Capital Market Imperfections and the Incentive to Lease* 1

24

ELSEVIER Journal of Financial Economics 39 (1995) 271-294 Capital market imperfections and the incentive to lease Steven A. Sharpe *, Hien H. Nguyen Federal Reserve Board, Washington, DC 20551, USA (Received September 1994; final version received April 1995) Abstract This paper evaluates the influence of financial contracting costs on public corpora- tions’ incentives to lease fixed capital. We argue that firms facing high costs of external funds can economize on the cost of funding by leasing. We construct several measures of leasing propensity, plus some a priori indicators of the severity of financial con- straints facing firms. We find that the share of total annual fixed capital costs attributable to either capital or operating leasesis substantially higher at lower-rated, non-dividend-paying, cash-poor firms - those likely to face relatively high premiums for external funds. Key words: Leasing; Asymmetric information; Capital structure JEL classijication: G31; G32; E22 1. Introduction The corporate lease-versus-buy decision is typically analyzed under the Miller-Modigliani framework of financial structure irrelevance, that is, studies usually begin by invoking the assumptions of perfectly competitive capital markets with no transaction costs or information asymmetries. The popularity of this approach owes largely to the finance literature’s emphasis on tax-related incentives (e.g., Miller and Upton, 1976; Myers, Dill, and Bautista, 1976). Indeed, *Corresponding author. The views expressed herein are the authors’ and do not necessarily reflect those of the Board of Governors or the staff of the Federal Reserve System. We would like to thank George Fenn, Jean Helwege, Hamid Mehran, Michael O’Malley, James Schallheim (referee), and Clifford Smith for helpful comments. 0304-405X/95/$09.50 0 1995 Elsevier Science S.A. All rights reserved SSDI 0304405X9500830 8

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Capital Market Imperfections and the Incentive to Lease* 1

ELSEVIER Journal of Financial Economics 39 (1995) 271-294

Capital market imperfections and the incentive to lease

Steven A. Sharpe *, Hien H. Nguyen Federal Reserve Board, Washington, DC 20551, USA

(Received September 1994; final version received April 1995)

Abstract

This paper evaluates the influence of financial contracting costs on public corpora- tions’ incentives to lease fixed capital. We argue that firms facing high costs of external funds can economize on the cost of funding by leasing. We construct several measures of leasing propensity, plus some a priori indicators of the severity of financial con- straints facing firms. We find that the share of total annual fixed capital costs attributable to either capital or operating leases is substantially higher at lower-rated, non-dividend-paying, cash-poor firms - those likely to face relatively high premiums for external funds.

Key words: Leasing; Asymmetric information; Capital structure JEL classijication: G31; G32; E22

1. Introduction

The corporate lease-versus-buy decision is typically analyzed under the Miller-Modigliani framework of financial structure irrelevance, that is, studies usually begin by invoking the assumptions of perfectly competitive capital markets with no transaction costs or information asymmetries. The popularity of this approach owes largely to the finance literature’s emphasis on tax-related incentives (e.g., Miller and Upton, 1976; Myers, Dill, and Bautista, 1976). Indeed,

*Corresponding author.

The views expressed herein are the authors’ and do not necessarily reflect those of the Board of Governors or the staff of the Federal Reserve System. We would like to thank George Fenn, Jean Helwege, Hamid Mehran, Michael O’Malley, James Schallheim (referee), and Clifford Smith for helpful comments.

0304-405X/95/$09.50 0 1995 Elsevier Science S.A. All rights reserved SSDI 0304405X9500830 8

272 S.A. Sharp, H.H. Nguyen/Journal ofFinancial Economies 39 (1YY.i) 271-294

a thorough characterization of just the tax implications of the lease-versus-buy decision and its interaction with a firm’s overall capital structure, even under the assumption of complete markets, can be quite complex (Lewis and Schallheim, 1992).

On the other hand, the economics of leasing are widely recognized as going well beyond tax minimization strategies. Perhaps the most common set of motivations underlying the lease-versus-buy decision involve the use of leases to minimize transaction costs that arise when a firm expects the life of capital equipment to exceed its prospective usefulness (see, e.g., Flath, 1980; and Smith and Wakeman, 1985). The valuation of options embedded in leasing agreements is another fertile area of research (see, e.g., McConnell and Schallheim, 1983).

Perhaps some of the most interesting factors in the lease-versus-buy decision have received surprisingly little attention in the modern corporate finance literature. These are the ‘financial contracting’ motivations suggested by Smith and Wakeman but precluded by the complete markets framework. Such motiva- tions arise when outside investors are less informed than firm insiders regarding ongoing operations or future prospects, or when conflicts of interest between classes of corporate claimants are costly to resolve. The influence of such financial market imperfections on corporate capital structure and financing policy has been the subject of extensive analysis (e.g., see review by Harris and Raviv, 1992), yet, little theoretical or empirical research in that area gives more than cursory consideration as to how leasing fits into that equation.

Similarly, much of the recent research on the behavior of capital expendi- tures- beginning with Fazzarri, Hubbard, and Petersen (1988) - examines the influence of capital market information imperfections on investment behavior. Here too, the option of leasing is virtually ignored, despite the fact that leased equipment now accounts for roughly a third of all equipment investment by business.

In this paper, we explore the role of leasing in alleviating financial contracting costs, and attempt to gauge empirically the influence of such costs on the propensity of public corporations to lease capital. We hypothesize that firms facing high costs of external funding may be able to economize on fixed capital costs by leasing. In particular, financing with a lease may reduce the premium on external funds that arises from severe asymmetric information (Myers and Majluf, 1984), or from agency problems that give rise to costly monitoring (Smith and Warner, 1979), or from underinvestment (Myers, 1977; Stulz and Johnson, 1985). To examine our hypothesis, we draw on commonly invoked identifying assumptions that firms which (i) pay little or no dividends, (ii) generate little current cash flow, or (iii) have low credit ratings face relatively high premiums for external funds. By estimating the effects of these proxies on the propensity to lease, we test the hypothesis that leasing lowers average capital costs for firms facing high premiums.

S.A. Sharpe, H.H. Nguyen JJournal of Financial Economics 39 (I 995) 271-294 213

The empirical analysis employs Standard and Poor’s Compustat data from 1985 to 1991. We define ‘firm propensity to lease’ as the fraction of a firm’s total fixed capital costs - costs associated with the employment of property, plant, and equipment - that can be attributed to fixed capital on lease. Our estimate of the ‘total lease share’ of a firm’s fixed capital costs is based on both income statement and balance sheet information, as it includes both capitalized and off- balance-sheet, or operating, leases. We also consider a narrower, somewhat more conventional measure of leasing propensity, which equals the proportion of property, plant, and equipment on the balance sheet that is attributable to capitalized leases.

We find strong support for the hypothesis that firms likely to face high financial contracting costs also have a significantly greater propensity to lease: the proportion of their total annual costs of fixed-capital usage incurred under leases is substantially higher than at firms relatively unhampered by such financial constraints. These results hold up even when controlling for firm size. Not surprisingly, the use of operating leases is negatively related to firm size, since firm size is likely correlated with financial, but also other, factors that influence the lease-versus-buy decision. On the narrower measure of leasing propensity, there is some, albeit weaker, evidence that financially con- strained firms finance a greater share of their on-balance-sheet fixed capital via capital leases. Finally, all else the same, both measures of leasing propensity show more leasing by firms that appear to have lower current and future tax liabilities.

2. Background, analytical framework, and related research

This section begins with a brief description of leasing contracts, then lays out our theoretical arguments, and, finally, discusses previous research related to our central hypothesis.

2. I. Financial contracting rationales for leasing

Justifying any particular financial contracting cost argument as an induce- ment to lease necessitates a discussion of certain institutional features of lease obligations. A lease contract can be classified in one of two categories, depend- ing on whether the lessor or lessee technically ‘owns’ the leased item, and what the attendant risks and benefits are. Ownership risks and costs include respons- ibility for casualty loss, wear and tear, and obsolescence, while ownership benefits entail the right of use, entitlement to gains from asset value appreci- ation, and ultimate possession of the property title. Whether or not a lessor retains ownership depends on whether it has retained a meaningful residual interest in the equipment under the lease agreement.

