Benefits of Risk Pooling

15

On the Benefits of Risk Pooling in Inventory Management Oded Berman, Dmitry Krass Joseph L. Rotman School of Management, University of Toronto, Toronto, ON M5S 3E6, Canada [email protected], [email protected] M. Mahdi Tajbakhsh Department of Industrial Engineering, Dalhousie University, Halifax, NS B3J 2X4, Canada, [email protected] W e analyze the benefits of inventory pooling in a multi-location newsvendor framework. Using a number of common demand distributions, as well as the distribution-free approximation, we compare the centralized (pooled) system with the decentralized (non-pooled) system. We investigate the sensitivity of the absolute and relative reduction in costs to the variability of demand and to the number of locations (facilities) being pooled. We show that for the distributions considered, the absolute benefit of risk pooling increases with variability, and the relative benefit stays fairly constant, as long as the coefficient of variation of demand stays in the low range. However, under high-variability conditions, both measures decrease to zero as the demand variability is increased. We show, through analytical results and computational experiments, that these effects are due to the different operating regimes exhibited by the system under different levels of variability: as the variability is increased, the system switches from the normal operation to the effective and then complete shutdown regimes; the decrease in the benefits of risk pooling is associated with the two latter stages. The centralization allows the system to remain in the normal operation regime under higher levels of variability compared to the decentralized system. Key words: risk pooling; stochastic inventory models; high demand variability; distribution-free approach History: Received: June 2009; Accepted: December 2009 by Eric Johnson; after 2 revisions. 1. Introduction Risk pooling in inventory management, a.k.a. inven- tory pooling, refers to the consolidation of inventory across locations into a single (real or virtual) location, from which the demands at the individual locations are served. Since one of the primary functions of the inventory is to protect the system against the vari- ability in demand, one would intuitively expect inventory pooling to be beneficial, as the centralized location faces less demand variability (as measured by the coefficient of variation) than the individual loca- tions. Moreover, since the reduction in variability is greatest when the demand faced by the individual locations has high variability, one would expect the benefits of inventory pooling to increase with the variability of demand. It is well known that (in the absence of additional costs such as transshipment costs and/or increase in lead times) inventory pooling is indeed beneficial (see Eppen (1979), Schwarz (1981), Chen and Lin (1989), and Cherikh (2000) as well as a recent review in Ger- chak and He (2003)). However, the behavior of risk pooling benefits as a function of variability of demand is less clear-cut. When the demands faced by the individual loca- tions are independent and Normally distributed, it is indeed not hard to show that the benefits of risk pooling increase with variability (see Example 1 in section 2). However, the Normal distribution cannot be a reasonable approximation of the distribution of demand when the variability is high, since it may lead to a significant probability of negative demands; for this reason Silver et al. (1998) present a rule of thumb: if the coefficient of variation of demand is > 0.5, one should consider a distribution other than the Normal distribution. In contrast to the results for the Normal distribution, Gerchak and He (2003) provide an ex- ample where increased variability of the individual demands reduces the risk pooling benefits. Benjaafar et al. (2005) show that in the production-inventory systems (also called make-to-stock queues), inventory pooling leads to little benefit if the variability of the location demands is very high. They argue that the inconsistency between their result and those obtained for pure inventory systems is partly due to the as- sumption of independent demands (or lead-time demands) in the inventory models. However, the vanishing benefits of inventory pooling are, in fact, 57 PRODUCTION AND OPERATIONS MANAGEMENT Vol. 20, No. 1, January–February 2011, pp. 57–71 ISSN 1059-1478|EISSN 1937-5956|11|2001|0057 POMS DOI 10.1111/J.1937-5956.2010.01134.x r 2010 Production and Operations Management Society

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Benefits of Risk Pooling

On the Benefits of Risk Pooling inInventory Management

Oded Berman, Dmitry KrassJoseph L. Rotman School of Management, University of Toronto, Toronto, ON M5S 3E6, Canada

[email protected], [email protected]

M. Mahdi TajbakhshDepartment of Industrial Engineering, Dalhousie University, Halifax, NS B3J 2X4, Canada, [email protected]

We analyze the benefits of inventory pooling in a multi-location newsvendor framework. Using a number of commondemand distributions, as well as the distribution-free approximation, we compare the centralized (pooled) system with

the decentralized (non-pooled) system. We investigate the sensitivity of the absolute and relative reduction in costs to thevariability of demand and to the number of locations (facilities) being pooled. We show that for the distributions considered,the absolute benefit of risk pooling increases with variability, and the relative benefit stays fairly constant, as long as thecoefficient of variation of demand stays in the low range. However, under high-variability conditions, both measures decreaseto zero as the demand variability is increased. We show, through analytical results and computational experiments, that theseeffects are due to the different operating regimes exhibited by the system under different levels of variability: as thevariability is increased, the system switches from the normal operation to the effective and then complete shutdown regimes;the decrease in the benefits of risk pooling is associated with the two latter stages. The centralization allows the system toremain in the normal operation regime under higher levels of variability compared to the decentralized system.

Key words: risk pooling; stochastic inventory models; high demand variability; distribution-free approachHistory: Received: June 2009; Accepted: December 2009 by Eric Johnson; after 2 revisions.

1. IntroductionRisk pooling in inventory management, a.k.a. inven-tory pooling, refers to the consolidation of inventoryacross locations into a single (real or virtual) location,from which the demands at the individual locationsare served. Since one of the primary functions of theinventory is to protect the system against the vari-ability in demand, one would intuitively expectinventory pooling to be beneficial, as the centralizedlocation faces less demand variability (as measured bythe coefficient of variation) than the individual loca-tions. Moreover, since the reduction in variability isgreatest when the demand faced by the individuallocations has high variability, one would expect thebenefits of inventory pooling to increase with thevariability of demand.

It is well known that (in the absence of additionalcosts such as transshipment costs and/or increase inlead times) inventory pooling is indeed beneficial (seeEppen (1979), Schwarz (1981), Chen and Lin (1989),and Cherikh (2000) as well as a recent review in Ger-chak and He (2003)). However, the behavior of riskpooling benefits as a function of variability of demandis less clear-cut.

When the demands faced by the individual loca-tions are independent and Normally distributed, it isindeed not hard to show that the benefits of riskpooling increase with variability (see Example 1 insection 2). However, the Normal distribution cannotbe a reasonable approximation of the distribution ofdemand when the variability is high, since it may leadto a significant probability of negative demands; forthis reason Silver et al. (1998) present a rule of thumb:if the coefficient of variation of demand is > 0.5, oneshould consider a distribution other than the Normaldistribution. In contrast to the results for the Normaldistribution, Gerchak and He (2003) provide an ex-ample where increased variability of the individualdemands reduces the risk pooling benefits. Benjaafaret al. (2005) show that in the production-inventorysystems (also called make-to-stock queues), inventorypooling leads to little benefit if the variability of thelocation demands is very high. They argue that theinconsistency between their result and those obtainedfor pure inventory systems is partly due to the as-sumption of independent demands (or lead-timedemands) in the inventory models. However, thevanishing benefits of inventory pooling are, in fact,

57

PRODUCTION AND OPERATIONS MANAGEMENTVol. 20, No. 1, January–February 2011, pp. 57–71ISSN 1059-1478|EISSN 1937-5956|11|2001|0057

POMSDOI 10.1111/J.1937-5956.2010.01134.x

r 2010 Production and Operations Management Society

easy to demonstrate for inventory systems with inde-pendent demands—see Example 2 in section 2, as wellas results in sections 3 and 4.

