CaixaBI R&C 2011_EN.docx

245

ANNUAL REPORT Separate and Consolidated Operations, 2011

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of CaixaBI R&C 2011_EN.docx

ANNUAL REPORT

Separate and Consolidated Operations, 2011

Annual Report – 2011

2

Index

Board of Directors’ Report ......................................................................... 4

1 Statutory bodies...............................................................................................................5

2 Organogram ....................................................................................................................6

3 Key consolidated financial indicators ...............................................................................7

4 Overview of CaixaBI ........................................................................................................8

4.1 Prizes and rankings................................................................................................................................... 8

4.2 Main operations ...................................................................................................................................... 10

5 Macroeconomic environment.........................................................................................13

5.1 International............................................................................................................................................ 13

5.2 Domestic ................................................................................................................................................ 16

5.3 Capital markets....................................................................................................................................... 17

6 Strategy and business model.........................................................................................19

6.1 Project finance ........................................................................................................................................ 20

6.2 Structured finance................................................................................................................................... 22

6.3 Corporate finance – advisory ................................................................................................................... 24

6.4 Debt capital market ................................................................................................................................. 28

6.5 Equity capital market ............................................................................................................................... 30

6.6 Financial brokerage................................................................................................................................. 32

6.7 Research ................................................................................................................................................ 32

6.8 Financing and structuring area................................................................................................................. 33

6.9 Syndication and sales ............................................................................................................................. 35

6.10 Venture capital ........................................................................................................................................ 35

6.11 Outlook for 2012 ..................................................................................................................................... 41

7 Results ..........................................................................................................................44

8 Human resources ..........................................................................................................47

9 Qualified equity investors...............................................................................................49

10 Acknowledgments .........................................................................................................50

11 Proposal for the appropriation of net income .................................................................51

Financial statements, notes and opinions ............................................... 52

1 Consolidated and separate financial statements............................................................53

2 Notes to the consolidated financial statements ..............................................................64

3 Notes to the separate financial statements ..................................................................126

Annual Report – 2011

3

4 Reports and opinions...................................................................................................185

Report on corporate governance........................................................... 197

I Corporate governance ..................................................................... 198

1 Assessment of compliance with good governance principles.......................................199

2 Management guidelines, mission, objectives and policies ...........................................201

3 General operating principles........................................................................................204

4 Relevant transactions with related parties....................................................................205

5 Corporate model..........................................................................................................208

5.1 Statutory bodies .................................................................................................................................... 209

5.2 Specialised committees......................................................................................................................... 222

6 Remuneration of members of statutory bodies ............................................................226

7 Control system ............................................................................................................227

7.1 Internal control system .......................................................................................................................... 227

7.2 Control system on the protection of the company’s investments and its assets........................................ 230

7.3 Control system for safeguarding customers’ assets held under CaixaBI’s custodian services................... 230

8 Disclosure of relevant information................................................................................232

8.1 Market relations representative.............................................................................................................. 232

8.2 Disclosure of relevant information .......................................................................................................... 232

8.3 Diagramme of CaixaBI investments ....................................................................................................... 232

8.4 Share capital and dividends policy ......................................................................................................... 233

9 Analysis of economic, social and environmental sustainability.....................................234

9.1 Economic considerations....................................................................................................................... 237

9.2 Environmental considerations................................................................................................................ 238

9.3 Social considerations ............................................................................................................................ 238

II Compliance with legal guidelines ....................................................... 240

Annual Report – 2011

4

Board of Directors’ Report

Annual Report – 2011

5

1 Statutory bodies

Shareholders’ meeting

Chairman

José Lourenço Soares

Secretaries

Salomão Jorge Barbosa Ribeiro

António Pereira Grada Ferreira

Board of directors

Chairman of the board of directors

Jorge Humberto Correia Tomé

Chairman of executive committee

Jorge Telmo Maria Freire Cardoso

Members of executive committee

Gonçalo Vaz Gago da Câmara de Medeiros Botelho

Francisco José Pedreiro Rangel

Members of the board of directors

Rui Manuel do Vale Jordão Gonçalves Soares

José Pedro Cabral dos Santos

José Manuel Carreiras Carrilho

Fiscal board

Chairman

Miguel José Pereira Athayde Marques

Members

Pedro António Felício

Maria Rosa Tobias Sá

Deputising

João Barata da Silva

Statutory auditors

Acting

Deloitte & Associados, SROC represented by João Carlos Henriques Gomes Ferreira

Deputising

Carlos Luís Oliveira de Melo Loureiro

Annual Report – 2011

6

2 Organogram

Board of Directors

ExecutiveBoard

Compliance Office

Ália Silva

CorporateDebt FinanceDivision

Paulo Serpa Pinto

Primary Equities MarketDivision

Ana Santos Martins

Corporate Advisory Division

Paulo Oliveira Silva

Syndicationand Sales

Leonor Canedo

Project FinanceDivision

Daniel Santos

Structured FinanceDivision

Paulo Henriques

Finance and StructuringDivision

Francisco Santos

Research Office

João Miguel Lourenço

Internal Audit Office

Fernando Oliveira

Financial BrokerageDivision

Valentim Martins

Legal Affairs Office

Ana Andrade

Strategic Planning andOrganisationDivision

Rita Lourenço

Human and AdministrativeResources

António Carlos Alves

OperationsDivision

Miguel Freire

Marketing andCommunicationOffice

António Gregório

AccountsDivision

João Gonçalves

InformationSystems

Ema Campos

Business Areas

Support Areas

Annual Report – 2011

7

3 Key consolidated financial indicators

Results indicators

(EUR thousand) 2010 2011

Net interest income 33,313 29,052

Net commissions 73,712 61,793

Income from financial assets (16,688) (31,283)

Other operating income 1,609 (519)

Net operating income 91,946 59,043

Net operating income – adjusted (1)

94,247 86,729

Provisions and impairment (9,656) (31,896)

Structural costs (29,018) (24,774)

Income before tax 53,272 2,373

Tax (13,611) 6,220

Non-controlling interests 492 (40)

Net income 40,153 8,553

Performance ratios

Cost-to-income - adjusted (1)

30.5% 28.1%

(1) Adjusted for impairment on financial assets

Balance sheet indicators

(EUR thousand) 2010 2011

Credit portfolio 787,912 699,133

Securities portfolio 671,516 537,241

Derivatives portfolio (active position) 428,578 715,196

Derivatives portfolio (passive position) (418,469) (735,111)

Customer resources 104,996 114,069

Net assets 2,000,188 2,161,679

Share capital 81,250 81,250

Shareholders’ equity 275,520 213,816

Performance ratios

ROE 15.0% 3.5%

ROA 2.0% 0.4%

Annual Report – 2011

8

4 Overview of CaixaBI

4.1 Prizes and rankings

Caixa - Banco de Investimento, S.A. (CaixaBI or Bank) in performing its operations, in 2011, furthered

the internationalisation strategy it has been implementing over the last few years. The Bank’s good

performance in terms of its core business has continued to merit the recognition of its customers and

partners and has been rewarded by the distinctions afforded by international analysts and in its

leading positions in the main sector rankings.

