Badal & Harter 2014 Gender Diversity and business performance

13

http://jlo.sagepub.com/ Organizational Studies Journal of Leadership & http://jlo.sagepub.com/content/21/4/354 The online version of this article can be found at: DOI: 10.1177/1548051813504460 2014 21: 354 originally published online 23 September 2013 Journal of Leadership & Organizational Studies Sangeeta Badal and James K. Harter Gender Diversity, Business-Unit Engagement, and Performance Published by: http://www.sagepublications.com On behalf of: Midwest Academy of Management can be found at: Journal of Leadership & Organizational Studies Additional services and information for http://jlo.sagepub.com/cgi/alerts Email Alerts: http://jlo.sagepub.com/subscriptions Subscriptions: http://www.sagepub.com/journalsReprints.nav Reprints: http://www.sagepub.com/journalsPermissions.nav Permissions: What is This? - Sep 23, 2013 OnlineFirst Version of Record - Sep 24, 2014 Version of Record >> by guest on September 25, 2014 jlo.sagepub.com Downloaded from by guest on September 25, 2014 jlo.sagepub.com Downloaded from

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Badal & Harter 2014 Gender Diversity and business performance

http://jlo.sagepub.com/Organizational StudiesJournal of Leadership &

http://jlo.sagepub.com/content/21/4/354The online version of this article can be found at:

DOI: 10.1177/1548051813504460

2014 21: 354 originally published online 23 September 2013Journal of Leadership & Organizational StudiesSangeeta Badal and James K. Harter

Gender Diversity, Business-Unit Engagement, and Performance

Published by:

http://www.sagepublications.com

On behalf of:

Midwest Academy of Management

can be found at:Journal of Leadership & Organizational StudiesAdditional services and information for

http://jlo.sagepub.com/cgi/alertsEmail Alerts:

http://jlo.sagepub.com/subscriptionsSubscriptions:

http://www.sagepub.com/journalsReprints.navReprints:

http://www.sagepub.com/journalsPermissions.navPermissions:

What is This?

- Sep 23, 2013OnlineFirst Version of Record

- Sep 24, 2014Version of Record >>

by guest on September 25, 2014jlo.sagepub.comDownloaded from by guest on September 25, 2014jlo.sagepub.comDownloaded from

Journal of Leadership &Organizational Studies2014, Vol. 21(4) 354 –365© The Authors 2013Reprints and permissions: sagepub.com/journalsPermissions.navDOI: 10.1177/1548051813504460jlo.sagepub.com

Article

Over the past 25 years, the percentage of women in the U.S. workforce has steadily increased. Today women are almost on par with men in the workforce (53.4% men and 46.6% women; U.S. Department of Labor, 2011a). This demo-graphic shift, prompted by the civil rights movement and promoted by government legislation, has led to an increased interest among businesses in managing diversity issues effectively (Kochan et al., 2003; Mannix & Neale, 2005). Private businesses quickly realized that fulfilling the legal mandates is not enough, and the diversity movement shifted from “valuing diversity” to a much more focused approach emphasizing the “business utility” for supporting diversity (Mannix & Neale, 2005). The business utility approach states that a more diverse workforce promotes innovation and creativity and allows the organization to be competitive in the global marketplace (Jehn & Bezrukova, 2004; Myaskovsky, Unikel, & Dew, 2005).

The research exploring linkages between diversity and performance has shown contradictory results. One view of diversity states that team-heterogeneity creates value and has a positive impact on business-unit processes due to the unique cognitive resources that team members bring to the team (Cox & Blake, 1991; Easley, 2001; Frink et al., 2003; Hambrick, Cho, & Chen, 1996; Horwitz, 2005; Kochan et al., 2003; Mannix & Neale, 2005). Another view of diver-sity states that homogenous groups generate better commu-nication, are more cohesive, have less conflict, and are more productive (Ancona & Caldwell, 1992; Böhren & Ström, 2005; Campbell & Mínguez-Vera, 2008; Gallego-Alvarez et al., 2009; Jimeno & Redondo, 2007; Konrad, Winter, & Gutek, 1992; Milliken & Martins, 1996; O’Reilly, Caldwell, & Barnett, 1989; Rose, 2007; Tsui, Egan, & O’Reilly, 1992;

Wharton & Baron, 1987, 1991; Williams & O’Reilly, 1998). Some experts suggest that the relationship between diver-sity and performance is both theoretically and empirically more complex than captured by any one perspective and thus it is important to consider the effect of context, such as interpersonal congruence, employee engagement levels, and human resource practices on the diversity-performance relationship (Carter, D’Souza, Simkins, & Simpson, 2007; Horwitz, 2005; Kochan et al., 2003; Pelled, 1996; Pelled, Eisenhardt, & Xin, 1999).

In this study, we seek to address two major research goals: our main goal is to further our understanding of the gender diversity–performance relationship by testing the impact of gender diversity, a key surface-level observable attribute, on the financial bottom-line of businesses. We spe-cifically chose to focus just on gender diversity, as studies have shown that it is better to treat each demographic diver-sity variable as a distinct theoretical construct. Combining different diversity categories together may mask the real impact of each on organizational outcomes (Herring, 2009; Smith, DiTomaso, Farris, & Cordero, 2001; Zenger & Lawrence, 1989). Moreover, a focus on gender diversity is critical since studies (Heilman & Haynes, 2005; Heilman & Okimoto, 2007) have found that women often suffer the con-sequences of gender stereotyping when they work in teams with men, hindering team performance and

504460 JLOXXX10.1177/1548051813504460Journal of Leadership & Organizational StudiesBadal and Harterresearch-article2013

1Gallup, Omaha, NE, USA

Corresponding Author:Sangeeta Badal, Gallup, 1001 Gallup Drive, P.O. Box 2277, Omaha, NE 68102, USA. Email: [email protected]

Gender Diversity, Business-Unit Engagement, and Performance

Sangeeta Badal1 and James K. Harter1

AbstractThis study investigates the relationship between gender diversity and financial performance at the business-unit level and whether employee engagement moderates this relationship. Using more than 800 business units from two companies belonging to two different industries, we found that employee engagement and gender diversity independently predict financial performance at the business-unit level. One implication is that making diversity an organizational priority and creating an engaged culture for the workforce may result in cumulative financial benefits.

Keywordsgender diversity, employee engagement, business-unit performance

by guest on September 25, 2014jlo.sagepub.comDownloaded from

Badal and Harter 355

overall organizational functioning. Our secondary goal is to examine the role of employee engagement as a potential moderator in the gender diversity–performance relationship. Employee perception of their work environment depends on their day-to-day interactions and relationships with their coworkers (Harter, Schmidt, Asplund, Killham, & Agrawal, 2010). These interpersonal and intergroup relationships in turn affect many important organizational outcomes such as sales and profit. Thus, this study adds significantly to the existing literature by providing a deeper look at the links between gender diversity, interpersonal and intergroup rela-tionships, and business performance. Furthermore, we extend the literature by outlining the psychological under-pinnings of the gender diversity–business performance link-age. This theory-based approach to understanding the gender diversity–engagement–performance linkage provides the practitioners with tools on how to manage gender diversity to drive organizational performance. Furthermore, this is the first study that links gender diversity to financial perfor-mance at the business-unit level. Studies at the firm level ignore the variability of performance across business units within firms. Prior studies (Harter, Schmidt, & Hayes, 2002; Harter et al., 2010) show that engagement varies substan-tially across business units within firms and is a predictor of business-unit outcomes. It is reasonable to postulate that diversity also varies substantially across business units within firms. In fact, the business units in the two organiza-tions in this article vary widely in gender diversity. For instance, in the retail organization, business-unit diversity values range from .09 (9% of the team is one gender and 91% in the other gender) to .48 (48% of the team is one gen-der and 52% in the other gender) with the average diversity of .24 (24% of the business unit is one gender and 76% in the other gender). Studying the gender diversity–performance linkage at the firm level may mask such variations. Harter and Schmidt (2006) explain that unit-level studies provide a more accurate view of the intergroup relations that affects many of the ultimate outcomes the units are working to achieve. Last, this is the first study that looks at objective financial performance measures in real organizations. If we are looking at the diversity–performance linkage from a business utility perspective, then it is important to study the impact of diversity on a business-unit’s financial bottom-line in real organizations rather than testing gender diversity effects in simulated environments.

