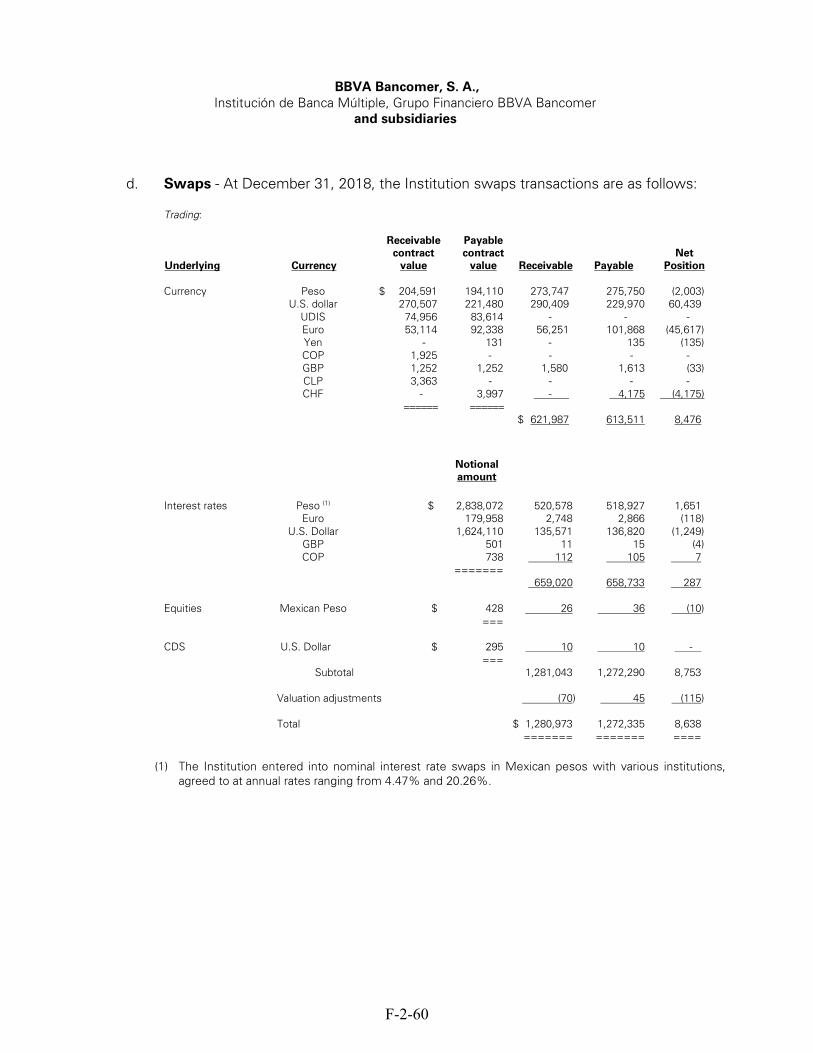

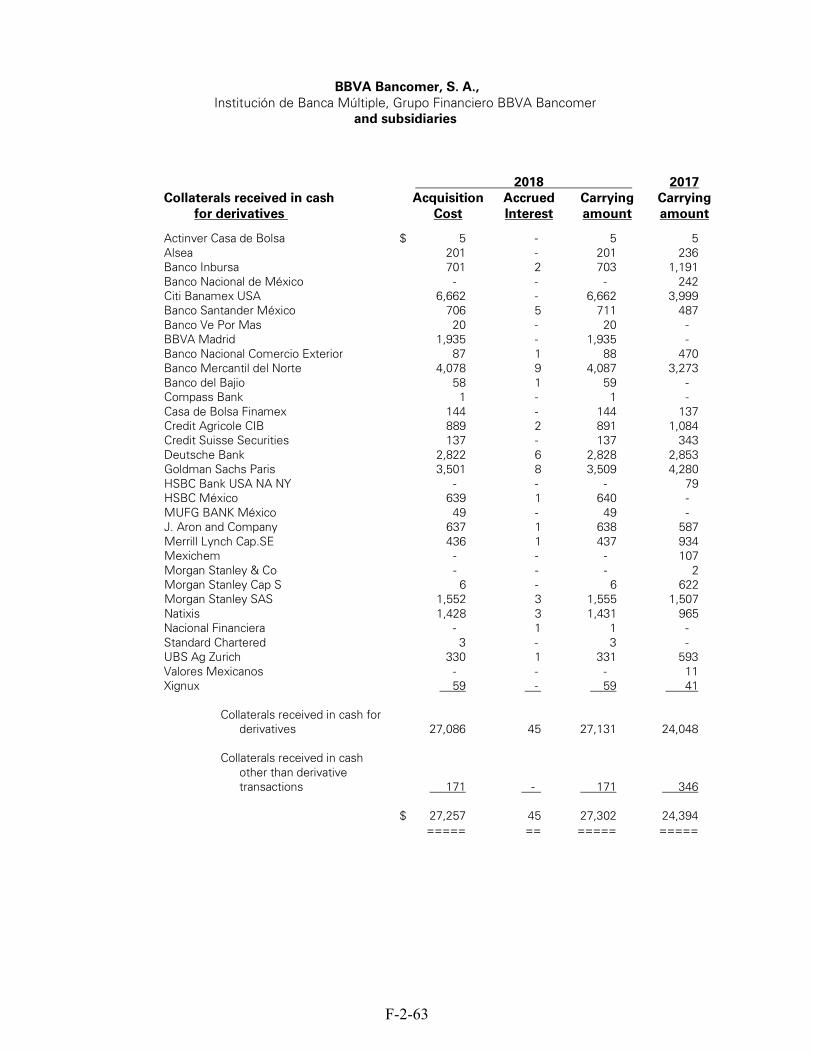

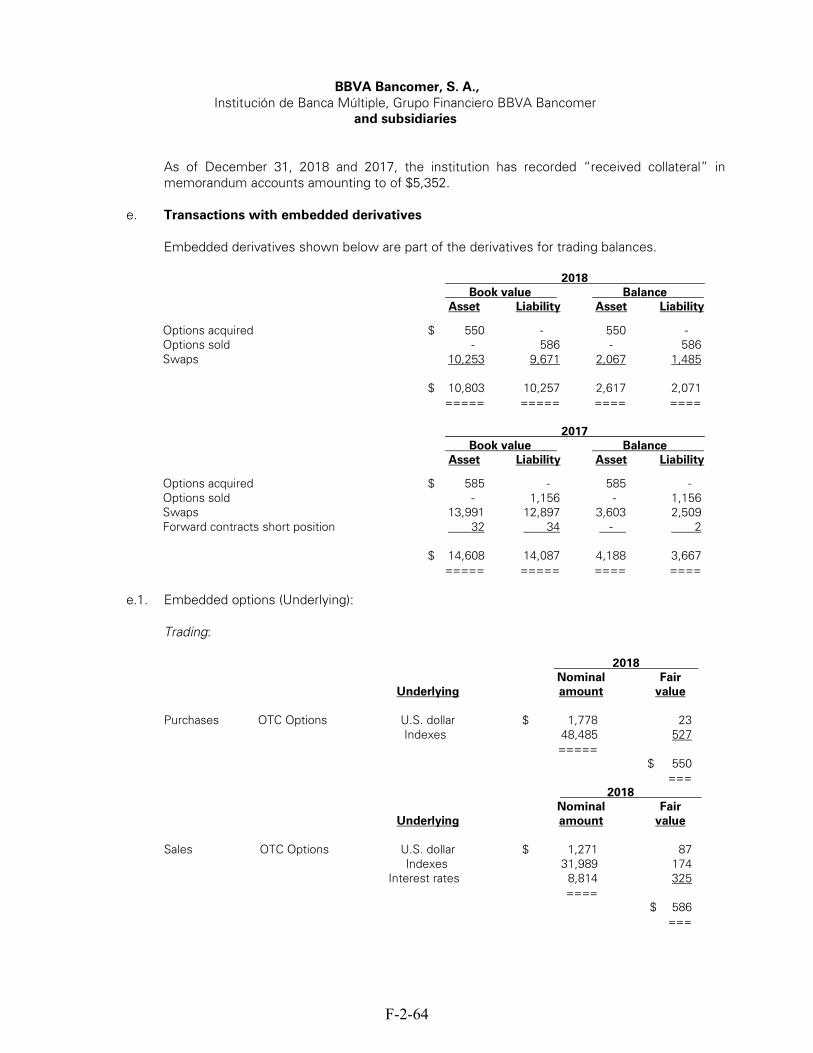

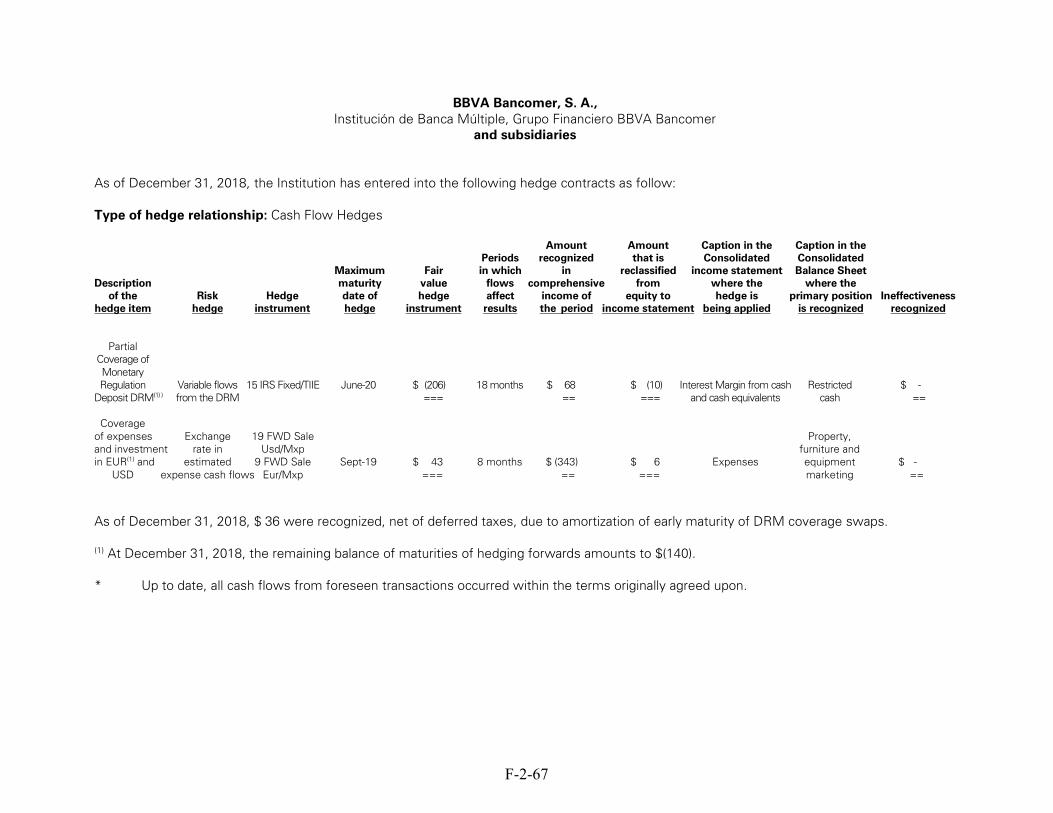

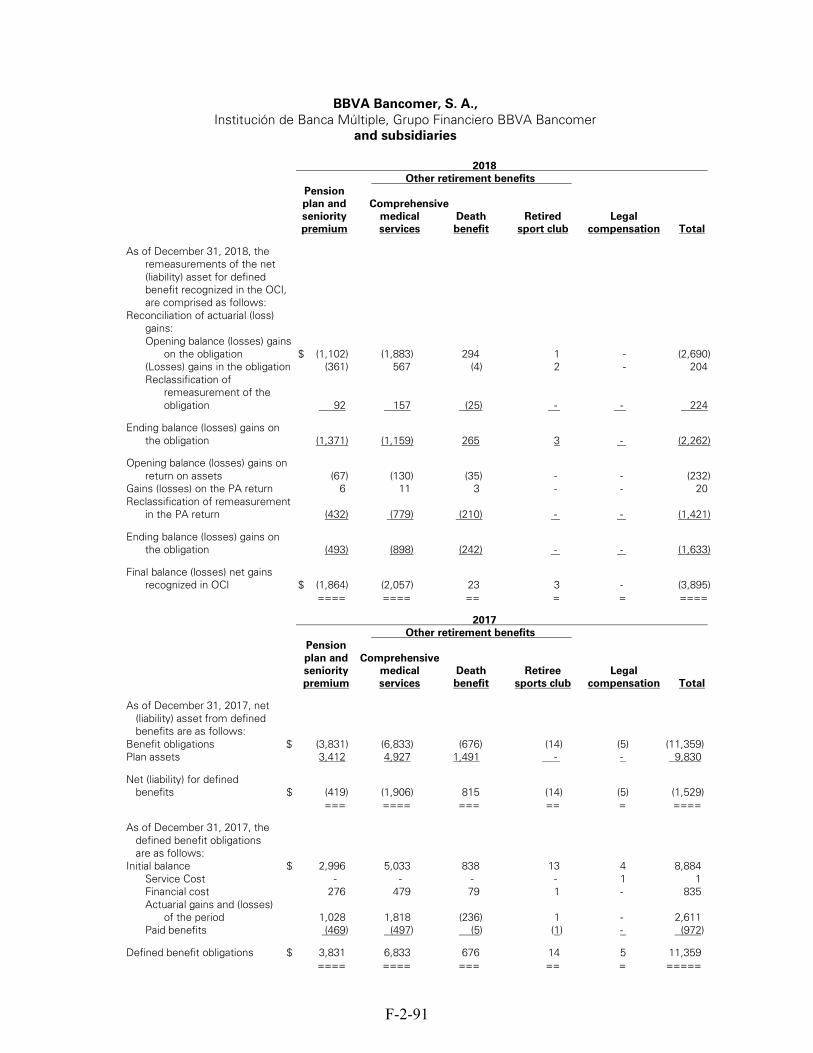

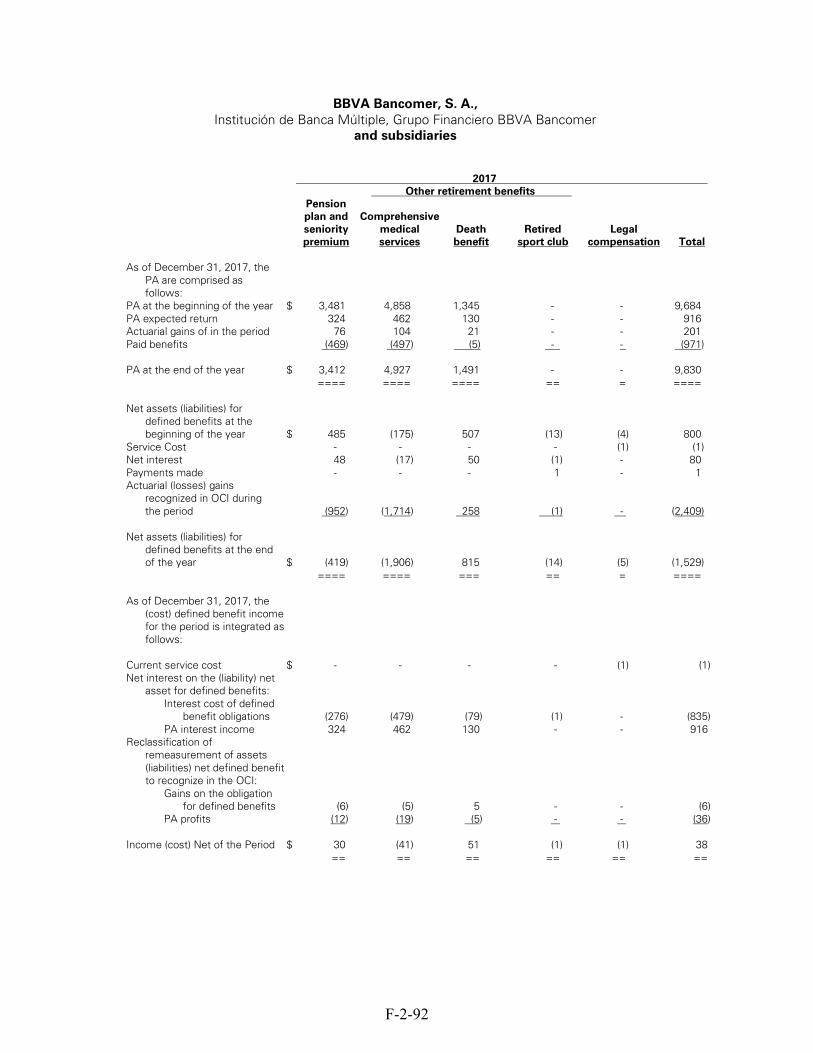

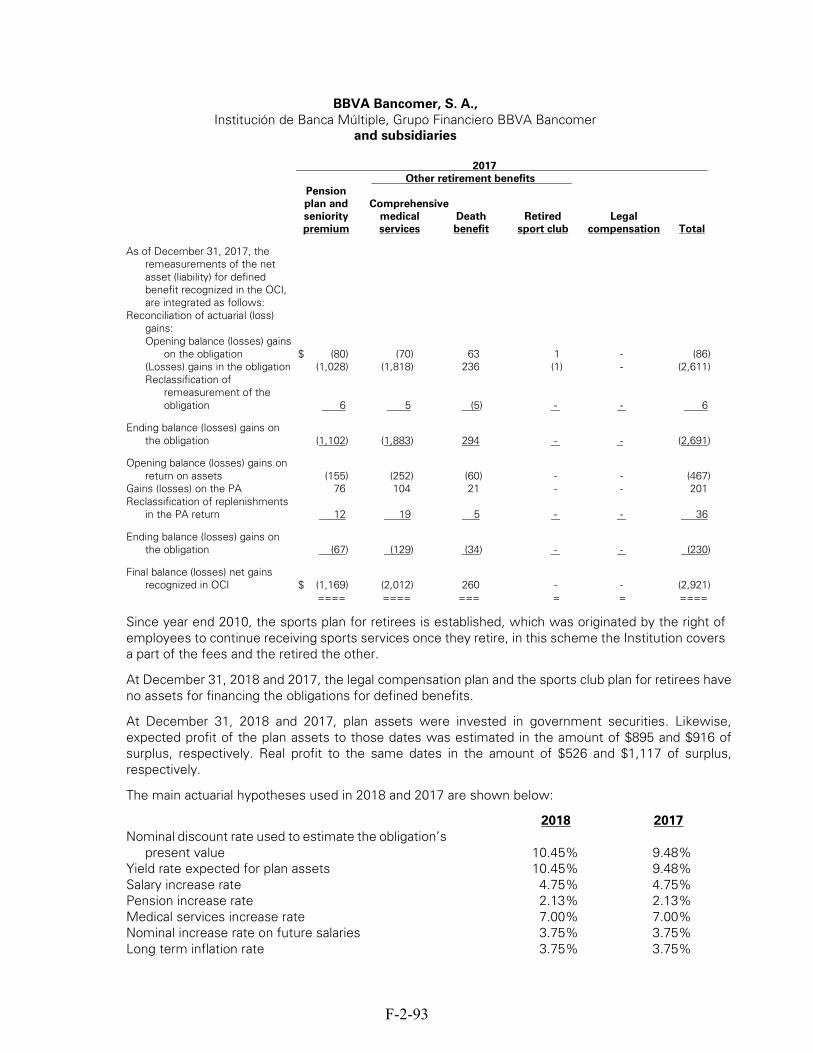

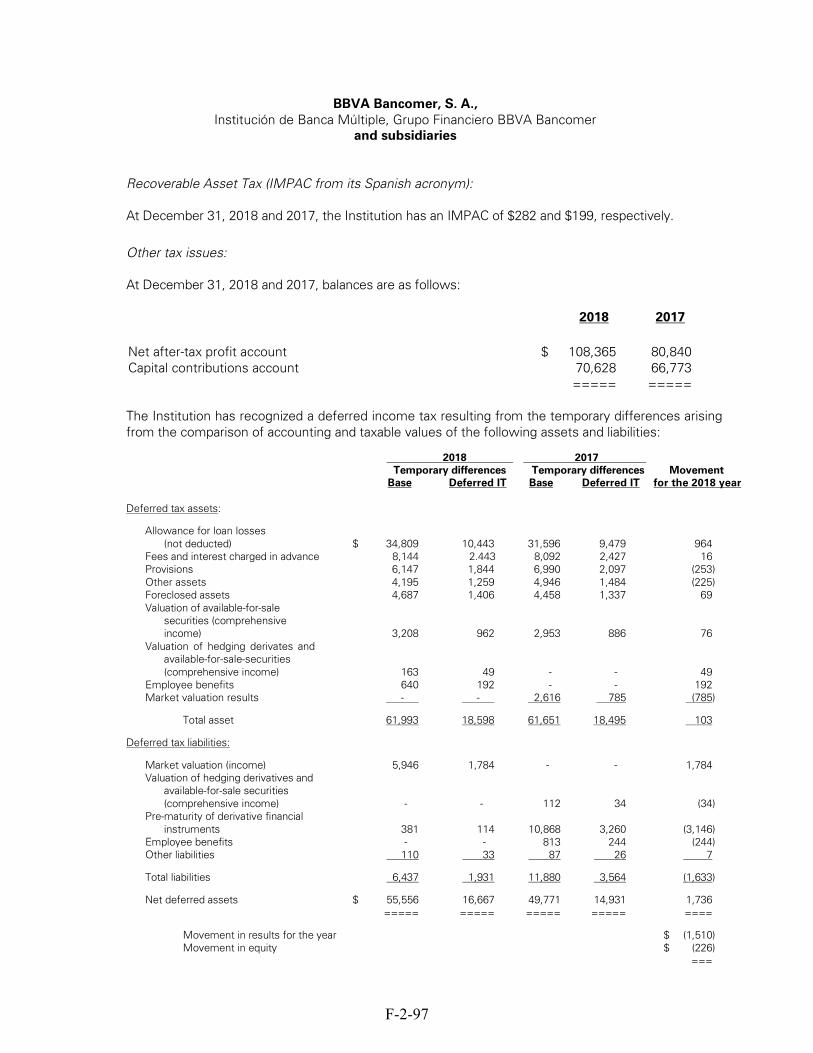

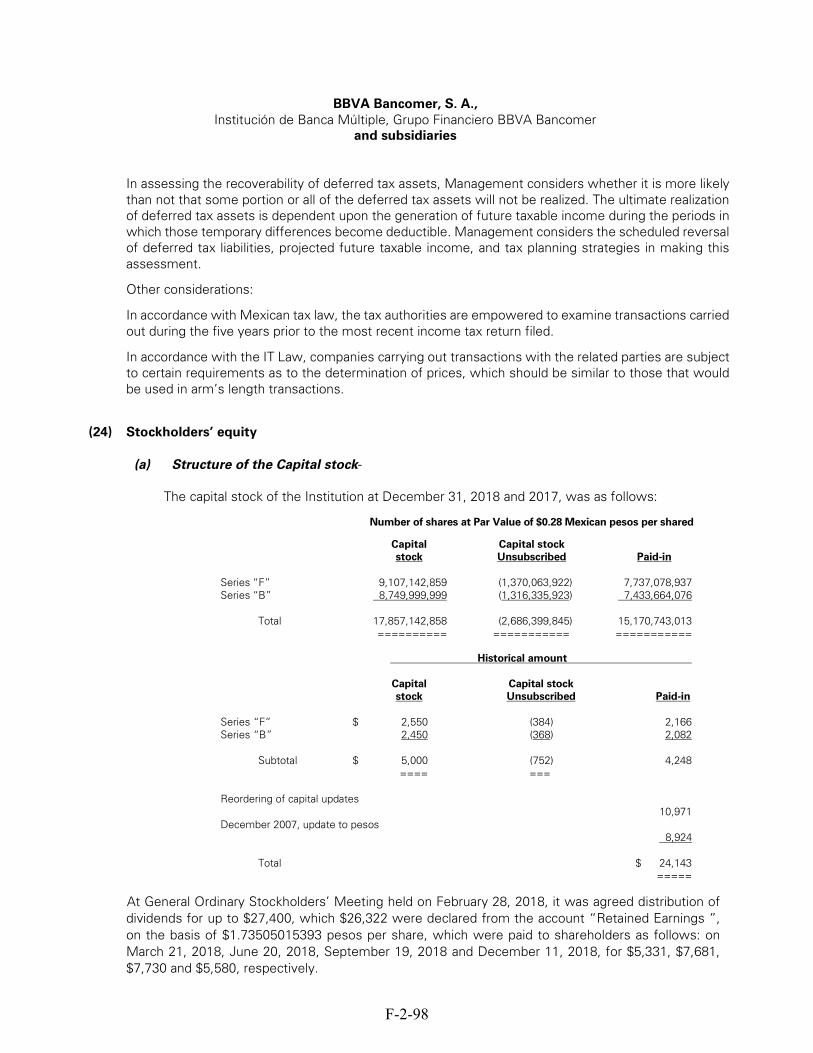

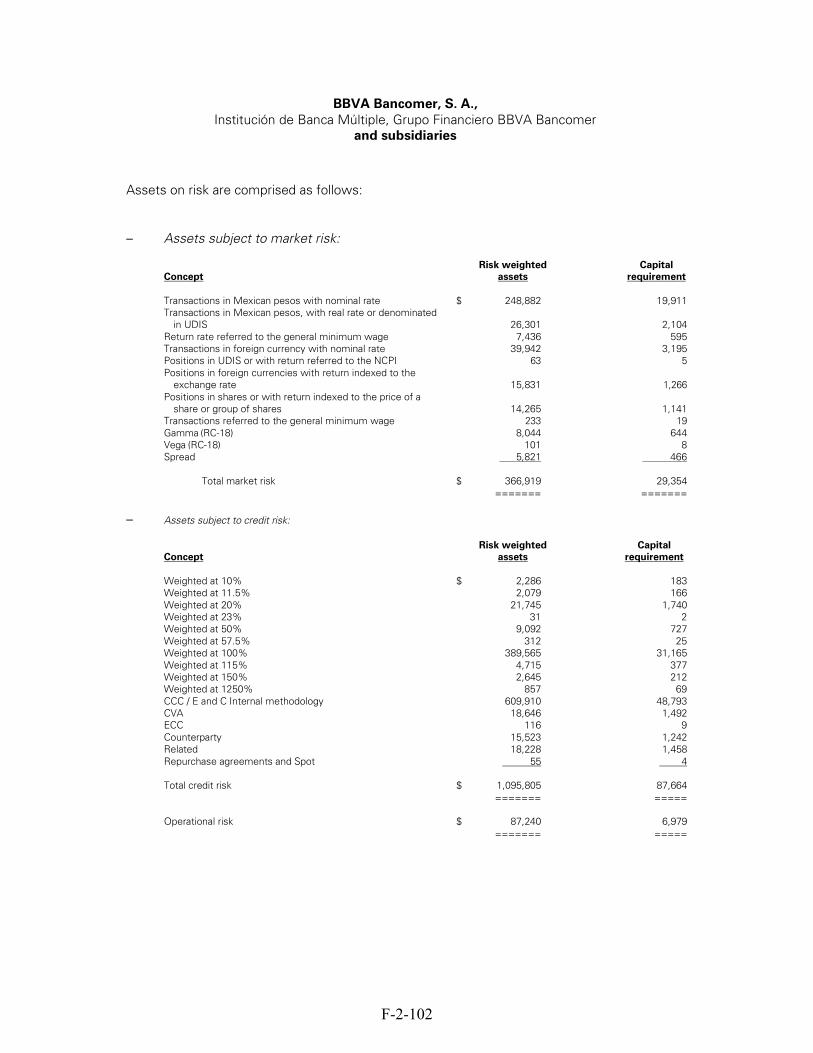

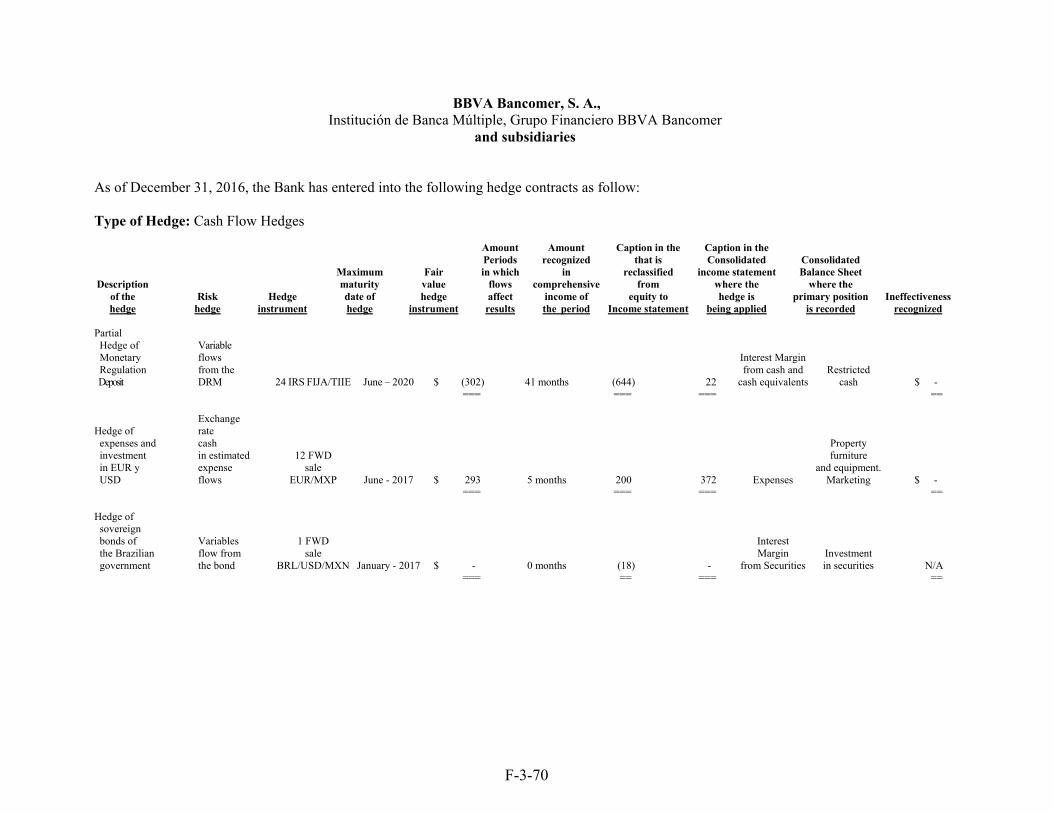

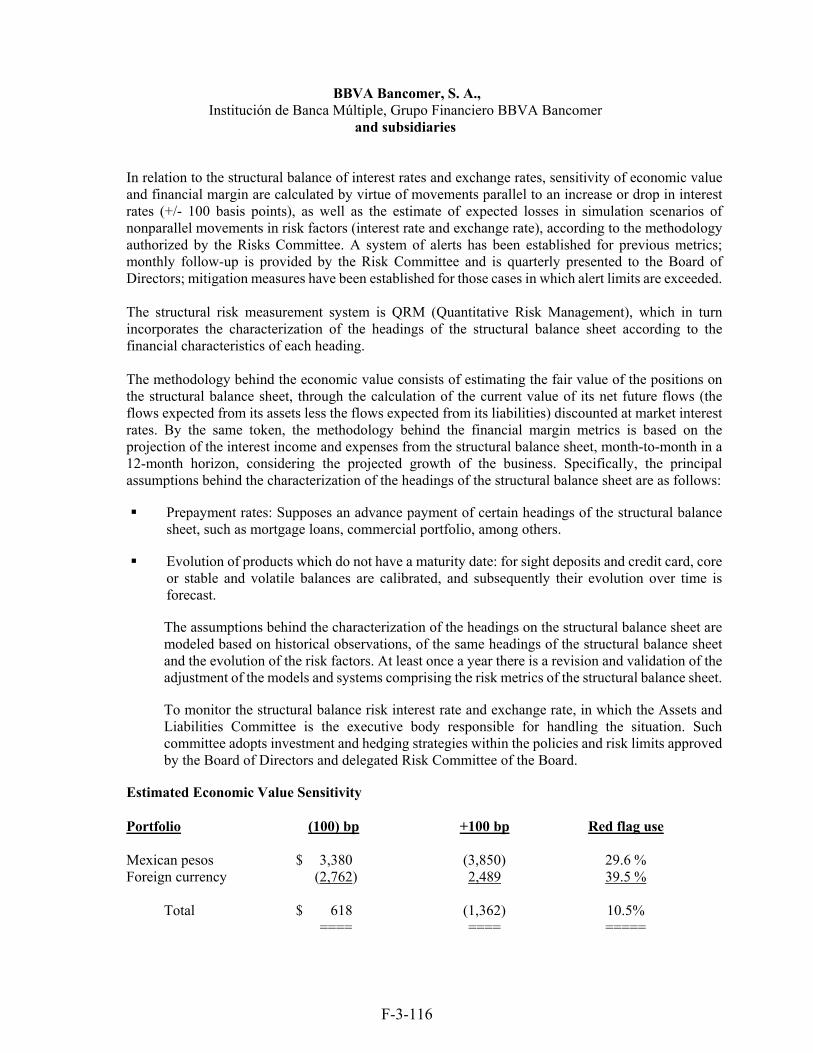

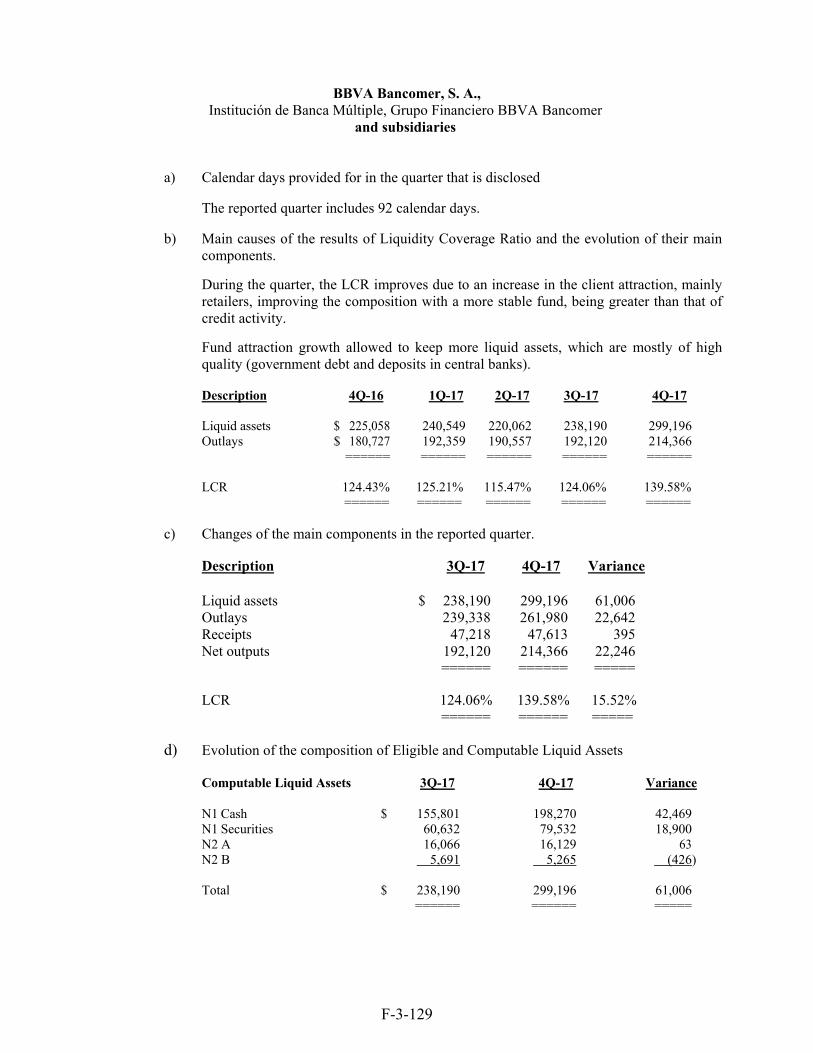

DBA-: Interpreta las relaciones entre el crecimie - Institución ...

Upload

khangminh22Category

view

0download

0

BBVA Bancomer, S.A., Institución de Banca Múltiple,

Grupo Financiero BBVA Bancomer,

acting through its Texas Agency

U.S.$750,000,000 5.875% Fixed Reset Subordinated Preferred Tier 2

Capital Notes Due 2034

under the

U.S.$10,000,000,000 Medium-Term Notes Program

FINAL OFFERING MEMORANDUM

ISSUE DATE: SEPTEMBER 13, 2019

EXECUTION VERSION

PRICING SUPPLEMENT

As of September 5, 2019

PROHIBITION OF SALES TO EEA RETAIL INVESTORS – The Notes are not intended to be

offered, sold or otherwise made available to and should not be offered, sold or otherwise made available to

any retail investor in the European Economic Area (“EEA”). For these purposes, a retail investor means a

