Brokers' Adoption of Net Stock Trading: A Study

11

ISSN (Print): 2328-3734, ISSN (Online): 2328-3696, ISSN (CD-ROM): 2328-3688 American International Journal of Research in Humanities, Arts and Social Sciences AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 14 AIJRHASS is a refereed, indexed, peer-reviewed, multidisciplinary and open access journal published by International Association of Scientific Innovation and Research (IASIR), USA (An Association Unifying the Sciences, Engineering, and Applied Research) Available online at http://www.iasir.net Brokers’ Adoption of Net Stock Trading: A Study Dr. Arwinder Singh Assistant Professor, Department of Business Management Guru Nanak Dev University Regional Campus Hardochanni Road, Gurdaspur, India (Punjab) Abstract: The purpose of this paper was to examine whether brokers who adopted Net stock trading perceived differently from those of non-net based brokers. The primary data based on 196 brokers (92 brokers and 104 non-net based brokers) were analyzed using advanced multivariate techniques like factor analysis and discriminant analysis besides percentages, means, and Z-test. Results clearly indicated that demographics relative to attitude dimensions were fairly strong in classifying brokers as Net brokers or non-Net brokers. As regards demographics, young brokers were more adaptable to the latest Internet technology as a medium of providing trading facility in comparison to aged and experienced brokers due to lack of education and awareness about this medium. As for as the attitude dimensions were concerned, ‘economic, convenience and transparency’ contributed significantly in discriminating between Net brokers and non-Net brokers. Keywords: Net stock trading; Brokers; Attitude; Demographic variables; Discriminant analysis; India. I. Introduction Internet, which has emerged as a result of convergence between telecommunication and computers, is revolutionizing the way business is done. The natural extension of e-commerce in the securities market is Net broking services (Nagree and Monie, 2001). In the mid-nineties, screen-based trading changed the face of Indian stock markets. Thereafter, dematerialization emerged, which further increased the comfort factor for investors. Now, it is Internet trading that is promising to take the investing experience to another plane (Chhabria, 2000). The Securities and Exchange Board of India introduced the Internet-based securities trading and services guidelines on January 31, 2000. While the National Stock Exchange was the first exchange to grant approval to its members for providing Internet-based trading services, the members of the stock exchange, Mumbai could avail of Internet trading services through BSE WEBX (Nagree and Monie, 2001). Internet-based trading is essentially a combination of the capabilities of the internet and trading services to facilitate virtual stock transactions. With the availability of internet trading, investors can now examine their portfolios, issue instructions, and buy and sell stocks over the internet. Furthermore, internet trading houses also provide stock market information such as real time stock quotes, information on stocks and the companies, on their web sites for customers. The convenience of the internet has allowed stock investors fast and easy access to stock trading thus allowing more people to invest in the stocks (Insight Xplorer, 2007). Besides, with the increase in internet trading, geographic location has become irrelevant with the ability for foreign investors to trade from overseas (Yap and Lin, 2001). Online trading offers broking service industry with high profit and is one of the areas which completely satisfy ecommerce (Wu et al., 2012). E-brokerages have also allowed brokers wider access to a variety of different people, therefore increasing their client base and allowing them to offer many different types of services to their customers. Ameritrade and E-Trade are examples of firms that have found new ways to deliver traditional services and new services (Barber and Odean, 2001). Significance and objectives of the study There is no denying the fact that in the past two decades information technology has become the most rapidly changing industry in the world. But more than the rate of change, what is remarkable is the way IT has changed the paradigms of business in other industries. One industry that has really felt the impact of IT is the share broking business (Dasgupta, 2002). The stockbroking industry is one of the most successful industries in the adoption and diffusion of ICT in its operations (Shankar, 2002). Safe Scrypt is the first licensed certifying authority in the country to issue digital signatures under the Information Technology Act, 2000. ICICI Web Trade is the first corporate entity and brokerage to get digital signatures (Gajra, 2002). Since Internet stock trading is relatively a recent phenomenon in India, little work has been done in this regard in the Indian context. No attempt has been made to study as to why demographics and attitudes of Net brokers differ from those of non-Net brokers in relation to Internet as a medium of trading. Therefore, there is need to identify the factors responsible for the adoption of net trading by the brokers. Main purpose of the study is to

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Brokers' Adoption of Net Stock Trading: A Study

ISSN (Print): 2328-3734, ISSN (Online): 2328-3696, ISSN (CD-ROM): 2328-3688

American International Journal of Research in Humanities, Arts and Social Sciences

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 14

AIJRHASS is a refereed, indexed, peer-reviewed, multidisciplinary and open access journal published by International Association of Scientific Innovation and Research (IASIR), USA

(An Association Unifying the Sciences, Engineering, and Applied Research)

Available online at http://www.iasir.net

Brokers’ Adoption of Net Stock Trading: A Study Dr. Arwinder Singh

Assistant Professor, Department of Business Management

Guru Nanak Dev University Regional Campus

Hardochanni Road, Gurdaspur, India (Punjab)

Abstract: The purpose of this paper was to examine whether brokers who adopted Net stock trading perceived

differently from those of non-net based brokers. The primary data based on 196 brokers (92 brokers and 104

non-net based brokers) were analyzed using advanced multivariate techniques like factor analysis and

discriminant analysis besides percentages, means, and Z-test. Results clearly indicated that demographics

relative to attitude dimensions were fairly strong in classifying brokers as Net brokers or non-Net brokers. As

regards demographics, young brokers were more adaptable to the latest Internet technology as a medium of

providing trading facility in comparison to aged and experienced brokers due to lack of education and

awareness about this medium. As for as the attitude dimensions were concerned, ‘economic, convenience and

transparency’ contributed significantly in discriminating between Net brokers and non-Net brokers. Keywords: Net stock trading; Brokers; Attitude; Demographic variables; Discriminant analysis; India.

I. Introduction

Internet, which has emerged as a result of convergence between telecommunication and computers, is

revolutionizing the way business is done. The natural extension of e-commerce in the securities market is Net

broking services (Nagree and Monie, 2001). In the mid-nineties, screen-based trading changed the face of Indian

stock markets. Thereafter, dematerialization emerged, which further increased the comfort factor for investors.

Now, it is Internet trading that is promising to take the investing experience to another plane (Chhabria, 2000).

The Securities and Exchange Board of India introduced the Internet-based securities trading and services

guidelines on January 31, 2000. While the National Stock Exchange was the first exchange to grant approval to

its members for providing Internet-based trading services, the members of the stock exchange, Mumbai could

avail of Internet trading services through BSE WEBX (Nagree and Monie, 2001).

Internet-based trading is essentially a combination of the capabilities of the internet and trading services to

facilitate virtual stock transactions. With the availability of internet trading, investors can now examine their

portfolios, issue instructions, and buy and sell stocks over the internet. Furthermore, internet trading houses also

provide stock market information such as real time stock quotes, information on stocks and the companies, on

their web sites for customers. The convenience of the internet has allowed stock investors fast and easy access to

stock trading thus allowing more people to invest in the stocks (Insight Xplorer, 2007). Besides, with the

increase in internet trading, geographic location has become irrelevant with the ability for foreign investors to

trade from overseas (Yap and Lin, 2001). Online trading offers broking service industry with high profit and is

one of the areas which completely satisfy ecommerce (Wu et al., 2012). E-brokerages have also allowed brokers

wider access to a variety of different people, therefore increasing their client base and allowing them to offer

many different types of services to their customers. Ameritrade and E-Trade are examples of firms that have

found new ways to deliver traditional services and new services (Barber and Odean, 2001).

Significance and objectives of the study There is no denying the fact that in the past two decades information technology has become the most rapidly

changing industry in the world. But more than the rate of change, what is remarkable is the way IT has changed

the paradigms of business in other industries. One industry that has really felt the impact of IT is the share

broking business (Dasgupta, 2002). The stockbroking industry is one of the most successful industries in the

adoption and diffusion of ICT in its operations (Shankar, 2002). Safe Scrypt is the first licensed certifying

authority in the country to issue digital signatures under the Information Technology Act, 2000. ICICI Web

Trade is the first corporate entity and brokerage to get digital signatures (Gajra, 2002).

