Business Logic for Sustainability

288

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Business Logic for Sustainability

Business Logic for Sustainability

This page intentionally left blank

Business Logic forSustainability A Food and Beverage Industry Perspective

Aileen Ionescu-Somers and Ulrich Steger

© Aileen Ionescu-Somers and Ulrich Steger 2008Foreword © James P. Leape

All rights reserved. No reproduction, copy or transmission of this publication may be made without written permission.

No paragraph of this publication may be reproduced, copied or transmitted save with written permission or in accordance with the provisions of the Copyright, Designs and Patents Act 1988, or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, 90 Tottenham Court Road, London W1T 4LP.

Any person who does any unauthorized act in relation to this publicationmay be liable to criminal prosecution and civil claims for damages.

The authors have asserted their rights to be identified as the authors of this work in accordance with the Copyright, Designs and Patents Act 1988.

First published 2008 byPALGRAVE MACMILLANHoundmills, Basingstoke, Hampshire RG21 6XS and 175 Fifth Avenue, New York, N.Y. 10010Companies and representatives throughout the world

PALGRAVE MACMILLAN is the global academic imprint of the Palgrave Macmillan division of St. Martin’s Press, LLC and of Palgrave Macmillan Ltd. Macmillan® is a registered trademark in the United States, United Kingdomand other countries. Palgrave is a registered trademark in the EuropeanUnion and other countries.

This book is printed on paper suitable for recycling and made from fully managed and sustained forest sources. Logging, pulping and manufacturingprocesses are expected to conform to the environmental regulations of thecountry of origin.

A catalogue record for this book is available from the British Library.

A catalogue record for this book is available from the Library of Congress.

10 9 8 7 6 5 4 3 2 117 16 15 14 13 12 11 10 09 08

ISBN 978-1-349-36214-1 ISBN 978-0-230-58350-4 (eBook)DOI 10.1057/9780230583504

Softcover reprint of the hardcover 1st edition 2008 978-0-230-55131-2

Contents

List of Tables viii

List of Figures ix

Acknowledgements xii

List of Abbreviations xiv

Foreword by James P. Leape, Director General, WWF International xvi

Preface xvii

Executive Summary xix

Part I Building the Business Logic 1

Chapter 1 Introduction 3

1 Background: the conundrum 42 Conceptual framework 6

2.1 The BCS project 73 Research questions and objectives 84 Terminology 95 Research instruments 10

5.1 Survey results 105.2 Interviews with corporate executives and stakeholders 115.3 Participating companies 12

6 The roadmap 13

Chapter 2 Industry and Competitive Analysis 15

1 Introduction 152 Industry definition and profile 163 Demographics, consumption trends and markets 174 Competitive analysis 20

4.1 Degree of rivalry 214.2 Barriers to entry 224.3 Threat of substitutes 234.4 Supplier power 234.5 Buyer power 24

5 Synthesis 27

v

Chapter 3 The Economic Relevance of Sustainability Issues 29

1 Introduction 292 Industry awareness of sustainable development and issues 303 The food and beverage value chain 364 What are the issues? 375 Upstream 41

5.1 Raw materials and natural resource depletion 415.2 Social impacts 505.3 Market distortions 525.4 Power of multinationals 54

6 Operations and downstream 596.1 Manufacturing operations 596.2 Traceability and health 62

7 Synthesis 74

Chapter 4 The Pressure of Stakeholders 78

1 Introduction 782 Food and beverage industry stakeholders 79

2.1 Deterring stakeholders 802.2 Promoting stakeholders 94

3 Synthesis 108

Chapter 5 The Value of Value Drivers 112

1 Introduction 1122 The concept of shareholder value 1133 Food and beverage industry value drivers 117

3.1 Reputation enhancement and brand value 1213.2 Attracting and retaining talent 1283.3 Innovation and revenue increase 132

4 Synthesis 143

Part II Rolling Out the Business Logic 147

Chapter 6 Corporate Sustainability Management 149

1 Introduction 1492 Corporate culture, vision and the mindsets of managers 1513 Sustainability strategy design 160

3.1 What good is a sustainability strategy? 1604 Organizational structure 166

4.1 Structure and interaction between key business units 166

vi Contents

5 Importance of functions: ‘Opposers’ and ‘Promoters’ 1745.1 Top management 1785.2 The ‘second layer’ 1805.3 The ‘old guard’ 1805.4 ‘New age’ managers 1815.5 Supply chain and purchasing officers 1825.6 Brand and marketing managers 185

6 Processes and systems 1916.1 Issue tracking, mapping and prioritization 1936.2 Integrating issues into strategic decision-making 1996.3 Implementation: working with mindsets and getting 205

managers on board7 Synthesis 235

References 239

Index 249

Contents vii

List of Tables

5.1 Areas of focus for companies seeking new business 141models

6.1 Issue tracking within food and beverage companies 1956.2 Tools available to F&B companies to promote 208

implementation of sustainability strategies6.3 Tools used in the food and beverage sector to promote 230

sustainability internally in companies

viii

List of Figures

1.1 Relationship between economic and environmental/ 7social performance beyond compliance – the ‘Smart Zone’

1.2 Food and beverage companies involved in the BCS food 12and beverage interview research

3.1 Managers’ familiarity with sustainable development: 31all industries

3.2 Managers’ familiarity with sustainable development: 32food and beverage industry

3.3 Business managers’ view on whether SD as a concept 32would grow in the future: all sectors

3.4 Business managers’ view on whether SD as a concept 33would grow in the future: F&B industry only

3.5 Industry progress in adopting more sustainable business 34practices

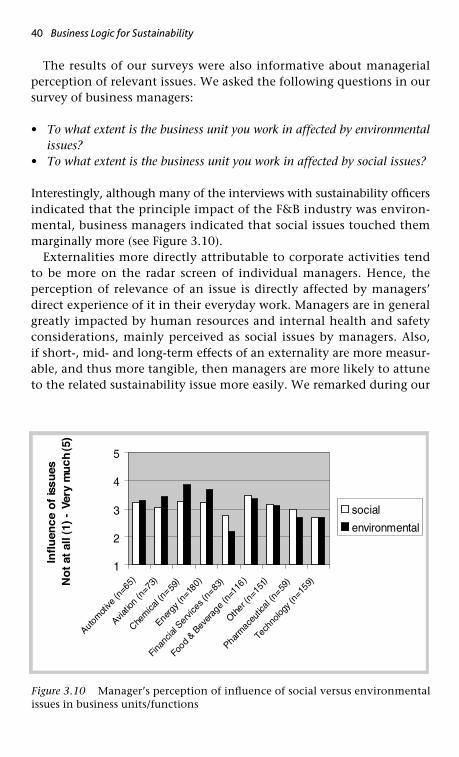

3.6 Food and beverage industry value chain 363.7 Nature of issues identified by business managers 373.8 How business units respond to issues 383.9 Issues in the food and beverage value chain 393.10 Manager’s perception of influence of social versus 40

environmental issues in business units/functions3.11 World trends indicating land and food availability and 42

population increase3.12 Potential risks and opportunities along the F&B product 60

chain4.1 Main barriers to success with sustainability initiatives 81

(business managers)4.2 Expected reaction of capital markets to improved 88

sustainability performance in the next five years (business managers, all sectors)

4.3 Expected reaction of sustainability performance in the 89next five years (business managers, food and beverage sector)

