Taxing International Emissions Trading

36

TAXING INTERNATIONAL EMISSIONS TRADING Valeria Costantini - Alessio D’Amato - Chiara Martini Maria Cristina Tommasino - Edilio Valentini - Mariangela Zoli Working Paper n° 143, 2011

Transcript of Taxing International Emissions Trading

TAXING INTERNATIONAL EMISSIONS TRADING

Valeria Costantini - Alessio D’Amato - Chiara Martini

Maria Cristina Tommasino - Edilio Valentini - Mariangela Zoli

Working Paper n° 143, 2011

I Working Papers del Dipartimento di Economia svolgono la funzione di divulgare tempestivamente, in

forma definitiva o provvisoria, i risultati di ricerche scientifiche originali. La loro pubblicazione è

soggetta all'approvazione del Comitato Scientifico.

Per ciascuna pubblicazione vengono soddisfatti gli obblighi previsti dall'art. l del D.L.L. 31.8.1945, n.

660 e successive modifiche.

Copie della presente pubblicazione possono essere richieste alla Redazione.

REDAZIONE:

Dipartimento di Economia

Università degli Studi Roma Tre

Via Silvio D'Amico, 77 - 00145 Roma

Tel. 0039-06-57335655 fax 0039-06-57335771

E-mail: [email protected]

TAXING INTERNATIONAL EMISSIONS TRADING

Valeria Costantini - Alessio D’Amato - Chiara Martini

Maria Cristina Tommasino - Edilio Valentini - Mariangela Zoli

Comitato Scientifico:

Fabrizio De Filippis

Anna Giunta

Paolo Lazzara

Loretta Mastroeni

Silvia Terzi

1

Taxing International Emissions Trading

Valeria Costantini, University Roma Tre - Italy1 Alessio D’Amato, University Tor Vergata - Italy Chiara Martini, University Roma Tre - Italy Maria Cristina Tommasino, ENEA - Italy Edilio Valentini, University “G. D’Annunzio” Chieti-Pescara - Italy Mariangela Zoli, University Tor Vergata - Italy

Abstract Most tradable permit regimes have ignored the role of emission allowance taxation whereas the OECD and the European Union have emphasized the need for further investigation of the related efficiency and effectiveness consequences. The aim of our paper is to take a first step in this direction. We illustrate a theoretical model featuring I representative competitive firms/countries. Our theoretical results show that accounting for permit taxation implies a distortion in the equilibrium price as well as an impact on emissions distribution across countries. The specific features of these distortions are then investigated through a Computable General Equilibrium model in which several options for taxes on net sellers’ permit revenues and defiscalization of net buyers’ permit costs are simulated. Welfare analysis is performed, suggesting that the design of permit taxation is relevant in determining how welfare gains and losses are distributed across countries.

JEL codes: H230; Q580. Keywords: international emissions trading, permit taxation, computable general equilibrium model.

1. Introduction

In the context of international environmental negotiations, cap-and-trade systems are regarded as

a cost-effective instrument for achieving abatement targets. Despite the fact that an extensive

literature has examined various aspects of the functioning of permit markets, the tax treatment of

revenues that arise in a permit trading market has not been fully addressed to date. Not

accounting for permit revenues/cost taxation issues however may lead to wrong conclusions in

terms of their efficiency and effectiveness as well as their impact on industry relocation decisions

(Estrada et al., 2009).

In this paper we aim to contribute to the literature on cap-and-trade regimes by investigating

how the tax treatment of emission allowances may affect the permit market in terms of cost

effectiveness, abatement decisions and welfare effects.

Most existing tradable permit systems have ignored the role of corporate and personal income

tax and Value Added Tax (VAT), implicitly assuming that tradable permits would be outside

1 Corresponding author [email protected]. We are grateful for helpful comments we received from participants to the 2011 EAERE and SIE conferences held in Rome, the 2011 GCET conference held in Madrid, the 2011 SIEP conference held in Pavia. Suggestions received by Simone Borghesi, Ester Camiña, Bouwe Dijkstra, Iñaki Bilbao Estrada and Massimiliano Mazzanti are also gratefully acknowledged.

2

these fiscal regimes or that the impact of taxes would be neutral. For instance, Directive

2003/87/EC establishing a Greenhouse Gas (GHG) allowance trading scheme within the

European Union makes no reference to the accounting and fiscal repercussions of the allocation

and transfer of emission permits. This is surprising, as the fiscal treatment of emission permits

turns out to be a crucial aspect (Kane, 2009), especially when regulated countries differ in terms of

the accounting nature of emission rights, the burden of initial allocation and transfer, the

deductible character of penalties resulting from non-fulfilment of the delivery obligation and the

tax breaks for emission rights transfers. As Fisher (2006) notes, the existence of tax differentials

raises relevant design questions in emission control policies by affecting the allocation of

abatement efforts within multinationals, across countries and across firms.

In this work the effects of the tax treatment of emission allowances are first analysed

theoretically and then investigated through numerical simulations performed with a Computable

General Equilibrium (CGE) model, allowing us to examine complex features of the international

emissions trading system.

In the analytical model, we consider I countries and I representative competitive firms, one in

each country. Firms take emission permit taxation as well as permit endowment as given and

choose their emissions level and their selling or buying behaviour accordingly. Our results show

that permit taxation involves distortions both in the equilibrium permit price and in the

distribution of the environmental target across countries. Emissions trading taxation in a given

country implies an upward shift in the equilibrium price as well as an increase in that country’s

emissions and a decrease in other countries’ emissions. As a consequence, the effect of permit

taxation on tax revenues depends on countries’ position in the permit market: if a country is a net

buyer of permits, its tax revenue is always decreasing both in its own tax rate and in other

countries’ tax rates; on the other hand, if a country is a net seller of permits, its tax revenue is

always increasing in other countries’ tax rates but it may decrease in its own tax rate. The entity

of all these effects depends in a complex way on countries’ specific characteristics, as technology,

competitiveness, and energy mix. Countries’ specificities are therefore explicitly considered in

simulations carried out in the CGE model, based on a modified version of the GTAP-E model,

where international emissions trading (IET) is allowed and permit fiscal treatment is explicitly

modelled. Finally, the cost effectiveness assessment of permits taxation is completed with a

welfare evaluation based on equivalent variation effects occurring in net sellers and net buyers.

According to our analysis we can argue that adverse welfare effects induced by taxation are

minimized for buyers when sellers impose the highest tax rate whilst no fiscal deduction is

allowed to net buyers.

Despite simulations are based on realistic parameter values and results are not far from real life

in many respects, they should be intended as qualitative, rather than quantitative, suggestions

3

about the potential effects of permit taxation in an ideal world emissions trading market featuring

heterogeneous countries. In this respect, our paper has relevant policy implications, although

more specific geographical and economic features must be included in simulations to make our

insights suitable for applied IET designs.

From a theoretical point of view, the bulk of existing contributions considering emissions

trading jointly with tax issues deals with the pros and the cons of overlapping regulatory

instruments (Böhringer et al., 2008; Borghesi, 2010; Brechet and Peralta, 2007; Eichner and

Pethig, 2009; Gruell and Taschini, 2011; Johnstone, 2003). In a slightly different modelling

framework, Fischer (2006) investigates the interaction between multinational taxation and

abatement activities under an IET scheme, mainly focusing on the impact of differentiated

corporate income tax on abatement efforts by taking the equilibrium permit price as exogenous.

