capital market – an overview - Conference

31

171 | Page “CAPITAL MARKET – AN OVERVIEW” Part of my thesis on "Impact of Foreign Institutional Investors on Indian Capital Market Volatility By RAM KUMAR GOYAL Research Scholar Registration No.: 13BSUJPPH004, ICFAI University, Jaipur

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of capital market – an overview - Conference

171 | P a g e

“CAPITAL MARKET – AN OVERVIEW”

Part of my thesis on

"Impact of Foreign Institutional Investors on Indian Capital

Market Volatility

By

RAM KUMAR GOYAL

Research Scholar

Registration No.: 13BSUJPPH004,

ICFAI University, Jaipur

172 | P a g e

CHAPTER 1

CAPITAL MARKET- AN OVERVIEW

1.1 Introduction to Capital Market

1.1.1 Structure of Capital Market

1.1.2 Major Players in the Market

1.1.3 Functions of Capital Market

1.1.4 Types of Capital Market

1.2 History and Development of Capital Market

1.2.1 World

1.2.2 History and Development of Capital Market in India

1.3 Primary Market

1.3.1 Introduction

1.3.2 Type of Issues in Primary Market

1.3.3 Type of Investors in Primary Market

1.3.4 Pricing Issues in Primary Market

1.3.5 The Book Building Process

1.3.6 Some New Concepts of Primary Market

1.3.7 Resource Mobilization from International Capital Market

1.4 The Secondary Market

1.4.1 Introduction

1.4.2 Development of Stock Market in India

1.4.3 Functions of Secondary Market

1.4.4 Stock Market Index

1.5 The Bombay Stock Exchange Limited (BSE)

1.6 National Stock Exchange Limited (NSE)

173 | P a g e

1.1 Introduction to Capital Market:

Capital markets are financial markets which can be defined as “The market for long-term funds where securities

such ascommon stock, preferred stock, and bonds are traded as well as long term funds (both equity and debt funds)

are raised within and outside the country”. Both the primary market for new issues andthe secondary market for

existing securities are part of the capital market.

In other words capital market deals with all operations of new issues – primary market and buying & selling of

securities – secondary market. New issues made by companies constitute the primary market, while trading

inexisting securities comprise secondary market. In simple terms, capital market covers all activities of financial

institutions, non banking finance companies etc to meet long term financial requirements which is normally

considered as more than one year period.

The capital market helps in mobilizing savings of the economic sectors anddirecting them towards productive

usewhich aids in maintaining economic growth. Following measures are adopted to facilitate mobilization of savings

from economic sectors:

New issues „primary securities‟ - „primary market‟: Mobilization of funds from cash surplus sector to cash

deficit sector such as the government and the corporate sector.

Issue of „secondary securities‟ - „primary market‟: Mobilization of funds from cash surplus sector to

financial intermediaries such as banking as non-banking financialinstitutions.

Secondary market – buying & selling of securities facilitateliquidity in the market.

Secondary market plays pivotal role in mobilizing funds by attracting investors as this market ensures quick exit at

nominal cost. To maintain growth, market liquidity plays an important role. Number of profitableprojects requires

long term financial investment. Many investors are reluctant to invest in such long gestation project as they

relinquish control over their savings. Secondary market provides a platform by ensuring investors quick exit at

nominal cost and helps in mobilization of funds. Hence, existence of an efficient capital market is necessary for

creating conductive climate for investment and economic growth.

1.1.1 Structure of Capital Market:

Capital market in India is very vast which constitute number of sub-markets. With the passage of time, in the recent

years, capital market structure has undergone changes to match the international developments.

The sub-markets of capital market are as below:

Market for Corporate Securities: The market for corporate securities - primary and secondary market are utilized

by business establishments / corporates for funds mobilizing.

174 | P a g e

Market for Government Securities: The market for government securities includesthemarket for T-bills and long

term government debts.

Market for Derivatives: This market is considered as part of corporate securities orgovernment securities but due

to the increasing popularity ofderivatives, now derivatives market is considered as separate section of the

capitalmarket.

The Market for Debt Instruments: This market includes debenturesand bonds of private sector, bonds of PSUs,

public financial institutions etc.

The Market for Mutual Funds: This isnew development in Indian capitalmarkets. Earlier, only UTI was

authorized to act as mutual fund. However, now evenprivate enterprises can also enter in the mutual funds market.

Therefore, mutualfund market is fast developing and has become an important part of capital market.

As far as individual investors are concernedthe market of corporate securities, derivatives and mutual funds are more

relevant.

1.1.2 Major Players in the Market:

The players in the capital market can be divided into following two broad areas.

Players in Primary Market:

A) Merchant Banker: For the success of primary market, merchant bankers plays very crucial role. Merchant

bankers acts as issue managers, lead managers, co-managers and areresponsible to the company and SEBI.They are

authorized to take all policy decisions for and on behalf of company in connection new issue. They also coordinate

with different agencies and responsible to provide “Due Diligence” certificate to the SEBI for true disclosures in

compliance to law and SEBI guidelines.

B) Registrars: In the success primary market, role of registrars is equally important. Registrars are responsible for

collecting applications for new issues, cheque, stock invest etc., classify and computerizethem. Registrars are also

responsible for making allotments in consultation with the regional stockexchanges in the event of over subscription

and in presence of publicrepresentative.

Registrars are responsible to dispatch the letters of allotments, refund orders and share certificates withinthe time

schedules stipulated under the companies act as well as in compliance of guidelines issued by SEBI, Government,

and RBI. In addition, Registrars have to comply with the listing requirements and get the new issue listed at one or

more stock exchanges.

C) Collecting and Coordinating bankers: The collecting and coordinating banks may besame or different.

Collecting bankers are responsible to collect cash, cheque, stock invests etc.Coordinating bankers are required to

collect the information on subscriptions and co-ordinate & monitor the collection work and submit their report to

registrars and merchant bankers for informing the company.

175 | P a g e

D) Underwriters and Brokers: Underwriters are responsible to mobilize the subscription up to specified / agreed

limit. They may be financial institutions, banks, mutualfunds, brokers etc. In case of shortfall of subscription,

underwriters have to subscribe the shortfall up to the agreed limit. Brokers are responsible to market the new issues

utilizing their network of clients / branch offices, sub-brokers etc

E) Printers, advertising and mailing agencies: These are other service providers helping in success of new issues

by providing specific services.

Secondary Market Intermediaries:

In the secondary market, the main functionaries are issuers ofsecurities, companies, intermediaries like brokers, sub-

brokers etc., andinvestors who bring in their savings and funds into the market.

The stock brokers are of various categories, namely:

Member Brokers: They are members of stock exchanges and do simple broking between buyers and sellers. They

are responsible for settlement of accounts between client and exchanges.

Sub-Brokers: They carry out broking activities between client and member brokers.They are responsible for

settlement of accounts between client and member broker.

Arbitrageurs: The brokers, who do inter market deals for a profit through differences inprices as between markets,

say buy in BSE & sell in NSE and visa-versa.

1.1.3 Functions of Capital Market:

There are following functions of efficient capital market:

Mobilizing savings to finance long-term investments.

Provide risk capital in form of equity or quasi-equity to entrepreneurs.

Encourage broader ownership of productive assets.

Provide liquidity with a mechanism enabling the investors to sell financial assets.

Lower the cost of transaction and information.

Improve the efficiency of capital allocation through competitive pricing mechanism.

Disseminate into efficiently for enabling participants to develop an informed opinionabout investment,

disinvestment, reinvestment or holding a particular financial asset.

Enable quick valuation of financial institutes both equity & debt.

Provide insurance against market risk on price risk through derivative trading anddefault rise through

investment protection fund.

Enable wider participation by enhancing the width of the market by encouraging individuals.

Provide operational efficiency through.

176 | P a g e

Simplified transaction procedures;

Lowering settlement timings; and

Lower transaction cost,

Develop integration among.

Real and financial sectors,

Equity and debt instruments,

Long-term & short-term funds,

Long-term & short-term invest cost,

Private & government sectors, and

Domestic &external funds,

Directthe flow of funds into efficient channels through investment, disinvestment &reinvestment.

