties created by the ad hoc nature of some of these charges and thedifficulties they add to interstate transactions constitute a form of non-tariff barrier to trade. Additionalnon-tariff barriers take the form of policies such as procurement guidelines, at the levels of provincialor lower level govermments, which may restrict imports or exports.

1.10 Both central and lower level government policies also affect factor mobility. The mobilityof capital refers to investment flows as well as credit flows, across provincial boundaries. Capitalmobility is essential for efficient resource allocation in a market economy, if investment is to flow intoits most productive uses, and in the most geographicaliy suitable areas. Labor mobility includes the

I In India, however, there is an interstate 'octroi', which takes the form of an ad valorem sales tax ongoods crossing state boundaries. bItersfrte sales tax registrion procedures are also cumbersome andact as a de facto constraint on intemal trade.

ability of both skilled and unskilled labor to seek jobs in alternative occupations and locations, alsopermitting industries to have access to the labor skills they require. Policies affecting the developmentand functioning of markets for capital and labor are therefore integral elements of the creation of anefficient internal market.

1.1' ~In additional to these policies, the functioning of the internal market will increasingly beaffected by the regulations of the government which monitor market behavior to safeguard competitionand guard against the abuse of market power. The issues alluded to here lead to the question of thefuture role of the government in the support of the market economy. As the government retracts fromits close involvement in market administration, its role in a more liberal market requires definition.While the government may no longer be setting prices, there may be a need for monitoring price settingin some contexts, for example, if there are possibilities of monopoly or oligopoly. This requires thecreation of a legal framework which permits this to be undertaken, as well as the setting up, oreinforcement, of appropriate agencies to perform these functions. The reduction in the role of state

planning also requires the proper functioning of contractual mechanisms, as well as the enactment andenforcement of mechanisms to protect consumers, for example against fraudulent trade or falseadvertising.

1.12 Finally, in parallel to these policies and regulations, the physical framework for transportand communication that permits the flow of goods and factors across the country will also criticallydetermine how well the market functions. At present China does not have sufficient capacity in itsransportation system to sustain its high rates of growth, and transportation is a particular impediment tothe development of an internal market, leading to production stoppages due to lack of inputs, the holdingof excessive inventory, and the spoilage of perishable goods, awaiting shipment.

Objectives of this Report

1.13 The everall objective of this report Is to evaluate the extent to which China, in its processof transition towards a market economy, has really been able to establish well-functioning and efficientmarkets which transmit accurate signals to economic agents in terms of production decisions and factorallocation, and permit the efficient exchange and distribution of goods. To this end, the report examinesthe present efficiency of markets and evaluates policies which affect market formation. Both the regionalor spatial aspect of market functioning, and the 'vertical' issue, of the movement from plan to market,are exaniined. Following a policy evaluation, the report analyzes 'real' aspects of market formation, interms of the new systems for allocating and distributing goods, which have evolved in the aftermath ofthe diminished role of planning. The present framework of regulation for the new markets is alsoexamined to evaluate its adequacy in the changing enviromnent.

1.14 In the following section, the report begins by pointing out the potential benefits of well-functioning and regionally integrated internal markets and shows how greater market integration has beenrealized in other countries. In this context, the report examines China's present industrial structure andshows that there is little evidence, so far, of a well-integrated structure, and that, relative to othercountries, China appears to be below its potential.

1 .1S Next, the report aims to analyze and evaluate policy measures which affect the functioningof the internal market (Chapter 2), including, first, policies relating to the price mechanism, and second,policies direcdy affecting the iterregional flows of goods and factors of production. The report showsthat, despite some success in the integration of plan and market pricing, regional integration, in terms

-6-

of the regional price convergence, has met with less success. Moreover, regional flow of goods, as wellas interregional investments and capital flows, appear to have declined, at least relative to the growth oftotal retail sales, or provincial GDP. Issues relating to regional mobility of labor are also examined,particularly in terms of recent developments, which suggest that there has been some progress in thisdirection, although further gains may be realized.'

1.16 Third, on the real side, the report evaluates changes in the distribution system and pointsout its present botdenecks (Chapter 3) It shows that the role of the state remains surprisingly large interms of distribution, despite Its withdrawal from planned allocation. However the state distributionmechanisms themselves have adapted to the new market environment While the evolution of new formsof distribution in China has been in the right direction, there a&e still constraints and limitations,compared to best practice in market economies, and areas in which Improvements may be achieved arepointed out. Constraints to distribution caused by transportation difficulties are also examined.

