Internal Audit Report on accounts Addl. District & Session ...

Upload

khangminh22Category

view

1download

0

_________________________________________________________

INTERNAL AUDIT MEMORANDUM

To: Senior Manager, Corporate Services Cc: Manager, Human Resource

From: Senior Manager, Internal Audit

Audit Project Ref: 11-2018/19 (02)

Date: 05 April 2019

Subject: Audit Report of Performance Management System

In terms of the Internal Audit Work Plan, approved by the Audit Committee, for the FY2018/19

an audit of the Performance Management System processes and controls was conducted.

The review focused on the design of system and processes within the Human Resource.

The purpose of this report is to provide management with an opinion on the internal controls

of Performance Management System to ensure that risks identified are appropriately mitigated

or managed.

We attach the final report for your management comments and action. You are requested to

treat the audit report with confidentiality. The distribution of the report to persons other than

those on the memo page should only be done after consultation with the Senior Manager,

Internal Audit.

The audit report has been structured as follows: -

Section A: Executive Summary Section B: Detailed report detailing the audit findings relating to the audit conducted

together with Internal Audit’s recommendations. Appendix A: Definitions of the rating classifications

Internal Audit Function follows a collaborative approach with management towards a shared

objective of strengthening the internal control environment of ELRC. In executing this

mandate, the audit report must provide an open and honest communication while

management will work proactively with Internal Audit Function in owning the control

environment.

Should you have any queries or comments relating to matters contained in this report, please

do not hesitate to contact the Senior Manager, Internal Audit at [email protected]

Yours sincerely

Senior Manager, Internal Audit

04 April 2019

Internal Audit Report – Performance Management System

2

Final Internal Audit Report

Audit of Human Resource’s Performance

Management System Internal Audit Reference: 11-2018/19 (2)

Internal Audit Report – Performance Management System

3

Table of Contents

1. Introduction

2. Background

3. Audit Objective and Scope

4. Results

5. Conclusion

6. Acknowledgments

7. Disclaimer

8. Distribution List

Internal Audit Report – Performance Management System

4

SECTION A - EXECUTIVE SUMMARY

1. Introduction

1.1. Internal Audit conducted a review of Human Resource’s Performance Management

System in terms of the approved annual audit plan. This audit aimed at testing the

effectiveness of system and processes currently in place and compliance with the laws

and regulations governing the Performance Management System.

2. Background

2.1. Managing employee or system performance and aligning their objectives facilitates the

effective delivery of strategic and operational goals. There is a clear correlation between

using performance management programs and improved business and organisational

results. 2.2. Performance Management System (PMS) is process of managing the performance of

the Council and individuals tasked with the duties. It includes performance appraisal and

employee development. Therefore, performance assessments help managers to

understand how well the organisation, divisions within the organisation and individuals

are performing. Clear indicators of performance allow clear targets to be set, and people

to be clear about what level of performance is expected, as well as describing whether

the required level of performance has been achieved, assisting also in allocation of

resources. 2.3. Performance indicators for individuals “must” be linked to the program’s objectives and

mandates. 2.4. To monitor the operations and practices of the Performance Management System,

Human Resource is guided by the Performance Management policy and procedure

manual, which sets out the standard practices, process flow description and

performance deliverables.

3. Audit Objective and Scope

3.1. The objective of this audit was to identify and test the design and operating effectiveness

of key controls in relation to:

• Reliability and integrity of PMS reporting information;

• Compliance with the Performance Management System policy and procedure

manual; and

• Effectiveness and efficiency of monitoring the MPS operations.

3.2. Our scope entailed the audit of the way Performance Management System is operating

to ensure that all transactions are processed accurately, promptly and with appropriate

authority, and compliance is maintained always, and was limited to processes and

controls outlined in the PMS policy and procedures for the period April 01, 2018 through

to March 25, 2019.

4. Summary of Results

For definitions of finding ratings, refer to Appendix A.

