Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements

14

International Journal of Auditing Int. J. Audit. 9: 187–200 (2005) ISSN 1090-6738 © Blackwell Publishing Ltd 2005. Published by Blackwell Publishing, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA. Blackwell Publishing Ltd.Oxford, UK and Malden, USAIJAUInternational Journal of Auditing1090-67382005 Blackwell Publishing Ltd.200593187200 Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing RequirementsH. Haron et al. Correspondence to: Hasnah Haron, School of Management, Univeristi Sains Malaysia, 11800 Penang, Malaysia. Email: [email protected] Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements Hasnah Haron, 1 Muhamad Jantan 2 and Eow Gaik Pheng 3 1 School of Management, Universiti Sains Malaysia 2 Centre for Policy Research, Universiti Sains Malaysia 3 6Q, Changkat Sg.Ara 3, Desa Ara, 11900, Penang This research investigated the extent of companies’ compliance with the Kuala Lumpur Stock Exchange (KLSE) listing requirements in relation to audit committees. Additionally, the research set out to identify any significant differences in compliance between PN4 companies, that is companies that fall under Practice Notes 4 of KLSE’s revamped listing requirements and are required to regularize their financial condition in a timely manner, and non-PN4 companies. One hundred and twenty companies were selected from 852 public listed companies on the KLSE. Year 2002 annual reports were the source of data for this study. The study investigated the ten listing criteria related to the five core KLSE disclosures to be complied with, which are with respect to: (1) audit committee composition, (2) written terms of reference, (3) audit committee meetings and attendance, (4) audit committee activities and (5) internal audit activities. Only 45% of the sample population complied with all ten listing criteria. This comprised 40.3% for companies listed on the main board, 57.1% for those listed on the second board and 38.5% for PN4 companies. The percentage of independent directors present at meetings ranged from 0% to 100%, with an average attendance of 78%. This indicated a deviation in practice from the KLSE listing requirement that requires 100% of all the meetings to have a majority of independent directors present. No significant difference between PN4 companies and non-PN4 companies with regard to audit committee compliance was found. Key words: corporate governance, audit committee, compliance level.

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements

International Journal of AuditingInt J Audit 9 187ndash200 (2005)

ISSN 1090-6738copy Blackwell Publishing Ltd 2005 Published by Blackwell Publishing 9600 GarsingtonRoad Oxford OX4 2DQ UK and 350 Main Street Malden MA 02148 USA

Blackwell Publishing LtdOxford UK and Malden USAIJAUInternational Journal of Auditing1090-67382005 Blackwell Publishing Ltd200593187200Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing RequirementsH Haron et al

Correspondence to Hasnah Haron School of ManagementUniveristi Sains Malaysia 11800 Penang Malaysia Emailhhasnahusmmy

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements

Hasnah Haron1 Muhamad Jantan2 and Eow Gaik Pheng3

1School of Management Universiti Sains Malaysia2Centre for Policy Research Universiti Sains Malaysia36Q Changkat SgAra 3 Desa Ara 11900 Penang

This research investigated the extent of companiesrsquo compliancewith the Kuala Lumpur Stock Exchange (KLSE) listingrequirements in relation to audit committees Additionallythe research set out to identify any significant differences incompliance between PN4 companies that is companies thatfall under Practice Notes 4 of KLSErsquos revamped listingrequirements and are required to regularize their financialcondition in a timely manner and non-PN4 companies Onehundred and twenty companies were selected from 852 publiclisted companies on the KLSE Year 2002 annual reports werethe source of data for this study The study investigated the tenlisting criteria related to the five core KLSE disclosures to becomplied with which are with respect to (1) audit committeecomposition (2) written terms of reference (3) audit committeemeetings and attendance (4) audit committee activities and (5)internal audit activities Only 45 of the sample populationcomplied with all ten listing criteria This comprised 403for companies listed on the main board 571 for those listedon the second board and 385 for PN4 companies Thepercentage of independent directors present at meetingsranged from 0 to 100 with an average attendance of 78This indicated a deviation in practice from the KLSE listingrequirement that requires 100 of all the meetings to havea majority of independent directors present No significantdifference between PN4 companies and non-PN4 companieswith regard to audit committee compliance was found

Key words corporate governance audit committee compliancelevel

188 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

SUMMARY

The recent financial crisis in emerging markets andcorporate scandals inevitably focused on the lackof corporate as well as governmental oversightThe Malaysian government initiated severalmeasures in its efforts to create a world-classcapital market Amongst the measures taken toensure a smooth implementation of theseinitiatives was to revise the listing requirements tomake it mandatory for all public listed companiesto form an audit committee by 1 August 1994 TheMalaysian Code of Corporate Governance issuedin 2001 requires that the board of directorsestablish an audit committee of at least threedirectors with the majority comprising of non-executive director The independence of the auditcommittee is critical to ensure that the board fulfilsits oversight role and holds managementaccountable to shareholders

The audit committee is an important boardcommittee that assists the board of directors inoverseeing and ensuring adequate functioning ofinternal control mechanisms monitoring andfocusing on reviewing financial risk and riskmanagement Audit committee helps determineindicators of problems and address theseproblems mitigate possible damage and enhanceshareholder value The audit committee is effectiveonly if it is able to fulfil the roles stipulated in therules and regulations The first step towardseffectiveness should be complete compliance withthe rules and regulations provided by the KLSElisting requirement

The listing requirements require that all publiclisted companies include the Audit CommitteeReport in their annual reports The AuditCommittee report should have the following tenrequirements (1) the audit committee shouldcomprise at least three members (2) the majorityof the audit committee should be independentdirectors (3) at least one member of the auditcommittee is financially literate (4) the chairmanof the audit committee is an independent director(5) no alternate director of the audit committee isappointed as a member (6) there are written termsof reference for the audit committee to refer to(7) the number of meetings should be noted (8)the majority attending the meeting should beindependent directors (9) there should be asummary of audit committee activities and (10) asummary of internal audit activities should alsobe produced

There is evidence to support that there is ahigh audit committee compliance level with allten KLSE listing requirements However thecompliance level for having majority independentdirectors in the committee and majorityindependent directors attending the meeting isrelatively low There is also evidence thatcompliance levels for PN4 companies and non-PN4 companies are similar The study also foundthat most of the companies have a standardizedformat of reporting and that the level ofinformation provided in the audit committeereports are quite limited For example the terms ofreference did not disclose any fact concerning howstereotype disclosure in the audit committee reportcreate concerns about the disclosure as merelyfulfiling the KLSE listing requirements Therespective governance body in Malaysia shouldtake appropriate steps to ensure compliance withthe ten requirements and more importantly toensure that these requirements are appropriatelyimplemented

INTRODUCTION

An audit committee (AC) is a standing committeeof the board constituted with the aim ofcontributing to effective corporate governanceespecially with regard to the boardrsquos responsibilityfor the reliability of financial disclosures and itsoversight of the effectiveness of risk managementinternal control and audit Good corporategovernance is expected to increase investorsrsquoconfidence and thus enhance shareholder value Itcan also be argued that good corporate governanceresults in reduced costs of doing business whichin turn increase shareholdersrsquo wealth (Kala 2001)

Reporting requirements and compliance mattersform essential parts of the corporate governanceprocess Without adequate reporting mechanismsone cannot be assured that the affairs of thecompany are being run for its benefit in a prudentmanner Tate (2002) observed that appropriateAC compliance helps spot and address redflags mitigates possible damage and enhancesshareholdersrsquo value Thus ACsrsquo emphasis oncompliance with rules and regulations is expectedto improve the effectiveness of the AC Continuedlisting on the Kuala Lumpur Stock Exchange(KLSE) requires constant compliance with itslisting requirements and it is compliance withthese requirements that is measured in this study

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 189

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

This study investigates reporting behaviourusing compliance that can be identified throughdisclosures as a measure of potential ACeffectiveness and also examines whether financialdistress in companies is associated with varyinglevels of compliance (and hence effectiveness) Theprimary objectives of the research are thereforeto (1) measure the level of audit committeesrsquocompliance with KLSE requirements and (2)examine differences between PN4 and non-PN4companies with respect to their compliance levelPN4 companies are listed companies that fail tomeet the financial conditions (due to liquidityproblems and deficits in shareholdersrsquo equity) forcontinued trading and listing on KLSE Thesecompanies need to regularize their financialconditions within 6ndash12 months and are underconstant scrutiny and monitoring by the StockExchange

The development of ACs in Malaysia began in1991 when the Malaysian Institute of CertifiedPublic Accountants (MICPA) the MalaysianInstitute of Accountants (MIA) and the Instituteof Internal Auditors (IIA) of Malaysia jointlysubmitted a memorandum to the Registrar ofCompanies (ROC) the Capital Issue Commission(CIC) and the KLSE1 to recommend that ACs bemade mandatory for all listed companies inMalaysia Subsequently Section 15A of the KLSEListing Requirement was introduced whichrequired all listed companies to form an AC byAugust 1 1994

