Bureau of Internal Revenue - U.S. Government Publishing Office

416

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Bureau of Internal Revenue - U.S. Government Publishing Office

, T

g yr q .

Treasury Department: . :: Bureau of Internal Revenue f

Internal Revenue Bulletin

Cumulative Bulletin XI-1

JANUARY — JUNE, 1932

SPECIAL ATTENTION m directed to the cant unary notice on this page that p~ lished rulings of the Bureau do not have the force and effect

of Treasury Decisions and that they are applicable only to facts presented in the published case

&Tteeeuvr~oe artment::::: Bureau ef tutetuel Reveuue .

c'Internal Revenue Bullebq=; NF

Y

Cumulative Bulletin XI — ' & l &

t'ai

tfig

JANUARY-JUNF. , 1932

IN THIS ISSUE

Introductory Notes . Contents Rulings Nos. 5339-5531—

Board of Tax Appeals Income Tax-

Part 1 (1928 Act) Part II (1926 Act) . Part HI (1924 Act) Part IV (1921 and Prior Acts) .

Estate Tax Sales Tax Capital Stock Tax Miscellaneous .

Index

Page

III v-vnl

1-12

13-144 145-215 216-235 236-323 324-337 338-361 362 — 367 368-383 385-396

35Q i

The raUngs repertml in tbe Internal Revasue BaUctin are fm the information of taxpayers and their eoonuel as ~ bowing the tread of ofbriai opinion in tho administratian of thc Bureau ol internal Revenue; the rulings othm than

Treasury Decisions have none ol the force or egeet of Trcasary Derisiuns and do not commit the Departmetn to ~ ny interpretation of the law which hss not been formally sppreved und promulgated by thc Secretary ol the

Treasury. Each ruling embodies tbe adm'uuutrstive applicatioa of the law aad Treasury Decisions to the entire

state of facts upon which a particular case rests. It is cspeciagy te be noted that the same resmt wiU net ncces. eerily bo reached in aaotbcr case unless aU the material facts sre identical with those of the reported case. As it is not always fcaribfe to publish a complete statement ol tbe facts uaderlying each ruling. there caa be no assurance

that any new case is identical with the reported casa As beatisg oat this distiaction, it msy be observed that the

rulings pablisbed from time to time may appear to rcrerse ralings previously publishotk

Ogircrs of tbo Bureau of Internal Revenue arc cspeciaUy cautioned against reaching a conclusion ia any casu

merely en thc basis uf similarity to a published ruling, aad should base thoir judgment on the application of aU per.

thrust proviiioas ol tbe law and Treasury Dccisiens to aU thc facts in each casa. These r slings should be used as sids

in studying the lsw snd its lormal construction as made iu the regulations sad Treasury Decisioas previously isuacd.

tu addition to pablisbiug aU Internal Beveauc Trcssary Decisions, it is the policy ol the Baresu of lnterasl Revenue

ta publish aU rulings and dccisioas, induding opinions of the General Counsel for thc Bureau of Internal Revenue,

which, because they announce s raling er decision upon s novel question ur upon a qaestios in regard to which

there exists no previously published ruling or decision, or lor other reasons. are ot such imsmtsnm as to be of

general interest It is also the policy of the Bureau tu publish uU rulings or decisions which revoke, modily, amcad,

or aacct in aay manner whatever aay published ruling or decision. In many instances opinions of tbe General

Coansel for tbe Bureau of Internal Rcvcauc arc not of general intcrcst because tbey anaounce no new ruling or no

now construction of the revenue laws but simply apply rulings already made public to certain situations of fact which

arc without special significance. It is not the policy of the Bureau to publish such ojuuous. Therefore, tbc uambers

asmgned to tbe published opinions of the General Counsel lor tbe Bureau of internal Revenue are not consecutive.

No anpubbshed rulisg or decision wiU be cited or relied upon by aay ofhcer or employee of the Bureau ol Internal

Revenue ss a precedent in the dispositioa ofother cases. Unless otherwise specificuUy iadicated. sU published

rugngs sud decisions have received the cousiderstioa sud approval of the General Coaasel for the Bureau ol

Internal Revenne.

UNITED STATES GOVERNMENT PRINTING OPEICR, WASHINGTON t 1932

psr sale by tbe Supcriutcadent ol Documents, Wasbingtoae D. C ~ - - Scc buck of title lor prices

The Internal Revenue Bulletin service for 1988 will weekly bulletins and semiannual cumulative bulletins.

The weekly bulletins will coutain the rulings and decisions to be made public and all Treasury Department decisions (known as Treas- ury decisions) pertaining to Internal Revenue matters. The annual cumulative bulletins will contain all rulin s and decisions (including Treasury decisions) published during the previous six months.

The complete Bulletin service may be obtained, on a subscription basis, from the Superintendent of Documents, Government Printing Office, Washington, D. C. , t'or $2 per year. Single copies of the weekly Bulletin, 5 cents each.

New subscribers and others desiring to obtain the 1919, 1920, and 1921 Income Tax Service may do so from the Superintendent of Docu- ments at prices as follows: Digest of Income Tax Rulings No, 19 (containing digests of all rulings appearing in Cumulative Bulletins 1 to 5, inclusive), 50 cents per copy; Cumulative Bulletins Nos. 1 to 5, containing in full all rulings published since April, 1919, to and in- cluding December, 1921, as follows: No. 1, 80 cents; No. 2, 25 cents; No. 8, 80 cents; No. 4, 80 cents; No. 5, 25 cents.

Persons desiring to obtain the Sales Tax Cumulative Bulletins for January — June and July — December, 1921, may procure then& from the Superintendent of Documents at 5 cents each per copy.

Persons desirin to obtain the Internal Revenue Bulletin- service for the years 1922, 1928, 1924, 1925, 1926, 1927, 1928, 1929, 1980, 1981, and 1982 may do so at prices as follows:

Cumulative Bulletin I — 1 (January — June, 1922) Cumulative Bulletin I — 2 ( July — December, 1922) 80 cents Cumulative Bulletin II — 1 (January — June, 1928) 80cents Cumulative Bulletin II — 2 (July — December, 1928) 40cents Cumulative Bulletin III — 1 ( January — June, 1924) 50 cents Cumulative Bulletin III — 2 (July — December, 1924) 50 cents Digest No. 18 ( January, 1922 — December, 1924) 60 cents Cumulative Bulletin IV — 1 ( January — June 1925) 40 cents Cumulative Bulletin IV — 2 ( July — Deceruber 1925) 85 cents Digest No. 17 (January — December, 1925) 25 cents Cumulative Bulletin V — 1 (January — June, 1926) 40 cents Cumulative Bulletin V — 2 ( July — December, 1926) 80 cents Digest No, 2l (Ja. nuary — December, 1926) 15 cents Cumulative Bulletin VI — 1 (January — June 1927) 40 cents Cumulative Bulletin VI — 2 ( July — December, 1927) 40 cents Digest No. 22 ( January, 1925 — December, 1927) 85 cents Cumulative Bulletin VII — 1 ( January — June, 1928) 85 cents Cumulative Bulletin VII — 2 (July — December, 1928) 50 cents Cumulative Bulletin VIII — 1 (Januarv — June, 1929) 50 cents Cumulative Bulletin VIII — 2 ( July-December, 1929) 55 cents Cumulative Bulletin IX — 1 ( January — June 1980) 50 cents Cumulative Bulletin IX — 2 ( Ju!v — December, 1980) 50 cents Cumulative Bulletin X-1 ( January — June, 1981) 65 cents Cumulative Bulletin X — 2 ( July — December, 1981) 80 cents Cumulative Bulletin XI-1 (January — June 1982) -- 80 cents

All inquiries in regard to these publications and subscriptions should be sent to the Superintendent of Documents, Government Printing Office, Washington, D. C,

INTRODUCTORY iVOTES.

The Internal Revenue Cumulative Bulletin XI — 1, in addition to all decisions of the Treasury Department (called Treasury decisions) pertaining to Internal Revenue matters, contains General Counsel's opinions, and rulings and decisions pertaining to income, estate, sales, capital stock, and miscellaneous taxes, as indicated on the title-page of this Bulletin, published in the weekly Bulletins (Volume XI — 1, Nos. 1 to 26, inclusive) for the period January 1 to June 80, 1982. It also contains a cumulative list of announcements relating to deci- sions of the United States Board of Tax Appeals published in the Internal Revenue Bulletin Service from January 1 to June 80, 1982.

Income Tax rulings are printed in four parts. Rulings under the Revenue Act of 1928 are published as Part I, the section headings corresponding with the sections of that law and the article headings corresponding with the article headings of Regulations 74. Rulings under the Revenue Act of 1926 are published as Part II, the section and article headings corresponding with the section and article head- ings of the Revenue Act of 1926 and Regulations 69. Rulings under the Revenue Act of 1924 are printed as Part III, the section and article headings corresponding with the section and article headings of the Revenue Act of 1924 and Regulations 65. Rulings under tl&e Revenue Act of 1921 or earlier Acts are printed as Part IV. the section and article headings corresponding with the section and article headings of the Revenue Act of 1921 and Regulations 62.

ABBRZVIATIOKS.

The following abbreviations are used throughout. the Bulletin: A, B; C, etc. — The names of individuals. A. R. M. — Committee on Appeals and Review memorandum. A. R. R, — Committee on Appeals and Review recommendation. B. T. A. — Board of Tax Appeals. C. B. — Cumulative Bulletin. Ct. D. — Court decision. C. S. T. — Capital Stocit Tax Division. D. C. — Treasury Department circular. E. T. — Estate Tax Division. G. C. M. — General Counsel's memorandum. L T. — Income Tax Unit. M, N, X, Y, Z, etc. — The names of corporations, places, or businesses, accord-

ing to content. Mim. — Mimeographed letter. MS. — Miscellaneous Division. O. or L. O. — Solicitor's law opinion. O. D. — OSce decision. Op. A. G. — Opinion of the Attorney General. S. T. — Sales Tax Division.

(ux)

S. M. — Solicitor's memorandum. Sol. Op. — Solicitor's opinion. S. B. — Solicitor's recommendation. T. — Tobacco Division. T. B. AI. — Advisory Tax Board memorandum. T. B. R. — Advisory Tax Board recommendation. T. D. — Treasury decision. e and y are used to represent certa. in numbers, and when used with the word

"dollars" represent sums of money.

The practice of promulgating Treasury Decisions that embody court decisions relating to the internal revenue has been discontinued. Hereafter opinions of the courts, with appropriate headnotes for the information and guidance of taxpayers and ofFIcers and employees of the Bureau of Internal Revenue, will be published in the Internal Revenue Bulletin without formal approval and promulgation by the Secretary of the Treasury.

