CEBoK Module 09 Cost and Schedule Risk Analysis

96

© 2002-2013 ICEAA. All rights reserved. v1.2 Unit III - Module 9 1 Cost and Schedule Risk Analysis: Basic How to adjust your estimate for uncertainty and historical cost and schedule growth “As we know, / There are known knowns. / There are things we know we know. We also know / There are known unknowns. / That is to say We know there are some things / We do not know. But there are also unknown unknowns, / The ones we don't know / We don't know.” - “The Unknown” from Pieces of Intelligence: The Existential Poetry of Donald Rumsfeld, Hart Seely, 2003 [DoD news briefing, 02/12/2002] Presented at the 2017 ICEAA Professional Development & Training Workshop www.iceaaonline.com/portland2017

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of CEBoK Module 09 Cost and Schedule Risk Analysis

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 1

Cost and Schedule Risk Analysis Basic

How to adjust your estimate for uncertainty and historical cost and schedule growth

ldquoAs we know There are known knowns There are things we know we know We also know There are known unknowns That is to say

We know there are some things We do not know But there are also unknown unknowns The ones we dont know We dont knowrdquo

- ldquoThe Unknownrdquo from Pieces of Intelligence The Existential Poetry of DonaldRumsfeld Hart Seely 2003 [DoD news briefing 02122002]

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Acknowledgmentsbull ICEAA is indebted to TASC Inc for the

development and maintenance of theCost Estimating Body of Knowledge (CEBoKreg)ndash ICEAA is also indebted to Technomics Inc for the

independent review and maintenance of CEBoKreg

bull ICEAA is also indebted to the following individuals who have made significant contributions to the development review and maintenance of CostPROF and CEBoK reg

bull Module 9 Cost and Schedule Risk Analysisndash Lead authors Richard L Coleman Jessica R Summerville

Eric R Druker Richard C Leendash Senior reviewers Richard L Coleman Michael F Jeffers Kevin

Cincotta Fred K Blackburnndash Reviewer Bethia L Cullisndash Managing editor Peter J Braxton

2Unit III - Module 9

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 3

Unit IndexUnit I ndash Cost EstimatingUnit II ndash Cost Analysis TechniquesUnit III ndash Analytical Methods

6 Basic Data Analysis Principles7 Learning Curve Analysis8 Regression Analysis9 Cost and Schedule Risk Analysis10Probability and Statistics

Unit IV ndash Specialized CostingUnit V ndash Management Applications

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 4

Risk Overviewbull Key Ideas

ndash Risk bias (accuracy)ndash Uncertainty (precision)ndash Cost realismndash Risk vs Sensitivityndash Inputs vs Outputs Risk

bull Practical Applicationsndash Probabilistic Cost Estimates

bull S-Curvesbull Budgeting to Percentiles

ndash Risk Scoring and Mapping

bull Analytical Constructsndash Probability Distributions for Riskndash Percentilesndash Prediction Intervals (PI)ndash Correlation

bull Related Topicsndash Data Collection for

Risk Analysisndash Monte Carlo Simulationndash Risk Managementndash Schedule Analysis

10

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Agendabull Cost Risk Analysis

ndash Introductionndash Distributions

bull Fitting distributions to historical databull Measuring technical uncertaintybull Measuring estimating uncertainty

ndash Aggregating riskbull Simulationbull Method of momentsbull Correlation

ndash Risk measuresndash Risk allocationndash Joint confidence level analysisndash Practical exercises

bull Comparing simulation with method of moments

Unit III - Module 9 5

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 6

Introductionbull Cost estimates in many cases project many years in the future

ndash Cost estimates are inherently uncertain regardless of whether risk is included (modeled)

bull Sources of uncertainty include (but are not limited to)ndash Scope and requirements (what is being estimated)ndash Technology readinessndash Manufacturing readinessndash Inflationndash Model uncertainty

bull The cost analysis profession recognizes the importance of risk and has incorporated risk analysis as an integral part of the estimating process

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Risk Analysis Termsbull Risk is the chance of uncertainty or loss

bull Uncertainty is the indefiniteness about the outcome of a situationndash Includes both favorable and unfavorable events

bull Cost Risk is a measure of the chance that due to unfavorable events the planned or budgeted cost of a project will be exceeded

bull Cost Uncertainty Analysis is a process of quantifying the cost estimating uncertainty due to variance in the cost estimating models as well as variance in the technical performance and programmatic input variables

bull Cost Risk Analysis is a process of quantifying the cost impacts of the unfavorable events

Unit III - Module 9 7

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 8

Are Our Costs Realisticbull We claim our costs are realisticbull We claim we estimate costs at the 50th percentile

ndash This should mean we have 50 low and 50 high outcomes

bull But we have an unchanging cost growth pattern showing only 12 of our estimates are high (underrun) and 88 are low (overrun)ndash As shown in the graphic on the next slide

bull The conclusion is inescapable our costs are not realistic

bull This also means our costs are at the 12th percentile not the 50th percentile

What Percentile Are We At Now (And Where Are We Going) R Coleman E Druker P Braxton B Cullis C Kanick SCEA 2009 DoDCAS 2010

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

88 Dollars ( in millions)

Co

st G

row

th F

acto

r

0

1

2

3

4

5

6

7

8

0 5000 10000 15000 20000 25000 30000 35000

lsquoUnit III - Module 9 9

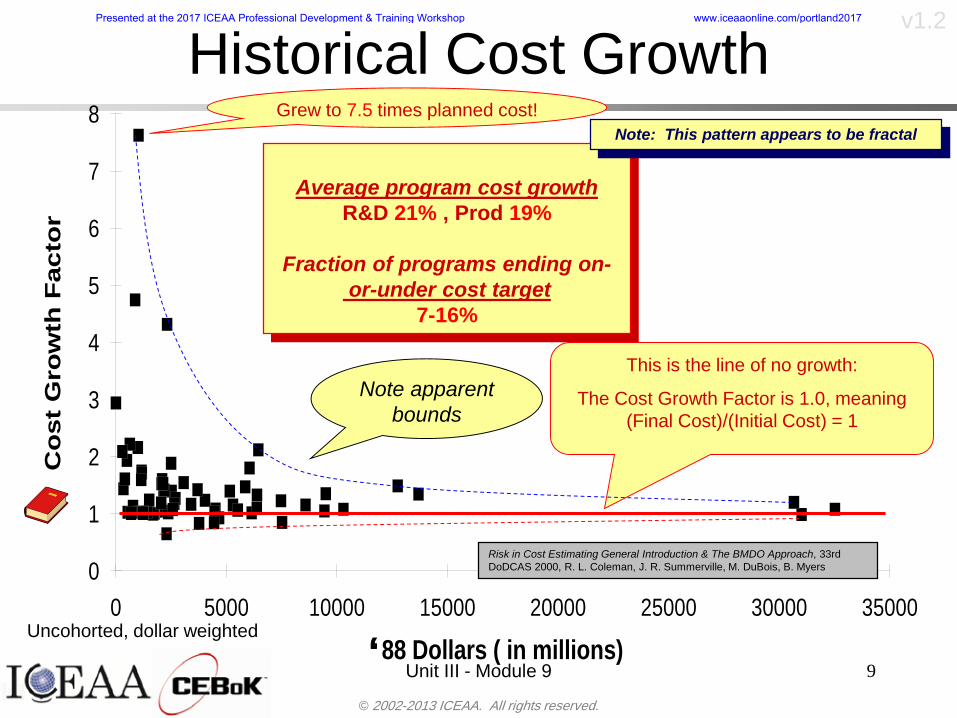

Historical Cost Growth

Average program cost growthRampD 21 Prod 19

Fraction of programs ending on-or-under cost target

7-16

Note This pattern appears to be fractal

Uncohorted dollar weighted

This is the line of no growth

The Cost Growth Factor is 10 meaning (Final Cost)(Initial Cost) = 1

Grew to 75 times planned cost

Risk in Cost Estimating General Introduction amp The BMDO Approach 33rd DoDCAS 2000 R L Coleman J R Summerville M DuBois B Myers

Note apparent bounds

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

88 Dollars ( in millions)

Cost Growth Factor

0

1

2

3

4

5

6

7

8

0

5000

10000

15000

20000

25000

30000

35000

copy 2002-2013 ICEAA All rights reserved

v12

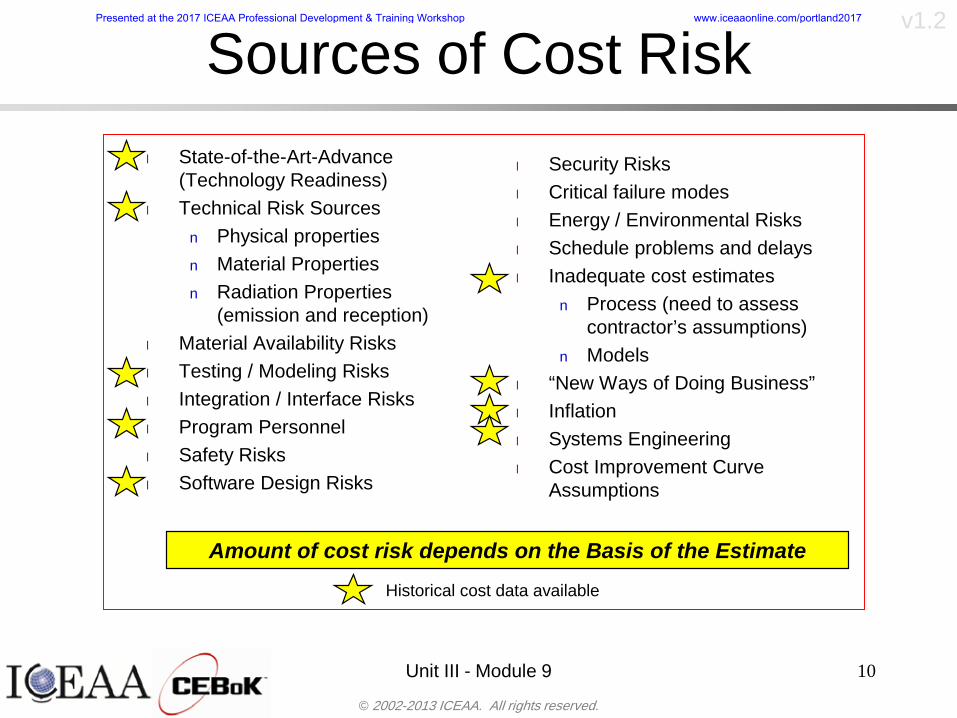

Sources of Cost Risk

Unit III - Module 9 10

l Security Risksl Critical failure modesl Energy Environmental Risksl Schedule problems and delaysl Inadequate cost estimates

n Process (need to assess contractorrsquos assumptions)

n Models l ldquoNew Ways of Doing Businessrdquol Inflationl Systems Engineeringl Cost Improvement Curve

Assumptions

l State-of-the-Art-Advance (Technology Readiness)

l Technical Risk Sourcesn Physical propertiesn Material Propertiesn Radiation Properties

(emission and reception)l Material Availability Risksl Testing Modeling Risksl Integration Interface Risksl Program Personnell Safety Risksl Software Design Risks

Historical cost data available

Amount of cost risk depends on the Basis of the Estimate

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

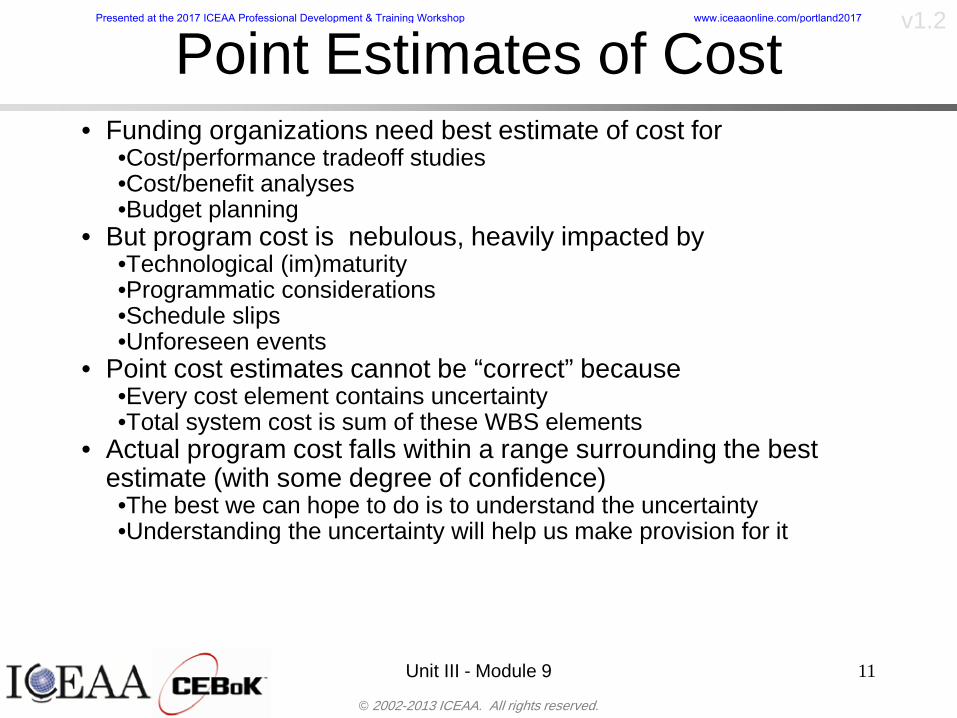

Point Estimates of Costbull Funding organizations need best estimate of cost for

bullCostperformance tradeoff studiesbullCostbenefit analysesbullBudget planning

bull But program cost is nebulous heavily impacted bybullTechnological (im)maturitybullProgrammatic considerationsbullSchedule slipsbullUnforeseen events

bull Point cost estimates cannot be ldquocorrectrdquo becausebullEvery cost element contains uncertaintybullTotal system cost is sum of these WBS elements

bull Actual program cost falls within a range surrounding the best estimate (with some degree of confidence)bullThe best we can hope to do is to understand the uncertaintybullUnderstanding the uncertainty will help us make provision for it

Unit III - Module 9 11

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 12

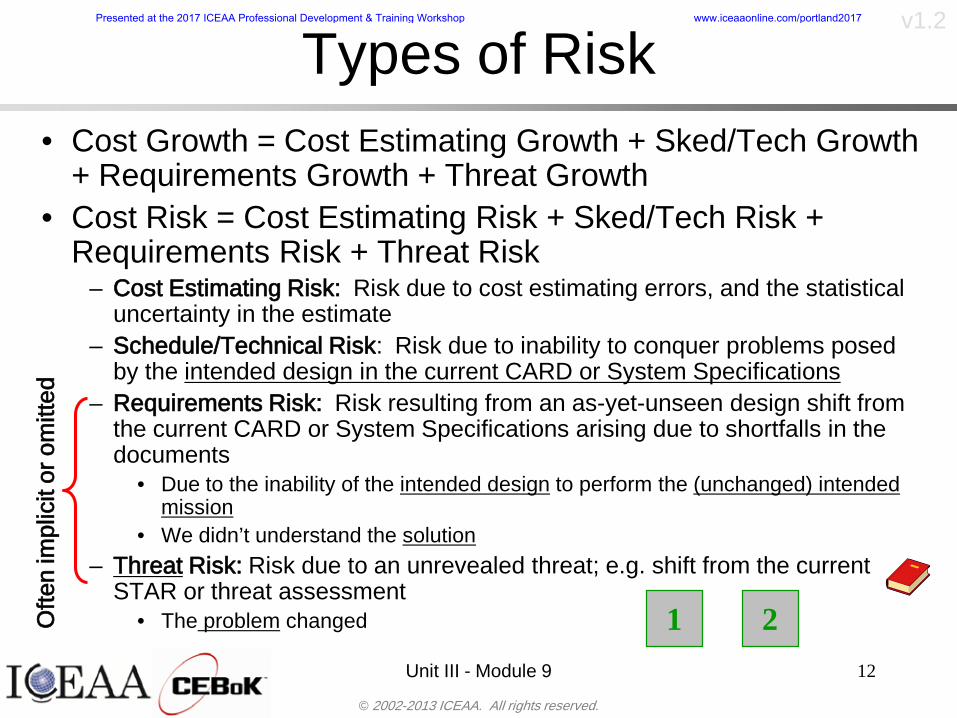

Types of Riskbull Cost Growth = Cost Estimating Growth + SkedTech Growth

+ Requirements Growth + Threat Growthbull Cost Risk = Cost Estimating Risk + SkedTech Risk +

Requirements Risk + Threat Riskndash Cost Estimating Risk Risk due to cost estimating errors and the statistical

uncertainty in the estimate ndash ScheduleTechnical Risk Risk due to inability to conquer problems posed

by the intended design in the current CARD or System Specificationsndash Requirements Risk Risk resulting from an as-yet-unseen design shift from

the current CARD or System Specifications arising due to shortfalls in the documents

bull Due to the inability of the intended design to perform the (unchanged) intended mission

bull We didnrsquot understand the solutionndash Threat Risk Risk due to an unrevealed threat eg shift from the current

STAR or threat assessmentbull The problem changedO

ften

impl

icit

or o

mitt

ed

1 2

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

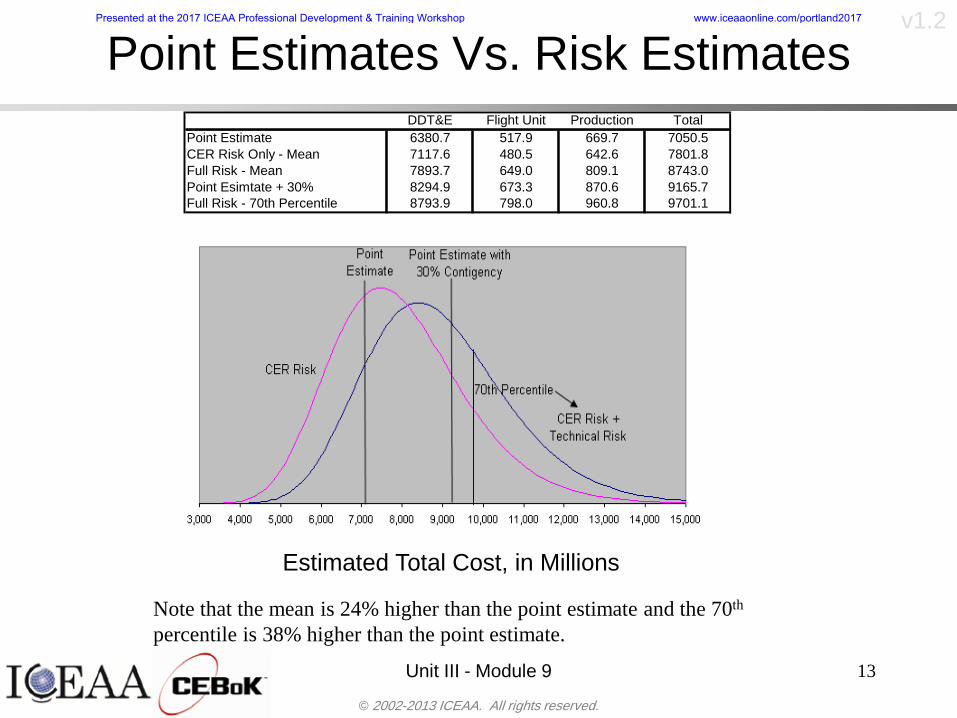

Point Estimates Vs Risk Estimates

Unit III - Module 9 13

DDTampE Flight Unit Production TotalPoint Estimate 63807 5179 6697 70505CER Risk Only - Mean 71176 4805 6426 78018Full Risk - Mean 78937 6490 8091 87430Point Esimtate + 30 82949 6733 8706 91657Full Risk - 70th Percentile 87939 7980 9608 97011

Estimated Total Cost in Millions

Note that the mean is 24 higher than the point estimate and the 70th

percentile is 38 higher than the point estimate

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

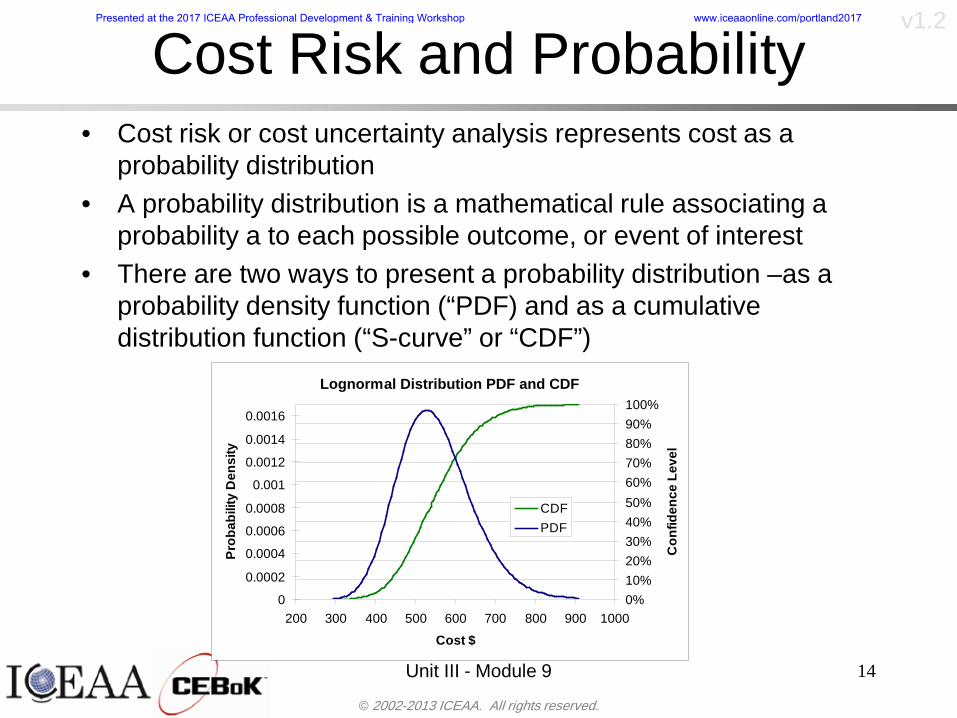

Cost Risk and Probabilitybull Cost risk or cost uncertainty analysis represents cost as a

probability distributionbull A probability distribution is a mathematical rule associating a

probability a to each possible outcome or event of interestbull There are two ways to present a probability distribution ndash as a

probability density function (ldquoPDF) and as a cumulative distribution function (ldquoS-curverdquo or ldquoCDFrdquo)