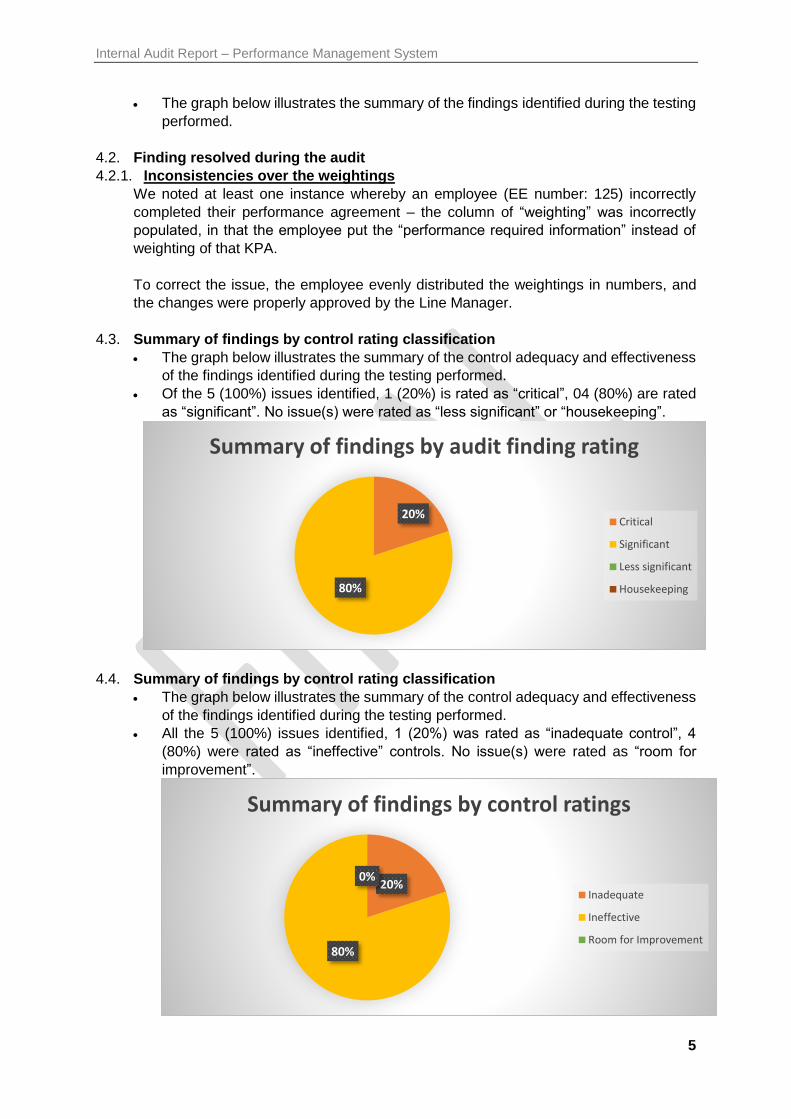

4.1. Summary of findings by audit finding rating

Internal Audit Report – Performance Management System

5

• The graph below illustrates the summary of the findings identified during the testing

performed.

4.2. Finding resolved during the audit

4.2.1. Inconsistencies over the weightings

We noted at least one instance whereby an employee (EE number: 125) incorrectly

completed their performance agreement – the column of “weighting” was incorrectly

populated, in that the employee put the “performance required information” instead of

weighting of that KPA.

To correct the issue, the employee evenly distributed the weightings in numbers, and

the changes were properly approved by the Line Manager.

4.3. Summary of findings by control rating classification

• The graph below illustrates the summary of the control adequacy and effectiveness

of the findings identified during the testing performed.

• Of the 5 (100%) issues identified, 1 (20%) is rated as “critical”, 04 (80%) are rated

as “significant”. No issue(s) were rated as “less significant” or “housekeeping”.

