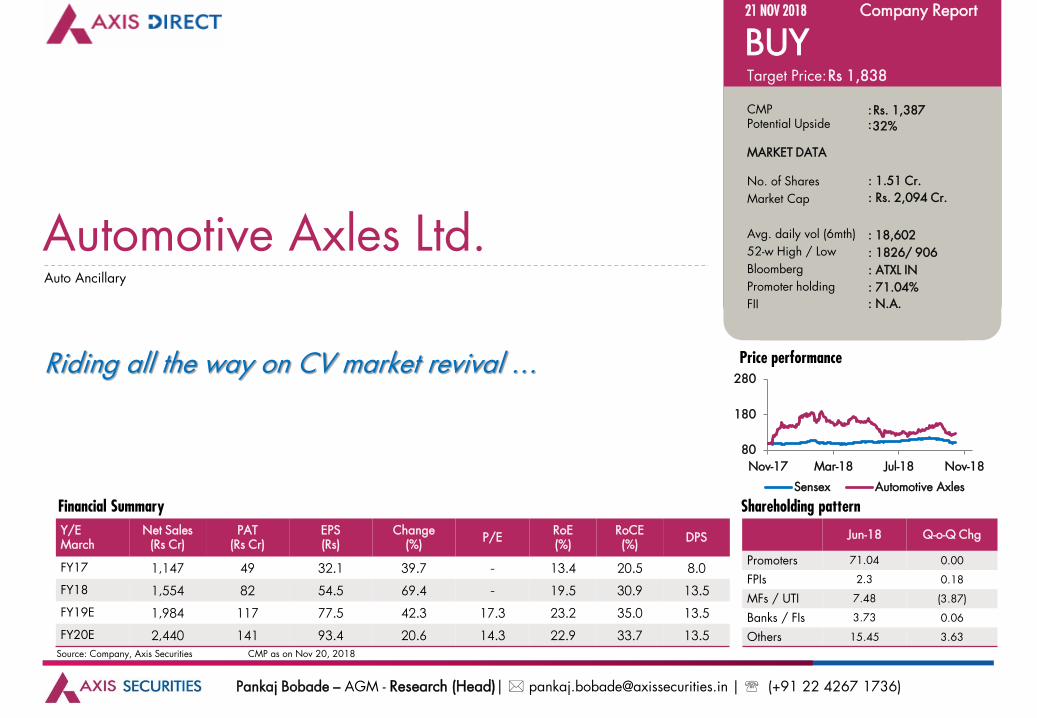

Automotive Axles Ltd - Axis Direct

25

Automotive Axles Ltd CV market revival to benefit the company…

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Automotive Axles Ltd - Axis Direct

Automotive Axles Ltd

CV market revival to benefit the company…

Y/EMarch

Net Sales(Rs Cr)

PAT (Rs Cr)

EPS (Rs)

Change (%)

P/ERoE(%)

RoCE(%)

DPS

FY17 1,147 49 32.1 39.7 - 13.4 20.5 8.0

FY18 1,554 82 54.5 69.4 - 19.5 30.9 13.5

FY19E 1,984 117 77.5 42.3 17.3 23.2 35.0 13.5

FY20E 2,440 141 93.4 20.6 14.3 22.9 33.7 13.5

Riding all the way on CV market revival …

Auto Ancillary

Price performance

Target Price:

CMPPotential Upside

MARKET DATA

No. of Shares

Market Cap

Avg. daily vol (6mth)

52-w High / Low

Bloomberg

Promoter holding

FII

21 NOV 2018 Company Report

BUYRs 1,838

Rs. 1,387::

: 1.51 Cr.

: Rs. 2,094 Cr.

:

: 1826/ 906

: ATXL IN

: 71.04%

: N.A.

Automotive Axles Ltd.

Shareholding patternFinancial Summary

Source: Company, Axis Securities CMP as on Nov 20, 2018

Jun-18 Q-o-Q Chg

Promoters 71.04 0.00

FPIs 2.3 0.18

MFs / UTI 7.48 (3.87)

Banks / FIs 3.73 0.06

Others 15.45 3.63

18,602

32%

Pankaj Bobade – AGM - Research (Head)| [email protected] | (+91 22 4267 1736)

80

180

280

Nov-17 Mar-18 Jul-18 Nov-18

Sensex Automotive Axles

3

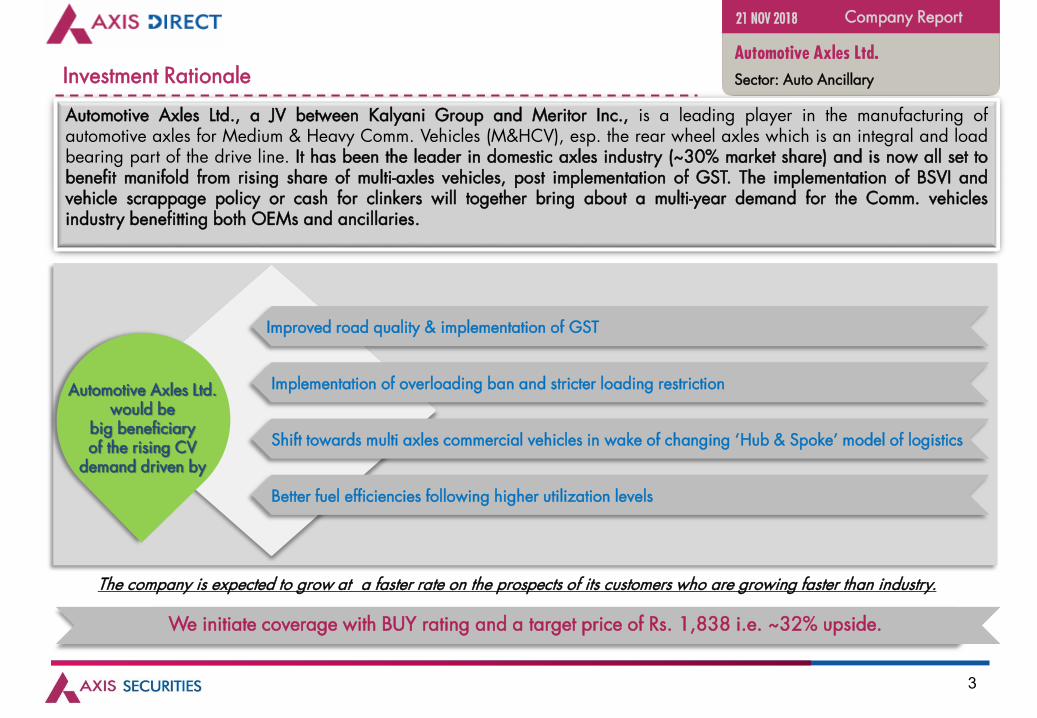

Investment Rationale

We initiate coverage with BUY rating and a target price of Rs. 1,838 i.e. ~32% upside.

Improved road quality & implementation of GST

Implementation of overloading ban and stricter loading restriction

Shift towards multi axles commercial vehicles in wake of changing ‘Hub & Spoke’ model of logistics

Better fuel efficiencies following higher utilization levels

The company is expected to grow at a faster rate on the prospects of its customers who are growing faster than industry.

Automotive Axles Ltd., a JV between Kalyani Group and Meritor Inc., is a leading player in the manufacturing ofautomotive axles for Medium & Heavy Comm. Vehicles (M&HCV), esp. the rear wheel axles which is an integral and loadbearing part of the drive line. It has been the leader in domestic axles industry (~30% market share) and is now all set tobenefit manifold from rising share of multi-axles vehicles, post implementation of GST. The implementation of BSVI andvehicle scrappage policy or cash for clinkers will together bring about a multi-year demand for the Comm. vehiclesindustry benefitting both OEMs and ancillaries.

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

21 NOV 2018

Automotive Axles Ltd. would be

big beneficiary of the rising CV

demand driven by

4

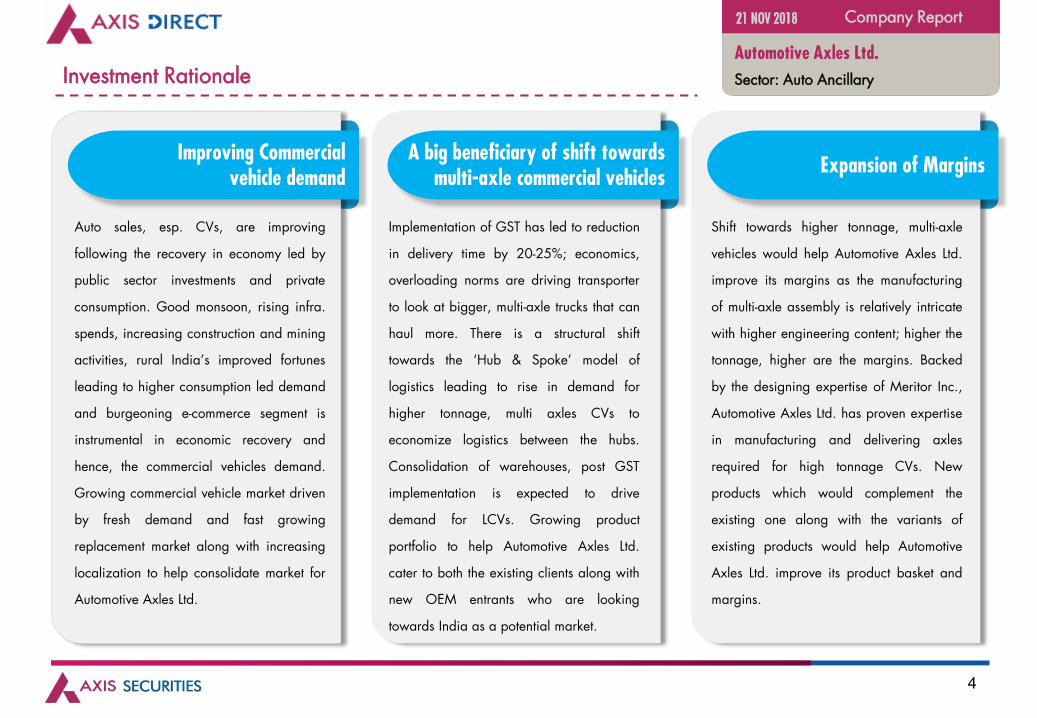

Investment Rationale

A big beneficiary of shift towards multi-axle commercial vehicles

Improving Commercial vehicle demand

Expansion of Margins

Auto sales, esp. CVs, are improving

following the recovery in economy led by

public sector investments and private

consumption. Good monsoon, rising infra.

spends, increasing construction and mining

activities, rural India’s improved fortunes

leading to higher consumption led demand

and burgeoning e-commerce segment is

instrumental in economic recovery and

hence, the commercial vehicles demand.

Growing commercial vehicle market driven

by fresh demand and fast growing

replacement market along with increasing

localization to help consolidate market for

Automotive Axles Ltd.

Implementation of GST has led to reduction

in delivery time by 20-25%; economics,

overloading norms are driving transporter

to look at bigger, multi-axle trucks that can

haul more. There is a structural shift

towards the ‘Hub & Spoke’ model of

logistics leading to rise in demand for

higher tonnage, multi axles CVs to

economize logistics between the hubs.

Consolidation of warehouses, post GST

implementation is expected to drive

demand for LCVs. Growing product

portfolio to help Automotive Axles Ltd.

cater to both the existing clients along with

new OEM entrants who are looking

towards India as a potential market.