To the best of our knowledge the only contributions that have explicitly addressed the impact

of emissions trading revenues taxation are Kane (2009) and Yale (2008). The former provides a

very detailed descriptive analysis on how different options for the fiscal treatment of permits affect

firms’ behaviour on emission trading markets, i.e. their buying (or selling) and banking (or

borrowing) permits. The study also highlights that the fiscal treatment of abatement costs is an

important component to be considered in the analysis of the taxation of emission trading markets,

and concludes that heterogeneous tax treatment regimes among firms or jurisdictions are very

likely to affect allocative efficiency in a multi-periods context.

The latter theoretically examines the extent to which income taxation interferes with cap-and-

trade environmental regulation, reaching two opposite conclusions according to the time horizon

under scrutiny. Within a single tax period, taxing returns from permits does not distort firms’

choices at the margin between using and selling permits or between buying permits and abating.

Conversely, taxes may distort firms’ decisions regarding whether and to what extent they find

permit banking convenient. This is particularly true when permits are provided for free and their

value is excluded from taxable income (holders with a zero basis in their permits). In this case, the

permit price will rise up to the point where tax exemption is capitalized into the price of permits.

Accordingly, tax rules can modify the relative costs of abatement in present and future periods by

affecting the cost-effective allocation of emission reduction.

Our contribution departs from Yale (2008) by theoretically and empirically modelling an

international permit market where permit price as well as emissions abatement decisions are

endogenous. By this framework we can easily show that, differently from Yale (2008), emission

trading taxation leads to distortions even in a static context.

A policy oriented report by Copenhagen Economics (2010) further focuses on cost distortions

related to the existence of differentiated tax treatment of permits across member States in the EU,

concluding that such distortions are not expected to be significant. This work however is based on

4

limiting assumptions such as, for instance, that equilibrium prices are fixed. We generalize

Copenhagen Economics (2010) by performing a broader welfare analysis and adopting a

framework where the IET market functioning is modelled in a more realistic way, as all variables

(including equilibrium price) are endogenously defined. In this setting the price and welfare

impacts of permit taxation turn out to be significant.

Our paper fits in the stream of literature that evaluates emissions trading performance and

design using general equilibrium modelling strategies, as recent works by Böhringer et al. (2011)

and Carbone et al. (2009), in order to better capture the role of countries’ specific features as well

as the role of alternative climate/energy policy designs. Our findings are also relevant in the

debate upon environmental tax reform (Ekins, 2011; Ekins and Salmons, 2010; Ekins et al., 2011a,

2011b), as tax revenues from fiscal treatment of emission permits may be exploited for enhancing

investment efforts in green technologies or for reducing potential negative distribution effects due

to climate change policies. This last point leaves room for further research questions which could

be investigated in the future.

The rest of the paper is organized as follows: Section 2 presents the theoretical model whereas

Section 3 provides some details on the CGE model used for numerical simulations. Section 4

describes the results from simulations and in Section 5 we provide some specific comments on

welfare effects. Section 6 concludes.

2. The theoretical model

We consider a stylized model representing a set of I countries, indexed by . There are a

large number of atomistic identical firms in each country; we can therefore assume that each

country features one representative firm, labelled firm i ( ). Each firm generates polluting

emissions . Firm i’s benefits from pollution, , are assumed to be increasing and strictly

concave in emissions, i.e. and . The shape of synthesizes the effect

related to each firm/country’s industrial and technological features.

Each firm i receives an exogenous amount of emission permits, , that can be traded on a

perfectly competitive international market. Given the after-trade price p arising in the permit

market, each firm chooses the level maximizing the net benefits from pollution, defined as

,

5

where is the tax rate on revenues (costs) generated by , i.e. the amount of permits sold

(when ) or bought (when ). Note that our model is general enough so that we do not

need to specify the nature of permit trading taxation. Possible examples for our purposes could be

the application of (or exemption from) VAT, or differentiated income taxation.

The first order condition of the firm’s maximization problem is

(1)

This condition suggests that, whenever ( ; and ) the taxation

(defiscalization) of revenues (costs) arising from permit trading generates a violation of the cost

effectiveness condition (i.e. ).2 Though expected, this result deserves

further consideration. Indeed, as Kane (2009) underlines, it is not obvious that cost effectiveness

continues to hold when permit taxation is in place. Condition (1) offers simple but rigorous proof

of such an assumption provided that tax rates are different for at least two countries: in fact, if

for any , we go back to the same conclusions yielded by Yale (2008) within a

single tax period.

By totally differentiating (1) we get:

which implies the following comparative statics results:

(2)

and

. (3)

The signs in (2) and (3) define how the level of changes when, for a given level of , p

increases and when, for a given level of p, increases respectively. Both results can be easily

2 In the rest of the paper we will refer to a fiscal policy oriented to reduce the cost of acquiring permit in a net buyer country as defiscalization or rebate interchangeably.

6

explained: when p increases, the net benefit of polluting decreases because buying (selling) permits

becomes more expensive (remunerative); on the other hand, because the net cost of a

permit, for any given permit price, is lowered by taxation, thus reducing the opportunity cost of

emissions. From a deeper analysis of (2) and (3), we can observe the following:

Remark 1. The reactivity of w.r.t. p decreases with and with the concavity of whereas the

reactivity of w.r.t. increases with p and decreases with the concavity of .

As it is reasonable, a country in which marginal benefits from emissions decrease more with

emissions themselves (due, for example, to a mature technology) will ceteris paribus react less to

changes in the permit price and/or in the tax rate. On the other hand, a country featuring a lighter

tax burden will react more to changes in price. From Remark 1, we would expect tax and

technological features to play a crucial role in affecting the effectiveness and efficiency of a cap and

trade program.

The equilibrium in the permit market is defined by the following condition:

. (4)

By totally differentiating (4), we get:

.

If we assume that , , we can rewrite the total differential as

,

so that the equilibrium price increases with tax rates of any country i, that is,

7

. (5)

We can then derive the following observation:

Remark 2. The reactivity of p w.r.t. increases with and decreases with .

Since the intensity of both and depends on the concavity of , Remark 2

suggests that the reactivity of p w.r.t. also depends on the concavity of the benefit functions in

all involved countries/firms. However, the overall effect of the concavity of (or loosely

speaking, the effect of industrial characteristics of country i) is indeterminate in this theoretical

framework, unless some ad hoc specifications are introduced on the functional form of .

Indeed, a change in for some affects the absolute values of both at the numerator

and at the denominator.

We now turn to the overall effect of permit taxation. Eq. (3) tells us that there is a positive

direct effect. Nonetheless, there is also an indirect effect passing through the equilibrium price of

permits. By equations (2) and (5) we know that an increase in implies an increase in which,

in turn, implies a reduction of . The overall impact can then be rewritten as:

where the first addendum on the right hand side is the direct effect whereas the second addendum

is the indirect effect, driven by the permit price in equilibrium. After substituting (3), (2) and (5)

into the expression for , we can rewrite the overall effect of on as follows:

8

. (6)

We can conclude from (6) that an increase in the tax rate in any country i increases equilibrium

emissions in the same country. In other words, the positive direct effect always dominates the

negative indirect (or equilibrium) effect.

By looking at the effect of a country taxation on emissions produced by another country, we

can also observe from (5) that there is a negative relation between the emissions level of any

country and the tax rate imposed by the i-th country:

(7)

since and .

The impact of changes in can be summed up as follows.

Remark 3. An increase in in any country , ceteris paribus, generates an increase in emissions (and

permit demand) in country i and a decrease in emissions (and permit demand) in all other countries.

We turn now to evaluate the effect of permit taxation on the related tax revenue, defined as

.

