@^cf}+ - Nepal Stock Exchange

138

वारक तिवेदन २०७६ / ७७ @^cf}+

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of @^cf}+ - Nepal Stock Exchange

वार्षिक प्रतिवेदन२०७६ / ७७

@^cf}+

;~r

fns

;ld

lt

>L b

Lks

sfs

L{;~rfns

>L d

's'Gb

gfy

9'·

]n;~rfns

>L O

{Gb| a

xfb'/

yfk

f;~rfns

>L P

=cf/

=Pd

= gh

d';

;ls

acWoIf

>Ld

tL s

d¿

g g

x/ c

xdb

;~rfns

>L D

ff]xd

b ;

fx c

fnd

;/j

/;~rfns

a}+ssf] ljQLo l:yltsf] emns

lgIf]k -?= xhf/df_

shf{ tyf ;fk6L -?= xhf/df_

Aofh cfDbfgL -?= xhf/df_

नेपाल बङ्गलादेश बैंक ललमिटेड 1

v'b gfkmf -?= xhf/df_

nfef+z -af]g; z]o/ ;d]t_ -?= xhf/df_

k|fylds k'+hL -¿ xhf/df_

नेपाल बङ्गलादेश बैंक ललमिटेड2

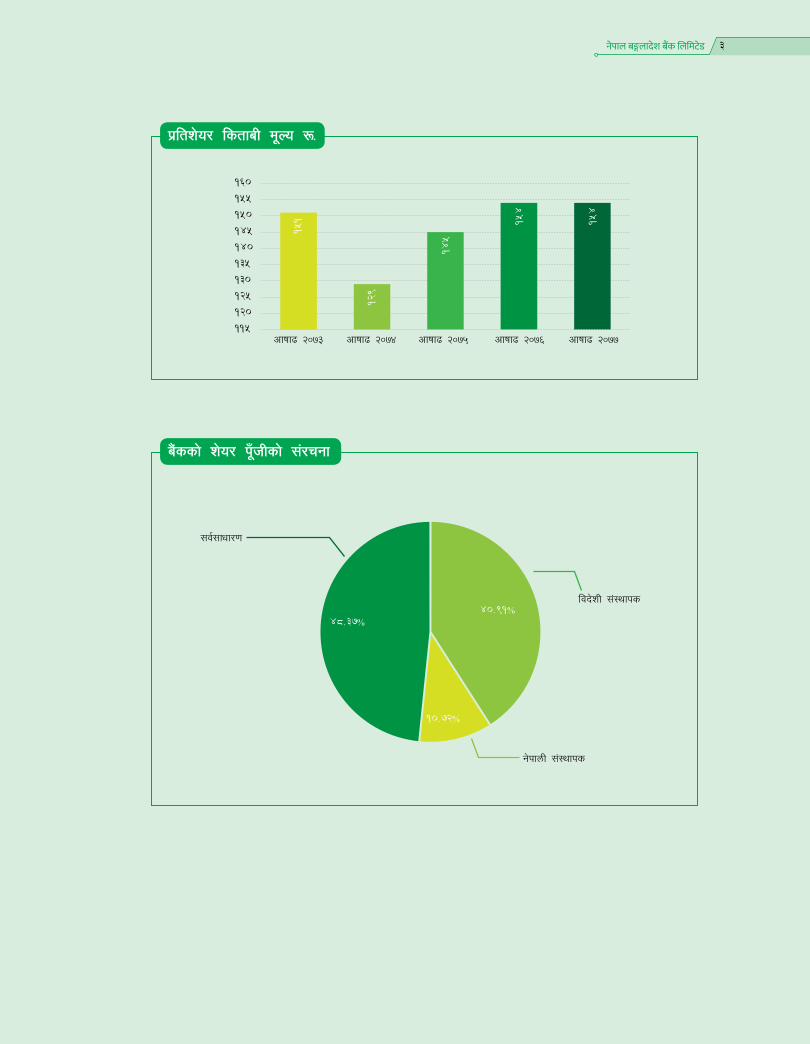

k|ltz]o/ lstfaL d"No ?=

a}+ssf] z]o/ k"FhLsf] ;+/rgf

ljb]zL ;+:yfks

g]kfnL ;+:yfks

;j{;fwf/0f

नेपाल बङ्गलादेश बैंक ललमिटेड 3

ljifo ;"rL

k|ltlglw — kq -k|f]S;L kmf/d_

5lAa;f}+}+ jflif{s ;fwf/0f;ef ;DaGwL ;"rgf tyf yk hfgsf/L

;~rfns ;ldltsf] k|ltj]bg

lwtf]kq btf{ tyf lgisfzg lgodfjnL;Fu ;DalGwt ljj/0f

k|d'v sfo{sf/L clws[tsf] k|lta4tf

cf=j= @)&^÷&& sf] n]vfk/LIfssf] k|ltj]bg

cf=j= @)&^÷&& sf] Plss[t ljQLo ljj/0f tyf cg';"rLx?

cf=j= @)&^÷&& sf] k|d'v n]vf gLltx? tyf n]vf ;DaGwL l6Kk0fL

g]kfn /fi6« a}+ssf] :jLs[tL kq

tLg dxn] ljj/0f

k|fb]lzs tyf zfvf sfof{nox?

%

&

!!

@)

@!

@$

@*

^%

!@*

!@(

!#)

k]h g+=

नेपाल बङ्गलादेश बैंक ललमिटेड4

k|ltlglw — kq -k|f]S;L kmf/d_ >L ;~rfns ;ldlt,

g]kfn aËnfb]z a}+s ln=

sdnfbL, sf7df8f}+ .

ljifoM k|ltlglw lgo'Qm u/]sf] af/] .

dxfzo,

========================================================================================================================= lhNnf =========================================================================================================== g=kf=÷uf=kf= j8f g+= ========================= a:g]

d÷xfdL =========================================================================================================================================================================================== n] To; a}+ssf] z]o/wgLsf] x}l;otn] @)&& ;fn

kf}if dlxgf @^ ut], cfOtaf/ x'g] 5AaL;f}+ jflif{s ;fwf/0f ;efdf pkl:yt eO{ 5nkmn tyf lg0f{odf ;xefuL x'g g;Sg]

ePsf]n] pQm ;efdf efu lng tyf dtbfg ug{sf nflu ======================================================================================================= lhNnf ====================================================

g=kf=÷uf=kf= j8f g+= ======================== a:g] To; a}+ssf z]o/wgL >L ===============================================================================================================================================================================================,

z]o/wgL g+=÷BOID No. ================================================================================================== nfO{ d]/f]÷xfd|f] k|ltlglw dgf]gog u/L k7fPsf] 5'÷5f}+ .

lgj]bs

b:tvt M ===========================================================================================================

gfd M =======================================================================================================================

7]ufgf M =================================================================================================================

z]o/wgL g+=÷BOID No. =======================================================================

z]o/ ;+Vof M =================================================================================================

ldlt M ======================================================================================================================

b|i6Jo M

!_ k|ltlglw -k|f]S;L_ d's// ubf{ z]o/wgL afx]s c?nfO{ ug{ kfOg] 5}g .

@_ of] lgj]bg ;fwf/0f ;ef x'g'eGbf $* 306f cufj} a}+ssf] s]lGb|o sfof{no, sdnfbLl:yt z]o/ zfvfdf k]z ul/;Sg' kg]{5 .

k|j]z kq

z]o/wgL g+=÷BOID No. ===========================================================================================================================================================================================================================================================================================================

z]o/wgLsf] gfd >L ===================================================================================================================================================================================================================================================================================================================

z]o/ ;+Vof M ====================================================================================================================================================

@)&& ;fn kf}if dlxgf @^ ut], cfOtaf/ o; g]kfn aËnfb]z a}+s ln= sf] 5AaL;f}+ jflif{s ;fwf/0f ;efdf pkl:yt x'g

hf/L ul/Psf] k|j]z—kq .

_________________________ _________________________

z]o/wgLsf] x:tfIf/ cflwsfl/s b:tvt

b|i6Jo M

!_ z]o/wgL cfkm}+n] vfnL sf]i7x? eg'{ xf]nf .

@_ ;efsIfdf k|j]z ug{ of] k|j]z—kq clgjfo{ ?kdf lnO{ cfpg'x'g cg'/f]w 5 .

नेपाल बङ्गलादेश बैंक ललमिटेड 5

नेपाल बङ्गलादेश बैंक ललमिटेड6

5lAa;f}+ aflif{s ;fwf/0f ;efsf] ;"rgfcfb/0fLo z]o/wgL dxfg'efjx¿,o; a}+ssf] ldlt @)&&÷)(÷)# df a;]sf] ;~rfns ;ldltsf] lg0f{ofg';f/ a}+ssf] 5lAa;f}+ jflif{s ;fwf/0f ;ef lgDg lnlvt ldlt, :yfg / ;dodf lgDg lnlvt k|:tfjx¿ pk/ 5nkmn ug{sf] nflu a:g] ePsf]n] ;Dk'0f{ z]o/wgL dxfg'efjx?sf] hfgsf/Lsf] nflu of] ;"rgf k|sflzt ul/Psf] 5 .

;ef x'g] ldlt, ;do tyf :yfgldltM– @)&& ;fn kf}if @^ cfOtaf/ . -tbg';f/ !) hgj/L, @)@!_;doM– laxfg !!M#) ah] .:yfgM– xfn sf]le8–!( sf] dxfdf/Lsf] hf]lvdsf sf/0f ;fwf/0f ;efdf cgnfOg -Zoom Cloud Meetings_ sf]

dfWodaf6 eRo'{cn ¿kdf ;xefuL x'g ;Sg] u/L z]o/wgL dxfg'efjx¿nfO{ Meeting ID / Password pknAw u/fpg] tyf a}+ssf] clkml;on k]m;a's k]haf6 k|ToIf k|zf/0f ug]{ Joj:yf ul/Psf] 5 .

5nkmnsf laifox?M-s_ ;fdfGo k|:tfj M!= cf=a= @)&^÷)&& sf] ;~rfns ;ldltsf] jflif{s k|ltj]bg 5nkmn u/L kfl/t ug]{ .@= o; a}+ssf] n]vfk/LIf0f k|ltj]bg ;lxtsf] cf=j= @)&^÷)&& sf] jflif{s ljQLo ljj/0fx? -jf;nft, gfkmf÷gf]S;fg

lx;fa, gub–k|jfxljj/0f cflb_ pk/ 5nkmn u/L kfl/t ug]{ .#= o; a}+ssf ;xfos sDkgLx¿ g]kfn a+unfb]z Soflk6n lnld6]8 / PgaLaLPn ;]So'l/l6h lnld6]8 ;lxtsf] cf=j=

@)&^÷)&& sf] PsLs[t jflif{s ljQLo ljj/0f pk/ 5nkmn u/L kfl/t ug]{ .$= cf=a= @)&&÷&* sf] n]vfk/LIf0f ug{sf] nflu a}+ssf] n]vfk/LIf0f ;ldltåf/f l;kmfl/z ul/P adf]lhd n]vfk/LIfsnfO{

lgo'lQm ug]{ / lghsf] kfl/>lds tf]Sg] . -xfnsf n]vfk/LIfs >L ;'lw/ s'df/ zdf{, S & S Associates, Chartered Accountants k'gM lgo'lQmsf nflu of]Uo /xg' ePsf]_.

%= ;~rfns ;ldltaf6 k|:tfj u/] cg';f/ cf=a= @)&^÷)&& sf] d"gfkmf /sdaf6 @)&& cfiff9 d;fGtdf sfod /x]sf] r"Qmf k"FhLsf] @=$@ k|ltzt -af]g; z]o/ tyf gub nfef+zdf nfUg] s/ ;d]t u/L_ sf b/n] gub nfef+z ljt/0f ug{ :jLs[lt k|bfg ug]{ .

^= o; a}+ssf] ldlt @)&&÷#÷@$ df ;DkGg #%^ cf}F ;~rfns ;ldltsf] a}7sn] lg0f{o u/] cg';f/ o; a}+ssf ;+:yfks z]o/wgL >L cfO{PkmcfO{;L a}+saf6 k|ltlglw ;~rfnssf ¿kdf ldlt @)&$ d+l;/ # ut] ePsf] ;fwf/0f ;efaf6 lgjf{lrt x'g'ePsf ;~rfns÷cWoIf >L hnfn cxdbsf] :yfgdf pxfFsf] afFsL sfo{sfnsf nflu cfO{PkmcfO{;L a}+saf6 dgf]lgt x'g'ePsf >L P=cf/=Pd= ghd'; zlsanfO{ o; a}+ssf] ;~rfns÷cWoIfdf lgol'Qm u/]sf] lg0f{onfO{ cg'df]bg ug]{ .

-v_ ljz]if k|:tfj M!= ;~rfns ;ldltn] k|:tfj u/] adf]lhd cf=a= @)&^÷)&& sf] d"gfkmf /sdaf6 @)&& cfiff9 d;fGtdf sfod /x]sf]

r"Qmfk"FhLsf] ^ k|ltztsf b/n] af]g; z]o/ hf/L ug]{ / o;/L af]g; z]o/ ljt/0f ubf{ s'g} z]o/wgLn] kfpg] af]g; z]o/ vl08s[t x'g cfPdf gk'u /sd ;DalGwt z]o/wgLn] kfpg] gub nef+zaf6 s§f u/L ljBdfg k"FhL ;+/rgf kl/jt{g gx'g] u/L k"0f{s[t z]o/ hf/L ug]{ / ;f]xL adf]lhd k|aGwkq tyf lgodfjnL ;+zf]wg :jLs[lt k|bfg ug]{ .

@= a}+ssf] k|jGwkq tyf lgodfjnLdf ;d;fdlos ;+zf]wg :jLs[t ug]{ .#= k|:tfljt ;+zf]wgdf lgodgsf/L lgsfo -g]kfn /fi6« a}+s, sDkgL /lhi6«f/sf] sfof{no cfbL_ n] kl/dfh{g÷km]/abn

ug{ ;'emfj jf lgb]{zg lbPdf ;f] cg'?k cfjZos ;dfof]hg ug{ ;~rfns ;ldltnfO{ clwsf/ k|bfg ug]{ .

-u_ ljljw .!= o; a}+ssf] #^! cf}F ;~rfns ;ldltsf] a}7sn] lg0f{o u/] adf]lhd a}+ssf] s'g} klg ;~rfns sf]le8–!( sf]

;ª\j|md0faf6 u|l;t eO{ c:ktfn egf{ x'g] cj:yfdf lghsf] c:ktfnsf] jf:tljs lan cg';f/ -a9Ldf b'O{ nfv ?k}ofF_ pkrf/ vr{ pknAw u/fpg] k|:tfj cg'df]bg ug]{ .

@= cGo -s'g} ePdf_ . ;~rfns ;ldltsf] cf1fn] sDkgL ;lrj

नेपाल बङ्गलादेश बैंक ललमिटेड 7

!= a+}ssf] z]o/ bflvn vf/]h ldlt @)&& ;fn kf}if !) ut] -Ps lbg_ aGb /xg]5 .

@= 5lAa;f}+ jflif{s ;fwf/0f ;ef tyf af]g; z]o/ / gub nfef+z k|of]hgsf] nflu ldlt @)&&.)(.)( ut] ;Dd g]kfn :6s PS;r]Gh lnld6]8df ePsf] z]o/ sf/f]jf/ ;DaGwL lnvt Pj+ sfuhftx? ldlt @)&&.)(.!& ut] ;Dddf a}+ssf] z]o/ /lhi6«f/ g]kfn aËnfb]z Soflk6n lnld6]8df a'emfO{ z]o/ gfd;f/L u/fpg' x'g cg'/f]w ub{5f}+ . pQm lbg ;Dd z]o/wgL btf{ lstfadf sfod z]o/wgLx?n] dfq ;fwf/0f;efdf cgnfOg -Zoom Cloud Meetings_ sf] dfWodaf6 eRo'{cn ¿kdf efu lng ;Sg]5g\ tyf nfef+z k|fKt ug]{5g\ .

#= ;Dk"0f{ z]o/ wgL dxfg'efjx?nfO{ z]o/wgLnutdf sfod /x]sf] lghx?sf] 7]ufgfdf ;fwf/0f ;efsf] ;'rgf / a}+ssf] jflif{s ;+lIfKt cfly{s ljj/0f k7fOg] Joj:yf ul/Psf] 5 . 7]ufgf k'/f gePsf tyf pQm sfuhft k|fKt gug{' x'g] z]o/wgL dxfg'efjx?n] jflif{s cfly{s ljj/0f ;~rfns ;ldltsf] k|ltj]bg / n]vfkl/Ifssf] k|ltj]bg lg/LIf0f ug{ o; a}+ssf] s'g} klg zfvf sfof{nox?df ;Dks{ ug{ ;Sg'x'g]5 . ;fy} pk/f]Qm pNn]lvt ljj/0f k|ltj]bgx? o; a}+ssf] j]j;fO6 https://www.nbbl.com.np df ;d]t upload ul/Psf] 5 .

$= ljZjJoflk ?kdf km}lnPsf] sf]/f]gf efO/; -sf]le8 !(_dxfdf/L /f]syfd tyf lgoGq0fsfn nflu g]kfn ;/sf/af6 hf/L ul/Psf :jf:Yo ;DjGwL lgb]{zg Pj dfkb08x?sf] ;Ddfg Pj kl/kfng ub]{ cgnfOg -er'{cn_ Zoom Cloud Meetings sf] dfWodaf6 ;efdf ;xefuL x'g], cfkm\gf] dGtJo /fVg] tyf dtbfg ug{ ;Sg] Joj:yf ;d]t ldnfPsf] x'bf sf]/f]gf efO/; -Covid-19_ sf] ;qmd0faf6 aRg / arfpg oyf;So cgnfOg er'{cn (Zoom) dfWodaf6 pkl:yt eO{lbg' x'g ;Dk"0f z]o/wgL dxfg'efjx¿nfO{ cg'/f]w 5 .

% cgnfOg er{'cn zoom dWodaf6 pkl:yt eO{ ;fwf/0ff ;efdf ;xefuL x'g] tyf dGtJo /fVg rfxg' x'g] z]o/wgL dxfg'efjn] ;ef x'g' eGbf $* 306f cufj} cfkm\gf] kl/rokq ;lxt a}+sn] hf/L u/]sf] z]o/ k|df0fkq DMAT vftf vf]lnPsf] k|df0fsf] :Sofg skL ;dfj]z u/L sDkgL ;lrjsf] Od]n 7]ufgf [email protected] df Od]n jf whatsApp dfk{mt\ k7fpg' kg]{5 . o;/L k|fKt ePsf] Od]n jf whatsApp df cgnfOg er'{cn (Zoom) dfWodaf6 ;efdf ;xefuL x'gsf nfuL cfjZos Meeting sf] ID / Password pknJw u/fOg] 5 . o; k|lqmofjf6 pkl:yt x'g'x'g] z]o/wgL dxfg'efjx?nfO{ ;ef:yndf pkl:yt eP;/x dfGotf lbg] Joj:yf ul/Psf] 5 . ;efdf cfkm\gf] /fo ;'emfj email dfkm{t klg lbg ;Sg] Joj:yf ldnfOPsf] 5 . o; ;DaGwL hfgsf/L sDkgL ;lrjsf] sfof{nosf] kmf]g g+= )!–$@##&*)÷*!–*% -PS;\6]G;g g+= $^@_ df ;Dks{ u/L k|fKt ug{ ;lsg] 5 .

^= ;fwf/0f ;efdf efu lng k|ltlglw k|f]S;L lgo'Qm ug{ rfxg] z]o/wgLx¿n] a}+ssf] csf]{ z]o/wgLnfO{ dfq k|ltlglw lgo'Qm ug{ ;Sg'x'g]5 . k|rlnt sDkgL sfg"gn] tf]s]sf]

9fFrfdf k|ltlglw k|f]S;L kmf/d e/L ;ef z'? x'g'eGbf sDtLdf $* 306f cufj} cyf{t @)&&÷)(÷@$ ut] laxfg ( jh] leq a}+ssf] /lhi6«f/ sfof{no sdnfbL sf7df8f}+df btf{ u/fO{ ;Sg'kg]{5 .

