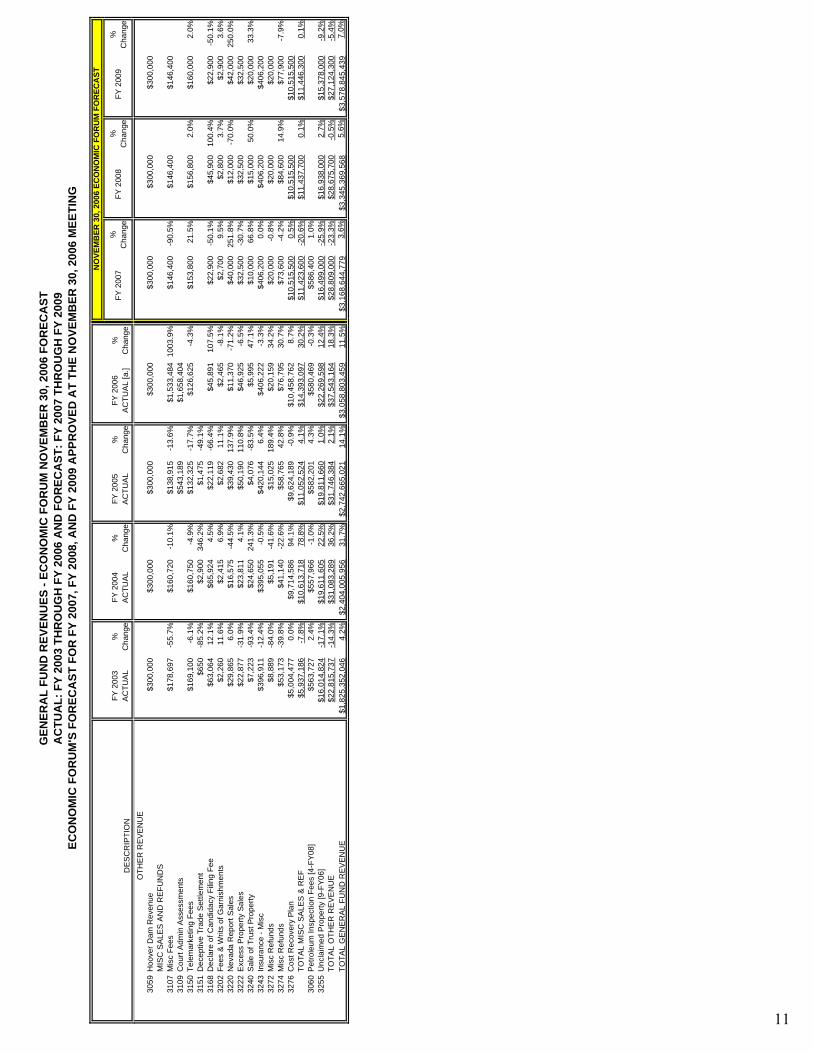

REVENUE REFERENCE MANUAL - Nevada Legislature

175

REVENUE REFERENCE MANUAL FISCAL ANALYSIS DIVISION JANUARY 2007

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of REVENUE REFERENCE MANUAL - Nevada Legislature

REVENUE REFERENCE MANUAL

FISCAL ANALYSIS DIVISION JANUARY 2007

TABLE OF CONTENTS

I. APPROPRIATIONS AND REVENUE CHARTS

A. NEVADA GENERAL FUND APPROPRIATIONS, 2005-2007 Biennium ................3 B. NEVADA GENERAL FUND REVENUE, Forecast 2007-2009 Biennium.................4

Actual Collections by Revenue Source: FY 2003 to FY 2006 ................…………………5

II. TAX REVENUE SUMMARIES

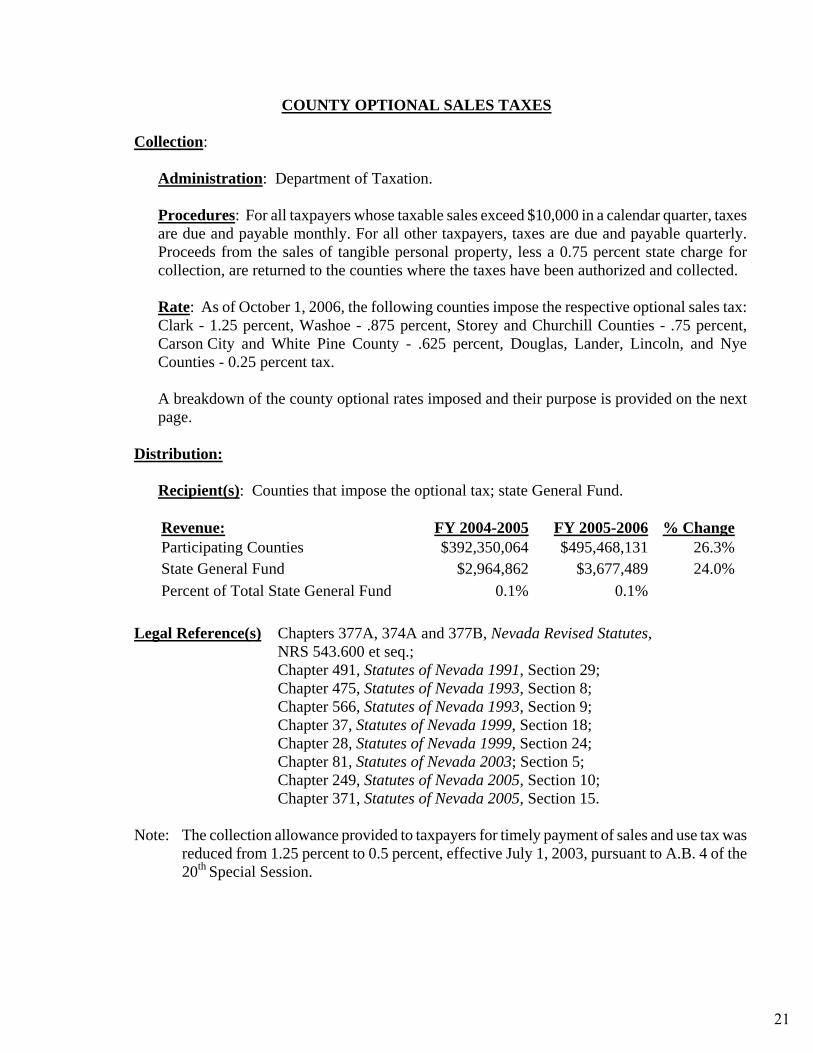

A. SALES TAXES

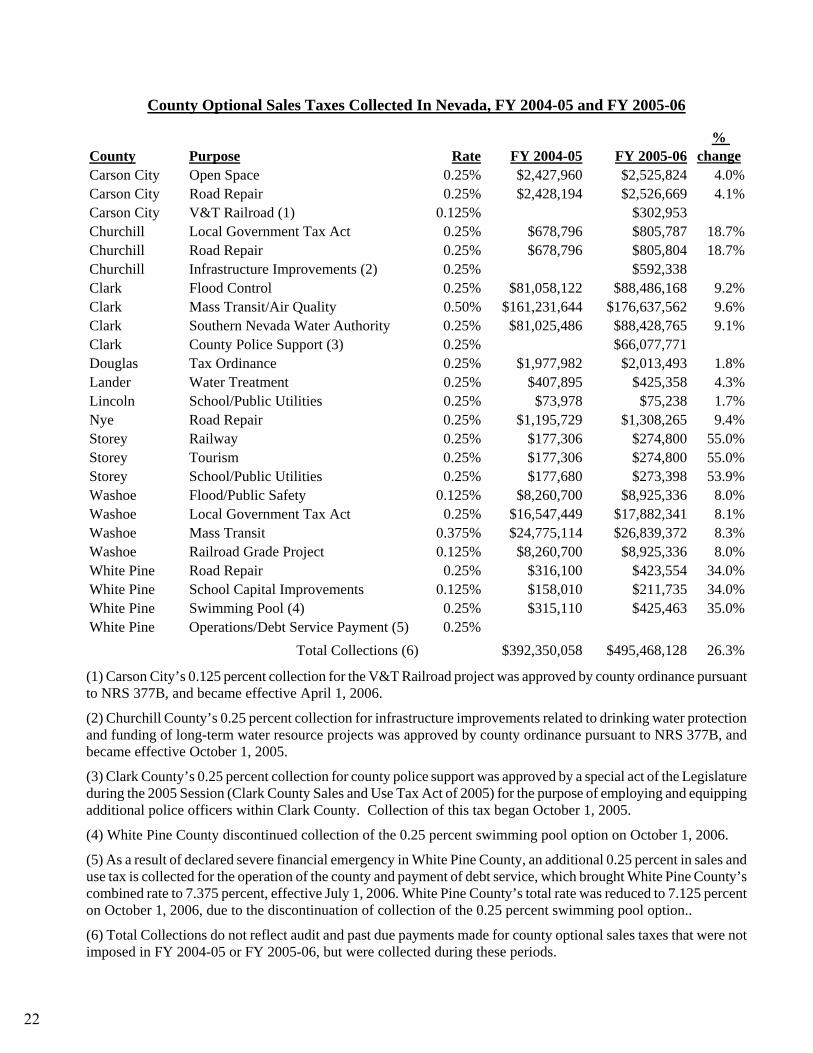

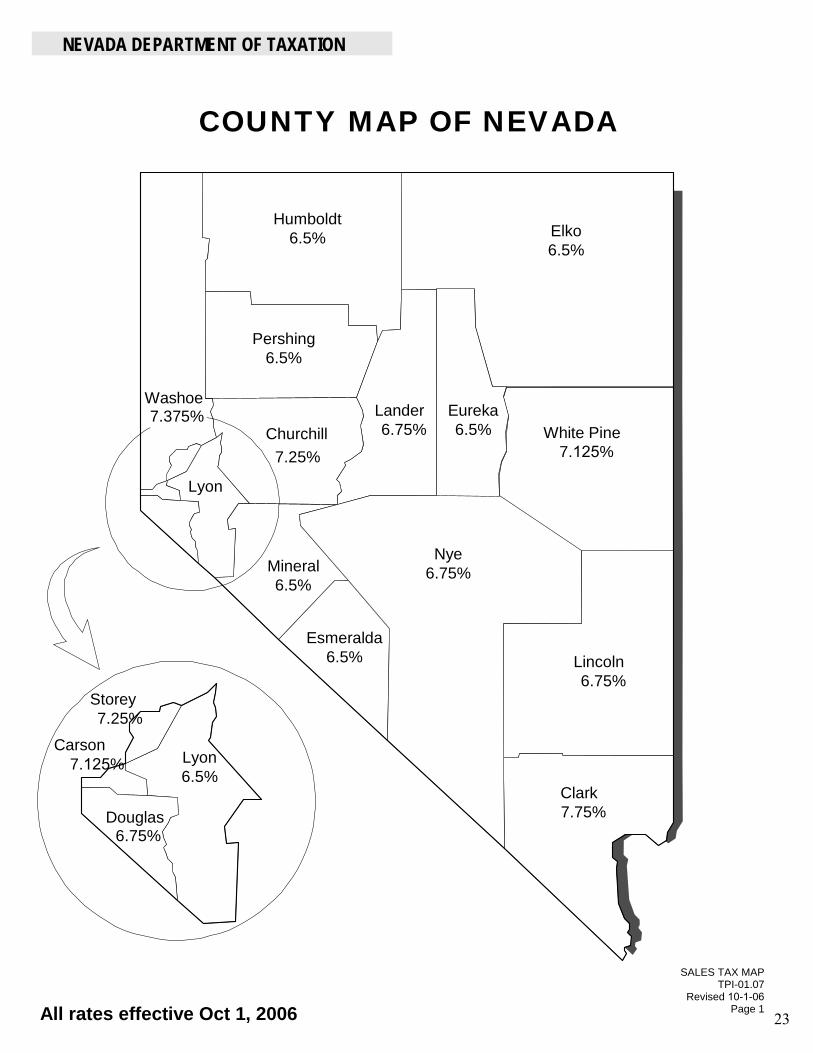

Sales and Use Tax..............................................................................................................17 Basic City-County Relief Tax (BCCRT)...........................................................................18 Supplemental City-County Relief Tax (SCCRT) ..............................................................19 Local School Support Tax (LSST) ....................................................................................20 County Optional Sales Taxes.............................................................................................21

B. GAMING TAXES

Gaming Percentage Fee .....................................................................................................27 Non-Restricted Slot License Fee .......................................................................................28 Restricted Slot License Fee................................................................................................29 Flat Fee on Games .............................................................................................................30 Advance License Fee ........................................................................................................31 Annual Slot Tax .................................................................................................................32

C. PROPERTY TAXES

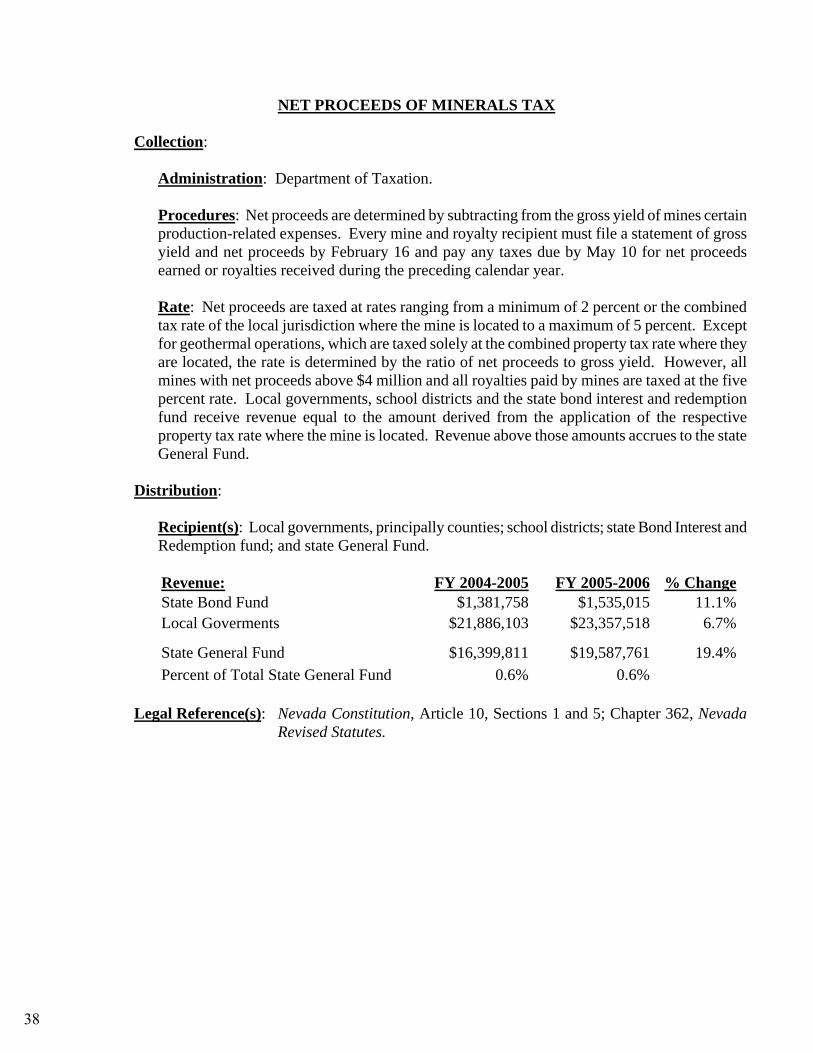

Property Tax.......................................................................................................................35 Net Proceeds of Minerals Tax............................................................................................38