274 S.A. Sharpe, H.H. NguyeniJournal of’ Financial Economk 39 (1995) 271 294

This dichotomy is complicated somewhat by the fact that the determination of ownership may differ, depending on whether it is made for financial ac- counting purposes or for legal and tax considerations. For financial accounting purposes, a lease is classified either as an operating or a capital lease. SFAS No. 13, ‘Accounting for Leases’, defines the criteria that differentiate operating and capital leases. Leases that do not substantially transfer the risks and benefits of ownership from the lessor to the lessee are classified as operating leases. In particular, a capital lease is defined by the following criteria: (i) ownership of the leased asset is transferred to the lessee by the end of the lease term; (ii) a bargain purchase option is available; (iii) the lease term is equal to 75% or more of the remaining economic life of the leased asset; or (iv) the present value of the minimum lease payments equals or exceeds 90% of the asset’s market value.

At the inception of a capital lease, the lessee capitalizes the leased asset and records the corresponding debt obligation on the balance sheet. Subsequently, the lessee depreciates the leased asset and amortizes the debt liability. Thus, from an accounting perspective, capital leases closely resemble purchases by the lessee and, therefore, require disclosures similar to asset purchases. In contrast, operating leases represent off-balance-sheet financing for the lessee, and are reflected on the income statement as rent expense.

From a legal and tax point of view, when the lessor retains ownership, the agreement is said to be a ‘true’ lease; if not, it is a lease ‘intended as security’, and the lessor’s claim is essentially viewed as a secured debt. Though our empirical analysis is based upon the financial accounting classification, the analytical arguments behind our hypotheses rest, in large part, upon the legal character- istics.’

Financial contracting rationales for the use of secured debt, as opposed to unsecured debt or equity, are offered by Smith and Warner (1979a) and Stulz and Johnson (1985). First, securing debt with a borrower’s assets may be a cost-effective way of reducing asset substitution risks and may help to econom- ize on lender monitoring costs. In addition, Stulz and Johnson demonstrate that a firm and its creditors can mitigate the underinvestment problem (analyzed by Myers, 1977) by allowing subsequent debt to be secured by the assets such borrowings can finance.

‘The distinctions between true and nontrue leases are not stressed in our empirical analysis, owing to the fact that financial accounting data only distinguishes between operating and capital leases. However, basing our analytical arguments for leasing on the legal characteristics of leases ought not lead to major incongruencies with the empirical analysis. While the two classification systems do not yield a one-to-one mapping, the discrepancies are, in principle, minor. Operating leases are usually true leases, and most capital leases are likely to be treated as leases intended as security. Regardless, the main focus of our analysis is on differences between lease and nonlease financing, rather than the choice among types of leases.

S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271.-294 215

The financial contracting advantages of a true lease may be even stronger than those for secured debt. One key difference between secured debt (or any other debt) and a true lease is in their treatment under a Chapter 11 bankruptcy filing. After filing for bankruptcy, the lessee has the option of either ‘assuming’ or ‘rejecting’ a true lease, that is, accepting or breaching all obligations entailed by the lease. If the lessee rejects an obligation, then the lessor may immediately recover possession of the equipment, re-lease or sell it, and file an unsecured claim against the lessee for economic losses incurred, including unpaid rents, late charges, and the present value of expected future rental shortfalls. In contrast, an automatic stay normally prevents secured creditors from repossessing their security after a bankruptcy filing.

If the financially troubled lessee chooses instead to assume the lease, and thus retain the equipment, the lessor is entitled to continue receiving compen- sation in accordance with the original lease agreement, since such obligations are classified as administrative expenses in the bankruptcy code. In fact, the lessor’s entire claim, including delinquencies, late fees, and other damages suffered, is classified as an administrative claim that must be paid immediately or ‘within a reasonable period (Sweig, 1993).2 Thus, when a true lease is not rejected, the lessor will continue to receive full compensation even after the lessee files for bankruptcy, while other outstanding creditor claims, including those of secured creditors, are accrued against the bankrupt firm with no assurance of being met.

By financing via true lease, as long as the leased asset is not returned prematurely to the lessor, the firm effectively puts the financial obligation on a par with other admininistrative expenses - such as employee and manage- ment compensation - that have a higher priority than normal debt. This aspect of a lease contract makes it a highly desirable financial contract in the presence of asymmetric information, since it would appear to put leasing at the top of the pecking order of external financing options. Apart from the potential for a few missed payments, under a true lease, the main risk borne by the lessor arises from the uncertainty of the value of the leased asset in the event that the obligation is rejected and the asset must be re-leased. In other words, much of the risk assumed by the lessor is only indirectly tied to the idiosyncratic, and perhaps concealable, aspect of the leasing firm’s prospects.

‘Not until the adoption of Article 2A of the Uniform Commercial Code in 1987 were the rights and remedies of lessor and lessee clearly defined (Zall, 1993; Strauss, 1991). Before Article 2A, there was considerable ambiguity about the criteria required for a lease to be treated as a true lease in bankruptcy. Article 2A has in effect broadened the definition of leases that meet the test of a ‘true’ lease

216 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294

2.2. Related empirical studies

Among previous analyses of the incentives to lease, Krishnan and Moyer (1994) is perhaps closest in spirit to our study. They hypothesize that leasing reduces bankruptcy costs in comparison to financing with ordinary debt, and argue that leases have all the advantages of secured debt and then some. As a consequence, leases should be more widely used by riskier, less established firms. This hypothesis is supported by their empirical finding that firms with lower and less stable operating earnings are more likely to lease. Nonetheless, their analysis examines the use of capital leases and ignores operating leases.

Other empirical analyses have attempted to gauge the effect of capitalized leases on overall debt capacity, but such studies fail to control for the underlying factors that determine debt capacity. Ang and Petersen (1984) examine the relation between the book value of capital leases and a firm’s use of other debt. They find that leases are complementary to debt, that is, firms with leases also appear to have more nonlease debt (relative to book equity). As pointed out by Smith and Wakeman (1985), this result probably reflects the difficulty of control- ling for debt capacity, that is, firms with higher debt capacity may also have (omitted) characteristics that make leasing relatively attractive. Bayless and Diltz (1988) control for such considerations by using an experimental setting in which banks are queried regarding the amount they would be willing to lend under various hypothetical circumstances. Bayless and Diltz found that, in the case of a term loan decision, banks did not treat outstanding capital leases and debt differently; however, leases had a somewhat negative relative effect on credit line decisions. They conclude that the fungibility of leases and other debt should generally depend upon the particular use for which the firm’s other debt has been targeted.

Our empirical design controls for such considerations by reorienting the problem so that the firm chooses among contracts for financing services from fixed capital. That is, we begin by estimating the amount of fixed capital services a firm ‘pays for’ over a given year, and measure the proportion of those services acquired under lease agreements. Moreover, we use both operating as well as capital leases in our measures of firm ‘leasing intensity’.

As previous researchers have pointed out, leasing gives rise to its own set of transactions costs and agency problems. Prominent among these is the lessee’s reduced incentive to preserve the value of the leased asset through appropriate use and maintenance, since the lessee does not have a claim to the entire service life of the asset (e.g., Flath, 1980; Wolfson, 1985). Consequently, a firm’s propen- sity to lease is a function of the type of capital required and the extent of leasing-related transactions costs associated with such assets. While it is difficult to control directly for such factors with the available data, we control for them indirectly by analyzing a firm’s propensity to lease relative to other firms in its own industry.