Theoretical Foundation and Hypotheses

The literature includes a number of well-established theo-ries that provide a conceptual framework to understand why and how gender diversity affects performance: resource-dependence theory, resource-based view of the firm, and psychological presence theory. These theories and the hypotheses are discussed below.

Pfeffer and Salancik’s (1978) resource-dependency the-ory seeks to explain how organizations employ strategies to manage complex business environments by accessing scarce external resources. It proposes that diversity is a vehicle for accessing critically valuable resources for the firm’s success (Aldrich & Pfeffer, 1976; Pfeffer & Salancik, 1978).

A growing degree of uncertainty in world affairs—evi-denced by recent economic downturn, market failures, and dissatisfaction with local and national governance bodies—makes it imperative for organizations to garner all resources at their behest to stay competitive and viable. Hiring a demographically diverse workforce is one such strategy to get access to critical resources for firm survival and success (Gallego-Alvarez, Garcia-Sanchez, & Rodriguez-Dominguez, 2009). For instance, Hillman, Shropshire, and Cannella (2007) found that companies that are heavily dependent on female employees or ones with ties to other companies who have women as board members are likely to strategically place women on their corporate boards to mir-ror the environment in which they operate. Other studies (Dalton, Daily, Ellstrand, & Johnson, 1998; Siciliano, 1996) have found that a diverse workforce is likely to establish interactions and external links that may result in easier access to resources such as diverse credit sources, multiple information sources, wider knowledge of the industry, or a bigger customer base. For instance, a diverse workforce may benefit from interactions with an increasingly diverse customer base (Carter, Simkins, & Simpson, 2003). In addi-tion, gender diversity in the employee base also enables companies to attract and retain talent from a wider pool of human capital (Gallego-Alvarez et al., 2009; Jimeno & Redondo, 2008).

These studies suggest that hiring female employees can provide a strategic advantage to these companies, affecting their performance positively. Currently, there are 71 million women in U.S. workforce, and the Bureau of Labor Statistics forecasts indicate that in the next decade women’s labor force growth will continue to be greater than men’s—a resource that companies cannot afford to ignore and may be the source of power in interorganizational relations (U.S. Department of Labor, 2011b).

The resource-based view (RBV) is a valuable conceptual framework to understand the way firms manage their inter-nal resources, in this case human resources, to achieve a competitive advantage. The theory postulates that a firm can gain a competitive advantage by using its valuable, rare, inimitable, and nonsubstitutable resources (Barney, 1991). Levels of human capital available to management can be a source of competitive advantage for a firm (Barney, 2001). Studies supporting this theory found that gender diversity is one such resource with no strategically equiva-lent substitute and can be a source of competitive advantage (Ali, Kulik, & Metz, 2009).

by guest on September 25, 2014jlo.sagepub.comDownloaded from

356 Journal of Leadership & Organizational Studies 21(4)

Theoretical support for the positive link between gender diversity and performance is based on the notion that men and women bring different viewpoints, diversity in creativ-ity and innovation, diverse market insights, and broader repertoire of skills that enable superior problem solving and decision making (Farrell & Hersch, 2001; Shrader, Blackburn, & Iles, 1997; Smith, Smith, & Verner, 2006; Watson, Kumar, & Michaelsen, 1993). Studies have found that gender-diverse teams perform better than single-gender teams (Kanter, 1977; Martin, 1985; Orlitzky & Benjamin, 2003). Similarly, Stewart (2006) found that heterogeneity is desirable in teams consisting of knowledge workers who are engaged in creative tasks. Wood (1987) conducted a meta-analysis of the findings from past laboratory research and concluded that mixed-sex groups slightly outperformed same-sex groups. Similarly, a recent McKinsey study (Desvaux, Devillard-Hoellinger, & Meaney, 2008) found that senior management teams with a higher proportion of women had better organizational performance. Similarly, Catalyst (2004), Dezso and Ross (2008), and Krishnan and Park (2005) found a strong positive correlation between female participation in top management and financial indi-cators of performance.

Both resource-dependency theory and RBV assert that hiring and managing a demographically diverse workforce can be a source of competitive advantage to the firm. Hence, we hypothesize that gender diversity at the business-unit level will be positively associated with financial performance.

Hypothesis 1: There is a positive relationship between gender diversity and financial performance at the business-unit level.

Kahn’s (1990) psychological presence model proposes that intergroup relations affect the psychological context at work, thus influencing personal engagement of employees. In his seminal work, Kahn (1990, 1992) defines engage-ment as an individual’s physical, cognitive, and emotional presence at work influenced by individual, interpersonal, group, intergroup, and organizational factors. According to this framework, work contexts create conditions (meaning-fulness, safety, and availability) that influence an individu-al’s engagement or disengagement. May, Gilson, and Harter (2004) empirically tested Kahn’s model and found that role fit and opportunities to grow in their jobs were positive pre-dictors of meaningfulness (a sense of self-worth, being use-ful, and being valued); supportive relationships between coworkers and between employees and supervisor predicted safety (open, trusting relationships with coworkers, clear expectations and control over their work, and supportive managerial environments); and access to resources posi-tively predicted psychological availability (having the physical, emotional, or psychological resources to person-ally engage in the role). Studies supporting this theory

found that when employees feel adequately supported by coworkers, it results in higher engagement with the job and higher levels of job satisfaction (Dignam, Barrera, & West, 1986). Similarly, Polzer, Milton, and Swann (2002) found that when demographically diverse groups have high levels of interpersonal congruence (open, trusting, and supportive relationships with coworkers and supervisors), conflict lev-els decrease, which in turn affects productivity positively. Conversely, the authors found that diversity in workgroups can lead to lowered productivity if group members catego-rize themselves into in-groups/out-groups and have lower interpersonal congruence. In another study, Tougas, Rinfret, Beaton, and de la Sablonniére (2005) found that women in the police force who felt they experienced relative disad-vantage compared to men (interpersonal incongruence) psychologically disengaged from their work, possibly lead-ing to inferior performance in the role. Jones and Harter (2005) assessed the combined effects of employee engage-ment and racial composition of employee–supervisor dyad on turnover intent. They found that at lower levels of engagement, different-race dyads show higher turnover intent, but at high levels of engagement, intent to stay with the organization was higher for different-race dyads. Similarly, Hobman, Bordia, and Gallois (2003) found that perceived openness to diversity moderated the relationships between diversity and workgroup conflict. In this investiga-tion, we conceptualize engagement levels as a manifesta-tion of intergroup relations at work and measure it using Gallup’s Q12 (Harter, Schmidt, & Hayes, 2002).

Based on Kahn’s (1990, 1992) work, we propose that high engagement levels at the business-unit level (indica-tive of positive intergroup relations) perpetuate a secure psychological environment in which gender-diverse groups may be able to achieve high levels of interpersonal congru-ence, thus reducing dysfunctional conflict and positively affecting business outcomes. Conversely, low engagement levels (indicative of negative intergroup relations) may trig-ger dysfunctional conflict among males and females, thus affecting business outcomes negatively. Based on psycho-logical presence theory and research, we hypothesize that the gender diversity–performance link is moderated by business-unit level engagement.

