BBA-7 Management Accounting Block-1 Introduction To Cost ...

38

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of BBA-7 Management Accounting Block-1 Introduction To Cost ...

Bachelor of Business Administration

(BBA)

BBA-7

Management Accounting

Block-1

Introduction To Cost AccountingUnit-1 Cost Accounting

Unit-2 Classification of Cost

Unit-3 Cost Sheet

Subject Experts

Professor Nripendra Narayan Sarma, Maniram Dewan School of Mangement, KKHSOU Professor Munindra Kakati, VC, ARGUCOM Professor Rinalini Pathak Kakati,Dept.of Busniess Administration, GU

Course Coordinator : Dr. Smritishikha Choudhury, Asst. Prof., KKHSOU

Dr.Chayanika Senapati, Asst. Prof., KKHSOU

SLM Preparation Team

UNITS CONTRIBUTORS1-3 Dr. Pradeep Kr. Jain

Gauhati University

Editorial TeamContent : Dr. Arup Roy, Tezpur University

Structure, Format and Graphics : Dr. Smritishikha Choudhury,KKHSOUDr. Chayanika Senapati, KKHSOU

November, 2018

This Self Learning Material (SLM) of the Krishna Kanta Handiqui State Open University is made available under a Creative Commons Attribution-Non Commercial-ShareAlike4.0 License (International) : http.//creativecommons.org/licenses/by-nc-sa/4.0

UNIT 1: COST ACCOUNTING

UNIT STRUCTURE

1.1 Learning objectives

1.2 Introduction

1.3 Meaning of Cost Accounting

1.4 Objectives of Cost Accounting

1.5 Cost accounting, financial accounting and management

accounting

1.5.1 Difference between cost accounting and financial

accounting

1.5.2 Meaning of management accounting

1.5.3 Difference between Cost accounting and management

accounting

1.6 Advantages of Cost Accounting

1.7 Limitations of Cost Accounting

1.8 Let Us Sum Up

1.9 Further Reading

1.10 Answers to Check Your Progress

1.11 Model Questions

1.1 LEARNING OBJECTIVES

After going through this unit, you will be able to

explain the meaning & objectives of Cost Accounting

explain the difference between Cost Accounting and Financial

Accounting

describe the meaning of Management Accounting

outline differences between Cost Accounting and Management

Accounting

discuss the advantages and limitations of Cost Accounting

1.2 INTRODUCTION

In this unit we are going to discuss the meaning and objectives

of cost accounting and its various advantages and disadvantages. Cost

accounting means keeping account of the costs of items in production.

After that you will get a fair idea on the meaning of management

accounting.

The difference between cost accounting, financial accounting and

management accounting will also be discussed.

1.3 MEANING OF COST ACCOUNTING

Cost Accounting is one of the important disciplines of accountancy

to give proper information required to the management for effectively

discharging its functions such as planning, organizing, controlling, directing,

co-coordinating and decision making. In this regard, Financial accounting

is concerned with record keeping directed towards the preparation of

Profit and Loss Account and Balance Sheet. It provides information about

the enterprise in a general way. Accordingly Financial Accounts are

prepared as per the requirement of the Companies Act and Income Tax

Act. The main purpose of financial accounting is to ascertain profit or

loss of a concern as a whole for a particular period. Thus, financial

accounting does not serve as the needs of management for effective

control, determination of prices, making effective plan for future operations

and formulating various policy decision.

To overcome the limitations of the financial accounting, the cost

accounting is a recent development born in response to the needs of

management for detailed information about cost of a product or a unit

of services. Every business firm is expected to make profit in the long

run and keep costs within control. Recently the Companies Act has

made obligatory the keeping of cost records in some manufacturing

companies. In essence, therefore Cost Accounting is now widely used

by large manufacturing and non-manufacturing operations.

1.4 OBJECTIVES OF COST ACCOUNTING

The following are the important objectives of Cost Accounting :

1) Ascertainment of cost.

2) Determination of selling price.

3) Cost control and cost reduction.

4) Ascertainment of profit of each activity.

5) Assisting Management in decision making.

6) Formulating business policy.

7) Matching costs with revenue.

1.5 COST ACCOUNTING, FINANCIAL ACCOUNTING ANDMANAGEMENT ACCOUNTING

In this section we will discuss about the difference between cost

accounting, financial accounting, and management accounting.

1.5.1 Difference between Cost accounting and FinancialAccounting

The following are the differences between Financial Accounting

and Cost Accounting:

Point of Financial Accounting Cost AccountingdifferencePurpose It is prepared for The main purpose of

providing information Cost Accounting is toabout the final results provide information toof the business the management foractivities as a whole the proper planning,for a particular period control and decisionto its proprietors, making.outsiders etc.

Need Financial Accounts are Cost accounts aremaintained as per maintained to meetthe requirements of the requirement ofCompanies Act and the management

Income Tax Act.

Cost accounting:

It is the process ofrecording, classifying,analysing and allocatingcosts associated with aprocess and developingcourses of action tocontrol the costs.

Recording Transactions are In cost accounting,

classified, recorded transactions are

and analysed classified recorded

subjectively. and analysed

objectively according

to the purpose for

which costs are

incurred.

Analysis of Financial accounting Cost Accounting

reveals the profit of shows the profit

a business as a made on each

whole. product, job or

process

Accounting Financial accounts are Cost reports are

Period prepared for a definite prepared frequently

period. and submitted to the

management may be

daily, weekly etc.

Stock In financial accounts, Cost accounting

stocks are valued at stocks are valued at

cost price or market cost.

price which ever is

less.

Dealings Financial accounts Cost account lays

deal with actual facts emphasis on both

and figures. actual facts and

estimates or

predetermined cost.