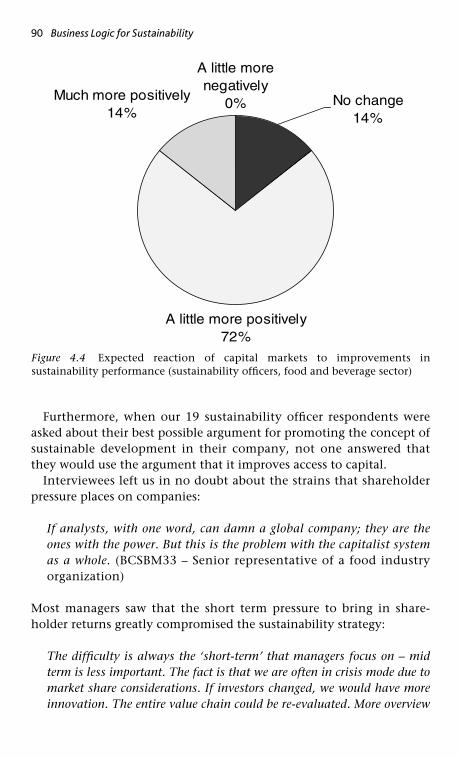

4.4 Expected reaction of capital markets to improvements in 90sustainability performance (sustainability officers, food and beverage sector)

ix

4.5 Pro-activeness of responsible parties in promoting 95sustainability (business managers)

4.6 Pro-activeness of responsible parties in promoting 95sustainability (sustainability officers)

4.7 Causes of incidents damaging corporate reputation over 98the past three years (business managers)

4.8 Significance to (business managers) of incidents affecting 99reputation

4.9 The food and beverage industry: stakeholder pressure and 109industry response

5.1 CSM’s contributions to value drivers 1155.2 Arguments for promoting the concept of sustainable 118

development in F&B companies (sustainability officers)5.3 System of value drivers 1195.4 Importance of brand or reputation to the company 123

(business managers – all sectors)5.5 Importance of brand or reputation for the company 123

(business managers – food and beverage sector)5.6 Cross industry analysis – importance of brand and 125

reputation5.7 Industry value driver response 1446.1 Approaches used by food and beverage companies to 154

overcome barriers to sustainability internally (sustainability officers)

6.2 Barriers to success of sustainability initiatives – all sectors 158(business managers)

6.3 Barriers to success of sustainability initiatives – F&B sector 158(business managers)

6.4 Main barriers to sustainability – all sectors (sustainability 159officers)

6.5 Main barriers to sustainability – food and beverage sector 159(sustainability officers)

6.6 Perception of company’s integration of environmental 162and social criteria into business strategy and operations(business managers)

6.7 Perception of company’s integration of environmental 162and social criteria into business strategies and operations(sustainability officers)

6.8 Steps in building an environmental strategy 1656.9 Collaboration with sustainability officers – business 170

managers in all sectors

x List of Figures

6.10 Collaboration with sustainability officers – business 170managers in the food and beverage industry

6.11 Contribution of increased collaboration to more 171sustainable practices in the company – business managers in all sectors

6.12 Contribution of increased collaboration to more 172sustainable practices in the company – business managers in food and beverage sector

6.13 Strongest opposition to implementing sustainability 175initiatives (responses from sustainability officers)

6.14 Strongest opposition to implementing sustainability 176initiatives (responses from business managers)

6.15 Functions that can most promote sustainability 177(responses from sustainability officers)

6.16 Functions that can most promote sustainability 177(responses from business managers)

6.17 Stages in the system of issue management 1926.18 Elaborating the ‘What?’, ‘Why?’ and ‘How?’ of 203

sustainability benefit measurement6.19 Tools and systems used by companies relating to the 206

concept of sustainable development (responses from business managers – food and beverage industry)

6.20 Most effective means of improving relationships with 219stakeholders

6.21 Changing managers’ mindsets 226

List of Figures xi

Acknowledgements

This may be the first attempt to write a book specifically on the businesslogic for sustainability in the food & beverage sector. For their supportwith this ground-breaking initiative, we would first like to thank themember companies of the Forum for Corporate Sustainability Manage-ment (Forum for CSM) at the International Institute for ManagementDevelopment (IMD) that pushed for an all out effort to ‘crack’ thebusiness case for sustainability (BCS) in nine industry sectors (seewww.imd.ch/research/ centers/csm). For their contributions to the con-tent of this book we would like to acknowledge the food & beveragecontingent amongst the CSM member companies; Hans Jöhr (Nestlé),Claus Conzelmann (Nestlé), Niels Christiansen (Nestlé), Tim Wolfe(Nestlé), Hans-Joachim Richter, (Nestlé Nespresso), Dean Sanders(Nestlé Nespresso), Richard Heathcote (Scottish & Newcastle), Jan-KeesVis (Unilever), Anne Weir (Unilever), Dierk Peters (Unilever), Jens Rupp(Coca Cola HBC) as well as the many others to whom we had accesswithin these companies. Both Unilever and Nestlé acted as ‘referencecompanies’, giving us exceptional access either to company informa-tion or to their senior management staff. This enabled us to carry outvaluable in-depth interviews in these companies over a prolongedperiod of time (2002 to 2007) to explore many of the dimensions of thebusiness logic for sustainability in the food & beverage industry.

We would also like to thank other managers that facilitated extensiveinterviewing at non-Forum for CSM member companies that also par-ticipated in our research: Lars Krause-Kjær (Aarhus United), GeorgesJaksch (Chiquita), Salvatore Gabola (Coca Cola), Will Peskett (Diageo),Bruno Kistner (DSM), Paul Hebblethwaite (Cadbury Schweppes), SorenHjuler Vogelsang (Danisco), Bernard Giraud (Danone), Kerr Dow(Heinz) Albrecht Schmidt (Kraft), Reid Hole (Nutreco), and Peter White(Procter & Gamble). All of these managers, and those to whom theyfacilitated access, ensured that we were able to ‘join the dots’ and pre-sent as holistic a picture of the status of business logic for sustainabilityin the F&B industry as possible. The strong survey response was alsomainly due to their support.

We thank our partner and friends from the World Wide Fund forNature (WWF International) for the invaluable support they gave to thisbook: Jim Leape (Director General), Paul Steele (Chief Operating Officer),

xii

and Jean-Paul Jeanrenaud and Maria Boulos of WWF’s Business andIndustry Unit. The food & beverage sector research presented in thisbook benefited greatly from WWF’s keen interest in bringing many ofthe difficult challenges of sustainable development to executive’s ‘frontof mind’. Jean-Paul was also a member of the BCS advisory council andwe also kindly acknowledge the other members: Margaret Flaherty ofWBCSD, Thomas Streiff of Swiss Re, Jeroen Bordewijk and Jan-Kees Visof Unilever as well as Reinier de Mann and Heike Leitschuh-Fecht. TheEuropean Academy for Business in Society (EABIS), and in particularDr. Gilbert Lenssen provided invaluable opportunities to present thefindings of the food & beverage research in several forums.

We would like to especially thank IMD president Peter Lorange, IMDfaculty Professor Benoit Leleux, IMD staff Philip Koehli, John Evans andPetri Lehtivaara for their continued interest in corporate sustainabilityand enthusiastic support for the objectives and continued existence ofIMD’s Forum for CSM.

We are also most grateful to the other members of the CSM team,Oliver Salzmann and Kay Richiger. Kay provided all manner of supportduring this project and without Oliver’s painstakingly careful andthoughtful contributions to data analysis and as a ‘sounding board’ formany of the conclusions reached in this book, things would have beena lot more difficult. Thanks also to Elaine Holt for much needed admin-istrative support, and to Michelle Perrinjaquet (IMD editorial team)and Keith Povey for their professional help with preparation of themanuscript.

Finally, warm thanks to Professor Robert (Bob) Briscoe of the NationalUniversity of Ireland (University College Cork) and who gave invaluablesupport to the doctoral work of Aileen Ionescu-Somers that contributedvaluable content to this book.

The authors take full responsibility for any flaws, errors and/oromissions in the book.