Unit III - Module 9 14

Lognormal Distribution PDF and CDF

0102030405060708090100

200 300 400 500 600 700 800 900 1000Cost $

Con

fiden

ce L

evel

0

00002

00004

00006

00008

0001

00012

00014

00016

Prob

abili

ty D

ensi

ty

CDFPDF

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 15

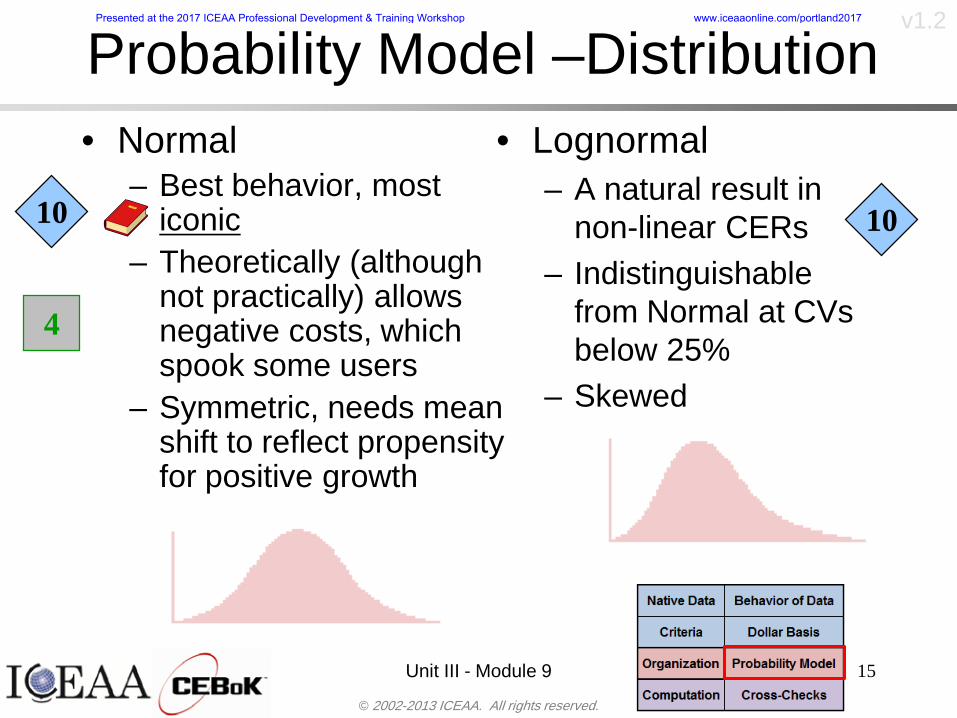

Probability Model ndash Distributionbull Normal

ndash Best behavior most iconic

ndash Theoretically (although not practically) allows negative costs which spook some users

ndash Symmetric needs mean shift to reflect propensity for positive growth

bull Lognormalndash A natural result in

non-linear CERsndash Indistinguishable

from Normal at CVs below 25

ndash Skewed

10

4

10

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 16

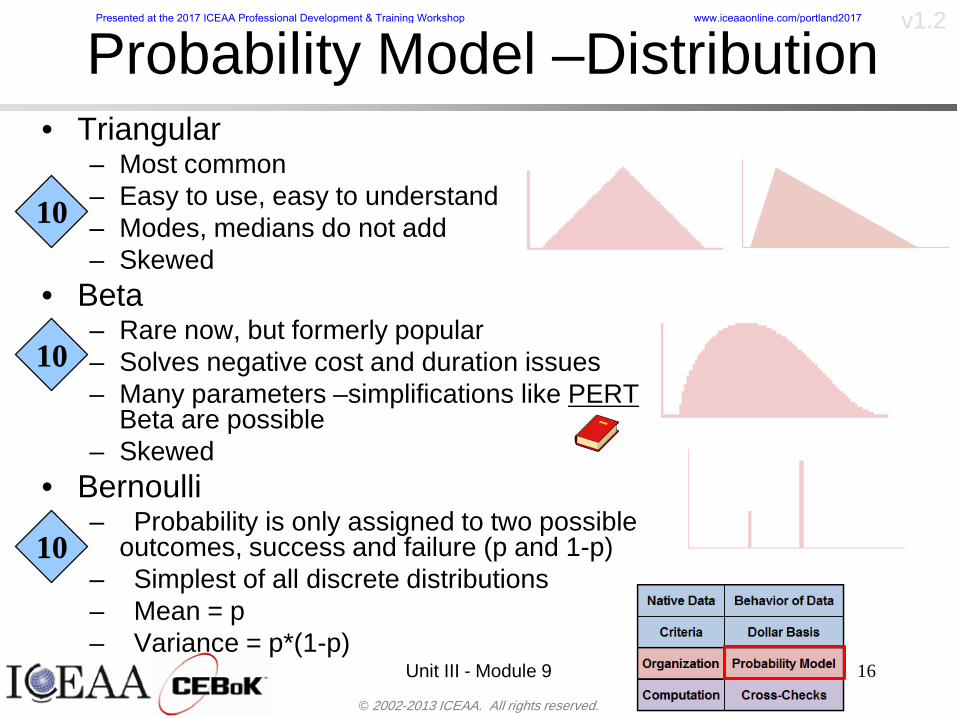

bull Triangularndash Most commonndash Easy to use easy to understandndash Modes medians do not addndash Skewed

bull Betandash Rare now but formerly popularndash Solves negative cost and duration issuesndash Many parameters ndash simplifications like PERT

Beta are possiblendash Skewed

bull Bernoullindash Probability is only assigned to two possible

outcomes success and failure (p and 1-p)ndash Simplest of all discrete distributionsndash Mean = pndash Variance = p(1-p)

10

Probability Model ndash Distribution

10

10

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

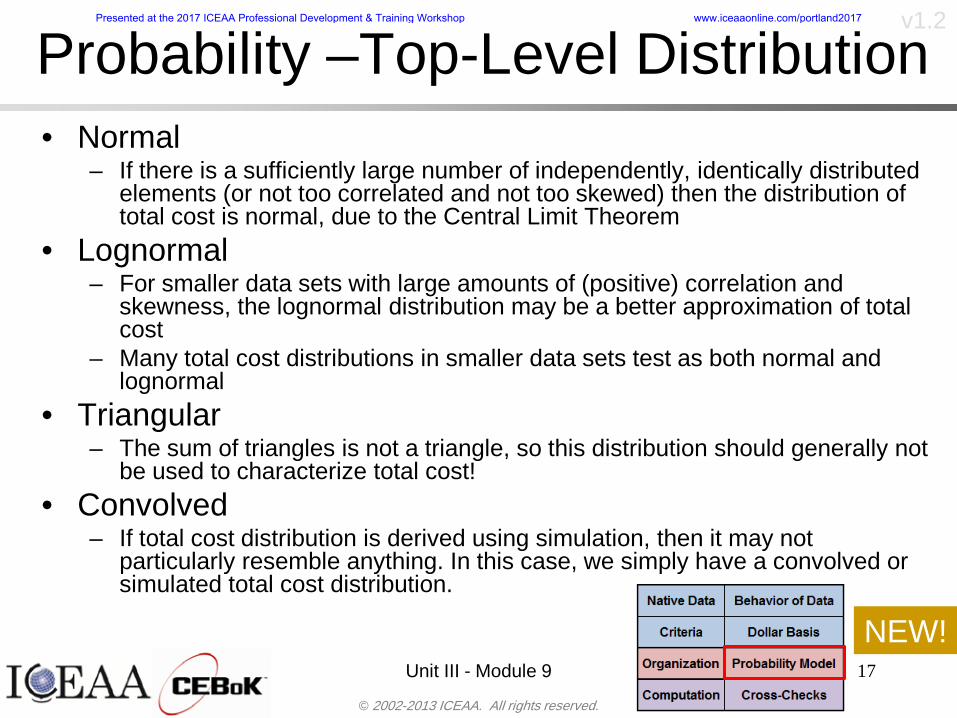

Unit III - Module 9 17

bull Normalndash If there is a sufficiently large number of independently identically distributed

elements (or not too correlated and not too skewed) then the distribution of total cost is normal due to the Central Limit Theorem

bull Lognormalndash For smaller data sets with large amounts of (positive) correlation and

skewness the lognormal distribution may be a better approximation of total cost

ndash Many total cost distributions in smaller data sets test as both normal and lognormal

bull Triangularndash The sum of triangles is not a triangle so this distribution should generally not

be used to characterize total costbull Convolved

ndash If total cost distribution is derived using simulation then it may not particularly resemble anything In this case we simply have a convolved or simulated total cost distribution

Probability ndash Top-Level Distribution

NEW

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

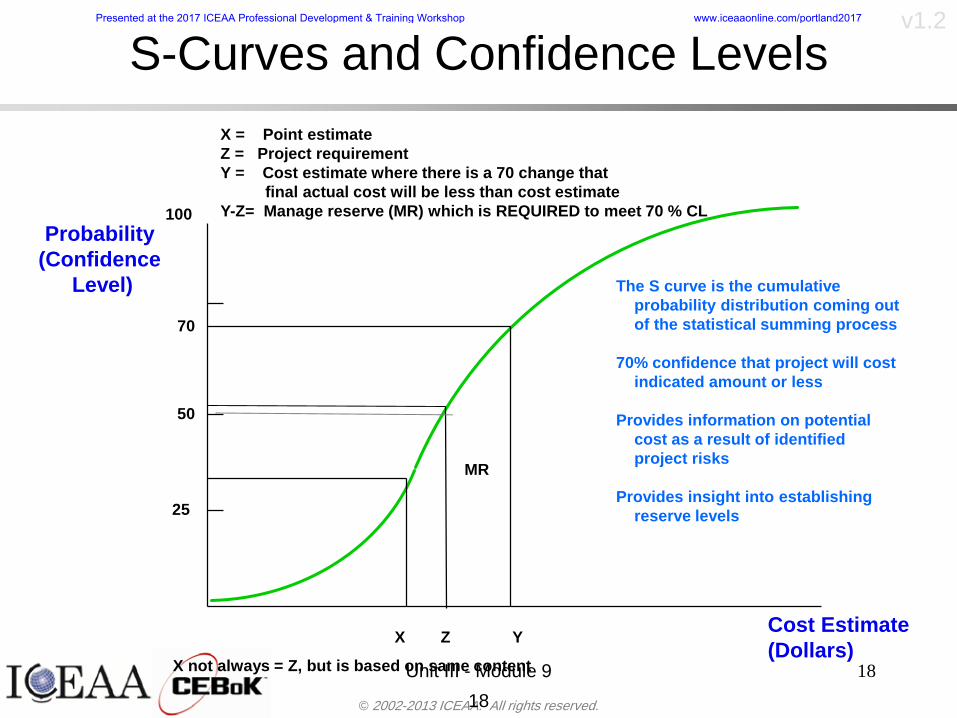

S-Curves and Confidence Levels

Unit III - Module 9 1818

100

70

25

Probability(Confidence

Level)

Cost Estimate(Dollars)

50

The S curve is the cumulative probability distribution coming out of the statistical summing process

70 confidence that project will cost indicated amount or less

Provides information on potential cost as a result of identified project risks

Provides insight into establishing reserve levels

X Y

MR

X = Point estimateZ = Project requirementY = Cost estimate where there is a 70 change that

final actual cost will be less than cost estimateY-Z= Manage reserve (MR) which is REQUIRED to meet 70 CL

Z

X not always = Z but is based on same content

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

19

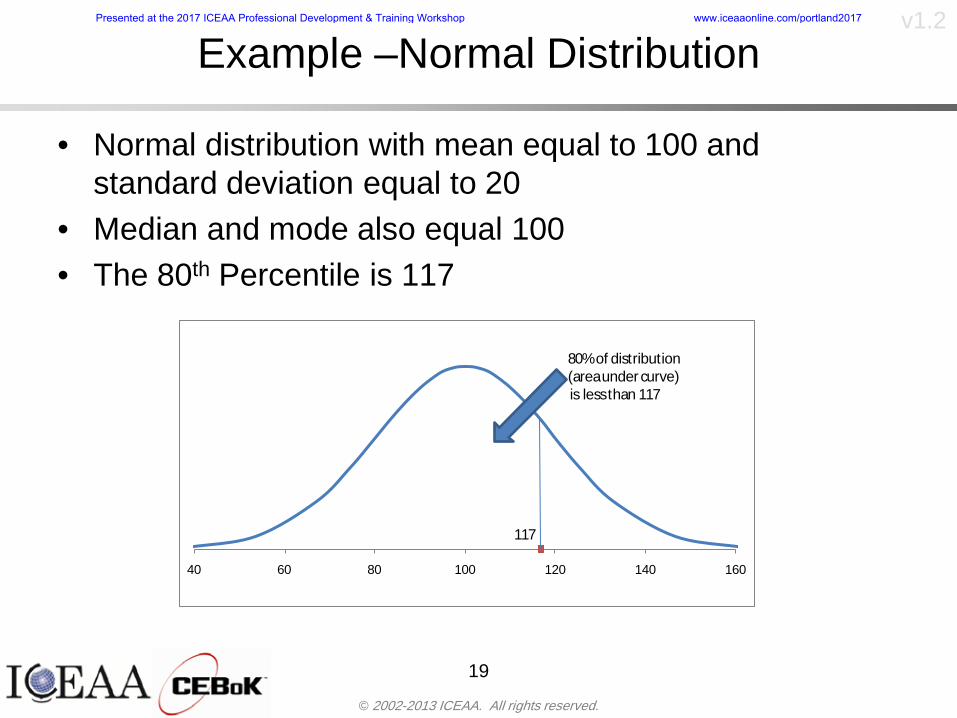

Example ndash Normal Distribution

bull Normal distribution with mean equal to 100 and standard deviation equal to 20

bull Median and mode also equal 100bull The 80th Percentile is 117

40 60 80 100 120 140 160

80 of distribution(area under curve)is less than 117

117

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

20

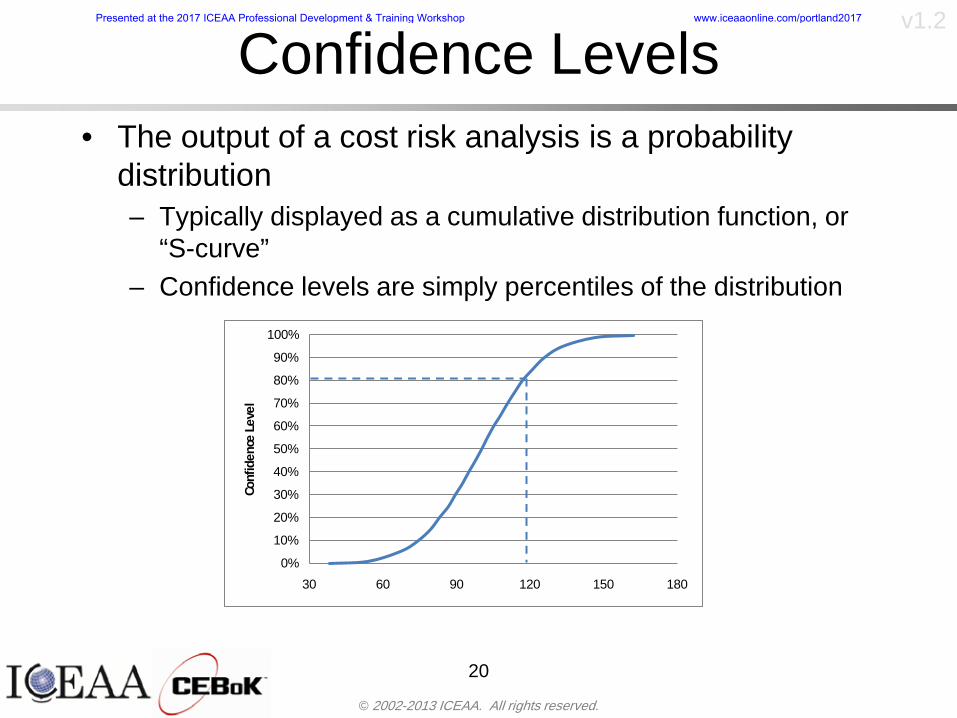

Confidence Levelsbull The output of a cost risk analysis is a probability

distributionndash Typically displayed as a cumulative distribution function or

ldquoS-curverdquondash Confidence levels are simply percentiles of the distribution

0

10

20

30

40

50

60

70

80

90

100

30 60 90 120 150 180

Conf

iden

ce L

evel

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Measuring Parametric Model Uncertainty

bull When developing estimates using cost-estimating relationships (CERs) there are two major sources of uncertaintyndash Technical (model input) uncertaintyndash Estimating uncertainty

bull Technical uncertainty reflects the uncertainty inherent in the model inputsndash Typical parametric model inputs include weight lines of code

heritage and other performance and management inputs

bull Estimating uncertainty measures the uncertainty inherent in the model due to the modelrsquos inability to capture all aspects of variability in the data

21

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Parametric Model Examplebull The NASAAir Force Cost Model (NAFCOM) is a

parametric model for estimating acquisition costs for spacecraft and launch vehicles

bull The CERs in NAFCOM have the formCost = C WeightVNewDesignWTechnicalXManagementY ClassZ

bull There is technical uncertainty about each of the parametersndash Parametric models are applied early in a program so there

is significant amount of uncertainty in the weightndash Heritage is also tricky it is inherently subjective and project

personnel are typically optimisticndash Technical characteristics can also change as a program

matures and requirements change

22

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

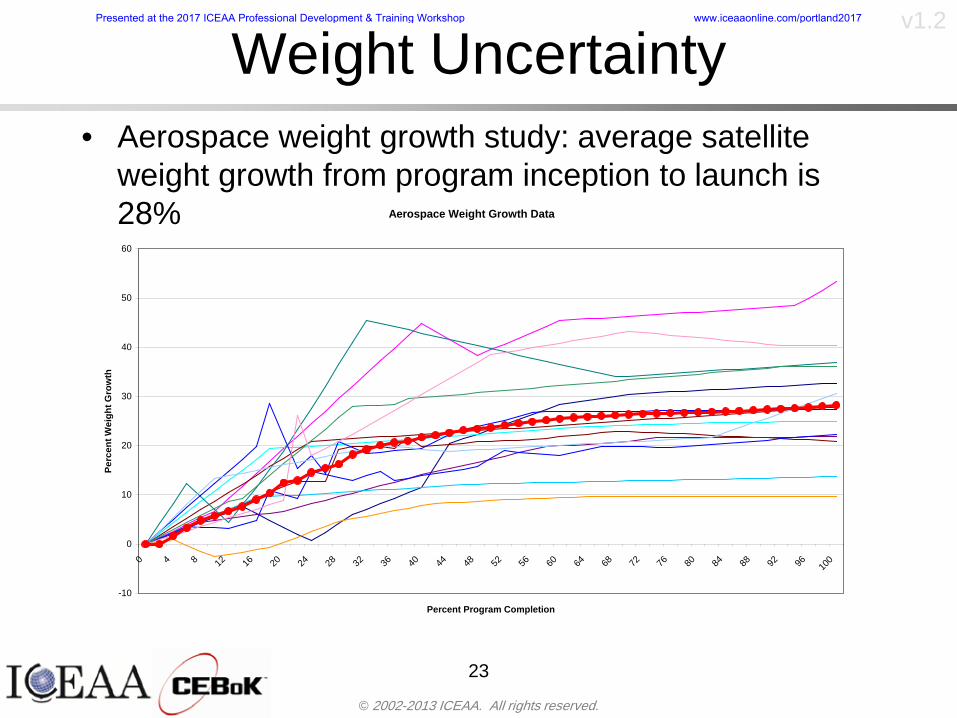

Weight Uncertaintybull Aerospace weight growth study average satellite

weight growth from program inception to launch is 28

23

Aerospace Weight Growth Data

-10

0

10

20

30

40

50

60

0 4 8 12 16 20 24 28 32 36 40 44 48 52 56 60 64 68 72 76 80 84 88 92 96 100

Percent Program Completion

Perc

ent W

eigh

t Gro

wth

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

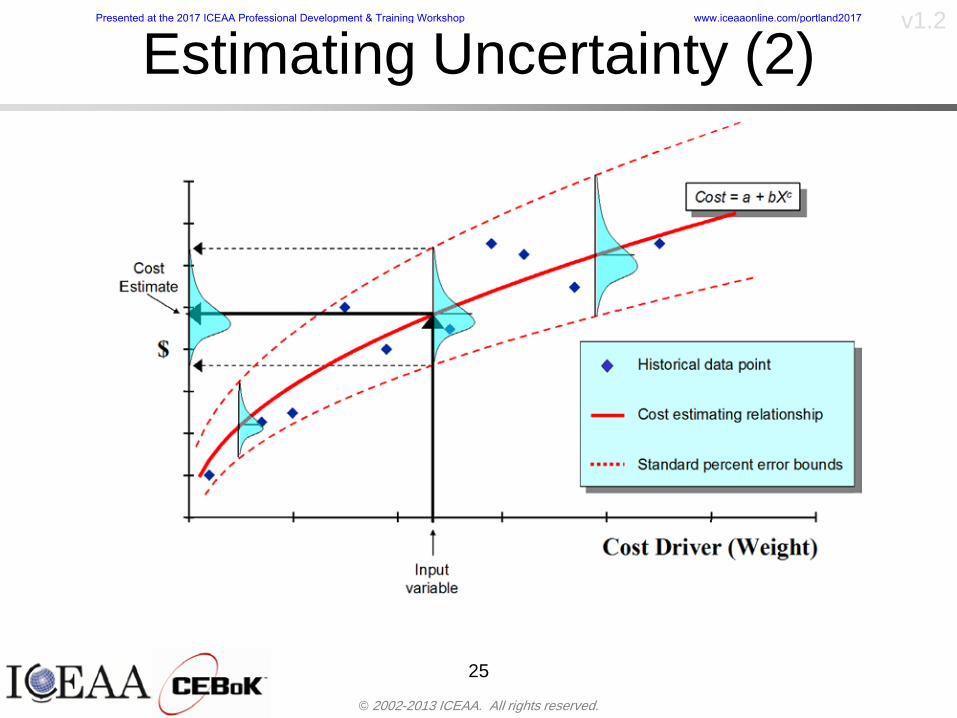

Estimating Uncertaintybull CERs do not perfectly fit the historical data

ndash There are non-repeatable random effects that cannot be predicted

bull For examplendash Parts breaking during testingndash Strikes which are difficult to predict

bull This results in an underlying uncertainty distribution about an estimatendash The outcome of a CER represents only one point on an

uncertainty distributionbull Typically mean or median depending upon the CER

methodology

24

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Estimating Uncertainty (2)

25

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Estimating Uncertainty (3)bull In the case of a linear regression the estimating

uncertainty follows a normal distributionndash The estimate is the mean and the standard error of the

estimate from the regression is the standard deviation of the normal distribution

bull In the case of a log-transformed linear regression the estimating uncertainty follows a lognormal distributionndash The estimate is the median of the lognormal and the

standard error of the estimate from the regression is the standard deviation of the normal distribution (in log-space)

bull There is additional uncertainty about an estimate based upon the distance of what is being estimated from the mean of the input datandash This results in a prediction interval