D. EXCISE TAXES

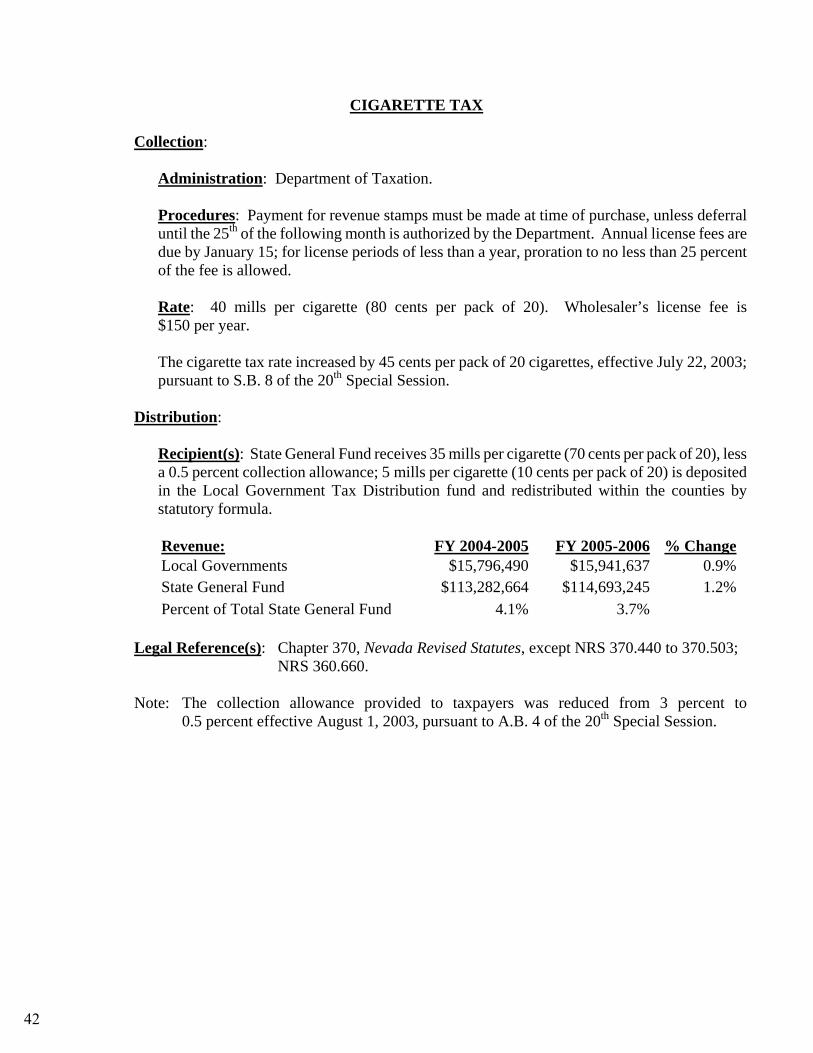

Liquor Tax .........................................................................................................................41 Cigarette Tax......................................................................................................................42 Tax on Other Tobacco Products ........................................................................................43

E. FUEL AND MOTOR VEHICLE TAXES

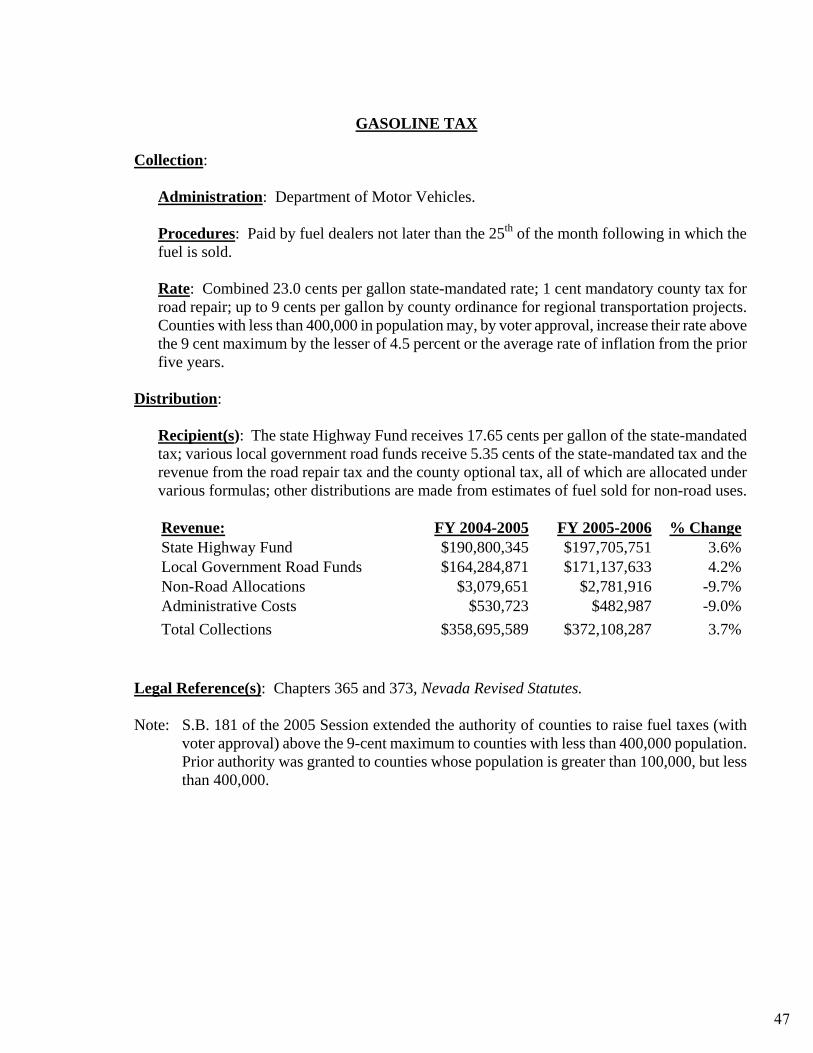

Gasoline Tax ......................................................................................................................47 Tax on Special Fuel ...........................................................................................................48 Jet Fuel Tax........................................................................................................................49 Petroleum Products Cleanup Fee .......................................................................................50 Governmental Services Tax...............................................................................................51

i

F. OTHER TAXES AND FEES

Insurance Premium Tax .....................................................................................................55 Modified Business Tax – Financial Institutions ................................................................56 Modified Business Tax – General Businesses ...................................................................57 Branch Bank Excise Fee ....................................................................................................58 Business License Tax ........................................................................................................59 Business License Fee ........................................................................................................60 Short-Term Car Rental Fee................................................................................................61 Real Property Transfer Tax................................................................................................62 Live Entertainment Tax .....................................................................................................63 Estate Tax...........................................................................................................................67 Room Tax...........................................................................................................................68

III. TAX LEGISLATION HISTORY – 1979 TO 2005

1979 Tax Reduction...........................................................................................................71 1981 Tax Reform ...............................................................................................................72 1983 Tax Package ..............................................................................................................73 1985 Tax Package ..............................................................................................................75 1987 Tax Package ..............................................................................................................76 1989 Tax Package ..............................................................................................................77 1991 Tax Package ..............................................................................................................78 1993 Tax Legislation .........................................................................................................79 1995 Tax Legislation .........................................................................................................80 1997 Tax Legislation .........................................................................................................81 1999 Tax Legislation .........................................................................................................82 2001 Tax Legislation .........................................................................................................83 2003 Tax Legislation .........................................................................................................84 State Revenue Bills - 2003.................................................................................................85 2005 Tax Legislation .........................................................................................................88 Property Tax Abatements ..................................................................................................88 State Revenue Bills - 2005.................................................................................................90

IV. TAXATION INFORMATION

A. TAX GLOSSARY .......................................................................................................99 B. DEPARTMENT OF TAXATION PUBLICATIONS...............................................111

V. TAX EXEMPTIONS

A. SALES TAX

Sales and Use Tax Act Exemptions .................................................................................119 Local School Support Tax and City/County Relief Tax Exemptions..............................123 Local School Support Tax and City/County Relief Tax Abatements..............................123

ii

B. PROPERTY TAX

Property Tax Abatements (A.B. 489 and S.B. 509 of the 2005 Session)….. ..................127 Property Tax Exemptions Granted Under Statute ...........................................................128 Partial Abatements Authorized by Commission on Economic Development .................134

C. GOVERNMENTAL SERVICES TAX….. ...............................................................137 D. REAL PROPERTY TRANSFER TAX.....................................................................141

VI. LOCAL GOVERNMENT FINANCE ISSUES

A. LIMITATIONS ON PROPERTY TAX RATES.......................................................147 B. ASSESSMENT STANDARDS AND PRACTICES.................................................151 C. FEE LIMITATIONS

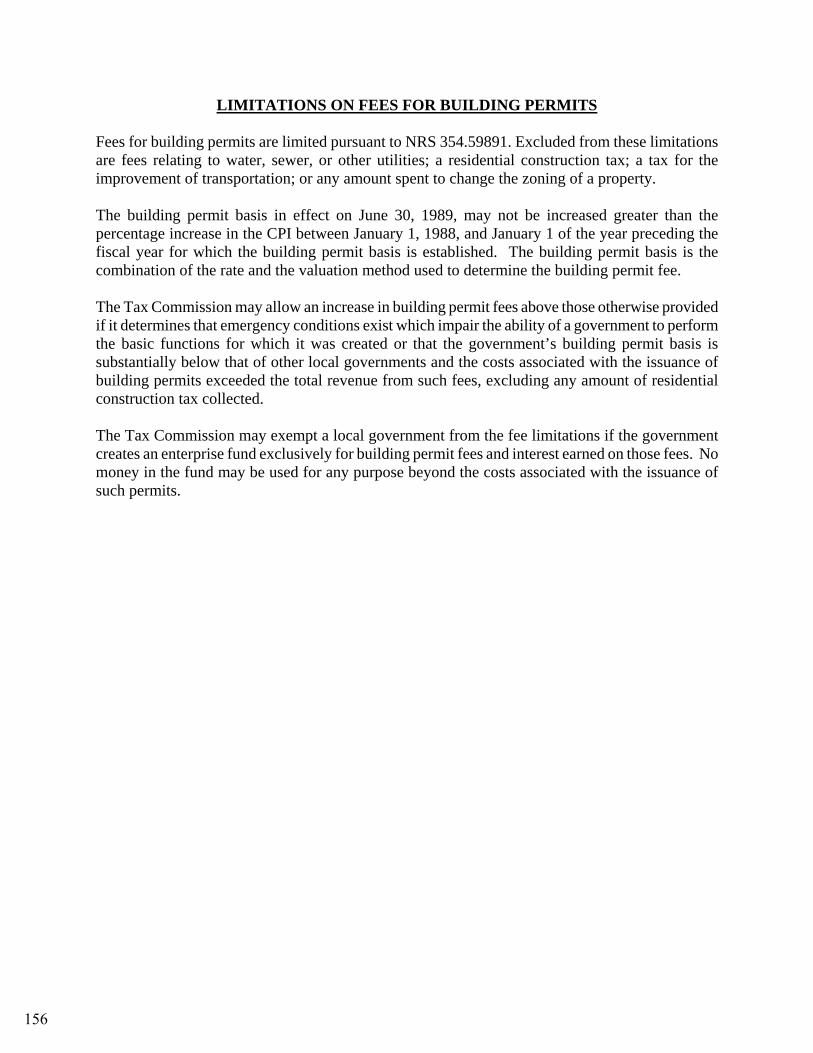

Limitations on Fees for Business Licenses......................................................................155 Limitations on Fees for Building Permits........................................................................156

VII. EDUCATION FUNDING INFORMATION

THE NEVADA PLAN ....................................................................................................161 VIII. FISCAL NOTES INFORMATION..............................................................................169

iii

THIS PAGE INTENTIONALLY LEFT BLANK

I. APPROPRIATIONS AND REVENUE CHARTS

1

THIS PAGE INTENTIONALLY LEFT BLANK

2

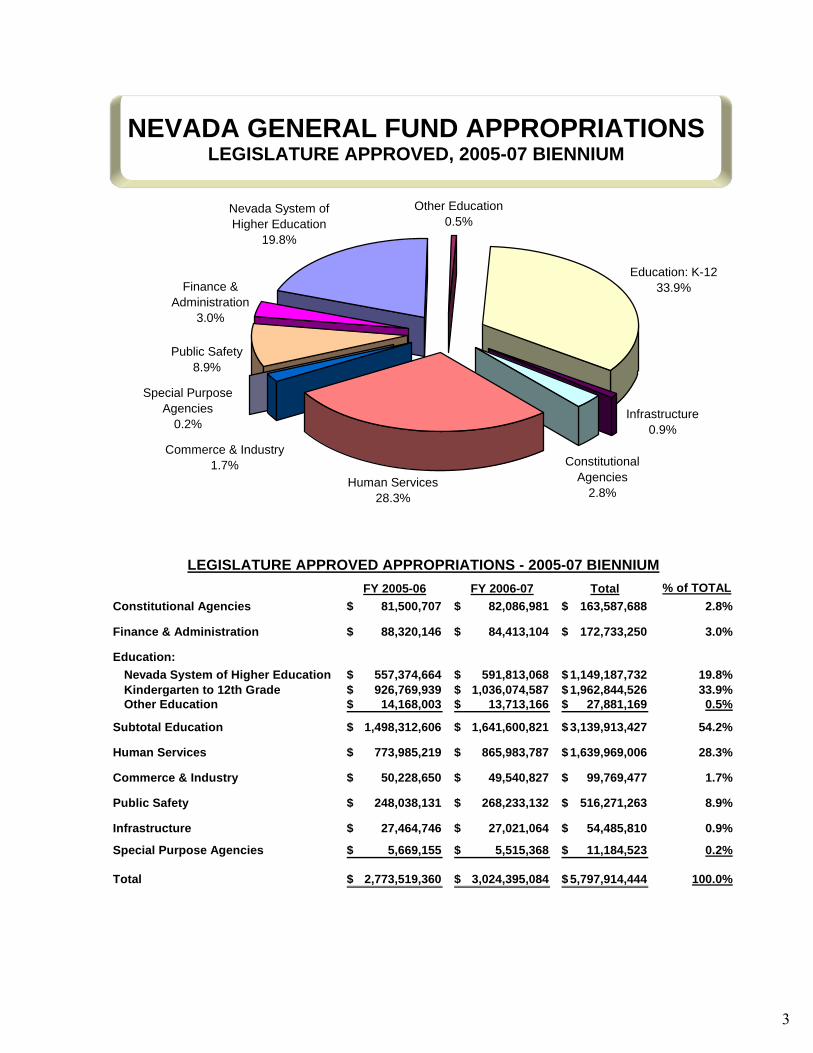

NEVADA GENERAL FUND APPROPRIATIONS LEGISLATURE APPROVED, 2005-07 BIENNIUM

Nevada System of Higher Education

19.8%

Other Education0.5%

Education: K-1233.9%

Human Services28.3%

Finance & Administration

3.0%

Constitutional Agencies

2.8%

Infrastructure0.9%

Commerce & Industry1.7%

Special Purpose Agencies

0.2%

Public Safety8.9%

FY 2005-06 FY 2006-07 Total % of TOTALConstitutional Agencies 81,500,707$ 82,086,981$ 163,587,688$ 2.8%

Finance & Administration 88,320,146$ 84,413,104$ 172,733,250$ 3.0%

Education:Nevada System of Higher Education 557,374,664$ 591,813,068$ 1,149,187,732$ 19.8%Kindergarten to 12th Grade 926,769,939$ 1,036,074,587$ 1,962,844,526$ 33.9%Other Education 14,168,003$ 13,713,166$ 27,881,169$ 0.5%

Subtotal Education 1,498,312,606$ 1,641,600,821$ 3,139,913,427$ 54.2%

Human Services 773,985,219$ 865,983,787$ 1,639,969,006$ 28.3%

Commerce & Industry 50,228,650$ 49,540,827$ 99,769,477$ 1.7%

Public Safety 248,038,131$ 268,233,132$ 516,271,263$ 8.9%

Infrastructure 27,464,746$ 27,021,064$ 54,485,810$ 0.9%

Special Purpose Agencies 5,669,155$ 5,515,368$ 11,184,523$ 0.2%

Total 2,773,519,360$ 3,024,395,084$ 5,797,914,444$ 100.0%

LEGISLATURE APPROVED APPROPRIATIONS - 2005-07 BIENNIUM

3

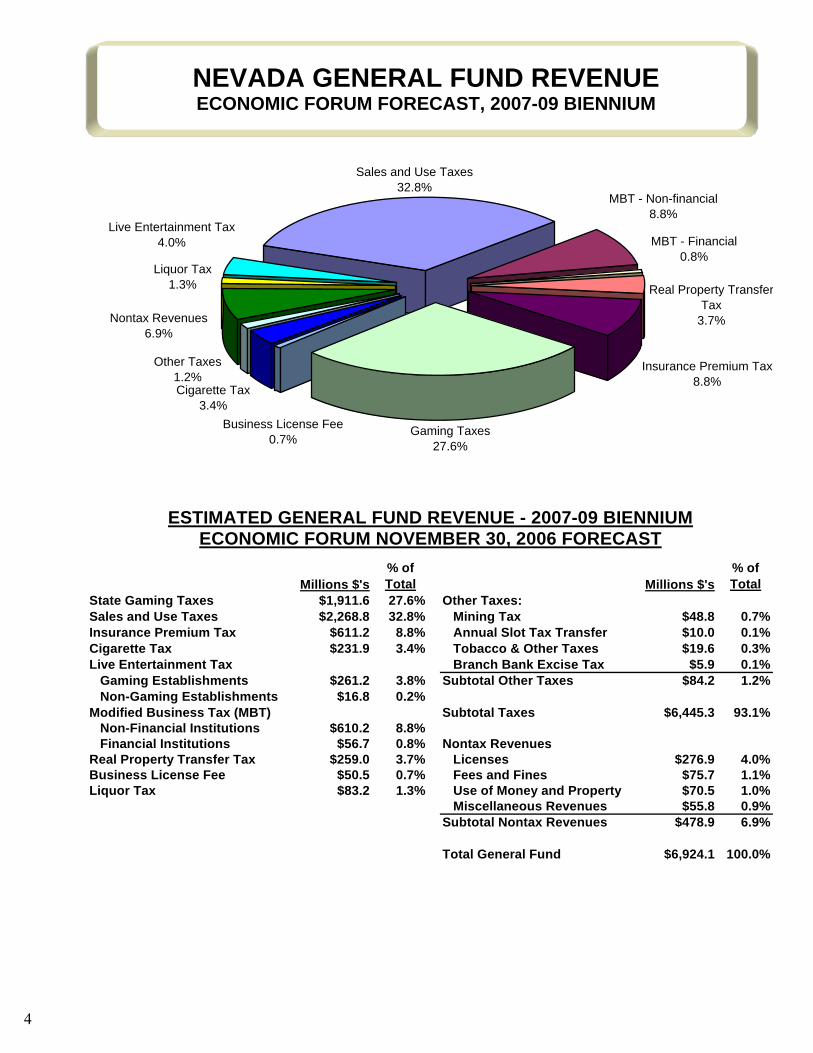

NEVADA GENERAL FUND REVENUE ECONOMIC FORUM FORECAST, 2007-09 BIENNIUM

Nontax Revenues6.9%

Other Taxes1.2%

Liquor Tax1.3%

Live Entertainment Tax4.0%

Business License Fee0.7%

Insurance Premium Tax8.8%

MBT - Financial0.8%

Real Property TransferTax

3.7%

Gaming Taxes27.6%

Sales and Use Taxes32.8%

Cigarette Tax3.4%

MBT - Non-financial8.8%

Millions $'s% of Total Millions $'s

% of Total

State Gaming Taxes $1,911.6 27.6% Other Taxes:Sales and Use Taxes $2,268.8 32.8% Mining Tax $48.8 0.7%Insurance Premium Tax $611.2 8.8% Annual Slot Tax Transfer $10.0 0.1%Cigarette Tax $231.9 3.4% Tobacco & Other Taxes $19.6 0.3%Live Entertainment Tax Branch Bank Excise Tax $5.9 0.1%