For additional information which will be of assistance in the use of the Internal Revenue Bulletin service read the Introductory Notes to the latest Digest.

ANNOUNCEMENT RELATING To BOARD OF TAX APPEALS DECISIONS.

Under the provisions of the recent Revenue Acts, relating to appeals to the Board of Tax Appeals, the Commissioner may ac- quiesce in the decision of the Board or he may, if the appeal was heard by the Board prior to the passage of the 1926 Act, cause to be instituted a proceeding in court for the collection of any part of a tax determined by the Commissioner to be due but disallowed by the Board, provided that such proceeding is commenced within one year after final decision of the Board. As to appeals heard by the Board after the passage of the 1926 Act, the Commissioner may, within six months after the Board's decision is rendered, file a petition for a review of the decision by a Circuit Court of Appeals or by the Court of Appeals of the District of Columbia; however, as to deci- sions rendered on and after June V, 1982, petitions for review must be filed within three months after the decision is rendered. In order that taxpayers and the general public may be informed as to whether or not the Commissioner has acquiesced in a decision of the Board of Tax Appeals disallowing a tax determined by the Commissioner to be due. announcement will be made in the weekly Bulletin at the earliest practicable date. A notice that the Commissioner has ac- quiesced or has nonacquiesced in a Board, decision relates, however, only to the issue or issues decided in favor of the taxpaye'r. Deci- aions so acquiesced in should be relied upon by ofFicers and employees of the Bureau of Internal Revenue as precedents in the disposition of other cases before the Bureau.

CONTENTS.

Ruling No. Page. Ruling. Ruling No. Page,

Treasury decisions: 330 4

331 4 433 2 ----- 4 333 4 334 4 335 4 336

Court decisions: 4 35 4 36 4 37 4 38 4 39 44 0 4 41 44 2 44 3 444 44 5 4 46 44 7--- --------. . --------- 48

44 9 4 50 4 51 4 52 4 53

54 4 55 4 56 4 57 4 58 4 g 5g 4 60 46 1 46 2-- 4 63 4 64 4 65 4 6 66 4 7 67 4 8 68 4 9 69 4n 7n 4 1 71 4 72 4 3 73 4 4 74 4 5 75 4 6 76 47 4 8 78 4 9 79 4 0 80 4 81 4 2 S2 483 4 4 84 4 85 4 86 4 87 4 8 88 4 89 4 90 4 91 4 92 4 3 gg 4 4 94 4 95 4 497 4 4 99

( XI-2-5352 XI-2-5353 RI-2-5354 RI-7-5390

XI-14-5438 KI-15-5440 RI-16-5457 XI-16-5456 XI-16-5455

XI-1-5343 XI-1-5344 RI — 1 — 5345 Xl-2-5350 KI — 2 — 5351 RI — 3 — 5362 XI — 3 — 5361 R 1~5368 XI~5366 XI-5-5374 XI — 5-5375 Xl fr-538G XI-6-5381 XI-7-5388 XI-7-5389 Xl ti-5395 XI — 8-5396 XI-9-5400 R 1~5402

XI — 10-5406 XI-10-5407 XI-11 — 5412 XI-11-5413 XI — 12 — 5419 RI-12-5420 XI-12-5421 XI-13-6426 XI-13-5427 XI-13-5428 XI-14-5433 XI-14-5436 XI — 14-5434 XI — 14-5436 XI — 15-5444 XI-15-5443 XI-15-5445 XI-16-5452 RI-1 6-5451 XI — 16-5453 XI-17-5461 XI-17-5462 RI-17-5463 XI-18-5469 XI-18-5470 XI-18-5468 XI-19-5473 RI-19-5474 XI-19 — 5476 RI-20-5481 XI-20-5482 XI-20-5480 XI-21 — 5488 XI — 21-5489 RI — 21-5487 XI-22 5495 XI — 22-5494 XI-22-5496 XI — 23-5502 Xl-23 — 5503 XI — 23-5504 XI-23 — 5505 XI-24-5509 XI-24-5511 XI-24-5512 XI-24-5514

368 370 370 33G 57 31

334 333 329

213 232 318 230 278 315 246 145 130 201 252 149 271 167 348 163 280 160 341 161 338 274 370 177 219 282 196 198 286 305 35S 353 334 205 187 331 308 195 324 174 209 311 164 242 151 216 238 211 362 364 265 182 322 128 256 138 320 153 154 260 263 124 191 250 293

Court Decisions — Continued. 600 60 1 50 2 503 504 50 5 606 5

General Counsel's memoranda: 9953 9 1

10100 10110 1 29 0 2g 10168 10170 10198 1 10260 10273 10299 10307 10384 10401 10416 10431 10452 10486 10557 10607 10613 10624 10627

Board of Tax Appeals: 3725 4017 5389

7435 8 9 290 9447 9764 1 0202 10299 10755 10980 12052 12231 13104 13319 14862 15822 15823 15824 16229 16275 16354 16355 16356 16429 16552 16627 16985 1/717 17911 1 18089 18591 18592 18593

XI-24-5515 RI-25-5519 KI-25-5521 XI — 25-5MO XI — 25-5MS XI-26-5527 XI-26-5529 XI-26-5MS XI-26 — 5530

XI~5365 XI-1 — 5342 RI — 2 — 5349 XI-3-5360 XI~5367 XI~5369 XI — 1-5340 XI~5372 XI~5378 XI — 7 — 5387 XI-8 — 5393

XI-13 — 5424 XI-11-5411 X. l-l 4-5432 XI — 12-5418 XI — 15-5442 XI-17 — 5459 XI-15-5441 KI-16-5449 Xl — 23-5499 XI — 22 — 5492 XI — 26 — 5525 KI-25-551S XI-24-5513 XI-24-5510 XI-26-5526

XI-g- 5398 XI — 9-5398 XI-9-5398 XI-9-5398 XI — 9-5398

Xl-26-5M4 XI if-5398 XI — 9-5398 XI-7-5385 Xi ft-5398 XI-9-5398 XI-9-5398 Xi 9 539S XI-ii-5392 XI- 9-5398 XI — 8 — 5392

XI — 19-5471 Xl-19 — o471 RI-12-5416 Xl-12-5416 Xl-12-5416 XI-3 — 5358

XI-12-5416 XI-14-5430 KI-12 — 5416 XI — 12 — 5416 XI — 20-5478 Kl — 20-5478 XI-19-5471 XI — 9-5398

XI-14-5430 XI-3-5358 XI — 3 — M58 Xl-3-5358

XI — 23 — 5498 RI-23 — 5498 KI-23 — 5498

336 225 2g6 267 299 179 223 184 340

13 135 114 72

131 236 38 17 15

158 68 79

169 104 133 49 59 41 37 18 14 21

108 173 145 26

11 9 9

12 10 8

10 8

10 8 8 8 9

4, 9 11

4, 9 11 3 5 5 5 1 4 5 5 5

9 10 3 5

7, 12 6, 11

2 1 5

Ruling. Ruling No. Page. Ruling. Ruling No- Page.

Board of Tax Appeals — Con. 18876 18987 19011 20074 20337 20658 20703 20705 20765 20766 20767 20768 20769 20770 20771 20772- 20773-- 20774 20775 20776 20899 21047 211M 21715 220 07 220 22009 22313 22348 23085 23601 23943 23969 24 223 24 446 24489 24520 24837 25030 25194 2 Fil 58$3 2 5854 258 81 25 984 25985 25986 26238 26239 262 0 50 26369 26717 26747-26757 26747 26748 26749 2 750 6 26751 26752 26753 26754 26755 26756 26757 27095 27616 27623 27624 27625 27626 27627 27628 27G29 27G30 27768 28369 28396 28M4 28618 28927 29104 29 0 10 05 2g 106 29138

XI — 12-5416 XI — 3 5358

XI-11-5410 XI — 17 — 5458 XI-4 — 5364 X 1-9-5398

XI — 12 — 5416 XI — 12 — 5416 Xl — 3 — 5358 Xl-3-5358 XI — 3 — 5358 XI — 3-5358 XI-3 — 5358 XI — 3-5358 XI — 3-5358 XI — 3 — r 358 Xl-3-5358 XI — 3 — 5358 XI — 3-53N XI — 3 — 5358

Xl-20-5478 XI — 13 — 5423 XI — 1g — 5471 KI-~75508 XI-8-5392 XI — 8 — 5392 XI — 8-N92

XI-12 — 5416 XI — 8-5392 XI-4 — 5364 XI — 6 — 5377

XI — 11 — 5410 XI — 9-5398 XI — 9 — 5398 XI — 3 — 53N

XI — 24-5508 XI-22-5491 Xl-23 — 549S XI — 4-5364 XI — 3 — 5358

XI-15-5439 XI — 15 — 5439 XI — 11 — 5410 XI — 12 — 5416 XI-12-5416 XI — 12-5416 XI — 15-5439 XI — 15 — 5439 XI-15-5439 XI — 11 — 5410 XI — 5-5371

Xl-21-5484 XI — 21 — 5484 XI — 21 — 5484 XI-21-5484 XI — 21 — 5484 XI — 21-5484 XI — 21 — 5484 XI — 21 — 5484 XI — 21-5484 XI — 21 — 5484 KI-21-o484 XI — 21 — 5484 XI — 17-5458 XI — 1 — 5339 XI-6-5377 XI — 6 — 5377 XI — 6- 5377 XI — 6 — 5377 XI — 6-5377 XI — 6-5377 X 1-6-5377 XI — 6 — 5377

XI — 19 — 5471 XI — 3-5358

XI-24- 5508 XI — 3 — 5358

XI-18-5465 KI-21 — 5484 XI — 23 — 5498 XI-23-5498 XI-23 — 5498 XI-16-5448

6 2 3 2

12 8 3

11 1 5 7 7 7 6 6 5 6 3 3 2 4 5

11 6

4, 9 4, 9 4, 9

6 12 3

10 11 8 2

11 6

5, 10 2, 8 12 I 5 7 7 5 5 5 6 5 5

10 4

1, 7 I 5 5 2 2 6 5 3 1 6 1 2 2 1 7

6 6 3 3 4

11

3 10 6 7 1 5 2 6

Board of Tax Appeals — Can. 29154

9oo Q

2927 $ 29291 29399 29635 29" 29 30183 30 30 3 30311 30 3096 30992 31018 31029 3

31632 3 3 1668 3 ~ 1690 31769 31801 31869 31931 3217? 3 32307 3 3 2438 3 2439 3 3 2459 3 2584 3 2609 3 32735 32841 aooro 3 2984 3 2997. 33041 3 3076 3 3159 33177 3 244 32 3 3279 33374 3' 375 75 3 '33 83 ' 33 ' '392 33464 33 46 33469 33516 33517 33533 33610 33694 33799 33826 33938 33971 340 88 34113 34499 34630 34939 34945 34946 34964 35015 35038 35098 35443 35472 35955 361'12 36116