Best investment bankin Portugal

Global Finance

Best investment bankin Portugal

EMEA Finance

Best debt housein Portugal

Euromoney Award for Excellence

Best investment bankin Portugal

Global Finance

Americas transport deal of the year

Project Finance International

Latin America transport deal of the year

Euromoney Project Finance

Best Investment Bank

In Portugal

2011

Best Investment Bank

In Portugal

2010

Best Debt House

In Portugal

2011

Nº 1 Corporate

Bond House

2011

Americas TransportDeal of the Year 2011

MANDATED LEAD ARRANGER | 2011

IDB (B LOAN): USD 330,000,000IDB (A LOAN): USD 100,000,000

Latin America Transport Deal of the Year 2011

MANDATED LEAD ARRANGER | 2011

IDB (B LOAN): USD 330,000,000IDB (A LOAN): USD 100,000,000

Annual Report – 2011

9

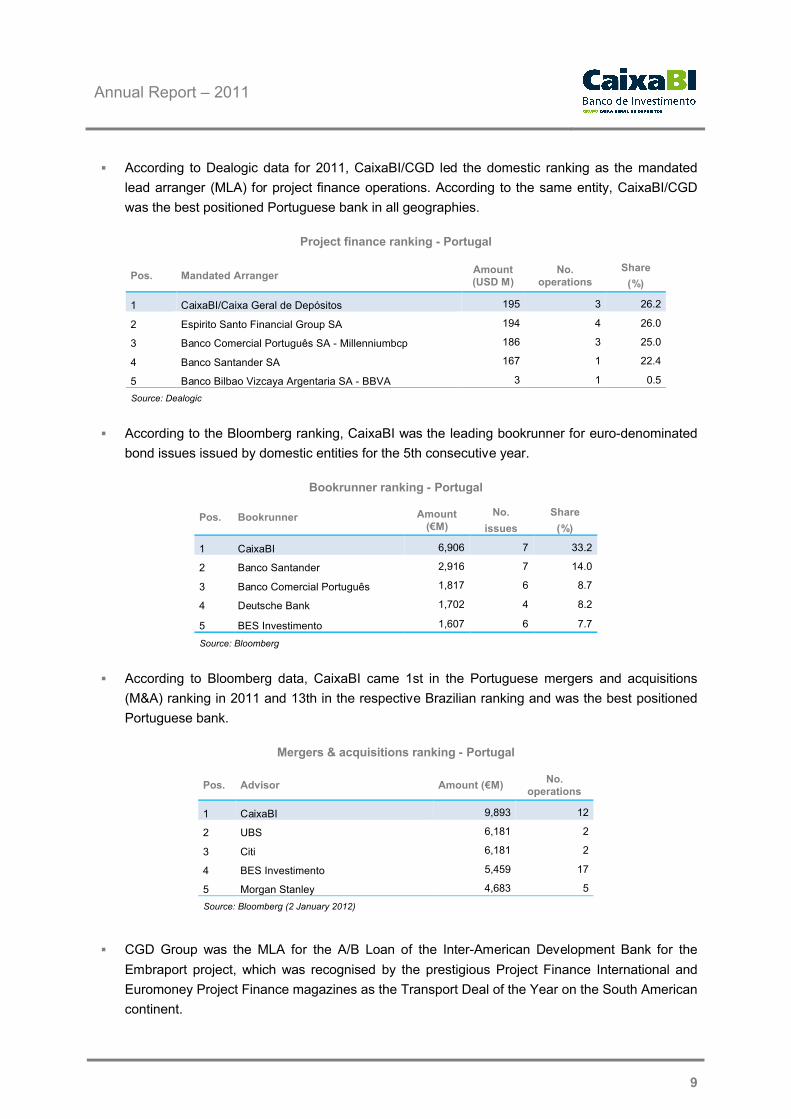

According to Dealogic data for 2011, CaixaBI/CGD led the domestic ranking as the mandated

lead arranger (MLA) for project finance operations. According to the same entity, CaixaBI/CGD

was the best positioned Portuguese bank in all geographies.

Project finance ranking - Portugal

Pos. Mandated ArrangerAmount(USD M)

No. operations

Share

(%)

1 CaixaBI/Caixa Geral de Depósitos 195 3 26.2

2 Espirito Santo Financial Group SA 194 4 26.0

3 Banco Comercial Português SA - Millenniumbcp 186 3 25.0

4 Banco Santander SA 167 1 22.4

5 Banco Bilbao Vizcaya Argentaria SA - BBVA 3 1 0.5

Source: Dealogic

According to the Bloomberg ranking, CaixaBI was the leading bookrunner for euro-denominated

bond issues issued by domestic entities for the 5th consecutive year.

Bookrunner ranking - Portugal

Pos. Bookrunner Amount(€M)

No.

issues

Share

(%)

1 CaixaBI 6,906 7 33.2

2 Banco Santander 2,916 7 14.0

3 Banco Comercial Português 1,817 6 8.7

4 Deutsche Bank 1,702 4 8.2

5 BES Investimento 1,607 6 7.7

Source: Bloomberg

According to Bloomberg data, CaixaBI came 1st in the Portuguese mergers and acquisitions

(M&A) ranking in 2011 and 13th in the respective Brazilian ranking and was the best positioned

Portuguese bank.

Mergers & acquisitions ranking - Portugal

Pos. Advisor Amount (€M)No.

operations

1 CaixaBI 9,893 12

2 UBS 6,181 2

3 Citi 6,181 2

4 BES Investimento 5,459 17

5 Morgan Stanley 4,683 5

Source: Bloomberg (2 January 2012)

CGD Group was the MLA for the A/B Loan of the Inter-American Development Bank for the

Embraport project, which was recognised by the prestigious Project Finance International and

Euromoney Project Finance magazines as the Transport Deal of the Year on the South American

continent.

Annual Report – 2011

10

4.2 Main operations

CaixaBI was involved in various emblematic business deals, strengthening its leading position as an

investment bank. Reference should be made to the following highlights in terms of its main business

areas.

Project finance

CGD Group, through CaixaBI, was involved in operations for a global amount of close to €389 million,

of which around €231 million in Portugal. CaixaBI came 1st in the Dealogic ranking for its role as an

MLA in project finance operations in Portugal and was the best positioned Portuguese bank in all

geographies.

On an international level, reference should be made to the progressive geographical expansion of the

Bank’s operations, associated with operations in Angola and Mozambique and, together with Banco

Caixa Geral – Brasil, S.A. (BCG Brasil), on structuring and/or financial advisory operations for a

diverse series of projects in Brazil. These prize-winning endeavours are exemplified by the award of

the highly ranked Project Finance International and Euromoney Project Finance magazines’ Transport

Deal of the Year prize for the Embraport operation in which CGD Group was the MLA.

Structured finance

In the sphere of structured operations on a corporate basis, CaixaBI geared its operations to

identifying mandates guaranteeing it MLA status of which special reference should be made to its

financial advisory services to Secil for funding the acquisition of an equity stake in Betecna from the

Lafarge Group.

Corporate finance – advisory

Notwithstanding the unfavourable macroeconomic environment and reduced level of M&A operations

activity on a global level, CaixaBI’s work and endeavours have been reflected in the Bloomberg

ranking in which the Bank came 1st, in Portugal, based on its involvement in 12 M&A operations for an

aggregate amount of around €10 billion.

In Brazil, according to the same ranking, CaixaBI, together with BCG Brasil and following only two full

years of activity in the country, came 13th in the investment banks’ ranking in terms of volume of

announced/completed M&A operations and is the best positioned Portuguese bank with an aggregate

amount of around R$17.8 billion.

During the course of 2011, reference should be made to the financial advisory operation for

Parpública’s disposal of a 21.35% equity investment in EDP, as part of the company’s highly

successful 8th reprivatisation stage. Reference should also be made to the financial advisory services

on Galp Energia’s disposal of a 30% equity investment in Petrogal Brasil, for around USD 4.8 billion.

Reference should, lastly, be made to the financial advisory operations for Portugal Telecom’s equity

investment in the Brazilian Oi Group, following the disposal of its equity investment in Vivo, in which

Annual Report – 2011

11

CaixaBI was also involved in a financial advisory capacity. This was one of the biggest operations

involving Portuguese companies over the last few years and represents yet another success for

CaixaBI’s Portugal – Brazil cross-border activities.

Debt capital market

CaixaBI’s leading position in the debt capital market and structured asset financing operations, in

2011, won another important international recognition with Euromoney’s Award of Excellence for the

Best Debt House in Portugal for the second time running.

Reference should also be made to the NYSE Euronext Lisbon Awards, awarded for the first time in

2011, with the main objective of promoting and recognising the activities of capital market players,

which distinguished CaixaBI with its No. 1 Corporate Bond House prize.

Notwithstanding the extraordinarily challenging environment in the debt markets, notably in the bond

sector, CaixaBI, over the course of 2011, led seven primary market bond issues. This performance,

according to the Bloomberg ranking, positioned the Bank as the number one bookrunner for euro-

denominated domestic bond issues for the fifth year running.

Activity in the commercial paper segment was strongly conditioned by the growing balance sheet

restrictions faced by domestic financial institutions, in 2011. However, despite the unfavourable

environment, CaixaBI retained a leading position in this market in Portugal, having organised and led

thirteen new commercial programmes1, totalling around €2.5 billion, last year.

Equity capital market

CaixaBI developed and successfully completed four capital market operations in 2011.

In the international sphere, it was involved as co-lead for the Bankia international public offering (IPO)

as the only Portuguese bank in the banking syndicate for one of the biggest offerings in Europe in

2011, and as co-manager for the international tranche of the Sonae Sierra Brasil IPO and secondary

public subscription for EDP Energias do Brasil, strengthening its international presence in the capital

market area.