The marginal effect of an increase in the tax rate on Ri is

(8)

which allows us to state that:

9

Remark 4. If country i is a net seller (i.e. ), its revenue increases if

whereas, if country i is a net buyer (i.e. ), its revenue always decreases (i.e. the rebate increases) with

the tax rate.

In other words, when a country is a net seller of permits, the revenue increases if the impact of

a change in the tax rate on the tax base (i.e. permits sold) is sufficiently small and/or the change in

unit tax revenue is sufficiently large.

It should be noted that there is also a tax related spillover, indeed

(9)

implying that:

Remark 5. The revenue in country j always increases with if country j is a net seller, whereas if country j

is a net buyer, its revenue decreases (i.e. the rebate increases) with if .

Remarks 1-5 put forward how equilibrium price, emission abatement decisions and tax

revenues change when the tax rate in a given country changes. A significant role played by

countries’ specificities is also suggested.3 When we move to the impact of changes in tax rates in

several (i.e. more than one) countries, we can observe more complex effects, and the same holds

with respect to welfare analysis. Instead of resorting to specific functional forms - that could be an

option open to a certain degree of arbitrariness - we examine how the international permit price

reacts to variations in the tax regimes of different countries through CGE simulations, where we

will introduce some elements of realism in order to achieve a deeper understanding of the involved

mechanisms.

!"

A graphical intuition of previous theoretical results is available in Appendix 1, examining the case of homogenous taxation across countries.

10

3. The CGE model for numerical simulations

In this paper we rely on the CGE GTAP-E model as an energy-environmental version of the

standard GTAP model specifically designed to simulate policies in the context of carbon emissions

mitigation. It includes an explicit treatment of energy demand, inter-factor and inter-fuel

substitution, carbon dioxide emissions accounting; it also features climate policies in terms of both

domestic actions, such as carbon taxes, and flexible mechanisms, such as emissions trading

(Burniaux and Truong, 2002; Mc Dougall and Golub, 2007).

Emissions trading is modelled by defining bloc-level emissions and quotas assuming that only

regulated countries can exchange permits in an international market. By exogenously defining

abatement targets for each regulated country, a carbon tax value can be endogenously computed

so that each country meets its commitments at the lowest domestic cost. When emissions trading

is allowed, carbon tax represents the equilibrium value of the marginal cost of abatement, which is

equalized across countries that participate in IET; such value identifies the equilibrium permits

price.

Each country is characterized by a specific abatement cost function. On this basis - and

considering its abatement target - the country becomes a net seller (buyer) if the permit price is

higher (lower) than the domestic abatement cost.

The standard GTAP-E formulation does not account for taxation related to emissions trading

revenues and costs, nor it considers how it affects equilibrium CO2 emissions. Hence a series of

specific modifications to the model equations have been implemented4.

Another significant adjustment is related to the fact that the theoretical model assumes that

each country features a single representative firm, and the selling or buying choices are taken by

representative firms with the aim of maximizing profits. In our CGE model, on the other hand,

abatement decisions are taken in a decentralized way by private agents, namely heterogeneous

firms and consumers that are located in countries participating to the IET. The amounts of abated

emissions by private agents are then summed up and compared with the emissions target at

national level, leading to an aggregate selling or buying behaviour at each country level. In order

to translate private agents’ decisions into the national abatement level, in this GTAP-E version,

the emission permits are taxed by acting directly in the demand price function.5 To simulate the

impact of IET taxation, the carbon equilibrium price (nominal carbon tax given by the

international market) faced by agents is increased by an ad valorem permit tax, thus influencing

the fossil fuel consumption behaviour of each economic agent. More precisely, the tax rate

4 For a flavour of how the theoretical model in Section 2 translates into GTAP-E see Figure A1 in Appendix 1. 5 In more detail, the taxation on revenues from the emission permits’ sale is modelled as directly affecting the emission permit price, and the same approach is adopted concerning the defiscalization of the costs related to emission permits’ purchase.

11

introduced into the GTAP-E model is uniform among economic sectors and differentiated

between countries, allowing the effects related to homogeneous or heterogeneous rates to be

simulated.

In this paper, according to Antimiani et al. (2011), two major changes in the standard GTAP-E

version are also introduced, enhancing the robustness of simulation results.

First of all, we adopt the updated GTAP Database version 7.1 (base year 2004) as well as the

latest version of the combustion-based CO2 emissions data provided by Lee (2008) for all GTAP

sectors and regions6.

Second, some elasticity parameters in the energy nests have been replaced with those proposed

by Beckman and Hertel (2010) for the substitution elasticity between the capital-energy composite

and the other endowments as well as for the Armington elasticities according to Hertel et al.

(2007).7

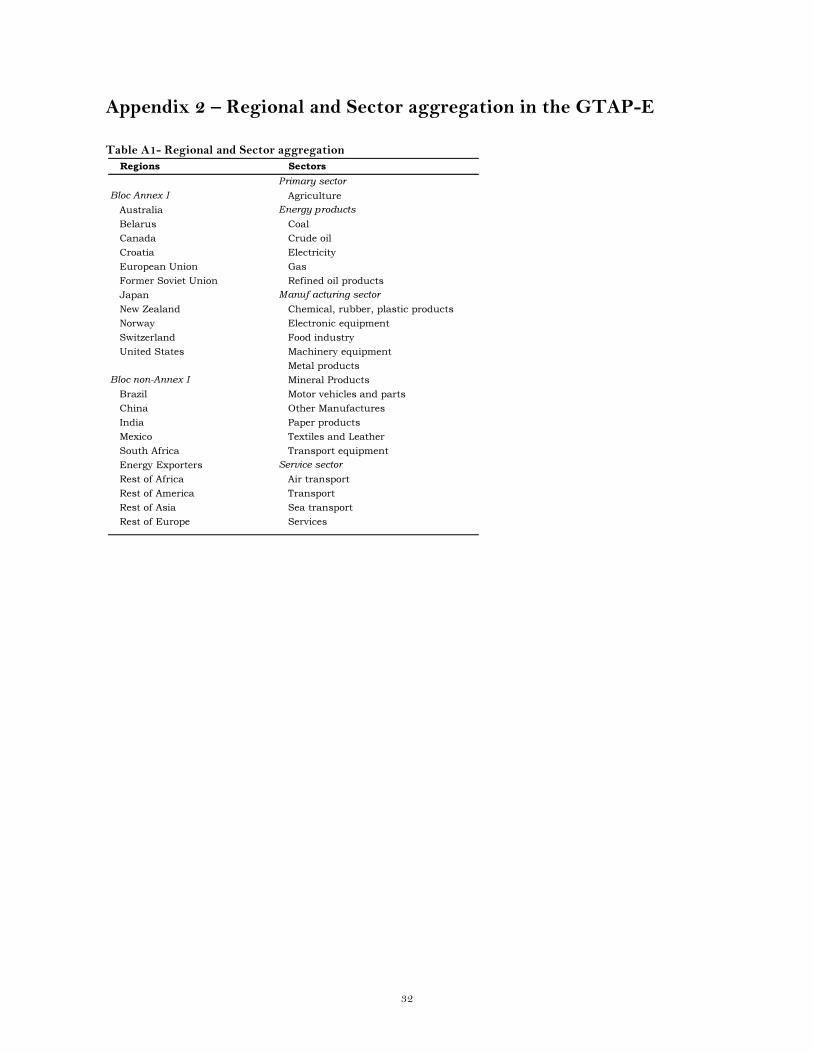

The model settings include an aggregation of 21 sectors and 21 regions (Table A1 in Appendix

2). With regard to regional aggregation, we consider as an ideal case a complete Kyoto Protocol

environment with 11 regulated countries/regions featuring country-specific CO2 reduction

commitments by 2012, where regional aggregation follows a simple criterion based on differences

in abatement targets. Therefore, the EU is considered as a single region since its bargaining

power has been exploited by obtaining a single abatement target (-8% compared with 1990

emission levels) whereas Croatia and Switzerland are treated separately since they have

negotiated two distinct emission targets.8

As far as sectoral aggregation is concerned, we single out energy sectors such as coal, crude oil,

gas, refined oil products and electricity as well as other energy intensive sectors (cement, paper,

steel and aluminium) since they are candidates for the main sources of production reallocation, and

other manufacturing non-energy intensive sectors as described by the IEA Energy Balances.