Xl-3-53N Xi — 19-5471 Xl-23-o498 XI-23-5498 XI-16-5448 XI-20. 5478 Xl-5 — 5371

XI-13-51% XI — 5 — 5371 XI-7 — 5385 XI-+-5364 Xl- 4 — 5364 Xl-4-5364

Xl — 12-5416 XI-20-5478 Xl-10-5404 Xl — 14- 5430 XI — 24-5508 KI — 26 — 5524 XI-26 — 5524 XI — 21 — 5484 XI — 12 — 5416 XI — 12-5416 XI — 6-r377

XI — 20-5478 X 1-3-535S

XI-19-5471 X. I — 22-6491 XI-20-o478 XI — 16 — 544S XI — 4-5364 Xl-3-535S XI~5364

XI-16 — 5448 X. l-16 — 5448 XI-24- MOS XI-14-5430 Kl-26-5524 XI — 16-5448 XI — 16-5448 XI — 21 — 5484 XI — 23-5498 XI — 9-5398

XI-10-5404 XI-12-541$ XI 16-5448 XI — 12-5416 XI-16-5448 KI-22-5491 KI — 16 — 5448 XI-12-5416 XI-6-537? KI SS-5377 XI-3-535S

XI — 10 — 5404 XI — 26 — 5524 XI-26-5524 XI-18. 5465 XI fr-5377 XI SS-N?7 Xl fi-5377

XI — 13-5423 XI-13-5423 XI-7-5385

XI-19-5471 XI-19 — 5471 Xi fi-5377

X 1-20-5478 Xl — 20-5478 XI — 17-54N XI-1$-5465 XI-20-5478 XI-3-53N XI — 3-53N K I-rg-5398 XI-5 — 5371 XI-3-53N XI-I-533g XI~5364

XI — 12-5416 KI-18-5465 XI-20-5478 XI-20-5478

4 9 7 6 9 9 6 3 4

10 3 2 3 8 3 3 7 3 7 7

2, 8 9 8 6 9

11 3

217 I 8

10 9 1

11 11

10, 12 8

2, 8 4 2 8 4 8 3

10 9 4 6 5

11 4 4 4

11 10 7 7 8

12 12 9 6

3, 9 10 7

11 5 9 5

2, 6 4 9

5, 10 6, 11

2 3

10 2

4, 5 2, 3 '2 12 8

Ruling. Ruling No. Page. Ruling. Rul! ng No. Page.

Board of Tax Appeals — Can. 36379 . 36393 . 36411 36438 M502 36867 M940 37001 37095 37102 37323 37324 37395 37447 37499 37534 37535 a75M 37552 87573 . 87574 87693 37694 37695 37696 37762

37835

88687 387]] 88726 88853 3886S 3S880 39167 39242 39255 39291 39406 39525 39647 39841 39873 aooao

40071 40081 4 40083 40115 40147 40229 40230 40231 40232 40233 40267 40446 40546 40553 40554 40565 40634 40659 40765 40873 4OBGO

40939 40948 40949 41023 41024 41026 41034 41072 41343 41344 41345 41346 41645 4]646

XI-20-5478 XI — 16-5448 Xl 9-539S

XI-24-5508 XI — 16-5448 XI-17 — 5458 XI-18-5465 XI~5364

XI-20-5478 XI-5-5371 XI-7 — 5385 XI-7 — 5386 XI — 7-5386

XI-26-5524 XI — 17-5458 XI-7-5385 R 1-7-5385 XI-7-5385 XI-7-5385 RI-6-5377 X 1-6-5377 XI — 3-5358 XI — 3 — 5358 RI — 3 — 5358 XI-3-5358 XI-7-5385

X 1-22-5491 XI — 7-5385

RI-19-5471 RI-5-5371 XI-3-5358

XI-13-5423 Xl f]-5377

XI — 21-5484 XI-3-5358

XI-22m 5491 XI — 19 — 5471 XI — ]3-5423 XI~5364

RI-22 — 5491 RI-19-5471 RI-22-5491 XI — 19-5471 XI-3-5358

XI-10 — M04 XI-12-5416 XI-7 — 5385 XI — 7-538li

XI — 13-5423 XI-13-5423 XI-13-M23 XI-16-5448 RI — 1 — 5339

XI — 14 — 5430 XI-]4-5430 XI-14-5430 XI-14-5430 KI-14-5430 XI — 16 — 5448 XI-24-5508 XI — 3 — 5358

XI — 24-5508 XI — 24 — 5508 XI-3-5358

RI — 12-5416 XI — 15-6448 XI — 19 — 5471 XI-16-5448 XT — 17-5458 RI-]3-5423 XI — 12-5416 RI-]2-M] f! RT — 3-5358 XI-3-"358 XI — 7 — 5385 XI-3-5358

XI — 16-5448 XI-13 — 5423 XI-13-5423 XI-]3-5423 XI-13 — 5423 X I-19-5471 RI — 19-5471

10 6

6, 11 3, 4

11 9 4 5

11 9

10 8 8 6

11 10 11

3, 8 6 2 1 1 1 1 4 4 6 8 6 1 6 a

ll 7

10 1, 4 '2

9 6 3

6, 11 11 4 9 1 6 4

3, 9 4, 10 7, 11

2 2

af7 1 7 4 7 4 8 1 6 2

12 9 6

8, 11 6

9, 10 2 8 8

10 10 5 1 6

3, 9 4, 10 4, ]0 7, 11

10 8

Board of Tax Appeals — Con. 41647 42032 42062 42340 42341 42460 42619

42743 42908 42917 43121 43176 43667 43795 43850 43912 43972 43973 439 85 44153 44321 445 83 44f!84 44742 44768 4476 9 44809 44845 44939 44992 45032 45065 45164 45169

0 46215 45320 4M30 45537 45616 45714 45741 46778 45780 45781 45863 45864 45957 4595S 45979 46055 46056 46057 4605s 46059 46060 46061 46G62 46079 46270 46272 46291 46292 46569 46583 46585 48293 48528 48692 48930 49422 49668 50059 50178 60305 50981 51012 51507 61858 53647 63791 53792

8 11 5 7 7 8

2, 3 8 2 6

11, 12

3 9

10 5 7 7

3, 7 9

2, 8

4 2, 8

7

9 3 2 3 5

11 9

XI-19-5471 XI-l~d-5416 XI — 7 — 5386

XI — 26-5524 XI-26-5524 XI-13 — 5423 XI — 21-5484 RI-18-5465 XI-]9 — 5471 XI-]2-5416 XI — 4 — 5364

XI-26-5524 XI — G-M71

XI-21-5484 XI-21-5484 XI-]3 — 5423 XI — 16 — 544S XI — 14-5430 XI-14-5430 XI — 4 — 5364

XI — ~5524 XI — 19-5471 XI-7-5385

XI-26-5524 XI-]3-5423 XI-26-5524 XI-26-5524 RI-15-5439 XT — 12 — 54]6 XI — 19-5471 XI — 16-5448 XI~5364 XI-9 — 5398

RT — 2]-5484 XI-3-5358, XI — 3-5358

XI-19-5471 XI-4-5364 XI-4-5M4

RT — 19-5471 XI — 19 — 5471 X 1-2-5347

XT-13-5423 XT — 13-5423 XI — 3-535S Xl — 3-5358 XI-3-5368 XI-3-5358

XI — 26-5524 XI-26-5524 XI-8-5392 XI — 9-539S RI-9-5398 XI-9-5398 RI-9-5398 XI-9-5398 XI-9-5398 XI-9-5398 RI — 9-5398

XI — 24-5508 XI — 13 — 5423 XI-24-5508 XI-4 — 5364 XI ]-5364

XI — 20-5478 XI-24- 5508 XI-6-5377

XI-11-5410 Rl i]-5398

XI-24-5508 XI-11-5410 XI — 20-5478 XI — 22~91 XI-1 1-5410 XI — 19 — 5471 XI-1~465 RI-24-5508 XT-12 — 5416 RI — 13-5423 XI-19-5471 XI-24-5508 Xl — 3-5358 X. I-3-5358

8, 9, 11 8, 9, 11

3 , 11

9 9 8 8 2 5 8 9

10 10 7 7 6 2 2 2 2 5 6 6 7 2 6

12 ]2 1

3, 4 5

6, 11 6

9, 11 1 6 8 2 8 4 4 2

4, ]0 3, 9

11 8

VIII

Ruling. Ruling No. Page. Ruling. Ruling No. Page.

Board of Tsx Appeals — Con. 53793 55755 56877 57835 59655

Offfce decisions (I. T. ): 2610 . 2611 2612 2613 2614 2615 2616 261 7 2618 2619

2621

XI — 3 — 5358 XI — 26-5524 XI — 24 — 5508 XI — 21 — 5484 XZ-21-5484

XI — 1 — 5341 XI — 2-5348 XI — 3 — 5359 XI-5-5373 Xl fl-5379 XI (f — 5394 XI — 9-5401

XI-10-5405 XI-12-4417 XI-13-5425 XI-14 — 5431 XI-16-6450 XI — 17-5460 XI-18-5467 XI-19-6472

8 11

4, 5 2

41 36 30

48 112 161 29 22

137 44 67 65 71

122

Oflice decisions (I. T. ) — Con. 2625 2626. 262? . 2628 2629 2630 2631

Office decisions (MS. ): 1 123 1 24 125 126 127 .

Mffneogrsphs: 3926 3931 3932 3937 3942

MisceHsneous

XI-20-5479 XI-21-5485 XI-21-5486 XI — 22-5493 XI-23 — 5500 XI-23-6501 XI-25-6517

XI-2-5355 XI-I}-5382

XI-10-5408 XI-15-5446 XI-19-5475 XI-23-5506

XI-2-5357 XI-?-5386 XI-ff-5383 XI (f-5399

XI-11-5414 XI-26-5531

25 66

119 34 20 54 60

376 376 377 378 379 380

380 33

381 61

124 381

CONTENTS OF CUMULATIVE BULLETINS (L T. ) I TO gl S. T. FOR 1920 AND 1921; INTERNAL REVENUE I — 1, 1-2, H-l, H-2, m-l, H1-2, IV-I, IV-2, V-l, V-2, VI-I, VI — 2, VH — 1, VH — 2, VIH-I, VHI-2, IX-I, IX-2, X-l, X-2 ~ AND Xl-l.