Acknowledgements xiii

List of Abbreviations

BCS Business case for sustainabilityBOP Bottom of pyramidBSE Bovine Spongiform EncephalopathyCAP Common Agricultural PolicyCARU Children’s Advertising UnitCGIAR Consultative Group on International Agricultural

ResearchCIES Comité International d’Entreprìses à Succursales –

International Committee of Food Retail ChainsvCJD variant Creutzfeldt-Jacob diseaseCNIE Canadian Network for Innovation in EducationCS Corporate sustainabilityCSA Community Supported AgricultureCSL Corporate Social LeadershipCSM Corporate sustainability managementCSR Corporate Social responsibilityEABIS European Academy for Business in SocietyEAS Early Awareness SystemECR Efficient Consumer ResponseEFFAT European Federation of Food, Agriculture and

Tourism Trade UnionsEHS Environmental, health & safetyEMS Environmental Management SystemESP Environmental and social performanceEU European UnionEurepGAP Euro Retailer Produce Working GroupF&B Food and beverageFAO Food and Agriculture OrganizationFDA Food and Drug AdministrationFMCG Fast-moving consumer goodsForum for CSM Forum for Corporate Sustainability ManagementFSA Food Standards AgencyGATT General Agreement on Tariffs and TradeGM Genetically ModifiedGMO Genetically modified organismsGRI Global reporting initiative

xiv

H&S Health and SafetyHCR Harvest Control RoomIACFO International Association of Consumer Food

OrganizationsIGO International Governmental OrganizationsIIASA International Institute for Applied Systems AnalysisIIED International Institute for Environment and

DevelopmentILO International Labour OrganisationIMD International Institute for Management

DevelopmentKPI Key Performance IndicatorsLTO Licence to operateMAP Management Appraisal ProcessMSC Marine Stewardship Council MSCI Morgan Stanley Capital InternationalNGO Non-governmental organizationNPV Net present valueOECD Organization for Economic Cooperation and

DevelopmentP&G Procter and GambleR&D Research and DevelopmentSAI Sustainable Agriculture InitiativeSAIN Sustainable Agriculture Initiative NestléSD Sustainable DevelopmentSFL Sustainable Food LaboratorySHGs Self-help groupsSME Small and/or medium-sized enterpriseSRI Socially responsible investingTNC Transnational corporationUNEP United Nations Environmental ProgramUNICEF United Nations International Children’s Emergency

FundVCJD Variant Creutzfeldt-Jakob DiseaseWBCSD World Business Council for Sustainable

DevelopmentWHO World Health OrganizationWWF World Wide Fund for Nature

List of Abbreviations xv

Foreword by James P. Leape, Director General, WWF International

From the time we wake up in the morning to a cup of coffee until wetoast another day at sundown, the food and beverage industry plays avital role in the lives of billions of people every day. Over the years,social and economic trends have had an impact on the industry, butultimately it is the environment – which has been largely undervaluedto date – that will decide the industry’s future.

Freshwater is a good example. Only 3 per cent of all water on earth isfreshwater, and only 1 per cent of this amount is useable. So it is ama-zing to think that while it takes three litres of water to produce one litreof carbonated soda, it takes up to 250 litres of water to produce the sugarused to flavour it. Even more astounding is the fact that it takes fivethousand litres to produce one fast-food hamburger meal. With increas-ing threats to freshwater ecosystems – from climate change to pollution– the business case for sustainability (BCS) in the food and beverageindustry should no longer be an open debate, but unfortunately it is.

This timely and in-depth study follows on the heels of an earlierpublication that WWF supported from 2002 to 2004, which exploredthe BCS across a broad range of industry sectors from aviation topharmaceuticals. Surprisingly, according to this latest work, most com-panies in the food and beverage industry are not yet taking sustain-ability seriously enough in order to assure sustainable development forfuture generations.

WWF has recently partnered with Coca-Cola, which publicly com-mitted to reduce, recycle and replenish the water that it uses. WWFhopes such partnerships will serve as both a catalyst and a standard forothers to follow. More broadly, we hope this study will challenge thesector to identify its critical path to sustainability before it is too late forbusiness and the planet.

xvi

Preface

This book presents the food and beverage (F&B) sector results of theIMD Forum for Corporate Sustainability Management’s research on thebusiness case for corporate sustainability (the BCS project) across nineindustry sectors from 2002 to 2004. It also reflects additional qualitativework carried out up to mid-2007 to further benchmark the resultsalready available and update developments within the industry onemerging business logic for sustainability.

Very often, perception defines reality when it comes to sustainability,and it is also difficult to break through the current ‘hype’ around theseconcepts. The topic of sustainability, or sustainable development, isoften perceived as ‘fuzzy’ by hard-nosed managers impatient for moremeasurable and tangible criteria by which to make their judgements.The topic is fascinating for researchers and a real ‘head-scratcher’ forsustainability professionals keen to make breakthroughs.

We reveal the economic logic behind the sustainability strategies ofglobally active companies in the industry. We assumed that such com-panies, being economic entities, will only take serious action uponsustainability issues beyond compliance if there is inherent businesslogic for so doing, and as long as that business logic can be communi-cated internally within companies. Our findings from a cross-industrycomparison were that the BCS is definitely industry-specific, and caneven be company or unit-specific; hence the value of this book for F&Bmanagers, and also for any manager who is working on integratingsustainability concepts in business strategy.

The F&B industry is a ‘front-line’ industry; given that people aroundthe world have to eat every day, it is ‘front of mind’ for consumers andfor industry stakeholders. That is reflected in many of the detailed con-clusions presented in this book. Within, you will find industry-specificdata that is extensively analysed, processed and compared also to theoverall BCS project results. A related diagnostic toolset can be down-loaded free of charge at: http://www.imd.ch/research/centers/csm.

The book is organized as follows. First we present an executivesummary with our general findings, assessing the business case anddiscussing what can reasonably be expected of companies in responseto articulated expectations of NGOs, governments and other stake-holders. The rest of the book has two parts, one devoted to our findings

xvii

about how managers build the business case for sustainability in theF&B industry. Here we focus mainly on the competitive framework ofthe industry, the economically relevant issues with which companiesare confronted, the nature of stakeholder pressure and the perceivedcontribution of sustainability to corporate value drivers. The secondpart of the book looks in detail at how F&B managers roll out the busi-ness case within companies and covers the full waterfront of activitiesinvolved in aligning F&B organizations behind strategies.

While it is clear that the business case in the F&B industry is probablystronger than any other sector considered in IMD’s BCS research, thecase is nevertheless not fully exploited by the industry and there still isa long way to go before sustainable development is fully integrated intobusiness strategy. We hope that this book will provide some of the toolsrequired by managers to bolster their business cases, so that it appearsless and less elusive to the grand majority.

xviii Preface

Executive Summary

Assessment of the Business Logic forSustainability in the Food andBeverage Industry

1 Introduction

In this volume, we address the complexities and challenges of buildingand implementing a business case for the integration of environmentaland social (sustainability) aspects into business strategy in the food andbeverage (F&B) industry. Our preliminary literature review revealed thatresearch contributing to the conception, building and roll out of indus-try-specific cases was lacking. Using comprehensive industry surveys,desk research and interviews with managers at global F&B companies aswell as industry stakeholders carried out over a period of five years, wepropose ‘building blocks’ for the business case for sustainability (BCS) inthe F&B industry. In our study, we also cover the full waterfront of man-agement aspects related to the potential for a BCS for globally active com-panies in the F&B industry, from strategy conception to implementation.

Since our research is primarily based on the perception of managers –what one could call an ‘inside out’ perspective – hard-lined, pragmaticmanagers may be tempted to write it off as too ‘soft’ an approach. Butour view and experience are that the successful promotion of a BCSdepends on how managers react to the related concepts as and whenthey are confronted with them. The ‘Smart Zone’ – the business area inwhich companies create additional economic value by improving envir-onmental and social performance beyond that required by legislation –is thus dependent on whether managers see a business reason for actionand whether they are able to build, communicate and implement thatbusiness case. Manager’s perception of business logic for sustainabilityis fundamental to the development of a BCS and also to its successfulroll out within companies.

It will always be a challenge for managers to work out the extent towhich they should go beyond a focused corporate profit objective andregulation to take responsibility for the host of unregulated yet negativesocial and environmental consequences of their economic decisions.

xix

The Smart Zone will therefore be unfixed and dynamic, and will dependon how much effort companies put into defining their businessrationale, the level of pressure companies receive from stakeholders, thechanging political climate, the corporate culture and type of peoplewithin organizations and so on.

In the following sections, we summarize our findings.

2 Building the business case

Is there a BCS in the F&B industry, a business case for internalizingsocial and environmental issues? Is the case robust, or elusive? One ofour advisory council members put it in a nutshell:

The business case is not just ‘found’, it has to be built.