S.A. Sharpe, H.H. Nguyen/Journal ofFinancial Economics 39 (1995) 271-294 211

3. Data and measurement issues

Firm level data used in this study are taken from the May 1993 Compustat files. Included in our panel are annual observations from 1986-1991 for firms on the active file for which 1985 data is available as well as firms on the research file that have data for 1985 and 1990. Foreign incorporated companies and a few industries are excluded.3 We require that each observation have complete data for the relevant variables. After discarding observations with missing data, our sample contains an average of about 2000 observations per year. Firms are categorized into one of six industry groups by their primary SIC code (Table 1).

3. I. Leasing propensity

To measure the propensity to use capital leases, we calculate the capital lease share of property, plant, and equipment, or the proportion of fixed assets accounted for by capital leases. This is based on net book values reported on the balance sheet for both items:4

net capital leases net PPE ’ (1)

Due to off-balance-sheet financing of operating leases, reported fixed capital understates the stock of total property, plant, and equipment utilized in produc- tion processes. Therefore, the critical task is to quantify the relative importance of operating leases. We do this by comparing an estimate of the annual flow of rented capital services to an estimate of the annual flow of capital services implicit in the level of property, plant, and equipment reported on the balance sheet. The annual flow of services from noncapitalized leases is approximated by the amount of rental commitments due in one year on noncancellable, non- capitalized leases, as reported at the end of the previous year in a footnote to the balance sheet. The annual flow of capital services from balance-sheet capital is

3Aside from financials (two-digit SIC codes: 6@69) and utilities (49), excluded industries include those where real property or natural resources are a large portion of firms’ capital (detailed property, plant, and equipment components were not disclosed) [petroleum refining (29), mining (10-14) agriculture and fishery (l-9)] as well as those where the main line of business involves leasing [auto repair (75) computer rental and leasing (73)].

4By accounting standards, capital lease assets (at cost) should always be greater than or equal to the corresponding liability, since the debt obligation is amortized over time. However, in about 5% of our observations, the disclosed lease asset is less than the debt obligation. This is probably because some lease assets are not reported separately, but are combined under the broader category of property, plant, and equipment, even though the corresponding liability may be fully disclosed. In situations where this occurs, the capital lease share of fixed capital is defined as the ratio of the capital lease liability (instead of asset) to net property, plant, and equipment.

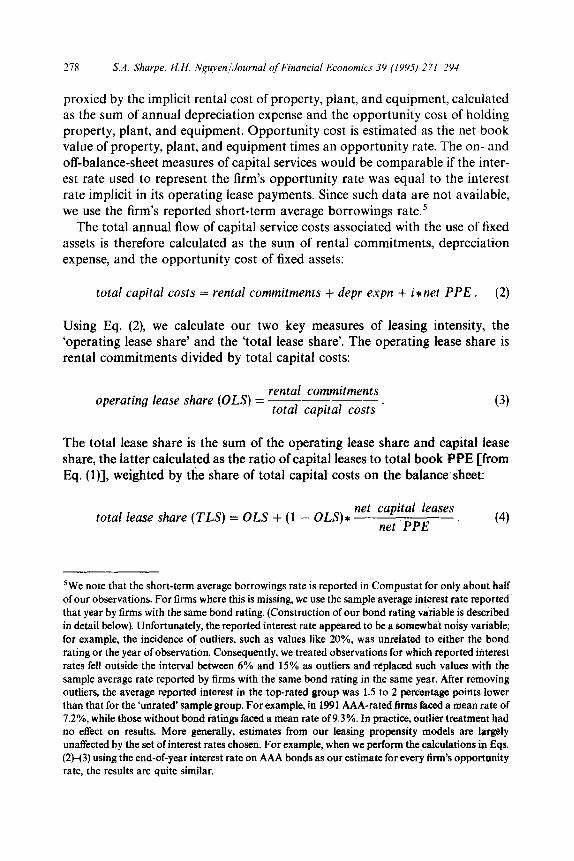

278 S.A. Sharpe. H.H. Nguyen/Journal @Financial Economics 39 (1995) 271-294

proxied by the implicit rental cost of property, plant, and equipment, calculated as the sum of annual depreciation expense and the opportunity cost of holding property, plant, and equipment. Opportunity cost is estimated as the net book value of property, plant, and equipment times an opportunity rate. The on- and off-balance-sheet measures of capital services would be comparable if the inter- est rate used to represent the firm’s opportunity rate was equal to the interest rate implicit in its operating lease payments. Since such data are not available, we use the firm’s reported short-term average borrowings rate.5

The total annual flow of capital service costs associated with the use of fixed assets is therefore calculated as the sum of rental commitments, depreciation expense, and the opportunity cost of fixed assets:

total capital costs = rental commitments + depr expn + i*net PPE . (2)

Using Eq. (2), we calculate our two key measures of leasing intensity, the ‘operating lease share’ and the ‘total lease share’. The operating lease share is rental commitments divided by total capital costs:

operating lease share (OLS) = rental commitments total capital costs ’ (3)

The total lease share is the sum of the operating lease share and capital lease share, the latter calculated as the ratio of capital leases to total book PPE [from Eq. (l)], weighted by the share of total capital costs on the balance sheet:

total lease share (TLS) = OLS + (1 - OLS)* net capital leases

net PPE ’ (4)

sWe note that the short-term average borrowings rate is reported in Compustat for only about half of our observations. For firms where this is missing, we use the sample average interest rate reported that year by firms with the same bond rating. (Construction of our bond rating variable is described in detail below). Unfortunately, the reported interest rate appeared to be a somewhat noisy variable; for example, the incidence of outiiers, such as values like 20%, was unrelated to either the bond rating or the year of observation. Consequently, we treated observations for which reported interest rates fell outside the interval between 6% and 15% as outliers and replaced such values with the sample average rate reported by firms with the same bond rating in the same year. After removing outiiers, the average reported interest in the top-rated group was 1.5 to 2 percentage points lower than that for the ‘unrated’ sample group. For example, in 1991 AAA-rated firms Faced a mean rate of 7.2%, while those without bond ratings faced a mean rate of 9.3%. In practice, outlier treatment had no effect on results. More generally, estimates from our leasing propensity models are largely unaffected by the set of interest rates chosen. For example, when we perform the calculations in Eqs. (2)-(3) using the end-of-year interest rate on AAA bonds as our estimate for every firm’s opportunity rate, the results are quite similar.

S.A. Sharpe. H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294 279

3.2. Proxies for asymmetric information costs

To test our hypothesis that firms that face high costs of external capital owing to financial contracting costs are more inclined to lease, we construct several explanatory variables that act as indicators of a firm’s information-cost related premium on external funds. Young, fast-growing, innovation-intensive firms are likely to have many investment opportunities. Such firms can face severe information asymmetry problems, and consequently may be forced to finance projects largely from retained earnings. Since firms that pay no cash dividends are likely to be among those most burdened by asymmetric information, a dummy variable equal to one for non-dividend-paying firms is used as an indicator for firms facing high capital market information costs.6

An alternative interpretation of our no-dividend indicator that is nonetheless consistent with our general hypothesis is suggested in Smith and Watts (1992). They argue that dividend payout should be lowest for those firms at greatest risk of facing the underinvestment problem. Firms with more growth opportunities ‘can tolerate more restrictions on dividends before the expected benefits of controlling payout are offset’ by the risk of triggering negative net present value investments. Thus, a finding that non-dividend-paying firms have a greater propensity to lease may alternatively be viewed as evidence that leasing helps to alleviate some of the expected costs associated with the underinvestment problem.

We develop two additional sets of proxies for gauging relative marginal funding costs. All else equal, firms generating poor cash flows probably face higher funding costs; in addition to providing cheap funds directly, greater cash flow enhances firm debt capacity. Our measure of cash flow is equal to the ratio of operating income to sales. We define cash flow as operating income before interest, depreciation, rent, and taxes. Rent expense is added back into cash flow in order to avoid creating a cash flow measure that is influenced by the choice of renting versus buying. In addition, the ratio is truncated at zero to avoid using a variable that is highly negatively skewed. Otherwise, large negative values appear for firms with low sales. Results are not sensitive to variations of the truncation point between zero and - 1, or to the inclusion of a dummy indicating firms with cash flow ratios lower than the truncation point.