Cumulative Bulletin. Ruling Nos.

Income Tax: December, 1919 (No. I) January — June, 1920 (1 o. 2) July — December, 1920 (No. 3) January — June, 1921 (No. 4) July — December, 1921 (No. 5)

Sales Tax: 1920 (ST. 1 — 20) January-June, 1921 July — December, 1921

Internal Revenue Bulletin: January — June, 1922 (No. I — 1) July — December, 1922 (No. I — 2) January — June, 1923 (No. II — 1) July — December, 1923 (No. II — 2) January — June, 1924 (No. III — 1) July — December, 1924 (No. III — 2) January — June, 1925 (No. IV — 1) July — December, 1925 (No. IV — 2) January — June, 1926 (No. V — 1) July — December, 1926 (No. V — 2) January — June, 1927 (No. VI — 1) July — December, 1927 (No. VI — 2) January — June, 1928 (No. VII — 1) July — December, 1928 (No. VII — 2) January — June, 1929 (No, VIII — 1) July — December, 1929 (No. VIII — 2) January — June, 1930 (No. IX — 1) July — December, 1930 (No. IX — 2) January — June, 1931 (No. X — 1) July — December, 1931 (No. X — 2) January — June, 1932 (No. XI — 1)

1-655 656-1033

103W1368 1369-1710 1711-1996

1-112 113-265 266-356

1-383 384-665 666-956

957-1276 1277-1641 1642-1949 1950-2251 2252-2523 2524-2813 2814-3026 3027-3291 3292-3557 3558-3784 3785-4052 4053-4248 4249-4487 4488-4683 4684-4887 4888-5124 5125-5338 5339-5531

(lx)

BOARD OF TAX APPEALS.

CUMULATIVE LIST OF ANNOUNCEMENTS RELATING TO . DECISIONS OF THE UNITED STATES BOARD OF TAX APPEALS PUBLISHED IN THE INTERNAL REVENUE BUL- LETIN SERVICE FROM JANUARY 1 TO JUNE 30, 1932, INCLUSIVE.

[announcements relating to the acquiescence or nonacquiescence of the Commissioner in decisions of the United States Board of Tax Appeals, as published in the weekly Internal Revenue Bulletin, from December 22, 1924, to December 31 1931, inclusive, are printed in Cumulative Bulictin X — 2, pages 1 — 103. The list below therefore, contains only such announcements published in the weekiv Bu11elins from January 1 to J'une 30, 1932, inclusive. l

' XI — 06 — 5M4

The Commissioner acquiesces in the following decisions of the United States Board of Tax Appeals:

Taxpayer. Docket b o.

Board of Tsx Appesis.

Volume. Page.

A.

Abeles, Charles T Abeles, Clifford Abeles, Francis, estate of Abeles, John T Abeles, Katherine Abeles, 1Villiemene H

Acme Manifolding Co. , Inc Adelaide Park Land et al. , trustees Albert Lea Packing Co. , Inc American Cigar Co American Feature Film Co American Security & Trust Co. et al. , executors '

40546 37695 37693 37694 37696 41034 25194 38687 39980 20765 16229 27623 39167

24 24 24 24 24 24

~4

25 24 21 24 24

435 435 435 435 435 435

429 211 376 464 18

334

Baldwin, Florence G Balfour, Sir Robert Barber, Arthur Barber, Philip C Barber, St. George Barber Trusts, Sarah P

32387 40230 26747 26755 26757

26?4?- 26757

23 25 25 25 25 25

512 154 513 513 513 513

Beaumont, Louis D

Bellows Falls Power Co

49422 18592

474

195

~Ruling No. 6524 includes sii acquiescence snd nonscquieseence notices pubiished in the Internal Revenue Bulletin service from January 1 to June 30, 1932.

& Estate tsx decision.

(I)

AcclurEscErrcEs — Continued.

Taxi, aver. Docket No.

Board of Tax Appeals

Volume Page

Birdner k Realty Coriioration

Biscavne Bay Islands Co

B!oodgood, Edith B

Blum, Julius, trustee

Borg 4: Beck Co

Buck, John A. , estate of '

Buck et al. , Mary M. , executors '

Bullock, George ' Butler, U. H

C.

46079

(

27616 35098 40147 26750 39242 40939 45741 51507 24223 34964

{ 32584 44153

( 44684 ( 32584

44158 44684 31209 46055

25

23

25

25

24

25

25

28 24

1084

731

518

119

995

780

780

710 506

Camp Manufacturing Co

Carman, F. J

Cooke, Beatrice B Coombs, Elizabeth M Coombs, J. Howard

Cooper, John I Cornwell, F. L Cotton, G. E Cromwell et al. , William Nelson, executors Crowley, Joseph J. , estate of 4

Crowninshield Shipbuilding Co Culver, Wilmer T

s

Carnie-Goudie Manufacturing Co Cathey, George Cathey, Luke Central Marl-et Street Co. ' Central Rendering Corporation City Bank Farmers Trust Co. et al. , executors 4

Clark et al. , James, executors Clements, W. L Clinchfield Securities Co Columbian Carbon Co. s

Connecticut River Power Co

85955

(

44821 44939 50178 20074 27095 46056 46057 24837 20776 31869 84499 46058 40554 42743 18591 29106 26751 44768 44769 32610 40115 80303 59655 42619 35472 18987 87574

)

25

24

24 24 25 24 28 24 24 25 25 25

25 25 25 24

24 25 24 25 24 24

537

162

679 506 506 499 376 668

1285 506 446 456 195 513

1820 1820 216 915 866 461 340 925

1013 t Estate tax decision; acquiescence relates to value of certain real estate in San Francisco and value of stock of Lsngendorf Baking Co. for estate tax purposes; and reasonableness of Corumissioner's allowance for support of the widow.

r ' Acquiescence relates to issue 2 of decision. r Acquiescence relates to issue regarding spportionruent of taxes among afliliated corporations. ~ Estate tsx decision. s Nonscquiescence published in Bulletin XI-14, page 1, revoked. s Estate tax decision; nonscquiescence published in Cumulative Bulletin X-2, pages 84, 88, revoked.

AoqurzscKtvozs — Continued.

Taxpayer. Docket No.

Board of Tsx Appeala

Volume. Page.

D.

Dahl, Andrew H. , estate of Dahl et al. , Julia, executors Davis, John A Detroit Trust Co. et al. , executors ' Dickinson, Albert G

Dirksen, Anna L. , executrix Dirksen, Theodore H. , estate of Douglas Co. , John Drexel Packing Co Duff, Robert C. s

E.

Eagle Pass h Piedras Negras Bridge Co Enameled Metals Co Evergreen Cemetery Association

F. Fame Canning Co Federal Street dt Pleasant Valley Passenger Ry. Co

Fidelity Savings dt Loan Association

First National Bank of Boston, administrator

Folk, H. B

Forres, Lord

Foster, N. C. , estate of ' Foster et al. , Willard, executor '

G. Ginsberg, Albert A Ginsberg, Nathan A Golden, Edward A Goldman, Maxwell Grand River Gravel Co Green, Robert D. '

Gulf Coast Irrigation Co. '

Gurnee, Augustus Coe, estate of '

44845 44845 20708 35472 85015 48176 17717 17717 38726 20775 37552

42460 19011 30726

20774 29758 14862 81801 39406 45215 36438 46583 28396 81018

( 40229 48978 82984 82984

27628 27629 27625 80802 28085 53647

{ 88694 40081 41848 42619

24 24 24 25

23 24 24 23 24 23

23 25 25

24 24

25

25

25

25 25

24 24 24 24 22 24

24

24

1167 1167

86 340

1211 1152 1152 1307 376

1342

1337 186 544

376 262

1059

252

599

154 414 414

18 18 18

915 1124 719

958

461

Hailey-Ola Coal Co Halladay, Sarah P Hamburg, jr. , Sam Hanscom, Edward E. , estate of ' Hanscom et al. , Melville, executors '

30962 26754 80804 44992 44992

24 25 24 24 24

895 513 915 173 173

t Estate tax decision. t Acquiescence relates to issue l of decision. e Acquiescence relates to transactions 1, 2, 3, and 4. & Acquiescence relates to all issues except sifihation issue. ~ Estate tsx decision; nonacquiescence published in Cumulative Bulletin ~-2, pages S4, SS revoked,

AcqmzscErsozs — Continued.

Taxpayer. Docket No.

Board of Tsx Appeals.

Volume. Page.

Harbeson Lumber Co. , W. B Havard, Charles Hay, W. H Hayman Co. , B Hess, Nathaniel J Hoffer, Anita, Ov, cns Hoffer, T. B Houston Bros. ' Houston, George T. ' Houston, Horace K ' Houston, Philip D. '

Huyler's, Inc

33076 ( 61012

32841 37499 16552 33279 33374 33375 12052

( 13104 22008 22009 22007

(

28369 29154 39841

24

25 25 25 24 24 24 22

22

22 22

24

542

1161 96

736 475

22 22 51 61 51 61

425

Ingalls, Charles C. , estate of ' Interstate Realty Co

Iten Biscuit, Co

57835 46272 60981

20899

25

25

773 728

880

Kasch, Ed Kasch, Theodora Kraemer, Samuel

Kuhn, Ida I&

48293 48293 37822 32609

1 40267

25 25 25 24

284 284 686 216

Lalte Charles Naval Stores Landers, Douglas J. , estate of ' Lawson, John

Liberty Farms Co Lincoln, Robert Todd, estate of ' Littauer, Eugene, estate of s

Littauer et al. , Lucius N. , execiitors s

Logel, Joseph F

Longyear, Mary B. , estate of Lourie, David A

34630 i

36940 i

35443 40232

j 26717 - 7 29899

39167 51858 61858

I 37762 I 40071

36438 —

l. 46583 27630

)

)

)

25 21 25

22

24 25 25

24

25

24

173 1347

154 1298 334 21 21

798

252

18

Markham Irrigation Co 4

Martin Hotel Co. and affiliated corporations Martin et al. , J. Earle, trustees Martin, T. S. , estate of Matagarda Canal Co. '

41344 16275 44583 44583

( 40082 41345

24 24 24 24

24

958 899 862 862 958

i Acquiescence relates only to deduction for business expenses in 1920 and to number of ber cut during 1919. 1 Estate tsx decision. s Estate tsx decision; acquiescence relates to issues 4, 5, and 7 of decision. 4 Acquiescence relates to sll issues except affiliation issue.

feet of ti~

AogfrrrzsczfvcEs — Conti cued.

