Barings ASEAN Frontiers Equity Strategy

75

Barings ASEAN Frontiers Equity Strategy 1Q 2022 For Investment Professionals only (HK: 22/2186947)

-

Upload

khangminh22 -

Category

Documents

-

view

9 -

download

0

Transcript of Barings ASEAN Frontiers Equity Strategy

Barings ASEAN Frontiers Equity Strategy

1Q 2022

For Investment Professionals only

(HK: 22/2186947)

For investment professionals only 2

Barings Overview

1. Includes third party, external AUM only.

All figures are as of March 31, 2022 unless otherwise indicated. Assets shown are denominated in USD. Percentages may not equal 100 due to

rounding.

Investment Offices Global Headquarters Other Locations

• Barings is a GLOBAL INVESTMENT MANAGER sourcing differentiated

opportunities and building portfolios across public and private fixed income,

real estate and specialist equity markets

• A subsidiary of MASSMUTUAL, we have the financial stability and flexibility to

take a long-term approach

• Our GLOBAL FOOTPRINT gives us a broad perspective and the ability to truly

partner with our clients to invest across North America, Europe and Asia Pacific

• We are committed to SUSTAINABLE PRACTICES AND RESPONSIBLE

INVESTMENT as we aim to serve our clients, communities and employees

ASSETS UNDER MANAGEMENT

1,200+EXTERNAL CLIENTS

1,800+PROFESSIONALS GLOBALLY

EXTERNAL AUM BY REGION1

38%

31%

31%

Americas Asia Pacific EMEA

B$371+

For investment professionals only 3

PUBLIC EQUITIES & MULTI ASSET2

Aims to deliver superior risk-adjusted returns through fundamental

analysis and high-conviction, high-active share solutions

GLOBAL & INTERNATIONAL EQUITIES

$3.3 B AUM

EMERGING MARKET EQUITIES

$7.4 B AUM

SMALL CAP EQUITIES

$3.3 B AUM

MULTI ASSET

$2.6 B AUM

Global Investment Capabilities

1. Excludes the Korean fixed income strategy totaling $1.6 billion in AUM.

2. Excludes the Korean domestic equities strategy, which has $9.5 billion in AUM and other equities of $0.1 billion.

3. Includes the EM Corporate Debt strategy, which has $5.9 billion in AUM.

4. Represents dedicated capital solutions accounts and does not include assets managed in other cross-platform portfolios.

5. Projected AUM figures.

6. Includes real estate debt assets that are managed as part of affiliated fixed income portfolios.

All figures are as of March 31, 2022 unless otherwise indicated. Assets shown are denominated in USD.

Barings leverages its DEPTH AND BREADTH OF EXPERTISE across public

and private markets to help meet our clients’ evolving investment needs

PUBLIC FIXED INCOME1

Provides access to strategies ranging from investment grade

to high yield across developed and emerging markets

INVESTMENT GRADE

$110.5 B AUM

HIGH YIELD BONDS & LOANS3

$61.0 B AUM

STRUCTURED CREDIT

$22.7 B AUM

GLOBAL SOVEREIGN DEBT & CURRENCIES

$15.8 B AUM

PRIVATE CREDIT

Offers a diverse range of private debt financing

solutions by partnering with our broad industry network

GLOBAL PRIVATE FINANCE

$35.9 B AUM

INFRASTRUCTURE & PRIVATE PLACEMENTS

$42.6 B AUM

REAL ESTATE5

Provides a broad spectrum of solutions across

private real estate debt and equity

REAL ESTATE DEBT6

$29.2 B AUM

REAL ESTATE EQUITY

$17.4 B AUM

PRIVATE EQUITY5

Leverages our global presence in an effort to identify

unique risk-adjusted return opportunities

DIRECT PRIVATE EQUITY

$2.6 B AUM

FUNDS & CO-INVESTMENTS

$5.3 B AUM

MULTI STRATEGY

Utilize our expansive asset market coverage to offer solutions such as income, target return and absolute return

PUBLIC

PRIVATE

CAPITAL SOLUTIONS4

$0.8 B AUM

For investment professionals only 4

Barings achieved a LEED GOLD CERTIFICATION for our global Charlotte headquarters, a BREEAM

EXCELLENT RATING for our London office, and a LEED GOLD CERTIFICATION for our Shanghai office.

Our dedicated resources help develop and

deliver our sustainability and ESG strategy, policy,

partnerships, research, training and reporting.

We are a signatory to the Principles

for Responsible Investment, a member of the

United Nations Global Compact and Climate

Action 100+, and public supporters of the Task

Force on Climate-related Financial Disclosures.

We work to advance the missions of these

industry partnerships.

Our Sustainability Committee consists of senior

business leaders and is tasked with supporting

sustainability strategy execution.

Our Sustainability Working Groups focus on long-

term strategic projects and regularly meet and

report to the Sustainability Committee.

FORMAL GOVERNANCE DEDICATED RESOURCES INDUSTRY PARTNERS

WE ARE DELIBERATE IN OUR DIRECTION, PARTNERSHIPS AND

DECISION MAKING TO ACHIEVE LONG-TERM, LASTING CHANGE

We integrate environmental, social

and governance information into our analysis

and decision-making across our investment

teams and business lines.

We are active stewards of the entities in which

we invest; this goes hand-in-hand with our active

investment approach. We believe the best way to

advance change is by rewarding progress.

ESG is ingrained in our business activities

through our corporate responsibility program. This

includes our Barings Social Impact philanthropic

program, as well as our focus on diversity, equity

and inclusion across our business.

ESG INTEGRATION STEWARDSHIP CORPORATE RESPONSIBILITY

OUR SUSTAINABILITY GOVERNANCE, RESOURCES AND PARTNERSHIPS

Investing in Lasting Change, Together

For investment professionals only 5

Our Commitment To Diversity, Equity & Inclusion

To foster an EQUITABLE AND INCLUSIVE environment where everyone can succeed

PHILOSOPHY OUR APPROACH CULTURE

The varying backgrounds, life experiences and

perspectives of our people influence our

approach to investing and creating culture.

Outcome and impact-centered global strategy

tailored to regional needs. Leaders first.

Managers model. Everyone’s responsible.

Maintain a culture of respect and integrity that

prioritizes genuine interactions and courageous

conversations to encourage authenticity,

belonging and psychological safety.

PEOPLE FOCUS COMMUNITY IMPACT PARTNERSHIPS

Six Employee Resource Groups (ERG) support

overall strategy and help build community,

utilizing culture surveys and focus groups to

collect qualitative data and regularly assess

impact.

Cross-collaboration with Barings Social Impact

and other teams to effectuate broader impact for

diverse communities.

Evaluate talent opportunities and gaps,

and actively partner with organizations to

broaden access to entry, mid- and

senior-level diverse talent.

MISSION

For investment professionals only 6

Equity Platform with Research at its CentreEquity Platform with Research at its Centre

Research57 Investment

Professionals

Globally

Source: Barings, March 31, 2022.

Number in brackets indicates years of industry experience as at March 31, 2022.

*AUM in USD as at March 31, 2022. AUM excludes BAMK, Active Passive and Active Quant.

Three groups served by a central research hub supporting an active investment platform

• Manage $14.2bn* of equity strategies across Developed and Emerging

markets.

• Investment approach characterized by:

– Active management and active ownership

– Differentiated fundamental research;

– Portfolio construction informed by asset class characteristics

• Ability to tailor strategies to meet client requirements.

PLATFORM OVERVIEW

• Centralized research team, with continuous interaction across groups.

• Regional expertise and global sector-focused teams for Resources,

Healthcare, and Technology.

• Specialist investment teams draw on the broader research platform in

addition to dedicated resources.

• Supported by 5 Dealers, 6 Client Portfolio Managers and Investment

Specialists.

RESEARCH AND PORTFOLIO TEAM

CORE PRODUCT OFFERING

EmergingWilliam Palmer (28)

Michael Levy (26)

$7.5bn*

Small and Mid CapNicholas Williams (31)

$3.3bn*

Global & InternationalDavid Bertocchi (23)

$3.4bn*

Research45+ Investment

Professionals

Globally

For investment professionals only 7

Barings ASEAN Frontiers Equity Strategy

Source: Barings, March 31, 2022.

*Relative to the MSCI AC ASEAN (Total Net Return) Index. Investors should bear in mind that these are return targets, rather than actual returns, and the fund may

experience substantial loss. There can be no assurance that such return targets will be achieved. AUM rounded to the nearest US$10m, gross assets. ** Barings

ASEAN Frontiers Fund was endorsed by RSMR as a Rated fund in 2021. Barings ASEAN Frontiers Fund was awarded BENCHMARK Fund of the Year Awards 2020

ASEAN Equity—Best-in-Class in Hong Kong, based on its performance between October 1, 2019 and September 30, 2020. Barings ASEAN Frontiers Fund was

awarded BENCHMARK Fund of the Year Awards 2019 ASEAN Equity—Best-in-Class in Hong Kong, based on its performance between October 1, 2018 and

September 30, 2019. The Fund was awarded Bloomberg Businessweek (Chinese Edition) Top Fund Awards 2019 ASEAN Equity—Best Performer, based on its

performance between October 2, 2014 to September 30, 2019. . Please note that Barings ASEAN Frontiers Fund is not available to US investors.