In order to compare economic and environmental effects of abatement decisions consistent with

our ideal Kyoto environment, a 2012 baseline has been constructed based on the GTAP 7.1

database that uses year 2004 data. To this end, we have considered a business as usual scenario for

emissions data with slow adoption of clean technologies according to IEA Business as Usual

6 Emissions in our version do not account for all other GHG emissions since they only relate to fossil fuels combustion, thus providing a lower bound estimate of the abatement targets. The underestimation is quite homogeneous across regions and sectors with the exceptions of the agriculture and chemicals sectors. 7 For a comprehensive discussion of substitution elasticities in the energy sector, see Koetse et al. (2008), Okagawa and Ban (2008), while Panagarya et al. (2001) and Welsch (2008) discuss the role of import demand elasticities in international trade. In our model parameters for substitution elasticities in the production function are:

,

, , , referred in the order to the nests including: capital and energy, electric and non electric energy, coal and non coal energy sources, non coal energy sources.

8 Considering the Rest of the World, we singled out the major emerging economies such as Brazil, China, India, Mexico, and South Africa. Nonetheless, in our simulations we are not interested in investigating the effects on non-regulated countries, since the IET mechanism is allowed in regulated countries only. Final regional and sector aggregation is described in Table A1 in Appendix 2."

12

Scenario (IEA, 2010b), economic projections to 2012 based on International Monetary Fund and

World Bank information on effective growth rates after the financial and economic crisis.

We have also accounted for potential distortions arising when transition economies are allowed

to sell permits in the carbon market. The huge potential supply by these countries would produce

substantial distortions, partially invalidating the role of an IET scheme. These uncertainties may

be included in the so-called “hot air” debate which also addresses the role of other flexible

mechanisms required by the Protocol (World Bank, 2010). In order to reduce potential market

failures brought about by this feature, we have adopted a partial adjustment to emission targets

for Belarus and Former Soviet Union (FSU). For these specific countries, the emissions level by

year 2012 - rather than the usual 1990 period - has been taken as the reference to which the 0%

target scheduled in the Protocol must be applied, reducing their potential permit supply

substantially.

As noted in the introduction, though linked to relatively realistic parameters, our simulations

are not to be intended as “real life” policy scenarios. Rather, we aim at using numerical simulations

to assess specific consequences of permits taxation that cannot be analysed in our simple

theoretical framework.

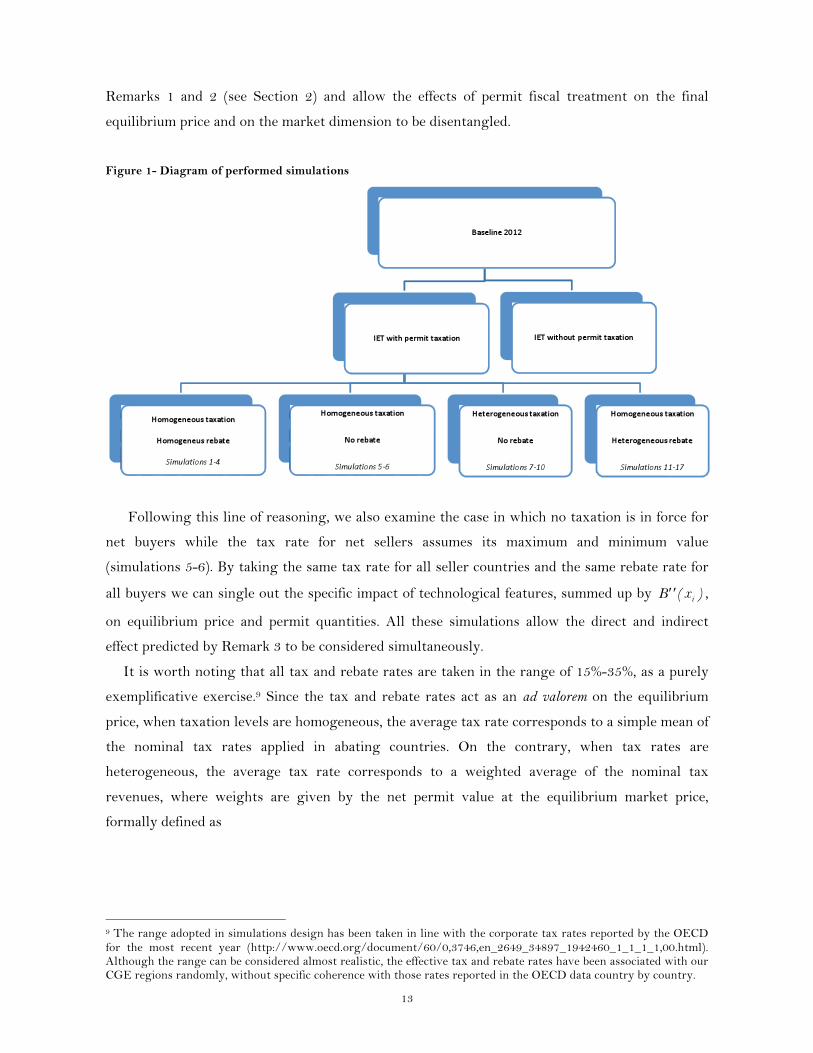

4. Simulation results

The different simulations we propose follow the main results obtained in the theoretical paper and

are summed up in Figure 1.

The baseline simulation considers an IET system without taxation of carbon permits (hereafter

referred as IET no Tax). This simulation represents the baseline for assessing the relative impact

of different options for fiscal treatment of emission permit revenues compared with a no tax

situation.

Starting from this benchmark, from the first set of simulations (Table 1) we can assess the

impact of the introduction of a tax rate on emission permit revenues (or a rebated tax rate on

permits costs) compared with an IET no tax situation. In particular, we test the overall effects on

the permit equilibrium price as well as on emission abatement decisions when homogeneous tax

rates across countries are implemented (simulation 1 for a low tax rate, simulation 2 for a high tax

rate). We then assess the effects related to the magnitude of the gap between the tax rates in net

selling and net buying countries, specifically assuming that tax rates are at their maximum level in

net selling countries while rebates are reduced in net buyers (simulations 3-4). In this case, the

gap only depends on net buyers’ decisions concerning the fiscal treatment of emission permit

purchase costs. These simulations are related to the partial equilibrium analysis addressed in

13

Remarks 1 and 2 (see Section 2) and allow the effects of permit fiscal treatment on the final

equilibrium price and on the market dimension to be disentangled.

Figure 1- Diagram of performed simulations

Following this line of reasoning, we also examine the case in which no taxation is in force for

net buyers while the tax rate for net sellers assumes its maximum and minimum value

(simulations 5-6). By taking the same tax rate for all seller countries and the same rebate rate for

all buyers we can single out the specific impact of technological features, summed up by ,

on equilibrium price and permit quantities. All these simulations allow the direct and indirect

effect predicted by Remark 3 to be considered simultaneously.