Taxpayer. Docket b, o.

Board of Tax Appeals.

Volume. Page.

Matthews, J. P Msuldin, I. M McCool, Bess McGrew, Elizabeth 55 Mercantile-Commerce National Bank in St. Louis

et al. , executors and trusteer 1

Metropolitan Properties Corporation Milgrim rtr Bros. , Inc. H. x

Mississippi Packing C. o. , Inc Mobile Light 6r Railroad Co. ' Moorehead William A Murths 5x kchmohl Co

26250 26239 46059 26753

35443 45032 33177 20772

i 4]026 42062 25853 17911

22 22 24 25

21 24 24 24 o3

22 17

858 858 606 513

1347 2'20 853 376 543 858 442

N.

National Contracting Co. ' National Mill Supply Co National Packing Corporation

Newell et al, , Sterling, executors ' New England Power Co New York Chicago 8; St. Louis R. R. Co . . Northern Aoal Co. '

24620 37001

f 31668 -E 33971

5"q36 18593 -( 29105 21047 34946

25

24

25

25

23 24

407 1362

773 195 177 307

O.

Oakley, Richard H

P.

46778 108'2

Paine et ai. , Francis Ward, executors. . Paine, Willialn A. , estate of Palm Beach Mather Co

Peavy-Byrnes Lumber Co

Peavy-Moore Lumber Co

Peavy-%'ilson I umber Co

Pennsylvania Investors Co Pershouse, Alice E Pershouse, Mabel B Pizitz Dry Goods Co. , Louis

34113 34113 43860

{ 15824 16354 25984

t

f 15823 16355 25986

J ~

2 15822 16356 25985 20766 26749 26748 46585

25 25

25

25

26

24 25 25 22

764 764 536

oo3

223

376 513 513 161

t Estate tsx decision. ' Acquiescence relates to issue 1 of decision. ~ Acquiescence relates to following issues: 1. Whether payments received by s trustee on behalf of peti-

tioner m the taxable years in accordance with s written agreement entered into by snd between petitioner snd another in 1906 constitute taxable payments of rent or nontaxable payments on the selling price of assets, 2, Whether petitioner sustained statutory net losses for 1926 and 1926 which csn be deducted from its income for 1925 snd 1926, respectively.

~ Acquiescence in Board's decision that petitioner had the right to allocate overhead expenses to each contract on completed basis snd that formula used by petitioner wss permissible; and issue relative to negligence.

~ Acquiescence relates to inventory issue.

Aoqur fcsoENoEs — Continued.

Taxpayer. Docket Nc,

Board of Tax Appeals.

Pope, Olive R Price, Laura M Price, W. E Prosser, Constance B

29274 40659 41072 26752

Volume.

25 24 24 25

Page.

1161 216 216 513

Rapp, John W. , estate of Reardon f)c Sons Co. , John Rialto Mining Corporation Richards k Hirschfeld, Inc Rodeo-Vailejo Ferry Co. '

Rosenberg, Louis Roy 4t Titcomb, Inc Russell, C. C Russell, Mrs. C. C

28618 20773 48692 56877 21715 36411 48528 27626 29138 46060 46061

24 24

25 24

24

24 24 24 24

1061 376 980

1289 936

18 969 506 506

San Carlos Milling Co. , Ltd. ' San Martinez Oil Co

Schepp Co. , L Scruggs, Gross R Scruggs Investment Co Scruggs, Marian P Seaconnet Coal Co. s

Searles Real Estate Trust Securities Co Sells Sporting Goods Co Shand, Gadsden Shaw, David, estate of Shea, R P

Smith et al. , Elizabeth D. , executors

Smith, I. N. , estate of Smith, Jessie, executrix Smith, Mrs. Jessie Smith, Louis, estate of Sprague 8c Son Co. , C. H. s

Sprunt k Son, Inc. , Alexander Standard Beef Co

Standard Conveyor Co

Stauffen, Theodora B Stearns, Robert L Stevens, John H Stoneman, David Sunburst Oil k Refining Co

39525 37447 43121 42908 33610 46270 38711 18089 24489 40553 20771 26238 34499 37835 40034 39291 49668 39291 49668 18876 22313 18876 34946 38408 20770

(

33159 36393 40873 26756 37573 29685 2?627 45979

24

25 25 24 24 24 24 25 25 24 22 24

24

25

25 24 24 24 24 24 24

25

25 24 24 24 23

1132 218 419

1174 1174 1174 307

1115 446 376 858

1235 798

291

291 807 807 807 307 599 376

281

513 1013

52 18

829 ' Acquiescence relates to deduction of contribution to Victory Highxray Association. r Acquiescence relates to issue 2 of decision. s Acquiescence relates to inventory issue.

Acqmzscfrn cgs — Continued.

Board of Tax Appeals.

Taxpayer. Docket iVo.

Volume. Page.

Texas Irrigation Co. '

Tifft, Charles

Tifft, Lewis E

Tobey, Maurice Tolerton 4 Warfield Co. ' Turrish, Henry

40083 41346 31029 33464 42340 45957 31030 33465 42341 45958 27624 45820 44742

24

25

24 23 24

958

986

986

18 892 913

Ulster dr Delaware R. R. Co Union Lard Corporation United States Trust Co. of New York, trustee

28927 20769

26747- 26757

25 24 25

109 376 513

Walker, George H. , estate of s

Ward Bros. Co Washington Market Co White Oak Transportation Co. Whitson, Thomas J Williams, Ella J Williams, W, W

Williamson, Alexander B

Williamson, Archibald (Lord Forres)

Wilson 4r Co. , Inc. , of California Wilson Commission Co Wilson ik Co. , Lee Wray, Eliza J Wright, George M

31869 30992 43912 18088 40233 29273 46062 40281 43972

( 40229 43973 20768 20767 33826 25881 25854

23 24 25 24 25 25 24

25

25 24 24 25 24 22

663 989 576 307 154

1161 506 154

154 376 376 840 94

858

Young, Ethel P 38868 24 815

' Acquiescence relates to sll issues except sf5listion issue. r Acquiescence relates to issue regarding deduction of loss sustained by petitioner during nona@listed

period. r Estate tax decision. r hcquiescence relates to inventory issue.

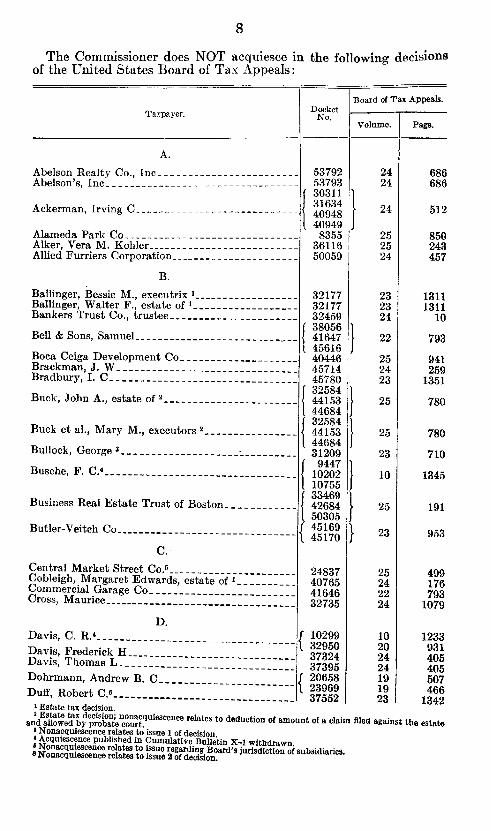

The Commissioner does NOT acquiesce in the following decisions of the United States Board of Tax Appeals:

Taxpayer, Docket No.

Board of Tax Appeals.

Volume. Page.

Abelson Realty Co. , Inc Abelson's, Inc

Ackerman, Irving C

Alameda Park Co Alker, Vera M. Kohler Allied Furriers Corporation

58792 53798 30311 31634 40948 40949 8355

36116 50059

24 24

24

25 25 24

686 686

512

850 243 457

Ballinger, Bessie M. , executrix ' Ballinger, Walter F. , estate of ' Bankers Trust Co. , trustee

Bell Jr Sons, Samuel

Boca Ceiga Development Co Brackman, J. W Bradbury, I. C

Buck, John A. , estate of '

Buck et al. , Mary M. , executors '

Bullock, George s

Busche, F. C. 4

Business Real Estate Trust of Boston

Butler-Veitch Co

32177 32177 32459

(

38056 41647 45616 40446 45714 45780,

(

32584 '

44153 44684

(

32584 44153 44684 31209

{ 9447

10202 10755

c

33469 42684 50305 45169 45170

23 23 24

22

25 24 23

25

2o

23

10

25

23

1311 1311

10

793

941 259

1351

780

780

710

1345

191

953

Central Market Street Co. ' Cobleigh, Margaret Edwards estate of ' Commercial Garage Co Cross, Maurice

D. Davis C. R. ' Davis, Frederick H Davis, Thomas L Dohrmann, Andrew B. C Duff, Robert C. s

24837 40765 41646 32735

c 10299 32950 37324 37895

( 20658 23969 37552

25 24 22 24

10 20 24 24 19 19 23

499 176 793

1079

1233 931 405 405 507 466

1342 4 Estate tax decision. 4 Estate tax decision; nonscquiescence relates to deduction of amount of a claim filed snd allowed by probate court. 4 Nonacquiescence relates to issue 1 of decision, 4 Acquiescence published in Cumulative Bulletin X-1 withdrawn. 4 Nonscquiescenoe relates to issue regarding Board's jurisdiction of subsidiaries. e Nonscquiescence relates to issue g of decision.

against the estate

NoNAcqnxEscENcEs — Continued.

Taxpayer. Docket No.

Board of Tax Appeals.

Volume. Page.