&= gfafns jf dfgl;s ¿kdf czQm z]o/wgLx?sf] tkm{jf6 a}+ssf] z]o/ nut btf{ lstfadf ;+/Ifssf] ?kdf gfd btf{ ePsf dxfg'efjx?n] ;efdf cgnfOg er'{cn (Zoom) dfWodaf6 efu lng jf k|ltlglw tf]Sg ;Sg' x'g]5 .

*= ;+o'Qm ?kdf z]o/ v/Lb ul/Psf] cj:yfdf z]o/wgLx?sf] nut btf{ lstfadf klxn] gfd pNn]v ePsf] JolQm cyjf ;j{;Ddtjf6 k|ltlglw lgo'Qm ul/Psf] Ps JolQmn] dfq ;efdf efu lng jf dtbfg ug{ kfpg]5 .

(= ;efdf efu lng k|ltlglw lgo'Qm ul/;s]kl5 ;DalGwt z]o/wgL cfkm}n] efu lng jf k|ltlglw km]/jbn ug{ rfx]df ;ef ;'? x'g'eGbf sDtLdf #^ 306f cufj} ;f] sf] ;'rgf a}ssf] /lhi6«f/ sfof{no sdnfbL sf8df8f}+df btf{ u/fO;Sg' kg]{ 5 cGoyf k|ltlglw km]/jbn x'g ;Sg] 5}g . t/ ;efdf ;DjlGwt z]o/wgL :jod\ pkl:yt ePdf z]o/wgLn] ul/lbPsf] clVtof/gfdf :jt jb/ x'g]5 .

!)= 5nkmndf ljifo dWo] ljljw zLif{s cGt{ut s'g} ljifodf ;fwf/0f ;efdf 5nkmn ug'{kg]{ eP OR5's z]o/ wgLn] ;ef x'g'eGbf & lbg cufj} ;f] ljifo sDkgL ;lrj dfkm{t\ ;~rfns ;ldltsf cWoIfnfO{ lnlvt ?kdf lbg'kg]{5 .

!!= ;efdf cgnfOg er'{cn dfWod -Zoom Cloud Meetings_ af6 cfkm\gf] dGtJo /fVg rfxg] z]o/wgL dxfg'efjx¿n] ;ef x'g'eGbf $* 306f cufl8;Dd a9Ldf # ldg]6;Ddsf] cfkm\gf] dGtJo lnlvt ¿kdf sDkgL ;lrjnfO{ a'emfpg' kg]{5 .

!@= z]o/wgL dxfg'efjx?n] AoQm ug'{ ePsf dGtAo tyf k|Zgx?sf] ;DaGwdf ;~rfns ;ldltsf] tkm{af6 ;fd"lxs ?kn] jf ;~rfns ;ldltaf6 cfb]z kfPsf JolQmn] pQ/ lbg]5g\ .

!#= ;ef z"? eGbf ! 306f cufj} cgnfOg er'{cn dfWod -Zoom Cloud Meetings_ v'Nnf ul/g] 5 .

!$= cGo hfgsf/Lsf] nflu a}+ssf] s]Gb|Lo sfof{no, sdnfbL, sf7df8f+}df sfof{no oyf;doleq ;Dks{ /fVg'x'g cg'/f]w 5 .

k'gZrM sDkgLsf] ;+lIfKt cfly{s ljj/0f z]o/wgL dxfg'efjx?n] pknAw u/fPsf] 7]ufgfdf k7fOPsf] 5 . ;fy} sDkgL P]g @)^# -klxnf] ;+zf]wg, @)&$_ cg';f/sf] jflif{s cfly{s ljj/0f, ;~rfns ;ldltsf] k|ltj]bg / n]vfk/LIfssf] k|ltj]bg z]o/wgL dxfg'efjx?n] sDkgLsf] s]Gb|Lo sfof{no, sdnfbL tyf o; a}+ssf] z]o/ /lhi6\«f/ g]kfn aËnfb]z Soflk6n ln=, sdnfbLdf cfO{ lg/LIf0f ug{ / k|fKt ug{ ;Sg] Aoxf]/f ;d]t hfgsf/Lsf nflu ;"lrt ul/G5 . cfly{s ljj/0f nufot jflif{s ;fwf/0f ;efdf k]z x'g] ;Dk"0f{ k|:tfjx¿ a}+ssf] j]j;fO{6 www.nbbl.com.np df klg x]g{ ;Sg'x'g]5 .

;fwf/0f ;ef ;DaGwL cGo hfgsf/L

नेपाल बङ्गलादेश बैंक ललमिटेड8

;~rfns ;ldlt

>L P=cf/=Pd= ghd'; ;lsacWoIf

>L d's'Gb gfy 9'Ë]n ;~rfns -;j{;fwf/0f ;d"x_

>L bLks sfsL{;~rfns -;j{;fwf/0f ;d"x_

cfGtl/s n]vfk/LIfslk=h]= yfkf P08 sDkgLrf6{8{ PsfpG6]G6\;\

sDkgL ;lrj>L ljZjk|sfz kf}8]n

n]vfk/LIfsP; P08 P; P;f]l;P6\;\

rf6{8{ PsfpG6]G6\;\

>L O{Gb| axfb'/ yfkf ;~rfns -;j{;fwf/0f ;d"x_

>L Dff]xdb ;fx cfnd ;/j/;~rfns -;+:yfks ;d"x_

>LdtL sd¿g gx/ cxdb;~rfns -;+:yfks ;d"x_

नेपाल बङ्गलादेश बैंक ललमिटेड10

P=cf/=Pd ghd'; ;lsacWoIf, ;~rfns ;ldlt

!= /fli6«o tyf cGt/fli6«o cfly{s ultljlwcGt/f{li6«o cfly{s l:yltsf]le8–!( sf] dxfdf/L kl5 ljZj cy{tGq ;g\ !(#) sf] bzssf] dxfdGbL kl5sf] ;j}eGbf 7"nf] ;+s'rgdf uPsf] 5 . ljZjn] Ps} k6s :jf:Yo ;+s6 / cfly{s ;+s6 Joxf]g'{ k/]sf sf/0f ul/aL, a]/f]huf/L / cfo c;dfgtf a9\g]] cg'dfg 5 . sf]le8–!( ;+qmd0f lgoGq0f tyf /f]syfdsf nflu ljZjJofkL ?kdf cjnDag ul/Psf pkfox?af6 pTkfbgb]lv cfk"lt{;Ddsf >[+vnf cj?4 eO{ ljZj cy{tGq ;+s'rgdf uPsf] 5 .

sf]le8–!( sf sf/0f ljZje/ g} >d ahf/ / ljk|]if0f cfk|jfx k|efljt x'g] cg'dfg 5 . k|d'v >duGtJo d'n'sx? cfly{s ;+s'rgdf uP;Fu} ljk|]if0f cfk|jfxdf sdL cfPdf ;f] sf] c;/ a}+lsË If]qsf] ;fwg kl/rfng, jfXo If]q ;Gt'ng tyf ul/aL lgjf/0fdf kg]{ b]lvPsf] 5 .

ljsl;t d'n'sx?sf] cy{tGq ;g\ @)!( df !=& k|ltztn] lj:tf/ ePsf]df ;g\ @)@) df * k|ltztn] ;+s'rg x'g]] cGt/f{li6«o d'b|fsf]ifsf] k|If]k0f 5 . PlzofnL cy{tGq ;g\ @)@) df !=^ k|ltztn] ;+s'rg x'g] cGt/f{li6«o d'b|fsf]ifsf] k|If]k0f 5 . o;dWo] ef/tsf]] cy{tGq $=% k|ltztn] ;+s'rg x'g] / rLgsf] cy{tGq ! k|ltztn] lj:tf/ x'g] k|If]k0f 5 . g]kfnsf] cfly{s j[l4 eg] ! k|ltztdf ;Lldt x'g] cGt/f{li6«o d'b|fsf]ifsf] k|If]k0f 5 .

;~rfns ;ldltsf] k|ltj]bg

cfb/0fLo z]o/wgL dxfg'efjx?,

g]kfn aËnfb]z a}+s lnld6]8sf] 5lAa;f}+ jflif{s ;fwf/0f ;efdf pkl:yt ;Dk"0f{ z]o/wgLx?, ljleGg

lgodgsf/L lgsfoaf6 kfNg'ePsf k|ltlglwx? tyf pkl:yt ;Dk"0f{ dxfg'efjx?nfO{ ;~rfns ;ldltsf]

tkm{af6 xflb{s :jfut tyf clejfbg ub{5f}+ . ljZJofkL sf]/f]gf dfxfdf/Ln] ;+;f/e/L ;a} k|s[ltsf Joj;fodf

k|lts'n kl/l:ylt >[hgf u/]sf] 5 . ljZj cy{tGq sf]/f]gfsf] k|lts'n kl/l:yltdf h'Wg k/]sf] cj:yf /x]sf]

5 . o;} cg'?k g]kfnsf] cy{tGq klg sf]/f]gfsf] dxfdf/Laf6 lgs} k|efljt /x\of] . o:tf] sl7g kl/l:ylt

afah'b a}+sn] cfly{s jif{ &^÷&& df klg lgs} r'gf}tLx?nfO{ ;fdgf ub}{ ;du|df pT;fxhgs pknAwL xfl;n

ug{ ;kmn ePsf] 5 . pkl:yt dxfg'efjx? ;dIf d @)&& cfiff9 d;fGtsf] a}+s tyf a}+ssf] ;xfos sDkgL

;d]tsf] PsLs[t ljQLo cj:yfsf] ljj/0f, cfly{s jif{ @)&^÷&& sf] PsLs[t gfkmf gf]S;fg ljj/0f, PsLs[t

cGo lj:t[t cfDbfgLsf] ljj/0f, PsLs[t gub k|jfx ljj/0f, OlSj6Ldf ePsf] kl/jt{g nufot cGo ljQLo

ljj/0fx? tyf ;f];Fu ;DalGwt cg';"rLx? ;efsf] :jLs[ltsf nflu k|:t't ug'{ cl3 /fli6«o tyf cGt/f{li6«o

cfly{s cj:yf Pj+ o;n] kf/]sf] k|efj tyf cf=j= @)&^÷&& df a}+sn] u/]sf s]xL pNn]Vo sfo{x?sf] ;dLIff

/ efjL sfo{qmdx? af/]df pNn]v ug{ rfxG5' .

cfly{s j[l4 / d"No l:yltcfly{s jif{ @)&%÷&^ df & k|ltzt cfly{s j[l4 xfl;n ePsf]df cfly{s jif{ @)&^÷&& df @=@* k|ltztdf ;Lldt /x]sf] s]Gb|Lo tYof° ljefusf] k|f/lDes cg'dfg 5 . s[lif If]qsf] j[l4b/ @=^ k|ltzt, pBf]u If]qsf] #=@ k|ltzt tyf ;]jf If]qsf] j[l4b/ @ k|ltzt /x]sf] cg'dfg 5 . cfly{s jif{ @)&^÷&& df s'n ufx{:Yo pTkfbg;Fusf] s'n ufx{:Yo artsf] cg'kft !*=! k|ltzt / s'n /fli6«o artsf] cg'kft $^ k|ltzt /x]sf] cg'dfg 5 . cl3Nnf] jif{ oL cg'kftx? qmdzM !( k|ltzt / $*=( k|ltzt /x]sf lyP . cfly{s jif{ @)&^÷&& df s'n ufx{:Yo pTkfbgdf s'n l:y/ k'FhL lgdf{0fsf] cg'kft @*=! k|ltzt / s'n k'FhL lgdf{0fsf] cg'kft %)=@ k|ltzt /x]sf] cg'dfg 5 . cl3Nnf] jif{ oL cg'kftx? qmdzM ##=& k|ltzt / %^=^ k|ltzt /x]sf lyP .

@)&& h]7df jflif{s ljGb'ut pkef]Qmf d'b|f:kmLlt $=%$ k|ltzt /x]sf] 5 . cfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf cf};t pkef]Qmf d'b|f:kmLlt ^=@* k|ltzt /x]sf] 5 . cl3Nnf] jif{sf] ;f]xL cjlwdf o:tf] d'b|f:kmLlt $=%! k|ltzt /x]sf] lyof] .

cfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf lgof{t )=@ k|ltztn] a9]/ ?= ** ca{ / cfoft !%=# k|ltztn] 36]/ ?= !!)) ca{ *! s/f]8 ePsf] 5 . o; cjlwdf Jofkf/ 3f6fdf !^=$ k|ltztn] ;'wf/ cfPsf] 5 eg]

नेपाल बङ्गलादेश बैंक ललमिटेड 11

ljk|]if0f cfk|jfx # k|ltztn] 36]/ ?= &&$ ca{ *& s/f]8 sfod ePsf] 5 . cfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf rfn' vftf 3f6f ?= &! ca{ ̂ $ s/f]8 / zf]wgfGt/ art ?= !&( ca{ #& s/f]8 sfod ePsf]] 5 . cfly{s jif{ @)&%÷&^ sf] ;f]xL cjlwdf rfn' vftf 3f6f ?= @$( ca{ * s/f]8 / zf]wgfGt/ 3f6f ?= () ca{ *# s/f]8 /x]sf] lyof] .

;dLIff jif{df ljk|]if0f cfk|jfx !^=% k|ltztn] j[l4 eO{ ?= *&( ca{ @& s/f]8 k'u]sf] 5 . cl3Nnf] jif{ ljk|]if0f cfk|jfx *=^ k|ltztn] j[l4 ePsf] lyof] . clGtd >d :jLs[ltsf cfwf/df a}b]lzs /f]huf/Ldf hfg] g]kfnLsf] ;+Vof cfly{s jif{ @)&%÷&^ df ut jif{sf] t'ngfdf #@=^ k|ltztn] 36]sf] 5 . cl3Nnf] jif{sf] ;f]xL cjlwdf o:tf] ;+Vof (=# k|ltztn] 36]sf] lyof] . cl3Nnf] jif{ ?= @$& ca{ %& s/f]8n] 3f6fdf /x]sf] rfn" vftf 3f6f ;dLIff jif{df j:t' cfoft pRr b/n] a9]sf] sf/0f ?= @^% ca{ #& s/f]8n] 3f6fdf uPsf] 5 . To;}u/L, cl3Nnf] jif{ ?= (^ s/f]8n] artdf /x]sf] ;du| zf]wgfGt/ l:ylt ;dLIff jif{df ?= ^& ca{ $) s/f]8n] 3f6fdf /x]sf] 5 .

@)&^ c;f/ d;fGtdf !@%( /x]sf] g]K;] ;"rsf° @)&& c;f/ d;fGtdf !#^@=#$ sfod ePsf]]] 5 . To;}u/L, @)&^ c;f/ d;fGtdf ahf/ k'FhLs/0f ?= !%^& ca{ %) s/f]8 /x]sf]df @)&& c;f/ d;fGtdf ?= !&(@ ca{ &^ s/f]8 /x]sf] 5 .

jfl0fHo a}+sx?nfO{ bL3{sfnLg C0fkq hf/L u/L ljQLo ;fwg kl/rfng ug{ k|f]T;flxt ul/Psf sf/0f lwtf]kq ahf/df pks/0fut ljljwLs/0f k|f/De ePsf] 5 . cfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf !& jfl0fHo a}+s / @ ljQ sDkgL u/L !( ;+:yfn] ?= $% ca{ @% s/f]8sf] C0fkq lgisfzg ug{ :jLs[lt k|fKt u/]sf 5g\ . @)&& h]7 d;fGtdf a}+s tyf ljQLo ;+:yfsf] ?= %$ ca{ @( s/f]8sf] C0fkq bfloTj /x]sf] 5 .

@= a}+s tyf ljQLo If]qsf] ;fwg tyf ;|f]tx?sf] kl/rfngcfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf a}s tyf ljQLo ;+:yfsf] lgIf]k kl/rfng !#=# k|ltztn] j[l4 eO{ ?= #^^^ ca{ ^@ s/f]8 k'u]sf] 5 . cl3Nnf] jif{sf]] ;f]xL cjlwdf ;d]t lgIf]k kl/rfng !#=# k|ltztn] j[l4 eO{ ?= #!)% ca{ &$ s/f]8 k'u]sf] lyof] .

cfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf a}s tyf ljQLo ;+:yfsf] nufgLdf /x]sf] shf{ !)=& k|ltztn] j[l4 eO{

?= #!&@ ca{ (* s/f]8 k'u]sf] 5 . cl3Nnf] jif{sf]] ;f]xL cjlwdf o:tf] shf{ !*=@ k|ltztn] a9]/ ?= @*#^ ca{ & s/f]8 k'u]sf] lyof] . @)&^ r}t d;fGtdf a}+s tyf ljQLo ;+:yfsf] nufgLdf /x]sf] shf{dWo] ?= !% nfv;Ddsf] shf{ !% k|ltzt, ?= !% nfvb]lv ?= %) nfv;Ddsf] shf{ @$=( k|ltzt, ?= %) nfvb]lv ?= ! s/f]8;Ddsf] shf{ !)=@ k|ltzt, ?= ! s/f]8b]lv ?= % s/f]8;Ddsf] shf{ @@=# k|ltzt / ?= % s/f]8 dflysf] shf{ @&=^ k|ltzt /x]sf] 5 .

@)&& h]7 d;fGtdf a}+s tyf ljQLo ;+:yf -n3'ljQ ljQLo ;+:yfx? ;d]t_ sf] r'Qmf k'FhL] @)&^ c;f/sf] t'ngfdf *=@ k|ltztn] j[l4 eO{ ?= #$( ca{ %( s/f]]8 k'u]sf] 5 . To;}u/L, o; cjlwdf k'FhLsf]if (=* k|ltztn] a9]/ ?= %!* ca{ % s/f]8 sfod ePsf]] 5 . @)&& h]7 d;fGtdf jfl0fHo a}+sx?sf] k'FhL sf]if kof{Kttf cg'kft !#=$ k|ltzt, ljsf; a}+sx?sf] !#=$ k|ltzt / ljQ sDkgLx?sf] !*=& k|ltzt /x]sf] 5 . @)&^ c;f/ d;fGtdf oL cg'kftx? qmdzM !$ k|ltzt, !^ k|ltzt / @)=$ k|ltzt /x]sf lyP .

a}+s tyf ljQLo ;+:yfx?sf] lgliqmo shf{ cg'kft @)&^ c;f/ d;fGtdf !=%@ k|ltzt /x]sf]df @)&^ r}t d;fGtdf !=*! k|ltzt k'u]sf] 5 . @)&^ r}t d;fGtdf jfl0fHo a}+sx?sf] lgliqmo shf{ cg'kft !=&@ k|ltzt, ljsf; a}+sx?sf] !=$* k|ltzt / ljQ sDkgLx?sf] ^=&^ k|ltzt /x]sf] 5 .

a}+s tyf ljQLo ;+:yfsf zfvf lj:tf/;Fu} ljQLo kx'Fr a9]sf] 5 . a}+s tyf ljQLo ;+:yfsf] zfvf ;+Vof @)&^ c;f/ d;fGtdf *^*^ /x]sf]df @)&& h]7 d;fGtdf (&!^ k'u]sf] 5 . pQm cjlwdf k|lt a}+s zfvf hg;+Vof ##^# af6 36]/ #)&% sfod ePsf] 5 .

df}lb|s If]qaf6 k|jfx x'g] shf{dWo] cfGtl/s shf{sf] j[l4b/ @$ k|ltzt / lghL If]qtk{msf] shf{sf] j[l4b/ @! k|ltztdf ;Lldt ug]{ k|If]k0f ul/Psf]]]df @)&& h]7 d;fGtdf oL shf{sf] jflif{s ljGb'ut j[l4b/ qmdzM !^=( k|ltzt / !# k|ltzt /x]sf] 5 .

cfly{s jif{ @)&^÷&& df ?= @!( ca{ !% s/f]8 t/ntf k|jfx ePsf] 5 . o; cGt{ut l/kf]dfkm{t ?= !!% ca{ *& s/f]8 / :yfoL t/ntf ;'ljwfdfkm{t ?= !)# ca{ @* s/f]8 k|jfx ePsf] 5 .

cfly{s jif{ @)&^÷&& df o; a}+sn] jfl0fHo a}+sx¿af6 cd]l/sL 8n/ $ ca{ @) s/f]8 v'b vl/b u/L ?= $(@ ca{ @$ s/f]8 t/ntf k|jfx u/]sf] 5 . ;f]xL

नेपाल बङ्गलादेश बैंक ललमिटेड12

cjlwdf kl/jTo{ ljb]zL d''b|f laqmL u/L ?= $$@ ca{ !# s/f]8sf] ef=?= vl/b u/]sf] 5 . cfly{s jif{ @)&^÷&& df jfl0fHo a}+sx¿aLr ?= !%)! ca{ $% s/f]8 / a}+s tyf ljQLo ;+:yfx¿ -jfl0fHo a}+sx¿aLr afx]s_ aLr ?= !@( ca{ $) s/f]8sf] cGt/a}+s sf/f]af/ ePsf] 5 .

