Board of Directors - CareerSource Pinellas

177

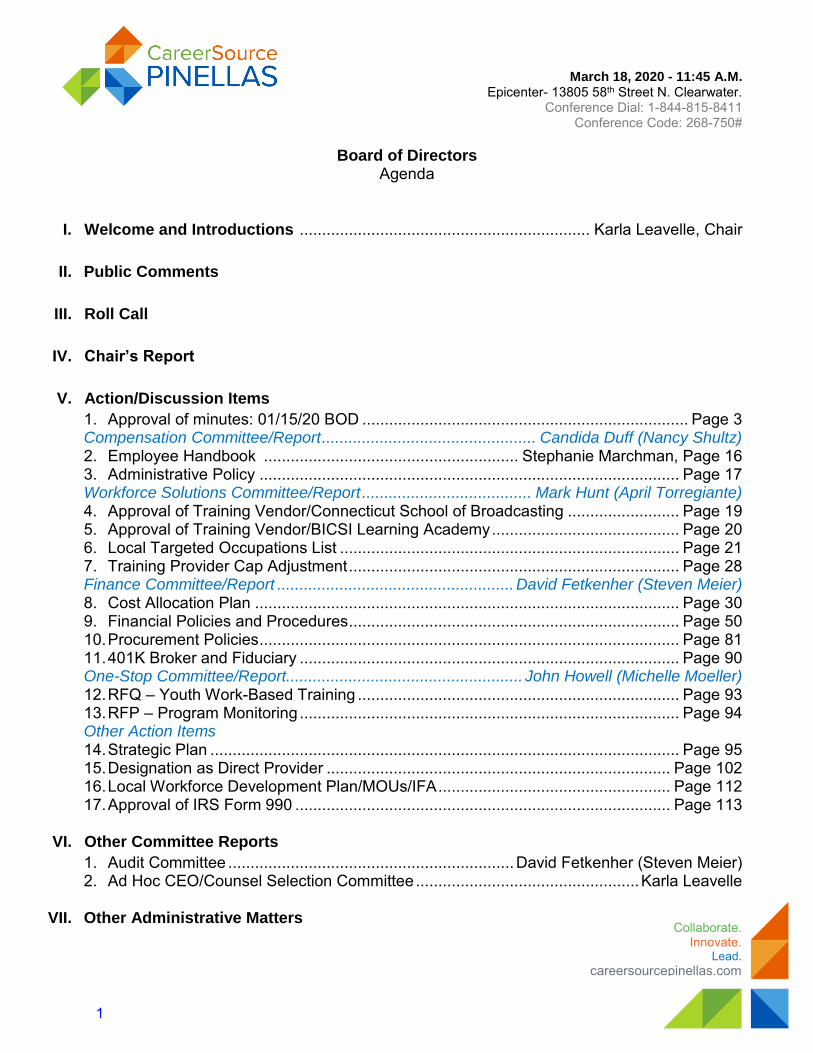

Collaborate. Innovate. Lead. careersourcepinellas.com March 18, 2020 - 11:45 A.M. Epicenter- 13805 58 th Street N. Clearwater. Conference Dial: 1-844-815-8411 Conference Code: 268-750# Board of Directors Agenda I. Welcome and Introductions ................................................................. Karla Leavelle, Chair II. Public Comments III. Roll Call IV. Chair’s Report V. Action/Discussion Items 1. Approval of minutes: 01/15/20 BOD ......................................................................... Page 3 Compensation Committee/Report ................................................ Candida Duff (Nancy Shultz) 2. Employee Handbook ......................................................... Stephanie Marchman, Page 16 3. Administrative Policy .............................................................................................. Page 17 Workforce Solutions Committee/Report ...................................... Mark Hunt (April Torregiante) 4. Approval of Training Vendor/Connecticut School of Broadcasting ......................... Page 19 5. Approval of Training Vendor/BICSI Learning Academy .......................................... Page 20 6. Local Targeted Occupations List ............................................................................ Page 21 7. Training Provider Cap Adjustment .......................................................................... Page 28 Finance Committee/Report ..................................................... David Fetkenher (Steven Meier) 8. Cost Allocation Plan ............................................................................................... Page 30 9. Financial Policies and Procedures.......................................................................... Page 50 10. Procurement Policies.............................................................................................. Page 81 11. 401K Broker and Fiduciary ..................................................................................... Page 90 One-Stop Committee/Report..................................................... John Howell (Michelle Moeller) 12. RFQ – Youth Work-Based Training ........................................................................ Page 93 13. RFP – Program Monitoring ..................................................................................... Page 94 Other Action Items 14. Strategic Plan ......................................................................................................... Page 95 15. Designation as Direct Provider ............................................................................. Page 102 16. Local Workforce Development Plan/MOUs/IFA .................................................... Page 112 17. Approval of IRS Form 990 .................................................................................... Page 113 VI. Other Committee Reports 1. Audit Committee ................................................................ David Fetkenher (Steven Meier) 2. Ad Hoc CEO/Counsel Selection Committee .................................................. Karla Leavelle VII. Other Administrative Matters 1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Board of Directors - CareerSource Pinellas

Collaborate. Innovate.

Lead. careersourcepinellas.com

March 18, 2020 - 11:45 A.M. Epicenter- 13805 58th Street N. Clearwater.

Conference Dial: 1-844-815-8411 Conference Code: 268-750#

Board of Directors Agenda

I. Welcome and Introductions ................................................................. Karla Leavelle, Chair

II. Public Comments

III. Roll Call

IV. Chair’s Report

V. Action/Discussion Items

1. Approval of minutes: 01/15/20 BOD ......................................................................... Page 3 Compensation Committee/Report ................................................ Candida Duff (Nancy Shultz) 2. Employee Handbook ......................................................... Stephanie Marchman, Page 16 3. Administrative Policy .............................................................................................. Page 17 Workforce Solutions Committee/Report ...................................... Mark Hunt (April Torregiante) 4. Approval of Training Vendor/Connecticut School of Broadcasting ......................... Page 19 5. Approval of Training Vendor/BICSI Learning Academy .......................................... Page 20 6. Local Targeted Occupations List ............................................................................ Page 21 7. Training Provider Cap Adjustment .......................................................................... Page 28 Finance Committee/Report ..................................................... David Fetkenher (Steven Meier) 8. Cost Allocation Plan ............................................................................................... Page 30 9. Financial Policies and Procedures .......................................................................... Page 50 10. Procurement Policies .............................................................................................. Page 81 11. 401K Broker and Fiduciary ..................................................................................... Page 90 One-Stop Committee/Report..................................................... John Howell (Michelle Moeller) 12. RFQ – Youth Work-Based Training ........................................................................ Page 93 13. RFP – Program Monitoring ..................................................................................... Page 94 Other Action Items 14. Strategic Plan ......................................................................................................... Page 95 15. Designation as Direct Provider ............................................................................. Page 102 16. Local Workforce Development Plan/MOUs/IFA .................................................... Page 112 17. Approval of IRS Form 990 .................................................................................... Page 113

VI. Other Committee Reports

1. Audit Committee ................................................................ David Fetkenher (Steven Meier) 2. Ad Hoc CEO/Counsel Selection Committee .................................................. Karla Leavelle

VII. Other Administrative Matters

1

Collaborate. Innovate.

Lead. careersourcepinellas.com

VIII. Information Items 1. Compliance Review…………………………………………….……………………….Page 154 2. DEO Daily Governor’s Report ............................................................................... Page 155 3. Performance Dashboard (as of 02/29/20) ............................................................ Page 156 4. Financial Reports through December 31, 2019 .................................................... Page 158 5. Organizational Chart ............................................................................................. Page 170 6. Iguanas ................................................................................................................. Page 172

IX. CEO Report……………………………………………………………………….Jennifer Brackney

X. Open Discussion

XI. Adjournment

Workforce Solutions Committee - April 14, 2020 One-Stop Committee - April 23, 2020 Finance Committee - April 29, 2020

Compensation Committee - TBD Next Board of Directors Meeting – May 20, 2020

*All parties are advised that if you decide to appeal any decision made by the Board with respect to any matter considered at the meeting or hearing, you will need a record of the proceedings, and that, for such purpose, you may need to ensure that a verbatim record of the proceedings is made, which record includes the testimony and evidence upon which the appeal is to be based.

*If you have a disability and need an accommodation in order to participate in this meeting, please contact Cindy Hockridge at 727-608-2426 or [email protected] at least two business days in advance of the meeting.

2

Action Item 1

Approval of Minutes

In accordance with Article VII, Section 1(H), of the approved WorkNet Pinellas By-Laws: Minutes shall be kept of all Board and Committee meetings. Minutes shall be reviewed and approved at the next CareerSource Pinellas Board or Committee meeting as appropriate. The official minutes of meetings of the Board and Committees of the Board are public record and shall be open to inspection by the public. They shall be kept on file by the Board Secretary at the administrative office of CareerSource Pinellas as the record of the official actions of the Board of Directors. The draft minutes from the January 15, 2020 meeting of the Board of Directors have been prepared and are enclosed.

RECOMMENDATION Approval of the draft minutes, to include any amendments necessary.

3

1

CareerSource Pinellas Board of Directors Minutes

Date: Wednesday, January 15, 2020 at 11:45 A.M. Location: Pinellas Technical College, 901 34th St. S, Rm G-8, St. Petersburg, FL. Call to Order Chairwoman Leavelle called the meeting to order at 11:45 a.m. and welcomed all participants. There was a quorum present with the following board members. Board Members in attendance Vivian Amadeo (phone), William Apple (phone), Jody Armstrong, Manny Bhuller, Candida Duff (phone), James England (phone), Celeste Fernandez (phone), David Fetkenher, Commissioner Patricia Gerard (phone), Barclay Harless, Mark Hunt, John Howell, Mark Hunt, Michael Jalazo, Carolyn King, Samuel Kolapo (phone), Karla Leavelle, Russell Leggette, Michael Logal, Michael Meidel, Dr. Rebecca Sarlo (phone), Sheryl Sheppard (phone), Amy Van Ness (phone), Scott Wagman, Zachary White (phone), Kenneth Williams (phone). Board Members Absent Jack Geller, Andrea Henning, Joanne Lentino, Kay McKenzie, Debbie Passerini, Chad Simpson, Glenn Willocks. Board Counsel Stephanie Marchman, Gray-Robinson Guests Rolando Torres, Abacode Dan McGrew, Dynamic Workforce Solutions Staff in attendance Jennifer Brackney, Don Shepherd, Steven Meier, Michelle Moeller, April Torregiante, Nancy Schultz, Mary Jo Schmick, René Davisson, Cindy Hockridge and Carlows Ellis. Welcome & Introductions Chairwoman Leavelle welcomed all the participating members. She highlighted a few topics: She introduced and asked the Board to welcome three new staff members: Mary Jo Schmick, Special Projects Director, René Davisson, Director of Administrative Services and Cindy Hockridge, Administrative Assistant.

