Australian plantation inventory: ownership changes, availability and policy.

43

Australian Plantation Inventory: Ownership Changes, Availability, and Policy Ian Ferguson 1 1 Department of Forest & Ecosystem Science The University of Melbourne Parkville, Vic. 3000 [email protected] Summary The Australian National Plantation Inventory has collected and collated plantation information since 1993 and has periodically published forecasts of availability based on those data. This paper outlines the past methodology and summarizes updates of the most recent forecasts. The failures of some Managed Investment Scheme forestry companies have drawn attention to the risks and difficulties involved in forecasting plantation wood yields for species and areas where few data are available. These issues have important implications for forecasts of availability but several unknowns still exist, especially in relation to future replanting. The accuracy of prospectus forecasts of yields from several Managed Investment Schemes is examined. The methods used in national and selected regional forecasts are reviewed and some of the underlying policy issues for Australian plantations and forestry are critically examined. Keywords: National Plantation Inventory, availability, forecasts, plantation growth and yield, Managed Investment Schemes, plantation policy Introduction

Transcript of Australian plantation inventory: ownership changes, availability and policy.

Australian Plantation Inventory:Ownership Changes, Availability, and

PolicyIan Ferguson1

1 Department of Forest & Ecosystem ScienceThe University of Melbourne

Parkville, Vic. [email protected]

Summary

The Australian National Plantation Inventory has collected and

collated plantation information since 1993 and has periodically

published forecasts of availability based on those data. This paper

outlines the past methodology and summarizes updates of the most

recent forecasts. The failures of some Managed Investment Scheme

forestry companies have drawn attention to the risks and difficulties

involved in forecasting plantation wood yields for species and areas

where few data are available. These issues have important

implications for forecasts of availability but several unknowns still

exist, especially in relation to future replanting. The accuracy of

prospectus forecasts of yields from several Managed Investment

Schemes is examined. The methods used in national and selected

regional forecasts are reviewed and some of the underlying policy

issues for Australian plantations and forestry are critically

examined.

Keywords: National Plantation Inventory, availability, forecasts,

plantation growth and yield, Managed Investment Schemes, plantation

policy

Introduction

The National Plantation Inventory (NPI) is now a program within the

Australian Bureau of Agricultural and Resource Economics and Sciences

(ABARES), a research organization within the Australian Government

Department of Agriculture, Fisheries and Forestry. The NPI was

established in 1993 to collect and collate grower information, to

allow up-to-date quantitative reporting of Australia’s plantation

resource, and to build on a 1988 Commonwealth-State project, the

National Forest Inventory, to establish uniform datasets. The first

comprehensive and spatially based inventory of Australia’s industrial

plantations was developed by the NPI in close consultation with

industry and growers and released in 1997 (Howell et al., 1997).

Figures were reported nationally and regionally, based on 15

plantation resource regions (NPI regions) identified at the time by

industry as the most appropriate economic wood supply zones.

Figures compiled through the first report of the NPI in 1997 provided

the baseline for the ‘Plantations for Australia: the 2020 Vision’ (Pl

antation 2020 Vision Implementation Committee, 1997), a strategic par

tnership between industry and the Australian, state and territory gov

ernments which was developed with a contentious target to treble the

extent of Australia’s plantations to 3 million hectares by 2020. The

release of the strategy in late 1997 was followed by a rapid increase

in the rate of hardwood plantation establishment.

In addition to supplying regular updates on annual planting and the

extent, distribution, planting date, and species involved, there have

been periodic analyses to collate and use area and other information

to forecast the likely availability of Australian-grown plantation

wood in 1997, 2001, 2006 and 2012 (National Forest Inventory, 1997;

Turner et al., 1997; Ferguson et al., 2002; Parsons et al., 2006;

Gavran et al., 2012).

2

The term ’availability’ is used here in preference to ‘log supply’ or

‘wood flows’ because future technologies and production costs may

change. Supply is conditional on price and many other factors. In any

event, supply in itself does not provide a forecast of consumption –

that requires the interaction of both supply and demand. Demand

itself is also subject to change from that anticipated now, as

incomes, tastes and other demand influences change.

Availability is therefore only a very rough proxy for future

consumption (and production) and assumes that the present setting of

real prices, costs, and most other characteristics of demand and

supply will change little, if at all, in the future. The major

influence on future availability is the amount of plantation wood at

any future point in time that meets current market specifications and

practices. Furthermore, ‘availability’ also assumes harvesting will

take place at that prescribed future point in time and that

replanting will follow automatically. These are definitional matters

that must underpin any use of the forecasts for policy or other

purposes.

Gavran et al., (2012) compiled the last official report on national

forecasts. The period from 2005 to 2012 was marked by a sequence of

natural disasters, together with failures of many Managed Investment

Scheme (MIS) forestry companies, all of which left their mark on the

Australian plantation estate. This paper deals first with the

failures of MIS forestry schemes because they raise a number of

policy issues with implications for national and regional

availabilities. It then deals with MIS growth and yield estimates,

reviews the methods used and presents updates of the national

forecasts and selected regional forecasts. Finally, it discusses

some of the underlying policy issues for Australian plantations and

the forestry sector.

3

Managed Investment Scheme Failures

Managed Investment Schemes are not confined to forestry and

agriculture but are quite common in Australian investment where they

play an especially important role in the property and commercial real

estate markets. However, the special taxation provisions relating to

forestry and agriculture MIS schemes set them apart.

A ‘Managed Investment Scheme’1 under Chapter 5c of the Corporations

Act 2001 (Cth) is any pooled direct investment in a venture that is

managed by some other company or person. A direct investment is where

investors are directly involved in the business or property as owners

or beneficial owners, or in which investors are directly contracting

for services to be carried out on their behalf. Holding shares or

debentures in a company does not qualify because share or debenture

holders do not own the business - the company does. Nor do investors

automatically receive profits from the business, only receiving such

dividends as the directors determine.

Any MIS prospectus (the ‘product disclosure statement’) has to meet

requirements laid down by the Australian Securities and Investment

Commission. The prospectus is subject to approval by the Australian

Taxation Office through a formal Product Ruling that enables

investors to be secure regarding the application of the taxation

provisions applying to their investment. An important provision (the

13-month prepayment provision) enables an individual investor to

charge their initial investment (including interest on funds borrowed

for the purpose) in planting against income tax in the financial year

in which the prospectus is approved, even though much of the actual

expenditure on planting might be delayed until later in the planting

season in the next financial year. This provision recognizes

plantation establishment has to be undertaken when seasonal

1 This section draws heavily on Ferguson et al., (2009).

4

conditions are suitable and therefore generally straddles the end of

a financial year.

The MIS model was effective in raising retail investment funds for

plantation establishment. Within Australia, some ten major MIS

companies and approximately seven other smaller entities raised funds

totaling about A$705 million in 2007-08 for forestry projects

(Australian Agribusiness Group, 2008). In total, these companies

offered twenty-two different forestry projects in 2007-08. MIS

companies listed on the Australian Stock Exchange raised 85 per cent

of funds invested in forestry in 2007-08 (Australian Agribusiness

Group, 2008). MIS forestry companies (Parsonson, 2010, citing

Advisor Edge as source) raised some A$5.3 billion from 1995 to 2008,

of which Parsonson estimated that:

· 80 per cent was spent on short rotation hardwoods at an average

cost of $7,000 ha-1

· 13 per cent on tropical species at an average cost of A$30,000

ha-1, and

· 7 per cent on longer rotation softwoods at an average cost of

$8,000 ha-1.

Figure 1 shows the net areas planted for six of the major MIS

forestry companies (Parsonson, 2010, citing Advisor Edge as source).

[Figure 1. Major MIS Hardwood plantation ownership]

A change of Australian Government policy in 2000 withdrawing the 13-

month prepayment provision led to the collapse of several companies

because it restricted their ability to raise new funds and thus

remain solvent while awaiting the age at which harvesting revenues

began to flow. In response to this collapse, a 12-month prepayment

provision was re-introduced in 2002. Very high external debt, and

delays in the commencement of exports of wood chips due to

5

infrastructure delays or market downturn led to the demise of others.

Some failed due to site and climatic conditions impacting on the

growth of particular species. Most of those that failed had become

dependent on the next prospectus to raise funds to bridge operations

until sufficient revenues were generated. Some have referred to this

as entering a Ponzi-like mode of operation (Parliamentary Joint Commi

ttee on Corporations and Financial Services, 2009: p35 - Submission b

y Piper Alderman).