Hypothesis 2: Employee engagement moderates the relationship between gender diversity and performance.

Method

Context and Data

We identified two different companies from two industries, retail (Study 1) and hospitality (Study 2), to examine the relationship between gender diversity and performance at the business-unit level. The main reason for using this approach is that the group processes and outcome variables

by guest on September 25, 2014jlo.sagepub.comDownloaded from

Badal and Harter 357

for each company are unique to their industry type, thus necessitating a detailed contextual analysis of the relation-ship between gender diversity and performance. For instance, the average male–female ratio in a business unit in the retail company is three males to one female, whereas the average ratio in the hospitality company is 1.13 females to 1 male. The critical outcome variable for the retail company is the year over year change in revenue, whereas for the hospitality company it is the quarterly net profit for each unit. Thus, each study draws on somewhat different kinds of data to address the issue of gender diversity at the busi-ness-unit level and its impact on performance. The store (retail organization) or restaurant (hospitality organization) is considered as the unit of analysis since this is the organi-zational unit where management decisions are made, and day-to-day interactions happen between coworkers. It is also the unit at which financial data are available.

The retail organization provided data from 532 electron-ics retail stores in the United States. The stores range in size from 64 to 220 full- and part-time employees (SD = 20.67), 4 to 5 assistant managers, and 1 general manager. The data collection involved both an objective financial measure (comparable revenue) at the store level and self-reported data from the employee engagement survey conducted for all employees in the company (92% response rate), which then is aggregated to a store level to match the financial data.

The hospitality organization provided data from 284 res-taurants in the United States. The restaurants range in size from 26 to 106 employees with almost 90% of the restau-rants having 50 or more employees. Due to slightly lower overall response rates, only restaurants with over 50 employ-ees and a response rate of 50% or above on the employee engagement survey were included in this analysis (range 50-106 employees, SD = 11.03). The excluded smaller res-taurants were not directly comparable to regular sized stores since they were quick-service mall/in-line restaurants rather than stand-alone restaurants. Each restaurant in the study has one general manager. We collected an objective financial measure (quarterly net profit) at the restaurant level and employee engagement data at the individual employee level, which was aggregated to the restaurant level.

Independent Variables

Proportional Diversity Index. The majority of the studies have defined gender composition as the percentage of heteroge-neity (heterogeneity index; Pelled, Eisenhardt, & Xin, 1999). The heterogeneity index is noninterval, that is, the difference in index scores between a group with one woman and a group with two women is larger than the difference in index scores between a group with two women and a group with three women (Williams & Mean, 2004), making it less well suited for regression analyses. This weakening of effect with distance from homogeneity also predetermines

nonlinearity in the representation of the diversity construct. For our study, we have used the proportional diversity index, which is the percentage of minority group members present within each business unit. This is on an interval scale and more appropriate since it does not predetermine nonlinearity in the diversity construct. Conceptualized within the diversity approach, the proportional diversity measure assumes that gender diversity among group mem-bers is an important determinant of group functioning, not the proportion of a particular gender (male or female; Wil-liams & Mean, 2004). The index calculates the proportion of minority members in each business unit and has values ranging from 0 to 0.5, where 0.5 denotes a business unit with an equal number of males and females, and 0 denotes a group with just one gender (male or female). Studies indi-cate that business units with one gender (index value of 0) lack the different viewpoints, diversity in creativity and innovation, diverse market insights, and broader repertoire of skills that the RBV of the firm postulates to be important for firm growth (Ali et al., 2009). As the proportion of males and females approaches parity the interaction between male and female members produces the benefits hypothesized by the RBV of the firm (Ali et al., 2009; Wil-liams & Mean, 2004).

Demographic breakdown of the stores and restaurants was obtained from company records at the time of each employee engagement measurement. In both studies, we use the proportional diversity approach to calculate the gen-der composition of business-units. For the retail study (Study 1), the average proportional diversity index is .24. This indicates that, on an average, one fourth of the team is one gender while three fourths is the other gender. Values range from 0.09 to 0.48.

For the hospitality study (Study 2), the average propor-tional diversity index is .43. This indicates that in this study, on average, 43% of the team is one gender while 57% is the other gender. Values range from .22 to .50 (.50 denotes a business unit with an equal number of males and females).

Employee Engagement. Both organizations (Study 1 and Study 2) measured employee engagement using the Gallup Q12 measure (Harter et al., 2002; Harter et al., 2010), which is a 12-item measure of employee engagement workplace conditions (clarity of expectations, interpersonal relation-ships between coworkers and with the supervisor, recogni-tion for good work, opportunities to develop, connection to the purpose of the organization, opportunities to learn and grow, etc.), the composite of which is highly statistically convergent with other direct measures of engagement cited by Macey and Schneider (2008) in their review of the employee engagement construct (Harter & Schmidt, 2006, 2008). Gallup’s instrument is a formative measure of engagement that captures the psychological and contextual

by guest on September 25, 2014jlo.sagepub.comDownloaded from

358 Journal of Leadership & Organizational Studies 21(4)

conditions that influence the state of engagement in the workplace. Kahn’s “meaningfulness” is measured by items like “received recognition for good work,” “opinions count,” “mission of my company makes me feel my job is important,” and “I have had opportunities to learn and grow.” Kahn’s “safety” is measured by items like “I know what is expected of me,” “I have a best friend at work,” “my associates are committed to doing quality work,” “my supervisor cares about me as a person,” “someone at work has talked to me about my progress,” and “there is someone at work who encourages my development.” Finally, “psy-chological availability” is measured by “I have the materi-als and equipment I need to do my work” and “at work, I have the opportunity to do what I do best every day.” When these psychological and contextual conditions are met, it creates a secure psychological environment that facilitates effective integration of divergent perspectives, increased levels of communication between group members and between employees and supervisors, and stronger interper-sonal relationships, thus enhancing group functioning and positively affecting organizational performance (Harter et al., 2002; Harter, Schmidt, Killham, & Asplund, 2006; Schaufeli & Bakker, 2004).

A particular strength of the Q12 is its prior meta-analytic evidence of causal impact of employee perceptions on the performance of the firm and high test–retest reliability (Harter et al., 2010). Since our primary research questions here involve the examination of the role of gender diversity in business-unit level performance, it is important that we include a measure that has prior empirical evidence of per-formance relatedness (particularly, known generalizable correlations with financial measures). A second strength is that the Q12 measure is a measure of psychological condi-tions at work that many organizations have found action-able. The Q12 is used in hundreds of organizations around the world and has been administered to more than 22 mil-lion respondents. In addition to capturing variance in global workplace attitudes (satisfaction, commitment, involve-ment, dedication, etc.), the instrument is a practical measure that managers can use in understanding the perceptions of their work teams with regard to Kahn’s hypothesized psy-chological conditions at work. In both studies the average engagement score for the 12 items is used to assess the level of engagement among business units. Employee engage-ment surveys were administered at the individual employee level in both studies. The data were then aggregated into business units at the direct manager level and subsequently rolled-up up to the store and restaurant level in each com-pany. This allows us to examine the predictive relationship between employee engagement at point one and the finan-cial performance at a subsequent time at the business-unit level. Engagement data were aggregated up to the store and restaurant level since this is the lowest unit at which finan-cial data was available.

For the retail study (Study 1), the engagement survey results were collected during the second quarter of 2004 with an average response rate of 92%.

For the hospitality study (Study 2), the employee engage-ment survey results were collected in March 2002 with an average response rate of 72%.

Dependent Variable

For the retail study (Study 1), Comparable Revenue 2005 was obtained from company records for each store. The comparable revenue is a key performance metric in the organization and computed as percent change in revenue from the previous year, 2004. Extreme values were removed to make Comparable Revenue normally distributed. This was then matched to Q12 measurement from the 2nd quar-ter of 2004.