26

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

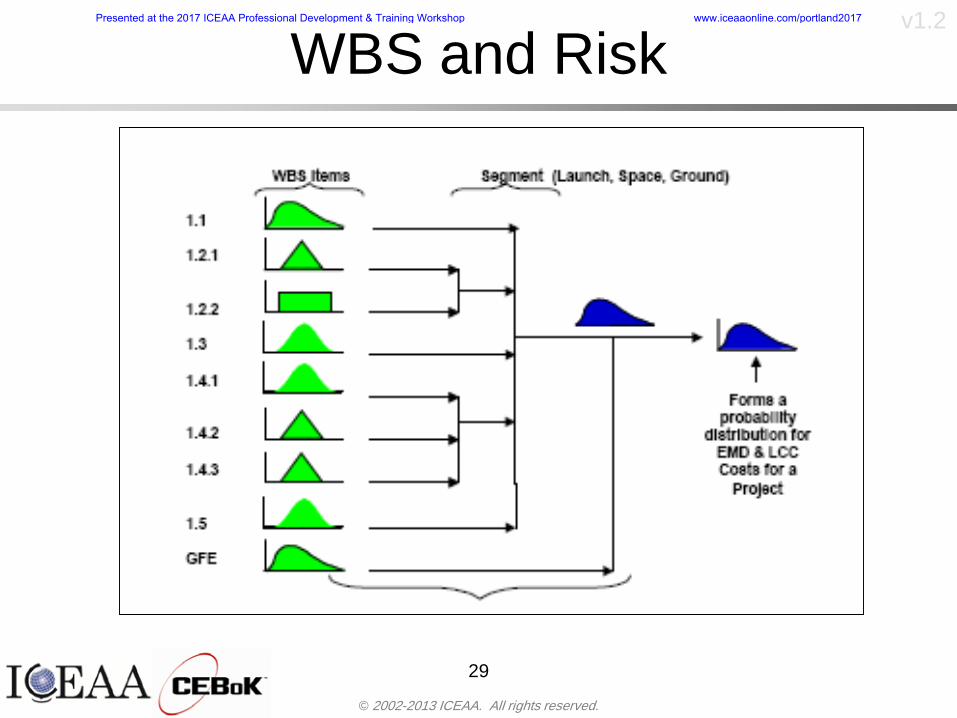

Aggregating Riskbull Risk is typically applied at the same level at

which we estimate cost that is at the Work Breakdown Structure (WBS) level

bull The estimates for each WBS are developedndash These estimates sum to yield the total system cost

bull For an n-element WBS the total cost is the sum of the cost for each of the n elements

27

nXXXCostSystem +++= 21

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

WBS Examplebull Launch Vehicle

ndash Structurebull Vehicle Structurebull Tank Structure

ndash Thermal Controlbull Active Thermal Controlbull Induced Thermal Controlbull Tank Thermal Control

ndash Main Propulsion Systemndash Liquid Rocket Enginendash Electric Power and Distributionndash Command Control and Data Handlingndash System Integration

28

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

WBS and Risk

29

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

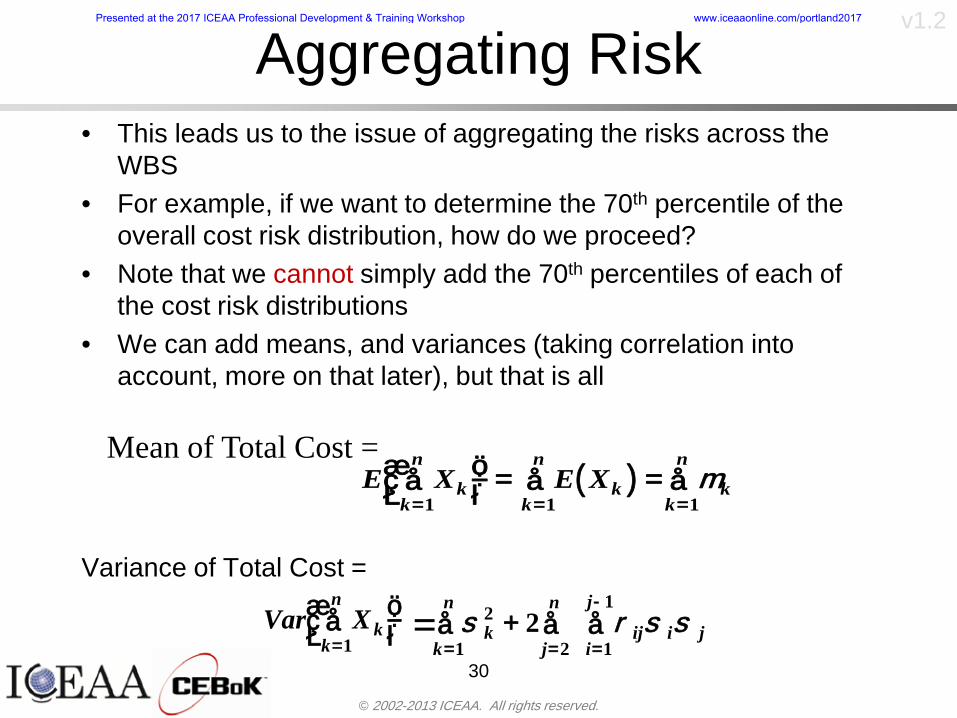

Aggregating Riskbull This leads us to the issue of aggregating the risks across the

WBSbull For example if we want to determine the 70th percentile of the

overall cost risk distribution how do we proceed bull Note that we cannot simply add the 70th percentiles of each of

the cost risk distributionsbull We can add means and variances (taking correlation into

account more on that later) but that is all

Variance of Total Cost =

30

Mean of Total Cost = ( )E X E Xk

k

n

kk

n

kk

n

= = =aringaelig

egraveccediloumloslashdivide

= =aring aring1 1 1

m

Var X kk

n

=aringaelig

egraveccediloumloslashdivide1

= s r s skk

n

iji

j

i jj

n2

1 1

1

22+aring aringaring

= =

-

=

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

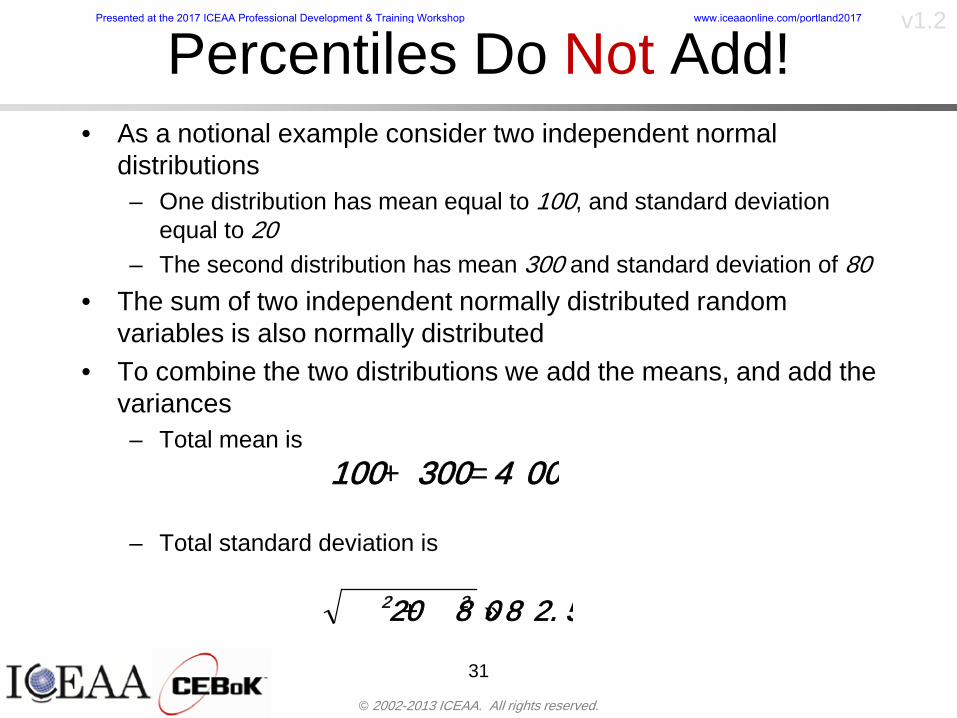

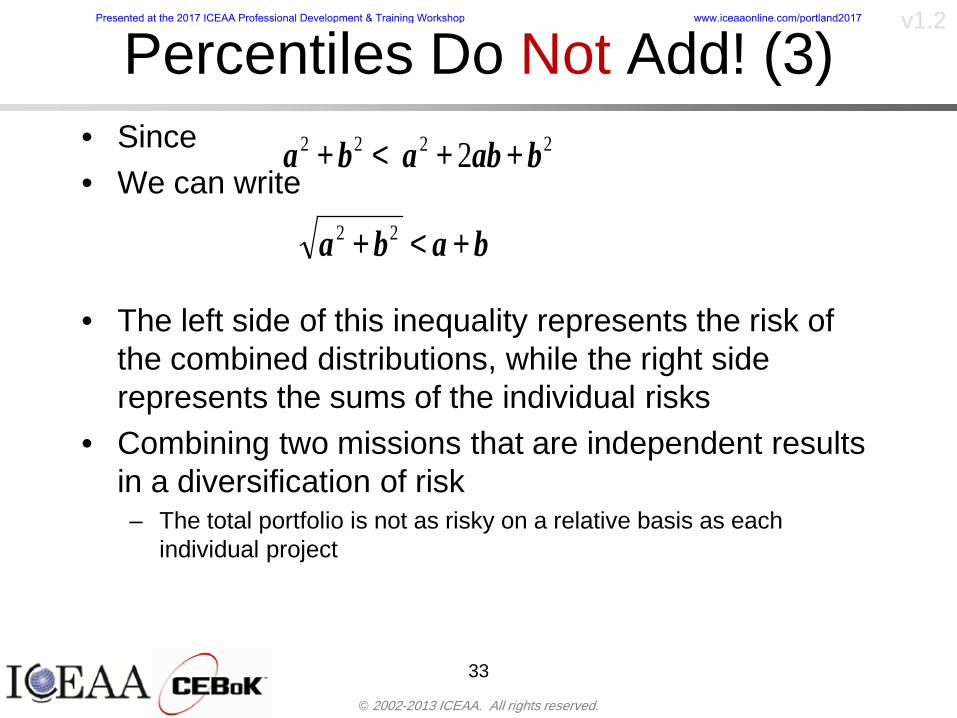

Percentiles Do Not Addbull As a notional example consider two independent normal

distributionsndash One distribution has mean equal to 100 and standard deviation

equal to 20ndash The second distribution has mean 300 and standard deviation of 80

bull The sum of two independent normally distributed random variables is also normally distributed

bull To combine the two distributions we add the means and add the variancesndash Total mean is

ndash Total standard deviation is

31

400300100 =+

8258020 22 raquo+

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

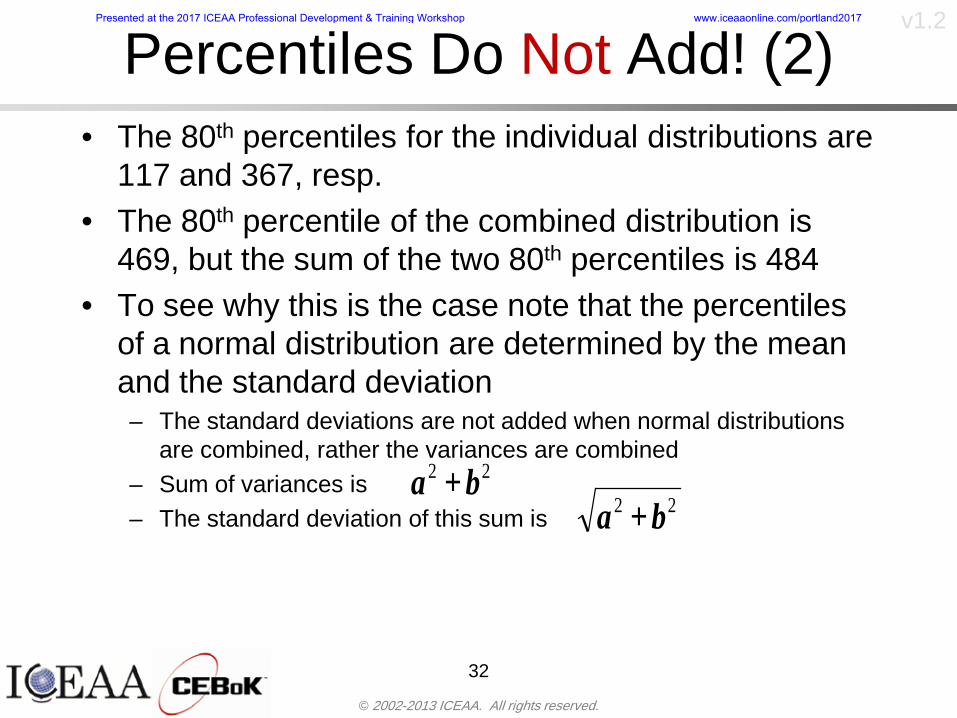

Percentiles Do Not Add (2)bull The 80th percentiles for the individual distributions are

117 and 367 respbull The 80th percentile of the combined distribution is

469 but the sum of the two 80th percentiles is 484bull To see why this is the case note that the percentiles

of a normal distribution are determined by the mean and the standard deviationndash The standard deviations are not added when normal distributions

are combined rather the variances are combinedndash Sum of variances is ndash The standard deviation of this sum is

32

22 ba +22 ba +

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Percentiles Do Not Add (3)bull Since bull We can write

bull The left side of this inequality represents the risk of the combined distributions while the right side represents the sums of the individual risks

bull Combining two missions that are independent results in a diversification of riskndash The total portfolio is not as risky on a relative basis as each

individual project

33

2222 2 bababa ++lt+

baba +lt+ 22

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

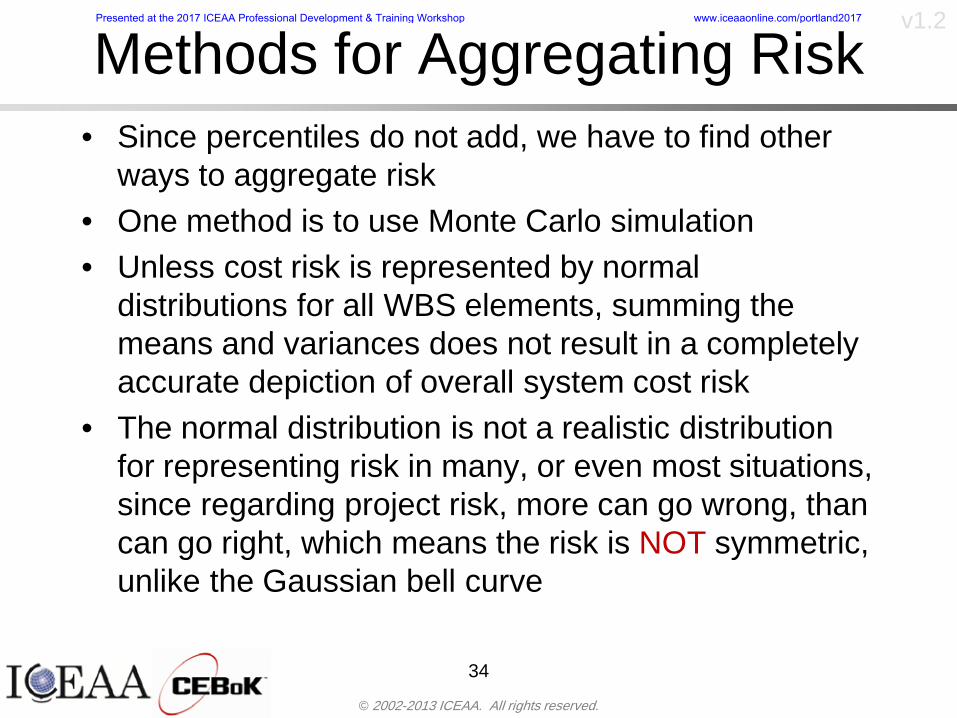

Methods for Aggregating Riskbull Since percentiles do not add we have to find other

ways to aggregate riskbull One method is to use Monte Carlo simulationbull Unless cost risk is represented by normal

distributions for all WBS elements summing the means and variances does not result in a completely accurate depiction of overall system cost risk

bull The normal distribution is not a realistic distribution for representing risk in many or even most situations since regarding project risk more can go wrong than can go right which means the risk is NOT symmetric unlike the Gaussian bell curve

34

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 35

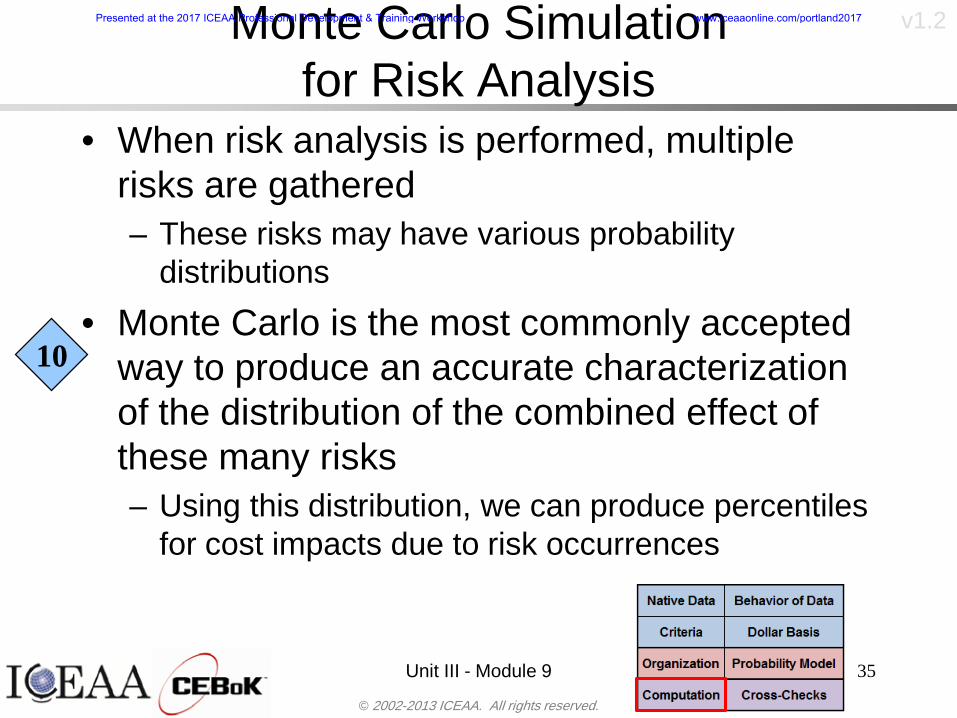

Monte Carlo Simulationfor Risk Analysis

bull When risk analysis is performed multiple risks are gatheredndash These risks may have various probability

distributions

bull Monte Carlo is the most commonly accepted way to produce an accurate characterization of the distribution of the combined effect of these many risksndash Using this distribution we can produce percentiles

for cost impacts due to risk occurrences

10

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

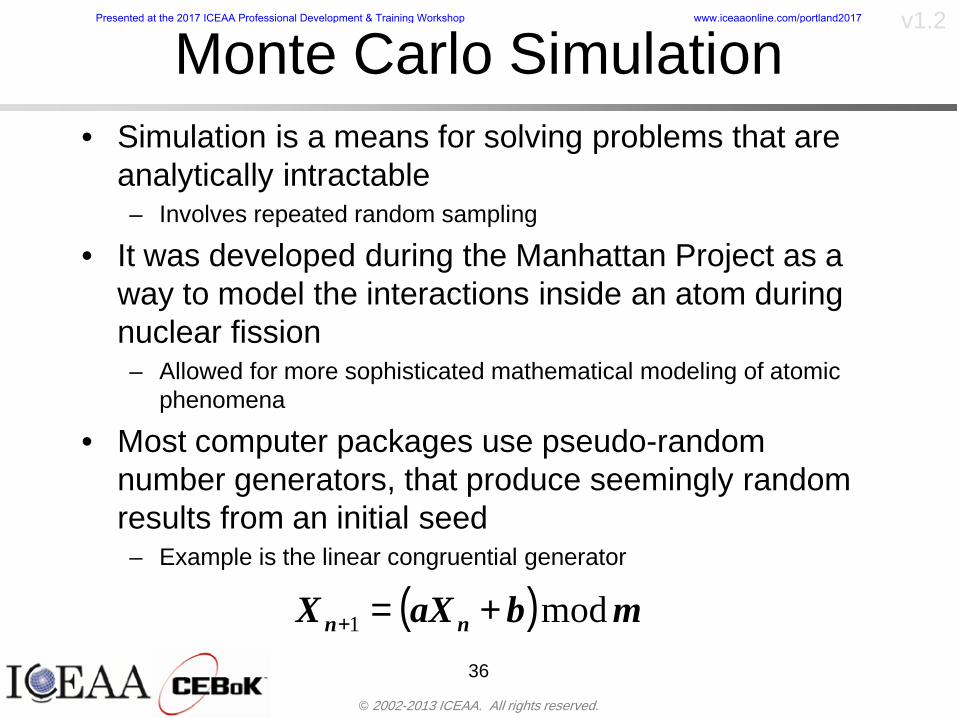

Monte Carlo Simulationbull Simulation is a means for solving problems that are

analytically intractablendash Involves repeated random sampling

bull It was developed during the Manhattan Project as a way to model the interactions inside an atom during nuclear fissionndash Allowed for more sophisticated mathematical modeling of atomic

phenomena

bull Most computer packages use pseudo-random number generators that produce seemingly random results from an initial seedndash Example is the linear congruential generator

36

( ) mbaXX nn mod1 +=+

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

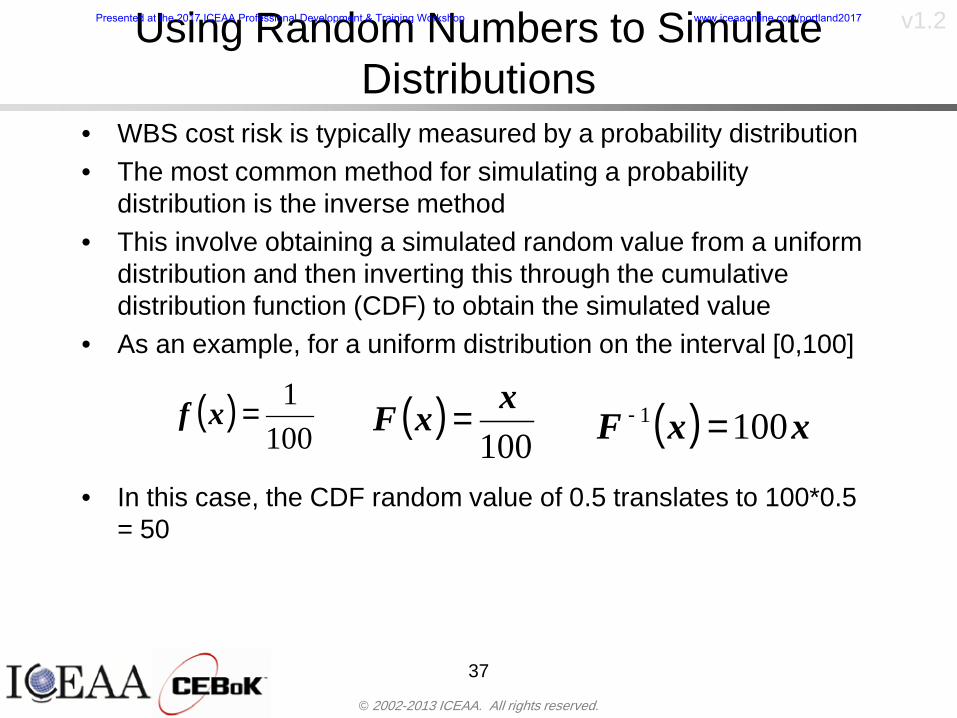

v12Using Random Numbers to Simulate Distributions

bull WBS cost risk is typically measured by a probability distributionbull The most common method for simulating a probability

distribution is the inverse methodbull This involve obtaining a simulated random value from a uniform

distribution and then inverting this through the cumulative distribution function (CDF) to obtain the simulated value

bull As an example for a uniform distribution on the interval [0100]

bull In this case the CDF random value of 05 translates to 10005 = 50

37

( )100

1=xf ( )

