Business Forum Switzerland - SWIFT

16

Business Forum Switzerland 22 March 2018 | Zürich | Switzerland WRAP–UP REPORT CONTENTS #BFSwitzerland From doing to implementing Trends and challenges in financial crime compliance Interesting times A new standard for cross- border payments From bricks and mortar to service networks Meeting the needs of the community Exploiting the potential of AI Securing the financial ecosystem The customer is key

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Business Forum Switzerland - SWIFT

Business Forum Switzerland

22 March 2018 | Zürich | Switzerland

WRAP–UP REPORT

CONTENTS

#BFSwitzerland

From doing to implementing

Trends and challenges in financial crime compliance

Interesting times

A new standard for cross-border payments

From bricks and mortar to service networks

Meeting the needs of the community

Exploiting the potential of AI

Securing the financial ecosystem

The customer is key

22

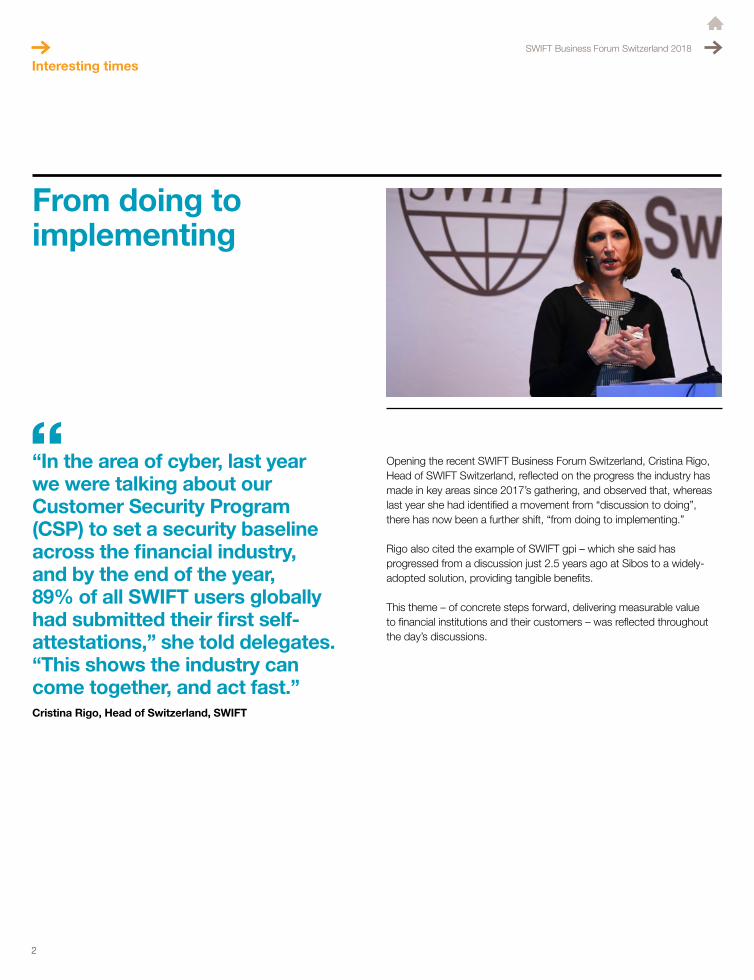

Opening the recent SWIFT Business Forum Switzerland, Cristina Rigo, Head of SWIFT Switzerland, reflected on the progress the industry has made in key areas since 2017’s gathering, and observed that, whereas last year she had identified a movement from “discussion to doing”, there has now been a further shift, “from doing to implementing.”

Rigo also cited the example of SWIFT gpi – which she said has progressed from a discussion just 2.5 years ago at Sibos to a widely-adopted solution, providing tangible benefits.

This theme – of concrete steps forward, delivering measurable value to financial institutions and their customers – was reflected throughout the day’s discussions.

“In the area of cyber, last year we were talking about our Customer Security Program (CSP) to set a security baseline across the financial industry, and by the end of the year, 89% of all SWIFT users globally had submitted their first self-attestations,” she told delegates. “This shows the industry can come together, and act fast.”Cristina Rigo, Head of Switzerland, SWIFT

From doing to implementing

Interesting timesSWIFT Business Forum Switzerland 2018

33

“We still see fraudulent MT103s,” Leibbrandt acknowledged, “but the losses are very limited. We can say we have been successful so far in preventing another Bank of Bangladesh.” However, he cautioned, “past success is no guarantee of future success.”