In Portugal and notwithstanding the low level of activity in the primary share market, CaixaBI was

responsible for organising and structuring the Inapa rights issue, through the issue of non-voting

preference shares as one of the main capital market operations in 2011.

Financial brokerage

The performance of the share segment of the capital market over the course of 2011 was extremely

negative, reflecting current uncertainty over fundamental variables for the evolution of share markets.

The domestic share market was particularly penalised by this environment, owing to greater investor

risk aversion to Portuguese assets which fuelled a decline of the volumes brokered in the market.

1

Includes fully or partly renewed programmes maturing in 2011.

Annual Report – 2011

12

According to CMVM data, market turnover to the end of August was down 34% over the same period

of 2010, naturally affecting the Bank’s financial brokerage activity.

There were no primary market operations, in Portugal, in 2011. CaixaBI was, however, actively

involved in the Bankia IPO in Spain and as co-manager for the Sonae Sierra Brasil IPO and for the

EDP offer for its EDP Energias do Brasil subsidiary.

Financing and structuring area

Public debt market-making activity in the secondary market, in 2011, was characterised by extremely

difficult conditions with low liquidity levels, historically high bid-offer spreads and major volatility.

Notwithstanding such market constraints, CaixaBI came 1st out of all the primary dealers in IGCP’s

general performance ranking.

In its activity as a liquidity provider, CaixaBI is a benchmark operator and Euronext has awarded its

maximum “A” ratings on all securities and categories in which it operates.

Syndication and sales

CaixaBI was involved, in 2011, as joint lead manager, for the issue of €600 million in Portugal

Telecom bonds and a Portuguese Treasury Bond issue for the amount of €3.5 billion. It was also

responsible for 341 commercial paper issues totalling €12 billion, with €4.8 billion in placements.

Venture capital

CaixaBI’s venture capital area has five venture capital funds, enabling it to provide a transversal level

of cover for different target segments over the course of the corporate life cycle and which, in one

specific case, was geared to a sectoral focus:

Caixa Empreender+

Caixa Mezzanine

CGD Group

Energias Renováveis and

Desenvolvimento e Reorganização Empresarial, set up in 2011.

During the course of 2011, 210 investment opportunities were analysed, with 32 operations totalling

€60 million having been approved, of which 21 were completed, involving an investment of €17 million.

There were also 8 disinvestments at a realisation price of €15 million.

Of total assets under direct Caixa Capital management, the amount invested in subsidiaries totalled

€344 million, at the end of 2011, invested in 75 companies of which 40% over the last three years

period.

Annual Report – 2011

13

5 Macroeconomic environment

5.1 International

2011 was characterised by the heightening of the sovereign debt crisis, started in 2010, and

particularly affecting the eurozone’s more peripheral countries such as Greece, Ireland and Portugal,

which were provided by financial assistance programmes from the IMF, ECB and European

Commission (Troika), but which, at certain times also penalised Spain and Italy.

The main rating agencies successively downgraded their ratings on countries with the greatest fiscal

difficulties, in 2011, keeping open the possibility of new short/medium term downgrades in the event of

failure to comply with the adjustment programmes and/or worsening economic outlook. This

environment led investors to reduce their exposure to such countries’ debt securities, with a highly

negative impact on the evolution of the respective yields spreads in relation to German public debt

securities with an identical maturity, pursuant to its role as a safe currency in periods of the greatest

turmoil, leading to historically low yields on these securities.

The Troika accordingly announced support measures to European countries experiencing difficulties

in accessing the markets, complemented by their commitment to strengthening and accelerating the

fiscal consolidation process as well as carrying out structural reforms designed to improve their

competitiveness and fuel their future growth. Countries with bailouts ceased to issue debt in the longer

maturity markets, performing only short term operations (treasury bills or similar securities) with the

aim of satisfying their short term liquidity requirements. The ECB also endeavoured to dampen the

yields on sovereign debt based on market acquisition of public debt securities of member states under

the greatest pressure.

On an economic level, the austerity programmes submitted by governments to guarantee compliance

with the respective adjustment programmes ended up by fuelling pessimism over the growth of

short/medium term economic activity, not only in the countries directly involved but also on a global

level.

The indicators of other non EU countries also showed imbalances in their public finance indicators.

This had a penalising effect, at certain times, on the performance of financial markets, such as in the

US, with an impact on an increase in the intrinsic risk on their public debt securities.

Growing concerns over the significant slowdown of growth in the main economies led the central

banks in the main economic zones to opt for clearly more expansionary monetary policies. This was

the case with the ECB which, at its November and December meetings, lowered its key rates by 0.5%

to 1.0%. At the end of the year, the ECB also announced two three year liquidity injection operations

to meet the needs of the financial system which was greatly penalised by the virtual closure of credit

markets, particularly in the case of southern European institutions.

Annual Report – 2011

14

FED, ECB, BoE and BoJ intervention rates

Source: Bloomberg, CaixaBI

The start of 2012 is likely to continue to be characterised by investors’ risk aversion to the financial

assets of the eurozone’s more peripheral countries, reflected in the continuation of relatively high risk

premiums on such countries. An improvement in the global assessment of the risks associated with

these countries will essentially depend on their capacity to evidence effective improvements in their

current fiscal consolidation processes, by complying with the objectives defined in the respective

financial assistance or stability programmes, pursuant to which investors are likely to attach great

importance to the main fiscal performance indicators achieved in the first few months of 2012.

In mid January, the IMF published an update to its World Economic Outlook which reflected a high

level of uncertainty regarding world economic performance, incorporating the risks associated with the

sovereign debt crisis and banking sector problems in the eurozone. According to the data published,

the world economy is thought to have grown by an average of 3.8% over 2011 against an estimate of

4.0% in the September report and 5.2% in 2010.

The IMF has reduced its growth estimates for the world economy, in 2012, indicating GDP growth of

around 3.3%. This will be a two tier growth, with the most developed economies recording more

moderate growth in activity and with unemployment remaining high. The more peripheral eurozone

countries will be penalised by pressure on their credit spreads and fiscal consolidation measures. The

IMF has downgraded the growth prospects for the countries by an amplitude of -0.7% for 2012, with

an estimate of GDP changes of 1.2.

ECB

FED

BoE

BoJ0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

Ma

r-0

7

Ju

n-0

7

Se

p-0

7

De

c-0

7

Ma

r-0

8

Ju

n-0

8

Se

p-0

8

De

c-0

8

Ma

r-0

9

Ju

n-0

9

Se

p-0

9

De

c-0

9

Ma

r-1

0

Ju

n-1

0

Se

p-1

0

De

c-1

0

Ma

r-1

1

Ju

n-1

1

Se

p-1

1

De

c-1

1

Evo

lutio

n o

f C

en

tra

l B

an

ks'

inte

rve

ntio

n r

ate

s (

%)

Annual Report – 2011

15

Developing economies are likely to post more significant growth rates, albeit with an increase of

inflationary pressures owing to higher commodity prices, particularly in first half 2011. China, India and

Brazil are likely to be highly dynamic notwithstanding the IMF’s downwards revisions of GDP growth.

GDP growth in the main world economies

2008 2009 2010 2011e 2012e

Eurozone 0.5% -4.2% 1.9% 1.5% 0.3%

Germany 1.0% -4.7% 3.7% 3.0% 0.6%

France 3.0% -2.4% 1.5% 1.7% 0.4%

Spain 0.9% -3.7% -0.1% 0.7% -1.0%

Portugal 0.0% -2.5% 1.4% -1.5% -3.1%

Italy -1.3% -5.0% 1.5% 0.4% -1.3%

United Kingdom -1.0% -4.9% 1.8% 0.9% 0.6%

US 0.0% -2.6% 3.0% 1.7% 1.8%

Japan -1.2% -6.3% 4.1% -0.9% 1.7%

Brazil 5.1% -0.7% 7.5% 3.0% 3.0%

World economy 2.8% -0.6% 5.0% 3.8% 3.3%

Source: IMF, EC, ESN, OECD, CaixaBI

According to the IMF, financial markets are likely to continue to be characterised by high levels of

volatility, reflecting investors’ concerns over sovereign risk, particularly in the eurozone. The

progressive stabilisation of financial markets may support a gradual acceleration of the rate of growth

of economic activity on an international level.