100xxF = ( ) xxF 1001 =-

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

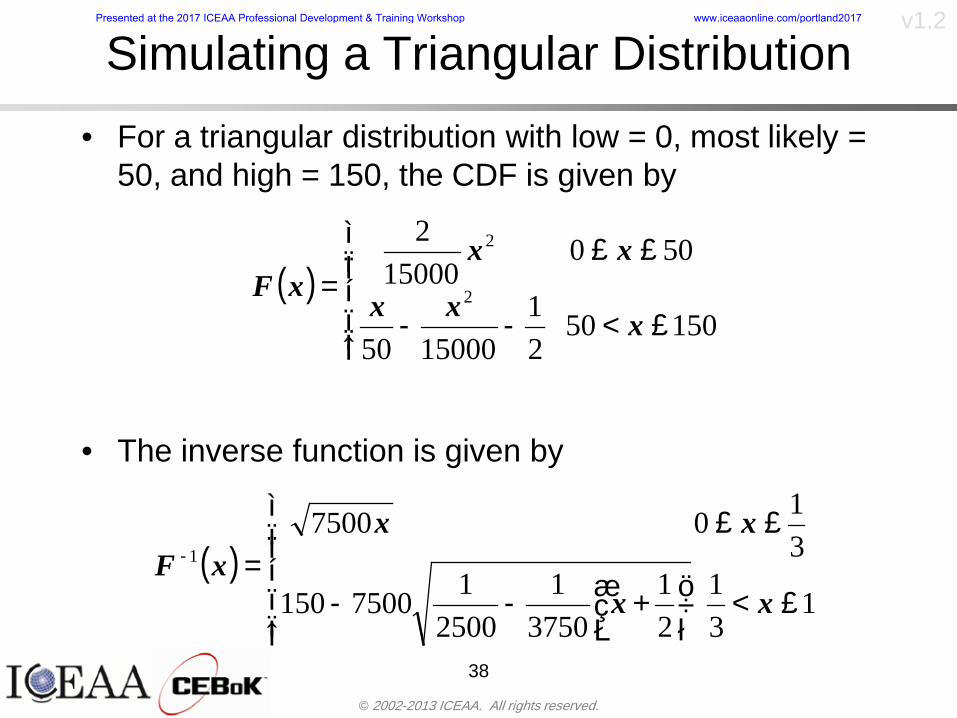

Simulating a Triangular Distribution

bull For a triangular distribution with low = 0 most likely = 50 and high = 150 the CDF is given by

bull The inverse function is given by

38

( )iumliumlicirc

iumliumliacute

igrave

poundlt--

poundpound=

1505021

1500050

50015000

2

2

2

xxx

xxxF

( )iumliumlicirc

iumliumliacute

igrave

poundltdivideoslashouml

ccedilegraveaelig +--

poundpound=-

131

21

37501

250017500150

3107500

1

xx

xxxF

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

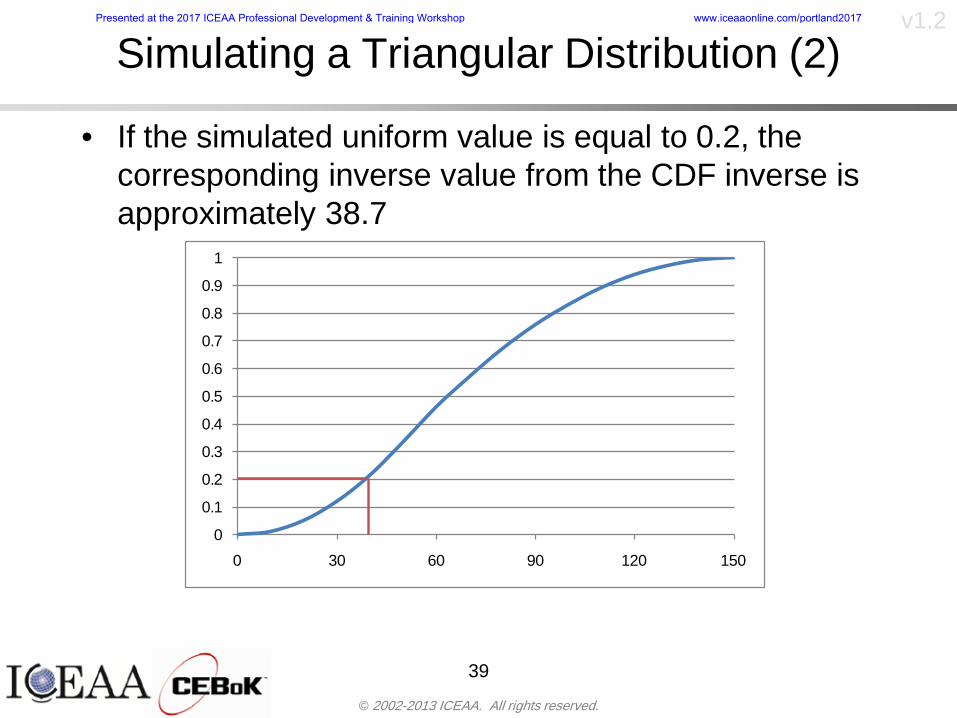

Simulating a Triangular Distribution (2)

bull If the simulated uniform value is equal to 02 the corresponding inverse value from the CDF inverse is approximately 387

39

0

01

02

03

04

05

06

07

08

09

1

0 30 60 90 120 150

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Monte Carlo and the WBSbull Simulation involves repeated trials

40

WBS Draw1 2 3 4 5

System 2912 3566 4390 2954 4655 Sum

Structure 80 105 55 80 57 SumVehicle Structure 50 70 30 40 20Tank Structure 30 35 25 40 37

Thermal Control 32 36 35 29 33 SumActive Thermal Control 10 15 12 7 10Induced Thermal Control 12 14 13 14 14Tank Thermal Control 10 7 10 8 9

Main Propulsion System 100 150 125 140 100

Liquid Rocket Engine 1000 1100 1800 900 2200

Electric Power and Distribution 100 125 150 75 90

Command Control and Data Handling 200 250 225 230 275

System Integration 1400 1800 2000 1500 1900

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

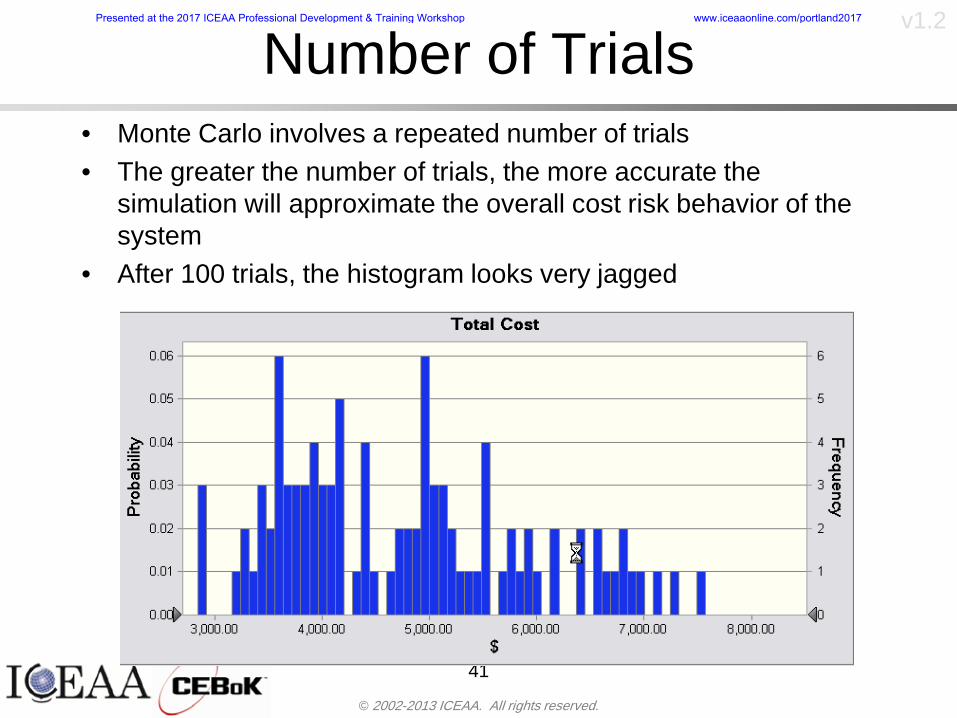

Number of Trialsbull Monte Carlo involves a repeated number of trialsbull The greater the number of trials the more accurate the

simulation will approximate the overall cost risk behavior of the system

bull After 100 trials the histogram looks very jagged

41

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

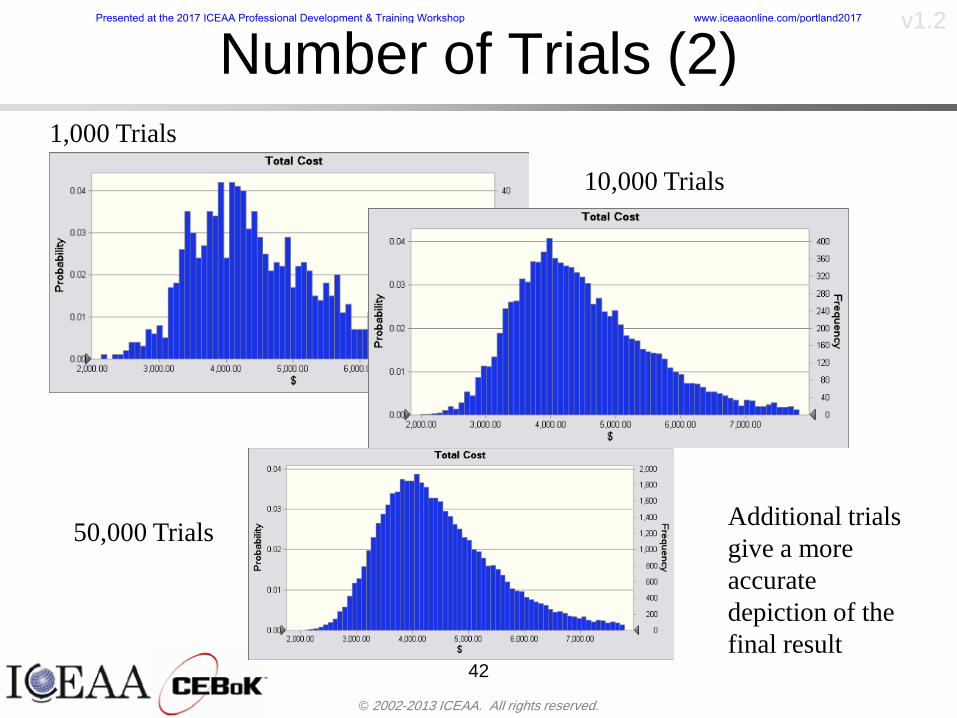

Number of Trials (2)

42

1000 Trials

10000 Trials

50000 Trials Additional trials give a more accurate depiction of the final result

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

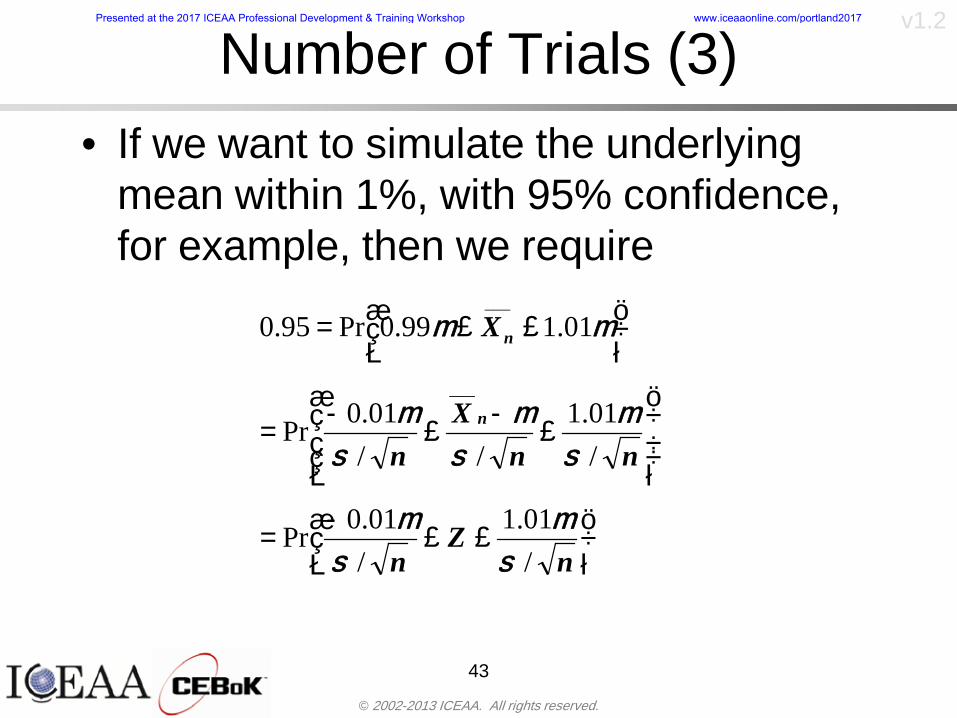

Number of Trials (3)bull If we want to simulate the underlying

mean within 1 with 95 confidence for example then we require

43

divideoslash

oumlccedilegrave

aelig poundpound-

=

dividedividedivide

oslash

ouml

ccedilccedilccedil

egrave

aeligpound

-pound

-=

divideoslashouml

ccedilegraveaelig poundpound=

nZ

n

nnX

n

X

n

n

011

010Pr

011

010Pr

011990Pr950

___

___

sm

sm

sm

sm

sm

mm

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

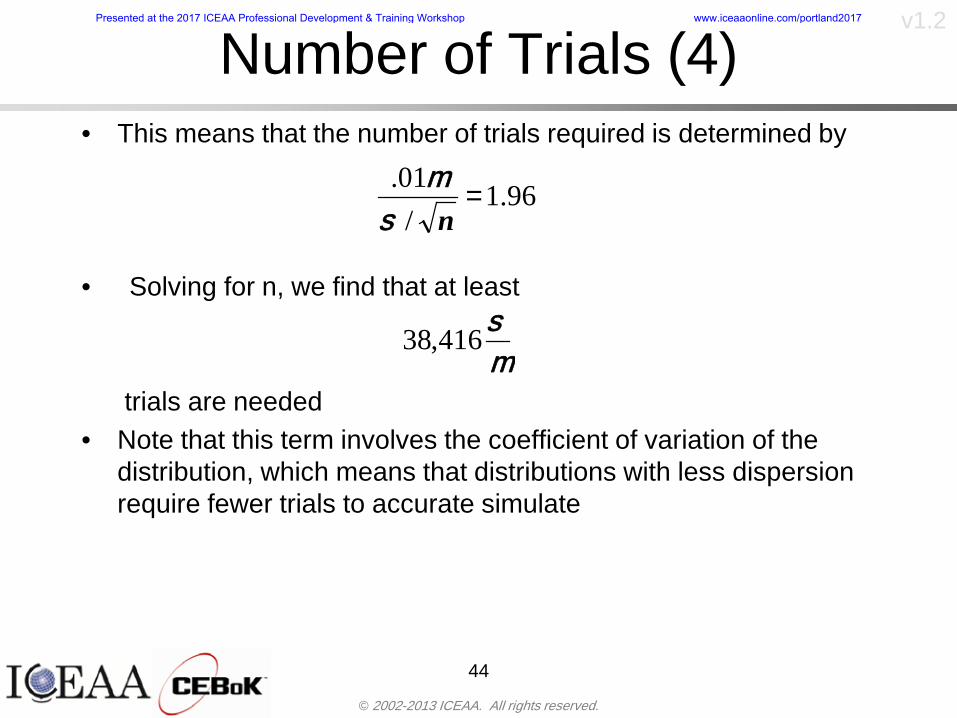

Number of Trials (4)bull This means that the number of trials required is determined by

bull Solving for n we find that at least

trials are neededbull Note that this term involves the coefficient of variation of the

distribution which means that distributions with less dispersion require fewer trials to accurate simulate

44

96101

=ns

m

ms41638

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

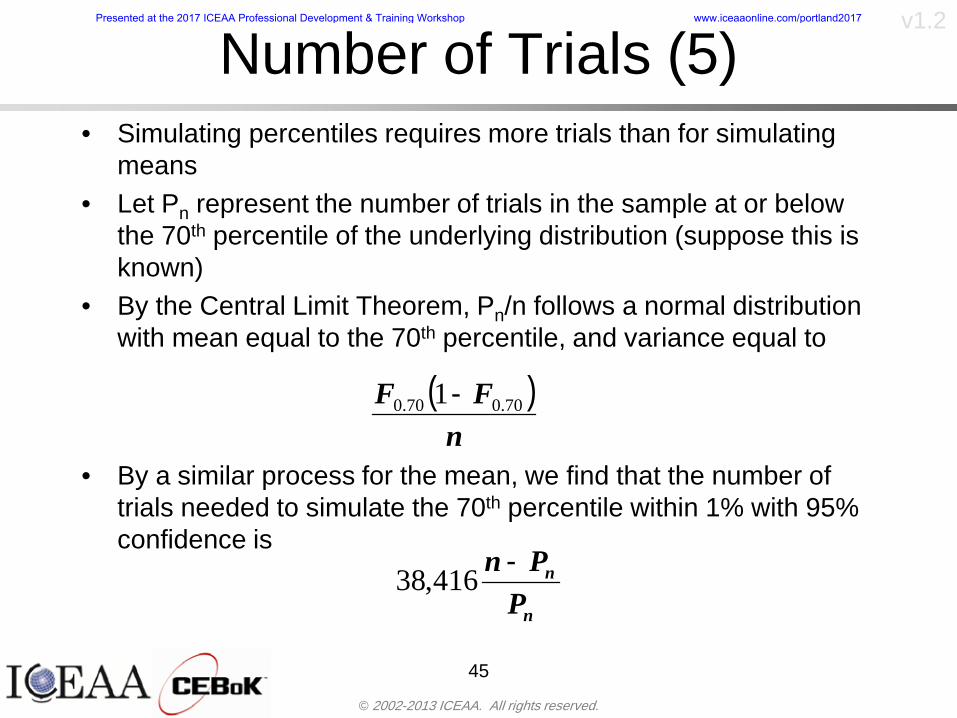

Number of Trials (5)bull Simulating percentiles requires more trials than for simulating

meansbull Let Pn represent the number of trials in the sample at or below

the 70th percentile of the underlying distribution (suppose this is known)

bull By the Central Limit Theorem Pnn follows a normal distribution with mean equal to the 70th percentile and variance equal to

bull By a similar process for the mean we find that the number of trials needed to simulate the 70th percentile within 1 with 95 confidence is

45

( )n

FF 700700 1-

n

n

PPn -41638

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

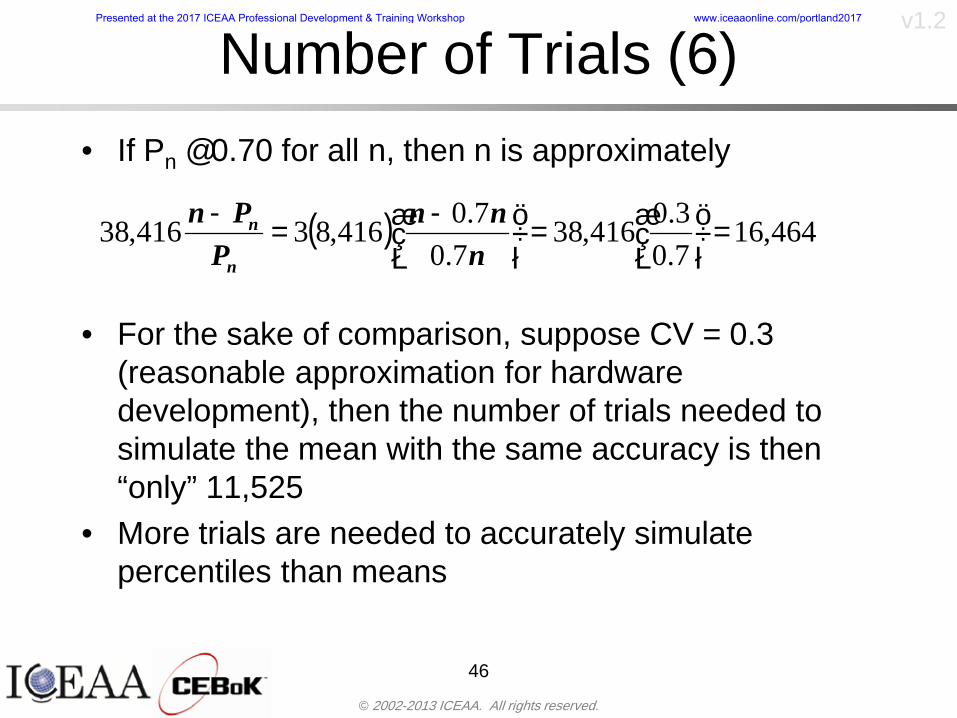

Number of Trials (6)bull If Pn 070 for all n then n is approximately

bull For the sake of comparison suppose CV = 03 (reasonable approximation for hardware development) then the number of trials needed to simulate the mean with the same accuracy is then ldquoonlyrdquo 11525

bull More trials are needed to accurately simulate percentiles than means

46

( ) 46416703041638

70704168341638 =divide

oslashouml

ccedilegraveaelig=divide

oslashouml

ccedilegraveaelig -

=-

nnn

PPn

n

n

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

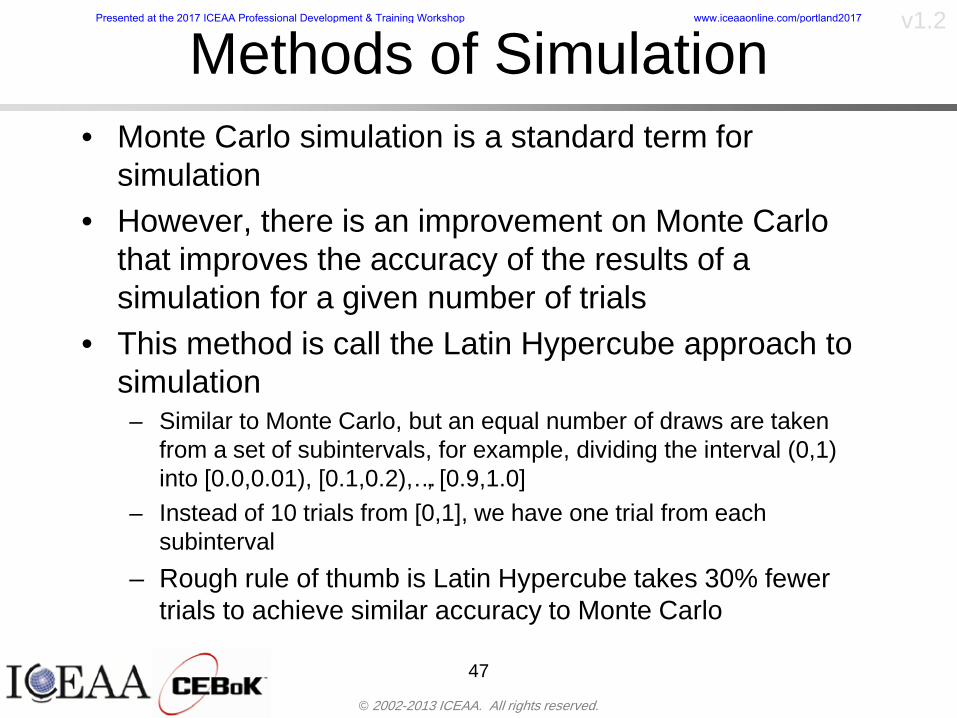

Methods of Simulationbull Monte Carlo simulation is a standard term for

simulationbull However there is an improvement on Monte Carlo

that improves the accuracy of the results of a simulation for a given number of trials

bull This method is call the Latin Hypercube approach to simulationndash Similar to Monte Carlo but an equal number of draws are taken

from a set of subintervals for example dividing the interval (01) into [00001) [0102)hellip [0910]

ndash Instead of 10 trials from [01] we have one trial from each subinterval

ndash Rough rule of thumb is Latin Hypercube takes 30 fewer trials to achieve similar accuracy to Monte Carlo