Technology-driven change is another challenge to be reckoned with, the SWIFT CEO told delegates. “Cloud, APIs, AI, DLT – these are all reshaping the world of retail payments,” he said. Fresh from a trip to China, he shared an interesting statistic with the Swiss audience. In Germany, two-thirds of payments at the point of sale are carried out using cash, with a third done using cards. In China, a third of payments at point of sale are cash, and the other two-thirds are done using Alipay and WeChat – with only 2% done using cards.

In the US-China corridor, more than 25% of all cross-border payments are already gpi. They are all trackable. They are all cleared within one day. Half are cleared in half an hour, many within minutes. That’s a fundamental rethink of cross-border banking and a credit to the community for making it happen.”Gottfried Leibbrandt, Chief Executive Officer, SWIFT

One outcome for SWIFT of this change is the advent of “real competition,” Leibbrandt acknowledged. “A lot of people are interested in cross-border payments,” he said. “Yes, they are mostly in the EUR 500-1000 range, a segment not well-served by banks, but I have learned that if new entrants disrupt the lower end, we should be worrying about them moving up the value chain. Innovating ourselves is the answer, and these new technologies enable existing players to do that just as well as new entrants.”

Interesting times

SWIFT CEO Gottfried Leibbrandt built further on Rigo’s observations. “The past two years have been very interesting,” he said. “The Bank of Bangladesh was two years ago in February 2016, and this went to the heart of the banking franchise as we know it.”

CSP has been an effective response to the cyber challenge, he suggested, and went on to remind delegates of the five elements of the programme: information sharing, implementing protection within software, self-attestation to establish a baseline of security, detection and control services, and working with the industry to create an ecosystem of security vendors able to help smaller banks in remote geographies up their game in this critical area.

SWIFT Business Forum Switzerland 2018

44

SWIFT gpi is an example of successful innovation in practice, with “staggering results”, he claimed. “In the US-China corridor, more than 25% of all cross-border payments are already gpi. They are all trackable. They are all cleared within one day. Half are cleared in half an hour, many within minutes. That’s a fundamental rethink of cross-border banking and a credit to the community for making it happen.”

The next step is to make SWIFT gpi the ‘default’, Leibbrandt said. “We are looking at what would be a realistic timeframe for that, perhaps two to three years. And if we can do that, we will have upped our game, and protected our franchise.”

Another force for change in payments is real-time, he continued – and he said SWIFT is looking closely at opportunities to link domestic real-time payments systems to facilitate cross-border payments. “At the end of the day, there is still a big role for banks here,” Leibbrandt reassured his audience. “My vision is that gpi is the fabric that overlays all of this, connecting real-time systems across the globe, and providing a great customer experience.”

In addition to linking real-time payments systems to gpi, SWIFT is also ‘selectively’ enabling them on SWIFTNet, he added. “Australia is already up and running with very high volumes – up to 100,000 transactions a day – and we are also working with the EBA and the ECB to put RT1 and TIPS on the SWIFT network.”

Alongside these developments, SWIFT is also “seriously looking” at migrating cross-border payments to ISO 20022, the CEO said. “This is not easy, but is becoming easier. Translation was always a problem because who would take responsibility? But now we can use APIs to support co-existence, translate between smaller players using MTs while bigger players use more ISO 20022 messages. We will bring the discussion to the community in the coming months, with a timeframe of 2021/2022 to 25 for transition.”

Highlighting other areas of progress, Leibbrandt turned to financial crime compliance, and reminded delegates of the success of the SWIFT KYC Registry. “More than half of our banks are on it. It has real traction, and the big banks say it has cut the cost of onboarding new financial institutions by 30%.”

Overall “we have a lot on our plate as a community”, the CEO said, and – again referencing his China trip – “we live in interesting times”. But, he emphasised, “it’s exciting”, and SWIFT has a “multi-pronged approach” to tackling the challenges and leveraging the opportunities that lie ahead.

Meeting the needs of the community

The next step is to make SWIFT gpi the ‘default. We are looking at what would be a realistic timeframe for that, perhaps two to three years. And if we can do that, we will have upped our game, and protected our franchise.” Gottfried Leibbrandt, Chief Executive Officer, SWIFT

SWIFT Business Forum Switzerland 2018

55

SWIFT Business Forum Switzerland 2018

Returning to the cyber theme, Zimmerman emphasised that “we are all aware that cybercrime is part of our reality”. “We must have an awareness of our vulnerability, not just in the part we can defend, but in every single piece of the chain,” he told delegates.