@)&& c;f/df (!–lbg] 6«]h/L ljnsf] efl/t cf};t Aofhb/ !=@& k|ltzt / jfl0fHo a}+sx¿aLrsf] efl/t cf};t cGt/a}+s b/ )=#% k|ltzt /x]sf] 5 . @)&^ c;f/df oL b/x? qmdzM $=(& k|ltzt / $=%@ k|ltzt /x]sf lyP . jfl0fHo a}+sx?sf] cf};t cfwf/ b/ @)&^ c;f/df (=%& k|ltzt /x]sf]df @)&& h]7df *=^^ k|ltzt sfod ePsf] 5 . To;}u/L @)&& h]7df shf{sf] efl/t cf};t Aofhb/ !)=$# k|ltzt / lgIf]ksf] efl/t cf};t Aofhb/ ̂ =!& k|ltzt sfod ePsf] 5 . @)&^ c;f/df shf{sf] efl/t cf};t Aofhb/ !@=!# k|ltzt / lgIf]ksf] efl/t cf};t Aofhb/ ^=^) k|ltzt /x]sf lyP .

a}+s tyf ljQLo ;+:yfx?n] ;+:yfut ljb]zL lgIf]kstf{ tyf u}/–cfjf;Lo g]kfnLaf6 Go"gtd @ jif{ cjlwsf] ljb]zL d'b|f d'2tL lgIf]k :jLsf/ ug{;Sg] Joj:yf ul/Psf]df cfly{s jif{ @)&^÷&& sf] P3f/ dlxgfdf * nfv *! xhf/ cd]l/sL 8n/ lgIf]k kl/rfng ePsf] 5 . a}+s tyf ljQLo ;+:yfn] s'n :jb]zL d'b|f lgIf]ksf] a9Ldf %) k|ltzt;Dd ;+:yfut lgIf]k kl/rfng ug{ kfpg] Joj:yf ul/Psf]df @)&& h]7df o:tf] lgIf]ksf] cf};t c+z $%=! k|ltzt /x]sf] 5 . a+}s tyf ljQLo ;+:yfn] cfgf] s'n :jb]zL lgIf]ksf] clwstd !) k|ltzt;Dd dfq Ps ;+:yfaf6 lgIf]k kl/rfng ug{ kfpg] Joj:yf /x]sf] 5 .

jfl0fHo a}+sx?n] cfgf] r'Qmf k'FhLsf] Go"gtd @% k|ltzt a/fa/ C0fkq hf/L ug'{kg]{ Joj:yf ul/Psf]df cfly{s jif{ @)&^÷&& df !@ jfl0fHo a}+sn] C0fkqdfkm{t ?= @^ ca{ ( s/f]8sf] ;fwg kl/rfng u/]sf 5g\ .

pTkfbgzLn ultljlw tyf lgof{tnfO{ k|f]T;flxt ug]{ p2]Zon] g]kfn /fi6« a}+saf6 ;x'lnot b/df k|bfg ul/+b} cfPsf] k'g/shf{ @)&& c;f/ d;fGtdf ?= & ca{ $( s/f]8 nufgLdf /x]sf] 5 . o; cGtu{t ;fwf/0f k'g/shf{ ?= % ca{ ** s/f]8 / e'sDk kLl8tnfO{ k|jfx ul/Psf] k'g/shf{ ?= ! ca{ ^! s/f]8 /x]sf] 5 .

jfl0fHo a}+sx?n] cfgf] s'n shf{sf] Go""gtd !) k|ltzt s[lif If]qdf k|jfx ug'{kg]{ Joj:yf /x]sf]df @)&& h]7 d;fGtdf ?= @^! ca{ !% s/f]8 cyf{t s'n shf{sf] (=& k|ltzt k|jfx ePsf] 5 . o;}u/L phf{ tyf ko{6gdf !% k|ltzt shf{ k|jfx ug'{kg]{ Joj:yf /x]sf]df phf{df ?= !$$ ca{ !$ s/f]8 cyf{t s'n shf{sf] %=# k|ltzt / ko{6gdf ?= !@( ca{ &) s/f]8 cyf{t s'n shf{sf] $=* k|ltzt shf{ k|jfx ePsf] 5 .

jfl0fHo a}+s, ljsf; a}+s / ljQ sDkgLn] cfgf] s'n shf{ nufgLsf] Go"gtd % k|ltzt ljkGg ju{df k|jfx ug'{kg]{ Joj:yf /x]sf]df @)&& h]7 d;fGtdf jfl0fHo a}+s, ljsf; j}+s / ljQ sDkgLx?sf]] ljkGg ju{df ?= !*( ca{ &! s/f]8 shf{ nufgL ePsf] 5 . of] /sd s'n shf{ nufgLsf] %=( k|ltzt x'g cfpF5 .

s[lif, 3/]n' tyf ;fgf pBd nufotsf Joj;fo ;~rfngdf shf{ k|jfx a9fpFb} pTkfbg tyf /f]huf/L clej[l4 ug{] p2]Zon] ;~rflnt ;x'lnotk"0f{ shf{ sfo{qmdaf6 @)&& h]7 d;fGt;Dd @( xhf/ !%& C0fL nfeflGjt ePsf 5g\ eg] ?= %% ca{ %$ s/f]8 shf{ nufgLdf /x]sf] 5 .

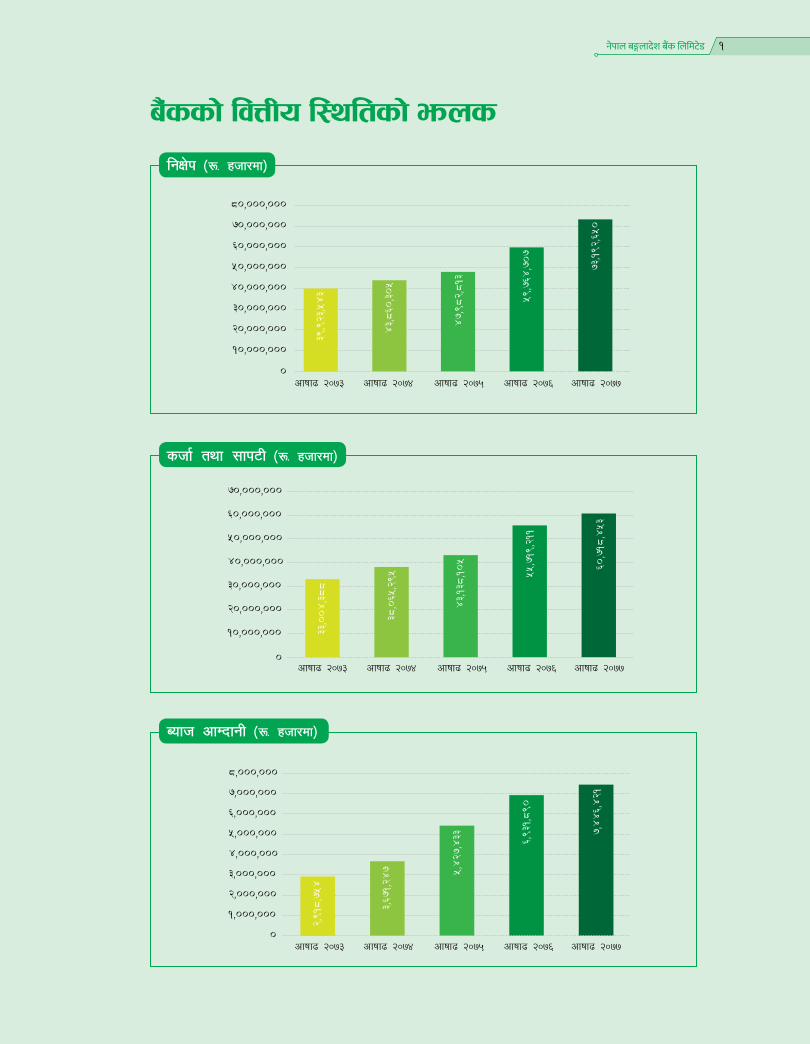

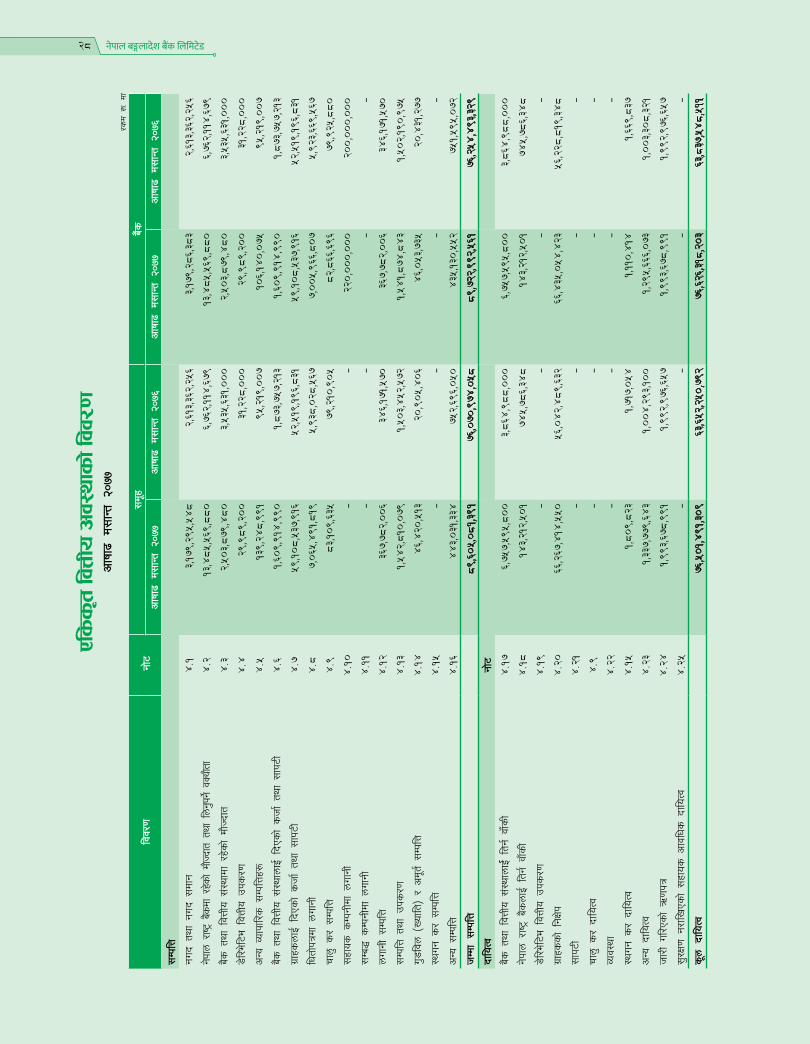

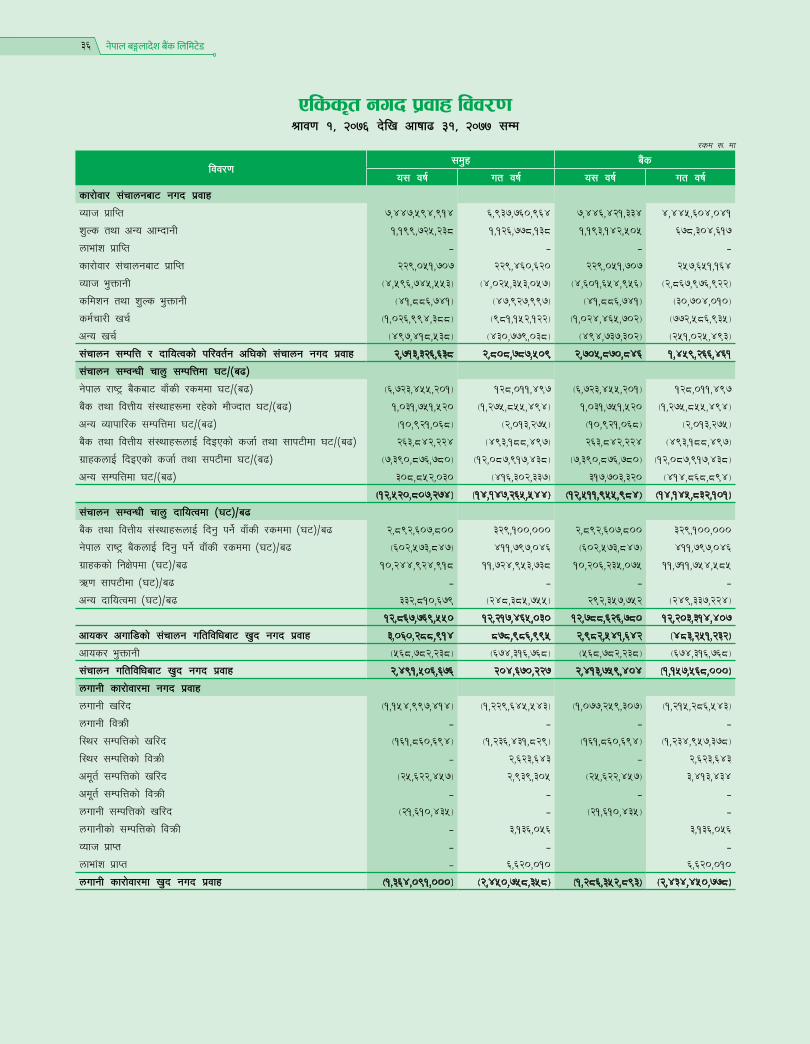

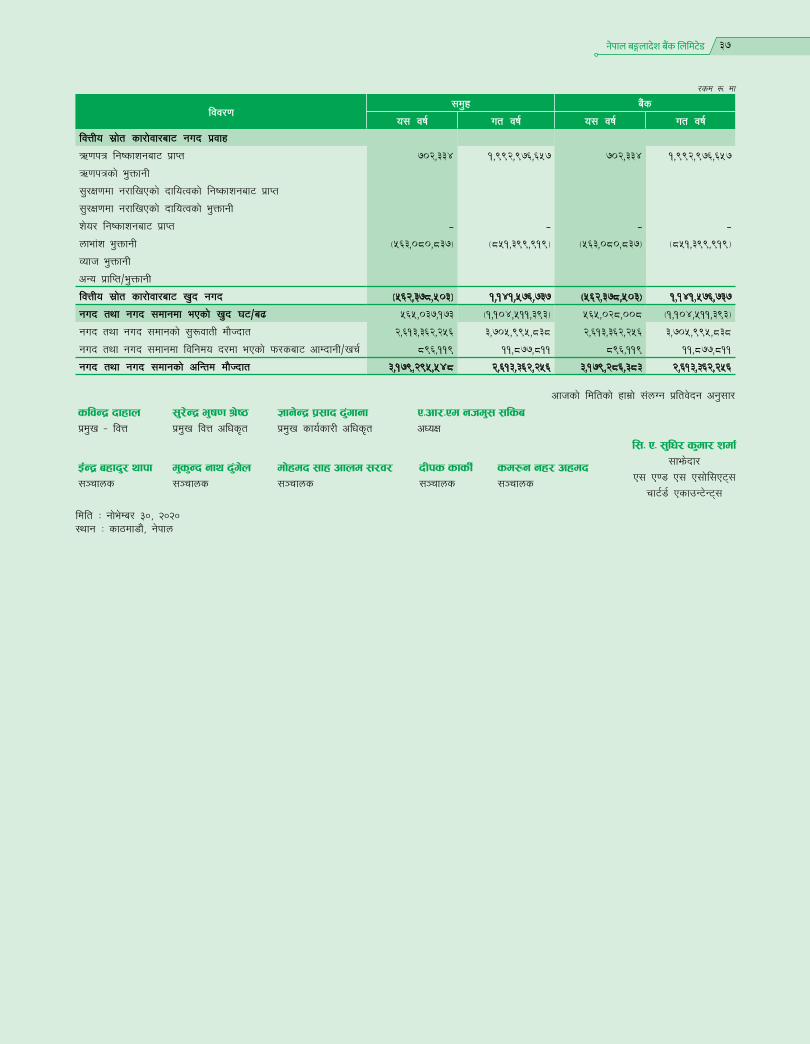

#= ;ldIff jif{df a}+ssf] sf/f]jf/sf] l;+xfjnf]sg#=! cf=j @)&^÷&& df a}+ssf] ljQLo cj:yfcfly{s jif{ @)&^÷&& / cfly{s jif{ @)&%÷&^ df a}+ssf] ljQLo l:yltsf] t'ngfTds ljj/0f b]xfo adf]lhd /x]sf] 5 .

-?= xhf/df_lzif{s cf=j= @)&%÷&^ cf=j= @)&^÷&& j[l4÷-x|f;_ k|ltzts'n lgIf]k 59,764,707 73,192,650 22.47 s'n shf{ tyf ;fk6L 55,719,211 60,718,453 8.97s'n ;DklQ 76,254,493 89,722,993 17.66 nufgL 6,123,670 9,835,986 60.62 v'b Aofh cfDbfgL 2,906,537 2,844,766 (2.13);+rfng cfDbfgL 4,199,950 4,221,689 0.52 ;+rfng d'gfkmf 2,272,028 1,837,076 (19.14)v'b d'gfkmf 1,587,960 1,244,847 (21.61)k"FhL sf]if 13.63% 13.59% -0.04%lgis[o shf{ 1.74% 2.89% 1.15%

नेपाल बङ्गलादेश बैंक ललमिटेड 13

lgIf]k ;+sngM cf=j= @)&%÷&^ df ?= %(=&^ ca{ lgIf]k ;+sng u/]sf]df cf=j= @)&^÷&& Dff @@=$& k|ltztn] j[l4 eO{ ?= &#=!( ca{ k'u]sf] 5 . s'n lgIf]k dWo] cf=j= @)&%÷&^ df rNtL tyf dflh{g lgIf]k, art lgIf]k, d'2tL lgIf]k / sn lgIf]ksf] dfqf qmdzM !#=$^, @$=%$, $&=&^ / !$=@$ k|ltzt /x]sf]df cf=j= @)&^÷&& df qmdzM @!=$&, @#=*!, $^=@(, *=$$ k|ltzt /x]sf] 5 .

shf{ tyf ;fk6L kl/rfngM cf=j= @)&%÷&^ df ?= %%=&@ ca{ shf{ tyf ;fk6L kl/rfng u/]sf]df cf=j= @)&^÷&& Dff *=(& k|ltztn] j[l4 eO{ ?= ^)=&@ ca{ k'u]sf] 5 . cf=j= @)&^÷&& sf] s'n shf{ tyf ;fk6Ldf dflh{g n]l08Ë shf{ )=%! k|ltzt / l/on :6]6 shf{ %=@! k|ltzt dfq /x]sf] 5 . ;fy} s'n shf{ tyf ;fk6Ldf lgis[o shf{sf] dfqf @=*( k|ltzt /x]sf] 5 h'g ut jif{ !=&$ k|ltzt /x]sf] lyof] .

s'n ;DklQM a}+ssf] s'n ;DklQ cf=j= @)&^÷&& Dff !&=^^ k|ltztn] j[l4 eO{ ?= *(=&@ ca{ k'u]sf] 5 . cf=j= @)&%÷&^ df s'n ;DklQ ?= &^=@% ca{ dfq /x]sf] lyof] .

v'b Aofh cfDbfgL cf=j= @)&%÷&^ sf] t'ngfdf cf=j= @)&^÷&& df @=!# k|ltztn] x|f; ePsf] 5 eg] ;+rfng cfDbfgL cf=j= @)&^÷&& Dff )=%@ k|ltztn] j[l4 ePsf] 5 . ljz]iftM COVID – 19 sf] sf/0f Aofh cfDbfgLdf lbOPsf] 5'6 / lgIf]ksf] t'ngfdf shf{sf] a[l4b/ sd ePsf]n] v'b Aofh cfDbfgLdf x|f; cfPsf] 5 . t/ COVID – 19 sf afjh'b u}x| sf]ifdf cfwfl/t shf{ kl/rfngdf ePsf] j[l4sf] sf/0fn] ;]jf z'Ns nufotsf cfDbfgLdf ePsf] j[l4n] ;+rfng cfDbfgLdf j[l4 ePsf] 5 .