1. Thank you to those Board Members who have agreed to go through the Strategic Planning process and who have joined the Focus Group. They are dedicating four days during the course of January and February.

2. Thank you to all of those who worked on the Science Center Committee and helped to make that sale happen. Since the sale of the Science Center, we now have two satellite offices open, which expands our footprint and our ability to serve the community. Those offices are the EpiCenter and Tarpon Springs.

3. The employment rate continues to be quite low in this area and continues to be a struggle to fill positions. Our CareerSource Center continues to work with both employees and employers to get those positions that are open filled.

Action Item 1 – Approval of the Minutes – 11.20.2019 Board of Directors The minutes of the November 20, 2019 Board of Directors meeting were presented for approval. Motion: Mark Hunt Second: Barclay Harless The minutes were approved as presented. This motion carried unanimously. There was no further discussion.

4

2

Action Item 2 – Proceeds from the sale of the Science Center CareerSource Pinellas closed on the sale of the Science Center on November 20, 2019. Net proceeds in the amount of $2,461,659.07 were received on that day.

Purchase Price $3,150,000.00

Payoff of Mortgage - Hancock Whitney Bank (585,279.12)

Payoff of Debt on HVAC (24,016.81)

Realtor Commission to Smith and Smith (79,045.00)

Proceeds Received $2,461,659.07

Commitment for Iguana Sanctuary (40,000.00)

Science Center Expenditures-Operating,

etc. (estimated through 11/30/19) (45,000.00)

Estimated Proceeds Available $2,376,659.07

Recommendation

Designate the net proceeds from the sale of the Science Center as unrestricted, subject to the reduction of expenses related to the sale and closing, and pending the completion of the DOL compliance review.

Motion: Scott Wagman Second: Russell Leggette The Board of Directors approved to designate the sale of the Science Center as unrestricted subject to the reduction of expenses, and pending the completion of the DOL compliance review. There was no further discussion. The motion carried unanimously. Action Item 3 – Release of Capital Improvement Funds to Unrestricted On October 30, 2015, the CareerSource Pinellas Finance Committee approved a modification to the Organization’s Fixed Asset Policy. One aspect of this modification was the implementation of a capital improvement account. The capital improvement account was maintained within the general fund. The account was designated to track cash value for capital improvements to buildings as they became necessary. The capital improvement account balance as of November 30, 2019 is $176,159.16. Recommendation Release the remaining $176,159.16 in the Capital Improvement Fund as of 11/20/2019 to unrestricted. Discussion: The Finance Committee decided to designate the funds as unrestricted and identify where the funds came from. Motion: Mark Hunt Second: Jody Armstrong

5

3

The Board approved releasing the funds as unrestricted, and as a line item to satisfy where the funds came from. The motion carried unanimously. Action Item 4 – RFP Issuance: EDMS, IT & Website Services CareerSource Pinellas currently contracts with Complete Technology Solution to provide all IT-related services. The contract provides a bundle of IT-related services, including help desk, information technology, infrastructure management, network management, Electronic Document Management System (EDMS) and website. As a result of the post-malware incident review, it is recommended that CSPIN move forward with a process to “unbundle” IT services in an effort to provide a more secure IT environment. Consequently, staff would like to issue a Request for Proposals for the provisions of its Information Technology needs across all offices, career centers, and satellite sites. Services to be included in the request for proposal include the following: I. EDMS: Manage a multi-faceted EDMS system to include electronic document management, online programs, e-courses and online scheduler. Provide development of new functionality or modules within the application as needed. II. Information Technology Services: Management of the overall administration of information technology systems and support of day-to-day operations. III. Website Services: Develop, maintain and manage website services. IV. Cybersecurity: Maintain and manage internal controls, security, and disaster recovery. *RFP for Cybersecurity has been issued and a vendor recommendation is forthcoming. Action

Date

Issue RFP 2/03/2020 Question and Answer period 2/07/2020 – 2/14/2020 RFP Due/Official Opening 2/28/2020 Evaluation and Selection Begins 03/02/2020 Award date 04/01/2020 Recommendation: Approval of the issuance of an RFP for the provision of EDMS, IT & Website Services. Discussion: There will be one RFP with three items-EDMS, IT and Website Services. Cybersecurity has already been sent out in an RFQ. Essentially, we are un-bundling our IT Services and looking at all options as we move forward to provide a secure environment for our computer systems. Potentially, we could have one vendor or three separate vendors but they will be issued in one RFP.

Motion: David Fetkenher Second: Barclay Harless

The Board approved the issuance of an RFP for the provision of EDMS, IT & Website services. The motion carried unanimously. Action Item 5 – RFQ Selection: Cybersecurity As a result of the malware incident in October 2019, CSPIN engaged Abacode, a computer forensic firm for further investigation. Based on best practices, it was recommended that CSPIN procure Cybersecurity services to provide a full spectrum of cybersecurity consulting services to help plan, implement and maintain governance and/or compliance, assess security posture and train staff to create a culture of security. On November 20, 2019, the Board approved the issuance of an RFQ for Cybersecurity services. CSPIN issued an RFQ, received and reviewed seven (7) proposals, which included provision for 24/7 monitoring. Three of the proposals did not meet the RFQ criteria.

6

4

In the short term, the 24/7 monitoring was determined to be a critical protective measure. The contract services for monthly monitoring were scheduled to expire on Friday, December 13, 2019. These are not offered on a month-to-month renewal basis, only on a one (1) year contract. To ensure continuous services for CSPIN’s 24/7 cyber monitoring platform, Abacode was selected as the vendor to offer 24/7 Cyber Lorica SIEM/SOC Monitoring for a one-year period at the cost of $5,050/month. The remaining services outlined in the proposal include the following: 1) Cybersecurity Policy Review and Development 2) External/Internal Vulnerability & Security Controls Assessment 3) Network, Physical and Wireless Penetration Tests 4) Phishing Exercise 5) Managed Cybersecurity Awareness Training. Four proposals were reviewed by staff, the costs of these services ranged from $14,470 to $92,650. Vendor Fixed 24/7 Total Abacode $48,270 $60,600 $108,870 MGT Consulting $51,100 $26,775 $77,875 Stealthentry $92,650 $35,500 $128,150 Infosight $14,470 $87,360 $101,830 Recommendation: To negotiate and enter into a contract with Abacode to secure the additional Cybersecurity services, as stated in the scope of work above, totaling $48,270.

Motion: David Fetkenher Second: Barclay Harless

The Board of Directors approved to negotiate and enter into contract with Abacode as stated in the scope of work. The motion carried unanimously.

Action Item 6 – Annual Financial Audit for the Fiscal Year Ended June 20, 2019

The audit firm of Powell & Jones, CPAs has completed the annual financial audit for WorkNet Pinellas, Inc. for the fiscal year ended June 30, 2019. Enclosed is a copy of the audit report. Representatives from the firm presented the results to the Audit Committee on January 15, 2020. Recommendation: The Audit Committee recommends approval of the Annual Financial Audit for the fiscal year ended June 30, 2019. Discussion: Richard Powell, CPA, reviewed the audit report. He highlighted the following:

(a) Note 14-Contingent Liability. The ETA documented seventeen findings regarding grant administration of DOL funds totaling $17,643,410. Approximately $5,557,469 relates to funds administered by CareerSource Pinellas. The DEO, along with the two CareerSource agencies involved have requested technical assistance from ETA to address and resolve the findings. CareerSource Pinellas has identified approximately $2.55 million in unrestricted funds that could be utilized to repay any final disallowed costs.

(b) Note 16-Subsequent Events. The Sale of the Science Center on November 20, 2019. Net proceeds were $2,461,659 and will be classified as unrestricted reserves of WorkNet.

(c) Subrecipient Monitoring-CareerSource Pinellas had three subrecipients of its grant funds totaling approximately $573,567 in pass-through funds. It is recommended that CareerSource Pinellas implement procedures to assure that all subrecipients of its federal funds are fully monitored as required by Section D of the Uniform Guidance.

7

5

(d) Current Year Findings-2019-2 Indirect Cost Allocation. This had not been completely documented at the time of the audit. Subsequently, the Organization received an approved provisional rate from the DOL for the year ended June 30, 2019 and 2020.

The Board discussion on DOL update/expectation for findings: In November DOL requested DEO to work with CareerSource Pinellas and Tampa Bay to submit additional information, which has been submitted. There has been no feedback regarding that. DEO has requested technical assistance meetings with USDOL. Once those meetings are completed, DEO will gather all recommendations from USDOL and meet with CareerSource Pinellas to review. After discussion regarding the total funds in Note 14, it was decided that Richard will add an additional comment stating that it is not possible to estimate a final liability at this time. Motion: Scott Wagman Second: Mark Hunt

The Board of Directors approved the Annual Financial Audit for the fiscal year ended June 30, 2019 with the stipulation that there will be an additional comment added to Note 14. The motion carried unanimously. Other Administrative Matters – DEO forwarded a copy of an anonymous letter to CareerSource Pinellas. In line with our commitment to promote transparency, a copy of the letter was presented to the Board of Directors. The Board asked the CEO to provide a response with the understanding a full response is not possible due to the anonymity of the letter. Presentations: Rolando Torres, Abacode – An overview of the company, cybersecurity framework, managing the risk & security program and highlighting the high-level gaps at the time of incident were made. Stephanie Marchman, Sunshine Law – The following recommendations were made: It is recommended that public comment be moved to the beginning of the agenda or for the Chair to allow public comment before each agenda item is voted upon. It is recommended that in addition to the website, future agendas also include the following language:

All parties are advised that if you decide to appeal any decision made by the Board with respect to any matter considered at the meeting or hearing, you will need a record of the proceedings, and that, for such purpose, you may need to ensure that a verbatim record of the proceedings is made, which record includes the testimony and evidence upon which the appeal is to be based.

If you have a disability and need an accommodation in order to participate in this meeting, please contact [insert name] at [phone number and email] at least two business days in advance of the meeting.