1.1.4 Types of Capital Market:

There are following three types of capital marketbased on their functions & type of operations:

Primary Market

Secondary Market and

Debt Market.

These markets have been explained in detail later in this chapter.

1.2 The History and Development of Capital Market:

With the passage of time, there have been changes in the capital market to meet investor needs as well as minimize

the risk to investor‟s community. Researcher has studied the available literature and summarized the development

story ofcapital market at world and India level as under:

1.2.1 World

1.2.1.1 Introduction:

In order to raise capital, securities (shares) are issued by companies in favor of investors which are traded on stock

exchanges. Capital collected by issuance of shares by companies is not to be returned and shareholders are co-owner

of company and have the right to influence corporate decision making as well as to receive dividend from the

company profits (paid out to shareholders). This is in contrast to debt market where collected funds have to be

returned along with agreed interest. In case of bankruptcy, share holders have right to obtain their share from sale

proceedings of company assets after repayment of debts. The transactions of issuance of shares directly by company

177 | P a g e

to investors are known as primary stock market. Buying & selling of stocks between investors & traders are known

as secondary stock market.

From the above, it is learnt that existence of stock market needs securities (stocks) which can be issued by

companies. Hence, there is a requirement of companies / joint-stock companies / corporations for existence of

capital market. Formation of Joint Stock Companies were started in early seventeenth century including the Dutch

East India Company which in the year 1617 had 954 shareholders (Davies 1961). However, free incorporation of

companies became widespread only in nineteenth century (after removing the need of government authorization –

the purpose of authorization) in United States and played a prominent role in raising capital which helped United

Status to become industrial power (Braithwaite and Drano‟s 2000). In reality, formation of corporations /

companies transformed the whole economy as dependence on family firms avoided. To run the business,

Corporation / companies were able to raise capital from thousands / millions of investor‟s scattered all over the

places and there was no single owner.

As primary stock markets are necessary for issuance of shares to investors, secondary stock market is required for

trading of stocks between investors and traders, Both are dependent of each other and are required for survival of

capital market. Initially trading was done directly between investors on an over – the – counter (OTC) market.

Slowly, for overwhelming share, trading became centralized at meeting places of professional stock traders. These

either used to collect orders from investors or trade on their account. The concentration of trading between specified

time and space resulted in easier trading for traders & exchange information‟s etc. led to creation of stock exchanges

for stock trading with established rules (Laulajainen 2003).

The world first stock exchange at Amsterdam was established in 1602 to trade the shares of Dutch East India

Company. In 1795 French troops invaded Amsterdam resulting London Stock Exchange (LSE) emerging as premier

stock exchange which dominated the market until 1914.

During this period, New York Stock Exchange led in terms of size.

In mid-nineteenth century, due to free incorporation of corporations / companies in Europe and North America, the

formation of new corporation / companies was at fast pace resulting in creation of stock exchange in most of the

major cities. In addition, exchanges were also developed in Latin America, Africa, Asia, Australia, and Oceania. The

invention of telegraph and telephone helped transfer of information‟s at fast pace resulting in integration of

exchanges.

With the growth of economy, one of main objective of stock exchanges was to establish the value of individual

company shares. Large number of transactions, high liquidity of security in stock market leads to price discovery.

178 | P a g e

There was no upper limit on share price and lower limit was ZERO. Therefore, investment in stocks was considered

risky which may give higher returns in long run in comparison to the safe investment.

For example – US markets have yielded an arithmetic average 8.7 percent per year aboveinflation from 1900 to

2000 with the standard deviation of 20.2% compared to US bonds with real returns of 2.1% per year with standard

deviation of 10% (Dimson et al. 2002).

In US during 1929, there was crash in stock market mainly due to great depression. This triggered milestone for

regulation. The Securities and Exchange Act was passed in 1933 which was followed by establishment of Securities

and Exchange Commission in 1934 and introduced:

o Strict entry requirements for companies willing to list on stock exchanges,

o Reporting duties for listed companies,

o Separation of investment from universal banking to insulate universal banking from stock market volatility

This regulatory model of stock market was adopted in many parts of the world (with significant modifications).

Number of countries emulated it. For example, Japan was persuaded to adopt the same by US military in 1940‟s.

From the above, it is to be noted that, till 1930‟s, stock exchanges were largely private clubs of traders. From

1940‟s, these exchanges were either government controlled or semi – public institutions. From 1970‟s, there were

gradual globalization of stock markets.

With the development and adoption of new technology by stock exchanges, there was no need of traders meeting at

one place. Orders are processed automatically and making virtual trading possible. In response, number of stock

exchanges become private publicly listed companies and redefined them with new IT technology.

In view of economy and technology development, many companies went for international listing after raising capital

from international market. Investors also started trading in these securities which has necessitated the requirement of

international regulation. Considering the investors risk, in 1983, International Organization of Securities

Commissions was established. Within European Union, number of steps were undertaken to stream the process of

listing rules as well as clearing and settlement.

Currently, in terms of size significance, stock markets are no more linear and are a continuous process of expansion.

First World War resulted in subdued stock market activity n Europe (with equitycrowded out by government

borrowing). However, it continued to boom in the United States, with unprecedented spread of corporate ownership,

exemplified by ATT owned by approx. 0.5 millionpeople in 1930. The Great Depression in US halted this

development. In 1939, the turnover of NYSE was less than 10 per cent of that in 1929 and less than half of 1920

(Michie 2006). Also stock market activity remained subdued even after Second World War. Stock market activities

179 | P a g e

picked up in late 1970‟s with deregulation of stock exchanges, rise of institutionalinvestors, privatization of the

corporate sector, as well as technological advancement.

1.2.1.2 Unprecedented recent growth with a qualification

Stock markets are playing very important role in the development of world economy as it can beseen in the start of

twenty-first century.There is unprecedented growth in spread of stockmarkets globally. In 1980, when the

UnitedNations (UN) had 154 member states, fifty-nine countries had a stock exchange (Clayton et al.2006). In July

2010, out of 192 members of the UN, 134 hosted a stock exchange and furtherthirteen are covered by regional stock

exchange arrangement (East Caribbean SecuritiesExchange and West Africa Regional Exchange). There are only

twenty-one countries with apopulation over one million, which did not have stock exchange. In these countries,

delay in spread of exchanges is not due to economic activities but mainly centers around the political will.

The recent growth of stock markets has also been unprecedented in terms of size. In 2010, therewere approx. 45,000

listed companies in the world, almost twice more than twenty years earlier(World Federation of Exchanges 2010).

Since 1990, companies around the world have raisedapprox. $2.5 trillion through IPOs. The global stock market

capitalization, the total market value ofoutstanding publicly traded equity at the end of 2015 was close to $81

trillion, eight times that in1990 (Figure 1.1). This represented nearly 100 per cent of the world‟s gross domestic

product

(GDP), while in 1913 (at the end of a long period of dynamic stock market development) the ratiowas close to 50

per cent (Rajan and Zingales 2003b). This growth was most spectacular inemerging markets. Figure 1.2 shows the

change in market capitalization (MC) since 2002. The topof the graph is occupied by emerging market economies,

many with more than a fivefold growth,despite the downturn of 2008. The very notion of emerging markets has

been commonly associatedwith stock markets rather than any other part of their economies or financial markets.

180 | P a g e

Figure 1.1 Stock Market Capitalizations, 2000-2015

Stock markets have grown not only in terms of extensity (geographical spread) and intensity (sizein relation to the

economy), but also in terms of velocity. Since 2000, the total number of stocktrades has increased eightfold (World

Federation of Exchanges 2010). While in late 1980s, stockexchanges could boast of executing tens of trades per

second, in 2010 some exchanges can handle amillion transactions within a second. The increased velocity has been

enabled by technology butalso deregulation driving the trading costs down.