Gaming Establishments $261.2 3.8% Subtotal Other Taxes $84.2 1.2%Non-Gaming Establishments $16.8 0.2%

Modified Business Tax (MBT) Subtotal Taxes $6,445.3 93.1%Non-Financial Institutions $610.2 8.8%Financial Institutions $56.7 0.8% Nontax Revenues

Real Property Transfer Tax $259.0 3.7% Licenses $276.9 4.0%Business License Fee $50.5 0.7% Fees and Fines $75.7 1.1%Liquor Tax $83.2 1.3% Use of Money and Property $70.5 1.0%

Miscellaneous Revenues $55.8 0.9%Subtotal Nontax Revenues $478.9 6.9%

Total General Fund $6,924.1 100.0%

ESTIMATED GENERAL FUND REVENUE - 2007-09 BIENNIUMECONOMIC FORUM NOVEMBER 30, 2006 FORECAST

4

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

TAXE

STO

TAL

MIN

ING

TA

XE

S$1

0,64

1,10

013

.0%

$16,

817,

927

58.0

%$1

6,44

9,30

4-2

.2%

$19,

661,

886

19.5

%$2

3,61

9,00

020

.1%

$24,

132,

000

2.2%

$24,

648,

000

2.1%

TOTA

L S

ALE

S A

ND

US

E T

AX

[1-F

Y04

][1-F

Y07

]$6

93,5

28,8

235.

9%$7

90,6

02,6

6714

.0%

$913

,895

,384

15.6

%$1

,005

,054

,248

10.0

%$1

,042

,630

,000

3.7%

$1,0

96,0

26,0

005.

1%$1

,172

,748

,000

7.0%

TOTA

L G

AM

ING

TA

XE

S [2

-FY

04][3

-FY

04][1

-FY

06][1

-FY

08]

$596

,260

,210

1.1%

$714

,653

,673

19.9

%$7

49,6

55,6

224.

9%$8

38,0

94,2

9611

.8%

$866

,378

,900

3.4%

$919

,452

,700

6.1%

$992

,125

,200

7.9%

CA

SIN

O/L

IVE

EN

TER

TAIN

ME

NT

TAX

[4a&

4b-F

Y04

][2-F

Y06

][2-F

Y08

]$7

0,21

2,81

58.

3%$8

9,20

1,82

727

.0%

$107

,884

,337

20.9

%$1

17,1

09,2

888.

6%$1

25,3

29,0

007.

0%$1

33,2

81,0

006.

3%$1

44,7

18,0

008.

6%IN

SU

RA

NC

E P

RE

MIU

M T

AX

$174

,133

,841

11.2

%$1

94,4

57,0

5811

.7%

$215

,948

,970

11.1

%$2

38,6

27,9

8910

.5%

$262

,538

,600

10.0

%$2

90,8

27,0

0010

.8%

$320

,346

,100

10.2

%LI

QU

OR

TA

X [5

-FY

04]

$16,

531,

358

3.3%

$33,

025,

941

99.8

%$3

5,49

0,87

47.

5%$3

7,34

7,24

05.

2%$3

9,21

5,00

05.

0%$4

0,97

9,00

04.

5%$4

2,20

9,00

03.

0%C

IGA

RE

TTE

TA

X [6

-FY

04]

$44,

019,

969

5.2%

$106

,770

,729

142.

6%$1

13,2

82,6

646.

1%$1

14,6

93,2

451.

2%$1

15,2

00,0

000.

4%$1

15,7

00,0

000.

4%$1

16,2

00,0

000.

4%O

THE

R T

OB

AC

CO

TA

X [7

-FY

04]

$5,9

16,3

016.

4%$6

,927

,276

17.1

%$7

,557

,607

9.1%

$8,1

78,5

938.

2%$8

,792

,000

7.5%

$9,4

07,0

007.

0%$1

0,06

6,00

07.

0%LA

ETR

ILE

& G

ER

OV

ITA

L M

FG.

HE

CC

TR

AN

SFE

R$5

,000

,000

$5,0

00,0

00$5

,000

,000

$5,0

00,0

00$5

,000

,000

$5,0

00,0

00$5

,000

,000

BU

SIN

ES

S L

ICE

NS

E F

EE

[8-F

Y04

][3-F

Y06

][4-F

Y06

]$7

39,5

618.

6%$1

1,85

1,75

215

03%

$14,

486,

315

22.2

%$2

1,89

7,09

551

.2%

$23,

000,

000

5.0%

$24,

500,

000

6.5%

$26,

000,

000

6.1%

BU

SIN

ES

S L

ICE

NS

E T

AX

[9-F

Y04

]$7

9,02

6,13

20.

8%$2

2,21

6,50

0-7

1.9%

$1,2

97,3

83-9

4.2%

$431

,986

-66.

7%$2

50,0

00$1

00,0

00M

OD

IFIE

D B

US

INE

SS

TA

XM

BT-

NO

NFI

NA

NC

IAL

[10-

FY04

][5-F

Y06

][6-F

Y06

][3-F

Y08

]$1

46,1

61,8

12$2

05,3

48,1

7040

.5%

$232

,760

,812

13.3

%$2

62,1

58,0

0012

.6%

$293

,355

,000

11.9

%$3

16,8

23,0

008.

0%M

BT-

FIN

AN

CIA

L [1

1-FY

04][5

-FY

06]

$15,

487,

677

$21,

575,

335

39.3

%$2

2,49

1,11

04.

2%$2

4,71

2,00

09.

9%$2

7,07

5,00

09.

6%$2

9,64

2,00

09.

5%B

RA

NC

H B

AN

K E

XC

ISE

TA

X [1

2-FY

04][7

-FY

06]

$1,5

08,1

92$3

,084

,456

104.

5%$2

,819

,210

-8.6

%$2

,905

,000

3.0%

$2,9

40,0

001.

2%$2

,975

,000

1.2%

RE

AL

PR

OP

ER

TY T

RA

NS

FER

TA

X [1

3-FY

04][8

-FY

06]

$88,

024,

738

$148

,730

,974

69.0

%$1

64,8

41,5

0610

.8%

$123

,735

,000

-24.

9%$1

24,1

66,0

000.

3%$1

34,8

80,0

008.

6%TO

TAL

TAX

ES

$1,6

96,0

10,1

114.

5%$2

,242

,707

,768

32.2

%$2

,559

,687

,394

14.1

%$2

,829

,008

,504

10.5

%$2

,925

,462

,500

3.4%

$3,1

06,9

40,7

006.

2%$3

,338

,380

,300

7.4%

LIC

ENSE

SIN

SU

RA

NC

E L

ICE

NS

ES

$10,

076,

143

29.1

%$1

0,57

8,74

45.

0%$1

1,35

8,65

17.

4%$1

2,53

6,52

910

.4%

$13,

163,

000

5.0%

$13,

822,

000

5.0%

$14,

513,

000

5.0%

BA

NK

ING

LIC

EN

SE

S [1

6-FY

04]

$20,

400

-13.

6%M

AR

RIA

GE

LIC

EN

SE

S$5

87,7

120.

0%$5

94,5

881.

2%$5

99,8

900.

9%$5

59,9

74-6

.7%

$567

,300

1.3%

$571

,200

0.7%

$574

,200

0.5%

TOTA

L S

EC

RE

TAR

Y O

F S

TATE

[14-

FY04

]$5

4,02

6,46

17.

9%$7

5,31

2,84

639

.4%

$84,

122,

084

11.7

%$1

01,1

39,6

2620

.2%

$105

,400

,700

4.2%

$113

,277

,200

7.5%

$121

,761

,100

7.5%

PR

IVA

TE S

CH

OO

L LI

CE

NS

ES

$207

,145

14.4

%$2

51,7

0521

.5%

$274

,132

8.9%

$246

,102

-10.

2%$2

55,0

003.

6%$2

59,0

001.

6%$2

64,0

001.

9%P

RIV

ATE

EM

PLO

YM

EN

T A

GE

NC

Y$2

9,10

00.

3%$2

6,00

0-1

0.7%

$18,

700

-28.

1%$1

8,00

0-3

.7%

$17,

500

-2.8

%$1

7,50

0$1

7,50

0TO

TAL

RE

AL

ES

TATE

[15-

FY04

][16-

FY04

]$1

,548

,788

-8.4

%$2

,653

,740

71.3

%$2

,628

,035

-1.0

%$3

,167

,643

20.5

%$3

,259

,500

2.9%

$3,3

56,5

003.

0%$3

,457

,500

3.0%

TOTA

L FI

NA

NC

IAL

INS

TITU

TIO

NS

[16-

FY04

]$1

,926

,415

7.3%

ATH

LETI

C C

OM

MIS

SIO

N F

EE

S

$1,9

01,3

5711

.4%

$2,2

58,3

0618

.8%

$2,4

62,4

479.

0%$3

,042

,779

23.6

%$2

,500

,000

-17.

8%$2

,500

,000

$2,5

00,0

00TO

TAL

LIC

EN

SE

S$7

0,32

3,52

010

.1%

$91,

675,

929

30.4

%$1

01,4

63,9

3910

.7%

$120

,710

,653

19.0

%$1

25,1

63,0

003.

7%$1

33,8

03,4

006.

9%$1

43,0

87,3

006.

9%

FEES

AN

D F

INES

VIT

AL

STA

TIS

TIC

S F

EE

S [1

7-FY

04]

$647

,213

12.2

%$7

59,5

8717

.4%

$845

,362

11.3

%$9

01,0

946.

6%$9

23,6

002.

5%$9

46,7

002.

5%$9

70,4

002.

5%D

IVO

RC

E F

EE

S$2

01,0

702.

1%$2

05,5

352.

2%$2

08,0

101.

2%$2

11,1

461.

5%$2

05,0

00-2

.9%

$210

,000

2.4%

$215

,000

2.4%

CIV

IL A

CTI

ON

FE

ES

$1,3

22,5

185.

8%$1

,376

,653

4.1%

$1,4

12,8

982.

6%$1

,396

,729

-1.1

%$1

,400

,000

0.2%

$1,4

10,0

000.

7%$1

,420

,000

0.7%

INS

UR

AN

CE

FE

ES

$617

,132

-14.

2%$6

24,1

491.

1%$5

76,0

35-7

.7%

$1,3

70,0

9713

7.8%

$656

,900

-52.

1%$6

56,9

00$6

56,9

00TO

TAL

RE

AL

ES

TATE

FE

ES

$436

,415

9.9%

$1,0

97,8

4715

1.6%

$1,2

43,1

7613

.2%

$1,4

52,9

7416

.9%

$1,3

66,7

00-5

.9%

$1,3

09,7

00-4

.2%

$1,3

07,8

00-0

.1%

SH

OR

T-TE

RM

CA

R L

EA

SE

$22,

208,

165

12.9

%$2

5,63

8,55

615

.4%

$26,

793,

014

4.5%

$26,

659,

712

-0.5

%$2

9,82

0,00

011

.9%

$29,

517,

000

-1.0

%$3

0,40

3,00

03.

0%A

THLE

TIC

CO

MM

ISS

ION

LIC

EN

SE

S/F

INE

S$2

10,9

2071

.6%

$109

,825

-47.

9%$1

22,5

1511

.6%

$690

,076

463.

3%$3

00,0

00-5

6.5%

$300

,000

$300

,000

WA

TER

PLA

NN

ING

FE

ES

STA

TE E

NG

INE

ER

SA

LES

$1,5

90,4

281.

2%$1

,698

,473

6.8%

$2,0

77,4

3222

.3%

$2,2

49,1

858.

3%$2

,000

,000

-11.

1%$2

,000

,000

$2,0

00,0

00S

UP

RE

ME

CO

UR

T FE

ES

$212

,035

2.0%

$219

,042

3.3%

$208

,203

-4.9

%$1

95,6

80-6

.0%

$201

,500

3.0%

$207

,700

3.1%

$214

,000

3.0%

MIS

C. F

INE

S/F

OR

FEIT

UR

ES

$350

,947

103.

4%$2

61,4

21-2

5.5%

$484

,199

85.2

%$1

,269

,520

162.

2%$8

64,1

00-3

1.9%

$836

,600

-3.2

%$8

41,6

000.

6%TO

TAL

FEE

S A

ND

FIN

ES

$27,

796,

842

11.7

%$3

1,99

1,08

815

.1%

$33,

970,

845

6.2%

$36,

396,

214

7.1%

$37,

737,

800

3.7%

$37,

394,

600

-0.9

%$3

8,32

8,70

02.

5%

USE

OF

MO

NEY

AN

D P

RO

PER

TYLY

ON

CO

UN

TY R

EP

AY

ME

NTS

OTH

ER

RE

PA

YM

EN

TS [1

8-FY

04]

$2,4

05,2

7715

8.1%

$2,0

08,7

38-1

6.5%

$2,1

00,0

784.

5%$2

,200

,892

4.8%

$2,9

32,0

1533

.2%

$2,8

34,6

04-3

.3%

$2,8

59,2

750.

9%M

AR

LETT

E R

EP

AY

ME

NT

$10,

512

$10,

512

$10,

512

$10,

664

1.4%

$10,

664

$10,

664

$10,

664

INTE

RE

ST

INC

OM

E$5

,990

,047

-52.

1%$4

,528

,633

-24.

4%$1

3,68

5,86

920

2.2%

$32,

933,

368

140.

6%$4

8,52

9,80

047

.4%

$35,

709,

900

-26.

4%$2

9,05

4,90

0-1

8.6%

TOTA

L U

SE

OF

MO

NE

Y A

ND

PR

OP

ER

TY$8

,405

,836

-37.

5%$6

,547

,883

-22.

1%$1

5,79

6,45

814

1.2%

$35,

144,

924

122.

5%$5

1,47

2,47

946

.5%

$38,

555,

168

-25.

1%$3

1,92

4,83

9-1

7.2%

OTH

ER R

EVEN

UE

HO

OV

ER

DA

M R

EV

EN

UE

$300

,000

$300

,000

$300

,000

$300

,000

$300

,000

$300

,000

$300

,000

MIS

C. S

ALE

S A

ND

RE

FUN

DS

$932

,709

-34.

9%$8

99,1

32-3

.6%

$1,4

28,3

3558

.9%

$3,9

34,3

3517

5.4%

$908

,100

-76.

9%$9

22,2

001.

6%$9

30,8

000.

9%C

OS

T R

EC

OV

ER

Y P

LAN

$5,0

04,4

770.

0%$9

,714

,586

94.1

%$9

,624

,189

-0.9

%$1

0,45

8,76

28.

7%$1

0,51

5,50

00.

5%$1

0,51

5,50

0$1

0,51

5,50

0P

ETR

OLE

UM

INS

PE

CTI

ON

FE

ES

[4-F

Y08

]$5

63,7

272.