Barings Global Emerging Markets Equity

AUM $570 million

Benchmark MSCI AC ASEAN (Total Net Return) Index

Objective 3% gross outperformance of benchmark*

Team Location Singapore, Hong Kong

Vehicles UCITS, Separate accounts

ESG Integrated ESG and Active Engagement (SFDR: Article 8)

Awards**

BARINGS ASEAN FRONTIERS EQUITY STRATEGY

Investment Process

For investment professionals only 9

Barings’ ASEAN Frontiers Equity Strategy Overview

Philosophy, Style and Process

Investment Philosophy

Investment Style

Investment Process

• We believe that Equity markets are both inefficient and risky

• Attractive risk-adjusted returns can be achieved through fundamental bottom-up stock selection and a

disciplined portfolio construction process

• Growth at a Reasonable Price (GARP)

• Our Key Differentiators:

• Extensive primary research supported by a large team of experienced EM professionals

• Proprietary fundamental analysis evaluating companies over a 5 year research horizon

• Fully integrated dynamic ESG assessment and active engagement

• Macro considerations incorporated through our Cost of Equity approach

• Proprietary risk management tools support portfolio construction

For investment professionals only 10

Barings ASEAN Frontiers Equity Strategy

Source: Barings, March 31, 2022.

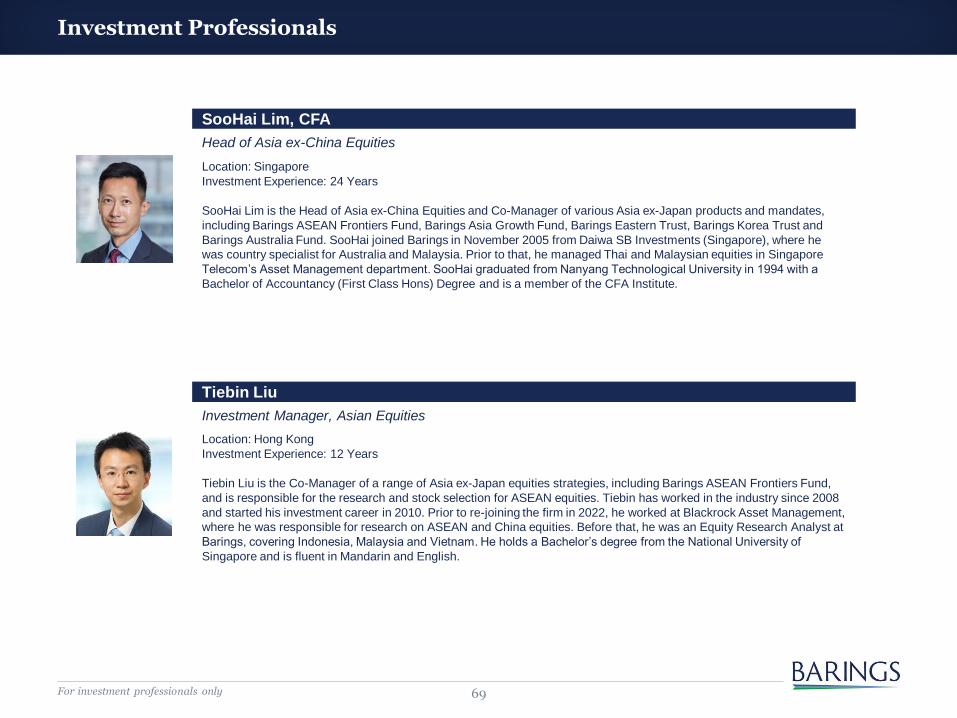

SooHai Lim and Tiebin Liu are the co-managers of the Barings ASEAN Frontiers Equity Strategy,

and are essentially the strategy’s ultimate decision makers

Investment Experience: 24 Years

Firm Tenure: 16 Years

Investment Experience: 12 Years

Firm Tenure: <1 Year

SooHai LimHEAD OF ASIA EX-CHINA EQUITIES

Tiebin LiuINVESTMENT MANAGER

For investment professionals only 11

Asia Equity Investment Team

Barings Asian Equity Investment Team also leverages the expertise of dedicated HK China Equity investment

professionals for portfolio management

*Based in Shanghai. **Shared Resources

Source: Barings, April 2022. Years of investment experience as at March 31, 2022.

Manager/Analyst

Investment

Experience

(Years)

Hong Kong China equities

William Fong 21

Nicola Lai 15

Baiding Rong 13

Nathan Jiang* 12

Alick Lu 12

Alan Lee 9

Freya Liu* 6

Stephen Yin 4

Salinas Zhang 3

Resources (Asia)

Maggie Sheng** 7

SooHai LimHead of Asia ex-China Equities

24 years of investment experience

Based in Singapore

Eunice HongInvestment Manager

15 years of investment experience

Based in Singapore

Barings Hong Kong China Equity Investment Team

Kuldeep KhanapurkarInvestment Manager

15 years of investment experience

Based in Hong Kong

Julie LeeInvestment Analyst

14 years of investment experience

Based in Singapore

Tiebin LiuInvestment Manager

12 years of investment experience

Based in Hong Kong

Yvonne TsaiInvestment Analyst

13 years of investment experience

Based in Taiwan

Zachary OngInvestment Analyst

6 years of investment experience

Based in Singapore

For investment professionals only 12

Global Emerging Markets Equity Team Research Capabilities

The Global Emerging Markets equity team leverages the expertise of 29 dedicated investment professionals:

• 14 years average investment experience

• Diversity across regional teams with 15+ different nationalities represented

• Providing in-depth research coverage of 500 emerging market companies

Source: Barings: Team Snapshot as of April 2022; number in brackets indicates years of industry experience as of March 31, 2022.

*Global Head of Equities; **Dual role as Equity Business Analyst

Global Emerging Markets Equity Leadership

William Palmer (28) – Asia Pacific (ex-Japan)

Co-Head of Global Emerging Markets Equity

Michael Levy (26) – EM (ex-Asia)

Co-Head of Global Emerging Markets Equity

Asia Pacific

Soo-Hai Lim (24)

Eunice Hong (15)

Kuldeep Khanapurkar (15)

Tiebin Liu (12)

Julie Lee (14)

Yvonne Tsai (13)

Zachary Ong (6)

China

William Fong (21)

Nicola Lai (15)

Baiding Rong (13)

Nathan Jiang (12)

Alick Lu (12)

Alan Lee (9)

Maggie Sheng (7)

Freya Liu (6)

Stephen Yin (4)

Salinas Zhang (3)

EMEA

Matthias Siller (24)

Ghadir Cooper (26)*

Maria Szczesna (15)

Adnan El-Araby (12)

Timothy Eklund (11)

Alay Patel (10)

LATAM

Mike Simpson (23)

Luis Alves De Lima (16)

Isabelle Irish (16)

ESG Equity Coordinator

Marios Halloumis (5)**

For investment professionals only 13

Refining the Investment Universe

From the unconstrained universe to portfolio candidates

Liquidity assessment

– Exclude companies with insufficient liquidity

Identifying GARP investible universe

– Growth at a reasonable price characteristics

– Commitment and competence of the management

– Accounting practices and transparency (ESG factors)

In-depth fundamental research

– Company meetings and fundamental analysis with all research

centrally stored and accessible to all investment professionals

Portfolio candidates

– Presented and debated with the investment team during various

collaborative interactions

Unconstrained

Equity

Universe

Liquidity

Evaluation

GARP

Universe

In-depth

fundamental

research

Portfolio

candidates

For investment professionals only 14

Fundamental Research – Consistent Company Scorecard

A consistent research approach helps evaluate companies and determine attractiveness by country and sector

Each company is rated on a scale of 1-5, with a 1 score being the most favourable and a 5 score, the least attractive.

Source: Barings, March 2022.

Growth Quality Valuation

- Historical – last 3-years’ earnings growth

- Near-term – next 12-months’ earnings growth

- Long-term – next 5-years’ forecast earnings

growth

- Franchise – competitive advantage,

efficiency, stability

- Management – competence, commitment

and alignment with shareholder Interest

- Balance sheet – cash flow, working capital,

capital structure analysis

- Barings valuation Approach – 5-years

discounted by our Cost of Equity to set price

target and determine upside

Company Score [1-5]

Sector / Industry / Macro Dynamics

5 Year Proprietary Financial Forecasts

ESG considerationsKey I

np

uts

Company Meetings

For investment professionals only 15

Fundamental Research – Company Meetings

Our EM Equity platform completed approximately 2500 company interactions in 2021

Source: Barings.

*Data representative of typical format split, based on 2019 data.

5 Year Proprietary Financial Forecasts

Sector / Industry / Macro Dynamics

ESG Considerations

Company Meetings

Is your market share sustainable?

What is the trend in profit margins?

How will the product mix change?

What is the industry likely to grow at?

What will be your effective tax rate?

40%

37%

23%

Meeting Format*

One to One Meeting Group Meeting Management Call

For investment professionals only 16

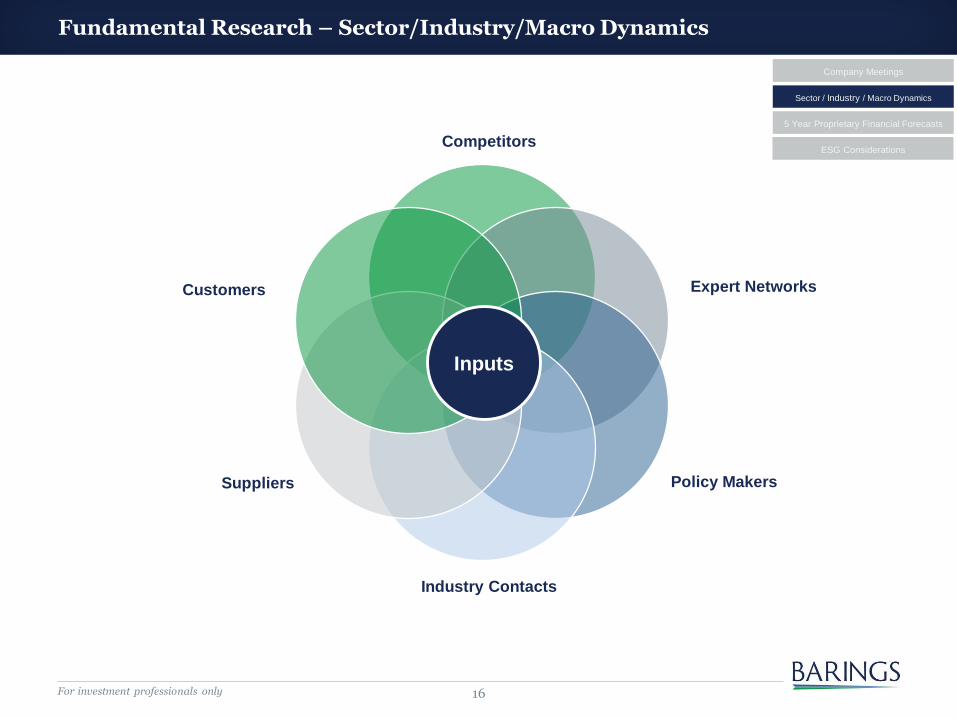

Competitors

Expert Networks

Policy Makers

Industry Contacts

Suppliers

Customers

Inputs

Fundamental Research – Sector/Industry/Macro Dynamics

5 Year Proprietary Financial Forecasts

Sector / Industry / Macro Dynamics

ESG Considerations

Company Meetings

For investment professionals only 17

Fundamental Research – 5 Year Proprietary Financial Forecasts

We produce financial models and earnings forecasts over a five-year research horizon

For illustrative purposes only.