47

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

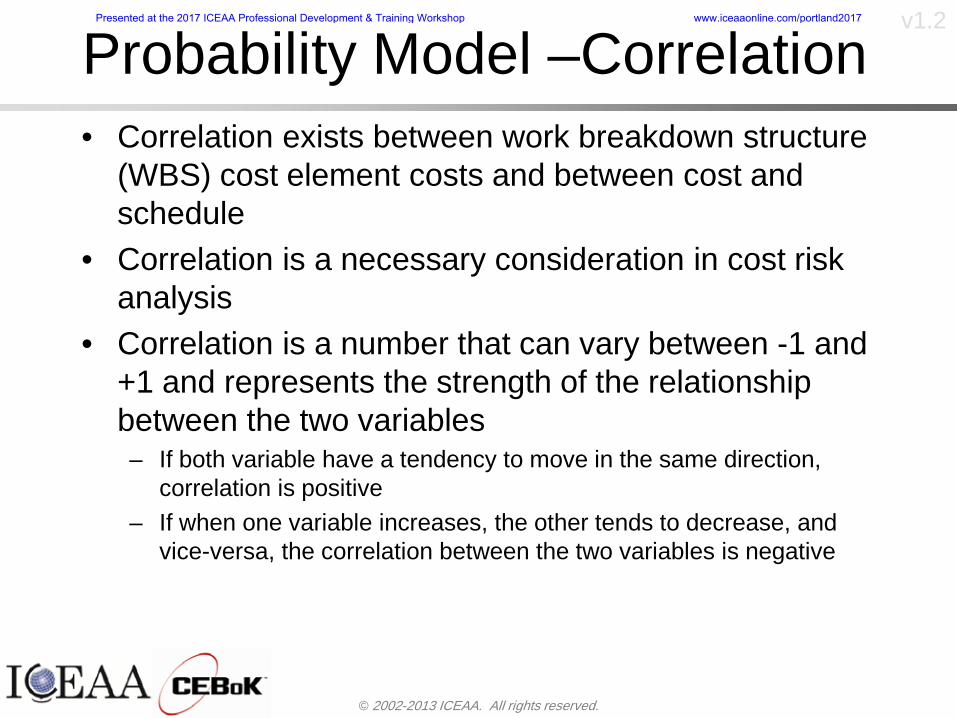

Probability Model ndash Correlationbull Correlation exists between work breakdown structure

(WBS) cost element costs and between cost and schedule

bull Correlation is a necessary consideration in cost risk analysis

bull Correlation is a number that can vary between -1 and +1 and represents the strength of the relationship between the two variablesndash If both variable have a tendency to move in the same direction

correlation is positivendash If when one variable increases the other tends to decrease and

vice-versa the correlation between the two variables is negative

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Correlation And Causationbull Note that correlation is not causation however

causation implies correlationndash For example shark attacks and ice cream sales at the beach

bull For example for a launch vehicle structure increasing the diameter will not only result in an increase in the structures cost but will also result in higher costs for thermal coating (paint etc)

bull Also simply because two subsystems do not appear to be related does not mean they are not correlatedndash For example structures and computer equipment seemingly

have little relation to one another however an external factor such as a funding cut or a strike will impact all subsystems leading to delays and increasing cost across the board

ndash Thus everything in a WBS has some correlationUnit III - Module 9 49

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

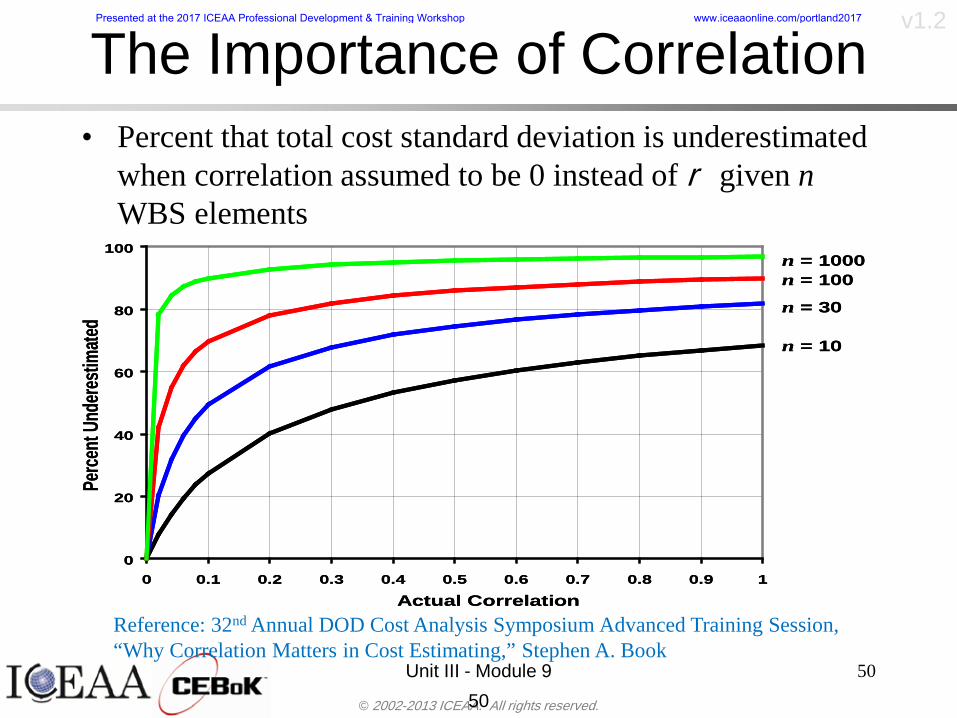

The Importance of Correlationbull Percent that total cost standard deviation is underestimated

when correlation assumed to be 0 instead of r given nWBS elements

Unit III - Module 9 5050

0

20

40

60

80

100

0 01 02 03 04 05 06 07 08 09 1Actual Correlation

Perce

nt Un

deres

timate

d

n = 10

n = 30

n = 100n = 1000

0

20

40

60

80

100

0 01 02 03 04 05 06 07 08 09 1Actual Correlation

Perce

nt Un

deres

timate

d

n = 10

n = 30

n = 100n = 1000

Reference 32nd Annual DOD Cost Analysis Symposium Advanced Training Session ldquoWhy Correlation Matters in Cost Estimatingrdquo Stephen A Book

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

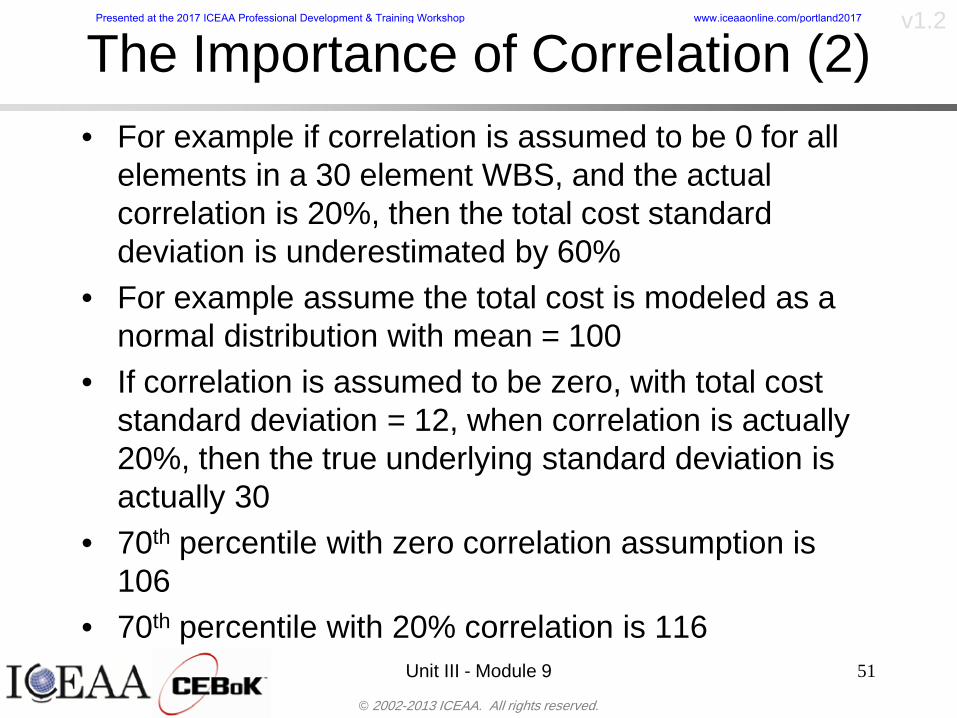

The Importance of Correlation (2)bull For example if correlation is assumed to be 0 for all

elements in a 30 element WBS and the actual correlation is 20 then the total cost standard deviation is underestimated by 60

bull For example assume the total cost is modeled as a normal distribution with mean = 100

bull If correlation is assumed to be zero with total cost standard deviation = 12 when correlation is actually 20 then the true underlying standard deviation is actually 30

bull 70th percentile with zero correlation assumption is 106

bull 70th percentile with 20 correlation is 116 Unit III - Module 9 51

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Measures of Correlationbull Two measures of correlation are commonly used in

cost risk analysesndash Pearsonrsquos product-moment correlation coefficient ndash Spearmanrsquos rank correlation coefficient

bull Garvey and others recommend using Pearsonrsquos product-moment correlation coefficient correlation for cost risk analysesndash Method of moments uses this but there are two options in

simulationndash Popular simulation packages like Risk and Crystal Ball use

rank correlation but in practice this has been found to make little difference

ndash Pearson product-moment correlation has been incorporated into Risk+

52

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

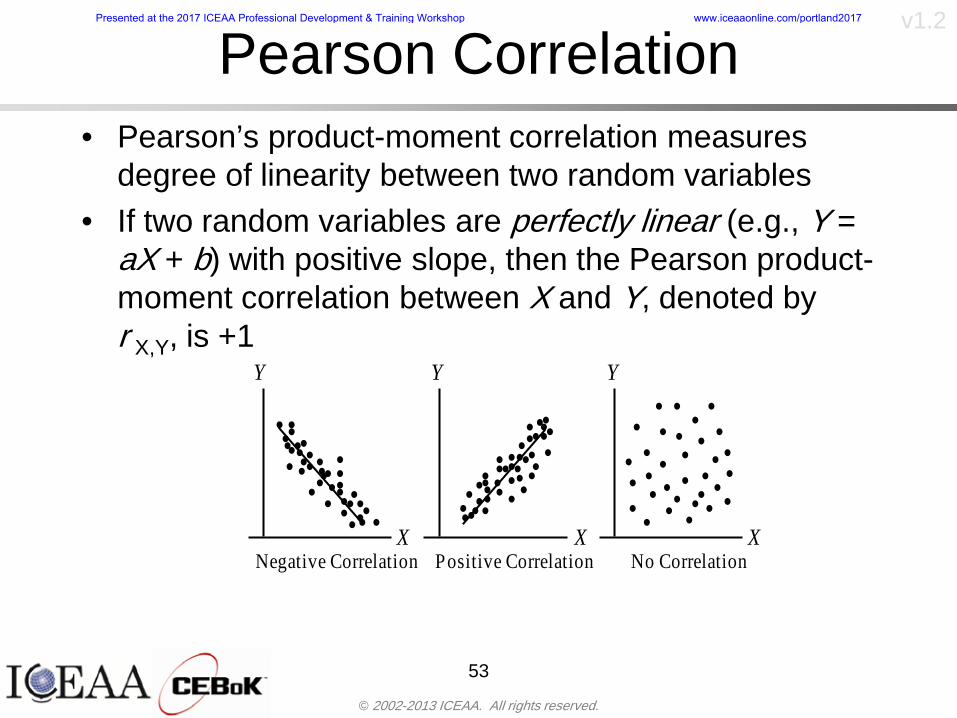

Pearson Correlationbull Pearsonrsquos product-moment correlation measures

degree of linearity between two random variables bull If two random variables are perfectly linear (eg Y =

aX + b) with positive slope then the Pearson product-moment correlation between X and Y denoted by rXY is +1

53

X X

Y Y Y

XNegative Correlation Positive Correlation No Correlation

middotmiddot

middotmiddot

middotmiddot middotmiddot

middotmiddot

middot

middot

middotmiddotmiddot

middotmiddot

middotmiddot

middotmiddot middot

middot

middot

middotmiddotmiddotmiddotmiddotmiddotmiddotmiddot

middotmiddotmiddotmiddot

middotmiddot

middotmiddot middotmiddotmiddotmiddot

middotmiddotmiddot

middotmiddotmiddotmiddot

middotmiddotmiddot

middotmiddotmiddot

middotmiddot

middot

middot middotmiddot

middot middotmiddotmiddotmiddot middotmiddot middot middotmiddot middot middot

middotmiddot middot

middotmiddotmiddotmiddotmiddot middot middotmiddot

middotmiddot

middot

middotmiddot

middotmiddot middot

middot middot middot

middotmiddot middot

middotmiddotmiddot

middotmiddot

middot middot

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

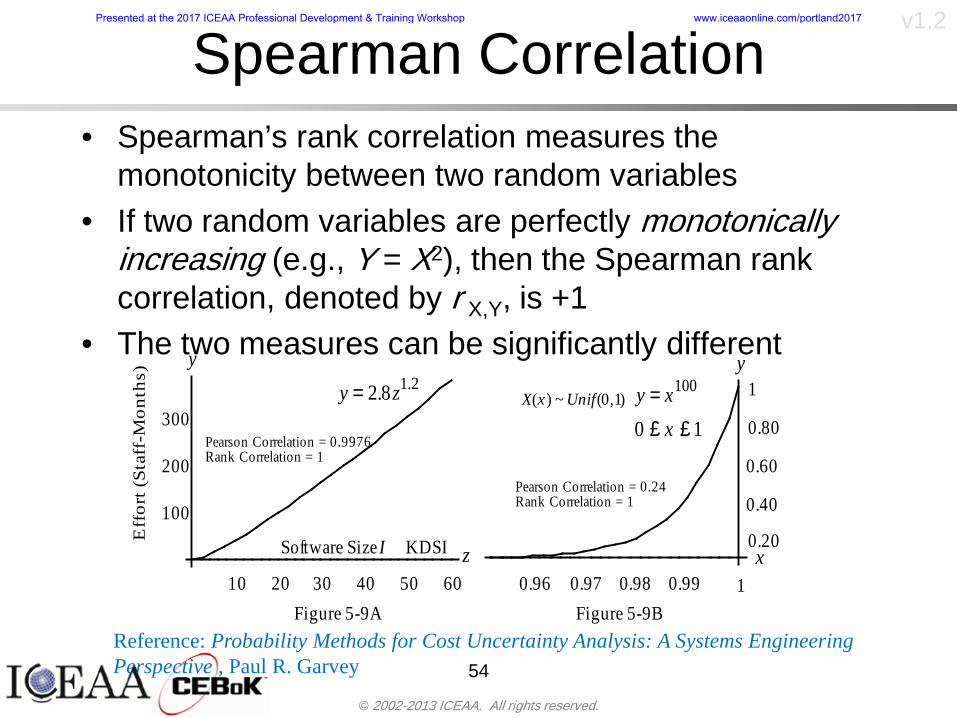

Spearman Correlationbull Spearmanrsquos rank correlation measures the

monotonicity between two random variablesbull If two random variables are perfectly monotonically

increasing (eg Y = X2) then the Spearman rank correlation denoted by rXY is +1

bull The two measures can be significantly different

54

10 20 30 40 50 60

100

200

300

096 097 098 099 1

1

060

020

040

080

Eff

ort (

Staf

f-M

onth

s)

Software Size I KDSI

y = 28z12y

z x

yy = x100

0 pound x pound 1

Figure 5-9A Figure 5-9B

Pearson Correlation = 09976 Rank Correlation = 1

Pearson Correlation = 024 Rank Correlation = 1

X(x ) ~ Unif(01)

Reference Probability Methods for Cost Uncertainty Analysis A Systems Engineering Perspective Paul R Garvey

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 55

200

250

300

350

400

1000 1200 1400 1600 1800 2000

Recurring Production

SEPM

200

250

300

350

400

1000 1200 1400 1600 1800 2000

Recurring Production

SEPM

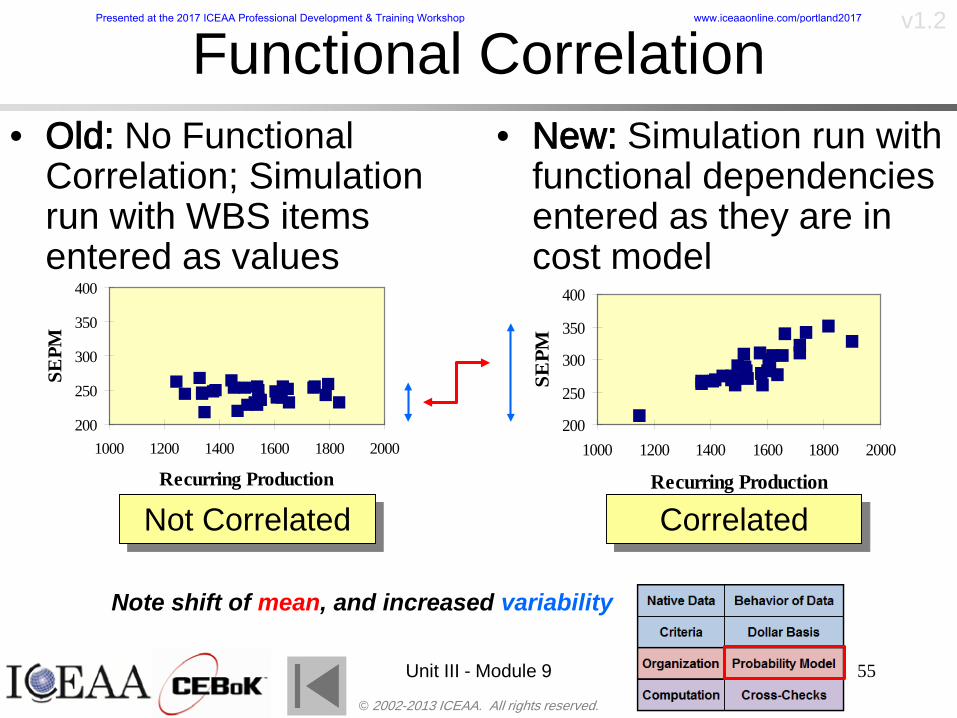

Functional Correlationbull Old No Functional

Correlation Simulation run with WBS items entered as values

bull New Simulation run with functional dependencies entered as they are in cost model

CorrelatedNot Correlated

Note shift of mean and increased variability

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Risk Measuresbull ldquoWestern Europe conquered the word because of a

technological revolution that started because of attempts to measure the worldrdquo ndash Phillipe Jorion ndash In the same way attempts to measure risk will lead to better project

managementbull Risk management for DoD and NASA agencies focuses

primarily on funding projects to a single percentile ndash NASA policy explicitly mentions 70 and 50ndash This is known as ldquoValue at Riskrdquo and is prevalent in the banking and

financial industry

56

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Value at Risk (VaR)bull VaR is a percentile of the cost risk

distributionndash VaR funding at the 70th percentile means that

there is a 30 chance of final project cost exceeding the funded amount (budget)

bull VaR has some meritsndash Common measure can be used to compare

different projects and programsndash Easily understood by senior managers and

decision makers

57

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

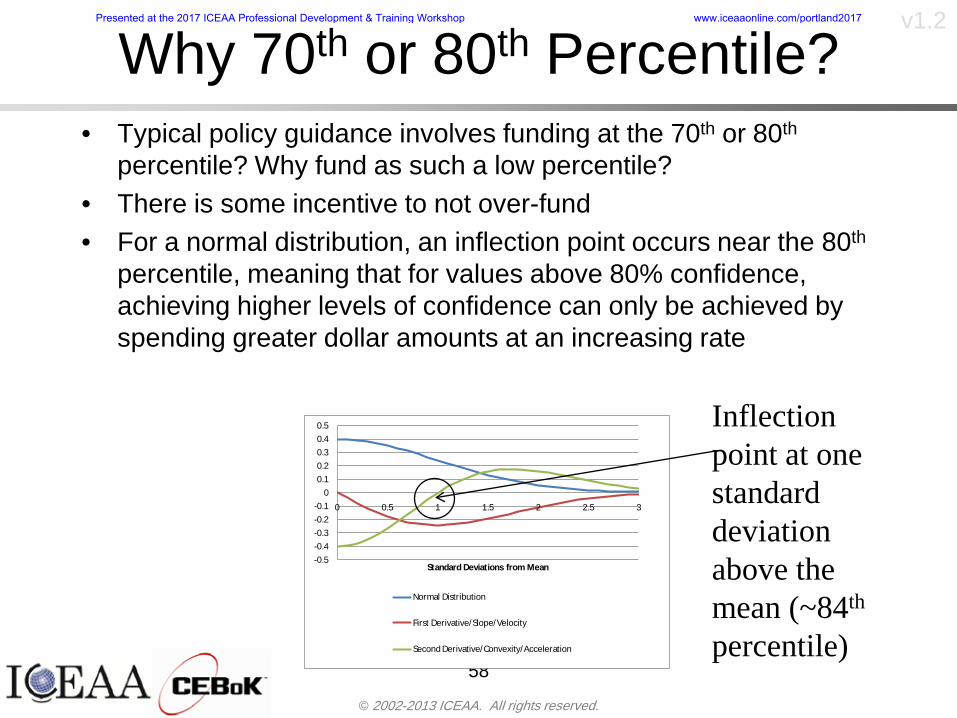

Why 70th or 80th Percentilebull Typical policy guidance involves funding at the 70th or 80th

percentile Why fund as such a low percentilebull There is some incentive to not over-fundbull For a normal distribution an inflection point occurs near the 80th

percentile meaning that for values above 80 confidence achieving higher levels of confidence can only be achieved by spending greater dollar amounts at an increasing rate