Despite these failures, the timber and land (where relevant) assets

of individual MIS investors were nominally secure, provided they were

able to maintain any payments that were due. However, continuing

ownership often became difficult if the funds had to be borrowed or

if some MIS investors in a particular project (i.e. Prospectus

offering in a particular year) failed to meet their payment

obligations. Most MIS projects pooled the costs and revenues to

woodlot owners across the project, with a pro rata allocation to

individual owners. Failure to meet contractual costs triggered a

change of ownership to the Trustee or, if the MIS project was deemed

to be uneconomic, to sale. When a MIS forestry company failed, the

trees and, if owned by the company, the land on which the trees were

planted, became the subject of the formidable legal processes of

administration, receivership and liquidation.

Five of the MIS forestry companies in Figure 1 existing prior to 2009

failed and only two others, Macquarie and TFS, remain. TFS is

concerned with sandalwood plantations: a very different species,

product and market to those considered in this paper. As a result of

the processes of administration and receivership, the Great Southern

Plantations (GSL) forestry assets are now owned by New Forests, an

Australian-based Timberland Investment Management Organization

(TIMO), that also owns substantial areas of (non-MIS) softwood

plantation in South Australia and Tasmania. Recently, Elders Forestry

6

(2011), formerly ITC, sold most of its forestry assets in the Albany

and Bunbury NPI Regions of Western Australia and the Green Triangle

to Global Forest Partners. The former Timbercorp forestry assets are

now 92 per cent also owned by Global Forest Partners under the name

of Australian Blue Gum Plantations Pty Ltd. Those of Forest

Enterprises Australia (FEA) and Gunns Ltd are in administration and

receivership pending the outcome of legal proceedings.

All these changes have implications for forecasts of availability:

none more so than the resolution of ownership and the management

intent of the new owner in relation to future wood production. These

issues hinge on what capability the woodlots have for future

production, so a prior question that potentially affects all

estimates of future availability is - what growth rates and yields

were and will be achieved by these plantations? This also raises a

peripheral issue of some importance to the forestry profession - how

accurate were the prospectus forecasts provided by MIS forestry

companies?

MIS Growth and Yield Forecasts

Official reports on the failures of many of the MIS companies provide

access to some data that enable assessment of the yield estimates and

on the accuracy of forecasts set out in the prospectuses promoting

various of the MIS schemes. I have attempted to collate the limited

available evidence to assess the accuracy of the MIS yield forecasts.

Unfortunately, most of these lack sufficient detail and clarity to

provide a good audit base. Further research would be desirable once

future ownership issues are resolved.

7

Short rotation MIS schemes

The overwhelming majority of MIS investment has been in short

rotation (10 to 12 y) plantations, mainly of blue gum (Eucalyptus

globulus) in southern Australia, with the expectation that the sole

product would be pulpwood to be exported as wood-chips or processed

domestically. This review will focus on blue gum plantations because

they are the most extensive and best documented in terms of growth

and yield.

The monitoring of outcomes in relation to yields and risks was

largely left to private sector rating agencies. Some collected

inventory data but, with some exceptions, little of it was subjected

to detailed analysis and critical appraisal and very little was made

available in the public domain.

Although some preliminary research was undertaken in the years before

and during the early years of MIS planting, no substantive studies on

MIS growth and yield were published prior to 2004. After 2004, a

number were published (e.g. Strandgard et al., 2005; Nambiar and

Ferguson, 2005; and Wang and Baker, 2007; Harper et al., 2009; Miehle

et al., 2009; Goodwin’s farm forestry toolbox (Private Forestry,

Tasmania, 2011). Nevertheless, some of these were available and being

circulated earlier than the date of publication shown. My

recollection is that researchers and many plantation management

experts at this time were widely critical of and concerned about the

values being used in prospectuses. However, they were constrained in

making public comment because very little independent research was

funded and published until too late. This highlights one of the

shortcomings of the main regulatory agencies (arguably the Australian

Securities and Investment Commission and the Australian Taxation

Office) in not promoting research to monitor what was a fundamental

component of the program. While the agencies cannot be responsible

8

for the profitability of the proposed investment, some verification

and monitoring of the accuracy of Prospectus data fundamental to the

outcome is desirable and in the public interest.

The first major independent study of growth and yield of MIS

plantations was initiated when one of the major companies got into

financial difficulties. KPMG (2008) undertook a comprehensive audit

of the expected blue gum yields for a major MIS company across four

States based on measurements of temporary plots at ages of 5 to 9

years. The results are summarized in Table 1.

[Table 1: Estimates of blue gum plantation production, Great Southern

Plantations]

As with most such aggregate statistics, a number of qualifications

need to be made in reviewing them. In much of southern Australia,

especially in the NPI Regions of Western Australia and the Green

Triangle, the period involved spans a long drought of varying

intensity, resulting in reductions in growth and yield. Towards the

latter years of this period, the supply of the most productive land

had declined as the competition for MIS land intensified and this

reduced average yields. On the other hand, planting and later tending

techniques were refined progressively over this period and led to

improvements in growth and yield. It is not possible to unravel the

impacts of these conflicting influences from aggregate data of this

kind.

What is clear is that, with the exception of a small area at Bunbury

in Western Australia, the blue gum yields in the Albany area and

Green Triangle region fell well short of the conventional wisdom of

20 to 25 m3 ha-1 y-1 (or even 27.5 m3 ha-1 y-1, see Adviser Edge,

2008:p16), which was used in many of the MIS company prospectuses2. 2 The Independent Forester’s Report (p34) of the Timbercorp (2005) Product Disclosure Statement states that ‘Timbercorp Forestry advises

9

Other data (ITC Project Management Limited, 2009) are available on

actual harvest yields in green metric tonnes (gmt) that broadly

support the average yields for the Albany region of Western Australia

reported in Table 1.The ages at ITC harvest varied from 10 to 13

years but the actual values were not reported, so no details are

reported here. The lack of transparency in such reports is a matter

of concern, as is the disparity between prospectus and actual yields

The Australian Agribusiness Group (2010) reported MIS results shown

in Table 2 for blue gum plantations located in the Geelong, Gippsland

and Portland areas. While limited in scope and imprecise because they

were based on tree measurement at 3 years of age, these highlight the

variability from planting year to planting year and/or location to

location.

[Table 2: Estimates of blue gum plantation production in Geelong,

Gippsland and Portland areas, Macquarie Forestry]

In 2008, Forest Enterprises Australia (FEA, 2008) reported a

comparison (Table 3) of prospectus forecasts of mean annual

increments and the weighted average values, based on measurement at

age 5 years, for plantations in Tasmania and northern New South

Wales. Some of these plantations were of species other than blue gum.

Details of the analysis are not available, making geographic

interpretation impossible.

[Table 3: Prospectus forecasts and estimates of mean annual increment

for FEA plantations in Tasmania and northern New South Wales]

Independent data and analyses

that only land that in aggregate with all other land in the Project will continue to provide the target weighted average yield of 275m3 ofpulpwood per hectare between 8-12 years after planting will be included in the Project’.

10

Data from field inventories of several hundred properties carrying

blue gum plantations were made available by a private industry

organization for this study. Most of the inventories were carried out

at 7.5 years, some at 4.5 years, and the data were used to predict

the expected yield per hectare at age 10 years. Although details are

not known, it seems likely that the predictions were made using early

versions of the Prophecy model (Strandgard et al., 2005). Prophecy

is a computer-based simulation model designed to predict the standing

volume and financial outcomes of blue gum plantations under a various

silvicultural regimes. The predictive functions in Prophecy were

based on data from collaborating organisations and MIS companies.

The plantation region (Green Triangle or the South-West of Western

Australia) and average rainfall was identified for each plantation,

together with net planted area, year of planting, the age at which

measurement was carried out, and the tenure of the land (freehold or

lease). Dummy variables were used in the multiple regression analysis

to identify the categorical variables in this set.

The data were edited to remove observations with missing values of

the predicted volume or rainfall and two of which were nonsensical

due to data entry errors. This greatly reduced the number of

observations available. There were too few to allow second rotation

options of replanting or coppicing to be explored. The remaining

data fell into two distinct groups – those in the Green Triangle

Region (277 observations) and those in the South-West of Western

Australia (90 observations).