4%$5

57,9

66-1

.0%

$582

,201

4.3%

$580

,469

-0.3

%$5

86,4

001.

0%U

NC

LAIM

ED

PR

OP

ER

TY [9

-FY

06]

$16,

014,

824

-17.

1%$1

9,61

1,60

522

.5%

$19,

811,

660

1.0%

$22,

269,

598

12.4

%$1

6,49

9,00

0-2

5.9%

$16,

938,

000

2.7%

$15,

378,

000

-9.2

%TO

TAL

OTH

ER

RE

VE

NU

E$2

2,81

5,73

7-1

4.3%

$31,

083,

289

36.2

%$3

1,74

6,38

42.

1%$3

7,54

3,16

418

.3%

$28,

809,

000

-23.

3%$2

8,67

5,70

0-0

.5%

$27,

124,

300

-5.4

%

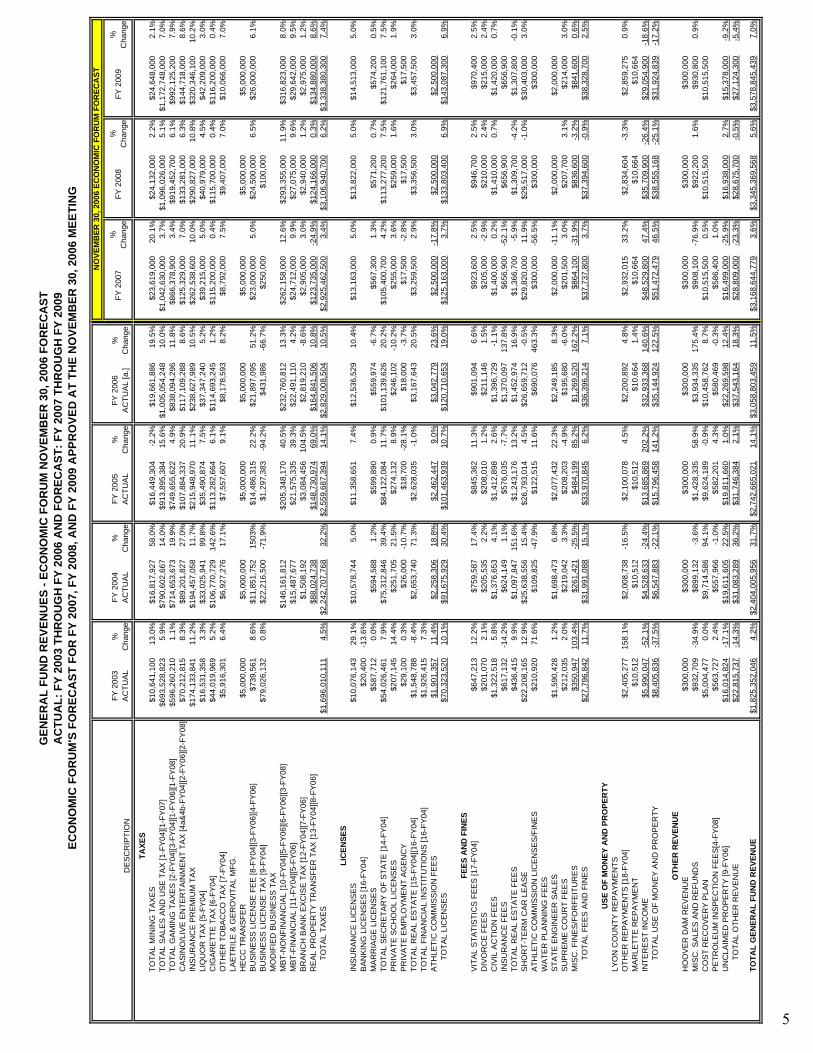

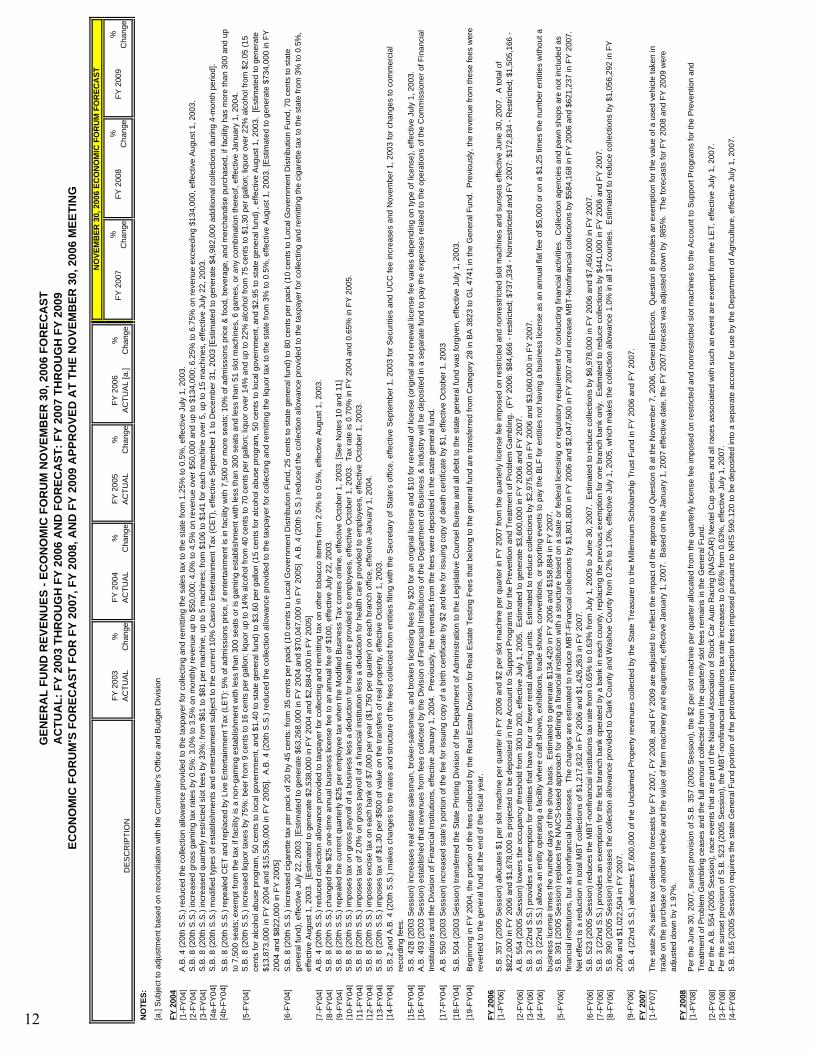

TOTA

L G

ENER

AL

FUN

D R

EVEN

UE

$1,8

25,3

52,0

464.

2%$2

,404

,005

,956

31.7

%$2

,742

,665

,021

14.1

%$3

,058

,803

,459

11.5

%$3

,168

,644

,779

3.6%

$3,3

45,3

69,5

685.

6%$3

,578

,845

,439

7.0%

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU

M N

OVE

MB

ER 3

0, 2

006

FOR

ECA

ST

NO

VEM

BER

30,

200

6 EC

ON

OM

IC F

OR

UM

FO

REC

AST

AC

TUA

L: F

Y 20

03 T

HR

OU

GH

FY

2006

AN

D F

OR

ECA

ST: F

Y 20

07 T

HR

OU

GH

FY

2009

ECO

NO

MIC

FO

RU

M'S

FO

REC

AST

FO

R F

Y 20

07, F

Y 20

08, A

ND

FY

2009

APP

RO

VED

AT

THE

NO

VEM

BER

30,

200

6 M

EETI

NG

5

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU

M N

OVE

MB

ER 3

0, 2

006

FOR

ECA

ST

NO

VEM

BER

30,

200

6 EC

ON

OM

IC F

OR

UM

FO

REC

AST

AC

TUA

L: F

Y 20

03 T

HR

OU

GH

FY

2006

AN

D F

OR

ECA

ST: F

Y 20

07 T

HR

OU

GH

FY

2009

ECO

NO

MIC

FO

RU

M'S

FO

REC

AST

FO

R F

Y 20

07, F

Y 20

08, A

ND

FY

2009

APP

RO

VED

AT

THE

NO

VEM

BER

30,

200

6 M

EETI

NG

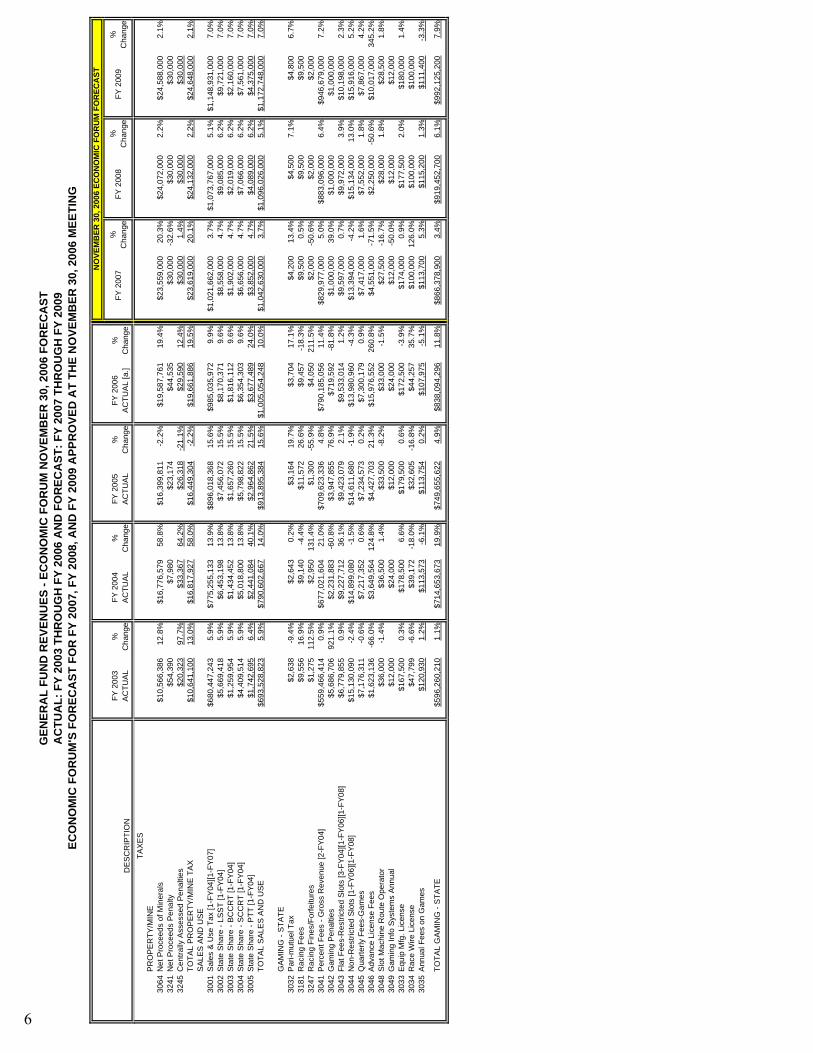

TAX

ES

PR

OP

ER

TY/M

INE

3064

Net

Pro

ceed

s of

Min

eral

s$1

0,56

6,38

612

.8%

$16,

776,

579

58.8

%$1

6,39

9,81

1-2

.2%

$19,

587,

761

19.4

%$2

3,55

9,00

020

.3%

$24,

072,

000

2.2%

$24,

588,

000

2.1%

3241

Net

Pro

ceed

s P

enal

ty$5

4,39

0$7

,980

$23,

174

$44,

535

$30,

000

-32.

6%$3

0,00

0$3

0,00

032

45C

entra

lly A

sses

sed

Pen

altie

s$2

0,32

397

.7%

$33,

367

64.2

%$2

6,31

8-2

1.1%

$29,

590

12.4

%$3

0,00

01.