Shift towards higher tonnage, multi-axle

vehicles would help Automotive Axles Ltd.

improve its margins as the manufacturing

of multi-axle assembly is relatively intricate

with higher engineering content; higher the

tonnage, higher are the margins. Backed

by the designing expertise of Meritor Inc.,

Automotive Axles Ltd. has proven expertise

in manufacturing and delivering axles

required for high tonnage CVs. New

products which would complement the

existing one along with the variants of

existing products would help Automotive

Axles Ltd. improve its product basket and

margins.

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

21 NOV 2018

5

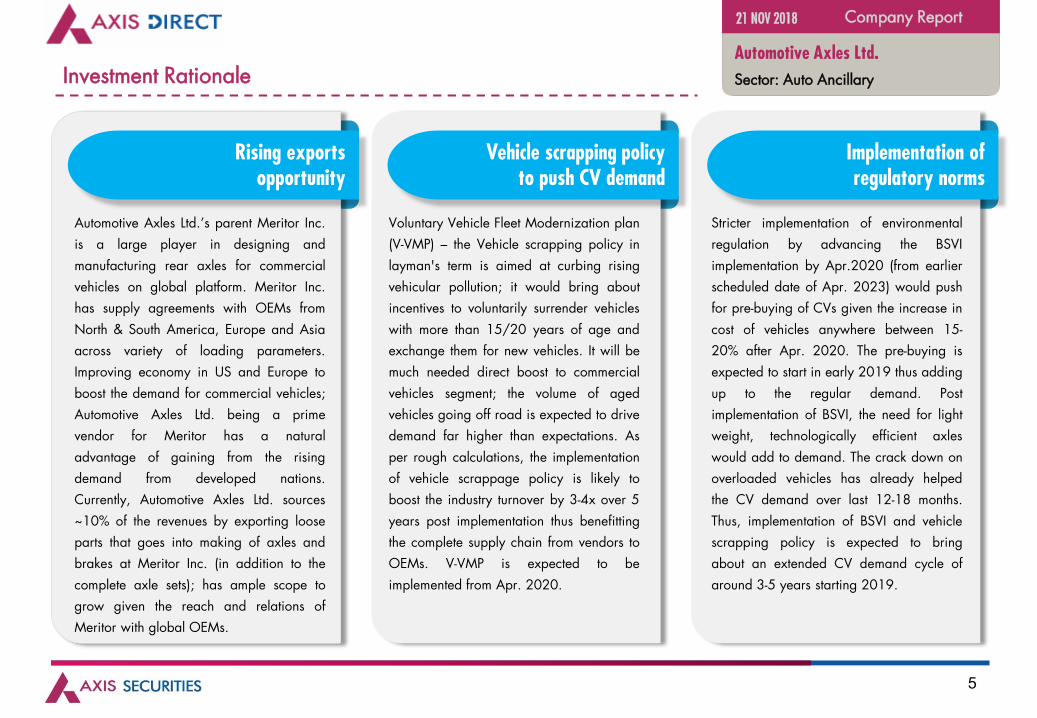

Investment Rationale

Vehicle scrapping policy to push CV demand

Rising exports opportunity

Implementation of regulatory norms

Automotive Axles Ltd.’s parent Meritor Inc.

is a large player in designing and

manufacturing rear axles for commercial

vehicles on global platform. Meritor Inc.

has supply agreements with OEMs from

North & South America, Europe and Asia

across variety of loading parameters.

Improving economy in US and Europe to

boost the demand for commercial vehicles;

Automotive Axles Ltd. being a prime

vendor for Meritor has a natural

advantage of gaining from the rising

demand from developed nations.

Currently, Automotive Axles Ltd. sources

~10% of the revenues by exporting loose

parts that goes into making of axles and

brakes at Meritor Inc. (in addition to the

complete axle sets); has ample scope to

grow given the reach and relations of

Meritor with global OEMs.

Voluntary Vehicle Fleet Modernization plan

(V-VMP) – the Vehicle scrapping policy in

layman's term is aimed at curbing rising

vehicular pollution; it would bring about

incentives to voluntarily surrender vehicles

with more than 15/20 years of age and

exchange them for new vehicles. It will be

much needed direct boost to commercial

vehicles segment; the volume of aged

vehicles going off road is expected to drive

demand far higher than expectations. As

per rough calculations, the implementation

of vehicle scrappage policy is likely to

boost the industry turnover by 3-4x over 5

years post implementation thus benefitting

the complete supply chain from vendors to

OEMs. V-VMP is expected to be

implemented from Apr. 2020.

Stricter implementation of environmental

regulation by advancing the BSVI

implementation by Apr.2020 (from earlier

scheduled date of Apr. 2023) would push

for pre-buying of CVs given the increase in

cost of vehicles anywhere between 15-

20% after Apr. 2020. The pre-buying is

expected to start in early 2019 thus adding

up to the regular demand. Post

implementation of BSVI, the need for light

weight, technologically efficient axles

would add to demand. The crack down on

overloaded vehicles has already helped

the CV demand over last 12-18 months.

Thus, implementation of BSVI and vehicle

scrapping policy is expected to bring

about an extended CV demand cycle of

around 3-5 years starting 2019.

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

21 NOV 2018

6

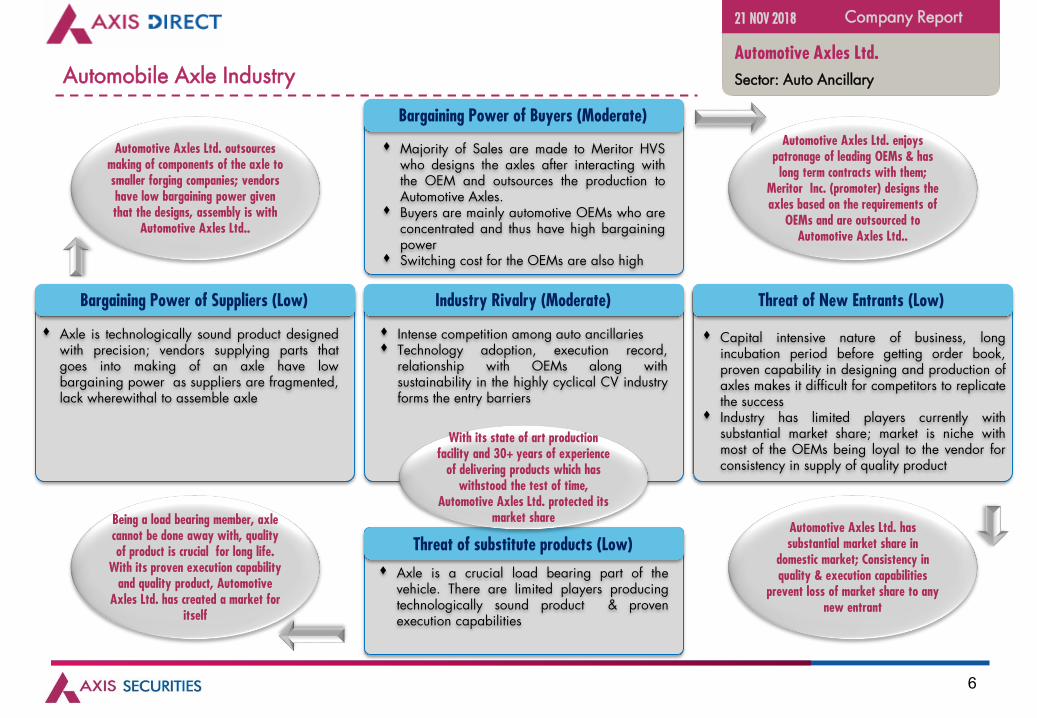

Automobile Axle Industry

Company Report

Sector: Auto Ancillary

Automotive Axles Ltd. enjoys patronage of leading OEMs & has

long term contracts with them; Meritor Inc. (promoter) designs the axles based on the requirements of

OEMs and are outsourced to Automotive Axles Ltd..

Being a load bearing member, axle cannot be done away with, quality of product is crucial for long life.

With its proven execution capability and quality product, Automotive

Axles Ltd. has created a market for itself

Automotive Axles Ltd. has substantial market share in

domestic market; Consistency in quality & execution capabilities

prevent loss of market share to any new entrant

Automotive Axles Ltd. outsources making of components of the axle to smaller forging companies; vendors have low bargaining power given that the designs, assembly is with

Automotive Axles Ltd..

21 NOV 2018

Axle is technologically sound product designedwith precision; vendors supplying parts thatgoes into making of an axle have lowbargaining power as suppliers are fragmented,lack wherewithal to assemble axle

Capital intensive nature of business, longincubation period before getting order book,proven capability in designing and production ofaxles makes it difficult for competitors to replicatethe success

Industry has limited players currently withsubstantial market share; market is niche withmost of the OEMs being loyal to the vendor forconsistency in supply of quality product

Intense competition among auto ancillaries Technology adoption, execution record,

relationship with OEMs along withsustainability in the highly cyclical CV industryforms the entry barriers

Bargaining Power of Suppliers (Low) Industry Rivalry (Moderate) Threat of New Entrants (Low)

Majority of Sales are made to Meritor HVSwho designs the axles after interacting withthe OEM and outsources the production toAutomotive Axles.

Buyers are mainly automotive OEMs who areconcentrated and thus have high bargainingpower

Switching cost for the OEMs are also high

Bargaining Power of Buyers (Moderate)

Axle is a crucial load bearing part of thevehicle. There are limited players producingtechnologically sound product & provenexecution capabilities

Threat of substitute products (Low)

With its state of art production facility and 30+ years of experience

of delivering products which has withstood the test of time,

Automotive Axles Ltd. protected its market share

Automotive Axles Ltd.

7

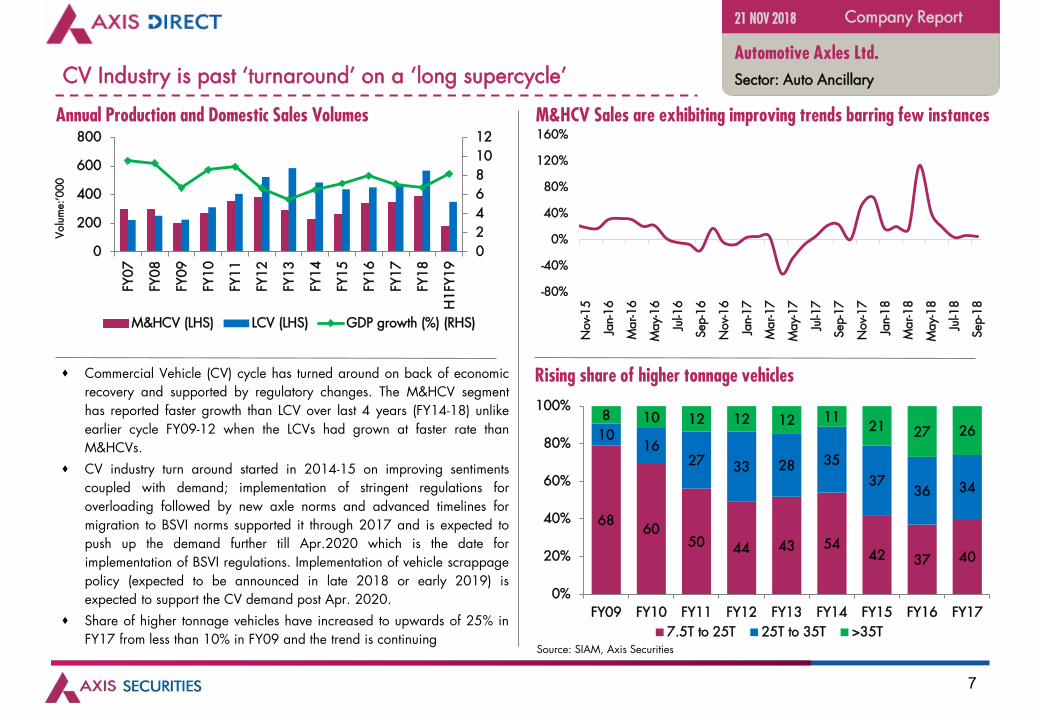

CV Industry is past ‘turnaround’ on a ‘long supercycle’

Commercial Vehicle (CV) cycle has turned around on back of economic

recovery and supported by regulatory changes. The M&HCV segment

has reported faster growth than LCV over last 4 years (FY14-18) unlike

earlier cycle FY09-12 when the LCVs had grown at faster rate than

M&HCVs.