The BCS is not only industry specific, but business unit and projectspecific. Its foundations must take account of both the tangible andthe quantifiable actions that are based on incremental continuousimprovement mechanisms, as well as the more intangible value con-structs; reputation/brand value, licence to operate, attracting andretaining talent, which allow corporate sustainability management(CSM) to contribute to important company value drivers.

However, the BCS is challenging for F&B companies to build, eventhough we identified many sustainability issues that had a direct rela-tionship with the industry’s core business. While the financialconsequences of F&B companies not internalizing key social andenvironmental issues are rarely permanent, sustainability issues havenevertheless shown themselves to impact the bottom line, at least ona short-term basis, increasingly regularly. Given the increasinglyshort-term earnings orientation of major shareholders, and thereliance of share price on a host of criteria including corporate imageand reputation, this should be is a cause for concern for senior man-agers, who very often are on a short-term mandate themselves, andare thus concerned about not ‘rocking the boat’.

However, the risks and opportunities presented by sustainabilityissues are often not immediately apparent to business managers. Themultiplicity of both the issues and relevant stakeholders serve to createa complex and fragmented business context over which companies willonly ever have very partial control. Many F&B companies still lack evenbasic capacity to gather and process economically relevant data, andthose that do manage to do this cannot hope to solve many of the sus-

xx Executive Summary

tainability issues they identify as relevant without working within thescope of stakeholder alliances and partnerships.

2.1 The F&B industry competitive framework

The personal and cultural nature of F&B implies that societal trends areof key importance for the sustainability agenda of companies in thissector. Since the sector’s potential customer base is, ultimately, made upof the entire population of the planet – assuming that one day even thepoorest may be prospective customers – focusing on consumer and soci-etal trends (health, traceability, consumer behaviour) are of paramountimportance for the industry. Here, the F&B sector has recourse to a con-siderable store of economic arguments that lend themselves to a robustBCS. These arguments have causal relationships based on industrydynamics that would not hold the same weight in other industries.

Consumer power is weak in key countries where population growth isat its highest. Consumption is stagnating in key markets such as theUnited States and Europe where populations are falling. Companies willhave to be increasingly creative to capitalize on the potential of devel-oping markets. However, we noted that the F&B industry has been rel-atively slow to innovate in order to anchor a foothold in these markets– yet innovate it must. We observed that exploiting reputation andbrand value constructs through radical strategic innovation around sus-tainability concepts is currently not part of the inbuilt DNA of theindustry. To a large extent, this is because this industry is inherentlyconservative and, like many mature industries, risk-averse. Also, there isstill substantial scope to exploit already existing products and processesand make substantial profits, without the risk and investment involvedin more radical innovation.

However, sustainability can present an opportunity for learning aboutnew markets and this may have been underestimated by F&B com-panies. And we are all the more convinced of this since, even in devel-oped markets, the industry was late to ‘get on the boat’ with the obesityissue and was forced into a race to product redevelopment and reviewof product strategies as a result. And even in spite of the formidablepressure still building around this specific issue, much of the industrystill remains anchored to old business models. Throughout the study,we have argued that with an integrated and strategic approach to sus-tainability issues, companies will be more in tune with their currentsocietal realities. This is in their business interest. A statistical ‘buying’trends approach will not be enough in the future given rapidly chang-ing consumption scenarios.

Executive Summary xxi

In addition, the differentiation opportunities that sustainabilitypresents are not being exploited to the full by companies. Yet, in anincreasingly consolidated market, with easily imitable products, F&Bcompanies probably need to be looking at and analysing each and everyopportunity available. Accessing immediate and short-term profits usingfamiliar, time-tested formulas and incremental improvements on exist-ing processes and systems is still dominating the agenda. It is simply stilltoo profitable in the short-term to do this than for the industry to investin research and development in radical innovation and to take the asso-ciated risks. Some leading companies are already demonstrating that thismay well be a blinkered strategy.

2.2 The business relevance of the key social and environmentalissues

The diversity and number of social and environmental issues faced bythe F&B industry is exceptional, given the way food permeates the dailylives of each and every living being on the planet. This compromises theidentification of a focused company-specific corporate sustainabilityagenda. Within the factory gates, managers in the industry demonstratea quiet confidence in their companies’ ability to manage environmentalissues directly related to production, while managing social issues aresomewhat taken for granted in Europe. But the industry’s major issues ofeconomic relevance are outside those gates, much further up – sustain-able agriculture, human rights, child labour – or down – public health,alcohol abuse, animal welfare – the supply chain. The sandwiched posi-tioning of the industry between its suppliers and retailers, which in turnare often interfacing with increasingly worried, health-conscious con-sumers, exposes the industry to sustainability related business risks rightthrough the value chain. However, because of the complexity, we dis-covered that even the primary players in the industry have a long way togo, and much to learn on the way, before they can state that they are ‘ontop of’ these issues. In any case, it is important for economicallysqueezed F&B companies to identify which of many sustainability issues‘out there’ are of economic importance to them, and to clarify for theirshareholders the materiality of social and environmental risks andpotential links to the bottom line.

Some sustainability issues touch the ‘soft underbelly’ of the F&Bindustry and the simple equation ‘no resource = no business’ presents astrong economic argument for adopting and promoting a more sustain-able approach. Experiencing a decrease in the raw material base uponwhich the industry relies is a considerable threat and a true business risk

xxii Executive Summary

to the industry’s economic viability. However, this generates consider-able complexity in the work place, given the way the industry’s currentsocio-economic framework is currently set up. Disappearing fishresources allowed some companies in the industry to use a tangibleexample to build an industry business case for the key issue of agricul-tural sustainability. It makes a lot of sense to use such a model toanalyse similar risk with bigger bottom-line effects, and to learn fromthe experience of a solid business case based on significant business riskwithin a tight time perspective of five years – and thus, within a timehorizon to which most managers relate.

During the period of research, we were able to observe and learn fromthe lack of readiness of the industry to handle major issues that hit thebottom line of companies and that have both socially and environmen-tally relevant global impacts, such as obesity and coffee issues. While theindustry bears the brunt of the blame for some major sustainability prob-lems and can be directly punished if not seen to be actively dealing withthem, actually doing something tangible involves interfacing with manyother players in public partnerships and coalitions. This is an activity thatthe industry is not yet adept at handling since it implies a new approachoften radically different to tried and tested ways of doing business.

2.3 Stakeholder dynamics: promoting and deterring factions

The perceived visibility and significance of issues has a direct bearing onthe extent to which stakeholders are demanding the industry either toresolve these issues or in some way to mitigate them using its weight andinfluence. Sustainability issues achieve their economic relevance in thecorporate business arena primarily through the pressuring effects fromthe industry’s stakeholders and the reward and punishment measuresthat they take to show satisfaction or otherwise with the industry’s inter-nalization of these issues into corporate strategy. Stakeholders that pro-mote sustainability agendas maintain companies in their Smart Zone,preventing sustainability projects from crossing into corporate oblivion.

Since many global F&B companies are moving out of direct sourcing,the F&B value chain is becoming ever longer and more complex, andthere are significant associated risks. At the end-user side, particularlywhen it concerns a health risk for consumers, there is pressure for fulltraceability of products from food industry customers (retailers) andlegislators. The move of the major players in the industry out of directsourcing comes at a time when pressures to ensure transparency in thesupply chain are strongest. This means that close supplier relation-ships, carefully monitored and measured, have become much more of a

Executive Summary xxiii

priority for global companies. This has an added buffer impact of givinga new business rationale to supplying companies – including SMEs – tobehave in a more sustainable manner.

Managers perceive NGOs as very proactive stakeholders. They havebecome more streamlined, strategic and professional in recent years,and they drive the corporate sustainability agenda increasingly byadopting a political lobbying stance. However, NGOs struggle to lever-age action in F&B companies when not supported by consumers, retail-ers and shareholders. Although partnerships and platforms with NGOsare more common now than even ten years ago, managers remain scep-tical – and sometimes cynical – about NGOs, especially their potentialto undermine hard-won stellar global brands and corporate reputation.The media, used by NGOs and others as a willing transmission agent forand amplifier of their concerns, are perceived by business managers asconveyers of bad news who ignore the good stories that can be toldabout positive action taken. Managers regret that industry is not givenmore credit by non-business stakeholders for fulfilling their primaryresponsibility of achieving profits, with the positive externalities theireconomic activities trigger.