Information Items

Information Item 1 – USDOL Compliance Review Update USDOL/ DEO Compliance Review Background: CareerSource Pinellas received the U.S. Department of Labor Employment and Training Administration (USDOL/ETA) Compliance Review of CareerSource Tampa Bay (CSTB) and Career Source Pinellas (CSPIN) on May 16, 2019. The report was submitted to Ken Lawson, Executive Director Florida Department of Economic Opportunity (DEO) and was issued by the Atlanta Regional Office on May 15, 2019. On June 28, 2019, the Florida Department of Economic Opportunity (DEO) submitted to the U.S. Department of Labor, Employment and Training Administration (ETA), Atlanta Regional Office, responses to the Findings contained in the ETA’s May 15, 2019 report of the Compliance Review. On October 14, 2019, USDOL/ETA issued a letter of response to DEO. USDOL/ETA acknowledged DEO efforts in working with CareerSource Tampa Bay and CareerSource Pinellas to begin to implement many of the corrective actions that are required to resolve the Findings. However, as reflected in the

8

6

Compliance Review Report, the documentation provided and corrective actions taken to date are insufficient to fully address the required actions in the Findings. As a result, 16 of the 17 Findings remain unresolved. In response, DEO requested supplemental information from both CSTB and CSPIN. The supplemental information was due to DEO for review on or before November 12, 2019. DEO will review this information in an effort to provide a written response to USDOL/ETA as required by November 28, 2019. In December, DEO submitted a request for technical assistance to the USDOL.

Information Item 2: Local Workforce Development Board Plan

The Department of Economic Opportunity has finalized the WIOA Local Plan Guidelines for the development of the comprehensive Local Workforce Development Board four-year plan (2020-2024).

Key Dates are as follows:

Event Date (On or Before)

Local Plan Guidelines Issued November 1, 2019 Labor Market Analysis Sent to Local Boards December 6, 2019 Local Plans Due March 16, 2020 WIOA Statewide Unified Plan Due March 30, 2020 WIOA Statewide Unified Plan Approved May 1, 2020 Local Plans Approved June 4, 2020 WIOA Program Year 2020 Begins July 1, 2020

The draft LWDP will be posted for the required 30 day public review period beginning in February. The final draft along with comments will be presented at the March Board of Directors Meeting for approval and, subsequently, submitted to the Board of County Commissioners for review and approval.

Information Item 3: MOU/IFA Renewals

As part of the Local Workforce Development Plan, CareerSource Pinellas is renewing Memorandums of Understanding (MOU) agreements.

MOUs establish joint processes and procedures that enable Partner integration into the One-Stop Delivery System resulting in a seamless and comprehensive array of education, human service, job training, and other workforce development services to persons with disabilities in Pinellas County.

The updated MOU & IFA’s will be presented at the March CSPIN Board of Directors meeting on March 18, 2020 for review and approval. MOU’s will subsequently be forwarded to the Board of County commissioners.

9

7

MOU/IFA Renewals

Partner

Program

Partner

Organization Authorization/Category Contact Information

Pending

Items

AARP Foundation SCSEP

AARP Foundation

Senior Community Service Employment Program (SCSEP) authorized under title V of the Older Americans Act of 1965 (42 U.S.C. 3056 et seq.) Gina Kravitz, [email protected]

Pending Both MOU and IFA; with

AARP legal department

Career, Technical & Adult Education Programs

Pinellas County School Board

WIOA title II Adult Education and Family Literacy Act (AEFLA) Program Mark Hunt, [email protected]

Pending Signed IFA; Signed MOU

Received

Career, Technical & Adult Education Programs

Pinellas County School Board

Career and technical education programs at the postsecondary level, authorized under the Carl D. Perkins Career and Technical Education Act of 2006 (20 U.S.C. 2301 et seq.) Mark Hunt, [email protected]

Pending Signed IFA; Signed MOU

Received

Community Services Block Grant

Pinellas Opportunity Council

Employment and training activities carried out under the Community Services Block Grant Act (CSBG) (42 U.S.C. 9901 et seq.) Carolyn King, [email protected]

Signed MOU and IFA

Received

Division of Blind Services

FL Department of Education

State Vocational Rehabilitation (VR) Services program authorized under title I of the Rehabilitation Act of 1973 (29 U.S.C. 720 et seq.), as amended by WIOA title IV

Nancy Brown, District Administrator- [email protected]

Marcela Blanchett- Employment Placement Specialist- [email protected]

MOU and IFA

Approved; DBS requests

to be final signature

Job Corps Odle Management

Job Corps, WIOA Title I, Subtitle C

Tim Foley, [email protected] Samuel Kolapo, [email protected]

Signed MOU and IFA

Received

Vocational Rehabilitation

FL Department of Education

State Vocational Rehabilitation (VR) Services program authorized under title I of

John Howell, [email protected]

Pending Both MOU and

IFA; with VR

10

8

the Rehabilitation Act of 1973 (29 U.S.C. 720 et seq.), as amended by WIOA title IV

legal department

Information Item 4: Strategic Plan

As the New Year begins, we look forward to working with board members and key stakeholders to develop “CareerSource Pinellas 2020.”

This comprehensive strategic initiative will be a brainstorming and planning process to define our aspirations at CareerSource Pinellas, and examine our existing resources and leadership’s role in

workforce development and the community.

To assist us with the facilitation of this project, we have engaged Strumpf & Associates. Lori Strumpf is an experienced consultant who will guide several opportunities for input and conversation to ensure an effective CareerSource Pinellas 2020 action plan.

As a key stakeholder, you are personally invited to join the Strategic Planning Team or Focus Group, as your input is important as we establish goals, set priorities and look to the future.

Strategic Planning Team

This Team will consist of 10-15 board members, partners and key stakeholders. The Charter of the

Strategic Planning Team is to develop a comprehensive strategic plan that will help to sustain growth and

provide direction to the organization over the next three years. The plan will also address steps to

implement new strategies and approaches. The team will submit the plan as a recommendation to the

Local Workforce Development Board (LWDB) for approval.

The current schedule is as follow, and members of the Strategic Planning Team are being asked to commit to attending all scheduled sessions for the most effective outcome.

Friday, January 17, 2020 Strategic Planning Team Meeting #1

9:00 am to 2:00 pm (including working lunch) Begin identifying strategic challenges and SWOT analysis.

Wednesday, January 29, 2020 Strategic Planning Team Meeting #2

8:30 am to 12:30 pm Continue SWOT analysis and begin to define what needs to be accomplished over the next three (3) years.

Friday, February 7, 2020 Strategic Planning Team Meeting #3

8:30 am to 12:30 pm Use data from the Focus Groups to refine goals and strategies. Begin to define vision, mission and values.

Tuesday, February 25, 2020 Strategic Planning Team Optional Meeting #4

8:30 am to 12:30 pm If needed, fourth meeting to finalize the plan and discuss next steps.

11

9

Focus Groups

Friday, January 17, 2020 Focus Group #1

2:30 pm to 4:00 pm Board Members

Wednesday, January 29, 2020 Focus Group #2

1:30 pm to 3:00 pm Partners

Wednesday, January 29, 2020 Focus Group #3

3:30 pm to 5:00 pm Employees

Friday, February 7, 2020 Focus Group #4

1:30 pm to 3:00 pm Employers

Friday, February 7, 2020 Focus Group #5

3:30 pm to 5:00 pm Job Seekers

Information Item 5: DEO Daily Governor’s Report

DEO Daily Governor’s Report – (Placement as reported in the Employ Florida system) Local Tracking for Program Year 2019-2020 and 2018-2019

CareerSource Pinellas

PY 19/20 Placements Composite Score Ranking Statewide

Placements

July 371 104.17% 11 8,426

August 341 117.58% 12 6,985

September 385 120.49% 11 7,974

October 370 88.83% 14 9,831

November 210 83.33% 12 6,391

December 234 96.23% 11 6,807

January

February

March

April

May

June

Totals 1,911 101.77% 11.8 46,414

CareerSource Pinellas

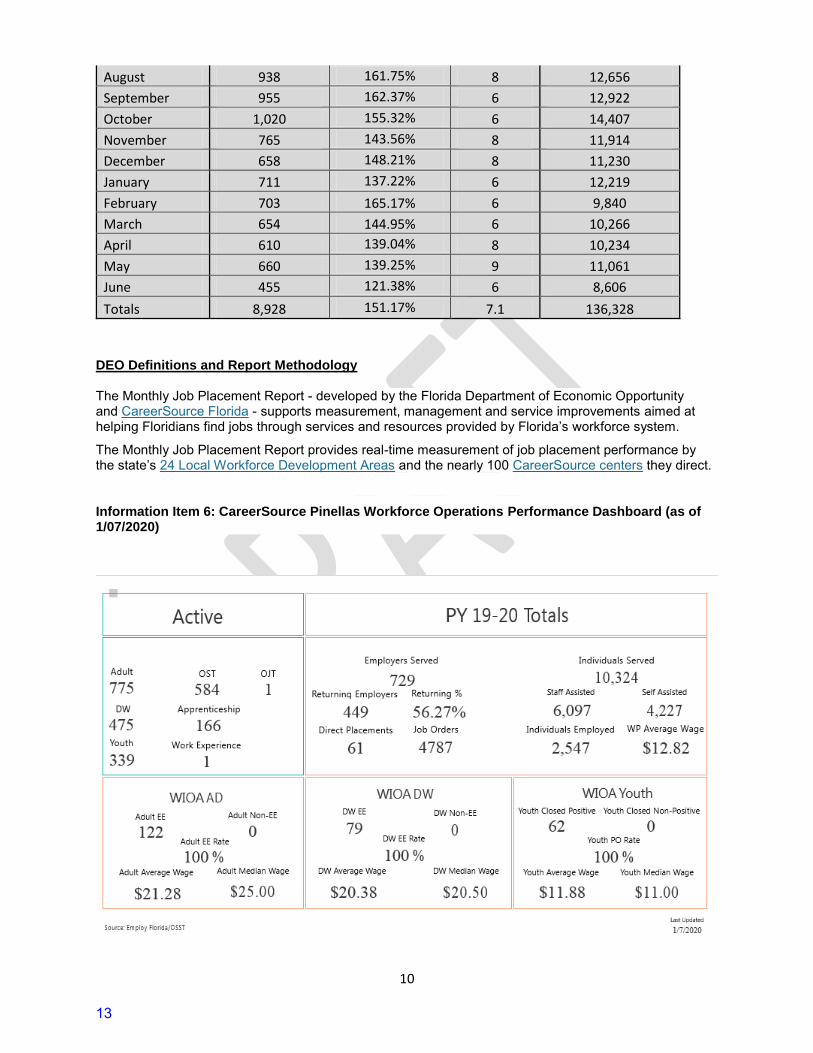

PY 18/19 Placements Composite Score Ranking Statewide

Placements

July 799 166.01% 8 10,973

12

10

August 938 161.75% 8 12,656

September 955 162.37% 6 12,922

October 1,020 155.32% 6 14,407

November 765 143.56% 8 11,914

December 658 148.21% 8 11,230

January 711 137.22% 6 12,219

February 703 165.17% 6 9,840

March 654 144.95% 6 10,266

April 610 139.04% 8 10,234

May 660 139.25% 9 11,061

June 455 121.38% 6 8,606

Totals 8,928 151.17% 7.1 136,328

DEO Definitions and Report Methodology

The Monthly Job Placement Report - developed by the Florida Department of Economic Opportunity and CareerSource Florida - supports measurement, management and service improvements aimed at helping Floridians find jobs through services and resources provided by Florida’s workforce system.