Other incentives for economic growth will, however, continue to be necessary and may, in the current

European context, be restricted to monetary-like instruments for which key reference rates are likely to

remain low for a relatively long period. In general, the reduction of inflationary pressures, owing to the

decline in the prices of the main commodities and contraction of consumption with economic

deleveraging and high unemployment rates will favour the maintenance of expansionary monetary

policies in the main economic blocs.

Various risk factors on the main economies, however, remain and may lead to a lower level of

economic activity. They include, inter alia:

Expectation of continued high unemployment for a relatively long period, owing to the gap

between the positive change in GDP and a shift towards job creation, which, if occurring, could

lead to less dynamic domestic demand in different countries.

Continuing credit restrictions, reflecting the banks’ needs to deleverage their balance sheets and

continue to increase their capital to comply with the new regulatory requirements.

Greater unwillingness by financial institutions to assume uncollateralised risks, having opted to

invest cash surpluses in short term investments with central banks at relatively low rates.

Danger of contagion of the sovereign debt crisis to other countries which will continue to

condition fiscal policies for a relatively long period.

Annual Report – 2011

16

5.2 Domestic

Notwithstanding the fact that the Portuguese Republic’s borrowing requirements up to 2013 are largely

guaranteed by the financial assistance programme signed in May 2011, funding restrictions on the

domestic economy and deleveraging requirements remain. This will have a negative impact on GDP

over the last few months of 2011 and predictably over a large part of 2012.

The Portuguese economy contracted by 1.5% in 2011, according to the snapshot estimates disclosed

by the INE, against growth of 1.0% in 2010. Reference should be made to negative quarter-on-quarter

changes over the last five quarters. This performance derived from the negative contribution of private

and public consumption and a huge drop in investment, notwithstanding the good performance of net

exports.

Up to third quarter 2011, net external demand made a positive contribution to GDP, with exports up

7.8%, notwithstanding the world economic slowdown. The 2.8% decline in imports particularly derived

from lower domestic demand.

The fiscal deficit reduction objective, which led to the implementation of austerity measures under the

financial assistance programme for Portugal, caused a retraction of domestic demand and investment,

with a downturn of 3.0% in private consumption, 2.5% in public consumption and 9.8% in gross fixed

capital formation in the first nine months of the year.

GDP and main components

Source: INE, CaixaBI Equity Research

The Harmonised Index of Consumer Prices (HICP) in Portugal, for December 2011 posted average

year-on-year growth of 3.6%, reflecting the changes in VAT rates and increase in the prices of the

main commodities in the international markets in the first half of the year.

The unemployment rate in fourth quarter 2011 was 14.0%, in comparison to the preceding quarter’s

12.4% and 11.1% at the end of 2010 (values not adjusted for INE’s new methodology).

-4

-3

-2

-1

0

1

2

3

-20

-15

-10

-5

0

5

10

15

1T

07

2T

07

3T

07

4T

07

1T

08

2T

08

3T

08

4T

08

1T

09

2T

09

3T

09

4T

09

1T

10

2T

10

3T

10

4T

10

1T

11

2T

11

3T

11

GD

P e

vo

lutio

n (

Yo

Y %

)

GD

P c

om

po

ne

nts

(Y

oY

%)

GDP Investment Domestic Demand Exports Imports

Annual Report – 2011

17

5.3 Capital markets

Money market

Interest rates in the eurozone money market tended to increase slightly over the course of the first half

year followed by stabilisation up to November, which witnessed the start of a downwards movement

as a reaction to the fall in the ECB’s refinancing rate.

Overnight and Euribor 3, 6 and 12 month rates

Source: Thomson Reuters, CaixaBI

Foreign exchange market

The performance of the single European currency against the dollar, in 2011, was heterogeneous,

appreciating significantly in the first quarter followed by a period of stabilisation up to September and

then depreciating, to a rate of less than 1.30 at the end of December. Performance against the yen

followed the same trend up to May after which the drop in the value of the euro was more pronounced

and lasting, ending the year close to 99.50 yen. The euro’s performance against sterling was more

stable as shown in the following chart.

EUR/USD, EUR/GBP and EUR/JPY (base100)

Source: Thomson Reuters, CaixaBI

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11

Euribor 3M Euribor 6M Euribor 12M EONIA

90

95

100

105

110

115

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11

EUR/USD EUR/GBP EUR/JPY

Annual Report – 2011

18

Share market

The euro crisis, which took the form of a broad rating downgrades movement in several eurozone

countries and external interventions in Ireland, Greece and Portugal, had economic and financial

repercussions which translated into a significant increase of risk premiums in most European share

markets.

A comparative analysis shows that US share benchmarks posted a more positive level of performance

than their European counterparties. Movements on the Bovespa were similar to those of European

indices but recorded the highest fall between January and August, as a consequence of the contagion

of the euro crisis. In 2011, the PSI20 was down 28.2%, Bovespa down 18.1%, the EuroStoxx50 down

17.5%, the Dax down 14.5%, the IBEX35 down 13.1% with the S&P500 recording a nil change and

the Dow Jones Industrial up 5.5%.

Main stock markets

Source: Thomson Reuters, CaixaBI

Bond market

Investors’ flight to such quality assets as German sovereign debt, led to a fall in long term yields in the

eurozone, although the yields on the peripheral euro countries increased significantly. As shown in the

following chart, the downwards movement in euro core yields was relatively parallel along the curve.

Yield curve at start and end 2011

Source: Thomson Reuters, CaixaBI

60

70

80

90

100

110

120

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11

PSI20

DJ Ind

S&P 500

IBEX

BovespaStoxx50

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 15Y 20Y 30Y

Dec-11

Jan-11

Annual Report – 2011

19

6 Strategy and business model

CaixaBI is the autonomous unit within CGD Group that concentrates all of its investment banking

activity, operating in tandem with CGD’s commercial structures to maximise the opportunity for cross-

selling with commercial banking activity.

The Bank develops products and services for customers operating in its target market segments of

large and medium sized companies, public institutes and local councils, institutional investors and

major domestic and regional project developers, as well as private individual investors in the trading

area.

CaixaBI has concentrated on markets targeted by Portuguese companies. In line with this strategy it

has carved out a highly competitive position in the Portugal – Spain – Brazil - Lusophone Africa

perimeter, without losing sight of other geographies of interest to its customers. The Bank’s

commercial organisation, with the aim of applying the referred to strategic model, is based on a

product divisions approach, involving both domestic and international aspects. CaixaBI’s high level of

specialisation is reflected in its provision of a comprehensive portfolio of premium financial services

including all relevant investment banking areas activity:

Project finance

Structured finance

Corporate finance - advisory

Debt capital market

Equity capital market

Financial brokerage

Research

Financing and structuring area

Syndication and sales

Venture capital.

Annual Report – 2011

20

6.1 Project finance

Notwithstanding the difficult economic-financial context felt over the course of 2011, CaixaBI was

responsible for structuring several operations giving it first place, in Portugal, in Dealogic’s MLA

ranking for project finance operations in 2011. The same organisation classified CaixaBI as the best

positioned Portuguese bank in all geographies.

CaixaBI was involved in various project finance operations, entailing global CGD Group investment of

approximately €389 million2, in 2011, most of which allocated to operations in Portugal.

Reference should be made to the following successfully completed operations in 2011:

Embraport: construction of a port terminal which, at a first stage

will be capable of handling 1.2 million TEU and will have the

capacity to handle bulk liquids, improving the capacity of the Port of

Santos (Brazil) to receive new generation deep keel cargo vessels.

The project’s promoters are Odebrecht Transport, Dubai Port

World and Coimex. The project was financed by an A/B Loan of the

Inter-American Development Bank (USD 430 million) and by a loan

from the Caixa Económica Federal (in Brazilian reais equivalent to

around USD 330 million).

CGD Group was the MLA for the A/B Loan of the Inter-American

Development Bank, in an operation in which only four commercial

banks participated, based on an invitation from the promoters and which was singled out by the

prestigious Project Finance International and Euromoney Project Finance magazines as the

Transport Deal of the Year on the South American continent.

ELOS Poceirão – Caia: CaixaBI was the MLA in the concession

contract for the design, construction, financing, maintenance and

supply of rail infrastructures (excluding signalling and

telecommunications systems) on the section between the Poceirão

and Caia zones as an integral part of the high speed Lisbon –

Madrid rail link. It was also MLA for the concession for the rail

infrastructures on the section of standard line east of the current

station in Évora and the border between Portugal and Spain, in the

Caia zone, which is an integral part of the standard Sines-Elvas-

Caia line, referred to as the “RAV Poceirão-Caia”.