CV industry turn around started in 2014-15 on improving sentiments

coupled with demand; implementation of stringent regulations for

overloading followed by new axle norms and advanced timelines for

migration to BSVI norms supported it through 2017 and is expected to

push up the demand further till Apr.2020 which is the date for

implementation of BSVI regulations. Implementation of vehicle scrappage

policy (expected to be announced in late 2018 or early 2019) is

expected to support the CV demand post Apr. 2020.

Share of higher tonnage vehicles have increased to upwards of 25% in

FY17 from less than 10% in FY09 and the trend is continuing

Company Report

Annual Production and Domestic Sales Volumes

Source: SIAM, Axis Securities

M&HCV Sales are exhibiting improving trends barring few instances

Sector: Auto Ancillary

Rising share of higher tonnage vehicles

21 NOV 2018

6860

50 44 43 5442 37 40

1016

27 33 28 35

3736 34

8 10 12 12 12 1121 27 26

0%

20%

40%

60%

80%

100%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

7.5T to 25T 25T to 35T >35T

Volu

me:

‘000

0

2

4

6

8

10

12

0

200

400

600

800FY

07

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

H1FY

19

M&HCV (LHS) LCV (LHS) GDP growth (%) (RHS)

Automotive Axles Ltd.

-80%

-40%

0%

40%

80%

120%

160%

Nov-

15

Jan-

16

Mar-1

6

May-

16

Jul-1

6

Sep

-16

Nov-

16

Jan-

17

Mar-1

7

May-

17

Jul-1

7

Sep

-17

Nov-

17

Jan-

18

Mar-1

8

May-

18

Jul-1

8

Sep

-18

8

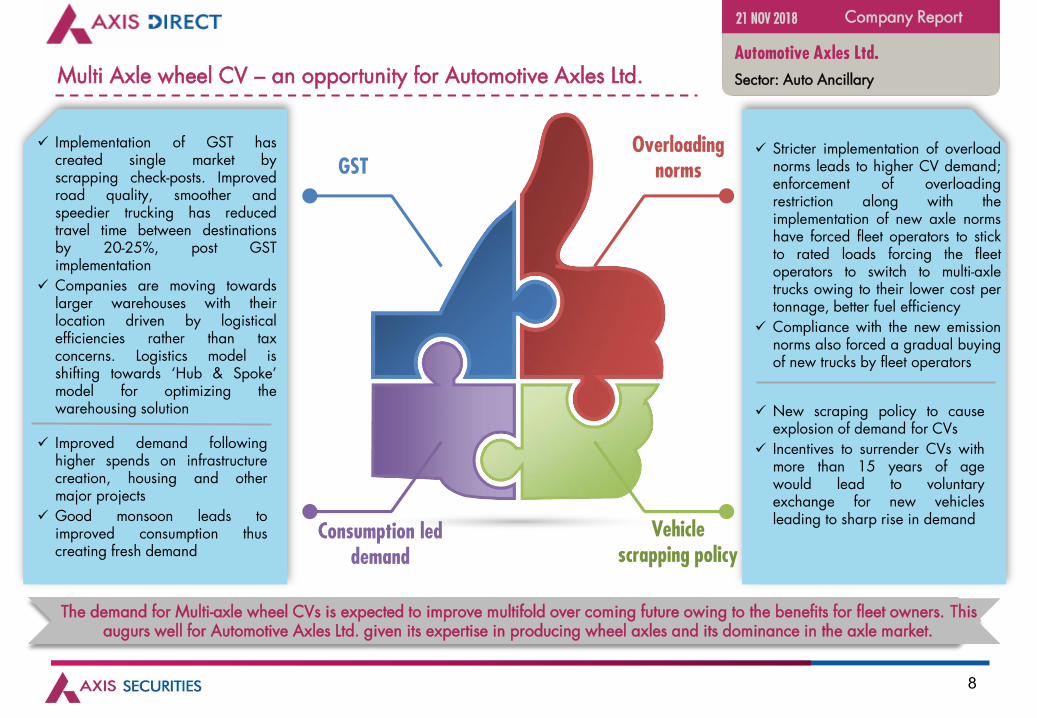

GSTOverloading

norms

Vehicle scrapping policy

Consumption led demand

Implementation of GST hascreated single market byscrapping check-posts. Improvedroad quality, smoother andspeedier trucking has reducedtravel time between destinationsby 20-25%, post GSTimplementation

Companies are moving towardslarger warehouses with theirlocation driven by logisticalefficiencies rather than taxconcerns. Logistics model isshifting towards ‘Hub & Spoke’model for optimizing thewarehousing solution

Stricter implementation of overloadnorms leads to higher CV demand;enforcement of overloadingrestriction along with theimplementation of new axle normshave forced fleet operators to stickto rated loads forcing the fleetoperators to switch to multi-axletrucks owing to their lower cost pertonnage, better fuel efficiency

Compliance with the new emissionnorms also forced a gradual buyingof new trucks by fleet operators

New scraping policy to causeexplosion of demand for CVs

Incentives to surrender CVs withmore than 15 years of agewould lead to voluntaryexchange for new vehiclesleading to sharp rise in demand

Improved demand followinghigher spends on infrastructurecreation, housing and othermajor projects

Good monsoon leads toimproved consumption thuscreating fresh demand

Multi Axle wheel CV – an opportunity for Automotive Axles Ltd.

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

21 NOV 2018

The demand for Multi-axle wheel CVs is expected to improve multifold over coming future owing to the benefits for fleet owners. This augurs well for Automotive Axles Ltd. given its expertise in producing wheel axles and its dominance in the axle market.

9

Product Portfolio

Company Report

Sector: Auto Ancillary

Source: Company, Axis Securities, ACMA

21 NOV 2018

Automotive Axles Ltd.

Product Range

Automotive Axles Ltd.

10

Marquee customers

Company Report

Sector: Auto Ancillary

21 NOV 2018

Automotive Axles Ltd.

11

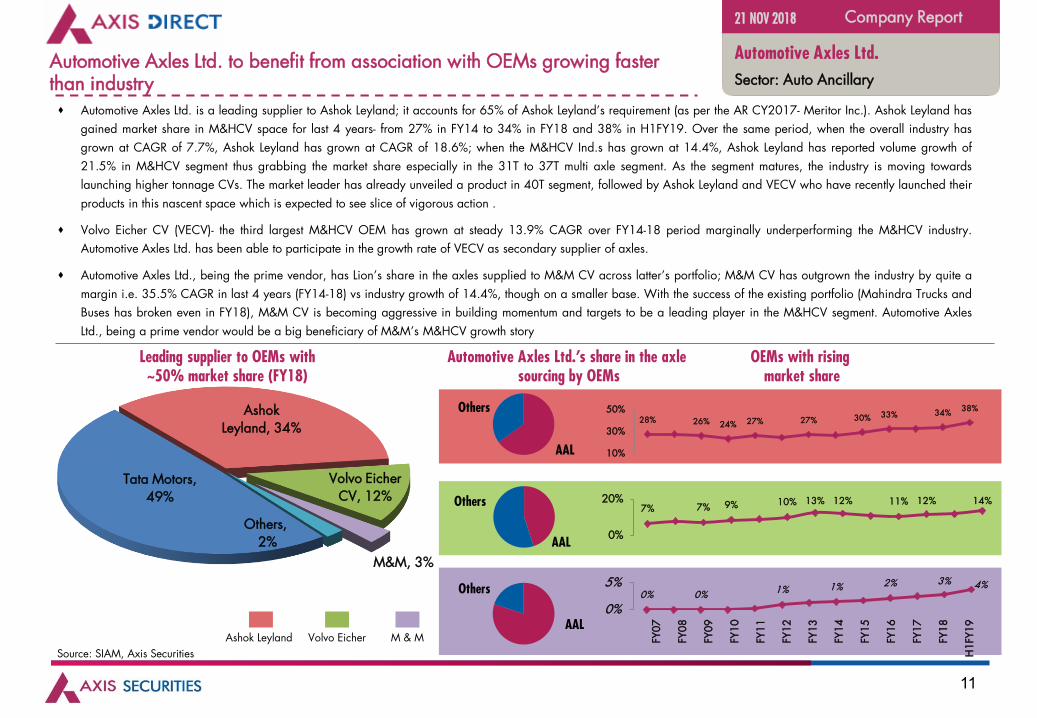

Automotive Axles Ltd. to benefit from association with OEMs growing faster than industry Automotive Axles Ltd. is a leading supplier to Ashok Leyland; it accounts for 65% of Ashok Leyland’s requirement (as per the AR CY2017- Meritor Inc.). Ashok Leyland has

gained market share in M&HCV space for last 4 years- from 27% in FY14 to 34% in FY18 and 38% in H1FY19. Over the same period, when the overall industry has

grown at CAGR of 7.7%, Ashok Leyland has grown at CAGR of 18.6%; when the M&HCV Ind.s has grown at 14.4%, Ashok Leyland has reported volume growth of

21.5% in M&HCV segment thus grabbing the market share especially in the 31T to 37T multi axle segment. As the segment matures, the industry is moving towards

launching higher tonnage CVs. The market leader has already unveiled a product in 40T segment, followed by Ashok Leyland and VECV who have recently launched their

products in this nascent space which is expected to see slice of vigorous action .

Volvo Eicher CV (VECV)- the third largest M&HCV OEM has grown at steady 13.9% CAGR over FY14-18 period marginally underperforming the M&HCV industry.

Automotive Axles Ltd. has been able to participate in the growth rate of VECV as secondary supplier of axles.

Automotive Axles Ltd., being the prime vendor, has Lion’s share in the axles supplied to M&M CV across latter’s portfolio; M&M CV has outgrown the industry by quite a

margin i.e. 35.5% CAGR in last 4 years (FY14-18) vs industry growth of 14.4%, though on a smaller base. With the success of the existing portfolio (Mahindra Trucks and

Buses has broken even in FY18), M&M CV is becoming aggressive in building momentum and targets to be a leading player in the M&HCV segment. Automotive Axles

Ltd., being a prime vendor would be a big beneficiary of M&M’s M&HCV growth story

Company Report

OEMs with rising market share

Leading supplier to OEMs with ~50% market share (FY18)

Sector: Auto Ancillary

Source: SIAM, Axis Securities

21 NOV 2018

Tata Motors, 49%

Ashok Leyland, 34%

Volvo Eicher CV, 12%

M&M, 3%

Others,2%

Automotive Axles Ltd.’s share in the axle sourcing by OEMs

AAL

Others

AAL

Others

AAL

Others

28% 26% 24% 27% 27% 30% 33% 34%38%

10%

30%

50%

7% 7% 9% 10% 13% 12% 11% 12% 14%

0%

20%

0% 0% 1% 1% 2% 3% 4%

0%

5%

Ashok Leyland Volvo Eicher M & M

0

2

4

6

8

10

12

0

100

200

300

400

500

600

700

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

H1FY

19

M&HCV (LHS) LCV (LHS) GDP growth (%) (RHS)

Automotive Axles Ltd.