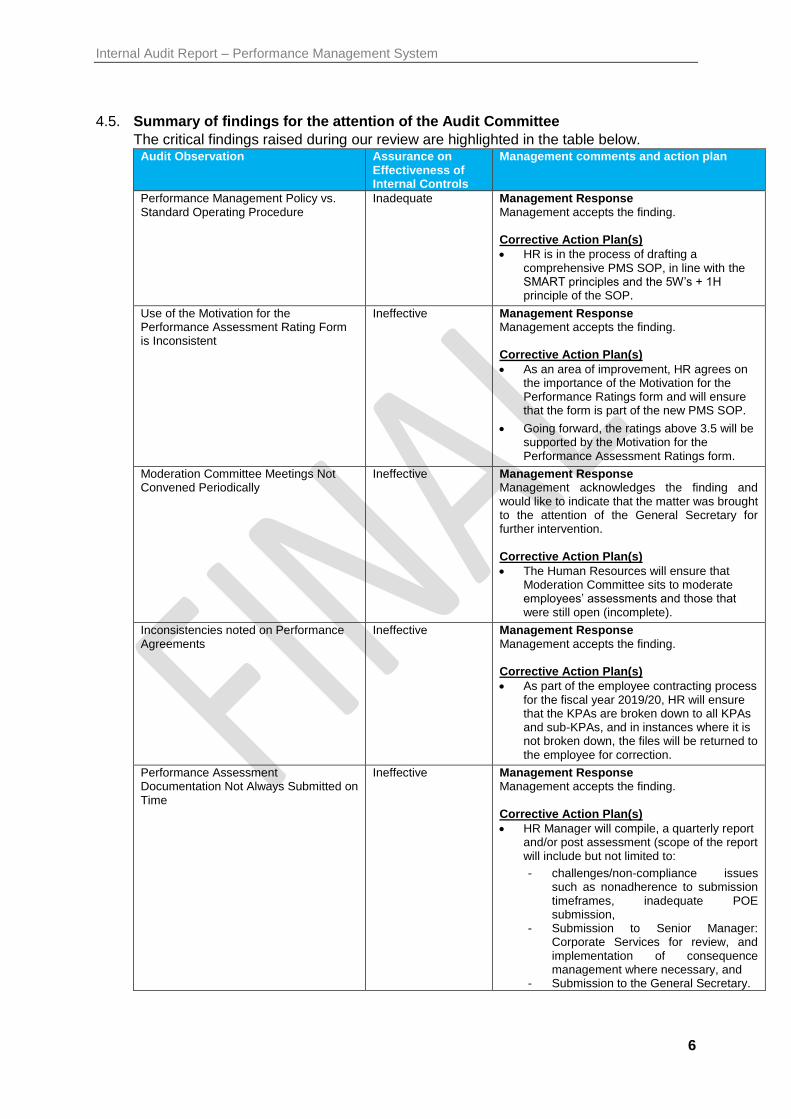

4.4. Summary of findings by control rating classification

• The graph below illustrates the summary of the control adequacy and effectiveness

of the findings identified during the testing performed.

• All the 5 (100%) issues identified, 1 (20%) was rated as “inadequate control”, 4

(80%) were rated as “ineffective” controls. No issue(s) were rated as “room for

improvement”.

20%

80%

Summary of findings by audit finding rating

Critical

Significant

Less significant

Housekeeping

20%

80%

0%

Summary of findings by control ratings

Inadequate

Ineffective

Room for Improvement

Internal Audit Report – Performance Management System

6

4.5. Summary of findings for the attention of the Audit Committee

The critical findings raised during our review are highlighted in the table below. Audit Observation Assurance on

Effectiveness of Internal Controls

Management comments and action plan

Performance Management Policy vs. Standard Operating Procedure

Inadequate Management Response Management accepts the finding. Corrective Action Plan(s)

• HR is in the process of drafting a comprehensive PMS SOP, in line with the SMART principles and the 5W’s + 1H principle of the SOP.

Use of the Motivation for the Performance Assessment Rating Form is Inconsistent

Ineffective Management Response Management accepts the finding. Corrective Action Plan(s)

• As an area of improvement, HR agrees on the importance of the Motivation for the Performance Ratings form and will ensure that the form is part of the new PMS SOP.

• Going forward, the ratings above 3.5 will be supported by the Motivation for the Performance Assessment Ratings form.

Moderation Committee Meetings Not Convened Periodically

Ineffective Management Response Management acknowledges the finding and would like to indicate that the matter was brought to the attention of the General Secretary for further intervention. Corrective Action Plan(s)

• The Human Resources will ensure that Moderation Committee sits to moderate employees’ assessments and those that were still open (incomplete).

Inconsistencies noted on Performance Agreements

Ineffective Management Response Management accepts the finding. Corrective Action Plan(s)

• As part of the employee contracting process for the fiscal year 2019/20, HR will ensure that the KPAs are broken down to all KPAs and sub-KPAs, and in instances where it is not broken down, the files will be returned to the employee for correction.

Performance Assessment Documentation Not Always Submitted on Time

Ineffective Management Response Management accepts the finding. Corrective Action Plan(s)

• HR Manager will compile, a quarterly report and/or post assessment (scope of the report will include but not limited to:

- challenges/non-compliance issues such as nonadherence to submission timeframes, inadequate POE submission,

- Submission to Senior Manager: Corporate Services for review, and implementation of consequence management where necessary, and

- Submission to the General Secretary.

Internal Audit Report – Performance Management System

7

5. Conclusion

Overall Audit Opinion

Full assurance

Full assurance that the system of internal control meets the organisation’s objectives and controls are consistently applied.

Significant assurance

Significant assurance that there is a generally sound system of control designed to meet the organisation’s objectives. However, some weaknesses in the design or inconsistent application of controls put the achievement of some objectives at some risk.