Since Internet stock trading is relatively a recent phenomenon in India, little work has been done in this regard

in the Indian context. No attempt has been made to study as to why demographics and attitudes of Net brokers

differ from those of non-Net brokers in relation to Internet as a medium of trading. Therefore, there is need to

identify the factors responsible for the adoption of net trading by the brokers. Main purpose of the study is to

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 15

examine the differences in perceptions between net-brokers and non-net brokers regarding the adoption of

Internet as a novel medium of trading. To achieve the main objective, the following were set as sub-objectives:

To analyze whether demographics such as age, income, education and occupational background, trading

experience influence the adoption of Net as a novel channel of trading by the brokers ; and

To investigate whether attitude factors affect the adoption of Net trading by the brokers.

It may be mentioned that in the present study, Net brokers are defined as those who offer a variety of functions

ranging from full trading through the website to features like online stock quotes, information and analysis etc.

(Patel, 2001). ICICIdirect and Indiabulls are fall in the category of Net Brokers. On the other hand, Non-net

brokers are defined as traditional brokers.

II. Literature review

Internet technology use in stock market has become more prevalent with the growth of the Internet and

increasing availability of broadband Internet access. Stockbroking firms have openly adopted information and

communication technology to improve their competitiveness and responsiveness in market conditions. Net

brokers and non-net brokers might be differentiated according to the demographics and attitudinal factors.

Demographics factors such as age and gender were found significant factors in the adoption of Windows 95

(Chau and Hui, 1998). Web-users have been profiled on the basis of their demographic characteristics,

suggesting the influence of sex, education, age and income in the use of several Web-based services. Web-users

were found to be male, highly-educated, with average income and middle-aged or young (Korgaonkar and

Wolin, 1999). In another study, Income and education levels were especially relevant in explaining the use of

Internet services and other technological devices (Guillén, 2002). With regard to the use of online shopping

services, sex, age and income were found significant factors (Bain, 1999). Online shoppers were found to be

predominantly male, younger and wealthier than non-online shoppers (Swinyard and Smith, 2003; Teo, 2001).

Attitude is an important determinant influencing the intention to adopt the system (Davis, 1993; Taylor and

Todd, 1995) and has been found to be an influential element for intention behavior in the use of a spreadsheet

package (Mathieson, 1991). Hartwick and Barki (1994) also identified attitude to be an important factor in

determining an adopter’s intention to continue using the system.

Bhasin (2006) examined e-brokering and how e-brokerage firms can market financial services. He discussed the

benefits of the lower transaction costs and the convenience of online trading for the investor. In a separate article

by Phelan (2001), the difference between full service brokers and online brokers is presented and a discussion

about the need for good online security is examined. Another study by Globerman et al. (2001) assessed how e-

commerce has added to the retail brokerage business. Brokers are now online and thus can provide lower costs

to their customers along with a larger variety of investment information. Yap and Lin (2001) examined how

online trading systems are changing. They think that future online discount brokerage firms will evolve from

systems that provide basic services like low transaction costs, speed, and boundary spanning to systems that will

eventually be able to provide the one-on-one personal advice that online brokerage firms are now missing. Teo

et al. (2004) evaluated the attitudes of people who traded stocks online as well as the attitudes of those who did

not trade online in the Singapore marketplace. Goswami (2003) examined the needs of investors that were

trading online in India. He compared the needs of the investors to what online investing websites were offering

and then tried to bridge the gap between the two. A study of Gopi and Ramayah (2007) identified the factors

that influenced the intention to use internet stock trading among investors in Malaysia. Findings showed that

attitude, subjective norm and perceived behavioral control had a direct positive relationship towards behavioral

intention to use internet stock trading. A study by Huang et al. (2005) indicated that five decision factors such as

organization scale, IT maturity, compatibility, marketing supply, and the cost of web site significantly

distinguished the adopters from the non-adopters in terms of the brokers' decision to adopt an online stock

trading system in Taiwan. Sohail and Shanmugham (2003) found the three major factors affecting the adoption

of Internet banking services, namely, Internet accessibility, awareness, and attitude towards change in Malaysia.

Gharavi et al. (2004) developed a conceptual framework to explore the ICT diffusion in the stockbroking

industry in the context of environmental evolution and selection.

A study by Srijumpa et al. (2007) examined customer satisfaction and dissatisfaction with interpersonal vs.

internet service encounters in Thai retail stockbrokerage. Results showed that customers actually had slightly

higher satisfaction on the Internet than with interpersonal encounters, but dissatisfaction on the internet was

much greater. Orbit-e Consultant's (2000) case study of BSE in India provided technology and business rules

compliance audit of stockbrokers wanting to trade on BSE using the Internet based trading through order routing

system (ITORS). The audit ensured that there were no unfair trade practices being used by a broker's site.

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 16

In recent study, Abroud et al. (2010) found that the variables, namely attitude, subjective norms, usefulness,

knowledge, and self-efficiency had strong relationship with intention to use electronic trading. Furthermore, the

risk variable had a negative relationship with attitude. Besides, the perceived behavioral control, social

demography, and ease of use had weak relationship and proved to possess no effect on the intention of the

investors to engage in internet stock trading at Tehran stock exchange. In another more recent study, Majali

(2012) attempted to investigate empirically the factors that could predict customer’s attitude toward using of ITS

in Jordan through applications of Innovation Diffusion Theory (IDT). The research model consists of six

exogenous variables: perceived usefulness, perceived ease of use, compatibility, trial ability, trust and awareness

and one endogenous variable: attitude toward using of ITS. The structural model demonstrated significant and

positive direct relationships between all of six exogenous variables and ITS. On the basis of the objectives of the

study and literature review, the following hypotheses (H) were proposed :

H1: Age discriminates significantly between net brokers and non-net brokers.

H2: Stock trading experience discriminates significantly between net brokers and non-net brokers.

H3: Education level discriminates significantly between net brokers and non-net brokers.

H4: Occupational background discriminates significantly between net brokers and non-net brokers.

H5: Income discriminates significantly between net brokers and non-net brokers.

H6: Economic, convenience, and transparency discriminates significantly between net brokers & non-net brokers.

H7: Variety, value-added services, and awareness discriminates between significantly net brokers & non-net brokers.

H8: Liquidity and safety discriminates significantly between net brokers and non-net brokers.

III. Research methodology

The instrument

The study was based on primary data generated by using a well-structured, non-disguised and pre-tested

questionnaire. The questionnaire was divided into two major parts : demographics and 7-point attitudinal Likert

scale (1 = strongly disagreed; 7 = strongly agreed). The scale comprised of 22 statements that were designed by

consulting relevant literature (Bagchi, 2002; K-Mailer Universe, 2002; Sharenet Company Ltd., 2003; Patel,

2001) and on-line brokers, investors and financial securities analysts.

The sample

Random sampling was used for data collection. Survey was conducted mainly in North India. Mail response was

very poor despite two reminders. In all, 250 respondents (125 Net brokers and non-Net brokers each) were

contacted and served the questionnaires personally in North India. However, filled up and usable questionnaires

from 196 respondents (92 net brokers and 104 non-net brokers) could be collected. So, the response rate of the

survey was as high as 78 per cent. The profile of sampled net brokers and non-net brokers is shown in Table I. Statistical tools

To analyze the data, multivariate statistical techniques, viz., factor analysis and discriminant analysis were used

besides Z-test. For bringing out the factors discriminating between two groups, discriminant analysis was

employed. The dependent variable was categorized as Net brokers and non-Net brokers. The independent

variables included two sets of dimensions. These were: (i) demographic dimensions, viz., age, income,

education, occupational background of parents/guardians, and stock trading experience; and (ii) attitude

dimensions. It may be mentioned that attitude dimensions were derived through a sequential two-step procedure

of Z-test and factor analysis. Initially, Z-test was conducted to identify attitude items which aided in

discriminating between the two groups. The resulting significant items were subjected to factor analysis to

derive the attitude dimensions/factors.

Reliability

A reliability analysis was performed using Cronbach’s alpha. The Cronbach’s alpha values for all factors ranged

from 0.77 to 0.88 (Table III) that indicated reliability of the sub-scales measuring the attitude of brokers (Hair

et al., 2005). The data, therefore, was found reliable. The composite alpha for entire scale was as high as 0.91.