For the hospitality study (Study 2), Net Profit after con-trollable expenses for the second quarter of 2002 was used in this analysis. Natural Log of Net Profit was used to achieve a normal distribution of the dependent variable. Net Profit was matched to the Q12 measurement conducted in March 2002. Both studies measured employee engagement (Q12 measurement) and diversity at Time 1 and outcomes at Time 2, making it a predictive study of business-unit-level performance.

Analyses

We use the hierarchical multiple linear regression approach to test our hypotheses. This approach is appropriate to test how each new variable or block of variables add to the pre-diction produced by the previously entered variables. We enter employee engagement first, since it has prior estab-lished meta-analytic evidence of relationship to financial outcomes (Harter et al., 2002; Harter et al., 2010). Once accounting for the variance captured by engagement, we enter the gender diversity variable to assess its unique prediction of financial performance, and finally the engagement–gender diversity interaction term, to test for significant moderation.

Results for Study 1: A Large Retailer

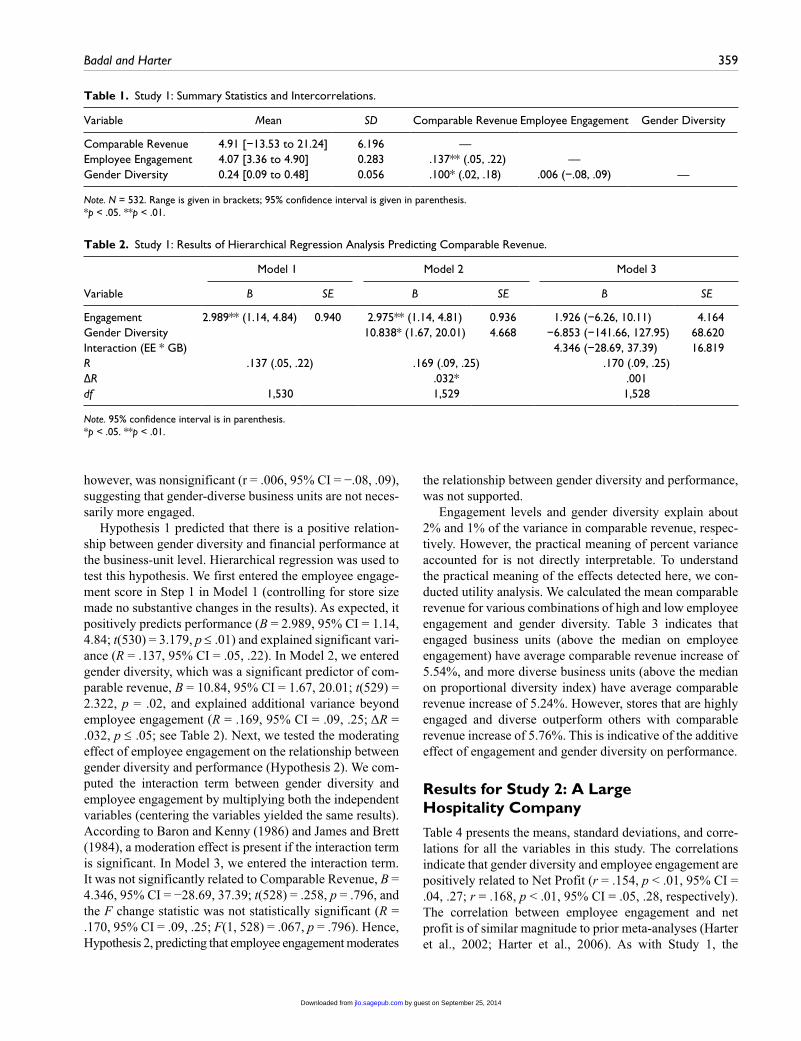

Table 1 presents the means, standard deviations, and corre-lations for all the variables in this study. The correlations indicate that gender diversity and employee engagement are positively related to Comparable Revenue (r = .100, p < .05, 95% confidence interval [CI] = .02, .18; r = .137, p < .01, 95% CI = .05, .22, respectively). The observed correlation of engagement to Comparable Revenue is of similar magni-tude as meta-analytic observed correlations reported in Harter et al. (2002) and Harter et al. (2006). The correlation between gender diversity and employee engagement,

by guest on September 25, 2014jlo.sagepub.comDownloaded from

Badal and Harter 359

however, was nonsignificant (r = .006, 95% CI = −.08, .09), suggesting that gender-diverse business units are not neces-sarily more engaged.

Hypothesis 1 predicted that there is a positive relation-ship between gender diversity and financial performance at the business-unit level. Hierarchical regression was used to test this hypothesis. We first entered the employee engage-ment score in Step 1 in Model 1 (controlling for store size made no substantive changes in the results). As expected, it positively predicts performance (B = 2.989, 95% CI = 1.14, 4.84; t(530) = 3.179, p ≤ .01) and explained significant vari-ance (R = .137, 95% CI = .05, .22). In Model 2, we entered gender diversity, which was a significant predictor of com-parable revenue, B = 10.84, 95% CI = 1.67, 20.01; t(529) = 2.322, p = .02, and explained additional variance beyond employee engagement (R = .169, 95% CI = .09, .25; ΔR = .032, p ≤ .05; see Table 2). Next, we tested the moderating effect of employee engagement on the relationship between gender diversity and performance (Hypothesis 2). We com-puted the interaction term between gender diversity and employee engagement by multiplying both the independent variables (centering the variables yielded the same results). According to Baron and Kenny (1986) and James and Brett (1984), a moderation effect is present if the interaction term is significant. In Model 3, we entered the interaction term. It was not significantly related to Comparable Revenue, B = 4.346, 95% CI = −28.69, 37.39; t(528) = .258, p = .796, and the F change statistic was not statistically significant (R = .170, 95% CI = .09, .25; F(1, 528) = .067, p = .796). Hence, Hypothesis 2, predicting that employee engagement moderates

the relationship between gender diversity and performance, was not supported.

Engagement levels and gender diversity explain about 2% and 1% of the variance in comparable revenue, respec-tively. However, the practical meaning of percent variance accounted for is not directly interpretable. To understand the practical meaning of the effects detected here, we con-ducted utility analysis. We calculated the mean comparable revenue for various combinations of high and low employee engagement and gender diversity. Table 3 indicates that engaged business units (above the median on employee engagement) have average comparable revenue increase of 5.54%, and more diverse business units (above the median on proportional diversity index) have average comparable revenue increase of 5.24%. However, stores that are highly engaged and diverse outperform others with comparable revenue increase of 5.76%. This is indicative of the additive effect of engagement and gender diversity on performance.

Results for Study 2: A Large Hospitality Company

Table 4 presents the means, standard deviations, and corre-lations for all the variables in this study. The correlations indicate that gender diversity and employee engagement are positively related to Net Profit (r = .154, p < .01, 95% CI = .04, .27; r = .168, p < .01, 95% CI = .05, .28, respectively). The correlation between employee engagement and net profit is of similar magnitude to prior meta-analyses (Harter et al., 2002; Harter et al., 2006). As with Study 1, the

Table 1. Study 1: Summary Statistics and Intercorrelations.

Variable Mean SD Comparable Revenue Employee Engagement Gender Diversity

Comparable Revenue 4.91 [−13.53 to 21.24] 6.196 — Employee Engagement 4.07 [3.36 to 4.90] 0.283 .137** (.05, .22) — Gender Diversity 0.24 [0.09 to 0.48] 0.056 .100* (.02, .18) .006 (−.08, .09) —

Note. N = 532. Range is given in brackets; 95% confidence interval is given in parenthesis.*p < .05. **p < .01.

Table 2. Study 1: Results of Hierarchical Regression Analysis Predicting Comparable Revenue.