It is worth noting that all tax and rebate rates are taken in the range of 15%-35%, as a purely

exemplificative exercise.9 Since the tax and rebate rates act as an ad valorem on the equilibrium

price, when taxation levels are homogeneous, the average tax rate corresponds to a simple mean of

the nominal tax rates applied in abating countries. On the contrary, when tax rates are

heterogeneous, the average tax rate corresponds to a weighted average of the nominal tax

revenues, where weights are given by the net permit value at the equilibrium market price,

formally defined as

9 The range adopted in simulations design has been taken in line with the corporate tax rates reported by the OECD for the most recent year (http://www.oecd.org/document/60/0,3746,en_2649_34897_1942460_1_1_1_1,00.html). Although the range can be considered almost realistic, the effective tax and rebate rates have been associated with our CGE regions randomly, without specific coherence with those rates reported in the OECD data country by country."

14

(10)

where is the total amount of permits sold/bought by country i, given by the difference

between emission targets and current emissions.

Table 1- Alternative homogeneous tax rates

As far as the baseline simulation (IET no tax) is concerned, we can single out net sellers and

net buyers by comparing the abatement targets (first column in Table 2) with the effective

emission levels in an IET context (second column). We have four net sellers, namely Belarus, EU,

FSU and Switzerland, whereas all other regulated countries reduce CO2 emissions to a lower

extent compared with their abatement targets, matching the difference by buying permits on the

international market (as illustrated by simulated MACs in Figures A2 and A3 in Appendix 3).10

The corresponding equilibrium price equals 22.86 US$ per ton of CO2 which is reasonably

consistent with the permit price values registered in the European Union carbon market (ETS)

corresponding approximately to 19-20 US$ per ton of CO2 on average for 2010.11

The homogeneous taxation case allows us to conclude that the higher the tax rate, the higher

the equilibrium price of permits. Indeed, the introduction of a 15% homogeneous taxation

10 Country-specific MAC curves are represented in Figures A2 and A3 in the Appendix 3 for small and large economies modelled in our GTAP-E version. Domestic marginal abatement costs for each national emissions target may be compared with the permit equilibrium price derived in an IET scenario, thus obtaining information on the relative position of each country in the carbon market within a general equilibrium context."11 Countries result as net sellers or buyers depending on multiple dimensions such as the current energy mix, the production structure as well as the specific abatement targets. Hence, our simulations are only representative of what could happen on the permits market for sellers and buyers in general, not at a country-specific level. Results may in fact change according to different model settings or simulation designs.

15

(simulation 1) implies an increase in the price of permits from 22.86 to 27.05. Increasing the tax

rate to a (homogenous) 35% (simulation 2) implies a further increase of the equilibrium price to

35.82. The increase in the equilibrium price is not, in general, the same as the tax rate, so that we

can confirm (as shown in the theoretical model, see equation (5)) that the economic structure of

involved countries plays indeed a role. More specifically, the price increase is 18% when a 15% tax

rate is introduced and around 57% when a 35% tax rate is introduced.

Table 2- Emission levels (tons of CO2) and permit price with homogeneous tax and rebate rates

By looking at simulations 1 to 4 in Table 2, we can conclude that there is a more general direct

link between the equilibrium permits price and the average tax rate. Turning to abatement levels,

and again coherently with our theoretical predictions (see equation (1)) in a fully homogeneous

case, emission abatement decisions remain fairly constant both for net sellers and buyers. On the

other hand, when net buyers’ taxation changes with respect to net sellers, a significant decrease in

abatement seems to be matched to increases in the gap between net buyers and net sellers’

taxation (see, in particular, simulations 3, 4 and 5).

Specific country features explain the relative strength of the indirect price effect and of the

effect directly related to taxation in terms of abatement decisions. Although the direct tax-related

effect always prevails, consistently with eq. (6) and Remark 3, net sellers feature a differentiated

impact in terms of emissions increase. The relative position of MACs for these countries explains

this result. If we compare Belarus with Switzerland (Figure A2) and FSU with EU (Figure A3) it

is worth noting that in both cases the portions of the MAC curves which are above the IET no

Tax equilibrium price diverge, with Switzerland and FSU showing higher abatement costs

16

compared with Belarus and EU respectively, giving a flavour of the role played by countries’

technological features12.

We finally turn to the effect of changes in tax rates on the (positive or negative) revenue (Table

3). In the homogeneous tax case, as expected, an increase in the tax rate (simulations 1 and 2)

implies a gain for net sellers and a loss for net buyers, due to the equilibrium permits price

increase brought by a higher tax rate. From Table 3 we can also conclude that lowering the tax

rate for net buyers reduces the loss for the corresponding countries but also generates lower gains

for net sellers due to a decrease in the equilibrium price of allowances.

Table 3- Net permit value, revenues and rebates with homogeneous tax and rebate rates

Our simulations lead to results which are more clear cut than in Remark 4: revenue always

increases with the tax rate for net sellers, while (negative) revenue decreases with the tax rate for

12 The MAC curve for FSU remains slightly above the MAC curve for EU up to the equilibrium price in the IET no Tax case, and then starts to grow more rapidly for abatement efforts corresponding to domestic carbon tax levels above the calculated equilibrium price. This result is hardly surprising if we consider that within the EU aggregate all new EU member States are included, which are characterized by low abatement costs. In addition, specialization patterns in the productive structure may also help explaining the relative higher costs for FSU above a threshold level.

17

net buyers. Additional interesting results can be singled out if we set the tax rates for net sellers

at 35% in line with simulation 2 and reduce the corresponding rates for net buyers to 25%, 15%

and 0% respectively. We can conclude that the larger the tax wedge, the smaller the permits price,

the larger emissions and the smaller the revenue for net permits sellers. By contrast, quite

reasonably, for net permits buyers we observe that an increasing tax difference implies smaller

emissions and a lower absolute value for the (negative) revenue.

The extreme cases in which a tax rate is imposed by net sellers whereas net buyers rates are set

to zero seems to confirm previous results in terms of the related price impact. Also, net sellers

react consistently with the theoretical model (Remark 1), reducing their abatement efforts

(increasing their emissions). Emissions for net permits buyers react in the opposite way, given the

overall target.

The second set of simulations (Table 4) considers a case where the tax rate for net buyers is set

to 0 (i.e. no rebate takes place), while a uniform 15% tax rate for sellers is taken as a benchmark

(simulation 6 from Table 1). This baseline is then compared with cases where one of the net sellers

imposes a larger tax rate (i.e. a tax rate equal to 35%). This exercise allows us to consider the

relative impact of country specific features, including heterogeneous tax rates, on the permit

market for net sellers.

Looking at abatement decisions (Table 5), net sellers’ behaviour respects the condition ,

since the emission level for a country with (tax rate equal to 35%) is always higher than

the benchmark case (simulation 6) where an homogenous 15% tax rate is applied. In this way, we

can single out the direct and indirect effect of the tax and price channel on abatement decisions.

Also, results in Table 5 show that the theoretical result

holds in our simulations, as an

increase in the tax rate in one country always leads to decreases in emissions in other countries.

As expected, the impact is less significant when the tax rate is increased in relatively small

countries.

The same holds with respect to the impact in terms of the equilibrium price of permits: when

the tax is increased in relatively small sellers, the change in the permits price is small.