12

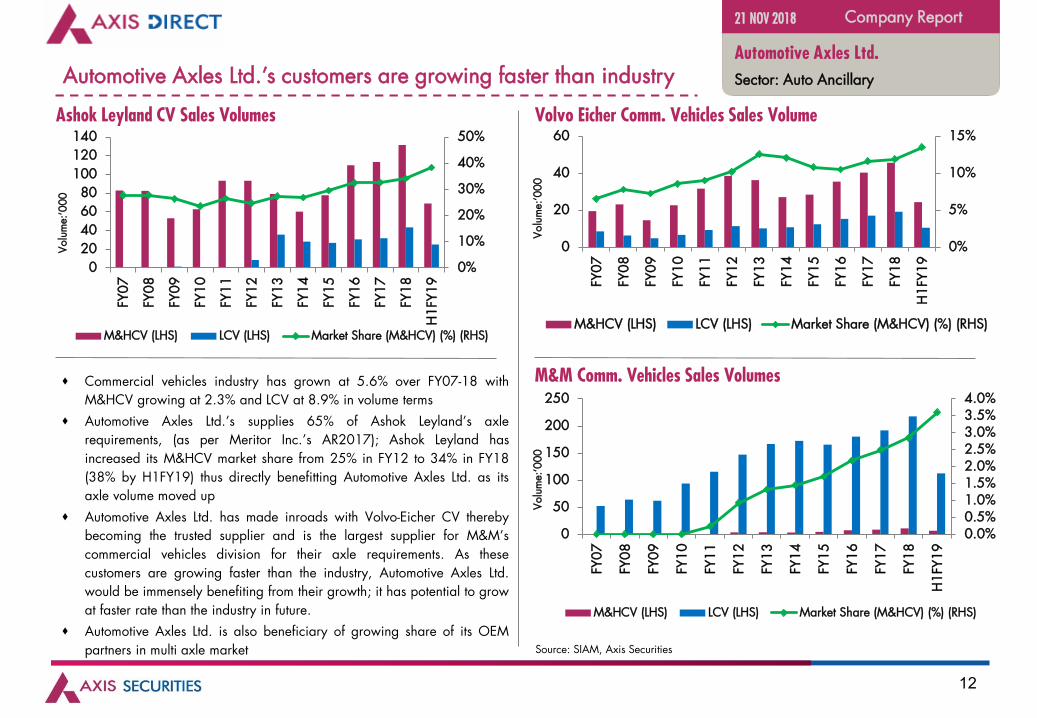

Automotive Axles Ltd.’s customers are growing faster than industry

Commercial vehicles industry has grown at 5.6% over FY07-18 with

M&HCV growing at 2.3% and LCV at 8.9% in volume terms

Automotive Axles Ltd.’s supplies 65% of Ashok Leyland’s axle

requirements, (as per Meritor Inc.’s AR2017); Ashok Leyland has

increased its M&HCV market share from 25% in FY12 to 34% in FY18

(38% by H1FY19) thus directly benefitting Automotive Axles Ltd. as its

axle volume moved up

Automotive Axles Ltd. has made inroads with Volvo-Eicher CV thereby

becoming the trusted supplier and is the largest supplier for M&M’s

commercial vehicles division for their axle requirements. As these

customers are growing faster than the industry, Automotive Axles Ltd.

would be immensely benefiting from their growth; it has potential to grow

at faster rate than the industry in future.

Automotive Axles Ltd. is also beneficiary of growing share of its OEM

partners in multi axle market

Company Report

Ashok Leyland CV Sales Volumes

Source: SIAM, Axis Securities

Volvo Eicher Comm. Vehicles Sales Volume

Sector: Auto Ancillary

M&M Comm. Vehicles Sales Volumes

21 NOV 2018

Volu

me:

‘000

Volu

me:

‘000

Volu

me:

‘000

0%

10%

20%

30%

40%

50%

0

20

40

60

80

100

120

140FY

07

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

H1

FY1

9

M&HCV (LHS) LCV (LHS) Market Share (M&HCV) (%) (RHS)

0%

5%

10%

15%

0

20

40

60

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

H1

FY1

9

M&HCV (LHS) LCV (LHS) Market Share (M&HCV) (%) (RHS)

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%

0

50

100

150

200

250

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

H1

FY1

9

M&HCV (LHS) LCV (LHS) Market Share (M&HCV) (%) (RHS)

Automotive Axles Ltd.

13

200

300

400

500

600

FY15 FY16 FY17 FY18

M&HCV LCV

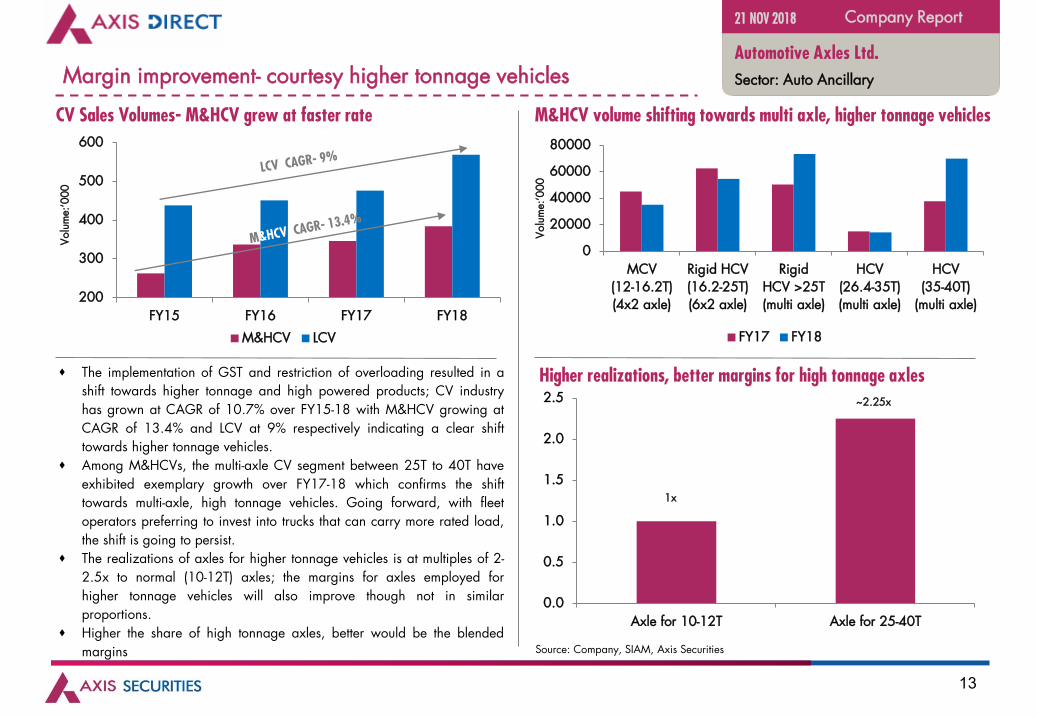

Margin improvement- courtesy higher tonnage vehicles

The implementation of GST and restriction of overloading resulted in a

shift towards higher tonnage and high powered products; CV industry

has grown at CAGR of 10.7% over FY15-18 with M&HCV growing at

CAGR of 13.4% and LCV at 9% respectively indicating a clear shift

towards higher tonnage vehicles.

Among M&HCVs, the multi-axle CV segment between 25T to 40T have

exhibited exemplary growth over FY17-18 which confirms the shift

towards multi-axle, high tonnage vehicles. Going forward, with fleet

operators preferring to invest into trucks that can carry more rated load,

the shift is going to persist.

The realizations of axles for higher tonnage vehicles is at multiples of 2-

2.5x to normal (10-12T) axles; the margins for axles employed for

higher tonnage vehicles will also improve though not in similar

proportions.

Higher the share of high tonnage axles, better would be the blended

margins

Company Report

CV Sales Volumes- M&HCV grew at faster rate

Source: Company, SIAM, Axis Securities

M&HCV volume shifting towards multi axle, higher tonnage vehicles

Sector: Auto Ancillary

Higher realizations, better margins for high tonnage axles

21 NOV 2018

Volu

me:

‘000

0.0

0.5

1.0

1.5

2.0

2.5

Axle for 10-12T Axle for 25-40T

0

20000

40000

60000

80000

MCV(12-16.2T)(4x2 axle)

Rigid HCV(16.2-25T)(6x2 axle)

RigidHCV >25T(multi axle)

HCV(26.4-35T)(multi axle)

HCV(35-40T)

(multi axle)

FY17 FY18

Volu

me:

‘000

1x

~2.25x

Automotive Axles Ltd.

14

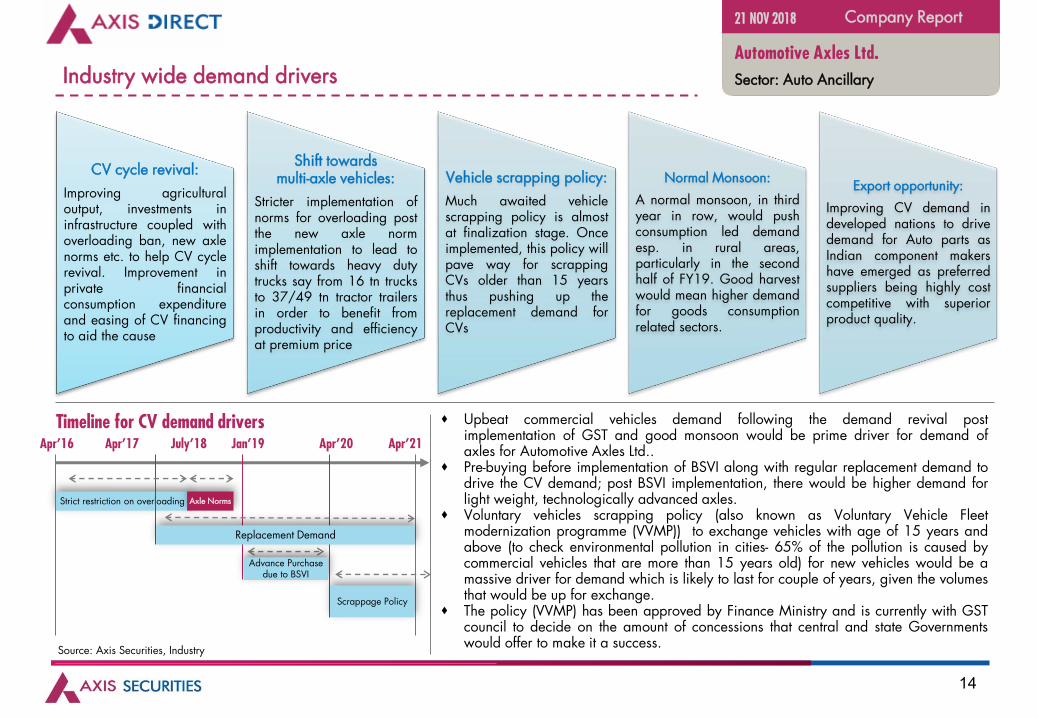

Industry wide demand drivers

Company Report

Sector: Auto Ancillary

CV cycle revival:

Improving agriculturaloutput, investments ininfrastructure coupled withoverloading ban, new axlenorms etc. to help CV cyclerevival. Improvement inprivate financialconsumption expenditureand easing of CV financingto aid the cause

Shift towards multi-axle vehicles:

Stricter implementation ofnorms for overloading postthe new axle normimplementation to lead toshift towards heavy dutytrucks say from 16 tn trucksto 37/49 tn tractor trailersin order to benefit fromproductivity and efficiencyat premium price

Vehicle scrapping policy:

Much awaited vehiclescrapping policy is almostat finalization stage. Onceimplemented, this policy willpave way for scrappingCVs older than 15 yearsthus pushing up thereplacement demand forCVs

Normal Monsoon:

A normal monsoon, in thirdyear in row, would pushconsumption led demandesp. in rural areas,particularly in the secondhalf of FY19. Good harvestwould mean higher demandfor goods consumptionrelated sectors.