Each observation was based on an inventory of a separate property.

The net plantable area on each property varied from 6 ha to 1370 ha.

However, as Figures 2 and 3 show, the distributions of net plantable

areas in the Green Triangle and Western Australia NPI Regions were

markedly skewed towards smaller areas. The two regions are fairly

11

similar in the distributions, the relative frequencies of new

plantable areas under 40 ha being 15 to 17 per cent, while those for

net plantable areas under 80 ha were 33 and 36 per cent respectively.

Given the differences in soils and climate, the two groups were

analysed separately using multiple regression analysis.

Green Triangle Region

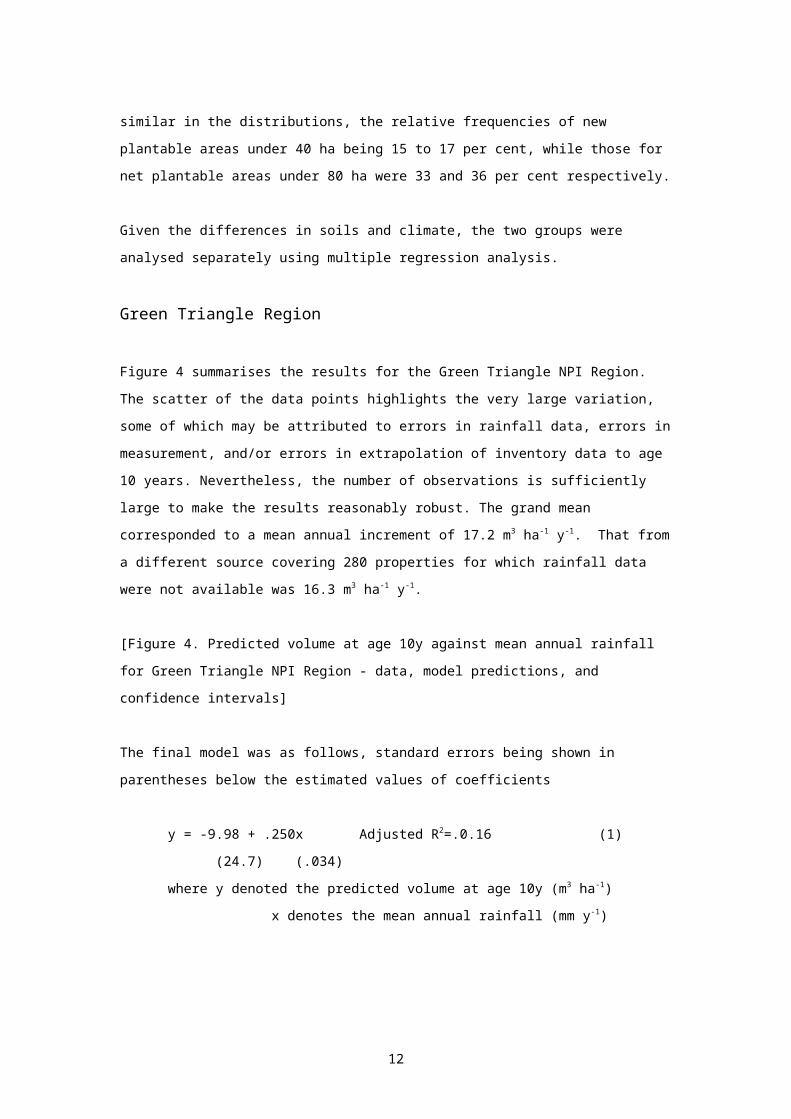

Figure 4 summarises the results for the Green Triangle NPI Region.

The scatter of the data points highlights the very large variation,

some of which may be attributed to errors in rainfall data, errors in

measurement, and/or errors in extrapolation of inventory data to age

10 years. Nevertheless, the number of observations is sufficiently

large to make the results reasonably robust. The grand mean

corresponded to a mean annual increment of 17.2 m3 ha-1 y-1. That from

a different source covering 280 properties for which rainfall data

were not available was 16.3 m3 ha-1 y-1.

[Figure 4. Predicted volume at age 10y against mean annual rainfall

for Green Triangle NPI Region - data, model predictions, and

confidence intervals]

The final model was as follows, standard errors being shown in

parentheses below the estimated values of coefficients

y = -9.98 + .250x Adjusted R2=.0.16 (1)

(24.7) (.034)

where y denoted the predicted volume at age 10y (m3 ha-1)

x denotes the mean annual rainfall (mm y-1)

12

Various alternative models including the other independent variables

were analyzed. None had coefficients that were significantly

different from zero at the 95 per cent probability level.

Western Australia NPI Region

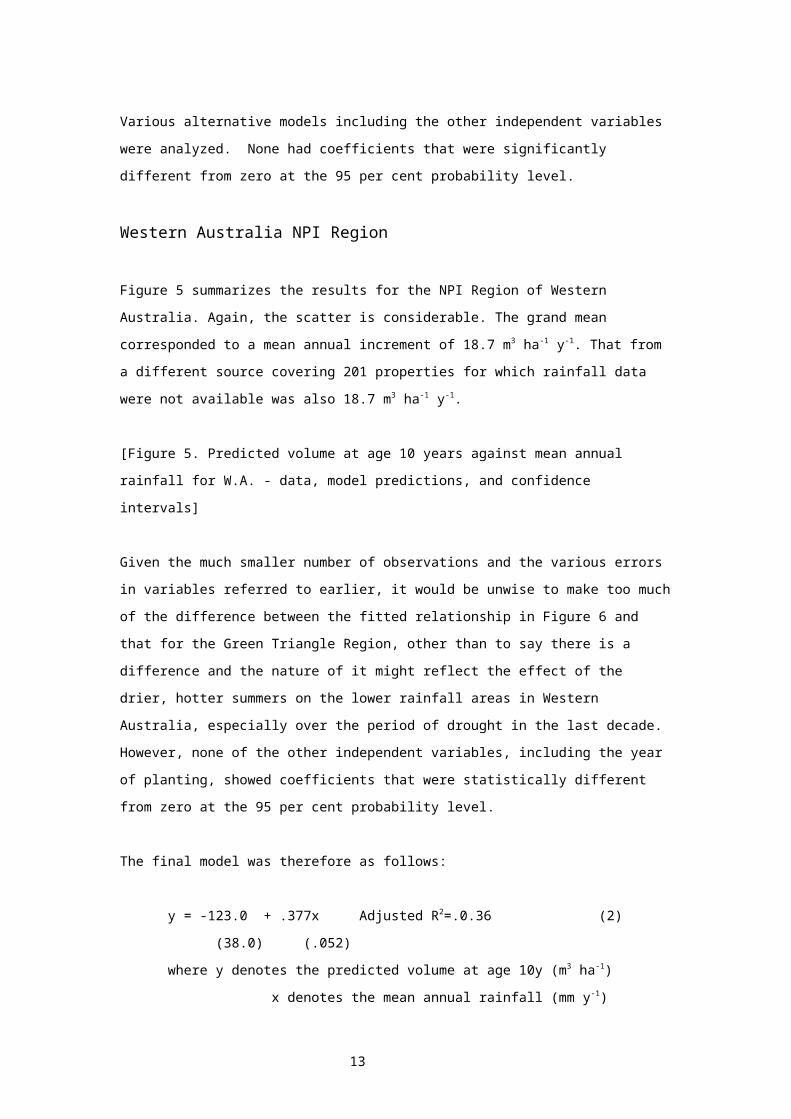

Figure 5 summarizes the results for the NPI Region of Western

Australia. Again, the scatter is considerable. The grand mean

corresponded to a mean annual increment of 18.7 m3 ha-1 y-1. That from

a different source covering 201 properties for which rainfall data

were not available was also 18.7 m3 ha-1 y-1.

[Figure 5. Predicted volume at age 10 years against mean annual

rainfall for W.A. - data, model predictions, and confidence

intervals]

Given the much smaller number of observations and the various errors

in variables referred to earlier, it would be unwise to make too much

of the difference between the fitted relationship in Figure 6 and

that for the Green Triangle Region, other than to say there is a

difference and the nature of it might reflect the effect of the

drier, hotter summers on the lower rainfall areas in Western

Australia, especially over the period of drought in the last decade.