4%$3

0,00

0$3

0,00

0TO

TAL

PR

OP

ER

TY/M

INE

TA

X$1

0,64

1,10

013

.0%

$16,

817,

927

58.0

%$1

6,44

9,30

4-2

.2%

$19,

661,

886

19.5

%$2

3,61

9,00

020

.1%

$24,

132,

000

2.2%

$24,

648,

000

2.1%

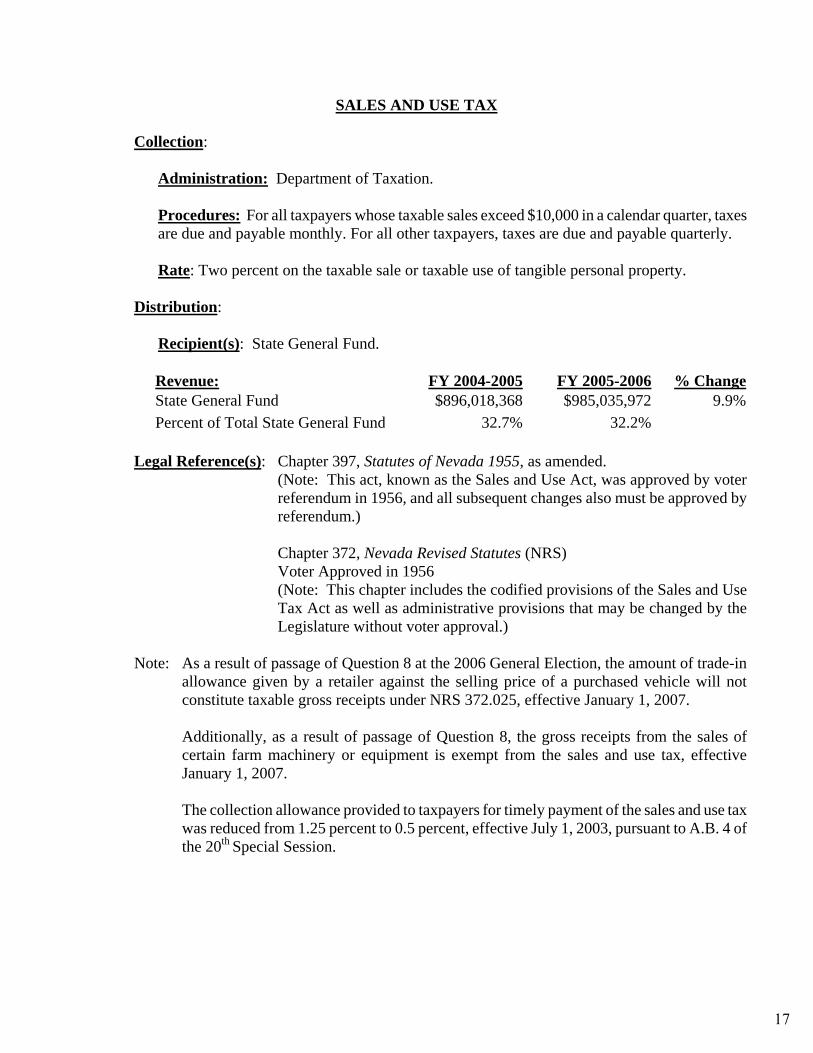

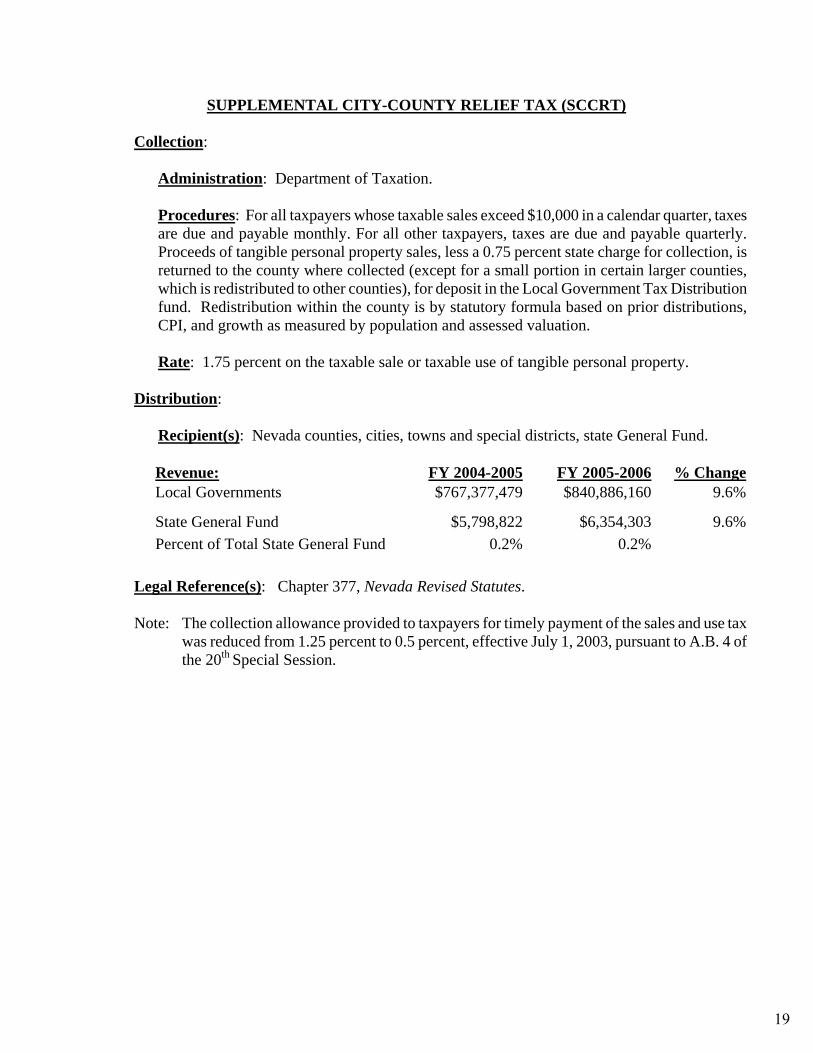

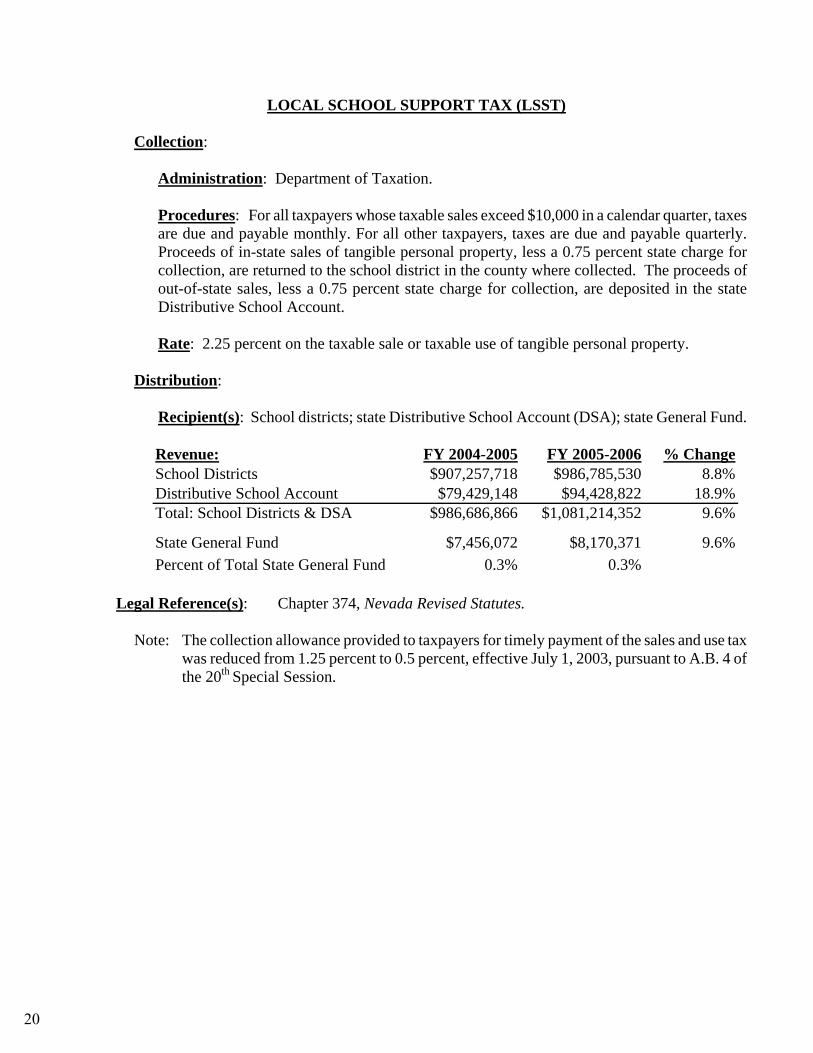

SA

LES

AN

D U

SE

3001

Sal

es &

Use

Tax

[1-F

Y04

][1-F

Y07

]$6

80,4

47,2

435.

9%$7

75,2

55,1

3313

.9%

$896

,018

,368

15.6

%$9

85,0

35,9

729.

9%$1

,021

,662

,000

3.7%

$1,0

73,7

67,0

005.

1%$1

,148

,931

,000

7.0%

3002

Sta

te S

hare

- LS

ST

[1-F

Y04

]$5

,669

,418

5.9%

$6,4

53,1

9813

.8%

$7,4

56,0

7215

.5%

$8,1

70,3

719.

6%$8

,558

,000

4.7%

$9,0

85,0

006.

2%$9

,721

,000

7.0%

3003

Sta

te S

hare

- B

CC

RT

[1-F

Y04

]$1

,259

,954

5.9%

$1,4

34,4

5213

.8%

$1,6

57,2

6015

.5%

$1,8

16,1

129.

6%$1

,902

,000

4.7%

$2,0

19,0

006.

2%$2

,160

,000

7.0%

3004

Sta

te S

hare

- S

CC

RT

[1-F

Y04

]$4

,409

,514

5.9%

$5,0

18,8

0013

.8%

$5,7

98,8

2215

.5%

$6,3

54,3

039.

6%$6

,656

,000

4.7%

$7,0

66,0

006.

2%$7

,561

,000

7.0%

3005

Sta

te S

hare

- P

TT [1

-FY

04]

$1,7

42,6

956.

4%$2

,441

,084

40.1

%$2

,964

,862

21.5

%$3

,677

,489

24.0

%$3

,852

,000

4.7%

$4,0

89,0

006.

2%$4

,375

,000

7.0%

TOTA

L S

ALE

S A

ND

US

E$6

93,5

28,8

235.

9%$7

90,6

02,6

6714

.0%

$913

,895

,384

15.6

%$1

,005

,054

,248

10.0

%$1

,042

,630

,000

3.7%

$1,0

96,0

26,0

005.

1%$1

,172

,748

,000

7.0%

GA

MIN

G -

STA

TE30

32P

ari-m

utue

l Tax

$2,6

38-9

.4%

$2,6

430.

2%$3

,164

19.7

%$3

,704

17.1

%$4

,200

13.4

%$4

,500

7.1%

$4,8

006.

7%31

81R

acin

g Fe

es$9

,556

16.9

%$9

,140

-4.4

%$1

1,57

226

.6%

$9,4

57-1

8.3%

$9,5

000.

5%$9

,500

$9,5

0032

47R

acin

g Fi

nes/

Forfe

iture

s$1

,275

112.

5%$2

,950

131.

4%$1

,300

-55.

9%$4

,050

211.

5%$2

,000

-50.

6%$2

,000

$2,0

0030

41P

erce

nt F

ees

- Gro

ss R

even

ue [2

-FY

04]

$559

,466

,414

0.9%

$677

,021

,604

21.0

%$7

09,6

23,3

364.

8%$7

90,1

85,0

5611

.4%

$829

,977

,000

5.0%

$883

,096

,000

6.4%

$946

,679

,000

7.2%

3042

Gam

ing

Pen

altie

s$5

,686

,706

921.

1%$2

,231

,883

-60.

8%$3

,947

,855

76.9

%$7

19,5

92-8

1.8%

$1,0

00,0

0039

.0%

$1,0

00,0

00$1

,000

,000

3043

Flat

Fee

s-R

estri

cted

Slo

ts [3

-FY

04][1

-FY

06][1

-FY

08]

$6,7

79,8

550.

9%$9

,227

,712

36.1

%$9

,423

,079

2.1%

$9,5

33,0

141.

2%$9

,597

,000

0.7%

$9,9

72,0

003.

9%$1

0,19

8,00

02.

3%30

44N

on-R

estri

cted

Slo

ts [1

-FY

06][1

-FY

08]

$15,

130,

090

-2.4

%$1

4,89

9,08

0-1

.5%

$14,

611,

680

-1.9

%$1

3,98

0,96

0-4

.3%

$13,

394,

000

-4.2

%$1

5,13

4,00

013

.0%

$15,

916,

000

5.2%

3045

Qua

rterly

Fee

s-G

ames

$7,1

76,3

11-0

.6%

$7,2

17,3

520.

6%$7

,234

,573

0.2%

$7,3

00,1

790.

9%$7

,417

,000

1.6%

$7,5

52,0

001.

8%$7

,867

,000

4.2%

3046

Adv

ance

Lic

ense

Fee

s$1

,623

,136

-66.

0%$3

,649

,564

124.

8%$4

,427

,703

21.3

%$1

5,97

6,55

226

0.8%

$4,5

51,0

00-7

1.5%

$2,2

50,0

00-5

0.6%

$10,

017,

000

345.

2%30

48S

lot M

achi

ne R

oute

Ope

rato

r$3

6,00

0-1

.4%

$36,

500

1.4%

$33,

500

-8.2

%$3

3,00

0-1

.5%

$27,

500

-16.

7%$2

8,00

01.

8%$2

8,50

01.

8%30

49G

amin

g In

fo S

yste

ms

Ann

ual

$12,

000

$24,

000

$12,

000

$24,

000

$12,

000

-50.

0%$1

2,00

0$1

2,00

030

33E

quip

Mfg

. Lic

ense

$167

,500

0.3%

$178

,500

6.6%

$179

,500

0.6%

$172

,500

-3.9

%$1

74,0

000.

9%$1

77,5

002.

0%$1

80,0

001.

4%30

34R

ace

Wire

Lic

ense

$47,

799

-6.6

%$3

9,17

2-1

8.0%

$32,

605

-16.

8%$4

4,25

735

.7%

$100

,000

126.

0%$1

00,0

00$1

00,0

0030

35A

nnua

l Fee

s on

Gam

es$1

20,9

301.

2%$1

13,5

73-6

.1%

$113

,754

0.2%

$107

,975

-5.1

%$1

13,7

005.

3%$1

15,2

001.

3%$1

11,4

00-3

.3%

TOTA

L G

AM

ING

- S

TATE

$596

,260

,210

1.1%

$714

,653

,673

19.9

%$7

49,6

55,6

224.

9%$8

38,0

94,2

9611

.8%

$866

,378

,900

3.4%

$919

,452

,700

6.1%

$992

,125

,200

7.9%

6

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU

M N

OVE

MB

ER 3

0, 2

006

FOR

ECA

ST

NO

VEM

BER

30,

200

6 EC

ON

OM

IC F

OR

UM

FO

REC

AST

AC

TUA

L: F

Y 20

03 T

HR

OU

GH

FY

2006

AN

D F

OR

ECA

ST: F

Y 20

07 T

HR

OU

GH

FY

2009

ECO

NO

MIC

FO

RU

M'S

FO

REC

AST

FO

R F

Y 20

07, F

Y 20

08, A

ND

FY

2009

APP

RO

VED

AT

THE

NO

VEM

BER

30,

200

6 M

EETI

NG

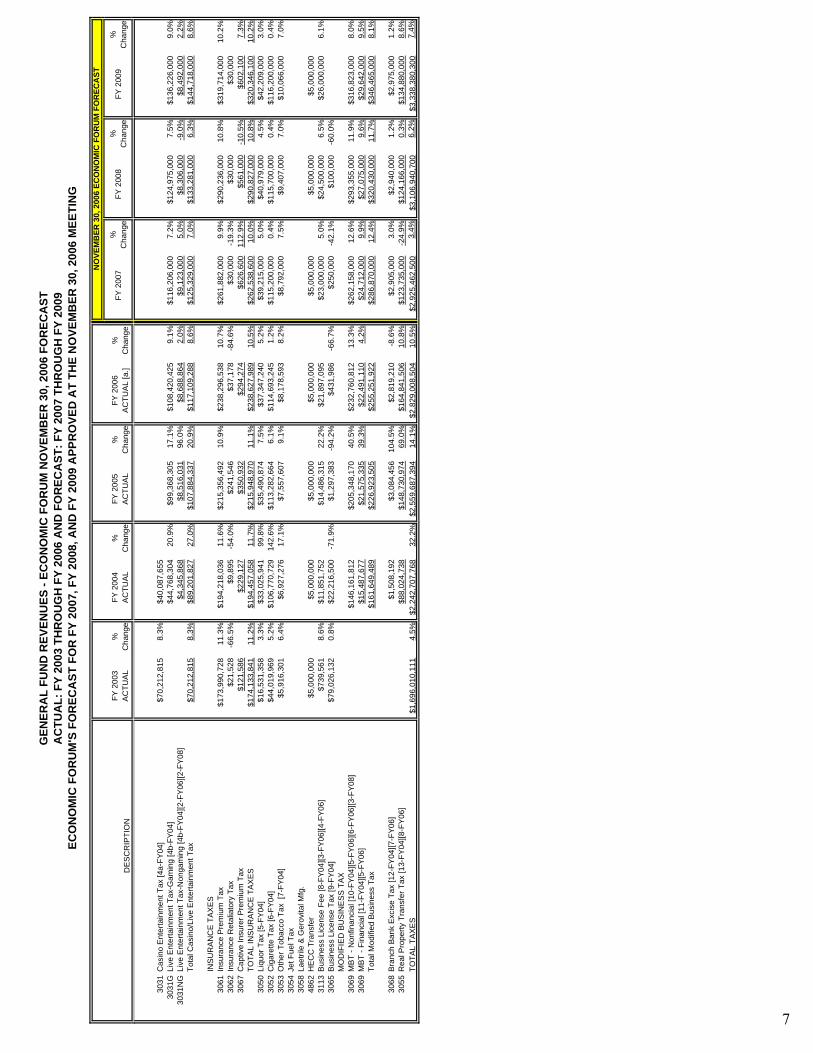

3031

Cas

ino

Ent

erta

inm

ent T

ax [4

a-FY

04]

$70,

212,

815

8.3%

$40,

087,

655

3031

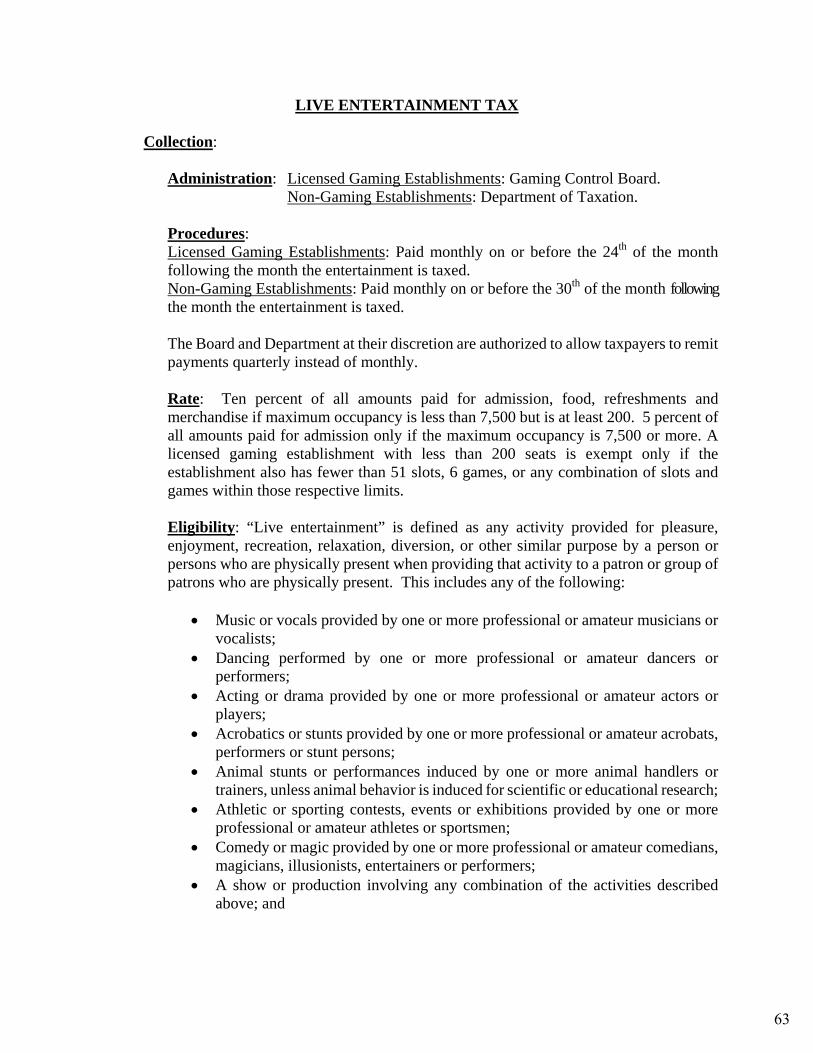

GLi

ve E

nter

tain

men

t Tax

-Gam

ing

[4b-

FY04

]$4

4,76

8,30

420

.9%

$99,

368,

305

17.1

%$1

08,4

20,4

259.

1%$1

16,2

06,0

007.

2%$1

24,9

75,0

007.

5%$1

36,2

26,0

009.