Interestingly, when the tax is increased in the EU, the price increases from 24.49 to 25.80, while

when the increase takes place in the Former Soviet Union increases slightly less (to 25.74). This

happens in spite of the (much) larger average tax rate arising when the tax increase takes place in

the FSU, being the latter the largest net seller. Such outcome suggests how specific features of

involved countries might affect the equilibrium outcome.

18

Table 4- Alternative heterogeneous tax rates with no rebate

Table 5- Emission levels (tons of CO2) and permit price with heterogeneous tax rates (no rebate)

Results in Table 6 confirm that each country’s revenue is increasing in own tax rate, with the

exception of Switzerland where apparently the condition

is not

respected (see Remark 4). This result, however, can be explained by considering the relatively low

influence of small economies’ taxing decisions on the equilibrium permit price. The prevailing

force is then likely to be associated with domestic emission abatement decisions, implying that the

right hand side of the above inequality is larger than the left hand side. Finally, it is also clear

from Table 6 that each net seller’s revenue increases with other countries taxation; the absolute

value of the impact depends on each country’s dimension, larger countries featuring a larger

impact on permits market and, therefore, on other countries’ revenue.

19

The third set of simulations (Table 7) completes our analysis by assessing the impact of tax

rates heterogeneity among net buyers, while keeping a homogenous tax rate for net sellers.

Table 6- Net permit value, and revenues with heterogeneous tax rates (no rebate)

Table 7- Alternative heterogeneous rebate rates (homogeneous tax)

20

We address the links among emissions, equilibrium price and revenues taking as a benchmark

the case where a homogeneous 15% tax rate is present in net buying countries (simulation 4). For

the sake of simplicity, simulations are classified according to a decreasing average tax rates for net

buyers.

Looking at Table 8, we can see that theoretical results, Remarks 1 and 2 in particular, are again

confirmed by simulations. Indeed, the equilibrium price of permits and emissions in the country

featuring a relatively high tax rate are larger, whilst emissions in other countries are lower and

the significance of the impact is lower the lower the dimension of the involved country.

Turning to the impact on public revenue, we find again a non monotonic relationship: revenue

decreases in all cases (i.e., increases in absolute value) and the reduction is larger the larger the

dimension of the buyer (simulation 11).

Table 8- Emission levels (tons of CO2) and permit price with heterogeneous rebate rates (homogeneous tax)

Interestingly, Table 9 confirms the existence of a revenue related spillover effect or, in other

terms, a change in the tax rate in one country implies a change in other countries’ revenue, being

them net sellers or net buyers. The sign of the relationship is expected to depend on the condition

summed up in Remark 5.

Summing up, simulation results mainly confirm our theoretical insights, but also extend them

to account for countries specificities.

Additional conclusions stemming from simulations can be briefly summarized as follows:

• the change in equilibrium permits price can be significantly larger than the tax rate change

(simulation 2). Though not explicitly modelled, we can expect that a 57% increase in the

equilibrium permits price can lead to a significant change in regulated firms’ behaviour in the long

run (in terms of the adopted energy technology for instance);

21

• countries can be expected to benefit or lose from increases in their own as well as other

countries’ tax rates; Switzerland, for example, as a net seller of permits, exhibits a decreasing tax

revenue in its own tax rate, given its small impact on the equilibrium permits price;

• countries’ features, such as marginal costs, tax rates and initial endowments, can significantly

affect the impact of taxation on the permits market.

Table 9- Net permit value, revenues and rebates with heterogeneous rebate rates

Clearly, not all results coming from different simulation settings have been reported here. The

choice of specific simulations turned out to be useful in order to arrange the welfare analysis

performed in the next section. We have dropped other simulations such as, for instance, the case

for asymmetric tax rates in which a 0 tax rate was imposed for net sellers while a 35% tax rate was

imposed for net buyers. We should note however that other possible combinations of tax rates do

not affect our results in qualitative terms.

5. Welfare analysis

The impact of permit taxation on welfare is expected to depend both on “pure” cost effectiveness

considerations and on broader effects related to the interaction of the permit market with the

whole economy.

22

Let us first discuss some broad considerations on the cost effectiveness of carbon market

taxation for net sellers and buyers. In Figure 2 we represent the simplest case where permits are

taxed in selling countries and buyers do not apply any rebate.

We focus on a two country/two representative firm economy and assume that marginal

abatement costs are homogenous among countries, corresponding to the case where

. In this case, the marginal abatement cost curve is the same for the two

countries that we label A and B (MACA,B). The two countries differ in their abatement

commitment that we assume is relatively higher for B (CB) than for A (CA). As a result, in the

absence of emissions trading, country A should introduce a carbon tax (CTaxA = PA) which is

smaller than the corresponding one in country B (CTaxB = PB); when emissions trading is instead

allowed, incentives to trade arise.13

In a two country model equilibrium, the permit quantity demanded by B is by construction

equal to the supply provided by A. Hence, the market is confined to the quantities associated with

the PA-PB price range. The equilibrium price (PE) corresponds to the point on the MACA,B where

country A decides to reduce emissions beyond its target until the domestic abatement costs of the

two countries are equalized.

We first derive the standard cost effectiveness property of emissions trading by comparing

abatement costs and permit revenues in the two cases, with and without IET. Country A (the

seller) will face a total abatement cost equal to 0ACA or to 0DRA,B in the case of domestic actions

or participation in a carbon market, respectively. In the case of IET, the increasing total

abatement cost is more than compensated by permit revenue (CABDRA,B) leading to a net gain

equal to the area ABD. On the contrary, country B will face a reduction in total abatement costs

equal to RA,BDECB covered only partially by payments for emission allowances on the carbon

market (RA,BDFCB), resulting in a net gain (DEF). We can therefore demonstrate the (standard)

cost effectiveness result for IET with regard to domestic actions (no IET).

Turning to the case where emissions trading taxation is present, let us assume that country A

imposes a tax rate on permits sold in the carbon market; the corresponding MAC curve shifts to

the left and the new equilibrium price increases to P’E , with country B buying less permits. The

new net gain compared with a no IET case for buyers will result in IEL with a net loss equal to

DILF. For country A, the final result is not obvious. The new MAC’A corresponds to a net gain

compared with a no IET case given by the area AGH, which has to be compared with area ABD.

The difference is determined by the relative size of areas BGHM and AMD. For country A, we

should also consider a pure revenue effect, which results in a net public revenue for country A

government, equal to the area TGHS. Net loss from raising abatement costs is instead given by

13 For a more detailed analysis see Appendix 1.

23

the areas AUS+SND, since a portion of the negative effect (namely the area UMNS) is

compensated by public revenue gains. Net selling country A can therefore experience a net gain

or loss depending on the comparison between gains TBMU+BGHN and losses AUS+SND. The

net impact depends on the extent to which the tax rate is transferred on the market equilibrium

price, or in other words, the relative elasticity of supply and demand curves, which in turn depends

on MAC curves.

Figure 2 - Effects of permit taxation on abatement costs for sellers and buyers

The net result for regulated countries as a whole is not obvious as well. The area QILF is by

construction equal to BGHN, so the corresponding gains and losses compensate reciprocally. We

are left with gains equal to area TBMU in country A and losses equal to AUS+SND in country A

and to DIQ in country B. In Figure 2, global losses are characterized by light grey, while global

gains are in dark grey. As it clearly emerges, no general conclusion can be derived.

Other factors may enter the picture as well. Indeed, the welfare analysis performed so far only

tells us one part of the story, since it only considers abatement costs and revenue related effects (in

a partial equilibrium setting as described in the theoretical model) whereas a general equilibrium

approach would provide more realistic MAC curves, also considering sector specialization as well

as terms of trade effects including non-regulated countries.