However, none of the other independent variables, including the year

of planting, showed coefficients that were statistically different

from zero at the 95 per cent probability level.

The final model was therefore as follows:

y = -123.0 + .377x Adjusted R2=.0.36 (2)

(38.0) (.052)

where y denotes the predicted volume at age 10y (m3 ha-1)

x denotes the mean annual rainfall (mm y-1)

13

The trends in Figures 5 tally broadly with research findings of

Harper et al., (2005: Tables 8 & 9) regarding the impact of average

rainfall but the Harper et al. study takes account of many other

variables as well.

The trends in Figures 4 and 5 are also broadly consistent with data

collated and similar regressions estimated by Knott (2011). Knott’s

presentation3, regrettably as yet unpublished, was based on more

numerous data drawn from across Victoria and south-eastern South

Australia and also provides some valuable insights on short-term

variations in rainfall, tree breeding and soils.

Precision of Prospectus Forecasts

The sets of confidence intervals shown in Figures 4 and 5 may help to

correct seeming misconceptions in some of the prospectus statements

of some consulting foresters. To avoid confusion over terminology,

let us define a:

· planting block as an area planted on a specific land title, and

a

· project area as the aggregate of planting blocks covered by

common conditions in a Prospectus.

The inner curves (dashed lines) around the predicted values are the

confidence intervals attached to the mean of the population value of

predicted volume at age 10 years across all planting blocks having a

given value of mean annual rainfall. For a given rainfall, these

3 In subsequent correspondence, Knott estimated the following function for merchantable volume (y) at age 10 years based on averageannual rainfall following planting (Rf) and 1612 plots: y= -1084.5+184.74*log(Rf). This is substantially lower than Equation 3, but somewhat closer to Equation 4 for lower rainfall. Unlike thoseequations it shows diminishing returns for high rainfall.

14

intervals reflect the sampling distribution of the mean predicted

volume at age 10 years if sampling was or could be repeated many

times for that rainfall and all those project areas in the sample

used to derive the mean and confidence interval. While it may be more

impressive to cite these intervals, they do not reflect the

circumstances that most consultants face in the field. Most

consultants are asked to report on a specific project area.

The outer confidence intervals (solid lines) reflect the sampling

distribution of the predicted volume at age 10 years for an

individual planting block at a specified mean annual rainfall under

repeated sampling. They are very much larger than the former because

the confidence interval comprises two separate components - a

variance attributable to the sample data used and a variance

attributable to the individual planting blocks not included in the

sample.

MIS plantations were generally sold to investors on the basis of a

project area that was effectively divided for sale of woodlots to

individual owners. Notwithstanding the subdivision and identification

of a specific area, timber yields and revenues were typically pooled

across the entire project area: a pro rata share going to the

individual owner. This means that the confidence intervals for a

particular project area lie between the two extremes described in

Figures 4 and 5.

A consultant would normally be asked to evaluate a Prospectus project

area that comprises a number of individual properties. For

simplicity, let us assume a consultant is asked to prepare or

evaluate a predicted yield at age 10 years for a new project area and

Prospectus. The effect of having more than one planting block will

draw the confidence interval for the project area in towards those of

the mean across all planting blocks. However, for most practical

15

situations (say 4 to 20 planting blocks in a project area), the

reduction will be small, as the change is less than proportional to

the square root of the number of blocks. Hence, when estimates of

variability are reported in prospectuses, the MIS lessons show that

consultants need to be clear as to the basis they are applying, as

the differences are substantial. Furthermore, confidence intervals

will be larger, the further the mean annual rainfall of the project

area is from the general mean of annual rainfall of the sample

relationship.

Data on Actual Yields

Table 4 summarizes one of the very few sets of data available to date

on the actual harvest yields using aggregated data from the NPI and

relate to blue gum MIS schemes established in South-east Australia.

The average values are similar to those in Figures 5 and 6 for first

rotation plantations. Mean annual increments were not adjusted for

the differences in harvest age, which ranged from 11 to 13 y.

[Table 4: Actual harvest yields of some blue gum plantations in

South-east Australia]

Sawlog rotation MIS schemes

Forecasts of plantation sawlog availability raise issues beyond those

already canvassed, because of the extended period of time required to

capture sufficient data on which to develop accurate growth and yield

models and to reflect the product out-turns and the risks involved

with respect to pests, diseases and natural disasters.

Where the species has been planted widely and the growth and yield

characteristics are well-documented, as in the case of radiata pine

(Pinus radiata), southern pines (P. caribbea, P. elliottii and

16

hybrids), or maritime pine (P. pinaster) in Western Australia, the

risks are much smaller.

Concerns expressed in evidence to some Parliamentary inquiries (e.g.

Parliamentary Joint Committee on Corporations and Financial Services,

2009: paras 3.37-3.49) over some inflated forecasts of growth and

yield in MIS prospectuses seem well founded. Some of the reports of

the consulting foresters in the MIS prospectuses for blue gum and

other hardwoods suggest that misplaced optimism was a more powerful

force than the literature and published research - there being little

(sometimes no) reference to that research or analysis of risks and

much reliance on undocumented experience and observation.

In fairness to those involved, however, comparatively little

published research was available about the growth and yields of the

hardwood species used in sawlog rotation projects. This partly

reflects the bias in those government agencies towards funding

experimental plantings, rather than later research that monitors and

analyses the outcomes (see Nambiar and Ferguson, 2005, for a

heartfelt account). What is available bears testimony to the

desirability of widely spread experimental plantings to sort out some

of the major risks, together with a preparedness to wait for a long

period, if not a full rotation, to ensure that early trends are borne

out.

The history of such plantings has many cases of failure or relative

failure following early promise. Most of the hardwood plantings in

Central and North Queensland failed for reasons discussed later. Yet

earlier analyses (Venn, 2005) based on expert estimates (though

little data) suggested these could be economically viable. Later age

failures include blue gum, a widely planted species that after early

promise yielded disappointing later-age growth when grown on the

duplex soils in Gippsland, Victoria. These disappointing outcomes

17

simply highlight the tendency to underestimate the risks involved,

even when assessed by knowledgeable local experts.

Some MIS marketing organizations deliberately sought to promote a mix

of plantings of lesser-known hardwood species with plantings of long-

established softwood species, each in geographically distant areas,

to better attract investors. For example, Willmott Forests (2010)

offered a blend of radiata pine (Southern NSW and Victoria) and

intermixtures of silky oak - Grevillea robusta - and Casuarina spp

(Northern NSW). Elders Forestry (2010) offered a blend of teak -

Tectona grandis (Far North Qld), African mahogany - Khaya

senegalensis (Far North Qld), sandalwood (northern WA) and blue gum

(southern States). How much of this was an attempt to appeal to an

innate preference of MIS investors for native Australian species as

against exotic species; how much was to appear to hedge long rotation

returns by blending long and short rotation returns; and how much was

to deliberately attract high-risk investors, is unclear and warrants

further investigation. The obvious difference in risk between long-

established and new species, generally pointed out explicitly in MIS

prospectuses, seemed to count for little with MIS investors as the

these options were widely taken up.

A referee suggested that this behavior may just reflect that

investors were rational in seeking to maximise the risk-adjusted

value of their investment, and that MIS companies and their promoters

were simply seeking to assist this endeavor. However, because of the

ASIC strictures against providing financial forecasts in the

Prospectuses, the information provided would scarcely enable a

rational analysis of the risks-adjusted returns.

Summary

18

What is clear is that MIS investors were not, in general, rational

investors in the sense of weighing return against risk. Or is it

simply that having avoided paying some tax, one might just as well

have a flutter on the ultimate returns in what largely constitutes a

bet at the Government’s expense? As a professional colleague engaged

in financial analysis of MIS investments forcefully pointed out, many

MIS investors were only interested in the tax avoidance and never

read the fine print of prospectuses anyway.

Such an opinion does not provide an excuse for a consulting forester

to neglect these issues. Sooner or later, an irate and informed MIS

investor (or group thereof) will trigger litigation about misleading

estimates. Consulting foresters need to address this and pay greater

attention to published literature and journal papers to establish

better their forecasts of likely yields or growth rates and to engage

in more explicit analyses of the risks. This is not just a matter of

citing current research. The essential lessons stem from

understanding the long-known and well-documented principles that

underpin forest growth and yield:

1. Experimental planting results generally exceed those achieved

in large-scale plantings- partly due to the inevitable

variations in site, treatment and climate within the latter4.