Source, Barings, Factset, March 2022. *Estimates based on weighted average constituents of MSCI AC ASEAN index.

5 Year Proprietary Financial Forecasts

Sector / Industry / Macro Dynamics

ESG Considerations

Company Meetings

Cash Flow Statement

($ Mn) 2021 2022e 2023e 2024e 2025e 2026e

Depreciation & Amortization 1,420 1,557 1,694 1,824 1,970 2,126

Capital expenditures 3,175 3,407 3,654 3,917 4,197 3,175Balance Sheet

($ Mn) 2021 2022e 2023e 2024e 2025e 2026e

Assets

Total current assets 20,289 21,163 22,100 23,219 24,561 26,146

Total non-current assets 20,541 22,222 24,003 25,905 27,928 30,080

Liabilities

Total liabilities 27,727 29,785 31,991 34,323 36,814 39,467

Equity 13,103 13,600 14,112 14,801 15,675 16,759

Income Statement

($ Mn) 2021 2022e 2023e 2024e 2025e 2026e

Revenues 141,576 151,992 163,091 174,910 187,494 200,892

Cost of sales 123,152 132,213 141,867 152,148 163,095 174,749

Gross profit 18,424 19,780 21,224 22,762 24,400 26,143

EBIT 4,480 4,811 5,168 5,548 5,952 6,382

Pre-tax profit 4,442 4,744 5,161 5,520 5,911 6,366

Net profit 3,134 3,634 3,716 3,974 4,256 4,584

DPS 1.47 1.79 2.05 2.35 2.69 3.09

EPS 7.09 8.35 8.67 9.40 10.21 11.14

Limited Sell Side Forecast

0

2

4

6

8

10

12

14

16

18

2022e 2023e 2024e 2025e 2026e

SELL SIDE ANALYST ESTIMATES PER COMPANY*

For investment professionals only 18

For illustrative purposes only. We will not directly invest in companies that violate International Conventions – please refer to our Active Engagement policy

for further details. Source: Barings, March 2022.

Unfavorable Not improving Improving Exemplary

Fundamental Research – ESG Integration

How ESG adds value

• Uncover risks not apparent from traditional fundamental analysis

• Highlights more sustainable business practices and investment opportunities

Our dynamic approach

• We look for signs of improving or deteriorating ESG standards

Proprietary assessment

• ESG due diligence is based on our company knowledge and regular management interaction

• Each company is evaluated on 9 key ESG topics scored from “Unfavorable” to “Exemplary”

• Overall assessment score impacts the Barings Cost of Equity (COE), valuation and Company Scorecard

• We engage with companies on material ESG issues

-1% to COE+2% to COE

Part of our fundamental research due diligence

5 Year Proprietary Financial Forecasts

Sector / Industry / Macro Dynamics

ESG Considerations

Company Meetings

2020 UNPRI

SCORE

BARINGS

SCORE

MEDIAN

SCORE

Incorporation A+ A

Active

EngagementA B

For investment professionals only 19

Change to Cost of Equity: +0.67%

9 key topicsScore /

Rationale

Data / Issues to

consider

Sustainability

Of The

Business Model

(Franchise)

1 Employee Satisfaction Improving

Astra provides a comprehensive, structured and tiered competence and leadership development

program. Employees remuneration policies are tied by the consideration of internal fairness and

external competitiveness, which are reviewed annually. Safety training is provided to all manufacturing

employees. Its plants are ISO45001 (Occupational health and safety), OHSAS 180010, SMK3 certified.

2 Resource Intensity UnfavorableThe mining segment is one of the major emitters of greenhouse gases and it produces fossil energy

resources that also significantly contributes to global CO2 emissions.

3Traceability / Security In

Supply ChainUnfavorable

Its commodity businesses (mainly CPO and mining) are subjected to environmental related risks. Its

CPO business is subject to deforestation and wild fire risks, while mining is subjected to mining

accident risks. Based on our conservation with management, we concluded that Astra and its

subsidiaries have strict environmental and safety protocols, detailed policies and processes for each

commodity business to mitigate such risks but do not fully eliminate them.

Corporate

Governance

Credibility

(Management)

4Effectiveness Of Supervisory

/ Management BoardNot improving

Only 3 independent commissioners out of 10. Only 1 female director in its Board of Directors.

Management is working on improving board diversity and independence.

5Credibility Of Auditing

ArrangementsImproving

Audit Committee comprises 4 members, Chairman of the Committee, 2 independent members, and 1

special member with no voting rights. The Chairman of the Audit Committee is an Independent

Commissioner and appointed by the Board of Commissioners.

6Transparency & Accountability

Of ManagementNot improving

Board of Directors (BoD) remuneration structure comprises salary, bonus and fixed or variable

allowances. However, BoD salary amount were not disclosed. IR team is accessible.

Hidden Risks

On The

Balance Sheet

(Balance Sheet)

7 Environmental Footprint Not improving

Although Astra has shown positive progression on carbon emission reduction with an average GHG

Emission Reduction Intensities/year of 5%, there is no set long-term targets. It implements Astra Green

Energy in its energy conservation program such as energy efficiency program and adoption of energy-

saving technologies. PHEV / EV, clean tech auto sales remain insignificant due to affordability and lack

of supporting infrastructure. It is working closely with Toyota and the government on initiatives to

promote and increase adoption; eg. partnering with Ministry of Industry to implement pilot projects

studies on the use of EV vehicles in a number of regions in Indonesia.

8Societal Impact of Products

/ ServicesExemplary

Social contribution is carried out by all organizations through CSR programs that focus on 4 main

pillars: Health, Education, Environment and Entrepreneurship. Examples in the area of health include

the provision of assistance to 1,698 community clinics, support in the provision of free healthcare

service to 132,180 patients and donation of eyeglasses, mostly for children living in the outermost,

remote and rural regions.

9 Business Ethics Improving The company has whistle blowing program that reports to the internal Audit Group.

PT Astra International – ESG Analysis

Source: Barings, December 2021.

Stock sample is for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions. Any

prediction, projection or forecast is not necessarily indicative of the future or likely performance.

For investment professionals only 20

Our Approach to Active Engagement

Driving positive change through engagement over blanket exclusions of entire sectors

Policy available here: https://barings-web.azureedge.net/assets/user/media/Barings-Public-Equities-ESG-Integration-Active-Engagement-Policy.pdf

DESIGN

ENGAGEMENT

PLAN AND

MEASURE

EFFECTIVENESS

ENGAGEMENT FRAMEWORK

BARINGS ESG

ANALYSIS

IDENTIFIES

NEED FOR

ENGAGEMENT

WHAT DO WE AIM TO ACHIEVE?

• To influence (or identify the need to influence) ESG practices

• To improve disclosure

• Improve investment returns

HOW DO WE DECIDE WHERE TO ENGAGE?

The prioritization of engagement activities is driven by:

• In-depth company knowledge of the company and regular interactions

• Commitments to the UN PRI, UN Global Compact and Barings values

• Sustainability Accounting Standard Board’s (SASB) material issues

IMPACT ON THE INVESTMENT RATIONALE

Successful Engagement

• Upgrade of quality score, Reduction in COE

• Unlock shareholder value

Unsuccessful Engagement

• Downgrade of quality score, Increase in COE

• Deterioration in investment rationale - Potential Divestment

ENGAGEMENT

SUCCESSFUL

OR ONGOING

=

RETAIN

INVESTMENT

ENGAGEMENT

UNSUCCESSFUL

=

POTENTIAL

DIVESTMENT

MONITOR

ESCALATE

For investment professionals only 21

Integrating Macro – Barings Cost of Equity Used in Company Valuation

A discount rate is used to determine a target price

Enables price target comparisons across sectors and geographies

Cost of

Equity

(Discount

rate)

Risk

Free Rate

Equity Risk

Premium

Stock

Specific

Risk

ESG= + + +

Systematic Idiosyncratic

Base Assumptions

4% - Developed Markets

5% - Emerging Markets

6% - Frontier Markets

2.25% + 5Y IMF CPI

forecast

Can add (0 to 2%) Can add ( -1% to 2%)

For investment professionals only 22

•Research recommendations are presented to the investment teams for debate through a series of formal and informal meetings

• Investment team review and challenge assumptions of the investment thesis and underlying financial model

•This process continues until investment case is validated or rejected

Validating the investment thesis

Valuation Output – Is There Unrecognised Growth?

For illustrative purposes only.