COVID – 19 sf] sf/0f Aofh cfDbfgLdf ePsf] x|f; / lgis[o shf{df ePsf] a[l4n] a}+ssf] ;+rfng d'gfkmf tyf v'b d'gfkmfM cf=j= @)&%÷&^ sf] t'ngfdf qmdzM !(=!$ / @!=^! k|ltztn] x|f; eO{ cf=j= @)&^÷&& Dff qmdzM ?= !=*$ ca{ / ?= !=@$ ca{ k'u]sf] 5 .

#=@ a}+ssf] zfvf lj:tf/a}+sn] cfkm\gf] ;~hfnnfO{ lj:tf/ ug]{ qmddf cfly{s jif{ @)&^÷&& df yk ^ j6f zfvf ;~rfngdf NofPsf] 5 . ;dLIff cjlwdf l;Gw'kfNrf]s lhNNffsf] tftf]kfgL, bfË lhNNffsf] t'n;Lk"/, nlntk'/ lhNnfsf] vf]sgf, sf7df08f} lhNNffsf] ltnuËf, sfF8f3f/L / d+l8vf6f/df u/L yk ^ j6f zfvf sfof{nox? ;+rfng u/]sf] 5 . cfiff9 d;fGt @)&& Dff a}+ssf] s'n zfvf ;+Vof (&

tyf PS;6]G;g sfpG6/ & j6f ;+rfngdf /xsf] 5 . To;} u/L zfvf lj:tf/ cleofgnfO{ lg/Gt/tf lb+b} rfn' cfly{s jif{df klg cGo yk zfvfx? ;+rfngdf Nofpg] of]hgf /x]sf] 5 . o;} u/L ;ldIff cjlwdf b]zsf ljleGg :yfgdf a}+ssf] &(, j6f Pl6Pdx? ;+rfngdf /x]sf 5g\ .

#=# lgIf]k of]hgf / ;'ljwfa}+sn] cfkm\gf] :yfkgf sfnb]lv g} lgIf]kstf{x?nfO{ pRrtd k|ltkmn lbg] / C0fLx?nfO{ plrt Aofhb/df shf{ k|jfx ug]{ p2]Zo /fv]sf]n] cGo a}+sx? eGbf ;fGble{s Aofhb/ lb+b}÷ln+b} cfPsf] 5 . ;a} ju{sf u|fxsx?nfO{ ;d]6\g] lx;fjn] ljleGg vfnsf lgIf]k of]hgfx? ;+rfngdf /x]sf 5g\ . !^ jif{ d'lgsf afnaflnsfx?sf] nfuL afn art vftf, z]o/wgLx?sf] nflu z]o/wgL art vftf, u[lx0fL dlxnfx?sf] nflu u[lx0fL art vftf, j[4 tyf czQmx?sf] nflu ;fdflhs ;'/Iff vftf cflb lgIf]k vftfx? ;+rfngdf /x]sf 5g\ . a}+sn] cfkm\gf lgIf]k of]hgfx?nfO{ ;do;fk]If kl/dfh{g ug]{ u/]sf] 5 / gofF–gofF lgIf]k of]hgfx? klg Nofpg] u/]sf] 5 . To;} u/L a+}+sn] xfn;fn} sd{rf/Lx?sf] art a[l4 ug]{ pb]Zon] cfsif{s ladf ;'lawf ;lxtpRrtd Jofh k|bfg ug]{ u/L sd{rf/L art vftf ;+rfngdf NofPsf] 5 .

shf{ tkm{ klg dWod ju{sf u|fxsx?nfO{ nlIft u/]/ Go"gtd Aofhb/ sfod ul/ 3/hUuf, cfjf;sf] nflu Pgla xf]d nf]g, ;jf/L ;fwg vl/bsf] nflu Pgla c6f] nf]g, b]zsf] ljsf; lgdf{0fdf v6]sf 7]s]bf/x¿nfO{ sG6«ofS6 nf]g nufotsf shf{x? k|jfx ul//x]sf] 5 . ;fy} cfkm\gf u|fxsx?sf] shf{sf] dfunfO{ Wofgdf /flv shf{ of]hgfx?df ;do;fk]If kl/dfh{g klg ul//x]s]f 5 . o;} qmddf a}+sn] shf{ cjlwe/ Aofhb/ :yL/ /xg] 3/ shf{, k|f]km];gn shf{, uf8L shf{, cfjlws lwtf] shf{ tyf lzIff shf{ ;~rfngdf NofPsf] 5 .

a}+sn] u|fxsx?nfO{ a}+lsË ;]jfsf] ;fy ;fy} cGo ;]jfx? klg cfkm\gf] k|fyldstfdf /fvL k|bfg ub}{ cfO/x]sf] 5 .

#=$ shf{ ckn]vg tyf c;"nLa}+sn] ljut jif{x?df ljljw sf/0fn] lstfaL ?kdf ckn]vg u/]sf shf{x?sf] c;"nLnfO{ k|efjsf/L?kn] cuf8L a9fPsfn] cf=j= @)&^÷&& df ckn]vg ul/Psf shf{x?af6 ?= !=!# s/f]8 c;"nL u/]sf] 5 . a}+ssf] k|wfg sfof{nodf /x]sf] shf{ c;'nL ljefun] lg/Gt/

नेपाल बङ्गलादेश बैंक ललमिटेड14

?kdf ;DalGwt zfvfsf] ;dGjodf o; k|sf/sf ckn]lvt shf{x?df c;'nLsf] k|lqmofnfO{ cufl8 a9fO{/x]sf] 5 . ;fy} a}+sn] cf=j= @)&^÷&& df ?= )=&) s/f]8 shf{ ckn]vg u/]sf] 5 .

$= ;+:yfut ;fdflhs pQ/bfloTja}+sn] ;+:yfut ;fdflhs pQ/bfloTj cGtu{t ljljw ;fdflhs sfo{ tyf cleofgx?df ljleGg lsl;dn] ;xeflutf hgfO{ ljljw ;xof]u u/]sf]] 5 . ;dLIff cjlwdf a}+sn] kz'klt If]qleq a[Iff/f]k0f,g]kfn ;/sf/sf] ljQLo hfu/0f cleofg cGtu{t “;Da[l4;Fu hf]8f}+ gftf, ;a} g]kfnLsf] a}+s vftf”sf nflu ljleGg sfo{qmdsf] nflu cfly{s ;xof]u, lj/f6 alx/f :s"nsf] nflu 8]:s tyf a]~rx? ;xof]u, Go" g]kfn ;f];fO6LnfO{ cgfyx?sf] nflu 3/ k'glg{df0f ug]{sf] nflu cfly{s ;xof]u, l6r km/ g]kfnsf] ljljw sfo{sf] nflu cfly{s ;xof]u, /Tg k':tfsfnonfO{ k':tsx? ;xof]u, g]kfn ;/sf/n] :yfkgf u/]sf] COVID fund df ;xof]u, g]kfn k|x/Lsf nflu cfjZos df:s ;xof]u, COVID-19 sf] dxfdf/ L;+u h'Wgsf nflu cfjZos kg]{ sanitary ;fdfgx?sf] ljt/0f nufotsf cGo ;fdflhs sfo{qmdx¿df cfkm\gf] ;lqmo ;xelutfnfO{ hf/L /fv]sf] 5 . To;}u/L a}+sn] x/]s aif{ k|j]lzsf k/LIffdf /fd|f] glthf Nofpg] a}+ssf rf/ hgf sd{rf/Lx?sf 5f]/f 5f]/Lx?nfO{ dfl;s ?= @,)))=)) sf b/n] b'O{ jif{;Ddsf] nflu 5fqj[lQ klg k|bfg ub}{ cfPsf] sfo{nfO{ o; jif{ klg lg/Gt/tf lbPsf]5 .

%= dfgj ;+;fwg;dLIff cljlwdf a}+sdf :yfoL / c:yfoL u/L s'n (&( hgf sd{rf/Lx? sfo{/t /x]sf 5g\ . a}+ssf] ;du| pGgltdf sd{rf/Lsf] d'Vo e"ldsf /xg] tYonfO{ cfTd;ft u/L pgLx?sf] l;h{gzLntf, sfo{s'zntf, Joj;flos bIftf tyf Joj:yfkg ;Lk a[l4sf nflu lgoldt ?kdf tflndsf] Joj:yf ug]{ gLlt a}+ssf] /x]sf] 5 . o;}qmddf ;dLIff jif{df ljljw ljifox?df sd{rf/Lx?nfO{ /fli6«o tyf cGt/f{li6«o :t/sf Joj;flos tflndx? k|bfg ul/Psf] lyof] . To:t} a}+sn] cfjZostf cg';f/ u'0ffTdstfsf] cfwf/df gofF sd{rf/L egf{ ug]{ / cfjZos tflnd tyf k|lzIf0f k|bfg ug]{ sfo{ ;d]t ul//x]sf] 5 . cf=j= @)&^÷&& df sd{rf/Lx?sf] :jb]zL tyf ljb]zL tflndx?sf] nflu ?= !=^( s/f]8 vr{ ePsf] lyof] . sd{rf/Lsf] bIftf clej[l4sf] nflu ul/g] ljleGg k|sf/sf tflnd tyf k|lzIf0f sfo{qmdx?nfO{ cfufdL lbgx?df klg lg/Gt/tf lbOg] 5 .

^= ;+:yfut ;'zf;g;+:yfut ;'zf;g ;+:yfsf] lbuf] ljsf; Pj+ :yfloTjsf] d"n cfwf/ xf] eGg] dfGotfnfO{ cfTd;ft ub}{ ;+:yfut ;'zf;gsf d"ne"t cfwf/x? kf/blz{tf, OdfGbfl/tf / hjfkmb]lxtfnfO{ a}+sn] b[9tfsf ;fy kl/kfngf ub}{ cfPsf] 5 . a}+sn] k|rlnt P]g lgod, g]kfn /fi6« a}+s Pj+ cGo lgofds lgsfox?åf/f hf/L lgb]{zg tyf a}+ss} cfGtl/s gLlt lgod adf]lhd sfo{ ;+rfng ub}{ cfPsf] 5 . a}+sn] cfkm\gf Joj;flos lqmofsnfk ;+rfng ug{ cfjZos kg]{ gLltut Joj:yf ug{ Pj+ a}+ssf] sfo{ ;Dkfbg cem r':t / k|efjsf/L agfpg ;~rfns ;ldlt cGtu{t ljleGg pk—;ldltx? u7g u/]sf] 5 . To;}u/L ;~rfns tyf sd{rf/Lx?n] kfngf ug'{kg]{ cfrf/ ;+lxtf sfof{Gjogdf NofO{ kfngf u/fO{/x]sf] 5 . a}+sn] cfkm\gf ljQLo ljj/0fx? tyf lgodgsf/L lgsfoåf/f lgwf{/0f ul/Psf ;"rgf tyf k|ltj]bgx? ;/f]sf/jfnf lgsfox? ;dIf ;dodf g} k]z ug'{sf ;fy} ;fj{hlgs ;/f]sf/sf ;"rgfx? tyf ljj/0fx? lgoldt ?kdf k|sfzg ub}{ cfPsf] 5 .

&= cfGtl/s lgoGq0f k|0ffnL tyf hf]lvd Aoj:yfkga}+lsË Joj;fodf lglxt hf]lvdx? shf{, ;+rfng, ahf/ tyf cGo hf]lvdx?nfO{ b[li6ut ul/ a}+sn] cfkm\gf] cfGtl/s lgoGq0f k|0ffnLnfO{ r':t b'?:t agfpg] gLlt lnP adf]lhd Joj;fosf] qmddf cfO{kg{ ;Sg] ;a} k|sf/sf hf]lvdx?nfO{ Go"lgs/0f ug{ a}+sn] cfGtl/s n]vfk/LIf0f, hf]lvd Joj:yfkg tyf cg"kfngfsf sfo{x? dfkm{t\ cfGtl/s lgoGq0f k|0ffnLnfO{ Jojl:yt t"NofPsf] 5 . a}+sdf u}/ sfo{sf/L ;~rfnssf] ;+of]hsTjdf /x]sf] hf]lvd Joj:yfkg ;ldltsf] lgu/fgLdf /xg] ul/ hf]lvd Joj:yfkg ;+oGq agfOPsf] 5 . k|d'v hf]lvd clws[t dfkm{t hf]lvd ;DalGw ;Dk"0f{ sfo{x? ;+rfng eO{/x]sf 5g\ . ;f]xL cg'?k k|d'v hf]lvd clws[t dftxtdf /xg] ul/ shf{ / ;+rfng hf]lvd Joj:yfgsf] nflu hf]lvd Joj:yfkg ljefu u7g ul/Psf] 5 . xfn pQm ljefun] shf{ k|jfx ubf{ tyf gjLs/0f ubf{ hf]lvdsf] dfqfx?sf] af/]df ljZn]if0f ug]{, a}+s ;+rfng ;DaGwL hf]lvd, ahf/ hf]lvd nufot cGo hf]lvdx? ljZn]if0f ug]{ / plrt /fo ;Nnfx lbg] sfo{ ug]{ u/]sf] 5 . ;fy} lgoldt ?kdf hf]lvd Joj:yfkgsf] af/]df hf]lvd Joj:yfkg ;ldltdf 5nkmn ug]{ u/]sf] 5 . o;sf ;fy} cfGtl/s lgoGq0f k|0ffnL tyf hf]lvd Joj:yfkgnfO{ yk r':t b'?:t agfpg] k|of]hgsf] nflu gfoj k|d'v sfo{sf/L clws[tsf] ;+of]hsTjdf ;+rfng hf]lvd Joj:yfkg ;ldlt ;d]t u7g ul/Psf]

नेपाल बङ्गलादेश बैंक ललमिटेड 15

5 . To:t} a}+ssf x/]s sd{rf/Lx?sf] JolQmut lhDd]jf/L / bfloTjnfO{ :yflkt ub{} sfo{ ;Dkfbgdf cfk;L lgoGq0f / ;Gtn'g k|0ffnLnfO{ k|efjsf/L ?kdf sfof{Gjog ub}{ cfPsf] 5 .

*= ;DklQ z'l4s/0f -dgL nfp08l/Ë_ lgjf/0fa}+sdf s]lGb|o:t/df Pp6f 5'6\6} cg'kfng (Compliance) ljefusf] u7g ul/Psf] / zfvfut ?kdf cg'kfng clws[t -Compliance Officer) tf]s]/ ljBdfg ;DklQ z'l4s/0f -dgL nfp08l/Ë_ lgjf/0fsf ;DaGwdf hf/L ePsf gLlt, lgod, lgb]{zgx?sf] kngf k'0f{?kn] ug]{ sfo{ eO{/x]sf] 5 .

(= n]vfk/LIf0fa}+ssf] rf}aL;f}+ jflif{s ;fwf/0f ;efn] cfly{s jif{ @)&^÷&& sf] afXo n]vfk/LIf0f ug{sf] nflu >L P; P08 P; P;f]l;P6\;\, rf6{8{ PsfpG6]G6\;\nfO{ n]vfk/LIf0f ;ldltsf] l;kmfl/zdf lgo'Qm u/]sf] lyof] / ;f]xL cg';f/ ;dLIff cjlwsf] n]vfk/LIf0f sfo{ ;DkGg ePsf] lyof] . sDkgL P]g @)^# sf] k|fjwfg cg';f/ xfnsf axfnjfnf n]vfk/LIfs >L P; P08 P; P;f]l;P6\;\, rf6{8{ PsfpG6]G6\;\nfO{ cfly{s jif{ @)&&÷&* sf] nflu klg n]vfk/LIfsdf lgo'lQmsf] nflu of]Uo /x]sf] / lghn] lgo'lQmsf] nflu cfkm\gf] ;xdlt klg lbPsfn] n]vfk/LIf0f ;ldltn] l;kmfl/z u/]adf]lhd o; ;efsf] Ps Ph]G8fsf] ?kdf lghsf] lgo'lQm klg /x]sf] 5 / ;f] nfO{ cg'df]bg ug{sf] nflu ;ef ;dIf cg'/f]w ub{5' .

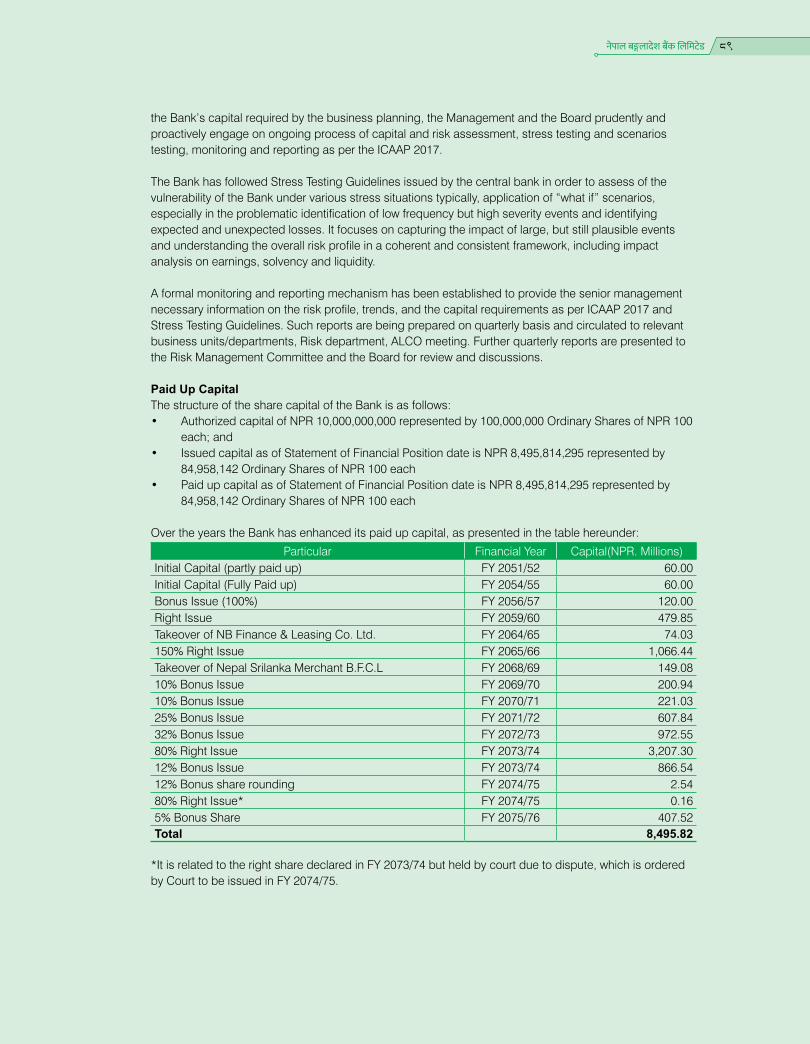

!)= g]kfn /fi6« a}+ssf] lgb]{zg / k"FhL of]hgfcfly{s jif{ @)&@÷&# sf] df}lb|s gLlt tyf g]kfn /fi6« a}+sn] ldlt @! ;fpg @)&@ df hf/L u/]sf] lgb]{zg adf]lhd a}+sx?n] cf=j= @)&#÷&$ ;Dddf cfkm\gf] r'Qmf k"+hL ?= * ca{ k'¥ofpg kg]{ lgb]{zg u/] adf]lhd a}+sn] cf=j= @)&#÷&$ leqg} a}+s cfkm}n] xsk|b z]o/ tyf af]gz z]o/ hf/L u/]/ tf]lsP adf]lhdsf] r'Qmf kF"hL j[l4 ul/;s]sf] 5 . a}+ssf] cfkm\gf] Joj;flos of]hgf cg';f/ k"FhL a[l4 ug]{ of]hgf /x]sf] 5 . a}+ssf] k"FhL a[l4 of]hgf cg'?k g} cf=j= @)&%÷&^ sf] cGTodf ?= @ ca{ /sdsf] C0fkq hf/L u/L ;s]sf] 5 eg] o; cf= j= @)&^÷&& df r'Qmf k"FhLsf] ^ k|ltzt af]g; z]o/ hf/L u/L r'Qmf k"FhL a[l4 ug{ o; ;efsf] Ps Ph]08fsf] ?kdf /flvPsf] 5 . ;f]nfO{ cg'df]bg ug{sf] nflu ;ef ;dIf cg'/f]w ub{5' .