He acknowledged that “CSP is bringing in a baseline set of standards”, but it is not without its challenges for banks. “It is costly, it makes operations more cumbersome, and banks have to do a lot of things to comply,” he said. At the same time, he called on SWIFT to think about the

We must have an awareness of our vulnerability, not just in the part we can defend, but in every single piece of the chain.”Stephan Zimmerman, Vice-Chairman, UBS Wealth Management and Deputy Chairman of the Board of Directors of SWIFT

next phases of development in this area. “We are at the stage where 90% of banks have self-attested, so what do we do next? Do we interact in the contractual relationship with our customers and their customers? We also need to work with audit companies to make sure it is embedded in risk systems to drive it forward with the idea that in the end we will all benefit – so that who we can operate with doesn’t further shrink, and that we can stop other systems making headway in a way that wouldn’t be good for the community.”

Meeting the needs of the communityLeibbrandt was then joined on stage by Stephan Zimmerman, Vice-Chairman, UBS Wealth Management and Deputy Chairman of the Board of Directors of SWIFT. Zimmerman confirmed as well that the industry is facing “transformational questions”, the more important of which for the Swiss community is “what will be our relationship with our neighbours in this climate of geopolitical uncertainty? Will we be able to access other countries?” he asked. Close behind are the impact of digitalisation on banks and regulatory pressure, he added.

Self-attestation will only be successful if banks consume the data,” he said. “Consumption is only now really getting started – with banks beginning to embed it into their overall processes for the evaluation of counterparties. It would be good if banks really got that going in earnest in 2018.”Gottfried Leibbrandt, Chief Executive Officer, SWIFT

66

to receive,” he said. “SR2018 requires them to be able to send it – and to pass it on if they receive it. This will make the gpi tracker capable of being universally adopted, and we are working with the community to foster adoption, to make this consumable. We will see corporates asking their banks for this service,” Leibbrandt suggested.

Asked about the likely speed of change prompted by new technology, Leibbrandt predicted that “legacy will take time to evolve out”. “We will see the fastest changes in the markets where there is no legacy – for example China,” he told delegates. In addition, some of the higher profile new technologies still need time to mature, he contended.

“We ran a large PoC on DLT for nostro reconciliations, effectively a private blockchain between banks. We used about 500 chains and this was the biggest Hyperledger implementation outside IBM. There are about 1.5m RMA bilateral relationships on SWIFT. To cope with that you’d need 1.5m blockchains. There is no way Hyperledger is developed enough to handle that kind of scale. It is all solvable, but it is not easy. It will take at least 10 years – although we may see the first implementations where there is no legacy.”

At the same time, the success of emerging technologies does not rule out the ongoing involvement of banks, Leibbrandt added. “Take crypto – and we are very close here in Zurich to the Crypto Valley of Europe – the

Leibbrandt agreed that there needs to be a constant emphasis on further raising the security bar. “At the end of the day, the cyber problem is not going away,” he said. “It’s getting more sophisticated, and the approach has to be similar to that we all take with home security: you secure your house in the hope that the thieves will go to your neighbour’s house not yours. The ultimate success will be if the criminals start moving away and looking elsewhere, and we are seeing that. So CSP will stay relevant.”

He too called for a move to the next stage of CSP. “Self-attestation will only be successful if banks consume the data,” he said. “Consumption is only now really getting started – with banks beginning to embed it into their overall processes for the evaluation of counterparties. It would be good if banks really got that going in earnest in 2018.”

In a similar vein, Zimmerman also called on SWIFT and the industry to keep raising the bar with SWIFT gpi. “It’s a new dimension – having control of where we send payments, when we send them, and all the gpi features,” he said. “But we want to not just send more data to enable a payment we can do today: we want to seamlessly integrate into the business processes of our customers.”