Our paper seeks to shed some light on these seem-ingly counter-intuitive behaviors. Namely, we want tounderstand how the benefits of risk pooling behaveunder increasing variability of demand and what ac-counts for this behavior. To this end, we examine asimple system consisting of n identical locations fac-ing identically distributed, independent demands andoperating as newsvendor systems (no fixed costs). Thecentralized system faces combined demands from theindividual locations with no additional transshipmentcosts or increases in lead times. We define two mea-sures of inventory pooling savings—the absolute andthe relative decrease in costs—and analyze how thebenefits of pooling change with the increase in thevariability of demand (at each location) and the num-ber of locations. The analysis is carried out under avariety of common demand distributions at each lo-cation, including the Normal, Uniform, Laplace,Logistic, Lognormal, Gamma, and Weibull (for a com-prehensive discussion on the applicability of differentdemand distributions to inventory control, the readeris referred to Burgin (1975), Silver et al. (1998), and thereferences therein). We classify these distributions intotwo groups depending on whether the negative de-mand can occur: Category I distributions (comprisedof the first four on our list) that admit negative de-mands and Category II distributions (the last three)that do not. Category I distributions can be analyzedonly under the low demand variability (coefficient ofvariation under 0.5), while Category II distributionscan be used under any level of variability. Our mainresults can be summarized as follows:� We show, both analytically (where possible) and

numerically (through Monte-Carlo simulations),that while the absolute benefits of pooling do in-crease with variability of demand under the low-variability conditions (as suggested by the intu-ition and by the analysis for the Normaldistribution), the behavior changes drastically athigher variability levels. Indeed, the benefits ofpooling (both absolute and relative) decrease rap-idly once the coefficient of variation of demand(at each location) exceeds a certain threshold, anddisappear entirely as the variability continues togrow. This behavior occurs for all Category IIdistributions. With respect to the number of lo-cations being pooled, under a given level ofvariability the benefits of pooling do increasewith the number of locations. However, underhigh-variability conditions, a certain minimumnumber of locations may need to be pooledbefore any appreciable benefits of pooling can berealized.

� The reasons for this behavior have to do with thefact that the optimal order-up-to level of thenewsvendor system operating under Category IIdistributions tends to decrease with variabilityonce a certain threshold value of the coefficient ofvariation is exceeded. This results in the followingthree-state regime for an optimally operatingnewsvendor system. At low levels of variability,both overage and underage costs increase withvariability; we call this the normal operation re-gime. Above a certain level of the coefficient ofvariation, the overage costs begin to decrease,while the underage costs continue to increase withvariability. Essentially, the system refuses to ac-cept overage risk; we call this the effective shutdownregime. At still higher levels of variability, the or-der-up-to levels as well as the overage costs areessentially equal to 0—the system holds no in-ventory and accepts the full costs of unmetdemand. We call this the complete shutdown re-gime. While both the decentralized and thecentralized systems go through all three regimesas the variability is increased, the decentralizedsystem enters them at lower levels of the varianceof demand. Our results indicate that the absolutesavings due to pooling grow (and the relativesavings stay approximately constant) while bothsystems are in the normal operation regime. Theabsolute savings peak when the decentralizedsystem enters the effective shutdown regimewhile the centralized system is still in the normaloperation regime. The benefits of pooling decreaseonce both systems are in the effective shutdownregime, and approach 0 once both systems enterthe complete shutdown regime. Note that Cate-gory I systems only operate under low-variabilityconditions and thus are always in the normal op-eration regime. This accounts for the difference inbehavior between the two types of distributions.

� These results suggest that an inventory systemfacing a certain distribution of demand has a cer-tain ‘‘variability threshold’’ above which normaloperations are not possible. Since, managerially, itprobably does not make sense to operate a systemunder the effective or complete shutdown regime,the benefits of pooling do behave as intuitivelyexpected in the range where the system operatesnormally. Moreover, inventory pooling allows thesystem to continue to operate normally underhigher levels of variability by delaying the onsetof the effective shutdown regime. Under veryhigh levels of variability at the individual loca-tions, a number of locations may need to bepooled before the variability of the centralizedsystem is reduced sufficiently to allow normaloperations.

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management58 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

� We note that while it is possible to analyze theexact behavior of the decentralized system underall of the distributions listed earlier (we supplythe closed-form expressions for optimal order-up-to levels and costs for the distributions not pre-viously analyzed in the literature), the exactanalysis is generally not available for the central-ized system since, in most cases, the distributionof demand cannot be derived in closed form. Toovercome this difficulty, we employ the ‘‘distri-bution-free’’ approximation (e.g., see Gallego andMoon (1993)). We observe that the behavior ofsavings due to pooling is similar to the behaviorobserved for other distributions in our numericaltests.

The remainder of this paper is organized as follows.In section 2, we present the general model and thepreliminary results based on the Normal and Gammadistributions. In section 3, we conduct numericalanalysis of the effects of centralization. In section 4,we follow the distribution-free approach and deriveseveral theoretical results on the benefits of risk pool-ing. In section 5, we present the different operatingregimes described above and present further compu-tational results. Finally, section 6 presents conclusionsand problems for further research.

2. The Model and Preliminary ResultsWe consider a multi-location newsvendor problemwith n locations having identical cost structure. Weassume that the per-period demands at all locationsare independent and identically distributed (i.i.d.).There are no transshipment costs between locations.The two alternative system designs are the decentral-ized (non-pooled) system, where each location servicesits own demand, and the centralized (pooled) system,where all demand is served from a single location.One should note that both systems are centrallyowned, i.e., under a single decision maker.

2.1. Decentralized (Single-Location) NewsvendorSystemLet y (the decision variable) be the stock level afterordering at the beginning of the period, which is alsoknown as the order-up-to level. We will use D to rep-resent the per-period demand, which has cumulativedistribution function (c.d.f.) F, mean m, and standarddeviation s; we also assume that a probability densityfunction (p.d.f.) f of D is well defined. Letting co and cu

represent the unit overage and underage costs, re-spectively, the expected cost per period is given by(e.g., see Porteus (2002))

LðyÞ ¼ coEðy�DÞþ þ cuEðD� yÞþ

¼ coðy� mÞ þ ðco þ cuÞEðD� yÞþ:ð1Þ

To avoid trivial cases, we will assume that s, co, cu40.The optimal order-up-to level y� that minimizes (1) isgiven by

Fðy�Þ ¼ cu

co þ cu� a;

where a is known as the ‘‘critical ratio’’ or the ‘‘Type Iservice level.’’ Using (1), we can express the minimumexpected cost per period as follows:

Lðy�Þ ¼ cum� ðco þ cuÞZ y�

�1xfðxÞdx: ð2Þ

The system above describes the inventory operation ateach of the n locations. The total expected cost for thedisaggregated system is given by nLðy�Þ.

2.2. Centralized (Pooled) System and EfficiencyMeasuresLet Di be the per-period demand at location i, fori 5 1, . . ., n, and DT 5 D11 � � �1Dn the total pooled de-mand in the system, where the demands at eachlocation are assumed to be i.i.d. random variables. Asbefore, we will use mT, sT, fT, FT, y�T, and LT to rep-resent the mean, the standard deviation, p.d.f., c.d.f.,the optimal order-up-to level, and the total expectedcost of the centralized system. Note that mT 5 nm,sT ¼

ffiffiffinp

s, and y�T satisfies FTðy�TÞ ¼ a.We define two efficiency measures allowing us to

compare the decentralized and the centralized sys-tems: the absolute savings of the centralized system

D ¼ nLðy�Þ �LTðy�TÞ;

and the relative savings in percent (or the percentagesavings) of the centralized system

C ¼ 100 1�LTðy�TÞnLðy�Þ

� �:

It is easy to show that the total expected cost of thecentralized system is lower than that of a decentral-ized system (see, e.g., Chen and Lin (1989), Eppen(1979)) LTðy�TÞonLðy�Þ, and thus, both measuresabove are positive and well defined. We are primarilyinterested in how the absolute and relative savingsbehave with respect to the variability of demand sand the number of inventory locations n. In the case ofNormally distributed demand, this analysis isstraightforward, as shown below.