In the last decade the growth in secondary stock markets outpaced that in primary stock markets. Insimple terms, the

stock market development took the form of much larger trading activity for stocksalready listed, rather than bringing

new companies to the stock market. While the United Kingdom and particularly emergingmarkets steamed ahead

with new listings, in the United States the number of listed companies fellby 28 per cent. In many Western European

countries, primary stock markets also contracted orstagnated. The year 2000 was the peak of the Internet boom,

which brought thousands of newcompanies around the world to stock market. When the bubble burst, hundreds of

companiesleft the public stock market. In some developed economies,theprimary stock market still has not

recovered

1.2.2 History and Development of Capital Market in India:

1840-50 Half a dozen brokers‟ commenced trading under a banyantree near called Horniman

Circle at Mumbai known as BSE.

1856 Government implemented Securities Contract (Regulation) Act to strengthenthe role of

government in Indian Capital Market.

1860-65 Number of brokers increased to about 250in BSE but they were finding difficult to find

a place for their regular meetings.

1874 The broking community find a place in what is now called Dalal Street

to conduct their dealings in securities without hindrance and informalassociationcame

into existence.

July 1875 Share and Stock Broker Association with aim of „protecting the

character, status and interests‟ of 3,128 members were formed who pay an entrance fee

of one rupee.

181 | P a g e

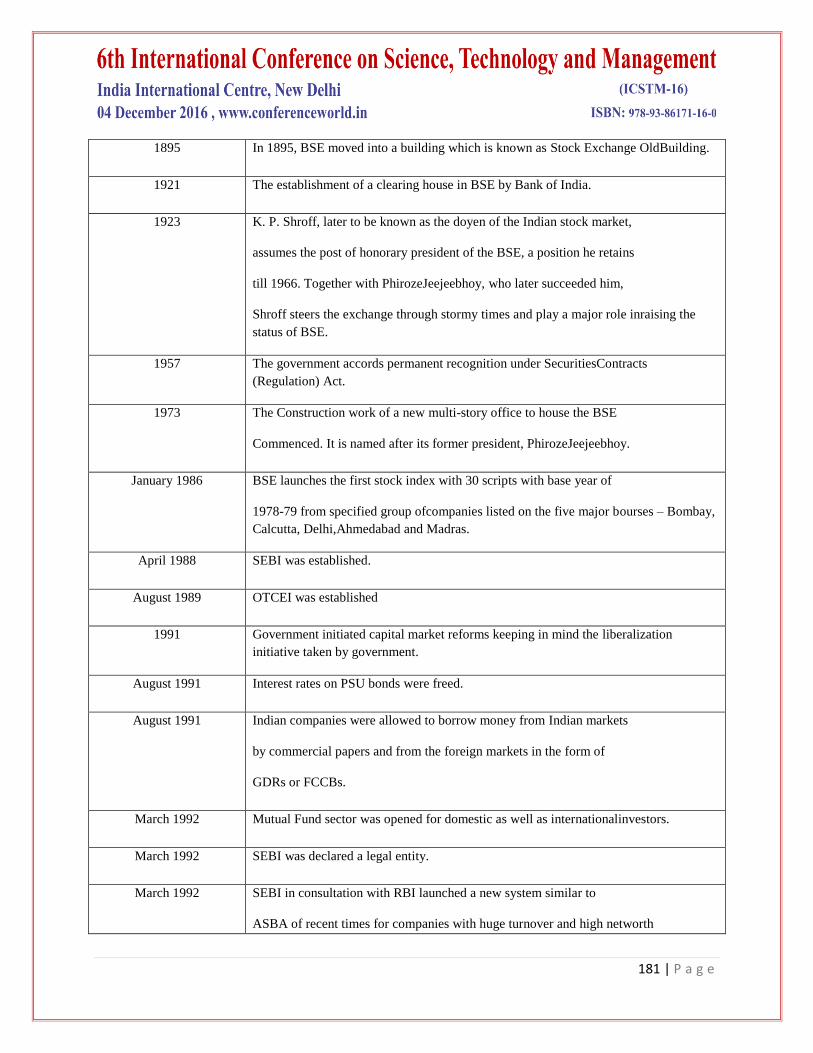

1895 In 1895, BSE moved into a building which is known as Stock Exchange OldBuilding.

1921 The establishment of a clearing house in BSE by Bank of India.

1923 K. P. Shroff, later to be known as the doyen of the Indian stock market,

assumes the post of honorary president of the BSE, a position he retains

till 1966. Together with PhirozeJeejeebhoy, who later succeeded him,

Shroff steers the exchange through stormy times and play a major role inraising the

status of BSE.

1957 The government accords permanent recognition under SecuritiesContracts

(Regulation) Act.

1973 The Construction work of a new multi-story office to house the BSE

Commenced. It is named after its former president, PhirozeJeejeebhoy.

January 1986 BSE launches the first stock index with 30 scripts with base year of

1978-79 from specified group ofcompanies listed on the five major bourses – Bombay,

Calcutta, Delhi,Ahmedabad and Madras.

April 1988 SEBI was established.

August 1989 OTCEI was established

1991 Government initiated capital market reforms keeping in mind the liberalization

initiative taken by government.

August 1991 Interest rates on PSU bonds were freed.

August 1991 Indian companies were allowed to borrow money from Indian markets

by commercial papers and from the foreign markets in the form of

GDRs or FCCBs.

March 1992 Mutual Fund sector was opened for domestic as well as internationalinvestors.

March 1992 SEBI was declared a legal entity.

March 1992 SEBI in consultation with RBI launched a new system similar to

ASBA of recent times for companies with huge turnover and high networth

182 | P a g e

individuals.

May 1992 SEBI Act established ( An Act to protect, develop and regulate the

securities market)

May 1992 Capital Issues (Control) Act repealed

June 1992 Securities Appellate Tribunal (SAT) Established BSE.

October 1992 OTCEI started its functioning.

November 1992 National Stock Exchange (NSE) India‟s first electronicstock exchange was

incorporated.

1992-1995 Opening of Indian economy by permitting foreign investment in Indian companies.

April 1993 NSE was recognized as stock exchange.

June 1994 Wholesale Debt market goes live on NSE.

November 1994 Capital market (equities) goes live on the NSE.

March 1995 BSE introduced On-Line Trading System BOLT.

March 1995 NSE establishes investors Grievances Cell.

April 1995 Establishment of NSCCL, the first clearing corporation.

July 1995 Establishment of the Investors Protection Fund by NSE.

October 1995 NSE becomes the largest stock exchange of the country.

January 1996 Badlatrading now limited to only few group A scripts.

March 1996 SEBI formulated guidelines of mandatory disclosures for listedcompanies.

April 1996 Commencement of clearing and settlement by NSCCL

April 1996 Launch of the S&P CNX Nifty.

June 1996 Establishment of Settlement Guarantee Fund by BSE

November 1996 Setting up of the National Securities Depository Limited, first depositoryin India, co-

183 | P a g e

promoted by the NSE.

December 1996 Commencement of trading/settlement in de-materialised securities on

NSE.

1997 BSE On-Line Trading (BOLT) system expands nation wide

March 1999 Central Depository Services Limited (CDSL) was launched by BSE.

June 2000 Equity Derivatives were introduced in India by BSE.

June 2000 Commencement of Derivative trading on NSE (Index Futures).

February 2001 BSE Webx Launched

December 2001 All securities turn to T+5 for settlement on BSE.

April 2002 T+3 trading introduced on BSE.

April 2003 BSE introduces T+2 Settlement.

August 2005 Incorporation of Bombay Stock Exchange Limited.BSE now becomes a corporate

entity.

March 2007 Singapore Stock Exchange Limited entered into an agreement to invest a

5% stack in BSE.

August 2008. Launch of Currency Derivatives on NSE.

October 2008 Launch of Currency Derivatives on BSE.

February 2010 Launch of Currency Futures on additional currency pairs

September 2010 BSE for the first time in India launched Mobile- Based trading.

Source: BSE, NSE, OTCEI and SEBI composed by researcher.