Finally, firms that have low-rated or unrated debt are probably closer to exhausting their debt capacity as well as their internal funding. Thus, they ought to face higher information- or agency-cost premiums on marginal financing.

6The use of low dividend payout as an indicator of the likelihood of facing financing constraints due to asymmetric information on investment is proposed, for example, by Fazzari, Hubbard, and Petersen (1988). Calomiris and Hubbard (1993) find historical support for this identifying assump- tion.

280 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271 -294

Based largely upon Standard & Poor’s senior debt ratings, five indicator variables are used in a four-tier rating system with the fifth group being unrated firms. For companies without senior debt ratings, we use subordinated debt ratings if available. Failing this condition, we check for commercial paper ratings. Companies that do not have any such ratings are classified as unrated. The rating groups are partitioned according to: AAA through AA - (or Al + for commercial paper); A + through A - (or Al for cp); BBB + through BBB - (or A2 for cp); and BB -t- through D (or B, C, D for cp).

3.3. Other variables

Because firm size is correlated with the quality of outsider information about firms’ operations and prospects, smaller firms are more likely to lease for financial contracting reasons. In fact, as evidence that firm size is negatively related to risk, Schallheim et al. (1987) find that yields charged on financial leases are higher for leases to smaller firms. If leasing reduced the information- cost premium on outside funds, then a decline in issuer size would be associated with an even steeper rise in yields on straight debt.

In addition, leasing propensity will be greater for smaller firms if there are significant nonconvexities, or indivisibilities, associated with the use of certain fixed assets. For example, smaller firms may not need an entire building. Also, such firms may face greater uncertainty on their future needs for any particular piece of capital equipment. Thus, leasing could minimize the transaction costs associated with resale. Larger firms are more likely to have alternative uses for equipment that is no longer needed in its originally intended use, and they may also have better developed mechanisms for remarketing equipment.

This alternative rationale for a firm-size influence on leasing propensity suggests some caution in interpreting size effects. We gauge firm size by the log of the number of employees. Since proportional changes in size might matter less once some threshold size is obtained, we allow for a more general functional form by including the square of size in those specifications where size is highly significant. Results are similar when the log of sales is used as the proxy of size. Using the standard measure of size - total assets - is inappropriate here because of its endogeneity. In particular, all else equal, firms that lease more will have a lower level of book assets. We choose the number of employees because, like assets, this is a measure of inputs to production, though, unlike assets, it should be roughly invariant to the leasing choice.

As we noted earlier, leasing is also motivated by tax incentives. Where the lessee faces a lower marginal tax rate than the lessor, both p&ties may benefit from a leasing-related transfer of tax shields to the lessor (see Brealey add Myers, 1984). This motivation might have been particularly influential under the tax code prior to the 1986 reform, as, in addition to providing for investment tax credits (ITCs), the code contained relatively generous tax depreciation rules.

S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294 281

Moreover, the influence of the pre-1987 tax code probably lingered for several years, as firms that had invested heavily during the early and mid-1980s only were able to fully utilize the associated deductions over time. In fact, about 75 of the firms in our sample - firms with a relatively high proportion of purchased, rather than leased, capital - continued to show ITCs on their balance sheets for several years after that benefit was eliminated on new investment.’

We construct two alternative proxies for a firm’s tax status. First, we approx- imate a firm’s tax rate with tax expense divided by pre-tax income; all else equal, firms paying little or no taxes should be more prone to lease. Ideally, we would like a measure of expected marginal tax rate (in the absence of lease financing). As an admittedly noisy proxy for this, we use the firm’s average financial tax rate. The tax rate variable is truncated so as to fall between zero and one. It is set at zero for all firms with nonpositive tax expense, regardless of pre-tax income, and set at one for firms that have positive taxes and negative income. Coefficient estimates on the tax rate are largely unaffected by dropping observations characterized by such anomalies. Also, using realized future tax rates does not enhance the variable’s explanatory power.

A better proxy of tax-motivated leasing incentives could be derived from tax-loss carry-forwards reported in the financial statements. Firms with signifi- cant tax-loss carry-forwards will be ‘tax-exhausted for a period of years, and thus unable to take full advantage of the tax benefits of ownership, including those from accelerated depreciation and investment tax credits. Since over two-thirds of the firms in any year have no tax-loss carry-forwards, and because of the highly skewed distribution of this variable for firms reporting a loss carry-forward, we employ dummy variables that indicate the presence of a ‘high or ‘low’ (versus ‘no’) loss carry-forward. Companies with tax-loss carry-forwards exceeding current year operating earnings (before depreciation, interest, and taxes) are placed into the high tax-loss carry-forward category, while those with positive loss carry-forwards that fail this criterion are labeled low tax-loss carry-forward firms. (We considered using the ratio of tax-loss carry-forwards to scaling variables such as operating income or sales, but, due to the highly skewed distribution of loss carry-forwards, this proved inferior to using dum- mies in the sense of having less explanatory power.)

To control for the characteristics of the property, plant, and equipment, we include industry dummies defined by broad industry categories or else use industry-adjusted values based on narrower, two-digit SIC industries. We also control for technological differences across firms by using a measure of capital

‘As discussed in detail by O’Malley (1994), the implementation of the Alternative Minimum Tax in 1986 probably helped sustain tax-motivated leasing. That provision limited the extent to which firms could use depreciation (as well as other items) to shield income against taxes, a constraint which was binding for many capital-intensive firms.

282 S.A. Sharpe, H.H. NguyenlJournal of Financial Economics 39 (1995) 271 294

intensity, the ratio of total annual capital costs [Eq. (2)] to the number of employees. The capital intensity of production processes may be negatively correlated with leasing intensity to the extent that firms that are more capital- intensive firms use specialized equipment that is less appropriate for leasing. Also, failing to control for differences in the capital-labor ratio may result in spurious estimated effects for variables such as operating earnings.

We also attempt to directly control for economic motivations arising in market environments characterized by a great deal of uncertainty. Firms in these environments could have asset needs that are unpredictable or temporary; leasing alleviates the problem of owning assets that are not expected to have productive use full-time. We construct a proxy for the anticipated variation in demand equal to the firm’s realized variance of annual sales growth measured over the years during which the firm is in the panel. This variable should be positively related with the option value of a short-term lease, and should be correlated with (expected) instability of earnings. Thus, it can also proxy for tax-motivated leasing, as predicted in Lewis and Schallheim (1992).

Finally, because of inflation, measuring fixed assets at book value results in an underestimate of the true value of these assets, and hence an underestimate of capital costs. Consequently, leasing propensity measured as the lease share of total capital costs will be biased upward. This problem will be more severe for firms with older equipment. We construct a proxy for equipment age equal to one minus the ratio of net PPE to gross PPE. A firm with an entirely nonde- preciated stock of equipment will have zero for equipment age, while firms with mostly depreciated equipment will have values approaching unity for equipment age.

4. Empirical results

In this section, we begin by examining the means and correlations of our leasing measures and explanatory variables; then, we describe the empirical models and, finally, the model estimates.

4. I. Sample statistics and simple correlations

Mean values of firm leasing intensity are shown for the 1986 sample shown in Table 1, which groups firms by broad industry category and their size relative to the industry. The first measure of leasing intensity (col. 1) shows capital leases as a share of net property, plant, and equipment on the balance sheet. Numbers in square brackets are the fraction of firms reporting any capital leases. Except for the retail industry, where stores’ square footage accounts for most of firms’ fixed asset costs, capital leases usually account for less than 15% of net book property, plant, and equipment. Moreover, fewer than two-thirds of the nonretail

S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294 283

Table 1 Measures of 1986 leasing intensity: Means by industry and firm size

Capital lease share of PPE is net capital leases divided by net book property, plant, and equipment. Operating lease share of total capital costs equals current-year rental commitments divided by total capital costs, where total capital costs is the sum of rental commitments and an estimate of the implicit annual rental cost of net property, plant, and equipment. Total lease share of total capital costs is the sum of the operating lease share and the capital lease share of total capital costs, the latter calculated as the capital lease share of net PPE multiplied by one minus the operating lease share. Firm size classification is determined by dividing each industry into firms above and below the median size, as measured by the number of employees.