person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of Directive

2014/65/EU (as amended, “MiFID II”); (ii) a customer within the meaning of Directive (EU) 2016/97 (the

“Insurance Distribution Directive”), where that customer would not qualify as a professional client as

defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined in Regulation

(EU) 2017/1129 (the “Prospectus Regulation”). Consequently no key information document required by

Regulation (EU) No 1286/2014 (as amended, the “PRIIPs Regulation”) for offering or selling the Notes

or otherwise making them available to retail investors in the EEA has been prepared and therefore offering

or selling the Notes or otherwise making them available to any retail investor in the EEA may be unlawful

under the PRIIPs Regulation.

PURSUANT TO CIRCULAR 3/2012 ISSUED BY BANCO DE MÉXICO AND PUBLISHED IN

THE FEDERAL OFFICIAL GAZETTE (DIARIO OFICIAL DE LA FEDERACIÓN) ON

MARCH 2, 2012, AND AS AMENDED FROM TIME TO TIME, INCLUDING THE

AMENDMENT PUBLISHED ON NOVEMBER 14, 2018, IN THE FEDERAL OFFICIAL

GAZETTE THROUGH CIRCULAR 16/2018, NO RELATED PARTY OF THE ISSUER, AS

DEFINED IN ARTICLE 73 OF THE MEXICAN BANKING LAW, MAY ACQUIRE, DIRECTLY

OR INDIRECTLY, ANY NOTES TO BE ISSUED PURSUANT TO THE OFFERING

MEMORANDUM.