Research on audit committees in developedcountries has covered various aspects relating totheir formation role and functions following theimportance attached to the AC as a componentof corporate governance by bodies such as theUS Treadway Commission and the UK CadburyCommittee On September 28 1998 the SEC(Securities amp Exchange Commission) NYSE (NewYork Stock Exchange) and the NASD (NationalAssociation of Securities Dealers) announced thecreation of the Blue Ribbon Committee (BRC)to improve the effectiveness of corporate ACThe BRCrsquos charter was to lsquoundertake an intensivestudy of the effectiveness of ACs in dischargingtheir oversight responsibilities and makeconcrete recommendations for improvementrsquoThe BRC made ten recommendations aimed atstrengthening the independence of ACs makingthem more effective and increasing theiraccountability along with that of outside auditorsand management

These ten recommendations were adoptedby AICPA (American Institute of CertifiedPublic Accountants) NYSE NASD and SECSubsequently these ten recommendations werelooked upon as the guiding benchmark for manycountries including Malaysia

Resulting from these ten recommendations inDecember 1999 the NYSE and NASDAQ (NationalAssociation of Securities Dealers AutomatedQuotation System) modified their requirements forACs so as to require firms to maintain committeeswith the majority of members being independentdirectors In broad terms independent directorsare those who are free of any business or otherrelationship which might interfere with theexercise of independent judgement

The paper is structured as follows The nextsection sets the study in the context of the existingliterature This is followed by sections which inturn describe the background and content ofthe KLSE requirements for ACs discuss themethodology applied present the results obtainedand comment on the implications of those resultsFinally some limitations and possibilities for futureresearch are noted

LITERATURE REVIEW

Discussions of the financial crises in emergingmarkets and of corporate scandals across the worldhave inevitably focused on the lack of corporateas well as governmental oversight The Malaysiangovernment initiated several measures in itsefforts to create a world-class capital marketAmong the measures taken to ensure a smoothimplementation of these initiatives were measuresto revise the listing requirements to make itmandatory to form an effectively functioning AC(Shamsher amp Zulkarnain 2001)

Though every listed company was required tohave an AC from 1993 thus far only one study(Zulkarnain et al 2001a) has been conducted toevaluate the compliance with Section 344A KLSElisting rules The study found that it was not until1998 that all 556 listed firms had formed an ACeven though it was mandated in 1993 They weregiven a grace period of one year to comply

In the international arena previous researchhas examined the relationship between thepresence of an AC and the quality of financialstatements (Beasley 1996 DeFond amp Jiambalvo1991 McMullen 1996) Other researchers haveexamined issues relating to the voluntary

190 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

formation of ACs (Bradbury 1990 Pincus et al1989) Most of the studies supported the viewthat the presence of an AC will reduce financialreporting problems and improve the transparencyand disclosure of financial reports

Audit committee

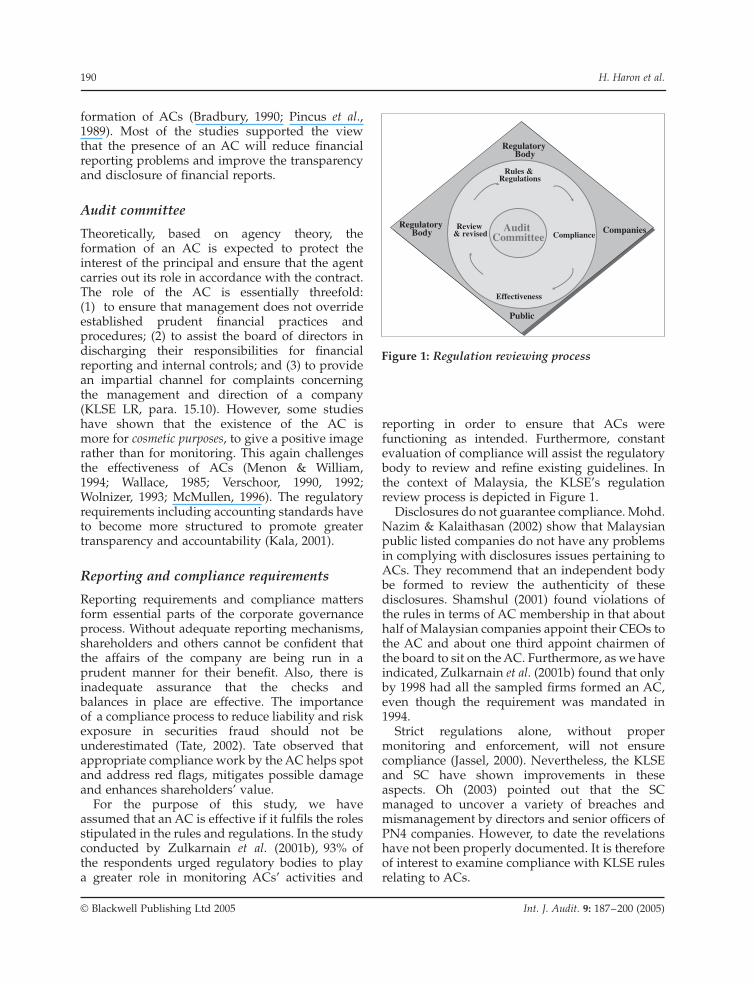

Theoretically based on agency theory theformation of an AC is expected to protect theinterest of the principal and ensure that the agentcarries out its role in accordance with the contractThe role of the AC is essentially threefold(1) to ensure that management does not overrideestablished prudent financial practices andprocedures (2) to assist the board of directors indischarging their responsibilities for financialreporting and internal controls and (3) to providean impartial channel for complaints concerningthe management and direction of a company(KLSE LR para 1510) However some studieshave shown that the existence of the AC ismore for cosmetic purposes to give a positive imagerather than for monitoring This again challengesthe effectiveness of ACs (Menon amp William1994 Wallace 1985 Verschoor 1990 1992Wolnizer 1993 McMullen 1996) The regulatoryrequirements including accounting standards haveto become more structured to promote greatertransparency and accountability (Kala 2001)

Reporting and compliance requirements

Reporting requirements and compliance mattersform essential parts of the corporate governanceprocess Without adequate reporting mechanismsshareholders and others cannot be confident thatthe affairs of the company are being run in aprudent manner for their benefit Also there isinadequate assurance that the checks andbalances in place are effective The importanceof a compliance process to reduce liability and riskexposure in securities fraud should not beunderestimated (Tate 2002) Tate observed thatappropriate compliance work by the AC helps spotand address red flags mitigates possible damageand enhances shareholdersrsquo value

For the purpose of this study we haveassumed that an AC is effective if it fulfils the rolesstipulated in the rules and regulations In the studyconducted by Zulkarnain et al (2001b) 93 ofthe respondents urged regulatory bodies to playa greater role in monitoring ACsrsquo activities and

reporting in order to ensure that ACs werefunctioning as intended Furthermore constantevaluation of compliance will assist the regulatorybody to review and refine existing guidelines Inthe context of Malaysia the KLSErsquos regulationreview process is depicted in Figure 1

Disclosures do not guarantee compliance MohdNazim amp Kalaithasan (2002) show that Malaysianpublic listed companies do not have any problemsin complying with disclosures issues pertaining toACs They recommend that an independent bodybe formed to review the authenticity of thesedisclosures Shamshul (2001) found violations ofthe rules in terms of AC membership in that abouthalf of Malaysian companies appoint their CEOs tothe AC and about one third appoint chairmen ofthe board to sit on the AC Furthermore as we haveindicated Zulkarnain et al (2001b) found that onlyby 1998 had all the sampled firms formed an ACeven though the requirement was mandated in1994

Strict regulations alone without propermonitoring and enforcement will not ensurecompliance (Jassel 2000) Nevertheless the KLSEand SC have shown improvements in theseaspects Oh (2003) pointed out that the SCmanaged to uncover a variety of breaches andmismanagement by directors and senior officers ofPN4 companies However to date the revelationshave not been properly documented It is thereforeof interest to examine compliance with KLSE rulesrelating to ACs

Figure 1 Regulation reviewing process

Public

RegulatoryBody

CompaniesRegulatory

BodyReview

amp revised

Rules ampRegulations

Effectiveness

ComplianceAudit

Committee

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 191

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

The role and responsibility of audit committee

The AC is an important committee that inter aliaassists the board of directors in overseeing andensuring adequate functioning of the internalcontrol mechanisms monitoring and focusing onreview of financial risk and other aspects of riskmanagement In this regard it is important to notethat the AC lsquoshould not and cannot be auditorsrsquo(Kala 2001)

In the United States the Blue Ribbon Committee(BRC) (1999) report on ACs specifically stated thatthe ultimate governance body in any corporationis the board of directors It also recommended thatthe members of the board serving on the ACshould be financially literate in order to detect theoccurrence of earnings management ACs arean integral part of the internal monitoringmechanisms that alert policy makers andregulators worldwide of irregularities TheCadbury Committee in the UK (1992) and the BRC(1999) further pointed out that ACs representthe full board providing an effective forum forpersonal contact and communication amongst andbetween the board the external auditors theinternal auditors the finance directors and theoperating executives

In the United States the former Secretary ofCommerce Barbara Hackman Franklin addressesthe fact that AC members fear being sued andthat because of this many directors are lessinclined to sit on the committees (Barr 1999) Thisis because in cases of fraudulent financialreporting such as Enron and WorldCom theauthorities tended to enquire whether the ACshad been performing their tasks responsibly andwhether there had been compliance with rulesand regulations

The Malaysian Code of Corporate Governancerequires the board of directors to establish anAC of at least three directors with a majority ofnon-executive directors The independence ofthe AC is critical to ensure that the board fulfilsits oversight role and holds managementaccountable to shareholders