IV. Empirics and analysis

Results

This section presents the empirics and analysis. As already mentioned, sequential two-step procedure of Z-test

and factor analysis was used to identify the attitude dimensions used as independent variables in discriminant

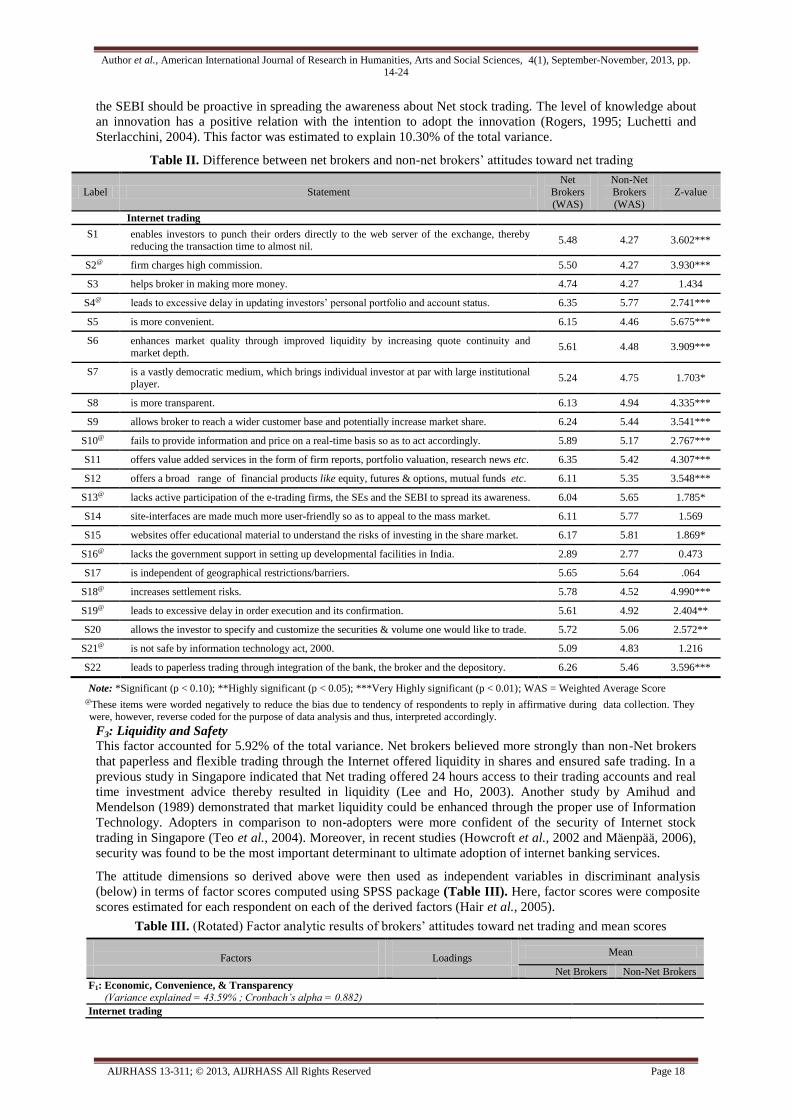

analysis. Results of Z-test employed on 22 attitude items are reported in Table II. It was found that significant

differences existed between the two groups of brokers with regard to 17 of the 22 attitude items. Thus, five

items, which did not contribute significantly for classifying the respondents as Net brokers or Non-Net brokers

were dropped from subsequent analysis.

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 17

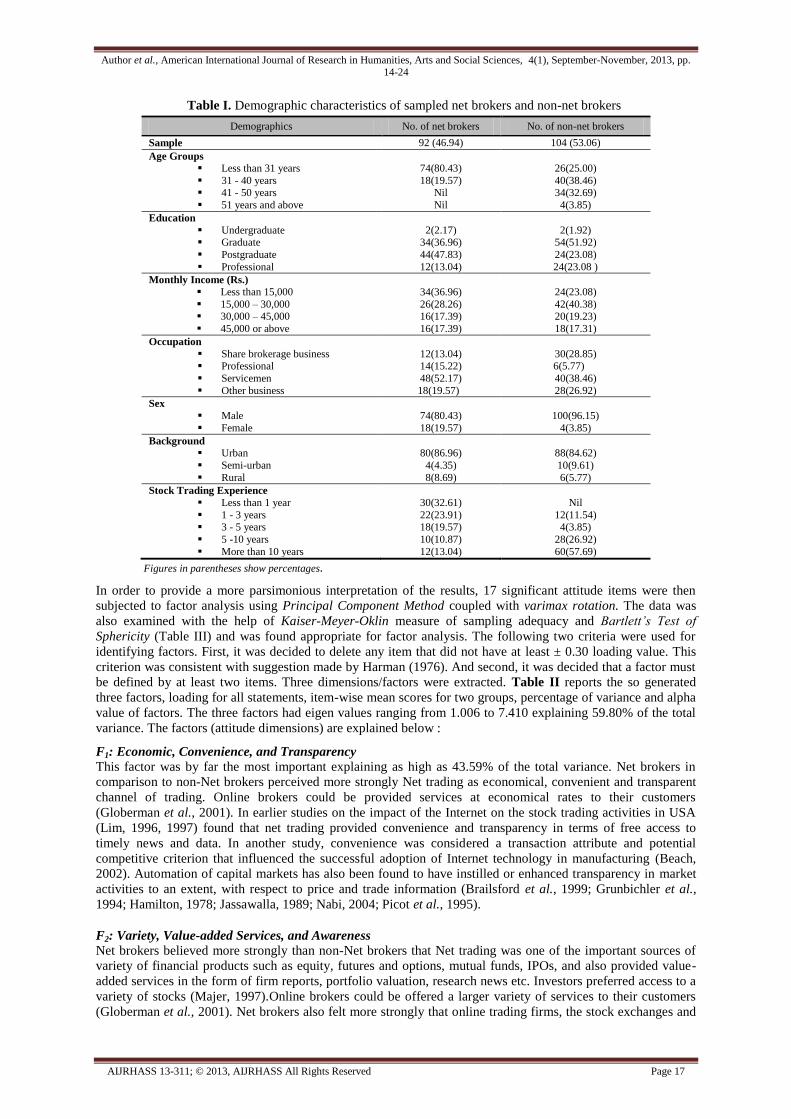

Table I. Demographic characteristics of sampled net brokers and non-net brokers

Demographics No. of net brokers No. of non-net brokers

Sample 92 (46.94) 104 (53.06)

Age Groups

Less than 31 years

31 - 40 years 41 - 50 years

51 years and above

74(80.43)

18(19.57) Nil

Nil

26(25.00)

40(38.46) 34(32.69)

4(3.85)

Education

Undergraduate Graduate

Postgraduate

Professional

2(2.17) 34(36.96)

44(47.83)

12(13.04)

2(1.92) 54(51.92)

24(23.08)

24(23.08 )

Monthly Income (Rs.) Less than 15,000

15,000 – 30,000 30,000 – 45,000

45,000 or above

34(36.96)

26(28.26) 16(17.39)

16(17.39)

24(23.08)

42(40.38) 20(19.23)

18(17.31)

Occupation

Share brokerage business Professional

Servicemen

Other business

12(13.04) 14(15.22)

48(52.17)

18(19.57)

30(28.85) 6(5.77)

40(38.46)

28(26.92)

Sex

Male

Female

74(80.43)

18(19.57)

100(96.15)

4(3.85)

Background

Urban

Semi-urban

Rural

80(86.96)

4(4.35)

8(8.69)

88(84.62)

10(9.61)

6(5.77)

Stock Trading Experience

Less than 1 year

1 - 3 years 3 - 5 years

5 -10 years

More than 10 years

30(32.61)

22(23.91) 18(19.57)

10(10.87)

12(13.04)

Nil

12(11.54) 4(3.85)

28(26.92)

60(57.69)

Figures in parentheses show percentages. In order to provide a more parsimonious interpretation of the results, 17 significant attitude items were then

subjected to factor analysis using Principal Component Method coupled with varimax rotation. The data was

also examined with the help of Kaiser-Meyer-Oklin measure of sampling adequacy and Bartlett’s Test of

Sphericity (Table III) and was found appropriate for factor analysis. The following two criteria were used for

identifying factors. First, it was decided to delete any item that did not have at least ± 0.30 loading value. This

criterion was consistent with suggestion made by Harman (1976). And second, it was decided that a factor must

be defined by at least two items. Three dimensions/factors were extracted. Table II reports the so generated

three factors, loading for all statements, item-wise mean scores for two groups, percentage of variance and alpha

value of factors. The three factors had eigen values ranging from 1.006 to 7.410 explaining 59.80% of the total

variance. The factors (attitude dimensions) are explained below :

F1: Economic, Convenience, and Transparency

This factor was by far the most important explaining as high as 43.59% of the total variance. Net brokers in

comparison to non-Net brokers perceived more strongly Net trading as economical, convenient and transparent

channel of trading. Online brokers could be provided services at economical rates to their customers

(Globerman et al., 2001). In earlier studies on the impact of the Internet on the stock trading activities in USA

(Lim, 1996, 1997) found that net trading provided convenience and transparency in terms of free access to

timely news and data. In another study, convenience was considered a transaction attribute and potential

competitive criterion that influenced the successful adoption of Internet technology in manufacturing (Beach,

2002). Automation of capital markets has also been found to have instilled or enhanced transparency in market

activities to an extent, with respect to price and trade information (Brailsford et al., 1999; Grunbichler et al.,

1994; Hamilton, 1978; Jassawalla, 1989; Nabi, 2004; Picot et al., 1995).