Further building on the value of gpi is in the plan, Leibbrandt confirmed. “Key here is the UETR – the unique transaction reference ID which Standards Release 2017 required banks to be able

Cross-border payments are SWIFT’s to lose, and the banks’ to lose, and if we play it well, we can remain relevant. I hope in 10 years’ time that gpi is universal, and anybody, anywhere can send payments, with a trusted bank in between.”Gottfried Leibbrandt, Chief Executive Officer, SWIFT

Securing the financial ecosystem

SWIFT Business Forum Switzerland 2018

crypto world is now discovering collateral, high powered money versus low, netting et cetera – everything banking has known about for a long time,” he said. “Cross-border payments are SWIFT’s to lose, and the banks’ to lose, and if we play it well, we can remain relevant,” he said. “I hope in 10 years’ time that gpi is universal, and anybody, anywhere can send payments, with a trusted bank in between.”

77

Securing the financial ecosystem

During a panel which delved deeply into the cyber challenge, delegates were left in no doubt that this threat is increasing all the time. Max Klaus, stv. Leiter MELANI, Eidg. Finanzdepartement EFD, Informatiksteuerungsorgan Bund ISB said: “It’s a fact that cyber attackers are getting more sophisticated every day. Even for IT experts, it’s harder to work out if something is malicious or not.”

The only response is a relentless focus on fighting back, suggested Carlo Hopstaken, CISO/Cyber Assurance, UBS Business Solutions. Echoing Leibbrandt’s earlier comments, he told delegates: “If it takes a lot of effort for cybercriminals, hopefully they will go to the neighbours instead.” However, acknowledging that the worst “could still happen,” banks need to have proper plans in place, he continued. “Think about worst case scenarios. If payment systems can’t be used, what would we do? If there are no systems at all, what would we do? How would we communicate?”

Preparing for the right threats is critical, added Michael Bartsch, Managing Director, Deutor Cyber Security Solutions Switzerland. “There is a difference between IT security and cybersecurity, where there is an active cyber attacker,”

he warned. “Last week we did a war game with a large German bank, compliant with every piece of IT security regulation possible. Twenty minutes in, they were entirely down - because they weren’t expecting an innovative cyber-attack.”

The approach of SWIFT and the SWIFT community to security through CSP has been a positive driver for change, confirmed Hopstaken – but the size of the challenge must not be under-estimated. “The CSP approach, with the workshops, has given us a good opportunity to understand the framework and provide feedback to SWIFT – and the exchanges with SWIFT have been very positive,” he said. “But it’s not that easy for smaller firms to be compliant and at the same time the bigger firms have a lot of legacy.”

He also highlighted the value of newer technologies in the cyber context. “A lot of the new products available use deception technology to attract the cyber attackers in by creating a fake system and credentials. The advantage of this is that if someone tries to break in it creates an alert, and if there is an alert from this route it is more or less 100% guaranteed to be malicious.”

SWIFT Business Forum Switzerland 2018

It’s a fact that cyber attackers are getting more sophisticated every day. Even for IT experts, it’s harder to work out if something is malicious or not.”Max Klaus, stv. Leiter MELANI, Eidg. Finanzdepartement EFD, Informatiksteuerungsorgan Bund ISB

88

But Bartsch sounded a note of caution around technology use. “One of the biggest problems is mixing buzzwords,” he said. “We hear that leveraging AI is the best way to prevent cyber-attacks – but remember that the hackers can use the same technology. How can we trust technology? You need a plan in place for when the technology fails. Even the best IT people are users: today, the developer is usually someone in Asia. We can’t test the source code. The environment is getting more complex, and crisis management for business – not IT – people is the best investment.”

On one new technology development Bartsch was more positive, however. “What we see for cyber-attacks is that cloud is more secure than on-premise,” he said. “Cloud brings other problems – data protection, trust, availability – but from what we see so far, if you go with a really good provider, cloud is more secure.

“Cloud is the end point of digitalisation, but you have to think about how you are going to implement it,” he continued. “You have to understand it otherwise you can’t manage it. You need to understand what the processes are, what the provider does and what you should do in a crisis situation.”

Another plus, he added, is that “cloud is so cheap, it also allows you to save some money to spend on IT security”.