Limited assurance

Limited assurance as weaknesses in the design or inconsistent application of controls put the achievement of the organisation’s objectives at risk in some of the areas reviewed.

No assurance

No assurance can be given on the system of internal control as weaknesses in the design and/or operation of key control could result or have resulted in failure(s) to achieve the organisation’s objectives in the area(s) reviewed.

5.1. System of internal control

• The system of PMS internal controls applied has been graded at significant

assurance, as a result of some weaknesses in the design consistent application of

controls put to achieve objectives and mitigate risks.

5.2. Testing opinion

• The assessment of compliance with established policies and standard operating

procedures has been graded at significant assurance. There is evidence that the

level of non-compliance with most of the controls may put some of the system's

objectives at risk and may leave the organisation open to risk.

5.3. Internal control environment

• In our opinion the control framework for Performance Management System, as

operated at the time of the audit provides significant assurance that leaving the

system open to significant error.

• Some issues have a material impact on the achievement of mitigation the risks

associated with PMS at individual, departmental and organisational levels.

• A number of findings, some of which are significant, have been raised. Where

action is in progress to address these findings and other issues known to

management, these actions will be at too early a stage to allow a satisfactory audit

opinion to be given.

6. Acknowledgement

6.1. Audit would like to thank staff involved for their assistance during this review.

7. Disclaimer

7.1. You are requested to treat the Final Internal Audit report with confidentiality. The

distribution of the report to persons other than staff and those on the distribution list

should only be done after consultation with the Internal Auditor.

7.2. Any queries relating to the interpretation/factual correctness of the findings within the

report must be routed to the Senior Manager, Internal Audit.

Internal Audit Report – Performance Management System

8

8. Distribution List

8.1. As required by the Internal Audit Charter, this report is distributed to:

• General Secretary;

• Senior Managers;

• Managers / Supervisors; and

• Audit Committee.

Internal Audit Report – Performance Management System

9

SECTION B – DETAILED AUDIT FINDINGS

1. Performance Management Policy vs. Standard Operating Procedure

Audit finding rating

Control rating classification

Risk rating Repeating finding

Inadequate High No

Criteria

A policy is a guiding principle used to set direction in an organisation, whereas, a procedure,

herein referred to an SOP, is a series of steps to be followed as a consistent and repetitive

approach to accomplish an end result.

Observation

1.1. The audit noted that the content of the procedure manual is the same as the policy, in

that it’s a copy and paste.

1.2. We expected that the Performance Management SOP would be specific to operation

that describes the activities necessary to complete tasks in accordance with ELRC

regulations and laws. However, this is not the case as the current SOP omitted crucial

activities within the performance management process such as:

• Handling of moderation committee review outcome

• Processes to be followed when there is a dispute

• Tools available for the quarterly assessments, for example, performance assessment

form, motivation for performance rating (3 and above score).

• Processes for employee performing below 3 – performance improvement plan and

monitoring thereof.

• Performance management process for employees on maternity leave or absent from

work for a period longer than a month.

1.3. The SOP still includes information no longer applicable to the ELRC, namely, clause 10

Performance Calculation was repelled by EXCO in May 2018, however HR has not

effected such deletion in the document.

1.4. There is no official procedure on how to implement paragraph 5.1.5 of the Performance

Management policy which state that the “Moderation Committee must examine

distribution of ratings, motivation for each rating and satisfy itself that the distribution is

justified”.

Root Cause(s)

• This was an error in that the policy was converted into an SOP.

Risk Arising / Consequence

• It is important to keep in mind that a good SOP doesn’t focus on what needs to be done

but rather how it should be done. So, in this case, it focuses on what needs to be done

and not how it should be done.

• Inconsistencies and unreliability of operations - people need consistency to achieve top

performance. Doing jobs the same way every time rather than wondering, “How does

the boss want it done today?” improves productivity. We are talking about consistency

in routines, not mind-numbing boredom

Internal Audit Report – Performance Management System

10

• Inefficiencies over operations - SOPs will reduce system variation, which is the enemy

of production efficiency and quality control.

• Irrelevant and not useful document.

• Likely to incur significant errors within the process.

• Miscommunication and failure to comply with business regulations.

Recommendation(s) – High Priority

• HR should revise the current PMS SOP by ensuring that the documents contains the

following:

- The document should in detail, describe the day to day processes around the PMS,

these includes but not limited to handling of moderation committee review outcome;

processes to be followed when there is a dispute; tools available for the quarterly

assessments, for example, performance assessment form, motivation for

performance rating (3 and above score); processes for employee performing below 3

– performance improvement plan and monitoring thereof; and performance

management process for employees on maternity leave or absent from work for a

period longer than a month.