2

Not all of the completed operations were eligible for the Dealogic ranking.

Latin America Transport Deal of the Year 2011

MANDATED LEAD ARRANGER | 2011

IDB (B LOAN): USD 330,000,000IDB (A LOAN): USD 100,000,000

ELOS – Ligações de Alta Velocidade, S.A.

Phase I – High Speed Railway

Line linking Portugal and Spain

(Poceirão-Caia)

Portugal

€1,088,384,493

MANDATED LEAD ARRANGER 2| 2011

Annual Report – 2011

21

Indáqua Santo Tirso: refinancing of the water and sewage

concession in the municipalities of Santo Tirso and Trofa, as

part of the process for restoring the concession’s economic-

financial balance. All of the original financing was taken out with

CGD.

On an international level, reference should be made to the Bank’s commitment to its geographical

expansion, focusing on Brazil, Mozambique and Angola, which endeavours continued to bear fruit in

2011, exemplified by its involvement in the referred to Embraport operation as well as financial

advisory services to EDP Energias do Brasil in the auction for a licence for the construction of a

combined 500 MW natural gas power station in Brasil.

Water and Sewage

Concession – Economic and

Financial Rebalancing

Portugal

€17,500,000

MANDATED LEAD ARRANGER 9 | 2011

Annual Report – 2011

22

6.2 Structured finance

In terms of operations financed and structured on a corporate basis, in 2011, reference should be

made to CaixaBI’s ongoing involvement in the identification of mandates giving it MLA status both in

Portugal and overseas.

In Portugal, reference should be made to the signing of the

promissory financing contract with SECIL, for an equity investment

in Betecna from the Lafarge Group, signed in July.

The Bank also played a highly active role in structuring various operations, particularly:

Ascendi: involvement in financing the Ascendi Group, reimbursed by the dividend flow received

by Ascendi Group SGPS.

José de Mello Saúde: structuring of short term finance for José de Mello Saúde for the

reimbursement of a tranche of the loan made by CGD Group to Escala Braga – Entidade

Gestora do Edifício, S.A. This financing operation was fully provided for by CaixaBI.

Also on an international level, CaixaBI endeavoured to be actively involved in advisory, structuring and

financial organisation on a typically corporate basis exemplified by the structured operation with

Rodovias do Tietê. In this operation, CGD Group, through BCG Brasil, was a member of a banking

syndicate which, in December 2010, arranged for a bridging loan with the Rodovias do Tietê

concessionaire, through the issue of promissory notes with a maturity of 6 months, latterly renewed in

June 2011, in the form of a new promissory notes issue with a maturity of 6 months.

The slow economic recovery and limited capacity of several companies to resolve their commitments,

vis-à-vis a scenario of liquidity restrictions maintained the trend noted in liabilities refinancing

operations, in which CaixaBI remained active in providing advisory services on several liabilities

refinancing operations.

Leveraged Buy -Out

Betecna(Grupo Lafarge)

€75,000,000

MANDATED LEAD ARRANGER 2 | 2011

Annual Report – 2011

23

As regards activity in the medium-sized enterprises segment, the environment of major restrictions on

access to liquidity, requirements for a reduction in leveraging imposed on the domestic economy and

significant increase in spreads were the reasons for greater concentration in accompanying

commercial paper programmes and the development and finalising of financial advisory mandates in

progress, particularly:

Eu-Steel Group: final closing stage of financial advisory services on refinancing liabilities,

involving negotiations with each of the lending banks.

Piedade Group: advisory service on refinancing the group’s liabilities, performed in collaboration

with PricewaterhouseCoopers, consisting of redefining the financing and negotiation structure

with each of the lending banks.

Annual Report – 2011

24

6.3 Corporate finance – advisory

M&A activity, in 2011, was down both worldwide and in Europe in comparison to 2010 (by 2.5% and

5.0% respectively), with very much lower amounts than in the last decade.

M&A activity

(€billion ) 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

World market 1,656 1,168 1,020 1,564 1,947 2,774 3,126 1,722 1,211 1,427 1,391

Growth rate. -51.6% -29.5% -12.7% 53.5% 24.5% 42.5% 12.7% -44.9% -29.7% 17.9% -2.5%

European market 683 619 451 636 863 1.331 1.573 890 404 533 507

Growth rate -51.2% -9.4% -27.2% 41.0% 35.7% 54.2% 18.2% -43.4% -54.6% 32.0% -5.0%

Source: Bloomberg

The world financial crisis, the major fiscal crisis affecting several countries in Western Europe,

uncertainty deriving from interbank market liquidity problems and rating downgrades on the sovereign

debt of a series of European countries are highly conditioning factors on M&A activities.

Notwithstanding the unfavourable macroeconomic context and reduced level of global mergers and

acquisitions activity CaixaBI’s endeavours over the course of 2011, namely its main M&A operations

on domestic entities are reflected in its current ranking in international benchmark league tables.

According to Bloomberg, CaixaBI came first in the domestic M&A ranking, in 2011, having been

involved in 12 operations for an aggregate amount of around €10 billion.

In Brazil, according to the same ranking, CaixaBI, in conjunction with BCG Brasil and following only

two full years of activity in this country, came 13th in terms of the announced/completed volume of

M&A operations and was the best positioned Portuguese bank with an aggregate amount of around

R$17.8 billion.

Special reference should be made to the following projects in 2011:

EDP: financial advisory services for Parpública’s disposal of an equity investment of 21.35% in

EDP, as part of the company’s 8th remarkably successful reprivatisation stage at a price of €3.45

per share corresponding to a premium of 53.6% over the company’s listed price. This

reprivatisation process was extremely competitive, and allowed

the Portuguese state and EDP to maximise their objectives.

The strategic partnership between EDP and China Three

Gorges represents a high level of value added for the company,

particularly as regards growth in new geographies with the

objective of achieving worldwide leadership in renewable

energies areas and obtaining new funding sources. The

operation will also make it possible to achieve high value offset

operations for the Portuguese economy in terms of potential

direct investment by Chinese companies in the industrial area

and R&D centres as well as financial support for Portuguese

Advisory in the sale of a

21.35% stake in

regarding the 8th Phase of

the Privatisation Process

FINANCIAL ADVISOR| 2011

Advisory in the sale of a

21.35% stake in

regarding the 8th Phase of

the Privatisation Process

FINANCIAL ADVISOR| 2011

Annual Report – 2011

25

companies and financial institutions.

Galp Energia: financial advisory services for Galp Energia’s

disposal of a 30% equity investment in Petrogal Brasil, through a

capital increase of around USD 4.8 billion in Sinopec. This

operation enabled Galp Energia to meet the borrowing

requirements associated with its exploration & production

activities in Brazil, resulting in direct proceeds from the

reimbursement of 30% of partners´ loans in Petrogal Brasil

(around USD 390 million). Reference should be made to the fact

that the capital increase announced is significantly higher than

the initial objectives indicated to the market by Galp Energia.

This strategic partnership with Sinopec, which still requires the

approval of the competent authorities is geared to the joint

development of Galp Energia’s current assets in Brazil, although there is a possibility that both

parties will continue to expand in the region.

Portugal Telecom: financial advisory services for Portugal

Telecom’s equity investment in the Brazilian Oi Group,

translating into an important level of support by CaixaBI to

enable Portugal Telecom to strengthen its internationalisation

and maintain a presence in a market with good growth prospects

following the disposal of its equity investment in Vivo, in which

CaixaBI also acted as the financial advisor.

The financial advisory operation for Portugal Telecom’s equity

investment in Oi was one of the largest operations involving

Portuguese companies over the last few years and represents

another example of CaixaBI’s successful Portugal – Brazil cross-

border operations.

SAG: financial advisory services for SAG’s disposal of an

investment of around 47% in Unidas, to the investment funds

managed by Gávea, Kinea and Vinci, in the form of a capital

increase of R$ 300 million. CaixaBI played a highly important role

in identifying suitable financial partners for the operation and in its

permanent involvement, enhancing the project’s value. This

operation was one of the largest private placements in Brazil, in

2011, in the case of Brazilian private equities.