5 Year Proprietary Financial Forecasts

2021 2022e 2023e 2024e 2025e 2026e

EPS 38.4 51.2 66.0 85.8 99.5 113.1

- Growth 16.9% 33.2% 29.1% 29.9% 15.9% 13.7%

DPS 0.0 2.1 3.4 4.3 5.0 5.7

Discounted by Barings Cost of Equity

Systematic

Inflation 5Y CPI + 2.25% 4.8%

Market risk premium 5.0%

Idiosyncratic

Company specific risk addition [0,2%] 0.3%

ESG impact [-1,2%] -0.1%

Barings discount rate 10.0%

0

50

100

150

200

250

300

CurrentShare Price

12M Price Target

US ($)

Unrecognised

Growth?

Output from Barings valuation methodology

Fully Valued /

Overvalued?

For investment professionals only 23

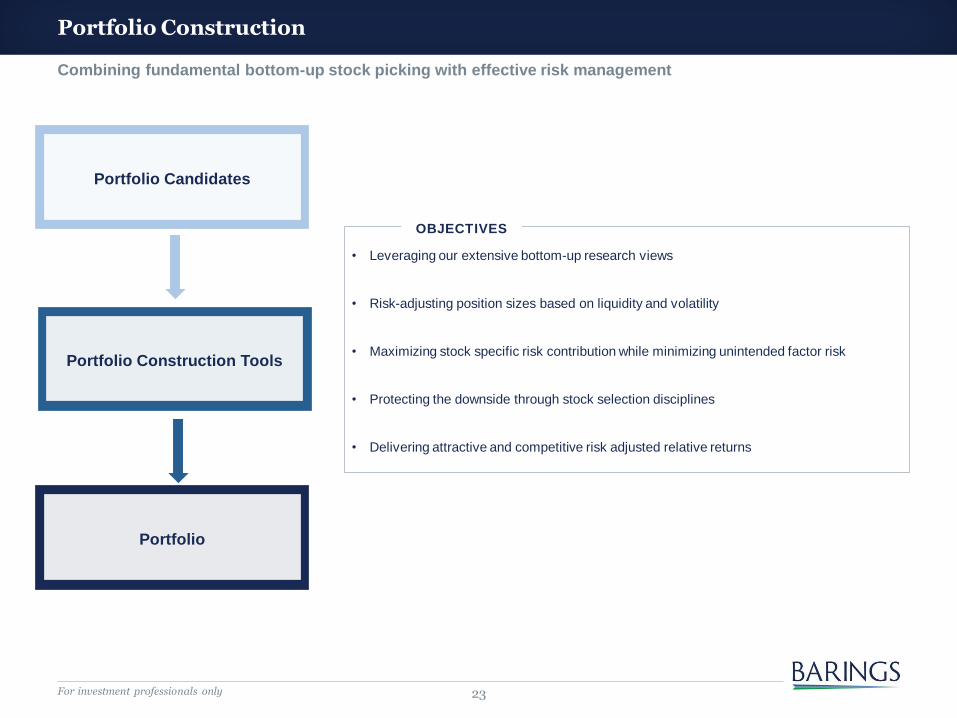

Portfolio Construction

Combining fundamental bottom-up stock picking with effective risk management

• Leveraging our extensive bottom-up research views

• Risk-adjusting position sizes based on liquidity and volatility

• Maximizing stock specific risk contribution while minimizing unintended factor risk

• Protecting the downside through stock selection disciplines

• Delivering attractive and competitive risk adjusted relative returns

Portfolio Candidates

Portfolio Construction Tools

Portfolio

OBJECTIVES

For investment professionals only 24

Proprietary Portfolio Construction Tools

Source: Barings, as of March 31, 2022. Data relates to the representative account of Barings ASEAN Frontiers Equity strategy.

Holdings are subject to change.

Style Horizon Analysis – Portfolio characteristics reflect GARP style

Macro Sensitivity Analysis

Minimal sensitivity to movements in macro events help avoid performance drawdown

-0.30 -0.21-0.07 -0.05

-0.23

0.22 0.300.10

0.29 0.28 0.20 0.290.07

0.29 0.39

-0.48

0.100.24 0.14

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50P

rice

to

Boo

k

Div

ide

nd

Yie

ld

Pri

ce

to

Earn

ings

Pri

ce

to

Earn

ings N

TM

Va

lue C

om

po

site

Re

turn

on E

qu

ity

Re

turn

on I

nve

ste

d C

apital

Ea

rnin

gs V

ola

tilit

y

De

bt

to E

quity

Qua

lity C

om

posite

Ea

rnin

gs G

row

th 3

Y H

IST

Sa

les G

row

th 1

Y H

IST

Ea

rnin

gs G

row

th N

TM

Su

sta

ina

ble

Gro

wth

Gro

wth

Com

posite

Mark

et C

ap

Mom

entu

m 6

Mth

Mom

entu

m 1

2 M

th

Mom

entu

m C

om

posite

Exp

osu

re (

Z s

co

re)

Exposures

5-year max

5-year avg

5-year min

-0.10

0.07 0.17

-0.03 -0.10

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

10Y USD Treasury+ 70bps

Asia ex. JapanEquities + 10%

Gold +10% USDJPY -8% Oil +25%

Acti

ve R

etu

rn (

%)

For investment professionals only 25

Portfolio Monitoring and Oversight

Investment

Team

Independent

Risk Team

Independent

Compliance

Team•The Risk Management department is organisationally and hierarchically independent from the portfolio management departments.

•Responsible for delivering the oversight and the tools, systems and advice necessary in identifying, managing and monitoring risks.

Independent Risk Team

•The Compliance department is organisationally and hierarchically independent from the portfolio management departments.

•Responsible for assessing and maintaining compliance with investment adviser policies, procedures, applicable regulations and monitoring client guidelines.

Independent Compliance Team

• Investment analysts monitor each investment thesis, continually integrating new information into their analysis.

•Our portfolio managers continually review and monitor the portfolio.

Investment Team

Portfolio managers continually review and monitor client portfolios supported by independent risk and

compliance functions

For investment professionals only 26

Sell Discipline

We consider selling when

The original mispricing has closed

The investment case has changed

There is a significantly more attractive idea

Characteristics & Performance

For investment professionals only 28

Portfolio Characteristics

Source: Barings, March 31, 2022. Data relates to the representative account of Barings ASEAN Frontiers Equity strategy.

Holdings and characteristics are subject to change.

*Ex-ante **Excludes cash and commitment

Barings ASEAN Frontiers

Equity StrategyMSCI AC ASEAN Index

Return on Equity (LTM) 14.1% 9.8%

EPS Growth (12 Month Forward) 15.9% 13.6%

Three Year EPS growth (Trailing) 3.1% -4.3%

Price to Book (Trailing) 2.4x 1.8x

P/E (NTM) 17.7x 17.2x

Number of Holdings 62 139

Active Share 55.0% --

Off Benchmark 27.2% --

Tracking Error* 4.1% --

Standard Deviation* 19.0% 18.3%

Beta* 1.01 --

Av. Market Cap (US$ Billion) 25.2 26.5

Small/ Mid Weight (<US$5Bn)** 28.6% 12.5%

For investment professionals only 29

Breakdown of Portfolio

Country and Sector Allocations as at March 31, 2022

Source: Barings. Allocations are subject to change. Figures may not add to 100% due to rounding.

Data relates to the representative account of Barings ASEAN Frontiers Equity strategy.

Country and sector breakdown are a by product of bottom-up stock selection

Country/Region Positions (%) Sector Positions (%)

Overweight Underweight

FundMSCI AC

ASEANRelative Weight

Information Technology 7.5 1.4

Materials 9.9 5.7

Cash 4.2 0.0

Industrials 11.7 9.2

Consumer Discretionary 6.9 4.6

Consumer Staples 8.1 7.8

Health Care 2.5 2.9

Utilities 2.9 3.7

Energy 1.0 4.4

Communication Services 10.7 14.9

Financials 32.6 37.3

Real Estate 2.0 8.1

Total 100.0 100.0

FundMSCI AC

ASEANRelative Weight

Indonesia 24.9 19.2

Cash 4.2 0.0

Vietnam 1.8 0.0

China 1.8 0.0

Philippines 6.0 8.5

Thailand 17.5 20.4

Malaysia 13.3 16.4

Singapore 30.5 35.6

Total 100.0 100.0

6.1

4.2

4.2

2.5

2.3

0.3

-0.4

-0.8

-3.4

-4.2

-4.7

-6.1

5.7

4.2

1.8

1.8

-2.5

-2.9

-3.1

-5.0

For investment professionals only 30

High Conviction Portfolio

Top Ten Active Holdings

Source: Barings, March 31, 2022. Holdings are subject to change. Figures may not add up due to rounding.

Data relates to the representative account of Barings ASEAN Frontiers Equity strategy.

Name % of active

weightCountry/Region Sector

PT Vale Indonesia 2.4 Indonesia Materials

PT Astra International 2.3 Indonesia Consumer Discretionary

International Container Terminal Services 1.9 Philippines Industrials

PT Bank Central Asia 1.7 Indonesia Financials

Vitrox 1.6 Malaysia Information Technology

PT Merdeka Copper Gold 1.6 Indonesia Materials

JMT Network Services 1.5 Thailand Financials

Press Metal Aluminium 1.5 Malaysia Materials

Frontken 1.5 Malaysia Industrials

Metropolitan Bank & Trust 1.5 Philippines Financials

Total 17.5

For investment professionals only 31

High Conviction Portfolio

Top Ten Largest Holdings

Source: Barings, March 31, 2022. Holdings are subject to change. Figures may not add up due to rounding .

Data relates to the representative account of Barings ASEAN Frontiers Equity strategy.