What we see for cyber-attacks is that cloud is more secure than on-premise. Cloud brings other problems – data protection, trust, availability – but from what we see so far, if you go with a really good provider, cloud is more secure.”Michael Bartsch, Managing Director, Deutor Cyber Security Solutions Switzerland

Trends and challenges in financial crime compliance

Last week we did a war game with a large German bank, compliant with every piece of IT security regulation possible. Twenty minutes in, they were entirely down – because they weren’t expecting an innovative cyber-attack.”Michael Bartsch, Managing Director, Deutor Cyber Security Solutions Switzerland

SWIFT Business Forum Switzerland 2018

99

During the next panel on financial crime compliance, the voice of caution on leaping too quickly into new technologies was further sounded. Stefan Neumann from Credit Suisse warned delegates to be careful with machine learning, for example. “There is a need to understand why the algorithm concluded what it did, and also to explain to the regulator how it came up with what it did,” he said. “Deep learning is a black box.”

The challenge with new technologies is “how risky they can be for banks”, he continued. “We have to formulate a risk appetite towards these new technologies. Crypto, bitcoin and digital currencies really are largely unregulated and as a second line of defence function there is no appropriate surveillance to have confidence in tracking the transactions. The risk exposure would be too high,” he suggested.

Technology should be adopted as it is needed and not before, agreed Thomas Steinebrunner, Head of Legal & Compliance, Rahn + Bodmer Co, and Chairman of the Board of the Swiss Association of Compliance Officers. “Two-thirds of the banks on SWIFT are Category 5 – small – and if you include

Category 4 banks, this accounts for 90% plus,” he said. “They are small, local businesses and are totally different to large universal banks. It’s a real challenge to be a compliance officer in a large bank. We are a private bank – with 4000/5000 big clients – and we don’t do commercial transactions. We have payments services, but is it that risky? We don’t have retailers coming in with cash every day. We have clients who deposit funds and leave them there. We have banks with clients who are all located in one valley: they know the clients really well and they are local economy focused businesses. So we ask the question, what do we actually need? Regtech has been around for 15 years. We get better at technology, but is anything actually new?”

Steinebrunner further questioned whether AI can really take the industry much further forward, if the focus is only on the technology. “Could AI have helped with Petrobras or FIFA? These big scandals could not have been avoided with technology alone – but only by business people keeping hold of their responsibilities, and not handing them off to systems.”The point, he emphasised, was the “simple might sometimes be

Could AI have helped with Petrobras or FIFA? These big scandals could not have been avoided with technology alone – but only by business people keeping hold of their responsibilities, and not handing them off to systems.”Thomas Steinebrunner, Head of Legal & Compliance, Rahn + Bodmer Co, and Chairman of the Board of the Swiss Association of Compliance Officers

SWIFT Business Forum Switzerland 2018

Trends and challenges in financial crime compliance

1010

better”. “The big banks might need technology, but they also must focus on getting on board people who can handle it.”

Luc Meurant, Chief Marketing Officer, SWIFT, agreed that “if you don’t understand the way the algorithm works, the regulator won’t accept it”. “You can’t say, someone else took the decision,” he told delegates. Another challenge, he added, is that “the key with machine learning is the learning, and for that you need a lot of transactions: that is easier with retail than B2B, where there are fewer transactions”.

That said, the pressure for banks – from regulators and their correspondents – to implement effective systems remains very high, Meurant continued. As a consequence, “this is a tipping point for utilities”, he alleged. “The banks want to work together and the regulators want to see it. At SWIFT, we are late to the utilities party, but this gives us an advantage because we are able to apply the latest technologies and we can mix and match information from different systems.”

Asked about the impact of increased use of real-time payment systems on transaction screening, Meurant acknowledged that “real-time and screening are like fire and water: they don’t go well together”. “The best filters today have a 2% false positive rate. In a retail shop, putting one in 50 transactions on hold would be very annoying.”

This challenge is not solved yet, he warned. “Typically, domestic transactions are not screened: two banks in the same country have the same regulator and there is a view that the KYC covers it. Today we have domestic real-time systems but in a couple of years we will have cross-border real-time systems – and then this will be much more of a concern.”

The banks want to work together and the regulators want to see it. At SWIFT, we are late to the utilities party, but this gives us an advantage because we are able to apply the latest technologies and we can mix and match information from different systems.”Luc Meurant, Chief Marketing Officer, SWIFT

A new standard for cross-border payments

SWIFT Business Forum Switzerland 2018

1111

SWIFT Business Forum Switzerland 2018

Martin Schlageter, Head of Treasury Operations, Roche Holding, giving the view of a corporate, confirmed the happiness referred to by Wachs. “We really wanted the banks to take this seriously, and I was still sceptical a year ago, but now it is tremendous to see what has come out of gpi,” he told delegates. “The number of banks, the amount of transactions, the access to information – this really stops us from having to call the bank because we can see the online tracking – and this is tremendous.”