Advisory in the sale of a stake in

FINANCIAL ADVISOR | 2011

Advisory in the sale of a 30% stake in

Petrogal Brasil

FINANCIAL ADVISOR| 2011

Advisory in the acquisition ofa stake in

FINANCIAL ADVISOR | 2011

Annual Report – 2011

26

CaixaBI successfully developed and completed other projects, in 2011, particularly:

Financial advisory services to DGTF for an economic-financial assessment and disposal of the

share capital of BPN, pursuant to the bank’s reprivatisation process.

Financial advisory services to Portugal Telecom for an equity investment in Contax and latter

merger with Dedic/GPTI.

Financial advisory services to EDP Energias do Brasil for the assessment and acquisition of

exploration rights to the Santo Antônio do Jari power plant.

Financial advisory services to DGTF for an economic and financial assessment of its equity

investment in Investment Opportunities.

Financial advisory to CGD for an economic and financial assessment of IHRU.

Financial advisory services to Parcaixa for an economic and financial assessment of Águas de

Portugal.

Financial advisory services to Parpública for an economic and financial assessment of TAP,

pursuant to its respective reprivatisation process.

Financial advisory services to Parpública for an economic and financial assessment of REN, as

part of the 2nd stage of its reprivatisation process.

Financial advisory services to A. Silva & Silva for the iZi/Mestre Maco disposal process.

Financial advisory services to REN for an economic and financial assessment of EDM –

Telefibra.

Financial advisory services to Parpública for an economic and financial assessment of

Hidroeléctrica de Cahora Bassa.

Financial advisory services to Caixa Seguros e Saúde for an economic and financial assessment

of HPP Saúde.

Annual Report – 2011

27

Advisory in thesale of theshare capital of

regarding the PrivatisationProcess

FINANCIAL ADVISOR | 2011

Advisory in theacquisition of a stake in

FINANCIAL ADVISOR | 2011

Advisory in theacquisitionof the

exploitationrightsin

Usina Hidroeléctrica

Santo António do Jari

FINANCIAL ADVISOR| 2011

Economicand Financial Valuationof

InvestmentOpportunities

FINANCIAL ADVISOR | 2011

Economic and Financial Valuation of

FINANCIAL ADVISOR | 2011

Economic and Financial Valuation of

FINANCIAL ADVISOR | 2011

PARCAIXA SGPS, SA

Economicand Financial Valuation of

regarding thePrivatisation Process

| 2011FINANCIAL ADVISOR

Economicand Financial Valuation of

regarding the 2nd Phase of

the Privatisation Process

| 2011FINANCIAL ADVISOR

Advisory in the sale of theshare capital of

FINANCIAL ADVISOR | 2011

Economicand Financial Valuation of

EDM TELEFIBRA

FINANCIAL ADVISOR | 2011

Economicand Financial Valuation of

FINANCIAL ADVISOR | 2011

CAIXA SEGUROS E SAÚDE, SGPS, SA

Economic and Financial Valuation of

FINANCIAL ADVISOR | 2011

Annual Report – 2011

28

6.4 Debt capital market

CaixaBI’s leading position in the debt capital market and structured assets financing in Portugal, was

afforded yet another important international recognition, in 2011, with the Award of Excellence for the

Best Debt House in Portugal from Euromoney, for the second year running. Reference should also be

made to the No. 1 Corporate Bond House prize from the NYSE Euronext Lisbon Awards.

Bond loans

The worsening crisis situation in Europe’s debt markets, major constraints which, since first quarter

2010 have restricted Portuguese issuers’ access to the market, various rating downgrades on the

Portuguese Republic and the main domestic banks and companies, in addition to the growing balance

sheet restrictions faced by Portuguese financial institutions, are factors which, in 2011, severely

limited the development of the Bank’s activity in these aspects of its operations.

Notwithstanding this environment, CaixaBI, in 2011, continued to be the Portuguese market

benchmark operator in the debt component of the capital market, particularly in the bonds and

commercial paper segments. CaixaBI’s performance in leading seven primary bond market issues

continued to position the Bank, according to the Bloomberg ranking as the leading bookrunner for

euro-denominated bonds issued by domestic entities for the fifth year running.

Its proactive management of opportunities enabled CaixaBI to operate as the bookrunner in two of the

three bond issues organised by domestic issuers in 2011. These operations, both of which took place

in the very limited window of opportunity available to several Portuguese issuers between end January

and early February, involved the issue of new benchmarks with a maturity of 5 years by Portugal

Telecom (€600 million) and the Portuguese Republic (€3.5 billion).

CaixaBI was also dealer manager in a CGD exchange offer, involving an exchange of securities for

four subordinated issues in circulation (two Tier I and two Upper Tier II issues) for securities pertaining

to a new senior issue maturing in 2015, for the amount of €367.3 million.

5,625% Notes due 2016

€600,000,000

01| 2011

PT International Finance B.V.

JOINT LEAD MANAGER & BOOKRUNNER

6,4% Obrigações do

Tesouro Benchmarkdue

2016

€3,500,000,000

JOINT LEAD MANAGER & BOOKRUNNER 02|2011

Change

of 2 Issues Upper Tier II

and of 2 Issues Tier I

for 8% Notes due 2015

€367,310,000

09| 2011J OINT DEALER MANAGER

8% Notes due 2015

€367,310,000

09| 2011JOINT LEAD MANAGER & BOOKRUNNER

Annual Report – 2011

29

CaixaBI also led four new CGD bond issues, two of which for covered bonds and two Portuguese

state-backed issues totalling €6.1 billion.

Commercial paper

Activity in the commercial paper segment was strongly conditioned by the growing balance sheet

restrictions faced by domestic financial institutions in 2011. However, notwithstanding the

unfavourable environment, CaixaBI retained a leading position in this market in Portugal having in the

last year, organised and led thirteen new commercial paper programmes3, totalling around €2.5 billion,

particularly:

3

Includes fully or partly renewed programmes maturing in 2011.

Floating Rate Mortgage

Covered Bonds due 2021

# 12

€750,000,000

04| 2011LEAD MANAGER & BOOKRUNNER

Floating Rate Mortgage

Covered Bonds due 2021

# 13

€750,000,000

04| 2011LEAD MANAGER & BOOKRUNNER

Guaranteed Floating

Rates Notes

€1,800,000,000

07| 2011LEAD MANAGER & BOOKRUNNER

Guaranteed Floating

Rates Notes

€2,800,000,000

12| 2011LEAD MANAGER & BOOKRUNNER

Commercial Paper

Programme

€ 200,000,000

04| 2011SOLE ARRANGER

Commercial Paper

Programme

€ 620,000,000

06| 2011SOLE ARRANGER

Commercial Paper

Programme

€ 1,000,000,000

06| 2011JOINT ARRANGER

Commercial Paper

Programme

€ 70,000,000

09| 2011SOLE ARRANGER

SONAE INVESTIMENTOS, SGPS, S.A.

Commercial Paper

Programme

€ 300,000,000

10| 2011JOINT ARRANGER

Commercial Paper

Programme

€ 100,000,000

10| 2011SOLE ARRANGER

Commercial Paper

Programme

€ 50,000,000

10| 2011SOLE ARRANGER

Annual Report – 2011

30

6.5 Equity capital market

A significant slowdown of activity in primary share markets was witnessed over the course of 2011

with a decline of 30.3% in the number of offers and 42.6% in terms of funds secured in comparison to

2010. This slowdown was more sharply felt in the second half of the year, with 3rd quarter 2011

having been the least active period in terms of new issues since 2009.

In Portugal and in light of the negative macroeconomic environment, 2011 was characterised by an

absence of new issues and relevant capital increases, with only two exceptions in the financial sector.

International investors continued to display major risk aversion. The effective recovery of the capital

market is dependent upon the general evolution of the economic situation and investor sentiment.

Capital market activity in Spain was also limited on account of the poor performance of the economy in

general, except for banking sector offerings in the sphere of the reorganisation and recapitalisation

process of the Spanish cajas. These included the Bankia IPO, which was one of the biggest offers this

year in Europe.

As regards the Brazilian market, in 2011, although there is still a relevant pipeline of offers, only

several of the smaller offers proceeded, with a significant number of offers having been postponed

owing to high interest rates, downwards revisions of the economy’s growth rate estimates and the

situation of instability in the main world stock markets.

In 2011, CaixaBI successfully achieved four capital market operations: the Bankia IPO, Sonae Sierra

Brasil IPO, the secondary public subscription for EDP – Energias do Brasil and Inapa’s capital

increase.