- The best SOP is one that accurately transfers the relevant information and facilitates

compliance with reading and using the SOP.

• Management should thereafter, train staff on the revised SOP to ensure that they

understand and adhere to the prescripts of this document.

• Management should ensure at all times that the SOP prescripts are strictly adhered to,

and where applicable, enforce consequence management.

Management Response

Management accepts the finding.

Corrective Action Plan(s)

• HR is in the process of drafting a comprehensive PMS SOP, in line with the SMART

principles and the 5W’s + 1H principle of the SOP.

SMART Principles 5W’s + 1H principle of the SOP

Specific – Specific processes and provide detailed instructions on how to carry out a task so that any employee can carry out a task correctly every time (uniformity).

What - What is the purpose of this SOP

Measurable – quantify or at least suggest an indicator of progress.

Where - Where this SOP is applicable (areas)

Achievable – specify the purpose of the SOP, who does what, where, when, which and how (5W’s + H).

Who - Who are responsible and accountable for this SOP

Realistic – state what results can realistically be achieved, given available resources, and the tasks performed.

When - When this SOP should be used. (frequency)

Time-related – specify when the result(s) of the process can be achieved

Which - Which are the documents relates to this SOP

How - How the procedure should be followed.

Internal Audit Report – Performance Management System

11

Responsible Official(s):

Senior Manager, Corporate Services

Manager, Human Resources

Agreed Action Implementation Date

Draft PMS SOP – 16 April 2019

Submission of the draft PMS SOP to General Secretary for approval – 26 April 2019.

Auditor’s Conclusion

Corrective action plan is noted, and follow-up will be done at the end of first quarter,

FY2019/20.

Internal Audit Report – Performance Management System

12

2. Use of the Motivation for the Performance Assessment Rating Form is

Inconsistent

Audit finding rating

Control rating classification

Risk rating Repeating finding

Ineffective Medium No

Criteria

Paragraph 5.1.5 of the Performance Management Policy requires that the Moderation

Committee must examine distribution of ratings, motivation for each rating and satisfy itself

that the distribution is justified.

The sound practice is that performance scores above 3.5 should be motivated (using the

motivation for performance assessment rating template and supported (in a form of

submission of portfolio of evidence). These information/records should form part of the

quarterly assessment pack, where applicable.

Observation

HR have designed a performance review system which is used to set goals and targets for all

employees, monitor performance and provide feedback to stimulate improvement. However,

the following gaps were identified within the process:

2.1. The following employees has performance ratings of 3.5 and above on their quarterly

performance assessment, however, the motivation for performance assessment rating

is not attached in their performance management personal files:

• Manager, Information Communication Technology

• Information Communication Technology Officer

• Manager, Human Resource

• Manager, Collective Bargaining Services

• Human Resource Officer

• Dispute Management Services Officers

• Dispute Management Services Administrator

2.2. Internal audit requested the Motivation for Performance Assessment Ratings for the

individuals noted in 2.1. above, and we were informed by the auditee that “this document

is not compulsory”. Yet it is a requirement for Senior Managers (whose performance is

assessed by the General Secretary) to complete and submit this during their

assessments. This is an indication of practises not streamlined.

2.3. The above raised a concern that HR is not adequately monitoring this process, in that,

inconsistent activities or practices are left unattended, and not adopted and imbedded

in the procedures as a compulsory process.

2.4. The motivation for assessment rating for employee number 058 was not duly signed-off

by the respective line manager.

Root Cause(s)

• The HR focused on the fact that the POE for each score that is 3.5 and above is provided

other than looking for the motivation form.

Internal Audit Report – Performance Management System

13

Risk Arising / Consequence

• Inconsistencies in the application of processes.

• Lengthy and unproductive processes of the moderation committee meetings.

• Increased likelihood of personal opinions as opposed to factual evidence.

• Intentional or unintentional biases become a challenge for the moderation committee to

detect.

Recommendation(s) – High Priority

• HR should streamline processes within PMS for consistency and synergy.

• As a requirement of paragraph 5.1.5 of the PMS Policy, the motivation for performance

assessment rating form should be a mandatory requirement for all ratings above 3.5.,

and HR should ensure that when checking the completeness of the quarterly

performance portfolio for each employee, all the required documents are submitted.

Management Response

Management accepts the finding.

Corrective Action Plan(s)

• As an area of improvement, HR agrees on the importance of the Motivation for the

Performance Ratings form and will ensure that the form is part of the new PMS SOP.