The main objectives of the AC as stated by Kala(2001) are as followsbull to assist the board of directors to fulfill its

responsibilities for the companyrsquos financialreporting for management of financial andcontrol risks and for monitoring internalcontrol systems

bull to serve as an independent and objectiveparty to review financial informationprepared by management prior to itsrelease to shareholders and the generalpublic and

bull to communicate with the board of directors anddeal directly with the external auditors internalauditors and financial management on specificissues where appropriate

Over time the functions of an AC have expandedACs are under pressure to accept additionaloversight responsibilities while facing the everrising cost of directorsrsquo liability

THE KLSE LISTING REQUIREMENTS ON AUDIT COMMITTEE

Malaysian PLCs are required to adhere to KLSEListing Rules Compared to the rules set by the SECin the US in respect of ACs the KLSE listingrequirements are less stringent (Mohd Nazim ampKalaithasan 2002)

The listing requirements cover several importantsections on composition of ACs terms of referencethe functions of ACs attendance of other directorsand employees rights to discharge dutiesquorums for meetings and reporting to theExchange on the non-compliance with KLSErequirements At the end of each financial yearthe Malaysian AC is required to prepare a reportwhich must be incorporated in the annual reportof the company Table 1 summarizes the KLSErequirements relating to ACs These appear to gofurther than other environments such as the UK atthe time of study In the UK the AC has not beenrequired to prepare any report but rather a reportis required from the board with respect to itscorporate governance (which would includereferences to its AC)

In the US the Blue Ribbon Committee requestedthe SEC to include a letter from the AC in thecompanyrsquos annual report to shareholders statingwhether for the fiscal year management hadreviewed the financial statements with the ACand that the external auditors had also discussedwith the AC amongst others the quality of theaccounting principles applied by the company andthat the AC after weighing the facts discussed withmanagement and the external auditors believedthat the companyrsquos financial statements were fairlypresented

The Malaysian AC report must cover compliancewith five core requirements and the extent of

192 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

compliance should be disclosed in the reportThese are listed in the following sub-sections

Composition of the audit committee

The AC must comprise at least three directors anda majority should be independent directors Atleast one director must be a member of theMalaysian Institute of Accountants (MIA) or he orshe must have at least three years relevant workingexperience and have passed the examinationsspecified in Part I of the First Schedule of theAccountants Act 1967 or be a member of one of theassociations of accountants specified in Part II ofthe First Schedule of the Accountants Act 1967 TheChairman of the audit committee should be anindependent director and no alternate director is tobe appointed An independent director as definedin KLSE listing requirement Para 101 and PracticeNote No 62001 is independent of managementfree from any business relationship and not a majorshareholder of the listed company or of any of itsrelated corporations

In terms of the number of members theminimum requirement of three is in line with thatof NYSE and NASDAQ whereas the requirementthat the majority is made up of independentdirectors is to ensure independence asrecommended by the Treadway Commission(1987) the Cadbury Committee (1992) and theBlue Ribbon Committee (1999) The stipulationregarding experience and qualifications of ACmembers is to ensure effectiveness (Blue RibbonCommittee 1999 Dezoort 1998 Kalbers amp Fogarty1993 Treadway Commission 1987 GAO 1991 Leeamp Stone 1997) Currently in the UK under the newUK 2003 Combined Code all members of the AC

must now be independent non-executive directorsIn the US this has been the case for several yearsunder the NYSE rules and the Sarbanes-Oxley Act

Terms of reference

Terms of reference are statements in written formthat describe the ACrsquos authority function andscope of duties and responsibilities One of theimportant functions of a Malaysian AC to bespecified in the terms of reference is to reportto the KLSE any conflict of interest or anyunsatisfactorily resolved matters

The statement of terms of reference disclosedin the report is important to ensure that the ACperforms its fiduciary role in ensuring that thefirmrsquos management complies with the relatedregulatory requirements (Accountant InternationalStudy Group 1997) to safeguard the interest of theusers (Menon amp Williams 1994 Beasley 1996)

Audit committee meetings

The attendance of other directors and employeesat Malaysian AC meetings is prohibited unlessthey are invited ACs may regulate their ownprocedures in particular with respect to thecalling of meetings notice given of such meetingsvoting and proceedings of such meetings keepingof minutes and custody production andinspection of such minutes The quorum for anaudit committee meeting is a majority of themembers who are independent

Even though the regulations do not stipulatea minimum number of meetings Kang (2001)suggests that at least five meetings annually arerequired to gain sufficient insight into the firmrsquos

Table 1 Checklist drawn up by KLSE to assist listed companies in complying with listing requirements

KLSE requirement relating to audit committee Paragraph number of listing requirements

1 Audit committee composition1a Comprises at least three members Para 1510(1)(a)1b Majority are independent directors Para 1510(1)(b)1c At least one member is financially literate Para 1510(1)(c)1d Chairman is an independent director Para 15111e No alternate director is appointed as member Para 1510(2)

2 Written terms of reference Para 1516(3)(b)3 Meeting

3a Number of meeting Para 1516(3)(c)3b Majority attendants must be independent directors Para 1516(3)(c)

4 A summary of audit committee activities Para 1516(3)(d)5 A summary of internal audit activities Para 1516(3)(e)

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 193

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

financial situation Further the frequency ofmeetings will enhance AC effectiveness since themeetings are important vehicles for directors tomonitor financial reporting (Menon amp William1994) protect shareholdersrsquo interest (Veschoor ampLiotta 1990) and improve shareholdersrsquo value(Vafeas 1999) However the BRC (1999) requiresthe minimum number of meetings to be four

A summary of audit committeersquos activities

Apart from its duties as set out in its terms ofreference the AC is required to prepare a summaryof activities in carrying out its functions and dutiesfor the financial year This report should contain astatement of the scope of the committeersquos reviewFor example it may include a review of thecorporate audit policy statement and relatedinternal and external auditing plans and results forthe period of review the system of accountingcontrol and the activities coordinated between theinternal and external auditors It could also includereference to the establishment of committees suchas a Risk Management Committee that would beable to assist the AC in identifying the principalrisks of the company and how to mitigate thoserisks

Internal audit activities

Malaysian ACs are required to prepare a summaryof the principal internal audit activities andfunctions which will include audit of financialmanagement and operations human resourceoperations and security controls Amongst theimportant points that could be mentioned in thereport are that the AC has approved the InternalAudit Plan at the beginning of each year and thatit receives regular reports from the Group ChiefInternal Auditor on audit work and activities priorto the committee meetings In addition the AC isrequired to satisfy itself that the internal auditorshave worked closely with the external auditors toresolve issues that were raised by the externalauditors pertaining to the accounting and controlissues of the organization

METHODOLOGY

This study is exploratory in nature with theprimary purpose of estimating the level ofcompliance with the KLSE requirements on auditcommittees by listed companies and to explore the

difference (if any) in compliance levels betweenPN4 and non-PN4 companies The data wasobtained from secondary sources by examining the2002 annual reports of companies listed on both themain board and the second board of the KLSEThere were 510 main board 248 second board and94 PN42 companies listed in the 11 differentindustrial sectors in the year 2002

The companies listed on the main board of theKLSE are those with minimum paid-up capital ofRM60 million comprising ordinary shares of notless than 10 cents each and at least 25 per cent ofthe companyrsquos issued and paid-up capital at thetime of listing being in the hands of publicshareholders The company should also have anuninterrupted after-tax profit record for the pastthree to five full financial years an aggregate after-tax profit of at least RM30 million over the periodof uninterrupted after-tax profit and a minimumafter-tax profit of RM8 million for the most recentfinancial year

Under the second board of the KLSE minimumpaid-up capital of RM40 million is requiredcomprising ordinary shares of not less than 10cents each and at least 25 per cent of the companyrsquosissued and paid-up capital at the time of listingbeing in the hands of public shareholders Thecompany should have an uninterrupted after-taxprofit record for the past three to five full financialyears an aggregated after-tax profit of at leastRM12 million over the period of interrupted after-tax profit and a minimum after-tax profit of RM4million for the most recent financial year