However, he added, “it is more the beginning than the end”. “It is a great platform. Now we need to add more banks, shape standards and shape future messaging,” he said. “We are very positive about this after one year but there is a different speed of adoption within

the banks. It is up to the corporates to speak to the banks and as much as possible get them to exploit this service. We are glad for the call to action by SWIFT and that the banks listen now, but not all banks are yet on the system, and it is only really useful when the whole ecosystem is on gpi.”

Natalia Blatter, Product and Market Development, Corporate and Institutional Clients, UBS, agreed that there is more to be done. “With gpi, we have seen unprecedented co-creation and co-opetition,” she said. “We realised either we succeed together or fail together. But this is not just interbank. We need all the support we can get from local banking communities and MIs, so we can track every payment from end to end.

A new standard for cross-border payments

The subsequent discussion on SWIFT gpi returned to the earlier theme of how to drive out the next level of benefits from this solution. In a brief update on progress so far, Stanley Wachs, Global Head of Bank Engagement, SWIFT global payments innovation, emphasised the benefits gpi brings in terms of speed, transparency, tracking and remittance information. He told delegates that 155+ banks are committed, and 45 are live, of which 29 are top 50. Currently 17% of cross-border MT103s are sent as gpi. Wachs reported that “corporates are very happy” and that SWIFT is “looking at making it easier for small and medium-sized banks to implement gpi.”

I am hoping at some point that every bank in the world will be able to join gpi. Corporates are still asking banks to add more value, and the journey has just begun.”Natalia Blatter, Product and Market Development, Corporate and Institutional Clients, UBS

1212

“I am hoping at some point that every bank in the world will be able to join gpi. Corporates are still asking banks to add more value, and the journey has just begun.”

Implementing gpi has not been plain sailing for the banks, as Paula Roels, Head of Market Infrastructures & Industry Initiatives in Cash Management, Deutsche Bank, pointed out. “When gpi was born, it came as a disruption, halfway through a budget cycle. But we realised it was addressing customer pain points, and that new competitors were beating on us. We understood in early 2016 that our corporate customers wanted it as soon as possible – without changes on their side.”

Deutsche Bank’s approach was to set up a global gpi implementation team, she told delegates. “It was important to sell the story internally. The business case was not going to come from growing revenues. It was going to come from improving relationships and meeting customer needs.”

Recognising that the industry is “in the middle of a transformation”, the bank wanted to ensure that whatever it built was strategic, not tactical – and its choice was to use APIs. Roels echoed Leibbrandt’s earlier commentary around the UETR and leveraging investment in this to go one step further and implement GPI. “SR2018 goes beyond the normal messaging change, and I am not sure if the industry has understood this,” she said. “This is triggered by the use of the UETR in the MT103, and it affects the back end of the payments engine as well because it requires every single SWIFT user to be able to receive the UETR and populate the field if the message is sent on. This is important for the gpi community

because corporate customers have these expectations, and it enables those banks who move first to deliver to clients’ expectations. So why not gpi-enable your operations at the same time to gain from efficiency and deliver a better customer experience?”

Overall, it’s important to think ahead, Roels said. “We are just starting this journey. The corporates are asking for the information in a way that can be integrated, i.e. using APIs. The corporates gave us a push in the first place, and it is now time to start looking at what else we can do. Can we look to apply it for other client segments, for example in trade finance or securities settlement? Can we find other use cases for ourselves based on the 202 being trackable – say in cash management processes?”

Roche’s Schlageter closed with another call to action. “We need every bank on this. Every flow should be automated and not stop somewhere. If we now have these standards, everyone should comply. The more you empower your corporates, the less you need operational teams replying to emails all day.

“The speed of this might be scary”, he said, but, he warned, “there is competition out there which is creeping into the cross-border business.”

“We need every bank on this. Every flow should be automated and not stop somewhere. If we now have these standards, everyone should comply. The more you empower your corporates, the less you need operational teams replying to emails all day.Martin Schlageter, Head of Treasury Operations, Roche Holding

From bricks and mortar to service networks

It was important to sell the story internally. The business case was not going to come from growing revenues. It was going to come from improving relationships and meeting customer needs.”Paula Roels, Head of Market Infrastructures & Industry Initiatives in Cash Management, Deutsche Bank

SWIFT Business Forum Switzerland 2018

1313

Fending off competition was also a key theme in the innovation panel, as the bankers on stage grappled with the new business model options ahead of them in a world of open banking.