• Going forward, the ratings above 3.5 will be supported by the Motivation for the

Performance Assessment Ratings form.

Responsible Official(s):

Senior Manager, Corporate Services

Manager, Human Resources

Agreed Action Implementation Date

26 April 2019

Auditor’s Conclusion

Corrective action plan is noted, and follow-up will be done at the end of first quarter,

FY2019/20.

Internal Audit Report – Performance Management System

14

3. Moderation Committee Meetings Not Convened Periodically

Audit finding rating

Control rating classification

Risk rating Repeating finding

Ineffective Medium No

Criteria

Paragraph 5.4.6 of The Performance Management Policy state that “The committee shall

convene every quarter after the assessment by both the Line Manager and the Employee”.

The purpose of moderation is to ensure that:

• Supervisors evaluate performance in a consistent way;

• There is a common understanding of the standards required at each level of the rating

scale

• The integrity of the system is protected.

Observation

The audit noted that the Moderation Committee does not meet quarterly as required by the

policy, for example:

3.1. At the time of the audit (March 2019), the Moderation Committee has set for the 3rd

quarter performance assessments, however, the process was not finalised at the time

of the audit. Therefore, there is no evidence of action plan to finalise quarter 2 and 3

outstanding issues before the end of the quarter and/or financial year.

3.2. The audit further noted that the 2nd quarter moderation is not yet complete. The following

units were still outstanding:

• Collective Bargaining Services, and

• Finance.

Root Cause(s)

• 3.1 The Moderation Committee did sit for the 3rd quarter, the initial meeting was

scheduled for the 15th February and was postponed due to the unavailability of the CBS

Senior Manager, again the Human Resources Department scheduled another meeting

on 21 February 2019, however, the meeting was not concluded since there were some

problems with the CBS assessments. The meeting was once again postponed to a later

date.

• 3.2 Senior Manager: CBS was meant to address the outstanding assessments for Q2.

This was not done due to postponement of the meeting.

• 3.2 An employee from Finance department was on maternity leave and their assessment

was meant to be addressed on Q3.

Risk Arising / Consequence

• If the responsibility and duties of the moderation committee are not efficiently and

effectively executed, then any deficiencies affecting the integrity of the system might not

be timely detected and corrected resulting to the system being compromised.

• Noncompliance with the Performance Management policy.

• Credibility and consistency of the system can be undermined.

Recommendation(s) – High Priority

Internal Audit Report – Performance Management System

15

• Management should come up with a solution on ensuring that the Moderation

Committee sits as per the requirement of the policy. It should be on only rare exceptional

cases were the moderation sitting is delayed, however, it should not be made a norm

that the quarterly moderation meetings don’t see or are delayed.

Management Response

• Management acknowledges the finding and would like to indicate that the matter was

brought to the attention of the General Secretary for further intervention.

Corrective Action Plan(s)

• The Human Resources will ensure that Moderation Committee sits to moderate

employees’ assessments and those that were still open (incomplete).

Responsible Official(s):

Senior Manager, Corporate Services

Manager, Human Resources

Agreed Action Implementation Date

23 April 2019, and going forward.

Auditor’s Conclusion

Corrective action plan is noted, and follow-up will be done at the end of first quarter,

FY2019/20.

Internal Audit Report – Performance Management System

16

4. Inconsistencies noted on Performance Agreements

Audit finding rating

Control rating classification

Risk rating Repeating finding

Ineffective Medium No

Criteria

Paragraph 21.1 of the PMS policy requires that the individual score is determined by scoring

each Key Performance Area and determining the weighted average based on the results of

each Key Performance Area.

Observation

4.1. The standard practice is that every Key Performance Area is allocated a scoring weight.

However, we noted inconsistencies whereby a scoring weight is allocated for the overall

Key Performance Area instead of distributing the weight evenly to all Sub-KPA falling

under that overall Key Performance Area. This relates to Performance Agreements of

employees’ number 142 and 084.

4.2. EE number: 058 and 051 – there is no breakdown of the overall KRAs score and allocate

it to each of the identified KPIs (weights).

Root Cause(s)

• An error where the employee did not evenly distribute the weightings and HR was at the

assumption that the weighting did not necessarily have to be put under sub-KPAs, as

long as they were distributed on the main KPAs.

Risk Arising / Consequence

• Inability to adequately assess the employee’s performance and give them the accurate

weightings.

• The above could also result in the increase disputes and prolonging of the assessment

of the employee.

Recommendation(s) – High Priority

• HR should streamline processes within PMS for consistency and synergy.