Industry # companies

Manufacturing 1167

Transportation 63

Communications 74

Wholesale 135

Retail 254

Services 331

Capital lease share of PPE [% w cap. lease]

Small Large

0.10 0.05 [OSS] CO.611

0.05 0.09 [0.58] CO.871

0.08 0.01 co.531 CO.811

0.13 0.12 co.451 [0.68]

0.25 0.24 [O.Sl] co.933

0.12 0.07 CO.641 [0.65]

Small

0.27

Large Small Large

0.16 0.34 0.20

0.32 0.16 0.36 0.23

0.17 0.04 0.23

0.34 0.27

0.41 0.32

0.36 0.32

0.43

0.55

0.44

0.05

0.35

0.47

0.37

Operating lease Total lease share of total share of total capital costs capital costs

firms in our sample report any capital leases. The capital lease fraction of fixed assets tends to be higher for smaller firms (those with fewer than the industry median number of employees), although, in most industries, larger firms more frequently report a positive number for capital leases.

The second measure of leasing intensity is the operating lease share of total capital costs. Within each industry, operating leases account for a higher-than- average share of total capital costs for smaller firms, and in most cases, substan- tially more. Taken by industry group, the operating lease share ranges from a low of 4% for large communication firms to a high of 41% for small retail firms.

Statistics for the total lease share of total capital costs, the most comprehen- sive measure of leasing intensity, appear in the right two columns. The total lease share is generally 5 to 10 percentage points higher than the operating lease share, and the pattern across industry and size groups follows that depicted for

284 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294

the operating lease share. Finally, though not shown, the pattern of industry average total leasing shares shows little movement over time. However, there appears to have been some shifting toward operating leases from capital leases. (Two notable exceptions are in the transportation and communication indus- tries; the average total lease share of large transportation firms grew about 7 percentage points, while that for small communication firms declined about 13 percentage points.)

Table 2 shows sample means and correlations among our measures of leasing intensity and explanatory variables (in 1986). Correlations are calculated using two-digit SIC industry-adjusted variables, that is, after subtracting 1986 indus- try mean values from each observation. Means are shown in the second column, correlations between measures of leasing intensity and explanatory variables are presented in the first three rows, and correlations among the explanatory variables constitute the remainder.

Since ‘no dividend’, ‘no rating’, and the two tax-loss carry-forward variables are all indicator (dummy) variables, their mean values equal the proportion of firms having such characteristics. Thus, 59% of our firms paid no dividends, 79% of them were not rated, and almost one-quarter of them had large tax-loss carry-forwards. The average number of employees reported by firms in our sample is about 800 (avg. firm size z ln[800]).

The correlations suggest that, by all three measures, leasing intensity is positively related to the no dividend and no rating indicators, and negatively related to contemporaneous operating income (before rent expense). In addition, leasing propensity is positively correlated with the presence of large tax-loss carry-forwards and negatively correlated with the tax rate. Leasing propensities are negatively related to firm size and positively related to the variance of sales growth. This is consistent with the economic rationale related to the option value of leasing. Finally, our three indicators of information- or agency-cost premiums on marginal funding - the no-dividend and no-rating dummies and EBITDA/sales - all show substantial correlations with firm size, the tax-loss carry-forward indicator, and the tax rate, suggesting that these controls are potentially important for a convincing test of our hypothesis.

4.2. Regression models

Before examining the main hypothesis, we consider the subset of our informa- tion relating to capital equipment only on the balance sheet. In particular, we examine whether firms facing greater financial constraints are likely to lease a greater proportion of the fixed assets reported on their balance sheet. As noted earlier, such a test avoids what could be the most troublesome measurement problems. Strictly speaking, however, this test only makes sense if the operating lease option can be ignored when estimating the decision to purchase equipment outright or acquire it under a capital lease. In other words, the test presumes

Tabl

e 2

1986

sam

ple

stat

istic

s fo

r va

riabl

es:

Mea

ns

and

two-

digi

t in

dust

ry-a

djus

ted

corre

latio

ns

Cor

rela

tions

ar

e ca

lcul

ated

af

ter

subt

ract

ing

1986

two-

digi

t in

dust

ry

mea

n va

lues

fro

m e

ach

obse

rvat

ion;

th

ose

deno

ted

with

an

ast

eris

k (*

) ar

e si

gnifi

cant

at

the

1%

lev

el (

two-

tail

test

). C

apita

l le

ase/

net

PPE

is n

et c

apita

l le

ases

div

ided

by

net

boo

k pr

oper

ty,

plan

t, an

d eq

uipm

ent.

Ope

ratin

g le

ase

shar

e eq

uals

cu

rrent

-yea

r re

ntal

co

mm

itmen

ts

divi

ded

by t

otal

ca

pita

1 co

sts,

whe

re t

otal

ca

pita

l co

sts

are

the

sum

of

rent

al

com

mitm

ents

an

d an

est

imat

e of

the

im

plic

it re

ntal

co

st o

f ne

t pr

oper

ty,

plan

t, an

d eq

uipm

ent.

Tota

l le

ase

shar

e is

the

sum

of

the

oper

atin

g le

ase

shar

e an

d th

e ca

pita

l le

ase

sham

of

tota

l ca

pita

l co

sts,

th

e la

tter

calc

ulat

ed

as th

e ca

pita

l le

ase

shar

e of

net

PPE

mul

tiplie

d by

one

min

us

the

oper

atin

g le

ase

shar

e of

tot

al

capi

tal

cost

s. N

o di

vide

nd

(no

debt

ra

ting)

eq

uals

one

if f

irm p

aid

no d

ivid

end

(was

unr

ated

) th

at y

ear,

and

is z

ero

othe

rwis

e.

EBIT

DA

is e

arni

ngs

befo

re i

nter

est,

taxe

s, d

epre

ciat

ion,

an

d re

nt

expe

nse.

Tax

ra

te

is t

ax

expe

nse

divi

ded

by p

re-ta

x in

com

e.

Larg

e ta

x-lo

ss

carry

-forw

ard

(CF)

is

one

if

firm

ha

d a

tax-

loss

ca

rry-fo

rwar

d ex

ceed

ing

curre

nt-y

ear

EBIT

DA.

Fi

rm

size

is th

e na

tura

l lo

g of

the

num

ber

of fu

ll-tim

e em

ploy

ees.

Ag

e of

PPE

equ

als

one

min

us t

he r

atio

of

net

PPE

to

gros

s PP

E.

Cap

ital

inte

nsity

is

tot

al

capi

tal

cost

s di

vide

d by

the

num

ber

of e

mpl

oyee

s.

Var(s

ales

gr

owth

) is

the

var

ianc

e of

the

ann

ual

chan

ge

in I

n(sa

les)

fro

m

1985

5199

1.

Sam

ple

mea

ns

(N =

202

4)

No

EBIT

DA

No

divi

dend

sa

les

ratin

g Ta

x ra

te

Larg

e ta

x-lo

ss

CF

Firm

si

ze

Age

of

PPE

Cap

ital

inte

nsity

Varia

nce

sale

s gr

owth

Cap

. le

ase/

Net

PP

E O

per.

leas

e sh

are

Tota

l le

ase

shar

e

0.10

0.

10*

- 0.

06*

0.08

* -

0.07

* 0.

09*

- 0.

11*

- 0.

02

0.00

-

0.01

0.

26

0.26

* -

0.21

* 0.

17*

- 0.

14*

0.19

* -

0.31

* 0.

21*

- 0.

05

0.09

* 0.

33

0.26

* -

0.21

* 0.

18;

- 0.

15*

0.21

* -

0.31

* 0.

15*

0.05

* 0.