Relative Financial accounts do Cost account provides

Efficiency not reveal the relative information on the

efficiency of each relative efficiencies of

department or section. various plant and

machinery

Financial accounting:

It is the process ofrecording, summarisingand reporting themyriad of transactionsresulting from businessoperations over a periodof time.

1.5.2 Meaning of Management Accounting

Management Accounting: Management Accounting helps

the management in effectively performing its functions of planning,

organizing, controlling, coordinating and decision making.

The Institute of Cost and Management Accountants,

London, has defined Management Accounting as “the application

of professional knowledge and skill in the preparation of accounting

information in such a way as to assist management in the

formation of policies, and in the planning and control of the

operations of the undertaking.”

1.5.3 Difference between Cost Accounting andManagement Accounting

Cost Accounting Vs Management Accounting

The following are the main distinctions between Cost

Accounting and Management Accounting :

1) Cost Accounting deals with cost ascertainment, cost allocation,

cost apportionment and cost control. Management Accounting

provides all accounting in formations to the management for

discharge of its functions effectively.

2) Management Accounting has a wider scope as compared to

cost accounting. Therefore management accounting uses

more advanced techniques of Management reporting.

3) Management accounting deals with both Cost Accounting and

Financial Accounting. But cost accounting deals with cost

data.

4) Standard Costing, Budgetary Control, Break-Even Analysis,

Inventory Control etc. are the basic tools and techniques used

in Cost Accounting. But in Management Accounting, fund flow

analysis, cash flow analysis, ratio analysis etc. are the

important tools used for analysis and interpretation of financial

statement.

1.6 ADVANTAGES OF COST ACCOUNTING

Cost Accounting helps the management to ascertain the true

cost of every operation, through setting objectives and standard of

operation, comparison of actual performance with standard to reveal the

discrepancies or variances. If the variances are adverse, the management

takes up corrective measure to eliminate variations. The following are

the advantages of cost accounting to the management, to the employees,

to the creditors, to the government and to the public.

Advantages to the management

1) Facilitates planning.

2) Helps in formulating policies.

3) Useful in setting up objectives and standards of performance.

4) Facilitates cost comparison.

5) Leads to effective cost control.

6) Determines the selling price.

7) Ascertains profit of each activity.

8) Assists the Management in decision making.

9) Facilitates cost reduction.

10) Measures performance.

Advantages to the Employees

1) Ensures fair incentive wage schemes.

2) Facilitates job security, recognition and promotion.

3) Useful in measuring operating efficiency of the employees.

Advantages to the Creditors

1) Measures the financial strength and creditworthiness of the

business.

2) Attract investors for extending their credit facilities.

3) Creates trustworthiness among the creditors, debenture

holders, banks etc.

Advantage to the Government

1) It helps to formulate business policies and national plans for

industrial development.

2) It facilitates assessment of taxation, and establishment of

indexes.

3) It assists in effective utilization of resources, i.e. materials,

labour and machines etc.

4) It assists the government for cost reduction, price fixation,

export and import and granting subsidy etc.

Advantage to the public

1) It helps in elimination of wastages and inefficiencies.

2) It facilitates the consumers to pay fair price for products.

3) It leads to progress of national economic growth.

4) Creates employment opportunities.

5) Increases the living standards of the people.

1.7 LIMITATIONS OF COST ACCOUNTING

The following are some of the limitations of cost accounting :

1) There is lack of uniformity in regard to its procedure and practices.

2) Cost are classified and interpreted in such different manners that

though given the same title, they are computed on a different basis.

3) Lack of consistency becomes more acute when projections are

made beyond the recorded cost data.

4) Inherent limitations of cost accounting objections raised by different

sections of business societies against the introduction of cost

accounting.

5) Cost accounting is unnecessary for recently established industries.

And also modern methods of costing systems are not suitable for

all types of industries.

6) Cost accounting system involves considerable amount of

expenditure at the installation stage. Thus costing system is not

economical for a small concern.

7) Cost accounting involves accounting procedures and record-

keeping. These are far more detailed and difficult than those required

in financial accounting.

CHECK YOUR PROGRESS:

Q1: Fill in the blanks :

a) Cost accounting is used by large

................................... and ................................

operations

b) Cost accounting deals with ……………… , ………………..

and ………………………………

c) Cost accounting stocks are valued at ………………………

d) Financial accounts are prepared for a …………….. period

e) Cost accounting shows the profit made on each …………,

……………………. and process.

Q2: State two objectives of cost accounting.

.......................................................................................................

.......................................................................................................

1.8 LET US SUM UP

Cost Accounting is one of the important disciplines of accountancy

to give proper information required to the management for effectively

discharging its functions such as planning, organizing, controlling,

directing, co-coordinating and decision making

The following are the important objectives of Cost Accounting :

1) Ascertainment of cost.

2) Determination of selling price.

3) Cost control and cost reduction.

4) Ascertainment of profit of each activity.

5) Assisting Management in decision making.

6) Formulating business policy.

7) Matching costs with revenue

Management Accounting helps the management in effectively

performing its functions of planning, organizing, controlling, and

coordinating and decision making.

We have also discussed the difference between cost accounting

and management accounting and financial accounting.

At the end we discussed the advantages and disadvantages of

cost accounting.

1.9 FURTHER READING

1. Jain P K & Khan MY(2017); Management Accounting,7edition

Mcgraw Higher Ed, India

2. Narang K.L. & Jain S.P.(2015), Cost Accounting, Kalyani Publications

3. Narang K.L. & Jain S.P(2015), Cost And Management Accounting,

4. Lal J & Srivastava S (2013), Cost & Management Accounting;

Mcgraw Higher Ed

5. Banerjee(2013);Cost Accounting: Theory and Practice; PHI Learning

Pvt Ltd; New Delhi

1.10 ANSWERS TO CHECK YOUR PROGRESS

Ans to Q1. a. manufacturing, non-manufacturing

b. cost ascertainment, cost allocation and cost control

c. Cost

d. definite

e. product, job and process

Ans to Q2. i) Ascertainment of cost.

ii) Determination of selling price.