F2: Variety, Value-added Services, and Awareness

Net brokers believed more strongly than non-Net brokers that Net trading was one of the important sources of

variety of financial products such as equity, futures and options, mutual funds, IPOs, and also provided value-

added services in the form of firm reports, portfolio valuation, research news etc. Investors preferred access to a

variety of stocks (Majer, 1997).Online brokers could be offered a larger variety of services to their customers

(Globerman et al., 2001). Net brokers also felt more strongly that online trading firms, the stock exchanges and

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 18

the SEBI should be proactive in spreading the awareness about Net stock trading. The level of knowledge about

an innovation has a positive relation with the intention to adopt the innovation (Rogers, 1995; Luchetti and

Sterlacchini, 2004). This factor was estimated to explain 10.30% of the total variance.

Table II. Difference between net brokers and non-net brokers’ attitudes toward net trading

Label Statement

Net

Brokers

(WAS)

Non-Net

Brokers

(WAS)

Z-value

Internet trading

S1 enables investors to punch their orders directly to the web server of the exchange, thereby reducing the transaction time to almost nil.

5.48 4.27 3.602***

S2@ firm charges high commission. 5.50 4.27 3.930***

S3 helps broker in making more money. 4.74 4.27 1.434

S4@ leads to excessive delay in updating investors’ personal portfolio and account status. 6.35 5.77 2.741***

S5 is more convenient. 6.15 4.46 5.675***

S6 enhances market quality through improved liquidity by increasing quote continuity and

market depth. 5.61 4.48 3.909***

S7 is a vastly democratic medium, which brings individual investor at par with large institutional player.

5.24 4.75 1.703*

S8 is more transparent. 6.13 4.94 4.335***

S9 allows broker to reach a wider customer base and potentially increase market share. 6.24 5.44 3.541***

S10@ fails to provide information and price on a real-time basis so as to act accordingly. 5.89 5.17 2.767***

S11 offers value added services in the form of firm reports, portfolio valuation, research news etc. 6.35 5.42 4.307***

S12 offers a broad range of financial products like equity, futures & options, mutual funds etc. 6.11 5.35 3.548***

S13@ lacks active participation of the e-trading firms, the SEs and the SEBI to spread its awareness. 6.04 5.65 1.785*

S14 site-interfaces are made much more user-friendly so as to appeal to the mass market. 6.11 5.77 1.569

S15 websites offer educational material to understand the risks of investing in the share market. 6.17 5.81 1.869*

S16@ lacks the government support in setting up developmental facilities in India. 2.89 2.77 0.473

S17 is independent of geographical restrictions/barriers. 5.65 5.64 .064

S18@ increases settlement risks. 5.78 4.52 4.990***

S19@ leads to excessive delay in order execution and its confirmation. 5.61 4.92 2.404**

S20 allows the investor to specify and customize the securities & volume one would like to trade. 5.72 5.06 2.572**

S21@ is not safe by information technology act, 2000. 5.09 4.83 1.216

S22 leads to paperless trading through integration of the bank, the broker and the depository. 6.26 5.46 3.596***

Note: *Significant (p < 0.10); **Highly significant (p < 0.05); ***Very Highly significant (p < 0.01); WAS = Weighted Average Score @These items were worded negatively to reduce the bias due to tendency of respondents to reply in affirmative during data collection. They

were, however, reverse coded for the purpose of data analysis and thus, interpreted accordingly.

F3: Liquidity and Safety

This factor accounted for 5.92% of the total variance. Net brokers believed more strongly than non-Net brokers

that paperless and flexible trading through the Internet offered liquidity in shares and ensured safe trading. In a

previous study in Singapore indicated that Net trading offered 24 hours access to their trading accounts and real

time investment advice thereby resulted in liquidity (Lee and Ho, 2003). Another study by Amihud and

Mendelson (1989) demonstrated that market liquidity could be enhanced through the proper use of Information

Technology. Adopters in comparison to non-adopters were more confident of the security of Internet stock

trading in Singapore (Teo et al., 2004). Moreover, in recent studies (Howcroft et al., 2002 and Mäenpää, 2006),

security was found to be the most important determinant to ultimate adoption of internet banking services.

The attitude dimensions so derived above were then used as independent variables in discriminant analysis

(below) in terms of factor scores computed using SPSS package (Table III). Here, factor scores were composite

scores estimated for each respondent on each of the derived factors (Hair et al., 2005).

Table III. (Rotated) Factor analytic results of brokers’ attitudes toward net trading and mean scores

Factors

Loadings Mean

Net Brokers Non-Net Brokers

F1: Economic, Convenience, & Transparency

(Variance explained = 43.59% ; Cronbach’s alpha = 0.882)

Internet trading

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 19

@firm charges high commission. 0.764 5.50 4.27

is more convenient. 0.702 6.15 4.46

enhances market quality through improved liquidity, by increasing quote

continuity and market depth 0.665 5.61 4.48

enables investors to punch their orders directly to the web server of the exchange, thereby reducing the transaction time to almost nil.

0.631 5.48 4.27

is a vastly democratic medium, which brings individual investor at par with

large institutional player. 0.605 5.24 4.75

@increases settlement risks. 0.596 5.78 4.52 @leads to excessive delay in order execution and its confirmation. 0.594 5.61 4.92

is more transparent. 0.589 6.13 4.94 @fails to provide information & price on a real-time basis so as to act

accordingly. 0.424 5.89 5.17

F2 : Variety, Value-added Services, and Awareness

(Variance explained = 10.30% ; Cronbach’s alpha = 0.825)

Internet trading

offers a broad range of financial products, such as equity, futures and

options, mutual funds, initial public offerings etc. 0.801 6.11 5.35

offers value added services in the form of firm reports, portfolio valuation,

research news, mutual fund data etc. 0.759 6.35 5.42

leads to excessive delay in updating investors’ personal portfolio and account status.

0.656 6.35 5.77

websites provide educational and other guidance material to understand the

risks of investing in the share market. 0.638 6.17 5.81

@lacks active participation of the online trading firms, the stock exchanges and

the SEBI to spread its awareness. 0.574 6.04 5.65

allows broker to reach a wider customer base and potentially increase market share.

0.553 6.24 5.44

F3 : Liquidity and Safety

(Variance explained = 5.92% ; Cronbach’s alpha = 0.766)

Internet trading

leads to paperless trading through integration of the bank, the broker and the

depository. 0.723 6.26 5.46

allows the investor to specify and customize the securities and volume one would like to trade.

0.678 5.72 5.06

websites provide educational and other guidance material to understand the

risks of investing in the share market. 0.625 6.17 5.81

@fails to offer information & price on a real-time basis so as to act accordingly. 0.555 5.89 5.17 @lacks active participation of the online trading firms, the stock exchanges and

the SEBI to spread its awareness. 0.441 6.04 5.65

@increases settlement risks. 0.432 5.78 4.52

Total variance explained = 59.80%; Overall Cronbach’s alpha = 0.914 Note: @ = Same as Table 2

Discriminant Analytic Results

In order to identify which of the factors (demographic and attitude dimensions) were significant in

discriminating between Net brokers and non-Net brokers, simultaneous discriminant analysis was used.