1.3 The Primary Market

1.3.1 Introduction:

184 | P a g e

Primary market is the market through which company‟s issues securities directly to investors to raise fresh capital

through prospectus, right issues, & private placement. Bonus shares are issued to investors from the free reserves

generated by company. Hence, bonus shares do not bring fresh capital to company but company capital is

restructured.

Higher the free reserves, higher are the chances of a bonus issue forthcoming from the corporate. Issue of bonus

shares creates excitement among investors and is well appreciated as they do not have to pay and they add to their

wealth.

There are number of reasons to issue bonus share by companies:

For better investor confidence and fulfill their expectations,

Improved liquidity of stocks: bonus shares expand equity base by increasing free float,

Lower the share price: Normally retail investors prefer to buy low price stocks,

Restructure the capital

1.3.2 Type of Issues in Primary Market:

Basically, stocks can be classified as Public issues, Rights issues and preferential issues (Private placements)as

detailed below:

Public issue: Shares are issued by company to investors either through Initial Public Offering (new or unlisted

company), offer for sale by existing company, or both for the first time to the public. This provides a gateway

for listing & trading of stocks.

185 | P a g e

Rights Issue: shares are issued to existing share holders on right basis,

Preferential issue / Private placement: In this case shares or convertible securities are issued to selected group of

people under Section 81 of the Companies Act, 1956. This is a faster way to raise capital.

1.3.3 Types of Investors in Primary Market:

SEBI has classified investors into following major categories:

Retail Investors: Individual investors spread over across the country. Financial limit of retail investors is INR

150,000/=

Qualified institutional Buyers: Financial institutions, banks, FIIs & Provident funds investors.

Non-Institutional Investors: Investors which do not fall in the above categories.

As per SEBI guidelines, of the entire amount, maximum limit of QIBs, Retail and Non-Institutional investors

are 50%, 35%, and 15% respectively.

1.3.4 Pricing Issues in Primary Market:

Prior to 1992, Controller of Capital Issue (CCI) used to regulate the primary market under Capital Issue (Control)

Act 1947 and issue price of stocks (issued through primary market) was decided by them within specified

guidelines. To calculate the issue price, basic consideration was net asset value and price earning value. The

permission was mandatory to issue capital beyond 1,00,00,000 or any amount from public at premium.

In 1992, all controls relating to pricing the issue were removed. SEBI has no major role to play in pricing the issue.

The issuer and merchant bankers were allowed to decide issue price without any restriction by disclosing the

financial & non-financial parameters which are considered in pricing the issue. This gave the way of issue pricing.

Number of promoters and merchant bankers entered the capital market with rosy and unrealistic projections & sold

the shares at very high price. These projections never materialized and killed the primary market. Out of 4000 issues

during 1992 – 96, more than 3000 were issued at very high premium. On the day of listing, majority of issues quoted

below issue price.

1.3.4.1 Free Pricing and SEBI Guidelines:

Under free pricing policy issuer Company, in consultation with merchant banker and shareholder approval, are free

to decide the share price. Companies are now free to raise funds from capital market to meet various type of

186 | P a g e

business requirement by providing adequate information in the offer document to safeguard investor‟s interest.

Companies are keen on raising maximum capital (issue with higher premium) to get more capital at cheap rate.

In accordance of SEBI guidelines of free pricing on capital issues, following categories of companies are permitted

to price their offers freely:

o New companies established by individual promoters.

o Existing companies with 4 years track record of consistent profitability.

o Existing listed companies.

o Existing closely held companies and other unlisted companies with or without 3 years track record of

consistent profitability.

New companies are required to price their issues at par. According to SEBI‟s guidelines, clause 8.8.1, subscription

list of public issues shall be keptopen for at least 3 working days and not more than 10 working days. In case of

book builtissues, the minimum & maximum period for which binding will be open is 3 to 7 days which is extendable

by 3 days in case of revision in the price-band. The issue of Infrastructure Company, meeting requirements in clause

2.4.1(iii)of chapter II, may be kept open for a maximumperiod of 21 working days. As per clause 8.8.2, rights issues

shall be kept open for at least 30days and not more than 60 days.The investors are entitled to receive a confirmatory

allotment note (CAN) in case they havebeen allotted shares, within 15 days from the date of closures of a book built

issue. The registrarhas to ensure that the DEMAT credit or refund as acceptable is completed within 15 days fromthe

date of closure of the book built issue.The listing on the stock exchanges is to be done within 7 days from the

finalization of the issue.

1.3.4.2 Types of Pricing Issues:

For pricing the issue, following two methods are followed.

Fixed Pricing:

The issuer company, in consultation with merchant banker and shareholder approval, decides the issue price and

provide the adequate information in the offer document along with basis of calculating the cost of premium, if

applicable. The issuer company is required to discloseindetail the various qualitative & quantitative factors that have

been considered and havebeen instrumental in demining the issue price. These shares are to be listed within 37 days

post issue closure.

Book Building:

In accordance of SEBI guidelines, book building is defined as“process under taken by which a demand for the

securities proposed to be issued by acorporate body is elected, built up & the price for the such securities is accessed

for thequantum of such securities to be issued by means of a notice, circular, advertisement orinformation

memoranda or offer document.” In case of book building issue, price of an issue is discovered based on demandfor

the equity at various pricelevels. Book building is the process of pricediscovery. Price band is disclosed by the

187 | P a g e

company to the market before opening the issue of offered securities based on the demands received at various

levels. Thus, book building process gives anopportunity to the market to discover price for individual securities.

The issuer company has to disclose in the offer document based on which it has setthe price band. So the issuer

company along with its merchant bankers disclosesin detail the various qualitative & quantitative factors that are

considered and areimportant in justifying the issuer price. After the bidding process is complete, the cut-offrate is

decided.

1.3.5 The Book Building Process:

There are following steps in book building to complete the task of price discovery:.

o The issuer appoints a merchant banker,

o The merchant banker prepares the document in accordance with SEBI guidelines and submits the same as

draft document to SEBI and obtains the acknowledgement card.

o The issuer and merchant banker decide to price band of offer shares,

o Offers regarding the demand for securities at different price levels are invited from Syndicate mutual funds

and others. The advertisement should mention the opening andclosing date for the bids. A bid usually

opens for a minimum of 5 working days.

o Based on the bids received the issuer arrives at the final cut-off price and complete the allocationin

consultation with merchant banker & lead manager.

o The issuer and merchant banker may impose restrictions on number of allotted sharesto avoid takeover

threat.

o Thereafter, final prospectus is filled with the registrar of companies (ROC) along with all necessary

documents,

o The placement portion opens only After filing the prospectus with ROC, placement process starts,

o QIB portion closes one day before closing of public offer.

o Lastly, public portion opens, shatter are allotted which is followed by listing of shares.

As per SEBI guidelines, book built issue shall offer:

Not less than 50 per cent to Qualified Institutional Buyers (QIBs)

Not less than 25 percent to retail investors.

Rest may be allotted to non-individual buyers or high network individuals.

1.3.5.1 Benefits of Book Building Method:

The benefits of book building issues can be divided into two following portion:

188 | P a g e

Benefits to the Issuer:

Helps issuer to maximize benefits arising from price & demand discovery.

Less chances of under subscription,

Lesser cost and time in execution,

Simplified procedure.

Benefits to Investors:

Can trust the price as syndicate members have purchased the securities at the same price,

Remote chances of price falling below par afterlisting.

1.3.5.1 Limitations of Book Building:

In India book building process is still at its nascent stage and is quite different from that of developed countries

which are detailed as below:

o In developed countries, road shows are held and issue price is arrived few hours before the issue opens.