1.11 MODEL QUESTIONS

Q1. What do you understand by Cost Accounting?

Q2. What are the important objectives of Cost Accounting?

Q3. What are the differences between financial account and cost

accounting?

Q4. Distinguish between cost accounting and management accounting.

Q5. Cost Accounting has become an essential tool of management.

Give your comments on this statement.

Q6. Indicate the various advantages and limitations of Cost Accounting.

*** ***** ***

UNIT 2: CLASSIFICATION OF COST

UNIT STRUCTURE

2.1 Learning objectives

2.2 Introduction

2.3 Cost concept

2.4 Techniques of costing

2.5 Classification of Cost

2.6 Let Us Sum Up

2.7 Further Reading

2.8 Answers to Check Your Progress

2.9 Model Questions

2.1 LEARNING OBJECTIVES

After going through this unit, you will be able to

describe the cost concepts

explain the techniques of costing

discuss the Classification of Cost

2.2 INTRODUCTION

In the earlier unit, we come to know about the concept of cost

accounting and its different objectives. Now in this unit we are going to

discuss the classification of cost and the various techniques of costing.

You will find this unit interesting, as it discuss about the costing methods

like job and process costing and the five different techniques of costing.

2.3 COST CONCEPT

The term ‘methods’ and ‘systems’ are used synonymously to

indicate an integrated set of procedures based on a complex concept

of ideas, principles and concepts. The term method of costing refers to

cost ascertainment. Different methods of costing for different industries

depend upon the production activities and the nature of business. For

these, costing methods can be grouped into two broad categories : (1)

Job costing and (2) Process costing.

1. Job Costing: Job costing is also termed as specific Order Costing

(or) Terminal Costing. In job costing, costs are collected and

accumulated according to jobs, contracts, products or work orders.

Each job is treated as a separate entity for the purpose of costing.

The material and labour costs are complied through the respective

abstracts and overheads are charged on predetermined basis to

arrive at the total cost. Job costing is used in printing, furniture

making, ship building etc.

Job costing is further classified into (a) Contract costing (b) Cost

plus contract and (c) Batch costing.

a) Contract Costing : This method of costing is applicable

where the job work is big like contract work of building. Under

this method, costs are collected according to each contract

work. Contract costing is also termed as Terminal costing.

The principles of job costing are applied in contract costing.

b) Cost plus Contract : These contracts provide for the

payment by the contracted of the actual cost of manufacture

plus a stipulated profit. The profit to be added to the cost. It

may be a fixed amount or it may be a stipulated percentage

of cost. These contracts are generally entered into when at

the time of undertaking a work, it is not possible to estimate

its cost with reasonable accuracy due to unstable condition

of material, labour etc. When the work is spread over a long

period of time, the prices of materials, rates of labour etc.

are liable to fluctuate.

Costing Methods

Job Costing Process Costing

Complied :Act in accordance withsomeone’s rules, commandsor wishes.Overheads :The expense of maintainingproperty

c) Batch Costing : In Batch Costing, a lot of similar units

which comprise the batch may be used as a cost unit for

ascertainment of cost. Separate Cost Sheet is maintained

for each batch by assigning a batch number. Cost per unit

of product is determined by dividing the total cost of a batch

by the number of units of the batch. Batch Costing is used

in drug industries, ready-made garments industries, electronic

components manufacturing T V Sets, etc.

2. Process Costing: This costing method refers to continuous

operation or continuous process costing. Process costing method

is applicable where goods or services pass through different

processes to be converted into finished goods. Process costing is

used in Cement industries, Sugar industries, Textiles, Chemical

industries etc.

The following are the important variants of process costing system.

a) Operation Costing : It is concerned with the determination

of the cost of each operation rather than process. It offers

scope for computation of unit operation cost at the end of

each operation by dividing the total operation cost by total

output of units.

b) Operating Costing : Operating costing is also termed as

service costing. Operating costing is similar to process

costing and is used in service industries. This method of

costing is suitable for concerns rendering services. For

example, Hospitals, Transport, Canteen, Hotels etc.

c) Output Costing : Output costing is also called Unit Costing

(or) Single Costing. This method of costing is applicable

where a concern undertakes mass and continuous production

of single unit or two or three types of similar products or

different grades of the same products. Under this method,

cost per unit is measured by dividing the total cost by number

of units produced. Output Costing is used in industries like

Cement, Cigarettes, Pencils, Quarries etc.

d) Multiple Costing : This method of costing means

combination of two or more methods of costing like operation

costing and output costing. Under this method, the cost of

different sections of production are combined after finding

out the cost of each and every part manufactured. This

method of costing is suitable for the industries manufacturing

motor cars, engines, aircraft, tractors, etc.

2.4 TECHNIQUES OF COSTING

Costing is the technique and process useful to allocation of

expenditure, cost ascertainment and cost control. In order to fulfill the

needs of the management, it supplies necessary information to the

management. The following are the various techniques of costing:

a. Uniform Costing

b. Marginal Costing

c. Standard Costing

d. Historical Costing

e. Absorption Costing

a) Uniform Costing: Uniform Costing is not a distinct method of

costing. In fact when several undertakings start using the same

costing principles and or practices, they are said to be following

uniform costing. The basic idea behind uniform costing is that the

different firms in an industry should adopt a common method of

costing and apply uniformly the same principles and techniques

for better cost comparison and common good.

b) Marginal Costing: The C.I.M.A. London defines marginal costing

as “a technique of costing which aims at ascertaining marginal

costs, determining the effects of changes in costs, volume, price

etc. on the Company’s profitability, stability etc. and furnishing the

relevant data to the management for enabling it to take various

management decisions by segregating total costs into variable

and fixed costs.”