Export opportunity:

Improving CV demand indeveloped nations to drivedemand for Auto parts asIndian component makershave emerged as preferredsuppliers being highly costcompetitive with superiorproduct quality.

Timeline for CV demand drivers

Source: Axis Securities, Industry

Upbeat commercial vehicles demand following the demand revival postimplementation of GST and good monsoon would be prime driver for demand ofaxles for Automotive Axles Ltd..

Pre-buying before implementation of BSVI along with regular replacement demand todrive the CV demand; post BSVI implementation, there would be higher demand forlight weight, technologically advanced axles.

Voluntary vehicles scrapping policy (also known as Voluntary Vehicle Fleetmodernization programme (VVMP)) to exchange vehicles with age of 15 years andabove (to check environmental pollution in cities- 65% of the pollution is caused bycommercial vehicles that are more than 15 years old) for new vehicles would be amassive driver for demand which is likely to last for couple of years, given the volumesthat would be up for exchange.

The policy (VVMP) has been approved by Finance Ministry and is currently with GSTcouncil to decide on the amount of concessions that central and state Governmentswould offer to make it a success.

21 NOV 2018

Strict restriction on overloading

Apr’16 Apr’17 July’18 Jan’19 Apr’20 Apr’21

Axle Norms

Replacement Demand

Advance Purchase due to BSVI

Scrappage Policy

Automotive Axles Ltd.

15

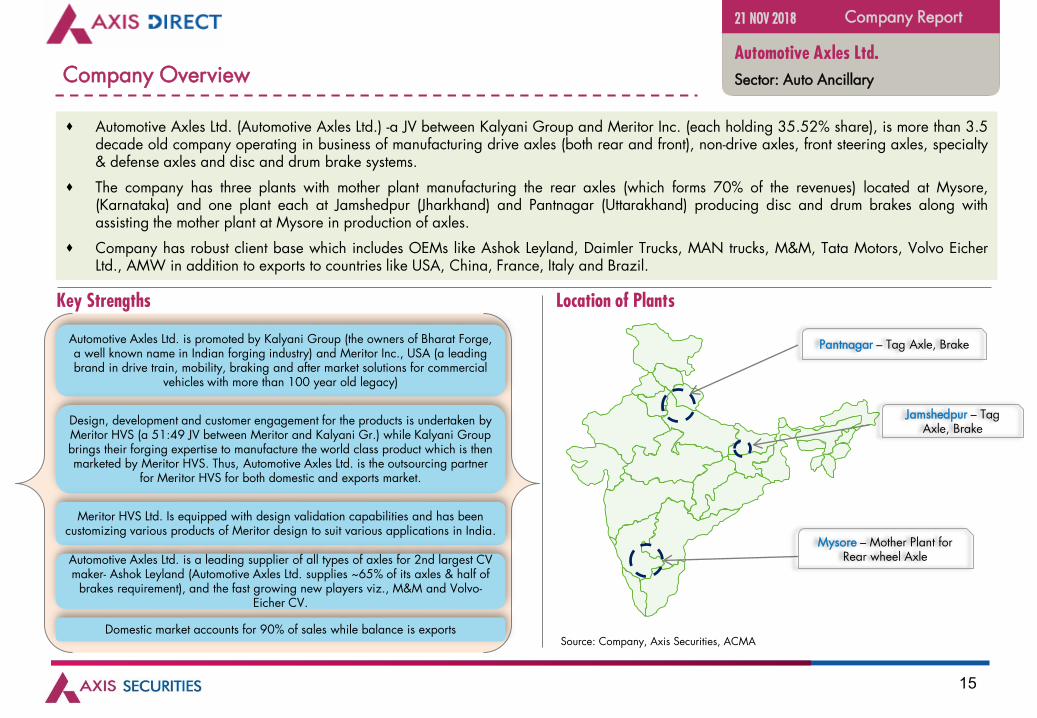

Company Overview

Automotive Axles Ltd. (Automotive Axles Ltd.) -a JV between Kalyani Group and Meritor Inc. (each holding 35.52% share), is more than 3.5decade old company operating in business of manufacturing drive axles (both rear and front), non-drive axles, front steering axles, specialty& defense axles and disc and drum brake systems.

The company has three plants with mother plant manufacturing the rear axles (which forms 70% of the revenues) located at Mysore,(Karnataka) and one plant each at Jamshedpur (Jharkhand) and Pantnagar (Uttarakhand) producing disc and drum brakes along withassisting the mother plant at Mysore in production of axles.

Company has robust client base which includes OEMs like Ashok Leyland, Daimler Trucks, MAN trucks, M&M, Tata Motors, Volvo EicherLtd., AMW in addition to exports to countries like USA, China, France, Italy and Brazil.

Company Report

Sector: Auto Ancillary

Key Strengths

Automotive Axles Ltd. is promoted by Kalyani Group (the owners of Bharat Forge, a well known name in Indian forging industry) and Meritor Inc., USA (a leading brand in drive train, mobility, braking and after market solutions for commercial

vehicles with more than 100 year old legacy)

Design, development and customer engagement for the products is undertaken by Meritor HVS (a 51:49 JV between Meritor and Kalyani Gr.) while Kalyani Group brings their forging expertise to manufacture the world class product which is then marketed by Meritor HVS. Thus, Automotive Axles Ltd. is the outsourcing partner

for Meritor HVS for both domestic and exports market.

Domestic market accounts for 90% of sales while balance is exports

Meritor HVS Ltd. Is equipped with design validation capabilities and has been customizing various products of Meritor design to suit various applications in India.

Automotive Axles Ltd. is a leading supplier of all types of axles for 2nd largest CV maker- Ashok Leyland (Automotive Axles Ltd. supplies ~65% of its axles & half of

brakes requirement), and the fast growing new players viz., M&M and Volvo-Eicher CV.

Location of Plants

Pantnagar – Tag Axle, Brake

Mysore – Mother Plant for Rear wheel Axle

Jamshedpur – Tag Axle, Brake

Source: Company, Axis Securities, ACMA

21 NOV 2018

Automotive Axles Ltd.

16

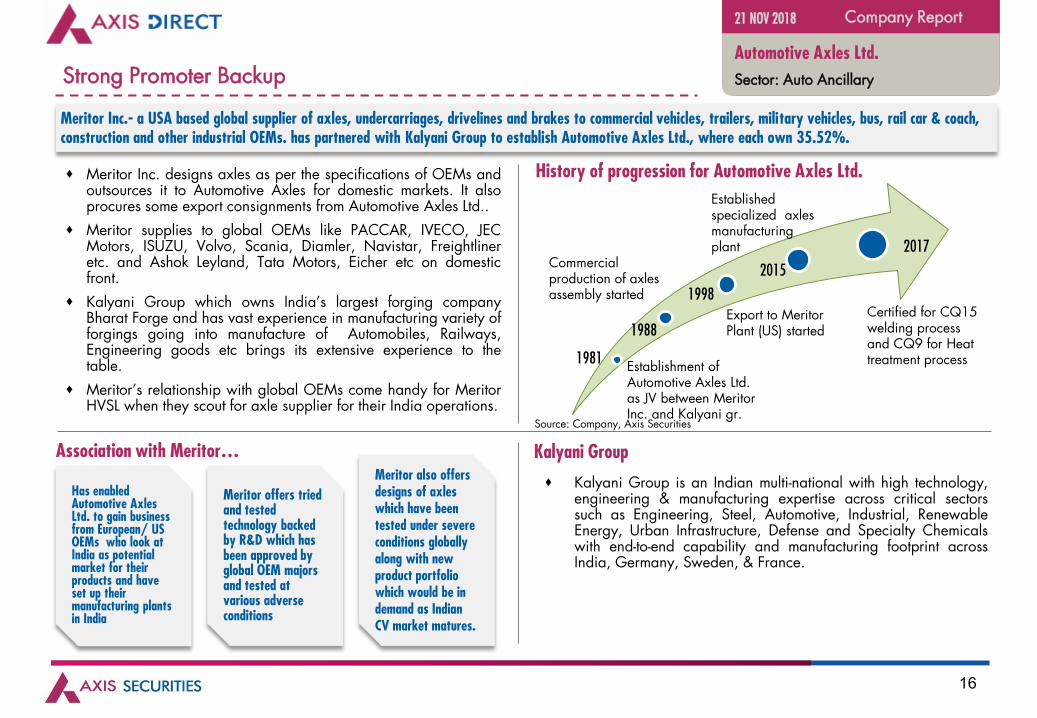

Strong Promoter Backup

Meritor Inc. designs axles as per the specifications of OEMs andoutsources it to Automotive Axles for domestic markets. It alsoprocures some export consignments from Automotive Axles Ltd..

Meritor supplies to global OEMs like PACCAR, IVECO, JECMotors, ISUZU, Volvo, Scania, Diamler, Navistar, Freightlineretc. and Ashok Leyland, Tata Motors, Eicher etc on domesticfront.

Kalyani Group which owns India’s largest forging companyBharat Forge and has vast experience in manufacturing variety offorgings going into manufacture of Automobiles, Railways,Engineering goods etc brings its extensive experience to thetable.

Meritor’s relationship with global OEMs come handy for MeritorHVSL when they scout for axle supplier for their India operations.

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

Has enabled Automotive Axles Ltd. to gain business from European/ US OEMs who look at India as potential market for their products and have set up their manufacturing plants in India

Meritor also offers designs of axles which have been tested under severe conditions globally along with new product portfolio which would be in demand as Indian CV market matures.

Meritor offers tried and tested technology backed by R&D which has been approved by global OEM majors and tested at various adverse conditions

Kalyani Group is an Indian multi-national with high technology,engineering & manufacturing expertise across critical sectorssuch as Engineering, Steel, Automotive, Industrial, RenewableEnergy, Urban Infrastructure, Defense and Specialty Chemicalswith end-to-end capability and manufacturing footprint acrossIndia, Germany, Sweden, & France.

Kalyani Group

Establishment of Automotive Axles Ltd. as JV between Meritor Inc. and Kalyani gr.

Commercial production of axles assembly started

Export to Meritor Plant (US) started

Established specialized axles manufacturing plant

Certified for CQ15 welding process and CQ9 for Heat treatment process1981

1988

1998

2015

2017

History of progression for Automotive Axles Ltd.

21 NOV 2018

Source: Company, Axis Securities

Association with Meritor…

Meritor Inc.- a USA based global supplier of axles, undercarriages, drivelines and brakes to commercial vehicles, trailers, military vehicles, bus, rail car & coach, construction and other industrial OEMs. has partnered with Kalyani Group to establish Automotive Axles Ltd., where each own 35.52%.