EXAMPLE 1: Normally distributed demand. Assume thedemand Di�N(m, s) at each location i. Let f and Fdenote, respectively, the p.d.f. and the c.d.f. of thestandard normal random variable. Then the optimalorder-up-to level is given by y� ¼ mþ z�s, wherez� ¼ F�1ðaÞ, with the optimal expected cost ofLðy�Þ ¼ ðco þ cuÞsfðz�Þ. Since the convolution ofNormal random variables is also Normal,

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 59

DT � Nðnm;ffiffiffinp

sÞ, and thus LTðy�TÞ ¼ ðco þ cuÞ �ffiffiffinp

sfðz�Þ, implying that

D ¼ ðco þ cuÞfðz�Þðn�ffiffiffinpÞs; ð3Þ

C ¼ 100�1� 1ffiffiffi

np Þ ð4Þ

Observe that D is increasing in the standard deviations and that C is independent of s. Thus, the absolutesavings of the centralized system grow without boundat the linear rate as s increases, while the relativesavings do not depend on the demand variability.Also note that D increases approximately linearlywith the number of locations n, while C rapidly ap-proaches 100% as n increases.

The fact that the benefits of risk pooling are in-creasing in the number of locations has also beenobserved in other settings. Hanany and Gerchak(2008) study inventory pooling in cooperative, decen-tralized systems (with multiple decision makers)facing the symmetric multivariate Normal demand.Under transferable utility games, they show that theexpected profit per location is increasing in the num-ber of locations. Dong and Rudi (2004) studytransshipment—which is considered to be a specialform of risk pooling—in a distribution system, wherea single manufacturer sells to multiple locations (re-tailers) owned by a single decision maker. They againshow that under the symmetric multivariate Normaldistribution, the expected profit per location is in-creasing in the number of locations. Therefore, theresults suggest that when the location demands fol-low identical and Normal distributions, the benefits ofrisk pooling increase with the number of participatinglocations.

The case of the Normally distributed demand sug-gests that the centralized system should outperformthe decentralized system by a wide margin as the de-mand variability increases. This is quite intuitive,since we expect the inventory cost to increase with thevariability of the demand, and the coefficient of vari-ation of the total demand CVT 5 sT/mT is smaller (by afactor of

ffiffiffinp

) than the coefficient of variation of thedemand at each location CV 5 s/m. Note, however,that the derivations in Example 1 are somewhat mis-leading, as (given that the demand should be non-negative) once s4m/2, it is no longer reasonable toassume that the demand is Normal.

In fact, the results (and the intuition) above clearlydo not hold for the case when the demand has aGamma distribution, as discussed below.

EXAMPLE 2: Gamma distributed demand. Assume that foreach location i, the demand Di�Gamma(k, y) where theparameters of the Gamma distribution are related to

the mean m and the standard deviation s by m5 k/yand s2 5 k/y2. The centralized demand DT also fol-lows the Gamma distribution with parameters y andnk. The formulas for the optimal order-up-to level andthe optimal expected cost are derived in the OnlineSupplement and are summarized in Table 1. It can beshown that

Lðy�Þ ¼ ðco þ cuÞs2y�fðy�Þ� �

=m:

Unfortunately, y� depends on both s and m in a rathercomplex way, and thus, no closed-form expressionsfor D and C are available. However, it is not hard toshow (see Gallego et al. (2007)) that lims!1 y� ¼lims!1 y�T ¼ 0. Therefore, since for non-negative Di’swe can write

D ¼ ðco þ cuÞZ y�

T

0

xfTðxÞdx� n

Z y�

0

xfðxÞdx

� ;

C ¼ 100 1� ncum� ðco þ cuÞR y�

T0 xfTðxÞdx

ncum� nðco þ cuÞR y�

0 xfðxÞdx

!;

it can be seen that lims!1 D ¼ lims!1C ¼ 0. Thus,the benefits of risk pooling vanish as the variability ofdemand grows. The numerical results presented inthe next section confirm the asymptotic results above:while both D and C initially grow with s, at somepoint they start decreasing and eventually asymptot-ically approach 0.

The two examples above present two very differentpictures of the benefits of centralization. Further in-vestigations of this effect will be presented insubsequent sections.

3. Effects of Centralization:Computational Results

In this section, we investigate the behavior of D and Cmeasures for a number of common distributions ofdemand. The distributions we investigate are dividedinto two groups: Category I includes distributions thatallow both positive and negative values of demand,while Category II distributions allow only positivevalues of demand. The specific distributions we ex-amine are listed below:

Category I (distributions allowing negative demand):Normal, Uniform, Laplace, and Logistic.

Category II (non-negative distributions): Lognormal,Gamma, and Weibull.

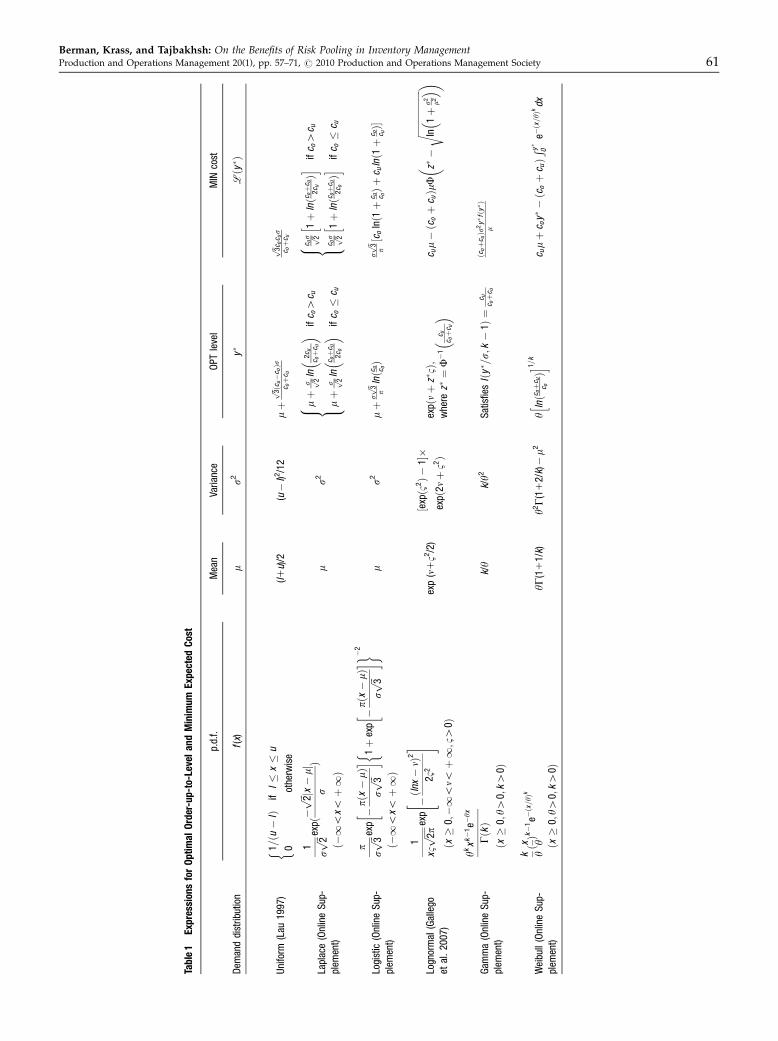

Table 1 provides closed-form expressions for calcu-lating the minimum expected cost and the optimalorder-up-to level for all the distributions listed above.These expressions can be used to evaluate the optimalcosts of the corresponding decentralized systems. Tothe best of our knowledge, the expressions for theLaplace, Logistic, Gamma, and Weibull distributionshave not appeared previously in the literature—the

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management60 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

Tabl

e1

Expr

essi

ons

for

Opt

imal

Ord

er-u

p-to

-Lev

elan

dM

inim

umEx

pect

edC

ost

p.d.