Needless to mention that while the attitude dimensions were metric, the demographic variables were non-metric.

Therefore, the latter were converted into dummy variables to make the data fit for discriminant analysis as

reported in Table III (Hair et al., 2005, pp. 83-85). The various statistics related to discriminant analysis (viz.,

Wilks’ Lambda, F-ratio, discriminant loadings) were reported in Table IV. This table also depicted frequency

percentages for demographics and group means for attitude dimensions. Column 3 of this table showed

significant test for equality of group means (Net brokers versus non-Net brokers) for each variable on the basis

of Wilks’ Lambda. While large values indicated that group means were not different, while small values

indicated that group means were different (Hair et al., 2005). It was observed that group means differed

significantly for four variables, X1, X8, X9 and X10.

Here, it was important to point out that even though Wilks’ Lambda might be statistically significant, yet it did

not provide enough information about the effectiveness of discriminant function in classification. In other

words, it would not be meaningful to interpret the analysis if the discriminant function estimate was not

statistically significant which was judged on the basis of a chi-square transformation of the Wilks’ Lambda

statistic (Malhotra, 2004). In testing for significance of discriminant function in this analysis, it might be noted

that the Wilks’ lambda associated with the function was worked out as 0.470, which transformed to a chi-square

value of 142.41 with 11 degrees of freedom. This was found statistically highly significant at 0.000 probability

level (see Table IV).

Further, the analyst should focus on making substantive interpretations of the findings only if the discriminant

function is statistically significant as also if the classification accuracy is acceptable (Hair et al., 2005). In our

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 20

paper, the discriminant function was already found to be highly statistically significant at 0.000 probability

level. Hence the next step would be to check if the classification accuracy was acceptable.

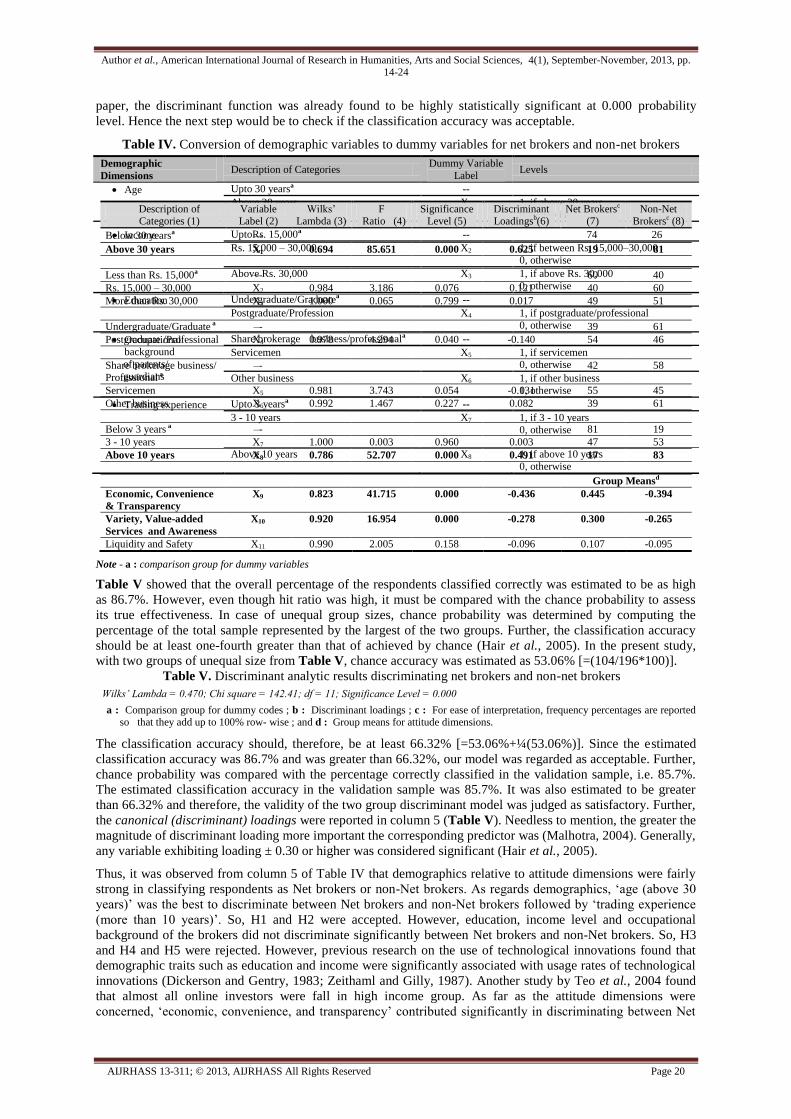

Table IV. Conversion of demographic variables to dummy variables for net brokers and non-net brokers

Note - a : comparison group for dummy variables

Table V showed that the overall percentage of the respondents classified correctly was estimated to be as high

as 86.7%. However, even though hit ratio was high, it must be compared with the chance probability to assess

its true effectiveness. In case of unequal group sizes, chance probability was determined by computing the

percentage of the total sample represented by the largest of the two groups. Further, the classification accuracy

should be at least one-fourth greater than that of achieved by chance (Hair et al., 2005). In the present study,

with two groups of unequal size from Table V, chance accuracy was estimated as 53.06% [=(104/196*100)].

Table V. Discriminant analytic results discriminating net brokers and non-net brokers

Wilks’ Lambda = 0.470; Chi square = 142.41; df = 11; Significance Level = 0.000

a : Comparison group for dummy codes ; b : Discriminant loadings ; c : For ease of interpretation, frequency percentages are reported so that they add up to 100% row- wise ; and d : Group means for attitude dimensions.

The classification accuracy should, therefore, be at least 66.32% [=53.06%+¼(53.06%)]. Since the estimated

classification accuracy was 86.7% and was greater than 66.32%, our model was regarded as acceptable. Further,

chance probability was compared with the percentage correctly classified in the validation sample, i.e. 85.7%.

The estimated classification accuracy in the validation sample was 85.7%. It was also estimated to be greater

than 66.32% and therefore, the validity of the two group discriminant model was judged as satisfactory. Further,

the canonical (discriminant) loadings were reported in column 5 (Table V). Needless to mention, the greater the

magnitude of discriminant loading more important the corresponding predictor was (Malhotra, 2004). Generally,

any variable exhibiting loading ± 0.30 or higher was considered significant (Hair et al., 2005). Thus, it was observed from column 5 of Table IV that demographics relative to attitude dimensions were fairly

strong in classifying respondents as Net brokers or non-Net brokers. As regards demographics, ‘age (above 30

years)’ was the best to discriminate between Net brokers and non-Net brokers followed by ‘trading experience

(more than 10 years)’. So, H1 and H2 were accepted. However, education, income level and occupational

background of the brokers did not discriminate significantly between Net brokers and non-Net brokers. So, H3

and H4 and H5 were rejected. However, previous research on the use of technological innovations found that

demographic traits such as education and income were significantly associated with usage rates of technological

innovations (Dickerson and Gentry, 1983; Zeithaml and Gilly, 1987). Another study by Teo et al., 2004 found

that almost all online investors were fall in high income group. As far as the attitude dimensions were

concerned, ‘economic, convenience, and transparency’ contributed significantly in discriminating between Net

Demographic

Dimensions Description of Categories

Dummy Variable

Label Levels

Age Upto 30 yearsa --

Above 30 years X1 1, if above 30 years

0, otherwise

Income UptoRs. 15,000a --

Rs. 15,000 – 30,000 X2 1, if between Rs. 15,000–30,000

0, otherwise

Above Rs. 30,000 X3 1, if above Rs. 30,000

0, otherwise

Education

Undergraduate/Graduatea --

Postgraduate/Profession

X4

1, if postgraduate/professional

0, otherwise

Occupational

background

of parents/

guardians

Share brokerage business/professionala --

Servicemen X5 1, if servicemen 0, otherwise

Other business X6 1, if other business

0, otherwise

Trading experience Upto 3 yearsa --

3 - 10 years X7 1, if 3 - 10 years

0, otherwise

Above 10 years

X8

1, if above 10 years

0, otherwise

Description of Categories (1)

Variable Label (2)

Wilks’ Lambda (3)

F Ratio (4)

Significance Level (5)