Segregating :Separate or isolate one thingfrom another.

c) Standard costing: Standard Costing is a technique of cost

accounting which compares the standard cost of each product or

service with actual cost to determine the efficiency of the operation,

so that any remedial action may be taken immediately.

d) Historical Costing: Historical costing is the ascertainment and

recording of actual costs when or after, they have been incurred

and is one of the first stages in the growth of the Cost Accountant’s

work. Actual costs refer to material cost, labour cost and overhead

cost.

e) Absorption Costing: Absorption Costing is also termed as Full

Costing (or) Orthodox Costing. It is the technique that takes into

account charging of all costs both variable and fixed costs to

operation processed or products or services.

CHECK YOUR PROGRESS

Q1: Fill in the blanks :

a) Costing methods can be grouped into two

.. broad categories: (1) ……………….......

(2) …………………………

b) Job costing is also termed as specific Order Costing

(or) …………………………………

c) Process Costing method refers to ………………………

d) Multiple Costing method of costing means combination

of …………………………………… methods of costing

Q2: What are the various techniques of costing?

a. ………………………………

b. ………………………………

c. ………………………………

d. ………………………………

e. ………………………………

2.5 CLASSIFICATION OF COST

Classification is the process of grouping costs according to their

common characteristics or features. There are various methods of

classifying costs on the basis of requirements.

The following are the important bases on which costs are

classified :

a) On the basis of Nature (or) Elements.

b) On the basis of Function

c) On the basis of Variability.

d) On the basis of Normality.

e) On the basis of Controllability and Decision Making.

The following chart can explain further the classifications cost:

1) On the basis of Nature or Elements: One of the important

classification cost is on the basis of nature or elements. Based on

elements, it is classified into Material Cost, Labour Cost and Other

Expenses. They can be further subdivided into Direct and Indirect

Material Cost, Direct and Indirect Labour Cost and Direct and

Indirect Other Expenses.

Classification of cost

Nature or Element

a. Material Costb. Labour Cost c. Other

expenses

Function

a. Production Costb. Administration

Cost c. Selling Costd. Distribution Cost

Variability

a. Fixed Costb. Variable Costc. Semi-

variable/fixedcost

Normality

a. Normal Cost b. Abnormal

Cost

Decision Making &

Controllability

a. Controllable Cost b. Uncontrollable

Costc. Sunk Cost d. Opportunity Coste. Replacement Costf. Conversion Cost

2) On the basis of Function: The classification of costs on the

basis of the various functions of a concern is known as function-

wise classification. Here, there are four important functional divisions

in the business organization. viz. (a) Production Cost (b)

Administration Cost (c) Selling Cost and (d) Distribution Cost.

3) On the basis of Variability : On the basis of variability with the

volume of production cost is classified into Fixed Cost, Variable

Cost and Semi Variable Cost. Fixed Costs are those costs which

remain constant with the volume of production. Rent and rates of

office and factory building are some example of fixed cost.

Variable costs are those costs incurred directly with the volume of

output. For example, cost of materials and wages to workers are

the expenses chargeable with direct proportion to the volume of

production.

Semi-Variable Costs are those costs incurred partly fixed and partly

variable, with the volume of production. Accordingly, it has both

fixed and variable features. For example, depreciations and

maintenance cost of plant and machinery.

4) On the basis of Normality: Costs are classified into normal costs

and abnormal costs on the basis of normality features. Normal

costs are those incurred normally within the target output or fixed

plan.

5) On the basis of Controllability and Decision Making: Based

on the managerial decision making and controllability the

classif ications are as follows: (a) Controllable Cost, (b)

Uncontrollable Cost, (c) Sunk Cost, (d) Opportunity Cost, (e)

Replacement Cost, (f) Conversion Cost.

a) Controllable Costs : Controllable Costs are the costs which

can be influenced by the action of a specified number of an

undertaking. Controllable Costs incurred in a particular

responsibility centre which is influenced by the action of the

executive heading. For example, direct materials and indirect

materials.

b) Uncontrollable Costs: Uncontrollable Costs are those costs

which cannot be influenced by the action of a specified

number of an undertaking. In fact, no cost is controllable; it

is only in relation to a particular individual that may specify

a particular cost to either controllable or non-controllable. For

example, rent and rates.

c) Sunk cost : These are historical costs which were incurred

in the past and are not relevant to the particular decision

making problem being considered. While considering the

replacement of a plant, the depreciated book-value of the old

asset is irrelevant as the amount is a sunk cost which is to

be written-off at the time of replacement. Unlike incremental

or decremental costs, sunk costs are not affected by increase

or decrease of volume. Examples of sunk cost include

dedicated fixed assets, development cost already incurred.

d) Opportunity Cost: Opportunity cost means the cost of

forgoing or giving up an opportunity. It is the notional value of

going without the next best use of time, effort and money.

These indicate the income or potential benefits sacrificed

because a certain course of action has been taken. An

example of opportunity costs is the market value forgone or

sacrificed when an old machine is being used.

e) Replacement Cost: Such expenses may be incurred due to

factors like change in method of production, an addition or

alteration in the factory building, change in flow of production

etc. All such expenses are treated as production overheads;

when amount of such expenses is large, it may be spread

over a period of time.

f) Conversion Cost: Conversion costs are those costs which

are incurred while converting materials into semi-finished or

finished goods. It is the aggregate of direct wages, direct

expenses and overhead costs of converting raw materials

into finished products.