0%30

31N

GLi

ve E

nter

tain

men

t Tax

-Non

gam

ing

[4b-

FY04

][2-F

Y06

][2-F

Y08

]$4

,345

,868

$8,5

16,0

3196

.0%

$8,6

88,8

642.

0%$9

,123

,000

5.0%

$8,3

06,0

00-9

.0%

$8,4

92,0

002.

2%To

tal C

asin

o/Li

ve E

nter

tain

men

t Tax

$70,

212,

815

8.3%

$89,

201,

827

27.0

%$1

07,8

84,3

3720

.9%

$117

,109

,288

8.6%

$125

,329

,000

7.0%

$133

,281

,000

6.3%

$144

,718

,000

8.6%

INS

UR

AN

CE

TA

XE

S30

61In

sura

nce

Pre

miu

m T

ax$1

73,9

90,7

2811

.3%

$194

,218

,036

11.6

%$2

15,3

56,4

9210

.9%

$238

,296

,538

10.7

%$2

61,8

82,0

009.

9%$2

90,2

36,0

0010

.8%

$319

,714

,000

10.2

%30

62In

sura

nce

Ret

alia

tory

Tax

$21,

528

-66.

5%$9

,895

-54.

0%$2

41,5

46$3

7,17

8-8

4.6%

$30,

000

-19.

3%$3

0,00

0$3

0,00

030

67C

aptiv

e In

sure

r Pre

miu

m T

ax$1

21,5

86$2

29,1

27$3

50,9

32$2

94,2

74$6

26,6

0011

2.9%

$561

,000

-10.

5%$6

02,1

007.

3%TO

TAL

INS

UR

AN

CE

TA

XE

S$1

74,1

33,8

4111

.2%

$194

,457

,058

11.7

%$2

15,9

48,9

7011

.1%

$238

,627

,989

10.5

%$2

62,5

38,6

0010

.0%

$290

,827

,000

10.8

%$3

20,3

46,1

0010

.2%

3050

Liqu

or T

ax [5

-FY

04]

$16,

531,

358

3.3%

$33,

025,

941

99.8

%$3

5,49

0,87

47.

5%$3

7,34

7,24

05.

2%$3

9,21

5,00

05.

0%$4

0,97

9,00

04.

5%$4

2,20

9,00

03.

0%30

52C

igar

ette

Tax

[6-F

Y04

]$4

4,01

9,96

95.

2%$1

06,7

70,7

2914

2.6%

$113

,282

,664

6.1%

$114

,693

,245

1.2%

$115

,200

,000

0.4%

$115

,700

,000

0.4%

$116

,200

,000

0.4%

3053

Oth

er T

obac

co T

ax [

7-FY

04]

$5,9

16,3

016.

4%$6

,927

,276

17.1

%$7

,557

,607

9.1%

$8,1

78,5

938.

2%$8

,792

,000

7.5%

$9,4

07,0

007.

0%$1

0,06

6,00

07.

0%30

54Je

t Fue

l Tax

3058

Laet

rile

& G

erov

ital M

fg.

4862

HE

CC

Tra

nsfe

r$5

,000

,000

$5,0

00,0

00$5

,000

,000

$5,0

00,0

00$5

,000

,000

$5,0

00,0

00$5

,000

,000

3113

Bus

ines

s Li

cens

e Fe

e [8

-FY

04][3

-FY

06][4

-FY

06]

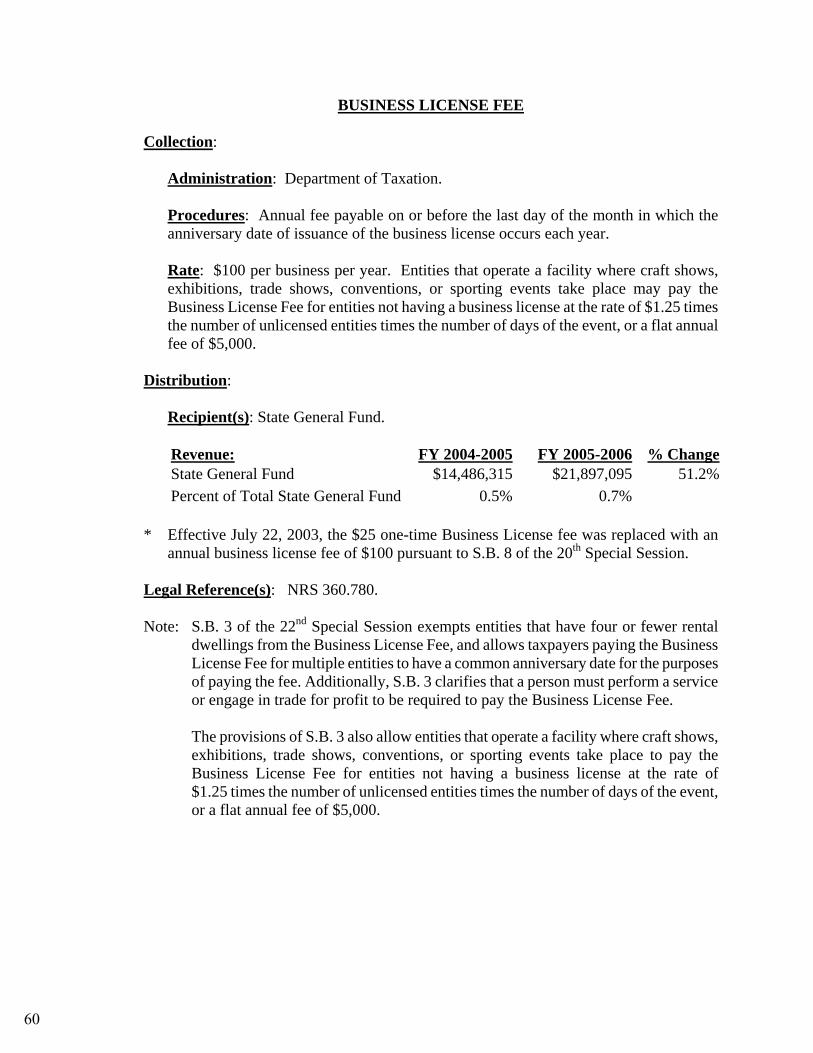

$739

,561

8.6%

$11,

851,

752

$14,

486,

315

22.2

%$2

1,89

7,09

5$2

3,00

0,00

05.

0%$2

4,50

0,00

06.

5%$2

6,00

0,00

06.

1%30

65B

usin

ess

Lice

nse

Tax

[9-F

Y04

]$7

9,02

6,13

20.

8%$2

2,21

6,50

0-7

1.9%

$1,2

97,3

83-9

4.2%

$431

,986

-66.

7%$2

50,0

00-4

2.1%

$100

,000

-60.

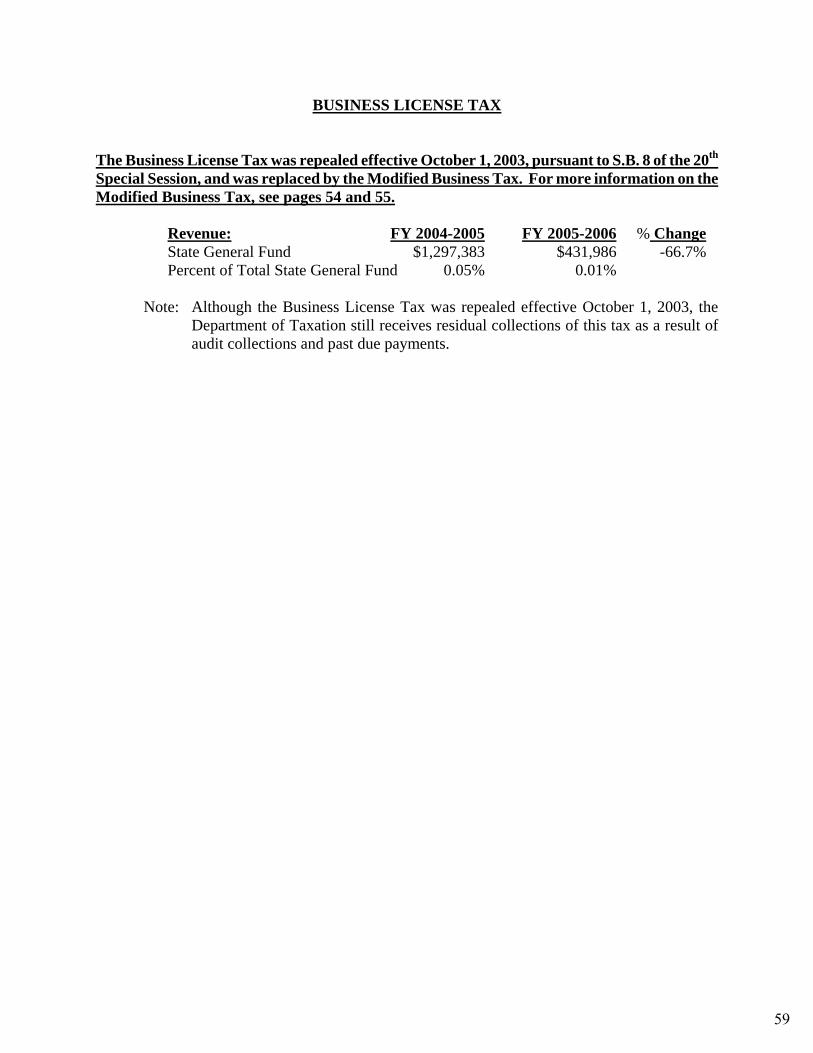

0%M

OD

IFIE

D B

US

INE

SS

TA

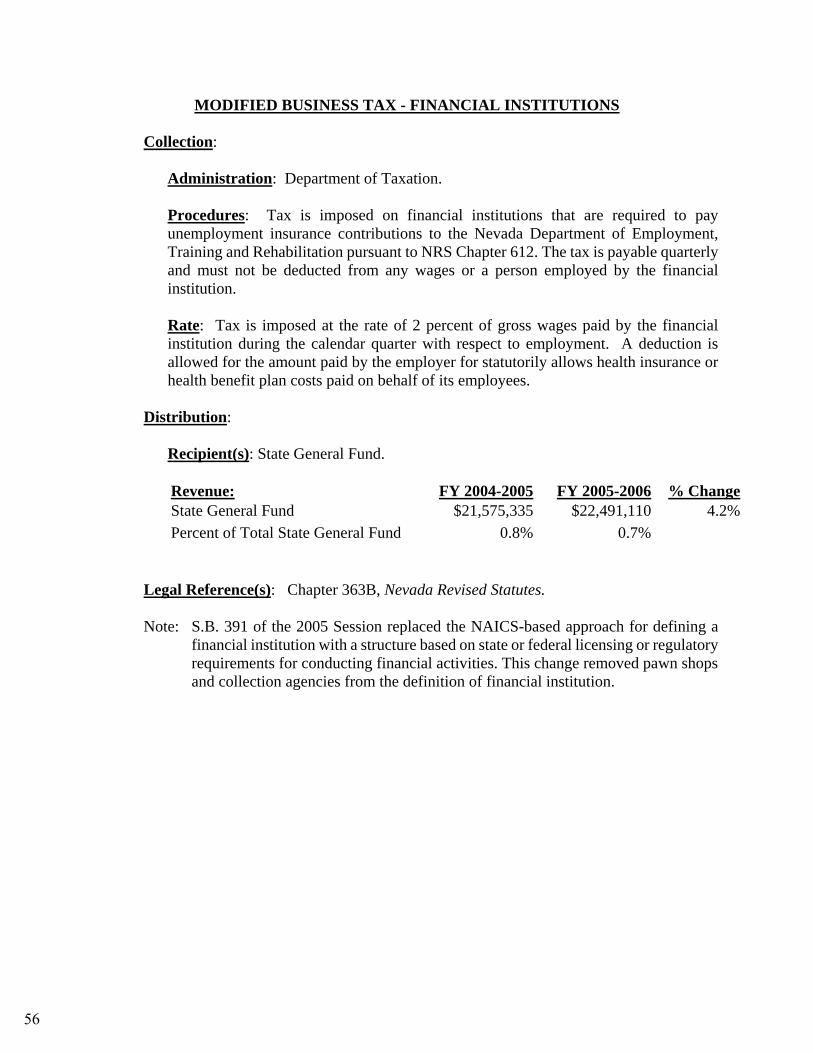

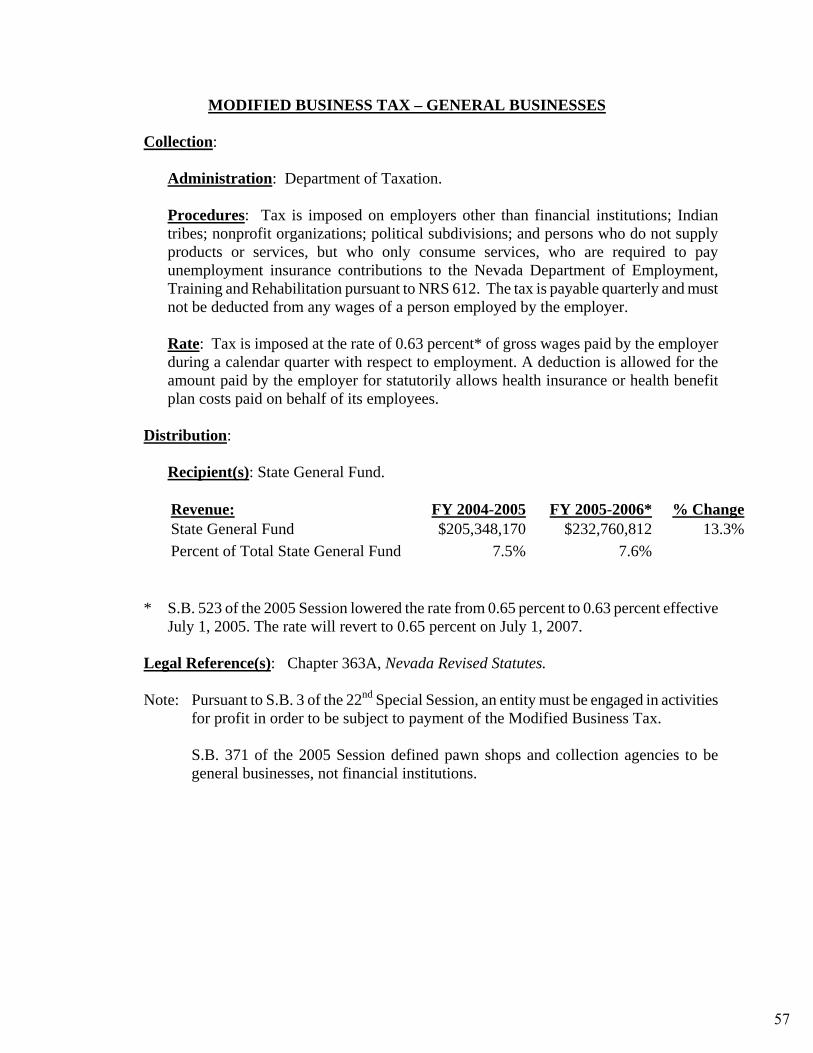

X30

69M

BT

- Non

finan

cial

[10-

FY04

][5-F

Y06

][6-F

Y06

][3-F

Y08

]$1

46,1

61,8

12$2

05,3

48,1

7040

.5%

$232

,760

,812

13.3

%$2

62,1

58,0

0012

.6%

$293

,355

,000

11.9

%$3

16,8

23,0

008.

0%30

69M

BT

- Fin

anci

al [1

1-FY

04][5

-FY

06]

$15,

487,

677

$21,

575,

335

39.3

%$2

2,49

1,11

04.

2%$2

4,71

2,00

09.

9%$2

7,07

5,00

09.

6%$2

9,64

2,00

09.