BBVA Bancomer S.A., Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer,

acting through its Texas Agency

Issue of U.S. $750,000,000 5.875% Fixed Reset Subordinated Preferred Tier 2 Capital Notes

Due 2034

under the U.S.$10,000,000,000

Medium-Term Notes Program

PART A – CONTRACTUAL TERMS

Terms used herein shall be deemed to be defined as such for the purposes of the terms and conditions set

forth in the section entitled “Description of the Notes” in the Offering Memorandum, dated August 6, 2019

and the supplement to it, dated August 28, 2019 (together, the “Offering Memorandum”). This document

constitutes the Pricing Supplement of the Notes described herein and must be read in conjunction with the

Offering Memorandum. Full information on the Issuer and the offer of the Notes is only available on the

basis of the combination of this Pricing Supplement and the Offering Memorandum. The Offering

Memorandum has been published on the website of the Irish Stock Exchange plc trading as Euronext Dublin

(“Euronext Dublin”).

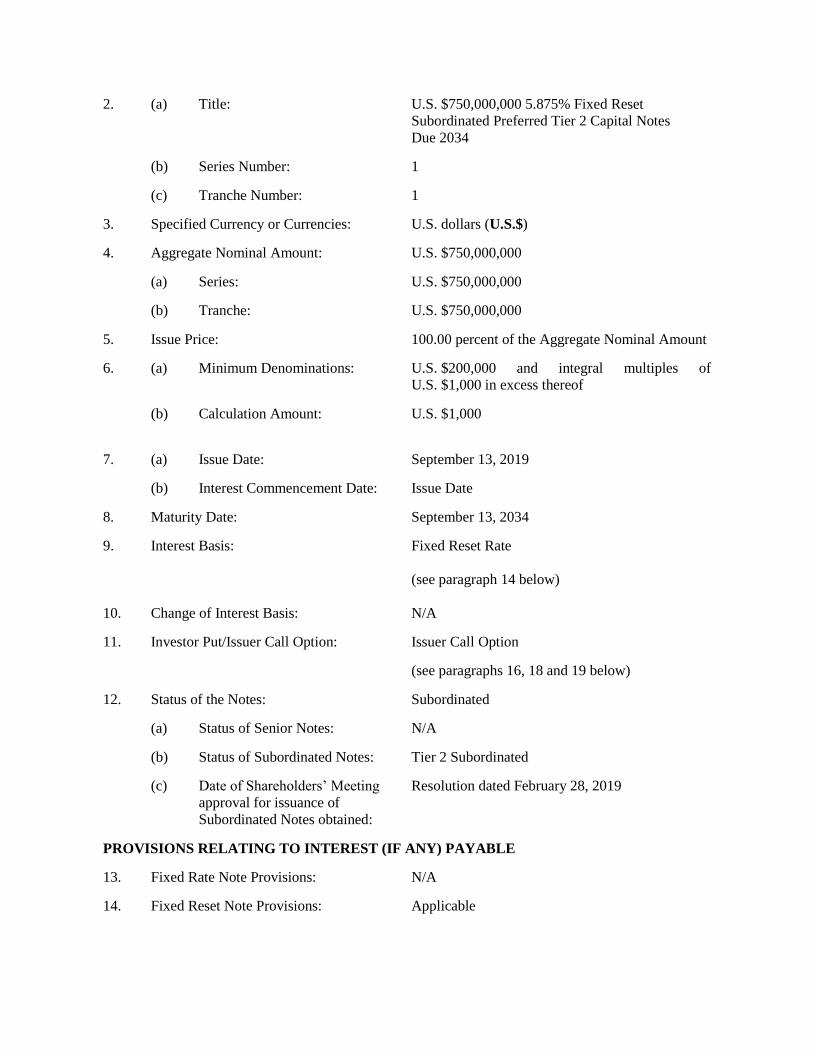

1. Issuer: BBVA Bancomer S.A., Institución de Banca

Múltiple, Grupo Financiero BBVA Bancomer,

acting through its Texas Agency

2. (a) Title: U.S. $750,000,000 5.875% Fixed Reset

Subordinated Preferred Tier 2 Capital Notes

Due 2034

(b) Series Number: 1

(c) Tranche Number: 1

3. Specified Currency or Currencies: U.S. dollars (U.S.$)

4. Aggregate Nominal Amount: U.S. $750,000,000

(a) Series: U.S. $750,000,000

(b) Tranche: U.S. $750,000,000

5. Issue Price: 100.00 percent of the Aggregate Nominal Amount

6. (a) Minimum Denominations: U.S. $200,000 and integral multiples of

U.S. $1,000 in excess thereof

(b) Calculation Amount: U.S. $1,000

7. (a) Issue Date: September 13, 2019

(b) Interest Commencement Date: Issue Date

8. Maturity Date: September 13, 2034

9. Interest Basis: Fixed Reset Rate

(see paragraph 14 below)

10. Change of Interest Basis: N/A

11. Investor Put/Issuer Call Option: Issuer Call Option

(see paragraphs 16, 18 and 19 below)

12. Status of the Notes: Subordinated

(a) Status of Senior Notes: N/A

(b) Status of Subordinated Notes: Tier 2 Subordinated

(c) Date of Shareholders’ Meeting

approval for issuance of

Subordinated Notes obtained:

Resolution dated February 28, 2019

PROVISIONS RELATING TO INTEREST (IF ANY) PAYABLE

13. Fixed Rate Note Provisions: N/A

14. Fixed Reset Note Provisions: Applicable

(a) Initial Fixed Reset Interest Rate: 5.875 percent per annum payable in arrears on

each Interest Payment Date up to, but excluding,

the Fixed Reset Date

(b) Interest Payment Dates: March 13 and September 13 in each year up to and

including the Maturity Date.

If any Interest Payment Date would otherwise fall

on a date that is not a Business Day, the required

payment of interest shall be made on the next

succeeding Business Day, with the same force and

effect as if made on such Interest Payment Date,

and no further interest shall accrue as a result of

the delay.

For purposes hereof, the term “Business Day” is

defined in the Indenture for the Notes as any day

other than a Saturday or a Sunday, or a day on

which banking institutions in The City of New

York, New York or Mexico City, Mexico are

authorized or required by law or executive or

administrative order to remain closed.

(c) Initial Fixed Reset Interest

Period:

From, and including, the Issue Date to, but

excluding, the September 13, 2029 (the “Optional

Call Date”).

(d) Regular Record Date(s): February 26 and August 29 in each year

(e) Fixed Coupon Amount to (but

excluding) the Reset Date:

U.S.$29.38 per Calculation Amount

(f) Fixed Day Count Fraction: 30/360

(g) Fixed Reset Date: September 13, 2029

(h) Subsequent Reset Date(s): N/A

(i) Reset Determination Date: 2 Business Days prior to the Fixed Reset Date

(j) Reset Reference Rate: Treasury Yield (as defined in the Offering

Memorandum)

(k) Reset Margin: +430.8 basis points

(l) Calculation Agent: Unless the Issuer has validly called all outstanding

Notes for redemption on or prior to the Fixed Reset

Date, the Issuer will appoint a calculation agent

with respect to the Notes prior to the Reset

Determination Date preceding the Fixed Reset

Date.

15. Floating Rate Note Provisions: N/A

PROVISIONS RELATING TO REDEMPTION

16. Tax Redemption: Applicable (in whole, but not in part)

17. Make-Whole Redemption: N/A

18. Special Event Redemption: Applicable (in whole, but not in part)

Notice Periods: Minimum period: 30 days

Maximum period: 60 days

19. Subordinated Notes Optional

Redemption:

Applicable (in whole or in part)

(a) Subordinated Notes Optional

Redemption Date:

September 13, 2029

(b) Notice Periods: Minimum period: 30 days

Maximum period: 60 days

20. Early Redemption Amount payable on

redemption for taxation reasons, on an

event of default or upon the occurrence

of a Special Event Redemption or

Subordinated Notes Optional

Redemption:

U.S. $1,000 per Calculation Amount

(For the avoidance of doubt, such amount shall

include accrued and unpaid interest due on, or with

respect to, the Notes, plus additional amounts, if any,

up to, but excluding, the date of redemption.)

21. Final Redemption Amount: U.S. $1,000 per Calculation Amount

(For the avoidance of doubt, such amount shall

include accrued and unpaid interest due on, or with

respect to, the Notes, plus additional amounts, if any,

up to, but excluding, the date of redemption.)

22. Investor Put: N/A

GENERAL PROVISIONS APPLICABLE TO THE NOTES

23. Form of Notes: Registered Notes:

Regulation S Global Note registered in the name of a

nominee for DTC

Rule 144A Global Note registered in the name of a

nominee for DTC

24. Additional Notes: N/A

25. Additional Events of Default: N/A

26. Other Terms: For the purposes of the Notes:

“Write-Down Amount” means an (i) amount of the

then-outstanding principal amount of the Notes that

would be sufficient, together with any concurrent

pro rata Write-Down or conversion of any other Tier

2 capital instruments issued by the Bank and the

then outstanding (after taking into account the effect

of the conversion or Write-Down of any loss-

absorbing Tier 1 capital instruments issued by the

Bank and then outstanding, if applicable), to return

its Fundamental Capital Ratio to the levels of then-

applicable Fundamental Capital Ratio required by

the CNBV in accordance with Section IX, b) of

Annex 1-S of the General Rules applicable to

Mexican Banks or any successor regulation, which

as of the date hereof is, including the Capital

Conservation Buffer, 7 percent plus the amount

required to restore any Countercyclical Capital

Supplement and any Systemically Important Bank

Capital Supplement to the minimum amounts

required under the Mexican Capitalization

Requirements on such Write-Down Date; or (ii) if

any Write-Down of the then-outstanding principal

amount, together with any concurrent pro rata

Write-Down or conversion of any other Tier 2

capital instruments issued by the Bank and the then

outstanding (after taking into account the effect of

the conversion or Write-Down of any loss-absorbing

Tier 1 capital instruments issued by the Bank and

then outstanding, if applicable), would be

insufficient to return the Bank’s Fundamental

Capital Ratio to the aforementioned amount

described in clause (i) above, then the amount

necessary to reduce the then-outstanding principal

amount of each outstanding Note to zero.

As required under the Mexican Capitalization

Requirements, a full Write-Down (whereby the

principal amount of the Notes has been written

down to zero) shall be completed (1) after giving

effect to the Write-Down or conversion of any loss

absorbing Tier 1 capital instruments issued by the

Bank and then outstanding, if applicable, and (2)

before any public funds are contributed or any

public assistance is provided to the Bank in the

terms of Article 148, Section II, Subsections a) and

b) of the Mexican Banking Law, including, among

others, in the form of (i) subscription of shares, (ii)

granting of loans, (iii) payment of the Bank’s

liabilities, (iv) granting of guaranties and (v) the

transfer of assets and liabilities.

PURPOSE OF PRICING SUPPLEMENT

This Pricing Supplement comprises the pricing supplement required for issue and admission to trading on

the exchange regulated market of Euronext Dublin (the “Global Exchange Market”) and for listing on the

Official List of Euronext Dublin of the Notes described herein pursuant to the listing of the

U.S.$10,000,000,000 Medium-Term Note Program of BBVA Bancomer S.A., Institución de Banca

Múltiple, Grupo Financiero BBVA Bancomer.

[Remainder of Page Intentionally Left Blank.]

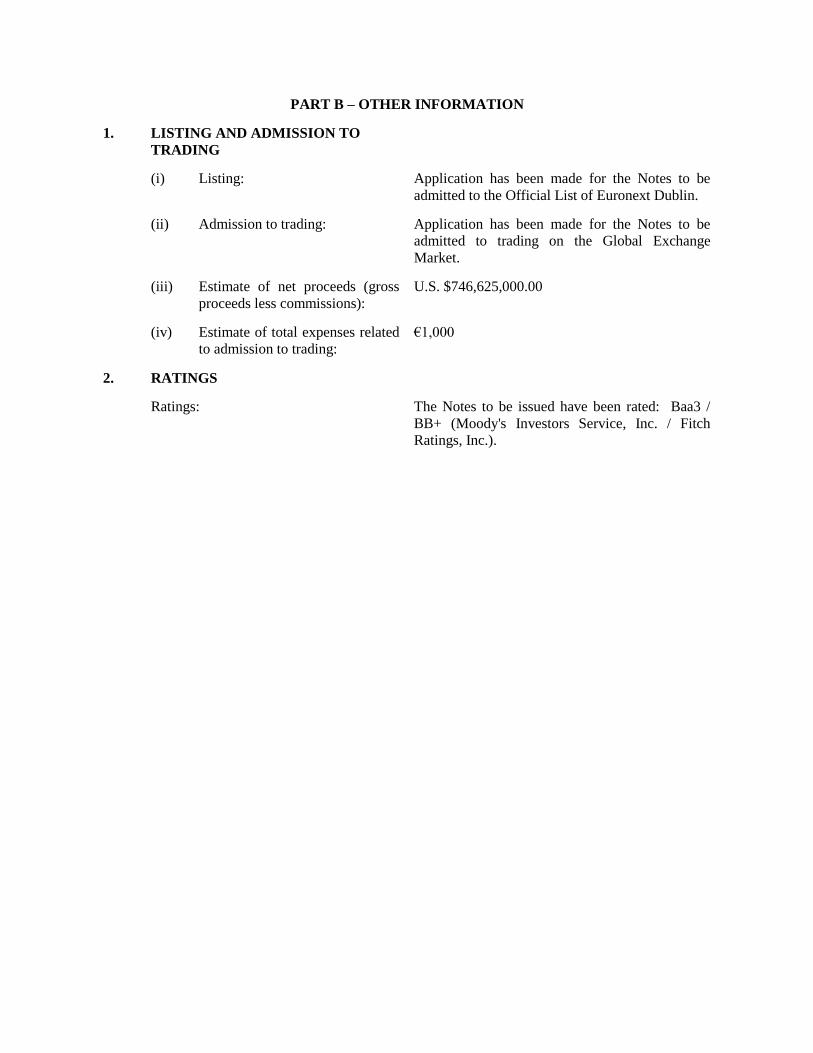

PART B – OTHER INFORMATION

1. LISTING AND ADMISSION TO

TRADING

(i) Listing: Application has been made for the Notes to be

admitted to the Official List of Euronext Dublin.

(ii) Admission to trading: Application has been made for the Notes to be

admitted to trading on the Global Exchange

Market.

(iii) Estimate of net proceeds (gross

proceeds less commissions):

U.S. $746,625,000.00

(iv) Estimate of total expenses related

to admission to trading:

€1,000

2. RATINGS

Ratings: The Notes to be issued have been rated: Baa3 /

BB+ (Moody's Investors Service, Inc. / Fitch

Ratings, Inc.).

3. INTERESTS OF NATURAL AND LEGAL PERSONS INVOLVED IN THE ISSUE

Save for any fees payable to the Dealers, so far as the Issuer is aware, no person involved in the offer of

the Notes has an interest material to the offer. The Dealers and their affiliates have engaged and may in

the future engage in investment banking and/or commercial banking transactions with, and may perform

other services for, the Issuer and its affiliates in the ordinary course of business.

4. USE OF PROCEEDS The Bank intends to use a portion of the net

proceeds to fund the purchase of the Tendered

Notes (as defined below) validly tendered and

accepted for payment in the offers to purchase the

Tendered Notes for cash. The Bank intends to use

any remaining net proceeds to strengthen its capital

ratios and for general corporate purposes.

“Tendered Notes” means up to U.S. $250,000,000

in aggregate principal amount of the Bank’s 7.25%

Non-Cumulative Fixed Rate Subordinated

Non-Preferred Notes due 2020, of which U.S.

$1,000,000,000 aggregate principal amount is

currently outstanding, and up to U.S. $500,000,000

in aggregate principal amount of its 6.500% Fixed

Rate Subordinated Preferred Notes due 2021, of

which U.S. $1,250,000,000 aggregate principal

amount is currently outstanding. The Tender Offers

are being made upon the terms and conditions set

forth in the Bank’s offer to purchase, dated August

28, 2019.

5. YIELD

Indication of yield: 5.875 percent per annum in respect of the Initial

Fixed Rate period.

The yield above is in relation to the Optional Call

Date and is calculated at the Issue Date on the basis

of the Issue Price. It is not an indication of future

yield.

6. OPERATIONAL INFORMATION

(i) ISIN Code: 144A Note: US05533UAG31

Reg. S Note: USP16259AN67

(ii) CUSIP: 144A Note: 05533U AG3

Reg. S Note: P16259 AN6

(iii) Common Code: N/A

(iv) Issuer Legal Entity Identifier

Code:

N/A

(v) Clearing System(s): DTC

Euroclear

Clearstream

(vi) Names and addresses of additional

Agent(s) (if any):

The Bank of New York Mellon will act as trustee,

registrar, transfer agent and paying agent.

240 Greenwich Street, Floor 7 East,

New York, New York 10286,

United States of America

(vii) Delivery: Delivery free of payment

7. DISTRIBUTION

(i) If syndicated, names and

addresses of Dealers and

underwriting commitments:

BBVA Securities Inc.

1345 Avenue of the Americas, 44th Floor

New York, NY 10105

Underwriting commitment: U.S.$ 187,500,000

Goldman Sachs & Co. LLC

200 West Street

New York, New York 10282

Underwriting commitment: U.S.$ 187,500,000

HSBC Securities (USA) Inc.