Lead manager offers two way quotes in the secondary market till trading picks up. In India, there is no such

provision.

o In developed countries, book building process relies on interaction between companies, merchant bankers

& investors. Same is missing in India and faith & reputation still plays key role in India. Lack of

transparency at critical steps & absence of strong regulation.

o Advertisements of book built issues to retail investors are not necessary. Hence, increased chances of

negotiated deals getting through.

o Price discovery mechanism is not proven. Number of issues has listedbelow their issue price.

o Issuers try to price the stock at maximum price due to collective bargaining power ofinstitutions.

o Larger institution holdings may affect the stock‟s liquidity resulting in volatile behavior.

o There is no role of retail investors in pricing the issue. Also, retailinvestors may not have the correct

information to judge the issue and thus, are not able to arriveat the correct pricing.

o Limits of allotments are flexible and can be adjusted based on market response. In case of low retail

demand, more then 75% of issue is allocated to the institutionalinvestors.

o Many IPOs after 1999 have badly failed and are still trading below issue price.

o In is necessary for SEBI to revise the guidelines of book building process pricing in the interest of investors

as well as gain market confidence.

o Low retail participation and needs a review and corrective action.

o There is a requirement of effective price discovery mechanism.

1.3.6 Some New Concepts of Primary Market

189 | P a g e

Reverse Book Building

This process is similar to reverse auction. In this process, shareholders are to bid the price on which they are willing

to offer their shares. This process helps in discovering the exit price in case of delisting the stock by companies.

Green-Shoe Option

While amending the guidelines in August 2003, SEBI has allowed allotment of shares in excess of issue and

operation of post listing price mechanism for a period not exceeding 30 days which is known as green-shoe option.

Stabilizing agent can buy shares from the market (up to 15% of issue) tostabilize the market price.

Online IPO:

The online issue of shares is permitted using electronic network of the stockexchanges as per guidelines of online

issue of shares which were incorporated in a newchapter in the SEBI (disclosure & investment protection)

guidelines, 2000. As per these guidelines, public issue can be made either through online system orthrough the

existing bank channels. The company proposing to have public issue viaonline method of stock exchange has to

comply with section 55-68A of theCompanies Act 1956 and Disclosure & Investor Protection (DIP) guidelines.

Also issuer is required to enter into an agreement with the stock exchanges which have therequisite system of

making online offer and has to appoint brokers & registrars.

1.3.7 Resource Mobilization from International Capital Markets:

In early 1990s, foreignexchange reserves of India depleted and the government was unable to meet the import

obligations of the Indian companies. Also, countryrating was been downgraded. To resolve these challenges,

Government of India allowed Indian companies to tap the equityand bond markets of internationally. Hence, capital

market reforms were initiated in 1991. One of the major policychanges was allowing Indian companies to raise

equity from international market. Before this policy change only debt was allowed to be raised from the

international market.The Indian companies has shown positive response to this policy change and raised capital

from international markets by way of GlobalDepositary Receipts (GDRs), American Depository

Receipts (ADRs), Foreign CurrencyConvertible Bonds (FCCBs) and External Commercial

Borrowings (ECBs).

1.3.7.1 Factors Leading to an Increase in the Popularity of International Market as a sourceof

Finance:

After 1991 capital market reforms and allowing Indian companies to raise equity capital from international market,

number of companies has opted for offshore primary market instead of Indian primary market for mobilizing funds.

The factors that attributed to this behavior are as follows:

190 | P a g e

o The time required to complete the entire public issue process of offshore primary market is shorter and the

issue costs are low using book building procedure.

o In case of offshore issue, Indian capital market ceiling are not applicable.

o Foreign Institutional Investors (FIIs) prefer euro issues as they do not have to register with SEBI nor they

have to pay the capital gain tax as on GDRs traded on International / foreign exchanges.

o Also, many times, arbitrage opportunities are available as GDR are priced at discount compared to domestic

price.

o Indian companies can mobilize large capital in foreign exchange frominternational markets which helps in

meeting business obligations at much cheaper cost.

o The increasing popularity of Euro bonds market among international borrowers meeting regulatory

requirements.

o Good GDP growth projections of India are preferred in overseas market.

o An overseas issue allows the company to get exposure of international investors resulting improved

visibility of Indian companies in the overseas market.

CONCLUSION:

Recently, primary market in India has showed some unprecedented growth but still there are number of changes

required in Indian primary (IPO) system. With the Introduction of ASBA in the IPO section, the retail investors are

now participating in the IPO process in large numbers. In spite of great successes of primary market in India, Indian

Primary Market needs attention to resolve some of the old problems which are still encountered by investors.

1.4 The Secondary Market:

1.4.1 Introduction:

The secondary market is a market where stocks / securities are traded. This market isalso known as stock market. In

India, secondary market consists of recognized stock exchangesoperating under the rules, by laws and regulations

duly approved by the government. These stockexchanges forms an organized market where securities issued by

central and state governments,public bodies and joint stock companies are traded. According to section 2(3) of The

SecuritiesContract (Regulation) Act, 1956 a stock exchange is defined as a body of individuals whether incorporated

or not, constitute for the purpose of assisting, regulating and controlling the businessof buying&selling and dealing

in securities. The major stock exchanges across the world are NASDAQ,New York Stock Exchange (NYSE),

London Stock Exchange (LSE), Dow Jones, Tokyo StockExchangeetc. The major stock exchanges in India are BSE,

NSE and OTCEI.

1.4.2 Development of Stock Market in India:

191 | P a g e

Origin of Indian stock market goes way back to 18th century when long term negotiablesecurities were issued.

However, mid 19th

century can be considered as actual beginning of stock market upon implementation of

Companies Act of 1850which introduced feature like limited liability andgenerated investor‟s interest in corporate

securities.The first stock exchange in India was formed in 1875 in the name of Native Stock Brokers‟ Association

which is now known as Bombay Stock Exchange. It was formed in the year 1875. This development led to reforms

throughout India with the formation of Ahmadabad Stock Exchange (1894), Calcutta Stock Exchange (1908), and

Madras(Chennai) Stock Exchange (1937).

Till 1960s, secondary market was largely dominated by the Calcutta Stock Exchange (CSE). Most of the companies

registered in India were listed on two major stockexchanges the CSE and the BSE. During 1961, out of the 1203

companies listed on the Indian stockexchanges 576 were listed on the CSE and 297 were listed on the BSE. The

shift of dominancefrom CSE to BSE started in the late 1960s. Till the early 1990s, the Indian secondary market was

full of uncertainties / limitations such as:

1. Uncertainty of execution price.

2. Uncertainty of delivery and settlement periods.

3. Front running, trading ahead of a client on knowledge of client order.

4. Lack of transparency.

5. High transaction cost.

6. Absence of risk management.

7. Systemic failure of entire market and market closure due to scams.

8. Club mentality of brokers.

9. Kerb trading (off market deals).

In 1991, after the liberalization of the Indian economy, the stock markets entered into an era ofreforms. The Indian

stock market then follows a three tier structure consisting of:

National Stock Exchange Ltd. (NSE),

Regional stock exchanges,

Over The Counter Exchange of India (OTCEI).

NSE was established in 1994 as first automated screen based exchange in India and was working on order matching

concept. The formation of NSE was a revolution to Indian stock market. Thereafter, all major stock exchanges

started electronic trading. Now, with technology revolution, traders / investors sitting in any part of the world can

buy or sell shares during the trading hours. The OTCEI wasestablished in 1992 to enable small and medium

enterprises to raise funds and generate capital atlow cost.

1.4.2.1 Organization, Management and Membership of Stock Exchanges:

192 | P a g e

Over a period of 140 years, stock exchanges have been set up in India from a small group of people to major

electronic stock exchange. In India, currently there are 21 stock exchanges.Their type & organization structure are as

detailed below:

Name Of The Exchange Type of Organization

Bombay , Ahmedabad, Patna, Indore Voluntary non-profit making association

Kolkata, Delhi, Bangalore, Cochin, Kanpur, Public limited company

Hyderabad, Pune, Rajkot, Magadh Company limited by guarantee

The National Stock Exchange A tax-paying company incorporated under

The Over the Counter Exchange of India A company under Section 25 of the

Source: website of SEBI

www.sebi.gov.in

Stock brokers are member of stock exchange, who can trade either on their own account or on behalfof clients. To

become a broker in India, person or company has to take a certificate of registrationfrom SEBI and then have to

comply with the prescribed code of conduct. Over the period of timemany proprietary and partnership firms have

converted themselves into corporate entities. BothNSE and OTCEI have laid strict membership criteria for new

admission. The criterion includescapital adequacy, track record, and education experience and so onto ensure quality

brokingservices.