07*

No

divi

dend

EB

ITD

A/Sa

les

No

ratin

g Ta

x ra

te

Larg

e ta

x-lo

ss

CF

Firm

si

ze

Age

of P

PE

Cap

ital

inte

nsity

0.59

0.

12

0.79

0.

34

0.25

6.

78

0.40

0.

12

- 0.

23*

0.33

* 0.

17*

0.2s

* -

0.56

’ 0.

00

- 0.

06

- 0.

17*

0.29

* -

0.39

* 0.

32*

- 0.

14*

0.08

* -

0.13

* 0.

12*

- 0.

53’

0.09

* 0.

00

- 0.

15*

0.26

* -

0.02

-

0.01

-

- 0.

38*

0.13

* 0.

07*

- 0.

11

- 0.

14*

- 0.

01

0.11

* -

0.15

* 0.

07*

- 0.

10*

0.16

* -

0.16

* -

0.01

0.

09*

286 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (199.5) 271 294

that the decision to acquire equipment under a capital lease is independent of the potential benefits of operating leases. Nonetheless, we explore the determi- nants of the capital lease share of property, plant, and equipment. Because many firms are observed to have no capital leases - capital lease share is truncated at zero - we estimate the determinants using a tobit specification, that is, we estimate Eq. (5) using maximum likelihood under the assumption of normality,

net capital leasesi net PPEi

= p’xi + ui if RHS 2 0, (5)

= 0 otherwise,

where Xi is a vector containing proxies for the firm’s external funding premium as well as control variables, including six dummies for the industry groups8

The results are presented in Table 3, in which estimates are shown for three separate years. The coefficient estimate of 0.03 on the no-dividend variable indicates that, all else equal, firms that fully retain their earnings have a capital lease fraction of property, plant, and equipment that is 3 percentage points higher compared with dividend-paying firms. In contrast, leasing propensity appears to have little relation to firm debt ratings. Perhaps surprising is the finding that leasing propensity is, if anything, positively related to cash flow (EBITDA/sales). Also, the coefficients on firm size and size-squared imply that the capital lease share is positively related to firm size for small and medium- sized firms. These latter two results suggest that it may be inappropriate to ignore the operating lease option when testing for the information-cost rationale behind leasing.

The significant positive coefficients on the high tax-loss carry-forward indi- cator and the negative coefficients on the tax rate in all three years suggest that capitalized leases are used more heavily by firms for which the tax benefits of ownership appear low. The strength of this result is somewhat surprising, in light of the ambiguous tax standing of capital leases and the finding by Krishnan and Moyer (1994) of no tax effects on the use of capital leases among a smaller sample of firms.

We examine the central hypothesis by modeling the cross-sectional pattern of the total lease share, or the proportion of total annual capital costs incurred under both capital and operating leases. Since, by construction, observations on this dependent variable vary over the interval between zero and one, we use a cumulative logistic transformation. The equation estimated is

1% TLSi

1 - TLSi = FXi + Ui 2

“We also consider a logit specification using the indicator variable for the presence of capital leases, which yields similar results.

S.A. Sharpe, H.H. NguyenJJournal of Financial Economics 39 (1995) 271-294 287

Table 3 Regression estimates of the capital lease share of PPE

Tobit regressions of net capital leases divided by net property, plant, and equipment, over three separate years (cross-sections). No dividend equals one if firm paid no dividend that year, and is zero otherwise. EBITDA is earnings before interest, taxes, depreciation, and rent expense. S&P rating is an indicator of the firm’s senior debt rating, the omitted category being unrated firms. Tax rate is tax expense divided by pre-tax income. Large (small) tax-loss CF is one if firm had a tax-loss carry-forward exceeding (not exceeding) current-year EBITDA. Size is the natural log of the number of employees divided by 10. Capital intensity is total capital costs divided by the number of employees. Variance of sales growth is the variance of the annual change in ln(sales) over 1985-1991. Also included but not shown are one-digit industry dummies. T-statistics are shown in parentheses.

Specification

No dividend

EBITDA/Sales

S&P ratings: AAA to AA -

A+ toA-

BBB + to BBB -

BB+ to D

Tax rate

Small tax-loss CF

Large tax-loss CF

Firm size

Firm size squared

Capital intensity

Variance of sales growth

# observations

- 0.03 ( - 0.83)

- 0.02 ( - 0.84)

- 0.06 ( - 2.68)

0.04 (2.04)

1986 1988 1991

0.03 0.02 0.04 (2.02) (2.06) (3.42)

0.01 0.12 0.11 (0.11) (2.32) (1.76)

- 0.06 - 0.03 0.01 ( - 1.55) ( - 1.02) (0.18)

- 0.01 - 0.03 - 0.03 ( - 0.42) ( - 1.04) ( - 0.93)

- 0.02 - 0.03 ( - 0.71) (0.92)

- 0.02 - 0.03 ( - 1.39) ( - 1.60)

- 0.04 - 0.04 ( - 2.10) ( - 2.11)

- 0.01 0.03 ( - 0.90) (1.86)

0.06 0.05 (4.44) (3.63)

0.26 0.32 (2.08) (2.32)

- 0.16 - 0.20 ( - 2.18) ( - 1.73) ( - 1.97)

- 0.01 - 0.02 - 0.00 ( - 0.43) ( - 0.84) (0.06)

- 0.01 - 0.01 - 0.01 ( - 1.20) ( - 0.60) ( - 1.28)

2024 2108 1978

0.06 (3.61)

0.42 (2.56)

- 0.25

288 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294

where TLS is the total lease share and Ui is assumed to be normally distributed. In this specification, we control for a firm’s industry by removing two-digit (year-specific) sample industry means from each variable and observation.

Regression results appear in Table 4, where three different specifications for 1986 are shown in the first three columns. In the second and third specifications, we omit either cash flow or firm size, respectively. We also report estimates of the complete specification for 1988 and 1991. In order to interpret estimated magnitudes as local derivatives, coefficients must be multiplied by a scaling factor, exp(@/lxJ/( 1 + exp(YZ/?xJ)2. However, since variables are demeaned by industry, regressor means are always zero, and thus the scaling factor equals 0.25.

Coefficient estimates indicate that non-dividend-paying firms are significantly more reliant on leasing, a result that is robust across all specifications. Accord- ing to the first specification, we estimate that firms that pay no dividends have a total lease share that is 8 percentage points higher (0.32/4) than dividend- paying firms. Perhaps not surprisingly, omitting firm size from the model (specification 3) results in a larger dividend effect. A firm’s reliance on leasing is also negatively related to cash flow (EBITDA/sales) in 1986, though not in later years. This is particularly evident in 1991, when the recession sharply reduced many firms’ cash flows.

The third proxy for information cost differentials is a firm’s bond rating. We find that firms with high bond ratings have a significantly and substantially lower propensity to lease. In fact, estimates suggest that, all else the same, the total lease share of firms in the highest rating category is 15 to 20 percentage points lower that that of the low-rated or unrated firms, while firms in the second-highest rating category fall in the middle.

Coefficient estimates on the large tax-loss carry-forward indicator, and on the tax rate in 1986, again appear to confirm that tax considerations are a significant motivation for leasing. It is interesting to note that the estimated effect of (large) tax-loss carry-forwards rises when cash flow is excluded; thus, cash flow may serve in part as a proxy for tax-related incentives to lease. Conversely, it is also possible that the tax-loss carry-forward variable picks up some of the cost- of-capital effect that cash flow is meant to capture.’

The influence of firm size is negative and significant. Moreover, the positive coefficient on the quadratic term suggests that size matters proportionateiy

‘We also considered ITCs (on the balance sheet) as an indicator of tax-exhaustion. About 4% of our sample firms indicated having deferred ITCs in 1986 and fewer in later years. However, this variable is highly endogeneous relative to the lease share (of outstanding capital), since the amount of a firm’s ITCs should be closely related and caused by the amount of capital the firm had purchased (rather than leased). Indeed, we find that the lease share is negatively and significantly reiated to the presence of ITCs when an indicator for their presence is included in our regressions. In principle, we could sidestep the endogeneity problem by examining the effect of outstanding ITCs on the incremental, or marginal, lease-versus-buy decision, an approach that would be interesting, but is beyond the scope of this paper.