f.M

ean

Vari

ance

OPT

leve

lM

INco

st

Dem

and

dist

ribu

tion

f(x)

ms2

y�

Lðy� Þ

Uni

form

(Lau

1997

)1=ðu�

lÞif

l

x

u

0ot

herw

ise

(l1

u)/2

(u�

l)2/1

2mþ

ffiffi 3pðc

u�

c oÞs

c oþ

c u

ffiffi 3p

c oc us

c oþ

c u

Lapl

ace

(Onl

ine

Sup

-

plem

ent)

1

sffiffiffi 2p

expð�

ffiffiffi 2pjx�mj

sÞ

ð�1o

xoþ1Þ

ms2

mþ

s ffiffi 2p

ln2c

uc oþ

c u

��

ifc o4

c u

mþ

s ffiffi 2p

lnc oþ

c u2c

o

��

ifc o

c u

8 > < > :c us ffiffi 2p

1þ

lnðc oþ

c u2c

uÞ

hi if

c o4

c u

c os ffiffi 2p

1þ

lnðc oþ

c u2c

oÞ

hi if

c o

c u

8 > < > :

Logi

stic

(Onl

ine

Sup

-

plem

ent)

p

sffiffiffi 3p

exp�pð

x�mÞ

sffiffiffi 3p

�� 1þ

exp�pð

x�mÞ

sffiffiffi 3p

��

�2

ð�1o

xoþ1Þ

ms2

mþ

sffiffi 3p p

lnðc u c oÞ

sffiffi 3p p½c o

lnð1þ

c u c oÞþ

c ulnð1þ

c o c uÞ

Logn

orm

al(G

alle

go

etal

.20

07)

1

xBffiffiffiffiffi 2pp

exp�ðln

x�nÞ

2

2B2

"#

ðx�

0;�1

onoþ1;B4

0Þex

p(n

1B2

/2)

½expðB

2Þ�

1�

expð

2nþB2Þ

expðnþ

z�BÞ;

whe

rez�¼

F�

1c u

c oþ

c u

��

c um�ðc

oþ

c uÞmF

z��

ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffi

ffiffiffiffiffiln

1þ

s2 m2

��

r�

Gam

ma

(Onl

ine

Sup

-

plem

ent)

ykx

k�

1e�

yx

GðkÞ

ðx�

0;y4

0;k4

0Þk/y

k/y2

Sat

isfie

sIðy� =s;

k�

1Þ¼

c uc oþ

c u

ðcoþ

c uÞs

2y� fðy� Þ

m

Wei

bull

(Onl

ine

Sup

-

plem

ent)

k yðx yÞ

k�

1e�ðx=yÞ

k

ðx�

0;y4

0;k4

0ÞyG

(11

1/k)

y2G

(11

2/k)�m2

ylnðc oþ

c uc oÞ

hi 1=k

c umþ

c oy��ðc

oþ

c uÞR y

�

0e�ðx=yÞ

kdx

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 61

relevant derivations can be found in the OnlineSupplement. It is interesting to note that for CategoryI distributions, the optimal cost Lðy�Þ depends onlyon the standard deviation of demand s, while forCategory II distributions it depends on both the meanand the standard deviation of demand.

Since in most applications, demand must be non-negative, Category I distributions can only be used toapproximate the distribution of demand when thelikelihood of negative values is low. We thus restrictour investigation of these distributions to the ranges m/2. For Category II distributions, we can exam-ine the effect of centralization for any value of s.

The distribution of the centralized demand is aconvolution of demands at individual locations, andfor the distributions listed above the closed-form ex-pressions for the convolutions are available in onlythree cases: Normal, Gamma, and Uniform (see Renyi(1970), Feller (1966) for the convolution of the Uniformdistribution). Therefore, we use computational exper-iments to evaluate the impact of s and n on D and C,as described in the following subsections. In section 4,we investigate the distribution-free system whereclosed-form expressions are available.

3.1. The Impact of the Variability of DemandFor the case of n 5 2 locations, fT is obtained as

fTðxÞ ¼Z 1�1

fðxÞfðx� xÞdx:

Thus, y�T can be determined by solving the followingequation:

FTðy�TÞ :¼Z y�

T

�1

Z 1�1

fðxÞfðx� xÞdxdx ¼ cu

co þ cu: ð5Þ

As noted earlier, for the Normal, Gamma, and Uni-form distributions, the form of fT is known, and thus,we are able to solve Equation (5) directly. For all otherdistributions, we applied the bisection method, im-plemented in the Mathematica 6 package, to solveEquation (5). This allows us to determine LTðy�TÞ andsubsequently to compute D and C. While, in principle,the same technique could be applied to n42 locations,the search for y�T becomes multi-dimensional andleads to numerical difficulties. We thus restricted ourexperiments in this section to the n 5 2 case.

In our experiments, we set co ¼ $1 and m5 100units. We tested a wide range of service level values,from low to high: a5 0.15, 0.35, 0.55, 0.75, 0.95 (notethat since a ¼ ½cu=ðco þ cuÞ, fixing a implicitly fixes cu

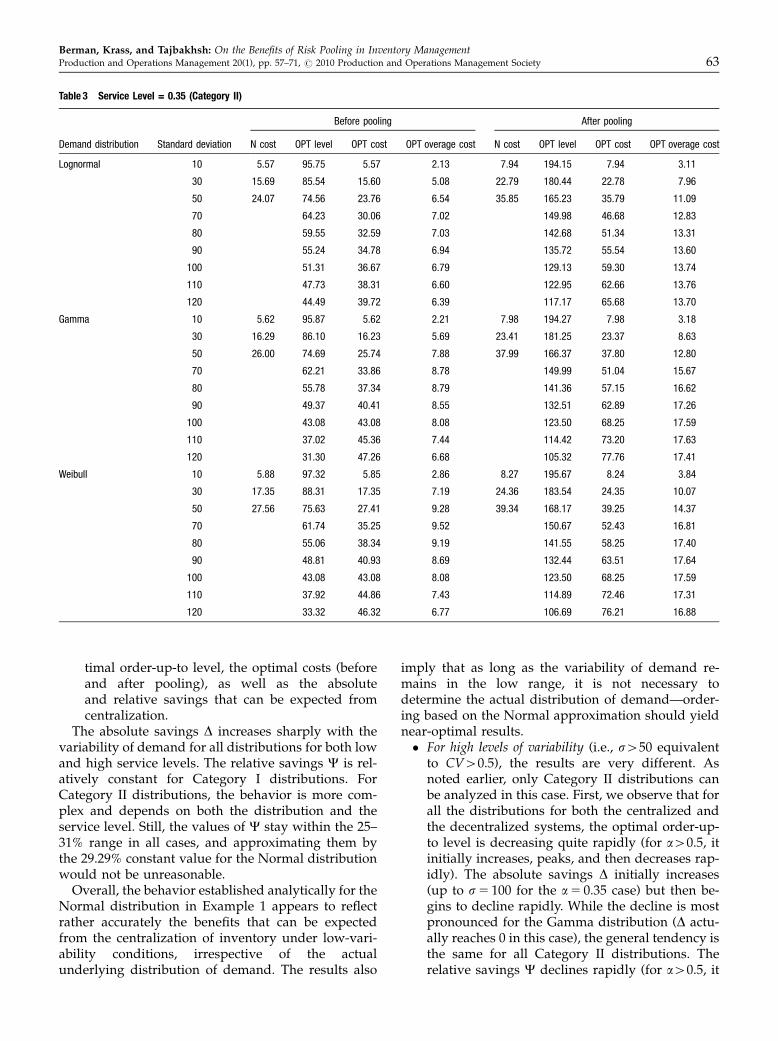

as well).Tables 2 and 3 contain the results for the service

level value of 0.35 (the results for a5 0.75 are pre-sented in the Online Supplement, and the results fora5 0.15, 0.55, 0.95 are similar and are available on re-quest from the authors). The columns labeled as ‘‘NCost’’ represent the cost of the Normal approximation.In this approximation, the optimal order-up-to level isapproximated by that of the Normal distribution andthen, the expected cost is evaluated using the actualdemand distribution. Figure 1 depicts the behavior ofD and C as functions of s for the service level 0.35.The plots in the right side of the figures are for Cat-egory II distributions only since CV40.5.