To this end, let us now enrich the discussion by turning to the global welfare effects and using

the net equivalent variation in a general equilibrium framework, derived from CGE simulation

24

results. In this way, apart from the already mentioned permits value and permits revenue effects,

we can also include the allocative efficiency effects of different abatement decisions (when

allocation of emission reductions changes according to different tax treatment) and terms of trade

effects related to the world market (related to changes in export to import relative prices), as

discussed by Hanslow (2000) and Hurt and Hertel (2000). Equivalent variations for all simulations

have been ranked according to the welfare changes relative to a domestic policy scenario without

emissions trading for two aggregate regions representing net sellers and net buyers.

Figure 3 shows different effects for sellers and buyers for three extreme cases compared to a

domestic policy simulation: the IET no Tax case; the case where tax rates are homogeneous

between sellers and buyers and set at the maximum level (Max Tax Rate - simulation 2); the case

where sellers impose the highest tax rate while no rebate is allowed for net buyers (Max Tax Lag

- simulation 5).

Figure 3 - Net welfare effects for countries participating in IET

The Max Tax Lag case shows the highest welfare gains at a global level with respect to a

domestic policy scenario, since total gains are higher than in the other two cases. The IET no Tax

case corresponds to the best scenario in welfare terms for net buyers since their welfare gains in

relation to a domestic policy scenario are maximized compared with all other cases.

Net sellers gain the most when a homogeneous tax rate is applied and the higher the tax rate,

the higher their welfare improvement. Moreover, the increase in net sellers’ equivalent variation is

larger when the distance between the tax and rebate rate is lower. As a result, highest gains for

net sellers are associated to the 35% homogenous tax rate with full rebate (Max Tax Rate); in this

case, net buyers are going to lose the most (compared with a no tax situation).

This specific result may well be explained by the combination of allocative efficiency effects

with effects related to permits value and defiscalization costs in the net buyers group. From

Figure 2, introducing a full rebate corresponds to a left-side shift of the MACB, thus resulting in a

-10.000

0

10.000

20.000

30.000

No Tax Max Tax Rate Max Tax Lag

Welfare effects

Total IET Net Sellers Net Buyers

25

net permit equilibrium price that is higher than in the IET no tax situation. Accordingly

abatement costs for net buyers increase, due to the higher permits value, and generates a larger

impact on public revenue in the net buying countries as well.

A decomposition of equivalent variation into its main components (Figures 4-5) helps

discovering the determinants of the welfare impact related to ETS taxation.

Figure 4 – Decomposition of welfare effects for net sellers

As Figure 4 shows, net selling countries experience the largest permits value under the Max

Tax Rate simulation, where the permits price is the largest possible. The same holds, as expected,

with respect to permits related revenue. In general, both permits value and permits revenues are

larger when emissions trading takes place as compared to the domestic policy case. The terms of

trade for sellers improve, leading to a larger welfare (with the largest effect again associated to the

Max Tax Rate case). Finally, allocative efficiency per se is damaged by permits taxation, as net

sellers perform additional emission reduction with respect to the optimal domestic level.

From Figure 5 we can conclude, as it is reasonable, that all changes underlined so far are

somewhat reversed in sign if we focus on net buying countries.

Summing up, when the overall welfare equivalent variations are scrutinized, the socially

desirable design of emissions trading taxation at a global level requires homogenous tax rates and

no rebate. Thus, the resulting equilibrium solution maximizing welfare gains seems to be

simulation 5, with the highest tax rate imposed by sellers and no rebate allowed by net buyers.

Finally, we can remark that allocative efficiency effects for net sellers are strongly driven by

domestic tax decisions. By considering simulations 7-10, where only net sellers adopt a tax

regime on emission permits, there is a direct relation between domestic tax rate and welfare (Wi)

in the form , where the relative magnitude of this relation is mainly explained by

country-specific features. For instance, when EU or FSU adopt a 35% tax rate whereas all other

sellers have a 15% rate (scenarios 7 and 8 respectively), the allocative efficiency gains are

-25.000

-5.000

15.000

35.000

No Tax Max Tax Rate Max Tax Lag

Net Sellers

Permits value Allocative efficiency

Terms of trade Permits revenue

26

relatively higher for EU than for FSU, and this is clearly explained by differences in MACs for the

two countries where permit equilibrium prices are higher than in an IET no tax situation.

Figure 5 – Decomposition of welfare effects for net buyers

6. Concluding remarks

Emissions trading is increasingly used in practice due to its desirable theoretical properties, the

most well-known being its ability to achieve a given emission reduction target at the lowest cost.

A substantial amount of literature has recently tested the robustness of these results to several

extensions. We put ourselves in this stream, by taking a first step in the evaluation of

environmental and welfare performance of emissions trading when permit revenues taxation and

permit costs rebates are explicitly accounted for.

This paper is intended to be a starting point. However, the main message of our work is both

theoretically and policy relevant. From a theoretical point of view, we add to the existing

literature by explicitly assessing the impact of permit taxation on equilibrium price and emissions

as well as on tax revenues. We complement theoretical results by developing a CGE simulation

model where the net buying or selling behaviour of countries as well as welfare effects are

investigated. Differently from previous works, we show that the design of permit trading taxation

is not expected to be neutral in terms of environmental effectiveness and economic efficiency.

Welfare analysis also suggests that the welfare optimum might not coincide with the most

preferred option for buyers or sellers.

From a policy perspective, our paper can have several applications and extensions. First of all,

our modelling strategy can be useful in addressing specific IET design issues, by adapting

parameter values and geographical settings to specific environmental quality problems and areas

(such as the case of the European ETS). Second, our paper suggests an additional source of

“green” revenues; this is likely to be an important side effect of IET taxation when considering it

-25.000

-5.000

15.000

35.000

No Tax Max Tax Rate Max Tax Lag

Net Buyers

Permits value Allocative efficiency

Terms of trade Permits revenue

27

in the broader view of environmental fiscal reforms. In this respect, our model already includes the

evaluation of welfare consequences related to raising public revenue, as clarified in Section 5, but a

more detailed analysis of the recycling of such revenue deserves further investigation.

Finally, given the significant impact on the equilibrium price of permits (up to 57% with respect

to the no taxation scenario), we can expect another side effect of IET taxation to be an increase in

incentives towards technological progress. This latter topic can be fruitfully explored by

extending our modelling strategy to a dynamic setting.

28

References

Antimiani A., Costantini, V., Martini, C., Salvatici, L., Tommasino, M.C., (2011), Cooperative and non-cooperative solutions to carbon leakage, Working Paper No. 136, Department of Economics, University Roma Tre, Italy.

Beckman, J.F., Hertel, T.W., (2010), Validating energy-oriented CGE models, GTAP Working Paper No. 54., GTAP, Purdue University.

Böhringer, C., Dijkstra, B., Rosendahl, K.E., (2011), Sectoral and regional expansion of emissions trading, Discussion Papers No. 654, May 2011, Statistics Norway, Research Department.

Böhringer, C., Koschel, H., Moslener, U., (2008), Efficiency losses from overlapping regulation of EU carbon emissions, Journal of Regulatory Economics, Vol. 33, pp. 299-317.

Brechet, T., Peralta, S., (2007), The race for polluting permits, CORE Discussion Paper 2007/27 and CEPR 6209.

Burniaux, J.M., Truong, T., (2002), GTAP-E: an energy-environmental version of the GTAP model, GTAP Technical paper No. 16.