58

-05-04-03-02-01

00102030405

0 05 1 15 2 25 3

Standard Deviations from Mean

Normal Distribution

First DerivativeSlopeVelocity

Second DerivativeConvexityAcceleration

Inflection point at one standard deviation above the mean (~84th

percentile)

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

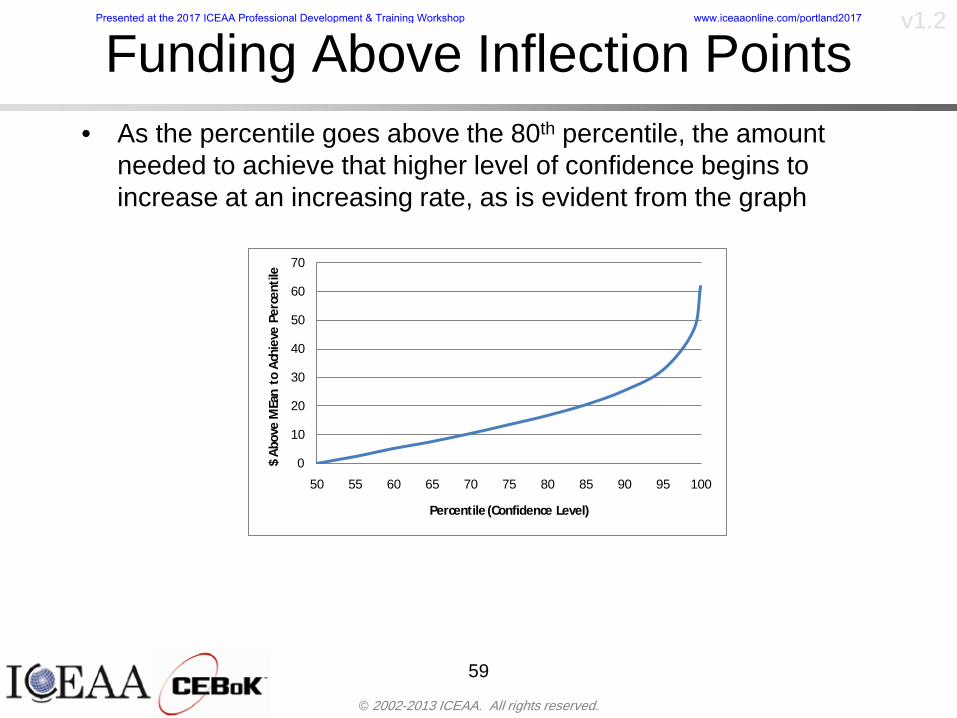

Funding Above Inflection Pointsbull As the percentile goes above the 80th percentile the amount

needed to achieve that higher level of confidence begins to increase at an increasing rate as is evident from the graph

59

0

10

20

30

40

50

60

70

50 55 60 65 70 75 80 85 90 95 100

$ Ab

ove

MEa

n to

Ach

ieve

Per

cent

ile

Percentile (Confidence Level)

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Why Budget to the 70th or 80thbull Government projects are funded at the 70th or 80th percentilesbull Why not the 90th or 99th percentile Wonrsquot that help prevent

overrunsndash As we have seen percentiles do not add across programs

bull The sum of the 80th percentiles does NOT equal the total 80th percentile

ndash This is because the individual programs are riskier than the entire suite of missions

bull Known as the ldquoPortfolio effectrdquo (more or this later)

ndash Funding at the 80th gives confidence that the entire portfolio will be adequately funded

bull And since there is an inflection point near the 80th percentile funding above that level quickly becomes cost prohibitive

60

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

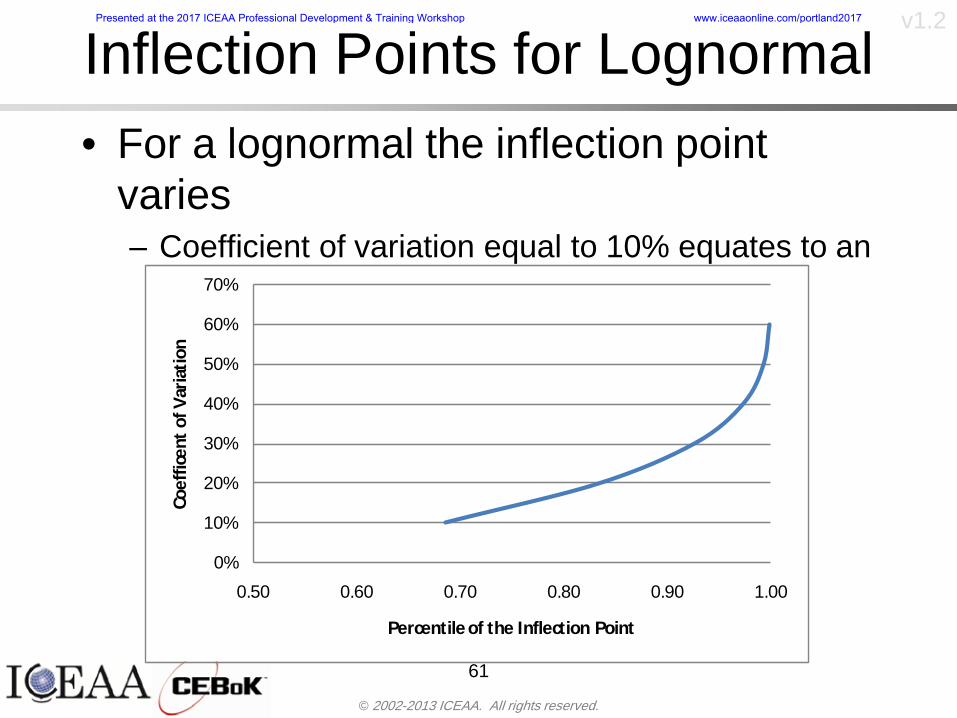

Inflection Points for Lognormalbull For a lognormal the inflection point

variesndash Coefficient of variation equal to 10 equates to an

inflection point at the 70th percentile

61

0

10

20

30

40

50

60

70

050 060 070 080 090 100

Coef

ficen

t of V

aria

tion

Percentile of the Inflection Point

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

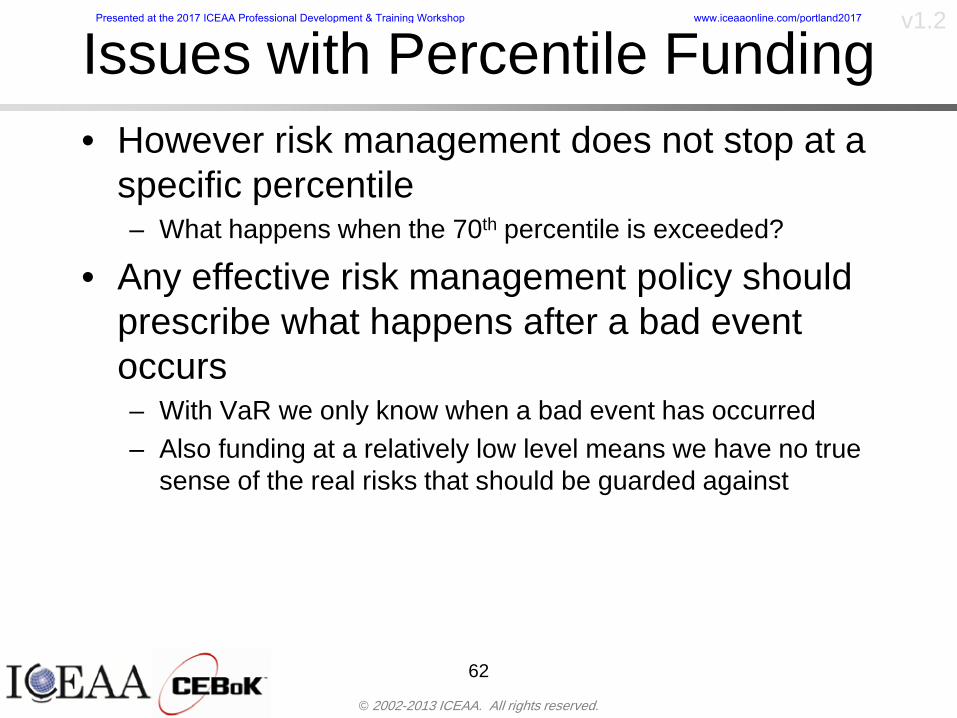

Issues with Percentile Fundingbull However risk management does not stop at a

specific percentilendash What happens when the 70th percentile is exceeded

bull Any effective risk management policy should prescribe what happens after a bad event occursndash With VaR we only know when a bad event has occurred ndash Also funding at a relatively low level means we have no true

sense of the real risks that should be guarded against

62

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

ldquoHere There Be Dragonsrdquobull On old maps uncharted territory was often

marked with monsters or dragons

63

A section of the Carta Marina by Olaus Magnus 16th Century

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

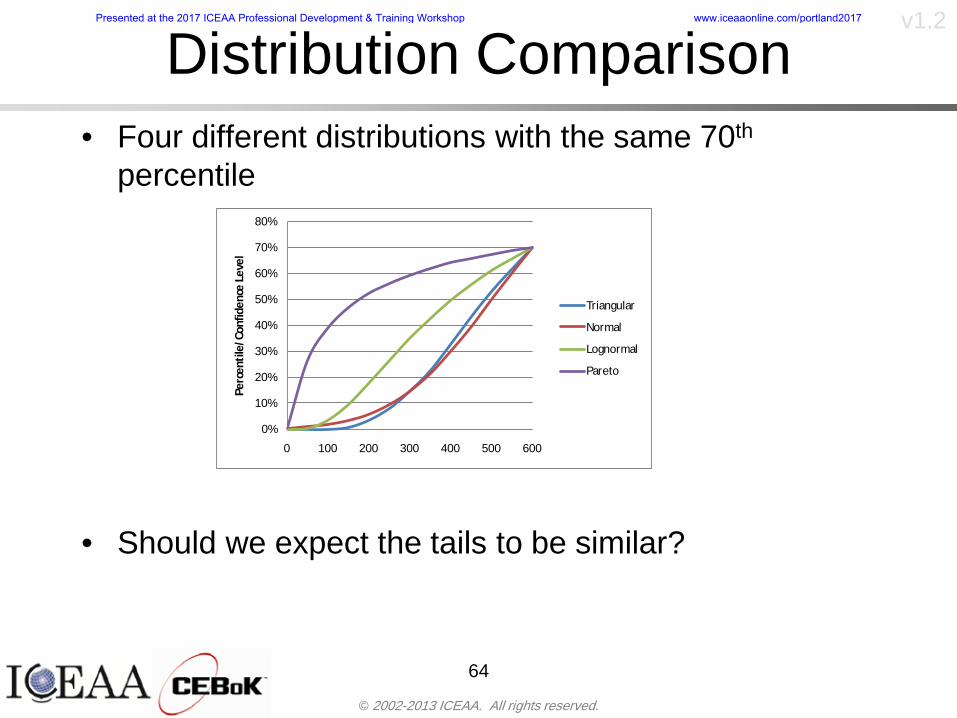

Distribution Comparisonbull Four different distributions with the same 70th

percentile

bull Should we expect the tails to be similar

64

0

10

20

30

40

50

60

70

80

0 100 200 300 400 500 600

Perc

entil

eCo

nfid

ence

Lev

el

Triangular

Normal

Lognormal

Pareto

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

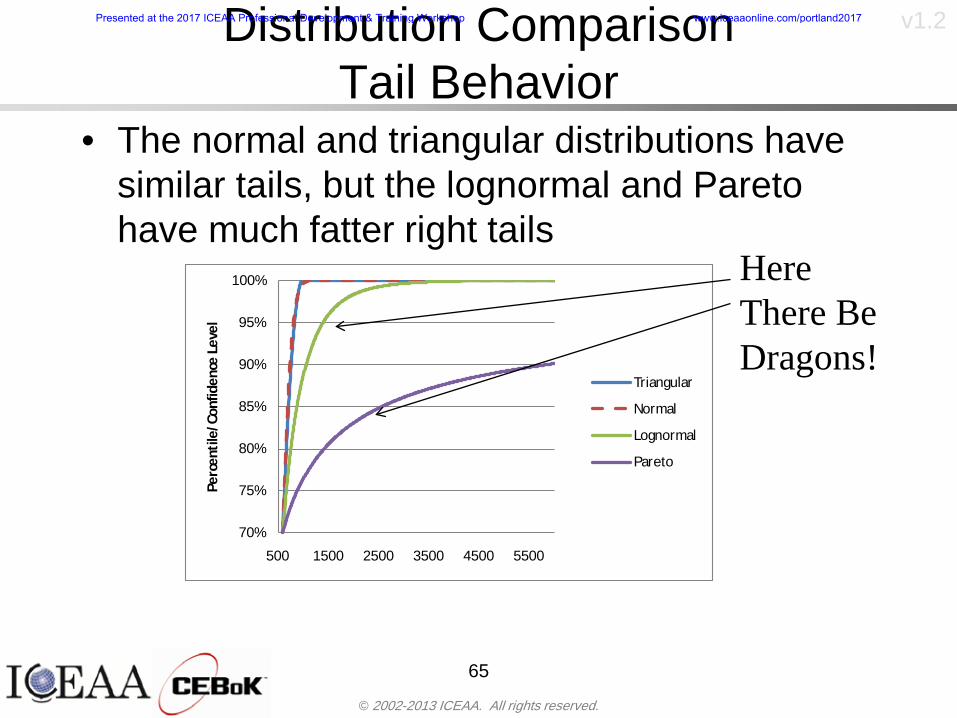

v12Distribution Comparison Tail Behavior

bull The normal and triangular distributions have similar tails but the lognormal and Pareto have much fatter right tails

65

70

75

80

85

90

95

100

500 1500 2500 3500 4500 5500

Perc

entil

eCo

nfid

ence

Lev

el

Triangular

Normal

Lognormal

Pareto

Here There Be Dragons

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

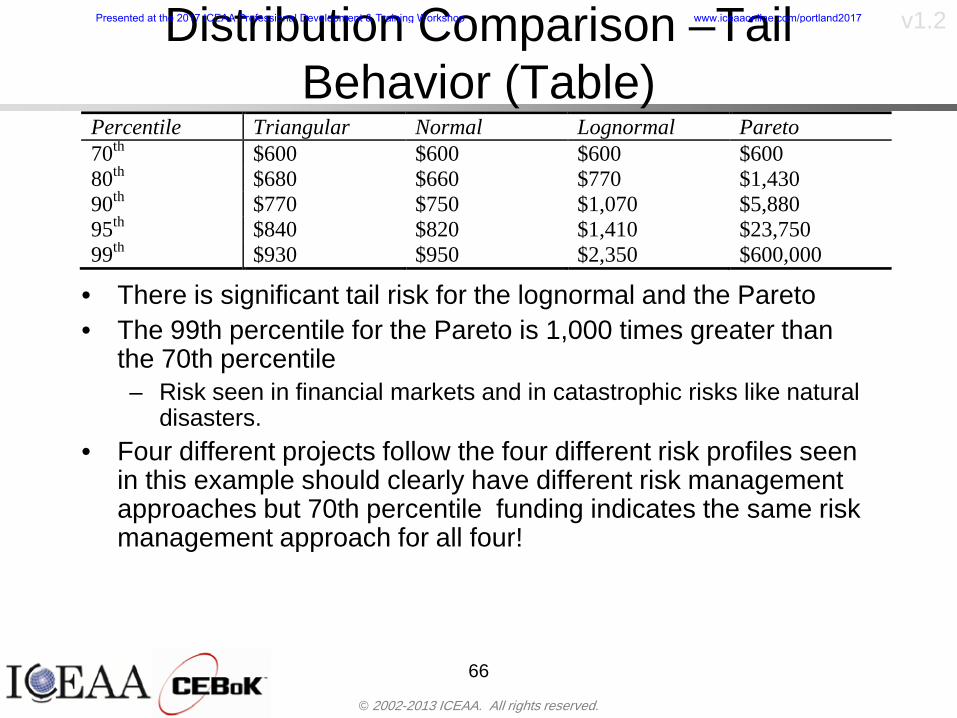

v12Distribution Comparison ndash Tail Behavior (Table)

bull There is significant tail risk for the lognormal and the Paretobull The 99th percentile for the Pareto is 1000 times greater than

the 70th percentilendash Risk seen in financial markets and in catastrophic risks like natural

disasters bull Four different projects follow the four different risk profiles seen

in this example should clearly have different risk management approaches but 70th percentile funding indicates the same risk management approach for all four

66

Percentile Triangular Normal Lognormal Pareto 70th $600 $600 $600 $600 80th $680 $660 $770 $1430 90th $770 $750 $1070 $5880 95th $840 $820 $1410 $23750 99th $930 $950 $2350 $600000

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Percentile Budgeting is Not Risk Management

bull Percentile budgeting ne effective risk management policybull Suppose that you are shopping for a new car You

mention that safety is your top concern The salesman says he has a great safe car available You ask about the air bags Do they work The salesman answers ldquoOf course Seventy percent of the time they work fine Only 30 of the time the air bags will fail to deployrdquo Would you buy such a car Hedge fund manager David Einhorn has stated ldquoRisk management is the air bag that must always work but only in the multi-sigma event where you have an accidentrdquo

67

Risk management is the air bag that must always work but only in the multi-sigma event where you

have an accident

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

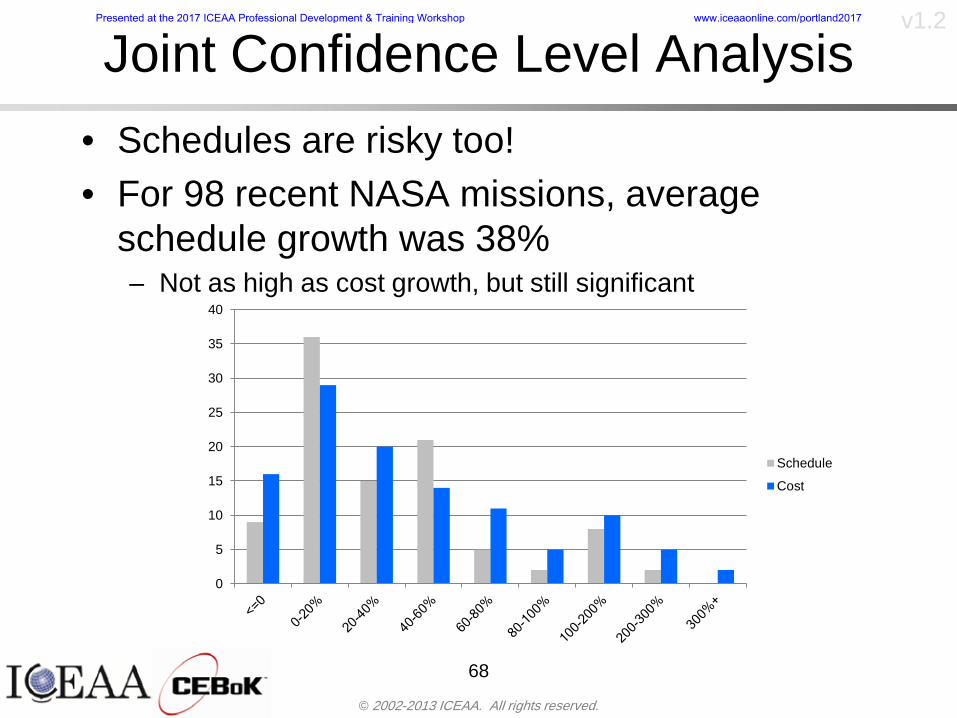

Joint Confidence Level Analysisbull Schedules are risky toobull For 98 recent NASA missions average

schedule growth was 38ndash Not as high as cost growth but still significant

68

0

5

10

15

20

25

30

35

40

Schedule

Cost

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Schedules Impact Costbull Changes in schedule can have enormous

impacts on cost ndash Schedule slips can lead to cost increases

bull Fixed programmatic costs must be paid on a regular basisndash Achieving schedule milestones early can result in cost

savings

bull Schedule is an important consideration in cost analysis including cost risk analysis

bull However we must be careful in correctly integrating cost and schedule riskndash Schedule is not simply an input but is dependent on many of

the same factors that drive cost

69

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

The Relationship of Cost to Schedulebull Cost and schedule are positively correlated

ndash A larger program with bigger scope with take longer to complete than a smaller simpler program

bull However longer schedules do not always equate to higher cost nor shorter schedules with lower costndash Highly compressed schedules relative to the

optimal schedule can lead to large overrunsbull Compressed schedules are commonplace for

many planetary missions

70

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

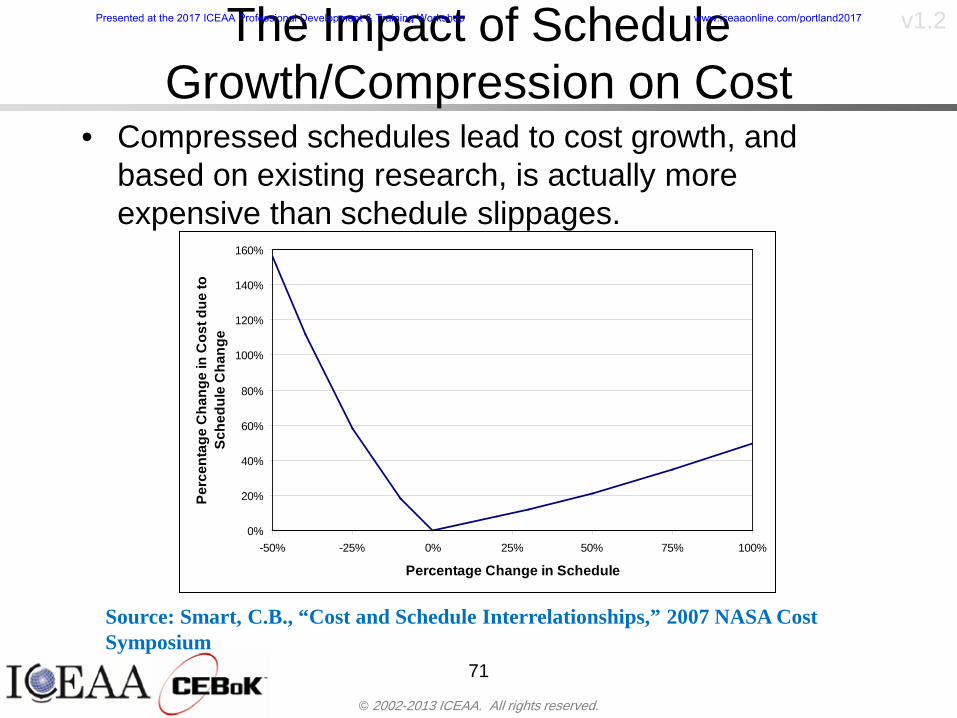

v12The Impact of Schedule GrowthCompression on Cost

bull Compressed schedules lead to cost growth and based on existing research is actually more expensive than schedule slippages