E Eifert, Earl C Elkins, Hallie D Emery, Mary M. , estate of

45781 39255 40899

23 24 25

1351 572 585

Fifth Street Building

Fletcher, Salathiel R {

16627 29264 45587 38041

24 876

75

Gassner, Louis ' Goldberg, Harry S. ' Green, Robert D. '

Gulf Coast Irrigation Co. s

H Hancock, G. Allan Harris, Allen ' Harris, Simon

Hawley Investment Co Hedrick, J. T Hcller, B. G Henn, A. W Hieronymus, Carl Richard, estate of Hill, D. F. , estate of ' Hill et al. , Paul F. , executors 4

Household Products, Inc Houston Baseball Association

Houston Bros. s

Houston, George T s

Houston, Horace K. s

Houston, Philip D. ' Hutchison Coal Co

4017 5389

53647

(

33694 40081 41343

3686? 10980 31632 45169 45170 33533 40634 37102 48930 29899 29399 44809 43985 45430 12052 13104 22008 22009 22007 84939

)

)

)

4 4

24

24

25 10 24 23 24 25 20 24 24 24 24

24

22

22

22 22 24

1071 1073 719

958

607 1374 612 953 444 259

1133 269

1144 1144 694 69 51 51 51 61

973

Imperial Investment Co Iten Biscuit Co Ives Dairy, Inc

29291 43667 45164 39873

23

23

1281 870 579

Jackson-Wermich Trust Jamison Coal 5t Coke Co

32307 31690 34088

24

24

160 564

1 Acquiescence published in Cumulative Bulletin X-1 withdrawn, s Nonacquiescence relates to transaction 3. ' Nonacquiescence relates to affiliation issue. ' Estate tax decision.

Nonacquiescence relates to March 1, 1913, value and to the basis for the deductipn fpr depletipn and fpr the computation of gain or loss upon subsequent sale of the tiruber.

10

NONAcQVIEscENcE~ontinued.

Taxpayer. Docket No.

Board of Tsx Appeals.

Volume. Page.

Kountze, Charles T Kountze et al. , Charles T. , executors Kountze, Luther L. , estate of Krull, Francis '

L Leetonia Furnace Co Levine, Hyman '

Liebes k Co. , H Littnuer Eugene, estate of ' Littauer et nl. , Lucius N. , executors s

Livingood, Charles J. , executor

37323 37535 37535 16985

32272 7435

(. . ' 28o44 35038 51858 5lgog 40899

24 24 24 10

23 8

) rs 25 25 25

405 405 405

1096

979 298

787 21 21

585

Manchester Coal Go Markham Irrigation Co. ' Matagarda Canal Co. s

McCrory, Iuke %. , trustee Miglietta, Olga K Moore Bread Co Morgarrite Brush Co. , Inc

Morriss et al. , Julia L

Morriss Realty Co. Trust No. 1

Morriss Realty Co. Trust Nn. 2 Murphy et al. , Fred T. , trustees Murphy Personal Property Trust Mutual Life Insurance Co. of New York

N.

33392 41344 40082

t 41345, 32444 36379 41645 26369 41023, 41024 45863

i 45864

c 41023 45863

( 41024 45864 43705 43795 9764

24 24

) 25 22 24

23

) ss

) rs 20 2u 23

577 958 958 994 243 703 776

1076

1076

1076 724 724 749

Nashville, Chattanooga 8: St. Louis National Contracting Co. 4

National Pipe Jc Foundry Co. s Neill, Ja, mes ' New York Life Insurance Co Nichols k Cox Lumber Co North American Investment Co Northern Coal Co. s

y----------- R 33799 24520 32997 9290

38880 23601 30183 34945

24 25 19 8

24 24 24 24

856 407 242 299

1217 54

419 307

t Acquiescence published in Cumulative Bulletin X-1 withdrawn. ~ Estate tsx decision; nonacquiescence in respect to that part of decision which holds that accrued interest paid on Federal income taxes for 1927 and 1928 from date of decedent's death to November 6, 1930 is a proper allowable administrative expense. I 4 Nonacquiescence relates to afQliation issue. 4 Nonacquiescence relates to issue 1 of decision and issue regarding deductibiiity of overhead costs in 1926. 4 Acquiescence published in Cumulative Bulletin IX-2, page 43, revol-ed. Revocation of prior acqui- escence aud present nonacquiescence are due to the failure of the Board's decision to limit the word "dh- tributed" to the cash distributions made to the stockholders. 4 Nonacquiescence relates to statute of limitations issue.

11

NoNAcqtfrzscENczs — Continued.

Tazpayer. Docket No.

Board of Tas Appeals.

Volume. Page.

O.

Oakman et al. , Mamie R Ogden, Hugh W Old Mission Portland Cement Co Olinger Mortuary Association

P Pacific Nash Motor Co

Peabody, Cornelia Haven, estate of ' Peabody et al. , Stephen, executors '

Phillips, William S

R. Roberts, Walter B Rodeo-Vallejo Ferry Co. ' Rosser, E. M. , executor 1

Roth, W. A. '

42917 28943 88853 86502

45169 45170 89647 89647 24446 31769

37534 36411 48528 40765 4'065

24 24 25 28

28

24 24

24

)4

24 22

84 1239 805

1281

953 787 787 98

405

986 176 587

St. Louis Southwestern Ry. Co

Salomon, Leon ' San Carlos Milling Co. , Ltd. s

Sand Springs Ry. Co

Seaconnet Coal Co. e

Small's, Inc Sprague & Son Co. , C. H. ' Spring City Foundry Co Stearns, Marshall, administrator Stockholms Enskfida Bank Sturgeon-Hubbard Trust Sturgeon et al, Rollin S. , trustees Suncrest Lumber Co Swisky, Toby W

13319 27768 83938

3725 12231 39525 82438 32439 18089 58791 34946 21169 48930 55755 37095 87095 33244 42032

24

4 8

24

21

24 24 24 25 24 25 25 25 25 25

917

1109 979

1182 1291 807 686 307 822 269

1328 368 368 375 259

Tennessee Consolids. ted Coal Co

Texas Irrigation Co. s

Titus, C. Dickson Todd, Willis Tolerton & Warfield Co. '

33383 40083 41846 20705 37586 45820

24

24

24 24 23

369 958

36 405 892

t Estate tax decision. r Nonscquiescence relates to issue 1 of decision, t Acqtriescenre published in Cumulative Bulletin X-1 withdrawn. ~ Nonacquiescence relates to statute of limitations i~us. 4 Nonacquiesccnce relates to afhliation issue. 4 Nonacquiescence relates to issue regarding deduction of loss sustained by two afliliated companies

during fiscaf year ended January 31, 1924, and the terable period February 1 to April 25, 1924, in computing the consolidated net income for taxable period April 25 to December 31, 1924, snd the year 1925.

12

NoNAcrluxnscarcczs — Continued.

Board of Tsx Appeals.

Tazpsrer. Docket No,

Volume. Page.

Union Trust Co. , trustee

W. Waggoner, Ella Waggoner, W. T Wall, Frank E. ' Wardman, Harry West Virginia-Pittsburgh Coal Co White Oak Transportation Co. ' White, Rita M. Kohler Wilson, Luke F. , estate of Wood Furniture Co. , J. A

42917

38517 38516

7859 22348 20887 25080 18088 36112 32444 40565

24

24 24

4 24

s4 24 25 25 21

657 657 915 102 284

307 243 994 564

Ziegler, Albert W Ziegler, Clifford E

46291 46292

23 23

1091 1091

t Acquiescence pnhlished in Cumulative Bulletin R-1 withdrawn. ' Nonacquiescence relates to statute of limitations issue.

INCOME TAX RULINGS. — PART I. REVENUE ACT OF 1928.

SUBTITLE B. — GENERAL PROVISIONS.

PART II. — COMPUTATION OF NET INCOME.

SECTION oo (a) . — GROSS INCOME: GENERAl. DEFINITION.

Art1zc1J. 51: What included in gross income.

air VENUE Acr Oir 1928.

XI~5865 G. C. M. 9958

Under section 161a of the Civil Code of California, which became effective July 29, 1027, a wife's earnings in California constitute community income. An agreement beta eeu husband and wife in California, entered into prior to the earning of Income, which pro- vided that the earnings of the wife, as dwell as those of the husband, should constitute the separate property of the spouse who per- formed the services, does not have the effect of shifting the burrlen of taxation from one to the other. As separate returns frere filed, the salary of the wife (as well as that of the husband) should be treated as community income and one-half thereof taxed to each spouse.

An opinion is requested whether, where a husband and wife domiciled in California. filed separate returns, a division of the per- sonal earnings of each is required, even though there is a written agreement entered into between the two spouses prior to the earn- ing of the income to the efFect that such earnings arc his or her separate property.

The husband and wife filed separate returns, the husband report- ing in his return a salary of 8. 78m dollars and the wife reporting in her' return a salary of 1. 6o. n dojlars. In General Counsel's Memo- randum 9988 (C. B. X — o, 115) the question was raised whether the earnings of a husband should be divided where separate returns were filed, whereas the instant case involves the question whether the earnings of both spouses should be divided. In the former case there w;is an agreement signed by the husband and wife to the efFect that all the earnings of the husband should constitute his separate property. In the instant case there v as an agreement to the efFect, that, the earnings of the wife, as well as those of the husband, should. constitute the separate property of the spouse who performed the services.

This once in General Counsel's Memorandum 9988, supra, held that, reo'ardless of the agreement existing between the husband and wife, the husband's salary earned after July o9. 1927, the efFective date of the amendment of the Civil Code of Cahfornia, was taxable

(13)

$22(a), Art. 52. ]

one-half to the wife and one-half to the husband, and that the agree- ment was not effective to preclude the taxation of such salary as

community income. The same question is involved in the instant case, except that in this case the agreement also provides that earn-

ings of the wife should constitute her separate property. In accord- ance with General Counsel's Memorandum 9938) supra, and on au-

thority of the decisions of the United States Supreme Court in Lsscas v. Earl (281 U. S. , 111) and by the Circuit Court of Appeals in Bla& v. Rofh (22 Fed. (2d), 932, T. D. 4152) C. B. VII — 1, 215, certiorari denied 277 U. S. , 588), it is believed that the agreement in the instant case was inelfectiv~e to shift the burden of tax from one spouse to another. In this connection it should be noted that in Blair v. Both, supra, the court stated that it concurred in the view of the Commissioner that "the instant they were received, the salaries were, by the law, impressed with the status of community property, and were taxable with reference to that status. " Under section 161a of the Civil Code of California, which became effective July 29, 1927, a wife's earnings in California became community property). AVllere separate returns are filed by husband and wife, community income in the form of salaries earned by either spouse on and after July 29, 1927) should be divided and one-half taxed to each. (See I. T. 2457, C. B. VIII-1, 89, and U. 8. v. 3falcolm, ) 282 U. S. ) 792. )

In view of the foregoing, it is the opinion of this offlce that even though the agreement in question may be valid for the purpose of changing property rights between the husband and wife, it does not have the effect of shifting the burden of taxation from one to the other. As separate returns were filed, the salary of the wife (as well as that of the husband) should be treated as communitv income and one-half thereof taxed to each spouse.