As part of its internationalisation strategy, CaixaBI was involved as

co-lead in the Bankia IPO as the only Portuguese bank in the banking

syndicate for one of the largest offerings in Europe, in 2011. Bankia is

the entity resulting from the aggregation of a series of Spanish cajas

(Caja Madrid, Bancaja, Caja Canarias, Caja de Ávila, Caixa Laietana,

Caja Segovia and Caja Rioja).

Notwithstanding the highly unfavourable environment in Europe in

general and the banking sector in Spain, in particular, it was possible

to successfully organise a major offering of €3.09 billion, in which

CaixaBI played an important role in promoting the Bankia offer and

investment case to a broad range of institutional investors in the

European market, notably in less obvious markets such Scandinavia.

CaixaBI also continued to carve out a position in Brazil, in partnership with BCG Brasil. Reference

should be made to CaixaBI´s involvement as co-manager for the Sonae Sierra Brasil IPO and the

EDP - Energias do Brasil secondary public offering, strengthening its international presence in the

capital market area. CaixaBI, as co-manager, contributed to the geographical diversification of the

placement in promoting contacts with a large number of institutional investors in the European market.

Initial Public Offering

€ 3,092,145,949

CO-LEAD | 2011

Annual Report – 2011

31

In Portugal, notwithstanding the reduced level of primary share market activity, CaixaBI was

responsible for organising and structuring the Inapa rights issue through its issue of non-voting

preference shares, as one of the main capital market operations in Portugal, in 2011.

SecondaryPublic Offering

R$ 810.724.020

CO-MANAGER | 2011

Initial Public Offering

R$ 465,020,860

CO-MANAGER | 2011

Share Capital Increase

through the issue of non-

voting preference shares

€ 54,176,479.38

ARRANGER | 2011

Annual Report – 2011

32

6.6 Financial brokerage

The highly negative performance of the share segment of the capital market over the course of 2011

reflected uncertainty over fundamental variables for the evolution of share markets, the slowdown of

the main world economies, the Europe-wide sovereign debt crisis and the main central banks’ needs

to adjust monetary policies. This framework led to a reduction of exposure to share risk by asset

managers, with negative repercussions on stockmarket turnover. The Portuguese share market was

particularly penalised by this environment, reflecting investors’ greater aversion to Portuguese assets

which is also reflected in a drop in brokerage volumes in the market, down 34% over 2010, according

to CMVM data.

CaixaBI was actively involved in the Bankia IPO and was co-manager for the Sonae Sierra Brasil IPO

and the EDP share offering on its EDP Energias do Brasil subsidiary, in 2011.

6.7 Research

CaixaBI’s equity research area aims to independently monitor the evolution of financial markets, with

the objective of assisting investors’ decision-making processes associated with the management of

equity investments in their financial assets portfolios.

Operating on a sell-side approach, the research area monitors the companies listed on the main

NYSE Euronext Lisbon (PSI20) index as well as other Portuguese mid and small caps selected on the

basis of their interest to investors.

CaixaBI is part of the ESN (European Securities Network), which is a pan European investment banks

and/or brokerage houses network working together in the capital markets in a wide range of areas

ranging from corporate equities and debt to the brokerage business (sales and trading) and equity

research areas.

Underlying the collaboration in the research area is a pan European approach whose methodology is

based on equity analysis standards to provide investors with local expertise while simultaneously

ensuring a more focused coverage of each company’s specific circumstances.

Reference should also be made to the fact that the ESN’s equity research teams are divided up into

various sectors based on the Footsie methodology, of which around 10 include Portuguese

companies, making it possible to supply research reports on European companies to domestic

investors while simultaneously providing information about domestic companies to a large number of

foreign investors on the same network, without the need for a global structure. Membership of the

ESN therefore allows CaixaBI’s analysts to form a consequently broader European perspective of the

evolution of capital markets, which is all the more important taking the current level of financial market

globalisation into account.

Annual Report – 2011

33

6.8 Financing and structuring area

Public debt

Market-making activity on public debt in the secondary market, in 2011, was characterised by

extremely difficult conditions, poor liquidity, historically high bid-offer spreads and major volatility. The

widening of spreads to historical maximums – above 1500 basis points on maturities of 5 years and

more than 1000 basis points on 10 year maturities in comparison to German bonds – also increased

the Bank’s difficulty in managing its positions.

Notwithstanding such market constraints, CaixaBI came top out of all of the primary dealers in IGCP’s

general performance ranking. The Bank’s strategy for this distinction was based on its best effort

compliance with obligations and in achieving relatively higher performance levels than in 2010, both in

terms of compliance and market share.

Liquidity providing

CaixaBI’s liquidity providing activities for various securities listed on Euronext Lisbon, such as Cofina,

Orey Antunes, Altri, Inapa, Ibersol and SAG Gest remained dynamic in 2011. This is a business area

in which CaixaBI was a pioneer and continues to be a benchmark operator with Euronext having

awarded its maximum “A” rating on all securities and categories.

CaixaBI continued to expand its contracts base in diversifying the type of instruments for which it is a

liquidity provider, maintaining its market-making activity on the Fundiestamo property fund and several

Tier I deeply subordinated perpetual issues, such as Finibanco, Millenniumbcp, BES and BESI.

Own portfolios

Access to wholesale funding by Portuguese issuers continues to be constrained, particularly for

financial issuers and only alleviated at the end of the year with the ECB’s three year maturity auction.

Owing to such constraints, CaixaBI has concentrated its trading activity in futures or shares. The

interaction between shares and credit teams has increased, implementing various models which have

been maintained, perfected or discontinued in line with market conditions or performance.

Corporate risk management advisory services

Instability in capital markets has geared the Bank’s activity to identifying new business opportunities

and intensifying customer contacts in order to minimise interest risk and mark-to-market variability.

With the decline of lending to companies, in a scenario of rates at historical minimums and strong

limitations on the taking of new risks, the positive performance noted essentially derives from

endeavours to find and secure new opportunities, particularly:

The extracting of some value from live structures, particularly through the identification of

operations for restructuring opportunities proposed to customers, owing to the stability/increase of

interest rates at the start of 2011.

Annual Report – 2011

34

Performance of hedge operations, essentially interest rate risk.

The performance of a series of highly profitable derivatives operations, leaving credit exposure

unchanged.

Deposit-taking operations, with a higher level of expression in second half 2011.

Annual Report – 2011

35

6.9 Syndication and sales

Syndication and sales activities, in 2011, were performed in a context of an extreme drop in secondary

market activity and the virtual non-existence of primary market operations.

Notwithstanding, CaixaBI succeeded in operating as joint lead manager in the following issues:

Portugal Telecom 5 years (January 2011): placement of a Portugal Telecom bond issue, for

the amount of €600 million, at a coupon rate of 5.625% maturing on 8 February 2016.

Benchmark 5 year Treasury Bonds (February 2011): placement of a Portuguese Republic

Treasury Bond Issue for the amount of €3.5 billion, at a coupon rate of 6.40% maturing on 15

February 2016.

Caixa Geral de Depósitos Exchange Offer (September 2011): exchange offer proposing an

exchange of secondary market subordinated debt in the institutional segment for a senior debt

bond maturing on 28 September 2015 at a coupon rate of 8%. The objective of this operation

was the strategic management of CGD’s financing and own funds structure and was very

successful in achieving a highly positive impact on investors holding such assets.

CaixaBI, as a specialised treasury securities operator was involved in Portuguese public debt auctions

in 2011:

January: treasury bonds auction (3.60%) – October 2014 and treasury bonds auction (4.80%)

January 2020;

March: treasury bonds auction (5.5%) – September 2013;

April: treasury bonds auction (5%) – June 2012 – extraordinary auction.

Treasury bills have been the Portuguese Republic’s main source of market funding, insofar as it

ceased to enjoy access to the medium and long term markets since its bailout application. CaixaBI, in

collaboration with CGD and IGCP, in order to promote treasury bill auctions secured orders for the

successful execution of all of the auctions occurring during the year.

CaixaBI performed 341 commercial paper issues, totalling €12 billion, in 2011, having placed €4.8

billion in coordination with CGD, particularly in the 4th quarter, at the time of the normalisation of the

treasury bills placement rates and restrictions raised by the Bank of Portugal (BdP) on banks’ interest

rates on deposits, with commercial paper having a good credit risk as an alternative for investors.