!!= cfly{s jif{ @)&&÷&* sf] cj:yfa}+sn] rfn' cfly{s jif{ @)&&÷&* df klg cfkm\gf] Joj;fonfO{ lgwf{/0f ul/Psf] nIo d'tfljs lj:tf/

ul//x]sf] 5 . lgIf]k ;+sng, shf{ k|jfx cflbdf k|ult xfl;n ul//x]sf] 5 . a}+sn] rfn' cfly{s jif{sf] k|yd qodf;sf] cGTo;Dddf ?= %& s/f]8 !! nfv v'b d'gfkmf cfh{g u/]sf] 5 .

!@= a}+ssf] efjL sfo{qmd tyf of]hgfx?a+}ssf] ;+:yfut gf/f ‘The Bank for Everyone’ nfO{ cfTd;ft ub{} u|fxsx? Dffem Ps e/kbf{] Pj+ ljZj;gLo a}+ssf] ?kdf cfkm\gf] :yfg sfod /fVb} z]o/wgLx?sf] lb3{sfnLg lxt ;+/If0f ug]{ sfo{nfO{ g} cfkm\gf] k|d'v nIo agfPsf 5f}+ . cfufdL lbgdf a}+ssf] sfo{qmdx? b]xfo adf]lhd /xg] 5g\ Ml a}+ssf] cfkm\gf] zfvf ;~hfn lj:tf/ of]hgf

cg';f/ / g]kfnsf] s'n hg;+Vofsf] 7"nf] lx:;f cem} a}+lsË k|0ffnLeGbf aflx/ /x]sf] oyfy{nfO{ dgg ub}{ tL If]qx?df a}+lsË ;]jf k'¥ofpg] sfo{nfO{ lg/Gt/tf lb+b} cGo yk zfvfx¿ ;+rfngdf Nofpg] of]hgf /x]sf] 5 .

l lgIf]ksf] cf}ift Aofhb/df sld Nofpg] lsl;dn] lgIf]ksf gofF of]hgfx? th'{df u/L sfof{Gjog ug]{ / ;+:yfut lgIf]ksf] dfqfnfO{ sd ub{} JolQmut lgIf]kstf{x?sf] cfwf/nfO{ j[l4 ug]{ of]hgf agfPsf] 5 .

l shf{sf] u'0f:t/nfO{ cem ;'wf/ ug]{ / shf{ lj:tf/ ubf{ s[ifL If]qsf ;fy} ;fgf tyf 3/]n' pBf]utkm{ nufgL a9fpg] of]hgf /x]sf] 5 . ;fy} ljutdf ckn]vg u/]sf shf{x?sf] c;'nLnfO{ pRr k|fyldstfdf /fVg] nIo lnOPsf] 5 .

l a}+sn] cfkm\g} ;xfos sDkgL cGtu{t 5'§} a|f]s/ sDkgL:yfkgf ul/;lsPsf] / cg'dlt k|fKt eP kZrft rfn' cfly{s jif{df ;+rfngdf Nofpg] of]hgf /x]sf] 5 .

l cfGtl/s lgoGq0f k|0ffnLnfO{ r':tb'?:t agfpg cfjZos dfqfdf cfGtl/s ;+/rgfnfO{ kl/dfh{g ug]{ / ;+:yfug ;'zf;gnfO{ cem a9L ;'b[9 agfpg] of]hgf agfPsf] 5 .

l a}+ssf] cfkm\gf] ;]jfnfO{ cem r':t b'?:t agfpg tyf ;+rfng vr{nfO{ s6f}tL ug]]{ p2]Zosf ;fy xfn ;+rfngdf /x]sf] Core Banking System (CBS) nfO{ kl/jt{g u/L yk k|efjsf/L Core Banking System (CBS)k|of]udf Nofpg] of]hgf cGtu{t cGt/f{li6«o :t/sf] Core Banking System (CBS) “FINASTRA” ;km\6j]o/ tyf ;f] ;km\6j]o/ ;+rfngdf Nopg cfjZos xf8{j]o/ h8fg u/L 8f6f dfO{u|]zg nufot cGo cfjZos dfO{u|]zg k|s[of o;} cfly{s jif{leq k"/f u/L ;+rfngdf NofOg] of]hgf 5 .

नेपाल बङ्गलादेश बैंक ललमिटेड16

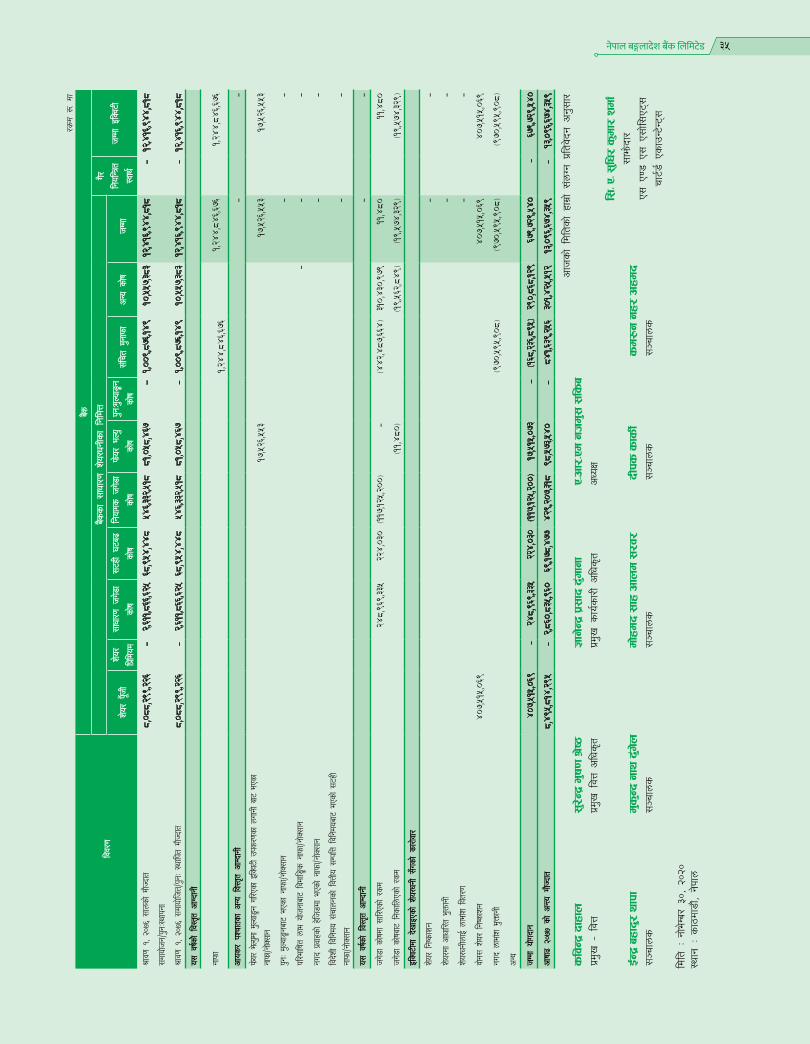

!#= ;~rfns ;ldlt!#=! ;~rfns ;ldltsf] a}7sa}+s ;~rfns ;ldltsf] a}7s cfly{s jif{ @)&^÷&& df hDdf !$ k6s a;]sf] lyof] . a}+ssf] k"FhL sf]ifsf] cj:yf, ;+:yfut ;'zf;g, shf{, ;+rfng tyf ahf/ hf]lvd nufot a}+sn] Wofg lbg'kg]{ cfjZos ;Dk'0f{ If]qsf ljifox? dfly uDeL/ ?kdf 5nkmn ub{} a}+snfO{ cem ;kmn / ;an agfpg ;~rfns ;ldltn] pko'Qm lg0f{ox? ub}{ cfO{/x]sf] 5 . cfufdL lbgx?df klg ;b}j a}+ssf] lxtnfO{ Wofgdf /fvL cfkm\gf] e'ldsf lgjf{x ug{ xfdL ;Dk'0f{ ;~rfnsx? k|ltj4 /x]sf 5f}+ .

!#=@ ;~rfns ;ldltdf ePsf] x]/km]/sDkgL P]g, a}+s tyf ljlQo ;+:yf ;DalGw P]g / a}+ssf] lgodfjnL adf]lhd ;~rfns ;ldltdf lgDg adf]lhdsf] x]/km]/ ePsf] 5 .

s= ;+:yfks ;d"x M ;+:yfks ;d"x cfO{PkmcfO{;L a}+s, a+unfb]zaf6 dgf]gLt # hgf ;+rfnsx¿ >L hnfn cxdb, >L df]xdb ;fx cfnd ;/ j/ / >L sd?g gx/ cxdbn] a}+ssf] ;+rfns ;ldltdf k|ltlglwTj ub{} cfpg'ePsf]df >L hnfn cxdbsf] :yfgdf ldlt h'nfO{ )*, @)@) b]lv >L P=cf/=Pd= ghd'; ;lsa dgf]gog ePcg';f/ lgDg adf]lhdsf ;+rfnsx¿n] ;+rfns ;ldltdf k|ltlglwTj ub{} cfpg'ePsf] 5 M >L P=cf/=Pd= ghd'; ;lsa >L df]xdb ;fx cfnd ;/j/>L sd?g gx/ cxdb

v= ;j{;fwf/0f ;d"x M cf=j= @)&^÷&& df ;j{;fwf/0f ;d"xdf s'g} kl/jt{g gePsf] .

u= Joj;flos ;~rfns M xfn l/Qm /x]sf] 5 .

!$= sDkgL P]g @)^# sf] bkmf !)( pkbkmf $ cg';f/ v'nfOPsf ljj/0fx?-s_ ljut jif{sf] sf/f]af/sf] l;+xfjnf]sg – ;~rfns

;ldltsf] k|ltj]bg sf] a'Fbf # df pNn]v ul/Psf] .-v_ /fli6«o tyf cGt/f{li6«o kl/l:yltaf6 sDkgLsf]

sf/f]af/nfO{ s'g} c;/ k/]sf] eP ;f] c;/ – ;f/e"t ?kdf k|ToIf c;/ gePsf] .

-u_ k|ltj]bg tof/ ePsf] ldlt;Dd rfn" jif{sf] pknlAw / eljiodf ug'{ kg]{ s'/fsf] ;DaGwdf ;~rfns ;ldltsf] wf/0ff – ;~rfns ;ldltsf] k|ltj]bg sf] a'Fbf !! / !@ df pNn]v ul/Psf] .

-3_ sDkgLsf] cf}Bf]lus jf Jofj;flos ;DaGw – a}+sn] cfkm";Fu cf}Bf]lus jf Jofj;flos ;DaGw

/fVg] ;Dk"0f{ ;+3 ;+:yfx?;Fu Jofj;flos Pj+ ;f}xfb{k"0f{ ;DaGw sfod u/]sf] 5 . a}+ssf] cGo lgsfox?;Fu sfod /x]sf] ;DaGwnfO{ Jofj;flostf tyf kf/blz{tfsf ;fy ;'b[9 agfpb} nluPsf] 5 / cfufdL jif{x?df ;f]xL adf]lhd lg/Gt/tf lbOg]5 .

-ª_ ;~rfns ;ldltdf ePsf] x]/km]/ / ;f]sf] sf/0f – ;~rfns ;ldltsf] k|ltj]bgsf] a'Fbf !# sf] æ;~rfns ;ldltÆ lzif{sdf pNn]v ul/Psf] .

-r_ sf/f]af/nfO{ c;/ kfg]{ d'Vo s'/fx¿ –!= a9\bf] k|lt:kwf{@= pRr t/ntfsf] bafa#= bIf hgzlQmsf] cefj $= sf]le8–!( sf sf/0f Joj;fox?df 5fPsf]

dGbL .-5_ n]vfk/LIf0f k|ltj]bgdf s'g} s}lkmot pNn]v

ePsf] eP ;f] pk/ ;~rfns ;ldltsf] k|lts[of – ;f/e't s}lkmot g/x]sf] .

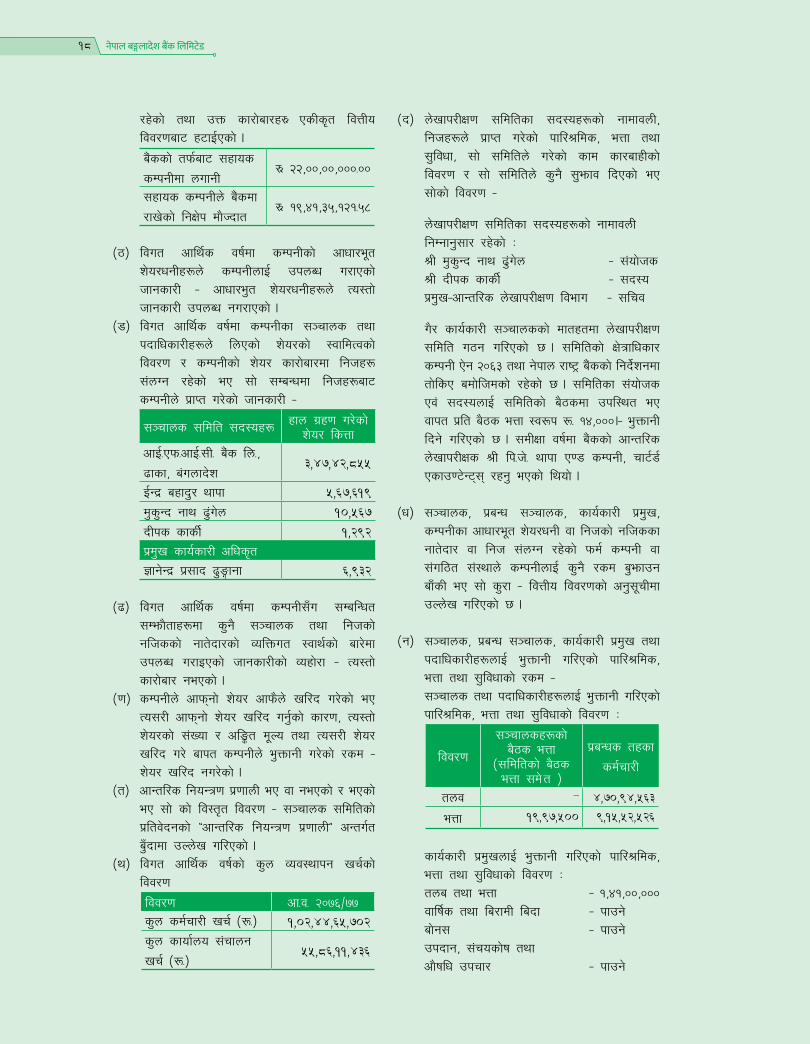

-h_ nfef+z afF8kmfF8 ug{ l;kmfl/; ul/Psf] /sd – a}+sn] @)&& cfiff9 d;fGtdf sfod /x]sf] r'Qmf k"FhLsf] ^ k|ltzt af]g; z]o/sf] nflu /sd ?= %),(&,$*,*%* / @=$@ k|ltzt gub nfef+z -nfef+z s/ k|of]hgsf] nflu ;d]t_ a/fa/sf] /sd ?= @),%^,**,!#^ afF8kmfF8 ug{] k|:tfj u/]sf] 5 .

em_ z]o/ hkmt ePsf] eP hkmt ePsf] z]o/ ;+Vof, To:tf] z]o/sf] cl°t d"No, To:tf] z]o/ hkmt x'g' eGbf cufj} ;f] afkt sDkgLn] k|fKt u/]sf] hDdf /sd / To:tf] z]o/ hkmt ePkl5 ;f] z]o/ laqmL u/L sDkgLn] k|fKt u/]sf] /sd tyf hkmt ePsf] z]o/afkt /sd lkmtf{ u/]sf] eP ;f]sf] ljj/0f – z]o/ hkmt gePsf] .

-`_ ljut cfly{s jif{df sDkgL / o;sf] ;xfos sDkgLsf] sf/f]af/sf] k|ult / ;f] cfly{s jif{sf] cGTodf /x]sf] l:yltsf] k'g/fjnf]sg–

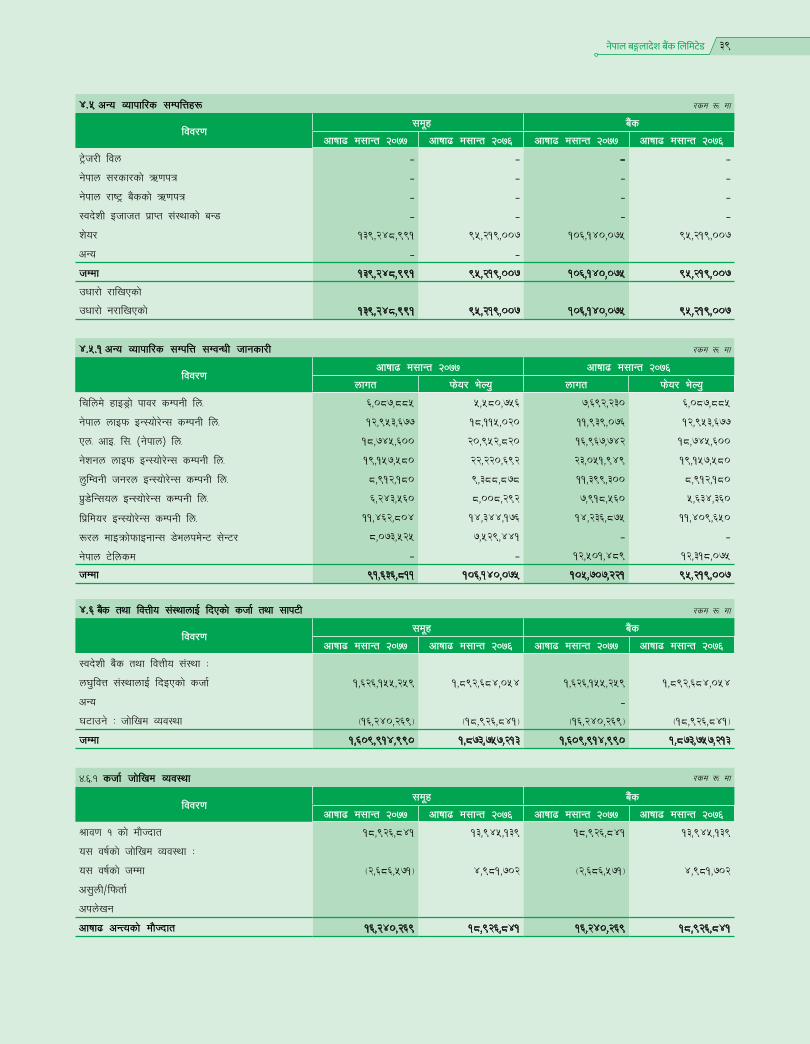

Af}+ssf] zt k|ltzt nufgL ePsf] Ps ;xfos sDkgL g]kfn a+unfb]z Soflk6n ln=n] ldlt @)&% kf}if @^ ut] lwtf]kq af]8{, g]kfnaf6 sf/f]af/ ug]{ cg'dlt k|fKt u/] kZrft ;+rfngdf /x]sf] 5 . ;fy} csf} ;xfos sDkgL PglalaPn ;]So"l/l6h ln=n] ;+rfng cg'dtL kfPsf] 5}g .