C. M. CIIAREsT) General Counsel) Bureats of Intervta/ Revenue.

ARTICI. E 52: Compensation for personal serv- ices.

XI — 22 — 5492 G. C. M. 10486

REVENUE ACT OF 1928 AND PRIOR REVENUE ACTS, ~

The reason that the commission allowed an insurance agent on a policy taken out on his own life is considered income is that the relationship of employer and employee exists between the insurance company and the agent and, inasmuch as the insurance company is under contract to pay the agent commissions on all policies of insurance secured by him, no distinction can logically be made be- tween a commission paid to the agent on account of a policy written on his own life und a commission paid to the agent on account of a policy written on the life of some one else.

Infortnation is requested relative to the basis on which a ruling relating to insurance commissions was made.

The particular ruling, which is one of several rulings contained in Treasury Decision 2187, reads as follows:

Co))))))ission retained t)y agent ou his o)on life insaranoe policy. — A commis- sion retained by a life insurance agent on his own life insurance policy is held to be income accruing to the agent, and should be included in his return of income for the assessment of the income tax.

15 [$22(a), Art. SS.

If a life insurance company reduces the standard charge of an -insurance policy to a purchaser and the relationship of employer and employee does not exist, the amount by which the policy is reduced can not be considered income at the time of purchase for the reason that it is not "gain derived from capital, from labor, or from both combined, " nor "profit gained through a s~ale or conversion of capital . assets" within the meaning of the definition of income as stated in Ezsner v. 3facomber (252 U. S. , 189, T. D. 3010, C. B. 3, 25). The Board of Tax Appeals has held that the purchase of property at a bargain price does not result in taxable income where the sale is con- summated by two persons dealing at arms' length. (See Appeal of 3fanomet Cranberry Co. , 1 B. T. A. , 706, C. B. IV — 1, 3. )

The reason that the commission allowed an insurance agent on a policy taken out on his own life is considered income is that the relationship of employer and etnployee exists between the insurance company and the agent, and inasmuch as the insurance company is under contract to pay the agent commissions on all policies of insur- ance secured by him, no distinction can logically be made between a commission paid to the agent on account of a policy written on his own life and a commission paid to the agent on account of a policy written on the life of some one else. The commission is paid to the agent as compensation for services rendered as an employee, i. e. , on account of business obtained, regardless of whose life is insured, and is "gain derived from labor, " and therefore taxable income. Furthermore, it is immaterial whether the agent remits to the com- pany the standard charge for such insurance (namely, the amount that would be charged any other person under like conditions) and receives a check for his commission, or whether he remits to the com- pany the standard charge minus his commission. The net result is the same. The agent receives taxable income to the extent of the commission, either actually or constructively. It follows that the amount of commission paid by the insurance company should be re- ported as income by the insurance agent.

C. M. CII. ~REST, General Counsel, Bureau of Internal Eev&enue.

ARTIGLE 58: Sale of stock and rights.

REVENUE ACT OF 1928.

XI — 6-5378 G. C. M. 10170

The taxpayer should be held to be bound by the election, made as authorized by article 58 of Regulations 74, to report as income the entire proceeds derived from the sale of stock rights.

An opinion is requested whether a taxpayer, after having exercised the option to include the entire proceeds from the sale of stock rights in gross income, pursuant to article 58 of Regulations 74, may later require the Bureau to compute the profit deriv~ed from the sale of the stock rights upon the theory that a portion of the proceeds derived from the sale thereof constituted a return of capital to the taxpayer.

It appears that for the calendar year 1928 an original income tax return was filed by A. A died on July 18, 1929„and an original re- turn tor the calendar year 1929, in which there was reported income

)22(a), Awt. 58. ] 16

received during the period January 1, 1929, to July 18, 1929, was

fil d by his executor. In both original returns the entire pro- c

ceeds derived from the sale of stock rights were reported as inco e

wl 'thout any deduction therefrom on account of cost or other basis, b and a capital net gain tax of 12&gz per cent paid thereon. Su se-

quently, amended returns for 1928 and 1929 were filed by the execu-

tor of the estate of A, in which certain amounts were deducted from

the proceeds derived from the sale of the stock rights, upon the

theory that such amounts represented the cost or other basis of the

stock rights. In this connection it is contended that taxable gain in

smaller amounts was realized from the sale of the stock rights in question, and claims for refund of taxes paid with respect to the taxable years 1928 and 1929 have been filed, based upon the ground that a portion of the proceeds from the sale of stock rights repre- sented a return of capital.

The field officers recommend disallowance of the claims upon the ground that the taxpayer, having exercised his option to include the entire proceeds from the sale of the stock rights in gross in-

come, pursuant to the provisions of article 58 of Regulations 74, is bound by the election in this respect. The pertinent provisions of article 58, Regulations 74, read as follows:

(I) If the shareholder does not exercise, but sells his rights to subscribe, the cost or other basis of the stock in respect of which the rights are issued shall be apportioned between the rights and the stock in proportion to the respective values thereof at the time the rights are issued, and the basis for determining gain or loss from the sale of a right on one hand or a share of stock on the other will be the quotient of the cost or other basis assigned to the rights or 5he stock, divided, as the case may be, by the number of rights issued or by the number of shares held.

The taxpayer may at his option include the entire proceeds from the sale oi' stock rights in gross income, in which case the basis for determining gain or loss from the subsequent sale of the stock in respect of which the rights were issued shall be the same as though the rights had not been issued.

From the foregoing, it is to be noted that under article 58 of Regu- lations 74 the taxpayer had the option of reporting the income in question upon either of two prescribed methods. In Lebolt ck Co. v. United States (67 Ct. Cl. , 422, Ct. D. 129, C. B. VIII — 2, 247) it was held that where there are two methods prescribed by regulations for the making of an income tax return, either one of which is legal and proper, aZd the taxpayer has made his return in accordance with one of these methods, then if the return is accepted and the taxes paid accordingly the taxpayer can not subsequently change to the other method of making a return and thereby become entitled to a refund. (See also Grant v. Rose, 24 Fed. (2d), 115, affirmed on ap- peal, 89 Fed. (2d), 340. ) It is, therefore, the opinion of this office that the taxpayer in the instant case is bound by the election to re- port as income the entire proceeds derived from the sale of the stock rights, and that the claims for refund should be denied.

C. M. Crr&REsT&

General Counsel, Bureau of Internal Revenue.

insurance poli

RI:VENVH ACT OF' Ious.

[$22(a), Art. 62.

XI — 5 — 5372 G. C. M. 10168

In determining the cash value or present worth of annuities, the uniform rate of 4 per cent should, in general, be employed in accordance with Table A in article 18 of Estate Tax Re ulations 70 (1929 edition). The ruling published a. I. T. 2891 (C. B. VII — 1, 90), in which the rate of o per «ent was used, should be followed as a precedent only in cases involving identical facts.

An opinion is requested relative to the interpretation to be placed upon I. T. 2397, in which the rate of 5 per cent is used in determining the present worth of an annuity instead of the rate of 4 per cent contained in Table A of article 13(10 of Estate Tax Regulations 70 (1929 edition).

In the case considered in I. T. 2397 the taxpayer transferred $50, 000 io the M College upon the agreement that he should receive an annuity of $2, 500 for life. The question there presented divas

whether any portion of the amount transferred should be considered as a contribution to the M College, an exempt organization, and hence deductible to the extent provided in section 214(a) 10 of the Revenue Act of 1926.

In that case it Ivas apparent thai the taxpayer had a double motive in making the contribution — that is, he wished to assure himself an annuity and also make a gift to the college. The conclusion neces- sitated the determination of what part of the amount actually re- ceived by the college represented a gift to it and what part repre- sented the purchase price of the annuity it undertook to pay the donor. In determining the value of the gift to the college it was necessary to reduce the amount actually received by the college by the present value of the amount it undertook to return to the donor in annual payments during his lifetime. The parties to the under- taking having adopted a presumed earning of 5 per cent per annum, there was, in the opinion of the Bureau, no justification for presum- ing that the fund would earn a lesser rate per annum for the purpose of determining the present worth of the annuity.

On reconsideration of the facts involved in the ruling published as I. T. 2397, in which the rate of 5 per cent was used in determining the value of the donor's life estate, it is believed that the ruling is sound and should be adhered to. However, tliat ruling should be followed as a precedent only in cases involving~ identical facts.

The cash value or present worth of annuities should, in general, be determined in accordance with Table A in article 13 of Estate Tax Regulations 70 (1929 edition), using the uniform rate of 4 per cent therein employed.

C. M. CiiAPRsT) General CotInee/, Bureau of Interna/ Revenue.

$22(b), Art. 84. ] 18

SECTION 22 (b) . — GROSS INCOME: EXCLUSIONS FROM GROSS INCOME.

ARTIGLE 84: Interest upon State obligations.

REVENUE ACT OF 1928.

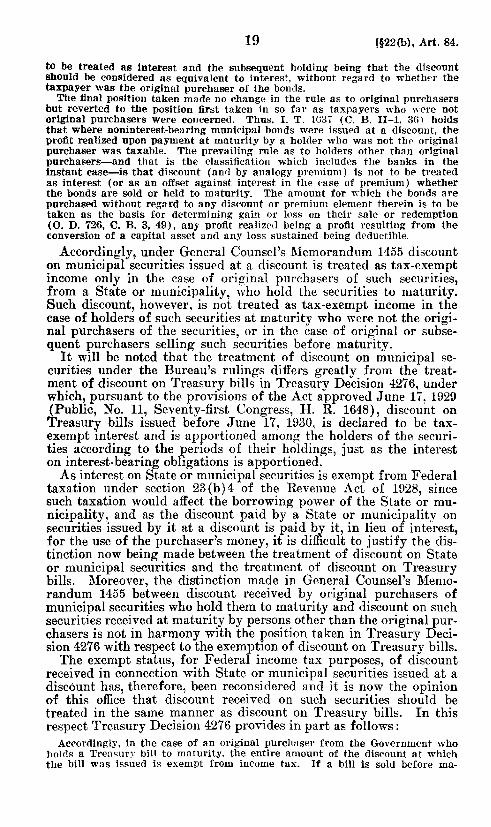

XI-23 — 5499 G. C. M. 10452

Cities and towns in the State of X meet expenses by the sale of notes. The notes are issued at a discount and are noninterest bearing.