We make the following observations:� For low levels of variability (i.e., when s 50,

which is equivalent to the coefficient of variationCV 0.5), it can be observed that the Normaldistribution provides an excellent approximationfor all other distributions with respect to the op-

Table 2 Service Level = 0.35 (Category I)

Demand distribution Standard deviation

Before pooling After pooling

N cost OPT level OPT cost N cost OPT level OPT cost

Normal 10 96.15 5.70 194.55 8.06

30 88.44 17.10 183.65 24.18

50 80.73 28.49 172.75 40.29

Uniform 10 6.10 94.80 6.06 8.25 194.34 8.25

30 18.31 84.41 18.19 24.75 183.03 24.75

50 30.51 74.02 30.31 41.25 171.71 41.24

Laplace 10 5.23 97.48 5.17 7.68 195.54 7.65

30 15.69 92.43 15.50 23.04 186.62 22.97

50 26.14 87.39 25.83 38.40 177.70 38.28

Logistic 10 5.50 96.59 5.49 7.96 194.89 7.94

30 16.49 89.76 16.47 23.71 184.70 23.68

50 27.49 82.94 27.46 39.52 174.48 39.51

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management62 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

timal order-up-to level, the optimal costs (beforeand after pooling), as well as the absoluteand relative savings that can be expected fromcentralization.

The absolute savings D increases sharply with thevariability of demand for all distributions for both lowand high service levels. The relative savings C is rel-atively constant for Category I distributions. ForCategory II distributions, the behavior is more com-plex and depends on both the distribution and theservice level. Still, the values of C stay within the 25–31% range in all cases, and approximating them bythe 29.29% constant value for the Normal distributionwould not be unreasonable.

Overall, the behavior established analytically for theNormal distribution in Example 1 appears to reflectrather accurately the benefits that can be expectedfrom the centralization of inventory under low-vari-ability conditions, irrespective of the actualunderlying distribution of demand. The results also

imply that as long as the variability of demand re-mains in the low range, it is not necessary todetermine the actual distribution of demand—order-ing based on the Normal approximation should yieldnear-optimal results.� For high levels of variability (i.e., s450 equivalent

to CV40.5), the results are very different. Asnoted earlier, only Category II distributions canbe analyzed in this case. First, we observe that forall the distributions for both the centralized andthe decentralized systems, the optimal order-up-to level is decreasing quite rapidly (for a40.5, itinitially increases, peaks, and then decreases rap-idly). The absolute savings D initially increases(up to s5 100 for the a5 0.35 case) but then be-gins to decline rapidly. While the decline is mostpronounced for the Gamma distribution (D actu-ally reaches 0 in this case), the general tendency isthe same for all Category II distributions. Therelative savings C declines rapidly (for a40.5, it

Table 3 Service Level = 0.35 (Category II)

Demand distribution Standard deviation

Before pooling After pooling

N cost OPT level OPT cost OPT overage cost N cost OPT level OPT cost OPT overage cost

Lognormal 10 5.57 95.75 5.57 2.13 7.94 194.15 7.94 3.11

30 15.69 85.54 15.60 5.08 22.79 180.44 22.78 7.96

50 24.07 74.56 23.76 6.54 35.85 165.23 35.79 11.09

70 64.23 30.06 7.02 149.98 46.68 12.83

80 59.55 32.59 7.03 142.68 51.34 13.31

90 55.24 34.78 6.94 135.72 55.54 13.60

100 51.31 36.67 6.79 129.13 59.30 13.74

110 47.73 38.31 6.60 122.95 62.66 13.76

120 44.49 39.72 6.39 117.17 65.68 13.70

Gamma 10 5.62 95.87 5.62 2.21 7.98 194.27 7.98 3.18

30 16.29 86.10 16.23 5.69 23.41 181.25 23.37 8.63

50 26.00 74.69 25.74 7.88 37.99 166.37 37.80 12.80

70 62.21 33.86 8.78 149.99 51.04 15.67

80 55.78 37.34 8.79 141.36 57.15 16.62

90 49.37 40.41 8.55 132.51 62.89 17.26

100 43.08 43.08 8.08 123.50 68.25 17.59

110 37.02 45.36 7.44 114.42 73.20 17.63

120 31.30 47.26 6.68 105.32 77.76 17.41

Weibull 10 5.88 97.32 5.85 2.86 8.27 195.67 8.24 3.84

30 17.35 88.31 17.35 7.19 24.36 183.54 24.35 10.07

50 27.56 75.63 27.41 9.28 39.34 168.17 39.25 14.37

70 61.74 35.25 9.52 150.67 52.43 16.81

80 55.06 38.34 9.19 141.55 58.25 17.40

90 48.81 40.93 8.69 132.44 63.51 17.64

100 43.08 43.08 8.08 123.50 68.25 17.59

110 37.92 44.86 7.43 114.89 72.46 17.31

120 33.32 46.32 6.77 106.69 76.21 16.88

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 63

reaches a peak and then decreases rapidly) for allthe distributions as s increases.

3.2. The Effect of the Number of LocationsHere, we investigate the sensitivity of the centraliza-tion savings to the number of locations n. We areparticularly interested in this behavior under thehigh-variability conditions. Thus, we limit ourselvesto Category II distributions in the current section. Werestrict the analysis to the Gamma distribution wherethe distribution of the centralized demand fT is avail-able in closed form.

We keep the values of parameters co, m, and a thesame as in the previous section. Let s5 100 and 400(corresponding to CV 5 1 and 4) and let n 5 2, . . ., 20.The results are displayed in Figure 2.

Based on our computational results, we make thefollowing observations:� For a given level of demand variability, pooling

inventory across larger number of locations in-creases both the absolute and the relative costsavings compared with the decentralized system.The rate of increase in both measures is largest

when the service level is high (this is naturalsince in this case, there is more inventory in thesystem).

� Under the moderate variability of demand (CV 5

1), we observe growth in the absolute and rela-tive cost savings for all service levels—this is inline with the results obtained for the Normallydistributed demand in Example 1.

� Under the high variability of demand (CV 5 4)and low-to-moderate service levels (a 0.55), theinventory must be pooled across a certain mini-mum number of locations n before any significantabsolute and relative cost savings are observed.For example, for a5 0.15, the savings are not sig-nificant and do not begin to grow until n 5 8,while for a5 0.35, the growth does not happenuntil n 5 5; for a5 0.55, the savings become sig-nificant when n 5 3.

4. Impact of Centralization: TheDistribution-Free Approach

In this section, we analyze the impact of centralizationunder the distribution-free approach. Under this

Figure 1 Pooling Savings as Functions of r for a = 0.35

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management64 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

approach, we assume that nothing is known about thedistribution of demand at each location, except for themean m and the standard deviation s. We then obtainan upper bound on the optimal inventory cost and thecorresponding ‘‘distribution-free’’ optimal order-up-to level.

This approach holds several advantages. First, itis quite practical since in many real-life situations,the form of the demand distribution may not beknown, however, estimates of m and s are likely tobe available. Second, as will be shown below,the bound on the optimal expected cost has a par-ticularly simple form, which allows us to deriveclosed-form expressions for D and C for thedistribution-free case. The analysis of these expres-sions provides some insights into the behavior ofthese measures. Finally, by applying the distribu-tion-free approach to the centralized system, wecan obtain lower bounds on D and C. We start bysummarizing the relevant results from Gallego andMoon (1993).