1.17 One striking development in Chinaes evolution towards a market economy are itsambitious recent experiments at setting up new forms of markets, in particular, the commoditiesexchanges, some of which engage in not only spot, but also forward and futures transactions. Aremarkable number of these new markets has been established in the last two to three years, notably ingrain, non-ferrous metals, petrochemicals, and agricultural commodities such as rubber and sugar. Thepresent report focuses particularly on the two non-ferrous metals exchanges as examples (Chapter 4).The report points out reasons why these markets are in many cases not functioning as intended. Areaswhere the efficiency and regulation of these markets could be strengthened are discussed. The report alsoprovides a demonstration of the links between markets for commodities and the market for services andforeign exchange. One of the difficulties faced by China, in its present situation of partly regulated andpardy liberated markets is that 'proxy markets' are beginning to evolve, where prices in liberated marketssometimes subsume the effects of price or quantity constraints in more controlled markets. Anotherdifficulty is the continued govermment intervention in different areas of price setting.

1.18 Finally, turning to market regulation, the report aims to provide a first assessment of theelements of the legal framework which are in place already, and to point out areas where extensions tothis would be required (Chapter 5). It also examines the institutions charged with the enforcement of thepresent system and evaluates their effectiveness, suggesting areas where reinforcement may be necessary.In the concluding chapter, the report pulls these different strands together to map out a feasible route forthe integration of the internal market, in terms of appropriate policy and regulatory instruments as wellas an adequate physical infrastructure. The report will discuss the specific 'real" and 'policy' variablesaffecing the mobility of goods and factors of production and will also describe the broader areas in thelegal and regulatory framework that require attention if internal competition is to be promoted.

7 Condrable attention has already been paid to this issue in a number of works, and therefore thetr_ant here is largely a summary of existing wor Evidence on the extent of labor mobility is_ummarized in World Bank (IM) Report No. 10266-CHA, and links between poverty levels and labormobility are discussed in World Bank (1992 October). Issues concerning the floating population ofurban labt and migrants are discussed in Banister (1989); Jefferson and Rawski (1992); Rutkowskd(1991); Solinger (1992 and 1992). New measures to enhance labor mobility are deAiled in Ody (1991).

-7-

B. The Potential Benefits of Internal Free Markets

1.19 The benefits of market determined prices and distribution systems are now wellrecognized in China. The case for allowing prices to be determined by demand and supply rests uponfirst, the long-run allocative efficiency that this will lead to, as resources flow towards their best uses,based upon price signals which reflect relative scarcities and needs; second, on the elimination of rent-seeking and parallel markets that arise, if prices are pegged at levels which do not reflect theirequilibrium values; third, a reduction in artificial losses (profits) in certain economic activities whereprices are set at levels below (above) their equilibrium values, and in addition, a reduction in direct orindirect subsidies that may be paid to loss-making economic agents, if these losses are due to policyconstrained prices. It is also accepted that greater flexibility in distribution systems which gives greaterflexibility to producers and consumers in procurement channels can reduce costs, cut inventoryrequirements and shorten delivery periods.

1.20 Economic gains from regional integration and its links to market efficiency are less wellunderstood and they are therefore the focus of this section. Regional economic integration, in its broadestsense, refers to the absence of economic discrimination and restrictions among economic agents of aregion." The process of integration requires the gradual elimination of economic frontiers and traderestricting instruments between territories within a region so that the mobility of goods, services andfactors is not constrained. This process of 'integration from below', can be reinforced by 'integrationfrom above', or the active promotion of economic cooperation between territories which may beencouraged through appropriate policies or institutions.9

Forms of Regional Integration

1.21 The core of most economic literature on regional integration refers to theories of customsunions. As a national unit, however, China is already a customs union, in the sense that it has a commonexternal tariff. The aim in the Chinese context is to go beyond the creation of a customs union, to theformation of a common market. The creation of a common market does not necessarily automaticallyfollow, within a customs union, as the example of Europe well illustrates. The customs union of the EECwas formed in 1957. However it was not till 1986 that the more ambitious goal of a 'market withoutfrontiers' was adopted, together with the wider goal of economic union in other areas. An economicunion, such as the EC aims to be, progresses beyond a customs union to monetary union and interlinkagesin internal (for example fiscal) economic policies. In China today, there is an anomalous situation wheremajor elements of economic union including a single currency and a common external tariff are combinedwith a lack of some basic features of a free trade area, such as the free movement of goods and factors.

8 In this chapter, thb analysis of regional integration is conducted at the level of intra-provincial tradeflow statistics. It would be interesting and valuable to examine intra-provincial trade flows as well,particularly in the larger provinces, to see whether similar patterns emerge. Lack of data haveprevented this from being included in the analysis.