S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294 289

Table 4 Regression estimates of the industry-adjusted total lease share of total capital costs

The dependent variable is the logistic transform of the total lease share (TLS): log[TLS/(l - TLS)]. Total lease share is the sum of operating lease share and capital lease share of total annual capital cost, where total capital cost is the sum of current-year rental commitments and an estimate of the implicit rental cost of net property, plant, and equipment. Operating lease share is current-year rental commitments divided by total capital cost. The capital lease share is the capital lease share of net PPE multiplied by one minus the operating lease share. No dividend equals one if firm paid no dividend that year, and is zero otherwise. EBITDA is earnings before interest, taxes, depreciation, and rent expense. S&P rating is an indicator of the firm’s senior debt rating, the omitted category being unrated firms. Tax rate is tax expense divided by pre-tax income. Large (small) tax-loss CF is one if firm had a positive carry-forward exceeding (not exceeding) current-year EBITDA. Size is the natural log of the number of employees. Variance of sales growth is the variance of the annual change in ln(sales) over 1985-1991. Two-digit industry means are subtracted from all variables.

1986

Specification (1) (4 (3)

No dividend

EBITDA/Sales

S&P ratings: AAA to AA -

A+ toA-

BBB + to BBB -

BB+ to D

Tax rate

Small tax-loss CF

Large tax-loss CF

Firm size

Firm size squared

Age of PPE

Capital intensity

Variance of sales growth

# observations Adjusted RZ

0.32 (5.28)

- 1.57 ( - 4.62)

- 0.67 ( - 5.42)

- 0.18 ( - 1.93)

- 0.19 (- 1.70)

- 0.00 (0.02)

- 0.17 ( - 1.82)

0.09 (1.25) 0.16 (2.49)

- 0.20 ( - 3.23)

0.01 (2.46) 0.71

(4.54) - 0.46

( - 2.06) - 0.01

( - 0.27) 2019 0.18

0.33 0.39 (5.53) (7.30)

- 1.73 (- 5.18)

- 0.82 - 0.72 ( - 6.29) ( - 6.73)

- 0.22 - 0.24 ( - 2.36) ( - 2.90)

- 0.19 - 0.26 (- 1.70) ( - 2.49)

0.01 - 0.07 (0.10) ( - 1.04)

- 0.28 - 0.24 ( - 3.07) ( - 2.65)

0.09 0.08 (1.33) (1.11) 0.26 0.23 (4.16) (3.54)

- 0.25 ( - 4.00)

0.01 (3.16) 0.80 0.76 (5.01) (4.85)

- 0.54 - 0.38 ( - 2.09) ( - 1.87)

0.00 0.00 (0.08) (0.07) 2019 2019 0.16 0.17

1988

0.25 (4.39)

- 0.61 ( - 1.62)

- 0.66 ( - 5.13)

- 0.27 ( - 2.52)

- 0.09 ( - 0.78)

0.04 (0.45)

- 0.04 ( - 0.43)

0.01 (0.19) 0.18

(2.87) - 0.28

( - 3.79) 0.01

(2.97) 1.07

(6.42) - 0.49

( - 3.89) 0.00 (0.07) 2107 0.17

1991

0.22 (4.08)

- 0.19 ( - 0.50)

- 0.72 - 4.69)

- 0.33 - 3.15)

0.05 (0.50) 0.02 (0.21)

- 0.10 - 1.25)

0.06 (0.9 1) 0.25 (3.77)

- 0.36 ( - 5.50)

0.02 (4.35) 1.33

(7.78) - 0.58

( - 7.23) - 0.02

( - 0.42) 1976 0.20

290 S.A. Sharpe, H.H. NguyenJJournal #Financial Economics 39 (199.5) 271~-294

Table 5 Regression estimates of the industry-adjusted operating lease share of total capital costs

The dependent variable is the logistic transformation of the operating lease share (OLS): log[OLS/(l - OLS)]. Operating lease share is current-year rental commitments divided by total capital cost, where total capital cost is the sum of current-year rental commitments and an estimate of the implicit rental cost of net property, plant, and equipment. No dividend equals one if firm paid no dividend that year, and zero otherwise. EBITDA is earnings before interest, taxes, depreciation, and rent expense. S&P rating is an indicator of the firm’s senior debt rating, the omitted category being unrated firms. Tax rate is tax expense divided by pre-tax income. Large (small) tax-loss CF is one if firm had a positive carry-forward exceeding (not exceeding) current-year EBITDA. Size is the natural log of the number of employees. Capital intensity is total capital costs divided by number of employees. Variance of sales growth is the variance of the annual change in ln(sales) over 198551991. Two-digit industry means are subtracted from all variables.

Specification 1986 1988 1991

No dividend

EBITDA/Sales

S&P ratings:

AAA to AA -

A+ toA-

BBB + to BBB -

BB+ to D

Tax rate

Small tax-loss CF

Large tax-loss CF

Firm size

Firm size squared

Age of PPE

Capital intensity

Variance of sales gowth

# observations

Adjusted RZ

0.30 (5.09)

- 1.46 ( - 4.22)

- 0.57 ( - 4.95)

- 0.16 ( - 1.75)

- 0.10 ( - 0.97)

0.06 (0.89)

- 0.10 ( - 1.10)

0.02 (0.26)

0.05 (0.81)

- 0.29 ( - 4.62)

0.02 (3.97)

1.11 (7.26)

- 0.46 ( - 1.97)

0.02 (0.52)

2023

0.17

0.20 (3.69)

- 0.75 ( - 2.61)

- 0.60 ( - 4.89)

- 0.29 ( - 2.69)

- 0.03 ( - 0.29)

0.10 (1.31)

0.06 (0.69)

0.05 (0.76)

0.08 (1.32)

- 0.33 ( - 4.76)

0.02 (4.04) 1.41

(8.65) - 0.48

( - 3.36)

- 0.01 ( - 0.13)

2107

0.17

0.15 (2.75)

- 0.23 ( - 0.61)

- 0.71 ( - 4.72)

- 0.30 ( - 2.87)

0.09 (0.88)

0.06 (0.64)

- 0.06 ( - 0.78)

- 0.02 ( - 0.30)

0.19 (2.93)

- 0.40 ( - 6.21)

0.02 (5.21)

1.58 (9.53)

- 0.57 ( - 7.41)

0.01 (0.30)

1977

0.21

S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294 291

more for small firms. For firms at the low end of the size spectrum, doubling in size is associated with a 5 to 7 percentage point decline in lease share. For firms in the range of 5000 employees (or a size of 8.5), doubling in size is associated with very little decline in lease share. Also, as predicted, we estimate that capital-intensive firms have a smaller total lease share. The positive coefficient on the control for equipment age suggests that the leasing share is substantially overstated because property, plant, and equipment is measured at book value. Finally, the variance of sales growth, our proxy for the option value of leasing, has no marginal predictive power for firm leasing propensity.

We estimate similar regressions for the operating lease share, or the propor- tion of total capital costs associated with rental commitments. As we show in Table 5, the estimated effects of most variables exhibit a pattern of results similar to those found for the total lease share. Again, low bond ratings and the policy of paying zero dividends are strong indicators of firms that are more reliant on leasing. One notable difference is that coefficients on the tax variables are substantially smaller and insignificant in 1988, and especially 1986, suggesting that prior to the implementation of the 1986 tax law, when the investment tax credit was eliminated, a lot of the tax benefits of leasing were obtained under longer-term capital leases.

Finally, we examine whether our framework produces similar inferences for within-firm changes in leasing propensity. We estimate our model for the total lease share - Eq. (6) - using three years of data (1986,1988, and 1991) and a fixed effects estimator on firms with data in at least two of these years. Since it can take several years for marginal financing incentives to be reflected in a firm’s average capital structure, coefficients generated from a within-firm estimator ought to be smaller than our estimates of the analogous cross-sectional effects. (Also, while the R-squares are much lower when compared with the cross- sectional regressions, mean squared errors in the panel (not shown) are about half the magnitude.)