1.4.3 Functions of Secondary Market:

The major functions of the secondary market are:

Facilitateliquidity and marketability of the outstanding equity and debt instruments.

o Contribution towards economic growth by allocation of funds to most efficient channels through

disinvestment and reinvestment.

o Provide instant valuation of securities due to change in environment (company and industry wide factors).

Such valuation facilitates assessment of the costof capital requirement and rate of return of economic

entities at the micro level.

o Ensure measure of safety and fair dealing to protect investors‟ interest.

193 | P a g e

o Induce companies to improve performance since the market price at the stock exchangereflects the

performance and this market price is readily available to the investors.

1.4.4 Stock Market Index:

To know the market sentiments & direction of market, stock market index have been developed by grouping

particular type securities listed on the exchange which is updated on contentious basis with change in prices of

stocks such as BSE SENSEX, NIFTY 50 etc.

The scrip selectedfor the Index formation should be with high capitalization and good liquidity. A stockmarket index

is a barometer of the market behavior. It reflects expectations from the economy as a whole. The major functions of

a stock market index are:

To serve as a barometer of the equity market.

To serve as a benchmark for portfolio of stocks.

To serve as underlying for futures and options contract.

1.4.4.1 Global Stock Market Indices:

The major stock market indices that exist around the world are:

1. Dow Jones industrial Average

2. NASDAQ composite Index

3. NASDAQ 100 Index

4. S&P 500 Index

5. The FTSE 100 Index

6. The MSCI Indices

All these indices help the investors to see and judge the movement of market.

1.4.4.2 Stock Market Indices in India:

There are two major indices in India: BSE SENSEX and S&P CNX Nifty 50. BSE SENSEX representsfor BSE

sensitive Index and was established in 1986. It comprises of 30 shares with the base year1978-79 and a base of 100

points. The all-time high of SENSEX is 29,844 points in January 2015. Criteria for selection of scrip for SENSEX

are large market capitalization& high liquidity.

Another index which has become very popular in a short span of last 15 years is the S&P CNX

Nifty50. The NSE began trading in November 1994, and its volume crossed BSE in short span of around 2 years.

The NSE and CRISIL under took a joint venture wherein they jointly promoted India IndexServices and Products, a

specializedorganization to provide stock index service. The organization developed scientifically devised indices of

194 | P a g e

stock prices in the NSE by technical partnership withStandard & Poor (S&P). The S&P CNX Nifty 50 was launched

on 8th July 1996.

1.5 The Bombay Stock Exchange Limited (BSE):

BSE is the oldest and one of the biggest stock exchanges in India and is voluntary non-profit making association

ofbroker members. It emerged as a premier stock exchange n 1960s. Since inception, BSE was operating as closed

club of members. Upon outburst of securities in 1992, regulators had to come in action and SEBI took over control

of market. Due to this, BSE brought changes in operation policies. Until March 1995, BSE followed the open floor

system of trading. However NSE, India first computerized and professionally stock exchange, gave stiff completion

to BSE and BSE was forced to change its trading system and introduced BSEOnline Trading System (BOLT).

Introduction of BOLT helped BSE in regaining its volumes. In 1995, BOLT was limited to Mumbai only, whereas

the NSE was functioning on nationallevel. As a result BSE was losing business. After lot of persuasion, SBEI

permitted BSE to use BOLT nationwide.

In February 2001 BSE launched its internet based systemBSE Webx. Thereafter, BSE launched India‟s first mobile

based trading system in 2010.

1.6 National Stock Exchange Limited (NSE):

1.6.1 Introduction

In 1990s the government of India decided for changes in the Indian StockMarket. Out of that, one change was to

establishment professionally managed fully supported by technology stock exchange which gave birth to NSE. NSE

was incorporated in November 1992 with the following objectives:

o Establish nationwide trading facility for equities, debt instruments andhybrids.

o Ensure investors gets equal access nationwide using appropriatenetwork.

o Provide fair, efficient and transparent securities market to investors.

o Establish shorter settlement cycles.

o Exchange should be in line with the current major exchanges operating across the globe & should be of

current international standards of the equity markets.

The NSE is a tax paying company incorporatedunder Companies Act, 1956. NSE was promoted by leading financial

institutions andbanks to provide automated and modern facilities for trading, clearing and settlement ofsecurities in a

transparent, fair and open manner with a country wide access. NSE is professionally managed. In order to upgrade

theprofessional standards of the market intermediaries, NSE give stress on factors suchas capital adequacy,

corporate structure, track record and educational experience.NSE membership is always on tap and anyone who

195 | P a g e

meets the criteria such as cash depositsand high net worth can become a member. A member, who wants to quit

business, can do sofreely and take refund of deposits after meeting all the liabilities.

NSE members are connected to the central computerlocated at the exchange through a satellite using VSAT (Very

Small Aperture Terminals).Members canplace their orders from their offices computers using connectivity. Also,

members are in full control and closely monitor the orders placed by them as well as by their authorized sub-

brokers.

Some of the special features of NSE are:

o First exchange in India to implement fully automated screen based trading.

o First exchange in India to go live using satellite communication.

o The first exchange in India to permit internet trading.

o The only exchange throughout the world to get first place in the country in the very first yearof operation.

CONCLUSION:

Recently, secondary market in India is developing at very fast pace. However, still it has a long way to improve

stability and control volatility. Indian capital market with two major stock exchanges namely BSE and NSE trying to

be the best meeting international standards and in return of their efforts, volumes at both these exchanges have

shown excellent growth.

REFERENCES:

1. Braithwaite J. and P. Drahos (2000) Global Business Regulation, Cambridge UniversityPress.

2. Budd, L. (1995), Globalization, territory and strategic alliances in different financial centers,Urban Studies 32,

345 – 360

3. Capital Market, various issues.

4. Clark M. R. (2000), “Cadillac Eldolarado, 1967- 1978 Performance Portfolio, CambridgeUniversity Press, June

2000.

5. Cortes, F, Lyon, M and Marsh, I W (2002), „Is there magic in corporate earnings?‟, Bank ofEngland Financial

Stability Review, December.

6. Gupta, L.C. (1998), “What Ails the Indian Capital Market?”Economic and Political Weekly, 23 (29-30).

7. Gupta, Ramesh (1999), „Retail Investors,‟ The Chartered Accountant, February 1999, pp.12-18.

8. Hansda, Sanjiv .K and Parthy Ray (2002), „BSE and NASDAQ: Globalisation, InformationTechnology and

Stock Prices,‟ Economic and Political Weekly, 12 February 2002, pp. 12-18.

9. Jain, S.K. (1995), ‘Euro Issues: Time to Take Stock,’ Analyst December 1995, pp. 38-40.

196 | P a g e

10. Karolyi, G. Andrew, 2006. "The Consequences of Terrorism for Financial Markets: WhatDo We Know?,"

Working Paper Series 2006-6, Ohio State University, Charles A. DiceCenter for Research in Financial

Economics.

11. Kumar, Sunil (1998), „Primary Market- will it ever Revive,‟ Dalal Street, vol. XII, no.12,pp. 56-58.

12. Laulajainen, Risto (2003) Routledge International Studies in Money and Banking ISBN:9780415278706 ISBN-

10: 0415278708 Publisher: Taylor & Francis

13. Malik, Debasis (2000), „Index Construction,‟ Chartered Financial Analyst, June 2000 pp.21-27.

14. Mehta, Aparna (2001), „Indian Stock Markets Towards Safer Havens,‟ Chartered Financial Analyst, June 2001,

pp.49-52.

15. Michie, Ranald C. (2008) "Reversal or Change? The Global Securities Market in the 20th

Century," New Global

Studies: Vol. 2 :Iss. 1, Article 1.

16. Michie, RC (2006). The Global Securities Market: a History. Oxford: Oxford University Press.

17. Naidu, Kumaraswamy G. And Ali MohamadAnwer (2003), „Market Cap to Free Floats:The Impact,‟ Portfolio

Organizer, September 2003, pp. 21-25.