Discriminant Loadingsb(6)

Net Brokersc (7)

Non-Net Brokersc (8)

Below 30 yearsa –- 74 26

Above 30 years X1 0.694 85.651 0.000 0.625 19 81

Less than Rs. 15,000a –- 60 40

Rs. 15,000 – 30,000 X2 0.984 3.186 0.076 0.121 40 60

More than Rs. 30,000 X3 1.000 0.065 0.799 0.017 49 51

Undergraduate/Graduate a –- 39 61

Postgraduate /Professional X4 0.978 4.294 0.040 -0.140 54 46

Share brokerage business/ Professional a

–- 42 58

Servicemen X5 0.981 3.743 0.054 -0.131 55 45

Other business X6 0.992 1.467 0.227 0.082 39 61

Below 3 years a –- 81 19

3 - 10 years X7 1.000 0.003 0.960 0.003 47 53

Above 10 years X8 0.786 52.707 0.000 0.491 17 83

Group Meansd

Economic, Convenience

& Transparency

X9 0.823 41.715 0.000 -0.436 0.445 -0.394

Variety, Value-added

Services and Awareness

X10 0.920 16.954 0.000 -0.278 0.300 -0.265

Liquidity and Safety X11 0.990 2.005 0.158 -0.096 0.107 -0.095

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 21

brokers and non-Net brokers followed by ‘variety, value-added services, and awareness’. In latest study on

investors’ adoption of Internet stock trading (Singh et al., 2010), ‘variety of financial products’ contributed

significantly in discriminating between adopters and non-adopters of internet stock trading followed by the

factors such as ‘convenience and transparency”. Therefore, H6 and H7 were accepted. Hence, H8 was rejected.

Summary of hypotheses and findings may be seen through Table VII.

Another aid to interpreting discriminant analytic results is to develop the characteristic profile for each group by

describing each group in terms of group means for the predictor variables. If the important predictors are

identified, then a comparison of the group means on these variables can assist in understanding the inter-group

differences (Malhotra, 2004). Column 6 and 7 of Table IV indicated that majority of the brokers (81%) aged

above 30 years were not providing trading facility through Internet to their clients. On the other hand, most of

the brokers (74%) aged below 30 years were offering Net trading facility to their clients. Brokers having trading

experience of more than 10 years were offering trading through screen-based channel, while brokers having

stock market exposure of less than 3 years adopted Internet as a medium of providing trading facility to their

clients.

As regards attitude dimensions, the mean rating on ‘economic, convenience and transparency’ showed that Net

brokers ( x = 0.445) in comparison to non-Net brokers ( x = –0.394) perceived more strongly Net trading as

economical, convenient and transparent medium that led to competitive commission.

The mean scores on ‘variety, value-added services and awareness’ indicated that Net brokers ( x = 0.299)

believed more strongly than non-Net brokers ( x = –0.265) that Net trading was one of the important sources

of variety of financial products and value-added services. Further, Net brokers felt more strongly that online

trading firms, the SEs and the SEBI should be proactive in spreading the awareness about Net stock trading.

Table VI. Classification accuracy results (net brokers versus non-net brokers)

Note : Figures in parentheses represent percentages; Analysis sample (Hit Ratio) = 86.7%; Validation sample (Hit Ratio) = 85.7%

Table VII. Summary of hypotheses and findings

Hypothesis Discriminate

significantly Results

Hypothesis Rejected /

Accepted

H1 Yes Age discriminated significantly between net brokers and non-net brokers.

Accepted

H2 Yes Trading experience discriminated significantly between

net brokers and non-net brokers. Accepted

H3 No Education did not discriminate significantly between net brokers and non-net brokers.

Rejected

H4 No Occupational background did not discriminate

significantly between net brokers and non-net brokers. Rejected

H5 No Income did not discriminate significantly between net brokers and non-net brokers.

Rejected

H6 Yes Economic, convenience, and transparency discriminated

significantly between net brokers and non-net brokers. Accepted

H7 Yes

Variety, value added services and awareness

discriminated significantly between net brokers and non-

net brokers.

Accepted

H8 No Liquidity and safety did not discriminate significantly between net brokers and non-net brokers.

Rejected

V. Discussion

The results of discriminant analysis indicated that, out of eight factors considered in the study, four factors were

found significant in discriminating between net brokers and non-net brokers. Demographics relative to attitude

dimensions were fairly strong in classifying respondents as Net brokers or non-Net brokers.Such considerations

were in line with previous research (Wan et al., 2005), demonstrating that demographic factors in contrast to

psychological ones were found strongly associated with consumers’ adoption of Internet banking in Hong Kong.

In another study (Sharif and Lowry, 2003), it was found that the demographic characteristics, age and education

level were the only significant factors affecting the adoption of the net by public relations practitioners in

Kuwait. However, in my latest study on investors’ adoption of Internet stock trading (Singh et al., 2010),

Predicted Total

Net Brokers Non-Net Brokers

Observed /Original

Cross-Validated

Net Brokers 78 (84.8) 14 (15.2) 92 (100.0)

Non-Net Brokers 12 (11.5) 92 (88.5) 104 (100.0)

Net Brokers 78 (84.8) 14 (15.2) 92 (100.0)

Non-Net Brokers 14 (13.5) 90 (86.5) 104 (100.0)

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 22

attitude dimensions in comparison to demographics contributed significantly in classifying investors as adopters

or non-adopters. However, the positive association between attitude dimensions and the intention to adopt the

innovation/technology was supported with the earlier studies (Mathieson, 1991; Ramayah et al., 2003; May,

2005; Ramayah and Suki, 2006; Abroud et al., 2010; Majali, 2012).

As regards demographics, ‘age (above 30 years)’ was the best to discriminate between Net brokers and non-Net

brokers followed by ‘trading experience (more than 10 years)’. It was worth mentioning over here that age

differences also identified in technology usage rates, suggesting that individuals' needs and preferences followed

a life-cycle orientation. Age was found to be negatively related to technology usage, usefulness perceptions and

positively related to perceived difficulty (Morris and Venkatesh, 2000). Further, the probability of Internet use is

expected to decline with the age of the computer operator. Older individuals are expected to be more

experienced in farming and thus value the information that can be attained from the Internet less than younger

farmers who have less experience (Gloy and Akridge, 2000). Researches on the adoption of new technology

indicated that those who adopted new communication technologies were more upscale and younger than non-

adopters (Dutton et al., 1987; Garramone et al., 1986; James et al., 1995; Lin, 1998; Rogers, 1995).

As for as the attitude dimensions were concerned, ‘economic, convenience and transparency’ contributed

significantly in discriminating between Net brokers and non-Net brokers followed by ‘variety, value-added

services and awareness’. According to Verdict Research Ltd. (2000), ‘cost effectiveness’ was the key reason for

the shoppers to buy online, followed by convenience and ease of purchase. The self-investing trend led to many

e-brokerages with lower fees than traditional brokerages (Teo et al., 2004). In a study on the impact of internet

on financial services industry, it was found that the internet was a convenient and transparent channel medium

of dealing (Menon, 2000). Another study by Norris (1997) found that customers preferred varieties that allowed

them to do things their way. In a recent study of adoption of computer and internet technologies in small firm

agriculture found that farmers who didn’t use computers or the Internet report being hindered primarily by lack

of knowledge (Burke and Sewake, 2008). A study by Chan and Mills (2002) found that small brokerages were

reluctant to adopt Internet-based trading where this was not regarded as compatible with business strategy.

VI. Implications, limitations, and future research direction

It might, therefore, be inferred that young brokers were more adaptable to the latest Internet technology as a

medium of providing trading facility in comparison to aged and experienced brokers who were reluctant to offer

Net trading facility due to lack of education and awareness about this medium. Government should, therefore,

encourage non-Net brokers to make use of computers and Internet for share market transactions as well as for

other tasks and also take active steps to set up the facilities to enable integrated Internet trading system in India.

The findings might be suggested that stock exchanges and perhaps the government should be proactive to

encourage online stock trading to non-net brokers and retail investors. They need to address investors’ concerns,

especially with regard to the trading interface and security issues. Perhaps, one solution is to incorporate click-

to-voice technology into the systems whereby dealers can assume the role of customer service officers.