The Monthly Job Placement Report provides real-time measurement of job placement performance by the state’s 24 Local Workforce Development Areas and the nearly 100 CareerSource centers they direct.

Information Item 6: CareerSource Pinellas Workforce Operations Performance Dashboard (as of 1/07/2020)

13

11

Information Item 7: Financial Reports through October 31, 2019

A brief overview of the financial reports provided in the agenda was given. Barclay Harless brought up the fact that several of the programs are up by double digits. Ms. Brackney explained that training enrollments are up due to a renewed focus on occupational training. We do want to continue to focus on work-based learning programs, especially Paid Work Experience (PWE). We have made a decision to take a step back in regards to On-The-Job Training to ensure program activities align with new guidance from USDOL/DEO.

Committee Meetings

1. Finance Committee (Fetkenher or Meier) The Finance Committee met on December 18. The Committee approved designating the net proceeds from the sale of the Science Center as unrestricted subject to the reduction of expenses related to the sale, closing and operating costs pending the completion of the DOL compliance review. Also, the Committee approved the release of approximately $175,000 in the Capital Improvement fund to unrestricted, also pending the completion of the DOL compliance review. The Committee also discussed entering into a contract with Abacode to perform 24/7 cybersecurity monitoring for one-year. The committee also reviewed the financial information that was included in today’s packet as information items. Lastly, information was submitted to the Department of Labor to obtain a provisional Indirect Cost Rate for 2018-2019. Since our meeting, the DOL provided a provisional indirect rate for 2018-2019 and 2019-2020 of 16.49% of Modified Total Direct Costs. As a reminder, CareerSource has been using the 10% de minimis rate.

The next Finance Committee Meeting is February 26, 2020.

2. Audit Committee (Fetkenher or Meier) The Audit Committee met immediately preceding today’s Board’s meeting. Representatives from Powell and Jones presented the audited statements that are included in today’s packet. The Audit Committee approved the audited financial statements as presented.

3. Ad Hoc CEO/Counsel Selection Committee (Leavelle) The Ad Hoc/Counsel Selection Committee did not meet this month.

4. Compensation Committee (Duff or Schultz) The Compensation Committee did not meet this month.

5. One-Stop Committee (Howell or Moeller) The One-Stop Committee did not meet this month. The next One Stop Committee meeting is scheduled for February 27, 2020

6. Workforce Solutions Committee (Hunt or Torregiante) The Workforce Solutions Committee did not meet this month. The next Workforce Solutions Committee is scheduled for February 11th, 2020

CEO Report:

The CEO introduced the leadership team. She also outlined a plan to upgrade the centers to allow for more customer-forward services. We are in the process of working with PCS to renovate the South County Career Resource Center which is why the meeting was held at PTC. Ms. Brackney welcomed everyone to join the tour.

14

12

The CEO thanked Mark Hunt for his hospitality and the use of the Pinellas Technical College.

Public Comments: None

Open Discussion:

Dr. Law has resigned. We are not required to fill that position. That reduces our count to 32. Also, the March meeting is going to be very important, as we have Local Workforce Development Plan, MOU’s/IFA’s, the budget and the work plan that have to go to the BOCC before June 30th for approval. There will also be a DEO presentation at the March Board Meeting.

Adjournment: The meeting was adjourned at 1:33 p.m.

15

Action Item 2

Employee Handbook

The following is a summary of the changes to the CareerSource Pinellas Employee Handbook approved by Compensation Committee after legal review:

Section Page Proposed Change Mission Statement 5 Reflect web page At Will Statement 6 Expanded statement Resignation 8 Once resignation is received may terminate without

completing final time given Complaint Police 10 No requirement to adhere to chain of command, may notify

any manager comfortable with to discuss the matter Flex Time 13 Flex time can only be used based on business need, must

be approved and used within the same week Modified Work Schedule 13 Removed specific hours of modified schedule Use, Owner and Return of Company System and Property

15 Robust and comprehensive description of proprietary information systems, information and property.

Lunch Periods 19 Must be taken between the hours of 11am-2pm. PTO 28 PTO may not exceed a total of 480 hours. Changed from

800 hours. Nursing Mothers Accommodations 29 Added new policy Leave for Emergency Closing 31 Increased from 3 to 4 days a year. No flex time may be used

for personal reasons. Personal Days 38 Rewrote this section – added up to 4 days paid maximum,

may be taken in 15 minute increments Absenteeism and Tardiness 40 Eliminated the reference to rolling 12 month period. Appearance Policy 41 Updated to professionalism with unacceptable appearance/

clothing Company Car 43 Added this section Safe Driver 45 Added this section Nepotism 48 Added employee in authority unable to make personnel

decisions, and added to relations Outside Employment 49 Added new policy Employee Discipline 57 Rewrote this section Problem Resolution 59 Expanded reporting process

RECOMMENDATION: Approval of the CareerSource Pinellas Employee Handbook, effective April 1, 2020.

Link: https://careersourcepinellas.com/wp-content/uploads/2020/03/4.1-Employee-Handbook-with-2-4-2020-comp-committee-modification.pdf

16

Action Item 3

Administrative Policies

As part of the Compliance Review, USDOL/DEO have requested CareerSource Pinellas review and update three (3) Administrative Policies. The modification of these policies helps ensure alignment with rules and regulations outlined by United States Department of Labor (USDOL), Department of Economic Opportunity (DEO) and CareerSource Florida (CSF). CSF Strategic Policies are high level principles or directional statements to inform or clarify federal or state legislation, policies or workforce system strategies that are approved by CSF Board. On November 14, 2019, the following CareerSource Pinellas Administrative policies were presented and approved by the Compensation Committee.

Ethics and Transparency Conflict of Interest Authorization of Bonuses and Pay Raises

On November 20, 2019, the Board of Directors approved a motion to withdraw the Authorization of Bonuses and Pay Raises Policy from Action Item 9 and send it back to the Compensation Committee and suggested the following language be considered: “The Local Workforce Development Board will approve all performance evaluation increases/stipends, bonuses, pay ranges, and benefit stipends.” On February 4, 2020, the Compensation Committee approved the following language to be sent to the Board of Director’s March meeting for final approval: “The Local Workforce Development Board will approve policies related to the budget, performance evaluations, bonuses, pay ranges and benefit stipends.”

RECOMMENDATION: Approval of the Authorization of Bonuses and Pay Raises Policy.

17

Page 1 of 1

Policy

SECTION: HUMAN RESOURCES POLICY # PAGE 1 OF 1

TITLE: Authorized Compensation

Policy

EFFECTIVE DATE: TBD

APPROVED BY: REPLACES: N/A

PURPOSE: The purpose of this policy is to formalize the Worknet Pinellas, Inc. dba CareerSource Pinellas (“CareerSource”) policy regarding authorization of a compensation policy.

BACKGROUND: As a recommendation outlined in the United States Department of Labor Compliance Review, all increases in compensation should be approved by the Local Workforce Development Board.

POLICY: The Local Workforce Development Board will approve policies related to the budget, performance evaluations, bonuses, pay ranges and benefit stipends.

POLICY AMENDMENTS OR REVOCATION: Notwithstanding any of the foregoing, CareerSource reserves the right to revise or revoke this policy at any time.

This policy is written to establish local policy and is not intended to supersede any applicable laws or regulations. Failure of CareerSource to adhere strictly to the steps outlined within this policy shall not be construed as a violation of rights or administrative procedures.

INQUIRIES: Any question about this policy should be directed to the HR Business Partner.

18

Action Item 4

Approval of Training Vendor Connecticut School of Broadcasting (ID# 5422)

3901 Coconut Palm Dr., Suite 105, Tampa, FL 33619

Connecticut School of Broadcasting has a license from the Commission for Independent Education. Staff conducted a site visit on Friday, 1.03.2020. Connecticut School of Broadcasting has begun reporting to FETPIP.

Courses/Certificate/Diploma Programs

Program – Course # - Type of Degree or

Certificate

Books & Supplies

Tuition & Fees

Total Cost

Duration Of

Training

Completion Rate

Average Wage At

Placement

Retention Rate

Radio and Television Broadcasting Program $100 $13,890 $13,990 112 hours 90.63% $12-18 93.75%

* Intro to Mobile Application Design & Development

Included $3,990 $3,990 112 hours N/A Anticipated $26.24 N/A

* Intro to Web Design & Development Included $4,990 $4,990 112 hours N/A Anticipated

$18-30 N/A

* Social Media Marketing Specialist Included $3,990 $3,990 112 hours N/A Anticipated

$18 N/A

* New programs approved by Florida Department Education on 11.29.2018

Years in operation: 16 years Total enrollments for prior year: 17

RECOMMENDATION: Approval of Connecticut School of Broadcasting as an approved training vendor for LWDB 14.

19

Action Item 5

Approval of Training Vendor Building Industry Construction Service International dba BICSI

Learning Academy 8610 Hidden River Pkwy., Tampa, FL 33637

BICSI Learning Academy has a license from the Commission for Independent Education. Staff conducted a site visit on Friday, 1.17.2020. BICSI Learning Academy will begin reporting to FETPIP.

Courses/Certificate/Diploma Programs

Program – Course # - Type of Degree or

Certificate

Books & Supplies

Tuition & Fees

Total Cost

Duration Of

Training

Completion Rate

Average Wage At

Placement

Retention Rate

Cabling Installation Program – Course IN101 – Installer 1

$260 $2,010 $2,270 35 hours N/A Anticipated $14-16 N/A

Cabling Installation Program – Course IN225

$260 $2,530 $2,790 35 hours N/A Anticipated $14-16 N/A

Cabling Installation Program – Course IN250

$260 $2,730 $2,990 35 hours N/A Anticipated $16-18 N/A

Cabling Installation Program – Course TE350

$260 $2,830 $3,090 35 hours N/A Anticipated $18-20 N/A

* New programs approved by Florida Department Education on 11.29.2018

Years in operation: 32 years Total enrollments for prior year: 330 for all courses in the Cabling Installation Program

We are also requesting approval to add occupational to the 2019-2020 RTOL for LWDB 14 under SOC Code 49-9052. RECOMMENDATION: Approval of BICSI Learning Academy as an approved training vendor for LWDB 14.