Companies are rapidly learning what their own weaknesses are whenconfronted with activist pressure, and they have been rectifying thesequite effectively. The ensuing learning process has brought very positivedevelopments in terms of bringing sustainability to the global negoti-ation table. Although the issues are so complex that no one company –no one industry in fact – can deal with them in isolation, the currentincreased drive towards coalitions and public–private partnerships con-veys hope for the sustainability agenda in the mid-term.

However, there are limits to the BCS in the sector unless substantialexternal political and economic pressure is applied to the industry. It iscurrently simply not in the immediate economic interest of companiesto move towards sustainability in more than incremental steps leading,granted, to continuous improvement but on a scale far below academicexpectations of breakthrough innovation and new business models andfar lower than that required for truly sustainable development in theshort to medium term. It is likely that there will be increased legislativepressures on companies in Europe, particularly on labelling efforts, butno ‘quantum leap’ effects will ultimately make the difference to the BCSin the short to medium term.

Retailers move in a cut-throat, competitive environment themselves,and ‘squeezed’ F&B companies try to find no-cost solutions for their sus-tainability efforts. The most prevalent reason is that, apart from a niche

xxiv Executive Summary

market, consumers will not pay for sustainable products unless they also perceive a direct benefit for themselves. A rising wave of hard-discounters in Europe, have not been quick in introducing more respons-ible sustainable sourcing policies, since they perceive this as increasingcosts. However, of late (2006 to 2007), some important players in theretail sector (Wal-Mart, Tesco and others) have begun to more activelypromote the sustainability agenda and their actions are starting to makea real difference in food supply chains. What we see emerging thereforeis a ‘race to the bottom’ at the same time as a ‘race to the top’. It is stillnot clear which side will conquer; the jury is still out.

Consumers are perceived by managers as the least proactive of all inpushing a sustainability agenda. Although the niche of aware consumersis growing (particularly in view of recent intense exposure of issuesrelated to climate change), many are still ‘head in the sand’ or just sim-ply ignorant about sustainable development. With the current weakstandards of product labelling, it is very difficult to point the finger atconsumers for choosing products that are not sustainable. Yet, sustainedpush from customers and consumers is the single factor that can makemost difference to the BCS in that they can influence all strategic busi-ness decisions in the industry. Since retailers are under extreme pressurefrom their own competitors, and because the consumer is not ‘votingwith his wallet’ by paying for more sustainable products, significantchange may continue to be halting. Recent increases in food pricesworldwide owing to shortfalls in world markets as subsidized cereals areswitched to biofuel production may also not help the situation.

National governments, careful about the whims of their electorates, do not put companies under significant pressure and in the absence of a‘level playing field’ very much take things step by step also so as not tojeopardize national competitiveness in the global markets. Neither doinvestors and shareholders currently push the sustainability agenda ofF&B companies significantly enough, because of a short-term results focuswhich is counter to a strategic long-term perspective required for an effec-tive sustainability agenda. The perspective from shareholders is veeringtowards ever more short-term, not only because of the structure of ourcapitalist model, but also because of the exclusion of social and environ-mental risks from the materiality issues affecting stocks. There are positiveindicators that socially and environmentally responsible investmentfunds are on the increase, but trends have not yet entered the main-stream. The corporate drive to feature on new sustainability indices isreally a mantra of major global players, leaving a substantial part of theindustry uninvolved. Nevertheless, trends at the consumer level – and

Executive Summary xxv

experience with the evolution of the obesity issue, in particular – shouldindicate to the financial services industry that it needs to have its ‘earmore firmly pinned to the wall’, so as to identify and monitor impendingenvironmental and social risks more rigourously than currently.

So, owing to lack of pressure from the most relevant stakeholders,leaders in the industry will either continue to seek sustainable ‘no extracost’ approaches to resolving key issues, or look for tangible ways inwhich sustainability can back up an added-value proposition using thebrand and allowing the charge of a sustainability premium. The bottomline is that, it does not pay (yet) for companies in the F&B industry tobe entirely sustainable and the result is that business models are beingevolved cautiously at the margins. It is hard to blame companies; to doany differently would put them at risk and ‘up for grabs’.

2.4 Sustainability’s contribution to corporate value drivers

Leading global F&B companies have moved beyond the more straight-forward cost-saving approach to sustainability (picking the low-hangingfruits of easily attainable pay-offs through, for example, increased eco-efficiency or Health and Safety (H&S) performance). They have evolvedtowards more elaborate business logic for sustainability. Given the indus-try’s front-line exposure to consumers, the identified value constructs ofreputation, brand and licence to operate have become strong drivers ofthe BCS in these companies.

Profit margins are low for this industry and it does not offer lucrativeremuneration rewards to staff compared with others. However, it isincreasing its scientific base to produce ever more sophisticated foodoptions, with health benefits, for example. This requires highly trainedand competent staff. The contribution of corporate sustainabilityactions to attracting and retaining talent is increasingly providing a BCSto the industry in European countries in general and Nordic countriesin particular.

CSM’s contribution to key value drivers through the strengthening ofreputation and brand value seem strong enough to convince the pro-gressive thinkers in the industry to give more than lip service to sus-tainability. The industry sustainability leaders say that they are notinvolved in sustainability programmes for monetary purposes only, butbecause it is the ‘right thing to do’, primarily because they present anopportunity for their companies to establish leadership positions in theindustry. But while this is laudable, there are dangers in adopting anentirely normative as opposed to strategic approach, as the support sys-tems are weaker and alignment cannot be guaranteed, especially in the

xxvi Executive Summary

ranks of influential managers that turn over rather quickly. The rigourof the classical economics paradigm, with its profits maximization andeconomic efficiency principles, becomes more nuanced when it comesto business logic behind sustainability actions. The BCS is strongest ifmeasured by a dual approach, drawing on aspects that are both valid-ated and non-validated by measurement.

Leading companies believe that, by lobbying hard within the indus-try and showing by example, laggards will eventually follow, thusreducing risk of competitive disadvantage. However, neither can theleaders sacrifice their competitive position in the meantime. Hence,investments in sustainability are heavily weighted against other activ-ities. Although interesting and promising coalitions have been devel-oped with a view to testing and eventually mainstreaming sustainabilityconcepts, we did not find significant examples of sustainable agriculturepilot projects hitting the mainstream. This, in itself, reveals the conser-vative, no-risk industry approach and the still relatively weak positionof the BCS against the prospect of shorter-term gain.

To assure that sustainability projects do not remain in the pilot ranksfor as long as they seem to, sustainability officers need to continuepushing the frontiers of quantification, and developing the businesslogic on a multidimensional basis. The fact that the BCS is primarilyfocused on soft, complex and intangible value constructs poses a signi-ficant problem in that managers are accustomed to hard figures and tan-gible outputs.

Cost savings based on eco-efficiency and H&S performance are rela-tively easy to quantify, and accounting systems are already equipped fortracking the ensuing financial benefits and reaping the ‘low hangingfruits’ first. On the other hand, brand value or licence to operate driversare heavily influenced by a host of other, non-sustainability related fac-tors, such as political agendas or, indeed, market performance. The con-structs themselves have to be leveraged in order to increase financialperformance. There is a cascading effect that makes the business logiccomplicated; for example, sustainability actions contribute to increasedbrand recognition, which in turn contributes to higher market shares.Increased licence to operate leads to fewer workplace disruptions andaccelerates permit authorizations implying cost reductions overall.Retaining talent through improved employee welfare leads to improvedindustrial relations and therefore fewer strikes, and reduced trainingcosts through lower staff turnover. Isolating the corporate sustainabilitycontribution to these constructs is considered so time-consuming andexpensive an exercise as to make the task undesirable from a business

Executive Summary xxvii

logic standpoint. Sustainability officers tend to still dream about a morequantified case, as they would welcome any opportunity to build astronger BCS. While this is particularly true for laggards, as clearly it iseasier to present tangibles than intangibles to sceptics, even sustain-ability officers at progressive companies found that the potential forquantification had far from been exhausted.