Besides, more traditional brokers would need to offer internet-based stock broking services. However, they

should not go completely online as a majority of the investors like the security of knowing that there is an actual

physical location where they can go if they need expert advice. Also, brokers would need to set up a

combination of both online trading and traditional trading services. Traditional brokers should consider offering

other services such as estate planning and tax planning, which will not be as easy to offer online.

As net trading services are still relatively new in India, this study might have been unable to measure the actual

usage behavior of such services. Further, a few respondents may not have experience and knowledge about

some features of Net trading, so they might have given a neutral response in such cases. As the scope of this

study is confined to the northern region of India, the sample should not be generalized as the belief and intention

towards using Internet stock trading of the whole Indian population. The present study covered only individual

brokers. Besides, future studies may also be carried out to include other regions of India, more demographic

variables, and contextual variables. Rather, future studied can be conducted cross-culturally to give inclusive,

comparative, and more general applicable results.

VII. Conclusion

Results of this study clearly indicated that demographics relative to attitude dimensions were fairly strong in

classifying brokers as Net brokers or non-Net brokers. As regards demographics, ‘age (above 30 years)’ was the

best to discriminate between Net brokers and non-Net brokers followed by ‘trading experience (more than 10

years)’. As for as the attitude dimensions were concerned, ‘economic, convenience and transparency’

contributed significantly in discriminating between Net brokers and non-Net brokers followed by ‘variety,

value-added services and awareness.

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 23

VIII. References

1) Abroud, Alireza, Choong, Yap Voon and Muthaiyah, Saravanan (2010).“Preparation of Measurement Tools of the Effective Factors

for the Acceptance of Online Stock Trading”, European Journal of Economics, Finance and Administrative Sciences, 19. 2) Amihud, Y. and Mendelson, H. (1989), “The effects of computer based trading on volatility and liquidity”, in Lucas, H.C. and

Schwartz, R.A. (Eds.), The challenge of information technology for the securities markets: Liquidity, volatility, and global trading,

The Saloman Brothers Centre for the Study of Financial Institutions, pp. 59-85. 3) Bagchi, A. (2002), “Online trading - issues and concerns”, Chartered Financial Analyst, December, available at: www.icfai.org

(accessed on June 19, 2003).

4) Bain, M.G. (1999), “Business to consumer ecommerce: an investigation of factors related to consumer adoption of the Internet as a purchase channel”, Centre for Marketing Working Paper: London, pp. 99-806.

5) Barber, B.M. and Odean, T. (2002). “Online Investors: Do the Slow Die First?” The Review of Financial Studies, Vol.15, pp. 455-87.

6) Beach, R. (2002), “Operational factors that influence the successful adoption of internet technology in manufacturing”, W Paper No 2/23, available at: www.brad.ac.uk/acad/management/external/pdf/workingpapers/booklet_02-23.pdf (accessed on October 19, 2007).

7) Bhasin, M.L. (2005-2006), “E-brokering as a tool for marketing financial services in the global market”, Journal of Services Research, Vol. 5 No. 2, pp. 151-67.

8) Brailsford, T.J., Frino, A., Hodgson, A. and West, A. (1999), “Stock market automation and the transmission of information between

spot and futures markets”, Journal of Multinational Financial Management, Vol. 9 No. 3-4, pp. 247-64. 9) Burke, K. and Sewake, K. (2008), “Adoption of computer and Internet technologies in small firm agriculture: a study of flower

growers in Hawaii”, Journal of Extension, Vol. 46 No. 3, available at: www.joe.org/joe/2008.html (accessed on January 3, 2009).

10) Chan and Mills (2002), “Internet Adoption by Small Firms”, available at: www.encyclopedia.jrank.org/articles/pages/6640/internet-adoption-by-small-firms.html (accessed on January 26, 2008).

11) Chau, Y.K. and Hui, K.L. (1998), “Identifying early adopters of new IT products: A case of Windows 95”, Information and

Management, Vol. 33 No. 5, pp. 225-30. 12) Chhabria, V. (2000), “Here's how you can make net gains”, available at: www.outlookmoney.com (accessed on December 28, 2003).

13) Dasgupta, P. (2002), “Future of e-banking in India” available at: www.projectshub.com (accessed on December 28, 2003).

14) Davis, F.D. (1993), “User acceptance of information technology: system characteristics, user perceptions and behavioral impacts”, International Man-Machine Studies, Vol. 38 No. 3, pp. 475-487.

15) Dickerson, M.D. and Gentry, J.W. (1983), “Characteristics of adopters and non-adopters of home computers”, Journal of Consumer

Research, Vol. 10 No. 2, pp. 225-35. 16) Dutton, W.H., Rogers, E.M. and Jun, S.H. (1987), “Diffusion and social impacts of personal computers”, Communication Research,

Vol. 14 No. 2, pp. 219-50.

17) Gajra, R. (2002), “Virtually no physical notes”, available at: wwwf.outlookmoney.com (accessed on December 29, 2003). 18) Garramone, G., Harris, A. and Anderson, R. (1986), “Uses of political computer bulletin boards”, Journal of Broadcasting and

Electronic Media, Vol. 30 No. 3, pp. 325-39.

19) Gharavi, H., Love, P.E.D. and Cheng, E.W.L. (2004), “Information and communication technology in the stockbroking industry: an evolutionary approach to the diffusion of innovation”, Industrial Management & Data Systems, Vol. 104 No. 9, pp. 756-65.

20) Globerman, S., Roehl, T.W., and Standifird, S. (2001), “Globalization and electronic commerce: inferences from retail brokering”,

Journal of International Business Studies, Vol. 32, pp. 749- 68.

21) Gloy, B.A. and Akridge, J.T. (2000), “Computer and internet adoption on large U.S. farms”, International Food and Agribusiness

Management Review, Vol. 3 No. 3, pp. 323-38.

22) Gopi, M. and Ramayah, T. (2007), “Applicability of theory of planned behavior in predicting intention to trade online: some evidence from a developing country”, Malaysia International Journal of Emerging Markets, Vol. 2 No. 4, pp. 348-60.

23) Goswami, C. (2003), “How Does net Stock Trading in India Work?”,Vikalpa: Journal for Decision Makers, Vol. 28 No.1, pp. 91-98.

24) Green, P.E., Tull, D.S. and Albaum, G. (1996), Research for Marketing Decisions, 5th edition, Prentice Hall of India, New Delhi. 25) Grunbichler, A., Longstaff, F.A. and Schwartz, E.S. (1994), “Electronic screen of trading and the transmission of information: An

empirical examination”, Journal of Financial Intermediation, Vol. 3, pp.166-87.

26) Guillén, M.F. (2002), “What is the best global strategy for the Internet?”, Business Horizons, Vol. 45 No. 3, pp. 39-46. 27) Hair, J.F., Anderson, R.E., Tatham, R.L. and Black, W.C. (2005), Multivariate Data Analysis, Pearson Education: New Delhi.

28) Hair, J.F., Bush, R.P. and Ortinau, D.J. (2003), Marketing Research – Within a Changing Information Environment, Tata McGraw-

Hill Publishing Company Limited, New Delhi. 29) Hamilton, J. (1978), “Marketplace organization and marketability: NASDAQ, the stock exchange, and the national market system”,

Journal of Finance, Vol. 33, pp. 478-503.

30) Harman, H.H. (1976), Modern Factor Analysis, University of Chicago Press: Chicago. 31) Hartwick, J. and Barki, H. (1994), “Explaining the role of user participation in information system use”, Management Science, Vol. 40

No. 4, pp. 440-65.

32) Howcroft, B., Hamilton, R. and Hewer, P. (2002), “Consumer attitude and the usage and adoption of home-based banking in the United Kingdom”, International Journal of Bank Marketing, Vol. 20 No. 3, pp. 111-121.

33) Huang, S.M., Hung, Y.C. and Yen, D.C. (2005), “A study on decision factors in adopting an on-line stock trading system by brokers in

Taiwan”, Decision Support Systems, Vol. 40 No. 2, pp. 315-28. 34) Insight Xplorer (2007), “Measuring online stock trading performance”, available at :www.insightxplorer.com (accessed 10 Feb, 2009).