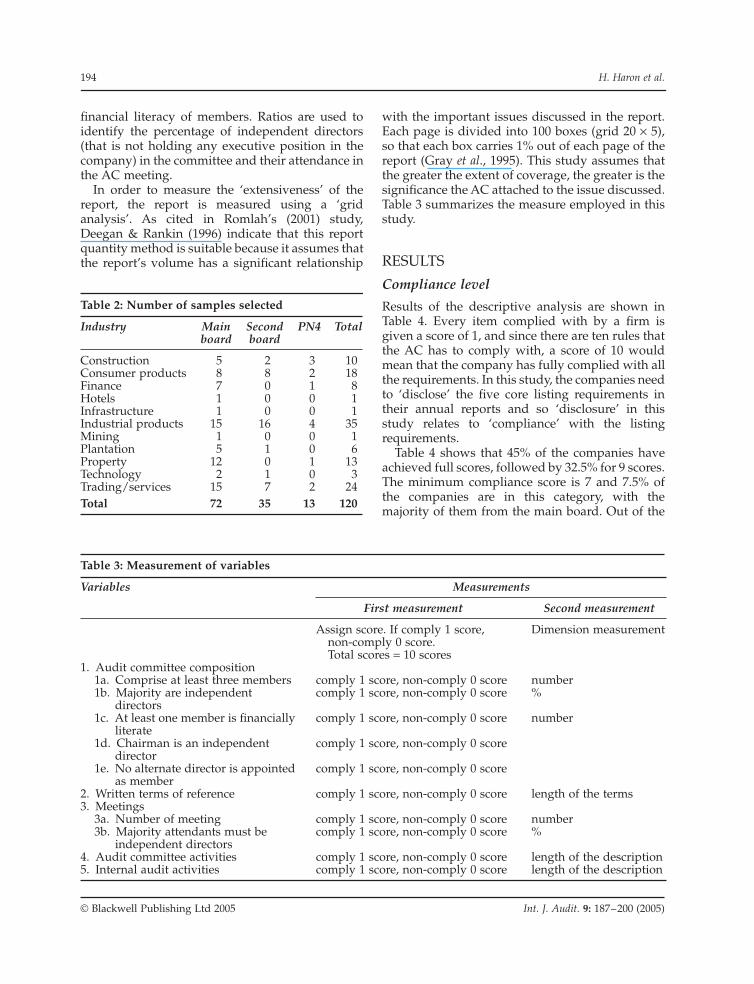

The population of the study is all the companieslisted on the KLSE in the year 2002 Howevercompanies whose fiscal year ends from October toDecember were excluded as their annual reportswere not available at the time of the study UsingRoscoersquos rule of thumb3 a sample of 120 companieswas deemed appropriate and these companieswere selected randomly across the variousindustrial sectors Table 2 below provides a profileof the selected sample

To assess the compliance level this study utilizesa scoring system as follows If the companycomplies with a particular requirement it gets ascore of one and zero otherwise The sum overall requirements forms the compliance level fora particular company Additionally in order toenrich this study the extent of compliance withspecific requirements was measured in thefollowing manner Numbers were used to measurethe AC members independent directors and the

194 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

financial literacy of members Ratios are used toidentify the percentage of independent directors(that is not holding any executive position in thecompany) in the committee and their attendance inthe AC meeting

In order to measure the lsquoextensivenessrsquo of thereport the report is measured using a lsquogridanalysisrsquo As cited in Romlahrsquos (2001) studyDeegan amp Rankin (1996) indicate that this reportquantity method is suitable because it assumes thatthe reportrsquos volume has a significant relationship

with the important issues discussed in the reportEach page is divided into 100 boxes (grid 20 times 5)so that each box carries 1 out of each page of thereport (Gray et al 1995) This study assumes thatthe greater the extent of coverage the greater is thesignificance the AC attached to the issue discussedTable 3 summarizes the measure employed in thisstudy

RESULTS

Compliance level

Results of the descriptive analysis are shown inTable 4 Every item complied with by a firm isgiven a score of 1 and since there are ten rules thatthe AC has to comply with a score of 10 wouldmean that the company has fully complied with allthe requirements In this study the companies needto lsquodisclosersquo the five core listing requirements intheir annual reports and so lsquodisclosurersquo in thisstudy relates to lsquocompliancersquo with the listingrequirements

Table 4 shows that 45 of the companies haveachieved full scores followed by 325 for 9 scoresThe minimum compliance score is 7 and 75 ofthe companies are in this category with themajority of them from the main board Out of the

Table 2 Number of samples selected

Industry Mainboard

Secondboard

PN4 Total

Construction 5 2 3 10Consumer products 8 8 2 18Finance 7 0 1 8Hotels 1 0 0 1Infrastructure 1 0 0 1Industrial products 15 16 4 35Mining 1 0 0 1Plantation 5 1 0 6Property 12 0 1 13Technology 2 1 0 3Tradingservices 15 7 2 24Total 72 35 13 120

Table 3 Measurement of variables

Variables Measurements

First measurement Second measurement

Assign score If comply 1 scorenon-comply 0 scoreTotal scores = 10 scores

Dimension measurement

1 Audit committee composition1a Comprise at least three members comply 1 score non-comply 0 score number1b Majority are independent

directorscomply 1 score non-comply 0 score

1c At least one member is financiallyliterate

comply 1 score non-comply 0 score number

1d Chairman is an independentdirector

comply 1 score non-comply 0 score

1e No alternate director is appointedas member

comply 1 score non-comply 0 score

2 Written terms of reference comply 1 score non-comply 0 score length of the terms3 Meetings

3a Number of meeting comply 1 score non-comply 0 score number3b Majority attendants must be

independent directorscomply 1 score non-comply 0 score

4 Audit committee activities comply 1 score non-comply 0 score length of the description5 Internal audit activities comply 1 score non-comply 0 score length of the description

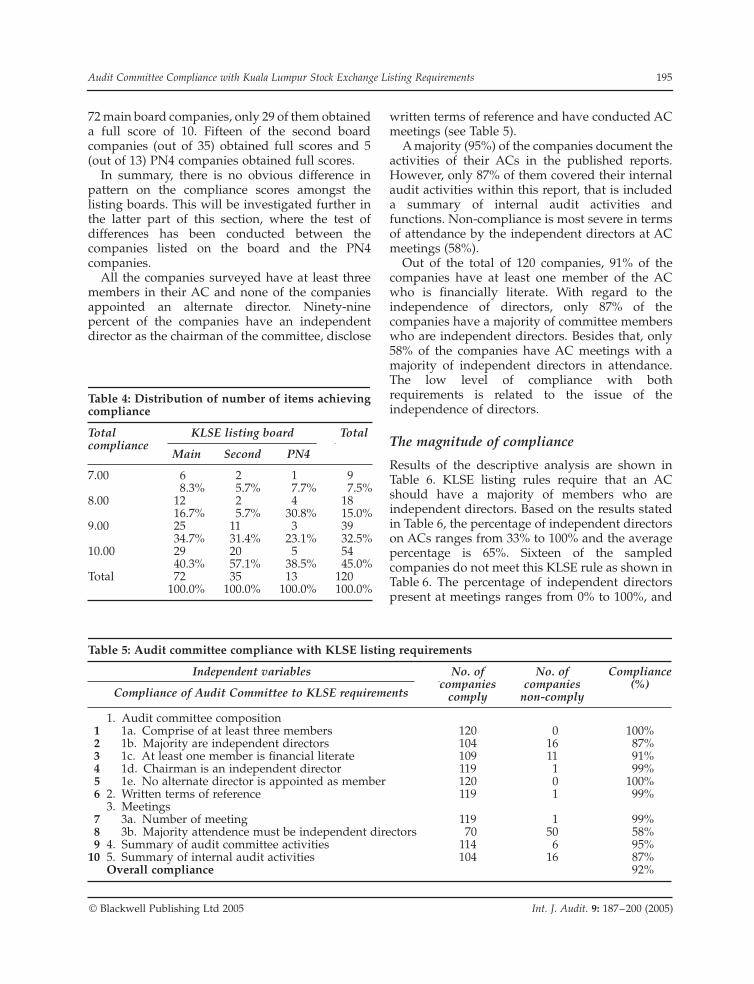

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 195

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

72 main board companies only 29 of them obtaineda full score of 10 Fifteen of the second boardcompanies (out of 35) obtained full scores and 5(out of 13) PN4 companies obtained full scores

In summary there is no obvious difference inpattern on the compliance scores amongst thelisting boards This will be investigated further inthe latter part of this section where the test ofdifferences has been conducted between thecompanies listed on the board and the PN4companies

All the companies surveyed have at least threemembers in their AC and none of the companiesappointed an alternate director Ninety-ninepercent of the companies have an independentdirector as the chairman of the committee disclose

written terms of reference and have conducted ACmeetings (see Table 5)

A majority (95) of the companies document theactivities of their ACs in the published reportsHowever only 87 of them covered their internalaudit activities within this report that is includeda summary of internal audit activities andfunctions Non-compliance is most severe in termsof attendance by the independent directors at ACmeetings (58)

Out of the total of 120 companies 91 of thecompanies have at least one member of the ACwho is financially literate With regard to theindependence of directors only 87 of thecompanies have a majority of committee memberswho are independent directors Besides that only58 of the companies have AC meetings with amajority of independent directors in attendanceThe low level of compliance with bothrequirements is related to the issue of theindependence of directors

The magnitude of compliance

Results of the descriptive analysis are shown inTable 6 KLSE listing rules require that an ACshould have a majority of members who areindependent directors Based on the results statedin Table 6 the percentage of independent directorson ACs ranges from 33 to 100 and the averagepercentage is 65 Sixteen of the sampledcompanies do not meet this KLSE rule as shown inTable 6 The percentage of independent directorspresent at meetings ranges from 0 to 100 and

Table 4 Distribution of number of items achievingcompliance

Totalcompliance

KLSE listing board Total

Main Second PN4

700 6 2 1 983 57 77 75

800 12 2 4 18167 57 308 150

900 25 11 3 39347 314 231 325

1000 29 20 5 54403 571 385 450

Total 72 35 13 1201000 1000 1000 1000

Table 5 Audit committee compliance with KLSE listing requirements

Independent variables No ofcompanies

comply

No ofcompanies

non-comply

Compliance()