Owing largely to a conservative stance within the industry, managersdo not generally perceive sustainability as an opportunity to innovate,although with some of the major players, this thinking has finallychanged in the last two to three years. This value construct is probablyundervalued, both in terms of product and process innovations, and interms of radical innovation for new markets. Too many managers stillperceive sustainability projects as being the remit of ‘the sustainabilityor corporate responsibility people’ rather than something for Researchand Development (R&D), marketing and business managers to take on.However, F&B companies must seek new businesses and new market-places in order to remain profitable. Innovation through sustainabilitymay be able to contribute to building up critical mass in the markets oftomorrow. Also, by creating high quality, added-value products, we sug-gested that brand values and consumer trust might eventually be usedin marketing and selling products. New aspects of managing the mar-keting value of a brand that are different to traditional approachesmight emerge as a result. Solid arguments based on scientific fact areconvincing but these must be qualified by a communicating absolutebenefits that consumers value. It follows that if a company’s initiativesare successfully communicated to consumers, building not only onconsumers emotions, while assuring them of quality and personalbenefits, confidence in the company’s food supply chain will increase,ultimately affecting profitability.

A more robust case for sustainability can probably be built right here andnow by each and every sustainability officer in the F&B industry. Strategiccorporate frameworks can, and should, incorporate parameters that areless fixed, since industries are moving in a dynamic environment where allelements; consumer behaviour, legislation, technology, economies andcompetitive features are changing and, indeed, expected to change.

3 Exploiting the business case

We found many areas where the industry was still either in an experi-mental stage with sustainability concepts and principles, or at the begin-ning of stakeholder engagement processes that will assure corporate

xxviii Executive Summary

learning about new angles on environmental and social issues. Currently,F&B companies do not comprehensively address the sustainability issuesthat are of economic, and thus strategic, importance to them, althoughthe leaders in the industry have a high awareness of what those issues areand have initiated action. Better access to the economic reasoning behindadopting internalization of the sustainability issue as part of businessstrategy appears to be lacking, given that many managers had not actu-ally thought about such a rationale until asked at our interviews.

Even sustainability leaders had not managed the difficult process ofassuring organizational alignment behind relatively well-worked outsustainability principles. For this reason, strategies are in danger of notbeing implemented by key business functions and a diluting effect cantake hold, which means that key messages about corporate sustain-ability strategies are not transmitted up and down through value chainas far as suppliers and consumers. The industry can most probablyachieve significant progress with designing and applying sustainabilitystrategies by opting for a more comprehensive and structured approach.

3.1 Promoting factors and barriers to roll out

While on the one hand, the rationale for the BCS is very definitelysector-specific, based on its own sets of issues, stakeholders and valuedrivers, on the other hand its application and interpretation are oftenculturally based. Open and transparent national cultures, such as thoseof the Nordic countries, are the ones that lend themselves best to thebottom-up processes that best promote corporate sustainability.

The decentralized nature of the F&B industry is currently perceivedas a barrier to implementation of sustainability objectives, but we sug-gest that this could be converted to an opportunity if sustainabilitybecomes one of the essential ‘glue’ elements that hold global com-panies together – such as by reinforcing tenuous corporate cultures ina global environment, and allowing access to much needed skilled andtalented personnel.

While sustainability officers see top management commitment as anessential prerequisite to promoting the BCS both internally and exter-nally, neither do they believe that this criterion is sufficient to assure suc-cess. Along with the top management commitment, an organizationalcommitment to integration of sustainability strategy into business strat-egy is essential. The identification of informal networks of sustainabilitychampions positioned in key strategic areas throughout companies hasproved in some companies to be a substantial contributor to success, andengagement of the ‘second layer’ of senior decision-makers is essential.

Executive Summary xxix

Overcoming internal constraints to rollout of a sustainability strategypresents the most immediate potential for further exploitation of thebusiness case that sustainability offers within organizations. Mindset ofmanagers, lack of knowledge and organizational culture are the mostsignificant perceived barriers, but these are also areas that are entirelywithin the corporation’s direct sphere of influence. The potential forfurther exploitation of the business case is therefore substantial, as man-agerial and staff development is within the competence and control ofeach and every organization.

A major inherent difficulty is the fact that, pushed by investors andcustomers, managers in business and industry look to the short-termbusiness result, while sustainability benefits are undisputedly long-term.The F&B industry is far from being alone in this respect (Steger, 2004).We found that the ‘right’ language must be used to convince decision-makers in the industry of the benefits of more long-term business plan-ning in the short-term.

The industry is nevertheless moving, albeit relatively slowly, in thedirection of taking more of a long-term view into account, but suchconsiderable change will not happen overnight. A major strategic chal-lenge is that key companies in the industry join forces both in spirit andin action, and share experiences in order to create new industry stan-dards and benchmarks. Despite a proliferation of EnvironmentalManagement System (EMS) tools and various standards available tomanagers, they still require help to manage the increasingly complexbusiness environment within which they operate.

Major companies have a policy of not holding a sustainability func-tion but are working instead on integrating sustainability across theorganization. In progressive companies, cross-functional teams fulfil theneed for an effective and much needed feedback process. There is never-theless room for better coordination across units and departments inorganizations, with scope for increased collaboration between sustain-ability officers and other functional units within organizations.

Hard-line sceptics in companies who are sometimes at senior man-agement must be reached, – particularly at decision-making level. Keymarketing and sales managers are largely left out of the sustainabilityequation at present and, because of this, product development, greatlyinfluenced by marketing managers, is also strongly affected. Indeed,engaging sales and marketing staff at an early stage of development ofa sustainability strategy – for example, by including them in strategiccoordination committees, task forces or issue groups – would greatlycontribute to breaking down the lack of knowledge that prevents these

xxx Executive Summary

managers from exploiting the concept of sustainability to its fullestextent. Finding the right language for communicating with consumersabout sustainability is a major challenge that marketing managers (con-servative by nature and with ever more short-term targets) are unwillingto take on, and indeed they currently lack the skills for so doing.Relatively little has as yet been attempted by the industry to change thedynamics between the industry and the consumer. We identified somekey players that are seeking breakthroughs through linking sustain-ability with other more personal benefits to consumers, thus usingsustainability as a driver to enhance the brand, and trying to prove thatsustainability does, in fact, sell.

So currently, there are cut-off points that ensure that companies can-not go all the way with their sustainability strategies. In general, morebuilding of awareness and internal education on sustainable develop-ment could eventually change the way F&B companies relate to theconsumer, as this would change mindsets over time. More radical inno-vation than today, based on sustainability concepts, could go beyondexperimental projects as a result. Today, support frameworks for such amove are still lacking.

Managers in global F&B companies regard stakeholder interaction aspart and parcel of today’s business model, and are in a learning processin this regard. There are some excellent, successful and leading exam-ples of partnerships with stakeholders. Companies are still feeling theground in this respect, but to varying degrees and depending on thecompany-specific business case for doing so. We have confidence thatthe learning processes that the industry has engaged in will bear fruitfor a more robust business case in the future.

Problems with alignment are, in fact, largely due to the absence ofcomprehensive integration of sustainability strategies into organiza-tional processes. We identified large gaps in the incentives programmesto stir managers to action. What is encouraging is that leading com-panies seem to be aware of such gaps. They intend to address them – eventually. But it was clear that, in the current very competitiveeconomic climate, urgency was lacking.

3.2 Effectiveness of approaches used to exploit the BCS in companies

To create a robust BCS, leading companies are focusing on enhancingactivities where an impact can be made and where a direct link can bemade to the business product, and then on communicating these ‘earlywins’ internally. Being able to share and exploit better practice and win-win success stories and, in the words of one manager, ‘communicate,

Executive Summary xxxi

communicate, communicate’; these are key components of both buildingand promoting a BCS.