20

Action Item 6

Local Targeted Occupations List The Department of Economic Opportunity’s (DEO) Bureau of Labor Market Statistics (LMS) published the 2019-2020 Statewide Demand Occupational Lists on the Department’s website. The Statewide Demand Occupations list identifies the labor market needs of Florida’s business community and encourages job training based on those needs, with emphasis on jobs that are both in high demand and high skill/high wage, and is used as a baseline for establishing the local Targeted Occupations List (TOL). The Local Workforce Development Boards (LWDBs) develop and use their TOLs to identify occupations for which eligible adults and dislocated workers may receive training assistance under the Workforce Innovation and Opportunity Act (WIOA). The TOL also governs Occupational skills training, Paid-Work Experience, and On-the-Job training programs, including Apprenticeships. A TOL must be updated when occupations are deleted or added. Each LWDB must update and publish the updated TOL to its website and submit a link to DEO with revisions. Staff have reviewed the current TOL and are submitting two additions for consideration. Accompanying Labor Market Information has been received through DEO to support the addition of these occupations to the 2019-2020 TOL for LWDB 14.

Potential Occupational Title Additions

SOC Code

SOC Title 2018 2026 Growth Percent Growth

Total Job Openings

2017 Medial Hourly Wage

($)

FL BLS

37-3011

Landscaping and Groundskeeping

Workers 3,991 4,507 516 12.9 4,531 12.29 NR NR

49-9052

Telecommunications Line Installers and

Repairers 473 494 21 4.4 401 19.32 PS HS

*Education Levels are abbreviated as follows for both Florida and USDOL, Bureau of Labor Statistics. HS: High School diploma or GED; NR: No Formal Educational credential required; PS: Post-secondary non-degree award

RECOMMENDATION: Approval of the updated Targeted Occupations list for CSPIN.

21

Workforce Development Area 14 - Pinellas County

Selection Criteria:12 80 annual openings and positive growth3 Mean Wage of $15.10/hour and Entry Wage of $12.29/hour4 High Skill/High Wage (HSHW) Occupations:

Mean Wage of $23.68/hour and Entry Wage of $15.10/hour

Annual FLDOE In EFIPercent Annual Training Targeted Data Youth/WT

SOC Code† HSHW†† Occupational Title† Growth Openings Mean Entry Code Industry? Source††† Only

132011 HSHW Accountants and Auditors 1.78 584 33.58 21.68 5 Yes R113011 HSHW Administrative Services Managers 1.91 89 53.00 25.92 4 Yes R413011 Advertising Sales Agents 0.15 1,496 27.95 13.30 3 Yes S493011 HSHW Aircraft Mechanics and Service Technicians 1.19 1,294 26.95 16.11 3 Yes S532011 HSHW Airline Pilots, Copilots, and Flight Engineers 1.52 557 88.88 45.87 4 Yes S173011 HSHW Architectural and Civil Drafters 1.38 733 24.37 16.33 3 Yes S274011 Audio and Video Equipment Technicians 1.84 638 19.22 12.61 4 Yes S493021 Automotive Body and Related Repairers 1.36 1,217 19.60 12.46 3 No S493023 Automotive Service Technicians and Mechanics 0.92 132 18.29 12.19 3 No R433031 Bookkeeping, Accounting, and Auditing Clerks 0.48 792 18.19 12.74 4 Yes R Youth/WT493031 Bus and Truck Mechanics and Diesel Engine Specialists 1.35 1,349 22.18 15.65 3 Yes S533022 Bus Drivers, School or Special Client 1.51 292 16.36 13.01 3 No R533021 Bus Drivers, Transit and Intercity 1.28 83 16.36 12.67 3 Yes R Youth/WT131199 HSHW Business Operations Specialists, All Other 1.87 577 32.22 18.84 4 No R435011 Cargo and Freight Agents 1.60 677 21.18 13.04 3 Yes S472031 Carpenters 1.72 275 18.30 12.88 3 No R472051 Cement Masons and Concrete Finishers 2.07 1,794 17.44 12.53 3 No S351011 Chefs and Head Cooks 1.42 1,333 25.97 14.71 3 No S111011 HSHW Chief Executives 0.45 91 91.48 37.59 5 Yes R399011 Child Care Workers 1.25 8,947 10.76 9.15 3 No S Youth/WT 131031 HSHW Claims Adjusters, Examiners, and Investigators 0.61 142 29.31 19.09 3 Yes R532012 HSHW Commercial Pilots 1.51 559 44.11 24.76 3 Yes S131041 HSHW Compliance Officers 1.21 1,657 29.94 16.83 3 No S113021 HSHW Computer and Information Systems Managers 1.81 80 64.54 39.49 5 Yes R151143 HSHW Computer Network Architects 1.37 94 42.35 24.57 3 Yes R151152 HSHW Computer Network Support Specialists 1.49 990 27.90 16.75 3 Yes S151131 HSHW Computer Programmers -0.26 768 37.18 22.28 3 Yes S Youth/WT151121 HSHW Computer Systems Analysts 1.43 97 38.78 23.73 4 Yes R151151 HSHW Computer User Support Specialists 1.98 279 24.16 15.21 3 Yes R474011 HSHW Construction and Building Inspectors 1.57 1,019 27.71 18.20 3 No S119021 HSHW Construction Managers 1.63 110 40.32 25.43 4 No R131051 HSHW Cost Estimators 1.76 94 29.01 18.33 4 No R434051 Customer Service Representatives 1.73 36,239 15.39 10.88 3 Yes S Youth/WT151141 HSHW Database Administrators 1.65 658 40.74 25.63 4 Yes S319091 Dental Assistants 2.70 157 18.87 14.04 3 Yes R292021 HSHW Dental Hygienists 2.21 1,000 30.31 22.54 4 Yes S472111 Electricians 1.28 259 20.04 14.44 3 No R252021 HSHW Elementary School Teachers, Except Special Education 1.24 258 28.57 21.44 5 No R292041 Emergency Medical Technicians and Paramedics 3.05 31 16.80 11.39 4 Yes R Youth/WT132051 HSHW Financial Analysts 1.89 86 38.52 23.81 5 Yes R113031 HSHW Financial Managers 2.84 150 67.07 35.45 5 Yes R332011 HSHW Firefighters 1.21 118 24.11 17.78 3 No R471011 HSHW First-Line Supervisors of Construction Trades and Extraction Workers 1.89 283 29.32 19.35 4 No R371011 First-Line Supervisors of Housekeeping and Janitorial Workers 1.65 2,043 18.90 12.51 3 No S371012 First-Line Supervisors of Landscaping, Lawn Service, and Groundskeeping Workers 1.72 2,016 23.07 13.92 3 No S491011 HSHW First-Line Supervisors of Mechanics, Installers, and Repairers 1.29 157 29.79 19.33 3 No R411012 HSHW First-Line Supervisors of Non-Retail Sales Workers 1.17 216 41.84 21.05 4 Yes R431011 HSHW First-Line Supervisors of Office and Administrative Support Workers 0.95 660 27.12 17.64 4 Yes R391021 First-Line Supervisors of Personal Service Workers 1.73 2,075 20.18 12.70 3 No S511011 HSHW First-Line Supervisors of Production and Operating Workers 0.89 211 29.04 18.30 3 Yes R411011 First-Line Supervisors of Retail Sales Workers 0.74 640 21.17 13.85 3 No R531031 HSHW First-Line Supervisors of Transportation and Material-Moving Machine and Vehicle Operators 1.29 1,392 25.39 15.24 3 Yes S119051 Food Service Managers 1.55 96 28.62 12.87 4 No R111021 HSHW General and Operations Managers 1.60 484 58.54 26.49 4 Yes R472121 Glaziers 1.96 658 17.80 13.89 3 No S271024 Graphic Designers 0.94 104 22.67 14.62 4 Yes R292099 Health Technologists and Technicians, All Other 1.92 1,011 19.75 12.98 3 Yes S499021 Heating, Air Conditioning, and Refrigeration Mechanics and Installers 1.76 309 19.59 14.57 3 No R533032 Heavy and Tractor-Trailer Truck Drivers 1.46 328 19.86 12.63 3 Yes R311011 Home Health Aides 3.85 4,744 10.80 9.58 3 Yes S Youth/WT131071 HSHW Human Resources Specialists 1.72 312 29.07 18.62 5 No R172112 HSHW Industrial Engineers 1.84 95 34.36 20.98 5 Yes R499041 Industrial Machinery Mechanics 1.18 1,374 23.30 15.99 3 Yes S151122 HSHW Information Security Analysts 3.22 553 41.33 26.32 3 Yes S413021 HSHW Insurance Sales Agents 1.66 287 32.96 16.25 3 Yes R271025 Interior Designers 1.36 671 23.70 13.77 4 Yes S292061 Licensed Practical and Licensed Vocational Nurses 1.98 328 20.87 16.97 3 Yes R533033 Light Truck or Delivery Services Drivers 1.16 6,980 16.66 10.46 3 Yes S434131 Loan Interviewers and Clerks 2.23 143 18.78 14.11 3 Yes R132072 HSHW Loan Officers 2.03 134 37.18 20.95 4 Yes R514041 Machinists 0.73 123 19.64 14.31 3 Yes R499071 Maintenance and Repair workers, General 1.44 10,322 17.00 11.61 3 No S Youth/WT131111 HSHW Management Analysts 2.34 368 39.82 23.89 5 Yes R131161 HSHW Market Research Analysts and Marketing Specialists 3.12 273 33.46 18.74 5 Yes R292012 Medical and Clinical Laboratory Technicians 1.95 656 24.78 15.07 4 Yes S292011 Medical and Clinical Laboratory Technologists 1.52 895 24.78 15.07 4 Yes S119111 HSHW Medical and Health Services Managers 2.11 92 53.99 32.94 5 Yes R319092 Medical Assistants 3.77 460 15.42 12.37 3 Yes R Youth/WT292071 Medical Records and Health Information Technicians 1.82 937 19.67 12.75 4 Yes S436013 Medical Secretaries 2.31 161 16.32 12.83 3 Yes R319094 Medical Transcriptionists 1.21 81 19.18 12.87 3 Yes R131121 Meeting, Convention, and Event Planners 1.84 1,102 22.66 13.72 4 No S

2017 Hourly Wage

2019-20 Regional Demand Occupations List

Sorted by Occupational Title

FLDOE Training Code 3 (PSAV Certificate), 4 (Community College Credit/Degree), or 5 (Bachelor's Degree)