Compliance of Audit Committee to KLSE requirements

1 Audit committee composition1 1a Comprise of at least three members 120 0 1002 1b Majority are independent directors 104 16 873 1c At least one member is financial literate 109 11 914 1d Chairman is an independent director 119 1 995 1e No alternate director is appointed as member 120 0 1006 2 Written terms of reference 119 1 99

3 Meetings7 3a Number of meeting 119 1 998 3b Majority attendence must be independent directors 70 50 589 4 Summary of audit committee activities 114 6 95

10 5 Summary of internal audit activities 104 16 87Overall compliance 92

196 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

the average percentage is 78 This is a deviationfrom the KLSE listing requirement that requiresthat 100 of all the meetings should have amajority of independent directors present

In the sample the maximum number offinancially literate members on the AC was 4 butthis was the case in only one company There were11 companies that had violated the requirementin respect of financial literacy by not havingany financially literate member on the committeeThis may be due to a lack of qualified andexperienced financially literate individuals willingto participate on board committees

In terms of length on average the ACrsquos terms ofreference account for 496 of the total volume ofthe AC reports As KLSE listing requirements donot specify the content to be included in the termsof reference there is some inconsistency in termsof the content Certain companies place theauthority and composition of the AC as part of theterms of reference However there are companiesthat have treated these matters under separateheadings In this sense the use of a lengthmeasurement is just to give an indication as to theextensiveness of coverage of the report

The maximum number of AC meetings heldduring the year was 21 and the mean number ofmeetings per year is 48 This result is lower thanthe six meetings found by Mohd Nazim andKalaithasan (2002)

The results presented in Table 6 indicate thatthe report on the audit committeersquos activitiesrepresented 10 of the total length of AC reportson average The average discussion of internalaudit activities was 6 of the reports ACs overseethe internal audit function that is they are requiredto ensure that there are proper internal audit plansand also to assist in circumstances where internal

auditors are experiencing problems with theconduct of their activities

Audit committee compliance levels between the PN4 and non-PN4 companies

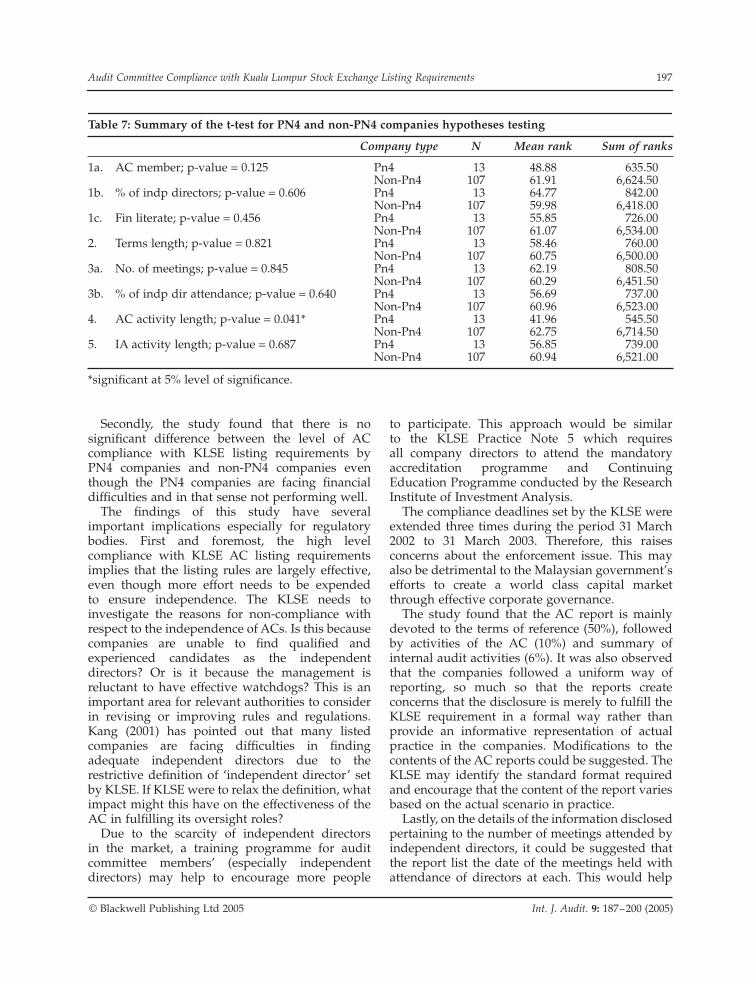

For the comparison between PN4 and non-PN4companies we used a non-parametric Mann-Whitney test due to the small number of PN4companies and the problem of normality of themeasurement The results are shown in Table 7Results of the independent sample t-test indicatethat there is no significant difference incompliance level between PN4 and non-PN4companies This means that even though PN4companies are facing lsquoliquidity problemsrsquo anddeficits in shareholdersrsquo equity4 their compliancelevel with respect to the AC is equally high asnon-PN4 companies

DISCUSSION AND IMPLICATIONS

Firstly taking all requirements together the auditcommittee reports indicate that the overallcompliance level with KLSE listing requirementsis 92 which can be considered satisfactory asmost of the requirements are being met Howeverwhile 87 of the companies comply with therequirement to have a majority of independentdirectors on the committee only 58 compliedwith the attendance requirement This can beconsidered to be relatively low and of concern Thisis critical given that the independence of thecommittee is at the core of the integrity of the AC(Treadway Commission 1987 Cadbury Committee1992 Blue Ribbon Committee 1999) In view ofthis the KLSE should implement more effectivemonitoring to ensure better compliance

Table 6 The magnitude of the audit committee compliance with KLSE listing requirements descriptive statistics

Unit of measurement N Minimum Maximum Mean Std deviation

1a AC member Quantity 120 3 6 343 0681b of indp directors Percentage 120 033 1 065 0131c Fin literate Quantity 120 0 4 103 0512 Terms length Length of the content 120 0 1 050 0173a No of meetings Quantity 120 0 21 484 1973b of indp dir attendance Percentage 120 0 1 078 0344 AC activity length Length of the content 120 0 033 010 0065 IA activity length Length of the content 120 0 023 006 004Total compliance scores Quantity 120 7 10 915 094

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 197

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

Secondly the study found that there is nosignificant difference between the level of ACcompliance with KLSE listing requirements byPN4 companies and non-PN4 companies eventhough the PN4 companies are facing financialdifficulties and in that sense not performing well

The findings of this study have severalimportant implications especially for regulatorybodies First and foremost the high levelcompliance with KLSE AC listing requirementsimplies that the listing rules are largely effectiveeven though more effort needs to be expendedto ensure independence The KLSE needs toinvestigate the reasons for non-compliance withrespect to the independence of ACs Is this becausecompanies are unable to find qualified andexperienced candidates as the independentdirectors Or is it because the management isreluctant to have effective watchdogs This is animportant area for relevant authorities to considerin revising or improving rules and regulationsKang (2001) has pointed out that many listedcompanies are facing difficulties in findingadequate independent directors due to therestrictive definition of lsquoindependent directorrsquo setby KLSE If KLSE were to relax the definition whatimpact might this have on the effectiveness of theAC in fulfilling its oversight roles

Due to the scarcity of independent directorsin the market a training programme for auditcommittee membersrsquo (especially independentdirectors) may help to encourage more people

to participate This approach would be similarto the KLSE Practice Note 5 which requiresall company directors to attend the mandatoryaccreditation programme and ContinuingEducation Programme conducted by the ResearchInstitute of Investment Analysis

The compliance deadlines set by the KLSE wereextended three times during the period 31 March2002 to 31 March 2003 Therefore this raisesconcerns about the enforcement issue This mayalso be detrimental to the Malaysian governmentrsquosefforts to create a world class capital marketthrough effective corporate governance

The study found that the AC report is mainlydevoted to the terms of reference (50) followedby activities of the AC (10) and summary ofinternal audit activities (6) It was also observedthat the companies followed a uniform way ofreporting so much so that the reports createconcerns that the disclosure is merely to fulfill theKLSE requirement in a formal way rather thanprovide an informative representation of actualpractice in the companies Modifications to thecontents of the AC reports could be suggested TheKLSE may identify the standard format requiredand encourage that the content of the report variesbased on the actual scenario in practice

Lastly on the details of the information disclosedpertaining to the number of meetings attended byindependent directors it could be suggested thatthe report list the date of the meetings held withattendance of directors at each This would help

Table 7 Summary of the t-test for PN4 and non-PN4 companies hypotheses testing

Company type N Mean rank Sum of ranks

1a AC member p-value = 0125 Pn4 13 4888 63550Non-Pn4 107 6191 662450

1b of indp directors p-value = 0606 Pn4 13 6477 84200Non-Pn4 107 5998 641800

1c Fin literate p-value = 0456 Pn4 13 5585 72600Non-Pn4 107 6107 653400

2 Terms length p-value = 0821 Pn4 13 5846 76000Non-Pn4 107 6075 650000

3a No of meetings p-value = 0845 Pn4 13 6219 80850Non-Pn4 107 6029 645150

3b of indp dir attendance p-value = 0640 Pn4 13 5669 73700Non-Pn4 107 6096 652300

4 AC activity length p-value = 0041 Pn4 13 4196 54550Non-Pn4 107 6275 671450

5 IA activity length p-value = 0687 Pn4 13 5685 73900Non-Pn4 107 6094 652100

significant at 5 level of significance

198 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

to identify whether a meeting is held without amajority of independent directors

In summary the enforcement of therequirements could be further improved by havingmore refined requirements and more robustfollow-up actions to ensure that remedial steps aretaken by non-compliant companies to improvetheir compliance level