71

0

20

40

60

80

100

120

140

160

-50 -25 0 25 50 75 100

Percentage Change in Schedule

Perc

enta

ge C

hang

e in

Cos

t due

to

Sche

dule

Cha

nge

Source Smart CB ldquoCost and Schedule Interrelationshipsrdquo 2007 NASA Cost Symposium

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Schedule as an Independent Variable

bull Why not simply add schedule as an input to cost-estimating relationships (CERs)

bull Schedule is often treated as an independent variable ndash schedules are often determined independently of cost considerationsndash Cost may not be considered explicitly although budgets and

schedules are determined based on scope and other common factors

bull In 2006 SAIC undertook a research task to determine the impact of schedule on cost and added schedule as an independent variable to the CERs in the NASAAir Force Cost Model (NAFCOM) to see if schedule provided any improvement in goodness of fit

72

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Schedule is a Dependent Variablebull Since NAFCOM includes an exhaustive list of cost drivers the inclusion

of schedule should give an indication of whether there is any additional independent value added from schedule independent of the cost drivers

bull In the study schedule was added to 10 subsystem-level CERs

ndash In each case the addition of schedule did NOTimprove the goodness of fit and schedule was NOT found to be a statistically significant cost driver (given the presence of the other variables) for any of the 10 CERs

bull Standard errors for the CERs increased due to decrease in degrees of freedom

bull Thus schedule as an independent variable did not provide any additional explanation of variation in historical cost

bull This is because schedule is truly NOT an independent variable but a dependent variable and is a function of the same factors that drive cost

73

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

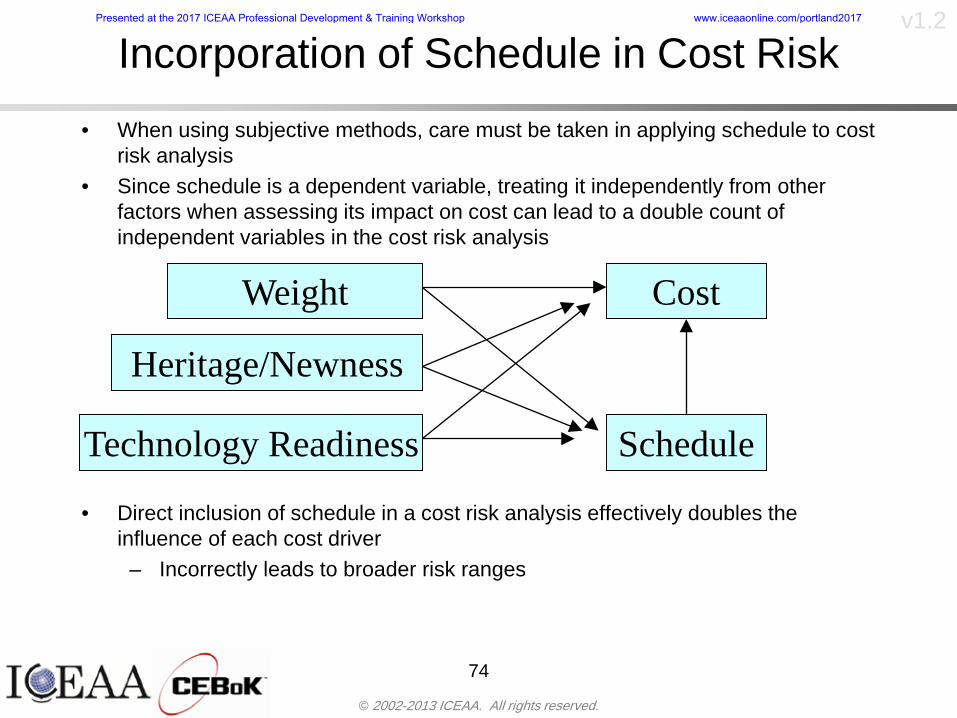

Incorporation of Schedule in Cost Risk

bull When using subjective methods care must be taken in applying schedule to cost risk analysis

bull Since schedule is a dependent variable treating it independently from other factors when assessing its impact on cost can lead to a double count of independent variables in the cost risk analysis

bull Direct inclusion of schedule in a cost risk analysis effectively doubles the influence of each cost driver

ndash Incorrectly leads to broader risk ranges

74

CostWeight

HeritageNewness

Technology Readiness Schedule

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

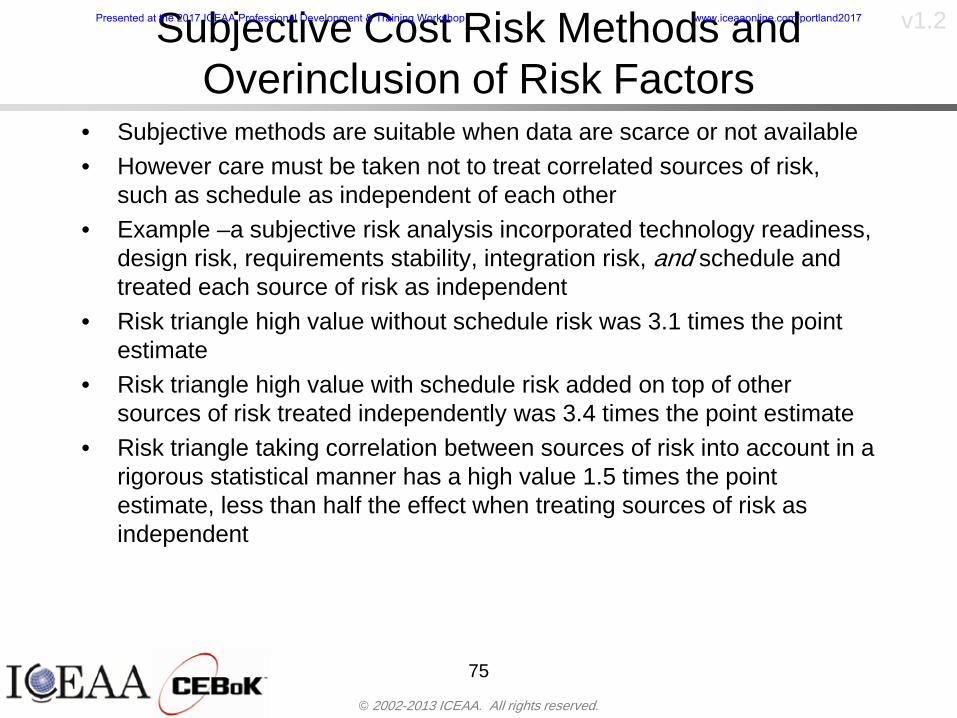

v12Subjective Cost Risk Methods and Overinclusion of Risk Factors

bull Subjective methods are suitable when data are scarce or not availablebull However care must be taken not to treat correlated sources of risk

such as schedule as independent of each otherbull Example ndash a subjective risk analysis incorporated technology readiness

design risk requirements stability integration risk and schedule and treated each source of risk as independent

bull Risk triangle high value without schedule risk was 31 times the point estimate

bull Risk triangle high value with schedule risk added on top of other sources of risk treated independently was 34 times the point estimate

bull Risk triangle taking correlation between sources of risk into account in a rigorous statistical manner has a high value 15 times the point estimate less than half the effect when treating sources of risk as independent

75

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Fundamental Equation of Cost and Schedule Interrelationships

bull The Fundamental Equation of the Relationship Between Cost and Schedule is

Time = Moneybull This is a well known adage that time is money Your boss at

work may even mention this to you from time to time or if you are the boss you are all too aware of this iron law

bull Because time is money cost and schedule risk should be modeled jointly not with schedule as an independent cost driver

bull Note that cost and schedule are not perfectly correlatedndash Cost can sometimes ldquobuy downrdquo schedule extra money can be

spent to meet a deadline since in some cases additional effort to hasten the completion of a task

76

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12How to (Correctly) Incorporate Schedule into Cost Risk Analysis

bull The best way to model cost and schedule risk is to develop a joint cost and schedule model based on the same data

bull Since such models are not currently available the next best approach is to model cost and schedule independently and then integrate cost and schedule risk analyses using joint probability distributions taking into account correlation between cost and schedulendash This approach pioneered by Paul Garvey and Steve Book is

considered industry best practicendash This is a practical method mathematically tractable and follows

naturally from the Fundamental Equation of Cost and Schedule Interrelationships

77

Book S A ldquoQuantifying the Relationship Between Cost and Schedulerdquo The Measurable News Winter 2007-2008 pp 11-15Garvey PR Probability Methods for Cost Uncertainty Analysis A Systems Engineering Perspective New York Marcel Dekker 2000 pp 308-335

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Joint Lognormal and Normal Distributions

bull Cost and schedule are typically modeled as some combination of Normal and Lognormal probability distributionsndash Studies by The Aerospace Corporation the MITRE

Corporation Wyle Labs and SAIC have found that the Lognormal probability distribution almost always serves as a good model for both the schedule distribution and the cost distribution

ndash The Normal distribution may also be appropriate in some instances and depending upon the level of confidence at which budgets are set may even be more conservative and logically consistent than the Normal distribution

ndash Joint Lognormal and Normal distributions are defined by a pair of mean and standard deviations and a level of correlation between the two

78

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Modeling Cost and Schedule as a Bivariate Distribution

bull In the approach set forth by Book and Garvey cost risk is assessed and the top-level distribution is modeled as a Lognormal (or Normal) distribution schedule risk is assessed and the overall schedule risk is modeled as a Lognormal (or Normal) distribution

bull The two distributions are combined into a Bivariate distribution by assigning a correlation between the two and by treating the two distributions as the marginal distributions of a Bivariate Lognormal distributionndash Other combinations include a Bivariate Normal or a Bivariate

Normal-Lognormal

79

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Bivariate Lognormal Distribution for Cost and Schedule

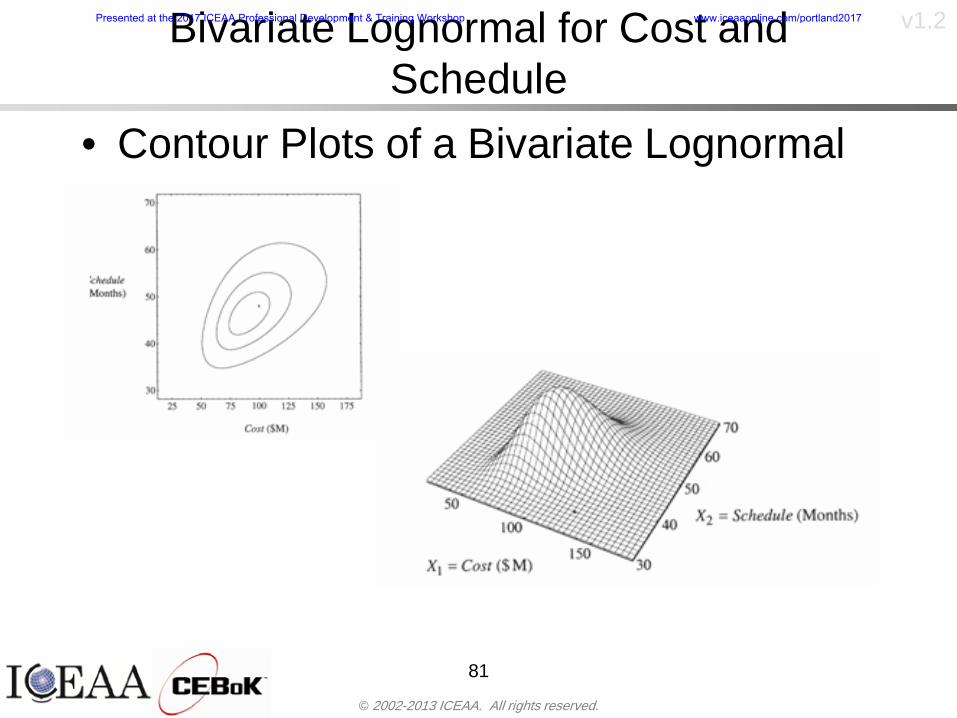

bull Cost is often observed to be Lognormal when strong positive correlations are present among the systemrsquos WBS cost element costs

bull A systemrsquos schedule is often observed (from Monte Carlo simulations) to be Lognormal if it is the sum of many positively correlated schedule activities in an overall schedule network

bull If Lognormal distributions characterize a systemrsquos cost and schedule then the Bivariate Lognormal could serve as an assumed model of their joint distributionndash In this case the marginal distribution of each of cost and schedule is

Lognormalbull Other possibilities for modeling cost and schedule as a Bivariate

distribution include a Bivariate Normal or a Bivariate Normal-Lognormal distributionndash All these combinations are analytically tractable

80

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Bivariate Lognormal for Cost and Schedule

bull Contour Plots of a Bivariate Lognormal

81

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

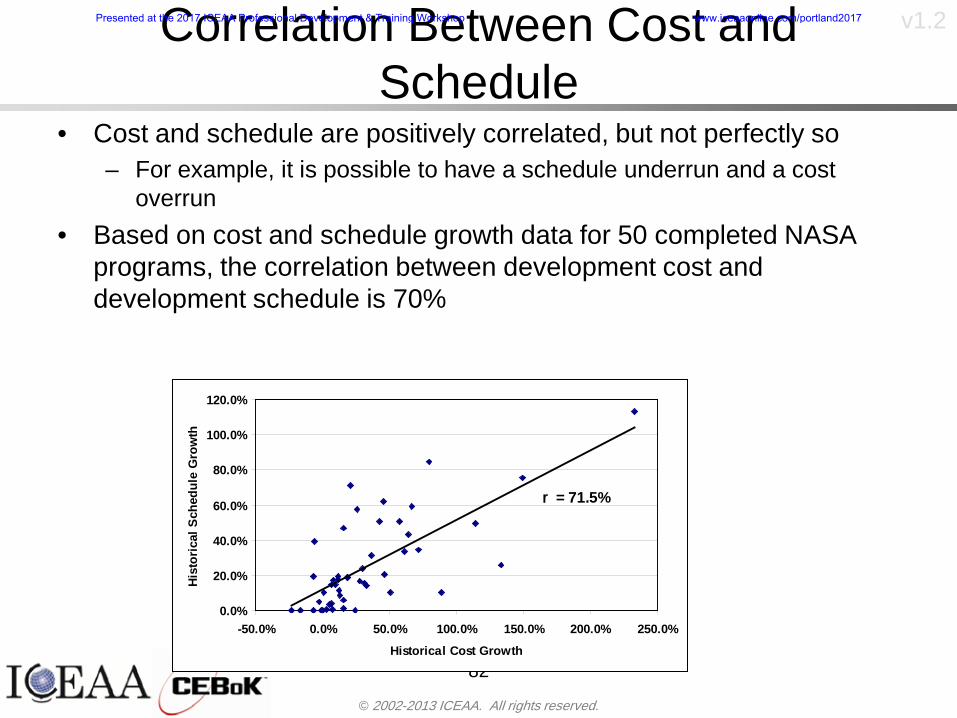

v12Correlation Between Cost and Schedule

bull Cost and schedule are positively correlated but not perfectly sondash For example it is possible to have a schedule underrun and a cost

overrunbull Based on cost and schedule growth data for 50 completed NASA

programs the correlation between development cost and development schedule is 70

82

00

200

400

600

800

1000

1200

-500 00 500 1000 1500 2000 2500Historical Cost Growth

Hist

oric

al S

ched

ule

Gro

wth

r = 715

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Correlation Between Cost and Schedule Caveats

bull Based on historical data recommended correlation between cost and schedule is 70 but this could be higher or lower depending upon program circumstancesndash If program is budget constrained cost and schedule will be

more highly correlated (go as you pay)ndash If program is schedule constrained cost and schedule will

have lower correlation perhaps even negative correlation ndash Smaller programs have smaller correlation between cost and

schedule riskbull Relatively easy to ldquohurry uprdquo and finish on time or even early if

needed

83

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

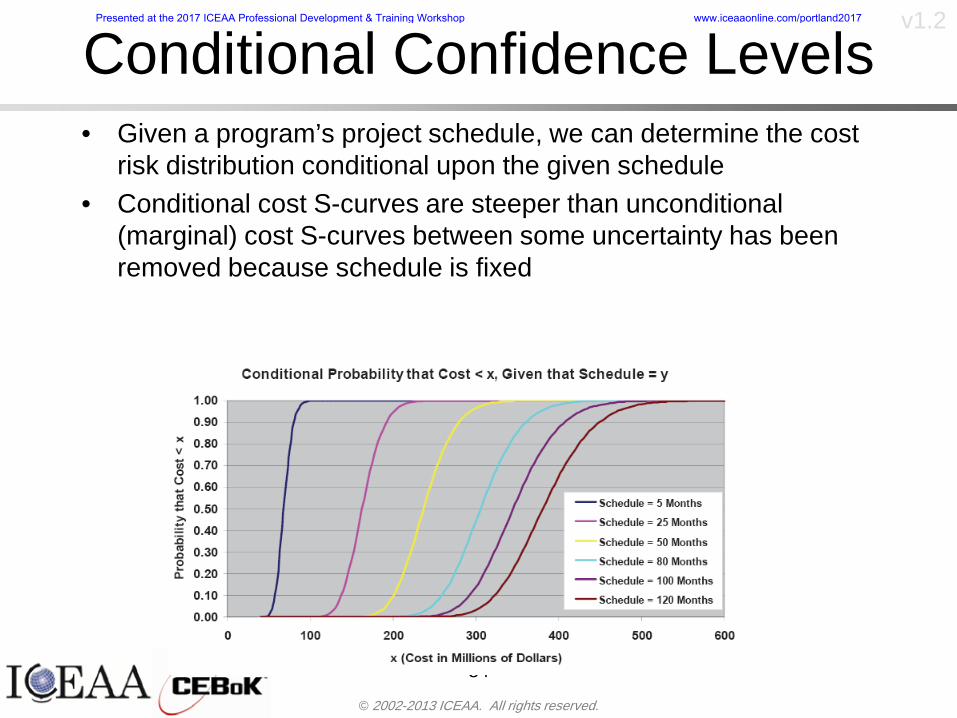

Conditional Confidence Levelsbull Given a programrsquos project schedule we can determine the cost

risk distribution conditional upon the given schedulebull Conditional cost S-curves are steeper than unconditional

(marginal) cost S-curves between some uncertainty has been removed because schedule is fixed

84

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

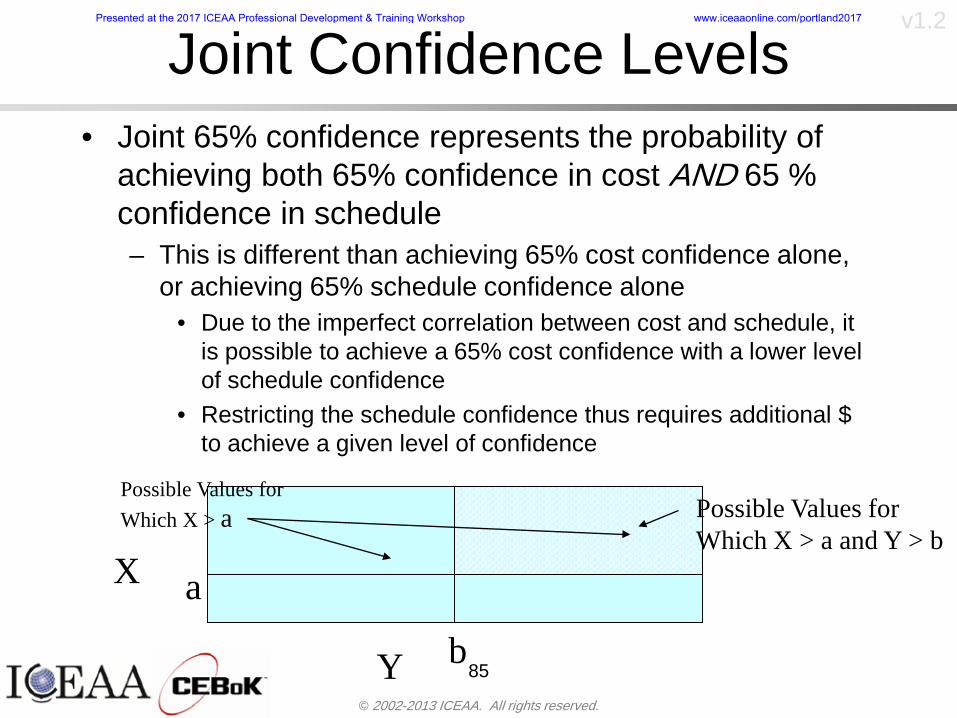

Joint Confidence Levelsbull Joint 65 confidence represents the probability of

achieving both 65 confidence in cost AND 65 confidence in schedulendash This is different than achieving 65 cost confidence alone

or achieving 65 schedule confidence alonebull Due to the imperfect correlation between cost and schedule it

is possible to achieve a 65 cost confidence with a lower level of schedule confidence

bull Restricting the schedule confidence thus requires additional $ to achieve a given level of confidence