22

252022 HSHW Middle School Teachers, Except Special and Career/Technical Education 1.25 115 29.14 23.41 5 No R493042 Mobile Heavy Equipment Mechanics, Except Engines 1.51 636 21.91 15.35 3 Yes S151142 HSHW Network and Computer Systems Administrators 1.18 101 37.88 24.58 4 Yes R311014 Nursing Assistants 2.28 14,476 12.88 10.76 3 Yes S Youth/WT472073 Operating Engineers and Other Construction Equipment Operators 1.82 97 18.10 12.97 3 No R472141 Painters, Construction and Maintenance 1.77 183 18.31 12.95 3 No R Youth/WT232011 HSHW Paralegals and Legal Assistants 2.10 168 24.49 16.58 3 Yes R132052 HSHW Personal Financial Advisors 1.78 103 46.57 18.32 5 Yes R292052 Pharmacy Technicians 1.24 43 14.88 11.86 3 No R Youth/WT312021 HSHW Physical Therapist Assistants 3.42 939 30.15 23.70 4 Yes S472151 Pipelayers 1.38 666 19.14 13.62 3 No S472152 Plumbers, Pipefitters, and Steamfitters 1.68 212 21.49 14.87 3 No R333051 HSHW Police and Sheriff's Patrol Officers 1.16 172 26.87 20.18 3 No R435031 Police, Fire, and Ambulance Dispatchers 1.35 705 19.53 13.95 3 No S119141 Property, Real Estate, and Community Association Managers 1.72 229 26.29 13.97 4 No R273031 HSHW Public Relations Specialists 1.53 88 29.89 19.54 5 Yes R131023 HSHW Purchasing Agents, Except Wholesale, Retail, and Farm Products 0.02 91 28.87 18.03 4 Yes R292034 HSHW Radiologic Technologists 1.74 1,016 26.55 19.26 3 Yes S419021 Real Estate Brokers 1.27 765 35.04 14.50 3 No S419022 Real Estate Sales Agents 1.37 222 31.82 14.34 3 No R493092 Recreational Vehicle Service Technicians 1.49 141 17.34 10.01 3 No S291141 HSHW Registered Nurses 1.58 783 32.21 24.31 4 Yes R291126 HSHW Respiratory Therapists 2.60 735 27.58 22.61 4 Yes S112022 HSHW Sales Managers 1.55 95 65.57 32.60 5 Yes R414012 Sales Representatives, Wholesale and Manufacturing, Except Technical and Scientific Products 1.14 553 28.66 12.88 3 Yes R414011 HSHW Sales Representatives, Wholesale and Manufacturing, Technical and Scientific Products 1.16 236 36.93 17.31 3 Yes R252031 HSHW Secondary School Teachers, Except Special and Career/Technical Education 1.25 146 30.85 23.40 5 No R436014 Secretaries, Except Legal, Medical and Executive 1.12 22,778 16.52 11.44 3 Yes S Youth/WT413031 HSHW Securities, Commodities, and Financial Services Sales Agents 1.12 190 37.68 17.47 5 Yes R492098 Security and Fire Alarm Systems Installers 1.52 867 20.40 14.48 3 No S472211 Sheet Metal Workers 1.49 1,087 18.70 13.19 3 No S151132 HSHW Software Developers, Applications 3.13 262 44.06 26.24 4 Yes R151133 HSHW Software Developers, Systems Software 1.49 113 45.75 27.56 5 Yes R472221 Structural Iron and Steel Workers 2.13 687 20.48 14.48 3 No S292055 Surgical Technologists 1.65 764 20.82 16.36 3 Yes S173031 Surveying and Mapping Technicians 1.51 733 19.30 13.37 3 Yes S259041 Teacher Assistants 1.24 250 15.65 12.49 3 No R Youth/WT253097 Teachers and Instructors, All Other, Except Substitute Teachers 1.78 98 24.41 14.75 5 No R131151 HSHW Training and Development Specialists NR NR 27.32 16.18 5 Yes R151134 HSHW Web Developers 1.76 950 29.89 18.24 3 Yes S514121 Welders, Cutters, Solderers, and Brazers 0.92 107 18.18 13.46 3 Yes R

†SOC Code and Occupational Title refer to Standard Occupational Classification codes and titles.

††HSHW = High Skill/High Wage.

†††Data Source:

R = Meets regional wage and openings criteria based on state Labor Market Statistics employer survey data. Regional data are shown.S = Meets statewide wage and openings criteria based on state Labor Market Statistics employer survey data. Statewide data are shown.NR = Not releasable.

EFI - Enterprise Florida, Inc.

23

Workforce Development Area 14 - Pinellas County

Selection Criteria:12 80 annual openings and positive growth3 Mean Wage of $15.10/hour and Entry Wage of $12.29/hour4 High Skill/High Wage (HSHW) Occupations:

Mean Wage of $23.68/hour and Entry Wage of $15.10/hour

Annual FLDOE In EFIPercent Annual Training Targeted Data Youth/WT

SOC Code† HSHW†† Occupational Title† Growth Openings Mean Entry Code Industry? Source††† Only

131151 HSHW Training and Development Specialists NR NR 27.32 16.18 5 Yes R311011 Home Health Aides 3.85 4,744 10.80 9.58 3 Yes S Youth/WT319092 Medical Assistants 3.77 460 15.42 12.37 3 Yes R Youth/WT312021 HSHW Physical Therapist Assistants 3.42 939 30.15 23.70 4 Yes S151122 HSHW Information Security Analysts 3.22 553 41.33 26.32 3 Yes S151132 HSHW Software Developers, Applications 3.13 262 44.06 26.24 4 Yes R131161 HSHW Market Research Analysts and Marketing Specialists 3.12 273 33.46 18.74 5 Yes R292041 Emergency Medical Technicians and Paramedics 3.05 31 16.80 11.39 4 Yes R Youth/WT113031 HSHW Financial Managers 2.84 150 67.07 35.45 5 Yes R319091 Dental Assistants 2.70 157 18.87 14.04 3 Yes R291126 HSHW Respiratory Therapists 2.60 735 27.58 22.61 4 Yes S131111 HSHW Management Analysts 2.34 368 39.82 23.89 5 Yes R436013 Medical Secretaries 2.31 161 16.32 12.83 3 Yes R311014 Nursing Assistants 2.28 14,476 12.88 10.76 3 Yes S Youth/WT434131 Loan Interviewers and Clerks 2.23 143 18.78 14.11 3 Yes R292021 HSHW Dental Hygienists 2.21 1,000 30.31 22.54 4 Yes S472221 Structural Iron and Steel Workers 2.13 687 20.48 14.48 3 No S119111 HSHW Medical and Health Services Managers 2.11 92 53.99 32.94 5 Yes R232011 HSHW Paralegals and Legal Assistants 2.10 168 24.49 16.58 3 Yes R472051 Cement Masons and Concrete Finishers 2.07 1,794 17.44 12.53 3 No S132072 HSHW Loan Officers 2.03 134 37.18 20.95 4 Yes R292061 Licensed Practical and Licensed Vocational Nurses 1.98 328 20.87 16.97 3 Yes R151151 HSHW Computer User Support Specialists 1.98 279 24.16 15.21 3 Yes R472121 Glaziers 1.96 658 17.80 13.89 3 No S292012 Medical and Clinical Laboratory Technicians 1.95 656 24.78 15.07 4 Yes S292099 Health Technologists and Technicians, All Other 1.92 1,011 19.75 12.98 3 Yes S113011 HSHW Administrative Services Managers 1.91 89 53.00 25.92 4 Yes R132051 HSHW Financial Analysts 1.89 86 38.52 23.81 5 Yes R471011 HSHW First-Line Supervisors of Construction Trades and Extraction Workers 1.89 283 29.32 19.35 4 No R131199 HSHW Business Operations Specialists, All Other 1.87 577 32.22 18.84 4 No R131121 Meeting, Convention, and Event Planners 1.84 1,102 22.66 13.72 4 No S172112 HSHW Industrial Engineers 1.84 95 34.36 20.98 5 Yes R274011 Audio and Video Equipment Technicians 1.84 638 19.22 12.61 4 Yes S292071 Medical Records and Health Information Technicians 1.82 937 19.67 12.75 4 Yes S472073 Operating Engineers and Other Construction Equipment Operators 1.82 97 18.10 12.97 3 No R113021 HSHW Computer and Information Systems Managers 1.81 80 64.54 39.49 5 Yes R253097 Teachers and Instructors, All Other, Except Substitute Teachers 1.78 98 24.41 14.75 5 No R132052 HSHW Personal Financial Advisors 1.78 103 46.57 18.32 5 Yes R132011 HSHW Accountants and Auditors 1.78 584 33.58 21.68 5 Yes R472141 Painters, Construction and Maintenance 1.77 183 18.31 12.95 3 No R Youth/WT151134 HSHW Web Developers 1.76 950 29.89 18.24 3 Yes S131051 HSHW Cost Estimators 1.76 94 29.01 18.33 4 No R499021 Heating, Air Conditioning, and Refrigeration Mechanics and Installers 1.76 309 19.59 14.57 3 No R292034 HSHW Radiologic Technologists 1.74 1,016 26.55 19.26 3 Yes S391021 First-Line Supervisors of Personal Service Workers 1.73 2,075 20.18 12.70 3 No S434051 Customer Service Representatives 1.73 36,239 15.39 10.88 3 Yes S Youth/WT119141 Property, Real Estate, and Community Association Managers 1.72 229 26.29 13.97 4 No R131071 HSHW Human Resources Specialists 1.72 312 29.07 18.62 5 No R371012 First-Line Supervisors of Landscaping, Lawn Service, and Groundskeeping Workers 1.72 2,016 23.07 13.92 3 No S472031 Carpenters 1.72 275 18.30 12.88 3 No R472152 Plumbers, Pipefitters, and Steamfitters 1.68 212 21.49 14.87 3 No R413021 HSHW Insurance Sales Agents 1.66 287 32.96 16.25 3 Yes R371011 First-Line Supervisors of Housekeeping and Janitorial Workers 1.65 2,043 18.90 12.51 3 No S292055 Surgical Technologists 1.65 764 20.82 16.36 3 Yes S151141 HSHW Database Administrators 1.65 658 40.74 25.63 4 Yes S119021 HSHW Construction Managers 1.63 110 40.32 25.43 4 No R435011 Cargo and Freight Agents 1.60 677 21.18 13.04 3 Yes S111021 HSHW General and Operations Managers 1.60 484 58.54 26.49 4 Yes R291141 HSHW Registered Nurses 1.58 783 32.21 24.31 4 Yes R474011 HSHW Construction and Building Inspectors 1.57 1,019 27.71 18.20 3 No S119051 Food Service Managers 1.55 96 28.62 12.87 4 No R112022 HSHW Sales Managers 1.55 95 65.57 32.60 5 Yes R273031 HSHW Public Relations Specialists 1.53 88 29.89 19.54 5 Yes R532011 HSHW Airline Pilots, Copilots, and Flight Engineers 1.52 557 88.88 45.87 4 Yes S292011 Medical and Clinical Laboratory Technologists 1.52 895 24.78 15.07 4 Yes S492098 Security and Fire Alarm Systems Installers 1.52 867 20.40 14.48 3 No S532012 HSHW Commercial Pilots 1.51 559 44.11 24.76 3 Yes S493042 Mobile Heavy Equipment Mechanics, Except Engines 1.51 636 21.91 15.35 3 Yes S173031 Surveying and Mapping Technicians 1.51 733 19.30 13.37 3 Yes S533022 Bus Drivers, School or Special Client 1.51 292 16.36 13.01 3 No R493092 Recreational Vehicle Service Technicians 1.49 141 17.34 10.01 3 No S472211 Sheet Metal Workers 1.49 1,087 18.70 13.19 3 No S151133 HSHW Software Developers, Systems Software 1.49 113 45.75 27.56 5 Yes R151152 HSHW Computer Network Support Specialists 1.49 990 27.90 16.75 3 Yes S533032 Heavy and Tractor-Trailer Truck Drivers 1.46 328 19.86 12.63 3 Yes R499071 Maintenance and Repair workers, General 1.44 10,322 17.00 11.61 3 No S Youth/WT151121 HSHW Computer Systems Analysts 1.43 97 38.78 23.73 4 Yes R351011 Chefs and Head Cooks 1.42 1,333 25.97 14.71 3 No S472151 Pipelayers 1.38 666 19.14 13.62 3 No S173011 HSHW Architectural and Civil Drafters 1.38 733 24.37 16.33 3 Yes S419022 Real Estate Sales Agents 1.37 222 31.82 14.34 3 No R151143 HSHW Computer Network Architects 1.37 94 42.35 24.57 3 Yes R