6.10 Venture capital

CaixaBI’s venture capital area is geared to strengthening the competitive capacity of domestic

companies in wider markets, promoting the appearance and development of well structured business

projects with high appreciation potential and a return on invested capital.

Activity in 2011 was naturally highly constrained by the recessionary context and uncertain business

environment. In general and together with companies’ reluctance to assume aggressive growth

strategies, a drop in the level of economic performance and depreciation of assets was witnessed.

Annual Report – 2011

36

The strategy adopted was therefore to fuel the development of industry in Portugal, consolidating CGD

Group’s leading position in the sector and fundamentally providing companies with capital instruments

adjusted to their development stage.

CGD Group has allocated around €700 million to venture capital resources in its twofold capacity as

an investor in highly specialised funds under third party management or with a suitable aptitude and

fundamentally as a direct operator using its own vehicles managed by Caixa Capital.

During the course of the year a fresh boost was given to the network operating model, comprising a

vast range of partnerships with different types of entities for securing, examining, and assessing

business projects, which, in addition to giving Caixa Capital a central role in its “ecosystem”, made it

possible to support a vast range of communicational initiatives in conjunction with CGD.

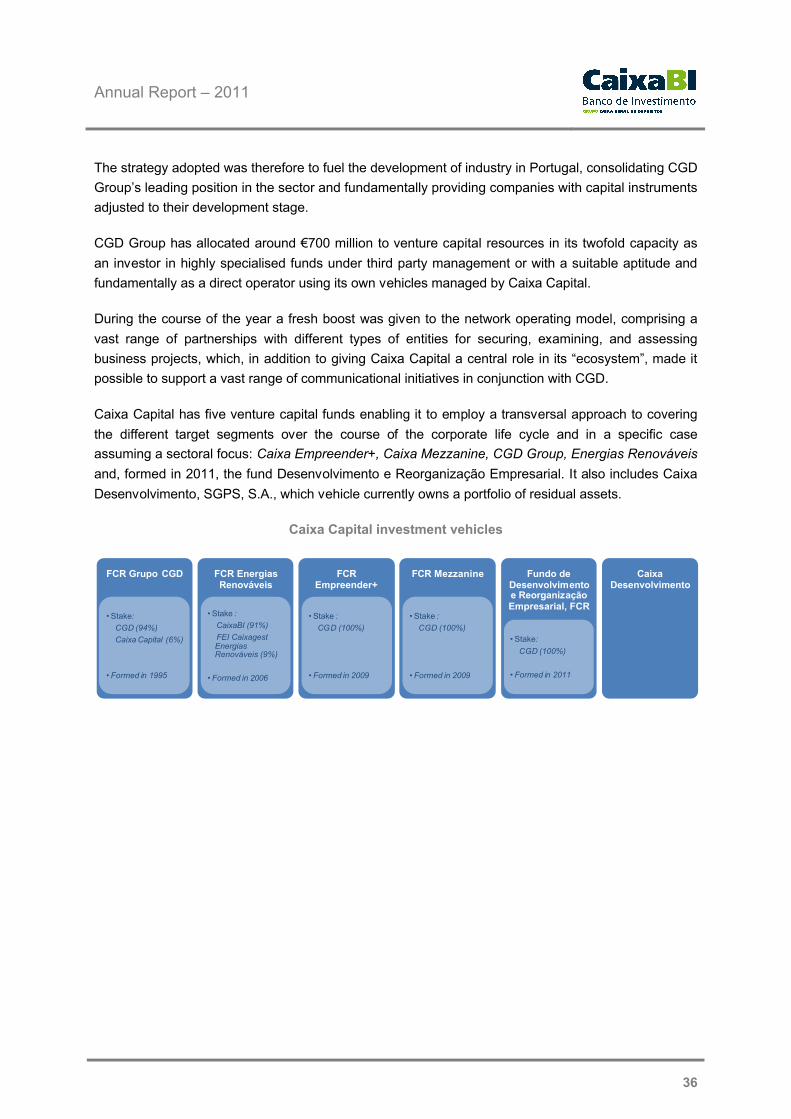

Caixa Capital has five venture capital funds enabling it to employ a transversal approach to covering

the different target segments over the course of the corporate life cycle and in a specific case

assuming a sectoral focus: Caixa Empreender+, Caixa Mezzanine, CGD Group, Energias Renováveis

and, formed in 2011, the fund Desenvolvimento e Reorganização Empresarial. It also includes Caixa

Desenvolvimento, SGPS, S.A., which vehicle currently owns a portfolio of residual assets.

Caixa Capital investment vehicles

FCR Energias Renováveis

• Stake :

CaixaBI (91%)

FEI CaixagestEnergias Renováveis (9%)

• Formed in 2006

FCR Grupo CGD

• Stake:

CGD (94%)

Caixa Capital (6%)

• Formed in 1995

FCR Empreender+

• Stake :

CGD (100%)

• Formed in 2009

FCR Mezzanine

• Stake :

CGD (100%)

• Formed in 2009

Fundo de Desenvolvimento e Reorganização Empresarial, FCR

• Stake:

CGD (100%)

• Formed in 2011

Caixa Desenvolvimento

Annual Report – 2011

37

Investments

The investment volume, in terms of total assets under direct Caixa Capital management, at the end of

2011 totalled €344 million in 75 companies. It should be noted that 40% of the portfolio comprised

investments made over the last three years.

210 investment opportunities were analysed during the course of the year, mainly in the form of seed

capital/start-ups. 32 operations totalling €60 million were approved and 21, involving investment of €17

million, completed. Industry (25%), services (23%) and information technology projects (22%)

predominated in sectoral terms.

Projects analysed in 2011

Status Type

By sector

210

21

11

130

48

Total

Implemented

Approved but not implemented

Filed

Under analysis

210

109

15

75

11

Total

Seed / Start-Up

Acquisition

Expansion

Reorganisation

Information Techonology

22%

PrivateEquity

1%

Industry25%

Services23%

Commerce10%

Agro industry4%

Tourism1%

Others3%

Energy11%

Annual Report – 2011

38

The referred to investments are split up into €3 million on 18 new investments and €14 million on

additional investment in 14 subsidiary companies, as follows:

CGD Group FCR

FCR Turismo Inovação (Tourism Innovation): 10% equity capital investment in the Turismo

Inovação – FCR, venture capital fund managed by Turismo Capital – SCR, S.A. with the

corporate objective of “contributing to the innovation, modernisation and internationalisation of

tourism SMEs and tourism projects enhancing the value of supply”. The fund has a capital of €20

million and its investors have paid up 30% of the subscribed capital, signifying a €600,000

investment for FCR CGD Group.

Mota-Engil and AICEP: partnership with Mota-Engil Indústria e Inovação, SGPS, S.A. and

AICEP Capital Global – Sociedade de Capital de Risco, S.A., with the corporate aim of promoting

joint participation in innovative, differentiated, industry based projects with high growth and value

creation potential, upon which work has still to start or is at its start-up stage, predominantly

outside domestic territory and preferably in external markets in which the companies belonging to

CGD and Mota-Engil groups and their respective subsidiaries operate.

ME3I: subscription for 19.4% of the equity capital of ME3I, SGPS, S.A., a company formed on

the basis of the above referred to agreement, as a corporate vehicle to which smaller

investments will be allocated. In 2011, this company approved a 49% equity investment in the

Solargus company’s internationalisation project for the Peruvian market, to set up a metalworking

area plant, starting 2012.

Capital increases: additional investment in portfolio companies totalled €11.32 million and

involved A. Silva & Silva – Imobiliário e Serviços, S.A., Logoplaste Latam, SGPS, S.A., Onyria

Internacional, S.A., Logoplaste Investimento, SGPS, S.A., Artlant PTA, S.A. and Eurofrozen –

Indústria e Comércio de Produtos Alimentares, S.A.

FCR Energias Renováveis (Renewable energies)

Pinewells: a €526 000 investment in Pinewells, S.A., following its October capital increase, in

which the Fund increased its investment from 20% to 22.69%.

FCR Empreender+ (entrepreneurialism)

Biosurfit: payment of the last investment tranche in Biosurfit, S.A., for the amount of €333,000,

comprising approximately 9.4% of the respective capital increase. The Biosurfit investment was

part of a global capital increase aimed at completing the SpinIT technology industrialisation