CHECK YOUR PROGRESS

Q3: What are the important bases on which costs

are classified ?

a) ...................................................................................................

b) ...................................................................................................

c) ...................................................................................................

d) ...................................................................................................

e) ...................................................................................................

Q4: What are the important bases on which managerial decision

making and controllability is classified?

..................................................................................................

..................................................................................................

..................................................................................................

2.6 LET US SUM UP

In this unit we discussed the following concepts:

Costing methods can be grouped into two broad categories:

(1) Job costing and (2) Process costing.

In job costing, costs are collected and accumulated according to

jobs, contracts, products or work orders.

Job costing is further classified into (a) Contract costing (b) Cost

plus contract and (c) Batch costing.

Process costing method is applicable where goods or services

pass through different processes to be converted into finished

goods.

Costing Methods

Job Costing Process Costing

The following are the important variants of process costing

system.

a) Operation Costing

b) Operating Costing

c) Output Costing

d) Multiple Costing

Costing is the technique and process useful to allocation of

expenditure, cost ascertainment and cost control

The following are the various techniques of costing:

a. Uniform Costing

b. Marginal Costing

c. Standard Costing

d. Historical Costing

e. Absorption Costing

The following are the important bases on which costs are

classified :

a) On the basis of Nature (or) Elements.

b) On the basis of Function

c) On the basis of Variability

d) On the basis of Normality

e) On the basis of Controllability and Decision Making.

2.7 FURTHER READING

1. Jain P K & Khan MY(2017); Management Accounting,7edition

Mcgraw Higher Ed, India

2. Narang K.L. & Jain S.P.(2015), Cost Accounting, Kalyani

Publications

3. Narang K.L. & Jain S.P(2015), Cost And Management Accounting,

4. Lal J & Srivastava S (2013), Cost & Management Accounting;

Mcgraw Higher Ed

5. Banerjee(2013);Cost Accounting: Theory and Practice; PHI

Learning Pvt Ltd; New Delhi

2.8 ANSWERS TO CHECK YOURPROGRESS

Ans to Q1: a. (1) Job costing and (2) Process costing.

b. Terminal Costing

c. continuous process costing.

d. two or more

Ans to Q2: The following are the various techniques of costing:

a. Uniform Costing

b. Marginal Costing

c. Standard Costing

d. Historical Costing

e. Absorption Costing

Ans to Q3: The following are the important bases on which costs are

classified :

a) On the basis of Nature (or) Elements.

b) On the basis of Function

c) On the basis of Variability.

d) On the basis of Normality.

e) On the basis of Controllability and Decision Making.

Ans to Q4: Based on the managerial decision making and controllability

the classifications are as follows: (a) Controllable Cost,

(b) Uncontrollable Cost, (c) Sunk Cost, (d) Opportunity Cost,

(e) Replacement Cost, (f) Conversion Cost.

2.9 MODEL QUESTIONS

Q1. What are the important methods of Costing? Describe each of

them briefly.

Q2. What are the important techniques of costing?

Q3. What method of costing would you recommend for the following

industries? Give reason.

a) Ship Building

b) Ready-made Garment

c) Sugar Industries

d) Hospitals

e) Cigarettes

f) Motor Cars manufacture.

Q4. Describe the different classification of cost in detail.

Q5. What are the important basic requisites for classification of cost?

Explain them briefly.

Q6. Write short notes on:

a) Uniform Costing.

b) Historical Costing

c) Marginal Costing.

d) Standard Costing

e) Sunk Costing

Q7. What are the differences between controllable costs and

uncontrollable costs?

*** ***** ***

UNIT : COST SHEET

UNIT STRUCTURE

.1

.2

.3

.4

.5

.6

.7

.8

Learning Objectives

Introduction

Elements Of Cost

.3.1 Materials Cost

.3.2 Labour Cost

.3.3 Expenses

Specimen of Cost Sheet

Let Us Sum Up

Further Reading

Answers to Check Your Progress

Model Questions

.1 LEARNING OBJECTIVES

After going through this unit, you will be able to

• explain elements of Cost.

• define material cost, labour cost and Expenses.

• explain Overheads and Cost Sheets.

• outline specimen of Cost Sheet

.2 INTRODUCTION

In the earlier unit, you have been acquainted with job costing and

contract costing. In this unit we are going to discuss another important

topic, i.e. cost sheet and the various items associated with it. One

important area to claim your attention is “elements of cost” which includes

different costs, materials cost, labour costs and expenses. A detailed

examination of each of these items is expected to enlighten you on the

main subject of this unit i.e. Cost Sheet.