THEOREM 1 (Gallego and Moon). Let D be a randomvariable with mean m and variance s2. Then,

1. For an order-up-to level y � 0,

EðD� yÞþ

ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffis2 þ ðy� mÞ2

q� ðy� mÞ

2:

Moreover, the upper bound on the expected costLðyÞ is given by

LðyÞ ¼ coðy� mÞ þ ðco þ cuÞ

�

ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffis2 þ ðy� mÞ2

q� ðy� mÞ

2:

There exists a distribution of D (the ‘‘maximal dis-tribution’’) for which LðyÞ is the actual expected costof the corresponding newsvendor model.

2. The function LðyÞ is strictly convex and is maxi-mized at

y� ¼ mþ ðcu�coÞs2ffiffiffiffiffifficocup if CVo

ffiffiffiffiffiffiffiffiffiffifficu=co

p;

0 otherwise;

(ð6Þ

where CV 5 s/m is the coefficient of variation of D.3. Let y� be the optimal order-up-to level (under the actual

distribution of D). Then Lðy�Þ Lðy�Þ, and this up-per bound above is tight for the maximal distribution.

Figure 2 Pooling Savings as Functions of n for Gamma Distribution

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 65

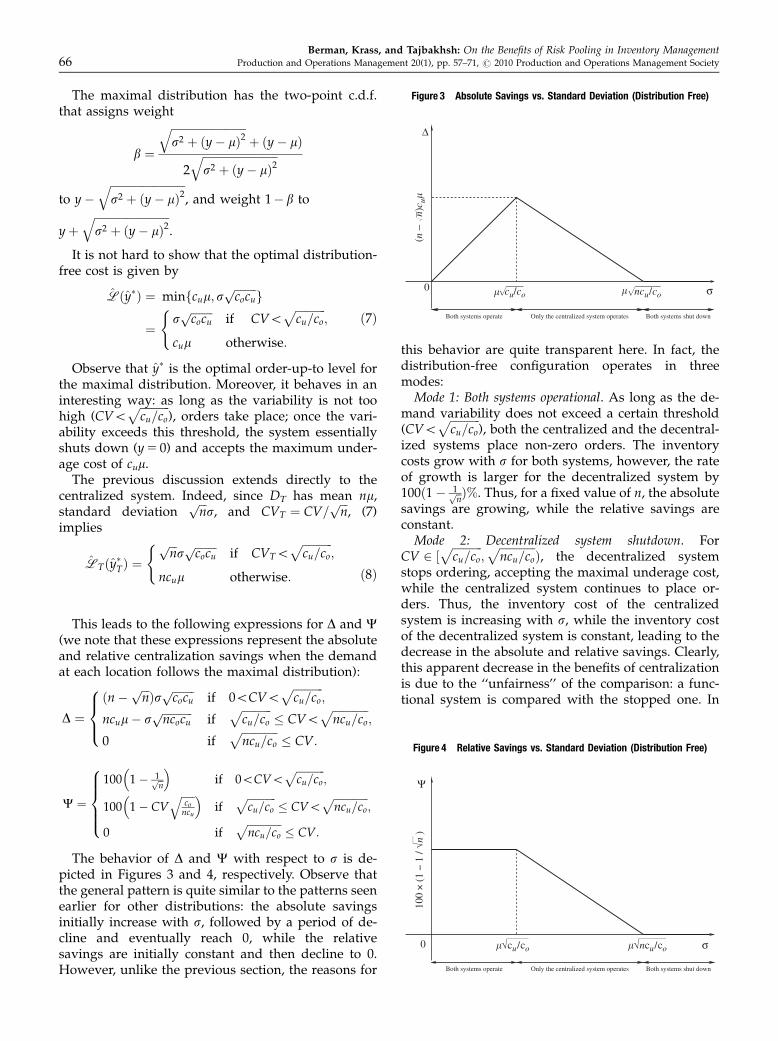

The maximal distribution has the two-point c.d.f.that assigns weight

b ¼

ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffis2 þ ðy� mÞ2

qþ ðy� mÞ

2ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffis2 þ ðy� mÞ2

qto y�

ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffis2 þ ðy� mÞ2

q, and weight 1� b to

yþffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffis2 þ ðy� mÞ2

q.

It is not hard to show that the optimal distribution-free cost is given by

Lðy�Þ ¼ minfcum; sffiffiffiffiffiffiffifficocup g

¼sffiffiffiffiffiffiffifficocup

if CVoffiffiffiffiffiffiffiffiffiffifficu=co

p;

cum otherwise:

(ð7Þ

Observe that y� is the optimal order-up-to level forthe maximal distribution. Moreover, it behaves in aninteresting way: as long as the variability is not toohigh (CVo

ffiffiffiffiffiffiffiffiffiffifficu=co

p), orders take place; once the vari-

ability exceeds this threshold, the system essentiallyshuts down (y 5 0) and accepts the maximum under-age cost of cum.

The previous discussion extends directly to thecentralized system. Indeed, since DT has mean nm,standard deviation

ffiffiffinp

s, and CVT ¼ CV=ffiffiffinp

, (7)implies

LTðy�TÞ ¼ffiffiffinp

sffiffiffiffiffiffiffifficocup

if CVToffiffiffiffiffiffiffiffiffiffifficu=co

p;

ncum otherwise:

(ð8Þ

This leads to the following expressions for D and C(we note that these expressions represent the absoluteand relative centralization savings when the demandat each location follows the maximal distribution):

D ¼ðn�

ffiffiffinpÞs ffiffiffiffiffiffiffiffi

cocup

if 0oCVoffiffiffiffiffiffiffiffiffiffifficu=co

p;

ncum� sffiffiffiffiffiffiffiffiffiffiffincocup

ifffiffiffiffiffiffiffiffiffiffifficu=co

p CVo

ffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

p;

0 ifffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

p CV:

8><>:

C ¼

100 1� 1ffiffinp

� �if 0oCVo

ffiffiffiffiffiffiffiffiffiffifficu=co

p;

100 1� CVffiffiffiffiffico

ncu

q� �if

ffiffiffiffiffiffiffiffiffiffifficu=co

p CVo

ffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

p;

0 ifffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

p CV:

8>>><>>>:

The behavior of D and C with respect to s is de-picted in Figures 3 and 4, respectively. Observe thatthe general pattern is quite similar to the patterns seenearlier for other distributions: the absolute savingsinitially increase with s, followed by a period of de-cline and eventually reach 0, while the relativesavings are initially constant and then decline to 0.However, unlike the previous section, the reasons for

this behavior are quite transparent here. In fact, thedistribution-free configuration operates in threemodes:

Mode 1: Both systems operational. As long as the de-mand variability does not exceed a certain threshold(CVo

ffiffiffiffiffiffiffiffiffiffifficu=co

p), both the centralized and the decentral-

ized systems place non-zero orders. The inventorycosts grow with s for both systems, however, the rateof growth is larger for the decentralized system by100ð1� 1ffiffi

np Þ%. Thus, for a fixed value of n, the absolute

savings are growing, while the relative savings areconstant.

Mode 2: Decentralized system shutdown. ForCV 2 ½

ffiffiffiffiffiffiffiffiffiffifficu=co

p;ffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

pÞ, the decentralized system

stops ordering, accepting the maximal underage cost,while the centralized system continues to place or-ders. Thus, the inventory cost of the centralizedsystem is increasing with s, while the inventory costof the decentralized system is constant, leading to thedecrease in the absolute and relative savings. Clearly,this apparent decrease in the benefits of centralizationis due to the ‘‘unfairness’’ of the comparison: a func-tional system is compared with the stopped one. In

0 � cu/co σ

Δ

� ncu/co

(n −

n)c u

�

Figure 3 Absolute Savings vs. Standard Deviation (Distribution Free)

0 �√cu/co σ

Ψ

�√ncu/co

100

× (1

− 1

/ √n

)

Figure 4 Relative Savings vs. Standard Deviation (Distribution Free)

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management66 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

fact, centralization of inventory (and the resulting de-crease in variability) is what allows the centralizedsystem to continue operating in this range.