That bias needs to be factored into early estimates of growth

and yield for large-scale plantings. My own rule of thumb is to

reduce initial estimates by at least one third.

2. Once measurable, current annual increment in volume or mass

exceeds mean annual increment up to the point of maximum mean

annual increment. Current annual increments during young ages

4 Experimental sites are generally better than average and more uniform in site productivity than a large plantation estate. Local geographic or temporal variations in climate, treatment, and the depredations of pests and diseases all contrive to lower yields in the latter relative to the former.

19

can be very misleading as to mean annual increment. Measurable

current annual increment may not start until year two but

escalates very rapidly only to decline rapidly thereafter.

These differences are profound for very short rotations of

order 10 years.

3. Growth rates for well-stocked plantations are generally

markedly influenced by rainfall. There is sufficient evidence

now available to factor the effect of mean average rainfall

into any estimates for many species in southern Australia but

more research is needed for sub-tropical and tropical regions.

4. Prolonged drought, other natural disasters and attack by

disease or pests can have devastating impacts. Risks, including

those of fire, drought, cyclone and hail, need to be assessed

from historical records and other research and applied to the

economic analyses. Any adjustments for risks should be

additional to the adjustments mentioned in #1. Risks from

disease and pests may be especially high for newly introduced

plantation species, as the Queensland experience with E.

grandis hybrids and E. dunnii shows.

5. A substantial number of permanent plots measured over periods

that approach the chosen rotation age are needed to establish

an adequate basis for estimation of growth and yield. Inventory

and the preparation of growth and yield models need to be a

line item that is specifically included in the MIS company

budget from inception and implemented for large-scale

plantings.

6. The predicted volume or mass at harvest needs to be reconciled

against actual volume or mass sold because factors including

markets, harvest technologies, and management can have marked

impacts on the amounts actually sold.

National Plantation Inventory Forecasting Methods

20

The preceding review of MIS plantations is a necessary building block

to understanding and interpreting the NPI forecasts, as MIS

plantation interests account for a substantial proportion of the

national plantation estate. Hence the following review of the

methods used to derive those forecasts, the assumptions that underpin

them and the resulting policy issues.

Net plantation areas

Net plantation areas represent a set of basic data whose accuracy

underpins all later forecast of aggregate growth and yield.

In the NPI, area data are collected from growers. In the case of

industrial plantations (estates exceeding 1,000 ha), all growers have

supplied detailed data on areas and, in most instances, species

planted on an annual basis. Confidentiality of the data is critical

and ABARES and its predecessors have established an excellent

reputation in this respect. Gross areas were validated and sometimes

more detailed checks were carried out by reference to remote sensing

data. Tabular area data have been updated annually (Gavran, 2012). A

more comprehensive update using spatial data provided by plantation

growers is undertaken every five years, the most recent available

being for 2010 (Gavran and Parsons, 2011). These area data reflect

additions due to new plantings and reductions due to re-measurements

of areas, changes in land use after harvesting, and losses due to

wildfire or pests or diseases up to 2010.

A National Farm Forestry Inventory (Sun et al., 1997) was established

in 1998 to collect and collate data from plantations of less than

1,000 ha owned by individual (rather than company, joint venture or

leasehold) growers. A further inventory was carried out in 2000. The

data were collected on a confidential basis through an extensive

21

network of regional and State farm forestry groups. The project

lapsed for lack of funds in 2001 and subsequent estimates have relied

on ad hoc updates supplied by some individual growers and informal

regional contacts. In 2001 (Wood et al., 2001), farm forestry

plantations constituted less than 5 per cent of the total plantation

estate and that proportion has declined substantially since that

date, so although an objective sample is currently lacking, it is

probably not a major defect in the present estimates.

Figure 6 summarizes the cumulative areas planted annually by species

type. The decline in new planting with the progressive failure of

many of the MIS schemes is evident. Aggregate areas planted can

readily be identified from remotely sensed imagery. However, checking

losses due to fire, drought, cyclone, pests and diseases is more

difficult, especially by age class, which is critical to forecasting

later yields.

[Figure 6. Total plantation areas by species type, 1995-2009.]

Plantation yields

Most industrial growers provided estimates of aggregate yields by

years or average plantation yields, under their planned silvicultural

regime. Some provided aggregate annual estimates that smoothed

marked irregularities in the past time pattern of ‘new planting’5 but

others did not. Some only provided data for currently planted areas

and did not assume replanting. Several did not supply estimates of

yields at all. Scientists responsible for national forecasts had to

fill the gaps, variously using extrapolation from previous data

5 The distinction between ‘new planting’ (i.e. planting of land previously in other uses) and ‘replanting’ (i.e. planting of land previously under plantations) is important, as later discussion will show. For simplicity, coppice regeneration is included under the heading of planting.

22

and/or estimates from similar estates, while maintaining strict

confidentiality. The estimates for farm forests required even more

gap filling although the general level of grower knowledge displayed

was surprisingly high.

The data supplied by growers were standardized and developed into

consistent records that could be aggregated within and between the 15

NPI Regions. In some regions, the temporal pattern of annual new

planting was markedly irregular, leading to spikes and gaps in the

collated estimates of availability. The number of regions with marked

irregularities diminished in the successive forecast reports of 1997,

2001, 2006 and 2012 reflecting a greater stability in rates of new

planting, so the need for smoothing was much reduced in the 2006 and

2012 forecasts.

Gavran et al. (2012) noted that their 2012 forecast of national

availability of softwood logs (sawlogs plus pulplogs) were 1.3 per

cent higher than those of the 2010-2045 period in the 2009 forecasts

by Gavran and Parsons (2009), based on a corresponding 3.4 per cent

increase in plantation area in that period. Gavran et al. (2012) also

noted that a much higher proportion of growers provided wood flow

forecasts for the 2012 forecasts. This difference in softwood

availability is not material, however, especially relative to the

uncertainties that underpin some of the other assumptions involved.

That said, there are some major differences in particular Regions

such as South-east and North Queensland that reflect events described

later.

The official national forecasts for hardwood pulpwood or other

categories did not simply accept prospectus forecasts or later

industrial and MIS forestry company forecasts. In the 2009 forecasts,

yield estimates supplied by MIS and industrial companies covered less

that 40 per cent of the plantation area involved. All such estimates

23

were checked for reasonableness. Yields for the remainder of the area

(60 per cent) were based on personal estimates by the respective

authors as documented in the reports – for example, an average of 17

m3 ha-1 y-1 was applied to that 60 per cent of blue gum growers, rather

than the prospectus figures of 20 to 25 m3 ha-1 y-1 commonly used in

the main growing regions. Even so, it is now apparent from the MIS

data and 2012 national forecasts for hardwoods that the actual mean

annual increment may be closer to 15 m3 ha-1 y-1.

The 2012 forecast of hardwood availability (sawlog plus pulplogs) was

15 per cent lower than the 2009 forecasts for the period 2010-2019,

notwithstanding an increase in the hardwood plantation area of 31.4

per cent over the period 2005-2012. This period is used here because

it is least affected by assumptions about replanting, given that the

overwhelming majority of the harvest will be for pulpwood grown on

short rotations. According to Gavran et al. (2012), the 2012 changes

reflect hardwood growers revising downwards their projected yields

together with some adjustment for losses of area due to pests,

diseases and cyclones. A much higher response by growers was also

apparent compared with the 2009 forecasts. Comparisons of individual

Regions indicate that the national decrease was largely due to

decreases in Western Australia, Green Triangle, Tasmania and South-

east Queensland, where the largest areas of hardwood plantations lie.

Another very significant change between the 2009 and 2012 forecasts

is the reduction in hardwood sawlog yields and increase in pulpwood

yields with the realization that to obtain quality sawlogs, pruning

and thinning will be needed (Nolan et al., 2005) and was not done on

much of the earlier sawlog planting.

Some senior figures in the industry have argued that the MIS forestry

company forecasts of future ‘log supply’ were much too high and by

inference that present and past national forecasts of availability

24

were also much too high (Parsonson, 2010). However, little difference

exists between the values given by a leading industry source

(Parsonson, 2010) and those in this paper for national hardwood

pulpwood availability in 2015-2019, those in 2012 national forecast

being generally slightly lower.