Model 1 Model 2 Model 3

Variable B SE B SE B SE

Engagement 2.989** (1.14, 4.84) 0.940 2.975** (1.14, 4.81) 0.936 1.926 (−6.26, 10.11) 4.164Gender Diversity 10.838* (1.67, 20.01) 4.668 −6.853 (−141.66, 127.95) 68.620Interaction (EE * GB) 4.346 (−28.69, 37.39) 16.819R .137 (.05, .22) .169 (.09, .25) .170 (.09, .25)ΔR .032* .001df 1,530 1,529 1,528

Note. 95% confidence interval is in parenthesis.*p < .05. **p < .01.

by guest on September 25, 2014jlo.sagepub.comDownloaded from

360 Journal of Leadership & Organizational Studies 21(4)

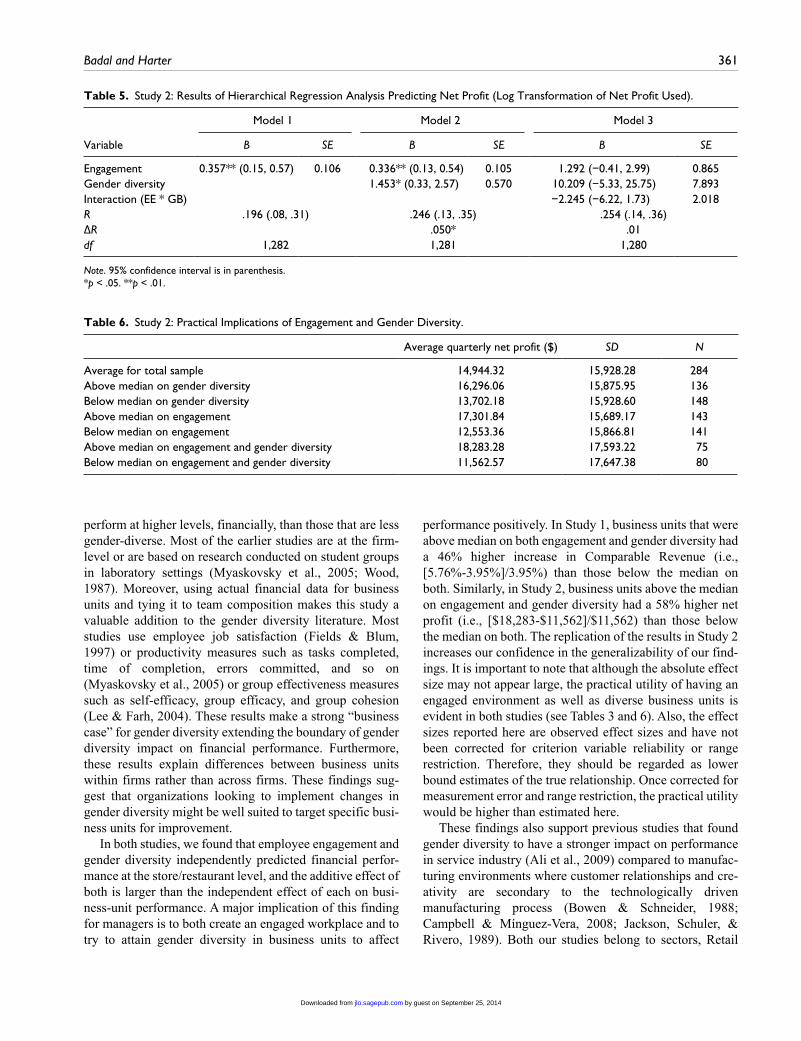

correlation between gender diversity and employee engage-ment was nonsignificant (r = .078, 95% CI= −.04, .19).

Hypothesis 1 predicted that there is a positive relation-ship between gender diversity and financial performance at the business-unit level (log transformation of Net Profit used). To test this hypothesis, we first entered employee engagement in Model 1. Employee engagement is posi-tively related to log transformed Net Profit (B = 0.357, 95% CI = .15, .57; t(282) = 3.365, p < .001) and explains sizeable proportion of variance (R = .196, 95% CI = .08, .31). The estimated regression coefficient of employee engagement is β

1 = 0.357. This indicates that an increase of one unit in

employee engagement will result in (eβ1 − 1) * 100 percent-age change in Y, that is, approximately 35.7% increase in Net Profit. In Model 2, we entered gender diversity, which, as with Study 1, by itself is a significant predictor of Net Profit, B = 1.453, 95% CI = .33, 2.57; t(281) = 2.551, p = .01, and explained additional variance (R = .246, 95% CI = .13, .35; ΔR = .05, p ≤ .01; see Table 5). Next, we tested the moderating effects of employee engagement on the rela-tionship between gender diversity and performance (Hypothesis 2). As with Study 1, we computed the interac-tion term between gender diversity and employee engage-ment by multiplying both the independent variables. In Model 3, we entered the interaction term. It was not signifi-cantly related to Net Profit, B = −2.245, 95% CI = −6.22, 1.73; t(280) = −1.112, p = .267, and the F change statistic was nonsignificant (R = .254, 95% CI = .14, .36; F(1, 280) = 1.237, p = .267). Hence, Hypothesis 2, predicting that employee engagement moderates the relationship between gender diversity and performance, was not supported. The

results of Study 2 are remarkably consistent with those from Study 1.

In this study, engagement and gender diversity each explain 3% to 4% of variance in Net Profit. Again, percent variance accounted for has no direct practical meaning on its own. As with Study 1, we conducted utility analysis, cal-culating the mean net profit for various combinations of high/low employee engagement and gender diversity. Table 6 indicates that engaged business units have average quar-terly net profit of $17,301.84, and gender-diverse business units have average quarterly net profit of $16,296.06; how-ever, stores that are highly engaged and have high gender diversity outperform others, with net profit of $18,283.28. This is again indicative of the additive effect of engagement and gender diversity on performance.

Discussion

In this investigation, our goal was to determine if there is a relationship between gender diversity and financial perfor-mance at the business-unit level and whether employee engagement moderates this relationship. Previous studies of diversity’s impact on performance have been inconsistent in their findings, suggesting a need to use a more complex theoretical framework. The present study draws on three well-established theories (resource-based view of the firm, resource dependency theory, and psychological presence theory) to explain the gender diversity–performance link-age. Using a total of 816 business units from two studies belonging to two different industries (retail and hospitality), the results suggest that more gender-diverse business units

Table 3. Study 1: Practical Implications of Engagement and Gender Diversity.

Average comparable revenue (%) SD N

Average for total sample 4.91 6.20 532Above median on gender diversity 5.24 6.55 266Below median on gender diversity 4.58 5.81 266Above median on engagement 5.54 6.45 262Below median on engagement 4.31 5.88 270Above median on engagement and gender diversity 5.76 7.27 137Below median on engagement and gender diversity 3.95 6.08 141

Table 4. Study 2: Summary Statistics and Intercorrelations.

Variable M SD Net Profit Employee Engagement Gender Diversity

Net Profit 14944.32 [−16,700 to 71,418] 15928.28 — Employee Engagement 3.94 [3.07 to 4.79] 0.281 .168** (.05, .28) — Gender Diversity 0.43 [0.22 to 0.50] 0.052 .154** (.04, .27) .078 (−.04, .19) —

Note. N = 284. Range is given in brackets; 95% confidence interval is given in parenthesis.*p < .05. **p < .01.

by guest on September 25, 2014jlo.sagepub.comDownloaded from

Badal and Harter 361

perform at higher levels, financially, than those that are less gender-diverse. Most of the earlier studies are at the firm-level or are based on research conducted on student groups in laboratory settings (Myaskovsky et al., 2005; Wood, 1987). Moreover, using actual financial data for business units and tying it to team composition makes this study a valuable addition to the gender diversity literature. Most studies use employee job satisfaction (Fields & Blum, 1997) or productivity measures such as tasks completed, time of completion, errors committed, and so on (Myaskovsky et al., 2005) or group effectiveness measures such as self-efficacy, group efficacy, and group cohesion (Lee & Farh, 2004). These results make a strong “business case” for gender diversity extending the boundary of gender diversity impact on financial performance. Furthermore, these results explain differences between business units within firms rather than across firms. These findings sug-gest that organizations looking to implement changes in gender diversity might be well suited to target specific busi-ness units for improvement.