Name % of Strategy Country/Region Sector

DBS 7.3 Singapore Financials

PT Bank Central Asia 6.3 Indonesia Financials

United Overseas Bank 5.6 Singapore Financials

Sea 5.2 Singapore Communication Services

PT Bank Rakyat Indonesia 4.2 Indonesia Financials

PT Astra International 3.7 Indonesia Consumer Discretionary

Bangkok Dusit Medical Services 2.5 Thailand Health Care

International Container Terminal Services 2.5 Philippines Industrials

Oversea-Chinese Banking 2.4 Singapore Financials

PT Vale Indonesia 2.4 Indonesia Materials

Total 42.2

For investment professionals only 32

Relative Contributors and Detractors to Performance

12 months to March 31, 2022

Source: Barings, March 31, 2022. Holdings are subject to change.

Data relates to the representative account of Barings ASEAN Frontiers Equity strategy.

Contributors Detractors

CompanyContribution to

Portfolio (%)

Sea 2.4

International Container Terminal Services 1.1

PT Merdeka Copper Gold 1.0

PT Vale Indonesia 1.0

JMT Network Services 1.0

CompanyDetraction from

Portfolio (%)

Grab -1.5

Nanofilm Technologies -0.9

Pentamaster -0.5

PT Bukalapak.com -0.5

R. S. -0.5

For investment professionals only 33

Historical Performance

Past performance is no indication of current or future performance. For periods greater than one year, returns are annualized.

Source: Barings, Morningstar, March 31, 2022. Performance is based on the Barings ASEAN Frontiers Equity composite in USD. The benchmark is MSCI

All Country ASEAN (Total Net Return) Index. *Inception date of the strategy and the composite under GIPS rules is August 1, 2008.

** Quartile ranking based on the representative account of Barings ASEAN Frontiers Equity strategy. Ranking is based on Morningstar Category –

ASEAN Equity, Morningstar fractional weighting methodology applied. © 2022 Morningstar, Inc. All Rights Reserved.

A Global Investment Performance Standards (GIPS®) Report for the Composites contained in this presentation can be found on page 70 and 71.

-4.6

3.3

10.510.0

8.4

2.6 2.7

-0.3

2.5

4.2

-7.1

0.6

10.8

7.3

4.0

-12.0

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

12.0

3 months 1 year 3 years (ann.) 5 years (ann.) Since inception* (ann.)

Barings ASEAN Frontiers Equity Strategy

MSCI AC ASEAN Index

Relative Performance

GROSS PERFORM ANC E (%)

Morningstar Peer Group Ranking**

Quartile 4th 3rd 1st 1st --

For investment professionals only 34

Performance – Barings ASEAN Frontiers Equity Strategy

Past performance is no indication of current or future performance. The portfolio holdings are subject to change.

Source: Morningstar, Barings, as of March 31, 2022. Batting average, Sharpe and information ratio performance based on the representative account of

Barings ASEAN Frontiers Equity strategy, and ranked against Morningstar Category – ASEAN Equity, Morningstar fractional weighting methodology

applied. Calculation benchmark used is MSCI AC ASEAN (Total Net Return) Index. Batting average is a Morningstar measure of a manager's ability to

consistently beat the market. It is calculated by dividing the number of months in which the manager beat or matched the fund's primary benchmark

index by the total number of months in the period. The top and bottom 5 percentiles are removed from the presentation as outliers.

Peer Group Rankings: Risk-Adjusted Return

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

0%

25%

50%

75%

100%

Sharpe Ratio Information Ratio Sharpe Ratio Information Ratio

3 Years (Ann.) 5 Years (Ann.)

Barings ASEAN Frontiers Equity Strategy

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

0

10

20

30

40

50

60

70

80

3 Years 5 Years

Barings ASEAN Frontiers Equity Strategy

%

Batting Average Quartiles

3 Years (Ann., %) 5 Years (Ann., %)

Sharpe

Ratio

Information

Ratio

Sharpe

Ratio

Information

Ratio

Barings ASEAN

Frontiers Equity

Strategy

0.40 1.00 0.42 0.79

Morningstar Peer

Group Median0.13 0.38 0.16 0.20

For investment professionals only 35

Downside Protection along with Upside Participation

Strong performance in both down- and up-markets driven by stock selection

72 and 56 observations in the peer group for 3 and 5 years respectively. Down Capture ratio is inversely ranked.

Source: Morningstar as of March 31, 2022. All data shown in USD, total return net of fees. Strategy returns based on the representative account of

Barings ASEAN Frontiers Equity strategy. Ranked against the Morningstar Category – ASEAN Equity and currency hedged = NA. Group calculation

benchmark used is MSCI AC ASEAN NR USD. Morningstar Methodology for peer group ranking applied.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

3 Years (%) 5 Years (%)

Up

Capture

Down

Capture

Up

Capture

Down

Capture

Barings ASEAN Frontiers Equity Strategy 126.66 85.17 119.22 88.07

Morningstar Peer Group Median 106.85 91.22 100.43 94.68

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

0%

25%

50%

75%

100%

Up Capture Down Capture Up Capture Down Capture

Barings ASEAN Frontiers Equity Strategy

Median

3 Years 5 Years

For investment professionals only 36

Active Management is Key to Address ASEAN Markets Inefficiencies

Source: MSCI, FactSet, January 2022. Note: Dec-15 is around 2 years before MIFID II (Markets in Financial Instruments Directive II) became effective

in January 2018.

Analyst Coverage for Stocks within MSCI Indices

ASEAN already an under researched region, more so after MIFID II

0

5

10

15

20

25

30

ASEAN Asia ex-Japan US

Average Number of Analysts for Stocks with Index Weight >0.2%

Dec-15 Dec-21

For investment professionals only 37

ASEAN – Relative Inefficiency Allows Alpha Generation through Stock Selection

Proven track record of identifying successful growth companies way ahead of index inclusion

*Stock Cumulative Return: total return over the period from first bought until index inclusion announcement, monthly returns in local currency terms.

Source: Bloomberg, Barings, data as of July 2021. Data relates to the representative account of Barings ASEAN Frontiers Equity strategy. Index: MSCI

AC ASEAN (Total Net Return) Index. Reference to the performance comparator index is for comparative purpose only.

Stock samples are for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Stock Name Position Initiation in the Strategy Stock Cumulative Return* Index Return

Vietnam Dairy Product June 2009 1696% 159%

My E.G. Services January 2014 526% 50%

Srisawad February 2015 117% 2%

ACE Hardware Indonesia June 2017 73% 17%

Osotspa October 2018 54% -4%

SEA October 2017 1579% 1%

-200

0

200

400

600

800

1000

1200

1400

1600

1800

-20

0

20

40

60

80

100

120

140

160

180

Total Cumulative Returns:from First Investment in Barings ASEAN Frontiers Equity Strategy to Index Inclusion

SAWAD ACES OSP VNM (RHS) MYEG (RHS) SEA (RHS)

% %

For investment professionals only 38

FUND AWARDS – BARINGS ASEAN FRONTIERS FUND

Barings ASEAN Frontiers Equity Strategy

Long established fund with proven track record

Source: Barings. Strategy size data as of March 31, 2022, rounded to the nearest US$10m, gross assets. Please note that Barings ASEAN Frontiers

Fund is not available to US investors.

• Awarded BENCHMARK Fund of the Year Awards 2020 – Best-in-Class across Hong Kong

and Singapore in ASEAN Equity Category, Retail Class

2020

2021

• Awarded Bloomberg Businessweek – Top Fund Awards 2021 – Best Performer in ASEAN Equity category on strong

risk-adjusted performance relative to peers over 1 year and 5 years

• Won 2021 Best of the Best Awards by Asia Asset Management for delivering consistent, strong risk-adjusted returns

relative to its peers over 10 years

• Won 2021 REFINITIV Lipper Fund Awards for consistently strong, risk-adjusted returns relative to

its peers for 3-year and 5-year performance

STRATEGY DETAILS

Inception Date of Strategy August 1, 2008

Strategy Size US$570 Million

Base Currency USD

Portfolio Managers SooHai Lim / Tiebin Liu

2022

• Won REFINITIV Lipper Fund Awards 2022 Taiwan for consistently strong, risk-adjusted returns relative to its peers for

3-year and 5-year performance

For investment professionals only 39

Our Key Differentiators

Our Key Differentiators:

• Extensive primary research supported by a large team of experienced EM professionals

• Proprietary fundamental analysis evaluating companies over a 5 year research horizon

• Fully integrated dynamic ESG assessment and active engagement

• Macro considerations incorporated through our Cost of Equity approach

• Proprietary risk management tools support portfolio construction

Investment Vehicles

For investment professionals only 41

Key Terms – Barings ASEAN Frontiers Fund

Source: Barings, March 31, 2022.

1. Further details regarding the subscription and redemption process is available in the Fund Prospectus.

2. The ongoing charges figure is based on the ongoing expenses chargeable to the respective unit class for the 12-month period ended October 31,

2021 expressed as a percentage of the average net asset value of the respective unit class for the same period. This figure may vary from year to

year.

Such terms and conditions are qualified in their entirety by the provisions of the final Fund documents which should be reviewed carefully before a

decision to invest in the fund is made. Please note that Barings ASEAN Frontiers Fund is not available to US investors.

Barings ASEAN Frontiers Fund

Domiciliation Ireland, UCITS Fund

Umbrella Barings International Umbrella Fund

Investment Manager Baring Asset Management Limited

Base Currency USD

Dealing Frequency Daily1

Fee Schedule

Management FeesClass A –1.25% per annum

Class I – 0.75% per annum

Ongoing Charges to

Fund (OCF)2

Class A – 1.70%

Class I – 1.00%

For investment professionals only 42

Identifiers – Barings ASEAN Frontiers Fund

Share Class ISIN Bloomberg ID

Barings ASEAN Frontiers Fund - Class A USD Inc IE0000830236 BRGPACI ID

Barings ASEAN Frontiers Fund - Class A EUR Inc IE0004868828 BRGPACE ID

Barings ASEAN Frontiers Fund - Class A GBP Inc IE00B3BC5T90 BASEANG ID

Barings ASEAN Frontiers Fund - Class A EUR Acc IE00B4MTNB49 BABAFAE ID

Barings ASEAN Frontiers Fund - Class A USD Acc IE00B59JG481 BAFRAUA ID

Barings ASEAN Frontiers Fund - Class I EUR Acc IE00B3BC5X37 BASEIEA ID

Barings ASEAN Frontiers Fund - Class I GBP Acc IE00B3BC5W20 BARAFIG ID

Barings ASEAN Frontiers Fund - Class I USD Acc IE00B3BC5V13 BARFIUA ID

Barings ASEAN Frontiers Fund - Class I USD Inc IE00BKQMYD06 BABAFIU ID

Please note that Barings ASEAN Frontiers Fund is not available to US investors.