National Forecasts of Availability

Figures 7 and 8 summarize the 2012 national forecasts of availability

based on an assumption that there will be replanting of the areas

following harvesting.

[Figure 7. Australian sawlog availability forecasts, 2010-54]

[Figure 8. Australian pulpwood availability forecasts, 2010-54]

The general picture painted by these national forecasts of

availability is

(1) The dominance of softwood over hardwood sawlog

availability right through to the 2054.

(2) The very small increase in softwood sawlog availability

over the next 20 years.

(3) The relatively static availability of softwood pulpwood

to 2054.

(4) The very large increase in hardwood pulpwood availability

over the next ten years, noting that the 2010 harvest

(plantation and native forest) was 4.3 million m3.

These data and observations hide some major issues and assumptions

that need to be recognized, not least the impact of the failures of

many MIS forestry companies and the uncertainty attached to

replanting.

25

Some areas have also been the subject of losses that were not fully

apparent at the time of the last collection of area data (2009-2010)

or to losses subsequent to that collection of data. North Queensland

has suffered major losses of earlier plantings through pests and

disease problems and cyclone damage. Elders Forestry (previously ITC)

wrote off 25,650 ha of pulpwood plantations in Central Queensland

(Elders Ltd, 2010). Kirramyces spp, a fungal pathogen, attacked E

grandis x E. camaldulensis hybrids severely. Quambalaria spp, another

pathogen, attacked Corymbia citriodora sub, variegata solidwood

plantations somewhat less severely and most were replanted to other

species. In part,the 2012 forecasts reflect these problems and some

cyclone damage between 2006 and 2010, but the full effect of pests

and diseases may further reduce the hardwood availabilities.

In addition, the 2011 cyclone6 destroyed nearly 20,000 ha of softwood

and hardwood plantations in the Cardwell area now owned by FPQ

Plantations Pty Ltd. Lindsay and Dickinson (2012) subsequently

carried out a comprehensive analysis of the influence of cyclonic

winds on hardwood plantations in North Queensland. These cyclone

losses are not fully reflected in the Gavran et al. (2012) forecasts

as the damage came after the collection of area data and other

statistics. As is the case of damage due to pests and diseases, some

hardwood species appear more resistant to wind damage than others and

genetic variation may provide more resistant provenances (e.g. Luo et

al., 2006).

Blue gum plantations at Esperance in Western Australia also suffered

lower growth rates than expected due to drought and higher port and

harvesting costs than expected (Elders Ltd, 2010), such that they are

6 Former students of Dr. Max Jacobs may be prompted to remember his cautionary tale of why tropical coastal forests in North Queensland fail to attain the height of their Southern counterparts, despite generally better growing conditions.

26

unlikely to be replanted if harvest proves viable. It seems likely

that this change was not reflected in the forecasts for Western

Australia.

Is the Current Methodology Tenable in

Future?

National forecasts provide an overall picture that can help with

assessments of national supply and demand, but they are not all that

useful in guiding investment decisions, which are regionally based.

This shift from national to regional focus will place additional

pressures on the accuracy of the NPI. While the 2012 forecasts were

aided by a much better response on wood flows from the large growers,

I doubt that that situation will remain.

The competitive nature of what is now a largely privately-owned

industry places great strain on the willingness of individual

companies to provide such data, unless legally required to do so.

Most would argue that a legal requirement to do so would be unfair

and costly, relative to other industries. The NPI has done an

excellent job in maintaining confidentiality of data, but that

becomes harder to manage with respect to the publication of the final

results as growers and processors agglomerate and individual entities

become more dominant in individual regions and even across regions.

Moreover, there is no national definition of standards of the

description of log products, as witness KPMG (2012) comments on the

structure of the log price index for softwoods. Furthermore, the

numbers of hardwood log assortments are increasing, as witness the

27

Tasmanian situation of high quality sawlogs, lesser quality sawlogs,

veneer logs, peeler arisings and pulpwood (Gavran et al., 2012).

When area data are received from growers, they are verified using pre

viously supplied data and remote sensing. Yields are verified using A

BARES data, published information and expert knowledge to ensure that

they are within an expected range. However, there are no penalties

for supplying incorrect data and the opportunities for checking are

limited. Some MIS data provided prior to 2012 were clearly based on

early Prospectus statements and had to be reduced substantially.

While valuable, the present methodology lacks a scientific basis in

which data definitions and sampling are consistent, objective and

capable of audit, and allowing error bounds to be estimated. The

bounds attached to all past estimates are probably very large, even

ignoring the uncertainties of the assumptions about automatic

replanting. More importantly, some marked changes in log products mix

have taken place between the 2009 to the 2012 forecasts, especially

involving previously categorized sawlogs being reclassified and sold

as pulpwood, making it more difficult to assess change in the

standing volume of both those products over time. This is not a

criticism of the 2012 forecasts because the changes appear well-

founded but it highlights the past lack of objective reconciliation

data that enable structural changes in product mix to be assessed as

part of the ongoing changes that inevitably go on, in addition to

growth.

Finally, plantation inventory of the availability of timber resources

is based on a largely independent process to that of the inventory of

forest carbon sources and sinks by the Australian Government, and

overlaps some of the same inventory issues. The technology now

available for remote sensing of plantation areas and productivities

provides a possible platform for a better and different form of NPI

28

in which the interactions with industrial plantation owners may be

more to do with:

· continuing to ensure consistent and objective area data,

· establishing a modest national sampling base to estimate key

growth and yield metrics,

· reconciling actual against predicted volumes harvested,

· surveying landowner attitudes to replanting,

· adapting the carbon measurement tools for application to grower

data on net growth and removals, and

· estimating error bounds.

This is in contrast to the present system that includes requesting

commercially sensitive data on predicted wood flows from growers

that, in my view, may become increasingly difficult to obtain and

interpret at a regional level. As a referee has pointed out, such

regional data collection might better be left to commissioned studies

by consultants.

Regional Forecasts

The major investment decisions are made regionally because they

relate to large-scale processing and the need for access to rail and

road infrastructure to service major cities, and ports to service

exports. So let us examine some of the major regions and see what the

most recent forecasts (Gavran et al., 2012) reveal or hide in relation

to policy issues–it is a bit of both.

Short-rotation plantations

The Western Australia and Green Triangle forecasts for hardwood

pulpwood in Figure 9 tell a similar story. They both involve a very

large increase in annual volumes available from the present levels of

harvest. No significant new planting is likely, at least in the next

29

five to ten years: indeed, there is likely to be a significant shift

to replanting blue gum areas with radiata pine on better sites in

some areas, thereby reducing the levels of hardwood pulpwood

availability shown beyond 2020.

The initial upward step in the Tasmanian forecast in Figure 9 in part

reflects the progressive impact of pruning and thinning of sawlog

plantations as they age, as well as an earlier increase in pulpwood-

only plantations. Commercial thinning of hardwood plantations plays

an important role in accelerating plantation hardwood sawlog supply,

to which later reference will be made.

The situation regarding new planting in Tasmania is uncertain,

pending resolution of negotiations in progress under the Tasmanian

Forest Agreement (2013). Substantial Commonwealth and State funding

of new sawlog plantations is likely if the negotiations are

satisfactorily concluded. Such plantations would also contribute to

future pulpwood availability through thinnings.

[Figure 9. Plantation Hardwood Pulpwood Availability in Major

Hardwood Regions of Australia]

Long rotation plantations - Hardwoods

Figure 10 (a) shows forecasts of hardwood sawlog availability for

South-east Queensland. The Queensland Government initially opted out

of the Commonwealth-State Regional Forest Agreement process and, in

2000, negotiated an agreement with the hardwood industry and the

Greens to phase out native forest harvesting in the region by 2025.

It provided substantial funds to invest in new hardwood sawlog

plantations that were expected to come into production by 2025.

30

In 2005, the Queensland Government committed additional funds to ‘new

planting’ up to 2015. Success hinges on species selection and

breeding to ameliorate the pest and disease issues (e.g. Angel et

al., 2005; Whyte et al., 2011) and on the maintenance of new planting

rates beyond 2015. However, the promise of a transition at the same

scale (circa 150,000 m3/y including poles) from native forest to

plantation hardwood sawlogs by 2025 cannot be realized. Continuity of

hardwood sawmilling in South-east Queensland therefore rests on the

supply from private property native forests bridging the hiatus or a

partial reversal of existing policy.