• The KRA and the KPI should be adequately allocated weights in numbers, and the

respective Line Managers should ensure that before they sign the PA, the document is

accurately completed and that all weights are allocated and tally.

Management Response

Management accepts the finding.

Corrective Action Plan(s)

• As part of the employee contracting process for the fiscal year 2019/20, HR will ensure

that the KPAs are broken down to all KPAs and sub-KPAs, and in instances where it is

not broken down, the files will be returned to the employee for correction.

Responsible Official(s):

Senior Manager, Corporate Services

Manager, Human Resources

Internal Audit Report – Performance Management System

17

Agreed Action Implementation Date

30 April 2019

Auditor’s Conclusion

Corrective action plan is noted, and follow-up will be done at the end of first quarter,

FY2019/20.

Internal Audit Report – Performance Management System

18

5. Performance Assessment Documentation Not Always Submitted on Time

Audit finding rating

Control rating classification

Risk rating Repeating finding

Ineffective Medium No

Criteria

The performance management policy required that compulsory and formal performance

reviews or appraisals be conducted quarterly during the financial year (July, October, January

and March). The quarterly review results must be submitted to the Manager, Human Resource

and the General Secretary.

The standard practice for submission of quarterly submission of performance assessments is

that Human Resource will issue a communique to Managers and Senior Managers of the

performance assessments date for the quarter under review.

Observation

We noted that performance assessments submission dates are not always adhered to by staff.

Human Resource’s Ins and Outs Register (register kept by HR for all incoming and outgoing

documents) showed late submission of quarterly performance assessments and portfolio of

evidence. The following are examples of such:

Official HR’s Date of Submission

EE Name EE’s Date Submitted (Ins and Outs Register)

Department

13/07/2018 S Makinta 17/07/2018 Dispute Management Service

13/07/2018 L Kutumela 17/07/2018 Dispute Management Service

25/01/2019 M Milne 01/02/2019 Collective Bargaining Service

25/01/2019 N Make 01/02/2019 Collective Bargaining Service

25/01/2019 M Molopi 01/02/2019 Collective Bargaining Service

25/01/2019 D Singh 01/02/2019 Collective Bargaining Service

25/01/2019 A Ndabankulu 01/02/2019 Collective Bargaining Service

25/01/2019 K Molebaloa 01/02/2019 Collective Bargaining Service

Root Cause(s)

• CBS department requested the extension date to submit their assessments as the

Senior Manager was on leave and the POE for provincial employees was still held from

the post office.

• Non adherence of due date by DMS department.

Risk Arising / Consequence

• Possible delay in finalisation of the quarterly assessment process / inability of

moderation committee convening a meeting to execute its mandate / quarterly

assessment outcome not reported to the General Secretary.

• Non-compliance with the policy.

• Disturbance of Human Resource’s operational plan resulting to HR not meeting their

performance targets.

Recommendation(s) – High Priority

• The submission deadlines for quarterly performance assessments are communicated to

staff well in advance (in this case, the communique was issued in the first quarter of the

Internal Audit Report – Performance Management System

19

financial year), therefore, HR should enforce consequence management in cases of

non-adherence to this, depending on the merits of late submission.

• The once off requests for extension are allowed, however, where it is a norm, it becomes

a problem.

• In instances where Senior Managers request submission extension, such must be

documented and approved as per the Delegation of Authority (an audit trail must exist).

Management Response

Management accepts the finding.

Corrective Action Plan(s)

• HR Manager will compile, a quarterly report and/or post assessment (scope of the report

will include but not limited to:

- challenges/non-compliance issues such as nonadherence to submission timeframes,

inadequate POE submission,

- Submission to Senior Manager: Corporate Services for review, and implementation of

consequence management where necessary, and

- Submission to the General Secretary.

Responsible Official(s):

Senior Manager, Corporate Services

Manager, Human Resources

Agreed Action Implementation Date

4th quarter assessments and going forward.

Auditor’s Conclusion

Corrective action plan is noted, and follow-up will be done at the end of first quarter,

FY2019/20.