5%To

tal M

odifi

ed B

usin

ess

Tax

$161

,649

,489

$226

,923

,505

$255

,251

,922

$286

,870

,000

12.4

%$3

20,4

30,0

0011

.7%

$346

,465

,000

8.1%

3068

Bra

nch

Ban

k E

xcis

e Ta

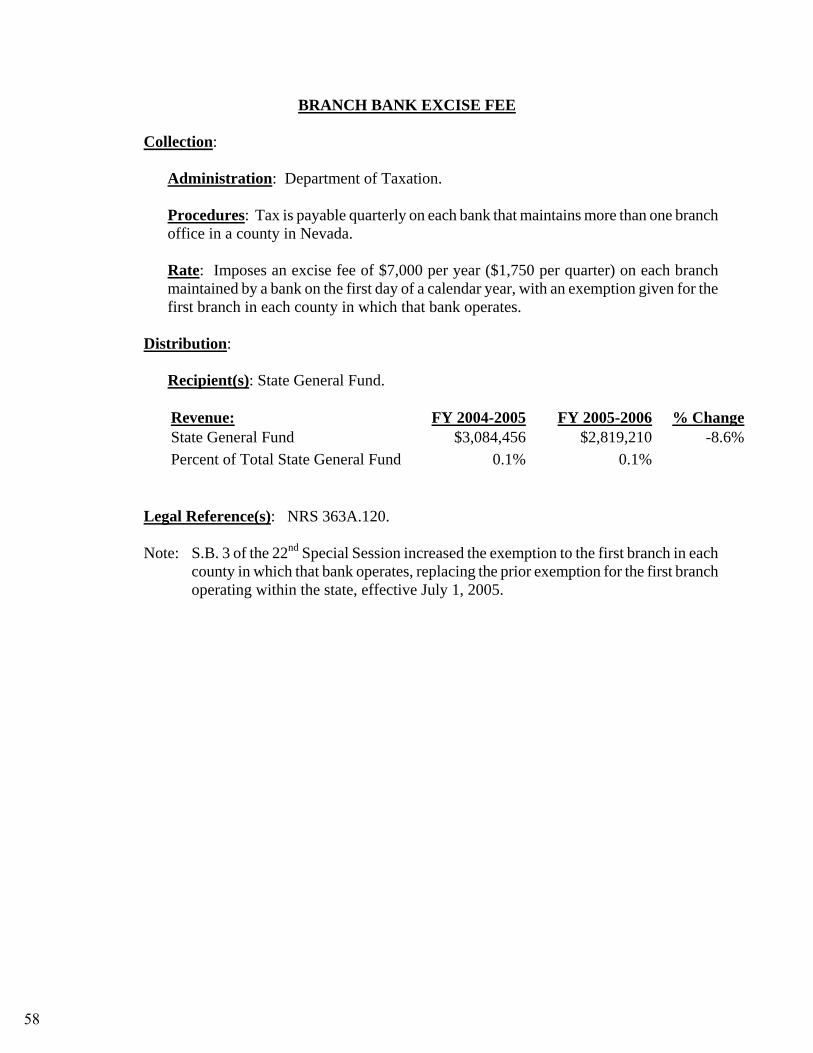

x [1

2-FY

04][7

-FY

06]

$1,5

08,1

92$3

,084

,456

104.

5%$2

,819

,210

-8.6

%$2

,905

,000

3.0%

$2,9

40,0

001.

2%$2

,975

,000

1.2%

3055

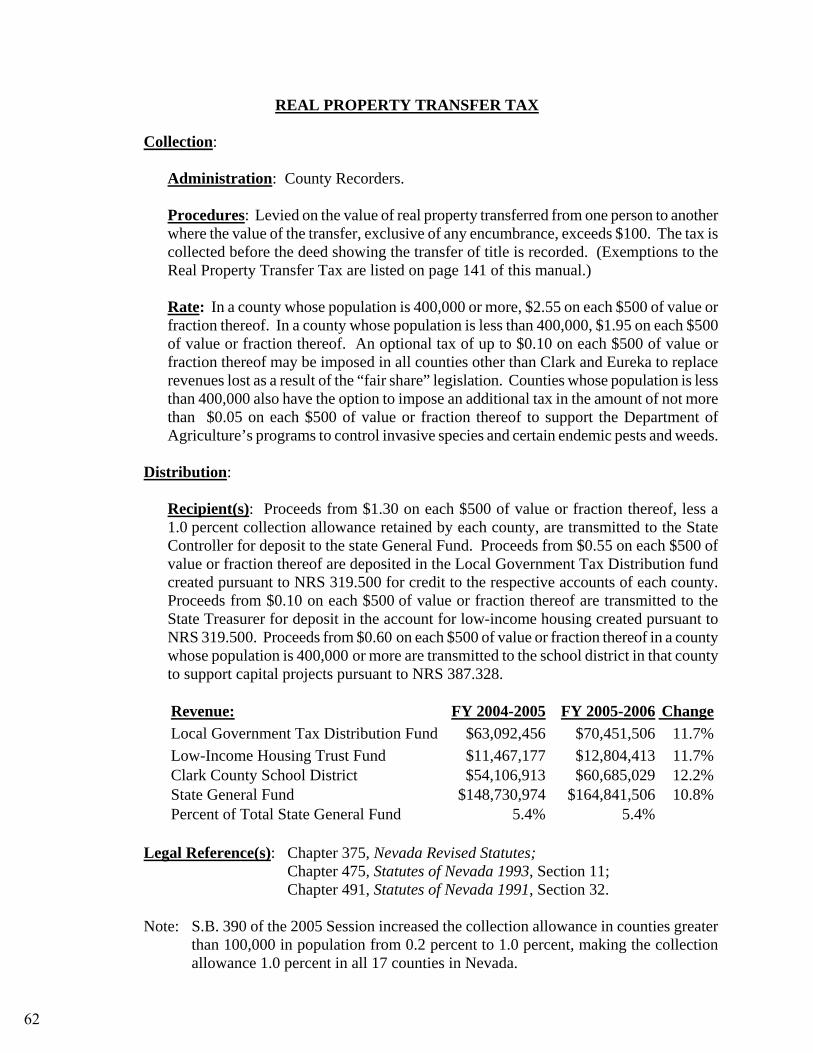

Rea

l Pro

perty

Tra

nsfe

r Tax

[13-

FY04

][8-F

Y06

]$8

8,02

4,73

8$1

48,7

30,9

7469

.0%

$164

,841

,506

10.8

%$1

23,7

35,0

00-2

4.9%

$124

,166

,000

0.3%

$134

,880

,000

8.6%

TOTA

L TA

XE

S$1

,696

,010

,111

4.5%

$2,2

42,7

07,7

6832

.2%

$2,5

59,6

87,3

9414

.1%

$2,8

29,0

08,5

0410

.5%

$2,9

25,4

62,5

003.

4%$3

,106

,940

,700

6.2%

$3,3

38,3

80,3

007.

4%

7

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU

M N

OVE

MB

ER 3

0, 2

006

FOR

ECA

ST

NO

VEM

BER

30,

200

6 EC

ON

OM

IC F

OR

UM

FO

REC

AST

AC

TUA

L: F

Y 20

03 T

HR

OU

GH

FY

2006

AN

D F

OR

ECA

ST: F

Y 20

07 T

HR

OU

GH

FY

2009

ECO

NO

MIC

FO

RU

M'S

FO

REC

AST

FO

R F

Y 20

07, F

Y 20

08, A

ND

FY

2009

APP

RO

VED

AT

THE

NO

VEM

BER

30,

200

6 M

EETI

NG

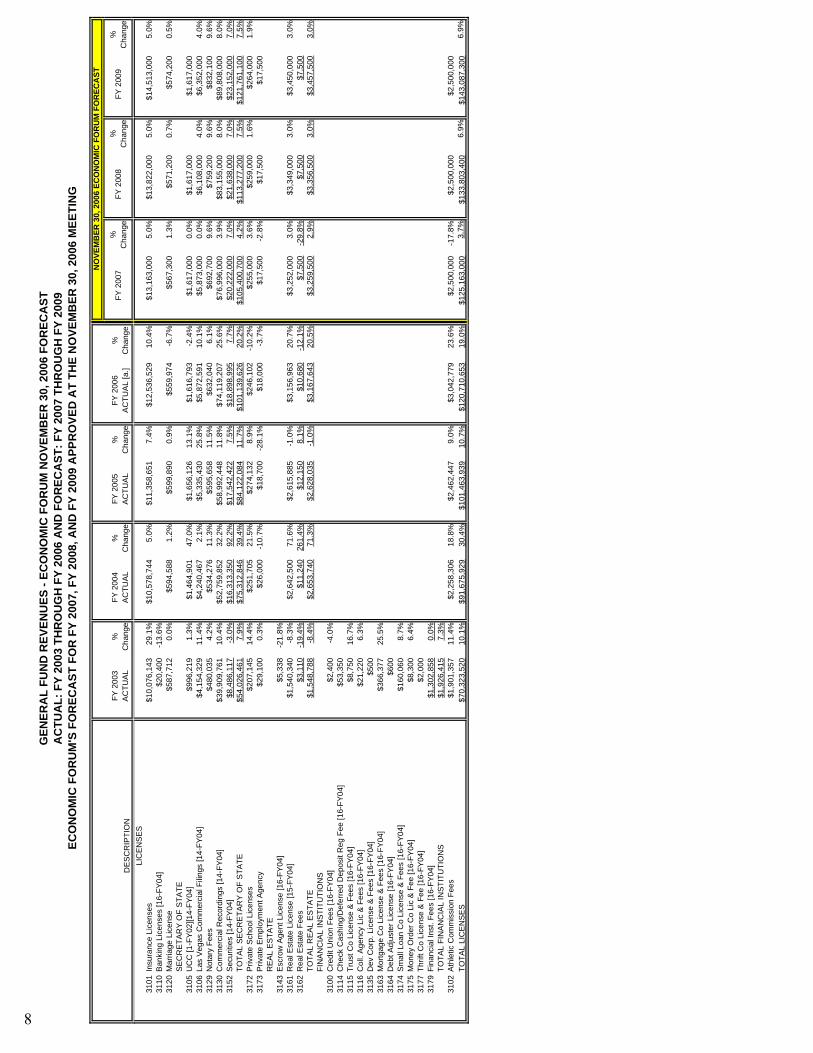

LIC

EN

SE

S31

01In

sura

nce

Lice

nses

$10,

076,

143

29.1

%$1

0,57

8,74

45.

0%$1

1,35

8,65

17.

4%$1

2,53

6,52

910

.4%

$13,

163,

000

5.0%

$13,

822,

000

5.0%

$14,

513,

000

5.0%

3110

Ban

king

Lic

ense

s [1

6-FY

04]

$20,

400

-13.

6%31

20M

arria

ge L

icen

se$5

87,7

120.

0%$5

94,5

881.

2%$5

99,8

900.

9%$5

59,9

74-6

.7%

$567

,300

1.3%

$571

,200

0.7%

$574

,200

0.5%

SE

CR

ETA

RY

OF

STA

TE31

05U

CC

[1-F

Y02

][14-

FY04

]$9

96,2

191.

3%$1

,464

,901

47.0

%$1

,656

,126

13.1

%$1

,616

,793

-2.4

%$1

,617

,000

0.0%

$1,6

17,0

00$1

,617

,000

3106

Las

Veg

as C

omm

erci

al F

iling

s [1

4-FY

04]

$4,1

54,3

2911

.4%

$4,2

40,4

672.

1%$5

,335

,430

25.8

%$5

,872

,591

10.1

%$5

,873

,000

0.0%

$6,1

08,0

004.

0%$6

,352

,000

4.0%

3129

Not

ary

Fees

$480

,035

4.2%

$534

,276

11.3

%$5

95,6

5811

.5%

$632

,040

6.1%

$692

,700

9.6%

$759

,200

9.6%

$832

,100

9.6%

3130

Com

mer

cial

Rec

ordi

ngs

[14-

FY04

]$3

9,90

9,76

110

.4%

$52,

759,

852

32.2

%$5

8,99

2,44

811

.8%

$74,

119,

207

25.6

%$7

6,99

6,00

03.

9%$8

3,15

5,00

08.

0%$8

9,80

8,00

08.

0%31

52S

ecur

ities

[14-

FY04

]$8

,486

,117

-3.0

%$1

6,31

3,35

092

.2%

$17,

542,

422

7.5%

$18,

898,

995

7.7%

$20,

222,

000

7.0%

$21,

638,

000

7.0%

$23,

152,

000

7.0%

TOTA

L S

EC

RE

TAR

Y O

F S

TATE

$54,

026,

461

7.9%

$75,

312,

846

39.4

%$8

4,12

2,08

411

.7%

$101

,139

,626

20.2

%$1

05,4

00,7

004.

2%$1

13,2

77,2

007.

5%$1

21,7

61,1

007.

5%31

72P

rivat

e S

choo

l Lic

ense

s$2

07,1

4514

.4%

$251

,705

21.5

%$2

74,1

328.

9%$2

46,1

02-1

0.2%

$255

,000

3.6%

$259

,000

1.6%

$264

,000

1.9%

3173

Priv

ate

Em

ploy

men

t Age

ncy

$29,

100

0.3%

$26,

000

-10.

7%$1

8,70

0-2

8.1%

$18,

000

-3.7

%$1

7,50

0-2

.8%

$17,

500

$17,

500

RE

AL

ES

TATE

3143

Esc

row

Age

nt L

icen

se [1

6-FY

04]

$5,3

38-2

1.8%

3161

Rea

l Est

ate

Lice

nse

[15-

FY04

]$1

,540

,340

-8.3

%$2

,642

,500

71.6

%$2

,615

,885

-1.0

%$3

,156

,963

20.7

%$3

,252

,000

3.0%

$3,3

49,0

003.

0%$3

,450

,000

3.0%

3162

Rea

l Est

ate

Fees

$3,1

10-1

9.4%

$11,

240

261.

4%$1

2,15

08.

1%$1

0,68

0-1

2.1%

$7,5

00-2

9.8%

$7,5

00$7

,500

TOTA

L R

EA

L E

STA

TE$1

,548

,788

-8.4

%$2

,653

,740

71.3

%$2

,628

,035

-1.0

%$3

,167

,643

20.5

%$3

,259

,500

2.9%

$3,3

56,5

003.

0%$3

,457

,500

3.0%

FIN

AN

CIA

L IN

STI

TUTI

ON

S31

00C

redi

t Uni

on F

ees

[16-

FY04

]$2

,400

-4.0

%31

14C

heck

Cas

hing

/Def

erre

d D

epos

it R

eg F

ee [1

6-FY

04]

$53,

350

3115

Trus

t Co

Lice

nse

& F

ees

[16-

FY04

]$8

,750

16.7

%31

16C

oll.

Age

ncy

Lic

& F

ees

[16-

FY04

]$2

1,22

06.

3%31

35D

ev C

orp.

Lic

ense

& F

ees

[16-

FY04

]$5

0031

63M

ortg

age

Co

Lice

nse

& F

ees

[16-

FY04

]$3

66,3

7725

.5%

3164

Deb

t Adj

uste

r Lic

ense

[16-

FY04

]$6

0031

74S

mal

l Loa

n C

o Li

cens

e &

Fee

s [1

6-FY

04]

$160

,060

8.7%

3175

Mon

ey O

rder

Co

Lic

& F

ee [1

6-FY

04]

$8,3

006.

4%31

77Th

rift C

o Li

cens

e &

Fee

[16-

FY04

]$2

,000

3179

Fina

ncia

l Ins

t. Fe

es [1

6-FY

04]

$1,3

02,8

580.

0%TO

TAL

FIN

AN

CIA

L IN

STI

TUTI

ON

S$1

,926

,415

7.3%

3102

Ath

letic

Com

mis

sion

Fee

s $1

,901

,357

11.4

%$2

,258

,306

18.8

%$2

,462

,447

9.0%

$3,0

42,7

7923

.6%

$2,5

00,0

00-1

7.8%

$2,5

00,0

00$2

,500

,000

TOTA

L LI

CE

NS

ES

$70,

323,

520

10.1

%$9

1,67

5,92

930

.4%

$101

,463

,939

10.7

%$1

20,7

10,6

5319

.0%

$125

,163

,000

3.7%

$133

,803

,400

6.9%

$143

,087

,300

6.9%

8

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU

M N

OVE

MB

ER 3

0, 2

006

FOR

ECA

ST

NO

VEM

BER

30,

200

6 EC

ON

OM

IC F

OR

UM

FO

REC

AST

AC

TUA

L: F

Y 20

03 T

HR

OU

GH

FY

2006

AN

D F

OR

ECA

ST: F

Y 20

07 T

HR

OU

GH

FY

2009

ECO

NO

MIC

FO

RU

M'S

FO

REC

AST

FO

R F

Y 20

07, F

Y 20

08, A

ND

FY

2009

APP

RO

VED

AT

THE

NO

VEM

BER

30,

200

6 M

EETI

NG

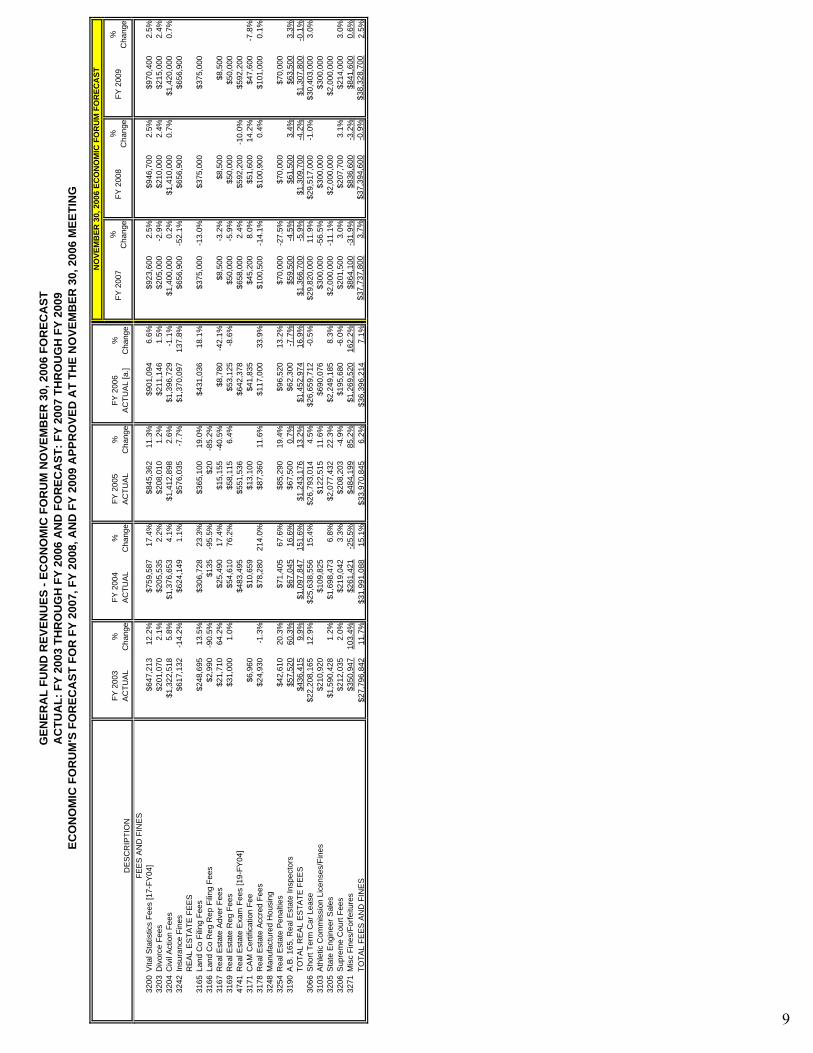

FEE

S A

ND

FIN

ES

3200

Vita

l Sta

tistic

s Fe

es [1

7-FY

04]

$647

,213

12.2

%$7

59,5

8717

.4%

$845

,362

11.3

%$9

01,0

946.