[Figure 10. Plantation Hardwood Sawlog Availability in Major

Hardwood Regions of Australia]

Tasmania (Figure 10(b)) has had a program of growing hardwood

plantations on long rotations for a longer period than most other

States. Pitt & Sherry and Esk (2012) provide more recent estimates of

sawlog availability from privately-owned hardwood plantations that

have a shorter history of plantings, with much less pruning and

thinning. The rapid step-up in the availability of hardwood sawlogs

shown in Figure 10 reflects the past history of plantings, largely by

Forestry Tasmania. As noted earlier, further increases through

commitments to future planting may follow. The longer term policy

issue is whether the quantity and quality (see Ferguson, 2012) of

plantation sawlogs will be adequate to service a viable sawmilling

and veneer industry in Tasmania, given the reduction in the supply of

native forest sawlogs from Forestry Tasmania (Tasmanian Forest

Agreement, 2013).

Long rotation plantations - Softwoods

31

Figure 11 shows the availabilities for plantation softwood sawlog in

the three NPI Regions with the largest softwood sawlog productions -

Green Triangle, Murray Valley and South-east Queensland.

[Figure 11. Plantation Softwood Sawlog Availability in Major Softwood

Regions

of Australia]

Given that the shortest possible rotation for softwood sawlog

production is about 25 years, all three regions shown in Figure 11

have very little if any scope for expansion of processing until 2035.

Beyond 2035, further sustained increases in softwood sawlog

availability and processing will hinge on the rate of new planting

from 2010 onwards or on the conversion of blue gum sites after

harvesting to radiata pine, in the case of Green Triangle and Murray

Valley Regions. Scope for similar conversion to softwood in

Queensland is limited by the commitment to expand hardwood

plantations, assuming the pest and disease problems can be overcome,

and the high price of land.

Future rates of replanting and new planting

The previous forecasts all rest on a tenuous assumption. Will

existing land-owners and growers replant following harvest? If they

don’t, availability will decline rapidly beyond 2020 and the

Australian Government will be left with carbon stock reductions it

does not want.

In some cases, the process of liquidation of failed MIS companies has

led to the purchase of the woodlots by a TIMO, in which case the

continuity of coppice or replanting seems likely. However,

restructuring of some failed MIS companies is yet to be completed, so

the future availability in subsequent rotations is uncertain in those

32

cases. Brand (2012), Managing Director of New Forests Pty Ltd - now

one of the largest owners of former MIS plantation land, stated that,

for the former Great Southern Plantation estate, he expected that

about one third of those hardwood plantations may revert to

agricultural uses and one third may convert to softwood plantation,

leaving one third as hardwood plantation. Changes of such magnitude,

especially if applied to other former MIS blue gum estates as well,

will have major implications for land prices, rural employment, and

investment in processing industries and/or export facilities.

One factor favoring retention of coppice or replanting is that

reversion from plantation to pasture or other crops incurs a

substantial cost - indicatively, between $750 ha-1 and $1500 ha-1. The

receipt of a major cash flow at the time of harvest may also

encourage owners to let the coppice grow or to replant non-coppicing

species. But owners will still need to invest further in some tending

and protection and, where relevant, to pay lease fees. That is where

assistance may be vital to the remaining small woodlot (as distinct

from TIMO) owners, especially in creating confidence as to the future

markets. In any event, the attitude of owners to replanting will be

critical to realizing these forecasts of availability in the long

term.

What, if any, policy provisions should support replanting? The

plantation industry will not be eligible to receive Renewable Energy

Certificates enabling carbon trading (Australian Government, 2011).

Unlike new planting (see later), the public benefit from replanting

rests on carbon sequestration alone, for which the only provision is

the waiver on the carbon tax on fuel used in forest-based harvesting

and haulage. Unless other measures are introduced, replanting will

rest solely on the attitude of the owner to the costs and benefits of

wood production. MIS tax avoidance provisions are likely to be much

less important in encouraging replanting now that much of the

33

hardwood plantation estate is owned by TIMOs who are likely to reduce

the costs of management and control by progressively winding up

rather than expanding MIS schemes.

‘New planting’ is planting on new sites previously cleared for

agriculture prior to 1990 (i.e. new ‘Kyoto forest’). It has clear

public benefits in the form of structural adjustment assistance that

enables ageing farm-owners to realize on their assets and retire

(Mackarness and Malcolm, 2006), as well as potential benefits from

carbon sequestration (Garnaut, 2008). These two benefits provide the

major policy rationale for MIS-type arrangements, albeit with much

tighter regulation in the future.

Future rates of new planting are extremely uncertain in the short

term because of the impact of the current mining boom on the exchange

rate, together with the impact of high prices of suitable land

spawned by competition for land by MIS forestry companies and other

factors (Schirmer, 2009), the uncertainties pertaining to Tasmania,

and the possible conversion of substantial areas on MIS hardwood

plantation back to agriculture or to softwood plantation.

The current mining boom has resulted in a major change in exchange

rates such that imports of sawn timber from Northern Europe into

Eastern Australia have risen from almost zero to about 14 per cent in

2010-11, placing the domestic producers under severe competitive

stress. Experience from the previous mining boom suggests that the

impact of the boom will ease progressively and exchange rates will

drop, gradually easing the competition from European imports,

especially once the European economy recovers. Nevertheless, the next

three years or so will not be conducive to new planting because of

the high, albeit declining, exchange rate and because of the high

prices for land engendered by the MIS schemes.

34

Some observers argue that current land prices make softwood planting

or replanting uneconomic and predict an absolute halt to expansion.

However, over the next 5 to 10 years, inflation and the MIS

plantation use changes predicted by Brand (2012) will progressively

reduce the real (inflation free) price of land from the current high

prices engendered by the MIS boom. Moreover, between 1 and 3 per cent

of agricultural properties in NPI regions are sold each year

(Schirmer, 2009). If those properties are strategically located or

provide economies of scale so that they are accretive to overall

returns, existing plantation companies will buy them. The possibility

of a complete halt to new planting is overstated – an initially slow

but progressively increasing rate of replanting is more likely.

In southern Australia, much hinges on a possible shift of some areas

from blue gum to radiata pine. While the Western Australia, Green

Triangle and Murray Regions are likely to have low levels of ‘new

planting’ under present policies, they may see substantial change

from blue gum to radiata pine on the more productive sites as

harvesting of the former proceeds, assuming the returns are

accretive.

Nevertheless, virtually all the available volume from existing

plantations is presently committed in the key regions and the

projected increases in the domestic availability beyond 2020 are

unlikely to accommodate expected future increases in domestic demand

for softwood timber. Much therefore rests on the future trends in

timber, stumpage and land prices. If European imports decline

markedly beyond 2015 and domestic timber and stumpage prices rise as

a result, a modest expansion of new planting of softwoods could be

engendered, conditional on agricultural land prices remaining stable

or declining at the that time. Too large an increase in stumpage

price, however, would in turn reduce the demand for sawn structural

timber and advantage competitive materials and imports somewhat.

35

For both replanting and new planting, much also depends on carbon

sequestration policies: in particular, the price imposed on carbon,

especially as it affects competitive materials such as steel and

cement. Present indications are that subsidies to the steel industry

will largely (94.5 per cent) offset the proposed carbon tax for the

next three years and, if recent media reports are to be believed,

possibly up to 2017. The pegged Australian price for carbon is

currently markedly above the European market price. International

trading of emissions credits is scheduled to commence in July 2015,

introducing volatility in carbon prices thereafter. The threat of the

Federal Opposition to abandon the emissions trading scheme in favour

of incentives, if it is elected to govern, has created even more

uncertainty.

In addition, much hinges on future development in the mining sector

and its impact on the Australian economy and, in turn, on continuing

economic growth in China and India; exports of pulpwood and lower

grades of softwood sawlog being very much linked to these

developments. Australia is a relatively small trade-exposed economy

and must now ride the cyclical waves of the global economy.

All of these trends and associated uncertainties add weight to the

need for an integrated national forest policy on plantations. Given

the dominance of private ownership in the processing industry and

now, the plantation estate, such a policy should aim principally at

providing information on the national plantation estate and reducing

impediments to invest in both the plantation estate and processing,

to better enable the plantation sector to ride those cyclical waves.