18. National Stock Exchange, Indian Securities Market: A Review, volume IV, 2001.

19. Prasuna, D.G. (2001), „Governance Matters,‟ Chartered Financial Analyst, June 2001, pp.20-25.

20. Priyadarshi, Atul (2000), „Rolling Settlement: Roll over to Efficiency,‟ Chartered FinancialAnalyst, March

2000, pp.56-58.

21. RaoRashmi (2002), „Bite of Reforms,‟ Capital Market, January 21- February 3, 2002, pp.4-8.

22. Reserve Bank of India, Annual Report, various issues.

23. Reserve Bank of India, Handbook of Statistics on Indian Economy, various issues.

24. Reserve Bank of India, Report on Currency and Finance, various issues.

25. The Economic Times,The Investors Year Book, 2001-2009

26. The Economic Survey of India Report, Government of India,2009

27. Pandey, Anand (2003), „Efficiency of Indian Stock Market,‟Thepaper is a part of TimeSeries Course by Dr.

Susan Thomas.

28. Raju, M.T. and Gosh, Anirban (2004), „Stock Market Volatility- An internationalComparison,‟ SEBI working

paper, downloaded from

http://www.sebi.gov.in/workingpaper/stock.pdf last visited on July 03, 2011.

29. Roxburgh et al. (2009). “Global Capital Markets: Entering a new era,” McKinsey GlobalInstitute.

30. Scott, David L. (2003), Wall Street Words 180, (3rd Edition. 2003).

31. www.sebi.gov.in

32. www.bseindia.com

33. www.nsendia.com

34. www.rbi.org.in

197 | P a g e

35. www.moneycontol.com

36. www.world-exchanges.org

37. Alves, F. 2013. Doing Business and Investing in Brazil. Price Waterhouse Coopers.

38. Bertrand, A., Kothe, E. 2013. FDI in figures.OECD Investment Division Quarterly Report.

39. Fagan, D.N. 2008. The U.S. Regulatory and Institutional Framework. Deloitte US Chinese Services Group.

40. http://www.investmentuk.net/institutional-investment.php Accessed on April 15, 2014

41. Jain, P. 2007. Determinants and Impact of Foreign Institutional Investors: An Indian Perspective. The University

of Nottingham.

42. Jain, M., Meena, P.L., Mathur, T.N. 2012. Impact of foreign institutional investment on stock market with

special reference to BSE: a study of last one decade. Asian Journal of Research in Banking and Finance.

43. Lall, S. 1997. Attracting Foreign Investment: New Trends, Sources and Policies.Commonwealth Secretariat

44.Mishra, B, M (1997), “Fifty Years of Indian Capital Market: 1947-97”, RBI Occasional Papers, VOL. 2& 3,

June/Sept.

45. Prasanna, P.K (2008), Foreign Institutional Investors: Investment preferences in India, JOAAG, Vol. 3, No-3.

46. Rosenn, K.S. 1991. Foreign investment in Brazil. Westview Press.

47. Saha, M. 2009. Stock markets in India and foreign institutional investments: An appraisal. Journal of business

and economic issues.

48. Singh, A and Bruce, A.W (1998), “Emerging Stock Markets, Portfolio Capital Flows and Long Term Economic

Growth: Micro and Macro Economic Perspectives”, World Development, VOL.26, (4), PP-607-22.

49. Singh, Ajit (2002), “Capital Account Liberalization, Free Long-term Capital Flows, Financial Crises and

Economic Development”, Paper Presented in Queen’s College, University of Cambridge..

50. Stanley Morgan (2002),“FII‟s influence on Stock Market”, Journal: Journal of impact of Institutional Investors

on ism. Vol. 17. Publisher: Emerald Group Publishing Limited.

51. Walia, K., Walia, R., Jain, M. 2012. Impact of foreign institutional investment on stock market.International

journal of computing and corporate research.

52. Wilkins, M. 2009. The History of Foreign Investment in the United States. Harvard university press.

53. JitendraLoomba, International Journal of Marketing, Financial Services & Management Research Vol.1 Issue 7,

July 2012, ISSN 2277 3622

54. Akaike, Hirotugu (1974). "A new look at the statistical model identification". IEEE Transactions on Automatic

Control 19 (6): 716-723. doi:10.1109/TAC.1974.1100705.MR0423716.

55. Akaike, Hirotsugu (1980). "Likelihood and the Bayes procedure", Bayesian Statistics, Ed. J.M.Bernardo et al.,

Valencia: University Press. p.143-166.

56. Anderson, D.R. (2008), Model Based Inference in the Life Sciences, Springer.

57. Brockwell, P.J., and Davis, R.A. (2009). Time Series: Theory and Methods, 2nd ed. Springer.

198 | P a g e

58. Brooks, Chris. Introductory Econometrics for Finance, Cambridge University Press 2ed edition,2002 pp. 345-

376.

59. Burnham, K. P., and Anderson, D.R. (2002). Model Selection and Multimodel Inference: APractical

Information-Theoretic Approach, 2nd ed. Springer-Verlag. ISBN 0-387-95364-7.[This has over 10000 citations

on Google Scholar.]

60. Burnham, K. P., and Anderson, D.R. (2004), " Multimodel inference: understanding AIC and BIC in Model

Selection

(http://www.sortie-nd.org/lme/Statistical Papers/Burnham_and_Anderson_2004_Multimodel_Inference.pdf)",

Sociological Methods andResearch, 33: 261-304.

61. Cavanaugh, J.E. (1997). "Unifying the derivations of the Akaike and corrected Akaikeinformation criteria",

Statistics and Probability Letters, 31: 201-208.

62. Claeskens, G, and N.L. Hjort (2008). Model Selection and Model Averaging, Cambridge.

63. Fang, Yixin (2011). " Asymptotic equivalence between cross-validations and Akaike Information Criteria in

mixed-effects models (http://www.jdsonline.com/file_download/278/JDS-652a.pdf)", Journal of Data Science,

9:15-21.

64. Groeneveld, RA; Meeden, G. (1984). "Measuring Skewness and Kurtosis".The Statistician33(4): 391–

399.doi:10.2307/2987742. JSTOR 2987742.

65. Gujarati, Damodaran. Basic Econometrics, Tata McGraw-Hill Publication, 5th edition 2004, pp735-790

66. Hurvich, C. M., and Tsai, C.-L. (1989). "Regression and time series model selection in smallsamples",

Biometrika, 76: 297-307.

67. Jeevanandanam, C. Foreign Exchange and Risk Management, Sulltan Chand Publication, 4th

edition, 2004 pp.

445-467.

68. Lukacs, P.M., et al. (2007). "Concerns regarding a call for pluralism of information theory andhypothesis

testing", Journal of Applied Ecology, 44:456-460.

69. McQuarrie, A. D. R., and Tsai, C.-L. (1998). Regression and Time Series Model Selection.World Scientific.

ISBN 981023242X.

70. Takeuchi, K. (1976). "Distribution of informational statistics and a criterion of model fitting",Suri-Kagaku

(Mathematical Sciences), 153: 12-18.(In Japanese).

71. Yang, Y. (2005). "Can the strengths of AIC and BIC be shared?",Biometrika, 92: 937-950.

72. Bekaert, G., and C.R. Harvey. 2000. Foreign speculators and emerging market equity markets, Journal of

Finance, Vol. 55 (2), 565-613.

73. Brennan, M.J., and H.H. Cao. 1997. International portfolio investment flows, Journal of Finance, Vol. 52, 1855-

1880."

74. Coval, J.D., and T.J. Moskowitz. 1999. Home bias at home: Local equity preference in domestic portfolios,

Journal of Finance, Vol. 54 (6), 2045-2073.

199 | P a g e

75. Elkins/McSherry. 2000. Global Universe. New York: ElkinslMcSherry Inc. Elton, E., and M. Gruber. 1995.

Modem Portfolio Theory and Investment Analysis. New York: Wiley.

76. Errunza, V. 1997. Research on emerging markets: Past, present and future, Emerging Markets Quarterly, Vol. 1,

5-18.