LIMITATIONS AND SUGGESTION FOR FUTURE RESEARCH

Although this study provides some interestinginsights about AC compliance with KLSE listingrequirements it is subject to a few limitationsFirstly due to time constraints the scope of studywas limited to PLCs with year end January toSeptember 2002 During the study the compliancedeadlines set by the KLSE were extended threetimes during the period 31 March 2002 to 31 March2003 This has created some difficulties indetermining the cut-off date for compliance Thestudy has assumed that as long as the requirementswere stated in the KLSE listing requirementsChapter 15 they can be considered as mandatoryand companies in the sample would have tocomply with them

Another limitation of the study would be thatit assumes that disclosure of the mandatoryrequirements would assume compliance by thecompanies Companies that do not disclose therequirements would thus be assumed to be non-compliant

Finally as a study of effectiveness the studyis based on the secondary data available in thecompaniesrsquo annual reports As such certain auditcommittee characteristics which are qualitative innature for instance the relationship between theboard management and shareholders the scope ofthe terms of reference for the AC the quality of itsactivities and the efficiency of the internal auditdepartment to support the AC which can also havean impact on firm performance are not take intoconsideration in this study

The present study found that only 58 of the 120companies have a majority of independentdirectorsrsquo attending for all the audit committeemeetings This figure is low and violated the KLSElisting requirement Therefore future researchneeds to be done to investigate the reasons for this

This study focused solely on the compliancelevel for AC requirements This study assumesthat compliance is something good or positive

As discussed earlier the mandated requirementsare intended to ensure that the AC dischargesits functions effectively thus ensuring soundcorporate governance (management controls)which in the long run is expected to improvethe performance of the company Whether thisproposition holds true that is compliance affectsperformance can be subjected to empiricalinvestigation in future research It is alsorecommended that future studies includeinterviews with the AC chairs to understand theunderlying reasons as to why the empirical resultspertain Other factors affecting the compliance levelsuch as management support to observe the rulesof the KLSE could also be investigated

NOTES

1 Referred to as Bursa Malaysia Securities Berhadfrom April 2004

2 PN4 companies are companies that the KLSEhas categorized as facing financial problemsFor example they may have deficits in theiradjusted shareholdersrsquo equity and also havereceived an adverse or disclaimer report by theauditors with respect to their latest financialyear end This category came into effect onFebruary 15 2001 The PN4 compels listedcompanies to improve the state of their financialcondition within 6 to 12 months If it fails tocomply with the obligations set out under thisPractice Note it may be suspended andor de-listed Please refer to Practice Note 4 paragraph814 of KLSE listing requirements for detailedcriteria of PN4 companies

3 According to Roscoersquos rule of thumb (Sekaran2002) the sample size for multivariate researchshould be several times (preferably 10 times ormore) as large as the number of variables in thestudy The basis to derive the 120 companiesis 5 (core independent variables) plus 1(dependent variable) and then times 20

4 Please refer to Practice Notes 4 paragraph 814of KLSE listing requirements for detailed criteriaof PN4 companies

REFERENCES

Accountants International Study Group (1997)Responsibilities of the Directors for the FinancialStatements Audit Committee Current Practices inCanada The United Kingdom and the United StatesLondon ICAEW

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 199

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

Barr S (1999) Watchdogs or lapdogs CFO Vol 15No 5 p 64

Beasley M S (1996) lsquoAn empirical analysis of therelation between the board of director compositionand financial statement fraudrsquo The AccountingReview Vol 71 No 4 pp 443ndash465

Blue Ribbon Committee (1999) Report andRecommendations of the Blue Ribbon Committee onImproving the Effectiveness of Corporate AuditCommittees New York NYSE

Bradbury M E (1990) lsquoThe incentives for voluntaryaudit committee formationrsquo Journal of Accountingand Public Policy Vol 9 No 1 pp 19ndash36

Cadbury Committee (1992) The Financial Aspects ofCorporate Governance London HMSO

Deegan C amp Rankin M (1996) lsquoDo Australiancompanies report environmental news objectivelyAn analysis of environmental disclosure by firmsprosecuted successfully by the EnvironmentalProtection Authorityrsquo Accounting Auditing ampAccountablity Journal Vol 9 No 2 pp 50ndash67

DeFond M L amp Jiambalvo J (1991) lsquoIncidence andcircumstances of accounting errorsrsquo The AccountingReview Vol 66 pp 643ndash655

Dezoort F T (1998) lsquoAn analysis of experience effectson audit committee membersrsquo oversightjudgmentsrsquo Accounting Organizations and SocietyVol 23 No 1 pp 1ndash21

GAO (General Accounting Office) (1991) Auditcommittees Legislation needed to strengthen bankoversight Report to Congressional Committees

Gray R Kouchy R amp Lavers S (1995) lsquoCorporatesocial and environmental reporting a review ofthe literature and a longitudinal study of UKdisclosurersquo Accounting Auditing and AccountabilityJournal Vol 8 No 2 pp 47ndash77

Jassel G K (2000) lsquoCorporate governance on theright trackrsquo Akauntan Nasional Vol 13 pp 6ndash8

Kala Anandarajah (2001) Corporate Governance APractical Approach Singapore Butterworth Asia

Kalbers L P amp Fogarty T J (1993) lsquoAudit committeeeffectiveness An empirical investigation of thecontribution of powerrsquo Journal of Practice amp TheoryVol 12 No 1 pp 24ndash49

Kang S M (2001) The Listing Requirements of KualaLumpur Stock Exchange What Directors and SeniorManagement Need to Know Malaysia Malayan LawJournal Sdn Bhd

Lee T amp Stone M (1997) lsquoEconomic agency andaudit committees responsibilities and membershipcompositionrsquo International Journal of Auditing Vol1 pp 97ndash116

McMullen D A (1996) lsquoAudit committeeperformance An investigation of the consequencesassociated with audit committeesrsquo Auditing AJournal of Practice amp Theory Spring pp 87ndash103

Menon K amp William J D (1994) lsquoThe use of auditcommittee for monitoringrsquo Journal of Accountingand Public Policy pp 121ndash139

Mohd Nazim Abdul Rahman amp KalaithasanKuppusamy (2002) lsquoCompliance of Audit

Committee in Public Listed Companies with theProvisions in the KLSE Listing Requirementrsquo Paperpresented at International Conference on CorporateGovernance Trend and Challenges in the MilleniumOctober 2002 Kuala Lumpur

New York Stock Exchange webiste httpwwwnysecomsearchsearchhtml Date accessedMarch 2004

Oh Errol (2003) lsquoIn pursuit of transparencyrsquo NewStrait Times January 18 2003

Pincus K Rubarsky M amp Wong J (1989) lsquoVoluntaryformation of corporate audit committees amongNASDAQ firmsrsquo Journal of Accounting and PublicPolicy Vol 8 No 4 pp 239ndash265

Romlah binti Jaffar (2001) lsquoThe reliability of thedisclosure of environmental informationrsquo PhDThesis National University of Malaysia Penang

Sekaran Uma (2002) Research Methods for Business ASkill-Building Approach 4th edn New York Wiley

Shamsher Mohamad amp Zulkarnain Muhamad Sori(2001) lsquoThe wealth effect ndash on announcementsof audit committee formationrsquo Akauntan NasionalVol 14 No 6 pp 22ndash24

Shamsul Nahar Abdullah (2001) lsquoCharacteristicsof board directors amp audit committees ndash amongMalaysian listed companies in period leading to1997 financial crisisrsquo Akauntan Nasional Vol 14No 10 pp 18ndash21

Tate D W (2002) lsquoIs your audit committee upto speedrsquo httpusersrcncomtateattyDownloaded on January 3 2003

Treadway Commission (1987) Report of the NationalCommission on Fraudulent Financial ReportingWashington DC

Vafeas N (1999) lsquoBoard meeting frequency and firmperformancersquo Journal of Financial Economics Vol 53No 1 pp 113ndash142

Verschoor C C (1990) lsquoMiniScribe A new exampleof audit committee ineffectivenessrsquo InternalAuditing Spring pp 13ndash19

Verschoor C C (1992) lsquoInternal auditing interactionswith the audit committeersquo Internal Auditing Spring

Verschoor C C amp Liotta J P (1990) lsquoCommunicationwith audit committeesrsquo Internal Auditor Aprilpp 42ndash47

Wallace W A (1985) lsquoAre outside directors put onthe board just for showrsquo The Wall Street JournalJanuary p 22

Wolnizer P W (1993) lsquoAudit committees ndashIndependent monitors of the financial aspects ofcorporate governancersquo Presented at the WardsTrust Seminar

Zulkarnain Muhamad Sori Shamsher Mohmad ampMohamad Ali Abdul Hamid (2001a) lsquoAuditcommittee The chairmanrsquos perspectiversquo AkauntanNasional Vol 14 No 2 pp 4ndash6

Zulkarnain Muhamad Sori Shamsher Mohmad ampMohamad Ali Abdul Hamid (2001b) lsquoAuditcommittee The institutional investorrsquosperspectiversquo Akauntan Nasional Vol 14 No 7pp 16ndash18