Sustainable agriculture pilot projects focus on opportunities to createvalue in areas of strategic business concern, and introduce measurableindicators of sustainability performance, thus linking business perfor-mance and improved sustainability performance. The creation of valuein these areas can contribute in turn to product differentiation, eventu-ally enabling companies to demand a product price premium or accessincreased brand loyalty. It remains to be seen whether experimentalpractices in the industry will move into the mainstream. Currently, toomany pilot projects remain in the wings, with no one company willingto go out on a limb and mainstream on its own: the competitive dis-advantages involved are still far too great.

The price of raw materials is small compared with the processing andmarketing costs of final products. Although efforts related to the BCS inleading companies are currently focused upstream – on the supplychain – there is substantial potential to work on downstream efforts andany current initiatives are very much in their infancy. Raising awarenessin the company that sustainability can be about gaining major reputa-tion and brand value benefits from little or no additional investmentneeds to be a key part of the communication strategy around the BCS.As sustainability is an essential prerequisite for the long-term security ofthe supply chain, progressive managers feel that it should ultimately bepossible to sell the concept to consumers. However, first, a muchstronger and tangible link needs to be made between the growing nicheof consumers that have a broader concern for environmental and socialissues, and the application of their principles to their buying habits.

4 So what’s the bottom line?

So is corporate sustainability just a buzzword in the F&B industry or isit bringing the triple bottom line ‘win-win-win’ solutions that some ofthe hype around the concept suggests? To this question, one of themanagers we interviewed responded:

Maybe corporate sustainability is not ‘the next big thing’ – but that is prob-ably good because for me, ‘next big thing’ is consultancy-speak for the nextthing that will be forgotten. (BCS47 – Business manager, Supply chain)

We identified enough enterprising initiatives to show that sustainabilityis firmly on the agenda of major companies and it is there to stay on

xxxii Executive Summary

corporate agendas of the future. Several pioneering companies aretaking on the complexities and challenges of sustainability and pushingthe boundaries of environmental and social business improvements.

But the BCS clearly has its limits under prevailing economic condi-tions. For a quantum leap forward, leaders in the industry will have tojoin with trade initiatives to support changes to the economic andpolitical framework within which the industry is operating. The indus-try would also do well to support more mainstreamed labellinginitiatives and the establishment of a ‘level playing field’ through reg-ulation that makes sense. This view is encompassed in these rather dis-enchanted comments; one from a stakeholder, one from a businessmanager:

The economic case will have its limits – even with the best resourcescarcity arguments, and cost savings and any other economic justifica-tions to impress the financial managers, there is a limit of 5 per cent plusor minus of overall company turnover that can be influenced by CSR. Therest is the daily grind of business and maximizing shareholder value.(BCSBM10 – Senior policy director, WWF)

If there was a really robust business case for sustainability, there wouldn’tbe need for so many publications. It is a real case of ‘the lady doth protesttoo much’. (BCS40 – Senior sustainability officer)

While CSM’s contributions to corporate reputation, brand value andattracting and retaining talent are stronger drivers for the BCS in theF&B industry than in most other industries, the level of this contribu-tion is still unlikely to be sufficiently strong to drive the business caseas far throughout organizations as is necessary for truly sustainabledevelopment. Food industry experts were not optimistic:

Current moves are on such a small scale that it’s difficult to see aquantum leap taking place. There are many vested interests in maintain-ing the current system. I’m not optimistic that the current corporatecontrol of food can be successfully challenged. The scales need to fall fromthe eyes of the industry. No single major company has reinvented itselfthroughout to fundamentally challenge the status quo. We need tougherincremental change. (BCSBM6 – Food industry expert)

However, we observed over the period of research that there was an evo-lution in awareness in the industry about the relevance of sustainability

Executive Summary xxxiii

concepts to business. We met managers who perceived potential forlarge, global companies to make a difference mid-term:

If large companies change, then the markets will change. It will progres-sively become clear that all the work in the supply chain will only get sofar and the consumption side of the equation will have to kick in. I see ahuge change, not in the next five years maybe, but certainly within a fiveto ten year perspective. (BCS43 – Senior business manager, Marketing)

Any research is but a snapshot of an existing state of affairs. Already in2007, it seemed that there was a shift in the issues that were ‘top ofmind’ for the global players in the industry. According to a recent pub-lished industry survey of food industry executives,1 corporate socialresponsibility (CSR) is now one of their major stated preoccupations,prompted mainly by a surge of interest in health and climate changeissues in 2006/07. However, complacency would be misplaced; ourresearch clearly showed that there is often a gap between attitudes andpositive actions. Moreover, change overnight is unfeasible as the issuesare both controversial and complex and resistance in the ranks of man-agers needs to be dealt with. To be able to take more ‘giant steps’, thefocus of the F&B industry BCS in the future must turn to addressingthe gap between consumer awareness and the positive steps that somecompanies are making.

In the current unprecedented context of high fuel prices, shifts ofcereal production to bio-fuels provoking the highest food prices indecades, emerging economies vying with developed countries forresources from energy to metals to food, and uncertain global econom-ic and social stability, it is by no means a foregone conclusion that cor-porate action in the F&B industry will substantially accelerate the causeof sustainable development in the short or even medium term. But let’snot underrate the power of marginal improvements that companiestend to opt for in this environment. Such changes will at least be long-lasting.

Our research conclusions are very much ‘out of the horses mouth’; weallowed F&B managers to articulate their perceptions of the BCS in theindustry. So we leave the last word to a visionary CEO of one of thecompanies involved in our research:

The questions are: Is there a consumer who recognizes and is prepared tobuy sustainable products? Will there be a market to allow companies tohave a decent return on their investment? Using reputation management

xxxiv Executive Summary

as a driver of sustainability is not a viable business strategy. Things haveto change – biodiversity is important. If the industry doesn’t change – thisis a dead end road. (BCS39 – Top management, CEO)

Note1 CIES – the Food Business Forum; Top of Mind 2007.

Executive Summary xxxv

Part I

Building the Business Logic

1Introduction

We live in the golden age of the internet, the mobile phone and theconstant and unrelenting exchanging of information across vast dis-tances from one end of the world to the other. For this reason, onlythe most ‘head in the sand’ person nowadays will have missed theincreasing attention devoted to sustainable development, particularlywith the recent unprecedented focus on climate change in Europe andthe United States. To read the press, it seems that everyone, from non-governmental organizations (NGOs) to governments to companies, is‘on the bandwagon’, and must be seen to be doing at least somethingabout sustainable development.1 But does the rhetoric match reality ormuch of it a matter of hype?

In this volume we do not pretend to present a complete answer to thisquestion, given that our focus is on the global company, and at that,global companies in the food and beverage (F&B) industry. Our purposehere is to show how global corporations in this particular sector, as pri-marily economic entities, take action on social and environmental issuesbeyond compliance only if clearly defined business logic to justify suchactions is identified, and as we do so, we will understand the extent towhich the reality meets the hype at least for the F&B industry.

We present the results of a research project incorporating data collectedover five years on the perceived economic rationale – or ‘business case’ –for including environmental and social sustainability programmes andagendas in business strategy in F&B companies, and on the extent towhich such programmes are strategically integrated. Many quantitativeand qualitative empirical results contributing to this research were col-lected in the context of a more extensive research initiative covering nineindustry sectors by the Forum for Corporate Sustainability Management(Forum for CSM), a research platform at the International Institute for

3

Management Development (IMD) business school in Switzerland during2001–04: ‘Building a Robust Business Case for Corporate Sustainability’ –‘the BCS project’ (Steger, 2004). Qualitative research continued during theperiod 2004 to mid-2007 and included additional benchmarking inter-views with consumer organizations, supply chain managers, participantsin corporate sustainability partnerships and other F&B industry stake-holders.