Stock Examples

For investment professionals only 44

SEA Ltd. – ASEAN’s Alibaba & Tencent in One

1. Source: Goldman Sachs Global Investment Research, Barings, December 2021.

2. Source: Company data, Barings, December 2021.

3. Source: Company data, Barings, Morgan Stanley Research, Credit Suisse Research, April 2022.

Stock sample is for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions. Any

prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Growth Upside / Valuation Quality

• The company has delivered superior growth in

terms of MAU, DAU, GMV and revenue

• Strong potential for take rate to increase as the

scale of the e-commerce business continues

to grow. Higher take rate will drive profitability

up

• Opportunities for Free Fire and Free Fire Max,

Garena’s highly successful self developed

games, to expand into new markets and

increase in-game monetization in existing

markets

• SEA has great potential given its experienced

management team and the growing presence

in many underpenetrated markets

• Among all its ecommerce markets, Taiwan and

Malaysia are the most prominent right now in

terms of profitability. We continue to see

strong potential for the other markets to

gravitate towards higher profitability

• SEA’s game business, Garena, is one of the

best game developers/operators in south east

Asia. They have come up with super games

and host the e-sports activities in the region

• Shopee, the company’s e-commerce platform,

has had good presence in some ASEAN

countries, plus Taiwan

• Although e-commerce is still in the investment

phase, strong cash flow generated from the

game business will give strong support for the

longer term growth

Score: 1.0 Score: 2.3 Score: 1.0

Strong Growth Driven by User Base Expansion1

Riding on the E-Commerce Trend2 Room for Take Rate to increase3

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

100

200

300

400

500

600

700

QAU (mn) QPU (mn) Paying Ratio

USD, bn

0.0%

8.5%

4.1% 3.6%

14.1%

16.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Shopee(FY16)

Shopee(4Q21)

Alibaba(FY21)

PDD(FY21)

Momo(4Q21)

MecardoLibre

(FY21)

Take Rate18.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

GMV (Gross Merchandise Volume)

For investment professionals only 45

6.8 7.2 7.5 7.9 7.9 8.38.7 9

9.4 9.8

0

2

4

6

8

10

12

14

16

2016 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Southeast Asia Market Size of Outsourced CX Services (US$ bn)

Traditional Economy New Economy

TDCX

1. Source: Frost & Sullivan, Goldman Sachs Global Investment Research, October 2021. E=Estimates.

2. Source: Company data, Barings, June 2021.

Stock sample is for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions. Any

prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Strong Growth Potential of Outsourced CX Services in Southeast Asia1

High Exposure to the New Economy Sector2

Growth Upside / Valuation Quality

• Secular tailwinds in the digital customer

experience services (CX) industry given the

rise of commercial digitalization trends,

migration towards online commerce, and

proliferation of new economy services

• Success in developing high value-added digital

capabilities has helped it acquire New

Economy clients, including Fortune 500 firms

• Leveraged to the high growth in the new

economy sector as TDCX derives more than

90% of revenue from new economy

customers. Geographically, TDCX is also well

placed to capture growth in the ASEAN region

where CX outsourcing growth is the highest

• Potential for TDCX to re-rate given the higher

growth relative to the overall CX industry,

favorable geographical exposure, and potential

market share gains

• The lack of listed comparable in the ASEAN

markets may allow TDCX to command a

scarcity premium

• Focusing on high value added digital services

enables TDCX to drive overall productivity up,

measured by revenue per employee, and to

command superior margins over peers

• Ability to retain talent in a high attrition rate

sector is a key merit. TDCX’s historical attrition

rate of 22-25% is significantly lower than the

APAC industry average of 30-35%

• TDCX runs a net cash balance sheet and has

strong free cash flow generation ability

Score: 1.0 Score: 2.0 Score: 2.7

92.20%

0%

20%

40%

60%

80%

100%

Revenue

Revenue exposure to New Economy clients

2018 2019 2020 1H2021

14.1

For investment professionals only 46

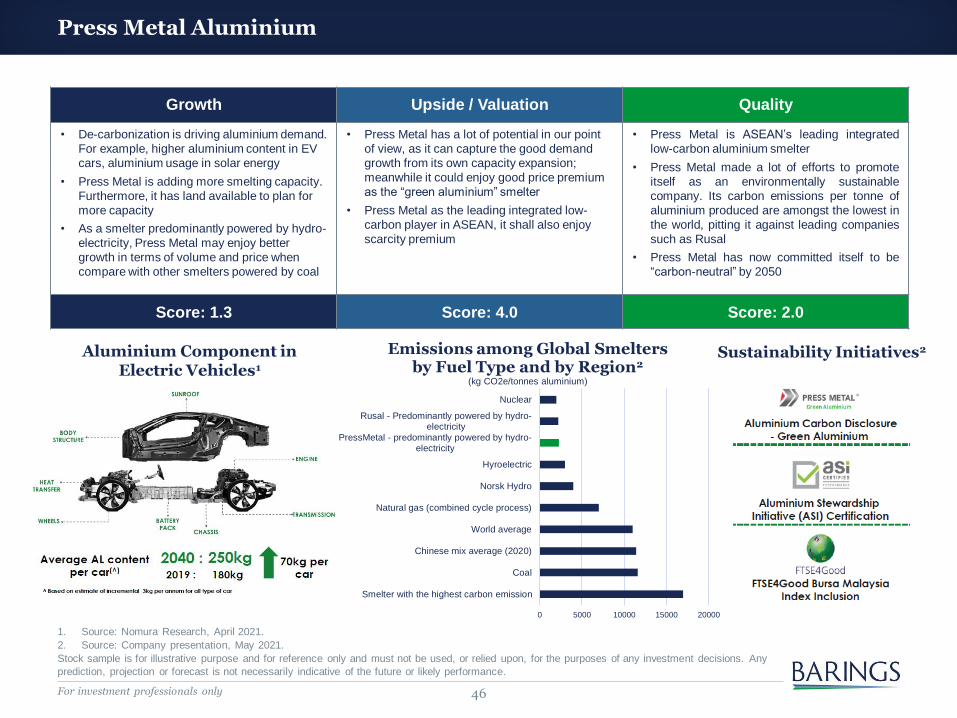

Press Metal Aluminium

1. Source: Nomura Research, April 2021.

2. Source: Company presentation, May 2021.

Stock sample is for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions. Any

prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Growth Upside / Valuation Quality

• De-carbonization is driving aluminium demand.

For example, higher aluminium content in EV

cars, aluminium usage in solar energy

• Press Metal is adding more smelting capacity.

Furthermore, it has land available to plan for

more capacity

• As a smelter predominantly powered by hydro-

electricity, Press Metal may enjoy better

growth in terms of volume and price when

compare with other smelters powered by coal

• Press Metal has a lot of potential in our point

of view, as it can capture the good demand

growth from its own capacity expansion;

meanwhile it could enjoy good price premium

as the “green aluminium” smelter

• Press Metal as the leading integrated low-

carbon player in ASEAN, it shall also enjoy

scarcity premium

• Press Metal is ASEAN’s leading integrated

low-carbon aluminium smelter

• Press Metal made a lot of efforts to promote

itself as an environmentally sustainable

company. Its carbon emissions per tonne of

aluminium produced are amongst the lowest in

the world, pitting it against leading companies

such as Rusal

• Press Metal has now committed itself to be

“carbon-neutral” by 2050

Score: 1.3 Score: 4.0 Score: 2.0

0 5000 10000 15000 20000

Smelter with the highest carbon emission

Coal

Chinese mix average (2020)

World average

Natural gas (combined cycle process)

Norsk Hydro

Hyroelectric

PressMetal - predominantly powered by hydro-electricity

Rusal - Predominantly powered by hydro-electricity

Nuclear

Emissions among Global Smelters by Fuel Type and by Region2

(kg CO2e/tonnes aluminium)

Aluminium Component in Electric Vehicles1

Sustainability Initiatives2

For investment professionals only 47

ViTrox

1. Source: Company Report, December 2021. E=Estimates.

2. Source: Macquarie Research, March 2022.

Stock sample is for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions. Any

prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Growth Upside / Valuation Quality

• The company has delivered remarkable

growth in revenue and profit, led by its

competitive products

• It will continue to benefit from the growing

needs for automation and semiconductor

presence across devices, such as EV

• Benefitting from tech companies looking for

alternative sources of equipment amid de-

globalization

• There is a great potential upside from the

company by capturing the IT capex spending

in the region

• EV segment, contributing 22% of the group

revenue, is one of the most promising end-

demand areas for the company in the medium

to long term

• ViTrox is an equipment design and

manufacturer that provides automated board

inspections and machine vision solutions

• One of the few ASEAN tech companies that

owns IP as a result of R&D focus, rather than

providing labor intensive assembly and testing

services

• Diversified customer base and applications,

with over 300 customers in automotive,

telecom, consumer, medical and

semiconductor industries

Score: 2.0 Score: 4.7 Score: 2.7

Key EndCustomersKey Top

Customers

ViTrox

Celestica

Cisco

Juniper

IBM

Jabil

Cisco

Apple

HP

Flex

Apple

Nike

Ford

ASE

Renesas

STMicro

Infineon

A Diversified Client Base2

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021E

Revenue and R&D Spending1

Revenue R&D R&D as % of Rev

(MYR mn)