200 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

AUTHOR PROFILES

Hasnah Haron is the chairperson of Accountingprogramme at the School of ManagementUniversiti Sains Malaysia Her research interest isin the area of auditing financial reporting andeducation She has written several books andmodules on management and financialaccounting She has presented various articles inthese areas at local and international conferencesShe sits on the Editorial Board of MalaysianAccounting Review and is the Assistant Editor forthe Asian Academy of Management Journal ofAccounting and Finance She has also beenappointed as reviewers for international journalsand has acted as editors of auditing textbooksOther than teaching research and consultationactivities Dr Hasnah is also active in professionalactivities She is currently a member of MIAPenang Branch and the Accounting and AuditingCommittee

Muhamad Jantan is a professor of operationsmanagement at the University Science of MalaysiaHis research interests are in the area of qualitymanagement information and technologymanagement He has presented various articlesin these areas at International Conferences inthe region He also sits on the Editorial Board forAsian Academy of Management Journal and theInternational Journal of Quality and Productivityand has reviewed articles for internationaljournals He has done various consultancy projectsfor big national corporations and conductedexecutive development programs for both localand multinational companies

Eow Gaik Pheng a Bachelor degree ofAccountancy (Honours) from Northern Universityof Malaysia a Master degree of BusinessAdministration from University Science Malaysiaand a member of Malaysian Institute of Accountants(MIA) She has more than 10 years experience inaccounting and corporate management

188 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

SUMMARY

The recent financial crisis in emerging markets andcorporate scandals inevitably focused on the lackof corporate as well as governmental oversightThe Malaysian government initiated severalmeasures in its efforts to create a world-classcapital market Amongst the measures taken toensure a smooth implementation of theseinitiatives was to revise the listing requirements tomake it mandatory for all public listed companiesto form an audit committee by 1 August 1994 TheMalaysian Code of Corporate Governance issuedin 2001 requires that the board of directorsestablish an audit committee of at least threedirectors with the majority comprising of non-executive director The independence of the auditcommittee is critical to ensure that the board fulfilsits oversight role and holds managementaccountable to shareholders

The audit committee is an important boardcommittee that assists the board of directors inoverseeing and ensuring adequate functioning ofinternal control mechanisms monitoring andfocusing on reviewing financial risk and riskmanagement Audit committee helps determineindicators of problems and address theseproblems mitigate possible damage and enhanceshareholder value The audit committee is effectiveonly if it is able to fulfil the roles stipulated in therules and regulations The first step towardseffectiveness should be complete compliance withthe rules and regulations provided by the KLSElisting requirement

The listing requirements require that all publiclisted companies include the Audit CommitteeReport in their annual reports The AuditCommittee report should have the following tenrequirements (1) the audit committee shouldcomprise at least three members (2) the majorityof the audit committee should be independentdirectors (3) at least one member of the auditcommittee is financially literate (4) the chairmanof the audit committee is an independent director(5) no alternate director of the audit committee isappointed as a member (6) there are written termsof reference for the audit committee to refer to(7) the number of meetings should be noted (8)the majority attending the meeting should beindependent directors (9) there should be asummary of audit committee activities and (10) asummary of internal audit activities should alsobe produced

There is evidence to support that there is ahigh audit committee compliance level with allten KLSE listing requirements However thecompliance level for having majority independentdirectors in the committee and majorityindependent directors attending the meeting isrelatively low There is also evidence thatcompliance levels for PN4 companies and non-PN4 companies are similar The study also foundthat most of the companies have a standardizedformat of reporting and that the level ofinformation provided in the audit committeereports are quite limited For example the terms ofreference did not disclose any fact concerning howstereotype disclosure in the audit committee reportcreate concerns about the disclosure as merelyfulfiling the KLSE listing requirements Therespective governance body in Malaysia shouldtake appropriate steps to ensure compliance withthe ten requirements and more importantly toensure that these requirements are appropriatelyimplemented

INTRODUCTION

An audit committee (AC) is a standing committeeof the board constituted with the aim ofcontributing to effective corporate governanceespecially with regard to the boardrsquos responsibilityfor the reliability of financial disclosures and itsoversight of the effectiveness of risk managementinternal control and audit Good corporategovernance is expected to increase investorsrsquoconfidence and thus enhance shareholder value Itcan also be argued that good corporate governanceresults in reduced costs of doing business whichin turn increase shareholdersrsquo wealth (Kala 2001)

Reporting requirements and compliance mattersform essential parts of the corporate governanceprocess Without adequate reporting mechanismsone cannot be assured that the affairs of thecompany are being run for its benefit in a prudentmanner Tate (2002) observed that appropriateAC compliance helps spot and address redflags mitigates possible damage and enhancesshareholdersrsquo value Thus ACsrsquo emphasis oncompliance with rules and regulations is expectedto improve the effectiveness of the AC Continuedlisting on the Kuala Lumpur Stock Exchange(KLSE) requires constant compliance with itslisting requirements and it is compliance withthese requirements that is measured in this study

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 189

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

This study investigates reporting behaviourusing compliance that can be identified throughdisclosures as a measure of potential ACeffectiveness and also examines whether financialdistress in companies is associated with varyinglevels of compliance (and hence effectiveness) Theprimary objectives of the research are thereforeto (1) measure the level of audit committeesrsquocompliance with KLSE requirements and (2)examine differences between PN4 and non-PN4companies with respect to their compliance levelPN4 companies are listed companies that fail tomeet the financial conditions (due to liquidityproblems and deficits in shareholdersrsquo equity) forcontinued trading and listing on KLSE Thesecompanies need to regularize their financialconditions within 6ndash12 months and are underconstant scrutiny and monitoring by the StockExchange

The development of ACs in Malaysia began in1991 when the Malaysian Institute of CertifiedPublic Accountants (MICPA) the MalaysianInstitute of Accountants (MIA) and the Instituteof Internal Auditors (IIA) of Malaysia jointlysubmitted a memorandum to the Registrar ofCompanies (ROC) the Capital Issue Commission(CIC) and the KLSE1 to recommend that ACs bemade mandatory for all listed companies inMalaysia Subsequently Section 15A of the KLSEListing Requirement was introduced whichrequired all listed companies to form an AC byAugust 1 1994

Research on audit committees in developedcountries has covered various aspects relating totheir formation role and functions following theimportance attached to the AC as a componentof corporate governance by bodies such as theUS Treadway Commission and the UK CadburyCommittee On September 28 1998 the SEC(Securities amp Exchange Commission) NYSE (NewYork Stock Exchange) and the NASD (NationalAssociation of Securities Dealers) announced thecreation of the Blue Ribbon Committee (BRC)to improve the effectiveness of corporate ACThe BRCrsquos charter was to lsquoundertake an intensivestudy of the effectiveness of ACs in dischargingtheir oversight responsibilities and makeconcrete recommendations for improvementrsquoThe BRC made ten recommendations aimed atstrengthening the independence of ACs makingthem more effective and increasing theiraccountability along with that of outside auditorsand management

These ten recommendations were adoptedby AICPA (American Institute of CertifiedPublic Accountants) NYSE NASD and SECSubsequently these ten recommendations werelooked upon as the guiding benchmark for manycountries including Malaysia

Resulting from these ten recommendations inDecember 1999 the NYSE and NASDAQ (NationalAssociation of Securities Dealers AutomatedQuotation System) modified their requirements forACs so as to require firms to maintain committeeswith the majority of members being independentdirectors In broad terms independent directorsare those who are free of any business or otherrelationship which might interfere with theexercise of independent judgement

The paper is structured as follows The nextsection sets the study in the context of the existingliterature This is followed by sections which inturn describe the background and content ofthe KLSE requirements for ACs discuss themethodology applied present the results obtainedand comment on the implications of those resultsFinally some limitations and possibilities for futureresearch are noted

LITERATURE REVIEW

Discussions of the financial crises in emergingmarkets and of corporate scandals across the worldhave inevitably focused on the lack of corporateas well as governmental oversight The Malaysiangovernment initiated several measures in itsefforts to create a world-class capital marketAmong the measures taken to ensure a smoothimplementation of these initiatives were measuresto revise the listing requirements to make itmandatory to form an effectively functioning AC(Shamsher amp Zulkarnain 2001)

Though every listed company was required tohave an AC from 1993 thus far only one study(Zulkarnain et al 2001a) has been conducted toevaluate the compliance with Section 344A KLSElisting rules The study found that it was not until1998 that all 556 listed firms had formed an ACeven though it was mandated in 1993 They weregiven a grace period of one year to comply

In the international arena previous researchhas examined the relationship between thepresence of an AC and the quality of financialstatements (Beasley 1996 DeFond amp Jiambalvo1991 McMullen 1996) Other researchers haveexamined issues relating to the voluntary

190 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

formation of ACs (Bradbury 1990 Pincus et al1989) Most of the studies supported the viewthat the presence of an AC will reduce financialreporting problems and improve the transparencyand disclosure of financial reports