The aim of the BCS project research was threefold:

• To identify and describe the perceived business and economic ra-tionale used by managers in global corporations for integratingenvironmental and social criteria into business strategy – the busi-ness case for sustainability (BCS)

• To understand how the perceived business and economic rationalefor implementing action on environmental and social problems orissues differs from industry to industry, to analyze the extent to whichcompanies in different industries have exhausted its potential, and toidentify reasons preventing companies from exploiting the potentialof the BCS

• To design a set of diagnostic tools for each sector, using the empiricalfindings of the research as a basis for tool development, thus increas-ing its relevance and assisting companies to understand and buildtheir individual BCS.2

1 Background: the conundrum

The concept of sustainable development was born out of a pressing needfor making trade-offs between economic activities and the quality andsustainability of the natural environment. In 1987, the World Com-mission for Environment and Development – the Brundtland Commis-sion – came up with what became the most widely adopted definition ofthis concept:

Sustainable development is any development which meets the needs of the present without compromising the ability of future generations to meettheir needs. (World Commission on Environment and Development,1987)

The commission recognized that unconstrained economic growth, con-sumption and social injustice would ultimately lead to environmentaldestruction and poverty. The ‘new twist’ of the Brundtland definition

4 Business Logic for Sustainability

at the time was the link that it made between current and future needs ofhumankind with environmental and resource bases, while at the sametime incorporating the notion of equity within and across geographicalzones as well as across generations. Thus, sustainable development cameto encompass the full range of human and natural systems including eco-logical, economic and socio-cultural aspects; the three so-called ‘pillars ofsustainability’.

This had significant implications not only for governments and policymakers, but also business and industry. The commission recognized thepotential to leverage the increasing power of global corporations to pro-mote sustainable development. As a net contributor to unsustainablebehaviour through its intense use of natural and human resources andthe impacts of production and consumption patterns, industry wouldalso have to be brought into the foray.

Since then, there has been growing momentum behind the idea thatcompanies have broader societal responsibilities, particularly during amore recent period of growing privatization of functions and processesformerly under governmental responsibility. This has coincided with a period of unprecedented growth in size of the modern corporationand at the same time, a proliferation of NGOs and not to be forgotten,a highly active anti-globalization movement.

The list of corporate governance scandals in recent years, such as thosesurrounding Enron, WorldCom, Ahold, Parmalat, and Adecco leadingto massive loss of investor savings (and prompting the establishmentof the Sarbanes–Oxley Act to assure more transparency and accuracy in corporate financial reporting), focused media and public attentionnot only on corporate governance and reputation issues but also onbusiness social responsibility, while at the same time increasing publiccynicism about corporations.

As we shall explore in this volume, modern day industrialized foodsystems cause significant social and environmental impacts. F&B cor-porate behaviour in the environmental and social domain has, as pre-dicted by many eminent academics, increasingly become part of thepublic’s criteria for judging companies (Carroll, 1979), but in spite ofthis we find survey reporting that only one third of European con-sumers believe that global companies act in the interests of society atleast some of the time (Bonini et al., 2006). The extent of distrust of Euro-pean consumers about the F&B industry, for example, has been heavilyimpacted by numerous food scandals (see Chapter 3). The full extent of public mistrust of the industry is demonstrated by a study releasedby Tate & Lyle in 2005 which shows that as many as 65 per cent of

Introduction 5

consumers agree with the statement that ‘often brands that claim to behealthy aren’t healthy at all’ (Sleep, 2005).

But, as with all additional complexity, external social expectations ofcompanies increase both corporate risks and opportunities. This book willalso explore these dynamics in the context of the food and beverageindustry.

2 Conceptual framework

The Forum for CSM is a membership-driven research initiative. In May2001, a representative of one of its member companies, a fast movingconsumer goods (FMCG) company, wrote:

Our senior management takes a compliance driven view of environment,health and safety. This creates a dilemma for me when trying to deal withcorporate social responsibility. They are not against, they just do notunderstand. I need to defend everything that my group does outside ofcompliance. Can you provide robust arguments about the contribution toshareholder value of ‘sustainability’ management? I need pragmatic,defensible information that cannot be challenged as being ‘contrived’ orbiased towards an ‘environmentalist’ philosophy.

This request typifies the dilemma often faced by those trying to promotethe BCS in today’s corporate environment. It contains some of the prin-ciple ingredients of what promoters of sustainability are often up againstin their organizations; a sceptical management demonstrating a prag-matic ‘what’s in it for us’ approach, a demand for as ‘quantified’ a busi-ness case as possible, with indisputable proof that sustainability positivelyimpacts the corporate bottom line.

The correlation between sustainability and economic performance lead-ing to a U shaped distribution curve has been used by several researchersas a model for promoting the case for ‘win-win’ BCS solutions (Lan-kowski, 2000; Steger, 2004). Steger refers to the positioning of a companyon the curve as the search for the ‘Smart Zone’ (Steger, 2004), where com-panies can ‘kill three birds with one stone’ and create additional econ-omic value by improving environmental and social performance (seeFigure 1.1).

The most profitable sustainability projects are likely to be carried outfirst by companies (low hanging fruits), and moving along the curve,the company will finally reach a ‘crossover point’ where the invest-ment becomes unprofitable. Allocating capital to projects that are not

6 Business Logic for Sustainability

as profitable as other competing projects then becomes a dilemma sincecorporate decision-makers weigh up the benefits and drawbacks of eachand every project brought to their attention. Thus, the BCS must draw on as many elements as possible in order to make it robust and water-tight. This book is intended to provide robust ‘Smart Zone’ arguments tomanagers in the F&B industry.

Members of the Forum for CSM felt that the question of whether thebusiness case differs across industries is hardly ever addressed inresearch, although there are researchers that have identified the needfor an industry or even company-specific business case.3 The Forum forCSM therefore elected to approach the issue on a sector-specific basis soas to provide research perspectives and conclusions offering a moredetailed and representative insight on the BCS across industries.

2.1 The BCS project

The BCS project was designed in partnership with the World WideFund for Nature (WWF) and was endorsed by the European Academyfor Business in Society (EABIS). The project covered nine industries:chemical, pharmaceutical, automotive, technology, utilities, oil and gas,aviation, financial services and, last but not least, the industry that isthe subject of this study, the F&B industry. The nine industry sectors

Introduction 7

Activity y

Activity x

I:NPV > 0

II:NPV < 0

III :NPV < 0

Absolute economicperformance

Compliance level

even with discount rate = 0

Environmental andsocial performance (ESP)

The Smart Zone:Economic and

environmental/socialperformance both

increase

Economic performance decreases through further ESPimprovements

Company isspending “realcash”

Figure 1.1 Relationship between economic and environmental/social performance beyond compliance – the ‘Smart Zone’

were chosen based on their significant economic relevance and socialand environmental impacts, and included a diversity of industries thathad both similarities and differences.

The BCS project team acted within a solid framework of support andpeer review from various entities; IMD itself, the members of the Forumfor CSM, the project team, and an appointed Advisory Council thatincluded representatives of the Forum for CSM member companies, theWorld Business Council for Sustainable Development (WBCSD) andWWF.

3 Research questions and objectives

For the sector-specific study on the F&B industry, we formulated severalresearch questions based on a number of assumptions:

Here, we seek arguments to constitute as robust a business case as poss-ible. We aim to evaluate the extent to which managers are or are not con-vinced that by integrating sustainability issues into business strategy andfocusing on the business opportunities they bring, F&B companies canbetter create economic value. In this way, we can assess the strength ofthe business case in the industry and its application. After all, when itcomes to such value-loaded concepts, perception represents reality. Also,if managers are not convinced of the value of a proposition, then it isunlikely that they will act effectively upon it. We propose lookingspecifically at four areas and therefore formulate four sub-questions:

Research question 1a: What is the competitive framework withinwhich the industry is operating and how does this influence the sustain-ability agenda?Research question 1b: What are the key social and environmentalissues of economic relevance to the industry and why are they relevant?Research question 1c: What stakeholder dynamics influence the busi-ness case for sustainability in the F&B industry; in particular, to what extentdo different stakeholder groups promote or deter progress on application ofa business case for sustainability in the industry?Research question 1d: What are the value drivers prompting the industryto take action on sustainability issues and how are they currently operating?

8 Business Logic for Sustainability

Research question 1:What is the perceived economic rationale behind the business case forsustainability in the F&B industry?