17

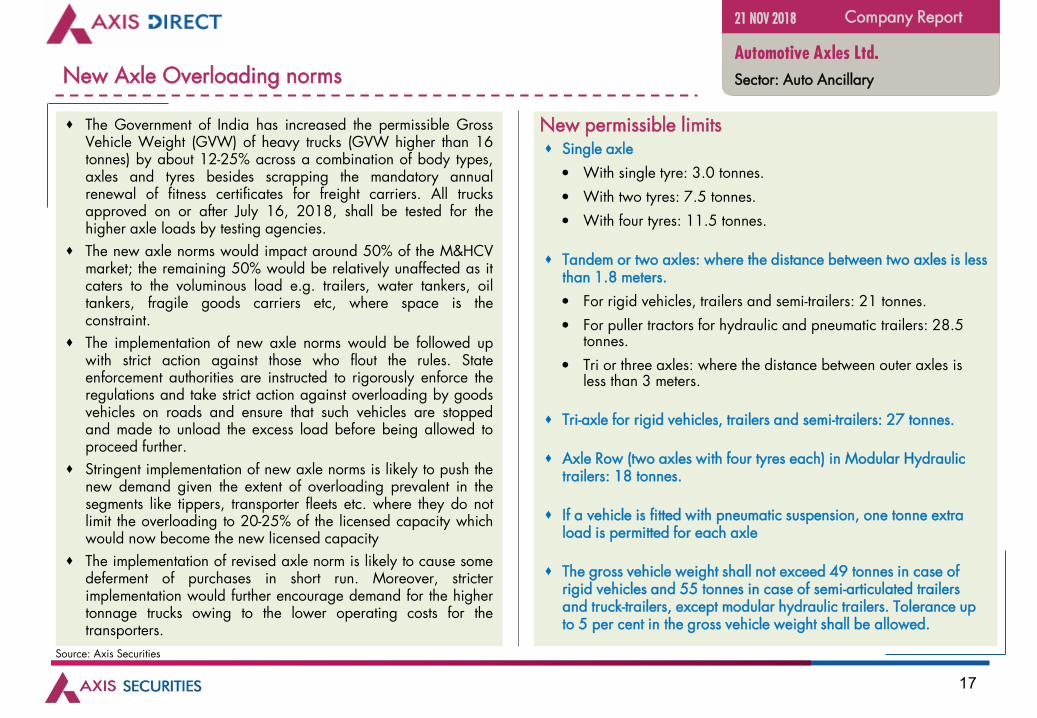

New Axle Overloading norms

Single axle

With single tyre: 3.0 tonnes.

With two tyres: 7.5 tonnes.

With four tyres: 11.5 tonnes.

Tandem or two axles: where the distance between two axles is less than 1.8 meters.

For rigid vehicles, trailers and semi-trailers: 21 tonnes.

For puller tractors for hydraulic and pneumatic trailers: 28.5 tonnes.

Tri or three axles: where the distance between outer axles is less than 3 meters.

Tri-axle for rigid vehicles, trailers and semi-trailers: 27 tonnes.

Axle Row (two axles with four tyres each) in Modular Hydraulic trailers: 18 tonnes.

If a vehicle is fitted with pneumatic suspension, one tonne extra load is permitted for each axle

The gross vehicle weight shall not exceed 49 tonnes in case of rigid vehicles and 55 tonnes in case of semi-articulated trailers and truck-trailers, except modular hydraulic trailers. Tolerance up to 5 per cent in the gross vehicle weight shall be allowed.

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

New permissible limits

Source: Axis Securities

21 NOV 2018

The Government of India has increased the permissible GrossVehicle Weight (GVW) of heavy trucks (GVW higher than 16tonnes) by about 12-25% across a combination of body types,axles and tyres besides scrapping the mandatory annualrenewal of fitness certificates for freight carriers. All trucksapproved on or after July 16, 2018, shall be tested for thehigher axle loads by testing agencies.

The new axle norms would impact around 50% of the M&HCVmarket; the remaining 50% would be relatively unaffected as itcaters to the voluminous load e.g. trailers, water tankers, oiltankers, fragile goods carriers etc, where space is theconstraint.

The implementation of new axle norms would be followed upwith strict action against those who flout the rules. Stateenforcement authorities are instructed to rigorously enforce theregulations and take strict action against overloading by goodsvehicles on roads and ensure that such vehicles are stoppedand made to unload the excess load before being allowed toproceed further.

Stringent implementation of new axle norms is likely to push thenew demand given the extent of overloading prevalent in thesegments like tippers, transporter fleets etc. where they do notlimit the overloading to 20-25% of the licensed capacity whichwould now become the new licensed capacity

The implementation of revised axle norm is likely to cause somedeferment of purchases in short run. Moreover, stricterimplementation would further encourage demand for the highertonnage trucks owing to the lower operating costs for thetransporters.

18

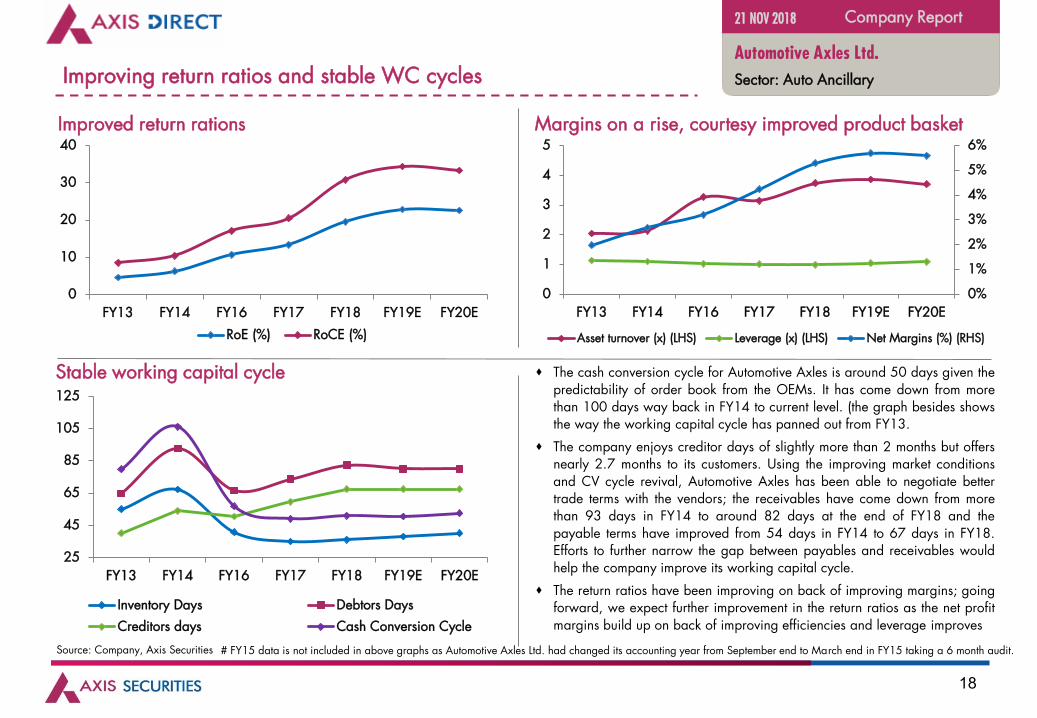

Improving return ratios and stable WC cycles

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

Stable working capital cycle

Margins on a rise, courtesy improved product basket

Source: Company, Axis Securities

The cash conversion cycle for Automotive Axles is around 50 days given thepredictability of order book from the OEMs. It has come down from morethan 100 days way back in FY14 to current level. (the graph besides showsthe way the working capital cycle has panned out from FY13.

The company enjoys creditor days of slightly more than 2 months but offersnearly 2.7 months to its customers. Using the improving market conditionsand CV cycle revival, Automotive Axles has been able to negotiate bettertrade terms with the vendors; the receivables have come down from morethan 93 days in FY14 to around 82 days at the end of FY18 and thepayable terms have improved from 54 days in FY14 to 67 days in FY18.Efforts to further narrow the gap between payables and receivables wouldhelp the company improve its working capital cycle.

The return ratios have been improving on back of improving margins; goingforward, we expect further improvement in the return ratios as the net profitmargins build up on back of improving efficiencies and leverage improves

21 NOV 2018

Improved return rations

# FY15 data is not included in above graphs as Automotive Axles Ltd. had changed its accounting year from September end to March end in FY15 taking a 6 month audit.

0

10

20

30

40

FY13 FY14 FY16 FY17 FY18 FY19E FY20E

RoE (%) RoCE (%)

0%

1%

2%

3%

4%

5%

6%

0

1

2

3

4

5

FY13 FY14 FY16 FY17 FY18 FY19E FY20E

Asset turnover (x) (LHS) Leverage (x) (LHS) Net Margins (%) (RHS)

25

45

65

85

105

125

FY13 FY14 FY16 FY17 FY18 FY19E FY20E

Inventory Days Debtors Days

Creditors days Cash Conversion Cycle

19

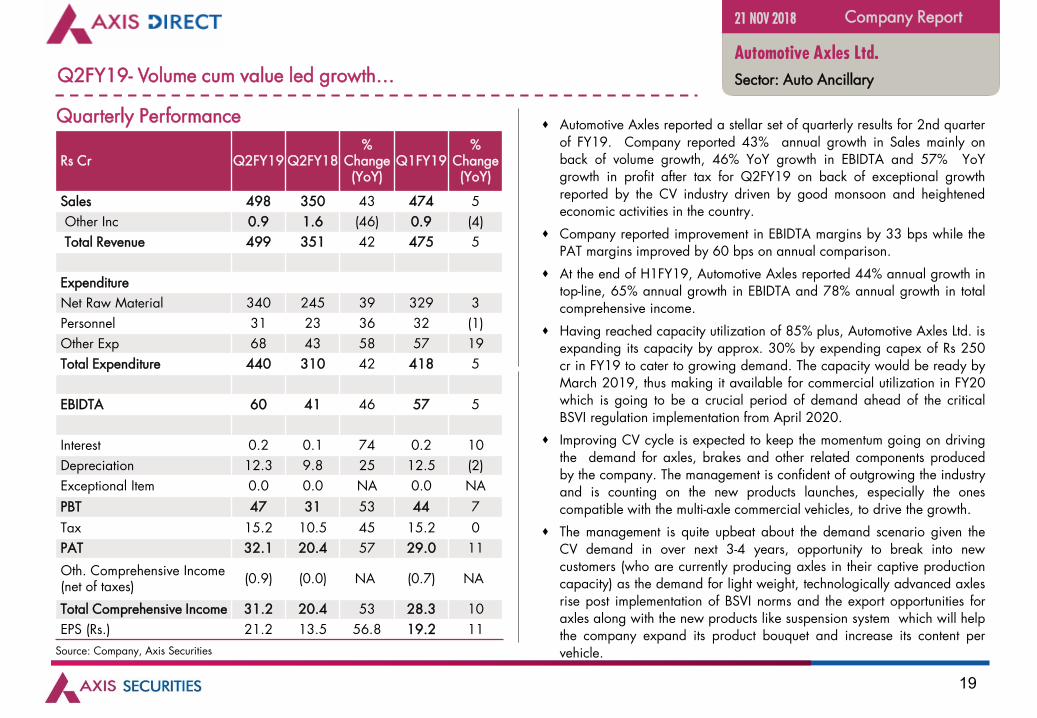

Q2FY19- Volume cum value led growth…

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

Automotive Axles reported a stellar set of quarterly results for 2nd quarterof FY19. Company reported 43% annual growth in Sales mainly onback of volume growth, 46% YoY growth in EBIDTA and 57% YoYgrowth in profit after tax for Q2FY19 on back of exceptional growthreported by the CV industry driven by good monsoon and heightenedeconomic activities in the country.

Company reported improvement in EBIDTA margins by 33 bps while thePAT margins improved by 60 bps on annual comparison.

At the end of H1FY19, Automotive Axles reported 44% annual growth intop-line, 65% annual growth in EBIDTA and 78% annual growth in totalcomprehensive income.