Carbone, J.C., Helm C., Rutherford, T.F., (2009), The case for international emission trade in the absence of cooperative climate policy, Journal of Environmental Economics and Management, Vol. 58, pp. 266-280.

Copenhagen Economics, (2010), Tax treatment of ETS allowances, Report prepared for EC DG TAXUD, October 2010.

EEA, (2010), Annual European Union greenhouse gas inventory 1990-2008, EEA Inventory report, Luxembourg.

Eichner, T., Pethig, R., (2009), CO2 emissions control with national emissions taxes and an international emissions trading scheme, European Economic Review, Vol. 53, pp. 625-635.

Ekins, P., (2011), The price mechanism and eco-efficiency: The role of green fiscal reform, Journal of Industrial Ecology, Vol. 15, pp. 663-666.

Ekins, P., Salmons, R., (2010), Making reform happen in environmental policy, in making reform happen: lessons from OECD countries, OECD, Paris, pp.129-157.

Ekins, P., Pollitt, H., Barton, J., Blobel, D., (2011a), The implications for households of environmental tax reform (ETR) in Europe, Ecological Economics, Vol. 70(12), pp. 2472-2485.

Ekins, P., Summerton, P., Thoung, C., Lee, D., (2011b), A major environmental tax reform for the UK: Results for the economy, employment and the environment, Environmental and Resource Economics, Vol. 50, pp. 447-474.

Estrada, I.B., Fargas Mas, L.M., Ansòtegui, A.I.M., (2009), Emission rights and corporate income tax in the EU, INTERTAX, Vol. 37, Issue 11.

Fischer, C., (2006), Multinational taxation and international emissions trading, Resource and Energy Economics, Vol. 38, pp. 139-159.

Gruell, G., Taschini, L., 2011, Cap-and-trade properties under different hybrid scheme designs, Journal of Environmental Economics and Management, Vol. 61, pp. 107-118.

Hanslow, K.J., (2000), A general welfare decomposition for CGE models, GTAP Technical Paper No. 19.

Hertel, T.W., Hummels, D., Ivanic, M., Keeney, R., (2007), How confident can we be of CGE-based assessments of free trade agreements?, Economic Modelling, Vol. 24, pp. 611-635.

Hurt, K.M., Hertel, T.W. (2000), Decomposing welfare changes in the GTAP model, GTAP Technical Paper No. 5.

IEA, (2010a), CO2 Emissions from fuel combustion- Highlights, International Energy Agency Statistics, Paris.

IEA, (2010b), World Energy Outlook, International Energy Agency, Paris. Johnstone, N., (2003), The use of tradable permits in combination with other environmental policy

instruments, OECD Environmental Directorate, ENV/EPOC/WPNEP(2002)28/ FINAL, OECD, Paris.

Kane, M., (2009), Taxation and global cap and trade, New York School of Law Colloquium on Tax Policy and Public Finance, NYU School of Law, U.S.

29

Koetse, M., de Groot, H., Florax, R., (2008), Capital-energy substitution and shifts in factor demand: a meta-analysis. Energy Economics, Vol. 30, pp. 2236-2251.

Lee, H., (2008), An emissions data base for integrated assessment of climate change policy using GTAP.

Ludena, C., (2007), CO2 Emissions in GTAP-E: Ready-for-aggregation GTAP 6.0 data. McDougall, R., Golub, A. (2007), GTAP-E Release 6: A revised energy-environmental version of

the GTAP model, GTAP Technical Paper No. 15. Okagawa, A., Ban., K., (2008), Estimation of substitution elasticities for CGE Models. Discussion

Paper 08-16, Graduate School of Economics and Osaka School of International Public Policy, Osaka, Japan.

Panagarya, A., Shah, S., Mishra, D., (2001), Demand elasticities in international trade: are they really low?, Journal of Development Economics, n. 64, pp. 313-342.

Sorrell, S., Sijm, J., (2003), Carbon trading in the policy mix, Oxford Review of Economic Policy, Vol. 19, pp. 420-437.

Welsch, H., (2008), Armington elasticities for energy policy modeling: evidence from four European countries, Energy Economics, Vol. 30, pp. 2252-2264.

World Bank, (2010), State and trends of the carbon market 2010, Carbon Finance at the World Bank, Environment Department, World Bank, Washington DC., USA.

Yale, E., (2008), Taxing cap and trade environmental regulation, The Journal of Legal Studies, Vol. 37, pp. 535-550.

30

Appendix 1 – Linking theoretical model with CGE: a graphical analysis

In this appendix, we provide a graphical intuition of how the permit market is affected by taxation

in the homogeneous taxation case in order to provide a useful link between theoretical formulation

and the implementation of fiscal treatment of emission permits into the CGE model here adopted.

We will focus on a two country/two representative firm economy and assume that marginal

abatement costs are homogenous among countries, corresponding to the case where

. In this case, the marginal abatement cost curve (bottom side of Figure A1) is

the same for the two countries that we label A and B (MACA,B). The two countries differ in their

abatement commitment that we assume is relatively higher for B (CB) than for A (CA). As a result,

in the absence of emissions trading, country A should introduce a carbon tax (CTaxA = PA) which

is smaller than the corresponding one in country B (CTaxB = PB); permit trade incentives would

therefore arise.

In a two country model, the permit quantity demanded by B is by construction equal to the

supply provided by A. Hence, the market is confined to the quantities associated with the PA-PB

price range in the bottom part of the graph. The equilibrium price (PE) corresponds to the point

on the MACA,B where country A decides to reduce emissions more than its target until the

domestic abatement costs of the two countries are equalized. In equilibrium, by definition, permits

sold by one country equal permits bought by the other. We can therefore represent the permit

market in a standard demand/supply graph, as in the top of Figure A1, where the exchanged

equilibrium quantity is 0QE= CARA,B= RA,BCB.

Suppose now that country A (the net seller) introduces a tax on permit revenue whereas no

rebate is allowed in country B. Country B stays on its previous MACA,B while country A’s MAC

shifts leftward to MAC’A (bottom of Figure A1), as the opportunity cost of emissions decreases

and the related marginal cost increases;14 this reduces the propensity to sell permits and therefore

implies a leftward shift in the supply curve (top of Figure A1). As a result, the equilibrium price

increases (P’E) and the exchanged quantity decreases (CAR’A=R’BCB= Q’E).

Let us now assume that a positive tax rate is present also in the net buying country, but the

corresponding tax rate is lower than that adopted in country A (tA). The new country B MAC

would be MAC’B resulting in a new demand curve (D’). As it clearly emerges from Figure A1, if a

positive tax rate also hits net buyers, the price increases more compared with a the case where

taxation only takes place in net selling country (P’’E) whereas the amount of permits exchanged is

14 Clearly MAC’A differs from MACA only when permits are sold, i.e. on the right of level CA in the bottom part of Figure A1.

31

closer to the no tax case (CAR’’A=R’’BCB= Q’’E). In an extreme case where tA=tB, MAC’B will

coincide with the new MAC’A.

Figure A1- Permit taxation with homogeneous abatement costs

This would result in a net equilibrium price increase of the same magnitude as the tax rate so

that the after tax price and the quantity exchanged in equilibrium would not change compared

with a no tax situation.

32

Appendix 2 – Regional and Sector aggregation in the GTAP-E

Table A1- Regional and Sector aggregation

33

Appendix 3 – Estimated MAC curves for different abatement levels

Figure A2 – MAC curves for small countries participating in IET calculated by GTAP-E

Figure A3 – MAC curves for large countries participating in IET calculated by GTAP-E