The role for direct subsidies is probably small and mainly confined

to small landowners and small processors, based on clear public

benefits such as structural adjustment, innovation, infrastructure

and rural employment and diversification.

36

Conclusions

Plantation policy in Australia is approaching critical crossroads.

The Australian Government, State Governments and forestry industry

need to develop a coherent national plantation policy if they wish to

maintain and expand rural manufacturing and employment that is

internationally cost-competitive and contributing significantly to

carbon sequestration and other environmental values. Restoring

community and investor confidence about future investment in the

plantation estate and processing industry is an important component

of that policy. Ongoing support for the NPI facility is needed to

ensure it can develop the methodologies and the systems to meet the

challenges to delivering a less intrusive but more objective

inventory at a national level.

More attention also needs to be given to the need for expansion of

industrial softwood plantations in key regions to facilitate

progressive scaling up of manufacturing industry, in the battle to

maintain an internationally competitive manufacturing base. This

necessitates a greater focus on encouragement and assistance to

expanding the plantation base in key regions, in concert with

measures relating to carbon sequestration, reducing risk and

transaction costs, and rural structural adjustment.

Acknowledgements

Special thanks go to Claire Howell, Mark Parsons, and Stuart Davey

and Blair Freeman for their comments. The work of the first four and

of others in ABARES in maintaining the present form of the NPI merits

special recognition. The participants of the plantation growing and

management sector also merit thanks for their significant ongoing

37

commitment and contribution to the NPI since its establishment in the

mid-1990s.

A preliminary version of this paper was presented at the 2011 ANZIF

Conference in Auckland. In the course of this revision, data errors

were discovered in MIS data supplied by a confidential source. Most

of the results still hold but reporting of some results with low

sample numbers could no longer be justified. The author takes sole

responsibility for the views expressed and acknowledges a vested

interest as a Director of a major softwood plantation company.

Literature CitedAdviser Edge (2008). 2007-2008 Timbercorp (Single Payment) Timberlot

Project. The author, Melbourne, 24pp.

Angel, P.J., Nichols, J.D. and Stone, C., 2003. Growth increments of

Eucalyptus dunnii subsequent to damage by Creiis literatus

(Hemiptera:Psyllidae). p192-5 in E.G Mason and C.J.Perley (Eds),

Proceedings 2003 ANZIF Conference, Queenstown, New Zealand,

Ministry of Agriculture and Forestry, Wellington.

Australian Agribusiness Group (2008). Agribusiness MIS Industry Repo

rt of Funds Raised, July 2008. The author, Melbourne, 10pp.

Australian Agribusiness Group (2010). Macquarie Forestry Investment

2010: Retail Investment Research- May 2010. The author, Melbourn

e, 10pp.

Australian Government, (2011). Working together for a Clean Energy Fu

ture: Forest Activities. Available on http://www.cleanenergyfutu

re.gov.au/forest-activities/

Brand, D. (2012). Investing in a Sustainable Australian Forest Secto

r. Remarks by David Brand to the Forestworks ‘Australian Forest

Industry Development Conference’, Canberra, October 2012. New Fo

rests, Sydney, 7pp.

Elders Forestry (2010). Diversified Forestry Project, 2010. Product D

38

isclosure Statement. Elders Forestry, Melbourne, 64pp

Elders Ltd, (2010). Completion and Outcome of Forestry Asset Review,

3 May 2010. Company Announcements Office, Australian Securities

Exchange, 8pp

Elders Ltd, (2011). Completed and intended asset sales and earnings e

xpectations. Elders Ltd, Adelaide, 3 pp.

FEA (2008). Canopy, Winter 2008. Forest Enterprises Australia,

Launceston.

Ferguson, Ian (2012). Forestry Tasmania’s Sustainable Yield under the

Australian Forestry Standard. Report commissioned by NSC

International, Melbourne, 40pp. Available on

http://www.forestrytas.com.au/uploads/File/pdf/pdf2012/appendix_

a_ferguson_report.pdf

Ferguson, I., Bull, L. and Gorrie, G. (2009). Improving the

Investment Climate for Australian Forest Industries. Paper

prepared for the Asia-Pacific Forestry Commission, May 2009, The

authors, Melbourne, 50pp

Ferguson, I., Fox, J., Baker, T., Stackpole, D. and Wild, I. (2002).

Australian and regional wood availability, 2001-2044.

Consultant’s report for the 2002 National Plantation Inventory,

Bureau of Rural Sciences, Canberra, 88pp.

Garnaut, R. (2008). The Garnaut Climate Change Review: Final Report.

Cambridge University Press, Cambridge, Canberra, 680pp.

Gavran, M. and Parsons, M. (2011). Australia’s plantations statistics

2011. Australian Bureau of Agricultural and Resource Economics

and Sciences, Canberra. 43pp.

Gavran, M., Frakes, I., Davey, S. and Mahendrarajah, S. (2012). Austr

alia’s plantation log supply 2010–2054, Australian Bureau of

Agricultural and Resource Economics and Sciences, Canberra, 55p

p. Available on http://adl.brs.gov.au/data/warehouse/afplsd9abfe

001/afplsd9abfe00120120515/AustLogSupply2012_2054_v.1.0.0.pdf

GSP (2006). Great Southern Plantations 2005 & 2006 Projects, Product

Disclosure Statement, the author, Perth, 84pp.

39

Harper, R. J., Smettem, K.R.J. and Tomlimson, R.J. (2005). Using soil

and climatic data to estimate the performance of trees, carbon

sequestration and recharge potential at the catchment scale.

Australian Journal of Experimental Agriculture 45:1189-1401

Howell, C. and Mutendeudzi, M. (1997) National Plantation Inventory

of Australia. Proceedings of the Australia New Zealand

Institute of Foresters, Canberra, April 1997 p321-328

ITC Project Management Limited (2009). Diversified Forestry Project

2009, Supplementary Product Disclosure Statement. ITC Project

Management Limited, Melbourne, 4pp.

Knott, Jim (2011) Estimating plantation productivity: Lessons learnt

from a Blue Gum Retrospective. Powerpoint presentation to a

Continuing Professional Development Workshop organised by the

Australian Consulting Foresters Association of the Institute of

Foresters of Australia, Melbourne, 2011. Available on

http://www.forestry.org.au/news/articlefiles/1821-Jim

%20Knott.pdf

KPMG (2008). Independent Forestry Specialist Review of Valuation Data

5, Great Southern Blue Gum Projects 1998 to 2002, October 2008.

KPMG Corporate Finance (Aust) Pty. Ltd.

KPMG (2012). Australian Log Price Index (Stumpage), January to June,

2012. KPMG, Melbourne, 19pp.

Lindsay, A. and Dickinson, G. (2012). Influence of cyclonic winds on

the performance of hardwood plantations in tropical north

Queensland. Queensland Department of Agriculture, Fisheries and

Forestry, Brisbane, 38pp.

Luo, J., Arnold, R.K. and Aken, K. (2006). Genetic variation in

growth and cyclone resistance in Eucalyptus pellita in south-

western China. Australian Forestry 69 (1):32-47

Mackarness, P. and B. Malcolm (2006). Public policy and managed

investment schemes for hardwood plantations. Extension Farming

Systems Journal 2(1):105-116

40

Miehle, P., Battaglia. M., Sands, P.J., Forrester, D.I., Feikema, P.

M.,Livesley, S.J., Morris, J.M. and Arndt, S.K. (2009). A compar

ison of four process-based models and a statistical regression m

odel to predict growth of Eucalyptus globulus plantations. Ecolo

gical Modelling 220:734-746

Nambiar, S. and Ferguson I. (2005). (Eds) New Forests: Wood

Production and Environmental Services. CSIRO Publications,

Melbourne.

National Forest Inventory (1997). National Plantation Inventory of Au

stralia, Bureau of Rural Sciences, Canberra, 96pp.

Nolan, G., Greaves, B., Washusen, R., Parsons, M. & Jennings, S.

(2005). Eucalypt Plantations for Solid Wood Products in

Australia - A Review, ‘If you don’t prune it, we can’t use it’.

FWPRDC project Report PN04.3002, Forest & Wood Products

Research & Development Corporation, Melbourne: 138pp.

Parliamentary Joint Committee on Corporations and Financial Services