Having reached capacity utilization of 85% plus, Automotive Axles Ltd. isexpanding its capacity by approx. 30% by expending capex of Rs 250cr in FY19 to cater to growing demand. The capacity would be ready byMarch 2019, thus making it available for commercial utilization in FY20which is going to be a crucial period of demand ahead of the criticalBSVI regulation implementation from April 2020.

Improving CV cycle is expected to keep the momentum going on drivingthe demand for axles, brakes and other related components producedby the company. The management is confident of outgrowing the industryand is counting on the new products launches, especially the onescompatible with the multi-axle commercial vehicles, to drive the growth.

The management is quite upbeat about the demand scenario given theCV demand in over next 3-4 years, opportunity to break into newcustomers (who are currently producing axles in their captive productioncapacity) as the demand for light weight, technologically advanced axlesrise post implementation of BSVI norms and the export opportunities foraxles along with the new products like suspension system which will helpthe company expand its product bouquet and increase its content pervehicle.

21 NOV 2018

Source: Company, Axis Securities

Rs Cr Q2FY19 Q2FY18%

Change (YoY)

Q1FY19%

Change (YoY)

Sales 498 350 43 474 5

Other Inc 0.9 1.6 (46) 0.9 (4)

Total Revenue 499 351 42 475 5

Expenditure

Net Raw Material 340 245 39 329 3

Personnel 31 23 36 32 (1)

Other Exp 68 43 58 57 19

Total Expenditure 440 310 42 418 5

EBIDTA 60 41 46 57 5

Interest 0.2 0.1 74 0.2 10

Depreciation 12.3 9.8 25 12.5 (2)

Exceptional Item 0.0 0.0 NA 0.0 NA

PBT 47 31 53 44 7

Tax 15.2 10.5 45 15.2 0

PAT 32.1 20.4 57 29.0 11

Oth. Comprehensive Income (net of taxes)

(0.9) (0.0) NA (0.7) NA

Total Comprehensive Income 31.2 20.4 53 28.3 10

EPS (Rs.) 21.2 13.5 56.8 19.2 11

Quarterly Performance

20

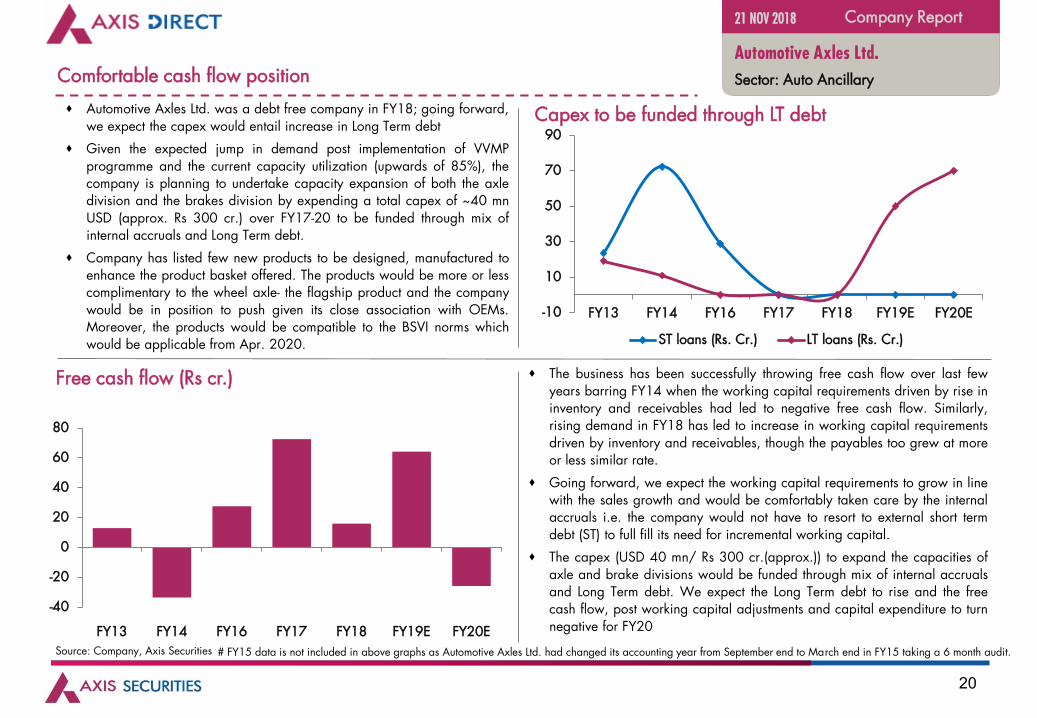

Comfortable cash flow position

Automotive Axles Ltd. was a debt free company in FY18; going forward,we expect the capex would entail increase in Long Term debt

Given the expected jump in demand post implementation of VVMPprogramme and the current capacity utilization (upwards of 85%), thecompany is planning to undertake capacity expansion of both the axledivision and the brakes division by expending a total capex of ~40 mnUSD (approx. Rs 300 cr.) over FY17-20 to be funded through mix ofinternal accruals and Long Term debt.

Company has listed few new products to be designed, manufactured toenhance the product basket offered. The products would be more or lesscomplimentary to the wheel axle- the flagship product and the companywould be in position to push given its close association with OEMs.Moreover, the products would be compatible to the BSVI norms whichwould be applicable from Apr. 2020.

Capex to be funded through LT debt

Company Report

Automotive Axles Ltd.

Sector: Auto Ancillary

Free cash flow (Rs cr.) The business has been successfully throwing free cash flow over last fewyears barring FY14 when the working capital requirements driven by rise ininventory and receivables had led to negative free cash flow. Similarly,rising demand in FY18 has led to increase in working capital requirementsdriven by inventory and receivables, though the payables too grew at moreor less similar rate.

Going forward, we expect the working capital requirements to grow in linewith the sales growth and would be comfortably taken care by the internalaccruals i.e. the company would not have to resort to external short termdebt (ST) to full fill its need for incremental working capital.

The capex (USD 40 mn/ Rs 300 cr.(approx.)) to expand the capacities ofaxle and brake divisions would be funded through mix of internal accrualsand Long Term debt. We expect the Long Term debt to rise and the freecash flow, post working capital adjustments and capital expenditure to turnnegative for FY20

# FY15 data is not included in above graphs as Automotive Axles Ltd. had changed its accounting year from September end to March end in FY15 taking a 6 month audit.

21 NOV 2018

Source: Company, Axis Securities

-10

10

30

50

70

90

FY13 FY14 FY16 FY17 FY18 FY19E FY20E

ST loans (Rs. Cr.) LT loans (Rs. Cr.)

-40

-20

0

20

40

60

80

FY13 FY14 FY16 FY17 FY18 FY19E FY20E

21

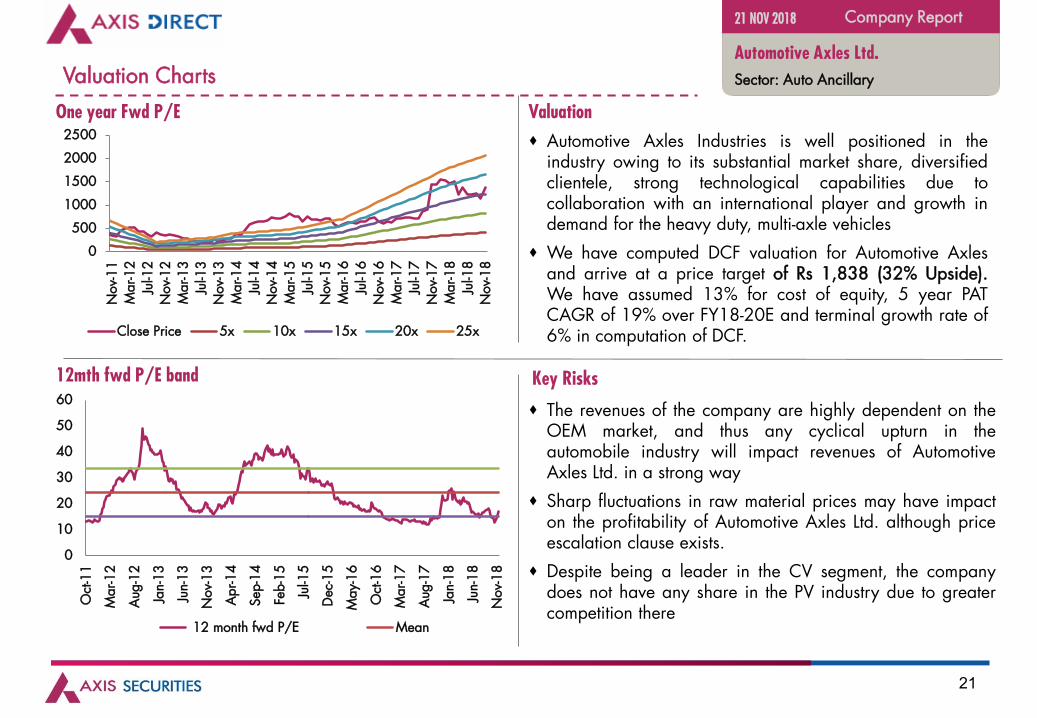

Valuation Charts

Company Report

Key Risks

The revenues of the company are highly dependent on theOEM market, and thus any cyclical upturn in theautomobile industry will impact revenues of AutomotiveAxles Ltd. in a strong way

Sharp fluctuations in raw material prices may have impacton the profitability of Automotive Axles Ltd. although priceescalation clause exists.

Despite being a leader in the CV segment, the companydoes not have any share in the PV industry due to greatercompetition there

21 NOV 2018

12mth fwd P/E band

Valuation

Automotive Axles Industries is well positioned in theindustry owing to its substantial market share, diversifiedclientele, strong technological capabilities due tocollaboration with an international player and growth indemand for the heavy duty, multi-axle vehicles

We have computed DCF valuation for Automotive Axlesand arrive at a price target of Rs 1,838 (32% Upside).We have assumed 13% for cost of equity, 5 year PATCAGR of 19% over FY18-20E and terminal growth rate of6% in computation of DCF.

One year Fwd P/E

Automotive Axles Ltd.