On the move to a services model, August Benz, Deputy CEO of the Swiss Bankers’ Association and Head of Private Banking & Asset Management, SwissBanking, pointed out that “if you move more into a services model, you have to provide more services”. “That’s how the industry moves forward, he suggested – adding services, without building them.”

The challenge of this is less about technology than about mindset, suggested Andreas Iten, Managing Director, SIX, Board member and Co-Founder of F10. “Are we willing to share and build up an ecosystem?” he asked. “That mindset is still not there – and it will take some time to develop,” he said.

Once again, a note of caution on leaping too quickly into new developments was struck, as UBS’s Zimmerman, asked about the impact of the Internet of Things on banking, said “banks need to get into these things as they become bank relevant”. “I recently spoke to a surgeon in London who told me that in a recent operation he was about to make the final scalpel cut when the lights went out and the computer giving the instructions was gone. There are risks to be faced when we rely on these new technologies too heavily.”

Banks will inevitably change, the panellists acknowledged. In 10 years’ time “there will be fewer of them”, predicted Benz, “and those that follow an internal digitalisation approach and try to replace everything internally will fail – while those who embrace new platforms and build new products and services will probably survive”.

The physical representation of banks will certainly be different, suggested Zimmerman. “They will not be fixed structures and buildings,” he said. “Rather, they will be services networks.”

Those that follow an internal digitalisation approach and try to replace everything internally will fail – while those who embrace new platforms and build new products and services will probably survive.”August Benz, Deputy CEO of the Swiss Bankers’ Association and Head of Private Banking & Asset Management, SwissBanking

Are we willing to share and build up an ecosystem. That mindset is still not there – and it will take some time to develop.”Andreas Iten, Managing Director, SIX, Board member and Co-Founder of F10

From bricks and mortar to service networks

Exploiting the potential of AI

SWIFT Business Forum Switzerland 2018

1414

If banks will still be here in 10 years’ time, so will banks’ operations people, suggested Nino Ciganovic, Head of Client Support and Member of the Management Committee, SIX Securities Services, in his presentation on how AI will transform customer services.

“Will AI change things? Yes. Will it replace me? No,” he told delegates. “Think about self-driving cars and how they will deal with construction signs. The answer is very simple – human operators will remain in ultimate control.”

The securities servicing business has little choice but to exploit the potential of AI, he contended, as a result of demographic changes alone. “The challenge today in securities services is that we have very high internal costs from repetitive enquiries. Generation Alpha – the kids of the Millennials who are currently 4 or 5 years old – will grow up completely different to us. They will want everything to happen unbelievably fast. We have to do something.”

AI is a major part of the solution, he contended, enabling financial services firms to elevate user experience, decrease costs, increase revenues and reduce risks.

Ciganovic gave a simple but compelling example of the speed and efficiency AI can unlock – citing one big bank which has implemented an AI based solution to process block trades. “These take a lot of time, allocating the trades that make up the block to the right accounts,” he said. “Typically, it can take 45 minutes per block trade. AI got it down to 2 minutes.”

Exploiting the potential of AI

The customer is keySWIFT Business Forum Switzerland 2018

1515

Every model has two sides, and though digital increases customer satisfaction, these are people businesses. Don’t lose touch with the customer through digital – because the customer is key.”Nicole Diermeier, Director, Global Marketing and Member of the Executive Board of Switzerland Tourism

The customer is key

The final speaker in the programme, Nicole Diermeier, Director, Global Marketing and Member of the Executive Board of Switzerland Tourism, shared her insights on the impact of digitalisation in her industry, drawing parallels with its impact in financial services.

Reflecting two of the strong themes of the day – that technology is unlocking powerful change, but that it must also be approached with care and caution and applied in the right areas – Diermeier issued a timely warning to the delegation.

SWIFT Business Forum Switzerland 2018

SWIFT © 2018

For more information about SWIFT visit swift.com

SWIFT Business Forum SwitzerlandPapiersaalAlte SihlpapierfabrikKalanderplatz 6 (Sihlcity)8045 Zürich

#BFSwitzerland