2017 Hourly Wage

2019-20 Regional Demand Occupations List

Sorted by Annual Percentage Growth

FLDOE Training Code 3 (PSAV Certificate), 4 (Community College Credit/Degree), or 5 (Bachelor's Degree)

24

493021 Automotive Body and Related Repairers 1.36 1,217 19.60 12.46 3 No S271025 Interior Designers 1.36 671 23.70 13.77 4 Yes S493031 Bus and Truck Mechanics and Diesel Engine Specialists 1.35 1,349 22.18 15.65 3 Yes S435031 Police, Fire, and Ambulance Dispatchers 1.35 705 19.53 13.95 3 No S531031 HSHW First-Line Supervisors of Transportation and Material-Moving Machine and Vehicle Operators 1.29 1,392 25.39 15.24 3 Yes S491011 HSHW First-Line Supervisors of Mechanics, Installers, and Repairers 1.29 157 29.79 19.33 3 No R472111 Electricians 1.28 259 20.04 14.44 3 No R533021 Bus Drivers, Transit and Intercity 1.28 83 16.36 12.67 3 Yes R Youth/WT419021 Real Estate Brokers 1.27 765 35.04 14.50 3 No S399011 Child Care Workers 1.25 8,947 10.76 9.15 3 No S Youth/WT 252022 HSHW Middle School Teachers, Except Special and Career/Technical Education 1.25 115 29.14 23.41 5 No R252031 HSHW Secondary School Teachers, Except Special and Career/Technical Education 1.25 146 30.85 23.40 5 No R259041 Teacher Assistants 1.24 250 15.65 12.49 3 No R Youth/WT292052 Pharmacy Technicians 1.24 43 14.88 11.86 3 No R Youth/WT252021 HSHW Elementary School Teachers, Except Special Education 1.24 258 28.57 21.44 5 No R319094 Medical Transcriptionists 1.21 81 19.18 12.87 3 Yes R131041 HSHW Compliance Officers 1.21 1,657 29.94 16.83 3 No S332011 HSHW Firefighters 1.21 118 24.11 17.78 3 No R493011 HSHW Aircraft Mechanics and Service Technicians 1.19 1,294 26.95 16.11 3 Yes S499041 Industrial Machinery Mechanics 1.18 1,374 23.30 15.99 3 Yes S151142 HSHW Network and Computer Systems Administrators 1.18 101 37.88 24.58 4 Yes R411012 HSHW First-Line Supervisors of Non-Retail Sales Workers 1.17 216 41.84 21.05 4 Yes R533033 Light Truck or Delivery Services Drivers 1.16 6,980 16.66 10.46 3 Yes S414011 HSHW Sales Representatives, Wholesale and Manufacturing, Technical and Scientific Products 1.16 236 36.93 17.31 3 Yes R333051 HSHW Police and Sheriff's Patrol Officers 1.16 172 26.87 20.18 3 No R414012 Sales Representatives, Wholesale and Manufacturing, Except Technical and Scientific Products 1.14 553 28.66 12.88 3 Yes R436014 Secretaries, Except Legal, Medical and Executive 1.12 22,778 16.52 11.44 3 Yes S Youth/WT413031 HSHW Securities, Commodities, and Financial Services Sales Agents 1.12 190 37.68 17.47 5 Yes R431011 HSHW First-Line Supervisors of Office and Administrative Support Workers 0.95 660 27.12 17.64 4 Yes R271024 Graphic Designers 0.94 104 22.67 14.62 4 Yes R493023 Automotive Service Technicians and Mechanics 0.92 132 18.29 12.19 3 No R514121 Welders, Cutters, Solderers, and Brazers 0.92 107 18.18 13.46 3 Yes R511011 HSHW First-Line Supervisors of Production and Operating Workers 0.89 211 29.04 18.30 3 Yes R411011 First-Line Supervisors of Retail Sales Workers 0.74 640 21.17 13.85 3 No R514041 Machinists 0.73 123 19.64 14.31 3 Yes R131031 HSHW Claims Adjusters, Examiners, and Investigators 0.61 142 29.31 19.09 3 Yes R433031 Bookkeeping, Accounting, and Auditing Clerks 0.48 792 18.19 12.74 4 Yes R Youth/WT111011 HSHW Chief Executives 0.45 91 91.48 37.59 5 Yes R413011 Advertising Sales Agents 0.15 1,496 27.95 13.30 3 Yes S131023 HSHW Purchasing Agents, Except Wholesale, Retail, and Farm Products 0.02 91 28.87 18.03 4 Yes R151131 HSHW Computer Programmers -0.26 768 37.18 22.28 3 Yes S Youth/WT

†SOC Code and Occupational Title refer to Standard Occupational Classification codes and titles.

††HSHW = High Skill/High Wage.

†††Data Source:

R = Meets regional wage and openings criteria based on state Labor Market Statistics employer survey data. Regional data are shown.S = Meets statewide wage and openings criteria based on state Labor Market Statistics employer survey data. Statewide data are shown.NR = Not releasable.

EFI - Enterprise Florida, Inc.

25

Workforce Development Area 14 - Pinellas County

Selection Criteria:12 80 annual openings and positive growth3 Mean Wage of $15.10/hour and Entry Wage of $12.29/hour4 High Skill/High Wage (HSHW) Occupations:

Mean Wage of $23.68/hour and Entry Wage of $15.10/hour

Annual FLDOE In EFIPercent Annual Training Targeted Data Youth/WT

SOC Code† HSHW†† Occupational Title† Growth Openings Mean Entry Code Industry? Source††† Only

131151 HSHW Training and Development Specialists NR NR 27.32 16.18 5 Yes R434051 Customer Service Representatives 1.73 36,239 15.39 10.88 3 Yes S Youth/WT436014 Secretaries, Except Legal, Medical and Executive 1.12 22,778 16.52 11.44 3 Yes S Youth/WT311014 Nursing Assistants 2.28 14,476 12.88 10.76 3 Yes S Youth/WT499071 Maintenance and Repair workers, General 1.44 10,322 17.00 11.61 3 No S Youth/WT399011 Child Care Workers 1.25 8,947 10.76 9.15 3 No S Youth/WT 533033 Light Truck or Delivery Services Drivers 1.16 6,980 16.66 10.46 3 Yes S311011 Home Health Aides 3.85 4,744 10.80 9.58 3 Yes S Youth/WT391021 First-Line Supervisors of Personal Service Workers 1.73 2,075 20.18 12.70 3 No S371011 First-Line Supervisors of Housekeeping and Janitorial Workers 1.65 2,043 18.90 12.51 3 No S371012 First-Line Supervisors of Landscaping, Lawn Service, and Groundskeeping Workers 1.72 2,016 23.07 13.92 3 No S472051 Cement Masons and Concrete Finishers 2.07 1,794 17.44 12.53 3 No S131041 HSHW Compliance Officers 1.21 1,657 29.94 16.83 3 No S413011 Advertising Sales Agents 0.15 1,496 27.95 13.30 3 Yes S531031 HSHW First-Line Supervisors of Transportation and Material-Moving Machine and Vehicle Operators 1.29 1,392 25.39 15.24 3 Yes S499041 Industrial Machinery Mechanics 1.18 1,374 23.30 15.99 3 Yes S493031 Bus and Truck Mechanics and Diesel Engine Specialists 1.35 1,349 22.18 15.65 3 Yes S351011 Chefs and Head Cooks 1.42 1,333 25.97 14.71 3 No S493011 HSHW Aircraft Mechanics and Service Technicians 1.19 1,294 26.95 16.11 3 Yes S493021 Automotive Body and Related Repairers 1.36 1,217 19.60 12.46 3 No S131121 Meeting, Convention, and Event Planners 1.84 1,102 22.66 13.72 4 No S472211 Sheet Metal Workers 1.49 1,087 18.70 13.19 3 No S474011 HSHW Construction and Building Inspectors 1.57 1,019 27.71 18.20 3 No S292034 HSHW Radiologic Technologists 1.74 1,016 26.55 19.26 3 Yes S292099 Health Technologists and Technicians, All Other 1.92 1,011 19.75 12.98 3 Yes S292021 HSHW Dental Hygienists 2.21 1,000 30.31 22.54 4 Yes S151152 HSHW Computer Network Support Specialists 1.49 990 27.90 16.75 3 Yes S151134 HSHW Web Developers 1.76 950 29.89 18.24 3 Yes S312021 HSHW Physical Therapist Assistants 3.42 939 30.15 23.70 4 Yes S292071 Medical Records and Health Information Technicians 1.82 937 19.67 12.75 4 Yes S292011 Medical and Clinical Laboratory Technologists 1.52 895 24.78 15.07 4 Yes S492098 Security and Fire Alarm Systems Installers 1.52 867 20.40 14.48 3 No S433031 Bookkeeping, Accounting, and Auditing Clerks 0.48 792 18.19 12.74 4 Yes R Youth/WT291141 HSHW Registered Nurses 1.58 783 32.21 24.31 4 Yes R151131 HSHW Computer Programmers -0.26 768 37.18 22.28 3 Yes S Youth/WT419021 Real Estate Brokers 1.27 765 35.04 14.50 3 No S292055 Surgical Technologists 1.65 764 20.82 16.36 3 Yes S291126 HSHW Respiratory Therapists 2.60 735 27.58 22.61 4 Yes S173011 HSHW Architectural and Civil Drafters 1.38 733 24.37 16.33 3 Yes S173031 Surveying and Mapping Technicians 1.51 733 19.30 13.37 3 Yes S435031 Police, Fire, and Ambulance Dispatchers 1.35 705 19.53 13.95 3 No S472221 Structural Iron and Steel Workers 2.13 687 20.48 14.48 3 No S435011 Cargo and Freight Agents 1.60 677 21.18 13.04 3 Yes S271025 Interior Designers 1.36 671 23.70 13.77 4 Yes S472151 Pipelayers 1.38 666 19.14 13.62 3 No S431011 HSHW First-Line Supervisors of Office and Administrative Support Workers 0.95 660 27.12 17.64 4 Yes R151141 HSHW Database Administrators 1.65 658 40.74 25.63 4 Yes S472121 Glaziers 1.96 658 17.80 13.89 3 No S292012 Medical and Clinical Laboratory Technicians 1.95 656 24.78 15.07 4 Yes S411011 First-Line Supervisors of Retail Sales Workers 0.74 640 21.17 13.85 3 No R274011 Audio and Video Equipment Technicians 1.84 638 19.22 12.61 4 Yes S493042 Mobile Heavy Equipment Mechanics, Except Engines 1.51 636 21.91 15.35 3 Yes S132011 HSHW Accountants and Auditors 1.78 584 33.58 21.68 5 Yes R131199 HSHW Business Operations Specialists, All Other 1.87 577 32.22 18.84 4 No R532012 HSHW Commercial Pilots 1.51 559 44.11 24.76 3 Yes S532011 HSHW Airline Pilots, Copilots, and Flight Engineers 1.52 557 88.88 45.87 4 Yes S151122 HSHW Information Security Analysts 3.22 553 41.33 26.32 3 Yes S414012 Sales Representatives, Wholesale and Manufacturing, Except Technical and Scientific Products 1.14 553 28.66 12.88 3 Yes R111021 HSHW General and Operations Managers 1.60 484 58.54 26.49 4 Yes R319092 Medical Assistants 3.77 460 15.42 12.37 3 Yes R Youth/WT131111 HSHW Management Analysts 2.34 368 39.82 23.89 5 Yes R533032 Heavy and Tractor-Trailer Truck Drivers 1.46 328 19.86 12.63 3 Yes R292061 Licensed Practical and Licensed Vocational Nurses 1.98 328 20.87 16.97 3 Yes R131071 HSHW Human Resources Specialists 1.72 312 29.07 18.62 5 No R499021 Heating, Air Conditioning, and Refrigeration Mechanics and Installers 1.76 309 19.59 14.57 3 No R533022 Bus Drivers, School or Special Client 1.51 292 16.36 13.01 3 No R413021 HSHW Insurance Sales Agents 1.66 287 32.96 16.25 3 Yes R471011 HSHW First-Line Supervisors of Construction Trades and Extraction Workers 1.89 283 29.32 19.35 4 No R151151 HSHW Computer User Support Specialists 1.98 279 24.16 15.21 3 Yes R472031 Carpenters 1.72 275 18.30 12.88 3 No R131161 HSHW Market Research Analysts and Marketing Specialists 3.12 273 33.46 18.74 5 Yes R151132 HSHW Software Developers, Applications 3.13 262 44.06 26.24 4 Yes R472111 Electricians 1.28 259 20.04 14.44 3 No R252021 HSHW Elementary School Teachers, Except Special Education 1.24 258 28.57 21.44 5 No R259041 Teacher Assistants 1.24 250 15.65 12.49 3 No R Youth/WT414011 HSHW Sales Representatives, Wholesale and Manufacturing, Technical and Scientific Products 1.16 236 36.93 17.31 3 Yes R119141 Property, Real Estate, and Community Association Managers 1.72 229 26.29 13.97 4 No R419022 Real Estate Sales Agents 1.37 222 31.82 14.34 3 No R411012 HSHW First-Line Supervisors of Non-Retail Sales Workers 1.17 216 41.84 21.05 4 Yes R472152 Plumbers, Pipefitters, and Steamfitters 1.68 212 21.49 14.87 3 No R511011 HSHW First-Line Supervisors of Production and Operating Workers 0.89 211 29.04 18.30 3 Yes R413031 HSHW Securities, Commodities, and Financial Services Sales Agents 1.12 190 37.68 17.47 5 Yes R