Sector: Auto Ancillary

0

500

1000

1500

2000

2500

Nov-

11

Mar-1

2Ju

l-12

Nov-

12

Mar-1

3Ju

l-13

Nov-

13

Mar-1

4Ju

l-14

Nov-

14

Mar-1

5Ju

l-15

Nov-

15

Mar-1

6Ju

l-16

Nov-

16

Mar-1

7Ju

l-17

Nov-

17

Mar-1

8Ju

l-18

Nov-

18

Close Price 5x 10x 15x 20x 25x

0

10

20

30

40

50

60

Oct

-11

Mar-1

2

Aug

-12

Jan-

13

Jun-

13

Nov-

13

Apr-1

4

Sep

-14

Feb-1

5

Jul-1

5

Dec

-15

May-

16

Oct

-16

Mar-1

7

Aug

-17

Jan-

18

Jun-

18

Nov-

18

12 month fwd P/E Mean

22

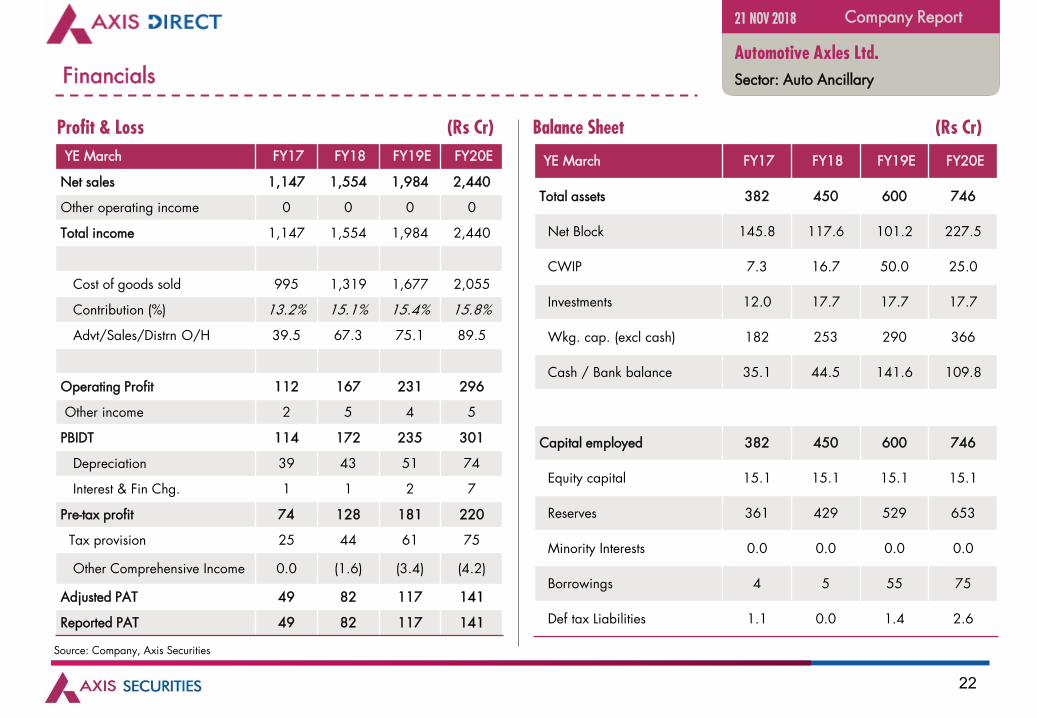

Financials

YE March FY17 FY18 FY19E FY20E

Net sales 1,147 1,554 1,984 2,440

Other operating income 0 0 0 0

Total income 1,147 1,554 1,984 2,440

Cost of goods sold 995 1,319 1,677 2,055

Contribution (%) 13.2% 15.1% 15.4% 15.8%

Advt/Sales/Distrn O/H 39.5 67.3 75.1 89.5

Operating Profit 112 167 231 296

Other income 2 5 4 5

PBIDT 114 172 235 301

Depreciation 39 43 51 74

Interest & Fin Chg. 1 1 2 7

Pre-tax profit 74 128 181 220

Tax provision 25 44 61 75

Other Comprehensive Income 0.0 (1.6) (3.4) (4.2)

Adjusted PAT 49 82 117 141

Reported PAT 49 82 117 141

YE March FY17 FY18 FY19E FY20E

Total assets 382 450 600 746

Net Block 145.8 117.6 101.2 227.5

CWIP 7.3 16.7 50.0 25.0

Investments 12.0 17.7 17.7 17.7

Wkg. cap. (excl cash) 182 253 290 366

Cash / Bank balance 35.1 44.5 141.6 109.8

Capital employed 382 450 600 746

Equity capital 15.1 15.1 15.1 15.1

Reserves 361 429 529 653

Minority Interests 0.0 0.0 0.0 0.0

Borrowings 4 5 55 75

Def tax Liabilities 1.1 0.0 1.4 2.6

Profit & Loss (Rs Cr) Balance Sheet (Rs Cr)

Source: Company, Axis Securities

Company Report21 NOV 2018

Automotive Axles Ltd.

Sector: Auto Ancillary

23

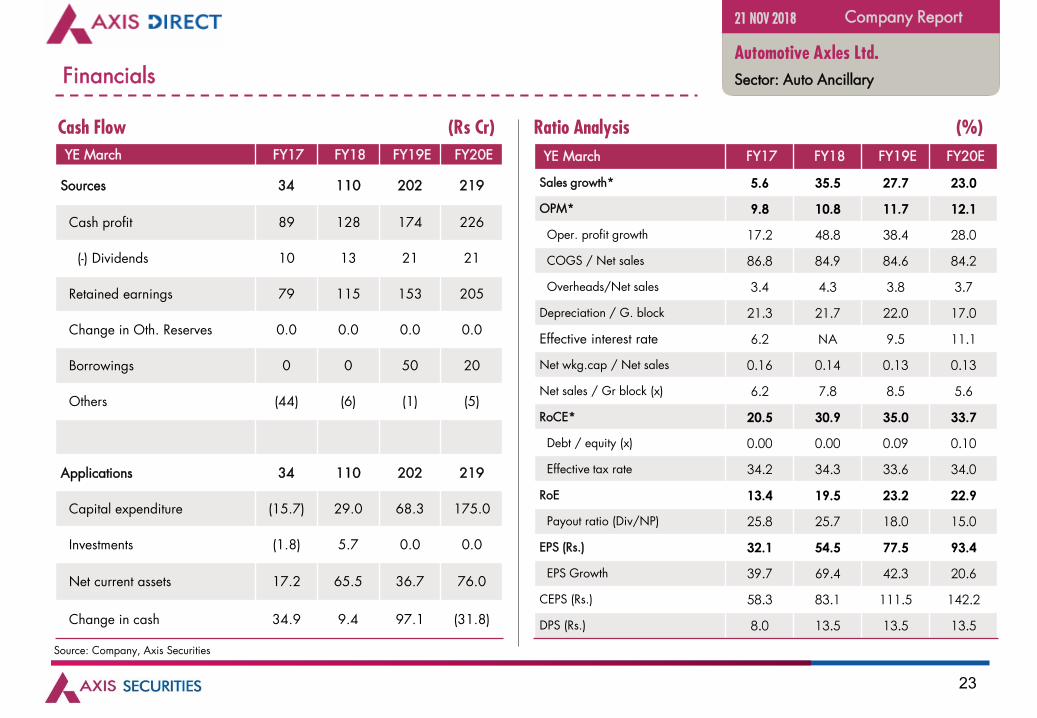

Financials

YE March FY17 FY18 FY19E FY20E

Sources 34 110 202 219

Cash profit 89 128 174 226

(-) Dividends 10 13 21 21

Retained earnings 79 115 153 205

Change in Oth. Reserves 0.0 0.0 0.0 0.0

Borrowings 0 0 50 20

Others (44) (6) (1) (5)

Applications 34 110 202 219

Capital expenditure (15.7) 29.0 68.3 175.0

Investments (1.8) 5.7 0.0 0.0

Net current assets 17.2 65.5 36.7 76.0

Change in cash 34.9 9.4 97.1 (31.8)

YE March FY17 FY18 FY19E FY20E

Sales growth* 5.6 35.5 27.7 23.0

OPM* 9.8 10.8 11.7 12.1

Oper. profit growth 17.2 48.8 38.4 28.0

COGS / Net sales 86.8 84.9 84.6 84.2

Overheads/Net sales 3.4 4.3 3.8 3.7

Depreciation / G. block 21.3 21.7 22.0 17.0

Effective interest rate 6.2 NA 9.5 11.1

Net wkg.cap / Net sales 0.16 0.14 0.13 0.13

Net sales / Gr block (x) 6.2 7.8 8.5 5.6

RoCE* 20.5 30.9 35.0 33.7

Debt / equity (x) 0.00 0.00 0.09 0.10

Effective tax rate 34.2 34.3 33.6 34.0

RoE 13.4 19.5 23.2 22.9

Payout ratio (Div/NP) 25.8 25.7 18.0 15.0

EPS (Rs.) 32.1 54.5 77.5 93.4

EPS Growth 39.7 69.4 42.3 20.6

CEPS (Rs.) 58.3 83.1 111.5 142.2

DPS (Rs.) 8.0 13.5 13.5 13.5

Cash Flow (Rs Cr) Ratio Analysis (%)

Source: Company, Axis Securities

Company Report21 NOV 2018

Automotive Axles Ltd.

Sector: Auto Ancillary

24

Disclaimer

Disclosures:

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations).

1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in the Regulations, is engaged in the business ofproviding Stock broking services, Depository participant services & distribution of various financial products. ASL is a subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed publiccompany and one of India’s largest private sector bank and has its various subsidiaries engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital,Stock Broking, the details in respect of which are available on www.axisbank.com.

2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the Association of Mutual Funds of India (AMFI) fordistribution of financial products and also registered with IRDA as a corporate agent for insurance business activity.

3. ASL has no material adverse disciplinary history as on the date of publication of this report.

4. I/We, Pankaj Bobade– AGM, Research, CFA (ICFAI), author/s and the name/s subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflectmy/our views about the subject issuer(s) or securities. I/We also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) orview(s) in this report. I/we or my/our relative or ASL does not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates may have beneficialownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Since associates of ASL are engaged in variousfinancial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. I/we or my/ourrelative or ASL or its associates do not have any material conflict of interest. I/we have not served as director, officer or employee in the subject company in the last 12-month period.

Any holding in stock – No

5. ASL or its associates has not received any compensation from the subject company in the past twelve months. ASL or its Research Analysts has not been engaged in market making activity for thesubject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its associates may have:

i. Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research report and / or;ii. Managed or co-managed public offering of the securities from the subject company of this research report and / or;iii. Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this research report;

ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in connection with this report

Term& Conditions:

This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not be altered inany way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ASL. The report is based on thefacts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained from publicly availablemedia or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer documentor solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all customers may receive thisreport at the same time. ASL will not treat recipients as customers by virtue of their receiving this report.

Company Report21 NOV 2018

Instead of a company visit, we have done a conference call with the company’s management.

Automotive Axles Ltd.

Sector: Auto Ancillary

25

Disclaimer

Disclaimer:

Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the recipient’s specific circumstances.The securities and strategies discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must make their own investment decisions, based on their owninvestment objectives, financial positions and needs of specific recipient.

This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as it deems necessary to arrive atan independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks involved), and should consult its own advisors to determine the meritsand risks of such an investment. Certain transactions, including those involving futures, options and other derivatives as well as non-investment grade securities involve substantial risk and are notsuitable for all investors. ASL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or anyaction taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend orincome, etc. Past performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance. Investors are advised to see Risk Disclosure Documentto understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions andmay be subject to change without notice.

ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the company(ies) mentioned herein or (b)be engaged in any other transaction involving such securities or earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein oract as an advisor or investment banker, lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related informationand opinions. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting this document.

ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this report should be aware that ASLmay have a potential conflict of interest that may affect the objectivity of this report. Compensation of Research Analysts is not based on any specific merchant banking, investment banking orbrokerage service transactions. ASL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the United States or Canada ordistributed or redistributed in Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such country, especially, USA, the same may be ignored and broughtto the attention of the sender. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or otherjurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ASL to any registration or licensing requirement within suchjurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors.

The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. TheCompany reserves the right to make modifications and alternations to this document as may be required from time to time without any prior notice. The views expressed are those of the analyst(s)and the Company may or may not subscribe to all the views expressed therein.Copyright in this document vests with Axis Securities Limited.

Axis Securities Limited, Corporate office: Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 18002100808/022-61480808, Regd. off.- Axis House, 8th Floor, Wadia International Centre, Pandurang Budhkar Marg, Worli, Mumbai – 400 025. Compliance Officer: Anand Shaha, Email: [email protected], Tel No: 022-42671582.

Company Report21 NOV 2018

DEFINITION OF RATINGS

Ratings Expected absolute returns over 12 months

BUY More than 10%

HOLD Between 10% and -10%

SELL Less than -10%

Automotive Axles Ltd.

Sector: Auto Ancillary