452 Fifth Avenue

New York, NY 10018

Underwriting commitment: U.S.$ 187,500,000

J.P. Morgan Securities LLC

383 Madison Avenue

New York, New York 10179

Underwriting commitment: U.S.$ 187,500,000

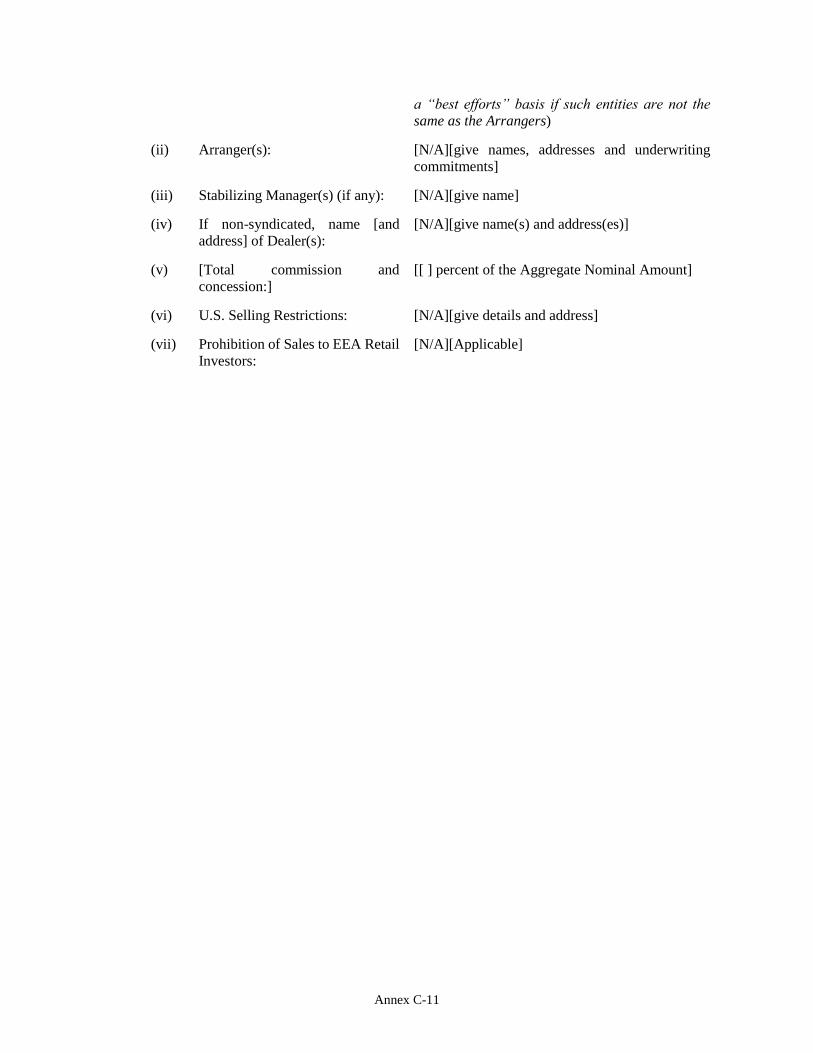

(ii) Arranger(s): N/A

(iii) Stabilizing Manager(s) (if any): N/A

(iv) If non-syndicated, name and

address of Dealer(s):

N/A

(v) Total commission and concession: 0.45 percent of the Aggregate Nominal Amount

(vi) U.S. Selling Restrictions: Reg. S Compliance Category 2, Rule 144A

(vii) Prohibition of Sales to EEA Retail

Investors

Applicable

THE NOTES WILL BE UNSECURED AND WILL NOT BE INSURED OR

GUARANTEED BY ANY OF THE BANK’S SUBSIDIARIES OR AFFILIATES,

INCLUDING OUR PARENT COMPANY OR BY THE SAVINGS PROTECTION

AGENCY (INSTITUTO PARA LA PROTECCIÓN AL AHORRO BANCARIO, OR

“IPAB”) OR ANY OTHER MEXICAN GOVERNMENTAL AGENCY, AND THE NOTES

ARE NOT CONVERTIBLE, BY THEIR TERMS, INTO ANY OF OUR DEBT

SECURITIES, SHARES OR ANY OF OUR EQUITY CAPITAL OR ANY DEBT

SECURITIES, SHARES OR EQUITY CAPITAL OF ANY OF ITS SUBSIDIARIES OR

AFFILIATES. THE NOTES WILL BE GOVERNED BY NEW YORK LAW; HOWEVER,

CERTAIN REGULATORY AND TAX MATTERS AFFECTING THE NOTES WILL BE

GOVERNED BY THE LAWS OF MEXICO AS DESCRIBED UNDER “DESCRIPTION

OF THE NOTES—GOVERNING LAW; CONSENT TO JURISDICTION” IN THE

OFFERING MEMORANDUM.

WE HAVE THE OPTION, BUT NOT THE OBLIGATION, TO REDEEM THE NOTES,

SUBJECT TO CERTAIN CONDITIONS SET OUT IN THE OFFERING

MEMORANDUM, ON THE OPTIONAL CALL DATE (AS DEFINED IN THE

OFFERING MEMORANDUM), OR AT ANY TIME UPON THE OCCURRENCE OF A

WITHHOLDING TAX EVENT (AS DEFINED IN THE OFFERING MEMORANDUM)

OR UPON THE OCCURRENCE OF A SPECIAL EVENT (AS DEFINED IN THE

OFFERING MEMORANDUM) AFFECTING THE NOTES. SEE “DESCRIPTION OF

THE NOTES—OTHER TERMS AND CONDITIONS APPLICABLE TO THE SENIOR

AND SUBORDINATED NOTES—SUBORDINATED NOTES OPTIONAL

REDEMPTION AND SPECIAL EVENT REDEMPTION OF SUBORDINATED NOTES”

AND “—REDEMPTION OF NOTES PRIOR TO MATURITY SOLELY FOR TAXATION

REASONS” IN THE OFFERING MEMORANDUM. PRINCIPAL AND INTEREST ON

THE NOTES WILL BE DEFERRED AND WILL NOT BE PAID UNDER CERTAIN

CIRCUMSTANCES. IF A TRIGGER EVENT (AS DEFINED IN THE OFFERING

MEMORANDUM) OCCURS, THE PRINCIPAL AMOUNT OF THE NOTES WILL BE

WRITTEN DOWN AS DESCRIBED IN THE OFFERING MEMORANDUM. IF A

WRITE-DOWN OCCURS, THE WRITTEN-DOWN PRINCIPAL, AND ANY INTEREST

ACCRUED WITH RESPECT THERETO DURING ANY SUSPENSION PERIOD, WILL

BE CANCELLED. THE DEFERRAL OF INTEREST IN ACCORDANCE WITH THE

PROCEDURES SET FORTH IN THE SUBORDINATED NOTES INDENTURE AND THE

OFFERING MEMORANDUM WILL NOT CONSTITUTE AN EVENT OF DEFAULT

UNDER THE SUBORDINATED NOTES INDENTURE. SEE “DESCRIPTION OF THE

NOTES—TRIGGER EVENT AND WRITE DOWN” IN THE OFFERING

MEMORANDUM. IF A CAPITAL RATIOS EVENT OR A MEXICAN REGULATORY

EVENT (IN EACH CASE, AS DEFINED IN THE OFFERING MEMORANDUM)

OCCURS, WE WILL SUSPEND PAYMENT OF INTEREST ON THE NOTES OR

PAYMENT OF PRINCIPAL AT MATURITY UNTIL THE END OF THE RELATED

SUSPENSION PERIOD (AS DEFINED IN THE OFFERING MEMORANDUM),

SUBJECT TO THE OCCURRENCE OF A WRITE-DOWN IN THE EVENT THAT

DURING SUCH SUSPENSION PERIOD A TRIGGER EVENT SHALL HAVE

OCCURRED. SEE “DESCRIPTION OF THE NOTES—TREATMENT OF INTEREST

AND PRINCIPAL DURING A SUSPENSION PERIOD” IN THE OFFERING

MEMORANDUM.

SUPPLEMENT, DATED AUGUST 28, 2019, to the Base Offering Memorandum, dated August 6, 2019

BBVA Bancomer, S.A.,

Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer,

acting directly or through its Texas Agency

U.S. $10,000,000,000 Medium-Term Note Program

BBVA Bancomer, S.A., Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer, a multi-purpose bank

incorporated in accordance with the laws of the United Mexican States, or Mexico (the “Bank”), acting through its

Texas Agency unless the applicable pricing supplement specifies that the Bank is acting directly (the “Issuer”), has

prepared this supplement (this “Supplement”) to supplement and be read in conjunction with the base offering

memorandum, dated August 6, 2019 (the “Offering Memorandum”), which constitutes listing particulars for the

purposes of listing of Notes on the Global Exchange Market of the Irish Stock Exchange plc trading as Euronext

Dublin (“Euronext Dublin”).

THE NOTES WILL BE UNSECURED AND WILL NOT BE INSURED OR

GUARANTEED BY ANY OF THE BANK’S SUBSIDIARIES OR AFFILIATES,

INCLUDING OUR PARENT COMPANY OR BY THE SAVINGS PROTECTION

AGENCY (INSTITUTO PARA LA PROTECCIÓN AL AHORRO BANCARIO, OR

“IPAB”) OR ANY OTHER MEXICAN GOVERNMENTAL AGENCY, AND THE

SUBORDINATED PREFERRED TIER 2 CAPITAL NOTES ARE NOT CONVERTIBLE,

BY THEIR TERMS, INTO ANY OF OUR DEBT SECURITIES, SHARES OR ANY OF

OUR EQUITY CAPITAL OR ANY DEBT SECURITIES, SHARES OR EQUITY

CAPITAL OF ANY OF ITS SUBSIDIARIES OR AFFILIATES. THE NOTES WILL BE

GOVERNED BY NEW YORK LAW; HOWEVER, CERTAIN REGULATORY AND TAX

MATTERS AFFECTING THE SUBORDINATED PREFERRED TIER 2 CAPITAL

NOTES WILL BE GOVERNED BY THE LAWS OF MEXICO AS DESCRIBED UNDER

“DESCRIPTION OF THE NOTES—GOVERNING LAW; CONSENT TO

JURISDICTION” IN THE OFFERING MEMORANDUM.

The Offering Memorandum does not comprise a prospectus for the purposes of Regulation (EU) 2017/1129 (the

“Prospectus Regulation”). The Offering Memorandum and this Supplement have not been reviewed or approved by

any regulator, which is a competent authority under the Prospectus Directive. Application has been made to Euronext

Dublin for the approval of this document as supplementary listing particulars. Copies of this Supplement and the

Offering Memorandum will be available on the website of Euronext Dublin.

Terms defined in the Offering Memorandum shall have the same meaning when used in this Supplement. To the extent

that there is any inconsistency between any statement in this Supplement and any other statement in the Offering

Memorandum, the statements in this Supplement will prevail.

The purpose of this Supplement is to:

Incorporate by reference into the Offering Memorandum the Unaudited Condensed Consolidated Interim

Financial Statements for the three-month and six-month periods ended June 30, 2019, together with the

independent auditors’ limited review report thereon (the “2Q19 Financial Statements”) and the related

Management’s Discussion and Analysis included herein.

Replace the sentence under sub-section “Significant Change in Financial or Trading Position” of the “General

Information” section of the Offering Memorandum with the following statement:

“There has been no significant change in the financial or trading position of the Bank since June 30, 2019.”

For the avoidance of doubt, if any documents incorporated by reference themselves incorporate any information or

other documents therein, either expressly or implicitly, such information or other documents will not form part of this

Supplement or the Offering Memorandum, except where such information or other documents are specifically

incorporated by reference or attached to this Supplement.

The Bank accepts responsibility for the information contained in this Supplement. To the best of the knowledge and

belief of the Bank (having taken all reasonable care to ensure that such is the case) the information contained in this

Supplement is in accordance with the facts and does not omit anything likely to affect the import of such information.

Except as disclosed in this Supplement, no significant new factor, material mistake or inaccuracy relating to the

information included in the Offering Memorandum has arisen or been noted, as the case may be, since the date of

publication of the Offering Memorandum.

We have not and will not register the Notes under the United States Securities Act of 1933, as amended (the

“Securities Act”), or any securities laws of any state or any other jurisdiction. The Notes may not be offered or

sold within the United States or to U.S. persons, except to qualified institutional buyers in reliance on the

exemption from registration provided by Rule 144A (“Rule 144A”) under the Securities Act and to certain non-

U.S. persons in offshore transactions in reliance on Regulation S (“Regulation S”) under the Securities Act.

You are hereby notified that sellers of the Notes may be relying on the exemption from the provisions of

Section 5 of the Securities Act provided by Rule 144A or any state securities laws. See “Plan of Distribution”

and “Transfer Restrictions” in the Offering Memorandum.

Neither the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores,

or the “CNBV”) nor the U.S. Securities and Exchange Commission, nor any state or foreign securities

commission or regulatory authority, has approved or disapproved of the Notes nor have any of the foregoing

authorities passed upon or endorsed the merits of an offering of the Notes or the accuracy, adequacy or

completeness of this Supplement or the Offering Memorandum. Any representation to the contrary is a

criminal offense.

THE NOTES HAVE NOT BEEN AND WILL NOT BE REGISTERED WITH THE MEXICAN NATIONAL

SECURITIES REGISTRY (REGISTRO NACIONAL DE VALORES, OR “RNV”) MAINTAINED BY THE

CNBV AND, THEREFORE, MAY NOT BE OFFERED OR SOLD PUBLICLY IN MEXICO, EXCEPT THAT

THE NOTES MAY PRIVATELY BE OFFERED OR SOLD TO INVESTORS THAT QUALIFY AS

INSTITUTIONAL OR QUALIFIED INVESTORS IN MEXICO SOLELY PURSUANT TO THE PRIVATE

PLACEMENT EXEMPTION SET FORTH IN ARTICLE 8 OF THE MEXICAN SECURITIES MARKET

LAW (LEY DEL MERCADO DE VALORES) AND REGULATIONS THEREUNDER. WE WILL NOTIFY

AND FILE CERTAIN DOCUMENTATION WITH THE CNBV OF THE TERMS AND CONDITIONS OF

THIS OFFERING OF THE NOTES OUTSIDE OF MEXICO. SUCH NOTICE WILL BE SUBMITTED FOR

INFORMATIONAL PURPOSES ONLY TO THE CNBV TO COMPLY WITH ARTICLE 7, SECOND

PARAGRAPH, OF THE MEXICAN SECURITIES MARKET LAW AND REGULATIONS THEREUNDER.

THE DELIVERY TO, AND RECEIPT OF SUCH NOTICE BY THE CNBV IS NOT A REQUIREMENT FOR

THE VALIDITY OF THE NOTES, AND DOES NOT CONSTITUTE OR IMPLY ANY CERTIFICATION

AS TO THE INVESTMENT QUALITY OF THE NOTES, OUR SOLVENCY, LIQUIDITY OR CREDIT

QUALITY OR THE ACCURACY OR COMPLETENESS OF THE INFORMATION SET FORTH IN THIS

SUPLEMENT OR THE OFFERING MEMORANDUM. THIS SUPLEMENT IS SOLELY OUR

RESPONSIBILITY AND HAS NOT BEEN REVIEWED OR AUTHORIZED BY THE CNBV, AND MAY

NOT BE PUBLICLY DISTRIBUTED IN MEXICO.

PURSUANT TO CIRCULAR 3/2012 ISSUED BY BANCO DE MÉXICO AND PUBLISHED IN THE

FEDERAL OFFICIAL GAZETTE (DIARIO OFICIAL DE LA FEDERACIÓN) ON MARCH 2, 2012, AND AS

AMENDED FROM TIME TO TIME, INCLUDING THE AMENDMENT PUBLISHED ON NOVEMBER 14,

2018, IN THE FEDERAL OFFICIAL GAZETTE THROUGH CIRCULAR 16/2018, NO RELATED PARTY

OF THE ISSUER, AS DEFINED IN ARTICLE 73 OF THE MEXICAN BANKING LAW, MAY ACQUIRE,

DIRECTLY OR INDIRECTLY, ANY NOTES TO BE ISSUED PURSUANT TO THIS SUPPLEMENT.

FOR SUBORDINATED NOTES ONLY:

WE HAVE THE OPTION, BUT NOT THE OBLIGATION, TO REDEEM THE

NOTES, SUBJECT TO CERTAIN CONDITIONS SET OUT IN THE OFFERING

MEMORANDUM, ON THE OPTIONAL CALL DATE (AS DEFINED IN THE

OFFERING MEMORANDUM), OR AT ANY TIME UPON THE OCCURRENCE

OF A WITHHOLDING TAX EVENT (AS DEFINED IN THE OFFERING

MEMORANDUM) OR UPON THE OCCURRENCE OF A SPECIAL EVENT (AS

DEFINED IN THE OFFERING MEMORANDUM) AFFECTING THE NOTES.

SEE “DESCRIPTION OF THE NOTES—OTHER TERMS AND CONDITIONS

APPLICABLE TO THE SENIOR AND SUBORDINATED NOTES—

SUBORDINATED NOTES OPTIONAL REDEMPTION AND SPECIAL EVENT

REDEMPTION OF SUBORDINATED NOTES” AND “—REDEMPTION OF

NOTES PRIOR TO MATURITY SOLELY FOR TAXATION REASONS” IN THE

OFFERING MEMORANDUM. PRINCIPAL AND INTEREST ON THE NOTES

WILL BE DEFERRED AND WILL NOT BE PAID UNDER CERTAIN

CIRCUMSTANCES. IF A TRIGGER EVENT (AS DEFINED IN THE OFFERING

MEMORANDUM) OCCURS, THE PRINCIPAL AMOUNT OF THE NOTES

WILL BE WRITTEN DOWN AS DESCRIBED IN THE OFFERING

MEMORANDUM. IF A WRITE-DOWN OCCURS, THE WRITTEN-DOWN

PRINCIPAL, AND ANY INTEREST ACCRUED WITH RESPECT THERETO

DURING ANY SUSPENSION PERIOD, WILL BE CANCELLED. THE

DEFERRAL OF INTEREST IN ACCORDANCE WITH THE PROCEDURES SET

FORTH IN THE SUBORDINATED NOTES INDENTURE AND THE OFFERING

MEMORANDUM WILL NOT CONSTITUTE AN EVENT OF DEFAULT UNDER

THE SUBORDINATED NOTES INDENTURE. SEE “DESCRIPTION OF THE

NOTES—CERTAIN TERMS AND CONDITIONS APPLICABLE TO

SUBORDINATED NOTES—TRIGGER EVENT AND WRITE-DOWN” IN THE

OFFERING MEMORANDUM. IF A CAPITAL RATIOS EVENT OR A MEXICAN

REGULATORY EVENT (IN EACH CASE, AS DEFINED IN THE OFFERING

MEMORANDUM) OCCURS, WE WILL SUSPEND PAYMENT OF INTEREST

ON THE NOTES OR PAYMENT OF PRINCIPAL AT MATURITY UNTIL THE

END OF THE RELATED SUSPENSION PERIOD (AS DEFINED IN THE

OFFERING MEMORANDUM), SUBJECT TO THE OCCURRENCE OF A

WRITE-DOWN IN THE EVENT THAT DURING SUCH SUSPENSION PERIOD

A TRIGGER EVENT SHALL HAVE OCCURRED. SEE “DESCRIPTION OF THE

NOTES—CERTAIN TERMS AND CONDITIONS APPLICABLE TO

SUBORDINATED NOTES—TREATMENT OF INTEREST AND PRINCIPAL

DURING A SUSPENSION PERIOD” IN THE OFFERING MEMORANDUM.