Market Outlook and Investment Themes

For investment professionals only 49

-80

-60

-40

-20

0

20

40

'21/01 '21/03 '21/05 '21/07 '21/09 '21/11 '22/01 '22/03

Google Mobility Index: Retail & Recreation Venues% from baseline, 7DMA

Indonesia Malaysia Philippines Singapore

Thailand Vietnam Korea India

63%

71%71%

80%

84%88%88%

92%

11%8%

2%

34%

48%

64%

46%

71%

PHIDINTHMYKRCNSG

Vaccination Progress in Asia

Vaccinated Partially vaccinated Booster Shot

Reopening Across Asia Expected to Continue with Rising Vaccination

1. Source: Our World in Data, latest available as of March 31, 2022.

2. Source: Google, Barings, March 31, 2022. 7DMA = 7-day moving average.

Most of the Asian Economies Have More than 50% of the Population Vaccinated1

Retail & Recreation Activities in Asia ex-China Are Recovering to Pre-COVID Levels2

Living with COVID, not zero-COVID

For investment professionals only 50

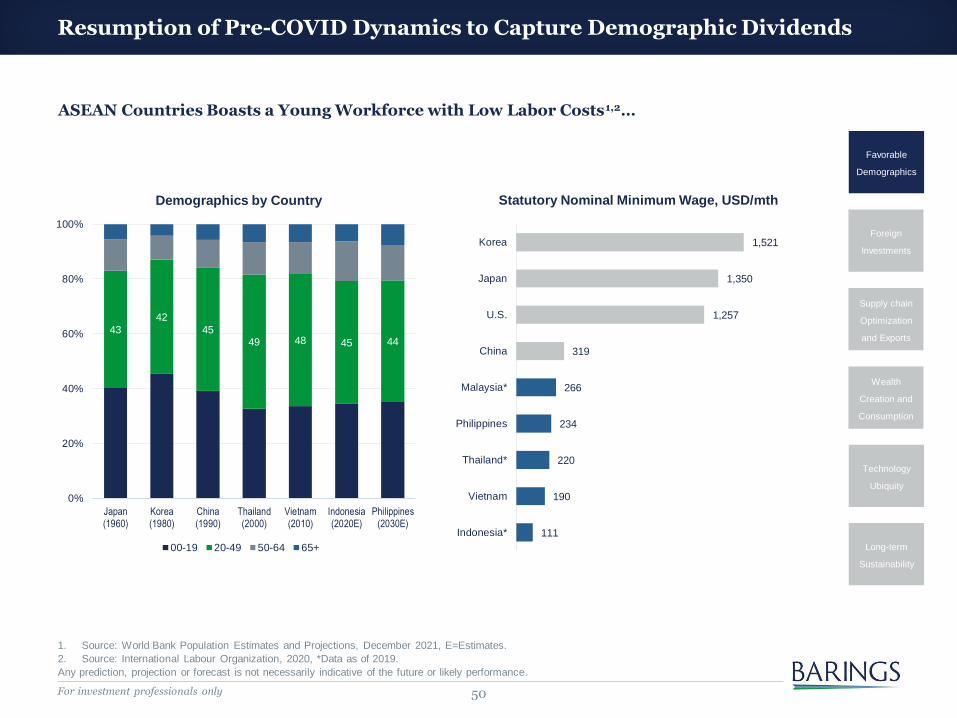

Resumption of Pre-COVID Dynamics to Capture Demographic Dividends

1. Source: World Bank Population Estimates and Projections, December 2021, E=Estimates.

2. Source: International Labour Organization, 2020, *Data as of 2019.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

1,521

1,350

1,257

319

266

234

220

190

111

Korea

Japan

U.S.

China

Malaysia*

Philippines

Thailand*

Vietnam

Indonesia*

Statutory Nominal Minimum Wage, USD/mth

ASEAN Countries Boasts a Young Workforce with Low Labor Costs1,2…

43

42

4549 48 45 44

0%

20%

40%

60%

80%

100%

Japan(1960)

Korea(1980)

China(1990)

Thailand(2000)

Vietnam(2010)

Indonesia(2020E)

Philippines(2030E)

Demographics by Country

00-19 20-49 50-64 65+

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 51

15%

20%

25%

30%

35%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Corporate Tax Rates, %3

Indonesia Malaysia Philippines

Singapore Thailand Vietnam

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

FDI into ASEAN, USD bn1

Indonesia Malaysia Philippines Singapore Thailand Vietnam

Foreign Investments at Historical Highs

1. Source: World Bank, data available as of December 2021. FDI = Foreign Direct Investments.

2. Source: CS Survey, Credit Suisse Research, October 2019.

3. Source: KPMG, data available as of December 2021.

Global Players Are Investing in ASEAN, Supported by Favorable Policies and Tax Regimes…

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

0% 20% 40% 60% 80% 100%

Tech. Hardware

Consumer Durables/Apparel

Capital Goods

Retailing

Countries/Regions Considered For Manufacturing2

ASEAN Other Asia Mexico EU US

For investment professionals only 52

ASEAN Is Becoming A Major Manufacturing Hub

Source: IMF, Bloomberg, Barings, data available as of March 31, 2022. ASEAN6 = Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam.

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

'08/12 '10/12 '12/12 '14/12 '16/12 '18/12 '20/12

ASEAN Exports to World

Exports, USD mn (Ls) % of World, 12MMA (Rs)

10%

18%

0%

5%

10%

15%

20%

25%

'02 '04 '06 '08 '10 '12 '14 '16 '18 '20

ASEAN Exports to U.S., % Total

ASEAN6 China

For investment professionals only 53

RCEP Could Further Reduce Trade Barriers

About 91% of the trade tariffs among members will be eliminated

Note: RCEP= Regional Comprehensive Economic Partnership.

1. Source: FactSet, IMF, December 2020. FTA= free trade agreement.

2. Source: ADB Estimates, December 2021.

3. Source: J.P. Morgan Estimates, December 2021.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

RCEP Member Countries

CHINA

AUSTRALIA

NEW

ZEALAND

INDONESIA

PHILIPPINES

JAPANSOUTH

KOREA

MYANMAR

THAILAND

LAOS

VIETNAM

CAMBODIA

BRUNEIMALAYSIA

SINGAPORE

0

10

20

30

0.0

0.5

1.0

1.5

2.0

2.5

RCEP NAFTA CPTPP EU

GDP, USD tn (Ls) Population, bn (Rs)

Largest FTA by Population and GDP1

45%

50%

55%

60%

65%

Philippines Indonesia Malaysia Thailand Singapore Vietnam

ASEAN trade with RCEP countries (% total trade)

0.0

0.2

0.40.6

0.8

1.0

SouthKorea

Malaysia Thailand Vietnam China Philippines Indonesia

Estimated Net Impact of RCEP on GDP by 2030, %

Inter-Regional Trade Stands to Benefit2

Catalyst for Long-term Economic Growth3

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 54

Wealth Creation Translates into Growth in Consumption and Investments

1. Source: World Bank, data available as of December 2021.

2. Source: IMF, data available as of December 2021.

3. Source: Bloomberg, data available as of December 2021.

324

545

1,715

2,839

0

500

1,000

1,500

2,000

2,500

3,000

1990 2000 2010 2020

Gross National Income, USD bn1

Indonesia Malaysia Philippines Singapore Thailand Vietnam

-

500

1,000

1,500

2,000

'99 '01 '03 '05 '07 '09 '11 '13 '15 '17 '19

Household Final Consumption, USD bn2

0

500

1,000

1,500

2,000

2,500

3,000

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

Stock Market Capitalization, USD bn3

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 55

Southeast Asia Is Entering the ‘Golden Age’ of Disposable Income

1. Source: Asia Partners Analysis, IMF, World Bank, Bloomberg, Angus Maddison Project Database 2018 (exclude telcos), September 2020.

2. Source: IMF, World Bank, Asia Partners Analysis, September 2020.

Stock examples are for illustrative purpose and for reference only and must not be used, or relied upon, for the purposes of any investment decisions.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Southeast Asia: GDP Per Capita in Real, Inflation-Adjusted Terms2

Three Powerful Precedents: A Consistent Pattern of Value Creation across 75 Years of Rising Middle Classes1

% of Current Tech Market Cap, by IPO Year (Cumulative)

Current Tech Market Cap (USD)

Real GDP Per Capita

Inflation Adjusted in 2018 USD (Log Scale)

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

USA

Japan

S.Korea

China

India

SEAsia

Expressed in Constant 2018 US Dollars

Bn $ Companies

$US Billions

$20-2,000bnAmazon, Apple,

Microsoft, Google, Meta,

Rakuten, Yahoo Japan, Netflix, Uber

$30-700bnAlibaba, Tencent, JD.com, Baidu, Xiaomi, Meituan

$2-100bnSea, Grab, GoTo,

Lazada, Tokopedia, Bukalapak.com

$0-1bnMpesa

$0.5-25bnZomato,

Paytm, Oyo

For investment professionals only 56

Digital Wallet Payments Volume (US$)Online Food Delivery GMV* (US$) Ride-Hailing GMV* (US$)

Southeast Asia Is Still in the Early Innings of Online Disruption

Source: Euromonitor, Grab, Credit Suisse Research, April 2021.

1. Based on % of total consumer foodservice that is ordered online (including online ordering for dine-in and takeaway). 2. Based on % of total consumer

expenditure on ride-hailing out of consumer expenditure on buses, coaches and taxis, and operation of personal transport equipment.