6%$9

23,6

002.

5%$9

46,7

002.

5%$9

70,4

002.

5%32

03D

ivor

ce F

ees

$201

,070

2.1%

$205

,535

2.2%

$208

,010

1.2%

$211

,146

1.5%

$205

,000

-2.9

%$2

10,0

002.

4%$2

15,0

002.

4%32

04C

ivil

Act

ion

Fees

$1,3

22,5

185.

8%$1

,376

,653

4.1%

$1,4

12,8

982.

6%$1

,396

,729

-1.1

%$1

,400

,000

0.2%

$1,4

10,0

000.

7%$1

,420

,000

0.7%

3242

Insu

ranc

e Fi

nes

$617

,132

-14.

2%$6

24,1

491.

1%$5

76,0

35-7

.7%

$1,3

70,0

9713

7.8%

$656

,900

-52.

1%$6

56,9

00$6

56,9

00R

EA

L E

STA

TE F

EE

S31

65La

nd C

o Fi

ling

Fees

$248

,695

13.5

%$3

06,7

2823

.3%

$365

,100

19.0

%$4

31,0

3618

.1%

$375

,000

-13.

0%$3

75,0

00$3

75,0

0031

66La

nd C

o R

eg R

ep F

iling

Fee

s$2

,990

-90.

5%$1

35-9

5.5%

$20

-85.

2%31

67R

eal E

stat

e A

dver

Fee

s$2

1,71

064

.2%

$25,

490

17.4

%$1

5,15

5-4

0.5%

$8,7

80-4

2.1%

$8,5

00-3

.2%

$8,5

00$8

,500

3169

Rea

l Est

ate

Reg

Fee

s$3

1,00

01.

0%$5

4,61

076

.2%

$58,

115

6.4%

$53,

125

-8.6

%$5

0,00

0-5

.9%

$50,

000

$50,

000

4741

Rea

l Est

ate

Exa

m F

ees

[19-

FY04

]$4

83,4

95$5

51,5

36$6

42,3

78$6

58,0

002.

4%$5

92,2

00-1

0.0%

$592

,200

3171

CA

M C

ertif

icat

ion

Fee

$6,9

60$1

0,65

9$1

3,10

0$4

1,83

5$4

5,20

08.

0%$5

1,60

014

.2%

$47,

600

-7.8

%31

78R

eal E

stat

e A

ccre

d Fe

es$2

4,93

0-1

.3%

$78,

280

214.

0%$8

7,36

011

.6%

$117

,000

33.9

%$1

00,5

00-1

4.1%

$100

,900

0.4%

$101

,000

0.1%

3248

Man

ufac

ture

d H

ousi

ng32

54R

eal E

stat

e P

enal

ties

$42,

610

20.3

%$7

1,40

567

.6%

$85,

290

19.4

%$9

6,52

013

.2%

$70,

000

-27.

5%$7

0,00

0$7

0,00

031

90A

.B. 1

65, R

eal E

stat

e In

spec

tors

$57,

520

60.3

%$6

7,04

516

.6%

$67,

500

0.7%

$62,

300

-7.7

%$5

9,50

0-4

.5%

$61,

500

3.4%

$63,

500

3.3%

TOTA

L R

EA

L E

STA

TE F

EE

S$4

36,4

159.

9%$1

,097

,847

151.

6%$1

,243

,176

13.2

%$1

,452

,974

16.9

%$1

,366

,700

-5.9

%$1

,309

,700

-4.2

%$1

,307

,800

-0.1

%30

66S

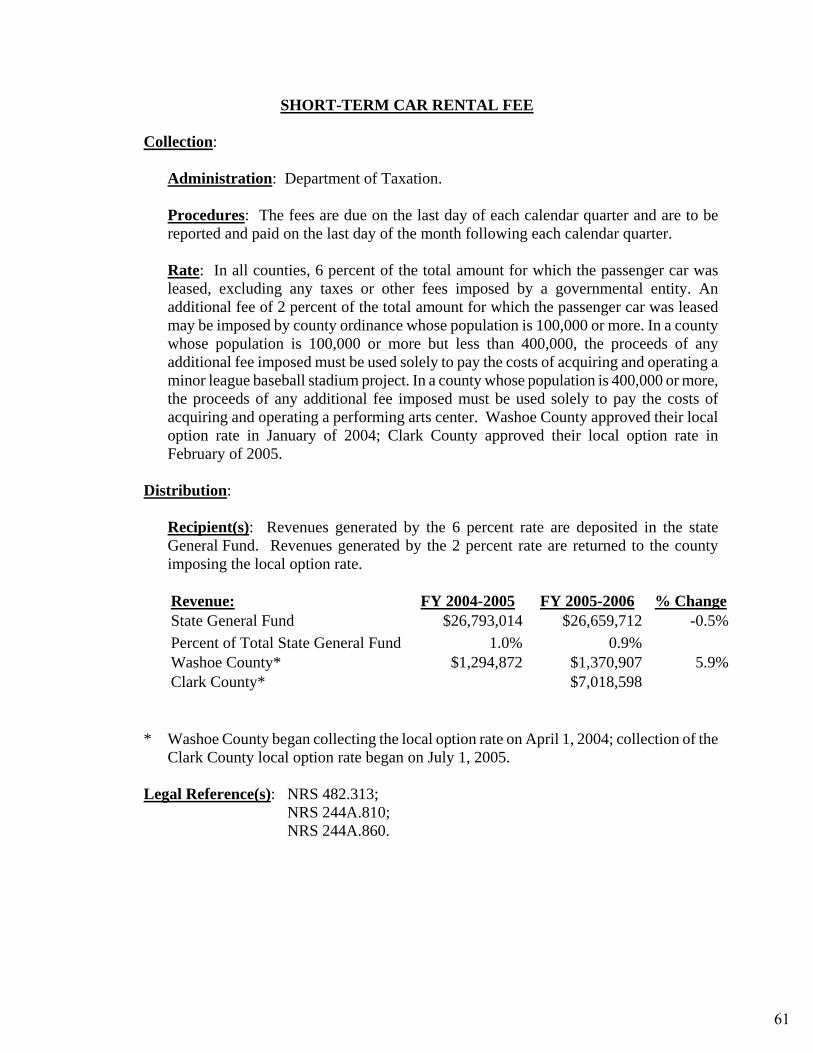

hort

Term

Car

Lea

se

$22,

208,

165

12.9

%$2

5,63

8,55

615

.4%

$26,

793,

014

4.5%

$26,

659,

712

-0.5

%$2

9,82

0,00

011

.9%

$29,

517,

000

-1.0

%$3

0,40

3,00

03.

0%31

03A

thle

tic C

omm

issi

on L

icen

ses/

Fine

s $2

10,9

20$1

09,8

25$1

22,5

1511

.6%

$690

,076

$300

,000

-56.

5%$3

00,0

00$3

00,0

0032

05S

tate

Eng

inee

r Sal

es

$1,5

90,4

281.

2%$1

,698

,473

6.8%

$2,0

77,4

3222

.3%

$2,2

49,1

858.

3%$2

,000

,000

-11.

1%$2

,000

,000

$2,0

00,0

0032

06S

upre

me

Cou

rt Fe

es$2

12,0

352.

0%$2

19,0

423.

3%$2

08,2

03-4

.9%

$195

,680

-6.0

%$2

01,5

003.

0%$2

07,7

003.

1%$2

14,0

003.

0%32

71M

isc

Fine

s/Fo

rfeitu

res

$350

,947

103.

4%$2

61,4

21-2

5.5%

$484

,199

85.2

%$1

,269

,520

162.

2%$8

64,1

00-3

1.9%

$836

,600

-3.2

%$8

41,6

000.

6%TO

TAL

FEE

S A

ND

FIN

ES

$27,

796,

842

11.7

%$3

1,99

1,08

815

.1%

$33,

970,

845

6.2%

$36,

396,

214

7.1%

$37,

737,

800

3.7%

$37,

394,

600

-0.9

%$3

8,32

8,70

02.

5%

9

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU

M N

OVE

MB

ER 3

0, 2

006

FOR

ECA

ST

NO

VEM

BER

30,

200

6 EC

ON

OM

IC F

OR

UM

FO

REC

AST

AC

TUA

L: F

Y 20

03 T

HR

OU

GH

FY

2006

AN

D F

OR

ECA

ST: F

Y 20

07 T

HR

OU

GH

FY

2009

ECO

NO

MIC

FO

RU

M'S

FO

REC

AST

FO

R F

Y 20

07, F

Y 20

08, A

ND

FY

2009

APP

RO

VED

AT

THE

NO

VEM

BER

30,

200

6 M

EETI

NG

US

E O

F M

ON

EY

AN

D P

RO

P44

20Ly

on C

ount

y R

epay

men

tsO

THE

R R

EP

AY

ME

NTS

4401

Hig

her E

duca

tion

Tuiti

on A

dmin

$1,8

68$2

5,00

0$2

5,00

0$1

25,0

00$1

75,0

00$2

25,0

00$2

75,0

0044

04B

ldg.

and

Gro

unds

Rep

aym

ents

$97,

421

$97,

421

$97,

421

$97,

421

$63,

157

$47,

413

$21,

103

4404

CIP

95-

C14

, Mai

lroom

Rem

odel

$21,

122

$21,

122

$21,

122

$21,

122

$21,

122

$21,

122

$21,

122

4405

Pris

on In

dust

ry R

epay

men

t$2

5,00

044

07P

rintin

g R

epay

men

t [18

-FY

04]

4408

Com

p/Fa

c R

epay

men

t$4

7,48

8$2

3,74

4$2

3,74

4$2

3,74

4$2

3,74

4$2

3,74

4$2

3,74

444

08C

omp/

Fac

- CIP

85-

6044

08C

IP 8

9-11

Com

pute

r Fac

ility

4408

CIP

95-

M1,

Sec

urity

Ala

rm

$5,9

95$2

,998

$2,9

98$2

,998

$2,9

98$2

,998

$2,9

9844

08C

IP 9

5-M

5, F

acili

ty G

ener

ator

$13,

748

$6,8

74$6

,874

$6,8

74$6

,874

$6,8

74$6

,874

4408

CIP

95-

S4F

, Adv

ance

Pla

nnin

g$1

,000

$1,0

00$1

,000

$1,0

00$1

,000

$1,0

00$1

,000

4408

CIP

97-

C26

, Cap

itol C

ompl

ex C

ondu

it S

yste

m, P

hase

I$1

27,0

00$6

2,54

2$6

2,54

2$6

2,54

2$6

2,54

2$6

2,54

2$6

2,54

244

08C

IP 9

7-S

4H, A

dvan

ce P

lann

ing

Add

ition

to C

ompu

ter F

acili

ty$9

6,24

0$9

,107

$9,1

07$9

,107

$9,1

07$9

,107

$9,1

0744

08S

.B. 2

01, 1

997;

Cos

t of P

BX

Sys

tem

$249

,967

$249

,967

$249

,967

$249

,967

$249

,967

$249

,967

$249

,967

4408

A.B

. 576

-Virt

ual T

ape

Sto

rage

$4

63,4

44$4

63,4

44$4

63,4

44Fo

rest

ry N

urse

ries

Fund

Rep

aym

ent (

05-M

27)

$26,

250

$26,

250

$26,

250

4409

Mot

or P

ool R

epay

- C

arso

n$2

0,17

6$2

0,17

6$2

0,17

6$2

0,17

6$2

0,17

644

09M

otor

Poo

l Rep

ay -

Ren

o$2

4,38

5$2

4,38

5$2

4,38

5$2

4,38

5$2

4,38

5$2

4,38

5$2

4,38

544

09M

otor

Poo

l Rep

ay -

LV$6

,638

$6,6

38$6

,638

$6,6

38$6

,638

$6,6

38$6

,638

NE

WE

qual

Rig

hts

Rep

aym

ent (

SB

387

)44

10P

urch

asin

g R

epay

men

t$1

5,23

7$1

5,95

7$1

6,72

2$1

7,53

7$1

8,40

4$1

9,32

6$2

0,30

848

65S

tate

Per

sonn

el IF

S R

epay

men

t; S

.B. 2

01, 1

997

Legi

slat

ure

$1,6

51,9

91$1

,441

,807

$1,5

32,3

81$1

,532

,381

$1,7

57,2

0814

.7%

$1,6

44,7

94-6

.4%

$1,6

44,7

94TO

TAL

OTH

ER

RE

PA

YM

EN

TS$2

,405

,277

158.

1%$2

,008

,738

-16.

5%$2

,100

,078

4.5%

$2,2

00,8

924.

8%$2

,932

,015

33.2

%$2

,834

,604

-3.3

%$2

,859

,275

0.9%

4406

Mar

lette

Rep

aym

ent

$10,

512

$10,

512

$10,

512

$10,

664

1.4%

$10,

664

$10,

664

$10,

664

4411

Col

orad

o R

iver

Rep

aym

ent

INTE

RE

ST

INC

OM

E32

90Tr

easu

rer

$5,9

27,4

49-5

2.5%

$4,4

71,1

64-2

4.6%

$13,

543,

085

202.

9%$3

2,66

5,64

714

1.2%

$48,

372,

000

48.1

%$3

5,50

3,00

0-2

6.6%

$28,

799,

000

-18.

9%32

91O

ther

$6

2,59

843

4.6%

$57,

469

-8.2

%$1

42,7

8414

8.5%

$267

,721

87.5

%$1

57,8

00-4

1.1%

$206

,900

31.1

%$2

55,9

0023

.7%

TOTA

L IN

TER

ES

T IN

CO

ME

$5,9

90,0

47-5

2.1%

$4,5

28,6

33-2

4.4%

$13,

685,

869

202.

2%$3

2,93

3,36

814

0.6%

$48,

529,

800

47.4

%$3

5,70

9,90

0-2

6.4%

$29,

054,

900

-18.

6%TO

TAL

US

E O

F M

ON

EY

& P

RO

P$8

,405

,836

-37.

5%$6

,547

,883

-22.

1%$1

5,79

6,45

814

1.2%

$35,

144,

924

122.

5%$5

1,47

2,47

946

.5%

$38,

555,

168

-25.

1%$3

1,92

4,83

9-1

7.2%

10

DE

SC

RIP

TIO

NFY

200

3 A

CTU

AL

%

Cha

nge

FY 2

004

AC

TUA

L%

C

hang

eFY

200

5 A

CTU

AL

%

Cha

nge

FY 2

006

AC

TUA

L [a

.]%

C

hang

eFY

200

7%

C

hang

eFY

200

8%

C

hang

eFY

200

9%

C

hang

e

GEN

ERA

L FU

ND

REV

ENU

ES -

ECO

NO

MIC

FO

RU