In both studies, we found that employee engagement and gender diversity independently predicted financial perfor-mance at the store/restaurant level, and the additive effect of both is larger than the independent effect of each on busi-ness-unit performance. A major implication of this finding for managers is to both create an engaged workplace and to try to attain gender diversity in business units to affect

performance positively. In Study 1, business units that were above median on both engagement and gender diversity had a 46% higher increase in Comparable Revenue (i.e., [5.76%-3.95%]/3.95%) than those below the median on both. Similarly, in Study 2, business units above the median on engagement and gender diversity had a 58% higher net profit (i.e., [$18,283-$11,562]/$11,562) than those below the median on both. The replication of the results in Study 2 increases our confidence in the generalizability of our find-ings. It is important to note that although the absolute effect size may not appear large, the practical utility of having an engaged environment as well as diverse business units is evident in both studies (see Tables 3 and 6). Also, the effect sizes reported here are observed effect sizes and have not been corrected for criterion variable reliability or range restriction. Therefore, they should be regarded as lower bound estimates of the true relationship. Once corrected for measurement error and range restriction, the practical utility would be higher than estimated here.

These findings also support previous studies that found gender diversity to have a stronger impact on performance in service industry (Ali et al., 2009) compared to manufac-turing environments where customer relationships and cre-ativity are secondary to the technologically driven manufacturing process (Bowen & Schneider, 1988; Campbell & Mínguez-Vera, 2008; Jackson, Schuler, & Rivero, 1989). Both our studies belong to sectors, Retail

Table 5. Study 2: Results of Hierarchical Regression Analysis Predicting Net Profit (Log Transformation of Net Profit Used).

Model 1 Model 2 Model 3

Variable B SE B SE B SE

Engagement 0.357** (0.15, 0.57) 0.106 0.336** (0.13, 0.54) 0.105 1.292 (−0.41, 2.99) 0.865Gender diversity 1.453* (0.33, 2.57) 0.570 10.209 (−5.33, 25.75) 7.893Interaction (EE * GB) −2.245 (−6.22, 1.73) 2.018R .196 (.08, .31) .246 (.13, .35) .254 (.14, .36)ΔR .050* .01df 1,282 1,281 1,280

Note. 95% confidence interval is in parenthesis.*p < .05. **p < .01.

Table 6. Study 2: Practical Implications of Engagement and Gender Diversity.

Average quarterly net profit ($) SD N

Average for total sample 14,944.32 15,928.28 284Above median on gender diversity 16,296.06 15,875.95 136Below median on gender diversity 13,702.18 15,928.60 148Above median on engagement 17,301.84 15,689.17 143Below median on engagement 12,553.36 15,866.81 141Above median on engagement and gender diversity 18,283.28 17,593.22 75Below median on engagement and gender diversity 11,562.57 17,647.38 80

by guest on September 25, 2014jlo.sagepub.comDownloaded from

362 Journal of Leadership & Organizational Studies 21(4)

and Hospitality, that gain from diverse perspectives, have more social interaction between team members, and higher interaction between employees and customers. In such environments, it is critical to capitalize on the benefits pro-vided by a diverse workforce.

While we found a practically meaningful relationship between gender diversity and performance, our findings suggest that engagement levels in the business unit may not be moderating this relationship. To our knowledge, this is the first study that uses employee engagement as a measure of intergroup relations at work and looks at its moderating effect on the gender diversity–performance link. A possible explanation for why engagement did not moderate the effect of gender diversity on performance is that the group mem-bers in these business units (retail stores in Study 1 and res-taurants in Study 2) spend a considerable amount of time with each other, working collaboratively to achieve specific goals. Hence, they have learned to anticipate and manage different viewpoints that may exist along the social catego-ries (Harrison, Price, Gavin, & Florey, 2002; Jehn & Bezrukova, 2004; Pelled et al., 1999). Prior research indi-cates that in collectivistic organizational cultures, such as retail or hospitality, the emphasis is on team performance rather than individual achievement. Team members depend on each other to achieve a common goal. In such cultures the organizational membership is far more important than membership based on demographic attributes (Chatman, Polzer, Barsade, & Neale, 1998). Turner, Oakes, Haslam, and McGarty (1994) term this “functional antagonism,” where, as the salience of one type of social categorization (organizational membership) increases, salience of the other type (gender, age, or race differences) decreases. In our study, the employees in a store or a restaurant work together to serve the customers’ needs and preferences and thus affect performance. There is a feeling of shared goals, leading members to consider more of their coworkers as members of the same group irrespective of their demo-graphic differences. Hence, interaction among males and females is likely to be much more harmonious in a collec-tivistic culture, reducing the role of engagement as a mod-erator. In individualistic work cultures like the manufacturing environment, limited interaction between male and female employees may lead to gender differences becoming more pronounced and thus hindering effective working of the unit (Ali et al., 2009). In such environments, the moderating effect of engagement may become more salient in harmo-nizing the relationships between gender groups and to fully leverage the benefits of gender diversity. Clearly, more research is needed to establish the role of engagement and gender diversity in different industry contexts.

Our study has several limitations that can be addressed by future research. The cross-sectional nature of the data makes it difficult to draw causal inferences from this study—a limitation that can be avoided by designing a

longitudinal study. A longitudinal study will also be able to capture how changes in gender diversity influence perfor-mance over time. Researchers should also explore the effect of organizational diversity goals on self-perception of women and its impact on intergroup relations, engagement, and organizational performance. Intergroup relations may be negatively affected if women feel they were hired to improve diversity levels. More research is also needed to uncover the mechanisms by which gender diversity drives business performance. Whether it is facilitating interactions with a diverse customer base or generating diverse market insights or bringing in a broader repertoire of skills into the workplace—understanding the means by which gender diversity can be a competitive advantage will enable organi-zations to use gender diversity as a lever for business growth. Future research should also look at the role of engagement as a moderator in industries other than retail and hospitality. It will be interesting to see the effect of engagement as a moderator in firms where demographic attributes may hinder business-unit performance. In addi-tion, future research should be focused on testing additional environmental and individual-level variables that could be better moderators of gender diversity–performance linkage in different industry settings. For instance, length of time the teams have been together, pattern and frequency of interaction among team members, and differential job types could possibly be better predictors of impact of gender diversity on business-unit performance. Arguably, the financial outcomes we included in this article are down-stream from potentially direct outcomes such as customer perceptions of service quality and employee turnover. Future research should focus on these direct outcomes and also explore the gender diversity link to nonfinancial out-comes, such as problem solving and innovation.

Conclusion

The current study is specifically focused on gender diver-sity. Even though there is an increasing body of literature assessing the relationship between different types of demo-graphic diversity (age, race, or gender) and performance, there are a limited number of empirical studies examining the independent effect of each demographic characteristic on performance—a fact pointed out by several researchers who tried to conduct a meta-analysis for each category (Horwitz & Horwitz, 2007). The results of this research support the contention that gender diversity at the business-unit level positively affects financial performance, which appears to have substantial practical implications. This financial utility suggests that making diversity an organiza-tional priority may realize financial benefits. We also showed that employee engagement separately and indepen-dently contributes to the company’s bottom-line. But diver-sity and engagement do not appear to be an either-or

by guest on September 25, 2014jlo.sagepub.comDownloaded from

Badal and Harter 363

proposition. They are relatively independent in their contri-bution to financial success, suggesting that organizations should focus both on selecting a diverse workforce and cre-ating an engaged culture.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

References

Aldrich, H. E., & Pfeffer, J. (1976). Environments of organiza-tions. Annual Review of Sociology, 2, 79-105.