Note: Southeast Asia statistics on this page refer to Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam. E= Estimates. *GMV = Gross

Merchandise Volume.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Large Addressable Southeast Asia Market Opportunity

2025E

$171bn Consumer Foodservice

Value

2025E

$28bn

2020

$9bn

2025E

$1,356bn Cash Transaction Value

2025E

$138bn

2020

$39bn

2025E

$235bn Consumer Expenditure

on Land Mobility

2025E

$19bn

2020

$4bn

21%

21%

11%

0% 5% 10% 15% 20% 25%

US

China

Southeast Asia

% 2020 online penetration

5%

15%

3%

0% 5% 10% 15% 20%

US

China

Southeast Asia

% 2020 online penetration

94%

95%

60%

82%

43%

17%

0% 50% 100%

US

China

Southeast Asia

% 2020 electronic transactions (volume)

% 2020 banked population (age >15)

ONLINE FOOD DELIVERY ON-DEMAND MOBILITY DIGITAL FINANCIAL SERVICES

1 2

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 57

Tech Adoption – Accelerating in ASEAN, Plateauing in China

1. Source: CEIC, Maybank Research, October 2021.

2. Source: Euromonitor, Maybank Research, October 2021.

China’s E-Commerce Penetration Rate at ~30%, Among the Highest Globally1

E-Commerce Penetration Rate in Malaysia, Philippines and Thailand Remain Below 10%2

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 58

0%

20%

40%

60%

80%

100%

120%

140%

160%

Singapore Thailand China Malaysia Philippines Indonesia

Smartphone penetration 4G Penetration

High Levels of Mobile Phone Penetration Rate Is Foundational to Digital Transformation in ASEAN

Source: Company data, World Bank, MCMC, IMDA, Credit Suisse estimates, October 2021.

Smartphone and 4G Penetration (2020) Remains High for ASEAN Nations Supporting the Digital Economy

COVID Has Accelerated Consumption of Mobile Data in ASEAN

0

2

4

6

8

10

12

14

16

18

20

Philippines Singapore Indonesia Thailand Malaysia

2015 2016 2017 2018 2019 2020

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

Average Data Use per Smartphone

Subscriber (GB/Month)

For investment professionals only 59

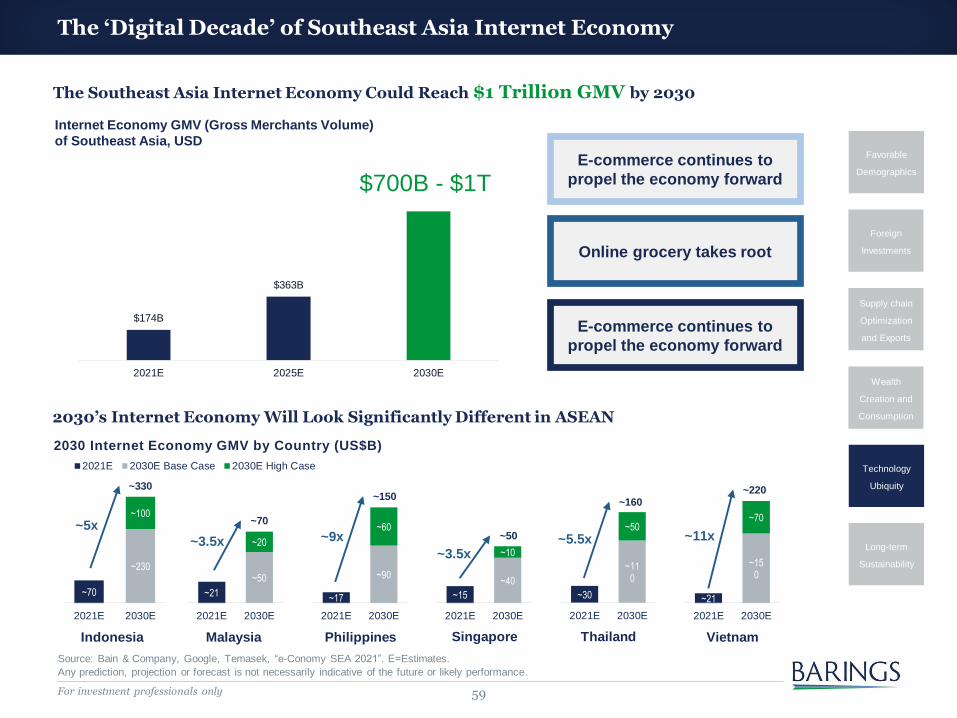

The ‘Digital Decade’ of Southeast Asia Internet Economy

Source: Bain & Company, Google, Temasek, “e-Conomy SEA 2021”. E=Estimates.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

The Southeast Asia Internet Economy Could Reach $1 Trillion GMV by 2030

2030’s Internet Economy Will Look Significantly Different in ASEAN

$174B

$363B

2021E 2025E 2030E

Internet Economy GMV (Gross Merchants Volume)

of Southeast Asia, USD

$700B - $1T

2030 Internet Economy GMV by Country (US$B)

~70

~230

~100

2021E 2030E

2021E 2030E Base Case 2030E High Case

Indonesia

~330

~5x

~21

~50

~20

2021E 2030E

~70

~3.5x

Malaysia

~17

~90

~60

2021E 2030E

~15

~40

~10

2021E 2030E

~30

~110

~50

2021E 2030E

~21

~150

~70

2021E 2030E

Philippines Singapore Thailand Vietnam

~150

~9x ~50

~3.5x

~160

~5.5x

~220

~11x

E-commerce continues to

propel the economy forward

Online grocery takes root

E-commerce continues to

propel the economy forward

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 60

2.4

5.56.4

7.8

3.34.5

5.9

7.1

8.65.6

3.8

3.0 0.8

5.6

0

2

4

6

8

10

12

14

16

2017 2018 2019 2020 H1 2020 H2 2020 H1 2021

Deal Value, USD bn

Other Unicorn

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2020 2021 2022E 2023E

Internet Sector Weight of MSCI ASEAN, %

Internet Unicorn Others

Healthy Pipeline of Unicorns to Transform ASEAN Markets

1. Source: Industry reports; VC partners; Bain analysis. Bain & Company, Google, Temasek, “e-Conomy SEA 2021”. E=Estimates. Note: Deals

include investments by venture capital, private equity and strategic investors.

2. Source: J.P. Morgan estimates, December 2021.

Southeast Asia’s Deal Landscape Is Thriving, with Global Capital Filtering into the Region in A Meaningful Manner1

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

Internet Sector Could be More Than 20% of MSCI ASEAN by 20232

For investment professionals only 61

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2011 2013 2015 2017 2019 2021E 2023E 2025E 2027E 2029E

Aluminium demand, per year, by green sector

Total Solar Demand Total Wind Demand Total EV Demand

Sustainability in Focus, But Green Transition Isn’t Only About Technology

1. Source: IEA, IRENA, Woodmac, CRU, Goldman Sachs Global Investment Research, October 2021. E= Estimates.

2. Source: Press Metal Company Presentation.

3. Source: Coordinating ministry for maritime and investment affairs of Indonesia, March 2021.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Climate Policies Driving Metal Deficits: Green Aluminium Demand Is Expected to Rise to 18% of Global Demand by 20301

Emissions among Global Smelters by Fuel Type and by Region2

28

87

87

200

Indonesia

Australia

Peru

Chile

Copper

7

16

20

21

Russia

Brazil

Australia

Indonesia

Nickel

7

111

4

5

7

Indonesia

Vietnam

Australia

Guinea

Bauxite

0.4

0.4

0.8

1.1

Brazil

Australia

Indonesia

China

Tin

0 5,000 10,000 15,000 20,000

Smelter with the highest carbonemission

Coal

Chinese mix average (2020)

World average

Natural gas (combined cycleprocess)

Norsk Hydro

Hyroelectric

PressMetal - predominantlypowered by hydro-electricity

Rusal - Predominantly poweredby hydro-electricity

Nuclear

(kg CO2e/tonnes aluminium)

Commodity Reserves by Country3 (Million Tons of Metal Compounds in 2019)

1

1

6

6

2

2

Indonesia’s Global Reserve Ranking

Indonesia’s Global Production Ranking

Favorable

Demographics

Foreign

Investments

Supply chain

Optimization

and Exports

Wealth

Creation and

Consumption

Technology

Ubiquity

Long-term

Sustainability

For investment professionals only 62

Economic and Earnings Momentum Shifts in Favor of ASEAN in 2022

1. Source: FactSet, I/B/E/S, MSCI, Haver, Goldman Sachs Global Investment Research, April 2022. GS = Goldman Sachs.

2. Source: Bloomberg Finance L.P., Ho Chi Minh City Securities Trading Center, TSE, Bursa Malaysia Berhad, JSE, PSE, April 2022. ASEAN

includes Singapore, Vietnam, Thailand, Malaysia, Indonesia and Philippines. Data for Singapore is till 28 Feb 2022 from EPFR Global. For

Malaysia – data starts at October 2009 and for Vietnam – data starts at January 2009.

3. Source: FactSet, Barings, April 22, 2022. E=Estimates.

Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

EPS Growth and Macro Forecasts1 Strong Rebound of Monthly Cumulative Flows of ASEAN YTD2

ASEAN Earnings May Rebound More Than Other Markets As They Have Not Yet Recovered to Pre-COVID Levels3

0.0

0.5

1.0

1.5

2.0

2.5

Ko

rea

Ta

iwa

n

India

EM

AxJ

Indo

ne

sia

Mala

ysia

Ho

ng

Ko

ng

Ch

ina

Th

aila

nd

Ph

ilip

pin

es

AS

EA

N

Sin

gap

ore

EPS Level vs. 2019, MSCI Indices

2021 2022E

For investment professionals only 63

Asia ex-Japan Portfolios Are Now Largely Greater China, ASEAN Neglected…

Source: FactSet, MSCI, Barings, March 31, 2022.

Greater China: MSCI Countries/Regions of China, Hong Kong, and Taiwan.

ASEAN5: MSCI Countries/Regions of Indonesia, Malaysia, Philippines, Singapore, Thailand.