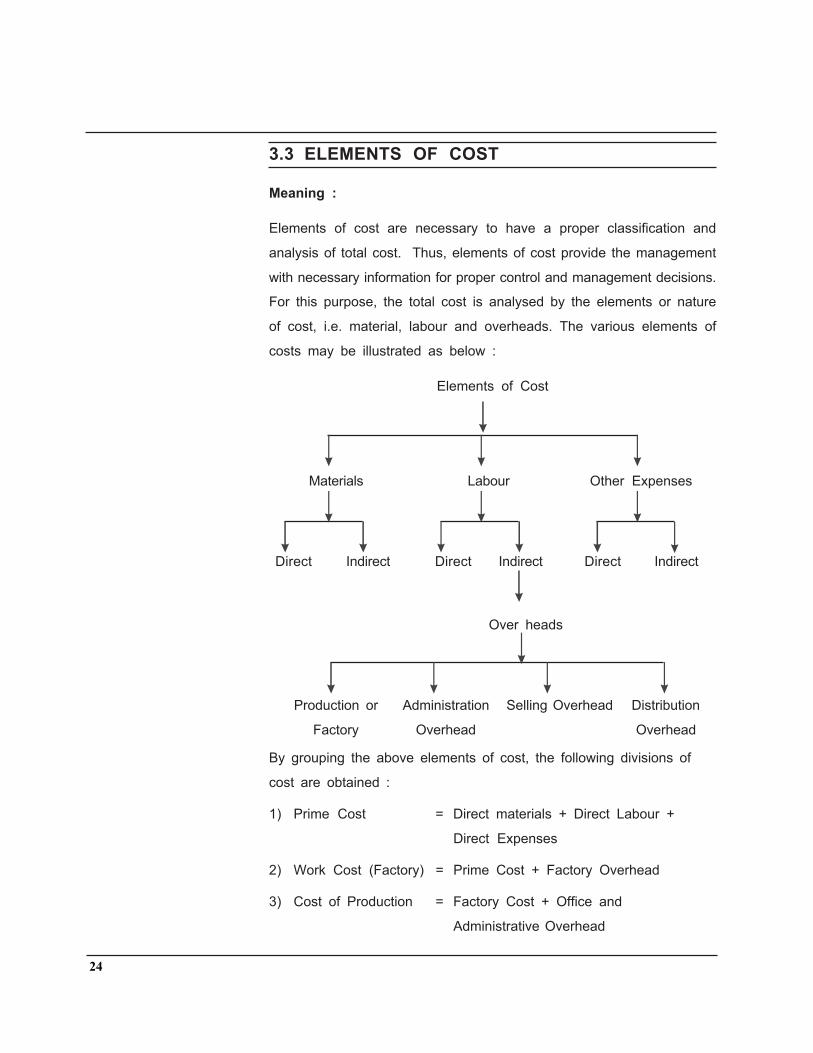

.3 ELEMENTS OF COST

Meaning :

Elements of cost are necessary to have a proper classification and

analysis of total cost. Thus, elements of cost provide the management

with necessary information for proper control and management decisions.

For this purpose, the total cost is analysed by the elements or nature

of cost, i.e. material, labour and overheads. The various elements of

costs may be illustrated as below :

Elements of Cost

Materials Labour Other Expenses

Direct Indirect Direct Indirect Direct Indirect

Over heads

Production or Administration Selling Overhead Distribution

Factory Overhead Overhead

By grouping the above elements of cost, the following divisions of

cost are obtained :