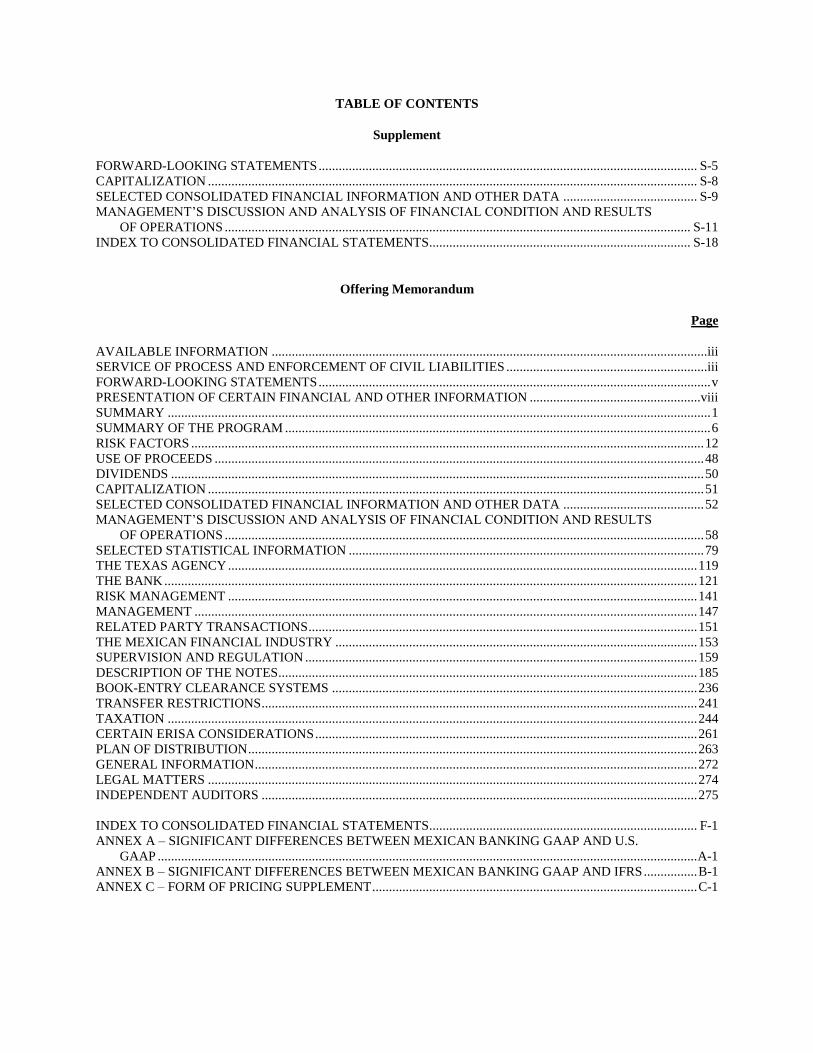

TABLE OF CONTENTS

Supplement

FORWARD-LOOKING STATEMENTS ................................................................................................................. S-5 CAPITALIZATION .................................................................................................................................................. S-8 SELECTED CONSOLIDATED FINANCIAL INFORMATION AND OTHER DATA ........................................ S-9 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS

OF OPERATIONS ........................................................................................................................................... S-11 INDEX TO CONSOLIDATED FINANCIAL STATEMENTS .............................................................................. S-18

Offering Memorandum

Page

AVAILABLE INFORMATION ..................................................................................................................................iii

SERVICE OF PROCESS AND ENFORCEMENT OF CIVIL LIABILITIES ............................................................iii

FORWARD-LOOKING STATEMENTS ..................................................................................................................... v

PRESENTATION OF CERTAIN FINANCIAL AND OTHER INFORMATION ...................................................viii

SUMMARY .................................................................................................................................................................. 1

SUMMARY OF THE PROGRAM ............................................................................................................................... 6

RISK FACTORS ......................................................................................................................................................... 12

USE OF PROCEEDS .................................................................................................................................................. 48

DIVIDENDS ............................................................................................................................................................... 50

CAPITALIZATION .................................................................................................................................................... 51

SELECTED CONSOLIDATED FINANCIAL INFORMATION AND OTHER DATA .......................................... 52

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS

OF OPERATIONS ............................................................................................................................................... 58

SELECTED STATISTICAL INFORMATION .......................................................................................................... 79

THE TEXAS AGENCY ............................................................................................................................................ 119

THE BANK ............................................................................................................................................................... 121

RISK MANAGEMENT ............................................................................................................................................ 141

MANAGEMENT ...................................................................................................................................................... 147

RELATED PARTY TRANSACTIONS .................................................................................................................... 151

THE MEXICAN FINANCIAL INDUSTRY ............................................................................................................ 153

SUPERVISION AND REGULATION ..................................................................................................................... 159

DESCRIPTION OF THE NOTES ............................................................................................................................. 185

BOOK-ENTRY CLEARANCE SYSTEMS ............................................................................................................. 236

TRANSFER RESTRICTIONS .................................................................................................................................. 241

TAXATION .............................................................................................................................................................. 244

CERTAIN ERISA CONSIDERATIONS .................................................................................................................. 261

PLAN OF DISTRIBUTION ...................................................................................................................................... 263

GENERAL INFORMATION .................................................................................................................................... 272

LEGAL MATTERS .................................................................................................................................................. 274

INDEPENDENT AUDITORS .................................................................................................................................. 275

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS ................................................................................ F-1

ANNEX A – SIGNIFICANT DIFFERENCES BETWEEN MEXICAN BANKING GAAP AND U.S.

GAAP ................................................................................................................................................................. A-1

ANNEX B – SIGNIFICANT DIFFERENCES BETWEEN MEXICAN BANKING GAAP AND IFRS ................ B-1

ANNEX C – FORM OF PRICING SUPPLEMENT ................................................................................................. C-1

S-5

FORWARD-LOOKING STATEMENTS

Certain statements contained in this Supplement relating to our plans, forecasts and expectations regarding future

events, strategies and projections are estimates. Examples of such forward-looking statements include, but are not

limited to: (i) statements regarding our results of operations and financial position, (ii) statements of plans, objectives

or goals, including those related to our operations, and (iii) statements of assumptions underlying such statements.

Words such as “may,” “might,” “will,” “would,” “shall,” “should,” “consider,” “can,” “could,” “believe,” “anticipate,”

“continue,” “expect,” “estimate,” “plan,” “intend,” “assume,” “foresee,” “seeks,” “predict,” “project,” “potential,” or

the negative of these terms, and other similar terms are used in this Supplement to identify such forward-looking

statements. Forward-looking statements included in this Supplement are based on our current expectations and

projections related to future events and trends that affect or would affect our business.

Forward-looking statements include risks, uncertainties and assumptions, since these refer to future events and,

therefore, do not represent any guarantee of future results. Therefore, our financial condition, results of operations,

strategies, competitive position and market environment may significantly differ from our estimates as a result of a

number of factors, including, but not limited to:

changes in requirements to make contributions to, or for the receipt of support from programs organized by,

the Mexican government;

financing plans and limitations on our access to sources of financing on competitive terms;

changes in general economic, business, trade, social, political or other conditions in Mexico, the United States

or elsewhere;

the ability or willingness of our customers to meet their payment obligations;

the monetary, foreign exchange and interest rate policies of Banco de México;

possible disruptions to commercial activities due to natural and man-made disasters, including health

epidemics, weather events, terrorist activities and armed conflicts;

material changes to, or withdrawals from, or renegotiations of free trade agreements to which Mexico is a

party, including the implementation of the new North American Free Trade Agreement;

competition in the banking and financial services industry in Mexico;

profitability of our businesses;

changes in exchange rates, market interest rates or the rate of inflation;

credit and other risks of lending, such as increases in default of borrowers;

limitations on our access to sources of financing on competitive terms;

failure to meet capital or other requirements;

additional capital requirements relating to our classification as a systemically important local bank and to

countercyclical risks;

limitations on our ability to freely determine interest rates, fees and commissions;

changes in reserve or capital requirements, changes in the laws or regulations applicable thereto, or the

interpretation of how such reserve or capital requirements are to be calculated;

S-6

our inability to hedge against market risks, including but not limited, to interest rate and exchange rate

movements;

changes in requirements to make contributions to or for the receipt of support from programs organized by

the Mexican government;

inability to timely and duly enforce our claims on collateral provided by borrowers;

changes in our or Mexico’s domestic and international credit ratings;

changes in regulations relating to the products we offer or otherwise;

changes in capital markets in general that may affect policies or attitudes towards investing in Mexico or

securities issued by companies in Mexico;

any failure or weakness in our operating controls or procedures or our risk management policies;

changes in consumer spending and saving habits;

a deterioration of labor relations with our employees;

our ability to implement new technologies and to safeguard against cyber-attacks and other breaches of our

information technology systems;

interruptions or failures in our technology systems;

actions taken by the Mexican Antitrust Commission (Comisión Federal de Competencia Económica) or the

Ministry of Finance and Public Credit (Secretaría de Hacienda y Crédito Público) with respect to our

business and the Mexican banking industry generally;

any adverse administrative or legal proceedings against us;

any failure to detect money laundering or other illegal or improper activities;

the impact of acquisitions and divestitures;

restrictions on foreign currency convertibility and remittance outside of Mexico;

the effect of changes in accounting principles, new legislation, intervention by regulatory authorities,

government directives or monetary or fiscal policy in Mexico; and

the other factors discussed under “Risk Factors” in the Offering Memorandum.

Therefore, our actual performance may be adversely affected and may significantly differ from the expectations set

forth in these forward-looking statements, which do not represent a guarantee of our future performance. Accordingly,

you should not place undue reliance on the estimates and forward-looking statements included in this Supplement to

make an investment decision.

Additional factors affecting our business may arise periodically and we cannot predict such factors, nor can we assess

the impact of all these factors on our business or the extent to which such factors or combination of factors could cause

our results to materially differ from those contained in any forward-looking statement. Although we consider the

plans, intentions, expectations and estimates reflected in, or suggested by, forward-looking statements included in this

Supplement to be reasonable, we cannot provide any assurance that our plans, intentions, expectations and estimates

S-7

will be achieved. Additionally, historical trends in our statements should not be interpreted as a guarantee that these

trends will continue in the future.

Forward-looking statements included herein are made only as of the date of this Supplement. Except as required by

law, we do not undertake any obligation to update any forward-looking statements to reflect events or circumstances

after the date hereof or to reflect the occurrence of anticipated or unanticipated events or circumstances.

S-8

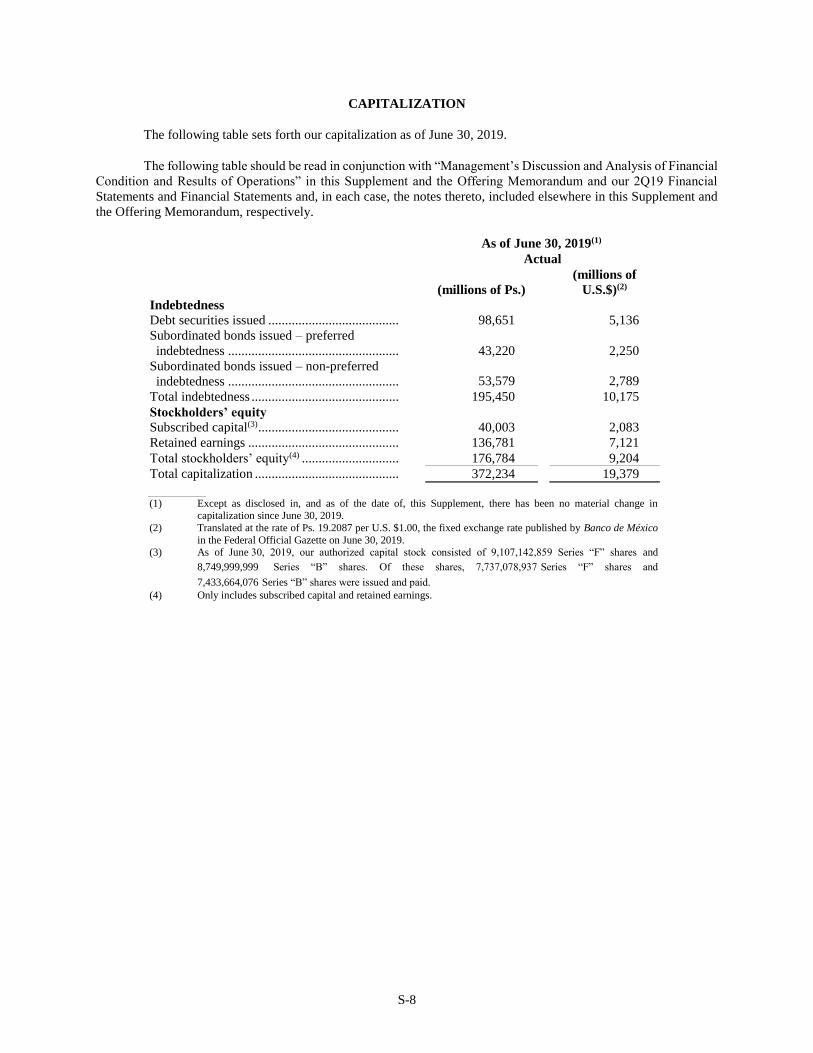

CAPITALIZATION

The following table sets forth our capitalization as of June 30, 2019.

The following table should be read in conjunction with “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” in this Supplement and the Offering Memorandum and our 2Q19 Financial

Statements and Financial Statements and, in each case, the notes thereto, included elsewhere in this Supplement and

the Offering Memorandum, respectively.

As of June 30, 2019(1)

Actual

(millions of Ps.)

(millions of

U.S.$)(2)

Indebtedness

Debt securities issued ....................................... 98,651 5,136

Subordinated bonds issued – preferred

indebtedness ................................................... 43,220 2,250

Subordinated bonds issued – non-preferred

indebtedness ................................................... 53,579 2,789

Total indebtedness ............................................ 195,450 10,175

Stockholders’ equity

Subscribed capital(3) .......................................... 40,003 2,083

Retained earnings ............................................. 136,781 7,121

Total stockholders’ equity(4) ............................. 176,784 9,204

Total capitalization ........................................... 372,234 19,379

(1) Except as disclosed in, and as of the date of, this Supplement, there has been no material change in capitalization since June 30, 2019.

(2) Translated at the rate of Ps. 19.2087 per U.S. $1.00, the fixed exchange rate published by Banco de México

in the Federal Official Gazette on June 30, 2019. (3) As of June 30, 2019, our authorized capital stock consisted of 9,107,142,859 Series “F” shares and

8,749,999,999 Series “B” shares. Of these shares, 7,737,078,937 Series “F” shares and

7,433,664,076 Series “B” shares were issued and paid.

(4) Only includes subscribed capital and retained earnings.

S-9

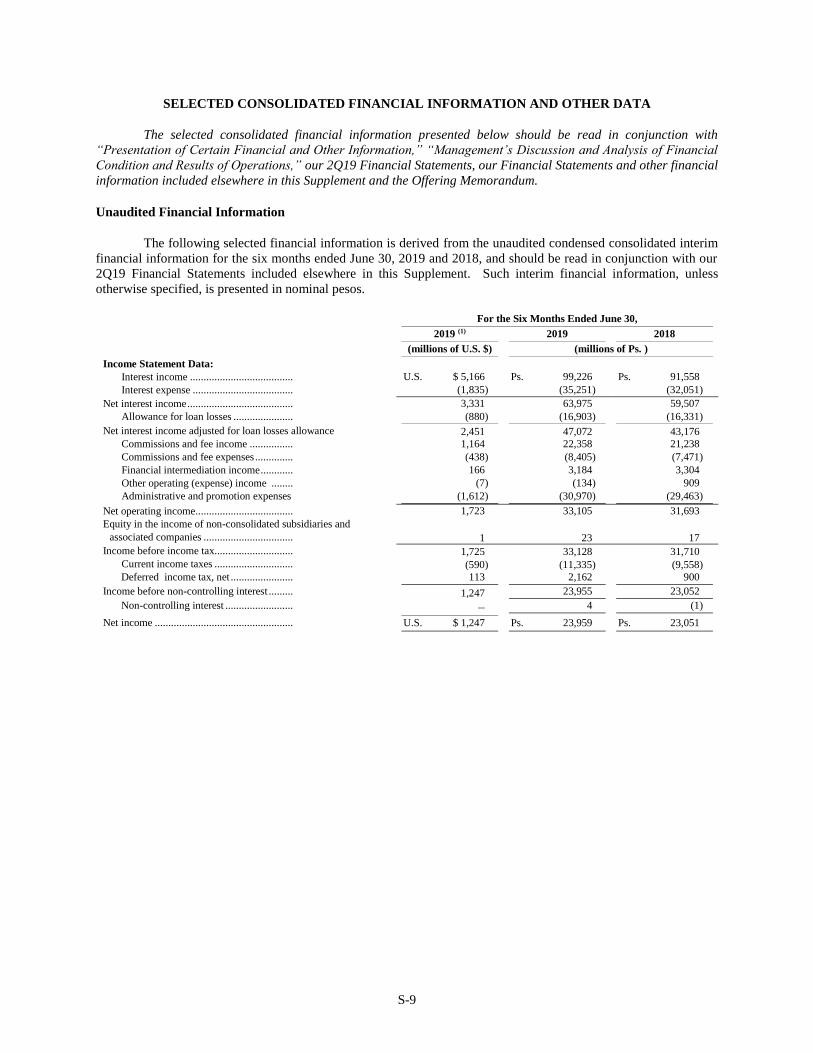

SELECTED CONSOLIDATED FINANCIAL INFORMATION AND OTHER DATA

The selected consolidated financial information presented below should be read in conjunction with

“Presentation of Certain Financial and Other Information,” “Management’s Discussion and Analysis of Financial

Condition and Results of Operations,” our 2Q19 Financial Statements, our Financial Statements and other financial

information included elsewhere in this Supplement and the Offering Memorandum.

Unaudited Financial Information

The following selected financial information is derived from the unaudited condensed consolidated interim

financial information for the six months ended June 30, 2019 and 2018, and should be read in conjunction with our

2Q19 Financial Statements included elsewhere in this Supplement. Such interim financial information, unless

otherwise specified, is presented in nominal pesos.