Audit committee

Theoretically based on agency theory theformation of an AC is expected to protect theinterest of the principal and ensure that the agentcarries out its role in accordance with the contractThe role of the AC is essentially threefold(1) to ensure that management does not overrideestablished prudent financial practices andprocedures (2) to assist the board of directors indischarging their responsibilities for financialreporting and internal controls and (3) to providean impartial channel for complaints concerningthe management and direction of a company(KLSE LR para 1510) However some studieshave shown that the existence of the AC ismore for cosmetic purposes to give a positive imagerather than for monitoring This again challengesthe effectiveness of ACs (Menon amp William1994 Wallace 1985 Verschoor 1990 1992Wolnizer 1993 McMullen 1996) The regulatoryrequirements including accounting standards haveto become more structured to promote greatertransparency and accountability (Kala 2001)

Reporting and compliance requirements

Reporting requirements and compliance mattersform essential parts of the corporate governanceprocess Without adequate reporting mechanismsshareholders and others cannot be confident thatthe affairs of the company are being run in aprudent manner for their benefit Also there isinadequate assurance that the checks andbalances in place are effective The importanceof a compliance process to reduce liability and riskexposure in securities fraud should not beunderestimated (Tate 2002) Tate observed thatappropriate compliance work by the AC helps spotand address red flags mitigates possible damageand enhances shareholdersrsquo value

For the purpose of this study we haveassumed that an AC is effective if it fulfils the rolesstipulated in the rules and regulations In the studyconducted by Zulkarnain et al (2001b) 93 ofthe respondents urged regulatory bodies to playa greater role in monitoring ACsrsquo activities and

reporting in order to ensure that ACs werefunctioning as intended Furthermore constantevaluation of compliance will assist the regulatorybody to review and refine existing guidelines Inthe context of Malaysia the KLSErsquos regulationreview process is depicted in Figure 1

Disclosures do not guarantee compliance MohdNazim amp Kalaithasan (2002) show that Malaysianpublic listed companies do not have any problemsin complying with disclosures issues pertaining toACs They recommend that an independent bodybe formed to review the authenticity of thesedisclosures Shamshul (2001) found violations ofthe rules in terms of AC membership in that abouthalf of Malaysian companies appoint their CEOs tothe AC and about one third appoint chairmen ofthe board to sit on the AC Furthermore as we haveindicated Zulkarnain et al (2001b) found that onlyby 1998 had all the sampled firms formed an ACeven though the requirement was mandated in1994

Strict regulations alone without propermonitoring and enforcement will not ensurecompliance (Jassel 2000) Nevertheless the KLSEand SC have shown improvements in theseaspects Oh (2003) pointed out that the SCmanaged to uncover a variety of breaches andmismanagement by directors and senior officers ofPN4 companies However to date the revelationshave not been properly documented It is thereforeof interest to examine compliance with KLSE rulesrelating to ACs

Figure 1 Regulation reviewing process

Public

RegulatoryBody

CompaniesRegulatory

BodyReview

amp revised

Rules ampRegulations

Effectiveness

ComplianceAudit

Committee

Audit Committee Compliance with Kuala Lumpur Stock Exchange Listing Requirements 191

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

The role and responsibility of audit committee

The AC is an important committee that inter aliaassists the board of directors in overseeing andensuring adequate functioning of the internalcontrol mechanisms monitoring and focusing onreview of financial risk and other aspects of riskmanagement In this regard it is important to notethat the AC lsquoshould not and cannot be auditorsrsquo(Kala 2001)

In the United States the Blue Ribbon Committee(BRC) (1999) report on ACs specifically stated thatthe ultimate governance body in any corporationis the board of directors It also recommended thatthe members of the board serving on the ACshould be financially literate in order to detect theoccurrence of earnings management ACs arean integral part of the internal monitoringmechanisms that alert policy makers andregulators worldwide of irregularities TheCadbury Committee in the UK (1992) and the BRC(1999) further pointed out that ACs representthe full board providing an effective forum forpersonal contact and communication amongst andbetween the board the external auditors theinternal auditors the finance directors and theoperating executives

In the United States the former Secretary ofCommerce Barbara Hackman Franklin addressesthe fact that AC members fear being sued andthat because of this many directors are lessinclined to sit on the committees (Barr 1999) Thisis because in cases of fraudulent financialreporting such as Enron and WorldCom theauthorities tended to enquire whether the ACshad been performing their tasks responsibly andwhether there had been compliance with rulesand regulations

The Malaysian Code of Corporate Governancerequires the board of directors to establish anAC of at least three directors with a majority ofnon-executive directors The independence ofthe AC is critical to ensure that the board fulfilsits oversight role and holds managementaccountable to shareholders

The main objectives of the AC as stated by Kala(2001) are as followsbull to assist the board of directors to fulfill its

responsibilities for the companyrsquos financialreporting for management of financial andcontrol risks and for monitoring internalcontrol systems

bull to serve as an independent and objectiveparty to review financial informationprepared by management prior to itsrelease to shareholders and the generalpublic and

bull to communicate with the board of directors anddeal directly with the external auditors internalauditors and financial management on specificissues where appropriate

Over time the functions of an AC have expandedACs are under pressure to accept additionaloversight responsibilities while facing the everrising cost of directorsrsquo liability

THE KLSE LISTING REQUIREMENTS ON AUDIT COMMITTEE

Malaysian PLCs are required to adhere to KLSEListing Rules Compared to the rules set by the SECin the US in respect of ACs the KLSE listingrequirements are less stringent (Mohd Nazim ampKalaithasan 2002)

The listing requirements cover several importantsections on composition of ACs terms of referencethe functions of ACs attendance of other directorsand employees rights to discharge dutiesquorums for meetings and reporting to theExchange on the non-compliance with KLSErequirements At the end of each financial yearthe Malaysian AC is required to prepare a reportwhich must be incorporated in the annual reportof the company Table 1 summarizes the KLSErequirements relating to ACs These appear to gofurther than other environments such as the UK atthe time of study In the UK the AC has not beenrequired to prepare any report but rather a reportis required from the board with respect to itscorporate governance (which would includereferences to its AC)

In the US the Blue Ribbon Committee requestedthe SEC to include a letter from the AC in thecompanyrsquos annual report to shareholders statingwhether for the fiscal year management hadreviewed the financial statements with the ACand that the external auditors had also discussedwith the AC amongst others the quality of theaccounting principles applied by the company andthat the AC after weighing the facts discussed withmanagement and the external auditors believedthat the companyrsquos financial statements were fairlypresented

The Malaysian AC report must cover compliancewith five core requirements and the extent of

192 H Haron et al

copy Blackwell Publishing Ltd 2005 Int J Audit 9 187ndash200 (2005)

compliance should be disclosed in the reportThese are listed in the following sub-sections

Composition of the audit committee

The AC must comprise at least three directors anda majority should be independent directors Atleast one director must be a member of theMalaysian Institute of Accountants (MIA) or he orshe must have at least three years relevant workingexperience and have passed the examinationsspecified in Part I of the First Schedule of theAccountants Act 1967 or be a member of one of theassociations of accountants specified in Part II ofthe First Schedule of the Accountants Act 1967 TheChairman of the audit committee should be anindependent director and no alternate director is tobe appointed An independent director as definedin KLSE listing requirement Para 101 and PracticeNote No 62001 is independent of managementfree from any business relationship and not a majorshareholder of the listed company or of any of itsrelated corporations

In terms of the number of members theminimum requirement of three is in line with thatof NYSE and NASDAQ whereas the requirementthat the majority is made up of independentdirectors is to ensure independence asrecommended by the Treadway Commission(1987) the Cadbury Committee (1992) and theBlue Ribbon Committee (1999) The stipulationregarding experience and qualifications of ACmembers is to ensure effectiveness (Blue RibbonCommittee 1999 Dezoort 1998 Kalbers amp Fogarty1993 Treadway Commission 1987 GAO 1991 Leeamp Stone 1997) Currently in the UK under the newUK 2003 Combined Code all members of the AC

must now be independent non-executive directorsIn the US this has been the case for several yearsunder the NYSE rules and the Sarbanes-Oxley Act

Terms of reference

Terms of reference are statements in written formthat describe the ACrsquos authority function andscope of duties and responsibilities One of theimportant functions of a Malaysian AC to bespecified in the terms of reference is to reportto the KLSE any conflict of interest or anyunsatisfactorily resolved matters

The statement of terms of reference disclosedin the report is important to ensure that the ACperforms its fiduciary role in ensuring that thefirmrsquos management complies with the relatedregulatory requirements (Accountant InternationalStudy Group 1997) to safeguard the interest of theusers (Menon amp Williams 1994 Beasley 1996)

Audit committee meetings

The attendance of other directors and employeesat Malaysian AC meetings is prohibited unlessthey are invited ACs may regulate their ownprocedures in particular with respect to thecalling of meetings notice given of such meetingsvoting and proceedings of such meetings keepingof minutes and custody production andinspection of such minutes The quorum for anaudit committee meeting is a majority of themembers who are independent

Even though the regulations do not stipulatea minimum number of meetings Kang (2001)suggests that at least five meetings annually arerequired to gain sufficient insight into the firmrsquos

Table 1 Checklist drawn up by KLSE to assist listed companies in complying with listing requirements

KLSE requirement relating to audit committee Paragraph number of listing requirements

1 Audit committee composition1a Comprises at least three members Para 1510(1)(a)1b Majority are independent directors Para 1510(1)(b)1c At least one member is financially literate Para 1510(1)(c)1d Chairman is an independent director Para 15111e No alternate director is appointed as member Para 1510(2)

2 Written terms of reference Para 1516(3)(b)3 Meeting