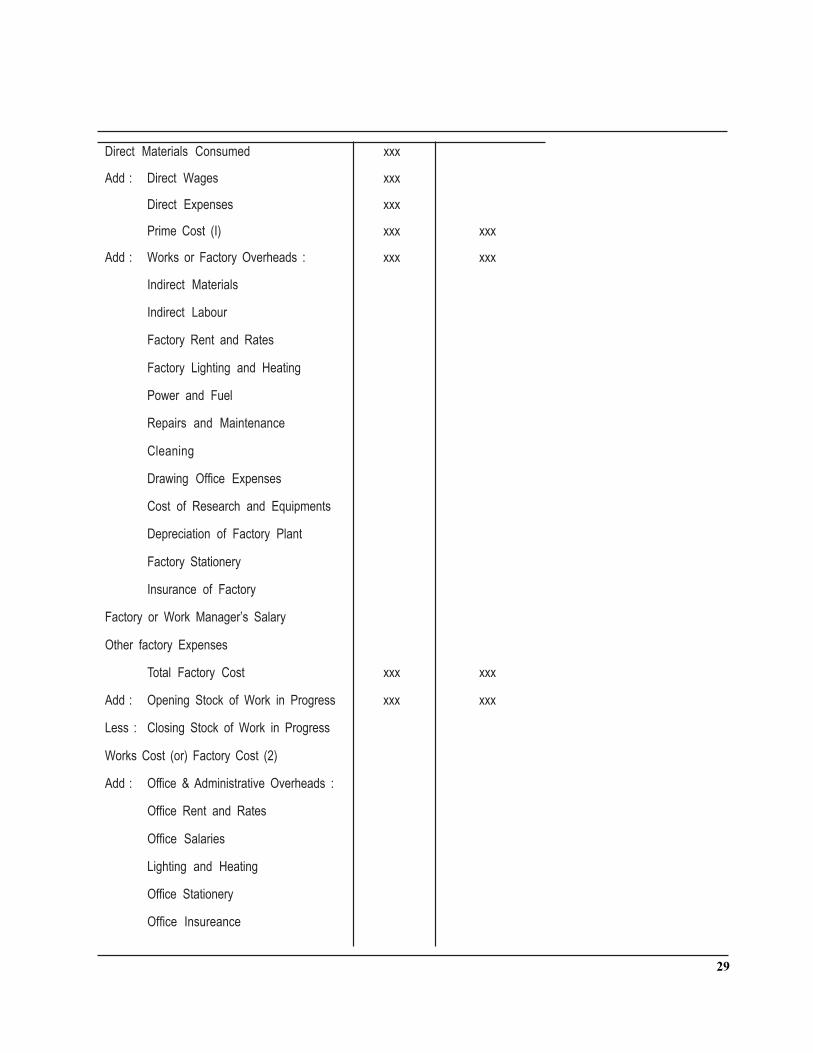

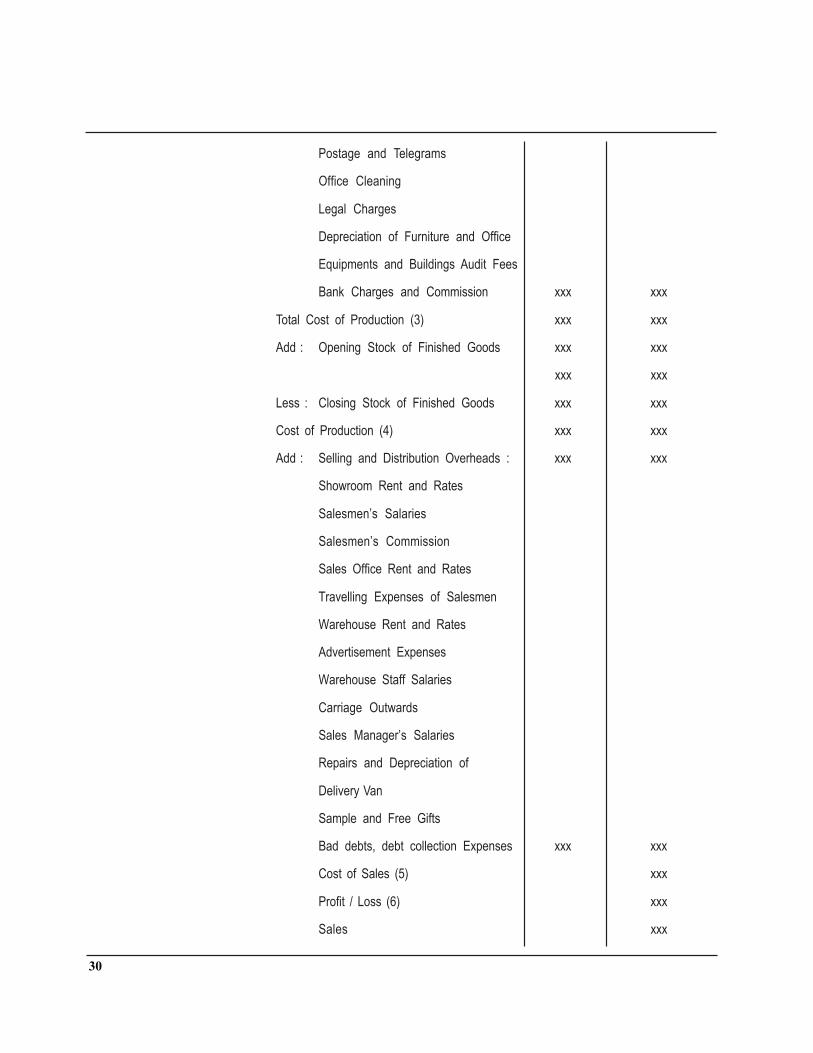

1) Prime Cost = Direct materials + Direct Labour +

Direct Expenses

2) Work Cost (Factory) = Prime Cost + Factory Overhead

3) Cost of Production = Factory Cost + Office and

Administrative Overhead

4) Cost of Sales (or)

Total Cost = Cost of production + Selling and

Distribution overhead

.3.1 Materials Cost

Materials Costs refer to cost of materials which are the major

substances used in production and are converted into finished

goods and semi-finished goods. Materials are grouped as direct

materials and indirect materials.

Direct Materials : Direct materials are those that form part of

product. Raw materials, semi finished products, and finished

products which can be identified with production of a product are

known as direct materials. Sugarcane, cotton, woods etc. are

examples of direct materials .The cost of materials involves

conversion of raw materials into finished products.

Indirect materials : Material costs, other than direct material

cost are known as indirect material cost. Indirect materials cannot

be identified with a particular unit of cost or product. Indirect

materials are indirectly used for producing the products. Lubricating

oil, consumable stores, fuel, design, layout etc. are examples of

indirect material cost.

.3.2 Labour Cost

In actual production of the product, labour is the prime factor

which is physically and mentally involved. The payment of

remuneration of wages is made for their effort. The labour costs

are grouped into (a) Direct Labour and (b) Indirect Labour.

a) Direct Labour : Direct labour cost or direct wages refer to

those, specifically incurred for or can be readily charged to

or identified with a specific job, contract, work order or any

other unit of cost are termed as direct labour cost. Wages

for supervision, Wages for foremen, Wages for labours who

are actually engaged in operation or process are examples

of direct labour cost.

b) Indirect Labour : Indirect labour is for work in general. The

importance of the distinction lies in the fact that whereas

direct labour can be identified with and charged to the job,

indirect labour cannot be so charged and has therefore to be

treated as part of the factory overheads to be included in the

cost of production. Examples are salaries and wages of

supervisors, store keepers, maintenance labour etc.

.3.3 Expenses

All expenses are other than material and labour that are incurred

for a particular product or process. They are defined by ICMA as

“The cost of service provided to an undertaking and the notional

cost of the use of owned assets.” Expenses are further grouped

into (a) Direct Expenses and (b) Indirect Expenses.

a) Direct Expenses : Direct expenses which are incurred

directly and identified with a unit of output or process are

treated as direct expenses. Hire charges of special plant or

tool, royalty on product, cost of special pattern etc. are the

examples of direct expenses.

b) Indirect Expenses : Indirect expenses are expenses other

than indirect materials and indirect labour, which cannot be

directly identified with a unit of output. Rent, power, lighting,

repairs, telephone etc. are examples of indirect expenses.

Indirect expenses are those expenses which are incurred

after the manufacturing of goods.