Indeed, as the results in Table 6 show, the signs of estimated coefficients are generally consistent with results from the cross-sectional models (Table 4) although smaller in magnitude. The coefficients on the ratings indicators are about one-quarter the size of the earlier regressions. Nonetheless, the coefficient on the second-highest bond rating indicator remains at least marginally signifi- cant. The coefficient on the no dividend indicator is similarly reduced, but is significant. Within-firm behavior thus offers further support for our interpreta- tion of cross-sectional findings.

5. Conclusions

In summary, we find strong evidence that a corporation’s propensity to lease is substantially influenced by the financial contracting costs associated with

292 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271 294

Table 6 Within-firm panel estimates of the total lease share of total capital costs using observations from 1986, 1988, 1991

The dependent variable is the logistic transformation of the total lease share (TLS): log[TLS/( 1 - TLS)]. Total lease share is the sum of operating lease share and capital lease share of total capital cost. No dividend equals one if firm paid no dividend that year, and is zero otherwise. EBITDA is earnings before interest, taxes, depreciation, and rent expense. S&P rating is an indicator of the firm’s senior debt rating, the omitted category being unrated firms. Tax rate is tax expense divided by pre-tax income. Large (small) tax-loss CF is one if firm had a positive tax-loss carry- forward exceeding (not exceeding) current-year EBITDA. Size is the natural log of the number of employees.

Specification

No dividend

EBITDA/Sales

S&P ratings:

AAA to AA -

A+ toA-

Model 1 Model 2 Model 3

0.06 0.07 (2.10) (2.19)

- 0.44 ( - 2.47)

- 0.10 -0.11 ( - 1.12) ( - 1.14)

- 0.08 - 0.08

0.09 (2.86)

- 0.51 - 2.77)

BBB + to BBB -

BB + to D

Tax rate

(- 1.51) ( - 1.55) ( - 2.25)

- 0.01 - 0.01 - 0.04 ( - 0.15) (-0.11) ( - 0.71)

0.00 0.00 - 0.03 (0.02) (0.02) ( - 0.67)

- 0.05 - 0.06 - 0.05 ( - 1.40) ( - 1.96) (- 1.54)

Tax-loss CF 0.01 (0.37)

Firm size

Age of PPE

- 0.13 ( - 4.87)

0.82 (7.61)

Year 1988 - 0.05 ( - 3.77)

Year 1991 - 0.01

0.02 0.02 (0.65) ( - 0.67)

- 0.13 - 4.98)

0.83 0.92 (7.72) (8.59)

- 0.05 - 0.07 - 3.93) ( - 5.09)

- 0.01 - 0.03 ( - 0.33) ( - 0.31) (- 1.67)

# observations 5771 5771 5771

Adjusted R2 0.05 0.05 0.04

S.A. Sharpe. H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294 293

information problems. The main results concern the total lease share, or the percentage of firms’ total annual costs of property, plant, and equipment use accounted for by capital or operating leases. After controlling for firm size and other factors, our estimates suggest that the total lease share of a low-rated firm that pays no cash dividends is about 25 percentage points higher than that of a highly rated dividend-paying firm. Not surprisingly, we also find that tax-related motivations help explain the relative propensity to lease.

Given that equipment under lease accounts for nearly a third of the total annual new equipment investment in the U.S. in recent years, the implications of these findings are clearly far-reaching. Our results suggest that a comprehensive analysis of corporate capital structure should not disregard the role of leasing, which serves as a means of alleviating financial contracting costs. Our results also suggest that microeconomic studies of fixed capital investment and its dynamics should consider the role of off-balance-sheet financing as reflected in rental expense. For example, our finding that leasing by small firms substantially exceeds that of large firms, particularly in manufacturing; suggests that current research focusing on the relative behavior of small- versus large-firm investment can generate misleading conclusions to the extent that these studies ignore the leasing option. Indeed, an examination of the dynamics of lease financing and equipment investment should prove fruitful in future research.

References

Ang, James and Pamela P. Peterson, 1984, The leasing puzzle, Journal of Finance 39, 105551065. Bayless, Mark E. and J. David Diltz, 1988, Debt capacity, capital leasing, and alternative debt

instruments, Akron Business and Economic Review 19, 77-88. Brealey, Richard and Stewart Myers, 1984, Principles of corporate finance (McGraw-Hill, New

York, NY) 629-645. Calomiris, Charles W. and R. Glenn Hubbard, 1993, Internal finance and investment: Evidence from

the undistributed profits tax of 193661937, Working paper (National Bureau of Economic Research, Cambridge, MA).

Fazzari, Steven M., Glenn R. Hubbard, and Bruce C. Petersen, 1988, Financing constraints and corporate investment, Brookings Papers on Economic Activity 1, 141-195.

Financial Accounting Standards Board, 1976, Accounting for leases, Statement of Financial Stan- dards No. 13 (FASB, Stamford, CT).

Flath, David, 1980, The economics of short-term leasing, Economic Inquiry 18, 243-255. Harris, Milton and Arthur Raviv, 1991, The theory of capital structure, Journal of Finance 46,

2977356. Krishnan, V. Sivarama and R. Charles Moyer, 1994, Bankruptcy costs and the financial leasing

decision, Financial Management 23, 3 l-42. Lewis, Craig M. and James S. Schallheim, 1992, Are debt and leases substitutes?, Journal of

Financial and Quantitative Analysis 27, 4977511. McConnell, John L. and James S. Schallheim, 1983, Valuation of asset leasing contracts, Journal of

Financial Economics 12, 237-261.

294 S.A. Sharpe, H.H. Nguyen/Journal of Financial Economics 39 (1995) 271-294

Miller, Merton and Charles Upton, 1976, Leasing, buying, and the cost of capital services, Journal of Finance 3 1, 761-786

Myers, Stewart C., 1977, Determinants of corporate borrowing, Journal of Financial Economics 5. 147-175.

Myers, Stewart C. and Nicholas S. Majluf, 1984, Corporate financing decision when firms have investment information that investors do not, Journal of Financial Economics 13, 1877220.

Myers, Stewart C., David A. Dill, and Albert0 J. Bautista, 1976, Valuation of financial lease contracts, Journal of Finance 31. 799-819.

O’Malley, Michael, 1994, The effects of taxes on leasing decisions: Evidence from panel data, Mimeo. (Federal Reserve Board, Washington, DC).

Schallheim, James C., Ramon E. Johnson, Ronald C. Lease, and John McConnell, 1987, The determinants of yields on financial leasing contracts, Journal of Financial Economics 19,45567.

Smith, Clifford W. and L. MacDonald Wakeman, 1985, Determinants of corporate leasing policy, Journal of Finance 40, 895-908.

Smith, Clifford W. and Jerold B. Warner, 1979, Bankruptcy, secured debt, and optimal capital structure: Comment, Journal of Finance 34, 247-251.

Smith, Clifford W. and Ross L. Watts, 1992, The investment opportunity set and corporate financing, dividend, and compensation policies, Journal of Financial Economics 32, 263-292.

Strauss, Robert D., 1991, Equipment lease under UCC Article 2A: Analysis and practice suggestions, Commercial Law Annual (Callaghan & Company, Atlanta, GA).

Stulz, Rent M. and Herb Johnson, 1985, An analysis of secured debt, Journal of Financial Economics 14, 501-521.

Sweig, Allan G. 1993, Why the equipment lessor will usually fare well in the bankruptcy of the equipment lessee, Presented in Conference on New Opportunities in Lease Finance (Institute for International Research, New York, NY).

Wolfson, Mark A., 1985, Tax, incentive, and risk-sharing issues in the allocation of property rights: The generalized lease versus buy decision, Journal of Business 58, 159-171.

Zall, Milton, 1993, The implications of UCC Article 2A, Equipment Leasing Today 5, Oct., 27-30.