85

X

Y

Possible Values for Which X gt a Possible Values for

Which X gt a and Y gt b

a

b

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

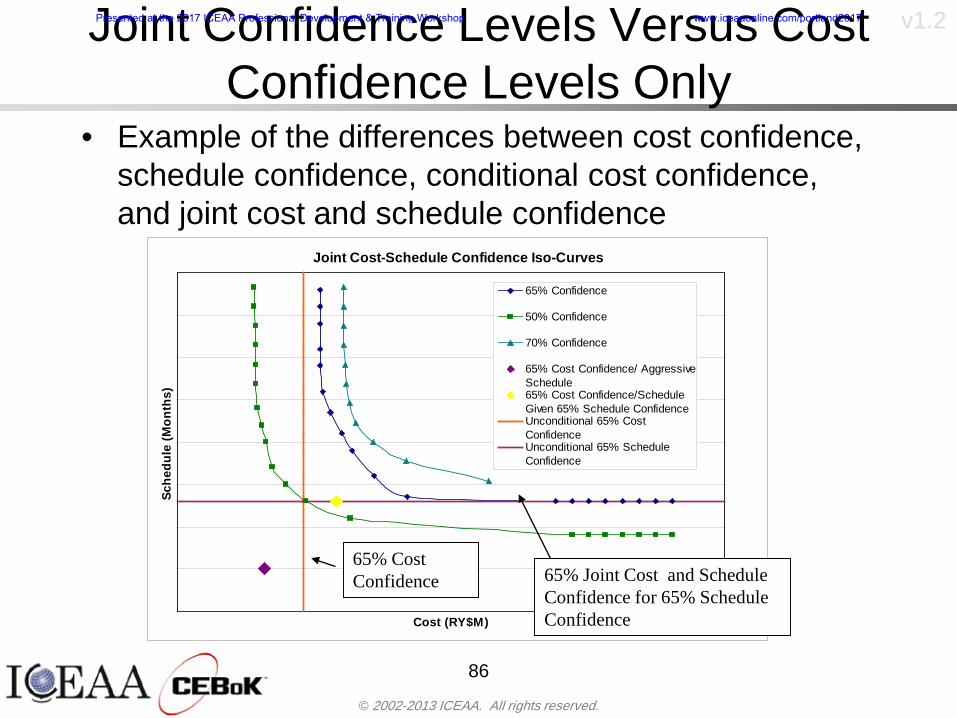

v12Joint Confidence Levels Versus Cost Confidence Levels Only

bull Example of the differences between cost confidence schedule confidence conditional cost confidence and joint cost and schedule confidence

86

Joint Cost-Schedule Confidence Iso-Curves

Cost (RY$M)

Sche

dule

(Mon

ths)

65 Confidence

50 Confidence

70 Confidence

65 Cost Confidence AggressiveSchedule65 Cost ConfidenceScheduleGiven 65 Schedule ConfidenceUnconditional 65 CostConfidenceUnconditional 65 ScheduleConfidence

65 Cost Confidence 65 Joint Cost and Schedule

Confidence for 65 Schedule Confidence

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Joint Cost and Schedule Confidence

bull Can examine pairs of cost and schedule that achieve a given level of confidence

bull Provides insights into the trade-offs between cost and schedule for a given level of confidencendash Possible to increase cost confidence by giving a

project more time in some instances or possible to ldquobuy downrdquo schedule

bull But these have limits and are shown in the iso-cost and schedule confidence curves

87

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Cost and Schedule Trade-offs for a Given Level of Joint Confidence

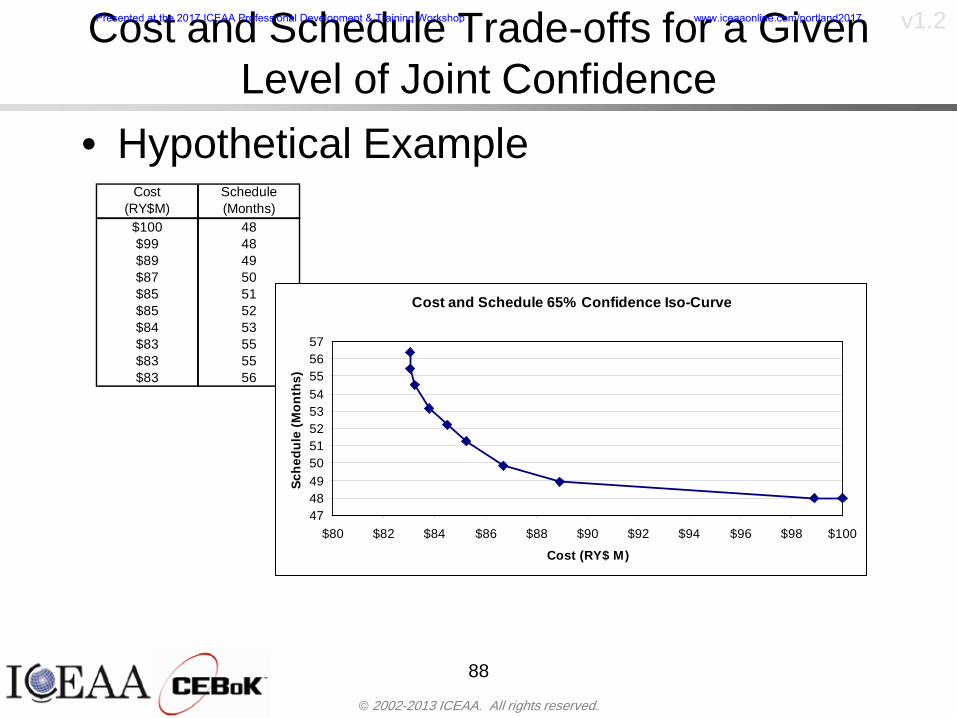

bull Hypothetical Example

88

Cost (RY$M)

Schedule (Months)

$100 48$99 48$89 49$87 50$85 51$85 52$84 53$83 55$83 55$83 56

Cost and Schedule 65 Confidence Iso-Curve

4748495051525354555657

$80 $82 $84 $86 $88 $90 $92 $94 $96 $98 $100

Cost (RY$ M)

Sche

dule

(Mon

ths)

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

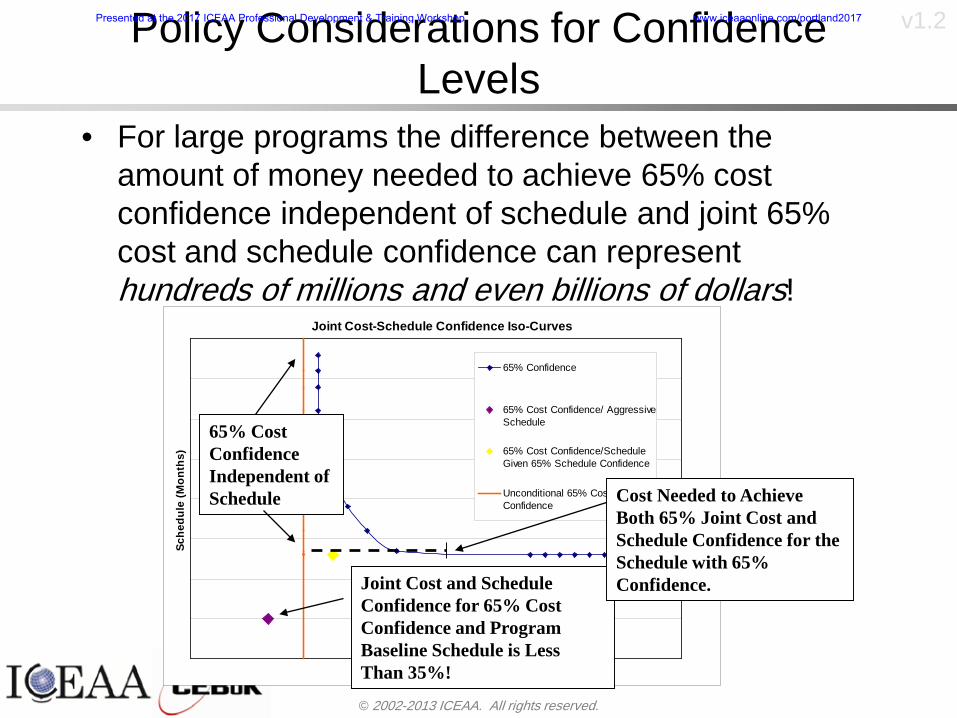

v12Policy Considerations for Confidence Levels

bull For large programs the difference between the amount of money needed to achieve 65 cost confidence independent of schedule and joint 65 cost and schedule confidence can represent hundreds of millions and even billions of dollars

89

Joint Cost-Schedule Confidence Iso-Curves

Cost (RY$M)

Sche

dule

(Mon

ths)

65 Confidence

65 Cost Confidence AggressiveSchedule

65 Cost ConfidenceScheduleGiven 65 Schedule Confidence

Unconditional 65 CostConfidence

Joint Cost and Schedule Confidence for 65 Cost Confidence and Program Baseline Schedule is Less Than 35

65 Cost Confidence Independent of Schedule Cost Needed to Achieve

Both 65 Joint Cost and Schedule Confidence for the Schedule with 65 Confidence

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

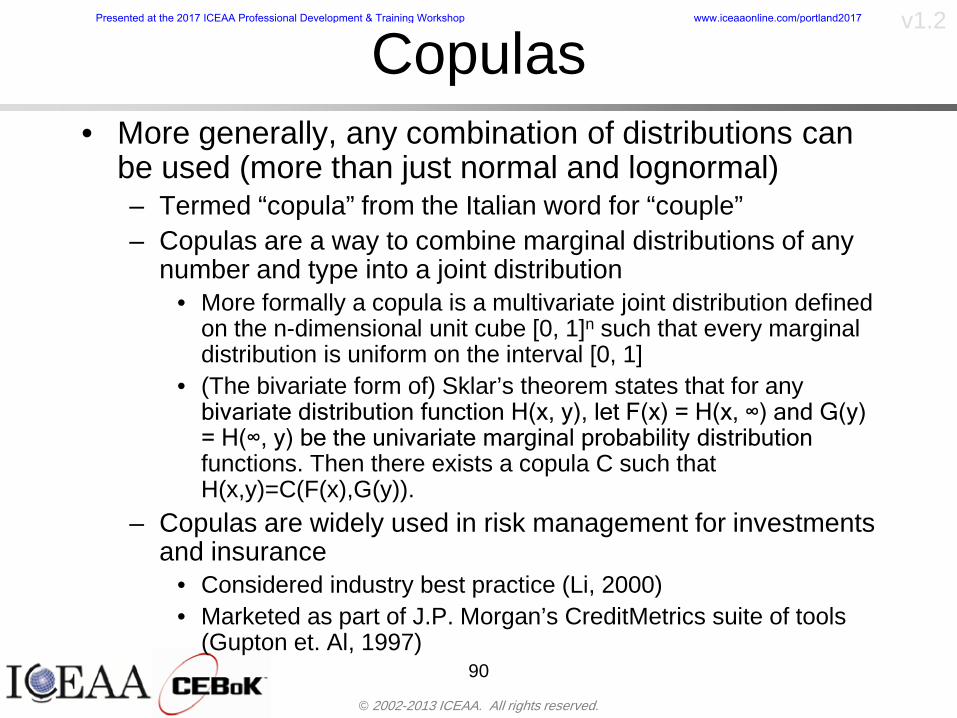

Copulasbull More generally any combination of distributions can

be used (more than just normal and lognormal)ndash Termed ldquocopulardquo from the Italian word for ldquocouplerdquondash Copulas are a way to combine marginal distributions of any

number and type into a joint distributionbull More formally a copula is a multivariate joint distribution defined

on the n-dimensional unit cube [0 1]n such that every marginal distribution is uniform on the interval [0 1]

bull (The bivariate form of) Sklarrsquos theorem states that for any bivariate distribution function H(x y) let F(x) = H(x infin) and G(y) = H(infin y) be the univariate marginal probability distribution functions Then there exists a copula C such that H(xy)=C(F(x)G(y))

ndash Copulas are widely used in risk management for investments and insurance

bull Considered industry best practice (Li 2000)bull Marketed as part of JP Morganrsquos CreditMetrics suite of tools

(Gupton et Al 1997)90

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Parametric Joint Cost and Schedule Analysis

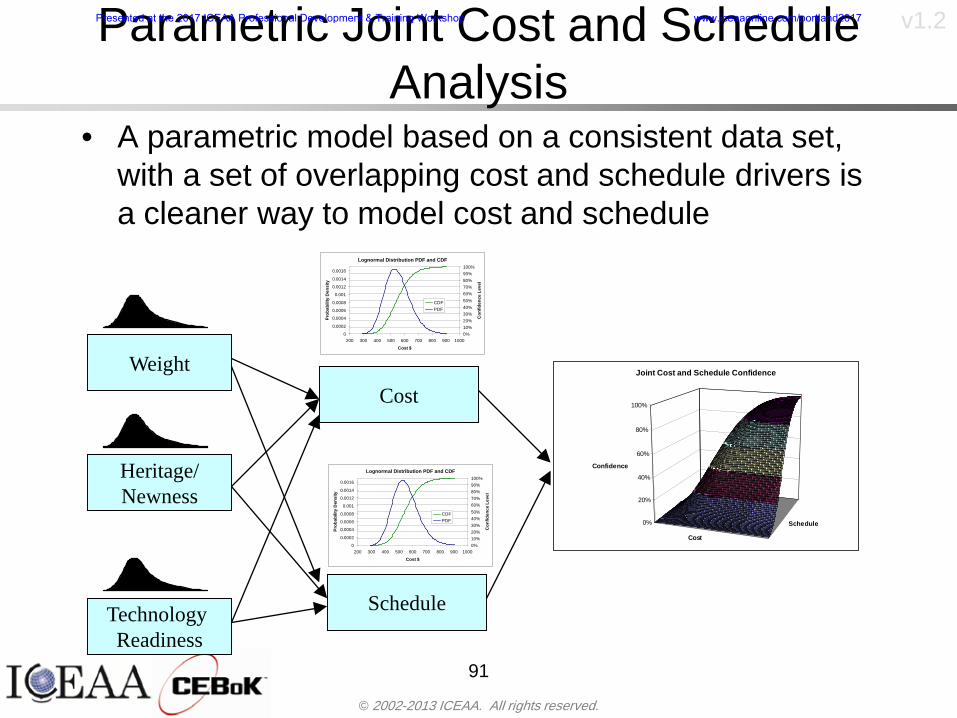

bull A parametric model based on a consistent data set with a set of overlapping cost and schedule drivers is a cleaner way to model cost and schedule

91

CostWeight

HeritageNewness

Technology Readiness

Schedule

0

20

40

60

80

100

Confidence

Joint Cost and Schedule Confidence

Schedule

Cost

Lognormal Distribution PDF and CDF

0102030405060708090100

200 300 400 500 600 700 800 900 1000Cost $

Con

fiden

ce L

evel

0

00002

00004

00006

00008

0001

00012

00014

00016

Prob

abili

ty D

ensi

ty

CDFPDF

Lognormal Distribution PDF and CDF

0102030405060708090100

200 300 400 500 600 700 800 900 1000Cost $

Con

fiden

ce L

evel

0

00002

00004

00006

00008

0001

00012

00014

00016

Prob

abili

ty D

ensi

ty

CDFPDF

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12Parametric Joint Cost and Schedule Analysis (2)

bull Joint cost and schedule risk analysis produced naturally by the integrated modelndash Addresses several issues with the copula

approachbull Tail dependencybull Correlation ndash no need to assign correlation

between cost and schedulebull Consistency of cost and schedule models

92

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Resource-Loaded Schedulesbull Involves assigning cost and schedule risks to a resource-loaded schedule

networkbull Bottom-up approach

ndash More labor intensive than parametrics but can also provide more insight

ndash Can answer questions than parametric typically cannot such as how much do reserve requirements decrease if a specific risk is retired

bull Currently being implemented in Constellation programbull Has same issue as all bottom-up models hard to count all the risks and model

them discretely

ndash As a result there is a tendency to reflect less risk than indicated by history

ndash ldquoThere are more things in heaven and earth Horatio than are dreamt of in your philosophyrdquo William Shakespeare Hamlet Act I Scene V

93

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

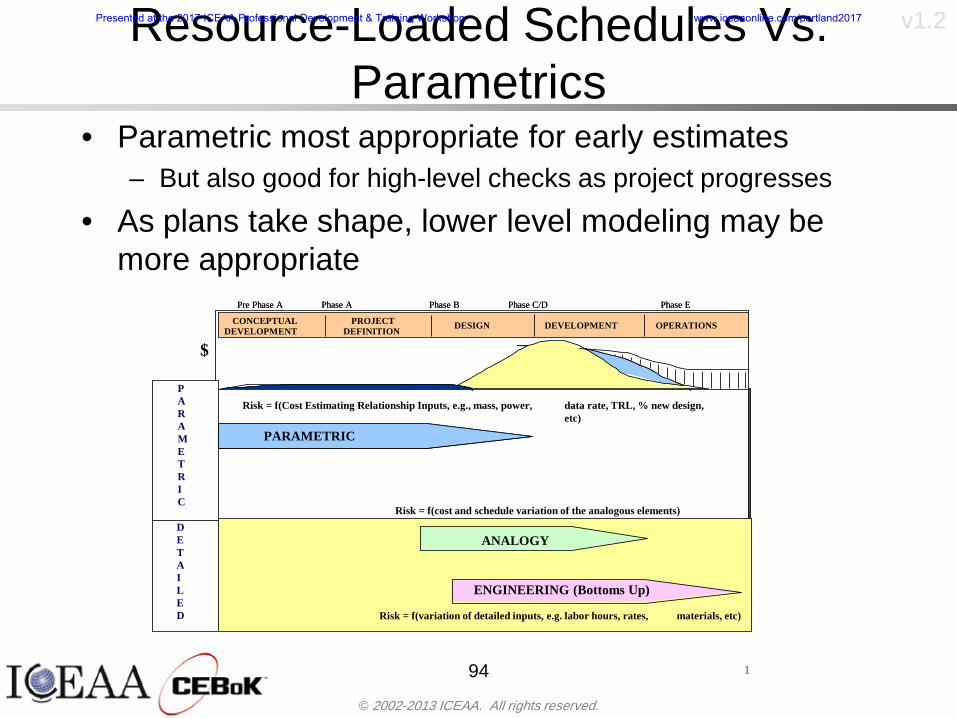

v12Resource-Loaded Schedules Vs Parametrics

bull Parametric most appropriate for early estimatesndash But also good for high-level checks as project progresses

bull As plans take shape lower level modeling may be more appropriate

94 1

CONCEPTUALDEVELOPMENT

PROJECTDEFINITION DESIGN DEVELOPMENT OPERATIONS

PARAMETRIC PARAMETRIC

ANALOGY

ENGINEERING (Bottoms Up)

$PARAMETRIC

DETAILED

$

Pre Phase A Phase B Phase CDPhase A Phase EPre Phase A Phase B Phase CDPhase A Phase E

Risk = f(Cost Estimating Relationship Inputs eg mass power data rate TRL new design etc)

Risk = f(cost and schedule variation of the analogous elements)

Risk = f(variation of detailed inputs eg labor hours rates materials etc)

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Resource-Loaded Schedulesbull Methodology has been demonstrated in other

industriesndash Construction oil and gasndash Analysis has not been traditionally done on highly uncertain

complex development projects bull Methodology focuses on project baseline schedule

ndash In baseline schedule all tasks are resource loaded to represent a baseline schedule and cost standpoint

ndash Resource loaded schedule is ldquorolledrdquo up to a manageable level

ndash Based on the risk and uncertainties identified schedule distributions are applied to each rolled up task

ndash Cost uncertainties are also applied to rolled up tasksbull Uncertainties include labor rate man power etc

ndash A Monte Carlo simulation is run to develop joint cost-schedule distributions

95

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

copy 2002-2013 ICEAA All rights reserved

v12

Unit III - Module 9 96

Execution ndash Cross Checksbull Means The mean cost growth factor for WBS items

can be compared to history as a way to cross check results

bull CVs The CV of the cost growth factors for WBS items can be compared to history as a way to cross check results

bull Inputs Checks are performed on inputs or other parameters to see if historical values are in line with program assumptionsndash Example Historical risk scores can be compared to program

risk scores to see if risk assessors are being realistic and to see if the underlying database is representative of the program

11

Presented at the 2017 ICEAA Professional Development amp Training Workshop wwwiceaaonlinecomportland2017

- Cost and Schedule Risk Analysis Basic

- Acknowledgments

- Unit Index

- Risk Overview

- Agenda

- Introduction

- Risk Analysis Terms

- Are Our Costs Realistic

- Historical Cost Growth

- Sources of Cost Risk

- Point Estimates of Cost

- Types of Risk

- Point Estimates Vs Risk Estimates

- Cost Risk and Probability

- Probability Model ndash Distribution

- Probability Model ndash Distribution

- Probability ndash Top-Level Distribution

- S-Curves and Confidence Levels

- Example ndash Normal Distribution

- Confidence Levels

- Measuring Parametric Model Uncertainty

- Parametric Model Example

- Weight Uncertainty

- Estimating Uncertainty

- Estimating Uncertainty (2)

- Estimating Uncertainty (3)

- Aggregating Risk

- WBS Example

- WBS and Risk

- Aggregating Risk

- Percentiles Do Not Add

- Percentiles Do Not Add (2)

- Percentiles Do Not Add (3)

- Methods for Aggregating Risk

- Monte Carlo Simulationfor Risk Analysis

- Monte Carlo Simulation

- Using Random Numbers to Simulate Distributions

- Simulating a Triangular Distribution

- Simulating a Triangular Distribution (2)

- Monte Carlo and the WBS

- Number of Trials

- Number of Trials (2)

- Number of Trials (3)

- Number of Trials (4)

- Number of Trials (5)

- Number of Trials (6)

- Methods of Simulation

- Probability Model ndash Correlation

- Correlation And Causation

- The Importance of Correlation

- The Importance of Correlation (2)

- Measures of Correlation

- Pearson Correlation

- Spearman Correlation

- Functional Correlation

- Risk Measures

- Value at Risk (VaR)

- Why 70th or 80th Percentile

- Funding Above Inflection Points

- Why Budget to the 70th or 80th

- Inflection Points for Lognormal

- Issues with Percentile Funding

- ldquoHere There Be Dragonsrdquo

- Distribution Comparison

- Distribution Comparison Tail Behavior

- Distribution Comparison ndash Tail Behavior (Table)

- Percentile Budgeting is Not Risk Management

- Joint Confidence Level Analysis

- Schedules Impact Cost

- The Relationship of Cost to Schedule

- The Impact of Schedule GrowthCompression on Cost

- Schedule as an Independent Variable

- Schedule is a Dependent Variable

- Incorporation of Schedule in Cost Risk

- Subjective Cost Risk Methods and Overinclusion of Risk Factors

- Fundamental Equation of Cost and Schedule Interrelationships

- How to (Correctly) Incorporate Schedule into Cost Risk Analysis

- Joint Lognormal and Normal Distributions

- Modeling Cost and Schedule as a Bivariate Distribution

- Bivariate Lognormal Distribution for Cost and Schedule

- Bivariate Lognormal for Cost and Schedule

- Correlation Between Cost and Schedule

- Correlation Between Cost and Schedule Caveats

- Conditional Confidence Levels

- Joint Confidence Levels

- Joint Confidence Levels Versus Cost Confidence Levels Only

- Joint Cost and Schedule Confidence

- Cost and Schedule Trade-offs for a Given Level of Joint Confidence

- Policy Considerations for Confidence Levels

- Copulas

- Parametric Joint Cost and Schedule Analysis

- Parametric Joint Cost and Schedule Analysis (2)

- Resource-Loaded Schedules

- Resource-Loaded Schedules Vs Parametrics

- Resource-Loaded Schedules

- Execution ndash Cross Checks

-