Overheads

All indirect material cost, indirect labour cost, and indirect

expenses are termed as overheads. Overheads may also be

classified into (a) Production or Factory Overhead (b) Office and

Administrative Overheads (c) Selling Overhead and (d) Distribution

Overhead.

a) Production Overhead : Production Overhead is also termed

as Factory Overhead. Factory overhead includes, indirect

material, indirect labour and indirect wages which are incurred

in the factory. For example, rent of factory building, repairs,

depreciation wages of indirect workers etc.

b) Office and Administrative Overhead : Office and

Administrative Overhead is the indirect expenditure incurred

in formulating the policies, establishment of objectives,

planning, organizing and controlling the operations of an

undertaking. All office and administrative expenses like rent,

staff salaries, postage, telegram, general expenses etc. are

example.

c) Selling Overhead : Selling Overhead is the indirect expenses

which are incurred for promoting sales, stimulating demand,

securing orders and retaining customers. For example,

advertisement, salesmen’s commission, salaries of salesmen

etc.

d) Distribution Overhead : These costs are incurred from the

time the product is packed until it reaches its destination.

Cost of warehousing, cost of packing, transportation cost

etc. are some of the examples of distribution overhead.

CHECK YOUR PROGRESS

Q1. What is overhead?

...........................................................................

.....................................................................................................

Q2. Give some exmaples of direct expenses.

.....................................................................................................

.....................................................................................................

.....................................................................................................

Q3. State true or false for the following statements:

(i) Lubricating oil, fuel, designs are some examples of direct

material cost.

(ii) Rent, power, telephone bills etc. are some of the example

of indirect expenses.

.4 SPECIMEN OF COST SHEET

Meaning : Cost Sheet or a Cost Statement is “a document which

provides for the assembly of the estimated detailed elements of cost in

respect of cost centre or a cost unit.” The analysis for the different

elements of cost of the product is shown in the form of a statement

called “Cost Sheet”. The statement summarises the cost of

manufacturing a particular list of product and discloses for a particular

period :

I) Prime Cost

II) Works Cost (or) Factory Cost;

III) Cost of Production;

IV) Total Cost (or) Cost of Sales.

Importance of Cost Sheet

1) It provides for the presentation of the total cost on the basis of the

logical classification.

2) Cost sheet helps in determination of cost per unit and total cost

at different stages of production.

3) Assists in fixing of selling price.

4) It facilitates effective cost control and cost comparison.

5) It discloses operational efficiency and inefficiency to the

management for taking corrective actions.

6) Enables the management in the preparation of cost estimates to

tenders and quotations.

SPECIMEN OF COST SHEETCost sheet for the Period ...........

Particulars Total Cost Cost Per Unit

Rs. Rs.

EXERCISE : 1

From the following particulars, prepare a Cost Sheetshowing (1) Cost of Materials Consumed (2) PrimeCost (3) Factory Cost (4) Cost of Production and (5)Profit.

Rs.Opening Stock of raw materials 20,000Opening Stock of work in Progress 10,000Opening stock of finished goods 50,000Raw materials purchased 5,00,000Direct wages 3,80,000Sales for the year 12,00,000Closing stock of raw materials 75,000Closing stock of work in progress 15,000Factory overhead 80,000Direct expenses 50,000Office and Administrative overhead 60,000Selling and distribution expenses 30,000

Solution : 1

Cost Sheet for the year ..................Particulars Amount Amount

Rs. Rs.

Particulars Amount Amount

Rs. Rs.

CHECK YOUR PROGRESS

Q4. What is cost sheet?

.........................................................................

.........................................................................

Q5. List three important factors of cost sheet.

.......................................................................................................

.......................................................................................................

.......................................................................................................

.5 LET US SUM UP

In this unit, we have discussed about cost sheet. Cost sheet is

the analytical presentation of total cost, i.e. material, labour and overhead

cost. Cost sheet is a document which provides for the assembly of the

estimated detail elements of cost in respect of a cost unit. Cost sheets

assist in fixing of selling price. It also enables the management in the

preparation of cost estimates to tenders and quotations.

.6 FURTHER READINGS

1. Management Accounting: Khan & Jain

2. Cost Accounting : Hongren

3. Cost & Management Accounting: Jain & Narang

4. Cost Accounting: B. Banerjee

.7 ANSWERS TO CHECK YOURPROGRESS

Ans to Q1. All indirect material cost, indirect labour cost, and indirect

expenses are termed as overheads

Ans to Q2. Hire charges of special plant or tool, royalty on product, cost

of special pattern etc. are the examples of direct expenses.

Ans to Q3. (i) False, (ii) True

Ans to Q4. Cost Sheet or a Cost Statement is “a document which

provides for the assembly of the estimated detailed elements of

cost in respect of cost centre or a cost unit.”

Ans to Q5. 1) It provides for the presentation of the total cost on the

basis of the logical classification.

2) Cost sheet helps in determination of cost per unit and total

cost at different stages of production.

3) Assists in fixing of selling price.

.8 MODEL QUESTIONS

Q1. What do you understand by cost sheet? Briefly explain with

specimen of cost sheet.

Q2. Explain the different elements of total costs.

Q3. Explain the importance of cost sheet.

Q4. Explain the different functional classification of overheads.

Q5. Distinguish between :

a) Direct material and Indirect material

b) Direct labour and Indirect labour.

c) Direct expenses and Indirect expenses.

Q6. From the following particulars of a manufacturing firm prepare a

statement showing :

1) Cost of Materials Consumed

2) Factory or Work Cost

3) Cost of Production

4) Profit

Cost of Production Rs.

Stock of materials on 1st January 2003 80,000

Purchases during the period 22,00,000

Stock of finished goods on 1st January 2003 1,00,000

Direct wages 10,00,000

Sales 48,00,000

Factory on cost 3,00,000

Office and Administrative Expenses 2,00,000

Stock of raw materials on 31st December 2003 2,80,000

Stock of finished goods on 31st December 2003 1,20,000

Ans. :

(1) Rs. 20,00,000 (2) Rs. 33,00,000 (3) Rs. 35,00,000

(d) Rs. 13,20,000

*** ***** ***