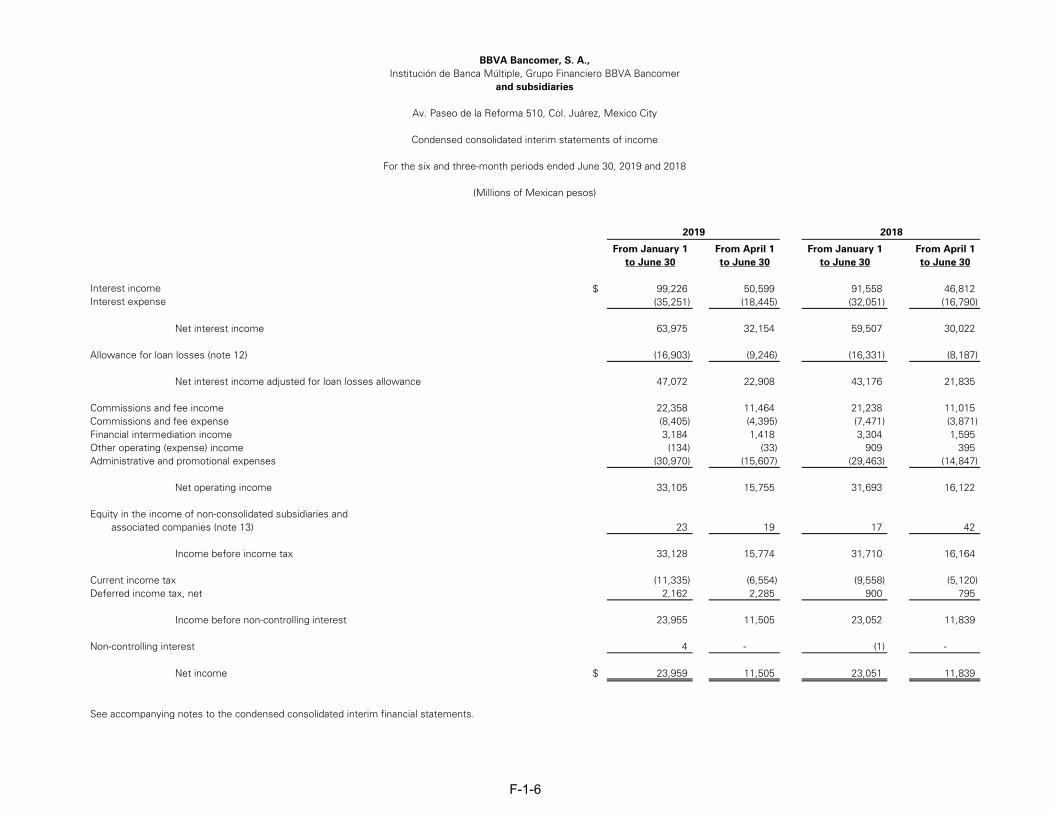

For the Six Months Ended June 30,

2019 (1) 2019 2018

(millions of U.S. $) (millions of Ps. )

Income Statement Data:

Interest income ...................................... U.S. $ 5,166 Ps. 99,226 Ps. 91,558

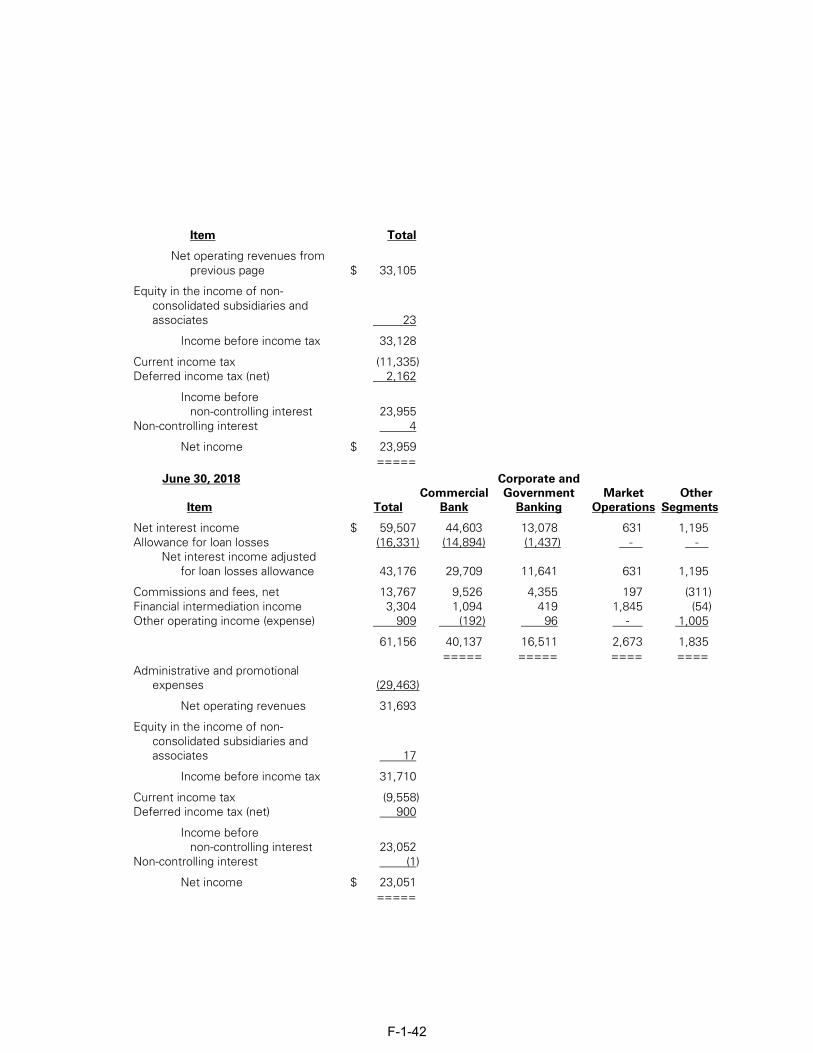

Interest expense ..................................... (1,835) (35,251) (32,051)

Net interest income ....................................... 3,331 63,975 59,507

Allowance for loan losses ...................... (880) (16,903) (16,331)

Net interest income adjusted for loan losses allowance 2,451 47,072 43,176

Commissions and fee income ................ 1,164 22,358 21,238

Commissions and fee expenses .............. (438) (8,405) (7,471)

Financial intermediation income ............ 166 3,184 3,304

Other operating (expense) income ........ (7) (134) 909

Administrative and promotion expenses (1,612) (30,970) (29,463)

Net operating income .................................... 1,723 33,105 31,693

Equity in the income of non-consolidated subsidiaries and

associated companies ................................. 1 23 17

Income before income tax............................. 1,725 33,128 31,710

Current income taxes ............................. (590) (11,335) (9,558)

Deferred income tax, net ....................... 113 2,162 900

Income before non-controlling interest ......... 1,247 23,955 23,052

Non-controlling interest ......................... – 4 (1)

Net income ................................................... U.S. $ 1,247 Ps. 23,959 Ps. 23,051

S-10

As of June 30,(1) As of December 31,(1)

2019(2) 2019 2018

(millions of U.S. $

except for percentages) (millions of Ps., except for percentages)

Balance Sheet Data:

Cash and cash equivalents ............................. 11,562 222,087 232,851

Margin Accounts ........................................... 672 12,912 10,548

Investment in securities ................................. 22,592 433,963 410,261

Loan portfolio ............................................... 62,360 1,197,858 1,163,593

Allowance for loan losses ............................. (1,769) (33,981) (31,811)

Deferred income tax and ESPS, net............... 953 18,308 16,667

All other assets .............................................. 13,283 255,144 266,150

Total assets ......................................................... U.S. $ 109,653 Ps. 2,106,291 Ps. 2,068,259

Total funding(3) ................................................... 71,389 1,371,289 1,317,779

Deposit funding (excluding debt securities issued) 60,379 1,159,805 1,112,727

Debt securities issued ................................... 5,136 98,651 88,162

Subordinated bonds issued ............................ 5,039 96,799 99,029

Banks and other borrowings .......................... 835 16,034 17,861

All other liabilities ........................................ 27,646 531,040 556,257

Total liabilities .................................................... U.S. $ 99,035 Ps. 1,902,329 Ps. 1,874,036

Total stockholders’ equity ................................... U.S. $ 10,618 Ps. 203,962 Ps. 194,223

Profitability and Efficiency:

Return on average total assets(4) .......................... – 2.3% 2.3%

Return on average stockholders’ equity(5) ........... – 24.1% 24.9%

Net interest margin on average total assets(6) ...... – 6.1% 6.1%

Efficiency ratio(7) ................................................ – 38.25% 38.24%

Capitalization:

Stockholders’ equity as a percentage of total assets – 9.68% 9.39%

Tier 1 Capital as a percentage of risk-weighted assets – 11.86% 12.44%

Total Capital as a percentage of risk-weighted assets – 14.17% 15.27%

Credit Quality Data:

Total current loan portfolio ................................. 61,079 1,173,256 1,140,319

Total past due loan portfolio ............................... 1,281 24,602 23,274

Total loans .......................................................... 62,360 1,197,858 1,163,593

Loans graded “C,” “D” and “E” .......................... 4,126 79,248 72,965

Allowance for loan losses ................................... (1,769) (33,981) (31,811)

Loan Recovery and Write-offs:

Past due loans – average balance(8) ..................... 1,208 23,196 23,010

Past due loans written-off ................................... 726

13,943 29,847

Recoveries in respect of past due loans ............... (37) (709) (1,538)

Recovered amounts as a percentage of average

past due loans .................................................. – 3.06% 6.68%

(1) Figures are as of such date, other than the Profitability and Efficiency Data, which reflect the six months and year ended periods ending on

such date.

(2) Translated at the rate of Ps. 19.2087 per U.S. $1.00, the fixed exchange rate published by Banco de México in the Federal Official Gazette on

June 30, 2019.

(3) Includes Deposit funding (excluding debt securities issued), Debt securities issued, Subordinated bonds issued and Banks and other

borrowings.

(4) Calculated by dividing net income by average total assets, based on beginning- and end-of-period balances. For the June 30 period, net

income is determined on an annualized basis.

(5) Calculated by dividing net income by average stockholders’ equity, based on beginning- and end-of-period balances. For the June 30 period,

net income is determined on an annualized basis.

(6) Represents net interest income divided by average total assets. Average total assets are determined based on beginning- and end-of-period

balances. For the June 30 period, net interest income is determined on an annualized basis.

(7) Efficiency ratio is equal to total non-interest expense as a percentage of the aggregate of net interest income and non-interest income (commission and fees, plus trading income, plus other operating income less administrative and promotional expenses). For this purpose, net

interest income and non-interest income are calculated before provision for loan losses.

(8) Calculated on an annualized basis based on the average of the beginning- and end-of-period balances.

S-11

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

The financial information presented in this section should be read in conjunction with the our Financial

Statements included elsewhere in this Supplement and the Offering Memorandum, as well as the Management’s

Discussion and Analysis of Financial Condition and Results of Operations in the Offering Memorandum. Our

Financial Statements have been prepared in accordance with Mexican Banking GAAP, which differs in significant

respects from U.S. GAAP and IFRS. For a discussion of significant differences between Mexican Banking GAAP and

U.S. GAAP and Mexican Banking GAAP and IFRS, see “Annex A—Significant Differences Between Mexican Banking

GAAP and U.S. GAAP” and “Annex B—Significant Differences Between Mexican Banking GAAP and IFRS,”

respectively, in the Offering Memorandum. No reconciliation of any of our Financial Statements to U.S. GAAP has

been prepared for this Supplement or the Offering Memorandum. Any such reconciliation could result in material

quantitative differences. See “Presentation of Certain Financial and Other Information” in the Offering

Memorandum.

Dividends

We paid dividends of Ps. 15,754 million for the six months ended June 30, 2019. For further information

regarding our dividends, see “Dividends” in the Offering Memorandum.

Results of Operations

The interim financial information presented in this section for the six months ended June 30, 2019 and 2018

has been derived from, and should be read in conjunction with, our 2Q19 Financial Statements and the notes thereto

included elsewhere in this Supplement. Such interim financial information, unless otherwise specified, is presented

in nominal pesos.

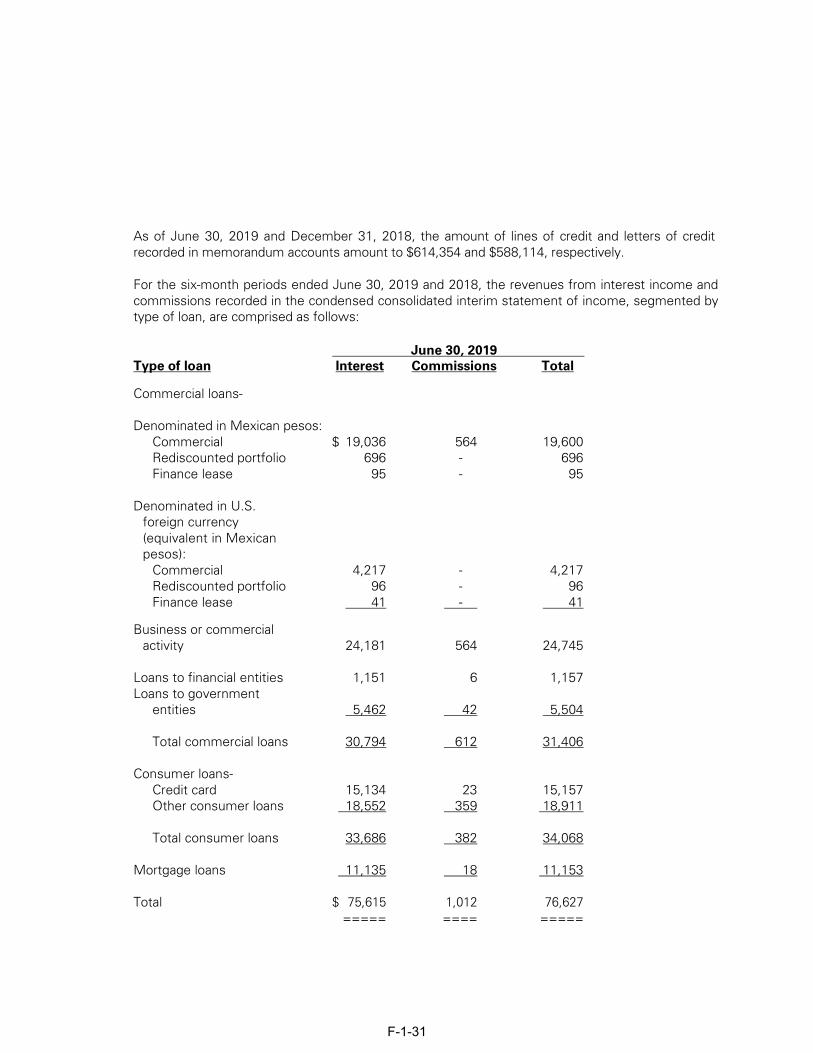

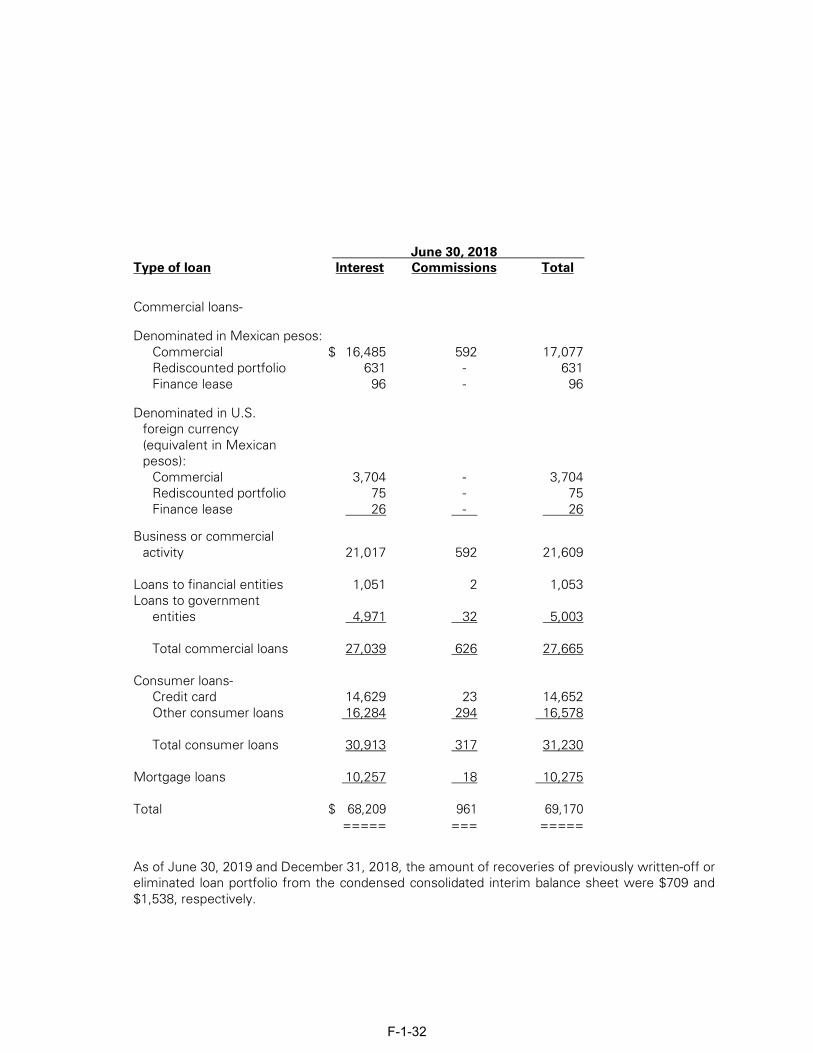

Net Interest Income

The following table sets forth the components of our net interest income:

For the Six Months Ended June 30,

2019 2018

(millions of Ps.)

Interest Income:

Interest and fees on loans ..................................................... 75,615 68,210

Interest on securities ............................................................ 17,681 18,171

Interest on cash and due from banks .................................... 2,734 2,378 Interest on repurchase agreements and securities lending .... 1,529 776

Interest on margin accounts ................................................. 128 257

Fees charged on initial loan ................................................. 1,012 961 Other ........................................................................................ 527 805

Total interest income ............................................................. 99,226 91,558

Interest Expense: Interest on demand deposits ................................................. 5,660 4,669

Interest on time deposits ...................................................... 8,412 6,357

Bank bonds .......................................................................... 3,272 2,836 Interest on interbank loans and loans from other entities ..... 846 911

Interest on subordinated debentures ..................................... 3,644 2,763

Interest on repurchase agreements and securities lending .... 12,601 13,626 Other .................................................................................... 816 889

Total interest expense ............................................................ 35,251 32,051

Financial margin .................................................................... 63,975 59,507

Financial margin for the six months ended June 30, 2019, totaled Ps. 63,975 million, an increase of 7.5%,

compared to Ps. 59,507 million for the six months ended June 30, 2018. This result was due primarily to a change in

the composition in the lending portfolio, as consumer loans grew at a higher rate than commercial loans.

S-12

Interest Income

Interest income was Ps. 99,226 million for the six months ended June 30, 2019, compared to Ps. 91,558

million for the six months ended June 30, 2018, an increase of Ps. 7,668 million, or 8.4%. This increase was primarily

the result of higher credit volumes in our consumer and mortgage lending portfolios.

Interest and fees on loans were Ps. 75,615 million for the six months ended June 30, 2019, compared to

Ps. 68,210 million for the six months ended June 30, 2018, an increase of Ps. 7,405 million, or 10.9%. This increase

was primarily attributable to an increase in the average volume of loans during the six months ended June 31, 2019,

especially in our consumer and mortgage lending portfolios, which increased by 8.7% and 10.2%, respectively, as

compared to the same period of 2018.

Interest on securities was Ps. 17,681 million for the six months ended June 30, 2019, compared to Ps. 18,171

million for the six months ended June 30, 2018, a decrease of Ps. 490 million, or 2.7%, resulting from a more volatile

environment in the financial markets compared to the same period of the previous year.

Interest on repurchase agreements and securities lending was Ps. 1,529 million for the six months ended June

30, 2019, compared to Ps. 776 million for the six months ended June 30, 2018, an increase of Ps. 753 million, or

97.0%, due to higher interest rates compared to the same period of 2018.

Interest Expense

Interest expense was Ps. 35,251 million for the six months ended June 30, 2019, compared to Ps. 32,051

million for the six months ended June 30, 2018, an increase of Ps. 3,200 million, or 10.0%. This increase was primarily

attributable to higher deposit volumes and interest rates.

Interest on demand deposits, time deposits and bank bonds was Ps. 17,344 million for the six months ended

June 30, 2019, compared to Ps. 13,862 million for the six months ended June 30, 2018, an increase of Ps.

3,482 million, or 25.1%. This increase was primarily attributable to an increase in the volume of deposits, a change

in the deposit mix from demand deposits to time deposits and higher interest rates applicable to bank bonds.

Allowance for Loan Losses

The allowance for loan losses charged against earnings was Ps. 16,903 million for the six months ended June

30, 2019, compared to Ps. 16,331 million for the six months ended June 30, 2018, an increase of Ps. 572 million, or

3.5%. This increase was primarily due to the increase in the loan portfolio and higher growth in retail loans, which

require a higher provision for loan losses than commercial loans.