-6_ sDkgL tyf To;sf] ;xfos sDkgLn] cfly{s jif{df ;DkGg u/]sf] k|d'v sf/f]af/x? / ;f] cjlwdf sDkgLsf] sf/f]af/df cfPsf] s'g} dxÎjk"0f{ kl/jt{g –

Af}+ssf] zt k|ltzt nufgL ePsf] b'O{ ;xfos sDkgLaLr jf;nft ldltdf lgDgfg';f/ sf/f]af/

नेपाल बङ्गलादेश बैंक ललमिटेड 17

/x]sf] tyf pQm sf/f]af/x¿ PsLs[t ljQLo ljj/0faf6 x6fO{Psf] . a}+ssf] tkm{af6 ;xfos

sDkgLdf nufgL ¿= @@,)),)),)))=))

;xfos sDkgLn] a}+sdf

/fv]sf] lgIf]k df}Hbft¿= !(,$!,#%,!@!=%*

-7_ ljut cfly{s jif{df sDkgLsf] cfwf/e"t z]o/wgLx?n] sDkgLnfO{ pknAw u/fPsf] hfgsf/L – cfwf/e't z]o/wgLx?n] To:tf] hfgsf/L pknAw gu/fPsf] .

-8_ ljut cfly{s jif{df sDkgLsf ;~rfns tyf kbflwsf/Lx?n] lnPsf] z]o/sf] :jfldTjsf] ljj/0f / sDkgLsf] z]o/ sf/f]af/df lghx? ;+nUg /x]sf] eP ;f] ;DaGwdf lghx?af6 sDkgLn] k|fKt u/]sf] hfgsf/L –

;~rfns ;ldlt ;b:ox? xfn u|x0f u/]sf] z]o/ lsQf

cfO{=Pkm=cfO{=;L= a}+s ln=,

9fsf, a+unfb]z3,47,42,855

O{Gb| axfb'/ yfkf 5,67,619d's'Gb gfy 9'+u]n 10,567bLks sfsL{ 1,292k|d'v sfo{sf/L clws[t

1fg]Gb| k|;fb 9'Ëfgf 6,932

-9_ ljut cfly{s jif{df sDkgL;Fu ;DalGwt ;Demf}tfx?df s'g} ;~rfns tyf lghsf] glhssf] gft]bf/sf] JolQmut :jfy{sf] af/]df pknAw u/fOPsf] hfgsf/Lsf] Joxf]/f – To:tf] sf/f]af/ gePsf] .

-0f_ sDkgLn] cfkm\gf] z]o/ cfkm}n] vl/b u/]sf] eP To;/L cfkm\gf] z]o/ vl/b ug'{sf] sf/0f, To:tf] z]o/sf] ;+Vof / cl°t d"No tyf To;/L z]o/ vl/b u/] afkt sDkgLn] e'QmfgL u/]sf] /sd – z]o/ vl/b gu/]sf] .

-t_ cfGtl/s lgoGq0f k|0ffnL eP jf gePsf] / ePsf] eP ;f] sf] lj:t[t ljj/0f – ;~rfns ;ldltsf] k|ltj]bgsf] æcfGtl/s lgoGq0f k|0ffnLÆ cGtu{t a'Fbfdf pNn]v ul/Psf] .

-y_ ljut cfly{s jif{sf] s'n Joj:yfkg vr{sf] ljj/0f

ljj/0f cf=j= @)&^÷&&s'n sd{rf/L vr{ -?=_ 1,02,44,65,702s'n sfof{no ;+rfng

vr{ -?=_55,86,11,436

-b_ n]vfk/LIf0f ;ldltsf ;b:ox?sf] gfdfjnL, lghx?n] k|fKt u/]sf] kfl/>lds, eQf tyf ;'ljwf, ;f] ;ldltn] u/]sf] sfd sf/afxLsf] ljj/0f / ;f] ;ldltn] s'g} ;'emfj lbPsf] eP ;f]sf] ljj/0f –

n]vfk/LIf0f ;ldltsf ;b:ox?sf] gfdfjnL lgDgfg';f/ /x]sf] M

>L d's'Gb gfy 9'+u]n – ;+of]hs >L bLks sfsL{ – ;b:o Kf|Df'v–cfGtl/s n]vfk/LIf0f ljefu – ;lrj

u}/ sfo{sf/L ;~rfnssf] dftxtdf n]vfk/LIf0f ;ldlt u7g ul/Psf] 5 . ;ldltsf] If]qflwsf/ sDkgL P]g @)^# tyf g]kfn /fi6« a}+ssf] lgb]{zgdf tf]lsP adf]lhdsf] /x]sf] 5 . ;ldltsf ;+of]hs Pj+ ;b:onfO{ ;ldltsf] a}7sdf pkl:yt eP jfkt k|lt a}7s eQf :j?k ?= !$,))).– e'QmfgL lbg] ul/Psf] 5 . ;dLIff jif{df a}+ssf] cfGtl/s n]vfk/LIfs >L lk=h]= yfkf P08 sDkgL, rf6{8{ Psfp06]G6\;\ /xg' ePsf] lyof] .

-w_ ;~rfns, k|aGw ;~rfns, sfo{sf/L k|d'v, sDkgLsf cfwf/e"t z]o/wgL jf lghsf] glhssf gft]bf/ jf lgh ;+nUg /x]sf] kmd{ sDkgL jf ;+ul7t ;+:yfn] sDkgLnfO{ s'g} /sd a'emfpg afFsL eP ;f] s'/f – ljQLo ljj/0fsf] cg';"rLdf pNn]v ul/Psf] 5 .

-g_ ;~rfns, k|aGw ;~rfns, sfo{sf/L k|d'v tyf kbflwsf/Lx?nfO{ e'QmfgL ul/Psf] kfl/>lds, eQf tyf ;'ljwfsf] /sd –

;~rfns tyf kbflwsf/Lx?nfO{ e'QmfgL ul/Psf] kfl/>lds, eQf tyf ;'ljwfsf] ljj/0f M

ljj/0f

;~rfnsx?sf] a}7s eQf

-;ldltsf] a}7s eQf ;d] t _

k|aGws txsf

sd{rf/L

tnj – 4,70,94,563

eQf 19,97,500 9,15,52,526

sfo{sf/L k|d'vnfO{ e'QmfgL ul/Psf] kfl/>lds, eQf tyf ;'ljwfsf] ljj/0f M

tna tyf eQf – !,$!,)),))) jflif{s tyf la/fdL labf – kfpg] af]g; – kfpg] pkbfg, ;+rosf]if tyf

cf}iflw pkrf/ – kfpg]

नेपाल बङ्गलादेश बैंक ललमिटेड18

cf=j= @)&^.&& df a}ssf] k|d'v sfo{sf/L clws[tsf] ?kdf >L 1fg]]Gb| k|;fb 9'+ufgf /xg' ePsf] 5 .

-k_ z]o/wgLx?n] a'lemlng afFsL /x]sf] nfef+zsf] /sd – cfiff9 d;fGt @)&& df e'QmfgL lng afFsL nfef+z ?= !$,^(,#%,@^( /x]sf] 5 .

-km_ bkmf !$! adf]lhd ;DklQ vl/b jf laqmL u/]sf] s'/fsf] ljj/0f – gePsf] .

-a_ bkmf !&% adf]lhd ;Da4 sDkgL aLr ePsf] sf/f]af/sf] ljj/0f – o;} k|ltj]bg cGtu{t ljQLo ljj/0fsf] l6Kk0fLsf] a'Fbf g+= %=^=^ tyf %=^=* df v'nfO{Psf] .

-e_ o; P]g tyf k|rlnt sfg"g adf]lhd ;~rfns ;ldltsf] k|ltj]bgdf v'nfpg' kg]{ cGo s'g} s'/f – o;} k|ltj]bg cGtu{t plrt 7fpFdf v'nfO{Psf] .

-d_ cGo cfjZos s'/fx? – o;} k|ltj]bg tyf ljQLo ljj/0fdf plrt 7fpFx?df v'nfO{Psf] .

wGojfb 1fkga}+ssf] lg/Gt/ pGgtL Pj+ k|ultdf ;bf ;fy lbg'x'g] cfb/0fLo u|fxs dxfg'efjx?, z]o/wgL dxfg'efjx? tyf lgodgsf/L lgsfox?, g]kfn ;/sf/, g]kfn /fi6« a}+s, g]kfn lwtf]kq af]8{, sDkgL /lhi6«f/sf] sfof{no, g]kfn :6s PS:r]Gh ln=sf ;fy} l;l8P; P08 lSnPl/Ë ln=af6 k|fKt ;xof]u tyf dfu{bz{gsf] nflu xflb{s s[t1tf 1fkgub}{ eljiodf klg o;}u/L oxfFx?sf] ;fy kfO{/xg] ljZjf; lnPsf] 5' .

;fy} o; a}+ssf k"j{ cWoIf >L hnfn cxdb Ho"n] pxfFsf] sfo{sfndf a}+ssf] lg/Gt/ pGglt Pj+ k|ultdf k'¥ofpg' ePsf] of] ubfg jfkb xflb{s wGojfb 1fkg ug{ rfxG5' .

cGTodf, a+}ssf] lxtsf] nflu lg/Gt/ lqmofzLn eO{ u|fxsju{sf] ;]jfdf ;+nUg ;Dk"0f{ sd{rf/Lx?, cfGtl/s tyf jfx\o n]vfk/LIfs, z]o/ /lhi6«f/ Pj+ ;Dk'0f{ z'e]R5'sx?nfO{ o; cj;/df xflb{s wGojfb lbg rfxG5' .

wGojfb .

;~rfns ;ldltsf] tkm{jf6P=cf/=Pd= ghd'; ;lsa cWoIfkf}if @^, @)&& .

नेपाल बङ्गलादेश बैंक ललमिटेड 19

qodf;clwstd d'No

Go'gtd d'No

clGtd d'No

s'n sf/f]af/ lbg

s'n sf/f]af/

z]o/ ;+Vofk|yd qodf; 216 190 243 64 3,653,963

bf];|f] qodf; 215 184 203 59 995,868

t];|f] qodf; 270 191 197 46 3,213,366

rf}yf] qodf; 210 169 209 15 308,516

!= ;~rfns ;ldltsf] k|ltj]bgMÜ ;DalGwt lzif{s cGtu{t /flvPsf] .

@= n]vfk/LIfssf] k|ltj]bgMÜ ;DalGwt lzif{s cGtu{t /flvPsf] .

#= n]vfk/LIf0fdf ePsf] ljQLo ljj/0fMÜ ;DalGwt lzif{s cGtu{t /flvPsf] .

$= sfg'gL sf/jfxL ;DaGwL ljj/0fM-s_ q}dfl;s cjlwdf ;+ul7t ;+:yfn] jf ;+:yfsf] lj?4 s'g} d'2f bfo/ ePsf] eP,Ü o; a}+sn] shf{ c;'nL k|lqmof cGtu{t shf{ c;'nL Gofolws/0fdf d'2f btf{ u/]sf] / shf{ c;'nLsf qmddf a}+s lj?4 xfn]sf d'2f afx]s cGo hfgsf/L g/x]sf] .

-v_ ;+ul7t ;+:yfsf] ;+:yfks jf ;~rfnsn] jf ;+:yfks jf ;~rfnssf] lj?4df k|rlnt lgodsf] cj1f jf kmf}Hbf/L ck/fw u/]sf] ;DaGwdf s'g} d'2f bfo/ u/]sf] jf ePsf] eP,Ü o; a}+ssf] hfgsf/Ldf g/x]sf] .

-u_ s'g} ;+:yfks jf ;+rfng lj?4 cfly{s ck/fw u/]sf] ;DaGwdf s'g} d'2f bfo/ ePsf] eP,Ü o; a}+ssf] hfgsf/Ldf g/x]sf] .

%= ;+ul7t ;+:yfsf] z]o/ sf/f]jf/ tyf k|ultsf] ljZn]if0f-s_ lwtf]kq ahf/df ePsf] ;+ul7t ;+:yfsf] z]o/sf] sf/f]af/ ;DaGwdf Joj:yfkgsf] wf/0ffÜ g]kfn :6s PS;r]Gh tyf lwtf]kq af]8{sf] ;'kl/j]If0f Joj:yfsf] clwgdf /xL sf/f]af/ /x]sf] .

-v_ cf=j= @)&^÷&& df ;+ul7t ;+:yfsf] z]o/sf] clwstd, Go'gtd / clGtd d"Nosf ;fy} s'n sf/f]af/ ;+Vof / sf/f]af/ lbg .

lwtf]kq btf{ tyf lgisfzg lgodfjnL, @)&# sf] lgod @^-@_ ;“u ;DalGwt ljj/0f

-v_ afx\o ;d:of tyf r'gf}tLÜ ljZjJofkL ?kdf km}lnPsf] dxfdf/L sf]le8–!( sf sf/0faf6

b] zsf] cy{tGqsf ljleGg If]qx?df x'g uPsf] gsf/fTds c;/ sf kmn:j?k shf{sf] ;fjfF tyf Aofh c;'nLdf ePsf] ;d:of .

Ü a}+s tyf ljQLo ;+:yfx? jLrsf] tLa| k|lt:kwf{ .Ü nufgLsf] cj;/df sdL .Ü hf]lvdo'Qm jftfj/0f .Ü ;"rgf k|ljlwsf If]qdf b]lvPsf r'gf}tLx? .

-u_ /0fgLltÜ ;+rfng ultljlwx?df ;|f]tsf] pRrtd kl/rfng ug]{ .Ü nufgL lj:tf/ tyf lgIf]k ;+sngsf] nflu gofF If]qx?sf]

klxrfg ug]{ .Ü ;do ;fIf]k k|ljlwdf cfwfl/t ;]jfx?sf] klxrfg ug]{ /

;+rfng ug]{ .Ü sd{rf/Lx?nfO{ cfkm\gf] sfo{Ifdtf j[l4 u/L :tl/o ;]jf k|bfg

ug{sf] nflu lg/Gt/ tflndx? pknAw u/fpg] tyf a}+sk|lt cfj4 / fVgsf] nflu oyf]lrt gLlt cjnDjg ug]{ .

Ü nfut tyf cGo vr{x? sd ug{] pkfox? cjnDag ug]{ .Ü ;"rgf k|ljlw;+u ;DalGwt hf]lvd Joj:yfkgnfO{ cem} r':t

agfpg] .Ü ljZjJofkL ?kdf km}lnPsf] dxfdf/L sf]le8–!( sf sf/0f

ljleGg If]qx?df k/]sf c;/x?af/] lj:t[t cWoog u/L cfgf C0fLx?sf ;d:of ;Daf]wg ug{ g]kfn /fi6« a}+ssf] lgb]{zg ;d] tsf] clwgdf /xL cfjZos /0fgLlt th'{df ug]{ .

&= ;+:yfut ;'zf;gÜ a}+sn] ;+:yfut ;'zf;gsf] kl/kfngfsf nflu g]kfn /fi6« a}+sn] hf/L u/]sf] gLlt, lgb]{zgx? Pj+ a}+ssf] cfkm\g} ;+rfng lgb]{lzsf, gLltlgodx?sf] kl/kfngf k"0f{?kdf ul//x]sf] 5 .

Ü a}+ssf] ;~rfnsx? k|efjsf/L ;+:yfut ;'zf;gsf] af/]df hfgsf/ /x]sf 5g\ . ;~rfns ;ldltdf lgoldt?kdf ;+:yfut ;'zf;gsf ljifox?nfO{ ;Daf]wg ug]{ sfo{ eO/x]sf] 5 .

Ü a}+ssf] cfly{s cj:yf, cfGtl/s lgoGq0f k|0ffnL, n]vfk/ LIf0f of]hgf cflbsf] af/]df k'g/fjnf]sg ug{ n]vfk/LIf0f ;ldlt, hf] lvd Joj:yfkg ;ldlt, dfgj ;+zfwg ;ldlt, ;"rgf k|ljlw ;ldlt cflb ;ldltx?sf] a}7s lgoldt ?kdf a:g] u/]sf] / tL ;ldltx?n] ;~rfns ;ldltnfO{ cfjZos l;kmfl/z ug] { ul//x]sf 5g\ .

Ü a}+ssf] ;DklQ tyf bfloTjsf] plrt / k|efjsf/L Joj:yfkgsf] nflu ;DklQ bfloTj Joj:yfkg ;ldlt (ALCO) lqmofzLn /x]sf] 5 .

*= ljj/0fkqdf k|If]k0f ul/Psf / n]vfkl/If0f ePsf] ljj/0fx?df aL; k|ltzt jf ;f] eGbf a9L km/s ;DaGwL ljj/0f MÜ gePsf]

^= ;d:of, r'gf}tL tyf /0fgLlt-s_ cfGtl/s ;d:of tyf r'gf}tLÜ a9\bf] ;+rfng vr{ .Ü bIf hgzlQmsf] cefj .Ü v'b Aofhb/ cGt/ ;Gt'ng ug]{ r'gf}tL .

नेपाल बङ्गलादेश बैंक ललमिटेड20

नेपाल बङ्गलादेश बैंक ललमिटेड 21

k|d'v sfo{sf/L clws[tsf] k|ltj4tf

cfb/0fLo z]o/wgL dxfg'efjx?,

@)&^ r}q dlxgf kZrft\ ljZjJofkL ?kdf km}lnPsf] sf]le8 ;+qmd0fn] ;Dk"0f{ Joj:ffodf k|lts'n k|efj kg{ uof] h;sf sf/0f a}+s tyf ljQLo ;+:yf sf] b}lgs ;+rfng klg lgs} r'gf}tL k"0f{ /x\of] . o;} cfly{s jif{df g]kfn a+unfb]z a}+sn] cfkm\gf] ;+:yfut ;fdflhs pQ/bfloTjnfO{ dgg ub}{ g]kfn ;/sf/sf] sf]/f]gf efO/; ;+qmd0f /f]syfd, lgoGq0f tyf pkrf/ sf]ifdf ?= !=$% s/f]8 k|bfg u/]sf] 5 / ;+o'Qm nufgLsf] a}+s cfO{PkmcfO{;L a}+s, cf}iflw pTkfbs a] lS;dsf] kmdf{:o'l6sn, a+unfb]zsf] ;+o'Qm kxndf sf]le8 ;+qmldt la/fdLx?sf] pkrf/df k|of]u x'g] hLjg/ Ifs cf}ifwL Remdisivir kf+r xhf/ yfg k|bfg ug{ nfUg] s'n / sd dWo] ?= &*=(( nfv a/fa/ o; a}+sn] ;xof]u u/]sf] 5 . o;/L g} cfufdL lbgdf klg a}+s ;+:yfut ;fdflhs pQ/bfloTj cGtu{t hg:jf:Yosf ljleGg If]qx?df ;xof]u ug{ tTk/ /xg] 5 . g]kfn /fi6« a}+sn] hf/L u/]sf] ljleGg gLlt lgb]{zgsf cwLgdf /xL a}+sn] sf]le8 !( sf] k|efjsf sf/0f a}+lsË If]qdf kg{ ;Sg] hf]lvd Go"gLs/0fsf pkfo cjnDag ub{} cfkm\gf] Joj;fo nfO{ lj:tf/ ul//x]sf] hfgsf/L u/fpFb5f} . o:tf] ljifd kl/l:yltsf afjh'b klg a}+sn] cf=j= @)&^.&& df *=$@ k|ltzt nfef+z k|bfg ug{ ;kmn ePsf] 5 / o; ;dodf a}+snfO{ ;fy lbg] ;Dk"0f{ u|fxs dxfg'efjx+?, a}+ssf sd+rf/L ju{, z]o/wgL dxfg'efjx? nfO{ xflb{s s[t1tf 1fkg ub{5' . xfn a}+lsË If]qdf cToflws t/ntfsf] cj:yf 5 / nufgLsf nflu sf]le8 dxfdf/Ln] ylkPsf r'gf}tfsf ljr casf lbgx?df a}+lsË Joj;fo gofF 9+un] cuf8L a9fpg' kg]{ cj:yf >[hgf ePsf] 5 . a}+sn] o; r'gf}tLk"0f{ ;dodf cfkm\gf ;]jfu|fxLx?nfO{ cgnfOg dfkm{t vftf vf]Ng] nufot cGo ;]jf k|bfg ug]{ sfo{qmd ;+rfngdf NofPsf] 5 / cfkm\gf u|fxsx?nfO{ ljleGg l8lh6n k|ljlwsf k|8S6x?af6 cfkm\gf] ;]jf lj:tf/ ub{} cfPsf] 5 . ca cfpg] lbgx?df a}+lsË Joj;fo k"0f{ k|ljwL d}qL jftfj/0fdf x'g uO/x]sf] cj:yfdf a}+sn] sfof{Gjogdf Nofpg nfu]sf] Finastra sf]/ a}+lsË l;:6dn] yk ;xof]u ldNg]5 eGg] cfzf lnPsf] 5' . a}+sn]] xfn k|of]u eO/x]sf] sf]/ a}+lsË l;:6d dfOu|]zgsf nflu rfn' cfly{s jif{sf] cGt ;Dddf :fDk"0f{ k|lqmof k'/f u/L Finastra ;km\6j]o/ live df n}hfg] of]hgf agfPsf] hfgsf/L u/fpFb5f}+ . o;} ;km\6j]o/ k|0ffnLdfkm{t\ a}+sn] u|fxsx?nfO{ ahf/df pknAw gePsf yk gf}nf ;]jfx? k|bfg ug]{ of]hgf agfPsf] 5 .

a}+sn] ;bf em}+ lgofds lgsfosf] lgb]{zg, ;+rfns ;ldltsf] dfu{bz{g tyf z]o/wgLx?sf] ;'emfjnfO{ cfTd;ft ub{} a}+ssf ;a} ;/f]sf/jfnf ju{nfO{ plrt k|ltkmn lbg yk cfjZos sfo{x? ug{df hf]8 lbg]5 . a}+lsË If]qdf b]lvPsf yk r'gf}tLx?nfO{ cfjZos Joj:yfkgsf pkfox? cjnDag ub}{ o; a}+snfO{ cem a9L ;an / ;Ifd a}+s agfpg] k|lta4tf JoQm ub{5' .