Mode 3: Complete system shutdown. Once CV �ffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

p, the centralized system stops placing orders

as well, leading to a constant inventory cost equal tothe maximal underage cost (same as for the decen-tralized system). Thus, both the absolute and therelative savings measures are 0 in this range.

We also observe that the behavior of D and C withrespect to the number of locations n for the distribu-tion-free approach is quite similar to the one observedfor other distributions in the previous sections: for afixed s (or CV) and a (or cu), both the absolute and therelative savings due to centralization generally in-crease with n, but a certain minimum number oflocations may have to be pooled before this increasestarts. Specifically,

1. If n CV2(co/cu), then D5C5 0.2. If n4CV2(co/cu), then both D and C are positive

and increasing in n. Note that limn!1C ¼ 100%.Of course, the reason for this behavior is that n has

to be large enough (in relation to CV) to enable thecentralized system to operate. When CV is sufficientlysmall so that the decentralized system is operating,the increase in D and C starts at n 5 2.

To summarize, we see that, at least in the case of the‘‘maximal’’ distribution, the seemingly counter-intu-itive behavior of the absolute and the relative savingsmeasures is easily explained by understanding theunderlying workings of the decentralized and thecentralized systems. In the following section, we willsee that similar (albeit modified) effects hold in thecase of other distributions as well.

We close the current section by pointing out that thedistribution-free approach can be used to obtain lowerbounds on the absolute and relative savings for thecases where the distribution of demand at each loca-tion is known but the distribution of the centralizeddemand cannot be derived. The following propositionfollows directly from Theorem 1, Equation (8), and thedefinitions of D and C.

PROPOSITION 2. Let Lðy�Þ be the optimal cost of the news-vendor model with per-period demand D and the coefficientof variation CV. Let L

�T ¼

ffiffiffinp

sffiffiffiffiffiffiffifficocup

if CVoffiffiffiffiffiffiffiffiffiffiffiffiffincu=co

pand L

�T ¼ ncum otherwise. Define

D ¼ nLðy�Þ � L�T; C ¼ 100 1� L

�T

nLðy�Þ

" #:

Then, D � D and C � C.The previous result can, for example, be applied to

all distributions listed in Table 1 for which Lðy�Þ isavailable in closed form.

5. Effective Shutdowns andCentralization Effects

In the previous section, we analyzed the behavior of Dand C measures with respect to s and n for the dis-tribution-free system. We were able to attribute theobserved patterns in the absolute and relative savingsto the shutdowns—first of only the decentralized sys-tem, and then of the centralized one as well.

It is tempting to look for the same effects in the caseof Category II distributions analyzed earlier in section3 (since D and C behave similarly). However, it isclear from Table 3 that ‘‘pure’’ shutdowns are notpresent in this case. While, as discussed earlier, it istrue that the optimal order-up-to levels y� and y�T ap-proach 0 as s approaches 1, nevertheless y� and y�Tremain positive for all s and thus, technically, neitherthe decentralized nor the centralized system evershuts down completely.

However, if we define ‘‘shutdown’’ to have oc-curred when y� (or y�T) is below some sufficientlysmall e40, then this certainly accounts for D5C � 0for sufficiently large s. On the other hand, this doesnot explain the behavior of the D measure, which firstincreases with s, peaks at a certain level, and thenbegins to decline. What triggers this decline?

We point out that the behavior of D is not (or, atleast not completely) accounted for by the behavior ofy� and y�T. For Category II distributions, y� first in-creases and then decreases with s for a40.5 anddecreases everywhere for a 0.5. This was estab-lished theoretically for the Gamma and Lognormaldistributions by Gallego et al. (2007) and numericallyfor the Weibull distribution in our earlier experiments;moreover, we observed the same behavior for y�T.However, as we saw in Figure 1, for a5 0.35 the ab-solute savings D goes through a period of increasefollowed by a decline even though from Table 3 wesee that y� and y�T are declining throughout.

The behavior of D appears to be driven by the op-timal expected overage cost coEðy� �DÞþ. Asillustrated in Figure 5a and b for the Gamma distri-bution (the patterns for all other distributions are verysimilar), the optimal expected overage cost first in-creases and then decreases with s. This parallels thebehavior of D and, we believe, provides an explana-tion for it.

Note that the newsvendor model is designed tobalance overage and underage risks. Thus, as thevariability (i.e., coefficient of variation) of demand in-creases, we would expect both the overage and theunderage costs to rise. However, at some high level ofvariability, the expected overage cost begins to fall to 0while the expected underage cost increases to themaximal level of cum. Thus, at some level of variability,the system is no longer ‘‘willing’’ to take the risk of

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 67

having too much inventory, accepting higher andhigher underage costs instead. We call this the ‘‘ef-fective shutdown’’ regime for the newsvendor system.This behavior occurs for both the decentralized and

the centralized systems but—because of the lowervariability—it sets in at a higher level of s in the lattercase. As we see from Figure 5 (and from Table 3), thepeak of the absolute savings due to centralization D

Figure 5 Optimal Costs (Overage Cost in ‘‘Black’’ and Underage Cost in ‘‘Grey’’) and Pooling Savings as Functions of r

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management68 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

occurs exactly during the period when the decentral-ized system has already entered into the effectiveshutdown regime, while the centralized system is stilloperational. Once both systems are in the effectiveshutdown regime, D declines rapidly to 0. The relativesavings measure C appears to be even more sensitiveto this effect: while C is fairly flat when both systemsare operational, it begins to decline rapidly with s assoon as the decentralized system enters the ‘‘effectiveshutdown’’ regime.

The observed pattern with respect to the number oflocations n for a given level of s is similarly explained.When the coefficient of variation of demand CV issufficiently high to place the decentralized systeminto the ‘‘effective shutdown’’ regime, a certain levelof n may be required before the coefficient of variationof the centralized system CVT is low enough to ensurethat the system is operational. Once this level isreached, both D and C increase with n as further de-creases in CVT give more and more advantage to thecentralized system.

To summarize, the newsvendor system for Cate-gory II distributions analyzed in this paper (and likelyfor many other distributions as well) goes through thefollowing three regimes as s increases:

Regime 1: Normal operation. At low levels of vari-ability, both the optimal overage and the optimalunderage costs increase with variability; we call thisthe normal operation regime.

Regime 2: Effective shutdown. Above a certain level ofthe coefficient of variation, the optimal overage costbegins to decrease while the optimal underage costcontinues to increase with variability; we call this theeffective shutdown regime.

Regime 3: Complete shutdown. At still higher levels ofvariability, the optimal order-up-to level as well as theoptimal overage cost are essentially equal to 0; we callthis the complete shutdown regime.

An intuitive explanation of the complete shutdownregime is as follows. When the variance is excessivelylarge and the mean is fixed, for any y40, there is ahigh probability that the demand is much smallerthan y and the overage cost is wasted. On the otherhand, for any y40, there is a high chance of havingdemand much larger than y, so the underage is stillvery large. Hence, by ordering nothing, we at leastsave on the overage cost, i.e., y� must be 0.

While both the decentralized and the centralizedsystems go through the above three regimes as thevariability is increased, the decentralized system en-ters them at lower levels of demand variability. Hence,when comparing the decentralized and centralizedsystems, we observe five modes as follows:

Mode 1: Both systems operational. As long as the de-mand variability does not exceed a certain threshold,the optimal overage cost increases with s for both the

decentralized and the centralized systems. The abso-lute savings D is growing while the relative savings Cis fairly constant in this range.