77. Griffin, J. M., and R.M. Stulz. 2001. International Competition and Exchange Rate Shocks: A Cross-Country

Industry Analysis of Stock Returns, Review of Financial Studies, Vol. 14 (1), 215-241.

78. Jorion, P., and D. Miller. 1997. Investing in emerging markets using depositary receipts, Emerging Markets

Quarterly, Vol. 1, 7-13.

79. Ramchad, L., and R. Susmel. 1998. Volatility and cross-correlations across major stock markets, Journal of

Empirical Finance, Vol. 5 (4), 397-416.

80. Scholl, R.B. 2000. The international investment position of the United States at yearend 1999, Survey of Current

Business, Vol. 80 (7), 46-56.

81. Solnik, B. 2000. International Investments.4th ed. Addison-Wesley.

82. Solnik, B., and A. de Freitas. 1988. International factors of stock price behavior, in S. Khoury and A. Ghosh.

eds. Recent developments in international finance and banking. Lexington: Lexington Books.

83. WSJ. 2000. ADR Issuance Surges as Firms Abroad Tap Market for Capital, The Wall Street Journal,

12/08/2000, C12.

84. Aggarwal, R ,Klapper, Land Wysocki, P.D.(2005), “Portfolio Prfrences of Foreign Institutional Investors.”

Journal of Banking and finance forthcoming.

85. Akula, Ravi (2011), “An Overview of Foreign Institutional Investment In India”, Indian Journal of Commerce

and Management Studies Vol. pp 100-104

86. Andy Lin Chih-Yuan Chen (2006), “The Impact of Qualified Foreign Institutional Investors on Taiwan‟s Stock

Market”, Journal: Journal of FII, their flow to India and Government policies Vol 23. Publisher: SSRN Group

Publishing Limited.

87. Bansal, Anand, Pasricha J.S, “Foreign institutional investor‟s impact on stock prices in India.” Journal of

Academic research in Economics, Volume 1, No. 2, October 2009.

88. Batra, Amita (2003), "The Dynamics of Foreign Portfolio Inflows and Equity Returns in India", ICRIECR

Working Paper 109.

89. Batra, Amit (2004), “Stock return volatility patterns in India” Indian council for research on international

economic relations, Working paper No.124,March, 2004

90. Bekaert Bose Suchismita and CoondooDipaankar (2005), “The Impact of FII Regulations in India”, Journal:

International Journal of financial market trends. Vol 30. Publisher: MCB UP Ltd.

91. Chakrabati, Rajesh 2001. In his study on “FII Flows to India: Nature & Causes.” ICRA Bulletin Money and

Finance, Oct-Dec: 61-81.

200 | P a g e

92. Dhamija, Nidhi (2007), “Foreign Institutional Investment in India”, Journal: Research on Indian Stock

Volatilty.Vol 14. Publisher: Emerald Group Publishing Limited.

93. Dr. Rahul Singh (2008) “A Study of FII Investment Flow and SENSEX Movement”, Working paper BIMTECH.

94. Ghosh, Saurabh and HerwadkarSnehal (2008),“Foreign Portfolio Flows and their Impact on Financial Markets in

India”, at IIFT Conference on Issues in International Trade and Finance, December 23-24, 2008

95. Guru, Anuradha and Parikh, Anokhi (2009), “Behavior of Foreign Institutional Investors in India: An Empirical

Study”, Indian Journal of Finance, Vol.3, No.8, August 2009.

96. Knill, April M.A.(2005), “Taking the Bad with the Good; Volatility of Foreign Portfolio Investment and

Financial Constraints of Small Firms.” WPS 3797, Working Paper series at World Bank.

97. Makwana, Chetna R. (2009), “FII & its Impact on Volatility of Indian stock market”,Narmada College of

Management ,Gujrat., CBS E-Journal, Biz n Bytes, Vol. 2, Dec., 2009

98. ManjinderKaur, Sharanjit S. Dhillon (2010), “Determinants of Foreign Institutional Investors‟ Investment in

India”, Eurasian Journal of Business and Economics 2010, 3 (6), 57-70.

99. Poshkwale, Sunil and Thapa, Chandra (2007), “Impact of foreign portfolio investments on market co-

movements; Emerging market group ESRC seminar on international equity markets co-movements and

contagion, Cass business school, London.

100. P. Krishna Prasanna (2008), in his study on “Foreign Institutional Investors: Investment Preferences in India.”

JOAAG, Vol.3. No.2

101. Raju M.T, GhoshAnirban (2004): “Stock Market Volatility – An International Comparison”, Journal: Research

on Indian Stock Volatilty. Vol 14. Publisher: Emerald Group Publishing Limited.

102. Rekha and Dutta, (2009) “Impact of FIIs and DIIs in Dynamism of Indian Capital Market.” 5th National

conference on Indian Capital Market: Retrospect and prospects.

103. Singh Sumanjeet&MinakshiPaliwal (2010), “Liberalization of FIIS in India: Magnitude, Impact assessment,

Policy Initiative and Issues” Global Journal of International Business Research Vol. 3. No.3. 2010

104. Srinivasan, P., M Kalaivani and K Sham Bhat (2010), “FII and Stock Market Return in India: Before &Dring

Global Financial Crisis”, The IUP Journal of Behavioral finance, vol.VII, Nos. 1 & 2, 2010, pp. 58-75

105. Stanley, Morgan (2002):“FII‟s influence on Stock Market”, Journal: Journal of impact of Institutional Investors

on ism.Vol 17. Publisher: Emerald Group Publishing Limited.

106. Takeshi Inoue (2008), “The casual relationships in mean & variance between stock returns & FII in India”,

South Asian Group, Area Studies Centre, IDE (Institute of developing economies) paper no.108 November,

2008.

107. Bekaert, G., and C.R. Harvey. 1998. Emerging equity market volatility, Journal of FinancialEconomics, Vol.

43, 29-77.

108. Chakrabarti, Rajesh (2001), “FII Flows to India: Nature and Causes”, Money & Finance,Vol. 2, No. 7.

201 | P a g e

109. Claessens, S., D. Klingebiel and S.L. Schmukler (2002), “Explaining the Migration ofStocks from Exchanges

in Emerging Economies to International Centers”, World BankWorking Paper No. 2816

110. De Santis, G., and B. Gerard. 1998. How big is the premium for currency risk? Journal, ofFinancial Economics,

Vol.48 (4), 15-26.

111. Diamonte, R.L., J.M. Liew, and R.L. Stevens. 1996. Political risk in emerging anddeveloped markets, Financial

Analysts Journal, Vol. 52 (3), 71-77.

112. Eun, C.S., and B.G. Resnick. 2001. International Financial Management, 2nd , McGraw-Hill

113. Griffin, J. M., and R.M. Stulz. 2001. International Competition and Exchange Rate Shocks:A Cross-Country

Industry Analysis of Stock Returns, Review of Financial Studies, Vol. 14(1), 215-241.

114. Hubbard, D.J., and R.K. Larson. 1995. American Depository Receipts: InvestmentAlternative or Quicksand?

CPA Journal, Vol. 65 (7), 70-73.

115. Lin, W.L., R.F. Engel, and T. Ito. 1994. Do bulls and bears move across borders?International transmission of

stock returns and volatility, Review of Financial Studies, Vol.7 (3), 507-538.

116. OECD. 1980. Experience with Controls on International Portfolio Operations in Shares andBonds. Paris:

OECD.

117. Papaioannou, M.G., and L.K. Duke. 1993. The Internationalization of Emerging EquityMarkets, Finance &

Development, Vol. 30 (3), 36-39.

118. Ramchad, L., and R. Susmel. 1998. Volatility and cross-correlations across major stockmarkets, Journal of

Empirical Finance, Vol. 5 (4), 397-416.

119. Solnik, B. 2000. International Investments.4th ed. Addison-Wesley.

![[ CONFERENCE TENTATIVE ]](https://static.fdokumen.com/doc/165x107/6332727f3108fad7760ea090/-conference-tentative-.jpg)