35) James, M.L., Wotring, C.E. and Forest, E.J. (1995), “An exploratory study of the perceived benefits of electronic bulletin board use

and their impact on other communication activities”, Journal of Broadcasting and Electronic Media, Vol. 39, pp. 30-50. 36) Jassawalla, M. (1989), “The impact of telematics on financial intermediaries and market interdependencies”, in Jassawalla, M. and

Okuma, T. (Eds.), Information technology and global interdependence, New York. 37) K-Mailer Universe (2002), “Online trading –a new dimension to stock trading”, available at: www.themanagermentor.com (accessed

on 30 January, 2002).

38) Korgaonkar, P.K. and Wolin, L.D. (1999), “A multivariate analysis of Web usage”, Journal of Advertising Research, Vol. 39 No. 2, pp. 53-68.

39) Lee, J.E. and Ho, P.S. (2003), “A retail investor’s perspective on the acceptance of internet stock trading”, Proceedings of the 36th

Hawaii International Conference on System Sciences (HICSS), pp. 1-11. 40) Lim, S. (1996), “The impact of the world wide web on individual investors and electronic stock market trading”, MBA Research

Project, Santa Clara University: USA, available at: http://www.employees.org (accessed on 30 March, 2008).

41) Lim, S. (1997), “The impact of the world wide web on individual investors and electronic stock market trading”, Ongoing Survey, Santa Clara University: USA, available at: http://www.employees.org/~slim/research.960816.html (accessed on 30 March, 2008).

Author et al., American International Journal of Research in Humanities, Arts and Social Sciences, 4(1), September-November, 2013, pp. 14-24

AIJRHASS 13-311; © 2013, AIJRHASS All Rights Reserved Page 24

42) Lin, C.A. (1998), “Exploring personal computer adoption dynamics”, Journal of Broadcasting and Electronic Media, Vol. 42 No. 1,

pp. 95-112. 43) Lucchetti, R. and Sterlacchini, A. (2004), “The adoption of ICT among SMEs: evidence from an Italian survey”, Small Business

Economics, Vol. 23 No. 2, pp. 151-68.

44) Mäenpää, K. (2006), “Clustering the consumers on the basis of their perceptions of the Internet banking services”, Internet Research, Vol. 16 No. 3, pp. 304-22.

45) Majali, Malek AL (2012). “No More Traditional Stock Market Exchange: A Study of Internet Trading Service in Jordan”, Journal of

Internet Banking and Commerce, 17(1). 46) Majer, A. (1997), “Net stock exchange survey”, available at: http://www.arraydev.com (accessed on 11 May, 08).

47) Malhotra, N.K. (2004), Marketing Research – An Applied Orientation, 3rd edition, Pearson Education Asia: India.

48) Mathieson, K. (1991), “Predicting user intention: comparing the technology acceptance model with the theory of planned behavior”, Information Systems Research, Vol. 2 No. 3, pp. 173-91.

49) May, O.S. (2005), “User acceptance of Internet banking in Penang: a model comparison approach”, MBA Thesis, School of

Management, University Sains Malaysia: Penang. 50) Menon, V. (2000), “Bank: virtues of internet banking”, The Business Times, Singapore.

51) Morris, M.G. and Venkatesh, V. (2000), “Age differences in technology adoption decisions: implications for a changing work force”,

Personnel Psychology, Vol. 53 No. 2, pp. 375-403. 52) Nabi, M.G. (2004), “Bangladesh Stock Markets: Their Necessity and Potential” available

at:http://www.csebd.com/cse/Publications/Portfoilio_Q1_2000/stockmarkets.htm (accessed 4 August, 2004).

53) Nagree, P. and Monie, D. (2001), “Where angels fear to trade”, available at: www.nishithdesai.com (accessed on 11 May, 2003). 54) Norris, J. (1997), “Electronic commerce”, Business & Economic Review, Vol. 43, pp. 23-25.

55) Orbit-e Consulting (2000), “Case study of BSE”, available at: www.orbit-e.com (accessed on 16 March, 2003).

56) Patel, B.A. (2001), Trading Online, Pearson Education: India. 57) Phelan, S. (2001), “The Internet as an investment tool”, Journal of Accountancy, Vol. 192 No. 2, pp. 27-31.

58) Picot, A., Bortenlaenger, C. and Roehrl, H. (1995), “The automation of capital markets”, Journal of Computer-Mediated

Communication, available at:http://www.ascusc.org/jcmc/vol1/issue3/picot.html (accessed on 4 August, 2004). 59) Ramayah, T. and Suki, N.M. (2006), “Intention to use mobile PC among MBA students: implications for technology integration in the

learning curriculum”, UNITAR E-Journal, Vol. 1 No. 2, pp. 1-10. 60) Ramayah, T., Noor, M.N.M., Nasurdin, A.M. and Hasan, H. (2003), “Students’ choice intention of a higher learning institution: an

application of the theory of reasoned action (TRA)”, Malaysian Management Journal, Vol. 7 No. 1, pp. 47-62.

61) Rogers, E.M. (1995), Diffusion of Innovations, 5th ed., Free Press: New York. 62) Sharenet Company Ltd. (2003), “Online vs. offline”, available at: www.sharenet.co.za (accessed on 16 March, 2003).

63) Shankar, G.D. (2002), “Impact of e-Business in stock broking”, Australian Computer Society Working Papers, available at:

www.acs.org.au/certification/Documents/EBus/Assign1Eb1GDShankar.pdf (accessed on 14 December, 2008). 64) Sharif, A.A. and Lowry, D. (2003), “Factors affecting the adoption of the internet by public relations practitioners in Kuwait: a

comparison of two social systems”, Ph.D. Thesis, Southern Illinois University: Carbondale, available at : portal.acm.org/citation.cfm

(accessed on 16 January, 2009). 65) Singh, A., Sandhu, H.S. and Kundu, S.C. (2010), “Investors’ adoption of internet stock trading : a study”, Journal of Internet Banking

and Commerce, Vol. 15 No 1, available at: www.arraydev.com/commerce/JIBC/2010-04/Singh.pdf (accessed on 14 December, 2008).

66) Sohail, S. and Shanmugham, B. (2003), “E-banking and customer preferences in Malaysia: An empirical investigation”, Information Sciences, Vol. 150, pp. 207-17.

67) Srijumpa, R., Chiarakul, T. and Speece, M. (2007), “Satisfaction and dissatisfaction in service encounters : retail stockbrokerage and

corporate banking in Thailand”, International Journal of Bank Marketing, Vol. 25 No. 3, pp. 173-194. 68) Swinyard, W.R. and Smith, S.M. (2003), “Why people (don't) shop online: a lifestyle study of the Internet consumer”, Psychology &

Marketing, Vol. 20 No. 7, pp. 567-97.

69) Taylor, S. and Todd, P.A. (1995), “Understanding information technology usage: a test of competing models”, Information Systems Research, Vol. 6 No. 2, pp. 144-76.

70) Teo, T.S.H. (2001), “Demographic and motivation variables associated with Internet usage activities”, Internet Research: Electronic

Networking Applications and Policy, Vol. 11 No. 2, pp. 125-37. 71) Teo, T.S.H., Tan, M. and Peck, S.N. (2004), “Adopters and Non-Adopters of Internet Stock Trading in Singapore”, Behaviour and

Information Technology, Vol. 23 No. 3, pp. 211-23.

72) Verdict Research Ltd. (2000), “UK verdict on electronic shopping – consumer research”, Verdict Research, March 31, London. 73) Wan, W.W.N., Luk, C.L. and Chow, C.W.C. (2005), “Consumers’ adoption of banking channels in Hong Kong”, International

Journal of Bank Marketing, Vol. 23 No. 3, pp. 255-72.

74) Wu, H.C., Tseng, C.M., Chan, P.C., Huang, S.F., Chu, W.W. and Chen, Y.F. (2012) , “Evaluation of stock trading performance of students using a web-based virtual stock trading system”, Computers and Mathematics with Applications, Vol. 64, pp. 1495-1505.

75) Yap, A.Y. and Lin, X. (2001), “Entering the arena of wall street wizard, euro brokers and cyber-trading samurais: a strategic

imperative for online stock trading”, Electronic Markets, Vol. 11 No. 3, pp. 193-205.

76) Zeithaml, V.A. and Gilly, M.C. (1987), “Characteristics affecting the acceptance of retailing technologies: a comparison of elderly and

nonelderly consumers”, Journal of Retailing, Vol. 63 No. 1, pp. 49-68.