S-13

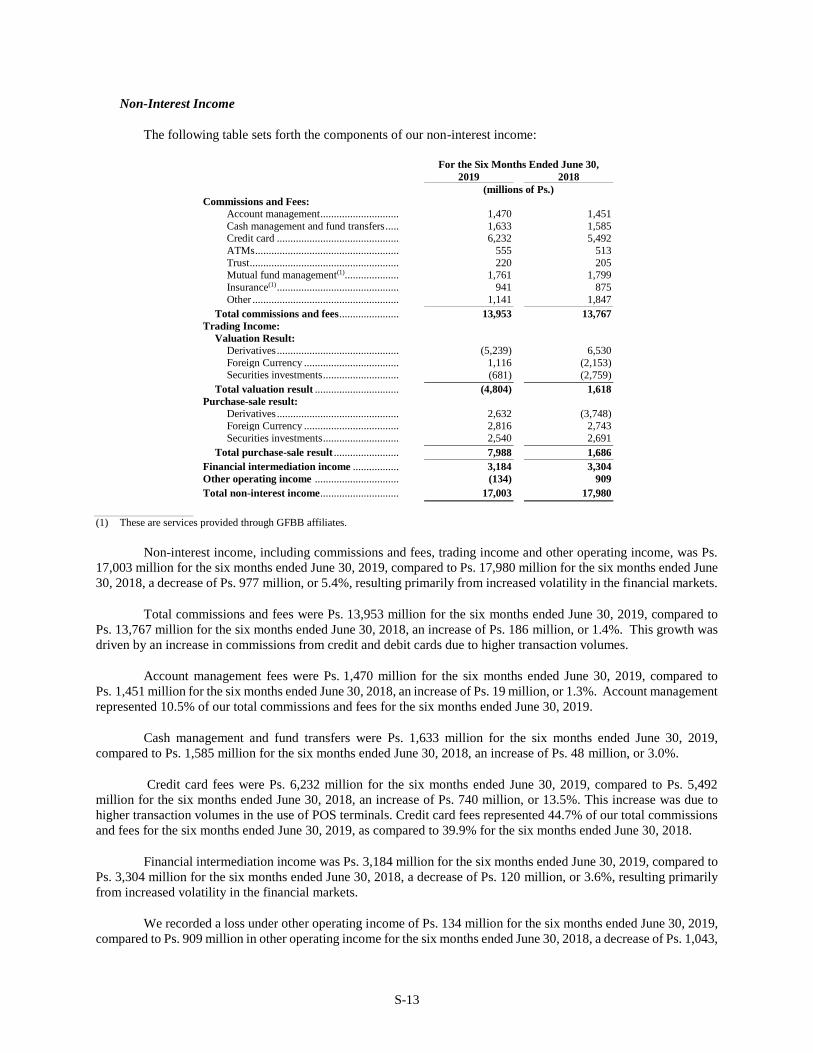

Non-Interest Income

The following table sets forth the components of our non-interest income:

For the Six Months Ended June 30,

2019 2018

(millions of Ps.)

Commissions and Fees:

Account management ............................. 1,470 1,451

Cash management and fund transfers ..... 1,633 1,585 Credit card ............................................. 6,232 5,492

ATMs ..................................................... 555 513

Trust ....................................................... 220 205 Mutual fund management(1) .................... 1,761 1,799

Insurance(1) ............................................. 941 875

Other ...................................................... 1,141 1,847

Total commissions and fees ...................... 13,953 13,767

Trading Income:

Valuation Result:

Derivatives ............................................. (5,239) 6,530

Foreign Currency ................................... 1,116 (2,153) Securities investments ............................ (681) (2,759)

Total valuation result ............................... (4,804) 1,618

Purchase-sale result:

Derivatives ............................................. 2,632 (3,748) Foreign Currency ................................... 2,816 2,743

Securities investments ............................ 2,540 2,691

Total purchase-sale result ........................ 7,988 1,686

Financial intermediation income ................. 3,184 3,304

Other operating income ............................... (134) 909

Total non-interest income ............................. 17,003 17,980

(1) These are services provided through GFBB affiliates.

Non-interest income, including commissions and fees, trading income and other operating income, was Ps.

17,003 million for the six months ended June 30, 2019, compared to Ps. 17,980 million for the six months ended June

30, 2018, a decrease of Ps. 977 million, or 5.4%, resulting primarily from increased volatility in the financial markets.

Total commissions and fees were Ps. 13,953 million for the six months ended June 30, 2019, compared to

Ps. 13,767 million for the six months ended June 30, 2018, an increase of Ps. 186 million, or 1.4%. This growth was

driven by an increase in commissions from credit and debit cards due to higher transaction volumes.

Account management fees were Ps. 1,470 million for the six months ended June 30, 2019, compared to

Ps. 1,451 million for the six months ended June 30, 2018, an increase of Ps. 19 million, or 1.3%. Account management

represented 10.5% of our total commissions and fees for the six months ended June 30, 2019.

Cash management and fund transfers were Ps. 1,633 million for the six months ended June 30, 2019,

compared to Ps. 1,585 million for the six months ended June 30, 2018, an increase of Ps. 48 million, or 3.0%.

Credit card fees were Ps. 6,232 million for the six months ended June 30, 2019, compared to Ps. 5,492

million for the six months ended June 30, 2018, an increase of Ps. 740 million, or 13.5%. This increase was due to

higher transaction volumes in the use of POS terminals. Credit card fees represented 44.7% of our total commissions

and fees for the six months ended June 30, 2019, as compared to 39.9% for the six months ended June 30, 2018.

Financial intermediation income was Ps. 3,184 million for the six months ended June 30, 2019, compared to

Ps. 3,304 million for the six months ended June 30, 2018, a decrease of Ps. 120 million, or 3.6%, resulting primarily

from increased volatility in the financial markets.

We recorded a loss under other operating income of Ps. 134 million for the six months ended June 30, 2019,

compared to Ps. 909 million in other operating income for the six months ended June 30, 2018, a decrease of Ps. 1,043,

S-14

or 114.7%, primarily related to a gain of Ps. 777.4 million on the sale of a real estate property recorded during the six

months ended June 30, 2018, and to our doubling our contribution to Fundación BBVA Bancomer, A.C. in the six

months ended June 30, 2019.

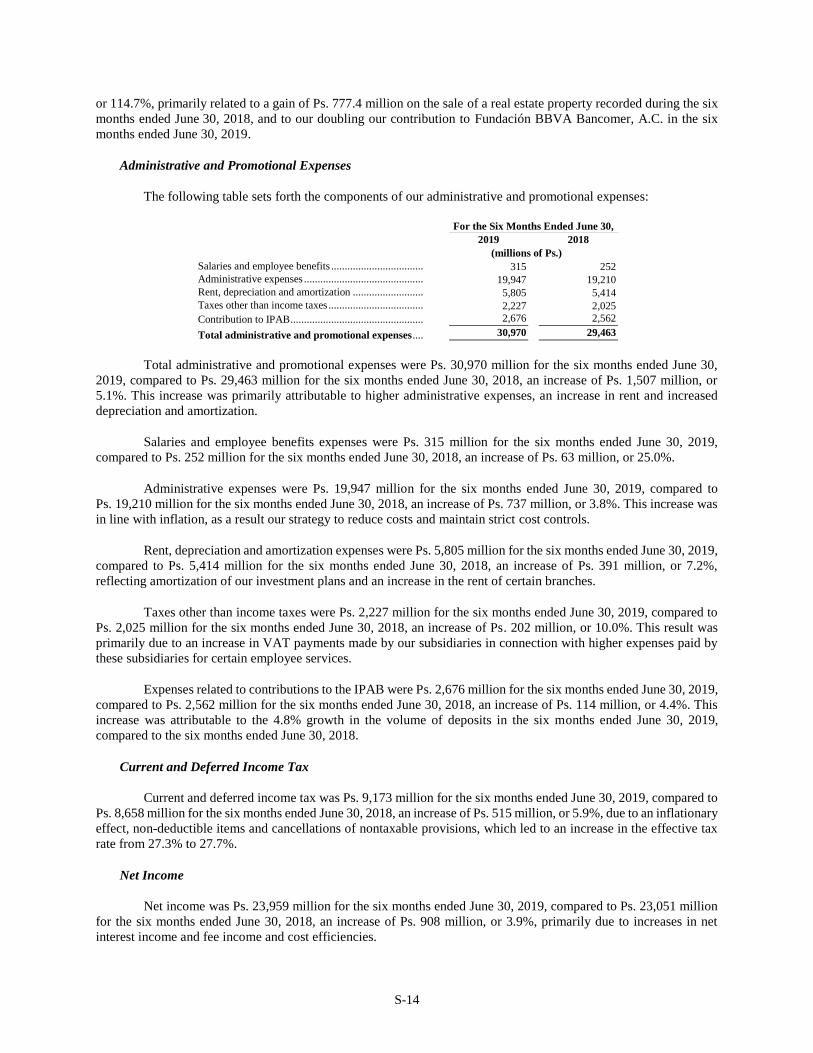

Administrative and Promotional Expenses

The following table sets forth the components of our administrative and promotional expenses:

For the Six Months Ended June 30,

2019 2018

(millions of Ps.)

Salaries and employee benefits .................................. 315 252

Administrative expenses ............................................ 19,947 19,210

Rent, depreciation and amortization .......................... 5,805 5,414

Taxes other than income taxes ................................... 2,227 2,025

Contribution to IPAB ................................................. 2,676 2,562

Total administrative and promotional expenses .... 30,970 29,463

Total administrative and promotional expenses were Ps. 30,970 million for the six months ended June 30,

2019, compared to Ps. 29,463 million for the six months ended June 30, 2018, an increase of Ps. 1,507 million, or

5.1%. This increase was primarily attributable to higher administrative expenses, an increase in rent and increased

depreciation and amortization.

Salaries and employee benefits expenses were Ps. 315 million for the six months ended June 30, 2019,

compared to Ps. 252 million for the six months ended June 30, 2018, an increase of Ps. 63 million, or 25.0%.

Administrative expenses were Ps. 19,947 million for the six months ended June 30, 2019, compared to

Ps. 19,210 million for the six months ended June 30, 2018, an increase of Ps. 737 million, or 3.8%. This increase was

in line with inflation, as a result our strategy to reduce costs and maintain strict cost controls.

Rent, depreciation and amortization expenses were Ps. 5,805 million for the six months ended June 30, 2019,

compared to Ps. 5,414 million for the six months ended June 30, 2018, an increase of Ps. 391 million, or 7.2%,

reflecting amortization of our investment plans and an increase in the rent of certain branches.

Taxes other than income taxes were Ps. 2,227 million for the six months ended June 30, 2019, compared to

Ps. 2,025 million for the six months ended June 30, 2018, an increase of Ps. 202 million, or 10.0%. This result was

primarily due to an increase in VAT payments made by our subsidiaries in connection with higher expenses paid by

these subsidiaries for certain employee services.

Expenses related to contributions to the IPAB were Ps. 2,676 million for the six months ended June 30, 2019,

compared to Ps. 2,562 million for the six months ended June 30, 2018, an increase of Ps. 114 million, or 4.4%. This

increase was attributable to the 4.8% growth in the volume of deposits in the six months ended June 30, 2019,

compared to the six months ended June 30, 2018.

Current and Deferred Income Tax

Current and deferred income tax was Ps. 9,173 million for the six months ended June 30, 2019, compared to

Ps. 8,658 million for the six months ended June 30, 2018, an increase of Ps. 515 million, or 5.9%, due to an inflationary

effect, non-deductible items and cancellations of nontaxable provisions, which led to an increase in the effective tax

rate from 27.3% to 27.7%.

Net Income

Net income was Ps. 23,959 million for the six months ended June 30, 2019, compared to Ps. 23,051 million

for the six months ended June 30, 2018, an increase of Ps. 908 million, or 3.9%, primarily due to increases in net

interest income and fee income and cost efficiencies.

S-15

Financial Position

The following discussion compares our consolidated financial position as of June 30, 2019, and the year

ended December 31, 2018.

Assets

As of June 30, 2019, we had total assets of Ps. 2,106,291 million, compared to Ps. 2,068,259 million as of

December 31, 2018, representing an increase of 1.8%. This increase was primarily attributable to a 2.9% increase in

total current loans, primarily in the consumer and mortgage loan portfolios.

Total Current Loans

As of June 30, 2019, we had total current loans of Ps. 1,173,256 million, compared to Ps. 1,140,319 million

as of December 31, 2018, an increase of 2.9%. This increase was primarily attributable to an increase in the volume

of our consumer and mortgage loan portfolios. As of June 30, 2019, current commercial loans represented 57% of

total current loans, current consumer loans represented 24% of total current loans, and current residential mortgage

loans represented 19% of total current loans.

Total Past Due Loans

Our total past due loans were Ps. 24,602 million as of June 30, 2019, compared to Ps. 23,274 million as of

December 31, 2018, an increase of Ps. 1,328 million, or 5.7%. This increase was the result of growth in the loan

portfolio. As of June 30, 2019, past due consumer loans represented 0.8% of our total loan portfolio, past due mortgage

loans represented 0.5% of our total loan portfolio, and past due commercial loans represented 0.7% of our total loan

portfolio. As of June 30, 2019, our past due business and commercial loans, past due consumer and past due residential

mortgage loans accounted for Ps. 8,926 million, Ps. 9,385 million and Ps. 6,291 million, respectively.

Liabilities

As of June 30, 2019, we had total liabilities of Ps. 1,902,329 million, compared to Ps. 1,874,036 million as

of December 31, 2018, representing an increase of 1.5%. This increase was mainly attributable to an increase in both

demand deposits and time deposits.

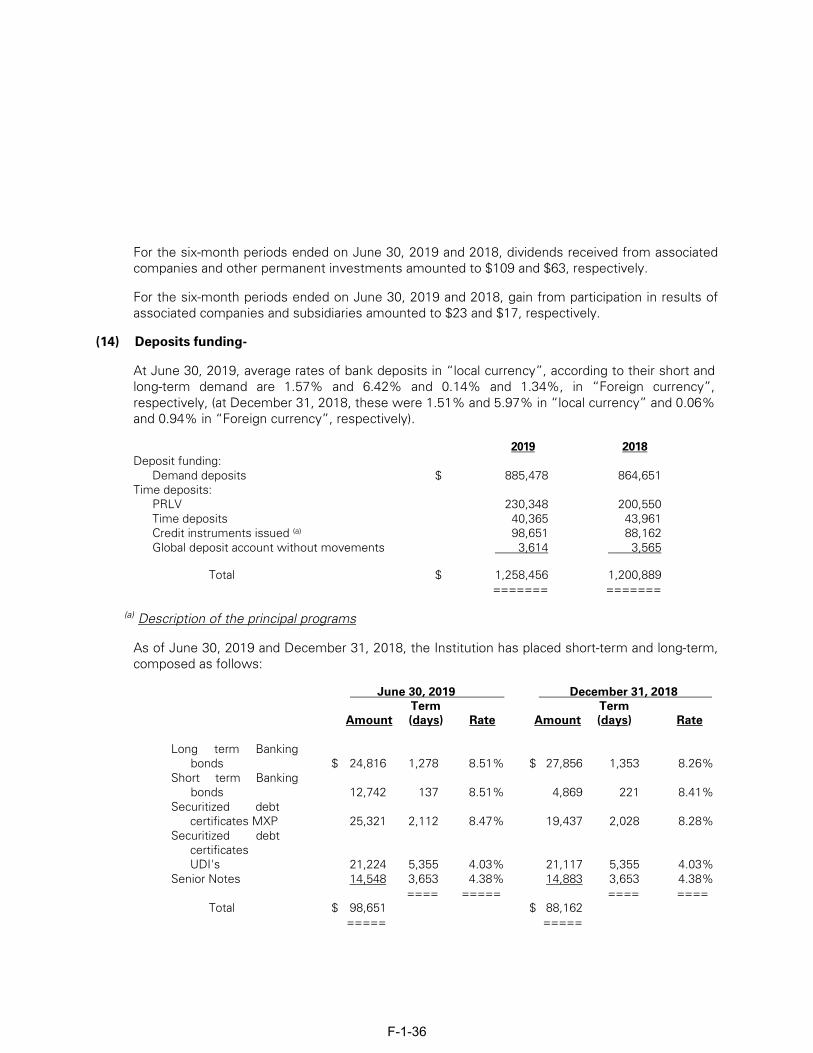

Deposits Funding

As of June 30, 2019, we had total deposit funding (including debt securities issued and deposits in global

accounts without movements) of Ps. 1,258,456 million, compared to Ps. 1,200,889 million as of December 31, 2018,

an increase of Ps. 57,567 million, or 4.8%. This result was primarily attributed to an increase in time deposits of

Ps. 26,202 million, as time deposits became more attractive for clients due to higher interest rates.

As of December 31, 2018, we had total deposit funding (including debt securities issued and deposits in

global accounts without movements) of Ps. 1,200,889 million, compared to Ps. 1,162,633 million as of December 31,

2017, an increase of Ps. 38,256 million, or 3.3%.

Bank and Other Borrowings

As of June 30, 2019, we had bank and other borrowings of Ps. 16,034 million, compared to Ps. 17,861 million

as of December 31, 2018, a decrease of Ps. 1,827 million, or 10.2%. This decline was the result of lower demand for

interbank loans and short-term loans from other entities. As of June 30, 2019, bank and other borrowings represented

0.8% of our total liabilities.

S-16

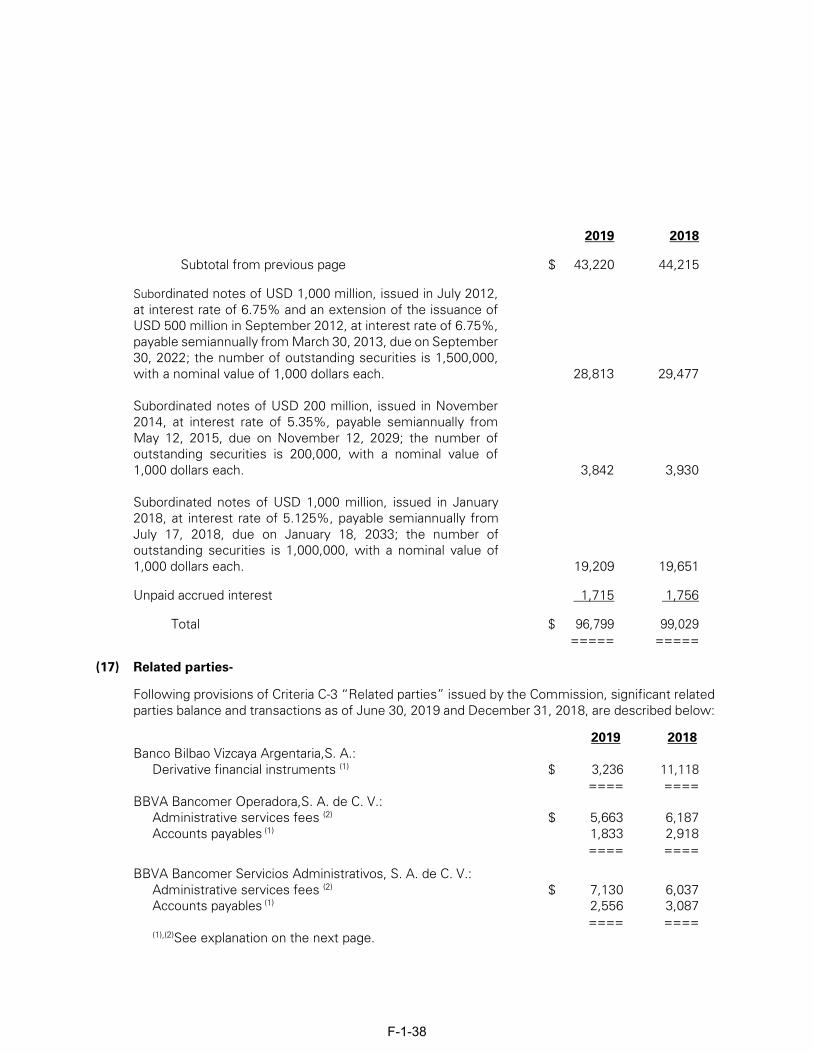

Subordinated Bonds Issued

As of June 30, 2019, we had Ps. 96,799 million of subordinated bonds issued, which represented 5.1% of our

total liabilities.