Held, that discount received in connection with State or municipal securities issued at a discount should be treated in the same man- ner as discount on Treasury bills is treated in Treasury Decision 4276 (C. B. VIII — 2, 83). General Counsel's Memorandum 1455 (C. B. VI-1, 87) is revdked in so far as it holds that discount on municipal securities issued at a discount may not be treated as tax-exempt income in the case of holders of the securities at ma- turity who were not the original purchasers of such securities, or in the case of original or subsequent purchasers selling such securities before maturity.

An opinion is requested regarding the treatment for Federal in- come tax purposes of the discount paid on noninterest-bearing mu- nicipal securities in the hands of persons other than the original purchasers.

Cities and towns in the State of X frequently meet their current operating expenses by the sale of notes which are liquidated when taxes are subsequently collected. These notes are noninterest bear- ing and are issued at a discount. The amount of discount is con- trolled, to some extent, by the condition of the current money market. These notes are purchased by the public and dealt in by the local banks. The question presented is whether the discount when paid may, in all cases, be considered as interest upon the obligation of a political subdivision of a State, and, therefore, exempt from taxation under section 23(b)4 of the Revenue A. ct of 1928, or whether the discount is exempt only if and to the extent that it is paid to the original purchasers.

The position of the Bureau regarding the status for Federal in- come tax purposes of discount received in connection with municipal bonds up to the present time is set out in the following extract from General Counsel's Memorandum 1455:

The position originally taken by the Bureau was that discount was to be dis- tinguished from interest in all cases, the excess of the amount received upon the maturity of a municipal bond over the purchase price being taxable profit whether or not the holder of the bond was the original purchaser. (0. D. 238, C. B. 1, 68. ) A fortiori, the excess was held to be taxable profit where the municipal bond was sold instead of being held to maturity. (0. D. 21, C. B. 1, 67; 0. D. 737, C. B. 3, 4S; 0. D. 774, C. B. 4, 31. )

This position was later modified to hold that the profit derived by purchasing municipal bonds at a discount and holding them to maturity was nontaxable where the profit was "in lieu of interest for the use of the taxpayer's money. " It was 'considered immaterial whether or not the taxpayer was the original pur- chaser of the bonds, but the exempted amount could in no case exceed the total discount at which the securities were originally sold by the municipality. (0. D. 647, C. B. 3, 123; 0. D. 856, C. B. 4, 110. ) But where the bonds instead of being held to maturity were sold by one other than the original purchaser (or even by the original purchaser) at a profit, the profit was taxable income and not exempt interest, even though the bonds were originally issued at a discount. (O. D. 762, C. B. 4, 31; I. T. 1187, C. B. I — 1, 27. )

The modification, it will be noted, related solely to the situation where the bonds were held to maturity, the first holding being that the discount was not

19 (()22(b), Art. 84.

to be treated as interest and the subsequent holding being that the discount should be considered as equivalent to interest, without regard to whether the taxpayer was the original purchaser of the bonds.

The final position taken made no change in the rule as to original purchasers but reverted to the position first taken in so far as taxpayers who were not original purchasers were concerned. Thus, I. T. 1682 (C. 8. II — I, 86) holds that where noninterest-bearing municipal bonds were issued at a discount, the profit realized upon payment at maturity by a holder who was not the original purchaser was taxable. The prevailing rule as to holders other than original purchasers — and that is the classification which includes the banks in the instant case — is that discount (and by analogy premium) is not to be treated as interest (or as an offset against interest in the case of premium) whether the bonds are sold or held to maturity. The amount for which the bonds are purchased without regard to any discount or premium element therein is to be taken as the basis for determining gain or loss on their sale or redemption (O. D. 726, C. B. 8, 49), any profit realized bein" a profit resulting from the conversion of a capital asset and any loss sustained being deductible.

Accordingly, under General Counsel's Memorandum 1455 discount on municipal securities issued at a discount is treated as tax-exempt income only in the case of original purchasers of such securities, from a State or municipality, ivho hold the securities to maturity. Such discount, howeveri is not treated as tax-exempt income in the case of holders of such securities at maturity who were not the origi- nal purchasers of the securities, or in the case of original or subse- quent purchasers selling such securities before maturity.

It will be noted that the treatment of discount on municipal se- curities under the Bureau's rulings divers greatly from the treat- ment of discount on Treasury bills in Treasury Decision 4276, under which, pursuant to the provisions of the Act approved June 17. 1929 (Public, No. 11, Seventy-first Congress, H. R. 1648), discount on Treasuq bills issued before June 17, 1930i is declared to be tax- exempt interest and is apportioned among the holders of the securi- ties according to the periods of their holdings, just as the interest on interest-bearing obligations is apportioned.

As interest on State or municipal securities is exempt from Federal taxation under section 23(b)4 of the Revenue Act of 1928, since such taxation would affect the borrowing power of the State or mu- nicipality, and as the discount paid by a State or municipality on securities issued by it at a discount is paid by it, in lieu of interest, for the use of the purchaser's money, it is difficult to justify the dis- tinction now being made between the treatment of discount on State or municipal securities and the treatment of discount on Treasury bills. Moreover, the distinction made in General Counsel's Memo- randum 1455 between discount received by original purchasers of municipal securities who hold them to maturity and discount on such securities received at maturity by persons other than the original pur- chasers is not in harmony with the position taken in Treasury Deci- sion 4276 with respect to the exemption of discount on Treasury bills.

The exempt status, for Federal income tax purposes, of discount received in connection with State or municipal securities issued at a discount has, therefore, been reconsidered and it is now the opinion of this office that discount received on such securities should be treated in the same manner as discount on Treasury bills. In this respect Treasury Decision 4276 provides in part as follows;

Accordingly, in the case of an original purchaser from the Govermnent who holds a Treasnry bill to maturity. the entire amount of the discount at which the bill was issued is exempt from iucome tax. If a bill is sold before ma-

$22(b), Art. 84. ] 20

turity, each respective holder is entitled to treat as exempt from income tax that proportion of the amount of the discount at which the bill was issued

which the number of days (computed on an actual calendar-day basis) the bill was owned by him bears to the total number of days (computed on an

actual calendar-day basis) from the date of the issuance of the bill to the

date of its maturity. In other words, the amount of the discount at which

the bill vvas issued is to be apportioned among the holders according to the periods of their holdings. The gain from the sale or other disposition of a Treasury bill (that is, the excess of the amount realized therefrom less dis-

count from the date of acquisition to the date of its disposition over the cost or other basis of the bill) is taxable as ordinary income. A loss from the sale or other disposition of a Treasury bill (that is, the excess of the cost or other basis of the bill over the amount realized therefrom less discount from the date of acquisition to the date of its disposition) is allowable as a deduction.

General Counsel's Memorandum 1455 is hereby revoked in so far as it holds that discount on municipal securities issued at a dis- count may not be treated as tax-exempt income in the case of holders of the securities at maturity who were not the original purchasers of such securities, or in the case of original or subse-

quent purchasers selling such securities before maturity. The Supreme Court of the United States in the case'of W'zllcats,

Collector, v. Bunn (282 U. S. , 216, Ct. D. 280, C. B. X — 1, 309) specifi- cally stated that it did not appear that the securities under consider- ation in that case were issued at a discomnt, so that the gain derived could be considered to be in lieu of interest, and that whatever ques tions might arise in cases of that sort were not before it. This OSce accordingly is of the opinion that the decision in WiUcuts, Collector, v. Berm, supra, does not acct the question of the treatment, for Federal income taxes, of discount received in connection with State or municipal securities issued at a discount, which is here under consideration. C. M. CHARE',

General Counse/, Bureau of Internal Ideeenue.

ARTIcLK 84: Interest upon State obligations.

RHVENUE ACT OF 1928.

XI-28-5500 I. T. 2629

'The city of Y sells 4 per cent bonds direct to the public. The bonds are sold at a discount to yield 4. 5 per cent.

Held, that the discount received in connection with State or municipal iuterest-bearing securities issued at a discount should be treated for income tax purposes in the same manner as dis- count on Treasury bills is treated in Treasury Decision 4276 (C. B. VIII — 2, 83).

Thc city of Y sells 4 per cent bonds direct to the public, and due to the market conditions at the present time the bonds are sold at a discount to yield 4. 5 per cent.

The question is raised whether, at the time these bonds mature and are paid at par, the owners will be s'ubject to a tax because of having purchased them at a discount.

The discount received in connection with State or municipal inter- est-bearing securities issued at a discount should be treated for in- come tax purposes in the same manner as discount on Treasury bills

21 [tj22(b), Art. 84.

;s treated in Treasury Decision 4276, which provides in part as follows:

Accordingly, in the ease of an original purchaser from the Government who holds a Treasurv bill to maturity, the entire amount of the discount at which the bill was issued is exempt from income tax. If a bill is sold befi re maturity, each respective holder is entitled to treat as exempt from income tax that proportion of the amount of the discount at which the bill was issued which the number of days (computed on an actual calendar-day basis) the bill was ovvned by him bears to the total number of days (computed on an actual calen- dar-day basis) from the date of the issuance of the bill to the date of its matu- rity. In other words, the amount of the discount at which the bill was issued is to be apportioned among the holders according to the periods of their holdings. The gain from the sale or other disposition of a Treasury bill (that is, the excess of the amount realized therefrom less discount from the date of acquisition to the date of its disposition over the cost or other ba. . is of the bill) is taxable as ordinary income. A loss from the sale or other disposition of a Treasury bill (that is, the excess of the cost or other basis of the bill over the Imount realized therefrom less discount from the date of acquisition to the date of its disposi- tion) is allowable as a deduction.

In this connection see General Counsel's ilemorandum 10452 [page 18], relating to the exempt status of discount received on noninterest- bearing municipal securities.

ARTICLE 84: Interest upon State obligations.

REvENVE ACT OF 1928.

XI — 26 — 5525 G. C. M. 10557

The University of the State of R has been held by the Supreme Court of the State to constitute an integral part of the free public school system of the State. The bonds here in question are issued by the trustees of the university and are regarded as instru- mentalities of the State issued for the purpose of carrying out an essential governmental function oi the State. The interest on such bonds is not subject to Federal income tax.

An opinion is requested whether the interest on the 41/i per cent firs mortgage union building bonds issued by the trustees of the University of the State of R is subject to Federal income tax

The issue has been thoroughly considered in connection with the decision of the United States Supreme Court in Burnet v. Coronado Oi7 ck Gas Co. (52 S. Ct. , 443 [Ct. D. 485, page 265]). In that case it was held that the income of a lessee of public school lands of the State of Oklahoma, derived from oil produced by the lessee from such school lands, was exempt from Federal income tax.

The following statements were made by the court: When Oklahoma undertook to lease her public lands for the benefit of the

public schools she exercised a function strictly governmental in character. 4