1fg]Gb| k|;fb 9'+ufgfk|d'v sfo{sf/L clws[t

sfF8f3f/L zfvf pb\3f6g ;df/f]x

dl08vf6f/ zfvf pb\3f6g

zfvf pb\3f6gsf emnsx?

नेपाल बङ्गलादेश बैंक ललमिटेड22

नेपाल बङ्गलादेश बैंक ललमिटेड 23

!= ;]G6/ km/ OlG8k]G8]G6 lnleËnfO{ lJxnlro/ ljt/0f sfo{qmd . @= 9fsf l:yt g]kfnL /fhb"tnfO{ %))) yfg /]d8]l;le/

x:tfGt/0f . #= sf]/f]gf efO/; ;+qmd0f /f]syfd, lgoGq0f tyf pkrf/ sf]ifdf ;xof]u . $= ltnu+uf zfvf l:yt :yflgo If] qdf

8:6lag ljt/0f . %= lkmlbdsf b[li6lxg afnaflnsfnfO{ d'b|f klxrfg ;DalGw tflnd . ^= ljQLo ;fIf/tf cGtu{t jfsfy'g

sfo{qmd .

;+:yfut ;fdflhs pQ/bfloTj sfo{qmdsf emnsx?

!

#

% ^

$

@

नेपाल बङ्गलादेश बैंक ललमिटेड24

नेपाल बङ्गलादेश बैंक ललमिटेड 25

नेपाल बङ्गलादेश बैंक ललमिटेड26

नेपाल बङ्गलादेश बैंक ललमिटेड 27

नेपाल बङ्गलादेश बैंक ललमिटेड28

ljj/0f

gf]6

;d"x

a}+s

cfiff9 d;fGt @)&&

cfiff9 d;fGt @)&^

cfiff9 d;fGt @)&&

cfiff9 d;fGt @)&^

;DklQ

gub

tyf gu

b ;dfg

4.1

3,1

79,2

95,5

48

2,6

13,3

62,2

56

3,1

79,2

86,

383

2,6

13,3

62,2

56

g]kfn /fi6« a}+sdf /x]s

f] df}Hbft t

yf lng'kg]{ jSof}tf

4.2

13,

485,

569,

880

6,7

62,1

14,6

79

13,

485,

569,

880

6,7

62,1

14,6

79

a}+s t

yf ljQLo ;

+:yfdf /x]sf] df}Hb

ft4.3

2,5

03,8

79,4

80

3,5

35,6

31,0

00

2,5

03,8

79,4

80

3,5

35,6

31,0

00

8]l/e]l6e

ljQ

Lo p

ks/0f

4.4

29,

989,

200

31,

228,0

00

29,

989,

200

31,

228,0

00

cGo Jofkfl/s ;

DklQx?

4.5

139

,248,9

91

95,

219,

007

106

,140,

075

95,

219,

007

a}+s t

yf ljQLo ;

+:yfnfO{ lbP

sf] shf{ ty

f ;fk6L

4.6

1,6

09,9

14,9

90

1,8

73,7

57,2

13

1,6

09,9

14,9

90

1,8

73,7

57,2

13

u|fxs

nfO{ lbP

sf] shf{ ty

f ;fk6L

4.7

59,

108,5

37,9

16

52,

519,

196,

831

5

9,10

8,5

37,9

16

52,

519,

196,

831

lwtf]kq

df n

ufgL

4.8

7,0

65,4

91,8

19

5,9

38,0

28,5

67

7,0

05,9

66,8

07

5,9

23,6

69,5

67

rfn' s

/ ;DklQ

4.9

83,

109,

635

79,

210,

905

82,

866

,696

7

9,92

5,880

;xfos

sDkgLdf n

ufgL

4.1

0 -

-

2

20,0

00,0

00

200

,000

,000

;Da4 s

DkgLdf n

ufgL

4.1

1 -

-

-

-

nufgL ;

DklQ

4.1

2 3

67,7

82,

006

346,

171,

570

367

,782,

006

346,

171,

570

;DklQ t

yf pks

/0f

4.1

3 1

,542,

810

,079

1

,503

,452

,572

1

,541,

874

,843

1,5

02,1

90,9

75

u'8ljn -Vo

flt_ / cd"t

{ ;DklQ

4.1

4 4

6,420

,513

2

0,90

5,406

4

6,05

3,73

5 2

0,431

,277

:yug

s/ ;DklQ

4.1

5 -

-

-

-

cGo ;

DklQ

4.1

6 4

43,

031,

334

752

,696

,050

4

35,1

30,5

52

751

,595

,072

hDdf ;DklQ

8

9,60

5,08

1,39

1 7

6,07

0,97

4,0

58

89,

722,

992,

561

76,

254,4

93,3

29

bfloTj

gf]6

a}+s t

yf ljQLo ;

+:yfnfO{{ ltg

{ jfFsL

4.1

7 6

,757

,595

,800

3

,864

,988,0

00

6,7

57,5

95,8

00

3,8

64,9

88,0

00

g]kfn /fi6

« a}+snfO{ ltg

{ jfFsL

4.1

8 1

43,

212,

501

745,

786,

348

143,

212,

501

745,

786,

348

8]l/e]l6e

ljQ

Lo p

ks/0f

4.1

9 -

-

-

-

u|fxs

sf] lgIf]k

4.2

0 6

6,26

7,414

,550

5

6,04

2,489,

632

66,

435

,054

,423

5

6,22

8,8

19,3

48

;fk6L

4.2

1 -

-

-

-

rfn' s

/ bfloTj

4.9

-

-

-

-

Joj:yf

4.2

2 -

-

-

-

:yug

s/ bfloTj

4.1

5 1

,809

,823

1

,717

,054

1

,110

,414

1

,669

,837

cGo b

floTj

4.2

3 1

,337

,779

,643

1,0

04,2

93,1

00

1,2

95,6

66,0

73

1,0

03,3

08,3

21

hf/L ul/Psf] C0fkq

4.2

4 1

,993

,678

,991

1

,992

,976

,657

1

,993

,678

,991

1

,992

,976

,657

;'/If0f g/flv

Psf] ;xfos

cfjlws b

floTj

4.2

5 -

-

-

-

s"n bfloTj

7

6,50

1,491

,309

6

3,65

2,25

0,79

2 7

6,62

6,31

8,2

03

63,

837

,548,5

11

Pls

s[t

ljQ

Lo c

j:y

fsf] l

jj/0

fcfiff9 d;fGt @)&&

/sd

?= df

नेपाल बङ्गलादेश बैंक ललमिटेड 29

ljj/0f

gf]6

;d"x

a}+s

cfiff9 d;fGt @)&&

cfiff9 d;fGt @)&^

cfiff9 d;fGt @)&&

cfiff9 d;fGt @)&^

OlSj6L

z]o/

k"FhL

4.2

6 8

,495

,814

,295

8

,088,2

99,2

26

8,4

95,8

14,2

95

8,0

88,2

99,2

26

z]o/

lk|ldo

d

-

-

-

-

;+lrt

d'gfkmf

8

46,

783,

487

1,0

11,6

54,5

97

841,

639,

256

1,0

09,8

76,1

49

hu]8

f sf]ifx?

4.2

7 3

,760

,992

,300

3

,318

,769

,442

3,7

59,2

20,8

07

3,3

18,7

69,4

42

z]o/wgLx?nfO{ jfF8kmfF8 of]Uo s'n OlSj6L

1

3,10

3,59

0,08

2 1

2,418

,723

,266

1

3,09

6,67

4,3

59

12,

416

,944,8

18

u}/ lgolGqt :jfy{

s'n OlSj6L

1

3,10

3,59

0,08

2 1

2,418

,723

,266

1

3,09

6,67

4,3

59

12,

416

,944,8

18

s'n bfloTj / OlSj6L

8

9,60

5,08

1,39

1 7

6,07

0,97

4,0

58

89,

722,

992,

561

76,

254,4

93,3

29

;+efljt

bfloTj t

yf k|ltj

4tf

4.2

8 7

1,78

7,21

2,31

9 6

2,14

9,30

9,35

2 7

1,78

7,21

2,31

9 6

2,14

9,30

9,35

2

k|lt

z]o/

v'b

;DklQ

1

54.1

5 1

53.5

2 1

54.1

5 1

53.5

2

slj

Gb| b

fxfn

k|d'v – ljQ

O{Gb

|| ax

fb'/

yfk

f;~r

fns

;'/]G

b| e

'if0f

>]i7

k|d'v ljQ

clws[t

d's

'Gb g

fy 9

'+u]n

;~r

fns

1fg

]Gb| k

|;fb

9'+u

fgf

k|d'v s

fo{sf/L clws[t

df]x

db

;fx

cfn

d ;

/j/

;~r

fns

bLk

s s

fsL{

;~r

fns

sd

?g

gx

/ c

xd

b;~r

fns

P=c

f/=P

d g

hd

'; ;

lsa

cWoIf

l;= P

= ;'lw

/ s

'df/

zd

f{;fem]bf/

P; P

08 P

; P

;f]l;

P6\;

rf6{8{ P

sfpG6]G6\;

cfhsf] ldltsf] xfd|f] ;

+nUg k

|ltj]b

g cg';

f/

ldlt M g

f]e]Da/ #), @)@)

:yfg M s

f7df8f}+, g]k

fn

/sd

?= df

नेपाल बङ्गलादेश बैंक ललमिटेड30

ljj/0f gf]6;d'x a}+s

o; jif{ ut jif{ o; jif{ ut jif{

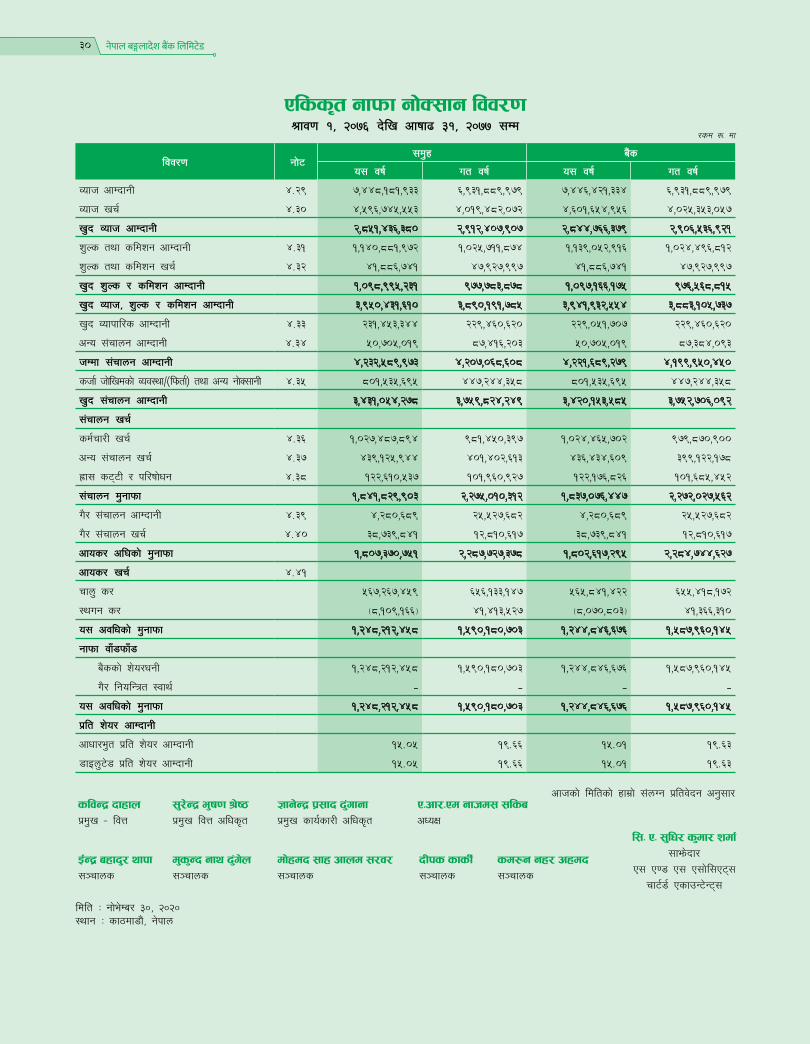

Jofh cfDbfgL 4.29 7,448,181,933 6,931,889,979 7,446,421,334 6,931,889,979

Jofh vr{ 4.30 4,596,745,553 4,019,482,072 4,601,654,956 4,025,353,057

v'b Jofh cfDbfgL 2,851,436,380 2,912,407,907 2,844,766,379 2,906,536,921

z'Ns tyf sldzg cfDbfgL 4.31 1,140,881,972 1,025,711,874 1,139,052,916 1,024,496,812

z'Ns tyf sldzg vr{ 4.32 41,886,741 47,927,997 41,886,741 47,927,997

v'b z'Ns / sldzg cfDbfgL 1,098,995,231 977,783,878 1,097,166,175 976,568,815

v'b Jofh, z'Ns / sldzg cfDbfgL 3,950,431,610 3,890,191,785 3,941,932,554 3,883,105,737

v'b Jofkfl/s cfDbfgL 4.33 231,453,344 229,460,620 229,051,707 229,460,620

cGo ;+rfng cfDbfgL 4.34 50,705,019 87,416,203 50,705,019 87,384,093

hDdf ;+rfng cfDbfgL 4,232,589,973 4,207,068,608 4,221,689,279 4,199,950,450

shf{ hf]lvdsf] Joj:yf÷-lkmtf{_ tyf cGo gf]S;fgL 4.35 801,535,695 447,244,358 801,535,695 447,244,358

v'b ;+rfng cfDbfgL 3,431,054,278 3,759,824,249 3,420,153,585 3,752,706,092

;+rfng vr{

sd{rf/L vr{ 4.36 1,027,487,894 981,450,397 1,024,465,702 979,870,900

cGo ;+rfng vr{ 4.37 439,125,944 401,402,613 436,434,609 399,122,178

Ãf; s6\6L / kl/iff]wg 4.38 122,610,537 101,960,927 122,176,826 101,685,452

;+rfng d'gfkmf 1,841,829,903 2,275,010,312 1,837,076,447 2,272,027,562

u}/ ;+rfng cfDbfgL 4.39 4,280,689 25,527,682 4,280,689 25,527,682

u}/ ;+rfng vr{ 4.40 38,739,841 12,810,617 38,739,841 12,810,617

cfos/ cl3sf] d'gfkmf 1,807,370,751 2,287,727,378 1,802,617,295 2,284,744,627

cfos/ vr{ 4.41

rfn' s/ 567,267,459 656,133,147 565,841,422 655,418,172

:yug s/ (8,109,166) 41,413,527 (8,070,803) 41,366,310

o; cjlwsf] d'gfkmf 1,248,212,458 1,590,180,703 1,244,846,676 1,587,960,145

gfkmf jfF8kmfF8

a}+ssf] z]o/wgL 1,248,212,458 1,590,180,703 1,244,846,676 1,587,960,145

u}/ lgolGqt :jfy{ - - - -

o; cjlwsf] d'gfkmf 1,248,212,458 1,590,180,703 1,244,846,676 1,587,960,145

k|lt z]o/ cfDbfgL

cfwf/e't k|lt z]o/ cfDbfgL 15.05 19.66 15.01 19.63

8fOn'6]8 k|lt z]o/ cfDbfgL 15.05 19.66 15.01 19.63

Plss[t gfkmf gf]S;fg ljj/0f>fj0f !, @)&^ b]lv cfiff9 #!, @)&& ;Dd

/sd ?= df

sljGb| bfxfnk|d'v – ljQ

O{Gb|| axfb'/ yfkf;~rfns

;'/]Gb| e'if0f >]i7k|d'v ljQ clws[t

d's'Gb gfy 9'+u]n;~rfns

1fg]Gb| k|;fb 9'+ufgfk|d'v sfo{sf/L clws[t

df]xdb ;fx cfnd ;/j/;~rfns

bLks sfsL{;~rfns

sd?g gx/ cxdb;~rfns

P=cf/=Pd gfhd; ;lsacWoIf

l;= P= ;'lw/ s'df/ zdf{;fem]bf/

P; P08 P; P;f]l;P6\;

rf6{8{ PsfpG6]G6\;

cfhsf] ldltsf] xfd|f] ;+nUg k|ltj]bg cg';f/

ldlt M gf]e]Da/ #), @)@):yfg M sf7df8f}+, g]kfn

नेपाल बङ्गलादेश बैंक ललमिटेड 31

ljj/0f

;d'x

a}+s

o; jif{

ut jif{

o; jif{

ut jif{

o; jif{sf] gfkmf

1

,248,2

12,4

58

1,5

90,1

80,

703

1,2

44,8

46,

676

1,5

87,

960,

145

cfos/ kl5sf] cGo lj:t[t cfDbfgL

s_ gfkmf÷gf]S;fg df k'gMjuL{s/0f gul/Psf a'Fbfx?

km]o/

e]No

'df d

'Nof°g

ul/Psf OlSj6L p

ks/0fsf nufgLaf6

ePsf gfkmf÷gf]S;

fg

2

7,33

9,78

2 (5

7,94

8,9

05)

25,

037,

933

(57,

948,9

05)

k'gM d'Nof°ga

f6 e

Psf gfkmf÷gf]S;

fg

kl/eflift n

fe o

f]hgfaf6

ljdfl°s g

fkmf÷gf]S;

fg

-

-

-

-

dfly p

Nn]v u

l/Ps

f j'Fb

fsf] cfos/

(8

,201

,935

) 1

7,38

4,6

71

(7,5

11,3

80)

17,

384,6

71

gfkmf÷gf]S;fgdf k'gMjuL{s/0f gul/Psf cGo v'b lj:t[t cfDbfgL

1

9,13

7,848

(40,

564,2

33)

17,

526,

553

(40,

564,2

33)

v_ gfkmf÷gf]S;fgdf k'gMjuL{s/0f ul/Psf jf ug{ ;lsg] a'Fbfx?