Ali, M., Kulik, C. T., & Metz, I. (2009, August). The impact of gender diversity on performance in services and manufactur-ing organizations. Academy of Management Annual Meeting Proceedings, Chicago, IL.

Ancona, D., & Caldwell, D. (1992). Demography and design: Predictors of new product team performance. Organization Science, 3, 321-341.

Barney, J. B. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17, 99-120.

Barney, J. B. (2001). Resource-based theories of competitive advantage: A ten-year retrospective on the resource-based view. Journal of Management, 27, 643-650.

Baron, R. M., & Kenny, D. A. (1986). The moderator-medi-ator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51, 1173-1182.

Böhren, O., & Ström, R. (2005). The value-creating board: Theory and evidence (Research Report No. 8/2005). Oslo, Norway: Department of Financial Economics, Norwegian School of Management.

Bowen, D. E., & Schneider, B. (1988). Services marketing and management: Implications for organizational behavior. In L. L. Cummings & B. M. Staw (Eds.), Research in organizational behavior (Vol. 10, pp. 43-80). Greenwich, CT: JAI Press.

Campbell, K., & Mínguez-Vera, A. (2008). Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics, 83, 435-451.

Carter, D. A., D’Souza, F., Simkins, B. J., & Simpson, W. G. (2007, September). The diversity of corporate board committees and firm financial performance (Working Paper). Retrieved from http://papers.ssrn.com/sol3/papers.cfm?abstract_id=9727631-30

Carter, D. A., Simkins, B. J., & Simpson, W. G. (2003). Corporate governance, board diversity and firm value. Financial Review, 38, 33-53.

Catalyst. (2004). The bottom line: Connecting corporate per-formance and gender diversity. Retrieved from http://www .catalyst.org/knowledge/bottom-line-connecting-corporate-performance-and-gender-diversity

Chatman, J., Polzer, J., Barsade, S., & Neale, M. (1998). Being different yet feeling similar: The influence of demographic

composition and organizational culture on work processes and outcomes. Administrative Science Quarterly, 43, 749-780.

Cox, T., & Blake, S. (1991). Managing cultural diversity: Implications for organizational competitiveness. Academy of Management Executive, 5, 45-56.

Dalton, D., Daily, C., Ellstrand, A., & Johnson, J. (1998). Meta-analytic review of board composition, leadership structure, and financial performance. Strategic Management Journal, 19, 269-290.

Desvaux, G., Devillard-Hoellinger, S., & Meaney, M. C. (2008). A business case for women. McKinsey Quarterly, 4, 27-33.

Dezso, C. L., & Ross, D. G. (2008). Girl power: Female partici-pation in top management and firm quality. Retrieved from http://ssrn.com/abstract=1088182

Dignam, J. T., Barrera, M., Jr., & West, S. G. (1986). Occupational stress, social support, and burnout among correctional offi-cers. American Journal of Community Psychology, 14, 177-193.

Easley, C. A., (2001). Developing, valuing and managing diversity in the new millennium. Organization Development Journal, 19, 38-50.

Farrell, K. A., & Hersch, P.L. (2001). Additions to corporate boards: Does gender matter? (Working Paper). Retrieved from http://papers.ssrn.com/sol3/papers.cfm?abstract_id=292281

Fields, D. L., & Blum, T. C. (1997). Employee satisfaction in business-units with different gender composition. Journal of Organizational Behavior, 18, 181-196.

Frink, D., Robinson, R. K., Reithel, B., Arthur, M. M., Ammeter, A. P., & Ferris, G. R. (2003). Gender demography and orga-nization performance: A two study investigation with conver-gence. Group and Organization Management, 28, 127-147.

Gallego-Alvarez, I., Garcia-Sanchez, I. M., & Rodriguez-Dominguez, L. (2009). The influence of gender diversity on corporate performance. Revista de Contabilidad—Spanish Accounting Review, 13, 53-88.

Hambrick, D., Cho, T., & Chen, M. (1996). The influence of top management team heterogeneity on firms’ competitive moves. Administrative Science Quarterly, 41, 659-684.

Harrison, D., Price, K., Gavin, J., & Florey, A. (2002). Time, teams and task performance: Changing effects of surface- and deep-level diversity on group functioning. Academy of Management Journal, 45, 1029-1045.

Harter, J. K., & Schmidt, F. L. (2006). Connecting employee sat-isfaction to business-unit performance. In A. I. Kraut (Ed.), Getting action from organizational surveys: New concepts, methods, and applications (pp. 33-52). San Francisco, CA: Jossey-Bass.

Harter, J. K., & Schmidt, F. L. (2008). Conceptual versus empirical distinctions among constructs: Implications for discriminant validity. Commentary on employee engagement. Industrial and Organizational Psychology, 1, 37-40.

Harter, J. K., Schmidt, F. L., Asplund, J. W., Killham, E. A., & Agrawal, S. (2010). Causal impact of employee work per-ceptions on the bottom line of organizations. Perspectives on Psychological Science, 5, 378-389.

Harter, J. K., Schmidt, F. L., & Hayes, T. L. (2002). Business-unit level relationship between employee satisfaction, employee engagement, and business outcomes: A meta-analysis. Journal of Applied Psychology, 87, 268-279.

by guest on September 25, 2014jlo.sagepub.comDownloaded from

364 Journal of Leadership & Organizational Studies 21(4)

Harter, J. K., Schmidt, F. L., Killham, E. A., & Asplund, J. W. (2006). Q12 meta-analysis (Technical Paper). Omaha, NE: Gallup.

Heilman, M. E., & Haynes, M. C. (2005). No credit where credit is due: Attributional rationalization of women’s success in male–female teams. Journal of Applied Psychology, 90, 905-916.

Heilman, M. E., & Okimoto, T. G. (2007). Why are women penal-ized for success at male tasks? The implied communality defi-cit. Journal of Applied Psychology, 92, 81-92.

Herring, C. (2009). Does diversity pay? Race, gender, and the business case for diversity. American Sociological Review, 74, 208-224.

Hillman, A., Shropshire, C., & Cannella, A. (2007). Organizational predictors of women on corporate boards. Academy of Management Journal, 50, 941-952.

Hobman, E. V., Bordia, P., & Gallois, C. (2003). Consequences of feeling dissimilar from others in a work team. Journal of Business and Psychology, 17, 301-325.

Horwitz, S. K. (2005). The compositional impact of team diversity on performance: Theoretical consideration. Human Resource Development Review, 4, 219-245.

Horwitz, S. K., & Horwitz, I. B. (2007). The effects of team diversity on team outcomes: A meta-analytic review of team demography. Journal of Management, 33, 987-1015.

Jackson, S. E., Schuler, R. S., & Rivero, J. C. (1989). Organizational characteristics as predictors of personnel practices. Personnel Psychology, 42, 727-786.

James, L. R., & Brett, J. M. (1984). Mediators, moderators, and tests for mediation. Journal of Applied Psychology, 69, 307-321.

Jehn, K. A., & Bezrukova, K. (2004). A field study of group diversity, business-unit context, and performance. Journal of Organizational Behavior, 25, 703-729.

Jimeno, F. J., & Redondo, M. (2007, September). Diversidad de género en el consejo de administración y características económico-financieras de las empresas [Gender diversity in the board of directors and financial characteristics of the com-panies]. Paper presented at XIV Congreso de la Asociación Española de Contabilidad y Administración de Empresas, Valencia, Spain.