Stockholders’ Equity

As of June 30, 2019, our stockholders’ equity was Ps. 203,962 million, compared to Ps. 194,223 million as

of December 2018, an increase of Ps. 9,739 million, or 5.0%. This was mainly the result of an increase in accumulated

results from previous years. Total stockholders’ equity represented 9.7% of our total assets as of June 30, 2019.

Liquidity and Funding

As of June 30, 2019, we had Ps. 157,761 million of notes outstanding, of which Ps. 60,962 million were

senior notes and Ps. 96,799 million were subordinated notes. As of December 31, 2018, we had Ps. 154,216 million

of notes outstanding, of which Ps. 55,187 million were senior notes and Ps. 99,029 million were subordinated notes,

which represented an increase of 14.1% and a decrease of 2.3%, respectively.

As reported to the CNBV, the average LCR for the six months ended June 30, 2019, was 138.12%.

Foreign Currency Position

As of June 30, 2019, our foreign currency-denominated assets, including derivative transactions, totaled

U.S. $15.8 billion (Ps. 303,196 million), representing 14% of our total assets. At that date, our foreign currency-

denominated liabilities, including derivative transactions, totaled U.S. $6.9 billion (Ps. 132,428 million), representing

7% of our total liabilities.

Risk-Based Capital

As of June 30, 2019, our Capital Ratios were (i) 14.17% in the case of Total Net Capital, (ii) 11.86% in the

case of Fundamental Capital and (iii) 11.86% in the case of Tier 1 Capital. As of December 31, 2018, our Capital

Ratios were (i) 15.27% in the case of Total Net Capital, (ii) 12.04% in the case of Fundamental Capital and (iii)

12.44% in the case of Tier 1 Capital. The table below presents our risk-weighted assets and Capital Ratios as of June

30, 2019 and December 31, 2018 and 2017, determined, as required by regulations, on an unconsolidated basis.

As of June 30, As of December 31,

2019 2018 2017

(millions of Ps., except for percentages)

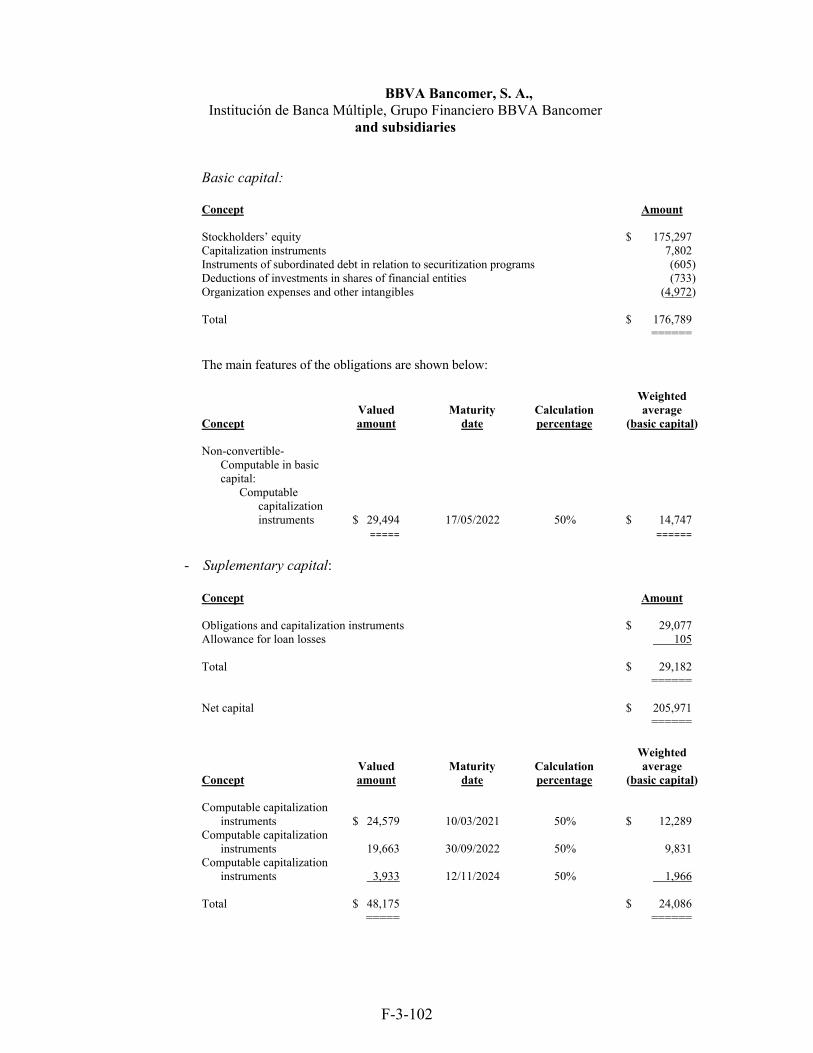

Tier 1 .......................................................................... 196,216 192,852 176,789

Tier 2 .......................................................................... 38,254 43,807 29,182

Total Capital ............................................................... 234,471 236,660 205,971

Risk-weighted assets:

Credit risk ................................................................... 1,133,747 1,095,804 1,001,708

Market risk ................................................................. 432,406 366,919 365,580

Operational risk .......................................................... 88,104 87,240 77,950

Total risk weighted assets ........................................... 1,654,258 1,549,963 1,445,238

Capital ratios (credit, market and operational risk):

Tier 1 Capital to risk-weighted assets ......................... 11.86% 12.44% 12.23%

Tier 2 Capital to risk-weighted assets ......................... 2.31% 2.83% 2.02%

Total Capital to risk-weighted assets .......................... 14.17% 15.27% 14.25%

Source: Banco de México

S-17

Off-Balance Sheet Arrangements

Off-balance sheet loan commitments to customers totaled Ps. 614,354 million as of June 30, 2019, and

Ps. 588,114 million as of December 31, 2018.

S-18

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

Page

Unaudited Condensed Consolidated Interim Financial Statements for the six-month and three-

month periods ended June 30, 2019 and 2018 ........................................................................................ F-1-1

Independent Auditors’ Limited Review Report.......................................................................................... F-1-2

Unaudited Condensed Consolidated Interim Balance Sheets as of June 30, 2019, with comparative

figures as of December 31, 2018 ................................................................................................................ F-1-4

Unaudited Condensed Consolidated Interim Statements of Income for the six-month and three-month

periods ended June 30, 2019, with Comparative Figures for the six-month and three-month periods

ended June 30, 2018 ................................................................................................................................... F-1-6

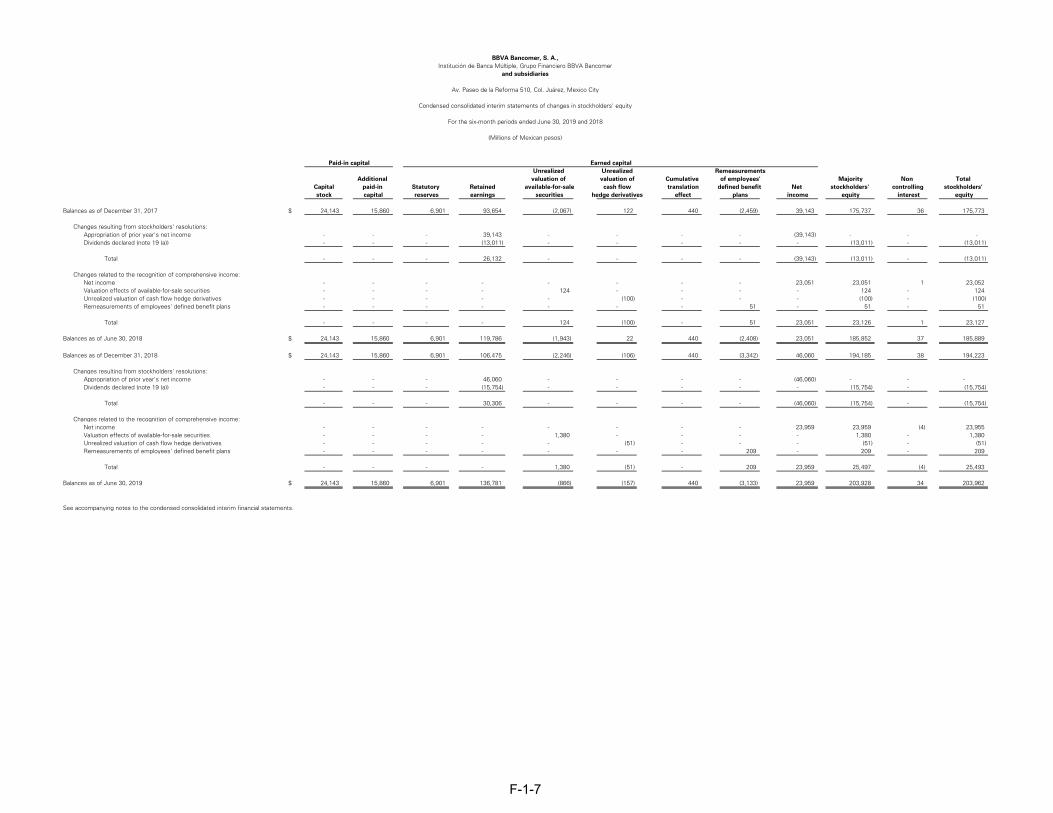

Unaudited Condensed Consolidated Interim Statements of Changes in Stockholders’ Equity for the six-

month period ended June 30, 2019, with comparative figures for the six-month period ended June 30,

2018 ............................................................................................................................................................ F-1-7

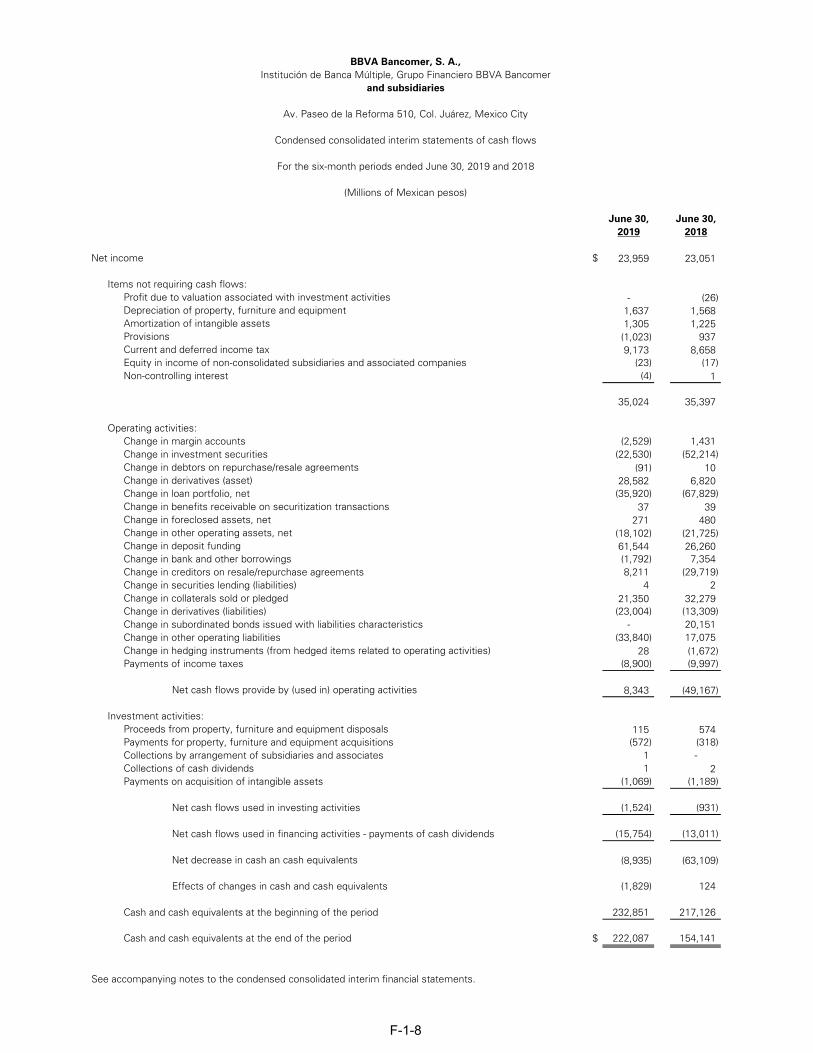

Unaudited Condensed Consolidated Interim Statements of Cash Flows for the six-month period ended

June 30, 2019, with comparative figures for the six-month period ended June 30, 2018 ........................... F-1-8

Notes to the Condensed Consolidated Interim Financial Statements as of June 30, 2019 with

comparative figures as of December 31, 2018 and for the six-month and three-month periods ended

June 30, 2018 .............................................................................................................................................. F-1-9

BBVA Bancomer, S. A., Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer and subsidiaries Unaudited condensed consolidated interim financial information June 30, 2019, December 31 and June 30, 2018 (With the Review Report of Independent Auditors)

F-1-1

Independent Auditors’ Report on Review of Condensed Consolidated Interim Financial Information

The Board of Directors and Stockholders of BBVA Bancomer, S. A. Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer: Introduction We have reviewed the accompanying condensed consolidated interim financial information as of June 30, 2019 (“the interim financial information”), of BBVA Bancomer, S. A. Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer and subsidiaries, which comprises:

• the condensed consolidated interim balance sheet as at June 30, 2019; • the condensed consolidated interim statements of income for the six-month and

three-month periods ended June 30, 2019; • the condensed consolidated interim statement of changes in stockholders’ equity for the

six-month period ended June 30, 2019; • the condensed consolidated interim statement of cash flows for the six-month period ended

June 30, 2019; and • notes to the condensed consolidated interim financial information.

Management is responsible for the preparation of this condensed consolidated interim financial information in accordance with the Accounting Criteria established by National Banking and Securities Commission (the “Commission”) included in the current General Provisions applicable to Credit Institutions in Mexico (the “Provisions”). Our responsibility is to express a conclusion on this condensed consolidated interim financial information based on our review. Scope of Review We conducted our review in accordance with the International Standard on Review Engagements 2410, Review of Interim Financial Information Performed by the Independent Auditor of the Entity. A review of interim financial information consists of making inquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with International Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion.

(Continued)

F-1-2

2 Conclusion Based on our review, nothing has come to our attention that causes us to believe that the accompanying condensed consolidated interim financial information as at June 30, 2019, is not prepared, in all material respects, in accordance with the accounting criteria established by the Commission. KPMG CÁRDENAS DOSAL, S. C.

Hermes Castañón Guzmán

August 23, 2019

F-1-3

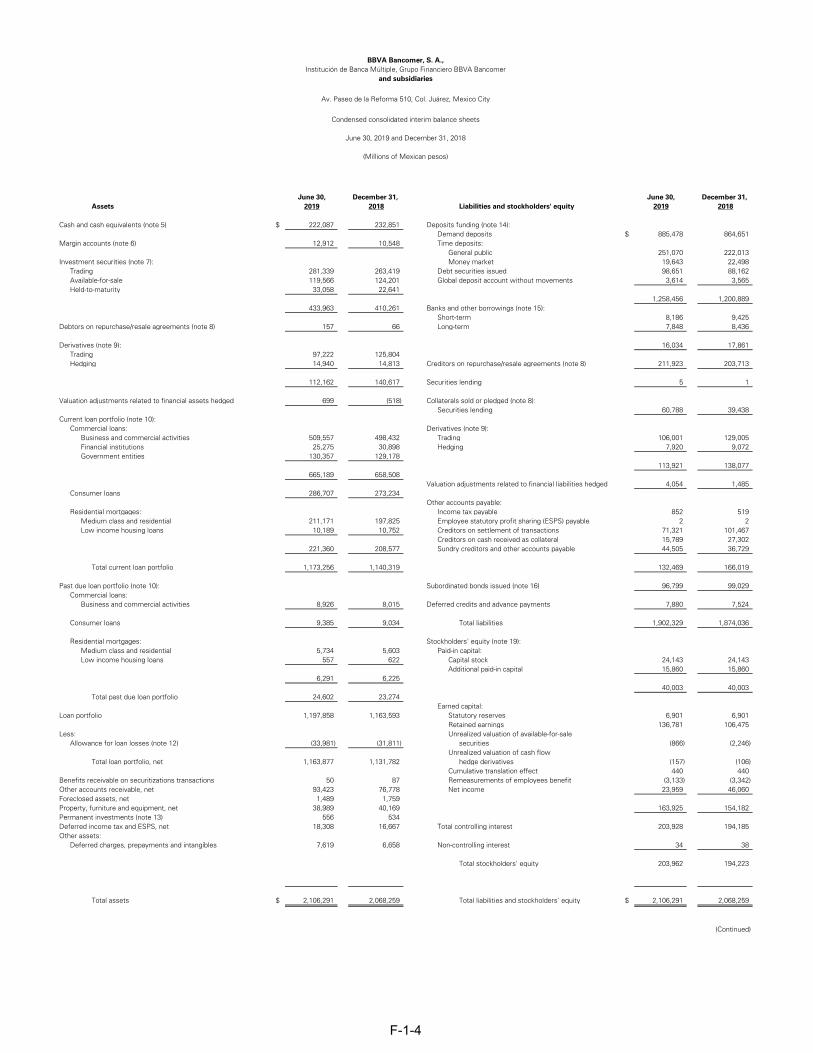

BBVA Bancomer, S. A.,Institución de Banca Múltiple, Grupo Financiero BBVA Bancomer

and subsidiaries

Condensed consolidated interim balance sheets

June 30, 2019 and December 31, 2018

(Millions of Mexican pesos)

June 30, December 31, June 30, December 31, Assets 2019 2018 Liabilities and stockholders' equity 2019 2018

Cash and cash equivalents (note 5) $ 222,087 232,851 Deposits funding (note 14):Demand deposits $ 885,478 864,651

Margin accounts (note 6) 12,912 10,548 Time deposits:General public 251,070 222,013

Investment securities (note 7): Money market 19,643 22,498 Trading 281,339 263,419 Debt securities issued 98,651 88,162 Available-for-sale 119,566 124,201 Global deposit account without movements 3,614 3,565 Held-to-maturity 33,058 22,641

1,258,456 1,200,889 433,963 410,261 Banks and other borrowings (note 15):

Short-term 8,186 9,425 Debtors on repurchase/resale agreements (note 8) 157 66 Long-term 7,848 8,436

Derivatives (note 9): 16,034 17,861 Trading 97,222 125,804 Hedging 14,940 14,813 Creditors on repurchase/resale agreements (note 8) 211,923 203,713

112,162 140,617 Securities lending 5 1

Valuation adjustments related to financial assets hedged 699 (518) Collaterals sold or pledged (note 8):Securities lending 60,788 39,438