2017 Hourly Wage

2019-20 Regional Demand Occupations List

Sorted by Annual Openings

FLDOE Training Code 3 (PSAV Certificate), 4 (Community College Credit/Degree), or 5 (Bachelor's Degree)

26

472141 Painters, Construction and Maintenance 1.77 183 18.31 12.95 3 No R Youth/WT333051 HSHW Police and Sheriff's Patrol Officers 1.16 172 26.87 20.18 3 No R232011 HSHW Paralegals and Legal Assistants 2.10 168 24.49 16.58 3 Yes R436013 Medical Secretaries 2.31 161 16.32 12.83 3 Yes R319091 Dental Assistants 2.70 157 18.87 14.04 3 Yes R491011 HSHW First-Line Supervisors of Mechanics, Installers, and Repairers 1.29 157 29.79 19.33 3 No R113031 HSHW Financial Managers 2.84 150 67.07 35.45 5 Yes R252031 HSHW Secondary School Teachers, Except Special and Career/Technical Education 1.25 146 30.85 23.40 5 No R434131 Loan Interviewers and Clerks 2.23 143 18.78 14.11 3 Yes R131031 HSHW Claims Adjusters, Examiners, and Investigators 0.61 142 29.31 19.09 3 Yes R493092 Recreational Vehicle Service Technicians 1.49 141 17.34 10.01 3 No S132072 HSHW Loan Officers 2.03 134 37.18 20.95 4 Yes R493023 Automotive Service Technicians and Mechanics 0.92 132 18.29 12.19 3 No R514041 Machinists 0.73 123 19.64 14.31 3 Yes R332011 HSHW Firefighters 1.21 118 24.11 17.78 3 No R252022 HSHW Middle School Teachers, Except Special and Career/Technical Education 1.25 115 29.14 23.41 5 No R151133 HSHW Software Developers, Systems Software 1.49 113 45.75 27.56 5 Yes R119021 HSHW Construction Managers 1.63 110 40.32 25.43 4 No R514121 Welders, Cutters, Solderers, and Brazers 0.92 107 18.18 13.46 3 Yes R271024 Graphic Designers 0.94 104 22.67 14.62 4 Yes R132052 HSHW Personal Financial Advisors 1.78 103 46.57 18.32 5 Yes R151142 HSHW Network and Computer Systems Administrators 1.18 101 37.88 24.58 4 Yes R253097 Teachers and Instructors, All Other, Except Substitute Teachers 1.78 98 24.41 14.75 5 No R151121 HSHW Computer Systems Analysts 1.43 97 38.78 23.73 4 Yes R472073 Operating Engineers and Other Construction Equipment Operators 1.82 97 18.10 12.97 3 No R119051 Food Service Managers 1.55 96 28.62 12.87 4 No R172112 HSHW Industrial Engineers 1.84 95 34.36 20.98 5 Yes R112022 HSHW Sales Managers 1.55 95 65.57 32.60 5 Yes R151143 HSHW Computer Network Architects 1.37 94 42.35 24.57 3 Yes R131051 HSHW Cost Estimators 1.76 94 29.01 18.33 4 No R119111 HSHW Medical and Health Services Managers 2.11 92 53.99 32.94 5 Yes R111011 HSHW Chief Executives 0.45 91 91.48 37.59 5 Yes R131023 HSHW Purchasing Agents, Except Wholesale, Retail, and Farm Products 0.02 91 28.87 18.03 4 Yes R113011 HSHW Administrative Services Managers 1.91 89 53.00 25.92 4 Yes R273031 HSHW Public Relations Specialists 1.53 88 29.89 19.54 5 Yes R132051 HSHW Financial Analysts 1.89 86 38.52 23.81 5 Yes R533021 Bus Drivers, Transit and Intercity 1.28 83 16.36 12.67 3 Yes R Youth/WT319094 Medical Transcriptionists 1.21 81 19.18 12.87 3 Yes R113021 HSHW Computer and Information Systems Managers 1.81 80 64.54 39.49 5 Yes R292052 Pharmacy Technicians 1.24 43 14.88 11.86 3 No R Youth/WT292041 Emergency Medical Technicians and Paramedics 3.05 31 16.80 11.39 4 Yes R Youth/WT

†SOC Code and Occupational Title refer to Standard Occupational Classification codes and titles.

††HSHW = High Skill/High Wage.

†††Data Source:

R = Meets regional wage and openings criteria based on state Labor Market Statistics employer survey data. Regional data are shown.S = Meets statewide wage and openings criteria based on state Labor Market Statistics employer survey data. Statewide data are shown.NR = Not releasable.

EFI - Enterprise Florida, Inc.

27

Action Item 7

Training Provider Cap Adjustment CareerSource Florida requires reporting and approval of a third-party contract valued at $25,000 or more involving a conflict of interest of board members or employees. This contracted amount must be approved by the Workforce Solutions Committee and a two-thirds vote of a quorum of Local Workforce Development Board (LWDB). Staff reviewed the Training Provider Financial Summary for the period of July 1, 2019 to December 31, 2019. It was determined that based on an increase in participant enrollment at UMA, spending will exceed the approved spending cap of $75,000. We anticipate a continued enrollment through June 30th because of a focus on enrollment in healthcare occupations. RECOMMENDATION: Approval of an increase in the spending cap from $75,000 to $150,000 for Ultimate Medical Academy to allow for continued enrollments through June 30, 2020.

28

Training Provider

Customer

Training

Approved

Spending (if

required) Remaining

# of

Participants Avg/ Per Part

Access Computer Training (Hillsborough)

Adam's State University 4,099$ 1 4,099$

American Manufacturing Skills Initiative (AmSkills) -

ATA, Career Institute of Florida, ( Hernando) -

BizTech Learning Centers, Inc., ( Pinellas) 5,000 1 5,000$

Brewster Technical Center

Center for Technology Training 23,995 5 4,799

Central Florida Heat and Frost Insulators J.A.C. (RA)

Computer Coach Training 111,295 23 4,839

Concorde Career Institute, (Hillsborough)

Eckerd College * -

Florida School of Traditional Midwifery, (Alachua)

Galen College of Nursing, (Pinellas) 150,023 55 2,728

Goodwill Industries - Suncoast 800 50,000 49,200 2 400

Hillsborough Community College

IEC- Independent Electrical Contractors, FAAC

International Union of Operating Engineers (RA)

Ironworkers (RA) *

JATC - Tampa Area Electrical JATC, (Hillsborough), FAAC (RA) * 28,214 100,000 71,786 31 910

Jersey College, ( Hillsborough) 24,866 6 4,144

Keiser University 1,842 1 1,842

LaSalle Computer Learning Center, (Hillsborough)

Learning Alliance Corporation

Masonry (RA)

National Aviation Academy, (Pinellas) 78,493 19 4,131