Jimeno, F. J., & Redondo, M. (2008, November). Efectos sobre los ratios financieros de la diversidad de género en los con-sejos de administración de empresas españolas [Gender diversity in the board of directors and the effects on the finan-cial performance of Spanish companies]. Paper presented at the First Workshop on Diversity, Gender, Governance and Accounting, Carmona, Seville, Spain.

Jones, J. R., & Harter, J. K. (2005). Race effects on the employee engagement-turnover intention relationship. Journal of Leadership and Organizational Studies, 11, 78-88.

Kahn, W. A. (1990). Psychological conditions of personal engage-ment and disengagement at work. Academy of Management Journal, 33, 692-724.

Kahn, W. A. (1992). To be fully there: Psychological presence at work. Human Relations, 45, 321-349.

Kanter, R. M. (1977). Men and women of the corporation. New York, NY: Basic Books.

Kochan, T., Bezyrkova, K., Ely, R., Jackson, S., Joshi, A., Jehn, K., . . . Thomas, D. (2003). The effects of diversity on business

performance: Report of the diversity research network. Human Resource Management, 42, 3-21.

Konrad, A. M., Winter, S., & Gutek, B. A. (1992). Diversity in business-unit sex composition: Implications for majority and minority workers. In S. Bacharach & P. Tolbert (Eds.), Research in the sociology of organizations (pp. 115-140). Greenwich, CT: JAI Press.

Krishnan, H., & Park, D. (2005). A few good women-on top man-agement teams. Journal of Business Research, 58, 1712-1720.

Lee, C., & Farh, J. (2004). Joint effects of group efficacy and gen-der diversity on group cohesion and performance. Applied Psychology: An International Review, 53, 136-154.

Macey, W. H., & Schneider, B. (2008). Meaning of employee engagement. Industrial and Organizational Psychology, 1, 3-30.

Mannix, E., & Neale, M. A. (2005). What differences make a dif-ference? The promise and reality of diverse teams in organiza-tions. Psychological Science in the Public Interest, 6, 31-55.

Martin, P. Y. (1985). Group sex composition in work organi-zations: A structural-normative model. Research in the Sociology of Organizations, 4, 311-349.

May, D. R., Gilson, R. L., & Harter, L. M. (2004). The psycho-logical conditions of meaningfulness, safety and availability and the engagement of the human spirit at work. Journal of Occupational and Organizational Psychology, 77, 11-37.

Milliken, F., & Martins, L. (1996). Searching for common threads: Understanding the multiple effects of diversity in organiza-tional settings. Academy of Management Review, 21, 402-433.

Myaskovsky, L., Unikel, E., & Dew, M. (2005). Effects of gender diversity on performance and interpersonal behavior in small business-units. Sex Roles, 52, 645-657.

O’Reilly, C., Caldwell, D., & Barnett, W. (1989). Business-unit demography, social integration and turnover. Administrative Science Quarterly, 34, 21-37.

Orlitzky, M., & Benjamin, J. D. (2003). The effect of sex composi-tion on small-group performance in a business school compe-tition. Academy of Management Learning and Performance, 2, 128-138.

Pelled, L. (1996). Demographic diversity, conflict, and business-unit outcomes: An intervening process theory. Organization Science, 7, 615-631.

Pelled, L., Eisenhardt, K., & Xin, K. (1999). Exploring the black box: An analysis of business-unit diversity, conflict, and per-formance. Administrative Science Quarterly, 44, 1-28.

Pfeffer, J., & Salancik, G. R. (1978). The external control of orga-nizations: A resource dependence perspective. New York, NY: Harper & Row.

Polzer, J. T., Milton, L. P., & Swann, W. B., Jr. (2002). Capitalizing on diversity: Interpersonal congruence in small work groups. Administrative Science Quarterly, 47, 296-324.

Rose, C. (2007). Does female board representation influence firm performance? The Danish evidence. Corporate Governance: An International Review, 15, 404-413.

Schaufeli, W. B., & Bakker, A. B. (2004). Job demands, job resources, and their relationship with burnout and engage-ment: A multi-sample study. Journal of Organizational Behavior, 25, 293-315.

Shrader, C. B., Blackburn, V. B., & Iles, P. (1997). Women in management and firm financial performance: An exploratory study. Journal of Managerial Issues, 9, 355-372.

by guest on September 25, 2014jlo.sagepub.comDownloaded from

Badal and Harter 365

Siciliano, J. I. (1996). The relationship of board member diversity to organizational performance. Journal of Business Ethics, 15, 1313-1320.

Smith, D. R., DiTomaso, N., Farris, G. F., & Cordero, R. (2001). Favoritism, bias and error in performance ratings of scientists and engineers: The effects of power, status, and numbers. Sex Roles, 45, 337-358.

Smith, N., Smith, V., & Verner, M. (2006). Do women in top management affect firm performance? A panel study of 2,500 Danish firms. International Journal of Performance Management, 55, 569-593.

Stewart, G. L. (2006). A meta-analytic review of relationships between team design features and team performance. Journal of Management, 32, 29-54.

Tougas, F., Rinfret, N., Beaton, A. M., & de la Sablonniére, R. (2005). Policewomen acting in self-defense: Can psycho-logical disengagement protect self-esteem from the negative outcomes of relative deprivation. Journal of Personality and Social Psychology, 88, 790-800.

Tsui, A., Egan, T., & O’Reilly, C. (1992). Being different: Relational demography and organizational attachment. Administrative Science Quarterly, 37, 549-588.

Turner, J. C., Oakes, P. J., Haslam, S. A., & McGarty, C. (1994). Self and collective: Cognition and social context. Personality and Social Psychology Bulletin, 20, 454-463.

U.S. Department of Labor. (2011a). Bureau of labor statis-tics: Labor force statistics from the current population sur-vey, 1942 to date. Retrieved from http://www.bls.gov/cps/cpsaat01.htm

U.S. Department of Labor. (2011b). Bureau of Labor Statistics: Employment outlook: 2010-2020. Labor force projections to 2020: A more slowly growing workforce. Retrieved from http://www.bls.gov/opub/mlr/2012/01/art3full.pdf

Watson, W. E., Kumar K., & Michaelsen, L. K. (1993). Cultural diversity’s impact on interaction process and performance: Comparing homogeneous and diverse task groups. Academy of Management Journal, 36, 590-602.

Wharton, A. S., & Baron, J. N. (1987). So happy together? The impact of gender segregation on men at work. American Sociological Review, 52, 574-587.

Wharton, A. S., & Baron, J. N. (1991). Satisfaction? The psy-chological impact of gender segregation on women at work. Sociological Quarterly, 32, 365-387.

Williams, H. M., & Mean, L. J. (2004). Measuring gender com-position in business-units: A comparison of existing methods. Organizational Research Methods, 7, 456-474.

Williams, K. Y., & O’Reilly, C. A., III. (1998). Demography and diversity in organizations: A review of 40 years of research. In B. M. Staw & L. L. Cummings (Eds.), Research in organi-zational behavior (Vol. 20, pp. 77-140). Greenwich, CT: JAI Press.

Wood, W. (1987). Meta-analytic review of sex differences in group performance. Psychological Bulletin, 102, 53-71.

Zenger, T. R., & Lawrence, B. S. (1989). Organizational demogra-phy: The differential effects of age and tenure distributions on technical communication. Academy of Management Journal, 32, 353-376.

Author Biographies

Sangeeta Badal is the primary researcher for Gallup's entrepre-neurship initiative and a Senior Consultant with the workplace practice. She has been employed with Gallup since 1999.

James K. Harter is Chief Scientist for workplace and well-being research at Gallup. He has been employed with Gallup since 1985.

by guest on September 25, 2014jlo.sagepub.comDownloaded from