Mode 2: Effective shutdown of the decentralized system.The decentralized system enters the effective shut-down regime: the optimal overage cost (as well as theoptimal order-up-to level y�) is decreasing as s grows.The centralized system is still in normal operation (theoptimal overage cost is growing with s). The absolutesavings D peaks in this range while the relativesavings C begins to decline.

Mode 3: Both systems in the effective shutdown regime.The centralized system also enters the effective shut-down regime. The optimal overage cost is decreasingas s grows for both systems. Both D and C aredecreasing.

Mode 4: Complete shutdown of the decentralized system.The decentralized system enters the complete shut-down regime: the optimal overage cost (as well as y�)is near 0 for the decentralized system. The centralizedsystem is still in the effective shutdown regime (theoptimal overage cost is decreasing as s grows). Both Dand C are approaching 0.

Mode 5: Complete system shutdown. The centralizedsystem also enters the complete shutdown regime.The optimal overage cost is near 0 for both systems.No orders are being placed—full underage cost isbooked. In this range, D5C5 0.

The managerial takeaway from this analysis is evensimpler: since, in practice, a system should not beoperated in the effective shutdown regime, the cen-tralization is always increasingly beneficial in therelevant operating range. Once the absolute savings ofcentralization begin to decline, it is a signal that thevariability is too large for the system (at least for thedecentralized configuration)—centralization across anumber of locations is required for the system tooperate effectively.

A harder question to answer is: how would onerecognize the on-set of the effective shutdown regimein practice, when the form of the distribution of Dmay not be known? Here, the distribution-free systemappears to be of use: the CV thresholds for the shut-down of the decentralized and centralizeddistribution-free systems appear to be good approx-imations for the on-set of the effective shutdowns inthe corresponding systems operating under variousCategory II distributions—see Table 4. For example, ifthe demand distribution is Lognormal and a5 0.15,the decentralized system enters the effective shut-down regime at CV 5 0.55 and the centralized systementers the effective shutdown regime when0.70oCV 0.90. Note that the distribution of thecentralized demand for the Lognormal and Weibulldistributions can only be computed numerically;therefore, we are only able to compute a range for

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 69

the CV values in those cases. Since the thresholds forthe distribution-free systems are computable from thevalues of unit overage and underage costs, they can beused as guidelines in practice.

6. Concluding RemarksWe consider risk pooling in a multi-location news-vendor problem and investigate the sensitivity of theinventory pooling benefits to the standard deviationof demands at each location and the number of loca-tions. We show that as long as the coefficient ofvariation of the demands is small (less than approx-imately 0.5), the behavior of savings due to pooling iswell approximated by the Normal distribution—theabsolute savings increases with the standard devia-tion of demand and the relative savings remains fairlyconstant. The growth in the absolute savings contin-ues as long as both the decentralized and thecentralized systems are in the ‘‘normal operation’’ re-gime characterized by the increase in both overageand underage costs with the standard deviation ofdemand. As the standard deviations of demand ateach location continue to grow, first the decentralizedand then the centralized systems enter the ‘‘effectiveshutdown’’ regime where the benefits of risk poolingdecrease; the pooling benefits vanish as both systemsenter the ‘‘complete shutdown’’ regime. Overall, ourresults indicate that pooling is beneficial in the ‘‘nor-mal operating range’’ of the system.

Many problems remain open in this line of research.First, a great deal of our analysis is based on MonteCarlo simulations due to the inability to analyze thebehavior of the centralized system analytically underCategory II distributions. Theoretical analysis sub-stantiating the three regimes described above wouldbe very valuable. Second, it is intuitively clear that ourresults do not apply to all demand distributions—only to those for which the order-up-to level ap-proaches 0 as the standard deviation of demandgrows. The behavior under other positive distribu-tions (i.e., the ones with positive support) that do notsatisfy the above condition remains to be analyzed.

Finally, we note that the lower bound on the ben-efits of pooling obtained via the distribution-free

approach in section 4 appears to be pretty weak. Ob-taining better bounds and/or approximations on theabsolute and relative savings of inventory poolingwould be of theoretical and practical interest.

AcknowledgmentsThis work was partially supported by NSERC grants of thefirst two authors. The authors would like to thank the senioreditor and the two referees for their valuable comments.

References

Benjaafar, S., W. L. Cooper, J.-S. Kim. 2005. On the benefits of pool-ing in production-inventory systems. Manage. Sci. 51(4): 548–565.

Burgin, T. A. 1975. The Gamma distribution and inventory control.Oper. Res. Q. 26(3): 507–525.

Chen, M.-S., C.-T. Lin. 1989. Effects of centralization on expectedcosts in a multi-location newsboy problem. J. Oper. Res. Soc.40(6): 597–602.

Cherikh, M. 2000. On the effect of centralization on expected profitsin a multi-location newsboy problem. J. Oper. Res. Soc. 51(6):755–761.

Dong, L., N. Rudi. 2004. Who benefits from transshipment? Exog-enous vs. endogenous wholesale prices. Manage. Sci. 50(5): 645–657.

Eppen, G. D. 1979. Effects of centralization on expected costs in amulti-location newsboy problem. Manage. Sci. 25(5): 498–501.

Feller, W. 1966. An Introduction to Probability Theory and its Applica-tions. Vol. 2. John Wiley & Sons, New York.

Gallego, G., K. Katircioglu, B. Ramachandran. 2007. Inventory man-agement under highly uncertain demand. Oper. Res. Lett. 35(3):281–289.

Gallego, G., I. Moon. 1993. The distribution free newsboy problem:Review and extensions. J. Oper. Res. Soc. 44(8): 825–834.

Gerchak, Y., Q.-M. He. 2003. On the relation between the benefits ofrisk pooling and the variability of demand. IIE Trans. 35(11):1027–1031.

Hanany, E., Y. Gerchak. 2008. Nash bargaining over allocationsin inventory pooling contracts. Nav. Res. Logist. 55(6): 541–550.

Lau, H.-S. 1997. Simple formulas for the expected costs in thenewsboy problem: An educational note. Eur. J. Oper. Res. 100(3):557–561.

Porteus, E. L. 2002. Foundations of Stochastic Inventory Theory. Stan-ford University Press, Stanford.

Renyi, A. 1970. Probability Theory. North-Holland, Amsterdam.

Schwarz, L. B. 1981. Physical distribution: The analysis of inventoryand location. AIIE Trans. 13(2): 138–150.

Silver, E. A., D. F. Pyke, R. Peterson. 1998. Inventory Management andProduction Planning and Scheduling. 3rd edn. John Wiley & Sons,New York.

Table 4 Effective Shutdown Threshold (CV) for Decentralized/Centralized Systems

Demand distribution

Service level a

0.15 0.35 0.55 0.75 0.95

Lognormal 0.55/(0.70, 0.90] 0.76/(1.00, 1.20] 1.02/(1.40, 1.60] 1.53/(2.20, 2.30] 4.54/(5.90, 6.10]

Gamma 0.55/0.78 0.75/1.07 1.01/1.43 1.48/2.09 3.54/5.01

Weibull 0.43/(0.60, 0.80] 0.63/(0.80, 1.00] 0.88/(1.20, 1.40] 1.32/(1.90, 2.10] 3.44/(4.80, 5.00]

Distribution-free 0.42/0.59 0.73/1.04 1.11/1.56 1.73/2.45 4.36/6.16

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory Management70 Production and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society

Supporting InformationAdditional supporting information may be found in theOnline Supplement of this article:

Appendix S1. Online Supplement.

Please note: Wiley-Blackwell is not responsible for thecontent or functionality of any supporting materials sup-plied by the authors. Any queries (other than missingmaterial) should be directed to the corresponding author forthe article.

Berman, Krass, and Tajbakhsh: On the Benefits of Risk Pooling in Inventory ManagementProduction and Operations Management 20(1), pp. 57–71, r 2010 Production and Operations Management Society 71