Internal Audit Report – Performance Management System

20

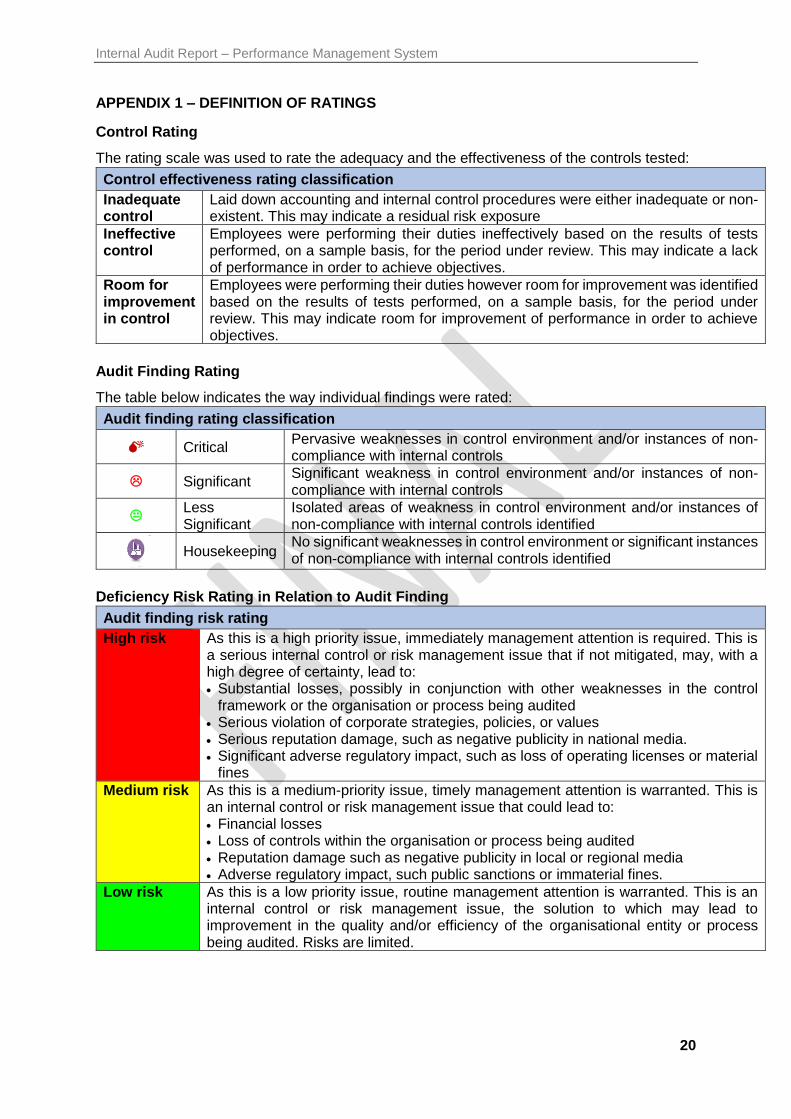

APPENDIX 1 – DEFINITION OF RATINGS

Control Rating

The rating scale was used to rate the adequacy and the effectiveness of the controls tested:

Control effectiveness rating classification

Inadequate control

Laid down accounting and internal control procedures were either inadequate or non-existent. This may indicate a residual risk exposure

Ineffective control

Employees were performing their duties ineffectively based on the results of tests performed, on a sample basis, for the period under review. This may indicate a lack of performance in order to achieve objectives.

Room for improvement in control

Employees were performing their duties however room for improvement was identified based on the results of tests performed, on a sample basis, for the period under review. This may indicate room for improvement of performance in order to achieve objectives.

Audit Finding Rating

The table below indicates the way individual findings were rated:

Audit finding rating classification

Critical Pervasive weaknesses in control environment and/or instances of non-compliance with internal controls

Significant Significant weakness in control environment and/or instances of non-compliance with internal controls

Less Significant

Isolated areas of weakness in control environment and/or instances of non-compliance with internal controls identified

Housekeeping

No significant weaknesses in control environment or significant instances of non-compliance with internal controls identified

Deficiency Risk Rating in Relation to Audit Finding

Audit finding risk rating

High risk As this is a high priority issue, immediately management attention is required. This is a serious internal control or risk management issue that if not mitigated, may, with a high degree of certainty, lead to: • Substantial losses, possibly in conjunction with other weaknesses in the control

framework or the organisation or process being audited • Serious violation of corporate strategies, policies, or values • Serious reputation damage, such as negative publicity in national media. • Significant adverse regulatory impact, such as loss of operating licenses or material

fines

Medium risk As this is a medium-priority issue, timely management attention is warranted. This is an internal control or risk management issue that could lead to: • Financial losses • Loss of controls within the organisation or process being audited • Reputation damage such as negative publicity in local or regional media • Adverse regulatory impact, such public sanctions or immaterial fines.

Low risk As this is a low priority issue, routine management attention is warranted. This is an internal control or risk management issue, the solution to which may lead to improvement in the quality and/or efficiency of the organisational entity or process being audited. Risks are limited.

Copyright © 2022 FDOKUMEN