gub

k|jfxsf] x]lhËaf6

ePsf] gfkmf÷gf]S;

fg

ljb]z

L ljlgdo

;+rfngs

f] ljQLo ;

DklQ ljlgd

oaf6 e

Psf] ;6x

L gfkmf÷gf]S;

fg

dfly p

Nn]v u

l/Ps

f j'Fb

fsf] cfos/

gfkmf÷gf]S;

fgdf k

'gMju

L{s/0f gu

l/Ps

f cGo v

'b lj:t[t

cfDb

fgL

gfkmf÷gf]S;fgdf k'gMjuL{s/0f ul/Psf jf ug{ ;lsg] cGo v'b lj:t[t cfDbfgL

-

- -

-

u_ OlSj6L tl/sfaf6 n

]vfª\sg ul/Psf] ;Da4 ;

+:yfsf] cGo lj:t[t cfDbfgLdf lx:;f

o; jif{sf] cfos/ kl5sf] cGo lj:t[t cfDbfgL

1

9,13

7,848

(40,

564,2

33)

17,

526,

553

(40,

564,2

33)

hDdf lj:t[t cfDbfgL

1

,267

,350

,306

1

,549,

616,

470

1

,262

,373

,229

1

,547,

395,

912

lj:t[t

cfDb

fgLsf] jfF8kmfF8M

a}+ssf] OlSj6L z

]o/wg

L

1,2

67,3

50,3

06

1,5

49,

616,

470

1

,262

,373

,229

1

,547,

395,

912

u}/ lgo

lGqt

:jfy{

-

-

-

-

hDdf lj:t[t cfDbfgL

1

,267

,350

,306

1

,549,

616,

470

1

,262

,373

,229

1

,547,

395,

912

Pls

s[t

cGo

lj:t

[t c

fDb

fgLs

f] ljj

/0f

>fj0f !, @)&^ b]lv cfiff9 #!, @)&& ;Dd

/sd

?= df

slj

Gb| b

fxfn

k|d'v – ljQ

O{Gb

|| ax

fb'/

yfk

f;~r

fns

;'/]G

b| e

'if0f

>]i7

k|d'v ljQ

clws[t

d's

'Gb g

fy 9

'+u]n

;~r

fns

1fg

]Gb| k

|;fb

9'+u

fgf

k|d'v s

fo{sf/L clws[t

df]x

db

;fx

cfn

d ;

/j/

;~r

fns

bLk

s s

fsL{

;~r

fns

sd

?g

gx

/ c

xd

b;~r

fns

P=c

f/=P

d g

hd

'; ;

lsa

cWoIf

l;= P

= ;'lw

/ s

'df/

zd

f{;fem]bf/

P; P

08 P

; P

;f]l;

P6\;

rf6{8{ P

sfpG6]G6\;

cfhsf] ldltsf] xfd|f] ;

+nUg k

|ltj]b

g cg';

f/

ldlt M g

f]e]Da/ #), @)@)

:yfg M s

f7df8f}+, g]k

fn

नेपाल बङ्गलादेश बैंक ललमिटेड32

OlSj6

Ldf e

Psf] k

l/jt

{gs

f] ljj

/0f

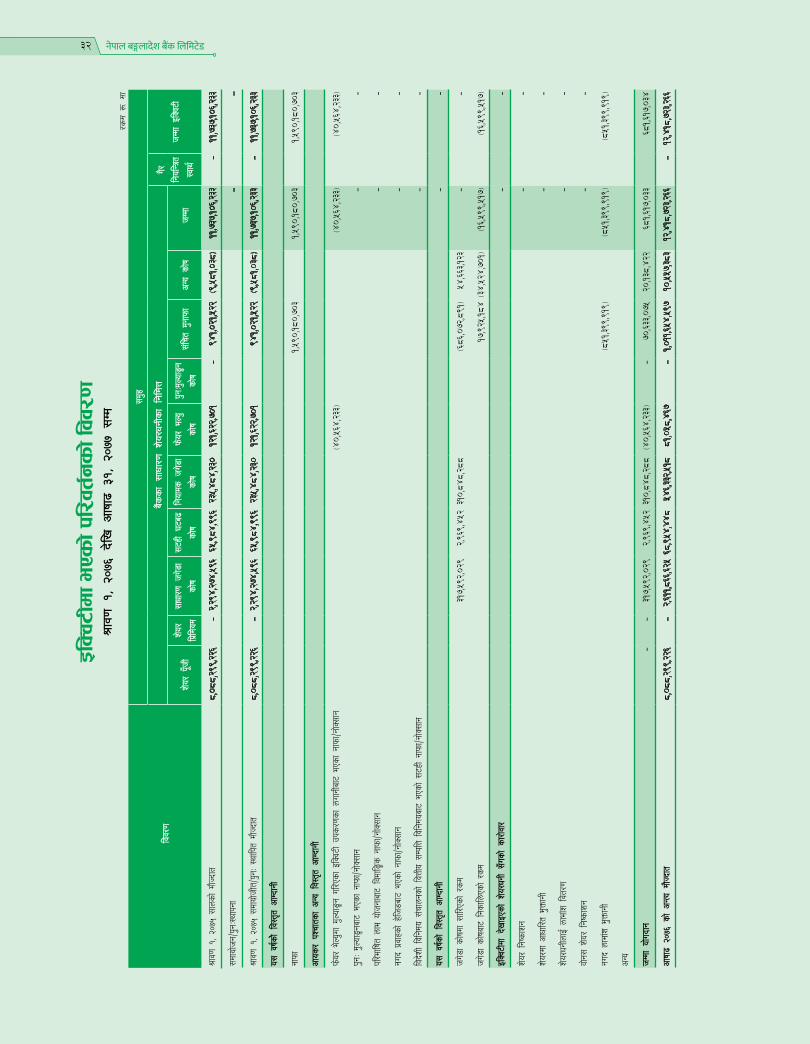

>fj0f !, @)&^ b]lv cfiff9 #!, @)&& ;Dd

ljj/0f

;d'x

a}+ssf ;fwf/0f z]o/wgLsf lgldQ

u}/

lgolGqt

:jfy{

hDdf OlSj6L

z]o/ k"Fh

Lz]o

/ lk|ldod

;fwf/0f hu]8f

sf]if

;6xL 36a9

sf]if

lgofds

hu]8f

sf]if

km]o/ eNo'

sf]if

k'gMd'Nof°g

sf]if

;+lrt d'gfkmf

cGo sf]if

hDdf

>fj0f !, @)&% ;fns

f] df}Hb

ft8,

088,

299,

226

-

2,29

4,27

4,59

6 6

5,98

4,99

6 2

35,4

84,2

30

121

,622,

701

-

941

,021

,522

(9

,581

,038

) 1

1,737

,106,2

33

-

11,7

37,10

6,233

;dfof]hg÷k'g

M:yfkgf

-

-

>fj0f !, @)&% ;d

fof]hLt÷k'gM :yflkt

df}Hb

ft8,

088,

299,

226

-

2,29

4,27

4,59

6 6

5,98

4,99

6 2

35,4

84,2

30

121

,622,

701

941

,021

,522

(9

,581

,038

) 1

1,737

,106,2

33

-

11,7

37,10

6,233

o; jif{sf]] lj:t[t cfDbfgL

gfkmf

1,5

90,18

0,70

3 1

,590

,180,

703

1,5

90,18

0,70

3

cfos

/ kZrfts

f cGo lj:t[t cfDbfgL

km]o/

e]No

'df d

'Nof°g

ul/Psf OlSj6L p

ks/0fsf nu

fgLaf6 e

Psf gfkmf÷g

f]S;fg

(40,

564,

233)

(40,

564,

233)

(40,

564,

233)

k'gM d'Nof°g

af6

ePsf gfkmf÷g

f]S;fg

-

-

kl/eflift n

fe o

f]hgfaf6

ljdfl°s g

fkmf÷gf]S;

fg

-

-

gub

k|jfxsf] x]lhªa

f6 e

Psf] gfkmf÷g

f]S;fg

-

-

ljb]z

L ljlgdo

;+rfng

sf] ljQLo

;DklQ

ljlgdo

af6

ePsf] ;6

xL g

fkmf÷gf]S;

fg

-

-

o; jif{sf] lj:t[t cfDbfgL

-

-

hu]8

f sf]ifdf ;

fl/Ps

f] /s

d 3

17,5

92,0

29

2,9

69,4

52 3

10,8

48,2

88

(686

,072

,891

) 5

4,66

3,123

-

-

hu]8

f sf]ifaf6

lgsfln

Psf] /s

d 1

7,92

5,18

4 (3

4,52

4,70

1) (1

6,599

,517

) (1

6,599

,517

)

OlSj6Ldf b]vfOPsf] z]o

/wgL ;

Fusf] sf/f]jf/

-

-

z]o/ lgisfzg

-

-

z]o/df cfwfl/t

e'QmfgL

-

-

z]o/wgLnfO{ nfef+z

ljt/0f

-

-

jf]g;

z]o/

lgisfzg

-

-

gub

nfef+z

e'Qmfg

L (8

51,39

9,91

9) (8

51,39

9,91

9) (8

51,39

9,91

9)

cGo

hDdf of]ubfg

-

-

317

,592

,029

2

,969

,452

310

,848

,288

(4

0,56

4,23

3) -

7

0,63

3,075

2

0,13

8,42

2 6

81,61

7,03

3 6

81,61

7,03

4

cfiff9 @)&^ s

f] cGTo df}Hbft

8,08

8,29

9,22

6 -

2

,611,8

66,62

5 68

,954

,448

5

46,33

2,51

8 8

1,058

,467

-

1

,011

,654,

597

10,

557,

383

12,

418,

723,2

66

-

12,

418,

723,2

66

/sd

?= df

नेपाल बङ्गलादेश बैंक ललमिटेड 33

ljj/0f

;d'x

a}+ssf ;fwf/0f z]o/wgLsf lgldQ

u}/

lgolGqt

:jfy{

hDdf OlSj6L

z]o/ k"Fh

Lz]o

/ lk|ldod

;fwf/0f hu]8f

sf]if

;6xL 36a9

sf]if

lgofds

hu]8f

sf]if

km]o/ eNo'

sf]if

k'gMd'Nof°g

sf]if

;+lrt d'gfkmf

cGo sf]if

hDdf

>fj0f !, @)&^ ;fns

f] df}Hb

ft8,

088,

299,

226

-

2,61

1,866

,625

68,9

54,4

48

546

,332,

518

81,0

58,4

67

-

1,0

11,65

4,59

7 1

0,55

7,38

3 1

2,41

8,72

3,266

-

1

2,41

8,72

3,266

;dfof]hg÷k'g

M:yfkgf

>fj0f !, @)&^ ;d

fof]hLt÷k'gM :yflkt

df}Hb

ft8,

088,

299,

226

-

2,61

1,866

,625

68,9

54,4

48

546

,332,

518

81,0

58,4

67

-

1,0

11,65

4,59

7 1

0,55

7,38

3 1

2,41

8,72

3,266

-

1

2,41

8,72

3,266

o; jif{sf]] lj:t[t cfDbfgL

gfkmf

1,2

48,2

12,4

58

1,2

48,2

12,4

58

1,2

48,2

12,4

58

cfos

/ kZrfts

f cGo lj:t[t cfDbfgL

-

-

km]o/

e]No

'df d

'Nof°g

ul/Psf OlSj6L p

ks/0fsf nu

fgLaf6 e

Psf gfkmf÷g

f]S;fg

19,

137,

848

19,

137,

848

19,

137,

848

k'gM d'Nof°g

af6

ePsf gfkmf÷g

f]S;fg

-

-

kl/eflift n

fe o

f]hgfaf6

ljdfl°s g

fkmf÷gf]S;

fg

-

-

-

gub

k|jfxsf] x]lhªa

f6 e

Psf] gfkmf÷g

f]S;fg

-

-

ljb]z

L ljlgdo

;+rfng

sf] ljQLo

;DklQ

ljlgdo

af6

ePsf] ;6

xL g

fkmf÷gf]S;

fg

-

-

o; jif{sf] lj:t[t cfDbfgL

-

-

hu]8

f sf]ifdf ;

fl/Ps

f] /s

d 2

48,9

69,33

5 2

24,0

30 (

117,

125,

200)

(442

,487

,664)

310,

430,

979

11,4

80

11,4

80

hu]8

f sf]ifaf6

lgsfln

Psf] /s

d (1

1,480

)(1

9,56

2,84

9) (1

9,57

4,32

9) (1

9,57

4,32

9)

OlSj6Ldf b]vfOPsf] z]o

/wgL ;

Fusf] sf/f]jf/

z]o/ lgisfzg

-

-

z]o/df cfwfl/t

e'QmfgL

-

-

z]o/wgLnfO{ nfef+z

ljt/0f

-

-

jf]g;

z]o/

lgisfzg

407

,515

,071

4

07,5

15,0

71

407

,515

,071

gub

nfef+z

e'Qmfg

L (9

70,5

95,9

08)

(970

,595

,908

) (9

70,5

95,9

08)

cGo

160

,196

160

,196

160

,196

hDdf of]ubfg

407

,515

,071

-

2

48,9

69,33

5 2

24,0

30 (

117,

125,

200)

19,

126,3

68

-

(164

,871

,113)

291

,028

,326

684

,866

,816

-

6

84,8

66,8

16

cfiff9 @)&& s

f] cGTo df}Hbft

8,49

5,81

4,29

5 -

2,

860,

835,

960

69,

178,

477

429

,207

,318

100

,184,

835

-

846

,783

,487

301

,585

,710

1

3,103

,590

,082

-

1

3,103

,590

,082

/sd

?= df

slj

Gb| b

fxfn

k|d'v – ljQ

O{Gb

|| ax

fb'/

yfk

f;~r

fns

;'/]G

b| e

'if0f

>]i7

k|d'v ljQ

clws[t

d's

'Gb g

fy 9

'+u]n

;~r

fns

1fg

]Gb| k

|;fb

9'+u

fgf

k|d'v s

fo{sf/L clws[t

df]x

db

;fx

cfn

d ;

/j/

;~r

fns

bLk

s s

fsL{

;~r

fns

sd

?g

gx

/ c

xd

b;~r

fns

P=c

f/=P

d g

hd

'; ;

lsa

cWoIf

l;= P

= ;'lw

/ s

'df/

zd

f{;fem]bf/

P; P

08 P

; P

;f]l;

P6\;

rf6{8{ P

sfpG6]G6\;

cfhsf] ldltsf] xfd|f] ;

+nUg k

|ltj]b

g cg';

f/

ldlt M g

f]e]Da/ #), @)@)

:yfg M s

f7df8f}+, g]k

fn

नेपाल बङ्गलादेश बैंक ललमिटेड34

ljj/0f

a}+s

a}+ssf ;fwf/0f z]o/wgLsf lgldQ

u}/

lgolGqt

:jfy{

hDdf OlSj6L

z]o/ k"FhL

z]o/

lk|ldod

;fwf/0f hu]8f

sf]if

;6xL 36a9

sf]if

lgofds h

u]8f

sf]if

km]o/ eNo'

sf]if

k'gMd'Nof°g

sf]if

;+lrt d'gfkmf

cGo sf]if

hDdf

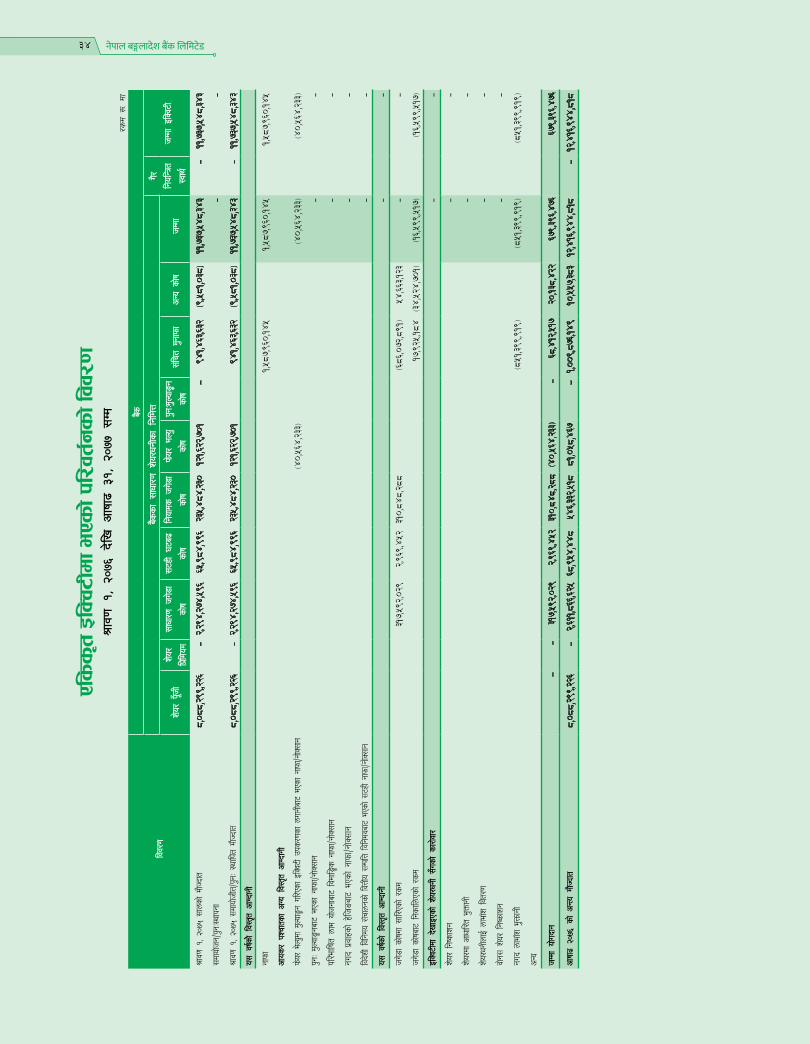

>fj0f !, @)&% ;fns

f] df}Hbft

8,08

8,29

9,22

6 -

2,

294,

274,

596

65,

984,

996

235

,484

,230

1

21,62

2,70

1 -

9

41,4

63,63

2 (9

,581

,038

) 1

1,737

,548

,343

-

11,7

37,5

48,34

3

;dfof]hg÷k'gM:y

fkgf

-

-

>fj0f !, @)&% ;d

fof]hLt÷k'gM :yflkt

df}Hbft

8,08

8,29

9,22

6 -

2,

294,

274,

596

65,

984,

996

235

,484

,230

1

21,62

2,70

1 9

41,4

63,63

2 (9

,581

,038

) 1

1,737

,548

,343

-

11,7

37,5

48,34

3

o; jif{sf]] lj:t[t cfDbfgL

gfkmf

1,5

87,9

60,14

5 1

,587

,960

,145

1,5

87,9

60,14

5

cfos

/ kZrftsf cGo lj:t[t cfDbfgL

km]o/ e

]No'df d

'Nof°g

ul/Psf OlSj6L p

ks/0fsf nu

fgLaf6 e

Psf gfkmf÷g

f]S;fg

(40,

564,

233)

(40,

564,

233)

(40,

564,

233)

k'gM d'Nof°g

af6

ePsf gfkmf÷g

f]S;fg

-

-

kl/eflift n

fe o

f]hgfaf6

ljdfl°s g

fkmf÷gf]S;

fg

-

-

gub

k|jfxsf] x]lhªa

f6 e

Psf] gfkmf÷g

f]S;fg

-

-

ljb]z

L ljlgdo

;+rfng

sf] ljQ

Lo ;

DklQ ljlgd

oaf6 e

Psf] ;

6xL gfkmf÷g

f]S;fg

-

-

o; jif{sf] lj:t[t cfDbfgL

-

-

hu]8

f sf]ifd

f ;fl/P

sf] /s

d 3

17,5

92,0

29

2,9

69,4

52

310,

848,

288

(686

,072

,891

) 5

4,66

3,123

-

-

hu]8

f sf]ifa

f6 lgs

flnPs

f] /s

d 1

7,92

5,18

4 (3

4,52

4,70

1) (1